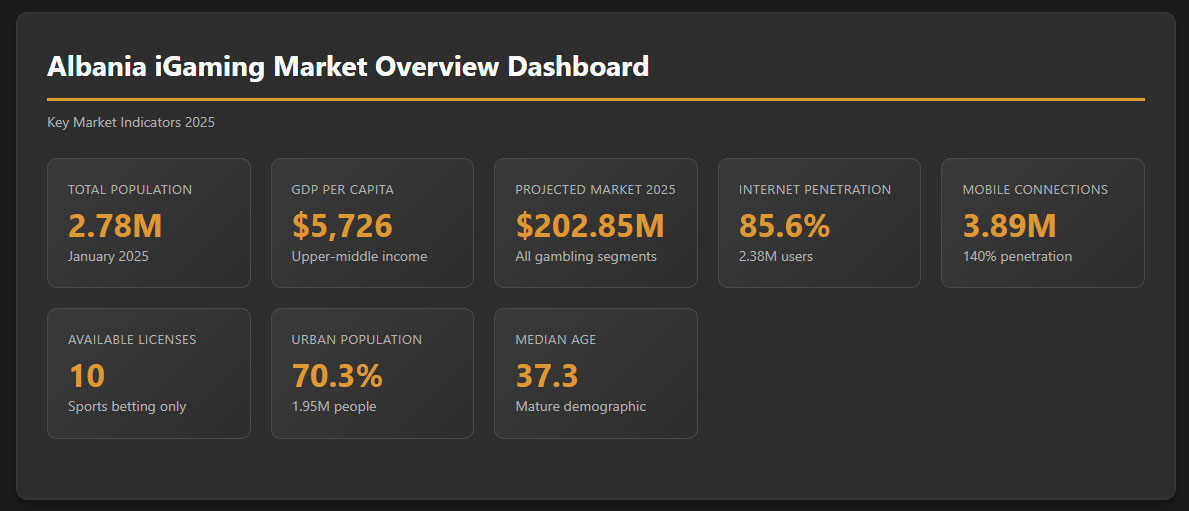

Albania presents an emerging iGaming opportunity following the 2024 regulatory shift that ended a five-year gambling ban and reintroduced online sports betting under strict licensing controls. With a population of 2.78 million, GDP per capita of approximately $5,700, and internet penetration exceeding 85 percent, the market demonstrates growing digital readiness.

The new framework limits licenses to just ten operators, creating a controlled competitive environment with significant entry barriers but substantial growth potential for qualified international operators.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Online Gambling Legal Status | Legal (Sports Betting Only) | Reinstated March 2024 |

| Number of Licenses Available | 10 licenses total | Competitive application process |

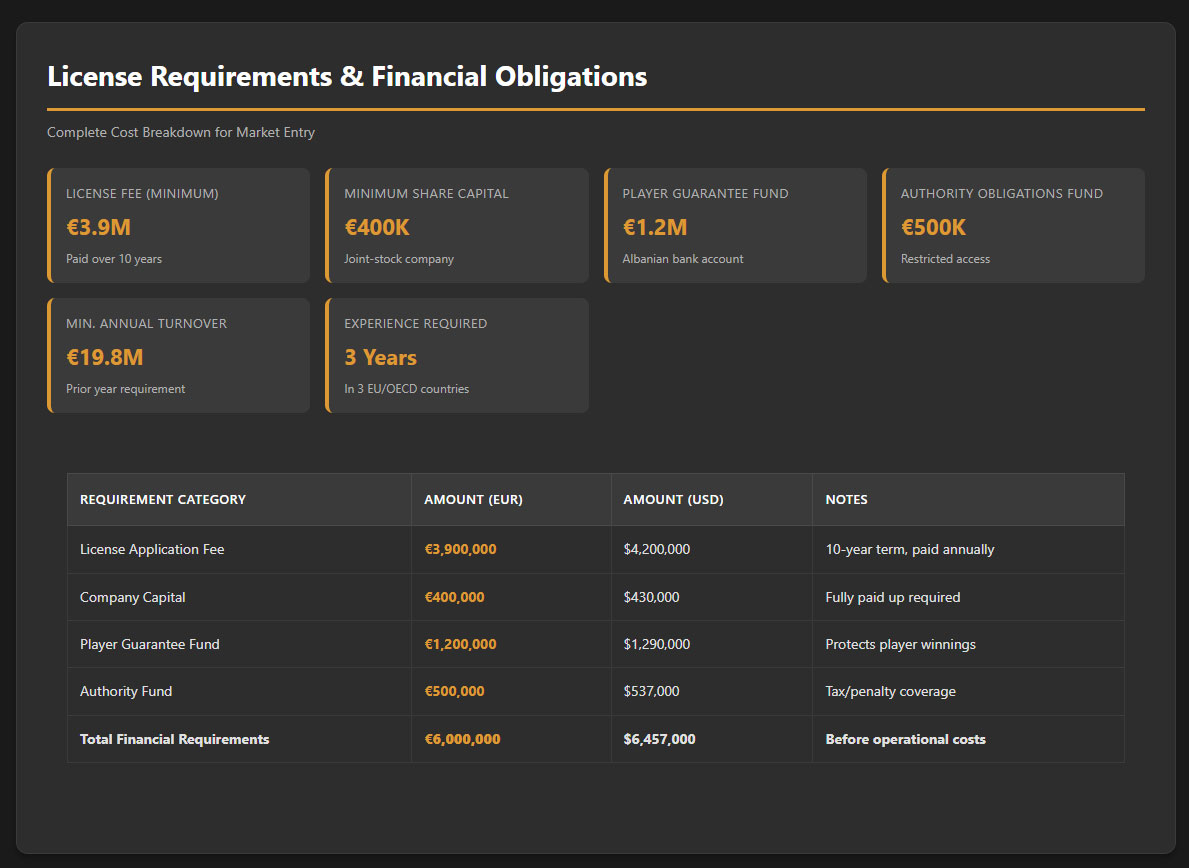

| License Fee | Minimum 400 million ALL | Approx. €3.9 million / $4.2 million |

| License Duration | 10 years | From issuance date |

| Minimum Share Capital | 40 million ALL | Approx. €400,000 / $430,000 |

| Experience Required | 3 years in 3 EU/OECD countries | Or via major shareholder |

| Minimum Annual Turnover | 2 billion ALL | Approx. €19.8 million / $21.3 million |

| Player Guarantee Fund | 120 million ALL | Approx. €1.2 million / $1.29 million |

| Authority Obligations Fund | 50 million ALL | Approx. €500,000 / $537,000 |

| Total Population | 2.78 million | January 2025 |

| Urban Population | 70.3% | 1.95 million people |

| Median Age | 37.3 years | Mature demographic profile |

| GDP (Nominal 2025) | $26.9 billion | 3.4% projected growth |

| GDP Per Capita | $5,726 – $9,474 | Various sources, growing trend |

| Internet Penetration | 85.6% | 2.38 million users |

| Mobile Connections | 3.89 million | 140% penetration rate |

| 4G/5G Coverage | 85.5% broadband connections | Growing 5G deployment |

| Social Media Users | 1.41 million | 50.7% of population |

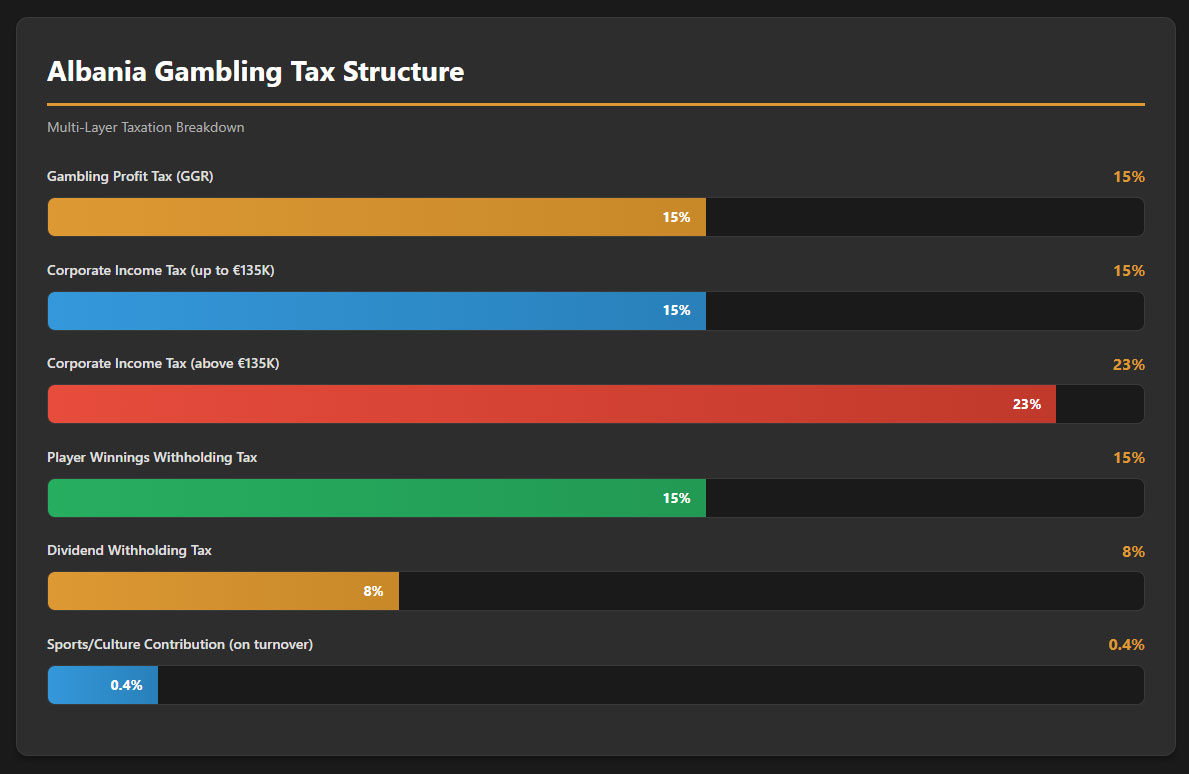

| GGR Tax Rate | 15% on profit | All gambling categories |

| Corporate Income Tax | 15% up to €135,000 | 23% above threshold |

| Player Winnings Tax | 15% | Withholding at payout |

| Minimum Player Age | 21 years | Strictly enforced |

| Advertising Restrictions | Prohibited in print/audiovisual | Strict limitations |

| Payment Methods | Digital only via financial agents | Cash transactions prohibited |

| Local Presence Required | Joint-stock company in Albania | Mandatory registration |

| Data Retention | 3 years minimum | Player and transaction data |

| Market Revenue 2024 | $9.79 million (online) | Growing segment |

| Projected Market Revenue 2025 | $202.85 million (total) | All gambling segments |

| Expected CAGR 2025-2029 | 3.43% – 4.59% | Varies by source |

| Estimated Annual Gambling Spend | €500-700 million | Historical estimates |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

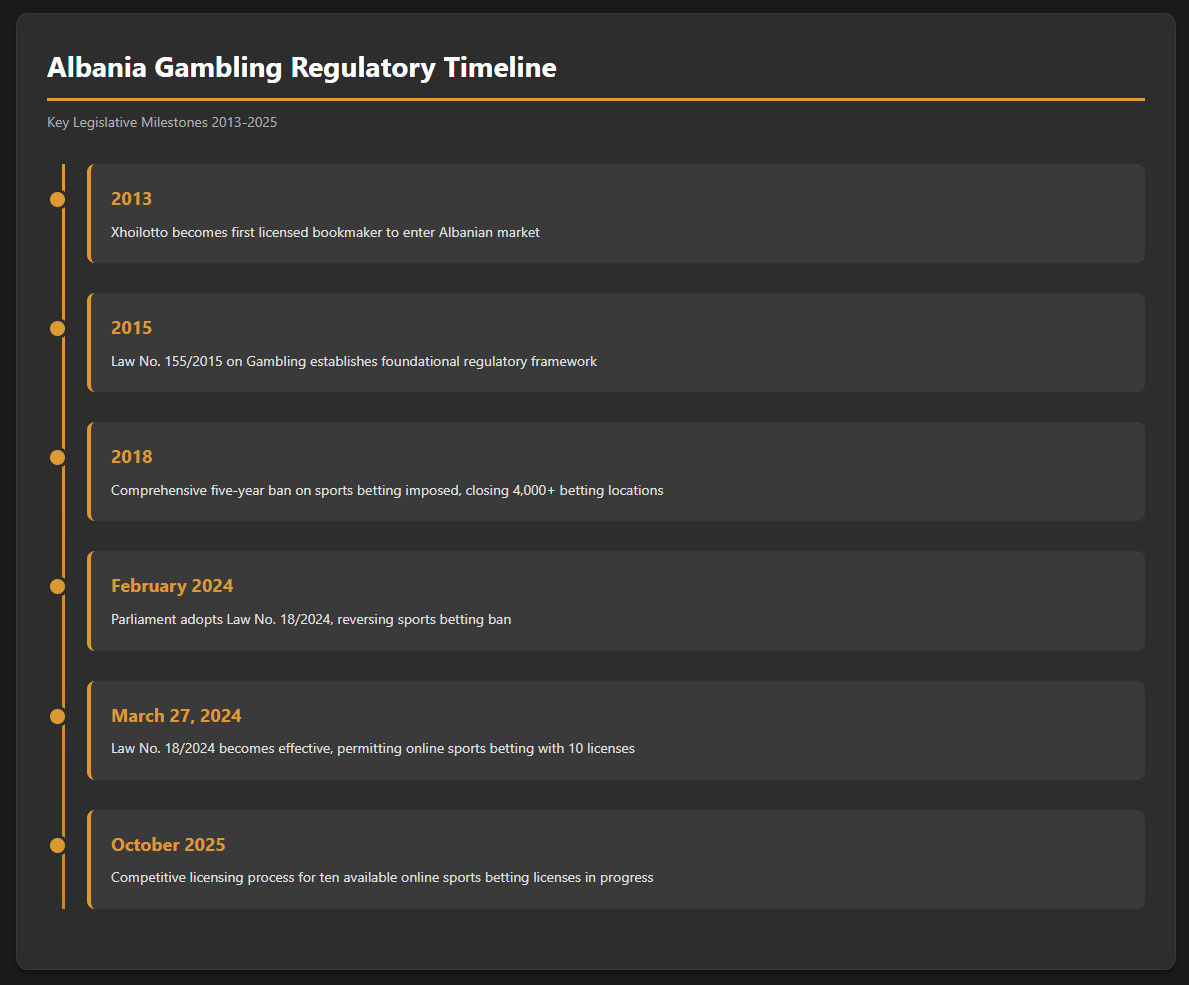

Albania underwent a dramatic regulatory transformation in early 2024 when Parliament adopted Law No. 18/2024 on February 15, amending the foundational Law No. 155/2015 on Gambling. This legislation, effective March 27, 2024, reversed a comprehensive five-year ban on sports betting that had been imposed in 2018. The regulatory shift represents a strategic government decision to bring underground gambling activity into a controlled, taxed, and monitored framework rather than maintaining an ineffective prohibition.

The current legal framework is highly restrictive, permitting only online sports betting under stringent licensing conditions while maintaining the ban on land-based betting shops. This creates a unique market structure where digital operations are the sole legal avenue for sports wagering, distinguishing Albania from most European jurisdictions that allow both land-based and online betting.

Land-Based Gambling Activities

Land-based gambling in Albania remains severely restricted following the 2018 reforms. Casino operations are exclusively permitted within five-star hotels and resort areas, creating an elite, tourism-focused gambling environment. The casino licensing fee structure reflects this premium positioning, with standard licenses costing 1 billion ALL (approximately €9.7 million or $10.4 million) for a 10-year period, while resort area establishments benefit from reduced fees of 70 million ALL (approximately €680,000 or $730,000).

Television bingo represents another permitted land-based gambling category, requiring a 10-year license fee of 40 million ALL (approximately €388,000 or $417,000). The state-operated national lottery continues to function as a monopoly offering. Sports betting venues and slot machine halls, which numbered over 4,000 locations before the 2018 ban, remain prohibited in physical form, with all sports betting activity now channeled exclusively to licensed online platforms.

Online Gambling Framework

The online gambling framework introduced in 2024 is narrowly focused on sports betting, representing a cautious regulatory approach to digital gambling. Only ten licenses will be issued for online sports betting operations, distributed through a competitive application process overseen by the newly established License Commission. This artificial scarcity creates significant value for successful applicants while allowing authorities to maintain tight control over market participants.

Online casino games, poker rooms, bingo, and other digital gambling products remain explicitly prohibited under current legislation. The government has indicated no immediate plans to expand the scope of permitted online gambling activities, maintaining sports betting as the sole authorized digital gambling category. This restriction reflects ongoing concerns about gambling addiction, money laundering, and social impacts that drove the original 2018 prohibition.

The regulatory authority structure combines oversight from the Ministry of Finance with operational enforcement by the Gambling Supervisory Authority (restructured following the 2018 reforms). The License Commission functions as a specialized collegial body specifically responsible for evaluating license applications, monitoring ongoing compliance, and making decisions regarding license renewals, suspensions, or revocations.

Licensed Operators and Market Players

As of October 2025, the competitive licensing process for the ten available online sports betting licenses is in various stages of completion. The market structure before the 2018 ban included approximately 10 licensed casino operators, 6 bookmakers, and 4 bingo operators, alongside the national lottery. However, the five-year prohibition eliminated most of these operators from the Albanian market.

International operators with regional Balkan experience are expected to dominate the new licensing round, given the stringent requirements for prior gambling experience in EU or OECD countries and minimum turnover thresholds. The licensing criteria effectively exclude small, inexperienced operators while favoring established European gambling companies with demonstrated track records and substantial financial resources.

The previous land-based market leader, Xhoilotto, was the first licensed bookmaker to enter the Albanian market in 2013 and maintained significant market presence until the 2018 closure. Whether existing pre-ban operators can successfully transition to the new online-only framework depends on their ability to meet the enhanced capital, experience, and technical requirements introduced in the 2024 legislation.

Market concentration is expected to be high given the limited number of licenses. With only ten operators serving a population of 2.78 million, each licensed operator theoretically serves approximately 278,000 potential customers, creating sustainable market positions if player acquisition and retention strategies prove effective. Competitive dynamics will likely focus on brand differentiation, betting product variety, competitive odds, mobile platform quality, and customer service excellence rather than price competition.

Licensing Framework and Requirements

Application Process and Eligibility

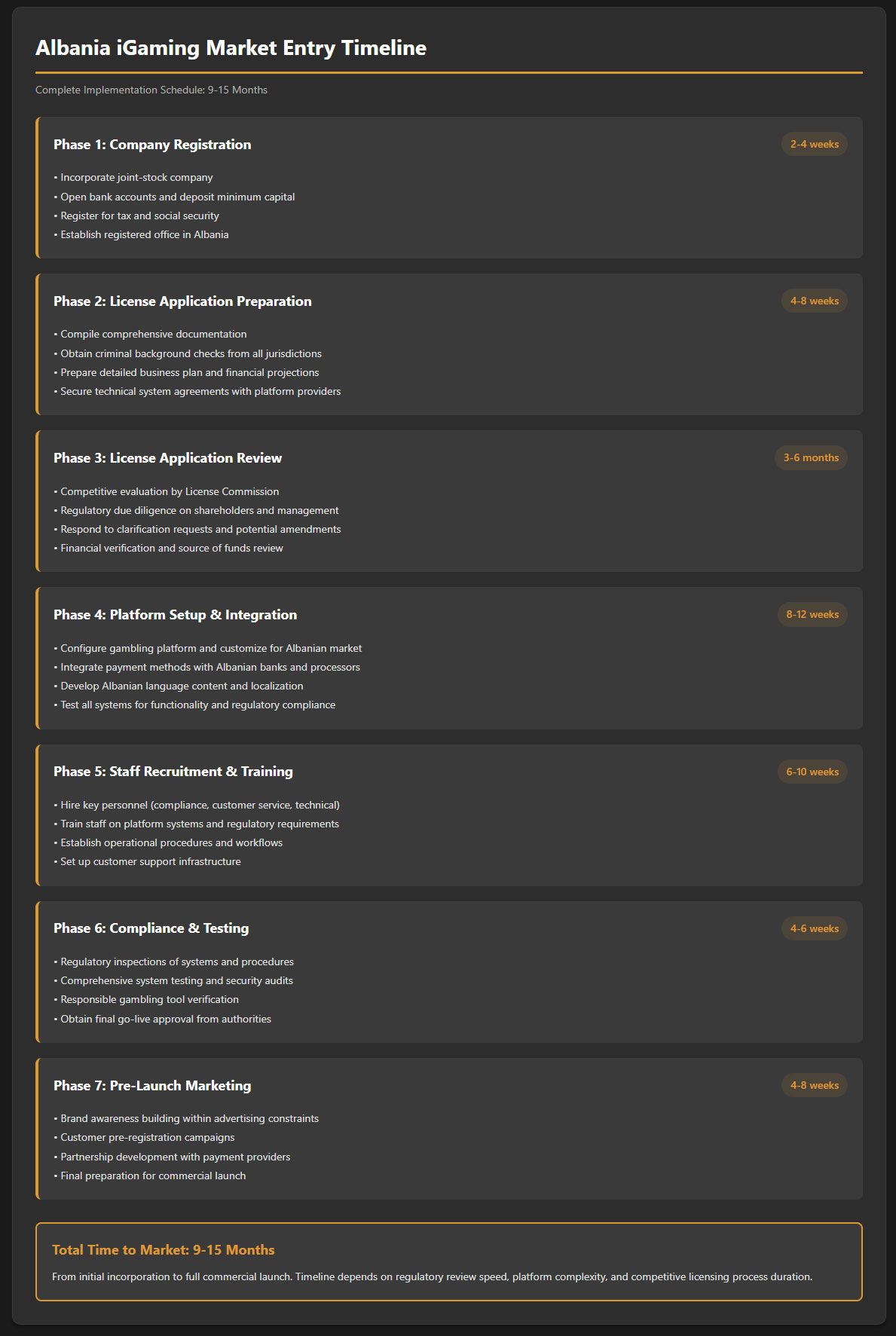

The licensing application process is administered by the License Commission, a specialized body established within the broader regulatory framework of the Gambling Supervisory Authority. The Commission operates as a collegial decision-making entity responsible for evaluating all applications against the statutory criteria and making binding license award determinations. Detailed procedural rules governing the competitive process were expected to be published following the law’s enactment in March 2024.

Applicants must demonstrate substantial gambling industry experience, specifically at least three consecutive years operating gambling activities in a minimum of three countries that are members of the European Union or the Organisation for Economic Co-operation and Development. This experience requirement can be satisfied either directly by the applicant entity or indirectly through a shareholder holding at least 30 percent of the company’s shares. The provision for shareholder experience creates opportunities for financial investors to partner with experienced operators.

Financial viability requirements are stringent. Applicants must document gambling-related turnover of at least 2 billion ALL (approximately €19.8 million or $21.3 million) in the most recent financial year prior to application. This substantial revenue threshold ensures that only established, financially stable operators with proven business models can enter the Albanian market. Supporting financial documentation, including audited financial statements and revenue verification from gambling regulatory authorities in operating jurisdictions, is mandatory.

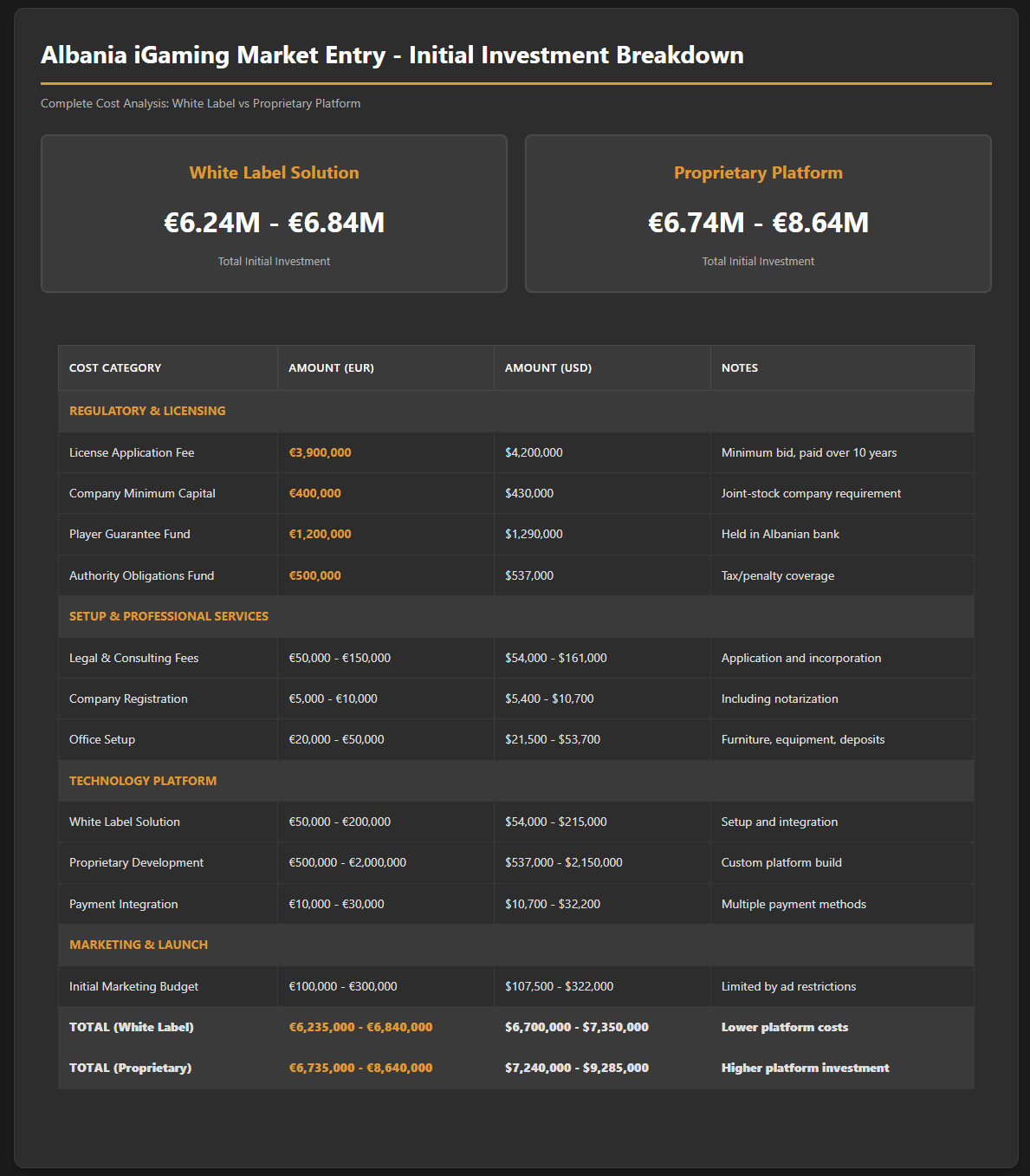

The license fee structure employs a competitive bidding mechanism. While the minimum license fee is set at 400 million ALL (approximately €3.9 million or $4.2 million), the actual fee paid by successful applicants equals the amount offered during the competitive process, provided it meets or exceeds this floor. License fees are payable in equal pro rata installments throughout the 10-year license term, reducing the immediate capital burden on new entrants while ensuring sustained financial commitment.

Local Presence and Operational Requirements

All licensed operators must establish legal presence in Albania as joint-stock companies registered under Albanian commercial law. This mandatory local incorporation requirement ensures operators are subject to Albanian corporate governance, taxation, and regulatory oversight. The minimum share capital for the joint-stock company is 40 million ALL (approximately €400,000 or $430,000), which must be fully paid up prior to license issuance.

Shareholders and senior management must satisfy rigorous fit and proper standards. All shareholders, regardless of ownership percentage, must be free from criminal convictions and provide documentation verifying the source of their capital investment. This anti-money laundering provision requires comprehensive beneficial ownership disclosure and background screening. Criminal record checks from all jurisdictions where shareholders and executives have resided during the previous ten years are standard requirements.

Operators must demonstrate administrative, organizational, and technical reliability capacities. This includes maintaining adequate staffing, implementing appropriate corporate governance structures, and deploying robust technical systems for platform operations, player management, responsible gambling tools, and regulatory reporting. A binding agreement with a technology provider for the necessary programs, systems, websites, and applications concerning online sports betting must be documented before license approval.

Domain and hosting requirements mandate that all player-facing platforms operate on servers and infrastructure that enable real-time monitoring by Albanian regulatory authorities. While the law does not explicitly require servers to be physically located in Albania, the platform architecture must provide the Gambling Supervisory Authority with continuous access to all transaction data, betting records, and player activities through secure technical interfaces.

Compliance Obligations and Monitoring

Player Protection and Identification

Player registration requirements are comprehensive. All individuals seeking to open betting accounts must register using their own personal data, including full legal name, date of birth, national identification number, residential address, and contact information. The minimum age for gambling participation is 21 years, strictly enforced through mandatory identity verification at account creation. Age verification must be completed before any deposits are accepted or bets are placed.

Know Your Customer and Anti-Money Laundering compliance obligations align with European standards. Operators must implement robust customer due diligence procedures, including identity document verification, address confirmation, and source of funds checks for high-value depositors. Enhanced due diligence applies to politically exposed persons and customers exhibiting unusual transaction patterns or behaviors indicative of money laundering risks.

Responsible gambling measures are mandated by law but specific implementation requirements remain subject to secondary regulations. Industry best practices suggest Albanian operators will need to provide deposit limits, loss limits, session time restrictions, reality checks, self-exclusion tools, and cooling-off periods. Mandatory player information disclosures must include responsible gambling messaging, links to problem gambling support resources, and clear explanations of odds, risks, and the statistical probability of losses.

A centralized self-exclusion system is expected to be implemented, allowing players to ban themselves from all licensed operators simultaneously. Self-exclusion requests must be honored immediately and maintained for specified periods, with robust technical controls preventing self-excluded individuals from creating new accounts or accessing betting services during their exclusion period. Operators must also monitor player behavior for signs of problem gambling and intervene with appropriate support measures when concerning patterns emerge.

Financial Monitoring and Reporting

Transaction monitoring systems must capture and record all financial activities, including deposits, withdrawals, bets placed, winnings paid, bonuses awarded, and any other fund movements. These records must be maintained in electronic format accessible for regulatory inspection for a minimum of three years from the transaction date. The centralized online monitoring system operated by the Gambling Supervisory Authority requires real-time connectivity from all licensed operators.

Audit and inspection procedures grant regulatory authorities broad powers to examine operator records, interview staff, test systems, and verify compliance with all licensing conditions. Unannounced inspections are permitted, and operators must provide immediate access to all premises, systems, and records upon request. Independent third-party technical audits of random number generators, payout percentages, and system security may be required periodically at operator expense.

The guarantee funds required from operators serve multiple protective functions. The 120 million ALL player guarantee fund ensures sufficient liquidity to pay all player winnings even if the operator experiences financial difficulties. The 50 million ALL authority obligations fund covers potential tax liabilities, regulatory fees, and penalties. Both funds must be maintained in designated Albanian bank accounts with restricted access, requiring regulatory approval for any withdrawals.

Taxation Structure and Financial Obligations

Player Taxation

Albanian players face taxation on gambling winnings under the country’s income tax regime. The standard withholding tax rate on gambling winnings is 15 percent, deducted directly at payout by the operator. This withholding applies to all categories of gambling income, including sports betting winnings, casino payouts, lottery prizes, and any other gambling-derived income.

The 15 percent withholding tax is applied without deduction of costs or losses, meaning the gross amount won is taxed regardless of how much the player wagered to achieve that win. For example, a player who wagers €1,000 and wins €1,500 pays 15 percent tax on the full €1,500 winnings, not on the €500 net profit. This tax treatment is less favorable than jurisdictions that allow offset of losses against winnings.

Players with substantial annual gambling income may face additional tax declaration requirements. If total annual income, including gambling winnings, exceeds certain thresholds under Albanian personal income tax law, players must include their gambling earnings in their annual tax returns. However, since the 15 percent tax has already been withheld at source, additional tax liability is unlikely unless the player has other income sources that push them into higher tax brackets.

Tax-free thresholds for small winnings do not appear to exist under current Albanian law, meaning even modest wins are subject to the 15 percent withholding. This differs from many jurisdictions that exempt smaller prizes from taxation. The operator is responsible for calculating, withholding, and remitting player winnings taxes to the Albanian tax authorities according to prescribed payment schedules.

Operator Taxation

Gambling operators in Albania face a multi-layered taxation structure. The primary gambling-specific tax is levied at 15 percent on the profit of the establishment or site for all categories of gambling. This profit-based taxation differs from the gross gaming revenue taxation common in many European markets, potentially providing more favorable treatment for operators with high operating costs relative to revenues.

Profit for tax purposes is calculated according to standard Albanian accounting principles, allowing deduction of legitimate operating expenses including staff salaries, technology costs, marketing expenses, payment processing fees, and license fees. The ability to deduct expenses before calculating the 15 percent gambling tax creates incentives for operators to invest in quality infrastructure, personnel, and responsible gambling programs.

Corporate income tax applies in addition to gambling-specific taxation. Under the Albanian Income Tax Law effective from January 2024, companies with annual taxable profits up to 14 million ALL (approximately €135,000 or $145,000) face a 15 percent corporate income tax rate. Profits exceeding this threshold are taxed at 23 percent for the excess amount. This progressive structure benefits smaller operators while ensuring larger, more profitable companies contribute proportionally more to state revenues.

Dividend taxation adds an additional layer. Distributed profits paid to shareholders face an 8 percent dividend tax, withheld at source by the distributing company. For foreign shareholders, international tax treaties may provide relief or credits against home country taxation, but the 8 percent Albanian withholding generally applies unless specifically exempted by treaty provisions.

License renewal fees are built into the initial license fee structure, with the substantial upfront payment covering the full 10-year license term. Annual operational fees or regulatory assessments beyond the initial license fee have not been publicly specified but may be introduced through secondary regulations. Operators should budget for potential additional regulatory fees, supervisory assessments, or contributions to problem gambling funds that could be imposed during the license period.

A special contribution requirement mandates operators contribute 0.4 percent of annual turnover to a fund supporting sports, culture, and technology projects. This social contribution, while relatively modest, represents an additional fixed cost that applies regardless of profitability. The contribution is calculated on gross turnover rather than profit or GGR, making it a consistent expense even during unprofitable periods.

Gambling Market Financial Performance

| Metric | Value | Period |

|---|---|---|

| Estimated Total Annual Gambling Spend | €500-700 million | Historical (pre-2018 ban) |

| Online Gambling Market Value | €50 million | 2022 estimate |

| Projected Online Revenue | $9.79 million | 2024 |

| Projected Total Gambling Revenue | $202.85 million | 2025 |

| Expected Annual Growth Rate (CAGR) | 3.43% – 4.59% | 2025-2029 |

| Estimated Tax Revenue from Sports Betting | €17.5 million annually | Government projection |

The Albanian gambling market historically represented a significant economic activity before the 2018 prohibition. Industry estimates suggested Albanians spent between €500 million and €700 million annually on gambling activities when over 4,000 betting locations operated throughout the country. This substantial expenditure in a nation of fewer than 3 million people indicated strong cultural acceptance of gambling and sports betting in particular.

The five-year ban from 2018 to 2024 did not eliminate gambling activity but rather drove it underground into unregulated channels. Data from the Gambling Supervisory Authority indicated that sports betting continued through informal networks, unlicensed websites, and offshore operators beyond Albanian jurisdiction. This persistence of demand despite legal prohibition motivated the government’s decision to reintroduce regulated sports betting to capture tax revenues and impose consumer protections.

Revenue projections for the newly legalized market vary among research sources. Conservative estimates place 2024 online gambling revenue at approximately $9.79 million, reflecting the initial stages of market development as the first licenses are awarded and platforms launch. More optimistic forecasts project total gambling revenue reaching $202.85 million by 2025, encompassing both the new online sports betting segment and continuing land-based casino and lottery activities.

Growth expectations for 2025-2029 range from 3.43 percent to 4.59 percent compound annual growth rate, depending on regulatory developments, market competition intensity, and broader economic conditions. These moderate growth projections reflect the controlled nature of the market with only ten licenses, balanced against pent-up demand from the five-year prohibition and increasing digital adoption among Albanian consumers.

Advertising and Marketing Restrictions

Albanian gambling advertising regulations are among the strictest in Europe. All gambling advertising in print media and audiovisual media is explicitly prohibited under the current regulatory framework. This comprehensive ban eliminates traditional marketing channels including television commercials, radio spots, newspaper advertisements, magazine placements, and outdoor billboards featuring gambling content.

The prohibition extends to sponsorship arrangements. Gambling operators cannot sponsor sports teams, sporting events, cultural activities, or other public entertainments in ways that create brand visibility or association with gambling products. This restriction significantly limits the marketing strategies available to operators seeking to build brand awareness and acquire customers in the Albanian market.

Digital marketing operates in a regulatory gray area. While the explicit prohibition covers print and audiovisual media, online advertising through search engines, social media platforms, affiliate websites, and email marketing is not specifically addressed in published regulations. Conservative legal interpretation suggests these digital channels may also be restricted under the broad advertising ban, but enforcement practices remain unclear.

Affiliate marketing programs commonly used by European gambling operators face uncertain legal status in Albania. If affiliate websites are deemed to constitute advertising that would otherwise be prohibited in print or audiovisual form, such arrangements could violate the advertising restrictions. Operators should seek specific legal guidance before implementing affiliate strategies to avoid regulatory sanctions.

Content restrictions for permitted marketing communications, if any channels are allowed, would logically prohibit appeals to minors, false or misleading claims about winning probabilities, encouragement of excessive gambling, or associations between gambling and financial success, social status, or sexual attractiveness. Responsible gambling messaging would likely be mandatory in any permitted communications.

The advertising restrictions create significant challenges for new market entrants seeking to build market share and customer bases. Without traditional brand-building tools, operators must rely on word-of-mouth, reputation effects, organic search visibility, superior product offerings, and customer referral programs. The first movers among the ten licensed operators may gain substantial advantages by establishing brand recognition early before competitors enter.

Recent Regulatory Changes and Their Impact

The February 2024 passage of Law No. 18/2024 represents the most significant regulatory change in Albanian gambling policy since the comprehensive 2018 ban. This reversal reflects a pragmatic governmental reassessment of gambling prohibition outcomes versus regulated market approaches. Key factors motivating the change included persistent underground gambling activity, foregone tax revenues, inability to impose consumer protections in illegal markets, and successful regulatory models in neighboring Balkan countries.

The decision to limit online sports betting licenses to just ten operators through competitive selection is a deliberate market structuring choice. This approach contrasts with open licensing systems where any qualified applicant receives authorization. The rationale appears to prioritize regulatory manageability, ensuring only financially sound and experienced operators participate, over market competition and consumer choice maximization.

Player taxation rules introduced in the 2024 Income Tax Law codified the 15 percent withholding rate on gambling winnings. Previously, taxation of gambling income existed in principle but lacked clear enforcement mechanisms. The new framework requires operators to withhold and remit taxes, shifting compliance responsibility from individual players to licensed operators with sophisticated accounting systems.

Bonus and promotion restrictions have not been extensively detailed in published regulations but likely will follow European norms limiting excessive inducements to gamble. Mandatory player information disclosure requirements reflect responsible gambling policy priorities, ensuring customers understand the risks and odds associated with sports betting before placing wagers.

Self-exclusion and cooling-off period requirements align Albania with EU gambling regulation standards. While specific implementation details await secondary regulations, the principle that players must have tools to restrict their own gambling activity is embedded in the licensing framework. The centralized monitoring system creates technical infrastructure to support national self-exclusion databases accessible to all licensed operators.

The impact on operator costs is substantial. The minimum €3.9 million license fee represents a significant upfront investment, paid over ten years but still requiring financial commitment and planning. Combined with the €400,000 minimum capital requirement, €1.2 million player guarantee fund, and €500,000 authority obligations fund, new entrants face approximately €6 million in financial requirements before considering operational technology, personnel, and marketing expenses.

Business strategy implications favor operators with existing Balkan regional presence who can leverage infrastructure, technology platforms, and operational expertise across multiple markets. Stand-alone Albanian market entry is economically challenging given the small population base and high entry costs. Most successful applicants are expected to be multi-market operators for whom Albania represents geographic expansion rather than primary market focus.

Upcoming regulatory changes may include the detailed competitive licensing process rules, technical standards for platform integration with the centralized monitoring system, specific responsible gambling tool requirements, reporting format specifications, and potentially an expansion of permitted gambling categories if online sports betting proves successful in addressing the concerns that motivated the 2018 prohibition.

Enforcement Mechanisms and Penalties

The Albanian regulatory framework provides enforcement authorities with graduated penalty structures designed to encourage compliance while maintaining the ability to impose severe sanctions for serious violations. Fines represent the most common enforcement tool, with amounts scaled to violation severity and operator size. Minor technical compliance failures may result in warnings or modest fines, while systematic rule violations or consumer harm triggers substantial financial penalties.

License suspension provides a powerful intermediate enforcement mechanism. Temporary suspension halts operator activities while allowing time for compliance remediation without the permanent market exit forced by revocation. Suspension duration can range from days to months depending on the violation nature and correction timeframe. During suspension, operators cannot accept new bets but must continue servicing existing obligations including paying outstanding winnings.

License revocation represents the maximum administrative penalty, permanently terminating the operator’s authorization to provide gambling services in Albania. Revocation is reserved for the most serious violations including fraud, money laundering facilitation, systematic consumer harm, refusal to pay legitimate winnings, providing gambling services to minors, or operating outside license conditions. Revoked licenses are not transferable, and the operator must cease all Albanian gambling activities immediately.

Recent enforcement actions remain limited given the market’s recent reopening in 2024. As the first ten licensed operators begin activities, enforcement patterns will emerge indicating regulatory priorities and tolerance levels for various violation types. Operators should anticipate an initial period of heightened regulatory scrutiny as authorities establish enforcement precedents and test compliance systems.

ISP blocking of unlicensed operators represents a technical enforcement tool targeting offshore websites serving Albanian customers without authorization. The Gambling Supervisory Authority can order Albanian internet service providers to block access to identified unlicensed gambling websites. Effectiveness of domain blocking in the modern internet environment with VPNs and alternative access methods is questionable, but it demonstrates regulatory intent to protect the licensed market from illegal competition.

Payment processor restrictions complement ISP blocking by targeting the financial infrastructure supporting unlicensed gambling. Albanian banks and payment institutions face legal obligations not to process transactions for unlicensed gambling operators. By cutting off deposit and withdrawal capabilities, regulators make unlicensed websites practically unusable for Albanian customers even if technically accessible.

Criminal penalties apply to the most egregious violations. Individuals operating unlicensed gambling businesses face potential criminal charges carrying fines starting at 500,000 ALL and possible imprisonment. Organizing gambling activities for minors, facilitating money laundering through gambling platforms, or systematically defrauding customers can result in prosecution under Albanian criminal law with sentences ranging from monetary fines to multi-year prison terms depending on offense severity and harm caused.

Compliance enforcement trends in Albania are expected to mirror broader European patterns emphasizing consumer protection, anti-money laundering effectiveness, and responsible gambling program implementation. Operators demonstrating proactive compliance cultures with robust internal controls, staff training programs, and customer protection measures will likely experience less intensive regulatory oversight than those taking minimalist compliance approaches or generating consumer complaints.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

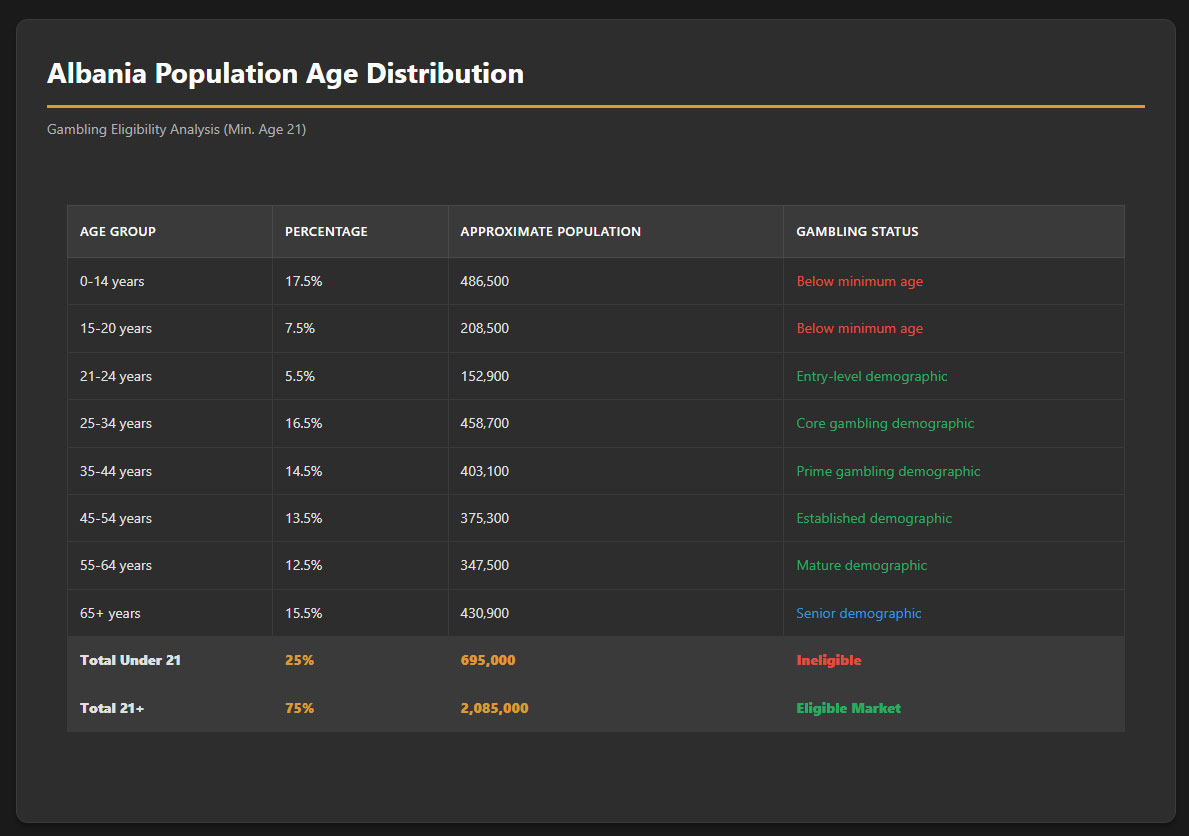

Albania’s population stood at 2.78 million in January 2025 according to United Nations data, though the official Albanian statistical office INSTAT reported 2.36 million residents as of January 2025, indicating some methodological differences in measurement. The population has experienced gradual decline, decreasing by approximately 20,000 people or 0.7 percent between early 2024 and 2025, continuing a long-term trend of emigration to Western Europe that accelerated after communism’s collapse in 1991.

The median age of 37.3 years positions Albania as a relatively mature market demographically, older than many developing countries but younger than most Western European nations. This median age suggests a population core in prime working years with disposable income potential, neither skewing extremely young nor elderly. The fertility rate of just 1.49 children per woman falls well below the 2.1 replacement level, contributing to the gradual population decline and aging trend.

Gender distribution is relatively balanced with slightly more males than females in younger age cohorts and the typical female longevity advantage producing more women in older age groups. Life expectancy at birth reaches approximately 79.8 years for both sexes combined, reflecting improved healthcare and living standards compared to the communist era but still trailing Western European averages by several years.

| Age Group | Approximate Percentage | Gambling Market Relevance |

|---|---|---|

| 0-14 years | 17-18% | Below minimum gambling age |

| 15-20 years | 7-8% | Below minimum gambling age |

| 21-24 years | 5-6% | Entry-level gambling demographic |

| 25-34 years | 16-17% | Core gambling demographic |

| 35-44 years | 14-15% | Prime gambling demographic |

| 45-54 years | 13-14% | Established gambling demographic |

| 55-64 years | 12-13% | Mature gambling demographic |

| 65+ years | 15-16% | Senior gambling demographic |

The population age structure shows approximately 25 percent of Albanians are under age 21 and therefore legally prohibited from gambling. This leaves roughly 2.1 million adults in the eligible gambling population. The concentration of population in the 25-54 age range, representing nearly 45 percent of total population, creates a substantial core market of working-age adults with income, digital literacy, and interest in sports betting entertainment.

Geographic Distribution

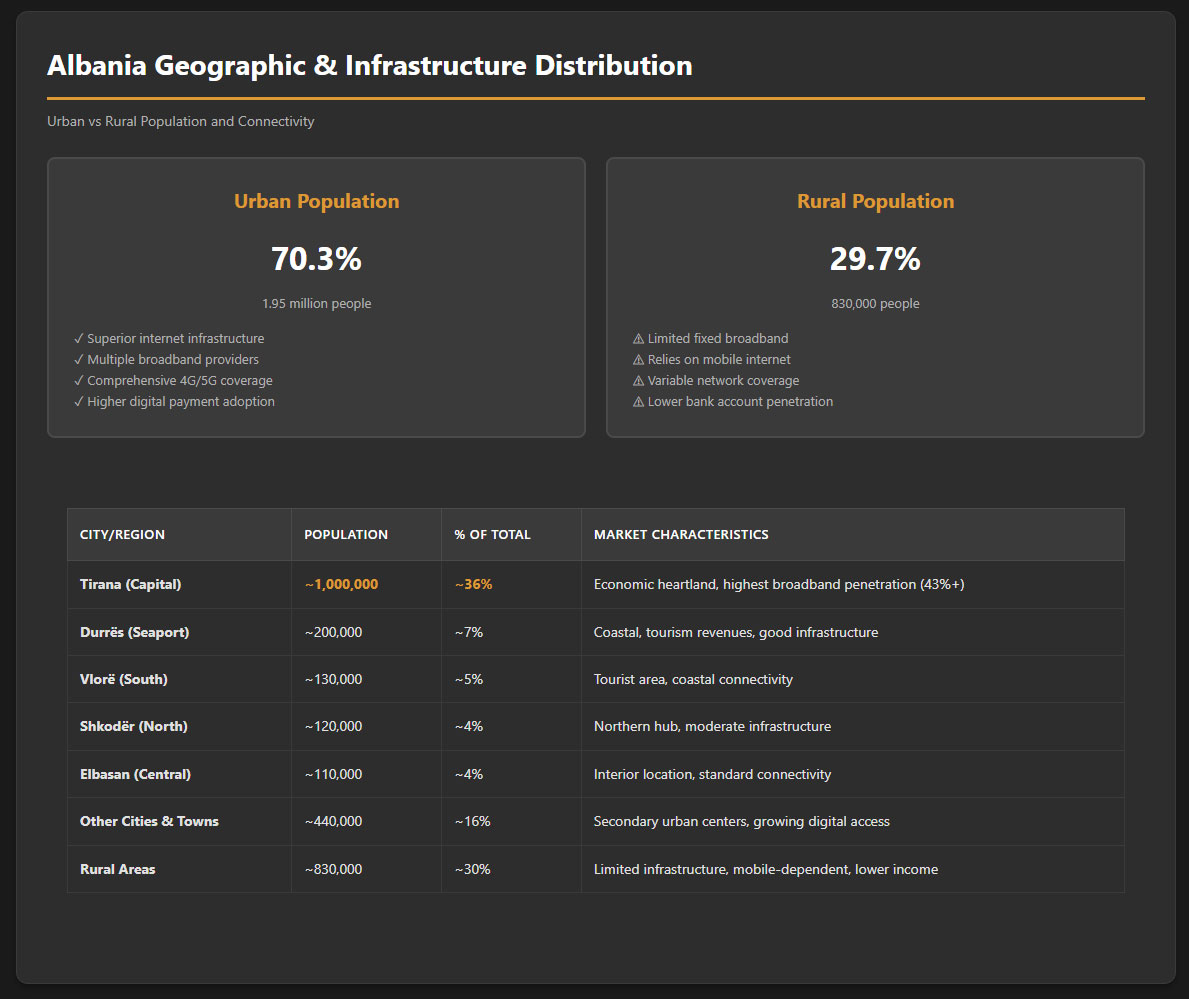

Urban population comprises 70.3 percent of Albania’s total, with 1.95 million people living in cities and towns while 34.3 percent or approximately 830,000 reside in rural areas. This high urbanization rate facilitates digital service delivery since urban areas enjoy superior internet infrastructure, mobile network coverage, and digital payment system access compared to rural regions.

Tirana, the capital and largest city, dominates Albania’s urban landscape with a population exceeding 500,000 in the city proper and approaching 1 million in the greater metropolitan area. Tirana alone represents roughly one-third of Albania’s total population, creating concentrated market opportunity. The capital exhibits the highest fixed broadband penetration, exceeding 43 percent of households by 2021, and offers the most developed digital infrastructure in the country.

Regional economic differences are pronounced. The Tirana-Durrës corridor represents Albania’s economic heartland, generating disproportionate shares of GDP, employment, and consumer spending. Coastal areas benefit from tourism revenues, while interior and mountainous regions remain more economically challenged with higher unemployment, lower incomes, and greater emigration. These disparities affect gambling market potential, with urban and coastal populations demonstrating higher discretionary spending capacity.

Internet access patterns closely track urbanization. Cities enjoy near-universal connectivity with multiple fixed broadband providers offering fiber, cable, and VDSL services, plus comprehensive 4G and emerging 5G mobile coverage. Rural areas lag significantly, often relying on mobile internet due to limited fixed infrastructure investment. However, the recent introduction of Starlink satellite internet in 2024 provides new connectivity options for remote regions, potentially expanding the addressable online gambling market to previously underserved areas.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Albania’s nominal GDP in 2025 is estimated at $26.9 billion, reflecting a developing economy with upper-middle income status. GDP per capita estimates vary by source and methodology, ranging from $5,726 to $9,474 depending on whether current exchange rates or purchasing power parity calculations are used. The lower figure represents nominal GDP per capita in current US dollars, while higher estimates reflect PPP adjustments accounting for lower living costs in Albania compared to developed economies.

Economic growth has been resilient, with 2024 growth reaching 3.3 percent and 2025 projections indicating 3.4 percent expansion. This moderate but consistent growth trajectory reflects recovery from pandemic disruptions, strong performance in tourism, construction activity, and services sectors, and ongoing structural reforms associated with EU accession candidacy. GDP growth forecasts for the next 3-5 years range from 3.5 to 3.8 percent annually, suggesting stable economic expansion.

The service sector dominates Albania’s economic structure, comprising 48.6 percent of GDP. Key service contributors include wholesale and retail trade, tourism and hospitality, real estate, logistics and transportation, and financial services. The industrial sector accounts for 20.2 percent of GDP, heavily influenced by construction activity. Agriculture, forestry, and fisheries represent 18.5 percent, while manufacturing contributes a modest 6.3 percent to total economic output.

Employment rates have improved following the pandemic, particularly in the private sector where wages grew by an average of 12.7 percent across all industries during the most recent year measured. This wage growth indicates tightening labor markets and improving living standards, both positive indicators for discretionary spending capacity. Inflation has been gradually easing from earlier peaks, supporting real income growth and consumer purchasing power.

| Indicator | Value | Year/Period |

|---|---|---|

| Nominal GDP | $26.9 billion | 2025 estimate |

| GDP Per Capita (nominal) | $5,726 – $9,474 | 2024-2025 |

| GDP Growth Rate | 3.3% – 3.4% | 2024-2025 |

| Projected GDP Growth 2025-2029 | 3.5% – 3.8% annually | Forecast period |

| Service Sector Share | 48.6% | GDP composition |

| Industrial Sector Share | 20.2% | GDP composition |

| Agricultural Sector Share | 18.5% | GDP composition |

| Private Sector Wage Growth | 12.7% average | Recent annual period |

| Tourism Visitors | 11.7 million | 2024 |

Income and Wealth Distribution

Average household income in Albania is challenging to precisely quantify due to substantial informal economic activity, but estimates suggest monthly household income ranges from €400 to €700 for median households, with significant variation between urban and rural areas. Tirana households earn substantially more than the national average, while rural agricultural regions fall below. Government statistics on household income should be interpreted cautiously given the large informal economy estimated at 30-40 percent of GDP.

Income inequality, measured by the Gini coefficient, positions Albania in the moderate inequality range for Europe. The coefficient has declined from high levels during the immediate post-communist transition period as economic development has proceeded and social safety nets have strengthened. However, substantial disparities remain between urban professionals and rural agricultural workers, between educated and less educated populations, and between those with remittance income from emigrant family members versus those without.

Disposable income trends have been positive, supported by wage growth outpacing inflation, improving employment rates, and continued remittance flows from the Albanian diaspora in Italy, Greece, Germany, and other Western European countries. Remittances represent a significant component of household income for many Albanian families, estimated at 10-15 percent of GDP annually. This external income source provides spending capacity beyond what domestic wages alone would support.

Consumer spending patterns in Albania allocate substantial portions of household budgets to food, housing, and utilities, reflecting the developing economy status. Entertainment and leisure spending, including gambling, competes with other discretionary categories like dining out, travel, electronics, and apparel. The historical evidence that Albanians spent €500-700 million annually on gambling before the 2018 ban suggests significant cultural acceptance and willingness to allocate disposable income to betting activities.

Middle class size and growth represent critical factors for gambling market potential. Albania’s middle class, defined as households with incomes sufficient for discretionary spending beyond basic necessities, has expanded steadily over the past two decades. Estimates suggest 35-45 percent of households now qualify as middle class, up from minimal levels during the 1990s transition period. This growing middle class provides the customer base with income, digital access, and cultural openness to support a sustainable online gambling market.

Market Size and Growth Projections

| Metric | Value | Source/Period |

|---|---|---|

| Historical Total Gambling Spend | €500-700 million annually | Pre-2018 ban estimates |

| Online Market Value 2022 | €50 million | Industry estimate |

| Online Revenue 2024 | $9.79 million | Market research projection |

| Total Gambling Revenue 2025 | $202.85 million | All segments projected |

| CAGR 2025-2029 | 3.43% – 4.59% | Growth forecast range |

| Projected Market Value 2029 | $230-240 million | Calculated from CAGR |

| Online Sports Betting Tax Revenue | €17.5 million annually | Government projection |

The current iGaming market in Albania is in early development following the March 2024 regulatory reopening. The historical baseline of €500-700 million annual gambling spend before the 2018 prohibition provides context for market potential, though direct comparison is complicated by the five-year gap, changed regulatory structure limiting activity to online sports betting, and broader economic evolution. The total gambling figure included land-based betting shops, casinos, bingo, and lottery, while current legal options are more restricted.

Online gambling specifically was valued at approximately €50 million in 2022, likely representing offshore unlicensed operators serving Albanian customers during the prohibition period. This figure demonstrates sustained demand despite legal restrictions. Conservative 2024 projections place online gambling revenue at $9.79 million, perhaps reflecting early stages as licenses are awarded and platforms launch with limited market awareness and customer acquisition.

The substantial jump to projected $202.85 million total gambling revenue in 2025 suggests expectations that the new legal framework will rapidly capture significant market share from both previously unlicensed online operators and pent-up demand from the prohibition period. This forecast likely aggregates online sports betting with continuing land-based casino, lottery, and other permitted activities.

Growth forecasts for 2025-2029 in the 3.43-4.59 percent CAGR range indicate moderate but sustainable expansion. These projections reflect several offsetting factors. Positive growth drivers include increasing digital adoption, improving internet access and speeds, growing smartphone penetration, rising disposable incomes, and market maturation as licensed operators establish brands and customer bases. Negative factors limiting growth include the restricted product offering (sports betting only), advertising restrictions hindering customer acquisition, high taxation reducing operator marketing budgets, and the small overall population base.

Revenue distribution by gambling type historically favored sports betting, which commanded the largest customer base and volume before the 2018 ban. The new online-only sports betting market likely will capture 40-50 percent of total gambling revenue once fully established, with land-based casinos, lottery, and other permitted activities comprising the remainder. Sports betting’s seasonal patterns tied to football seasons and major sporting events will create quarterly revenue fluctuations.

Education, Skills, and Digital Literacy

Educational Foundation

Albania’s literacy rate exceeds 98 percent for both males and females, reflecting universal primary education and high secondary school enrollment. This strong foundational literacy supports digital engagement and the ability to navigate online platforms, understand betting odds and terms, and engage with responsible gambling information. Educational attainment has improved dramatically since the communist era, when university access was highly restricted.

Tertiary education completion rates have risen substantially, with approximately 25-30 percent of young adults now obtaining university degrees or equivalent qualifications. Popular fields include business, engineering, medicine, and information technology. This expanding educated workforce demonstrates the cognitive sophistication to understand complex betting products, analyze sporting events, and manage gambling budgets responsibly.

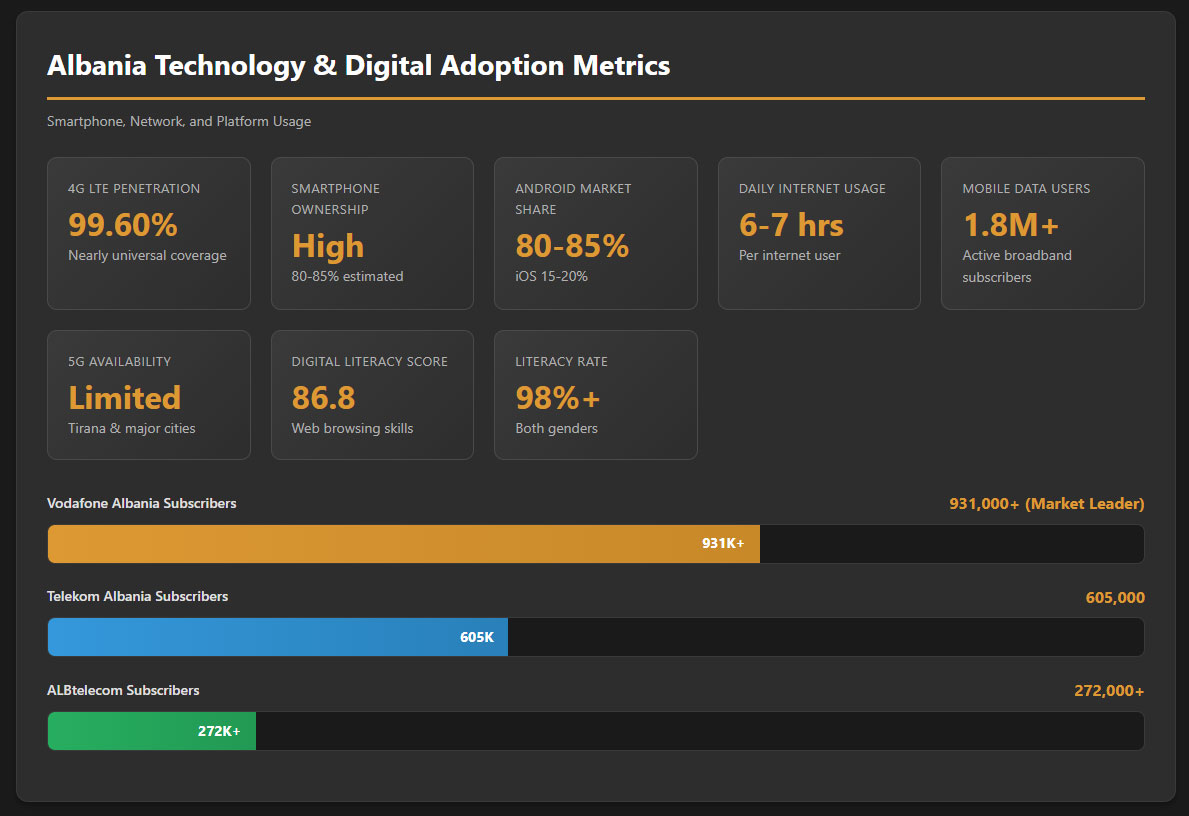

Digital literacy indicators position Albania favorably for online gambling adoption. The mobile connectivity index score of 66.1 out of 100 points in 2022 showed strong performance in consumer readiness, measuring the percentage of citizens with skills to browse the web, at 86.8 points. This high consumer digital competency means most Albanian adults can navigate online sports betting platforms without technical assistance.

English language proficiency is moderate and improving, particularly among younger demographics. While Albanian remains the primary language for all services including gambling platforms, many Albanians possess functional English enabling them to use international platforms if domestic options are unavailable. However, localized Albanian language platforms with customer support in Albanian will command competitive advantages.

Cultural and Social Factors

Communication and Language

Albanian is the primary language for daily life, business communication, and internet usage. The Albanian language exists in two main dialects, Gheg in the north and Tosk in the south, with standard Albanian based on Tosk. All gambling platforms must operate in Albanian to achieve mass market acceptance, though multilingual capabilities for expatriate users could provide marginal advantages.

Internet language preferences overwhelmingly favor Albanian for consumer-facing websites and applications. While English content is common in business and technology contexts, entertainment and gambling services succeed best when fully localized. Customer support must be available in Albanian during peak usage hours, which typically align with European football match schedules for sports betting.

Cultural Attitudes

Gambling acceptance in Albanian society is relatively high despite the Muslim-majority religious composition. Albania’s secular governmental tradition dating from the communist era and reinforced in the post-1991 democratic constitution creates separation between religious doctrine and social norms. Approximately 58 percent of Albanians identify as Muslim according to some surveys, but religious observance levels vary widely and religious prohibitions on gambling have limited practical impact on behavior.

The historical evidence of over 4,000 betting locations operating profitably before 2018 demonstrates cultural acceptance and participation in gambling activities. Sports betting in particular enjoys social legitimacy, viewed as skill-based entertainment connected to football fandom rather than pure chance gambling. The social aspect of discussing bets, sharing predictions, and collectively experiencing matches contributes to betting’s cultural integration.

Foreign brand perception is generally positive in Albania. The population’s historical orientation toward Western Europe, desire for EU membership, and extensive diaspora connections create favorable attitudes toward international brands. Well-established European gambling brands may enjoy prestige advantages over unknown local operators. However, trust-building requires localization, responsive customer service, and demonstrated commitment to the Albanian market.

Risk tolerance among Albanian consumers appears relatively high based on historical gambling participation rates and the entrepreneurial culture evident in high self-employment rates. Economic necessity during the difficult 1990s transition period cultivated resilience and willingness to take calculated risks, characteristics that may translate to gambling behavior. However, the 1997 pyramid scheme collapse that bankrupted many Albanian families created lasting skepticism toward financial schemes promising unrealistic returns.

Problem Gambling and Social Considerations

Comprehensive data on problem gambling prevalence in Albania is limited. The 2018 decision to ban sports betting and slot machines was motivated by governmental concerns about gambling addiction impacts on low-income families and the social problems associated with widespread betting availability. The estimated 4,000 betting locations in a country of fewer than 3 million people suggested high gambling density that authorities deemed excessive.

While specific problem gambling prevalence percentages have not been published from rigorous population studies, international benchmarks suggest approximately 0.5-2.0 percent of adult populations in countries with legal gambling exhibit severe problem gambling behaviors, with an additional 2-4 percent experiencing moderate difficulties. Applying these rates to Albania’s 2.1 million adults over age 21 suggests 10,000-40,000 individuals may struggle with problem gambling, with 40,000-85,000 experiencing subclinical issues.

At-risk populations include young males aged 21-35, individuals with other addictive behaviors or mental health conditions, those experiencing financial stress or unemployment, and people with easy access to gambling opportunities. Gender distribution of problem gambling typically skews male, particularly for sports betting products, though online gambling’s privacy and accessibility can increase female participation and associated problems.

Government response measures to problem gambling concerns include the minimum age 21 requirement, higher than the age 18 standard in many European jurisdictions. Mandatory self-exclusion capabilities, responsible gambling tools, and prohibitions on advertising represent additional protective measures. The centralized monitoring system creates technical infrastructure to identify problem gambling patterns, though its effectiveness depends on analytical capabilities and intervention protocols.

Treatment facilities and support services for problem gambling in Albania are underdeveloped compared to Western European standards. Mental health services generally face resource constraints and social stigma barriers. International operators entering the Albanian market should anticipate potential requirements to fund problem gambling awareness programs, treatment services, or research initiatives as part of corporate social responsibility expectations or future regulatory mandates.

Mandatory contributions to problem gambling funds are not currently specified in published regulations but could be introduced as the market develops and authorities gain experience with online gambling’s social impacts. The 0.4 percent of turnover contribution to sports, culture, and technology projects provides a precedent for earmarked social levies that could be expanded or redirected toward problem gambling prevention and treatment.

Political Structure and Governance

Albania operates as a parliamentary republic with a president serving as ceremonial head of state and a prime minister functioning as head of government with executive authority. The unicameral parliament exercises legislative power. The political system has demonstrated increasing stability since the turbulent 1990s, with peaceful transfers of power between competing parties becoming routine. Current governance emphasizes EU accession preparation, requiring legal and institutional reforms to align with European standards.

Political stability indicators show substantial improvement over time. The country has not experienced significant civil unrest, political violence, or governmental instability in recent years. The 1997 crisis triggered by pyramid scheme collapses marked the last major political breakdown. Contemporary political competition occurs within established democratic channels, with international observers generally validating electoral processes despite occasional concerns about campaign finance and media balance.

Regulatory consistency and predictability in the gambling sector specifically have been poor given the dramatic 2018 prohibition followed by 2024 reversal. This policy volatility creates uncertainty for potential investors despite current favorable regulations. Operators must assess the risk that future political changes could trigger another prohibition or major regulatory restructuring that disrupts business models and destroys invested capital.

Corruption perception remains a challenge for Albania. Transparency International’s Corruption Perceptions Index consistently ranks Albania in the middle to lower range globally, indicating widespread perceptions of public sector corruption. EU accession requirements are driving anti-corruption reforms and institutional strengthening, but legacy practices and informal relationships continue influencing business operations. Gambling licensing, given its high-value nature and limited supply, presents corruption risks that international operators must navigate carefully while maintaining compliance with anti-bribery laws in their home jurisdictions.

Albania’s EU candidate status represents a major political and economic driver. The country formally became an EU membership candidate in 2014 and opened accession negotiations in 2022. The accession process requires harmonizing Albanian law with EU directives across all sectors including gambling, consumer protection, data privacy, and anti-money laundering. This reform agenda generally favors business environment improvements, legal predictability, and regulatory quality enhancements that benefit foreign investors.

Technology Adoption and Digital Behavior

Internet and Digital Usage

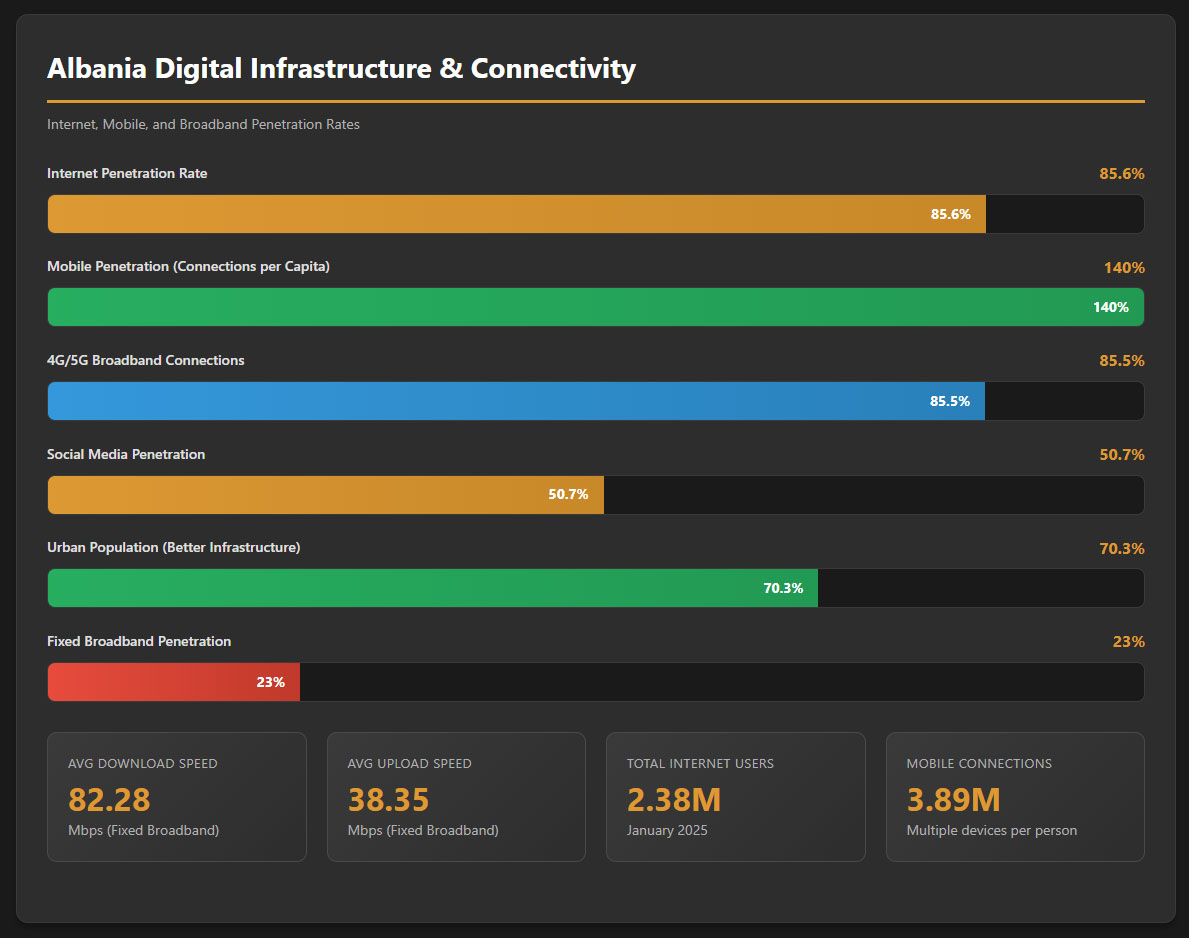

Internet penetration in Albania reached 85.6 percent in January 2025, with 2.38 million internet users in a population of 2.78 million. This high penetration rate places Albania favorably for online service delivery, though the 14.4 percent of the population remaining offline skews rural, elderly, and lower-income. Internet adoption showed slight decline of 17,000 users between January 2024 and January 2025, likely reflecting overall population decline rather than reduced internet usage rates.

Daily internet usage hours average approximately 6-7 hours among internet users, comparable to broader European patterns. Usage concentrates on social media, video content, messaging, and increasingly e-commerce and entertainment services. Mobile devices dominate internet access, with smartphones serving as the primary or sole internet-connected device for many Albanians, particularly younger demographics and those in areas with limited fixed broadband infrastructure.

Social media engagement is substantial with 1.41 million social media user identities representing 50.7 percent of the total population. Popular platforms include Facebook, Instagram, TikTok, and messaging applications like WhatsApp and Viber. This high social media adoption creates potential marketing channels if gambling advertising restrictions can be navigated, and indicates digital comfort levels supporting online gambling adoption.

E-commerce participation has grown steadily though remains below Western European levels. Albanian consumers increasingly shop online for clothing, electronics, and services, but cash-on-delivery payment options remain popular due to limited credit card penetration and trust concerns about online payments. The gambling market’s requirements for digital deposits and withdrawals necessitate customer education and trust-building around electronic payment security.

| Metric | Value | Date |

|---|---|---|

| Internet Penetration Rate | 85.6% | January 2025 |

| Total Internet Users | 2.38 million | January 2025 |

| Mobile Connections | 3.89 million | Early 2025 |

| Mobile Penetration Rate | 140% | Multiple devices per person |

| Broadband Mobile Connections | 85.5% | 3G/4G/5G networks |

| Social Media Users | 1.41 million | January 2025 |

| Social Media Penetration | 50.7% | Of total population |

| Fixed Broadband Penetration | 23% approximately | Recent estimate |

| Average Download Speed (Fixed) | 82.28 Mbps | August 2025 |

| Average Upload Speed (Fixed) | 38.35 Mbps | August 2025 |

Digital Payment Behavior

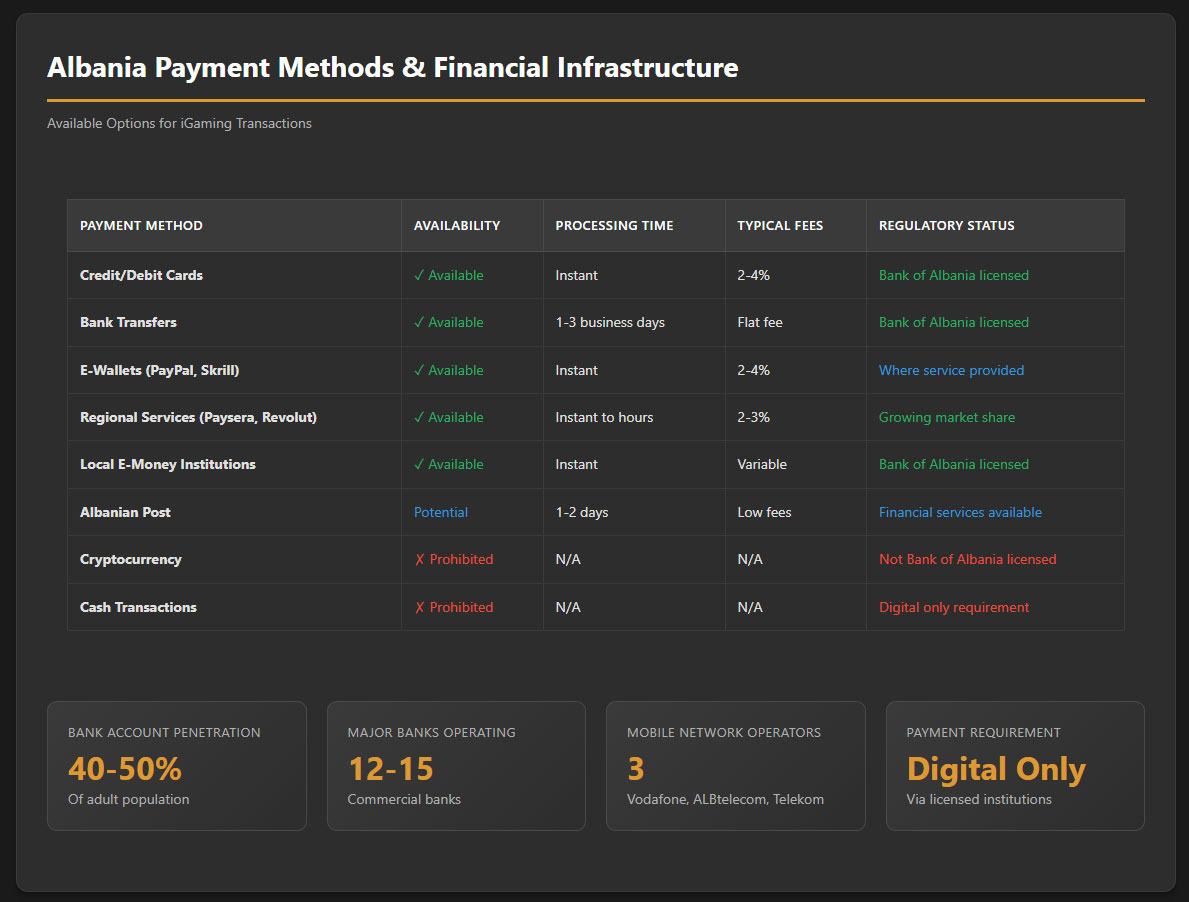

Payment method preferences in Albania favor cash for everyday transactions, but digital payments have gained ground particularly among urban, educated, and younger consumers. Credit and debit card penetration is growing but remains below Western European levels, with many Albanians lacking bank-issued payment cards or using them infrequently. Digital wallets and e-money services are expanding, driven by remittance services and increasing e-commerce adoption.

The most popular digital wallets include international services like PayPal where available, regional players like Paysera and Revolut gaining market share, and local e-money institutions licensed by the Bank of Albania. Online banking penetration has improved significantly, with all major Albanian banks offering internet and mobile banking services that enable account-to-account transfers for gambling deposits and withdrawals.

The regulatory requirement that all gambling payments be processed exclusively through authorized financial agents such as banks, licensed electronic currency institutions, and payment institutions licensed by the Bank of Albania eliminates cash transactions and creates a fully traceable payment environment. This restriction may initially limit market size by excluding unbanked populations but enhances anti-money laundering compliance and creates comprehensive transaction records.

Cryptocurrency adoption for gambling is legally ambiguous in Albania. While cryptocurrencies are not explicitly prohibited, the requirement for payments through Bank of Albania-licensed institutions effectively excludes direct cryptocurrency deposits and withdrawals. Some international payment processors may accept cryptocurrency funding behind the scenes while providing fiat currency interfaces to gambling operators, but this remains an uncertain legal area requiring clarification.

Gaming and Gambling Preferences

Current Market Participation

Precise current data on gambling participation rates is unavailable given the market’s recent reopening. Historical evidence from the pre-2018 period indicated very high participation rates, with the 4,000+ betting locations suggesting convenient access for most urban and many rural residents. Industry estimates suggested 30-40 percent of adult males participated in sports betting at least occasionally, with lower but growing female participation.

Online gambling participation during the 2018-2024 prohibition period likely occurred through offshore unlicensed websites, though quantifying this activity is difficult. The €50 million estimated online market value in 2022 suggests sustained demand despite legal restrictions. As licensed domestic platforms launch in 2024-2025, participation rates should increase due to local language support, trusted domestic brands, Albanian currency options, and marketing efforts by licensed operators.

Popular gambling activities historically centered on sports betting, particularly football which commands passionate following in Albania. The national team, Albanian players in international leagues, and major European competitions generate intense interest and betting volume. Basketball, tennis, and other international sports attract secondary interest. Casino games were available in land-based venues but commanded smaller customer bases than sports betting.

Lottery participation is widespread given the national lottery’s long-standing presence and low entry cost. Bingo enjoys modest popularity particularly among older demographics. The new online sports betting framework may expand product offerings over time to include virtual sports, esports betting, and potentially live dealer casino games if regulations evolve, but currently the market is limited to traditional sports wagering.

Consumer Behavior Patterns

Average spending per player is difficult to quantify precisely but can be estimated from aggregate market size. If 500,000 adults participate in online sports betting representing roughly 20-25 percent of the over-21 population, and the market reaches €100 million annually once established, average annual spending per active player would approximate €200, or roughly €17 monthly. High-value players likely spend multiples of this average while casual bettors contribute significantly less.

Typical bet sizes vary widely by player segment and event importance. Casual bettors may place small wagers of €2-10 on routine matches, while serious players bet €20-100 or more on major competitions. Accumulator bets combining multiple selections into single wagers with multiplied odds are popular, allowing small stakes to generate meaningful potential returns. Live in-play betting during matches attracts higher-frequency, lower-average-stake betting from engaged viewers.

Peak gambling times align with sporting event schedules. European football matches occurring primarily on weekend afternoons and evenings drive the highest betting volumes. Midweek Champions League and Europa League matches create secondary peaks. Summer months traditionally see reduced football betting but increased interest in tennis, basketball, and other sports. The seasonal pattern creates revenue fluctuations operators must manage through diversified sport offerings and operational planning.

Session length averages vary by betting type. Pre-match betting sessions may last just minutes as players research, select bets, and place wagers before matches begin. Live in-play betting extends sessions to match duration of 90+ minutes for football. Serious bettors may spend hours weekly researching teams, analyzing statistics, and managing multiple active bets across different events and sports.

Retention and loyalty patterns in gambling markets typically show high customer acquisition costs, making player lifetime value maximization critical. Successful operators achieve 6-12 month average player lifecycles before churn, with top-tier programs retaining valuable customers for years through loyalty rewards, VIP

programs, personalized offers, and superior service. Albanian market retention may benefit from limited licensed competition creating fewer switching opportunities once players establish accounts with preferred operators.

Bonus sensitivity and promotional response among Albanian players likely mirrors broader market patterns showing strong initial response to welcome bonuses and free bet offers. However, the regulatory framework may restrict bonus generosity through maximum bonus caps, wagering requirement minimums, or promotional frequency limitations. Sustainable player acquisition strategies must balance attractive introductory offers with long-term value proposition through competitive odds, product variety, and user experience quality.

Preferred game types by age group typically show younger males favoring live in-play betting, esports, and accumulator wagers, while older demographics prefer traditional pre-match betting on familiar sports. Female players, though smaller in number, often favor lower-risk betting types and demonstrate more cautious bankroll management. Operators should segment offerings and marketing to appeal across demographic profiles.

Deposit and withdrawal frequency patterns show most players depositing relatively infrequently, perhaps monthly or around major sporting events, while high-value players maintain more active transaction patterns. Withdrawal frequency typically lags deposits as many players recycle winnings into additional bets. Fast withdrawal processing becomes a competitive differentiator, with same-day or instant withdrawals commanding premium value to players compared to multi-day processing delays.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Albania’s internet infrastructure has improved substantially over the past decade, though quality remains uneven between urban and rural areas. Fixed broadband penetration stands at approximately 23 percent of the population, concentrated heavily in cities and towns. Urban centers like Tirana enjoy competitive markets with multiple providers offering fiber-to-the-home, cable, and VDSL services delivering speeds from 50 Mbps to 1 Gbps depending on package and location.

Average internet speeds for fixed broadband connections reached 82.28 Mbps download and 38.35 Mbps upload in August 2025 measurements, ranking Albania 79th and 80th globally respectively. These speeds suffice for online gambling applications requiring modest bandwidth for bet placement, live odds updates, and streaming of live sporting events. However, consistency and reliability matter more than peak speeds for gambling platforms where transaction completion and real-time data accuracy are critical.

Network reliability has improved as infrastructure investment has modernized equipment and expanded fiber backbone capacity. The main internet service providers have upgraded their core networks to handle increasing data traffic driven by video streaming, social media, and growing cloud service usage. Internet Society assessments give Albania a 50 percent internet resilience score, rated as medium, with good diversity of ISPs and upstream connections providing redundancy.

Infrastructure investment trends are positive, with government targets calling for half of users to have gigabit-capable connections by 2025. While this ambitious goal likely will not be fully achieved, it demonstrates policy commitment to digital infrastructure development. Major providers like One Albania are rolling out fiber-to-the-home in expanding geographic areas and connecting institutions like schools, universities, and government offices at 1 Gbps speeds.

Rural connectivity gaps remain significant challenges. While mobile internet provides basic access in most areas, fixed broadband infrastructure investment in sparsely populated regions is economically challenging for private providers. Government subsidy programs and universal service obligations may eventually extend fiber access more broadly, but the urban-rural digital divide will persist for years affecting the addressable online gambling market size.

5G and Future Technology Deployment

Current 4G coverage is extensive, with 85.5 percent of mobile connections classified as broadband, meaning they connect via 3G, 4G, or 5G networks. The three major mobile operators – Vodafone Albania, ALBtelecom (Eagle Mobile), and Telekom Albania – have deployed comprehensive 4G LTE networks covering all cities and most towns, with expanding coverage in rural areas. 4G network quality generally supports mobile gambling applications effectively.

5G rollout began in 2024 with initial deployments in Tirana and major cities. Network equipment vendor Ericsson is a principal supplier supporting Albanian operator 5G infrastructure investments. Some efforts have been made in conjunction with neighboring Kosovo to create a seamless 5G corridor along the highway connecting the countries, demonstrating regional cooperation on telecommunications infrastructure.

5G coverage currently reaches a small percentage of the population concentrated in urban centers, but expansion is progressing. The enhanced speeds, lower latency, and greater capacity of 5G networks will support richer gambling experiences including high-quality live streaming, virtual reality applications, and more sophisticated in-play betting features. However, 4G networks adequately serve current online sports betting needs, making 5G an enhancement rather than necessity.

Future infrastructure plans emphasize continued fiber expansion, 5G network densification, and satellite internet options for underserved areas. The 2024 introduction of Starlink satellite internet in Albania provides an important connectivity alternative for remote regions where terrestrial infrastructure investment is uneconomical. Starlink service costs approximately 42,500 ALL (€418) for hardware and 6,500 ALL (~$60) monthly subscription, delivering 50-200 Mbps speeds with low latency suitable for online gambling.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Albania’s mobile market features three major network operators: Vodafone Albania, ALBtelecom (operating the Eagle Mobile brand), and Telekom Albania (AMC). This competitive three-player market drives service quality improvements and competitive pricing. Market consolidation occurred in 2022 when 4iG acquired One Telecommunications and a majority stake in ALBtelecom, potentially leading to business integration that would reduce the market to effectively two major competitors.

Network operator market share breakdown shows Vodafone Albania serving over 931,000 mobile users as of recent data, Telekom Albania with approximately 605,000 users, and ALBtelecom with more than 272,000 users. Total active mobile users exceeded 2.7 million with almost 1.8 million active broadband subscribers. The mobile connection count of 3.89 million indicates many users maintain multiple SIM cards for coverage or pricing reasons.

Coverage quality varies by operator and location. All three operators provide strong coverage in Tirana and other major cities with overlapping 4G networks ensuring redundancy. Coastal tourist areas receive priority infrastructure investment ensuring quality service during peak summer seasons. Mountain and remote interior regions have more variable coverage, with some areas served by only one or two operators and falling back to 3G or even 2G connectivity.

4G/5G coverage maps show nearly complete 4G population coverage in urban areas declining to partial coverage in rural regions. 5G coverage remains limited to Tirana and select major cities as of 2024-2025, but expansion is ongoing. The 99.60 percent LTE penetration rate indicates comprehensive 4G availability for the vast majority of the population, with only 10,858 people reportedly limited to UMTS (3G) or slower speeds.

| Metric | Value | Notes |

|---|---|---|

| Total Mobile Connections | 3.89 million | 140% population penetration |

| Active Mobile Users | 2.7 million+ | Recent estimate |

| Mobile Broadband Subscribers | 1.8 million | 3G/4G/5G data users |

| Broadband Connection Percentage | 85.5% | 3G or better |

| 4G LTE Penetration | 99.60% | Very high coverage |

| Vodafone Albania Subscribers | 931,000+ | Market leader |

| Telekom Albania Subscribers | 605,000 | Second position |

| ALBtelecom Subscribers | 272,000+ | Third position |

| 5G Availability | Limited, expanding | Major cities only |

Device Penetration

Smartphone adoption rates in Albania are high, with the vast majority of mobile users owning smartphones capable of internet access and application installation. The 140 percent mobile penetration rate, while reflecting multiple devices per person rather than 140 percent smartphone ownership, indicates widespread mobile device access. Many Albanians own both personal and work phones, or maintain multiple SIM cards for network coverage or pricing advantages.

Device preferences favor mid-range Android smartphones from brands like Samsung, Xiaomi, Huawei, and other Asian manufacturers offering good functionality at accessible price points. Premium devices like Apple iPhones have growing but smaller market share concentrated among affluent urban consumers. Budget smartphones costing €100-200 provide entry-level access, while mid-range devices at €300-500 represent the volume market.

Android versus iOS market share strongly favors Android, likely commanding 80-85 percent of smartphones with iOS representing 15-20 percent. This distribution is typical for developing markets where iPhone premium pricing limits adoption. Gambling operators must prioritize Android app development and optimization while also serving the smaller but often higher-value iOS user base.

Average device specifications have improved substantially as even budget smartphones now offer adequate processors, RAM, and storage for gambling applications. Screen sizes of 5.5-6.5 inches are standard, providing sufficient display area for betting interfaces, live odds, and event information. Battery life, camera quality, and storage capacity matter more for general smartphone satisfaction than for gambling-specific functionality.

Mobile internet usage patterns show Albanians spending significant daily time on smartphones for social media, messaging, video content, and increasingly e-commerce and service access. Mobile data consumption has surged as 4G networks enable video streaming and content-rich applications. The convenience of mobile betting, allowing wager placement from anywhere with network coverage, makes mobile the dominant online gambling channel.

Financial Services and Payment Infrastructure

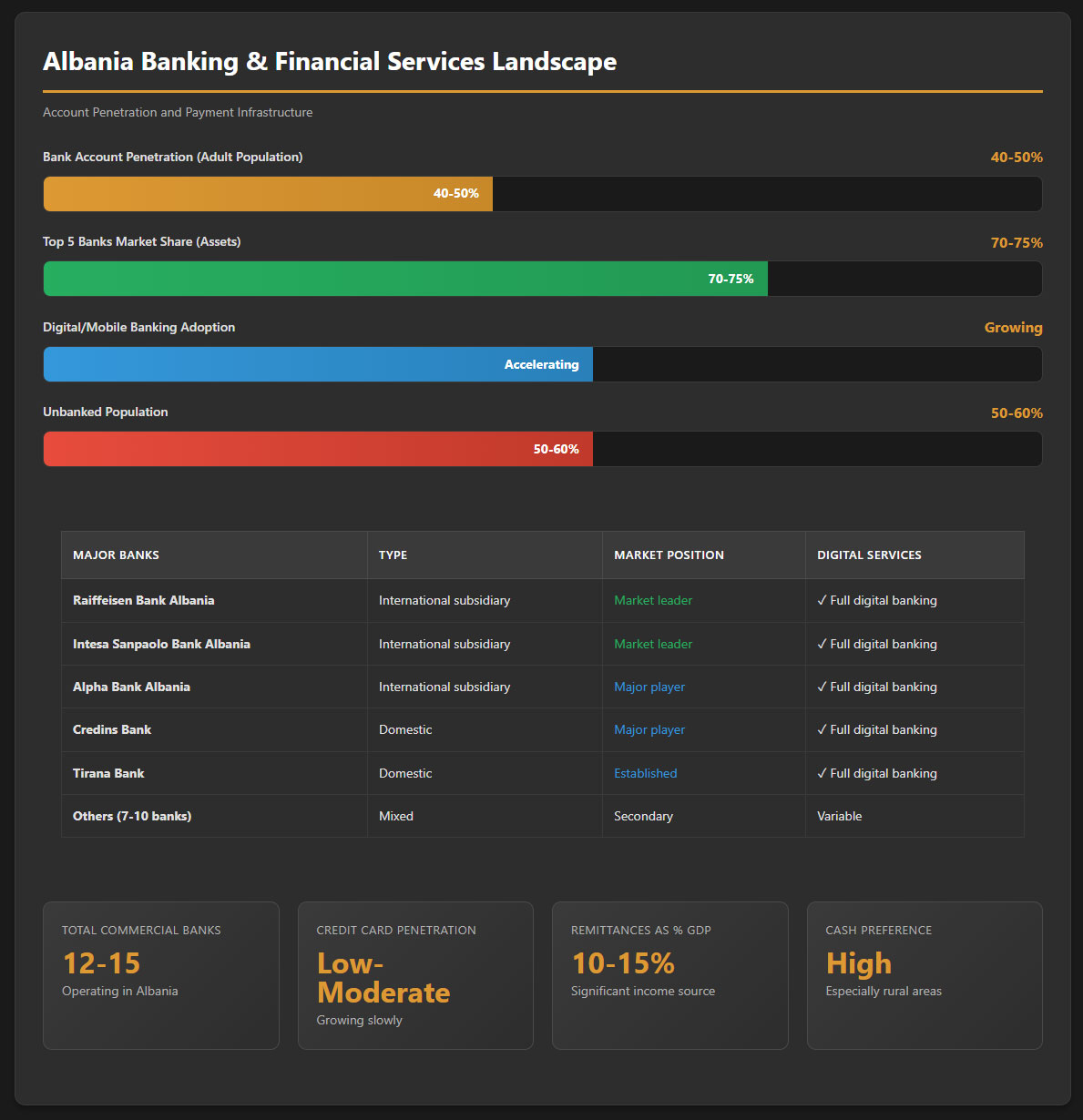

Banking System Structure

Albania’s banking sector features approximately 12-15 commercial banks operating in the country, including both domestic institutions and subsidiaries of international banking groups. Major banks include Raiffeisen Bank Albania, Intesa Sanpaolo Bank Albania, Alpha Bank Albania, Credins Bank, Tirana Bank, and others. The sector has consolidated over time, with several mergers and acquisitions reducing the number of institutions while strengthening remaining banks.

Bank market share is relatively concentrated among the top five institutions, which together command approximately 70-75 percent of total banking assets. Raiffeisen Bank Albania and Intesa Sanpaolo Bank Albania are market leaders by assets and customer base. The banking sector is generally stable, well-capitalized, and supervised by the Bank of Albania, the country’s central bank and financial regulatory authority.

Digital banking adoption has accelerated, particularly among urban and younger customers. All major banks offer internet banking and mobile banking applications enabling account management, transfers, payments, and other services remotely. Mobile banking penetration continues growing as smartphone ownership expands and user interfaces improve. However, many Albanians, particularly older and rural populations, still prefer in-person branch banking for complex transactions.

Account penetration rates have improved but remain below Western European levels. Approximately 40-50 percent of Albanian adults hold formal bank accounts, though rates are higher in urban areas and among employed individuals. Unbanked populations concentrated in rural areas, informal economy workers, and elderly citizens pose challenges for gambling operators since the regulatory requirement for digital payments through licensed financial institutions excludes cash transactions.

Credit and lending markets have developed slowly following the 1997 pyramid scheme crisis that destroyed public confidence in financial institutions. Banks maintain conservative lending practices, requiring substantial collateral and documentation. Consumer credit for purchases, personal loans, and mortgages is available but less accessible than in developed economies. Credit cards and overdraft facilities exist but with relatively low penetration compared to Western European norms.

Payment Processing Options

Available payment methods for iGaming in Albania must comply with the regulatory requirement that all gambling payments be processed exclusively through authorized financial agents. This category includes banks licensed by the Bank of Albania, licensed electronic currency institutions, licensed payment institutions, and potentially the Albanian Post which offers financial services. Direct cash deposits, unregulated payment intermediaries, and cryptocurrency payments are prohibited.