Kuwait presents a nuanced and highly regulated environment for the potential entry of the iGaming sector. The country’s strict stance on gambling activities, combined with a conservative legal framework, limits direct digital gaming operations.

Nevertheless, understanding the existing regulatory environment is crucial for any market entry strategy, especially given Kuwait’s strategic regional position and economic wealth.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

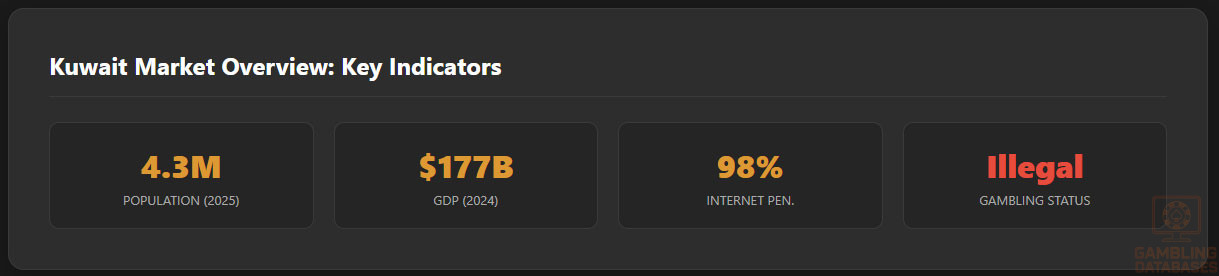

| Legal Status of Gambling | Illegal; No licensing framework for online or land-based gambling |

| Population | 4.3 million (2025 estimate) |

| GDP | $177 billion (2024) |

| Internet Penetration | 98% |

| Mobile Penetration | 105% |

| License Cost | N/A – Not available; market is unregulated |

| Taxation | None applicable; gambling activities are prohibited |

| Market Entry Barrier | High; prohibition and legal restrictions |

| Gambling Revenue | Essentially zero due to prohibition |

| Regulatory Timeline | Stable; no recent change in stance |

| Internet Infrastructure | Highly developed, regional hub |

| Business Environment | Restrictive; prohibitive of gambling operations |

| Market Size Projection | Minimal; excluded from formal sectors |

| Growth Forecast (CAGR) | 0%, as market is illegal |

| Average Revenue Per User (ARPU) | Not applicable |

| Market Penetration Rate | Zero for online gambling; high legal barriers |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

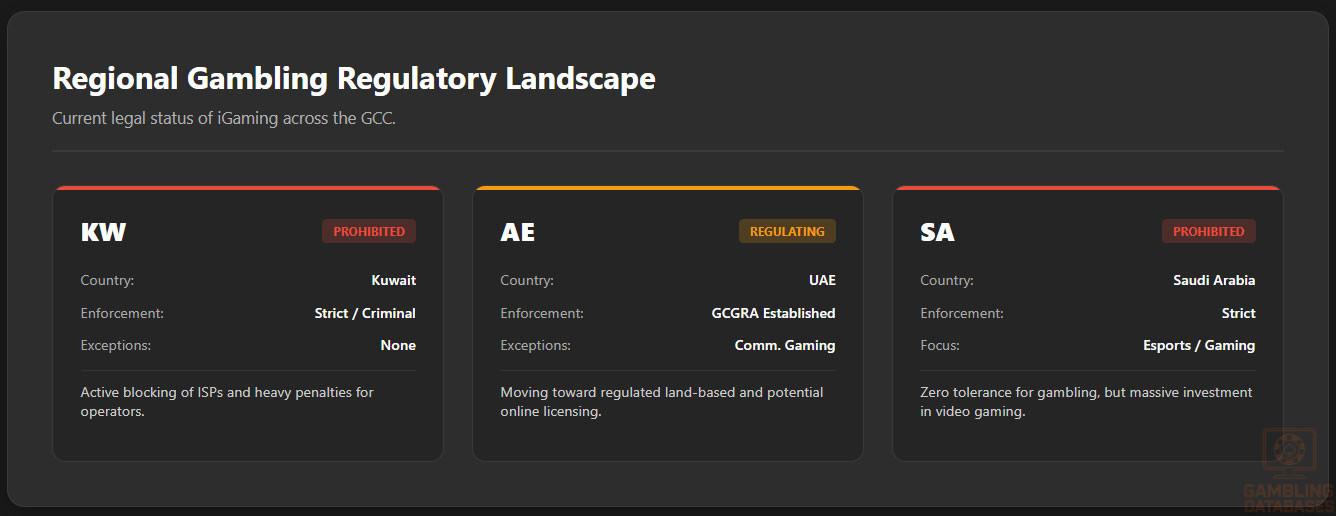

Kuwait enforces a strict ban on all forms of gambling, both land-based and digital. The nation’s legal stance explicitly prohibits any form of betting activities, and the government enforces comprehensive penalties for engagement or facilitation of gambling operations. There are no licensed operators or regulated markets for online gaming, making entry legally infeasible under current laws.

Land-Based Gambling Activities

The Kuwait legal framework explicitly bans casino operations, slot machine halls, sports betting venues, and any other land-based gambling activities.

The government maintains strict enforcement measures against illegal betting operations, with penalties including heavy fines and imprisonment. No licensed physical gambling venues exist within Kuwait, and there are no provisions for legal land-based gaming establishments.

Online Gambling Framework

The digital gambling environment is similarly prohibited under Kuwait law. The country’s legal system classifies online betting and casino activities as illegal, with no regulatory oversight or licensing regime in place.

Licensed Operators and Market Players

Since all gambling activities are illegal, there are no licensed operators or official market players in Kuwait’s iGaming landscape. Any existing online gambling websites are considered illicit, with government authorities aggressively pursuing enforcement actions against such entities.

The absence of a regulatory framework and the prohibition laws create a barrier to formal market entry, deterring legitimate operators from entering the Kuwaiti market.

Licensing Framework and Requirements

Kuwait does not offer legal licensing procedures for the gambling sector. The absence of regulatory provisions means no formal application process, eligibility criteria, or technical standards exist. All gambling-related activities are classified as criminal offenses, with penalties including fines and imprisonment for operators and players.

Local Presence and Operational Requirements

Regulations do not permit the establishment of gambling operations, hence there are no mandates for local presence, physical offices, or operational facilities.

Foreign ownership restrictions are not applicable in a legal context because no legal gambling operations are permissible. Any attempt to operate or facilitate gambling services is subject to criminal prosecution.

Compliance Obligations and Monitoring

There are no compliance obligations or monitoring mechanisms for online gambling, as all such activities are illegal. The government employs internet filtering, monitoring, and enforcement to ensure the prohibition is upheld, with severe penalties for violations. Player protection measures, responsible gambling, or AML standards are not applicable in this unlawful environment.

Taxation Structure and Financial Obligations

Gambling taxation is non-existent since all betting activities are illegal. The government does not impose taxes or fees related to gambling operations.

Any revenue generated from illegal activities remains unregulated, and enforcement agencies focus on criminal prosecution rather than tax collection.

Advertising and Marketing Restrictions

Advertisements promoting gambling are strictly prohibited under Kuwaiti law. The country enforces bans on gambling advertisements across all media channels, including online, television, and outdoor signage. Promotional activities or sponsorship linked to gambling are likewise unlawful, and violations attract significant penalties.

Recent Regulatory Changes and Enforcement

Kuwait has maintained its prohibition stance throughout recent years, with no notable amendments to its gambling laws. Enforcement efforts include internet restrictions, raids on illegal gambling operations, and criminal prosecutions. The legal environment remains highly restrictive, with no indications of liberalization in the foreseeable future.

Enforcement Mechanisms and Penalties

- Criminal penalties including imprisonment for operators and players

- Heavy fines for illegal gambling activities

- Internet filtering and blocking of gambling sites

- Raids and criminal prosecutions against illegal operators

- Asset seizure related to illegal gambling activities

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

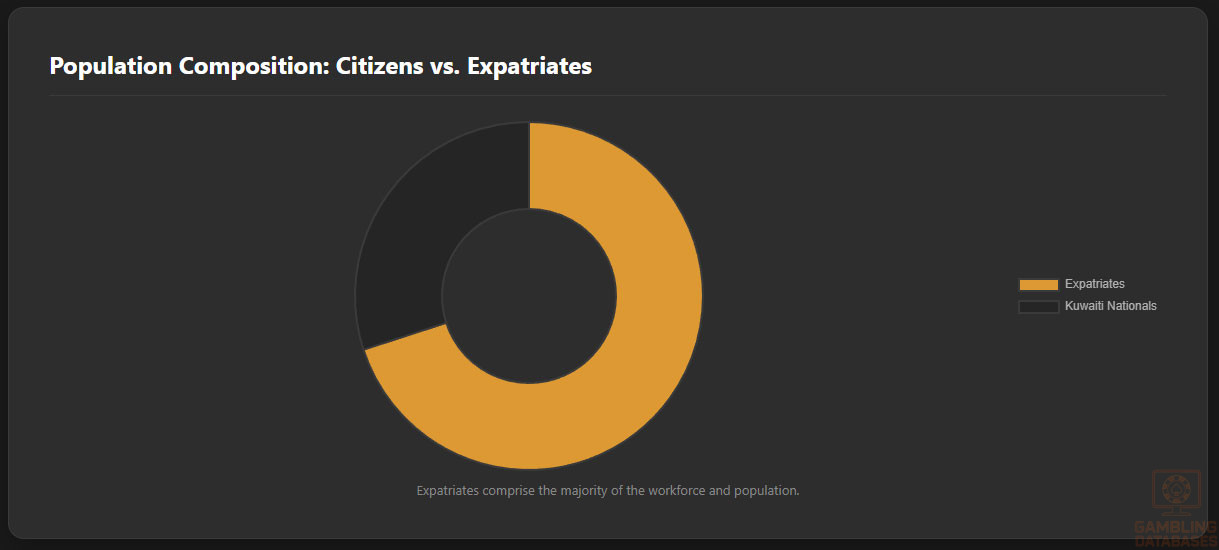

Kuwait’s population is approximately 4.3 million as of 2025, with a youthful demographic profile and a median age around 32 years. The gender ratio is slightly skewed toward males due to a substantial expatriate workforce, which comprises over 70% of the total population. Urbanization is high, with around 98% of residents living in urban areas.

The population is distributed unevenly, with concentrations in the capital and surrounding urban centers, reflecting economic and social infrastructure hubs. Rural areas are sparsely populated, leaning heavily on the urban cores for services and employment opportunities.

This urban concentration supports strong digital connectivity and potential consumer engagement for online services.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 23% |

| 15-24 years | 17% |

| 25-44 years | 38% |

| 45-64 years | 16% |

| 65+ years | 6% |

Geographic Distribution

The majority of Kuwait’s population is concentrated in five major cities that serve as economic and administrative centers. These cities command advanced telecommunications and broadband infrastructure enabling widespread internet access.

- Kuwait City, the capital, with an estimated population of 4 million in the metropolitan area

- Al Ahmadi, known for its oil industry-related population

- Hawalli, a mixed residential and commercial district

- Salmiya, a major commercial and entertainment hub

- Jahra, noted for its agricultural and industrial presence

Urban centers exhibit near-complete internet penetration rates, whereas rural areas, though limited in size, maintain basic digital access primarily via mobile networks. Gambling venues are essentially non-existent due to legal restrictions, but urban consumers have high exposure to digital platforms.

Economic Indicators and Consumer Spending Power

Kuwait holds a Gross Domestic Product (GDP) around $177 billion, with consistent growth supported by the hydrocarbon sector yet increasingly diversified towards services and finance. The country experienced an annual GDP growth rate near 2.5% pre-2025, with forecasts indicating moderate expansion driven by government economic plans.

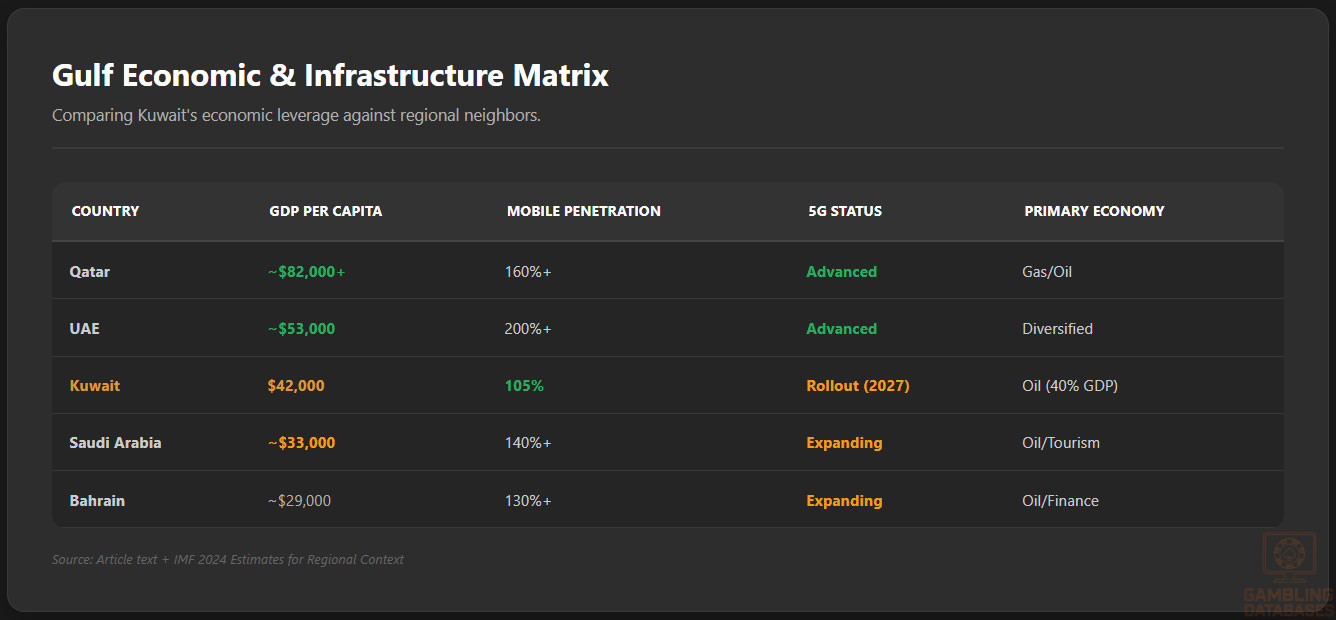

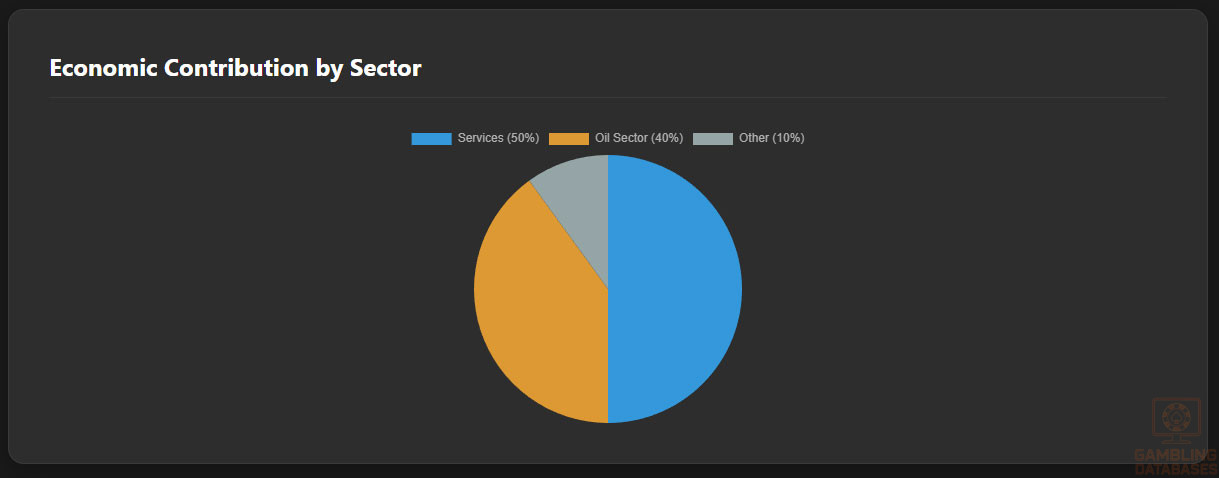

The economy is dominated by the oil sector (~40% of GDP), but services represent approximately 50%, demonstrating a transition toward a consumption-driven market. Per capita GDP is among the highest in the Gulf Cooperation Council (GCC) at over $42,000, underpinning substantial consumer purchasing power.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $177 billion |

| GDP Growth Rate (Annual) | 2.5% |

| GDP per Capita | $42,000 |

| Oil Sector Contribution to GDP | 40% |

| Service Sector Contribution to GDP | 50% |

| Unemployment Rate | 2.1% |

Household incomes vary widely, influenced by a large expatriate segment earning below national averages. The median household income for Kuwaiti nationals ranges between $50,000 and $70,000 annually, with disposable income elevated due to limited taxation.

Consumer spending emphasizes technology, entertainment, and digital services, suggesting potential for online market engagement despite iGaming legal constraints.

Income and Wealth Distribution

The wealth distribution in Kuwait is moderately unequal, with a Gini coefficient estimated around 30, reflecting broad affluence among nationals but disparities in expatriate earnings. High-income households dominate urban areas, fueling luxury consumption and online retail expansion.

Middle-income groups show increasing adoption of digital payment systems, while low-income expatriates have limited discretionary spending.

Market Size and Growth Projections

Although there is no formal iGaming market due to legal prohibitions, adjacent digital entertainment and technology service sectors show robust expansion.

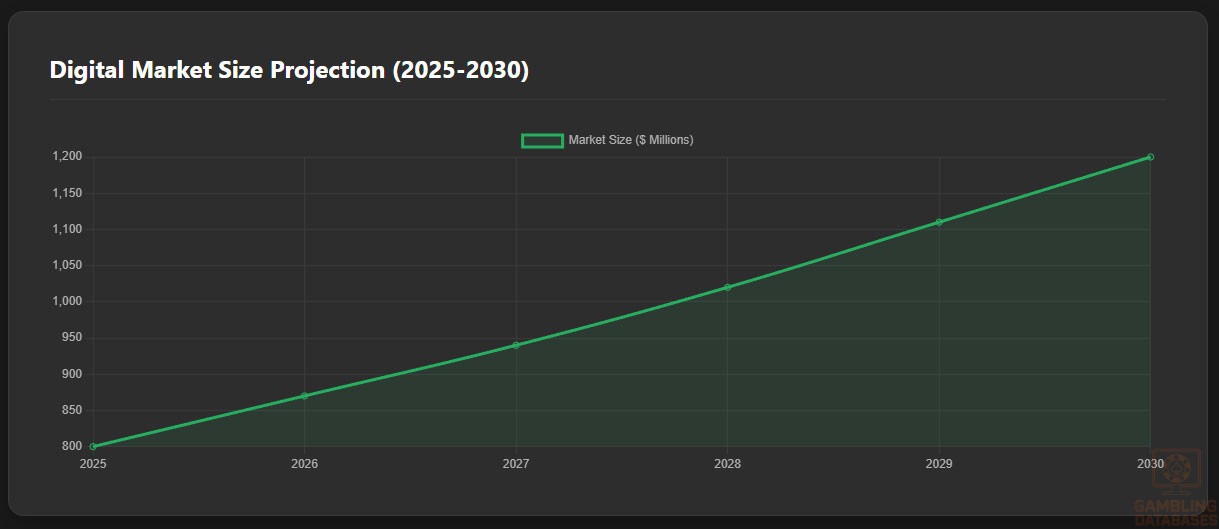

Online consumer markets are projected to grow at a compound annual growth rate (CAGR) of approximately 8% over the next five years as internet adoption deepens. This growth is fueled by high smartphone penetration and evolving digital consumption habits.

| Metric | 2025 Value | 2030 Forecast | CAGR |

|---|---|---|---|

| Digital Market Size (USD) | $800 million | $1.2 billion | 8% |

| Online Service Users (million) | 3.5 | 4.2 | 4% |

| Average Revenue Per User (ARPU) | $230 | $285 | 4.5% |

Education, Skills, and Digital Literacy

Kuwait boasts high literacy rates exceeding 97%, with a well-developed education system focusing on STEM subjects. The youth population is notably tech-savvy, exhibiting high proficiency in digital skills and fluency in English, which underpins their engagement with global digital content.

Cultural and Social Factors

Communication and Language

Arabic is the official language and cultural medium, but English is widely understood and used in business and online communication. Diverse expatriate communities speak multiple languages, including Urdu, Tagalog, and Hindi, reflecting Kuwait’s multicultural makeup.

- Arabic (official, primary)

- English (business and digital)

- Urdu (large expatriate group)

- Tagalog (significant Filipino population)

- Hindi (common among South Asian residents)

Cultural Attitudes

Kuwaiti society is deeply influenced by Islamic values, which shape strict cultural norms against gambling. Social acceptance of gambling is minimal due to religious prohibitions and legal restrictions.

Foreign brands related to entertainment or digital content are cautiously received, with preference for family-friendly and culturally sensitive offerings.

Problem Gambling and Social Considerations

Given the legal and cultural restrictions, formal data on problem gambling is scarce. However, underground gambling activities generate social concerns, prompting government advisories promoting awareness. Social responsibility efforts focus on education and deterrence rather than rehabilitation programs.

- Public awareness campaigns on risks of illegal gambling

- Religious guidance discouraging gambling behaviors

- Community-based outreach programs

- Legal enforcement actions to prevent gambling

- Support for at-risk youth through social services

Political Structure and Governance

Kuwait operates a constitutional emirate with a stable political environment and consistent regulatory regime. Governance emphasizes conservative social policies aligned with Islamic law, resulting in stringent regulatory controls, particularly in entertainment and digital sectors. Regulatory consistency supports predictability but restricts gambling-related business freedoms.

Technology Adoption and Digital Behavior

Internet and Digital Usage

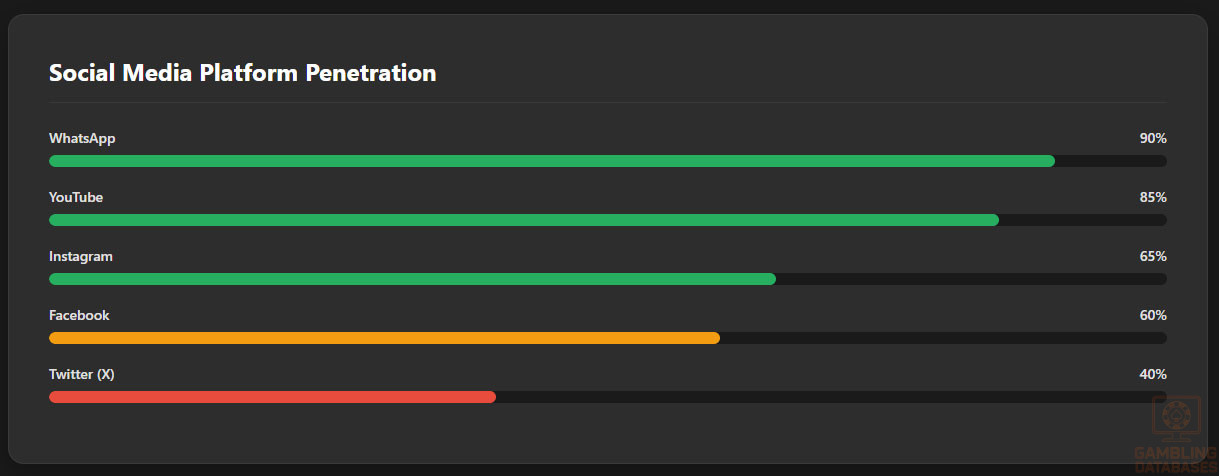

Kuwait’s internet penetration rate exceeds 98%, with users spending an average of 7.5 hours daily online across devices. Mobile subscription rates surpass 105% due to widespread multi-SIM use. Social media engagement is significant and diversified, including global and regional platforms.

- WhatsApp – primary messaging platform with 90% penetration

- Instagram – popular among youth and professionals with 65%

- YouTube – broad video consumption platform reaching 85%

- Twitter – key for news and government communication at 40%

- Snapchat – popular among younger demographics at 35%

- Facebook – steady user base of 60%, mostly older demographics

Digital Payment Behavior

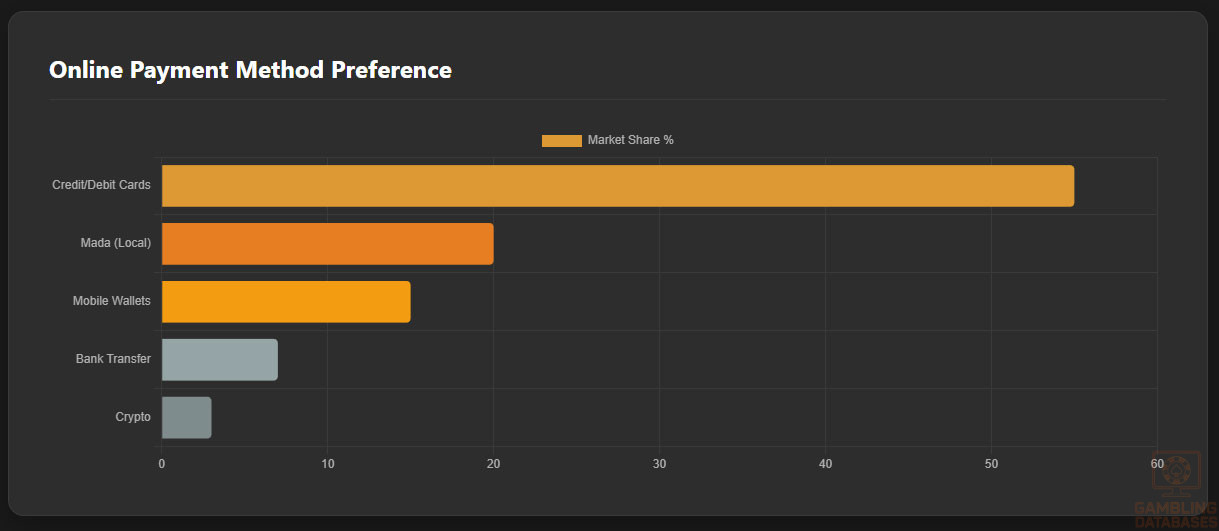

Consumers prefer a blend of traditional and modern payment methods for online transactions. Credit and debit cards lead transaction volumes, but rapid growth in e-wallets and mobile payments is evident among young and expatriate users. Cryptocurrency holds a niche but emerging presence.

- Credit and debit cards – 55% market share in online payments

- Mada (national card scheme) – 20%

- Mobile wallets (Apple Pay, STC Pay) – 15%

- Bank transfers – 7%

- Cryptocurrency payments – 3%, growing trend

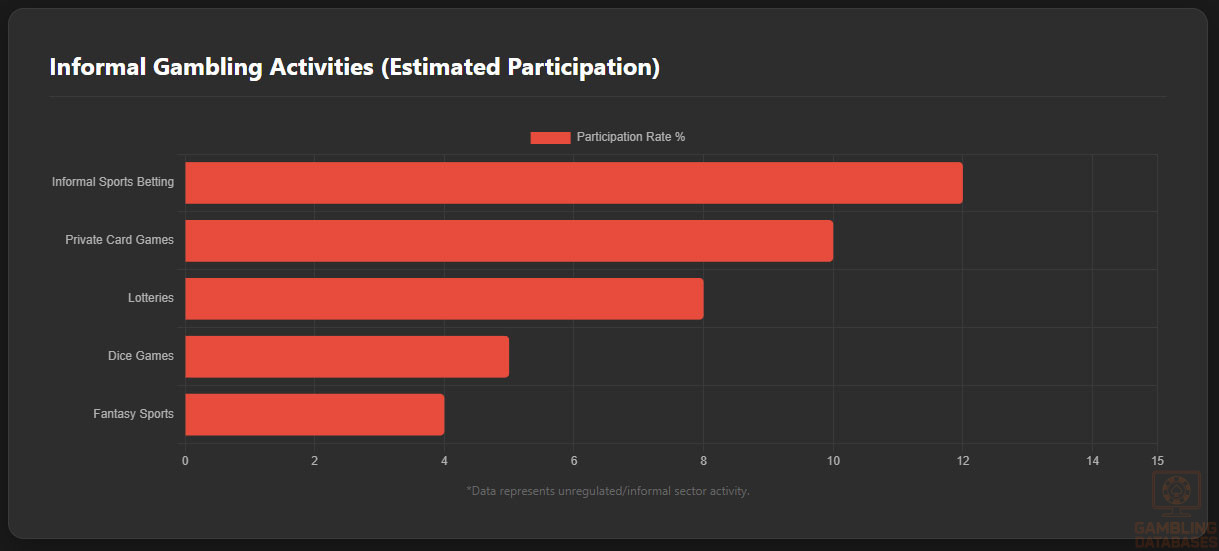

Gaming and Gambling Preferences

Despite legal prohibitions, informal gambling activities persist, primarily through social and private networks, with preferences leaning toward lotteries, informal sports betting, and card games.

Online gaming engagement remains strong in non-gambling categories such as casual games, esports, and fantasy sports.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Informal Sports Betting | 12% |

| 2 | Private Card Games | 10% |

| 3 | Lotteries (Underground) | 8% |

| 4 | Informal Dice Games | 5% |

| 5 | Fantasy Sports (Unofficial) | 4% |

Consumer behavior exhibits strong preference for mobile platforms due to convenience and discretion, with peak usage during evenings and weekends.

Retention depends on social engagement elements and culturally acceptable entertainment formats. Overall, digital entertainment adoption remains high but within cultural and legal boundaries.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Kuwait boasts one of the highest internet penetration rates globally, exceeding 98% among the population, supported by extensive broadband and mobile network infrastructure. Fixed broadband connections constitute approximately 40% of internet access, while mobile broadband dominates with over 60% due to widespread smartphone adoption.

Average internet speeds are highly competitive in the region, with fixed broadband averaging 150 Mbps download and 80 Mbps upload speeds. Network reliability is strong, backed by continuous investments in fiber-optic expansion and resilient infrastructure to support business and consumer demands.

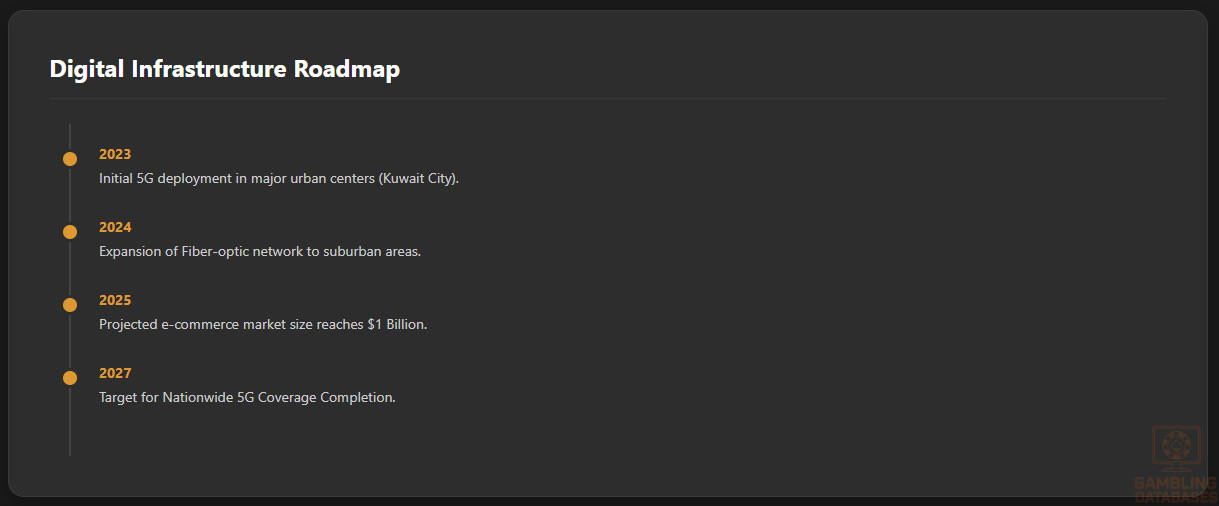

5G and Future Technology Deployment

Kuwait’s 5G rollout is well underway, with major urban centers enjoying widespread coverage. Deployment began in late 2023, with nationwide 5G expected by 2027. Telecom operators plan to leverage 5G for enhanced mobile broadband, Internet of Things (IoT) applications, and smart city projects, reinforcing Kuwait’s digital economy goals.

The competitive telecom market drives innovation and accelerates investments in next-generation technologies, positioning Kuwait as a regional digital hub.

Mobile Technology Ecosystem

Mobile Network Infrastructure

The mobile telecommunications market is served by multiple operators, fostering competitive pricing and extensive coverage. Coverage quality is strong across urban and most suburban areas, with rapid improvements in rural connectivity. Data costs are moderate relative to regional peers, supporting high mobile adoption and digital service consumption.

- Ooredoo Kuwait – Largest market share with over 45% subscribers

- Zain Group – Leading competitor holding about 40% market share

- VIVA Kuwait (now part of STC) – Approximately 15% market share

Device Penetration

Smartphone penetration penetrates over 95%, with consumers favoring high-end Android and Apple iOS devices. Device usage patterns indicate a preference for mobile internet over desktop, reflecting high engagement in social media, video streaming, and mobile applications. The proliferation of affordable 5G-enabled devices supports the shift toward an increasingly mobile-first digital ecosystem.

Financial Services and Payment Infrastructure

Banking System Structure

Kuwait’s banking sector is mature, with a mixture of national and international banks offering comprehensive digital banking services. Account penetration is high, with government initiatives promoting financial inclusion, especially digital wallets and contactless payments.

- National Bank of Kuwait (NBK) – Dominant market leader with extensive digital offerings

- Kuwait Finance House (KFH) – Major Islamic banking provider

- Burgan Bank – Significant regional presence with growing digital platform

- Commercial Bank of Kuwait – Focus on SME and consumer sectors

- Aman Bank – Emerging player targeting fintech integration

Payment Processing Options

Payment options in Kuwait span traditional card schemes, mobile wallets, and bank transfers. Debit and credit cards including Visa, Mastercard, and Mada dominate card usage. E-wallet adoption is rising, driven by youth and expatriate consumers seeking convenience and speed.

- Credit/Debit Cards (Visa, Mastercard, Mada)

- Mobile Wallets (STC Pay, Apple Pay, Samsung Pay)

- Bank Transfers via local ACH networks

- Cash on Delivery (for e-commerce)

- Cryptocurrency payments in growing niche segments

E-commerce and Digital Economy

The e-commerce market is rapidly expanding, with estimates placing total market size at approximately $1 billion in 2025. Consumer trust is robust, driven by improved digital payment security and enhanced delivery infrastructure.

Digital services, including entertainment, fintech, and online education, show dynamic growth aligned with rising digital literacy.

Business Environment and Regulatory Framework

Ease of Business Operations

Kuwait ranks moderately high on the World Bank’s Ease of Doing Business index, supported by efficient business registration procedures, investor protections, and regulatory stability.

Operational costs are higher than regional averages due to compliance requirements and market entry complexities in regulated industries.

- Preparation of legal documents for company formation and notarization

- Submission of incorporation application to the Ministry of Commerce

- Obtainment of commercial license and municipal approvals

- Registration for tax and social security at respective authorities

- Opening a corporate bank account and operational setup

Corporate Structure and Registration

Available corporate structures include Limited Liability Companies (LLCs), Joint Stock Companies, and Foreign Branches. LLCs are the most common for foreign investors due to flexible ownership structures and ease of management. Foreign ownership is permitted up to 100%, but some sectors may have restrictions or require local sponsorship.

- Limited Liability Company (LLC)

- Joint Stock Company

- Foreign Branch Office

- Representative Office (non-commercial activities)

- Special Economic Zone Entities

Registration timelines generally span 4-6 weeks, with comprehensive documentation required including corporate bylaws, shareholder agreements, and proof of capital. Mandatory compliance includes ongoing financial reporting and adherence to local labor and commercial laws.

Taxation Framework

Kuwait features a favorable tax environment for businesses, with no corporate or personal income tax on foreign entities and individuals. However, Kuwaiti shareholding companies pay a flat corporate income tax rate of 15%. Special Economic Zones provide tax holidays for qualifying companies.

International treaties support double taxation avoidance with over 15 countries, enhancing Kuwait’s attractiveness as a business hub.

- Bahrain

- United Arab Emirates

- Saudi Arabia

- France

- United Kingdom

Market Entry Considerations

Recommended entry strategies include local partnerships, utilization of digital platforms compliant with Kuwait law, and leveraging existing fintech infrastructure. Operators must prioritize cultural sensitivity and regulatory compliance to navigate the conservative business environment effectively.

- Forming joint ventures with local companies for market knowledge and compliance

- Utilizing digital-only platforms for non-gambling entertainment and skill-based games

- Leveraging mobile-first technology to reach the digitally engaged populace

- Engaging in corporate social responsibility initiatives to build brand trust

- Investing in localized content and customer support

Initial investments typically range from $500,000 for licensing, compliance, and technology setup to over $2 million for full market launch and marketing. Entry timelines span 6 to 12 months, influenced by regulatory approvals and infrastructure deployment.

| Cost Category | Estimated Cost (USD) |

|---|---|

| Licensing and Regulatory Fees | $150,000 – $400,000 |

| Technology Platform and Development | $200,000 – $600,000 |

| Marketing and Customer Acquisition | $100,000 – $500,000 |

| Operational and Staffing Costs | $100,000 – $300,000 |

| Legal and Consulting Fees | $50,000 – $100,000 |

FAQ: Frequently Asked Questions

1. Is online gambling legal in Kuwait?

Online gambling remains illegal under Kuwaiti law, with strict prohibitions on both land-based and digital betting activities. There is no licensing framework, and operators or players engaging in such activities face severe penalties. Businesses interested in this sector should explore alternative non-gambling digital entertainment opportunities that comply with local regulations.

2. What types of gambling licenses are available and what do they cover?

Since gambling is prohibited in Kuwait, no official license types exist for iGaming or gambling operations. Any attempts to operate gambling services violate legal statutes, and no regulatory authority issues or manages gambling licenses.

3. How much does an iGaming license cost and how long does it take to obtain?

As licensing for gambling activities is non-existent, it is not possible to obtain an iGaming license in Kuwait. This restricts lawful operations within the country, requiring businesses to consider jurisdictions with legal frameworks or alternative product offerings.

4. Can foreign companies obtain a gambling license?

Foreign companies cannot obtain gambling licenses in Kuwait as the activity itself is unlawful. Foreign businesses seeking to enter the Kuwaiti digital market should focus on compliant services and abide strictly by local laws.

5. What are the tax obligations for iGaming operators?

Since gambling operations are illegal, there are no tax obligations specific to iGaming operators. Businesses operating legally in other sectors benefit from Kuwait’s favorable tax regime, which includes no personal income tax and corporate tax only on Kuwaiti shareholding companies.

6. Are gambling winnings taxed for players?

Given the illegality of gambling, there is no formal tax framework for gambling winnings as the activity itself is prohibited. Players found participating in illicit gambling activities risk legal repercussions rather than standard tax treatment.

7. What are the typical operational costs for running an online casino or sportsbook?

Operating an online casino or sportsbook is not permissible under Kuwaiti law; hence, costs cannot be officially tabulated. However, in legal jurisdictions, major cost categories include platform licensing, compliance, marketing, payment processing, and customer service.

8. What is the expected ROI timeline for entering this market?

In Kuwait, expected ROI for iGaming ventures is not applicable due to legal restrictions. For compliant digital entertainment or fintech ventures, ROI timelines typically range between 18 to 36 months depending on investment scale and market traction.

9. What are the local presence requirements for operators?

There are no legal options for operators to establish gambling businesses locally. For other digital businesses, local presence may be required for licensing and regulatory compliance, including physical offices and local management.

10. What payment methods are available and recommended?

Payment methods favored by consumers include credit and debit cards, national card schemes, mobile wallets, and bank transfers. Cryptocurrency usage remains limited but growing among tech-savvy users.

11. What are the advertising and marketing restrictions?

Advertising for gambling is strictly banned. Marketing must comply with content appropriateness standards, focusing on non-gambling services and respecting cultural sensitivities. Digital platforms should avoid any references or promotions of betting-related activities.

12. What responsible gambling measures are mandatory?

No mandatory responsible gambling measures exist due to legal prohibitions. However, operators in alternative digital sectors are encouraged to promote responsible digital consumption and data privacy.

13. How large is the iGaming market and what is the growth potential?

The iGaming market in Kuwait is non-existent due to prohibitive laws. Adjacent digital entertainment sectors present growth opportunities fueled by rising internet penetration and digital literacy.

14. Who are the main competitors and what is their market share?

There are no legal gambling competitors in Kuwait. Digital entertainment and mobile gaming companies dominate the online market, serving the tech-savvy population with diverse content.

15. What are the player preferences and typical spending patterns?

Player preferences favor mobile access, social and casual games, with spending concentrated on in-app purchases and subscription models. Gambling or betting is relegated to informal and illegal settings.

16. What are the key success factors and main challenges for new entrants?

Success hinges on regulatory compliance, cultural adaptation, robust digital infrastructure, and strong local partnerships. Challenges include legal restrictions on gambling, market entry barriers, and strong government enforcement.

Sources and References

- KuwaitGambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Kuwait – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Gaming Industry Report – Regional Market Analysis 2024

- Kuwait Ministry of Communications – Technology & Infrastructure Reports 2024

- GCC Telecommunication Authority Reports 2024

- Kuwait Ministry of Commerce – Business Registration Guidelines 2024

- International Monetary Fund – Kuwait Country Report 2025

- Global Digital Payments Index 2024

- Middle East Economy and Digital Trends Report 2025

- Kuwait Central Statistical Bureau – Economic and Demographic Statistics

- Gambling Industry Compliance Analysis – Middle East Overview 2024

- Kuwait Ministry of Education – Literacy & ICT Curriculum Data 2024

- Arab Social Media Report 2025

- Global Internet and Mobile Usage Statistics 2025 – Digital Economy Insights

- World Economic Forum – Technology Competitiveness Report 2024

- Regional Fintech Adoption Study 2024

- Digital Entertainment Market Report – GCC 2025

- Kuwait Investment Authority Publications 2024

- International Telecommunications Market Data – Kuwait 2025

- Middle East Banking and Finance Report 2024

- Legal Framework for Digital Businesses – Kuwait Special Report 2025

- Industry Whitepaper – Compliance and Market Entry Challenges in GCC

- Kuwait Ministry of Tourism and Commerce – Digital Market Strategy 2025

- Global Regulatory Environment for iGaming – Comparative Study 2024

- Middle East Gaming and Esports Trends 2025

- Kuwait Economic Diversification and Vision 2035 Document

- Corporate Tax Treaties and International Agreements – Kuwait Ministry of Finance

🎯 Gambling Databases Country Rating: Kuwait

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.0/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 0.0/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 0.0/10 | ⛔️ COMPLETELY FORBIDDEN |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- TOTAL PROHIBITION: All forms of gambling (online, land-based, sports betting, casino) are CRIMINALLY ILLEGAL under Kuwaiti Penal Law based on Islamic Sharia principles.

- IMPRISONMENT RISK: Operators and players face mandatory prison sentences and heavy fines. This is not a civil offense; it is a serious crime.

- ACTIVE SURVEILLANCE: The government actively employs “intensive internet monitoring” and filtering to block gambling sites and track users.

- ASSET SEIZURE: Any revenue generated is considered “illicit gains” and is subject to total confiscation by the state.

- ADVERTISING BAN: All marketing is strictly prohibited across all channels; violation leads to immediate prosecution.

- NO LICENSING: There is no regulatory framework. Any “license” claiming to cover Kuwait is fraudulent or unrecognized by local authorities.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Illegal with strict enforcement (-1.0). Online casino prohibition (-1.5). Active ISP blocking and monitoring (-0.5). Affiliate prosecution risk (-0.5). Final Score capped at 0.0. |

| Licensing Process | 25% | 0.0/2.5 | No licensing available (0 points). No legal mechanism exists to apply for or hold a gambling license. |

| Taxation & Costs | 20% | 0.0/2.0 | While there is no “tax,” the effective cost is 100% of revenue due to asset seizure risks (-1.5). High risk of fines and legal defense costs (-0.5). Final Score: 0.0. |

| Operational Requirements | 15% | 0.0/1.5 | Excessive requirements (0 points). Operation requires total black-market obfuscation. Banking bans (-0.25). Crypto restrictions (-0.25). Local presence is a criminal liability risk. |

| Market Environment | 10% | 0.0/1.0 | Difficult environment (+0.25). Total advertising ban (-0.5). Active enforcement against operators (-0.25). Cultural hostility (-0.25). Final Score capped at 0.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.0/4.0 | Illegal with player penalties (0 points). Online casino/betting fully prohibited (-1.5). Players face criminal prosecution risk (-0.5). |

| Practical Accessibility | 30% | 0.0/3.0 | Severe restrictions, extensive blocking (+0.5). Banks block gambling MCC codes (-0.5). Intensive ISP filtering and monitoring (-0.5). VPN use is monitored (-0.5). Final Score: 0.0. |

| Player Penalties | 20% | 0.0/2.0 | Criminal penalties possible (0 points). Players can face imprisonment, fines, and public shaming. |

| Market Availability | 10% | 0.0/1.0 | No access (0 points). No licensed operators exist; offshore sites are aggressively blocked. |

🔍 Key Highlights

Strengths (If Any)

- High GDP Per Capita: ~$42,000, indicating high potential disposable income (theoretically).

- Digital Infrastructure: 98% internet penetration and 105% mobile penetration.

- Note: These “strengths” are irrelevant for legal operators due to total prohibition.

⛔️ CRITICAL RISKS AND CHALLENGES

- Criminal Liability: This is not a “grey market.” It is a black market. Participation equals criminal activity.

- Cyber Policing: Kuwait uses advanced filtering and monitoring technology to identify and prosecute gambling traffic.

- Financial Blockade: Local banks (NBK, KFH) strictly block payments to known gambling entities. Crypto is also under scrutiny.

- Expatriate Deportation: Non-citizens (70% of the population) caught gambling face immediate deportation after serving sentences.

- No Marketing Channels: Advertising on social media or search engines is blocked and can lead to platform bans or legal action against the advertiser.

- Asset Confiscation: Government has the authority to freeze and seize assets linked to illegal gambling operations.

Player-Specific Issues

- Players face social stigma and potential imprisonment.

- No consumer protection; players using black-market sites have no recourse for stolen funds.

- Access requires sophisticated VPNs, which are themselves subject to scrutiny if used for illegal acts.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: N/A (Legal entry impossible).

Monthly Operating Costs: Variable (High costs for obfuscation, mirrors, and payment processing laundering).

Effective Tax Rate on Revenue: 100% Risk of Seizure.

Customer Acquisition Cost: Extreme. Word-of-mouth only. Digital marketing is blocked.

Profitability Assessment: NON-EXISTENT FOR LEGAL OPERATORS. Any attempt to operate here is a criminal enterprise, not a business venture. The risk-to-reward ratio is catastrophic due to the high likelihood of domain seizures, payment freezing, and international warrants.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Site blocking, payment freezing, criminal charges in absentia, Interpol notices. |

| Licensed Sports Betting Operators | CRITICAL | Your license (MGA, UKGC, etc.) will be jeopardized by operating in a prohibited jurisdiction. |

| Affiliates/Advertisers | CRITICAL | Immediate prosecution if located in Kuwait. Domain bans and ad account bans globally. |

| Payment Processors | CRITICAL | Complicity in money laundering charges. Permanent ban from Kuwaiti banking system. |

| Company Directors/Executives | CRITICAL | Personal criminal liability, risk of arrest upon entry to GCC countries, extradition risks. |

🚨 Extradition and International Enforcement

Extradition Treaties: Kuwait has extradition agreements with the United Kingdom, India, Egypt, Turkey, and all GCC nations (Saudi Arabia, UAE, etc.). They are also members of Interpol.

Enforcement History: Kuwait actively polices “vice” crimes. While extradition for online gambling specifically is rare for Western directors, traveling to the GCC region poses a significant risk of arrest if an arrest warrant has been issued.

Travel Risk: EXTREME within the Middle East. Do not transit through Dubai, Doha, or Riyadh if you are operating illegally in Kuwait.

📋 Final Verdict

Kuwait receives an Operator Ease Score of 0.0/10 and a Player Access Score of 0.0/10, resulting in an overall market attractiveness rating of 0.0/10.

HONEST ASSESSMENT: Kuwait is a “No-Go” zone. The combination of strict Islamic law, active cyber-surveillance, and severe criminal penalties makes this market viable only for criminal syndicates, not legitimate businesses. There is no legal loophole, no grey area, and no tolerance. Operating here puts your freedom, assets, and other licenses at immediate risk.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NO ONE. There is no legal pathway for any operator.

❌ Definitely Avoid If You Are:

- EVERYONE. Specifically:

- Publicly Traded Companies: Operating here is a compliance violation that will tank your stock.

- Licensed Operators (MGA/UKGC): You risk losing your tier-1 licenses.

- Payment Providers: You risk money laundering charges.

- Affiliates: You cannot monetize traffic without risking fines or jail.

⚠️ BOTTOM LINE: Stay away. Kuwait is a strictly prohibited market with active enforcement and zero potential for legal revenue.