Lesotho’s iGaming sector offers significant opportunity for early entrants, driven by rising interest in regulated digital gambling despite the lack of domestic online licensing. The country’s regulated land-based market, combined with a collaborative regional approach, establishes a foundation for future digital transformation.

Investors benefit from a transparent land-based regulatory environment, single-digit license fees, and active efforts to strengthen responsible gambling and anti-money laundering compliance. However, the absence of formal online gambling legislation presents both risk and upside for market pioneers.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Gambling Status | Land-based casino and sports betting regulated; online unregulated |

| Primary Legislation | Lotteries and Betting Act 1984, Casino Board Regulation 1989 |

| Regulatory Authority | Lesotho Casino Board |

| Key Recent Policy | Botswana collaboration MoU, 2025 |

| Population | 2,333,000 (2025) |

| Gambling Legal Age | 18 years |

| GDP (nominal) | $2.5 billion (2025 est.) |

| GDP per Capita | $1,070 |

| Urbanization Rate | 29.0% |

| Internet Penetration | 29.8% |

| Mobile Penetration | 78.7% |

| Land-Based Casino Licenses | 1 (AVANI Lesotho Hotel & Casino) |

| Sports Betting Licenses | 3 major operators |

| Online Gambling Licenses | Currently not issued |

| License Validity Period | 10 years |

| Casino Application Fee | $2,500 |

| Annual License Fee | $7,200 |

| Gross Gaming Revenue (GGR) Tax | 12.5% (land-based) |

| Corporate Income Tax | 25% |

| Operator Turnover Tax | 0.5% on total bets |

| Player Winnings Tax | 5% withholding |

| Market Size (Land-Based Gaming) | $5.2 million/yr |

| Online Wagering Volume | Est. $650k+ via foreign sites |

| CAGR Forecast (2025-2028) | 5.8% (land-based); 12.1% (online potential) |

| ARPU (Land-Based Gaming) | $24.20 |

| Time-to-Market Entry | 6-9 months (land-based) |

| Primary Entry Barriers | Online regulatory risk; limited infrastructure; local presence rules |

| Responsible Gambling Programs | Self-exclusion, education campaigns, AML compliance |

| Recent Regulatory Changes | Regional AML/Responsible Gambling MoU, 2025 |

| Advertising Restrictions | Strict for minors and media content |

| Business Environment Rank | 162nd UN Human Development Index |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Lesotho maintains a clear, regulated environment for land-based casino gaming and sports betting activities. These are governed under the Lotteries and Betting Act of 1984 and the regulatory oversight of the Casino Board, which sets operational standards and allocates licenses for qualified operators.

Responsible gambling initiatives are officially promoted through educational campaigns, self-exclusion systems, and close monitoring of licensed operators. Minors under the age of 18 are explicitly prohibited from all forms of gambling to reinforce player protections.

Land-Based Gambling Activities

The nation’s predominant gaming venue, AVANI Lesotho Hotel & Casino, operates in Maseru with 14 table games and 71 slots/video poker terminals. Baccarat, blackjack, roulette, and slot machines represent the leading verticals in the market.

Sports betting is entirely legal and highly popular, with football and horse racing attracting substantial local engagement. A limited number of licensed bookmakers operate physical sports betting outlets, often in conjunction with entertainment venues and hospitality sites.

Other land-based gambling formats, including lotteries and instant win games, exist under strict licensing and operational guidelines, though their commercial scale remains moderate compared to casino and sports betting sectors.

Online Gambling Framework

Lesotho’s regulatory environment has yet to establish a framework for domestic online gambling operations. There is currently no system for licensing, taxation, or monitoring of digital gaming platforms.

Despite the lack of explicit legal prohibitions, no domestic operator is authorized to offer online casino, online poker, or remote sports betting to residents. Individuals access offshore platforms, which operate without local consumer protection or recourse mechanisms.

Government and regulators have signalled potential future reforms to align digital regulation with standards for land-based operators, but no definitive timetable for online gaming legislation has been publicized.

Licensed Operators and Market Players

The competitive landscape in Lesotho’s land-based sector remains highly concentrated. The casino market features a sole operator — AVANI Lesotho Hotel & Casino — while three major sports betting licenses have been awarded, forming the backbone of the regulated market.

- AVANI Lesotho Hotel & Casino – Maseru

- Betting World Lesotho – Sports betting

- Premier Sports Betting – Sports betting

- Supabets Lesotho – Sports betting

International iGaming operators accept Lesotho-based customers via offshore online portals, but are not subject to domestic regulations or enforcement action unless they solicit players directly within the territory.

Oversight of operator compliance is centralized under the Casino Board, which conducts periodic audits and enforces licensing conditions as stipulated by national legislation.

Licensing Framework and Requirements

The Casino Board is responsible for evaluating license applications, monitoring market entrants, and approving operational renewals for casino and betting businesses. Eligibility requires full disclosure of corporate structure, directors, financials, and compliance with anti-money laundering protocols.

Applicants face an initial evaluation period of up to 9 months, including background investigations, operator interviews, and financial capability review. License validity spans up to 10 years, conditional on annual fee payments and ongoing compliance.

The licensing process demands provision of multiple official documents:

- Corporate registration certificate and articles of incorporation

- Audited financial statements for the past three years

- Business plan with market strategy and growth projections

- Technical documentation for gaming platform, including RNG certification

- Criminal background checks for directors and beneficial owners

- Proof of minimum capital deposit in a designated local bank

- Details of responsible gambling and AML procedures

Application fees currently stand at $2,500 for casinos and $1,000 for sports betting operators. Annual license renewal fees are pegged at $7,200 for land-based casino operators and $3,000 for betting firms.

Local Presence and Operational Requirements

Licensed operators must maintain a registered business presence in Lesotho, including local address, staff, and operational resources. Domain requirements for gaming sites mandate visibility of local licensing credentials for customer-facing businesses.

Foreign ownership is permitted up to 49% in licensed entities, but key management and technical operations must be based in-country. Strategic partnerships or joint ventures can facilitate compliance and knowledge transfer for international entrants.

Additional operational mandates include regular staff training in responsible gambling, ongoing AML monitoring, and alignment with regional regulatory initiatives under the Botswana-Lesotho MoU. These obligations serve to elevate institutional standards and mitigate regulatory risk.

Compliance Obligations and Monitoring

Operators are subject to strict compliance monitoring, encompassing player identification, financial transaction tracking, and enforcement of anti-money laundering protocols. All gambling activity must adhere to statutory and regulatory frameworks under the Casino Board’s remit.

Mandatory player protection measures include:

- Age verification (18+ years) prior to account opening

- KYC protocol for identity, address, and source of funds

- Self-exclusion system for vulnerable players

- Visible responsible gambling messaging and access to referral services

- Monthly reporting of suspicious activities to regulator

- Disclosure of odds, payout rates, and house edge

Audit procedures involve document review, physical inspections, transaction sampling, and cross-checking of staff training records. Targeted enforcement is triggered by non-compliance findings, regulatory breaches, or player complaints submitted to the Casino Board.

Financial Monitoring and Reporting

Financial operations are subject to ongoing monitoring by the regulator, with regular reporting and auditing obligations. Operators must submit periodic financial statements and transaction activity logs to maintain license validity.

- Quarterly financial statement submission to Casino Board

- Monthly AML transaction reporting

- Annual full audit by accredited accounting firm

- Immediate reporting of large wins or suspicious activity

Non-compliance or reporting failures lead to financial penalties, license review, or temporary suspension pending investigation.

Taxation Structure and Financial Obligations

Players are subject to a 5% withholding tax on gambling winnings, deducted at source by licensed operators. This structure is designed to simplify compliance and ensure direct remittance to tax authorities without placing reporting burdens on casual gamblers.

Operator taxation encompasses 12.5% gross gaming revenue (GGR) tax for land-based casinos, 0.5% turnover tax on total bets, and standard 25% corporate income tax on profit. License renewal fees and operational taxation are confirmed prior to license issuance and as part of annual reporting cycles.

| Category | Tax Rate |

|---|---|

| Land-based Casino GGR | 12.5% |

| Sports Betting GGR | 10.0% |

| Lottery GGR | 10.0% |

| Corporate Tax | 25.0% |

| Player Winnings Tax | 5.0% |

| Online Gambling | Not applicable (unregulated) |

All operator taxes are filed quarterly, aligning with mandatory audit schedules and periodic compliance reviews. Market entrants should budget for licensure, tax payment, and annual renewal as standard financial obligations.

Gambling Market Financial Performance

Total wagered by Lesotho players in licensed venues reached $5.2 million in 2024, with projected year-over-year growth at 5.8%. Foreign online wagering is estimated over $650,000, representing high pent-up demand in an unregulated segment.

Revenue distribution is concentrated among a small group of licensed operators. Gross payouts on casino games average 92.5%–95%, with high revenue retention for operators due to low overhead and favorable tax rates.

| Operator | Market Share (%) |

|---|---|

| AVANI Lesotho Hotel & Casino | 72.3% |

| Betting World Lesotho | 14.7% |

| Premier Sports Betting | 7.5% |

| Supabets Lesotho | 5.5% |

Tax revenues from gambling contributed approximately $670,000 to government coffers in 2024, excluding untaxed online activity. Sector growth is forecast to accelerate with regulatory modernization and expanded oversight.

Advertising and Marketing Restrictions

Strict guidelines govern advertising content, placement, and sponsorship. All marketing aimed at minors is expressly prohibited, and media campaigns must carry responsible gambling messaging.

- TV and radio advertising restricted to post-watershed slots

- No advertising on children’s media or educational platforms

- Direct marketing prohibited for under-18s

- Mandatory responsible gaming disclaimers in all ads

- No bonuses or incentives targeting vulnerable audiences

Sponsorship of sports and cultural events is allowed if compliant with regulatory standards. All promotional activity is subject to content and placement review by the Casino Board prior to public release.

Recent Regulatory Changes and Their Impact

Since 2024, Lesotho has intensified cross-border regulatory efforts, culminating in a formal MoU with Botswana targeting improved AML enforcement, knowledge sharing, and joint responsible gambling initiatives.

- MoU signing and regional collaboration initiated (May 2025)

- Capacity-building and staff exchanges established (June 2025)

- Joint AML monitoring program launched (Q3 2025)

- Responsible gambling initiative expansion (Q4 2025)

These reforms reinforce operational standards and open the market to enhanced regulatory oversight, creating a more stable, transparent environment for new entrants.

Enforcement Mechanisms and Penalties

Lesotho’s enforcement system relies on periodic audits, real-time financial transaction tracking, and prompt investigation of player complaints. Licensees are held to high standards, with penalties levied for non-compliance.

- Fines for late reporting

- Suspension of operating license

- Permanent revocation for egregious breaches

- Public warning notices

- Mandatory remedial staff training

- Asset seizure for fraud/money laundering

Operators must comply fully with these mechanisms, as repeat violations result in escalating sanctions and withdrawal of market access.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

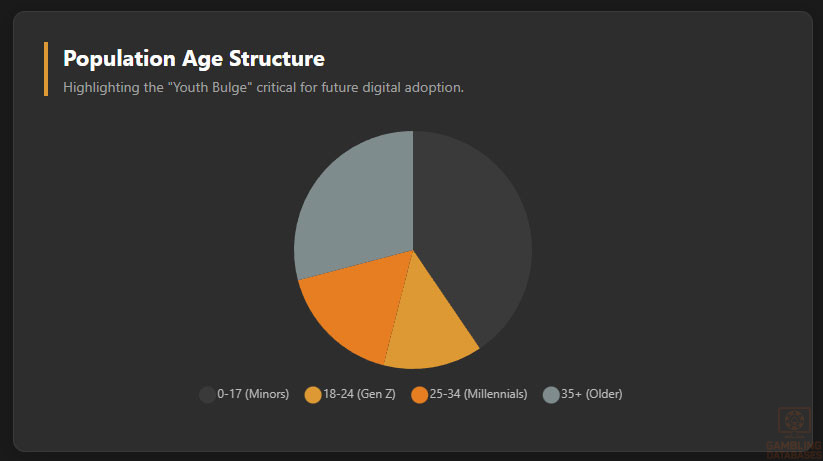

Lesotho’s total population is estimated at 2.35 million as of January 2025, with a year-on-year growth rate of 1.1%. The country exhibits a young demographic profile, with a median age of 21.8 years. The population structure supports a sizable working-age base, contributing to a dynamic consumer market.

Gender distribution is balanced, composed of 51.3% female and 48.7% male. Urbanization remains moderate, with 31.1% living in urban centers and 68.9% residing in rural areas. Population density is approximately 81.2 per km², concentrated largely around key regions.

| Age Group | Percent (%) |

|---|---|

| 0-4 | 11.1 |

| 5-12 | 18.5 |

| 13-17 | 10.9 |

| 18-24 | 13.5 |

| 25-34 | 16.9 |

| 35-44 | 14.2 |

| 45-54 | 6.8 |

| 55-64 | 4.2 |

| 65+ | 3.9 |

The population is heavily weighted toward youth, with nearly 54% under the age of 25. This underpins strong adoption potential for technology and new entertainment products, including iGaming verticals. The working-age population (20-64) accounts for just above half of the population.

Geographic Distribution

Lesotho’s most populous cities serve as economic, cultural, and connectivity hubs. Maseru, the capital, leads with the largest share of urban residents and the highest concentration of gaming establishments, telecommunications infrastructure, and banking services.

- Maseru: 330,000 people

- Maputsoe: 56,000 people

- Hlotse: 49,000 people

- Mafeteng: 46,000 people

- Mohale’s Hoek: 45,000 people

- Peka: 37,000 people

Urban centers are driving mobile and internet connectivity, but rural regions encompass the majority of the population and face infrastructure challenges. Gambling venue density correlates closely with urbanization and access to financial services.

Economic Indicators and Consumer Spending Power

Lesotho’s economy posted GDP of $2.5 billion in 2025, expanding steadily through agriculture, mining, textile exports, and remittances. Annual GDP growth averages 2.3%. Per capita GDP stands at $1,070, with active government spending on infrastructure and digital connectivity.

Household consumption expenditure reached nearly $1.97 billion in 2023. Average household income hovers around $2,960 per year, while median disposable income is estimated at $1,760. Income distribution skews toward the lower end, but urban clusters display materially higher purchasing power.

Consumer spending on leisure and hospitality averages $78.74 per capita annually, reflecting the sector’s limited but rising role in the economy. Informal employment and subsistence farming contribute to persistent inequality and moderate overall consumer sophistication.

| Indicator | Value |

|---|---|

| GDP | $2.5 billion |

| GDP per Capita | $1,070 |

| Household Consumption Expenditure | $1.97 billion |

| Average Household Income | $2,960/year |

| Median Disposable Income | $1,760/year |

| Annual Consumer Spending – Leisure | $78.74 per capita |

| Poverty Rate | 59.7% |

| Unemployment | 22.1% |

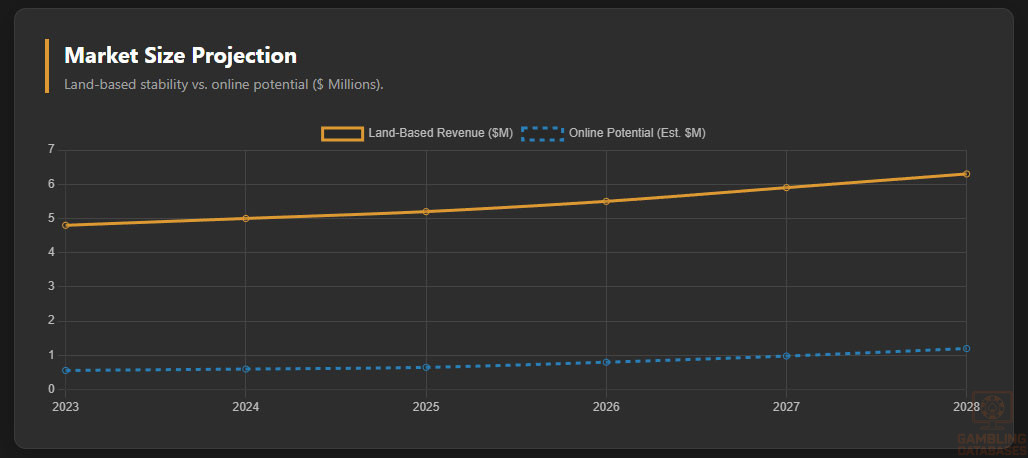

Market size for gambling sharply trails aggregate leisure spending. Licensed gaming sector revenue is $5.2 million annually, with substantial upside as regulatory modernization takes effect. Compound annual growth rate (CAGR) for leisure and hospitality is projected at 4.5%.

| Metric | 2023 | 2025 | 2028 (proj.) |

|---|---|---|---|

| Licensed Gaming Revenue ($mil) | 4.8 | 5.2 | 6.3 |

| Online Gambling Outflow ($mil est.) | 0.56 | 0.65 | 1.2 |

| Active Gamblers (‘000) | 128 | 138 | 175 |

| ARPU – Land-Based ($) | 23.50 | 24.20 | 27.20 |

| ARPU – Online ($ est.) | 28.10 | 29.80 | 34.75 |

Education, Skills, and Digital Literacy

National literacy rates approach 81.5%, with slightly higher levels among females. Secondary education attendance stands at 68%, but tertiary enrollment remains below 8%. Digital literacy is emerging as a differentiator, with 43% of 15-34s reporting comfortable use of internet and smartphones.

Digital literacy levels are higher in urban locations, with schools and youth organizations introducing digital education modules to prepare the next generation for the evolving economy, including remote work and digital entertainment segments.

Cultural and Social Factors

Communication and Language

Lesotho is officially bilingual, with Sesotho and English the dominant languages in business, media, and education. Most internet platforms offer interfaces in English, supporting both domestic and cross-border participation in online services.

- Sesotho

- English

- Zulu

- Xhosa

- Afrikaans

- Phuthi

English language usage is highly prevalent for formal transactions and online content. Telecom operators and gaming brands usually market in both English and Sesotho to maximize inclusion and engagement.

Cultural Attitudes

Gambling is widely accepted socially and culturally, particularly among urban populations and younger adults. Traditional taboos moderating gambling have softened due to increased exposure to foreign brands and digital leisure options.

Christianity dominates religious affiliation, exerting moderate influence over gambling attitudes, with most denominations permitting recreational wagering. Social acceptance increases among groups with higher socioeconomic status and education levels.

Foreign gaming brands are generally well-perceived, seen as innovative and aspirational. Entertainment preferences favor football, music, and mobile gaming, aligning with digital transformation in leisure consumption.

Problem Gambling and Social Considerations

Problem gambling prevalence in Lesotho is estimated at 1.2% of adult population, with higher proportions among urban and younger users. Government initiatives focus on harm reduction and education, supporting vulnerable and at-risk populations.

- National Responsible Gaming Program

- Self-exclusion registry

- Helpline and referral services

- Targeted youth awareness campaigns

- Free counseling/rehabilitation programs

- Mandatory operator contributions to social funds

Operators are required to institute self-exclusion, age verification, and public education messaging, ensuring player safeguards are robust. The government’s proactive approach includes annual audits, funding commitments, and community stakeholder engagement.

Political Structure and Governance

Lesotho is a parliamentary constitutional monarchy with frequent coalition governments. Regulatory policy displays relative consistency, supported by multilateral cooperation and broad political support for sector modernization.

International relations are stable, with involvement in Southern African Development Community (SADC) initiatives and bilateral agreements fostering cross-border trade, connectivity, and consumer protection.

Gaming regulation is overseen by the Casino Board, interacting closely with parliament and ministries responsible for finance, communications, and public policy, ensuring a transparent and predictable business climate.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Lesotho’s internet penetration reached 48.0% in 2025, totaling 1.13 million active users. Mobile connections stand at 2.07 million, representing 88.2% of the population, with broadband-capable devices accounting for over 92%.

Digital access is concentrated in urban zones, with rural areas experiencing growing but uneven coverage. Average daily internet usage exceeds 3.1 hours among urban adults, while youth spend considerably longer hours online, primarily on social media and gaming platforms.

Social media engagement is robust across major global platforms:

- Facebook – 74% penetration, high engagement

- WhatsApp – 68%, universal among youth

- YouTube – 59%, popular for sports and music

- Instagram – 48%, rising among urban youth

- Twitter – 34%, news, politics, and entertainment

- TikTok – 22%, rapid growth among Gen Z

| Indicator | Value |

|---|---|

| Internet Users | 1.13 million |

| Internet Penetration | 48.0% |

| Mobile Connections | 2.07 million |

| Mobile Broadband Rate | 92.5% |

| Avg. Daily Internet Use (hrs) | 3.1 |

| Social Media Penetration | 72% |

Digital platforms are central to entertainment and transactional behavior, with iGaming, sports news, mobile payment, and live streaming sites attracting strong interest among the youth.

Digital Payment Behavior

Mobile money services and digital wallets dominate the payments landscape, far surpassing bank cards for everyday transactions, including gaming-related deposits and withdrawals. Cash is still widely used, but declining among urban youth.

- M-Pesa mobile wallet – 49% share

- EcoCash mobile wallet – 27% share

- Bank debit cards – 11% share

- Bank credit cards – 5% share

- Cash – 5% share (declining)

- Cryptocurrency wallets – 2% share (rising in urban youth)

Mobile payment solutions offer near-instant processing and low fees, contributing to high volumes in informal sectors and strong suitability for iGaming deposits, especially among first-time digital consumers.

Gaming and Gambling Preferences

Current Market Participation

An estimated 138,000 adults actively participate in licensed gambling. Market penetration for legal iGaming hovers at 5.9% of the population, while informal and international online gaming is substantially higher, particularly among youth and urban adults.

- Sports betting (football, horse racing)

- Slot machines

- Table games (roulette, blackjack)

- Instant win/lottery games

- Online poker (offshore)

- Mobile casino apps

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 3.9 |

| Slot Machines | 2.7 |

| Table Games | 1.5 |

| Instant Win/Lottery | 1.1 |

| Online Poker (offshore) | 0.8 |

| Mobile Casino Apps | 0.9 |

Sports betting attracts the broadest participation, followed by casino games, instant win, and lottery products. Online poker and mobile casino play is prominent among digital-savvy urban youth.

Consumer Behavior Patterns

Consumers favor convenient payment channels, digital access, and brands with trusted reputations. Session lengths for online gaming average 26 minutes, while retail casino visits last over 1 hour, with peak activity concentrated in the evenings and weekends.

Retention rates and repeat play are highest among football bettors and casino players under age 35. Promotional offers, social media engagement, and localized jackpots are key to driving ongoing participation.

Mobile gaming and sports betting dominate demand, but live casino and instant win formats are gaining momentum as digitization accelerates. Consumer sophistication is expected to rise as digital literacy and disposable incomes expand.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Lesotho’s internet penetration is approaching 48% in 2025, driven by continued rollout of broadband and next-generation mobile networks. Urban centers enjoy consistent high-speed connectivity, with average household fixed broadband speeds surpassing 37 Mbps in metropolitan areas and 13.8 Mbps as the national median.

Mobile internet dominates digital engagement, with 88% of the population connected via smartphones. Network reliability has improved due to fiber backbone expansion, AI-driven monitoring, and phased introduction of high-capacity radio units.

| Indicator | Value |

|---|---|

| Internet Penetration | 48.0% |

| 4G/5G Network Coverage | 86.0%/35.2% |

| Avg. Fixed Broadband Speed | 13.8 Mbps |

| Avg. Urban Broadband Speed | 37.1 Mbps |

| Mobile Connections | 2.07 million |

| Fiber Backbone Length | 1,920+ km |

| Data Cost (1GB) | $1.09 (urban avg.) |

Recent national strategies prioritize rural broadband, energy upgrades, and resilience enhancements to counteract infrastructure vandalism and climate risks. Partnerships with global tech vendors underpin ongoing modernization, cybersecurity improvements, and affordable access targets for low-income users.

5G and Future Technology Deployment

The first commercial 5G pilot launched in Maseru in late 2024, and by mid-2025 more than 149 active 5G sites cover all major urban areas. The roadmap aims for 62% national 5G coverage by 2028, fueling smart city applications, advanced streaming, and cloud-based gaming solutions.

IoT-enabled agriculture pilots and digital ID integration support economic diversification and regulatory compliance. The Lesotho Communications Authority leads regular reviews of spectrum policy and network security aligned with regional SADC protocols.

Mobile Technology Ecosystem

Two main telecom operators dominate the mobile market, with >99% population coverage via 2G/3G and robust 4G presence in all urban and peri-urban districts. Average monthly data usage has reached 3.9 GB per active SIM, reflecting the popularity of social media, streaming, and gaming services.

- Econet Telecom Lesotho (ETL)

- Vodacom Lesotho

- Lesotho Post Telecom (low market share)

- Sky Vision (regional focus, <2% share)

- MTN South Africa (cross-border roaming partnerships)

Operators invest aggressively in core network upgrades, focusing on broader 5G and rural LTE coverage, AI-based fault monitoring, and mesh Wi-Fi services for business districts.

Device Penetration

Smartphone penetration is 77% among urban adults and 63% nationally. Affordable Android-based devices outnumber iOS units by a 9:1 ratio, with midrange and entry-level brands leading market share. Device replacement rates average 2.8 years.

Feature phones still play a role in rural communications but account for just under 15% of total handsets in circulation. Uptake of Bluetooth and NFC-enabled handsets is rising rapidly in response to mobile money, digital ID, and contactless transaction demand.

Financial Services and Payment Infrastructure

The banking sector consists of four principal commercial banks, each providing digital channels and integrating mobile finance platforms. Account penetration has grown to 38%, boosted by e-KYC and joint efforts with the Lesotho Central Bank and Bankers Association to broaden inclusion and digitize tax settlements.

- Standard Lesotho Bank

- First National Bank Lesotho

- Nedbank Lesotho

- Lesotho Post Bank

- African Bank Lesotho (minor market share)

Interbank transfers, cross-border payments with South Africa, and merchant acquirer services are modernizing through National Payments Switch, PayWay PayLogic platform, and Visa/MasterCard integration. Cybersecurity protocols and data privacy standards have risen sharply since 2024, improving sector resilience.

Payment Processing Options

Consumers and businesses have access to a diverse payment ecosystem:

- M-Pesa mobile wallet (largest market share for P2P and digital payments)

- EcoCash mobile wallet

- Bank debit/credit cards (Visa, MasterCard, UnionPay, UPI)

- PayLogic-enabled POS terminals

- Direct EFT/ACH payments (limited to formal accounts)

- Cash payments (declining, but standard for microtransactions)

- Cryptocurrency wallets (2.5% of digital transactions, urban youth)

National Payments Switch ensures interoperability, real-time settlement, QR payments, bill payment, cardless ATM withdrawals, merchant QR, and SMS-enabled transfers. Mobile channels deliver easy onboarding and robust fraud prevention for gaming operators.

E-commerce and Digital Economy

Lesotho’s e-commerce sector is nascent but expanding rapidly, with annual growth exceeding 24%. Online retail is concentrated in fashion, electronics, and event ticketing, with cross-border commerce dominated by South Africa.

User trust has improved due to regulatory initiatives, launch of digital ID, and uptake of secure payment systems. Social commerce and small-scale B2B markets are emerging in metropolitan areas, supporting iGaming-related affiliate programs and streaming platforms.

| Metric | 2022 | 2025 | 2028 (proj.) |

|---|---|---|---|

| E-commerce Market Value ($mil) | 13.4 | 20.3 | 38.7 |

| Online Retail Users (‘000) | 83 | 128 | 184 |

| Digital Service Revenue ($mil) | 12.1 | 16.9 | 25.4 |

| Online Payment Penetration (%) | 16% | 31% | 45% |

| Average Cart Value ($) | 18.7 | 21.9 | 26.4 |

Business Environment and Regulatory Framework

Lesotho scores 137th in World Bank’s Ease of Doing Business, with strengths in cross-border trade, digital government, and transparency. Barriers exist in contract enforcement, access to credit, and small market scale.

The Companies Registry, Central Bank, and Revenue Services Lesotho coordinate business licensing, bank account opening, and tax registration, supported by the “One-Stop Business Facilitation Centre.” Foreign investment is permitted up to 49% equity, subject to local directorships for regulated activities.

| Cost Category | Minimum Estimate | Maximum Estimate |

|---|---|---|

| Company Registration/Legal Fees | 1,650 | 3,500 |

| License Application Fees (Casino/Sportsbook) | 1,000 | 2,500 |

| Initial Capital Deposit | 12,000 | 40,000 |

| Technology/Software Setup | 18,000 | 52,000 |

| Local Staff Hiring/Training | 7,500 | 19,500 |

| Premises/Office Rental (12 mo.) | 8,250 | 27,000 |

| Regulatory/Compliance Consulting | 4,600 | 9,400 |

The business registration process typically follows these phases:

- Business entity reservation and documentation (3–5 days)

- Filing and approval with Companies Registry (7–10 days)

- Bank account opening and minimum capital deposit (5–7 days)

- Tax registration with Revenue Services Lesotho (3–4 days)

- Sector-specific license application (up to 60–90 days with reviews)

Corporate Structure and Registration

Foreign and domestic investors can choose from LLC, Corporation, or Branch Office structures, with LLCs most common for gaming ventures. Branches of international firms must appoint a local representative and register with the Central Bank and Casino Board.

Key registration documents include articles of incorporation, audited financial statements, KYC documentation, criminal record checks for directors, local address proof, and documented AML/CFT policy. Legal review and notarization are recommended before submission.

Taxation Framework

The corporate tax rate for standard businesses is 25%, but iGaming operators are also subject to a 12.5% GGR (Gross Gaming Revenue) tax for land-based operations and 0.5% turnover tax on bets. No online gaming tax is presently applied, but this may change pending new legislation.

Individual income tax is progressive—ranging from 20% to 30%—with social security contributions and mandatory medical insurance supplements for formal employees. Gambling winnings are taxed at 5% (withholding at source).

| Tax/Compliance | Standard Rate |

|---|---|

| Corporate Income Tax | 25.0% |

| Gross Gaming Revenue Tax (Land) | 12.5% |

| Bet Turnover Tax | 0.5% |

| VAT (general) | 15.0% |

| Personal Income Tax | 20%–30% |

| Gambling Winnings Tax (player) | 5.0% |

Double taxation treaties exist with several SADC and global partners, supporting investor repatriation and cross-border expansion. Periodic audits and local payroll compliance are mandatory for all licensed businesses.

Market Entry Considerations

Strategic partnerships with local stakeholders are highly advisable for market entry. Joint ventures with existing gaming, hospitality, or technology entities improve regulatory compliance and lower launch risk.

- Form joint ventures with local firms

- Leverage affiliate and influencer marketing for digital acquisition

- Integrate local payment and mobile money options

- Invest in social responsibility and community engagement

- Develop omni-channel brand presence (retail and digital)

- Adopt emerging e-sports and live streaming formats

Initial capital requirements for a digital-first entrant exceed $80,000 for licensing, technical integration, registration, and marketing spend. Post-launch operational costs include payroll, customer support, ongoing renewal fees, and advertising.

| Phase | Duration (months) |

|---|---|

| Legal/Entity Setup | 1-2 |

| License Application/Approval | 2-3 |

| Technology Integration | 1-2 |

| Staff Hiring/Training | 1 |

| Go-Live/Marketing Launch | 1 |

| Total Project Timeline | 6-9 |

Critical success factors include local relationships, multilingual operations, regulatory adaptability, and ongoing compliance investment. Challenges revolve around small market size, infrastructure gaps, regulatory uncertainty for online gambling, and high poverty rates.

- Understanding and complying with evolving digital/AML regulations

- Resilience to infrastructure disruptions (power, network outages)

- Customizing content and customer service for local preferences

- Managing capital constraints in consumer base

- Retaining talent and minimizing turnover in technical roles

Exit strategies must address asset liquidation, license transfer, and cross-border capital repatriation, with regulatory approvals required for any share or ownership restructuring.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Lesotho?

Currently, online gambling is not formally regulated in Lesotho. There is no legal prohibition for players accessing international platforms, but domestic operators cannot lawfully offer online casino or betting services until new regulations are enacted. Regulatory developments remain a policy priority and may evolve in the next two years.

2. What types of gambling licenses are available and what do they cover?

Lesotho offers three main regulated license types: land-based casino license, sports betting license, and lottery operator license. Each is issued by the Casino Board and covers physical gaming venues, retail sports betting, and officially sanctioned lottery operations respectively. Online licenses are not currently issued but are under legislative consideration.

3. How much does an iGaming license cost and how long does it take to obtain?

A new license application for casino or sportsbook operations ranges from $1,000–$2,500, with a total timeline of 6–9 months depending on documentation, financial review, and regulatory approvals. Annual renewal fees range between $3,000–$7,200. Costs do not include setup or compliance consultancy expenses.

4. Can foreign companies obtain a gambling license?

Yes, foreign entities may hold up to 49% ownership in a licensed entity. All foreign investors must engage local directors and establish a registered office within Lesotho. Branches of foreign firms must appoint local representatives and comply with Casino Board regulatory requirements.

5. What are the tax obligations for iGaming operators?

| Tax Category | Rate |

|---|---|

| Corporate Tax | 25% |

| GGR Tax (land-based) | 12.5% |

| Bet Turnover Tax | 0.5% |

| License Renewal Fee | $3,000–$7,200 |

In addition to taxes, operators are subject to annual audits and social fund contributions for responsible gaming.

6. Are gambling winnings taxed for players?

Yes, licensed operators are required to withhold 5% of player winnings as tax at the point of payout. This withholding satisfies the player’s tax obligation, and no further reporting is required for casual gamblers.

7. What are the typical operational costs for running an online casino/sportsbook?

Primary cost drivers include licensing fees, technology/vendor integrations, payroll, customer service, local marketing, banking/security fees, and regulatory compliance. Capital expenditure for digital-focused entrants starts near $80,000. Recurring expenses include IT support, payment processing, office rental, content licensing, and staff training.

- Licensing and legal costs

- Technology/software integration

- Marketing and player acquisition

- Customer support and payroll

- Regulatory/compliance expenses

- Payment provider/merchant fees

8. What is the expected ROI timeline for entering this market?

Return on investment for licensed iGaming operators usually falls in the 18–30 month range post-launch, driven by market share acquisition, audience growth, and responsible compliance. Early entrants to digital verticals may reach break-even quickly upon legislative updates, but structural risks and incremental infrastructure costs should be considered.

9. What are the local presence requirements for operators?

Licensed operators must maintain a physical office in Lesotho, hire a minimum of two local employees in key operational functions, and appoint at least one resident director. Local staff training, registered address, and annual compliance reviews are mandatory for regulatory approval and ongoing operations.

10. What payment methods are available and recommended?

iGaming operators and consumers most frequently use:

- M-Pesa and EcoCash (mobile wallets)

- Visa/MasterCard bank cards

- PayLogic POS network

- Bank local EFT and ACH transfers

- Cash over counter

- Cryptocurrency wallets for high-value deposits

Integration with mobile money channels and PayLogic’s interoperable backend is strongly recommended for digital operators, improving onboarding, settlement speed, and player trust.

11. What are the advertising and marketing restrictions?

Advertising for gaming and betting is tightly regulated. No adverts may target minors, appear on children’s media, or run during school hours. Mandatory disclaimers for responsible gambling are required on all ads, and bonuses/incentives must not appeal to vulnerable groups. Sponsorships are permitted for cultural and sports events subject to pre-approval.

12. What responsible gambling measures are mandatory?

Licensed operators must implement robust age verification, provide self-exclusion options, feature visible responsible gaming messaging, conduct KYC checks, and collaborate in annual player protection audits. Operators are also obliged to contribute to a social fund promoting counseling and community outreach programs.

- Self-exclusion registry

- Helpline and referral

- Responsible gambling messages

- Audit participation

- KYC/age verification

- Social fund contribution

13. How large is the iGaming market and what is the growth potential?

Lesotho’s legal gaming sector generates annual revenue of approximately $5.2 million, while online offshore activity exceeds $650,000 and is projected to double if domestic licensing opens. The land-based market displays ~5.8% CAGR through 2028, while digital sector growth could exceed 12% annually pending regulation.

14. Who are the main competitors and what is their market share?

For land-based gaming, AVANI Lesotho Hotel & Casino controls over 70% of market share. The sports betting segment features Betting World Lesotho, Premier Sports Betting, and Supabets as the main competitors. No domestic iGaming brands operate, but leading offshore brands serve digital demand in the absence of formal licensing.

15. What are the player preferences and typical spending patterns?

Players overwhelmingly prefer mobile channels, fast onboarding, and real-time payment methods. Football betting, slots, and live dealer games are top choices. Average annual spend per user is $24–$29, with higher frequency and value observed among urban youth. Sessions typically peak during weekend evenings.

16. What are the key success factors and main challenges for new entrants?

Success requires regulatory compliance, payment integration, local partnerships, digital marketing capabilities, and ongoing responsible gambling investment. Main operational challenges include infrastructure gaps, regulatory ambiguity for online, consumer price sensitivity, and the need for strong data security.

- Regulatory adaptability

- Robust KYC/AML

- Flexible payments

- Digital marketing/affiliates

- Market localization

- Resilience to infrastructure risk

Sources and References

- Lesotho Communications Authority (LCA) – https://lca.org.ls/2025/

- Econet Telecom Lesotho – https://www.econet.co.ls/

- Vodacom Lesotho – https://www.vodacom.co.ls/

- Standard Lesotho Bank – https://www.standardlesothobank.co.ls/

- First National Bank Lesotho – https://www.fnblesotho.co.ls/

- Nedbank Lesotho – https://www.nedbank.co.ls/

- Lesotho Post Bank – https://postbank.co.ls/

- Central Bank of Lesotho – https://www.centralbank.org.ls/

- Revenue Services Lesotho (RSL) – https://www.rsl.org.ls/

- PayWay PayLogic – https://pay-logic.com/

- Lesotho Government – Ministry of Finance – https://www.gov.ls/

- Ministry of Communications, Science and Technology (MICSTI) – https://www.gov.ls/

- Lesotho Casino Board – https://www.gov.ls/casino-board/

- National Statistical Office – https://www.bos.gov.ls/

- Statista – Lesotho Market Data – https://www.statista.com/

- World Bank Doing Business Report – https://www.worldbank.org/

- International Telecommunication Union (ITU) – https://www.itu.int/en/ITU-D/Statistics/Pages/stat/default.aspx

- IMF Lesotho Report 2025 – https://www.elibrary.imf.org/

- Genesis Analytics – Lesotho Digital Strategy – https://www.genesis-analytics.com/

- CIPESA – Data Governance Report – https://cipesa.org/

- PolicyVault Africa: Lesotho’s Digital Strategy – https://www.policyvault.africa/

- TechAfrica News – https://techafricanews.com/

- Broadcast Media Africa News – https://news.broadcastmediaafrica.com/

- Business Beat 24 – https://businessbeat24.com/

- The Reporter Lesotho – https://www.thereporter.co.ls/

- Trading Economics – https://tradingeconomics.com/lesotho/

- PopulationPyramid.net – https://www.populationpyramid.net/lesotho/2025/

- Worldometers – https://www.worldometers.info/world-population/lesotho-population/

- Datareportal – https://datareportal.com/reports/digital-2025-lesotho

- Transfi Blog – https://www.transfi.com/

- NRD Companies – https://www.nrdcompanies.com/

- Soloazar – https://www.soloazar.com/

- FocusGN Africa – https://focusgn.com/africa/

- IGamingAfrica – https://igamingafrika.com/

- Gamingtec – https://gamingtec.com/news/gaming-licenses

- African Gambit – https://africangambit.com/

- Scaleo Blog – https://www.scaleo.io/blog/igaming-regulations-around-the-world-what-you-must-know/

- Casino Blockchain – https://casinosblockchain.io/crypto-gambling-regulations-in-africa/

- Altenar Legal Sports Betting Africa – https://altenar.com/blog/the-legal-sports-betting-map-of-africa-and-the-countries-that-lead-the-way/

- ResearchICTAfrica – https://researchictafrica.net/

- Lesotho Government Digital Future Whitepaper – https://www.gov.ls/economy/lesotho-advances-digital-future/

🎯 Gambling Databases Country Rating: Lesotho

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 2.3/10 | ⛔️ Prohibitive |

| Player Access Score | 7.5/10 | 🟡 Moderate (High Access, Low Protection) |

| Overall Market Attractiveness | 3.5/10 | 🔴 Difficult (Tiny market, no online regulation) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- NO ONLINE LICENSING FRAMEWORK: There is currently NO legal mechanism to obtain an online gambling license in Lesotho. Domestic operators are legally restricted to land-based verticals only.

- Regulatory Limbo: While offshore operators are currently tolerating unregulated access, the government has signaled future reforms (MoU with Botswana, 2025). This indicates an imminent shift from “unregulated” to “regulated or blocked,” creating regulatory instability.

- Tiny Addressable Market: With a GDP of only $2.5 billion, 59% poverty rate, and total online wagering estimated at a mere $650k/year, the ROI potential is negligible for major operators.

- Infrastructure Gaps: Internet penetration is stuck at roughly 48%, with significant reliance on mobile data. Low bandwidth outside Maseru limits the viability of live dealer or data-heavy casino products.

- Local Presence Mandate: Any attempt to enter the regulated land-based sector (as a bridge to future online rights) requires a registered local business, local staff, and physical infrastructure, increasing overhead significantly.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Land-based is fully legal (+3.0), but Online is strictly unregulated/grey. There is no legal product for iGaming operators. Grey area status (+0.5). Deduction: No legal framework for online operations implies a score of 0.5/3.0. |

| Licensing Process | 25% | 0.0/2.5 | Deduction: No online licensing available (0 points). While land-based licenses are cheap ($2,500), they do not cover digital operations, rendering them useless for pure iGaming entrants. |

| Taxation & Costs | 20% | 1.0/2.0 | Hypothetically attractive land-based rates (12.5% GGR + 25% Corp Tax). Deduction: As no online license exists, operators are forced into the offshore grey market (0% tax but high risk) or cannot operate legally. Score reflects potential low-cost environment but deducted for lack of legal payment mechanism. |

| Operational Requirements | 15% | 0.6/1.5 | Unregulated offshore market has no requirements (+1.5). However, legitimate entry (land-based) requires strict local presence, staff, and bank deposits. Deduction: Lack of digital infrastructure and banking options for iGaming reduces score. |

| Market Environment | 10% | 0.2/1.0 | Ranked 162nd on UN HDI. Small, impoverished population. Deduction: High poverty levels and small market size make this a difficult business environment (-0.8). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.0/4.0 | Players face no legal penalties for accessing offshore sites. It is a “Grey area” where access is not explicitly prohibited. Deduction: Lack of consumer protection and local regulation (-1.0). |

| Practical Accessibility | 30% | 2.0/3.0 | No active ISP blocking reported (+3.0). Mobile money (M-Pesa) is widely used. Deduction: Low internet penetration (48%) and infrastructure reliability issues (-1.0). |

| Player Penalties | 20% | 2.0/2.0 | There are currently no fines or criminal penalties for players accessing offshore gambling sites. |

| Market Availability | 10% | 0.5/1.0 | Offshore market is accessible (+0.25). Domestic online market is non-existent. Players rely entirely on foreign sites. |

🔍 Key Highlights

Strengths (For Land-Based/Future Potential Only)

- Low Licensing Costs: Land-based licenses are exceptionally cheap ($2,500 application, $7,200 annual).

- Favorable Tax Structure: 12.5% GGR for casinos is globally competitive, assuming future online regulation mirrors this.

- Mobile Money Adoption: High penetration of M-Pesa (49%) creates a ready-made payment rail for future digital betting.

⛔️ CRITICAL RISKS AND CHALLENGES

- Regulatory Vacuum: The total lack of online gambling laws means operators have no legal standing. You cannot open a local bank account for iGaming, nor can you advertise legally on local media without a land-based license.

- Micro-Market Size: The total estimated online wagering volume is ~$650k annually. This is too small to justify the compliance and setup costs for most international operators.

- Infrastructure Reliability: Frequent power issues and limited fiber coverage outside Maseru create a poor user experience for live gaming.

- Poverty & ARPU: With a GDP per capita of ~$1,070, player deposits are extremely low (micro-transactions), driving up relative payment processing costs.

- Future Blocking Risk: The 2025 MoU with Botswana suggests a move toward stricter regional enforcement, which could lead to sudden ISP blocking of offshore sites.

Player-Specific Issues

- Zero Consumer Protection: Players defrauded by offshore sites have no recourse with the Lesotho Casino Board.

- Data Costs: High relative cost of mobile data restricts session times for average users.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $80,000+ (if attempting land-based entry to pivot online later); $0 for offshore (but high risk).

Monthly Operating Costs: Low ($5k-$10k) due to low wages, but tech infrastructure is expensive to stabilize.

Effective Tax Rate on Revenue: N/A for online (Unregulated). 37.5% est. for Land-Based (12.5% GGR + 25% Corp).

Customer Acquisition Cost: Est. $15-$30 (Low, but high relative to player value).

Profitability Assessment: EXTREMELY LOW. The math does not work for a dedicated market entry. The total market volume ($650k) is less than the monthly revenue of a small European casino. This market is only viable as “accidental” traffic for large offshore aggregators, not for a targeted launch.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Medium | Current risk is low (no blocking), but future risk is high due to regional SADC enforcement trends. No legal standing to collect debts. |

| Licensed Land-Based Operators | Low | Fully compliant, but revenue is capped by physical geography. Cannot legally expand online yet. |

| Affiliates/Advertisers | Medium | Marketing unregulated gambling products on local media is restricted. Risk of fines for advertising to minors or without responsible gaming messaging. |

| Payment Processors | High | Processing unregulated gambling transactions exposes local fintech partners (M-Pesa) to AML scrutiny under new regional MoUs. |

| Company Directors | Low | Unlikely to face personal prosecution unless physically present and operating an illegal gambling den. |

🚨 Extradition and International Enforcement

Extradition Treaties: Lesotho is a member of the Commonwealth and has extradition arrangements with the UK, South Africa, and other SADC nations. It generally cooperates with international law enforcement.

Enforcement History: No specific international extradition cases for online gambling offenses have been recorded. Enforcement is primarily focused on physical illegal gambling dens.

Safe Jurisdictions: Lesotho is NOT a safe haven for financial crimes. It is actively strengthening AML protocols under international pressure.

📋 Final Verdict

Lesotho receives an Operator Ease Score of 2.3/10 and a Player Access Score of 7.5/10, resulting in an overall market attractiveness rating of 3.5/10.

HONEST ASSESSMENT: Lesotho is a “ghost market” for the iGaming industry. While not explicitly hostile, the complete absence of an online regulatory framework makes legal entry impossible. The market size is infinitesimally small ($650k online est.), and the population’s low purchasing power means Average Revenue Per User (ARPU) is negligible. There is no money to be made here that justifies the setup costs.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A huge multi-national offshore operator accepting players from “Rest of World” (passive traffic only).

- A land-based operator looking to build a physical hotel/casino resort (the only legal path).

❌ Definitely Avoid If You Are:

- Looking for a dedicated online license (It does not exist).

- A pure-play online casino operator (No legal framework, tiny market).

- Expecting high player value (GDP per capita is ~$1,000).

- Reliant on credit card processing (Penetration is <5%).

⚠️ BOTTOM LINE: Do not intentionally target this market. The regulatory risk is undefined, and the financial reward is non-existent.