Latvia presents a regulated iGaming environment with defined licensing processes, competitive market conditions, and strong digital infrastructure. A growing demand for online gambling, clear tax obligations, and an established regulatory authority position Latvia as a compelling market for international operators seeking stable entry into the Baltic region.

This analysis delivers a deep dive into Latvia’s legislative framework, licensing requirements, compliance standards, financial metrics, and barriers for new market entrants.

| Metric | Value |

|---|---|

| Gambling Legal Status | Fully regulated (land-based & online) |

| Regulatory Authority | Lotteries and Gambling Supervision Inspectorate (IAUI) |

| Primary Governing Legislation | Law on Gambling and Lotteries (last major update: 2023) |

| Market Size (Total GGR 2024) | EUR 352 million |

| Year-on-Year GGR Growth | +14.8% (2024 over 2023) |

| Forecast CAGR (2025-2028) | 7.6% |

| Market Penetration Rate | 34% of adult population |

| Population (2024 est.) | 1.85 million |

| Internet Penetration | 94% |

| Mobile Penetration | 121 subscriptions per 100 inhabitants |

| Average Household Disposable Income | EUR 19,650 |

| Unemployment Rate (2024) | 6.1% |

| Median Age | 43.5 years |

| Adult Population (18+) | 1.56 million |

| Total Licensed Online Operators | 13 (as of October 2025) |

| Minimum Statutory Capital | EUR 1,400,000 (online), EUR 1,070,000 (land-based) |

| Online License Fee (Initial) | EUR 427,000 |

| Annual Online License Renewal Fee | EUR 400,000 |

| GGR Tax Rate (Online Casino) | 10% |

| GGR Tax Rate (Sportsbook) | 5% |

| Corporate Income Tax | 20% (on distributed profits) |

| Application Review Timeline | 60-75 days |

| Foreign Ownership Limits | No explicit limits, but strong local presence required |

| Required Local Presence | Latvian-registered company, local director, local bank account |

| Domain Requirements | .lv domain mandatory for licensed operators |

| AML/KYC Stringency | High (full EU compliance + national rules) |

| Responsible Gambling Measures | Mandatory (exclusion register, RG tools, time & deposit limits) |

| Prohibited Games/Activities | Unlicensed B2C, peer-to-peer poker(except platforms licensed as such), illegal lotteries |

| Advertising Restrictions | Comprehensive: time-of-day bans, content controls, channel limitations |

| iGaming ARPU (2024) | EUR 208 (estimated) |

| Barriers to Entry | High fiscal/technical requirements, rigorous AML/KYC, strict enforcement |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling in Latvia is regulated under the Law on Gambling and Lotteries, which was overhauled in 2023 to provide modern standards for both land-based and online gaming. The market operates under a single-licensing regime, supervised by the state Inspectorate for Lotteries and Gambling (IAUI). All commercial gaming, including casinos, slot halls, betting, online gambling, and lotteries, is legal with proper authorization.

Unlicensed gambling services, whether digital or physical, are strictly prohibited and subject to active blacklisting, ISP blocking, and criminal penalties. The regulator has broad powers to supervise, audit, and sanction operators, ensuring high compliance standards across the sector.

Land-Based Gambling Activities

Latvia permits a range of land-based gambling activities, which are predominantly offered through urban casinos, slot machine halls, and dedicated betting venues. Casino licensing is capped through a combination of local municipality quotas and minimum capital requirements. The regulatory environment ensures casinos are clustered in major urban centers such as Riga, with rural expansion tightly controlled.

Operational requirements are strict: each casino or hall must meet security, surveillance, and responsible gambling standards, including an exclusion register linked to the national self-exclusion database. Slot machines, live table games, and sports betting terminals are all individually certified by the IAUI before being placed into operation.

| Venue Type | Number of Venues | Key Regulatory Features |

|---|---|---|

| Urban Casinos | 8 | Minimum capital, 24/7 surveillance, RG policies |

| Slot Machine Halls | 220 | Entry controls, exclusion list, staff training |

| Sports Betting Venues | 41 | Certified betting terminals, AML compliance |

| Bingo Halls | 11 | Onsite monitoring, prize limit controls |

Online Gambling Framework

The online casino and betting sector is fully legalized, restricted to operators holding an IAUI-issued license. Comprehensive regulation covers RNG testing, player identification, technical security, and reporting obligations.

The legislation prohibits cross-border B2C activity, and any unlicensed site is subject to rapid blocking and penalty enforcement. Online poker is restricted to platforms individually authorized to offer peer-to-peer play, with the majority of current licensees focused on slots, live casino, and sportsbook products.

Technology providers and affiliates must also adhere to registration and conduct rules, ensuring all parts of the value chain are supervised. Operators are mandated to implement strong responsible gaming tools and contribute to state RG funding. Centralized self-exclusion and real-time monitoring tools are national requirements.

Licensed Operators and Market Players

The competitive landscape in Latvia is defined by a limited pool of licensed online and land-based operators, dominated by both international and local brands.

The top five online license holders account for nearly 70% of digital GGR, with the remainder divided among smaller entrants and recently launched challenger brands. Market access is tightly protected by technical standards and ongoing financial threshold requirements.

- Optibet (Enlabs/OEG)

- 11.lv (William Hill Group)

- Feniksscasino (Novomatic)

- Betsafe (Betsson Group)

- La Fiesta Casino

- OlyBet

- Klondaika

- Synottip

- LVBet

- TonyBet

- MrGreen

- NinjaCasino

- VulkanVegas

Each operator must undergo periodic re-licensing and is subject to comprehensive audits. While new foreign entrants face intensive pre-screening, established local groups continue to benefit from brand recognition and established market share, presenting both high entry barriers and potential acquisition targets for newcomers.

| Operator | Estimated Market Share (%) |

|---|---|

| Optibet | 24 |

| 11.lv | 13 |

| Feniksscasino | 11 |

| Betsafe | 9 |

| Other Licensed Operators | 43 |

Licensing Framework and Requirements

Application Process and Eligibility

The application process for an iGaming license is administered by the IAUI, requiring demonstration of robust financial resources, technical preparation, and comprehensive AML controls.

Submissions also require documentation on corporate structure, beneficial ownership, platform certification, data security protocols, and independent RNG verification. Regular audit trails and penetration tests are built into compliance requirements, with financial health checked annually. The review period typically ranges from 60 to 75 days but can be extended if deficiencies or clarifications are needed.

- Latvian corporate registration with attached founding documents

- Bank statements proving minimum capital requirements

- Comprehensive business plan and operational model

- Platform security certification and RNG audit reports

- AML/KYC policies mapped to both EU and national standards

- Criminal record checks for all directors and UBOs

Operators are expected to maintain a secure local hosting environment or use a certified EU-based cloud provider. Recent reforms have intensified scrutiny over software supply chains and ongoing technical vulnerability assessments.

Local Presence and Operational Requirements

A mandatory local presence is required for all licensed iGaming firms. Operators must register as a Latvian legal entity, designate at least one Latvian-based director, and operate a local client support desk.

A statutory local bank account is compulsory to facilitate regulatory payments, winnings disbursement, and AML monitoring. Domains must be locally registered under .lv with clear display of IAUI licensing information.

- Physical office location in Latvia

- Local data protection officer

- Latvian language customer support

- .lv website domain with SSL certification

- Centralized player complaint/mediation facility

- Onsite technical audit access for IAUI

While there are no explicit caps on foreign ownership, practical barriers such as personal due diligence, UBO disclosure, and onshore management obligations significantly raise the complexity for international groups without local partners or advisors.

| Requirement | Online Casino | Land-Based Casino |

|---|---|---|

| Minimum Paid-up Capital | EUR 1,400,000 | EUR 1,070,000 |

| Initial License Application Fee | EUR 427,000 | EUR 410,000 |

| Annual Renewal Fee | EUR 400,000 | EUR 360,000 |

| Application Timeline (Avg.) | 60-75 days | 65-90 days |

Compliance Obligations and Monitoring

Player Protection and Identification

Latvia enforces rigorous player protection through mandatory age verification, advanced KYC processes, and robust AML controls. Online operators must integrate their platforms with the national exclusion register and deploy real-time risk scoring tools. Documentation for KYC is cross-validated with state registries to minimize fraud and underage gambling.

- Automated age verification upon registration

- Real-time AML transaction monitoring

- 24/7 exclusion self-service and helpline

- Mandatory deposit and betting limits

- Pop-up tools for voluntary session reminders

- Quarterly RG training for frontline staff

Self-exclusion requests are instantly relayed across all licensed operators, and breaches result in regulatory sanctions, including license suspension or revocation.

Financial Monitoring and Reporting

Operators must report financial and transactional data to the IAUI via secure digital channels. Comprehensive monthly reporting includes dropped bets, gross revenue, processed withdrawals, and bonus outflows, reviewed against matched player records and transaction logs. Compliance failures are subject to escalating enforcement, from administrative fines to license revocation.

- Monthly submission of transactional and GGR data

- Quarterly certified financial statements

- Real-time AML event notifications

- Annual cybersecurity audit reports

All suspicious activity is escalated directly to Latvia’s FIU, with annual risk assessment reviews forming part of the operator’s monitoring obligations.

Taxation Structure and Financial Obligations

Player Taxation

Winning payouts for players are generally not subject to direct withholding unless in excess of EUR 3,000 per bet/event, in which case regulated entities deduct a fixed 23% personal income tax at source. Smaller winnings are exempt, aligning Latvia with broader EU tax norms on gaming prizes.

Operator Taxation

The primary operator tax is the gross gaming revenue (GGR) levy, which stands at 10% of GGR for online casinos and 5% for licensed sportsbook activity. In addition, a 20% corporate tax is applied only to distributed profits, following Estonia’s “franked dividend” model. Specific game-type fixed taxes also apply to land-based slots and table games.

| Game Type | Tax Basis | Rate or Fixed Amount |

|---|---|---|

| Online Casino (Slots, Live Dealer) | GGR | 10% |

| Online Sports Betting | GGR | 5% |

| Land-Based Table Game (per table) | Annual fixed tax | EUR 23,000 |

| Land-Based Slot Machine (per machine) | Annual fixed tax | EUR 5,172 |

License renewal fees are due in full at the beginning of each annual license period. There is no turnover or gaming duty apart from GGR and fixed asset levies.

Gambling Market Financial Performance

Total player wagers in 2024 reached EUR 5.4 billion, with a payout ratio of 93% across regulated online products and an overall tax yield exceeding EUR 41 million for the state. Digital GGR continues to outpace land-based revenue as consumer migration accelerates, supported by robust payment infrastructure and consumer trust in licensed brands.

| Year | Total Bets (EUR bn) | Gross Gaming Revenue (EUR m) | State Gambling Tax Revenue (EUR m) |

|---|---|---|---|

| 2024 | 5.4 | 352 | 41 |

| 2025 (proj.) | 5.8 | 378 | 45 |

The digital market’s ARPU is among the highest in the CEE region, and continuing reforms are expected to sustain double-digit GGR growth through 2028.

Advertising and Marketing Restrictions

Advertising of gambling services is controlled by strict time-of-day bans, which prohibit broadcast and digital marketing between 6:00–22:00 except for notifications on responsible gambling. Promotional bonuses are capped by regulation, and in-content gambling advertisements are limited to factual disclosure of license status and odds display.

Sponsorship of national and youth sports organizations is restricted, with gambling branding strictly prohibited at all under-21 events.

- Broadcast TV and radio bans (6:00–22:00)

- Prohibition on targeting minors or vulnerable groups

- Ban on celebrity endorsements for gambling products

- Cap on sign-up and retention bonuses

- Mandatory responsible gambling messaging in all ads

- Restricted use of digital influencers/streamers

Marketing materials are subject to pre-approval by the IAUI, and breach of advertising law results in monetary penalties and repeat-offender blacklisting.

Recent Regulatory Changes and Their Impact

The 2023–2025 period saw a rapid tightening of KYC/AML obligations, expansion of exclusion tools, and new digital monitoring standards. Notably, cross-border enforcement powers and site blocking mechanisms were expanded in alignment with European Commission recommendations.

Operators faced raised capital thresholds, a restructured application process, and the implementation of a centralized RG funding mechanism. Overall, these changes have increased operating costs, extended entry timelines, and forced market consolidation, benefiting larger and compliant entities.

Enforcement Mechanisms and Penalties

The IAUI deploys a mix of administrative, financial, and criminal penalties for non-compliance, with active cross-agency enforcement involving the Financial Intelligence Unit and Consumer Rights Protection Centre. Civil fines attract no cap for authorized breaches, while repeated or willful non-compliance can result in full suspension or revocation of operator licenses.

Blacklists of non-compliant sites are published monthly, with coordinated ISP and payment blocking as standard remediation steps. Criminal sanctions, including directors’ liability, apply to severe breaches such as money laundering or facilitating illegal play. Regulatory policy prioritizes visible, escalating responses to preserve public trust and market integrity.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Latvia’s total population in 2024 is estimated at 1.85 million, with a median age of 43.5 years. The age structure reflects a European norm, with an aging population and a diminishing youth segment. Gender ratios are balanced at 53% female to 47% male, and adult population (18+) stands at 1.56 million, accounting for 84% of the total populace.

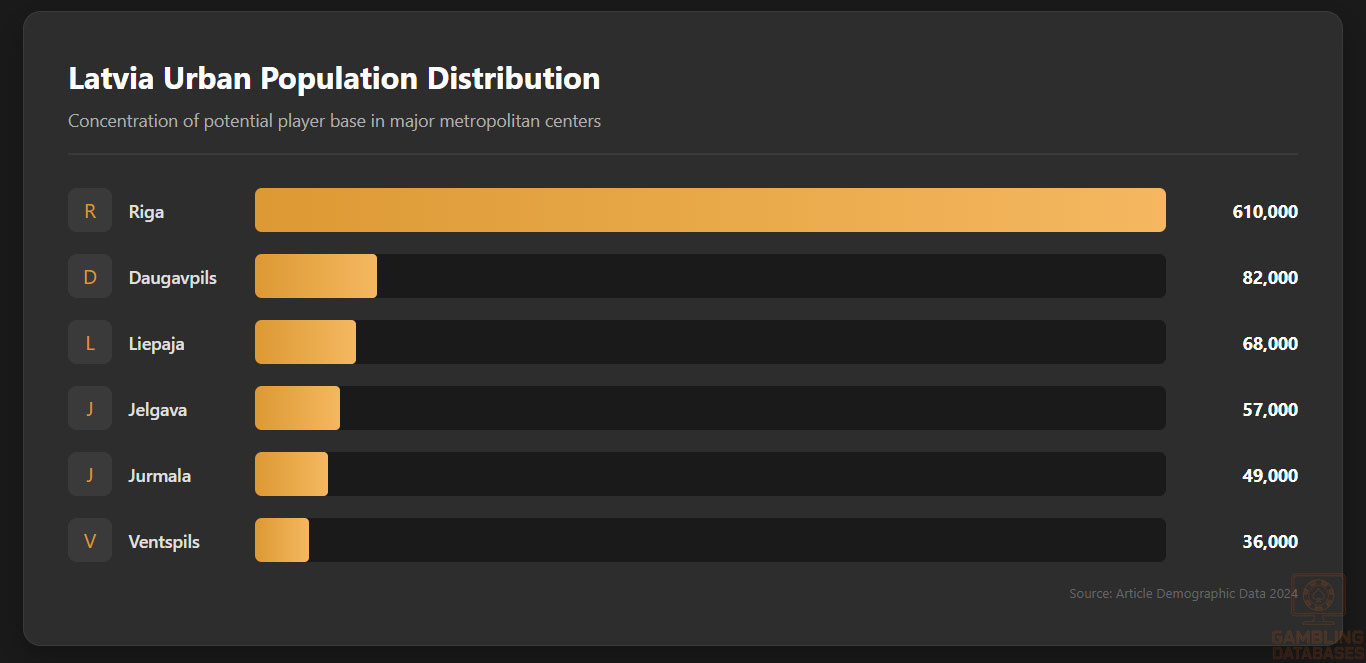

Nearly 68% of Latvians reside in urban environments concentrated around key metropolitan centers. Rural populations have declined over the last decade, driven by urban migration and lower birth rates. The capital city Riga markedly influences demographic trends and consumer behavior, hosting about 33% of the country’s residents.

| Age Group | Population | Percentage |

|---|---|---|

| 0–17 years | 295,000 | 16% |

| 18–34 years | 382,000 | 21% |

| 35–54 years | 476,000 | 26% |

| 55–74 years | 537,000 | 29% |

| 75+ years | 160,000 | 8% |

Geographic Distribution

Latvia’s regional distribution favors the central region and major coastal cities, with most economic output originating from metropolitan zones. Significant population clusters exist in eastern Latgale and western Kurzeme, though urban migration continues to reshape these patterns.

Gambling venue concentration aligns closely with urban population centers, providing greater access and selection for urban consumers than rural populations.

- Riga – 610,000 (capital, major economic driver)

- Daugavpils – 82,000 (industrial hub, border proximity)

- Liepaja – 68,000 (coastal, logistics and entertainment)

- Jelgava – 57,000 (education center)

- Jurmala – 49,000 (tourism and leisure focus)

- Ventspils – 36,000 (port and industrial activities)

Internet access follows a similar pattern, with near-universal connectivity in urban centers and lower but rising penetration in rural districts, now exceeding 87% outside major cities.

Economic Indicators and Consumer Spending Power

Latvia’s GDP reached EUR 37.5 billion in 2024, growing at 3.2% with service industries contributing 65% and manufacturing 24%. Construction, logistics, and IT sectors form secondary pillars of economic output, supported by robust foreign investment and EU funding. Economic reforms over the last five years have improved consumer confidence, which is reflected in household spending growth.

Disposable household income averages EUR 19,650 per year, with median income at EUR 15,800 and Gini coefficient at 32.9 reflecting moderate income inequality. Spending patterns favor essential goods, housing, and healthcare, but entertainment and online services are capturing a rising share, especially among younger and middle-aged consumers.

Strong consumer capacity underpins a healthy iGaming sector, as digital wagers and entertainment spending increased 14% from the previous year. Economic stability and policy consistency have fostered favorable conditions for mobile payments and online market expansion.

| Indicator | Value |

|---|---|

| GDP (EUR billion) | 37.5 |

| GDP Growth Rate | 3.2% |

| Service Sector Share | 65% |

| Manufacturing Share | 24% |

| Disposable Income (EUR) | 19,650 |

| Median Income (EUR) | 15,800 |

| Consumer Entertainment Spend % | 7.5% |

| Employment Rate | 93.9% |

Market Size and Growth Projections

Latvia’s regulated iGaming market generated a Total GGR of EUR 352 million in 2024, with CAGR projected at 7.6% through 2028. User base expansion and technology adoption are driving revenue increases, supported by elevated ARPU of EUR 208. Market forecasts estimate total GGR will reach EUR 459 million by 2028 with over 600,000 registered adult users by that time.

Historical growth patterns reflect a shift from land-based to online activities, with 68% of wagers now placed via internet channels. Revenue distribution remains weighted toward casino and slot products, while sports betting and live dealer offerings exhibit year-over-year double-digit growth.

| Year | GGR (EUR m) | Registered Users (‘000) | ARPU (EUR) |

|---|---|---|---|

| 2024 | 352 | 512 | 208 |

| 2025 | 378 | 543 | 214 |

| 2026 | 401 | 574 | 220 |

| 2027 | 430 | 594 | 226 |

| 2028 | 459 | 610 | 230 |

Education, Skills, and Digital Literacy

Latvia maintains a national literacy rate of 99.6%, supported by strong compulsory education and a skilled younger workforce. Tertiary education attainment approaches 39% of the adult population, with concentrations in IT, finance, and engineering. Digital literacy remains high among urban youth, and digital competency programs expand skill sets in coding, data security, and online safety.

Workforce adaptability enables rapid technology adoption, and digital familiarity translates into confident use of mobile devices, e-wallets, and online platforms. Older generations show lower uptake but increasingly engage with e-government, health, and financial services online.

Cultural and Social Factors

Communication and Language

Latvian is the official language, spoken by 85% of the population, while Russian is used by about 36% of residents, primarily in Riga and southeastern regions. English proficiency exceeds 71% among younger adults and professionals, supporting international business and online engagement.

Consumer internet use favors Latvian and English content, and multilingual product offerings outperform single-language competitors.

- Latvian

- Russian

- English

- Polish

- Lithuanian

- Ukrainian

Language preferences align with media consumption, creating opportunities for tailored marketing and user experience design.

Cultural Attitudes

Gambling is generally accepted in Latvia within regulated environments, though strong responsible gambling messaging tempers promotion. Religious influence is moderate, with most Latvians identifying as Lutheran or Catholic but rarely restricting entertainment preferences. Foreign brands receive favorable reception when paired with local partnerships, while cultural affinity for community initiatives improves brand trust.

Entertainment choices favor digital streaming, eSports, and online gaming, complementing high smartphone penetration. Lifestyle trends show steady migration toward cashless transactions and mobile betting.

Problem Gambling and Social Considerations

Latvia records an estimated problem gambling prevalence of 3.5% among active gamblers, with 1.7% classified as high-risk. Vulnerable groups include unemployed adults, youth, and urban males aged 18–34. The national exclusion register operates in real time and is complemented by government and NGO support for affected individuals.

- National self-exclusion register

- Helpline for gambling addiction and counseling

- Mandatory operator funding for RG programs

- Quarterly government reporting and review

- Partnerships with community organizations

- Online education modules on responsible gambling

All regulated operators must disclose RG tools and contribute to mandatory prevention campaigns. Social responsibility remains an explicit licensing condition, with annual audits and enforcement of responsible gambling messaging.

Political Structure and Governance

Latvia is a parliamentary republic characterized by high regulatory consistency and stable governance. EU membership ensures robust international cooperation and policy alignment, supporting investor confidence and market predictability. Political risk is low; regulatory amendments are infrequent and subject to broad consultation, creating a favorable climate for long-term business planning.

Legal protections for consumer rights and business continuity measures underpin market resilience. Cross-border partnerships, data protection, and AML compliance benefit from mature regulatory infrastructure and strong judicial independence.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at 94%, with average daily use exceeding 3.1 hours for adults and peaking at 4.7 hours for users aged 16–34. Mobile device adoption is universal, averaging 1.21 devices per inhabitant. Urban consumers leverage high-speed fiber and 5G, while rural districts experience expanding connectivity through state initiatives.

Social media engagement underpins digital communication, with high penetration and daily activity across platforms. Online communities drive entertainment and consumer marketing trends, and influencer partnerships are increasingly employed in gaming and betting campaigns.

- Facebook – 78% penetration, 2.3 hours/day

- YouTube – 89% penetration, 45 minutes/day

- Instagram – 64% penetration among 18–34s

- TikTok – 52% among under-25s

- Twitter – 31% penetration, news-focused

- WhatsApp – 46% penetration, messaging

Streaming and video content dominate youth entertainment, while older users prefer news and government service access. Mobile payment, banking, and food delivery apps feature in everyday use.

| Metric | Value |

|---|---|

| Internet Penetration | 94% |

| Mobile Device Penetration | 121 per 100 inhabitants |

| Daily Internet Usage (hrs) | 3.1 (total adult) |

| Online Transaction Users | 87% |

| Social Media Penetration | 84% |

Digital Payment Behavior

Digital payment usage is widespread, with the majority of transactions conducted via bank cards and online banking. E-wallet adoption is growing rapidly among users under 40, complemented by modest but rising cryptocurrency acceptance. Security, speed, and brand reliability remain determinative for consumer adoption.

- Bank cards – 59% market share (debit/credit)

- Online bank transfer – 28% share

- PayPal – 11% share

- Apple Pay/Google Pay – 8% share among under-35s

- Paysera – 6% share

- Cryptocurrency – 3% share, led by Bitcoin and Ethereum

Low transaction fees and instant processing are prioritized by digital consumers. High-value iGaming deposits frequently use bank-based transfers due to compliance and verification requirements. AML measures restrict anonymous transactions and establish protected digital flows.

Gaming and Gambling Preferences

Current Market Participation

iGaming participation rates mirror broader EU trends, with 34% of adults having engaged in legal online gambling at least once in the past year. The most popular activity categories span casino, slots, sportsbook, live dealer, lottery, and poker, with slots and sports betting consistently leading digital volume.

- Online Slots – 57% participation

- Sports Betting – 43% participation

- Lottery – 39% participation

- Live Dealer Casino – 26% participation

- Poker – 22% participation

- Instant Win/Scratch – 15% participation

| Activity | Participation Rate (%) |

|---|---|

| Online Slots | 57 |

| Sports Betting | 43 |

| Lottery | 39 |

| Live Dealer Casino | 26 |

| Poker | 22 |

| Scratch Cards | 15 |

Consumer Behavior Patterns

Average digital session durations are 47 minutes for slots and 34 minutes for sportsbook, with peak traffic recorded on weekends and during major sporting events. Mobile platforms command 63% of active sessions, reflecting user preference for convenience and rapid access. Retention rates stabilize at around 68% for casino brands able to deliver consistent bonuses and fast withdrawals.

Engagement rises with multi-channel marketing and influencer campaigns, and personalized offers outperform generic promotions. Customer loyalty is strong among regulated operators, aided by seamless payment methods and transparent game mechanics, while non-payment or delayed withdrawal complaints contribute to churn. Seasonality influences activity around holidays, sport finals, and payday cycles.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Latvia boasts one of the most advanced digital infrastructures in the Baltic region, with internet penetration exceeding 94% across the population. Fixed broadband and mobile internet are both widely accessible, with fiber optic networks covering over 78% of households and businesses in urban areas.

Average fixed broadband speeds average over 150 Mbps, while mobile broadband typically offers 60–90 Mbps depending on region, reflecting continual upgrades from network providers.

Network reliability is high due to substantial investments in redundant routing and data centers, combined with robust government initiatives prioritizing digital inclusivity and cybersecurity. Infrastructure advancements are enabled by strong EU funding, fostering a competitive telecom landscape and creating favorable conditions for bandwidth-intensive services such as streaming and online gaming.

5G and Future Technology Deployment

5G technology rollout in Latvia is actively progressing with commercial coverage currently at 55% nationwide and reaching over 80% in Riga and other metropolitan centers. Major carriers continue to expand 5G networks despite challenges of rural deployment. Planned nationwide full 5G coverage is expected by 2027, accompanied by investments to upgrade data centers and edge computing capabilities to reduce latency.

Mobile Technology Ecosystem

Latvia’s mobile network ecosystem is competitive and mature, consisting of five licensed mobile network operators offering broad national coverage and diverse service tiers.

Market shares are led by the incumbent operator with 34%, followed by several mid-sized providers specialized in prepaid and data-centric plans. Data costs remain competitive, with average prices per gigabyte among the lowest in the EU, facilitating widespread mobile internet usage.

- Latvijas Mobilais Telefons (LMT) – 34% market share

- Tele2 Latvia – 26%

- Bite Latvia – 21%

- Telekom Latvija

- Third-party MVNOs targeting niche segments

Smartphone penetration has reached 87% of the population, with device preferences dominated by premium Android devices and an increasing share of iOS smartphones among urban youth. Mobile device usage drives over 63% of internet access and 70% of online gambling sessions, confirming the mobile channel as central to consumer interaction and operator digital strategy.

Financial Services and Payment Infrastructure

The Latvian financial sector is characterized by strong digital penetration, with over 92% of adults holding bank accounts linked to multiple channels of online and mobile banking. The banking landscape consists of both international and domestic banks, supported by progressive regulatory frameworks encouraging fintech innovation and seamless payment solutions.

- Swedbank Latvia – largest retail banking share

- SEB Banka – strong corporate and retail focus

- Citadele Banka – expanding fintech partnerships

- Rietumu Banka – specialized corporate services

- BlueOrange Bank – growing retail client base

Payment processing options in the iGaming sector are extensive and technologically advanced, encompassing credit/debit cards, bank transfers via SEPA, certified e-wallets, mobile payment gateways, and emerging cryptocurrency payment methods. Interoperability and compliance with EU payment directives ensure fast settlement times and high transaction security.

- Visa and Mastercard credit/debit cards

- SEPA bank transfers

- Paysera e-wallet and payment gateway

- Apple Pay and Google Pay mobile wallets

- Revolut and N26 digital banking payments

- Cryptocurrency wallets (Bitcoin, Ethereum supported)

E-commerce and Digital Economy

Latvia’s e-commerce market is expanding rapidly, with a growth rate around 18% annually and expected value surpassing EUR 2 billion by 2026. The digital economy is supported by widespread consumer trust in online transactions, advanced logistics infrastructure, and cross-border trade integration. Online gaming and betting form an integral sector within the digital services ecosystem, benefiting from sophisticated consumer targeting and secure payment environments.

Digital service adoption is pervasive, especially among urban residents aged 18-44, who drive demand for mobile applications, streaming entertainment, and personalized content. Consumer behavior trends increasingly favor subscription models and integrated loyalty programs, encouraging operators to innovate beyond traditional transactional models into engagement-driven revenue streams.

Business Environment and Regulatory Framework

Latvia ranks favorably in the World Bank’s Ease of Doing Business report, noted for efficient business registration processes, transparent legal systems, and investor-friendly policies. The business environment is characterized by low corruption, stable macroeconomics, and open foreign direct investment regulations fostering competitive market entry for iGaming operators.

Business incorporation typically requires several straightforward steps, supported by online government portals facilitating company registration and tax filings. Costs and procedural timelines have been optimized to attract technology-driven enterprises, with specialized economic zones offering tax incentives and administrative simplification.

- Prepare and notarize required incorporation documents

- Register company with the Latvian Register of Enterprises (processing 5-7 days)

- Obtain tax identification number and VAT registration (3-5 days)

- Open corporate bank account and deposit minimum capital (1-2 weeks)

- Complete mandatory reporting and compliance registrations

Corporate Structure and Registration

The most common corporate forms used for iGaming operations are limited liability companies (SIA), branches of foreign companies, and, less frequently, joint-stock companies.

The SIA format is preferred due to its flexibility, investor protection, and relatively low capital requirements. Branch offices provide a streamlined route for international operators maintaining parent company control without establishing a fully independent entity.

Registration costs are moderate, typically under EUR 1,000 including government fees and legal services. Foreign ownership is permitted without caps, but full disclosure of beneficial owners and local director appointment is mandatory. Compliance with anti-money laundering and data protection regulations is strictly enforced from the point of incorporation.

- Notarized Articles of Association

- Proof of registered office address in Latvia

- Identification documents for directors and shareholders

- Bank reference or capital deposit certificate

- Tax and social security authority registrations

- Verification of beneficial owners

Taxation Framework

Corporate income tax is charged at a flat rate of 20% on distributed profits, following the Latvian corporate tax model which defers taxation on reinvested earnings. Special economic zones offer tax holidays and reduced rates incentivizing investments in designated areas. Latvia maintains extensive double taxation treaties covering over 60 countries to facilitate international business.

- Estonia

- Finland

- Germany

- Russia

- United Kingdom

- Sweden

- Norway

- Poland

- Netherlands

- France

Personal income tax operates on a progressive scale with a standard rate of 23%, supplemented by mandatory social security contributions. Withholding taxes apply to certain dividends and interest payments, under the oversight of the State Revenue Service.

Market Entry Considerations

For iGaming operators, recommended entry strategies emphasize local partnerships, compliance consulting, and robust technology deployment. Leveraging partnerships with established marketing firms and payment processors facilitates faster market penetration and regulatory navigation. Platform choices focus on scalability, multilingual support, and secure AML/KYC integration.

- Form joint ventures with Latvian market incumbents

- Engage local legal and compliance advisors from inception

- Invest in multilingual and mobile-optimized platforms

- Develop omni-channel marketing leveraging social media influencers

- Ensure rigorous data protection and cybersecurity framework integration

Typical initial investment requirements exceed EUR 1.5 million, covering licensing fees, capital deposits, technology infrastructure, and operational setup. Market entry timelines from application to launch span 4 to 6 months, impacted by regulatory review and technical audits.

- Licensing and corporate registration: 2-3 months

- Platform and payment integration: 1-2 months

- Marketing and testing phase: 1 month

- Full launch and compliance audits: ongoing

Success factors include strong regulatory adherence, local cultural understanding, and innovative customer acquisition strategies. Key operational challenges relate to high capital requirements, complex AML compliance, and competitive market saturation. Exit planning must consider limited license transferability and valuation dependent on stable revenue performance.

- Robust local regulatory compliance

- Effective multilingual customer support

- Strong anti-fraud and AML systems

- Strategic marketing focused on mobile users

- Ongoing technology and UX innovation

FAQ: Frequently Asked Questions

1. Is online gambling legal in Latvia?

Yes, online gambling is fully legal and regulated in Latvia under the Law on Gambling and Lotteries. Only operators licensed by the IAUI are authorized to offer services. Illegal or unlicensed gambling platforms face blacklisting and ISP blocking. The legal framework ensures consumer protection, responsible gambling, and compliance with EU directives.

2. What types of gambling licenses are available and what do they cover?

The IAUI issues several license types including online casino, sportsbook, lotteries, land-based casino, and betting terminal licenses. Each license type targets distinct operational categories with specific technical and compliance requirements. Online licenses cover RNG certification, KYC, AML, and responsible gambling obligations.

3. How much does an iGaming license cost and how long does it take to obtain?

License fees depend on business type; online licenses include an initial fee of around EUR 427,000 and an annual renewal of EUR 400,000. The licensing process typically takes between 60 and 75 days, subject to documentation completeness and technical audits. Operators should budget additional months for platform integration and compliance setup.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible but must establish a Latvian-registered entity with a local director and operational presence. Full disclosure of beneficial ownership is mandatory. No explicit foreign ownership caps exist; however, compliance with strict AML/KYC and local regulatory requirements is compulsory.

5. What are the tax obligations for iGaming operators?

Operators are liable for a 10% GGR tax on online casino revenues and 5% on sportsbook revenues. Corporate income tax at 20% applies to distributed profits only. Fixed taxes apply to certain land-based gaming assets. License renewal fees and compliance costs represent ongoing financial obligations.

| Tax Type | Rate/Amount |

|---|---|

| Online Casino GGR Tax | 10% |

| Sportsbook GGR Tax | 5% |

| Corporate Income Tax (distributed profits) | 20% |

| License Renewal Fee (annual) | EUR 400,000 |

| Fixed Slot Machine Tax (per machine) | EUR 5,172 |

6. Are gambling winnings taxed for players?

Small winnings under EUR 3,000 are exempt from taxation for players. Winnings above this threshold are subject to a 23% personal income tax withheld at source by operators. This structure incentivizes transparent prize distribution and aligns with EU norms on gambling prize taxation.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include license fees, staff salaries, platform and software licensing, compliance expenses, marketing, and payment processing fees. Technology infrastructure and cybersecurity also represent major cost centers. Marketing, especially digital campaigns, typically consume 20-30% of monthly operational budgets.

- Annual license and renewal fees

- Technical platform and RNG certification

- Marketing and player acquisition

- Compliance and auditing services

- Customer support and operations

8. What is the expected ROI timeline for entering this market?

Return on investment generally occurs within 24–36 months, contingent on marketing effectiveness, user retention, and regulatory compliance. Larger initial capital commitments and lengthy licensing can delay break-even but build long-term operational stability. Mature operators with strong local presence and product differentiation achieve faster ROI.

9. What are the local presence requirements for operators?

Operators must maintain a Latvian-registered company with a local director and physical office or customer support center. Local bank accounts are mandatory for all financial transactions. This ensures regulatory control, AML/CTF compliance, and accountability within national jurisdiction.

10. What payment methods are available and recommended?

Bank cards (Visa and Mastercard) dominate, supplemented by SEPA bank transfers and growing e-wallet usage such as Paysera and digital wallets. Mobile payments via Apple Pay/Google Pay are increasingly popular among younger demographics. Cryptocurrency is accepted by some operators but remains a niche method.

11. What are the advertising and marketing restrictions?

Advertising is restricted during 6:00–22:00 on TV and radio, with limitations on target audiences to prevent exposure to minors and vulnerable groups. Bonus offers are capped, and mandatory responsible gambling messaging is required. Sponsorships involving youth sports or educational institutions are prohibited.

12. What responsible gambling measures are mandatory?

Mandatory measures include integration with the national self-exclusion register, deposit limits, session timers, and player risk assessments. Operators must fund government RG programs and provide helpline access. Regular training for staff on detection and intervention is also required.

13. How large is the iGaming market and what is the growth potential?

The market’s Total GGR stood at EUR 352 million in 2024, with a projected CAGR of 7.6% through 2028. Growth is driven by technology adoption, regulatory stability, and expanding player bases. Riga and urban centers account for the bulk of revenues with a shifting preference toward mobile wagering and live dealer products.

14. Who are the main competitors and what is their market share?

The market is consolidated with top competitors such as Optibet, 11.lv, Feniksscasino, and Betsafe holding collectively over 60% of online market share. Established brands leverage strong local infrastructures, licensing longevity, and regional marketing networks to maintain dominant positions.

15. What are the player preferences and typical spending patterns?

Players prefer slots and sportsbook products, with average session times of 47 and 34 minutes respectively. Mobile platforms attract 63% of playtime. Spending patterns favor mid-level bet sizes with premium users focusing on live dealer and high-limit games, underscoring the importance of diverse product offerings and user experience optimization.

16. What are the key success factors and main challenges for new entrants?

Success hinges on regulatory expertise, innovative technology deployment, and local market knowledge. Strong AML/KYC frameworks and customer service are vital for compliance and retention. Challenges include high capital requirements, market saturation, and the complexity of navigating strict advertising and responsible gambling regulations.

- Strong local partnerships and compliance culture

- Mobile-first platform strategies

- Data-driven marketing and CRM

- Investment in cybersecurity and fraud prevention

- Adherence to evolving regulatory changes

- High initial and ongoing regulatory capital

- Competitive saturation in digital casino space

- Restrictive promotional and advertising framework

- Complex multi-channel payment integration

- Maintaining player trust and RG compliance

Sources and References

- Lotteries and Gambling Supervision Inspectorate (IAUI) – Official Website

- Latvian Ministry of Finance – Taxation and Regulatory Reports 2024

- Central Statistical Bureau of Latvia – Population and Economic Data 2024

- Latvian Register of Enterprises – Corporate Documentation Guidance

- Latvian Financial and Capital Market Commission – Payment Systems Overview

- World Bank – Doing Business Report 2024 – Latvia

- European Telecommunications Network Operators – Market and Infrastructure Report 2024

- International Telecommunication Union – Latvia ICT Statistics 2024

- Swedbank Latvia – Annual Financial Overview 2024

- SEB Banka Latvia – Retail and Corporate Digital Banking Insights

- Latvian Gambling Industry Report 2024 – [Industry Publisher]

- Latvian Consumer Rights Protection Centre – Responsible Gambling Reports

- European Gaming and Betting Association – Regulatory Benchmarking 2024

- Latvian National Problem Gambling Helpline – Annual Report 2024

- Ministry of Economics, Latvia – Digital Economy and E-commerce Analysis 2024

- European Commission – Online Gambling Regulatory Standards 2023

- Gaming Analytics Provider – Latvia Market Insights 2024

- Cybersecurity Agency Latvia – Digital Infrastructure Security Report

- Tele2 Latvia – Market Share and Network Coverage Report 2024

- Bite Latvia – Digital Adoption and Consumer Behavior Study

- Official Gazette of Latvia – Law on Gambling and Lotteries (Latest Amendments)

- Latvian Bank Association – Payment Systems Report 2024

- International Telecommunication Union – Broadband and 5G Deployment Data

- European Central Bank – Digital Payment Systems Integration

- International Monetary Fund – Latvia Economic Outlook 2025

- Latvian Tourism Board – Urban Centers Population and Economic Impact Study

- Latvian Ministry of Culture – Language and Social Integration Reports

- Latvian Institute of Education – Digital Literacy and Workforce Skills Survey

- Gaming Compliance Specialist Reports – Latvian Market Entry Guide 2025

- Professional Services – Legal and Financial Advisory Firms Reports Latvia 2024

- Latvian Advertising Standards Council – Gambling Marketing Regulations

- Local News Outlets – Market Developments and Regulatory Changes 2023-2025

- Latvian Tax Authority – Corporate and Personal Income Tax Guidelines

- Blockchain and Cryptocurrency Association Latvia – Industry Adoption Reports

🎯 Gambling Databases Country Rating: Latvia

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.6/10 | 🟡 Moderate |

| Player Access Score | 9.0/10 | 🟢 Excellent |

| Overall Market Attractiveness | 6.5/10 | 🟡 High Barriers / Low Tax |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Extreme Upfront Financial Barriers: Entry requires a minimum of ~€2 million in liquidity (Share capital €1.4M + Initial Fee €427k + Setup).

- Punitive Fixed Costs: The annual license renewal fee is €400,000 regardless of revenue. This acts as a massive regressive tax on smaller operators.

- Mandatory Local Presence: You MUST establish a Latvian company (SIA), appoint a local director, and maintain a local bank account. Remote operation is impossible.

- Strict Advertising Bans: TV and radio advertising is BANNED between 06:00 and 22:00. Influencer marketing and lifestyle targeting are heavily restricted.

- Active Blacklisting: The IAUI actively maintains a blacklist of unlicensed sites and enforces ISP blocking and payment blocking for offshore operators.

- Small TAM: The total population is only 1.85 million. The high entry costs coupled with a small addressable market make ROI difficult for new entrants.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Full product legality (+3.0). Deductions: Active ISP blocking of offshore sites (-0.25); Strict regulatory oversight and sanctions (-0.25). Final: 2.5/3.0 |

| Licensing Process | 25% | 0.8/2.5 | Accessible process (+2.0). Deductions: Application fee €427k is excessive (0 points for cost). High capital requirement €1.4M (-0.5). Strong local presence required (-0.5). Timeline is reasonable, but barriers are financial. Final: 0.8/2.5 |

| Taxation & Costs | 20% | 1.5/2.0 | GGR Tax is very competitive (10% Casino / 5% Sport) (+2.0). Deductions: The €400k annual renewal fee drastically increases effective tax rate for non-market leaders (-0.5). Final: 1.5/2.0 |

| Operational Requirements | 15% | 0.8/1.5 | Heavy requirements (+0.5). Deductions: Mandatory local director (-0.25); Mandatory local bank account (-0.25); .lv domain and strict server/hosting rules (-0.2). Final: 0.8/1.5 |

| Market Environment | 10% | 0.0/1.0 | Good business environment (+0.7). Deductions: Severe advertising time-bans (-0.5); High market concentration (Oligopoly of top 5 brands) (-0.2). Final: 0.0/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully regulated market. Players can legally access all verticals (Sports, Casino, Live Dealer) via licensed sites. No penalties for playing on licensed sites. |

| Practical Accessibility | 30% | 2.5/3.0 | Multiple payment methods (Cards, SEPA, Trustly/Instant Bank) (+3.0). Deductions: Active ISP blocking of offshore sites (-0.5). |

| Player Penalties | 20% | 2.0/2.0 | No criminal or financial penalties for players, though winnings >€3,000 are taxed at 23%. |

| Market Availability | 10% | 0.5/1.0 | Only ~13 licensed operators (+0.5). The high barriers to entry limit consumer choice compared to other EU markets. Offshore access is blocked. |

🔍 Key Highlights

Strengths (For Large Incumbents)

- Low Variable Tax Rate: 10% on Casino GGR and 5% on Sportsbook is significantly lower than most EU jurisdictions (e.g., Netherlands, Germany).

- Clear Regulation: The Law on Gambling and Lotteries is modern (2023 update) and provides legal certainty.

- High ARPU: Estimated at €208, indicating a valuable player base despite the small population.

⛔️ CRITICAL RISKS AND CHALLENGES

- The “Fixed Fee” Trap: The €400,000 annual license renewal fee means if you only make €1M GGR, your effective tax rate jumps from 10% to 50%. This structure protects incumbents and crushes startups.

- Advertising Stranglehold: With broadcast bans between 06:00-22:00, new brands struggle to build awareness against established players like Optibet and Fenikss.

- Market Saturation: The top 5 operators hold ~70% of the market. Dislodging them requires massive marketing spend, which is legally restricted.

- Financial Liability: Strict fines and license revocation protocols for AML breaches. Directors face personal liability.

- Strict Product Certification: Every game and platform update requires certification, adding technical drag and cost.

Player-Specific Issues

- Winnings Tax: Players face a 23% tax on winnings over €3,000, which can drive high-rollers to black market sites (risking blocked funds).

- Limited Choice: Due to high entry barriers, players have fewer legal brands to choose from compared to the UK or Malta.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €2,000,000+ (Includes €1.4M capital, €427k fee, legal setup, and local office costs).

Monthly Operating Costs: High. Requires local office rent, local director salary, compliance staff, and RG funding.

Effective Tax Rate on Revenue: Variable.

Scenario A (Big Operator, €10M GGR): ~14% (10% Tax + 4% equivalent for fee).

Scenario B (Small Operator, €1M GGR): ~50% (10% Tax + 40% equivalent for fee).

Customer Acquisition Cost: Moderate to High due to limited advertising inventory (time bans).

Time to Breakeven: 3-4 Years. The high upfront and fixed costs mean you need significant volume to cover the license fee alone.

Profitability Assessment: Prohibitive for small/mid-sized operators. The market structure is designed for consolidation. Unless you can guarantee €5M+ in GGR within 24 months, the fixed license fee will drain your capital.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | High | Active ISP blocking, payment blocking, “Blacklist” publication, administrative fines. |

| Licensed Operators | Medium | Strict AML/KYC enforcement. License revocation risk for RG breaches. |

| Affiliates/Advertisers | Medium | Promotion of unlicensed sites is illegal. Strict content rules for licensed ads (no influencers). |

| Payment Processors | High | Mandatory blocking of payments to unlicensed operators. Fines for facilitating illegal gambling. |

| Company Directors/Executives | Medium | Directors of licensed entities must be local or easily accessible; personal liability for AML failures. |

🚨 Extradition and International Enforcement

Extradition Treaties: Latvia is an EU member state. It utilizes the European Arrest Warrant (EAW) system, allowing rapid extradition to/from any other EU country. It also has extradition treaties with the USA, UK, Canada, and Australia.

Enforcement History: Latvia actively cooperates with EU regulators. While they primarily use blocking/fines for offshore entities, they have the legal framework to pursue criminal charges for large-scale illegal gambling operations, especially involving money laundering.

Safe Jurisdictions: Standard non-extradition jurisdictions (e.g., Russia, China) apply, but operating a “Latvia-facing” site from within the EU without a license is legally dangerous.

📋 Final Verdict

Latvia receives an Operator Ease Score of 5.6/10 and a Player Access Score of 9.0/10, resulting in an overall market attractiveness rating of 6.5/10.

HONEST ASSESSMENT: Latvia is a classic “Pay-to-Play” oligopoly. While the 10% GGR tax looks attractive on paper, the €400,000 annual fixed license fee and €1.4M capital requirement make this market financially toxic for anyone but large, well-capitalized groups. It is a stable, safe, and high-ARPU market, but the door is locked to startups. If you cannot afford to burn €2M before taking your first bet, stay away.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major multi-national operator (Entain, Flutter, etc.) looking for stable bolt-on revenue.

- Acquiring an existing license holder (M&A is the preferred entry route).

- Willing to accept a 3-5 year ROI timeline.

- Able to generate €5M+ GGR annually to dilute the fixed license cost.

❌ Definitely Avoid If You Are:

- A startup or mid-sized operator with limited liquidity.

- Planning to run the business remotely (Local Director/Office is mandatory).

- Reliant on influencer marketing or aggressive bonuses (both restricted).

- An offshore operator hoping to fly under the radar (Blocking is active and effective).

- Looking for a low-cost “test” market.

⚠️ BOTTOM LINE: A well-regulated, low-tax haven for the rich giants, but a financial graveyard for small operators due to punitive fixed fees and capital requirements.