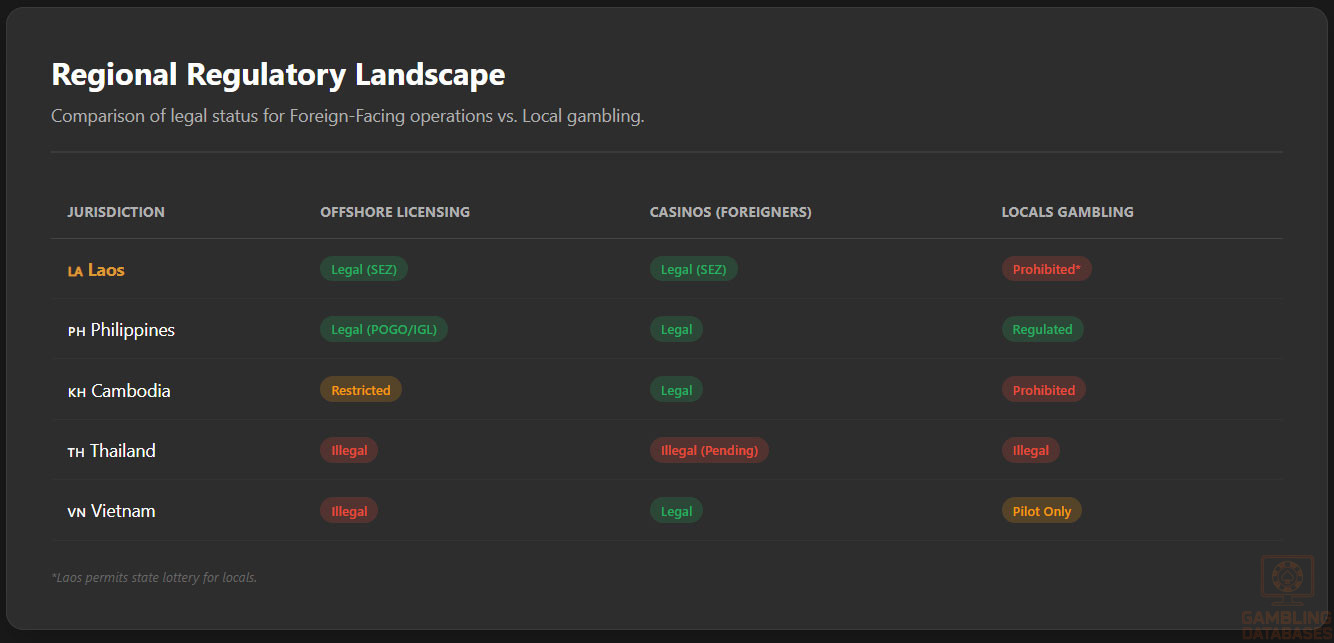

Laos presents a unique iGaming market opportunity centered around its Special Economic Zones (SEZs) catering primarily to foreign players. The regulatory framework is evolving to formalize casino operations while maintaining strict prohibitions on local gambling activities.

This analysis covers the comprehensive regulatory environment, licensing requirements, taxation policies, and compliance obligations shaping Laos’s iGaming landscape.

| Metric | Value |

|---|---|

| Gambling Legal Status | Illegal for residents except state lottery; casinos legal in SEZs for foreigners only |

| Regulatory Framework | Ministry of Planning and Investment (MPI) licensing; multiple ministries oversee sectors |

| Licensed Gambling Types | Casinos, state lottery, limited sports betting in SEZs |

| Population | Approx. 7.5 million (2025 estimate) |

| GDP (Nominal) | USD 20 billion (2024 est.) |

| GDP per Capita | Approx. USD 2,700 |

| Internet Penetration Rate | Approx. 65% |

| Mobile Penetration Rate | Over 85% |

| License Authority | Ministry of Planning and Investment (MPI) |

| License Duration | 10 to 20 years |

| License Application Fee | Varies; typically USD 50,000+ depending on casino size |

| Annual License Fee/Tax | Flat-rate tax USD 3–8 million based on gaming tables and slot machines |

| Player Taxation | No direct tax on player winnings |

| Operator Tax Structure | Flat-rate tax by casino category; excludes income and dividend taxes |

| Market Entry Barriers | Strict regulatory scrutiny, investment size, SEZ location requirements |

| License Application Process | Multiple steps including background checks, due diligence, technical audits |

| Local Presence Requirement | Mandatory employment of Laotian nationals; local business registration required |

| Foreign Ownership Restrictions | Permitted under controlled conditions; partnership encouraged |

| Compliance Obligations | AML/KYC, responsible gaming policies, audits, advertising restrictions |

| Prohibited Activities | Local residents betting, online gambling for locals, unlicensed sports betting |

| Market Size | USD 450 million+ annual estimated revenue from casinos in SEZs |

| Revenue Growth Forecast (CAGR) | 6–8% over next 5 years |

| Average Revenue Per User (ARPU) | Approx. USD 2,300 (foreign players) |

| Market Focus | Foreign tourists, offshore online players only |

| Regulatory Updates | 2024 Law on Investment Promotion amended; 2025 Presidential Ordinance on casino taxation |

| Advertising Restrictions | Strict with channel limitations and content controls |

| Enforcement and Penalties | Fines and imprisonment for illegal/local gambling activities |

| Technology Infrastructure | Improving Internet and mobile access supporting offshore gaming |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling activities in Laos are tightly regulated, with the Lao Penal Law strictly prohibiting residents from engaging in most gambling forms except for the state-run lottery. The government maintains a strong stance against local gambling to mitigate social and economic risks while allowing foreign participation in authorized venues.

Online gambling is banned for residents, yet Laos has developed specialized licensing frameworks for offshore iGaming operators targeting international customers. This model resembles the Philippine Offshore Gaming Operator (POGO) system, permitting licensed operators to run online games exclusively for non-resident players.

Land-Based Gambling Activities

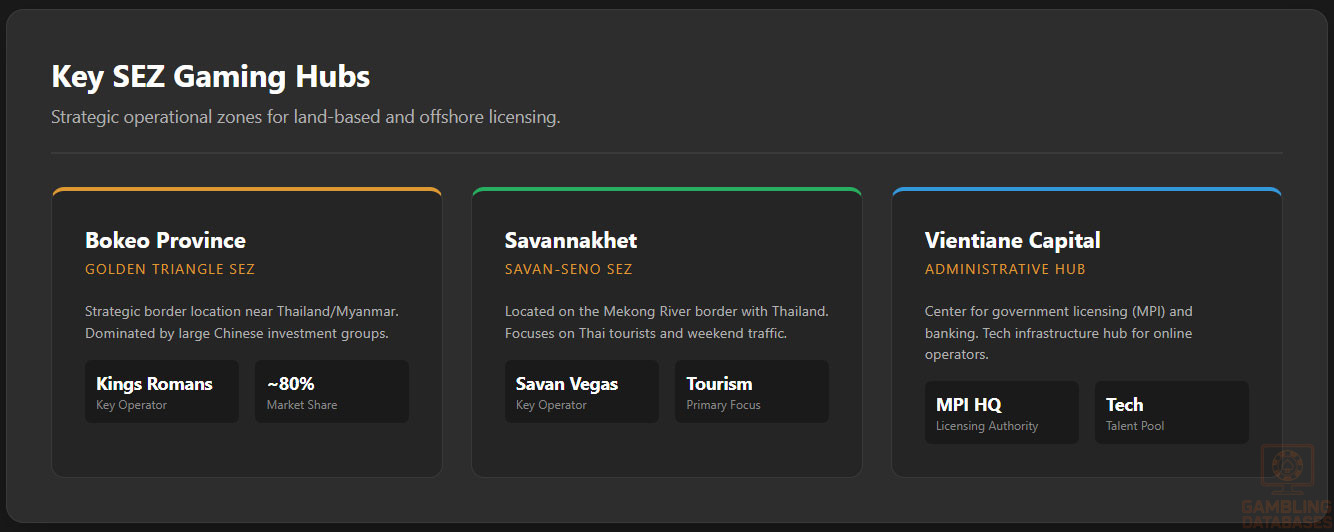

Casino operations in Laos are concentrated in SEZs, with prominent establishments including the Kings Romans Casino in Bokeo Province and the Savan Vegas Hotel and Casino in Savannakhet Province. These casinos offer a range of services such as gaming tables, slot machines, and entertainment amenities aimed mainly at foreign clientele.

Sports betting remains illegal for residents but is permitted under tightly controlled conditions within SEZs primarily for foreign bettors. Slot machine halls and other gambling venues operate solely within these zones under strict licensing and monitoring by authorities.

Other land-based gambling forms are legally restricted, and enforcement is vigorous to prevent unauthorized operations. Gambling advertising is heavily regulated, with limits imposed on promotional activities both inside and outside SEZs.

Online Gambling Framework

Laos has instituted specific regulations that prohibit online gambling for residents while simultaneously providing licenses to offshore operators targeting international markets. The Ministry of Planning and Investment (MPI) governs licensing issuance for these operators under a regulatory structure established in 2022.

This framework forbids local population access to online gambling platforms and enforces strict oversight to ensure compliance with AML standards, responsible gaming, and technical integrity. The licensing conditions parallel successful regional offshore frameworks, facilitating Laos’s aspiration to become a competitive regional hub for offshore iGaming.

The online gambling law mandates technical certification of gaming software, regular audits, and comprehensive financial reporting obligations to maintain transparency and protect players abroad, aligning with international best practices.

Licensed Operators and Market Players

The market is dominated by large casino groups operating within the SEZs, primarily foreign enterprises from China and Hong Kong. The Kings Romans Group holds an estimated 80% market share in the Golden Triangle SEZ, benefiting from its strategic location and strong investor backing.

Licensed offshore online operators are emerging under new licensing schemes, focusing on sports betting, online poker, and esports for foreign users. Competitive dynamics favor investors capable of navigating Laos’s regulatory framework and maintaining compliance with comprehensive tax and operational rules.

Foreign investments are encouraged but subject to rigorous due diligence, and operators must implement local employment policies aimed at increasing government jobs and sustaining social acceptability.

Licensing Framework and Requirements

Application Process and Eligibility

The Ministry of Planning and Investment (MPI) is the regulatory authority responsible for issuing licenses for casino and online gambling operations. The application process is multi-staged and requires meeting strict eligibility standards, including financial stability, proven track record in gaming, and sound reputation.

The licensing process involves submitting detailed documentation on ownership structure, management, technical systems, and compliance policies, followed by MPI’s thorough due diligence checks.

The minimum licensing period ranges between 10 and 20 years, affording operational stability but requiring ongoing adherence to prescribed operational frameworks, including architectural designs, game types permitted, and wager limits.

Technical audits and compliance verification form integral parts of the approval stages with MPI conducting background checks and interviews of key personnel to assess suitability.

The license application fees vary according to the casino size and scope, with additional fees imposed for exceeding authorized gaming tables or slot machines.

Required Documentation for Licensing

- Corporate registration certificate and articles of incorporation

- Detailed business plan covering market strategy and financial projections

- Audited financial statements for the past three years

- Technical documentation of gaming platforms and RNG certification

- Criminal background checks for all beneficial owners and directors

- Proof of minimum capital deposit in licensed financial institution

- Responsible gambling and AML/KYC policy documents

- Details of local employment and operational compliance measures

Local Presence and Operational Requirements

Operators must maintain a physical presence in Laos, including business registration and office facilities within approved SEZs. Mandatory employment quotas require operators to engage Laotian nationals across operational and managerial roles to support local workforce development.

Foreign ownership is permitted under controlled conditions, often necessitating partnerships or joint ventures with local entities to meet government expectations for social and economic inclusion.

Domain registration for online operators must be compliant with Lao regulatory authority controls to prevent unauthorized access by local users and ensure jurisdictional oversight.

Operational Compliance Requirements

- Maintain local registered office within SEZ or approved jurisdiction

- Employment of a prescribed percentage of Laotian nationals in workforce

- Implementation of AML and KYC policies compliant with Lao law

- Technical systems and software certification as per MPI standards

- Regular compliance reporting and operational audits

- Adherence to responsible gambling measures and player protection

Compliance Obligations and Monitoring

Player Protection and Identification

Strict age verification is enforced to prevent underage gambling. Operators must comply with rigorous KYC and AML standards designed to identify and prevent fraud, money laundering, and other illicit activities.

Responsible gambling mandates require implementing self-exclusion tools, deposit limits, and information disclosure policies designed to protect vulnerable players and promote sustainable gaming behaviors.

Mandatory player protection measures include:

- Age and identity verification for all players

- Implementation of self-exclusion and cooling-off options

- Deposit and wager limit controls

- Ongoing monitoring of player behavior for signs of problem gambling

- Transparent disclosure of game odds and risk information

Financial Monitoring and Reporting

Operators are required to maintain transparent transaction records subject to periodic reviews by regulators. Monthly and annual financial reporting includes details of wagers, winnings, tax payments, and suspicious activity reports forwarded to the Ministry of Finance and MPI.

An internal compliance officer is often mandated to oversee adherence to reporting timelines and ensure audit readiness.

- Submission of monthly financial and activity reports to MPI

- Independent annual audit by approved external auditor

- Tax payment reconciliation and reporting to Ministry of Finance

- AML report submission on suspicious transactions

Taxation Structure and Financial Obligations

Player Taxation

There is no explicit taxation on player winnings in Laos, as gambling for residents is largely illegal. Offshore players using licensed platforms face no withholding obligations imposed by the operator.

Operator Taxation

| Tax Category | Rate/Amount |

|---|---|

| Flat-Rate Tax on Gaming Tables | USD 3 million to 8 million annually depending on table count |

| Flat-Rate Tax on Slot Machines | USD 3,000 per machine annually |

| Corporate Income Tax | Standard rate applied separately (~24%) |

| License Renewal Fee | Variable, depending on license and operational scale |

| Entry Fee (per customer) | USD 200 per entry to casino premises |

Gambling Market Financial Performance

The total annual revenue derived from casinos in SEZs is estimated at over USD 450 million, driven by high-stakes foreign players. The flat-rate taxation system simplifies tax administration but requires operators to carefully manage operational scale.

Year-over-year growth is projected in the 6 to 8% range, supported by increased foreign tourism and expanding offshore gaming licenses. The market maintains a high average revenue per user (ARPU), supported by VIP segments and significant foreign spending power within SEZs.

Advertising and Marketing Restrictions

Marketing efforts for gambling must comply with strict regulations intended to minimize societal harm. Advertising is restricted to certain channels and formats, with prohibition on targeting local residents or minors.

Sponsorships in sports and entertainment are limited and subject to regulatory approval. Time-of-day restrictions apply, limiting gambling promotions during specific hours to reduce exposure to vulnerable populations.

Advertising channels and restrictions include:

- Permitted channels: SEZ-limited print media, authorized online platforms for foreign users

- Prohibited channels: Local TV, radio, and public spaces accessible to residents

- Content restrictions: No promotion of gambling as wealth creation or solution to financial issues

- Mandatory responsible gambling messages on all adverts

- Restrictions on bonuses and inducements targeting frequent players

Recent Regulatory Changes and Their Impact

Key regulatory reforms in late 2024 and early 2025 include the revision of the Law on Investment Promotion removing casinos from the highest scrutiny list, facilitating smoother licensing processes. Concurrently, the May 2025 Presidential Ordinance introduced a structured flat-rate tax scheme on casino operations.

These changes have lowered barriers for international investors and formalized tax collection, providing greater regulatory clarity and business predictability while maintaining tight control over local gambling participation.

Enforcement Mechanisms and Penalties

Penalties for illegal gambling activities in Laos are severe, including fines and imprisonment. Law enforcement actively targets unauthorized operators and gambling activities involving residents.

Regulatory authorities employ strict monitoring regimes and collaborate with provincial internet management committees to shut down illegal gambling outlets and internet cafes involved in unauthorized betting.

- Monetary fines commensurate with offense severity

- Seizure of illegal gambling equipment

- License suspension or revocation for non-compliance

- Imprisonment for operators and participants in illegal gambling

- Internet and telecommunications monitoring to block unauthorized sites

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

The total population of Laos in 2025 is estimated at 7.87 million people, with a median age of 24.9 years, reflecting a young demographic profile. The gender ratio is relatively balanced, with slightly more males at approximately 50.2% compared to 49.8% females.

Urbanization stands at around 39.2%, with the majority still residing in rural areas, which impacts accessibility and consumer behavior related to gambling and digital services.

| Age Group | Percentage of Population |

|---|---|

| 0-4 years | 10.0% |

| 5-12 years | 16.0% |

| 13-17 years | 9.5% |

| 18-24 years | 12.7% |

| 25-34 years | 17.2% |

| 35-44 years | 13.9% |

| 45-54 years | 9.4% |

| 55-64 years | 6.4% |

| 65+ years | 4.8% |

Major urban centers concentrate economic activities and digital connectivity. The population is unevenly distributed, with significant clusters in the capital and provincial hubs, facilitating targeted iGaming marketing and service delivery.

- Vientiane – approx. 820,000 residents

- Savannakhet – approx. 130,000 residents

- Luang Prabang – approx. 56,000 residents

- Pakse – approx. 57,000 residents

- Thakhek – approx. 49,000 residents

Internet access and gambling operations are most prevalent in these cities, with rural areas largely underserved, creating market segmentation between urban tech-savvy users and rural populations with limited digital participation.

Economic Indicators and Consumer Spending Power

Laos’s nominal GDP reached approximately USD 20 billion in 2024, with a projected growth slowdown to around 3.5% in 2025 amid external economic pressures. The GDP per capita stands near USD 2,700, marking gradual improvement but reflecting modest disposable income levels for most consumers.

The economy is dominated by the service sector, accounting for over 40% of GDP, supported by growing tourism and trade, followed by agriculture and industry. Inflation remains elevated but is easing from previous peaks, impacting consumer confidence and discretionary spending.

| Indicator | Value |

|---|---|

| GDP (Nominal) 2024 | USD 20 billion |

| GDP Growth Rate 2025 (Projected) | 3.5% |

| GDP per Capita | USD 2,700 |

| Inflation Rate (2025 estimate) | 10-12% |

| Service Sector GDP Contribution | 41% |

| Agriculture Sector GDP Contribution | 30% |

| Industry Sector GDP Contribution | 29% |

Household income distribution is skewed towards lower middle-income brackets, with many families maintaining subsistence living standards. Urban center residents generally enjoy higher incomes and more disposable spending power, especially in Vientiane and SEZ areas where foreign investment drives economic growth.

Consumer spending patterns show increasing interest in digital and entertainment services, supported by rising mobile penetration. However, lower-income brackets limit mass-market gambling participation, making premium, foreign-player-focused services more viable in Laos.

Market Size and Growth Projections

| Metric | Value/Projection |

|---|---|

| Current Market Revenue (2025 est.) | USD 450 million |

| Projected CAGR (2025-2030) | 6-8% |

| Estimated Player Base | 190,000 active foreign users |

| Average Revenue per User (ARPU) | USD 2,300 |

| Market Penetration Rate (Internet users) | 54% |

The Laos iGaming market is concentrated on foreign tourists and offshore users, with growth fueled by expanding SEZ casino operations and offshore online gambling licenses. Growth forecasts indicate steady expansion supported by infrastructure improvements and regulatory certainty.

Education, Skills, and Digital Literacy

Literacy rates in Laos exceed 85%, with ongoing government efforts to improve educational access. While formal education attainment levels remain modest outside urban areas, digital literacy is increasing rapidly due to expanded mobile connectivity and internet accessibility.

Cultural and Social Factors

Communication and Language

The primary official language is Lao, spoken by over 90% of the population. French and English are widely used in business, education, and tourism sectors, especially in urban and SEZ locations. Minority groups speak various languages, reflecting Laos’s ethnolinguistic diversity, though these have limited direct impact on gaming market targeting.

- Lao (National language and majority usage)

- French (Business and historical education)

- English (Tourism, business, and international communication)

- Khmu and Hmong (Ethnic minority languages)

- Other tribal languages (Localized use in rural areas)

Cultural Attitudes

Gambling in Laos holds a complex cultural position; traditionally viewed as social entertainment sometimes intertwined with cultural ceremonies, gambling is also stigmatized due to societal and religious norms emphasizing restraint. The Lao Buddhist majority often perceives gambling as a potential moral hazard.

Foreign gambling brands are commonly accepted within SEZs and urban tourist areas but are largely invisible or inaccessible to most local populations due to legal restrictions. Entertainment preferences favor communal activities, sports, and music, with growing openness to digital engagement for younger demographics.

Problem Gambling and Social Considerations

Problem gambling prevalence is a recognized social issue, particularly among certain demographics engaged in both legal and illegal betting activities. Government and NGOs have initiated early-stage response programs focused on awareness, counseling, and behavioral health support.

- Public awareness campaigns on gambling risks

- Gambling addiction counseling services

- Community support groups and family education programs

- Mandatory responsible gaming policies for operators

- Expansion of helplines and online support portals

Social responsibility in the gambling industry is increasingly emphasized through regulatory mandates requiring operator contributions to funding problem gambling and social welfare programs.

Political Structure and Governance

Laos operates as a single-party socialist republic under the Lao People’s Revolutionary Party, providing a stable though centralized political environment. Regulatory consistency for foreign investment, including gambling ventures, remains focused on promoting economic growth while maintaining social order.

International relations, particularly with China, Vietnam, and Thailand, influence business frameworks. The government encourages foreign direct investment within designated SEZs as part of broader economic modernization and poverty reduction strategies.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration has reached approximately 64% in 2025, fueled by mobile broadband expansion and infrastructure upgrades. Daily internet usage averages 3-4 hours for most urban users, predominantly accessed via smartphones.

Social media engagement is robust, with an estimated 54% of the population active on social networks, mostly within the 18-34 age group. This engagement offers lucrative channels for digital marketing and customer acquisition for iGaming companies.

- Facebook with 63% penetration of internet users

- YouTube with 60% penetration and high video consumption

- Instagram rapidly growing among younger users

- TikTok gaining momentum for entertainment consumption

- Twitter used mainly for news and celebrity updates

Digital Payment Behavior

Digital payments are increasingly preferred in Laos’s urban centers and SEZs. Consumers adopt a range of payment methods, including mobile wallets, bank cards, and mobile money services linked to telecom providers.

Cryptocurrency adoption is nascent but rising among tech-savvy demographics, supported by growing fintech innovation and cross-border transaction needs in gambling and tourism sectors.

- Mobile money wallets (e.g., M-Pay, Lao Telecom wallets)

- Debit and credit cards issued by local banks

- Bank transfers for online services

- QR code payments through mobile apps

- Cryptocurrency usage for niche online payments

Gaming and Gambling Preferences

Current Market Participation

Gambling participation is primarily concentrated among foreign visitors and expatriate residents due to local prohibitions. Popular activities include casino table games, slot machines, and limited legal sports betting within SEZs.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Casino Table Games (Roulette, Blackjack) | 52 |

| 2 | Slot Machine Play | 38 |

| 3 | Sports Betting (Legal SEZ Markets) | 24 |

| 4 | Online Offshore Betting | 18 |

| 5 | Lottery and Raffles | 15 |

Consumer Behavior Patterns

Laotian gambling consumers, primarily foreign players in SEZs, prefer high-stakes table games and frequent long-duration sessions often marked by VIP service models. Online users increasingly demand fast payouts, mobile-friendly platforms, and diverse betting options including esports and virtual games.

Peak gaming times align with evening hours and weekends, correlating with tourist visitation patterns. Retention is driven by loyalty programs and personalized promotions within regulatory limits.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Laos’s internet penetration reached approximately 64% in 2025, predominantly driven by mobile broadband connectivity. Fiber-optic infrastructure is under gradual expansion in urban centers and Special Economic Zones (SEZs), improving broadband speed and reliability for commercial users. Average fixed broadband speeds hover around 40 Mbps, while mobile networks average 20-25 Mbps, suitable for streaming and gaming applications.

Despite progress, rural regions experience limited connectivity due to topographical challenges and infrastructure costs, restricting digital service reach. The government prioritizes investment in digital infrastructure, aiming to reduce urban-rural divides and improve network resilience to international standards.

5G and Future Technology Deployment

5G technology rollouts began in selected urban areas and SEZs in late 2024, with coverage expected to reach 40% of the population by 2027. The rollout is driven by the two dominant telecom operators coordinating with government agencies for spectrum allocation and infrastructure upgrades without major regulatory delays. 6G research initiatives are still nascent but part of long-term digital strategy frameworks.

Industry stakeholders actively monitor technology trends for emerging opportunities in low-latency networks, essential for advanced gaming experiences and cloud-based services. Planned fiber expansions and 5G coverage improvements provide a solid foundation for iGaming operators.

Mobile Technology Ecosystem

Mobile Network Infrastructure

The mobile market hosts three major operators with diverse market shares, improving competition and service quality. Market penetration exceeds 90%, bolstered by affordable smartphones and expanding 4G LTE coverage. Data prices have gradually decreased, supporting increased consumer data consumption.

- Lao Telecom – State-owned, largest market share (~50%)

- Unitel – Joint venture, second largest with ~35%

- MPT – Third operator, ~15% market share with regional focus

Device Penetration

Smartphone adoption surpasses 75% of the population, concentrated in urban and semi-urban locales. Android dominates with over 85% share, favored due to price accessibility and ecosystem support; iOS holds a niche affluent-user segment. Device usage patterns emphasize multimedia consumption, mobile payments, and social media, facilitating mobile-first engagement in iGaming.

Financial Services and Payment Infrastructure

Banking System Structure

Laos’s banking sector is composed of state-owned and private institutions, with ongoing reforms accelerating digital banking solutions and increasing account penetration. Around 36% of adults have formal bank accounts, though digital wallet adoption is rapidly increasing among younger demographics. Financial inclusion remains a priority to support economic modernization and service sector growth.

- Banque Pour Le Commerce Exterieur Lao (BCEL) – Market leader with extensive network

- Joint Development Bank (JDB) – Large private bank focusing on SME lending

- Phongsavanh Bank – Growing in retail digital banking

- Southeast Asia Commercial Bank (E-SANPA) – Specialized in trade finance

- ANZ Bank Laos – Focus on corporate and international banking

Payment Processing Options

A broadening spectrum of payment methods supports digital transactions, including gambling-related payments. Popular options include bank card payments, mobile wallets, and bank transfers, integrated with improved POS systems and enhanced security mechanisms. Cryptocurrency remains niche but is emerging within tech-savvy groups.

- Mobile wallets: M-Pay, Lao Telecom’s mobile money services

- Debit and credit card payments via UnionPay, Visa, and Mastercard

- Bank transfers, including real-time online banking options

- QR code payments integrated into popular apps

- Cryptocurrency use mainly for offshore online platforms

E-commerce and Digital Economy

Laos’s e-commerce market has expanded, driven by improved logistics, rising digital literacy, and growing consumer confidence in online shopping. Despite infrastructural challenges, urban consumers increasingly transact via popular platforms offering electronics, fashion, and digital services, including entertainment subscriptions. Payment gateway upgrades facilitate smoother cross-border transactions pertinent for iGaming operators targeting foreign users.

Business Environment and Regulatory Framework

Ease of Business Operations

Laos ranks mid-tier in regional ease of doing business indices, with improvements in business registration, licensing, and operational processes aiding foreign investor confidence. Despite occasional bureaucratic hurdles, recent regulatory reforms have streamlined permissions for SEZ-based entities, including gambling operators.

- Preparation and notarization of required documents (2-3 weeks)

- Submission and review by Ministry of Planning and Investment (5-7 business days)

- Tax registration and acquisition of tax ID number (3-5 days)

- Opening corporate bank account and depositing minimum capital (1-2 weeks)

- Final license and operational confirmation issuance (2-3 days)

Corporate Structure and Registration

Foreign enterprises typically establish Limited Liability Companies (LLCs) or branch offices within SEZs for iGaming operations. LLCs provide flexibility and limited liability protections; branch offices offer simpler setups but depend on parent company governance. Joint ventures with local partners are common to meet ownership expectations and facilitate regulatory approvals.

- Limited Liability Company (LLC) – Most common for foreign investors

- Branch Office – Subsidiary operations under parent company

- Joint Venture – Partnership with local entities

- Representative Office – Market research and liaison functions only

- Special Economic Zone Company – Optimized for operations inside SEZs

Registration timelines average 4-6 weeks, contingent on document completeness and regulatory responses. Foreign ownership is allowed but subject to government review and limitations to encourage domestic participation.

Registration Requirements

- Certificate of incorporation or equivalent

- Shareholder and director information

- Business plan and financial projections

- Proof of capital deposit

- Lease agreement for local office premises

- Tax registration documents

- Technical and operational compliance certificates

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate is approximately 24%, with preferential regimes in SEZs offering tax holidays and reduced rates for initial years. Laos holds multiple double taxation treaties facilitating tax efficiency for foreign investors including agreements with ASEAN countries, China, Vietnam, and others.

- China

- Vietnam

- Thailand

- South Korea

- Singapore

- Malaysia

- Japan

Personal Income Tax

Individuals are subject to progressive income tax rates ranging from 0% to 24%, with withholding tax applied on salaries and gambling-related income where applicable. Social security contributions are mandatory for employed persons, and tax residency is defined by physical presence exceeding 180 days annually.

Market Entry Considerations

Recommended Entry Strategies

Successful market entry typically combines partnership with local entities to meet regulatory and cultural expectations. Leveraging SEZ advantages such as tax incentives and streamlined licensing accelerate time to market. Adopting mobile-first technology platforms and compliance-centric operational models mitigates risks and enhances customer acquisition.

- Forming joint ventures with local firms

- Applying for SEZ-based licenses to capitalize on tax breaks

- Integrating mobile payment and marketing ecosystems

- Investing in compliance and responsible gaming systems

- Engaging in targeted digital marketing for foreign user acquisition

Typical Costs and Timelines

Initial investment includes licensing fees, regulatory compliance, platform development, and marketing expenditures. Operational costs are influenced by staff salaries, technical infrastructure, and taxation. Market entry timelines from application to operation commonly span 6 to 12 months depending on licensing approval rounds and infrastructure deployment.

- License application and approval: USD 50,000–150,000

- Operational setup (office, staff, technology): USD 200,000–500,000

- Marketing and customer acquisition: USD 100,000+

- Monthly operational costs (staff, tech): USD 30,000–60,000

- Compliance and audit expenses: USD 15,000–30,000 annually

Success Factors and Challenges

Key success factors include robust regulatory compliance, strong local partnerships, tailored marketing strategies for foreign audiences, and investment in advanced technology platforms. Challenges involve navigating regulatory complexity, mitigating illegal gambling competition, and addressing infrastructure gaps outside urban centers.

- Clear understanding of local regulatory environment

- Effective AML and responsible gambling systems

- Strong alliances with local stakeholders

- Agile marketing strategies aimed at foreign users

- Investment in scalable technology infrastructure

Exit Strategy Planning

Exit planning involves consideration of license transferability restrictions, valuation multiples based on market share and revenue, and potential regulatory approvals. Market liquidity for gambling assets remains limited but improving through increasing foreign investor interest and maturing regulatory frameworks.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Laos?

Online gambling for residents is illegal under Lao law. However, licensed offshore operators can legally provide online gambling services exclusively to foreign players. The government restricts access for locals through monitoring and enforcement to prevent illegal local online gambling. Authorized operators must comply with tight regulatory controls and ensure no local user access.

2. What types of gambling licenses are available and what do they cover?

Laos primarily issues licenses for land-based casinos in Special Economic Zones and offshore online gambling operators targeting non-residents. Casino licenses allow operation of tables and slot machines within SEZs. Offshore licenses cover online sports betting, poker, and casino games for foreign users only. No standalone sports betting licenses exist for local markets as betting is illegal locally.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees generally start around USD 50,000, increasing with casino scale or additional gaming tables. The review and approval process takes between six to twelve months, depending on documentation completeness and regulatory scrutiny. Renewal fees and ongoing fixed taxes are also imposed annually on operators.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain gambling licenses typically by establishing locally registered entities within SEZs. Foreign ownership is permitted but often requires partnership with local investors or compliance with government-set ownership limits. Due diligence and financial stability assessments are strict, ensuring operator suitability.

5. What are the tax obligations for iGaming operators?

Operators pay flat-rate taxes based on gaming tables and slot machine counts alongside standard corporate income tax. These flat fees simplify tax calculation but require operators to precisely manage operational scale. No direct taxes are applied on player winnings. Tax holidays and reductions may apply in SEZs.

6. Are gambling winnings taxed for players?

Residents are generally prohibited from gambling, so no personal tax arises on winnings. Foreign players visiting SEZ casinos or using offshore platforms are not subject to Lao withholding taxes on winnings. This creates a favorable environment for foreign high-stakes players.

7. What are the typical operational costs for running an online casino/sportsbook?

Key operational costs include licensing and regulatory fees, technology platform development and maintenance, staffing, customer acquisition marketing, and compliance expenses. Monthly technology and staffing costs range from USD 30,000 to 60,000, with marketing budgets flexible depending on scale. Responsible gaming and AML systems constitute ongoing compliance expenses.

8. What is the expected ROI timeline for entering this market?

ROI typically materializes within two to four years post-launch, depending on market penetration, operational efficiency, and effective user acquisition. SEZ tax incentives and growing foreign demand improve profitability potential, though upfront capital and marketing investments extend breakeven timelines.

9. What are the local presence requirements for operators?

Operators must maintain registered business premises in SEZs, employ a specified percentage of local staff, and maintain operational headquarters for regulatory oversight. Physical offices and local representation ensure compliance with tax and reporting obligations and facilitate government cooperation.

10. What payment methods are available and recommended?

Payment acceptance should include popular mobile wallets, debit and credit cards, bank transfers, and emerging cryptocurrency options for offshore clients. Mobile money services are essential for local adaptation, while card and e-wallet payments align with international user expectations. Cryptocurrency remains emerging but promising for niche markets.

11. What are the advertising and marketing restrictions?

Advertising is restricted to channels targeting foreign players, with bans on local TV, radio, and public space promotions. Content must include responsible gambling messages and avoid misleading claims. Sponsorships and promotions undergo regulatory approval, and bonus offers are limited to avoid encouraging excessive gambling.

12. What responsible gambling measures are mandatory?

Mandatory measures include strict age verification, self-exclusion programs, deposit and wagering limits, player activity monitoring for early problem detection, and transparent disclosure of odds and risks. Operators must contribute to problem gambling programs financially and maintain open communication channels for player support.

13. How large is the iGaming market and what is the growth potential?

The market is estimated at USD 450 million annually, with projected growth rates between 6-8% CAGR through 2030. Growth drivers include expanding SEZ developments, improving digital infrastructure, and rising foreign tourist volumes. Offshore online gaming licenses further broaden revenue potential targeting global players.

14. Who are the main competitors and what is their market share?

Key competitors include large casino groups operating in SEZs, notably the Kings Romans Group dominating 80% market share in border-region SEZs. Emerging offshore online operators diversify the landscape but remain smaller. Market consolidation is gradual, with foreign capital primarily controlling major assets.

15. What are the player preferences and typical spending patterns?

Foreign players favor high-stakes table games, slot machines, and online esports betting platforms. Spending patterns emphasize evening and weekend sessions with VIP loyalty benefits driving retention. Mobile and online usage is increasing, shaping a shift towards digitally accessible gaming experiences.

16. What are the key success factors and main challenges for new entrants?

Success depends on robust regulatory compliance, technology investment, strategic local partnerships, and effective marketing to foreign players. Challenges include navigating complex licensing regimes, infrastructure gaps outside urban hubs, and competition from illegal operators.

Sources and References

- LaosGambling Regulatory Authority – Official Website – https://legalpilot.com/country/laos/

- Ministry of Planning and Investment (MPI) – Licensing and Investment Laws – https://laotradeportal.gov.la

- National Statistical Office of Laos – Population and Demographic Data 2025 – https://worldometers.info/world-population/laos-population/

- World Bank – Lao Economic Monitor May 2025 – https://worldbank.org/en/country/lao/publication/lao-economic-monitor-may-2025

- International Telecommunication Union – ICT Statistics Laos 2025 – https://itu.int/statistics/ict/laos-2025

- Digital 2025 Report Laos – Datareportal – https://datareportal.com/reports/digital-2025-laos

- Laos Special Economic Zones Regulatory Framework – Government Publications

- Gaming Industry Reports 2024-2025 – iGaming Today and Altenar

- Central Bank of Laos – Banking and Financial Services Reports 2024

- Lao Ministry of Finance – Tax Regulations and Treaties – https:// mof.gov.la

- Telecommunications Operators Market Data – Lao Telecom, Unitel, MPT annual reports

- Academic Studies on Gambling and Social Impact in Laos – University of Laos, 2019-2025

- News Reports on Laos Gambling Policies and Dealer Networks – Various news agencies 2024-2025

- Social Media Statistics Laos 2025 – Statcounter and NapoleonCat

- E-Commerce Market Analysis Laos 2025 – Local and regional consulting firms

- Responsible Gambling Frameworks and Policy Guides – laos-proceed.com

- Foreign Investment Regulatory Amendments 2024-2025 – Official Gazette of Laos

- International Tax Treaty Lists – Lao Ministry of Finance Publications

- Mobile Payment Adoption Reports – Telecom Sector Analyses 2025

- Global Online Gambling Trends and Compliance Standards 2025

- Laos Digital Infrastructure Development Plans – Ministry of Posts and Telecommunications

- Industry Whitepapers on iGaming Success Factors – Consulting Firms 2025

- Market Entry Strategy Publications for Southeast Asia – Asia-Pacific Business Insights 2025

- Investment Promotion Laws and Ordinances Laos – Official Legal Publications 2024-2025

- Laos Social and Cultural Studies Reports – National Research Institutes 2025

- Consumer Behavior and Digital Usage Surveys – Laos Market Research Firms 2025

- World Bank Doing Business 2025 Report – Laos Section

- International Financial Institutions Statistical Reports – IMF, ADB 2025

- Technical Certification and Audit Standards for iGaming – Local Regulatory Authorities

- Cross-border Gambling Network Investigations – Governmental Reports 2025

🎯 Gambling Databases Country Rating: Laos

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 4.2/10 | [🔴 Difficult 3-4] |

| Player Access Score | 2.0/10 | [⛔️ Illegal (For Residents)] |

| Overall Market Attractiveness | 3.1/10 | [⛔️ Restricted / Offshore Hub Only] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE LOCAL BAN: Gambling is strictly illegal for Laos residents. The market exists SOLELY as an export hub for foreign players. Targeting locals creates immediate criminal liability.

- IMPRISONMENT RISK: The Lao Penal Law enforces severe penalties, including fines and imprisonment, for operators and participants involved in unauthorized local gambling.

- MANDATORY PHYSICAL PRESENCE: Licenses are tied to Special Economic Zones (SEZs). You cannot operate remotely; you must establish a physical office, register a business, and employ local staff.

- HIGH CAPITAL BARRIERS: Flat-rate taxation (up to USD 3-8 million for land-based/large scale) and SEZ investment requirements make this market accessible only to well-capitalized enterprises, not startups.

- STRICT ADVERTISING RESTRICTIONS: Any promotion targeting the local population or appearing in public spaces accessible to residents is prohibited.

- GEOPOLITICAL ENFORCEMENT: Laos cooperates heavily with neighbors (China, Thailand, Vietnam). Operators targeting these nationals from Laos face cross-border enforcement risks and extradition pressure.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 1.5/3.0 | Partial Legality/Dual System. The framework is a “POGO-style” offshore model. • Offshore/Foreign: Legal and Regulated (+2.0). • Local Market: Strictly Prohibited (-1.5). • Enforcement: Active monitoring of internet cafes and local betting (-0.5). • Result: Legal only for export; domestic market is a zero-revenue zone. |

| Licensing Process | 25% | 1.0/2.5 | Complex & Restrictive. • Availability: Available via Ministry of Planning and Investment (MPI) but tied to SEZs (+1.0). • Costs: Application fees $50k+, but “investment size” requirements are high (-0.5). • Complexity: Requires background checks, technical audits, and multi-ministry oversight (-0.5). • Timeline: Lengthy due diligence process (-0.5). |

| Taxation & Costs | 20% | 0.7/2.0 | High Fixed Costs. • Structure: Flat-rate tax system (USD 3M–8M for casinos). While efficient for massive operators, this is prohibitively expensive for new or mid-sized entrants (-1.0). • Setup Costs: SEZ physical setup, mandatory local employment quotas, and infrastructure investment creates very high overhead (-0.5). |

| Operational Requirements | 15% | 0.5/1.5 | Heavy Burden. • Presence: Must maintain registered office within an SEZ (-0.5). • Staffing: Mandatory employment of Laotian nationals (quotas) (-0.25). • Tech: Servers/operations often required to be within the zone/jurisdiction for oversight (-0.25). |

| Market Environment | 10% | 0.5/1.0 | Moderate/Difficult. • Political: Stable single-party rule, but heavily influenced by foreign policy (China/Thailand) (+0.5). • Risk: Recent crackdowns in the Golden Triangle SEZ regarding illegal activities create reputational and operational scrutiny (-0.5). • Ads: Strict restrictions on marketing (-0.25). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.5/4.0 | Illegal. • Residents: Strictly prohibited from all forms of online gambling except state lottery (-1.5). • Foreigners: Allowed in SEZs. • Score reflects the status for the local population (7.5M people). |

| Practical Accessibility | 30% | 1.0/3.0 | Restricted. • Blocking: Government collaborates with ISPs to block unauthorized sites (-1.0). • Payments: Local banking system does not process gambling transactions; access requires offshore methods or crypto (which is niche) (-1.0). |

| Player Penalties | 20% | 0.5/2.0 | Severe. • Penalties: Fines and imprisonment are codified in the Penal Law for illegal gambling participation. This is not just a theoretical ban; enforcement exists. |

| Market Availability | 10% | 0.0/1.0 | Zero Domestic Options. • No licensed operators are permitted to serve the local resident market. Access is strictly via black-market offshore sites using VPNs. |

🔍 Key Highlights

Strengths (For Offshore Hub Operators Only)

- Low Variable Tax: The flat-rate tax model creates a ceiling on tax liability, which is advantageous only for operators with massive revenue volumes.

- Strategic Location: Proximity to Thailand, Vietnam, and China makes it a logistical hub for targeting these grey/black markets (despite legal risks).

- License Duration: Long license terms (10-20 years) provide operational stability for infrastructure investors.

⛔️ CRITICAL RISKS AND CHALLENGES

- Zero Domestic Market: You cannot legally monetize the 7.5 million local residents. Revenue must come 100% from foreign markets.

- High Barrier to Entry: The requirement to physically operate inside an SEZ, build/rent offices, and pay flat-rate taxes (often in the millions) eliminates small-to-mid-sized competition.

- Reputational Risk: Laos SEZs (specifically the Golden Triangle) have been associated with human trafficking and scam centers, leading to heightened scrutiny from international banking partners and regulators.

- Infrastructure Gaps: While urban internet is improving, reliability in SEZs can vary, and recruitment of highly skilled technical staff often requires importing talent (which has visa costs).

- Enforcement & Jail: Unlike grey markets where the risk is a fine, Laos imposes criminal penalties for violations regarding local gambling.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $500,000 – $1,000,000+ (Includes licensing, SEZ setup, mandatory capital deposits, and physical office construction/rental).

Monthly Operating Costs: $50,000 – $100,000+ (Local staff quotas, expatriate salaries, technical infrastructure maintenance).

Effective Tax Rate: Regressive. If your revenue is low, the flat tax (e.g., $3M+) could represent >100% of your GGR. If revenue is $100M, the rate is negligible.

Profitability Assessment: Prohibitive for 99% of Operators. The Laos model is built for massive land-based casino groups expanding into online verticals to serve their existing VIP databases. It is NOT a viable jurisdiction for a standalone online gambling startup. The fixed costs will bankrupt a small operator before the first bet is taken.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Critical | If targeting locals: Immediate criminal prosecution and asset seizure. If targeting foreigners: Banking instability due to SEZ reputation. |

| Licensed Operators (SEZ) | Medium/High | Compliance burden is heavy; risk of “guilt by association” with illegal operators in the same SEZ; geopolitical pressure from China. |

| Affiliates/Advertisers | High | Strict bans on local advertising. Promoting gambling to Lao residents is a criminal offense. |

| Company Directors | Critical | Personal liability including imprisonment if operations inadvertently accept local players or violate SEZ terms. |

🚨 Extradition and International Enforcement

Extradition Treaties: Laos has active extradition treaties and strong law enforcement cooperation with China, Vietnam, Thailand, and Cambodia. It also cooperates with ASEAN nations on transnational crime.

Enforcement History: There have been multiple high-profile raids and deportations of Chinese nationals operating illegal gambling and scam centers within Lao SEZs in 2023-2024. The government is under pressure to clean up SEZs.

Safe Jurisdictions: Laos is NOT a safe haven for operators targeting Chinese or Vietnamese nationals illegally. Authorities frequently hand over suspects to these neighboring governments.

📋 Final Verdict

Laos receives an Operator Ease Score of 4.2/10 and a Player Access Score of 2.0/10, resulting in an overall market attractiveness rating of 3.1/10.

HONEST ASSESSMENT: Laos is a “Landlord Market” designed for physical casino moguls, not digital entrepreneurs. The regulatory framework requires heavy physical infrastructure (SEZ presence), massive fixed tax payments, and strict prohibitions on the local population. It functions solely as a high-risk operational base for targeting other Asian countries.

For the average iGaming operator, the entry costs are too high, the reputational risks of the SEZs are too great, and the local market value is zero (illegal).

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A massive Asian-facing land-based casino group (e.g., operating in Macau or Cambodia) needing an online extension.

- Capable of paying $3M+ annually in flat taxes regardless of revenue.

- Willing to station staff physically in a Special Economic Zone.

❌ Definitely Avoid If You Are:

- A pure-play online startup or mid-sized European operator.

- Looking to target the local Laotian population (Prison risk).

- Unwilling to relocate staff and infrastructure to Southeast Asia.

- Reliant on Tier-1 banking partners (who will likely reject Lao SEZ transactions).

- Operating with less than $5M in initial capital.

⚠️ BOTTOM LINE: Avoid this market. It is an expensive, complex, and high-risk jurisdiction suitable only for large-scale conglomerates with specific regional strategies.