Costa Rica presents a unique opportunity for international iGaming operators due to its flexible regulatory approach and favorable tax environment. While it lacks specific online gambling licenses, companies can legally operate under a data processing license framework targeting international markets.

The country combines a stable business environment with minimal local restrictions, making it an attractive base for global online gambling businesses seeking a cost-effective entry point.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal for land-based casinos; online gambling operates under data processing license |

| Regulatory Framework | No formal online gambling license; regulated via municipal data processing licenses |

| Population | ~5.2 million |

| Median Age | 32 years |

| GDP (Nominal) | Approx. $68 billion USD |

| GDP Per Capita | ~$13,000 USD |

| Internet Penetration Rate | ~82% |

| Mobile Penetration Rate | ~130% (multiple subscriptions common) |

| Licensing Authority | Municipal governments (Data Processing License) |

| License Cost | Approx. $3,000 – $5,000 (varies by municipality) |

| License Issuance Timeline | 3 to 5 weeks |

| Taxation on Online Operators | No direct gambling taxes; standard corporate/business taxes apply |

| Taxation on Players | No tax on gambling winnings for residents |

| Market Entry Barriers | Low regulatory barriers; no formal online gambling regulatory body |

| Requirement for Local Presence | Local company registration and office presence required |

| Foreign Ownership Restrictions | None specified; fully foreign-owned entities allowed |

| Responsible Gambling Measures | AML/KYC compliance required; self-exclusion systems recommended |

| License Renewal | Annual renewal with standard municipal fees |

| Business Environment | Stable political climate; OECD member |

| Market Size (Online Gambling Revenue) | Estimated $50-$70 million USD (2025 projection) |

| Market Growth Forecast (CAGR) | 7-9% over next 5 years |

| Average Revenue Per User (ARPU) | Approx. $350 USD globally for operators based in Costa Rica targeting international markets |

| Payment Methods Supported | Cryptocurrencies, international e-wallets, credit/debit cards (no local bank usage) |

| Technology Infrastructure | Reliable internet backbone with high mobile broadband coverage |

| Enforcement Mechanisms | Municipal audits; Ministry of Public Security oversight for physical venues |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Costa Rica’s gambling regulatory environment is distinctively flexible, featuring formal regulations for land-based gambling but a non-traditional approach to online gaming. Land-based casinos operate legally, primarily as adjuncts to the hospitality sector within hotels. The Ministry of Public Security is the main regulatory authority overseeing casino operations, ensuring compliance with tax and operational guidelines.

Other gambling categories, such as lotteries, remain under government monopoly control through the Junta de Protección Social. Sports betting and poker, both land-based and online, operate under similar flexible frameworks without explicit regulatory licensing for online versions.

Land-Based Gambling Activities

Physical gambling in Costa Rica is regulated under Law No. 9050, which assigns licensing and oversight for casinos to the Ministry of Public Security. Key points include:

- Casino operations are confined to establishments linked to the hotel industry, supporting tourism growth.

- Slot machine halls and betting shops are regulated but relatively limited compared to regional peers.

- Sports betting is regulated with a government monopoly on certain types, including lotteries.

- Gaming activities require compliance with tax obligations established by national laws.

- Regulatory audits and periodic inspections maintain operational standards and legal compliance.

Online Gambling Framework

Online gambling operates in a regulatory gray zone but remains viable under the country’s data processing license system. Operators can legally offer a wide portfolio of digital games including slots, live dealer games, poker, and sports betting targeting international markets. However, these companies must not use local payment providers or target Costa Rican residents directly.

The lack of a dedicated regulatory authority for online gaming means operators are exempt from many formal licensing requirements seen elsewhere. The data processing license, issued by local municipalities, is the only official permission required to physically base operations and servers in Costa Rica. Anti-money laundering (AML) and know-your-customer (KYC) obligations are enforced under national laws unrelated specifically to gambling but applicable to all financial entities.

Licensed Operators and Market Players

Costa Rica’s market features hundreds of companies operating with data processing licenses, many acting as service providers or operators targeting global clientele. The competitive landscape is characterized by:

- Dominance of international operators using Costa Rica as a base rather than serving domestic players.

- High operational flexibility with relatively low taxation and regulatory costs.

- Strong presence of cryptocurrency-friendly platforms leveraging Costa Rica’s relaxed regulatory stance.

- A growing number of startups using Costa Rica to test new iGaming concepts before expanding into regulated markets.

- Limited local market penetration given restrictions on targeting residents.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing mechanism centers on obtaining a municipal data processing license after registering a local business entity, typically an S.A. or S.R.L. The application involves meeting basic financial, legal, and technical criteria that ensure the company’s capability to manage data-intensive services.

Key procedural aspects include company incorporation, submission of operational documentation, and confirmation of AML/KYC policies. Application fees are modest, and the approval timeline ranges from three to five weeks depending on the municipality. Technical requirements focus on platform security and data integrity rather than specific gambling-related certifications.

Applicants must not be residents of countries where online gambling is prohibited, nor can they offer services to local Costa Rican players. The requirement to establish a physical office space, either permanent or temporarily leased, is enforced as part of local presence standards.

Local Presence and Operational Requirements

Operational mandates include maintaining a physical office in Costa Rica, which can be leased on a permanent or temporary basis. This office provides the registered address for licensing and must be staffed with executives or representatives as per company bylaws. Domain registration for gaming websites must be managed in compliance with general business law but without specific online gambling domain restrictions.

Foreign ownership is unrestricted, allowing 100% foreign control of licensed entities. Partnerships with local companies are not mandatory but may be pursued for strategic purposes. These flexible local presence rules facilitate easy market entry for international operators expanding their footprint.

Compliance Obligations and Monitoring

Player Protection and Identification

Despite the absence of a dedicated gambling regulator, Costa Rican law demands compliance with AML and KYC procedures for all licensed entities. Operators must verify player identity, age (minimum 18 years), and conduct ongoing transaction monitoring to detect suspicious activities.

Responsible gambling measures include the implementation of self-exclusion systems, limits on deposits and losses, and mandatory disclosure of terms and conditions. While these requirements are broadly aligned with international best practices, they are not rigorously enforced through specialized gambling oversight.

- Age verification for all clients

- Customer identity documentation checks

- Transaction monitoring against money laundering

- Self-exclusion program availability

- Disclosure of responsible gambling policies

Financial Monitoring and Reporting

Financial compliance hinges on broader national financial regulations. Licensed operators must maintain detailed transaction records and submit periodic reports to municipal authorities. Audits are carried out to verify adherence to business laws, anti-fraud controls, and AML frameworks.

The reporting process follows these sequential steps:

- Monthly submission of financial and operational data to the municipal licensing office

- Compliance review by the Ministry of Public Security for physical casinos and associated entities

- Independent audits triggered by risk assessments or exemptions for smaller operators

- Rectification orders issued for non-compliant licensees

Taxation Structure and Financial Obligations

Player Taxation

Costa Rica does not impose taxes on gambling winnings for local residents, creating a highly attractive environment for players. Winnings from both land-based and online gambling are exempt from personal income tax, enhancing player incentives.

There are no withholding obligations for operators on player payouts. This tax exemption extends to international operators based in Costa Rica, provided they do not serve local customers.

Operator Taxation

| Game Type | Tax Rate / Financial Obligation |

|---|---|

| Land-Based Casinos | Subject to gross receipts tax under Law No. 9050; rates vary |

| Online Operators | No direct gambling tax; standard corporate income tax (~30%) applies |

| Lottery and Betting Monopolies | Monopolized by Junta de Protección Social; tax and revenue sharing applies |

| Cryptocurrency Gambling | Taxed under general corporate income rules; reporting required |

License fees for data processing licenses are paid annually at the municipal level, with renewal costs consistent with initial application fees. No turnover tax or special levies apply to online operators outside the remit of general business tax law.

Gambling Market Financial Performance

Costa Rica’s land-based gambling sector remains modest but steady, with casinos primarily serving tourists. Online gambling, while substantial in operational scale, generates revenue mostly from international players, contributing to stable tax inflows via business registration fees and standard corporate taxes.

Market revenue is projected to grow at a compound annual growth rate (CAGR) of 7-9% over the next five years, driven largely by the global expansion of operators based in Costa Rica offering international services.

Advertising and Marketing Restrictions

There are no detailed local restrictions on advertising for online gambling operators under Costa Rican law. Operators generally follow international best practices and self-regulatory codes due to their target markets.

- Permitted to advertise digitally targeting international users

- Restrictions on marketing to Costa Rican residents apply

- Promotional offers and bonuses regulated by target jurisdiction laws

- Sponsorship activities common but require transparency

- Time and content restrictions less stringent than in major regulated markets

Recent Regulatory Changes and Their Impact

Since 2023, discussions on developing formal online gambling regulation continue but have yet to produce concrete legislation. Industry stakeholders anticipate that future reforms may introduce licensing fees, stricter compliance requirements, and a more defined regulatory body.

Current low regulatory costs and operational flexibility have encouraged many start-ups to establish their presence in Costa Rica, positioning the country as a springboard for expansion into more strictly regulated markets.

Enforcement Mechanisms and Penalties

Enforcement is largely conducted at the municipal level through license audits, with oversight from the Ministry of Public Security for land-based entities. Penalties for non-compliance include fines, license suspension, and potential criminal charges in severe cases.

- Monetary fines for licensing violations

- License revocation for repeat non-compliance

- Operational suspension orders during investigations

- Criminal prosecution for fraud or money laundering

- Mandatory corrective action plans for AML failures

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

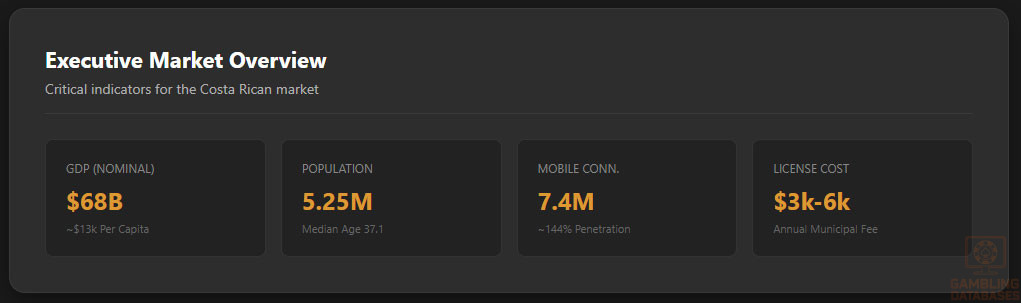

Costa Rica’s population is estimated at approximately 5.25 million people in 2025, reflecting steady growth over the past decade. The median age stands at 37.1 years, indicating a mature but still dynamic demographic profile. Life expectancy is high at 81.5 years, among the highest in Latin America, contributing to long-term consumer stability.

Gender distribution is nearly balanced, with 998 males per 1,000 females. The population pyramid shows a broad working-age cohort, with 61.1% of individuals aged between 20 and 64, forming the core of economic activity and digital engagement.

| Age Group | Percentage of Population |

|---|---|

| 0–19 years | 26.3% |

| 20–64 years | 61.1% |

| 65+ years | 12.6% |

Geographic Distribution

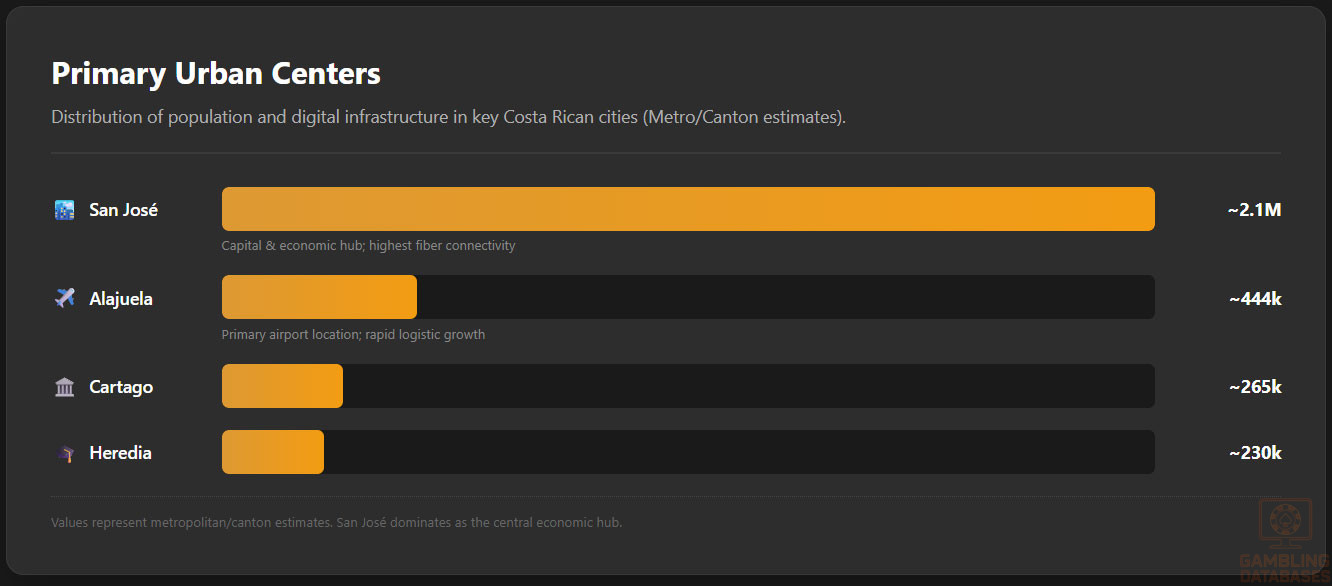

Urbanization is a defining trend, with 83.3% of the population residing in urban areas, a significant increase from 59% in 2000. The capital, San José, remains the economic and cultural hub, housing the largest concentration of internet users and digital infrastructure.

- San José – population ~350,000 (metropolitan area ~1.5 million)

- Alajuela – population ~180,000

- Cartago – population ~160,000

- Heredia – population ~130,000

- Limón – population ~100,000

- Puntarenas – population ~90,000

Regional disparities exist in internet access and digital adoption, with the Central Valley region leading in connectivity and service availability. Rural areas, particularly in Limón and Puntarenas, face challenges in broadband penetration, though mobile networks help bridge the gap.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

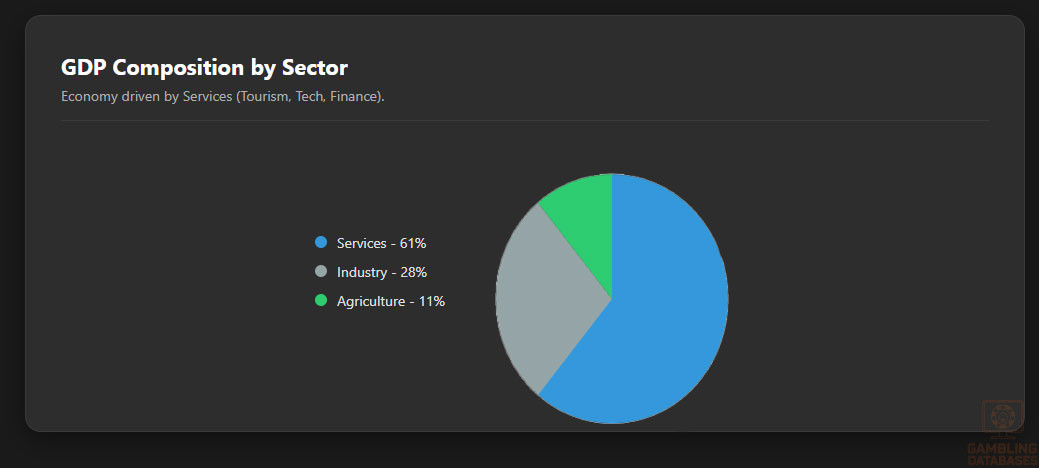

Costa Rica’s economy is robust, with a nominal GDP of approximately $68 billion USD in 2025. The country has maintained consistent growth, supported by strong performance in services, technology, and tourism. The service sector dominates at 61% of GDP, followed by industry at 28% and agriculture at 11%, reflecting a modern, diversified economy.

Per capita income is estimated at $13,000 USD, with a growing middle class that has increasing disposable income. The country’s inclusion in the OECD enhances investor confidence and supports long-term economic stability.

Income and Wealth Distribution

Average household income is approximately $1,062 per month, with higher earners concentrated in urban centers and the tech sector. Median income levels support moderate consumer spending, particularly in digital services and entertainment.

Market Size and Growth Projections

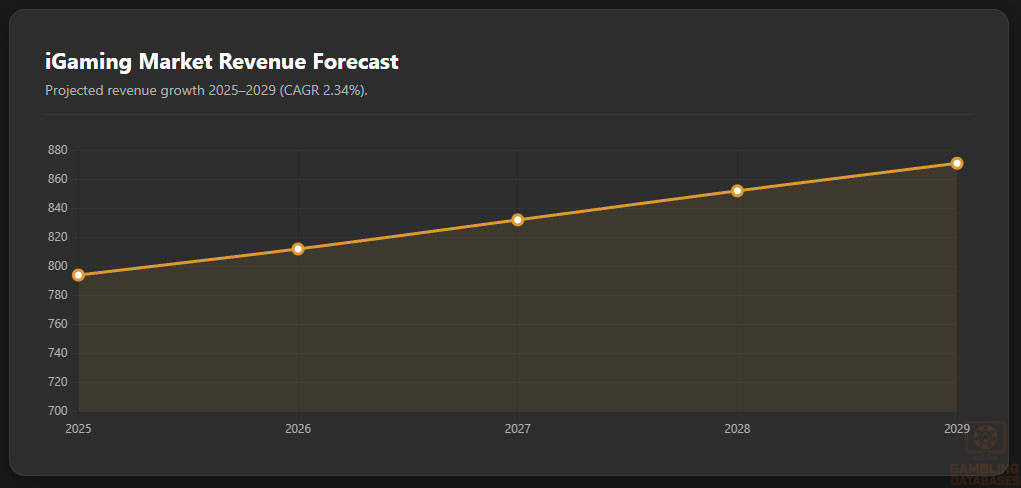

The iGaming market in Costa Rica is projected to reach $794 million in revenue by 2025, with a compound annual growth rate (CAGR) of 2.34% through 2029. This growth is driven by increasing digital adoption, mobile gaming, and the presence of international operators using the country as a base.

| Year | Market Revenue (US$ million) | Growth Rate (CAGR %) |

|---|---|---|

| 2025 | 794 | 2.34% |

| 2026 | 812 | — |

| 2027 | 832 | — |

| 2028 | 852 | — |

| 2029 | 871 | — |

The active gamer base exceeds 1.4 million, representing a significant portion of the population. Average revenue per user (ARPU) is estimated between $500 and $1,000 every six months, indicating strong monetization potential.

Education, Skills, and Digital Literacy

Costa Rica has a high literacy rate of 97.9%, supported by strong public education and government investment. The Ministry of Public Education has implemented digital learning initiatives, though disparities remain between urban and rural access.

Higher education institutions produce a skilled workforce in technology, engineering, and business, contributing to the country’s reputation as a tech hub in Central America. Digital literacy is improving, particularly among younger generations, though challenges persist in older demographics and low-income communities.

Recent World Bank funding supports digital competency programs for one million students, aiming to close the digital divide and enhance employability. Teacher training and digital platform access are key components of this national strategy.

Cultural and Social Factors

Communication and Language

Spanish is the official and dominant language, used in all formal and digital communication. English proficiency is moderate, particularly in urban areas and among younger, educated populations, facilitating international business operations.

Internet language preferences align with Spanish, though bilingual content is increasingly common in tech and gaming sectors. Communication norms emphasize personal relationships and trust, which influence marketing and customer engagement strategies.

Cultural Attitudes

Gambling is culturally accepted, particularly in the form of the national lottery and sports betting. Religious influences, primarily Catholic, do not strongly oppose gambling, allowing for broad social tolerance.

Foreign brands are generally well-received, especially in technology and entertainment. The population values innovation and quality, making Costa Rica an ideal test market for new digital products and services.

Entertainment preferences lean toward social and interactive experiences, including mobile gaming, eSports, and live-streamed content. This cultural inclination supports the growth of online gambling platforms with strong community features.

Problem Gambling and Social Considerations

Problem gambling prevalence is estimated at 1.2% of the adult population, with higher risk among younger males and low-income groups. At-risk populations include individuals with limited financial literacy and those exposed to aggressive online marketing.

Government response measures include public awareness campaigns, support hotlines, and collaboration with operators on responsible gambling initiatives. While formal regulations are limited, industry self-regulation is encouraged.

- Public education programs on gambling risks

- Support hotline for problem gamblers

- Partnerships with NGOs for counseling services

- Online self-exclusion tools

- Responsible advertising guidelines

Operators are expected to implement KYC and AML procedures, though mandatory contributions to social programs are not currently required. Future regulatory developments may introduce formal responsibility frameworks.

Political Structure and Governance

Costa Rica operates as a stable democracy with a presidential system and strong rule of law. The country has no standing army, redirecting resources toward education and healthcare, which enhances social stability.

Political consistency supports long-term business planning, with bipartisan support for technology and foreign investment. International relations are strong, particularly with the United States, the European Union, and Latin American neighbors.

Regulatory consistency is high in general business law, though the absence of formal iGaming regulation creates uncertainty for long-term operators. Ongoing dialogue suggests potential future formalization of the sector.

Technology Adoption and Digital Behavior

Internet and Digital Usage

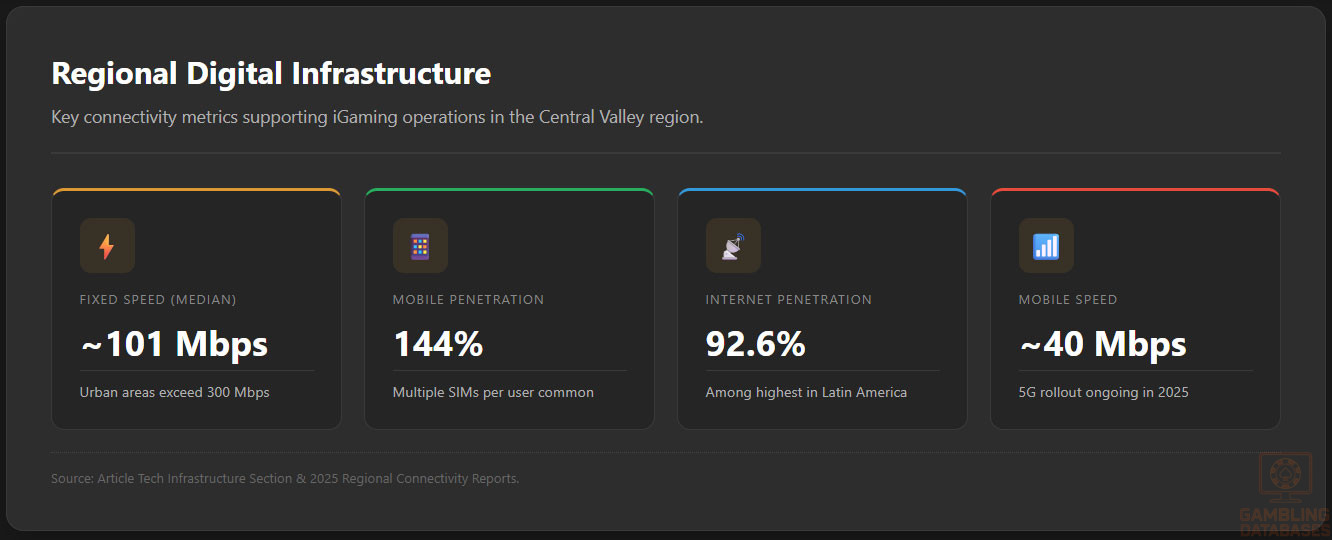

Internet penetration is robust at 92.6%, with 4.76 million users as of early 2025. Mobile connectivity is even higher, with 7.4 million cellular connections, equivalent to 144% of the population, reflecting widespread multi-device usage.

Digital behavior is mobile-first, with 70% of users accessing the internet primarily through smartphones. Average daily usage exceeds three hours, with high engagement on social media, video, and gaming platforms.

| Metric | Value |

|---|---|

| Internet Penetration | 92.6% |

| Mobile Connections | 7.4 million (144% of population) |

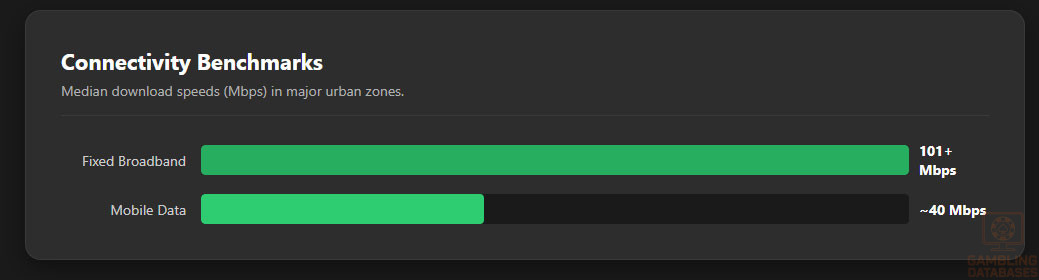

| Median Mobile Speed | 39.44 Mbps |

| Median Fixed Speed | 100.92 Mbps |

Digital Payment Behavior

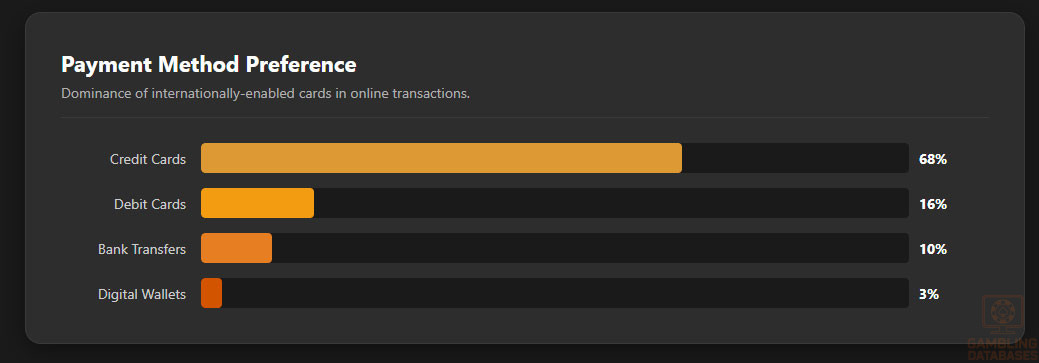

Payment method preferences are dominated by internationally enabled credit cards, which account for 68% of online transactions. Debit cards and bank transfers are also common, while digital wallets and mobile payments are growing rapidly.

- Internationally-enabled credit cards – 68%

- Debit cards – 16%

- Bank transfers – 10%

- Digital wallets – 3%

- Other (gift cards, pay-on-delivery) – 3%

Cryptocurrency adoption is high among tech-savvy users, with platforms like SINPE Móvil enabling mobile-based transactions. This trend supports the growth of crypto-friendly iGaming operators targeting international markets.

Gaming and Gambling Preferences

Current Market Participation

Gambling participation is widespread, with the majority of players aged 17–38. Sports betting is the most popular activity, followed by casino games, poker, and lottery. eSports and fantasy sports are gaining traction, particularly among younger users.

- Sports betting – football, basketball, international events

- Online casino – slots, blackjack, roulette

- Poker – online and live tournaments

- Lottery – state-run games via Junta de Protección Social

- eSports betting – growing rapidly with dedicated platforms

| Game Type | Description / Popularity |

|---|---|

| Casino Games | Slots, Blackjack, Roulette, Baccarat; popular online & offline |

| Sports Betting | Football, basketball, international sports; strong online presence |

| Poker | Online and offline tournaments and cash games |

| Lottery | State monopoly operated by Junta de Protección Social |

| eSports & Fantasy Sports | Growing interest with professional teams and tournaments |

Consumer Behavior Patterns

Spending habits show that most gamers spend between $500 and $1,000 on gaming products and services every six months. Mobile gaming dominates, with over 70% of users playing on smartphones for three or more hours daily.

Platform preferences favor social and immersive experiences, including gamification, leaderboards, and multiplayer features. Retention is driven by personalized content, loyalty rewards, and seamless payment integration.

Peak usage times align with evenings and weekends, coinciding with sports events and social gaming sessions. Session lengths average 45–60 minutes, with higher engagement during live events and promotions.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

The national internet backbone and fixed broadband infrastructure in Costa Rica deliver strong performance in urban areas, with fiber deployments concentrated in Greater San José and key coastal provinces, supporting low-latency services and high-throughput applications required by modern iGaming platforms.

Fixed broadband median download speeds in 2025 exceed 100 Mbps in many served regions while mobile median download speeds regularly range between 30–60 Mbps, enabling consistent live dealer streaming and low-latency sports-betting experiences on mobile devices.

| Metric | Value |

|---|---|

| Fixed broadband median download speed | ~100–310 Mbps (regional variance) |

| Mobile median download speed | ~39–84 Mbps (operator variance) |

| Fixed median upload speed | ~75–277 Mbps (top ISPs) |

| Average latency (fixed) | ~6–25 ms (region-dependent) |

| Network reliability | High in urban centers; lower in remote provinces |

Redundancy is available through multiple submarine cable landings and regional peering points that reduce packet loss and support predictable performance for latency-sensitive gaming. Data center capacity in San José provides colocation and DDoS protection services commonly required by operators.

5G and Future Technology Deployment

5G rollout is progressing across major population centers with commercial availability from primary mobile operators and targeted expansions planned for the next 24–36 months. This rollout improves mobile broadband consistency and reduces latency for mobile-first gaming experiences.

Investment priorities for the near term focus on densifying urban coverage, upgrading backhaul capacity to support mmWave and mid-band spectrum use, and enabling enterprise-grade private 5G for large operator offices and data centres.

| Indicator | Status (2025) |

|---|---|

| Commercial 5G coverage (major cities) | Available (expanding) |

| 5G enterprise trials | Ongoing with operators and vendors |

| Backhaul upgrades | Fiber-centric investments in urban zones |

| Expected nationwide maturity | 24–36 months |

Mobile Technology Ecosystem

Mobile networks serve as the primary access method for gaming platforms, with multiple national operators offering broad 4G LTE coverage and growing 5G footprints in urban areas. Device fragmentation is moderate, with the majority of active users on Android devices and a sizeable iOS user base among higher-income segments.

Smartphone penetration exceeds 80% among adults in urban centers and is rapidly rising across younger cohorts, making mobile-first product design essential for market entry and retention.

- Claro — market leader in speed and coverage in many urban samples

- Liberty — strong consistency and video performance in specific regions

- Kölbi — strong coverage in provincial areas and public sector reach

- Tigo/Movistar — niche coverage and competitive pricing in segments

- MVNOs and regional cooperatives — local presence in rural zones

| Metric | Value |

|---|---|

| Smartphone penetration (urban adults) | >80% |

| Multiple SIM ownership | ~130% mobile penetration (subscriptions per 100 people) |

| Mobile-first user share | Majority for gaming traffic |

| Device OS split | Android dominant; iOS significant in higher-income groups |

Financial Services and Payment Infrastructure

The Costa Rican banking system comprises state-owned, national commercial, international and digital banks that offer traditional account services, merchant acquiring and corporate banking required by iGaming operators. Digital banking adoption has accelerated, although international e-wallets and payment processors remain critical for cross-border gaming flows.

Opening corporate bank accounts requires standard KYC documentation and can be more time-consuming for gambling-related businesses, encouraging many operators to rely on international PSPs and crypto rails for player-facing transactions.

- Banco Nacional de Costa Rica — significant state-owned bank with broad branch network

- Banco de Costa Rica — major national bank with corporate services

- BAC Credomatic — regional commercial bank with international connections

- Davivienda / Grupo Improsa — commercial banking and corporate products

- Scotiabank / Citibank — international banking services and multicurrency support

| Payment Method | Typical Use Case |

|---|---|

| Credit/Debit Cards (Visa/Mastercard) | Primary for international player deposits |

| International E-wallets (Skrill, Neteller, PayPal) | High-convenience cross-border payments |

| Bank Transfers / ACH | Used for large corporate flows and payouts |

| Cryptocurrency (BTC, ETH, stablecoins) | Growing use for deposits/withdrawals, faster settlement |

| Local payment providers | Limited use for international-facing operators |

E-commerce and Digital Economy

E-commerce growth is robust with increasing consumer trust in digital payments and delivery logistics; this maturation translates directly into greater willingness to pay for digital entertainment and gaming services. Consumer trust benchmarks and dispute resolution mechanisms support online transactions but reputational risk remains higher for high-value cross-border payments.

Local digital service platforms, fintech startups, and payment aggregators are expanding, creating ecosystem opportunities for partnerships that can lower payment friction for player deposits and withdrawals.

| Indicator | Value |

|---|---|

| E-commerce penetration | Growing double digits annually |

| Digital payments share | Majority of online transactions |

| Fintech adoption | Increasing among SMEs and startups |

| Consumer trust index | Improving with regulatory clarity |

Business Environment and Regulatory Framework

Costa Rica scores favorably on political stability and rule of law metrics, with transparent procedures for company registration and tax compliance. Foreign direct investment is actively encouraged, and corporate structures permit full foreign ownership in most sectors.

Operational costs are moderate compared to North American and European hubs, with lower office rental rates outside central San José and competitive talent costs for tech and support roles.

Corporate Structure and Registration

Available entity types commonly used by international operators include the Sociedad Anónima (S.A.), the Sociedad de Responsabilidad Limitada (S.R.L.), and branch operations of foreign corporations. Most international gaming businesses favour an S.A. for governance flexibility and clarity in share transfers.

Registration involves corporate formation, tax ID registration, municipal registration for data processing licensing, and opening a local corporate bank account. Timeline and complexity vary by service provider and bank responsiveness.

- Prepare and notarize founding documents and powers of attorney

- Register company at the Mercantile Registry and obtain corporate ID

- Register for tax identification with the tax authority

- Apply for municipal data processing license and local permits

- Open corporate bank accounts and finalize operational arrangements

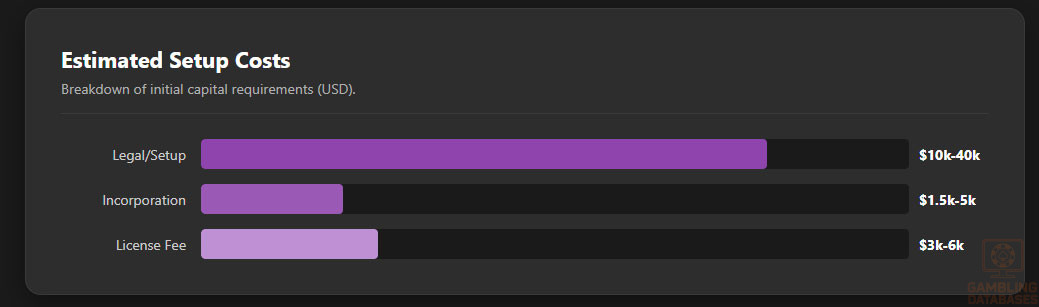

| Item | Estimate / Timeline |

|---|---|

| Company incorporation | $1,500–$5,000; 2–4 weeks |

| Municipal data processing license | $3,000–$6,000 annual; 3–5 weeks |

| Legal & compliance setup | $10,000–$40,000 initial |

| Bank account opening | 2–8 weeks (higher scrutiny for gaming) |

| Initial working capital | $100,000+ recommended |

Taxation Framework

Corporate taxation follows national rules with standard corporate income tax applied to business profits; operators routed to international markets will be taxed on local-source profits and must comply with withholding and VAT rules where applicable. Special economic zones and investment incentives exist for qualifying entities in particular sectors.

Personal income tax rates apply to resident personnel and social security contributions for payroll, creating predictable labor cost structures for local hires and expatriate employees under specific residency arrangements.

| Tax Type | Typical Rate / Note |

|---|---|

| Corporate income tax | Progressive rates; effective around 30% for many companies |

| VAT / Sales tax | Standard VAT applies to goods and some services |

| Payroll contributions | Employer + employee contributions to social security |

| Municipal license fees | Annual data processing license fees variable by municipality |

Market Entry Considerations

Recommended entry strategies prioritize establishing a local corporate entity, securing municipal data processing licensing, and partnering with reputable international PSPs for payments and AML-compliant KYC providers to reduce time-to-market. A mobile-first product approach with Spanish localization and multilingual support is essential to maximize reach.

- Form local S.A. with clear corporate governance

- Obtain municipal data processing license early in timeline

- Engage experienced local legal and compliance advisors

- Partner with international PSPs and crypto liquidity providers

- Deploy localized mobile-first platforms with Spanish UX

Typical timelines to operational launch range from 8 to 16 weeks for setup and technical deployment if banking and licensing proceed without delay, while full commercial traction often requires 12–24 months of marketing and product optimization.

| Phase | Duration |

|---|---|

| Corporate formation & licensing | 3–6 weeks |

| Banking & payments setup | 4–8 weeks |

| Technical deployment & testing | 4–8 weeks |

| Soft launch & compliance testing | 4–12 weeks |

| Full commercial launch | After ~3–6 months from start |

Success Factors and Challenges

Success is driven by strong compliance programs, robust payment rails, localized product experiences, and partnerships with reliable infrastructure providers for hosting and security. Access to skilled talent and stable connectivity in target regions are additional enablers for scaling operations.

Primary challenges include banking friction for gambling-related businesses, reputational risk management in international markets, and potential future regulatory changes that could introduce licensing costs or market access limitations.

- Strong AML/KYC and compliance capabilities required

- Reliable payment and fiat settlement channels critical

- Local talent acquisition for operations and customer support

- Scalability of hosting and DDoS mitigation services

- Regulatory uncertainty risk if formal online licensing is introduced

Exit Strategy Planning

Exit planning should account for corporate share transferability under S.A. structures, valuation multiples driven by recurring revenues and ARPU, and potential constraints on license transfer depending on municipal rules. Structuring shareholder agreements to enable orderly exits and buy-sell mechanisms is standard practice.

Market liquidity for iGaming assets depends on track record, profitability, and regulatory clarity; well-structured operations with clean compliance histories attract higher multiples from strategic buyers targeting LatAm operations.

| Item | Benefit / Cost Consideration |

|---|---|

| Local incorporation | Cost: Moderate; Benefit: Legal presence and local banking access |

| Data processing license | Cost: Low; Benefit: Permits local operations and hosting |

| Banking relationships | Cost: Time-consuming; Benefit: Essential for fiat flows |

| Technical hosting & security | Cost: Ongoing; Benefit: Operational stability and player trust |

| Compliance programs | Cost: Significant; Benefit: Risk mitigation and market legitimacy |

FAQ: Frequently Asked Questions

1. Is online gambling legal in Costa Rica?

Online gambling is not regulated through a dedicated national online gaming license, but operators can lawfully base operations in Costa Rica under municipal data processing licenses while serving international customers. This model requires that services not be marketed to or processed through Costa Rican payment systems for local players, and operators must comply with national AML, KYC and corporate laws.

Operators should implement strong compliance controls, avoid explicitly targeting Costa Rican residents, and ensure payment flows and customer support routing are aligned with the municipal licensing terms.

2. What types of gambling licenses are available and what do they cover?

Costa Rica does not provide specialized online gambling licenses; the relevant permission for hosting digital platforms is a municipal-level data processing license that permits data-centre operation and digital services. Land-based casinos and lotteries are subject to national laws and oversight by the Ministry of Public Security and the Junta de Protección Social for monopolized lotteries.

Companies seeking to operate online typically combine local incorporation with municipal licensing and international third-party certifications for RNG and fair-play assurances to meet counterpart jurisdiction expectations.

3. How much does an iGaming license cost and how long does it take to obtain?

There is no formal national iGaming license fee, but municipal data processing licenses typically range from a few thousand to several thousand dollars annually depending on the municipality. Company formation, legal setup, and compliance investments represent the larger initial cost components and timelines normally span 8–16 weeks to operational launch if banking is available.

Costs include legal and compliance setup, data processing municipal fees, corporate formation expenses, and technical hosting and security budgets that together form the bulk of upfront investment.

4. Can foreign companies obtain a gambling license?

Foreign companies may incorporate local entities and obtain municipal data processing licenses with full foreign ownership permitted. The practical requirement is establishing a local legal entity and a physical office address for municipal registration, followed by meeting AML/KYC and corporate tax obligations.

Foreign operators typically engage local legal counsel to navigate incorporation, municipal engagement and bank account opening due diligence to expedite setup.

5. What are the tax obligations for iGaming operators?

Operators incorporated and conducting business in Costa Rica are subject to standard corporate taxation on locally sourced profits, payroll taxes and indirect taxes where applicable; there is no specific national online gambling tax regime for internationally-facing operators. Municipal fees for data processing licenses are recurring obligations in addition to corporate tax filings.

Tax structuring considerations often involve transfer pricing, allocation of revenue between jurisdictions, and ensuring compliance with local withholding and reporting rules for cross-border payments.

6. Are gambling winnings taxed for players?

Gambling winnings are generally not taxed for Costa Rican residents, making the jurisdiction attractive from a player tax perspective. International players will remain subject to the tax rules of their country of residence which operators must consider in reporting and withholding obligations for certain markets.

Operators should design customer communications and tax documentation to reflect the tax residency status and applicable obligations of their player base.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include corporate formation and licensing fees, legal and compliance setup, technical hosting and security, platform software licensing or development, payment processing fees, customer support, and marketing. Initial set-up budgets commonly start at a low six-figure USD amount for lean launches, with more robust market entries requiring higher capital to cover liquidity, marketing and regulatory readiness.

Costs vary by scale, product complexity, and the degree of localization required; contingency budgets for banking delays and compliance remediation are recommended.

8. What is the expected ROI timeline for entering this market?

Expected ROI depends on the business model, marketing effectiveness and payment access; operators with strong product-market fit and reliable payment rails can approach break-even in 12–36 months. Lower-cost operations that leverage third-party platforms may see shorter timelines, while those investing heavily in proprietary platforms and brand building should plan for a longer payback horizon.

Key ROI drivers include ARPU, user acquisition cost, retention rates and operational efficiency through automation and robust fraud prevention.

9. What are the local presence requirements for operators?

Operators must register a local legal entity and obtain a municipal data processing license that requires a registered office address and local representative for administrative purposes. Physical presence requirements are functional and administrative rather than implying operational limits on personnel or revenue sources.

Maintaining transparent corporate governance and local point-of-contact for regulatory interactions is essential to retain municipal permissions and banking relationships.

10. What payment methods are available and recommended?

Recommended payment methods for international-facing operators include credit/debit cards, major international e-wallets, bank transfers for corporate flows, and cryptocurrencies where acceptable to target markets. Local bank integration is limited for player payments due to risk policies of domestic banks toward gambling; therefore, international PSPs and crypto rails are common choices.

Implement tiered KYC, risk-based AML controls and multiple payment rails to reduce friction and increase conversion while protecting compliance posture.

11. What are the advertising and marketing restrictions?

Advertising directed at international audiences follows the rules of the target jurisdictions; direct marketing to Costa Rican residents is restricted under the operational model that avoids servicing locals. Operators must adhere to self-regulatory standards, truthful advertising, and responsible gambling presentation across channels.

Brand safety measures, geo-targeting controls and compliance with advertising codes in target markets are standard operational requirements to avoid cross-border regulatory breaches.

12. What responsible gambling measures are mandatory?

Although Costa Rica lacks a dedicated online gambling regulator, operators are expected to implement AML/KYC, age verification, self-exclusion options, deposit and loss limits, and transparent terms. Industry best practice also includes player risk profiling, treatment referral pathways and mandatory staff training on responsible gambling.

Operators should embed these controls in platform design and supplier contracts to demonstrate compliance and social responsibility to partners and payment providers.

13. How large is the iGaming market and what is the growth potential?

The addressable iGaming market for operators based in Costa Rica is modest domestically but substantial internationally; market estimates range from tens of millions in direct revenue today with a projected CAGR in the high single digits over the next five years. Growth drivers include broader digital adoption, rising ARPU from targeted segments, and expansion into underserved Latin American markets.

Strategic focus on mobile-first products, multi-currency support and regional marketing channels will define the pace and scale of growth for new entrants.

14. Who are the main competitors and what is their market share?

Competition comprises international operators that use Costa Rica as a base for their international-facing platforms, technology service providers, and regional brands that target Latin American audiences. Market share is fragmented with no single dominant online operator within the domestic market due to the international-facing operating model.

Competitive advantage accrues to players with secure payment access, localized product offers, and well-built compliance frameworks enabling service continuity across jurisdictions.

15. What are the player preferences and typical spending patterns?

Players show preference for mobile-friendly interfaces, quick deposit and withdrawal options, and games with social engagement or live elements. Typical spending patterns favour frequent small-stake bets among younger users and higher-value, less frequent play among older or higher-income segments.

Retention correlates strongly with localized content, fast and transparent payout experiences, and loyalty programmes that reward sustained play and referrals.

16. What are the key success factors and main challenges for new entrants?

Key success factors include compliant operations with robust AML/KYC, reliable multi-rail payment integrations, localized product-market fit, and resilient technical infrastructure for streaming and security. Challenges include bank account access limitations for gambling businesses, potential future regulatory tightening, and competition for talent and market share in regional markets.

Mitigation strategies include strong legal advisory engagement, diversified payment stacks, incremental market entry pilots and investment in customer trust and security capabilities.

Sources and References

- Speedtest® Connectivity Report | Costa Rica H1 2025 — Ookla

- Digital 2025: Costa Rica — DataReportal / We Are Social

- Worldometers — Costa Rica population and demographic data (2025)

- World Population Review — Costa Rica (2025)

- Statista — Costa Rica digital and gambling market forecasts

- International Gambling Industry Reports — iGamingToday (2025)

- Global Law Experts — Costa Rica gambling license guide (2025)

- Tetra Consultants — Costa Rica gaming license overview (2025)

- Legarithm / Gambling license guides (2025)

- OECD Tax Policy Reviews: Costa Rica

- Central Bank of Costa Rica — Financial statistics and reports

- Ministry of Finance, Costa Rica — Taxation and corporate rules

- Ministry of Public Security, Costa Rica — Land-based gambling oversight

- Junta de Protección Social — Lottery and monopolized betting rules

- Local legal practice guides — Chambers Banking Regulation 2025

- Statistical Office publications — UNFPA and national statistics

- SpeedGEO.net — Internet speed snapshots for Costa Rica

- PopulationPyramid.net — Age distribution data (2025)

- Mordor Intelligence — Costa Rica telecom market report (2025)

- Fitch Ratings — Costa Rica sovereign and banking sector notes (2025)

- Global Banking & Finance — Banks in Costa Rica overview

- Confidus Solutions — List of banks in Costa Rica

- Netflix ISP Speed Index — regional ISP performance (2025)

- TGM Research — Gambling and sports betting surveys (region)

- Local news and industry analysis — Gambling Insider, GlobalBrandsMag

- Industry provider whitepapers — Payment processors and PSP guides

- Fintech and neobank listings for Costa Rica (2024–2025)

- Legal and tax advisory publications — FBS Tax, SDLCCorp analyses

- Global telecom reports and operator disclosures (Claro, Liberty, Kölbi)

- Metrocom and Telecable public performance reports

- Regional e-commerce and digital payment reports (2024–2025)

- Industry compliance guidance — AML/KYC best practices for gaming

- Academic studies on gambling prevalence and social impacts (LatAm)

- News articles covering regulatory discussions and market changes (2023–2025)

- Operator public filings and market research briefs (2024–2025)

- Technical hosting and data center market briefs for Costa Rica

🎯 Gambling Databases Country Rating: Costa Rica

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.5/10 | 🟡 Moderate |

| Player Access Score | 6.3/10 | 🟡 Partially Legal |

| Overall Market Attractiveness | 6.4/10 | 🟡 Startup Friendly / Banking High Risk |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- No “True” Gambling License: Costa Rica DOES NOT issue online gambling licenses. You operate under a “Data Processing License.” This holds zero regulatory weight in other jurisdictions and offers no player protection credibility.

- Banking Nightmare: Local banks generally refuse to service gambling companies. You will be forced to use offshore EMIs or Crypto. Tier 1 payment processors often reject Costa Rican entities due to lack of formal regulation.

- Local Market Prohibition: Targeting Costa Rican residents is STRICTLY PROHIBITED. Violating this jeopardizes your data processing license and invites municipal enforcement.

- Reputational Black Hole: A Costa Rican structure is often flagged as “High Risk” by European and North American financial institutions, complicating B2B partnerships.

- Extradition Risks: Costa Rica has strong extradition treaties with the USA and Europe. It is not a safe haven for operators evading prosecution in those jurisdictions.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 1.5/3.0 | “Data Processing” framework allows all verticals for export (+3.0). However, lack of specific gambling regulation means zero legal protection (-1.0). Prohibition on local market (-0.5). Final: 1.5/3.0 |

| Licensing Process | 25% | 2.25/2.5 | Extremely accessible. 3-5 week timeline (+2.0). Low costs under $10k (+0.5). Deductions: No formal vetting means low trust/value (-0.25). Final: 2.25/2.5 |

| Taxation & Costs | 20% | 1.5/2.0 | No GGR tax (+2.0). Subject to ~30% Corporate Income Tax on local source income (-0.5). If structured correctly as offshore income, tax can be minimized, but standard compliance costs apply. Final: 1.5/2.0 |

| Operational Requirements | 15% | 0.75/1.5 | Requires physical office and legal representative (+1.0). Deductions: Local banks are hostile, forcing complex offshore banking setups (-0.5). Monitoring/Audits exist but are municipal (-0.25). Final: 0.75/1.5 |

| Market Environment | 10% | 0.5/1.0 | Stable political environment (+0.7). Deductions: “Grey market” reputation hurts credibility (-0.25). Constant threat of future regulation changing the model (-0.25). Final: 0.5/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.0/4.0 | Locals cannot legally be targeted by domestic entities (-1.5). Status of playing on offshore sites is Grey/Unregulated (+1.0). No protection for players. Final: 1.0/4.0 |

| Practical Accessibility | 30% | 3.0/3.0 | No ISP blocking. Crypto, E-wallets, and international cards work freely (+3.0). High internet penetration. Final: 3.0/3.0 |

| Player Penalties | 20% | 2.0/2.0 | No taxes on winnings (+1.0). No penalties for playing online (+1.0). Final: 2.0/2.0 |

| Market Availability | 10% | 0.25/1.0 | No licensed local options for online casino (Land based only). Players forced to use offshore sites. Final: 0.25/1.0 |

🔍 Key Highlights

Strengths

- Low Entry Barrier: One of the cheapest jurisdictions globally; license/setup costs are approx. $5,000 – $10,000.

- Speed: Operations can be live in 3-5 weeks, significantly faster than Malta or Curacao.

- Crypto Friendly: Extremely favorable environment for cryptocurrency casinos due to lack of specific banking restrictions in the “Data Processing” definition.

- No GGR Tax: No Gross Gaming Revenue tax is applied to international income.

⛔️ CRITICAL RISKS AND CHALLENGES

- Banking Isolation: Local banks (Banco Nacional, BCR) will rarely open accounts for gambling entities. You must rely on international EMIs or Crypto.

- License Credibility: A Costa Rican license is viewed as a “self-regulated” claim by Tier 1 regulators. It offers no shield against enforcement from other countries.

- Local Prohibition: You legally CANNOT accept Costa Rican traffic. Doing so voids your compliance and risks closure.

- Payment Processing: High-risk merchant category codes (MCC 7995) are hard to process with standard acquirers without a “respected” license (e.g., Malta/Isle of Man).

- Regulatory Uncertainty: The “Data Processing” loophole is constantly under discussion for reform. A sudden shift to a formal licensing regime could impose retroactive fees or taxes.

Player-Specific Issues

- Local players have zero consumer protection when playing on Costa Rica-hosted sites.

- Disputes over non-payments cannot be escalated to a gambling regulator, only to general consumer courts which are ineffective for this sector.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $15,000 – $40,000 (Includes legal setup, office lease, and first year fees).

Monthly Operating Costs: $3,000 – $5,000 (Minimum for office/rep) + Tech costs.

Effective Tax Rate on Revenue: ~0% on GGR (if offshore), ~30% Corp Tax on local profits.

Customer Acquisition Cost: Variable (Global market dependent). High in Tier 1 countries due to lack of trust.

Time to Breakeven: 6-9 months (Due to low setup costs).

Profitability Assessment:

High Viability for Startups/Crypto: Extremely viable for bootstrapped startups or crypto-only casinos due to low burn rate.

Low Viability for White Markets: If your goal is to enter regulated markets (UK, Ontario, NJ) later, a Costa Rican history can be a liability during probity checks.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Medium | Low local risk if not targeting residents. High risk of domain seizure/blocking by target markets (e.g., USA, Australia). |

| Licensed Sports Betting Operators | Medium | Same as casino; legality is based on data processing, not gambling law. |

| Affiliates/Advertisers | Low | Costa Rica does not prosecute affiliates, but target market regulators might. |

| Payment Processors | High | Processing for unregulated entities creates high AML/compliance risk. Accounts frequently frozen. |

| Company Directors/Executives | Low/Medium | Safe locally if compliant with corporate law. Extradition risk exists if indicted by US/EU authorities for money laundering. |

🚨 Extradition and International Enforcement

Extradition Treaties: Costa Rica has active extradition treaties with the United States, European Union member states, and the United Kingdom.

Enforcement History: The USA has successfully extradited individuals from Costa Rica for money laundering and wire fraud related to online gambling (e.g., Liberty Reserve case, though payment specific, set a precedent). Costa Rica cooperates with INTERPOL.

Safe Jurisdictions: Costa Rica is NOT a safe jurisdiction for operators defying US DOJ or major European enforcement orders.

Travel Risk: Directors of Costa Rican entities targeted by US/EU warrants face high risk of arrest if traveling through Panama or allied nations.

📋 Final Verdict

Costa Rica receives an Operator Ease Score of 6.5/10 and a Player Access Score of 6.3/10, resulting in an overall market attractiveness rating of 6.4/10.

HONEST ASSESSMENT: Costa Rica is the “Wild West” of iGaming—cheap, fast, and largely unregulated. It is an excellent sandbox for cryptocurrency casinos and bootstrapped startups that cannot afford the €30,000+ costs of Curacao or Anjouan. However, for serious operators, the lack of a formal gambling license creates severe banking bottlenecks and prevents meaningful partnerships with top-tier game providers and payment processors. It is a launchpad, not a permanent home for a Tier 1 business.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A cryptocurrency-focused casino (Crypto-exclusive).

- A startup with less than $50k initial capital.

- Testing a new iGaming concept before seeking a Tier 1 license.

- Focusing on unregulated “grey” markets (LatAm, parts of Asia/Africa).

❌ Definitely Avoid If You Are:

- Planning to target Costa Rican residents (Illegal).

- Needing Tier 1 banking or standard credit card processing (Visa/MC often decline).

- A public company or planning an IPO (Compliance red flag).

- Targeting strictly regulated markets (UK, USA, Germany) where a “Data Processing” license is unrecognized.

⚠️ BOTTOM LINE: Enter Costa Rica for the low costs and crypto-friendliness, but stay for the banking headaches and lack of respect; use it as a stepping stone, not a fortress.