Kyrgyzstan’s iGaming market is emerging as a key opportunity in Central Asia, following the legalization of gambling activities starting in 2022. The country’s regulatory landscape establishes a framework for both land-based and online gambling, targeting foreign operators with significant restrictions for local players.

With a growing internet penetration and underdeveloped competition, Kyrgyzstan presents potential for iGaming operators seeking to enter a nascent but rapidly developing market supported by evolving regulation and tax incentives.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling legal status | Fully legalized with restrictions since 2022 |

| Primary governing legislation | “Gambling Activities in the Kyrgyz Republic” Law |

| Regulatory authorities | Financial Regulation Service (land-based), Communications Regulation Service (online) |

| Population | ~6.8 million (2025 estimate) |

| Urbanization rate | ~36% |

| GDP (nominal) | Approx. $9.3 billion (2025 estimate) |

| GDP per capita | ~$1,370 |

| Internet penetration | ~70% |

| Mobile penetration | ~110% (multiple SIM ownership) |

| Licensed online casinos | 5 (including Palmium, Internet Technologies Venice) |

| Licensed land-based casinos | 3 (mainly foreigner-only, located in Bishkek and Issyk-Kul) |

| License costs (online casinos) | Up to $1.1 million |

| License costs (land-based casinos) | $500,000 – $1.1 million depending on region |

| GGR tax rate (online casinos) | 4% |

| Fixed tax (land-based casinos) | ~600,000 KGS ($6,850) per gaming table |

| Corporate income tax | 10% |

| VAT rate | 12% |

| Minimum casino size | 200 sqm minimum gaming area |

| Minimum casino tables (Bishkek) | 10 gaming tables |

| Minimum casino tables (other regions) | 5 gaming tables |

| Slot machines per hall | At least 30 slot machines |

| Yearly market revenue forecast | $113 million (2025 forecast) |

| Annual gambling tax revenue | Approx. 60 million KGS (Q1-Q2 2025) |

| Local player restrictions | Locals banned from land-based casinos |

| Payment currency for online gambling | KGS only legally; foreign currency under discussion |

| Responsible gambling requirements | Self-exclusion, age verification mandatory |

| Video surveillance requirements | Real-time recording at all cash and registration points |

| Operational restrictions | Casinos only in designated zones; no credit loans for gambling |

| Market growth forecast (CAGR 2025-2030) | Approx. 8%-10% |

| Average Revenue Per User (ARPU) | Estimated $250 – $350 annually |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Kyrgyzstan fully legalized gambling in 2022 after a decade-long ban, with a distinct legal framework covering land-based and online sectors. The core legal act is the “Gambling Activities in the Kyrgyz Republic” law, which defines categories of gambling including casinos and virtual casinos.

The law authorizes both physical casinos and online platforms but imposes strict operational requirements and geographic restrictions primarily favoring foreign players in land-based establishments. Local residents are currently banned from accessing land-based casinos, though online gambling remains more loosely regulated toward domestic users.

Land-Based Gambling Activities

Land-based casinos are restricted to specific zones, including Bishkek and the Issyk-Kul region, with a minimum size regulation of 200 square meters for gaming floors. Casinos in Bishkek must have at least 10 gaming tables, while others require a minimum of 5 tables. Slot machine halls must host at least 30 machines.

Online Gambling Framework

Online and virtual casinos operate under a separate regulatory regime controlled by the State Service for Regulation and Supervision of Communications. These platforms are licensed independently from land-based casinos but must conform to software standards and provide secure and transparent operations.

The online sector experiences less stringent regulatory enforcement currently; the government is considering tightening oversight. Online casinos cater primarily to foreign customers, with domestic regulations still evolving in terms of currency acceptance and payment mechanisms. Two official online casino licenses have been issued to date, indicating a nascent but growing digital gambling market.

Licensed Operators and Market Players

The market currently includes a small number of licensed online casinos, including Palmium and Internet Technologies Venice, alongside three licensed land-based casinos. The competitive landscape is emerging, with operators focusing on high-end tourist venues due to restrictions on local player participation.

Market entry strategies need to account for regulatory opacity regarding local player access, adherence to operational mandates, and a focus on servicing foreign tourists and online international players. Operators benefit from relatively low GGR tax rates on online platforms but face high licensing costs and operational restrictions on land-based venues.

Licensing Framework and Requirements

Application Process and Eligibility

Licensing authority is split between two regulators: the Financial Regulation and Supervision Service under the Ministry of Economy for land-based operations and the Communications Regulation Service under the Ministry of Digital Development for online casinos. Both require adherence to financial stability, technical capabilities, and compliance with regulatory standards.

Application fees vary depending on location and type, with online casino licenses costing up to $1.1 million and land-based licenses ranging from $500,000 to $1.1 million. The licensing process involves comprehensive submission of documentation and technical certifications, including RNG certification and platform security verification.

Licenses are typically valid for multi-year periods, with renewal contingent on compliance reviews and adherence to tax obligations. The authorities maintain the right to suspend or revoke licenses upon violation of regulatory provisions.

Local Presence and Operational Requirements

Land-based operators must maintain physical casino establishments within designated regions and comply with minimum establishment sizes and facility standards. Online operators must register within Kyrgyzstan and use national domains but benefit from fewer location-based restrictions.

Foreign ownership is permitted; however, operators must demonstrate operational control within the country and ensure compliance with KYC and AML requirements. Partnership with local entities is encouraged to facilitate regulatory compliance and market navigation.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators must verify player age, implement robust KYC and AML procedures, and enforce self-exclusion mechanisms. Responsible gambling measures include mandatory display of risk warnings and tools for voluntary play limits.

- Age verification at registration

- Rigorous KYC data collection and verification

- Implementation of AML transaction monitoring

- Self-exclusion options for players

- Display of responsible gambling messages on platforms

- Training of staff on identifying problematic gambling behavior

Operators must maintain logs of player interactions and comply with data protection regulations. Regular audits by the regulator ensure ongoing compliance with player protection norms.

Financial Monitoring and Reporting

Operators are obliged to maintain detailed records of all transactions, including deposits, withdrawals, and payouts. Monthly financial reports, including tax filings, must be submitted to regulatory bodies for review.

- Monthly submission of gross gaming revenue (GGR) reports

- Quarterly financial audits by independent firms

- Annual tax return filings

- Immediate reporting of suspicious transactions

- Retention of financial data for minimum 5 years

Taxation Structure and Financial Obligations

Player Taxation

Players are generally not taxed directly on winnings; taxation is imposed on operators. No withholding tax is charged on player winnings, maintaining player-friendly conditions. However, all financial transactions must comply with anti-money laundering standards.

Operator Taxation

| Activity Type | Tax or Fee | Rate/Amount |

|---|---|---|

| Online Casinos | Gross Gambling Revenue Tax (GGR) | 4% |

| Land-Based Casinos | Flat tax per gaming table | 600,000 KGS (~$6,850) |

| Slot Machines | Flat tax per slot machine | 15,000 KGS (~$170) |

| Bookmakers | License fee per betting shop | 500,000 KGS (~$5,700) |

| Corporate Income Tax | On net profits | 10% |

| Value Added Tax (VAT) | Applied on services | 12% |

License renewal fees and other operational levies apply depending on the business scale and region. The tax regime for gambling is designed to attract investment while maintaining government revenue stability through predictable fixed and variable components.

Gambling Market Financial Performance

The Kyrgyz gambling market is forecasted to generate revenues exceeding $110 million in 2025. Tax contributions from gambling rose significantly in early 2025, with casinos contributing the majority share of over 58 million KGS in Q1-Q2.

Year-on-year growth is projected at 8%-10%, driven by gradual legalization and regulatory improvements. The split between land-based and online revenue is shifting as online platforms gain traction supported by growing internet penetration and mobile device usage.

Advertising and Marketing Restrictions

Advertising of gambling services is subject to restrictions including bans on targeting local residents for land-based casinos. Promotions must avoid misleading content and comply with age-limit warnings. Advertising channels are limited to regulated media and premises with consumate control on time restrictions.

- Prohibition of targeting minors and locals in ads

- Restrictions on advertising hours on TV/radio

- Ban on promoting credit or loan use for gambling

- Mandated inclusion of responsible gambling messaging

- Prohibition of outright bonus inducements in certain media

Sponsorship of sports and cultural events is permitted under strict guidelines requiring transparency and exclusion of minors. The advertising framework balances sector growth stimulation with social responsibility.

Recent Regulatory Changes and Their Impact

Since legalization in 2022, Kyrgyzstan has implemented several regulatory updates enhancing surveillance, compliance, and tax structures. Key changes include mandates for video surveillance in casinos, minimum venue size requirements, and consolidation of betting operations within casinos.

New laws propose reducing some land-based tax burdens to attract investment while considering future tightening of online gambling controls. Market growth is encouraged by incremental regulatory clarity and investment incentives, although restrictions on local access and licensing costs remain challenges.

Enforcement Mechanisms and Penalties

Regulators maintain strong enforcement powers including license suspension and revocation for violations, fines, and criminal prosecution for illegal gambling operations. Penalties apply to unlicensed operators, breaches of player protection, and failure to submit timely reports.

- License suspension or revocation for non-compliance

- Monetary fines based on violation severity

- Criminal charges for illegal gambling operations

- Confiscation of gaming equipment used unlawfully

- Public blacklisting of offending operators

Law enforcement continues to identify and shut down underground casinos, and compliance monitoring continues to tighten, especially for land-based establishments.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Kyrgyzstan’s population is estimated at approximately 6.8 million in 2025, with a youthful median age of 29.7 years. The population divides into about 40.2% aged 19 or younger, 53.6% between 20 and 64 years, and 6.2% over 65 years.

The gender ratio shows slightly more women than men, with approximately 980 men per 1,000 women. Population growth remains steady at around 1.1% annually, driven by a fertility rate of 2.67 children per woman.

Urban residents account for roughly 38.1% of the population and are concentrated primarily in a handful of cities, while the majority lives in rural areas, reflecting Kyrgyzstan’s agrarian economic base. Population density stands at about 35 people per square kilometer, with gradual urbanization projected to increase over the coming years.

| Age Group | Population Percentage |

|---|---|

| 0-19 years | 40.2% |

| 20-64 years | 53.6% |

| 65 years and above | 6.2% |

Internet access and gambling venue availability are heavily urban-centric, with greater penetration in Bishkek and Issyk-Kul. Rural regions experience comparatively lower digital penetration and economic activity, influencing consumer behavior and gaming accessibility.

- Bishkek: Approx. 995,000 residents

- Osh: Approx. 243,000 residents

- Jalal-Abad: Approx. 89,000 residents

- Karakol: Approx. 80,000 residents

- Kara-Balta: Approx. 70,000 residents

Economic Indicators and Consumer Spending Power

Kyrgyzstan’s GDP reached roughly $9.3 billion by 2025, reflecting robust growth averaging 6.8% projected for the year amid an economic recovery spurred by domestic demand and investment. Key sectors include manufacturing, agriculture, and services, with trade and construction acting as growth anchors.

Consumer spending shows cautious growth, with entertainment and digital services gaining traction among younger urban populations, offering a strong base for future iGaming market expansion.

| Indicator | Value |

|---|---|

| GDP (nominal) | $9.3 billion |

| GDP growth rate (2025 projected) | 6.8% |

| GDP per capita | $1,370 |

| Inflation rate | Single-digit (estimated 7%) |

| Unemployment rate | Approx. 7-9% |

| Average household income | Varies by region, ~ $3,500 per year urban average |

The iGaming market size is forecasted to expand considerably, driven by increased disposable incomes in urban centers and a rising digital economy. Revenue projections show market growth at a CAGR of 8-10%, with user base expansion supported by enhanced internet penetration and mobile device adoption.

| Year | Estimated Market Revenue (USD Million) | Annual Growth Rate (CAGR) | Estimated User Base (Thousands) |

|---|---|---|---|

| 2025 | 113 | 8% | 450 |

| 2026 | 122 | 8% | 490 |

| 2027 | 131 | 8% | 530 |

| 2028 | 141 | 8% | 570 |

| 2029 | 152 | 8% | 610 |

| 2030 | 164 | 8% | 660 |

Education, Skills, and Digital Literacy

Kyrgyzstan maintains a high literacy rate approaching 99%, with most of the population completing secondary education. Higher education enrollment is improving, especially in urban areas, enhancing workforce capabilities in technology and services sectors.

Digital literacy is growing rapidly, boosted by government initiatives and private sector investments in IT infrastructure. Most urban youth display strong familiarity with mobile and internet technologies, supporting digital entertainment uptake, though rural broadband access remains limited.

Cultural and Social Factors

Communication and Language

Kyrgyz and Russian are the official languages, with Russian widely used in business and online communication. Kazakh and Uzbek minorities also contribute to linguistic diversity, though Kyrgyz remains dominant in public life.

- Kyrgyz – majority language

- Russian – business, media, and online use

- Uzbek – regional minority areas

- Tajik – small minority usage

- Other Turkic dialects – localized presence

Cultural Attitudes

Gambling has traditionally been viewed with skepticism, influenced by Orthodox and Muslim religious values discouraging games of chance. However, younger generations show growing acceptance, particularly in urban settings, and foreign brands are largely welcomed as symbols of modernization and entertainment.

Social attitudes remain cautious due to concerns about addiction and financial harm, creating a dual market environment wherein legalized gambling targets foreigners while domestic regulation emphasizes player protection.

Problem Gambling and Social Considerations

The prevalence of problem gambling is relatively low but rising awareness has prompted government initiatives to address potential social harms. Public education campaigns, mandatory responsible gambling measures by operators, and treatment programs are part of this emerging framework.

- Public awareness and educational programs

- Operator contributions to social responsibility funds

- Self-exclusion programs across licensed platforms

- Government-supported treatment centers

- Collaboration with NGOs on addiction research

Political Structure and Governance

Kyrgyzstan operates as a parliamentary republic with a history of political volatility but relative stability since 2023. The government prioritizes economic development and regulatory transparency, positioning gambling legalization as a fiscal stimulus. Consistent regulatory updates reflect attempts to balance growth with social responsibility and international relations.

Technology Adoption and Digital Behavior

Internet and Digital Usage

The country’s internet penetration stands at an advanced 88.5% of the total population in 2025, with approximately 6.4 million users. Mobile internet speeds average a median download of 39.7 Mbps, facilitating rich digital experiences.

Social media engagement is robust among young adults, driving digital content consumption, communication, and online gambling interest.

- YouTube – 89% penetration, popular for video content

- Facebook – 78% penetration with high daily usage

- Instagram – 64% among 18-34 demographic

- TikTok – rapidly growing at 52% under 25

- VK (VKontakte) – popular Russian-language platform

- Telegram – widely used for messaging and channels

Digital Payment Behavior

Payment methods exhibit diversity with an increasing shift towards digital wallets and card-based payments in urban markets. Cash remains dominant in rural areas but mobile money and QR-based payments are rapidly expanding.

- Visa and Mastercard cards widely accepted

- Local payment system ELQR using QR codes

- Apple Pay and Google Pay adoption growing

- Bank transfers for large-ticket transactions

- Emerging use of cryptocurrencies in niche segments

Gaming and Gambling Preferences

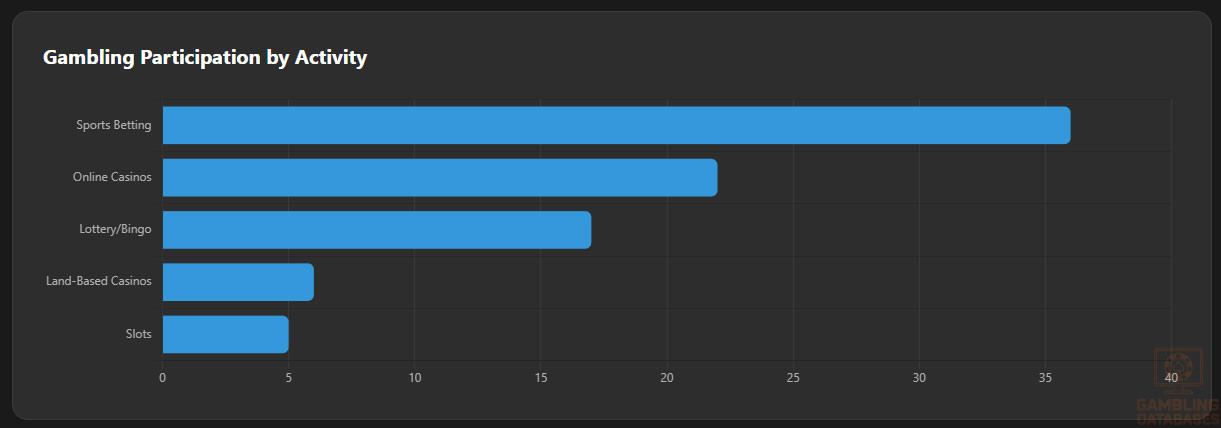

Current Market Participation

Gambling participation is currently limited by law, especially for local residents in land-based casinos. However, participation in online gambling and sports betting is on the rise, driven by younger demographics comfortable with digital entertainment.

| Activity | Estimated Participation Rate (%) |

|---|---|

| Sports Betting | 36% |

| Online Casinos | 22% |

| Lottery and Bingo | 17% |

| Land-Based Casinos (Foreigners Only) | 6% |

| Slot Machine Gaming | 5% |

Consumer Behavior Patterns

Operators report peak activity in evening hours and weekends with session lengths averaging around 35-45 minutes. Urban consumers prefer mobile platforms for gaming access, showing high retention rates when platforms offer localized content and easy payment options.

Spending patterns reveal cautious but growing budgets for entertainment, with ARPU estimated between $250 and $350 annually, driven by affinity for sports betting and popular casino games among the younger demographic.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Kyrgyzstan boasts an internet penetration rate of approximately 88.5% as of 2025, reflecting notable growth driven by urban adoption of broadband and mobile internet. Fixed broadband connections remain limited, accounting for about 25% of users, with mobile broadband serving the majority through affordable 3G and 4G networks.

Connectivity is characterized by average download speeds near 40 Mbps, adequate for delivering rich online gaming experiences. However, rural and mountainous regions suffer from limited infrastructure, impacting service reliability and latency. The government has prioritized investments in fiber optic expansion and satellite technologies to enhance nationwide coverage.

5G and Future Technology Deployment

The rollout of 5G in Kyrgyzstan is in early phases, with commercial coverage currently in Bishkek and several regional urban centers. A full national 5G network is projected for 2027-2028, backed by partnerships between government and leading mobile operators to accelerate digital transformation.

Mobile Technology Ecosystem

The mobile market includes several operators competing on coverage and data pricing. Mobile data is affordable relative to income, facilitating widespread smartphone usage and online service accessibility, crucial for iGaming growth.

- Beeline Kyrgyzstan – Market share approx. 37%

- Megacom – Market share approx. 33%

- O! (Sky Mobile) – Market share approx. 20%

- Sputnik – niche operator focused on rural areas

- AloCom – emerging competitor with expat focus

Smartphone adoption rates exceed 80% in urban areas, with popular device brands including Samsung, Xiaomi, and Apple. User preferences favor devices supporting fast mobile internet and seamless app experiences, reinforcing mobile-first strategies for iGaming operators.

Financial Services and Payment Infrastructure

The banking sector remains dominated by a few large institutions with growing digital banking platforms enabling easier access to financial services. Bank account penetration is approximately 45% of the population, with digital wallets and mobile money rapidly increasing in popularity.

- National Bank of Kyrgyzstan – Largest retail and corporate bank

- Optima Bank – Known for advanced digital solutions

- Kyrgyz Investment and Credit Bank – Major commercial lender

- Demir Kyrgyz International Bank – Strong regional presence

- First Microfinance Bank – Serving SMEs and rural clients

iGaming payment acceptance benefits from various options, including card networks, e-wallets, and bank transfers. Cryptocurrency adoption is nascent but observed in niche operator platforms.

- Visa and Mastercard debit/credit cards widely supported

- Qiwi and Yandex.Money local e-wallet alternatives

- Bank transfers through domestic clearing systems

- Mobile payment systems such as ELQR regional QR-code payments

- Emerging acceptance of Bitcoin and Ethereum for select platforms

E-commerce and Digital Economy

While still maturing, Kyrgyzstan’s e-commerce sector grows by double digits annually, spurred by rising digital payments and consumer confidence. Online retail penetration stands near 20%, with younger demographics driving demand for digital entertainment, fostering expansion of sectors like online gambling.

Consumer trust in digital services has improved thanks to fraud mitigation, better regulation, and increased mobile connectivity. These trends create a fertile environment for sustained iGaming market development.

Business Environment and Regulatory Framework

Kyrgyzstan ranks favorably in regional ease of doing business indices thanks to streamlined company registration processes and investor-friendly policies. The government encourages foreign direct investment, though some regulatory complexities and bureaucratic delays remain notable challenges.

- Prepare notarized incorporation documents with apostille where required

- Submit registration applications to Companies Registry, 5-7 business days

- Register with tax authorities, receive Tax Identification Number (TIN) within 3 days

- Open corporate bank accounts with minimum capital deposits

- Obtain industry-specific licenses including gambling permits

Corporate structure options include Limited Liability Companies (LLCs), Joint Stock Companies, and foreign Branch Offices. LLCs remain the preferred form for iGaming due to flexible governance and limited liability. Foreign ownership is permitted fully, though active local presence requirements apply for gambling licenses.

- Limited Liability Company (LLC) – common for small/medium enterprises

- Joint Stock Company – suitable for larger operations and capital raising

- Branch Office – subsidiaries of foreign companies registered locally

- Representative Office – limited activities, not allowed for gambling

- Nonprofit organizations – excluded from iGaming activities

Registration requires submission of multiple documents as well as compliance with financial and operational standards enforced by regulatory authorities, including KYC and AML protocols.

- Incorporation charter and founding documents

- Proof of registered office address

- Identification of directors and shareholders

- Tax registration certificate

- Licenses and permits specific to gambling activities

Taxation Framework

The corporate income tax rate in Kyrgyzstan stands at a flat 10%, with certain Special Economic Zones (SEZs) offering tax holidays and incentives to attract foreign operators. The country maintains double taxation treaties with multiple jurisdictions to prevent tax base erosion and encourage investment.

- Russia

- China

- Kazakhstan

- Turkey

- Singapore

- Switzerland

- United Arab Emirates

Personal income tax is withheld at progressive rates with a top marginal rate of 20%. Employers are responsible for withholding taxes and social security contributions. Residency for tax purposes applies to individuals spending more than 183 days annually in Kyrgyzstan.

Market Entry Considerations

Key entry strategies recommend forming joint ventures with local partners to navigate regulatory environment, developing mobile-optimized platforms localized linguistically and culturally, and leveraging digital payment ecosystems robustly integrated with local banking.

- Partnership with established local firms for compliance and market access

- Developing mobile-first platforms given smartphone prevalence

- Localized language support (Kyrgyz and Russian)

- Robust KYC/AML systems adapted to Kyrgyz legal standards

- Investment in marketing through approved channels respecting advertising restrictions

Initial setup and operational costs can be substantial due to licensing fees and compliance expenses, requiring careful budgeting for a break-even period typically ranging 12 to 24 months.

- License application and renewal fees

- Legal and consulting services

- Technology platform development/customization

- Marketing and customer acquisition expenses

- Personnel and operational infrastructure

- Pre-application market research and feasibility (1-2 months)

- Document preparation and licensing application (3-4 months)

- Platform development and integration (3-6 months)

- Launch and initial marketing (1-2 months)

- Ongoing compliance and growth scaling (continuous)

Operator success relies heavily on agile adaptation to regulatory changes, strong compliance culture, and effective customer engagement strategies balancing entertainment and responsible gambling.

- Understanding and adapting to evolving regulation

- Transparent compliance and reporting

- Investment in cybersecurity and payment security

- Building trusted brand presence locally

- Leveraging data analytics for user retention and growth

Exit options remain limited due to licensing restrictions, requiring strategic planning around ownership transfer and valuation considerations focusing on operational profitability and market position.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Kyrgyzstan?

Yes, online gambling is legally permitted under Kyrgyz law, with licenses issued to operators meeting regulatory standards. The government regulates online casinos separately from land-based casinos, requiring compliance with technical, financial, and player protection norms. Foreign and local operators can obtain licenses, though restrictions remain on local player participation in certain venues.

2. What types of gambling licenses are available and what do they cover?

Kyrgyzstan issues licenses for land-based casinos, online casinos, sports betting operations, slot machine halls, and betting shops. Each license covers specific activities authorized within designated geographic zones or online platforms, with separate regulatory obligations and fees. Operators must apply to the respective regulatory bodies overseeing financial and communications sectors.

3. How much does an iGaming license cost and how long does it take to obtain?

License fees vary by type and location, with online casino licenses costing up to $1.1 million and land-based casino licenses ranging between $500,000 and $1.1 million. The application process typically requires 3 to 6 months for review, including technical verification and compliance assessment before final issuance.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain gambling licenses provided they establish a local legal entity complying with Kyrgyz regulations. They must demonstrate operational presence, financial stability, and adhere to player protection measures. Joint ventures with local partners are common to facilitate regulatory navigation and market entry.

5. What are the tax obligations for iGaming operators?

Operators pay a 4% gross gaming revenue tax on online operations and fixed taxes per gaming table or slot machine for land-based venues. Corporate income tax is levied at 10%, with additional VAT obligations on services. Regular financial reporting and tax filings are mandatory to maintain licensing status.

6. Are gambling winnings taxed for players?

Players are generally not taxed directly on gambling winnings. Tax obligations fall predominantly on operators. This structure encourages player participation while ensuring government revenue through operator tax compliance.

7. What are the typical operational costs for running an online casino/sportsbook?

Major operational costs include licensing fees, platform development and maintenance, payment processing charges, marketing and customer acquisition, and personnel expenses. Compliance and cybersecurity investments are also significant to meet regulatory requirements and protect player data.

8. What is the expected ROI timeline for entering this market?

Return on investment is expected between 12 to 24 months, depending on scale and market response. Effective market penetration, localized offerings, and compliance adherence influence the speed of profitability.

9. What are the local presence requirements for operators?

Operators must establish a local legal entity, maintain registered office premises, and have designated compliance personnel within Kyrgyzstan. These measures ensure regulatory oversight and facilitate communication with authorities.

10. What payment methods are available and recommended?

Recommended payment options include Visa and Mastercard, local e-wallets like Qiwi and Yandex.Money, bank transfers, and mobile payment systems utilizing QR codes. Cryptocurrency acceptance is limited but growing within niche platforms.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors and local residents for land-based gambling. Restrictions exist on broadcast times, content prohibitions on credit or loan promotion, and mandatory responsible gambling warnings. Sponsorship activities require regulatory approval and transparency.

12. What responsible gambling measures are mandatory?

Operators are required to implement age verification, KYC/AML procedures, self-exclusion programs, responsible gambling messaging, and staff training to identify gambling problems. Periodic audits ensure compliance and player protection.

13. How large is the iGaming market and what is the growth potential?

The iGaming market is currently estimated at near $113 million in 2025, with projected growth rates of 8-10% annually. Increasing internet penetration and disposable incomes, especially in urban centers, support strong medium-term expansion.

14. Who are the main competitors and what is their market share?

The market hosts a handful of licensed operators including Palmium and Internet Technologies Venice for online platforms, and three licensed land-based casino operators focused on tourists. Market share is fragmented but consolidating as regulation matures.

15. What are the player preferences and typical spending patterns?

Players favor sports betting and online casinos, with average annual spend (ARPU) estimated between $250 and $350. Mobile platforms dominate access, with peak usage in evenings and weekends. Retention relies on localized content and seamless payment integration.

16. What are the key success factors and main challenges for new entrants?

Success hinges on compliance agility, local partnership, robust digital infrastructure, and culturally adapted offerings. Challenges include regulatory complexity, high licensing costs, competition for customer trust, and infrastructural limitations outside urban areas.

Sources and References

- Gambling in Kyrgyzstan: Obtaining a License & Legalization – Slotegrator, 2025

- Open a Casino in Kyrgyzstan | Turnkey Gambling Business – 2wpower.com, 2025

- Games – Kyrgyzstan | Statista Market Forecast, 2025

- Kyrgyzstan Population (2025) – Worldometers, 2025

- Demographics of Kyrgyzstan – Wikipedia, 2024

- Kyrgyzstan: Economic Outlook 2025 – Khan Teniri Capital, 2025

- Digital 2025: Kyrgyzstan – Datareportal, 2025

- Payment Processing in Kyrgyzstan – Novalnet, 2025

- List of Cities in Kyrgyzstan by Population 2025 – Chislennost, 2024

- Kyrgyzstan Gambling Regulatory Authority – Official Government Publications, 2024-2025

- Corporate Taxation in Kyrgyzstan – Revera Legal, 2025

- Kyrgyzstan Online Casinos – Star Gambling, 2025

- World Bank – Doing Business Report 2025

- International Telecommunication Union – ICT Statistics 2025

- Central Bank of Kyrgyzstan – Annual Financial Report 2025

- Ministry of Finance Kyrgyzstan – Tax Regulations 2025

- IMF – Kyrgyz Republic Economic Data 2025

- Kyrgyzstan Gambling Market Analysis – Gambling Insider, 2025

- Nova News – Gambling Tax Revenue Kyrgyzstan, 2025

- Regional Telecom Infrastructure Reports – 2024-2025

- Kyrgyzstan Digital Economy Outlook – 8b.world, 2025

- Consumer Payment Preferences in Kyrgyzstan – YOGONET, 2025

- Stargambling.net – Kyrgyzstan Casino Reviews & Ratings 2024

- Kyrgyzstan Government Official Gazettes – 2022 to 2025

- Gaming Industry Reports – Various Publishers 2024-2025

- Local News Reports on Gambling Legislation – AKChabar and others 2024-2025

🎯 Gambling Databases Country Rating: Kyrgyzstan

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.2/10 | 🟡 Moderate |

| Player Access Score | 8.8/10 | 🟢 Excellent |

| Overall Market Attractiveness | 5.5/10 | 🟡 Moderate / Risky |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Exorbitant License Fees vs. Market Value: Online casino licenses cost up to $1.1 million. In a country with a GDP per capita of ~$1,370, this creates an incredibly difficult ROI path.

- Local Player Restrictions (Land-Based): While online is “loosely regulated” for locals, land-based casinos are strictly BANNED for Kyrgyz citizens. There is a significant risk that this ban could extend to online platforms in future regulatory updates to align with social/religious protections.

- Currency & Payment Restrictions: Legally, payments must be settled in KGS (Kyrgyz Som). While foreign currency is “under discussion,” current laws restrict flexible multi-currency operations.

- Political & Regulatory Instability: Kyrgyzstan has a history of political volatility and “regulatory opacity.” The framework is new (2022), and enforcement mechanisms are still evolving, leading to unpredictability.

- Infrastructure Limitations: While mobile penetration is high, rural connectivity is poor, and high-speed broadband is limited to Bishkek and major urban centers.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Fully legalized in 2022 (+3.0). Deductions for regulatory opacity regarding local player access online vs. land-based bans (-0.5). |

| Licensing Process | 25% | 1.0/2.5 | Licenses are available (+2.0). MASSIVE deduction for prohibitive cost ($1.1M) relative to market size (-1.0). Process involves complex technical certs and bureaucratic hurdles. |

| Taxation & Costs | 20% | 1.8/2.0 | Extremely favorable GGR tax of 4% (+2.0). Corporate tax 10%. Slight deduction for mandatory fixed costs and potential hidden administrative fees (-0.2). |

| Operational Requirements | 15% | 0.5/1.5 | Requires local registration, national domain, and server/control presence (+1.0). Deductions for KGS currency restriction (-0.25) and strict physical presence mandates (-0.25). |

| Market Environment | 10% | 0.4/1.0 | Low GDP per capita limits revenue potential significantly (-0.3). Political volatility and history of gambling bans (-0.3). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.5/4.0 | Online gambling is legal for players (+4.0). Slight deduction due to the ambiguity of the land-based ban for locals potentially bleeding into online interpretation (-0.5). |

| Practical Accessibility | 30% | 2.5/3.0 | Payments via cards and local wallets (ELQR) work well (+2.5). Rural internet instability reduces universal access (-0.5). |

| Player Penalties | 20% | 2.0/2.0 | No current penalties for players accessing licensed online sites. |

| Market Availability | 10% | 0.8/1.0 | 5 licensed online casinos (+0.7) plus accessible offshore sites (though regulation is tightening). |

🔍 Key Highlights

Strengths (If Any)

- Extremely Low Tax Rate: A 4% GGR tax is globally competitive and arguably the market’s only major selling point for operators.

- High Mobile Penetration: 110% mobile penetration and growing smartphone usage create a decent foundation for mobile-first iGaming.

- First Mover Advantage: Only 5 licensed online casinos currently exist, offering low competition for those who can afford the entry ticket.

⛔️ CRITICAL RISKS AND CHALLENGES

- Financial Mismatch: The $1.1M license fee is priced for a Tier-1 European market, but the player base is a low-income Tier-3 Central Asian market.

- Market Size Cap: With a population of 6.8m and low disposable income (ARPU $250-350/year), the total addressable market is small.

- Local Player Ban Risk: The government strictly bans locals from entering land-based casinos to “protect” them. It is highly probable this logic will eventually be applied to online casinos, potentially wiping out the domestic user base overnight.

- Currency Isolation: Forcing KGS (Som) usage complicates treasury management and exposes operators to currency fluctuation risks.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $1.5M – $2.0M (Includes $1.1M license fee, local setup, and technical compliance).

Monthly Operating Costs: $50k – $100k (Low labor costs, but high compliance/reporting overhead).

Effective Tax Rate on Revenue: ~14-16% (4% GGR + 10% Corporate Tax + VAT considerations).

Customer Acquisition Cost: Moderate ($20-$50), but player lifetime value (LTV) is also low.

Time to Breakeven: 3-4 Years.

Profitability Assessment: POOR for most. To recoup a $1.1 million license fee with an ARPU of $300, you need ~3,700 active, depositing users just to pay the license principal—before taxes, salaries, or marketing. Given the poverty levels, acquiring thousands of high-value players is difficult. This market makes sense ONLY if the Kyrgyz license allows you to accept players from other jurisdictions (acting as a hub), or if you are a massive land-based operator cross-selling to tourists.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Medium | ISP blocking is not yet sophisticated but “tightening oversight” is planned. Risk of being blacklisted. |

| Licensed Operators | High | Regulatory volatility; risk of sudden ban on local players online; high sunk costs ($1.1M) that cannot be recovered if laws change. |

| Affiliates/Advertisers | Medium | Advertising is restricted; bans on targeting locals for land-based casinos create a minefield for online ad compliance. |

| Company Directors/Executives | Low/Medium | Physical presence required creates jurisdiction; financial crimes (AML) are taken seriously. |

🚨 Extradition and International Enforcement

Extradition Treaties: Kyrgyzstan is a CIS member and has strong extradition and legal cooperation treaties with Russia, Kazakhstan, Uzbekistan, and China. Treaties with Western nations are limited, but Kyrgyzstan cooperates with Interpol.

Enforcement History: The government actively raids illegal land-based gambling dens. Online enforcement is currently focused on “identifying” operators, but physical raids on local offices of non-compliant entities are a real possibility.

📋 Final Verdict

Kyrgyzstan receives an Operator Ease Score of 6.2/10 and a Player Access Score of 8.8/10, resulting in an overall market attractiveness rating of 5.5/10.

HONEST ASSESSMENT: The economics of this market are fundamentally broken for the average operator. While the 4% tax rate is attractive, the $1.1 million license fee is completely detached from the reality of the local economy (GDP/capita ~$1,370). You are essentially paying a Premium UK/USA entry price for a developing Central Asian market.

Furthermore, the strict ban on locals entering land-based casinos suggests a regulatory philosophy that views gambling as a “vice for foreigners.” This poses an existential risk to online operators: if the government decides to harmonize online and land-based rules, you could lose your entire domestic player base instantly.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A large regional operator (CIS focus) expanding a multi-national footprint.

- Able to utilize the Kyrgyz license to target traffic from other “grey” Central Asian jurisdictions (if legally permissible).

- A land-based casino operator in Bishkek looking to extend LTV from tourists.

❌ Definitely Avoid If You Are:

- A startup or mid-sized operator (The $1.1M fee will kill your cash flow).

- Looking for a quick ROI (Breakeven is 3+ years away).

- Reliant on local mass-market players (Low ARPU and risk of future bans).

- Unwilling to establish a physical office and staff in Kyrgyzstan.

⚠️ BOTTOM LINE: A tax haven trap. The low tax rate baits you in, but the high license fee and low player value will bleed you dry unless you have a unique cross-border strategy.

Quick question, does the article mention how sports betting operators in New York handle player data security?

Regarding player data security, the article actually touches on the fact that New York sports betting operators are required to adhere to strict regulations, including the use of encryption and secure servers to protect player information. For example, operators like FanDuel and DraftKings have implemented robust security measures, such as two-factor authentication and regular security audits, to ensure the integrity of player data.