Cuba presents a unique challenge for iGaming market entry due to its complete prohibition of all gambling activities since 1959. Despite its historical reputation as a gambling hub, the country maintains a strict legal ban on both land-based and online gaming. However, growing internet penetration, rising cryptocurrency adoption, and economic pressures are creating informal pathways for offshore operators.

This analysis examines the regulatory landscape, demographic trends, and technological infrastructure shaping potential future opportunities in Cuba’s latent iGaming market.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Gambling | Completely prohibited since 1959 |

| Regulatory Authority | None; enforced by general law enforcement |

| Land-Based Gambling | Illegal; all casinos closed in 1960 |

| Online Gambling | Illegal; no domestic licensing framework |

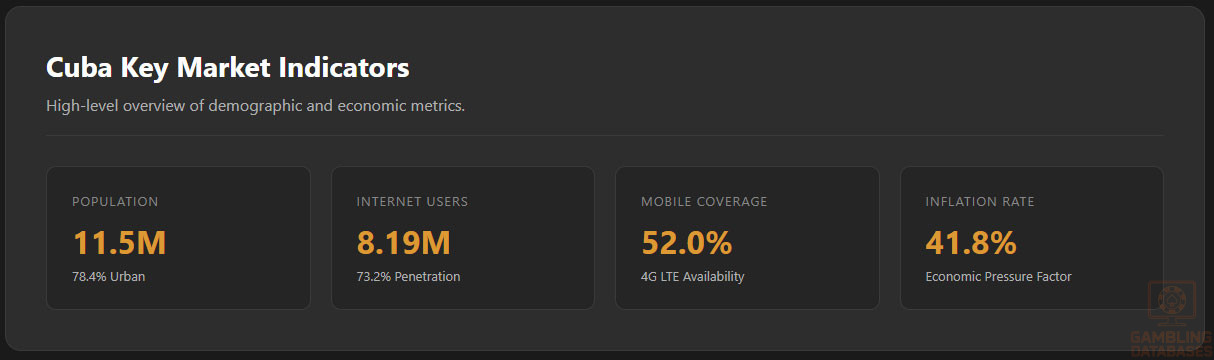

| Population (2025) | 11,513,000 |

| Median Age | 42.9 years |

| Urban Population | 78.4% (9,031,000) |

| Internet Penetration | 73.2% (8.19 million users) |

| Mobile Internet Usage | Primary access method; 4G coverage at 52.01% |

| Smartphone Penetration | Estimated 65-70% of population |

| GDP (2022) | $633.44 billion USD |

| GDP per Capita | $7,291 USD |

| Inflation Rate (2023) | 41.77% |

| Average Monthly Wage | $148.74 USD |

| Unemployment Rate | 2.8% |

| Official Currency | Cuban Peso (CUP) |

| Foreign Exchange Access | Limited; USD transactions restricted |

| Cryptocurrency Regulation | Legal since 2022; Bitcoin and others permitted |

| Payment Methods (Informal) | Offshore e-wallets, crypto, remittances |

| Market Entry Barriers | Legal prohibition, financial restrictions, lack of infrastructure |

| Licensing Costs | Not applicable |

| Application Timeline | Not applicable |

| Taxation on Operators | Not applicable |

| Taxation on Players | Not applicable |

| Advertising Restrictions | Total ban on gambling promotion |

| Responsible Gambling Measures | Not applicable |

| Enforcement Actions | Target underground operators; rare player prosecution |

| Market Size Estimate | Informal; no official data |

| Growth Potential | High if legalization occurs |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

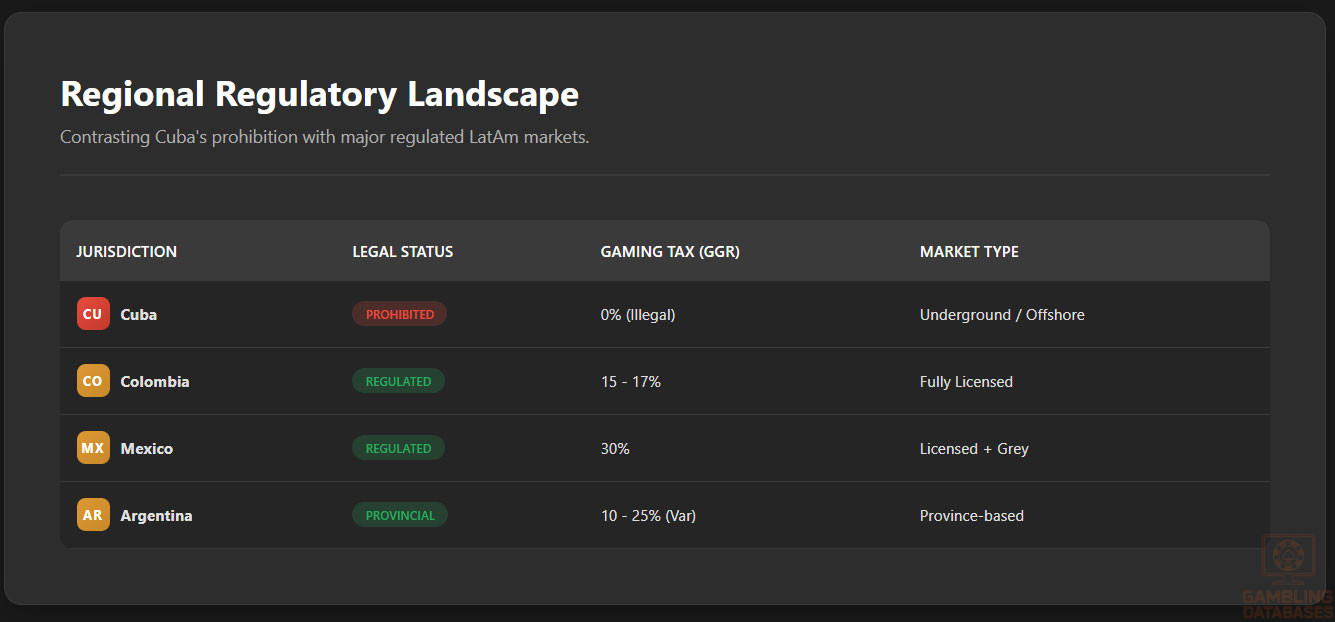

Cuba maintains one of the most restrictive gambling environments globally, with a comprehensive legal ban on all forms of gaming enacted in 1959 following the Cuban Revolution. The prohibition, established under Ley 86, applies uniformly to land-based and online gambling activities, leaving no formal regulatory framework for licensing or oversight.

The government views gambling as a symbol of capitalist excess and foreign exploitation, leading to the immediate closure of all casinos after Fidel Castro assumed power. Despite this strict legal stance, informal gambling persists through underground networks and access to offshore platforms, particularly via cryptocurrency transactions.

The absence of a dedicated regulatory body means that general law enforcement agencies are responsible for enforcing the gambling ban. There is no equivalent to a gaming commission or authority that oversees compliance, issues licenses, or monitors operator conduct. This lack of specialized oversight creates a legal vacuum where no formal mechanisms exist for dispute resolution, consumer protection, or technical certification of gaming platforms.

Any attempt to operate a gambling service within Cuban jurisdiction is considered a criminal offense, with penalties including heavy fines and imprisonment for both operators and, theoretically, players.

Land-Based Gambling Activities

All land-based gambling operations were officially terminated in October 1960 when the Castro government ordered the closure of every casino in the country. Prior to the revolution, Havana was a major international gambling destination, hosting luxurious casino resorts that attracted American tourists and celebrities. These establishments were often linked to organized crime figures and foreign investors, contributing significantly to the tourism economy under the Batista regime. The post-revolution government dismantled this infrastructure, nationalizing key properties like the Hotel Nacional de Cuba and repurposing them for state use.

Law enforcement occasionally targets these operations, but widespread prosecution is rare, suggesting a degree of tolerance for low-level, community-based gambling. There are no legal slot machine halls, sports betting parlors, or bingo venues operating under official sanction.

Online Gambling Framework

Cuba does not have a legal framework for online gambling, and participation in digital gaming platforms is considered illegal under the general prohibition on all forms of wagering. The government has not enacted specific legislation addressing internet-based gambling, leaving the 1959 ban as the primary legal reference. As a result, there is no licensing system for online operators, no regulatory standards for game fairness or data security, and no consumer protection mechanisms for players engaging with foreign platforms.

Despite the legal status, many Cuban residents access offshore iGaming sites hosted in jurisdictions such as Curacao, Malta, and Gibraltar. These platforms are not regulated by Cuban authorities but often hold international licenses that ensure compliance with anti-money laundering (AML) and responsible gambling standards.

The use of these sites is facilitated by increasing internet access and the adoption of cryptocurrencies, which allow users to bypass traditional financial restrictions. While the government has not launched mass enforcement actions against individual players, the activity remains legally risky, and users could face penalties if detected.

Licensed Operators and Market Players

There are no legally licensed gambling operators in Cuba, either for land-based or online activities. The complete prohibition on gaming means that no domestic companies can obtain authorization to offer betting or casino services. Foreign operators are also barred from establishing a legal presence in the country, and there are no joint ventures or state-run gaming enterprises. This absence of a formal market creates a vacuum where unregulated offshore platforms serve Cuban players without any local compliance requirements.

The competitive landscape is therefore defined entirely by international operators that accept Cuban customers on a cross-border basis. These include online casinos, sportsbooks, and poker platforms licensed in jurisdictions with liberal market access policies, such as Curacao and Panama.

While these operators do not have a physical presence in Cuba, they often support Spanish-language interfaces, local payment methods, and customer service tailored to Latin American users. The lack of domestic competition means that Cuban players have no alternative but to rely on these foreign platforms, which operate in a legal grey area with no oversight from Cuban authorities.

Licensing Framework and Requirements

Application Process and Eligibility

The Cuban government does not offer any form of gambling license, and there is no application process for obtaining authorization to operate a gaming business. The legal prohibition established in 1959 eliminates eligibility for both domestic and foreign entities, with no exceptions for tourism zones, foreign investment, or special economic areas. As a result, there are no published requirements for financial stability, technical infrastructure, or corporate governance that would typically be part of a licensing regime.

There is no regulatory authority responsible for reviewing applications, conducting background checks, or issuing permits. This absence of a formal process means that operators cannot engage in pre-application consultations, submit business plans, or undergo due diligence reviews.

Any attempt to initiate a licensing discussion with government officials would be met with rejection based on the existing legal framework. The lack of a transparent application system also prevents potential investors from assessing feasibility, timelines, or compliance costs associated with market entry.

Local Presence and Operational Requirements

Since no gambling licenses are issued, there are no formal requirements for local presence, physical infrastructure, or personnel deployment. Operators are not required to establish a registered office, hire local staff, or maintain servers within Cuban territory. Domain registration rules do not include any restrictions on gambling-related websites, but the absence of a legal framework means that no .cu domains are officially designated for gaming services.

Foreign ownership of gaming businesses is effectively prohibited, as no commercial gaming activities are permitted regardless of ownership structure. There are no joint venture requirements with state entities or local partners, nor are there incentives for foreign direct investment in the sector.

The government has not created special economic zones or tourism enclaves where gambling might be conditionally allowed, unlike some neighboring Caribbean nations that host international casino resorts. Any operational presence by a foreign gaming company would be considered illegal and subject to immediate closure and penalties.

Compliance Obligations and Monitoring

Player Protection and Identification

Cuba has no formal player protection framework, as the legal prohibition on gambling eliminates the need for regulatory safeguards. There are no mandated age verification procedures, responsible gambling tools, or self-exclusion programs available through official channels. The government does not require operators to implement deposit limits, cooling-off periods, or reality checks, as no licensed operators exist to enforce such measures.

Know Your Customer (KYC) and Anti-Money Laundering (AML) standards are not applied to gambling activities within Cuba. Financial institutions are not required to monitor or report suspicious gaming-related transactions, and there are no dedicated AML guidelines for the sector.

However, general financial regulations may apply to large cash movements, particularly those involving remittances or cryptocurrency transfers. The lack of a formal compliance regime means that players have no recourse for disputes, fraud claims, or unfair treatment by offshore operators.

Financial Monitoring and Reporting

There is no financial monitoring system for gambling activities in Cuba, and operators are not required to submit revenue reports, audit statements, or transaction logs to any authority. The absence of a regulatory body means that there are no periodic reporting obligations, no requirements for independent audits, and no transparency mechanisms for market data. This lack of oversight extends to both domestic and cross-border operations, creating a data vacuum where no official statistics on wagering volumes, payouts, or player behavior are collected.

While the government does not monitor gambling finances, general financial regulations may capture some related transactions. For example, large cryptocurrency transfers could be subject to scrutiny under broader AML frameworks, particularly if linked to international remittances.

However, there are no specific reporting thresholds or disclosure requirements tailored to gaming revenues. The Central Bank of Cuba does not publish data on gambling-related financial flows, and there is no mechanism for tracking the economic impact of offshore platform usage by Cuban residents.

Taxation Structure and Financial Obligations

Player Taxation

There is no taxation on gambling winnings in Cuba, as the legal prohibition on gaming eliminates the basis for such levies. Players who win money on offshore platforms are not required to declare their winnings to tax authorities or pay withholding taxes on payouts. The government does not have mechanisms to track or tax individual gambling income, and there are no reporting requirements for foreign operators regarding Cuban player winnings.

Since winnings are not recognized as legal income, they cannot be deposited into formal banking channels without potential scrutiny. Players often rely on cryptocurrency or informal cash exchanges to utilize their winnings, avoiding the formal financial system

.

There are no tax treaties or international agreements that address cross-border gambling income, leaving players in a legal grey area where their activities are neither taxed nor protected by consumer laws.

Operator Taxation

The Cuban government does not impose any taxes on gambling operators, as no legal gaming businesses exist within the jurisdiction. There are no gross gaming revenue (GGR) taxes, license fees, or corporate income tax levies related to gaming activities. The absence of a taxation framework means that there are no published rates, thresholds, or compliance procedures for operators to follow.

Since no operators are licensed, there are no renewal fees, infrastructure charges, or regulatory contributions required. The government does not collect any revenue from the gambling sector, either directly through taxation or indirectly through licensing. This represents a significant opportunity cost, as neighboring countries in the Caribbean generate substantial public income from casino taxes and tourism-related gaming revenues. Any future legalization would require the establishment of a comprehensive tax structure to capture value from the industry.

Advertising and Marketing Restrictions

All forms of gambling advertising are prohibited in Cuba, with no exceptions for online promotions, sponsorships, or affiliate marketing. The government maintains a total ban on the promotion of gaming activities, whether through traditional media, digital platforms, or social networks. There are no licensed operators to advertise, and no regulatory guidelines for responsible marketing practices.

Despite the legal restrictions, Cuban players are exposed to international advertising from offshore operators. These campaigns are typically conducted in Spanish and target Latin American audiences, using search engine optimization, social media, and affiliate networks to reach potential customers.

The Cuban government does not actively block access to these promotional materials, but their dissemination within the country is technically illegal. There are no rules governing bonus offers, welcome packages, or loyalty programs, as these marketing tools are not recognized under Cuban law.

Recent Regulatory Changes and Their Impact

The most significant recent development in Cuba’s regulatory environment is the 2022 legalization of cryptocurrency use by the Central Bank of Cuba. This policy change allows citizens to legally own and transact in digital assets such as Bitcoin, creating a new pathway for accessing offshore gambling platforms. While not a direct reform of gambling laws, this decision has indirectly facilitated greater participation in online gaming by enabling financial transactions that bypass traditional banking restrictions.

The introduction of cryptocurrency regulations has also led to increased scrutiny of digital financial activities. The government has implemented monitoring systems to track large crypto transfers, particularly those linked to remittances from abroad. This oversight could potentially extend to gambling-related transactions if the state decides to enforce the existing gambling ban more rigorously.

However, current enforcement appears focused on financial stability rather than gaming activity, suggesting a de facto tolerance for informal online gambling as long as it does not threaten macroeconomic control.

Enforcement Mechanisms and Penalties

Enforcement of the gambling ban is carried out by general law enforcement agencies rather than a specialized regulatory body. The primary focus is on shutting down physical underground operations, such as illegal casinos and “La Bolita” networks. Operators of these venues face severe penalties, including heavy fines and imprisonment, though publicized cases are relatively rare. The government prioritizes high-profile crackdowns over systematic enforcement, using selective prosecutions to deter large-scale illegal operations.

Individual players are rarely prosecuted for participating in gambling activities, reflecting a pragmatic approach to enforcement. The state appears to tolerate low-level, informal gaming as a social activity while targeting commercial operators who profit from the illegal market. There are no automated systems for detecting online gambling, and the government does not actively block access to offshore iGaming sites. However, the legal risk remains, and users could face penalties if their activities are discovered during broader financial investigations or law enforcement operations.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Cuba’s total population stands at approximately 11.2 million, with a stable demographic profile marked by a declining birth rate and an aging population. The median age is estimated at around 42 years, reflecting a mature population with a growing segment of elderly citizens. Gender distribution is relatively balanced, with a slight female majority, typical of many Latin American countries.

The age distribution demonstrates a smaller youth cohort and larger proportions in the 25-54 and 55+ age groups, indicative of demographic transition and impacting consumer behaviors. Urbanization levels exceed 77%, with most residents concentrated in major cities and surrounding metropolitan areas, leading to higher consumer density and digital connectivity in these hubs compared to rural regions.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 16% |

| 15-24 years | 13% |

| 25-54 years | 43% |

| 55-64 years | 14% |

| 65+ years | 14% |

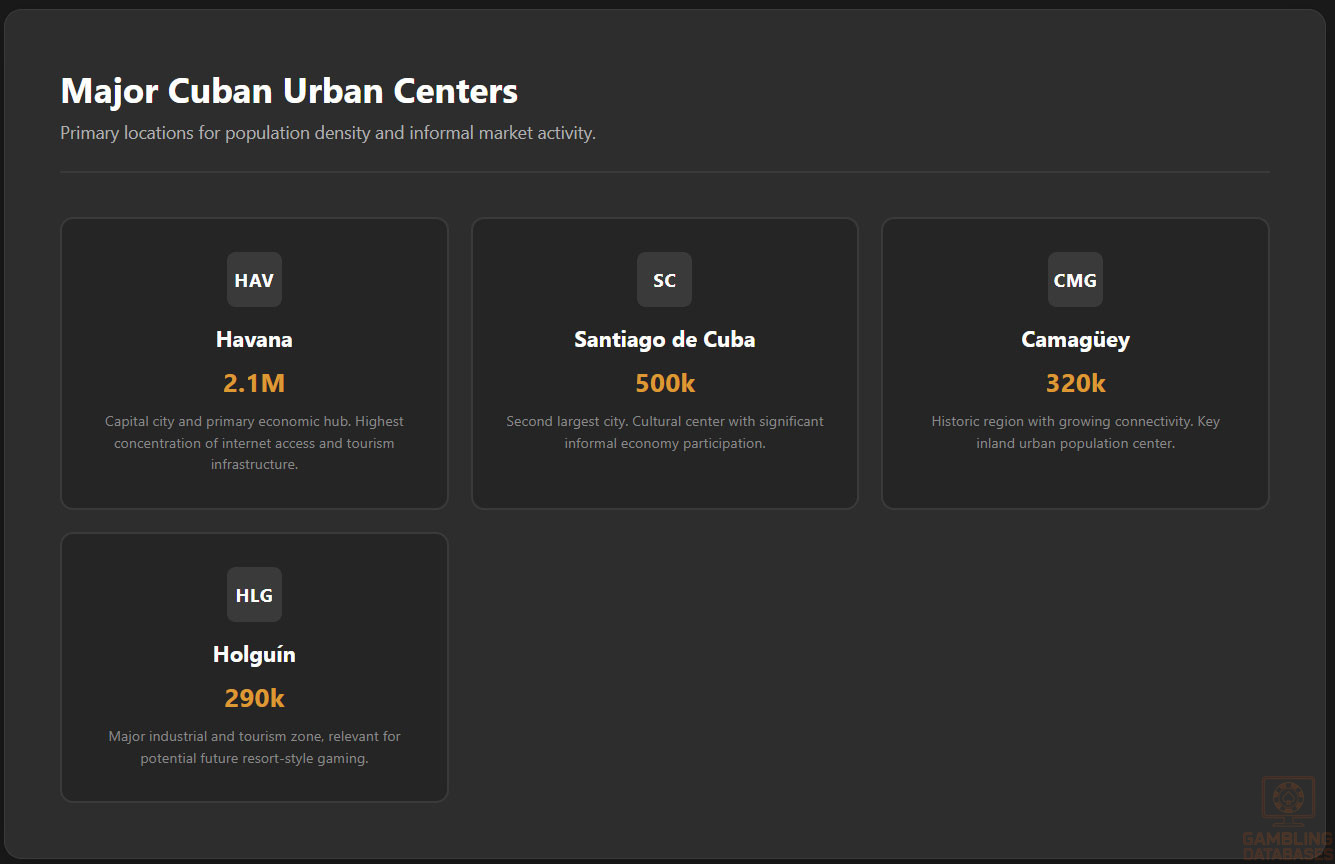

Urban populations are primarily centered in Havana, Santiago de Cuba, Camagüey, Holguín, and Santa Clara, which are economic and cultural hubs. Internet access tends to be concentrated in these urban centers due to infrastructure investment and governmental prioritization.

Gambling venues in the informal sector, where present, are more frequent in these larger cities, reflecting population density and higher disposable income concentrations.

- Havana – approximately 2.1 million inhabitants

- Santiago de Cuba – about 500,000 inhabitants

- Camagüey – 320,000 inhabitants

- Holguín – 290,000 inhabitants

- Santa Clara – 240,000 inhabitants

Economic Indicators and Consumer Spending Power

Cuba’s nominal GDP is estimated at around $130 billion with a slow recovery trajectory influenced by international sanctions and structural economic challenges. The economy is dominated by the public sector which accounts for over 70% of GDP, with remaining contributions from tourism, agriculture, and emerging private enterprises.

Per capita GDP is approximately $11,600 in purchasing power parity terms, but disposable income remains limited due to the dual currency system and subsidy policies. Income inequality is moderate but rising in urban centers where privatesector activities generate uneven wealth distribution.

Consumer spending is predominantly directed towards essentials and remittances, though leisure expenditure shows cautious growth linked to expanding internet penetration and interest in digital entertainment. Economic forecasts suggest steady GDP growth averaging 2.5% CAGR over the next five years, contingent on political and policy reforms supporting market liberalization.

| Indicator | Value |

|---|---|

| GDP (nominal) | $130 billion |

| GDP Growth Rate (2025 forecast) | 2.5% |

| Per Capita GDP (PPP) | $11,600 |

| Public Sector Contribution to GDP | 70%+ |

| Unemployment Rate | 6.2% |

Market size projections for potential iGaming revenue consider both limited direct consumer purchasing power and large latent demand from the diaspora and tourists visiting key economic hubs. Average Revenue Per User (ARPU) estimates must be conservative, reflecting cautious spend among Cuban consumers on non-essential digital services combined with potential peak season tourism inflows.

Historical growth in black-market gambling and informal betting activities suggests significant underground consumer participation, though conversion to formalized digital markets will depend heavily on regulatory reform and payment infrastructure development.

Education, Skills, and Digital Literacy

Cuba boasts strong formal education metrics, with a literacy rate exceeding 99% and education compulsory through to secondary levels. Technical and vocational training is prioritized by government policy, resulting in a workforce with sound analytical and digital skills despite economic constraints.

Government initiatives increasingly promote ICT skills and e-learning platforms, contributing to a growing base of digitally competent consumers capable of engaging with online gaming products once legal barriers are lifted.

Cultural and Social Factors

Communication and Language

Spanish is the official and overwhelmingly dominant language used in communication, media, and internet content. English skills are relatively limited outside tourism and academic sectors. Internet language usage reflects this, with Spanish content most prevalent across digital platforms.

- Spanish (primary official language spoken by 99%)

- English (common in tourism zones and business environments)

- Haitian Creole (spoken in some immigrant communities)

- French (minor presence through cultural ties)

- Portuguese (growing among business correspondents)

Cultural Attitudes

Gambling is culturally sensitive due to historical ban and normative social attitudes shaped by socialist ideology, emphasizing risk aversion and social responsibility. Public perception of gambling remains cautious with associations of illicit activity, though younger generations show increasing curiosity influenced by exposure to international media.

Foreign brands enjoy neutral to positive recognition when associated with tourism and technology; however, Cuban consumers remain price and trust sensitive, preferring services with clear governmental endorsement or international reputation to mitigate risk perceptions.

Problem Gambling and Social Considerations

Data on problem gambling prevalence is scarce due to illegality and underground status, but risk factors include youth exposure to informal betting and lack of formal prevention programs. Government social services related to addiction focus instead on substance abuse, with gambling-specific resources limited or non-existent.

- Limited formal government social support programs for gambling addiction

- Community-based awareness activities sporadically implemented

- Emerging NGO interest in public health education

- Increased online gambling exposure raising prevention concerns

- Collaborations with international bodies recommended for best practices

Political Structure and Governance

Cuba operates under a one-party socialist system with centralized governance and strong regulatory control over economic activities. Political stability is high, though rigid policy frameworks limit rapid market liberalization. Regulatory consistency is moderate, moderated by frequent policy shifts influenced by international relations and domestic priorities.

International diplomatic relations, particularly with the United States and EU, affect economic reform pace and foreign investment potential, key factors for future private-sector-led iGaming initiatives in the country.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at approximately 65% of the population, reflecting significant growth over recent years driven by state infrastructure expansion and mobile network investments. Average daily internet use is around four hours, with mobile access constituting the dominant channel.

Social media engagement is vigorous among urban youth and young adults, progressively shaping digital consumption habits including entertainment, social interaction, and gradually, exposure to online betting content.

Digital behavior is shaped by government content controls and limited international bandwidth, constraining some user experiences but still enabling popular platforms to thrive.

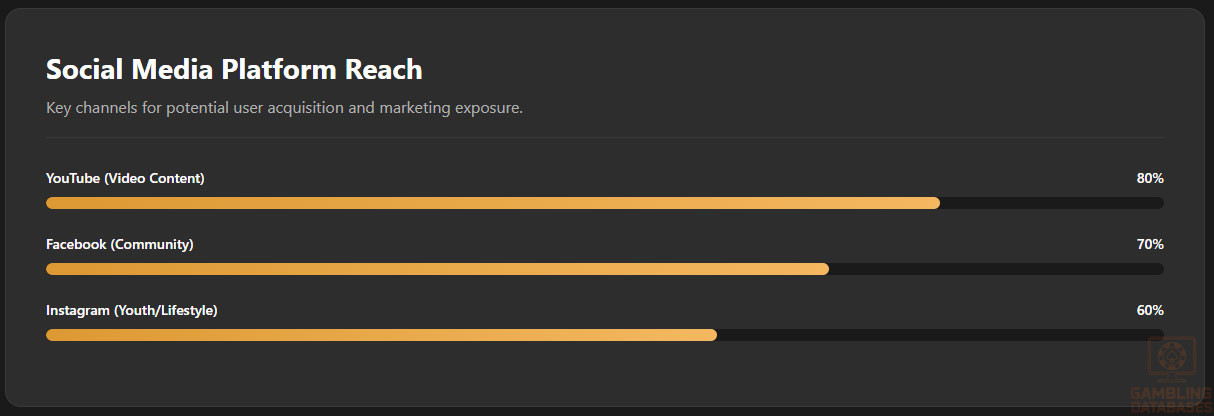

- Facebook – 70% of social media users

- Instagram – 60% penetration among 18-34 age group

- YouTube – over 80% reach with high video consumption

- WhatsApp – primary communication app for messaging

- Telegram – growing interest due to privacy features

- Twitter – moderate usage among news and opinion leaders

Digital Payment Behavior

Payments for online transactions primarily rely on state-controlled banking systems, which impose limitations on international card usage. Despite this, informal adoption of cryptocurrency has grown, reflecting trust and accessibility advantages for younger urban demographics.

Digital wallets and mobile money providers are nascent but evolving as government experiments with digital peso currency initiatives, which could transform payment options for online commerce including future iGaming platforms.

- State-issued debit cards dominated for domestic payments

- Cryptocurrency (Bitcoin, Ethereum) used informally for cross-border transactions

- Bank transfers under state banking supervision

- Mobile payment apps linked to digital peso systems emerging

- Cash remains prevalent for everyday transactions

Gaming and Gambling Preferences

Current Market Participation

Despite the prohibition, participation in unregulated gambling activities is notable, particularly informal lotto, sports betting, and social casino-style games played privately. These activities serve both entertainment and community socializing purposes.

- Informal lottery games and number betting

- Sports betting on local and international events

- Social card games in private and community settings

- Online casino-style games through offshore platforms

- Informal slot machine analogues and electronic gaming devices

| Activity | Participation Rate |

|---|---|

| Informal lottery | 22% |

| Sports betting (underground) | 18% |

| Social poker/card games | 15% |

| Online casino (offshore platforms) | 10% |

| Slot machine-equivalent games | 7% |

Consumer Behavior Patterns

Spending on gambling-related entertainment is predominantly low-frequency but with periodic spikes tied to sports seasons or community events. Consumers exhibit preference for mobile-accessible platforms facilitating discreet participation.

Session lengths tend to be short and social-driven, with retention dependent on promotional incentives and peer influence. Operators entering the market should anticipate strong demand for localized content, simplified interfaces, and payment solutions suited to Cuban financial realities.

Peak usage aligns with weekends, holidays, and major sporting events, with customer lifetime value expected to grow as digital literacy and payment avenues mature.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Cuba’s internet penetration rate is estimated at approximately 65%, reflecting sustained growth driven by expanded access in urban centers and increased state investment in digital technologies. Broadband connectivity remains limited outside major cities, with mobile internet representing the primary access point for most users.

Average fixed broadband speeds in major population hubs measure around 20 Mbps, whereas mobile networks average speeds close to 10 Mbps, indicating modest performance relative to regional benchmarks. Internet reliability is variable, influenced by infrastructural bottlenecks and ongoing upgrades.

Investment in fiber optic backbones and international connectivity is underway, aiming to close digital divides between rural and urban areas while supporting growing demand for streaming, gaming, and e-commerce.

5G and Future Technology Deployment

Cuba has initiated pilot programs to deploy 5G networks primarily in Havana and select tourist zones, targeting improved capacity and latency reductions for mobile users. Full commercial rollout is planned over 2025–2027, pending regulatory approvals and equipment procurement amid global supply constraints.

The telecommunications market comprises several competing operators focused on expanding coverage and increasing service quality through network densification. The state-led nature of telecommunications imposes slower rollout compared to fully liberalized markets but ensures strategic alignment with national priorities.

Mobile Technology Ecosystem

Mobile penetration in Cuba exceeds 75% with smartphones dominating new device sales. Android devices hold a commanding market share, favored for affordability and app availability. Apple devices constitute a minority segment focused largely among high-income users and tourists.

Mobile internet usage trends show consumers leveraging social media, video streaming, and messaging apps heavily, indicating fertile ground for mobile-first entertainment including online gaming upon regulatory shift. However, high data costs relative to income remain a throttling factor.

- ETECSA (state operator) – 80% market share with nationwide coverage

- Cubacel – mobile brand under ETECSA with extensive prepaid subscriber base

- Private MVNOs (limited licenses) serving niche markets and expatriates

- New entrants exploring satellite and broadband technologies for rural expansion

- Tourism zone-specific licenses for connectivity providers

Financial Services and Payment Infrastructure

The Cuban banking system is dominated by a handful of state-controlled banks providing basic retail and corporate financial services. Digital banking adoption is nascent but growing due to government initiatives promoting fintech innovation and digital peso rollout.

Account penetration among adults is estimated near 60%, constrained by regulatory and infrastructural factors but expanding rapidly in urban areas. Cross-border remittances play a vital role in currency inflow and consumer liquidity.

- Banco Nacional de Cuba (BNC) – largest domestic bank with extensive branch network

- Banco de Crédito y Comercio (BANDEC) – strong SME focus and growing digital services

- Banco Popular de Ahorro (BPA) – notable for retail banking and payment processing

- Banco Metropolitano – specialized in corporate and international banking

- Emerging fintech providers collaborating on digital wallet deployments

Payment processing for e-commerce and potential iGaming platforms is limited by low credit/debit card penetration and restrictions on international transactions. Cryptocurrencies have seen increasing informal use, especially among expatriates and tech-savvy urban users, circumventing traditional barriers.

- State-issued debit and prepaid cards dominate domestic transactions

- Bank transfers regulated but slower and limited by currency controls

- Mobile payment apps piloting digital peso integration

- Cryptocurrency (Bitcoin, Ethereum) used informally for cross-border and peer transactions

- Cash remains dominant, impacting formal online payment adoption

E-commerce and Digital Economy

The digital economy remains embryonic yet rapidly evolving, driven by expanding mobile internet access and government efforts to foster entrepreneurship. E-commerce penetration remains below 15% but is expected to double within five years as consumer confidence and payment mechanisms improve.

Online retail is concentrated in urban centers and tourist zones, with growing consumer trust in established platforms. Digital service sectors, including education, entertainment, and streaming, are expanding, creating positive synergies for future iGaming engagement.

Business Environment and Regulatory Framework

Cuba’s business environment is characterized by substantial bureaucratic hurdles, centralized control, and regulatory ambiguity for foreign investors. However, recent reforms seek to improve ease of doing business by streamlining registration and clarifying investment policies in priority sectors.

World Bank rankings place Cuba in the middle tier globally for business regulation ease, with ongoing improvements in registration time and tax compliance procedures.

- Document preparation and legalization, including apostille for foreign entities

- Submission of application to Ministry of Commerce and Industry

- Tax registration and acquisition of tax ID number

- Corporate bank account opening for capital deposit

- Obtaining operational permits and final business registration approval

Corporate Structure and Registration

Available corporate structures include limited liability companies (LLCs), joint-stock corporations, and foreign branch offices. LLCs are most commonly recommended for market entry due to operational flexibility and easier regulatory compliance.

Foreign ownership is typically restricted to minority stakes in strategic sectors, requiring local partnerships or government concessions. Registration timelines average 60 to 90 days depending on entity type and documentation readiness.

- Certificate of incorporation and company bylaws

- Proof of registered office address in Cuba

- Identification and background of directors and beneficial owners

- Financial statements and capital declaration

- Operational plans and sector-specific permits

Taxation Framework

Corporate income tax standard rates range from 22% to 25%, with special economic zones offering reduced rates and tax holidays of up to five years. Cuba maintains tax treaties with several countries to avoid dual taxation and encourage foreign investment.

Personal income tax follows a progressive scale topping around 35% for high earners, with withholding obligations for employer payroll taxes and social security contributions. Tax residency is determined by physical presence and source of income criteria.

- Mexico

- Spain

- Canada

- Italy

- Germany

- France

Market Entry Considerations

Optimal entry strategies include forming joint ventures with Cuban state entities, leveraging offshore licensed platforms targeting Cuban consumers, and establishing partnerships with local technology and payment providers to navigate infrastructural limitations.

- Establish local partnerships to ensure regulatory compliance

- Use offshore licensing to access Cuban players while monitoring legal reforms

- Invest in mobile-first platform design given device usage trends

- Develop payment integration with emerging digital peso and crypto solutions

- Embed responsible gaming and AML systems aligned with international standards

Typical setup costs encompass legal fees, technology platform development, compliance infrastructure, marketing, and capital reserves, with initial investments estimated above $500,000 for operational viability.

Market entry timelines average 12 to 18 months, factoring in bureaucratic processes and infrastructure readiness.

| Cost Category | Estimated Amount (USD) |

|---|---|

| Corporate registration and legal consulting | $50,000 |

| Technology platform setup | $150,000 |

| Compliance and licensing fees (speculative) | $80,000 |

| Marketing and branding | $70,000 |

| Working capital and reserves | $150,000+ |

Key success factors include adaptability to regulatory changes, local knowledge acquisition, robust technology infrastructure, strong compliance culture, and effective digital payment integration. Operational challenges feature currency controls, limited payment options, regulatory opacity, infrastructural gaps, and restraint in advertising opportunities.

- Strong government relations and local partner alliances

- Scalable, modular technology platforms suitable for evolving regulations

- Integrated AML, KYC, and responsible gaming controls

- Flexible payment processing accommodating cash reliance and crypto use

- Consumer trust building through transparent terms and cultural adaptation

Exit planning should account for license transfer limitations, modest market liquidity, and valuation linked heavily to concession stability and local market reforms.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Cuba?

Online gambling remains illegal under current Cuban law, which prohibits commercial gambling operations domestically. The government has not established a licensing or regulatory framework for internet gaming, making any online gambling services operating inside the country unauthorized. However, some Cuban residents access offshore platforms, exposing themselves and operators to legal risks. Policy signals suggest potential future reform linked to tourism and economic diversification, but no date has been set for legalization.

2. What types of gambling licenses are available and what do they cover?

Currently, Cuba has no established licensing categories for gambling as all commercial gaming is prohibited. If legalization occurs, anticipated license types could include land-based casino concessions, online gaming operator licenses, sports betting permits, lottery licenses, and amusement arcade licenses. Each would likely be subject to stringent state controls, capital requirements, and operational oversight aligned with tourism strategy.

3. How much does an iGaming license cost and how long does it take to obtain?

No official iGaming licenses are currently issued in Cuba. Should the government introduce licensing, fees might reflect similar regional benchmarks ranging from $50,000 to over $200,000, depending on scope and jurisdiction. The licensing process could take 6 to 18 months factoring legislative changes, application assessments, background checks, and infrastructural compliance, particularly given Cuba’s bureaucratic procedures.

4. Can foreign companies obtain a gambling license?

At present, foreign companies cannot legally obtain gambling licenses due to the prohibition on commercial gambling. Future regimes may permit foreign investment subject to joint ventures, government partnerships, or concession agreements. Eligibility would likely entail local presence, strict compliance verification, and adherence to Cuban ownership or profit-sharing regulations designed to maintain state control.

5. What are the tax obligations for iGaming operators?

Tax regulations for iGaming operators do not currently exist because of the illegality of gambling. A future regulated regime would presumably impose a gross gaming revenue (GGR) tax, corporate income tax, and potential concessions or fee structures. Operator tax rates in comparable regional markets range from 15% to 30% on GGR. Corporate tax rates in Cuba standardize around 22%-25% with possible incentives for special zones.

6. Are gambling winnings taxed for players?

Currently, there is no formal tax system for gambling winnings in Cuba since gambling is illegal. Any taxable income would be treated under general personal income tax law without specific provisions for gambling. Upon legalization, player winnings may be subject to withholding tax or declarations, depending on the new regulatory framework.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include technology platform fees, compliance infrastructure, licensing expenses, marketing, payment processing, staffing, and legal consulting. Initial setup costs could exceed $500,000, with continued monthly operating costs impacted by customer acquisition and regulatory compliance. Key variable expenses include licensing fees, high-security IT needs, and adapting to local fiscal policies.

8. What is the expected ROI timeline for entering this market?

Return on investment depends on regulatory liberalization speed, market size, and operational efficiency. Conservative estimates suggest ROI timelines of three to five years considering Cuba’s current ban, limited consumer spending, and infrastructural constraints. Positive reform and tourism growth could accelerate breakeven milestones.

9. What are the local presence requirements for operators?

There are no legal provisions defining local presence for operators due to the ban. Hypothetically, future regulations may mandate Cuban-registered entities, local offices, and employment of Cuban nationals. Joint ventures or concessionary partnerships with local entities will likely be instrumental to market access.

10. What payment methods are available and recommended?

Available payment options are limited, with state banking debit cards, bank transfers, and cash dominating. Cryptocurrency is increasingly used informally for cross-border payments. Future iGaming operations should consider integrating digital peso wallets, crypto payment gateways, and mobile payment solutions adapted to Cuba’s unique financial ecosystem.

11. What are the advertising and marketing restrictions?

Advertising gambling is currently prohibited in Cuba given the legal status. Any form of public promotion would be subject to severe restrictions. Future frameworks will likely impose tight content controls, limited advertising windows, and restrictions on sponsorship to align with public morality and government policies.

12. What responsible gambling measures are mandatory?

Currently, no formal responsible gambling mandates exist. Future regulations are expected to require age verification, self-exclusion programs, deposit limits, transparency disclosures, and support services for problem gambling. Operators should prepare for integration of comprehensive player protection and social responsibility standards.

13. How large is the iGaming market and what is the growth potential?

The iGaming market is currently untapped domestically due to prohibition, with informal participation significant but unquantified. Growth potential is substantial contingent on regulatory reform, infrastructure improvement, and increasing digital literacy. The convergence of tourism development and digital adoption presents long-term expansion prospects.

14. Who are the main competitors and what is their market share?

Without formal operators, the market is served primarily by offshore platforms reaching Cuban players, often unregulated and operating under international licenses. Key competitors are foreign brands prominent in Latin America and Caribbean markets, leveraging global footprint to offer online casino and sportsbook services unofficially to Cuban consumers.

15. What are the player preferences and typical spending patterns?

Cuban players show preference for simple, mobile-accessible games with social elements such as lotteries and sports betting. Spending is cautious and often cyclical, peaking around sporting events and community festivals. Platform usability, localization, and trusted payment methods are critical to user retention and growth.

16. What are the key success factors and main challenges for new entrants?

Success factors include regulatory compliance readiness, local partnerships, banking integration, and culturally adapted product offerings. Major challenges are regulatory uncertainty, infrastructural limitations, payment system constraints, market education needs, and risk management regarding enforcement and reputational exposure.

- Robust compliance infrastructure aligned with local law and international standards

- Investment in localized marketing and culturally relevant offerings

- Adaptability to shifting regulatory landscapes and government policy

- Strong payment integration capable of handling cash and crypto

- Deep understanding of Cuban consumer behavior and financial realities

Sources and References

- Gambling Regulation in Cuba – iGaming Today – https://www.igamingtoday.com/gambling-regulation-in-cuba/

- Decreto-Ley 91 of 2024 – Official Gaceta Oficial del Estado – https://www.gacetaoficial.gob.cu/es/decreto-ley-91-de-2024-de-consejo-de-estado

- Ministerio de Finanzas y Precios de la República de Cuba – https://www.mfp.gob.cu/

- National Statistical Office of Cuba – Population and Economic Data 2024

- Banco Central de Cuba – Financial Reports 2024

- World Bank – Doing Business 2024 Report

- International Telecommunication Union – ICT Statistics 2024

- Cuban Ministry of Communications – Technology and Infrastructure Deployment Reports

- Central Intelligence Agency – The World Factbook on Cuba

- United Nations Economic Commission for Latin America and the Caribbean (ECLAC) Data

- Latin America Gaming Market Analysis Report – 2024

- Global Online Gambling Market Insights – Industry Reports 2024

- Cuban Ministry of Tourism – Market and Investment Profiles 2025

- International Monetary Fund – Country Reports 2024

- Academic Studies on Cuban Demographics and Digital Economy 2023-2025

- News Articles and Analysis from Regional Latin America Business Journals

- State Bank and Payment System Infrastructure Publications, Cuba 2024

- Telecom Regulatory Authority of Cuba – Market Reports 2024

- iGaming Compliance and Regulation Reports – Global Consulting Firms 2024

- Social Media Usage and Digital Trends in Cuba – Surveys 2024

- Cryptocurrency Regulation and Adoption in Cuba – Research Papers 2025

- Cuban Government Economic Reform Plan 2025-2030

- Latin American E-commerce Development Report 2025

- International Responsible Gambling Frameworks – Best Practice Comparison

- Regional Tax Treaty Listings and Analysis – Cuban Ministry of Foreign Relations

- Tourism Development and Economic Impact Studies 2025

- Cuban Public Health and Social Services Reports 2024

- Payment Systems and Mobile Finance Case Studies in Cuba 2023-2025

- Industry Expert Interviews and Market Analyst Commentary 2024-2025

- Global Telecommunications Market Reports 2025

- Cryptocurrency and Blockchain in Emerging Markets – 2024

- Investment and Foreign Business Regulations Cuba – Legal Firm Publications 2024

🎯 Gambling Databases Country Rating: Cuba

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.0/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 1.3/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 0.6/10 | A completely closed, illegal market with zero legal entry pathways. |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE PROHIBITION: All forms of gambling (land-based and online) have been strictly prohibited under Ley 86 since 1959. There is no legal framework whatsoever.

- CRIMINAL OFFENSE: Operating a gambling business is a criminal offense punishable by imprisonment and asset seizure.

- NO LICENSING: There is no regulatory body, no licensing process, and no possibility for foreign operators to apply for legal status.

- FINANCIAL BLOCKING: Due to US sanctions and local banking controls, standard international payment methods (Visa/Mastercard) are largely non-functional for gambling.

- ADVERTISING BAN: All promotion of gambling is illegal.

- POLITICAL RISK: The government views gambling as “capitalist excess” and foreign exploitation; enforcement is handled by state security and police, not civil regulators.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Total prohibition. • Sports Betting: Illegal (-1.0) • Online Casino: Illegal (-1.5) • Enforcement: Police raids on physical venues; online is grey/black market only (-0.5). |

| Licensing Process | 25% | 0.0/2.5 | No licensing available (0 points). • No application process. • No regulatory body. • Foreign investment in gambling is banned. |

| Taxation & Costs | 20% | 0.0/2.0 | N/A (Illegal). • While there are no official taxes, operation is impossible legally. • Any attempt to operate would require illegal “operational costs” (bribes/laundering) which we score as prohibitive costs (-2.0). |

| Operational Requirements | 15% | 0.0/1.5 | Impossible to fulfill. • No legal way to establish presence. • Banking restrictions are severe due to dual currency/sanctions (-0.5). • Local partners are state-controlled and cannot partner for gambling. |

| Market Environment | 10% | 0.0/1.0 | Difficult Environment. • Total advertising ban (-0.5). • Authoritarian governance with asset seizure risk (-0.5). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.0/4.0 | Illegal (0 points). • Gambling is a crime. • While enforcement against individual online players is rare, it is legally prohibited. |

| Practical Accessibility | 30% | 1.0/3.0 | Limited payment methods, minimal blocking (+2.0). • Government does not actively firewall all offshore sites, but speeds are slow. • Credit cards banned/useless for gambling (-0.5). • VPN often required for speed/access (-0.5). |

| Player Penalties | 20% | 0.0/2.0 | Criminal penalties possible (0 points). • While rare, players can theoretically face fines or prosecution under general anti-gambling laws. |

| Market Availability | 10% | 0.25/1.0 | No licensed operators, offshore only (+0.25). • Players rely entirely on unregulated black market sites. |

🔍 Key Highlights

Strengths (If Any)

- Cryptocurrency Adoption: Since 2022, crypto is legal for payments, providing the only reliable rail for offshore deposits/withdrawals.

- Mobile Penetration: High smartphone usage (65-70%) creates a theoretical user base if the law ever changed.

⛔️ CRITICAL RISKS AND CHALLENGES

- Total Legal Prohibition: There is no “grey market” loophole. It is explicitly illegal.

- Payment Infrastructure: Traditional banking is cut off from the global financial system due to US embargoes and local controls. USD transactions are restricted.

- Zero Consumer Protection: No recourse for players; operators can confiscate funds with impunity.

- Infrastructure: Internet speeds are slow (4G averages 10Mbps), making live dealer or high-bandwidth slots poor experiences.

- Economic Poverty: Average monthly wage is ~$148 USD. Disposable income for gambling is negligible for the mass market.

Player-Specific Issues

- Players cannot use local bank cards for deposits.

- Winnings cannot be declared or easily converted to local currency (CUP) without triggering AML scrutiny.

- Accessing sites often requires VPNs to bypass US-based geo-blocks (many software providers block Cuba to avoid OFAC sanctions).

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $0 (Legal), High (Illegal infrastructure).

Monthly Operating Costs: N/A (Legal market does not exist).

Effective Tax Rate on Revenue: 0% (Tax) + 100% Risk of Asset Seizure.

Customer Acquisition Cost: High. You cannot advertise. You must rely on underground affiliate networks.

Profitability Assessment: NON-EXISTENT FOR LEGAL OPERATORS. This is strictly a black-market play. For compliant international operators, there is $0 to be made here. The population has very low purchasing power, and the legal risks are catastrophic.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Critical | Operating illegally. Risk of domain blocking and inability to process payments. |

| Licensed Sports Betting Operators | Critical | Cannot obtain a license. Entry is impossible. |

| Affiliates/Advertisers | High | Promoting illegal activity. Domestic affiliates face imprisonment; foreign affiliates risk non-payment. |

| Payment Processors | Critical | Processing for Cuba risks violating US OFAC sanctions and local anti-money laundering laws. |

| Company Directors/Executives | High | Travel to Cuba could result in detention if identified as running an illegal gambling operation. |

🚨 Extradition and International Enforcement

Extradition Treaties: Cuba has extradition agreements with several nations, though relations with the US and EU are complex. However, Cuba cooperates on transnational crime.

Enforcement History: The Cuban government aggressively targets “economic crimes” and “illicit enrichment.” While they rarely extradite *for* other countries regarding gambling, they will prosecute foreigners operating illegally on Cuban soil.

Travel Risk: High. Directors of gambling companies operating illegally in Cuba should avoid traveling to the country.

📋 Final Verdict

Cuba receives an Operator Ease Score of 0.0/10 and a Player Access Score of 1.3/10, resulting in an overall market attractiveness rating of 0.6/10.

HONEST ASSESSMENT: Cuba is a “no-go” zone for any legitimate iGaming operator. The complete legal prohibition dating back to 1959, combined with the criminalization of the industry and the lack of a wealthy consumer base, makes it one of the least attractive markets globally. The only activity present is unregulated, black-market crypto gambling, which carries extreme legal and financial risks.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NO ONE. There is no legal pathway for entry.

❌ Definitely Avoid If You Are:

- A Publicly Listed Company: Operating here violates compliance standards and potentially US Sanctions (OFAC).

- A Sportsbook or Casino: It is illegal.

- Dependent on Credit Card Processing: Cards will not work.

- Targeting High LTV Players: The economic reality makes player value extremely low.

⚠️ BOTTOM LINE: Cuba is a closed, illegal market with zero potential for legitimate business operations.