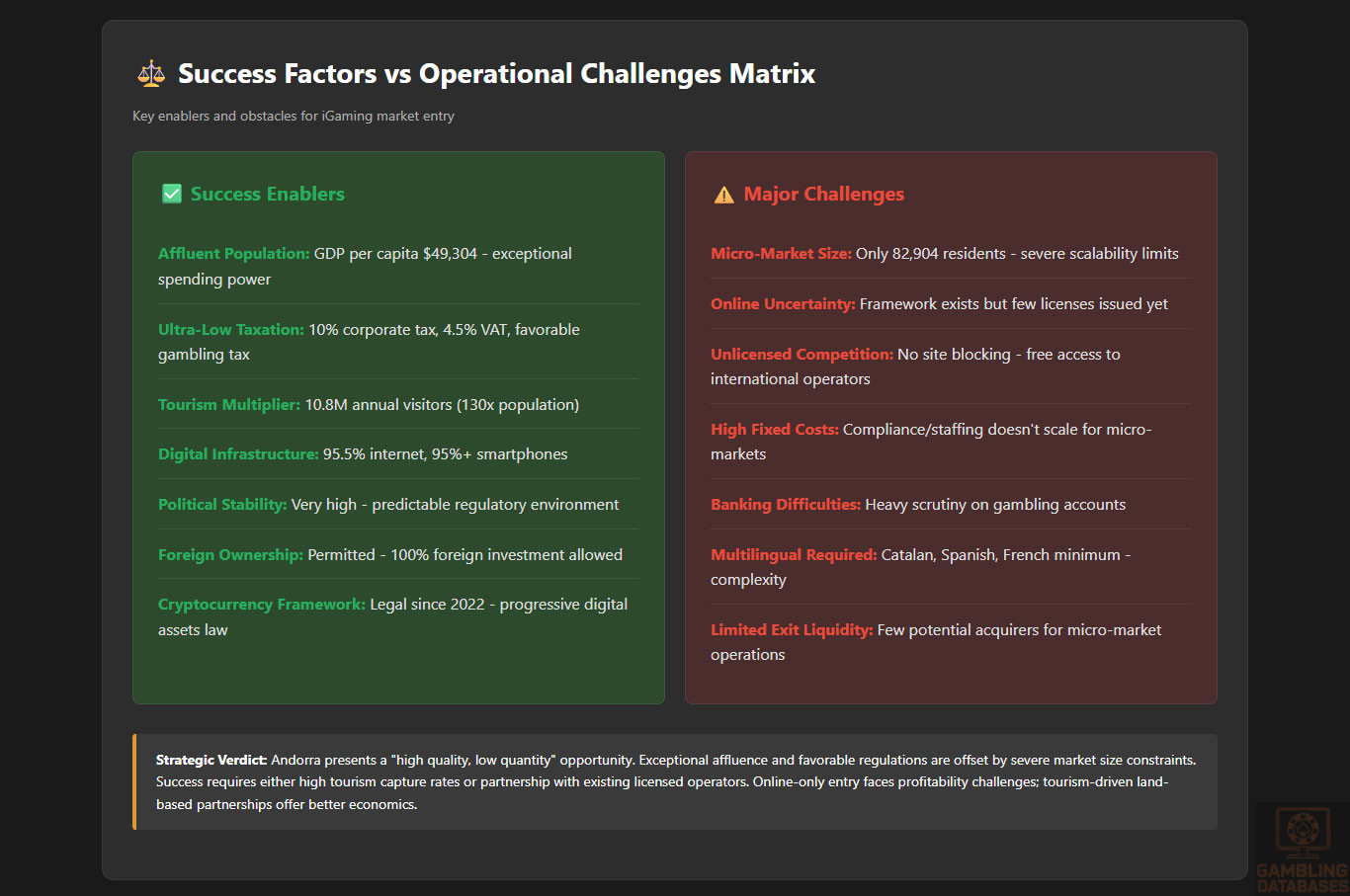

Andorra presents a unique opportunity for iGaming operators seeking entry into a microstate with evolving gambling regulations. The Principality has transitioned from a complete gambling prohibition to a regulated framework under Law 4/2021, offering both land-based and emerging online gambling opportunities.

With a highly affluent population, exceptional internet penetration of 95.5%, and one of Europe’s lowest tax regimes, Andorra combines strategic geographic positioning between France and Spain with tourism-driven economic dynamics that create distinctive market characteristics for gambling operators.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Gambling Legal Status | Legal and Regulated | Law 4/2021 governs both land-based and online gambling |

| Regulatory Authority | CRAJ (Consell Regulador Andorrà del Joc) | Established regulatory and control entity |

| Online Gambling Status | Regulated but limited licensing | Framework exists, few licenses issued to date |

| Total Population (2025) | 82,904 | Among smallest markets in Europe |

| Population Density | 176 per km² | Highly concentrated urban population |

| Median Age | 43.9 years | Mature demographic profile |

| Urban Population | 82.3% | 68,233 people in urban areas |

| GDP Total (2024) | $6.00 billion USD | Developed economy driven by tourism and finance |

| GDP Per Capita | $49,304 USD (2024) | 325% of world average, 16th richest country |

| GDP Growth Rate | 1.4% (2023) | Stable economic growth |

| Currency | Euro (EUR) | Monetary agreement with EU since 2011 |

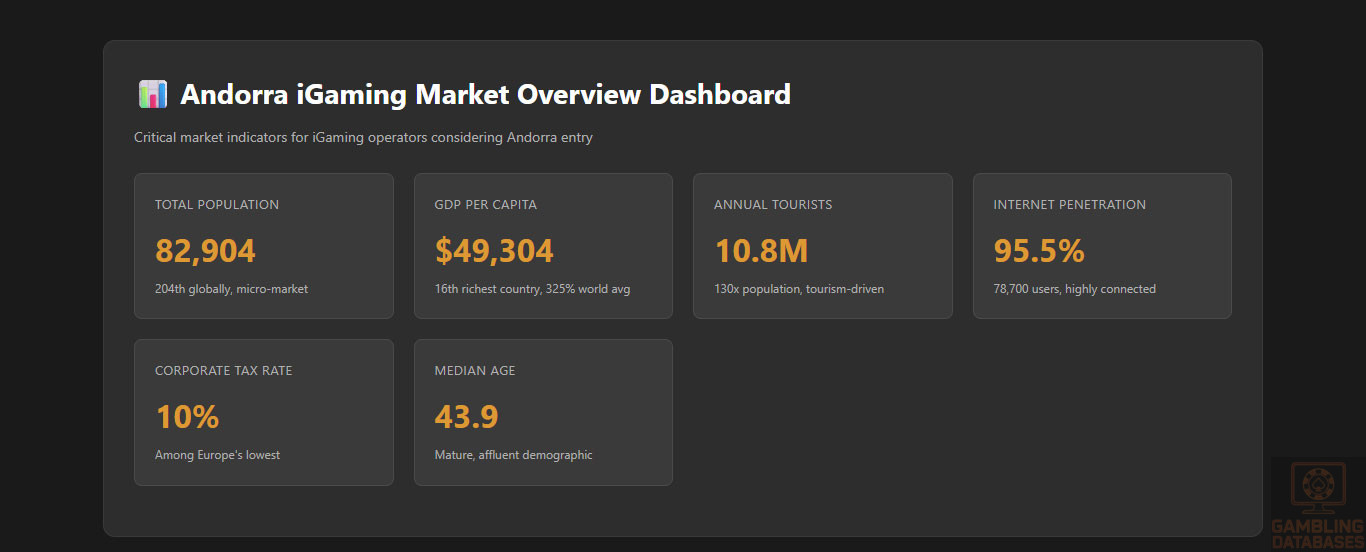

| Internet Penetration | 95.5% | 78,700 internet users (January 2025) |

| Mobile Connections | 126,000 | 153% of total population |

| Social Media Penetration | 58.2% | 48,000 social media users |

| Smartphone Penetration | High (est. 95%+) | Advanced mobile ecosystem |

| Corporate Tax Rate | 10% standard | Among lowest in Europe; 2-5% for new businesses first 3 years |

| Personal Income Tax | 0-10% progressive | €24,000 exempt, max 10% above €40,000 |

| VAT Rate (IGI) | 4.5% standard | One of Europe’s lowest; 9.5% for financial services |

| Dividend Tax (Domestic) | 0% | No withholding on Andorran company dividends |

| Minimum Legal Gambling Age | 18 years | Strictly enforced |

| Annual Tourist Visitors | 10.8 million (2008 est.) | Tourism-driven economy, visitors far exceed residents |

| Official Language | Catalan | Spanish, French, Portuguese widely spoken |

| Market Entry Timeline | 6-12 months estimated | Company formation + licensing process |

| License Duration | 17 years (casino) | Renewable upon expiration |

| Foreign Ownership | Permitted | 100% Andorran ownership may provide competitive advantage |

| Business Environment Rank | Favorable | Streamlined processes, low bureaucracy |

| Political Stability | Very High | Stable parliamentary democracy |

| Market Size Classification | Micro-market | Limited by small population; tourism provides expansion potential |

| Estimated iGaming Market Value | Developing | No comprehensive revenue data available yet |

| Market Maturity | Emerging | Recent regulatory framework, evolving landscape |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

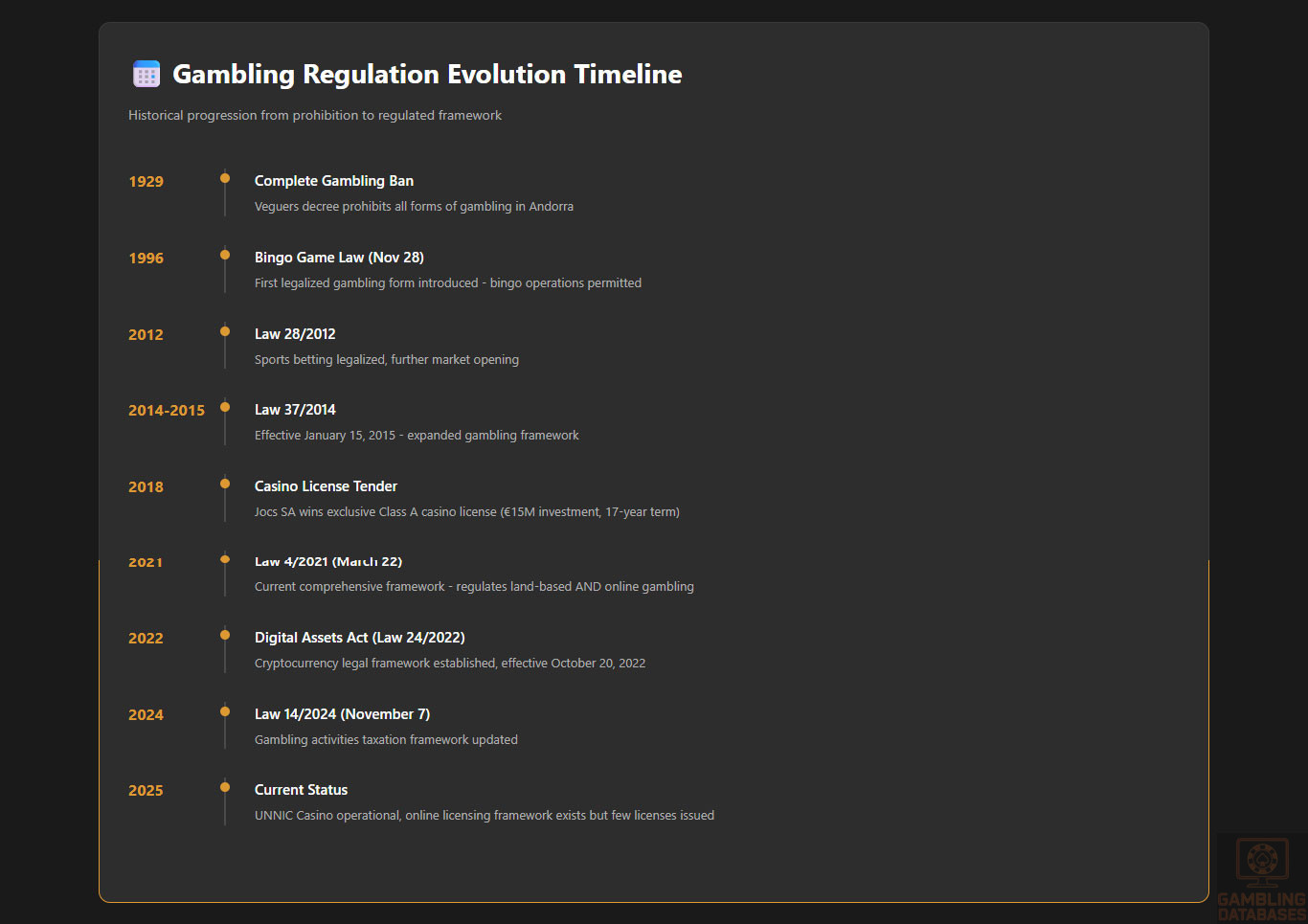

Andorra has undergone a dramatic transformation in gambling regulation over the past decade. Historically, all forms of gambling were prohibited under a 1929 decree by the Veguers of Public Order and Residence of Foreigners.

This blanket ban persisted for nearly 70 years until the Bingo Game Law of November 28, 1996, marked the first step toward regulated gambling. The evolution accelerated with Law 28/2012, followed by Law 37/2014 (effective January 15, 2015).

The current comprehensive legal framework is governed by Law 4/2021, dated March 22, 2021, which establishes the consolidated text for the regulation of games of chance. This legislation provides a structured approach to both land-based and online gambling activities.

The regulatory authority, Consell Regulador Andorrà del Joc (CRAJ), was established as an independent administrative body with legal personality, exclusively responsible for regulating, controlling, and supervising all gambling activities in the Principality.

Land-Based Gambling Activities

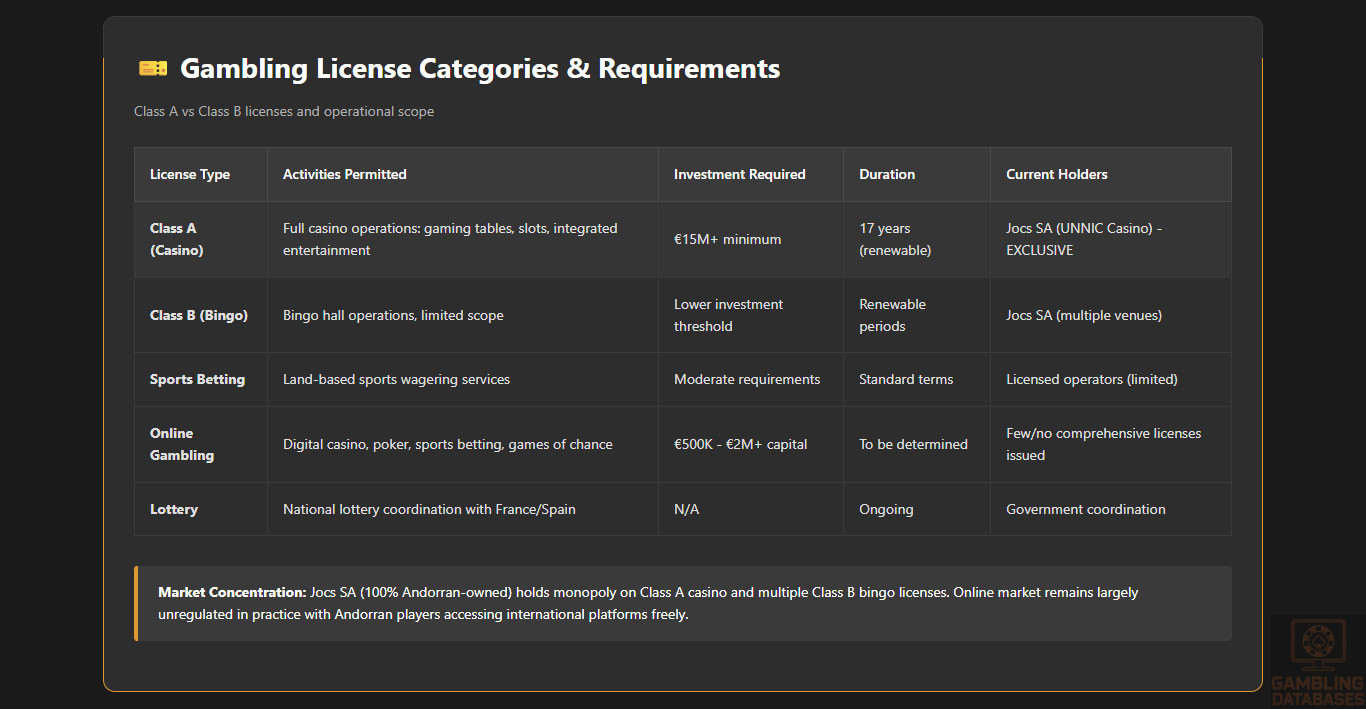

Casino Operations: Andorra has authorized land-based casino gambling through a competitive licensing process. In 2018, Andorran company Jocs SA was awarded the sole Class A casino license after a tender that attracted 13 international bidders.

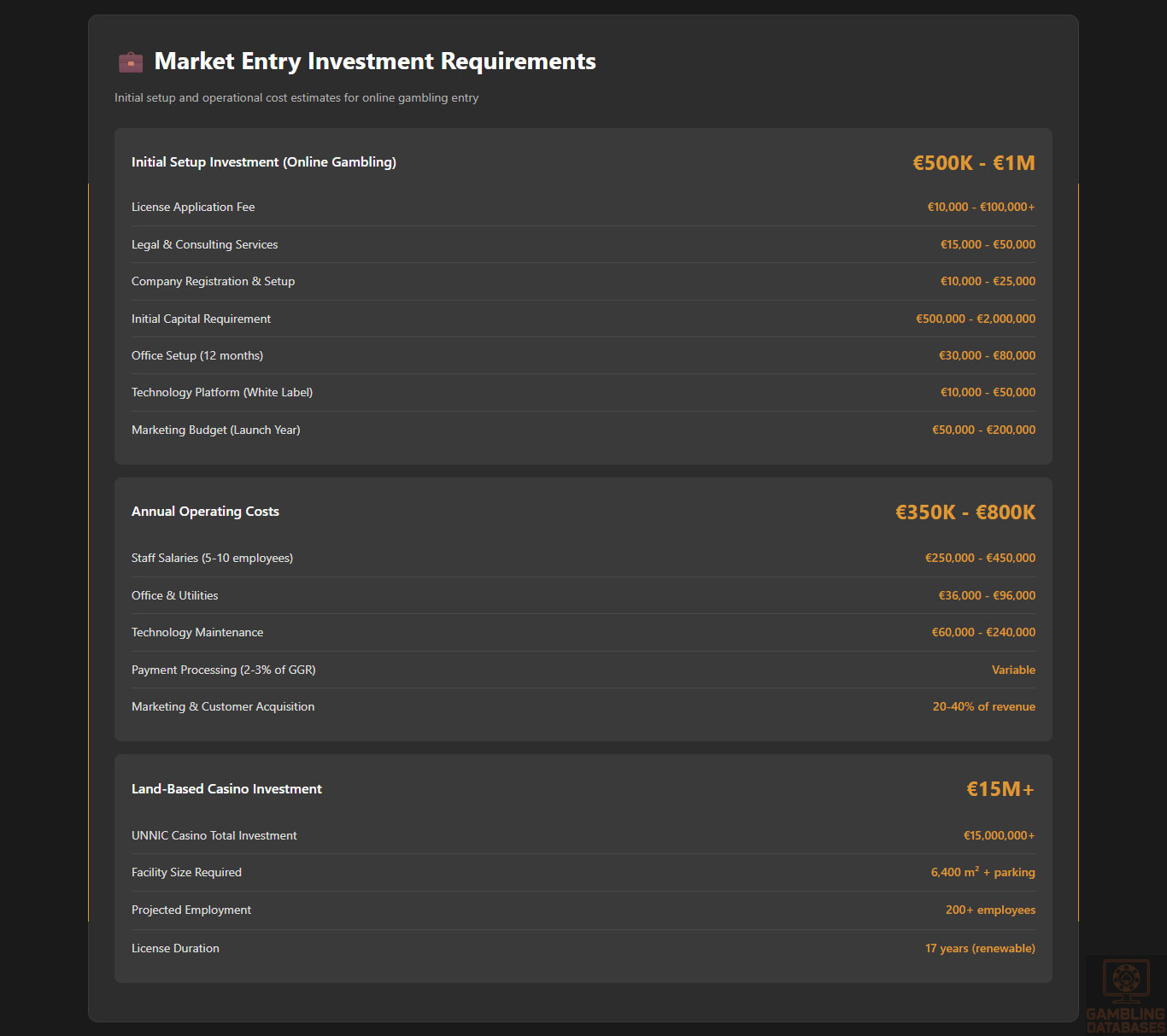

The winning bid involved a €15 million casino complex in Andorra la Vella, expected to accommodate approximately 1,500 people and create over 160 jobs. The license was granted for 17 years from the effective opening date, with renewal possibilities.

After regulatory delays and appeals, the UNNIC Casino eventually opened, representing a significant milestone in Andorra’s gambling market development. The casino features gaming tables, slot machines, and integrated entertainment facilities.

Sports Betting Venues: Sports betting has been legal in Andorra since 2012. Licensed operators can offer land-based sports wagering services, though the market remains relatively small due to population size constraints.

Bingo Operations: Bingo was the first legalized form of gambling in Andorra. Class B licenses permit bingo hall operations, with Jocs SA also managing bingo venues throughout the Principality.

The traditional “Quintos” bingo format remains popular and has cultural significance in Andorran society. Regulations specify operational requirements, prize structures, and responsible gambling measures for bingo operators.

Lottery and Other Games: National lottery operations function in coordination with similar lotteries in France and Spain, reflecting Andorra’s geographic and cultural connections with neighboring countries.

Online Gambling Framework

Regulatory Status: Law 4/2021 explicitly provides for the regulation of online gambling activities, distinguishing between in-person and digital gaming modalities. The legal framework categorizes online operators separately from land-based establishments.

However, implementation has been gradual. While the legislation authorizes CRAJ to issue online gambling licenses, the regulatory body has been slow to grant such licenses, creating a transitional regulatory environment.

Permitted Online Activities: The law encompasses online casino games, sports betting, poker, and other games of chance delivered through digital platforms. Operators must comply with specific technical standards and player protection requirements.

Current Market Reality: As of early 2025, Andorra has not established a robust licensed online gambling market. Few if any comprehensive online gambling licenses have been issued to operators.

Andorran residents currently access offshore online gambling sites without legal restrictions or enforcement actions. The CRAJ has not implemented blocking mechanisms against unlicensed international operators, creating a de facto open market situation.

This regulatory gap may represent either an opportunity or uncertainty for prospective operators, depending on how quickly CRAJ moves to implement comprehensive online licensing frameworks and whether access to unlicensed sites continues.

Licensed Operators and Market Players

Land-Based Market: Jocs SA holds the exclusive Class A casino license and operates multiple Class B bingo licenses, making it the dominant licensed gambling operator in Andorra.

The company is 100% Andorran-owned, which proved advantageous in the competitive bidding process against international gaming corporations including Genting Group, CIRSA, Partouche, and Casinos Austria AG.

Jocs SA partnered with Austrian technology provider Novomatic as the strategic technology supplier for the UNNIC Casino, combining local ownership with international gaming expertise and equipment.

Online Market: No comprehensive data exists on licensed online gambling operators in Andorra. The online market remains largely unregulated in practice, with Andorran players accessing international platforms.

Market Concentration: The land-based gambling market exhibits extreme concentration, effectively operating as a monopoly or duopoly structure with Jocs SA controlling the primary licensed operations.

Licensing Framework and Requirements

Application Process and Eligibility

Regulatory Authority: The Consell Regulador Andorrà del Joc (CRAJ) is the sole entity responsible for issuing gambling licenses in Andorra. The authority operates from C/ Doctor Vilanova, 9 – Edifici Thaïs, 3a planta – despatx D, AD500 Andorra la Vella.

Contact: +376 822 922, Email: [email protected]. The CRAJ website (www.craj.ad) provides official information, though predominantly in Catalan.

License Categories: Law 4/2021 distinguishes six categories of gambling operators, classified by activity type and delivery method (face-to-face or online). Categories include pure games of chance, lotteries, mixed games of chance and skill.

Class A licenses authorize casino operations with the most comprehensive gaming rights. Class B licenses permit bingo operations with more limited scope and investment requirements.

Application Process: Operators must submit comprehensive applications to CRAJ including business plans, financial documentation, technical specifications, responsible gambling policies, and evidence of financial capacity.

For the casino license, CRAJ conducted an international public tender that required detailed proposals covering investment amounts, job creation projections, economic impact assessments, architectural plans, and operational strategies.

The winning bidder had 15 days to submit the formal license application after tender selection. CRAJ then issued the license within approximately two months following application submission.

Financial Requirements: Specific capital requirements vary by license type and are not publicly disclosed in detail. The casino license required demonstrated financial capacity to execute a minimum €15 million investment.

Operators must prove sufficient financial resources to sustain operations, meet player liabilities, implement technical systems, and fulfill ongoing compliance obligations. Banking relationships in Andorra typically require extensive due diligence.

Background Checks: All license applicants and beneficial owners undergo rigorous background investigations. Required documentation includes criminal record certificates with Hague Apostille, valid for maximum three months from issuance.

Passport copies with Hague Apostille, detailed CVs, business plans, and documentation explaining work profiles and business models must be submitted. Andorra maintains high standards for anti-money laundering compliance and reputational integrity.

Application Fees: Law 4/2021 Article 94 specifies that license applications are subject to administrative fees. Exact fee schedules are not publicly published and likely vary by license category.

Prospective operators should contact CRAJ directly for current fee structures. Based on the casino tender experience, expect substantial fees commensurate with exclusive licensing privileges and market access value.

Local Presence and Operational Requirements

Company Incorporation: Foreign operators must establish a legal entity incorporated under Andorran law to obtain gambling licenses. Acceptable structures include limited liability companies (SL – Societat Limitada) or corporations (SA – Societat Anònima).

The company must have its registered office in Andorra and conduct effective management from the Principality. Managers must perform their functions from Andorra, and board meetings must take place within the country.

Failure to maintain genuine Andorran management creates tax residence risks, potentially subjecting the company to taxation in other jurisdictions where effective control occurs.

Physical Presence: Land-based gambling licenses obviously require physical premises meeting CRAJ’s technical, security, and accessibility standards. The casino required a 6,400-square-meter facility with parking for 80 vehicles.

Online gambling operations require registered office space in Andorra, though the extent of physical infrastructure requirements remains unclear given limited online licensing precedents.

Staffing Requirements: Operators must employ personnel in Andorra. The casino license projected over 200 employees, contributing to the economic impact evaluation that influenced license award decisions.

Key management positions, compliance officers, and customer service functions likely require Andorran-based staff, though specific mandates are not publicly detailed.

Technology and Hosting: Technical requirements for online gambling are specified in CRAJ regulations but not comprehensively published. Operators should anticipate requirements for certified gaming platforms, random number generator testing, and responsible gambling tools.

Whether server infrastructure must be hosted within Andorra or can operate from other jurisdictions remains unclear. The small market size suggests flexibility, but confirmation from CRAJ is essential.

Foreign Ownership: Foreign investment in Andorran companies is permitted under the Foreign Investment Law. Non-residents can invest in and own Andorran gambling operators.

However, the casino tender outcome suggests 100% Andorran ownership may provide competitive advantages in licensing decisions, particularly for high-value exclusive licenses where economic impact and local benefit are evaluation criteria.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification: The minimum legal gambling age in Andorra is 18 years. Operators must implement robust age verification systems preventing minors from accessing gambling services.

CRAJ enforces strict compliance with age restrictions. Marketing materials, premises access control, and online registration processes must include effective age verification mechanisms.

Anyone appearing under 25 years of age must present identification documentation. Violations of minor protection regulations result in severe penalties including license suspension or revocation.

KYC/AML Requirements: Andorra maintains rigorous anti-money laundering standards aligned with international best practices. Despite its favorable tax regime, the Principality complies with OECD guidelines and has established over 15 tax information exchange agreements.

Gambling operators must implement comprehensive Know Your Customer procedures, including identity verification, source of funds checks, and ongoing transaction monitoring. Customer due diligence must meet standards applied by Andorran financial institutions.

Beneficial ownership information must be identified and verified. Politically exposed persons require enhanced due diligence. Suspicious transaction reporting to Andorran authorities is mandatory.

Responsible Gambling Measures: Law 4/2021 emphasizes responsible gambling as a core regulatory objective. Operators must implement measures to prevent excessive gambling and identify problem gambling behaviors.

UNNIC Casino prominently features responsible gambling information and support resources. The website advises: “Gambling without control is not healthy gambling. When you stop enjoying yourself, gambling becomes an addiction.”

Required measures include self-assessment tools, deposit limits, loss limits, session time limits, reality checks, and self-exclusion options. Marketing must include responsible gambling messaging and avoid targeting vulnerable populations.

Self-Exclusion Systems: Operators must maintain self-exclusion registries allowing players to voluntarily ban themselves from gambling activities. Self-exclusion periods must be enforceable across all operator platforms.

The CRAJ may maintain a centralized exclusion registry applicable across all licensed operators, though specific implementation details for Andorra’s system are not publicly documented.

Player Information Disclosures: Gambling platforms must display clear information about game rules, odds, return-to-player percentages, and terms and conditions. Players must understand the risks and mechanics before participation.

Promotional terms must be transparent, including wagering requirements, withdrawal restrictions, and expiration dates. Misleading advertising is prohibited.

Financial Monitoring and Reporting

Transaction Monitoring: Operators must implement systems to detect unusual betting patterns, potential money laundering, match-fixing, or fraud. Automated monitoring tools should flag suspicious activities for investigation.

Large cash transactions, structured deposits, and high-value winnings trigger enhanced scrutiny. Gambling operators function as gatekeepers in Andorra’s financial system and bear compliance responsibilities accordingly.

Reporting Obligations: Licensed operators must submit regular reports to CRAJ covering financial performance, player statistics, responsible gambling metrics, and compliance activities. Reporting frequency likely includes monthly or quarterly submissions.

Annual audited financial statements must be filed with both CRAJ and Andorran commercial registry authorities. Tax declarations to the Andorran Tax Administration must accurately report gambling revenues.

Audits and Inspections: CRAJ retains authority to conduct on-site inspections, examine records, test gaming equipment, and audit compliance systems. Operators must cooperate fully with regulatory examinations.

Independent third-party audits of gaming systems, random number generators, and financial controls may be required to maintain licensing compliance.

Data Retention: Player records, transaction histories, gaming logs, and compliance documentation must be retained for specified periods. Based on general European standards, expect minimum 5-year retention requirements.

Taxation Structure and Financial Obligations

Player Taxation

Winnings Tax: Gambling winnings in Andorra are subject to personal income tax treatment. However, winnings from gambling activities authorized in the Principality benefit from favorable exemptions.

For savings income (which includes certain gambling winnings), the first €3,000 is entirely exempt from taxation. Amounts exceeding €3,000 are taxed at 10%.

This creates a de facto tax-free threshold for casual players, with only significant winners facing moderate taxation on excess amounts.

Offshore Gambling Income: Andorran tax residents receiving gambling income from unauthorized international gambling sites or foreign casinos do not benefit from the €3,000 exemption for locally authorized gambling.

Such winnings are considered general savings income taxed at 10% from the first euro, though enforcement and reporting challenges exist for offshore winnings.

Professional Gamblers: Individuals earning income from professional poker playing or gambling activities may be taxed differently. Income from poker tournament winnings, team salaries, affiliate marketing, and prizes in kind goes to the general tax base.

The general tax base provides €24,000 fully exempt, then 5% on income between €24,000-€40,000, and 10% on income exceeding €40,000. Maximum effective taxation for professional gamblers remains capped at 10%.

Professional gamblers must navigate banking challenges, as financial institutions often view gambling-related accounts skeptically. Many register as digital marketing professionals to facilitate banking relationships.

Operator Taxation

Gambling Activities Tax: Licensed gambling operators are subject to a specific tax on gambling activities under Law 14/2024 (November 7, 2024). This tax regime applies to all licensed gambling operations.

Exact tax rates by game type are not publicly disclosed in available sources. Andorran authorities have indicated intentions to keep gambling taxation “really low” to attract investors and operators.

Based on the regulatory environment, operators should anticipate GGR-based taxation, though rates likely fall below European averages given Andorra’s general low-tax positioning.

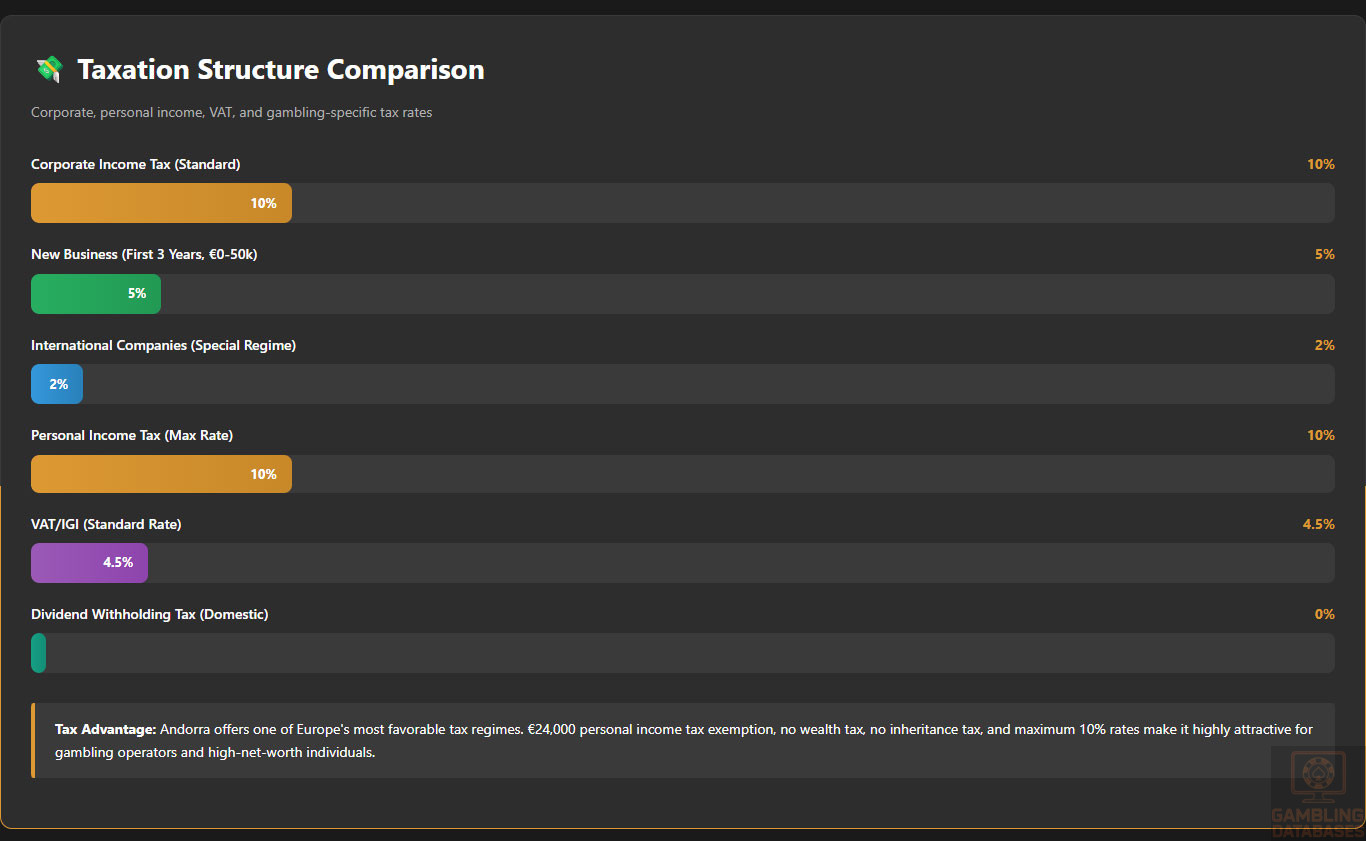

Corporate Income Tax: Gambling operators operating as Andorran companies are subject to standard corporate income tax (IS – Impost de Societats) at 10% on company profits.

New companies benefit from reduced rates during the first three years: 5% on the first €50,000 of taxable income and 10% on income exceeding €50,000 (for companies with income below €100,000).

International gambling companies and holding structures may qualify for reduced 2% taxation, though specific applicability to gambling operations requires expert confirmation.

License Fees and Renewal Costs: Initial license application involves administrative fees under Article 94 of Law 4/2021. Exact amounts are not published and vary by license class.

The casino license, being exclusive and high-value, likely commanded substantial fees. Annual license maintenance fees and periodic renewal fees should be anticipated.

The 17-year casino license duration suggests renewal fees will apply upon expiration, though terms are negotiated based on market conditions and regulatory policy at renewal time.

Other Operational Taxes: Value Added Tax (IGI – Impost General Indirecte) applies at 4.5% standard rate in Andorra, among Europe’s lowest. Financial services face a 9.5% increased rate.

Gambling services’ IGI treatment requires clarification – they may be zero-rated, standard-rated, or subject to special provisions. Social security contributions for employees must be paid to CASS (Andorran social security).

Employment-related contributions can escalate quickly and represent significant operational costs beyond headline tax rates.

Gambling Market Financial Performance

Market Revenue Data: Comprehensive gambling market revenue statistics for Andorra are not publicly available. The market is in early development stages, particularly for online gambling.

The UNNIC Casino opening represents the first major modern casino, making historical revenue data limited. Bingo operations have existed since 1996 but represent a small market segment.

Projected Economic Impact: Jocs SA’s casino license application projected the facility would attract 200,000 international visitors annually and contribute over €90 million to Andorra’s economy.

These figures remain projections and actual performance data is not publicly disclosed. The casino’s economic contribution includes direct gaming revenue, employment creation, tourism spending, and secondary economic effects.

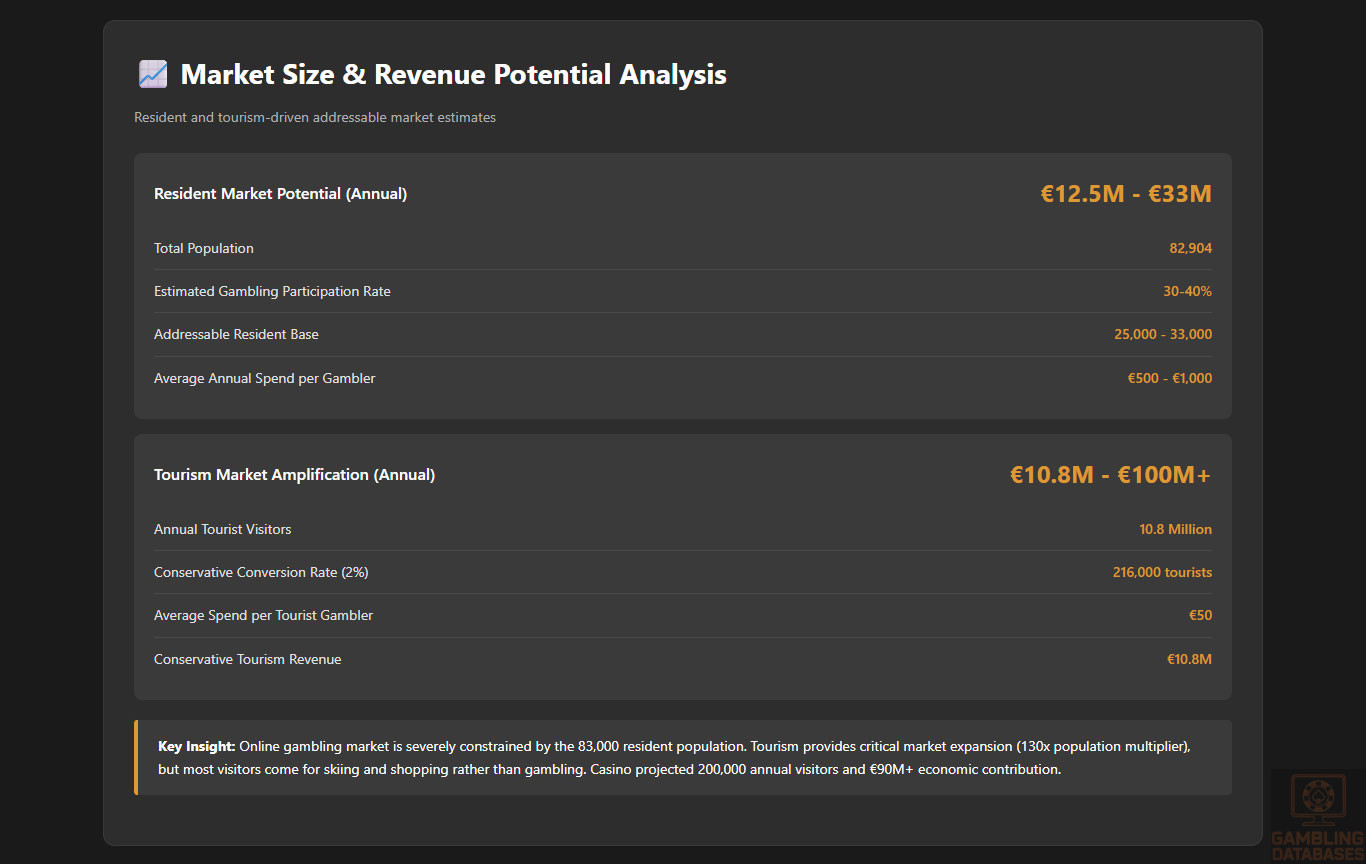

Market Size Estimation: Given Andorra’s population of 82,904 and tourism influx of approximately 10.8 million annually, the addressable market for gambling significantly exceeds the resident base.

However, most tourists visit for shopping and skiing rather than gambling. Converting meaningful percentages of tourist visitors to casino patrons requires strong marketing and compelling entertainment offerings.

Online gambling market potential is constrained by small resident population unless licenses permit broader European market access, which seems unlikely given Andorra’s non-EU status.

Growth Trends: Insufficient historical data exists to establish reliable year-over-year growth trends. The market is essentially in a formation phase with the recent casino opening and evolving online framework.

Expected growth drivers include increased casino awareness, potential online licensing expansion, tourism recovery post-COVID, and Andorra’s growing international profile as a business and residence destination.

Advertising and Marketing Restrictions

Permitted Channels: Andorran gambling advertising regulations are not comprehensively detailed in available public sources. Law 4/2021 addresses advertising but specific permitted channels require regulatory clarification.

Land-based casino marketing appears permitted through standard channels including outdoor advertising, print media, digital platforms, and tourism promotional materials.

Content Restrictions: Marketing must comply with responsible gambling principles. Advertisements cannot target minors, vulnerable populations, or create false impressions about winning probabilities.

Promotional content must include responsible gambling warnings and information about support resources. Age restrictions must be clearly communicated.

Bonus and Promotion Rules: Specific restrictions on bonus offers, wagering requirements, or promotional caps are not detailed in available sources. Online casinos serving Andorran players typically offer bonuses.

Operators should anticipate requirements for fair terms, transparent disclosures, and reasonable wagering requirements aligned with general European consumer protection principles.

Sponsorship Regulations: Sports sponsorships, event sponsorships, and team partnerships are common in European gambling markets. Andorra’s small size limits major sports franchise opportunities.

Given tourism focus and international visibility goals, gambling operators may find sponsorship opportunities with ski resorts, cycling events (Andorra hosts Tour de France and Vuelta stages), and cultural festivals.

Affiliate Marketing: Online affiliate marketing rules for Andorra are undefined. As online licensing develops, expect regulations governing affiliate relationships, promotional accuracy, and compliance responsibilities.

Recent Regulatory Changes and Their Impact

Law 4/2021 Implementation: The March 22, 2021 enactment of the consolidated gambling regulation represented the most significant recent regulatory development. This law replaced Law 37/2014 and created the current comprehensive framework.

Law 4/2021 clarified operator categories, licensing procedures, compliance obligations, and the CRAJ’s regulatory authority. It established foundation for both land-based and online gambling regulation.

Law 14/2024 Tax Update: November 7, 2024 saw the approval of Law 14/2024 on gambling activities taxation. This recent legislation governs the tax collection framework for gambling operations.

The law is managed by CRAJ, which handles both regulation and tax collection for gambling activities. Specific rate changes or new obligations introduced by this law are not publicly detailed.

Casino License Saga: The 2018-2020 period saw significant regulatory drama with the casino license. Jocs SA initially won the tender in 2018 but faced license withdrawal in 2019 due to documentation deficiencies.

After appeals and resubmission of revised documentation, the license was ultimately granted, but delays created uncertainty. In February 2020, CRAJ again rejected aspects of Jocs’ concession.

These regulatory flip-flops demonstrated CRAJ’s stringent standards but also raised questions about regulatory consistency and predictability for prospective operators.

Online Licensing Delays: Despite Law 4/2021 authorizing online gambling licenses, CRAJ has been slow to implement comprehensive online licensing. This creates ongoing uncertainty about when and how online gambling will be fully regulated.

The delay may reflect cautious regulatory approach, resource constraints at CRAJ, or policy debates about appropriate online gambling frameworks for such a small market.

Enforcement Mechanisms and Penalties

CRAJ Authority: The Consell Regulador Andorrà del Joc possesses comprehensive enforcement powers including license suspension, license revocation, financial penalties, and criminal referrals for serious violations.

The regulatory body can conduct inspections, seize equipment, order operational changes, and impose corrective action plans on licensed operators.

Penalty Structures: Specific fine amounts and penalty schedules are not publicly detailed. Violations are likely categorized by severity (minor, serious, very serious) with escalating penalties.

License suspension prevents operations until compliance is restored. License revocation permanently terminates the operator’s authorization, forfeiting investments and market position.

Enforcement Precedents: The casino license withdrawal and subsequent restoration demonstrates CRAJ’s willingness to enforce standards rigorously, even against the sole casino licensee representing significant economic investment.

This precedent suggests CRAJ prioritizes regulatory integrity over economic considerations, creating accountability but also potential unpredictability risks for operators.

Unlicensed Operator Blocking: Andorra has not implemented systematic ISP-level blocking of unlicensed international gambling sites. Residents access offshore operators freely without restrictions.

This hands-off approach may change as CRAJ develops online licensing frameworks. Future enforcement could include website blocking, payment processing restrictions, or advertising prohibitions against unlicensed operators.

Payment Processor Restrictions: No evidence exists of restrictions on payment processors handling gambling transactions. Andorran banks maintain rigorous compliance standards but process legitimate gambling-related payments.

Criminal Penalties: Operating unlicensed gambling activities in Andorra likely constitutes criminal offenses under the general prohibition framework. Penalties may include fines, imprisonment, or both for serious violations.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Total Population: Andorra’s population stands at approximately 82,904 as of mid-2025, ranking 204th globally and 43rd in Europe. The population has shown modest growth of approximately 1.08% annually.

This represents one of the world’s smallest national populations, creating inherent market size constraints for gambling operators but also enabling focused marketing and customer service approaches.

Population Growth: Between 2024 and 2025, Andorra added approximately 260 people, reflecting natural increase as births exceed deaths. Net migration contributes positively with approximately 1,061 net migrants in 2023.

The steady but slow population growth suggests a stable market base with limited organic expansion potential from demographic factors alone.

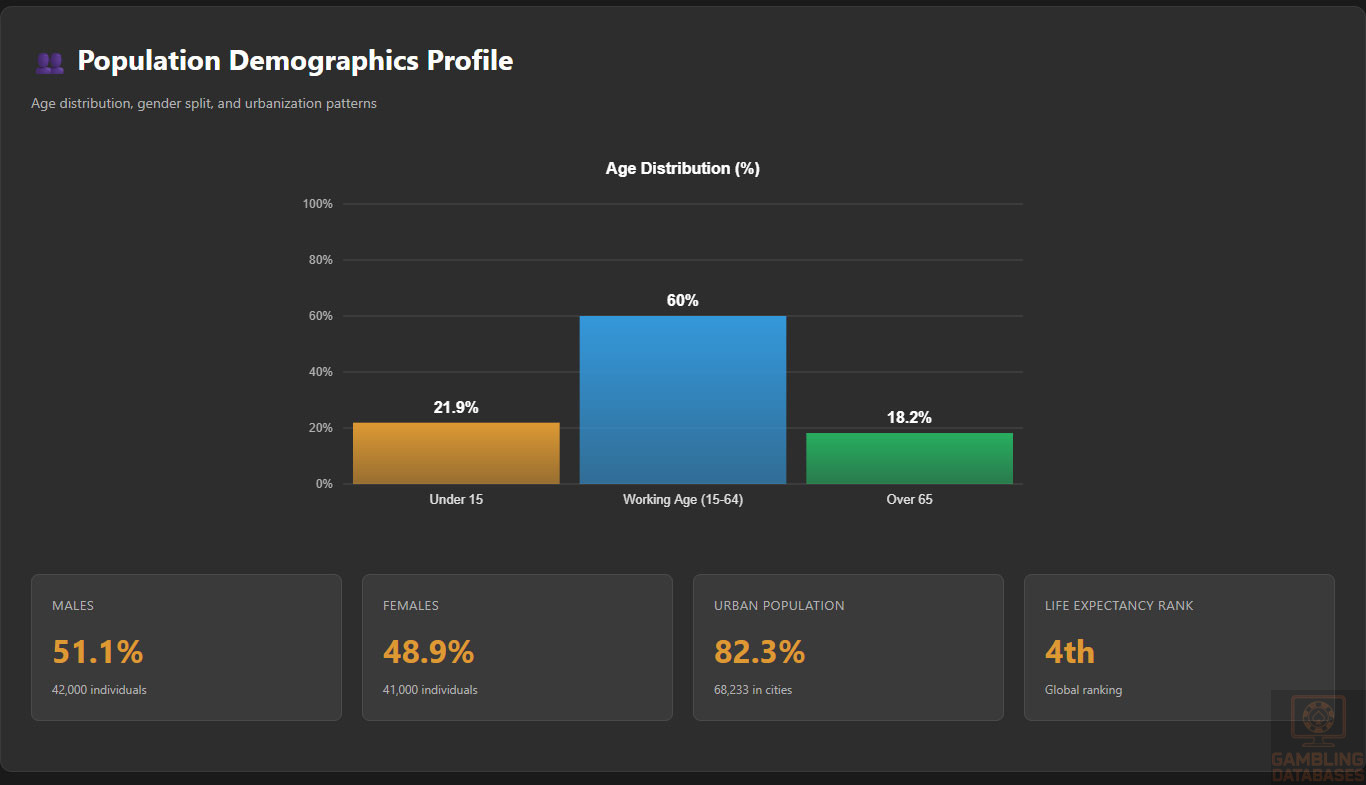

Age Distribution: The median age of 43.9 years indicates a mature population profile. Approximately 21.9% of the population is under 15 years (child dependency ratio).

The working-age population (15-64 years) comprises the majority, while 18.2% are aged 65+ (aged dependency ratio). The total dependency ratio of 40% is relatively low.

For gambling operators, the mature demographic suggests an audience with established income, discretionary spending capacity, and familiarity with entertainment expenditures. Youth market segments are limited.

Gender Distribution: Andorra has 42,000 males and 41,000 females, creating a sex ratio of 104.48 males per 100 females. The male population represents 51.09% while females comprise 48.9%.

The slight male majority may influence gambling participation rates, as males typically show higher engagement in sports betting and casino gambling across European markets.

Life Expectancy: Andorra boasts the 4th highest life expectancy globally, reflecting excellent healthcare, high living standards, and quality of life. Long life expectancy correlates with affluent, health-conscious populations.

Geographic Distribution

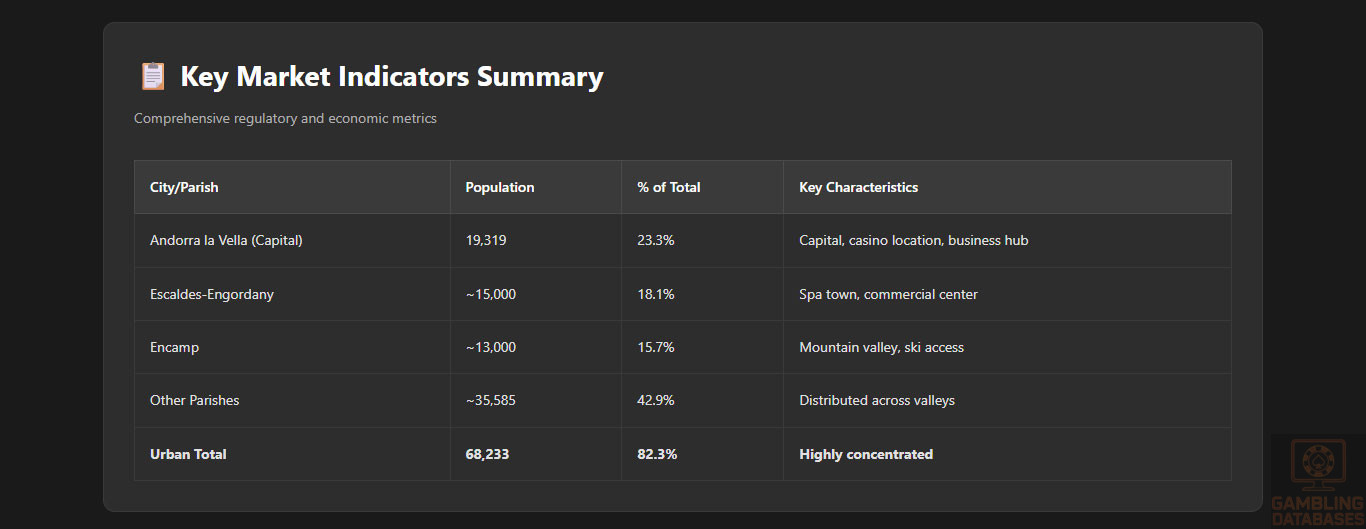

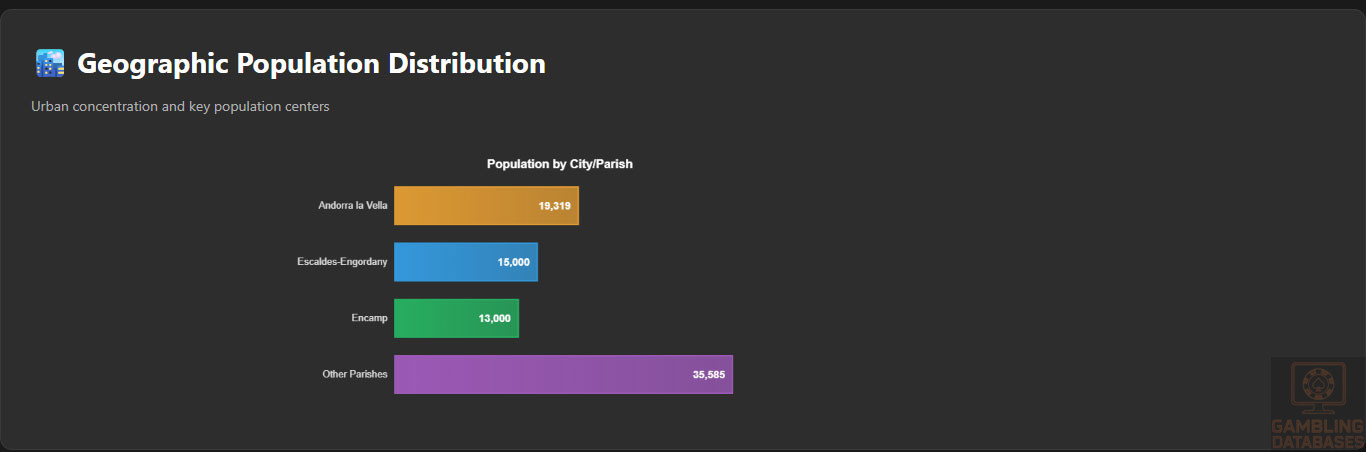

Urbanization Rate: An impressive 82.3% of Andorra’s population lives in urban areas, totaling approximately 68,233 urban residents. This high urbanization facilitates marketing, service delivery, and land-based venue accessibility.

Capital City: Andorra la Vella serves as the capital and largest city with a population of 19,319. The city is Europe’s highest elevation capital, situated in the central valley.

The UNNIC Casino is strategically located in Andorra la Vella at Prat de la Creu, maximizing accessibility to both residents and tourist traffic.

Population Centers: Beyond Andorra la Vella, population concentrates in seven urbanized valleys. Key population centers include Escaldes-Engordany, Encamp, La Massana, and Sant Julià de Lòria.

The compact geography (470 km² total area) means the entire population is within short driving distance of central locations, simplifying land-based gambling accessibility.

Regional Economic Patterns: Economic activity concentrates in Andorra la Vella and Escaldes-Engordany, where financial services, retail, and tourism infrastructure cluster. These areas attract the highest visitor densities during ski seasons.

Tourism Geography: Mountain resort areas in parishes like Canillo, La Massana, and Ordino drive winter tourism. Shopping districts in Andorra la Vella attract cross-border visitors from Spain and France year-round.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

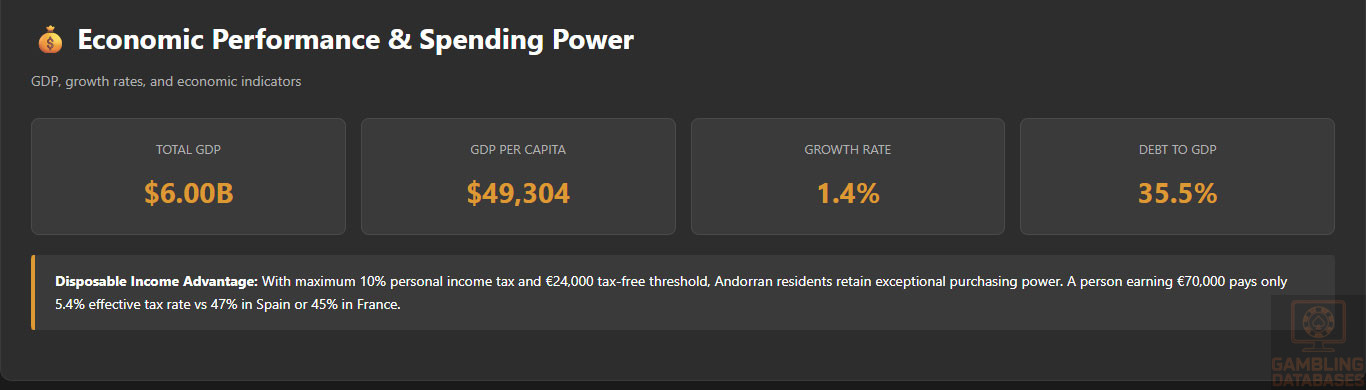

GDP Total: Andorra’s GDP reached $6.00 billion USD in 2024, ranking 166th globally. For such a small population, this represents substantial economic output.

GDP Per Capita: At $49,304 USD in 2024 (some sources cite $41,034-$46,414 depending on methodology), Andorra’s per capita GDP equals 325% of the world average.

The country ranks as the 16th richest globally by GDP per capita, creating an affluent market with significant discretionary spending capacity. This wealth level surpasses many large European economies.

GDP Growth: Economic growth reached 1.4% in 2023, reflecting steady expansion. Over the past decade, Andorra averaged 1.5-2.2% annual GDP growth, demonstrating economic stability.

While growth rates are modest, the stable trajectory provides confidence in sustained consumer spending and business environment predictability.

Economic Structure: Services dominate at 54.5% of GDP, followed by industry at 33.6% and agriculture at 11.9%. Financial services, tourism, and commerce account for 75% of gross value added.

The service-oriented economy aligns well with gambling and entertainment industry development. Tourism dependence creates seasonal revenue fluctuations but also substantial visitor spending potential.

Public Debt: National debt stood at €1.242 billion ($1.343 billion) in 2023, representing a 35.47% debt-to-GDP ratio. This low debt level reflects sound fiscal management and economic stability.

Public debt per capita equals €14,594 ($15,782), modest compared to most developed nations and indicative of governmental financial health.

Income and Wealth Distribution

Income Levels: Specific average household income data for Andorra is limited in public sources. However, the exceptionally high GDP per capita suggests average household incomes far exceed European medians.

Estimates suggest average annual incomes in the €40,000-€70,000+ range for employed individuals, with significant variation by sector and position.

Disposable Income: Andorra’s ultra-low tax regime dramatically increases disposable income compared to neighboring countries. With maximum 10% personal income tax, €24,000 tax-free, and no wealth or inheritance taxes, residents retain exceptional purchasing power.

A person earning €70,000 annually pays approximately €3,800 in income tax (5.4% effective rate), leaving substantially more disposable income than in Spain (up to 47% tax) or France (up to 45% tax).

Wealth Concentration: Andorra attracts high-net-worth individuals seeking favorable tax treatment, creating a population with above-average wealth concentration. Many residents are business owners, investors, or professionals from financial services.

The Gini coefficient and detailed income inequality measures are not published, but the small, affluent population suggests relatively compressed income distribution at high levels.

Consumer Spending Patterns: High disposable income supports robust consumer spending on entertainment, dining, travel, and luxury goods. The tourism-driven retail sector thrives on both resident and visitor spending.

Gambling expenditure capacity is substantial, though cultural factors and small population limit absolute market size. Average spend per gambler may exceed regional averages due to affluence.

Market Size and Growth Projections

Current Market Status: Comprehensive iGaming market revenue data for Andorra does not exist in public sources. The online gambling market remains largely undeveloped from a licensed operator perspective.

Land-based gambling is nascent with the recent casino opening. Bingo operations provide historical baseline but represent limited revenue scope.

Resident Market Potential: With approximately 83,000 residents and assuming 30-40% participation in gambling annually (typical European rates), the addressable resident base is 25,000-33,000 potential customers.

If average annual spend per gambler reaches €500-€1,000 (conservative given affluence), resident market potential approximates €12.5-€33 million annually across all gambling forms.

Tourism Market Amplification: The critical market expansion factor is tourism. With 10.8 million annual visitors, even minimal conversion rates dramatically expand the addressable market.

If 2% of tourists engage in gambling spending an average €50 per visit, tourism adds €10.8 million. Higher conversion rates and spending levels could push tourism gambling revenue to €50-100 million+.

Online Market Constraints: Online gambling market size is severely constrained by the small resident base. An 83,000 population cannot support substantial online gambling revenues comparable to larger markets.

Unless Andorran online licenses permit cross-border service delivery to EU markets (highly unlikely given regulatory frameworks), online gambling remains a niche opportunity.

Growth Projections: Insufficient baseline data prevents reliable CAGR calculations. However, market growth drivers include casino establishment phase, potential online licensing expansion, and tourism sector recovery and expansion.

Optimistic scenarios project 10-15% annual growth over 5 years as the market develops from a low base. Conservative scenarios assume 5-8% growth reflecting modest population increases and gradual market penetration expansion.

ARPU Estimates: Average Revenue Per User in Andorra likely exceeds European averages due to exceptional affluence. ARPUs of €800-€1,500 annually for active online gamblers are plausible.

Land-based casino ARPU may reach higher levels given tourism visitor spending patterns and the premium entertainment positioning required in such a small market.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy Rate: Andorra maintains essentially universal literacy at 100% for both genders, reflecting developed nation educational standards and compulsory education requirements.

Education System: The education system offers instruction in Catalan, Spanish, or French, reflecting multilingual national character. Both public and private schools operate to high European standards.

Tertiary education completion rates are substantial, with many Andorrans pursuing university education in Spain, France, or other countries before returning home.

Digital Literacy: With 95.5% internet penetration and advanced smartphone adoption, digital literacy is exceptionally high. The population comfortably navigates online platforms, digital payments, and technology services.

This digital sophistication supports online gambling platform adoption, though cultural preferences and regulatory frameworks ultimately determine market development.

Language Skills: Most Andorran residents are multilingual, typically speaking Catalan plus Spanish, French, and often English. This linguistic diversity facilitates consumption of international content and services.

For gambling operators, multilingual platform support is expected. Catalan language offerings demonstrate local commitment, while Spanish and French reach broader audiences.

Cultural and Social Factors

Communication and Language

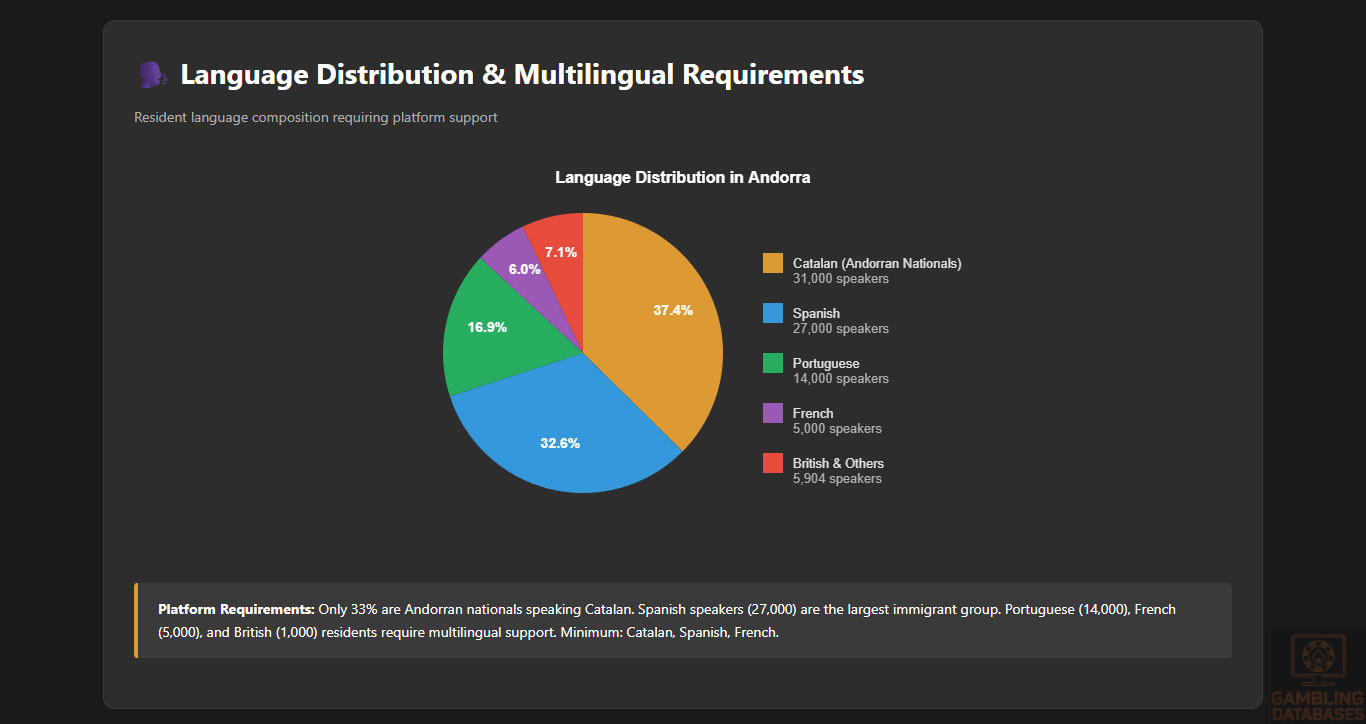

Official Language: Catalan is the sole official language, spoken by virtually all Andorran nationals. However, only 31,000 (33%) of residents are Andorran nationals.

Immigrant Languages: Spanish speakers number approximately 27,000 (primarily from Spain), Portuguese speakers total 14,000, French speakers reach 5,000, and British residents number around 1,000.

This linguistic diversity requires gambling platforms to support multiple languages. Catalan demonstrates local respect, Spanish reaches the largest user group, and French serves the northern valley communities.

Business Communication: Business typically operates in Catalan and Spanish, with French common in certain sectors. English proficiency is growing, particularly in tourism-facing and international business contexts.

Gambling customer service should offer Catalan, Spanish, and French as minimum language support. English capability enhances international visitor service quality.

Cultural Attitudes Toward Gambling

Historical Context: Gambling was prohibited for decades under the 1929 decree, creating a cultural background of restricted access. This prohibition reflected conservative social values and concerns about moral impacts.

The gradual legalization since 1996 suggests evolving attitudes, but gambling doesn’t enjoy the cultural integration seen in some European countries.

Religious Influence: Over 90% of the population is Roman Catholic, though religiosity levels and church attendance vary. Catholic teaching traditionally views gambling cautiously.

However, moderate gambling for entertainment is generally accepted. The cultural environment likely supports responsible recreational gambling rather than high-stakes or problem gambling behaviors.

Social Acceptance: Bingo has existed since 1996 and enjoys social acceptance as community entertainment. The casino opening in a central Andorra la Vella location signals governmental and social acceptance of gambling.

Online gambling acceptance mirrors general European trends, with younger demographics more comfortable with digital entertainment including gambling.

Foreign Brand Perception: Andorra’s economy relies heavily on international tourism and foreign investment. Residents regularly interact with international brands and services.

Well-established international gambling brands would likely be viewed positively, particularly if partnered with local entities. Pure foreign operators without local presence may face skepticism.

Risk Tolerance: The affluent, educated population likely exhibits moderate risk tolerance in financial matters. However, gambling risk tolerance varies individually.

Conservative investment cultures and stable economic preferences suggest moderate rather than aggressive gambling behaviors. Skill-based games and sports betting may appeal more than pure chance games.

Problem Gambling and Social Considerations

Prevalence Data: No published studies or statistics exist specifically measuring problem gambling prevalence in Andorra. The small population and recent gambling legalization mean systematic research is lacking.

Extrapolating from European averages (0.5-2% problem gambling prevalence), Andorra might have 400-1,600 problem gamblers, though actual numbers could differ significantly.

At-Risk Populations: Demographic groups typically at higher risk include young males (25-35 years), individuals with substance use issues, and those experiencing financial stress.

Andorra’s affluence may reduce financial stress-driven gambling, but accessibility and normalization could increase participation rates across demographics.

Regulatory Response: Law 4/2021 explicitly prioritizes preventing excessive gambling and problem gambling behaviors. CRAJ’s mandate includes preventing pathological gambling.

Required responsible gambling measures, self-exclusion systems, and operator obligations reflect proactive regulatory positioning to prevent problem gambling before it escalates.

Treatment Services: Information about specialized gambling addiction treatment services in Andorra is not publicly available. The small population may limit dedicated facilities.

Residents likely access treatment through general mental health and addiction services or seek specialized care in Spain or France if needed.

Support Resources: CRAJ provides contact information (Tel: +376 822 922, Email: [email protected]) as a regulatory resource. Whether dedicated helplines or support services exist is unclear.

The UNNIC Casino displays responsible gambling information directing players to regulatory contact points and encouraging self-awareness about gambling control.

Mandatory Contributions: Whether operators must contribute financially to problem gambling prevention, research, or treatment funds is not specified in available sources.

European regulatory norms increasingly require such contributions, so Andorran operators should anticipate potential requirements even if not yet formalized.

Political Structure and Governance

Government System: Andorra is a parliamentary co-principality, unique among world governments. The heads of state are the President of France and the Bishop of Urgell (Spain) serving as co-princes.

The General Council (parliament) exercises legislative power, and the Head of Government leads executive functions. This unusual structure has proven stable for centuries.

Political Stability: Andorra enjoys exceptional political stability with peaceful democratic transitions, low corruption, and consistent policy frameworks. Political risk is minimal.

For gambling operators, this stability provides confidence in regulatory continuity and predictable business environment over license terms.

Regulatory Consistency: While the casino licensing process showed some inconsistency with the Jocs SA approval-rejection-approval sequence, overall regulatory frameworks are professional and transparent.

CRAJ operates as an independent authority reducing political interference risks. Regulatory decisions follow legal frameworks rather than arbitrary political considerations.

Corruption Levels: Andorra maintains low corruption levels typical of developed European nations. Transparency International and similar indices rate the country favorably.

Business licensing and regulatory processes function professionally. Bribery or corrupt practices in licensing would be highly unusual and legally risky.

International Relations: Andorra maintains strong relationships with France and Spain. The country is a UN member, participates in the OSCE, Council of Europe, IMF, and has WTO observer status.

A Monetary Agreement with the EU (2011) allows euro usage. An Association Agreement with the EU is under negotiation, subject to a 2025 referendum.

EU Relationship: Andorra is not an EU member state and does not participate in the EU VAT area, though a customs union exists. The non-EU status limits certain cross-border service freedoms.

For gambling licensing, this means Andorran licenses do not benefit from EU passporting rights. Operators cannot leverage an Andorran license to serve other EU markets.

Technology Adoption and Digital Behavior

Internet and Digital Usage

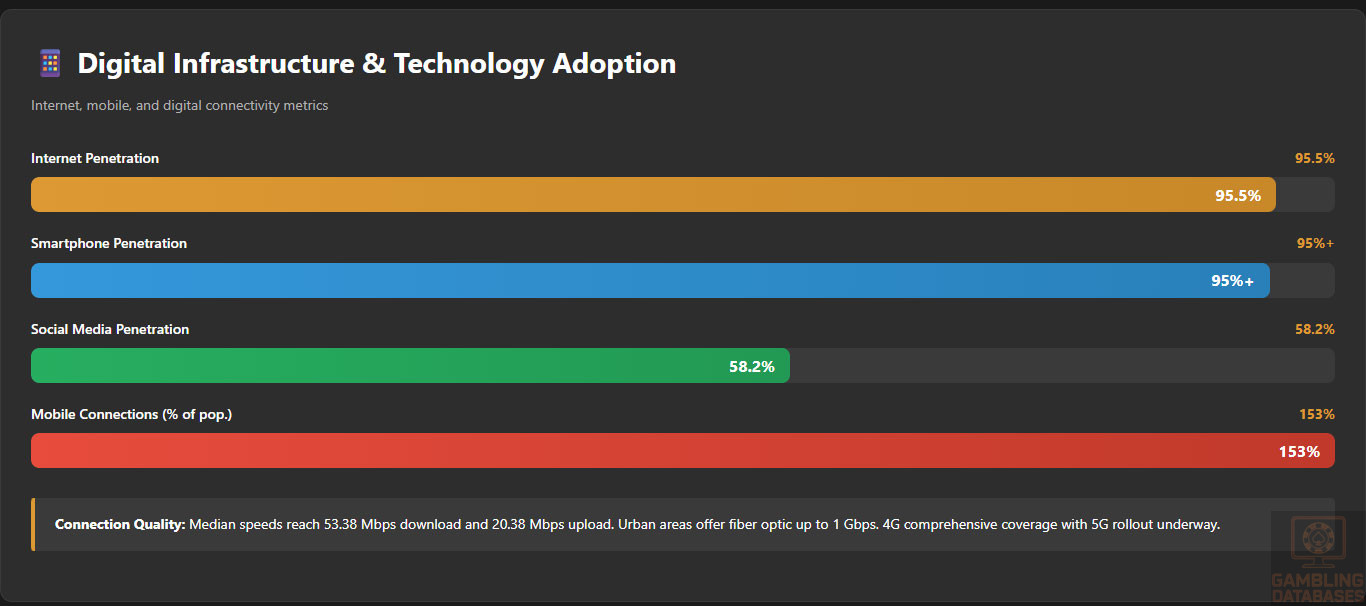

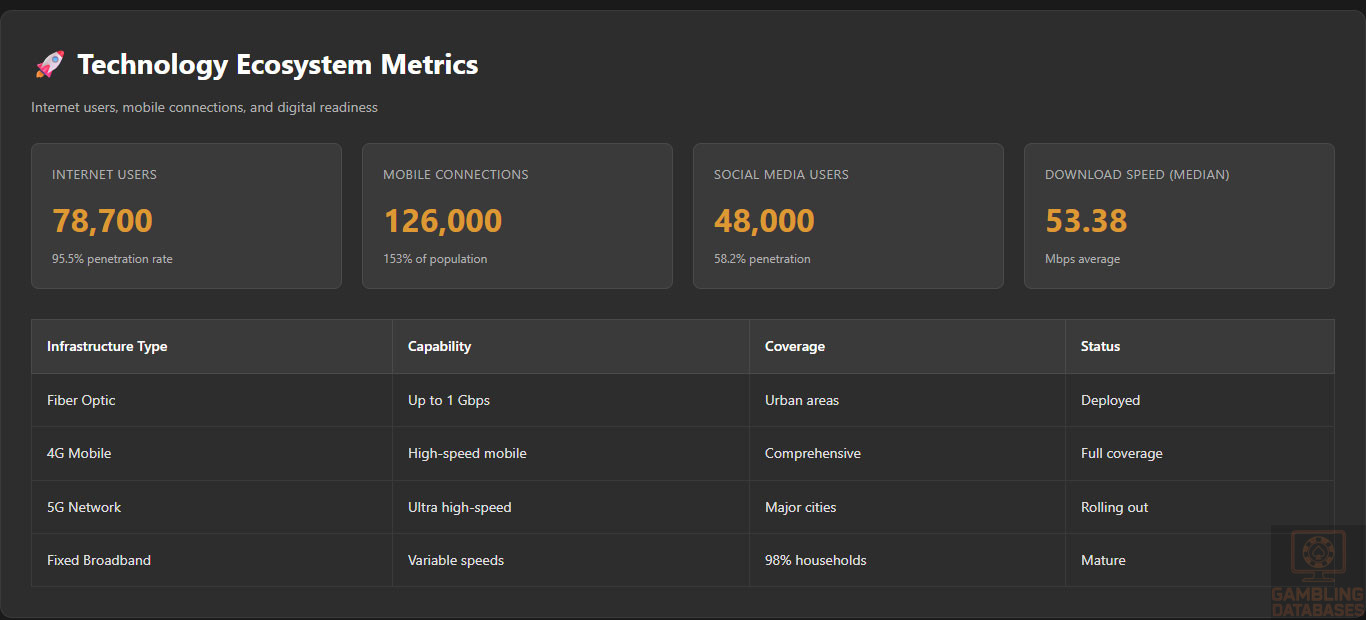

Internet Penetration: With 95.5% internet penetration (78,700 users) as of January 2025, Andorra ranks among the world’s most connected nations. This exceeds many large European countries.

Year-over-year growth reached 1.3% (992 new users) between January 2024 and 2025, reflecting near-saturation with incremental gains from population growth and elderly adoption.

Connection Quality: Internet speeds in Andorra show variable performance. Median speeds reach 53.38 Mbps download and 20.38 Mbps upload, representing decent broadband performance.

However, mountainous terrain creates coverage variability. Urban areas enjoy excellent connectivity with fiber optic networks, while remote valleys may experience limitations.

Andorra Telecom offers 1 Gbps fiber connections in urban areas, providing infrastructure for bandwidth-intensive applications including live dealer casino gaming.

Daily Usage: Specific daily internet usage hours for Andorra are not published. However, European averages suggest 5-7 hours daily, with Andorra’s affluent, digitally-literate population likely at the higher end.

Mobile Internet: Mobile internet is widespread with 4G/5G coverage ensuring smooth connectivity. 5G rollout is progressing, with Andorra Telecom leading network infrastructure development.

E-commerce Participation: E-commerce adoption is substantial, reflecting the small retail market’s limitations and consumers’ comfort with online purchasing. Cross-border online shopping from Spain and France is common.

This e-commerce familiarity translates well to online gambling adoption, as users are accustomed to digital transactions and remote service consumption.

Social Media Engagement: Social media penetration reaches 58.2% with 48,000 user identities. This moderate penetration reflects demographic factors including older population segments less active on social platforms.

Popular platforms likely mirror Spanish and French markets: Facebook, Instagram, YouTube, and WhatsApp dominate. Social media provides viable marketing channels for gambling operators.

Digital Payment Behavior

Banking Infrastructure: Andorra maintains a sophisticated banking sector aligned with European standards. Digital banking adoption is high, with most residents using online and mobile banking routinely.

Account penetration approaches universal levels among adults. The banked population percentage likely exceeds 95%, facilitating electronic payment integration for gambling.

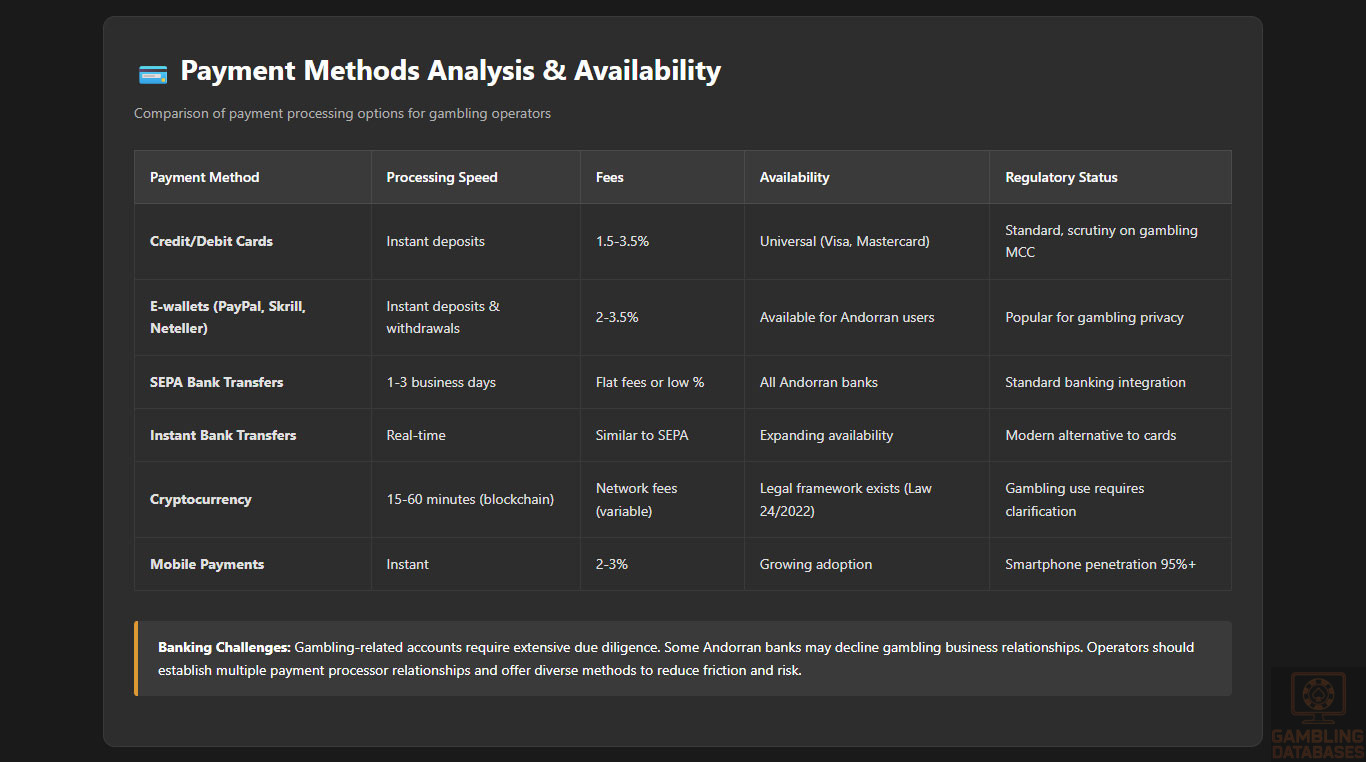

Payment Method Preferences: Credit and debit card usage is standard for transactions. Cards issued by Andorran banks function throughout the euro zone and globally.

Bank transfers through SEPA (Single Euro Payments Area) systems provide efficient euro-denominated transactions. Instant transfer capabilities are increasingly available.

E-wallet Adoption: Information on specific e-wallet (PayPal, Skrill, Neteller, etc.) adoption in Andorra is limited. Given European integration and cross-border commerce, major e-wallets likely function for Andorran users.

For gambling deposits and withdrawals, e-wallets provide privacy and transaction speed advantages that appeal to users. Operators should support popular European e-wallet options.

Cryptocurrency Adoption: Andorra approved the Digital Assets Act (Law 24/2022) on June 30, 2022, effective October 20, 2022. This law provides comprehensive legal framework for digital asset issuance, custody, exchange, and supervision.

Cryptocurrency is legal to hold and trade in Andorra. However, specific regulations on cryptocurrency use for gambling transactions are not detailed in available sources.

Given the progressive digital asset framework, crypto-based gambling may be permitted if operators comply with AML requirements and obtain appropriate authorizations.

Transaction Security Trust: Trust in online payment systems is high, reflecting strong banking regulation, low fraud rates, and sophisticated consumer protection. Andorran residents regularly conduct high-value online transactions.

For gambling operators, this trust environment facilitates larger deposit sizes and reduces payment friction, though responsible gambling guardrails remain essential.

Gaming and Gambling Preferences

Current Market Participation

Overall Gambling Participation: Specific data on what percentage of Andorran residents gamble annually is not published. Extrapolating from European averages suggests 30-50% participation rates.

Given recent legalization and limited land-based venues, actual participation may fall below European averages. As market matures and awareness grows, participation rates should increase.

Online Gambling Participation: With no licensed domestic online gambling operators and free access to international sites, online gambling participation occurs but is unmeasured.

Digital literacy and internet penetration support online gambling adoption. Younger demographics (25-44 years) likely show higher online gambling engagement.

Popular Activities: Bingo has historical cultural acceptance in Andorra. Sports betting gained legal status in 2012, suggesting market demand exists.

The casino opening introduces table games, slot machines, and potentially poker rooms. Tourist preferences for slots and roulette may drive land-based casino product mix.

Sports Betting Preferences: Specific sports betting preferences align with broader Spanish and French cultural interests: football dominates, followed by basketball, tennis, cycling, and Formula 1.

Winter sports betting (skiing, snowboarding) may show elevated interest given Andorra’s mountain culture and hosting of international skiing events.

Casino Game Preferences: Data on specific casino game preferences is unavailable. However, European trends suggest slots generate highest revenue volumes, followed by roulette, blackjack, and baccarat.

Live dealer games combining online convenience with authentic casino atmosphere are growing in popularity across Europe and likely appeal to Andorran players.

Lottery Participation: National lottery participation occurs through coordination with French and Spanish lottery systems, indicating cultural acceptance of lottery products.

Consumer Behavior Patterns

Spending Levels: Average gambling spending per active player in Andorra is not documented. However, high disposable income suggests above-average spending capacity.

Monthly spending of €50-€200 per active gambler represents reasonable estimates, with high-value players potentially spending significantly more.

Platform Preferences: Mobile vs desktop usage patterns are not specifically measured for Andorran gambling. European trends show 60-70% mobile gambling adoption.

Andorra’s high smartphone penetration (95%+) and mobile connectivity support mobile-first gambling consumption. Operators must prioritize mobile optimization.

Peak Usage Times: Peak gambling times typically align with leisure hours: evenings (20:00-24:00), weekends, and holiday periods.

Seasonal patterns may show increased activity during ski season (December-March) when tourist populations peak and leisure entertainment demand rises.

Session Characteristics: Average session lengths and frequency are not published. European patterns suggest online gambling sessions of 30-60 minutes, with 2-4 sessions weekly for regular players.

Deposit/Withdrawal Behavior: Affluent players may make larger deposits with less frequency, while recreational players deposit smaller amounts more regularly.

Withdrawal preferences favor speed and convenience. E-wallets offering same-day withdrawals are increasingly expected by European players.

Bonus Sensitivity: European players generally respond to bonuses but increasingly scrutinize wagering requirements and terms. Andorran players likely share this sophisticated approach.

Fair, transparent bonuses build loyalty. Overly complex or restrictive terms damage brand reputation and customer retention.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Internet Quality Assessment: Andorra maintains developed digital infrastructure supporting advanced connectivity. Urban areas, particularly Andorra la Vella and Escaldes-Engordany, offer excellent broadband access.

Fixed Broadband: Fiber optic networks deliver up to 1 Gbps connections in urban zones through Andorra Telecom, the national telecommunications provider.

Fixed broadband penetration is high among households and businesses, providing stable connectivity for bandwidth-intensive applications.

Mobile Internet: Mobile broadband complements fixed connections. 4G coverage is comprehensive across populated areas, with 5G deployment underway.

126,000 mobile connections (153% of population) reflect multiple device ownership and robust mobile ecosystem.

Speed Performance: Median internet speeds reach 53.38 Mbps download and 20.38 Mbps upload. However, variability exists with recorded speeds ranging from 0.04 Mbps to 346.55 Mbps download.

Mountainous terrain creates coverage challenges in remote valleys, but population concentration in urban areas means most residents and businesses enjoy reliable high-speed connectivity.

Network Reliability: Andorra Telecom operates as the primary network operator, maintaining infrastructure to European standards. Uptime and reliability meet expectations for developed markets.

Infrastructure Investment: Ongoing investments in fiber expansion and 5G rollout demonstrate commitment to maintaining competitive digital infrastructure.

5G and Future Technology Deployment

5G Rollout: 5G deployment is progressing with Andorra Telecom leading implementation. Specific coverage percentages and deployment timelines are not publicly detailed.

Urban areas likely receive priority for 5G coverage, with gradual expansion to smaller parishes following.

Coverage Plans: 4G coverage currently serves the majority of populated areas. 5G expansion aims to enhance mobile broadband speeds and support emerging technologies.

Network Competition: Andorra Telecom dominates as the primary telecommunications provider. The small market limits room for multiple competing network operators.

This concentration provides network consistency but may limit competitive pricing compared to markets with multiple carriers.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Network Operators: Andorra Telecom is the principal mobile network operator providing comprehensive coverage throughout the Principality.

The company offers mobile plans with roaming included in many European destinations, reflecting cross-border connectivity importance for residents and tourists.

Coverage Quality: Mobile coverage quality is generally strong in populated areas. Mountainous terrain creates natural challenges in remote locations.

Skiing areas and tourist zones receive infrastructure priority ensuring connectivity where visitor densities are highest.

Data Costs: Specific cost-per-GB pricing is not detailed in available sources. However, Andorra’s competitive market positioning and European integration suggest reasonable data pricing.

Mobile plans include data allowances, with unlimited or high-capacity plans increasingly standard.

Mobile Payments: Mobile payment integration is advancing with smartphone-based payment options including contactless payments and mobile banking apps.

Mobile wallet adoption supports digital transaction ecosystems essential for mobile gambling integration.

Device Penetration

Smartphone Adoption: Smartphone penetration exceeds 95% of the population, reflecting affluence and technology adoption characteristics.

Multiple device ownership is common, with individuals often maintaining separate work and personal smartphones.

Device Preferences: Specific brand preferences are not published, though European markets show mixed iOS and Android adoption.

Gambling operators must ensure cross-platform compatibility supporting both operating systems and various device types.

Device Capabilities: Average device specifications are high given the affluent market. Recent smartphone models with advanced processors, high-resolution displays, and 5G capability are common.

This device quality supports sophisticated mobile gambling applications including live dealer streaming and high-quality graphics.

Financial Services and Payment Infrastructure

Banking System Structure

Banking Sector: Andorra maintains a sophisticated banking sector with multiple institutions serving the domestic market and international clients.

Major banks include Andbank, MoraBanc, Crèdit Andorrà, and others. The sector underwent significant reform and transparency improvements over the past decade.

Regulatory Framework: Banking regulation aligns with European standards through Laws 35/2010, 7/2013, 7/2024, and others governing financial institutions.

The Andorran Financial Authority (AFA) supervises the banking sector ensuring stability and compliance with international standards.

Digital Banking: All major Andorran banks offer comprehensive online and mobile banking platforms. Digital banking adoption is very high.

Account management, transfers, bill payments, and investment services are accessible remotely, supporting digital economy participation.

Account Access: Essentially all adults maintain bank accounts. Account penetration approaches universal levels, facilitating electronic payment integration.

Deposit Protection: The Andorran Guarantee Deposit Fund (FAGADI) protects deposits up to €100,000, with additional coverage up to €300,000 for specific exceptional situations.

Payment Processing Options

Card Payments: Credit and debit cards are standard payment methods. Visa and Mastercard are widely accepted, with cards issued by Andorran banks functioning throughout Europe.

For gambling operators, card processing is essential. However, gambling-related merchant category codes may face additional scrutiny from payment processors.

E-wallet Availability: Popular European e-wallets including PayPal, Skrill, Neteller, and others likely function for Andorran users, though specific availability should be verified.

E-wallets provide privacy, speed, and convenience advantages for gambling transactions. Operators should integrate multiple e-wallet options.

Bank Transfers: SEPA bank transfers enable efficient euro-denominated transactions. Instant payment capabilities are expanding, though traditional transfers may require 1-3 business days.

Bank transfers suit larger deposits but lack the immediacy players increasingly expect for gambling funding.

Cryptocurrency Payments: The Digital Assets Act (Law 24/2022) provides legal framework for cryptocurrency operations. Whether gambling operators can accept crypto payments requires regulatory clarification.

If permitted, cryptocurrency offers privacy and international transaction advantages, though volatility and regulatory compliance create challenges.

Processing Fees: Payment processing fees vary by method. Card transactions typically incur 1.5-3.5% merchant fees. E-wallets charge similar percentages. Bank transfers may involve flat fees.

These processing costs represent significant operational expenses for gambling operators and should be factored into financial modeling.

Transaction Timelines: Card deposits are instant. E-wallet deposits are instant. Bank transfers require 1-3 business days unless instant payment rails are used.

Withdrawal processing times vary by operator policies and payment method. E-wallets typically enable fastest payouts (same-day to 24 hours). Cards and bank transfers may require 3-5 business days.

International Capabilities: Andorran payment infrastructure integrates with international systems. Cross-border euro transactions function smoothly within SEPA zone.

Currency conversion for non-euro transactions is available but involves exchange rate spreads and fees.

Gambling Payment Restrictions: Specific restrictions on payment processing for gambling are not detailed. However, banking institutions maintain strict compliance standards.

Gambling-related accounts require enhanced due diligence. Some banks may decline gambling business relationships, making payment processor selection critical.

E-commerce and Digital Economy

Digital Market Development

E-commerce Market Size: Specific e-commerce market size data for Andorra is not published. However, the small retail market and sophisticated population drive substantial online purchasing.

Cross-border e-commerce from Spain, France, and international platforms is significant given limited local retail selection.

Online Retail Penetration: Online purchasing complements rather than replaces physical retail. Duty-free shopping remains a major draw for tourism-driven retail sector.

However, convenience goods, specialized products, and services are increasingly purchased online.

Consumer Trust: Trust in online transactions is high, supported by strong consumer protection, low fraud rates, and sophisticated banking security.

This trust environment facilitates online gambling adoption as users are comfortable with digital service consumption and electronic payments.

Popular Platforms: International e-commerce platforms (Amazon, eBay, etc.) serve Andorran consumers. Spanish and French online retailers are frequently accessed.

Digital service consumption includes streaming entertainment, software subscriptions, and online gaming, creating familiarity with digital entertainment business models.

Business Environment and Regulatory Framework

Ease of Business Operations

Business Climate: Andorra offers a favorable business environment characterized by low taxation, political stability, and streamlined regulatory processes.

The government actively promotes economic diversification and foreign investment, particularly in technology, real estate, and financial services sectors.

Registration Efficiency: Business registration processes are relatively efficient compared to many European jurisdictions. Company formation typically completes within 1-3 months.

Required documentation is substantial, reflecting rigorous anti-money laundering standards, but processes are professional and predictable.

Foreign Investment Policy: The Foreign Investment Law permits non-residents to invest in Andorran companies. Foreign ownership is allowed, though 100% Andorran ownership may provide advantages in certain licensing situations.

Operational Costs: Office rent in Andorra la Vella reflects limited commercial space availability but remains moderate compared to major European cities.

Salary levels for qualified professionals are competitive with Spain and France, though lower than Switzerland or Luxembourg. Utilities and business services are reasonably priced.

Labor Market: The small labor pool creates talent acquisition challenges for specialized positions. Many businesses recruit from Spain and France.

Work permits for foreign nationals require employer sponsorship and demonstration of unavailable local talent. Multilingual professionals are particularly valued.

Corporate Structure and Registration

Available Entity Types

Limited Liability Company (SL): Societat Limitada is suitable for small to medium operations. Minimum capital requirements are moderate, governance structures are flexible, and administrative burdens are lower than corporations.

Corporation (SA): Societat Anònima provides structure for larger operations, public offerings, or situations requiring more formal governance. Higher capital requirements and stricter reporting apply.

Branch Office: Foreign companies can establish branch offices in Andorra, though this structure may not satisfy gambling licensing requirements for fully independent Andorran entities.

Recommended Structure: For iGaming operators, an SL or SA incorporated under Andorran law is most appropriate. The choice depends on scale, governance preferences, and capital availability.

SL offers simplicity for smaller operations. SA provides structure for larger casino or multi-product gambling businesses.

Registration Requirements

Registration Timeline: From application to full registration approval typically requires 1-3 months, depending on documentation completeness and due diligence complexity.

Registration Costs: Government fees for company registration are moderate. Legal and consulting fees for documentation preparation, notarization, and process management typically range €3,000-€8,000+.

Total registration costs including capital deposits, legal fees, and initial setup expenses typically total €10,000-€25,000 depending on entity type and complexity.

Required Documents: Criminal record certificates with Hague Apostille (valid 3 months), passport copies with Hague Apostille, detailed CVs, business plans, financial projections, and source of funds documentation.

All foreign documents require apostille authentication. Banking relationships require extensive KYC documentation.

Foreign Ownership Rules: No specific percentage limits restrict foreign ownership in most sectors. Gambling licensing evaluation may favor Andorran ownership but does not prohibit foreign-owned applicants.

Capital Requirements: Minimum capital varies by entity type. SLs require modest minimum capital (specific amounts not detailed in sources). SAs require higher capitalization.

For gambling licenses, demonstrated financial capacity far exceeding minimum legal requirements is essential.

Ongoing Compliance: Annual financial statements must be filed. Tax declarations are required. Corporate governance meetings must be documented.

Companies must maintain updated shareholder registers, comply with employment regulations, and fulfill social security obligations.

Taxation Framework

Corporate Income Tax Structure

Standard Rate: Corporate income tax is levied at 10% on company profits (revenues minus expenses). This rate is among Europe’s lowest.

New Business Incentives: New companies with income below €100,000 benefit from reduced rates for the first three years: 5% on the first €50,000 taxable income, 10% on income exceeding €50,000.

First-year operations receive 50% reduction in settlement fees, further reducing initial tax burdens.

Special Regimes: International companies, holding companies, and intra-group financial management entities may qualify for 2% maximum taxation under specific conditions.

Patent Box regime reduces effective tax to 2% for companies engaged in research and development predominantly in Andorra, rewarding innovation.

Loss Carryforward: Negative tax bases can be carried forward and applied against future profits for up to 10 years, providing flexibility during development or loss periods.

Tax Treaties: Andorra has established over 15 double taxation treaties with countries including Spain, France, Portugal, Luxembourg, and others.

These treaties prevent double taxation of business income and facilitate international operations. Transfer pricing documentation may be required for related-party transactions.

Withholding Taxes: Dividends from Andorran companies to residents incur 0% withholding tax. Dividends to non-residents also face 0% withholding in Andorra (though recipient country taxation may apply).

Interest and royalty payments may face withholding depending on treaty provisions.

Personal Income Tax

Tax Brackets: Personal income tax (IRPF) applies progressively: €0-€24,000 exempt (0% rate), €24,000-€40,000 taxed at 5%, income exceeding €40,000 taxed at 10%.

Maximum effective tax rates remain well below 10% for all income levels due to exemptions and lower bracket rates.

Employee Withholding: Employers must withhold income tax from employee salaries and remit to tax authorities. Social security contributions to CASS are also withheld.

Social Security: Employer and employee contributions to CASS (social security) are required. Contribution rates are complex and can escalate quickly, representing significant employment costs.

Total social security burden (employer + employee) can reach 20%+ of gross salaries, substantially increasing true employment costs beyond headline wages.

Foreign Employees: Foreign nationals working in Andorra are subject to Andorran income tax on their worldwide income if they become tax residents (residing 183+ days annually).

Tax residency planning is essential for mobile workers and executives splitting time between jurisdictions.

Market Entry Considerations

Recommended Entry Strategies

Licensing vs Partnership: Direct licensing pursuit requires full Andorran entity establishment, substantial capital investment, and navigating CRAJ’s stringent requirements.

Partnership with existing licensed operators (particularly Jocs SA for land-based operations) may provide faster market access with reduced capital requirements and regulatory complexity.

Local Partnership Benefits: Partnering with 100% Andorran-owned entities provides local market knowledge, regulatory relationships, and competitive advantages demonstrated in casino licensing outcomes.

Local partners navigate cultural nuances, language requirements, and government relationships more effectively than pure foreign entrants.

White Label vs Proprietary: For online gambling (if/when licensing becomes available), white label solutions reduce technology development costs and accelerate time-to-market.

However, proprietary platforms provide greater control, differentiation potential, and long-term strategic flexibility.

Technology Leveraging: Given the micro-market size, leveraging existing technology platforms and shared infrastructure optimizes economics.

Building custom technology solely for Andorra’s 83,000 population is economically challenging. Multi-jurisdiction platforms amortize development costs.

Marketing Localization: Despite small size, marketing must address multilingual requirements (Catalan, Spanish, French) and cultural sensitivities.

Tourism marketing targeting French and Spanish visitors requires different positioning than resident-focused campaigns.

Payment Provider Selection: Establishing banking relationships in Andorra requires extensive due diligence. Operators should engage banking advisors early.

Multiple payment method integration (cards, e-wallets, bank transfers) is essential. Backup payment processors mitigate relationship termination risks.

Typical Costs and Timelines

Initial Setup Investments

License Application: Casino license fee amounts are not disclosed but are substantial given exclusive 17-year rights. Online license fees (when available) should be anticipated at €10,000-€100,000+ depending on scope.

Legal and Consulting: Legal services for entity formation, license application preparation, contract negotiation, and compliance setup typically total €15,000-€50,000+.

Company Registration: Entity formation costs including government fees, notarization, and initial setup total €10,000-€25,000.

Initial Capital: Minimum capital depends on entity type. However, demonstrated financial capacity for gambling operations requires significant reserves.

Casino operations demanded €15+ million total investment. Online operations might require €500,000-€2,000,000+ in accessible capital.

Office Setup: Commercial office space rental, furnishing, IT infrastructure, and utilities for initial 12 months total €30,000-€80,000+ depending on size and location.

Technology Platform: Proprietary platform development costs €200,000-€1,000,000+. White label solutions involve setup fees of €10,000-€50,000 plus ongoing revenue shares.

Marketing Budget: Initial marketing to establish brand awareness, acquire customers, and generate launch momentum requires €50,000-€200,000+ for first 12 months.

Total Initial Investment: Conservative estimates for online gambling market entry total €300,000-€500,000 minimum. Realistic budgets considering all contingencies approach €500,000-€1,000,000.

Land-based casino operations require €15,000,000+ as demonstrated by UNNIC Casino investment levels.

Operational Cost Estimates

Staff Salaries: Minimum viable team includes general manager, compliance officer, customer service representatives, and technical support. Monthly salaries total €15,000-€30,000.

Including social security contributions, annual personnel costs reach €250,000-€450,000+ depending on team size and seniority.

Office and Utilities: Monthly rent, utilities, internet, and office maintenance total €3,000-€8,000, or €36,000-€96,000 annually.

Technology Maintenance: Platform hosting, software licenses, security systems, and technical support cost €5,000-€20,000 monthly or €60,000-€240,000 annually.

Payment Processing: Transaction fees at 2-3% of gross gaming revenue represent variable costs. For €1,000,000 GGR, processing fees total €20,000-€30,000.

Marketing and CAC: Customer acquisition costs vary by channel. Digital marketing, affiliates, and promotions typically consume 20-40% of revenue during growth phases.

For €1,000,000 annual GGR, marketing budgets of €200,000-€400,000 support customer acquisition and retention.

Total Annual Operating Costs: Fixed costs (staff, office, technology) total €350,000-€800,000 annually. Variable costs (payment processing, marketing) scale with revenue.

Breakeven requires substantial GGR generation, challenging in a market of only 83,000 residents.

Timeline Expectations

Company Registration: 1-3 months from application to approval and commercial registry inscription.

License Application: Timeline varies significantly. Casino license tender to award took months. Online license timelines are unknown as few have been issued.

Prudent planning assumes 6-12 months for gambling license application review and decision.

Platform Setup: White label platform integration requires 4-8 weeks. Proprietary platform development requires 4-12 months depending on scope.

Total Time-to-Market: From initial decision to operational launch, realistic timelines span 9-18 months including entity formation, licensing, platform development, payment integration, and marketing preparation.

Resource Requirements