Angola represents an emerging opportunity in the African iGaming landscape, with a newly established regulatory framework that commenced accepting operator licenses in February 2025. The country’s evolving digital infrastructure, growing internet penetration, and young demographic profile create favorable conditions for market entry.

With 23 licensed operators currently active and government projections targeting 100 million USD in annual gaming sector contributions, Angola is positioning itself as a competitive iGaming jurisdiction. However, operators must navigate complex licensing requirements, moderate taxation levels, and infrastructure challenges that characterize this developing market.

Executive Summary: Key Market Indicators

| Indicator | Value | Details |

|---|---|---|

| Gambling Legal Status | Regulated | New licensing framework active from February 18, 2025 |

| Online Gambling Status | Legalized | Sports betting, online casinos, and lottery games permitted |

| Regulatory Authority | ISJ | Instituto de Supervisão de Jogos |

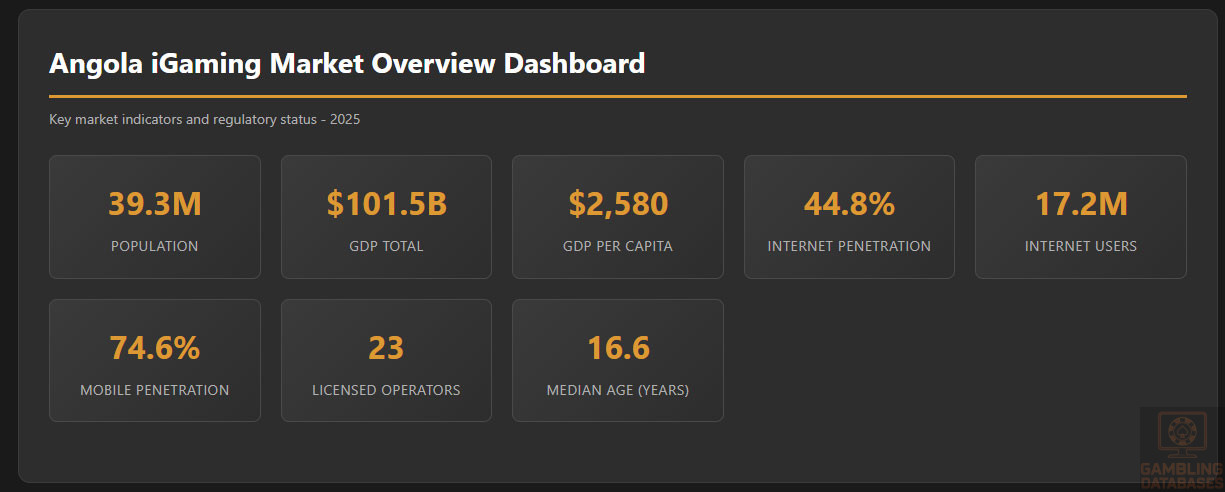

| Total Population | 39.3 million | 2025 estimate |

| Median Age | 16.6 years | One of Africa’s youngest populations |

| GDP Total | $101.5 billion | 2024 estimate |

| GDP Per Capita | $2,580 | 2024 estimate |

| GDP Growth Rate | 4.4% | 2024 actual; 3.2% projected for 2025 |

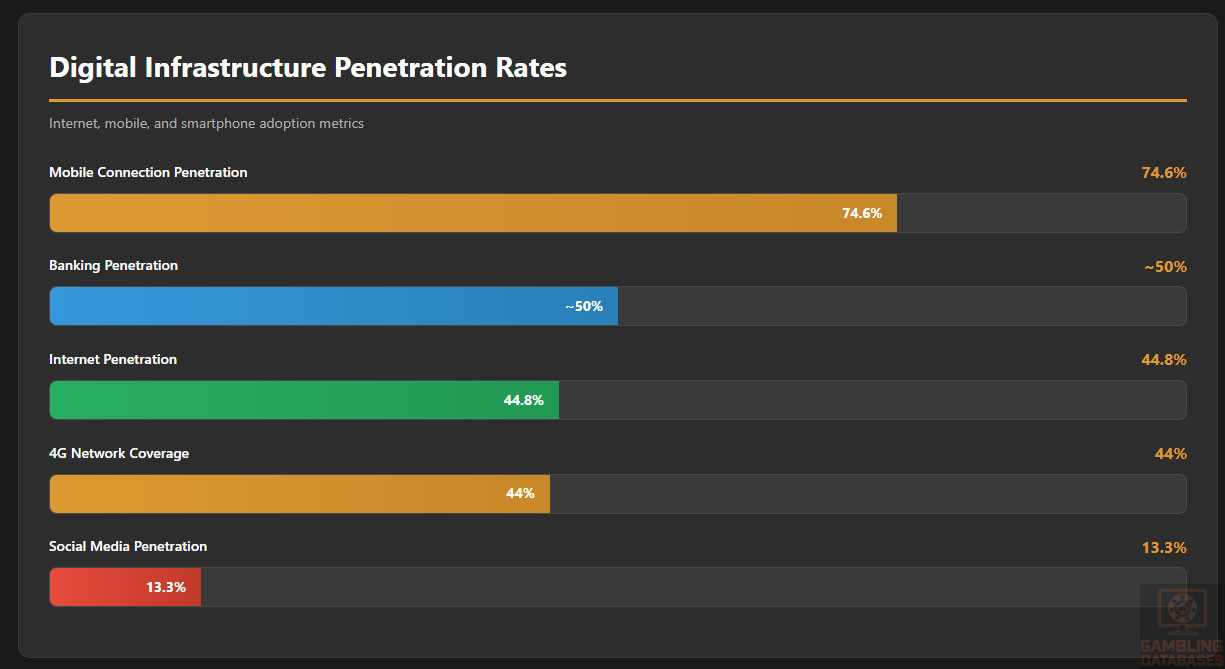

| Internet Penetration | 44.8% | 17.2 million users (January 2025) |

| Mobile Connections | 28.7 million | 74.6% penetration rate |

| Smartphone Penetration | Moderate | Growing rapidly in urban areas |

| License Duration | 10 years | Renewable for successive 3-year periods |

| GGR Tax Rate Range | 1.1% – 20% | Varies by gambling category |

| Player Winnings Tax | 10% – 15% | Varies by game type |

| Corporate Tax Rate | 25% | Standard rate for businesses |

| Licensed Operators | 23 | 10 gaming, 3 sports betting, 10 online (2024) |

| Gambling Tax Revenue | 10.1 billion AOA | $10.6 million USD (2023) |

| Urban Population | 68% | Concentrated in Luanda and major cities |

| Inflation Rate | 19.8% | May 2025; declining from 27.5% peak |

| Currency | Angolan Kwanza | AOA; experienced depreciation against USD |

| Legal Gambling Age | 18 years | Strictly enforced with KYC requirements |

| Foreign Ownership | Permitted | Must establish local company |

| Banking Penetration | ~50% | Significant underbanked population |

| Mobile Money Adoption | Growing | Multiple providers active (Unitel Money, Afrimoney) |

| Average Internet Speed | 12.7 Mbps | Mobile download; 19.96 Mbps fixed-line |

| Doing Business Rank | 177th | World Bank ranking; reforms underway |

| HDI Ranking | 150th | 0.591 index score (2022) |

| Primary Language | Portuguese | Official and business language |

| Market Entry Timeline | 6-12 months | License application to market launch |

| Projected Sector Growth | $100 million | Government target for annual contributions |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

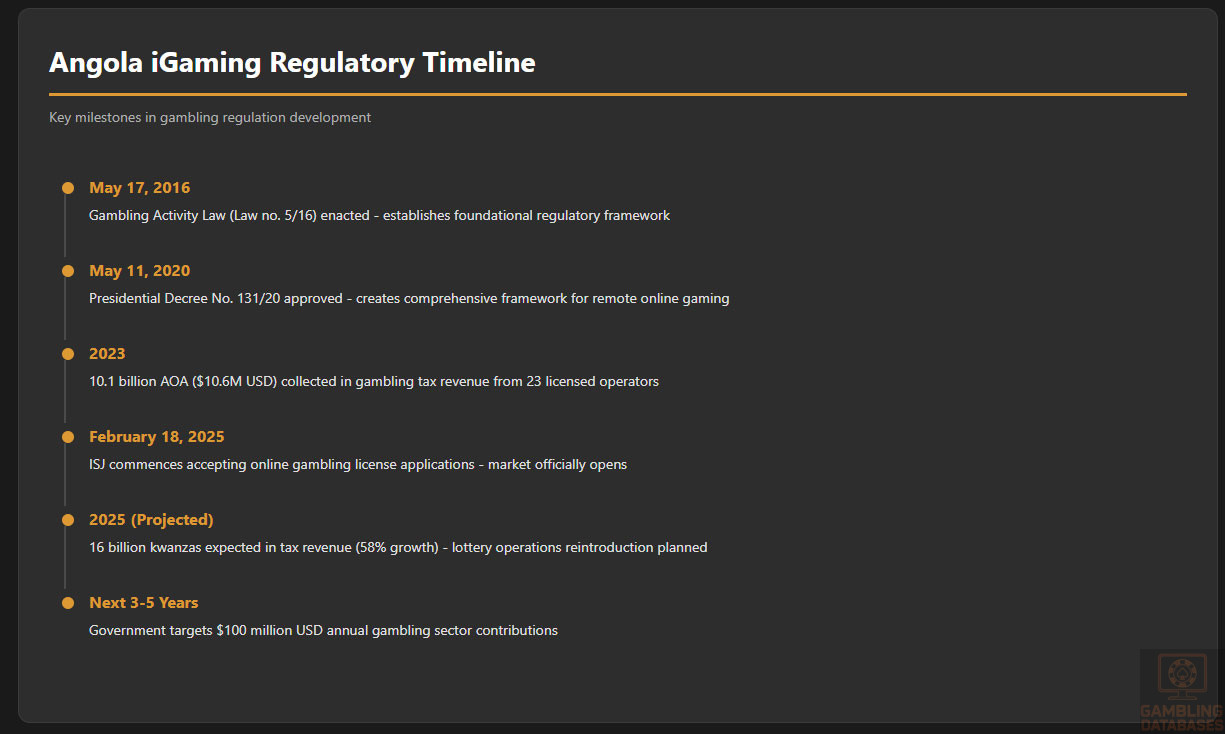

Angola’s gambling sector operates under a comprehensive regulatory framework established by the Gambling Activity Law (Law no. 5/16 of May 17, 2016) and subsequent amendments. The Instituto de Supervisão de Jogos (ISJ) serves as the primary regulatory authority responsible for licensing, supervision, and enforcement of all gambling activities within the country.

In a significant development for the African gambling market, Angola announced in February 2025 that ISJ would commence accepting license applications from operators seeking to enter the Angolan market starting February 18, 2025. This marks a pivotal expansion of the country’s online gambling regulatory framework, signaling Angola’s commitment to establishing a well-regulated and competitive gaming sector.

The fundamental principle governing Angola’s gambling sector is that exploitation rights are reserved to the Angolan State. However, these rights can be acquired through concession agreements as established in Article 5 of the Gambling Activity Law. This creates a structured pathway for private operators to participate in the market while maintaining governmental oversight and control.

Land-Based Gambling Activities

Angola permits various forms of land-based gambling operations, each subject to specific licensing requirements and operational standards. Casino operations represent the most established segment of the land-based gambling market, with facilities concentrated primarily in Luanda and other major urban centers. Operators must meet stringent security, transparency, and responsible gaming requirements.

Slot machine halls and gaming venues constitute another permitted category, falling under the broader casino and gaming hall regulations. The Gaming Law establishes minimum distance requirements between establishments to protect competition and prevent market saturation in specific geographic areas. This special regime allows multiple companies to operate casinos in the same geographical area provided they respect competitive spacing requirements.

Social games and certain lottery operations also fall under the land-based regulatory framework. The government is actively working to reintroduce lottery games, with concession contract negotiations underway for the winner of a public tender held by the State. This expansion is expected to launch by the end of 2025.

Online Gambling Framework

The Regulation on the Exploitation of Remote Online Gaming in Angola, approved by Presidential Decree No. 131/20 of May 11, 2020, establishes the comprehensive framework for online gambling operations. This regulation applies to the exploration and practice of online games and betting conducted remotely using electronic, computer, telematic, and interactive media or any other technological means.

The new licensing framework encompasses three primary categories of online gambling. Sports betting operations represent a major focus, allowing operators to offer wagering on sporting events through digital platforms. Online casino games including slots, table games, and live dealer options are permitted under appropriate licensing. Gambling-related lotteries conducted through digital channels complete the trio of authorized online gambling categories.

Online gambling and betting can only be carried out under a license granted to a public limited company (sociedade anónima). This corporate structure requirement ensures appropriate capitalization, transparency in ownership, and accountability mechanisms for regulatory oversight. The framework explicitly requires that all online gambling platforms implement responsible gambling measures, display information about responsible gambling practices, and implement strict age verification systems to prevent access by minors.

Prohibited activities and restrictions apply to operations that fail to obtain proper licensing or that target vulnerable populations. The regulatory framework mandates clear boundaries between different gambling categories, requiring operators to maintain distinct systems for different gambling activities to ensure appropriate regulatory oversight and consumer protection for each category.

Licensed Operators and Market Players

As of 2024, Angola’s gambling market comprises 23 licensed operators distributed across different gambling categories. The market structure includes 10 operators in the gaming sector (primarily casino operations), 3 operators holding territorial sports betting licenses, and 10 operators licensed for online gambling activities.

The market demonstrates moderate concentration with established players holding significant market positions. Unitel, one of Angola’s major telecommunications operators, has leveraged its mobile network infrastructure to develop Unitel Money, creating synergies between mobile payments and gambling activities. This convergence of telecoms and gaming represents an emerging trend in the Angolan market.

International operators can participate in the Angolan market by establishing local companies. Foreign investors are permitted to own gambling licenses without mandatory local partnerships, provided they create an Angolan-registered legal entity. This flexibility in ownership structure has attracted interest from international gaming operators seeking to expand their African footprint.

The competitive landscape is evolving rapidly following the February 2025 opening of the online licensing framework. The government projects that the gambling sector should contribute amounts in kwanzas equivalent to 100 million dollars over the coming years, indicating expectations for significant market expansion. This growth will likely intensify competition as new entrants challenge established operators.

| Category | Number of Operators | Market Characteristics |

|---|---|---|

| Gaming Sector (Casinos) | 10 | Primarily land-based operations in major cities |

| Territorial Sports Betting | 3 | Land-based betting venues with regulatory approval |

| Online Gambling | 10 | Digital platforms for sports betting, casino games, lottery |

| Total Licensed Operators | 23 | Active as of 2024; growth expected post-February 2025 |

Licensing Framework and Requirements

Application Process and Eligibility

The Instituto de Supervisão de Jogos (ISJ) administers the licensing process for all gambling operations in Angola. Operators seeking to enter the market must submit comprehensive applications demonstrating financial stability, technical capability, and commitment to responsible gaming principles. The regulatory framework requires rigorous criteria including financial capacity, adherence to security protocols, and proven responsible gaming practices.

License duration varies based on the regulatory regime. Under the exclusive regime, licenses to operate online gaming and betting are valid for 10 years and are renewable. For operations outside the exclusive regime, licenses are valid for 5 years with renewal options. Following initial issuance, licenses can be extended for successive periods of 3 years upon successful renewal applications.

Only entities with regular contributory and tax status qualify for licensing consideration. Applicants must demonstrate full compliance with Angolan tax obligations and social security contributions. This requirement ensures that only financially responsible operators with established local presence participate in the regulated market.

Background check procedures apply to all natural or legal persons wishing to acquire, directly or indirectly, qualifying holdings in a gaming operator. Prior authorization from ISJ is mandatory for shareholding acquisitions that reach or exceed the limits of 20%, 33%, or 50% of a gaming operator. The ISJ must also approve any entity that acquires control of a gaming operator regardless of the percentage shareholding.

Local Presence and Operational Requirements

Operating entities must establish meaningful local presence in Angola to qualify for and maintain gaming licenses. Companies must maintain a bank account with an Angolan financial institution at a national address for all transactions related to online gambling and betting activities. This ensures that financial flows remain visible to regulatory authorities and subject to Angolan banking oversight.

All licensed companies must have their registered office in Angola. The regulatory framework specifies that licenses outside the exclusive regime may be awarded to private legal persons governed by Angolan law and having their registered office in Angola. This physical presence requirement creates accountability and ensures operators can be effectively supervised by regulatory authorities.

The totality of share capital of exploiting entities must be represented by shares that allow the issuer of the license to know the identity of respective holders. Operators are obligated to communicate to ISJ all acts or businesses that imply the acquisition, transmission, or encumbrance of shares within 30 days from the date the company became aware of the act or business. This transparency requirement prevents unknown beneficial ownership and supports anti-money laundering efforts.

Companies are also required to ensure compliance with current Angolan laws on the prevention of money laundering and financing of terrorism. This includes implementing robust customer due diligence procedures, transaction monitoring systems, and suspicious activity reporting mechanisms aligned with international standards and Angolan regulatory expectations.

Technical and Infrastructure Requirements

Operating entities must install and maintain a technical system for the exploitation of online gaming and betting that meets ISJ’s technical standards. The system must be capable of creating a registration and an account for each player, tracking all gambling activities, and generating comprehensive reports for regulatory compliance purposes.

The framework establishes specific technical requirements for different gambling categories. Sports betting operators face distinct requirements from online casino platforms, reflecting the technical differences between these gambling sectors. This specialized approach ensures appropriate regulation for each gambling category while maintaining flexibility for operators to innovate within their licensed verticals.

All gambling platforms must implement strict age verification systems to prevent access by minors. The legal gambling age in Angola is 18 years, and operators must employ robust verification mechanisms during registration and potentially at transaction points to ensure compliance. Failure to prevent underage gambling represents a serious regulatory violation subject to penalties including license suspension or revocation.

Statistical monitoring requirements form part of the technical framework. Licensed operators must maintain detailed records of gambling activities, providing regulatory authorities with data for market analysis and compliance monitoring. This data-driven approach enables evidence-based policy adjustments and helps ISJ identify emerging risks or compliance issues.

Compliance Obligations and Monitoring

Player Protection and Identification

Operating entities are obligated to collect and maintain comprehensive personal data on all registered players. Required information includes full name, date of birth, nationality, profession, address and residence, telephone contact, email address, and identification document details. This information supports both regulatory compliance and responsible gambling initiatives.

KYC (Know Your Customer) and AML (Anti-Money Laundering) compliance standards align with international best practices. Operators must verify player identity during registration, implement ongoing monitoring for suspicious transactions, and report potential money laundering or terrorist financing activities to appropriate authorities. The Data Protection Law (Law no. 22/11 of June 17, 2011) governs the processing of personal data, and the Agência de Proteção de Dados (APD) oversees compliance.

Operators must create mechanisms that prevent minors and other socially vulnerable groups from registering. Age verification goes beyond simple checkbox confirmations, requiring document verification and potentially additional checks for accounts exhibiting suspicious activity. Operators failing to prevent underage gambling face severe penalties including fines, license suspension, and potential criminal charges.

Responsible gambling measures mandated by law include displaying information about responsible gambling practices prominently on all platforms. Players have the right to clear information on the rules of games, to receive their winnings promptly, and to have their personal data protected in accordance with applicable legislation. Operators must inform players about data processing activities and limit data collection to what is strictly necessary for gambling operations.

Self-exclusion system requirements enable players to voluntarily exclude themselves from gambling activities for specified periods. Operators must implement effective self-exclusion mechanisms that prevent excluded players from accessing gambling services across all platforms operated by the license holder. Cross-operator self-exclusion systems may be required as the regulatory framework matures.

Financial Monitoring and Reporting

Transaction monitoring systems must track all financial activities including deposits, wagers, winnings, and withdrawals. Operators must implement automated systems capable of identifying unusual transaction patterns that may indicate money laundering, fraud, or problem gambling behaviors. These systems should generate alerts for manual review by compliance personnel.

Reporting requirements and schedules vary by regulatory category and operator size. Operators must submit regular reports to ISJ documenting gambling activities, financial performance, player statistics, and compliance metrics. Monthly or quarterly reporting cycles are typical, with annual comprehensive reviews required for license renewals.

Audit and inspection procedures grant ISJ authority to examine operator records, systems, and facilities to verify compliance with licensing conditions. Operators must cooperate fully with regulatory inspections, providing access to relevant documentation and technical systems upon request. Independent third-party audits may be required periodically to verify the integrity of gaming systems and financial reporting.

Data retention requirements mandate that operators preserve transaction records, player communications, and compliance documentation for specified periods. These records must be readily accessible for regulatory review and may be required for dispute resolution, investigation of complaints, or enforcement proceedings. Typical retention periods range from 5 to 7 years depending on the nature of the records.

Taxation Structure and Financial Obligations

Player Taxation

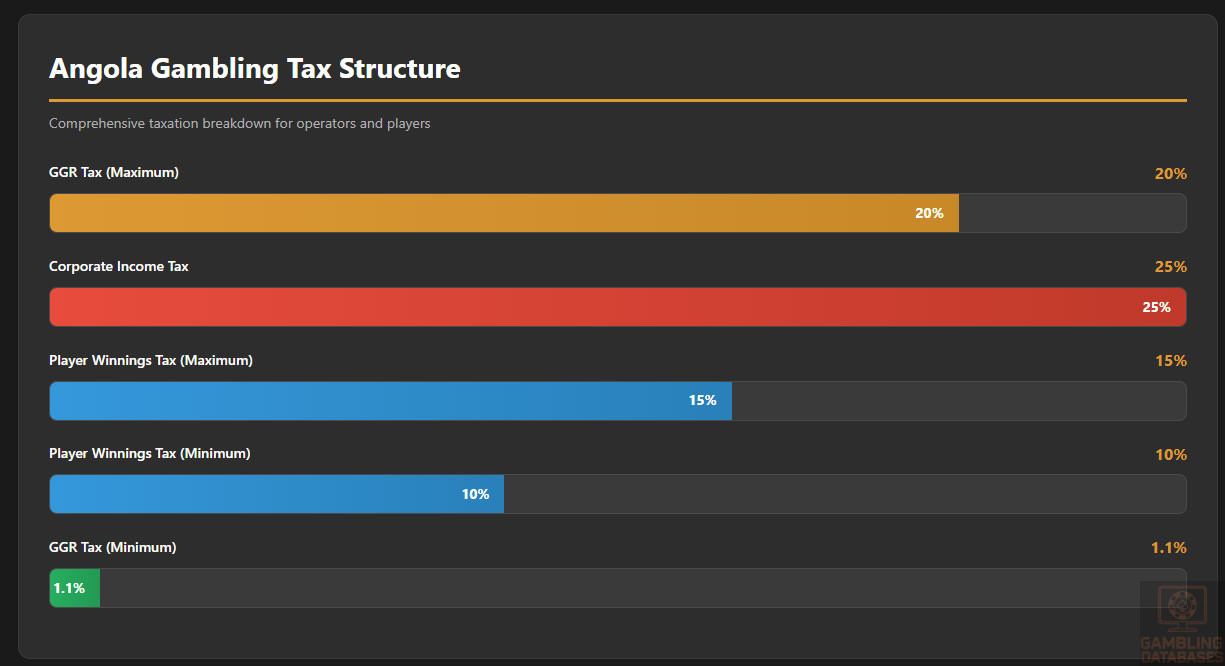

The total value of prizes awarded to players is subject to tax, with rates varying between 10% and 15% depending on the type of game. This player winnings tax is withheld by operators at the point of payout, reducing the administrative burden on individual players while ensuring tax collection. The tax applies to gross winnings before deduction of the original stake.

Players are entitled to receive their net winnings after applicable withholding taxes. Operators must clearly communicate the tax treatment of winnings to players, ensuring transparency about the amounts retained for tax purposes. Dispute resolution mechanisms must be available for players who believe winnings taxes were incorrectly calculated or withheld.

Tax-free thresholds may apply to smaller winnings, though specific threshold amounts have not been publicly disclosed in available regulatory documentation. The tax framework aims to balance revenue collection with maintaining player engagement and ensuring the competitiveness of legal, regulated gambling compared to unlicensed alternatives.

Operator Taxation

The Gaming Law provides for different rates of special tax on gambling, ranging from a minimum of 1.1% to a maximum of 20% of the gross revenue from gambling activities, depending on the form of gambling in question. This graduated tax structure recognizes different margin profiles across gambling verticals and aims to create an equitable tax burden across the industry.

Historical context shows that gambling tax rates in Angola have been subject to significant pressure from industry stakeholders. The president of the Games Association noted that the association managed to reduce the tax from 45% two years ago to 25% currently, with expectations for further reductions to 18% or 20%, and ongoing advocacy for rates around 12%. Industry representatives argue that Angola’s gambling taxes remain higher than international norms.

Corporate income tax applies to gambling operators at standard Angolan rates. As of current regulations, the standard corporate tax rate is 25% on taxable profits. This applies in addition to gambling-specific taxes, creating a combined tax burden that operators must account for in financial planning and pricing strategies.

Fixed operational taxes and annual fees include license application fees, license renewal fees, and potentially other regulatory charges. While specific fee schedules have not been publicly disclosed in available documentation, these represent significant upfront and ongoing costs that operators must budget for when planning market entry.

| Tax Type | Rate/Amount | Application |

|---|---|---|

| GGR Tax (Gambling) | 1.1% – 20% | Varies by gambling category |

| Player Winnings Tax | 10% – 15% | Withheld at payout; varies by game type |

| Corporate Income Tax | 25% | Standard rate on taxable profits |

| License Application Fee | Not disclosed | One-time payment upon application |

| License Renewal Fee | Not disclosed | Required for license extensions |

| Annual Regulatory Fee | Not disclosed | Ongoing compliance and oversight costs |

Gambling Market Financial Performance

In 2023, the Angolan State collected 10.1 billion kwanzas from the gaming sector, equivalent to approximately $10.6 million USD. This represents revenue from 23 licensed operators across all gambling categories. The government projected that tax revenues would reach 16 billion kwanzas in 2024, representing a 58% increase and signaling strong sector growth.

Looking forward, the Director-General of ISJ stated that over the next few years, the gaming sector should contribute amounts in kwanzas equivalent to 100 million dollars. This ambitious projection reflects expectations that the new online licensing framework will significantly expand the regulated market and attract substantial new investment from both domestic and international operators.

Total market size in terms of gross gaming revenue has not been publicly disclosed, but can be estimated based on tax collections and known tax rates. Assuming an average effective GGR tax rate of 15-20%, the 2023 tax collection of $10.6 million would imply total GGR in the range of $53-70 million. This represents a developing market with substantial room for growth as internet penetration increases and the online gambling framework matures.

Year-over-year growth trends show accelerating expansion. The projected increase from 10.1 billion kwanzas in 2023 to 16 billion kwanzas in 2024 represents 58% growth, significantly outpacing general economic growth rates. This rapid expansion reflects pent-up demand for regulated gambling services and the positive impact of regulatory modernization on market development.

Advertising and Marketing Restrictions

Angola’s gambling regulations include provisions governing advertising and marketing activities, though detailed restrictions have not been fully elaborated in public documentation. Operators must ensure that all marketing communications promote responsible gambling and do not target vulnerable populations, particularly minors.

Prohibition on marketing to minors is strictly enforced. All gambling advertisements must include clear age restrictions and warnings about the risks of gambling. Marketing materials cannot feature minors or appeal to underage audiences through themes, imagery, or placement in media consumed primarily by children.

Promotional limitations apply to bonus offers and wagering requirements. While specific caps on bonus amounts or maximum wagering requirements have not been publicly specified, operators must ensure that promotional terms are fair, transparent, and do not encourage excessive gambling. Misleading advertising regarding odds, payout rates, or terms and conditions is prohibited.

Content restrictions require that advertising accurately represents gambling products and does not make false claims about winning probabilities or potential returns. Testimonials and endorsements must be genuine and not create unrealistic expectations. Gambling cannot be portrayed as a solution to financial problems or as a risk-free activity.

Recent Regulatory Changes and Their Impact

The most significant recent regulatory change occurred in February 2025 when ISJ announced it would commence accepting license applications for online gambling operations starting February 18, 2025. This marked a comprehensive expansion of Angola’s online gambling market and represented the culmination of regulatory development efforts that began with Presidential Decree No. 131/20 in May 2020.

The new licensing framework timing provides operators with structured entry pathways into a market that previously operated with limited formal oversight of online activities. The two-week preparation period between announcement and activation allowed potential operators to gather necessary documentation and align operations with regulatory requirements.

The Gambling Activity Law enacted in 2016 (Law no. 5/16) established the foundational regulatory framework, but has been supplemented by subsequent decrees and regulations. The 2020 Presidential Decree on Remote Online Gaming (Decree No. 131/20) specifically addressed the digital gambling environment, creating the legal basis for the 2025 licensing launch.

Impact on operator costs and business strategy has been significant. Lower tax rates improve unit economics for operators, potentially enabling more competitive bonusing, better odds for players, and sustainable business models. However, operators must still navigate substantial compliance costs related to technical systems, reporting requirements, and regulatory fees.

Enforcement Mechanisms and Penalties

The Gaming Law establishes a comprehensive penalty structure for gambling-related offenses. Depending on the nature of the offense, violators can be sentenced to up to two years’ imprisonment or fines up to AOA 50,000,000 (fifty million kwanzas, approximately $52,000 USD at recent exchange rates).

License suspension and revocation constitute the most severe administrative penalties available to ISJ. Operators who fail to maintain compliance with licensing conditions, engage in fraudulent activities, or repeatedly violate regulatory requirements risk having their licenses suspended pending remediation or permanently revoked.

Recent enforcement actions and precedents are not extensively documented in public sources, but the regulatory framework clearly empowers ISJ to investigate complaints, conduct inspections, and take corrective action. The emphasis on data protection, responsible gambling, and anti-money laundering compliance suggests these areas receive particular regulatory scrutiny.

ISP blocking of unlicensed operators represents a potential enforcement tool, though Angola’s approach to blocking foreign gambling sites is not well documented. The government’s focus on channeling gambling activity into the regulated market suggests that blocking unlicensed operators could intensify as the domestic licensing framework matures.

Payment processor restrictions may be employed to prevent unlicensed operators from serving Angolan players. Banks and payment service providers can be directed not to process transactions for unlicensed gambling operators, creating operational barriers for offshore sites attempting to serve the Angolan market without proper authorization.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

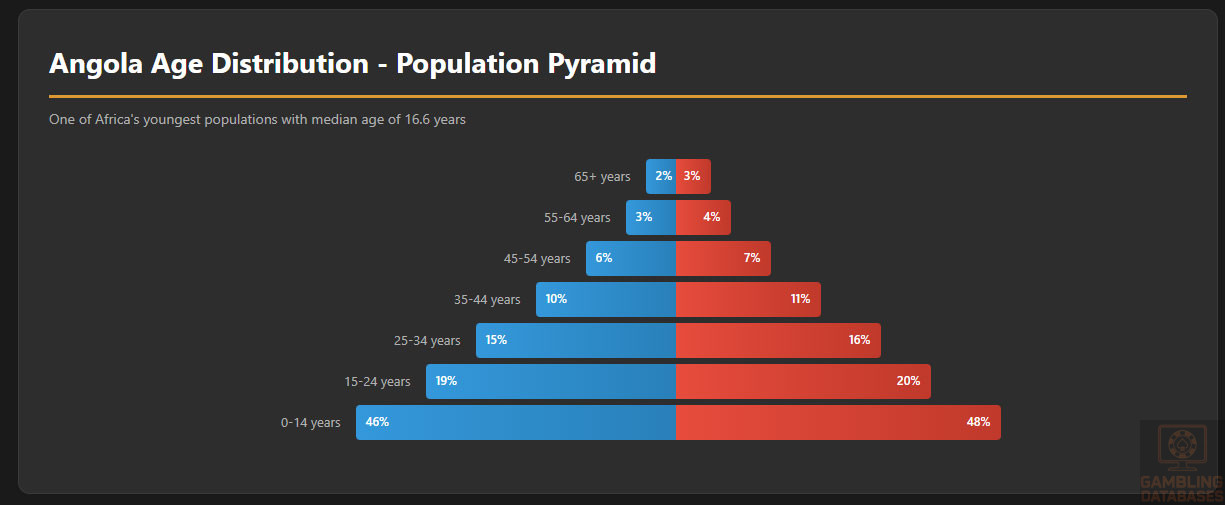

Angola’s total population stands at approximately 39.3 million people as of 2025, making it the 39th largest country globally by population. The population continues to grow at a robust rate of approximately 3.1% annually, reflecting high fertility rates and improving healthcare outcomes. This growth rate significantly exceeds global averages and creates an expanding consumer base for digital services including iGaming.

The median age of 16.6 years makes Angola one of the youngest populations globally. This extraordinarily young demographic profile has profound implications for the gambling market. While only those 18 and older can legally gamble, the large cohort approaching gambling age and the tech-savvy nature of younger consumers creates favorable long-term growth prospects.

Age distribution demonstrates a classic expansive population pyramid with a wide base of young people. The 0-14 age group comprises approximately 46-48% of the population. The 15-24 age group represents roughly 19-20% of the total. The 25-34 age bracket, a key gambling demographic, accounts for approximately 15-16% of the population. The 35-44 group represents about 10-11%, while those 45-54 comprise 6-7%. The 55-64 age group accounts for 3-4%, and those 65 and older represent only 2-3% of the total population.

Gender ratios are relatively balanced with slight male predominance in younger age groups. Life expectancy has improved significantly in recent years, though it remains below global averages at approximately 61-63 years. The young population structure combined with improving life expectancy suggests sustained population growth for decades to come.

Geographic Distribution

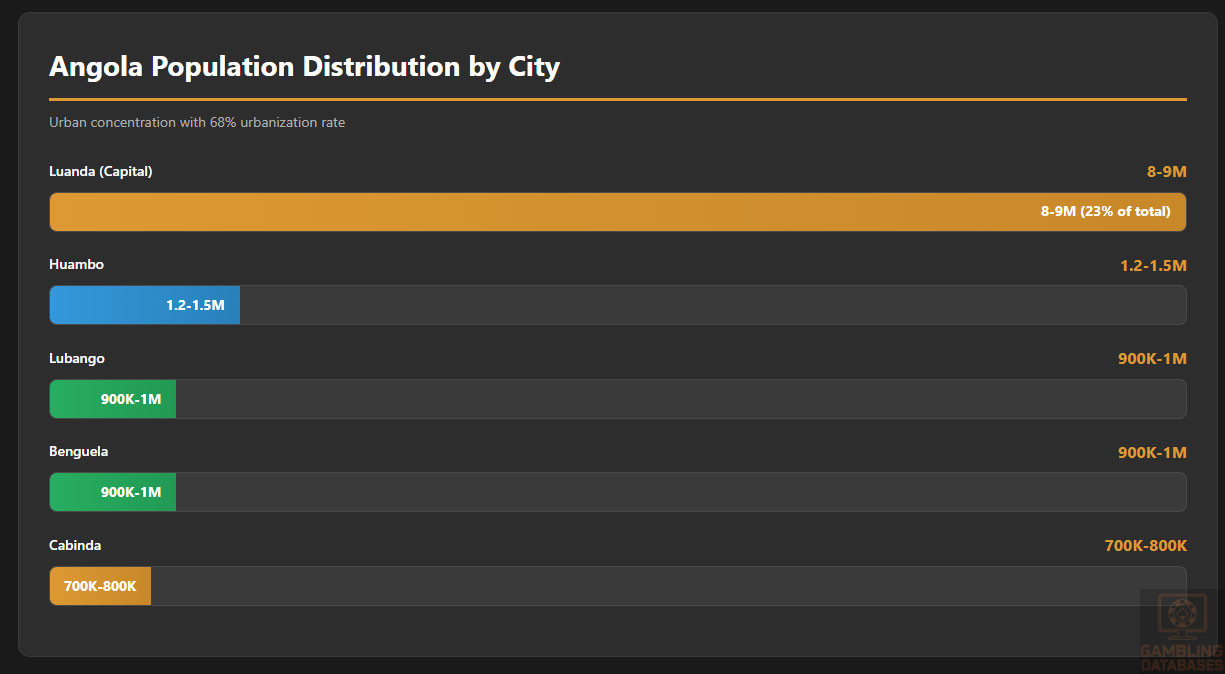

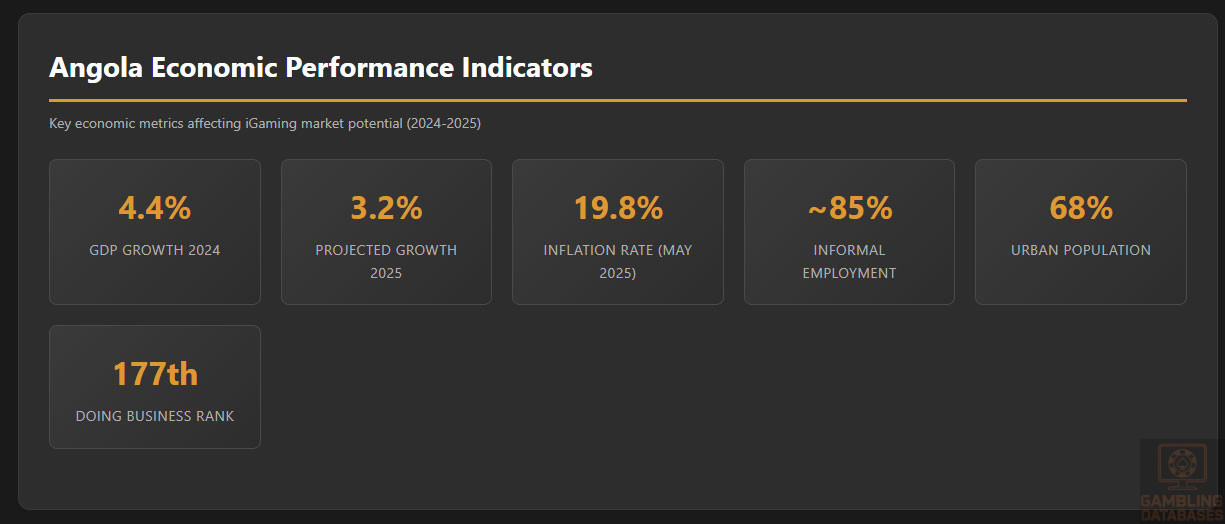

Angola demonstrates high levels of urbanization with approximately 68% of the population residing in urban areas. This urban concentration creates favorable conditions for iGaming operators, as urban residents typically have better internet access, higher incomes, and greater exposure to digital entertainment options compared to rural populations.

Luanda, the capital city, dominates the urban landscape with a population estimated at 8-9 million people, representing approximately 20-23% of the national population. This massive concentration of population, wealth, and infrastructure in a single city creates a natural focal point for iGaming operators. Luanda offers the best internet connectivity, highest concentration of banked individuals, and greatest consumer purchasing power in the country.

Other major population centers include Huambo with approximately 1.2-1.5 million residents, Lubango with 900,000-1 million, Benguela with 900,000-1 million, and Cabinda with 700,000-800,000 residents. These secondary cities represent important regional markets with growing digital infrastructure and rising consumer demand for online entertainment services.

Regional economic differences are substantial. Luanda and coastal provinces benefit from oil industry wealth, port infrastructure, and government investment. Interior provinces remain more agricultural and less developed with limited digital infrastructure. This geographic divide means iGaming operators will likely see highly concentrated demand from urban coastal areas, particularly Luanda, in the near to medium term.

Internet access geographic patterns reflect this urban-rural divide. Urban areas, especially Luanda, enjoy relatively good 4G coverage and increasingly available fixed broadband. Rural areas often rely on 2G or 3G mobile networks with inconsistent coverage, making online gambling access challenging for rural residents despite their inclusion in the total addressable market.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Angola’s GDP totaled approximately $101.5 billion in 2024, positioning the country as the 75th largest economy globally by nominal GDP. This substantial economic base reflects Angola’s status as one of Africa’s major oil producers, though the government is actively pursuing economic diversification to reduce dependence on petroleum exports.

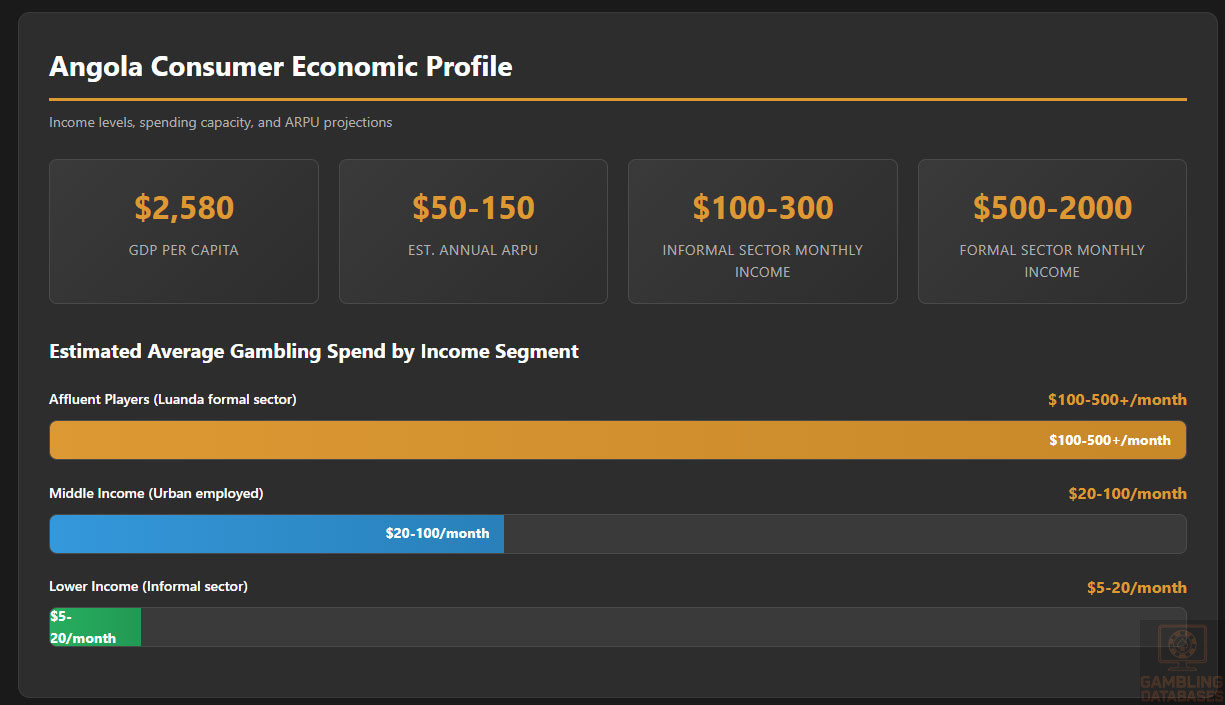

GDP per capita stood at approximately $2,580 in 2024, placing Angola in the lower-middle income category by World Bank classifications. While this figure is modest by global standards, it represents significant purchasing power in the African context and indicates a consumer base capable of discretionary spending on entertainment including gambling.

The economy recorded its strongest growth performance in five years in 2024, with real GDP expanding 4.4%, well above the 1.1% growth of 2023. This recovery was driven mainly by the non-oil sector, with agriculture and fisheries’ share of GDP more than doubling from 6.2% in 2010 to 14.9% in 2023, underscoring Angola’s commitment to economic diversification.

GDP growth forecasts project more modest expansion of 3.2% in 2025, mostly driven by strong dynamism of the non-oil sectors, as the oil sector is expected to return to its declining trend. The African Development Bank projects growth to reach 4.1% in 2024 and strengthen to 4.5% in 2025, though these forecasts vary across institutions.

Economic sector composition shows oil remains central to the economy, accounting for 28.9% of GDP and 95% of total exports. However, the services sector is growing rapidly, driven by commerce and telecommunications. Agriculture, fisheries, and mining (particularly diamonds) are expanding, creating a more balanced economic foundation that supports sustainable growth in consumer spending.

Employment rates and wage levels vary significantly between formal and informal sectors. Approximately 85% of the workforce operates in the informal economy according to Angola’s national statistics institute. Formal sector employment offers higher wages but remains limited. Informal sector workers often have irregular income streams, creating challenges for consistent gambling participation but also demand for mobile-accessible entertainment.

Inflation represents a significant challenge for consumer purchasing power. Inflation accelerated from 20.4% in 2023 to 27.5% in early 2025, driven by higher food prices and diesel price adjustments. However, inflation has been declining recently, reaching 19.8% in May 2025. This high inflation environment erodes real incomes and creates uncertainty that may impact discretionary spending including gambling.

| Indicator | Value | Trend |

|---|---|---|

| GDP Total | $101.5 billion | Growing |

| GDP Per Capita | $2,580 | Modest growth |

| Real GDP Growth 2024 | 4.4% | Strong recovery |

| Projected Growth 2025 | 3.2% | Moderating |

| Inflation Rate (May 2025) | 19.8% | Declining from peak |

| Oil Sector GDP Share | 28.9% | Declining |

| Agriculture/Fisheries Share | 14.9% | Growing |

| Informal Employment | ~85% | Stable |

| Public Debt to GDP | ~70% | Declining from 89% |

| Currency (AOA vs USD) | Depreciated 10% in 2024 | Stabilizing |

Income and Wealth Distribution

Income inequality in Angola is substantial, though specific Gini coefficient data is not readily available in recent public sources. The concentration of wealth in Luanda and among those connected to the oil industry creates stark disparities between urban and rural populations, and between formal and informal sector workers.

Average household income varies dramatically by region and employment sector. Formal sector employees in Luanda may earn monthly salaries equivalent to $500-2,000 or more, while informal sector workers and rural populations often subsist on $100-300 monthly or less. This creates a bifurcated market where a minority of relatively affluent consumers account for disproportionate spending power.

Banking penetration of approximately 50% indicates that half of Angolans have bank accounts, though many are “underbanked,” meaning they use accounts primarily to withdraw salaries as cash once or twice monthly rather than for active transaction management. The remaining 50% unbanked population represents both a challenge and opportunity for mobile money-enabled gambling solutions.

Disposable income trends are pressured by high inflation, particularly food price increases that consume a large share of household budgets for lower-income families. However, the growing middle class in urban areas, particularly Luanda, demonstrates increasing capacity for discretionary spending on entertainment, dining, and digital services including potential gambling activities.

Consumer spending patterns in Angola reflect the dominant role of cash transactions, though digital payment adoption is growing rapidly. Mobile money services like Unitel Money and Afrimoney are expanding financial access and creating new payment channels that could facilitate online gambling participation even among unbanked or underbanked consumers.

Market Size and Growth Projections

Current iGaming market revenue in Angola is estimated at approximately $50-70 million based on government tax collection data and estimated effective tax rates. This represents a developing market with substantial room for expansion as regulatory frameworks mature and internet penetration increases.

Historical revenue growth has been strong, with the government reporting gambling tax collections of 10.1 billion kwanzas ($10.6 million) in 2023 and projecting 16 billion kwanzas ($16.8 million) in 2024. This 58% year-over-year growth in tax collections indicates rapid market expansion driven by new operator entries and growing consumer adoption.

Revenue forecasts for the next 3-5 years are ambitious. The government projects the gambling sector should contribute amounts in kwanzas equivalent to $100 million over the coming years. If this represents annual tax contributions, and assuming a 15-20% effective tax rate, it would imply total market GGR of $500-670 million, representing roughly 7-10x growth from current levels.

Expected CAGR (Compound Annual Growth Rate) would need to exceed 40-50% annually to achieve the government’s $100 million tax collection target within 3-5 years. While aggressive, such growth rates are not unprecedented in emerging African iGaming markets experiencing regulatory formalization, rising internet penetration, and mobile technology adoption.

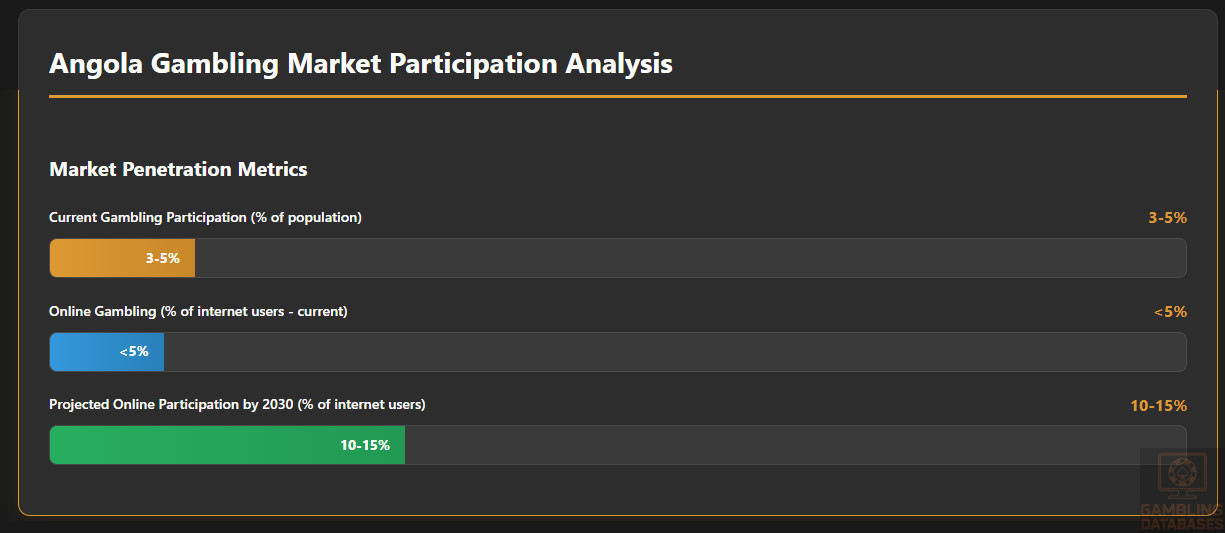

Projected user base growth depends on expanding internet access and gambling participation rates. With 17.2 million internet users in early 2025 and internet penetration growing 3.1% annually, the addressable market is expanding rapidly. If gambling participation rates among internet users reach 10-15% over the next 5 years (comparable to more mature markets), Angola could see 1.7-2.6 million active gamblers by 2030.

Average Revenue Per User (ARPU) in Angola is likely modest compared to developed markets, perhaps $50-150 annually based on income levels and spending patterns. However, ARPU should grow as the market matures, payment methods improve, and operators develop more sophisticated player retention and monetization strategies.

Market penetration rates currently remain low, with gambling participation estimated at less than 5% of internet users. As regulatory clarity improves, payment options expand, and operators invest in marketing and localization, penetration rates should increase toward 10-15% of internet users, creating substantial growth potential even before accounting for rising internet access.

Online versus land-based revenue split currently favors land-based operations given the longer establishment of casino and betting shop licenses. However, online gambling should capture increasing market share as mobile access improves, digital payment adoption grows, and operators launch compelling mobile-first products tailored to local preferences.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy rates in Angola have improved significantly but remain moderate by global standards. Overall adult literacy is estimated at 70-75%, with higher rates among younger cohorts who have benefited from expanded educational access. Gender gaps in literacy persist but are narrowing, particularly in urban areas.

Education levels show that primary school completion has risen substantially, though secondary and tertiary completion rates remain limited. Many Angolans complete primary education but do not progress to secondary school due to economic pressures, limited school availability in rural areas, or early entry into informal employment.

Digital literacy varies dramatically between urban and rural populations and across age groups. Young urban Angolans demonstrate strong digital skills, comfortable navigating smartphones, social media, and mobile applications. Older and rural populations show lower digital literacy, creating a divide in potential gambling platform adoption.

Workforce skill levels are constrained by limited tertiary education and vocational training. The gambling sector employs approximately 6,000 people according to industry association data, with 1,703 in administrative and operational roles and 4,177 as game mediators. Attracting technical talent for platform development and operations represents a challenge for operators.

Technology adoption readiness is high among younger, urban populations who have embraced smartphones and mobile internet rapidly. This tech-savvy demographic cohort represents the core target market for online gambling operators and demonstrates willingness to adopt new digital services including gaming and gambling applications.

Cultural and Social Factors

Communication and Language

Portuguese serves as Angola’s official language and the primary language for business, government, and formal communication. All gambling operations, websites, marketing materials, and customer service must be available in Portuguese to effectively serve the Angolan market. English proficiency is limited outside of educated urban elites.

Internet language preferences heavily favor Portuguese, with minimal English language consumption except among highly educated professionals. Operators attempting to serve the Angolan market with English-only platforms will fail to connect with the mass market and may face regulatory challenges regarding accessibility and consumer protection.

Business communication norms in Angola reflect Portuguese colonial heritage combined with African cultural traditions. Formality in initial business interactions is expected, with relationships developing over time. Local partnerships or hiring experienced Angolan business development professionals can accelerate market entry and regulatory navigation.

Cultural Attitudes Toward Gambling

Gambling acceptance levels in Angolan society appear moderate to positive based on the established presence of casinos, betting shops, and the government’s active promotion of the gambling sector for economic development and tax revenue generation. Unlike some African countries where religious opposition constrains gambling development, Angola’s regulatory expansion suggests social acceptance.

Religious influences on gambling perception exist but do not appear to dominate policy discussions. Angola’s population is predominantly Christian (Catholicism and Protestant denominations), with small Muslim and indigenous belief communities. While some religious groups may oppose gambling, the government’s pursuit of gambling sector growth indicates this opposition has not blocked market development.

Foreign brand perception and trust is generally positive, particularly for established international brands with quality reputations. Angola’s history as a Portuguese colony and ongoing economic ties to Portugal, Brazil, and other lusophone countries means Portuguese and Brazilian brands may enjoy cultural affinity advantages. However, foreign operators must demonstrate commitment to the local market through appropriate licensing, local employment, and Portuguese language service.

Risk tolerance indicators suggest Angolans demonstrate entrepreneurial spirit, evidenced by the 85% informal sector employment rate. This entrepreneurial orientation may correlate with higher risk tolerance and openness to gambling as a form of entertainment and potential income supplementation, though research specifically measuring gambling-related risk tolerance is unavailable.

Problem Gambling and Social Considerations

Prevalence of gambling addiction in Angola has not been extensively studied or published in available research. As the gambling market expands, particularly online gambling which can present higher addiction risks due to accessibility and speed of play, problem gambling rates will likely increase and require regulatory and industry response.

Government response measures to problem gambling are embedded in the regulatory framework through requirements for responsible gambling information, self-exclusion systems, and player protection measures. However, comprehensive treatment infrastructure, public awareness campaigns, and research into gambling harm appear limited compared to more mature gambling jurisdictions.

Social responsibility requirements for operators include displaying responsible gambling information, implementing age verification systems, providing self-exclusion mechanisms, and limiting data collection to necessary purposes. As the market matures, regulators may introduce additional requirements such as mandatory spending limits, session time restrictions, or contributions to problem gambling treatment funds.

Political Structure and Governance

Angola operates as a presidential republic with President João Lourenço serving since 2017. The government has pursued economic reforms aimed at diversification, anti-corruption measures, and attracting foreign investment. Political stability has improved compared to the civil war era that ended in 2002, though governance challenges persist.

Political stability indicators show Angola ranks moderately in terms of political risk. The country scores 150th out of 193 countries on the Human Development Index with a score of 0.591, indicating development challenges. The Corruption Perception Index ranking suggests corruption remains an issue, though anti-corruption efforts have intensified under the current administration.

Regulatory consistency and predictability are improving as Angola modernizes its legal and regulatory frameworks. The structured approach to gambling regulation, with clear laws, defined regulatory authority, and transparent licensing processes, demonstrates government commitment to creating a stable operating environment that can attract legitimate investment.

International relations impact on business is generally positive, with Angola maintaining relationships with Portugal, Brazil, China, and other major economies. Trade agreements and investment treaties provide some protection for foreign investors, though operators should conduct thorough due diligence on investment protection frameworks before committing substantial capital.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at 44.8% of the population, with 17.2 million internet users as of January 2025. This represents 3.1% annual growth, adding 513,000 new users between January 2024 and January 2025. While penetration lags the continental average and significantly trails leaders like Morocco (92%), the growth trajectory is positive and creates expanding market opportunities.

Daily internet usage hours among connected Angolans are not precisely documented in available sources, but mobile internet dominates access patterns given the 28.7 million mobile connections versus limited fixed broadband penetration. Users likely spend 2-4 hours daily on mobile internet for social media, messaging, entertainment, and information consumption.

Social media engagement is substantial, with 5.10 million social media user identities in Angola as of January 2025, equating to 13.3% of the total population. Facebook represents the dominant platform, with advertising reach of approximately 5 million users. Social media provides important marketing channels for gambling operators to reach engaged digital consumers.

E-commerce participation rates remain modest but are growing rapidly. Digital payment adoption through mobile money services (Unitel Money, Afrimoney, Multicaixa Express) and banking apps is expanding, creating the payment infrastructure necessary for online gambling transactions. Consumers increasingly comfortable with e-commerce transactions for retail goods will more readily adopt online gambling.

Digital Payment Behavior

Payment method preferences in Angola reflect a transitioning economy moving from cash dominance toward digital transactions. Mobile money represents the most accessible digital payment option for many Angolans, particularly the unbanked or underbanked 50% of the population. Bank cards (debit more than credit) serve the banked population in urban areas.

Most popular digital wallets include Multicaixa Express with over 1 million Google Play Store downloads, making it likely the most used digital wallet in Angola. Unitel Money, operated by major telecom Unitel, positions itself as the “National Mobile Bank of Angola” and serves millions of users. Afrimoney, launched by Africell in April 2023, targets the underbanked population and is growing rapidly.

Other digital wallet solutions include e-Kwanza (BAI bank), Agiliza (Banco Millennium Atlântico), and AKI, which operate through app-based or USSD channels. International e-wallets like Skrill and Neteller are available but serve primarily more affluent, internationally-oriented consumers rather than the mass market.

Online transaction patterns reflect mobile-first behavior with small, frequent transactions dominating. Average transaction sizes are modest given income levels, likely in the range of $5-50 for typical consumer purchases. Gambling transactions will likely mirror this pattern with small deposits and frequent micro-transactions rather than large deposits.

Trust in online payment systems is developing. The expansion of mobile money and digital banking demonstrates growing consumer comfort with digital financial services, particularly when provided by trusted brands like major banks or telecommunications companies. International payment brands like Visa and Mastercard also carry trust advantages.

Cryptocurrency adoption for gambling remains minimal in Angola. While some international gambling sites accept crypto, local regulatory framework does not specifically address cryptocurrency gambling, and adoption rates are low among the general population. Crypto is unlikely to represent a significant payment channel in the near term for the mainstream Angolan gambling market.

| Payment Method | Market Position | Gambling Suitability |

|---|---|---|

| Multicaixa Express | Leading digital wallet (1M+ downloads) | High – widely adopted, mobile-friendly |

| Unitel Money | Major mobile money provider | High – large user base, instant transfers |

| Afrimoney | Growing mobile money (launched 2023) | Medium – expanding, targets unbanked |

| Bank Cards (Visa/Mastercard) | Moderate penetration, urban focused | Medium – trusted but limited reach |

| Bank Transfers | Available for banked population | Medium – secure but slower |

| e-Kwanza, Agiliza, AKI | Smaller digital wallet providers | Low-Medium – niche but growing |

| International e-wallets | Limited (Skrill, Neteller available) | Low – small, affluent audience only |

| Cryptocurrency | Minimal adoption | Very Low – regulatory uncertainty |

Gaming and Gambling Preferences

Current Market Participation

Percentage of population that gambles is difficult to quantify precisely given limited market research data, but industry observers estimate that perhaps 3-5% of Angolans participate in gambling activities at least occasionally. With 39.3 million total population, this would suggest 1.2-2 million people engage in some form of gambling, primarily through land-based casinos, betting shops, and informal channels.

Percentage that gambles online is even smaller, likely 1-2% of the population or less currently. With 17.2 million internet users, if 5-10% participate in online gambling, this would suggest 860,000 to 1.7 million online gamblers. However, given the recent licensing framework launch, actual online gambling participation through licensed Angolan operators is probably lower, with many users accessing unlicensed international sites.

Popular gambling activities likely follow patterns observed across Africa and globally. Sports betting, particularly football (soccer) betting, represents the most popular form of gambling given Africa’s passion for football and the social nature of sports wagering. Casino games including slots and table games attract players seeking variety and potentially larger payouts.

Sports betting versus casino games preference appears to tilt toward sports betting based on general African market patterns and the presence of three territorial sports betting operators among the 23 total licensees. However, casino games (particularly slots) represent substantial revenue generators and appeal to players seeking more diverse gaming experiences.

Lottery participation rates are difficult to assess given that lottery operations were previously limited and are only now being reintroduced through public tender processes. Historical lottery participation may have been high given lottery’s accessibility and low entry costs, and renewed lottery operations could capture significant market share.

Consumer Behavior Patterns

Average spending per player varies dramatically by income level and gambling vertical. Lower-income players might wager $5-20 monthly on sports betting or slots, while more affluent players could spend $100-500+ monthly. Average monthly spend across all players might range from $20-50, though comprehensive data is unavailable.

Platform preferences strongly favor mobile over desktop given Angola’s mobile-first internet access pattern. With smartphones representing the primary internet access device for most Angolans, gambling operators must prioritize mobile-optimized websites or dedicated mobile applications. Desktop/laptop gambling will remain niche, concentrated among office workers and more affluent consumers.

Peak gambling times likely align with leisure hours – evenings after work, weekends, and around major sporting events. For sports betting specifically, match times (often European football matches in evening Angolan time) drive concentrated betting activity. Paydays early in each month may see increased gambling activity as consumers receive salaries.

Bonus sensitivity and promotional response among Angolan players is likely high given income constraints and the value-seeking behavior typical in emerging markets. Welcome bonuses, free bets, and deposit matches will effectively attract new players. However, operators must balance aggressive bonusing with sustainable economics and regulatory requirements.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

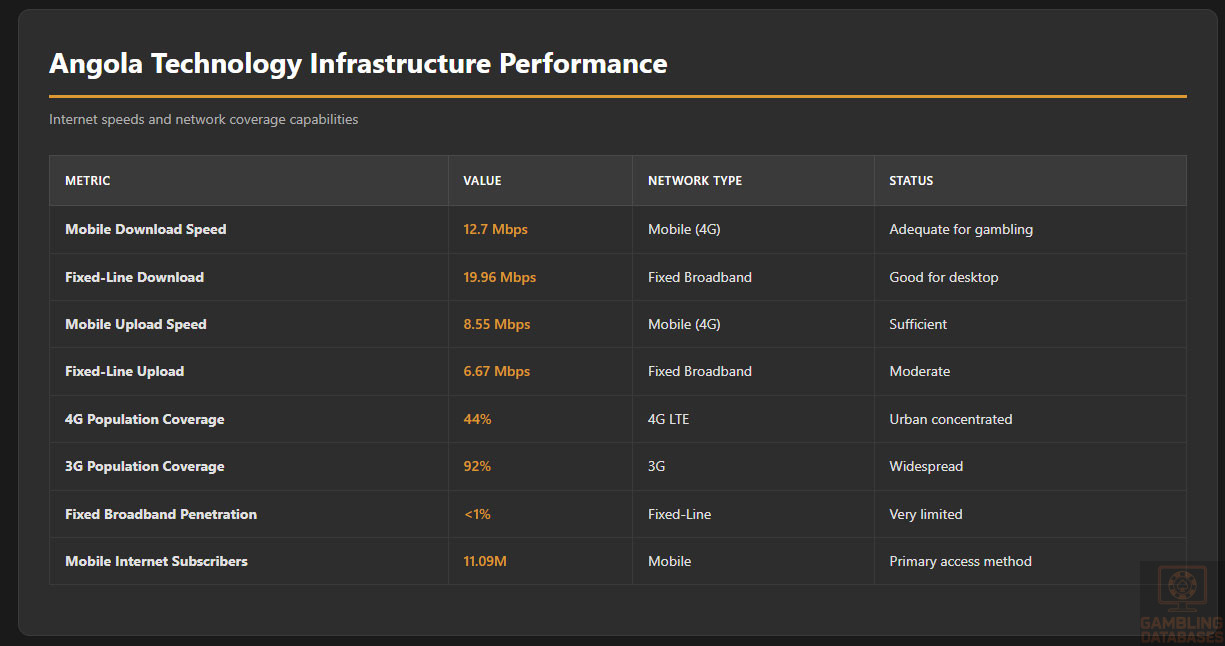

Internet penetration of 44.8% (17.2 million users) places Angola slightly above the continental average but well behind African leaders. Fixed broadband penetration remains very low at under 1% of the population, with only 137,705 fixed-line internet subscribers as of September 2023 according to INACOM data. Mobile internet dominates, with 11.09 million mobile internet subscribers.

Average internet speeds are modest but improving. As of February 2024, Angola recorded median mobile download speeds of 12.7 Mbps and upload speeds of 8.55 Mbps. Fixed-line connections averaged 19.96 Mbps download and 6.67 Mbps upload. These speeds are less than half the global median for mobile and less than a tenth the global median for fixed-line, but are adequate for most gambling applications.

Network reliability and uptime face challenges due to infrastructure limitations and frequent power outages. The fractured electricity system served 75% of urban populations as of 2021 but only 7.3% of rural populations as of 2018. Power outages remain frequent, impacting both network infrastructure and user devices, creating frustrations for real-time gambling experiences.

Infrastructure investment trends are positive, with government prioritizing digital infrastructure expansion. The expansion of the terrestrial fiber optic network, Angola’s accession to the 2África submarine fiber optic cable, and the consolidation of the national space program with commercialization of Angosat 2 satellite capacity represent major initiatives improving connectivity foundations.

Fixed internet speeds improved approximately 18% from 2024 to 2025, likely due to new fiber deployments and upgrades in urban centers. However, mobile median speeds saw a decline of about 28% during 2023, perhaps due to more users crowding onto networks or technical issues, highlighting the volatility in quality as networks expand and user bases grow.

5G and Future Technology Deployment

Current 4G coverage reached approximately 44% of the Angolan population as of 2022 according to GSMA Mobile Connectivity Index data, while 92% of the population was covered by 3G wireless network access. This indicates that while basic mobile internet is widely available, higher-speed 4G coverage remains concentrated in urban areas and along major transportation corridors.

5G rollout commenced in late 2021 when the Ministry of Telecommunications set up a 5G hub to assess use cases. Licenses were granted to Africell, Movicel, and Unitel to offer 5G services using spectrum in the 3.3-3.7GHz range. While initial deployments have begun in Luanda, nationwide 5G coverage remains years away.

Future infrastructure plans include continued fiber optic network expansion with approximately 2,000 kilometers of installation prepared, the implementation of digital terrestrial television, and interconnection with border countries via terrestrial optical fiber. These investments will gradually improve network capacity, speeds, and reliability supporting data-intensive applications like live gambling streams.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Angola has three mobile network operators. Unitel, launched in 2001, is the market leader and historically held a near-monopoly on mobile internet. Movicel, which started as a state-owned mobile division, became the second operator. Africell entered the market in 2022, ending the long-standing duopoly and introducing new competition.

4G coverage quality varies significantly by operator and geography. Unitel expanded 4G services substantially from 2021 onward and maintains the most extensive 4G footprint. Africell, having entered recently with modern infrastructure, is building comprehensive networks and aims for nationwide coverage by 2025. Movicel’s 4G deployment has lagged competitors.

Data costs and pricing models have become more competitive with Africell’s market entry. While specific pricing is not detailed in available sources, the entrance of a third operator has increased price competition, benefiting consumers through lower data costs and more generous data bundles. Prepaid models dominate given limited credit history and banking penetration.

Mobile payment integration through carrier billing or mobile money wallets is well-established through services like Unitel Money and Afrimoney. These services enable gambling operators to offer payment options accessible even to unbanked users, potentially expanding market reach beyond the 50% banked population.

Device Penetration and Usage

Smartphone adoption rates are high among internet users but moderate across the total population. With 17.2 million internet users in a population of 39.3 million, and assuming most internet users access via smartphones, smartphone penetration likely ranges from 40-50% of the population. Urban areas show much higher penetration while rural areas lag significantly.

Android versus iOS market share heavily favors Android, likely representing 85-95% of the smartphone market. This reflects price sensitivity and the availability of affordable Android devices from Chinese manufacturers. iOS devices remain luxury items for affluent consumers. Gambling operators must prioritize Android app development and optimization.

Average device specifications trend toward mid-range and entry-level smartphones. While flagship devices are available, most Angolans use smartphones in the $50-200 price range with modest processing power, limited RAM, and smaller storage capacity. Applications must be optimized for lower-spec devices to reach the mass market.

Mobile internet usage patterns show smartphones serve as the primary internet access device for most users. Time spent on mobile internet, data consumption for video and social media, and comfort with mobile applications all point to mobile-first design as essential for gambling products targeting the Angolan market.

Financial Services and Payment Infrastructure

Banking System Structure

Angola has 26 commercial banks registered to operate, though the market is highly concentrated. Five banks – Banco Angolano de Investimentos (BAI), Banco Economico, Banco de Fomento Angola (BFA), Banco BIC Angola (BIC), and Banco de Poupança e Crédito (BPC) – control over 80% of total banking assets, deposits, and loans.

Digital banking adoption has grown substantially, particularly accelerated by the COVID-19 pandemic and government encouragement of cashless transactions. Major banks offer mobile banking apps and internet banking platforms. However, usage often remains limited to checking balances and basic transfers rather than full transaction management.

Account penetration rates of approximately 50% mean half of Angolans have bank accounts, representing significant progress from historical levels below 10%. However, many account holders are “underbanked,” using accounts primarily to receive salary deposits and immediately withdrawing cash, limiting the utility of traditional bank-based payment methods for gambling.

Payment Processing Options for iGaming

Available payment methods for iGaming in Angola must include mobile money given its market dominance and accessibility to unbanked populations. Multicaixa Express, Unitel Money, and Afrimoney should be priority integrations. Bank transfers serve banked populations but process more slowly than mobile payments.

Credit and debit card penetration is moderate in urban areas but limited nationally. Visa and Mastercard are the dominant international card networks, with Multicaixa serving as the national card scheme. Card payments require integration with Multicaixa networks and potentially individual bank partnerships for optimal acceptance.

E-wallet options beyond local mobile money include international services like Skrill and Neteller, which some Angolans use, particularly for international transactions or remittances. However, these serve a niche market and should be considered supplementary rather than primary payment methods.

Processing fees and typical charges vary by payment method and provider. Mobile money transactions often carry percentage-based fees of 1-3% or flat fees depending on transaction size. Bank transfers may be free for account holders or carry minimal fees. Card processing typically costs 2-4% of transaction value.

Transaction processing timelines favor mobile money and cards for instant deposits. Bank transfers may process same-day or require 1-2 business days. Withdrawals to mobile money or bank accounts typically process within 24-48 hours depending on operator policies and KYC verification requirements.

Regulatory restrictions on gambling payments require that operators maintain bank accounts with Angolan financial institutions for all gambling-related transactions. All prizes must be paid in national currency (kwanza) and through bank transfers, ensuring traceability and regulatory oversight while complicating cryptocurrency or foreign currency transactions.

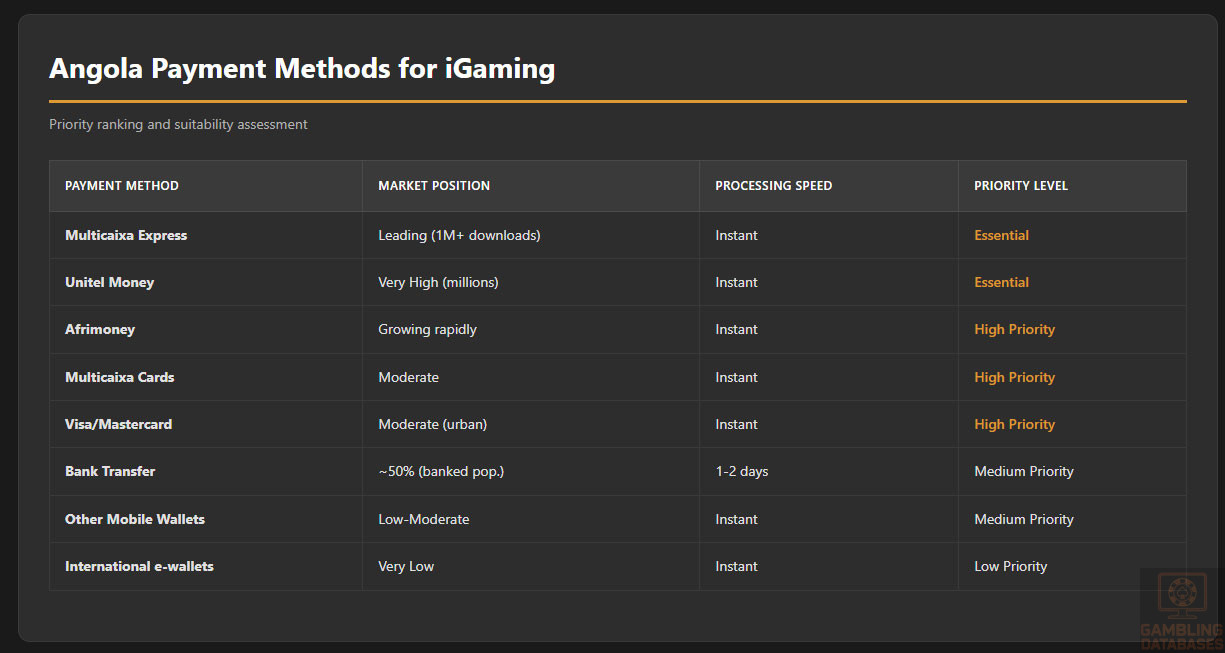

| Payment Method | Penetration | Processing Speed | Recommended Priority |

|---|---|---|---|

| Multicaixa Express | High (1M+ users) | Instant | Essential |

| Unitel Money | Very High (millions) | Instant | Essential |

| Afrimoney | Growing rapidly | Instant | High Priority |

| Multicaixa Cards | Moderate | Instant | High Priority |

| Visa/Mastercard | Moderate (urban) | Instant | High Priority |

| Bank Transfer | ~50% (banked pop.) | 1-2 days | Medium Priority |

| Other Mobile Wallets | Low-Moderate | Instant | Medium Priority |

| International e-wallets | Very Low | Instant | Low Priority |

E-commerce and Digital Economy

Digital Market Development

E-commerce market size in Angola is growing but remains in early stages of development. Online retail penetration represents a small percentage of total retail, with most commerce still conducted through physical stores and informal markets. However, the COVID-19 pandemic accelerated digital adoption, and younger urban consumers increasingly embrace online shopping.

Digital service adoption rates are rising across multiple sectors. Mobile banking, digital payments, online media consumption, and app-based services are all experiencing growth. This broader digital transformation creates favorable conditions for online gambling adoption as consumers become comfortable with digital transactions and services.

Consumer trust in online transactions is developing but requires careful nurturing. Partnerships with recognized brands (major banks, telecommunications operators, established international gambling operators) can transfer trust and credibility. Clear communication about security measures, licensing status, and player protection builds confidence among cautious consumers.

Popular e-commerce platforms are emerging but the sector remains fragmented. Many businesses use social media (particularly Facebook and Instagram) as sales channels, conducting transactions through messaging apps and mobile money payments. This informal e-commerce model demonstrates consumer comfort with mobile-mediated commerce that gambling operators can leverage.

Business Environment and Regulatory Framework

Ease of Business Operations

Angola ranks 177th in the World Bank’s Doing Business index, indicating significant challenges in the business regulatory environment. This low ranking reflects complexities in starting businesses, registering property, enforcing contracts, and navigating bureaucratic processes. However, the government has undertaken reforms to improve the business climate and attract foreign investment.

Business registration processes require navigating multiple government agencies and can be time-consuming. The standard process involves name reservation, document preparation and notarization, registration with the commercial registry, tax registration, and social security registration. Each step involves fees, documentation requirements, and processing times.

Time required to start a business has improved from historical levels but remains longer than in many countries. Entrepreneurs should expect the company registration process to take 4-8 weeks or more depending on entity type, documentation completeness, and efficiency of legal and consulting support engaged.

Foreign investment policies have become more welcoming under recent government reforms. The Private Investment Law (Law 10/18) provides the framework for foreign investment, offering equal treatment to foreign and domestic investors in most sectors. Special incentives may be available for investments in priority sectors or less-developed regions.

Operational cost structures in Angola reflect the country’s oil-driven economy and import dependence. Office rent in prime Luanda locations can be expensive by African standards, though rates have moderated from historical peaks. Salaries for skilled professionals are competitive regionally, while less-skilled labor costs less but may require significant training.

Labor market conditions present both opportunities and challenges. Angola’s young population provides a large potential workforce, but skill gaps exist particularly in technical and management roles. Operators may need to combine local hiring for customer service and operational roles with expatriate recruitment or extensive training for specialized technical and management positions.

Corporate Structure and Registration

Available entity types in Angola include the Sociedade por Quotas (similar to LLC), Sociedade Anónima (corporation/public limited company), branch offices of foreign companies, and representative offices. For iGaming operations, a Sociedade Anónima is required as the Gaming Law specifies that online gambling and betting licenses are granted only to public limited companies.

The Sociedade Anónima structure requires that the totality of share capital be represented by shares, enabling transparency in ownership as required by gambling regulations. This corporate form allows for multiple shareholders, professional management structures, and the formal governance frameworks expected by regulators for licensed gambling operations.

Registration requirements include preparing articles of association, appointing directors and statutory auditor, obtaining notarization of founding documents, registering with the Commercial Registry, obtaining tax identification numbers, and registering with social security. Foreign shareholders are permitted without requiring local partners for most business activities including gambling operations.

Registration costs include government fees for commercial registry, notary fees for document authentication, legal fees for documentation preparation and filing, and initial capital deposit requirements. Total costs for establishing a Sociedade Anónima might range from $5,000 to $15,000 or more depending on complexity and professional services engaged.

Minimum capital requirements vary by entity type. While specific minimums for gambling-licensed companies have not been publicly disclosed, operators should expect substantial capital requirements demonstrating financial stability sufficient to honor player deposits and winnings. Capital in the range of $100,000 to $500,000 or higher is likely necessary.

Ongoing compliance requirements include annual financial statement preparation and filing, annual general meetings of shareholders, maintaining statutory books and records, annual tax returns, and audits by statutory auditor. Gaming operators face additional reporting obligations to ISJ including regular activity reports, financial statements, and compliance certifications.

Taxation Framework

Standard corporate tax rates in Angola are 25% on taxable profits for most business activities. This rate applies to gambling operators’ profits after deduction of allowable expenses and gambling-specific taxes. The corporate tax burden combines with GGR taxes (1.1-20%) to create the total tax load on gambling operations.

Tax holidays or reduced rates for new businesses may be available under the Private Investment Law for investments in priority sectors or less-developed regions. However, gambling operations are unlikely to qualify for preferential tax treatment given their profitability potential and government interest in maximizing gambling tax revenues.

International tax treaties provide some protection against double taxation for operators structured with foreign parent companies. Angola has tax treaties with Portugal, Cape Verde, and other countries. Operators should structure ownership and profit repatriation strategies considering treaty benefits and transfer pricing requirements.

Withholding tax on dividends, interest, and royalties applies when profits are distributed to foreign shareholders or when payments are made to foreign service providers. Dividend withholding tax is typically 10% for companies and 15% for individuals, though treaty rates may differ. Interest and royalty payments face 15% withholding tax unless reduced by treaty.

VAT/GST does not apply to gambling services themselves as gambling is typically exempt or zero-rated. However, VAT at standard rates (currently 14%) applies to purchases of goods and services by gambling operators. Operators can generally reclaim input VAT on business purchases against output VAT on any taxable supplies they make.

Personal Income Tax

Individual tax rates in Angola follow a progressive structure with brackets ranging from approximately 0% on very low incomes up to marginal rates of 25% on higher incomes. Employees are subject to withholding tax on salaries, with employers responsible for calculating, withholding, and remitting taxes to authorities on behalf of employees.

Social security contributions represent additional costs for both employers and employees. Employer contributions are approximately 8% of gross salary for social security purposes. Employee contributions are around 3% of gross salary. These contributions fund pension, disability, and other social protection programs.

Taxation of foreign employees depends on residency status. Tax residents (generally those present in Angola for 183 days or more in a calendar year) are taxed on worldwide income. Non-residents are taxed only on Angola-source income. Foreign employees typically qualify for residency and face taxation on their full compensation.

Market Entry Considerations

Recommended Entry Strategies

Direct licensing represents the optimal market entry approach for operators with experience in regulated markets and sufficient capital to navigate the licensing process. Establishing an Angolan Sociedade Anónima, applying for an ISJ license, and building proprietary operations provides maximum control and long-term value capture.

Local partnerships, while not mandatory for ownership, can provide significant advantages in regulatory navigation, market understanding, and operational execution. Engaging experienced Angolan consultants, legal counsel, and potentially operational partners accelerates market entry and reduces execution risk despite not being legally required.

White label versus proprietary platform considerations depend on operator resources and strategic objectives. White label solutions enable faster market entry with lower upfront technology costs but sacrifice differentiation and long-term platform control. Proprietary platforms require greater investment but enable customization, unique player experiences, and avoidance of ongoing platform fees.

Technology infrastructure leveraging strategies should prioritize mobile optimization given Angola’s mobile-first internet access pattern. Cloud-based platforms with content delivery networks optimized for African users ensure acceptable performance despite infrastructure limitations. Integration with local payment methods (Multicaixa, Unitel Money, Afrimoney) is non-negotiable for market success.

Marketing and localization requirements demand Portuguese language across all touchpoints including website, mobile apps, customer service, marketing materials, and responsible gambling information. Localization extends beyond translation to include local sports coverage (Angolan football leagues, African competitions), culturally relevant promotions, and local currency display and transaction handling.

Payment provider selection should prioritize integration with dominant mobile money platforms (Unitel Money, Afrimoney, Multicaixa Express) as primary deposit and withdrawal methods. Card processing through Multicaixa network and major international schemes (Visa, Mastercard) serves the banked urban population. Partnerships with multiple payment providers ensures redundancy and maximum market coverage.

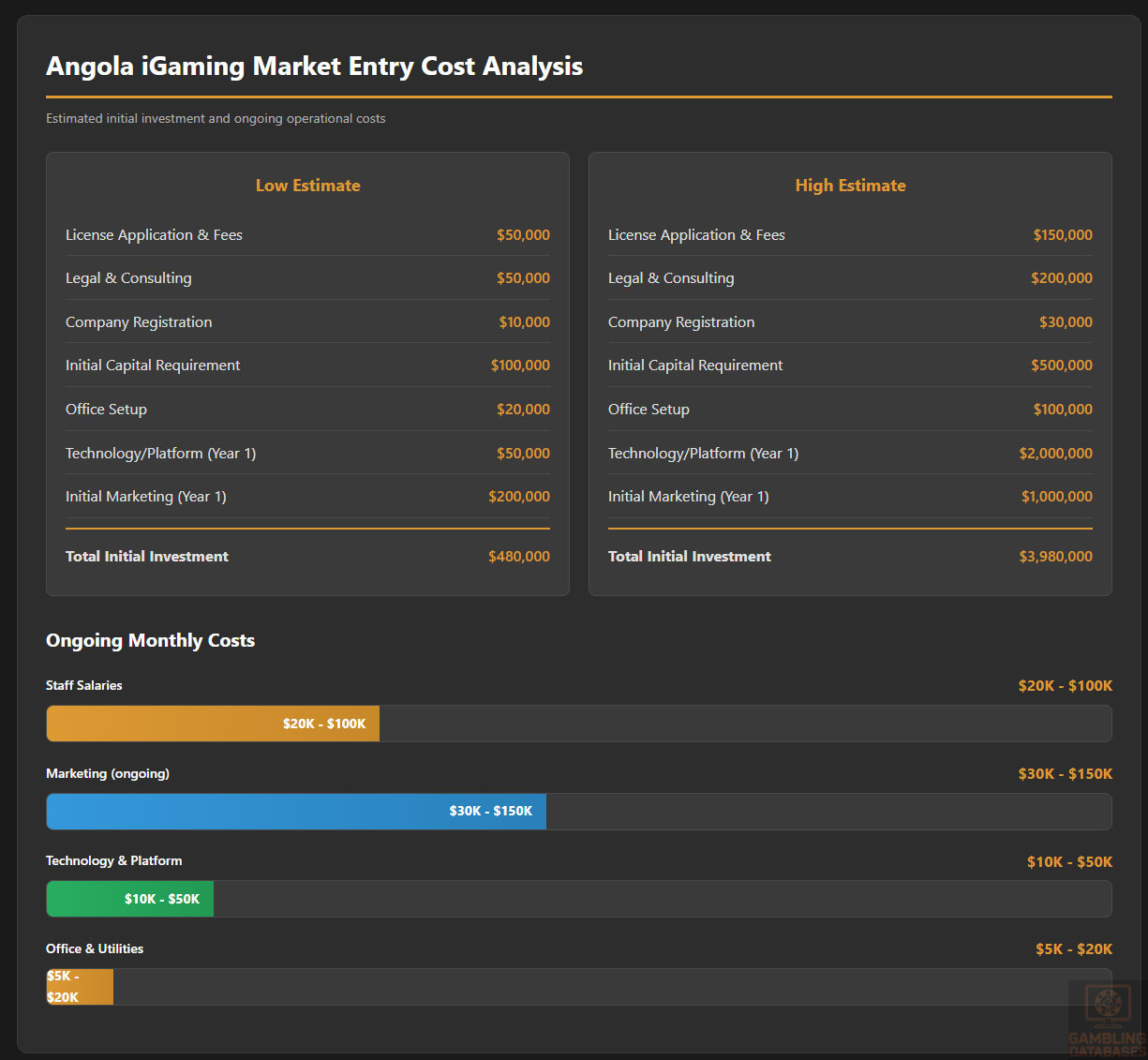

Typical Costs and Timelines

Initial setup investments breakdown into several major categories. License application and fees likely range from $50,000 to $150,000 or more including application fees, regulatory assessments, and compliance documentation. Legal and consulting fees for entity formation, license application, regulatory compliance, and ongoing counsel might total $50,000 to $200,000 depending on complexity.

Company registration costs including entity formation, notarization, registration fees, and initial capital deposit might total $10,000 to $30,000. Initial capital requirements mandated by gambling regulations could range from $100,000 to $500,000 or higher depending on license type and regulatory expectations for financial stability.

Office setup costs for physical presence in Angola including rent deposits, furniture, equipment, and telecommunications infrastructure might require $20,000 to $100,000 depending on location quality and office size. Technology and platform costs vary dramatically between white label ($50,000-200,000 annually) and proprietary development ($500,000-2,000,000+ for initial build).

Initial marketing budget for brand launch, player acquisition, promotional offers, and initial campaigns should be substantial given competitive pressures. Operators should budget $200,000 to $1,000,000+ for the first year of marketing depending on market share ambitions and competitive intensity.

Operational cost estimates include monthly staff salaries for local team (customer service, operations, compliance, management) potentially ranging from $20,000 to $100,000+ monthly depending on team size and seniority. Office rent and utilities in Luanda might cost $5,000 to $20,000 monthly for adequate space. Technology maintenance including platform fees, hosting, support, and development ranges from $10,000 to $50,000+ monthly.

Payment processing fees typically consume 2-4% of processed volumes depending on payment methods and negotiated rates. Marketing and customer acquisition costs on an ongoing basis might represent 30-50% of revenue in competitive markets. Total monthly operational costs could range from $100,000 to $500,000+ depending on scale ambitions.

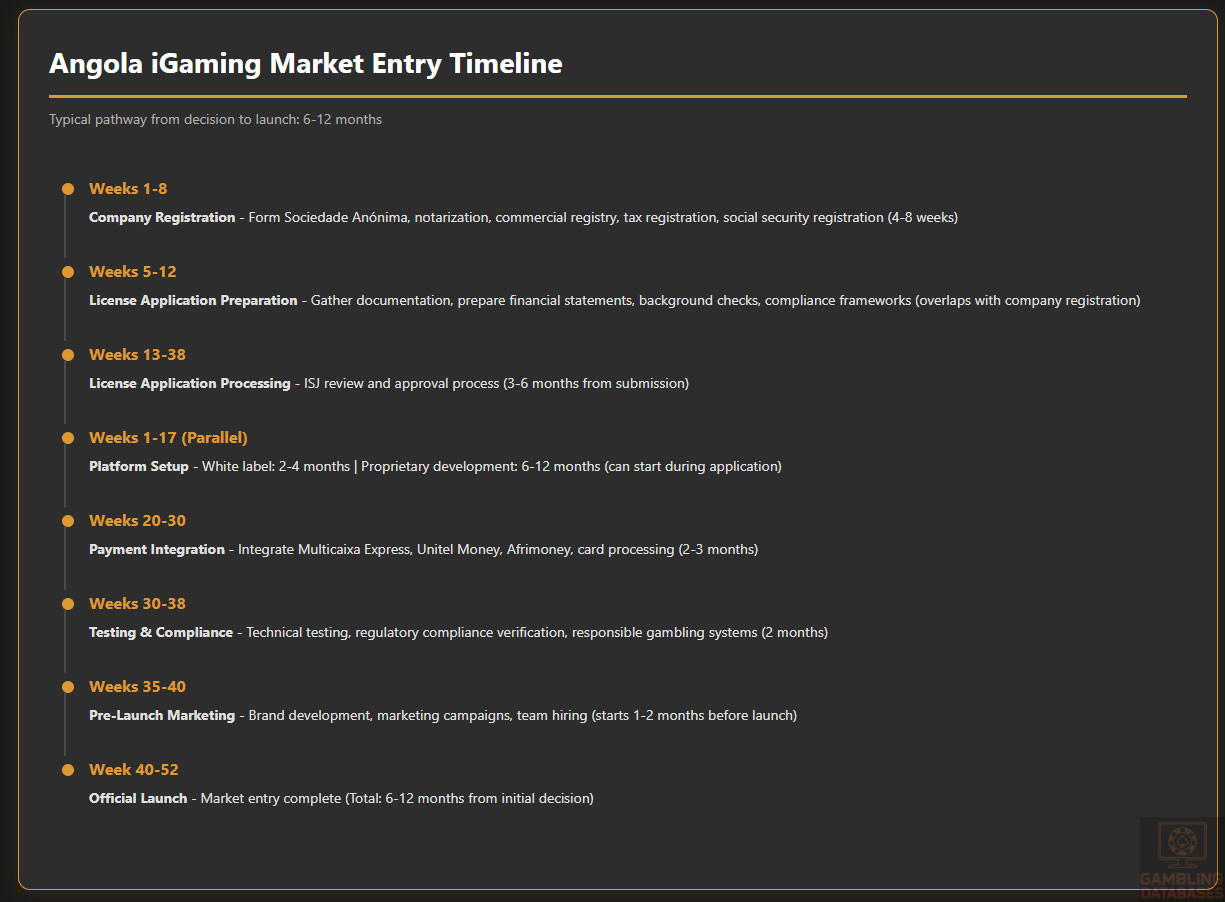

Timeline expectations for market entry begin with company registration requiring 4-8 weeks. License application processes may span 3-6 months from submission to approval depending on application quality and regulatory workload. Platform setup for white label solutions might require 2-4 months, while proprietary platform development could take 6-12 months. Total time from market entry decision to launch could range from 6-12 months for streamlined execution to 18-24 months for more complex implementations.