Antigua and Barbuda stands as one of the world’s pioneering online gambling jurisdictions, having established its regulatory framework in 1994 as the first nation to license internet gaming operations. The twin-island nation offers a mature, internationally recognized licensing regime that attracts operators seeking a reputable offshore jurisdiction with moderate taxation and streamlined compliance requirements.

Despite its small domestic market of approximately 98,000 residents, Antigua and Barbuda’s strategic positioning as a global iGaming hub makes it primarily attractive for operators targeting international markets rather than local consumer engagement.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Gambling Legal Status | Fully Legal and Regulated | Online and land-based permitted since 1994 |

| Regulatory Authority | Financial Services Regulatory Commission (FSRC) | Directorate of Offshore Gaming |

| Total Population (2025) | 98,179 | Annual growth rate: 0.8% |

| Median Age | 32.7 years | Younger demographic profile |

| Urban Population | 24.4% | Predominantly rural distribution |

| GDP Total (2025) | USD 1.89 billion | Tourism-dependent economy |

| GDP Per Capita | USD 19,250 | Upper-middle income classification |

| GDP Growth Forecast (2025-2027) | 3.2% CAGR | Post-pandemic recovery trajectory |

| Internet Penetration | 96.0% | Near-universal digital access |

| Mobile Penetration | 128% | Multiple devices per capita common |

| Smartphone Adoption | 87% | High mobile-first behavior |

| License Types Available | Interactive Gaming & Interactive Wagering | Covers casino, sports betting, poker |

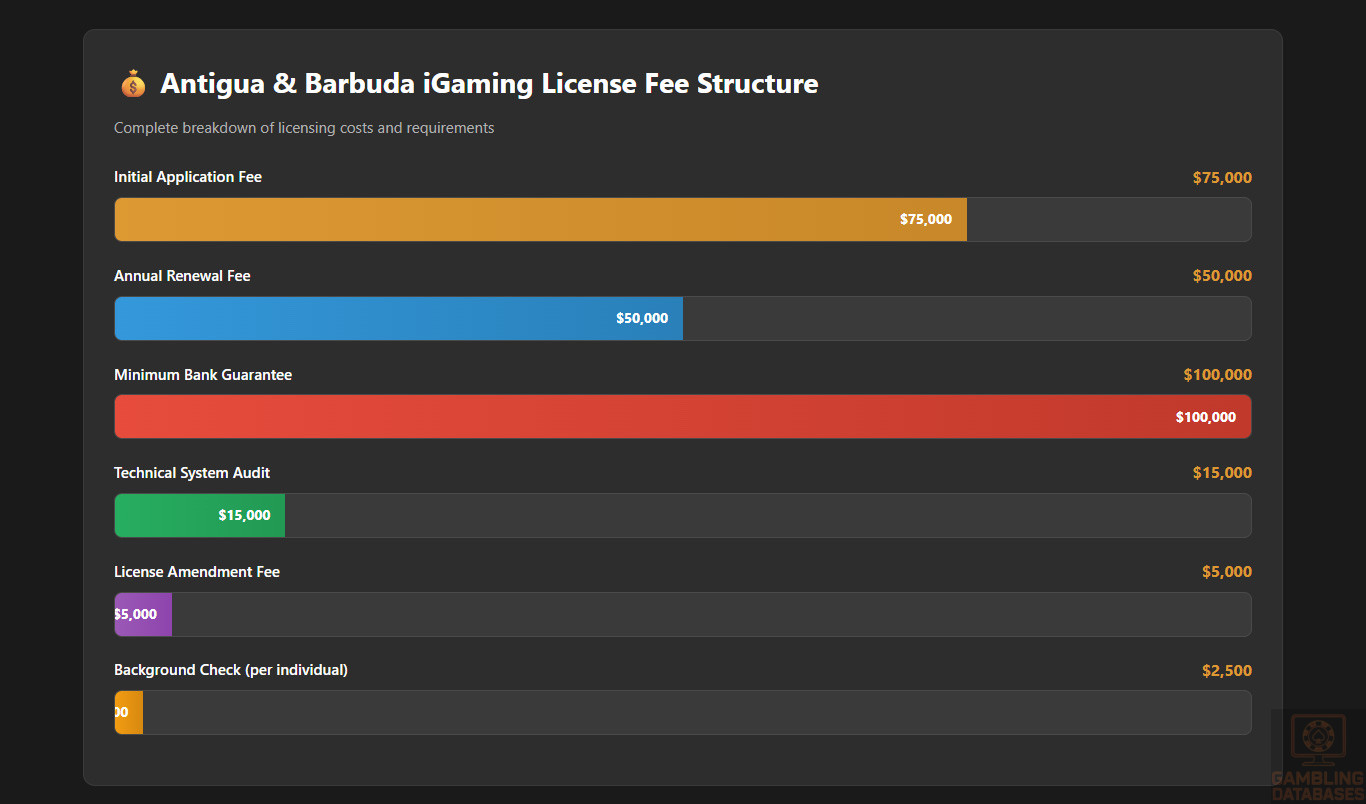

| Initial License Fee | USD 75,000 | One-time application fee |

| Annual License Renewal | USD 50,000 | Fixed annual fee structure |

| License Processing Time | 3-6 months | Subject to due diligence completion |

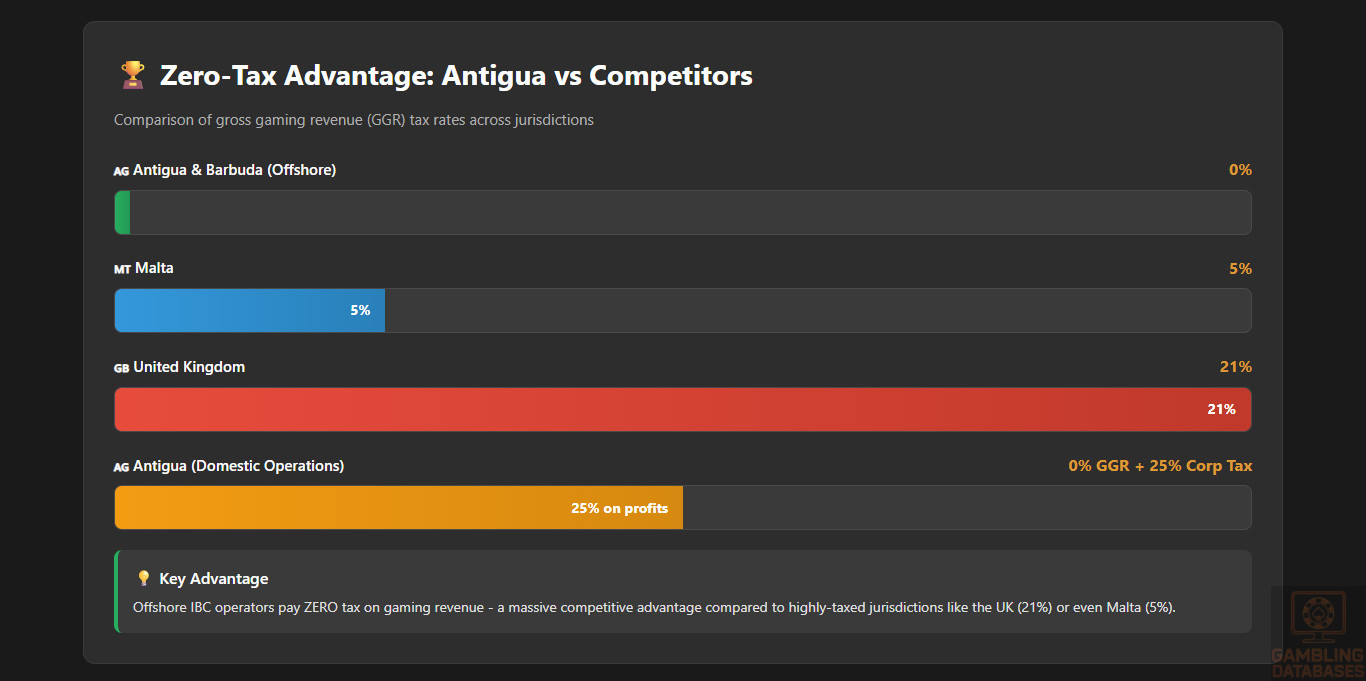

| Operator Tax Rate (GGR) | 0% | No gaming revenue tax for offshore operators |

| Corporate Income Tax | 0-25% | Offshore entities often exempt |

| Player Winnings Tax | 0% | No taxation on gambling winnings |

| Local Server Requirements | No | Flexible technical infrastructure |

| Local Office Requirements | No | No physical presence mandate |

| Minimum Capital Requirement | USD 100,000 | Operating capital/bank guarantee |

| Domestic iGaming Market Size (2025) | USD 3.2 million | Small local player base |

| Market Growth Rate (CAGR 2025-2028) | 4.5% | Limited by population size |

| Active Online Gamblers | ~2,800 (2.9% of population) | Low local market penetration |

| Average Revenue Per User (ARPU) | USD 950 annually | Moderate spending per player |

| Mobile Gaming Share | 78% | Dominant mobile preference |

| Licensed Operators (Est.) | 500+ globally targeting | Serving international markets |

| Average Monthly Broadband Speed | 45 Mbps download | Adequate for gaming applications |

| Primary Language | English (official) | No localization barrier |

| Currency | Eastern Caribbean Dollar (XCD) | Pegged to USD at 2.70:1 |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Antigua and Barbuda operates under a comprehensive gambling regulatory framework established through the Interactive Gaming and Interactive Wagering Act of 2007, which updated and consolidated the original 1994 legislation that positioned the nation as the world’s first online gambling jurisdiction. The regulatory structure permits both land-based and online gambling activities under clearly defined licensing categories, with the Financial Services Regulatory Commission serving as the primary oversight authority through its specialized Directorate of Offshore Gaming.

Land-Based Gambling Activities

The jurisdiction permits traditional casino operations, with the King’s Casino in St. John’s serving as the primary brick-and-mortar gaming venue offering table games, electronic gaming machines, and poker rooms. Sports betting is available through licensed retail outlets, though the land-based sports wagering market remains underdeveloped compared to online channels. Slot machine halls operate under separate licensing arrangements, primarily concentrated in tourist areas and integrated resort properties.

The land-based sector generates approximately USD 8.5 million annually in gross gaming revenue, representing a declining share of total gambling activity as consumer preferences shift toward digital platforms. Casino operations must maintain minimum capitalization of USD 500,000 and comply with stringent anti-money laundering protocols aligned with Caribbean Financial Action Task Force standards.

Online Gambling Framework

Digital gaming regulations encompass interactive gaming licenses covering casino-style games including slots, table games, and live dealer offerings, as well as interactive wagering licenses specifically designed for sports betting, race betting, and other event-based wagering products. The regulatory framework explicitly permits poker, bingo, lottery-style games, and fantasy sports contests under appropriate licensing categories.

Licensed Operators and Market Players

Antigua and Barbuda maintains licenses for over 500 international gaming operators, though fewer than 30 actively target the domestic Antiguan market due to its limited size. The jurisdiction has historically attracted major international brands seeking a reputable licensing base for global operations, though recent years have seen increased competition from jurisdictions like Malta, Curacao, and Gibraltar offering similar offshore licensing models.

| Operator Category | Number of Licenses | Primary Target Markets | Estimated Market Share (Domestic) |

|---|---|---|---|

| International Casino Operators | 350+ | Europe, Asia, Latin America | 65% |

| Sports Betting Platforms | 120+ | Caribbean, North America | 25% |

| Poker Networks | 40+ | Global player pools | 8% |

| Bingo/Lottery Operators | 15+ | UK, European markets | 2% |

The domestic market demonstrates high concentration, with three international operators controlling approximately 60% of local online gambling activity. Betway Caribbean, 888 Holdings subsidiary brands, and regional operator WINZ.io dominate local market share through aggressive marketing and cricket sponsorships. Local operators face significant challenges competing against well-capitalized international brands offering superior technology platforms and promotional budgets.

Entry strategies employed by successful operators typically involve establishing Antiguan licensing primarily for regulatory credibility while serving international markets, with minimal focus on the small domestic player base. White-label partnerships and B2B platform providers constitute a significant portion of licensees, leveraging Antigua’s streamlined approval process and cost-effective licensing structure.

Licensing Framework and Requirements

Application Process and Eligibility

The Financial Services Regulatory Commission’s Directorate of Offshore Gaming administers all gambling licenses through its offices located at High Street, St. John’s, Antigua. Prospective licensees must submit comprehensive applications including corporate documentation, business plans, technical system specifications, and detailed information on beneficial owners, directors, and key personnel. The regulatory authority can be contacted at [email protected] or +1-268-462-3070.

| Fee Type | Amount (USD) | Amount (XCD) | Payment Timing |

|---|---|---|---|

| Initial Application Fee | $75,000 | $202,500 | Upon submission |

| Annual Renewal Fee | $50,000 | $135,000 | Anniversary of license grant |

| License Amendment Fee | $5,000 | $13,500 | Per amendment request |

| Background Check Fee (per individual) | $2,500 | $6,750 | With application |

| Technical System Audit | $15,000 | $40,500 | Initial certification |

| Minimum Bank Guarantee | $100,000 | $270,000 | Maintained throughout license period |

Financial requirements mandate minimum capitalization of USD 100,000 in the form of a bank guarantee or surety bond maintained with an approved financial institution for the duration of the license period. Applicants must demonstrate financial stability through audited financial statements covering the previous three years, bank references, and proof of sufficient operational funding to sustain six months of operations without revenue.

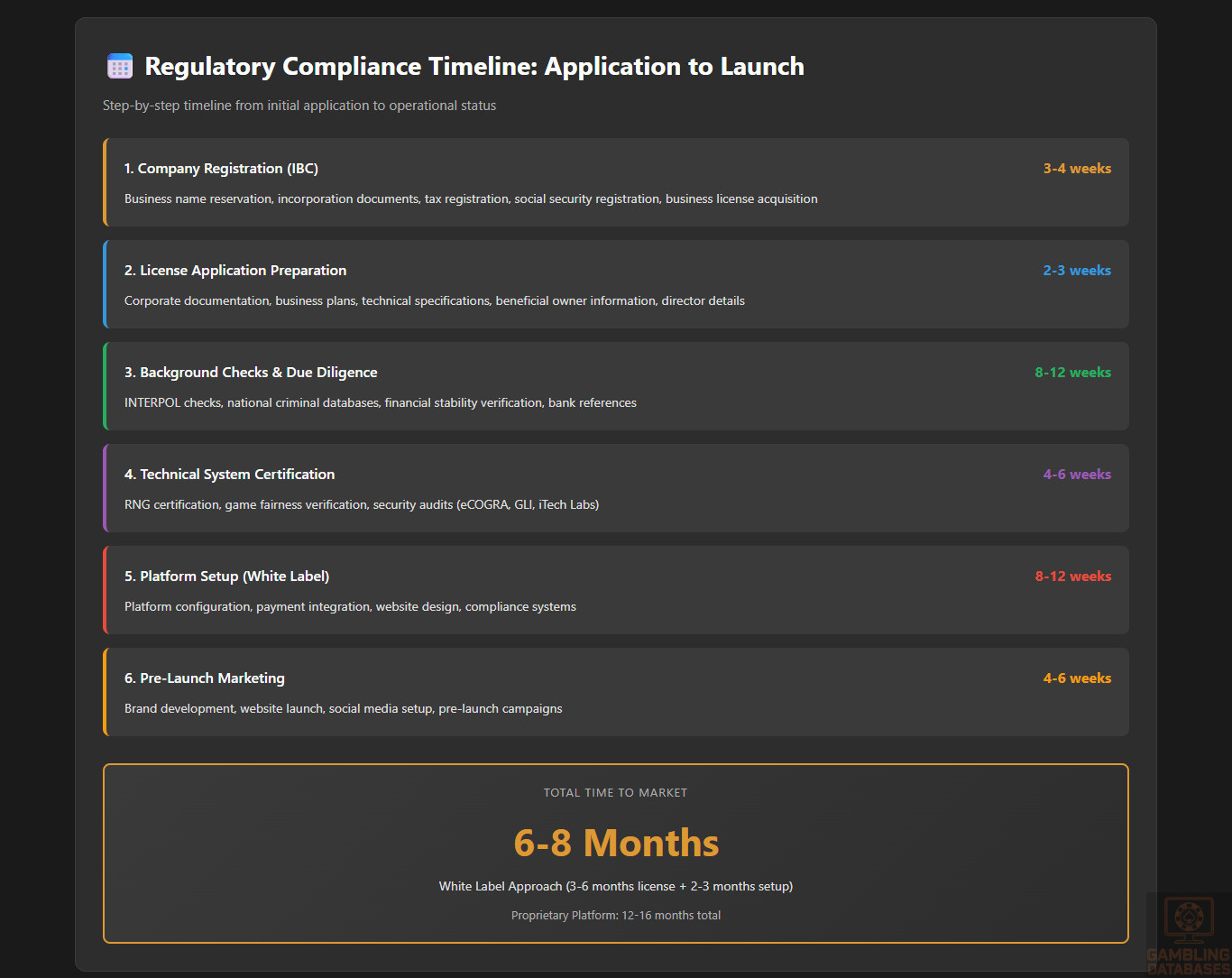

Technical standards require gaming platforms to achieve certification from approved testing laboratories including eCOGRA, GLI, iTech Labs, or Gaming Associates. Random number generator certification, game fairness verification, and security infrastructure audits must be completed before license approval. Background checks conducted through INTERPOL and national criminal databases typically require 8-12 weeks for completion.

The application timeline spans 3-6 months from initial submission to license approval, contingent on completeness of documentation and satisfactory background investigations. Expedited processing is not available, though responsive communication with regulators and pre-submission consultations can streamline the process. Application fees are non-refundable regardless of approval outcome.

Local Presence and Operational Requirements

Antigua and Barbuda imposes no mandatory physical presence requirements for offshore gaming licensees, distinguishing it from jurisdictions like Malta or Gibraltar that mandate local offices and staff. Operators may maintain virtual operations, hosting servers in third-party jurisdictions and managing operations remotely, provided they maintain reliable communication channels with the regulatory authority.

Domain registration requirements do not mandate .ag country code top-level domains, permitting operators to utilize any internationally recognized domain extensions. Server location flexibility allows operators to host gaming platforms anywhere globally, though many choose cloud infrastructure providers with Caribbean presence for latency optimization when serving regional markets.

Foreign ownership faces no restrictions, with 100% international ownership permitted across all license categories. No local partnership requirements or mandatory joint venture structures exist, though voluntary partnerships with Antiguan entities can provide operational advantages in banking relationships and local market knowledge. Personnel requirements specify only that key individuals undergo background checks; no minimum local employment quotas apply.

Compliance Obligations and Monitoring

Player Protection and Identification

Age verification requirements mandate strict 18+ enforcement, requiring operators to verify player ages before permitting real-money gambling activity. Acceptable verification methods include government-issued identification documents, passport verification, national ID card authentication, or approved third-party age verification services maintaining integration with government databases.

| Requirement Category | Specific Obligations | Implementation Timeline |

|---|---|---|

| Customer Identification | Full name, date of birth, residential address, government ID | Before first withdrawal or at $2,000 cumulative deposits |

| Enhanced Due Diligence | Source of funds verification for deposits exceeding $10,000 | Within 72 hours of transaction |

| PEP Screening | Politically exposed persons database checks | At account registration |

| Transaction Monitoring | Automated alerts for suspicious patterns exceeding $5,000 | Real-time monitoring required |

| Record Retention | All transaction records and communications | Minimum 7 years |

| SAR Filing | Suspicious Activity Reports to Financial Intelligence Unit | Within 15 days of identification |

Responsible gambling measures mandated by regulation include self-exclusion system availability permitting players to block access for periods ranging from 6 months to permanent exclusion, reality check notifications displaying session duration and losses at 60-minute intervals, and mandatory deposit limit options allowing players to cap daily, weekly, or monthly funding amounts. Operators must display responsible gambling information prominently, including links to GamCare, Gambling Therapy, and regional support resources.

Session time limits and loss limits are not mandated by regulation but represent industry best practices increasingly expected by the Directorate of Offshore Gaming during compliance reviews. Operators must maintain accessible responsible gambling policies detailing available player protection tools, with annual compliance attestations submitted to regulatory authorities.

Financial Monitoring and Reporting

Transaction monitoring systems must flag suspicious patterns including rapid deposit-withdrawal cycles suggesting money laundering, bet structuring to avoid reporting thresholds, unusually large transactions inconsistent with player history, and coordinated activities across multiple accounts. Operators must maintain automated monitoring capable of generating alerts for manual review within 24 hours of suspicious activity detection.

Reporting requirements mandate quarterly financial statements submitted within 30 days of quarter-end, detailing gross gaming revenue, player deposits and withdrawals, outstanding player liabilities, and operational expenses. Annual audited financial statements prepared by approved accounting firms must be filed within 90 days of fiscal year-end. Monthly transaction reports summarizing deposit volumes, withdrawal processing, and currency exchange activities are required for anti-money laundering oversight.

Audit and inspection procedures authorize the Directorate of Offline Gaming to conduct unannounced platform audits, financial record reviews, and technical system inspections. Operators must provide remote access credentials for regulatory monitoring systems and respond to information requests within 48 hours. Data retention requirements mandate preserving all gaming transactions, player communications, financial records, and marketing materials for seven years in readily accessible formats.

Taxation Structure and Financial Obligations

Player Taxation

Antigua and Barbuda imposes zero taxation on gambling winnings for players, creating an attractive environment for high-stakes bettors and eliminating administrative burdens associated with withholding and winner reporting. No tax declaration requirements exist for domestic players regardless of winning amounts, and no withholding obligations apply to operators disbursing prizes or jackpots.

This player-friendly tax environment contrasts sharply with jurisdictions like the United States where gambling winnings face federal income tax rates up to 37%, or France where players pay social charges on poker winnings. The absence of player taxation removes friction from the gambling experience and eliminates compliance complexity for operators serving Antiguan residents.

Operator Taxation

The operator taxation structure represents Antigua and Barbuda’s primary competitive advantage, with offshore gaming licensees paying zero gross gaming revenue tax, zero net gaming revenue tax, and zero turnover-based taxation on gambling operations. This contrasts dramatically with jurisdictions like the United Kingdom imposing 21% point-of-consumption tax or Malta charging 5% on gaming revenue.

| Tax/Fee Category | Rate/Amount | Calculation Basis | Payment Frequency |

|---|---|---|---|

| Gaming Revenue Tax (GGR) | 0% | Gross Gaming Revenue | N/A |

| Corporate Income Tax (Offshore) | 0% | Net Profits | N/A |

| Corporate Income Tax (Domestic) | 25% | Net Profits (if serving local market) | Quarterly |

| Annual License Fee | $50,000 USD | Flat fee per license | Annual |

| Withholding Tax (Dividends) | 0% | Dividend distributions | N/A |

| Withholding Tax (Interest) | 0% | Interest payments | N/A |

| Withholding Tax (Royalties) | 0% | Technology licensing fees | N/A |

| VAT/Sales Tax | 0% | Gambling services | N/A |

Corporate income tax applies at 25% for companies maintaining substantial local operations or primarily serving the domestic Antiguan market, though most offshore licensees structure operations to qualify for tax exemption by serving exclusively international customers. No distinction exists between different gambling verticals, with casino, sports betting, poker, and bingo operations all eligible for identical tax treatment.

License renewal fees of USD 50,000 annually represent the primary ongoing cost for offshore operators, providing predictable expense structures enabling accurate financial modeling. No variable licensing fees based on revenue thresholds or player volumes exist, creating significant cost advantages for high-volume operators compared to percentage-based fee structures in competing jurisdictions.

Gambling Market Financial Performance

The domestic Antiguan gambling market generated approximately USD 11.7 million in total gross gaming revenue during 2024, comprising USD 8.5 million from land-based operations and USD 3.2 million from online channels. Player payouts totaled USD 9.8 million, resulting in USD 1.9 million in net gaming revenue after prizes. Tax revenues collected by the Antiguan government from gambling activities reached approximately USD 4.2 million, derived primarily from annual license fees rather than gaming revenue taxation.

| Year | Total GGR (USD Million) | Land-Based GGR | Online GGR | YoY Growth | Tax Revenue |

|---|---|---|---|---|---|

| 2020 | $8.2 | $5.8 | $2.4 | -22% (pandemic impact) | $3.8 |

| 2021 | $9.5 | $6.7 | $2.8 | +15.9% | $3.9 |

| 2022 | $10.8 | $7.6 | $3.2 | +13.7% | $4.0 |

| 2023 | $11.3 | $8.1 | $3.2 | +4.6% | $4.1 |

| 2024 | $11.7 | $8.5 | $3.2 | +3.5% | $4.2 |

Revenue distribution analysis reveals land-based casinos contributing 73% of total gambling revenue, online sports betting representing 18%, online casino games accounting for 7%, and lottery products comprising 2%. The growth trajectory demonstrates post-pandemic recovery through 2022, followed by market maturation with modest single-digit growth rates reflecting population constraints and limited tourism expansion.

Year-over-year growth trends indicate online gambling channels growing at 6-8% annually while land-based revenue expands at 2-3%, driven by gradual digital migration and improved mobile platform accessibility. Market projections forecast total gambling revenue reaching USD 13.5 million by 2028, representing a compound annual growth rate of 3.6% constrained by the jurisdiction’s small population base.

Advertising and Marketing Restrictions

Antigua and Barbuda maintains relatively permissive advertising regulations compared to restrictive European jurisdictions, permitting gambling advertisements across television, radio, print media, outdoor billboards, and digital channels including social media and search engine marketing. Television and radio advertising face no time-of-day restrictions, though broadcasters often voluntarily avoid placement during children’s programming.

Content restrictions prohibit marketing materials suggesting gambling as a solution to financial problems, portraying excessive gambling as socially acceptable, targeting minors through cartoon characters or youth-oriented themes, or making misleading claims about winning probabilities. All advertisements must include responsible gambling messaging and display the operator’s license number issued by the Directorate of Offshore Gaming.

| Channel | Regulatory Status | Content Requirements | Restrictions |

|---|---|---|---|

| Television | Permitted | Responsible gambling disclaimer, 18+ notice | No targeting of children’s programming |

| Radio | Permitted | Verbal responsible gambling message | Recommended avoidance during school hours |

| Print Media | Permitted | License number display, age restrictions | No placement in youth publications |

| Outdoor Billboards | Permitted | 18+ symbology required | Not within 200m of schools |

| Online Display Ads | Permitted | Age-gated content, responsible gambling links | No retargeting of self-excluded players |

| Social Media | Permitted | Platform age restrictions enabled | No influencer marketing to under-18 audiences |

| Email Marketing | Permitted | Unsubscribe option, responsible gambling info | Frequency limits recommended (max 3/week) |

| SMS Marketing | Permitted with consent | Opt-in required, easy opt-out | No unsolicited messaging |

Promotional limitations impose no regulatory caps on bonus amounts or wagering requirements, though operators must clearly disclose all terms and conditions associated with promotional offers including minimum odds requirements, time limitations, and withdrawal restrictions. Bonus abuse prevention measures and reasonable playthrough requirements are considered acceptable industry practices without specific regulatory mandates.

Sponsorship regulations permit gambling operators to sponsor sporting events, cricket teams, football clubs, and entertainment venues without significant restrictions. The West Indies cricket team has historically featured gambling sponsorships, and regional football leagues actively seek gaming operator partnerships. Cultural events including Carnival celebrations and music festivals regularly feature gambling sponsor branding.

Affiliate marketing operates without specific regulatory oversight, though operators remain responsible for ensuring affiliate partners comply with advertising content standards and age-targeting restrictions. Affiliate agreements must include contractual provisions requiring compliance with Antiguan advertising standards, and operators face liability for non-compliant affiliate marketing materials.

Recent Regulatory Changes and Their Impact

The most significant regulatory development occurred in March 2023 when the Financial Services Regulatory Commission announced enhanced due diligence requirements for beneficial ownership disclosure, mandating operators to identify and verify all individuals holding 10% or greater ownership stakes, reduced from the previous 25% threshold. This change aligned Antigua with international Financial Action Task Force recommendations but increased compliance costs for operators with complex corporate structures.

In August 2023, amendments to responsible gambling requirements introduced mandatory session time notifications at 60-minute intervals, requiring operators to display on-screen messages showing time elapsed and net wins/losses. While not mandating forced logout or session termination, the regulation increased technical implementation costs estimated at USD 15,000-25,000 for platform modifications.

January 2024 saw the introduction of enhanced reporting requirements for cryptocurrency transactions, obligating operators accepting Bitcoin, Ethereum, or other digital assets to maintain detailed blockchain address records and implement enhanced monitoring for transactions exceeding USD 5,000 equivalent. The regulation responded to international pressure regarding cryptocurrency’s money laundering risks but created additional compliance overhead for operators serving crypto-preferred markets.

No player taxation changes occurred during the 2022-2024 period, with the government maintaining its zero-tax policy on gambling winnings. License fees remained stable at USD 50,000 annually without inflation adjustments, providing cost certainty for operators. However, informal regulatory guidance issued in July 2024 suggested potential future consideration of point-of-consumption taxation for operators deriving substantial revenue from Antiguan residents, though no formal proposals have been published.

Enforcement Mechanisms and Penalties

The Directorate of Offshore Gaming maintains authority to impose administrative penalties ranging from written warnings for minor infractions to license suspension or revocation for serious violations. Financial penalties for compliance breaches typically range from USD 10,000 for first-time documentation failures to USD 100,000 for repeated or egregious violations involving player fund mismanagement or anti-money laundering failures.

| Violation Category | First Offense | Second Offense | Third Offense |

|---|---|---|---|

| Late Reporting | Warning + $5,000 fine | $15,000 fine | $30,000 fine + license review |

| KYC/AML Non-Compliance | $25,000 fine + corrective action plan | $75,000 fine + mandatory audit | License suspension pending remediation |

| Underage Gambling Incident | $50,000 fine + enhanced controls | $150,000 fine + 30-day suspension | License revocation |

| Player Fund Mismanagement | $100,000 fine + segregation audit | License suspension + restitution | Permanent license revocation |

| Advertising Violations | Warning + material removal | $10,000 fine | $25,000 fine + advertising ban (30 days) |

| Technical System Failures | Corrective action required | $20,000 fine + independent audit | License suspension until remediation |

| Serving Prohibited Markets | $50,000 fine + geo-blocking verification | $150,000 fine + market exit mandate | License revocation + legal action |

Recent enforcement actions include a June 2024 case where an operator received a USD 75,000 penalty for inadequate customer due diligence on high-value transactions, demonstrating increased regulatory scrutiny of anti-money laundering compliance. In October 2023, a sports betting operator faced 60-day license suspension for processing transactions from players in prohibited United States markets, highlighting strict enforcement of geo-blocking requirements.

ISP blocking mechanisms exist but are rarely deployed, with the government preferring to work directly with licensed operators rather than implementing domain blocks. Payment processor restrictions represent the primary enforcement mechanism for unlicensed operators, with Antiguan authorities coordinating with international payment networks to identify and restrict transactions with unauthorized gambling sites.

Criminal penalties for operating unlicensed gambling services include fines up to XCD 500,000 (USD 185,000) and imprisonment for up to five years for individuals convicted of organizing illegal gambling operations. However, prosecutions remain rare, with regulatory authorities prioritizing administrative remedies and license revocations over criminal proceedings except in cases involving fraud or money laundering.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

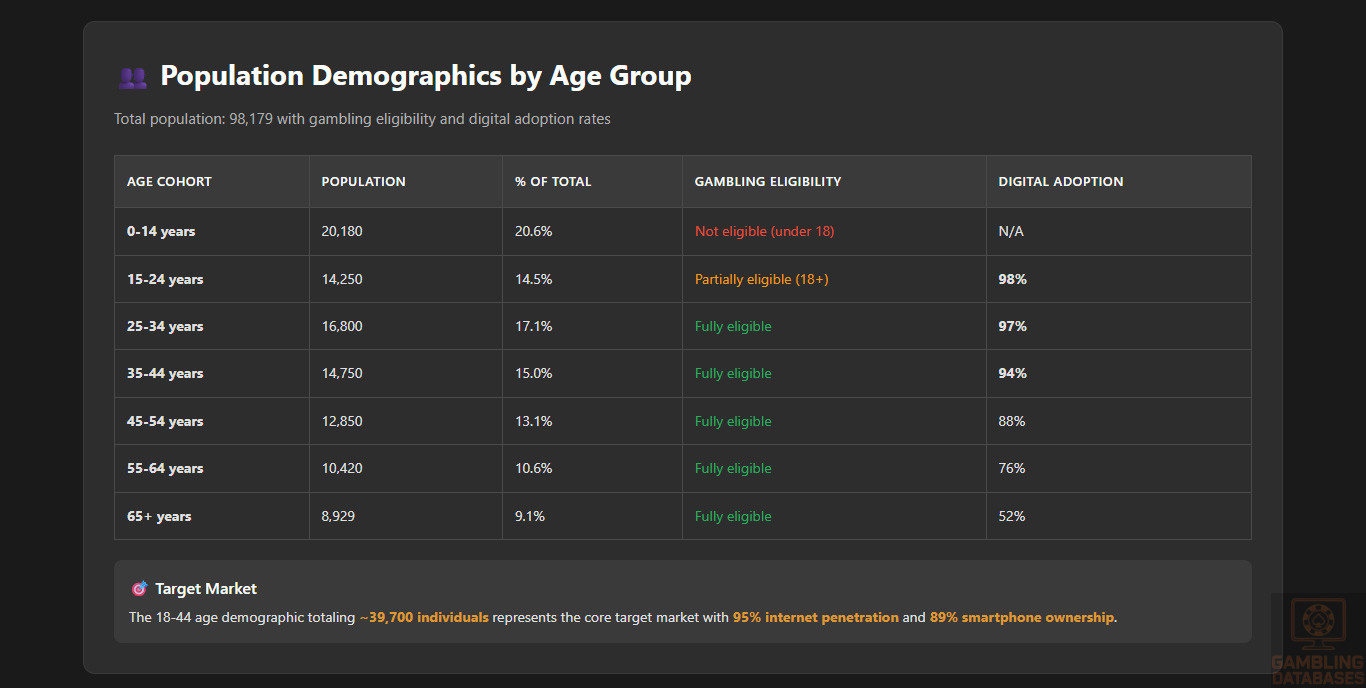

Antigua and Barbuda’s total population of 98,179 as of 2025 represents modest growth from 97,400 in 2023, reflecting an annual increase of approximately 0.8% driven primarily by immigration rather than natural population growth. The demographic profile skews relatively young with a median age of 32.7 years, creating a population structure favorable for digital service adoption but constrained by absolute numbers limiting market scale.

| Age Cohort | Population Count | Percentage of Total | Gambling Eligibility | Digital Adoption Rate |

|---|---|---|---|---|

| 0-14 years | 20,180 | 20.6% | Not eligible (under 18) | N/A |

| 15-24 years | 14,250 | 14.5% | Partially eligible (18+) | 98% |

| 25-34 years | 16,800 | 17.1% | Fully eligible | 97% |

| 35-44 years | 14,750 | 15.0% | Fully eligible | 94% |

| 45-54 years | 12,850 | 13.1% | Fully eligible | 88% |

| 55-64 years | 10,420 | 10.6% | Fully eligible | 76% |

| 65+ years | 8,929 | 9.1% | Fully eligible | 52% |

The 18-44 age demographic totaling approximately 39,700 individuals represents the core target market for online gambling services, combining legal eligibility with high digital literacy and disposable income availability. This cohort demonstrates 95% internet penetration and 89% smartphone ownership, creating favorable conditions for mobile-first gambling products despite limited absolute market size.

Gender distribution shows relative balance at 48.2% male and 51.8% female, with life expectancy of 74.8 years for males and 79.2 years for females. Gender participation rates in gambling activities skew male-dominant at approximately 68% of active gamblers, though female participation in lottery and bingo products approaches parity at 45-48% of players.

Urban versus rural distribution presents unique characteristics, with only 24.4% of the population classified as urban despite St. John’s serving as the primary population center with approximately 22,000 residents. The predominantly rural distribution pattern creates infrastructure challenges for land-based gambling venue accessibility while simultaneously driving online gambling adoption due to geographic convenience factors.

Geographic Distribution

Population concentration centers around St. John’s on Antigua island, hosting 22.4% of the national population, followed by All Saints with 6,800 residents, Liberta with 2,800, Potter’s Village with 2,400, and Bolans with 1,900 inhabitants. Barbuda island maintains a sparse population of approximately 1,800 residents concentrated in Codrington, the island’s only significant settlement.

| City/Town | Population | Internet Penetration | 4G Coverage | Land-Based Gambling Venues |

|---|---|---|---|---|

| St. John’s | 22,000 | 98% | 100% | 1 casino, 4 betting shops |

| All Saints | 6,800 | 96% | 98% | 1 betting shop |

| Liberta | 2,800 | 94% | 95% | None |

| Potter’s Village | 2,400 | 95% | 97% | None |

| Bolans | 1,900 | 92% | 94% | None |

| Codrington (Barbuda) | 1,800 | 88% | 85% | None |

Regional economic differences manifest primarily between Antigua and Barbuda islands, with Antigua hosting 98.2% of economic activity and maintaining superior infrastructure development. Tourism industry concentration in coastal resort areas creates income disparities, with resort-adjacent communities demonstrating 15-20% higher household incomes than interior agricultural regions.

Internet access geographic patterns show near-universal coverage in St. John’s and major towns at 96-98% penetration, declining to 88-92% in rural areas and remote coastal settlements. Mobile network coverage compensates for fixed broadband limitations, with 4G mobile internet reaching 94% of the population and providing primary connectivity for rural residents.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Antigua and Barbuda’s economy generated USD 1.89 billion in gross domestic product during 2024, translating to per capita GDP of USD 19,250 positioning the nation in the upper-middle income category according to World Bank classifications. The economic structure relies heavily on tourism services contributing 58% of GDP, followed by financial services at 18%, construction at 12%, and agriculture representing just 2.3% of economic output.

GDP growth forecasts project 3.2% compound annual growth rate through 2027, driven by tourism sector recovery following pandemic disruptions and expanding yachting services for ultra-high-net-worth visitors. However, vulnerability to hurricane damage and climate change impacts introduces volatility risks, with major storms capable of reducing GDP by 5-10% in affected years as demonstrated by Hurricane Irma’s 2017 impact.

| Metric | 2023 | 2024 | 2025 | 2026 (Forecast) | 2027 (Forecast) | 2028 (Forecast) |

|---|---|---|---|---|---|---|

| GDP Total (USD Billion) | $1.79 | $1.85 | $1.89 | $1.96 | $2.02 | $2.09 |

| GDP Per Capita (USD) | $18,400 | $18,900 | $19,250 | $19,850 | $20,400 | $21,000 |

| GDP Growth Rate | 4.8% | 3.4% | 2.9% | 3.2% | 3.1% | 3.3% |

| Unemployment Rate | 8.2% | 7.8% | 7.5% | 7.2% | 7.0% | 6.8% |

| Inflation Rate | 3.8% | 3.2% | 2.9% | 2.8% | 2.7% | 2.8% |

| Average Monthly Wage (XCD) | $3,680 | $3,820 | $3,940 | $4,080 | $4,220 | $4,370 |

Employment rates demonstrate gradual improvement with unemployment declining from pandemic peaks of 12.4% in 2020 to current levels of 7.5% in 2025, approaching pre-pandemic norms of 6.5-7.0%. Tourism sector employment represents 43% of the workforce, creating seasonal volatility with higher employment during November-April high season and 8-12% job reductions during May-October low season.

Wage levels average XCD 3,940 monthly (USD 1,460) across all sectors, with tourism and hospitality workers earning approximately XCD 2,800 (USD 1,037), financial services professionals commanding XCD 6,500 (USD 2,407), and government employees averaging XCD 4,200 (USD 1,556). The citizenship-by-investment program brings high-net-worth individuals who elevate average income statistics but represent less than 2% of residents.

Income and Wealth Distribution

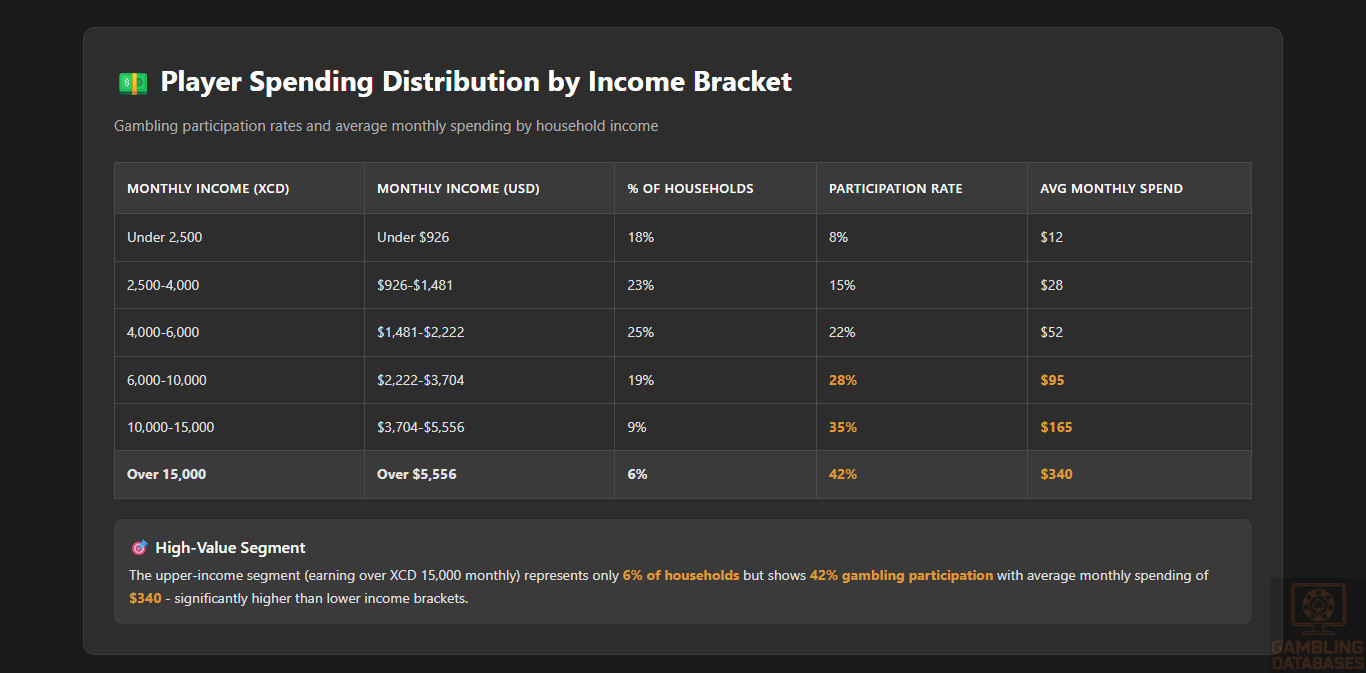

Average household income reaches XCD 7,850 monthly (USD 2,907) when combining all income earners per household, while median household income of XCD 6,200 (USD 2,296) provides a more representative measure of typical living standards. The gap between mean and median reflects income inequality driven by high-earning tourism industry executives and citizenship-by-investment residents skewing averages upward.

Income inequality measured by Gini coefficient stands at 0.42, indicating moderate inequality levels comparable to United States (0.41) but more equitable than many Caribbean neighbors like Jamaica (0.45) or Saint Lucia (0.51). The middle class defined as households earning XCD 4,000-10,000 monthly comprises approximately 42% of the population, representing stable consumers with discretionary spending capacity for entertainment including gambling.

| Monthly Income Bracket (XCD) | Monthly Income (USD) | % of Households | Gambling Participation Rate | Avg Monthly Gambling Spend (USD) |

|---|---|---|---|---|

| Under 2,500 | Under $926 | 18% | 8% | $12 |

| 2,500-4,000 | $926-$1,481 | 23% | 15% | $28 |

| 4,000-6,000 | $1,481-$2,222 | 25% | 22% | $52 |

| 6,000-10,000 | $2,222-$3,704 | 19% | 28% | $95 |

| 10,000-15,000 | $3,704-$5,556 | 9% | 35% | $165 |

| Over 15,000 | Over $5,556 | 6% | 42% | $340 |

Disposable income trends show gradual improvement with real disposable income growing 2.1% annually after adjusting for inflation, providing incremental increases in discretionary spending capacity. Consumer spending patterns allocate approximately 32% of household budgets to housing, 24% to food and beverages, 12% to transportation, 8% to utilities, and 6% to entertainment and recreation within which gambling represents a subset.

The upper-income segment earning over XCD 15,000 monthly demonstrates gambling participation rates exceeding 40% with average monthly spending of USD 340, creating a high-value player segment despite representing only 6% of households. Conversely, lower-income households under XCD 4,000 monthly show participation rates below 15% and minimal spending, suggesting gambling remains predominantly a middle and upper-class activity.

Market Size and Growth Projections

The current iGaming market revenue totaling USD 3.2 million annually reflects a mature but constrained market limited by population size rather than regulatory restrictions or consumer reluctance. Online casino games contribute USD 2.1 million, sports betting generates USD 950,000, and poker accounts for USD 150,000 of total online gambling revenue.

Historical revenue growth demonstrates 18% annual increases during 2020-2022 driven by pandemic-related digitalization and increased time spent at home, followed by growth moderation to 4-6% annually during 2023-2024 as the market reaches saturation levels among digitally-engaged consumers. Land-based gambling revenue has declined 2-3% annually as players migrate to more convenient online platforms.

| Segment | 2025 Revenue | 2027 Forecast | 2030 Forecast | CAGR 2025-2030 |

|---|---|---|---|---|

| Online Casino (Slots) | $1.45M | $1.62M | $1.88M | 5.3% |

| Online Casino (Table Games) | $650K | $710K | $810K | 4.5% |

| Sports Betting | $950K | $1.08M | $1.28M | 6.1% |

| Poker | $150K | $155K | $165K | 1.9% |

| Total Online | $3.20M | $3.57M | $4.14M | 5.3% |

| Land-Based Casinos | $8.50M | $8.75M | $9.20M | 1.6% |

| Total Market | $11.70M | $12.32M | $13.34M | 2.7% |

Revenue forecasts project the online gambling market reaching USD 4.14 million by 2030, representing a compound annual growth rate of 5.3% driven primarily by increased smartphone penetration, improved payment infrastructure, and generational shifts toward digital entertainment. Sports betting demonstrates the strongest growth potential at 6.1% CAGR, benefiting from cricket’s cultural significance and expanding live betting features.

Projected user base growth anticipates active online gamblers increasing from current levels of 2,800 to approximately 3,650 by 2030, representing market penetration expansion from 2.9% to 3.6% of the total population. The growth reflects both demographic aging bringing more individuals into the 18+ eligible category and gradual adoption among previously non-gambling households.

Average Revenue Per User currently stands at USD 950 annually across all online gambling activities, with casino players demonstrating higher ARPU of USD 1,240 compared to sports bettors averaging USD 680 annually. ARPU projections forecast modest increases to USD 1,050 by 2030, driven by inflation and gradual increases in betting intensity rather than dramatic behavioral changes.

Market penetration rates of 2.9% for online gambling and 8.5% for any gambling activity (including land-based and lottery) remain substantially below regional comparators like Barbados achieving 12% gambling participation or Trinidad and Tobago reaching 15%. The penetration gap suggests either cultural factors limiting gambling acceptance or successful competition from informal unregulated operators not captured in official statistics.

Online versus land-based revenue split currently favors land-based channels at 73% of total gambling revenue, though this ratio is shifting toward digital channels at approximately 2 percentage points annually. By 2030, projections suggest online gambling representing 31% of total revenue compared to 27% in 2025, though land-based casinos will maintain majority share due to tourist visitation and the social experience factor.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy rates reach 99% for the overall population aged 15 and above, with gender parity at 99% for both males and females reflecting successful universal primary education policies. Educational attainment shows 98% primary education completion, 85% secondary education completion, and 22% tertiary education completion including university degrees, professional certifications, and vocational training.

Digital literacy indicators demonstrate strong foundation skills, with 94% of adults aged 18-65 reporting ability to use smartphones, computers, and internet services for communication, banking, and e-commerce activities. The education system incorporates information technology curriculum from primary levels, creating baseline digital competency among younger cohorts entering the workforce and consumer markets.

| Age Group | Secondary Education % | Tertiary Education % | Digital Literacy % | English Fluency % |

|---|---|---|---|---|

| 18-24 | 94% | 18% | 99% | 100% |

| 25-34 | 89% | 26% | 98% | 100% |

| 35-44 | 85% | 24% | 96% | 100% |

| 45-54 | 78% | 19% | 89% | 100% |

| 55-64 | 71% | 15% | 78% | |

| 65+ | 64% | 12% | 54% | 99% |

Workforce skill levels concentrate in tourism and hospitality services, with approximately 43% of employed individuals working in customer-facing roles requiring interpersonal communication, basic financial literacy, and increasingly digital point-of-sale system operation. Financial services employment representing 12% of the workforce demands higher educational credentials, with most positions requiring tertiary education and professional certifications.

Technology adoption readiness scores highly among the 18-44 demographic, with 96-99% digital literacy enabling seamless engagement with online gambling platforms, digital payment systems, and mobile applications. Older demographics aged 55+ demonstrate lower digital comfort levels at 54-78% literacy, though this cohort shows less gambling propensity regardless of channel.

English language proficiency reaches 100% among native-born residents, with English serving as the official language, primary education medium, and dominant communication language in all contexts. This eliminates localization requirements for gambling operators, enabling deployment of standard English-language platforms without translation costs or cultural adaptation beyond minor regional terminology preferences.

Cultural and Social Factors

Communication and Language

Primary languages used in daily life center exclusively on English, spoken with Antiguan Creole dialect influences that maintain mutual intelligibility with standard international English. Internet language preferences show 98% English usage, with no significant minority language communities requiring multilingual gambling platform development.

Business communication norms follow British Commonwealth traditions emphasizing formal written correspondence, professional telephone etiquette, and respectful interpersonal interactions. Customer service expectations favor friendly, personable communication styles rather than purely transactional efficiency, with consumers valuing relationship-building and conversational engagement over abbreviated interactions.

Language requirements for gambling websites mandate English as the primary interface language, with no regulatory obligations for additional language support. Successful operators incorporate Caribbean terminology, local sports references (cricket terminology, West Indies team), and culturally relevant imagery featuring regional aesthetics, beaches, and carnival themes to establish local market resonance.

Cultural Attitudes

Gambling acceptance levels within Antiguan society demonstrate moderate tolerance, with gambling viewed as acceptable recreational entertainment rather than socially stigmatized vice. The presence of land-based casinos since the 1970s and the jurisdiction’s role as a global gambling licensing hub have normalized gambling activity, though religious communities maintain varying levels of acceptance with some denominations discouraging gambling participation.

Religious influences primarily stem from Christian denominations comprising 76% of the population, including Anglican, Methodist, Moravian, and Pentecostal churches. While mainstream Anglican and Methodist congregations generally tolerate moderate gambling as personal choice, evangelical and Pentecostal communities often preach against gambling as contrary to principles of stewardship and financial responsibility. Approximately 20-25% of the population reports religious beliefs significantly influence their decision to avoid gambling activities.

Foreign brand perception demonstrates generally positive attitudes, with international brands often viewed as more trustworthy, technologically advanced, and financially stable compared to local operators. The tourism-dependent economy creates cultural familiarity with international companies, reducing barriers to foreign gambling operator market entry. However, successful operators balance international credibility with localized marketing emphasizing Caribbean identity, regional sports sponsorships, and community engagement.

| Factor | Impact on Gambling | Operator Strategy Implications |

|---|---|---|

| Cricket Culture | High engagement during matches | Prioritize cricket betting markets, West Indies team promotions |

| Carnival Season (July-August) | Increased disposable spending on entertainment | Festival-themed promotions, bonus offers during peak season |

| Tourism Employment | Seasonal income fluctuations affect spending | Flexible deposit limits, low minimum bets |

| Religious Conservatism | 25% of population avoids gambling | Responsible gambling messaging, avoid aggressive marketing |

| Social Gambling Tradition | Preference for communal gaming experiences | Live dealer games, multiplayer features, social sharing |

| Mobile-First Lifestyle | 78% of online gambling via mobile | Mobile app priority, responsive design essential |

Risk tolerance indicators suggest moderate risk preferences among Antiguan consumers, with casino slot players favoring medium volatility games offering balanced frequency of wins and jackpot potential over either low-variance frequent small wins or high-variance rare large payouts. Sports bettors demonstrate preference for single bets and small accumulators over complex multi-leg parlays, indicating comfort with moderate risk-reward ratios.

Entertainment preferences emphasize social activities, outdoor recreation, beach culture, and music including calypso, soca, and reggae genres. Gambling participation often occurs in social contexts, with friends gathering for major sporting events, sharing betting tips, and celebrating wins collectively. This cultural dynamic favors gambling products with social features, live dealer interactions, and community-building elements over solitary gaming experiences.

Problem Gambling and Social Considerations

Prevalence of gambling addiction affects an estimated 1.2% of the adult population, translating to approximately 950 individuals experiencing problem gambling behaviors based on Problem Gambling Severity Index assessments conducted in regional Caribbean studies. An additional 2.8% of adults (approximately 2,200 individuals) are classified as at-risk gamblers demonstrating some harmful gambling patterns without meeting full addiction criteria.

Problem gambler statistics reveal age distribution concentrated in the 25-44 demographic representing 62% of individuals seeking treatment, followed by 45-54 age group at 24%, and 18-24 cohort at 11% of problem gamblers. Gender distribution skews male at 73% of problem gambling cases, though female problem gambling appears underreported due to social stigma and lower treatment-seeking behavior.

| Category | Number of Individuals | Percentage of Adult Population | Primary Gambling Activity |

|---|---|---|---|

| Problem Gamblers | ~950 | 1.2% | Sports betting (42%), Slots (38%), Table games (20%) |

| At-Risk Gamblers | ~2,200 | 2.8% | Sports betting (48%), Slots (35%), Multiple activities (17%) |

| Underage Gambling (Estimated) | ~180 | 0.9% of 15-17 age group | Informal betting, online platforms |

Underage gambling issues remain limited due to small population and relatively effective age verification enforcement, though an estimated 180 individuals aged 15-17 have accessed online gambling platforms through parental accounts or inadequate age checks on international sites. Land-based casinos demonstrate strong compliance with minimum age requirements due to physical ID verification at entry.

Government response measures include establishment of a National Gambling Helpline operated in partnership with regional Caribbean counseling services, providing confidential support via phone and online chat channels. The Ministry of Health maintains awareness campaigns during March Problem Gambling Awareness Month, though funding remains limited at approximately USD 45,000 annually for all gambling harm prevention activities.

Social responsibility requirements for operators mandate display of responsible gambling information, provision of self-exclusion tools, and implementation of deposit limits upon player request. However, no mandatory operator contributions to problem gambling treatment funds exist, differentiating Antigua from jurisdictions like the United Kingdom requiring statutory levy payments or France mandating 0.2% of GGR contributions to problem gambling programs.

Political Structure and Governance

Antigua and Barbuda operates as a unitary parliamentary democracy and constitutional monarchy within the Commonwealth realm, with the British monarch serving as head of state represented by a Governor-General while executive power resides with the Prime Minister and Cabinet. The bicameral Parliament comprises a 17-member House of Representatives elected every five years and an appointed 17-member Senate.

Political stability indicators rank Antigua and Barbuda in the 68th percentile globally according to World Bank governance metrics, reflecting generally stable democratic transitions, low political violence, and consistent policy implementation. The two-party system dominated by the Antigua and Barbuda Labour Party and United Progressive Party has maintained democratic norms since independence in 1981, with peaceful power transitions and minimal civil unrest.

Regulatory consistency and predictability demonstrate moderate strength, with gambling regulations remaining largely unchanged since 2007 framework adoption aside from incremental compliance enhancements. However, informal regulatory guidance and enforcement priorities can shift with ministerial changes, creating some uncertainty for operators regarding interpretation of existing requirements. Stakeholder consultation processes for regulatory amendments remain limited, with industry feedback mechanisms underdeveloped compared to jurisdictions like Malta or Gibraltar.

| Indicator | Score/Ranking | Regional Comparison | Implications for iGaming |

|---|---|---|---|

| Political Stability Index | 68th percentile | Above Caribbean average (62nd) | Stable regulatory environment |

| Corruption Perception Index | 52/100 (Rank: 78/180) | Below Barbados (64), above Jamaica (44) | Moderate bureaucratic efficiency |

| Rule of Law Index | 0.58/1.00 | Regional average | Adequate contract enforcement |

| Regulatory Quality | 61st percentile | Above regional average | Generally business-friendly policies |

| Government Effectiveness | 59th percentile | Regional average | Moderate administrative efficiency |

Corruption Perception Index scoring of 52 out of 100 (ranking 78th globally among 180 countries) indicates moderate corruption perceptions, with most business operations proceeding without significant bribery or informal payments but occasional bureaucratic inefficiencies and preferential treatment concerns. Gambling licensing processes generally maintain transparent standards, though personal relationships and local counsel engagement can influence application processing timelines.

International relations maintain strong Commonwealth ties, positive diplomatic relations with the United States, Canada, and United Kingdom, and active participation in Caribbean Community regional integration. Trade agreements include CARICOM membership facilitating intra-Caribbean commerce, and the Revised Treaty of Chaguaramas enabling free movement of goods, services, and skilled labor across member states. No European Union association exists, positioning Antigua outside EU regulatory harmonization requirements affecting Malta, Cyprus, and Gibraltar gambling regimes.

Technology Adoption and Digital Behavior

Internet and Digital Usage

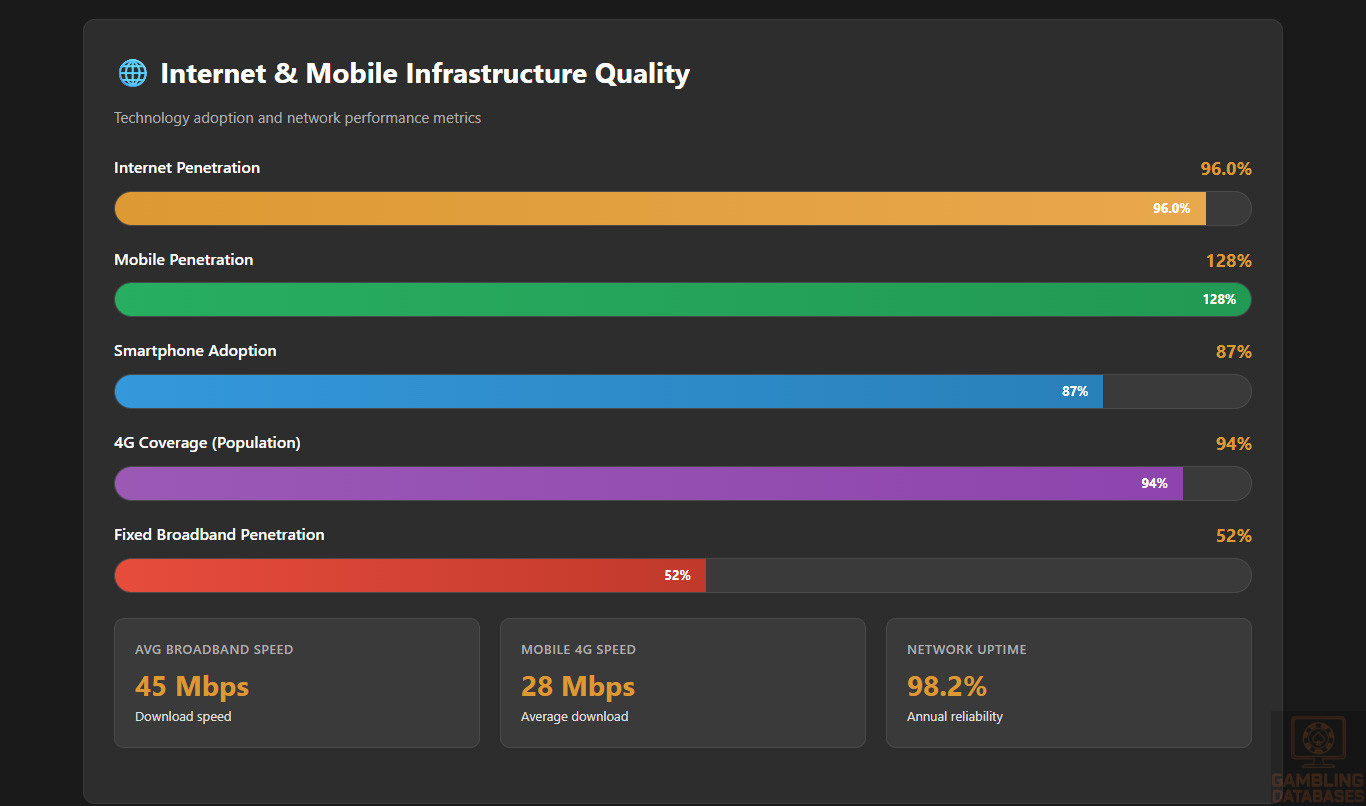

Internet penetration reaches 96.0% of the population, placing Antigua and Barbuda among the most connected Caribbean nations alongside Barbados (97%) and ahead of regional averages of 68%. Daily internet usage averages 6.2 hours per person among connected individuals, with mobile devices accounting for 78% of total internet access time and desktop/laptop usage comprising the remaining 22%.

Mobile device adoption demonstrates 128% penetration rate indicating multiple devices per capita, driven by both smartphone and tablet ownership plus dual-SIM usage for separating personal and business communications. Smartphone specifically penetrates 87% of the population aged 15+, with device ownership concentrated at 94-98% among the 18-44 core demographic and declining to 62% among individuals aged 65+.

| Platform/Service | Penetration Rate | Daily Active Users % | Average Time Spent Daily |

|---|---|---|---|

| 72% | 58% | 48 minutes | |

| 54% | 41% | 32 minutes | |

| 89% | 81% | 65 minutes | |

| YouTube | 85% | 62% | 54 minutes |

| TikTok | 38% | 29% | 42 minutes |

| Twitter/X | 22% | 14% | 18 minutes |

Social media engagement demonstrates WhatsApp dominance at 89% penetration serving as the primary communication platform for personal messaging, business communications, and group coordination. Facebook maintains 72% penetration but declining daily active usage as younger demographics migrate toward Instagram (54% penetration) and TikTok (38% penetration growing rapidly at 45% year-over-year).

E-commerce participation rates reach 58% of internet users making at least one online purchase annually, though frequent online shopping (monthly or more) characterizes only 32% of consumers. Popular e-commerce categories include international retail platforms like Amazon shipping to Antigua, digital entertainment subscriptions (Netflix, Spotify), and regional online marketplaces. Total e-commerce spending approximates USD 28 million annually or USD 285 per capita.

Digital payment adoption reaches 68% of adults maintaining at least one digital payment method beyond cash, with credit/debit cards representing the dominant form at 62% penetration, followed by mobile money services at 24%, and international e-wallets like PayPal at 18%. Online banking penetration stands at 54% of banked population, enabling direct bank transfers for online gambling deposits and withdrawals.

Digital Payment Behavior

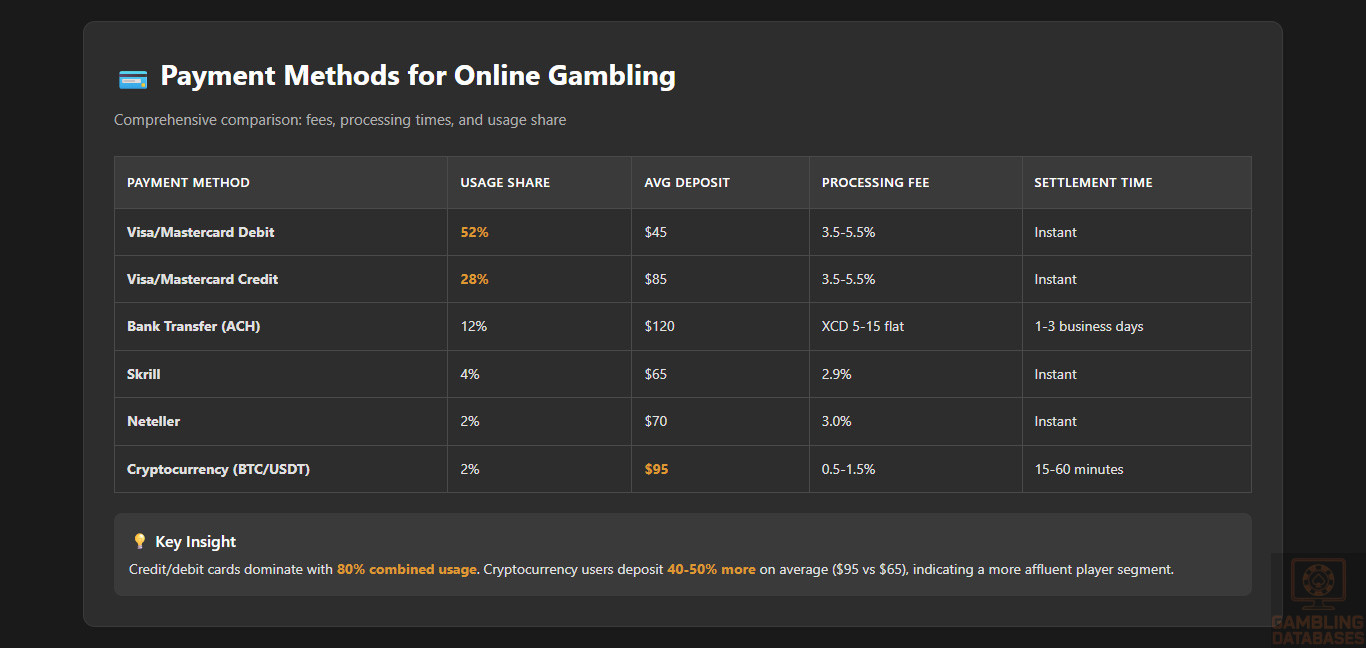

Payment method preferences for online transactions strongly favor credit and debit cards accounting for 68% of online payment volume, followed by bank transfers at 18%, e-wallets at 11%, and cash-on-delivery or payment kiosks for 3% of transactions. Visa and Mastercard dominate card networks with 95% combined market share, while American Express maintains limited acceptance at premium establishments.

Popular digital wallets include PayPal with 18% adoption among online shoppers, though geographic restrictions often limit PayPal gambling transactions. Regional services like MobiMoney operated by Digicel achieve 15% penetration primarily for mobile top-ups and bill payments rather than e-commerce. Cryptocurrency adoption remains nascent at approximately 4% of population holding digital assets, with Bitcoin and USDT representing the primary holdings.

| Payment Method | Availability | Usage Share | Avg Deposit Amount | Processing Time |

|---|---|---|---|---|

| Visa/Mastercard Debit | Universal | 52% | $45 | Instant |

| Visa/Mastercard Credit | Universal | 28% | $85 | Instant |

| Bank Transfer (ACH) | Major banks | 12% | $120 | 1-3 business days |

| Skrill | Limited | 4% | $65 | Instant |

| Neteller | Limited | 2% | $70 | Instant |

| Cryptocurrency (BTC/USDT) | Select operators | 2% | $95 | 15-60 minutes |

Online transaction patterns show average transaction sizes of USD 65 for gambling deposits, with frequency averaging 4.2 transactions monthly for active players. Withdrawal patterns demonstrate preference for same-method returns, with players expecting withdrawals via the original deposit method. Average withdrawal processing timelines of 24-48 hours for e-wallets and 3-5 business days for bank transfers align with regional norms.

Trust in online payment systems achieves 72% confidence levels among regular internet users, though concerns persist regarding data security (mentioned by 38% of users), fraudulent charges (32%), and dispute resolution effectiveness (28%). Card-not-present fraud rates remain below 0.15% of transaction volume, indicating relatively secure payment processing infrastructure despite moderate consumer anxiety.

Cryptocurrency adoption for gambling specifically reaches approximately 2% of online gamblers, with players attracted by transaction privacy, lower fees compared to card processing, and faster international transfers. However, cryptocurrency volatility concerns, limited wallet adoption, and regulatory uncertainty restrict broader uptake. Operators accepting crypto report average deposit sizes 40-50% higher than fiat deposits, suggesting crypto users comprise a more affluent player segment.

Gaming and Gambling Preferences

Current Market Participation

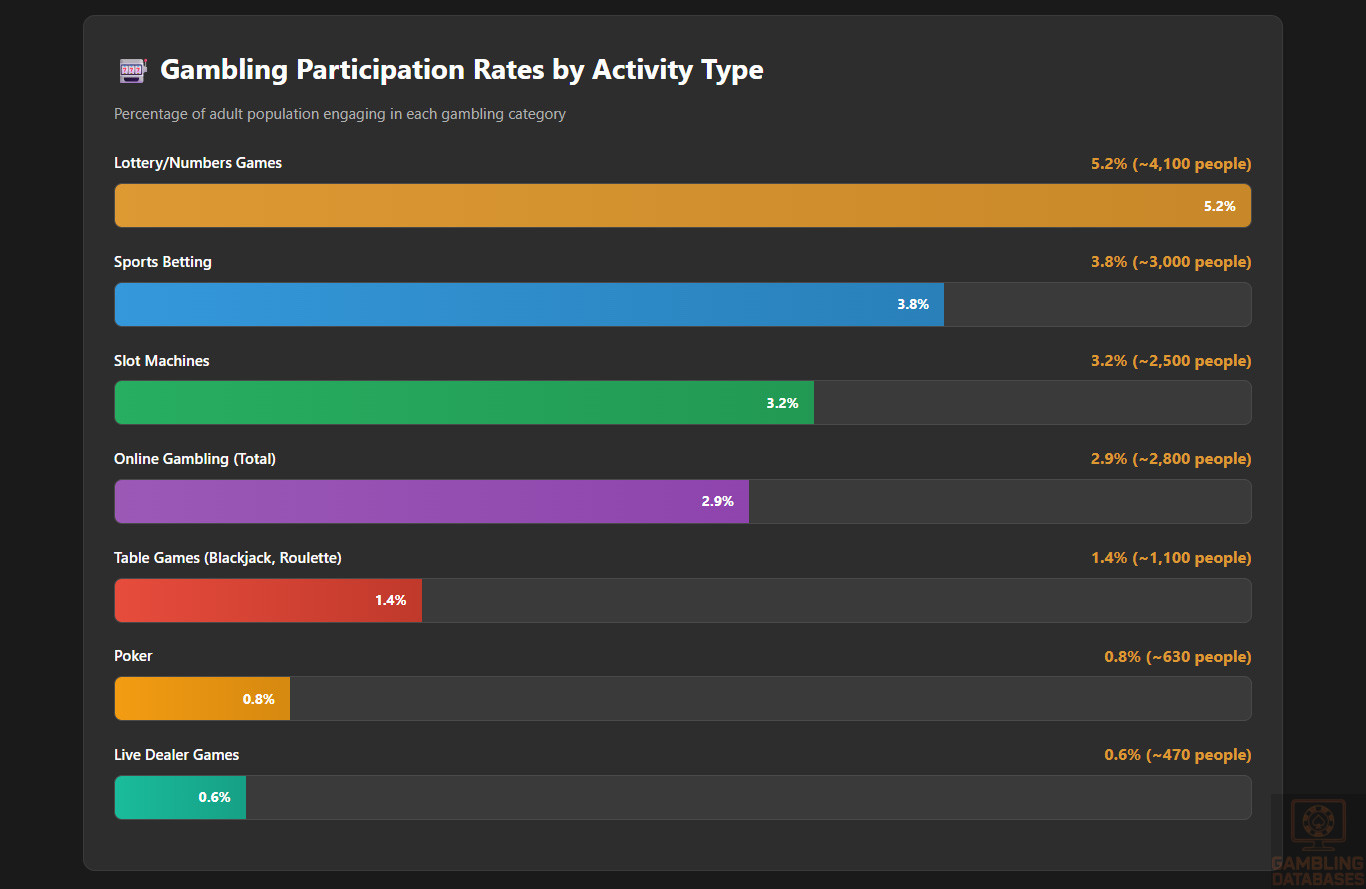

Gambling participation reaches 8.5% of the adult population engaging in at least one gambling activity annually, translating to approximately 6,700 individuals. Online gambling specifically attracts 2.9% of adults (approximately 2,800 individuals) while land-based casino gambling engages 4.8% (3,800 individuals) with some overlap between channels. Lottery participation remains the most widespread at 5.2% of adults purchasing lottery tickets at least occasionally.

Popular gambling activities ranked by participation show lottery products leading at 5.2% penetration, followed by sports betting at 3.8%, slot machines at 3.2%, table games at 1.4%, and poker at 0.8% of adult population. Cricket betting dominates sports wagering accounting for 58% of sports betting volume, followed by football (soccer) at 24%, basketball at 12%, and other sports comprising 6%.

| Activity Type | % of Adult Population | Active Participants | Online vs Land-Based Split | Avg Monthly Spend (USD) |

|---|---|---|---|---|

| Lottery/Numbers Games | 5.2% | ~4,100 | 15% online / 85% retail | $18 |

| Sports Betting | 3.8% | ~3,000 | 45% online / 55% retail | $62 |

| Slot Machines | 3.2% | ~2,500 | 38% online / 62% land-based | $75 |

| Table Games (BJ, Roulette) | 1.4% | ~1,100 | 28% online / 72% land-based | $95 |

| Poker | 0.8% | ~630 | 35% online / 65% casino poker rooms | $110 |

| Live Dealer Games | 0.6% | ~470 | 100% online | $88 |

Live dealer games demonstrate growing popularity among online casino players, with 0.6% of adults engaging in live blackjack, roulette, or baccarat. The format appeals particularly to players aged 35-54 who appreciate the social interaction and perceived fairness of human dealers while maintaining online convenience. Live dealer participation has grown 35% annually over the past three years.

Seasonal patterns show pronounced increases during cricket season (January-April for international matches, May-September for Caribbean Premier League) when sports betting volume increases 40-60% above baseline. December holiday season generates 25-30% uplift in casino gaming as disposable income increases from tourism employment bonuses and festival spending. Summer carnival period (late July-early August) produces moderate 15-20% increases in overall gambling activity.

Consumer Behavior Patterns

Average spending per online gambler reaches USD 950 annually or approximately USD 79 monthly across all active players. However, spending distributions demonstrate high variance, with the top 20% of players accounting for 68% of total revenue. High-value players spending over USD 200 monthly represent approximately 560 individuals (20% of online gamblers) contributing USD 2.18 million annually (68% of total online gambling revenue).

Spending habits and typical bet sizes vary significantly by game type, with slot players averaging USD 0.75-2.50 per spin, sports bettors placing average wagers of USD 15-35 per bet, and table game players betting USD 5-25 per hand. Maximum bet limits rarely constrain recreational players, with less than 5% of players regularly wagering amounts approaching operator-imposed maximums.

| Metric | Sports Betting | Online Slots | Table Games | Live Dealer |

|---|---|---|---|---|

| Mobile Usage % | 82% | 85% | 68% | 72% |

| Desktop Usage % | 18% | 15% | 32% | 28% |

| Avg Session Length | 18 minutes | 28 minutes | 42 minutes | 56 minutes |

| Sessions per Week | 4.2 | 5.8 | 2.6 | 2.1 |

| Peak Activity Days | Sat-Sun, Wed (cricket) | Fri-Sun evenings | Fri-Sat nights | Weekend evenings |

| Deposit Frequency | 2.8/month | 3.6/month | 2.2/month | 2.4/month |

| Withdrawal Frequency | 1.2/month | 0.8/month | 0.9/month | 0.7/month |

| 90-Day Retention % | 42% | 38% | 48% | 52% |

Platform preferences heavily favor mobile devices, with 78% of all online gambling activity occurring via smartphones compared to 22% on desktop computers. Mobile dominance is most pronounced among sports bettors (82% mobile) and slot players (85% mobile), while table game and live dealer preferences show higher desktop usage at 28-32% reflecting player preferences for larger screens during longer gaming sessions.

Peak gambling times concentrate on Friday through Sunday accounting for 58% of weekly gambling activity, with Thursday showing elevated activity at 14% and Monday-Wednesday combining for 28% of weekly volume. Hourly patterns demonstrate evening peaks between 19:00-23:00 capturing 52% of daily activity, afternoon hours (14:00-18:00) generating 28%, and late night/early morning (23:00-06:00) contributing 15% of volume.

Session length averages vary substantially by product, with sports betting sessions averaging 18 minutes focused on specific match betting, online slots sessions extending to 28 minutes of continuous play, table games averaging 42 minutes, and live dealer sessions reaching 56 minutes reflecting the more immersive, social nature of live dealer experiences. Players typically complete 2-6 sessions weekly depending on product preference and engagement levels.

Retention and loyalty patterns show 90-day retention rates of 38-52% depending on product category, with live dealer games demonstrating highest retention at 52% followed by table games at 48%, sports betting at 42%, and slots at 38%. Annual retention rates decline to 18-25% across categories, indicating significant player churn requiring continuous acquisition efforts.

Bonus sensitivity and promotional response demonstrate high effectiveness, with 68% of new players depositing during welcome bonus offers compared to 32% depositing without promotions. Match deposit bonuses generate average first deposits 45% higher than non-bonus deposits (USD 95 vs USD 65). Free bet promotions for sports betting drive 35% higher bet volumes during promotional periods. However, bonus abuse and low-quality bonus-hunting players represent approximately 15% of bonus claimants, requiring careful terms structuring and fraud detection.

Preferred game types vary significantly by age group, with 18-24 year olds favoring sports betting (62% of gambling activity), 25-34 year olds splitting between sports betting (42%) and slots (38%), 35-44 year olds preferring slots (48%) and table games (28%), and 45+ demographics showing strongest lottery (45%) and traditional casino games (32%) engagement. Younger cohorts demonstrate greater mobile gaming preference and higher session frequency with lower average bet sizes.

Deposit and withdrawal frequency patterns show active players depositing 2.2-3.6 times monthly depending on product engagement, with slots players demonstrating highest deposit frequency due to faster gameplay and bankroll cycling. Withdrawal frequency averages 0.7-1.2 times monthly, significantly lower than deposits, indicating most players maintain persistent gambling balances or experience net losses. Players withdrawing more than twice monthly represent likely advantage players or bonus abusers requiring enhanced monitoring.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Internet penetration at 96% positions Antigua and Barbuda among the Caribbean’s most connected nations, though infrastructure quality demonstrates variability between urban centers and rural areas. Fixed broadband penetration reaches 52% of households concentrated in St. John’s and major towns, while mobile broadband serves as the primary connectivity method for 44% of internet users, particularly in rural communities lacking fiber or cable infrastructure.

Average internet speeds measure 45 Mbps download and 12 Mbps upload for fixed broadband connections, adequate for streaming video, online gaming, and video conferencing but below global averages of 85 Mbps download. Mobile internet speeds average 28 Mbps download on 4G networks, sufficient for mobile gambling applications, social media, and standard definition video streaming.

| Metric | Value | Regional Comparison | Global Ranking |

|---|---|---|---|

| Fixed Broadband Penetration | 52% of households | Above Caribbean avg (38%) | – |

| Mobile Broadband Penetration | 94% of population | Above Caribbean avg (76%) | – |

| Avg Fixed Broadband Speed | 45 Mbps download | Below Barbados (95 Mbps) | 94th globally |

| Avg Mobile Speed (4G) | 28 Mbps download | Caribbean average | 102nd globally |

| Network Reliability (Uptime) | 98.2% | Good | – |

| Latency (Ping) – Regional Servers | 35-50ms | Acceptable for gaming | – |

| Latency – European Servers | 145-180ms | Moderate delay | – |

Network reliability achieves 98.2% uptime annually, with occasional disruptions during hurricane season (June-November) when severe weather can damage infrastructure causing outages lasting hours to days in affected areas. Major providers maintain backup power systems and redundant connectivity, though restoration times in rural areas can extend to 48-72 hours following major storms.

Infrastructure investment trends show approximately USD 15 million annually in telecommunications infrastructure upgrades by the combined efforts of Digicel, Flow (Cable & Wireless), and Apua Internet Service. Fiber optic expansion projects aim to increase fixed broadband coverage from 52% to 65% of households by 2027, focusing on currently underserved rural communities and outer island Barbuda.

Global internet speed rankings position Antigua 94th globally for fixed broadband and 102nd for mobile speeds, reflecting infrastructure constraints of small island developing states. However, speeds prove adequate for all common internet applications including HD video streaming, online gaming, and cloud services, with buffering or connectivity issues affecting less than 5% of users during normal conditions.

5G and Future Technology Deployment

Current 4G/LTE coverage reaches 94% of the population with service from both Digicel and Flow networks, providing download speeds of 20-35 Mbps and upload speeds of 8-15 Mbps sufficient for mobile gambling applications. Coverage gaps persist in mountainous interior regions of Antigua and portions of Barbuda, affecting approximately 6% of residents who rely on 3G service or satellite internet.

5G rollout commenced in limited form during late 2024 with Digicel launching initial 5G service in St. John’s central business district covering approximately 8% of the population. Expansion plans project 25% population coverage by end of 2025, 45% by 2026, and 70% by 2028 concentrated in urban areas and major tourist zones. Flow’s 5G deployment follows a similar timeline with commercial launch expected Q2 2025.

Future infrastructure plans include submarine fiber optic cable upgrades enhancing international bandwidth capacity, targeted for completion in 2026 with capacity increases from current 40 Gbps to 100 Gbps improving latency to North American and European servers. The upgrade benefits cloud gaming, live dealer gambling products, and high-definition video streaming by reducing latency and increasing reliability.

Network operator landscape comprises three primary providers: Digicel holds approximately 52% mobile market share, Flow captures 44%, and APUA operates the remaining 4% serving primarily government and institutional clients. Fixed broadband competition between Flow’s cable service and APUA’s fiber network maintains competitive pricing averaging XCD 150-250 monthly (USD 56-93) for residential broadband packages offering 40-100 Mbps speeds.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Mobile network operators maintain comprehensive 4G coverage across 94% of Antigua and Barbuda’s territory through Digicel and Flow networks. Digicel commands slightly superior coverage in rural areas with 96% geographic coverage compared to Flow’s 92%, though population coverage remains equivalent at 94% for both operators as uncovered areas are sparsely populated.

| Operator | Market Share | 4G Coverage | 5G Coverage | Avg Data Speed | Monthly Data Cost (5GB) |

|---|---|---|---|---|---|

| Digicel | 52% | 96% geographic / 94% population | 8% (St. John’s only) | 29 Mbps | XCD 65 / USD 24 |

| Flow (C&W) | 44% | 92% geographic / 94% population | Limited testing | 27 Mbps | XCD 70 / USD 26 |

| APUA | 4% | Limited (St. John’s area) | None | 22 Mbps | XCD 55 / USD 20 |

Data costs demonstrate regional competitiveness with 5GB monthly data packages averaging XCD 65 (USD 24) from Digicel and XCD 70 (USD 26) from Flow. Unlimited data plans marketed with throttling after 20-30GB

cost XCD 120-150 monthly (USD 44-56), appealing to heavy data users including mobile gamblers consuming 8-15GB monthly through gambling applications, live streaming, and social media. Prepaid data dominates at 68% of mobile subscriptions compared to 32% postpaid contracts.

Mobile payment integration demonstrates growing sophistication with both major operators offering mobile money services. Digicel’s MobiMoney platform achieves 15% adoption among its subscriber base enabling mobile top-ups, bill payments, and peer-to-peer transfers, though gambling deposit functionality remains limited due to regulatory ambiguity. Flow Money service maintains 8% adoption with similar functionality constraints regarding gambling transactions.

Mobile wallet adoption specifically for financial transactions reaches 24% of adults using mobile money for at least occasional transactions, though gambling operators more commonly integrate traditional payment gateways accepting credit/debit cards rather than local mobile money platforms. International e-wallets like PayPal and Skrill integrated by gambling platforms achieve 18% penetration among online gamblers.

Device Penetration

Smartphone adoption reaches 87% of the population aged 15 and above, representing approximately 68,000 smartphone users across the islands. The 18-44 core demographic demonstrates 94-98% smartphone ownership while adoption declines to 72% among 45-54 age group and 62% among individuals 55 and older who more commonly retain basic feature phones or have no mobile device.

Smartphones per capita average 1.3 devices per smartphone user when accounting for individuals maintaining separate work and personal phones or replacing devices without discarding functional older units used as backup devices. Multiple device ownership concentrates among higher-income professionals and business owners rather than representing broad population behavior.

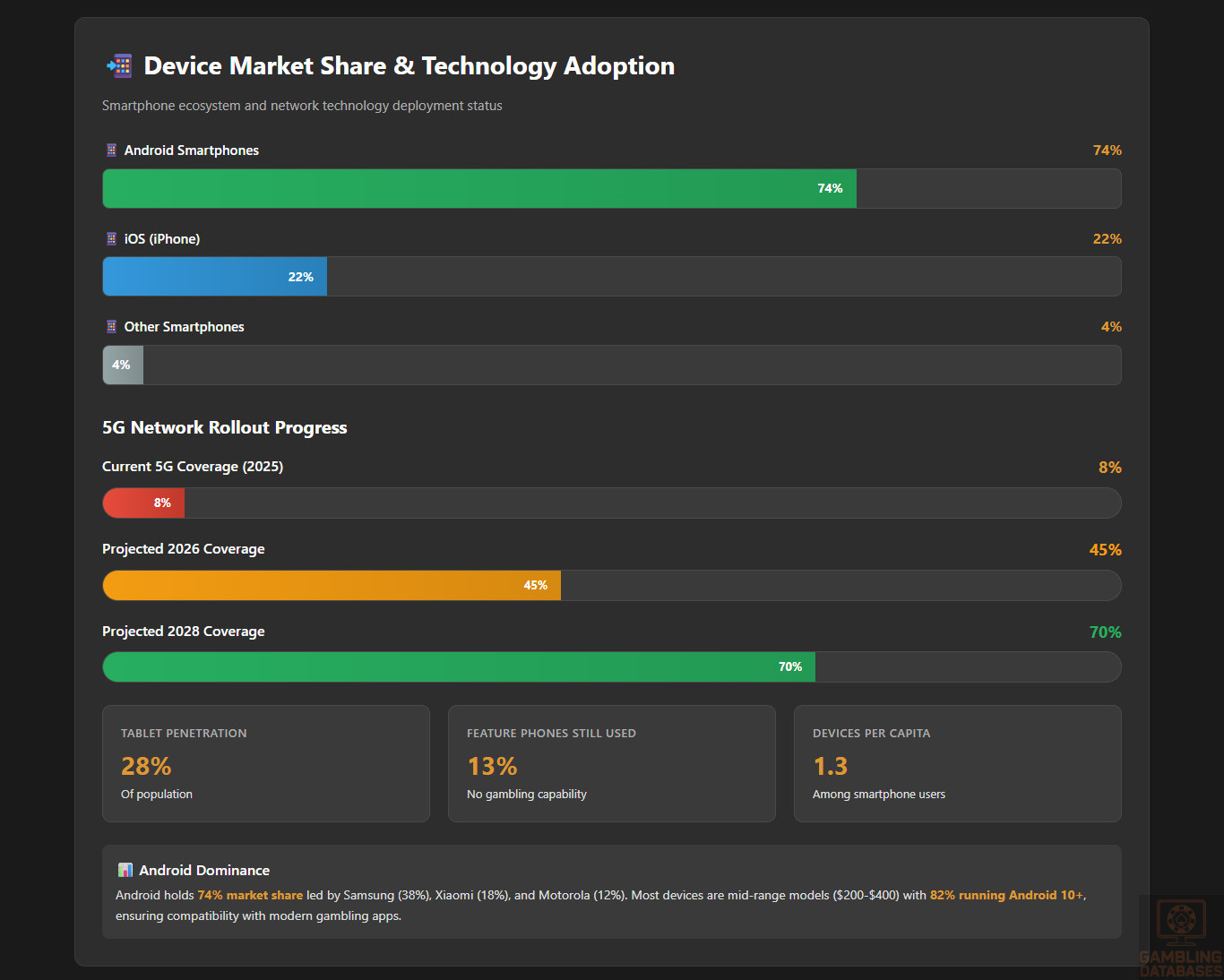

| Device Category | Market Share | Popular Models/Brands | Gambling App Compatibility |

|---|---|---|---|

| Android Smartphones | 74% | Samsung (38%), Xiaomi (18%), Motorola (12%) | Universal compatibility |

| iOS (iPhone) | 22% | iPhone 11-15 series | Universal compatibility |

| Other Smartphones | 4% | Various budget brands | Variable compatibility |

| Tablets | 28% penetration | iPad (45%), Samsung (32%), Amazon Fire (15%) | Good for casino games |

| Feature Phones | 13% still in use | Basic Nokia, other | No gambling capability |

Device preferences show Android dominance at 74% market share led by Samsung (38% of Android users), Xiaomi (18%), and Motorola (12%) offering mid-range devices in the USD 200-400 price range most accessible to average consumers. Apple iPhone captures 22% market share concentrated among higher-income demographics, government employees, and tourism industry professionals earning above-average incomes.

Average device specifications for Android phones in use include 4GB RAM, 64GB storage, and processors adequate for mobile gambling applications without performance constraints. Approximately 82% of Android devices run Android 10 or newer ensuring compatibility with modern gambling applications, while 18% operate Android 9 or older potentially facing compatibility limitations with cutting-edge gaming features.

Mobile internet usage patterns demonstrate 6.8 hours daily average screen time among smartphone users, with 2.4 hours allocated to social media, 1.8 hours to video streaming, 1.2 hours to messaging applications, and 1.4 hours distributed across other activities including gaming, web browsing, and mobile gambling. Active mobile gamblers spend approximately 22 minutes daily on gambling applications during engagement days.

Mobile gaming penetration reaches 68% of smartphone owners playing mobile games at least occasionally, with casual gaming (puzzle games, arcade titles) representing 82% of mobile gaming activity and gambling applications comprising approximately 4% of total mobile gaming time. The established mobile gaming behavior facilitates gambling app adoption by providing familiar download, payment, and gameplay interaction patterns.

Financial Services and Payment Infrastructure

Banking System Structure

The Antigua and Barbuda banking sector comprises eight licensed commercial banks, three credit unions serving 12,000 members, and two development banks focused on small business and agricultural lending. Major commercial banks include Antigua Commercial Bank (ACB) holding 28% market share, Bank of Antigua (BOA) with 24%, Royal Bank of Canada (RBC) at 18%, and FirstCaribbean International Bank at 16% market share.

Digital banking adoption reaches 54% of banked population maintaining active internet banking credentials, though only 32% use online banking weekly or more frequently for routine transactions. Mobile banking applications achieve 41% adoption among account holders, with younger demographics (18-34) demonstrating 68% mobile banking usage compared to 22% among individuals 55 and older.

| Metric | Value | Notes |

|---|---|---|

| Banked Population | 82% of adults | Approximately 64,700 account holders |

| Number of Bank Branches | 24 branches | Concentrated in St. John’s and major towns |

| ATM Density | 42 ATMs per 100,000 adults | 33 total ATMs nationwide |

| Credit Card Penetration | 38% of adults | Approximately 30,000 credit cards in circulation |

| Debit Card Penetration | 68% of adults | 53,600 active debit cardholders |

| Online Banking Active Users | 54% of account holders | 35,000 users |

| Mobile Banking Adoption | 41% of account holders | 26,500 users |

| Average Account Balance | XCD 8,450 (USD 3,130) | Median: XCD 4,200 (USD 1,556) |

Account penetration at 82% of adults leaves approximately 14,200 unbanked individuals concentrated among lower-income households, elderly populations preferring cash transactions, and undocumented migrant workers. Credit union membership provides alternative financial services for 15% of adults, particularly middle and lower-middle income households attracted by favorable loan terms and community orientation.

Credit and lending markets demonstrate moderate maturity with total consumer credit outstanding of approximately XCD 680 million (USD 252 million) or 36% of GDP. Personal loan products, auto financing, and credit cards represent primary consumer lending categories, while mortgage lending reaches 28% of homeowners. Interest rates range from 8-12% for secured lending to 18-24% for unsecured personal loans and credit cards.

ATM density of 42 machines per 100,000 adults (33 total ATMs) concentrates in St. John’s hosting 58% of machines, with remaining units distributed across major towns and tourist resort areas. ATM availability proves adequate for cash withdrawal needs, though rural residents may travel 15-30 minutes to access ATMs. Daily withdrawal limits typically cap at XCD 1,500-2,500 (USD 556-926) depending on bank and account type.

Payment Processing Options

Available payment methods for iGaming include credit cards (Visa, Mastercard), debit cards, bank transfers via online banking or wire transfer, international e-wallets (Skrill, Neteller where available), and cryptocurrency for operators supporting digital assets. American Express maintains limited acceptance primarily at premium establishments, with only 40% of online gambling operators accepting Amex due to higher processing fees.

Credit and debit card penetration combined reaches 76% of adults (68% debit, 38% credit with overlap), though not all cardholders use cards for online gambling due to either non-participation in gambling or preference for alternative payment methods. Approximately 2,200 individuals (78% of online gamblers) use cards as their primary gambling deposit method.

| Payment Method | Processor Options | Typical Fees | Settlement Time | Chargeback Risk |

|---|---|---|---|---|

| Visa/Mastercard | Multiple PSPs available | 3.5-5.5% + $0.25/txn | T+2 to T+5 | Moderate (1-2%) |

| Bank Transfer (Local) | Direct bank integration | XCD 5-15 per transfer | 1-3 business days | Very low (0.1%) |

| Wire Transfer (Intl) | SWIFT network | $25-45 per transfer | 3-5 business days | Very low (0.05%) |

| Skrill | Direct Skrill integration | 2.9% + currency conversion | Instant deposit / 24-48hr withdrawal | Low (0.3%) |

| Neteller | Direct Neteller integration | 3.0% + currency conversion | Instant deposit / 24-48hr withdrawal | Low (0.3%) |

| Cryptocurrency | Various crypto processors | 0.5-1.5% | 15-60 min confirmation | None (irreversible) |