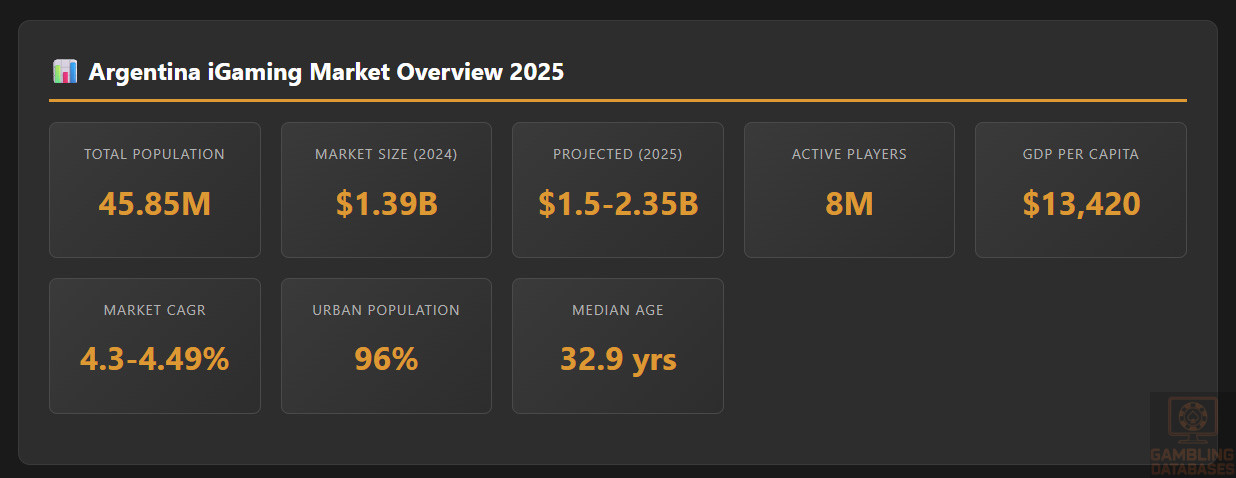

Argentina represents one of Latin America’s most dynamic and rapidly expanding iGaming markets, with projected revenues exceeding USD 1.5 billion by 2025 and nearly 8 million active players.

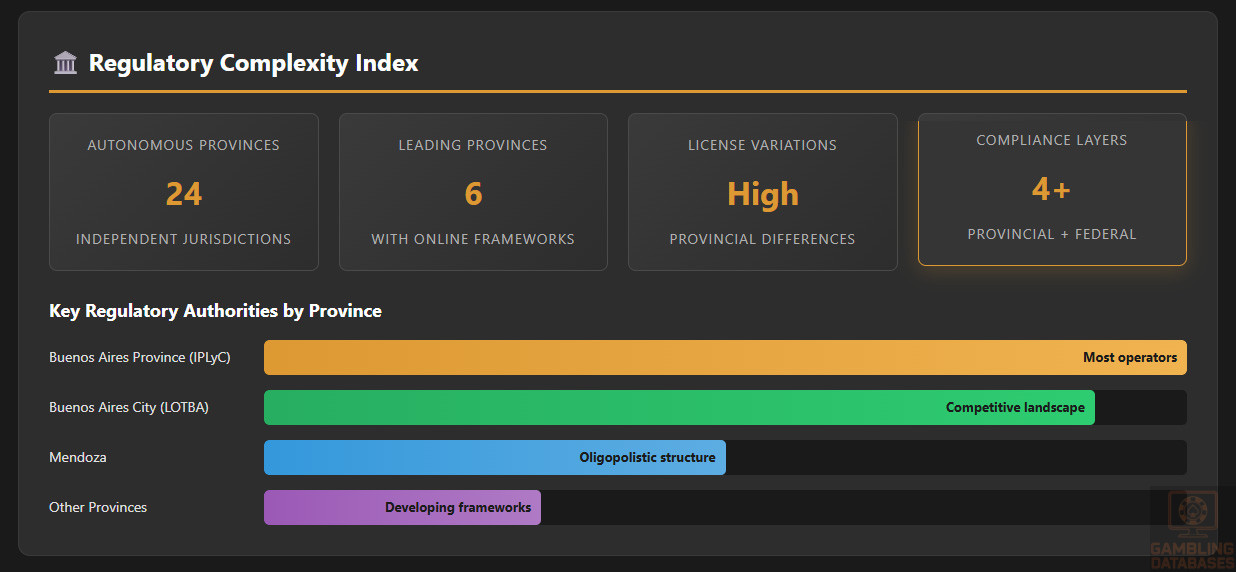

The country’s decentralized regulatory framework grants each of its 24 provinces autonomous control over gambling legislation, creating a complex but opportunity-rich landscape for operators.

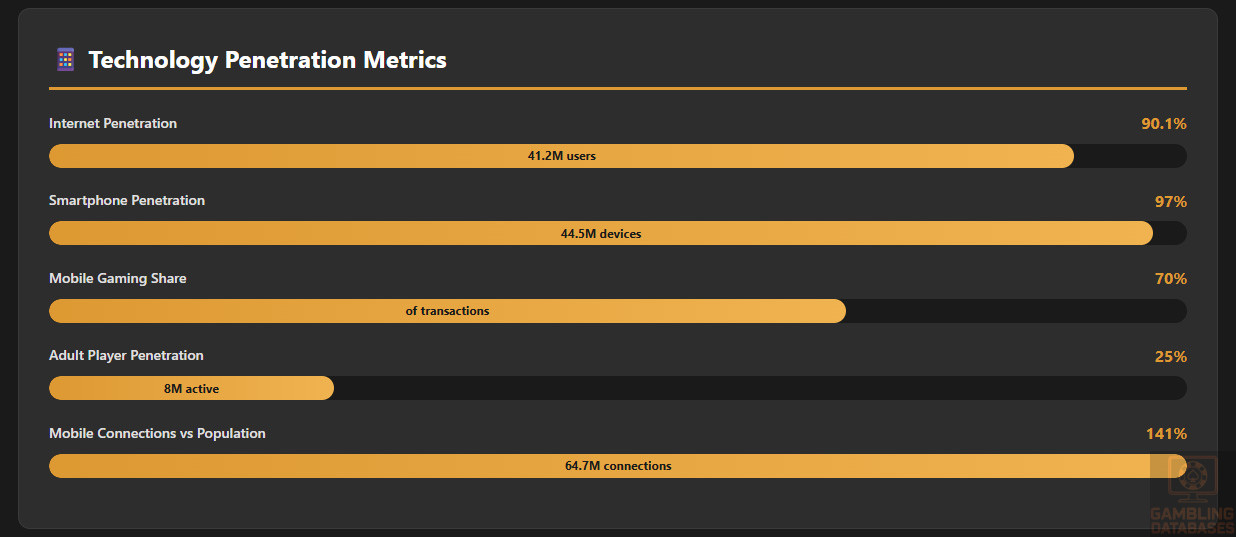

With 90 percent internet penetration, 97 percent smartphone adoption, widespread use of digital payment platforms like Mercado Pago, and a population passionate about sports betting, Argentina offers significant market potential.

However, operators must navigate provincial licensing requirements, evolving federal advertising restrictions, multi-layered taxation structures, and pending national legislation that could reshape the industry.

Executive Summary: Key Market Indicators

| Indicator | Value |

|---|---|

| Online Gambling Legal Status | Legal at provincial level (24 autonomous jurisdictions) |

| Total Population (2025) | 45.85 million |

| Urban Population | 96 percent (44 million) |

| Median Age | 32.9 years |

| GDP Per Capita (2024) | USD 13,420 |

| Internet Penetration | 90.1 percent (41.2 million users) |

| Mobile Connections | 64.7 million (141 percent of population) |

| Smartphone Penetration | 97 percent of population |

| Total iGaming Market Size (2024) | USD 1.39 billion (online only) |

| Projected Market Size (2025) | USD 1.5-2.35 billion |

| Market CAGR (2025-2029) | 4.3-4.49 percent |

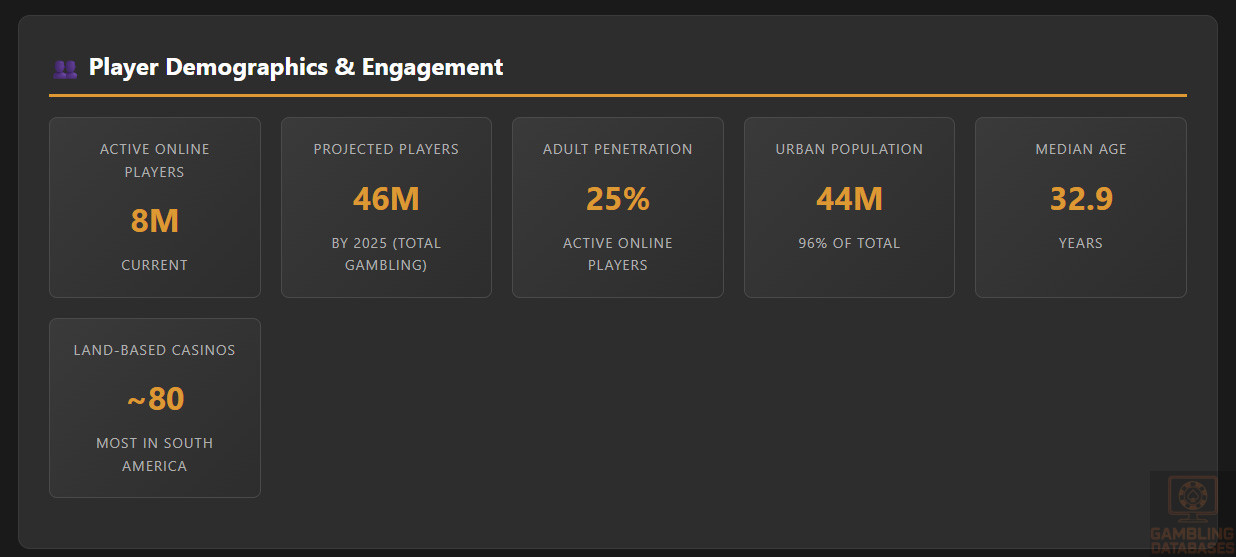

| Active Online Players | 8 million (25 percent adult penetration) |

| Projected Players by 2025 | 46 million (total gambling population) |

| Mobile Gaming Share | 70 percent of transactions |

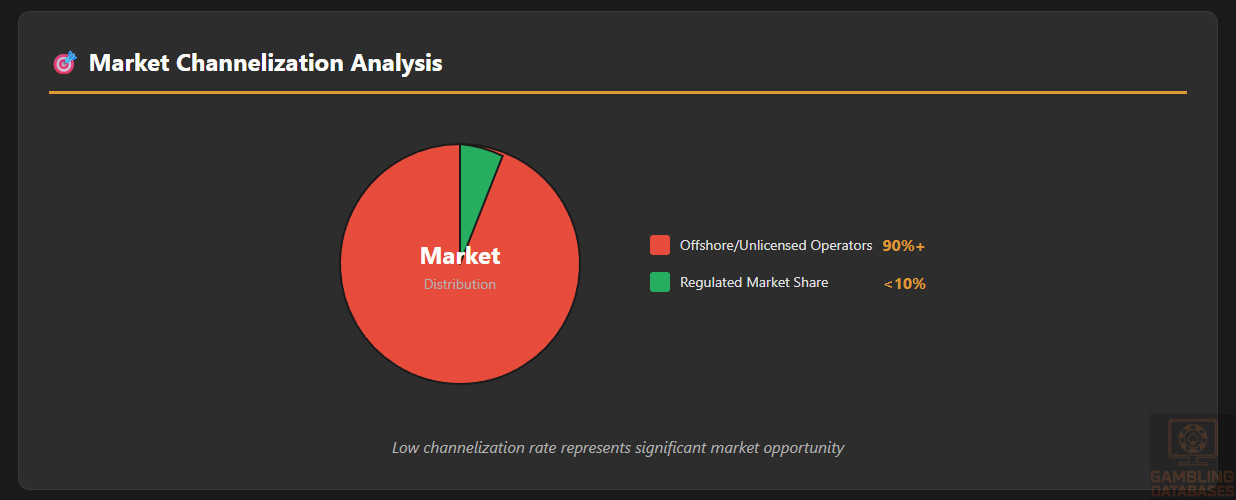

| Regulated Market Share | Less than 10 percent (90 percent+ offshore) |

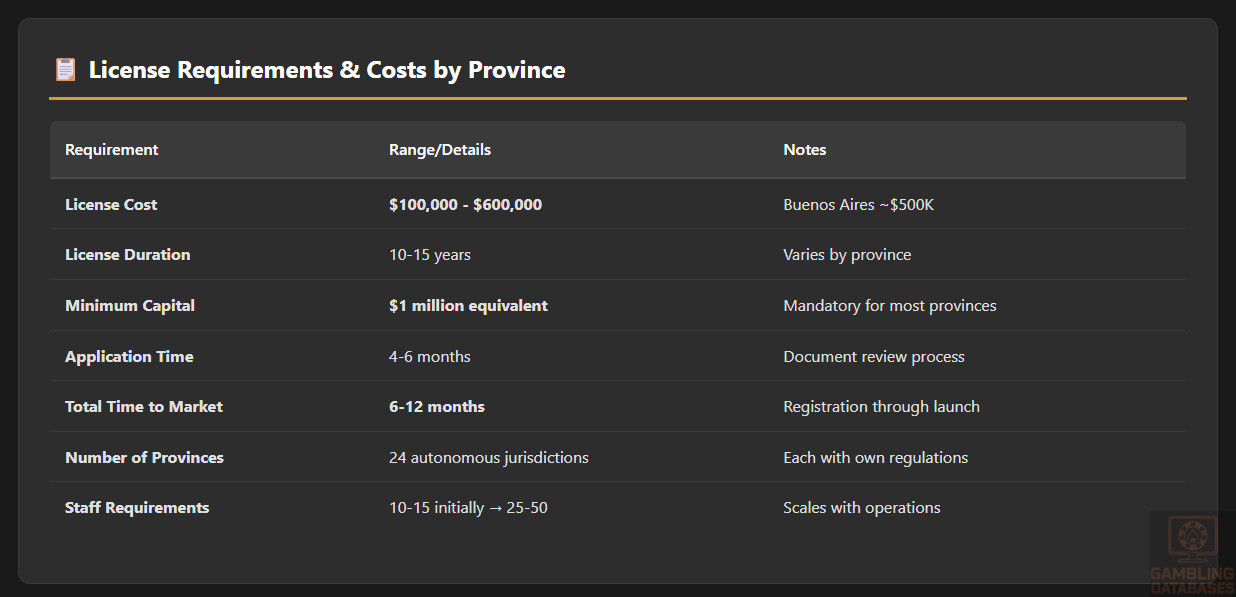

| Provincial License Cost Range | USD 100,000-600,000 |

| License Duration | 10-15 years (varies by province) |

| GGR Tax Rate (Online Casinos) | 10-12 percent (provincial) |

| GGR Tax Rate (Sports Betting) | 10 percent (provincial) |

| Federal Deposit Tax | 2.5-15 percent (based on operator status) |

| Corporate Income Tax | 25-35 percent |

| Minimum Capital Requirement | USD 1 million equivalent |

| Leading Payment Method | Mercado Pago (digital wallet) |

| Primary Language | Spanish |

| Currency | Argentine Peso (ARS) |

| Time to Market | 6-12 months (licensing process) |

| Primary Regulatory Challenge | Provincial fragmentation and pending federal legislation |

| Key Market Opportunity | Low channelization rate (90 percent+ market still offshore) |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Argentina operates under a federalized gambling regulatory system where each of the country’s 24 provinces and the Autonomous City of Buenos Aires exercises independent authority over gambling activities within their territories.

This decentralized structure was established constitutionally and confirmed through the 2016 National Gaming Law, which recognized provincial sovereignty while criminalizing unlicensed operations nationwide.

The fragmented approach creates both complexity for operators seeking national coverage and opportunities for strategic market entry through high-value jurisdictions.

Land-Based Gambling Activities

Argentina hosts approximately 80 land-based casinos, the most in South America, distributed across provinces with varying regulatory requirements.

Sports betting shops and lottery outlets operate extensively throughout urban centers, with provincial authorities issuing licenses and collecting gaming taxes.

Slot machine halls and bingo facilities require separate provincial licenses with specific technical certification standards and location restrictions based on local regulations.

Horse racing wagering facilities operate under specialized provincial regulations, often administered by entities separate from general gaming authorities.

Online Gambling Framework

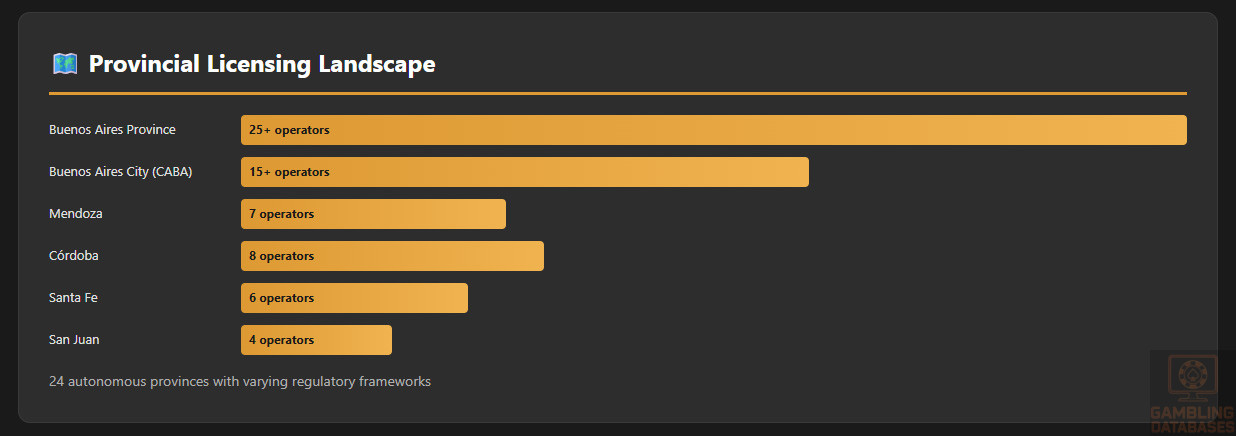

Online gambling regulation exists at the provincial level, with Buenos Aires City, Buenos Aires Province, Mendoza, Córdoba, Santa Fe, and San Juan leading in comprehensive digital gaming frameworks.

Permitted online activities typically include sports betting, casino games (slots, table games), live dealer games, poker, and provincially-authorized lottery products.

Geo-blocking technology and payment restrictions ensure players can only access platforms licensed in their province of residence, though enforcement remains challenging.

The regulatory framework mandates local server hosting in some jurisdictions, requires player funds segregation, and imposes strict responsible gambling protocols including self-exclusion systems.

Licensed Operators and Market Players

As of 2025, over 25 operators hold licenses in Buenos Aires Province alone, with Mendoza authorizing seven active operators and other provinces granting between 2-10 licenses each.

Major international operators include Betsson, Codere, Bet365 (operating through local partnerships), Coolbet, BetWarrior, and Playtech, alongside domestic players like Casino Trilenium Online and Bplay.

Market concentration varies significantly by province, with Buenos Aires City (CABA) featuring the most competitive landscape and provinces like Mendoza showing oligopolistic market structures.

International operators typically enter through partnerships with established local entities, leveraging existing regulatory relationships and market knowledge to navigate the complex provincial licensing system.

| Operator | Type | Provincial Presence | Estimated Market Position |

|---|---|---|---|

| Codere Online | International | Buenos Aires City, Buenos Aires Province | Leading sports betting operator |

| Bet365 | International (via partnerships) | Multiple provinces | Major sports betting platform |

| Betsson | International | Buenos Aires Province, Córdoba | Top casino and sports operator |

| BetWarrior | International | Buenos Aires Province | Growing sports betting presence |

| Casino Trilenium Online | Local | Buenos Aires Province | Leading local casino brand |

| Bplay | Local | Santa Fe, Córdoba | Regional sports betting leader |

| Coolbet | International | Córdoba | Sports betting specialist |

| Playtech | International (B2B/Platform) | Buenos Aires Province | Platform provider and operator |

| Lotería de la Provincia | State-run | Buenos Aires Province | Lottery and betting |

| Boldt | Local | Buenos Aires Province | Casino and sports betting |

Licensing Framework and Requirements

Application Process and Eligibility

Licensing authority varies by province, with Instituto Provincial de Lotería y Casinos (IPLyC) administering Buenos Aires Province licenses and Lotería de la Ciudad (LOTBA) overseeing Buenos Aires City operations.

Financial requirements typically mandate minimum authorized capital equivalent to USD 1 million, with Buenos Aires Province requiring investments of at least ARS 200 million for preferential tax treatment.

Technical certifications must be obtained from approved testing laboratories, with Random Number Generator (RNG) certification, game fairness verification, and responsible gambling system validation required before launch.

Background checks extend to all ultimate beneficial owners holding 5 percent or more equity, company directors, key management personnel, and significant shareholders, with processes taking 90-120 days.

| Province | License Cost | Duration | Annual Renewal | Min. Capital |

|---|---|---|---|---|

| Buenos Aires Province | USD 500,000 | 15 years | No renewal required | USD 1 million |

| Buenos Aires City | USD 300,000-500,000 | 15 years | No renewal required | |

| Mendoza | USD 400,000 | 10 years + 1 year extension | Up to 5 percent GGR | USD 1 million |

| Córdoba | USD 350,000-450,000 | 15 years | No renewal required | USD 1 million |

| Santa Fe | USD 250,000-400,000 | 10-15 years | Varies | USD 800,000 |

| San Juan | USD 200,000-350,000 | 10 years | Annual fee | USD 1 million |

Local Presence and Operational Requirements

Physical presence mandates vary significantly by province, with Buenos Aires City and Buenos Aires Province requiring registered office space, though full operational teams may operate remotely.

Domain requirements typically mandate use of provincial or national domains (.ar extensions), though some provinces permit international domains with geo-location verification systems.

Server and data hosting requirements differ by jurisdiction, with Buenos Aires Province and Buenos Aires City mandating state-owned bank payment processing and some provinces requiring local server infrastructure.

Foreign ownership faces no absolute restrictions in most provinces, though partnerships with local entities provide significant advantages in navigating regulatory processes and accessing banking relationships.

Compliance Obligations and Monitoring

Player Protection and Identification

Age verification requires biometric identity confirmation through RENAPER (Registro Nacional de las Personas), Argentina’s national digital ID system, with facial recognition technology mandated by pending federal legislation.

KYC/AML compliance follows Financial Action Task Force (FATF) standards, requiring collection of government-issued ID, proof of address, tax identification numbers, and source of funds verification for large transactions.

Responsible gambling measures include mandatory pre-play warnings, session time notifications, deposit limit options, cooling-off periods, and access to self-assessment tools with links to support services.

The National Self-Exclusion Registry (RENA) allows individuals to ban themselves from all licensed platforms, with operators required to check registrations daily and immediately block excluded players.

Financial Monitoring and Reporting

Transaction monitoring systems must flag suspicious activities including unusual betting patterns, rapid deposit-withdrawal cycles, and transactions exceeding reporting thresholds set by provincial authorities.

Reporting requirements typically include monthly gross gaming revenue declarations, quarterly player activity reports, semi-annual responsible gambling metrics, and annual financial audits by approved firms.

Data retention mandates require maintaining player transaction records, game outcomes, communications, and identity verification documents for minimum five to seven years depending on provincial regulations.

Audit procedures involve quarterly technical systems reviews, annual financial statement audits, and periodic game fairness testing by approved independent laboratories.

Taxation Structure and Financial Obligations

Player Taxation

Gambling winnings in Argentina are subject to personal income tax, with rates determined by total annual income brackets ranging from 5 percent to 35 percent.

Withholding obligations require operators to deduct taxes on significant winnings before payout, with thresholds varying by province but typically applying to prizes exceeding ARS 50,000-100,000.

Players must declare gambling income in annual tax returns filed with the Federal Administration of Public Revenue (AFIP), with operators providing year-end statements detailing wins and losses.

No tax-free threshold exists for professional or consistent gamblers, though recreational players may benefit from standard personal exemptions depending on total annual income.

Operator Taxation

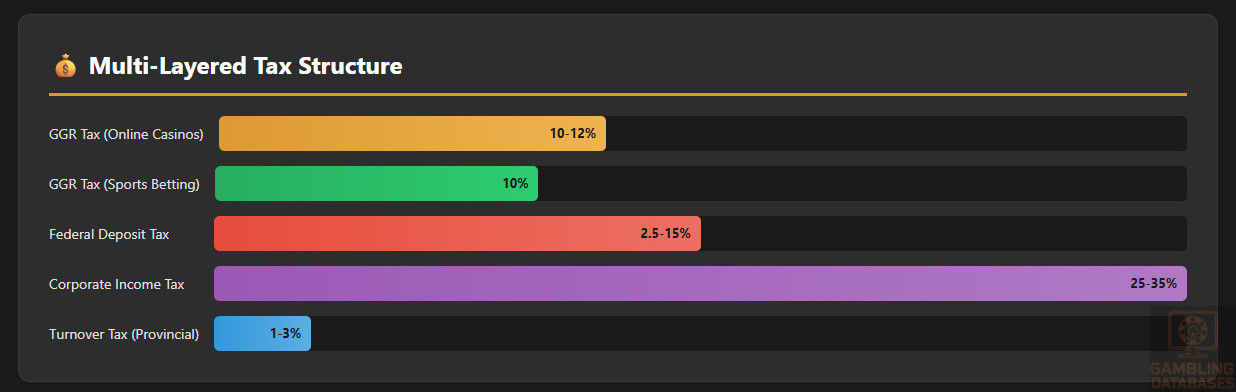

Gross Gaming Revenue taxation varies by province and game type, with online casinos typically taxed at 10-12 percent and sports betting at 10 percent of GGR.

The federal deposit tax, implemented in 2022 and modified through Decree 293/2022, ranges from 2.5 percent to 15 percent of player deposits based on operator registration status.

| Operator Status | Tax Rate | Requirements for Qualification |

|---|---|---|

| Registered with RCOSA + Investment Criteria | 2.5% | ARS 200M investment, 20% payroll increase, 20+ employees |

| Argentine Entity Registered with RCOSA | 5% | Local entity with tax ID, RCOSA registration |

| Non-Registered Argentine Entity | 7.5% | Local entity without RCOSA registration |

| Foreign Operator | 10% | Non-resident company, any status |

| Tax Haven/Non-Cooperative Jurisdiction | 15% | Based in blacklisted jurisdiction |

Corporate income tax applies at 25-35 percent on net profits, with rates depending on company structure and whether the entity qualifies for any special economic zone incentives.

Provincial turnover taxes levy additional charges on gross gaming revenue at rates ranging from 1-3 percent, calculated separately from provincial gaming taxes.

Municipal taxes may apply to operators maintaining physical office spaces, varying by location with Buenos Aires City incorporating these charges into broader provincial frameworks.

Gambling Market Financial Performance

Argentina’s total iGaming market reached approximately USD 1.39 billion in annual revenue during 2024, representing online gambling only without including land-based operations.

The broader gambling market including land-based casinos, sports betting, and lotteries generates between USD 2.5-3.8 billion annually, positioning Argentina as Latin America’s largest gambling economy.

Government tax revenues from regulated online gambling reached approximately USD 120-150 million in 2024, though this represents a small fraction of total gambling activity due to low channelization rates.

Year-over-year growth in regulated online gambling has averaged 15-20 percent since provincial markets opened, with Buenos Aires Province showing 1.8 million registered players generating USD 1.2 billion annual turnover.

| Gambling Type | Annual GGR | Market Share | Player Distribution |

|---|---|---|---|

| Online Sports Betting | USD 650-800 million | 47.3% | 3.8 million players |

| Online Lottery | USD 300-400 million | 21.6% | 3.3 million players |

| Online Slots | USD 250-350 million | 18.1% | 2.3 million players |

| Online Card Games/Poker | USD 140-190 million | 10.5% | 1.5 million players |

| Other Online Gaming | USD 50-80 million | 2.5% | 500,000 players |

Advertising and Marketing Restrictions

Current provincial regulations permit gambling advertising across most channels including television, radio, online platforms, outdoor billboards, and social media, though content restrictions apply universally.

Advertising content must include responsible gambling messages, display age restrictions prominently (18+), avoid targeting minors through youth-oriented content or influencers, and include problem gambling helpline information.

Promotional limitations exist in some provinces capping welcome bonus values, requiring transparent wagering requirements disclosure, and prohibiting misleading claims about winning probabilities.

Sponsorship regulations currently permit gambling operators to sponsor sports teams, stadiums, and events, with prominent jersey and stadium advertising visible across Argentine football leagues.

However, pending federal legislation passed by the Chamber of Deputies in November 2024 proposes comprehensive advertising bans including prohibition of all gambling advertising across media channels, elimination of sports team sponsorships, and restrictions on welcome bonuses and promotional offers.

If enacted by the Senate, the federal advertising ban would represent unprecedented federal intervention into provincial gambling regulation and could severely impact operator marketing strategies.

Time restrictions for television and radio advertising currently vary by province but typically prohibit gambling advertisements during programming with significant minor viewership, generally before 10 PM.

Recent Regulatory Changes and Their Impact

The Chamber of Deputies passed comprehensive federal gambling legislation in November 2024 with 139-36 vote, introducing biometric age verification, advertising bans, and enhanced player protection measures.

Biometric identification requirements mandate facial recognition verification through RENAPER for all online gambling accounts, with full implementation expected if Senate approval occurs before November 30, 2025.

The proposed advertising ban would eliminate all gambling promotion across social media, traditional media, billboards, sports sponsorships, and athlete endorsements, with licensed premises exempted if displaying responsible gambling warnings.

Payment method restrictions introduced in the pending legislation prohibit credit card usage for gambling deposits, limit debit card deposits to daily ATM withdrawal limits, and restrict e-wallet deposits to available balances.

Prohibition on using social welfare payment accounts (ANSeS) for gambling deposits aims to protect vulnerable populations, with operators required to screen and block these payment sources.

Córdoba Province finalized its first licensing round in 2023 with five operators, expanded to seven active operators by 2025, demonstrating provincial markets’ continued growth despite federal uncertainty.

San Juan Province opened its online market in 2024-2025, publishing regulatory frameworks and announcing public tender processes for license issuance, expanding the total addressable market for operators.

Buenos Aires Province licensing review, originally expected in late 2024, remains pending as authorities assess the potential impact of federal legislation before finalizing additional operator authorizations.

Enforcement Mechanisms and Penalties

Penalty structures vary by province but typically include fines ranging from USD 50,000 to USD 500,000 for minor violations, with license suspension for 30-180 days for moderate infractions.

License revocation represents the ultimate sanction for serious violations including money laundering facilitation, serving minors, manipulating games, or operating without valid authorization, with no refund of license fees.

Recent enforcement actions have focused on illegal offshore operators, with provincial regulators coordinating with federal authorities to block domains and restrict payment processing to unlicensed platforms.

ISP blocking of unlicensed operators occurs at the provincial level, with telecommunications providers required to implement DNS-level filtering based on regulatory blacklists updated monthly.

Payment processor restrictions mandate banks and fintech services to block transactions with unlicensed gambling sites, with fines up to USD 250,000 for financial institutions facilitating illegal gambling payments.

Criminal penalties under National Criminal Code Section 301 bis impose three to six years imprisonment for operating gambling services without proper provincial licenses, though enforcement primarily targets large-scale illegal operations.

The Federal Administration of Public Revenue (AFIP) actively pursues tax collection from operators, with particular focus on the federal deposit tax and ensuring compliance with reporting obligations.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Argentina’s population reached 45.85 million as of mid-2025, ranking 35th globally and third in South America after Brazil and Colombia, with annual growth averaging 0.8-1.0 percent.

Age distribution shows 20 percent of the population under 15 years, 65 percent in the economically active 15-64 age bracket, and 12 percent aged 65 and older, creating a mature demographic profile.

The median age of 32.9 years positions Argentina favorably for digital entertainment and gambling services, with the core gambling demographic (25-54 years) representing approximately 45 percent of the total population.

Gender ratios remain relatively balanced at 51 percent female and 49 percent male, with life expectancy averaging 77 years overall, 73.7 years for males and 80.4 years for females.

| Age Group | Population (millions) | Percentage | Gambling Market Relevance |

|---|---|---|---|

| 0-14 years | 9.2 | 20% | Prohibited (protection focus) |

| 15-24 years | 7.1 | 15.5% | Emerging market segment |

| 25-34 years | 7.8 | 17% | Core online gambling demographic |

| 35-44 years | 6.9 | 15% | High-value player segment |

| 45-54 years | 6.0 | 13% | Established gambling participants |

| 55-64 years | 4.6 | 10% | Traditional gambling preference |

| 65+ years | 5.5 | 12% | Land-based and lottery focus |

Geographic Distribution

Urban concentration reaches 96 percent of the population, with 44 million Argentines living in cities, creating highly accessible markets for digital services and concentrated marketing opportunities.

Buenos Aires Province contains 17.5 million residents, representing 38 percent of the national population, while the Autonomous City of Buenos Aires (CABA) adds 3 million, creating a metropolitan area exceeding 14 million.

Major urban centers include Córdoba (1.3 million metropolitan population), Rosario (1.3 million), Mendoza (1.0 million), Tucumán (900,000), La Plata (900,000), Mar del Plata (650,000), Salta (620,000), and Santa Fe (550,000).

Regional economic differences show significant disparities, with Buenos Aires, Córdoba, and Santa Fe provinces accounting for approximately 70 percent of GDP, while northern provinces display lower income levels and internet penetration.

Internet access follows urban-rural patterns, with urban areas achieving 92-95 percent connectivity while rural regions average 60-70 percent, though mobile internet is bridging gaps through 4G expansion.

Gambling venue concentration mirrors population distribution, with Buenos Aires metropolitan area hosting 30 percent of land-based casinos and the highest density of sports betting shops and lottery outlets.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Argentina’s GDP per capita reached USD 13,420 in 2024, with projections indicating growth to USD 15,530 by 2030 despite historical volatility and inflation challenges affecting purchasing power.

Total GDP stands at approximately USD 640 billion (nominal) or USD 1.8 trillion (PPP-adjusted), positioning Argentina as the second-largest economy in South America and among the G20 major economies.

Economic growth forecasts for 2025 range from 3.5 percent to 5.5 percent according to Goldman Sachs and BBVA respectively, driven by agricultural recovery, stabilization policies, and expanding services sector.

Economic sector composition shows services accounting for 60 percent of GDP, industry contributing 28 percent, and agriculture providing 12 percent, with technology and fintech sectors experiencing rapid expansion.

Employment rates fluctuate between 55-60 percent of working-age population, with formal employment challenged by high social security costs and inflation-driven wage pressures affecting disposable income.

Inflation remains Argentina’s persistent challenge, with rates declining from triple-digit levels in 2024 to projected sub-30 percent in 2025 under President Milei’s stabilization program, improving real purchasing power.

Income and Wealth Distribution

Average household income approximates USD 1,200-1,500 monthly (ARS 1.2-1.5 million at exchange rates), though significant regional variations exist with Buenos Aires incomes 40-60 percent above northern provinces.

Median household income sits lower at approximately USD 900-1,100 monthly, reflecting income inequality with the Gini coefficient measuring 0.42, indicating moderate inequality by Latin American standards.

Income distribution shows approximately 30 percent of households earning under USD 600 monthly, 45 percent in the USD 600-1,500 range, 20 percent between USD 1,500-3,500, and 5 percent exceeding USD 3,500.

The middle class encompasses approximately 35-40 percent of the population, with growth constrained by inflation but supported by formal employment expansion and entrepreneurial activity in services and technology.

Disposable income after essential expenses (housing, food, utilities) averages 25-35 percent of household income, with entertainment and discretionary spending recovering as inflation stabilizes under economic reforms.

Consumer spending patterns show 35-40 percent allocated to food and beverages, 20-25 percent to housing, 10-15 percent to transportation, 8-12 percent to clothing, with entertainment including gambling representing 5-8 percent.

Market Size and Growth Projections

Argentina’s online iGaming market reached USD 1.39 billion in 2024, with the broader gambling market including land-based operations generating USD 2.5-3.8 billion annually across all segments.

Historical revenue growth over the past three years (2022-2024) averaged 18-25 percent annually for online gambling, accelerating as provinces launched regulated markets and digital adoption increased.

| Year | Market Size (USD) | Active Players (millions) | ARPU (USD/year) | Penetration Rate |

|---|---|---|---|---|

| 2024 | $1.39 billion | 8.0 | $174 | 25% |

| 2025 | $1.50-2.35 billion | 8.5-9.0 | $176-261 | 26-28% |

| 2026 | $2.45 billion | 9.5-10.0 | $258 | 29-31% |

| 2027 | $2.56 billion | 10.5-11.0 | $244 | 32-34% |

| 2028 | $2.67 billion | 11.5-12.0 | $232 | 35-37% |

| 2029 | $6.60 billion* | 12.5-13.0 | $508-528 | 38-40% |

The Compound Annual Growth Rate (CAGR) for 2025-2029 projects at 4.3-4.49 percent for conservative estimates, though optimistic scenarios accounting for improved channelization suggest potential 15-20 percent growth.

Player base growth forecasts indicate 8.5-9.0 million active online gamblers by end-2025, expanding to 12.5-13.0 million by 2029 as regulatory clarity improves and additional provinces open markets.

Average Revenue Per User (ARPU) currently sits at USD 174 annually for online gambling, with projections showing growth to USD 250-528 by 2029 as player sophistication increases and higher-value segments expand.

Market penetration among adults (18+) currently reaches 25 percent for online gambling participation, with forecasts projecting 38-40 percent penetration by 2029, approaching mature European market levels.

Online versus land-based revenue split currently favors land-based at approximately 60-65 percent, but online is projected to reach 50-55 percent market share by 2027-2028 as digital adoption accelerates.

Regional comparison shows Argentina generating 2-3 times the online gambling revenue of Chile, approximately 40-50 percent of Brazil’s market, and representing 35-40 percent of total Latin American iGaming revenue.

Education, Skills, and Digital Literacy

Educational Foundation

Argentina achieves 98 percent literacy rate overall, with virtually no gender gap (98.04 percent male, 98.1 percent female), ranking among Latin America’s highest and supporting digital service adoption.

Education levels show 95 percent primary completion, 82 percent secondary completion, and 36 percent tertiary education enrollment, creating a highly educated workforce capable of engaging with complex digital platforms.

Digital literacy indicators rank favorably in regional comparisons, with 85-90 percent of internet users capable of conducting e-commerce transactions, managing digital wallets, and navigating sophisticated applications.

Workforce skill levels concentrate in services and technology sectors, with Buenos Aires hosting one of Latin America’s largest tech talent pools, though gambling-specific expertise remains limited requiring imported knowledge.

Technology adoption readiness scores highly, with Argentina producing one of the highest rates of unicorn startups per capita in Latin America, indicating entrepreneurial sophistication and innovation capacity.

English language proficiency among urban educated populations reaches 15-20 percent moderate fluency, though Spanish remains overwhelmingly dominant requiring full localization for consumer-facing gambling services.

Cultural and Social Factors

Communication and Language

Spanish serves as the primary language for 99 percent of the population, with Argentine Spanish featuring distinctive pronunciation and vocabulary requiring localization beyond standard Castilian Spanish.

Internet language preferences show 95 percent of users engaging in Spanish-language content, with English-language sites achieving limited penetration outside business and technology professional segments.

Business communication norms favor formal professional interactions initially, transitioning to warmer personal relationships as trust develops, important for B2B partnerships and regulatory relationships in gambling sector.

Language requirements for gambling websites mandate Spanish as primary interface language in all provinces, with customer support required in Spanish during local business hours minimum.

Cultural Attitudes

Gambling acceptance levels remain moderate to high in Argentine society, with sports betting particularly normalized through cultural association with football (soccer) passion and traditional lottery participation.

Religious influences show 76.5 percent Roman Catholic identification and 9 percent Protestant, though religious opposition to gambling remains muted compared to other Latin American markets, with cultural acceptance prevailing.

Foreign brand perception varies by sector, with international gambling operators viewed positively if demonstrating local commitment through Argentine partnerships, Spanish localization, and responsible gambling emphasis.

Risk tolerance indicators suggest Argentines display higher risk acceptance than regional averages, partly driven by economic volatility experience creating comfort with uncertainty and speculative activities.

Entertainment preferences center heavily on football (soccer), with 85 percent male participation in sports betting focusing on domestic and international football competitions, creating natural market entry point.

Social gambling culture emphasizes group activities and sports bar viewing experiences, though online gambling adoption has normalized solitary mobile gambling sessions, particularly among younger demographics.

Problem Gambling and Social Considerations

Problem gambling prevalence estimates range from 0.5-1.5 percent of adult population based on regional studies, translating to approximately 180,000-540,000 individuals experiencing gambling-related harm.

At-risk population statistics suggest an additional 2-3 percent of adult population (720,000-1.08 million individuals) display problematic gambling behaviors without meeting clinical addiction criteria.

Age groups most affected by gambling addiction concentrate in 18-35 year demographic, with increased online gambling access and sports betting proliferation raising concerns about youth gambling habits.

Gender distribution of problem gamblers shows 70-75 percent male and 25-30 percent female, reflecting broader gambling participation patterns though female online gambling participation is growing rapidly.

Underage gambling issues have intensified with online gambling expansion, with surveys indicating 8-12 percent of minors aged 15-17 reporting online gambling experience, driving pending federal legislation.

| Metric | Estimate | Notes |

|---|---|---|

| Problem Gamblers (adults) | 180,000-540,000 | 0.5-1.5% of adult population |

| At-Risk Gamblers | 720,000-1.08 million | 2-3% of adult population |

| Minors Reporting Online Gambling | 8-12% of 15-17 age group | Primary driver of regulatory concern |

| Male Problem Gamblers | 70-75% | Predominantly sports betting focused |

| Female Problem Gamblers | 25-30% | Growing with online casino adoption |

| Treatment Facilities | 50-75 nationwide | Concentrated in major urban centers |

Government response measures include the Interministerial Committee for Prevention and Treatment of Compulsive Gambling in Adolescents created in 2024, focusing on youth protection and public policy development.

Treatment facilities remain limited with 50-75 specialized gambling addiction centers nationwide, primarily concentrated in Buenos Aires, Córdoba, and other major cities, creating access barriers for rural populations.

Social responsibility requirements for operators include mandatory responsible gambling training for staff, player education materials, self-exclusion system integration, and deposit limit offerings as standard features.

Mandatory contributions to problem gambling funds vary by province, typically ranging from 0.5-2 percent of gross gaming revenue directed toward prevention, treatment, and research programs.

Recent studies on gambling harm increased significantly following online market expansion, with academic institutions and health ministries conducting prevalence surveys and publishing findings driving regulatory responses.

Political Structure and Governance

Argentina operates as a federal presidential republic with 24 provinces and one autonomous city (Buenos Aires), each exercising constitutional sovereignty over gambling regulation within their territories.

Political stability improved following President Javier Milei’s election in late 2023, implementing economic reforms and deregulation policies affecting telecommunications and gaming sectors, though federal-provincial tensions remain.

Regulatory consistency varies significantly across provinces, with Buenos Aires City and Buenos Aires Province maintaining sophisticated frameworks while smaller provinces display less developed regulatory capacity and enforcement mechanisms.

Corruption Perception Index ranks Argentina 94th out of 180 countries with a score of 38/100, indicating moderate corruption challenges requiring robust compliance programs and careful due diligence on local partnerships.

International relations generally support business operations, with Argentina maintaining trade agreements with Mercosur partners (Brazil, Paraguay, Uruguay) and bilateral investment treaties with major economies including United States and European Union members.

Argentina holds no EU membership or association status but maintains cooperative relationships with European regulatory bodies, facilitating information exchange on gambling regulation best practices and technical standards.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration reached 90.1 percent of the population in early 2025, representing 41.2 million users with annual growth of 1.3 percent (542,000 new users) between January 2024-2025.

Daily internet usage averages 5.3 hours per person, increased from 4.95 hours in 2022, with mobile devices accounting for 75-80 percent of total internet access time.

Mobile device adoption reaches 97 percent smartphone penetration with 41.1 million smartphone users in 2024, projected to grow to 44.15 million by 2029, ensuring universal access to mobile gambling platforms.

Social media engagement shows 32.2 million user identities (70.3 percent of population) active on platforms, with Facebook, Instagram, WhatsApp, and X (Twitter) dominating, creating marketing channels for gambling operators.

E-commerce participation reached 95 percent of connected adults having made online purchases, with 69 percent of e-commerce volume coming from mobile devices, demonstrating comfort with mobile transactions.

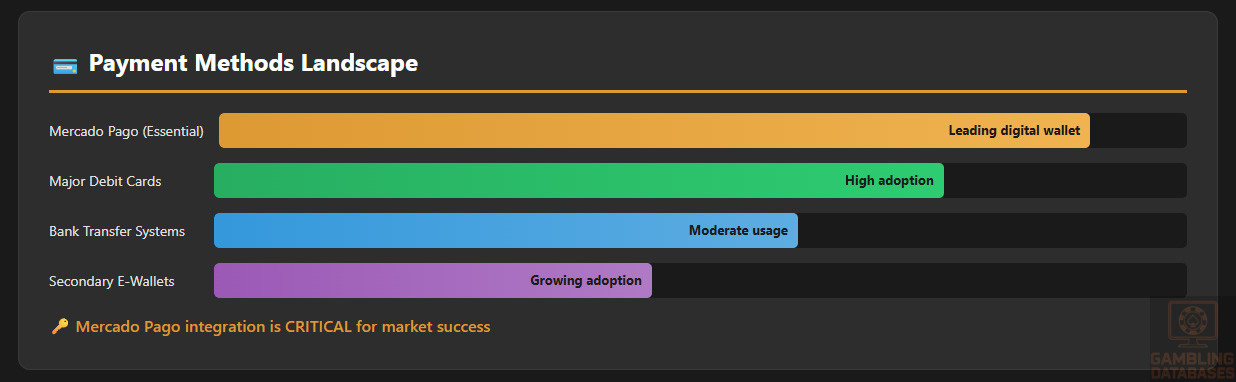

Digital payment adoption expanded dramatically with Mercado Pago achieving market-leading position, complemented by traditional bank cards and emerging fintech solutions supporting gambling payment requirements.

Online banking penetration reaches 65-70 percent of banked population, with mobile banking apps widely adopted and facilitating seamless integration between banking services and gambling deposit/withdrawal processes.

Digital Payment Behavior

Payment method preferences show Mercado Pago digital wallet dominating with approximately 40-45 percent market share for online transactions, followed by debit cards (30-35 percent) and bank transfers (15-20 percent).

Credit cards, while popular for e-commerce generally, face restrictions for gambling under pending federal legislation, with current usage representing 10-15 percent of gambling deposits before potential prohibition.

| Payment Method | Market Share | Gambling Suitability | Regulatory Status |

|---|---|---|---|

| Mercado Pago | 40-45% | Excellent – instant deposits/withdrawals | Permitted, widely integrated |

| Debit Cards | 30-35% | Good – instant deposits, 24-48hr withdrawals | Permitted with daily limits |

| Bank Transfers | 15-20% | Moderate – slower processing | Permitted, some instant options |

| Credit Cards | 10-15% | Good but facing restrictions | Pending federal prohibition |

| Cryptocurrency | 1-3% | Limited – not authorized for gambling | Not permitted for gambling transactions |

| Cash (lottery outlets) | 5-8% | Regional use for deposits | Permitted in some provinces |

Digital wallet alternatives include Ualá, Naranja X, Personal Pay, and traditional bank digital wallets (Brubank, Prex), providing multiple integration options for gambling operators beyond Mercado Pago.

Online transaction patterns show average gambling deposits ranging from USD 20-50, with withdrawal requests averaging USD 30-80, though high-value players may transact significantly larger amounts.

Transaction frequency among active players averages 2-4 deposits monthly for recreational players and 8-15 deposits monthly for regular gamblers, with instant deposit expectations standard across user base.

Trust in online payment systems rates highly at 75-80 percent of digital users expressing confidence in secure transactions, supported by strong fintech regulation and consumer protection frameworks.

Cryptocurrency adoption for gambling remains unauthorized under current regulations requiring peso-denominated transactions, though 5-10 percent of Argentines own cryptocurrency primarily for investment purposes.

Gaming and Gambling Preferences

Current Market Participation

Approximately 45-50 percent of Argentine adults (18+) participate in some form of gambling annually, including lottery, sports betting, casino gaming, and bingo across land-based and online channels.

Online gambling participation reached 25 percent of adults in 2024 with 8 million active online players, representing significant growth from 18-20 percent in 2022 as provincial markets matured.

Popular gambling activities ranked by participation show sports betting leading at 47.3 percent of gamblers, lottery at 41.8 percent, online slots at 29.1 percent, and card games including poker at 18.2 percent.

Sports betting focuses overwhelmingly on football (soccer) with Argentine Primera División, Copa Libertadores, European leagues, and international tournaments driving 80-85 percent of sports betting volume.

Live dealer games have gained significant popularity among casino players, particularly live roulette and live blackjack, with 35-40 percent of online casino revenue coming from live dealer products.

Lottery participation remains deeply culturally embedded with weekly draws attracting millions of participants across all demographic segments, often representing gateway gambling experience for older demographics.

Seasonal patterns show increased gambling activity during football season (February-December), summer holidays (December-February), and major tournament periods (World Cup, Copa America), with 20-30 percent volume increases.

Consumer Behavior Patterns

Average spending per online player ranges from USD 120-180 monthly for regular players, with recreational players averaging USD 40-60 monthly and high-value players exceeding USD 500-1,000 monthly.

Betting habits show typical sports wagers ranging from USD 5-20 for casual bets to USD 50-200 for serious punters, with casino game bets averaging USD 0.50-5.00 per spin/hand.

| Player Segment | Population % | Avg. Monthly Spend | Session Frequency | Primary Activity |

|---|---|---|---|---|

| Recreational | 60% | $40-60 | 2-4 times/month | Sports betting, lottery |

| Regular | 30% | $120-180 | 8-12 times/month | Sports betting, slots |

| High-Value | 8% | $500-1,000+ | 15-25 times/month | All products |

| VIP | 2% | $2,000-10,000+ | Daily | High-stakes betting, live casino |

Platform preferences decisively favor mobile with 70 percent of gambling transactions occurring on smartphones, 25 percent on desktop computers, and 5 percent on tablets.

Peak gambling times concentrate on evenings 7 PM-11 PM local time during weekdays, with weekend afternoons and evenings (2 PM-midnight) showing 40-50 percent higher activity than weekday averages.

Session length averages 15-25 minutes for sports betting focused on specific matches, 30-45 minutes for casino gaming sessions, and 60-90 minutes for poker or extended multi-event betting.

Retention patterns show 30-day retention rates of 35-45 percent for sports betting operators and 25-35 percent for casino operators, with loyalty programs significantly improving these metrics.

Bonus sensitivity rates highly among Argentine players, with 70-80 percent of new registrations driven by welcome bonus promotions and 50-60 percent of players regularly claiming reload bonuses.

Preferred game types vary by age, with 18-35 year-olds favoring sports betting and slots, 35-50 year-olds showing balanced preferences across products, and 50+ demographics preferring lottery and table games.

Deposit and withdrawal frequency shows active players depositing 2-4 times monthly on average, with withdrawal requests occurring 1-2 times monthly, though patterns vary significantly by player segment and gambling success.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Argentina’s internet penetration reached 90.1 percent in early 2025, representing 41.2 million connected users, positioning the country among Latin America’s most digitally connected markets.

Fixed broadband penetration stands at approximately 25 percent of households with dedicated connections, while the remaining population relies primarily on mobile internet through 4G and emerging 5G networks.

Average internet speeds show median fixed broadband download speeds of 92.62 Mbps and upload speeds of 40-50 Mbps, representing 22 percent annual improvement from 2024’s 75.89 Mbps.

Mobile internet download speeds averaged 35.16 Mbps in January 2025, showing remarkable 40.7 percent year-over-year growth from 25 Mbps in 2024, supporting seamless mobile gambling experiences.

| Connection Type | Median Speed | YoY Growth | Regional Ranking |

|---|---|---|---|

| Fixed Broadband Download | 92.62 Mbps | +22.0% | 3rd in Latin America |

| Fixed Broadband Upload | 40-50 Mbps | +18% | 4th in Latin America |

| Mobile Download | 35.16 Mbps | +40.7% | 5th in Latin America |

| Mobile Upload | 12-15 Mbps | +35% | 6th in Latin America |

Network reliability maintains 95-98 percent uptime in urban areas, with occasional instability during peak evening hours (7-11 PM) in residential zones due to bandwidth congestion.

Infrastructure investment trends show government and private sector commitments exceeding USD 2 billion annually for fiber expansion, 5G deployment, and rural connectivity projects through state-owned ARSAT.

Global internet speed rankings position Argentina as a mid-tier performer, trailing Chile and Uruguay in Latin America but surpassing Brazil and Colombia in fixed broadband performance.

The rural-urban connectivity gap remains significant with urban areas achieving 92-95 percent internet access while rural regions average 60-70 percent, though mobile 4G expansion is bridging this divide.

5G and Future Technology Deployment

Current 4G coverage reaches 85-90 percent of the population with three major network operators (Claro, Telefónica/Movistar, Telecom) providing extensive nationwide service supporting mobile gambling platforms.

5G spectrum auctions completed in October 2023 allocated frequencies to the three major operators, with commercial 5G services launching in Buenos Aires, Córdoba, Rosario, and other major cities throughout 2024-2025.

5G rollout timeline projects 20-25 percent population coverage by end-2025, expanding to 50-60 percent by 2027, with focus on urban centers where gambling activity concentrates.

Future infrastructure plans include additional spectrum auctions announced by the Milei administration for remaining frequencies originally allocated to regulatory authority Enacom, opening opportunities for new entrants.

Network operator landscape consists of Claro (América Móvil subsidiary), Telefónica Argentina (Movistar brand), and Telecom Argentina, with market shares approximately 35 percent, 33 percent, and 32 percent respectively.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Three major mobile network operators dominate the market, providing comprehensive coverage across urban areas and major transportation corridors, with rural coverage improving through government universal access programs.

Market share breakdown shows Claro leading with 35-36 percent, Telefónica/Movistar at 33-34 percent, and Telecom Argentina at 32-33 percent, creating competitive pricing and service quality environment.

Coverage quality varies by operator and geography, with all three providers offering excellent urban 4G service but Claro maintaining slight advantages in rural coverage breadth.

4G coverage maps show approximately 85-90 percent population coverage, with 5G expanding rapidly in major cities and operators planning nationwide 5G rollout completion by 2027-2028.

Data costs declined significantly following market deregulation in 2024, with average cost per GB ranging from USD 2-4 for prepaid plans and USD 1-2 for postpaid unlimited plans.

Mobile payment integration with operator billing remains limited for gambling due to regulatory restrictions, though operators partner with digital wallets like Mercado Pago for seamless payment experiences.

Mobile wallet adoption reaches 65-70 percent of smartphone users, with Mercado Pago alone serving over 30 million Argentine users and facilitating majority of online gambling transactions.

Device Penetration

Smartphone adoption rates reached 97 percent of the population in 2025, representing 41.1 million smartphone users with projections indicating growth to 44.15 million by 2029.

Smartphones per capita average 1.4 devices per person among adult population, with many users maintaining multiple devices for personal and work purposes or upgrading devices frequently.

Device preferences show Android dominating with 77.6 percent market share compared to iOS at 21-22 percent, with Android’s affordability and variety appealing to mass market consumers.

Average device specifications include 4-6 GB RAM, 64-128 GB storage, and processors capable of handling modern mobile gambling applications with high-quality graphics and live streaming.

Popular brands include Samsung (30-35 percent market share), Motorola (25-28 percent), Xiaomi (12-15 percent), Apple (21-22 percent), and various Chinese manufacturers comprising remaining market share.

Mobile internet usage patterns show daily average of 5.3 hours per user, with 75-80 percent of total internet access time occurring on mobile devices rather than desktop computers.

Mobile gaming penetration reaches 60-65 percent of smartphone users engaging with mobile games monthly, creating familiar context for mobile gambling adoption and user interface expectations.

Financial Services and Payment Infrastructure

Banking System Structure

Major banks operating in Argentina include Banco de la Nación Argentina (state-owned, largest by assets), Banco Santander Río, Banco Galicia, BBVA Argentina, Banco Macro, and Banco Itaú Argentina.

Market share concentration shows the top 10 banks controlling approximately 75-80 percent of banking assets, with Banco de la Nación alone accounting for 25-30 percent through extensive branch network.

Digital banking adoption accelerated dramatically with 65-70 percent of banked population actively using online banking services and 75-80 percent utilizing mobile banking applications for transactions.

Account penetration rates indicate approximately 70-75 percent of adults maintain formal bank accounts, with financial inclusion initiatives expanding access though significant unbanked population remains in rural areas.

Credit and lending markets show limited depth due to inflation volatility and economic instability, with consumer credit primarily short-term and mortgage lending constrained by peso depreciation concerns.

ATM density averages 40-50 ATMs per 100,000 adults in urban areas, with concentration in Buenos Aires metropolitan region and lower density in provincial cities and rural zones.

Payment Processing Options

Available payment methods for iGaming emphasize digital wallets (Mercado Pago, Ualá, Naranja X), debit cards, bank transfers, and cash deposits at lottery outlets in some provinces.

Credit and debit card penetration shows approximately 60-65 percent of adults holding debit cards and 40-45 percent with credit cards, though gambling regulations increasingly restrict credit card usage.

| Payment Method | Deposit Speed | Withdrawal Speed | Transaction Fees | User Preference |

|---|---|---|---|---|

| Mercado Pago | Instant | Instant-24 hours | 2-3% | 45% |

| Debit Cards | Instant | 24-48 hours | 3-4% | 30% |

| Bank Transfers | 1-2 hours | 24-72 hours | 1-2% | 15% |

| Other E-wallets (Ualá, etc) | Instant | Instant-24 hours | 2-3% | 8% |

| Cash (Lottery Outlets) | Instant (after deposit) | N/A | 3-5% | 2% |

E-wallet platforms beyond Mercado Pago include Ualá (5+ million users), Naranja X (3+ million users), Personal Pay, and bank-integrated wallets from major financial institutions.

Bank transfer systems offer both traditional ACH-equivalent transfers (24-72 hours) and instant CVU (Clave Virtual Uniforme) transfers enabling real-time payments between bank accounts and digital wallets.

Cryptocurrency acceptance for gambling remains prohibited by regulations requiring peso-denominated transactions, though 5-10 percent of Argentines own cryptocurrency primarily for investment and inflation hedging.

Processing fees typically range from 2-4 percent for deposits and 2-5 percent for withdrawals, with digital wallet transactions generally cheaper than card-based payments.

Transaction processing timelines show deposits clearing instantly for digital wallets and cards, while withdrawals process within 24-48 hours for e-wallets and 3-5 business days for bank transfers.

International payment capabilities remain limited due to foreign exchange controls and capital restrictions, requiring most gambling transactions to occur in Argentine pesos through local payment infrastructure.

Regulatory restrictions on gambling payments mandate use of state-owned banks in some provinces (Buenos Aires City and Province), limiting payment processor options and requiring specialized integration.

Chargebacks and dispute resolution follow standard banking protocols, with operators required to maintain documentation of transactions, bonus terms acceptance, and player communications for dispute defense.

E-commerce and Digital Economy

Digital Market Development

E-commerce market size reached USD 26.7 billion in transaction volume during 2023, with projections indicating 17 percent CAGR through 2027, reaching approximately USD 47-50 billion.

Online retail penetration represents approximately 4 percent of Argentina’s GDP and 12-15 percent of total retail sales, with growth accelerating following pandemic-driven digital adoption and economic volatility.

Digital service adoption extends beyond physical goods to financial services, entertainment subscriptions, online education, telemedicine, and gambling, creating sophisticated digital consumer behaviors.

Consumer trust in online transactions improved substantially with 80-85 percent of internet users expressing confidence in digital payment security, supported by improved fraud prevention and regulatory oversight.

Popular e-commerce platforms include Mercado Libre (dominant with 60-70 percent market share), followed by international players like Amazon Argentina and domestic retailers’ online channels.

Cross-border online shopping represents approximately 3-5 percent of e-commerce volume, with growth potential constrained by import duties, shipping costs, and peso depreciation affecting pricing competitiveness.

Digital goods and services consumption spans streaming entertainment (Netflix, Spotify, Disney+), software subscriptions, online gaming, gambling, and digital education platforms with high penetration among middle-class consumers.

Business Environment and Regulatory Framework

Ease of Business Operations

World Bank Doing Business ranking historically placed Argentina in the 120-130 range out of 190 countries, though the ranking was discontinued in 2021 following methodology controversies.

Ease of Starting a Business metrics showed Argentina requiring 11-12 procedures, 25-30 days, and costs equivalent to 5-7 percent of per capita income, placing it mid-range among Latin American nations.

Business registration processes involve name approval with General Inspection of Justice (IGJ), drafting articles of incorporation through notary public, capital deposit at Central Bank, publication in Official Gazette, and tax registration.

Foreign investment policies underwent significant liberalization under President Milei’s administration, eliminating many restrictions and simplifying registration requirements that previously required proof of foreign economic activity.

Operational cost structures vary by location, with Buenos Aires office rent ranging from USD 15-30 per square meter monthly for standard spaces and USD 30-60 for premium locations.

Labor market conditions offer access to educated talent pool with 98 percent literacy and strong technology skills, though formal employment costs include high social security contributions (approximately 17-27 percent employer burden).

Corporate Structure and Registration

Available Entity Types

Limited Liability Company (Sociedad de Responsabilidad Limitada – S.R.L.) requires minimum 2 shareholders, maximum 50 shareholders, with liability limited to capital contributions and relatively simple governance structure.

Stock Corporation (Sociedad Anónima – S.A.) requires minimum 2 shareholders, no maximum limit, with shares freely transferable and structure suitable for larger operations or future public listing.

Simplified Stock Company (Sociedad por Acciones Simplificada – S.A.S.) created in 2017 requires only 1 shareholder, minimal capital requirements, and streamlined formation process designed for startups and small businesses.

Branch Office allows foreign companies to establish local presence without creating separate legal entity, though requires local legal representative and limits operations to parent company’s scope.

Recommended structure for iGaming operators is typically S.R.L. or S.A., with S.R.L. preferred for smaller operations and S.A. suited for larger investments requiring complex capitalization structures.

| Entity Type | Min. Shareholders | Min. Capital | Formation Time | Best For |

|---|---|---|---|---|

| S.R.L. (LLC) | 2 (max 50) | USD 1,000-5,000 | 8-12 weeks | Small-medium operators |

| S.A. (Stock Corp) | 2 (no max) | USD 7,500+ | 10-14 weeks | Large operators, licensing |

| S.A.S. (Simplified) | 1 (no max) | Minimal | 4-6 weeks | Startups, testing market |

| Branch Office | N/A | None | 6-10 weeks | Limited operations only |

Registration Requirements

Registration timelines span 8-14 weeks from initial documentation to operational status, with S.R.L. averaging 8-12 weeks, S.A. requiring 10-14 weeks, and S.A.S. completing in 4-6 weeks.

Registration costs include government fees (USD 500-1,500), notary fees (USD 800-1,500), legal fees (USD 2,000-5,000), and publication costs (USD 200-500), totaling USD 3,500-8,500 for standard incorporation.

Required documents include shareholders’ identification (passport, national ID), proof of address for all shareholders, articles of incorporation drafted by notary, capital deposit certificate, and power of attorney if shareholders absent.

Foreign ownership rules impose no absolute restrictions on percentage of foreign ownership in most sectors including gambling, though local partnerships provide significant practical advantages for regulatory relationships.

Minimum capital requirements vary by entity type, with S.R.L. requiring minimal capital (USD 1,000-5,000 sufficient), S.A. mandating USD 7,500 minimum, and gambling licenses typically requiring USD 1 million operational capital.

Ongoing compliance requirements include annual financial statement filing with Public Registry of Commerce, monthly/quarterly tax returns to AFIP, maintenance of corporate books (shareholders, board meetings, accounting), and annual tax compliance certificates.

Corporate governance requirements mandate board of directors for S.A. (minimum 1 director) and managers for S.R.L., with majority of directors/managers required to be Argentine residents in most cases.

Taxation Framework

Corporate Income Tax Structure

Standard corporate income tax rates apply progressively based on annual taxable income: 25 percent on income up to ARS 5 million, 30 percent on ARS 5-50 million, and 35 percent on income exceeding ARS 50 million.

Special economic zones offer limited incentives in specific regions (Tierra del Fuego, free trade zones), though gambling operations typically cannot access these benefits due to sector-specific restrictions.

Tax holidays or reduced rates for new businesses remain unavailable for gambling sector, with full tax obligations applying from commencement of operations regardless of profitability or investment levels.

International tax treaties exist with numerous countries including Spain, Italy, Germany, France, United Kingdom, United States (limited scope), Brazil, Chile, and other nations, enabling reduced withholding rates on dividends and interest.

Transfer pricing rules require arm’s length pricing for related-party transactions, with documentation requirements for transactions exceeding specified thresholds and heavy penalties for non-compliance.

Withholding tax rates for non-residents include 7 percent on interest payments, 13 percent on royalties and technical services, and 35 percent on dividends, subject to treaty reductions where applicable.

VAT/IVA applies at standard 21 percent rate on most goods and services, though gambling services face specialized treatment with provincial gaming taxes substituting for VAT in most cases.

Personal Income Tax

Individual tax rates apply progressively from 5 percent on lowest income brackets to 35 percent on highest incomes exceeding ARS 2.5 million annually, with inflation-adjusted brackets updated periodically.

Withholding requirements for employees mandate monthly income tax withholding by employers, with final annual reconciliation through personal tax returns filed by individuals before June 30 each year.

Social security contributions include 17 percent employee contribution and approximately 17-27 percent employer contribution on gross salaries, covering retirement, health insurance, unemployment, and family benefits.

Tax residency rules define residents as individuals physically present in Argentina for more than 12 months in any 24-month period or maintaining principal residence/economic interests in Argentina.

Taxation of foreign employees follows standard progressive rates for resident employees, with non-residents taxed only on Argentine-source income at flat 35 percent rate on employment income.

Market Entry Considerations

Recommended Entry Strategies

Optimal market entry approaches prioritize Buenos Aires Province and Buenos Aires City as initial targets given 40 percent national population concentration, mature regulatory frameworks, and established licensing processes.

Local partnership requirements while not legally mandatory prove practically essential for navigating provincial regulatory relationships, accessing state-owned bank payment processing, and establishing credibility with authorities.

White label versus proprietary platform considerations favor proprietary platforms for operators planning multi-provincial expansion, while white label solutions suit testing market with lower capital commitment.

Technology infrastructure leveraging strategies emphasize cloud-based solutions hosted through approved providers meeting local data security requirements, avoiding expensive on-premise infrastructure where regulations permit.

Marketing and localization requirements demand full Spanish translation with Argentine dialect consideration, integration with local sports leagues and events, partnerships with Argentine sports personalities, and culturally appropriate promotional strategies.

Payment provider selection criteria prioritize Mercado Pago integration as essential, complemented by major debit cards, bank transfer systems, and secondary e-wallets to maximize payment success rates.

Risk mitigation strategies include phased provincial rollout starting with 1-2 provinces, local legal counsel retention, compliance monitoring systems, diversified payment providers, and contingency planning for regulatory changes.

Typical Costs and Timelines

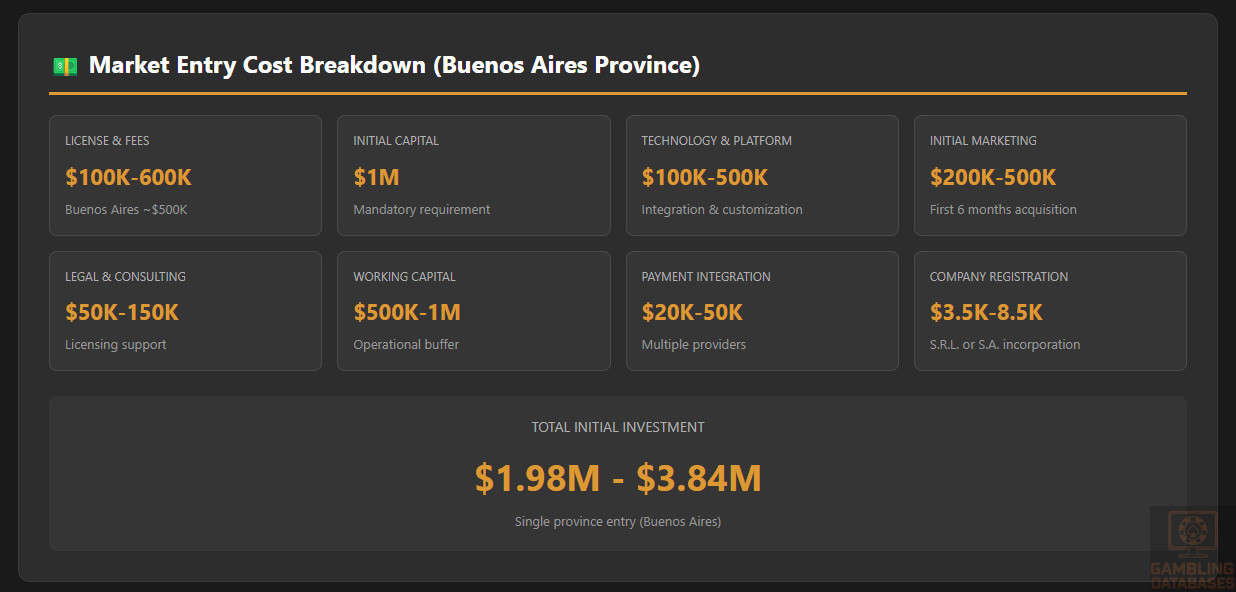

| Cost Category | Initial Investment (USD) | Notes |

|---|---|---|

| License Application & Fees | 100,000-600,000 | Varies by province; Buenos Aires ~$500k |

| Legal & Consulting Fees | 50,000-150,000 | Licensing support, regulatory compliance |

| Company Registration | 3,500-8,500 | S.R.L. or S.A. incorporation costs |

| Initial Capital Requirement | 1,000,000 | Mandatory for most provincial licenses |

| Office Setup | 10,000-30,000 | First 6 months rent, furnishing, equipment |

| Technology & Platform | 100,000-500,000 | Platform licensing, integration, customization |

| Payment Integration | 20,000-50,000 | Multiple provider setup, compliance |

| Initial Marketing Budget | 200,000-500,000 | First 6 months player acquisition |

| Working Capital Reserve | 500,000-1,000,000 | Player funds, operational buffer |

| TOTAL INITIAL INVESTMENT | 1.98-3.84 million | Single province entry (Buenos Aires) |

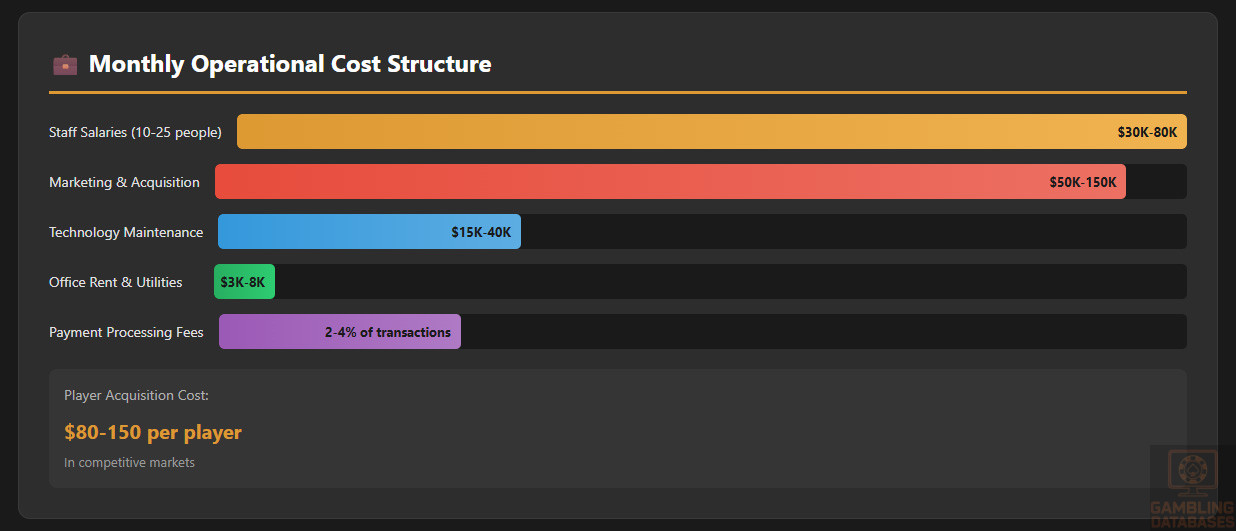

Operational cost estimates include monthly staff salaries (USD 30,000-80,000 for 10-25 person team), office rent and utilities (USD 3,000-8,000), technology maintenance (USD 15,000-40,000), payment processing fees (2-4 percent of transactions).

Marketing and customer acquisition costs typically range from USD 80-150 per acquired player in competitive markets, with total monthly marketing budgets of USD 50,000-150,000 for growing operations.

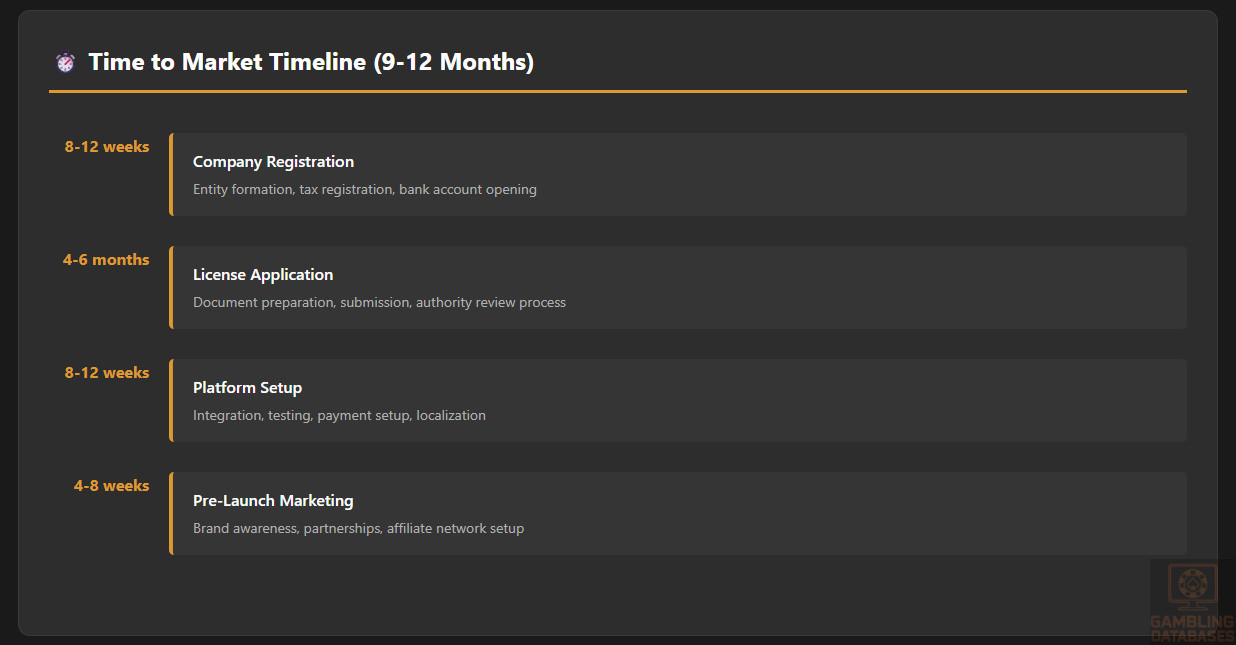

| Phase | Duration | Key Activities |

|---|---|---|

| Company Registration | 8-12 weeks | Entity formation, tax registration, bank account |

| License Application | 4-6 months | Document preparation, submission, authority review |

| Platform Setup | 8-12 weeks | Integration, testing, payment setup, localization |

| Pre-Launch Marketing | 4-8 weeks | Brand awareness, partnerships, affiliate setup |

| TOTAL TIME TO MARKET | 9-12 months | From decision to commercial launch |

Resource requirements include minimum 10-15 staff initially (management, customer support, compliance, marketing, finance), expanding to 25-50 employees for mature multi-provincial operations.

Key positions needed include Country Manager, Compliance Officer, Marketing Manager, Customer Support Team Lead, Finance Manager, IT/Platform Manager, and legal counsel (can be external).

Technology stack requirements encompass licensed gambling platform, payment gateway integrations, CRM system, responsible gambling tools, fraud detection systems, business intelligence/reporting tools, and customer support platforms.

Success Factors and Challenges

Key Success Enablers

Understanding local player preferences requires research into Argentine sports betting culture, particularly football passion, popular local leagues, and preferred betting types (match winner, over/under, accumulator bets).

Localized payment methods integration with Mercado Pago as priority, supplemented by all major debit cards and alternative e-wallets, ensures maximum payment success rates and player convenience.

Mobile-first approach proves essential with 70 percent of transactions on mobile devices, requiring responsive design, native apps for iOS/Android, and optimization for varying network speeds and device capabilities.

Effective marketing channels include social media marketing (Facebook, Instagram, X/Twitter), sports sponsorships (though pending federal restrictions), affiliate programs, influencer partnerships, and content marketing around football.

Strong customer support in Spanish with Argentine cultural sensitivity, available via WhatsApp (preferred channel), email, phone, and live chat during extended hours covering peak gambling times.

Competitive bonus and promotion strategy balances acquisition costs with lifetime value, offering welcome bonuses competitive with market leaders while maintaining sustainable wagering requirements and terms.

Responsible gambling commitment demonstrated through visible tools, support resource links, staff training, self-exclusion promotion, and partnership with problem gambling organizations builds regulatory trust and social license.

Local sports and events coverage emphasizes Argentine Primera División, Copa Libertadores, Argentine national team matches, international football, and secondary sports like basketball, rugby, and tennis.

Major Operational Challenges

Regulatory compliance complexity stems from managing multiple provincial frameworks simultaneously, each with distinct requirements for reporting, technical standards, advertising, and player protection.

High taxation burden combines provincial GGR taxes (10-12 percent), federal deposit taxes (2.5-15 percent), corporate income tax (25-35 percent), and turnover taxes (1-3 percent), significantly impacting profitability.

Payment processing restrictions in provinces mandating state-owned bank usage create integration challenges, limit provider flexibility, and may increase transaction costs and processing times.

Marketing and advertising limitations under pending federal legislation threaten to eliminate most promotional channels including sports sponsorships, welcome bonuses, and social media advertising, requiring strategy pivots.

Competition from established operators includes well-funded international brands with existing licenses, established player bases, brand recognition, and optimized operations creating high barriers to market share gain.

Player acquisition costs remain elevated in competitive markets with established operators, requiring substantial marketing investment and differentiated value propositions to attract players from incumbents.

Talent shortage exists for gambling-specific expertise including compliance specialists, responsible gambling professionals, and gambling platform specialists, requiring international recruitment or extensive training programs.

Economic volatility with inflation, currency depreciation, and changing foreign exchange policies creates planning challenges, affects player spending power, and complicates financial forecasting and capital management.

Cultural Considerations

Local holidays and peak seasons include summer vacation (December-February), football season intensity (March-November), World Cup/Copa America years with massive engagement spikes, and Christmas/New Year promotional opportunities.

Popular local sports beyond football include basketball (Liga Nacional), rugby (Los Pumas national team), tennis (strong Argentine tradition), polo, and motorsports, offering secondary betting market opportunities.

Preferred customer service channels emphasize WhatsApp as primary contact method for Argentine consumers, followed by direct phone support, with email considered slower and less personal option.

Communication style preferences favor warm, personal interactions over formal corporate language, with Argentine Spanish dialect usage and cultural references creating connection and authenticity with players.

Trust-building requirements for foreign brands include local partnerships, visible local presence, community engagement, transparent operations, responsive customer service, and sponsorship of local sports or cultural events.

Exit Strategy Planning

Market liquidity for operator sales remains moderate with international operators seeking Argentine market entry, regional consolidation activity, and local investors interested in established brands with proven licenses.

Regulatory requirements for ownership transfer include provincial authority approval of new owners, background checks on acquiring parties, and potential license modification procedures varying by jurisdiction.

License transferability generally permitted in most provinces subject to authority approval, with Buenos Aires and other mature markets having established transfer procedures including transfer fees.

Typical valuation multiples in Latin American gambling markets range from 5-8x EBITDA for profitable operations with established licenses, player bases, and multi-provincial coverage.

Process for closing operations legally requires customer notification periods, player fund withdrawals, regulatory approvals, license surrender procedures, tax clearances, and formal company liquidation through commercial registry.

FAQ: Frequently Asked Questions

Legal & Licensing

Is online gambling legal in Argentina?

Yes, online gambling is legal in Argentina, but regulation occurs at the provincial level rather than nationally. Each of Argentina’s 24 provinces and the Autonomous City of Buenos Aires has authority to regulate gambling within its territory.

As of 2025, several provinces have implemented comprehensive online gambling frameworks, including Buenos Aires Province, Buenos Aires City, Mendoza, Córdoba, Santa Fe, and San Juan. Other provinces maintain land-based only regulations or are developing digital gaming legislation.

The 2016 National Gaming Law confirmed provincial sovereignty while criminalizing unlicensed gambling operations nationwide, imposing three to six years imprisonment for operating without proper provincial authorization. This creates a complex regulatory landscape where operators must obtain separate licenses for each province they wish to serve.

Pending federal legislation passed by the Chamber of Deputies in November 2024 proposes national player protection standards, advertising restrictions, and biometric verification requirements. However, this legislation faces Senate review and potential constitutional challenges regarding federal intrusion into provincial regulatory authority.

What types of gambling licenses are available and what do they cover?

Provincial gambling licenses vary by jurisdiction but typically include separate authorizations for online sports betting, online casino games, online poker, and lottery products. Some provinces issue comprehensive licenses covering multiple products, while others require separate licenses for each vertical.

Buenos Aires Province and Buenos Aires City offer comprehensive online gambling licenses covering sports betting, casino games (slots, table games, live dealer), poker, and authorized lottery products within a single license framework. License duration reaches 15 years in both jurisdictions without renewal requirements.

Mendoza Province issues licenses for 10 years with possible one-year extension, covering online sports betting and casino products. The province conducted licensing rounds in 2023-2024, authorizing seven active operators as of 2025.

Córdoba Province provides 15-year licenses without renewal obligations, covering comprehensive online gambling products. Santa Fe and San Juan provinces have developed their own frameworks with varying terms, products covered, and requirements.

Each license specifies permitted gambling activities, technical standards, responsible gambling obligations, reporting requirements, and operational conditions. Operators seeking nationwide coverage must obtain separate licenses from each province, creating significant compliance complexity.

How much does an iGaming license cost and how long does it take to obtain?

License costs vary significantly by province, ranging from USD 100,000 to USD 600,000 as initial application and approval fees. Buenos Aires Province charges approximately USD 500,000, Buenos Aires City USD 300,000-500,000, Mendoza USD 400,000, and smaller provinces USD 200,000-350,000.

Beyond license fees, operators must demonstrate minimum authorized capital equivalent to USD 1 million for most provincial licenses. Additional costs include legal and consulting fees (USD 50,000-150,000), technical certifications (USD 20,000-50,000), and company incorporation expenses (USD 3,500-8,500).

The licensing timeline typically spans 4-6 months from application submission to final approval, assuming complete documentation and no complications. This period includes background checks on beneficial owners (90-120 days), technical system reviews, financial verification, and regulatory authority deliberation.

Total time to market including company registration (8-12 weeks), license application (4-6 months), platform setup (8-12 weeks), and pre-launch preparation (4-8 weeks) ranges from 9-12 months from initial decision to commercial launch.

Annual fees apply in some provinces, typically ranging from 2-5 percent of annual gross gaming revenue, though Buenos Aires Province and Buenos Aires City licenses do not require renewal as they grant 15-year terms without additional authorization processes.

Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain gambling licenses in Argentina without facing absolute restrictions on foreign ownership. Provincial regulations generally do not prohibit international operators from applying for and holding licenses directly.

However, practical requirements favor local partnerships or establishment of Argentine subsidiaries. Foreign applicants must incorporate a local entity (S.R.L. or S.A.) with Argentine tax identification, local bank account, and registered office address to apply for provincial licenses.

Local legal representatives are required for foreign-owned entities, handling regulatory communications, document submission, and ongoing compliance obligations. These representatives must be Argentine residents with power of attorney to act on the company’s behalf.

Recent regulatory changes under President Milei’s administration eliminated requirements for foreign entities to prove economic activity abroad, simplifying the entry process for international operators without prior operating history in other markets.

Partnership with established Argentine entities provides significant advantages including regulatory relationship navigation, payment processor access (especially state-owned banks in Buenos Aires jurisdictions), market knowledge, and credibility with provincial authorities. Many international operators enter through joint ventures or licensing agreements with local partners.

Financial & Taxation

What are the tax obligations for iGaming operators?

iGaming operators in Argentina face multi-layered taxation including provincial gaming taxes, federal deposit taxes, corporate income tax, and provincial turnover taxes. The combined tax burden significantly impacts profitability and requires careful financial planning.

Provincial gaming taxes apply to gross gaming revenue at rates ranging from 10-12 percent for online casinos and 10 percent for sports betting, varying by jurisdiction. Buenos Aires Province charges 12 percent on casino GGR and 10 percent on sports betting GGR.

Federal deposit tax, implemented through Decree 293/2022, ranges from 2.5 percent to 15 percent of player deposits based on operator status. Argentine entities registered with the Online Control Registry of the Betting System (RCOSA) and meeting investment criteria (ARS 200 million investment, 20 percent payroll increase, 20+ employees) qualify for 2.5 percent rate.

Standard registration with RCOSA without investment criteria results in 5 percent deposit tax, while unregistered Argentine entities pay 7.5 percent. Foreign operators face 10 percent tax, and operators based in tax havens or non-cooperative jurisdictions pay 15 percent.

Corporate income tax applies progressively: 25 percent on taxable income up to ARS 5 million, 30 percent on ARS 5-50 million, and 35 percent on income exceeding ARS 50 million annually. Provincial turnover taxes add 1-3 percent on gross gaming revenue.

VAT generally does not apply to gambling services as provincial gaming taxes substitute, though operators pay VAT on purchased goods and services. Social security contributions of 17-27 percent on employee salaries represent additional employer obligations.

Are gambling winnings taxed for players?