Armenia presents an evolving opportunity for iGaming operators as one of the regulated markets in the South Caucasus region. The country has established a licensing framework overseen by the Ministry of Finance, with comprehensive regulations covering online and land-based gambling activities.

Recent legislative reforms in 2025 have significantly transformed the tax structure and compliance requirements, introducing higher duties and stricter oversight mechanisms while maintaining market accessibility for licensed operators.

Executive Summary: Key Market Indicators

| Indicator | Value/Status |

|---|---|

| Gambling Legal Status | Legal and Regulated |

| Regulatory Authority | Ministry of Finance |

| Online Gambling Status | Licensed and Permitted |

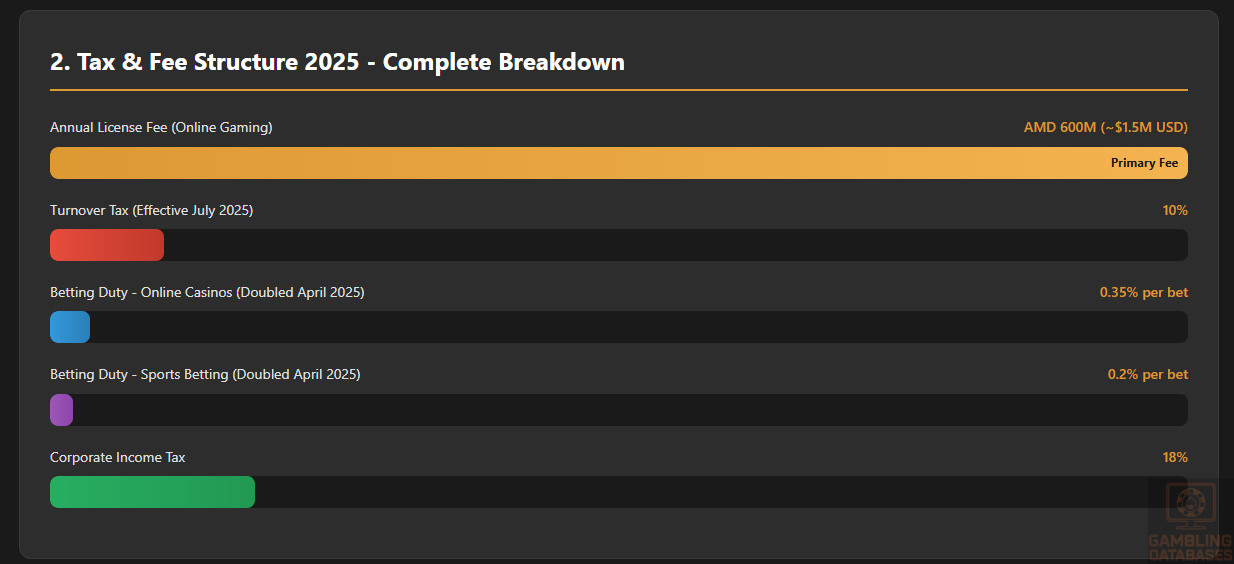

| Annual License Fee (Online Gaming) | AMD 600 million (~$1.5 million USD) |

| Gambling Tax Rate (2025) | 10% turnover tax (effective July 2025) |

| Betting Duty (Online Casinos) | 0.35% per bet (doubled from 0.175% in April 2025) |

| Betting Duty (Sports Betting) | 0.2% per bet (doubled from 0.1% in April 2025) |

| Corporate Income Tax | 18% |

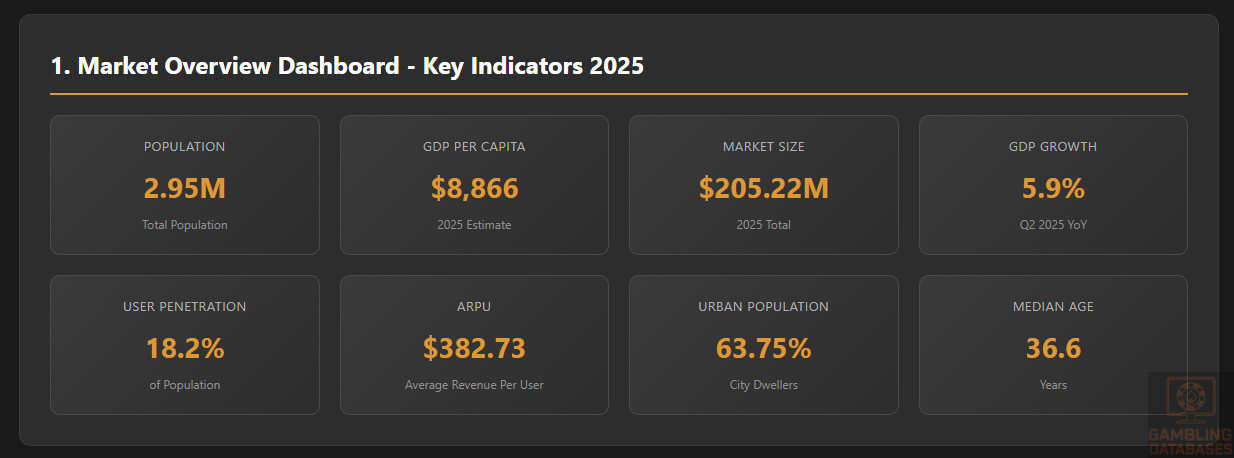

| Population (2025) | 2.95 million |

| Median Age | 36.6 years |

| Urban Population | 63.75% |

| GDP (2024) | $25.79 billion USD |

| GDP Per Capita (2025) | $8,866 USD |

| GDP Growth (Q2 2025) | 5.9% YoY |

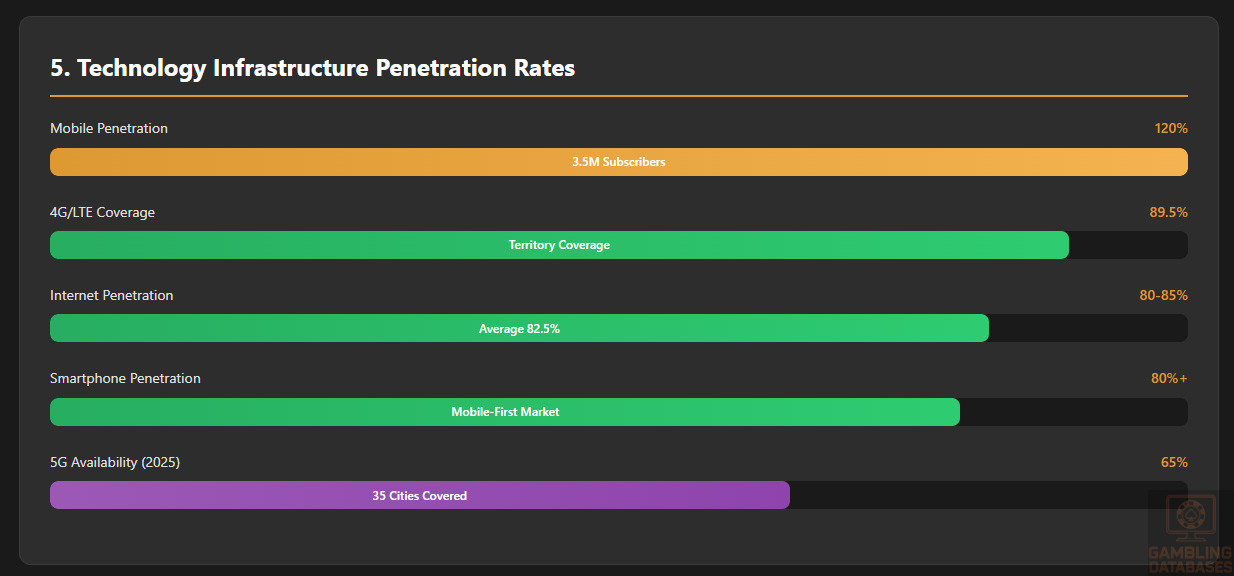

| Internet Penetration | 80-85% |

| Smartphone Penetration | 80%+ |

| Mobile Penetration | 120% (3.5 million subscribers) |

| 4G/LTE Coverage | 89.5% of territory |

| 5G Availability (2025) | 65% population coverage across 35 cities |

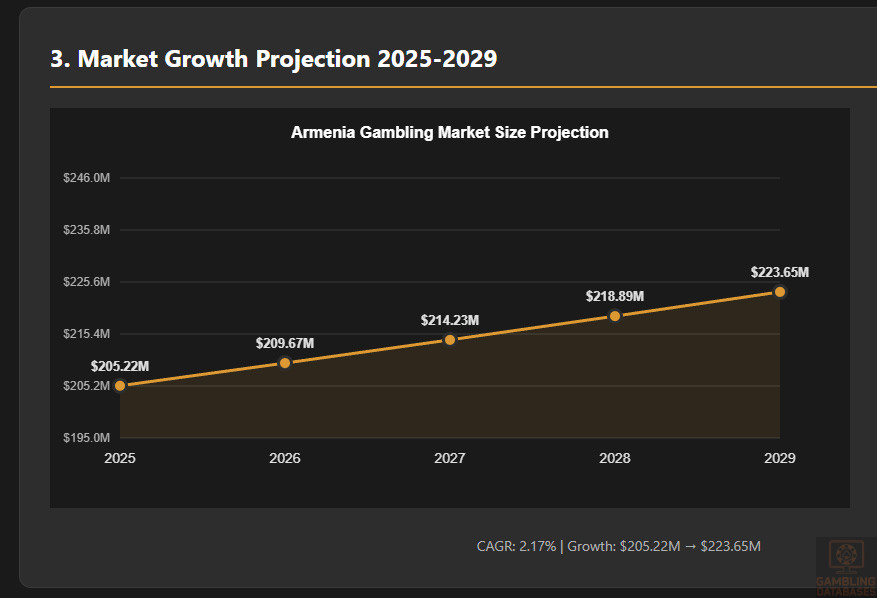

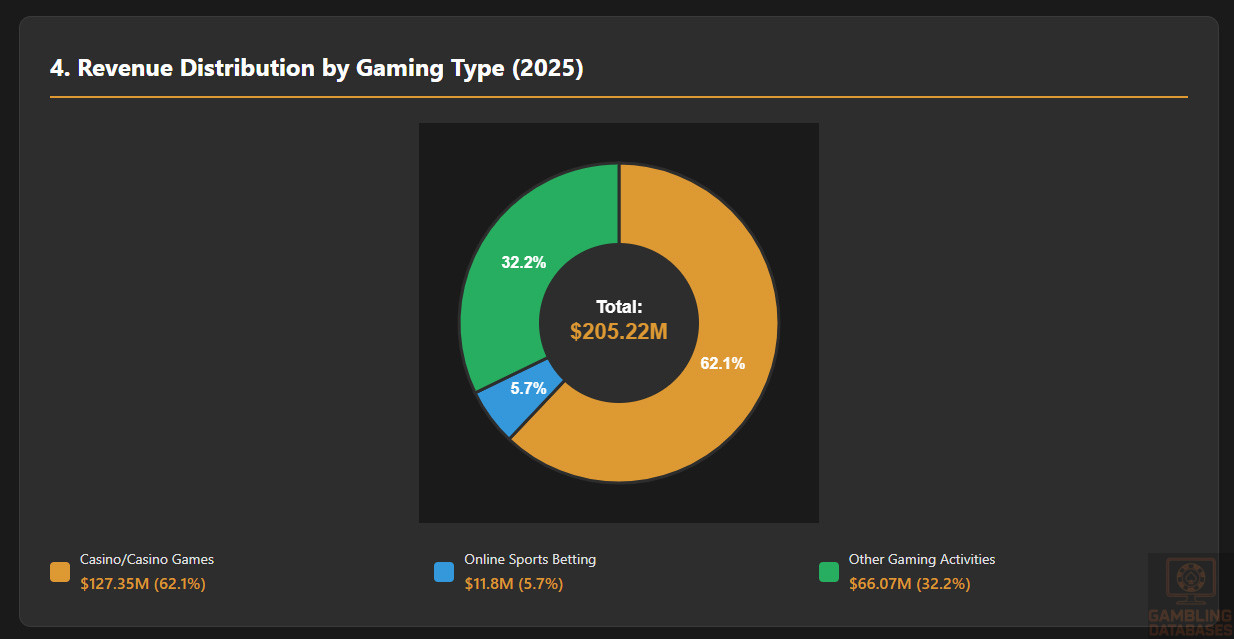

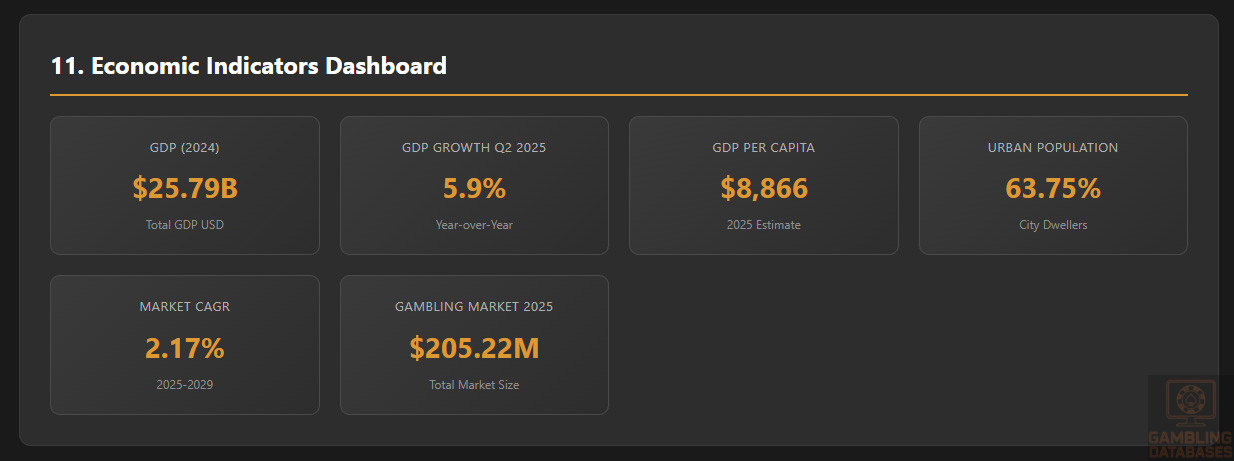

| Gambling Market Size (2025) | $205.22 million USD |

| Market CAGR (2025-2029) | 2.17% |

| Projected Market Size (2029) | $223.65 million USD |

| Casino/Casino Games Revenue (2025) | $127.35 million USD |

| Online Sports Betting Revenue (2025) | $11.8 million USD |

| Average Revenue Per User (ARPU) | $382.73 USD (2025) |

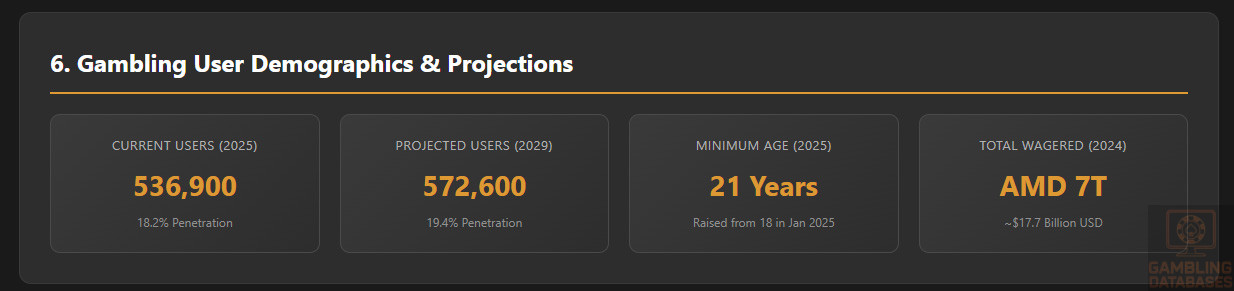

| Gambling User Penetration (2025) | 18.2% |

| Projected Users (2029) | 572,600 |

| Total Wagered (2024) | AMD 7 trillion (~$17.7 billion USD) |

| Minimum Gambling Age | 21 years (raised from 18 in January 2025) |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Armenia operates a regulated gambling market under comprehensive legislation that governs all forms of gaming activities. The primary regulatory framework is established through the Law of the Republic of Armenia “On Winning Games and Gambling Houses” which provides the foundation for licensing, operation, and supervision of gambling establishments.

Land-Based Gambling Activities

Land-based gambling in Armenia is categorized into three main types. Games of chance include activities organized on gaming tables and gaming machines where outcomes depend primarily on chance or predominantly on player skills, abilities, or knowledge such as poker, operated through mechanical or electronic devices.

Totos represent games where outcomes depend on the occurrence, non-occurrence, or manner of events predicted by players, where the betting events remain beyond the gambling operator’s control. These encompass sports betting and related activities in physical venues.

Casino operations face varying annual state duty requirements based on location. Tsakhkadzor commands AMD 180 million, Sevan requires AMD 150 million, Jermuk mandates AMD 100 million, and Meghri imposes AMD 35 million in annual fees for land-based casino licenses.

Online Gambling Framework

Digital gaming regulations in Armenia permit online casino games, internet-based winning games, and online sports betting under proper licensing. The regulatory scope covers all forms of internet gambling organized by Armenian-registered commercial entities holding valid licenses from the Ministry of Finance.

Significant legislative changes took effect January 1, 2025, through the new law “Regulation of Gaming Activities.” This legislation prohibits Armenian residents from participating in or accessing gambling organized in foreign jurisdictions and bans advertising of gambling services conducted outside Armenia or on non-Armenian domain names.

Technical infrastructure requirements mandate that operators maintain physical presence in Armenia, including servers, software, hardware, and gaming platforms located within the country. This localization requirement aims to ensure regulatory oversight and tax compliance while limiting offshore gambling access.

Prohibited activities include operating without valid Armenian licenses, accepting bets from jurisdictions where gambling is illegal, and providing services to individuals on the Ministry of Finance’s exclusion list. Unlicensed operators face IP blocking measures, payment processing restrictions, and potential criminal penalties.

Licensed Operators and Market Players

The Armenian gambling market consists of both local and international operators holding licenses from the Ministry of Finance. While specific market share data for individual operators remains limited, the market has attracted significant investment with operators collectively processing over AMD 811 billion in deposits during 2024.

Market concentration has increased substantially, with gambling activities growing seventeen-fold between 2018 and 2024. The majority of betting activity occurs online, reflecting global digital transformation trends and high smartphone penetration among Armenian consumers.

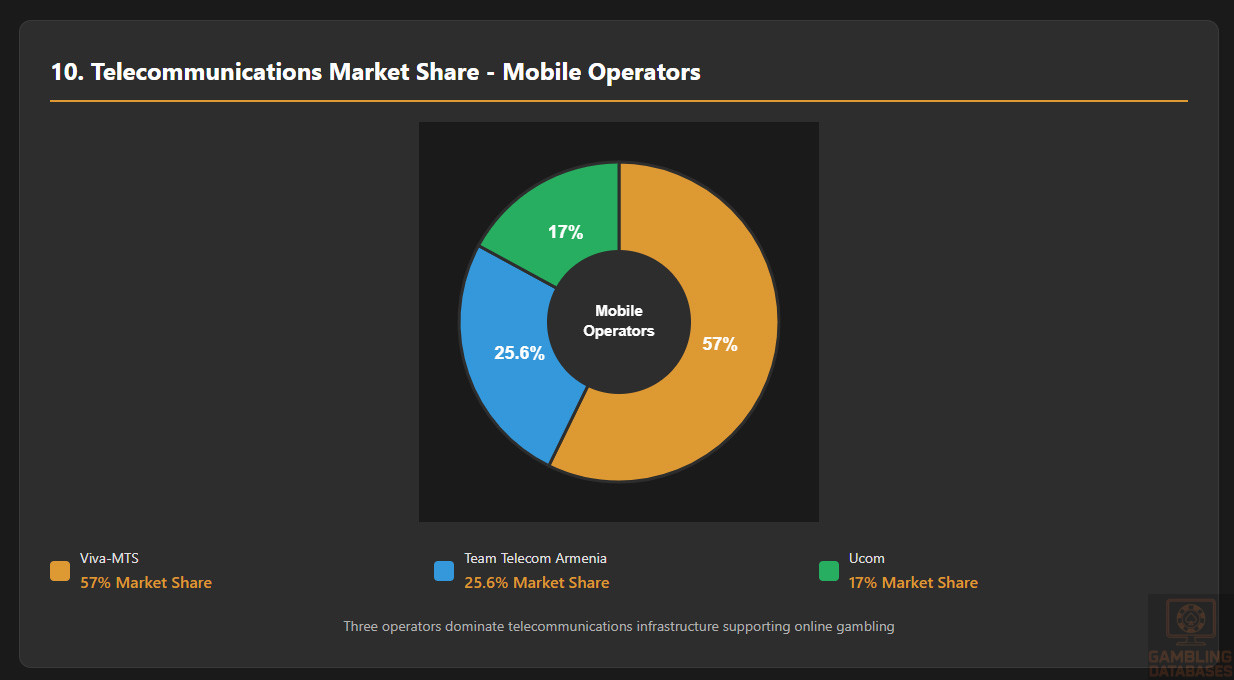

Three mobile network operators dominate telecommunications infrastructure supporting online gambling: Viva-MTS commands approximately 57% of mobile subscriptions, Team Telecom Armenia holds 25.6%, and Ucom maintains 17% market share. These providers enable the mobile-first gambling experience prevalent in the market.

International operators entering the Armenian market typically establish local subsidiaries to meet physical presence requirements. Foreign ownership is permitted under Armenian law, though operators must register commercial entities within Armenia and maintain operational infrastructure domestically.

Licensing Framework and Requirements

Application Process and Eligibility

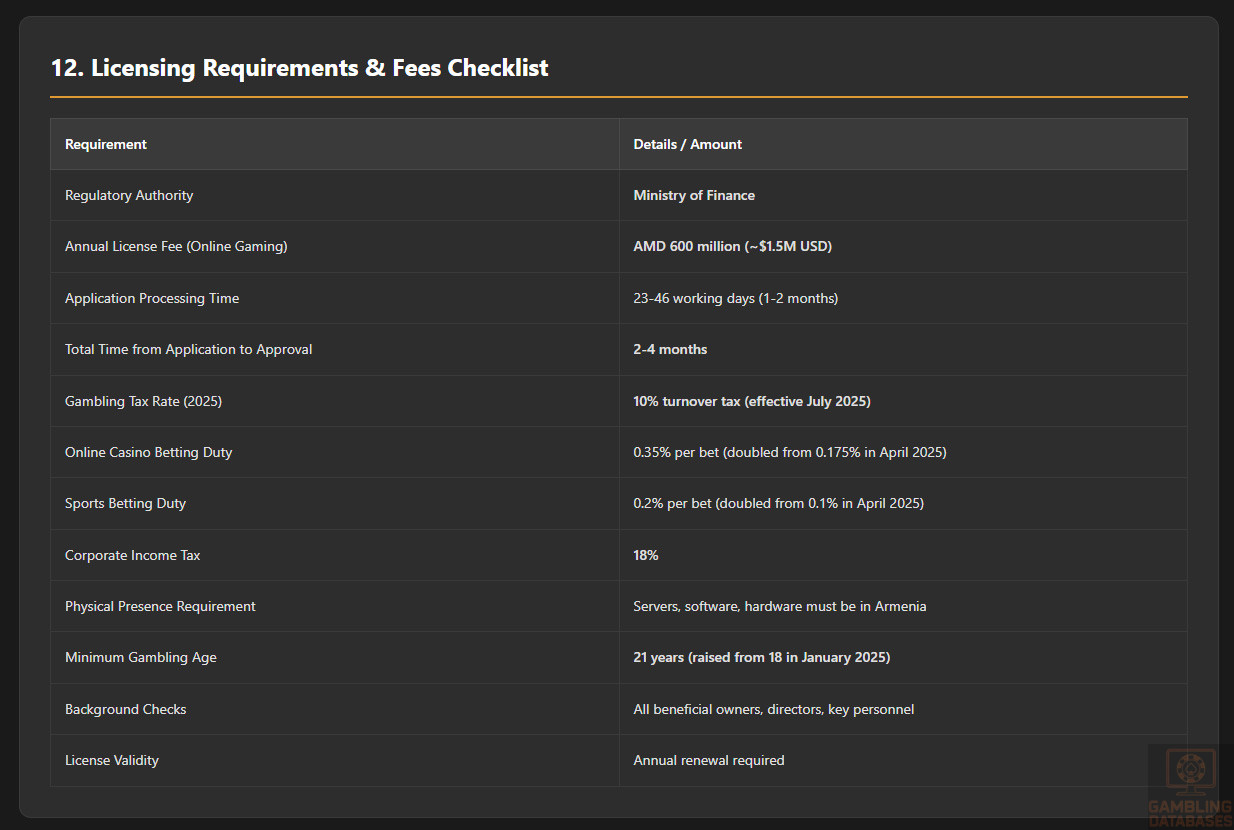

The Ministry of Finance serves as the primary licensing authority for all gambling activities in Armenia. Applications for licenses require submission of comprehensive documentation including company registration details, beneficial ownership information, technical system specifications, and financial stability evidence.

The licensing timeline spans 23 working days from application submission for initial review, with potential extension of an additional 23 working days if submitted documentation requires further study. Upon approval decision, licenses are issued within one month following payment of the first annual state duty installment.

Financial requirements for online gambling licenses include an annual state duty of AMD 600 million (approximately $1.5 million USD), which must be paid before license issuance. This represents a substantial entry barrier designed to ensure only financially stable operators enter the market.

Background check procedures examine all beneficial owners, directors, and key personnel associated with applicant companies. These investigations verify absence of criminal records, financial misconduct, or prior license revocations in any jurisdiction.

| License Type | Annual State Duty | Processing Time | Additional Requirements |

|---|---|---|---|

| Online Gambling/Casino | AMD 600 million (~$1.5M USD) | 23-46 working days | Local servers, Armenian entity |

| Sports Betting (Online) | AMD 600 million (~$1.5M USD) | 23-46 working days | Local servers, Armenian entity |

| Land-Based Casino (Tsakhkadzor) | AMD 180 million (~$453K USD) | 23-46 working days | Physical premises in designated zone |

| Land-Based Casino (Sevan) | AMD 150 million (~$378K USD) | 23-46 working days | Physical premises in designated zone |

| Land-Based Casino (Jermuk) | AMD 100 million (~$252K USD) | 23-46 working days | Physical premises in designated zone |

| Land-Based Casino (Meghri) | AMD 35 million (~$88K USD) | 23-46 working days | Physical premises in designated zone |

| Lottery | Varies by scope | 23-46 working days | Armenian founders only |

Local Presence and Operational Requirements

Physical presence mandates require online gambling operators to establish registered commercial entities in Armenia. All gaming servers, software systems, hardware infrastructure, and gaming platforms must be physically located within Armenian territory to qualify for licensing.

Domain requirements specify that licensed operators must use Armenian domain extensions or internationally recognized domains registered to Armenian entities. The recent 2025 legislation prohibits advertising of gambling services on non-Armenian domains, reinforcing the localization mandate.

Personnel obligations include employing qualified technical staff for server maintenance, customer support representatives fluent in Armenian, and compliance officers responsible for regulatory adherence. While specific minimum headcount requirements vary by operation scale, regulators expect adequate staffing for license scope.

Foreign ownership restrictions permit 100% foreign ownership of gambling operators, providing no citizenship requirements exist for founders of gaming companies. However, lottery operations maintain stricter requirements, permitting only Armenian citizens or Armenian-registered legal entities as founders.

Compliance Obligations and Monitoring

Player Protection and Identification

Age verification requirements mandate that all gambling operators verify participants have reached the minimum age of 21 years before allowing gambling activity. This age threshold increased from 18 to 21 years effective January 2025, applying to sports betting and lottery games.

KYC and AML compliance standards require operators to collect and verify player identity documents, maintain transaction records, and report suspicious activities to the State Revenue Committee. Enhanced due diligence applies to high-value transactions and politically exposed persons.

Responsible gambling measures mandated by law include providing self-exclusion mechanisms through the Ministry of Finance’s central exclusion list. The exclusion system covers all licensed operators, preventing excluded individuals from participating in any gambling activities across the entire market.

Operators must restrict access to individuals whose legal capacity has been limited due to placing their families in difficult financial situations through gambling. The Ministry maintains and distributes this exclusion list to all licensed operators who must check against it before allowing participation.

Financial Monitoring and Reporting

Transaction monitoring systems are required to track all deposits, withdrawals, wagers, and payouts in real-time. A new unified electronic system for monitoring all gambling activities is under development, scheduled for implementation by 2028 to enhance regulatory oversight and tax compliance verification.

Reporting requirements mandate operators to submit detailed financial statements on monthly and quarterly schedules. Tax obligations transitioned to self-reporting in 2025, though the forthcoming monitoring center will provide independent verification capabilities reducing reliance on voluntary operator disclosures.

Audit and inspection procedures grant the State Revenue Committee authority to conduct on-site inspections and desk audits of operator records. Documentary control and examination of submitted reports form the current supervisory framework pending the new monitoring authority’s establishment.

Data retention requirements obligate operators to maintain comprehensive records of all gambling transactions, player accounts, and compliance activities for periods specified by anti-money laundering legislation and tax authorities.

Taxation Structure and Financial Obligations

Player Taxation

Tax rates on winnings implement a two-tier structure effective 2025. Gambling companies act as tax agents withholding 5% at source for significant individual wins. When smaller wins accumulate throughout the year, operators must withhold 10% during the player’s annual income declaration process.

Withholding procedures require operators to deduct applicable taxes from player winnings before payout and remit these amounts to tax authorities according to prescribed schedules. This tax agent role transfers enforcement burden from individual players to licensed operators.

Player tax obligations include declaring gambling income in annual tax returns where winnings exceed specified thresholds. The dual taxation approach aims to capture revenue from both large single wins and accumulated smaller winnings throughout the tax year.

Tax-free thresholds remain undefined in current legislation, with all gambling winnings potentially subject to taxation depending on amount and frequency. The withholding system ensures collection occurs before players receive funds, maximizing government revenue capture.

Operator Taxation

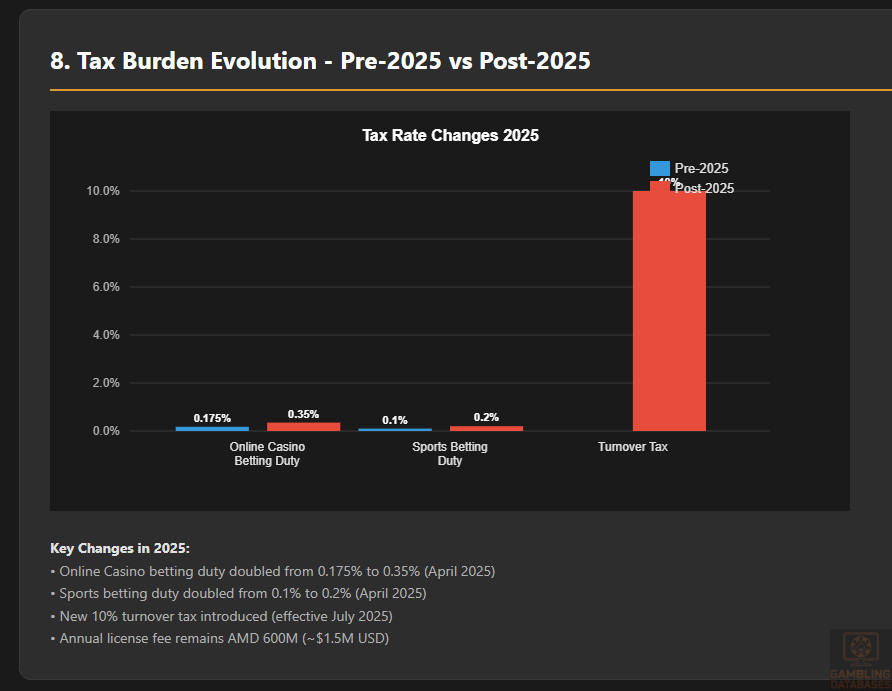

Armenia implemented dramatic tax reforms affecting gambling operators in 2025. The Parliament approved legislation introducing a 10% turnover tax on all licensed gambling activities effective July 1, 2025, replacing the previous per-bet duty structure for greater simplicity and transparency.

Prior to July 2025, a doubled per-bet tax structure applied: online casinos paid 0.35% per bet (increased from 0.175%), and sports betting operators paid 0.2% per bet (increased from 0.1%). These rates doubled effective April 1, 2025, as interim measures before the July turnover tax implementation.

Fixed operational taxes include the annual licensing fee of AMD 600 million for online gambling operations, representing substantial upfront capital requirements. This fee applies regardless of operational revenue, creating significant fixed cost pressure particularly for new market entrants.

Corporate income tax applies at the standard Armenian rate of 18% on net profits after accounting for gambling-specific duties and fees. This represents the only traditional tax applicable to gambling operations, as gambling activities receive exemption from most other standard business taxes due to the high licensing fees.

| Tax Type | Pre-2025 Rate | April-June 2025 | July 2025 Onward |

|---|---|---|---|

| Online Casino Bet Duty | 0.175% per bet | 0.35% per bet | – |

| Sports Betting Duty | 0.1% per bet | 0.2% per bet | – |

| Turnover Tax | N/A | N/A | 10% of turnover |

| Annual License Fee | AMD 600M (~$1.5M) | AMD 600M (~$1.5M) | AMD 600M (~$1.5M) |

| Corporate Income Tax | 18% | 18% | 18% |

| Projected Additional Revenue | – | AMD 13B annually | AMD 100B annually |

Gambling Market Financial Performance

Total amount wagered annually in Armenia reached extraordinary levels by 2024. Over AMD 7 trillion (approximately $17.7 billion USD) was wagered on gambling activities, marking a seventeen-fold increase compared to 2018 levels. The vast majority of this betting volume occurred through online channels.

Online casino deposits specifically exceeded AMD 811 billion (approximately $2 billion USD) in 2024 according to parliamentary testimony. This substantial deposit volume demonstrates both the market’s maturity and the scale of financial flows through the regulated gambling sector.

Revenue to government through gambling taxation showed significant growth trajectories. The 2022 gambling sector contributed AMD 18.8 billion (approximately $43.5 million USD) to state coffers, representing 10.4% of the entire services sector contribution.

Market revenue projections for 2025 estimate total gambling market revenue at $205.22 million USD, with the casino and casino games segment generating $127.35 million and online sports betting contributing $11.8 million. Alternative estimates place total market size at approximately $147 million with higher growth projections.

| Metric | 2021 | 2022 | 2024 | 2025 Projection |

|---|---|---|---|---|

| Total Wagered | – | – | AMD 7T ($17.7B) | – |

| Online Casino Deposits | – | – | AMD 811B ($2B) | – |

| Player Losses (GGR) | $150M | – | – | – |

| Government Tax Revenue | – | AMD 18.8B ($43.5M) | – | – |

| Total Market Revenue | – | – | – | $205.2M |

| Casino/Casino Games | – | – | – | $127.4M |

| Online Sports Betting | – | – | – | $11.8M |

Advertising and Marketing Restrictions

Permitted advertising channels for gambling operations face significant restrictions as of 2025. Only locally licensed operators may advertise gambling services in Armenia, with foreign gambling advertising completely prohibited under the January 2025 legislation.

Content restrictions mandate that all gambling advertisements target audiences aged 21 or older, aligning with the raised minimum gambling age. Television and radio advertising faces time restrictions, permitting broadcasts only between 10:00 PM and 6:00 AM to limit youth exposure.

Geographic advertising limitations prohibit gambling promotions at Armenian entry points including airports and border crossings. Hotel advertising also faces restrictions, with proposals to eliminate gambling advertisements even in four-star and higher-rated establishments to improve tourism perception.

Promotional limitations under discussion include potential caps on bonus offers and wagering requirement restrictions, though specific parameters remain under parliamentary review. The government aims to balance market competitiveness with responsible gambling objectives through these promotional controls.

Affiliate marketing rules require affiliates to adhere to the same advertising restrictions as operators, including age targeting and time limitations. Payment of affiliate commissions for directing Armenian residents to unlicensed foreign operators may face penalties under the new framework.

Penalty structures for advertising violations include fines of AMD 1 million (approximately $2,500 USD) for first offenses, escalating to AMD 4 million ($10,000) for second violations and AMD 8 million ($20,000) for third breaches. These graduated penalties aim to enforce compliance without immediately destroying operator businesses.

Recent Regulatory Changes and Their Impact

March 2025 marked a pivotal moment when the Armenian National Assembly approved comprehensive gambling tax reforms during a second reading on March 6. The legislation passed with 58 votes in favor, 2 against, and 17 abstentions, demonstrating substantial political support for stricter regulation.

The doubled betting duties implemented April 1, 2025 immediately increased operator costs. Online casinos saw per-bet taxation double from 0.175% to 0.35%, while sports betting operators faced increases from 0.1% to 0.2% per bet. These interim measures generated estimated additional monthly revenue of $2.7 million for the state.

July 2025 brought the most significant change: implementation of a 10% turnover tax replacing the per-bet duty structure. This fundamental shift simplifies tax calculation while increasing total tax burden, with government projections estimating AMD 100 billion (approximately $241.9 million) in additional annual state revenue.

The January 2025 law “Regulation of Gaming Activities” introduced sweeping changes including prohibition of Armenian participation in foreign-organized gambling, advertising bans for offshore operators, and server localization requirements. These measures aim to capture all Armenian gambling activity within the regulated domestic market.

Minimum gambling age increased from 18 to 21 years effective January 2025, reducing the addressable market size while aiming to protect younger adults from gambling-related harm. This change particularly affects sports betting and lottery participation demographics.

Future regulatory developments include establishment of a dedicated gambling monitoring center by 2028. Parliament included an escalation clause warning that if this regulatory body fails to become operational by the deadline, tax rates could increase three-fold, four-fold, or even five-fold, creating strong incentives for timely implementation.

Enforcement Mechanisms and Penalties

Penalty structures for unlicensed operations include potential criminal prosecution, though civil penalties dominate the current enforcement regime. ISP blocking measures target unlicensed foreign operators, with authorities gaining expanded powers under 2025 legislation to restrict access to offshore gambling websites.

Payment processor restrictions prevent Armenian banks and payment service providers from processing transactions with unlicensed gambling operators. This financial isolation strategy aims to make unlicensed operations commercially unviable within Armenia.

Recent enforcement actions have focused primarily on taxation compliance rather than unlicensed operations, with the State Revenue Committee conducting audits and inspections of licensed operators. The forthcoming unified monitoring system will dramatically enhance real-time compliance verification capabilities.

Compliance enforcement trends indicate government prioritization of revenue collection over prohibition. Prime Minister Pashinyan explicitly stated complete gambling bans remain impractical, as Armenian residents would simply use foreign websites, making taxation and regulation preferable to unsuccessful prohibition.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Total population of Armenia stands at approximately 2.95 million as of 2025, representing a small but economically active market in the South Caucasus region. The population has experienced modest decline from its 1992 peak of 3.63 million due to emigration related to economic challenges and regional conflicts.

Age distribution breakdown shows a mature population structure with significant working-age concentration. The 0-14 age group represents approximately 19% of the population, while 15-64 year-olds comprise about 68% of residents. The 65+ demographic accounts for roughly 13% of the total population.

The median age of 36.6 years positions Armenia as a relatively mature market with substantial purchasing power among middle-aged consumers. This demographic profile suits gambling market development, as disposable income and gambling propensity typically peak in the 35-54 age ranges.

Gender ratios show relative balance with women comprising approximately 53.4% of the population compared to 46.6% male representation. Life expectancy reaches 73.2 years overall, with significant gender disparity: males average 69.6 years while females reach 77.3 years.

| Age Group | Percentage | Estimated Population | Gambling Eligibility |

|---|---|---|---|

| 0-14 years | ~19% | ~561,000 | Prohibited |

| 15-20 years | ~6% | ~177,000 | Prohibited (under 21) |

| 21-34 years | ~20% | ~590,000 | Eligible |

| 35-44 years | ~16% | ~472,000 | Eligible |

| 45-54 years | ~14% | ~413,000 | Eligible |

| 55-64 years | ~12% | ~354,000 | Eligible |

| 65+ years | ~13% | ~384,000 | Eligible |

| Total Eligible (21+) | ~75% | ~2.21 million | Legal Market |

Geographic Distribution

Urban versus rural distribution patterns show strong urbanization with 63.75% of the population (approximately 1.88 million people) residing in urban areas. Rural populations account for 36.25%, though these areas face significant challenges in infrastructure and economic opportunity access.

Major cities and population centers concentrate in the capital Yerevan and several regional hubs. Yerevan dominates with over 1 million residents, serving as the commercial, cultural, and technological center. Other significant cities include Gyumri, Vanadzor, Vagharshapat, Hrazdan, and Abovyan.

Regional economic differences create varying consumer spending power and gambling participation rates. Yerevan residents enjoy substantially higher incomes and better access to both land-based and online gambling options compared to provincial areas.

Internet access geographic patterns follow urban-rural divides, with near-universal connectivity in cities but more limited rural access despite improving infrastructure. The 5G network rollout prioritizes urban centers, currently covering 65% of the population across 35 cities including both the capital and regional towns.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Current GDP reached $25.79 billion USD in 2024 according to World Bank data, demonstrating sustained economic growth despite regional challenges. The economy has transformed significantly from its Soviet-era industrial base to a more diversified services and technology-oriented structure.

GDP per capita stands at $8,866 USD in 2025 according to World Economics estimates, reflecting substantial growth from $4,269 in 2020. This represents more than doubling of per capita income over five years, indicating strong economic recovery and development momentum.

GDP growth forecasts remain robust with Q1 2025 posting 5.1% year-over-year growth and Q2 2025 achieving 5.9% expansion. The government’s 2025 budget projects 5.1% annual growth with inflation controlled at 3% (±1.5%), creating favorable conditions for consumer spending.

Economic sector composition has shifted toward services, which now dominate the economy. The gambling and gaming sector represents a measurable 10.4% of total services sector revenue, highlighting its economic significance beyond entertainment value.

Employment rates and wage levels show gradual improvement, though official unemployment stands at 17.3% with independent estimates suggesting potentially higher figures. Over one-third of Armenia’s population lives in poverty, constraining discretionary spending for gambling among lower-income segments.

Income and Wealth Distribution

Average household income data remains limited in public sources, though GDP per capita figures suggest monthly household incomes in the range of $600-800 for average families. Urban households, particularly in Yerevan, command significantly higher incomes enabling greater gambling participation.

Median household income likely falls below average figures due to income inequality, with wealth concentrated among urban professionals, business owners, and technology sector workers. The growing IT industry has created a new middle class with substantial disposable income.

Income inequality measures reflect typical post-Soviet patterns with emerging wealth gaps between urban and rural areas, employed and unemployed populations, and those with versus without higher education. This creates a tiered gambling market with different segments exhibiting vastly different spending capacities.

Disposable income trends show improvement alongside GDP growth, particularly for employed urban residents. The growing middle class represents the core target demographic for online gambling operators, combining digital literacy, financial resources, and entertainment spending willingness.

| Indicator | Value | Year | Trend |

|---|---|---|---|

| Total GDP | $25.79 billion | 2024 | Growing |

| GDP Per Capita | $8,866 | 2025 | Rising (+4.3% from 2024) |

| GDP Growth Rate (Q1) | 5.1% | 2025 | Strong |

| GDP Growth Rate (Q2) | 5.9% | 2025 | Accelerating |

| Projected Annual Growth | 5.1% | 2025 | Stable |

| Inflation Rate (July 2025) | 3.4% | 2025 | Controlled |

| Unemployment Rate (Official) | 17.3% | 2025 | High but improving |

| Poverty Rate | ~33% | 2025 | Gradual decline |

Market Size and Growth Projections

Current iGaming market revenue reached $205.22 million USD in 2025 according to Statista projections, with casino and casino games dominating at $127.35 million. Online sports betting contributes approximately $11.8 million, while the remaining revenue comes from lottery and other gambling verticals.

Historical revenue growth shows explosive expansion with total wagered amounts increasing seventeen-fold between 2018 and 2024. This growth trajectory reflects increasing digitalization, smartphone adoption, and operator marketing investments rather than proportional player base expansion.

Revenue forecasts for 2025-2029 project a compound annual growth rate of 2.17%, reaching $223.65 million by 2029 according to Statista. Alternative estimates suggest slightly higher growth rates of 4.73% CAGR, potentially driving market size to $147-160 million by 2029.

The projected user base growth anticipates 572,600 active gamblers by 2029, up from current penetration of 18.2% of the population. This represents approximately 536,000 current users based on 2025 population figures and penetration rates.

Average Revenue Per User currently stands at $382.73 USD annually in 2025, positioning Armenia as a mid-tier ARPU market. This figure reflects the balance between high-spending urban users and more modest rural or lower-income participants.

Market penetration rates at 18.2% in 2025 leave substantial room for growth compared to mature European markets where penetration can exceed 30-40%. However, the raised minimum age to 21 years constrains addressable market size relative to jurisdictions maintaining 18+ thresholds.

| Metric | 2025 | 2029 | CAGR |

|---|---|---|---|

| Total Market Revenue | $205.22M | $223.65M | 2.17% |

| Casino/Casino Games | $127.35M | ~$140M (est.) | ~2.4% |

| Online Sports Betting | $11.8M | ~$13.5M (est.) | ~3.4% |

| Active Users | ~536,000 | 572,600 | 1.7% |

| User Penetration | 18.2% | ~19.5% | +1.3pp |

| ARPU | $382.73 | ~$390 (est.) | ~0.5% |

| Total Wagered | ~$18B (est.) | ~$20B (est.) | ~2.7% |

Education, Skills, and Digital Literacy

Educational Foundation

Literacy rates in Armenia reach exceptionally high levels at 99.76% for adults, reflecting the strong educational legacy of the Soviet system. Male literacy stands at 99.81% while female literacy reaches 99.7%, showing negligible gender gaps in basic education.

Education levels demonstrate strong tertiary attainment with the 2011 census recording 539,394 persons (19.4% of population above 6 years) holding higher professional education qualifications. This creates a substantial pool of digitally capable, sophisticated consumers.

Digital literacy indicators position Armenia favorably among post-Soviet states. High smartphone penetration above 80% and internet usage reaching 80% of the population demonstrate widespread digital comfort and capability essential for online gambling adoption.

Workforce skill levels particularly in technology sectors have strengthened significantly, with Armenia developing as a regional IT and software development hub. This technical sophistication translates to consumer comfort with complex online platforms and digital payment systems.

Cultural and Social Factors

Communication and Language

Primary languages used in daily life center on Armenian, spoken by approximately 98% of the population. Yazidi and Kurdish serve as minority languages, with Russian maintaining widespread understanding due to Soviet-era education and continuing cultural ties.

Business communication norms blend post-Soviet formality with increasingly Western-influenced practices, particularly in Yerevan’s business community. Customer service expectations include responsive support in Armenian language during local business hours.

Language requirements for gambling websites mandate Armenian as the primary interface language, though multilingual options enhance appeal to diaspora users and international residents. Payment instructions, terms and conditions, and responsible gambling information must be clearly presented in Armenian.

Cultural Attitudes

Gambling acceptance levels in Armenian society show increasing tolerance despite traditional conservative values. The sector’s growth from $150 million in player losses in 2021 to over $200 million market size in 2025 indicates widespread participation overcoming cultural stigma.

Religious influences on gambling perception remain meaningful given Armenia’s identity as the first Christian nation (301 AD) and the Armenian Apostolic Church’s 93%+ affiliation rate. However, religious opposition has not translated into prohibition movements, with regulation preferred over bans.

Foreign brand perception and trust show openness to international operators, though local presence requirements ensure all operators establish Armenian identities. Consumers respond positively to international gambling brands operating under Armenian licenses.

Risk tolerance indicators suggest moderate-to-high risk appetite among Armenian gamblers, with substantial betting volumes relative to income levels. The $382 average annual spending per user represents meaningful discretionary income allocation despite modest national income levels.

Problem Gambling and Social Considerations

Prevalence of gambling addiction has increased dramatically according to psychology experts, with problem gambler numbers growing tenfold over the past five years. This alarming trend drove many of the 2025 regulatory tightening measures including age increases and advertising restrictions.

Number of problem gamblers remains difficult to quantify without comprehensive studies, though the $150 million in player losses reported for 2021 suggests thousands of individuals experiencing gambling-related harm. The 17-fold increase in wagering since 2018 likely corresponds to proportional addiction growth.

At-risk population statistics concentrate among young adults and lower-income individuals facing economic stress. Military suicides linked to gambling debt became a particular concern, with over half of 2024 military suicides attributed to gambling problems according to parliamentary testimony.

Underage gambling issues motivated the January 2025 age increase from 18 to 21 years. The government identified particular vulnerability among 18-20 year-olds who lacked sufficient financial maturity and risk awareness despite legal adult status.

Government response measures include the mandatory self-exclusion list maintained by the Ministry of Finance, judicial capacity limitation for individuals bankrupting families through gambling, and planned establishment of a dedicated monitoring center by 2028.

Treatment facilities and support services remain underdeveloped relative to problem gambling prevalence. The lack of comprehensive treatment infrastructure represents a gap that regulations attempt to address through prevention rather than intervention.

Political Structure and Governance

Government system operates as a parliamentary republic with Prime Minister Nikol Pashinyan leading since 2018. The political environment has stabilized following the 2020 Nagorno-Karabakh conflict and subsequent 2025 peace agreement with Azerbaijan.

Political stability indicators show improvement with the August 2025 peace declaration ending nearly four decades of conflict. This stability enhances business confidence and reduces geopolitical risk for international investors entering the gambling market.

Regulatory consistency and predictability have improved under current leadership, with systematic approaches to gambling regulation replacing ad-hoc policy changes. The comprehensive 2025 reforms demonstrate capacity for complex legislative initiatives despite political pressures.

Corruption perception remains a concern typical of post-Soviet states, though reform efforts continue. The gambling sector’s high licensing fees and reporting requirements aim to ensure transparency and reduce opportunities for corruption in licensing and oversight.

International relations impact on business includes deepening Western orientation, with Armenia pursuing EU membership. Parliament approved EU accession endorsement in February 2025, positioning Armenia for closer European integration that may influence future gambling regulations toward EU standards.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration rates reached 80-85% of the population in 2025, with approximately 2.37 million internet users. This high penetration enables widespread online gambling access, though the 15-20% offline population remains excluded from digital gaming opportunities.

Daily internet usage hours average substantial time online, driven by social media engagement, entertainment consumption, and increasingly remote work arrangements. High engagement levels create opportunities for gambling operators to reach consumers through digital marketing channels.

Mobile device adoption rates exceed 80% smartphone penetration, with 93.9% of residents owning phones of some type. The mobile-first nature of internet access in Armenia makes mobile-optimized gambling platforms essential rather than optional for market success.

Social media engagement shows high participation rates with 1.85 million social media users as of 2023, representing 66.6% of the population. Popular platforms include Facebook, Instagram, and international services, providing advertising channels despite gambling marketing restrictions.

E-commerce participation rates have grown substantially, with consumers increasingly comfortable making online purchases and digital transactions. This familiarity with e-commerce translates directly to comfort with online gambling deposits and withdrawals.

Digital Payment Behavior

Payment method preferences in Armenia favor bank cards and bank transfers, with digital wallets gaining traction. Traditional cash-based transactions still dominate retail, but online payments show rapid adoption particularly among younger, urban demographics.

Most popular digital wallets include international services like PayPal where available, regional payment solutions, and mobile operator payment systems. Local payment method integration proves essential for maximizing deposit conversion rates.

Online transaction patterns show increasing frequency and comfort with digital payments, accelerated by pandemic-driven digitalization. Average transaction sizes for e-commerce provide benchmarks for expected gambling deposit amounts.

Trust in online payment systems has improved significantly with banking sector modernization and regulatory oversight enhancements. Security concerns that previously limited online spending have diminished as infrastructure matures.

Cryptocurrency adoption for gambling remains limited given Armenia’s regulatory focus on licensed, monitored operations. The server localization and monitoring requirements make cryptocurrency-based gambling difficult to reconcile with compliance obligations.

Gaming and Gambling Preferences

Current Market Participation

Percentage of population that gambles annually reaches approximately 18.2% based on market penetration data, translating to roughly 536,000 active gamblers from the eligible 21+ population. This participation rate leaves substantial room for market expansion.

Percentage that gambles online dominates total gambling activity, with the vast majority of the AMD 7 trillion wagered in 2024 occurring through online channels. Desktop traffic currently leads at 66.97% versus 32.45% mobile, though mobile shows 19.5% growth indicating shifting preferences.

Popular gambling activities ranking by participation shows online casino games dominating revenue at $127.35 million, followed by online sports betting at $11.8 million. Lotteries maintain steady participation particularly in designated resort cities.

Sports betting versus casino games preference tilts heavily toward casino games based on revenue distribution. Casino gaming generates over 10 times the revenue of sports betting, suggesting either higher casino game participation or significantly higher spending per casino player.

Live dealer games popularity data remains limited, though global trends toward live casino suggest this represents a growth segment for operators. Armenian players’ preference for social interaction may favor live dealer formats over pure RNG games.

Consumer Behavior Patterns

Average spending per player annually reaches $382.73 based on ARPU calculations, though significant variance exists between casual players and high-rollers. This figure translates to approximately $32 monthly spending per active user.

Spending habits and typical bet sizes vary by game type and player segment. The substantial wagered amounts relative to market revenue suggest relatively high payout percentages or significant variance in betting volumes across the user base.

Platform preferences currently favor desktop at nearly 67% of traffic, contrasting with global mobile-first trends. However, the 19.5% mobile growth rate suggests rapid transition toward mobile-dominant usage patterns within 1-2 years.

Peak gambling times likely concentrate in evening hours after work and on weekends, following typical entertainment consumption patterns. Seasonal variations may align with salary payment cycles and holiday periods when discretionary spending increases.

Session length averages remain undocumented in available data, though the high annual wagered amounts relative to user counts suggest either long session durations or high session frequency among active players.

Retention and loyalty patterns appear strong given the dramatic growth in wagering volumes without proportional user base expansion. This suggests deepening engagement among existing users rather than primarily new customer acquisition driving growth.

Bonus sensitivity and promotional response likely remain high given the competitive market and operators’ efforts to differentiate offerings. However, the 10% turnover tax implementation may constrain promotional budgets, reducing bonus generosity.

| Metric | Value | Trend |

|---|---|---|

| Internet Penetration | 80-85% | Stable/Growing |

| Internet Users | 2.37 million | Stable |

| Smartphone Penetration | 80%+ | Growing |

| Phone Ownership | 93.9% | Stable |

| Social Media Users | 1.85 million (66.6%) | Growing |

| Desktop Web Traffic | 66.97% | Declining (-7.4% YoY) |

| Mobile Web Traffic | 32.45% | Rising (+19.5% YoY) |

| Gambling Participation | 18.2% of population | Growing |

| Active Gamblers | ~536,000 | Growing slowly |

| Annual Spending/User | $382.73 | Stable |

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Internet penetration rates reach 80-85% in 2025 with quality assessment showing solid mid-tier performance compared to regional neighbors. Armenia positions as neither the best nor worst connected South Caucasus nation, with Georgia slightly ahead but Armenia exceeding Azerbaijan in some metrics.

Fixed broadband versus mobile internet breakdown shows mobile dominance for access with 147.4% mobile penetration (4.10 million connections for 2.95 million population). Fixed broadband serves approximately 315,319 users (10.76 per 100 persons), with fiber accounting for 83.3% of fixed connections.

Average internet speeds reached 40.14 Mbps for fixed connections and 22.35 Mbps for mobile as of early 2023, representing a 43.7% annual increase for fixed speeds. These speeds adequately support online gambling platforms though lag behind top-tier European markets.

Network reliability and uptime statistics indicate stable service from major providers including Ucom, Viva Armenia, and Team Telecom Armenia. The competitive three-operator market drives infrastructure investment and service quality improvements.

5G and Future Technology Deployment

Current 4G/5G coverage shows comprehensive 4G/LTE deployment across 89.5% of Armenian territory covering 898 settlements. This near-universal 4G access provides the foundation for mobile gambling across both urban and rural areas.

5G rollout timeline accelerated dramatically in 2025 with Ucom launching the country’s largest 5G network reaching 65% of the population across 35 cities. The deployment uses non-stand-alone architecture maximizing reuse of existing 4G infrastructure for cost efficiency.

Future infrastructure plans include continued 5G expansion by all three mobile operators, with Team Telecom partnering with Ericsson for infrastructure upgrades. Millimeter-wave trials in Yerevan business districts promise gigabit speeds for dense urban areas.

Network operator landscape competition among Viva-MTS (57% market share), Team Telecom (25.6%), and Ucom (17%) drives innovation and infrastructure investment. Government spectrum policy favors operators over neighboring countries, accelerating deployment.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Number of mobile network operators stands at three: Viva-MTS, Team Telecom Armenia, and Ucom. This competitive but not fragmented market structure balances infrastructure investment with service competition.

Network operator market share breakdown shows Viva-MTS commanding 57% dominance, Team Telecom holding 25.6%, and Ucom maintaining 17%. All three offer 2G, 3G, 4G, and now 5G services with modern, reliable networks.

4G/5G coverage maps show near-complete 4G coverage with 5G rapidly expanding. Ucom’s aggressive 5G deployment extends to regional cities like Aparan, Martuni, and Sisian, not just the capital.

Data costs and pricing models remain competitive with budget options like Team’s AMD 1,500 tariff serving cost-conscious users. Unlimited data packages face slower uptake due to inflation constraints on discretionary spending.

| Operator | Market Share | 2G | 3G | 4G | 5G |

|---|---|---|---|---|---|

| Viva-MTS | 57% | Yes (99.3%) | Yes (98.1%) | Yes (48.5%) | Launching |

| Team Telecom | 25.6% | Yes (88.9%) | Yes (60%) | Yes (60%) | Planned |

| Ucom | 17% | Yes | Yes | Yes | Yes (65% pop) |

Device Penetration

Smartphone adoption rates exceed 80% of the population representing approximately 2.36 million smartphone users. This high penetration makes mobile-optimized gambling platforms essential for market penetration.

Smartphones per capita approach one device per person among the connected population, with many users owning multiple devices for personal and professional use.

Device preferences and popular brands favor affordable Android devices given economic constraints, though iPhone penetration exists among affluent urban consumers. Budget-friendly smartphone demand drives local manufacturer growth.

Android versus iOS market share heavily favors Android with approximately 81-85% dominance, similar to neighboring Azerbaijan’s 81.29% Android share. iOS accounts for roughly 15-19% of devices, concentrated among higher-income users.

Financial Services and Payment Infrastructure

Banking System Structure

Major banks operating in Armenia include both domestic institutions and international banking groups. The banking sector has modernized significantly since 2000s reforms breaking the ArmenTel telecommunications monopoly’s payment dominance.

Digital banking adoption rates show strong growth with online and mobile banking usage increasing among younger demographics. Traditional branch banking remains important for older users and rural populations.

Account penetration rates indicate moderate banking inclusion with significant urban-rural divides. Yerevan residents maintain near-universal banking access while rural areas lag in formal financial service usage.

Credit and lending markets maturity has improved with Armenian banks’ lending growing 10% in 2019 and continued expansion. Banking sector assets and credit exposures nearly doubled between 2012 and 2018.

Payment Processing Options

Available payment methods for iGaming include bank cards (credit and debit), bank transfers, and emerging digital wallet options. Traditional banking products dominate due to regulatory emphasis on traceable, monitored transactions.

Credit and debit card penetration shows moderate adoption concentrated among employed urban residents. Card usage for online transactions has grown substantially though cash remains king for in-person purchases.

E-wallet options availability includes some international services though local adoption lags European levels. PayPal, Skrill, and Neteller availability varies with some services restricted or limited in Armenia.

Cryptocurrency acceptance faces regulatory ambiguity with the gambling sector’s localization and monitoring requirements creating challenges for crypto integration. Licensed operators must maintain traceable, reportable payment flows incompatible with cryptocurrency anonymity.

Processing fees and typical charges vary by method with bank transfers often offering lowest-cost options and card payments incurring 2-4% merchant fees. International payment processing adds currency conversion costs.

Transaction processing timelines range from instant for domestic bank transfers to 1-3 business days for international card transactions. Withdrawal processing speed represents competitive differentiation among operators.

International payment capabilities exist for licensed operators requiring currency conversion and international banking partnerships. The Armenian Dram (AMD) serves as primary currency though USD and EUR acceptance facilitates diaspora player deposits.

Business Environment and Regulatory Framework

Ease of Business Operations

World Bank Doing Business ranking places Armenia in mid-tier globally, with particular strength in specific areas like contract enforcement while facing challenges in others. Overall business environment has improved under reform-oriented government leadership.

Business registration processes follow standardized procedures with clearly defined steps. Online registration systems streamline company formation for standard entity types.

Time required to start a business has decreased through digitalization initiatives, though the gambling sector faces additional licensing timeline requirements beyond standard business registration.

Foreign investment policies welcome international capital with 100% foreign ownership permitted for gambling operations. No special restrictions apply to foreign investors beyond those applicable to all operators.

Corporate Structure and Registration

Available Entity Types

LLC (Limited Liability Company) represents the most common structure for iGaming operators, offering liability protection and relatively simple administration. Corporations (joint stock companies) suit larger operations planning significant capitalization.

Branch office options exist for established foreign gambling companies seeking Armenian market entry, though full subsidiary registration often proves preferable for licensing and operational flexibility.

Recommended structure for iGaming operators typically involves Armenian LLC or CJSC (closed joint stock company) providing proper legal basis for license application while limiting shareholder liability.

Registration Requirements

Registration timelines span 1-3 weeks for standard commercial entity registration excluding gambling license processing. Combined entity registration plus license approval extends to 2-4 months total.

Registration costs include government fees of approximately $100-300 for entity registration plus legal and notarization fees of $500-2,000 depending on complexity and service provider selection.

Required documents include articles of association, shareholder information, beneficial ownership declarations, registered office address proof, and director appointment documentation. Notarization requirements apply to founding documents.

Foreign ownership rules permit 100% foreign ownership of gambling companies with no local partner requirements, unlike lottery operations restricted to Armenian citizen founders.

Minimum capital requirements vary by entity type with LLCs requiring minimal capital (AMD 100,000 or ~$250) while joint stock companies mandate higher capitalization. Gambling licenses require separate financial stability demonstration.

Taxation Framework

Corporate Income Tax Structure

Standard corporate tax rates stand at 18% on net profits, among the lower rates in the region. Gambling operators pay this standard rate on profits after accounting for gambling-specific duties and license fees.

Special economic zone benefits exist in Armenia though gambling operations typically operate under standard tax regimes rather than SEZ frameworks given regulatory oversight requirements.

International tax treaties cover numerous countries helping Armenian operations avoid double taxation on cross-border transactions and profit repatriation. Treaty network facilitates international holding structures.

Withholding tax on dividends, interest, and royalties applies according to domestic law and treaty provisions, typically ranging 5-10% for treaty countries and up to 15% for non-treaty jurisdictions.

Personal Income Tax

Individual tax rates apply to employee salaries with progressive or flat rate structures. Social security contributions require both employer and employee payments adding to total employment costs.

Tax residency rules determine obligation scope with residents taxed on worldwide income and non-residents on Armenian-source income only. Six-month presence typically establishes tax residency.

| Tax Type | Rate | Application |

|---|---|---|

| Corporate Income Tax | 18% | Net profits after gambling duties |

| Gambling Turnover Tax | 10% | Total turnover (from July 2025) |

| Online Casino Bet Duty | 0.35% | Per bet (April-June 2025) |

| Sports Betting Duty | 0.2% | Per bet (April-June 2025) |

| License Fee (Annual) | AMD 600M ($1.5M) | Online gambling operations |

| Player Winnings Tax | 5-10% | Withheld by operator |

| VAT | 20% | Not applicable to gambling |

| Dividend Withholding | 5-15% | Based on treaties |

Market Entry Considerations

Recommended Entry Strategies

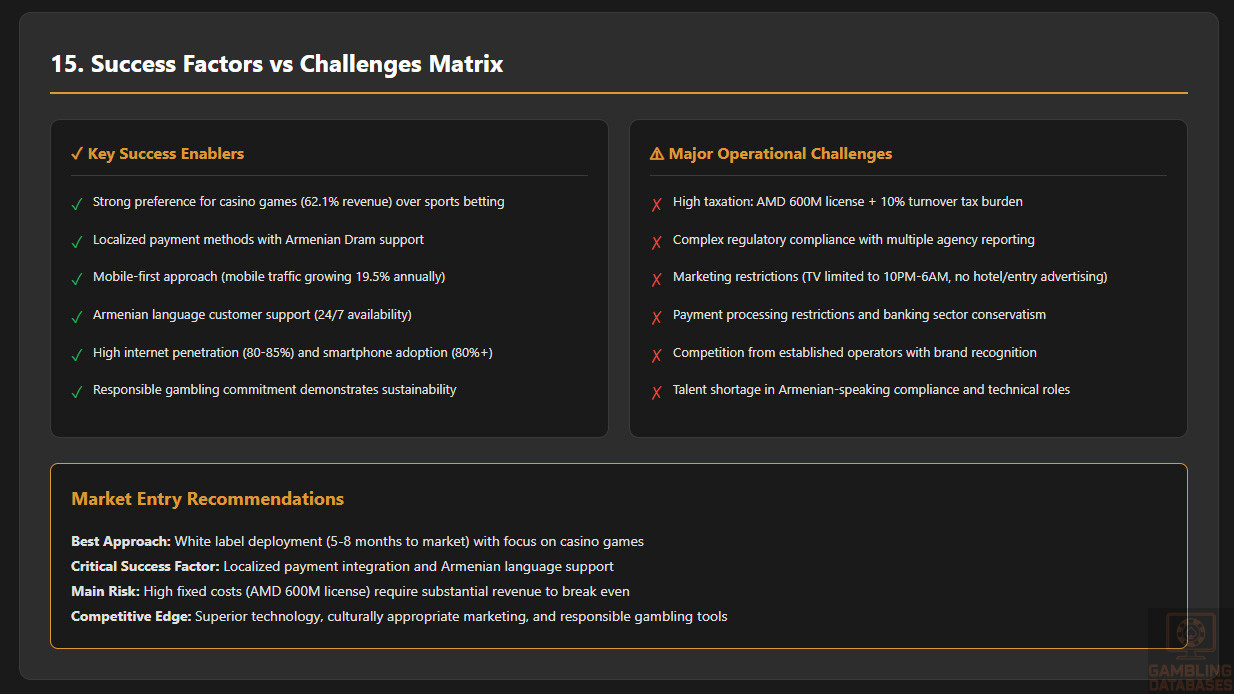

Optimal market entry approaches favor establishing wholly-owned Armenian subsidiaries meeting all localization requirements. Direct licensing proves more viable than partnership structures given 100% foreign ownership permissions.

Local partnership requirements remain optional rather than mandatory for online gambling operations, though partnerships with established Armenian businesses can facilitate market entry through operational knowledge and relationship networks. Payment provider partnerships prove essential given banking integration complexities.

White label versus proprietary platform considerations involve balancing speed-to-market against control and margins. White label solutions enable faster entry with 2-3 month deployment versus 6-12 months for proprietary platforms, though revenue sharing reduces long-term profitability.

Technology infrastructure leveraging strategies should emphasize mobile optimization given rapid mobile traffic growth despite current desktop dominance. Investment in Armenian language interfaces and local payment method integration proves essential rather than optional.

Marketing and localization requirements demand comprehensive Armenian language content across all customer touchpoints. Cultural sensitivity regarding gambling’s social impacts and alignment with responsible gambling messaging helps navigate the regulatory environment’s increasing scrutiny.

Payment provider selection criteria should prioritize local banking integration, AMD currency support, and compliance with transaction monitoring requirements. International payment processors must work alongside domestic banking relationships to serve both local and diaspora customers effectively.

Risk mitigation strategies include staged market entry with initial licensing followed by scaled marketing investment once operational stability confirms. Building cash reserves for the substantial AMD 600 million annual license renewals prevents liquidity crises.

Typical Costs and Timelines

Initial setup investments breakdown includes multiple significant cost categories. License application fees comprise the AMD 600 million (~$1.5 million) annual state duty representing the single largest entry cost and creating substantial barriers to entry for undercapitalized operators.

Legal and consulting fees for license application, entity registration, and ongoing compliance typically range $50,000-150,000 depending on complexity and external advisory requirements. Local legal counsel proves essential for navigating Armenian regulatory frameworks.

Company registration costs remain modest at $1,000-3,000 for standard entity formation including government fees, notarization, and basic legal services. This represents minimal expense relative to total entry investment.

Initial capital requirements beyond the license fee include working capital for operations prior to revenue generation, typically $200,000-500,000 depending on launch scale and marketing ambitions. Cash reserves must cover 3-6 months of operations.

Office setup costs for required physical presence range $20,000-100,000 annually depending on location and scale. Yerevan center locations command premium rents while peripheral or smaller city locations offer cost savings.

Technology and platform costs span $100,000-500,000 for white label solutions including integration, customization, and first-year licensing fees. Proprietary platform development escalates costs to $500,000-2,000,000 with longer development timelines.

Initial marketing budget requirements depend on competitive positioning strategy but typically demand $200,000-1,000,000 for market entry campaigns. Customer acquisition costs in competitive markets require substantial investment for meaningful market share capture.

| Cost Category | Low Estimate | High Estimate | Notes |

|---|---|---|---|

| License Application Fee | $1,500,000 | $1,500,000 | Annual fee, paid upfront |

| Legal & Consulting | $50,000 | $150,000 | License prep + ongoing |

| Company Registration | $1,000 | $3,000 | Entity formation |

| Initial Working Capital | $200,000 | $500,000 | 3-6 months runway |

| Office Setup | $20,000 | $100,000 | First year costs |

| Technology/Platform | $100,000 | $2,000,000 | White label vs proprietary |

| Initial Marketing | $200,000 | $1,000,000 | Launch campaigns |

| Server Infrastructure | $30,000 | $100,000 | Local hosting required |

| Payment Integration | $10,000 | $50,000 | Multiple methods |

| Compliance Systems | $20,000 | $80,000 | KYC/AML tools |

| TOTAL INITIAL INVESTMENT | $2,131,000 | $5,483,000 | First year |

Operational cost estimates on monthly and annual basis include staff salaries representing significant ongoing expenses. Technical staff command AMD 400,000-800,000 monthly ($1,000-2,000), customer support AMD 200,000-400,000 ($500-1,000), and management AMD 1,000,000+ ($2,500+) depending on experience.

Office rent and utilities in Yerevan range $1,000-5,000 monthly for suitable commercial space, with utilities adding $200-500 monthly. Smaller offices or regional locations reduce costs but may impact talent recruitment.

Technology maintenance includes platform licensing fees, hosting costs, software updates, and technical support, typically totaling $10,000-40,000 monthly depending on platform complexity and user volumes.

Payment processing fees consume 2-5% of transaction volumes depending on payment methods and processing partners. These variable costs scale with revenue but represent significant margin pressure.

Marketing and customer acquisition costs typically require $50,000-200,000 monthly for competitive market presence given advertising restrictions limiting channel options and increasing costs for remaining permitted channels.

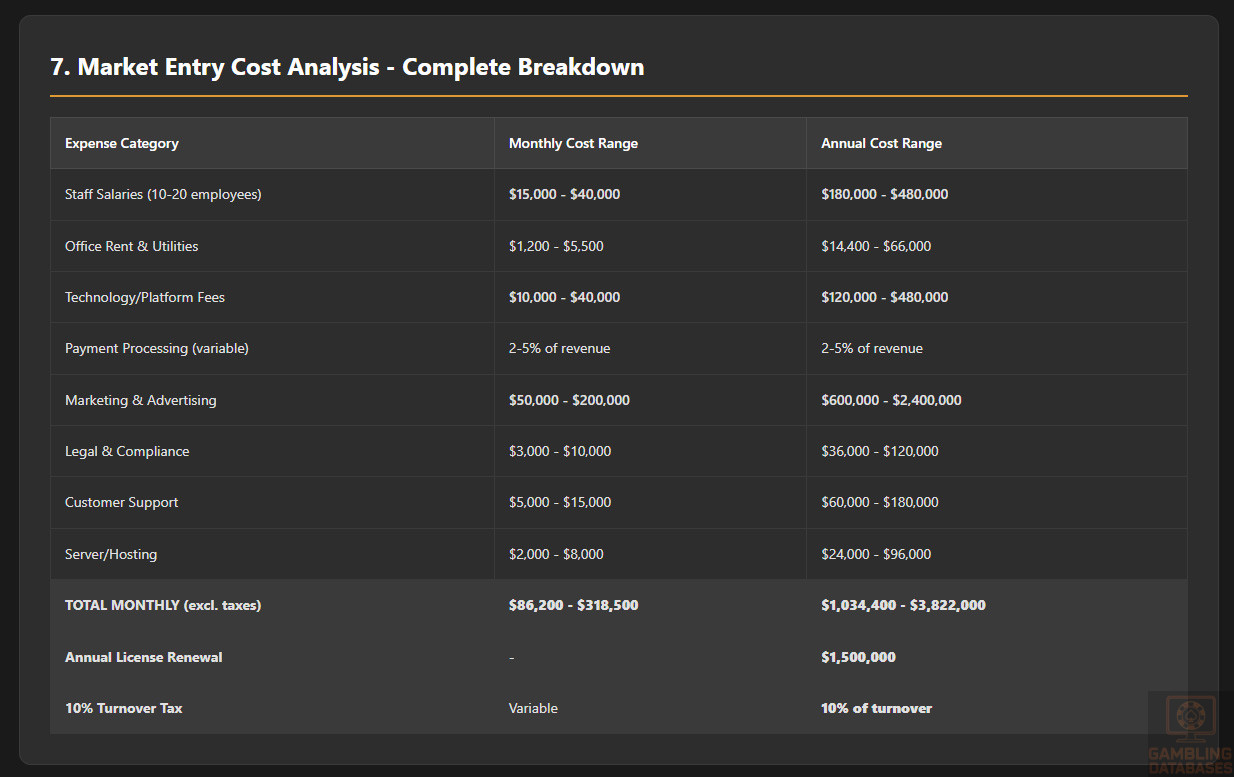

| Expense Category | Monthly Cost Range | Annual Cost Range |

|---|---|---|

| Staff Salaries (10-20 employees) | $15,000 – $40,000 | $180,000 – $480,000 |

| Office Rent & Utilities | $1,200 – $5,500 | $14,400 – $66,000 |

| Technology/Platform Fees | $10,000 – $40,000 | $120,000 – $480,000 |

| Payment Processing (variable) | 2-5% of revenue | 2-5% of revenue |

| Marketing & Advertising | $50,000 – $200,000 | $600,000 – $2,400,000 |

| Legal & Compliance | $3,000 – $10,000 | $36,000 – $120,000 |

| Customer Support | $5,000 – $15,000 | $60,000 – $180,000 |

| Server/Hosting | $2,000 – $8,000 | $24,000 – $96,000 |

| TOTAL MONTHLY (excl. taxes) | $86,200 – $318,500 | $1,034,400 – $3,822,000 |

| Annual License Renewal | – | $1,500,000 |

| 10% Turnover Tax | Variable | 10% of turnover |

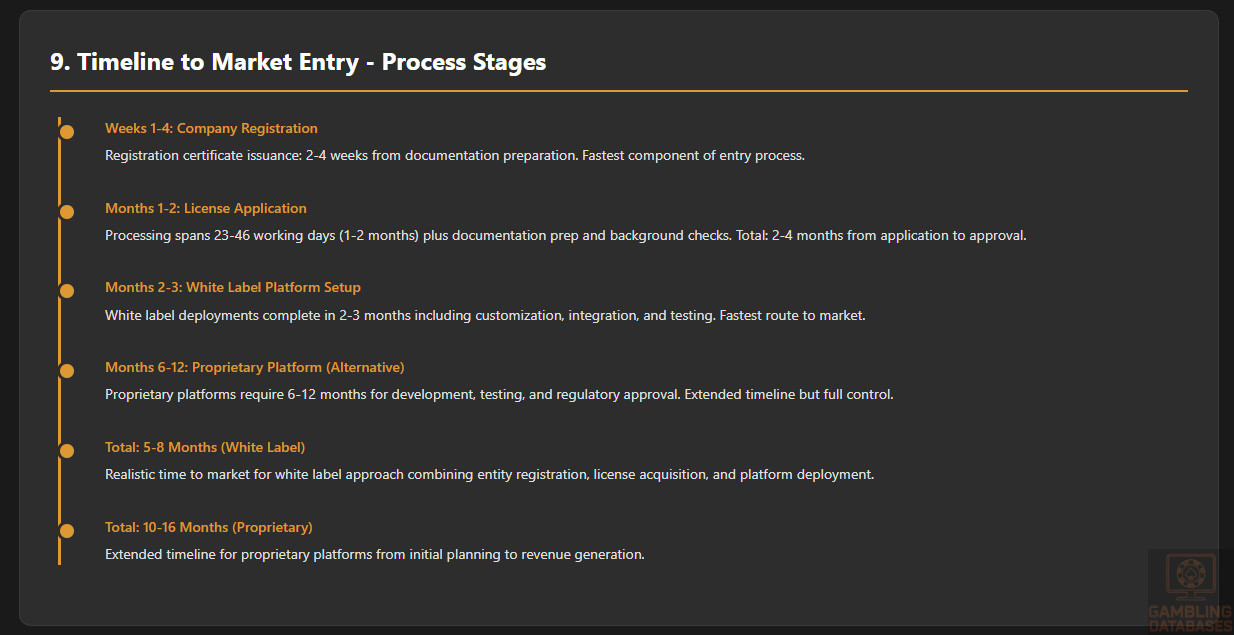

Timeline expectations for market entry include company registration requiring 2-4 weeks from documentation preparation to registration certificate issuance. This represents the fastest component of the entry process.

License application processing spans 23-46 working days (approximately 1-2 months) plus additional time for documentation preparation and stakeholder background checks. Expect 2-4 months total from initial application to license approval.

Platform setup timelines vary dramatically by approach: white label deployments complete in 2-3 months including customization, integration, and testing. Proprietary platforms require 6-12 months for development, testing, and regulatory approval.

Total time to market realistically spans 5-8 months for white label approaches combining entity registration, license acquisition, and platform deployment. Proprietary platforms extend timelines to 10-16 months from initial planning to revenue generation.

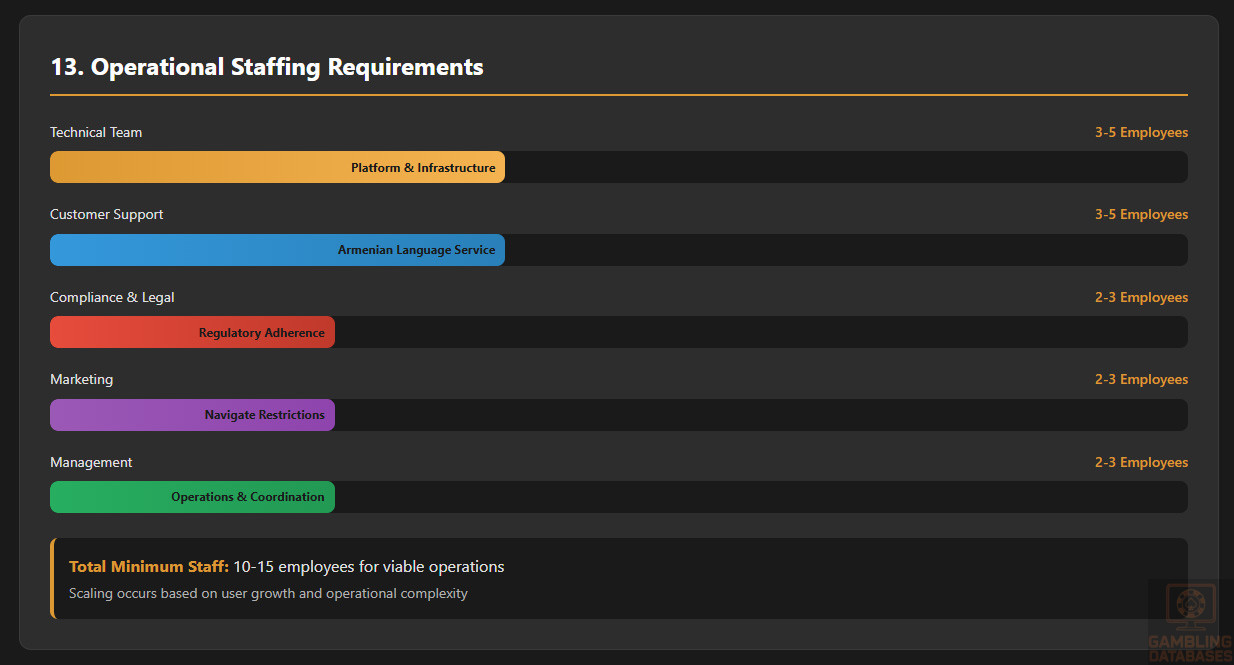

Resource requirements include minimum staff headcount of 10-15 employees for viable operations: technical team (3-5), customer support (3-5), compliance and legal (2-3), marketing (2-3), and management (2-3). Scaling occurs based on user growth.

Key positions needed encompass Technical Director managing platform and infrastructure, Compliance Officer ensuring regulatory adherence, Customer Support Manager handling Armenian-language service, Marketing Manager navigating advertising restrictions, and General Manager coordinating operations and stakeholder relationships.

Success Factors and Challenges

Key Success Enablers

Understanding of local player preferences proves essential with Armenian gamblers showing strong preference for casino games over sports betting based on revenue distribution. Operators must prioritize slot and table game libraries over sportsbook development.

Localized payment methods integration maximizes deposit conversion with Armenian Dram support, local bank transfer options, and familiar payment interfaces reducing friction. International payment methods serve diaspora players but cannot replace local integration.

Mobile-first approach becomes increasingly critical as mobile traffic grows 19.5% annually despite current desktop dominance. Responsive design and native mobile applications position operators for shifting usage patterns rather than reacting after market transition completes.

Effective marketing channels and partnerships face constraints from advertising restrictions limiting television, radio, hotel, and entry point promotions. Digital channels, affiliate partnerships, and brand building through permitted channels require creative approaches.

Strong customer support in Armenian language distinguishes operators in a market where language represents cultural identity. 24/7 support availability, rapid response times, and culturally appropriate communication styles build loyalty.

Competitive bonus and promotion strategy must balance player acquisition against the 10% turnover tax burden. Creative promotional structures emphasizing entertainment value rather than pure monetary incentives may prove necessary.

Responsible gambling commitment gains importance as government scrutiny intensifies following problem gambling increases. Proactive self-exclusion support, deposit limits, and responsible gambling tools demonstrate commitment to sustainable operations.

Major Operational Challenges

Regulatory compliance complexity increases substantially under 2025 reforms requiring comprehensive transaction monitoring, player taxation withholding, and reporting to multiple government agencies. The forthcoming unified monitoring system will further increase compliance burdens.

High taxation burden represents the most significant financial challenge with the AMD 600 million annual license fee creating fixed costs requiring substantial revenue to recoup. The 10% turnover tax dramatically reduces gross margins compared to GGR-based taxation markets.

Payment processing restrictions and banking sector conservatism limit payment method options compared to European markets. International payment processors may face difficulties establishing Armenian banking relationships necessary for local operations.

Marketing and advertising limitations severely constrain customer acquisition channels with television restricted to 10PM-6AM, hotel and entry point advertising banned, and foreign operator advertising prohibited. These restrictions increase customer acquisition costs through remaining channels.

Competition from established operators presents entry barriers as existing players hold market knowledge, customer databases, and brand recognition. New entrants must differentiate through superior technology, better bonuses, or niche targeting.

Player acquisition costs escalate in mature markets where most interested players already hold accounts with existing operators. Switching incentives must overcome switching costs and established loyalties.

Talent shortage in specific skills including Armenian-speaking customer support representatives with gambling industry knowledge, compliance professionals understanding Armenian regulations, and technical staff capable of managing localized infrastructure creates recruitment challenges.

Cultural Considerations

Local holidays and peak seasons influence gambling activity with increased participation during New Year, Christmas (January 6 in Armenian Apostolic tradition), and summer months when tourism and disposable income peak. Promotional calendars should align with these patterns.

Popular local sports and events for sports betting include football (soccer) with strong European league following, boxing, chess (Armenia consistently ranks among top chess nations), and wrestling. International sporting events generate betting spikes.

Preferred customer service channels emphasize direct communication with phone support remaining important alongside modern chat options. Armenian customers expect personal service rather than purely automated responses.

Communication style preferences blend post-Soviet directness with Armenian hospitality traditions. Customer support should balance efficiency with warmth, avoiding overly formal corporate communication or excessive casualness.

Trust-building requirements for foreign brands necessitate demonstrating Armenian commitment through local presence, Armenian language proficiency, and cultural awareness. Highlighting licensing from Armenian authorities rather than foreign credentials builds legitimacy.

Exit Strategy Planning

Market liquidity for operator sales remains limited given the small market size and high entry costs deterring potential acquirers. Strategic buyers would most likely come from regional gambling groups seeking portfolio expansion.

Regulatory requirements for ownership transfer involve Ministry of Finance approval ensuring new owners meet licensing criteria including background checks and financial stability demonstrations. License transfers require similar scrutiny to initial applications.

License transferability provisions allow license assignment to qualified buyers meeting all licensing requirements. The AMD 600 million annual fee remains payable regardless of ownership changes.

Typical valuation multiples in market remain difficult to establish given limited transaction history. Expect 2-4x annual EBITDA for profitable operations, though high licensing costs and tax burdens may compress multiples below global norms.

Process for closing operations legally requires Ministry of Finance notification, customer account closure with withdrawal processing, employee termination compliance, and final tax settlement. License surrender does not entitle fee refunds for unused annual periods.

FAQ: Frequently Asked Questions

Legal & Licensing

Is online gambling legal in Armenia?

Yes, online gambling is legal and regulated in Armenia under a comprehensive licensing framework administered by the Ministry of Finance. Both online casino games and sports betting are permitted for operators holding valid Armenian licenses. The legal framework was significantly updated in 2025 with new legislation titled “Regulation of Gaming Activities” taking effect January 1, 2025.

However, the 2025 reforms prohibited Armenian residents from participating in gambling organized outside Armenia and banned advertising of foreign gambling services. All licensed operators must maintain physical presence in Armenia including servers, software, and hardware located within the country.

The minimum gambling age increased from 18 to 21 years effective January 2025, applying to all forms of gambling including sports betting and lottery games. Operators must verify age through identification documentation before allowing participation.

What types of gambling licenses are available and what do they cover?

Armenia offers several gambling license types covering different activities. Online gambling licenses permit internet casino games, online winning games, and online sports betting operations. These licenses cost AMD 600 million (approximately $1.5 million USD) annually and require comprehensive compliance with localization and monitoring requirements.

Land-based casino licenses permit games of chance operated through gaming tables and machines in physical locations. License fees vary by designated zone: Tsakhkadzor (AMD 180 million), Sevan (AMD 150 million), Jermuk (AMD 100 million), and Meghri (AMD 35 million) annually.

Lottery licenses permit prize pool draws but face stricter ownership requirements than other gambling licenses. Only commercial organizations registered in Armenia with founders who are Armenian citizens or Armenian-registered legal entities may operate lotteries. Geographic restrictions limit lottery operations to the four designated resort cities.

Sports betting licenses for land-based operations fall under the toto category covering events where outcomes depend on occurrences beyond operator control. These licenses permit acceptance of bets on sports events and other predictive gaming in physical venues.

How much does an iGaming license cost and how long does it take to obtain?

An online gambling license in Armenia costs AMD 600 million (approximately $1.5 million USD) annually, representing one of the highest license fees in the region. This amount must be paid before license issuance and renews annually regardless of operational revenue or profitability.

The application processing timeline spans 23 working days from submission for initial review, with potential extension of an additional 23 working days if documentation requires further study. This translates to approximately 1-2 months for processing after application submission.

Upon approval, the Ministry of Finance issues the license within one month following receipt of the first annual state duty payment. Total timeline from initial application preparation to license receipt typically spans 2-4 months depending on documentation completeness and complexity.

Additional costs beyond the license fee include company registration ($1,000-3,000), legal and consulting fees ($50,000-150,000), and initial setup investments for technology, office space, and working capital totaling $500,000-2,000,000 depending on operation scale.

Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain gambling licenses in Armenia with 100% foreign ownership permitted. No local partnership requirements exist for online casino or sports betting operations, though lottery licenses require Armenian citizen founders.

Foreign operators must establish registered commercial entities in Armenia before license application. LLC (Limited Liability Company) or CJSC (Closed Joint Stock Company) structures work well for foreign-owned gambling operations, providing liability protection while meeting regulatory requirements.

All physical infrastructure including servers, software, hardware, and gaming platforms must be located within Armenian territory regardless of ownership nationality. This localization requirement ensures regulatory oversight and facilitates the government’s monitoring capabilities.

Background checks apply to all beneficial owners, directors, and key personnel regardless of nationality. These investigations examine criminal records, financial misconduct history, and prior gambling license issues in any jurisdiction worldwide.

Financial & Taxation

What are the tax obligations for iGaming operators?

Armenian gambling operators face multiple tax obligations creating substantial financial burdens. The primary gambling-specific tax is a 10% turnover tax on all licensed gambling activities implemented July 1, 2025, replacing previous per-bet duty structures.

The annual license fee of AMD 600 million (approximately $1.5 million USD) represents a significant fixed cost payable regardless of revenue generation. This fee renews annually for the duration of operations.

Corporate income tax applies at 18% on net profits after accounting for gambling duties and license fees. This standard Armenian corporate rate applies to all gambling operators without special exemptions.

Operators serve as tax agents for players, withholding 5% at source for significant individual wins and 10% for accumulated smaller winnings during annual income declarations. These withholding obligations create administrative burdens and payment processing complexities.

Prior to July 2025, a per-bet duty structure applied with online casinos paying 0.35% per bet and sports betting operators paying 0.2% per bet. These rates doubled from previous levels in April 2025 as interim measures before turnover tax implementation.

Are gambling winnings taxed for players?

Yes, gambling winnings are taxed for players in Armenia under a system implemented in 2025. Licensed gambling operators act as tax agents withholding applicable taxes before distributing winnings to players.

For significant individual wins, operators must withhold 5% tax at the source of the bet before paying out winnings. This applies to single wins exceeding specified thresholds set by tax authorities.

When players accumulate smaller wins throughout the year, gambling companies withhold 10% during the player’s annual income declaration process. This captures tax on cumulative winnings that individually fall below the significant win threshold.

Tax-free thresholds for gambling winnings remain undefined in current legislation, with all winnings potentially subject to taxation depending on amount and timing. The withholding system ensures collection before players receive funds rather than relying on voluntary tax reporting.

Players retain responsibility for declaring gambling income in annual tax returns, though the operator withholding system aims to capture the majority of tax liability automatically. Additional taxes may apply if operators under-withhold.

What are the typical operational costs for running an online casino or sportsbook?

Operational costs for Armenian online gambling operations are substantial due to high licensing fees and compliance requirements. Monthly operational expenses typically range $86,000-320,000 excluding gambling-specific taxes, translating to $1.0-3.8 million annually.

The AMD 600 million annual license fee ($1.5 million USD) represents the single largest fixed cost. This amount remains payable regardless of revenue or profitability, creating significant break-even requirements.

Staff salaries for a team of 10-20 employees cost $15,000-40,000 monthly ($180,000-480,000 annually). This covers technical staff, customer support representatives, compliance officers, marketing personnel, and management.

Technology and platform fees range $10,000-40,000 monthly ($120,000-480,000 annually) depending on whether operators use white label solutions or proprietary platforms. These costs include hosting, software licensing, and maintenance.

Marketing and customer acquisition expenses typically require $50,000-200,000 monthly ($600,000-2.4 million annually) for competitive market presence. Advertising restrictions increase costs by limiting available channels and intensifying competition for remaining options.

The 10% turnover tax adds significant variable costs directly proportional to betting volumes. For operators processing $20 million annual turnover, this represents $2 million in gambling tax beyond the license fee and corporate income tax.

What is the expected ROI timeline for entering this market?

ROI timeline for Armenian gambling market entry extends longer than many jurisdictions due to high fixed costs and substantial initial investment requirements. Total initial investment of $2.1-5.5 million creates significant capital requirements before revenue generation begins.