Australia presents a complex yet lucrative opportunity for iGaming operators, ranking among the world’s highest per-capita gambling markets with annual player losses exceeding AUD 24 billion. However, the Interactive Gambling Act 2001 strictly prohibits online casino operations while permitting licensed sports betting and lotteries, creating a unique regulatory landscape that requires careful navigation and strategic market entry planning.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Online Casino Gaming Legal Status | Prohibited | Banned under Interactive Gambling Act 2001 |

| Online Sports Betting Status | Legal (Licensed) | Pre-match only; in-play betting prohibited |

| Population (2025) | 27.5 million | Growing at 1.6% annually |

| Median Age | 38.3 years | Aging population trend |

| Urban Population | 86.5% | Highly concentrated in major cities |

| GDP (2025) | USD 1.82 trillion | 17th largest global economy |

| GDP Per Capita | USD 67,400 | High purchasing power |

| GDP Growth Rate (2024-25) | 1.3% | Lowest since early 1990s (excluding COVID) |

| Internet Penetration | 97.1% | 26.1 million users |

| Mobile Connections | 128% of population | 34.4 million connections |

| Smartphone Penetration | 97% | Among highest globally |

| Total Gambling Market (2025) | USD 15.43 billion | All gambling forms combined |

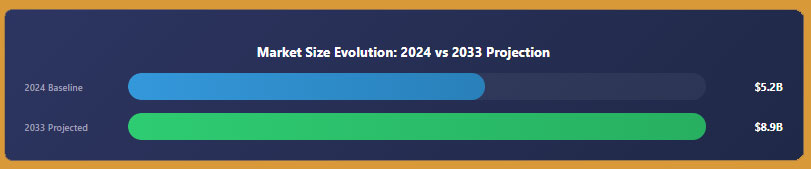

| Online Gambling Market (2024) | USD 5.2 billion | Sports betting and lotteries only |

| Market Growth CAGR (2025-2033) | 5.88% | Expected to reach USD 8.9 billion by 2033 |

| Sports Betting Market (2024) | AUD 6.81 billion | Fastest growing segment at 22.1% CAGR |

| Per Capita Gambling Losses (2022-23) | AUD 1,555 | Among world’s highest |

| Average Revenue Per User (ARPU) | USD 809.94 | High spending players |

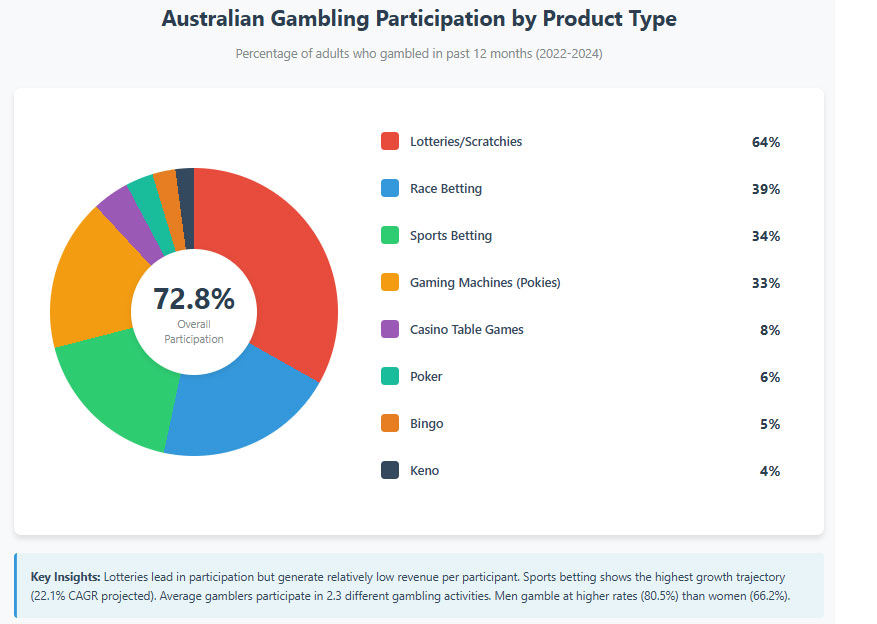

| Gambling Participation Rate | 72.8% | Of adults gambled in past 12 months |

| Market Penetration (2025) | 70.6% | Expected 19.4 million users by 2029 |

| Wagering License Application Fee | AUD 10,000-100,000 | Varies by state/territory |

| Casino License Application Fee | AUD 100,000+ | Land-based only; multi-million for major casinos |

| Corporate Income Tax Rate | 30% | Standard rate for gaming operators |

| Goods and Services Tax (GST) | 10% | Applies to most gaming services |

| Point of Consumption Tax | Varies by state | 8-15% on wagering revenue |

| Regulatory Authority (Federal) | ACMA | Australian Communications and Media Authority |

| Ease of Doing Business Rank | 14th globally | Strong business environment |

| Corruption Perception Index | 13th globally | High transparency and governance |

| Mobile Internet Speed (Median) | 103.46 Mbps | Up 10.2% year-over-year |

| Fixed Internet Speed (Median) | 77.90 Mbps | Up 43.2% year-over-year |

| Problem Gambling Prevalence | 0.6-1.0% | Approximately 160,000-270,000 adults |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Australia operates under a dual regulatory system where federal legislation governs online gambling through the Interactive Gambling Act 2001, while state and territory authorities regulate land-based operations and license online wagering providers. This creates a complex but well-defined legal framework that strictly prohibits certain online gambling forms while permitting others under license.

Land-Based Gambling Activities

Casino Operations: Australia hosts 13 major land-based casinos distributed across states and territories. Crown Melbourne and The Star Sydney represent the largest operations, though both have faced significant regulatory scrutiny in recent years. The Victorian Gambling and Casino Control Commission concluded in March 2024 that Crown Melbourne had returned to suitability after implementing extensive remediation programs.

Sports Betting Venues: Licensed sports betting operates through both physical TAB (Totalisator Agency Board) outlets and authorized bookmakers. Each state maintains its own TAB operation or equivalent, with Tabcorp historically dominating the retail wagering market. In August 2024, the Victorian Gambling and Casino Control Commission fined Tabcorp AUD 4.6 million for compliance failures, and in June 2024, Tabcorp received an additional AUD 370,417 fine for allowing minors to gamble. These actions demonstrate regulators’ zero-tolerance approach to violations.

Electronic Gaming Machines (Pokies): Australia operates 76 percent of the world’s pub and club poker machines despite having only 0.3 percent of global population. In financial year 2020-21, Australians wagered nearly AUD 150 billion through electronic gaming machines, resulting in player losses of AUD 12 billion. Per capita losses from pokies alone reached AUD 608, representing approximately half of total gambling losses. Victoria has implemented major reforms including reducing maximum machine deposits from AUD 1,000 to AUD 100 effective December 2025, mandatory pre-commitment systems, and venue closures between 4am and 10am (excluding Crown Casino).

Other Land-Based Activities: Legal land-based gambling extends to bingo halls, keno lounges, lotteries sold through retail outlets, charitable gaming operations, and raffles conducted by eligible organizations. Each activity requires specific licenses determined by state or territory regulations.

Online Gambling Framework

Digital Gaming Regulations: The Interactive Gambling Act 2001 forms the cornerstone of Australia’s online gambling regulation. The Act makes it illegal for operators to offer real-money online casino games, including slots, roulette, blackjack, and poker, to Australian residents. The legislation targets providers rather than players—accessing these services is not an offense for consumers, but offering them carries severe penalties including fines, prosecution, and ISP blocking.

Permitted Online Activities: Licensed operators may legally offer pre-match sports betting and race wagering to Australian customers through online and telephone channels. Online lottery ticket sales are also permitted under state lottery licenses. However, in-play sports betting (placing bets after an event has commenced) remains prohibited under the 2016 amendments to the Interactive Gambling Act, though this restriction is widely circumvented through telephone betting channels.

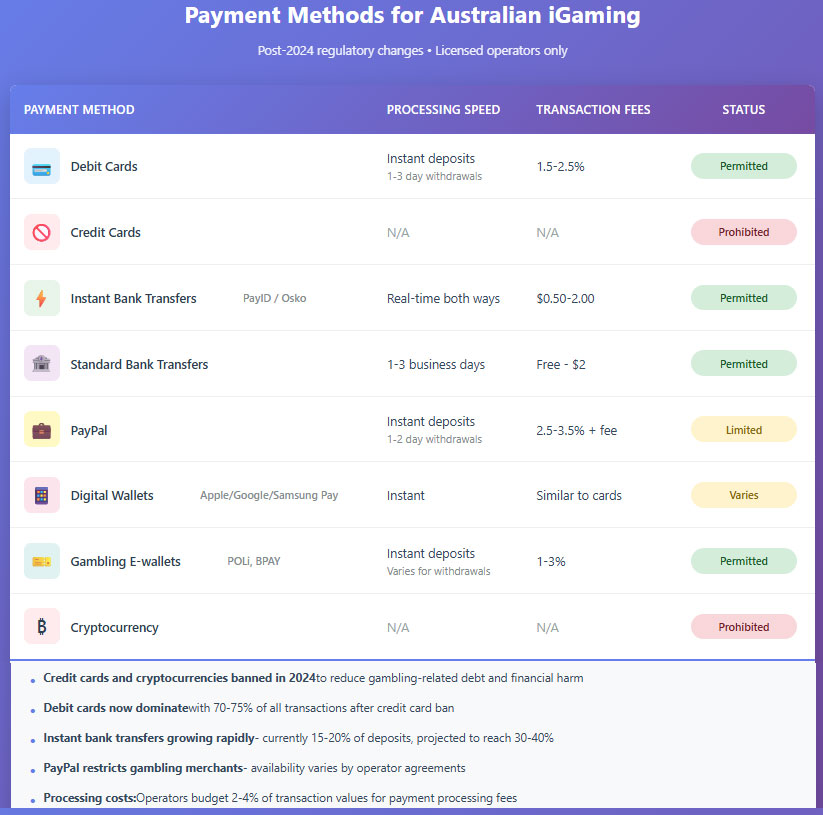

Prohibited Activities: Expressly banned online gambling services include casino-style games, poker rooms, in-play sports betting through digital channels, and any gambling services offered without an Australian license. In mid-2024, Australia banned credit cards and digital currencies for online wagering transactions to reduce gambling-related financial harm. Between October and December 2024, ACMA investigated 301 complaints and identified 16 breaches, resulting in 75 websites being referred for ISP blocking.

Regulatory Oversight Bodies: The Australian Communications and Media Authority operates at the federal level, monitoring and enforcing interactive gambling laws, maintaining a register of Australian-licensed providers, and coordinating ISP blocking of illegal offshore sites. As of September 2025, ACMA has requested ISPs block more illegal online gambling and affiliate sites, exercising expanded enforcement powers granted in recent legislative reforms.

State and territory regulators include the Victorian Gambling and Casino Control Commission, NSW Independent Liquor & Gaming Authority, Northern Territory Racing Commission, Queensland Office of Liquor and Gaming Regulation, and equivalent bodies in other jurisdictions.

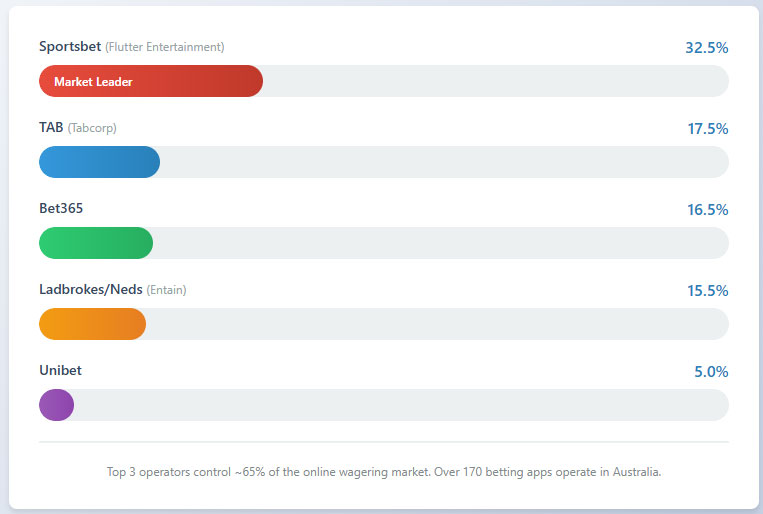

Licensed Operators and Market Players

Australia’s online wagering market features both major domestic operators and international brands holding Australian licenses. The Northern Territory has historically been the preferred licensing jurisdiction for online operators due to its streamlined processes and operator-friendly regulatory approach.

| Operator | Market Position | License Jurisdiction | Estimated Market Share |

|---|---|---|---|

| Sportsbet (Flutter Entertainment) | Market Leader | Northern Territory | 30-35% |

| TAB (Tabcorp) | Traditional Leader | Multiple State Licenses | 15-20% |

| Bet365 | International Major | Northern Territory | 15-18% |

| Ladbrokes (Entain) | Major Competitor | Northern Territory | 8-10% |

| Neds (Entain) | Growing Brand | Northern Territory | 5-8% |

| Unibet | International Player | Northern Territory | 4-6% |

| BlueBet | Australian-owned | Northern Territory | 2-4% |

| PointsBet | Australian-founded | Northern Territory | 2-3% |

Market Dynamics: The Australian wagering market exhibits significant concentration among top operators, with Sportsbet commanding approximately one-third of online sports betting activity. International operators including Bet365, Ladbrokes, and Unibet have successfully established strong market positions by combining global technology platforms with localized marketing campaigns focused on Australian sporting events including AFL, NRL, cricket, and horse racing. The market features over 170 licensed mobile betting applications, creating intense competition for customer acquisition and retention.

Competitive Landscape: Operators compete primarily on promotional offers, odds competitiveness, platform usability, event coverage breadth, and customer service quality. The cost of customer acquisition has increased substantially, with operators investing heavily in sponsorships of major sporting codes, teams, and media rights. Market consolidation continues, with Flutter Entertainment’s ownership of Sportsbet and Entain’s control of multiple brands demonstrating the scale advantages in this highly competitive market.

Licensing Framework and Requirements

Application Process and Eligibility

Regulatory Authority Selection: Prospective operators must first determine the appropriate licensing jurisdiction based on their intended business model. For online sports betting and race wagering, the Northern Territory Racing Commission represents the most popular choice, having licensed numerous major operators. Queensland’s Office of Liquor and Gaming Regulation handles lottery operator licenses. State-specific regulators oversee land-based operations including casinos, pokies venues, and retail betting outlets within their territories.

Financial Requirements: License applicants must demonstrate substantial financial capacity and stability. For online wagering licenses, operators typically must provide evidence of access to capital ranging from AUD 500,000 to several million dollars depending on projected scale of operations. Casino license applicants face significantly higher thresholds, often requiring proof of access to tens or hundreds of millions in capital. Financial guarantees or bonds may be required to ensure operators can meet ongoing obligations including player payouts and tax remittances.

Technical Standards: Gaming systems must undergo independent testing and certification to verify fairness, security, and integrity. Operators must demonstrate that random number generators meet international standards, that player funds are held in segregated trust accounts, and that systems include robust controls against fraud, money laundering, and underage gambling. Technical infrastructure must support responsible gambling tools including deposit limits, loss limits, time-out periods, and self-exclusion capabilities.

Background Checks and Probity: All directors, major shareholders (typically those holding 5% or more), key executives, and individuals in positions to influence operations must undergo comprehensive probity investigations. These checks examine criminal history, financial history, business conduct, associates, and overall suitability to be involved in gambling operations. The process typically takes 3 to 6 months for individuals and involves interviews, document verification, and potentially international inquiries for non-Australian applicants.

| License Type | Application Fee | Annual Fee | Processing Time |

|---|---|---|---|

| Online Wagering (Northern Territory) | AUD 10,000-50,000 | Based on turnover | 3-6 months |

| Interactive Gambling (Queensland) | AUD 2,147-21,460 | Quarterly fees negotiated | 6-12 months |

| Lottery Operator (Queensland) | AUD 21,460 | Quarterly (negotiated) | 6-12 months |

| Casino Operator (Major) | AUD 100,000-5,000,000 | AUD 1,000,000+ annually | 12-24 months |

| Venue Operator (Pokies – Victoria) | AUD 500-5,000 | Per machine fees | 8-16 weeks |

| Gaming Equipment Supplier | AUD 100-1,000 | AUD 500-2,000 | 4-12 weeks |

| Bookmaker License (Retail) | AUD 5,000-50,000 | Varies by state | 3-6 months |

Local Presence and Operational Requirements

Physical Presence: Most jurisdictions require licensed operators to maintain a physical office presence within Australia, though requirements vary by license type and state. Online operators typically must establish a registered business address and designate a responsible manager residing in Australia. Larger operations may need to demonstrate significant local employment and infrastructure investment. Some states mandate that key operational functions including customer service, compliance monitoring, and management occur within the licensing jurisdiction.

Domain and Hosting: While there is no absolute requirement for operators to use Australian-registered domain names, holding an Australian license provides legal protection and consumer trust that offshore operators lack. Server location requirements vary—some regulators require critical gaming servers to be located within Australia or in approved jurisdictions, while others permit international hosting provided data security and access standards are met. All operators must ensure their systems are accessible to regulators for audit and inspection purposes.

Personnel Requirements: Operators must employ appropriately qualified personnel in key positions including compliance officers, responsible gambling coordinators, anti-money laundering officers, and technical managers. Many jurisdictions require these individuals to hold specific certifications or undergo regulator-approved training. For casino operations, extensive staffing requirements cover gaming floor personnel, surveillance operators, security staff, and management, all of whom may require individual licenses or permits.

Foreign Ownership: Australia generally permits foreign ownership of gambling licenses, though conditions apply. Foreign-owned entities typically must establish an Australian subsidiary, demonstrate financial transparency, and show that ultimate beneficial owners meet probity standards.

Some jurisdictions impose restrictions on cumulative foreign ownership or require a minimum percentage of Australian ownership for certain license types. Recent regulatory inquiries at Crown Melbourne and The Star Sydney have intensified scrutiny of foreign ownership structures and corporate governance arrangements.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification: The minimum gambling age throughout Australia is 18 years for all gambling products. Operators must implement robust age verification before allowing any person to create an account or place wagers. Since September 2024, AUSTRAC requires all online gambling service providers to complete applicable customer identification procedures before establishing accounts or offering services. This requirement strengthens existing Know Your Customer protocols and aligns gambling operators with banking sector identification standards.

KYC and AML Compliance: Anti-money laundering and counter-terrorism financing obligations under the AML/CTF Act apply comprehensively to gambling operators. Operators must verify customer identity using reliable and independent documentation, monitor transactions for suspicious patterns, maintain records for seven years, and report designated transactions and suspicious matters to AUSTRAC. Several major corporate bookmakers have recently been required by AUSTRAC to appoint independent auditors to assess their AML/CTF compliance, with one entering into an enforceable undertaking. Further enforcement actions are expected throughout 2025.

Responsible Gambling Measures: The National Consumer Protection Framework for Online Wagering establishes minimum consumer protections across all jurisdictions. Mandatory measures include activity statements showing gambling expenditure, voluntary pre-commitment tools allowing customers to set deposit and loss limits, account closure mechanisms, and prohibition on extending credit to customers. Operators must display responsible gambling messages prominently, provide links to support services, and train staff in identifying and responding to problem gambling indicators.

Self-Exclusion Systems: BetStop, the National Self-Exclusion Register, launched in August 2023 and requires all betting providers to verify customers against the registry. Operators must not allow individuals on the register to create accounts or receive marketing communications. By the end of Q2 2024-25, 35,671 individuals had registered for self-exclusion, with 26,020 active registrations. State-level self-exclusion programs also operate for land-based venues, and New South Wales is implementing gaming reforms including a statewide exclusion register with potential facial recognition technology integration.

Information Disclosure: Recent regulatory changes mandate specific player information disclosures. Operators must provide clear information about odds, probabilities of winning, house edges on different products, and the mathematical disadvantage players face. Marketing materials and platforms must display warnings about gambling risks, and operators must send periodic activity statements to customers summarizing their gambling expenditure, wins, and net losses over specified timeframes.

Financial Monitoring and Reporting

Transaction Monitoring: Operators must implement automated transaction monitoring systems capable of detecting unusual patterns, potential money laundering, structuring behaviors, and other suspicious activities. These systems must generate alerts for manual review by trained compliance staff. Since the 2024 credit card ban, operators must ensure payment methods exclude prohibited instruments and verify that customers are not circumventing restrictions through alternative means.

Regulatory Reporting: Financial reporting obligations vary by jurisdiction but generally include monthly or quarterly submission of revenue data, tax calculations, player activity statistics, responsible gambling metrics (self-exclusions, account closures, limit activations), and compliance incident reports. Operators must maintain detailed records of all transactions, customer interactions, and system changes, making these available to regulators upon request. Some jurisdictions require real-time data access for regulatory monitoring.

Audit and Inspection: Regulators conduct regular audits of operator compliance, examining financial records, gaming systems, customer complaints handling, marketing materials, and adherence to license conditions. For major operators, regulators may require independent audits by accredited firms on annual or more frequent bases. Following the casino royal commissions, Crown Melbourne and The Star properties operate under continuous independent monitoring, with reports submitted to regulators assessing remediation progress against identified deficiencies.

Data Retention: Operators must retain comprehensive records for periods ranging from three to seven years depending on record type and regulatory requirements. This includes customer identification documents, transaction records, marketing communications, responsible gambling interactions, surveillance footage (for land-based operations), game outcomes, and all correspondence with regulators. Records must be maintained in formats accessible to regulators and preserved even after customers close accounts or operators cease operations.

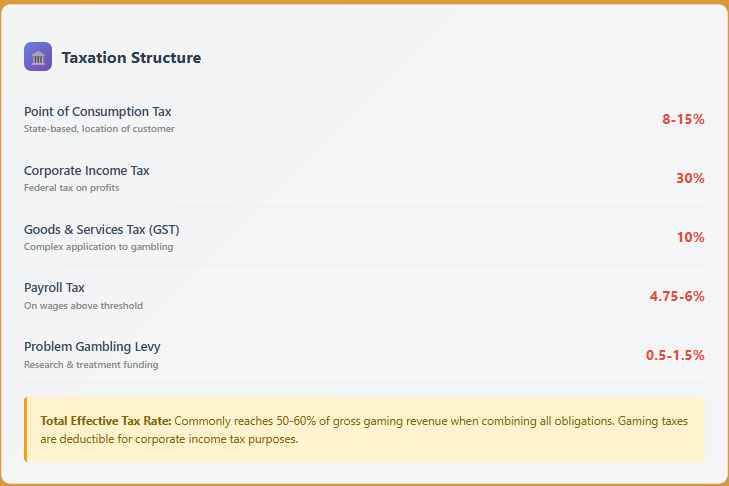

Taxation Structure and Financial Obligations

Player Taxation

Winnings Tax Status: Gambling winnings in Australia are generally not taxed for recreational players. This tax-free treatment applies whether the gambling activity occurs online or at land-based venues, and regardless of the amount won. Players are not required to report gambling winnings on personal income tax returns, and operators do not withhold taxes from payouts. This favorable tax treatment for players contributes to Australia’s high gambling participation rates and distinguishes it from many other jurisdictions where significant winnings trigger tax obligations.

Professional Gambler Treatment: Individuals who gamble as a business rather than recreation may have winnings treated as assessable income subject to taxation. The Australian Taxation Office examines factors including volume and frequency of gambling activity, systematic approaches to gambling, whether the person has other income sources, and business-like record keeping. This classification affects relatively few individuals and primarily impacts professional sports bettors and poker players operating at high levels.

Operator Taxation

Australia’s gambling taxation occurs primarily at the state and territory level, creating a complex mosaic of different tax regimes based on gambling product type, operator license type, and jurisdiction. This structure means operators must navigate multiple tax obligations simultaneously.

| Gambling Product | Tax Base | Typical Rate Range | Notes |

|---|---|---|---|

| Online Sports Betting | Net Revenue | 8-15% Point of Consumption | Varies by state where customer located |

| Online Race Betting | Net Revenue | 5-15% | Lower rates for racing to support industry |

| Casino Gaming (Land-based) | Gross Gaming Revenue | 10-30% tiered structure | Higher rates at higher revenue levels |

| Electronic Gaming Machines | GGR from machines | 25-50% | Varies significantly by state and venue type |

| Lottery (Lotto-style) | Gross Revenue | 73.48% (Queensland example) | Extremely high rates offset by exclusivity |

| Lottery (Instant Scratch) | Gross Revenue | 55% | Lower than lotto but still substantial |

| Keno | Player Loss | 20-30% | Varies by jurisdiction |

Point of Consumption Tax: Most states impose point of consumption taxes on online wagering, calculated based on the location of the customer rather than where the operator is licensed. When a Victorian customer places a bet with a Northern Territory-licensed operator, Victorian point of consumption tax applies to that transaction. Rates typically range from 8 to 15 percent of net wagering revenue (stakes minus payouts). Victoria pioneered this approach, and other states have followed, significantly increasing the tax burden on online operators compared to historical arrangements.

Corporate Income Tax: In addition to gambling-specific taxes, operators pay standard corporate income tax on profits at the 30 percent rate. Some smaller companies with turnover below AUD 50 million may qualify for the 25 percent small business rate, though most gambling operators exceed this threshold. Gaming-specific taxes are deductible expenses when calculating corporate income tax liability, somewhat offsetting the cumulative tax burden.

Goods and Services Tax: GST of 10 percent applies to most goods and services in Australia, including certain gambling activities. The application to gambling is complex—generally, gambling supplies are input-taxed, meaning operators cannot claim GST credits on related expenses. However, fees charged to customers for non-gambling services may attract GST. Lottery products have specific GST treatment with different rules for government-operated versus privately-operated lotteries.

License Fees and Levies: Beyond taxes on revenue, operators pay annual license fees that vary from thousands to millions of dollars depending on license type and jurisdiction. Queensland’s lottery operator pays quarterly license fees negotiated with government in addition to the 73.48 percent tax on gross revenue. Casino operators typically pay annual license fees of AUD 1 million or more. Additional levies may fund problem gambling research, treatment services, and regulatory administration.

Gambling Market Financial Performance

Australia’s gambling industry generates substantial revenue, reflecting the nation’s status as one of the world’s highest per-capita gambling markets. Financial data reveals both the market’s scale and its growth trajectory, though recent economic headwinds have moderated expansion rates in some segments.

| Metric | Value (AUD) | Value (USD) | Year-over-Year Change |

|---|---|---|---|

| Total Amount Wagered | AUD 244.3 billion | USD 164.3 billion | +18.2% |

| Total Gambling Expenditure (Player Losses) | AUD 32.0 billion | USD 21.5 billion | +13.8% |

| Per Capita Annual Losses | AUD 1,555 | USD 1,046 | +11.5% |

| Gaming Machines Turnover | AUD 191.2 billion | USD 128.6 billion | +20.9% |

| Gaming Machines Revenue | AUD 15.8 billion | USD 10.6 billion | +22.8% |

| Online Gambling Turnover | AUD 75.4 billion | USD 50.7 billion | +165.7% |

| Wagering Expenditure (Race and Sports) | AUD 5.815 billion | USD 3.91 billion | +27.3% |

| Land-Based Casino Turnover | AUD 20.0 billion | USD 13.4 billion | +22.6% |

| Keno Turnover | AUD 1.8 billion | USD 1.2 billion | +18.7% |

| Lottery Turnover | AUD 7.6 billion | USD 5.1 billion | -1.1% |

Revenue Distribution Analysis: Electronic gaming machines dominate Australia’s gambling landscape, accounting for approximately 49 percent of total gambling expenditure despite representing a smaller portion of total turnover. The AUD 15.8 billion in gaming machine revenue reflects their high house edge and the captive nature of venue-based gambling. Wagering on racing and sports contributed AUD 5.815 billion in 2020-21, with this figure experiencing explosive growth of 27.3 percent as online wagering platforms expanded aggressively and COVID-19 restrictions drove migration from retail to digital channels.

Online Gambling Surge: The 165.7 percent year-over-year increase in online gambling turnover to AUD 75.4 billion marks the most dramatic shift in Australia’s gambling landscape. This figure excludes racing and sports betting, representing primarily offshore casino gaming activity by Australian players despite its illegal status under Australian law. The surge prompted regulatory concern and contributed to ACMA’s intensified enforcement actions including ISP blocking of offshore operators. Online wagering per capita reached AUD 397.50, representing 31 percent of total gambling turnover—a proportion expected to continue growing.

Tax Revenue Generation: State and territory governments collect substantial revenue from gambling taxes, though exact figures vary by jurisdiction. Victoria’s gaming machine revenue alone generates approximately AUD 2 billion annually in state taxes. Point of consumption taxes on online wagering generated hundreds of millions in additional state revenue since implementation.

Total government gambling tax revenue across all jurisdictions and products exceeds AUD 6 billion annually, making gambling a significant contributor to state budgets and complicating policy reform efforts given fiscal dependencies.

Growth Trends: Historical data shows gambling expenditure increasing from AUD 21.243 billion in 2019-20 to AUD 24.039 billion in 2020-21, a 13.2 percent increase reflecting both COVID-19 impacts (venue closures driving online migration) and underlying market growth. Projections indicate continued expansion, with the online gambling market alone expected to grow from USD 5.2 billion in 2024 to USD 8.9 billion by 2033 at a 5.88 percent CAGR. Sports betting demonstrates even more aggressive growth projections of 22.1 percent CAGR, potentially reaching AUD 50.15 billion by 2034.

Advertising and Marketing Restrictions

Australia’s gambling advertising regulations have tightened substantially in recent years following public concern about pervasive marketing, particularly during sports broadcasts popular with children and young adults. The regulatory framework combines federal legislation, state rules, and industry self-regulation through codes of practice.

Broadcast Media Restrictions: Gambling advertisements are prohibited during live sports broadcasts on free-to-air television, pay television, and radio from five minutes before the event commences through five minutes after conclusion. This ban applies between 5:00 AM and 8:30 PM, protecting children from exposure during daytime and evening viewing hours.

Sports betting advertisements may still appear during breaks in live sports coverage outside the prohibited windows, though this remains controversial and subject to ongoing reform proposals. The Murphy Report recommended a complete ban on gambling advertising across all broadcast media, though the government has not yet implemented this comprehensive prohibition.

Online and Digital Marketing: Online gambling advertising faces fewer explicit restrictions, though the AANA Wagering Advertising and Marketing Communications Code establishes self-regulatory standards. Advertisements must not appeal strongly to minors, must not encourage excessive gambling, must include responsible gambling messages, and must not create misleading impressions about odds of winning. Social media platforms apply their own policies, generally prohibiting gambling advertising targeted at users under 18. Operators heavily utilize online channels including search engine marketing, display advertising, social media, and partnerships with sports websites and apps.

Outdoor and Transit Advertising: Victoria banned betting advertisements on roads, public transport, and within 150 meters of schools under section 4.7.1 of the Gambling Regulation Act 2003. These restrictions apply to static advertising including billboards, bus shelters, station platforms, bridges, and noise walls. Other states have implemented or are considering similar geographic restrictions to reduce gambling advertising exposure in public spaces.

Sponsorship Regulations: Sports sponsorships by gambling operators remain largely permissible, with major betting brands sponsoring AFL teams, NRL clubs, cricket competitions, and individual athletes. However, restrictions limit sponsor logo prominence during broadcasts subject to advertising bans, and naming rights for stadiums and competitions face increasing scrutiny. Some sporting codes have voluntarily reduced gambling sponsorships in response to community concerns, and future regulatory tightening appears likely.

Promotional Limitations: Bonus offers and promotional inducements must comply with responsible gambling principles. Operators cannot offer credit for gambling or promote betting as a solution to financial problems. Promotional terms and conditions must be clearly disclosed, including wagering requirements, time limits, and restrictions. Recent regulatory changes in some jurisdictions have limited the value or frequency of promotional offers, particularly introductory bonuses designed to attract new customers.

Content Restrictions: Marketing materials must not misrepresent the probability of winning, must not suggest gambling is a legitimate income source, must not encourage gambling as an escape from personal problems, and must not portray gambling as glamorous or a pathway to social acceptance. Advertisements must include responsible gambling messaging and helpline information. Testimonials and celebrity endorsements must not create false expectations about typical outcomes.

Affiliate Marketing Rules: Affiliate marketers promoting gambling services must adhere to the same advertising standards as operators. ACMA has increased enforcement against affiliate websites promoting illegal offshore casino services, with referrals for ISP blocking of sites that facilitate access to prohibited services. Operators remain responsible for ensuring their affiliates comply with advertising restrictions and must implement monitoring systems to detect and address violations.

Penalties for Violations: Breaches of advertising restrictions can result in formal warnings, mandatory corrective advertising, financial penalties, and in serious or repeated cases, license sanctions. Between October and December 2024, ACMA’s investigation of 301 complaints resulted in identification of 16 breaches, demonstrating active enforcement. Industry participants expect further advertising restrictions in 2025 and beyond, with comprehensive reform proposals under government consideration.

Recent Regulatory Changes and Their Impact

Australia’s gambling regulatory environment has experienced significant evolution in 2024-25, driven by casino royal commission findings, community concerns about gambling harm, and technological developments. These changes materially affect operator compliance costs, business strategies, and market entry planning.

Credit Card and Digital Currency Ban (2024): In mid-2024, Australia banned credit cards and digital currencies for online wagering transactions. This prohibition aims to reduce gambling-related debt and financial harm by preventing customers from gambling with borrowed funds or anonymous cryptocurrency. Operators must implement systems preventing these payment methods and verify customer payment sources. The ban increases operational complexity and potentially reduces conversion rates from customers preferring these payment options, though debit cards, bank transfers, and approved e-wallets remain available.

Enhanced Customer Identification Requirements (September 2024): AUSTRAC’s requirement that operators complete applicable customer identification procedures before establishing accounts or offering services took effect in September 2024 after a one-year transition period. This strengthens existing KYC obligations by aligning gambling operators with banking sector standards. Operators must verify customer identity using document verification, biometric checks, or approved digital identity services before allowing any gambling activity. The change increases onboarding friction and compliance costs while enhancing AML/CTF controls.

Victorian Gaming Machine Reforms (2024-25): Victoria implemented sweeping pokies reforms including reducing maximum deposits from AUD 1,000 to AUD 100 effective December 2025, mandatory pre-commitment becoming effective December 2025, and mandatory venue closures between 4:00 AM and 10:00 AM implemented August 2024 (excluding Crown Casino). These measures respond to community concerns about gaming machine harm and align with research demonstrating effectiveness of limit-setting tools. Venue operators face significant technology upgrade costs and potential revenue impacts from reduced player spending capacity.

Casino Operator Scrutiny and Remediation (2022-2025): The Victorian Gambling and Casino Control Commission determined Crown Melbourne returned to suitability in March 2024 after two years of remediation following royal commission findings. However, The Star Sydney’s license remains suspended until at least March 2025, with independent supervision continuing and a AUD 15 million fine imposed for regulatory breaches. These actions establish new compliance expectations for all casino operators including enhanced governance, culture change programs, continuous monitoring, and immediate reporting of significant incidents.

Western Australia Gambling Law Reforms (February 2025): Western Australia introduced tougher gambling laws providing the Gaming and Wagering Commission with expanded investigative powers and substantially higher fines for non-compliance. These reforms reflect a nationwide trend toward stricter enforcement and higher penalties for regulatory violations. Operators in Western Australia face increased compliance scrutiny and material financial consequences for breaches.

BetStop National Self-Exclusion Register (August 2023-ongoing): The mandatory national self-exclusion register requires all licensed operators to verify customers against the database and prohibit account creation or marketing to registered individuals. By Q2 2024-25, 35,671 people had registered, with 26,020 active exclusions. Operators must implement real-time checking systems and processes for immediately closing accounts when customers self-exclude. The register represents a significant operational requirement with ongoing compliance monitoring by regulators.

Advertising Reform Proposals (2024-2025): Following the Murphy Report’s recommendation for comprehensive gambling advertising bans, the federal government delayed implementation but continues consultation on reform options. Industry participants anticipate significant advertising restrictions in 2025 or 2026, potentially including bans on broadcast advertising outside sporting events, limits on digital marketing, and restrictions on sponsorships. Such changes would materially affect customer acquisition strategies and costs, potentially advantaging established operators with strong brand recognition over new entrants.

ISP Blocking Intensification (2024-2025): ACMA has accelerated ISP blocking of illegal offshore gambling sites and affiliates, requesting blocks of additional sites in September 2025. Between October and December 2024, 75 websites were referred for blocking after investigation of 301 complaints identified 16 breaches. This enforcement targets both offshore casino operators (whose services are illegal to offer to Australians) and affiliate sites promoting such services. The intensified blocking makes offshore operation increasingly untenable and reinforces the importance of obtaining proper Australian licensing.

Cashless Gaming Trials and Implementation: Several jurisdictions are implementing or trialing cashless gaming systems for electronic gaming machines and retail betting.

Impact on Business Strategy: Recent regulatory changes increase compliance costs, limit marketing effectiveness, potentially reduce customer lifetime values through tighter responsible gambling controls, and create uncertainty for business planning. New entrants must factor higher compliance infrastructure costs into launch budgets. Established operators must invest in remediation and system upgrades to meet evolving standards. The regulatory trajectory favors larger, well-capitalized operators capable of absorbing compliance costs while maintaining market presence, potentially consolidating the market further.

Enforcement Mechanisms and Penalties

Australian gambling regulators have demonstrated increasing willingness to exercise enforcement powers, with substantial penalties imposed on even major operators for compliance failures. The enforcement landscape establishes clear expectations that regulatory requirements are not merely aspirational but strictly enforced obligations.

Administrative Penalties: Regulators may impose warnings, conditions on licenses, requirements for remedial action, mandatory audits, and oversight regimes short of license suspension or revocation. Crown Melbourne and The Star properties operate under enhanced supervision with independent monitors reporting to regulators on remediation progress. Such arrangements impose substantial costs on operators while restricting operational flexibility.

Financial Penalties: Recent enforcement actions demonstrate regulators’ willingness to impose material fines. The Star Sydney received a AUD 15 million fine in October 2024 for regulatory breaches. Tabcorp was fined AUD 4.6 million in August 2024 for compliance failures and AUD 370,417 in June 2024 for allowing minor gambling. These penalties represent significant financial consequences designed to deter violations and demonstrate to the public that regulators take compliance seriously.

License Suspension and Revocation: The ultimate enforcement tool involves suspending or revoking an operator’s license, terminating their ability to conduct gambling activities. The Star Sydney’s license suspension since 2022 (continuing until at least March 2025) demonstrates regulators’ preparedness to use this power even against major operators when serious deficiencies are identified. While economic impacts on employees and connected businesses are considered, suitability concerns override financial considerations when operators demonstrate unwillingness or inability to meet regulatory standards.

ISP Blocking: For offshore operators offering illegal services to Australians, ACMA utilizes ISP blocking to disrupt access. This mechanism has proven increasingly effective, with 75 websites blocked between October and December 2024 alone. Once blocked, offshore operators lose Australian traffic and face brand damage. The blocking regime makes unlicensed operation in the Australian market commercially unviable for operators depending on legitimate payment processors and public visibility.

Payment Processor Restrictions: Regulators coordinate with financial institutions and payment processors to restrict transactions with unlicensed operators. Banks and payment providers face their own regulatory obligations to prevent facilitation of illegal gambling. This creates practical barriers to offshore operators receiving deposits from or making payouts to Australian customers, complementing ISP blocking efforts.

Criminal Penalties: Serious violations can trigger criminal proceedings. The Interactive Gambling Act creates criminal offenses for offering prohibited services, with penalties including imprisonment for individuals and substantial fines for companies. While criminal prosecution is less common than administrative action, the possibility creates significant deterrent effect and personal liability for directors and executives involved in illegal operations.

Precedent Setting: Recent enforcement actions against major casino operators, corporate bookmakers, and offshore operators establish precedents influencing all operators. The message is clear: regulatory compliance is non-negotiable, violations will be detected through enhanced monitoring, penalties will be substantial and proportionate to operator size, and remediation requirements are comprehensive and intrusive. This enforcement environment demands robust compliance systems and proactive rather than reactive approaches to regulatory obligations.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Australia’s population of 27.5 million as of March 2025 reflects continued growth despite recent economic headwinds, with demographic characteristics that create a favorable environment for iGaming operations. The population grew by 423,400 people or 1.6 percent in the year ending March 2025, driven primarily by net overseas migration of 315,900 and natural increase of 107,400.

| Age Group | Population (millions) | Percentage of Total | iGaming Relevance |

|---|---|---|---|

| 0-14 years | 5.1 | 18.5% | Below legal gambling age |

| 15-24 years | 3.3 | 12.0% | Entry-level gambling demographic |

| 25-34 years | 3.8 | 13.8% | High digital engagement, growing income |

| 35-44 years | 3.7 | 13.5% | Peak earning years, prime gambling demographic |

| 45-54 years | 3.5 | 12.7% | Established income, high disposable spending |

| 55-64 years | 3.0 | 10.9% | Pre-retirement, substantial wealth accumulation |

| 65+ years | 4.6 | 16.7% | Growing segment, increasing digital adoption |

| Legal Gambling Age Population (18+) | 21.4 | 77.8% | Total addressable market |

Median Age Implications: At 38.3 years, Australia’s median age positions the country as a mature developed market with substantial purchasing power concentrated in prime working ages. The median age has increased from 33.4 years in 1994, reflecting declining birth rates and increasing life expectancy. For iGaming operators, this aging demographic profile suggests emphasis on products appealing to middle-aged consumers while developing offerings for the growing 65-plus segment increasingly comfortable with digital platforms.

Gender Distribution: Australia’s population is 49.62 percent male and 50.38 percent female, with approximately 204,000 more females than males. Life expectancy stands at 81.1 years for males and 85.1 years for females, creating a larger female population in older age brackets. Gambling participation data shows 80.5 percent of men and 66.2 percent of women gambled in the past 12 months, with 48 percent of men and 28 percent of women gambling at least weekly. This gender gap presents opportunities for operators to develop products and marketing specifically targeting female players.

Urban Concentration: With 86.5 percent of Australians living in urban areas (23.3 million people), the population demonstrates extreme concentration in cities. Major cities are home to 73 percent of the population, with 25 percent in inner and outer regional areas and only 1.9 percent in remote and very remote regions. This urban concentration simplifies marketing and customer service logistics, as operators can effectively reach the vast majority of potential customers through metropolitan-focused campaigns.

Geographic Distribution

Australia’s population concentrates overwhelmingly in coastal cities along the eastern and southeastern seaboards, with vast interior regions remaining sparsely populated. This geographic distribution creates distinct target markets with different characteristics and gambling preferences.

| City/Metropolitan Area | Population (millions) | Key Characteristics |

|---|---|---|

| Greater Sydney (NSW) | 5.4 | Financial center, diverse population, high incomes |

| Greater Melbourne (VIC) | 5.2 | Cultural hub, sports-focused, multicultural |

| Greater Brisbane (QLD) | 2.6 | Fastest growing major city, subtropical lifestyle |

| Greater Perth (WA) | 2.2 | Mining wealth, isolated location, high wages |

| Greater Adelaide (SA) | 1.4 | Aging population, lower costs, wine region |

| Gold Coast (QLD) | 0.7 | Tourism hub, younger demographic, entertainment focus |

| Greater Canberra (ACT) | 0.5 | National capital, high education, government employment |

| Greater Newcastle (NSW) | 0.5 | Industrial heritage, growing service economy |

Regional Economic Differences: Western Australia and Northern Territory exhibit higher per-capita incomes driven by mining sector wages, though recent commodity price fluctuations have moderated growth. New South Wales and Victoria represent the largest markets by population and economic activity, accounting for approximately 60 percent of national GDP. Queensland experiences rapid population growth driven by interstate migration of retirees and families seeking lower housing costs and lifestyle benefits.

Internet Access Patterns: Urban areas enjoy superior internet infrastructure with fiber and 5G networks widely deployed, while regional and remote areas rely more heavily on fixed wireless and satellite connections. Internet penetration exceeds 97 percent even in regional areas, though connection speeds and reliability vary. This near-universal connectivity means operators can effectively reach customers regardless of location, though product optimization for varying connection qualities remains important.

Gambling Venue Concentration: Electronic gaming machines concentrate heavily in New South Wales and Victoria, which together account for approximately 70 percent of pokies in Australia. Queensland restricts pokies to casinos and reduces their density in communities.

Western Australia maintains the strictest gaming machine regulations with limited availability. This regulatory diversity means gambling product preferences vary regionally, with New South Wales and Victorian consumers more habituated to gaming machines while other states show different preferences.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Australia’s economy demonstrates resilience despite recent challenges including declining per-capita GDP, elevated inflation, and housing affordability pressures. Understanding current economic conditions is critical for operators assessing market entry timing and forecasting customer spending patterns.

| Indicator | Current Value | Trend | Regional Comparison |

|---|---|---|---|

| Total GDP (2025) | USD 1.82 trillion | Growing 1.3% FY 24-25 | 17th largest globally |

| GDP Per Capita (2025) | USD 67,400 | Declining in real terms | Top 20 globally |

| GDP Growth (Q2 2025) | 0.6% quarterly | Modest recovery underway | Below OECD average |

| Annual GDP Growth (June 2025) | 1.8% | Lowest since 1990s excluding COVID | Lagging developed peers |

| GDP Per Capita Growth | -0.4% annually | 7 consecutive quarterly declines | Worst among OECD nations |

| Inflation Rate (June 2025) | 2.1% annually | Returning to target band | Below recent peaks |

| Core Inflation (Sept 2024) | 3.5% | Persistent services inflation | Above RBA target midpoint |

| Unemployment Rate | 4.0-4.5% | Near full employment | Low by historical standards |

| Wage Growth (June 2025) | 3.4% annually | Moderating from 2024 peak | Below inflation in recent years |

Economic Challenges: Real GDP per capita fell for seven consecutive quarters through early 2024 before slight recovery, with another decline in March 2025 quarter. This performance positions Australia as an outlier among developed economies and reflects sustained erosion of purchasing power. While nominal wages grew 3.4 percent annually, this failed to keep pace with inflation running above 3.5 percent through much of 2024, resulting in declining real incomes. Food prices rose 11.7 percent and gas 33.9 percent since 2022, while energy rebates capped electricity increases that otherwise would have reached 14.9 percent.

Sector Performance: The service sector constitutes 61.1 percent of the economy and employs 79.2 percent of Australians, providing the foundation for economic activity. Mining remains crucial for exports and government revenue, particularly in Western Australia where iron ore and natural gas dominate. However, declining productivity growth—which fell below historical trends—limits the economy’s supply capacity and weighs on long-term growth prospects. The Reserve Bank of Australia lowered productivity growth assumptions, reducing GDP growth forecasts for outer years.

Consumer Implications: The cost-of-living crisis and declining real incomes create headwinds for discretionary spending categories including gambling. However, gambling often demonstrates counter-cyclical characteristics, with some consumers increasing gambling activity during economic stress as entertainment or hoped escape from financial pressures. The 13.8 percent increase in gambling expenditure from 2019-20 to 2020-21 occurred during COVID-19 economic disruptions, suggesting resilience in gambling demand even during economic weakness.

Income and Wealth Distribution

Australian household income levels support substantial consumer spending capacity, though wealth concentration and cost-of-living pressures affect different segments unevenly. Understanding income distribution helps operators identify target demographics and calibrate product offerings.

| Metric | Value (AUD) | Value (USD) | Commentary |

|---|---|---|---|

| Median Household Income (Annual) | AUD 91,000 | USD 61,200 | After-tax income |

| Average Household Income (Annual) | AUD 116,000 | USD 78,000 | Mean exceeds median due to high earners |

| Median Full-Time Weekly Earnings | AUD 1,923 | USD 1,293 | Before tax |

| Average Weekly Ordinary Time Earnings | AUD 1,838 | USD 1,236 | Full-time adult employees |

| Median Wealth per Adult | AUD 386,000 | USD 259,500 | Among world’s highest |

| Mean Wealth per Adult | AUD 660,000 | USD 444,000 | Reflects property ownership concentration |

| Gini Coefficient | 0.33 | – | Moderate inequality by global standards |

Income Distribution by Bracket: Approximately 23 percent of households earn below AUD 50,000 annually, representing lower-income segments including retirees, part-time workers, and single-income households. The AUD 50,000-100,000 bracket encompasses roughly 30 percent of households, forming the middle-income core. Households earning AUD 100,000-150,000 represent 20 percent, while those exceeding AUD 150,000 constitute 27 percent of the population. This distribution suggests strong purchasing power across broad segments, with particular depth in middle and upper-middle income ranges.

Disposable Income Trends: Real household disposable income declined sharply in 2023-24, with Australia experiencing the steepest fall among developed nations since 2019. Households absorbed elevated interest rates on mortgages, rising essential costs, and wage growth failing to match inflation. However, employment remained strong near full employment levels, preventing income collapse and maintaining baseline consumption capacity. As inflation moderates and wage growth continues, real income recovery appears likely through 2025-26.

Middle Class Characteristics: Australia’s substantial middle class exhibits home ownership rates around 65 percent nationally (varying by state and age cohort), significant superannuation (retirement savings) assets, and consumption patterns oriented toward services and experiences. This demographic demonstrates willingness to spend on entertainment and leisure including gambling, particularly when products are positioned as entertainment rather than investment vehicles. The middle class decline in purchasing power creates pressure but not elimination of discretionary spending capacity.

Wealth Concentration: Property ownership drives Australian wealth, with median wealth per adult among the world’s highest at approximately AUD 386,000. However, this wealth concentrates among homeowners predominantly in older age brackets, while younger Australians face severe housing affordability challenges.

In 2024, median home values exceeded AUD 1 million in Sydney and approached that level in Melbourne, requiring household incomes substantially above median for affordability. This creates generational wealth gaps, with implications for gambling participation—younger cohorts face tighter discretionary budgets while older homeowners control substantial assets.

Market Size and Growth Projections

Australia’s iGaming market demonstrates robust growth trajectories despite regulatory constraints, with online segments outpacing traditional land-based gambling. Multiple research sources provide converging estimates that together paint a comprehensive picture of market scale and future expansion.

| Metric | 2024 Baseline | 2025 Projection | 2029-2034 Projection | CAGR |

|---|---|---|---|---|

| Total Gambling Market | USD 15.1 billion | USD 15.43 billion | USD 16.88 billion (2029) | 2.26% |

| Online Gambling Market (Sports Betting & Lotteries) | USD 5.2 billion | USD 5.5 billion | USD 8.9 billion (2033) | 5.88% |

| Online Gambling (Alternative Estimate) | AUD 9.1 billion | AUD 9.8 billion | AUD 19.4 billion (2034) | 7.89% |

| Sports Betting Market | AUD 6.81 billion | AUD 8.3 billion | AUD 50.15 billion (2034) | 22.10% |

| Sports Betting (Alternative Estimate) | USD 2.44 billion | USD 2.8 billion | USD 5.10 billion (2030) | 13.2% |

| Casino & Casino Games Segment | – | USD 7.02 billion | – | – |

| Number of Users | 18.9 million | 19.0 million | 19.4 million (2029) | 0.66% |

| Market Penetration Rate | 70.3% | 70.6% | 71.8% (2029) | – |

| Average Revenue Per User (ARPU) | USD 798 | USD 809.94 | USD 870 (2029) | 1.86% |

Market Size Context: The total Australian gambling market of USD 15.43 billion in 2025 encompasses all legal gambling forms including land-based casinos, electronic gaming machines, wagering (racing and sports), lotteries, and keno. Within this total, online gambling represents approximately USD 5.2-5.5 billion or roughly 35 percent of the market, with this online share projected to increase substantially as digital migration continues.

Sports betting demonstrates the most aggressive growth trajectory, with some projections indicating the segment could expand from AUD 6.81 billion in 2024 to AUD 50.15 billion by 2034, representing a 22.1 percent CAGR driven by mobile adoption, live betting (via phone), event coverage expansion, and integration with sports viewing experiences.

Historical Growth Analysis: Online gambling turnover increased 165.7 percent year-over-year to AUD 75.4 billion in 2022-23, marking explosive growth. However, this figure includes significant illegal offshore casino activity by Australian players, explaining the dramatic surge. Legal online wagering on sports and racing grew 27.3 percent from AUD 4.567 billion to AUD 5.815 billion in 2020-21, demonstrating robust but more moderate expansion in licensed activities. Total gambling expenditure increased 13.8 percent to AUD 32.0 billion in 2022-23, recovering from COVID-19 disruptions and reflecting both increased participation and migration to online channels.

User Growth Projections: The number of gambling users is expected to grow modestly from 18.9 million in 2024 to 19.4 million by 2029, representing a 0.66 percent CAGR. This slow growth reflects market maturity, with 70.6 percent penetration already achieved. Future growth derives primarily from population increases and aging into legal gambling age rather than converting non-gamblers. The modest user growth contrasts with substantial revenue growth projections, indicating that increased spending per user rather than user base expansion drives market growth.

ARPU Expansion: Average revenue per user of USD 809.94 in 2025 ranks among the world’s highest, reflecting Australians’ propensity for gambling spending. ARPU is projected to increase to approximately USD 870 by 2029, representing 1.86 percent annual growth. This expansion suggests operators can increase customer lifetime values through product development, personalization, enhanced engagement, and effective promotional strategies. However, responsible gambling requirements including mandatory limits may constrain ARPU growth for some customer segments.

Online vs Land-Based Split: Online channels represent approximately 35 percent of total gambling revenue in 2025, projected to reach 50 percent or more by 2033 as digital migration continues. Sports betting demonstrates the highest online penetration at approximately 80 percent, while gaming machine gambling remains predominantly land-based at approximately 95 percent venue-based. Lotteries show mixed distribution with both retail and online channels significant. This shift to online creates opportunities for digital-first operators while pressuring traditional venue-based businesses.

Regional Comparison: Australia’s per-capita gambling losses of AUD 1,555 annually position it among global leaders, significantly exceeding regional neighbors. New Zealand’s per-capita gambling losses approximate AUD 800, roughly half Australia’s level. Asian markets including Singapore, Macau, and Philippines show different patterns with casino tourism dominating over distributed retail and online gambling. Australia’s combination of high penetration, high ARPU, and favorable regulatory environment (for licensed sports betting) creates unique market characteristics distinct from regional comparisons.

Education, Skills, and Digital Literacy

Educational Foundation

Australia’s highly educated population demonstrates strong digital literacy and technological adoption, creating favorable conditions for online gambling platforms requiring customer comfort with digital transactions, account management, and mobile applications.

Literacy and Education Levels: Australia achieves near-universal literacy at 99 percent, ensuring that online gambling platforms requiring text comprehension and navigation face minimal barriers. Approximately 60 percent of working-age Australians hold post-secondary qualifications including university degrees, diplomas, and vocational certificates. This educational attainment translates to workforce skills heavily concentrated in services, technology, and professional sectors. The high education levels correlate with comfort adopting new technologies, understanding terms and conditions, and managing financial transactions online—all critical capabilities for online gambling participation.

Digital Literacy Indicators: With 97.1 percent internet penetration and 97 percent smartphone ownership, Australians demonstrate exceptional digital engagement. Average daily internet usage approaches 6 hours across all age groups, with younger demographics (16-34) exceeding 7 hours daily. This extensive online time includes e-commerce transactions, online banking usage exceeding 90 percent of adults, and social media engagement at 77.9 percent penetration. Such digital immersion means online gambling platforms compete for attention within an already-crowded digital ecosystem but benefit from customers highly comfortable with online financial transactions.

Technology Adoption Readiness: Australia consistently ranks among early adopters of new consumer technologies. Smartphone penetration reached 97 percent, among the world’s highest. Contactless payment adoption exceeds 95 percent of card transactions, with mobile wallet usage growing rapidly (Apple Pay, Google Pay, Samsung Pay collectively account for significant transaction volumes). Cryptocurrency awareness and usage, while still minority activities, exceed regional averages. This technology enthusiasm creates receptive audiences for gambling innovation including live betting interfaces, augmented reality experiences, and gamification features.

English Language Proficiency: English serves as the primary language for approximately 72 percent of Australians, while 28 percent speak languages other than English at home. Major non-English languages include Mandarin (2.7%), Arabic (1.4%), Vietnamese (1.3%), Cantonese (1.2%), and Punjabi (0.9%). However, English proficiency among non-native speakers remains high due to education system requirements and workplace demands.

For gambling operators, English-language platforms serve the vast majority of customers effectively, though operators targeting specific ethnic communities may benefit from multilingual support, particularly in Mandarin for the substantial Chinese-Australian population.

Cultural and Social Factors

Communication and Language

Internet Language Preferences: English dominates online activity in Australia, with 95-plus percent of internet users conducting online activities primarily in English. This linguistic homogeneity simplifies content creation, customer service, and marketing compared to multilingual markets. However, operators should consider that ethnic communities may prefer content in native languages, particularly for complex gambling concepts, terms and conditions, and responsible gambling information. Mandarin and Arabic language support could provide competitive advantages for operators targeting these substantial demographic segments.

Business Communication Norms: Australian communication styles tend toward directness, informality, and egalitarianism compared to more hierarchical or formal Asian cultures. Customer service expectations emphasize friendly, efficient, and straightforward interactions rather than elaborate courtesy or formality. Gambling marketing successfully employing colloquial language, humor, and sports-focused messaging resonates with Australian audiences. However, this informality must balance with responsible gambling messaging requirements and avoid trivializing gambling risks.

Cultural Attitudes

Gambling Acceptance Levels: Australia exhibits exceptionally high cultural acceptance of gambling, with 72.8 percent of adults participating in gambling activities in the past 12 months (80.5 percent of men, 66.2 percent of women). Gambling integrates deeply into social rituals including Melbourne Cup sweepstakes in workplaces, AFL and NRL season betting among friend groups, and pokies venue visits as social outings.

This cultural normalization means gambling operators face minimal social stigma compared to markets where gambling carries stronger negative connotations. However, increasing awareness of gambling harm and problem gambling has begun moderating pure acceptance with growing emphasis on responsible gambling.

Religious Influences: Australia’s religious landscape shows declining identification with organized religion, with 38.9 percent identifying as having no religion in the 2021 census, up from 30.1 percent in 2016. Christianity remains the largest religious group at 43.9 percent (declining from 52.1 percent in 2016), with Catholics at 20 percent and Anglicans at 9.8 percent. Islam accounts for 3.2 percent, Buddhism 2.4 percent, and Hinduism 2.7 percent. Christian denominations in Australia generally do not prohibit gambling, though some conservative Protestant groups discourage it. Islamic prohibition on gambling affects Muslim communities, potentially limiting participation among this demographic. Overall, religious considerations present minimal obstacles to gambling industry operations given the secular orientation of most Australians.

Foreign Brand Perception: Australians demonstrate openness to international brands across consumer categories, with companies like Bet365 (UK-based) successfully establishing major market positions. However, local presence matters—brands must demonstrate commitment to Australian market through local sponsorships, Australian sporting event coverage, customer service based in Australia or compatible time zones, and compliance with Australian regulations. Successful international operators balance global brand strength with local market customization, avoiding perception as distant foreign entities extracting profits without contributing to Australian sporting and community ecosystems.

Risk Tolerance: Australian culture exhibits relatively high risk tolerance as evidenced by the gambling participation rates far exceeding global norms. This risk comfort extends beyond gambling to investment behavior, entrepreneurship rates, and consumer spending patterns. The cultural emphasis on “having a go” (taking chances) creates psychological compatibility with gambling activities. However, this risk tolerance coexists with increasing awareness that excessive gambling risks can lead to financial and personal harm, creating tension between cultural acceptance and harm prevention that shapes regulatory approaches.

Entertainment Preferences: Australians demonstrate passionate engagement with sports, particularly Australian Rules Football (AFL), Rugby League (NRL), cricket, horse racing, and increasingly soccer and basketball. Major sporting events including the Melbourne Cup, AFL Grand Final, State of Origin rugby series, and international cricket matches attract massive audiences and gambling activity. Sports betting operators achieve maximum engagement by offering comprehensive coverage of Australian sports, competitive odds, live streaming integration, and promotional campaigns aligned with sporting calendars. Beyond sports, Australians show strong interest in reality television, entertainment events, and cultural festivals, though these translate less directly to gambling opportunities under current regulations.

Problem Gambling and Social Considerations

Australia’s status as a high-gambling nation inevitably produces significant problem gambling impacts, creating regulatory pressures and corporate social responsibility expectations that operators must address.

| Indicator | Value | Details |

|---|---|---|

| Problem Gambling Prevalence | 0.6-1.0% | Percentage of adult population |

| Estimated Problem Gamblers | 160,000-270,000 | Based on adult population of 21.4 million |

| Moderate Risk Gamblers | 2.0-3.0% | At-risk but not yet problem level |

| Estimated Moderate Risk Population | 428,000-642,000 | Potential future problem gamblers |

| BetStop Registrations (August 2023-Q2 FY25) | 35,671 total | 26,020 currently active |

| Gender Distribution (Problem Gamblers) | 65% male, 35% female | Men over-represented relative to general participation |

| Age Groups Most Affected | 25-44 years | Peak problem gambling incidence |

| Primary Problem Products | Gaming machines, sports betting | High-frequency, high-intensity products |

Prevalence and Impact: Problem gambling affects between 160,000 and 270,000 Australian adults, representing 0.6 to 1.0 percent of the population—rates comparable to other developed gambling markets. An additional 2.0 to 3.0 percent exhibit moderate risk gambling behaviors, representing 428,000 to 642,000 adults who may progress to problem gambling without intervention. These individuals experience financial hardship, relationship breakdowns, mental health deterioration, and in severe cases, suicide ideation. For every problem gambler, an estimated 6 to 10 additional people (family members, employers, friends) experience negative impacts, meaning harm affects potentially 1.5 to 2.5 million Australians indirectly.

Demographic Patterns: Problem gambling disproportionately affects males, who represent 65 percent of problem gamblers despite 50 percent of the population. The 25-44 age range shows highest problem gambling prevalence, likely reflecting combination of gambling exposure, financial pressures, and risk-taking behaviors. Lower socioeconomic groups exhibit higher problem gambling rates, creating concerning patterns where those least able to afford losses experience disproportionate harm. Indigenous Australians show elevated problem gambling rates, partly attributable to gaming machine concentration in areas with significant Indigenous populations.

Product-Specific Risks: Electronic gaming machines generate the highest problem gambling rates due to continuous play, rapid bet-to-result cycles, near-miss features, and immersive characteristics. Research consistently identifies pokies as the most harmful gambling product. Online sports betting shows increasing problem gambling association, particularly among younger males, driven by 24/7 availability, in-app promotional offers, and integration with sports viewing. Race betting traditionally shows lower problem gambling rates than other products, though high-intensity online wagering can still produce harm.

Underage Gambling: Strict age verification requirements and penalties for allowing minor gambling keep direct underage participation relatively low. However, concerns persist about youth exposure to gambling advertising, normalization of betting through sports sponsorships, and simulated gambling in video games preparing pathways to real-money gambling. Recent regulatory actions including Tabcorp fines for allowing minor gambling demonstrate zero tolerance, though enforcement challenges remain particularly for online environments where age verification depends on document submission that may be circumvented.

Government Response Measures: The National Consumer Protection Framework for Online Wagering establishes minimum protections including activity statements, pre-commitment tools, account closure, and credit prohibition. BetStop National Self-Exclusion Register provides unified exclusion across all licensed operators. Individual states implement additional measures including gaming machine pre-commitment (Victoria), reduced stake limits, mandatory breaks in play, and cashless gaming trials. Gambling Help Online (1800 858 858) provides free 24/7 counseling and support services funded by gambling taxes and operator levies.

Treatment and Support Services: Each state operates problem gambling counseling services funded through gambling taxation and operator contributions. Services include financial counseling, psychological treatment, family support, and residential programs for severe cases. However, treatment capacity remains limited relative to problem gambling prevalence, with waiting lists common. Online counseling and self-help resources supplement face-to-face services, improving accessibility particularly in regional areas.

Operator Responsibility Requirements: Licensed operators must contribute to problem gambling research and treatment through levies typically ranging from 0.5 to 1.5 percent of revenue. Corporate social responsibility expectations include funding independent research, supporting treatment services, implementing sophisticated player protection technologies, training staff in harm minimization, and demonstrating genuine commitment to reducing harm rather than merely compliance with minimum requirements. Operators failing to demonstrate adequate social responsibility face reputational damage and regulatory scrutiny as evidenced by casino royal commission findings.

Political Structure and Governance

Government System: Australia operates as a federal parliamentary constitutional monarchy with Queen (now King) as titular head of state represented by a Governor-General, and a Prime Minister leading the elected government. The bicameral Parliament consists of the House of Representatives (lower house) and Senate (upper house). State and territory governments exercise substantial powers including gambling regulation, creating the complex dual regulatory structure affecting gaming operators.

Political Stability: Australia demonstrates high political stability with peaceful democratic transfers of power, strong institutional frameworks, independent judiciary, and low corruption. The current Labor government led by Prime Minister Anthony Albanese won office in May 2022, ending nine years of Coalition (Liberal-National) government.

Corruption Perception: Australia ranks 13th globally on Transparency International’s Corruption Perception Index, indicating high transparency and effective governance. This clean governance environment means licensing processes, regulatory decisions, and enforcement actions generally follow established rules rather than discretionary favoritism or corrupt influence. Operators can expect fair treatment provided they meet regulatory requirements, though recent casino inquiries revealed some instances of regulatory capture and insufficient oversight that reforms are addressing.

Regulatory Consistency: While gambling regulation varies across states and territories, creating complexity, each jurisdiction maintains relatively consistent and predictable regulatory approaches within its boundaries. License terms, tax rates, and compliance requirements remain stable over multi-year periods, allowing business planning. However, the recent wave of reforms following casino royal commissions demonstrates that major regulatory shifts can occur when problems are identified, creating some uncertainty about future requirements.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Australia’s technology infrastructure and digital adoption rates rank among the world’s highest, creating optimal conditions for online gambling platforms requiring reliable connectivity, sophisticated device capabilities, and customer digital literacy.

| Metric | Value | Year-over-Year Change | Global Comparison |

|---|---|---|---|

| Internet Penetration | 97.1% | +1.0% | Top 10 globally |

| Total Internet Users | 26.1 million | +256,000 | 0.33% of global users |

| Daily Internet Usage (Average) | 5 hours 51 minutes | Stable | Above global average |

| Daily Internet Usage (Ages 16-24) | 7 hours 11 minutes | +3% | Among highest globally |

| Daily Internet Usage (Ages 25-34) | 7 hours 4 minutes | +2% | Very high engagement |

| Mobile Internet Penetration | 97.4% | +0.8% | Near saturation |

| Mobile Connections | 34.4 million | +1.3% | 128% of population |

| Smartphone Penetration | 97% | +1% | Among world’s highest |

| Social Media Penetration | 77.9% | +2.1% | Above OECD average |

| Social Media Users | 20.9 million | +450,000 | High engagement levels |

| E-commerce Penetration | 13.8% | +0.8% | Below US/UK, above OECD |

| Online Banking Usage | 90%+ | +3% | Very high adoption |

Connectivity Quality: Median mobile internet speeds reached 103.46 Mbps in January 2025, up 10.2 percent year-over-year, providing ample bandwidth for data-intensive gambling applications including live streaming, high-definition graphics, and real-time betting interfaces. Fixed broadband median speeds of 77.90 Mbps increased 43.2 percent annually, reflecting NBN (National Broadband Network) upgrades and fiber deployment expansion. However, Australia’s fiber penetration of 28.3 percent lags the OECD average of 44.6 percent and neighbors like New Zealand (70.3 percent), with fixed wireless access filling gaps at 10 percent adoption. Despite infrastructure criticisms, actual speeds suffice for all current gambling applications.

Device Ecosystem: The 128 percent mobile connection rate (34.4 million connections for 27 million population) indicates widespread multi-device ownership with individuals maintaining multiple smartphones, tablets, and mobile broadband connections.

Android and iOS split the market approximately 55/45 percent, requiring gambling operators to develop for both platforms. Average device specifications have improved substantially, with budget smartphones now offering processing power, screen quality, and connectivity enabling sophisticated gambling applications previously requiring high-end devices.

Digital Engagement Patterns: Australians spend nearly 40 hours weekly online, roughly equivalent to full-time employment hours. This extensive digital time distributes across entertainment (streaming video, music, gaming), social media, e-commerce, information seeking, and increasingly, gambling. The challenge for gambling operators involves capturing attention within this crowded digital landscape through compelling user experiences, personalized engagement, and integration with other digital activities (particularly sports viewing for sports betting).

Digital Payment Behavior