Austria stands at a critical juncture in its iGaming evolution, presenting both significant opportunities and complex challenges for market entrants. With a population of 9.1 million and a mature gambling market valued at approximately $3.31 billion, the country maintains a monopoly system scheduled for potential reform by 2027.

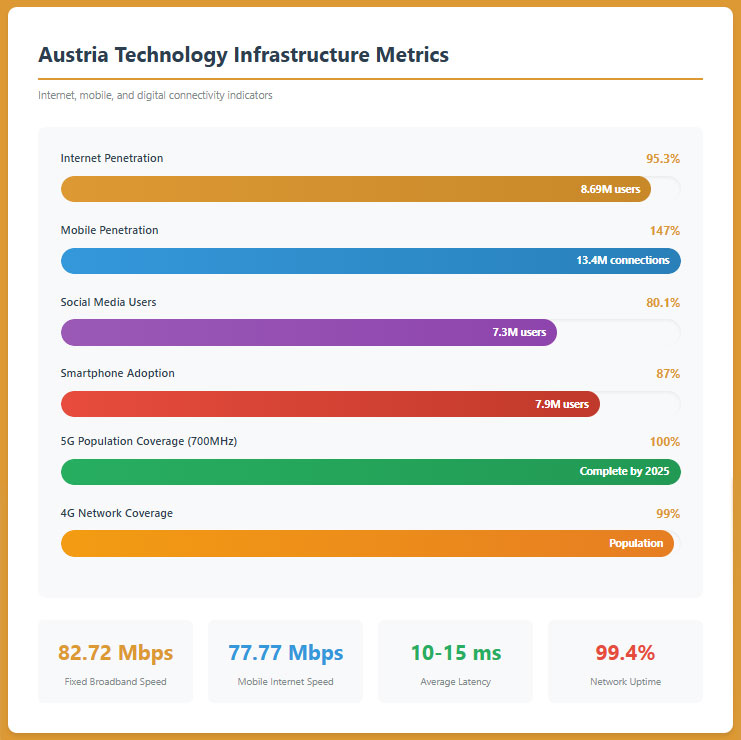

The Austrian market features high internet penetration at 95.3%, exceptional mobile connectivity with 147% mobile subscriptions per capita, and a GDP per capita of $58,669, positioning it among Europe’s wealthiest markets. However, operators face strict regulatory barriers, elevated taxation recently increased from 2% to 5% for betting activities, and a dominant state monopoly controlling online casino operations through Win2Day.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Gambling Legal Status | Monopoly System | Online casino monopoly, state-regulated sports betting |

| Online Casino Regulation | Single License Monopoly | Casinos Austria exclusive license until Sept 2027 |

| Sports Betting Status | State-Level Licensing | Regulated by 9 individual federal states |

| Total Population | 9.11 million | 0.11% of global population (2025) |

| Median Age | 43.6 years | Aging population, mature market |

| Urban Population | 58.6% | 5.34 million in urban areas |

| GDP (Total) | $495 billion | Q2 2025 estimate |

| GDP Per Capita | $58,669 | 13th highest globally (2024) |

| GDP Growth Forecast | -0.3% (2025), +1.0% (2026) | Economic slowdown period |

| Total Gambling Market | $3.31 billion | 2025 estimate, all gambling forms |

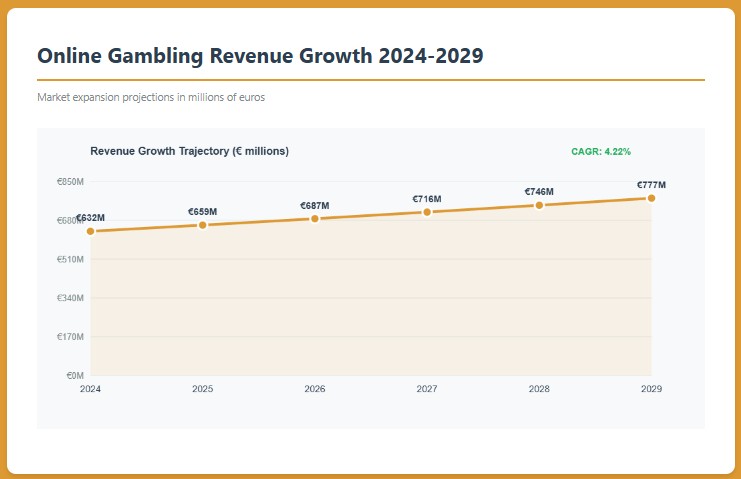

| Online Gambling Market | €632 million ($690 million) | 2024 figure, projected growth to €777M by 2029 |

| Market Growth CAGR | 4.22% | Online gambling 2024-2029 projection |

| Online Casino Revenue | €326.2 million | 2024 projection |

| Casinos Austria GGR | €1.48 billion | 2023 total (lotteries + casinos) |

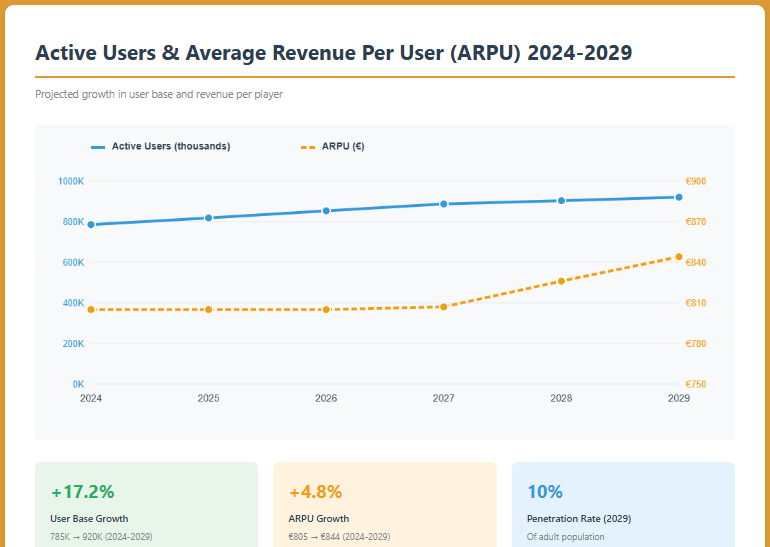

| Expected Online Users | 920,100 by 2029 | Growing digital gambling participation |

| Average Revenue Per User | $890 | Online gambling ARPU 2024 |

| User Penetration Rate | 8.6% | Online gambling participants 2024 |

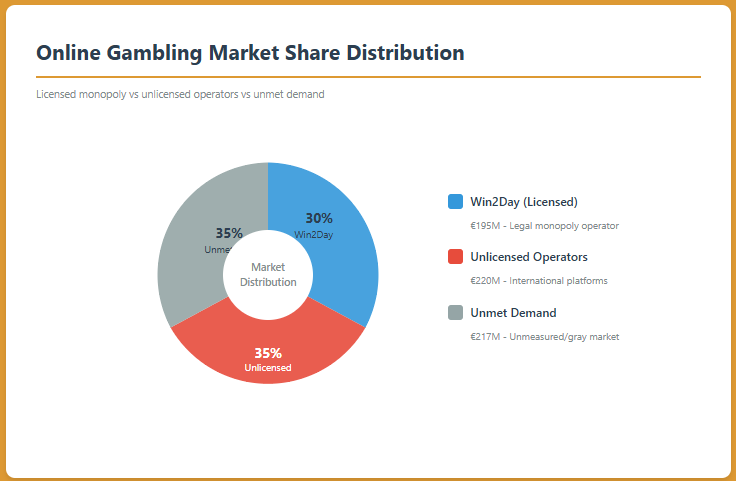

| Black Market Share | ~35% | Estimated unlicensed operator market |

| Monopoly Market Share | 30% | Win2Day online casino share |

| Internet Penetration | 95.3% | 8.69 million internet users (Jan 2025) |

| Mobile Penetration | 147% | 13.4 million active connections |

| Social Media Users | 7.3 million (80.1%) | High engagement for marketing |

| 5G Coverage | 100% population (700MHz) | Advanced mobile infrastructure by 2025 |

| Online Casino Tax | 40% GGR | High operator taxation |

| Sports Betting Tax | 5% (increased April 2025) | Previously 2%, staged increase implemented |

| Land-Based Casino Tax | 30% GGR | Plus additional operational fees |

| Corporate Income Tax | 25% | Standard rate for corporations |

| License Application Fee | Variable | Tender-based, historically single monopoly |

| Minimum Capital Requirement | €109 million | For lottery/casino license applicants |

| License Validity | 15 years maximum | Current monopoly expires Sept 2027 |

| Regulatory Reform Timeline | 2025-2027 | Potential market liberalization window |

| Tax Revenue Forecast | €240 million by 2031 | Government target, up from €50M in 2025 |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Austria operates under the Glücksspielgesetz (GSpG) or Law on Games of Chance, which establishes a federal monopoly system for gambling activities. The regulatory framework is complex, divided between federal and state jurisdictions, with the Federal Ministry of Finance serving as the primary regulatory authority through the Tax Office Austria (Finanzamt Österreich). This fragmented structure creates distinct regulatory pathways depending on the gambling category.

Land-Based Gambling Activities

Casino Operations: Austria maintains 15 land-based casino licenses, with Casinos Austria AG holding 12 active licenses. Three licenses have been revoked by courts. The casino licenses operate under federal jurisdiction and run until 2027 and 2030 respectively. Land-based casinos are subject to strict operational standards, geographical restrictions, and comprehensive player protection measures mandated by federal law.

Sports Betting Venues: Unlike casino operations, sports betting falls under state-level regulation, creating a fragmented landscape across Austria’s nine federal states. Each state maintains its own licensing regime, application procedures, and regulatory standards. Five states (Lower Austria, Upper Austria, Burgenland, Carinthia, and Styria) have opted to permit sports betting operations, while four states have chosen not to establish regulatory frameworks. This state-level control creates significant complexity for operators seeking nationwide coverage.

Slot Machine Halls: Gaming machine operations are similarly regulated at the state level, with five federal states (Lower Austria, Upper Austria, Burgenland, Carinthia, and Styria) having created specific legislative frameworks. These regulations govern the placement, operation, and taxation of slot machines outside of casino environments. The remaining four states do not permit standalone gaming machine operations.

Lottery Activities: The lottery sector operates under a strict federal monopoly. Österreichische Lotterien GmbH holds the exclusive license for all stationary lottery offerings, including Lotto, Toto, goal betting, letter lotteries, and scratch cards. This single license was awarded in October 2012 for the maximum statutory duration of 15 years and is scheduled to expire on September 30, 2027. The lottery monopoly has remained unchanged since the company’s inception, with no other operator ever receiving licensing consideration.

Online Gambling Framework

Digital Gaming Regulations: Online gambling in Austria operates under Section 12a of the GSpG, which defines “electronic lotteries” as encompassing all types of games of chance offered by electronic means, including casino-style online games. The current regulatory structure grants a single operator the exclusive right to provide online gambling services, effectively creating a digital monopoly mirroring the land-based lottery system.

Österreichische Lotterien GmbH operates the Win2Day platform, which serves as Austria’s only legal online gambling destination. The platform offers online casino games, sports betting, poker, and lottery products. This exclusive arrangement was established through the 2012 licensing tender and extends through the current license period ending September 30, 2027.

Prohibited Activities and Restrictions: Austrian law strictly prohibits cross-border supply of gambling activities. International operators offering services to Austrian residents without a valid Austrian license operate illegally under current legislation. The Ministry of Finance has announced intentions to implement domain name system (DNS) blocking and payment processor restrictions for unlicensed operators, though as of 2025, specific blocking legislation has not been fully enacted.

The regulatory framework explicitly prohibits advertising or facilitating advertising of games of chance where operators do not hold relevant Austrian licenses. This advertising ban applies to all media channels, including television, online platforms, outdoor advertising, and affiliate marketing. Violations of these advertising restrictions carry administrative penalties and potential criminal prosecution.

Regulatory Body Structure and Oversight

The Federal Ministry of Finance (Bundesministerium für Finanzen) serves as the principal regulatory authority, exercising control over licensing, taxation, compliance monitoring, and enforcement. The Tax Office Austria (Finanzamt Österreich) operates as the functional regulatory body for federal games of chance, handling day-to-day oversight and compliance enforcement.

For state-regulated activities, each of the nine federal states maintains its own regulatory structure through state government departments. District administrative authorities serve as enforcement agencies, imposing penalties for administrative offenses regarding violations of gambling regulations.

A significant regulatory development announced in the 2025-2029 governmental program includes the establishment of an independent gambling regulatory authority, separate from the Ministry of Finance. This proposed authority would assume responsibilities for licensing, compliance, and enforcement, addressing long-standing concerns about conflicts of interest arising from the Ministry’s dual role as regulator, tax collector, license grantor, and shareholder in monopoly operators. The European Gaming and Betting Association (EGBA) has strongly advocated for this independence to enhance consumer protection and market transparency.

The Ministry of Finance established a Staff Unit for Addiction Prevention and Counselling on December 1, 2010, dedicated to player protection, addiction prevention, and counseling services. This specialized unit provides technical support to the gambling regulatory authority and maintains oversight of responsible gambling initiatives mandated by Austrian law.

Licensed Operators and Market Players

Austria’s gambling market is characterized by extreme concentration, with state-controlled monopolies dominating legal operations. The market structure reflects decades of protectionist policy favoring established operators with government ownership stakes.

Current Licensed Operators

| Operator | License Type | Market Presence | Ownership Structure |

|---|---|---|---|

| Österreichische Lotterien GmbH | Federal Lottery & Online Monopoly | Win2Day platform, nationwide lottery | Government stake through Ministry of Finance |

| Casinos Austria AG | Land-Based Casino License (12 venues) | 12 casinos nationwide | 33.3% government ownership via Ministry of Finance |

| State-Level Betting Operators | Regional Sports Betting | Operations in 5 federal states | Various private and state-connected entities |

| Regional Slot Operators | State Gaming Machine Licenses | 5 federal states permit operations | Multiple private operators under state regulation |

Market Leaders and Estimated Market Share

Österreichische Lotterien GmbH / Win2Day: The monopoly operator generated gross gaming revenue of €1.48 billion in 2023, comprising €946.8 million from lottery operations and €304.5 million from casino operations. Despite its exclusive legal status, Win2Day captures approximately 30% of the online gambling market, indicating massive participation in unlicensed offshore platforms. The company operates Austria’s most visited legal gambling website and maintains the only permitted online casino, sports betting, and poker offerings.

Casinos Austria AG: Operating 12 physical casino properties across major Austrian cities, Casinos Austria dominates the land-based casino sector. The company maintains exclusive rights at premium locations including Vienna, Salzburg, Innsbruck, Linz, Graz, and other major population centers. The operator employs approximately 2,361 slot machines and 237 gaming tables across its network, offering traditional table games, electronic gaming machines, and exclusive VIP gaming salons.

Unlicensed International Operators: The Austrian market features significant participation from unlicensed international operators, primarily operating under Maltese, Curaçao, and Gibraltar licenses. Industry estimates suggest these operators collectively capture approximately 35% of the online gambling market, or roughly €220 million in annual revenue. Major international brands serving Austrian players without local licenses have faced increasing enforcement pressure, including payment blocking, domain seizures, and civil litigation from players seeking refunds.

Competitive Landscape Overview

The competitive environment in Austria remains heavily distorted by the monopoly structure. Win2Day’s 30% market share despite exclusive legal rights demonstrates fundamental weakness in the monopoly model, with Austrian consumers overwhelmingly choosing international platforms offering superior products, bonuses, game variety, and user experience. The monopoly system has failed to adequately address consumer demand, creating one of Europe’s largest gray and black markets relative to total market size.

The state-regulated sports betting sector shows greater competition, with multiple operators active across the five permitting states. However, fragmentation across nine different regulatory regimes creates operational complexity and prevents emergence of truly national betting brands beyond the Win2Day platform.

International operators have established strong brand recognition among Austrian players despite their unlicensed status. Popular platforms include major European betting and casino brands offering localized German-language interfaces, EUR currency transactions, Austrian payment methods, and targeted marketing to Austrian customers through affiliate networks and sports sponsorships outside Austria.

Licensing Framework and Requirements

Application Process and Eligibility

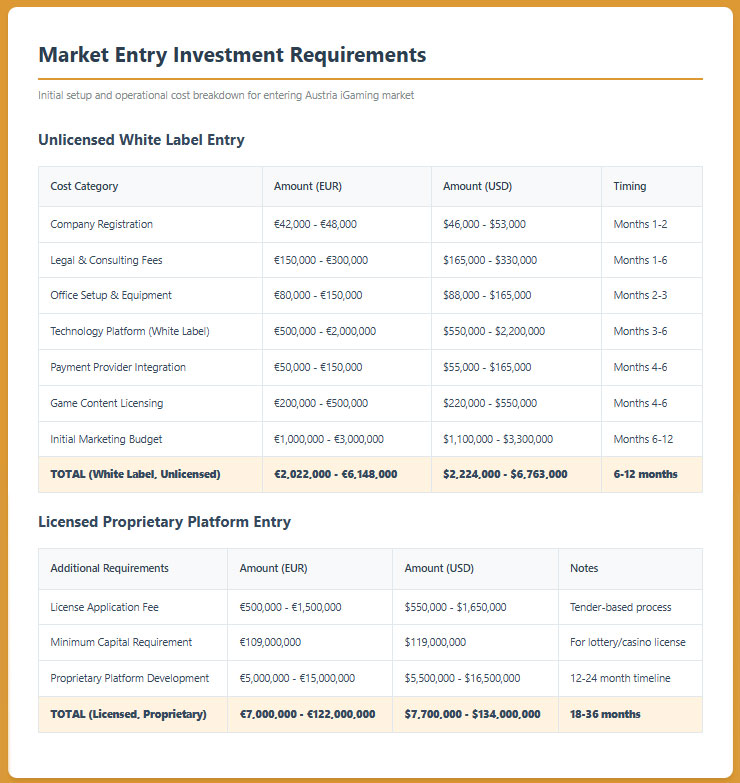

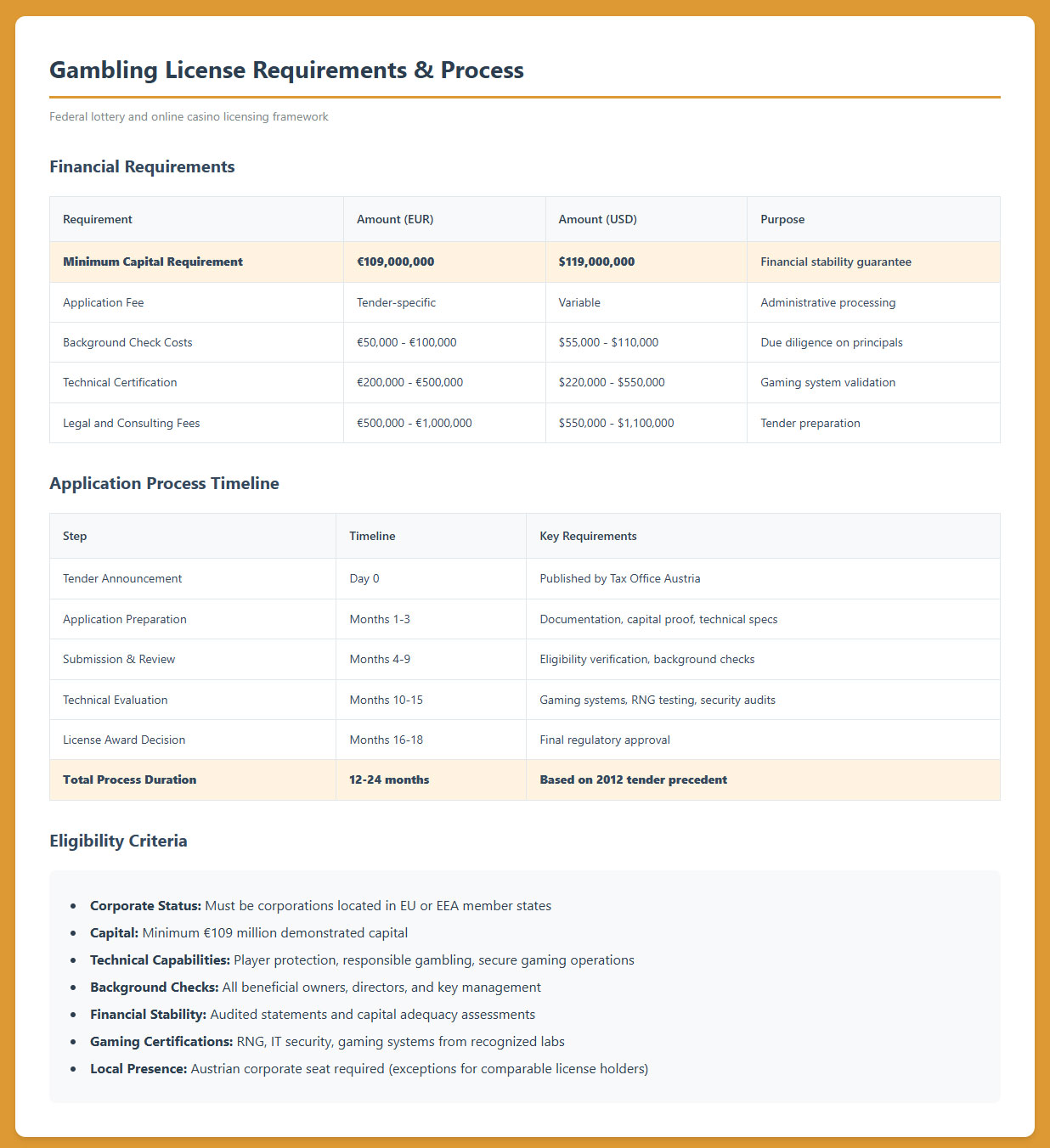

Federal Lottery and Online Casino License: The Tax Office Austria administers the single license for lotteries, electronic lotteries, and Video Lottery Terminals (VLTs) through a transparent public tender process. The licensing procedure follows statutory requirements outlined in the Glücksspielgesetz.

Eligibility Criteria:

- Applicants must be corporations located in European Union or European Economic Area (EEA) member states

- Minimum capital requirement of €109 million

- Demonstrated technical capabilities meeting Austrian standards for player protection, responsible gambling, and secure gaming operations

- Background checks on all beneficial owners, directors, and key management personnel

- Financial stability demonstrated through audited financial statements and capital adequacy assessments

- Technical certifications for gaming systems, random number generators, and IT security infrastructure

Local Presence Requirements: Successful applicants with registered offices outside Austria must establish a corporate seat in Austria as a condition of license issuance. However, exceptions exist for companies holding comparable lotteries licenses in their state of incorporation, subject to comparable gambling supervision and supervisory authority cooperation with Austrian regulators. For qualifying applicants, mere local presence (representative office) may suffice rather than full corporate establishment.

Application Timeline: The 2012 tender process, the most recent comprehensive licensing round, spanned approximately 18 months from announcement to final license award. The upcoming tender expected to commence in late 2025 or early 2026 will likely follow similar timelines. Given the license expiration date of September 30, 2027, authorities must initiate tender procedures by early 2025 to ensure seamless transition.

| Requirement | Amount (EUR) | Amount (USD Equivalent) | Purpose |

|---|---|---|---|

| Minimum Capital Requirement | €109,000,000 | $119,000,000 | Financial stability guarantee |

| Application Fee | Tender-specific | Variable | Administrative processing |

| Background Check Costs | €50,000 – €100,000 | $55,000 – $110,000 | Due diligence on principals |

| Technical Certification | €200,000 – €500,000 | $220,000 – $550,000 | Gaming system validation |

| Legal and Consulting Fees | €500,000 – €1,000,000 | $550,000 – $1,100,000 | Tender preparation and representation |

Ongoing Compliance Requirements

Reporting Obligations: Licensed operators must submit comprehensive financial reports on a monthly and quarterly basis to the Tax Office Austria. These reports include detailed revenue breakdowns by product category, player statistics, responsible gambling metrics, and tax calculations. Annual audited financial statements must be filed demonstrating compliance with capital maintenance requirements and financial obligations.

Technical Standards: Gaming systems must maintain certification throughout the license period, with regular testing of random number generators, game fairness, and payout percentages. Licensed operators must employ certified gaming technology meeting standards established by recognized international testing laboratories. Systems must maintain secure player databases with encryption standards meeting or exceeding EU data protection requirements.

Inspection and Audit Rights: Regulatory authorities maintain unrestricted rights to conduct audits and inspections at any time without prior notice. Failure to cooperate fully with regulatory examinations constitutes grounds for license suspension or revocation. Operators must maintain comprehensive records for minimum periods specified by regulation, typically seven years for financial records and three years for player transaction data.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification Requirements: The minimum legal age for gambling participation in Austria is 18 years without exception. All operators must implement robust age verification procedures before allowing any gambling activity. This verification typically involves checking official government-issued identification documents including passports, national identity cards, or driver’s licenses. Enhanced identification checks may be required for higher-value transactions or when risk thresholds are met.

Know Your Customer (KYC) and Anti-Money Laundering (AML) Compliance: Austrian gambling operators must comply with comprehensive KYC procedures aligned with EU Anti-Money Laundering Directives. Operators must verify player identity, residential address, and source of funds for significant transactions. Enhanced due diligence applies to politically exposed persons (PEPs), high-value players, and transactions involving jurisdictions identified as high-risk for money laundering.

Player identification procedures must include collection and verification of full legal name, date of birth, permanent residential address, nationality, and valid government-issued identification. Operators must screen players against international sanctions lists and maintain ongoing monitoring for suspicious transaction patterns.

Responsible Gambling Measures Mandated by Law: Austrian legislation requires comprehensive responsible gambling frameworks including deposit limits, loss limits, session time restrictions, and reality checks. Players must receive clear information about gambling risks, problem gambling symptoms, and available support resources. Operators must display responsible gambling messages prominently across all platforms.

Self-Exclusion System Requirements: Licensed operators must maintain self-exclusion systems allowing players to temporarily or permanently exclude themselves from gambling activities. The exclusion must apply across all products offered by the operator and must prevent account access, marketing communications, and bonus offers. Austria maintains a national self-exclusion register that licensed operators must integrate into their player management systems.

Mandatory Player Information Disclosures: Operators must provide comprehensive information to players including game rules, prize structures, odds of winning, return-to-player (RTP) percentages, and applicable fees or charges. Terms and conditions must be presented in clear German language, with unambiguous statements regarding player rights, dispute resolution procedures, and data protection practices. Players must receive transaction histories upon request, with complete records of deposits, wagers, winnings, and withdrawals.

Session Time Limits and Loss Limits: Recent regulatory developments emphasize enhanced player protection through mandatory time and loss limitations. Operators must implement systems that track cumulative playing time and financial losses, triggering warnings when predetermined thresholds are approached. Players must have the ability to set their own limits below maximum regulatory thresholds, with cooling-off periods required before increasing limits.

Financial Monitoring and Reporting

Transaction Monitoring Systems Required: Licensed operators must deploy sophisticated transaction monitoring systems capable of detecting unusual patterns indicative of money laundering, fraud, or problem gambling. These systems must generate alerts for investigation when transactions exceed defined thresholds or exhibit patterns consistent with financial crime typologies.

Reporting Requirements and Schedules: Austrian gambling operators submit monthly financial reports to the Tax Office Austria by the 15th day of the following month. These reports detail gross gaming revenue, taxes due, player counts, and product performance metrics. Quarterly reports provide additional detail on player demographics, responsible gambling interventions, and compliance activities. Annual reports include comprehensive financial statements, auditor certifications, and detailed operational statistics.

Audit and Inspection Procedures: Regulatory authorities conduct scheduled and unscheduled audits of licensed operators. Scheduled audits typically occur annually, examining financial records, gaming systems, player protection measures, and compliance documentation. Unscheduled inspections may occur based on complaints, suspicious activity reports, or routine surveillance. Operators must provide complete access to facilities, records, and personnel during regulatory examinations.

Data Retention Requirements: Financial records must be retained for seven years from the end of the relevant financial year. Player transaction data must be maintained for three years, with longer retention for records subject to ongoing investigations or litigation. Gaming system logs, including game outcomes, random number generator seeds, and technical events, must be preserved for three years. All records must be stored in formats allowing prompt retrieval and inspection by regulatory authorities.

Taxation Structure and Financial Obligations

Player Taxation

Tax Treatment of Gambling Winnings: Austria generally does not impose personal income tax on gambling winnings. Income that does not fall under the seven recognized types of taxable income in Austrian tax law remains untaxed, and gambling winnings typically fall into this category. This favorable treatment makes Austria attractive for high-stakes players and contributes to strong consumer participation in gambling activities.

Exception for Professional Gamblers: If gambling becomes a player’s primary or substantial source of income, tax authorities may classify winnings as taxable business income. This professional gambler designation requires consistent, systematic gambling activity demonstrating intent to generate regular income. Tax authorities examine factors including frequency of gambling, size of stakes, record-keeping practices, and proportion of total income derived from gambling.

Tax-Free Thresholds: No specific threshold triggers taxation on casual gambling winnings. However, players reporting large wins may face scrutiny regarding the source of funds used for gambling and whether gambling activity constitutes a business or profession. Winnings from foreign gambling operators may face different treatment depending on the jurisdiction and tax treaty provisions.

Operator Taxation

| Gambling Category | Tax Base | Tax Rate | Effective Date |

|---|---|---|---|

| Online Gambling (Casino) | Gross Gaming Revenue (GGR) | 40% | Current |

| Sports Betting | Gross Gaming Revenue (GGR) | 5% | April 1, 2025 (increased from 2%) |

| Land-Based Casinos | Gross Gaming Revenue (GGR) | 30% | Current |

| Casino Slot Machines | Net Gaming Revenue (NGR) | 30% | Current |

| Independent Slot Machines | Net Gaming Revenue (NGR) | 10% | Current |

| Lottery Stakes | Stakes/Turnover | 27.5% | Current |

| Video Lottery Terminals (VLTs) | Net Gaming Revenue (NGR) | 10% | Current |

| Corporate Income Tax | Net Profit | 25% | Standard rate |

Gross Gaming Revenue (GGR) Definition: GGR is calculated as total stakes or wagers minus winnings paid out to players. This calculation excludes promotional bonuses, jackpot contributions, and certain other deductions. Tax authorities closely scrutinize GGR calculations to ensure operators properly account for all gaming revenue and do not artificially reduce tax liability through improper deductions.

Net Gaming Revenue (NGR) Considerations: For certain gaming machine categories, taxation applies to Net Gaming Revenue, which may allow additional deductions beyond player payouts. These deductions typically include jackpot contributions, progressive pool allocations, and specific equipment costs. The distinction between GGR and NGR taxation creates significantly different effective tax burdens across gambling categories.

Recent Tax Increases and Impact: The April 1, 2025 increase in betting tax from 2% to 5% represents a 150% increase in tax burden for sports betting operators. This staged increase aims to align Austrian taxation with neighboring Germany’s rates while generating additional government revenue projected at €50 million in 2025, rising to €240 million by 2031. Industry stakeholders have criticized the increase as compressing operator margins and potentially driving players toward unlicensed offshore operators offering better odds.

License Renewal Fees: License renewal fees are determined through tender processes, with substantial costs associated with maintaining licenses through each renewal cycle. The 2012 monopoly license award to Österreichische Lotterien required significant financial commitments including upfront payments and ongoing annual fees beyond standard tax obligations.

Additional Financial Obligations: Licensed operators face mandatory contributions to problem gambling prevention programs, responsible gambling research, and addiction treatment services. These contributions typically range from 0.5% to 1% of gross gaming revenue, depending on the specific license category and regulatory requirements.

Gambling Market Financial Performance

| Year | Total GGR | Tax Revenue | Land-Based Revenue | Online Revenue |

|---|---|---|---|---|

| 2018 | €4.49 billion | €509.49 million | €4.18 billion | €310 million (est.) |

| 2023 | €4.85 billion (est.) | €575 million (est.) | €4.30 billion | €550 million |

| 2024 | €5.10 billion (est.) | €625 million (est.) | €4.45 billion | €632 million |

| 2025 (Forecast) | €5.25 billion | €675 million | €4.55 billion | €700 million |

Revenue Distribution by Gambling Type: Lottery operations constitute the largest segment of Austria’s gambling market, generating approximately €950 million annually. Land-based casinos contribute €315 million from table games and slots. Sports betting across all channels accounts for approximately €400 million. Online casino gaming through Win2Day generates approximately €305 million, though the total online gambling market including unlicensed operators exceeds €650 million.

Year-Over-Year Growth Trends: The Austrian gambling market has demonstrated steady but modest growth averaging 1.7% annually from 2020 to 2025. Online gambling has shown stronger growth at 4.22% CAGR, driven by increasing digital adoption, mobile gambling expansion, and growing acceptance of online gaming. Land-based operations have experienced slower growth, with some casino properties reporting declining revenues due to competition from online alternatives and economic headwinds.

Market Size Comparison: Austria’s gambling market represents approximately 1.2% of GDP, placing it in the mid-range among European countries. Compared to regional neighbors, Austria shows lower per-capita gambling spend than the United Kingdom (approximately €450 per capita vs. UK’s €550) but higher than Germany’s per-capita spend of €320. The relatively mature market with aging demographics suggests limited organic growth potential without regulatory liberalization.

Advertising and Marketing Restrictions

Permitted Advertising Channels: Operators holding valid Austrian licenses may advertise their gambling services across multiple media channels including television, radio, online platforms, outdoor advertising, and print media. However, advertising rights remain limited exclusively to licensed operators, creating a significant competitive advantage for the monopoly holder while effectively prohibiting international operators from marketing to Austrian consumers.

Television and Radio Advertising: Licensed operators may advertise during most broadcast hours but face restrictions on advertising during programs primarily targeted at minors. Time restrictions prevent gambling advertising during children’s programming and early morning hours when youth viewership is elevated. Broadcasters must ensure advertisements include responsible gambling messages and contact information for gambling addiction support services.

Online Advertising Restrictions: Digital advertising by licensed operators is permitted across search engines, social media platforms, content websites, and affiliate networks. However, operators must ensure advertising does not target minors through age-gating mechanisms, content targeting, and platform selection. Advertising on websites primarily frequented by minors remains strictly prohibited.

Content Restrictions and Guidelines: The Federal Ministry of Finance published non-binding interpretation guidelines detailing responsible standards for gambling advertising.

These guidelines require advertisements to avoid excessive promotion, must not portray gambling as a solution to financial problems, cannot suggest gambling enhances social acceptance or success, and must not display minors or appeal specifically to underage audiences. Advertisements must include clear responsible gambling messaging and problem gambling helpline information.

Bonus and Promotion Limitations: Promotional offers must comply with responsible gambling principles. Welcome bonuses cannot be excessively generous or create pressure to gamble beyond comfortable limits. Wagering requirements must be clearly disclosed with realistic terms allowing average players reasonable opportunity to meet conditions. Bonus abuse prevention measures must be implemented while ensuring fair treatment of legitimate players.

Sponsorship Regulations: Licensed operators may sponsor sports teams, events, and venues subject to responsible gambling standards. Sponsorships cannot target youth sports or events with predominantly minor audiences. Visible branding at sponsored events must include responsible gambling messaging. The monopoly structure has enabled Österreichische Lotterien and Casinos Austria to dominate sports sponsorships, creating significant brand visibility and marketing advantages.

Affiliate Marketing Rules: Affiliate marketing by licensed operators is permitted but subject to the same content and targeting restrictions as direct advertising. Affiliates promoting Austrian-licensed gambling services must ensure content meets responsible gambling standards, does not target minors, and includes appropriate disclaimers and problem gambling resources. Unlicensed operators are prohibited from advertising, including through affiliate channels, making affiliate promotion of international gambling sites technically illegal though widely practiced.

Advertising Ban for Unlicensed Operators: The Glücksspielgesetz explicitly prohibits advertising or facilitating advertising of games of chance where operators do not hold relevant Austrian licenses. This prohibition applies to all media channels, including online platforms, and extends to affiliates, advertising networks, and media publishers. Violations carry administrative penalties and potential criminal liability for serious or repeated infractions.

Enforcement of advertising restrictions against international operators has intensified, with authorities pursuing legal action against media outlets, advertising platforms, and affiliate networks facilitating promotion of unlicensed gambling services. Payment processors and banks face pressure to terminate relationships with entities involved in unlicensed gambling advertising.

Recent Regulatory Changes and Their Impact

Coalition Government Formation and Policy Direction (March 2025): Austria’s new coalition government comprising the center-right People’s Party (ÖVP), Social Democrats (SPÖ), and Liberal Party (NEOS) announced comprehensive gambling sector reform plans in their governmental program for 2025-2029. The coalition agreement signals retention of the online casino monopoly structure while introducing enhanced taxation, strengthened enforcement, and establishment of an independent regulatory authority.

Betting Tax Increase (April 1, 2025): The staged increase in betting tax from 2% to 5% of gross gaming revenue became effective April 1, 2025, representing the most significant recent regulatory change. This 150% tax increase affects all sports betting operators, compressing margins and forcing business model adjustments. Industry representatives have criticized the increase as implemented without transition period, creating immediate financial pressure on licensed betting operators while potentially driving players to unlicensed offshore alternatives offering better odds.

Announced Casino and Gambling Tax Increases (2025): The governmental program announced a 10% increase in general gambling taxes affecting land-based casinos and other gaming operations. Specific implementation details and effective dates remain under development, but operators should anticipate substantial tax burden increases over the 2025-2027 period. Combined with existing high tax rates (30% GGR for land-based casinos, 40% GGR for online casinos), these increases will create the most expensive gambling tax regime in Central Europe.

Independent Regulatory Authority Proposal: The coalition government committed to establishing an independent gambling regulatory authority separate from the Ministry of Finance. This structural reform addresses long-standing conflict-of-interest concerns arising from the Ministry’s simultaneous roles as regulator, tax collector, license grantor, and shareholder in monopoly operators. The proposed authority would assume responsibility for licensing, compliance monitoring, enforcement, and player protection oversight. Timeline for implementation remains uncertain, but stakeholders expect progress during 2025-2026 to enable operational authority before the 2027 license expiration.

Enhanced Enforcement Measures: The government announced “decisive” action against illegal gambling through internet blocking and payment blocking mechanisms. While DNS blocking legislation has been discussed since 2021, implementation has repeatedly delayed. The new coalition’s commitment suggests renewed urgency, with potential legislation in 2025-2026 implementing domain blocking, IP address blocking, and payment transaction restrictions for unlicensed operators.

Enforcement has intensified through existing mechanisms. In the first half of 2024, Austria’s financial police imposed fines totaling €962,000 for illegal gambling activities. Authorities increased cooperation with ISPs and banks to block unlicensed operator domains, IP addresses, and payment channels. The Ministry of Finance maintains active blocking lists, though effectiveness remains limited as operators deploy technical countermeasures.

Player Refund Litigation Developments: Austrian courts have issued judgments requiring unlicensed operators to refund player losses based on the monopoly’s legal status and prohibition of unlicensed gambling. These judgments have generated significant litigation volumes, with players supported by litigation funders pursuing claims against international operators. The litigation trend has created substantial financial exposure for unlicensed operators serving Austrian players.

Malta’s 2023 amendments to its Gaming Act (Bill 55) attempted to block recognition and enforcement of Austrian court judgments against Malta-licensed operators. The European Commission opened infringement proceedings against Malta in June 2025, arguing Malta’s legislation violates EU Regulation 1215/2012 on recognition and enforcement of judgments. This ongoing legal battle creates uncertainty for operators and players while highlighting tensions between national gambling monopolies and EU internal market principles.

Upcoming License Tender (2025-2026): With the current monopoly license expiring September 30, 2027, Austrian authorities must commence tender procedures in 2025 or early 2026. The tender represents a critical juncture, with three potential scenarios: renewal of the single monopoly license, limited multi-operator licensing, or comprehensive market liberalization.

Industry stakeholders including the Austrian Betting and Gaming Association (OVWG) and European Gaming and Betting Association (EGBA) strongly advocate for market liberalization through multi-operator licensing. The EGBA notes that 21 EU countries have adopted multiple licensing systems, positioning Austria alongside Poland as among Europe’s last monopoly markets. However, the coalition agreement language suggests preference for continuing monopolistic structures, describing plans for “further development” of the current monopoly rather than fundamental liberalization.

Enforcement Mechanisms and Penalties

Penalty Structures: Austrian gambling law establishes comprehensive penalty frameworks for violations ranging from administrative fines to criminal prosecution. Administrative penalties for unlicensed gambling operations can reach several hundred thousand euros per violation, with repeated infractions subject to escalating penalties. License holders face administrative sanctions for compliance failures, including warnings, temporary operational restrictions, financial penalties, and ultimately license suspension or revocation.

Administrative Penalties: Operating gambling services without appropriate Austrian licenses constitutes an administrative offense punishable by fines up to €22,000 per incident. Advertising unlicensed gambling services carries penalties ranging from €5,000 to €50,000 depending on violation severity and reach. Payment processors, banks, and media outlets facilitating unlicensed gambling face similar administrative penalties for knowingly supporting illegal operations.

Criminal Penalties: Serious violations, particularly those involving organized unlicensed gambling operations, fraud, or money laundering, may result in criminal prosecution. Criminal penalties include imprisonment for up to six months for individuals operating or facilitating illegal gambling, with longer sentences for aggravated circumstances. Confiscation of gambling equipment, financial assets, and proceeds of illegal gambling operations accompanies criminal convictions.

License Suspension and Revocation: Licensed operators face license suspension for material compliance violations, including failure to meet player protection standards, inadequate anti-money laundering controls, tax payment defaults, or providing false information to regulators. Suspension typically requires remediation within specified timeframes, with revocation following failure to correct deficiencies. Three land-based casino licenses have been revoked by Austrian courts, demonstrating regulatory willingness to employ this ultimate sanction.

Recent Enforcement Actions: Austrian authorities have intensified enforcement against unlicensed operators through multiple mechanisms. The financial police conducted raids on suspected illegal gambling operations in 2024, resulting in fines totaling €962,000 in just the first half of the year. These enforcement actions targeted both operators and intermediaries including payment processors, advertising networks, and affiliate marketers.

ISP Blocking of Unlicensed Operators: While comprehensive DNS blocking legislation remains pending, Austrian authorities have implemented targeted domain blocking through cooperation with Internet Service Providers. The Ministry of Finance maintains lists of unlicensed gambling domains, requesting ISPs to block access. However, effectiveness remains limited as technical circumvention through VPNs, mirror sites, and alternative domains allows continued player access. The government’s 2025-2029 program emphasizes more aggressive blocking implementation.

Payment Processor Restrictions: Austrian financial institutions face increasing pressure to terminate relationships with entities involved in unlicensed gambling. Banks and payment processors must implement screening procedures identifying gambling-related transactions and blocking payments to unlicensed operators. The regulatory framework includes provisions for financial institution liability when knowingly facilitating illegal gambling transactions.

Compliance Enforcement Trends: Regulatory enforcement has shifted from reactive complaint-based approaches to proactive surveillance and systematic enforcement campaigns. The Tax Office Austria employs specialized teams monitoring online gambling activities, identifying unlicensed operators, and pursuing enforcement actions. Coordination with international regulatory bodies and law enforcement agencies has enhanced cross-border enforcement capabilities.

The player refund litigation trend represents a novel enforcement mechanism, essentially deputizing players as private enforcers through civil litigation. Austrian courts have consistently ruled that contracts with unlicensed operators are void, requiring operators to refund player losses. This creates substantial financial risk for unlicensed operators while providing players with apparent loss recovery mechanisms, though actual enforcement of judgments against foreign operators remains challenging.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Austria’s population reached 9.11 million people as of mid-2025, representing 0.11% of global population and ranking 99th worldwide. The population has grown modestly over recent decades, increasing by approximately 1.62 million people between 1980 and 2024, though growth has followed an uneven trajectory rather than consistent upward progression. Population forecasts project steady but slow growth of approximately 150,000 people over the 2024-2030 period, reflecting mature demographic patterns typical of developed European nations.

Annual Growth Rate: Austria’s current population growth rate stands at approximately 0.3% annually, driven primarily by net immigration rather than natural increase. The low birth rate combined with aging population creates demographic challenges including labor force constraints and increasing dependency ratios. These demographic patterns have significant implications for the gambling market, suggesting limited organic growth potential from population expansion.

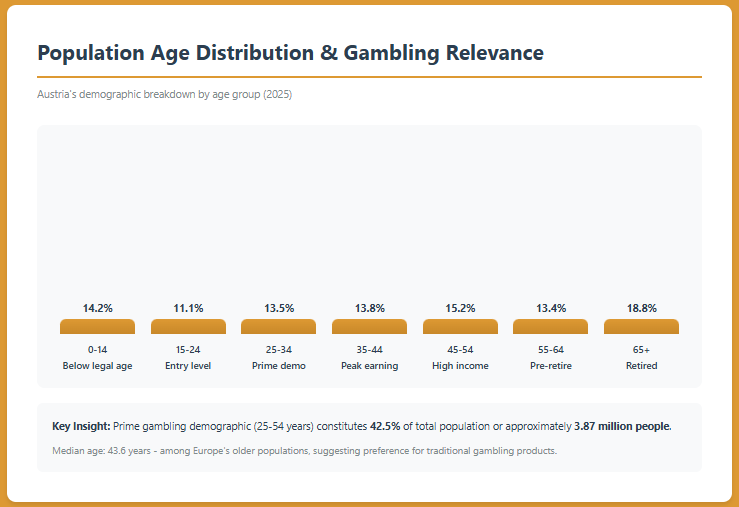

| Age Group | Percentage of Population | Total Population | Gambling Market Relevance |

|---|---|---|---|

| 0-14 years | 14.2% | 1.29 million | Below legal gambling age |

| 15-24 years | 11.1% | 1.01 million | Entry-level gamblers, digital natives |

| 25-34 years | 13.5% | 1.23 million | Prime gambling demographic, high digital engagement |

| 35-44 years | 13.8% | 1.26 million | Peak earning years, highest gambling participation |

| 45-54 years | 15.2% | 1.38 million | High disposable income, established gambling habits |

| 55-64 years | 13.4% | 1.22 million | Pre-retirement, significant gambling participation |

| 65+ years | 18.8% | 1.71 million | Retired, lottery preference, traditional gambling |

Median Age and Market Implications: Austria’s median age of 43.6 years positions it among Europe’s older populations, with significant implications for gambling market dynamics. The aging demographic suggests preference for traditional gambling products including lottery, land-based casinos, and sports betting over emerging formats like esports betting or cryptocurrency gambling.

Operators must balance appealing to older established customers while attracting younger digital-native players to ensure long-term market sustainability.

The prime gambling demographic (25-54 years) constitutes 42.5% of total population or approximately 3.87 million people. This cohort demonstrates highest gambling participation rates, strongest digital adoption, and greatest disposable income for entertainment spending. Marketing and product strategies must prioritize this demographic while recognizing the substantial 55+ population representing established lottery and casino customers.

Gender Distribution: Austria maintains relatively balanced gender distribution with approximately 50.4% female and 49.6% male population. Life expectancy shows typical patterns with females averaging 83.8 years compared to males at 78.9 years. Gender considerations influence gambling participation, with males historically representing approximately 70% of casino players and 75% of sports betting participants. However, female participation in online gambling has grown significantly, particularly in slots, bingo-style games, and lottery products.

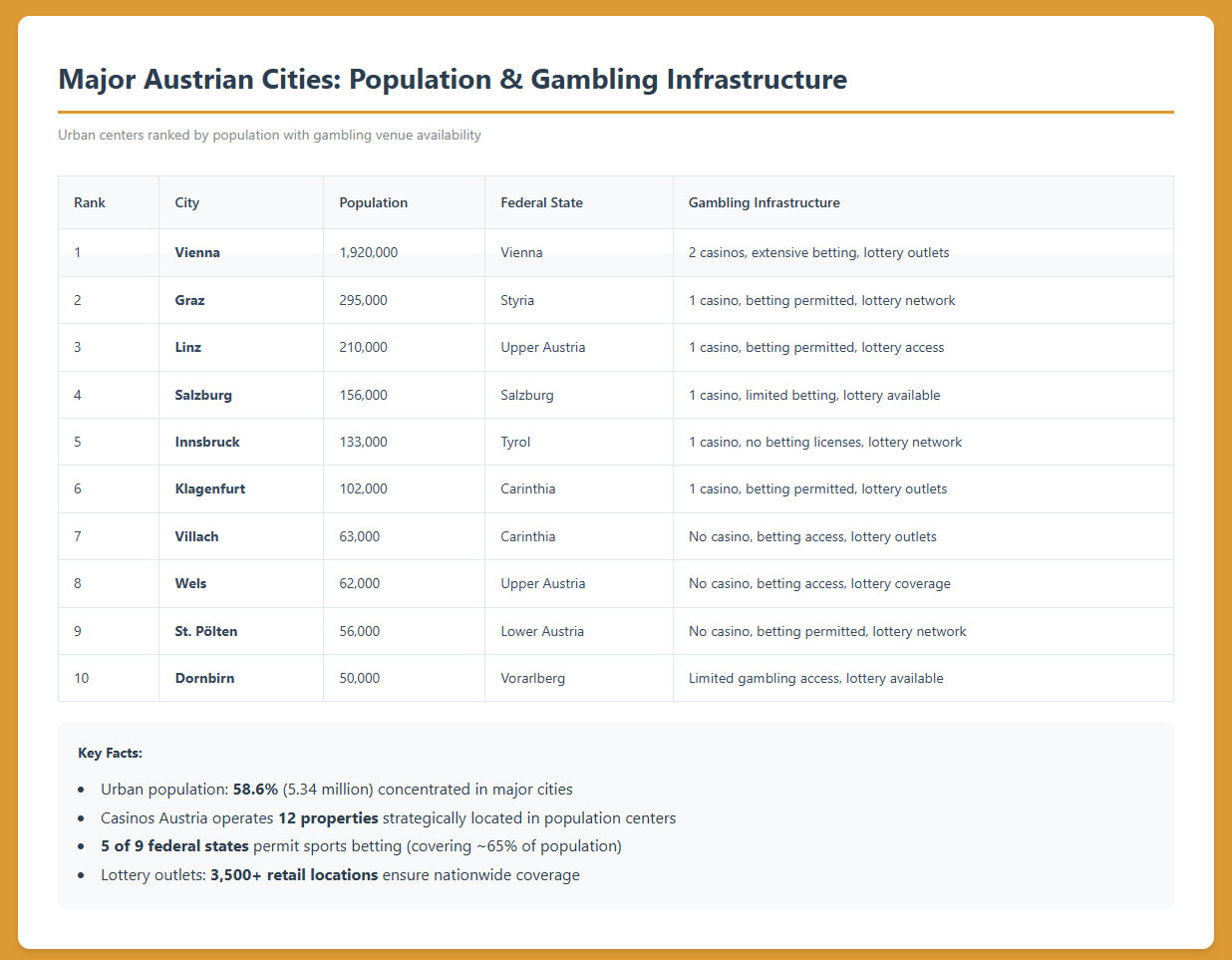

Urban vs Rural Distribution: Approximately 58.6% of Austria’s population resides in urban areas, totaling 5.34 million people concentrated in major cities and surrounding metropolitan regions. The remaining 41.4% or 3.77 million people live in rural and small-town environments. Urban populations demonstrate higher online gambling participation, greater exposure to marketing, and broader product preferences. Rural populations show stronger loyalty to traditional lottery products and occasional land-based casino visits.

Geographic Distribution

| City | Population | Federal State | Gambling Infrastructure |

|---|---|---|---|

| Vienna | 1,920,000 | Vienna | 2 casinos, extensive betting shops, lottery outlets |

| Graz | 295,000 | Styria | 1 casino, betting permitted, lottery network |

| Linz | 210,000 | Upper Austria | 1 casino, betting permitted, lottery access |

| Salzburg | 156,000 | Salzburg | 1 casino, limited betting, lottery available |

| Innsbruck | 133,000 | Tyrol | 1 casino, no betting licenses, lottery network |

| Klagenfurt | 102,000 | Carinthia | 1 casino, betting permitted, lottery outlets |

| Wels | 62,000 | Upper Austria | No casino, betting access, lottery coverage |

| St. Pölten | 56,000 | Lower Austria | No casino, betting permitted, lottery network |

| Dornbirn | 50,000 | Vorarlberg | Limited gambling access, lottery available |

| Villach | 63,000 | Carinthia | No casino, betting access, lottery outlets |

Regional Economic Differences: Vienna dominates Austria’s economic landscape, generating approximately 26% of national GDP despite housing only 21% of the population. Vienna’s GDP per capita of €38,632 significantly exceeds the national average, creating concentrated wealth and gambling potential. Other major urban centers including Salzburg, Innsbruck, and Graz maintain strong regional economies driven by tourism, manufacturing, and services. Rural regions, particularly in alpine areas, rely heavily on tourism and agriculture, creating seasonal economic and gambling participation patterns.

Internet Access Geographic Patterns: Urban areas achieve near-universal internet penetration exceeding 98%, with high-speed fiber and cable broadband widely available. Rural and mountainous regions face infrastructure challenges, though Austria’s Broadband Strategy 2030 targets nationwide gigabit connectivity. Current rural internet penetration stands at approximately 88%, with improving 4G and 5G mobile coverage compensating for fixed broadband limitations in some areas.

Concentration of Gambling Venues by Region: Casinos Austria operates 12 properties strategically located in major population centers, with Vienna housing two facilities. The five federal states permitting sports betting (Lower Austria, Upper Austria, Burgenland, Carinthia, Styria) contain approximately 65% of Austria’s population, creating uneven betting access across regions. Lottery outlets maintain nationwide coverage with over 3,500 retail locations, ensuring universal lottery product access regardless of geography.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Current GDP Metrics: Austria’s economy generated approximately $495 billion in total GDP during Q2 2025, positioning it as the 26th largest economy globally and among the wealthiest per capita. GDP per capita reached $58,669 in 2024, ranking Austria 13th highest worldwide and firmly establishing it as a high-income developed economy. Vienna ranks as the fifth richest NUTS-2 region within Europe with GDP per capita of €38,632, trailing only Inner London, Luxembourg, Brussels-Capital Region, and Hamburg.

GDP Growth Forecasts: Austria faces near-term economic headwinds with GDP projected to decline by 0.3% in 2025 before recovering to 1.0% growth in 2026. This marks a prolonged recession following contractions of 1.0% in 2023 and 1.2% in 2024. The economic slowdown reflects multiple factors including reduced industrial production (down 5.4% in 2024), high energy costs impacting manufacturing competitiveness, and declining investment particularly in industrial equipment.

Medium-term forecasts project gradual recovery with GDP growth returning to 1.5-2.0% annually from 2027 onwards. However, structural challenges including aging demographics, elevated government debt (84.0% of GDP in 2025, rising to 85.8% in 2026), and global economic uncertainty create downside risks. For gambling operators, the economic slowdown suggests constrained consumer discretionary spending and heightened price sensitivity in entertainment purchases.

Economic Sector Composition: Austria’s economy is dominated by services, accounting for approximately 70% of GDP. Manufacturing and industry contribute 27%, with agriculture representing less than 3%. The service sector’s dominance creates favorable conditions for gambling and entertainment industries, as services employment typically correlates with gambling participation. Tourism constitutes a significant economic driver, contributing approximately 15% of GDP and creating seasonal patterns in gambling participation particularly in alpine resort regions.

Employment and Wage Levels: The unemployment rate stood at 5.3% in 2025, representing a gradual increase from the post-COVID trough of 4.8% in 2022. The labor market remains relatively healthy by European standards, with labor force participation sustained by increasing female participation as the statutory retirement age for women gradually aligns with men’s by 2033. Monthly earnings averaged approximately €3,306 ($3,625) in December 2022, with wages growing more than 8% in 2024 as workers received inflation compensation through collective bargaining agreements.

Inflation Trends: Inflation surged to 3.3% in Q1 2025 driven by retail energy price increases following expiration of government relief measures and high wholesale oil and gas prices. Persistent services inflation contributes to elevated inflation rates. Projections suggest inflation moderating to 2.9% for full-year 2025 and further declining to 2.1% in 2026 as energy commodity prices stabilize and wage growth moderates. High inflation erodes real gambling budgets, requiring operators to adjust pricing strategies and promotional offers to maintain player engagement.

Income and Wealth Distribution

| Metric | Value | Implications for Gambling Market |

|---|---|---|

| Average Household Income (Annual) | €54,000 ($59,130) | Substantial discretionary income available |

| Median Household Income (Annual) | €48,000 ($52,560) | Typical household gambling budget capacity |

| Disposable Income Per Capita | €26,500 ($29,015) | High entertainment spending capacity |

| Gini Coefficient | 0.28 | Relatively equal income distribution, broad market access |

| At-Risk Poverty Rate | 14.8% | Approximately 1.35M people with limited gambling capacity |

| Median Wealth Per Adult | $95,000 | Significant accumulated wealth supporting gambling spend |

Income Inequality Measures: Austria maintains relatively equal income distribution with a Gini coefficient of 0.28, among the lowest in the OECD and indicating compressed income disparity compared to many developed economies. This equality translates to broad middle-class gambling participation rather than concentration among wealthy individuals. Approximately 85% of Austrian households report annual incomes between €30,000 and €80,000, creating a large addressable market for mainstream gambling products.

Disposable Income Trends: Real disposable income declined in 2023-2024 due to high inflation outpacing wage growth, forcing households to reduce discretionary spending and increase savings rates to historically high levels. The 2024 recovery in real wages, driven by 8%+ wage increases, has begun restoring disposable income. Gambling operators experienced pressure during the 2023-2024 period, with players reducing betting frequency, lowering average stakes, and becoming more promotion-sensitive.

Consumer Spending Patterns: Austrian households allocate approximately 3.5-4% of disposable income to recreation and entertainment, translating to roughly €1,000-1,200 annually per household. Gambling represents a subset of entertainment spending, competing with dining, travel, sports, and cultural activities. The mature market exhibits relatively stable gambling spend patterns, with economic cycles influencing betting frequency and stake sizes rather than fundamental participation rates.

Middle Class Size and Growth: Austria’s substantial middle class, defined as households earning 75-200% of median income, encompasses approximately 60% of the population or 5.5 million people. This demographic cohort demonstrates highest gambling participation rates, strongest brand loyalty, and greatest lifetime value for operators. Middle-class growth has stagnated in recent years due to inflation, housing cost pressures, and tax burdens, creating challenges for gambling market expansion.

Market Size and Growth Projections

| Year | Total Online Gambling | Online Casino | Sports Betting | Active Users | ARPU |

|---|---|---|---|---|---|

| 2024 | €632M ($692M) | €326M ($357M) | €210M ($230M) | 785,000 | €805 ($882) |

| 2025 | €659M ($722M) | €340M ($372M) | €220M ($241M) | 818,000 | €805 ($882) |

| 2026 | €687M ($753M) | €355M ($389M) | €230M ($252M) | 853,000 | €805 ($882) |

| 2027 | €716M ($784M) | €370M ($405M) | €241M ($264M) | 887,000 | €807 ($884) |

| 2028 | €746M ($817M) | €385M ($422M) | €252M ($276M) | 903,000 | €826 ($905) |

| 2029 | €777M ($851M) | €401M ($439M) | €263M ($288M) | 920,100 | €844 ($925) |

Historical Revenue Growth: The Austrian online gambling market has demonstrated consistent expansion from approximately €310 million in 2018 to €632 million in 2024, representing a compound annual growth rate of 12.7% over the six-year period. This growth significantly outpaces land-based gambling revenue, which has remained largely stagnant at approximately €4.3-4.5 billion annually. The shift toward online channels reflects broader digital transformation trends, with pandemic acceleration permanently elevating online gambling participation.

Expected CAGR: Projections indicate online gambling revenue will grow at a 4.22% CAGR from 2024 to 2029, reaching approximately €777 million by decade’s end. This moderating growth rate compared to historical performance reflects market maturation, economic headwinds, increased taxation, and demographic constraints. The 4.22% CAGR positions Austria below European online gambling market averages of 7-9% but consistent with other mature Western European markets.

Projected User Base Growth: Active online gambling users are expected to expand from approximately 785,000 in 2024 to 920,100 by 2029, representing 17.2% growth or 3.2% CAGR. User growth lags revenue growth, indicating increasing average revenue per user driven by higher engagement, larger average stakes, and product mix shifts toward casino gaming. The projected user base represents approximately 10% of Austria’s adult population by 2029, suggesting significant remaining growth potential if regulatory liberalization improves product quality and marketing capabilities.

Average Revenue Per User (ARPU) Analysis: Current ARPU stands at approximately €805-890 ($882-975) annually, positioning Austria in the mid-to-high range among European markets. This ARPU reflects the country’s high disposable income, mature gambling culture, and preference for casino products over lower-margin betting. Projections suggest ARPU will increase modestly to €844 ($925) by 2029, driven by product premiumization, live dealer game adoption, and high-value player acquisition rather than mass-market expansion.

Market Penetration Rates: Online gambling penetration currently reaches 8.6% of Austria’s total population, or approximately 13.7% of adults aged 18+. This penetration rate remains below leading European markets such as the United Kingdom (22%), Sweden (18%), and Denmark (15%), suggesting substantial growth potential under improved regulatory frameworks. The monopoly structure and limited product variety constrain penetration, with many Austrian players accessing international unlicensed platforms excluded from official statistics.

Online vs Land-Based Revenue Split: Online gambling represents approximately 13% of total gambling revenue in 2024, with land-based operations maintaining 87% share. This ratio reflects Austria’s strong land-based infrastructure, cultural preferences for physical casinos and lottery retail, and limitations in the online monopoly’s product offerings. International comparisons show online shares of 35-55% in liberalized markets, indicating Austria’s online sector remains significantly underdeveloped. Regulatory liberalization could accelerate online share growth to 25-30% by 2030.

Market Size Comparison with Regional Neighbors: Austria’s per-capita gambling spend of approximately €575 annually positions it above Germany (€320) and Switzerland (€450) but below Italy (€650) and significantly below the United Kingdom (€850). The monopoly structure constrains market development relative to competitive markets, with gray-market participation suggesting true gambling demand exceeds official statistics. Including estimated unlicensed operator revenue of €220 million, total online gambling approaches €850 million or approximately €93 per capita.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy Rates: Austria maintains universal literacy at 99%+ of the adult population, with no significant gender disparities. This high educational foundation supports sophisticated gambling product comprehension, including complex betting markets, game rules, and terms and conditions. Universal literacy enables effective responsible gambling messaging and player protection communications.

Education Levels: Approximately 86% of Austrians aged 25-64 have completed upper secondary education, placing Austria in the upper tier of OECD countries. Tertiary education completion reaches 40% of the adult population, with strong technical and vocational training traditions supplementing academic university pathways. Higher education levels correlate with online gambling adoption, financial literacy supporting bankroll management, and responsiveness to sophisticated marketing messages.

Digital Literacy Indicators: Austria ranks highly in digital skills assessments, with approximately 78% of adults demonstrating at least basic digital competencies. Advanced digital skills reach 38% of the population, supporting adoption of mobile gambling applications, cryptocurrency payments, and interactive live dealer products. Older demographics (55+) show lower digital literacy, preferring traditional lottery retail and land-based casinos over online alternatives.

Workforce Skill Levels: Austria’s highly skilled workforce, supported by renowned vocational training systems, creates favorable conditions for gambling industry employment. Technology development, customer service, compliance, and data analysis roles find ample qualified candidates. German language proficiency is essential, with English language skills supporting international business operations and software development partnerships.

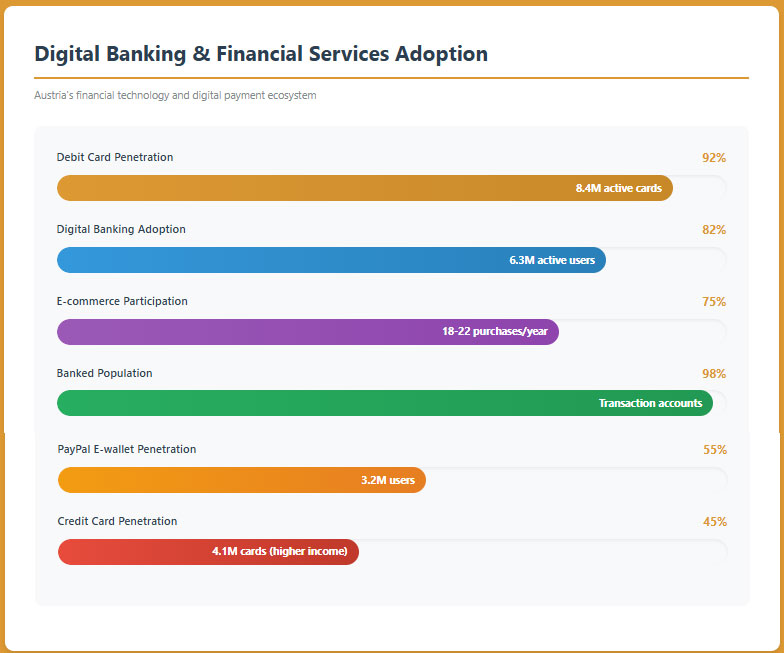

Technology Adoption Readiness: Austrian consumers demonstrate high technology adoption rates across digital banking (82% penetration), e-commerce (75% participation), and mobile applications. This technology comfort supports rapid adoption of gambling innovations including mobile-first products, biometric authentication, instant payment methods, and augmented reality features. Skepticism toward purely digital products remains lower than in southern European markets but higher than Scandinavian countries.

English Language Proficiency: Approximately 73% of Austrians report English language capabilities, with higher proficiency among younger demographics and urban populations. However, German remains the essential language for customer-facing gambling services. Operators must provide comprehensive German language support including websites, mobile applications, customer service, responsible gambling materials, and marketing content. English language capabilities support consumption of international gambling content and participation on English-language platforms.

Cultural and Social Factors

Communication and Language

Primary Languages: German serves as Austria’s official language and overwhelmingly dominant communication medium, spoken natively by approximately 88% of the population. Austrian German differs in vocabulary, pronunciation, and expressions from German spoken in Germany or Switzerland, requiring localization beyond simple translation. Minority languages include Turkish (2.3%), Serbian (2.2%), and Croatian (1.6%), with regional variations including distinctive dialects in Vienna, Tyrol, and Vorarlberg.

Internet Language Preferences: Approximately 92% of Austrian internet users prefer German language content, with English accepted for technical or specialized content but rarely preferred for consumer services. Gambling operators must deliver authentic Austrian German rather than German German, incorporating local terminology for betting, casino games, and payment methods. Poor localization immediately signals foreign operation, triggering trust concerns and regulatory scrutiny.

Business Communication Norms: Austrian business culture emphasizes formality, precision, and adherence to rules and procedures. Gambling customer service must balance efficiency with politeness, using formal address (Sie rather than du) unless explicitly invited to informal communication. Written communications should maintain professional standards with proper grammar and terminology. Response times, complaint handling, and problem resolution affect brand reputation significantly in Austria’s quality-conscious market.

Cultural Attitudes Toward Gambling

Gambling Acceptance Levels: Austrian society demonstrates high gambling acceptance, with lottery participation considered mainstream entertainment across all social classes. Casino gambling maintains upscale associations linked to tourism destinations like Baden bei Wien and luxury venues in Vienna. Sports betting has grown in social acceptance, particularly among younger demographics, though some stigma persists compared to lottery. Online gambling faces greater skepticism, associated with addiction concerns and unlicensed operator fraud stories prominently covered in Austrian media.

Religious Influences: Austria’s historically Catholic population (approximately 55% identify as Catholic, though active practice is lower) maintains generally permissive attitudes toward gambling. Catholic social teaching accepts moderate gambling as entertainment while condemning excessive or addictive behavior. Gambling is not viewed as sinful or immoral when practiced responsibly, distinguishing Austria from Protestant-influenced societies with stronger gambling restrictions. Islamic populations (8% of total) generally avoid gambling for religious reasons, creating demographic segments with minimal gambling participation.

Foreign Brand Perception: Austrian consumers demonstrate sophisticated attitudes toward international brands, generally viewing established European gambling companies positively while maintaining skepticism toward lesser-known offshore operations. Brands with strong German-speaking market presence (Germany, Switzerland) benefit from regional familiarity. British gambling brands carry prestige associations with established regulatory frameworks and premier league sports. However, unlicensed operation regardless of brand strength triggers regulatory risk concerns among informed consumers, particularly following high-profile player refund litigation cases.

Risk Tolerance Indicators: Austrian investment and insurance market behaviors suggest moderate risk tolerance, with preference for secure savings over equity investments but willingness to accept calculated risks for potential rewards. This translates to gambling preferences emphasizing games with understood odds and perceived skill elements (sports betting, poker) over pure chance games. Austrians respond well to promotional offers but demonstrate skepticism toward excessively generous bonuses suggesting unsustainable business practices.

Entertainment Preferences and Habits: Austrian entertainment culture balances traditional preferences (opera, classical music, outdoor recreation) with modern digital consumption patterns. Gaming and esports have grown significantly among younger demographics, creating crossover opportunities for gambling products. Sports culture emphasizes winter sports (skiing, ski jumping), football, and Formula 1, shaping sports betting product priorities. Seasonal patterns see gambling activity increase during major sports events and winter tourist seasons.

Social vs Solitary Gambling Preferences: Austrians exhibit mixed preferences, with lottery and sports betting often enjoyed as social activities discussed among friends and colleagues. Land-based casino gambling maintains strong social components, with group outings common particularly in tourist-focused venues. Online gambling trends toward solitary activity, though social casino features and multiplayer poker retain appeal. Live dealer casino games successfully bridge social and online preferences, explaining their strong growth trajectory.

Problem Gambling and Social Considerations

| Metric | Value | Percentage of Population |

|---|---|---|

| Problem Gamblers (Estimated) | 45,000 – 60,000 | 0.5% – 0.66% |

| At-Risk Gamblers | 180,000 – 250,000 | 2.0% – 2.75% |

| Underage Gambling Participants | 8,000 – 12,000 | 0.7% of minors |

| Treatment Facility Admissions (Annual) | 3,500 – 4,500 | N/A |

| Problem Gambling Helpline Calls (Annual) | 12,000 – 15,000 | N/A |

Prevalence of Gambling Addiction: Problem gambling affects an estimated 0.5-0.66% of Austria’s adult population, translating to 45,000-60,000 individuals experiencing significant gambling-related harm. This prevalence rate aligns with European averages and remains lower than liberalized markets like the United Kingdom (0.8%) but higher than restrictive jurisdictions like Poland (0.3%). The at-risk population, demonstrating problematic behaviors not yet reaching clinical addiction thresholds, encompasses an additional 2.0-2.75% or 180,000-250,000 people.

Demographics of Problem Gamblers: Problem gambling disproportionately affects males, representing approximately 75% of individuals seeking treatment. The most affected age groups span 25-45 years, coinciding with peak gambling participation and disposable income availability. Lower socioeconomic groups show higher problem gambling rates despite lower overall gambling participation, reflecting greater vulnerability to gambling harm among financially constrained populations.

Age Groups Most Affected: Young adults aged 18-24 demonstrate concerning problem gambling indicators, with approximately 1.2% meeting diagnostic criteria for gambling disorder. This elevated rate reflects developmental factors including impulsivity, peer influence, and digital natives’ comfort with online gambling. The 35-44 age group shows highest absolute problem gambling numbers, balancing elevated gambling participation with established financial obligations creating stress when gambling becomes problematic.

Gender Distribution: Males dominate problem gambling statistics at approximately 75% of cases, though female problem gambling is underreported due to stigma and help-seeking barriers. Female problem gamblers more commonly report electronic gaming machine (EGM) addiction, while males show higher rates of sports betting and casino game problems. Recent trends show narrowing gender gaps in online gambling participation, potentially foreshadowing convergence in problem gambling rates.

Underage Gambling Issues: Despite minimum age restrictions of 18 years, an estimated 8,000-12,000 Austrian minors participate in gambling activities annually, representing approximately 0.7% of the under-18 population. Underage participation occurs primarily through family members purchasing lottery tickets, inadequate age verification on international gambling websites, and unregulated gambling-style video game mechanics. Underage gambling correlates with elevated problem gambling risk in adulthood, making prevention a policy priority.

Government Response Measures: The Austrian government established the Staff Unit for Addiction Prevention and Counselling within the Federal Ministry of Finance in 2010, dedicated to gambling harm reduction. This unit coordinates research, prevention campaigns, treatment facility funding, and regulatory policy development. Public health campaigns target at-risk demographics, educate about problem gambling symptoms, and promote responsible gambling practices.

Treatment Facilities and Support Services: Austria maintains a network of approximately 85 specialized gambling addiction treatment centers and counseling services distributed across federal states. These facilities offer individual therapy, group counseling, family support, and relapse prevention programs. Annual treatment capacity accommodates 3,500-4,500 individuals, though demand exceeds capacity with waiting lists common in urban centers. Services are primarily publicly funded through healthcare systems and mandatory gambling operator contributions.

The national problem gambling helpline operates 24/7, receiving 12,000-15,000 calls annually providing crisis intervention, treatment referrals, and support for family members affected by gambling problems. Online counseling services supplement telephone support, recognizing that digital channels better reach younger problem gamblers.

Social Responsibility Requirements for Operators: Licensed operators face comprehensive social responsibility obligations including mandatory contributions to problem gambling prevention and treatment programs, typically 0.5-1% of gross gaming revenue. Operators must implement player protection tools including deposit limits, loss limits, time limits, reality checks, and self-exclusion systems. Advertising must include responsible gambling messages and helpline information. Staff training on problem gambling identification and intervention is mandatory.

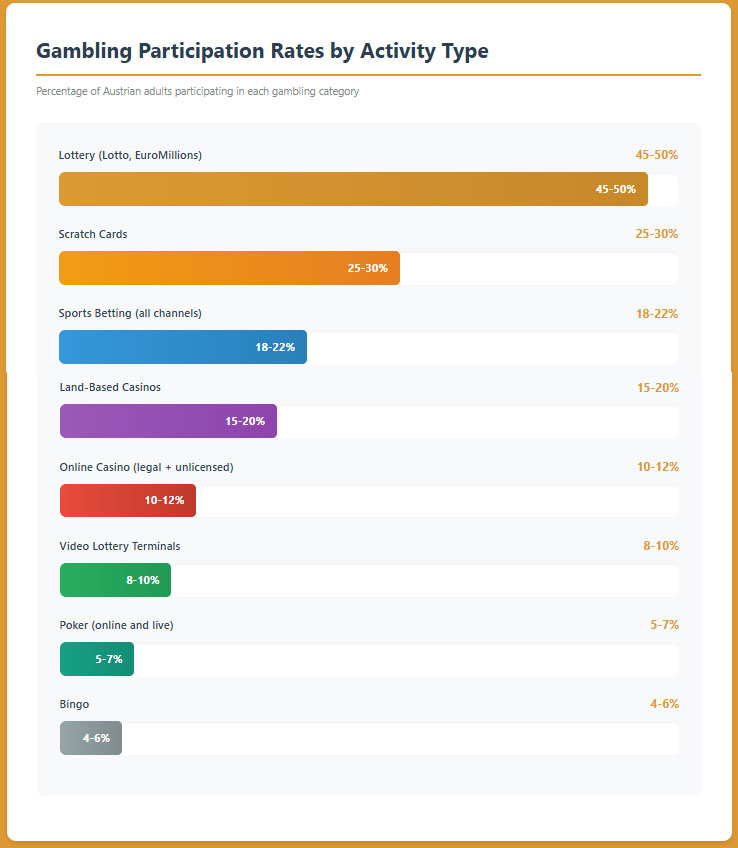

Recent Studies and Research: A 2024 study by TGM Research examined Austrian gambling participation and behavior, finding that 16.23% of respondents play casino games once monthly, with 14.42% playing several times monthly and 14.42% several times weekly. These participation rates suggest widespread gambling engagement, necessitating continued focus on harm minimization. Research emphasizes the effectiveness of early intervention, voluntary limit setting, and algorithmic detection of risky gambling patterns in reducing gambling harm.

Political Structure and Governance

Government System: Austria operates as a federal parliamentary republic comprising nine autonomous federal states (Bundesländer). The federal government exercises authority over national matters including fiscal policy, foreign relations, and federal-level gambling regulation, while states maintain significant autonomy over regional affairs including state-level gambling licensing. This federal structure creates regulatory complexity for gambling operators navigating both federal monopolies and state-specific regimes.

Current Political Situation (2025): Austria’s coalition government formed in March 2025 comprises the center-right People’s Party (ÖVP), Social Democrats (SPÖ), and Liberal Party (NEOS). This three-party coalition emerged after months of political uncertainty following September 2024 elections that failed to produce a clear majority. The coalition agreement addresses gambling through enhanced taxation, strengthened enforcement, and proposed establishment of an independent regulatory authority, but stops short of monopoly liberalization advocated by industry stakeholders.

Political Stability Indicators: Austria maintains strong political stability, ranking 13th globally on the World Bank’s Political Stability and Absence of Violence index. Democratic institutions function effectively, transitions of power occur peacefully through regular elections, and rule of law principles are well-established. However, coalition politics can create policy uncertainty as multiple parties negotiate compromises, as seen in the extended 2024-2025 government formation period.

Regulatory Consistency and Predictability: Austrian regulatory frameworks demonstrate high consistency and predictability in most sectors, with well-established legal traditions and judicial independence. However, gambling regulation shows greater uncertainty due to pending reforms, monopoly system challenges under EU law, and potential market liberalization. The extended delays in implementing announced gambling law amendments (originally expected in 2021, still pending in 2025) create planning challenges for operators and investors.

Corruption Perception: Austria scores 71 out of 100 on Transparency International’s Corruption Perceptions Index 2024, ranking 22nd globally and indicating relatively low corruption levels. However, this represents a decline from higher historical rankings, with concerns about political party financing, conflicts of interest in public procurement, and economic crimes. The gambling sector specifically faces conflict-of-interest criticism regarding the Ministry of Finance’s simultaneous roles as regulator, tax collector, and shareholder in monopoly operators.

EU Membership Impact: As a European Union member since 1995, Austria operates within EU internal market frameworks, creating tensions between national gambling monopolies and EU free movement principles. The European Court of Justice has repeatedly examined Austrian gambling restrictions, generally upholding monopoly structures while requiring genuine public interest justifications and proportionate restrictions. EU membership facilitates Austrian operators’ access to other EU markets while creating pressure to liberalize domestic markets. Future gambling reforms will need EU law compliance, particularly regarding non-discrimination and proportionality principles.

Trade Agreements: Austria benefits from EU trade agreements providing market access to numerous countries. For gambling and digital services, the EU’s digital single market initiatives and e-commerce directive shape regulatory frameworks. However, gambling remains an area where member states retain significant autonomy, limiting trade agreement impacts on market access. The EU-wide General Data Protection Regulation (GDPR) establishes data protection standards that gambling operators must meet when processing Austrian player data.

Technology Adoption and Digital Behavior

Internet and Digital Usage

| Metric | Value | Global/European Ranking |

|---|---|---|

| Internet Penetration | 95.3% | Top 15 globally |

| Total Internet Users | 8.69 million | N/A |

| Mobile Internet Users | 8.3 million (91%) | Top 20 globally |

| Daily Internet Usage (Average) | 6.2 hours | Above European average |

| Social Media Users | 7.3 million (80.1%) | High engagement |

| E-commerce Participation | 75% | Top 25 globally |

| Digital Banking Adoption | 82% | Leading European market |

| Mobile Connections per Capita | 147% | Multiple devices common |

Internet Penetration Quality: Austria’s 95.3% internet penetration positions it among Europe’s most connected countries, with 8.69 million people accessing the internet regularly. This near-universal connectivity creates optimal conditions for online gambling market development, eliminating infrastructure barriers that constrain adoption in less developed markets. Urban areas achieve 98%+ penetration, while rural regions maintain 88%+ access through combination of fixed broadband and mobile networks.

Daily Internet Usage Patterns: Austrians average 6.2 hours of daily internet usage, exceeding European averages and indicating deep digital integration across work, entertainment, and social activities. Peak usage occurs evenings between 7 PM and 11 PM, coinciding with prime gambling activity windows. Weekend usage increases further, creating elevated gambling participation Saturdays and Sundays. Mobile devices account for approximately 65% of internet usage time, emphasizing importance of mobile-optimized gambling products.