Azerbaijan presents a complex and evolving gambling market characterized by strict mainland prohibitions contrasted with emerging opportunities in designated zones. Following a 27-year gambling ban instituted in 1998, Azerbaijan passed groundbreaking legislation in July 2025 permitting casino operations exclusively on artificial islands in the Caspian Sea.

This regulatory shift signals potential market liberalization while maintaining strict controls. With a population of 10.4 million, 89 percent internet penetration, and rapid digital payment adoption, Azerbaijan demonstrates strong technological readiness.

However, market entry remains highly restricted, requiring careful navigation of regulatory constraints and emerging licensing frameworks for operators considering this frontier market.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Gambling Legal Status | Highly Restricted | Banned on mainland since 1998; casinos allowed only on artificial islands from 2025 |

| Online Gambling Status | Prohibited | No legal online casino licenses available; international sites operate in gray area |

| Legal Gambling Forms | State Lotteries, Sports Betting | Very limited; heavily regulated by Ministry of Finance |

| Total Population | 10.4 million | As of 2025; 0.6% annual growth |

| Median Age | 33.6 years | Young, digitally active population |

| Urban Population | 58.7% | Concentrated in Baku and major cities |

| GDP (Total) | $74.32 billion | 2024 estimate; oil-dependent economy |

| GDP Per Capita | $7,284 – $7,458 | 2024-2025 estimates |

| GDP Growth Rate | 3-4.1% | 2025 projection: 3%; 2024 actual: 4.1% |

| Internet Penetration | 89% | 9.23 million users; 0.6% YoY growth |

| Mobile Penetration | 118% | 12.2 million connections; multiple SIM ownership common |

| Smartphone Adoption | High | Android 81.3%, iOS 18.1%; mobile-first market |

| Social Media Users | 6.73 million | 64.9% of population; 87.6% growth 2023-2024 |

| Cashless Payment Adoption | 91% | As of early 2025; 9 of 10 transactions are cashless |

| Casino License Fee (Artificial Islands) | $200,000 annually | 340,000 AZN; new framework from 2025 |

| Regulatory Authority | Ministry of Finance | Controls all gambling licensing and oversight |

| Tax Structure | Not Yet Published | Artificial island casino taxation framework pending |

| Corporate Income Tax | 20% | Standard rate; special zones may offer incentives |

| Language | Azerbaijani | Russian widely spoken; limited English proficiency |

| Currency | Azerbaijani Manat (AZN) | 1 USD ≈ 1.70 AZN; 1 EUR ≈ 1.79 AZN |

| Average Monthly Salary | 1,098 AZN ($646) | January-July 2025 average |

| Mobile Internet Speed | 56.19 Mbps | Median download; 23.6% increase YoY |

| Fixed Internet Speed | 62.69 Mbps | Median download; 89.8% increase YoY |

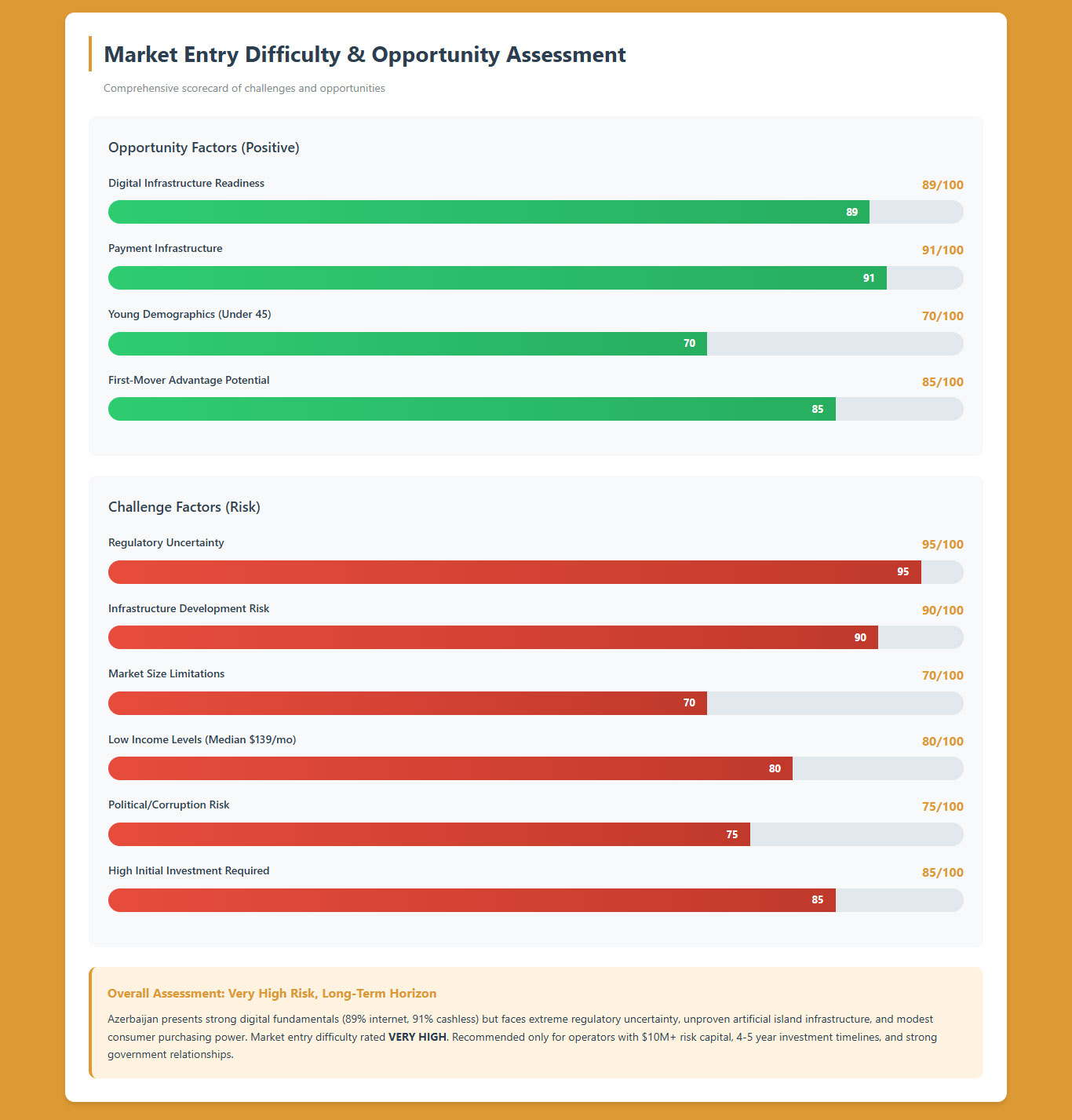

| Market Entry Difficulty | Very High | Extremely limited licensing; artificial island projects unproven |

| Political Stability | Stable but Authoritarian | Aliyev family regime; limited press freedom; high corruption perception |

| Religion | 95% Muslim | 85% Shia, 15% Sunni; conservative attitudes toward gambling |

| Investment Outlook | High Risk, Long-Term | Regulatory uncertainty; artificial island infrastructure unbuilt |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Historical Context and Recent Developments

Azerbaijan implemented a comprehensive gambling ban in 1998 under President Heydar Aliyev, prohibiting all forms of casino operations, slot machines, and table games. This ban remained firmly in place for 27 years as part of policies addressing concerns about gambling addiction and public safety.

The legislative shift followed earlier groundwork laid in May 2024 with the Law on Creation of Artificial Land Plots in the Azerbaijani Sector of the Caspian Sea. Prominent businessman Emin Agalarov publicly announced plans in fall 2024 to open a casino within his Sea Breeze entertainment complex.

Lawmakers justified the policy change by citing revenue generation potential, tourism development, job creation, and reducing capital flight. Azerbaijani citizens currently travel abroad or use online platforms to gamble, with the new law aimed at reducing the shadow market.

Land-Based Gambling Activities

Casino Operations: Casinos remain strictly prohibited throughout mainland Azerbaijan. The July 2025 legislation creates an exception permitting casino operations exclusively on designated artificial islands in the Caspian Sea under strict national regulations and licensing requirements.

Licensed casinos on artificial islands must pay an annual license fee of 340,000 AZN (approximately $200,000). The regulatory framework establishes legal and organizational principles for operating casinos on such territories while maintaining the prohibition elsewhere.

Sports Betting Venues: Land-based sports betting is permitted under heavily restricted conditions. Only state-approved operators with Ministry of Finance licensing can operate sports betting facilities. State-sponsored operators like Topaz dominate the limited legal sports betting market.

Slot Machine Halls: Slot machines and gaming halls are comprehensively prohibited throughout Azerbaijan. Organizing or operating slot machine facilities constitutes illegal gambling activity subject to significant administrative fines and potential criminal liability.

Lotteries: State-authorized lotteries represent one of few legal gambling forms. The Law on Lotteries governs lottery organization and conduct, with licensing restricted to legal entities registered in Azerbaijan meeting strict financial and operational criteria.

Online Gambling Framework

Digital Gaming Regulations: Online casino gambling is explicitly banned in Azerbaijan. No licenses are available for online casino operations within the country. The Ministry of Finance maintains strict prohibition against digital casino platforms targeting Azerbaijani residents.

International online casinos operate in a regulatory gray area. While not licensed locally, enforcement against international operators and players remains inconsistent. However, authorities actively restrict access to unauthorized gambling websites, and facilitating such access is punishable by law.

Sports Betting Online: Online sports betting exists in limited form through state-approved operators. Licensing is extremely restrictive, with the government maintaining tight control through designated platforms. All online gambling operators must obtain Ministry of Finance licensing to operate within legal boundaries.

Regulatory Enforcement: Recent crackdowns intensified against online casino advertisements on social networks. Lawyer Alimamed Nuriev emphasized that virtual gambling involving fraud is illegal, with participants facing long-term imprisonment and substantial fines for fraudulent virtual gambling schemes.

Licensed Operators and Market Players

Sports Betting Operators: Topaz operates as the largest state-sponsored sports betting platform in Azerbaijan, enjoying government backing and sponsoring the Azerbaijan Premier League. The market remains highly concentrated with minimal competition due to restrictive licensing.

Lottery Operators: State-approved lottery organizers hold exclusive licenses granted by the Ministry of Finance. Market participation is limited to entities with significant capital reserves, clean legal records, and demonstrated operational capability under strict government oversight.

International Operators: No international casino operators currently hold legal licenses for Azerbaijan. International online casinos serve Azerbaijani players from offshore jurisdictions without local authorization, operating outside the regulatory framework and at legal risk.

Artificial Island Casino Projects: As of October 2025, no casinos have opened on artificial islands despite the July 2025 legal authorization. The Sea Breeze entertainment complex project represents the most prominent announced development, though timelines remain uncertain and infrastructure unbuilt.

Licensing Framework and Requirements

Regulatory Authority Structure

Ministry of Finance: The Ministry of Finance serves as the primary regulatory body for all gambling activities in Azerbaijan. It issues licenses, enforces compliance, implements regulatory amendments, and oversees operations for lotteries, sports betting, and the new artificial island casino framework.

State Tax Office: The State Tax Office of Azerbaijan works alongside the Ministry of Finance to collect gambling revenues and ensure proper tax compliance. Both agencies coordinate to maintain industry oversight and prevent unauthorized activities.

Contact Information: Licensing applications and inquiries must be directed to the Ministry of Finance of the Republic of Azerbaijan, located in Baku. Specific contact protocols for artificial island casino licensing have not been publicly disclosed as the framework remains nascent.

Application Process and Eligibility

Lottery License Requirements: Lottery licenses are granted exclusively to legal entities registered in Azerbaijan meeting strict financial and operational criteria. Entities or individuals with criminal records or previous gambling law violations are generally ineligible for licensing consideration.

Applicants must demonstrate sufficient capital reserves to cover operational costs and player payouts. Additional financial guarantees or bonds may be required to ensure compliance and protect player funds throughout operations.

Sports Betting License: Sports betting licenses follow similar strict eligibility requirements under the Law on Physical Education and Sports. Licensing is limited, with preference given to state-affiliated entities or those with strong government connections.

Artificial Island Casino License: The new artificial island casino licensing framework requires annual fees of 340,000 AZN ($200,000). Detailed application procedures, eligibility criteria, financial requirements, and operational standards have not been fully published as of October 2025.

Background Checks and Timelines: All gambling license applications undergo rigorous background checks covering financial history, criminal records, business integrity, and operational capability. Processing timelines vary but typically extend several months to over a year depending on complexity.

Financial Requirements and Guarantees

License Fees: Artificial island casino licenses cost 340,000 AZN annually (approximately $200,000 at 1.70 AZN/USD exchange rate). Lottery and sports betting licenses involve separate fee structures set by the Ministry of Finance and not publicly disclosed.

Minimum Capital Requirements: Lottery operators must demonstrate substantial capital reserves sufficient to cover operational expenses and guarantee player payouts. Specific minimum amounts vary by operation scale and are determined during the licensing evaluation process.

Financial Guarantees: Operators must provide financial bonds or bank guarantees to secure license approval. These instruments protect player funds and ensure regulatory compliance throughout the license term, with amounts determined by the Ministry of Finance.

Local Presence and Operational Requirements

Physical Presence Mandates: All licensed gambling operators must establish legal entities registered in Azerbaijan. Lottery licenses are explicitly restricted to Azerbaijani-registered legal entities meeting operational and financial criteria set by regulatory authorities.

Artificial Island Operations: Casino operations on artificial islands must comply with specific territorial requirements. Casinos can operate only on designated artificial land plots in the Azerbaijani Caspian Sea sector, with operations prohibited elsewhere in the country.

Foreign Ownership Restrictions: Detailed foreign ownership limitations for artificial island casinos have not been published. Traditional Azerbaijani business regulations typically impose restrictions on foreign ownership in strategic sectors, suggesting similar constraints may apply to gambling.

Domain and Hosting: Online gambling operators serving Azerbaijan typically require local server presence or partnerships with approved technology providers. Specific technical requirements for state-approved sports betting platforms are determined by regulatory authorities on case-by-case basis.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification: Strict identification checks are implemented to prevent underage gambling and ensure regulatory compliance. The minimum legal gambling age in Azerbaijan is 18 years, with operators required to verify age before allowing participation.

Know Your Customer (KYC): All licensed operators must implement rigorous KYC procedures adhering to strict anti-money laundering and counter-terrorism financing regulations. Player identity verification is mandatory before account activation or transaction processing.

Responsible Gambling Measures: Operators must implement player protection mechanisms including self-exclusion systems and responsible gambling tools. The specific requirements vary by license type, with state-approved operators subject to Ministry of Finance oversight and enforcement.

Self-Exclusion Systems: Licensed operators must provide mechanisms allowing players to voluntarily exclude themselves from gambling activities. Self-exclusion duration options and implementation procedures are determined by regulatory guidelines established by the Ministry of Finance.

Financial Monitoring and Reporting

Anti-Money Laundering (AML): Strict adherence to AML and counter-terrorism financing regulations is mandatory for all licensed gambling operators. The Law on Prevention of Legalization of Criminally Obtained Funds governs financial monitoring requirements.

Transaction Monitoring: Operators must implement systems monitoring transactions for suspicious activity. Large transactions, unusual patterns, and high-risk behaviors require enhanced scrutiny and reporting to relevant authorities per AML regulations.

Reporting Obligations: Regular reporting to the Ministry of Finance on operations, financial performance, and compliance status is required for all licensed operators. Reporting frequency and specific requirements vary by license type and operational scale.

Audit and Inspection: The Ministry of Finance conducts periodic audits and inspections of licensed operators to ensure ongoing compliance with licensing conditions, financial requirements, player protection standards, and operational regulations.

Taxation Structure and Financial Obligations

Player Taxation

Winnings Tax: Tax treatment of player gambling winnings in Azerbaijan has not been comprehensively published. Based on regional norms, winnings may be subject to personal income tax above certain thresholds, though specific rates and exemption levels remain unclear.

Withholding Procedures: Licensed operators may be required to withhold taxes on player winnings above specified amounts. Implementation details for the new artificial island casino framework have not been published as of October 2025.

Player Obligations: Players may have declaration requirements for substantial gambling winnings under Azerbaijan’s personal income tax framework. Tax residency rules and international tax treaties affect obligations for foreign nationals gambling in Azerbaijan.

Operator Taxation

Gambling-Specific Taxes: The specific gross gaming revenue (GGR) tax rates, net gaming revenue (NGR) considerations, and turnover taxes for artificial island casinos have not been published. The Ministry of Finance will establish taxation frameworks as operators launch.

Annual License Fees: Artificial island casino operators pay 340,000 AZN ($200,000) annually in license fees. This represents a fixed operational cost separate from revenue-based taxation that may be implemented.

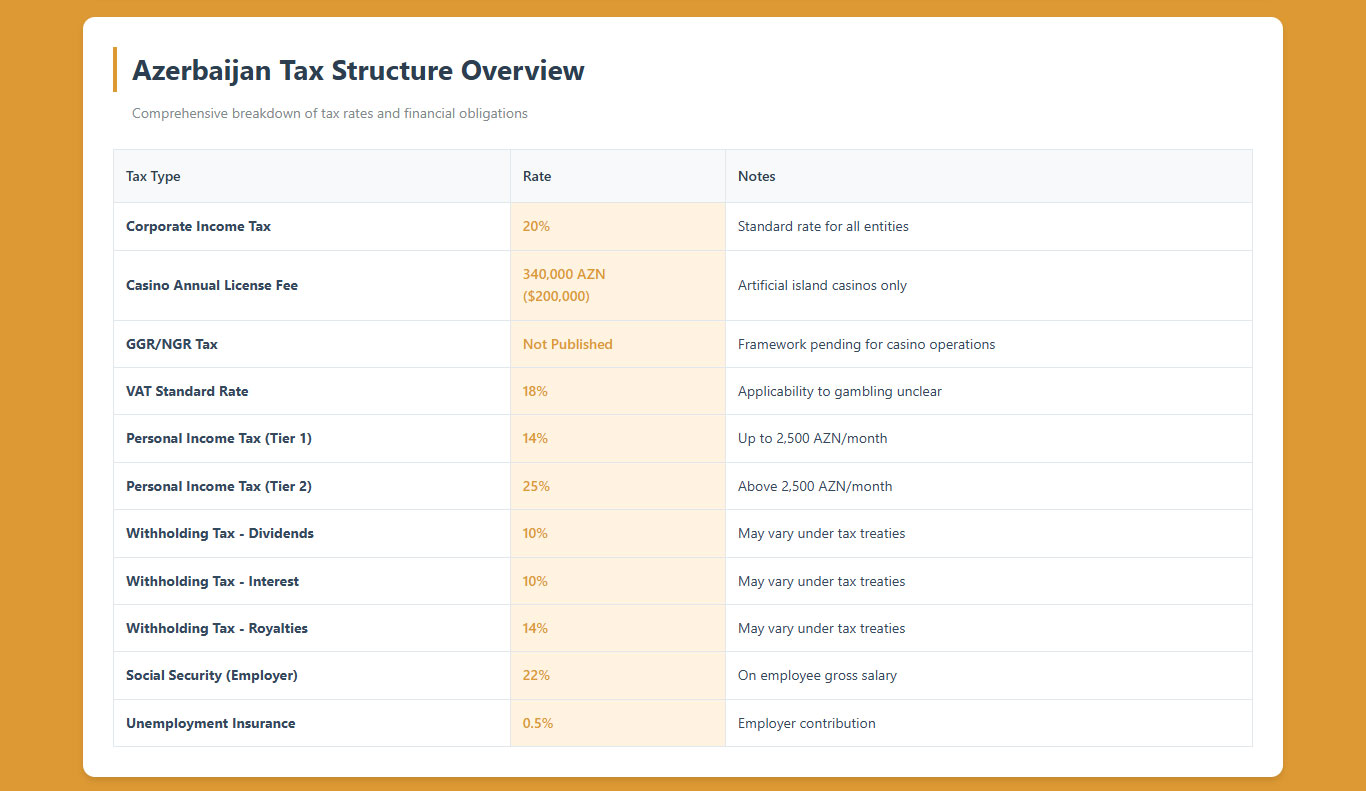

Corporate Income Tax: All Azerbaijani entities, including gambling operators, are subject to standard corporate income tax at 20 percent of taxable profits. Special economic zones may offer reduced rates or tax holidays for qualifying investments.

Value Added Tax (VAT): Azerbaijan applies VAT to most goods and services. The standard VAT rate and its applicability to gambling services have not been clearly defined for the new artificial island casino operations.

| Tax Type | Rate | Notes |

|---|---|---|

| Corporate Income Tax | 20% | Standard rate for all entities |

| Casino Annual License Fee | 340,000 AZN ($200,000) | Artificial island casinos only |

| GGR/NGR Tax | Not Published | Framework pending for casino operations |

| VAT Standard Rate | 18% | Applicability to gambling unclear |

| Withholding Tax – Dividends | 10% | May vary under tax treaties |

| Withholding Tax – Interest | 10% | May vary under tax treaties |

| Social Security (Employer) | 22-25% | On employee salaries |

Gambling Market Financial Performance

Market Size: Comprehensive data on Azerbaijan’s total gambling market size is not publicly available due to the sector’s restricted nature. The legal market consists primarily of state lottery sales and limited sports betting through approved platforms.

Gray Market Activity: Significant gambling activity occurs through international online platforms operating without local licenses. Azerbaijani citizens access offshore casino and betting sites, with market size estimates difficult to quantify due to the informal nature.

Capital Flight: Lawmakers cited substantial funds leaving Azerbaijan as citizens travel abroad to gamble or use foreign online platforms. The artificial island casino legislation aims to retain this spending domestically and generate tax revenues.

Projected Growth: The artificial island casino framework could generate significant tax revenues once operational, though projections remain speculative. Initial projects like the Sea Breeze complex have not disclosed investment amounts or expected revenues.

Advertising and Marketing Restrictions

Permitted Advertising Channels

State-Approved Gambling Only: Advertising and promotion are strictly forbidden for unauthorized gambling activities. Only state-approved gambling products including official lotteries and regulated sports betting may be advertised under government oversight.

Marketing Channel Restrictions: Specific regulations governing television, radio, online, outdoor, and print advertising for legal gambling products are enforced by the Ministry of Finance. All marketing materials must not target minors or vulnerable groups.

Online Advertising Crackdown: Recent enforcement actions intensified against online casino advertisements on social networks. Authorities monitor social media platforms and take legal action against entities promoting illegal gambling services to Azerbaijani residents.

Content and Promotional Restrictions

Misleading Advertising Prohibition: All gambling advertising must avoid misleading or aggressive content. Marketing materials undergo government scrutiny to prevent false claims about winning probabilities, payout rates, or guaranteed returns.

Minor Protection: Gambling advertisements must not appeal to minors or feature content attractive to underage audiences. Placement restrictions prevent gambling promotions during children’s programming or in media targeting youth demographics.

Bonus and Promotion Limits: Specific restrictions on bonus offers, wagering requirements, and promotional incentives have not been published for artificial island casinos. State-approved sports betting operators face limitations on promotional activities.

Recent Regulatory Changes and Their Impact

2021-2022 Legislative Amendments

Law on Amendments to Lotteries: The Amendment Law was adopted December 27, 2021, entering force January 1, 2022. This legislation introduced updated provisions and penalties for violations while clarifying legal boundaries for lottery operations.

Connected amendments modified laws on Telecommunications, Prevention of Money Laundering, Information Protection, Advertising, Physical Education and Sports, and the Tax Code. Telecommunication operators gained authority to block access to illegal gambling sites.

Gambling Definition Expansion: The amendments defined gambling games as lotteries, sports betting, and other betting games involving distribution of winnings based on uncertainty or coincidence, except for approved lotteries and sports betting conducted per specific laws.

Tax Code Changes: Significant Tax Code amendments effective January 1, 2022, addressed tax evasion prevention, provided certain exemptions, broadened tax burdens, and introduced new concepts affecting the gambling sector’s financial obligations.

2024-2025 Major Reforms

Artificial Land Plots Law: On May 7, 2024, Azerbaijan adopted the Law on Creation of Artificial Land Plots in the Azerbaijani Sector of the Caspian Sea, defining legal and organizational frameworks for artificial territories including construction rights.

Casino Legalization (July 2025): Parliament passed legislation in third reading permitting casino establishment on artificial islands. This marked the most significant gambling liberalization since the 1998 ban, creating new market entry possibilities.

The July 2025 law establishes regulations for business activity on artificial islands, creating conditions for investment and entrepreneurship promotion. Casinos outside artificial islands remain prohibited, maintaining the mainland ban.

Operator Impact: The regulatory change creates potential market entry opportunities for casino operators willing to invest in artificial island infrastructure. However, operational timelines remain uncertain as physical infrastructure development has not commenced at scale.

Enforcement Mechanisms and Penalties

Violation Penalties and Sanctions

Criminal Liability: Article 244-1 of the Criminal Code criminalizes unauthorized organization and conduct of gambling activities. Violators face significant administrative fines and potential criminal prosecution including imprisonment.

Fraud-Related Gambling: Virtual gambling involving fraud carries particularly severe penalties. Offenders face long-term imprisonment and substantial fines, as emphasized by legal authorities during recent enforcement campaigns against fraudulent gambling schemes.

License Violations: Operating without proper licensing or violating license conditions results in administrative fines, license suspension, or permanent revocation. The Ministry of Finance enforces compliance through regular inspections and investigations.

Enforcement Actions and Trends

Website Blocking: Access to unauthorized gambling websites is actively restricted through ISP-level blocking. Telecommunication operators must implement measures preventing organization and operation of gambling through telecommunications services and blocking access to foreign platforms.

Payment Processor Restrictions: Financial institutions face requirements preventing transaction processing for illegal gambling activities. Banks and payment providers must implement controls blocking transfers to unlicensed gambling operators.

Recent Enforcement: Intensified crackdowns occurred against online casino social media advertising, particularly targeting potentially fraudulent operations. Authorities pursue both operators and facilitators of illegal gambling access.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

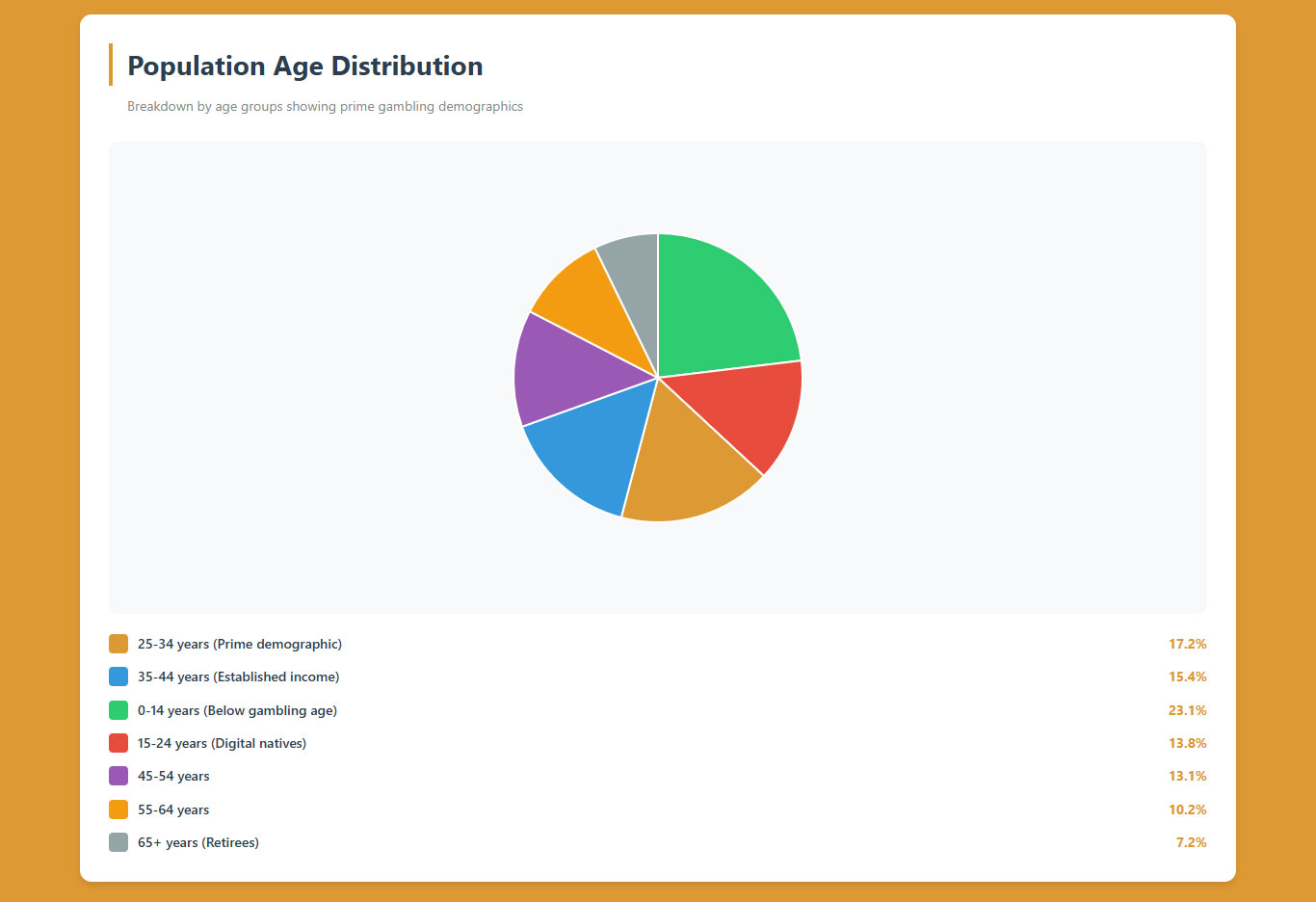

Azerbaijan’s population stands at 10.4 million as of 2025, representing modest growth of 0.6 percent year-over-year. The country ranks 94th globally by population size, accounting for 0.13 percent of total world population.

The median age is 33.6 years, indicating a relatively young and economically active demographic profile favorable for digital services adoption. This positions Azerbaijan younger than most European nations but older than many developing Asian markets.

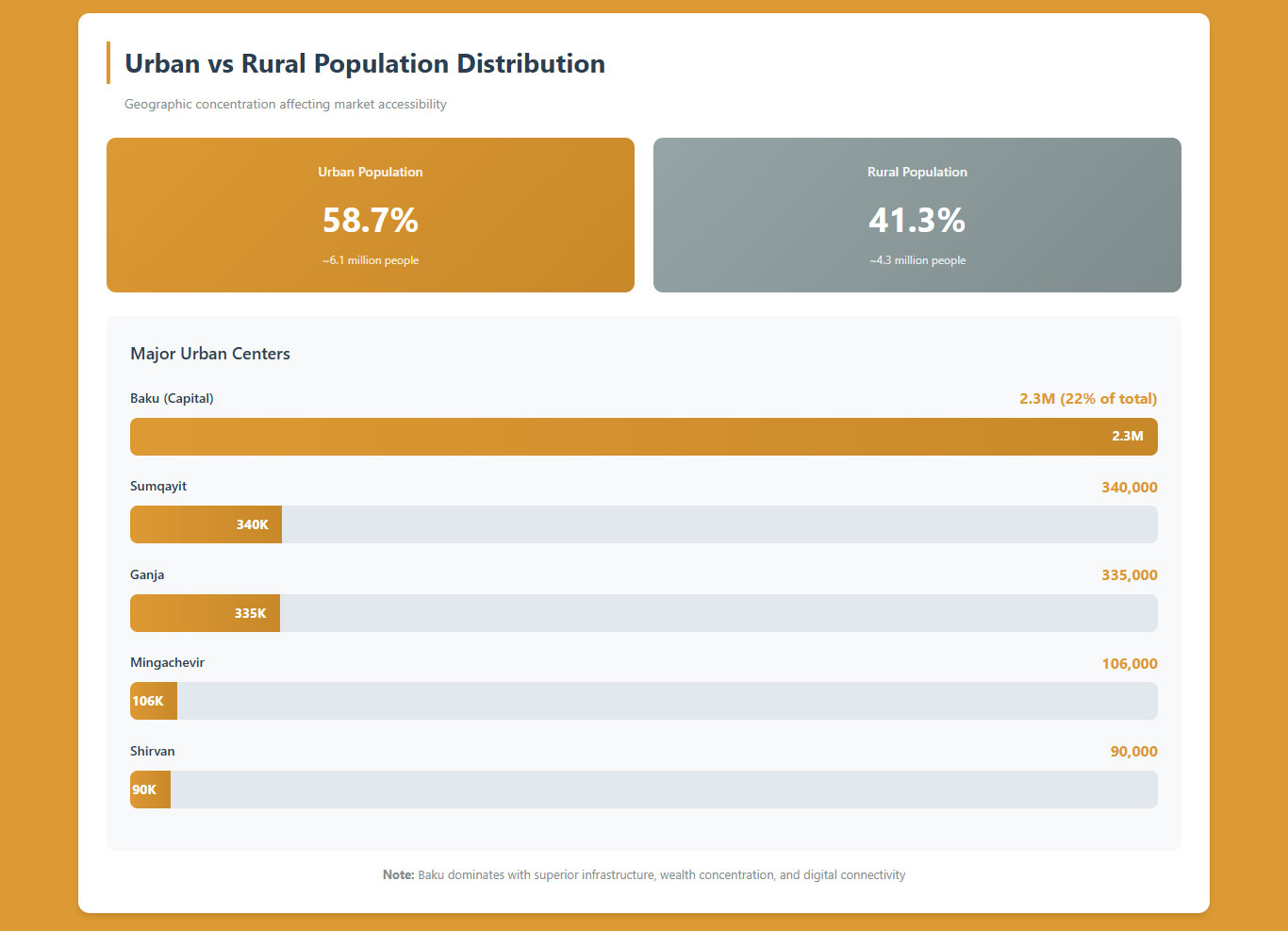

The urban-rural split shows 58.7 percent of the population residing in urban areas while 41.3 percent live in rural regions. Urban concentration facilitates digital infrastructure deployment and gambling market accessibility, though rural penetration remains substantial.

| Age Group | Percentage of Population | Characteristics |

|---|---|---|

| 0-14 years | 23.1% | Below gambling age; future market potential |

| 15-24 years | 13.8% | Digital natives; high mobile adoption |

| 25-34 years | 17.2% | Prime gambling demographic; peak earning years |

| 35-44 years | 15.4% | Established income; family responsibilities |

| 45-54 years | 13.1% | Higher disposable income; stability-focused |

| 55-64 years | 10.2% | Pre-retirement; conservative spending |

| 65+ years | 7.2% | Retirees; limited gambling participation |

The dependency ratio shows that the working-age population (15-64 years) must support a relatively modest dependent population. Child dependency stands at 33 percent while aged dependency reaches only 9.2 percent, indicating low pressure on productive population.

Annual population growth of 150,097 people is projected for 2025, driven by natural increase of 153,774 births exceeding deaths, partially offset by net emigration of 3,677 individuals. Migration patterns reveal more people leaving than arriving.

Literacy rates reach 99.8 percent among adults aged 15 and above, with male literacy at 99.9 percent and female literacy at 99.7 percent. This high educational foundation supports digital services adoption and online platform usage.

Geographic Distribution

Baku – Capital City: Baku dominates as the political, economic, and cultural center, housing approximately 2.3 million residents or roughly 22 percent of the national population. The capital concentrates wealth, infrastructure, and digital connectivity significantly above national averages.

Major Urban Centers: Secondary cities include Ganja (population approximately 335,000), Sumqayit (340,000), Mingachevir (106,000), and Shirvan (90,000). These urban centers provide regional economic hubs with developing infrastructure and growing middle-class populations.

Regional Economic Differences: Stark disparities exist between Baku and regions. Oil wealth concentrates in the capital while rural areas and secondary cities remain significantly underdeveloped. This creates bifurcated market conditions affecting consumer spending power.

Internet Access Patterns: Urban areas, particularly Baku, enjoy superior internet infrastructure with higher speeds and broader coverage. Rural connectivity has improved but remains limited compared to cities, affecting digital service accessibility.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Azerbaijan’s total GDP reached $74.32 billion in 2024, reflecting the country’s substantial but narrowly-based economic foundation. The economy remains heavily dependent on oil and gas, which constitute two-thirds of GDP and 90 percent of export revenues.

GDP per capita stands at $7,284 to $7,458 depending on calculation methodology, positioning Azerbaijan as an upper-middle-income country by World Bank classifications. However, this figure masks significant wealth concentration and regional disparities.

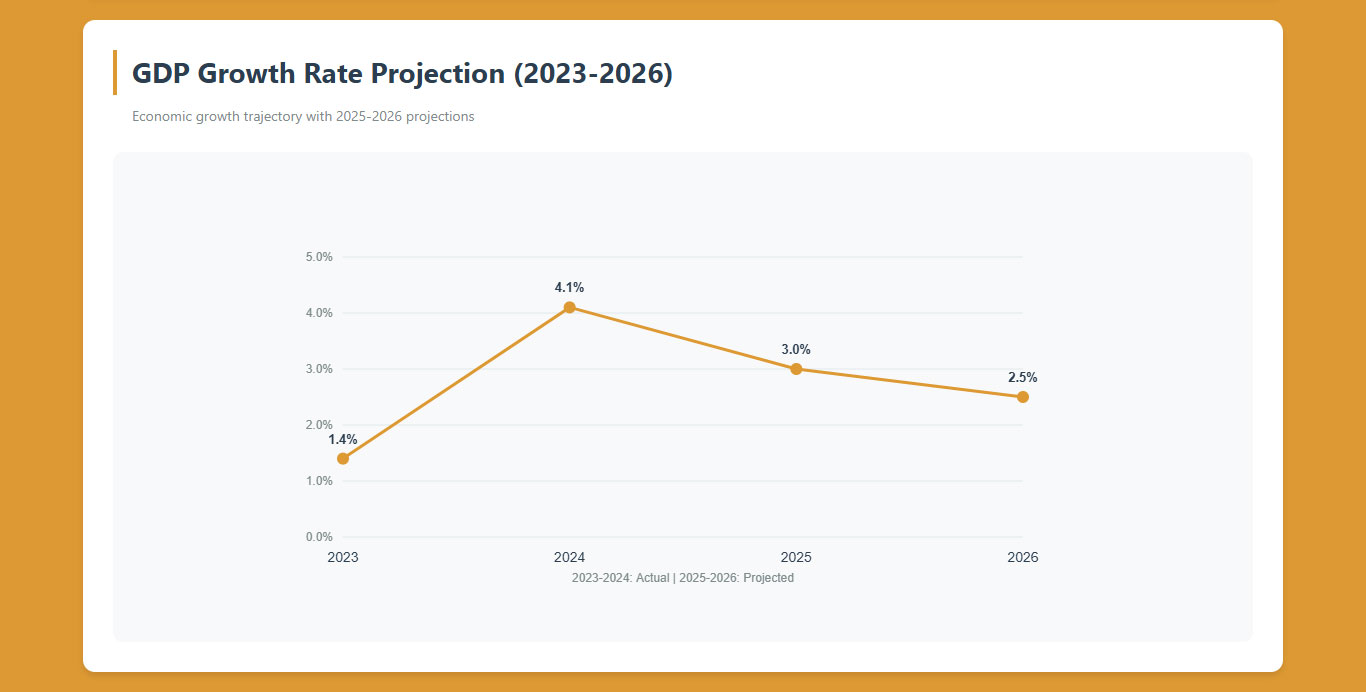

Economic growth reached 4.1 percent in 2024, driven primarily by non-oil sector expansion of 6.2 percent. The non-oil economy benefited from construction, ICT, transportation, and tourism growth supported by rising real incomes and infrastructure investment.

Growth projections for 2025 moderate to 3 percent with further slowdown to 2.5 percent expected in 2026. This deceleration reflects oil sector constraints, global commodity price sensitivity, and structural economic challenges beyond petroleum dependence.

| Indicator | 2023 | 2024 | 2025 Projection |

|---|---|---|---|

| Real GDP Growth | 1.4% | 4.1% | 3.0% |

| Non-Oil GDP Growth | 3.7% | 6.2% | 5.0% (est.) |

| GDP (Billion USD) | $72.5 | $74.32 | $77.0 (est.) |

| GDP Per Capita (USD) | $7,133 | $7,284 | $7,458 |

| Inflation Rate (Annual) | 8.8% | 4.9% | 4.5% (est.) |

| Unemployment Rate | 6.0% | 5.8% (est.) | 5.5% (est.) |

The petroleum sector dominance creates economic volatility tied to global oil prices. Oil and gas generate 60 percent of state finances, making government budgets and public spending highly sensitive to energy market fluctuations.

Average monthly nominal salary reached 1,098 AZN ($646) for January-July 2025, representing gradual improvement but remaining modest by international standards. Salary levels vary dramatically between oil sector workers and other industries.

Inflation moderated to 4.9 percent in August 2025 compared to the previous year, down from higher rates in 2023. Consumer price stability improves purchasing power but remains a concern for fixed-income households.

Income and Wealth Distribution

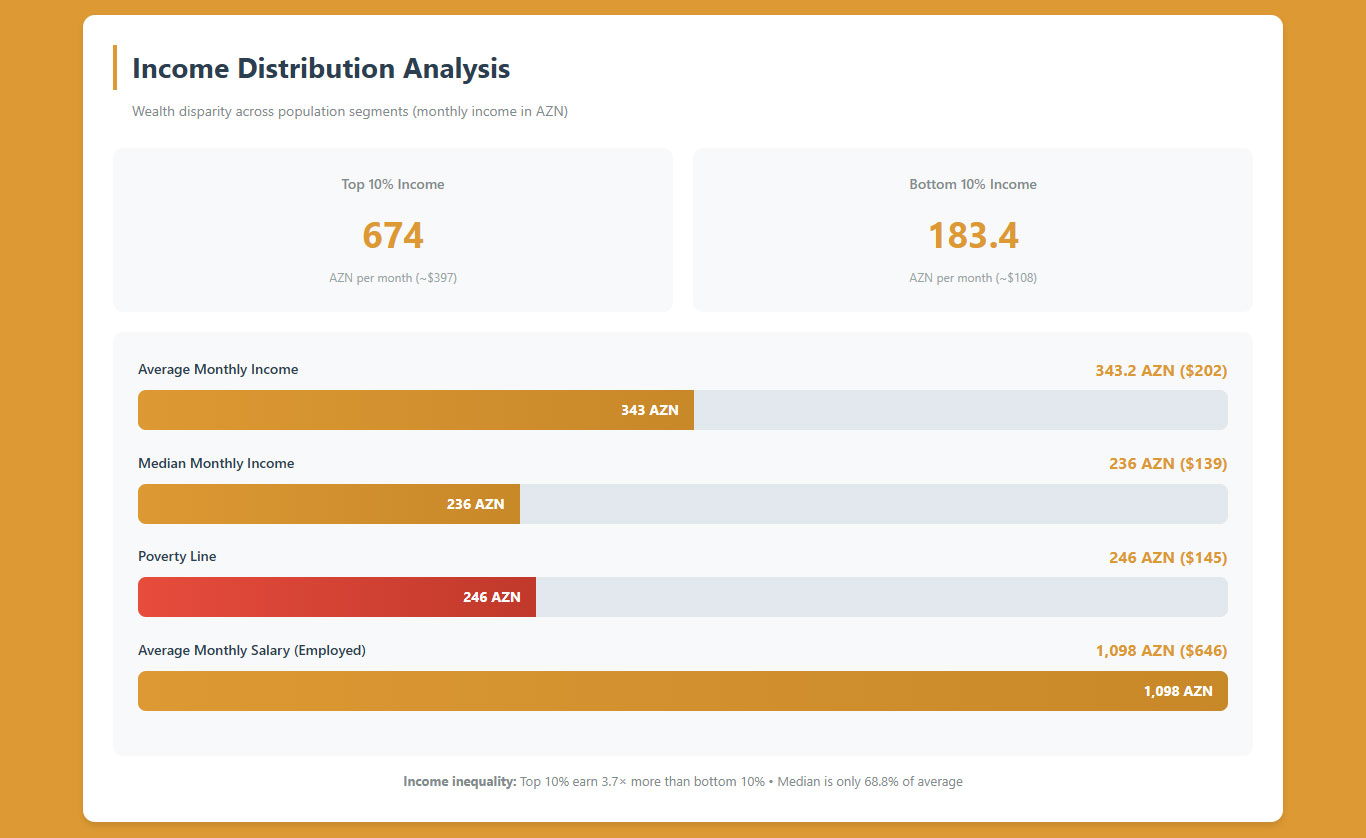

Average per capita monthly income stands at 343.2 AZN (approximately $200) according to official statistics, though independent researchers question this figure’s accuracy. Urban incomes exceed rural incomes by 7.5 percent, reflecting regional economic disparities.

The official poverty line (minimum subsistence level) is set at 246 AZN per person monthly. Average income sits only 28 percent above this threshold, indicating limited financial cushion for the typical citizen.

Median income calculations by the Baku Research Institute reveal significant inequality. The median monthly income equals approximately 68.8 percent of the average income, suggesting wealth concentration among higher earners skewing average figures upward.

Income distribution analysis shows the top 10 percent of earners command 674 AZN monthly while the bottom 10 percent struggle with 183.4 AZN monthly. This 3.7-fold disparity illustrates substantial income inequality within Azerbaijan’s population.

| Income Metric | Amount (AZN) | Amount (USD) | Notes |

|---|---|---|---|

| Average Monthly Income | 343.2 | $202 | Official statistics; reliability questioned |

| Median Monthly Income | 236 (est.) | $139 | 68.8% of average; BRI calculation |

| Poverty Line | 246 | $145 | Minimum subsistence level |

| Average Monthly Salary | 1,098 | $646 | Employed workers only |

| Top 10% Income | 674 | $397 | Per month |

| Bottom 10% Income | 183.4 | $108 | Per month |

Wealth concentration among ruling elites represents a defining economic characteristic. Oil revenues have enriched government-connected individuals while the broader population experiences limited prosperity gains despite official poverty reduction claims.

Leading economist Rovshan Aghayev states government poverty reduction claims remain unsubstantiated as Azerbaijan fails to provide transparent statistical data necessary to measure real income inequality and living standards accurately.

Transparency issues plague income statistics. Azerbaijan does not disclose income distribution by quintiles or deciles, share received by population groups, P80/20 and P90/10 ratios, poverty depth index, or chronic poverty assessments.

Remittances from abroad contribute to household incomes. Central Bank balance of payments data shows 2.8 billion AZN ($1.66 billion) in cash remittances during 2023, averaging 277 AZN per person annually or 23 AZN monthly.

Market Size and Growth Projections

Current iGaming Market Status: No legal regulated online iGaming market exists in Azerbaijan. The market consists exclusively of illegal gray market activity through international platforms and limited legal sports betting through state-approved operators.

Gray Market Estimates: Quantifying gray market size proves challenging due to the informal nature of offshore casino and betting participation. Azerbaijani citizens access international sites without regulatory oversight, with spending difficult to track systematically.

Sports Betting Market: The legal sports betting market remains small and concentrated around state-sponsored operators like Topaz. Market size data is not publicly disclosed, suggesting modest revenues under tight government control.

Artificial Island Casino Projections: Future market size depends entirely on artificial island casino development success. Annual license fees of $200,000 suggest operators anticipate substantial revenues to justify investment, though projections remain speculative.

Regional Comparison: Compared to neighboring Georgia (population 3.8 million with legal online gambling) and Turkey (population 85 million with strict prohibitions), Azerbaijan’s restrictive framework limits market development despite reasonable population size.

Long-Term Growth Potential: If Azerbaijan liberalizes online gambling regulations, market potential exists given 89 percent internet penetration, 91 percent cashless payment adoption, and young demographic profile. However, regulatory trajectory remains highly uncertain.

Education, Skills, and Digital Literacy

Educational Foundation

Azerbaijan maintains near-universal literacy with 99.8 percent of adults aged 15 and above able to read and write. This strong educational foundation supports digital technology adoption and online platform usage across age groups.

Educational attainment levels show substantial completion rates for primary and secondary education. The State Strategy on Development of Education prioritizes educational advancement as part of national development policy.

Digital literacy remains concentrated in urban areas and younger demographics. Baku residents and individuals under 40 demonstrate significantly higher comfort with digital technologies compared to rural and older populations.

English language proficiency is limited outside business and educated urban circles. Most Azerbaijanis communicate primarily in Azerbaijani with Russian as secondary language, requiring localization for consumer-facing services.

Cultural and Social Factors

Communication and Language

Primary Languages: Azerbaijani (Turkic language family) serves as the official state language and primary communication medium for 92 percent of the population. Russian remains widely spoken, particularly among older generations and in business contexts.

Internet Language Preferences: Online content in Azerbaijani is preferred by consumers, though Russian-language content reaches substantial audiences. English content has limited reach outside educated urban demographics and international business sectors.

Localization Requirements: Gambling operators must provide Azerbaijani-language interfaces, customer support, and promotional materials to effectively reach mainstream consumers. Russian language support extends market reach to older demographics.

Religious and Cultural Attitudes

Religious Composition: Approximately 95 percent of Azerbaijan’s population identifies as Muslim, with 85 percent Shia and 15 percent Sunni. Azerbaijan has the second-highest Shia population percentage globally after Iran.

Gambling Religious Perspective: Islamic teachings generally prohibit gambling, creating cultural resistance to gambling activities. However, Azerbaijan’s secular governance and Soviet legacy result in less strict religious adherence compared to Middle Eastern nations.

Social Gambling Acceptance: Despite religious prohibitions, gambling participation exists through offshore platforms and cross-border travel. The government’s artificial island casino authorization signals pragmatic economic prioritization over religious considerations.

Foreign Brand Perception: International brands often face trust barriers requiring substantial marketing investment and local partnerships. State connections and government endorsement significantly influence consumer confidence in service providers.

Problem Gambling and Social Considerations

Problem Gambling Data: Comprehensive statistics on gambling addiction prevalence in Azerbaijan are not publicly available. The 27-year gambling ban limited research into problem gambling rates, though offshore platform usage suggests participation exists.

Social Responsibility Framework: As artificial island casino regulations develop, problem gambling prevention requirements remain undefined. International operators should anticipate mandatory responsible gambling measures including self-exclusion systems and player protection tools.

Treatment Infrastructure: Dedicated gambling addiction treatment facilities are limited or non-existent given the historical gambling prohibition. As legal gambling emerges, treatment infrastructure may require development.

At-Risk Populations: Without research data, specific at-risk demographic identification proves challenging. Traditional patterns suggest young males represent higher-risk groups for problem gambling behaviors.

Political Structure and Governance

Government System and Stability

Azerbaijan operates as a presidential republic under the Aliyev family regime. President Ilham Aliyev succeeded his father Heydar Aliyev in 2003, maintaining authoritarian control over political, economic, and social spheres.

Political stability remains high from an investment continuity perspective, though achieved through authoritarian governance rather than democratic institutions. The regime maintains tight control over media, opposition, and civil society.

Corruption perception indexes rank Azerbaijan poorly, with endemic corruption characterizing government operations and business environments. Transparency International and similar organizations consistently highlight corruption concerns.

Oil wealth has significantly strengthened regime stability and enabled lavish international event hosting. The government uses petroleum revenues for political consolidation and international lobbying rather than broad economic development.

International Relations and Trade

Regional Positioning: Azerbaijan maintains complex relationships with neighboring countries including Russia, Iran, Turkey, Georgia, and Armenia. Recent conflict resolution with Armenia over Nagorno-Karabakh reshapes regional dynamics.

European Engagement: Azerbaijan is not an EU member but maintains Council of Europe membership and OSCE participation. The country serves as an energy supplier to Europe, particularly following Russia-Ukraine tensions.

Trade Corridors: Azerbaijan’s position along the Middle Corridor connecting China to Europe creates opportunities for transport and logistics sectors. Peace-building efforts may unlock new trade routes and investment flows.

Investment Climate: Foreign direct investment focuses heavily on petroleum sector. Non-oil sector foreign investment faces bureaucratic obstacles, corruption, and political favoritism affecting business predictability.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at 89 percent of the population, representing 9.23 million users as of January 2025. This high penetration rate increased by 57,000 users (0.6 percent) between January 2024 and January 2025.

Mobile internet dominates connectivity with 71.4 percent of total web traffic occurring via mobile devices. Desktop accounts for 27.3 percent while tablet usage remains minimal at 1.3 percent.

Daily internet usage averages are not precisely published but mobile-first behavior suggests substantial time spent online, particularly among younger demographics. Social media engagement reaches 6.73 million users (64.9 percent of population).

Social media user growth exploded by 87.6 percent from January 2023 to January 2024, though this dramatic increase may reflect measurement methodology changes rather than purely organic growth.

| Metric | Value | Penetration Rate |

|---|---|---|

| Internet Users | 9.23 million | 89.0% |

| Mobile Connections | 12.2 million | 118% |

| Social Media Users | 6.73 million | 64.9% |

| Mobile Web Traffic | 71.4% | Of total traffic |

| Fixed Broadband Subscribers | 2.15 million | 20.7% |

| Smartphone Adoption | High | Android 81.3%, iOS 18.1% |

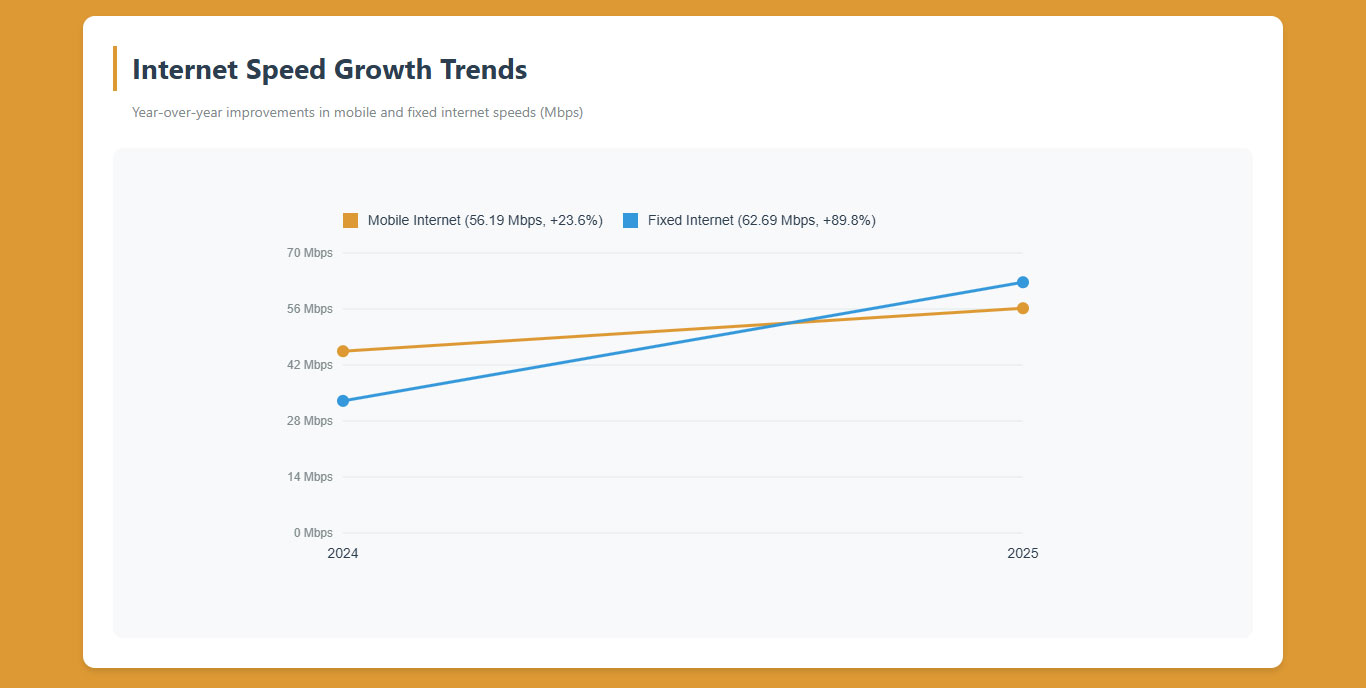

Internet speeds have improved dramatically. Median mobile internet download speed reached 56.19 Mbps, increasing 23.6 percent year-over-year. Fixed internet download speed hit 62.69 Mbps, surging 89.8 percent annually.

E-commerce participation is growing with increasing consumer trust in online transactions. Digital services consumption expands across payment, shopping, entertainment, and communication categories as infrastructure improves.

Digital Payment Behavior

Cashless payment adoption reached 91 percent of all transactions as of early 2025, representing dramatic transformation from cash-dominated economy. Nine out of ten payment card transactions now occur without physical currency.

Bank card transactions totaled 126 billion AZN ($74.1 billion) in 2024, growing 27 percent from 2023. Domestic cashless transactions increased 67 percent by volume and 91 percent by transaction count in the first four months of 2025.

The number of bank cards increased 17 percent year-over-year to 20.7 million in early 2025. This exceeds two cards per capita, indicating multiple card ownership and active participation in electronic payment systems.

Mobile wallet adoption is expanding with twelve licensed providers operating in Azerbaijan. Popular services include Apple Pay, Google Pay, PashaPay, GoldenPay, and TURAN e-wallet, offering contactless and instant payment solutions.

| Payment Method | Market Share | Notes |

|---|---|---|

| Mobile Payments | 58% | Dominant method; rapid growth |

| Credit Cards | 27% | Traditional but declining share |

| E-Wallets | 11% | Growing adoption; multiple providers |

| Bank Transfer | 1% | Direct transfers; limited for retail |

| Prepaid Cards | 1% | Minimal usage |

| Cash | 9% | Declining rapidly; 91% cashless adoption |

Popular digital wallets include international options like PayPal, Skrill, and WebMoney alongside local providers. AniPay, the Central Bank-launched instant payment system, facilitates rapid transfers and QR code payments.

Cryptocurrency awareness exists but regulatory status and adoption for gambling purposes remain unclear. Azerbaijan has not established comprehensive cryptocurrency frameworks affecting potential gambling payment integration.

Gaming and Gambling Preferences

Current Participation Rates: Precise gambling participation statistics are unavailable due to prohibition and gray market nature. However, lawmakers cited significant citizens gambling abroad or via online platforms as justification for artificial island casino legalization.

Sports Betting Popularity: Sports betting through state-approved operators represents the most accessible legal gambling form. Football (soccer) dominates betting interest given Azerbaijan Premier League and international competition following.

Casino Game Preferences: With no legal land-based casinos for 27 years, preferences remain based on offshore platform usage. International casino sites serving Azerbaijanis likely reveal preferences for slots, roulette, and blackjack.

Mobile vs Desktop Preference: Given 71.4 percent mobile web traffic dominance, gambling participation would likely skew heavily toward mobile platforms. Desktop usage would occur primarily in office or home settings.

Spending Patterns: Average spending per gambling participant cannot be quantified without market data. However, modest median incomes ($139 monthly) suggest recreational gambling at low stakes predominates over high-roller activity.

Seasonal Trends: Football season drives sports betting activity with peak interest during European championships and World Cup events. Holiday periods and major cultural celebrations may influence casino gaming participation.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Azerbaijan’s internet infrastructure has undergone rapid modernization, achieving 89 percent population penetration representing 9.23 million users. This positions the country among regional leaders in connectivity, surpassing many neighboring nations in digital access.

Fixed broadband subscriptions reached 2.15 million in 2023, representing approximately 20.7 percent household penetration. While lower than mobile internet adoption, fixed broadband provides stable high-speed connectivity for urban households and businesses.

Average internet speeds have improved dramatically year-over-year. Median mobile internet download speed reached 56.19 Mbps in January 2025, representing a 23.6 percent increase from the previous year and supporting bandwidth-intensive applications.

Fixed internet download speeds hit 62.69 Mbps median, surging 89.8 percent annually. This remarkable improvement reflects infrastructure investments and network upgrades bringing Azerbaijan closer to European connectivity standards.

| Connection Type | Download Speed | Year-over-Year Growth |

|---|---|---|

| Mobile Internet (Median) | 56.19 Mbps | +23.6% |

| Fixed Internet (Median) | 62.69 Mbps | +89.8% |

| Mobile Internet (Average – 2024) | 45.45 Mbps | +31.4% |

| Fixed Internet (Average – 2024) | 33.03 Mbps | +22.3% |

Network reliability and uptime statistics are not comprehensively published but infrastructure quality concentrates in Baku and major urban centers. Rural connectivity has improved but experiences lower speeds and reliability compared to cities.

The government prioritizes ICT sector development as part of economic diversification strategy. The Ministry of Digital Development and Transport spearheads infrastructure investment alongside telecommunications operators expanding coverage and capacity.

Global internet speed rankings position Azerbaijan competitively within the Caucasus region. While not matching Western European speeds, Azerbaijan outperforms many former Soviet republics in network performance and accessibility.

5G and Future Technology Deployment

4G/LTE coverage extends across most populated areas with major operators providing widespread service. Azercell, Bakcell, and Azerfon (operating as Nar Mobile) compete to expand LTE networks reaching rural territories previously underserved.

5G deployment remains in trial phases with commercial rollout delayed. Azercell and Bakcell completed 5G trials but postponed announcing commercial services due to insufficient demand, lack of suitable spectrum allocation, and questions about investment return.

Current LTE network capacity adequately meets demand for high-speed data and broadband services, reducing urgency for 5G deployment. Operators focus on optimizing 4G coverage and capacity rather than rushing 5G introduction.

Future infrastructure plans include gradual 5G rollout as spectrum becomes available and use cases justify investment. The timeline for widespread 5G deployment likely extends several years given market dynamics and infrastructure priorities.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Three mobile network operators dominate Azerbaijan’s telecommunications market. Azercell, the largest operator with over 35 percent market share, leads in subscribers and coverage. State-owned AzTelecom maintains participation in mobile operators.

Bakcell operates as the second-largest provider serving substantial subscriber base across Azerbaijan. Azerfon (Nar Mobile) represents the third operator, granted licensing in 2006 to increase market competition.

Mobile connections total 12.2 million, representing 118 percent population penetration. Multiple SIM card ownership is common, with individuals maintaining separate numbers for personal and business use or leveraging promotional pricing.

Network quality varies by operator and geography. Azercell generally leads in coverage comprehensiveness, while urban areas enjoy competitive service from all three operators. Rural coverage gaps persist despite expansion efforts.

| Operator | Market Share | Technology | Ownership |

|---|---|---|---|

| Azercell | ~35%+ | 2G/3G/4G | Partially state-owned (MCIT 35%) |

| Bakcell | ~30% | 2G/3G/4G | Private |

| Azerfon (Nar) | ~25% | 2G/3G/4G | State telecom participation |

| Catel | Minimal | Legacy | Limited operations |

Data costs remain relatively high compared to regional neighbors, possibly reflecting market consolidation and limited competition. Cost per gigabyte pricing affects consumer data consumption patterns and mobile internet usage intensity.

Mobile payment integration is rapidly advancing with operators supporting contactless payments, mobile wallet services, and value-added financial services. Network infrastructure increasingly enables fintech innovation beyond traditional telecommunications.

Device Penetration and Preferences

Smartphone adoption is high across Azerbaijan with Android dominating at 81.3 percent market share. iOS commands 18.1 percent, indicating Apple’s premium positioning appeals to affluent urban consumers but remains niche.

Device preferences skew toward mid-range Android smartphones balancing functionality with affordability. Samsung, Xiaomi, and Huawei represent popular brands, while iPhone ownership signals status among higher-income demographics.

Average device specifications support modern mobile applications including video streaming, gaming, and resource-intensive apps. Memory, processing power, and screen quality continue improving as consumers upgrade to newer models.

Mobile internet usage dominates with 71.4 percent of total web traffic occurring via mobile devices. This mobile-first behavior requires gambling operators to prioritize mobile-optimized platforms and native app development.

Financial Services and Payment Infrastructure

Banking System Structure

Azerbaijan’s banking sector includes numerous domestic and international banks competing for market share. Major banks include International Bank of Azerbaijan (IBA), Kapital Bank, Pasha Bank, AccessBank, Unibank, TuranBank, and YapiKredi Bank Azerbaijan.

International Bank of Azerbaijan operates as one of the largest institutions with extensive branch networks and digital banking services. Kapital Bank and Pasha Bank aggressively pursue digital transformation and fintech integration.

Digital banking adoption is accelerating with mobile banking apps gaining user acceptance. Banks invest in user-friendly interfaces, instant payments, and integrated financial services responding to consumer demand for convenience.

Account penetration rates have improved but remain below developed economy standards. Banking access concentrates in urban areas with rural populations less likely to maintain formal banking relationships.

Payment Processing Options

Cashless payment infrastructure has transformed dramatically with 91 percent of transactions now occurring electronically. This represents one of the highest cashless adoption rates globally, driven by government policy, infrastructure investment, and consumer behavior change.

Credit and debit cards dominate with Visa and Mastercard representing principal payment schemes. Domestic card brands AzeriCard (owned by International Bank of Azerbaijan) and MilliKart (owned by 17 banks and EBRD) maintain limited presence.

American Express and Diners Club cards are accepted at select merchants, primarily upscale hotels, restaurants, and international businesses. Coverage remains far below Visa and Mastercard acceptance levels.

| Payment Method | Availability | Usage Level |

|---|---|---|

| Visa/Mastercard | Widespread | Very High |

| AzeriCard | Limited | Low |

| MilliKart | Limited | Very Low |

| Mobile Wallets | Growing | High and Increasing |

| Bank Transfers | Universal | Moderate |

| Cryptocurrency | Unclear Legal Status | Low/Unknown |

| PayPal | Available | Moderate |

| Skrill/Neteller | Available | Moderate |

E-wallet options include international services like PayPal, Skrill, WebMoney, and Paysera alongside domestic providers. Twelve licensed mobile wallet providers operate including Apple Pay, Google Pay, PashaPay, GoldenPay, and the upcoming TURAN e-wallet.

Bank transfer systems support instant payments through AZIPS (Azerbaijan Interbank Payment System) for real-time large-value transactions and HÖP for retail payments. AniPay, the Central Bank instant payment system, enables QR code payments and rapid transfers.

Processing fees vary by payment method and provider. Card transaction fees typically range 1.5-3 percent for merchants, while bank transfers and mobile wallets may offer lower costs depending on transaction type.

Transaction processing timelines have accelerated with instant payment systems enabling real-time transfers. Traditional bank transfers complete within one business day domestically, while international transactions follow standard SWIFT timelines.

Cryptocurrency acceptance for gambling remains unclear given ambiguous regulatory status. Azerbaijan has not established comprehensive cryptocurrency frameworks, creating uncertainty about legal usage for iGaming transactions.

Regulatory restrictions on gambling payments are not yet defined for artificial island casinos. Traditional banking regulations may prohibit financial institutions from processing transactions for unlicensed gambling operators.

E-commerce and Digital Economy

Digital Market Development

E-commerce market size is growing with increasing consumer trust in online transactions. Card payment volumes of 126 billion AZN ($74.1 billion) in 2024 reflect substantial digital commerce activity across retail, services, and bill payments.

Domestic e-commerce transactions increased from 80.9 billion AZN in 2022 to 173.3 billion AZN in 2023, representing 114 percent growth. This explosive expansion demonstrates rapid consumer adoption of online shopping and digital services.

POS terminal payments surged 81 percent and e-commerce payments jumped 108 percent year-over-year in 2023. This growth trajectory positions Azerbaijan among the fastest-growing digital payment markets globally.

Popular e-commerce platforms include both international services and domestic marketplaces. Cross-border online shopping is common, with Azerbaijanis purchasing from Turkish, Russian, Chinese, and European retailers.

Consumer trust in online transactions has improved significantly as payment security, delivery reliability, and merchant professionalism advance. However, cash-on-delivery remains popular for consumers cautious about prepayment.

Business Environment and Regulatory Framework

Ease of Business Operations

Azerbaijan ranked 34th globally in the World Bank’s final 2020 Doing Business report, though this ranking was subject to controversy. The country specifically ranked 9th out of 190 countries for ease of starting a business.

It is important to note that the World Bank discontinued the Doing Business Index in 2021 following data manipulation scandals. Azerbaijan’s 2020 score was allegedly artificially lowered by World Bank officials, casting doubt on historical rankings.

The replacement Business Ready (B-READY) index launched in 2024 with initial coverage of 50 countries. Azerbaijan was not included in the first B-READY report, leaving current ease-of-doing-business assessment dependent on other sources.

Business registration processes have been streamlined with online systems reducing bureaucratic hurdles. The Ministry of Taxes provides efficient registration portals, though corruption and informal requirements may complicate procedures.

| Indicator | Value/Status | Notes |

|---|---|---|

| Doing Business Rank (2020) | 34th of 190 | Allegedly manipulated; index discontinued |

| Starting a Business Rank | 9th of 190 | 2021 data; streamlined procedures |

| Corruption Perception | High | Endemic corruption affects operations |

| Political Stability | Stable (Authoritarian) | Predictable but limited democratic freedoms |

| Private Sector Development | Weak | State dominates economy; over 50% work for government |

| Regulatory Transparency | Low | Limited public data; unclear requirements |

Foreign investment policies officially welcome FDI but practical barriers include corruption, bureaucratic obstacles, and political favoritism. Oil sector attracts most foreign investment while non-oil sectors face challenges.

Operational cost structures vary dramatically between Baku and regions. Office rent in central Baku approaches European levels while secondary cities offer substantially lower costs. Salaries, utilities, and services similarly show geographic disparities.

Labor market conditions provide educated workforce with strong technical skills, particularly in engineering, IT, and sciences. However, brain drain affects talent availability as skilled professionals emigrate for higher wages abroad.

Corporate Structure and Registration

Limited Liability Company (LLC): LLCs represent the most common structure for small and medium businesses in Azerbaijan. They offer liability protection, flexible ownership structures, and relatively straightforward compliance requirements.

Joint-Stock Company (JSC): Joint-stock companies suit larger enterprises and those seeking to issue shares. They require higher minimum capital, more stringent governance, and greater reporting obligations than LLCs.

Branch Office: Foreign companies can establish branch offices representing the parent entity without creating separate legal entities. Branches face restrictions on certain business activities and taxation differences.

Representative Office: Representative offices conduct limited non-commercial activities including market research and liaison functions. They cannot engage in revenue-generating operations or sign commercial contracts.

Recommended Structure for iGaming: Artificial island casino operators would likely require Azerbaijani-registered legal entities, probably LLCs or JSCs depending on scale. Specific requirements have not been published for casino licensing.

| Entity Type | Min. Capital | Liability | Best For |

|---|---|---|---|

| LLC | 2 AZN | Limited | Small-medium businesses; foreign investors |

| Joint-Stock Company | Higher (varies) | Limited | Large enterprises; public offerings |

| Branch Office | None | Parent company liable | Foreign company local presence |

| Representative Office | None | Parent company liable | Non-commercial activities only |

| Sole Proprietorship | None | Unlimited | Individual entrepreneurs |

Registration timelines have improved with efficient online systems. Company registration can complete within days for straightforward cases, though complex structures or foreign ownership may extend processing to several weeks.

Registration costs include government fees, legal fees, notarization, and translation expenses. Basic LLC registration costs several hundred dollars in official fees, with professional service provider fees adding substantially to total costs.

Required documents include founding agreements, articles of association, director identification, address confirmation, and beneficial ownership declarations. Notarization and translation to Azerbaijani may be required for foreign-language documents.

Foreign ownership rules generally permit 100 percent foreign ownership in most sectors, though strategic sectors face restrictions. Gambling sector foreign ownership rules are undefined for the new artificial island framework.

Ongoing compliance includes annual financial reporting, tax declarations, audit requirements for larger entities, and maintaining registered office and resident director where required. Compliance complexity varies by entity type and business activities.

Taxation Framework

Corporate Income Tax Structure

Standard corporate income tax is levied at 20 percent of taxable profits for all Azerbaijani entities. This rate applies to domestic and foreign companies earning Azerbaijan-source income.

Special economic zones may offer reduced corporate tax rates or tax holidays to incentivize investment. Specific incentives depend on sector, investment amount, and location within designated development zones.

International tax treaties exist with numerous countries affecting withholding tax rates on cross-border payments. Azerbaijan has signed double taxation avoidance agreements with major trading partners and investment source countries.

Transfer pricing rules govern transactions between related parties to prevent profit shifting. Documentation requirements apply to companies with related-party transactions, following international transfer pricing standards.

| Tax Type | Rate | Application |

|---|---|---|

| Corporate Income Tax | 20% | On taxable profits |

| VAT (Standard) | 18% | On goods and services |

| Personal Income Tax | 14% + 25% | 14% up to 2,500 AZN/month; 25% above |

| Withholding Tax – Dividends | 10% | May be reduced by treaty |

| Withholding Tax – Interest | 10% | May be reduced by treaty |

| Withholding Tax – Royalties | 14% | May be reduced by treaty |

| Social Security (Employer) | 22% | On employee gross salary |

| Unemployment Insurance | 0.5% | Employer contribution |

Personal Income Tax and Payroll

Individual income tax employs a two-tier progressive structure. Monthly income up to 2,500 AZN is taxed at 14 percent, while income exceeding this threshold faces 25 percent taxation on the excess amount.

Employers must withhold income tax from employee salaries and remit to tax authorities. Monthly tax returns and payments are required for all employers with staff.

Social security contributions are mandatory with employers contributing approximately 22 percent of gross salary covering pensions, healthcare, and disability insurance. Employees contribute 3 percent from their gross wages.

Unemployment insurance requires 0.5 percent employer contribution. Total employer payroll burden reaches approximately 22.5 percent above gross salary, significantly impacting employment costs.

Market Entry Considerations

Recommended Entry Strategies

For Artificial Island Casinos: Direct licensing and facility development represents the only legal path. Operators must secure 340,000 AZN annual licenses, invest in physical infrastructure on designated artificial islands, and comply with forthcoming operational regulations.

Partnership Approach: Given Azerbaijan’s business environment, partnerships with well-connected local entities may facilitate regulatory navigation, licensing approval, and operational success. Government connections significantly influence business outcomes.

Phased Development: Conservative operators should consider phased approaches – securing licensing first, developing minimal viable operations, and expanding based on market response and regulatory clarity.

For Sports Betting: Extremely limited licensing availability makes market entry through legal channels nearly impossible for new operators. The state maintains tight control through designated operators, leaving minimal opportunity for competition.

Online Gambling: No legal entry strategy exists for online casino operators as Azerbaijan prohibits digital gambling licensing. Operating offshore to serve Azerbaijanis carries legal risks and enforcement uncertainty.

Typical Costs and Timelines

Artificial Island Casino Setup Costs:

- Annual License Fee: 340,000 AZN ($200,000)

- Physical Infrastructure: Highly variable; millions of dollars for casino construction on artificial islands

- Company Registration: 500-2,000 AZN including professional services

- Legal and Consulting: $50,000-$200,000 for licensing, compliance, and setup advisory

- Initial Capital Requirements: To be determined by licensing authority

- Gaming Equipment: $500,000-$5,000,000+ depending on casino size and quality

- Technology Platform: $100,000-$500,000 for management systems

Monthly Operational Costs (Estimated):

- Staff Salaries: 50-200+ employees at 1,000-5,000 AZN average = $30,000-$600,000+ monthly

- Facility Operating Costs: Utilities, maintenance, security – highly variable

- Technology Maintenance: $5,000-$20,000 monthly

- Marketing: $20,000-$100,000+ monthly depending on scale

- Compliance and Regulatory: $10,000-$30,000 monthly

Timeline Estimates:

- Company Registration: 1-4 weeks

- License Application and Approval: Unknown; 6-18 months estimated

- Physical Infrastructure Development: 12-36+ months for casino construction

- Total Time to Market: 24-48+ months from initiation to casino opening

Success Factors and Challenges

Critical Success Enablers:

Understanding local consumer preferences is paramount given limited market research availability. Initial operators must invest in market intelligence to identify optimal gaming offerings, price points, and service expectations.

Government relationships and political connections significantly influence licensing success, regulatory navigation, and operational permissions. Engaging well-connected local advisors and partners proves nearly essential.

Premium positioning may attract affluent Azerbaijanis and regional tourists given limited legal gambling supply. Differentiation through luxury amenities, entertainment offerings, and unique experiences can justify premium pricing.

Localized marketing in Azerbaijani and Russian languages with culturally appropriate messaging maximizes market penetration. Understanding cultural sensitivities around gambling helps craft effective promotional strategies.

Major Operational Challenges:

Regulatory uncertainty dominates all planning as artificial island casino regulations remain incompletely defined. Tax rates, compliance requirements, and operational restrictions may emerge that fundamentally alter business models.

Infrastructure development on artificial islands faces unique challenges including construction logistics, utilities provision, transportation access, and environmental considerations. No precedent exists for this development model in Azerbaijan.

Limited market size constrains revenue potential – Azerbaijan’s 10.4 million population and modest incomes may not support multiple large casinos. Operators must attract regional tourists or accept limited market capacity.

Payment processing for international visitors may face challenges if banking relationships prove difficult to establish or if foreign card acceptance encounters restrictions.

Talent shortage in casino management, gaming operations, and hospitality may necessitate importing foreign expertise at high cost. Training local staff requires time and investment.

Competitive Dynamics:

First-mover advantages exist for early artificial island casino operators who can establish brand recognition and customer bases before competition emerges. However, first movers also bear regulatory uncertainty risks.

Turkish casino markets in North Cyprus pose competition for Azerbaijani gamblers who currently travel abroad. Artificial island casinos must offer compelling reasons to gamble domestically versus established foreign alternatives.

Offshore online casinos will continue serving Azerbaijanis regardless of artificial island casino development. Land-based operations cannot capture online gambling demand without regulatory liberalization.

Exit Strategy Planning

Market liquidity for casino sales in Azerbaijan is completely unknown given no historical precedent. Finding buyers for artificial island casino assets may prove challenging without established secondary market.

License transferability rules have not been published, creating uncertainty about whether licenses can be sold with casino businesses or require new application processes.

Typical valuation multiples cannot be determined without operational track record. Early operators should prepare for extended hold periods rather than expecting rapid exits.

Legal process for closing operations remains undefined under new framework. Operators should negotiate exit provisions in initial licensing agreements to preserve flexibility.

FAQ: Frequently Asked Questions

Legal and Licensing

1. Is online gambling legal in Azerbaijan?

No, online casino gambling is explicitly prohibited in Azerbaijan. The Ministry of Finance does not issue licenses for online casino operations, and operating or promoting online casinos targeting Azerbaijani residents is illegal.

Only state-approved lotteries and limited sports betting through government-designated operators are permitted in digital form. International online casinos operate in a gray area serving Azerbaijani players from offshore jurisdictions without local authorization.

Authorities actively restrict access to unauthorized gambling websites and prosecute those facilitating illegal gambling activities. Recent enforcement actions have intensified against social media advertising for online casinos, particularly fraudulent operations.

Players accessing international gambling sites face unclear legal risks. While enforcement focuses primarily on operators rather than individual players, using unlicensed platforms remains technically illegal and outside regulatory protections.

2. What types of gambling licenses are available and what do they cover?

Azerbaijan currently offers three extremely limited license types. Lottery licenses permit organization and operation of state-approved lotteries, restricted to Azerbaijani-registered legal entities meeting strict financial and operational criteria.

Sports betting licenses allow operation of betting facilities on sports events under the Law on Physical Education and Sports. Licensing is highly restricted with preference for state-affiliated entities.

Artificial island casino licenses, introduced in July 2025, permit casino operations exclusively on designated artificial land plots in the Azerbaijani sector of the Caspian Sea. Mainland casino operations remain prohibited.

No online gambling licenses are available. No slot machine hall licenses exist. No poker room licenses are granted. The gambling licensing framework is among the world’s most restrictive.

3. How much does an iGaming license cost and how long does it take to obtain?

Artificial island casino licenses cost 340,000 AZN (approximately $200,000) annually. This represents the only published licensing fee for the new casino framework introduced in July 2025.

Application timelines have not been officially published as the regulatory framework remains nascent. Based on regional comparisons and Azerbaijan’s bureaucratic environment, operators should anticipate 6-18 months for license application processing.

Additional costs include legal representation, compliance consulting, background check fees, and financial guarantee instruments. Total licensing costs could reach $250,000-$500,000 including professional services.

Lottery and sports betting license costs are not publicly disclosed. Given tight government control and limited availability, these licenses are effectively unavailable to new applicants without extraordinary political connections.

4. Can foreign companies obtain a gambling license?

Foreign ownership rules for artificial island casino licenses have not been explicitly published. However, licensing requires establishing an Azerbaijani-registered legal entity meeting Ministry of Finance criteria.

Lottery licenses explicitly restrict eligibility to legal entities registered in Azerbaijan. This suggests foreign companies must create local subsidiaries rather than operating through branch offices or foreign entities.

Foreign ownership percentages, if restricted, have not been disclosed. Azerbaijan’s general business regulations often impose limitations on strategic sector foreign ownership, suggesting similar constraints may apply to gambling.

Practical reality suggests foreign operators will need well-connected local partners to navigate licensing processes successfully. Political relationships and government connections heavily influence business outcomes in Azerbaijan’s authoritarian environment.

Financial and Taxation

5. What are the tax obligations for iGaming operators?

Specific gambling tax structures for artificial island casinos have not been published. The Ministry of Finance will establish gross gaming revenue (GGR) tax rates, net gaming revenue (NGR) considerations, and other gambling-specific taxation.

All Azerbaijani entities face standard corporate income tax at 20 percent of taxable profits. This applies to casino operators alongside any gambling-specific taxes that may be implemented.

Annual license fees of 340,000 AZN ($200,000) represent fixed operational costs separate from revenue-based taxation. License fees must be paid regardless of profitability.

Value-added tax at 18 percent applies to most goods and services in Azerbaijan. The applicability of VAT to gambling services has not been clarified for casino operations.

Withholding taxes on dividends (10 percent), interest (10 percent), and royalties (14 percent) apply to cross-border payments. International tax treaties may reduce these rates for qualifying entities.

6. Are gambling winnings taxed for players?

Player taxation on gambling winnings has not been comprehensively defined for artificial island casino operations. Based on regional norms, winnings may be subject to personal income tax above certain thresholds.

Azerbaijan’s personal income tax employs two tiers: 14 percent on monthly income up to 2,500 AZN and 25 percent on amounts exceeding this threshold. How gambling winnings factor into these brackets remains unclear.

Operators may be required to withhold taxes on player winnings above specified amounts, though specific thresholds and procedures have not been published. Implementation details will emerge as casinos begin operations.

Tax-free thresholds for small winnings may exist but have not been defined. Neighboring countries often exempt modest winnings from taxation while taxing substantial jackpots.

7. What are the typical operational costs for running an online casino or sportsbook?

Online casinos and sportsbooks cannot legally operate in Azerbaijan, making typical operational cost analysis impossible. However, for artificial island land-based casinos, costs are substantial.

Monthly staff costs for 50-200 employees at average salaries of 1,000-5,000 AZN could range $30,000-$600,000 depending on scale and expertise requirements. Casino managers and specialized staff command premium wages.

Facility operating expenses including utilities, maintenance, security, and cleaning vary dramatically based on casino size. Island location may inflate costs due to logistics and infrastructure limitations.

Marketing and customer acquisition costs could reach $20,000-$100,000+ monthly depending on promotional intensity and market competition. Attracting customers to island locations requires substantial marketing investment.

Technology platform maintenance, compliance monitoring, regulatory reporting, and payment processing add $15,000-$50,000 monthly. Gaming equipment maintenance and replacement represent ongoing capital expenditures.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines are highly speculative given zero operational precedent for artificial island casinos. Initial operators face extraordinary risks and uncertain financial outcomes.

Development timeline of 24-48 months from initiation to casino opening means investors must sustain capital deployment for 2-4 years before generating revenue. Construction and licensing costs accumulate during this period.

Initial ramp-up periods typically require 6-12 months post-opening to reach stable operations and customer base development. Break-even may require 3-5 years of operations depending on initial investment scale.

Total time to positive ROI could extend 5-8+ years from initial commitment. Only well-capitalized operators with long investment horizons should consider Azerbaijan market entry.

Market size limitations suggest modest revenue potential relative to investment requirements. Azerbaijan’s 10.4 million population with median income around $139 monthly cannot support unlimited casino capacity.

Operations and Compliance

9. What are the local presence requirements for operators?

Gambling operators must establish Azerbaijani-registered legal entities to obtain licensing. Branch offices or foreign entities operating without local registration cannot secure gambling licenses.

Physical presence on designated artificial islands is mandatory for casino operations. Casinos can only operate in specified zones on artificial land plots in the Caspian Sea.

Specific requirements for office space, management personnel, and local staffing have not been published. Regional gambling regulations typically mandate local offices and resident directors.

Domain and server hosting requirements for any digital components (player databases, surveillance systems) may require local infrastructure. Technology requirements await regulatory clarification.

10. What payment methods are available and recommended?

Credit and debit cards via Visa and Mastercard represent the most widely available payment methods with 91 percent cashless transaction adoption. Card acceptance is essential for any gambling operation.