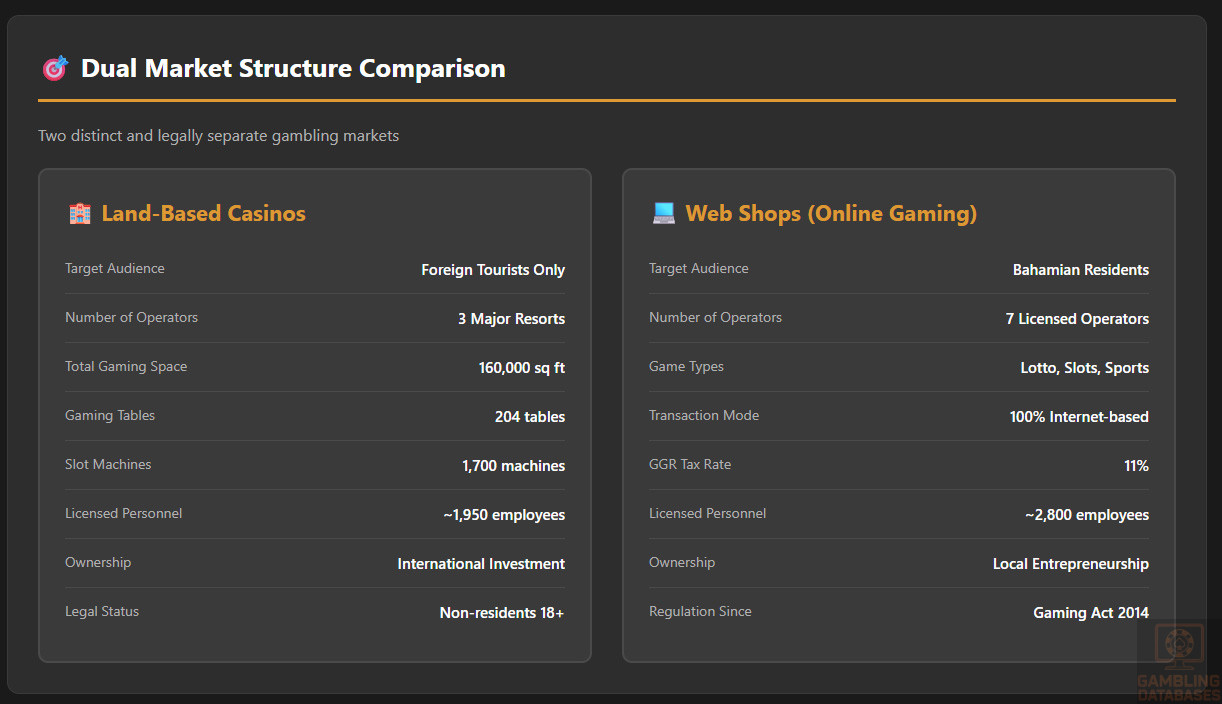

The Bahamas presents a unique and highly regulated iGaming opportunity characterized by a dual-market structure. Land-based casinos exclusively serve international tourists while domestic online gaming operates through licensed web shops serving local residents.

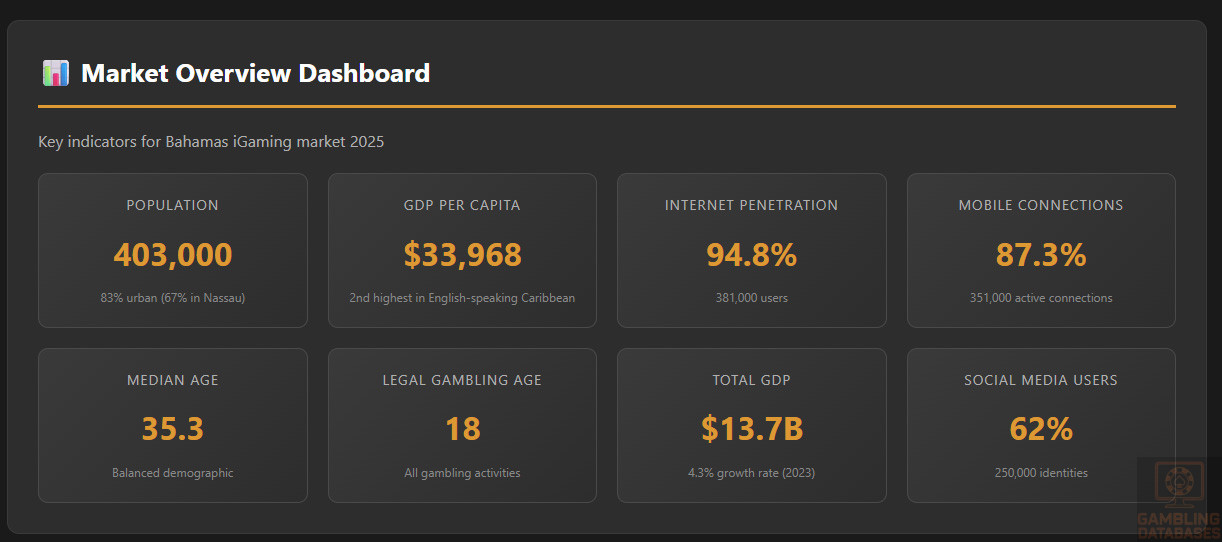

With a population exceeding 400,000, high internet penetration rates above 94%, and the second-highest GDP per capita in the English-speaking Caribbean at approximately $34,000, the archipelago nation offers substantial economic foundations.

The Gaming Act of 2014 established comprehensive regulatory frameworks overseen by the Gaming Board for The Bahamas, creating clear pathways for both casino operators and domestic gaming providers.

Executive Summary: Key Market Indicators

| Indicator | Value | Details |

|---|---|---|

| Population (2025) | 403,000 | Urban concentration: 83% (Nassau accounts for 67%) |

| GDP (2023) | $13.7 billion | Growth rate: 4.3% (2023), 2.64% (2023 actual) |

| GDP Per Capita (2024) | $33,968 | Second highest in English-speaking Caribbean |

| Internet Penetration | 94.8% | 381,000 users (January 2025) |

| Mobile Connections | 87.3% | 351,000 active cellular connections |

| Social Media Users | 62.0% | 250,000 user identities |

| Median Age | 35.3 years | Balanced demographic profile |

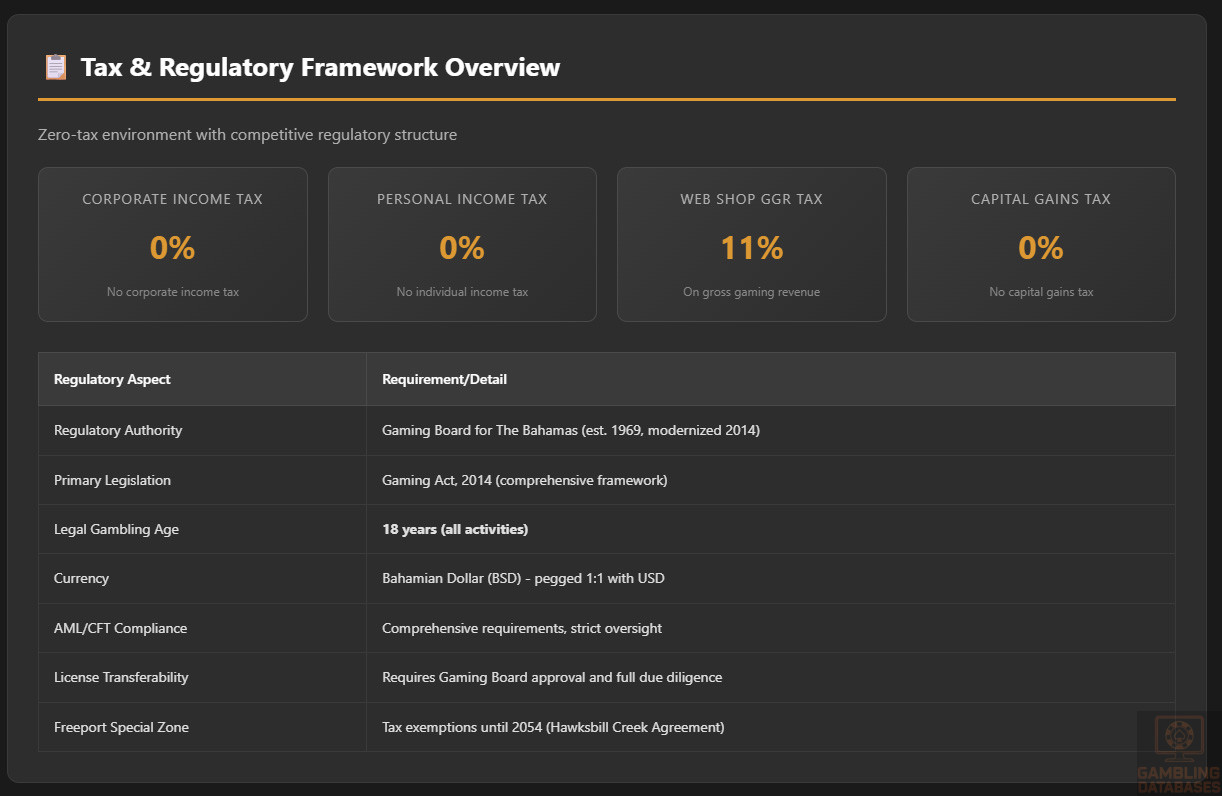

| Legal Gambling Age | 18 years | Applies to all gambling activities |

| Casino Gambling (Tourists) | Legal | Restricted to non-residents only |

| Online Gambling (Domestic) | Regulated | Web shops for Bahamian residents |

| Regulatory Authority | Gaming Board for The Bahamas | Established 1969, modernized 2014 |

| Primary Legislation | Gaming Act, 2014 | Comprehensive regulatory framework |

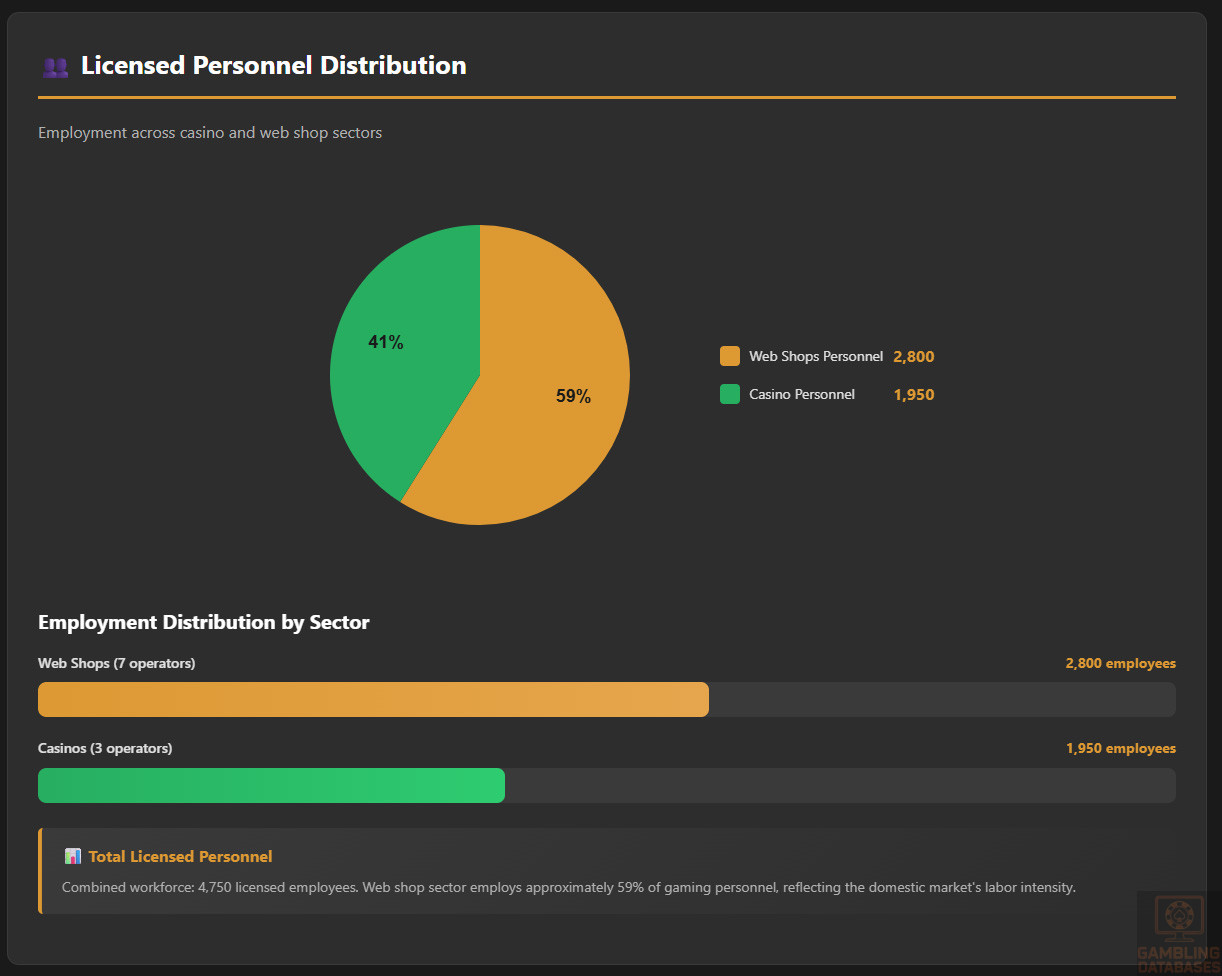

| Licensed Casinos | 3 operational | Atlantis, Baha Mar, Resorts World Bimini |

| Licensed Web Shops | 7 operators | Domestic online gaming providers |

| Casino License Availability | 7 total licenses | 6 in use, expansion opportunities exist |

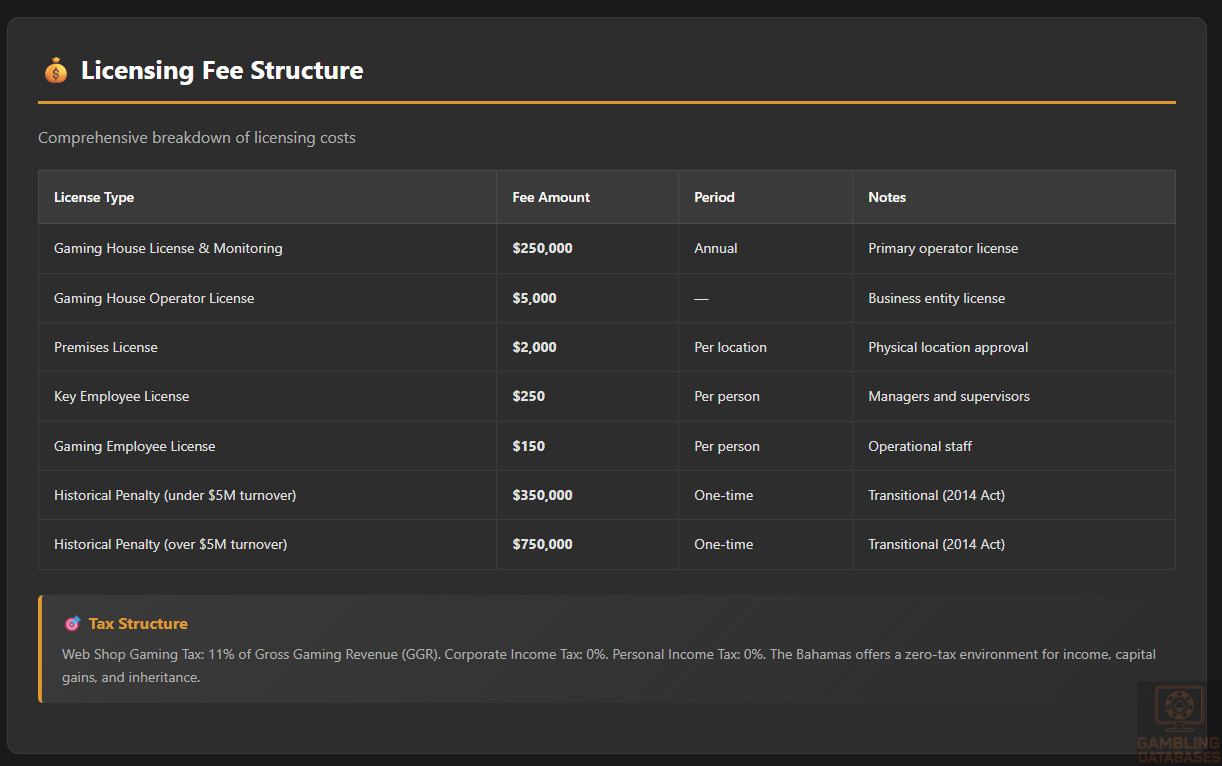

| Web Shop Gaming Tax | 11% GGR | Gross Gaming Revenue basis |

| Gaming House License Fee | $250,000 | Annual license and monitoring fee |

| Gaming Employee License | $150 | For operational staff |

| Key Employee License | $250 | For managers and supervisors |

| Corporate Income Tax | 0% | No corporate income tax |

| Personal Income Tax | 0% | No individual income tax |

| VAT Rate | Applicable | Applies to goods and services |

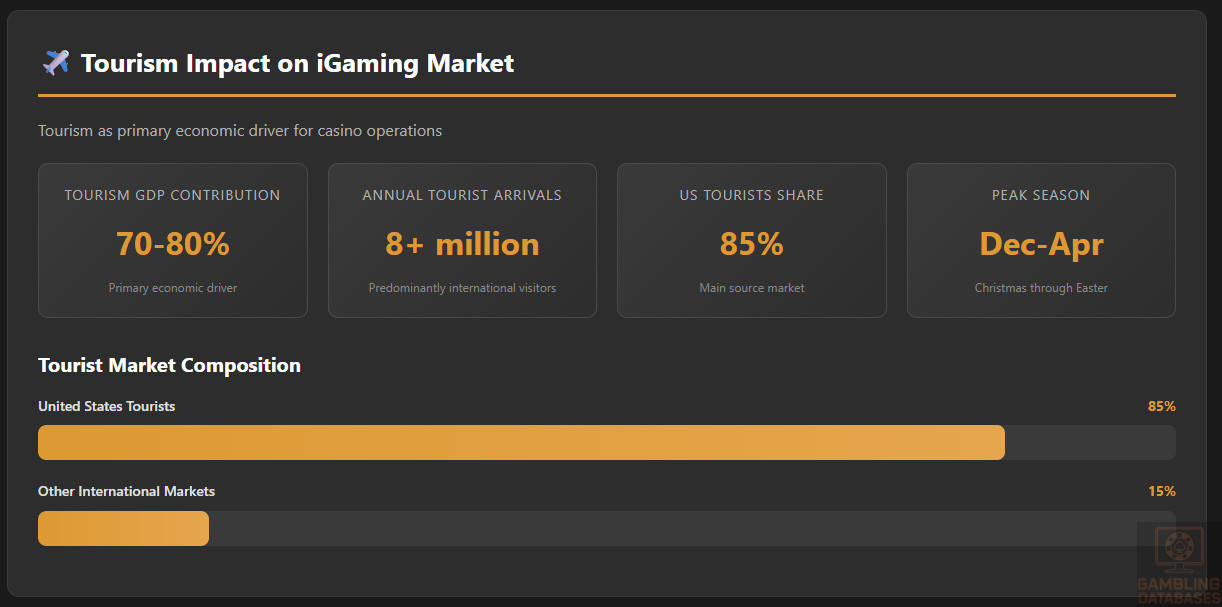

| Tourism GDP Contribution | 70-80% | Primary economic driver |

| Annual Tourist Arrivals | 8+ million | 85% from United States |

| Primary Language | English | Official language |

| Currency | Bahamian Dollar (BSD) | Pegged 1:1 with USD |

| Mobile Internet Speed (2022) | Average | Fixed broadband: 41.64 Mbps download |

| 4G LTE Coverage | 95%+ | Comprehensive across populated areas |

| 5G Status | Limited deployment | Focus remains on 4G improvement |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

The Bahamas operates under a unique dual-market gambling regulatory system established through the Gaming Act of 2014, which modernized and expanded the original Lotteries and Gaming Act of 1969.

This framework creates two distinct and legally separate gambling markets designed to serve different populations with minimal overlap.

Land-Based Gambling Activities

Casino gambling in the Bahamas is legally restricted to foreign tourists and non-residents aged 18 and over. Bahamian citizens, permanent residents, work permit holders, and their spouses are explicitly prohibited from participating in casino gaming.

This discriminatory restriction has faced criticism from industry leaders and is currently under review. Gaming Board Chairman Dr. Daniel Johnson has publicly advocated for legislative changes to permit Bahamian residents to gamble in casinos.

Proposed amendments were expected to reach Parliament, potentially bringing the gaming sector into the 21st century by allowing citizens choice in their entertainment activities.

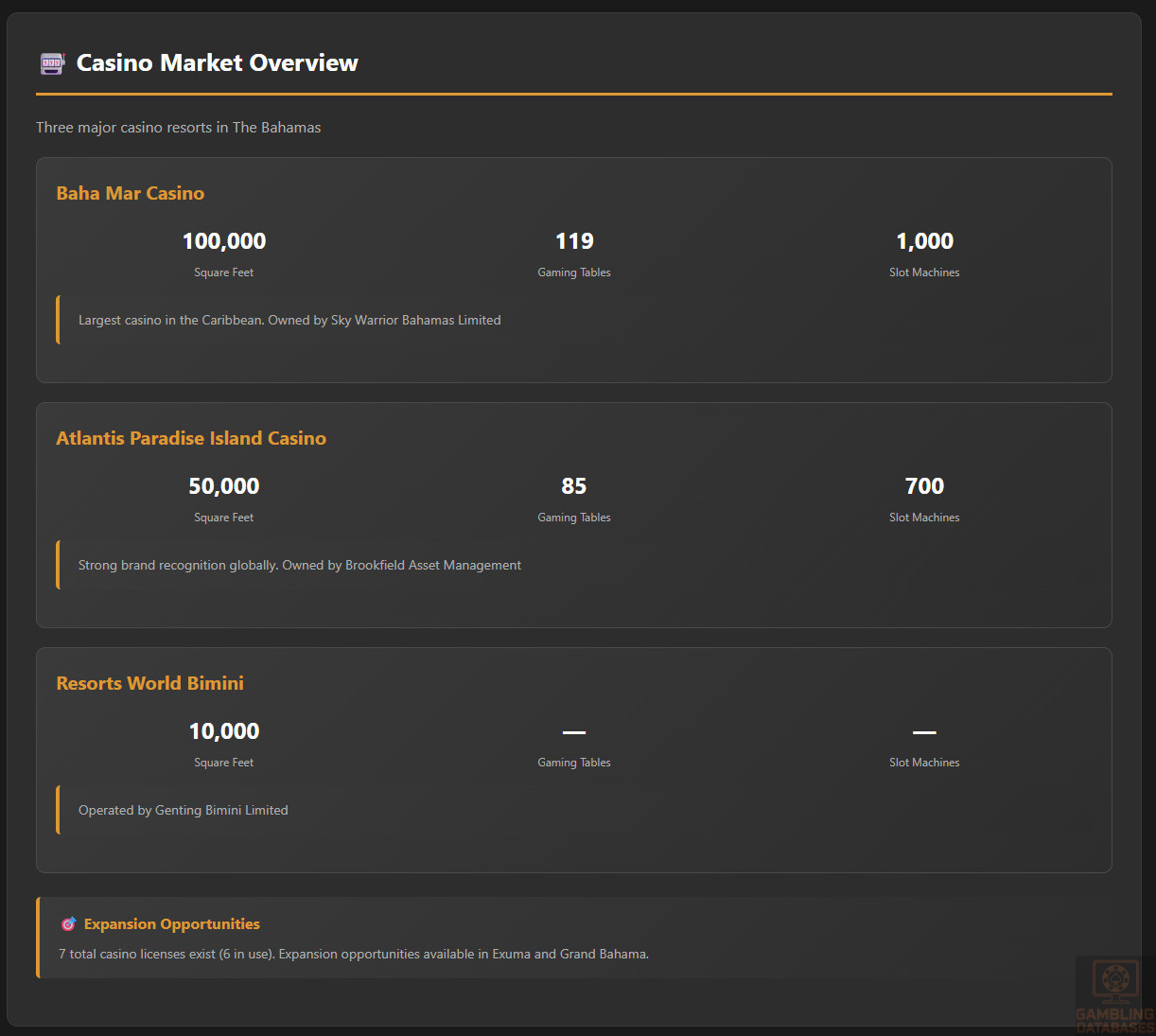

Baha Mar Casino operates the largest casino in the Caribbean at 100,000 square feet, offering 119 gaming tables and 1,000 slot machines. Resorts World Bimini maintains a 10,000 square foot facility.

Available casino games include Craps, Baccarat, various poker variants (Ultimate Texas Hold ’em, Let It Ride, Pai Gow), Roulette, Blackjack, and comprehensive sportsbook offerings.

All three casinos feature private gaming rooms for high-rollers and sports betting facilities. These venues collectively employ approximately 1,950 licensed personnel.

Online Gambling Framework

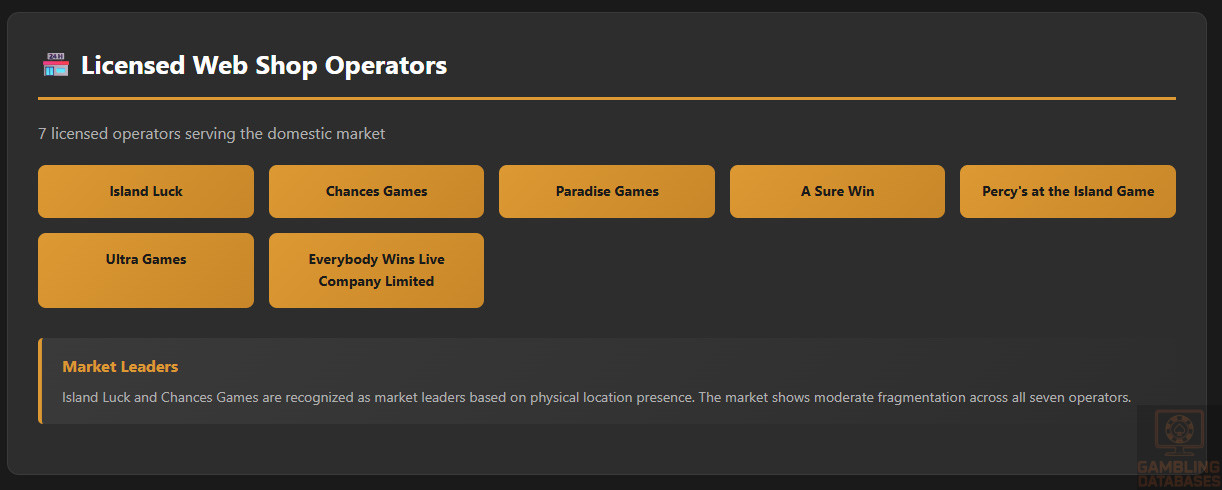

Domestic online gaming was formally regulated in 2014 through provisions specifically designed for Bahamian residents. This sector operates through Gaming House Operators, commonly called web shops.

Seven licensed operators currently serve the market: Island Luck, Chances Games, Paradise Games, A Sure Win, Percy’s at the Island Game, Ultra Games, and Everybody Wins Live Company Limited.

These gaming houses employ approximately 2,800 licensed personnel across their operations. Game offerings include lotto, slots, and sports betting, all conducted entirely via internet transactions.

The regulations permit mobile and proxy gaming while imposing restrictive controls on interactive gaming from licensed casinos. Online gaming from websites managed within The Bahamas for international markets remains prohibited.

Restrictive interactive gaming licenses allow players to bet online or on mobile devices within casino property boundaries but do not extend beyond the physical premises.

Licensed Operators and Market Players

The casino market demonstrates high concentration with three major international resort operators. Atlantis Paradise Island is owned and operated by Brookfield Asset Management, representing one of the most recognized casino brands globally.

Baha Mar Casino operates under Sky Warrior Bahamas Limited ownership, positioning itself as the Caribbean’s largest gaming facility. Resorts World Bimini functions under Genting Bimini Limited management.

Market share distribution favors Baha Mar based on gaming floor size and machine count, though Atlantis maintains strong brand recognition and attracts significant tourist traffic.

The domestic web shop market shows moderate fragmentation across seven licensed operators. Island Luck and Chances Games are generally recognized as market leaders based on physical location presence.

International versus local operator dynamics differ significantly between the two markets. Casino operations are entirely international investment-driven, while web shops represent predominantly local Bahamian entrepreneurship.

Seven casino licenses exist in total, with only six currently operational. Expansion opportunities exist in Exuma and Grand Bahama, with the Gaming Board actively seeking operators for these locations.

Licensing Framework and Requirements

Application Process and Eligibility

The Gaming Board for The Bahamas serves as the primary regulatory authority for all licensing matters. The Board operates from Centreville House, Second Terrace and Collins Avenue, Nassau.

Contact information includes phone (242) 397-9200, fax (242) 327-8864, and email at [email protected]. Dr. Daniel Johnson currently serves as Executive Chairman.

Application forms are available through the Board’s official website and cater to multiple license classes including new, temporary, and renewal applications.

The Gaming Act, 2014 Sections 39 through 51 provide detailed explanatory information regarding license categories and requirements. Applicants bear responsibility for selecting and completing correct application forms.

Financial requirements for gaming house operators include substantial capital provisions. Operators with gross turnover below $5 million face one-time penalties of $350,000 for historical unlicensed operations.

Those exceeding $5 million gross turnover must pay $750,000 penalties. These represent transitional measures from the 2014 regulatory modernization.

Technical standards require all gaming devices, systems, and software to be certified, authorized, and approved by registered independent gaming laboratories. Operators must use only approved gaming equipment meeting technical requirements.

Background check procedures involve comprehensive vetting through the Gaming Board’s investigative processes. All key personnel and operators undergo thorough scrutiny to ensure suitability.

Local Presence and Operational Requirements

Physical presence mandates require substantial local establishment. Gaming house operators must maintain licensed premises for all operations.

Employee licensing extends comprehensively throughout organizations. Every gaming employee, from cashiers to machine technicians, requires individual licensing at $150 per license.

Key employees including managers, supervisors, pit bosses, inspectors, and similar positions require separate key employee licenses at $250 each.

Foreign ownership restrictions apply differently to casino and web shop operations. Casino operations welcome international investment as evidenced by current operators.

Web shop operations historically emerged from domestic entrepreneurship, though specific foreign ownership percentage limits are not publicly detailed in available documentation.

Compliance Obligations and Monitoring

Player Protection and Identification

Age verification requirements strictly enforce the 18-year minimum gambling age. Individuals under 18 are categorically prohibited from entering gaming areas or engaging in any gambling form.

KYC and AML compliance standards align with Financial Action Task Force guidelines. All licensed operators must comply with comprehensive anti-money laundering and counter-financing of terrorism regulations.

The Gaming Board signed a Memorandum of Understanding with the Financial Intelligence Unit in September 2025, strengthening collaborative oversight of AML/CFT compliance.

Responsible gambling measures represent mandatory obligations. License holders must provide gamblers and potential problem gamblers with sufficient information and assistance to obtain proper counseling.

Access to appropriate support organizations must be facilitated. The Gaming Board can require operators to limit or cease gaming activities for individuals demonstrating problematic behavior.

Financial Monitoring and Reporting

Transaction monitoring systems follow Financial Transactions Reporting Act requirements. Licensed gaming operators must maintain detailed financial records and report suspicious transactions.

Regular reporting includes detailed compliance documentation submitted to the Gaming Board on schedules determined by regulatory requirements. Operators must maintain operational integrity and transparency in all activities.

Audit and inspection procedures allow the Gaming Board to conduct investigations and take enforcement actions as necessary. Comprehensive oversight ensures regulatory compliance across all licensed operations.

Taxation Structure and Financial Obligations

Player Taxation

The Bahamas maintains an attractive tax-neutral environment for gambling winnings. No income tax, capital gains tax, or inheritance tax applies to individuals.

This favorable regime extends comprehensively to online gambling winnings. Players face no tax obligations on their gambling proceeds regardless of amounts won.

No withholding procedures exist for player winnings. This creates a completely tax-free gambling experience for all participants, enhancing the jurisdiction’s appeal.

Operator Taxation

Gaming house operators face an 11 percent tax on Gross Gaming Revenue. GGR is defined as total amounts wagered minus winnings paid to players.

Annual licensing and monitoring fees for gaming house operators total $250,000. Additional operational license fees include $5,000 for gaming house operator licenses.

Gaming house premises licenses cost $2,000. Gaming house agent licenses require $1,000 fees. These fees apply per license category.

The Bahamas imposes no corporate income tax, representing a significant advantage for gaming operators. However, businesses must pay annual registration fees based on their operating structure.

Value-Added Tax applies to goods and services, potentially affecting gambling operators and related service providers. Operators must incorporate VAT into their pricing and operational cost structures.

Casino operators may negotiate specific tax rates and incentives as part of individual license agreements. Large-scale resort projects particularly benefit from customized arrangements.

Gambling Market Financial Performance

Comprehensive market revenue data for the Bahamas gambling sector remains limited in publicly available sources. The three major casinos contribute significantly to the Bahamian economy through investments, job creation, and tax revenues.

Gaming tax revenues support government operations though specific annual figures are not publicly detailed in accessible documentation. The 11 percent tax on web shop GGR generates ongoing revenue streams.

Year-over-year growth trends show recovery following Hurricane Dorian (2019) and COVID-19 pandemic impacts. The tourism sector’s rebound to 8+ million annual visitors drives casino revenue growth.

Advertising and Marketing Restrictions

Specific advertising restrictions and marketing regulations for gambling operators are not comprehensively detailed in available public documentation from the Gaming Board.

General regulatory oversight ensures responsible marketing practices. Operators must avoid targeting minors and maintain responsible gambling messaging in all promotional activities.

Marketing to Bahamian residents for casino gambling remains prohibited given the legal restrictions on local casino participation. Web shops can market to domestic audiences.

Recent Regulatory Changes and Their Impact

The Gaming Act of 2014 represents the most significant recent regulatory overhaul, completely modernizing the Bahamian gambling framework. This legislation replaced the 1969 Lotteries and Gaming Act.

Key changes included regulating previously unlicensed domestic gaming operations, expanding the range of permitted gaming services and products, and establishing an enhanced licensing regime.

The Gaming Regulations 2014, Gaming House Operator Regulations 2014, Gaming Rules 2015, and Financial Transactions Reporting (Gaming) Regulations 2014 provided comprehensive implementation frameworks.

Proposed amendments to permit Bahamian residents to gamble in casinos represent the most significant pending change. Gaming Board Chairman Dr. Daniel Johnson announced in May 2023 that legislation would be introduced.

This change would end the discriminatory prohibition and allow Bahamian citizens choice in gaming entertainment. Implementation timelines and specific regulatory details await legislative action.

Enforcement Mechanisms and Penalties

The Gaming Board maintains comprehensive enforcement authority. The Board conducts investigations, issues guidelines and directives, and takes enforcement actions as necessary to ensure regulatory compliance.

License suspension or revocation represents the most severe penalty for non-compliance. Operators failing to maintain standards risk losing authorization to operate.

Financial penalties apply for various violations though specific fine structures are not publicly detailed in accessible documentation. The Board maintains discretionary authority over penalty assessment.

Recent enforcement actions focus on anti-money laundering compliance. The September 2025 MoU between the Gaming Board and Financial Intelligence Unit strengthens collaborative enforcement capabilities.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

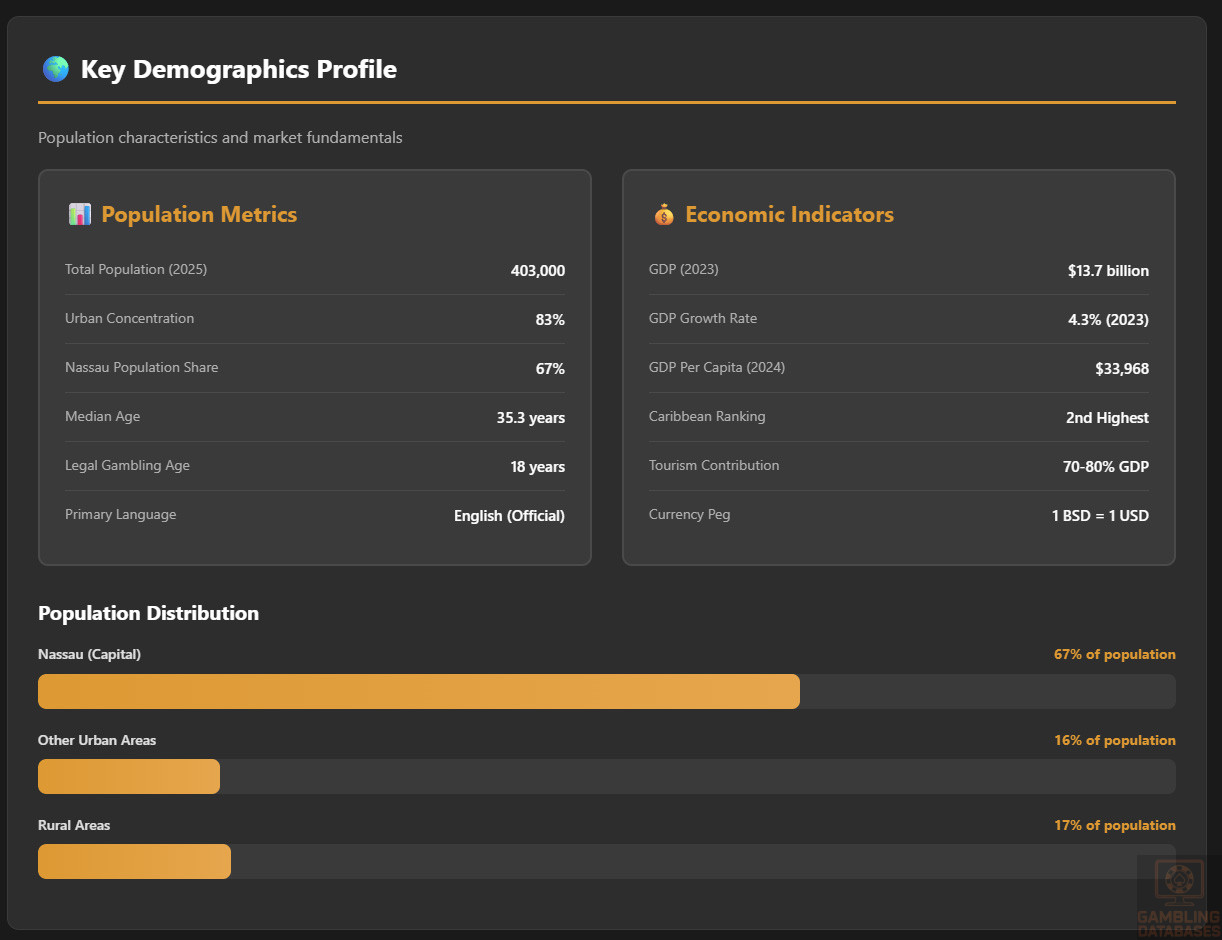

The Bahamas population reached approximately 403,000 in 2025, showing modest growth of 0.41 percent annually. This represents relatively stable demographic expansion.

Gender distribution shows 192,000 males (47.71%) and 211,000 females (52.29%), creating a sex ratio of 91.248 males per 100 females. This 18,000 female surplus reflects regional demographic patterns.

The median age stands at 35.3 years, positioning the population in a mature working-age demographic. This balanced age structure supports economic productivity while maintaining gambling market potential.

Life expectancy remains high by regional standards, contributing to population stability. The demographic profile supports sustained consumer spending across multiple age cohorts.

Geographic Distribution

Urban concentration reaches 83 percent of the total population, with approximately 67 percent living on New Providence Island where Nassau is located.

This extreme urban concentration creates highly efficient market targeting opportunities. Marketing and operational strategies can focus on Nassau with confidence of reaching the majority of potential customers.

The archipelago spans 700 islands and islets with approximately 30 inhabited islands. This geographic dispersion creates unique service delivery challenges beyond Nassau’s urban core.

Internet access follows urban-rural divides. Nassau enjoys comprehensive connectivity while family islands experience varying service quality. Starlink satellite internet has expanded to 9,000 users, particularly serving remote areas.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

The Bahamian economy reached $13.7 billion GDP in 2023, representing significant recovery from pandemic-era contractions. GDP per capita stands at $33,968 in 2024.

This represents the second-highest per capita GDP in the English-speaking Caribbean, establishing the Bahamas as a high-income developed economy with strong consumer purchasing power.

GDP growth forecasts project continued expansion. The economy grew 2.64 percent in 2023 after stronger 10.78 percent growth in 2022 reflecting post-pandemic recovery.

Tourism dominates the economic sector composition, contributing 70-80 percent of GDP. Financial services account for approximately 15 percent. Manufacturing and agriculture combined contribute less than 7 percent.

Income and Wealth Distribution

Average household income levels benefit from the high GDP per capita, though specific median household income figures are not publicly detailed in accessible documentation.

The tourism-driven economy creates employment for approximately half the workforce in tourism-related sectors. Unemployment stood at 8.8 percent in May 2023 labor force surveys.

Income inequality measures show moderate disparities though specific Gini coefficient data is not immediately available. The concentration of economic activity in Nassau versus family islands creates regional income variations.

Consumer spending patterns reflect high living costs typical of island economies. Import dependence drives prices upward, though strong incomes support discretionary spending including entertainment and gambling.

Market Size and Growth Projections

Specific Bahamas iGaming market revenue figures are not comprehensively available in public documentation. The domestic web shop sector serves approximately 400,000 potential customers.

Seven licensed operators indicate market viability supports multiple competitors. The 2,800 employees across these operations suggest substantial business scale.

Historical revenue growth follows tourism sector patterns. Strong tourist arrivals exceeding 8 million annually (projected to break records in 2023-2024) drive casino revenues.

Revenue forecasts depend heavily on regulatory changes. Permitting Bahamian residents to gamble in casinos would substantially expand the addressable market for casino operators.

Global online gambling market growth rates of 10-12 percent CAGR through 2030 provide context. The Bahamas market likely tracks similar growth patterns given high internet penetration and affluent demographics.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy rates exceed 95 percent, reflecting strong educational infrastructure. English as the official language eliminates translation requirements for English-language gaming platforms.

Digital literacy levels align with high internet penetration rates. The 94.8 percent internet penetration demonstrates widespread digital capability across the population.

Workforce skill levels support technology sector operations. Financial services contributing 15 percent of GDP require sophisticated technical skills, creating a capable labor pool.

Cultural and Social Factors

Communication and Language

English serves as the primary and official language across all social and business contexts. This linguistic uniformity simplifies all aspects of gambling operations.

Internet language preferences overwhelmingly favor English. Gaming platforms require no localization efforts beyond standard English-language interfaces.

Business communication norms follow British Commonwealth traditions given the Bahamas’ historical ties. Professional standards align with international business practices.

Cultural Attitudes

Gambling acceptance levels show interesting dualities. Tourist casino gambling has operated since 1969, demonstrating long-term societal acceptance of the industry.

However, the prohibition on Bahamian residents gambling in casinos reflects historical paternalistic attitudes. This restriction increasingly faces criticism as outdated and discriminatory.

The 2014 regulation of domestic web shops acknowledges widespread gambling participation among Bahamians. This represents pragmatic acceptance of market reality.

Foreign brand perception remains highly positive. The Bahamas’ 85 percent U.S. tourist dependence creates familiarity with American brands and comfort with international operators.

Problem Gambling and Social Considerations

Problem gambling prevalence data is not comprehensively available in public documentation. The regulatory framework includes provisions for protecting gambling addicts.

Gaming regulations require license holders to provide information and assistance enabling problem gamblers to obtain proper counseling and support organization access.

The Gaming Board can require operators to limit or cease gaming activities for individuals showing problematic patterns. This regulatory power enables intervention.

Treatment facilities and support services are mandated in regulations though specific program details are not publicly detailed in accessible documentation.

Political Structure and Governance

The Bahamas operates as a stable parliamentary democracy since 1729 within the Commonwealth realm. Queen (now King) Charles III serves as head of state represented by the Governor General.

Political stability has characterized the nation since independence in 1973. The Free National Movement and Progressive Liberal Party dominate political life, alternating governance.

Regulatory consistency and predictability rank favorably. The Gaming Board’s longstanding operation since 1969 provides institutional stability despite the 2014 modernization.

Corruption perception indices show moderate performance. Transparency International rankings place the Bahamas in the middle tier among Caribbean nations.

Technology Adoption and Digital Behavior

Internet and Digital Usage

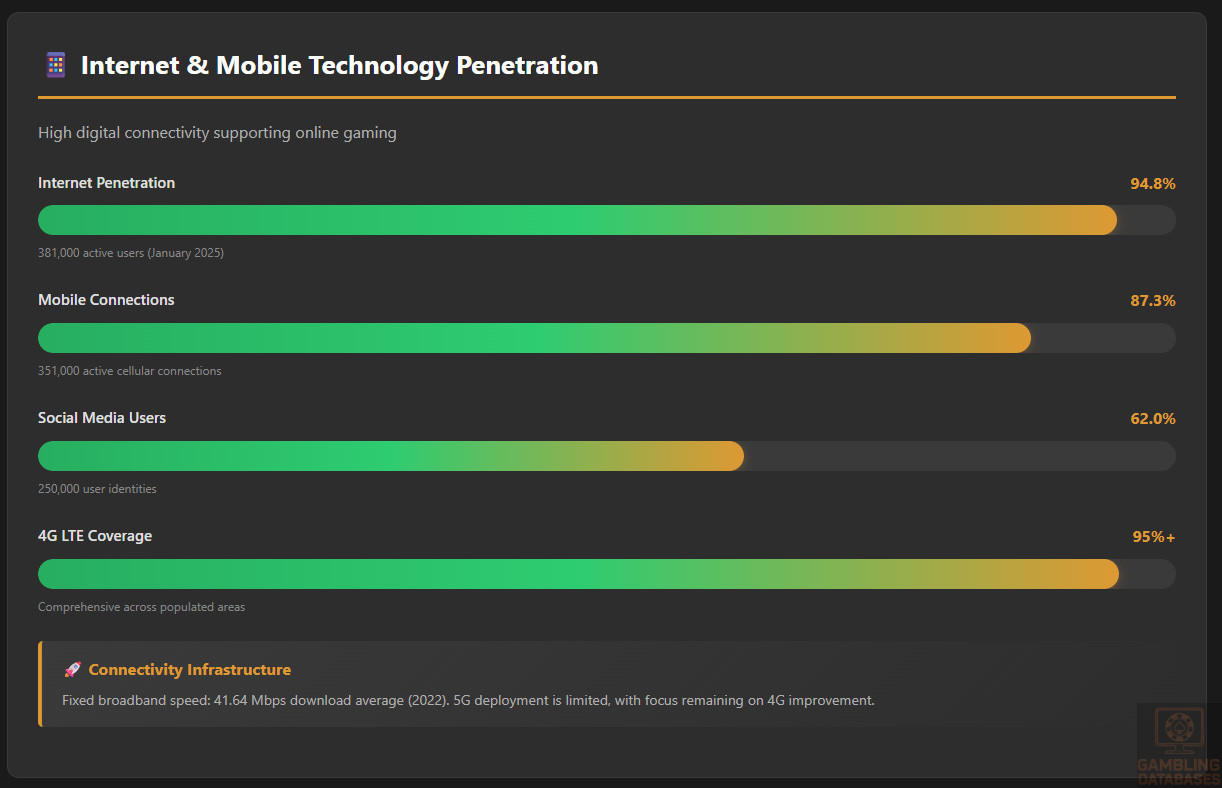

Internet penetration reached 94.8 percent in January 2025, representing 381,000 users. This increased by 1,739 users (0.5 percent) between January 2024 and January 2025.

Daily internet usage patterns align with global norms. High social media penetration at 62 percent (250,000 users) demonstrates active digital engagement.

Mobile device adoption reaches 87.3 percent with 351,000 active cellular connections. Smartphone usage dominates, with users accessing internet via mobile devices as primary method.

E-commerce participation rates show growing adoption. Digital banking penetration supports online transactions, creating favorable conditions for online gambling payment processing.

Digital Payment Behavior

Payment method preferences include traditional credit and debit cards supported by the well-developed banking sector. Digital wallets show increasing adoption.

The Bahamian dollar’s 1:1 peg with the U.S. dollar simplifies international transactions and payment processing. This removes currency conversion concerns for U.S.-based payment processors.

Online banking penetration supports digital payment adoption. The sophisticated financial services sector provides robust payment infrastructure.

Cryptocurrency adoption remains emerging. The Bahamas issued the Sand Dollar central bank digital currency, demonstrating government interest in digital payment innovation.

Gaming and Gambling Preferences

Current Market Participation

Gambling participation rates are not comprehensively quantified in public documentation. The existence of seven licensed web shops serving 400,000 residents suggests significant market engagement.

The 2,800 employees across web shop operations indicate substantial business volume. Popular gambling activities include lotto, slots, and sports betting based on licensed operator offerings.

Sports betting shows strong appeal given the comprehensive sportsbook facilities at all three major casinos and availability through web shops.

Consumer Behavior Patterns

Average spending per player data is not publicly available. Platform preferences strongly favor mobile given the 87.3 percent mobile connection rate.

Web shop operators’ success with internet-based models demonstrates market comfort with online gambling. Mobile and proxy gaming regulations acknowledge this preference.

Seasonal patterns likely align with tourism cycles. Peak tourist seasons from November through April drive casino activity. Local web shop patterns may follow different seasonal influences.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Internet penetration stands at 94.8 percent, representing highly developed digital infrastructure. This ranks among the highest penetration rates in the Caribbean region.

Fixed broadband versus mobile internet shows strong mobile dominance. Fixed broadband median download speeds reached 41.64 Mbps in August 2022, with upload speeds of 9.46 Mbps.

Network reliability benefits from dual-operator competition. BTC (Bahamas Telecommunications Corporation) and Cable Bahamas (operating as Aliv) provide comprehensive services.

Infrastructure investment continues with fiber optic upgrades in Nassau. The Bahamas Domestic Submarine Network links all major islands providing connectivity backbone.

5G and Future Technology Deployment

Current 4G/5G coverage shows limited 5G deployment. Both BTC and Aliv indicated 5G rollout is not yet economically viable given high investment requirements.

4G LTE coverage exceeds 95 percent of the population. Aliv reports over 97 percent population coverage with average download speeds exceeding 90 Mbps on compatible devices.

BTC maintains over 90 percent 4G population coverage with peak 5G availability only in New Providence and Grand Bahama. Real-world speeds typically range from 20-60 Mbps.

Future infrastructure plans focus on improving 4G coverage quality and expanding family island connectivity rather than rushing 5G deployment.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Two mobile network operators serve the market: BTC and Aliv. This duopoly structure provides competition while maintaining network investment viability.

Network operator market share shows BTC retaining largest customer base historically, though Aliv has gained market share since launching in 2016.

Coverage quality varies by island. Nassau and major tourism centers enjoy excellent coverage. Family islands experience varying quality with ongoing improvements.

Data costs and pricing models show competitive pressure driving improvements. Unlimited data plans and bundled offerings have become standard.

Device Penetration

Smartphone adoption rates exceed 80 percent based on the high mobile connection and internet penetration figures. The 351,000 mobile connections for a 403,000 population indicates near-universal mobile device access.

Android versus iOS market share follows global patterns with Android likely dominating given regional market trends. Device preferences favor mid-range to premium smartphones given high per capita income.

Mobile internet usage patterns show data consumption for social media, messaging, and increasingly for online services including gaming. Mobile-first strategies are essential for market success.

Financial Services and Payment Infrastructure

Banking System Structure

The Bahamas maintains a sophisticated banking sector reflecting its status as an international financial center. As of 1998, 418 banks and trust companies held licenses.

This extensive banking infrastructure supports both domestic needs and international financial services that contribute 15 percent of GDP. Digital banking adoption shows strong growth.

Account penetration rates exceed regional averages given high income levels. The well-capitalized banking sector provides stability and comprehensive services.

Credit and lending markets demonstrate maturity appropriate to a developed economy. Consumer credit availability supports discretionary spending including gambling activities.

Payment Processing Options

Available payment methods for iGaming include traditional credit and debit cards widely held by the affluent population. Major international card networks operate comprehensively.

E-wallet options including PayPal, Skrill, and Neteller face varying availability. Regulatory approval and banking partnerships determine specific e-wallet accessibility for gambling transactions.

Bank transfer systems operate efficiently. The sophisticated banking infrastructure supports various transfer mechanisms though instant transfer systems may be less developed than in larger markets.

Cryptocurrency acceptance remains emerging. While the Bahamas pioneered the Sand Dollar CBDC, private cryptocurrency adoption for gambling faces regulatory uncertainty.

Processing fees and typical charges align with regional standards. International payment processing may incur higher fees given the small market size.

Transaction processing timelines vary by method. Card transactions process quickly while bank transfers may require 1-3 business days.

E-commerce and Digital Economy

Digital Market Development

E-commerce market growth follows global trends though specific market size data for the Bahamas is limited. The 94.8 percent internet penetration supports online retail adoption.

Digital service adoption rates show strong uptake particularly in urban Nassau. Online banking, bill payment, and digital services are widely used.

Consumer trust in online transactions benefits from the sophisticated banking sector and established rule of law. The stable political environment supports confidence in digital commerce.

Cross-border online shopping is common given import dependence. Bahamians frequently purchase from U.S. online retailers, demonstrating comfort with international digital transactions.

Business Environment and Regulatory Framework

Ease of Business Operations

The Bahamas maintains an investment-friendly environment characterized by political stability, English-speaking workforce, and established rule of law. The stable parliamentary democracy since 1729 provides continuity.

Business registration processes follow standard Commonwealth legal frameworks. Company formation typically involves several weeks to complete documentation and registration.

Foreign investment policies are generally welcoming particularly in tourism and financial services sectors. The government actively promotes foreign direct investment through various incentive programs.

Operational cost structures reflect island economy realities. Office rent in Nassau commands premium rates. Salaries must compete with tourism and financial services sectors.

Corporate Structure and Registration

Available Entity Types

Standard corporate structures include International Business Companies (IBCs) established under the 1990 IBC Act, domestic corporations, and limited liability companies.

For iGaming operators, domestic corporate structures are required given the need for Gaming Board licensing. IBC structures may not qualify for gaming licenses.

The Gaming Act requires proper corporate formation with adequate capitalization, proper governance, and comprehensive regulatory compliance capabilities.

Registration Requirements

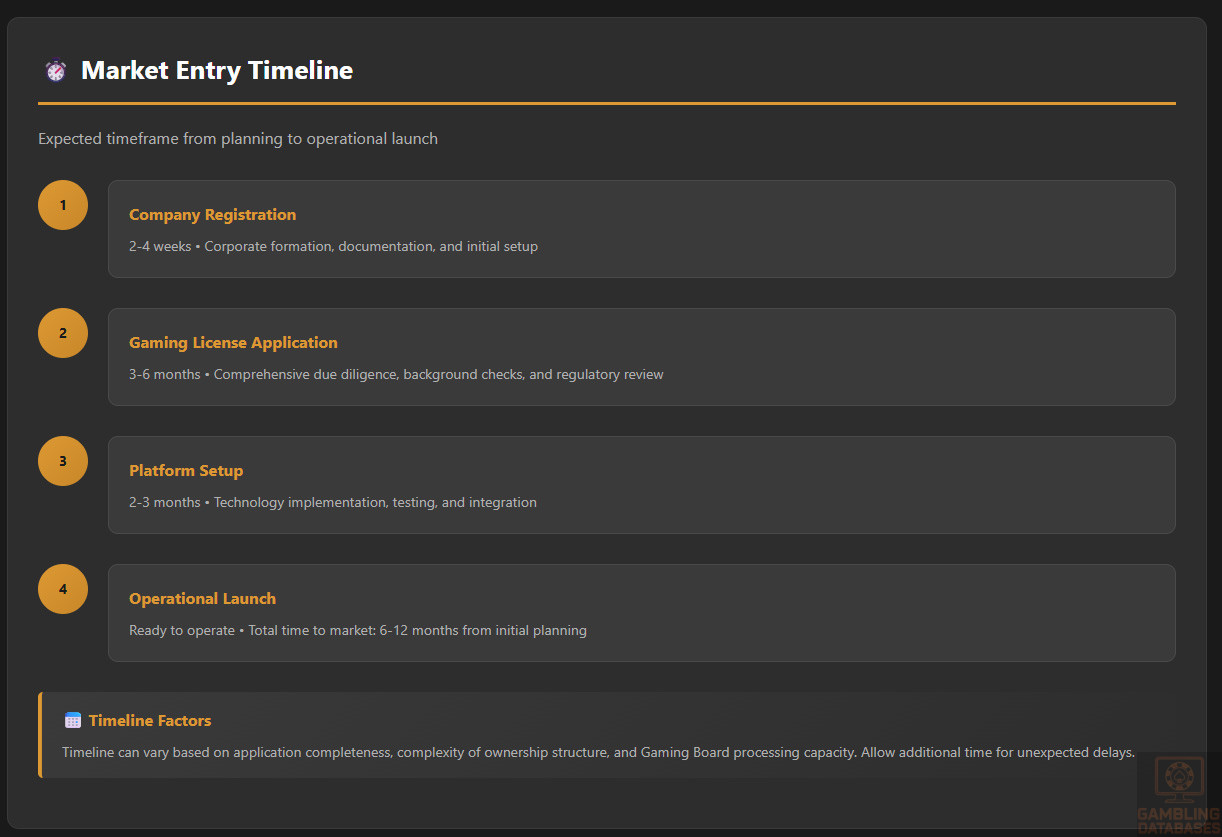

Registration timelines typically span several weeks for company formation plus additional months for gaming license applications. Complete market entry can require 6-12 months.

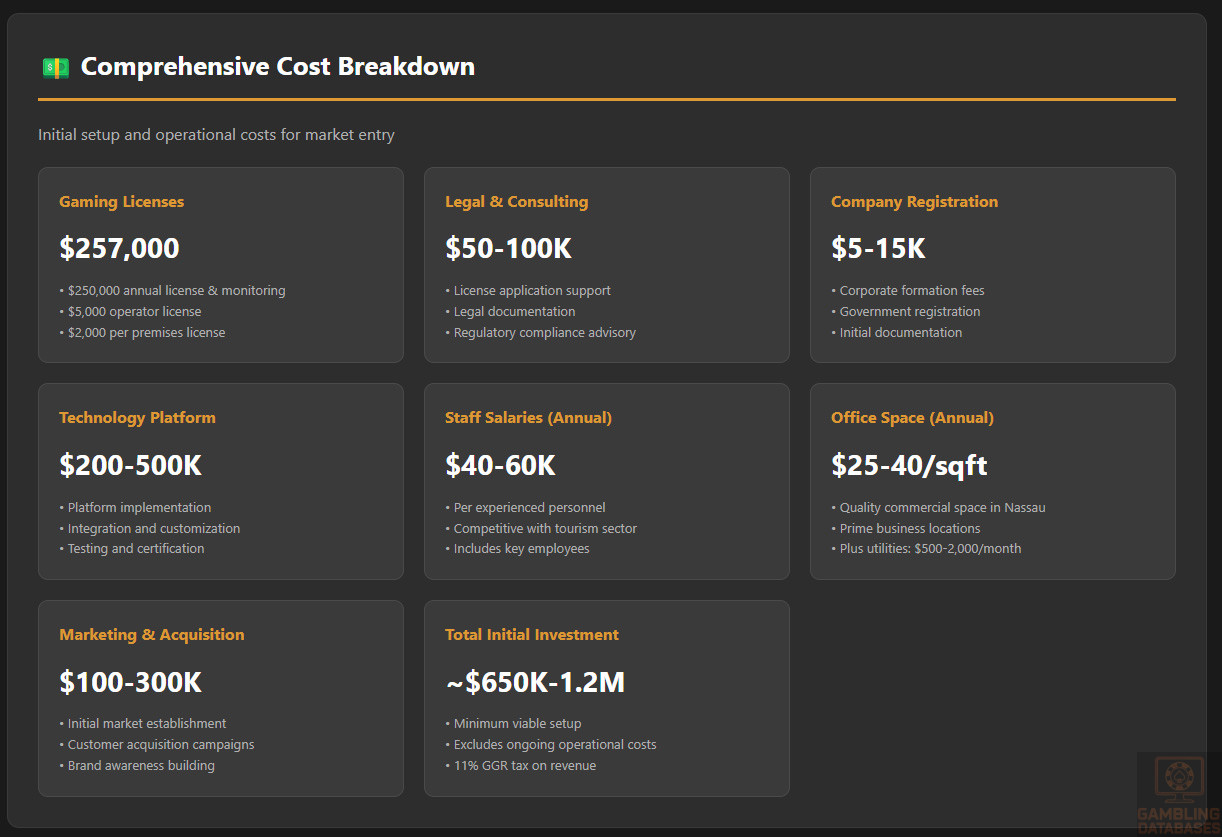

Registration costs include government fees for company formation, legal fees for documentation preparation, and gaming license application fees totaling $250,000 for gaming house operators.

Required documents include comprehensive business plans, financial statements, background information on all principals and key employees, and detailed operational procedures.

Foreign ownership rules permit international investment in casino operations as demonstrated by current operators. Web shop operations have historically been domestic-focused.

Taxation Framework

Corporate Income Tax Structure

The Bahamas imposes no corporate income tax, representing a major competitive advantage. This zero-tax environment extends to capital gains and inheritance taxes.

Special economic zones offer additional benefits. Freeport on Grand Bahama operates under the Hawksbill Creek Agreement guaranteeing tax exemptions until 2054.

Businesses in Freeport are exempt from real property, excise, import, and business taxes. This creates powerful incentives for operators considering establishment outside Nassau.

International tax treaties are limited. The absence of income tax reduces treaty network importance though agreements exist for specific purposes.

Personal Income Tax

No individual income tax applies in the Bahamas. This attracts high-net-worth individuals and creates favorable conditions for executive recruitment.

No withholding requirements exist for employee income. Social security contributions represent the primary payroll obligation for employers and employees.

This tax environment simplifies payroll administration and reduces employment costs compared to jurisdictions with income tax regimes.

Market Entry Considerations

Recommended Entry Strategies

For casino operators, establishing resort-integrated operations represents the proven model. All three current casinos operate within major resort properties serving the tourism market.

Partnership with established tourism operators may facilitate market entry. Integration with hotel, dining, and entertainment offerings creates comprehensive destination appeal.

For domestic web shop operations targeting Bahamian residents, local partnerships are essential. Understanding the domestic market and regulatory compliance requirements benefits from local expertise.

White label versus proprietary platform considerations depend on technical capabilities and resources. Established platforms may accelerate launch timelines.

Typical Costs and Timelines

Initial setup investments for gaming house operators include the $250,000 annual license and monitoring fee, $5,000 gaming house operator license, and $2,000 per premises license.

Legal and consulting fees for license applications can reach $50,000 to $100,000 or more depending on complexity. Company registration costs range from $5,000 to $15,000.

Technology and platform costs vary widely based on proprietary versus licensed solutions. Budget $200,000 to $500,000 for comprehensive platform implementation.

Operational costs include staff salaries competitive with tourism and financial services sectors. Expect $40,000 to $60,000 annually for experienced personnel.

Office rent in Nassau can reach $25 to $40 per square foot annually for quality commercial space. Utilities and internet connectivity add $500 to $2,000 monthly.

Marketing and customer acquisition costs require significant investment. Budget $100,000 to $300,000 for initial market establishment.

Timeline expectations include 2-4 weeks for company registration, 3-6 months for gaming license application processing, and 2-3 months for platform setup.

Total time to market typically spans 6-12 months from initial planning to operational launch.

Success Factors and Challenges

Key Success Enablers

Understanding local player preferences is crucial. Sports betting shows strong appeal. Lotto and slots dominate web shop offerings based on licensed operator game selections.

Localized payment methods integration must accommodate the Bahamian banking system. The USD peg simplifies international payment processing.

Mobile-first approach is essential given 87.3 percent mobile connection rates and smartphone dominance. Responsive design and mobile apps are critical.

Strong customer support in English aligns with the official language. However, understanding local communication styles and cultural nuances enhances customer relationships.

Competitive bonus and promotion strategies must balance player acquisition with the 11 percent GGR tax burden and regulatory compliance requirements.

Major Operational Challenges

Regulatory compliance complexity requires dedicated resources. The Gaming Board maintains strict oversight with comprehensive AML/CFT requirements.

The 11 percent GGR tax represents moderate burden compared to some jurisdictions though it impacts margin calculations.

Payment processing restrictions may limit some international payment methods. Banking relationships and regulatory approval are necessary.

Marketing and advertising limitations must be navigated. Responsible gambling messaging and avoiding minor targeting are mandatory.

Competition from established operators presents challenges. Seven licensed web shops already serve the domestic market. Three major casinos dominate tourist gaming.

Talent shortage in specialized gaming roles may require importing expertise. The small market limits the available pool of experienced gaming professionals.

Cultural Considerations

Local holidays and peak seasons align with tourism patterns. Christmas through Easter represents peak tourist season driving casino activity.

Popular local sports include basketball, track and field, and sailing. However, international sports particularly NFL, NBA, and soccer attract betting interest.

Preferred customer service channels emphasize personal relationships and responsive communication. Phone support remains important alongside digital channels.

Trust-building requirements for foreign brands benefit from the positive attitudes toward international operators demonstrated by casino success.

Exit Strategy Planning

Market liquidity for operator sales depends on gaming license transferability. The Gaming Board must approve all ownership changes.

License transferability requires comprehensive due diligence on prospective buyers. Background checks and suitability assessments mirror initial licensing processes.

Process for closing operations legally requires Gaming Board notification and orderly wind-down procedures ensuring customer protection.

FAQ: Frequently Asked Questions

Legal & Licensing

Is online gambling legal in Bahamas?

Yes, online gambling is legal and regulated in the Bahamas but operates under a dual-market structure. Domestic online gaming through licensed web shops serves Bahamian residents.

These operations offer lotto, slots, and sports betting via internet platforms. Seven operators currently hold licenses: Island Luck, Chances Games, Paradise Games, A Sure Win, Percy’s at the Island Game, Ultra Games, and Everybody Wins Live Company Limited.

Casino gambling is legal exclusively for foreign tourists and non-residents aged 18 and over. Bahamian citizens, permanent residents, and work permit holders cannot gamble in casinos.

This restriction is under review with proposed legislation to permit resident casino access. All gambling operations require Gaming Board licensing under the Gaming Act of 2014.

What types of gambling licenses are available and what do they cover?

The Bahamas offers several license types under the Gaming Act of 2014. Operator’s licenses are required for entities operating gaming establishments including casinos and web shops.

These comprehensive licenses mandate AML/CFT compliance, employee licensing, and operational integrity standards. Suppliers’ licenses are necessary for companies supplying gaming devices, software, hardware, or equipment repair services.

Gaming employee licenses are mandatory for all staff working in licensed establishments. This includes cashiers, dealers, machine technicians, and security personnel at $150 per license.

Key employee licenses at $250 cover managers, supervisors, pit bosses, and similar oversight positions. Gaming house premises licenses at $2,000 authorize specific physical locations for operations.

How much does an iGaming license cost and how long does it take to obtain?

Gaming house operator licenses cost $250,000 annually for the combined license and monitoring fee. Additional fees include $5,000 for the gaming house operator license itself.

Each premises requires a $2,000 gaming house premises license. Gaming house agent licenses cost $1,000. All employees must be individually licensed at $150 to $250 depending on position.

Historical penalties applied during the 2014 transition. Operators with gross turnover below $5 million paid $350,000 one-time penalties. Those exceeding $5 million paid $750,000.

Application timelines typically require 3-6 months for Gaming Board processing. This includes comprehensive background checks on all principals and key employees.

Complete market entry from company formation through licensing to operational launch generally spans 6-12 months depending on preparation quality and application completeness.

Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain gambling licenses as demonstrated by the three major casino operators. Atlantis Paradise Island is owned by Brookfield Asset Management.

Baha Mar operates under Sky Warrior Bahamas Limited. Resorts World Bimini functions under Genting Bimini Limited management. All represent substantial international investment.

Foreign operators must establish proper legal entities within the Bahamas. Local presence requirements include licensed premises, proper staffing, and comprehensive regulatory compliance infrastructure.

The Gaming Board evaluates all applicants on suitability regardless of nationality. Background checks, financial capability assessments, and technical standards compliance apply equally to foreign and domestic applicants.

Financial & Taxation

What are the tax obligations for iGaming operators?

Gaming house operators face 11 percent tax on Gross Gaming Revenue defined as total wagers minus winnings paid. This represents the primary gambling-specific tax obligation.

The Bahamas imposes no corporate income tax, creating significant advantages. Operators avoid income tax burdens that exist in most jurisdictions.

Value-Added Tax applies to goods and services, potentially affecting various business operations. Operators must incorporate VAT into operational cost planning.

Annual license and monitoring fees total $250,000 for gaming house operators. Additional operational license fees range from $150 to $5,000 depending on license type.

Casino operators may negotiate specific tax arrangements as part of individual license agreements. Large resort projects particularly benefit from customized tax structures.

Are gambling winnings taxed for players?

No, gambling winnings are not taxed in the Bahamas. The jurisdiction maintains a completely tax-neutral environment for individuals.

No income tax, capital gains tax, or inheritance tax applies. This extends comprehensively to all gambling winnings regardless of amount.

No withholding procedures exist for winnings. Players receive full payout amounts without tax deductions.

This favorable tax treatment enhances the Bahamas’ appeal as a gambling destination for tourists and creates attractive conditions for domestic players.

What are the typical operational costs for running an online casino/sportsbook?

Initial setup costs include $250,000 annual gaming license fees, $50,000-$100,000 in legal and consulting fees, and $5,000-$15,000 for company registration.

Platform and technology costs range from $200,000-$500,000 for comprehensive solutions depending on proprietary versus licensed platforms.

Monthly operational costs include staff salaries of $40,000-$60,000 annually per experienced employee. Office rent in Nassau reaches $25-$40 per square foot annually.

Payment processing fees typically range 2-5 percent of transaction values. Marketing and customer acquisition require $10,000-$30,000 monthly for sustained market presence.

Technology maintenance, hosting, and support services add $5,000-$15,000 monthly. Total operational costs easily exceed $100,000 monthly for properly resourced operations.

What is the expected ROI timeline for entering this market?

Return on investment timelines depend heavily on market segment and execution quality. The small population of 403,000 limits total addressable market size.

Initial investments of $500,000-$1,000,000 are typical for proper market entry. Breaking even may require 18-36 months of operation.

The seven existing web shop operators demonstrate market viability but also indicate competitive intensity. Market share must be captured from existing players.

Positive ROI within 3-5 years represents realistic expectations for well-executed operations. Superior technology, marketing, and customer service can accelerate timelines.

Operations & Compliance

What are the local presence requirements for operators?

Operators must maintain licensed physical premises within the Bahamas for all gaming operations. This includes proper commercial facilities meeting Gaming Board specifications.

All employees require individual gaming licenses. Staff must undergo background checks and maintain active licenses throughout employment.

Management must include licensed key employees meeting higher standards. The Gaming Board evaluates executives, directors, and operational managers for suitability.

Comprehensive compliance infrastructure is mandatory. This includes AML/CFT systems, responsible gambling programs, financial monitoring, and reporting capabilities.

What payment methods are available and recommended?

Traditional credit and debit cards from major international networks are widely available. Card acceptance is essential given high card penetration among the affluent population.

Bank transfers through the sophisticated Bahamian banking system provide reliable options. Direct bank integration supports both deposits and withdrawals.

E-wallet availability varies. PayPal, Skrill, Neteller, and similar services face regulatory approval requirements. Banking partnerships determine specific e-wallet accessibility.

The Bahamian dollar’s 1:1 peg with USD simplifies international payment processing. USD acceptance eliminates currency conversion complications.

Cryptocurrency remains emerging with uncertain regulatory status. While the Sand Dollar CBDC exists, private cryptocurrency adoption for gambling requires careful compliance evaluation.

What are the advertising and marketing restrictions?

Specific comprehensive advertising restrictions are not detailed in publicly available Gaming Board documentation. General responsible gambling principles apply.

Marketing to minors is strictly prohibited. All advertising must avoid targeting individuals under 18 years.

Responsible gambling messaging must be incorporated. Operators cannot promote excessive gambling or minimize risks.

Marketing Bahamian casino gambling to residents is prohibited given legal restrictions on local casino access. Web shops can market domestically.

What responsible gambling measures are mandatory?

License holders must provide gamblers and potential problem gamblers with sufficient information and assistance to obtain proper counseling.

Access to appropriate support organizations must be facilitated. Operators must maintain resources and referral capabilities.

The Gaming Board can require operators to limit or cease gaming activities for individuals demonstrating problematic behavior. Intervention authority enables player protection.

Age verification systems must prevent under-18 access. Comprehensive identity verification is mandatory for all participants.

AML/CFT compliance includes monitoring for problem gambling indicators. Financial transaction patterns may reveal concerning behavior requiring intervention.

Market Opportunity

How large is the iGaming market and what is the growth potential?

The Bahamas market serves a population of approximately 403,000 with high internet penetration at 94.8 percent. This creates an addressable market of 380,000+ potential online customers.

GDP per capita of $33,968 ranks second-highest in the English-speaking Caribbean, indicating strong purchasing power for discretionary spending including gambling.

Seven licensed web shop operators currently serve the domestic market, employing 2,800 personnel. This indicates substantial market scale supporting multiple competitors.

Growth potential benefits from regulatory changes. Proposed legislation permitting Bahamian residents to gamble in casinos would dramatically expand the addressable market.

Tourism sector growth with 8+ million annual visitors (85 percent from the United States) drives casino revenue expansion. Tourist gambling represents significant growth opportunity.

Who are the main competitors and what is their market share?

The casino market includes three major operators. Baha Mar operates the largest facility at 100,000 square feet with 119 tables and 1,000 slots.

Atlantis Paradise Island maintains 50,000 square feet with 85 tables and 700 slots. Resorts World Bimini operates 10,000 square feet with smaller scale.

Baha Mar likely holds largest market share based on size though specific revenue figures are not publicly available. Atlantis benefits from strong brand recognition and long operating history.

The domestic web shop market includes seven licensed operators: Island Luck, Chances Games, Paradise Games, A Sure Win, Percy’s at the Island Game, Ultra Games, and Everybody Wins Live Company Limited.

Island Luck and Chances Games are generally recognized as market leaders though specific market share data is not publicly disclosed.

What are the player preferences and typical spending patterns?

Player preferences favor sports betting based on comprehensive sportsbook presence at all casinos and web shop offerings. Slots and lotto represent other popular activities.

Mobile gaming strongly dominates given 87.3 percent mobile connection rates. Web shop operators’ success with internet-based models confirms mobile preference.

Spending patterns reflect high disposable income from $33,968 per capita GDP. Players can support regular gambling activity without financial strain.

Specific average spending figures per player are not publicly available. The 2,800 web shop employees serving 400,000 residents suggests substantial transaction volumes.

What are the key success factors and main challenges for new entrants?

Key success factors include mobile-first platform design matching the 87.3 percent mobile connection rate. Comprehensive sports betting offerings align with demonstrated preferences.

Strong payment integration with local banking systems is essential. Understanding the USD-pegged Bahamian dollar simplifies international payment processing.

Competitive marketing and customer acquisition strategies must overcome established competitor advantages. Superior technology and user experience can differentiate new entrants.

Main challenges include the small market size limiting total revenue potential. Only 403,000 residents restrict scaling opportunities.

Competition from seven established web shop operators creates market share acquisition difficulties. Customer loyalty to existing providers presents barriers.

High operational costs reflecting island economy realities impact profitability. Salaries, rent, and infrastructure costs exceed many comparable markets.

Regulatory compliance requires dedicated resources and expertise. Gaming Board oversight is comprehensive with strict standards.

Sources and References

- Gaming Board for The Bahamas – Official Website – https://www.gamingboardbahamas.com/

- Bahamas Government – Gaming and Casino Regulations – https://www.bahamas.gov.bs/gaming-and-casinos

- Gaming Act, 2014 – Bahamas Legislation – http://laws.bahamas.gov.bs/cms/images/LEGISLATION/PRINCIPAL/2014/2014-0040/2014-0040.pdf

- LegalPilot – Is Gambling Legal in Bahamas? Laws & Regulations Explained 2025 – https://legalpilot.com/country/bahamas/

- iGamingToday – Gambling Regulation in the Bahamas – https://www.igamingtoday.com/gambling-regulation-in-the-bahamas/

- Yogonet International – Bahamas Government to introduce legislation allowing residents to gamble in casinos – https://www.yogonet.com/international/news/2023/05/04/67029-bahamas-government-to-introduce-legislation-allowing-residents-to-gamble-in-casinos

- SDLC Corp – What are the Tax Implications of Online Gambling Winnings in the Bahamas? – https://sdlccorp.com/post/what-are-the-tax-implications-of-online-gambling-winnings-in-the-bahamas/

- Bahamas Local News – Web shop taxes, license fees unveiled – https://www.bahamaslocal.com/newsitem/107135/Web_shop_taxes_license_fees_unveiled.html

- Worldometer – Bahamas Demographics 2025 – https://www.worldometers.info/demographics/bahamas-demographics/

- StatisticsTimes – Bahamas demographics 2025 – https://statisticstimes.com/demographics/country/bahamas-demographics.php

- MacroTrends – Bahamas Population (1950-2025) – https://www.macrotrends.net/global-metrics/countries/bhs/bahamas/population

- MacroTrends – Bahamas GDP Growth Rate 1961-2025 – https://www.macrotrends.net/global-metrics/countries/BHS/bahamas/gdp-growth-rate

- DataReportal – Digital 2025: The Bahamas – https://datareportal.com/reports/digital-2025-bahamas

- Statista – Internet penetration in the Bahamas 2022 – https://www.statista.com/statistics/1055422/internet-penetration-bahamas/

- TS2 Space – Internet Access in The Bahamas – https://ts2.tech/en/internet-access-in-the-bahamas/

- eSIM Bahamas – Mobile Operators in the Bahamas: Which is the Best in 2025? – https://esimbahamas.com/operators/

- Travel Pander – Do You Get Service In The Bahamas? Mobile Internet And Coverage Explained – https://travelpander.com/do-you-get-service-in-the-bahamas/

- Statista – Mobile and fixed broadband internet speeds in the Bahamas 2022 – https://www.statista.com/statistics/1175901/bahamas-mobile-fixed-broadband-internet-download-upload-speed/

- Moody’s Analytics – Bahamas Economic Indicators – https://www.economy.com/bahamas/indicators

- Wikipedia – Economy of the Bahamas – https://en.wikipedia.org/wiki/Economy_of_the_Bahamas

- World Bank – GDP per capita (current US$) – Bahamas, The – https://data.worldbank.org/indicator/NY.GDP.PCAP.CD?locations=BS

- U.S. Department of State – Bahamas Investment Climate Statements 2020 – https://www.state.gov/reports/2020-investment-climate-statements/bahamas/

- U.S. Department of Commerce – Bahamas Market Overview – https://www.trade.gov/country-commercial-guides/bahamas-market-overview

- GF Magazine – The Bahamas GDP and Economic Data – https://gfmag.com/country/the-bahamas-gdp-country-report/

- Global Citizen Solutions – The List of the Richest Caribbean Countries by GDP in 2025 – https://www.globalcitizensolutions.com/which-caribbean-country-makes-the-most-money/

- Trading Economics – Bahamas GDP per capita – https://tradingeconomics.com/bahamas/gdp-per-capita

- Grand View Research – Online Gambling Market Size, Trends | Industry Report, 2030 – https://www.grandviewresearch.com/industry-analysis/online-gambling-market

- Grand View Research – North America Online Gambling Market Size Report, 2030 – https://www.grandviewresearch.com/industry-analysis/north-america-online-gambling-market-report

- Statista – Gambling Market Forecast Worldwide – https://www.statista.com/outlook/amo/gambling/worldwide

- Yahoo Finance – Online Gambling Market Research Report 2025 – https://finance.yahoo.com/news/online-gambling-market-research-report-095200878.html

- SkyQuest Technology – Online Gambling Market Size, Share, and Growth Analysis – https://www.skyquestt.com/report/online-gambling-market

- GM Insights – Online Gambling Market Size & Share, Growth Forecasts 2034 – https://www.gminsights.com/industry-analysis/online-gambling-market

- Blockchain Ads – What Is the Growth Rate of iGaming? Industry Statistics and Market Share – https://www.blockchain-ads.com/post/igaming-statistics

- Mordor Intelligence – Online Gambling Market Growth | Industry Analysis, Size & Forecast Report – https://www.mordorintelligence.com/industry-reports/online-gambling-market

- Grand View Research – U.S. Online Gambling Market Size | Industry Report, 2030 – https://www.grandviewresearch.com/industry-analysis/us-online-gambling-market-report

- GBO Licensing – Compare Gaming License Costs – https://gbo-licensing.com/compare-gaming-license/

- American Gaming Association – Commercial Gaming Revenue Tracker – https://www.americangaming.org/resources/commercial-gaming-revenue-tracker/

- American Gambler – Online Gambling in The Bahamas – https://www.americangambler.com/online-gambling-in-the-bahamas/

- Scaleo – iGaming Regulations Around The World: What You Must Know [2025 Update] – https://www.scaleo.io/blog/igaming-regulations-around-the-world-what-you-must-know/

- Slotegrator – Where Is Online Gambling Legal in 2025? Global Overview of iGaming Regulations – https://slotegrator.pro/analytical_articles/where-online-gambling-is-legal.html

🎯 Gambling Databases Country Rating: The Bahamas

| Rating Category | Score | Assessment |

|---|---|---|

| Operator Ease Score | 3.2/10 | ⛔️ CHALLENGING – Dual-market restrictions, tourist-only casinos, small domestic market |

| Player Access Score | 4.5/10 | ⚠️ RESTRICTED – Citizens banned from casinos, web shops only, limited options |

| Overall Market Rating | 3.9/10 | ❌ AVOID FOR MOST OPERATORS – Micro-market with discriminatory restrictions |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNING

🚨 EXTREME CAUTION REQUIRED:

- Discriminatory Dual-Market System: Bahamian citizens, permanent residents, and work permit holders are LEGALLY BANNED from casino gambling – casinos serve only foreign tourists

- Domestic Market Monopoly: Only 7 licensed web shop operators serve local residents with limited game offerings (lotto, slots, sports betting)

- International iGaming PROHIBITED: Online gaming for international markets from Bahamas-based websites is explicitly banned

- Micro-Market Economics: Population of only 403,000 creates extremely limited addressable market – not viable for large-scale operations

- Tourist Dependency Risk: Casino operations 100% dependent on foreign tourism (8M+ annual visitors, 85% American)

- Regulatory Uncertainty: Proposed changes to allow residents in casinos announced but not implemented – timeline uncertain

- No Licensing Path for Most: Only 7 total casino licenses exist, 6 already operational – minimal expansion opportunity

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | MATH: Started at +1.5 (partial legality – only tourist casinos and domestic web shops legal). DEDUCTIONS: -1.0 for discriminatory dual-market system (Bahamian citizens banned from casinos = eliminates 403,000 potential customers from casino operations), -0.5 for international online gaming prohibition (cannot operate Bahamas-based sites for global markets), -0.5 for regulatory uncertainty (proposed resident casino access legislation announced but not implemented = unreliable timeline). CRITICAL: This is NOT a normal regulated market – it’s two separate restricted markets serving different populations. |

| Licensing Process | 25% | 0.25/2.5 | MATH: Started at +0.5 (extremely limited – only 7 total casino licenses, 6 operational, applications require extensive capital). DEDUCTIONS: -0.25 for FIRB-style foreign investment scrutiny (Gaming Board controls limited licenses, prioritizes established international resort operators). APPLICATION COSTS: Casino operations require multi-million dollar resort investment ($250,000 annual license fee is minor compared to property development). Web shop licensing exists but market already saturated with 7 operators serving tiny population. REALITY: Licensing is theoretically available but practically inaccessible for most operators due to integrated resort requirements. |

| Taxation & Costs | 20% | 1.25/2.0 | MATH: Started at +1.5 (GGR tax 11% for web shops = under 15%). DEDUCTIONS: -0.25 for extreme customer acquisition costs in micro-market ($500+ per customer realistic given 403K population, 7 existing competitors, and need for aggressive marketing to gain share). POSITIVE: Zero corporate income tax and zero personal income tax are significant advantages. REALITY: While tax rates are favorable, operational costs on island economy are extremely high (salaries, rent, infrastructure all exceed comparable markets). Tourism casino operations face different tax structures not publicly disclosed. |

| Operational Requirements | 15% | 0.5/1.5 | MATH: Started at +1.0 (moderate requirements – local office and staff needed). DEDUCTIONS: -0.25 for complex dual-license system (separate requirements for casino vs web shop), -0.25 for extensive employee licensing requirements (all gaming staff must be individually licensed: Gaming House License $250K, Gaming Employee License $150, Key Employee License $250 – adds administrative burden). REALITY: Casino operators must build/operate integrated resorts. Web shops require physical locations across islands plus online platform. Remote operation is NOT possible. |

| Market Environment | 10% | 0.7/1.0 | MATH: Started at +1.0 (excellent business environment – high GDP per capita $33,968, strong tourism infrastructure, English-speaking, USD-pegged currency). DEDUCTIONS: -0.25 for regulatory instability (proposed changes to casino residency restrictions create uncertainty), -0.05 for market concentration risk (3 casino operators, 7 web shops already saturated in tiny market). POSITIVES: Pro-business environment, no income tax, stable currency, strong internet/mobile infrastructure (94.8% internet penetration). |

OPERATOR EASE TOTAL: 3.2/10

CALCULATION: (0.5×30% + 0.25×25% + 1.25×20% + 0.5×15% + 0.7×10%) × 10 = 3.2

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.5/4.0 | MATH: Started at +2.0 (partially legal – Bahamian residents can access web shops, tourists can access casinos). DEDUCTIONS: -0.5 for discriminatory restrictions (Bahamian citizens, permanent residents, work permit holders, and their spouses are LEGALLY BANNED from all casino gambling – this affects 100% of the 403,000 resident population). WHAT PLAYERS CAN ACCESS: Residents: Web shop gaming only (lotto, slots, sports betting). Tourists: Casino gaming only. WHAT’S PROHIBITED: Residents cannot enter casinos or play casino games. International online casino access for residents unclear/grey area. |

| Practical Accessibility | 30% | 2.5/3.0 | MATH: Started at +3.0 (multiple payment methods, no ISP blocking mentioned). DEDUCTIONS: -0.5 for limited product access (residents restricted to web shop offerings only, cannot access full casino product range available to tourists). PAYMENT METHODS: Local banking integration exists. Bahamian dollar pegged 1:1 with USD simplifies transactions. No mention of credit card bans or crypto restrictions. ACCESS: Web shops operate via internet/mobile platforms. 94.8% internet penetration and 87.3% mobile connection rate support accessibility. No VPN required. |

| Player Penalties | 20% | 2.0/2.0 | MATH: Full +2.0 points – no penalties for players mentioned. Players are not prosecuted for gambling in licensed web shops (residents) or licensed casinos (tourists). ENFORCEMENT: Regulations target operators, not individual players. Residents attempting to enter casinos are simply denied entry (enforcement at casino level, not criminal prosecution). |

| Market Availability | 10% | 0.5/1.0 | MATH: Started at +0.7 (2-4 licensed operators for resident market). DEDUCTIONS: -0.2 for extreme market segmentation (residents have access to 7 web shop operators but ZERO casino operators; tourists have access to 3 casino operators but cannot use web shops). REALITY: While 10 total licensed operators exist (3 casinos + 7 web shops), each population segment has restricted access. Web shop market already saturated serving 403K residents. |

PLAYER ACCESS TOTAL: 4.5/10

CALCULATION: (1.5×40% + 2.5×30% + 2.0×20% + 0.5×10%) × 10 = 4.5

🔍 Key Highlights

Strengths (Limited)

- Zero Income Tax Regime: No corporate income tax or personal income tax – significant financial advantage for profitable operations

- High GDP Per Capita: $33,968 (second-highest in English-speaking Caribbean) indicates strong purchasing power for discretionary gambling spending

- Excellent Digital Infrastructure: 94.8% internet penetration, 87.3% mobile connections, comprehensive 4G LTE coverage supports online/mobile gaming

- Tourism Infrastructure: 8+ million annual tourists (85% American) create substantial casino customer base – though residents cannot participate

- Currency Stability: Bahamian dollar pegged 1:1 with USD eliminates exchange rate risk, simplifies payment processing

- English-Speaking Market: Official language is English, reducing localization barriers and operational complexity

⛔️ CRITICAL RISKS AND CHALLENGES

- [Product Prohibitions – DISCRIMINATORY SYSTEM:] Bahamian citizens, permanent residents, and work permit holders are LEGALLY BANNED from casino gambling. This affects 100% of the 403,000 resident population. Casinos can only serve foreign tourists. This discriminatory dual-market system eliminates local casino revenue entirely and creates operational complexity. Gaming Board Chairman has called for changes, but legislation remains pending with no implementation timeline.

- [International Online Gaming BANNED:] Operating online gaming websites from The Bahamas targeting international markets is explicitly prohibited. This eliminates offshore operator business models entirely. Only licensed web shops serving domestic residents and licensed casinos serving tourists are permitted.

- [Micro-Market Economics:] Total population of only 403,000 creates extremely limited addressable market. Web shop market already saturated with 7 licensed operators competing for same small customer base. Tourism casino market limited to 8M annual visitors but highly seasonal and concentrated in Nassau (67% of population). Scaling challenges make this market economically unviable for large international operators.

- [Extreme Licensing Scarcity:] Only 7 total casino licenses exist, with 6 already operational. One remaining license has been available for years in Exuma/Grand Bahama without takers – suggesting poor commercial viability. Web shop licensing exists but market saturation makes new entry unprofitable. License availability does NOT equal opportunity.

- [Tourism Dependency Risk – 100%:] Casino operations are 100% dependent on foreign tourism. 85% of tourists are American – making operations extremely vulnerable to US economic conditions, travel restrictions (COVID demonstrated this), US-Bahamas relations, and airline capacity. No domestic casino revenue stream exists as backup.

- [High Island Operating Costs:] All operational costs significantly exceed comparable markets due to island economy. Salaries, rent, utilities, imported goods, and infrastructure costs are premium-priced. Despite favorable tax rates, total cost structure makes profitability challenging.

- [Integrated Resort Requirements:] Casino licensing requires development/operation of integrated resort properties with hotels, restaurants, amenities. This creates multi-hundred-million dollar capital requirements, eliminating pure iGaming operators from market consideration. Only major international resort developers can participate.

- [Regulatory Uncertainty:] Proposed legislation to allow Bahamian residents in casinos has been “coming soon” for years without implementation. Gaming Board Chairman publicly advocates for changes but Parliamentary action remains uncertain. Operators cannot build business plans around potential future reforms.

Player-Specific Issues

- Discriminatory Access Restrictions: Bahamian citizens, permanent residents, work permit holders, and their spouses are legally prohibited from entering casinos or playing casino games – despite casinos being located in their own country

- Limited Product Range for Residents: Residents can only access web shop gaming (lotto, slots, sports betting) – no access to full casino table games, poker, premium gaming experiences available to tourists

- No Choice of Operator Type: Residents cannot choose between casino and web shop experiences – legally restricted to web shops only regardless of preference or financial capability

- Market Saturation: Only 7 licensed web shop operators serve 403,000 residents – limited competitive pressure may result in less favorable player conditions (odds, bonuses, customer service)

- Tourist-Only Casino Policy: Creates two-tier system where wealthy Bahamians cannot gamble in world-class casinos in their home country while tourists can – social inequality criticism ongoing

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required:

- Casino Operator: $100M-500M+ (integrated resort development including hotel, casino, restaurants, amenities) – Baha Mar cost exceeded $3.5B

- Web Shop Operator: $2M-5M (physical locations across islands, online platform development, licensing, working capital)

Annual Operating Costs:

- Casino: $50M-150M+ annually (resort operations, 1,950+ licensed staff across 3 properties, premium island costs)

- Web Shop: $2M-8M annually (7 operators employ 2,800 total staff, physical locations, technology, compliance, marketing in saturated market)

Effective Tax Rate on Revenue:

- Web Shop: 11% GGR tax + 0% corporate tax = 11% total (excellent)

- Casino: Tax structure not publicly disclosed but likely favorable given zero corporate income tax regime

- ADVANTAGE: Zero income tax is significant benefit offsetting high operational costs

Customer Acquisition Cost:

- Web Shop Market: $500-1,000+ per customer (7 competitors fighting for 403K residents = aggressive marketing required, limited geographic scale makes digital marketing inefficient)

- Casino Market: Lower per-tourist due to resort integrated marketing, but tourism dependency creates volatility

Time to Breakeven:

- Casino: 7-15+ years (massive upfront resort investment, tourism seasonality, limited to Nassau/Freeport areas)

- Web Shop: 3-5 years IF you can capture meaningful market share from 7 entrenched competitors (unlikely for new entrant)

Time to Positive ROI:

- Casino: 10-20+ years for resort investment to generate positive returns

- Web Shop: 5-8 years if successful (but market saturation makes new entry success highly questionable)

Profitability Assessment:

CASINO OPERATIONS: Only viable for major international resort developers with $100M+ capital and integrated resort expertise. Casino gaming is secondary revenue stream supporting overall resort profitability – not standalone business. 100% tourism dependency creates extreme seasonality and external risk. Market limited to 3 licenses in prime locations (Nassau, Bimini). ROI timeline exceeds 10 years. NOT suitable for pure iGaming operators.

WEB SHOP OPERATIONS: Economics are PROHIBITIVE for new entrants. Market already saturated with 7 licensed operators serving only 403,000 residents. Customer acquisition costs of $500-1,000 in tiny market make scaling impossible. Even if you capture 10% market share (optimistic), that’s only 40,000 customers – insufficient to cover operational costs and generate meaningful returns. High island operating costs further compress margins. Market entry NOT recommended.

BOTTOM LINE: This micro-market only makes economic sense for existing operators defending market share or for resort developers where casino is amenity supporting broader hospitality business. Pure iGaming operators should avoid entirely.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Licensed Casino Operators | Low-Medium | Clear legal framework for tourist-serving casinos. Main risks: (1) Tourism dependency vulnerability to external shocks, (2) Regulatory change uncertainty if resident casino access approved, (3) Compliance burden with Gaming Board oversight, (4) Reputational risk from discriminatory access policies |

| Licensed Web Shop Operators | Low | Regulated domestic market with clear legal status. Risks: (1) Market saturation limiting growth, (2) Potential tax increases if government revenue needs increase, (3) Regulatory changes to product offerings, (4) Gaming Board compliance requirements and monitoring fees ($250K annual) |

| Unlicensed Offshore Operators | High | International online gaming from Bahamas-based websites is explicitly PROHIBITED. Operators attempting to use Bahamas as offshore base face: (1) Gaming Board enforcement action, (2) Website shutdown, (3) Financial penalties, (4) Potential criminal charges. No safe harbor exists. |

| International Online Operators Targeting Bahamians | Medium | Legal status unclear/grey area. Risks: (1) Potential ISP blocking if Gaming Board takes enforcement action, (2) Payment processing difficulties, (3) Regulatory uncertainty if government decides to enforce against international access, (4) Customer acquisition limited by small population (403K) |

| Affiliates/Advertisers | Low-Medium | Legal framework focuses on operator licensing – affiliate/advertiser enforcement not emphasized. Risks: (1) Potential restrictions on advertising if government tightens regulations, (2) Reputational risk from promoting casinos Bahamians cannot access, (3) Limited market size (403K residents) makes affiliate economics challenging |

| Payment Processors | Low | Banking system cooperates with licensed operators. Risks: (1) Must verify operator licensing status, (2) Potential restrictions if processing for unlicensed operators, (3) USD-pegged currency simplifies compliance |

| Company Directors/Executives | Low | Operating licensed casinos or web shops creates minimal personal liability. Risks: (1) Probity checks during licensing process, (2) Gaming Board oversight and potential penalties for violations, (3) Reputational risks if involved in unlicensed operations. No extradition risk for licensed operators. |

🚨 Extradition and International Enforcement

Extradition Treaties: The Bahamas maintains extradition agreements with: United States, United Kingdom, Canada, and various Commonwealth nations. Strong US-Bahamas relations (85% of tourists are American) create close law enforcement cooperation.

Enforcement History: No documented cases of gambling-related extradition from The Bahamas. Gaming enforcement focuses on licensing compliance rather than international prosecution. However, The Bahamas cooperates with US authorities on financial crimes, drug trafficking, and other serious offenses.

Safe Jurisdictions: Standard list applies – Russia, China, some CIS countries lack extradition agreements. Not relevant for legitimate licensed operators but critical for anyone considering unlicensed operations.

Travel Risk: LOW for licensed operators. Gaming Board provides clear legal framework – directors/executives of licensed casinos and web shops face no international travel restrictions. HIGH for anyone operating unlicensed gaming sites using Bahamas as base – could face arrest when traveling through countries with US/UK extradition agreements.