Bahrain presents a unique and highly challenging market for iGaming operators due to its complete prohibition of all gambling activities under Islamic law. Despite exceptional digital infrastructure, high GDP per capita, and sophisticated payment systems, the Kingdom maintains strict enforcement of gambling bans through legislative measures and technological censorship.

This comprehensive analysis examines the regulatory environment, market demographics, technology infrastructure, and business conditions in Bahrain. While legal gambling operations are not currently possible, this report provides essential insights for operators monitoring potential future regulatory developments in the Gulf region.

Executive Summary: Key Market Indicators

| Indicator | Value | Implications |

|---|---|---|

| Gambling Legal Status | Completely Illegal | All forms prohibited under Sharia law |

| Regulatory Framework | No Licensing System | Zero legal pathway for operators |

| Licensed Operators | 0 (Zero) | No legal iGaming market exists |

| Market Size | Not Applicable | Underground market only |

| Total Population | 1.64 million | Small but affluent market |

| GDP Per Capita | $30,616 (2022) | High disposable income levels |

| Internet Penetration | 99.0% | Exceptional digital connectivity |

| Mobile Connections | 2.52 million (155% of population) | High mobile device ownership |

| Median Age | 33.4 years | Young, tech-savvy population |

| Urbanization Rate | 100% | Entirely urban population |

| Penalty for Public Gambling | BD 300 fine + 3 months imprisonment | Severe legal consequences |

| Penalty for Operators | BD 1,000 fine + 1 year imprisonment | High enforcement risk |

| Website Blocking | ISP-level censorship | Systematic access restriction |

| Corporate Income Tax | 0% (general businesses) | No tax for non-oil sectors |

| Personal Income Tax | 0% | No individual taxation |

| VAT Rate | 10% | Standard consumption tax |

| Average Household Income | ~$50,000 annually | Strong purchasing power |

| Mobile Internet Speed | 118.36 Mbps (median) | 5th fastest globally |

| Fixed Internet Speed | 86.33 Mbps | Excellent broadband quality |

| Smartphone Penetration | 95%+ | Universal mobile access |

| Social Media Users | 1.19 million (73.2%) | High digital engagement |

| E-commerce Growth | Rapid expansion | Digital payment adoption |

| Banking Sector | 400+ financial institutions | Regional financial hub |

| Ease of Doing Business | 43rd globally (2019) | Business-friendly environment |

| Expatriate Population | 52.6% of total | Diverse international workforce |

| English Proficiency | High (business language) | International communication ease |

| Political Stability | Moderate | Stable but conservative governance |

| Regulatory Change Probability | Very Low (short-term) | Religious foundations unlikely to shift |

| Market Entry Recommendation | Not Viable | Legal operations impossible |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

The Kingdom of Bahrain maintains an absolute prohibition on all forms of gambling, rooted in Islamic Sharia law principles. As one of the earliest regions to convert to Islam in AD 628, Bahrain’s legal system is heavily influenced by religious jurisprudence.

Land-Based Gambling Activities

Casino Operations: Completely prohibited with no exceptions. No casino licenses exist, and no legal framework permits casino establishments. The construction or operation of any casino facility would result in immediate prosecution and business closure.

Sports Betting Venues: All sports betting is illegal, including wagering on international events such as the Bahrain Grand Prix and Formula One races. Despite Bahrain hosting major sporting events, no betting facilities or licensed bookmakers operate within the Kingdom.

Slot Machine Halls: Electronic gaming machines are entirely banned. No gaming establishments, amusement centers with gambling elements, or slot machine operations are permitted under any circumstances.

Lottery and Bingo: No state lottery exists, and private lottery operations are criminalized. Bingo halls, raffle competitions, and similar games of chance are prohibited regardless of charitable or commercial purposes.

Online Gambling Framework

Digital Gaming Regulations: Article 308 of the Bahrain Penal Code addresses gambling primarily in the context of public spaces but is interpreted to extend to all gambling forms. While the legislation does not explicitly mention online gambling, telecommunications regulators actively block access to gambling websites.

Prohibited Activities: All forms of online gambling are illegal, including online casinos, sports betting platforms, poker rooms, daily fantasy sports, esports betting, and virtual slot machines. The prohibition extends to both local operators and foreign platforms serving Bahraini residents.

Regulatory Body Structure: The Information Affairs Authority oversees internet censorship and blocks gambling-related websites at the ISP level. The Central Bank of Bahrain monitors financial transactions, though banks do not systematically block gambling-related payments. The Ministry of Interior enforces gambling laws through criminal prosecution.

Licensed Operators and Market Players

Licensed Operator Count: Zero legal operators exist. No iGaming licenses have been issued, and no regulatory pathway exists for obtaining gambling licenses of any kind.

Market Presence: International offshore operators serve Bahraini players through websites and mobile applications despite the prohibition. Players access these platforms using VPN technology to bypass ISP-level website blocking. No operator maintains legal status or physical presence in Bahrain.

Underground Market Characteristics: Bahraini residents access international gambling sites, particularly those accepting cryptocurrency payments and offering VPN-compatible platforms. Exact market size is impossible to quantify due to illegal status, but anecdotal evidence suggests thousands of Bahrainis engage in online gambling through offshore platforms.

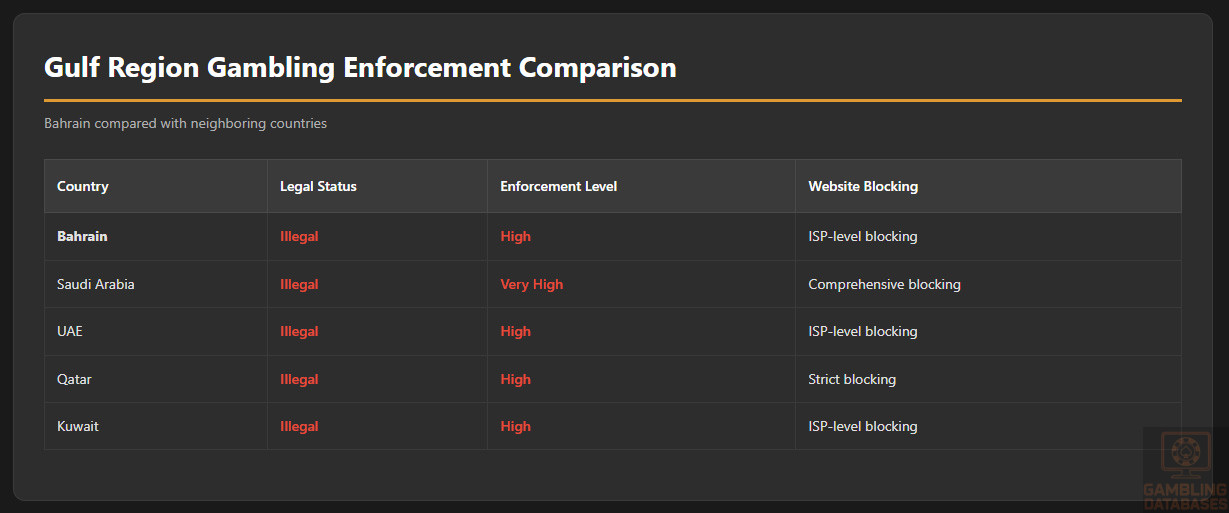

| Country | Legal Status | Enforcement Level | Website Blocking |

|---|---|---|---|

| Bahrain | Illegal | High | ISP-level blocking |

| Saudi Arabia | Illegal | Very High | Comprehensive blocking |

| UAE | Illegal | High | ISP-level blocking |

| Qatar | Illegal | High | Strict blocking |

| Kuwait | Illegal | High | ISP-level blocking |

Licensing Framework and Requirements

Regulatory Authority: No gambling regulatory authority exists in Bahrain. The government has not established any licensing framework, application process, or oversight body for gambling operations.

License Types: Not applicable. No gambling licenses are available, including for online casinos, sports betting, poker, bingo, lottery, or any other gambling category.

Application Process: No application process exists. Inquiries about gambling licenses would be rejected immediately, and persistent attempts could trigger investigation by authorities.

Application Process and Eligibility

Financial Requirements: Not applicable due to complete prohibition.

Technical Standards: Not applicable. No certification processes exist for gambling platforms or gaming equipment.

Background Checks: Not relevant, as no licensing pathway exists.

Minimum Capital Requirements: Not applicable.

Local Presence and Operational Requirements

Physical Presence Mandates: Establishing any gambling-related business entity would be illegal and result in immediate prosecution. Company registration systems would reject gambling-related business classifications.

Domain and Hosting: Bahraini domain registrars would refuse gambling-related domains. Local hosting providers cannot legally host gambling platforms. International operators attempting to serve Bahraini players face systematic ISP-level blocking.

Personnel Requirements: Employing staff for gambling operations would constitute criminal activity. Job postings for gambling-related positions would likely trigger regulatory scrutiny.

Foreign Ownership: Irrelevant, as no gambling operations can be legally established regardless of ownership structure.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification: Not applicable under current prohibition. Offshore operators serving Bahraini players implement their own age verification procedures based on their licensing jurisdiction requirements.

KYC/AML Compliance: No gambling-specific KYC requirements exist domestically. Banks and financial institutions follow standard Central Bank of Bahrain anti-money laundering regulations, which do not specifically address gambling transactions.

Responsible Gambling Measures: No mandated responsible gambling framework exists, as legal gambling operations do not exist. Offshore operators may offer responsible gambling tools based on their home jurisdiction requirements.

Self-Exclusion Systems: Not applicable domestically. Players accessing offshore platforms rely on those operators’ self-exclusion programs.

Financial Monitoring and Reporting

Transaction Monitoring: Banks do not systematically monitor or block gambling-related transactions, though authorities could potentially investigate suspicious payment patterns. Many Bahraini players use e-wallets and cryptocurrency to maintain anonymity.

Reporting Requirements: No gambling-specific reporting requirements exist because legal operations are prohibited.

Audit Procedures: Not applicable in absence of legal gambling operations.

Taxation Structure and Financial Obligations

Player Taxation

Tax on Winnings: Not applicable because gambling is illegal. Bahrain imposes no personal income tax on residents, so even if gambling were legal, winnings would likely be tax-free.

Player Tax Obligations: Players accessing offshore gambling sites face no tax obligations on winnings due to Bahrain’s zero personal income tax policy. However, engaging in illegal gambling exposes players to potential criminal penalties.

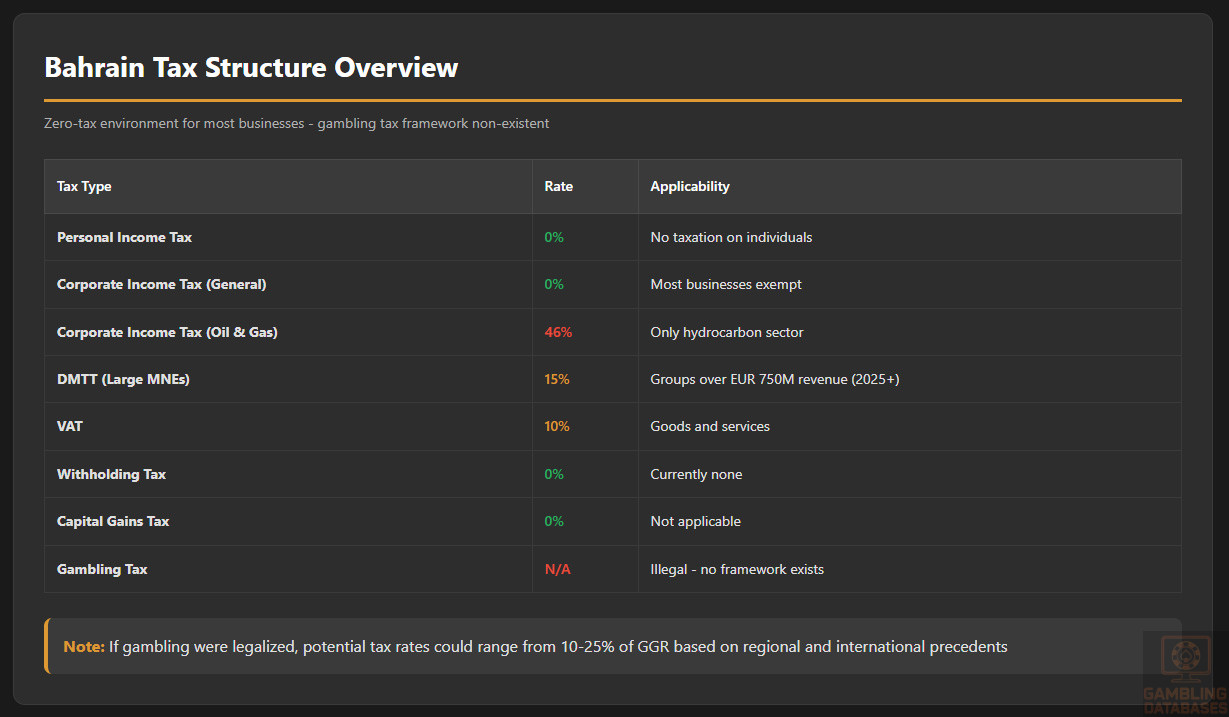

| Tax Type | Rate | Applicability |

|---|---|---|

| Personal Income Tax | 0% | No taxation on individuals |

| Corporate Income Tax (General) | 0% | Most businesses exempt |

| Corporate Income Tax (Oil & Gas) | 46% | Only hydrocarbon sector |

| DMTT (MNEs) | 15% | Large multinationals only (2025+) |

| VAT | 10% | Goods and services |

| Withholding Tax | 0% | Currently none |

| Capital Gains Tax | 0% | Not applicable |

Operator Taxation

Gambling-Specific Taxation: Not applicable. No legal operators exist, and no tax regime exists for gambling operations.

Hypothetical Taxation Scenario: If gambling were legalized, Bahrain’s zero corporate income tax policy would theoretically apply. However, the government would likely introduce gambling-specific taxation similar to VAT or excise taxes to generate revenue. Based on regional and international precedents, potential tax rates could range from 10% to 25% of gross gaming revenue.

Current Corporate Tax Environment: Bahrain implemented a 15% Domestic Minimum Top-Up Tax in January 2025 for multinational enterprise groups with consolidated annual revenues exceeding EUR 750 million. General businesses operating outside the oil and gas sector pay zero corporate income tax.

Future Tax Developments: Bahrain’s government presented draft 2025-26 budget plans including potential introduction of general corporate income tax for the first time. This represents a significant fiscal policy shift as the Kingdom diversifies away from oil dependency.

Gambling Market Financial Performance

Legal Market Revenue: Zero. No legal gambling market exists.

Underground Market Estimates: Impossible to quantify accurately. Bahraini residents accessing offshore gambling platforms likely generate millions of dollars in wagering volume annually, but no official data exists. These funds flow entirely to international operators, generating zero tax revenue for Bahrain.

Potential Market Size: Based on Bahrain’s affluent population, high internet penetration, and regional gambling participation rates in neighboring countries, a legalized gambling market could potentially generate $50-150 million in annual gross gaming revenue. This remains purely theoretical given the prohibition.

Advertising and Marketing Restrictions

Complete Advertising Ban: All gambling advertising is prohibited in Bahrain across every medium and channel. This prohibition applies to television, radio, print media, outdoor advertising, digital platforms, social media, and any other communication channel.

Permitted Channels: None. No gambling advertising is legally permitted.

Content Restrictions: Any content promoting, encouraging, or facilitating gambling is illegal. This extends to editorial content, sponsored articles, influencer marketing, and affiliate websites.

Sponsorship Regulations: Sports teams, events, and venues cannot accept gambling sponsorships. Despite Bahrain hosting international sporting events like Formula One, gambling company sponsorships visible in international broadcasts remain prohibited domestically.

Affiliate Marketing: Operating gambling affiliate websites targeting Bahraini players would be illegal. Earning commissions from directing Bahraini players to offshore gambling sites could constitute facilitation of illegal gambling.

Marketing to Minors: Extremely strict prohibition, though enforcement is unnecessary given the complete gambling ban.

Recent Regulatory Changes and Their Impact

No Liberalization Trend: Unlike some jurisdictions that have moved toward regulated gambling markets, Bahrain has maintained its absolute prohibition. No legislative proposals or policy discussions suggest any movement toward gambling legalization or regulation.

Strengthened Enforcement: In June 2014, Bahrain’s Parliament discussed implementing harsher penalties for gambling, reflecting the government’s commitment to strict enforcement. Proposed amendments included increased fines and longer prison terms for repeat offenders.

Internet Censorship Enhancement: Since 2009, Bahrain has significantly expanded website blocking through the Information Affairs Authority. Gambling sites are among the primary categories targeted for ISP-level blocking, making access increasingly difficult without VPN technology.

Financial Technology Regulations: While Bahrain has become a progressive fintech hub in the Gulf region, gambling-related payment processing remains strictly prohibited. The Central Bank’s regulatory sandbox and innovation initiatives explicitly exclude gambling technologies.

Enforcement Mechanisms and Penalties

| Offense | Fine (BHD) | Imprisonment | Additional Consequences |

|---|---|---|---|

| Public Gambling (First Offense) | 300 | Up to 3 months | Criminal record |

| Public Gambling (Repeat Offense) | 500 | Up to 1 year | Enhanced penalties |

| Operating Gambling House | 1,000 | 1 year | Business closure, license revocation |

| Commercial Gambling Venue | 1,000+ | 1 year+ | Permanent closure, asset seizure |

Criminal Prosecution: Article 308 of the Bahrain Penal Code defines gambling as a criminal offense. Conviction results in criminal record, affecting future employment, visa applications, and professional licensing.

Business Closure: Commercial establishments hosting gambling activities face immediate closure and permanent license revocation. The government shuts down venues and prevents reopening under any business classification.

ISP Blocking: Telecommunications regulators maintain blacklists of gambling websites and systematically block access at the ISP level. New gambling sites are added to blocking lists regularly, though VPN usage remains legal and common.

Payment Processor Restrictions: While banks do not systematically block gambling payments, financial institutions could face regulatory scrutiny for facilitating illegal activity. International payment processors operating in Bahrain generally comply with local gambling prohibitions.

Enforcement Priority: Authorities focus primarily on shutting down illegal gambling operations rather than prosecuting individual players. Cases of prosecution for private gambling are extremely rare, with enforcement targeting commercial operators and public gambling activities.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Bahrain’s population reached 1.64 million in 2025, representing one of the smallest but most affluent populations in the Gulf region. The Kingdom experiences steady population growth driven primarily by expatriate immigration rather than natural increase.

The median age of 33.4 years indicates a young, economically active population with strong technology adoption. This demographic profile typically correlates with higher digital service consumption and entertainment spending in markets where gambling is legal.

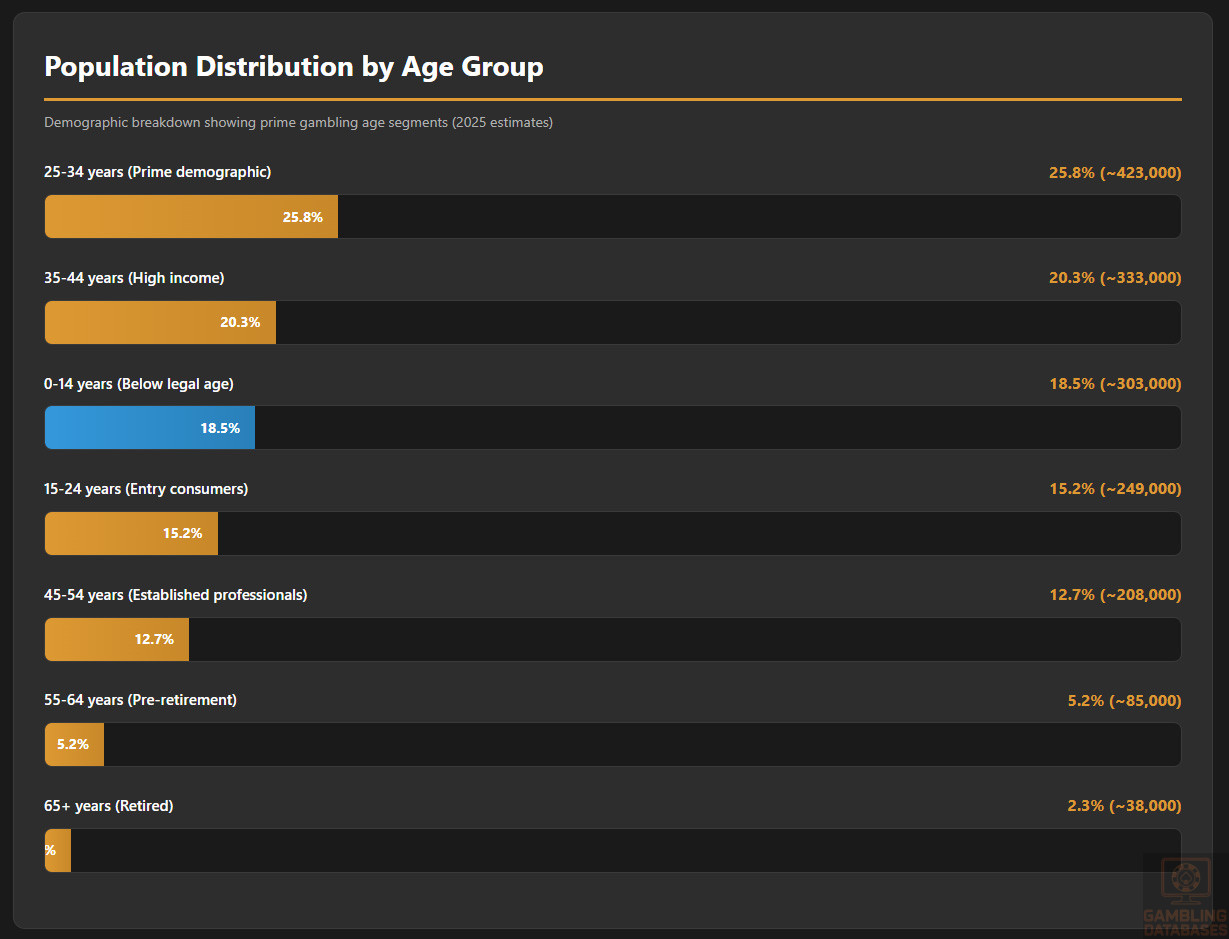

| Age Group | Percentage | Estimated Population | Gambling Market Relevance |

|---|---|---|---|

| 0-14 years | 18.5% | ~303,000 | Below legal age |

| 15-24 years | 15.2% | ~249,000 | Entry-level consumers |

| 25-34 years | 25.8% | ~423,000 | Prime gambling demographic |

| 35-44 years | 20.3% | ~333,000 | High disposable income |

| 45-54 years | 12.7% | ~208,000 | Established professionals |

| 55-64 years | 5.2% | ~85,000 | Pre-retirement cohort |

| 65+ years | 2.3% | ~38,000 | Retired population |

Gender Distribution: Males comprise approximately 63% of the total population (1.03 million), while females represent 37% (607,000). This male-skewed ratio results from large expatriate worker populations, predominantly male laborers in construction and service sectors.

Life Expectancy: Bahraini citizens enjoy life expectancy of 78.2 years (76 years for males, 80.3 years for females), reflecting excellent healthcare infrastructure and high living standards.

Geographic Distribution

Bahrain is 100% urbanized, with the entire population residing in urban areas across five governorates. This complete urbanization facilitates uniform internet access and digital service penetration.

| City/Governorate | Population | Economic Significance |

|---|---|---|

| Manama (Capital) | 157,000 (metro: 330,000) | Financial and business hub |

| Muharraq | ~200,000 | Industrial and residential |

| Northern Governorate | ~450,000 | Most densely populated |

| Central Governorate | ~350,000 | Mixed residential/commercial |

| Southern Governorate | ~210,000 | Oil industry presence |

Population Density: At 2,162 people per square kilometer, Bahrain ranks among the world’s most densely populated countries. The northern region is so densely populated it effectively functions as a single metropolitan area.

Internet Access Geographic Patterns: Universal internet penetration across all regions eliminates geographic barriers to digital service access. No significant urban-rural divide exists due to complete urbanization.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

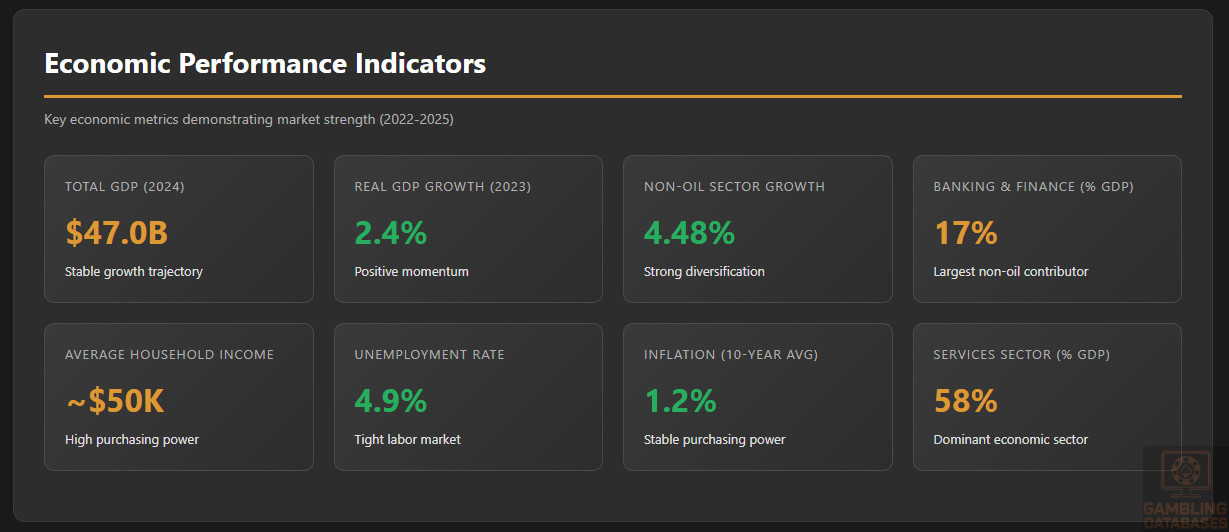

Bahrain’s economy demonstrates resilience and diversification success, moving beyond oil dependency toward financial services, manufacturing, and tourism. The Kingdom achieved 2.4% real GDP growth in 2023, with non-oil sector expansion of 4.48% highlighting successful economic diversification efforts.

| Indicator | Value | Trend |

|---|---|---|

| Total GDP (Nominal, 2024) | $47.0 billion | Stable growth |

| GDP Per Capita (2022) | $30,616 | High income economy |

| GDP Per Capita (2025 est.) | $29,142 | Slight adjustment |

| Real GDP Growth (2023) | 2.4% | Positive momentum |

| Non-Oil Sector Growth (2023) | 4.48% | Strong diversification |

| Banking & Finance (% of GDP) | 17% | Largest non-oil contributor |

| Average GDP Growth (2014-2023) | 2.9% | Stable decade average |

Economic Sector Composition: Services dominate at 58% of GDP, followed by industry at 39% and agriculture at 3%. The financial services sector alone contributes 17% of GDP, establishing Bahrain as the Gulf’s premier banking center.

Employment and Wages: Unemployment averages 4.9%, indicating a tight labor market. Mean wages reached $19.81 per man-hour in 2009 data, significantly higher than regional developing economies.

Inflation Trends: Bahrain maintained low inflation averaging 1.2% over the past decade, supporting stable purchasing power and consumer spending capacity.

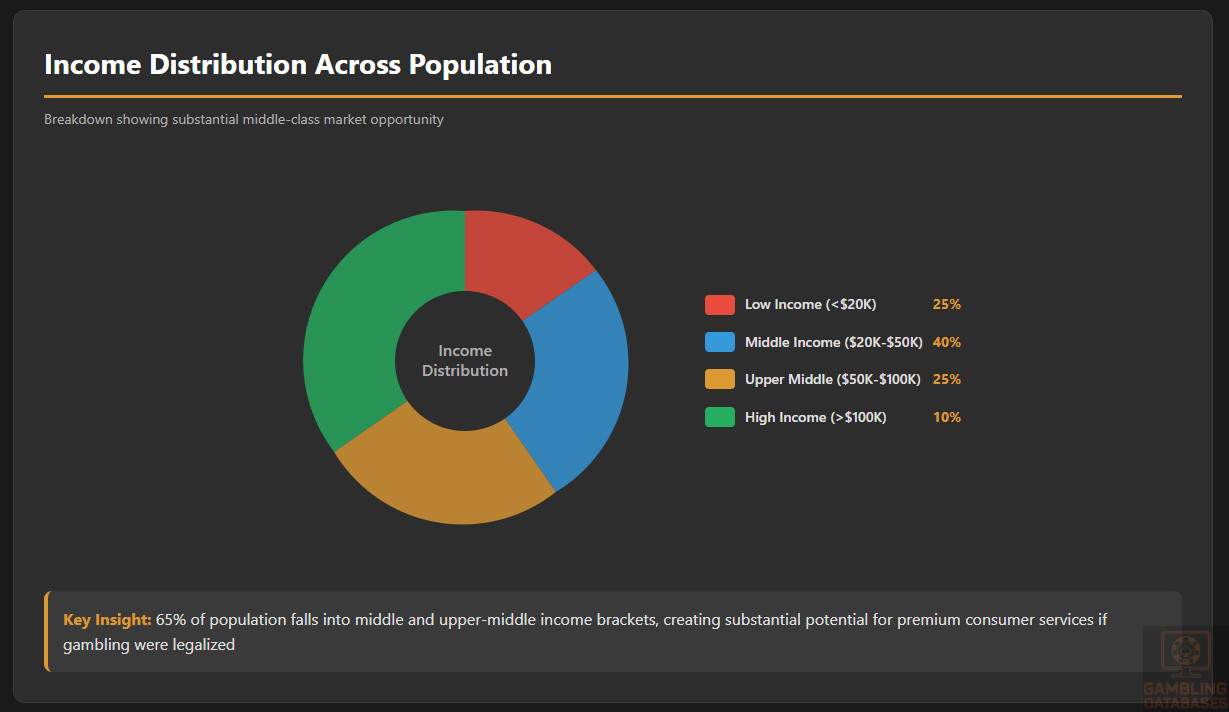

Income and Wealth Distribution

Average Household Income: Bahraini households average approximately $50,000 annually, placing the population among the Gulf’s most affluent. This high income level creates substantial disposable income for entertainment and discretionary spending.

Income Inequality: While specific Gini coefficient data is limited, Bahrain exhibits moderate income inequality typical of Gulf economies. The large expatriate population creates distinct income tiers, with high-earning professionals and low-wage laborers.

Disposable Income Trends: High income levels combined with zero personal income tax result in exceptional disposable income. Households retain full earnings after only modest social insurance contributions, maximizing spending capacity.

Consumer Spending Patterns: Bahrainis demonstrate strong propensity for discretionary spending on entertainment, dining, travel, and luxury goods. The population’s affluence supports premium service consumption when legal options exist.

| Income Bracket | Estimated % of Population | Characteristics |

|---|---|---|

| Low Income (<$20,000) | 25% | Primarily low-wage expatriate workers |

| Middle Income ($20,000-$50,000) | 40% | Skilled workers, mid-level professionals |

| Upper Middle ($50,000-$100,000) | 25% | Senior professionals, business owners |

| High Income (>$100,000) | 10% | Executives, wealthy Bahraini citizens |

Middle Class Size: Approximately 65% of the population falls into middle and upper-middle income brackets, creating substantial mass-market opportunity for consumer services in a legalized gambling environment.

Market Size and Growth Projections

Current iGaming Market: Zero legal market exists. All gambling activity occurs through offshore platforms accessed via VPN, generating no domestic economic benefit or tax revenue.

Theoretical Market Potential: Based on comparable markets with similar GDP per capita and internet penetration, Bahrain could support an iGaming market of $80-150 million in annual gross gaming revenue if legalized. This projection assumes 15-25% population participation at average annual spending of $300-500 per active player.

Regional Comparison: Legal gambling markets in countries with similar economic profiles typically achieve 20-35% adult participation rates. Applying conservative 15% participation to Bahrain’s adult population of 1.34 million yields approximately 200,000 potential players.

| Scenario | Participation Rate | Active Players | ARPU (Annual) | Market Size (GGR) |

|---|---|---|---|---|

| Conservative | 10% | 134,000 | $400 | $53.6 million |

| Moderate | 15% | 201,000 | $500 | $100.5 million |

| Optimistic | 20% | 268,000 | $600 | $160.8 million |

Growth Forecast: Not applicable given current prohibition. However, if legalization occurred, Bahrain’s market could achieve 15-25% CAGR in initial years based on pent-up demand and rapid digital adoption patterns.

Revenue Distribution Projection: Sports betting would likely capture 50-60% of market share given regional preferences, online casino games 30-40%, and lottery/other products 5-10%. Mobile gaming would dominate with 75-85% of activity.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy Rates: Bahrain achieves 95.65% adult literacy, with male literacy at 96.92% and female literacy at 93.46%. This high educational attainment supports sophisticated digital service adoption.

Education Levels: Significant portion of population holds tertiary education credentials. Bahrain invests heavily in education infrastructure, producing highly skilled workforce capable of complex technology utilization.

Digital Literacy: Near-universal digital literacy among working-age population reflects extensive smartphone usage, social media engagement, and e-commerce participation. The population navigates complex digital platforms with ease.

Workforce Skills: Bahrain ranks 4th globally in skilled labor and 10th in talent readiness. The workforce demonstrates exceptional capability in financial services, technology, and professional services requiring advanced digital competencies.

English Language Proficiency: High English proficiency among Bahraini nationals and expatriates facilitates interaction with international digital platforms. English serves as primary business language alongside Arabic.

Cultural and Social Factors

Communication and Language

Primary Languages: Arabic serves as official language, with widespread English usage in business and professional contexts. The large expatriate population (52.6% of total) brings diverse linguistic capabilities including Urdu, Hindi, Tagalog, and Bengali.

Internet Language Preferences: Digital content consumption occurs primarily in English and Arabic. International gambling platforms offering Arabic language interfaces would have significant advantage, though English-only platforms remain accessible to most users.

Business Communication Norms: Professional communications typically occur in English. Contract negotiations, technical documentation, and customer service commonly use English, particularly in international business contexts.

Cultural Attitudes

Gambling Acceptance Levels: Official societal stance strongly opposes gambling based on Islamic religious principles. However, underground gambling activity suggests divergence between public prohibition and private behavior among segments of population.

Religious Influences: Islam’s prohibition of gambling (maysir) creates fundamental opposition at religious and legal levels. Approximately 74% of population practices Islam, with strong Shia Muslim majority among Bahraini citizens and significant Sunni populations.

Foreign Brand Perception: Bahrain demonstrates openness to international brands and foreign investment across most sectors. The Kingdom hosts 400+ international financial institutions and welcomes foreign companies. However, gambling remains absolute exception to this openness.

Risk Tolerance: Despite gambling prohibition, Bahrainis demonstrate moderate-to-high risk tolerance in financial markets, entrepreneurship, and investment activities. The sophisticated financial services sector reflects comfort with calculated risk-taking in legal contexts.

Entertainment Preferences: Strong preferences for sports (particularly Formula One, football, and cricket), dining, travel, and digital entertainment. Cinema, gaming cafes, and social entertainment venues thrive, indicating demand for leisure activities.

Problem Gambling and Social Considerations

Prevalence Data: No official statistics exist regarding gambling addiction in Bahrain due to prohibition. The illegal nature of gambling prevents research, treatment infrastructure development, and public health monitoring.

At-Risk Populations: Impossible to identify without legal framework and research infrastructure. However, young males with disposable income and technology access likely face highest risk in markets where gambling is accessible.

Government Response: No problem gambling programs exist, as gambling prohibition theoretically eliminates the issue. Treatment resources for gambling addiction are unavailable, forcing affected individuals to seek help abroad or through general mental health services.

Social Responsibility Requirements: Not applicable under current prohibition. If legalization occurred, Bahrain would need to develop comprehensive responsible gambling frameworks from scratch.

Political Structure and Governance

Government System: Bahrain operates as constitutional monarchy with King Hamad bin Isa Al Khalifa as head of state. Bicameral legislature consists of appointed Consultative Council and elected Council of Representatives.

Political Stability: Moderate stability with occasional social tensions. The Kingdom experienced protests during 2011 Arab Spring but has maintained governmental continuity. Constitutional monarchy provides institutional stability.

Regulatory Consistency: High predictability in business regulations outside politically sensitive areas. Gambling prohibition remains absolute constant with zero indication of policy reconsideration.

Corruption Perception: Bahrain demonstrates relatively low corruption compared to regional standards, though specific index rankings vary by methodology. Business environment generally characterized by transparent processes in regulated sectors.

International Relations: Strong ties with Western nations, particularly United States and United Kingdom. Member of Gulf Cooperation Council alongside Saudi Arabia, UAE, Kuwait, Oman, and Qatar. These relationships influence economic policy but not gambling prohibition.

Technology Adoption and Digital Behavior

Internet and Digital Usage

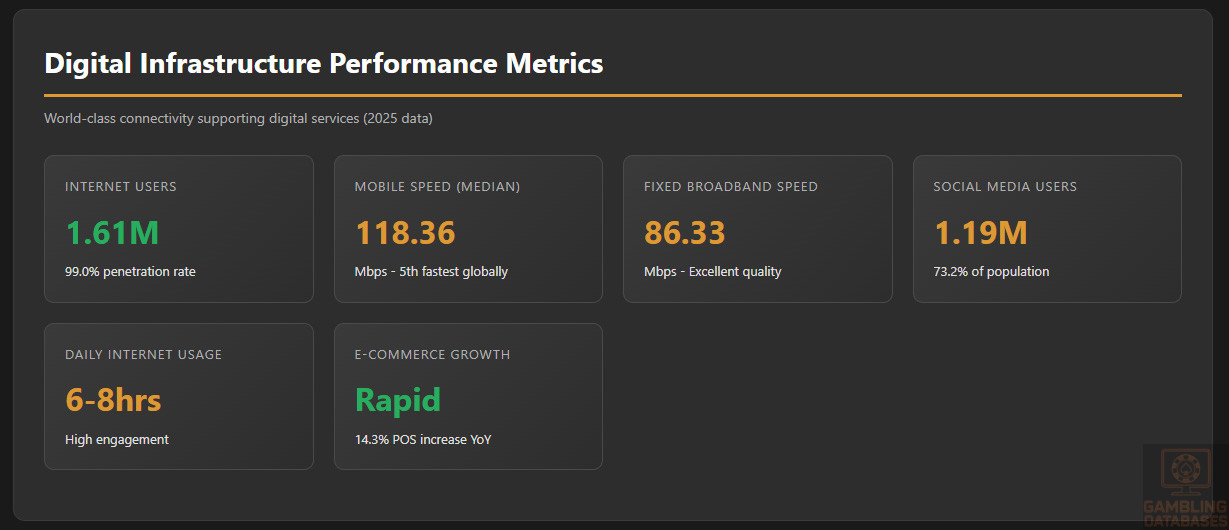

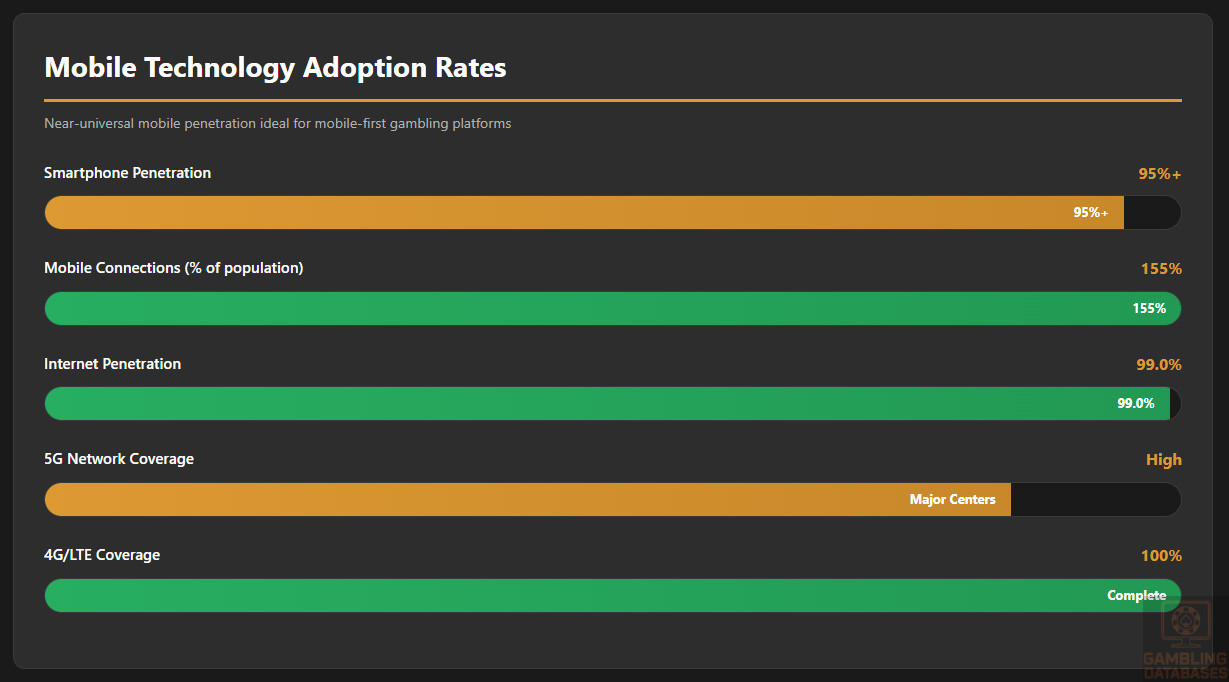

Bahrain leads the Gulf region in digital infrastructure and adoption. The Kingdom achieved 99% internet penetration in 2025, ranking among the world’s most connected nations. This exceptional connectivity creates ideal conditions for digital service delivery.

| Metric | Value | Global Ranking/Context |

|---|---|---|

| Internet Users | 1.61 million | 99.0% penetration rate |

| Year-over-Year Growth | +38,000 users | +2.4% increase |

| Mobile Connections | 2.52 million | 155% of population |

| Median Mobile Speed | 118.36 Mbps | 5th fastest globally |

| Median Fixed Broadband Speed | 86.33 Mbps | Excellent quality |

| Smartphone Penetration | 95%+ | Near-universal adoption |

| Social Media Users | 1.19 million | 73.2% of population |

| Daily Internet Usage | 6-8 hours | High engagement |

Mobile Device Adoption: Multiple mobile connections per capita indicate high device ownership. Users maintain separate personal and work devices, contributing to connection figures exceeding population count.

E-commerce Participation: Rapidly expanding online shopping ecosystem with increasing consumer confidence. Point-of-sale transactions rose 14.3% from 2018 to 2019, reflecting digital payment adoption momentum.

Social Media Engagement: Facebook, Instagram, Twitter, and TikTok dominate social media landscape. High engagement rates create opportunities for digital marketing in legal sectors but remain prohibited for gambling advertising.

Digital Payment Behavior

Bahrain has emerged as Gulf leader in digital payment innovation and adoption. The shift from cash to digital transactions accelerated dramatically, particularly following COVID-19 pandemic.

| Payment Method | Adoption Level | Primary Use Cases |

|---|---|---|

| Credit/Debit Cards | Very High | POS, online shopping, bills |

| BenefitPay | High | P2P transfers, bills, merchants |

| stc pay | High | Mobile payments, remittances |

| Max Wallet (Credimax) | Medium-High | Digital wallet services |

| Bank Transfers (EFTS/Fawri) | Very High | Large transactions, B2B |

| Apple Pay | Medium | Contactless retail payments |

| Cryptocurrency | Growing | Investment, international transfers |

| International E-wallets (PayPal) | Medium | International transactions |

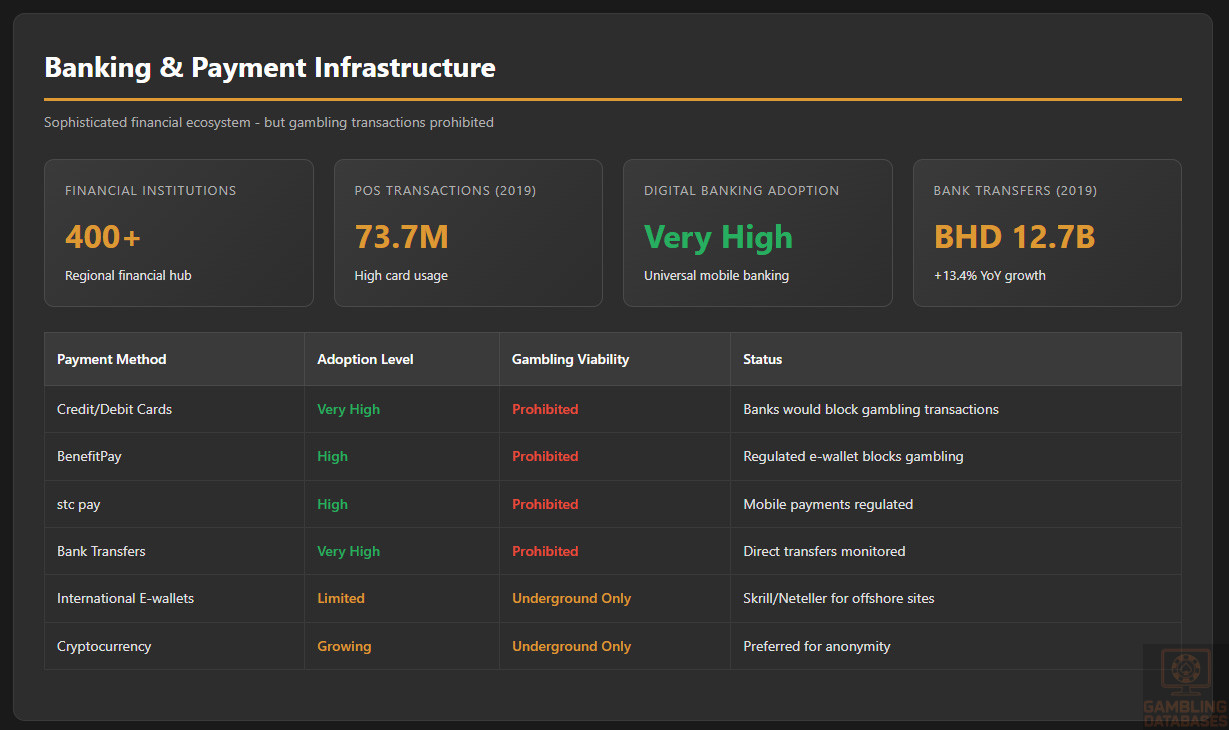

Payment Method Preferences: Card payments dominate with over 73.7 million POS transactions in 2019. E-wallet usage surged, with Electronic Fund Transfer System transfers reaching BHD 12.7 billion in 2019, representing 13.4% year-over-year growth.

Online Transaction Patterns: Increasing frequency and value of digital transactions. COVID-19 drove 1,257% increase in Fawri+ remittances in March 2020 alone, demonstrating rapid behavioral adaptation to digital channels.

Average Transaction Sizes: Varied by payment method. Card transactions average lower values for retail purchases, while bank transfers handle larger amounts for bills and B2B payments.

Trust in Online Payments: High consumer confidence in digital payment security. Sophisticated banking sector infrastructure and Central Bank oversight support trust. eKYC platform implementation further enhances security and user confidence.

Cryptocurrency Adoption: Growing interest in cryptocurrency, particularly Bitcoin and Ethereum. Bahrain positions itself as Gulf cryptocurrency hub, with Central Bank granting licenses to crypto payment service providers like BPay Global (Binance subsidiary) in April 2025.

Gaming and Gambling Preferences

Current Market Participation

Legal Gambling Participation: Zero, as all gambling is illegal. No official statistics measure gambling participation rates.

Underground Market Behavior: Anecdotal evidence suggests thousands of Bahrainis access offshore gambling platforms using VPN technology. Exact numbers remain unknown due to illegal status and users’ discretion.

Popular Activities: Among users accessing offshore platforms, sports betting appears most popular, particularly on football, cricket, and Formula One. Online casino games, especially slots and live dealer games, also attract significant interest.

Sports Betting Preferences: Strong interest in international football leagues (English Premier League, Spanish La Liga, UEFA Champions League), cricket (particularly Indian Premier League), and Formula One racing. Regional football competitions and tennis also generate betting interest.

Consumer Behavior Patterns

Spending Levels: Impossible to determine accurately given underground nature. However, Bahrain’s high disposable income suggests spending per player likely exceeds regional averages in legal markets.

Platform Preferences: Mobile dominance likely mirrors global trends, with 75-85% of activity occurring on smartphones and tablets. Universal smartphone adoption and fast mobile internet speeds support mobile-first gambling behavior.

Peak Activity Times: Likely concentrated in evenings and weekends, with spikes during major sporting events. Ramadan may see altered patterns, though gambling participation during holy month would be particularly controversial.

Session Length: Unknown without access to operator data. However, global iGaming standards suggest 15-30 minute average sessions for sports betting, 20-45 minutes for casino gaming.

Payment Preferences for Offshore Gambling: Users reportedly favor cryptocurrency (Bitcoin, USDT) and international e-wallets (Skrill, Neteller) for anonymity and ease of international transactions. Credit card usage risky due to potential bank scrutiny.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Bahrain boasts world-class internet infrastructure positioning it among global digital leaders. The Kingdom’s investment in telecommunications infrastructure delivers exceptional connectivity speeds and reliability.

Internet Penetration Quality: The 99% penetration rate reflects not merely access but quality connectivity. Fixed broadband and mobile internet both deliver speeds supporting seamless streaming, gaming, and cloud application usage.

| Metric | Performance | Year-over-Year Change |

|---|---|---|

| Median Mobile Download Speed | 118.36 Mbps | -0.68 Mbps (-0.6%) |

| Median Fixed Download Speed | 86.33 Mbps | +5.57 Mbps (+6.9%) |

| Mobile Speed Global Ranking | 5th | Top tier globally |

| Network Reliability | 99%+ uptime | Excellent stability |

Infrastructure Investment: Continuous telecommunications sector investment ensures future-ready infrastructure. Bahrain prioritizes digital economy development as core economic diversification strategy.

Rural-Urban Connectivity: No disparity exists as 100% urbanization ensures uniform infrastructure quality. All residents access identical network performance regardless of location.

5G and Future Technology Deployment

5G Coverage: Bahrain ranks among earliest 5G adopters globally, launching commercial 5G networks in 2019. Current 5G coverage extends across major population centers with ongoing expansion.

4G/LTE Ubiquity: Complete 4G LTE coverage provides backup and ensures connectivity even in areas where 5G deployment remains incomplete. Multiple mobile operators ensure competitive service quality.

Future Plans: Continued 5G expansion and network densification planned. Bahrain’s telecommunications operators invest heavily in infrastructure upgrades supporting emerging technologies including IoT, smart cities, and advanced mobile services.

Network Operator Landscape: Three major mobile operators (Batelco, stc Bahrain, Zain Bahrain) compete vigorously, driving service quality improvements and competitive pricing. This competition benefits consumers through better performance and value.

Mobile Technology Ecosystem

Mobile Network Infrastructure

| Operator | Market Position | Services Offered |

|---|---|---|

| Batelco (Beyon) | Market Leader | Mobile, fixed-line, broadband, data |

| stc Bahrain | Strong Competitor | Mobile, broadband, enterprise solutions |

| Zain Bahrain | Significant Player | Mobile, data services, digital solutions |

Network Quality: All operators deliver excellent 4G/5G coverage with minimal dead zones. Competition ensures continuous quality improvements and network expansion.

Data Costs: Competitive pricing with unlimited data plans widely available. Mobile data affordability supports high consumption rates, enabling video streaming, gaming, and intensive application usage without cost constraints.

Mobile Payment Integration: Seamless integration between mobile operators and payment systems. stc pay exemplifies operator-led mobile wallet success, combining telecommunications and financial services.

Device Penetration

Smartphone Adoption: Exceeding 95% smartphone penetration places Bahrain among world leaders. Multiple device ownership common, with individuals maintaining personal and work smartphones.

Device Preferences: Mix of iOS and Android devices, with slight Android majority reflecting global trends and diverse income levels. Premium device ownership high among affluent citizens and expatriate professionals.

Average Device Specifications: Modern devices with capabilities supporting sophisticated applications. Regular upgrade cycles ensure population uses relatively current hardware capable of latest application features.

Mobile Internet Usage Patterns: Users consume 20+ GB monthly data on average, significantly above global averages. Heavy usage includes video streaming, social media, messaging, and gaming.

Financial Services and Payment Infrastructure

Banking System Structure

Bahrain’s status as Gulf financial hub manifests in sophisticated banking infrastructure. The Kingdom hosts the region’s most diverse and advanced financial services ecosystem.

Bank Count and Diversity: Approximately 400 financial institutions operate in Bahrain, including commercial banks, Islamic banks, wholesale banks, investment banks, and specialized financial institutions. This density creates highly competitive, innovation-driven environment.

| Bank | Type | Market Significance |

|---|---|---|

| Ahli United Bank | Commercial | Leading retail and corporate bank |

| National Bank of Bahrain | Commercial | Largest domestic bank |

| BBK (Bank of Bahrain and Kuwait) | Commercial | Major retail presence |

| Al Baraka Banking Group | Islamic | Leading Islamic banking institution |

| Bahrain Islamic Bank | Islamic | Significant Sharia-compliant banking |

Digital Banking Adoption: Extremely high digital banking penetration with mobile banking apps standard across all major institutions. Banks invest heavily in digital transformation, offering sophisticated online and mobile services.

Account Penetration: High percentage of population maintains bank accounts. Banking infrastructure accessibility and regulatory requirements for employment ensure broad financial system participation.

Credit Markets: Well-developed consumer lending including personal loans, auto financing, and mortgages. Islamic finance products provide Sharia-compliant alternatives, expanding market reach.

Payment Processing Options

Card Infrastructure: All debit cards issued under BENEFIT scheme, Bahrain’s national ATM and POS switch network. This standardization ensures universal acceptance and interoperability.

Credit Card Penetration: High usage of Visa and Mastercard, with American Express and other networks also present. Cards accepted universally at merchants and for online transactions.

| Method | Availability | Gambling Viability | Notes |

|---|---|---|---|

| Credit/Debit Cards | Universal | Prohibited | Banks would block gambling transactions |

| BenefitPay | Widespread | Prohibited | Regulated e-wallet blocks gambling |

| Bank Transfers | Standard | Prohibited | Direct transfers monitored |

| International E-wallets | Limited | Underground Only | Skrill/Neteller used for offshore sites |

| Cryptocurrency | Growing | Underground Only | Preferred for anonymity |

Processing Fees: Competitive merchant fees typically 2-3% for card transactions. E-wallet and bank transfer fees vary by provider but generally remain reasonable.

Transaction Speed: Instant or near-instant processing for domestic transactions. International transfers may require 1-3 business days depending on correspondent banking relationships.

Gambling Payment Restrictions: While banks don’t systematically block all gambling transactions currently, establishing legal gambling payment processing would require Central Bank approval and regulatory framework development.

E-commerce and Digital Economy

Digital Market Development

E-commerce Growth: Explosive expansion in online retail, particularly accelerated by COVID-19 pandemic. Consumer confidence in online transactions reached high levels, supporting continued digital commerce growth.

Market Size: Regional e-commerce projected to grow from $8.3 billion (2017) to $28.5 billion (2022) across Middle East and North Africa, with Bahrain participating in this expansion.

Online Retail Penetration: Increasing percentage of total retail occurring online. Younger demographics drive adoption, with older consumers gradually embracing digital shopping.

Popular Platforms: Mix of international platforms (Amazon, Noon) and regional players. Local e-commerce sites serve specialized niches and capitalize on domestic market knowledge.

Cross-border Shopping: High engagement in international e-commerce. Consumers regularly purchase from global retailers, demonstrating comfort with international digital transactions and willingness to use foreign platforms.

Business Environment and Regulatory Framework

Ease of Business Operations

Bahrain earned reputation as Gulf’s most business-friendly jurisdiction through consistent regulatory reforms and foreign investment welcoming policies.

World Bank Rankings: Bahrain ranked 43rd globally in final Doing Business report (2019 data). The Kingdom improved from 62nd position in 2018, reflecting successful reform implementation.

| Indicator | Performance | Regional Context |

|---|---|---|

| Starting a Business | 3-7 days typical | Among fastest in Gulf |

| Registration Cost | BHD 200-500 | Very affordable |

| Online Registration | Sijilat portal available | Fully digital process |

| Foreign Ownership | 100% in most sectors | No local sponsor required |

| Economic Freedom | 1st in Arab World | Leading Gulf position |

Foreign Investment Policy: Liberal regime allowing 100% foreign ownership in most sectors. Notable exceptions include specific regulated industries, but general business environment highly welcoming to international investors.

Operational Costs: Lower than Dubai and other Gulf business hubs while maintaining quality infrastructure. Office space, salaries, and living costs more affordable than UAE competitors.

Labor Market: Access to skilled talent from local Bahraini workforce and large expatriate population. Unemployment at 4.9% indicates tight but functional labor market.

Corporate Structure and Registration

Available Entity Types

Limited Liability Company (WLL): Most common structure for foreign investors. Requires minimum 2 shareholders, maximum 50. Suitable for small-to-medium operations with liability protection.

Single Person Company (SPC): Allows 100% foreign ownership with single shareholder. Ideal for solo entrepreneurs and small operations. Simplified governance requirements compared to traditional WLL.

Branch Office: Extension of foreign parent company. Suitable for companies maintaining presence while conducting limited activities. Parent company assumes full liability for branch operations.

Representative Office: Non-trading entity for market research, liaison, and promotion. Cannot generate revenue or conduct commercial transactions. Useful for market exploration before full commitment.

| Entity Type | Minimum Capital | Foreign Ownership | Best For |

|---|---|---|---|

| WLL (Limited Liability) | BHD 20,000 | 100% permitted | Most businesses |

| Single Person Company | BHD 20,000 | 100% permitted | Solo entrepreneurs |

| Branch Office | No minimum | 100% (parent owned) | Foreign company presence |

| Representative Office | No minimum | 100% (parent owned) | Market research only |

| Free Zone Company | Varies by zone | 100% permitted | Export-oriented business |

Registration Requirements

Registration Timeline: Complete registration typically requires 3-7 working days for straightforward businesses. Complex structures or regulated industries may require 2-3 weeks including approval processes.

Registration Process via Sijilat: Bahrain’s online business registration portal streamlines company formation. Digital process eliminates need for physical paperwork submission and reduces processing time.

Required Documents: Passport copies of shareholders and directors, proof of address, business plan summary, Memorandum and Articles of Association, lease agreement for office space, and bank reference letters.

Notarization Requirements: Documents may require authentication by Bahrain embassy or consulate if originating from foreign jurisdictions. Local notarization available for documents prepared in Bahrain.

Foreign Ownership Rules: Complete 100% foreign ownership permitted in vast majority of sectors. No local sponsorship requirement for most business activities, distinguishing Bahrain from several Gulf neighbors.

Ongoing Compliance: Annual renewal of commercial registration required. Companies must maintain proper accounting records, submit annual returns, and comply with sector-specific regulations. Audited financial statements required for larger companies.

Corporate Governance: Standard corporate governance principles apply. Companies must maintain registered office address, hold annual general meetings, and maintain statutory registers of shareholders and directors.

Taxation Framework

Corporate Income Tax Structure

General Business Tax Rate: Currently 0% for general businesses outside oil and gas sector. This zero-tax environment represents major competitive advantage attracting international investment.

Oil and Gas Taxation: Companies in hydrocarbon extraction and refining face 46% corporate income tax on net profits. This sector-specific taxation funds government revenue while other industries remain tax-free.

Domestic Minimum Top-Up Tax (DMTT): Effective January 2025, multinational enterprises with consolidated annual revenue exceeding EUR 750 million face 15% minimum effective tax rate. This implements OECD Pillar Two global minimum tax framework.

| Business Category | Tax Rate | Applicability |

|---|---|---|

| General Businesses | 0% | Most companies |

| Oil & Gas Operations | 46% | Hydrocarbon sector only |

| Large MNEs (DMTT) | 15% | Groups over EUR 750M revenue |

| Gambling Operations | N/A | Illegal – no tax framework |

Future Tax Developments: Bahrain’s 2025-26 budget includes consideration of general corporate income tax introduction for first time. Specific rates and implementation timeline remain undetermined, but represents significant policy shift.

Tax Treaties: Bahrain maintains double taxation avoidance agreements with over 40 countries, facilitating international business and preventing double taxation on cross-border income.

Transfer Pricing: With potential corporate tax introduction, transfer pricing regulations may become relevant. Currently minimal transfer pricing requirements exist given zero-tax environment.

Value Added Tax (VAT)

VAT Rate: Standard 10% rate applies to most goods and services. Bahrain implemented VAT in January 2019 at 5%, increasing to 10% in January 2022.

VAT Registration Threshold: Businesses exceeding annual turnover thresholds must register for VAT. Registration enables input VAT recovery while requiring VAT collection and remittance.

Zero-Rated and Exempt Supplies: Certain goods and services receive 0% VAT treatment or exemption. Exports typically zero-rated. Financial services and residential property rentals often exempt.

Gambling VAT Treatment: Not applicable given prohibition. If legalized, gambling services would likely face standard 10% VAT rate based on international precedents.

Personal Income Tax

Zero Personal Tax: No individual income tax exists in Bahrain. Employees retain full salary after only social insurance contributions, creating significant disposable income advantage.

Social Insurance Contributions: Employers and employees contribute to Social Insurance Organization. Contribution rates vary by nationality and employment terms but remain modest compared to income tax regimes.

| Category | Employee Contribution | Employer Contribution | Total |

|---|---|---|---|

| Bahraini Nationals | 7% | 12% | 19% |

| GCC Nationals | 1% | 3% | 4% |

| Expatriates | N/A | 3% | 3% |

Tax Residency: No personal income tax means tax residency determination less critical than jurisdictions with progressive tax systems. However, residency affects social insurance requirements.

Expatriate Taxation: Foreign workers face no income tax in Bahrain, making Kingdom attractive destination for international professionals seeking tax-efficient employment.

Market Entry Considerations

Recommended Entry Strategies

Critical Disclaimer: No legal market entry strategy exists for iGaming operators in Bahrain given absolute gambling prohibition. The following analysis addresses hypothetical scenario where regulatory change occurs.

Hypothetical Licensing Approach: If legalization occurred, operators should pursue direct licensing rather than gray-market operations. Offshore operations targeting Bahraini players would likely face enforcement action once regulatory framework exists.

Local Partnership Considerations: Despite 100% foreign ownership generally permitted, gambling licensing (if introduced) might require local partnerships similar to other Gulf jurisdictions. Strategic local partners would provide market knowledge and regulatory navigation.

White Label vs. Proprietary Platform: White label solutions could enable faster market entry with lower capital requirements. However, proprietary platforms offer greater control and differentiation in competitive environment.

Technology Infrastructure: Leverage Bahrain’s exceptional internet infrastructure and mobile penetration. Mobile-first strategy essential given smartphone dominance and consumer behavior patterns.

Payment Provider Selection: Establish relationships with local banks and payment processors early. Regulatory approval for gambling payment processing would require Central Bank coordination and compliance infrastructure.

Typical Costs and Timelines

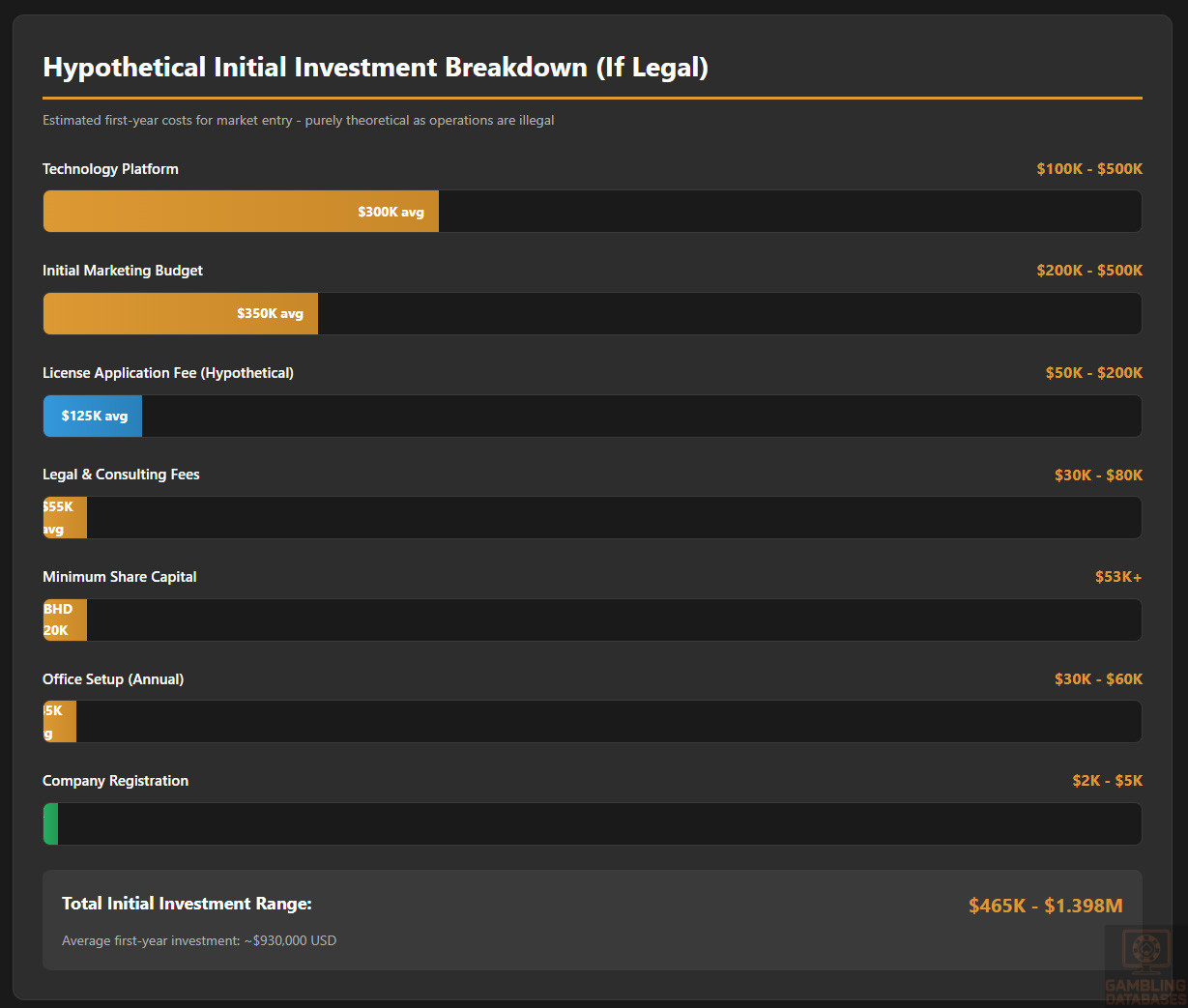

Hypothetical Setup Costs (If Gambling Were Legal):

| Cost Category | Estimated Range (USD) | Notes |

|---|---|---|

| License Application Fee | $50,000 – $200,000 | Hypothetical – no framework exists |

| Legal & Consulting Fees | $30,000 – $80,000 | Regulatory compliance setup |

| Company Registration | $2,000 – $5,000 | Standard incorporation costs |

| Minimum Share Capital | $53,000+ | BHD 20,000 minimum for WLL |

| Office Setup (Annual) | $30,000 – $60,000 | Rent, furniture, equipment |

| Technology Platform | $100,000 – $500,000 | White label or proprietary |

| Initial Marketing Budget | $200,000 – $500,000 | Brand launch campaign |

| Total Initial Investment | $465,000 – $1,398,000 | First year minimum |

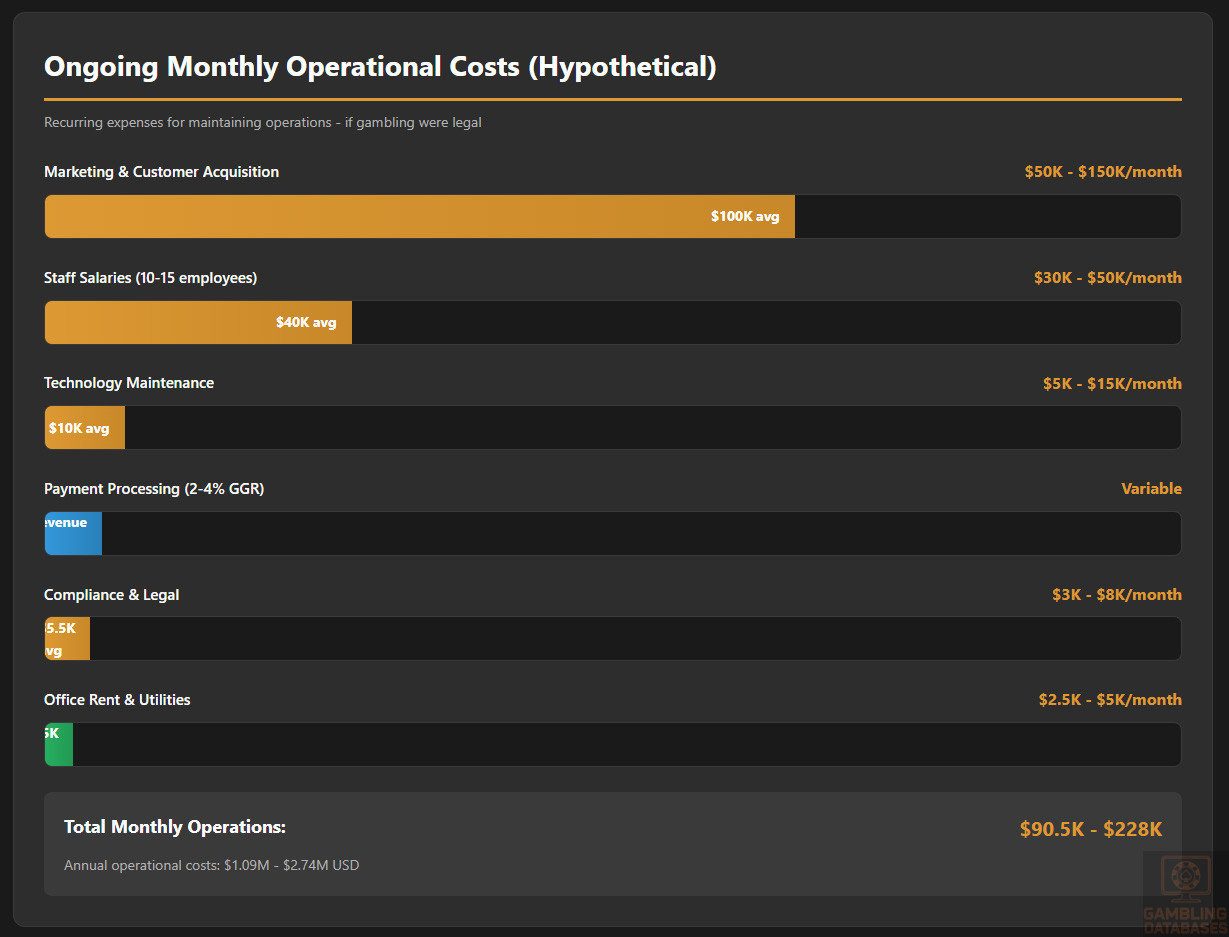

Operational Cost Estimates (Monthly):

| Expense Category | Monthly Cost (USD) | Annual Cost (USD) |

|---|---|---|

| Staff Salaries (10-15 employees) | $30,000 – $50,000 | $360,000 – $600,000 |

| Office Rent & Utilities | $2,500 – $5,000 | $30,000 – $60,000 |

| Technology Maintenance | $5,000 – $15,000 | $60,000 – $180,000 |

| Payment Processing (2-4% GGR) | Variable | $40,000 – $120,000 |

| Marketing & Customer Acquisition | $50,000 – $150,000 | $600,000 – $1,800,000 |

| Compliance & Legal | $3,000 – $8,000 | $36,000 – $96,000 |

| Total Monthly Operations | $90,500 – $228,000 | $1,086,000 – $2,736,000 |

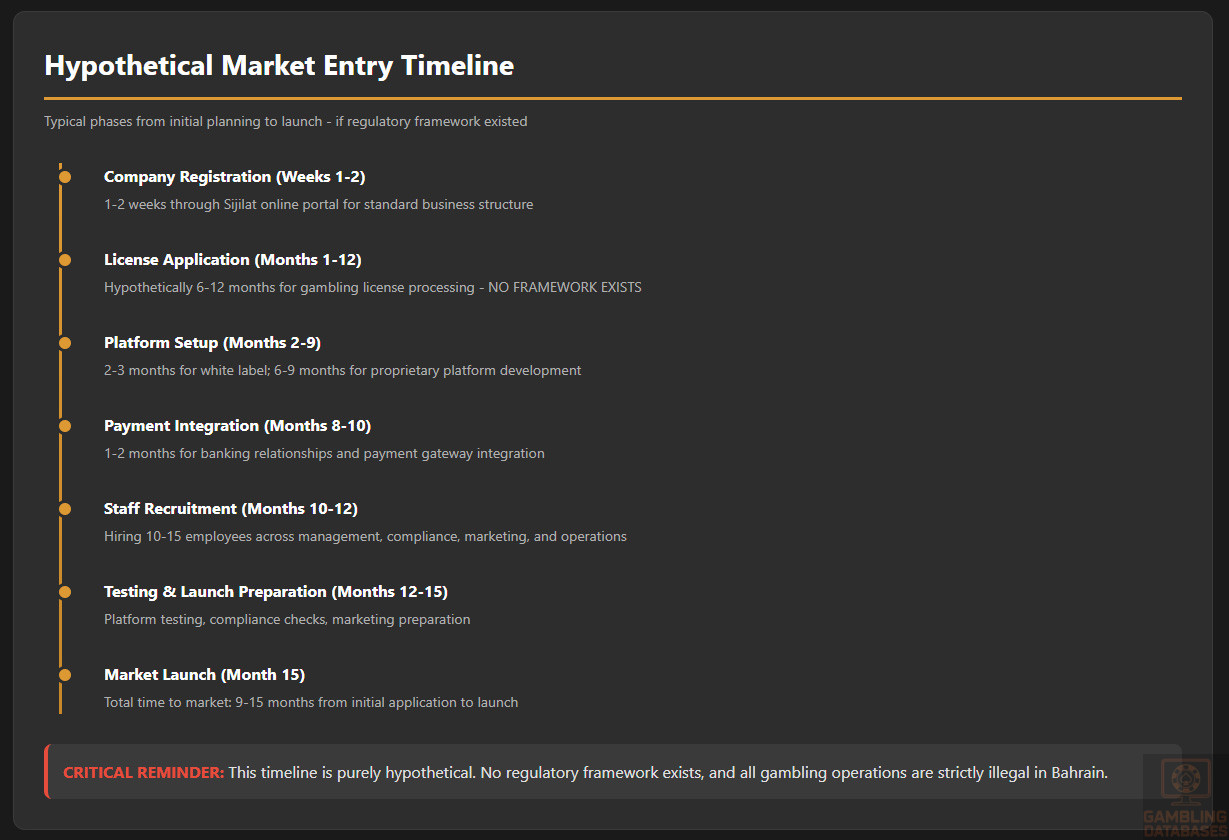

Timeline Expectations

Company Registration: 1-2 weeks through Sijilat online portal for standard business structure.

License Application: Not applicable currently. Hypothetically, 6-12 months typical for gambling license processing in jurisdictions with established frameworks.

Platform Setup: 2-3 months for white label implementation; 6-9 months for proprietary platform development.

Payment Integration: 1-2 months for banking relationships and payment gateway integration.

Total Time to Market: Hypothetically 9-15 months from initial application to launch, assuming regulatory framework exists.

Resource Requirements

Minimum Staff Headcount: 10-15 employees for initial operations including management, customer service, marketing, compliance, finance, and technical support.

Key Positions Needed: General Manager, Compliance Officer, Finance Manager, Marketing Manager, Customer Service Team Lead, IT/Platform Manager, Payment Operations Specialist.

| Department | Positions | Headcount | Monthly Salary Range (USD) |

|---|---|---|---|

| Management | General Manager, CFO | 2 | $12,000 – $20,000 |

| Compliance & Legal | Compliance Officer, Legal Counsel | 2 | $6,000 – $12,000 |

| Marketing | Marketing Manager, Digital Specialists | 3 | $6,000 – $10,000 |

| Customer Service | CS Manager, Agents | 4-5 | $4,000 – $7,000 |

| Technology | IT Manager, Support Staff | 2-3 | $5,000 – $10,000 |

| Finance & Payments | Finance Officer, Payment Specialist | 2 | $4,000 – $8,000 |

Technology Stack Requirements: Gaming platform (white label or proprietary), payment gateway integration, CRM system, fraud detection tools, responsible gambling tools, reporting systems, mobile applications (iOS and Android).

Success Factors and Challenges

Key Success Enablers (Hypothetical Legalization Scenario)

Local Market Understanding: Deep comprehension of Bahraini player preferences, cultural sensitivities, and spending patterns essential. Sports betting on football and cricket likely dominate over casino games.

Localized Payment Methods: Integration with BenefitPay, stc pay, and local bank transfers critical for user adoption. International payment methods alone insufficient for mass-market penetration.

Mobile-First Approach: Smartphone penetration exceeding 95% and exceptional mobile internet speeds demand superior mobile experience. Desktop optimization secondary priority.

Marketing Channel Selection: If advertising permitted post-legalization, digital channels including social media, search engines, and sports partnerships would drive customer acquisition. Traditional media less effective for target demographics.

Arabic Language Support: Comprehensive Arabic interface and customer service essential despite high English proficiency. Language localization demonstrates commitment to local market.

Competitive Promotions: Generous welcome bonuses and ongoing promotions necessary to compete against established offshore operators and potential new local competitors.

Responsible Gambling Commitment: Proactive responsible gambling measures build regulatory goodwill and protect vulnerable players. Self-exclusion, deposit limits, and reality checks should exceed minimum requirements.

Local Sports Coverage: Comprehensive odds on Bahrain Grand Prix, regional football, and popular international sports. Live betting capabilities essential for modern sports betting expectations.

Major Operational Challenges

Fundamental Legal Barrier: Absolute prohibition represents insurmountable challenge. No legal pathway exists, and no indication suggests policy change forthcoming. This eliminates all market opportunity.

Religious and Cultural Opposition: Deep-rooted Islamic prohibition of gambling creates societal resistance extending beyond legal framework. Even if legalization occurred, social acceptance challenges would persist.

Small Market Size: Population of 1.64 million limits total addressable market. Even with high participation rates, total market potential remains modest compared to larger jurisdictions.

Regulatory Uncertainty: No existing framework means complete regulatory uncertainty. Potential future regulations could impose severe restrictions, high taxation, or burdensome compliance requirements.

Payment Processing Restrictions: Even if legalized, conservative banking sector might resist gambling payment processing. Islamic banks would likely refuse involvement based on Sharia principles.

Marketing Limitations: Traditional advertising channels might remain restricted even post-legalization. Sponsorships and public promotions could face strict limitations.

Competition from Established Offshore Operators: Years of Bahraini players accessing international sites creates loyalty to established brands. New local operators face customer acquisition challenges against recognized names.

Talent Shortage: Limited local expertise in gambling operations, compliance, and risk management. Recruiting international talent would be necessary but culturally challenging.

Technology Infrastructure Adaptation: While internet infrastructure excellent, gambling-specific technology infrastructure non-existent. Building from scratch increases complexity and cost.

Cultural Considerations

Ramadan Observance: Holy month significantly impacts consumer behavior. Gambling activity would likely decline dramatically during Ramadan, affecting monthly revenue predictability.

Friday Prayer Times: Friday afternoon prayers represent important cultural moment. Business operations should respect prayer times even though gambling operations typically run 24/7.

Local Holidays and Events: Bahrain National Day, Eid celebrations, and cultural festivals affect spending patterns and engagement levels. Marketing calendars must account for cultural calendar.

Sports Event Preferences: Bahrain Grand Prix represents major annual event generating significant betting interest if legal. Regional football tournaments and cricket matches drive engagement spikes.

Customer Service Expectations: Bahraini consumers expect high service quality and rapid response times. Customer service must operate in both Arabic and English with cultural sensitivity.

Trust Requirements: Foreign brands require significant trust-building in financial services. Transparent operations, secure platforms, and reliable payouts essential for reputation establishment.

Exit Strategy Planning

Market Liquidity: Non-existent currently given illegal status. Even post-legalization, small market size would limit buyer pool for operator sales.

Regulatory Transfer Requirements: License transferability would depend on future regulatory framework. Many jurisdictions require regulatory approval for ownership changes.

License Transferability: Unknown without existing framework. Typically gambling licenses attach to specific entities with transfer subject to regulatory approval.

Valuation Multiples: Small emerging markets typically trade at 3-6x EBITDA compared to 8-12x in mature markets. Limited comparables would challenge valuation.

Closing Operations: Legal process for ceasing gambling operations would require regulatory notification, customer account settlement, and formal license surrender once framework exists.

FAQ: Frequently Asked Questions

Legal & Licensing

1. Is online gambling legal in Bahrain?

No. All forms of gambling, both online and land-based, are completely illegal in Bahrain. The Kingdom prohibits gambling under Islamic Sharia law, codified in Article 308 of the Bahrain Penal Code.

The law prescribes criminal penalties including fines up to BD 300 and imprisonment up to three months for individuals caught gambling in public places. Operators face BD 1,000 fines and one year imprisonment.

Online gambling receives no special exemption. Telecommunications regulators block gambling websites at the ISP level, preventing easy access to offshore gambling platforms. While no specific online gambling prohibition exists in statute, the general gambling ban extends to all forms regardless of delivery channel.

2. What types of gambling licenses are available and what do they cover?

No gambling licenses exist in Bahrain. The government has not established any licensing framework, regulatory authority, or application process for gambling operations of any kind.

This includes casino licenses, sports betting licenses, online gambling licenses, lottery licenses, bingo licenses, poker room licenses, or any other gambling authorization. No legal pathway exists for obtaining permission to operate gambling activities.

3. How much does an iGaming license cost and how long does it take to obtain?

Not applicable. No iGaming licensing system exists in Bahrain, making it impossible to apply for or obtain a gambling license at any cost or timeframe.

Any entity claiming to offer Bahrain gambling licenses would be fraudulent. Legitimate business operators should not pursue gambling licensing in Bahrain under current legal framework.

4. Can foreign companies obtain a gambling license?

No. Neither foreign nor domestic companies can obtain gambling licenses in Bahrain because no licensing framework exists. The absolute prohibition applies equally to local Bahraini companies, foreign corporations, and joint ventures.

While Bahrain generally welcomes foreign investment and permits 100% foreign ownership in most business sectors, gambling represents an absolute exception. No amount of foreign investment or economic contribution would enable gambling license acquisition.

Financial & Taxation

5. What are the tax obligations for iGaming operators?

No tax framework exists for gambling operators because gambling operations are illegal. However, understanding Bahrain’s general tax environment provides context for hypothetical scenarios.

Bahrain currently imposes zero corporate income tax on general businesses outside the oil and gas sector. If gambling were legalized, the government would likely introduce gambling-specific taxation potentially including gross gaming revenue taxes, license fees, and regulatory charges.

Based on international precedents, GGR tax rates could range from 10-25%. Bahrain recently introduced 10% VAT, which would likely apply to gambling services. The Kingdom also implemented 15% minimum top-up tax for large multinationals with revenue exceeding EUR 750 million.

6. Are gambling winnings taxed for players?

Not applicable under current prohibition. However, Bahrain imposes no personal income tax on individuals, meaning gambling winnings would theoretically remain tax-free if gambling were legalized.

This zero personal tax environment creates attractive proposition for players, as full winnings would be retained without tax withholding or declaration requirements. This represents significant advantage compared to jurisdictions taxing gambling winnings.

7. What are the typical operational costs for running an online casino/sportsbook?

Hypothetically, if gambling operations were legal in Bahrain, annual operational costs would likely range from $1-3 million for small-to-medium operators. This includes staff salaries ($360,000-600,000), technology and platform maintenance ($60,000-180,000), payment processing fees (2-4% of GGR), marketing and customer acquisition ($600,000-1,800,000), office and infrastructure ($30,000-60,000), and compliance and legal costs ($36,000-96,000).

Initial setup investment would require $465,000-1,400,000 covering license fees (if framework existed), legal and consulting fees, company registration, minimum capital requirements, office setup, technology platform, and initial marketing budget.

8. What is the expected ROI timeline for entering this market?

Cannot be calculated given illegal status. However, hypothetically if market opened, break-even would likely occur within 18-36 months for efficient operators in small market environment.

Small population base (1.64 million) limits revenue potential, requiring careful cost management for profitability. High customer acquisition costs and intense competition would extend payback periods. First-mover advantage would be critical for achieving faster ROI.

Operations & Compliance

9. What are the local presence requirements for operators?

Not applicable currently. However, if gambling were legalized, operators would likely face requirements similar to other regulated financial services including registered legal entity in Bahrain, physical office address in the Kingdom, minimum local staff employment, and Bahrain-based management representation.

Local server hosting or data center requirements might apply for gaming platforms. Domain registration under .bh TLD could be mandated. These requirements would ensure regulatory oversight and economic benefit to Bahrain.

10. What payment methods are available and recommended?

For legal gambling operations (if framework existed), recommended payment methods would include local options for maximum reach: BenefitPay (national e-wallet with widest adoption), stc pay (mobile operator wallet), bank transfers via EFTS/Fawri (instant domestic transfers), and credit/debit cards (Visa, Mastercard universally accepted).

International methods like Skrill, Neteller, and PayPal would provide alternatives for players comfortable with these platforms. Cryptocurrency integration could appeal to privacy-conscious users, though regulatory acceptance uncertain.

Currently, players accessing illegal offshore sites use cryptocurrency (Bitcoin, USDT), international e-wallets, and occasionally credit cards for anonymity and transaction ease.

11. What are the advertising and marketing restrictions?

Complete advertising ban currently exists. All gambling marketing is prohibited across every channel including television, radio, print media, outdoor advertising, digital platforms, social media, and any other medium.

If legalization occurred, advertising restrictions would likely remain severe given religious sensitivities. Potential restrictions might include prohibition on marketing to minors, restrictions on broadcast media advertising, limitations on outdoor advertising visibility, requirements for responsible gambling messaging, prohibition on celebrity endorsements, restrictions on bonus advertising and social media marketing limitations.

Sponsorship of sports teams and events would face scrutiny despite Bahrain hosting international sporting events.

12. What responsible gambling measures are mandatory?

No framework currently exists. However, if gambling legalization occurred, mandatory measures would likely include age verification systems (preventing under-18 access), identity verification and KYC compliance, self-exclusion program with cross-operator recognition, deposit and loss limits, reality check notifications during extended sessions, access to gambling addiction resources and helplines, mandatory responsible gambling messaging in all communications, and staff training on identifying problem gambling.

Operators should exceed minimum requirements, implementing voluntary exclusion options, affordability checks, behavioral analytics for early intervention, and contributions to problem gambling research and treatment.

Market Opportunity

13. How large is the iGaming market and what is the growth potential?

Legal market does not exist. Current market size is zero from legal operations perspective. Underground market size impossible to quantify due to illegal status, but Bahraini residents accessing offshore platforms likely generate millions in annual wagering volume.

Hypothetical legal market potential would be $80-150 million in annual GGR based on population size, GDP per capita, internet penetration, and regional comparisons. Growth potential would be strong initially (15-25% CAGR) driven by pent-up demand and rapid digital adoption, but would plateau quickly due to small population base.

Market maturity would occur within 3-5 years, limiting long-term growth potential. Regional expansion would be necessary for sustained growth beyond domestic market saturation.

14. Who are the main competitors and what is their market share?

No legal operators exist, meaning no legitimate market competition exists. Underground market served exclusively by international offshore operators including Bet365, 1xBet, 888sport, and others accepting Bahraini players despite prohibition.

These operators maintain no legal status and face systematic website blocking, though VPN usage enables access. Market share data unavailable due to illegal operations and lack of regulatory oversight. Competition occurs entirely outside Bahrain’s legal jurisdiction.

15. What are the player preferences and typical spending patterns?

Limited data available due to prohibition, but anecdotal evidence and regional patterns suggest sports betting dominates preferences with particular focus on football (English Premier League, UEFA Champions League, Spanish La Liga), cricket (especially Indian Premier League), and Formula One racing.

Online casino games attract secondary interest, with slots and live dealer games most popular. Lottery and bingo generate minimal interest. Mobile gaming dominates with estimated 75-85% of activity occurring on smartphones.

Spending patterns remain unknown without operator data access. However, Bahrain’s high disposable income ($50,000 average household income) and zero personal tax suggest spending per active player would exceed regional averages, potentially $400-600 annually per player.

16. What are the key success factors and main challenges for new entrants?

Success Factors (Hypothetical): First-mover advantage in newly legalized market, mobile-optimized platform leveraging exceptional mobile infrastructure, integration with local payment methods (BenefitPay, stc pay), Arabic language support with bilingual customer service, competitive welcome bonuses and ongoing promotions, comprehensive sports betting on local and international events, strong responsible gambling commitment, and partnerships with local businesses for credibility.

Main Challenges: Absolute legal prohibition representing fundamental barrier, religious and cultural opposition creating societal resistance, small market size limiting revenue potential and scalability, regulatory uncertainty with no existing framework, potential severe restrictions even if legalized, payment processing challenges with conservative banking sector, marketing limitations likely to persist post-legalization, competition from established offshore operators with existing customer loyalty, talent shortage in gambling expertise requiring international recruitment, and technology infrastructure requiring complete development from zero base.

Sources and References

- Bahrain Gambling Regulatory Framework – Bahrain Penal Code Article 308

- Law Outlook – Betting or Gambling Not Legal in Bahrain – https://www.onlinebe.mywhc.ca/legal/bahrain/

- LCB.org – Are Online Casinos Legal In Bahrain? – https://lcb.org/restrictions/bahrain

- Online Casino Bahrain – Is Gambling in Bahrain Legal and Safe? – https://onlinecasinobahrain.net/en/tips/gambling-law

- Cointelegraph – Online Casino Bahrain in 2025 – Trusted BH Casino Sites – https://cointelegraph.com/crypto-betting/real-money-casinos/bahrain/

- Play Today – List of Countries Where Gambling is Illegal – https://playtoday.co/blog/guides/countries-where-gambling-is-illegal/

- Arabian Betting – Bahrain Casinos – Play Casino Games Safely in 2025 – https://arabianbetting.com/en/country/online-casino-bahrain/

- Bookmakers.bet – Best Bahrain Betting Sites 2025 – https://www.bookmakers.bet/betting-sites/bahrain/

- Arabian Betting – Best Sports Betting Sites in Bahrain 2025 – https://arabianbetting.com/en/country/online-sports-betting-in-bahrain/

- Slotegrator – Where Is Online Gambling Legal in 2025? Global Overview – https://slotegrator.pro/analytical_articles/where-online-gambling-is-legal.html

- Worldometer – Bahrain Population (2025) – https://www.worldometers.info/world-population/bahrain-population/

- Wikipedia – Demographics of Bahrain – https://en.wikipedia.org/wiki/Demographics_of_Bahrain

- Worldometer – Bahrain Demographics 2025 – https://www.worldometers.info/demographics/bahrain-demographics/

- Ministry of Information, Kingdom of Bahrain – Population and Demographics – https://www.mia.gov.bh/kingdom-of-bahrain/population-and-demographics/

- World Bank – Population Data – Bahrain – https://data.worldbank.org/indicator/SP.POP.TOTL?locations=BH

- Countrymeters – Bahrain Population (2025) Live – https://countrymeters.info/en/Bahrain

- World Population Review – Bahrain Population 2025 – https://worldpopulationreview.com/countries/bahrain

- Macrotrends – Bahrain Population Growth Rate 1950-2025 – https://www.macrotrends.net/global-metrics/countries/bhr/bahrain/population

- World Health Organization – Bahrain Health Data Overview – https://data.who.int/countries/048

- World Economics – Bahrain’s GDP 2025 – https://www.worldeconomics.com/Country-Size/Bahrain.aspx

- Wikipedia – Economy of Bahrain – https://en.wikipedia.org/wiki/Economy_of_Bahrain

- Macrotrends – Bahrain GDP Per Capita – https://www.macrotrends.net/global-metrics/countries/bhr/bahrain/gdp-per-capita

- FocusEconomics – Bahrain Economy: GDP, Inflation, CPI & Interest Rates – https://www.focus-economics.com/countries/bahrain/

- Information & eGovernment Authority, Bahrain – Bahrain’s Economy Achieves Real Growth of 2.4% in 2023 – https://www.iga.gov.bh/en/article/bahrains-economy-achieves-real-growth-of-2-4-in-2023-compared-to-2022

- Global Finance Magazine – Bahrain GDP and Economic Data – https://gfmag.com/country/bahrain-gdp-country-report/

- DataReportal – Digital 2025: Bahrain – https://datareportal.com/reports/digital-2025-bahrain

- Wikipedia – Internet in Bahrain – https://en.wikipedia.org/wiki/Internet_in_Bahrain

- World Bank – Individuals using the Internet (% of population) – Bahrain – https://data.worldbank.org/indicator/IT.NET.USER.ZS?locations=BH

- Worldostats – Internet Penetration Rates by Country in 2025 – https://worldostats.com/country-stats/internet-penetration-by-country/

- World Population Review – Internet Penetration by Country 2025 – https://worldpopulationreview.com/country-rankings/internet-penetration-by-country

- Statista – Digital & Connectivity Indicators – Bahrain Forecast – https://www.statista.com/outlook/co/digital-connectivity-indicators/bahrain

- TechAfrica News – Bahrain Ranks 5th Globally for Fastest Mobile Internet Speeds – https://techafricanews.com/2025/09/23/bahrain-ranks-5th-globally-for-fastest-mobile-internet-speeds/

- BuddeComm – Bahrain – Telecoms, Mobile and Broadband Statistics and Analyses – https://www.budde.com.au/Research/Bahrain-Telecoms-Mobile-and-Broadband-Statistics-and-Analyses

- GeoStats Game – Top 10 Countries with Highest Internet Penetration 2025 – https://geostatsgame.com/resources/blog/top-10-highest-internet-penetration-2025

- Kingdom of Bahrain – eWallet Payment Solutions – https://bahrain.bh/wps/portal/en/BNP/HomeNationalPortal/ContentDetailsPage/

- Central Bank of Bahrain – CBB Grants License to BPay Global – https://www.cbb.gov.bh/media-center/central-bank-of-bahrain-grants-license-to-bpay-global/

- Bahrain Economic Development Board – From Pearl Trade to e-Wallets: The Rise of Digital Payments in the GCC – https://www.bahrainedb.com/bahrain-pulse/from-pearl-trade-to-e-wallets-the-rise-of-digital-payments-in-the-gcc

- Central Bank of Bahrain – Digital Payment Landscape Report 2022 – https://www.cbb.gov.bh/wp-content/uploads/2022/11/The-Digital-Payment-Landscape-Report-2022.pdf

- PayCEC – What is the Digital Wallet (e wallet) in Bahrain? – https://www.paycec.com/faq/what-is-the-digital-wallet-in-bahrain