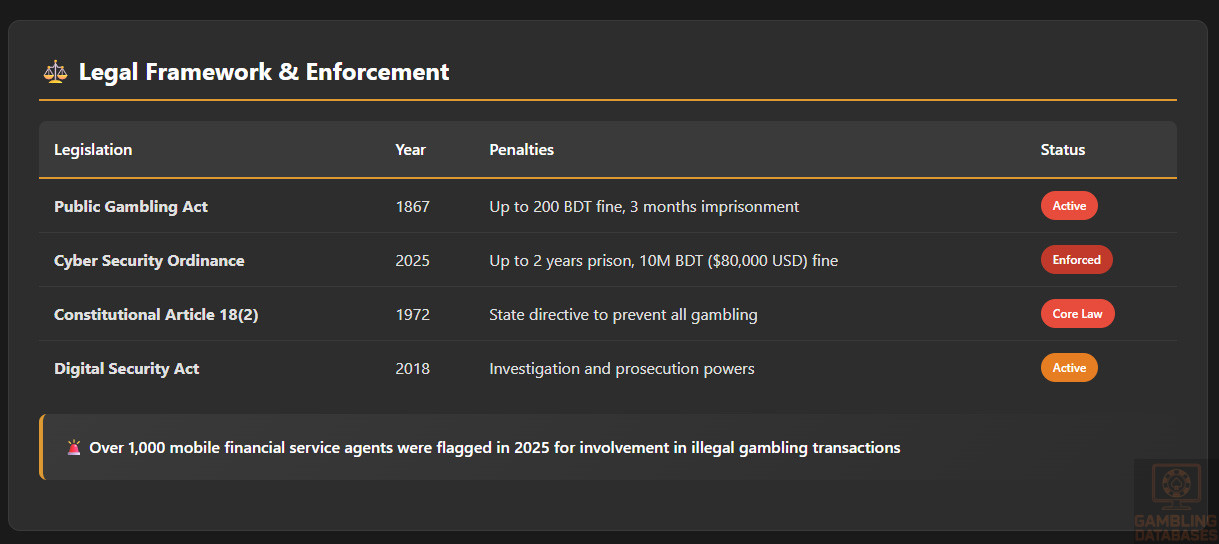

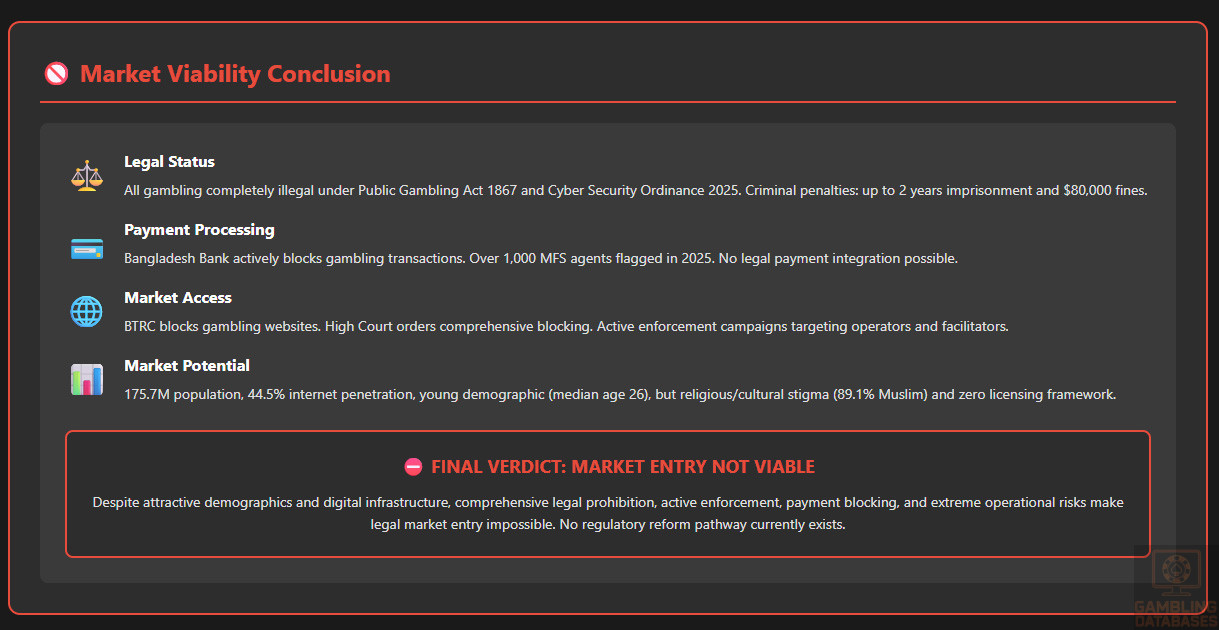

Bangladesh presents a highly restrictive market for iGaming operations due to comprehensive gambling prohibitions under Islamic law and colonial-era legislation. The Public Gambling Act of 1867 outlaws all forms of gambling except horse racing and government-authorized lotteries. With recent enforcement actions under the Cyber Security Ordinance 2025, authorities are actively cracking down on online gambling activities.

This analysis examines the complete regulatory landscape, demographic trends, technology infrastructure, and business environment factors relevant to understanding this challenging yet demographically compelling market.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

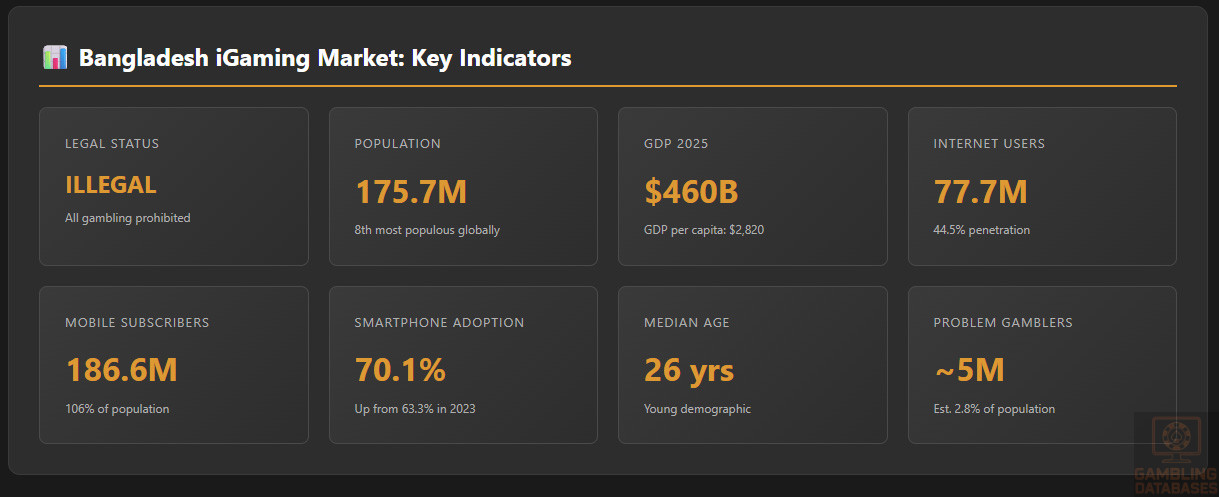

| Legal Status | Illegal | All gambling prohibited except horse racing and authorized lotteries |

| Primary Legislation | Public Gambling Act 1867 | Inherited from British colonial rule |

| Recent Enforcement Law | Cyber Security Ordinance 2025 | Up to 2 years imprisonment, fines up to BDT 10 million ($80,000 USD) |

| Licensing Available | No | No legal framework for operator licensing |

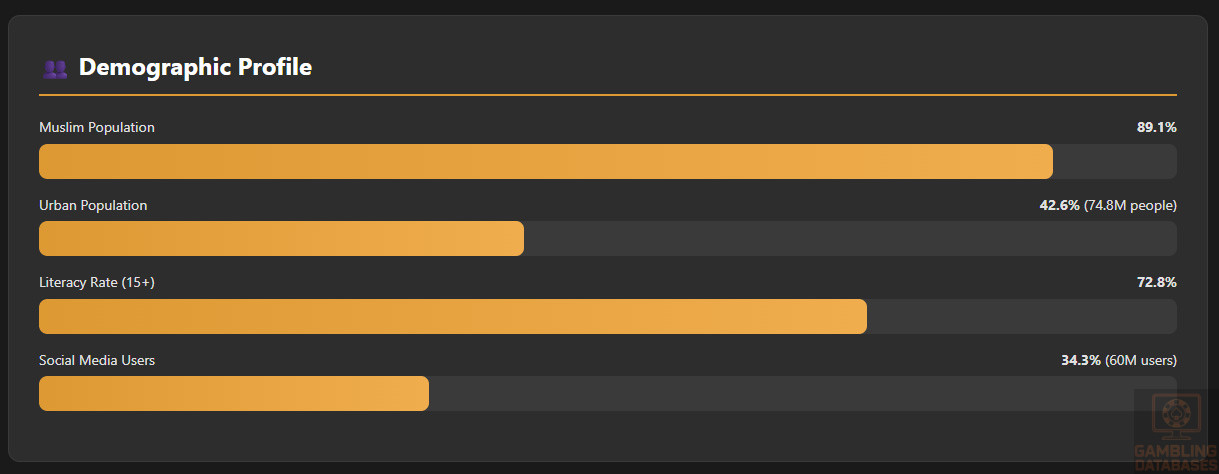

| Population | 175.7 million | 8th most populous country globally |

| Median Age | 26 years | Young, digitally-oriented demographic |

| Urban Population | 42.6% | 74.8 million people in urban areas |

| GDP 2025 | $460 billion USD | Nominal GDP |

| GDP Per Capita 2025 | $2,820 USD | Increased from $2,738 in FY24 |

| GDP Growth Rate FY25 | 3.97% | Lowest since COVID-19 pandemic |

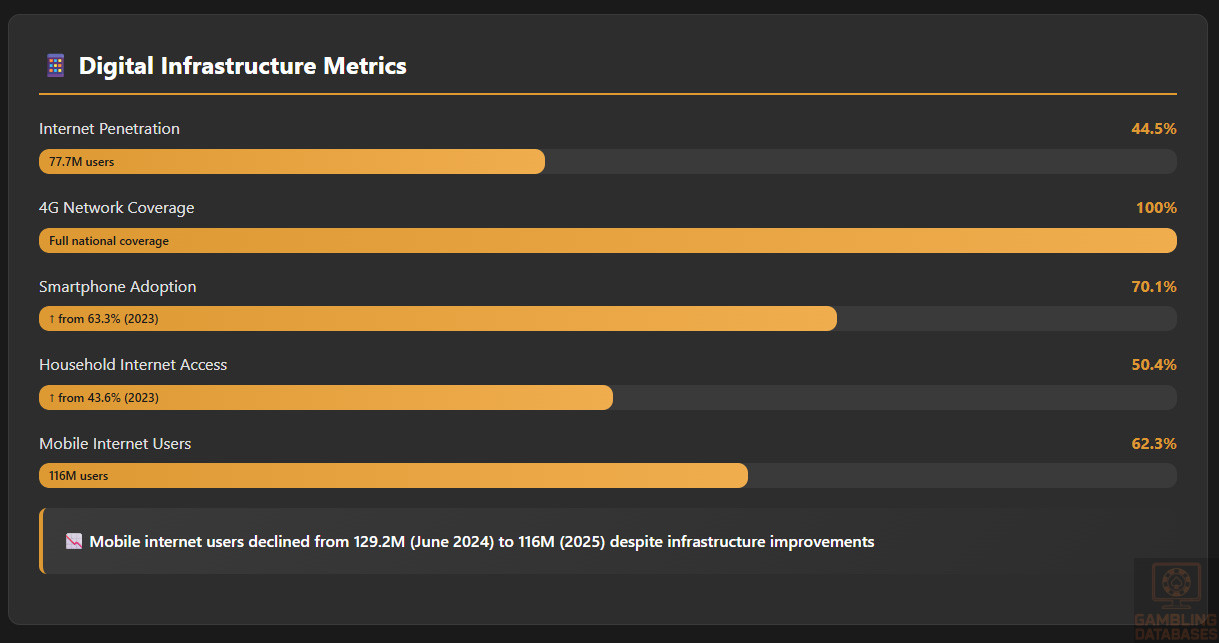

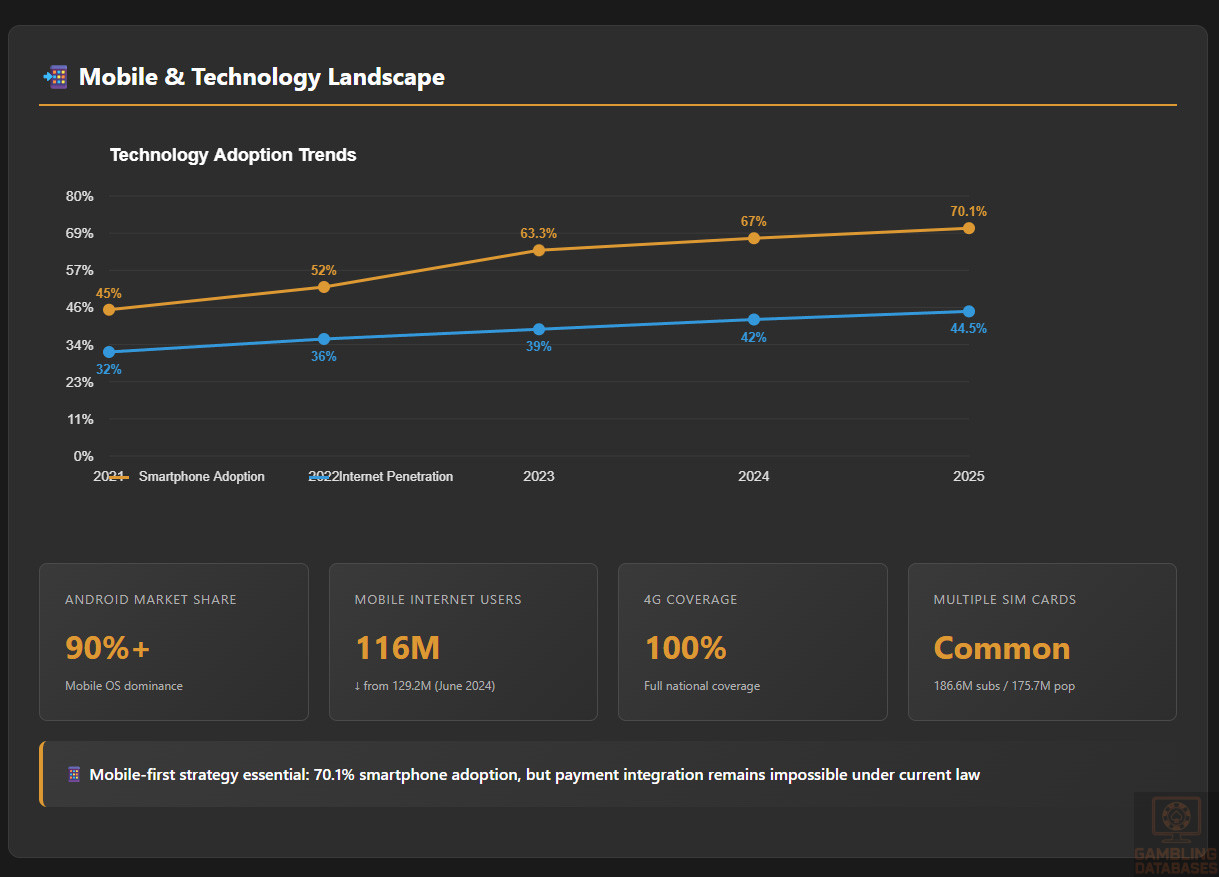

| Internet Penetration | 44.5% | 77.7 million internet users |

| Mobile Subscribers | 186.6 million | 106% of population (multiple SIM cards common) |

| Smartphone Adoption | 70.1% | Increased from 63.3% in 2023 |

| Mobile Internet Users | 116 million | Declined from 129.2 million in June 2024 |

| 4G Coverage | 100% | Full national 4G network coverage |

| Household Internet Access | 50.4% | Increased from 43.6% in 2023 |

| Social Media Users | 60 million | 34.3% of total population |

| Primary Religion | 89.1% Muslim | Islamic law prohibits gambling |

| Literacy Rate | 72.8% | Population aged 15+ |

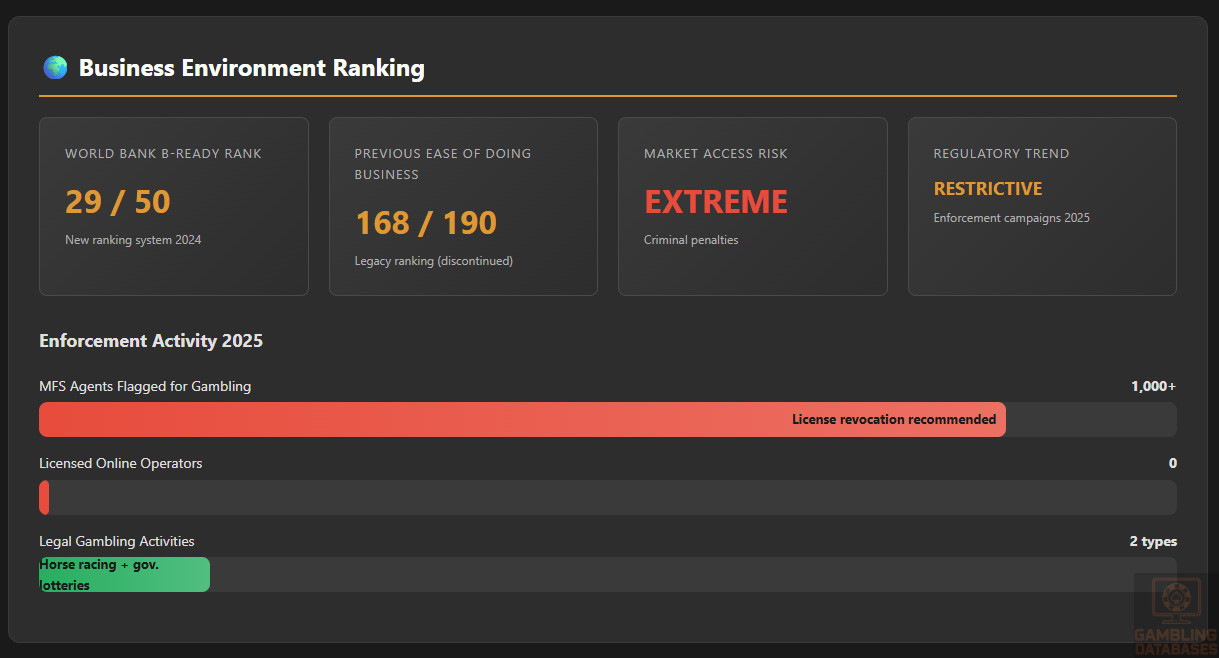

| World Bank B-Ready Rank | 29 of 50 | Previous Ease of Doing Business: 168 of 190 |

| Estimated Problem Gamblers | 5 million | Approximately 2.8% of population |

| Market Access Risk | Extreme | Criminal penalties, payment blocking, ISP restrictions |

| Regulatory Trend | Increasingly Restrictive | Active enforcement campaigns launched 2025 |

| Payment Provider Cooperation | High Risk | 1,000+ mobile financial agents flagged for gambling transactions |

| Estimated Underground Market | Unknown | No official data; widespread illegal activity reported |

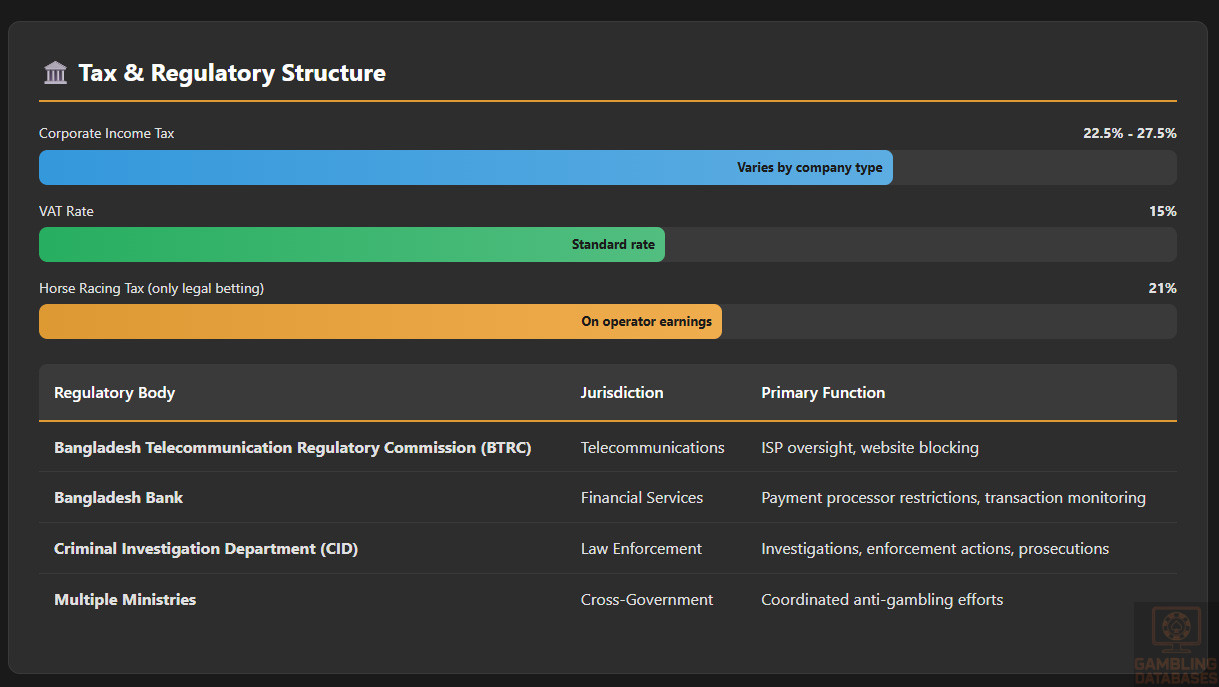

| Corporate Income Tax | 22.5% – 27.5% | Varies by company type and listing status |

| VAT Rate | 15% | Standard rate |

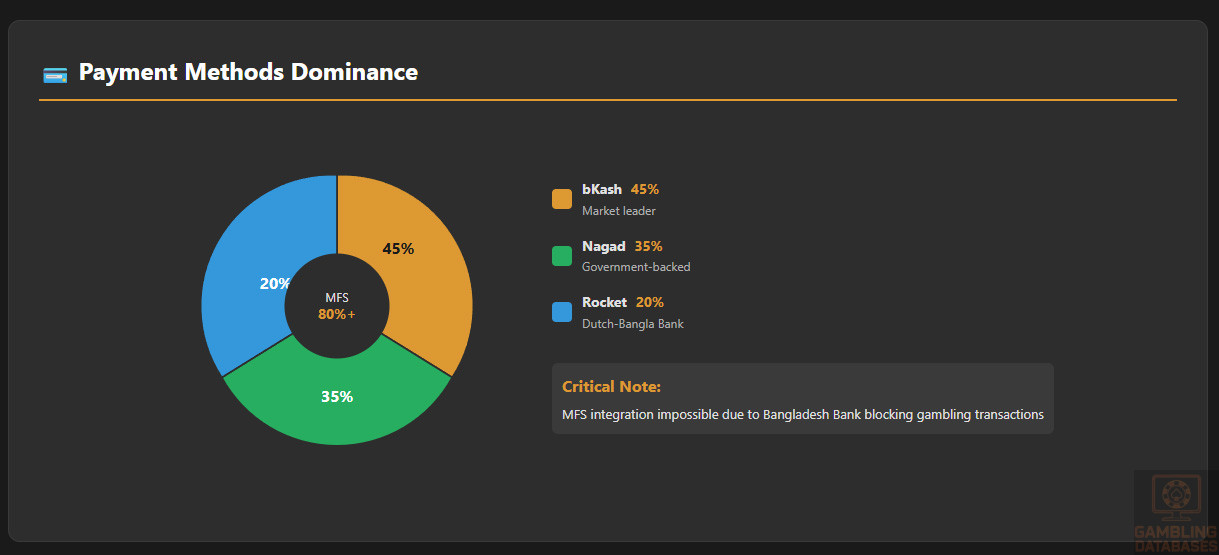

| Major Payment Methods | bKash, Nagad, Rocket | Mobile financial services dominate; 80%+ market share |

| Currency | Bangladeshi Taka (BDT) | Exchange rate approximately 120 BDT = 1 USD |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Bangladesh maintains one of the world’s strictest gambling prohibition regimes, rooted in both Islamic religious principles and British colonial legislation dating to 1867. The regulatory framework reflects the country’s constitutional commitment to prevent gambling activities and the religious beliefs of its predominantly Muslim population.

Land-Based Gambling Activities

Casino Operations: All casino operations are strictly prohibited throughout Bangladesh. No licenses are available for land-based casino establishments. Operating or maintaining a common gaming house constitutes a criminal offense under the Public Gambling Act of 1867. Penalties include fines up to 200 BDT ($1.67 USD) and imprisonment up to three months for venue operators.

Sports Betting Venues: Physical sports betting shops and bookmaking operations are illegal except for horse racing. Licensed horse racing betting is permitted under special provisions with operators subject to a 21% tax on earnings. All other forms of sports betting through physical venues face prosecution under existing gambling laws.

Slot Machine Halls: Electronic gaming machines, slot halls, and arcade gambling facilities are completely prohibited. No licensing framework exists for any form of electronic gaming equipment in public venues. The prohibition extends to all games of chance operated through mechanical or electronic devices.

Other Land-Based Activities: Government-authorized lotteries represent the only other legal gambling activity. These lotteries are classified as games of skill rather than gambling under Bangladesh law. Private lottery operations remain illegal. Traditional games involving stakes played in private settings technically violate the law but face minimal enforcement.

Online Gambling Framework

Digital Gaming Regulations: Online gambling exists in a legal grey area under the Public Gambling Act of 1867, which predates the internet era. The legislation contains no specific provisions addressing online gambling, creating ambiguity regarding digital platforms. However, Article 18(2) of the Bangladesh Constitution directs the state to prevent all forms of gambling, establishing a clear policy position against online gaming activities.

Prohibited Activities: The Cyber Security Ordinance 2025 explicitly criminalizes the creation, operation, and promotion of online gambling platforms. Section 20 of this ordinance addresses online gambling as a criminal offense punishable by up to two years imprisonment, fines up to 10 million BDT (approximately $80,000 USD), or both. Related offenses under Sections 21 and 22 prohibit fraud and manipulation in connection with gambling activities.

Enforcement Mechanisms: The Criminal Investigation Department (CID) launched nationwide enforcement campaigns in 2025 targeting online gambling operators and facilitators. Authorities employ multiple enforcement tools including ISP blocking of gambling websites, payment processor restrictions, investigation of mobile financial service agents, and prosecution under the Digital Security Act. Over 1,000 mobile financial service agents were identified in 2025 for involvement in illegal gambling transactions.

Regulatory Body Structure: Bangladesh lacks a dedicated gambling regulatory authority. The Bangladesh Telecommunication Regulatory Commission (BTRC) oversees internet service providers and can implement website blocking. The Bangladesh Bank monitors financial transactions and can restrict payment processing. The Criminal Investigation Department conducts investigations and enforcement actions. Multiple government ministries coordinate anti-gambling efforts including Post and Telecommunications, Information, Home Affairs, and Law ministries.

Licensed Operators and Market Players

Legal Operators: Zero licensed online gambling operators exist in Bangladesh due to the comprehensive prohibition. No legal framework permits the licensing of iGaming platforms. Horse racing operations and government lotteries represent the only authorized gambling activities, neither of which extend to online platforms under current regulations.

Unlicensed Foreign Operators: Numerous international gambling websites accept Bangladeshi players despite the legal prohibition. These offshore operators function without Bangladesh licenses or regulatory oversight. Many utilize local agents and mobile financial services for payment processing. The exact number of operators serving the Bangladesh market remains unknown due to the illegal nature of these operations.

Market Structure: The underground online gambling market in Bangladesh operates through foreign-licensed platforms, illegal local agents, and informal payment networks. Social media advertising on Facebook and YouTube drives significant traffic to gambling sites. Match-fixing syndicates in football leagues operate betting operations. Estimates suggest approximately 5 million Bangladeshis engage in online gambling despite the legal prohibition.

Competitive Landscape: No legitimate competitive market exists due to the blanket prohibition. Unlicensed operators compete for Bangladesh market share without regulatory constraints. Sports betting sites dominate, particularly those offering cricket betting given the sport’s popularity. International casino sites accepting Asian players commonly serve Bangladesh customers. Market concentration data is unavailable given the illegal status of all operations.

Licensing Framework and Requirements

Application Process and Eligibility

Licensing Authority: No gambling licensing authority operates in Bangladesh. No application process exists for obtaining gambling operation licenses. The regulatory framework provides no pathway for legal gambling licensing under current law. Constitutional provisions require the state to prevent gambling rather than regulate it.

Financial Requirements: Not applicable. No capital requirements, financial guarantees, or application fees exist because no licensing framework is available. Would-be operators cannot obtain licenses regardless of financial resources or technical capabilities.

Technical Standards: No technical certification requirements exist for gambling systems as no legal gambling operations are permitted. Gaming software, random number generators, and platform security cannot receive Bangladesh regulatory approval because no regulatory framework exists.

Background Checks: Not applicable. No probity investigations or background check procedures exist for gambling operator applicants given the absence of any licensing regime. Law enforcement focuses on identifying and prosecuting gambling operators rather than evaluating their fitness for licensing.

Local Presence and Operational Requirements

Physical Presence: Operating gambling activities from Bangladesh territory is illegal. No local office requirements exist because no legal operations are permitted. Foreign operators serving Bangladesh customers illegally do not maintain local presence to avoid prosecution.

Domain and Hosting: Bangladesh does not permit .bd domain registration for gambling websites. The BTRC blocks access to known gambling domains. No local server hosting is permitted for gambling platforms. International operators use foreign domains and offshore hosting to serve Bangladesh customers.

Personnel Requirements: No staffing requirements exist for gambling operations as none are legally permitted. Employing individuals in Bangladesh to facilitate gambling operations exposes both employer and employee to criminal prosecution.

Foreign Ownership: The question of foreign ownership is moot given that no domestic or foreign companies can legally operate gambling businesses in Bangladesh. No restrictions or permissions regarding foreign investment in gambling exist because the entire sector is prohibited.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification: No regulatory requirements for age verification exist as online gambling is illegal. Underground operators implement varying age verification standards, typically minimal. The legal gambling age question is irrelevant when all gambling is prohibited.

KYC/AML Compliance: No gambling-specific KYC or AML requirements exist in Bangladesh. Financial institutions must comply with general KYC/AML regulations under the Money Laundering Prevention Act 2012 and Anti-Terrorism Act 2009. These laws prohibit facilitating illegal activities including unlicensed gambling. Bangladesh Bank has directed financial institutions to use artificial intelligence to identify gambling-related transactions.

Responsible Gambling Measures: No mandated responsible gambling requirements exist for operators as legal operations are prohibited. Problem gambling support services are extremely limited. No charity services specifically address gambling addiction due to the illegal status and religious prohibition. International services like GamCare provide some support accessible to Bangladeshi players.

Self-Exclusion Systems: No regulatory requirement or framework exists for self-exclusion programs. Illegal operators may offer voluntary self-exclusion features but face no regulatory obligations. Players seeking to exclude themselves from gambling have no official registry or protection system.

Financial Monitoring and Reporting

Transaction Monitoring: Bangladesh Bank requires financial institutions to monitor transactions for illegal activities including gambling. The 2025 directive mandates AI-based systems to identify merchants and customers involved in online gambling. Mobile financial service providers must report suspicious gambling-related transactions. Over 1,000 MFS agents had licenses recommended for revocation in 2025 due to gambling transaction facilitation.

Reporting Requirements: Financial institutions must report suspicious transactions potentially related to money laundering or illegal activities. No gambling-specific reporting exists because operations are illegal. Law enforcement receives reports of gambling activity through multiple channels including financial institution alerts, public complaints, and investigative work.

Audit Procedures: No gambling operation audits occur as no legal operators exist. Financial institution audits may reveal gambling transaction processing. Law enforcement conducts investigations rather than regulatory audits when gambling activities are detected.

Data Retention: General data retention requirements apply to financial institutions per Bangladesh Bank regulations. No gambling-specific retention requirements exist. Evidence of illegal gambling transactions may be retained as part of criminal investigations.

Taxation Structure and Financial Obligations

Player Taxation

Winnings Tax: No specific tax on gambling winnings exists in Bangladesh tax law. Given that gambling is illegal, winnings from unlawful activities technically constitute illegal proceeds. Players do not report or pay taxes on illegal gambling winnings. Legal horse racing winnings and lottery prizes face taxation under general income tax provisions.

Withholding Procedures: No withholding mechanisms exist for online gambling winnings as operations are illegal. Legal lottery operators withhold taxes on prizes. Underground gambling operations make no tax withholdings.

Declaration Requirements: Bangladesh tax law requires declaration of all income sources. Gambling winnings from illegal activities should theoretically be declared but rarely are. No separate gambling income category exists on tax returns.

Tax-Free Thresholds: No gambling-specific tax-free thresholds exist. General income tax exemption limits apply to all income sources. The basic tax exemption threshold for individual taxpayers is 350,000 BDT ($2,917 USD) annually for the 2024-2025 tax year.

Operator Taxation

Gross Gaming Revenue Tax: No GGR tax framework exists as gambling operations are illegal. Legal horse racing operators face a 21% tax on earnings. This represents the only gambling-specific taxation in Bangladesh law.

Corporate Income Tax: If gambling operations were legal, they would face standard corporate income tax rates ranging from 22.5% to 27.5% depending on company type, listing status, and sector. Publicly traded companies enjoy lower rates. Banks and financial institutions face rates up to 37.5%.

License Fees: No license fees exist as no licensing framework is available. Government-authorized lottery operators may pay fees or revenue shares but these arrangements are not publicly disclosed.

Annual Operational Taxes: No gambling-specific operational taxes exist beyond standard business taxes. Legal businesses pay corporate income tax, VAT at 15%, and various local government fees.

Gambling Market Financial Performance

Total Market Size: No official data exists on gambling market size in Bangladesh due to the illegal status of most activities. Underground market estimates are unreliable. Media reports suggest millions of Bangladeshis participate in illegal online gambling. Anecdotal evidence indicates significant money flows to offshore gambling operators.

Government Revenue: The government collects minimal gambling-related revenue limited to horse racing taxes. No online gambling tax revenue exists. Enforcement actions may result in fines but these represent penalties rather than structured taxation.

Growth Trends: Media reports and enforcement agency statements indicate rapid growth in online gambling participation from 2020-2024. The COVID-19 pandemic accelerated online gambling activity. Recent enforcement campaigns aim to reverse this growth trend.

Revenue Distribution: Insufficient data exists to analyze revenue distribution by gambling type. Horse racing and government lotteries represent minimal legal activity. Underground sports betting and online casino games dominate illegal activity based on law enforcement reports.

Advertising and Marketing Restrictions

Permitted Channels: No gambling advertising is permitted in Bangladesh. All channels including television, radio, print media, outdoor advertising, and online platforms are prohibited from carrying gambling promotions. The constitutional mandate to prevent gambling extends to advertising restrictions.

Content Restrictions: All gambling advertising content is prohibited regardless of messaging. Educational campaigns about gambling risks are rare. Anti-gambling messaging occasionally appears in public service announcements.

Celebrity Endorsements: High-profile gambling advertising scandals have occurred involving Bangladeshi celebrities. Cricket star Shakib Al Hasan faced investigation and public backlash for promoting a sports betting website. His sister faced investigation related to the Mahadev betting app case. Such endorsements violate Bangladesh law and cultural norms.

Online Marketing: Despite prohibitions, gambling advertisements appear on social media platforms, particularly Facebook and YouTube. These advertisements typically originate from outside Bangladesh. The government has called for removal of gambling advertisements from social media platforms. A 2025 High Court petition demanded action against gambling ads on Facebook, YouTube, WhatsApp, Bigo Live, TikTok, Likee, and Google Play Store.

Affiliate Marketing: Affiliate marketing for gambling sites operates in Bangladesh despite legal prohibitions. Local agents recruit players and facilitate transactions. These activities are illegal but persist due to enforcement challenges. Affiliate marketers face prosecution if identified.

Sponsorship Regulations: Gambling-related sponsorship of sports teams, events, or other activities is prohibited. Historical evidence shows illegal gambling syndicates influence football clubs through financial incentives. Match-fixing and manipulation remain significant problems in lower-tier football leagues.

Recent Regulatory Changes and Their Impact

Cyber Security Ordinance 2025: The most significant recent development is the Cyber Security Ordinance 2025, which explicitly criminalizes online gambling operations. This ordinance represents the first comprehensive legal framework specifically addressing digital gambling. Maximum penalties of two years imprisonment and 10 million BDT fines provide stronger enforcement tools than the colonial-era Public Gambling Act.

CID Enforcement Campaign 2025: Bangladesh’s Criminal Investigation Department launched nationwide enforcement operations in 2025 targeting online gambling under the new cyber security law. This represents the first major coordinated enforcement effort specifically focused on digital gambling. Over 1,000 mobile financial service agents were identified for involvement in gambling transactions, with license revocation and penalties recommended.

High Court Intervention 2025: In May 2025, the Bangladesh High Court ordered a comprehensive report on online gambling within 30 days. The court issued rules requiring government explanation for why internet gateways to gambling platforms should not be removed. Another rule sought explanation for why a 24-hour monitoring cell should not be established to track online gambling activities. This judicial intervention reflects growing concern about online gambling proliferation.

Banking Sector Directives 2025: Bangladesh Bank issued directives to banks and financial institutions to deploy artificial intelligence systems for identifying gambling-related transactions. This technological approach to enforcement represents a significant escalation in anti-gambling efforts. Financial institutions face pressure to block gambling payments proactively.

Enforcement Mechanisms and Penalties

Criminal Penalties: Under the Public Gambling Act 1867, operating a common gaming house carries penalties of 200 BDT fine and up to three months imprisonment. Participating in gambling at such venues carries 100 BDT fine and up to one month imprisonment. Under the Cyber Security Ordinance 2025, creating, operating, or promoting online gambling platforms carries up to two years imprisonment, fines up to 10 million BDT ($80,000 USD), or both penalties.

Financial Penalties: Mobile financial service agents facilitating gambling transactions face license revocation and financial penalties. Banks and payment processors enabling gambling transactions may face regulatory sanctions from Bangladesh Bank. The exact financial penalty structures remain unclear but enforcement actions in 2025 target significant agent networks.

ISP Blocking: The Bangladesh Telecommunication Regulatory Commission blocks access to known gambling websites at the ISP level. Enforcement remains inconsistent as blocked sites often return under new domains. VPN usage allows some users to circumvent blocking. The High Court 2025 order demands comprehensive blocking of gambling site access.

Payment Restrictions: Bangladesh Bank restricts payment processing for gambling activities. Cryptocurrency transactions remain illegal under the Foreign Exchange Regulation Act 1947, Money Laundering Prevention Act 2012, and Anti-Terrorism Act 2009. These restrictions impede both legal and illegal gambling payment processing.

| Offense | Legislation | Maximum Fine | Maximum Imprisonment |

|---|---|---|---|

| Operating gambling venue | Public Gambling Act 1867 | 200 BDT ($1.67 USD) | 3 months |

| Gambling participation | Public Gambling Act 1867 | 100 BDT ($0.83 USD) | 1 month |

| Online gambling operation | Cyber Security Ordinance 2025 | 10,000,000 BDT ($80,000 USD) | 2 years |

| Gambling-related fraud | Cyber Security Ordinance 2025 Sections 21-22 | Variable | Variable |

| MFS agent facilitation | Bangladesh Bank regulations | License revocation + fines | Potential prosecution |

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Bangladesh ranks as the eighth most populous country globally with an estimated 175.7 million people in 2025. The population demonstrates a young demographic profile with a median age of just 26 years, positioning Bangladesh advantageously for digital service adoption. The population growth rate of 1.22% annually indicates continued expansion though at a moderating pace compared to historical levels.

Gender distribution shows 86.37 million males and 89.32 million females, creating a female majority of 2.96 million. The sex ratio stands at 96.7 males per 100 females. Life expectancy has improved to 73.4 years reflecting healthcare advancements. The young population structure creates a large working-age cohort with approximately 115 million people in the productive age groups.

| Age Group | Population (millions) | Percentage | Characteristics |

|---|---|---|---|

| 0-14 years | 47.5 | 27% | Youth dependency; future market |

| 15-24 years | 33.0 | 19% | Adolescents; early digital adopters |

| 25-34 years | 30.5 | 17% | Prime gambling demographic |

| 35-44 years | 26.4 | 15% | Peak earning years |

| 45-54 years | 19.3 | 11% | Established financial position |

| 55-64 years | 12.3 | 7% | Pre-retirement; lower digital adoption |

| 65+ years | 12.0 | 7% | Elderly dependency; minimal online activity |

The total fertility rate has declined dramatically from nearly 7 children per woman in the 1970s to approximately 2.1 in 2025, reaching replacement level. This demographic transition indicates maturing population structure. Approximately 28% of the population falls in the 10-24 age bracket, representing nearly 50 million young people who demonstrate high digital engagement and technology adoption rates.

Geographic Distribution

Bangladesh exhibits one of the world’s highest population densities at 1,350 people per square kilometer across its 130,170 square kilometer land area. Urban areas house 42.6% of the population totaling 74.8 million people, while 57.4% remain in rural areas. Urbanization accelerates at 3.13% annually, driving migration to cities for economic opportunities.

Dhaka, the capital and largest city, dominates the urban landscape with a sprawling metropolitan area housing over 20 million people in the greater Dhaka region. Other major urban centers include Chittagong (port city, second largest), Khulna (industrial hub), Rajshahi (silk city), Sylhet (tea region), and Barisal (river port). These cities concentrate internet connectivity, digital services, and disposable income.

| City | Population (millions) | Economic Profile | Internet Penetration |

|---|---|---|---|

| Dhaka | 20+ (metro) | Capital; commerce, government, services | Very High (78%+) |

| Chittagong | 5-6 | Port city; trade, shipping, industry | High (65-75%) |

| Khulna | 2-3 | Industrial center; manufacturing | Moderate-High (55-65%) |

| Rajshahi | 1-1.5 | Education; silk production | Moderate (50-60%) |

| Sylhet | 0.5-0.7 | Tea cultivation; remittance hub | Moderate (50-60%) |

| Rural areas | 100+ | Agriculture-based economy | Low-Moderate (46%) |

Regional economic disparities create significant variation in consumer purchasing power and technology access. Urban areas in Dhaka and Chittagong divisions demonstrate substantially higher internet penetration at 60-78% compared to rural areas at 46%. This digital divide affects market accessibility for online services including gambling platforms.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

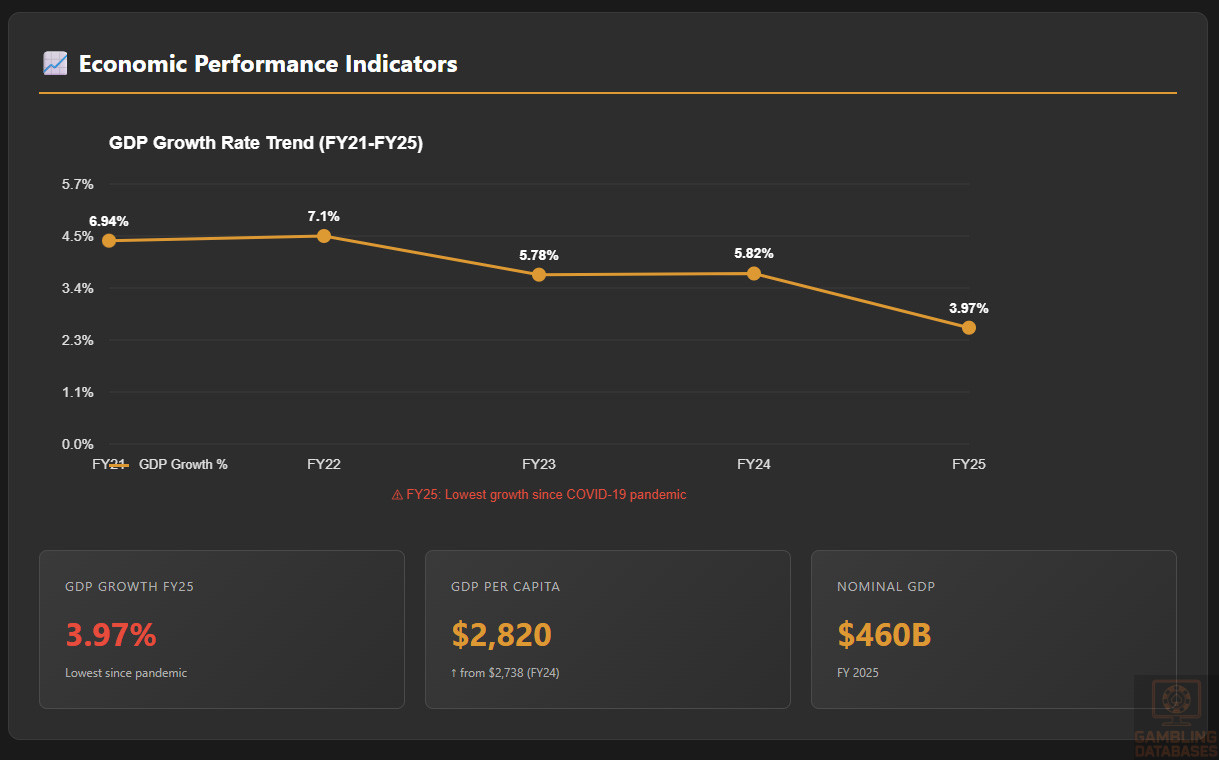

Bangladesh’s nominal GDP reached approximately $460 billion USD in 2022, positioning the country among significant emerging markets. GDP per capita increased to $2,820 USD in fiscal year 2024-2025 according to Bangladesh Bureau of Statistics provisional data, up from $2,738 the previous year. This represents continued income growth despite economic headwinds.

The GDP growth rate of 3.97% in FY25 represents the slowest expansion since the COVID-19 pandemic, reflecting global economic pressures and domestic challenges. The agriculture sector grew 1.79%, industry expanded 4.34%, and services increased 4.51%. Export-oriented garment manufacturing remains the economic backbone generating substantial foreign exchange.

| Indicator | Value | Year-over-Year Change |

|---|---|---|

| Nominal GDP | $460 billion USD | +10.54% (2022 vs 2021) |

| GDP Per Capita | $2,820 USD | +$82 (+3.0%) |

| GDP Growth Rate | 3.97% | -0.25 percentage points |

| Agriculture Growth | 1.79% | Impacted by natural disasters |

| Industrial Growth | 4.34% | Led by manufacturing sector |

| Services Growth | 4.51% | Steady expansion |

| Inflation Rate | 6.17% (Feb 2022) | Rising cost pressures |

Bangladesh graduated from Least Developed Country status in 2018 when it achieved Gross National Income of $1,724 per capita, demonstrating substantial development progress. Foreign exchange reserves faced pressure following the Ukraine conflict due to rising import costs, particularly for fuel and commodities. The country’s garment export sector generates over 80% of export earnings but faces challenges from tariff uncertainties.

Income and Wealth Distribution

Average household income in Bangladesh varies dramatically between urban and rural areas and across income quintiles. Urban households demonstrate significantly higher earnings with greater access to formal employment and business opportunities. The growing middle class represents an increasingly important consumer segment with rising disposable income for discretionary spending including entertainment and leisure activities.

Income inequality remains a significant challenge measured through the Gini coefficient and wealth concentration data. The wealthiest quintile captures a disproportionate share of national income while lower-income groups struggle with subsistence-level earnings. Remittances from overseas Bangladeshi workers contribute substantially to household incomes, particularly in rural areas and specific regions like Sylhet.

| Income Bracket | Monthly Household Income (BDT) | USD Equivalent | Population Share |

|---|---|---|---|

| Low Income | Below 15,000 | Below $125 | 35-40% |

| Lower-Middle Income | 15,000 – 30,000 | $125 – $250 | 25-30% |

| Middle Income | 30,000 – 60,000 | $250 – $500 | 20-25% |

| Upper-Middle Income | 60,000 – 120,000 | $500 – $1,000 | 8-12% |

| High Income | Above 120,000 | Above $1,000 | 3-5% |

Disposable income trends show gradual improvement as per capita income rises, though living costs also increase particularly in urban areas. Consumer spending patterns prioritize necessities including food, housing, and healthcare, with limited remaining budget for entertainment. However, the growing middle and upper-middle class segments demonstrate increasing willingness to spend on leisure activities, digital services, and entertainment including potential gambling expenditure.

Market Size and Growth Projections

Official data on gambling market size does not exist in Bangladesh due to the illegal status of most gambling activities. Underground market estimates prove unreliable given the clandestine nature of operations and reluctance of participants to acknowledge involvement. Media reports and law enforcement statements suggest millions of Bangladeshis participate in illegal online gambling, indicating substantial market activity despite legal prohibitions.

Anecdotal evidence from enforcement agencies indicates rapid growth in online gambling participation from 2020-2024, accelerated by COVID-19 pandemic lockdowns and increased internet access. High Court petitions in 2025 claimed approximately 5 million people suffer from online gambling addiction, representing roughly 2.8% of the population. If accurate, this suggests tens of millions may engage in occasional gambling activity.

| Metric | Conservative Estimate | Moderate Estimate | Notes |

|---|---|---|---|

| Active Participants | 5-8 million | 10-15 million | Based on enforcement data and media reports |

| Problem Gamblers | 3-5 million | 5-7 million | High Court petition cited 5 million |

| Market Penetration | 3-5% | 6-9% | Percentage of adult population |

| Annual Market Size | $200-400 million | $500 million – $1 billion | Highly speculative; no official data |

| ARPU (Annual) | $40-80 | $50-100 | Based on GDP per capita ratios |

| Growth Rate 2020-2024 | 15-25% | 25-40% | Accelerated during pandemic |

Market projections remain highly uncertain given the illegal status and aggressive enforcement actions launched in 2025. The Cyber Security Ordinance and coordinated crackdowns aim to suppress market growth significantly. Payment processing restrictions and ISP blocking create operational barriers for both operators and players. Future market trajectory depends heavily on enforcement effectiveness and whether legal reforms eventually emerge.

Education, Skills, and Digital Literacy

Educational Foundation

Bangladesh has achieved a literacy rate of 72.8% for the population aged 15 and above as of 2025, representing significant progress from historical levels but still lagging developed nations. Gender parity in education has improved substantially with near-equal enrollment rates in primary and secondary education. However, quality concerns persist regarding educational outcomes and skill development.

Tertiary education completion rates remain relatively low compared to regional competitors, though expanding. Universities produce graduates in various fields but skill mismatches with market demand create employment challenges. Digital literacy varies significantly by age cohort, urban-rural location, and education level. Younger urban populations demonstrate high digital competency while older rural residents lag substantially.

English language proficiency remains limited outside major cities and educated classes, though improving among youth. Most Bangladeshis prefer content and services in Bengali (Bangla) language. Technology adoption readiness is high among younger demographics who have grown up with mobile devices and internet access. The workforce increasingly possesses basic digital skills though advanced technical capabilities remain concentrated in urban areas and IT sector professionals.

Cultural and Social Factors

Communication and Language

Bengali (Bangla) serves as the primary language for 99% of the population and dominates daily communication, business transactions, and online content consumption. The language uses its own script which requires proper localization for websites and applications serving Bangladesh users. English functions as a secondary language for educated urban populations and business contexts but cannot serve as the primary interface for mass-market services.

Internet users strongly prefer Bengali language content and services. Successful digital platforms in Bangladesh provide Bengali interfaces, customer support, and localized content. Payment instructions, terms and conditions, and all customer communications must be available in Bengali to achieve broad market penetration. Regional dialects exist particularly in Chittagong and Sylhet but Bengali standardization enables communication across regions.

Cultural Attitudes Toward Gambling

Gambling faces strong cultural stigma in Bangladesh rooted in Islamic religious teachings that prohibit gambling as haram (forbidden). With 89.1% of the population identifying as Muslim, religious perspectives heavily influence social attitudes and policy positions. The Constitution’s directive for the state to prevent gambling reflects this cultural-religious consensus against gambling activities.

Foreign brands face trust challenges in Bangladesh particularly for financial services and high-risk categories. Bangladeshi consumers prefer locally-rooted businesses or internationally established brands with proven track records. For illegal gambling services, this manifests in reliance on international operators already serving Asian markets, accessed through local agent networks that provide Bengali-language support and familiar payment methods.

Problem Gambling and Social Considerations

Prevalence and Demographics

Problem gambling prevalence data remains limited given the illegal status of gambling and cultural stigma against acknowledging participation. A 2025 High Court petition claimed approximately 5 million Bangladeshis suffer from online gambling addiction, though this figure’s reliability is unclear. If accurate, this represents roughly 2.8% of the total population or potentially 4-5% of the adult population.

Media reports document serious social harms including individuals selling land and assets to finance gambling, family breakdowns, and suicides following gambling losses. The rapid growth of smartphone access and social media advertising has exposed younger populations to gambling platforms. Rural areas previously insulated from gambling access now face increased exposure through mobile internet connectivity.

| Indicator | Reported Impact | Most Affected Groups |

|---|---|---|

| Estimated Problem Gamblers | 3-5 million | Young males, urban and rural |

| Financial Harm Cases | Widespread asset sales reported | Families, land owners |

| Suicide Cases | Multiple media reports | Individuals with severe losses |

| Age Groups Affected | Teenagers to middle-aged | Concentration in 18-40 age range |

| Gender Distribution | Predominantly male | Limited female participation |

| Underage Gambling | Significant concern | Teenagers with smartphone access |

Government and Support Services

Bangladesh lacks dedicated problem gambling treatment facilities or support services. No charity organizations specifically address gambling addiction due to the illegal status and religious prohibition. Private mental health services may treat gambling-related issues within broader addiction or behavioral health frameworks but specialized gambling treatment programs do not exist.

International support services like GamCare provide telephone and online chat support accessible to Bangladeshi problem gamblers, though awareness of these resources remains limited. Language barriers and cultural factors inhibit help-seeking behavior. The stigma associated with gambling combined with its illegal status prevents many problem gamblers from seeking assistance.

Government response focuses on enforcement and prohibition rather than harm reduction or treatment. The 2025 enforcement campaign aims to eliminate gambling access rather than provide support for affected individuals. No mandatory contributions to problem gambling funds exist as no legal gambling operations function in Bangladesh. Public awareness campaigns about gambling risks remain minimal.

Political Structure and Governance

Government System and Stability

Bangladesh operates as a parliamentary democracy with a prime minister serving as head of government. Political stability has varied over recent decades with periodic tensions between major political parties. Governance quality faces challenges related to corruption, regulatory consistency, and institutional capacity. The Corruption Perceptions Index typically ranks Bangladesh in the lower half globally indicating significant governance issues.

Regulatory consistency and predictability pose concerns for businesses given policy changes, enforcement variation, and bureaucratic discretion. The business environment has improved in recent years with reforms aimed at attracting investment and modernizing regulations. However, institutional weaknesses persist in areas including contract enforcement, property rights protection, and regulatory transparency.

International relations generally remain stable with Bangladesh maintaining diplomatic and economic ties across major powers. The country is not an EU member but benefits from preferential trade access to European markets under Everything But Arms provisions. Bilateral and multilateral trade agreements facilitate export-oriented manufacturing particularly in the garment sector.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration reached 44.5% of the population in January 2025 with 77.7 million internet users according to DataReportal analysis. This represents growth of 1.2% or 939,000 new users compared to January 2024. However, recent data from Bangladesh Telecommunication Regulatory Commission shows decline in mobile internet users from 129.2 million in June 2024 to 116 million by January 2025, indicating market volatility.

Daily internet usage averages vary by demographic segment with younger urban users spending multiple hours online daily while older rural populations use internet sparingly if at all. Mobile devices dominate internet access with fixed broadband serving a small minority of users. Social media engagement is high among connected populations with 60 million social media users representing 34.3% of the total population.

| Metric | Value | Year-over-Year Change |

|---|---|---|

| Total Internet Users | 77.7 million | +939,000 (+1.2%) |

| Internet Penetration | 44.5% | +0.5 percentage points |

| Mobile Internet Users | 116 million | -13.2 million (-10.2%) |

| Household Internet Access | 50.4% | +6.8 percentage points |

| Urban Internet Access | 60.3% | Higher than national average |

| Rural Internet Access | 46% | Narrowing urban-rural gap |

| Social Media Users | 60 million | 34.3% penetration |

| Median Mobile Download Speed | 28.26 Mbps | +5.26 Mbps (+22.9%) |

| Median Fixed Download Speed | 48.91 Mbps | +9.08 Mbps (+22.8%) |

E-commerce participation grows steadily as trust in online transactions increases and digital payment infrastructure improves. Popular e-commerce platforms include Daraz, Pickaboo, and various local retailers establishing online presence. Digital service consumption spans entertainment streaming, food delivery, ride-hailing, and increasingly financial services through mobile banking applications.

Digital Payment Behavior

Mobile financial services dominate digital payments in Bangladesh with bKash, Nagad, and Rocket commanding over 80% combined market share. bKash leads with more than 60% of all mobile financial transactions and 70+ million registered users. Nagad, operated by Bangladesh Post Office, serves 74 million customers with daily transactions averaging $12 million. These platforms have revolutionized financial inclusion enabling millions without bank accounts to participate in digital economy.

Payment method preferences strongly favor mobile financial services over traditional banking for person-to-person transfers, bill payments, mobile recharges, and increasingly merchant payments. Credit and debit card penetration remains relatively low concentrated among urban middle and upper classes. Bank transfers occur primarily for larger transactions and formal business payments. Cryptocurrency adoption for payments remains illegal and minimal given Bangladesh Bank prohibitions.

| Payment Method | Market Share | Users (millions) | Primary Use Cases |

|---|---|---|---|

| bKash | 60%+ | 70+ | P2P transfers, merchant payments, bills, remittances |

| Nagad | 15-20% | 74 | Government services, transfers, payments |

| Rocket (DBBL) | 8-12% | Unknown | Bank-linked wallet services |

| Other MFS | 5-10% | 10-15 | Upay, SureCash, etc. |

| Credit/Debit Cards | 5-8% | 5-8 | Online shopping, ATM withdrawals |

| Bank Transfers | 3-5% | Variable | Large transactions, business payments |

| Cash | Declining | Universal | Still dominant in informal economy |

Trust in online payment systems has grown substantially though concerns about fraud and security persist. Average transaction sizes vary by payment type with P2P transfers typically ranging from 500-5,000 BDT while merchant payments and bill payments span wider ranges. Transaction frequency is high among active MFS users who may conduct multiple transactions weekly for various purposes including sending money to family, paying bills, and shopping online.

Gaming and Gambling Preferences

Current Market Participation

Reliable data on gambling participation rates does not exist given the illegal status and social stigma. Estimates based on enforcement reports and media coverage suggest 5-15 million Bangladeshis may engage in gambling activities at least occasionally. Sports betting dominates preferences particularly on cricket matches given the sport’s massive popularity in Bangladesh. Football betting also attracts participants especially during major tournaments.

Online casino games have gained traction with slots, roulette, and card games accessible through international platforms. Live dealer games appeal to players seeking more authentic casino experiences. Lottery participation occurs through legal government-authorized lotteries and illegal underground operations. Seasonal patterns align with major sporting events including cricket tournaments, football World Cups, and regional competitions.

Consumer Behavior Patterns

Average spending per player remains speculative without official data. Based on GDP per capita and regional comparisons, monthly gambling expenditure likely ranges from 1,000-5,000 BDT ($8-42 USD) for regular participants. Problem gamblers may spend substantially more, potentially exhausting available resources and selling assets to continue gambling. Bet sizes typically remain modest reflecting limited disposable income among most participants.

Mobile platforms dominate access given smartphone penetration and mobile-first internet usage patterns. Desktop usage is minimal outside office environments and internet cafes. Peak gambling times likely align with cricket match schedules and evening leisure hours when individuals have free time after work. Weekend activity may increase for sports betting corresponding to match schedules.

| Behavior Metric | Estimated Pattern | Notes |

|---|---|---|

| Average Monthly Spend | 1,000-5,000 BDT ($8-42) | Regular participants; problem gamblers much higher |

| Typical Bet Size | 100-500 BDT ($0.83-4.17) | Modest stakes reflecting income levels |

| Platform Preference | 85-90% mobile | Smartphone-based access dominates |

| Popular Game Types | Sports betting (cricket, football) | Slots and casino games secondary |

| Session Frequency | Multiple times weekly | Active participants; casual players less frequent |

| Peak Activity Times | Evenings, weekends, match days | Leisure time and sporting events |

| Deposit Frequency | Weekly or bi-weekly | Aligned with income receipt patterns |

| Withdrawal Behavior | Infrequent | Most players lose more than they win |

Retention and loyalty remain unclear without operator data. Bonus sensitivity is likely high given price consciousness among Bangladeshi consumers. Promotional offers and free bet incentives probably drive significant participation. Player preferences by age show younger participants (18-35) dominating online gambling while older demographics engage less frequently in digital gambling though may participate in traditional informal gambling.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Bangladesh has achieved 100% 4G network coverage with 3G reaching 99.80% of the population as of 2025. This near-universal mobile network availability provides the foundation for mobile internet access across urban and rural areas. Fixed broadband infrastructure remains limited serving primarily urban commercial and residential customers with only 14.3 million ISP/PSTN subscribers compared to 116 million mobile internet users.

Average internet speeds have improved significantly with median mobile download speeds reaching 28.26 Mbps in January 2025, up 22.9% year-over-year. Fixed broadband connections deliver median download speeds of 48.91 Mbps, up 22.8% annually. These speeds suffice for most online applications including video streaming, gaming, and web-based services though still lag behind developed markets and some regional competitors.

| Infrastructure Type | Coverage/Speed | Year-over-Year Improvement |

|---|---|---|

| 4G Network Coverage | 100% | Full coverage achieved |

| 3G Network Coverage | 99.80% | Near-universal |

| 5G Deployment | Not yet launched | Expected by 2026-2027 |

| Mobile Download Speed | 28.26 Mbps (median) | +5.26 Mbps (+22.9%) |

| Fixed Download Speed | 48.91 Mbps (median) | +9.08 Mbps (+22.8%) |

| Mobile Internet Users | 116 million | -13.2 million (concerning decline) |

| Fixed Broadband Subscribers | 14.3 million | Modest growth |

Network reliability and uptime generally prove adequate in urban areas though rural locations may experience intermittent connectivity. Infrastructure investment continues with operators expanding 4G coverage and preparing for 5G rollout. The government’s Digital Bangladesh initiative prioritizes connectivity expansion to underserved areas. However, recent decline in mobile internet subscriptions from 129.2 million to 116 million raises concerns about affordability and economic pressures affecting connectivity.

5G and Future Technology Deployment

5G network deployment has not yet commenced in Bangladesh as of 2025 though planning and preparation activities are underway. Major mobile operators including Grameenphone, Robi, Banglalink, and Teletalk are expected to begin 5G rollout in 2026-2027 pending spectrum allocation and infrastructure investment. Initial deployment will focus on major urban centers before expanding to secondary cities and eventually rural areas.

The timeline for nationwide 5G coverage extends beyond 2030 given the investment requirements and infrastructure buildout needed. However, existing 4G networks provide sufficient capacity for current online services including gaming and streaming applications. Future 5G deployment will enable enhanced mobile broadband experiences, lower latency for real-time applications, and support for emerging technologies.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Four mobile network operators serve Bangladesh: Grameenphone (market leader with 86.51 million subscribers), Robi (57.40 million), Banglalink (37.95 million), and state-owned Teletalk (6.59 million). Total mobile phone subscribers reached 186.6 million in January 2025, representing 106% of the population indicating multiple SIM card ownership is common.

Network operator competition drives service improvements and price reductions benefiting consumers. Grameenphone leads in overall mobile experience quality according to OpenSignal with video experience scores of 57.6 points and download speeds of 23.3 Mbps. Data costs have declined substantially making mobile internet more affordable, though recent economic pressures and taxation increases have constrained affordability for lower-income users.

| Operator | Subscribers (millions) | Market Share | Network Quality |

|---|---|---|---|

| Grameenphone | 86.51 | 46% | Leader in speed and experience |

| Robi | 57.40 | 31% | Strong challenger |

| Banglalink | 37.95 | 20% | Value-focused operator |

| Teletalk | 6.59 | 3% | State-owned operator |

| Total | 188.45 | 100% | Teledensity 106% |

Device Penetration

Smartphone adoption reached 70.1% of mobile phone users in 2025, up from 63.3% in 2023 and 52.1% in 2022. This rapid smartphone penetration enables access to mobile applications and mobile-optimized websites. An estimated 123-130 million smartphones are in use across Bangladesh concentrated in urban areas and among younger demographics.

Android devices dominate the market with estimated 90%+ share due to affordable device availability from Chinese manufacturers including Xiaomi, Oppo, Vivo, and Samsung. iOS/iPhone penetration remains minimal restricted to affluent urban consumers. Average device specifications improve continuously as low-cost smartphones offer increasingly capable features including larger screens, better processors, and adequate RAM for mobile applications.

Mobile internet usage patterns show heavy reliance on smartphones for all online activities including social media, messaging, entertainment, e-commerce, and financial services. Mobile data consumption per user averages 8.2 GB monthly as of 2025, up substantially from 1.2 GB in 2020. This growth reflects increased video streaming, social media engagement, and application usage driving demand for faster networks and larger data packages.

Financial Services and Payment Infrastructure

Banking System Structure

Bangladesh’s banking sector comprises over 60 commercial banks including state-owned, private domestic, and foreign banks. Major banks include Sonali Bank (largest state-owned), Dutch-Bangla Bank (DBBL), BRAC Bank, City Bank, Standard Chartered Bangladesh, and numerous others. Banking penetration has improved but remains limited with significant portions of the population lacking formal bank accounts.

Digital banking adoption grows steadily with major banks offering mobile banking applications and internet banking services. However, mobile financial services through bKash, Nagad, and Rocket reach far more Bangladeshis than traditional banking. Account penetration rates show approximately 50-60% of adults have some form of financial account including bank accounts or MFS accounts. Credit and lending markets remain underdeveloped with limited consumer credit availability outside major urban centers.

Payment Processing Options

Mobile financial services dominate payment processing in Bangladesh offering the most accessible and widely-used payment infrastructure. bKash processes millions of daily transactions for person-to-person transfers, merchant payments, bill payments, mobile recharges, and remittance receipts. Nagad and Rocket provide similar services with government service payment integration and bank linkages respectively.

Credit and debit card acceptance remains limited outside major retail chains, hotels, and online platforms. International card networks including Visa and Mastercard operate in Bangladesh but penetration is low. E-wallet options beyond local MFS platforms are largely unavailable – PayPal, Skrill, and Neteller do not officially serve Bangladesh market. Cryptocurrency transactions remain illegal under Bangladesh Bank directives citing Foreign Exchange Regulation Act, Money Laundering Prevention Act, and Anti-Terrorism Act violations.

| Payment Method | Availability | Processing Fees | Suitability for iGaming |

|---|---|---|---|

| bKash | Widely available | 1-2% MDR for merchants | Blocked for gambling; high risk |

| Nagad | Widely available | 1-2% MDR for merchants | Blocked for gambling; high risk |

| Rocket | Available | 1-2% MDR for merchants | Blocked for gambling; high risk |

| Credit/Debit Cards | Limited penetration | 3-4% MDR | Banks restrict gambling transactions |

| Bank Transfers | Available | Fixed fees vary | Slow; monitoring for gambling |

| International E-wallets | Not available | N/A | PayPal, Skrill, Neteller not operational |

| Cryptocurrency | Illegal | N/A | Prohibited by Bangladesh Bank |

| Cash Agents | Informal networks | Variable | Used by illegal operators; prosecution risk |

Processing fees for mobile financial services typically range 1-2% for merchant payments, significantly lower than the 3.5% charged for card transactions. Transaction processing timelines are near-instantaneous for MFS transfers. International payment capabilities remain restricted with limitations on cross-border transactions and foreign exchange controls. Chargebacks and dispute resolution mechanisms exist but vary by payment method with MFS platforms offering customer complaint processes.

For gambling operations, payment processing faces severe restrictions. Bangladesh Bank has directed financial institutions to identify and block gambling transactions. The 2025 enforcement campaign flagged over 1,000 mobile financial service agents for facilitating gambling payments, with license revocations and penalties recommended. This creates extreme operational risk for any gambling operator attempting to process payments through legitimate Bangladesh financial infrastructure.

E-commerce and Digital Economy

Digital Market Development

E-commerce market size in Bangladesh has grown substantially reaching several billion dollars annually with continued rapid expansion. The Digital Bangladesh initiative and improving internet connectivity drive online retail adoption. Popular e-commerce platforms include Daraz, Pickaboo, Othoba, Rokomari, and numerous specialized retailers across categories including fashion, electronics, books, and groceries.

Online retail penetration remains relatively low at 5-8% of total retail but grows quickly from a small base. Digital service adoption extends beyond shopping to food delivery (Foodpanda, Pathao Food), ride-hailing (Uber, Pathao), digital content streaming, and online education. Consumer trust in online transactions has improved as platforms demonstrate reliability and payment security, though concerns about counterfeit products and delivery reliability persist.

Cross-border online shopping faces limitations due to foreign exchange restrictions and customs procedures. Most e-commerce activity involves domestic merchants and local delivery. Digital goods and services consumption grows including mobile game in-app purchases, streaming service subscriptions, and software/application purchases. The digital economy contributed approximately 4.2% to GDP in 2025, exceeding earlier projections and creating an estimated 350,000 jobs.

Business Environment and Regulatory Framework

Ease of Business Operations

Bangladesh ranked 168th out of 190 economies in the final World Bank Ease of Doing Business report published in 2020. In the successor Business Ready (B-Ready) report released in 2024, Bangladesh ranked 29th among 50 countries evaluated in the initial phase. This represents significant improvement though comparability between the two methodologies is limited.

The B-Ready report scored Bangladesh at 56.99 for Regulatory Framework, 41.64 for Public Services, and 70.49 for Operational Efficiency. The relatively strong operational efficiency score contrasts with weaker public services delivery. Business registration processes have been streamlined though still involve multiple steps and approvals. Time required to start a business has decreased but remains longer than regional leaders.

| Indicator | Ranking/Score | Comparison |

|---|---|---|

| World Bank Ease of Doing Business 2020 | 168 of 190 | Behind India (63), Nepal (94), Pakistan (108) |

| B-Ready 2024 Overall | 29 of 50 | Behind Nepal, Indonesia; ahead of Pakistan (37) |

| B-Ready Regulatory Framework | 56.99 | Moderate scoring (50-70 range) |

| B-Ready Public Services | 41.64 | Low scoring (below 50) |

| B-Ready Operational Efficiency | 70.49 | High scoring (above 70) |

| Corruption Perceptions Index | Lower half globally | Governance challenges persist |

Foreign investment policies permit 100% foreign ownership in most sectors though some restrictions apply in strategic industries. Operational cost structures vary significantly between Dhaka and secondary cities. Office rent in Dhaka central business districts can be expensive while provincial cities offer lower costs. Labor market conditions provide access to large workforce at competitive wage rates though skill shortages exist in specialized technical areas.

Corporate Structure and Registration

Available Entity Types

Foreign companies can establish presence in Bangladesh through several entity structures including Private Limited Company, Public Limited Company, Branch Office, Liaison Office, and Representative Office. Private Limited Companies represent the most common structure for foreign businesses as they permit commercial operations and provide limited liability protection.

Private Limited Companies require minimum two shareholders and two directors with at least one director being a Bangladesh resident. Public Limited Companies must have minimum seven shareholders and three directors, suitable for larger operations or those planning stock exchange listing. Branch Offices allow foreign companies to conduct business using parent company name and capital but the parent bears full liability for branch activities.

Liaison Offices and Representative Offices permit limited activities focused on liaison, coordination, and information gathering without engaging in commercial transactions. These structures suit companies exploring the market before establishing full operations. For gambling operations, entity structure is irrelevant as licensing is not available under any corporate form.

Registration Requirements

Company registration in Bangladesh involves multiple steps including name clearance from Registrar of Joint Stock Companies and Firms (RJSC), preparation of incorporation documents, payment of registration fees, and obtaining registration certificate. Timeline from application to approval typically ranges 2-4 weeks for Private Limited Companies, though complications can extend this period.

Registration costs include government fees of approximately 3,000-5,000 BDT ($25-42 USD) plus legal fees ranging 20,000-50,000 BDT ($167-417 USD) depending on complexity and professional service providers engaged. Required documents include memorandum and articles of association, identification documents for shareholders and directors, registered office address proof, and various declarations and forms.

| Step | Timeline | Cost Range | Key Requirements |

|---|---|---|---|

| Name Clearance | 3-5 days | 600 BDT ($5) | Unique name not conflicting with existing |

| Document Preparation | 5-10 days | Legal fees variable | MOA, AOA, shareholder/director details |

| RJSC Registration | 7-14 days | 3,000-5,000 BDT | Submit complete documentation |

| TIN Certificate | 3-7 days | No fee | Tax identification number |

| Trade License | 7-15 days | 2,000-10,000 BDT | City corporation/municipality approval |

| VAT Registration | 5-10 days | No fee | If turnover exceeds threshold |

| Total Timeline | 1-2 months | 50,000-100,000 BDT | Including legal and professional fees |

Foreign ownership rules permit 100% foreign shareholding in Private Limited Companies for most business sectors. No local partnership is mandated for general businesses though some strategic sectors require government approval or local participation. Minimum capital requirements depend on whether foreign investment is involved – companies without foreign investment have no minimum capital requirement while those with foreign investment typically require $50,000 minimum capital brought through banking channels.

Ongoing compliance requirements include filing annual returns with RJSC, submitting audited financial statements, conducting annual general meetings, and maintaining statutory registers and records. Corporate governance requirements mandate proper board meetings, shareholder meetings, and documentation of corporate decisions. Foreign companies must appoint local directors and maintain registered office in Bangladesh.

Taxation Framework

Corporate Income Tax Structure

Corporate income tax rates in Bangladesh vary based on company type, listing status, and business sector. Publicly traded companies enjoy lower tax rates to incentivize stock market listings. Banks and financial institutions face higher rates. Standard rates for private companies range 22.5% to 27.5% depending on specific circumstances.

| Company Type | Tax Rate | Notes |

|---|---|---|

| Publicly Traded Company | 22.5% | Listed on stock exchange |

| Non-Publicly Traded Company | 27.5% | Private companies |

| One Person Company | 22.5% | Special structure for entrepreneurs |

| Bank, Insurance, Financial Institution | 37.5% | Higher rate for financial sector |

| Mobile Phone Operator | 40% | Telecom sector premium rate |

| Cigarette Manufacturer | 45% | Sin tax premium |

Special economic zones offer tax incentives including tax holidays for new businesses, reduced tax rates, and duty-free import of capital machinery. These incentives aim to attract foreign investment and promote industrial development. Tax treaties exist with numerous countries to prevent double taxation and facilitate cross-border investment, though gambling operations would not benefit from treaty protections given their illegal status.

Transfer pricing rules apply to related-party transactions requiring arm’s length pricing documentation. Withholding tax rates on dividends, interest, and royalties paid to non-residents typically range 10-20% depending on payment type and applicable tax treaties. VAT applies at standard rate of 15% to most goods and services with some exemptions and reduced rates for specific categories.

Personal Income Tax

Individual income tax in Bangladesh follows progressive rate structure with rates ranging from 0% to 25% depending on income levels. The basic tax exemption threshold for the 2024-2025 tax year is 350,000 BDT ($2,917 USD) for individual taxpayers, 400,000 BDT for female taxpayers, 450,000 BDT for senior citizens aged 65+, and 475,000 BDT for persons with disabilities.

| Income Bracket (BDT) | Tax Rate | Notes |

|---|---|---|

| 0 – 350,000 | 0% | Tax-free threshold (standard taxpayer) |

| 350,001 – 450,000 | 5% | Entry-level tax rate |

| 450,001 – 750,000 | 10% | Middle income bracket |

| 750,001 – 1,150,000 | 15% | Upper-middle income |

| 1,150,001 – 1,650,000 | 20% | High income bracket |

| Above 1,650,000 | 25% | Top marginal rate |

Employers must withhold income tax from employee salaries based on applicable rates. Social security contributions are minimal compared to developed countries with limited mandatory employer or employee contributions. Tax residency rules determine whether individuals pay tax on worldwide income or only Bangladesh-source income, with residents defined as those present in Bangladesh for 182 days or more in a tax year.

Market Entry Considerations

Legal Market Entry Assessment

Critical Finding: Legal market entry for iGaming operations is not possible in Bangladesh under current law. No licensing framework exists, no regulatory pathway is available, and all gambling operations face criminal prosecution. The following analysis addresses theoretical entry considerations if legal reforms were to occur, or for operators assessing illegal market access risks.

Illegal Operation Risks: Operating without license in Bangladesh carries severe penalties under the Cyber Security Ordinance 2025 including up to 2 years imprisonment and fines up to 10 million BDT ($80,000 USD). Payment processing faces active blocking with over 1,000 MFS agents flagged in 2025. ISP blocking prevents website access. Criminal Investigation Department conducts ongoing enforcement operations. Reputational and legal risks are extreme.

Theoretical Entry Strategies (If Legal Framework Existed)

If Bangladesh were to legalize and regulate gambling, optimal market entry approaches would likely include:

Local Partnership Strategy: Partnering with established Bangladesh business groups would provide local market knowledge, regulatory navigation capability, and customer trust. Joint ventures with telecommunications companies, banks, or large conglomerates could leverage existing customer bases and distribution networks. Local partnerships would be essential for payment processing, customer acquisition, and regulatory relationships.

White Label Approach: Licensing white label platform technology to local operators would minimize foreign operator exposure while enabling rapid market entry. Local partners would handle regulatory compliance, payment processing, and customer service while international technology providers supply gaming platforms, content, and operational expertise. This model reduces capital requirements and regulatory burden for international operators.

Mobile-First Strategy: Given 70%+ smartphone adoption and mobile-dominated internet usage, mobile-optimized or mobile-only platforms would be essential. Progressive web apps or native applications distributed through alternative app stores (not Google Play which restricts gambling apps) would reach the mass market. Mobile payment integration through bKash, Nagad, and Rocket would be mandatory for market penetration.

Localization Requirements

Successful market entry would require comprehensive localization including Bengali language interface for all customer-facing elements, customer support in Bengali, culturally appropriate marketing messaging, integration with local payment methods, local customer service hours, and content relevant to Bangladesh users particularly cricket betting given the sport’s dominant popularity.

Price point optimization would be critical given average GDP per capita of $2,820 USD. Low minimum bets, affordable deposit amounts, and bonus structures targeting value-conscious consumers would be necessary. Marketing channels would focus on social media particularly Facebook given its 60 million users in Bangladesh, cricket sponsorships and partnerships if permitted, and influencer marketing targeting young urban males.

Payment Strategy Requirements

Payment provider selection would be the most critical operational challenge. bKash, Nagad, and Rocket dominate payment preferences but actively block gambling transactions. Alternative payment solutions would need development potentially including cryptocurrency despite current prohibition, informal agent networks accepting extreme risk, international e-wallets if regulatory changes permitted their operation, or prepaid voucher systems distributed through retail networks.

Typical Costs and Timelines

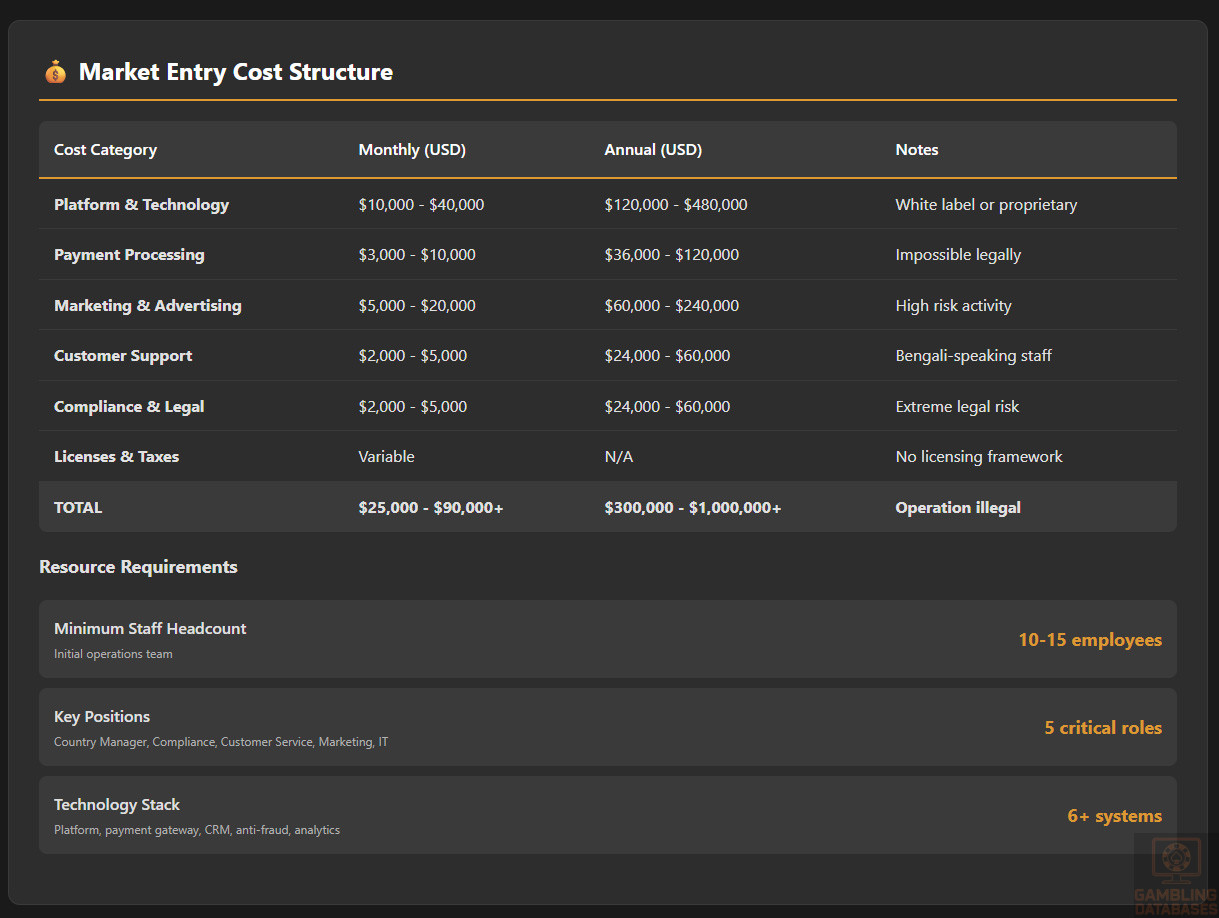

Initial Setup Investment Breakdown

| Cost Category | Estimated Amount (USD) | Notes |

|---|---|---|

| License Application Fee | N/A – No licensing available | Would likely be $50,000-200,000 if framework existed |

| Company Registration | $500-1,000 | Standard business registration costs |

| Initial Capital Requirement | $50,000 minimum | For foreign investment registration |

| Legal & Consulting Fees | $20,000-50,000 | Local legal counsel, regulatory advice |

| Office Setup (Annual) | $12,000-36,000 | Dhaka office space and utilities |

| Technology Platform | $100,000-500,000 | White label or proprietary development |

| Payment Integration | $20,000-50,000 | Technical integration if partnerships achieved |

| Initial Marketing Budget | $100,000-300,000 | Launch campaign and customer acquisition |

| Working Capital | $200,000-500,000 | Player balances, operational reserves |

| Total Initial Investment | $500,000-1,500,000+ | Highly variable based on scale and approach |

Monthly Operational Cost Estimates

| Expense Category | Monthly Cost (USD) | Annual Cost (USD) |

|---|---|---|

| Staff Salaries (10-15 employees) | $5,000-10,000 | $60,000-120,000 |

| Office Rent & Utilities | $1,000-3,000 | $12,000-36,000 |

| Technology Platform Fees | $5,000-15,000 | $60,000-180,000 |

| Payment Processing (% of GGR) | Variable | Typically 2-5% of transactions |

| Marketing & Customer Acquisition | $10,000-50,000 | $120,000-600,000 |

| Customer Support | $2,000-5,000 | $24,000-60,000 |

| Compliance & Legal | $2,000-5,000 | $24,000-60,000 |

| Licenses & Taxes | Variable | Depends on regulatory framework |

| Total Operating Costs | $25,000-90,000+ | $300,000-1,000,000+ |

Timeline Expectations

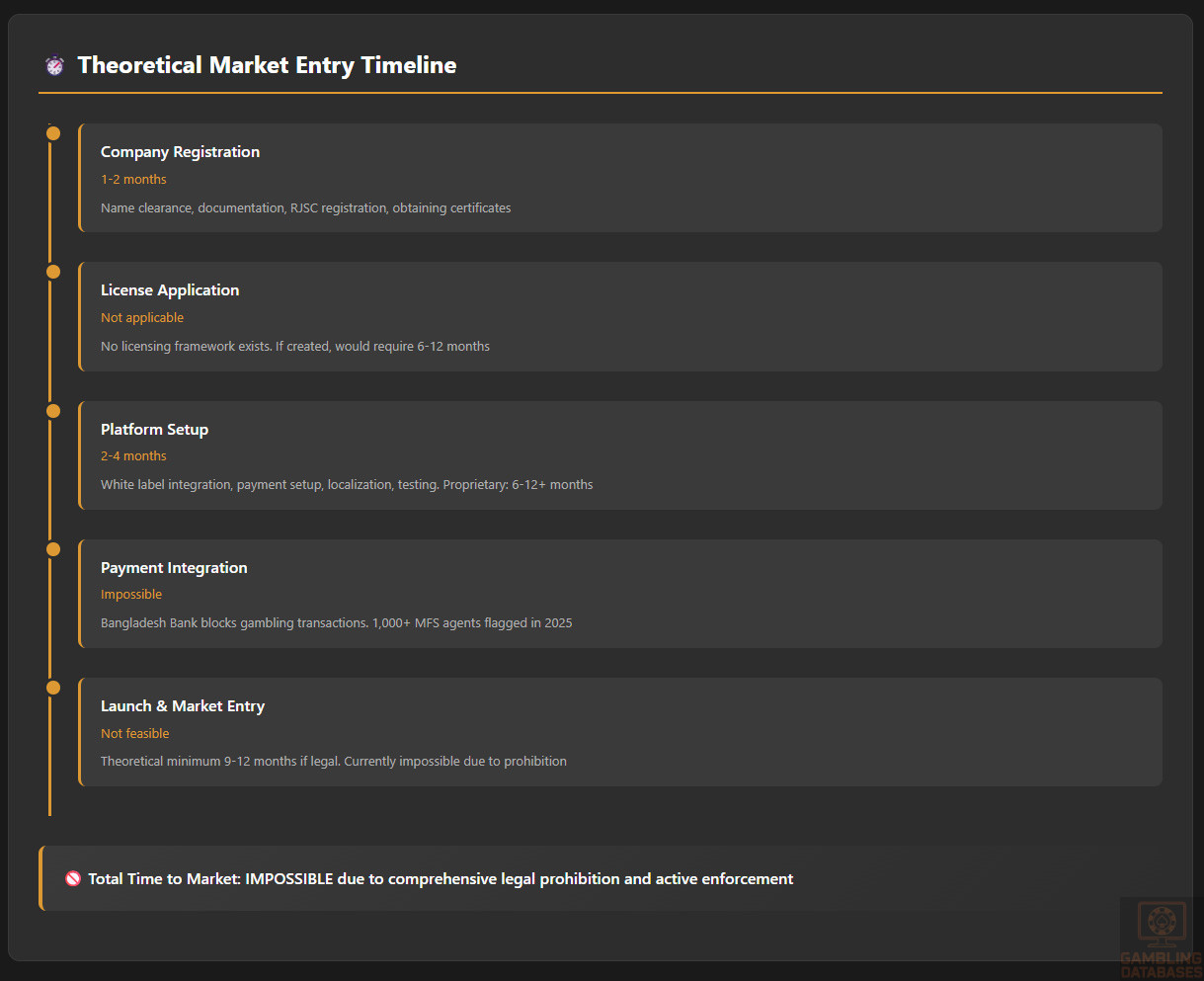

Company Registration: 1-2 months from initiation to completion including name clearance, documentation, RJSC registration, and obtaining necessary certificates.

License Application: Not applicable as no licensing framework exists. If framework were created, likely 6-12 months based on regional comparisons for comprehensive application review.

Platform Setup: 2-4 months for white label integration including payment integration, localization, testing, and launch preparation. Proprietary platform development would require 6-12+ months.

Total Time to Market: Impossible currently due to prohibition. Theoretical minimum 9-12 months if legal framework existed, assuming efficient execution across all workstreams.

Resource Requirements

Minimum Staff Headcount: 10-15 employees for initial operations including general manager, compliance officer, customer service representatives (Bengali-speaking), marketing manager, finance/accounting staff, IT support, and payment operations specialist.

Key Positions Needed: Country Manager with Bangladesh market experience and regulatory relationships; Compliance Manager familiar with financial services regulation; Customer Service Manager capable of building Bengali-language support team; Marketing Director with local market expertise; Technology Manager for platform operations and integration.

Technology Stack Requirements: Gaming platform (white label or proprietary), payment gateway integration with local MFS providers, customer relationship management system, responsible gambling tools, anti-fraud systems, data analytics and reporting tools, and mobile-optimized front-end interface.

Success Factors and Challenges

Key Success Enablers (Theoretical Legal Market)

Payment Method Integration: Successfully integrating bKash, Nagad, and Rocket would be absolutely critical as these methods dominate consumer preferences. Without these payment options, market penetration would be severely limited. Given current prohibition and active blocking of gambling transactions, achieving payment partnership would be the single most important success factor.

Mobile-First Excellence: Superior mobile experience is mandatory given device usage patterns. Fast-loading pages, intuitive navigation optimized for smaller screens, minimal data consumption, and offline-capable features where possible would differentiate successful operators. Android optimization is essential given 90%+ market share.

Localization Quality: Professional Bengali translation, culturally appropriate imagery and messaging, local sports coverage particularly cricket with Bangladesh national team and leagues, region-specific promotions aligned with festivals and cultural events, and Bengali-speaking customer support available during local business hours would build trust and engagement.

Competitive Value Proposition: Low minimum bets (10-50 BDT), attractive bonus structures with achievable wagering requirements, regular promotions targeting value-conscious consumers, loyalty programs rewarding frequent players, and transparent pricing without hidden fees would appeal to price-sensitive Bangladesh market.

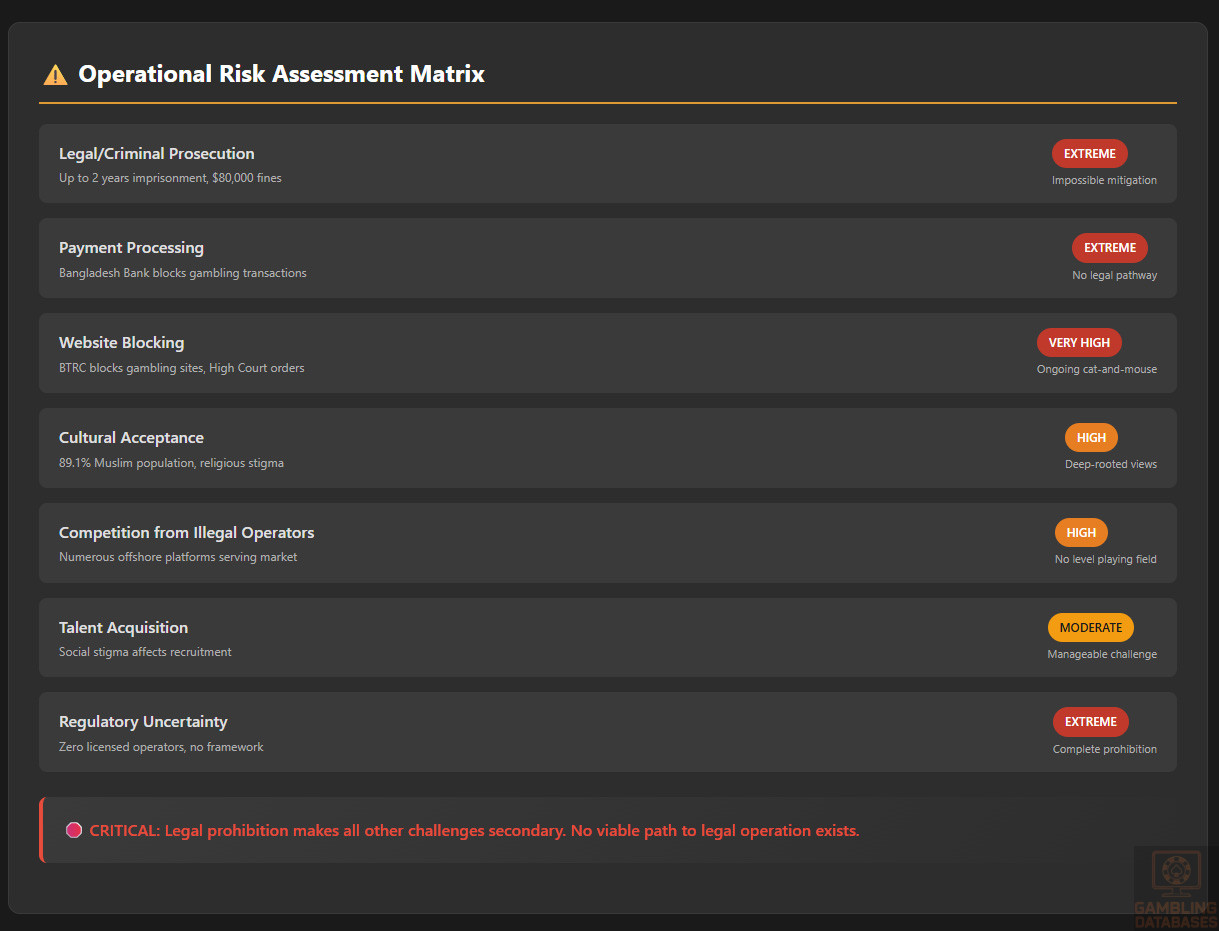

Major Operational Challenges

Legal Prohibition: The fundamental challenge is that gambling remains completely illegal. No pathway exists for legal operation. Criminal penalties under Cyber Security Ordinance 2025 create extreme risk. Enforcement campaigns actively target operators, payment facilitators, and agents. This prohibition makes all other challenges secondary to the core legal impossibility.

Payment Processing Restrictions: Bangladesh Bank directs financial institutions to block gambling transactions. Over 1,000 MFS agents faced license revocation recommendations in 2025 for facilitating gambling payments. Cryptocurrency is illegal. International e-wallets don’t operate in Bangladesh. Payment processing represents an insurmountable barrier without regulatory change or underground networks accepting significant legal risk.

ISP Blocking: Bangladesh Telecommunication Regulatory Commission blocks gambling websites. High Court orders demand comprehensive blocking of gambling platforms across all gateways and platforms. While VPNs enable circumvention, widespread blocking limits market accessibility and creates poor user experience for mainstream consumers.

Cultural and Religious Stigma: Islamic principles prohibit gambling creating social stigma. 89.1% Muslim population means gambling conflicts with religious values for vast majority. Cultural attitudes reinforce legal prohibition. Players may hesitate to gamble openly or discuss activity with peers. This stigma limits marketing effectiveness and word-of-mouth growth.

| Risk Category | Severity | Mitigation Difficulty |

|---|---|---|

| Legal/Criminal Prosecution | Extreme | Impossible without law reform |

| Payment Processing | Extreme | Impossible without regulatory change |

| Website Blocking | Very High | Very Difficult – ongoing cat-and-mouse |

| Cultural Acceptance | High | Difficult – deep-rooted religious views |

| Talent Acquisition | Moderate | Moderate – stigma affects recruitment |

| Competition from Illegal Operators | High | Difficult – no level playing field |

| Regulatory Uncertainty | Extreme | Impossible – no regulatory framework |

Cultural Considerations

Religious Festivals and Ramadan: During Ramadan, gambling participation would likely decline significantly as devout Muslims fast and focus on spiritual activities. Eid celebrations following Ramadan might see increased leisure activity but gambling remains inappropriate during religious observances. Marketing must be sensitive to religious calendar and avoid promotions during sacred times.

Cricket Season Peaks: Bangladesh cricket matches, particularly against rivals like India and Pakistan, drive massive engagement. Cricket World Cups, Asia Cups, and Bangladesh Premier League create prime betting opportunities. Successful operators would need comprehensive cricket coverage with competitive odds and live betting features.

Trust Building for Foreign Brands: International operators face skepticism from Bangladesh consumers who prefer local or well-established brands. Building trust requires local partnerships, Bengali-language customer service, transparent operations demonstrating financial stability and ability to pay winners promptly, and potentially licensing recognizable local brand ambassadors.

Communication Style: Direct, respectful communication works best. Overly promotional or aggressive marketing may be perceived negatively. Educational content helping players understand odds and make informed decisions could build credibility. Responsible gambling messaging, though required in regulated markets, resonates less in cultural context where gambling itself is prohibited.

Exit Strategy Planning

Market Liquidity: No legitimate market exists for selling Bangladesh gambling operations given the illegal status. If legalization occurred, market liquidity would depend on regulatory stability, profitability of operations, and interest from strategic acquirers or financial investors.