Barbados presents a unique opportunity for iGaming operators as the Caribbean nation stands at the threshold of online gambling regulation. The government announced plans in 2023 to introduce comprehensive betting and gaming legislation, creating anticipation for a regulated market in one of the region’s wealthiest and most technologically advanced countries.

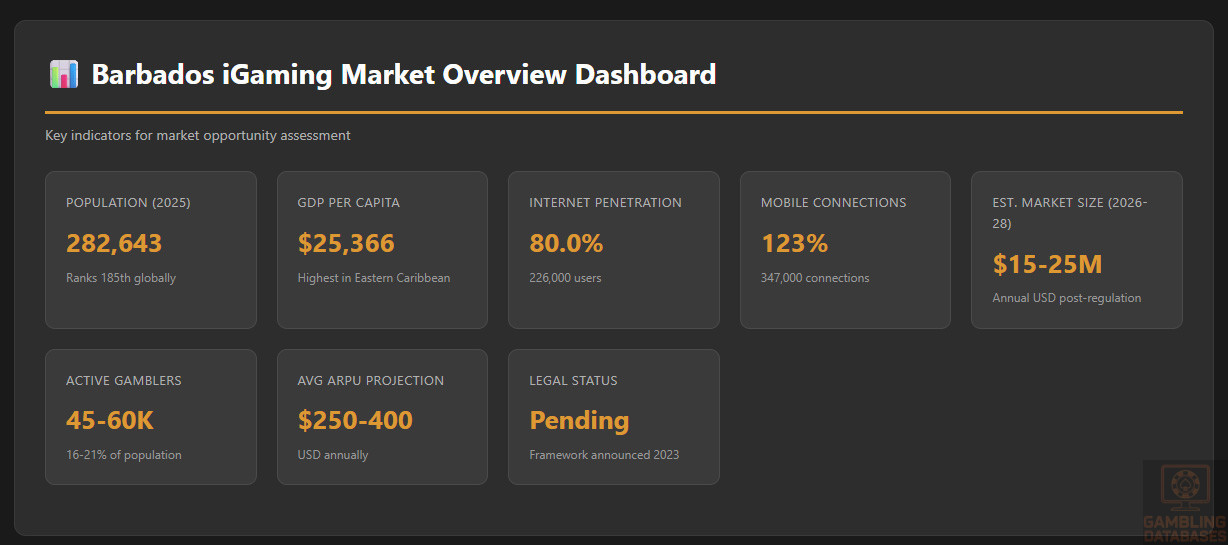

With a population of approximately 283,000, high internet penetration of 80%, and GDP per capita of $25,366, Barbados offers attractive fundamentals despite its small size.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Online Gambling Legal Status | Unregulated – Legislation Pending | Government announced framework coming 2023-2026 |

| Land-Based Gambling Status | Partially Regulated | Slots and horse racing permitted; table games prohibited |

| Total Population (2025) | 282,643 | Ranks 185th globally |

| Median Age | 39.4 years | Mature demographic profile |

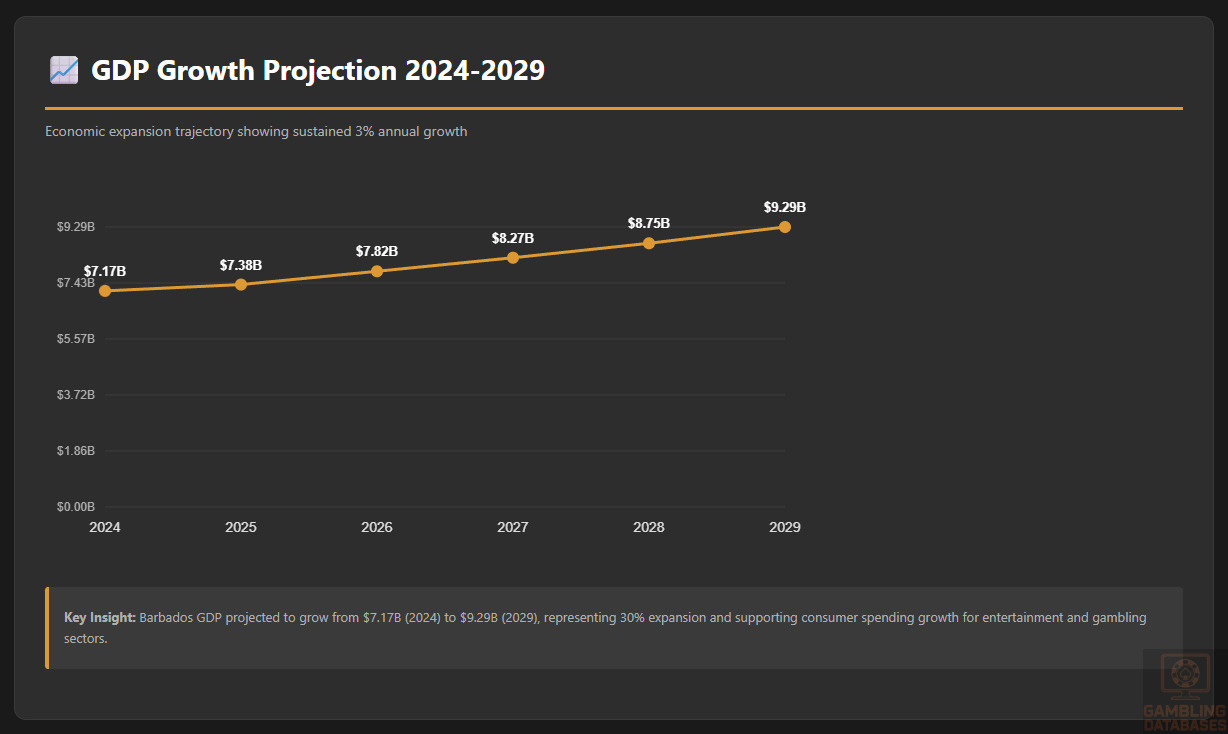

| GDP (Total, 2024) | $7.17 billion USD | Projected $9.29 billion by 2029 |

| GDP Per Capita (2024) | $25,366 USD | Highest in Eastern Caribbean |

| GDP Growth Forecast (2025) | 3.0% annually | Sustained growth expected through 2029 |

| Internet Penetration | 80.0% | 226,000 users; regional leader |

| Mobile Connections | 347,000 (123% penetration) | Multiple devices per capita common |

| Social Media Penetration | 63.7% | 180,000 active users |

| Urban Population | 32.47% | 91,766 people in urban areas |

| Primary Language | English | Official language; Bajan dialect informal |

| Currency | Barbadian Dollar (BBD) | Pegged 2:1 to USD |

| Regulatory Authority | Barbados Lottery Authority | Currently regulates land-based only |

| Expected iGaming License Cost | TBD | Framework under development |

| Corporate Income Tax | 1-5.5% | Competitive international business rates |

| Personal Income Tax | 17.5-35% | Progressive brackets |

| Expected Market Size (2026-2028) | $15-25 million USD annually | Estimated upon regulation |

| Estimated Active Gamblers | 45,000-60,000 | 16-21% of population currently using offshore sites |

| Average ARPU Projection | $250-400 USD annually | Based on regional comparables |

| Market Entry Timeline | 12-18 months | Post-regulation implementation |

| Ease of Doing Business Rank | 128 of 190 | Moderate business environment |

| Political Stability | High | Stable parliamentary democracy |

| Corruption Perception Index | Low corruption | Strong institutions and rule of law |

| Tourism Contribution to GDP | Major driver | Key economic sector alongside offshore finance |

| Time Zone | Atlantic Standard Time (AST) | Same as US Eastern +1 hour |

| Mobile Payment System Launch | BiMPay – March 2026 | National instant payment infrastructure |

| Banking Penetration | High | Well-banked population with strong financial services |

| Market Maturity Stage | Pre-Regulation | First-mover advantage opportunity |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Barbados currently operates under a partially regulated gambling framework that permits certain land-based activities while prohibiting others. The regulatory landscape is in transition, with the government actively developing comprehensive online gambling legislation announced in 2023.

Land-Based Gambling Activities

Casino Operations: Traditional table games including roulette, blackjack, and poker are explicitly prohibited in Barbados. No licensed casino facilities operate on the island, reflecting a conservative approach to gambling that prioritizes the country’s image as a relaxed, family-friendly tourism destination.

Slot Machines: Electronic gaming machines represent the primary legal gambling option in Barbados. Slots are widely available in tourist areas, particularly in St. Lawrence Gap and Holetown, where establishments like Lucky Horseshoe restaurants and Silver Fox Arcade offer these games. Hotels, restaurants, bars, and pools catering to tourists can legally operate slot machines under current regulations.

Horse Racing: Horse racing forms a significant part of Barbados’ gambling culture, with races held at Garrison Savannah, one of the world’s oldest racetracks. The facility hosts three racing seasons annually, allowing spectators to place wagers on race days. Visitors can observe training sessions, but betting is restricted to official race events.

Lotteries: The Barbados Lottery Authority operates several lottery products including Pick 3, Pick 4, Caribbean Keno, Jackpot Bingo, and Caribbean Lotto. Live lottery draws are broadcast on licensed local television and radio broadcasters, providing widespread access to these games.

Online Gambling Framework

Online gambling currently exists in a regulatory gray zone in Barbados. The country does not license domestic online gambling operators, and no iGaming sites are based in Barbados. However, the government does not prohibit residents from accessing international online casinos and sports betting platforms.

Player Activity: Barbadians freely access offshore gambling sites without legal repercussions. Popular international platforms serving Barbadian players include BGO, Black Lotus, 32Red, and numerous other licensed operators based in jurisdictions like Malta, Curacao, and the United Kingdom.

Upcoming Regulatory Framework: In March 2023, Finance Minister Ryan Straughn announced that legislation to oversee the online gaming sector would be introduced to Parliament. The new betting and gaming framework is designed to manage activities that pose “significant risks” to the financial sector and broader economy. The government is finalizing regulations expected within an 18-24 month timeframe from the announcement.

Licensed Operators and Market Players

The Barbadian market currently lacks licensed online operators, creating a first-mover advantage opportunity once regulations are enacted. The land-based sector features limited competition focused on slot machine operations in tourist areas and lottery services provided by the government-controlled Barbados Lottery Authority.

Current Market Structure: International operators serve Barbadian players from offshore jurisdictions without local licensing. These operators leverage established payment processing networks, international banking relationships, and marketing channels to reach Barbadian consumers. Market leaders include major European and Curacao-licensed brands with Caribbean market presence.

Market Concentration: The absence of local regulation means market share data is unavailable. However, industry estimates suggest 45,000-60,000 Barbadians actively use offshore gambling platforms, representing 16-21% of the population. This participation rate aligns with Caribbean regional averages for mature markets.

Licensing Framework and Requirements

Application Process and Eligibility

Regulatory Authority: The Barbados Lottery Authority currently regulates land-based gambling activities including slot machines, lotteries, and horse racing. Upon enactment of online gambling legislation, regulatory oversight will likely expand or transfer to a specialized gaming commission or division within the Financial Services Commission.

Contact Information: Barbados Lottery Authority oversees current gambling operations. Prospective operators should monitor announcements from the Ministry of Finance and the Financial Services Commission regarding the new regulatory framework. The Financial Services Commission website is https://www.fsc.gov.bb

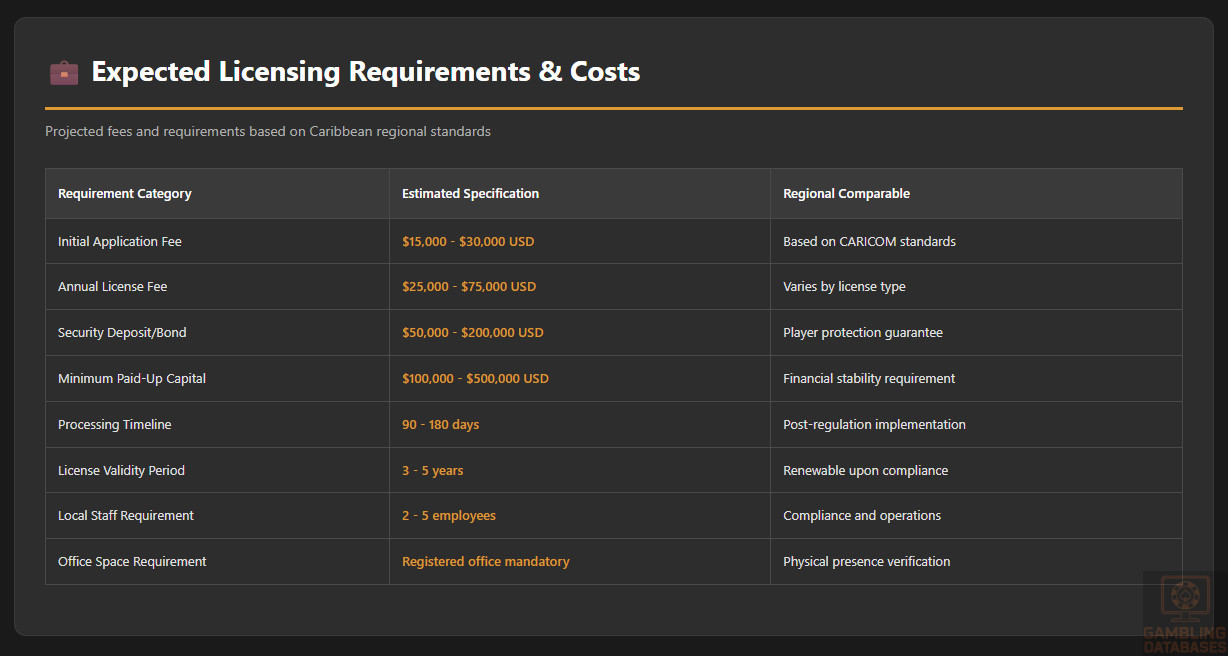

Expected Financial Requirements: While specific figures await regulatory framework publication, comparable Caribbean jurisdictions require initial license fees ranging from $15,000 to $50,000 USD annually, with security deposits between $50,000 and $200,000 USD. Minimum paid-up capital requirements typically range from $100,000 to $500,000 USD depending on license scope.

Technical Standards: Licensed operators will likely need to demonstrate compliance with internationally recognized gaming standards, including RNG certification from approved testing laboratories (GLI, eCOGRA, iTech Labs), server security protocols, game fairness verification, and responsible gambling tools integration.

Background Checks: Application processes in similar jurisdictions require comprehensive due diligence on all directors, shareholders holding more than 5-10% ownership, and key personnel. Expect requirements for police clearance certificates, proof of financial standing, and professional reference verification with processing timelines of 60-180 days.

Local Presence and Operational Requirements

Barbados’ approach to local presence requirements will likely balance attracting international operators with ensuring regulatory oversight and local economic benefit. Based on the government’s stated goals and regional precedents, operators should anticipate moderate localization requirements.

Physical Presence: Expected requirements may include maintaining a registered office in Barbados with local staff for compliance, customer service, and liaison functions. Caribbean jurisdictions typically require 2-5 full-time employees for operational licenses, though server and technical infrastructure may be hosted elsewhere.

Domain and Hosting: Domain requirements will likely mandate .bb ccTLD or recognized international domains (.com, .net) with geo-location verification. Server location requirements may be flexible, allowing cloud infrastructure hosted regionally or internationally provided regulators have access for monitoring purposes.

Foreign Ownership: Barbados has historically welcomed foreign investment in its offshore financial services sector. Online gambling licenses will likely permit 100% foreign ownership while requiring local representation through registered agents, attorneys, or compliance officers familiar with Barbadian regulations.

| Requirement Category | Estimated Specification | Regional Comparable |

|---|---|---|

| Initial Application Fee | $15,000 – $30,000 USD | Based on CARICOM standards |

| Annual License Fee | $25,000 – $75,000 USD | Varies by license type |

| Security Deposit/Bond | $50,000 – $200,000 USD | Player protection guarantee |

| Minimum Paid-Up Capital | $100,000 – $500,000 USD | Financial stability requirement |

| Processing Timeline | 90 – 180 days | Post-regulation implementation |

| License Validity Period | 3 – 5 years | Renewable upon compliance |

| Local Staff Requirement | 2 – 5 employees | Compliance and operations |

| Office Space Requirement | Registered office mandatory | Physical presence verification |

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification: Barbados will almost certainly adopt an 18+ minimum age requirement aligning with international standards and Caribbean regional norms. Operators must implement robust age verification at registration using government-issued ID documents, address verification, and database cross-checks.

KYC/AML Compliance: As a member of the Caribbean Financial Action Task Force (CFATF) and committed to international AML standards, Barbados will require stringent Know Your Customer procedures. Operators must collect and verify player identity, source of funds for high-value transactions, and monitor for suspicious activity patterns.

Responsible Gambling Measures: Expected mandatory features include deposit limits (daily, weekly, monthly), loss limits, session time limits, self-exclusion options (temporary and permanent), reality checks displaying time and money spent, and prominently displayed responsible gambling resources and helpline information.

Player Information Disclosures: Operators will likely need to provide clear terms and conditions in plain English, transparent odds and RTP percentages for all games, withdrawal processing timelines and any associated fees, bonus terms including wagering requirements, and privacy policies detailing data usage and protection.

Financial Monitoring and Reporting

Regulatory oversight will require comprehensive financial reporting to ensure tax compliance, player protection, and market integrity. Operators should prepare systems for detailed transaction monitoring and regular reporting submissions.

Reporting Requirements: Expected monthly reports on gross gaming revenue by game category, player deposit and withdrawal volumes, active player counts and new registrations, responsible gambling tool usage statistics, and customer complaints and resolutions. Quarterly financial statements including profit and loss accounts, balance sheets, and cash flow statements will likely be required.

Audit and Inspection: Licensed operators should anticipate annual independent audits of financial records, gaming systems, and RNG certification, with regulatory authority rights to conduct surprise inspections, system audits, and player fund verification at any time.

Data Retention: Standard requirements typically mandate retaining all transaction records for 7-10 years, player communications and complaint records for 5-7 years, and game outcome logs and RNG seeding data for 3-5 years.

Taxation Structure and Financial Obligations

Player Taxation

Caribbean jurisdictions typically do not tax player winnings, and Barbados will likely follow this model to remain competitive and avoid administrative complexity of tracking individual player profits across thousands of participants.

Withholding Procedures: If player taxation is implemented, it would likely apply only to large jackpot wins exceeding threshold amounts (e.g., $10,000 BBD / $5,000 USD), with operators responsible for withholding and remitting taxes on behalf of players.

Operator Taxation

Barbados’ taxation approach will aim to balance revenue generation with attracting operators to establish legitimate operations. The government will likely structure taxes to compete with regional gambling jurisdictions while generating meaningful fiscal returns.

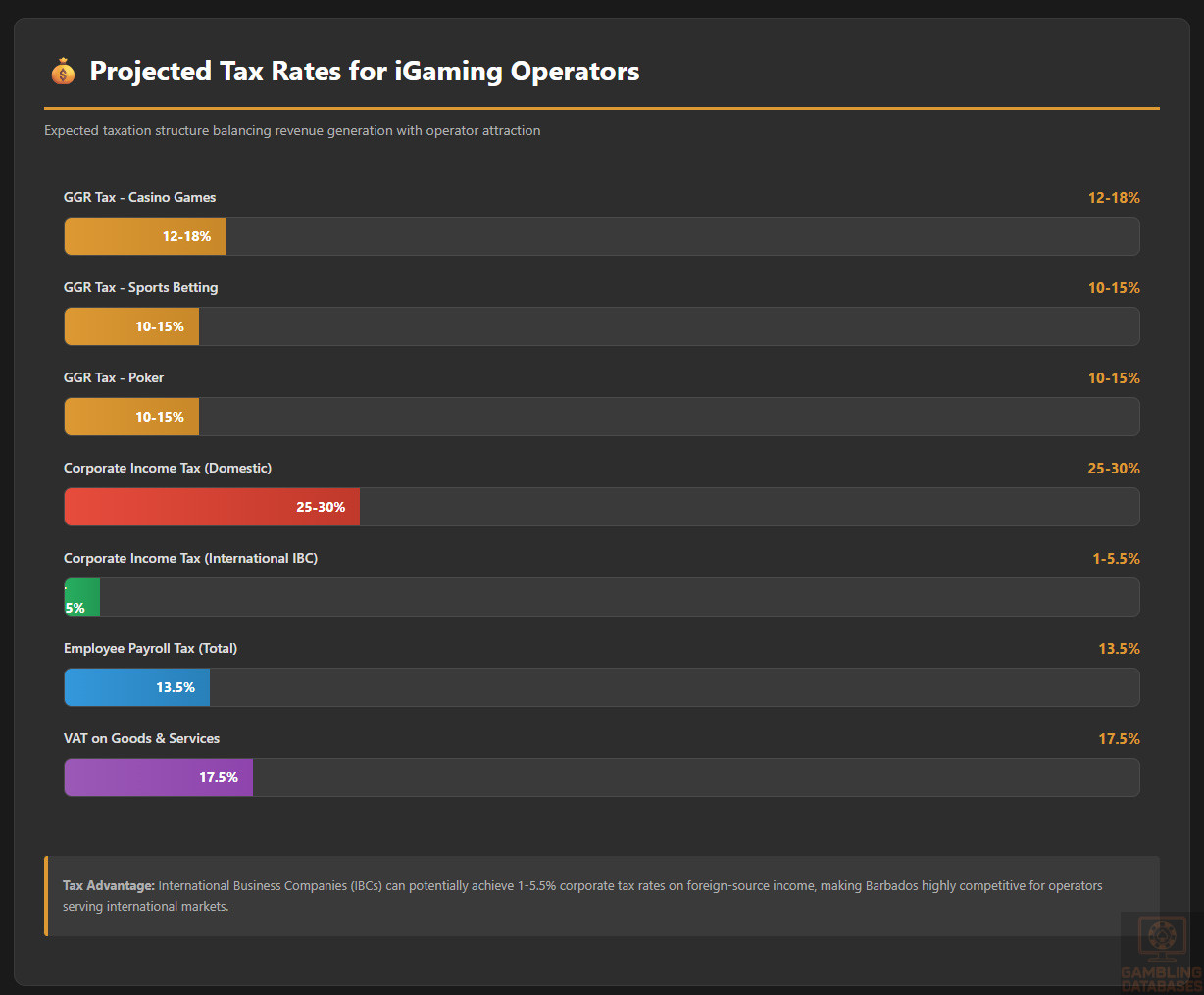

Gross Gaming Revenue (GGR) Tax: Expected rates range from 10-20% of GGR calculated as total stakes minus winnings paid. Caribbean comparables include Curacao (0-2% licensing fees), Antigua (3% GGR), and Costa Rica (no GGR tax but higher licensing fees).

Corporate Income Tax: Barbados offers attractive corporate tax rates for international business companies ranging from 1-5.5% on foreign-sourced income. Gaming operations serving international markets may qualify for these preferential rates, while domestic operations face standard 25-30% corporate tax rates.

License Fees: Annual renewal fees typically range $25,000-75,000 USD depending on license scope, with separate rates for casino licenses, sports betting licenses, poker licenses, and aggregator/platform provider licenses.

| Tax Type | Expected Rate | Calculation Basis |

|---|---|---|

| GGR Tax – Casino Games | 12-18% | Total stakes minus winnings |

| GGR Tax – Sports Betting | 10-15% | Total stakes minus winnings |

| GGR Tax – Poker | 10-15% | Rake and tournament fees |

| Corporate Income Tax (Domestic) | 25-30% | Net profits from local operations |

| Corporate Income Tax (International) | 1-5.5% | Preferential IBC rates |

| Annual License Renewal | $25,000-75,000 USD | Fixed fee by license type |

| Employee Payroll Tax | 13.5% | Split employer/employee contributions |

Gambling Market Financial Performance

Due to the current unregulated status of online gambling in Barbados, comprehensive market revenue data is unavailable. However, we can estimate market size based on population, gambling participation rates, and regional benchmarks.

Estimated Annual Market Size: With 45,000-60,000 active online gamblers spending $250-400 USD annually (regional ARPU), the total addressable market ranges from $11.25 million to $24 million USD annually. Upon regulation, this market would consolidate from offshore operators to licensed domestic platforms.

Land-Based Market: Slot machines and lottery operations generate an estimated $15-20 million BBD ($7.5-10 million USD) annually, with the majority from slot machines in tourist areas and lottery ticket sales.

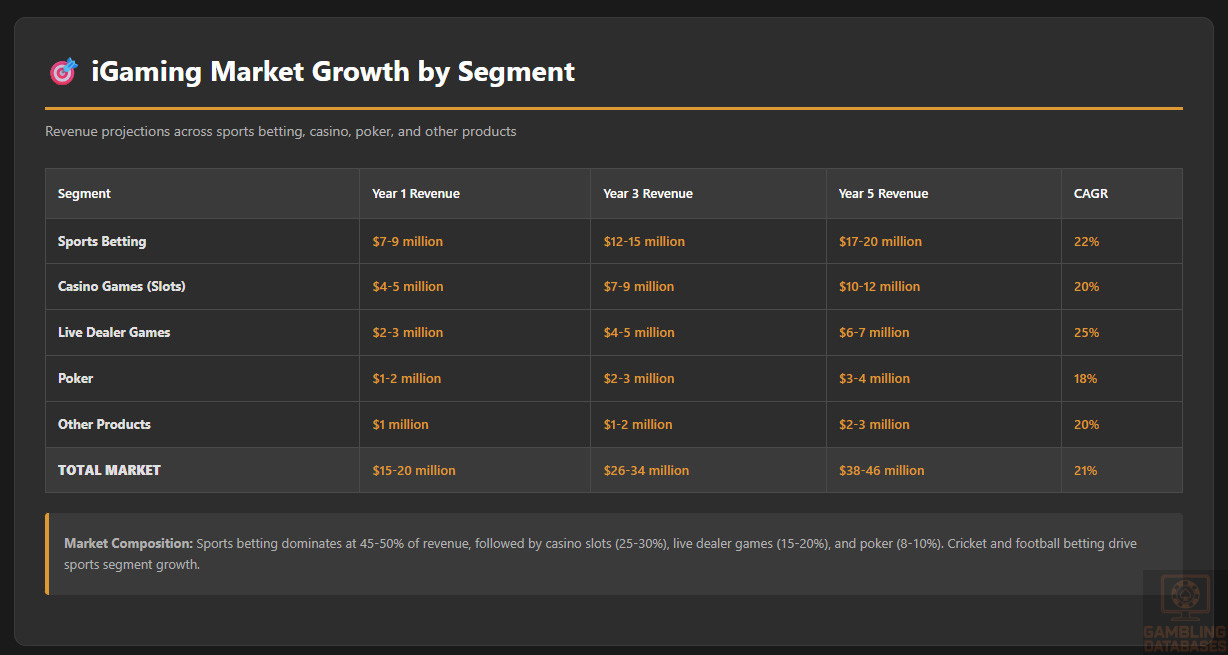

Revenue Distribution Projection: Upon market regulation, expected split would be approximately 45-50% sports betting, 35-40% casino games (slots, table games, live dealer), 10-15% poker, and 5-10% other products (bingo, lottery-style games).

Growth Trajectory: Regulated markets typically experience 15-25% annual growth in the first 3-5 years post-licensing as offshore activity migrates to licensed platforms and marketing increases awareness. Barbados could see the market expand from $15 million to $35-40 million USD by year five of regulation.

| Metric | Year 1 | Year 3 | Year 5 |

|---|---|---|---|

| Total Market Size (USD) | $15-18 million | $25-30 million | $35-40 million |

| Active Players | 50,000-55,000 | 60,000-70,000 | 70,000-80,000 |

| Average ARPU (USD) | $280-320 | $380-420 | $480-520 |

| Market Penetration Rate | 18-20% | 21-25% | 25-28% |

| Government Tax Revenue (USD) | $2-3 million | $4-5 million | $6-7 million |

| Annual Growth Rate | Baseline | 20-25% | 12-18% |

Advertising and Marketing Restrictions

While specific advertising regulations await finalization in the upcoming gambling legislation, Barbados will likely adopt restrictions balancing operator marketing needs with consumer protection concerns aligned with international best practices.

Permitted Channels: Online advertising (websites, social media, search engines), print media (newspapers, magazines), outdoor advertising (billboards in approved locations), and radio advertising during appropriate time slots are expected to be allowed with restrictions.

Content Restrictions: Marketing materials must avoid targeting minors, include responsible gambling messages and 18+ age warnings, accurately represent odds and winning probabilities, clearly state bonus terms and wagering requirements, and avoid suggesting gambling as a solution to financial problems or path to financial success.

Promotional Limitations: Bonus offers will likely face caps on maximum amounts or percentages, reasonable wagering requirements (20x-40x deposit plus bonus), clear expiration terms, and restrictions on free bet promotions without deposit requirements to protect vulnerable players.

Sponsorship Regulations: Sports team and event sponsorships may be permitted with restrictions on visibility during youth-oriented events, requirements for responsible gambling messaging, and prohibitions on branding that appeals to minors.

Time Restrictions: Television and radio advertising will likely be prohibited during children’s programming hours and may face restrictions during live sports broadcasts accessible to minors.

Recent Regulatory Changes and Their Impact

The most significant recent development is the March 2023 announcement by Finance Minister Ryan Straughn that comprehensive online gaming legislation is in final development stages. This marks Barbados’ first major step toward regulating the digital gambling sector.

Legislative Timeline: The government indicated the betting and gaming framework would be introduced to Parliament before end of June 2023, though as of October 2025, final legislation has not yet been enacted. This delay suggests thorough stakeholder consultation and careful consideration of international regulatory models.

Rationale for Regulation: The government explicitly cited the need to manage activities that pose “significant risks” to the financial sector and broader economy, while referencing lessons from the 2022 FTX cryptocurrency collapse in the Bahamas as motivation for robust regulatory oversight.

Industry Impact: Once implemented, regulations will create substantial market structure changes including migration of players from offshore to licensed platforms, establishment of local operator presence and employment, and formalization of tax revenue collection from an economic activity currently generating zero government income.

Enforcement Mechanisms and Penalties

Expected enforcement provisions will likely mirror established Caribbean gambling jurisdictions, with penalties designed to ensure compliance while allowing remediation opportunities before extreme sanctions.

Penalty Structures: Financial penalties for minor infractions ($5,000-25,000 BBD), suspension of license for serious violations (30-90 days), revocation of license for repeated or severe breaches, criminal penalties for operating without licenses, and confiscation of unlicensed gambling equipment and funds.

ISP Blocking: Barbados may implement DNS-level blocking of unlicensed international operators refusing to cease serving Barbadian customers, though enforcement complexity and VPN usage limit effectiveness of such measures.

Payment Processor Restrictions: Financial institutions and payment processors may be prohibited from processing transactions for unlicensed operators, creating barriers to market entry for non-compliant platforms.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Barbados maintains a stable, mature population with demographic characteristics favorable for certain gambling market segments. The population of 282,643 as of 2025 ranks the country 185th globally but delivers strong per-capita economic metrics.

Population Trends: Annual growth stands at just 0.05%, with population projected to reach approximately 292,930 by early 2026. This minimal growth reflects low birth rates typical of developed nations and net emigration as Barbadians seek opportunities abroad.

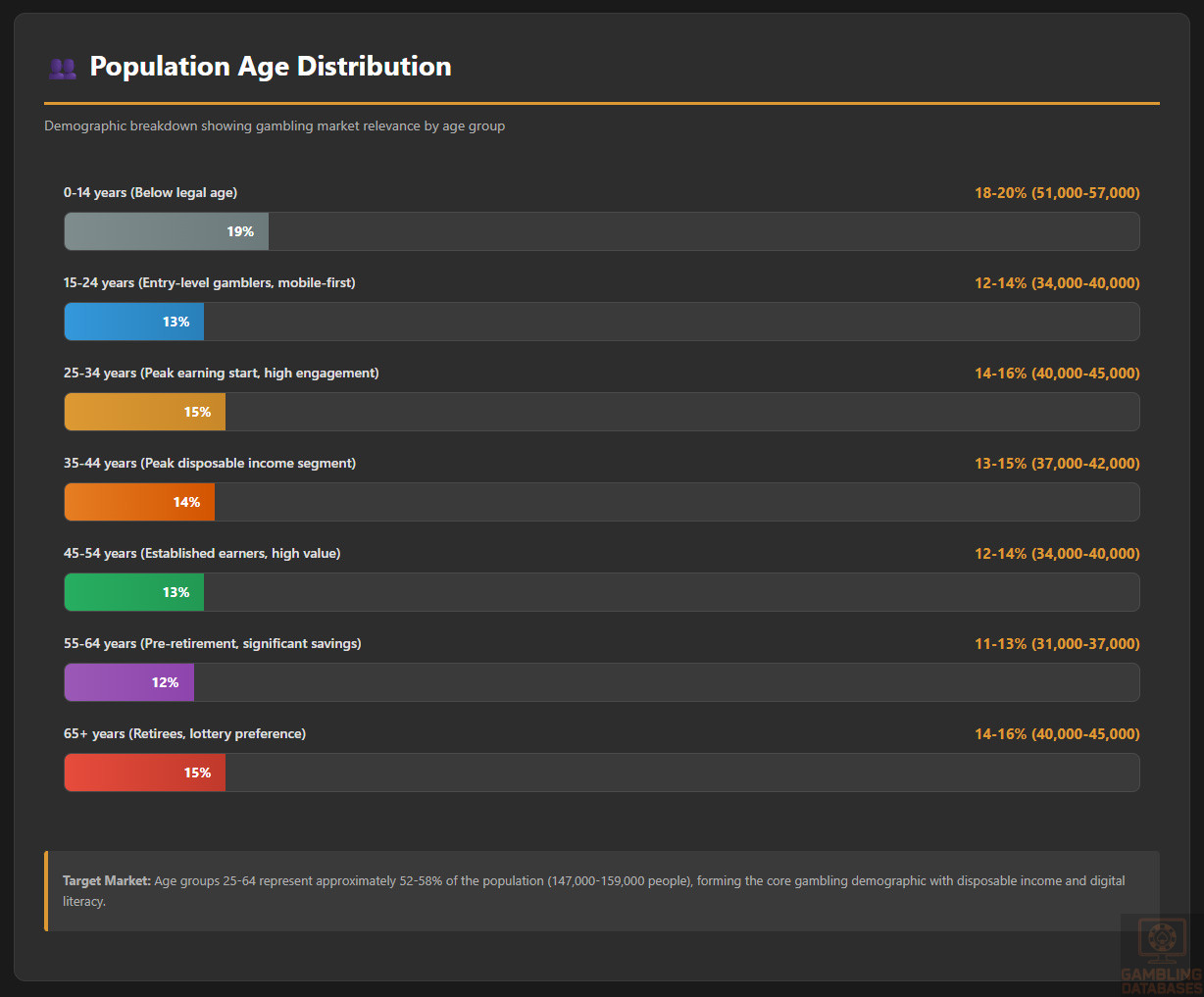

Age Distribution: The population skews toward middle-age demographics optimal for gambling products. Approximately 18-20% fall in the 0-14 age group, 65-68% in the critical 15-64 working-age segment, and 14-16% aged 65+. The median age of 39.4 years indicates a mature market with disposable income.

Gender Ratios: Females outnumber males with 52.05% female to 47.95% male, creating a gender ratio of approximately 92 males per 100 females. This gender imbalance persists across age groups and influences market targeting strategies.

Life Expectancy: High life expectancy of 80.9 years overall (79.1 for males, 82.8 for females) reflects excellent healthcare infrastructure and living standards. This longevity supports sustained customer lifetime value for gambling operators.

Urban vs Rural Distribution: Just 32.47% of the population resides in urban areas, with 91,766 people concentrated in cities while the majority live in suburban and rural settings. However, the island’s compact size of 430 square kilometers means even rural residents access urban services easily.

| Age Group | Percentage | Approximate Number | Gambling Market Relevance |

|---|---|---|---|

| 0-14 years | 18-20% | 51,000-57,000 | Below legal gambling age |

| 15-24 years | 12-14% | 34,000-40,000 | Entry-level gamblers, mobile-first |

| 25-34 years | 14-16% | 40,000-45,000 | Peak earning start, high engagement |

| 35-44 years | 13-15% | 37,000-42,000 | Peak disposable income segment |

| 45-54 years | 12-14% | 34,000-40,000 | Established earners, high value |

| 55-64 years | 11-13% | 31,000-37,000 | Pre-retirement, significant savings |

| 65+ years | 14-16% | 40,000-45,000 | Retirees, lottery preference |

Geographic Distribution

Barbados’ small geographic footprint creates unique market dynamics. Population density reaches 657 people per square kilometer, making it the 4th most densely populated country in the Americas and 15th globally.

Major Population Centers: Bridgetown, the capital and largest city, hosts approximately 110,000 residents with density of 7,300 people per square kilometer. Other significant population centers include Speightstown, Oistins, Holetown, and Bathsheba, though all remain easily accessible from any point on the island.

Regional Economic Differences: The south and west coasts concentrate tourism infrastructure, hotels, restaurants, and entertainment venues, creating higher employment and income levels. The eastern coast features more traditional fishing and agricultural communities with lower average incomes but strong community ties.

Internet Access Patterns: Urban areas enjoy near-universal fixed broadband and 4G coverage, while rural areas rely more heavily on mobile internet connections. However, the island’s small size ensures 80% overall internet penetration extends across geographic regions with minimal disparity.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Barbados stands as the wealthiest and most developed country in the Eastern Caribbean region, enjoying one of the highest per capita incomes. The economy has successfully diversified from historical sugar dependence into tourism, offshore financial services, light manufacturing, and information services.

Current GDP Metrics: Total GDP reached $7.17 billion USD in 2024, with GDP per capita of $25,366 USD positioning Barbados well above Caribbean regional averages. This wealth concentration creates attractive consumer spending power for discretionary entertainment like gambling.

GDP Growth Forecasts: The Central Bank of Barbados projects sustained real GDP growth of 3.0% annually through 2029, with total GDP forecast to reach $9.29 billion USD by 2029. This growth is driven by tourism recovery, infrastructure investments, renewable energy projects, and offshore financial services expansion.

Economic Sector Composition: Services dominate the economy at approximately 78%, with industry contributing 16% and agriculture just 6%. The service-sector focus aligns with high internet usage and digital transaction comfort necessary for online gambling adoption.

Employment and Wages: Unemployment rates have declined post-pandemic to approximately 8-10%, with labor force of 128,500 workers. Average wages in tourism and financial services sectors support disposable income for entertainment spending.

Inflation Trends: Inflation is expected to moderate in 2025-2026 to 1.5-2.5% annually as global commodity prices stabilize. This low inflation environment preserves consumer purchasing power and supports discretionary spending growth.

Income and Wealth Distribution

Understanding income distribution helps operators segment markets and set appropriate betting limits, bonus structures, and VIP tier thresholds for Barbadian consumers.

Average Household Income: Median household income is estimated at $3,500-4,500 BBD monthly ($1,750-2,250 USD), though significant variance exists between urban/rural areas and sectors. Tourism and financial services workers earn above-average wages while agricultural and informal sector workers earn less.

Income Inequality: As a developed small island nation, Barbados maintains moderate income inequality compared to larger Caribbean neighbors, though wealth concentration exists among business owners, professionals, and expatriate workers.

Disposable Income: After accounting for housing, utilities, food, and transportation, average households retain 25-35% of income for discretionary spending. This translates to $400-700 USD monthly for entertainment, dining, and leisure activities including gambling.

Middle Class Size: Approximately 45-55% of Barbadian households qualify as middle class with stable employment, home ownership, and discretionary spending capacity. This segment represents the core target market for online gambling operators.

| Indicator | 2024 | 2025 Projection | 2029 Projection |

|---|---|---|---|

| Total GDP (USD) | $7.17 billion | $7.38 billion | $9.29 billion |

| GDP Per Capita (USD) | $25,366 | $26,100 | $32,800 |

| Annual GDP Growth | 2.8% | 3.0% | 3.0% |

| Inflation Rate | 3.2% | 1.5-2.5% | 2.0% |

| Unemployment Rate | 8.5% | 7.8% | 6.5% |

| Tourism Contribution | High | Increasing | Sustained |

| Currency (BBD:USD) | 2:1 (pegged) | 2:1 (pegged) | 2:1 (pegged) |

Market Size and Growth Projections

The Barbadian iGaming market presents modest absolute size but attractive relative penetration and ARPU metrics. Market projections assume regulation implementation by 2026-2027 with gradual migration from offshore to licensed platforms.

Current Market Revenue: Barbadian players currently wager an estimated $15-25 million USD annually with offshore operators. This revenue flows entirely outside Barbados’ economy and tax system, representing significant opportunity cost for the government.

Historical Growth: Without regulation, precise historical growth data is unavailable. However, internet penetration growth from 65% in 2010 to 80% in 2025 suggests proportional gambling market expansion as more consumers gained digital access.

Revenue Forecasts: Year 1 post-regulation: $15-18 million USD as early adopters migrate to licensed platforms. Year 3: $25-30 million USD as marketing drives awareness and trust in local licenses. Year 5: $35-40 million USD representing market maturity with 25-28% population penetration.

Expected CAGR: The market should achieve 20-25% compound annual growth rate in years 1-3 post-regulation, moderating to 12-18% CAGR in years 4-5 as the market matures and growth normalizes.

Projected User Base Growth: Active gamblers should increase from 50,000-55,000 in year 1 to 70,000-80,000 by year 5, representing penetration growth from 18-20% to 25-28% of the adult population.

Average Revenue Per User: ARPU is projected to grow from $280-320 USD in year 1 to $480-520 USD by year 5 as players develop comfort with platforms, operators improve retention strategies, and product variety expands.

Online vs Land-Based Split: Online gaming should capture 55-60% of total gambling revenue by year 3, with land-based slots and lottery retaining 40-45%. The convenience and product variety of online platforms drives this shift.

Regional Comparison: Barbados’ projected market size aligns with other small Caribbean nations. Curacao (population 160,000) generates approximately $15-20 million in player value, while Antigua and Barbuda (population 98,000) sees similar per-capita gambling activity from its resident population.

| Segment | Year 1 Revenue | Year 3 Revenue | Year 5 Revenue | CAGR |

|---|---|---|---|---|

| Sports Betting | $7-9 million | $12-15 million | $17-20 million | 22% |

| Casino Games (Slots) | $4-5 million | $7-9 million | $10-12 million | 20% |

| Live Dealer Games | $2-3 million | $4-5 million | $6-7 million | 25% |

| Poker | $1-2 million | $2-3 million | $3-4 million | 18% |

| Other Products | $1 million | $1-2 million | $2-3 million | 20% |

| Total Market | $15-20 million | $26-34 million | $38-46 million | 21% |

Education, Skills, and Digital Literacy

Educational Foundation

Barbados boasts one of the highest literacy rates in the developing world, providing strong foundations for digital service adoption including online gambling platforms.

Literacy Rates: Overall literacy exceeds 99%, with near-universal primary and secondary school completion. This high educational attainment facilitates understanding of gambling odds, terms and conditions, and responsible gambling information.

Education Levels: Primary education completion reaches 100%, secondary completion approximately 95%, and tertiary enrollment rates of 55-60% rank among the Caribbean’s highest. The University of the West Indies Cave Hill campus in Barbados produces graduates in business, technology, and professional fields.

Digital Literacy: Widespread smartphone usage and social media engagement (63.7% of population) demonstrates comfort with digital interfaces. Younger demographics (18-44) show near-universal digital literacy, while older cohorts (55+) maintain functional digital skills for banking and communication.

Workforce Skills: The labor force demonstrates strong technical skills from the offshore financial services and technology sectors. This creates favorable conditions for customer support roles, compliance positions, and technical operations for licensed gambling operators.

English Language Proficiency: English serves as the official language and primary language of business, education, and government. While Bajan dialect is common in informal settings, all Barbadians speak standard English, eliminating language barriers for international operators.

Cultural and Social Factors

Communication and Language

Language uniformity simplifies market entry compared to multilingual Caribbean nations. English-language platforms, customer support, and marketing materials serve the entire population without translation requirements.

Internet Language Preferences: Barbadians consume English-language content online, follow English-speaking social media influencers, and engage with international brands using standard English. Local dialect (Bajan) appears in informal communications but not in business contexts.

Business Communication Norms: Formal, professional communication follows British Commonwealth standards. Customer service should maintain polite, respectful tones while remaining friendly and accessible. Barbadians appreciate efficient service balanced with personal warmth.

Cultural Attitudes Toward Gambling

Understanding cultural perceptions of gambling informs marketing strategies, product positioning, and responsible gambling messaging for the Barbadian market.

Social Acceptance: Gambling enjoys moderate social acceptance in Barbados, particularly lottery play and informal betting on sports and horse racing. However, the government’s historical prohibition of casinos reflects some cultural ambivalence about gambling’s place in society.

Religious Influences: Christianity predominates in Barbados, with Anglican, Methodist, and Pentecostal denominations holding significant influence. Conservative religious communities view gambling skeptically, though this hasn’t prevented widespread lottery participation or offshore online gambling.

Foreign Brand Perception: Barbadians demonstrate openness to international brands across retail, technology, and services sectors. Well-known gambling brands with strong reputations will find receptive audiences, though local partnerships and community engagement strengthen trust.

Risk Tolerance: As a population with relatively high financial literacy and offshore financial services experience, Barbadians demonstrate moderate risk tolerance in investment and entertainment decisions. This supports participation in gambling as calculated entertainment rather than desperate financial strategy.

Entertainment Preferences: Cricket dominates sports interest, followed by football (soccer), basketball, and horse racing. Cultural events like Crop Over festival, calypso and reggae music, and beach activities compete for entertainment spending. Gambling products must position as complementary entertainment rather than primary leisure activity.

Social vs Solitary Gambling: Lottery play and horse racing betting feature strong social components with friends and family discussing picks and outcomes. Online gambling’s solitary nature requires marketing emphasizing community features, social media integration, and shared experiences.

Problem Gambling and Social Considerations

While comprehensive problem gambling data for Barbados is unavailable, regional studies and international benchmarks provide insights into expected challenges and operator responsibilities.

Prevalence Estimates: International studies suggest 0.5-2.0% of adult populations experience gambling disorders, with an additional 2-4% at risk for problem gambling. Applied to Barbados’ 200,000 adults, this suggests 1,000-4,000 problem gamblers and 4,000-8,000 at-risk individuals.

At-Risk Demographics: Young males (18-35) face highest problem gambling risk, particularly with sports betting and casino games. Lower-income individuals chasing losses, those with substance abuse histories, and individuals experiencing depression or anxiety also show elevated risk.

Underage Gambling: With high smartphone penetration among teenagers and offshore sites often lacking robust age verification, underage gambling likely occurs. Licensed operators must implement stringent age verification to prevent minor access.

Government Response: The forthcoming regulatory framework will likely mandate responsible gambling measures, self-exclusion registries, operator contributions to problem gambling treatment funds, and public awareness campaigns about gambling risks.

Treatment Services: Barbados’ mental health infrastructure includes counseling services through the Psychiatric Hospital and community health centers. Specialized gambling addiction treatment programs are limited, requiring operators to provide resources and referrals as part of social responsibility commitments.

Social Responsibility Requirements: Expected operator obligations include displaying responsible gambling messages in marketing, providing reality checks and limit-setting tools, training customer service staff to identify problem gambling signs, funding public education campaigns, and contributing to treatment service development (typically 0.5-1.0% of GGR).

Political Structure and Governance

Political stability and governance quality significantly impact regulatory consistency, licensing security, and business environment predictability for gambling operators.

Government System: Barbados operates as a parliamentary republic within the Commonwealth, having transitioned from constitutional monarchy in 2021. The bicameral Parliament consists of the House of Assembly and Senate, with the Prime Minister leading the government.

Political Stability: Barbados maintains exceptional political stability with peaceful democratic transitions, strong rule of law, and respected institutions. The current Barbados Labour Party government under Prime Minister Mia Mottley holds strong parliamentary majority, providing policy consistency.

Regulatory Consistency: The government’s track record in offshore financial services demonstrates capacity for sophisticated regulation, international cooperation, and consistent policy implementation. These capabilities should transfer to gambling regulation.

Corruption Levels: Barbados scores well on Transparency International’s Corruption Perceptions Index, ranking among the Caribbean’s least corrupt nations. Strong institutions, independent judiciary, and professional civil service minimize corruption risks in licensing processes.

International Relations: As a CARICOM member, small island developing state voice in UN forums, and participant in international financial standards, Barbados maintains positive global relationships. These connections facilitate regulatory information exchange and payment processing relationships.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Barbados’ technology infrastructure and digital adoption rates create favorable conditions for online gambling market development, with connectivity and usage patterns supporting mobile-first and desktop experiences.

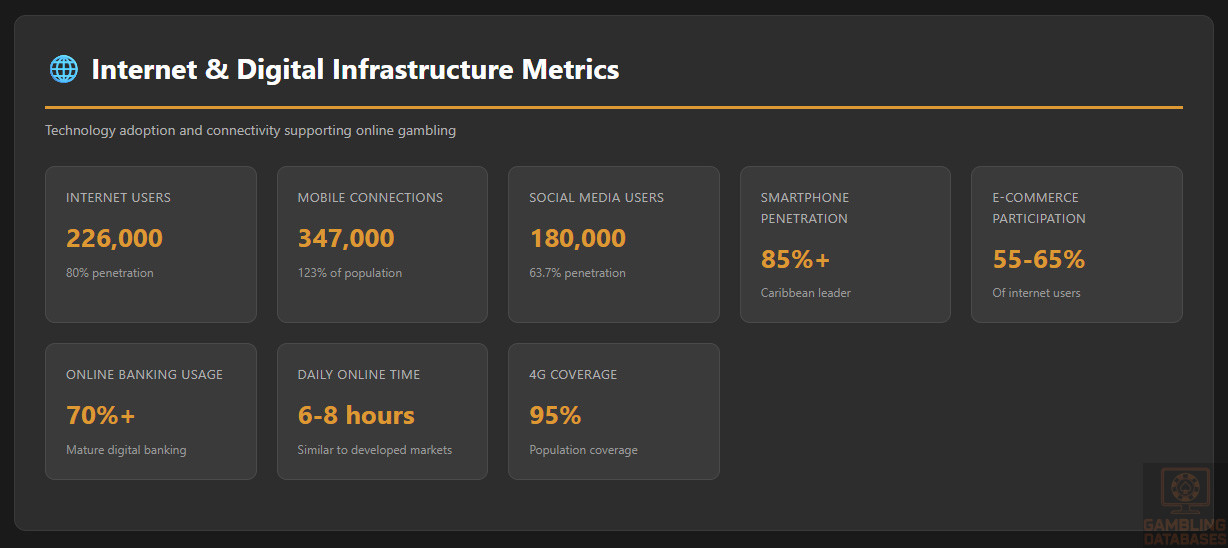

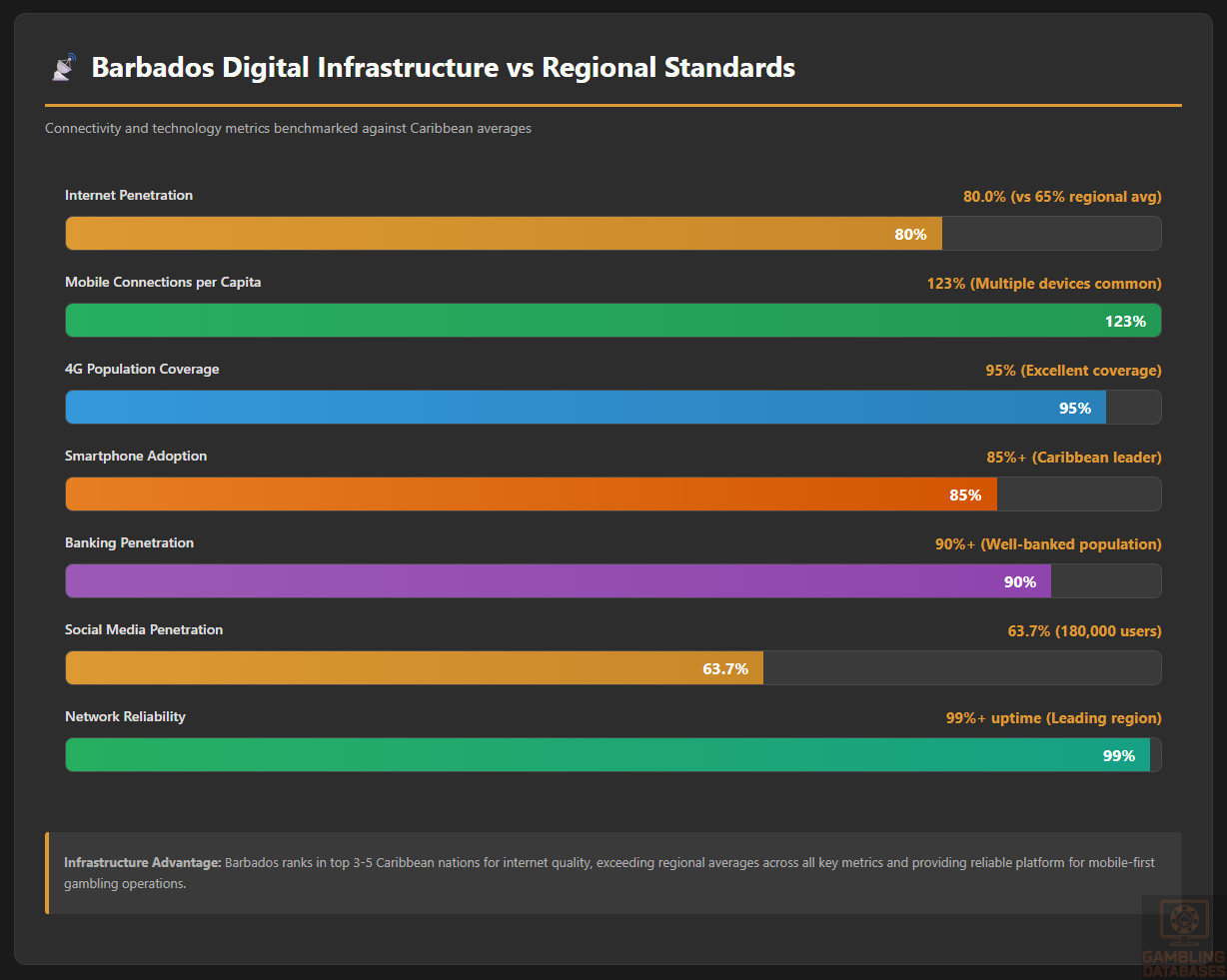

Internet Penetration: At 80.0% penetration with 226,000 users, Barbados leads the Caribbean region in internet access. This exceeds the global average of 67.5% and approaches developed market levels (85-95%).

Daily Usage Hours: Barbadians average 6-8 hours daily online across work and leisure activities. High connectivity during evenings (6pm-midnight) and weekends creates prime windows for gambling activity.

Mobile Device Adoption: Smartphone penetration exceeds 85%, with 347,000 mobile connections representing 123% of population. Multiple device ownership (smartphone, tablet, work phone) is common among middle-class consumers.

Social Media Engagement: 180,000 Barbadians (63.7% of population) actively use social media platforms. Facebook dominates with 140,000+ users, followed by Instagram (80,000+), WhatsApp (near-universal), and emerging TikTok adoption among younger demographics.

E-Commerce Participation: Online shopping adoption has grown significantly, with 55-65% of internet users making online purchases in the past year. International platforms like Amazon deliver to Barbados, while local e-commerce sites serve domestic markets.

Digital Payment Adoption: Credit/debit card usage is widespread for online transactions, with growing adoption of digital wallets and online banking. The upcoming BiMPay instant payment system launching March 2026 will further accelerate digital payment comfort.

Online Banking: Major banks (Sagicor Bank, FirstCaribbean, CIBC, Republic Bank) offer comprehensive online banking with mobile apps. Banking penetration exceeds 90% of adults, with majority utilizing digital banking services regularly.

| Metric | Value | Regional Comparison |

|---|---|---|

| Internet Users | 226,000 (80.0%) | Above Caribbean average (65%) |

| Mobile Connections | 347,000 (123%) | High multiple-device ownership |

| Social Media Users | 180,000 (63.7%) | Aligned with regional average |

| Smartphone Penetration | 85%+ | Leading Caribbean market |

| E-Commerce Participation | 55-65% | Above regional average |

| Online Banking Usage | 70%+ | Mature digital banking market |

| Average Daily Online Time | 6-8 hours | Similar to developed markets |

Digital Payment Behavior

Payment method availability and consumer preferences critically impact gambling operator success. Barbados’ evolving payment landscape offers expanding options for deposits and withdrawals.

Credit/Debit Cards: Visa and Mastercard dominate with widespread acceptance. Card penetration exceeds 70% of adults, with many holding multiple cards. Cards serve as primary online payment method for e-commerce and expected to dominate gambling deposits initially.

Digital Wallets: International wallets like PayPal, Skrill, and Neteller have limited direct Barbados support, though some residents access through workarounds. Local wallet adoption remains nascent but growing, with BiMPay instant payment system launching March 2026 potentially accelerating e-wallet adoption.

Bank Transfers: Direct bank transfers function for larger transactions but lack instant processing. Current settlement takes 1-3 business days through BACHSI clearing house, though BiMPay will enable real-time transfers between institutions beginning 2026.

Cryptocurrency: Crypto adoption remains limited in Barbados, with regulatory uncertainty dampening enthusiasm. Some technically sophisticated users hold Bitcoin, Ethereum, and other cryptocurrencies, but mainstream adoption is years away. Gambling operators should monitor regulatory development before integrating crypto payments.

Most Popular Methods: For online transactions, credit/debit cards hold 60-70% share, bank transfers 20-25%, and alternative methods 5-15%. Gambling deposits will likely mirror this distribution initially, evolving as BiMPay and digital wallets gain traction.

Transaction Patterns: Average online transaction values range $50-200 USD for e-commerce. Gambling deposits typically start smaller ($20-50) with higher-value players depositing $100-500 per transaction. Withdrawal preferences favor bank transfers for larger amounts despite longer processing times.

Payment Security Trust: Barbadians demonstrate high trust in established financial institutions and internationally recognized payment brands. Operators using secure, branded payment gateways with SSL encryption and PCI compliance will ease consumer concerns.

Gaming and Gambling Preferences

Current Market Participation

Understanding existing gambling participation patterns guides product development, marketing focus, and revenue forecasting for licensed operators entering the Barbadian market.

Overall Gambling Participation: An estimated 35-40% of Barbadian adults (70,000-80,000 people) engage in some form of gambling annually, including lottery, horse racing, slots, and offshore online platforms. This participation rate aligns with Caribbean regional averages.

Online Gambling Participation: Approximately 16-21% of adults (45,000-60,000 people) use offshore online gambling platforms, with higher penetration among males (25-30%) than females (8-12%) and concentrated in 25-54 age groups.

Popular Activities Ranking: 1) Lottery (highest participation ~25-30% of adults), 2) Offshore online sports betting (12-15%), 3) Offshore online casino games (8-12%), 4) Horse racing betting (5-8%), 5) Land-based slots (3-5%), 6) Poker (online and informal, 2-4%).

Sports Betting vs Casino Preference: Sports betting attracts more participants due to cricket and football fandom, but casino games generate higher per-player revenue. Ratio is approximately 60% sports bettors to 40% casino players among online gamblers, though many engage in both.

Live Dealer Popularity: Live dealer games appeal to Barbadian players seeking authentic casino experiences without travel. Blackjack, roulette, and baccarat variants attract players aged 35-55 with higher average bets than RNG slots.

Lottery Participation: Government lottery products enjoy widest social acceptance and participation, with 65,000-75,000 regular players spanning all demographics. Weekly lottery spending averages $5-15 BBD per participant.

Seasonal Patterns: Gambling activity spikes during major sporting events (Cricket World Cup, FIFA World Cup, NBA playoffs), Christmas holiday season, and Crop Over festival (July-August). Cricket season (January-September) drives sustained sports betting engagement.

Consumer Behavior Patterns

Detailed behavioral insights enable operators to optimize user experience, maximize customer lifetime value, and implement effective retention strategies for the Barbadian market.

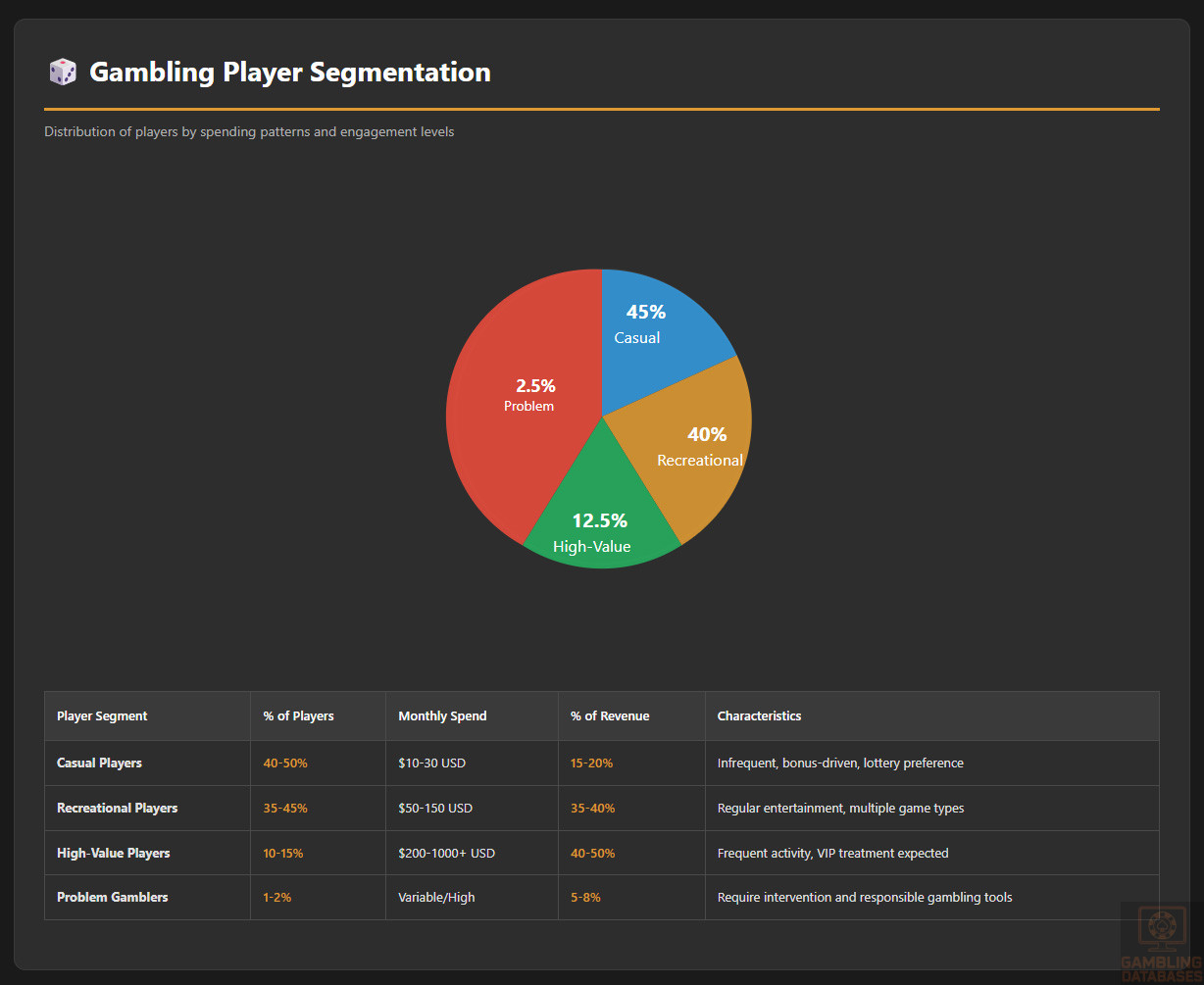

Average Monthly Spending: Online gamblers spend $40-80 USD monthly on average, with significant variance. Casual players ($10-30 monthly) comprise 40-50% of users, recreational players ($50-150) represent 35-45%, and high-value players ($200+) account for 10-15% but generate 40-50% of revenue.

Annual Spending Per Player: Average online gambling spend reaches $280-400 USD annually, projected to grow to $480-520 USD by year 5 post-regulation as market matures and player trust in licensed platforms increases.

Typical Bet Sizes: Sports betting: $5-20 BBD ($2.50-10 USD) per bet, with accumulators ranging higher. Casino slots: $0.25-2.00 BBD ($0.125-1.00 USD) per spin. Table games: $5-25 BBD ($2.50-12.50 USD) per hand. High rollers bet significantly more but represent small percentage of player base.

Platform Preferences: Mobile devices account for 65-70% of online gambling sessions, with smartphones dominating over tablets. Desktop usage (30-35%) occurs primarily during work hours and evening sessions at home. Operators must prioritize mobile-responsive design and native app development.

Peak Activity Times: Weekday evenings (7pm-11pm) see highest traffic, with Tuesday-Thursday showing strong engagement. Weekend afternoons and evenings (Saturday-Sunday 2pm-midnight) generate sustained high activity. Sports betting spikes during live match times.

Average Session Length: Casino sessions average 25-40 minutes, sports betting sessions 15-25 minutes for pre-match wagering, and live betting extends 60-90 minutes for match duration. Poker sessions run longest at 45-120 minutes.

Retention and Loyalty: First-year player retention rates typically reach 25-35% for online gambling, with strong correlation between welcome bonus value, early wins, and customer service quality. Loyalty programs offering comp points, cashback, and exclusive promotions improve retention to 40-50% among engaged players.

Bonus Sensitivity: Barbadian players respond strongly to welcome bonuses, with 70-80% of new registrations driven by promotional offers. Reload bonuses, free bets, and cashback offers effectively reactivate dormant players. However, transparency in wagering requirements is critical to maintaining trust.

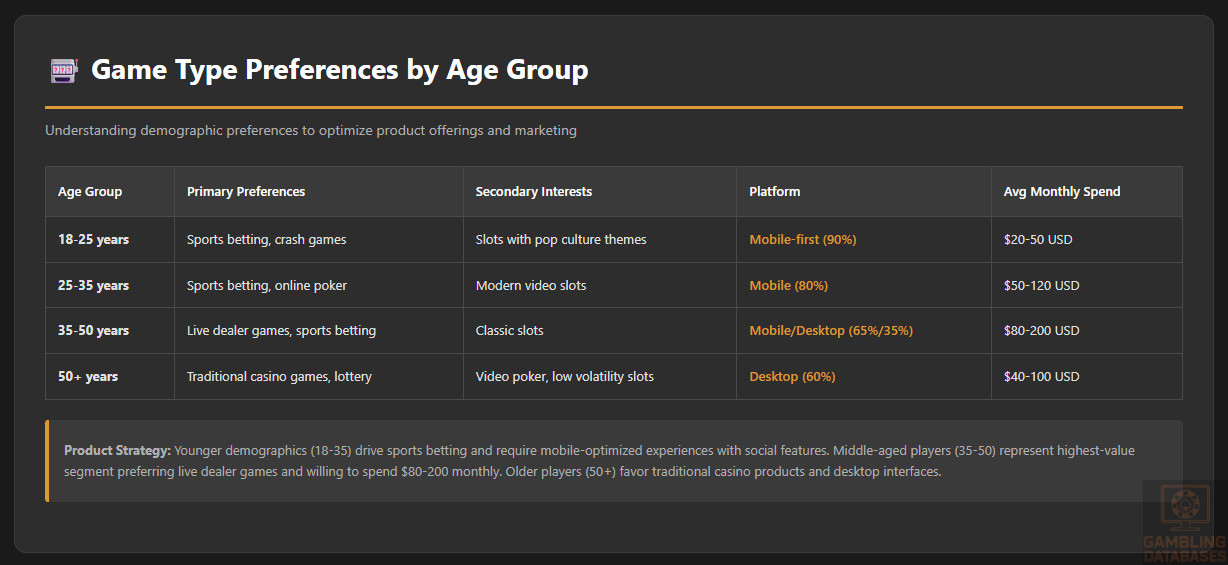

Game Type Preferences by Age: 18-25: Sports betting, slots with pop culture themes, crash games. 25-35: Sports betting, online poker, modern video slots. 35-50: Live dealer games, classic slots, sports betting. 50+: Traditional casino games, video poker, lottery-style games, lower volatility slots.

Deposit Frequency: Casual players deposit 2-4 times monthly, recreational players 4-8 times monthly, and high-value players 10-20+ times monthly. Average deposit amounts range $30-100 USD, with payment method and bonus availability influencing deposit timing and size.

Withdrawal Patterns: Players typically withdraw winnings after significant wins exceeding 5-10x deposit amount. Withdrawal frequency averages 1-2 times monthly for active players. Fast withdrawal processing (under 24 hours) strongly influences platform loyalty and positive word-of-mouth.

| Player Segment | % of Players | Monthly Spend | % of Revenue | Characteristics |

|---|---|---|---|---|

| Casual Players | 40-50% | $10-30 USD | 15-20% | Infrequent, bonus-driven, lottery preference |

| Recreational Players | 35-45% | $50-150 USD | 35-40% | Regular entertainment, multiple game types |

| High-Value Players | 10-15% | $200-1000+ USD | 40-50% | Frequent activity, VIP treatment expected |

| Problem Gamblers | 1-2% | Variable/High | 5-8% | Require intervention and responsible gambling tools |

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Barbados’ telecommunications infrastructure ranks among the Caribbean’s most advanced, providing reliable connectivity essential for online gambling platform operation and player experience.

Internet Penetration Quality: The 80% penetration rate reflects genuine broadband access rather than basic connectivity. Most connections support streaming video, real-time gaming, and high-quality video calls, indicating sufficient bandwidth for online gambling applications.

Fixed Broadband vs Mobile: Approximately 55-60% of connections are mobile internet via 4G/LTE networks, while 40-45% utilize fixed broadband through fiber, cable, or DSL. Urban areas enjoy widespread fiber-to-the-home availability, while rural areas rely more heavily on mobile networks.

Average Internet Speeds: Fixed broadband speeds average 50-100 Mbps download and 10-25 Mbps upload for residential plans, with business-tier services reaching 150-500 Mbps. Mobile 4G networks deliver 15-40 Mbps download speeds, sufficient for mobile gambling apps and responsive web platforms.

Network Reliability: Uptime statistics exceed 99% for major providers Flow and Digicel. Power outages occur infrequently, and cellular towers feature backup power ensuring continued mobile connectivity during disruptions. Submarine fiber optic cables provide redundant international connectivity.

Infrastructure Investment: The government and telecom operators continue investing in network expansion and modernization. Ongoing projects include fiber network extension to underserved areas, 5G preparation, and data center infrastructure development.

Global Rankings: Barbados ranks in the top 3-5 Caribbean nations for internet infrastructure quality, comparable to Trinidad and Tobago and ahead of Jamaica. While lagging developed nations, infrastructure meets requirements for online gambling operations.

Urban vs Rural Gap: Urban areas like Bridgetown enjoy near-universal coverage with multiple provider options and fastest speeds. Rural areas have good 4G mobile coverage but more limited fixed broadband choices. The island’s small size minimizes this gap compared to larger nations.

5G and Future Technology Deployment

Fifth-generation mobile networks represent the next evolution in connectivity, promising significantly enhanced speeds and reduced latency beneficial for live betting, live dealer games, and augmented reality gambling experiences.

Current 4G/5G Coverage: 4G LTE coverage reaches approximately 95% of the population across all parishes. Digicel and Flow provide comprehensive 4G networks supporting mobile gambling applications. 5G deployment remains in planning stages as of 2025.

5G Rollout Timeline: Commercial 5G launch is projected for 2026-2027 in Barbados, following spectrum allocation and infrastructure investment by major carriers. Initial deployment will focus on Bridgetown and high-density tourist areas before expanding island-wide.

Future Infrastructure Plans: The government’s digital transformation agenda includes telecommunications infrastructure modernization, public WiFi expansion in city centers, and continued submarine cable investments. These improvements will support growing data demands from streaming, gaming, and business applications.

Network Operator Competition: Two major operators (Flow and Digicel) maintain competitive networks, driving service quality improvements and keeping data costs reasonable. This duopoly structure ensures investment continues while providing consumer choice.

| Infrastructure Element | Current Status | Regional Ranking | Future Outlook |

|---|---|---|---|

| Fixed Broadband Speed | 50-100 Mbps average | Top 5 Caribbean | Improving with fiber expansion |

| Mobile Internet Speed | 15-40 Mbps (4G) | Top 3 Caribbean | 5G deployment 2026-2027 |

| Network Reliability | 99%+ uptime | Leading region | Sustained excellence |

| Coverage Geographic | 95% population | Excellent | Approaching universal |

| International Connectivity | Multiple submarine cables | Well-connected | Additional redundancy planned |

Mobile Technology Ecosystem

Mobile Network Infrastructure

Network Operators: Flow (Cable & Wireless) and Digicel dominate the Barbadian mobile market, both offering 4G LTE services, data plans, and bundled packages. Flow holds approximately 55-60% market share with Digicel capturing 40-45%.

Coverage Quality: Both operators provide excellent coverage in urban areas and main thoroughfares. Flow’s network receives marginally higher satisfaction ratings for consistency, while Digicel often leads in promotional pricing and data bundle value.

4G Coverage Maps: 4G LTE coverage extends across approximately 95% of inhabited areas. Only remote coastal areas and elevated interior regions experience occasional coverage gaps. Both providers offer coverage checkers on their websites.

Data Costs and Pricing: Mobile data costs have declined significantly in recent years. Current pricing averages $1.50-2.50 BBD per GB ($0.75-1.25 USD) for prepaid plans, with postpaid unlimited plans ranging $80-120 BBD monthly ($40-60 USD). These rates align with Caribbean regional averages.

Mobile Payment Integration: Both carriers support mobile money services enabling airtime purchases, bill payments, and peer-to-peer transfers. The upcoming BiMPay system launching March 2026 will provide instant bank-to-bank transfers accessible via mobile banking apps.

Mobile Wallet Adoption: Standalone mobile wallets remain underdeveloped in Barbados compared to mobile banking apps. Banks have invested heavily in their mobile applications, offering comprehensive financial services that reduce demand for third-party wallet solutions.

Device Penetration

Smartphone Adoption: Smartphone penetration exceeds 85% of the population, with near-universal ownership among adults under 55. Even seniors increasingly adopt smartphones, though feature phone usage persists among elderly populations for basic communication.

Devices Per Capita: Multiple device ownership is common, with many Barbadians owning both personal and work smartphones plus tablets. The 123% mobile connection rate (347,000 connections for 282,643 population) reflects this multi-device reality.

Device Preferences and Brands: Samsung leads Android market share at 35-40%, followed by Chinese brands like Xiaomi, Huawei, and OPPO (25-30% combined). Apple iPhones capture 20-25% market share, concentrated among higher-income demographics. Budget Android devices fill remaining market space.

Android vs iOS Market Share: Android dominates with 75-80% market share while iOS holds 20-25%. This distribution requires gambling operators to prioritize Android app development while maintaining iOS offerings for higher-value player segments.

Average Device Specifications: Mid-range smartphones (4-6GB RAM, 64-128GB storage, 6-6.5 inch screens) represent typical ownership. These specifications comfortably run gambling applications, stream video, and support responsive web platforms without performance issues.

Mobile Internet Usage: Barbadians spend 4-5 hours daily on mobile devices, consuming social media (2-3 hours), messaging (1-2 hours), entertainment/gaming (1-2 hours), and other activities. Peak mobile usage occurs during commutes, lunch breaks, and evening relaxation periods.

Mobile Gaming Penetration: Approximately 45-55% of smartphone users play mobile games (casual, social, competitive), demonstrating comfort with touch-based gaming interfaces and in-app payments. This familiarity transfers easily to mobile gambling applications.

Financial Services and Payment Infrastructure

Banking System Structure

Barbados maintains a sophisticated banking system reflecting its role as a regional financial services hub. This mature infrastructure supports diverse payment options for gambling operators and high consumer trust in digital financial services.

Major Banks and Market Share: Republic Bank (30-35% market share), FirstCaribbean International Bank (25-30%), Sagicor Bank (15-20%), CIBC FirstCaribbean (10-15%), and Scotiabank (8-12%) dominate the retail banking sector. These institutions offer comprehensive services including checking/savings accounts, credit cards, loans, and investment products.

Digital Banking Adoption: Digital banking penetration reaches 70-75% of account holders, with mobile banking apps showing strongest growth. All major banks offer feature-rich mobile applications supporting transfers, bill payments, account management, and customer service.

Account Penetration: Banking penetration exceeds 90% of adults, with most Barbadians maintaining accounts at one or more institutions. This high banked population percentage facilitates payment processing for gambling transactions without need for alternative financial services.

Credit and Lending Markets: Consumer credit is widely available through banks and credit unions. Credit card penetration reaches 60-70% of adults, with average credit limits of $3,000-8,000 BBD ($1,500-4,000 USD). Personal loans, mortgages, and vehicle financing are readily accessible to employed individuals with good credit histories.

ATM Density: ATMs are ubiquitous across Barbados with machines in all commercial areas, hotels, gas stations, and shopping centers. The island supports approximately 200-250 ATMs serving 283,000 residents, providing convenient cash access though digital payments increasingly replace ATM usage.

Payment Processing Options

Gambling operators require diverse payment method integration to maximize market penetration and accommodate player preferences. Barbados offers expanding options though some limitations exist compared to larger markets.

Credit/Debit Cards: Visa and Mastercard enjoy universal acceptance with near-complete merchant coverage. American Express and Discover have limited acceptance. All major banks issue Visa or Mastercard debit cards with most also offering credit cards. Cards represent the default online payment method with 65-70% of digital transactions.

E-Wallet Availability: International e-wallets face regional restrictions limiting Barbados support. PayPal does not officially service Barbados for merchant accounts, complicating integration for gambling operators. Skrill and Neteller have historically served Caribbean markets but have reduced regional presence. Operators may need to partner with regional payment processors or await BiMPay adoption.

Bank Transfer Systems: The Barbados Automated Clearing House System Initiative (BACHSI) processes electronic payments between banks, though current settlement times of 1-3 business days limit utility for gambling deposits requiring instant confirmation. BiMPay instant payment system launching March 2026 will revolutionize bank transfers with real-time settlement.

Cryptocurrency Status: Cryptocurrency remains in regulatory gray area in Barbados. The Central Bank has issued warnings about cryptocurrency risks but hasn’t prohibited usage. Bitcoin, Ethereum, and other cryptocurrencies see limited adoption primarily among tech-savvy younger demographics. Gambling operators should monitor regulatory clarity before integrating crypto payments.

Processing Fees: Credit card processing fees range 2.5-3.5% for merchants. International payment gateways charge 3.5-5.0% plus transaction fees of $0.20-0.40 USD. Bank transfers incur flat fees of $2-5 BBD domestically. These costs must factor into operator margin calculations.

Transaction Processing Timelines: Credit/debit card transactions settle instantly for deposits and 1-3 business days for refunds/withdrawals. Bank transfers currently take 1-3 business days but will become instant with BiMPay. E-wallet transactions typically settle within 24 hours when available.

International Payment Capabilities: Barbadian financial institutions maintain correspondent banking relationships enabling international transactions. However, some international payment processors exclude Caribbean jurisdictions due to perceived risk, requiring operators to establish relationships with processors experienced in the region.

Gambling Payment Restrictions: Current regulations don’t specifically prohibit gambling-related transactions, but banks may decline to process gambling payments without proper licensing. Upon regulation implementation, licensed operators should gain access to full payment processing infrastructure with banks obligated to service legitimate gaming businesses.

Chargeback and Dispute Resolution: Credit card chargeback procedures follow Visa/Mastercard international standards. Gambling transactions face scrutiny in disputes, making clear terms and conditions, transaction descriptions, and customer service documentation essential. Operators typically experience 0.5-2.0% chargeback rates depending on player satisfaction and dispute handling.

| Payment Method | Availability | Processing Time | Fees | Recommended Use |

|---|---|---|---|---|

| Credit/Debit Cards | Excellent | Instant deposits / 1-3 days withdrawals | 2.5-3.5% | Primary deposit method |

| Bank Transfers (Current) | Good | 1-3 business days | $2-5 BBD flat fee | Large withdrawals |

| Bank Transfers (BiMPay 2026+) | Excellent | Real-time | TBD (likely minimal) | Deposits and withdrawals |

| International E-Wallets | Limited | 24 hours | 3.5-5.0% | Alternative for experienced players |

| Cryptocurrency | Uncertain | 10-60 minutes | Blockchain fees | Wait for regulatory clarity |

| Mobile Payments | Emerging | Instant | 2.0-3.0% | Future opportunity |

E-commerce and Digital Economy

Digital Market Development

Barbados’ e-commerce maturity indicates readiness for online gambling adoption, as digital transaction comfort translates across industries. Understanding e-commerce trends provides insights into payment preferences and consumer digital behavior.

E-Commerce Market Size: The Barbadian e-commerce market generates an estimated $180-220 million USD annually and growing 12-15% per year. This includes both domestic online retail and international purchases from platforms delivering to Barbados.

Online Retail Penetration: E-commerce represents approximately 8-12% of total retail spending in Barbados, below developed market averages of 15-20% but growing steadily. COVID-19 pandemic accelerated adoption with many consumers maintaining digital shopping habits post-pandemic.

Digital Service Adoption: Beyond retail, Barbadians purchase digital services including streaming subscriptions (Netflix, Spotify, Amazon Prime), software licenses, online courses, and mobile apps. This demonstrates comfort with digital-only transactions and subscription models applicable to gambling products.

Consumer Trust in Online Transactions: Trust surveys indicate 65-75% of internet users feel comfortable making online purchases, though concerns about fraud and secure payment processing persist. Well-known brands and secure payment indicators (SSL certificates, recognized payment logos) significantly improve conversion rates.

Popular E-Commerce Platforms: International platforms Amazon, eBay, and AliExpress serve Barbadian consumers through shipping partners. Local e-commerce sites include Caribbean-focused marketplaces and domestic retailers with online ordering capabilities. Social media commerce through Facebook and Instagram is emerging.

Cross-Border Shopping Behavior: Barbadians frequently purchase from US and UK online retailers, utilizing freight forwarding services when direct shipping isn’t available. This international shopping experience makes offshore gambling brands familiar rather than concerning.

Digital Goods Consumption: Virtual products and services see strong adoption including gaming in-app purchases, music and video streaming, e-books, and software subscriptions. This comfort with digital-only value exchanges supports online gambling’s intangible product nature.

Business Environment and Regulatory Framework

Ease of Business Operations

Understanding Barbados’ business environment helps operators assess market entry complexity, operational costs, and regulatory burden beyond gambling-specific requirements.

World Bank Doing Business Ranking: Barbados ranks 128 of 190 countries in the World Bank’s Doing Business Index, indicating moderate ease of doing business. While not among global leaders, this ranking places Barbados in the middle tier suitable for established operators with international experience.

Ease of Starting a Business: Starting a business in Barbados requires navigating bureaucratic processes that, while not overly burdensome, involve multiple steps and government interactions. The country ranks 119 of 190 specifically for starting a business.

Business Registration Process: Company registration involves submitting Articles of Incorporation to the Corporate Affairs and Intellectual Property Office, obtaining tax registration from the Barbados Revenue Authority, registering for National Insurance, and obtaining necessary permits or licenses. Legal counsel or corporate service providers typically manage this process.

Time to Start Business: Company registration typically requires 18-31 days from initial application to operational status, assuming all documentation is properly prepared. Delays can extend timelines to 45-60 days if paperwork requires corrections or additional government approvals are needed.

Foreign Investment Policies: Barbados generally welcomes foreign investment with few restrictions. Foreign companies can establish wholly-owned subsidiaries in most sectors without requiring local partners. Some sectors like banking and insurance face additional regulatory requirements, but online gambling should permit 100% foreign ownership once regulated.

Operational Cost Structures: Office rent in Bridgetown ranges $15-35 BBD per square foot annually ($7.50-17.50 USD), with quality office space in commercial districts commanding premium rates. Professional salaries range $30,000-80,000 BBD annually ($15,000-40,000 USD) depending on role and experience. Utilities average $200-500 BBD monthly ($100-250 USD) for office spaces.

Labor Market and Talent: Barbados offers educated, English-speaking workforce with strong customer service culture. Talent availability for specialized roles like compliance officers, data analysts, and developers may require recruiting from regional markets or providing competitive compensation to attract skilled professionals from other industries.

Corporate Structure and Registration

Available Entity Types

Gambling operators can choose from several corporate structures when establishing Barbadian presence, each offering different benefits and compliance requirements.

Limited Liability Company (LLC): Standard structure for domestic operations, offering limited liability protection for shareholders while maintaining relatively straightforward compliance requirements. LLCs face 25-30% corporate tax rates on domestic income but can structure operations to minimize tax exposure.

International Business Company (IBC): Designed for companies primarily earning foreign-source income, IBCs enjoy preferential tax rates of 1-5.5%. This structure attracts international gambling operators serving markets beyond Barbados. However, the government has been reforming IBC provisions to meet international tax transparency standards.

Branch Office: Foreign companies can register Barbados branches rather than establishing separate legal entities. Branches simplify structure for multinational operators but offer less liability protection and may face less favorable tax treatment.

Recommended Structure: For iGaming operators, a Barbados IBC serving international markets offers optimal tax efficiency if regulations permit this structure for licensed gambling operations. For operators primarily targeting the domestic Barbados market, a standard LLC provides appropriate structure.

Registration Requirements

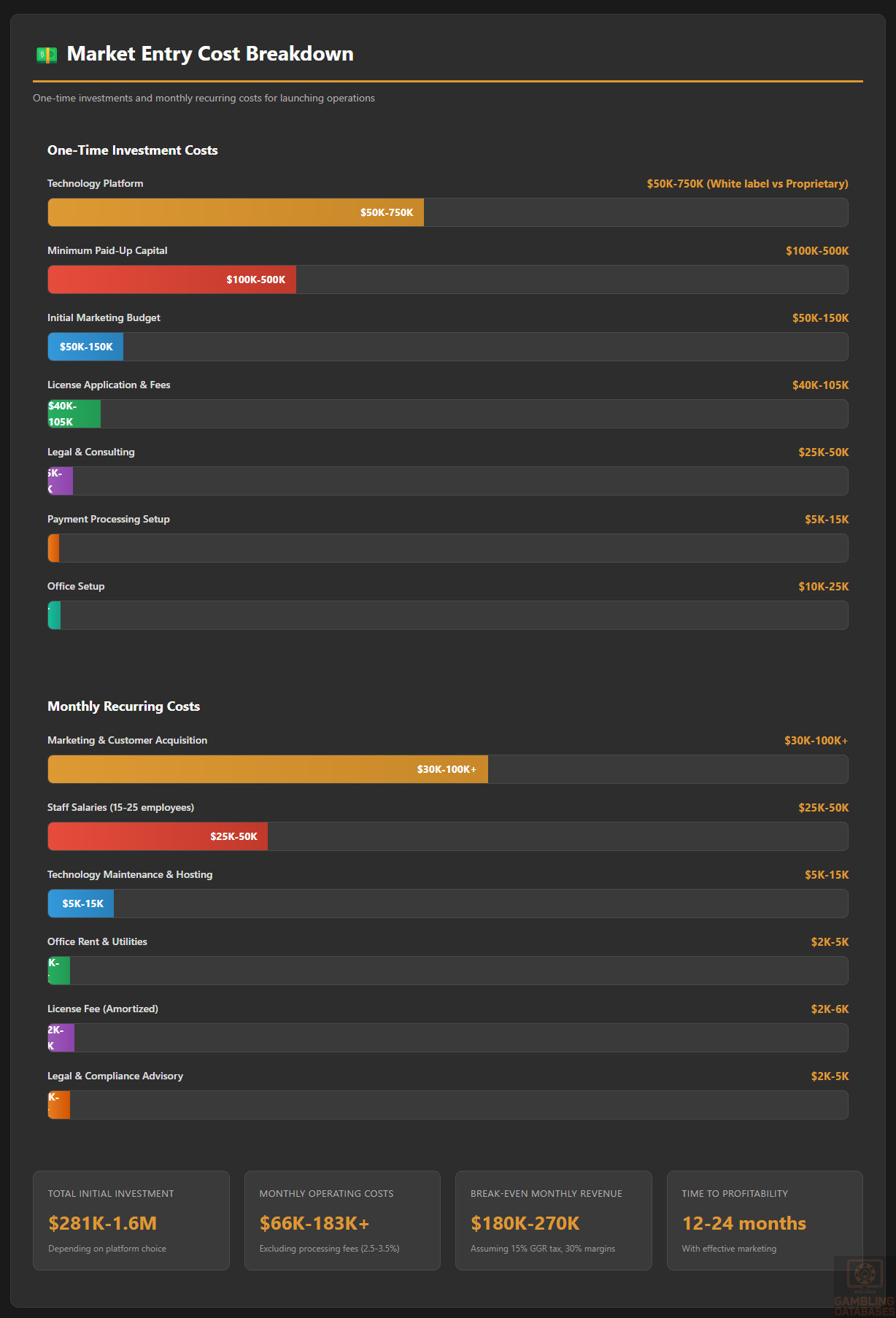

Registration Timeline: Incorporating a company in Barbados requires 18-31 days on average, with IBC registrations sometimes processing faster (10-15 days) through specialized corporate service providers. Adding gambling license application extends total time to market to 4-8 months post-regulation.

Registration Costs: Government incorporation fees range $375-550 BBD ($187.50-275 USD) depending on entity type and authorized share capital. Legal fees for preparation and filing add $1,500-3,500 BBD ($750-1,750 USD). Corporate service provider annual fees for registered office and agent services cost $1,200-2,500 BBD ($600-1,250 USD) annually.

Required Documents: Articles of Incorporation, Memorandum of Association, details of directors and shareholders (proof of identity, proof of address, professional references), registered office address in Barbados, and business plan or description of proposed operations. All foreign documents require apostille certification or notarization.

Foreign Ownership Rules: No restrictions on foreign ownership percentages for standard companies. Directors don’t need to be Barbadian citizens or residents, though at least one local director or registered agent is required for certain entity types.

Minimum Capital Requirements: No minimum paid-up capital for most company types, though gambling licenses will likely impose minimum capital requirements of $100,000-500,000 USD depending on license scope and business plan.

Ongoing Compliance: Annual returns must be filed with the Corporate Affairs Office, audited financial statements submitted to tax authorities for companies above certain revenue thresholds, and National Insurance contributions paid for all employees. Corporate service providers typically manage compliance calendars and filings for annual fees.

Corporate Governance Requirements: Companies must maintain minutes of director and shareholder meetings, keep accounting records showing financial position, and maintain registers of directors, shareholders, and charges. Publicly listed companies face additional governance requirements, though gambling operators typically remain private.

| Feature | Domestic LLC | International Business Company | Branch Office |

|---|---|---|---|

| Tax Rate | 25-30% | 1-5.5% | Variable |

| Setup Time | 18-31 days | 10-15 days | 20-35 days |

| Setup Cost | $1,000-2,000 USD | $1,200-2,500 USD | $800-1,500 USD |

| Annual Compliance | Moderate | Moderate | High |

| Foreign Ownership | 100% permitted | 100% permitted | 100% by definition |

| Liability Protection | Full | Full | Limited |

| Best Use Case | Domestic market focus | International operations | Extension of foreign entity |

Taxation Framework

Corporate Income Tax Structure

Tax planning significantly impacts gambling operator profitability. Understanding Barbados’ corporate tax system enables operators to structure operations efficiently while maintaining full compliance.

Standard Corporate Tax Rates: Domestic companies pay corporation tax of 25-30% on taxable profits. Small businesses with turnover below certain thresholds may qualify for reduced rates. Loss carryforward provisions allow offsetting future profits against prior losses.

International Business Company Rates: IBCs historically enjoyed rates of 1-2.5% on foreign-source income. Recent reforms have adjusted these rates upward to 1-5.5% while adding substance requirements including minimum employees, office space, and operational decision-making in Barbados. Gambling operators must verify IBC availability for gaming licenses.

Special Economic Zone Benefits: Barbados periodically offers tax incentives for specific industries or economic zones. Operators should investigate whether gambling operations qualify for any preferential tax treatment, expedited depreciation, or duty-free equipment imports.

Tax Treaties: Barbados maintains tax treaties with over 30 countries including the UK, Canada, China, and several EU nations. These treaties prevent double taxation and may offer withholding tax benefits for dividends, interest, and royalties paid to foreign shareholders.

Transfer Pricing Rules: Companies transacting with related parties must document that pricing reflects arm’s length terms. Gambling operators with international payment processing, technology licensing, or management service arrangements with affiliated companies must maintain transfer pricing documentation.

Withholding Taxes: Dividends paid to non-residents face 15% withholding tax (often reduced by treaty). Interest and royalty payments to non-residents incur 15% withholding. Management fees and other service payments may face withholding depending on circumstances and treaty provisions.

VAT/GST Applicability: Barbados imposes Value Added Tax (VAT) of 17.5% on most goods and services. Whether gambling services face VAT requires clarification in forthcoming regulations. Many jurisdictions exempt gambling from VAT, instead imposing specific gambling taxes.

Personal Income Tax

Personal income tax affects gambling operators through employee taxation, potentially attracting or deterring international talent, and through costs of employing local staff.

Individual Tax Brackets: Barbados operates progressive personal income tax with brackets approximately: First $25,000 BBD tax-free, $25,001-$35,000 BBD at 17.5%, $35,001-$75,000 BBD at 28.5%, Above $75,000 BBD at 35%. These rates apply to employed and self-employed individuals.

Employment Tax Obligations: Employers must withhold Pay As You Earn (PAYE) tax from employee salaries, calculate and remit amounts monthly to Barbados Revenue Authority, provide annual tax statements, and bear administrative compliance costs.

Social Security Contributions: National Insurance System requires contributions splitting between employers (8.5% of salary up to maximum) and employees (5% of salary up to maximum). These contributions fund pensions, unemployment benefits, and healthcare coverage. Total payroll burden reaches approximately 13.5%.

Tax Residency Rules: Individuals spending more than 182 days in Barbados during a tax year become tax residents, subjecting their worldwide income to Barbadian taxation. Operators employing expatriate staff must structure compensation considering residency and tax implications in both home and host countries.

Foreign Employee Taxation: Expatriate employees face the same tax rates as Barbadians, though tax treaties may provide relief from double taxation. Employers often gross-up compensation to offset higher tax burdens for international recruits relocating to Barbados.

| Tax Type | Rate | Application |

|---|---|---|

| Corporate Income Tax (Domestic) | 25-30% | Taxable profits from local operations |

| Corporate Income Tax (IBC) | 1-5.5% | Foreign-source income with substance requirements |

| Personal Income Tax | 0-35% progressive | Individual employment and business income |

| National Insurance | 13.5% total | 8.5% employer / 5% employee on salaries |

| Dividend Withholding | 15% (often reduced) | Dividends to non-residents |

| Interest/Royalty Withholding | 15% | Payments to non-residents |

| VAT | 17.5% | Most goods and services |

| Expected GGR Tax (Gaming) | 10-20% | Gross gaming revenue from gambling operations |

Market Entry Considerations

Recommended Entry Strategies

Successful market entry requires careful strategy selection balancing speed to market, investment requirements, risk exposure, and long-term positioning. Barbados’ emerging regulatory framework creates unique considerations.

Early Mover Licensing Strategy: Operators positioning for licenses immediately upon regulation gain first-mover advantages including brand establishment before competition intensifies, favorable negotiating position with payment processors and affiliates, and potential regulatory consultation opportunities shaping implementation. Risk includes uncertainty about final regulatory requirements and costs.

Partnership with Local Entities: Collaborating with established Barbadian businesses (tourism companies, retailers, lottery operators) provides local market knowledge, regulatory navigation assistance, payment processing relationships, and customer trust. Partners can assist with office setup, hiring, and government relations.