Belgium presents a complex yet potentially rewarding market for iGaming operators willing to navigate its strict regulatory framework and evolving compliance landscape. The country operates under a channeling policy that allows limited licensed operators to offer gambling services through a comprehensive licensing system managed by the Belgian Gaming Commission.

However, recent regulatory tightening including advertising bans, increased minimum gambling age to 21, and weekly loss limits of €200 create significant operational challenges that must be carefully weighed against market opportunities.

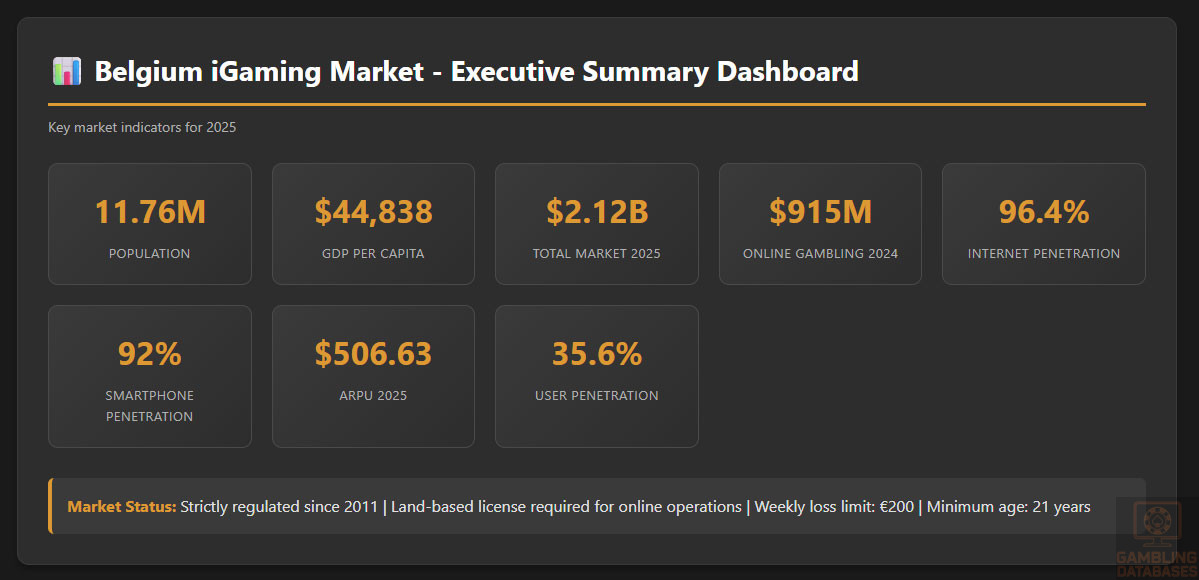

Executive Summary: Key Market Indicators

| Metric Category | Indicator | Value/Status |

|---|---|---|

| Legal Status | Online Gambling Legal | Yes, strictly regulated since 2011 |

| Regulatory Authority | Gaming Commission (BGC) | Belgian Gaming Commission (Kansspelcommissie) |

| Licensing System | Available License Types | A+ (Online Casino), B+ (Online Arcade), F1+ (Online Betting) |

| License Requirement | Land-Based Prerequisite | Yes – must hold corresponding land-based license |

| Population | Total Population 2025 | 11.76 million |

| Demographics | Median Age | 41.9 years |

| Demographics | Urban Population | 98.8% (11.6 million) |

| Economic Indicators | GDP (Total 2024) | Approximately $528 billion USD |

| Economic Indicators | GDP Per Capita 2024 | $44,838 USD |

| Economic Indicators | GDP Growth Forecast 2025 | 0.2-0.4% quarterly growth |

| Internet Infrastructure | Internet Penetration | 96.4% (11.3 million users) |

| Internet Infrastructure | Mobile Connections | 102% penetration (12 million connections) |

| Technology | Smartphone Penetration | 92% (10.4 million users by 2025) |

| Technology | Average Fixed Internet Speed | 107.01 Mbps download |

| Technology | Average Mobile Internet Speed | 88.69 Mbps download |

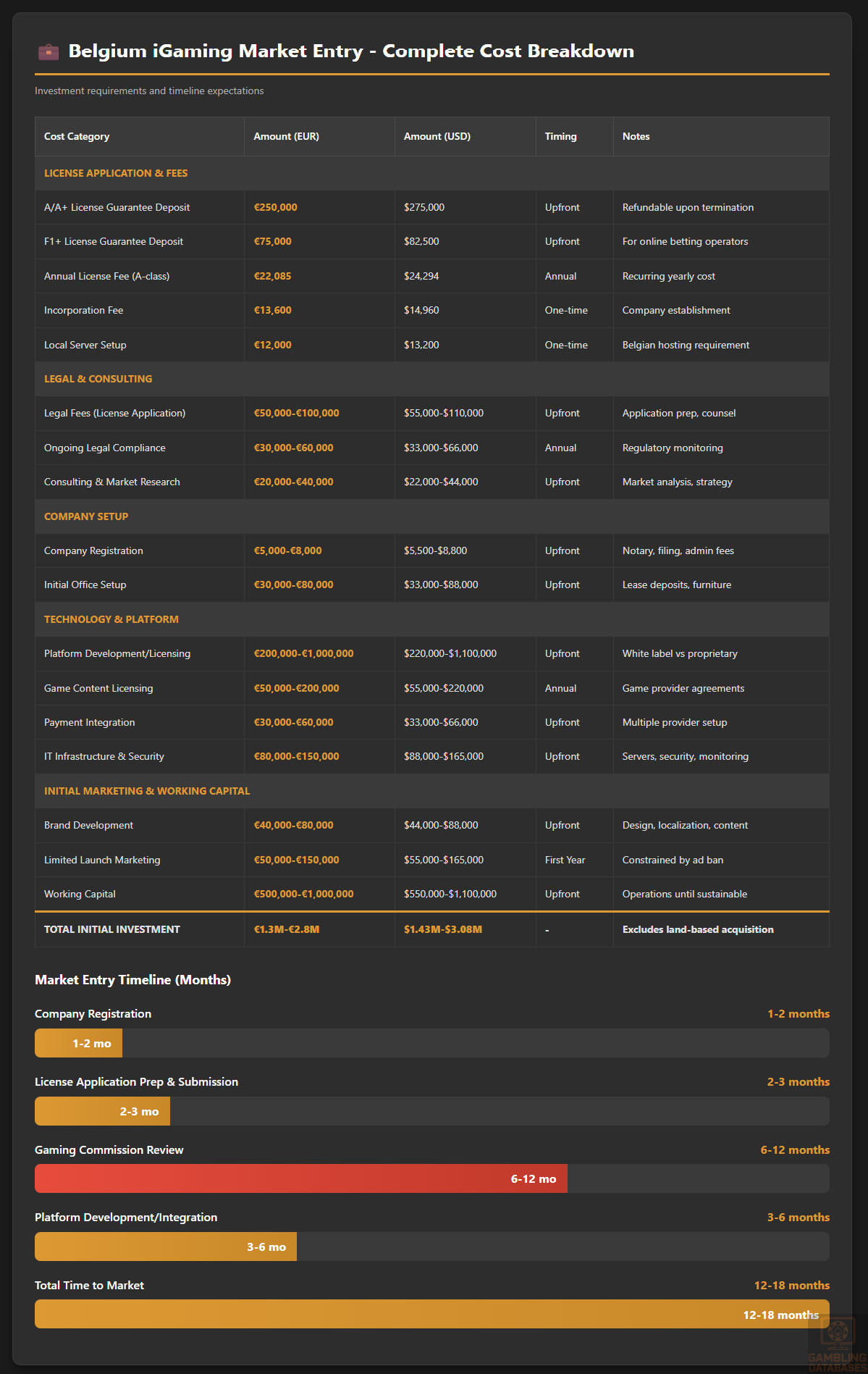

| Licensing Costs | A/A+ License Guarantee | €250,000 warranty deposit |

| Licensing Costs | F1/F1+ License Guarantee | €10,000 (F1) / €75,000 (F1+) warranty |

| Licensing Costs | Annual License Fee (A-Class) | €22,085 |

| Licensing Costs | Additional Setup Fees | €13,600 incorporation + €12,000 local server |

| Tax Rates | Online Gambling GGR Tax | 11% (varies by region) |

| Tax Rates | Corporate Income Tax | 25% (standard rate) |

| Tax Rates | VAT Rate | 21% |

| Player Regulations | Minimum Gambling Age | 21 years (as of September 2024) |

| Player Regulations | Weekly Loss Limit | €200 maximum per player per week |

| Market Size | Total Gambling Market 2025 | $2.12 billion USD (total gambling) |

| Market Size | Online Gambling Revenue 2024 | $914.80 million USD |

| Market Growth | Online Gambling CAGR 2024-2029 | 4.64% |

| Market Growth | Total Market CAGR 2025-2030 | 1.48% |

| Player Metrics | Average Revenue Per User (ARPU) | $506.63 (2025 projection) |

| Player Metrics | User Penetration Rate | 35.6% (2025) |

| Player Metrics | Expected Users by 2030 | 4.5 million gambling users |

| License Validity | Casino Licenses (A/A+) | 15 years (renewable) |

| License Validity | Betting Licenses (F1/F1+) | 9 years (renewable) |

| Processing Time | F1 License Application | 6 months (statutory maximum) |

| Processing Time | Documentation Review | 2-3 months (typical) |

| Market Entry Barriers | Advertising Restrictions | Near-total ban since July 2023 |

| Market Entry Barriers | License Availability | Limited number (numerus clausus) |

| Market Entry Barriers | Server Location Requirement | Must be hosted in Belgium |

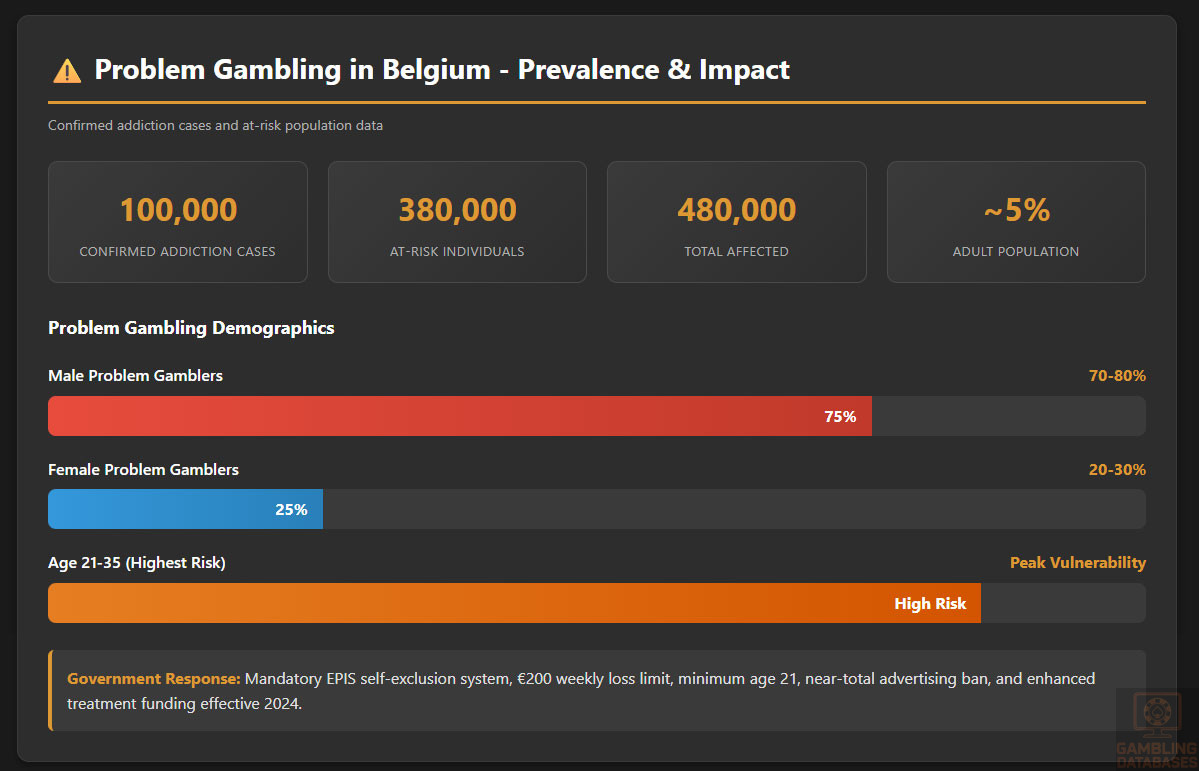

| Problem Gambling | Confirmed Addiction Cases | Approximately 100,000 people |

| Problem Gambling | At-Risk Gamblers | 380,000 individuals (5% of adult population) |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Belgium’s gambling regulatory framework operates on a fundamental principle that all games of chance are prohibited unless specifically authorized through a strict licensing system. The Belgian Federal Act of 7 May 1999 on games of chance, betting, gaming establishments and player protection serves as the cornerstone legislation, establishing a channeling policy designed to provide Belgian residents access to limited, safe, and strictly regulated gambling options while combating illegal operations. This approach represents a deliberate balance between prohibition and controlled commercialization, requiring constant regulatory fine-tuning to address technological developments and social concerns.

The regulatory environment underwent significant transformation in 2024 with the implementation of the Law of 18 February 2024, which came into force on September 1, 2024. This landmark reform standardized the minimum legal gambling age at 21 years across all gambling activities, eliminating previous age disparities where casinos required 21 but other sectors allowed 18. The legislation also introduced critical prohibitions including the combination of different online licenses on the same website and established stricter player protection measures. These changes reflect Belgium’s increasingly cautious approach to gambling regulation, prioritizing consumer protection and addiction prevention over market liberalization.

An important judicial clarification emerged in October 2024 when the Belgian Council of State ruled that virtual betting on non-real events does not constitute legal betting under Belgian law. The court specified that bets must be placed on real, uncertain events rather than virtual simulations, significantly impacting operators offering virtual sports betting. This ruling demonstrates the regulatory authorities’ strict interpretation of gambling legislation and their willingness to adapt oversight to emerging gambling formats, creating potential compliance risks for operators developing innovative betting products.

Land-Based Gambling Activities

Belgium permits carefully controlled land-based gambling operations through a strictly limited licensing system. Casino operations require Class A licenses, with only nine casinos authorized to operate throughout Belgium’s territory. The Gaming Act specifies the exact municipalities where casinos may be established, and each casino must conclude a concession agreement with the local municipality. These establishments must combine gambling activities with sociocultural offerings including shows, exhibitions, congresses, and hotel and catering services, positioning them as integrated entertainment destinations rather than pure gambling venues.

Gaming arcades operating slot machines require Class B licenses, with 180 licenses available nationwide and 175 currently active as of October 2024. These Class II gaming establishments focus specifically on automatic games of chance and must meet distinct operational requirements separate from full casinos. Additionally, drinking establishments may obtain Class C licenses permitting up to two gaming machines, provided these machines include strict age verification functions requiring ID card insertion before play. This tiered licensing structure creates multiple entry points into Belgium’s land-based gambling market, though each tier faces significant regulatory compliance obligations.

Sports betting venues operate under F1 and F2 licenses, with F1 licenses granted to primary betting operators and F2 licenses issued to retail agents and newspaper shops offering betting as an ancillary activity. The regulatory framework distinguishes between different types of betting establishments, with Type I through Type IV gaming establishments each subject to specific operational requirements. Recent legislative proposals may soon require C license applicants to obtain positive municipal opinions before license issuance, adding another layer of local government involvement in gambling regulation.

Online Gambling Framework

Online gambling has been regulated in Belgium since January 1, 2011, when the Gaming Act was amended to create a legal framework for digital gaming operations. However, a critical requirement distinguishes Belgium’s online gambling regime from many other jurisdictions: operators must hold a corresponding land-based license before obtaining permission to offer the same games online. This dual-licensing requirement means A+ licenses for online casinos can only be obtained by holders of A licenses for physical casinos, B+ licenses for online gaming arcades require B licenses, and F1+ licenses for online betting necessitate F1 licenses.

The mandatory physical presence requirement creates significant market entry barriers for international operators without Belgian land-based operations. The Gaming Commission enforces this policy as part of Belgium’s channeling approach, ensuring online operators maintain substantial local presence and commitment to Belgian market regulations. This structure has resulted in only nine active A+ licenses and limited B+ and F1+ licenses, corresponding exactly to the number of authorized land-based operations in each category.

Recent regulatory changes prohibit combining different online license types on the same website, effective September 1, 2024. Operators can no longer offer both casino games and sports betting through a single online platform even if they hold multiple license types. This separation requirement forces operators to maintain distinct websites for different gambling products, increasing operational complexity and costs while theoretically improving player protection through clearer product categorization.

Prohibited Activities and Restrictions

Belgian law explicitly prohibits several gambling activities and imposes strict content restrictions on permitted operations. Virtual betting on simulated events stands definitively prohibited following the October 2024 Council of State ruling, limiting F1 and F1+ license holders to offering bets exclusively on real sporting events and competitions. Operators cannot accept wagers on events whose outcomes are already known, activities contrary to public order or morality, or events lacking genuine uncertainty in their results.

The Gaming Act contains broad prohibitions against unlicensed gambling operations, with both civil and criminal penalties applicable to violators. The Gaming Commission maintains and regularly updates a blacklist of websites offering unlawful games of chance to Belgian players, published on the Commission’s website. Most Belgian Internet Service Providers block access to blacklisted websites, and the Commission has established cooperation with telecommunications regulators to enhance blocking effectiveness and raise awareness about illegal gambling risks.

Regulatory Body Structure and Oversight

The Belgian Gaming Commission serves as the primary regulatory authority, operating as an independent public body responsible for supervising, enforcing, and regulating all gambling activities covered by the Gaming Act. The Commission exercises threefold competence encompassing advisory functions, licensing authority, and supervisory powers. When requested by Parliament or ministers, the Commission provides expert advice on legislative and regulatory issues within the Gaming Act’s scope, influencing policy development and regulatory evolution.

The Commission’s licensing authority extends to granting and refusing license applications across all gambling categories, evaluating applicants against financial stability requirements, criminal record checks, and technical compliance standards. The Commission’s Control Unit conducts inspections at gaming establishments and on IT systems, investigates potential violations, requests relevant documents, and drafts official reports of infractions for submission to public prosecutors. Recent legislative proposals suggest expanding the Control Committee’s membership, signaling potential intensification of enforcement activities.

Enforcement mechanisms include warnings, operational suspensions, license revocations, and administrative fines. For serious violations, criminal prosecution may proceed independently of or alongside administrative sanctions. The Commission can also impose fines when public prosecutors decline to pursue criminal charges, ensuring violations face consequences even without criminal convictions. This multi-layered enforcement approach creates substantial compliance pressure on licensed operators and serves as a significant deterrent against unlicensed gambling activities.

Licensed Operators and Market Players

Belgium’s restricted licensing system has created a concentrated market with limited competition among established operators. As of October 2024, exactly nine A licenses and nine corresponding A+ licenses are active, matching the maximum number permitted by law. Similarly, 175 B licenses remain active from the 180 available, with corresponding B+ licenses for online operations. The F1 and F1+ licensing categories show similar constraint, though exact numbers vary as licenses are granted for renewable terms and may lapse if operators exit the market.

The Belgian National Lottery operates a legal monopoly on lottery products, commanding significant market presence with over 5 million monthly website visitors to its French-language portal and similarly strong traffic to its Dutch-language equivalent. This state-controlled monopoly controls a substantial portion of total gambling revenue, particularly in the lottery segment which generated €38 billion in European-wide revenue in 2024, with land-based lottery significantly outperforming online alternatives.

International operators with Belgian operations include major European gaming groups that have established land-based presence to qualify for online licenses. Gaming1 has emerged as a significant market player following partnerships with international content providers and expansion of its online casino and sports betting offerings. Market concentration remains high due to licensing restrictions, with established operators benefiting from first-mover advantages and substantial barriers to new entrant competition.

The market structure reflects Belgium’s deliberate policy choice to limit gambling availability while channeling player activity toward licensed, regulated operators. Market leaders focus on defending their positions through network quality, customer service excellence, and compliance with evolving regulatory requirements. However, this concentration has prompted concerns that overly restrictive regulation may push players toward unlicensed offshore operators that face fewer restrictions and can offer more attractive promotions, potentially undermining the channeling policy’s effectiveness.

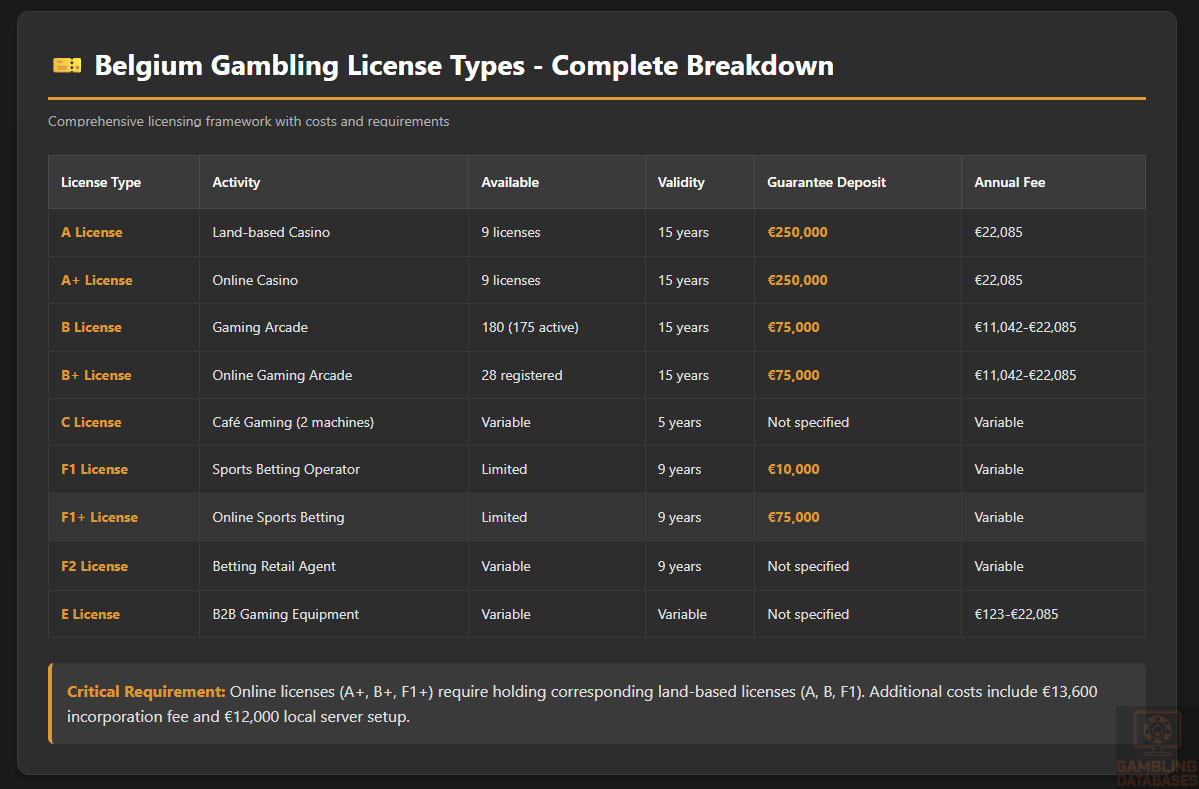

Licensing Framework and Requirements

Application Process and Eligibility

The Belgian Gaming Commission administers all license applications through structured procedures designed to ensure only qualified, financially stable operators receive authorization. Applicants must first complete detailed application forms enabling the Commission to assess suitability and identify all relevant parties involved in the proposed operation. The Commission reviews applications against multiple criteria including financial capacity, technical competence, criminal record history of management personnel, and compliance capability.

| License Type | Activity Authorized | Number Available | Validity Period | Guarantee Deposit | Annual Fee |

|---|---|---|---|---|---|

| A License | Land-based Casino | 9 licenses | 15 years (renewable) | €250,000 | €22,085 |

| A+ License | Online Casino | 9 licenses | Same as A license | €250,000 | €22,085 |

| B License | Gaming Arcade | 180 available (175 active) | 15 years (renewable) | €75,000 | €11,042-€22,085 |

| B+ License | Online Gaming Arcade | Limited (28 registered) | Same as B license | €75,000 | €11,042-€22,085 |

| C License | Café Gaming (max 2 machines) | Variable | 5 years | Not specified | Variable |

| F1 License | Sports Betting Operator | Limited | 9 years (renewable) | €10,000 | Variable |

| F1+ License | Online Sports Betting | Limited | Same as F1 license | €75,000 | Variable |

| F2 License | Betting Retail Agent | Variable | 9 years (renewable) | Not specified | Variable |

| E License | B2B Gaming Equipment | Variable | Variable | Not specified | €123-€22,085 |

Financial requirements represent substantial barriers to market entry. A and A+ license applicants must provide €250,000 warranty deposits, while B and B+ licenses require €75,000 guarantees. F1 licenses demand €10,000 warranties, but corresponding F1+ online licenses increase the requirement to €75,000. These deposits remain locked throughout the license validity period, representing significant capital commitments that must be maintained separate from operational funding requirements.

Beyond guarantee deposits, applicants face additional one-time costs including €13,600 incorporation fees and €12,000 local server setup fees for online operations. These mandatory infrastructure investments ensure operators establish genuine Belgian presence rather than operating purely from foreign jurisdictions. The Gaming Commission may request additional documentation or clarifications during review processes, potentially extending timelines and increasing legal and consulting expenses.

The Commission must process F1 license applications within six months of submission per statutory requirements. Documentation review typically requires 2-3 months when applications include all required materials. However, incomplete applications or requests for additional information can extend timelines significantly. Applicants should anticipate total time-to-market of 6-12 months from initial application submission through license approval and operational launch, though complex applications may require longer periods.

Local Presence and Operational Requirements

Belgium mandates physical presence within Belgian territory for all online gambling license holders. Operators cannot conduct online gambling purely through remote servers or foreign corporate structures. This requirement flows from the dual-licensing system requiring land-based operations before online authorization. A+ license holders must operate physical casinos, B+ operators need gaming arcades, and F1+ betting sites require land-based betting establishments or agency networks.

Server hosting requirements specify that all systems supporting online gambling operations must be located physically within Belgium. Operators cannot rely on cloud infrastructure or data centers in other jurisdictions, even within the European Union. This localization requirement increases operational costs and limits technical flexibility, but ensures Belgian authorities maintain direct oversight capabilities and can conduct physical inspections of IT infrastructure supporting gambling operations.

Domain registration requirements mandate Belgian domains for licensed operators, reinforcing the local presence requirement and making it easier for Belgian consumers to identify licensed operators. The Gaming Commission provides a list of licensed operators and their authorized domains on its website, helping players distinguish legal operators from unlicensed alternatives. Operators must use the “Always Play Legally” logo provided by the Gaming Commission, creating visual consistency across licensed gambling websites.

Personnel requirements include employment of Belgian residents or EU nationals with appropriate work authorization. Operators must maintain management teams capable of interfacing with Belgian authorities in French, Dutch, or German depending on their operational region. Foreign ownership faces no explicit percentage restrictions, allowing international companies to own 100% of Belgian gambling operations, but the requirement to hold land-based licenses before obtaining online permission creates practical limitations favoring operators willing to make substantial Belgian market commitments.

Compliance Obligations and Monitoring

Player Protection and Identification

Age verification requirements mandate operators verify that all players are at least 21 years old before permitting any gambling activity. This applies uniformly across casinos, betting operations, gaming arcades, and all online equivalents following the September 2024 regulatory changes. Operators must implement robust identification systems capable of confirming age through government-issued ID documents before account creation or any gambling participation.

Know Your Customer and Anti-Money Laundering compliance follows strict standards aligned with European Union directives. Operators must conduct enhanced due diligence on players making significant deposits or withdrawals, maintain detailed transaction records, and report suspicious activities to Belgian financial intelligence authorities. Customer identification verification must occur before processing significant financial transactions, with operators required to maintain secure databases of verified player information.

The Excluded Persons Information System operates as Belgium’s centralized self-exclusion database. Players can request indefinite exclusion from all licensed gambling operations through the Gaming Commission’s website. Once registered in EPIS, individuals cannot access any licensed casino or online gambling platform. Operators must check all players against EPIS before permitting gambling participation and face severe penalties for allowing excluded persons to gamble.

Expanded EPIS consultation requirements take effect in May 2025 for most operators, with F2 licensees in specific categories receiving extensions until May 2026. The Law of 7 May 2024 introduces specific identification requirements for newspaper shops offering sports betting, requiring certified IT systems capable of age verification and EPIS database checking. These expanding obligations increase compliance costs but aim to strengthen responsible gambling protections across all gambling channels.

Responsible gambling measures mandated by law include mandatory display of problem gambling information, limits on session times and loss amounts, cooling-off periods, and reality checks interrupting play to inform players of time and money spent. Operators must provide clear information about gambling risks, links to problem gambling support services, and mechanisms for players to set personal deposit and loss limits. The weekly loss limit of €200 per player applies across all licensed operators, requiring sophisticated systems to track and enforce cumulative limits.

Financial Monitoring and Reporting

Transaction monitoring systems must track all player deposits, wagers, winnings, and withdrawals in real-time. Operators need technical infrastructure capable of detecting unusual patterns, potential money laundering, underage gambling attempts, and violation of loss limits. These systems must integrate with EPIS to prevent excluded persons from gambling and must be available for inspection by the Gaming Commission’s Control Unit at any time.

Reporting requirements vary by license type but generally include monthly and quarterly submissions detailing gross gaming revenue, number of active players, total wagers, payouts, and compliance metrics. Operators must maintain detailed audit trails of all transactions and make these available to regulators upon request. Annual audits by independent certified auditors are mandatory, with audit reports submitted to the Gaming Commission demonstrating compliance with financial, technical, and responsible gambling requirements.

Audit and inspection procedures grant the Gaming Commission’s Control Unit broad powers to enter premises, examine IT systems, review documents, and interview personnel without prior notice. Operators must cooperate fully with inspections and provide requested information promptly. The Commission can seize documents, gaming machines, and evidence of potential violations. Inspection reports may lead to warnings, fines, license suspensions, or criminal referrals depending on violation severity.

Data retention requirements mandate operators maintain comprehensive records of all gambling transactions, player interactions, compliance checks, and system logs for specified periods. These records must be stored securely, protected against unauthorized access or tampering, and readily producible for regulatory review. Failure to maintain adequate records constitutes a serious violation potentially resulting in license suspension or revocation.

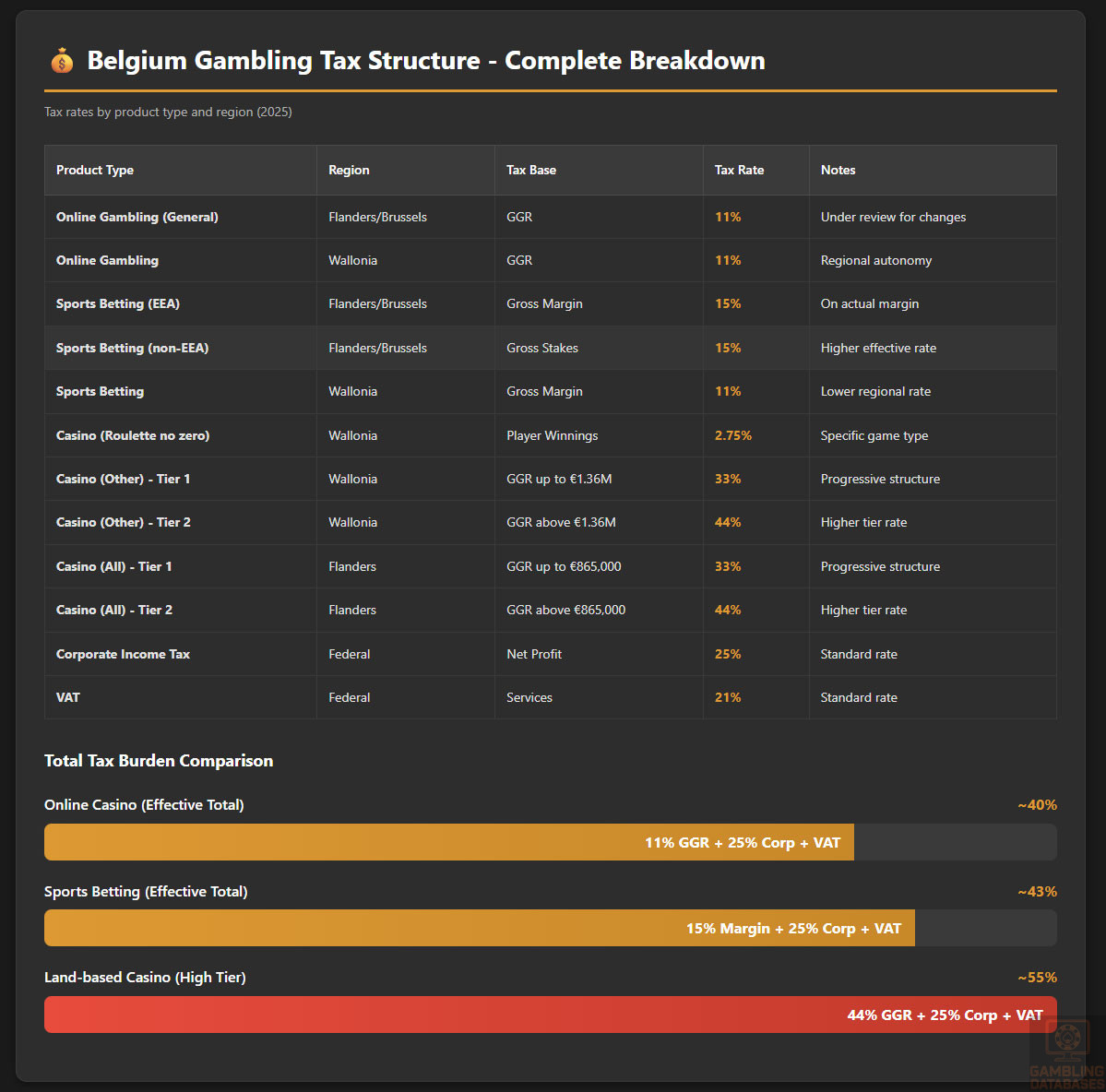

Taxation Structure and Financial Obligations

Player Taxation

Belgian tax law imposes taxes on certain gambling winnings, though the specific application varies by gambling type and amount won. Players generally do not pay taxes on most casino game winnings or sports betting profits. However, lottery winnings above certain thresholds may be subject to withholding tax, and players receiving large payouts may face tax obligations requiring declaration on annual tax returns.

The taxation framework deliberately avoids burdening most recreational gamblers with tax compliance obligations, simplifying administration and avoiding disincentives to use licensed operators. However, professional gamblers or individuals deriving substantial income from gambling may face income tax obligations on their gambling profits. Tax authorities can investigate unusually large or frequent gambling winnings to ensure appropriate tax treatment.

Operator Taxation

| Product Type | Region | Tax Base | Tax Rate | Additional Notes |

|---|---|---|---|---|

| Online Gambling (General) | Flanders/Brussels | Gross Gaming Revenue | 11% | Under review for potential changes |

| Online Gambling | Wallonia | Gross Gaming Revenue | 11% | Regional autonomy on rates |

| Sports Betting (EEA events) | Flanders/Brussels | Gross Margin | 15% | On actual gross margin realized |

| Sports Betting (non-EEA) | Flanders/Brussels | Gross Stakes | 15% | Higher effective rate |

| Sports Betting (General) | Wallonia | Gross Margin | 11% | Lower regional rate |

| Casino Games (Roulette no zero) | Wallonia | Player Winnings | 2.75% | Specific game type |

| Casino Games (Other) | Wallonia | GGR up to €1.36M | 33% | Tiered structure |

| Casino Games (Other) | Wallonia | GGR above €1.36M | 44% | Progressive higher rate |

| Casino Games (All) | Flanders | GGR up to €865,000 | 33% | Tiered structure |

| Casino Games (All) | Flanders | GGR above €865,000 | 44% | Progressive higher rate |

| Gaming Machines | All Regions | Per Machine | Fixed Annual Amount | Varies by machine type and license class |

| Corporate Income Tax | Federal | Net Profit | 25% | Standard corporate rate |

| VAT | Federal | Services | 21% | Standard rate |

Belgium’s federal structure grants its three regions significant taxation autonomy over gambling activities. The Flemish Region, Walloon Region, and Brussels-Capital Region each determine tax rates applicable to gambling operations within their territories. This creates complexity for operators serving players across multiple regions, requiring sophisticated systems to track player locations and apply appropriate regional tax rates to each transaction.

The Flemish Parliament is actively contemplating changes to online gambling tax rates, though specific details remain undisclosed as of 2025. Any rate changes could significantly impact operator profitability and business models, creating uncertainty for market planning. Operators must monitor regional legislative developments closely and prepare for potential tax increases that could materially affect financial projections.

Gross Gaming Revenue taxation applies to most online gambling operations, calculated as total player wagers minus winnings paid out. The 11% GGR tax rate common across regions represents a moderate burden compared to some European jurisdictions, but combined with corporate income tax, VAT, and other obligations, the total tax burden reaches substantial levels. Operators must maintain precise accounting systems capable of calculating GGR accurately across different game types and player jurisdictions.

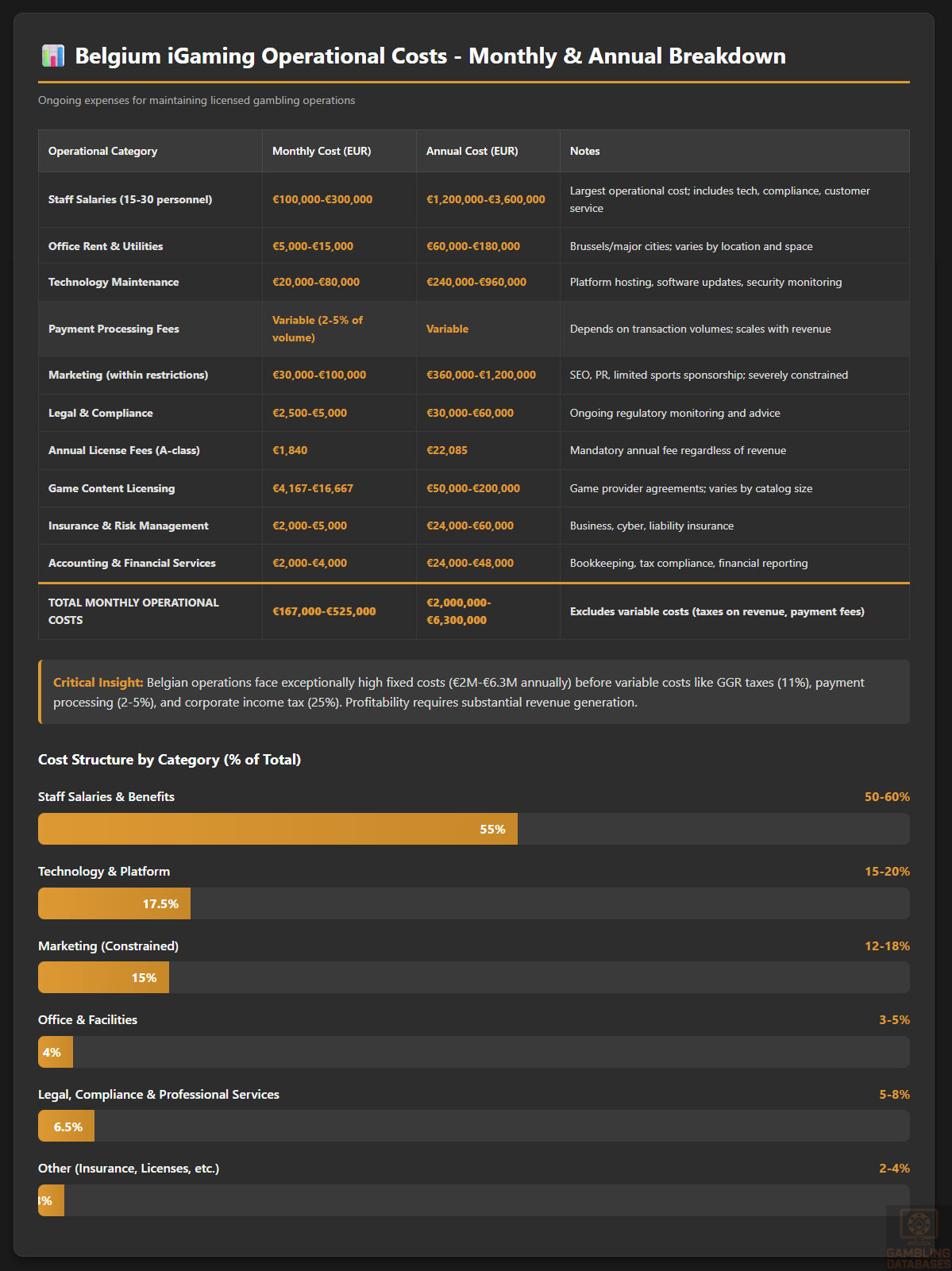

Fixed operational taxes and annual license fees add to the tax burden. A-class license holders pay €22,085 annually regardless of revenue performance, creating a significant fixed cost for smaller operators or those experiencing revenue challenges. Combined with guarantee deposits, infrastructure requirements, and compliance costs, the total financial commitment to maintain Belgian gambling operations exceeds €300,000 annually before considering variable taxes on revenue.

Corporate income tax at 25% applies to net profits after deducting operational expenses and gambling-specific taxes. Belgium maintains tax treaties with numerous countries to prevent double taxation, potentially benefiting international operators with Belgian subsidiaries. However, transfer pricing rules require arm’s-length pricing for transactions between related entities, limiting opportunities to shift profits to lower-tax jurisdictions through artificial pricing arrangements.

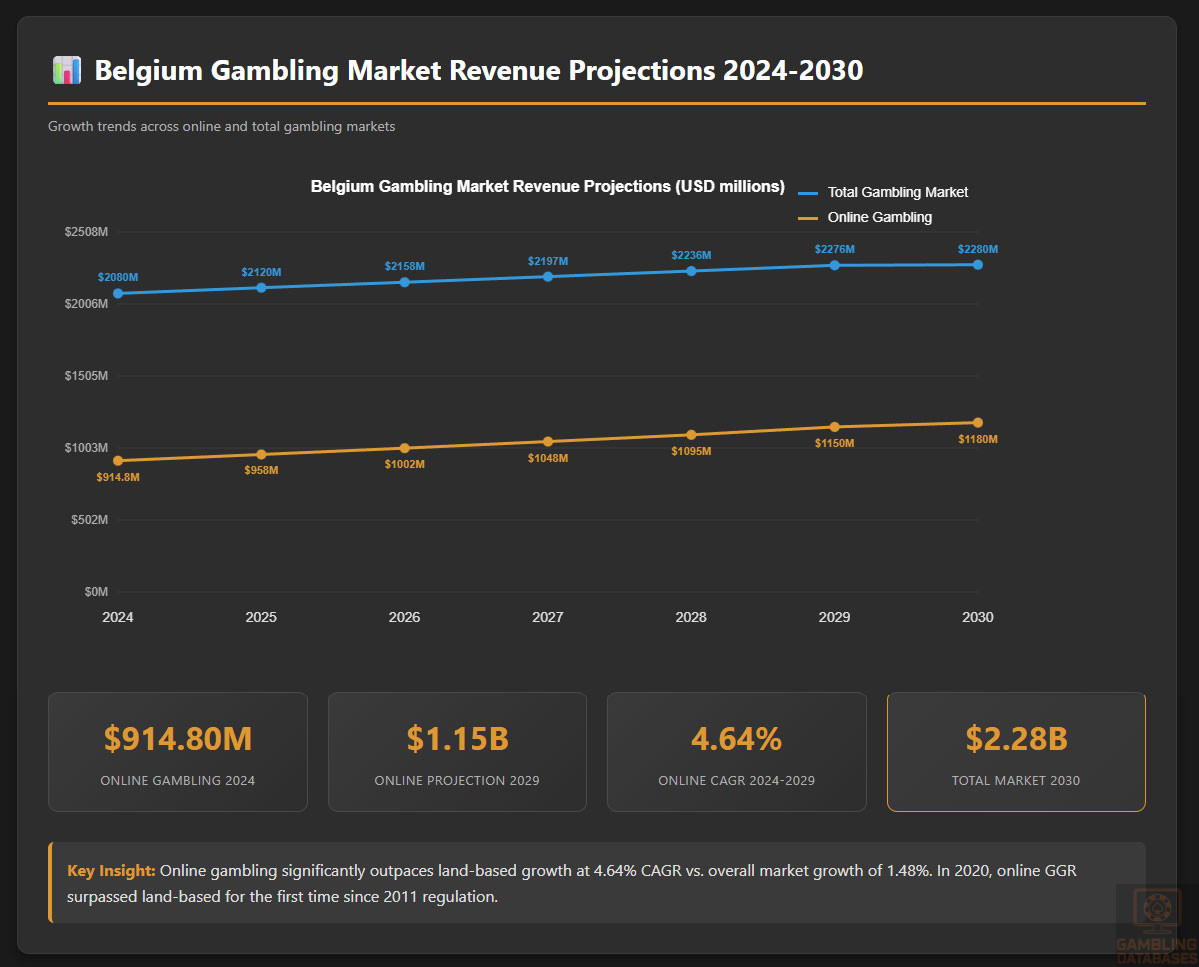

Gambling Market Financial Performance

Belgium’s total gambling market generated approximately €2.12 billion in revenue during 2025, encompassing land-based and online operations across casinos, betting, lottery, and gaming arcades. The market demonstrates moderate growth with a projected CAGR of 1.48% through 2030, reaching approximately €2.28 billion. This modest growth reflects market maturity, regulatory constraints, and demographic factors limiting rapid expansion.

Online gambling revenue reached €914.80 million in 2024 and continues growing at 4.64% CAGR, significantly outpacing land-based gambling growth. By 2029, online gambling is projected to reach €1.15 billion, representing an increasing share of total gambling revenue. This shift toward digital channels reflects broader consumer preferences for convenience and mobile access, though Belgium’s online growth lags behind less-regulated European markets.

In 2020, Belgium experienced a historic milestone when online gambling Gross Gaming Revenue surpassed land-based gambling for the first time since online regulation began in 2011. The Gaming Commission reported 18.03% online GGR growth in 2023 compared to 2022, while offline markets grew 15.18% during the same period. This accelerating digital transition creates opportunities for online-focused operators but also intensifies regulatory scrutiny of online gambling’s social impacts.

Revenue distribution by gambling type shows lottery commanding the largest overall product category at €38 billion European-wide, though Belgium’s specific lottery revenue concentrates with the National Lottery monopoly. Casino games generated approximately €30 billion across Europe in 2024, predominantly online at €21.5 billion versus land-based €8.5 billion. Sports betting produced €20.1 billion with online channels at €13.7 billion exceeding land-based betting revenue.

Tax revenues generated for Belgian federal and regional governments from gambling operations contribute substantially to public finances. The combination of GGR taxes, fixed license fees, corporate income taxes, and VAT on gambling services produces hundreds of millions in annual government revenue. This fiscal contribution strengthens political support for maintaining regulated gambling markets, though concerns about problem gambling social costs create ongoing debates about optimal regulatory balance.

Advertising and Marketing Restrictions

Belgium implemented sweeping advertising restrictions through the Royal Decree of 27 February 2023 and subsequent amendments to the Gaming Act in 2024. The regulatory framework now establishes a general prohibition on all gambling advertising, with only specifically authorized exceptions permitted. This represents one of Europe’s strictest advertising regimes, fundamentally reshaping how licensed operators can acquire customers and build brand awareness.

All permitted advertisements must include mandatory warnings displaying the minimum legal gambling age of 21 and prominent problem gambling prevention messages. These requirements ensure that even authorized advertising communications emphasize gambling risks rather than purely promotional content. The mandatory disclosures reduce advertising effectiveness and increase creative constraints on permitted marketing materials.

Incidental advertising connected to sports event coverage remains authorized, allowing gambling brand visibility during broadcasts of sporting competitions. However, this exception is narrowly construed and does not permit traditional commercial advertising slots. Sports sponsorship authorization continues for non-professional sports associations indefinitely, but professional sports sponsorship faces phased elimination creating significant implications for operators using sports marketing strategies.

Professional sports sponsorship restrictions implement a gradual phase-out schedule. Until January 1, 2025, gambling operators could display brand names and logos at sports practice locations. This permission ended as of 2025, eliminating stadium advertising opportunities. Sponsorship through sports clothing and team branding continues until January 2028, when all professional sports sponsorship by gambling companies becomes prohibited. Sponsorship expenses ceased being tax-deductible for gambling companies in 2024, increasing the effective cost of remaining sponsorship activities.

The advertising ban creates severe customer acquisition challenges for licensed operators, particularly new market entrants lacking established player bases. Traditional marketing channels that drive awareness and trial are unavailable, forcing reliance on organic search, direct navigation to known websites, and word-of-mouth referrals. Critics argue these restrictions disadvantage licensed operators while unlicensed offshore operators continue advertising through online channels difficult for Belgian authorities to block.

Affiliate marketing faces significant restrictions under the advertising ban interpretation. While not explicitly addressed in initial regulations, the general prohibition on gambling advertising appears to encompass affiliate websites promoting gambling services to Belgian consumers. Operators must carefully structure any affiliate relationships to avoid violating advertising restrictions, likely limiting affiliate marketing effectiveness compared to less-regulated markets.

Legal challenges to the advertising restrictions are pending before Belgian courts and potentially the European Court of Justice. Industry representatives argue the total ban violates EU principles of free movement of services and disproportionately restricts commercial speech. They contend that complete advertising prohibition pushes players toward unlicensed operators rather than protecting vulnerable consumers. However, initial court rulings have upheld Belgium’s advertising restrictions, and the regulatory trend continues toward tighter limitations.

Recent Regulatory Changes and Their Impact

The Law of 18 February 2024 represents the most significant gambling regulatory reform in recent years, implementing comprehensive changes affecting all licensed operators. The standardization of the minimum gambling age to 21 across all gambling activities eliminates a substantial player segment that previously accessed betting and gaming arcades legally at age 18. This age increase reduces the total addressable market and forces operators to implement more rigorous age verification systems.

Weekly loss limits decreased from €500 to €200 effective September 2024, representing a 60% reduction in the amount individual players can lose across all licensed gambling platforms. This consumer protection measure significantly impacts high-value players who previously exceeded €200 in weekly gambling expenditure. Operators must implement sophisticated tracking systems monitoring cumulative losses across their platforms and preventing players from exceeding limits through technical controls.

The prohibition on combining different online license types on single websites requires operators holding multiple licenses to maintain entirely separate digital properties. An operator with both A+ casino and F1+ betting licenses can no longer offer both products through a unified platform, forcing development and maintenance of distinct websites, apps, and customer databases. This separation increases technology costs, fragments customer experiences, and complicates cross-product marketing.

Bonus and promotion restrictions have intensified alongside advertising bans. While specific bonus limitations vary by interpretation, the general regulatory direction toward enhanced player protection suggests bonuses face increasing scrutiny. Operators must ensure any promotional offers comply with evolving responsible gambling standards and avoid encouraging excessive play or targeting vulnerable individuals. The €200 weekly loss limit effectively caps bonus value since players cannot wager beyond this threshold.

Mandatory player information disclosure requirements expanded through 2024 amendments. Operators must provide clearer, more prominent information about gambling risks, problem gambling resources, self-exclusion procedures, and loss limits before players begin gambling. These disclosures must appear during account registration, regularly during gameplay through reality checks, and whenever players approach loss limits. The increased disclosure requirements aim to ensure informed consent but add friction to customer onboarding processes.

Self-exclusion and cooling-off period requirements now mandate that all operators participate in the EPIS system and honor all exclusions immediately. Players can request temporary cooling-off periods preventing gambling access for specified durations or permanent indefinite exclusions. Operators cannot contact excluded players with marketing materials or incentivize them to return after self-exclusion, respecting players’ decisions to cease gambling activities.

License fee and tax rate changes remain under consideration, particularly in the Flemish Region where parliamentary discussions address potential online gambling tax increases. Any rate changes could materially impact operator profitability. The lack of specific details creates planning uncertainty, as operators cannot accurately forecast tax burdens or adjust business models in advance of regulatory changes.

The cumulative impact of recent regulatory changes substantially increases operator costs while limiting revenue potential. Higher age limits reduce player populations, loss limits cap individual player spending, advertising bans eliminate customer acquisition channels, and compliance requirements increase operational expenses. These changes demonstrate Belgium’s prioritization of player protection over gambling industry growth, creating a challenging environment for operators seeking to enter or expand in the Belgian market.

Enforcement Mechanisms and Penalties

The Belgian Gaming Commission employs comprehensive enforcement powers to ensure compliance with gambling regulations. The Control Unit conducts unannounced inspections of land-based establishments and remotely audits online gambling systems. During inspections, officials can access all areas of gambling facilities, examine gaming equipment, review financial records, and interview staff members. Operators must grant immediate access to all requested information and systems.

Penalty structures encompass administrative sanctions, financial penalties, and potential criminal prosecution. Administrative sanctions include formal warnings for minor first-time violations, temporary operational suspensions for more serious infractions, and license revocation for repeated violations or severe breaches. License suspension can apply to specific gaming machines, particular games, or entire operations depending on violation nature and scope.

| Violation Type | Potential Administrative Penalty | Potential Criminal Penalty | Additional Consequences |

|---|---|---|---|

| Operating Without License | License denial, blacklisting | Fines, imprisonment | ISP blocking, payment restrictions |

| Advertising Violations | Warning, fines | Possible criminal charges | Mandatory advertising cessation |

| Allowing Excluded Players | Fines, suspension | Criminal liability possible | Enhanced monitoring requirements |

| Underage Gambling | Severe fines, suspension | Criminal prosecution likely | Potential license revocation |

| Loss Limit Violations | Fines, system corrections mandated | Repeated violations: criminal | Technical audit requirements |

| Tax Evasion/Reporting Failures | Administrative fines | Tax fraud prosecution | Financial audits, increased scrutiny |

| AML/KYC Failures | Fines, operational restrictions | Money laundering charges | Enhanced compliance obligations |

| License Condition Breaches | Warning to revocation | Varies by severity | Corrective action requirements |

Financial penalties vary based on violation severity and operator size. Administrative fines can reach substantial amounts, particularly for serious violations endangering players or undermining regulatory objectives. The Gaming Commission publishes enforcement decisions to create transparency and deter violations by other operators. Public disclosure of violations can damage operator reputations and customer trust beyond direct financial penalties.

Criminal penalties for illegal gambling operations include fines and potential imprisonment for organizers, entrepreneurs, directors, representatives, and agents of unlicensed lotteries or games of chance. Article 302 of the Belgian Criminal Code establishes criminal liability for unauthorized gambling operations, creating personal criminal exposure for individuals involved in illegal gambling businesses. This criminal liability extends beyond corporate penalties to hold individuals accountable.

ISP blocking of unlicensed operators represents a key enforcement mechanism. The Gaming Commission maintains an updated blacklist of websites offering illegal gambling to Belgian consumers, published on the Commission’s official website. Belgian Internet Service Providers cooperate in blocking access to blacklisted domains, preventing Belgian consumers from reaching unlicensed gambling sites. While determined users might circumvent blocks through VPNs or proxy services, ISP blocking significantly reduces illegal operator accessibility.

Payment processor restrictions complement ISP blocking by preventing financial transactions between Belgian consumers and unlicensed gambling operators. Banks and payment service providers receive guidance to identify and block gambling-related transactions with unlicensed entities. This financial chokepoint creates substantial operational difficulties for illegal operators attempting to accept deposits or pay winnings to Belgian players.

Recent enforcement actions demonstrate the Commission’s willingness to take decisive action against violations. The Commission regularly adds websites to its blacklist, investigates complaints about unlicensed operations, and pursues both administrative and criminal penalties against violators. Licensed operators also face enforcement actions when they breach license conditions, with recent years seeing warnings, fines, and compliance orders issued for various regulatory violations.

Compliance enforcement trends indicate intensifying scrutiny of responsible gambling measures, advertising restrictions, and player protection requirements. The proposed expansion of the Control Committee membership suggests the Commission intends to increase inspection frequency and enforcement capability. Operators should anticipate more frequent audits, stricter interpretation of regulatory requirements, and lower tolerance for compliance failures.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Belgium’s population reached 11.76 million people as of 2025, representing a modest 0.2% annual growth rate. The country maintains a highly developed demographic profile characteristic of advanced European economies, with slow population growth driven primarily by immigration rather than natural increase. The population grew from 11.74 million in 2024 to current levels, adding approximately 62,000 inhabitants annually through the combination of births, deaths, and international migration.

| Age Group | Population Count | Percentage of Total | Gambling Market Relevance |

|---|---|---|---|

| 0-17 years (Minors) | 2,320,770 | 19.6% | Not eligible (min age 21) |

| 18-20 years | Approx. 360,000 | ~3% | Not eligible since Sept 2024 |

| 21-24 years | Approx. 480,000 | ~4% | Newly eligible, entry segment |

| 25-34 years | Approx. 1,400,000 | ~12% | Core digital gambling demographic |

| 35-44 years | Approx. 1,500,000 | ~13% | High disposable income segment |

| 45-54 years | Approx. 1,550,000 | ~13% | Peak earnings demographic |

| 55-64 years | Approx. 1,450,000 | ~12% | Pre-retirement segment |

| 65+ years | 2,405,315 | 20.3% | Retirement demographic |

| 18-64 years (Working Age) | 7,099,466 | 60% | Primary target market |

| 21+ years (Eligible Gamblers) | Approx. 9,100,000 | ~77% | Total addressable population |

The median age of 41.9 years reflects Belgium’s mature demographic structure and aging population trend. This median has increased from 38 years in 1995, demonstrating consistent population aging over recent decades. An aging population creates both opportunities and challenges for gambling operators. Older demographics typically show higher disposable income but may demonstrate lower digital adoption rates and different gambling preferences compared to younger cohorts.

Gender ratios stand relatively balanced at 97 men per 100 women, creating a nearly equal split between male and female populations. This gender balance differs from the gambling participation patterns, where males demonstrate substantially higher gambling rates than females across most gambling product categories. Life expectancy reached 82.28 years in 2023, with significant gender disparity showing female life expectancy at 84.30 years versus male life expectancy at 80.18 years.

The age distribution’s implications for gambling markets prove significant. The September 2024 increase in minimum gambling age to 21 eliminated approximately 360,000 individuals aged 18-20 from the legal gambling market. This regulatory change reduced the total addressable market by roughly 3%, impacting operators previously serving this younger demographic through betting and gaming arcade channels.

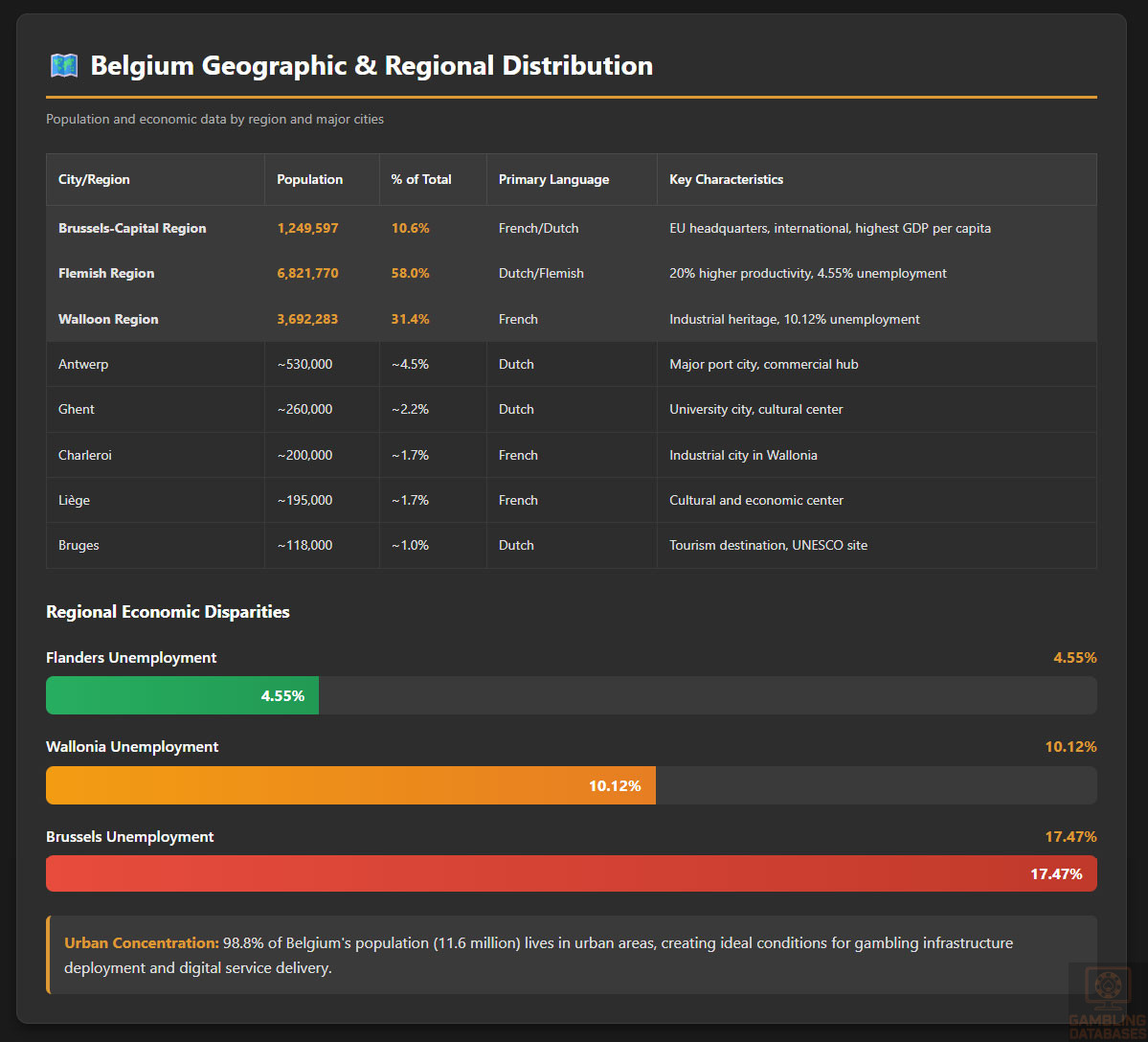

Geographic Distribution

Belgium’s urban population concentration stands at 98.8%, representing 11.6 million people living in urban areas. This exceptionally high urbanization rate creates favorable conditions for both land-based gambling establishment accessibility and digital infrastructure supporting online gambling. Urban concentration facilitates customer acquisition, reduces geographic dispersion challenges, and enables efficient marketing even under advertising restrictions.

| City/Region | Population | Percentage of Total | Primary Language | Key Characteristics |

|---|---|---|---|---|

| Brussels-Capital Region | 1,249,597 | 10.6% | French/Dutch (bilingual) | EU headquarters, international |

| Flemish Region | 6,821,770 | 58.0% | Dutch/Flemish | Higher per capita productivity |

| Walloon Region | 3,692,283 | 31.4% | French | Industrial heritage |

| Antwerp | Approx. 530,000 | ~4.5% | Dutch | Major port city, commercial hub |

| Ghent | Approx. 260,000 | ~2.2% | Dutch | University city, cultural center |

| Charleroi | Approx. 200,000 | ~1.7% | French | Industrial city in Wallonia |

| Liège | Approx. 195,000 | ~1.7% | French | Cultural and economic center |

| Bruges | Approx. 118,000 | ~1.0% | Dutch | Tourism destination, UNESCO site |

Regional economic differences significantly impact gambling market dynamics. Flanders demonstrates approximately 20% higher productivity per inhabitant compared to Wallonia, translating to higher disposable incomes and potentially greater gambling expenditure capacity. Brussels’ GDP per capita substantially exceeds both regions, though this figure is somewhat misleading as many Brussels workers reside in Flanders or Wallonia, artificially inflating Brussels’ per capita statistics.

Unemployment disparities reveal economic variations across regions. Flanders maintains unemployment around 4.55%, while Wallonia faces 10.12% unemployment, and Brussels experiences the highest rate at 17.47%. These employment differences correlate with income disparities and gambling participation patterns, with higher-employment regions typically showing greater gambling market development and higher average spending per player.

Internet access and digital infrastructure show relatively uniform distribution across geographic areas despite economic differences. Belgium’s small geographic size and high urbanization enable consistent broadband and mobile coverage nationwide. This infrastructure uniformity facilitates online gambling operations without the geographic access disparities that challenge operators in larger or less-developed countries.

The concentration of gambling venues varies by region, with casino licenses specifically allocated to nine designated municipalities and gaming arcade licenses distributed more broadly. The nine authorized casino locations include major cities and tourism destinations, creating geographic concentration of premium gambling offerings while gaming arcades provide broader geographic coverage across urban centers.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Belgium’s total GDP reached approximately $528 billion in 2024, positioning it among Europe’s significant economies despite its relatively small population. This economic scale reflects Belgium’s highly developed industrial base, advanced services sector, and strategic position as headquarters for European Union institutions and numerous international organizations. The economy’s diversification provides stability against sector-specific downturns affecting gambling industry performance.

GDP per capita stood at $44,838 in 2024, ranking Belgium among the world’s highest income countries. This affluence translates directly to gambling market potential, as higher per-capita income correlates strongly with discretionary spending capacity including entertainment and gambling expenditures. Projections indicate GDP per capita will reach approximately $64,690 by 2029, representing 15.25% growth over five years and suggesting continued income increases supporting gambling market expansion.

GDP growth forecasts for 2025 indicate modest quarterly expansion at 0.2-0.4%, reflecting mature economy characteristics and global economic uncertainties. While growth rates appear modest compared to emerging markets, Belgium’s economic stability provides predictable operating environment for gambling businesses. The consistent, if slow, economic growth supports gradual gambling market expansion without the volatility characterizing more dynamic economies.

Economic sector composition shows services dominating at 77.2% of GDP, with industry contributing substantially and agriculture representing only 0.7%. The services economy concentration aligns well with gambling operations, as service sector employment typically generates stable incomes and leisure spending patterns favorable to entertainment industries. Belgium’s position as a service economy hub creates a receptive market for leisure and entertainment offerings including gambling.

Employment rates remain strong despite regional variations, with overall labor market performance supporting consumer confidence and spending capacity. Wage levels across Belgium rank among Europe’s highest, though regional variations mirror unemployment disparities. Higher wages in Flanders and Brussels translate to greater disposable income available for gambling and other discretionary expenditures.

Inflation trends affect real income growth and consumer purchasing power. Recent years have seen elevated inflation challenging consumer budgets, though Belgium’s diversified economy and strong social safety nets moderate inflation’s impact on consumer spending. Operators must monitor inflation trends as they influence disposable income available for gambling and may affect price sensitivity to gambling taxes and fees.

Income and Wealth Distribution

Average household income in Belgium reaches substantial levels supporting discretionary spending capacity. While specific current figures vary by region, Belgian households enjoy among Europe’s highest average incomes, translating to approximately €3,500-€4,500 monthly household income depending on region and household composition. These income levels support significant leisure spending budgets within which gambling expenditures compete with other entertainment options.

Median household income provides a more representative measure than average income by excluding distortion from very high earners. Belgium’s median household income indicates strong middle-class prosperity, with majority of households achieving comfortable living standards. The robust median income demonstrates that gambling market potential extends beyond affluent segments to encompass broad middle-class participation.

Income inequality measures including the Gini coefficient show Belgium maintaining relatively equitable income distribution compared to many developed economies. This equality reflects Belgium’s strong social safety net, progressive taxation, and collective bargaining traditions. Lower inequality means gambling market opportunity distributes broadly across income levels rather than concentrating among wealthy elites, supporting mass-market gambling products over exclusively premium offerings.

Disposable income trends influence gambling spending capacity directly. After accounting for taxes, mandatory social contributions, and essential living expenses, Belgian households retain substantial discretionary income. This disposable income forms the budget from which gambling expenditures derive, competing with travel, dining, entertainment, and other leisure activities for consumer allocation.

Consumer spending patterns demonstrate Belgians allocate significant portions of discretionary budgets to entertainment and leisure activities. Cultural affinity for entertainment, strong social traditions around hospitality, and high urbanization supporting diverse leisure options create favorable context for gambling market development. However, the €200 weekly loss limit effectively caps individual gambling expenditure regardless of income level, limiting high-value player contributions.

The middle class size and growth provide crucial market foundation. Belgium’s substantial middle class, characterized by stable employment, homeownership, and discretionary income, represents the core gambling market demographic. Middle-class growth correlates with gambling market expansion as more households achieve income levels supporting regular gambling participation. Belgium’s mature middle class suggests stable rather than rapidly expanding market fundamentals.

Market Size and Growth Projections

| Market Segment | 2024 Revenue | 2025 Revenue | 2029/2030 Projection | CAGR | Growth Driver |

|---|---|---|---|---|---|

| Total Gambling Market | ~$2.08bn USD | $2.12bn USD | $2.28bn USD (2030) | 1.48% | Modest overall growth |

| Online Gambling | $914.80m USD | ~$958m USD | $1.15bn USD (2029) | 4.64% | Digital shift acceleration |

| Land-Based Gambling | ~$1.17bn USD | ~$1.16bn USD | ~$1.13bn USD (2030) | -0.7% | Gradual decline |

| Online Sports Betting | $439.70m USD | ~$470m USD | ~$580m USD (2029) | 5.7% | Sports popularity, mobile |

| Online Casino Games | ~$475m USD | ~$488m USD | ~$570m USD (2029) | 3.7% | Game variety expansion |

| European Total Market | €123.3bn EUR | €127.7bn EUR | €149.2bn EUR (2029) | 3.5% | Regional benchmark |

Current iGaming market revenue of $914.80 million in 2024 positions Belgium as a significant but not dominant European gambling market. The market size reflects Belgium’s population scale, affluent demographics, and regulatory maturity. However, strict advertising restrictions and recent regulatory tightening constrain growth below levels achieved in less-regulated European markets.

Historical revenue growth shows accelerating online gambling adoption. In 2020, online gambling GGR surpassed land-based gambling for the first time, marking a structural shift in Belgian gambling consumption. The 18.03% online GGR growth in 2023 demonstrates strong momentum, though this growth rate appears unsustainable long-term as market matures and regulatory restrictions intensify.

Revenue forecasts project online gambling reaching $1.15 billion by 2029, representing 25.7% growth over five years from 2024 levels. This 4.64% CAGR indicates healthy expansion but trails global online gambling growth rates averaging 11-12% annually. Belgium’s lower growth reflects regulatory constraints including advertising bans, loss limits, and age restrictions limiting market expansion potential.

The projected user base growth shows gambling participants increasing from current levels toward 4.5 million users by 2030. This represents approximately 38% penetration of Belgium’s total population or roughly 49% of the adult 21+ population. These penetration rates indicate substantial market maturity, with roughly half of eligible adults participating in gambling activities at least occasionally.

Average Revenue Per User of $506.63 in 2025 provides crucial profitability metric for operators. This ARPU indicates Belgian gamblers spend approximately €470 annually across all gambling products. The €200 weekly loss limit caps individual spending at €10,400 annually, though most players spend far less. ARPU trends will likely remain stable or decline as regulatory restrictions prevent monetization increases.

Market penetration rates at 35.6% in 2025 indicate over one-third of Belgians participate in some form of gambling during the year. This penetration encompasses lottery players, casino visitors, sports bettors, and gaming arcade patrons across both online and land-based channels. The high penetration suggests market maturity with growth depending more on increasing spending per existing player than dramatic expansion of player population.

Online versus land-based revenue split continues shifting toward digital channels. Online gambling represented approximately 44% of total gambling revenue in 2024, projected to reach 50% by 2029 as digital channels capture majority market share. This transition mirrors global gambling trends but proceeds slower in Belgium due to regulatory constraints and the requirement that online operators maintain land-based operations.

Market size comparison with regional neighbors shows Belgium performing moderately relative to population and economic scale. The Netherlands, with similar population and economy, shows comparable gambling market size. France and Germany, with larger populations, generate substantially more absolute gambling revenue but show similar or lower per-capita gambling expenditure. Belgium’s market positioning appears consistent with its demographic and economic profile.

Education, Skills, and Digital Literacy

Educational Foundation

Belgium maintains exceptionally high literacy rates approaching 100% of the adult population, reflecting comprehensive compulsory education and strong educational infrastructure. Universal literacy ensures gambling operators can rely on text-based communications, complex terms and conditions, and written responsible gambling information without accessibility concerns. This educational foundation supports sophisticated gambling products requiring player comprehension of rules, odds, and risks.

Education levels demonstrate strong tertiary education participation, with significant portions of the population completing university or advanced vocational training. High educational attainment correlates with digital literacy, sophisticated financial decision-making, and capacity to understand gambling mathematics. However, education also correlates with greater awareness of gambling risks, potentially moderating participation or encouraging more cautious gambling behaviors.

Digital literacy indicators show Belgium’s population demonstrates strong technology competency across age groups. While older demographics show somewhat lower digital adoption than younger cohorts, Belgium’s overall digital literacy supports widespread online gambling participation. Operators can deploy sophisticated digital platforms confident that target demographics possess necessary technical skills for account management, deposits, withdrawals, and gameplay.

Workforce skill levels rank among Europe’s highest, reflecting Belgium’s advanced economy and education system. The skilled workforce includes substantial technology sector employment, creating population segments highly comfortable with digital services including online gambling. Belgium’s position as European Union headquarters and international business center attracts educated professionals whose demographics align well with online gambling target markets.

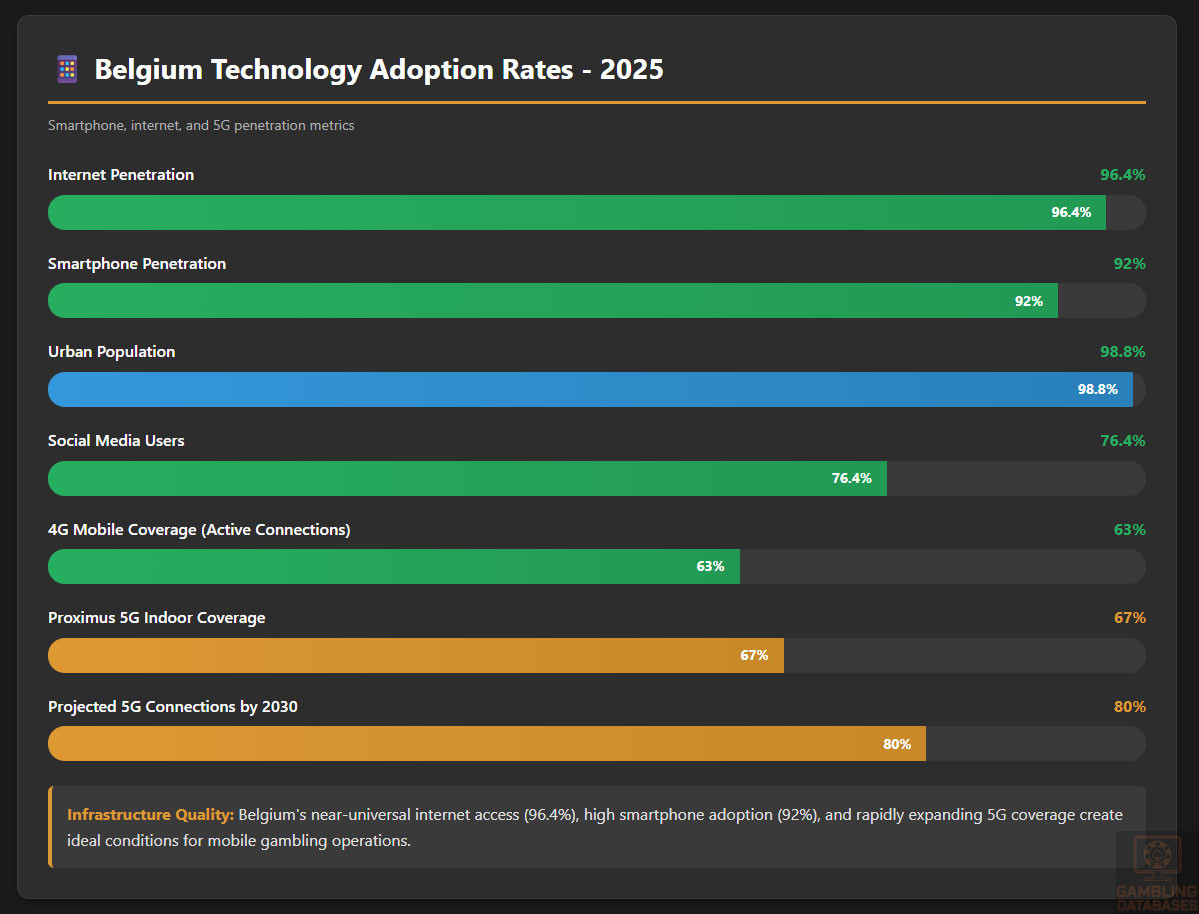

Technology adoption readiness shows Belgian consumers quickly embrace new digital services and platforms. Smartphone penetration at 92%, internet penetration at 96.4%, and strong e-commerce adoption demonstrate population-wide comfort with digital transactions. This readiness facilitates online gambling adoption, as players already familiar with online shopping and digital payments easily transition to online gambling when motivated.

English language proficiency varies but generally reaches moderate to high levels, particularly among younger demographics and urban populations. While operators must provide customer support and platforms in French and Dutch to serve all market segments effectively, substantial portions of the Belgian population can engage with English-language content. This multilingual capability, combined with Belgium’s international character, creates receptivity to international gambling brands and products.

Cultural and Social Factors

Communication and Language

Belgium’s linguistic complexity requires operators to navigate multiple language requirements across different regions. The Flemish Region predominantly speaks Dutch, the Walloon Region uses French, and Brussels operates bilingually in French and Dutch. A small German-speaking community of approximately 79,000 residents exists near the German border. This linguistic diversity necessitates multilingual operations for companies serving the entire Belgian market.

Internet language preferences generally align with regional linguistic patterns, with Flemish players preferring Dutch-language content and Walloon players favoring French. Brussels shows mixed language usage depending on individual linguistic backgrounds. Operators must maintain websites, customer service, marketing materials, and responsible gambling information in both French and Dutch as minimum requirements for comprehensive market coverage.

Business communication norms emphasize formality, precision, and multilingual capability. Belgian consumers expect professional communications in their preferred language, with customer service representatives fluent in French or Dutch depending on player location. The cultural emphasis on linguistic accommodation means operators cannot rely solely on English communications despite many Belgians speaking English as a second language.

Language requirements for gambling websites mandate that all player-facing content, terms and conditions, responsible gambling information, and customer communications appear in appropriate languages for target audiences. The Gaming Commission can require specific language provisions as license conditions, ensuring Belgian players receive information in languages they fully understand without relying on translation or foreign-language comprehension.

Cultural Attitudes

Gambling acceptance levels in Belgian society present mixed attitudes. Historical tolerance for lotteries and casino gambling suggests baseline acceptance of regulated gambling as legitimate entertainment. However, growing concern about gambling addiction, particularly affecting approximately 100,000 people with confirmed gambling problems and 380,000 at-risk individuals, has strengthened support for stricter regulation and player protection measures.

Religious influences on gambling perception remain moderate in contemporary Belgium. While the country has Catholic heritage and approximately 50% of the population identifies as Roman Catholic, religious practice has declined substantially. Active religious observance among younger demographics appears minimal, reducing religious objections to gambling. However, certain religious communities maintain opposition to gambling, potentially limiting participation in specific demographic segments.

Foreign brand perception and trust levels vary across Belgian market segments. Belgium’s international character as EU headquarters and diverse immigrant population creates general openness to foreign brands. However, Belgian consumers value local presence, customer service in local languages, and adherence to Belgian regulatory standards. International operators must demonstrate genuine Belgian market commitment rather than operating as pure offshore services to build consumer trust.

Risk tolerance indicators suggest Belgian culture demonstrates moderate risk-taking propensity. Financial conservatism and strong social safety nets reduce necessity-driven risk-taking, but affluence and education support calculated risk-taking in entertainment contexts. This moderate risk tolerance aligns well with recreational gambling participation but may limit extreme high-roller behavior compared to gambling cultures with greater risk acceptance.

Entertainment preferences and habits show Belgians engage actively with sports, particularly football, cycling, and tennis. Strong sports culture supports sports betting market development, with major sporting events generating intense interest and betting activity. Casino game preferences lean toward traditional offerings including roulette, blackjack, and slot machines, with emerging interest in live dealer games and innovative digital gambling products.

Social gambling versus solitary gambling preferences show mixed patterns. Land-based casino visits often occur in social contexts with friends or as part of entertainment outings. Online gambling demonstrates more solitary characteristics, though social features including chat functions and multiplayer games create some social interaction. The €200 weekly loss limit and responsible gambling emphasis may reduce extreme solitary gambling behaviors that characterize problem gambling.

Problem Gambling and Social Considerations

Prevalence of gambling addiction affects approximately 100,000 Belgian residents with confirmed gambling problems, representing roughly 0.85% of the total population or about 1.1% of adults. This rate aligns with European averages but generates substantial concern among policymakers, healthcare providers, and advocacy organizations. The confirmed addiction cases represent only diagnosed individuals, with actual problem gambling likely affecting larger populations.

At-risk population statistics indicate 380,000 individuals exhibit problematic gambling behaviors without meeting full addiction criteria. Combined with confirmed addiction cases, nearly 480,000 Belgians or approximately 5% of the adult population experience some level of gambling-related harm. These statistics drive regulatory tightening and intensified player protection requirements affecting all licensed operators.

Problem gambling demographics show young men particularly vulnerable to gambling addiction. Males demonstrate substantially higher problem gambling rates than females, with vulnerability peaking among men aged 18-35. The September 2024 increase in minimum gambling age to 21 specifically targets this high-risk demographic by preventing legal gambling access during years of peak vulnerability.

Gender distribution of problem gamblers shows males representing approximately 70-80% of diagnosed gambling addiction cases. Female problem gambling occurs but at substantially lower rates, typically manifesting through different gambling products and patterns. Women show higher representation among slot machine and bingo players, while male problem gamblers more commonly involve sports betting and casino games.

Government response measures include the mandatory EPIS self-exclusion system, enhanced regulatory requirements, advertising restrictions, loss limits, and public health campaigns. The government finances problem gambling treatment through mandatory operator contributions and general healthcare funding. Recent regulatory changes including age increases, loss limits, and advertising bans directly respond to problem gambling concerns.

Treatment facilities and support services receive government and operator funding to provide counseling, therapy, and support for problem gamblers and affected families. The self-exclusion system allows indefinite exclusion from all licensed gambling, creating permanent barriers to gambling access for individuals recognizing their addiction. Support services include telephone hotlines, online resources, residential treatment programs, and outpatient counseling.

Social responsibility requirements for operators include mandatory responsible gambling information, reality checks, session limits, loss limits, self-exclusion support, and employee training on identifying and assisting problem gamblers. Operators must monitor player behavior for addiction indicators and intervene when patterns suggest gambling problems. These requirements increase operational costs but serve as essential license conditions.

Mandatory contributions to problem gambling funds require operators to finance addiction research, treatment services, and prevention programs. These contributions come from license fees, specific levies, or requirements to fund particular initiatives. The financial obligations ensure gambling industry contributes to addressing harms its products create, aligning with public health and ethical gambling principles.

Political Structure and Governance

Belgium operates as a federal parliamentary constitutional monarchy with complex governance structures dividing power among federal, regional, and community governments. This multi-layered governance creates regulatory complexity for gambling operators as different authorities exercise jurisdiction over various gambling aspects. Federal legislation establishes core gambling law, while regions control taxation and certain operational aspects.

Political stability indicators generally rate Belgium favorably despite periodic governmental crises and coalition formation challenges. The country maintains strong democratic institutions, rule of law, and peaceful political transitions. For gambling operators, political stability translates to regulatory predictability and confidence that license rights will be respected across governmental changes.

Regulatory consistency and predictability face challenges from Belgium’s complex governance and evolving gambling policy priorities. Recent years have seen substantial regulatory changes including advertising restrictions, age increases, and enhanced player protection measures. While changes follow democratic legislative processes, the pace and scope of regulatory evolution create business planning challenges for operators requiring stable regulatory frameworks.

The Corruption Perception Index ranks Belgium favorably among global nations, indicating low corruption levels and strong governance quality. For gambling operators, low corruption means licensing processes operate transparently based on regulatory criteria rather than political connections or informal payments. However, the complex bureaucracy and multiple governmental layers can create administrative challenges navigating approval processes.

International relations impact on business remains generally positive. As EU headquarters and NATO home, Belgium maintains strong international relationships and embeds deeply in European and transatlantic institutional frameworks. EU membership provides legal stability through European Court of Justice oversight and ensures Belgium adheres to EU internal market principles including service provision freedom.

EU membership affects gambling regulation through European law requirements. While gambling regulation remains primarily national competence, EU law constrains Belgium’s regulatory choices through free movement of services principles. Operators licensed in other EU states can challenge Belgian restrictions as disproportionate barriers to cross-border service provision, creating tension between national regulatory autonomy and EU integration.

Trade agreements affecting iGaming remain limited as gambling generally falls outside international trade agreement coverage. However, EU internal market rules function similarly to trade agreements by requiring Belgium to justify restrictions on gambling services from other EU member states. These requirements prevent Belgium from discriminating against EU-licensed operators without proportionate justification based on public policy objectives.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration rates reached 96.4% of Belgium’s population in January 2025, representing 11.3 million internet users. This near-universal internet access creates ideal conditions for online gambling operations, ensuring virtually all potential players can access digital gambling platforms. The high penetration encompasses all age groups, though usage intensity and sophistication vary demographically.

| Metric | Value | Year-over-Year Change | Market Implication |

|---|---|---|---|

| Internet Users | 11.3 million | +21,000 (+0.2%) | Near-saturation market |

| Internet Penetration | 96.4% | Stable | Universal access achieved |

| Mobile Connections | 12.0 million | Growth continuing | 102% penetration rate |

| Smartphone Users | 10.4 million | Steady growth | 92% penetration (2025 projection) |

| Social Media Users | 8.98 million | Increasing | 76.4% of population |

| Fixed Internet Speed | 107.01 Mbps | +14.00 Mbps (+15.1%) | Supports high-quality streaming |

| Mobile Internet Speed | 88.69 Mbps | +19.36 Mbps (+27.9%) | Excellent mobile gaming performance |

| 4G Coverage | Extensive | Mature deployment | Reliable mobile connectivity |

| 5G Coverage | Expanding | Rapid rollout | Future-proof infrastructure |

| E-commerce Participation | High | Growing | Comfort with online transactions |

Daily internet usage hours average substantial portions of Belgians’ waking time, though specific current figures vary by demographic. Younger users demonstrate highest usage intensity, spending multiple hours daily online across mobile and desktop devices. This extensive internet engagement creates numerous touchpoints where gambling operators could reach consumers, though advertising restrictions severely limit commercial communications.

Mobile device adoption rates show smartphones becoming primary internet access devices for many Belgians. With 92% smartphone penetration representing 10.4 million users by 2025, mobile devices dominate internet access over desktop computers for substantial user segments. This mobile-first behavior necessitates operators prioritize mobile-optimized platforms and native applications to serve player preferences effectively.

Social media engagement reaches 76.4% of Belgium’s population with 8.98 million social media users. Popular platforms include Facebook, Instagram, LinkedIn, and TikTok, with usage patterns varying by age demographics. While social media represents significant advertising channel in other markets, Belgium’s gambling advertising restrictions limit operators’ ability to leverage social media for customer acquisition and brand building.

E-commerce participation rates demonstrate Belgians’ comfort with online purchasing and digital transactions. High e-commerce adoption indicates consumers overcome psychological barriers to online payments, trust in digital service delivery, and familiarity with account-based online interactions. These behaviors transfer directly to online gambling, reducing friction in converting potential players to active gambling participants.

Digital payment adoption shows widespread use of online banking, digital wallets, and contactless payments. Belgium’s advanced financial infrastructure and high banking penetration support seamless digital payments for gambling deposits and withdrawals. Consumer familiarity with digital financial services eliminates payment method barriers that challenge online gambling adoption in less digitally developed markets.

Online banking penetration approaches universal coverage among Belgian adults, with nearly all banking customers accessing accounts digitally. This digital banking saturation ensures players can fund gambling accounts through familiar banking interfaces and withdraw winnings to established bank accounts. The integration between banking and gambling platforms enables smooth financial flows essential to positive user experiences.

Digital Payment Behavior

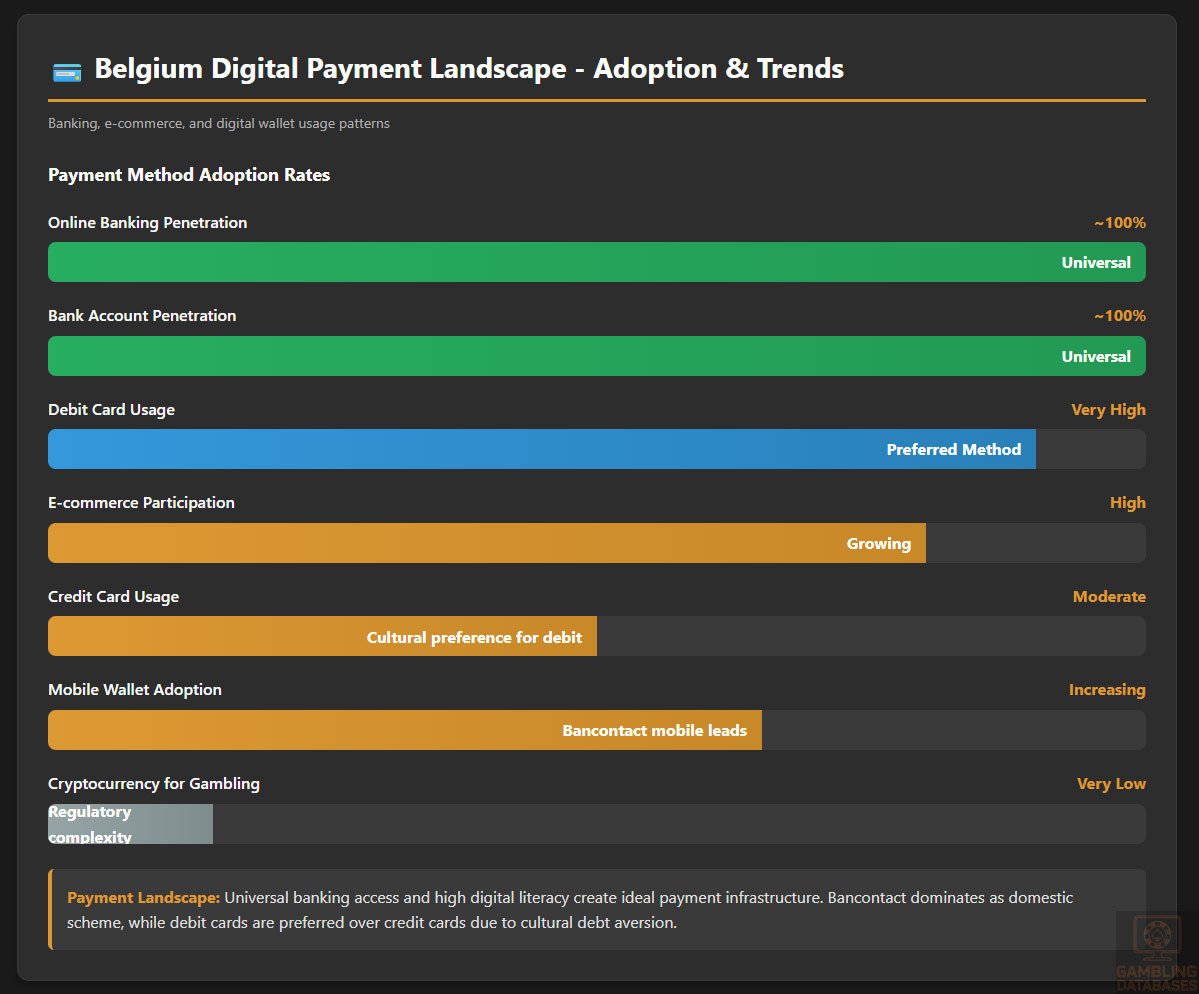

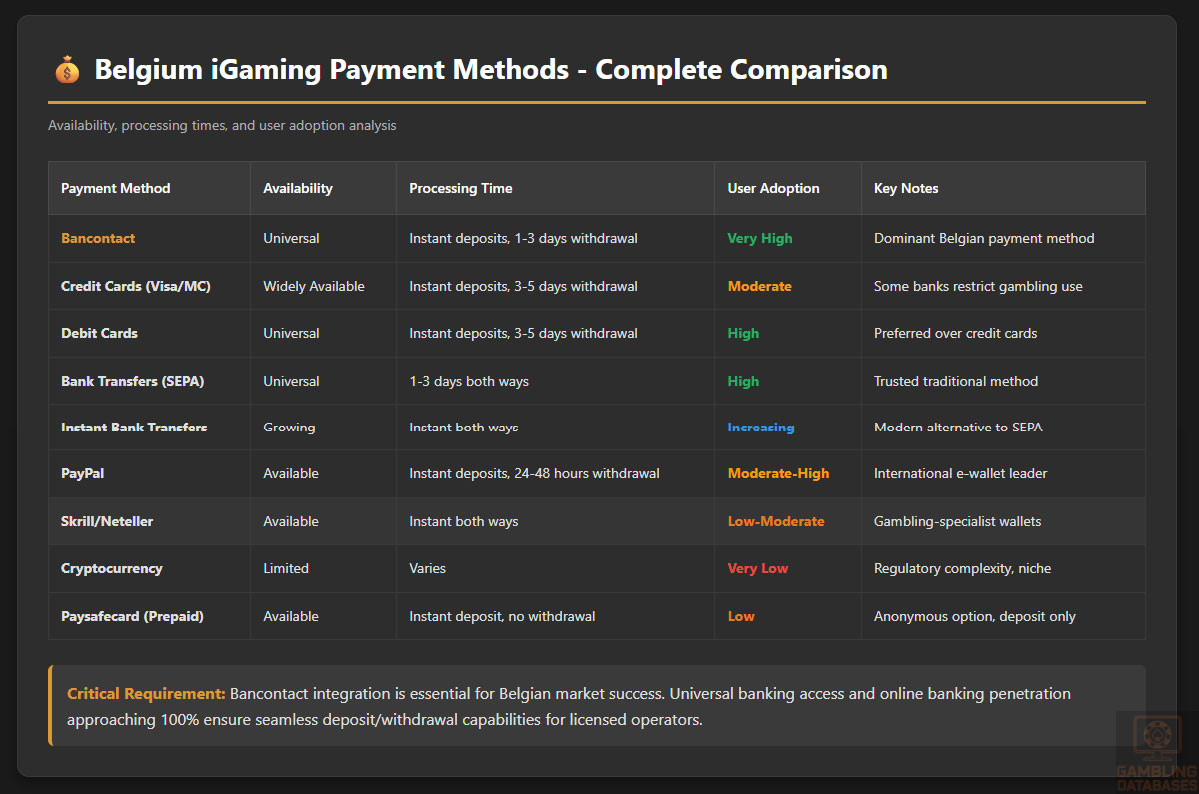

Payment method preferences among Belgian consumers span multiple options including credit and debit cards, e-wallets, bank transfers, and emerging payment technologies. Card penetration remains high with most adults holding at least one payment card. Debit cards see particularly widespread usage for everyday transactions, while credit card adoption remains moderate compared to some markets due to cultural preferences for avoiding debt.