Benin presents an emerging iGaming market opportunity in West Africa characterized by evolving regulatory frameworks and growing digital connectivity. The country enacted comprehensive gambling taxation in January 2025 under Law No. 2024-34, introducing a 10% tax on land-based gambling and 25% on online gambling winnings.

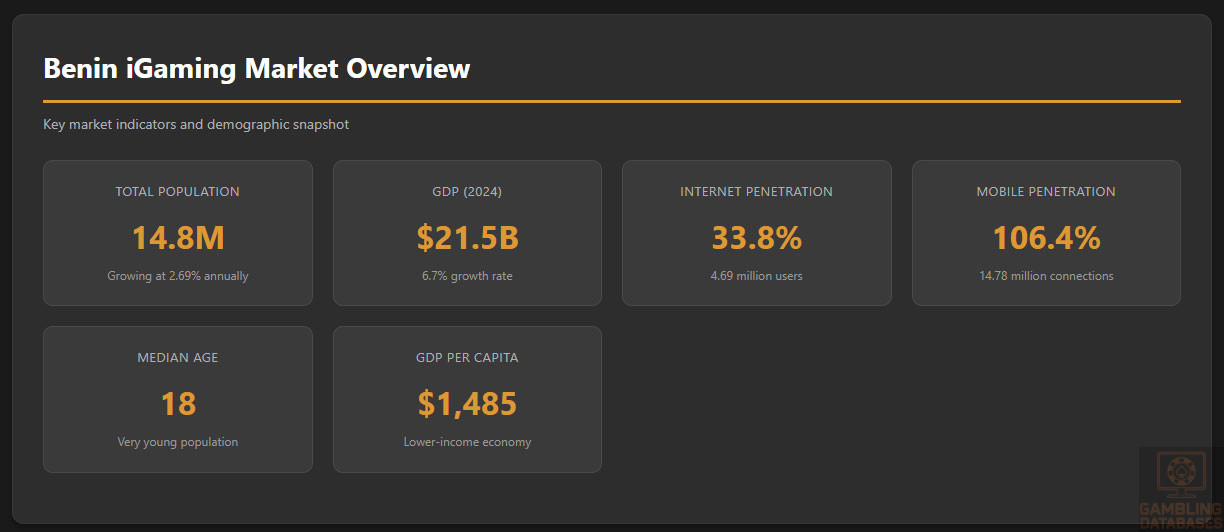

With a population of 14.8 million and internet penetration reaching 33.8%, the market remains largely untapped but shows promising growth potential. The National Lottery Authority oversees gambling operations, though online gaming regulation is still developing.

Executive Summary: Key Market Indicators

| Category | Indicator | Value |

|---|---|---|

| Legal Status | Online Gambling Legal Status | Partially regulated; land-based legal, online framework developing |

| Regulatory Body | Primary Authority | National Lottery Authority (LONAB) / Ministry of Finance |

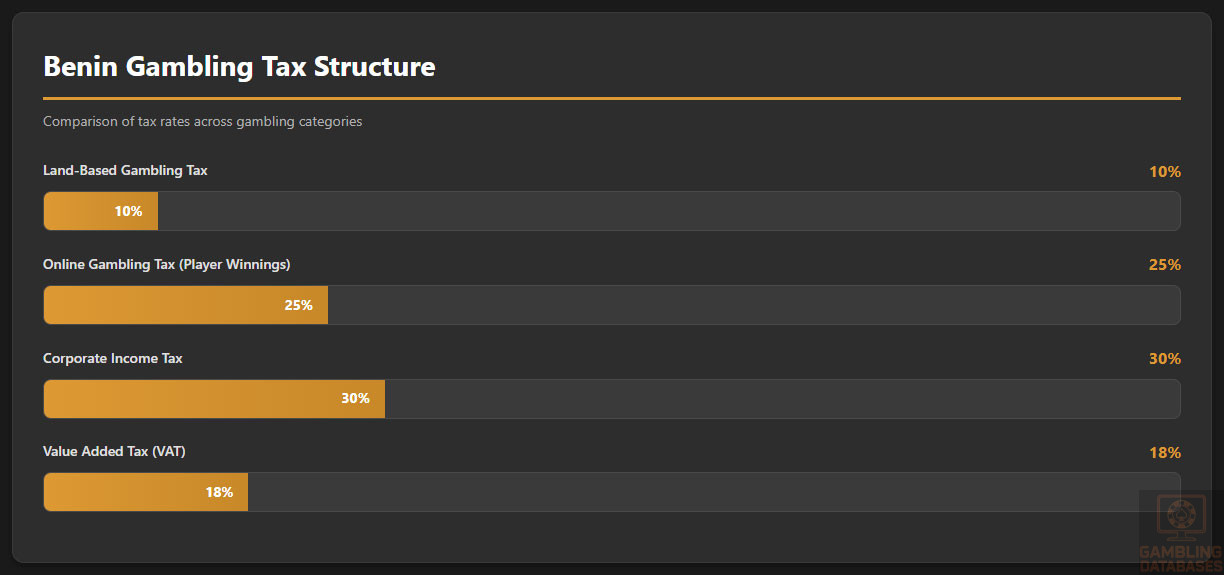

| Taxation | Land-Based Gambling Tax | 10% on turnover |

| Taxation | Online Gambling Tax | 25% on winnings |

| Demographics | Total Population (2025) | 14.8 million |

| Demographics | Median Age | 18 years |

| Demographics | Urban Population | 47.76% (7.1 million) |

| Demographics | Population Growth Rate | 2.69% annually |

| Economic Indicators | GDP (2024) | $21.5 billion |

| Economic Indicators | GDP per Capita | $1,485 USD |

| Economic Indicators | GDP Growth Rate (2024) | 6.7% |

| Economic Indicators | Inflation Rate (2024) | 1.2% |

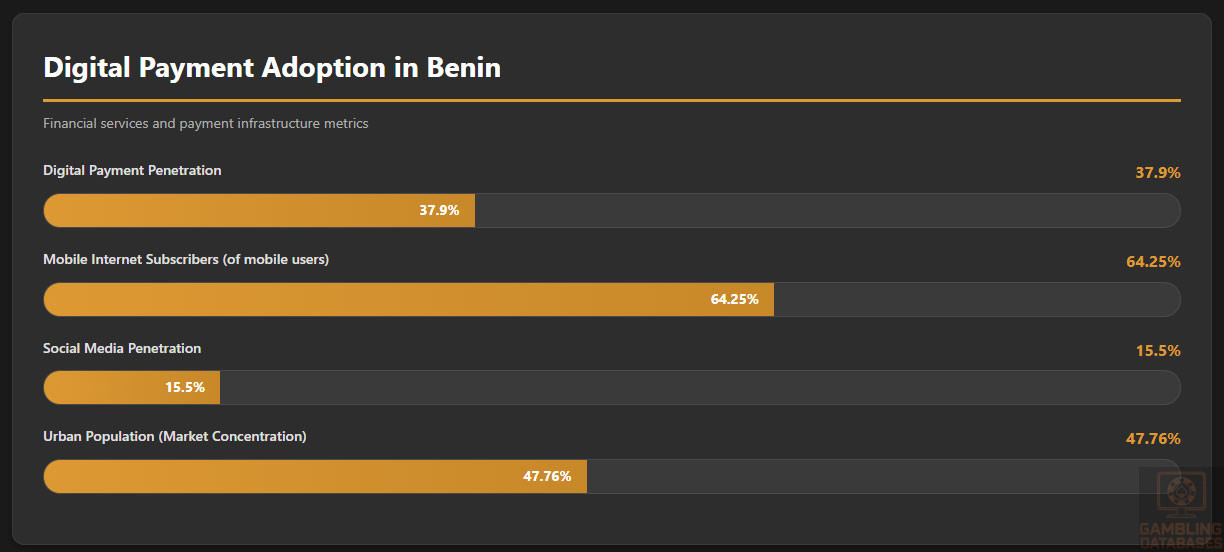

| Technology | Internet Penetration | 33.8% (4.69 million users) |

| Technology | Mobile Penetration | 106.4% (14.78 million connections) |

| Technology | Social Media Users | 2.15 million (15.5% of population) |

| Technology | 4G Coverage | 88% of population |

| Technology | Mobile Internet Speed | 30.56 Mbps (median) |

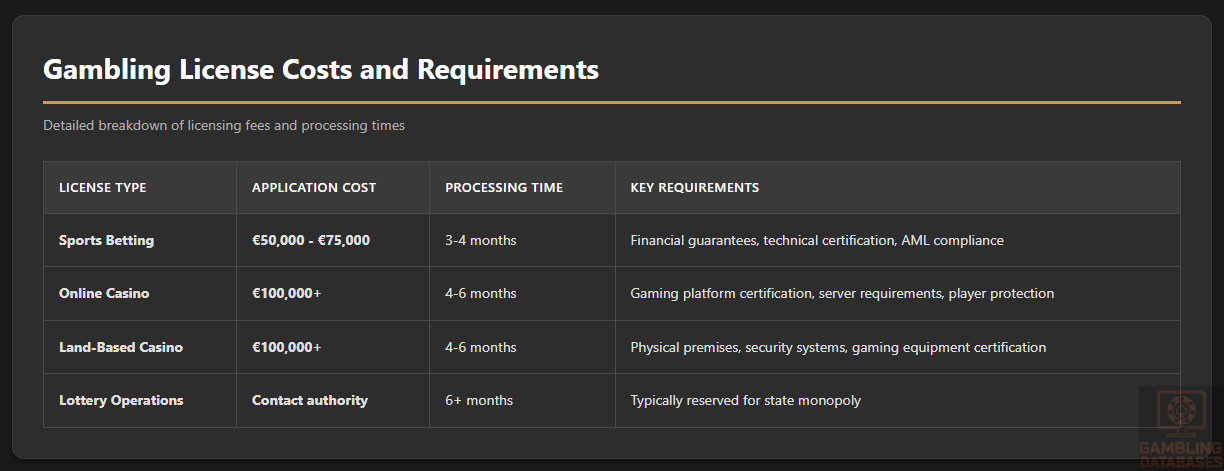

| Licensing | Sports Betting License Cost | €50,000 – €75,000 |

| Licensing | Casino License Cost | €100,000+ |

| Licensing | License Processing Time | 3-6 months |

| Market Projections | Annual Tax Revenue Target | $25 million (from gambling taxes) |

| Business Environment | Legal Gambling Age | 21 years |

| Business Environment | Currency | West African CFA Franc (XOF) |

| Business Environment | Primary Language | French (official) |

| Business Environment | Literacy Rate | 45.8% (2021) |

| Market Maturity | Online Gambling Market Stage | Emerging / Early Development |

| Competition | Licensed Land-Based Operators | Limited (few casinos, national lottery) |

| Payment Systems | Digital Payment Penetration | 37.9% (2017) |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Land-Based Gambling Activities

Benin has established legal frameworks for traditional gambling activities since 2002. The Gaming Act of 2002 regulates land-based gambling including casinos, lotteries, and sports betting venues. The country operates a National Lottery established in 1967 under the authority of the Loterie Nationale du Benin.

Land-based casinos operate in major cities, with the primary establishment located at the Benin Marina Hotel in Cotonou. These venues offer table games including roulette, slot machines, and video poker. The casino sector remains relatively small with limited expansion due to regulatory constraints and market size.

Sports betting is legal and has gained popularity in recent years. Both local and international bookmakers operate physical betting shops primarily in urban areas. Licensed sports betting operators accept wagers on football, basketball, tennis, and other international sporting events.

Online Gambling Framework

Online gambling in Benin exists in a regulatory gray area. The 2002 Gaming Act did not specifically address internet-based gambling as internet penetration was minimal at the time of enactment. International online gambling websites remain accessible to Beninese players without explicit legal restrictions.

The government announced plans in March 2023 to develop a digital monitoring system to better regulate and track online gambling activities. This proposed control platform aims to provide fairer treatment of operators, stimulate competition, strengthen anti-money laundering efforts, and enhance player protections.

The December 2024 Finance Law (Law No. 2024-34) represents a significant step toward formalizing online gambling regulation. By introducing specific taxation for online gambling winnings at 25%, the government acknowledged the sector’s existence and established groundwork for comprehensive regulation.

Licensed Operators and Market Players

The Beninese gambling market features limited licensed operators compared to more mature African markets. The National Lottery holds a monopoly on lottery operations and has expanded into digital channels. Several international sports betting operators have established physical presences in major cities.

The government’s regulatory modernization efforts aim to attract licensed international operators while protecting existing domestic operators. Market entry opportunities exist for operators willing to navigate evolving regulatory requirements and establish compliant local operations.

Licensing Framework and Requirements

Application Process and Eligibility

Gambling licenses in Benin are issued by the Ministry of Finance and Economic Development under oversight of the National Gambling and Lottery Regulatory Authority. The licensing process requires substantial documentation, financial guarantees, and technical certifications to demonstrate operational capability.

Applicants must submit comprehensive business plans detailing operational structures, responsible gambling measures, anti-money laundering procedures, and technical infrastructure. Background checks are conducted on all beneficial owners, directors, and key personnel to ensure suitability and prevent criminal involvement.

The application process typically takes 3-6 months depending on application completeness and gambling activity type. Sports betting licenses generally process faster than full casino licenses which require more extensive review of gaming systems and financial adequacy.

| License Type | Application Cost | Processing Time | Key Requirements |

|---|---|---|---|

| Sports Betting | €50,000 – €75,000 | 3-4 months | Financial guarantees, technical certification, AML compliance |

| Online Casino | €100,000+ | 4-6 months | Gaming platform certification, server requirements, player protection systems |

| Land-Based Casino | €100,000+ | 4-6 months | Physical premises, security systems, gaming equipment certification |

| Lottery Operations | Contact authority | 6+ months | Typically reserved for state monopoly |

Local Presence and Operational Requirements

Operators seeking licenses must demonstrate commitment to the Beninese market through local presence requirements. Specific requirements for physical office space, local staff employment, and operational infrastructure vary by license type but generally favor operators establishing substantive local operations.

The regulatory framework is expected to evolve with the planned digital monitoring system implementation. Future requirements may include mandatory server hosting within Benin or the West African Economic and Monetary Union region, local domain registration, and enhanced local partnership obligations.

Foreign ownership is generally permitted though the government may introduce preference mechanisms for local partnerships. Operators should anticipate requirements for local directors, designated compliance officers based in Benin, and minimum local staffing levels particularly for customer-facing operations.

Compliance Obligations and Monitoring

Player Protection and Identification

The legal gambling age in Benin is 21 years for all forms of gambling. Operators must implement strict age verification processes to prevent minors from accessing gambling services. Acceptable verification methods include national identity cards, passports, and voter registration documents.

Know Your Customer and Anti-Money Laundering compliance standards follow international best practices. Operators must collect and verify customer identity information, monitor transactions for suspicious activity, and report unusual patterns to authorities. The planned digital monitoring system will enhance regulatory oversight capabilities.

Responsible gambling measures are increasingly emphasized though not yet comprehensively mandated. Operators are encouraged to provide self-exclusion options, deposit limits, session time reminders, and problem gambling resources. Future regulations will likely formalize these requirements as player protection priorities increase.

Financial Monitoring and Reporting

Licensed operators face ongoing financial monitoring and reporting obligations. Transaction monitoring systems must track player deposits, withdrawals, and betting patterns to detect money laundering and ensure tax compliance. The digital monitoring platform under development will automate much of this oversight.

Reporting schedules vary by license type but typically include monthly revenue declarations, quarterly financial statements, and annual comprehensive audits. The National Lottery Authority and Ministry of Finance coordinate oversight activities with inspections conducted periodically to verify compliance.

Data retention requirements mandate operators maintain detailed records of all transactions, player communications, and operational activities for minimum periods typically ranging from 5-7 years. These records must be readily accessible for regulatory inspections and investigations.

Taxation Structure and Financial Obligations

Player Taxation

The 2025 Finance Law introduced significant changes to gambling taxation affecting both operators and players. Online gambling winnings now face a 25% withholding tax, representing one of the higher player taxation rates in West Africa and potentially impacting player attractiveness of licensed operators.

Land-based gambling winnings taxation follows similar principles though specific thresholds and rates may vary. Players receiving winnings above certain amounts face withholding obligations at the point of payout. Operators are responsible for calculating, withholding, and remitting player taxes to authorities.

Tax-free thresholds for small winnings may exist though specific amounts are not publicly detailed in available regulations. Players should maintain records of gambling activities for potential tax declaration requirements though enforcement of individual player tax obligations remains limited.

Operator Taxation

| Tax Type | Rate | Tax Base | Payment Frequency |

|---|---|---|---|

| Land-Based Gambling Tax | 10% | Turnover/Wagering | Monthly |

| Online Gambling Tax | 25% | Player Winnings | Monthly |

| Corporate Income Tax | 30% | Net Profits | Annual |

| License Renewal Fee | Varies | Annual fixed amount | Annually |

The 10% tax on land-based gambling applies to gross turnover, creating moderate tax burden compared to some African jurisdictions taxing Gross Gaming Revenue. Online gambling’s 25% tax on winnings effectively functions as a player-facing tax that operators must withhold and remit.

Corporate income tax at standard rates applies to gambling operators’ net profits after gambling-specific taxes. Value Added Tax applicability to gambling services varies by jurisdiction interpretation and service type. Operators should obtain specific tax rulings from Beninese authorities.

License renewal fees provide additional ongoing revenue obligations. Annual fees vary by license type and operator size though specific schedules have not been publicly detailed. Operators should budget for renewal costs equivalent to 10-25% of initial license fees.

Gambling Market Financial Performance

Comprehensive gambling market financial data for Benin remains limited due to the sector’s early development stage and historical lack of comprehensive regulation. The government projects gambling taxation will generate approximately $25 million annually under the new 2025 tax regime.

This revenue target suggests total gambling turnover in the tens of millions of dollars range, though exact Gross Gaming Revenue figures are not publicly available. The land-based sector historically dominated gambling activity with lottery ticket sales and limited casino operations forming the core market.

Online gambling market size remains largely unmeasured as most activity occurs through international unlicensed operators. The introduction of formal taxation and planned regulatory framework aims to capture this revenue stream and bring offshore operations under local oversight.

Advertising and Marketing Restrictions

Gambling advertising regulations in Benin remain underdeveloped compared to mature markets. Current frameworks do not impose extensive restrictions on advertising channels, content, or promotional activities though this may change as online gambling regulation formalizes.

Operators generally can advertise through television, radio, online channels, outdoor billboards, and print media. Content restrictions prohibit marketing to minors, misleading claims about winning probabilities, and promotion of gambling as income source. Responsible gambling messaging requirements may be introduced.

Sponsorship of sports teams, events, and cultural activities is permitted and represents effective market entry strategy in Benin. Popular football clubs and local sporting events provide visibility opportunities. Affiliate marketing operates without specific regulations though this will likely change.

Time restrictions on broadcast advertising and prohibition on advertising near schools or religious institutions may be implemented as regulations mature. Operators should anticipate increased scrutiny of bonus offers, wagering requirements, and promotional terms as player protection emphasis grows.

Recent Regulatory Changes and Their Impact

The December 2024 enactment of Law No. 2024-34 (Finance Law 2025) represents the most significant regulatory development in Benin’s gambling sector. This legislation introduced the first comprehensive taxation framework for both land-based and online gambling, marking Benin’s formal recognition of digital gambling.

The 10% levy on land-based casino turnover and 25% tax on online gambling winnings took effect January 1, 2025. These rates position Benin in the mid-to-high range for African gambling taxation, potentially impacting operator margins and market competitiveness versus unlicensed offshore alternatives.

In March 2023, the government announced development of a digital monitoring system to enhance regulatory oversight. This platform will track gambling activities in real-time, verify tax compliance, block illegal operators, and strengthen player protections including age verification and responsible gambling controls.

The Gaming Sector Supervisory Unit (Cellule de Supervision du Secteur des Jeux, CSJ) has increased collaboration with regional partners to modernize regulation. A November 2024 exchange with Liberia’s National Lottery Authority focused on best practices for security, compliance, and integrity in evolving gaming markets.

Enforcement Mechanisms and Penalties

Enforcement of gambling regulations in Benin faces significant challenges particularly regarding unlicensed online operators. The National Lottery Authority holds responsibility for compliance oversight but resource constraints limit effectiveness against sophisticated international operators.

The rise of unlicensed gambling venues operating without tax payments and often offering larger payouts undermines legal operators and complicates regulatory efforts. Experts call for stricter laws and increased enforcement resources to establish fair competitive environment.

Penalty structures for non-compliance include fines, license suspension, and license revocation. Criminal penalties may apply for operating without licenses or facilitating money laundering. The planned digital monitoring system will enhance enforcement capabilities through ISP blocking of unlicensed websites.

Payment processor restrictions represent another enforcement tool. Blocking financial transactions to unlicensed operators can effectively limit their market access. Implementation of comprehensive payment monitoring through the digital platform will strengthen this enforcement approach.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

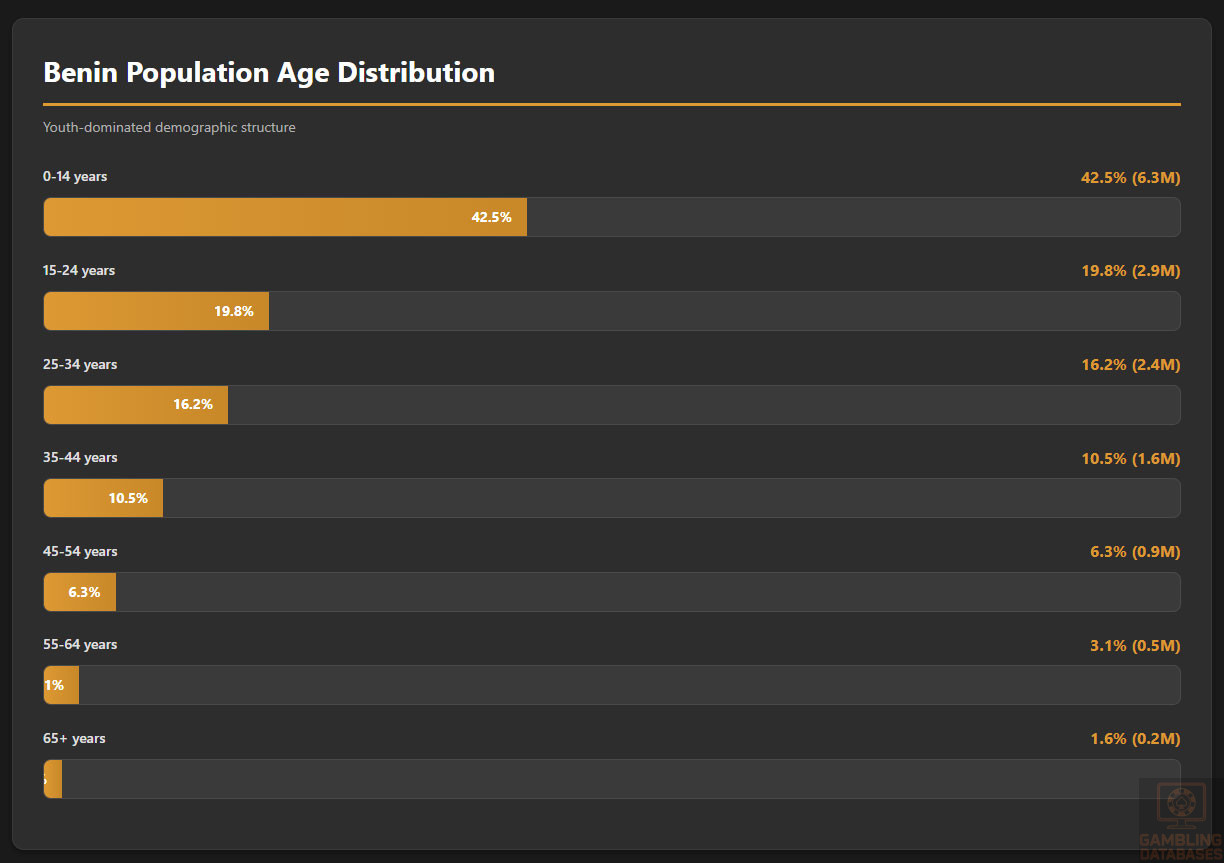

| Age Group | Percentage | Population (millions) |

|---|---|---|

| 0-14 years | 42.5% | 6.3 |

| 15-24 years | 19.8% | 2.9 |

| 25-34 years | 16.2% | 2.4 |

| 35-44 years | 10.5% | 1.6 |

| 45-54 years | 6.3% | 0.9 |

| 55-64 years | 3.1% | 0.5 |

| 65+ years | 1.6% | 0.2 |

Benin’s population reached 14.8 million in 2025 with robust annual growth of 2.69%. The extremely young demographic profile shows a median age of just 18 years, creating a pyramid-shaped age distribution characteristic of developing nations with high fertility rates.

The youth-dominated population structure presents both opportunities and challenges for iGaming operators. While 42.5% of the population remains under legal gambling age of 21, the large 15-34 age cohort of 5.3 million represents the core target demographic for digital gambling services.

Gender distribution shows relative balance with 974 males per 1,000 females. Life expectancy averages 61.2 years though this is improving with healthcare access expansion. The high dependency ratio of 90.1% means each working person must support themselves plus nearly one dependent.

Geographic Distribution

Urbanization reached 47.76% in 2025 with 7.1 million people living in cities. Urban population concentration facilitates internet infrastructure deployment and creates density for land-based gambling venues. The largest city Cotonou serves as the economic hub and primary market for gambling operations.

Major urban centers include Cotonou (largest city), Porto-Novo (capital), Parakou, Djougou, and Bohicon. These cities account for the majority of internet users, mobile banking adoption, and disposable income necessary for gambling participation. Rural areas lag significantly in connectivity and economic development.

Regional economic differences are pronounced with southern coastal regions significantly wealthier than northern areas. Internet access geographic patterns closely mirror economic development with urban southern regions showing penetration rates approaching developed markets while rural north remains largely offline.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

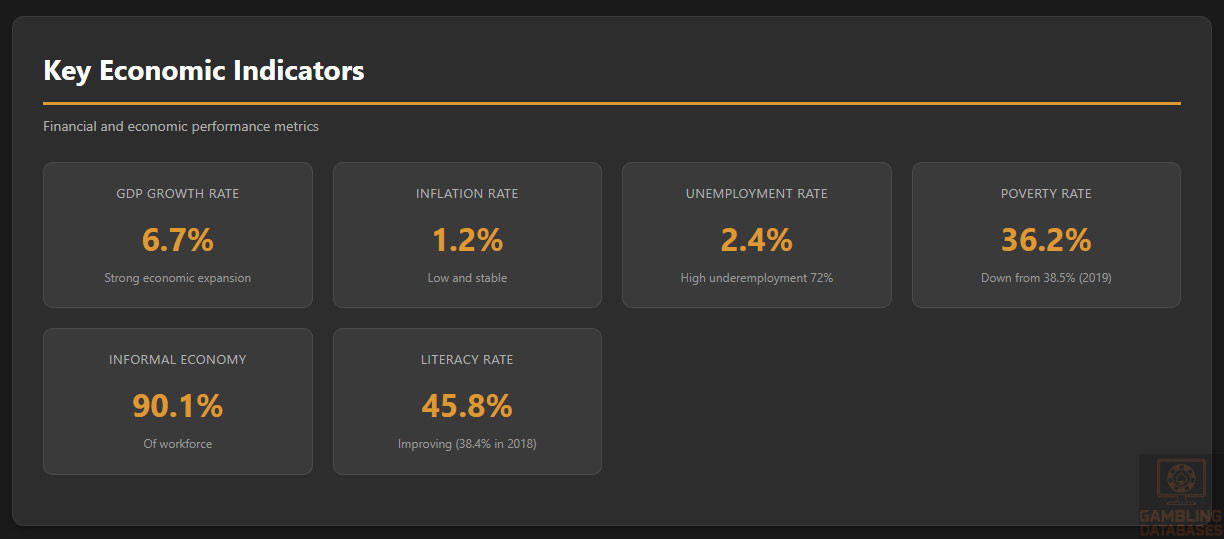

Benin’s economy demonstrated strong resilience with 6.7% GDP growth in 2024, up from 6.4% in 2023. Total GDP reached $21.5 billion positioning Benin as a small but growing West African economy. Per capita GDP of $1,485 USD places the country among lower-income nations globally.

Economic growth is projected to stabilize at 6.2% annually between 2024-2026, averaging 3.5% per capita growth. Growth drivers include the Glo-Djigbé Industrial Zone expansion, agricultural sector performance, and services sector resilience. The economy recovered strongly from COVID-19 impacts.

Inflation moderated significantly to 1.2% in 2024 from 2.8% in 2023, driven by lower energy and transport costs. Price stability enhances consumer purchasing power and creates favorable environment for discretionary spending including entertainment and gambling activities.

| Indicator | Value | Notes |

|---|---|---|

| GDP (2024) | $21.5 billion | 7.5% growth |

| GDP per Capita | $1,485 USD | 10% of world average |

| Agriculture % of GDP | ~25% | Cotton dominant export |

| Services % of GDP | ~52% | Growing sector |

| Industry % of GDP | ~23% | Light manufacturing |

| Unemployment Rate | 2.4% | High underemployment 72% |

| Informal Economy | 90.1% | Of workforce |

| National Poverty Rate | 36.2% | Down from 38.5% in 2019 |

Income and Wealth Distribution

Average household income remains modest with significant inequality. The informal economy dominates employment at 90.1% of the workforce, limiting formal income documentation and tax revenue collection. Cotton accounts for 40% of GDP and 80% of official exports, creating economic vulnerability to commodity price fluctuations.

Disposable income for gambling activities concentrates among urban middle-class and affluent populations. The poverty rate of 36.2% means a substantial portion of the population focuses on basic needs rather than discretionary entertainment spending. However, poverty has declined from 38.5% in 2018-2019.

The emerging middle class represents the key target demographic for iGaming operators. While small compared to total population, this segment shows growing disposable income, technology adoption, and openness to modern entertainment options including online gambling.

Market Size and Growth Projections

Benin’s iGaming market remains in early development with limited comprehensive revenue data. The government’s $25 million annual tax revenue target from gambling suggests gross wagering in the range of $100-250 million depending on tax calculation methodologies and compliance rates.

Historical market growth is difficult to quantify due to lack of regulation and data collection for online activities. Most online gambling occurs through unlicensed international operators making revenue estimation challenging. The introduction of formal regulation and taxation aims to capture and measure this activity.

Growth projections are highly speculative but favorable demographics, increasing internet penetration, and smartphone adoption suggest strong potential. Conservative estimates project market growth of 15-25% annually over the next 3-5 years as regulation formalizes and licensed operators enter.

The market split between online and land-based gambling heavily favors land-based activities currently due to limited internet access and regulatory uncertainty. As digital infrastructure improves and online regulation clarifies, the split will likely shift toward online channels matching regional trends.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy rates in Benin remain low at 45.8% as of 2021, up from 38.4% in 2018. This represents significant improvement but still falls below the sub-Saharan African average of 65.4% and least developed countries average of 62.7%.

Education completion rates show concerning patterns with many children not completing primary education. Secondary and tertiary education access remains limited particularly for rural populations and girls. The government has prioritized education investment including digital skills initiatives.

French serves as the official language and medium of education though many ethnic languages are spoken locally. English language proficiency is limited, presenting challenges for international operators but opportunities for French-language focused market entry strategies.

Cultural and Social Factors

Communication and Language

French dominates official communications, business, and education as Benin’s colonial language. However, local languages including Fon, Yoruba, Bariba, and Dendi are widely spoken in daily life. Gambling operators must provide French-language services at minimum with local language support enhancing accessibility.

Internet language preferences overwhelmingly favor French for formal content though social media shows mixing of French and local languages. International operators entering the market should prioritize French localization for all customer-facing materials, support channels, and regulatory communications.

Mobile communication dominates with SMS, WhatsApp, and voice calls serving as primary contact methods. Customer support strategies should emphasize mobile-friendly channels including click-to-call, WhatsApp support, and SMS notifications rather than email-heavy approaches.

Cultural Attitudes

Gambling acceptance in Beninese society is mixed with traditional lottery participation widely accepted while casino gambling carries more stigma. Religious influences vary with Christianity (48.5% of population), Islam (27.7%), and traditional Vodun religion (11.6%) all present and shaping attitudes.

Islamic communities generally oppose gambling on religious grounds though enforcement of prohibitions varies. Christian denominations show mixed attitudes with some viewing gambling as harmless entertainment and others condemning it. Traditional religions often incorporate elements of chance and divination.

Foreign brand perception in Benin is generally positive with international products and services associated with quality and modernity. However, trust must be earned through consistent service, secure payment processing, and transparent operations. Local partnerships can accelerate trust building.

Risk tolerance indicators suggest cautious approach to major financial decisions but willingness to participate in lottery-style gambling with small stakes. The popularity of lottery products reflects preference for low-cost participation with life-changing jackpot potential versus consistent small-stake betting.

Problem Gambling and Social Considerations

Comprehensive data on gambling addiction prevalence in Benin is lacking due to limited research and historical lack of regulatory focus on problem gambling. As gambling regulation evolves, social impact assessment and player protection will likely increase in priority.

Government response measures focus primarily on taxation and revenue generation currently. The planned digital monitoring system includes player protection objectives such as preventing underage gambling and promoting responsible gambling, though specific programs and treatment facilities remain underdeveloped.

Operators entering the market should proactively implement responsible gambling tools including deposit limits, self-exclusion options, and reality checks. Mandatory contributions to problem gambling funds may be introduced as regulations mature following patterns in more developed markets.

Social responsibility requirements for operators will likely expand as the regulatory framework develops. Proactive commitment to player protection can provide competitive advantages and position operators favorably with regulators while emerging regulations are established.

Political Structure and Governance

Benin operates as a democratic republic with President Patrice Talon elected in 2016 and re-elected in subsequent elections. The January 2023 legislative elections saw government-supporting parties win 81 of 109 National Assembly seats with main opposition party Les Démocrates holding 28 seats.

Political stability has improved significantly since the transition to democratic government in 1990. The regulatory environment shows increasing consistency though bureaucratic processes can be slow. The government prioritizes economic development and revenue generation supporting business-friendly reforms.

Corruption perception remains a concern though improvement efforts are ongoing. Operators should expect some bureaucratic challenges and ensure compliance with anti-bribery regulations in all interactions with government officials. Transparency in licensing processes varies by ministry and regulatory body.

International relations with neighboring Nigeria significantly impact business environment due to border trade dynamics. Benin is a member of the West African Economic and Monetary Union and Economic Community of West African States, facilitating regional economic integration.

Technology Adoption and Digital Behavior

Internet and Digital Usage

| Metric | Value | Growth/Comparison |

|---|---|---|

| Internet Users | 4.69 million | +2.7% YoY (123,000 users) |

| Internet Penetration | 33.8% | Below SSA average 39.3% |

| Offline Population | 9.20 million (66.2%) | Significant growth opportunity |

| Mobile Connections | 14.78 million | 106.4% of population |

| Mobile Internet Users | 11.7 million subscriptions | 64.25% adoption rate |

| Unique Mobile Internet Users | ~7 million (55.4%) | After multi-SIM adjustment |

| Regular Mobile Internet Users | 3.8 million (28%) | 48% of adults |

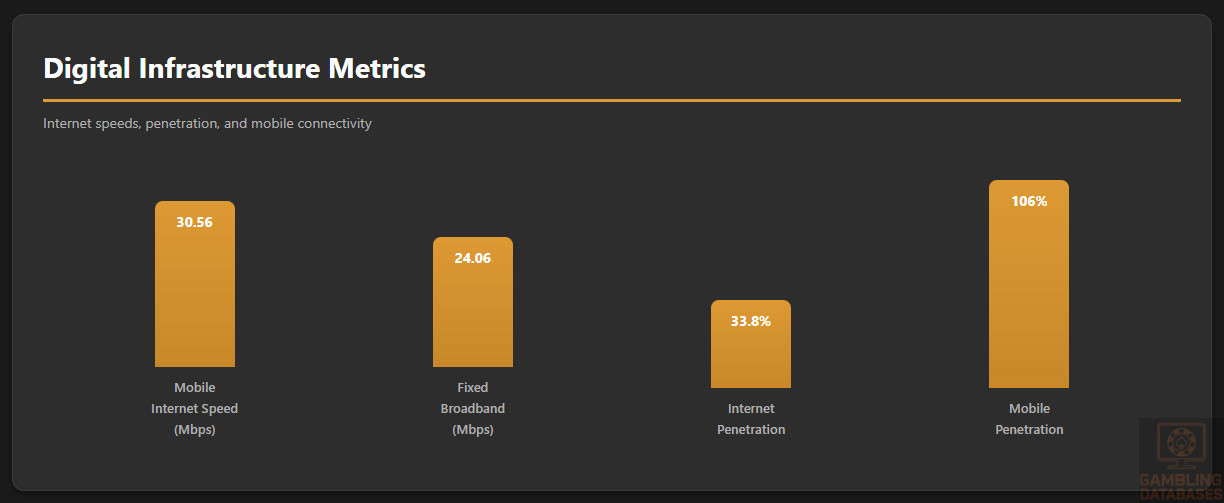

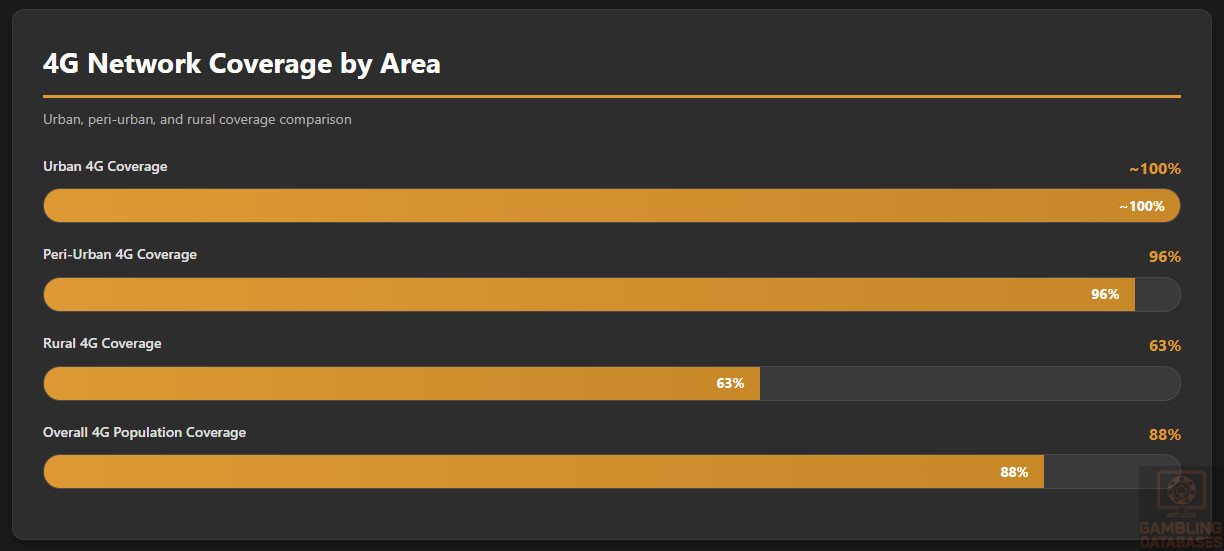

| 3G/4G Coverage | 90% of population | Above West Africa 77% average |

| 4G Coverage | 88% of population | Up from 62% three years prior |

| Social Media Users | 2.15 million | 15.5% penetration |

Internet penetration of 33.8% positions Benin below regional averages but shows steady growth. The gap between network coverage and actual usage represents significant opportunity. While 90% of the population has access to high-speed mobile networks, only 55.4% are unique internet users.

Daily internet usage hours and detailed behavior patterns are not comprehensively documented. However, mobile devices dominate internet access with smartphones serving as primary or only internet-enabled devices for most users. Desktop and laptop penetration remains extremely low outside business environments.

Social media engagement focuses primarily on Facebook and WhatsApp with Instagram and TikTok growing among younger urban users. X (formerly Twitter) shows minimal penetration. Social media usage concentrates in the 15-34 age demographic with engagement rates declining sharply in older populations.

E-commerce participation remains limited but growing. Only a small percentage of internet users regularly purchase goods or services online due to payment infrastructure limitations, trust concerns, and preference for physical inspection of goods before purchase.

Digital Payment Behavior

Digital payment adoption reached 37.9% in 2017, above the sub-Saharan Africa average of 34.2%. Mobile money services through MTN Mobile Money and other providers dominate digital payments due to low bank account penetration and mobile network ubiquity.

Payment method preferences strongly favor mobile money for small-value transactions with bank transfers used for larger amounts. Credit card penetration is minimal with most cards being debit cards linked to bank accounts. International payment methods like PayPal have limited adoption.

Online banking penetration lags behind mobile money with banks focused on serving businesses and higher-income individuals. The unbanked and underbanked populations rely heavily on mobile money, cash, and informal financial services for daily transactions.

Cryptocurrency adoption for gambling remains negligible in Benin. Regulatory clarity on cryptocurrency is limited and most consumers lack understanding of digital assets. Mobile money and bank transfers will dominate gambling payment methods for the foreseeable future.

Gaming and Gambling Preferences

Current Market Participation

Comprehensive data on gambling participation rates in Benin is not publicly available due to the market’s early development stage. Lottery participation is widely accepted with the National Lottery selling tickets through physical retail networks reaching rural and urban areas.

Sports betting has grown significantly in recent years particularly among young urban males. Football dominates betting interest with major European leagues, African competitions, and local matches attracting wagers. Basketball and tennis generate secondary interest.

Online gambling participation occurs primarily through unlicensed international operators. Players access offshore sports betting sites and online casinos despite lack of local regulation. Payment processing through international methods or cryptocurrency enables this cross-border activity.

Casino games show limited traction in the mass market with physical casinos serving primarily tourists and affluent locals. Online casino games may find broader appeal if marketed effectively to younger digital-native demographics with appropriate low minimum stakes.

Consumer Behavior Patterns

Average spending per player data is unavailable for Benin specifically. However, low GDP per capita and income levels suggest very modest average stakes compared to developed markets. Successful operators will need to accommodate micro-transactions and low minimum deposits.

Mobile device usage for gambling will dominate due to smartphone penetration far exceeding desktop/laptop availability. Platform preferences strongly favor mobile-optimized websites and dedicated mobile applications. Desktop gambling will remain niche among office workers and internet café users.

Peak gambling times likely align with major sporting events, evening hours after work, and weekends. Football match scheduling significantly influences sports betting activity. Lottery ticket sales spike around major draws and when jackpots grow large.

Retention and loyalty patterns in emerging markets typically show higher churn rates than mature markets. Players often maintain accounts with multiple operators and chase bonuses. Building loyalty requires competitive promotions, reliable payment processing, and excellent mobile experience.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

| Metric | Value | Global Ranking/Notes |

|---|---|---|

| Fixed Broadband Download Speed | 24.06 Mbps (median) | Ranked 133rd globally |

| Fixed Broadband Upload Speed | 9.7 Mbps | Ranked 140th globally |

| Mobile Internet Speed | 30.56 Mbps (median) | Faster than fixed broadband |

| Fixed Broadband Penetration | ~0% | Negligible household adoption |

| Fixed Broadband Growth (2023-2024) | +65.4% speed increase | +9.51 Mbps improvement |

| Urban 4G Coverage | Nearly 100% | Universal in cities |

| Peri-Urban 4G Coverage | 96% | Strong suburban coverage |

| Rural 4G Coverage | 63% | Improving but gaps remain |

Internet infrastructure in Benin shows significant urban-rural divide. Cities enjoy nearly universal 4G coverage with reliable mobile internet while rural areas lag with 63% coverage and lower speeds. This geographic disparity concentrates gambling market opportunity in urban centers.

Mobile internet outperforms fixed broadband in both speed and accessibility. The 30.56 Mbps median mobile speed exceeds fixed broadband’s 24.06 Mbps, reinforcing mobile-first strategy necessity. Fixed broadband remains essentially non-existent for consumers outside business and institutional users.

Network reliability has improved with major infrastructure investments by mobile operators. Uptime statistics are not comprehensively published but anecdotal reports suggest increasing stability particularly in major cities. Rural areas experience more frequent outages and coverage gaps.

The government launched a national fiber optic backbone network project in 2020 with World Bank and African Development Bank support. This infrastructure aims to improve broadband connectivity and reduce costs, though benefits will take years to fully materialize for end consumers.

5G and Future Technology Deployment

5G networks are not yet deployed in Benin as of 2024. The country focuses on expanding and optimizing 4G coverage which grew dramatically from 62% to 88% population coverage in just three years. This represents appropriate prioritization given the large offline population.

4G coverage expansion continues as the primary network development focus. The 90% population coverage for 3G/4G combined exceeds West Africa’s 77% average, positioning Benin relatively well for a lower-income country. However, the usage gap between coverage and actual adoption requires addressing.

Future infrastructure plans emphasize increasing internet affordability and device accessibility rather than advanced network technologies. The government recognizes that high data costs and smartphone prices represent primary barriers to internet adoption more than network availability.

Mobile Technology Ecosystem

Mobile Network Infrastructure

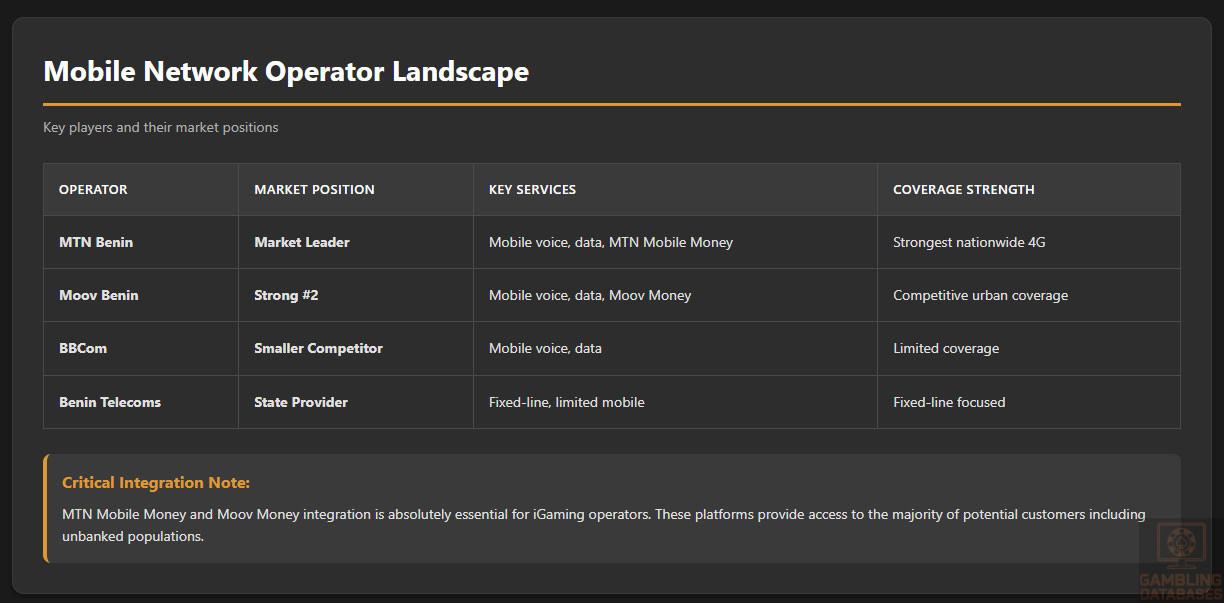

Benin’s mobile market features multiple operators with MTN holding market leadership. Moov ranks as the second-largest operator with BBCom and Benin Telecoms also active. Competition among operators has driven coverage expansion and price competition benefiting consumers.

Network operator market share data is not comprehensively published but MTN’s dominance is widely recognized. All major operators offer mobile money services integrated with their networks, creating payment infrastructure essential for gambling transactions.

Data costs remain significant barrier to internet adoption despite declining prices. The average monthly budget for mobile phone service was $11.20 in 2024. For a population with GDP per capita of $1,485, this represents substantial portion of income limiting discretionary data usage.

Mobile payment integration through operator-owned mobile money services is excellent. MTN Mobile Money penetration is particularly high. Gambling operators can integrate directly with these services for deposits and withdrawals, providing familiar payment methods to users.

Device Penetration

Smartphone adoption rates continue growing though exact penetration figures vary by source. The 14.78 million mobile connections against 7 million unique internet users suggests substantial smartphone penetration among internet users. However, basic feature phones remain common particularly in rural areas.

Device preferences favor budget Android smartphones from Chinese manufacturers including Tecno, Infinix, Itel, and Samsung. These brands offer affordable smartphones priced for emerging market consumers. Apple iOS devices remain luxury items with minimal market share.

Android dominates the smartphone market with estimates suggesting 85%+ share. This concentration simplifies mobile app development priorities. iOS app development can be deprioritized initially with Android-first or Android-only approaches appropriate for market entry.

Average device specifications skew toward entry-level with limited RAM, storage, and processing power. Gambling platforms must be optimized for low-end devices with efficient data usage, small app sizes, and minimal hardware requirements to maximize addressable market.

Financial Services and Payment Infrastructure

Banking System Structure

Benin’s banking sector underwent consolidation and privatization in the 1990s creating a shallow but functional financial system. Major banks include international institutions and regional West African banks with limited indigenous banks. The sector serves primarily businesses and higher-income individuals.

Account penetration rates remain low with majority of population unbanked. Exact figures are not current but estimates suggest less than 30% of adults hold formal bank accounts. This low bankarization creates both challenge and opportunity for gambling operators.

Digital banking adoption among account holders is growing with mobile banking apps and internet banking available from major banks. However, usage concentrates among urban professionals and businesses. Mobile money far exceeds bank-based digital payments in transaction volume.

No customer deposit insurance system exists, potentially contributing to limited trust in banking sector. The lack of deposit protection emphasizes importance of bank selection and diversification for operators managing large float balances.

Payment Processing Options

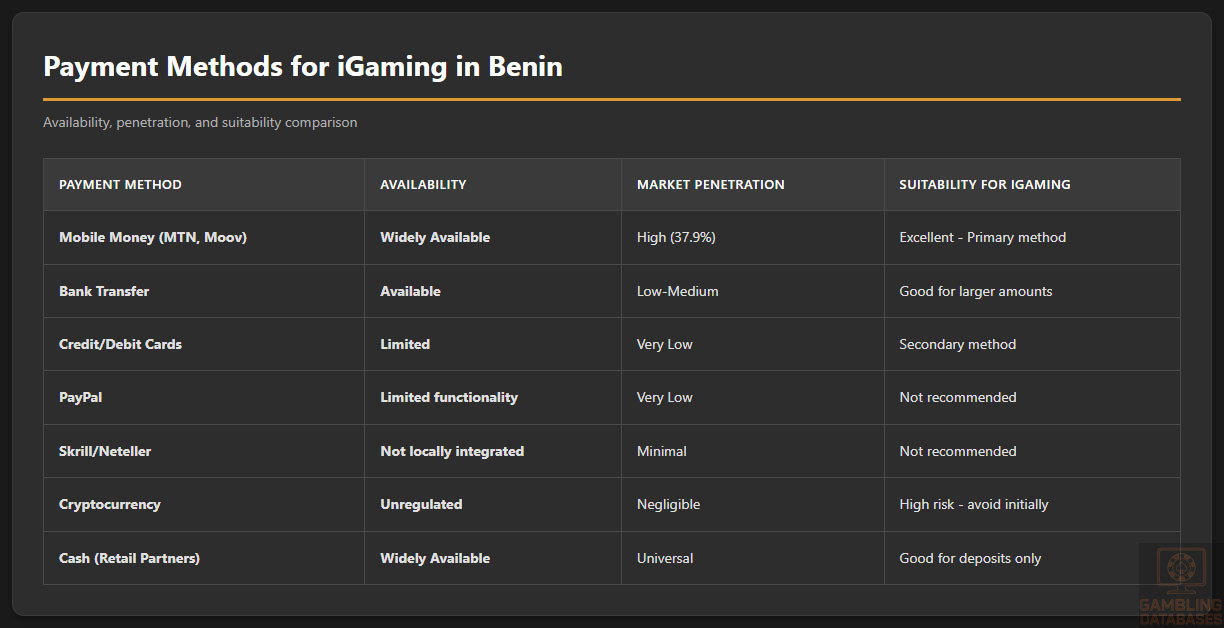

| Payment Method | Availability | Penetration | Suitability for iGaming |

|---|---|---|---|

| Mobile Money (MTN, Moov) | Widely available | High (37.9% digital payment adoption) | Excellent – Primary method |

| Bank Transfer | Available | Low-Medium (limited bank accounts) | Good for larger amounts |

| Credit/Debit Cards | Limited | Very Low | Secondary method |

| PayPal | Limited functionality | Very Low | Not recommended |

| Skrill/Neteller | Not locally integrated | Minimal | Not recommended |

| Cryptocurrency | Unregulated | Negligible | High risk – avoid initially |

| Cash (Retail Partners) | Widely available | Universal | Good for deposits only |

Mobile money represents the essential payment method for gambling operators in Benin. Integration with MTN Mobile Money and Moov Money enables serving the majority of potential customers including unbanked populations. These services offer instant deposits and fast withdrawals familiar to users.

Bank transfers serve as secondary payment method for customers with bank accounts and larger transaction amounts. SWIFT and regional WAEMU transfer systems function adequately though processing times can be slow. Real-time transfers within Benin through domestic payment systems exist but adoption is limited.

International payment processors like PayPal, Skrill, and Neteller have minimal penetration in Benin and should not be prioritized for market entry. These services face regulatory restrictions and limited local currency support making them impractical for mass market.

Processing fees vary by method with mobile money typically charging 1-5% depending on transaction size. Bank transfers carry fixed fees making them more economical for larger amounts. Operators should absorb deposit fees while potentially passing withdrawal fees to customers following local market norms.

E-commerce and Digital Economy

Digital Market Development

E-commerce market size in Benin remains small but growing. The UNCTAD B2C E-commerce Index ranked Benin 100th of 152 countries in 2019, up from 108th in 2018. The score of 36.6 out of 100 indicates significant development needs in internet use, secure servers, payments, and postal reliability.

Online retail penetration as percentage of total retail is minimal with most commerce occurring through physical channels. Trust in online transactions is gradually building but cash-on-delivery and physical inspection preferences dominate consumer behavior.

Popular e-commerce platforms are primarily international services including Jumia Africa and informal Facebook/WhatsApp-based commerce. Local e-commerce platforms exist but lack scale. Cross-border online shopping from China through platforms like AliExpress shows growing adoption.

Digital goods and services consumption focuses on mobile airtime, data bundles, mobile money transfers, and increasingly music/video streaming. These micro-transaction models trained consumers on digital payments creating foundation for gambling transactions.

Business Environment and Regulatory Framework

Ease of Business Operations

The World Bank discontinued its Doing Business report in 2021 following data integrity concerns. The last published rankings showed Benin in moderate positions for business environment though specific scores are outdated and should not be relied upon for current decision-making.

The replacement Business Ready (B-READY) framework launched in October 2024 but does not yet cover Benin comprehensively. Anecdotal evidence suggests business registration processes are improving with online systems reducing bureaucratic barriers though implementation remains inconsistent.

Foreign investment policies are generally welcoming with the government seeking to attract capital and expertise. Special economic zones including the Glo-Djigbé Industrial Zone offer incentives though applicability to gambling operations is unclear. Investors should clarify incentive eligibility early in planning.

Operational cost structures vary significantly between urban and rural areas. Office rent in Cotonou is moderate by regional standards while utilities including electricity can be unreliable requiring backup generators. Labor costs are relatively low though skilled technical talent is limited.

Corporate Structure and Registration

Available Entity Types

| Entity Type | Minimum Capital | Liability | Suitability for iGaming |

|---|---|---|---|

| SARL (LLC) | 1 million XOF (~$1,650) | Limited | Suitable for local operations |

| SA (Corporation) | 10 million XOF (~$16,500) | Limited | Preferred for larger operations |

| Branch Office | Varies | Parent company liable | Possible but less common |

| Representative Office | N/A | Parent company liable | Not suitable for operations |

Limited liability companies (SARL) suit small to medium operations with minimum capital of approximately $1,650. Corporations (SA) require higher minimum capital around $16,500 but provide structure appropriate for regulated gambling operations attracting investor capital.

Most foreign gambling operators should establish SA corporations to demonstrate substance and commitment to regulators. The higher capitalization requirement is modest relative to gambling license costs and signals serious market entry intent versus minimal compliance approaches.

Registration Requirements

Business registration timelines have improved with online systems reducing delays. Registration can be completed in 2-4 weeks for standard entity types though gambling-specific approvals add months to overall market entry timeline. The UNCTAD noted assistance helping Benin move registration online during COVID-19.

Registration costs include government fees, legal fees, and notarization charges totaling approximately $500-2,000 for standard entities. Gambling operations should budget significantly higher for specialized legal counsel to navigate licensing requirements and regulatory compliance.

Required documents include articles of incorporation, shareholder information, beneficial ownership declarations, registered office address proof, and director identification. Notarization requirements add time and cost. All documents must be in French or officially translated.

Foreign ownership is generally permitted at 100% though gambling regulations may impose local partnership requirements. Operators should clarify ownership restrictions during licensing discussions. Local directors may be required with at least one director resident in Benin.

Taxation Framework

Corporate Income Tax Structure

| Tax Type | Rate | Application |

|---|---|---|

| Corporate Income Tax | 30% | On net taxable profits |

| Branch Profit Tax | 30% | Same as corporate rate |

| Withholding Tax – Dividends | 10-15% | Depends on recipient jurisdiction |

| Withholding Tax – Interest | 10-15% | Varies by agreement |

| Withholding Tax – Royalties | 15-20% | On gross payments |

| VAT/GST | 18% | Applicability to gambling varies |

Corporate income tax at 30% applies to net profits after gambling-specific taxes and allowable deductions. The rate is standard for WAEMU member states. International tax treaties may provide relief from double taxation though Benin’s treaty network is limited.

VAT at 18% applicability to gambling services requires specific tax ruling. Some jurisdictions exempt gambling from VAT while others apply it to fees or services. Operators must obtain definitive guidance from tax authorities on VAT obligations before launching.

Transfer pricing rules apply to related-party transactions requiring arm’s length pricing documentation. Gambling operators using offshore platforms, software licenses, or management services from related entities must maintain comprehensive transfer pricing documentation.

Personal Income Tax

Individual tax rates follow progressive brackets with top marginal rates around 35-40% though specific current brackets are not publicly detailed. Withholding requirements apply to employee salaries with employers responsible for monthly tax remittance.

Social security contributions include employer and employee portions totaling approximately 20-25% of gross salary. Exact rates vary by category. These mandatory contributions cover pensions, health insurance, and employment injury insurance.

Tax residency rules determine liability with residents taxed on worldwide income and non-residents taxed only on Benin-source income. Foreign employees may face taxation in both Benin and home countries requiring careful tax planning.

Market Entry Considerations

Recommended Entry Strategies

Optimal market entry requires establishing licensed local operations rather than serving customers from offshore jurisdictions. The 2025 taxation framework and planned digital monitoring system signal government intent to regulate and tax all operators serving Beninese customers.

Local partnerships with experienced Beninese business people can accelerate market entry and navigate regulatory complexities. Partners should bring government relationships, local market knowledge, and operational capabilities rather than passive investment only.

White label platforms offer faster market entry than building proprietary technology but reduce differentiation and create ongoing dependency. For emerging markets like Benin, white label approaches can minimize initial investment while testing market viability before larger commitments.

Payment provider integration with MTN Mobile Money and Moov Money is absolutely essential. Operators should establish these relationships early as they determine operational feasibility. Multiple payment options provide redundancy against individual provider issues.

Typical Costs and Timelines

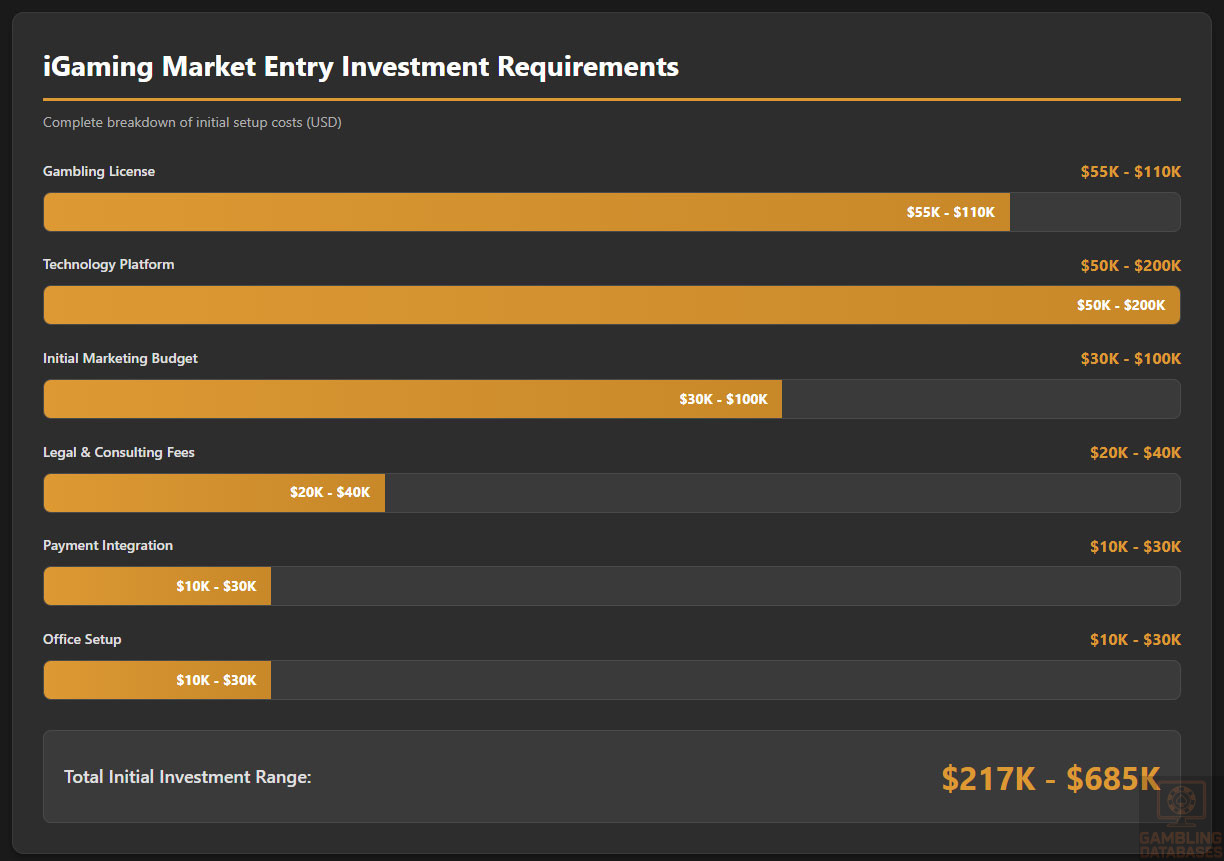

| Cost Category | Estimated Amount (USD) | Notes |

|---|---|---|

| Gambling License | $55,000 – $110,000 | Varies by license type |

| Legal and Consulting Fees | $20,000 – $40,000 | For licensing process |

| Company Registration | $1,000 – $3,000 | Including legal fees |

| Initial Capital Requirement | $17,000+ | For SA corporation minimum |

| Office Setup (Annual) | $12,000 – $36,000 | Rent, furniture, equipment |

| Technology Platform | $50,000 – $200,000 | White label vs proprietary |

| Payment Integration | $10,000 – $30,000 | Setup and initial float |

| Initial Marketing Budget | $50,000 – $150,000 | First 6-12 months |

| Total Initial Investment | $215,000 – $569,000 | Minimum to full-scale entry |

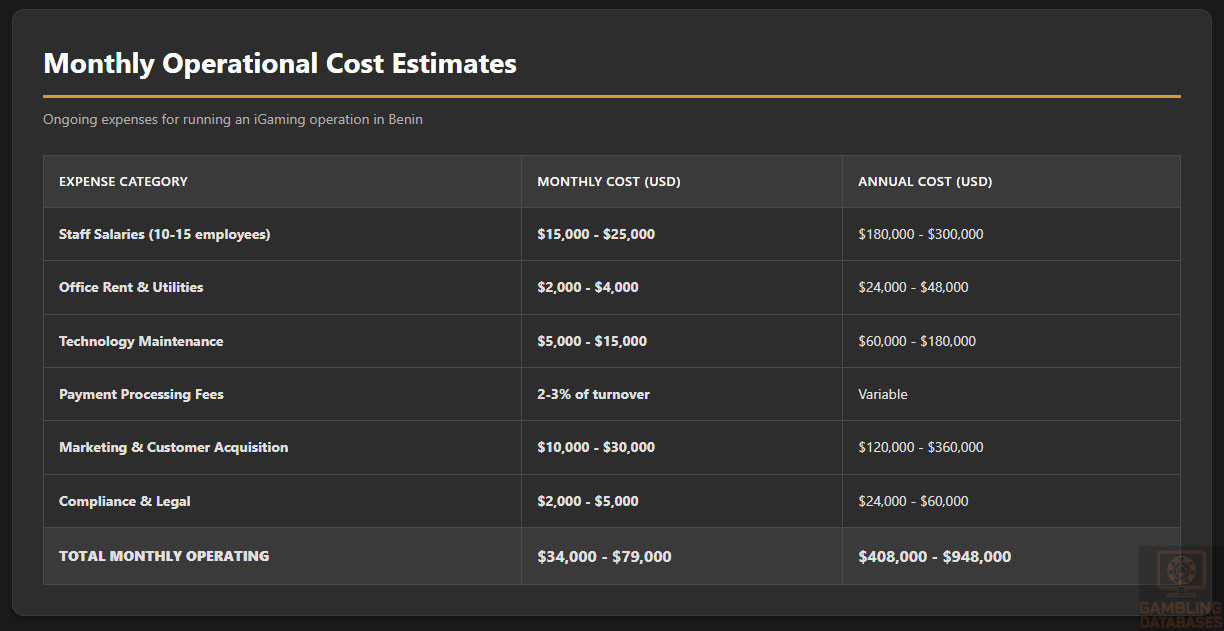

| Expense Category | Monthly Cost (USD) | Annual Cost (USD) |

|---|---|---|

| Staff Salaries (10-15 employees) | $8,000 – $15,000 | $96,000 – $180,000 |

| Office Rent and Utilities | $1,000 – $3,000 | $12,000 – $36,000 |

| Technology and Platform Fees | $5,000 – $15,000 | $60,000 – $180,000 |

| Payment Processing Fees | Variable (2-5% of volume) | Depends on turnover |

| Marketing and Acquisition | $8,000 – $25,000 | $96,000 – $300,000 |

| Regulatory Compliance | $2,000 – $5,000 | $24,000 – $60,000 |

| Total Monthly Operating | $24,000 – $63,000 | $288,000 – $756,000 |

| Phase | Duration | Key Activities |

|---|---|---|

| Company Registration | 2-4 weeks | Entity formation, bank account opening |

| License Application Preparation | 4-8 weeks | Documentation, technical specs, compliance frameworks |

| License Application Review | 3-6 months | Regulatory review, due diligence, clarifications |

| Platform Setup and Integration | 2-4 months | Technology deployment, payment integration, testing |

| Pre-Launch Marketing | 1-2 months | Brand building, partnership development |

| Total Time to Market | 8-16 months | Parallel activities can compress timeline |

Resource Requirements

Minimum staff headcount for viable operations ranges from 10-15 employees covering management, customer support, compliance, finance, marketing, and technology. Key positions include General Manager, Compliance Officer, Finance Manager, Customer Support Lead, and Marketing Manager.

Customer support requires French-speaking staff available during peak hours covering evenings and weekends. WhatsApp and phone support capabilities are essential with email support secondary. Outsourcing to specialized call centers can reduce costs.

Technology stack requirements depend on white label versus proprietary approaches. White label solutions include hosting, platform, and payment integration reducing technical staff needs. Proprietary development requires significant technical team or offshore development partnerships.

Success Factors and Challenges

Key Success Enablers

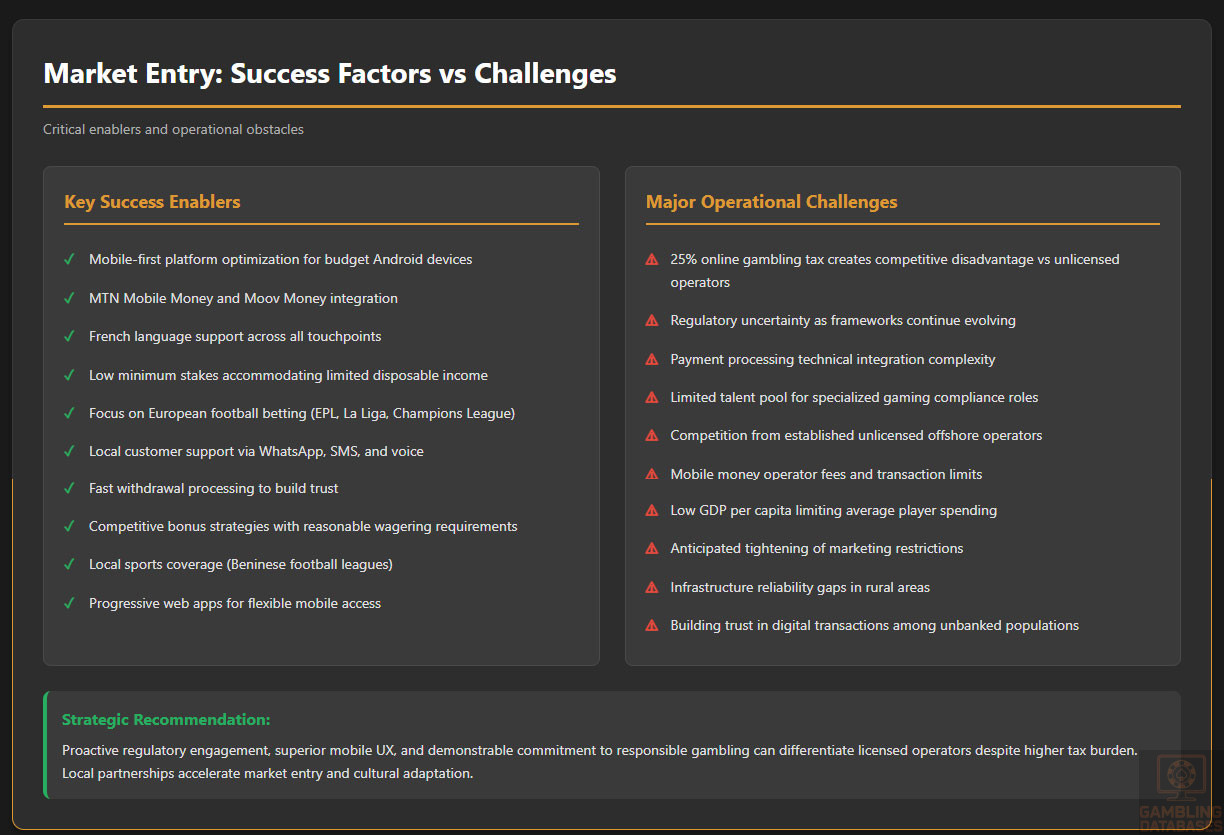

Understanding local player preferences is critical with focus on football betting, low minimum stakes, mobile optimization, and simple user interfaces. French language throughout all customer touchpoints is mandatory with local language support beneficial.

Mobile-first approach cannot be overstated with the vast majority of users accessing gambling exclusively via smartphones. Platforms must work flawlessly on budget Android devices with slow connections and limited data budgets.

Competitive bonus and promotion strategies must balance acquisition costs with player lifetime value. Micro-deposit bonuses attract users with limited funds while reasonable wagering requirements enable withdrawals building trust and word-of-mouth marketing.

Local sports and events coverage particularly Beninese football leagues creates differentiation versus international operators. Partnerships with local sports media and influencers can accelerate brand building and customer acquisition.

Major Operational Challenges

Regulatory compliance complexity will increase as frameworks formalize. Early entrants face uncertainty but can shape regulations through constructive regulator engagement. Compliance costs and ongoing obligations will rise requiring dedicated resources.

The 25% tax on online gambling winnings represents significant competitive disadvantage versus unlicensed offshore operators not collecting this tax. Licensed operators must offer superior service, security, and local payment methods to justify the tax burden.

Payment processing restrictions and mobile money integration challenges can delay implement responsible gambling measures including self-exclusion options, deposit limits, reality checks, and links to problem gambling resources. Mandatory contributions to problem gambling funds may be introduced as regulations mature following patterns in more developed markets.

Social responsibility requirements create market differentiation opportunities for operators demonstrating commitment to player welfare. Proactive implementation of responsible gambling tools positions operators favorably with regulators and builds consumer trust in emerging market.

Political Structure and Governance

Benin operates as a democratic republic with President Patrice Talon winning re-election through parties supporting him securing 81 of 109 parliamentary seats in January 2023 elections. The main opposition party Les Démocrates holds 28 seats, marking the opposition’s return after four-year absence.

Political stability has improved since the 1990 transition to democracy though concerns remain about democratic backsliding and civil liberties. The next general elections scheduled for 2026 will be governed by a new electoral code adopted in March 2024.

Corruption remains a concern with Benin ranking in the lower half of Transparency International’s Corruption Perceptions Index. Business operations require careful navigation of bureaucratic processes and relationship building with regulatory authorities to ensure smooth licensing and compliance.

Technology Adoption and Digital Behavior

Internet and Digital Usage

| Metric | Value | Year-over-Year Change |

|---|---|---|

| Internet Users | 4.69 million | +123,000 (+2.7%) |

| Internet Penetration | 33.8% | +0.7 percentage points |

| Mobile Connections | 14.78 million | N/A |

| Mobile Penetration | 106.4% | N/A |

| Social Media Users | 2.15 million | Revised methodology |

| Social Media Penetration | 15.5% | N/A |

| Mobile Internet Subscribers | 11.7 million | 64.25% of mobile users |

| 3G Subscribers | 6.8 million | N/A |

| 4G Subscribers | 4.4 million | Growing rapidly |

Internet penetration of 33.8% positions Benin slightly below the sub-Saharan African average of 39.3% but above the least developed countries average of 28.5%. The 66.2% of population remaining offline represents both challenge and opportunity as infrastructure expansion continues.

Daily internet usage patterns favor mobile access with smartphones serving as primary internet devices. Desktop and laptop usage remains limited to business and educational settings. E-commerce participation rates are growing but remain modest with 2019 B2C E-commerce Index ranking of 100th out of 152 countries.

Social media engagement centers on Facebook, WhatsApp, and increasingly TikTok among younger demographics. Platform preferences shift rapidly as new services gain popularity. Operators should monitor trending platforms for marketing and customer engagement opportunities.

Digital Payment Behavior

Payment method preferences strongly favor mobile money solutions over traditional banking products. MTN Mobile Money and Moov Money dominate the mobile payments landscape with widespread agent networks even in rural areas. Digital payment penetration reached 37.9% in 2017, above sub-Saharan African and least developed countries averages.

Credit card penetration remains very low with most consumers lacking access to traditional banking products. Debit card usage is growing slowly as bank account penetration increases but remains limited compared to mobile money adoption. This payment landscape requires operators to prioritize mobile money integrations.

Bank transfers are possible but cumbersome for most users due to limited banking access. Online banking penetration lags significantly behind mobile money adoption. E-wallets like PayPal, Skrill, and Neteller have minimal market presence due to regulatory restrictions and limited international payment corridor development.

Cryptocurrency adoption for gambling remains negligible due to regulatory uncertainty, limited technical knowledge, and preference for familiar payment methods. While some international operators accept cryptocurrency, local users show little interest or awareness of digital currency options.

Gaming and Gambling Preferences

Current Market Participation

Comprehensive gambling participation data for Benin is limited due to historical lack of market research and regulatory data collection. Lottery products attract the broadest participation across income levels with the National Lottery maintaining widespread recognition and accessibility through physical agent networks.

Sports betting has gained popularity particularly among young urban males interested in European football. International leagues including English Premier League, Spanish La Liga, and Champions League generate the highest betting volumes. Local and African football competitions also attract wagering interest.

Casino games remain niche products primarily accessed by higher-income urban residents. Online casino gaming through international operators is growing among tech-savvy younger demographics though overall participation remains low relative to sports betting and lottery products.

Consumer Behavior Patterns

Average spending per player data is not publicly available though anecdotal evidence suggests low average stakes reflecting limited disposable income. Lottery ticket purchases of small denominations dominate gambling expenditure patterns with occasional larger sports betting stakes among more engaged users.

Platform preferences strongly favor mobile access with limited desktop usage. The 106.4% mobile penetration rate versus 33.8% internet penetration indicates mobile-first internet access patterns. Operators must prioritize mobile-optimized experiences and native mobile applications.

Peak gambling times likely align with major sporting events, weekends, and evening hours after work. Local time zone considerations and African sporting event schedules should inform marketing timing and promotional strategies. Seasonal patterns around holidays and major tournaments create peaks in activity.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Benin’s internet infrastructure shows mixed performance with significant urban-rural divide. Fixed broadband remains limited with only 0.2% of population having dedicated high-speed connections. Mobile internet dominates connectivity with 3G and 4G networks covering approximately 90% of the population as of 2024.

Network performance varies significantly by location and operator. Median mobile internet speeds reached 30.56 Mbps in early 2024 according to Ookla data, sufficient for gambling applications. Fixed internet median speeds of 24.06 Mbps increased 65.4% year-over-year, showing rapid infrastructure improvements.

Network reliability in major cities is generally adequate though rural areas experience frequent outages and connectivity gaps. Infrastructure investment trends are positive with government prioritizing digital connectivity through the National Digital Strategy 2019-2025 and World Bank-supported fiber optic backbone deployment.

| Metric | Value | Global Ranking |

|---|---|---|

| Mobile Internet Speed | 30.56 Mbps | Mid-range for Africa |

| Fixed Broadband Speed | 24.06 Mbps | 133rd globally |

| Fixed Broadband Penetration | ~0.2% | Very low |

| 3G/4G Population Coverage | ~90% | Above West African average (77%) |

| 4G Population Coverage | 88% | Strong growth from 62% in 2021 |

| Urban 4G Coverage | ~100% | Nearly universal |

| Rural 4G Coverage | 63% | Improving |

5G and Future Technology Deployment

5G networks are not yet deployed in Benin as of 2024. The country focuses on expanding 4G coverage and improving existing network quality before transitioning to next-generation mobile technology. Regional 5G rollouts in larger African markets like Nigeria and South Africa will likely precede Benin deployment.

Future infrastructure plans emphasize fiber optic backbone expansion, improved international connectivity, and 4G network densification. The government launched a national fiber optic backbone project in 2020 with World Bank and African Development Bank support to improve broadband connectivity and reduce costs.

Timeline for 5G deployment remains uncertain though 2026-2028 represents realistic earliest introduction period. Operators should plan for 4G-based services for the medium term with mobile-optimized lightweight applications suited to moderate bandwidth constraints.

Mobile Technology Ecosystem

Mobile Network Infrastructure

The mobile telecommunications market features three primary operators: MTN Benin (market leader), Moov Benin (second-largest), and BBCom (smaller third player). Benin Telecoms operates as the state-owned fixed-line provider with limited mobile market presence.

MTN dominates the market with the largest subscriber base, widest network coverage, and strongest brand recognition. The operator provides extensive 4G coverage and operates MTN Mobile Money, the leading mobile payments platform. Moov competes aggressively on pricing and coverage, offering competitive mobile money services.

Network quality varies by operator and location with urban areas generally well-served by all operators. Rural coverage depends heavily on population density and economic activity with remote areas relying on 2G or 3G connectivity. Data costs have decreased significantly though remain expensive relative to income levels.

| Operator | Market Position | Key Services | Coverage Strength |

|---|---|---|---|

| MTN Benin | Market Leader | Mobile voice, data, MTN Mobile Money | Strongest nationwide 4G |

| Moov Benin | Strong #2 | Mobile voice, data, Moov Money | Competitive urban coverage |

| BBCom | Smaller Competitor | Mobile voice, data | Limited coverage |

| Benin Telecoms | State Provider | Fixed-line, limited mobile | Fixed-line focused |

Device Penetration

Smartphone adoption rates have grown rapidly though exact penetration figures vary by source. Estimates suggest 50-60% of mobile users own smartphones with adoption concentrated among urban, younger, and higher-income demographics. Feature phones remain prevalent particularly in rural areas and among older populations.

Android dominates the smartphone market with 85-90% market share. Budget Android devices from Chinese manufacturers including Tecno, Infinix, and Xiaomi lead sales due to affordability. iOS/iPhone usage remains limited to affluent consumers representing single-digit market share.

Average device specifications trend toward entry-level and mid-range smartphones with 2-4GB RAM, 32-64GB storage, and 720p-1080p displays. Operators should optimize applications for lower-specification devices to ensure broad compatibility and smooth performance.

Financial Services and Payment Infrastructure

Banking System Structure

Benin’s banking sector includes approximately 15-20 commercial banks with major institutions including Bank of Africa Benin, Ecobank Benin, and other regional banking groups. The sector underwent consolidation and privatization in the 1990s creating more stable and competitive banking environment.

Digital banking adoption grows among urban educated populations though overall bank account penetration remains low. Microfinance institutions play significant role with nearly 60% penetration of microfinance services according to 2003 Central Bank data, providing financial services to underbanked populations.

ATM density has improved in urban areas though rural access remains limited. Cash remains dominant payment method for everyday transactions with banking services concentrated in major cities. The formal banking sector serves primarily businesses and higher-income individuals.

Payment Processing Options

| Payment Method | Availability | Market Penetration | Suitability for iGaming |

|---|---|---|---|

| MTN Mobile Money | Widely Available | Very High | Essential – Primary method |

| Moov Money | Widely Available | High | Essential – Secondary method |

| Bank Transfer | Available | Low | Supplementary option |

| Credit/Debit Cards | Limited | Very Low | Minimal usage expected |

| International E-wallets | Restricted | Very Low | Not recommended |

| Cryptocurrency | Uncertain | Negligible | Not viable currently |

| Cash via Agents | Available | High potential | Useful for deposits |

Mobile money dominates digital payments with MTN Mobile Money and Moov Money providing essential infrastructure for iGaming payment processing. Operators must integrate both platforms to capture majority of potential users. Agent-based cash deposits into mobile money accounts extend reach beyond purely digital users.

International payment processors face regulatory restrictions and limited local partnerships. PayPal, Skrill, Neteller, and similar services show minimal market presence. Processing fees for mobile money typically range 1-3% for merchants with additional transaction fees for users.

Transaction processing timelines are near-instantaneous for mobile money transfers enabling smooth user experience. Bank transfers process within 1-3 business days. International payments face significant delays and costs making cross-border transactions inefficient.

E-commerce and Digital Economy

Digital Market Development

E-commerce in Benin remains underdeveloped with 2019 B2C E-commerce Index ranking of 100th out of 152 countries, improving from 108th in 2018. The index measures internet use, secure servers, credit card penetration, and postal reliability showing gradual progress.

Online retail penetration represents small percentage of total retail activity concentrated in electronics, fashion, and mobile phone accessories. Popular e-commerce platforms include regional players and local startups though market maturity lags Nigeria and other larger African markets.

Consumer trust in online transactions grows slowly requiring secure payment methods, clear refund policies, and reliable delivery mechanisms. Cash-on-delivery remains popular payment option for physical goods though not applicable to digital gambling services.

Business Environment and Regulatory Framework

Ease of Business Operations

The World Bank discontinued its Doing Business rankings in 2021 following data manipulation allegations. Historical rankings placed Benin in the mid-range for African countries with moderate ease of business operations. The replacement Business Ready framework launched in 2024 but Benin rankings are not yet available.

Starting a business in Benin requires navigating bureaucratic processes typical of West African nations. Reforms have simplified company registration though challenges remain with multiple agency approvals, notarization requirements, and varying interpretation of regulations by officials.

Foreign investment policies generally welcome international capital though specific sectors face restrictions. The gambling sector’s evolving regulatory framework creates uncertainty for foreign investors requiring careful legal advice and relationship building with authorities.

| Indicator | Value/Rating | Assessment |

|---|---|---|

| Business Registration Time | 7-14 days | Improving with online systems |

| Foreign Ownership Restrictions | Sector-dependent | Generally permissive |

| Labor Market Flexibility | Moderate | Informal sector dominates |

| Office Space Costs (Cotonou) | $8-15 per sqm/month | Moderate for region |

| Talent Availability | Limited | Skills gap in tech sectors |

| Corruption Perception | Below average | Requires careful navigation |

Corporate Structure and Registration

Available Entity Types

Foreign companies can establish presence in Benin through several corporate structures. Limited Liability Companies (SARL) represent the most common structure for small to medium businesses offering liability protection and operational flexibility. Joint Stock Companies (SA) suit larger operations requiring significant capitalization.

Branch offices of foreign companies are permitted allowing international operators to establish local presence without creating separate legal entities. Representative offices serve marketing and liaison functions without direct commercial operations. The optimal structure depends on operational scale, ownership preferences, and regulatory requirements.

For iGaming operators, SARL or SA structures typically align best with licensing requirements and operational needs. Regulators may prefer locally incorporated entities over branch offices to ensure adequate local commitment and regulatory jurisdiction.

Registration Requirements

Company registration in Benin has been streamlined with online systems reducing time from weeks to days in some cases. The process requires drafting articles of association, notarizing founding documents, registering with the commercial registry, obtaining tax identification, and social security registration.

Registration timelines vary from 1-4 weeks depending on documentation completeness and efficiency of processing. Costs include government fees typically $500-2,000 depending on company type plus legal and notary fees of $1,000-5,000 for professional assistance.

Foreign ownership faces no specific restrictions in most sectors though minimum capital requirements vary by company type. SARL requires minimum capital of XOF 1,000,000 (approximately $1,700) while SA requires substantially more. Gambling licenses likely impose additional minimum capital requirements.

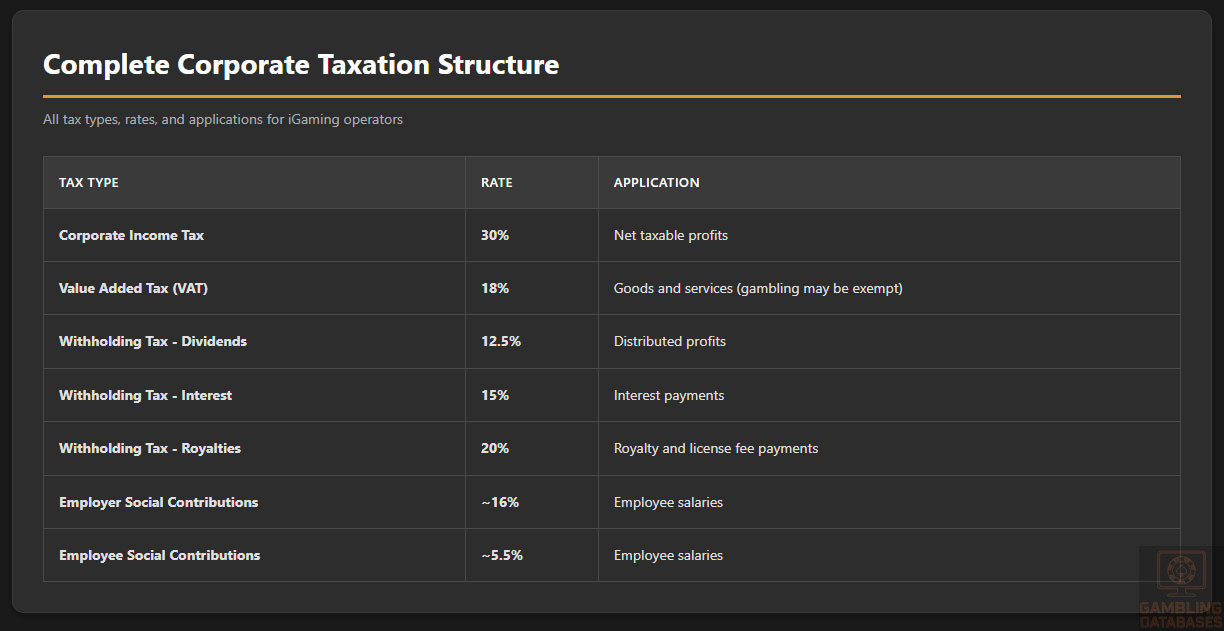

Taxation Framework

Corporate Income Tax Structure

| Tax Type | Rate | Application |

|---|---|---|

| Corporate Income Tax | 30% | Net taxable profits |

| Value Added Tax (VAT) | 18% | Goods and services (gambling may be exempt) |

| Withholding Tax – Dividends | 12.5% | Distributed profits |

| Withholding Tax – Interest | 15% | Interest payments |

| Withholding Tax – Royalties | 20% | Royalty and license fee payments |

| Employer Social Contributions | ~16% | Employee salaries |

| Employee Social Contributions | ~5.5% | Employee salaries |

Corporate income tax at 30% applies to net profits after deducting gambling-specific taxes and legitimate business expenses. Tax incentives may be available for operations in special economic zones or specific priority sectors though gambling typically does not qualify for preferential treatment.

VAT applicability to gambling services requires specific clarification as different jurisdictions treat gambling differently. Some exempt gambling from VAT while others apply reduced rates or full VAT. Operators should obtain tax rulings before launching operations.

Benin participates in the West African Economic and Monetary Union (WAEMU) tax harmonization framework. International tax treaties with various countries may reduce withholding tax rates on cross-border payments. Transfer pricing documentation is increasingly required for related-party transactions.

Market Entry Considerations

Recommended Entry Strategies

Market entry strategy for Benin should prioritize regulatory compliance, mobile-first technology, and local payment integration. Obtaining proper licensing through the Ministry of Finance and National Lottery Authority represents the critical first step ensuring legal operations and market access.

Local partnerships can accelerate market entry providing regulatory navigation expertise, cultural insights, and established business relationships. Potential partners include marketing agencies, payment processors, customer support providers, and even established lottery or betting shop operators seeking digital expansion.

White label solutions offer faster market entry versus building proprietary platforms though customization limitations may constrain competitive differentiation. Established gambling platform providers with African market experience can provide turnkey solutions reducing technical complexity and time to market.

Typical Costs and Timelines

| Cost Category | Estimated Amount (USD) | Notes |

|---|---|---|

| Initial Setup Costs | ||

| License Application Fee | $55,000 – $110,000 | Varies by gambling type |

| Legal & Consulting Fees | $20,000 – $40,000 | Regulatory navigation, compliance |

| Company Registration | $2,000 – $5,000 | Including notary and filing fees |

| Initial Capital Requirement | $50,000 – $200,000 | Regulatory minimum plus working capital |

| Office Setup | $10,000 – $30,000 | Rent, furniture, equipment for 6 months |

| Technology Platform | $50,000 – $200,000 | White label vs proprietary |

| Initial Marketing Budget | $30,000 – $100,000 | Launch campaign, brand building |

| Total Initial Investment | $217,000 – $685,000 | Minimum to substantial operation |

| Expense Category | Monthly Cost (USD) | Annual Cost (USD) |

|---|---|---|

| Staff Salaries (10-15 employees) | $15,000 – $25,000 | $180,000 – $300,000 |

| Office Rent & Utilities | $2,000 – $4,000 | $24,000 – $48,000 |

| Technology Maintenance | $5,000 – $15,000 | $60,000 – $180,000 |

| Payment Processing Fees | 2-3% of turnover | Variable |

| Marketing & Customer Acquisition | $10,000 – $30,000 | $120,000 – $360,000 |

| Compliance & Legal | $2,000 – $5,000 | $24,000 – $60,000 |

| Total Monthly Operating | $34,000 – $79,000 | $408,000 – $948,000 |

| Phase | Duration | Key Activities |

|---|---|---|

| Company Registration | 1-2 months | Entity formation, bank account setup |

| License Application | 3-6 months | Documentation, review, approval |

| Platform Setup | 2-4 months | Technology deployment, payment integration, testing |

| Pre-Launch Marketing | 1-2 months | Brand building, partnerships, compliance final review |

| Total Time to Market | 7-14 months | From initiation to full launch |

Success Factors and Challenges

Key Success Enablers

Understanding local player preferences represents critical success factor. Beninese users favor simple, mobile-optimized interfaces with French language support, popular local payment methods, and games matching cultural preferences. Sports betting on European football leagues combined with lottery-style products aligns well with market demand.

Mobile-first approach is non-negotiable given 106.4% mobile penetration versus 33.8% internet penetration. Applications must function smoothly on entry-level Android devices with optimization for lower bandwidth conditions. Progressive web apps can supplement native applications providing flexibility.

Payment method integration focusing on MTN Mobile Money and Moov Money enables access to majority of potential users. Cash-via-agent deposit options extend reach to users uncomfortable with purely digital transactions. Fast withdrawals build trust and encourage repeat usage.

Local customer support in French through mobile-friendly channels including WhatsApp, SMS, and voice calls enhances user experience. Email-only support alienates users preferring immediate mobile communication. Building local support team understanding cultural context improves satisfaction.

Major Operational Challenges

Regulatory compliance complexity and uncertainty pose significant challenges as frameworks continue evolving. The 25% tax on online gambling winnings creates substantial burden potentially making licensed operations uncompetitive versus unlicensed international operators not collecting taxes.

Payment processing faces technical integration challenges and cost pressures. Mobile money operator fees, transaction limits, and occasional system downtime can frustrate users. International payment restrictions limit deposit/withdrawal options for some user segments.