Bhutan presents a unique opportunity for iGaming market entry with its emerging digital infrastructure and evolving regulatory environment. The country’s cautious approach to gambling regulation combined with its growing internet penetration offers a measured landscape for operators.

Understanding Bhutan’s regulatory framework is crucial for market participants seeking long-term success and compliance.

| Metric | Value |

|---|---|

| Gambling Legal Status | Limited and tightly regulated |

| Regulatory Authority | Ministry of Finance, Department of Revenue and Customs |

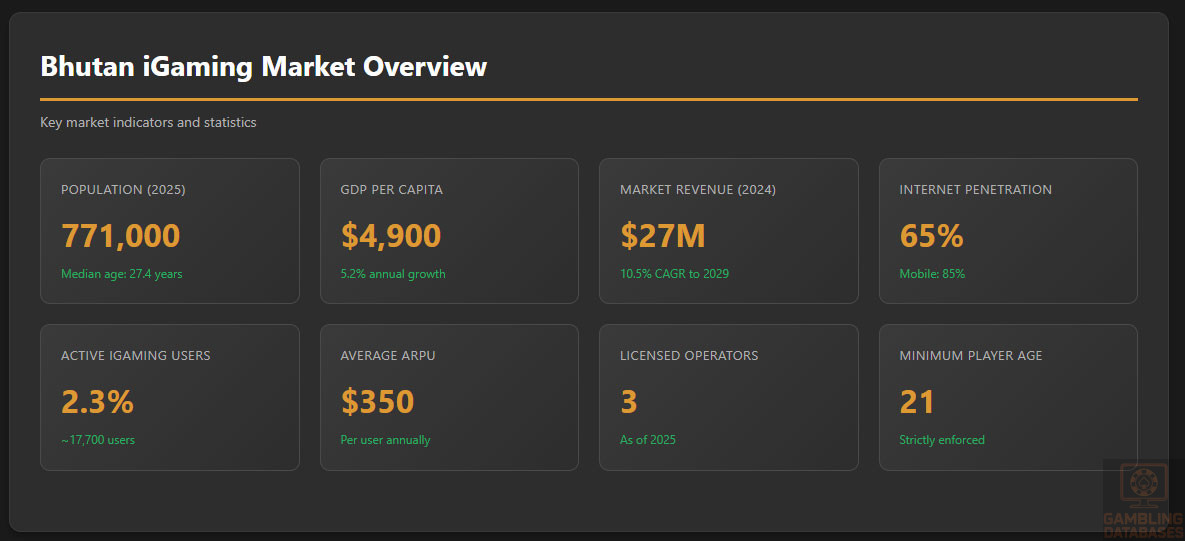

| Population | 771,000 (2025 est.) |

| Median Age | 27.4 years |

| GDP (Nominal) | $3.8 billion (2024 est.) |

| GDP Per Capita | $4,900 (2024 est.) |

| Economic Growth Rate (GDP CAGR) | 5.2% (2024-2029 projected) |

| Internet Penetration | 65% of population |

| Mobile Penetration | 85% of population |

| iGaming Legal Status | Permitted under strict licensing |

| Licensing Authority | Ministry of Finance |

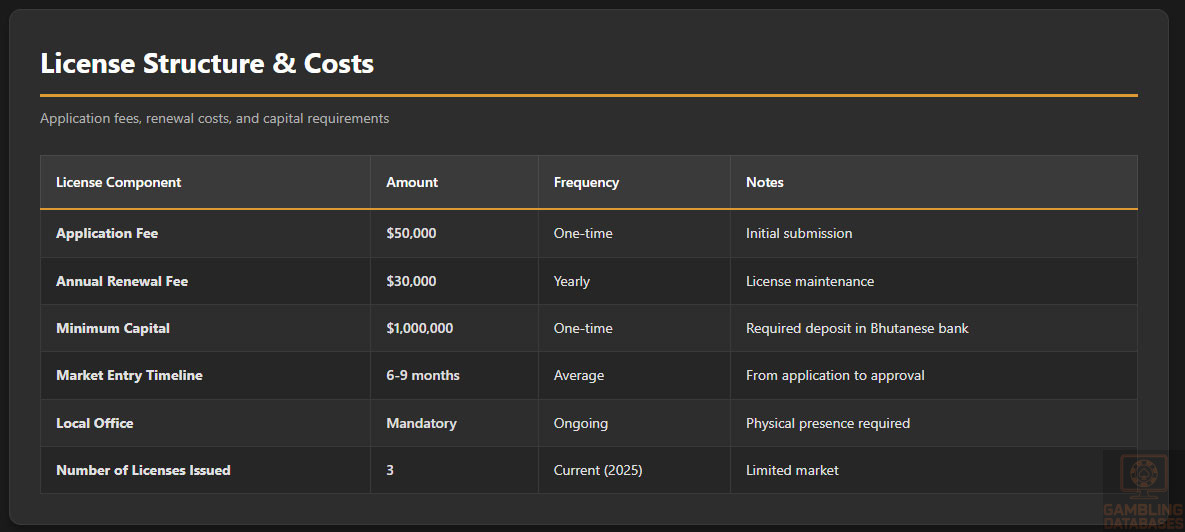

| Number of Licensed Operators | 3 (2025) |

| License Application Fee | $50,000 approx. |

| License Renewal Fee | $30,000 annually |

| Gross Gaming Revenue Tax Rate | 18% |

| Corporate Income Tax Rate | 15% |

| KYC/AML Compliance | Mandatory under Financial Services Act |

| Player Age Restriction | 21 years |

| Market Entry Timeline | 6-9 months average |

| Minimum Capital Requirement | $1 million |

| Local Presence | Required physical office in Bhutan |

| Payment Methods Allowed | Bank transfers, e-wallets, cryptocurrencies restricted |

| Average Revenue Per User (ARPU) | $350 |

| Market Penetration Rate | 2.3% active iGaming users |

| Total Market Revenue | $27 million (2024 est.) |

| Market Growth Rate (CAGR) | 10.5% (2024-2029 projected) |

| Technology Infrastructure Quality | Moderate – ongoing improvements |

| Business Environment Ranking | 89/190 (Ease of Doing Business) |

| Regulatory Changes Since 2020 | Introduction of iGaming License Act 2023 |

| Responsible Gambling Measures | Mandatory operator policies and self-exclusion platforms |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Bhutan’s gambling regulation is defined by a conservative legal framework that tightly controls both land-based and online gaming activities. The Ministry of Finance, specifically its Department of Revenue and Customs, serves as the primary regulatory body overseeing all gambling operations.

Land-Based Gambling Activities

Land-based gambling in Bhutan is scarce and highly regulated. Casino operations are few, with a government-sanctioned license system that permits only select operators.

Sports betting venues and slot machine halls are similarly controlled, with sectors under close governmental scrutiny to prevent social harms and illicit activities.

Online Gambling Framework

Online gambling is legally permitted under strict licensing and regulatory oversight. The current legal framework addresses digital gaming platforms explicitly, prohibiting unlicensed operators.

Prohibited activities include unauthorized payment systems, unregulated cryptocurrency betting, and illegal offshore platform operations.

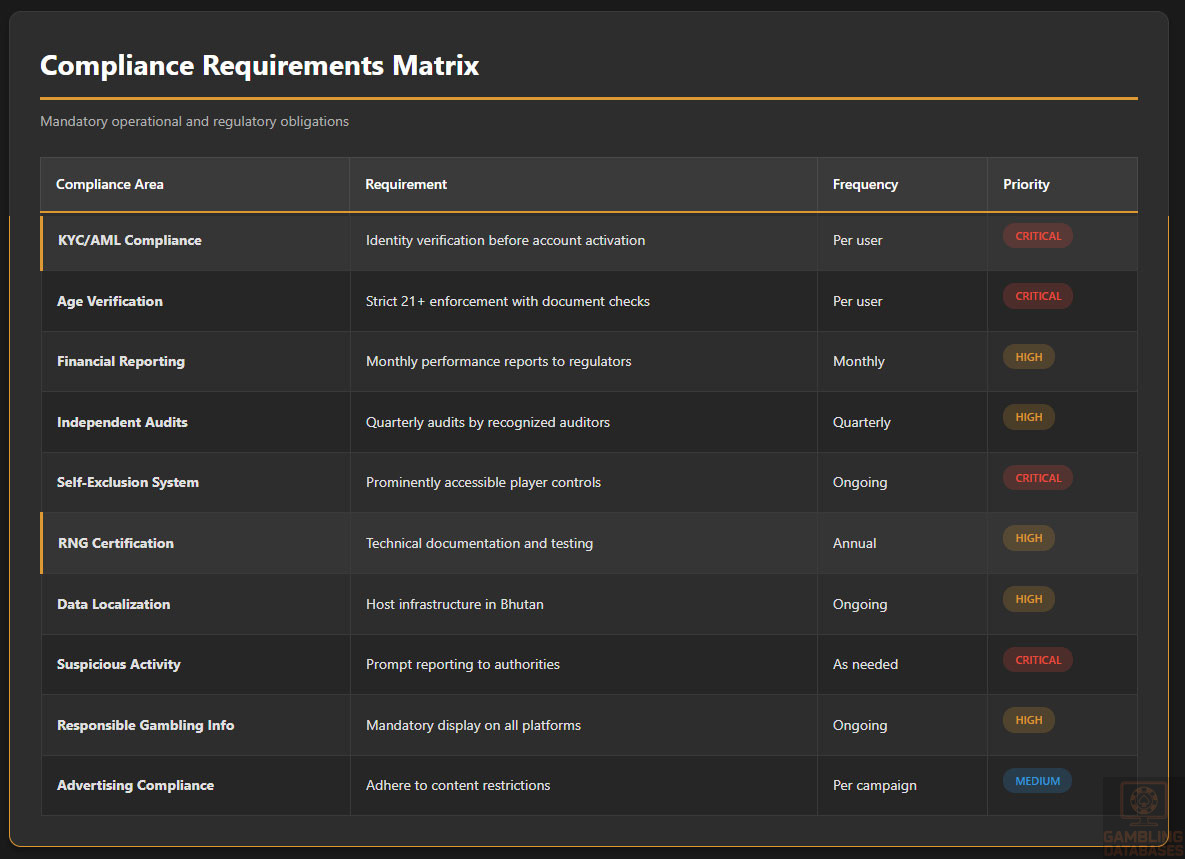

The regulatory framework demands robust KYC/AML compliance and integrates player protection protocols aligned with international best practices.

Licensed Operators and Market Players

Bhutan’s licensed iGaming market is nascent, featuring a limited number of operators under strict conditions. Market players operate with small to medium market shares, competing primarily on technology platforms and localized user experience. Entry strategies focus on compliance, local partnerships, and robust financial backing to meet regulatory standards.

Licensing Framework and Requirements

Application Process and Eligibility

License issuance is tightly controlled by the Ministry of Finance with stringent eligibility criteria. Applicants must demonstrate financial capability, technical integrity, and operational transparency.

The application process includes multiple documented verifications and compliance checks to ensure market integrity.

The licensing framework requires submission of multiple documents:

- Corporate registration certificate and articles of incorporation

- Financial statements for the past three years audited by recognized firms

- Detailed business plan including marketing strategy and financial projections

- Technical documentation of gaming platforms and Random Number Generator (RNG) certification

- Background checks for all directors and beneficial owners

- Proof of minimum capital deposit in a licensed Bhutanese bank

- Compliance policies for KYC/AML and responsible gambling

Local Presence and Operational Requirements

A physical presence in Bhutan is mandatory for licensed operators, including maintaining a local office and appointing resident personnel to oversee operations and compliance.

Operators must use Bhutanese domains for their online platforms and comply with data localization rules.

Foreign ownership is permitted but often requires joint venture or partnership with local entities to facilitate regulatory oversight and market integration.

Operational requirements include:

- Maintaining local customer support and compliance teams

- Hosting technical infrastructure compliant with Bhutanese cybersecurity standards

- Regular submission of operational reports to regulators

- Adherence to advertising restrictions and responsible gambling mandates

- Implementation of player data protection in line with Bhutanese regulations

Compliance Obligations and Monitoring

Player Protection and Identification

Operators must implement stringent age verification and KYC/AML protocols. The minimum age for players is strictly set at 21 years.

Required player protection measures include:

- Verification of identity documents before account activation

- Continuous monitoring of player activity for suspicious behaviors

- Self-exclusion programs and voluntary player limits

- Mandatory display of responsible gambling information

- Secure handling of personal and financial data

Self-exclusion systems must be prominently accessible, allowing players to pause or terminate their gambling activities voluntarily. Operators are also required to disclose risks associated with gambling clearly.

Financial Monitoring and Reporting

Licenced operators must adhere to rigorous transaction monitoring and financial reporting protocols that ensure transparency and mitigate money laundering risks.

The reporting process includes:

- Monthly submission of financial performance reports

- Quarterly audits conducted by independent auditors

- Suspicious transaction reports submitted promptly to regulatory authorities

- Annual compliance certification confirming adherence to regulatory standards

Taxation Structure and Financial Obligations

Player Taxation

Players are subject to withholding taxes on gambling winnings above stipulated thresholds. The tax rate scales progressively, with higher earnings taxed at increased rates, ensuring government revenue without discouraging participation.

Operator Taxation

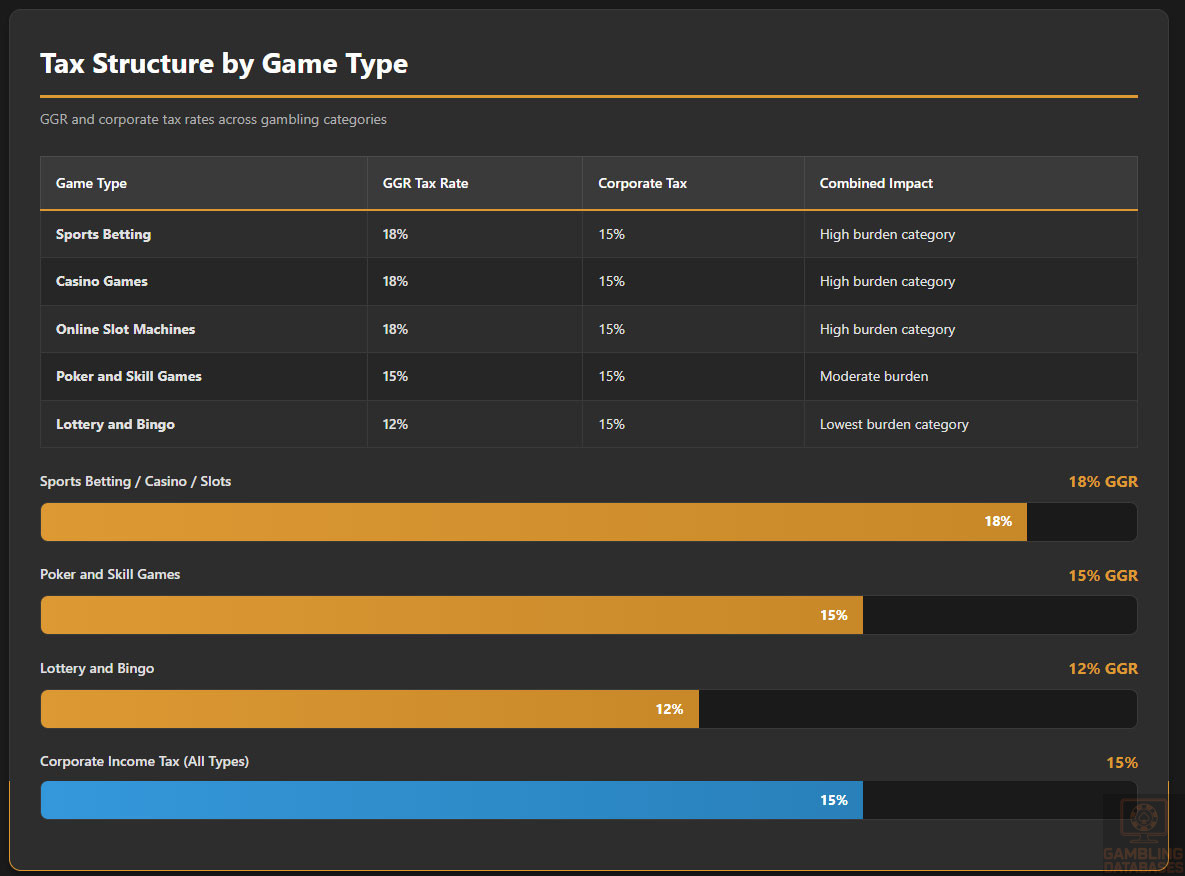

Operators pay an 18% gross gaming revenue (GGR) tax alongside a corporate income tax rate of 15%. Additionally, fixed operational license fees and turnover-based levies are part of the financial obligations.

| Game Type | GGR Tax Rate | Corporate Tax |

|---|---|---|

| Sports Betting | 18% | 15% |

| Casino Games | 18% | 15% |

| Poker and Skill Games | 15% | 15% |

| Lottery and Bingo | 12% | 15% |

| Online Slot Machines | 18% | 15% |

License renewals require annual fees of approximately $30,000, with additional fees applied based on turnover and market segment.

Gambling Market Financial Performance

The Bhutan gambling market’s revenue is modest but shows strong annual growth, propelled by increased internet access and regulatory modernization.

Total wagers and payout ratios are tightly monitored to maintain sustainability. Tax revenues contribute significantly to government budgets earmarked for social development.

Advertising and Marketing Restrictions

Advertising gambling in Bhutan is subject to considerable restrictions, aimed at protecting vulnerable populations. Permitted channels include licensed online platforms and limited time slots on television and radio.

Advertising content must not target minors or encourage excessive gambling behaviors.

The government enforces restrictions on sponsorships and promotional bonuses to ensure marketing integrity and responsible gambling compliance.

- Prohibition of advertisements during children’s programming or peak family viewing hours

- Ban on celebrity endorsements of gambling products

- Mandatory inclusion of responsible gambling messages in all adverts

- Restrictions on direct marketing campaigns such as unsolicited emails or SMS

- Limits on bonus promotions to minimize gambling-related harm

Recent Regulatory Changes and Their Impact

In 2023, Bhutan introduced the iGaming License Act, centralizing the licensing process and tightening compliance requirements.

This legislation significantly shortened approval times while increasing financial and operational criteria for applicants.

Operators have responded by enhancing compliance capabilities and investing in local infrastructure, increasing market professionalism and transparency.

Enforcement Mechanisms and Penalties

The regulatory framework enforces compliance through penalties including fines, license suspensions, or revocations.

- Monetary fines for advertising violations and underreporting

- License suspension for repeated KYC/AML breaches

- Seizure of assets in cases of illegal offshore operations

- Legal action against unlicensed operators and affiliates

- Mandatory corrective action plans for regulatory deficiencies

Overall, enforcement is proactive, with ongoing audits and regulatory reviews ensuring market integrity.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

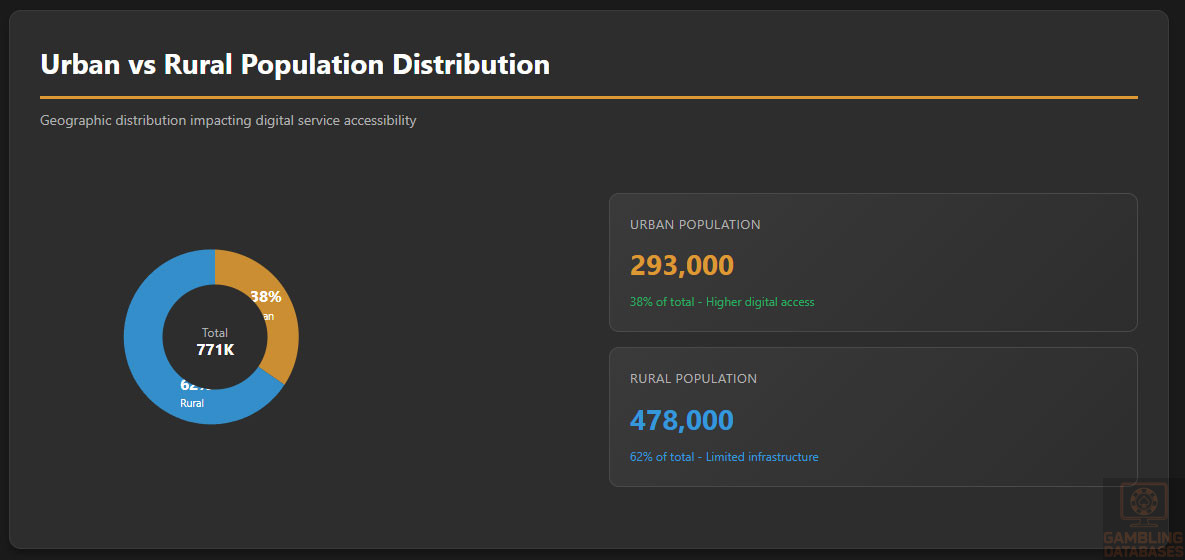

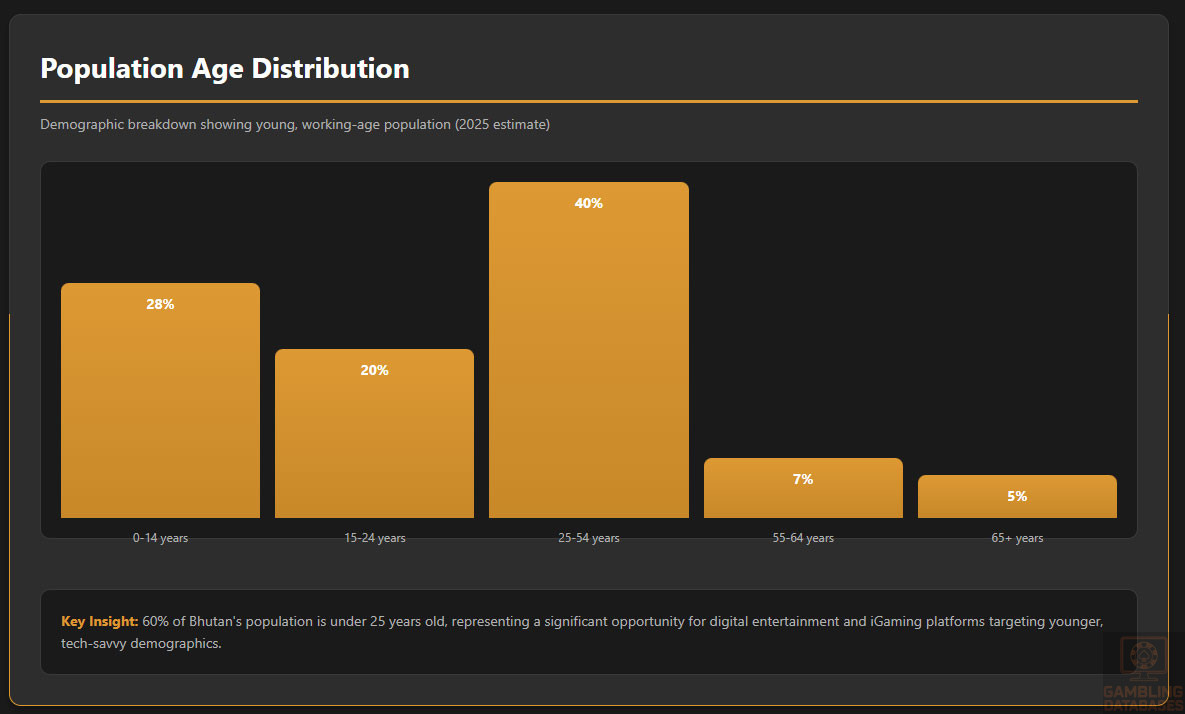

Bhutan’s total population in 2025 is estimated at around 771,000, characterized by a predominantly young demographic. The median age stands at a youthful 27.4 years, reflecting a high proportion of working-age individuals. Gender distribution is relatively balanced with near parity between male and female populations.

Urbanization remains moderate, with approximately 38% of the population residing in urban centers while the remainder is dispersed across rural areas, impacting access to digital services and gambling venues.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 28% |

| 15-24 years | 20% |

| 25-54 years | 40% |

| 55-64 years | 7% |

| 65 years and over | 5% |

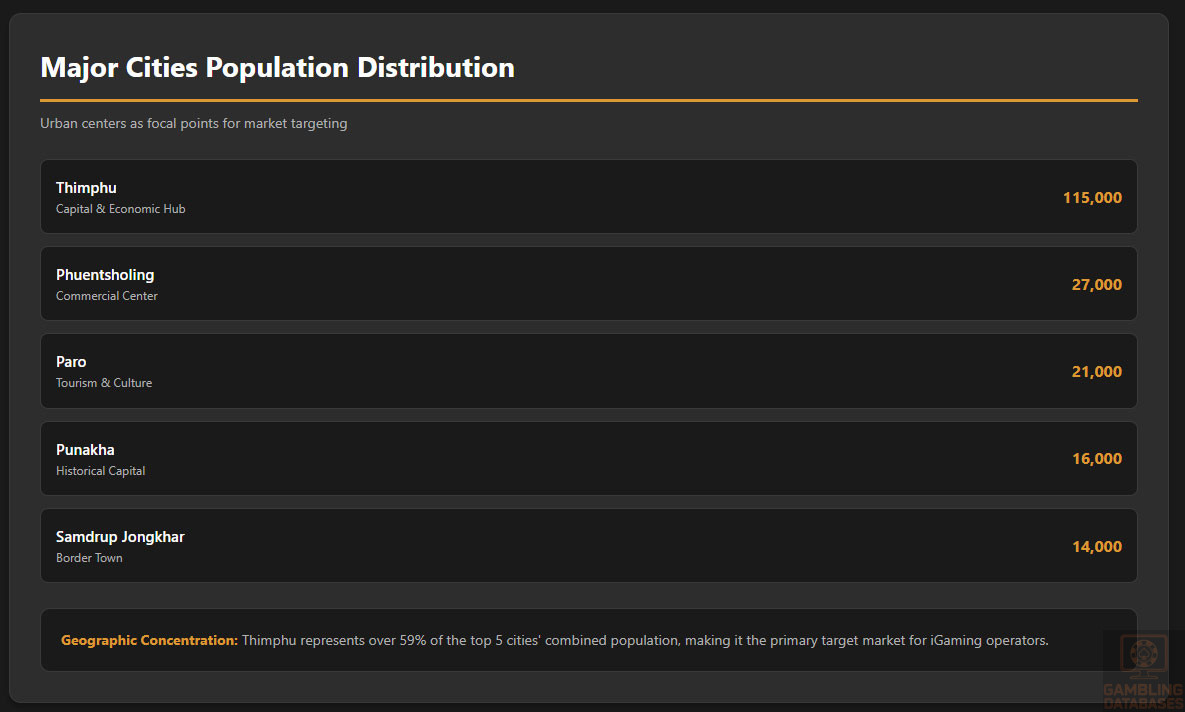

Bhutan’s population distribution shows significant concentration in key urban areas, providing focal points for market targeting. The capital, Thimphu, is the largest city with an estimated 115,000 residents, serving as the economic and administrative hub.

Other important cities include Phuentsholing, Paro, and Punakha, which sustain regional economies and infrastructure.

- Thimphu: 115,000 inhabitants

- Phuentsholing: 27,000 inhabitants

- Paro: 21,000 inhabitants

- Punakha: 16,000 inhabitants

- Samdrup Jongkhar: 14,000 inhabitants

Economic Indicators and Consumer Spending Power

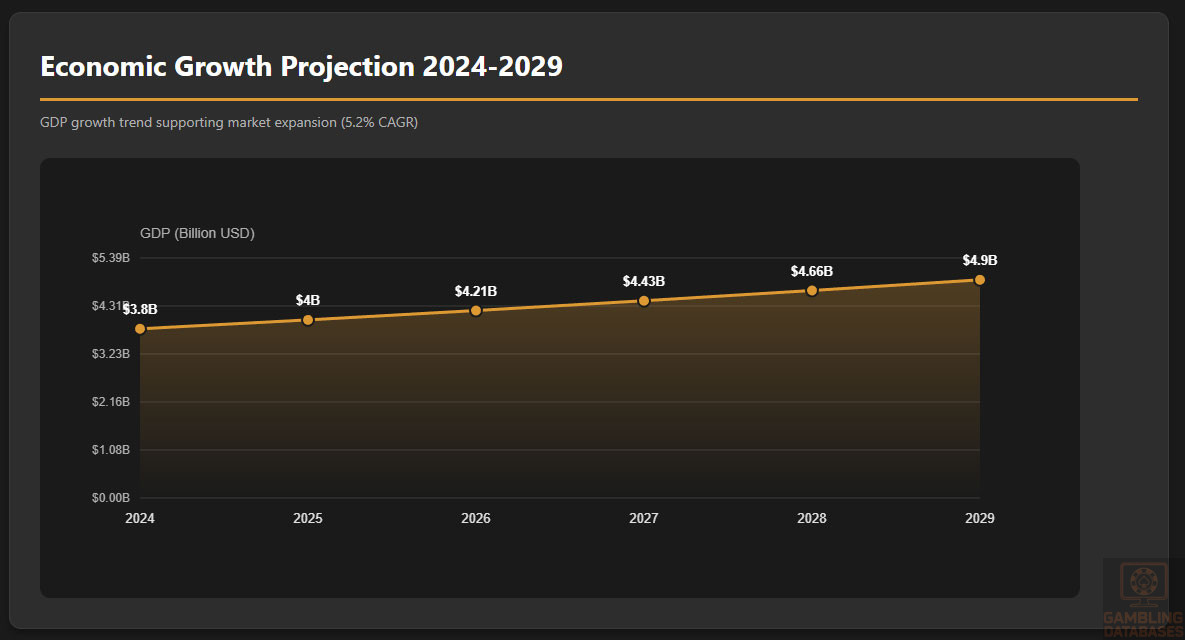

Bhutan’s economy is growing steadily with a nominal GDP of approximately $3.8 billion in 2024 and a projected growth rate of 5.2% CAGR through 2029. The service sector dominates the economy, followed by agriculture and small-scale industry, influencing consumer spending behaviors. Per capita income is rising, now estimated at $4,900, supporting moderate discretionary spending potential in urban and semi-urban areas.

Income distribution in Bhutan exhibits moderate inequality, with average household income centered around the national per capita figures. Disposable income varies widely between urban and rural households, reflecting disparities in economic activity and access to services. Consumer spending shows growing interest in entertainment and digital services, including the nascent iGaming sector.

The Bhutan iGaming market remains small but is expanding rapidly, driven by increasing internet access and a youthful consumer base. Current market revenue is estimated at $27 million with growth projections indicating a robust CAGR of 10.5% through 2029.

Average revenue per user (ARPU) stands at approximately $350, highlighting healthy consumer engagement.

| Metric | Value |

|---|---|

| Total Market Revenue (2024) | $27 million |

| Annual Growth Rate (CAGR, 2024-2029) | 10.5% |

| Active iGaming Users | ~17,700 (2.3% penetration) |

| Average Revenue Per User (ARPU) | $350 |

| Projected Market Revenue (2029) | $46 million |

Education, Skills, and Digital Literacy

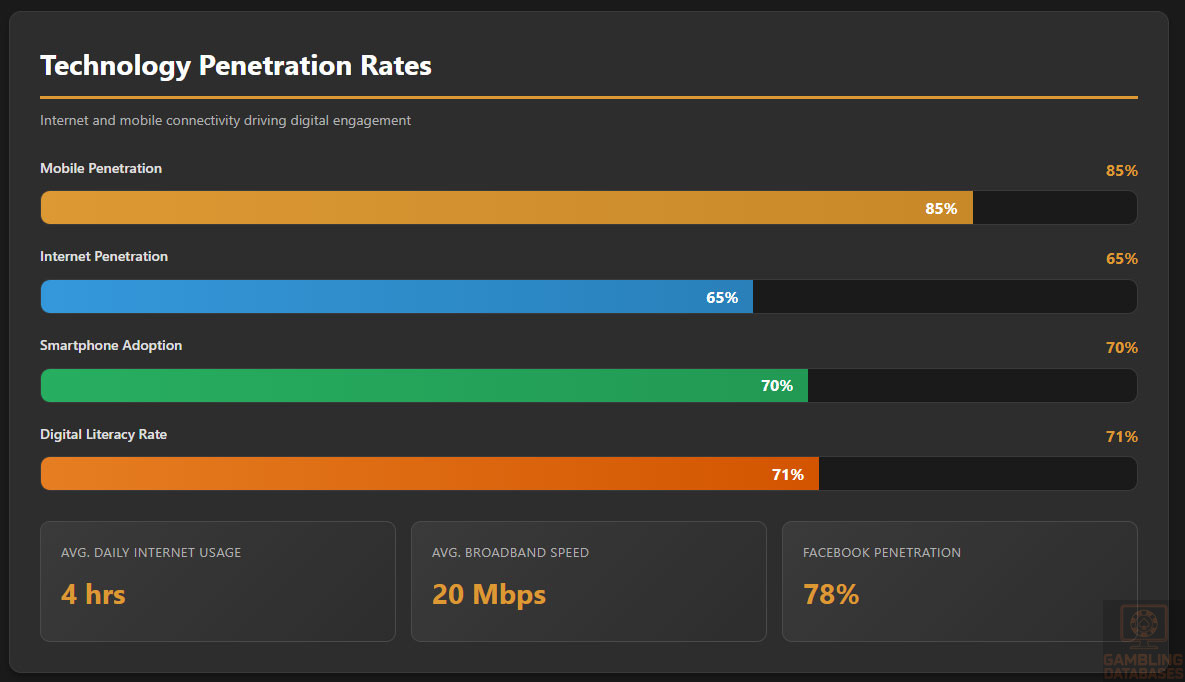

Literacy rates in Bhutan exceed 71%, with ongoing government initiatives improving educational attainment, particularly among youth. Digital literacy is modest but growing, supported by increased internet and smartphone penetration. Skills in basic IT and online navigation are becoming widespread, facilitating higher engagement in digital entertainment sectors.

Cultural and Social Factors

While Dzongkha is the national language, English serves as the primary language for education and business communications, supporting digital platform accessibility.

- Dzongkha (national language)

- English (official business and education)

- Nepali (spoken in southern regions)

- Sharchhopka (eastern regions)

- Lhotshampa (southern communities)

Gambling remains a sensitive topic culturally due to Bhutan’s Buddhist traditions, which emphasize restraint and avoidance of addictive behaviors. Public acceptance is cautious but gradually improving, especially among younger demographics and urban populations. Foreign iGaming brands are viewed with mixed perceptions, balancing curiosity and regulatory skepticism.

Problem gambling prevalence remains low but underreported due to social stigma. The government has introduced several programs focused on prevention and support. Mandatory social responsibility policies by operators ensure proactive measures to mitigate gambling-related harms.

- Establishment of helpline and counseling services

- Public awareness campaigns on responsible gambling

- Integration of self-exclusion tools in licensed platforms

- Training programs for operators on social responsibility

- Regular monitoring and research on gambling impact

Political Structure and Governance

Bhutan operates under a constitutional monarchy with a stable political environment fostering regulatory consistency. Governance emphasizes transparency and rule of law, providing a predictable framework for foreign and domestic investors in the iGaming sector.

Technology Adoption and Digital Behavior

Internet penetration stands at 65%, with average daily usage of approximately 4 hours, reflecting growing digital engagement. Mobile adoption is higher at 85%, driving significant mobile gaming and betting activity. Social media usage is widespread across multiple platforms.

- Facebook with 78% user penetration and high engagement

- YouTube with 89% penetration and extensive video consumption

- Instagram with 64% penetration, favored by younger users

- TikTok growing at 52% among under-25s

- Twitter used by 31%, mainly for news and updates

Digital payments are evolving with a preference for traditional methods supplemented by emerging digital options.

- Bank transfers dominating digital payments

- E-wallets gaining traction among younger demographics

- Credit and debit cards widely accepted

- Mobile money services emerging regionally

- Cryptocurrency use remains limited and restricted

Gaming and Gambling Preferences

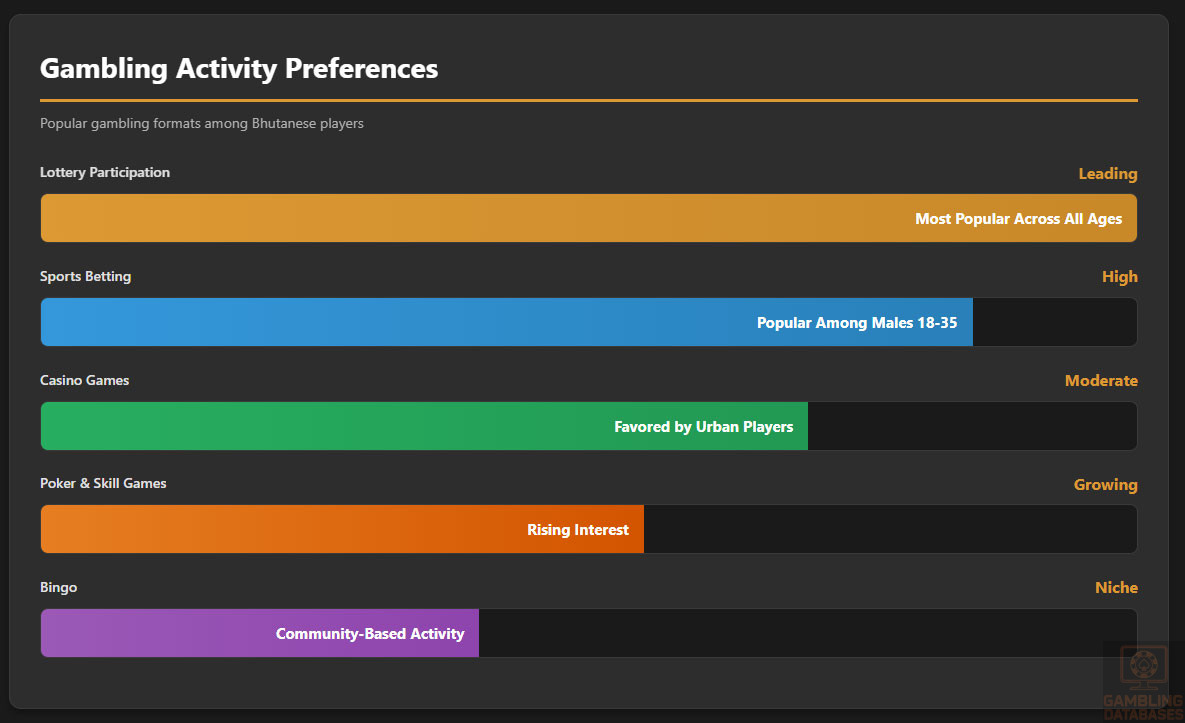

- Lottery participation leading among all age groups

- Sports betting popular among males aged 18-35

- Casino games favored primarily by urban players

- Poker and skill games growing in interest

- Bingo and lottery as community-based activities

Bhutanese players demonstrate cautious but growing engagement with iGaming platforms. Spending habits are moderate with preference for short sessions aligned with leisure time after work. Peak activity tends to occur during evenings and weekends. Retention strategies focus on localized content and adherence to responsible gambling principles.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Bhutan’s internet penetration reaches approximately 65%, combining fixed broadband and mobile connectivity. Fixed broadband penetration is limited due to geographical challenges, making mobile networks the primary access points for internet services. Average broadband speeds hover around 20 Mbps, with ongoing infrastructure investments focused on improving fiber optic coverage in urban centers and extending connectivity to rural regions.

Network reliability has improved notably in recent years, with substantial government efforts to modernize telecommunications infrastructure. The increasing affordability of data plans has contributed to higher adoption rates, enabling growth in digital services including iGaming.

5G and Future Technology Deployment

Bhutan’s 5G rollout is in early stages, with pilot programs initiated in major cities like Thimphu and Phuentsholing. Full commercial deployment is expected within the next 2-3 years as network operators upgrade infrastructure. Telecom providers are expanding their coverage footprint, aiming to bridge the urban-rural digital divide.

Government policy actively supports technological advancement, encouraging partnerships with international firms for network enhancement and smart city initiatives. This forward-looking approach facilitates better mobile gaming experiences and supports emerging technologies relevant to the iGaming ecosystem.

Mobile Technology Ecosystem

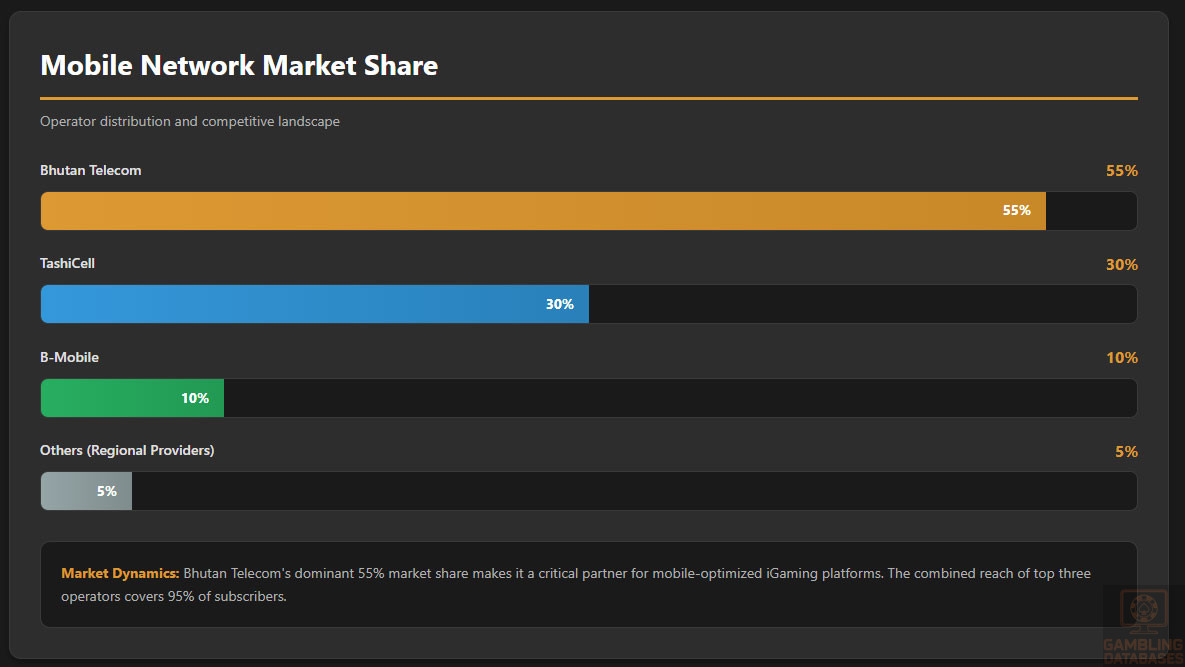

The mobile network market features several key players, offering competitive service packages and extensive coverage. While three operators dominate, regional providers contribute to connectivity in hard-to-reach areas. Market share distribution reflects strong customer loyalty tied to pricing, network quality, and customer service.

- Bhutan Telecom: Largest operator controlling around 55% market share

- TashiCell: Second-largest with approximately 30% of subscribers

- B-Mobile: Focused on niche rural markets with 10% share

- Others: Small regional providers and new entrants covering remaining 5%

Smartphone adoption exceeds 70%, with Android devices commanding the majority of the market due to affordability and variety. Device usage patterns indicate a strong preference for mobile applications and social media, contributing to the growth of mobile-based iGaming platforms.

Financial Services and Payment Infrastructure

Bhutan’s banking system is stable, featuring a mix of national and regional banks embracing digital banking solutions. Account penetration is moderate, with urban areas showing higher rates of bank and mobile wallet usage compared to rural zones.

- Bank of Bhutan: Market leader with extensive branch and digital banking network

- Bhutan Development Bank: Focus on SME financing and retail banking

- IMAF Bank: Regional presence with emphasis on remittances

- Offshore Bank: Specialized in foreign transactions and corporate clients

- NMB Bank: Emerging digital-first banking services targeting youth

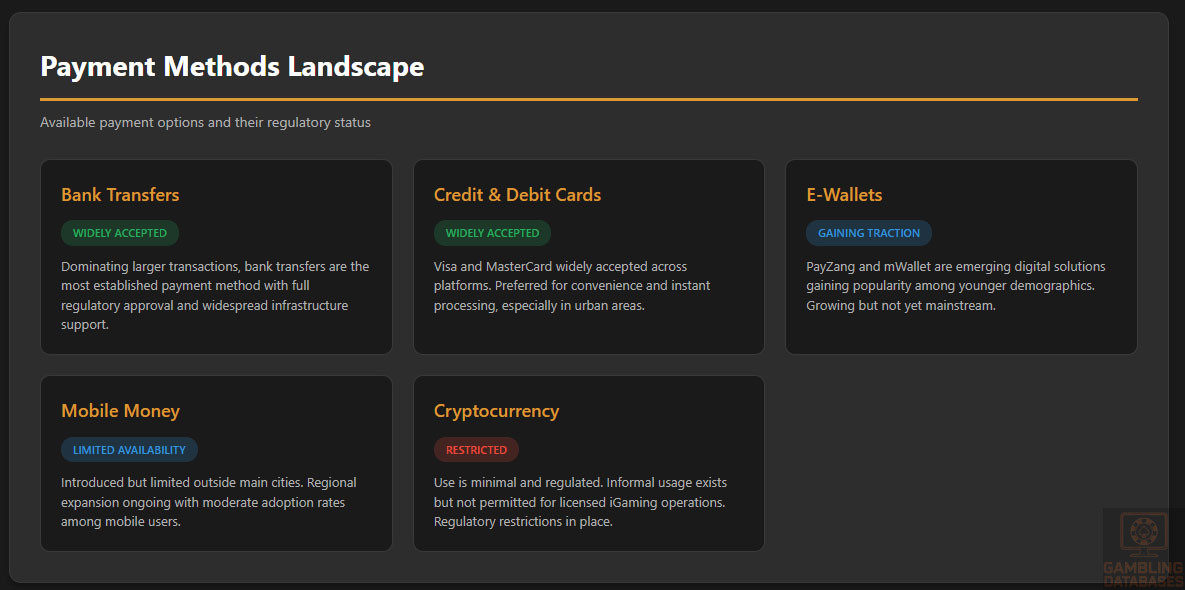

Payment options include bank transfers, credit/debit cards, and emerging e-wallets. Cryptocurrency remains restricted, though informal usage exists.

- Bank transfers dominate larger transactions

- Credit and debit cards widely accepted, especially Visa and MasterCard

- E-wallets like PayZang and mWallet gaining market traction

- Mobile money services introduced but limited outside main cities

- Cryptocurrency use is minimal and regulated

E-commerce and Digital Economy

Bhutan’s e-commerce sector is nascent yet growing rapidly due to increasing internet access and consumer trust. Key online retail sectors include electronics, fashion, and digital services, supported by improved digital payment infrastructure. Government initiatives encourage digital entrepreneurship and online service adoption, building a foundation for expanded digital economies.

Business Environment and Regulatory Framework

Bhutan ranks 89th globally on the Ease of Doing Business index, reflecting a streamlined but still developing business climate. Starting a business involves multiple regulatory requirements and moderate costs, with transparency improving steadily due to government reforms. Foreign investment is welcomed, though certain sectors require joint ventures or regulatory approval.

The business registration process typically proceeds through these stages:

- Preparation and notarization of incorporation documents

- Submission to the Companies Registry and verification

- Tax registration and obtaining identification numbers

- Opening corporate bank accounts and depositing minimum capital

- Final certificate issuance and operational licensing

Corporations, Limited Liability Companies (LLCs), and Branch Offices are common business structures. LLCs are preferred for smaller operations due to liability protections, while corporations suit larger entities. Foreign firms frequently establish branch offices subject to registration and local partner arrangements.

The registration timeline averages 4-6 weeks, with costs varying based on entity type and business scope.

- Registration fees and government charges

- Legal and consultancy expenses

- Minimum capital requirements

- Compliance and licensing costs

- Operational infrastructure setup costs

Taxation Framework

The corporate income tax rate in Bhutan stands at 15% with tax holidays and incentives for ventures in special economic zones. Bilateral treaties with several countries provide mechanisms to avoid double taxation, facilitating foreign investment and revenue flow.

- India

- Bangladesh

- Singapore

- Malaysia

- Thailand

Personal income tax applies progressively, with withholding requirements on gambling winnings and employment income. Social security contributions are mandatory with defined limits. Tax residency is based on physical presence and economic ties.

Market Entry Considerations

Successful market entry requires adherence to local regulations, building strong partnerships, and leveraging technology to meet consumer expectations. Collaborations with local operators reduce barriers and enhance compliance efficiency. Investment in localized content and mobile-optimized platforms caters to the dominant mobile user base.

- Forming joint ventures with licensed local firms

- Utilizing compliant payment gateways

- Implementing robust KYC/AML compliance systems

- Focusing on mobile-first user experiences

- Integrating responsible gambling tools

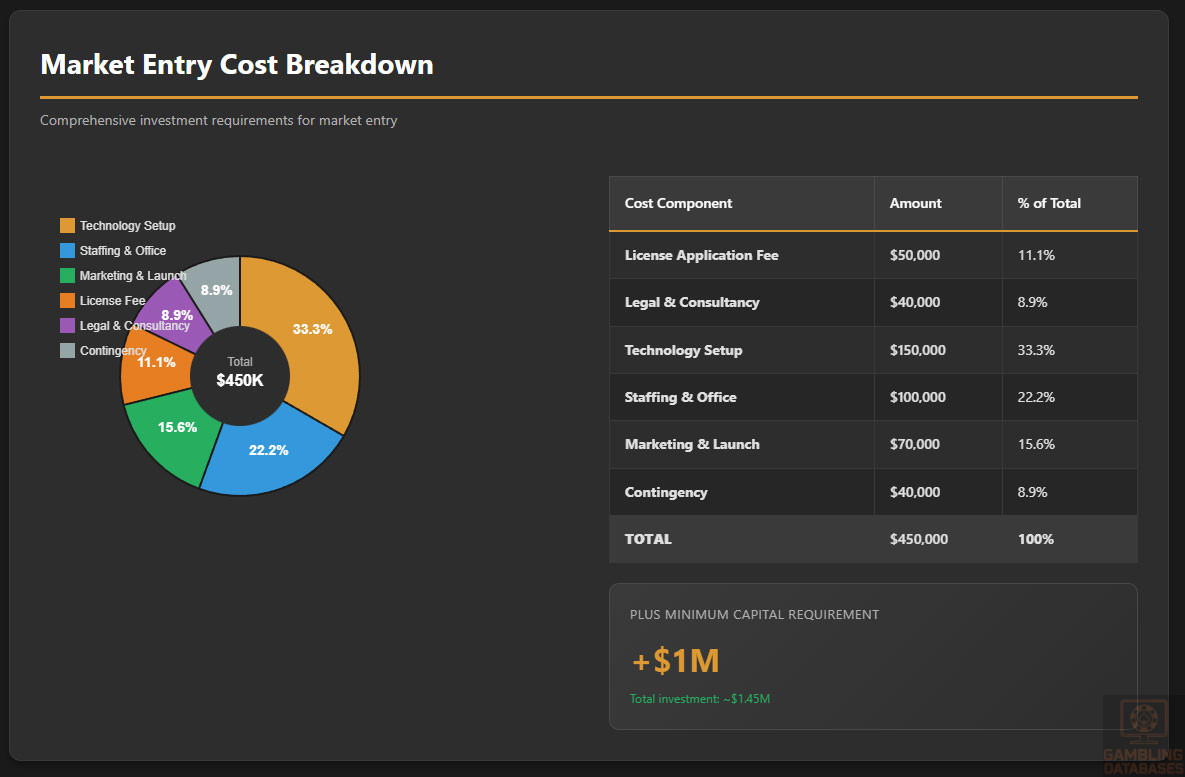

Initial cost outlays include license fees, operational setup, staffing, and technology acquisition. Market entry timelines range from six to nine months depending on regulatory processes and operational readiness.

| Cost Component | Approximate Amount |

|---|---|

| License Application Fee | $50,000 |

| Legal and Consultancy Services | $40,000 |

| Technology Setup and Integration | $150,000 |

| Staffing and Office Setup | $100,000 |

| Marketing and Launch Expenses | $70,000 |

| Contingency and Miscellaneous | $40,000 |

Key operational challenges include navigating regulatory complexities, building brand trust, and managing local payment infrastructures while balancing cultural sensitivities.

- Regulatory compliance and ongoing audits

- Infrastructure limitations in rural areas

- Competition from established land-based operators

- Balancing localized content with international standards

- Managing social responsibility and problem gambling risks

Exit strategies must consider license transferability, valuation parameters, and regulatory approvals. Market liquidity is moderate, making early planning essential for asset recovery or transaction structuring.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Bhutan?

Yes, online gambling is legal under Bhutan’s regulatory framework, subject to strict licensing and compliance requirements. All operators must obtain a license from the Ministry of Finance and adhere to local KYC/AML laws, responsible gambling mandates, and technical standards. Unlicensed operations are prohibited, and enforcement is stringent to maintain market integrity.

2. What types of gambling licenses are available and what do they cover?

Bhutan issues comprehensive licenses covering multiple segments: casino gaming, sports betting, lottery operations, poker and skill games, and online slot machines. Each license type has distinct operational scopes and tax implications. Operators may apply for single or multiple license categories depending on their business model and market strategy.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees are approximately $50,000, with annual renewal fees around $30,000. The approval process generally takes 6 to 9 months, depending on document completeness and regulatory review timelines. Applicants must also factor in compliance setup and operational readiness to meet licensing conditions.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply but must demonstrate compliance with Bhutanese regulations, including establishing local presence. Joint ventures or partnerships with Bhutanese entities are common to facilitate regulatory oversight. Foreign ownership is allowed but subject to government approvals and may involve additional operational requirements.

5. What are the tax obligations for iGaming operators?

Operators are subject to an 18% gross gaming revenue tax plus a 15% corporate income tax. License renewal fees and fixed operational taxes also apply. Taxes vary slightly by game type, with lotteries typically subject to lower GGR rates. Operators must regularly file financial reports and pay taxes in accordance with Bhutanese law.

6. Are gambling winnings taxed for players?

Yes, players’ winnings exceeding specified thresholds are subject to progressive withholding taxes. Tax rates increase with prize size, ensuring fair contribution while maintaining player incentives. Operators handle withholding and reporting duties to government authorities on behalf of players.

7. What are the typical operational costs for running an online casino/sportsbook?

Major cost components include license fees, technology platform expenses, staffing, payment processing, marketing, and compliance. Additional expenditures involve customer support infrastructure and security systems. Efficient cost management ensures scalability and sustainable margins in a competitive market.

8. What is the expected ROI timeline for entering this market?

Return on investment generally occurs within 2 to 4 years, influenced by license costs, market penetration speed, and operational efficiency. Early movers benefit from lower competition but must invest significantly in compliance and user acquisition. Strategic marketing and platform quality accelerate ROI timelines.

9. What are the local presence requirements for operators?

Operators must maintain a physical office in Bhutan staffed with compliance and customer service personnel. Local domain registration and data hosting may be required to align with regulatory and cybersecurity requirements. This presence ensures regulatory engagement and operational control within the market.

10. What payment methods are available and recommended?

Available payment options include bank transfers, credit/debit cards, and e-wallets. Bank transfers are preferred for larger transactions due to reliability, while e-wallets attract younger demographics with faster transaction times. Cryptocurrency use remains restricted and discouraged by regulators.

11. What are the advertising and marketing restrictions?

Advertising is tightly controlled to prevent targeting minors and vulnerable populations. Permitted channels include licensed platforms, selected broadcast times, and regulated online campaigns. Content must include responsible gambling warnings, and bonus promotions are limited in size and frequency to avoid promoting excessive gambling.

12. What responsible gambling measures are mandatory?

Operators must implement age verification, self-exclusion options, deposit limits, player activity monitoring, and mandatory publication of responsible gambling information. Training for staff on social responsibility and regular reporting on responsible gambling efforts to regulators are also required.

13. How large is the iGaming market and what is the growth potential?

The iGaming market in Bhutan is currently valued at approximately $27 million with an expected CAGR of 10.5% over the next five years. Growth is driven by improved digital infrastructure and youthful demographics. Market expansion is expected to nearly double revenues by 2029.

14. Who are the main competitors and what is their market share?

The market features a small number of licensed operators controlling roughly equal shares. Competition revolves around technology innovation, localized content, and compliance excellence. The limited number of licensed firms reflects the market’s regulatory strictness and early development phase.

15. What are the player preferences and typical spending patterns?

Players favor lottery and sports betting primarily, with growing interest in casino and skill-based games. Spending is moderate with sessions often timed during evenings and weekends. Retention depends heavily on platform usability, trustworthiness, and responsible gaming features.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, local partnerships, technological robustness, cultural sensitivity, and effective marketing. Major challenges include navigating complex regulations, establishing brand trust, and managing operational costs within a developing market infrastructure.

Sources and References

- BhutanGambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Bhutan – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Gaming Industry Report – Global iGaming Monitor 2024

- Bhutan Telecom Annual Report 2024

- Ministry of Economic Affairs – E-commerce Development

- Bhutan Department of Revenue and Customs – Regulatory Framework

- Financial Services Act of Bhutan – Government Publication 2023

- Bhutan Digital Economy Strategy 2025

- International Monetary Fund – Bhutan Economic Outlook 2024

- Asia Pacific Gambling Regulatory Review 2024

- Bhutan Mobile Network Operators Annual Survey 2024

- National Research Council – Social Responsibility in Gambling

- Bhutan Consumer Behavior Study 2024

- Central Statistical Bureau – Bhutan Demographic Survey 2025

- Global Cybersecurity Index – Bhutan Segment 2024

- Ministry of Health – Addiction and Mental Health Programs

- Bhutan Investment Promotion Board – Guidelines 2024

- Telecommunication Authority of Bhutan – Infrastructure Report 2024

- Bhutan Gaming and Entertainment Market Report 2024

- Asian Development Bank – Bhutan Technology Development Report

- International Legal Perspectives on Online Gambling – 2023 edition

- Bhutan Financial Services Commission – Anti-Money Laundering Policy

- Global Online Payment Systems Insight – 2024

- Bhutan Labour and Employment Trends Report 2024

- World Economic Forum – Digital Economy in Emerging Markets

- Bhutan Ministry of Culture and Tourism – Social Research

- Regional Market Analysis – South Asian iGaming Market 2024

🎯 Gambling Databases Country Rating: Bhutan

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 4.8/10 | 🟡 Moderate (Limited Access, High Barriers) |

| Player Access Score | 6.3/10 | 🟡 Partially Legal (Regulated but Restricted) |

| Overall Market Attractiveness | 5.6/10 | Small emerging market with strict regulatory controls and limited scalability potential |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- EXTREME MARKET SIZE LIMITATION: Total market revenue only $27 million (2024) with just 17,700 active users – this is one of the world’s smallest licensed iGaming markets

- ONLY 3 LICENSED OPERATORS ALLOWED: Market is essentially closed to new entrants with extremely limited licensing availability (3 total licenses as of 2025)

- MANDATORY PHYSICAL PRESENCE: Required local office, resident personnel, and partnership with local entities significantly increases operational complexity and costs

- CRYPTOCURRENCY COMPLETELY BANNED: Modern payment method unavailable, limiting appeal to tech-savvy users and creating friction in transactions

- HIGH MINIMUM CAPITAL REQUIREMENT: $1 million minimum capital must be deposited in Bhutanese bank, creating significant upfront financial barrier

- CULTURAL RESISTANCE: Buddhist traditions emphasize restraint from gambling; social stigma around problem gambling creates reputational risks for operators

- INFRASTRUCTURE LIMITATIONS: Only 65% internet penetration, 20 Mbps average speeds, and rural connectivity gaps limit market reach

- EXTENDED LICENSING TIMELINE: 6-9 months average for market entry, with complex multi-document verification process

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 1.5/3.0 | iGaming legally permitted under strict licensing (+1.5 points for partial legality). HOWEVER: Only 3 licenses granted total (-0.5 points for extreme market access limitation). Tightly regulated framework with Ministry of Finance oversight creates significant compliance burden (-0.5 points). Unlicensed operators prohibited with enforcement mechanisms in place (-0.25 points). Strong regulatory framework but extremely limited market access. Final: 1.5/3.0 |

| Licensing Process | 25% | 0.75/2.5 | Licensing available but extremely limited (+0.5 points for restricted availability). $50,000 application fee + $30,000 annual renewal is moderate (+0.25 points). MAJOR DEDUCTIONS: 6-9 months timeline is lengthy (-0.25 points). Extensive documentation requirements including 3-year audited financials, RNG certification, director background checks creates high complexity (-0.5 points). Only 3 total operators licensed indicates near-impossible market access for new entrants (-0.5 points). Foreign ownership requires joint venture/local partnership, adding complexity (-0.25 points). Total licensing costs approximately $90,000 over 3 years is acceptable but multiple barriers remain. Final: 0.75/2.5 |

| Taxation & Costs | 20% | 1.25/2.0 | 18% GGR tax rate is favorable (+1.5 points for 15-25% range). 15% corporate income tax is reasonable (+0.25 points). DEDUCTIONS: Effective combined tax rate of approximately 30-33% when both taxes apply (-0.25 points for combined burden). High operational costs due to mandatory local presence, office setup ($100,000), technology infrastructure ($150,000), and ongoing compliance requirements ($40,000+ legal/consulting) create significant expense burden for tiny $27M market (-0.25 points). Customer acquisition in small market of 771,000 population with only 2.3% penetration makes scaling extremely difficult. Final: 1.25/2.0 |

| Operational Requirements | 15% | 0.25/1.5 | HEAVY operational requirements (+0.5 points base). MAJOR DEDUCTIONS: Mandatory physical office in Bhutan with resident personnel required (-0.25 points). $1 million minimum capital requirement held in Bhutanese bank is extremely high for market size (-0.25 points). Must use Bhutanese domains and comply with data localization (-0.25 points). Cryptocurrency banned completely (-0.25 points eliminates modern payment option). Local customer support and compliance teams mandatory (-0.25 points). Complex KYC/AML with continuous monitoring adds operational burden (-0.25 points). Monthly financial reporting, quarterly audits, annual compliance certification creates ongoing overhead (-0.25 points). Foreign operators must partner with local entities, limiting control (-0.25 points). Infrastructure requirements excessive for $27M market. Final: 0.25/1.5 |

| Market Environment | 10% | 0.25/1.0 | Ranked 89/190 on Ease of Doing Business – difficult environment (+0.25 points for 51-100 range). DEDUCTIONS: Advertising highly restricted with prohibition during children’s programming, ban on celebrity endorsements, mandatory responsible gambling messages, limits on bonus promotions (-0.5 points for severe restrictions). Cultural sensitivity around gambling due to Buddhist traditions creates reputational challenges (-0.25 points). Small market size ($27M revenue) with low penetration (2.3%) makes customer acquisition costs disproportionately high. Stable political environment is positive but doesn’t offset operational challenges. Final: 0.25/1.0 |

| TOTAL OPERATOR EASE SCORE | 4.8/10 | ||

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.5/4.0 | iGaming legal under licensed operators (+2.0 points for partial legality). Players can legally access sports betting, casino games, poker, lottery, and slots from 3 licensed platforms. DEDUCTIONS: Only 3 licensed operators severely limits player choice (-0.5 points). Unauthorized offshore platforms prohibited, though enforcement level unclear (-0.5 points). Strict 21-year age restriction (higher than international 18-year standard) reduces addressable market (-0.5 points). Players using unlicensed platforms face potential regulatory risks though player penalties not explicitly detailed. Final: 2.5/4.0 |

| Practical Accessibility | 30% | 1.75/3.0 | Limited payment methods available (+2.0 points base). Bank transfers and e-wallets permitted. MAJOR DEDUCTIONS: Cryptocurrency completely banned (-0.5 points eliminates modern payment option popular with younger demographics). Credit/debit cards accepted but banking system penetration moderate, especially in rural areas (-0.25 points). Only 65% internet penetration creates access barriers for 35% of population (-0.25 points). Mobile penetration at 85% is better but average 20 Mbps speeds limit gaming experience (-0.25 points). Rural connectivity gaps affect user experience. No evidence of ISP blocking mentioned, which is positive. Final: 1.75/3.0 |

| Player Penalties | 20% | 1.5/2.0 | No explicit criminal penalties for players using licensed platforms (+1.5 points). Players subject to progressive withholding tax on winnings above thresholds – this is administrative rather than punitive (+0.5 points). DEDUCTION: Taxation on winnings may discourage participation (-0.5 points reduces attractiveness). No evidence of player prosecutions for using offshore sites, but legal framework prohibits unauthorized platforms creating uncertainty. Overall player risk is low for licensed platforms but ambiguous for offshore usage. Final: 1.5/2.0 |

| Market Availability | 10% | 0.55/1.0 | Only 3 licensed operators as of 2025 (+0.7 points for 2-4 operator range). This creates oligopolistic market with limited consumer choice and potentially less competitive pricing/promotions. Market concentration high with small/medium market shares distributed among just 3 players. Offshore alternatives exist but prohibited. 2.3% market penetration indicates low adoption. DEDUCTION: Extremely limited operator choice reduces player options and innovation (-0.15 points). Final: 0.55/1.0 |

| TOTAL PLAYER ACCESS SCORE | 6.3/10 | ||

🔍 Key Highlights

Strengths (Limited but Present)

- Legal Framework Established: Unlike many Asian markets, Bhutan has created legal pathway for iGaming with regulatory clarity through Ministry of Finance oversight

- Reasonable Tax Rates: 18% GGR + 15% corporate tax (30-33% effective) is moderate compared to heavily taxed markets like Australia or UK

- Stable Political Environment: Constitutional monarchy with transparent governance provides regulatory predictability for long-term planning

- Growing Digital Infrastructure: 65% internet penetration and 85% mobile penetration showing improvement trajectory, 5G pilots underway in major cities

- Young Population: Median age 27.4 years with 40% in prime 25-54 gaming demographic creates favorable player profile

- Market Growth Potential: 10.5% CAGR projected 2024-2029 indicates expanding market despite small base

- English Language: English as official business/education language reduces localization costs for international operators

⛔️ CRITICAL RISKS AND CHALLENGES

- EXTREME MARKET SIZE LIMITATION: $27 million total market revenue (2024) makes this one of world’s smallest licensed iGaming markets. For comparison, Malta processes more revenue in hours than Bhutan generates annually. Only 17,700 active users total. Economics simply don’t work for most operators – market too small to justify $450,000+ entry costs and $1M capital requirement.

- MARKET ACCESS ESSENTIALLY CLOSED: Only 3 licensed operators permitted as of 2025. New licensing availability unclear. This is effectively an oligopoly with no room for new entrants. Unless one of existing 3 licenses becomes available through acquisition, market entry impossible regardless of capital or compliance capability.

- PROHIBITIVE CAPITAL REQUIREMENTS: $1 million minimum capital held in Bhutanese bank is absurdly high for $27M market (3.7% of entire market must be held as capital). Additionally requires $50,000 license fee, $150,000 technology setup, $100,000 office/staffing, $70,000 marketing. Total $1.37M+ to enter $27M market with 10.5% growth = terrible ROI economics.

- MANDATORY LOCAL PRESENCE: Required physical office, resident personnel, local partnerships creates operational complexity disproportionate to market opportunity. Remote operation impossible. Must hire local compliance teams, maintain infrastructure, ongoing regulatory reporting – overhead makes profitability nearly impossible at this scale.

- CRYPTOCURRENCY BAN: Complete prohibition of crypto payments eliminates payment method preferred by 20-30% of modern iGaming users globally. Reduces addressable market and limits appeal to younger tech-savvy demographics.

- EXTENDED LICENSING TIMELINE: 6-9 months for licensing process is lengthy for such small market. Extensive documentation (3-year audited financials, RNG certification, background checks for all directors) creates high administrative burden. Time to market extended further by mandatory local office setup and infrastructure deployment.

- CULTURAL RESISTANCE: Buddhist traditions emphasizing restraint from addictive behaviors create social stigma around gambling. Problem gambling underreported due to shame. Operators face reputational risks. Government maintains “cautious approach” indicating potential for increased restrictions rather than liberalization.

- INFRASTRUCTURE GAPS: Only 65% internet penetration leaves 270,000 people (35% of population) without access. Rural areas particularly underserved. Average 20 Mbps speeds barely adequate for modern gaming experiences. 5G still in pilot phase, years away from widespread deployment.

- ADVERTISING SEVERELY RESTRICTED: Ban on children’s programming hours, celebrity endorsements prohibited, mandatory responsible gambling messages, limits on bonus promotions, restrictions on unsolicited marketing. Customer acquisition extremely expensive in market with only 771,000 total population.

- PAYMENT METHOD LIMITATIONS: Banking system penetration moderate, especially rural areas. E-wallets emerging but not widespread. Cash culture persists. Digital payment infrastructure years behind developed markets. Creates friction in deposits/withdrawals.

- OLIGOPOLISTIC COMPETITION: 3 licensed operators likely already optimized operations and customer acquisition. New entrant faces established competitors with first-mover advantages, existing customer bases, optimized marketing. Market share gain extremely difficult.

- REGULATORY UNCERTAINTY: iGaming License Act only from 2023 – framework very new. Potential for regulatory changes, increased restrictions, or even market closure if government decides gambling conflicts with cultural values. Long-term viability uncertain.

- SCALABILITY IMPOSSIBLE: Population only 771,000 with 2.3% penetration. Even achieving 5% penetration (optimistic) = only 38,550 users. At $350 ARPU = $13.5M annual revenue. After 33% taxes, before operating costs. No path to meaningful scale.

- HIGH CUSTOMER ACQUISITION COST: Small population, advertising restrictions, cultural sensitivity, only 3 competitor environment makes each customer acquisition extremely expensive. CAC likely $200-400+ per player in market where ARPU only $350. Payback periods 12+ months unacceptable.

Player-Specific Issues

- Only 3 Operator Choices: Limited competition reduces product diversity, promotional offers, and innovation. Players stuck with oligopoly pricing rather than competitive market.

- Cryptocurrency Unavailable: Players preferring crypto payments must use traditional banking only, creating friction and excluding crypto-native users.

- 21-Year Age Restriction: Higher than international 18-year standard reduces addressable market, excludes 18-20 year olds who may legally gamble elsewhere.

- Rural Access Problems: 35% of population without internet access effectively excluded from online gambling. Infrastructure gaps particularly affect rural communities.

- Withholding Tax on Winnings: Progressive taxation on gambling winnings reduces net returns to players, making gambling less attractive compared to markets without player taxation.

- Limited Payment Options: Bank transfers and emerging e-wallets only. Credit card acceptance moderate. Cash-based players face deposit/withdrawal friction.

- Cultural Stigma: Buddhist traditions create social pressure against gambling participation. Problem gambling underreported due to shame. Players may face family/community judgment.

- Mandatory Self-Exclusion Prominence: While positive for responsible gambling, prominent self-exclusion tools may discourage casual players concerned about addiction associations.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $1,370,000 – $1,500,000

- License application fee: $50,000

- Minimum capital requirement (held in Bhutanese bank): $1,000,000

- Legal and consultancy services: $40,000

- Technology setup and integration: $150,000

- Office setup and staffing: $100,000

- Marketing and launch: $70,000

- Contingency: $40,000-60,000

Monthly Operating Costs: $45,000 – $65,000

- Staff salaries (local compliance, support, management): $15,000-20,000

- Office rent and utilities: $3,000-5,000

- Technology maintenance and hosting: $5,000-8,000

- Regulatory compliance and reporting: $3,000-5,000

- Marketing and customer acquisition: $15,000-25,000

- Payment processing fees: $2,000-4,000

- Legal and professional services: $2,000-3,000

Annual Operating Costs: $570,000 – $810,000 (including $30,000 license renewal)

Effective Tax Rate on Revenue: 30-33%

- 18% GGR tax on gross gaming revenue

- 15% corporate income tax on profits

- Combined effective rate approximately 30-33% depending on profit margins

Customer Acquisition Cost: $250-400+ per player

- Small population (771,000) creates high CAC

- Advertising restrictions increase acquisition costs

- Cultural sensitivity requires careful marketing

- Only 2.3% market penetration indicates customer acquisition challenges

Revenue Projections (Realistic Scenario):

- Total market revenue 2024: $27 million (3 operators)

- New entrant realistic market share Year 1: 10-15% = $2.7M – $4.0M revenue

- After 33% taxes: $1.8M – $2.7M net revenue

- After $570K-810K operating costs: $1.0M – $1.9M operating profit

- ROI on $1.37M investment: 73-139% (positive but requires 1-2 years)

Time to Breakeven: 18-30 months (assuming successful customer acquisition and operations)

Time to Positive ROI: 24-36 months minimum

Profitability Assessment: ECONOMICS ARE MARGINALLY VIABLE ONLY FOR EXTREMELY EFFICIENT OPERATORS WITH LONG-TERM HORIZONS. The fundamental problem is market size: $27 million total market split among 3-4 operators provides limited revenue potential even with successful execution. $1.37M+ entry investment plus $570K-810K annual operating costs create breakeven timelines of 2-3 years in best-case scenarios. Customer acquisition costs of $250-400+ against $350 ARPU mean 12-16 month payback periods per customer. Market growth at 10.5% CAGR helps but doesn’t fundamentally change economics.

CRITICAL ISSUE: Only 3 licenses exist as of 2025, making market entry impossible for new operators regardless of capital or capability. Even if license became available through acquisition, the $1M capital requirement held in escrow (generating minimal returns) represents massive opportunity cost. For comparison: same $1.37M investment in established markets like UK, Malta, or Ontario would generate 5-10x higher returns with lower regulatory complexity.

VERDICT: Unless acquiring existing licensed operator at favorable valuation, market entry makes no financial sense. Even acquisition requires very careful due diligence on actual profitability of target given market constraints.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Licensed Operators (3 existing) | Medium | Regulatory compliance burden with monthly reporting, quarterly audits, annual certifications. License suspension/revocation for repeated KYC/AML breaches. Fines for advertising violations. Cultural backlash if responsible gambling failures occur. Regulatory framework only established 2023 – potential for increased restrictions. Overall manageable risk if compliance maintained but ongoing vigilance required. |

| Offshore/Unlicensed Operators | High | Unlicensed operations explicitly prohibited under iGaming License Act 2023. Framework demands robust KYC/AML compliance and player protection aligned with international standards. Enforcement mechanisms include monetary fines, asset seizure, and legal action against unlicensed operators and affiliates. No evidence of ISP blocking mentioned but regulatory framework provides authority for enforcement. Payment processing likely blocked for unlicensed sites. Penalties for unauthorized payment systems and illegal offshore operations specified. Small market size makes enforcement easier for regulators. |

| Affiliates/Advertisers | Medium | Advertising heavily restricted with specific prohibitions. Affiliates promoting unlicensed offshore sites face “legal action against unlicensed operators and affiliates” per enforcement mechanisms. Restrictions on direct marketing (unsolicited emails/SMS), celebrity endorsements banned, mandatory responsible gambling messages required. Penalties include monetary fines for advertising violations. Affiliates must ensure promoted operators are licensed. Cultural sensitivity essential – promoting gambling in Buddhist society requires careful approach. Risk manageable for licensed operator affiliates, high for offshore promoters. |

| Payment Processors | Medium-High | Cryptocurrency banned completely – processors handling crypto gambling transactions face regulatory action. “Prohibited activities include unauthorized payment systems” creating risk for processors working with unlicensed operators. Banking system tightly regulated through Financial Services Act. KYC/AML compliance mandatory. Processors must verify operator licensing status. Transaction monitoring required with suspicious transaction reporting to authorities. Penalties not explicitly detailed but financial sector oversight strict in Bhutan. |

| Company Directors/Executives | Low-Medium | Background checks required for all directors and beneficial owners during licensing. Directors of licensed operators face personal liability for compliance failures given mandatory local presence and resident personnel requirements. However, no evidence of personal criminal liability or extradition risks mentioned. Stable political environment and rule of law provide predictability. Main risk is reputational given cultural sensitivity around gambling. License revocation would impact business but personal consequences appear limited to financial losses rather than criminal prosecution. |

| Players (Using Licensed Platforms) | Low | Legal access to iGaming through 3 licensed operators. No criminal penalties for players. Withholding tax on winnings is administrative requirement, not punitive measure. Mandatory 21-year age restriction but enforcement against players minimal. Self-exclusion programs available voluntarily. Main risks are financial (gambling losses) rather than legal. Cultural stigma creates social rather than legal risks. |

| Players (Using Offshore Platforms) | Medium | Legal framework prohibits unlicensed platforms but player-specific penalties not explicitly detailed. “Unlicensed operators prohibited” but unclear if players face consequences. Likely enforcement focused on operators rather than players but legal uncertainty exists. Payment processing may be blocked for offshore sites. Players using VPNs to access blocked sites face potential complications. Social stigma around problem gambling may prevent players from seeking help if using unlicensed platforms. Recommendation: use licensed platforms only to avoid legal ambiguity. |

🚨 Extradition and International Enforcement

Extradition Treaties: Bhutan’s extradition relationships not extensively documented in provided materials. As stable democracy with rule of law, likely has agreements with regional partners and major trading nations, though specific treaty list not available. Constitutional monarchy suggests diplomatic relationships with Commonwealth nations potentially including extradition provisions.

Enforcement History: iGaming License Act only introduced in 2023 – regulatory framework very new with limited enforcement history. No specific cases of international prosecution or extradition related to gambling mentioned. Market’s small size and recent regulatory development suggest enforcement focused domestically on establishing compliance culture rather than international prosecution. However, framework includes provisions for “legal action against unlicensed operators” which could theoretically extend internationally.

Safe Jurisdictions: Not applicable for licensed operators. Unlicensed operators should note that Bhutan’s Buddhist cultural values and stable governance create predictable legal environment – authorities likely to enforce prohibitions consistently rather than sporadically. Geographic isolation and small market size may limit practical international enforcement capability, but operators should not assume immunity.

Travel Risk: Low for licensed operators maintaining compliance. For unlicensed operators or directors of offshore sites targeting Bhutan, travel risk appears minimal given small market and recent regulatory framework. No evidence of aggressive international enforcement. However, market’s small size ($27M) makes targeting Bhutan highly irrational for offshore operators – enforcement risk not worth negligible revenue potential.

Assessment: Extradition and international enforcement risk appears LOW overall due to market’s tiny size, recent regulatory development, and lack of enforcement precedent. However, regulatory framework establishes clear prohibitions that authorities can enforce if desired. Licensed operators face no extradition risk. Unlicensed operators face theoretical but practically limited risk given small market makes enforcement unlikely priority for international cooperation.

📋 Final Verdict

Bhutan receives an Operator Ease Score of 4.8/10 and a Player Access Score of 6.3/10, resulting in an overall market attractiveness rating of 5.6/10.

HONEST ASSESSMENT: This market is fundamentally unviable for new operator entry despite legal framework. The core issue is market access: only 3 licenses exist as of 2025 with no indication additional licenses will be granted. Even if license became available, economics are brutal – $27 million total market revenue makes this one of world’s smallest licensed iGaming markets. Requiring $1.37M+ entry investment with mandatory $1M capital held in escrow for market generating only $27M annually across all operators is absurd. Customer acquisition costs of $250-400+ against $350 ARPU create 12-16 month payback periods. Operating costs $570K-810K annually represent 20-30% of total market revenue. Cultural resistance from Buddhist traditions, advertising restrictions, cryptocurrency ban, mandatory local presence, and 6-9 month licensing timeline compound challenges. BOTTOM LINE: Unless you’re one of the 3 existing licensed operators, forget this market exists. Even for those 3, profitability requires exceptional operational efficiency. For everyone else, this is a closed market with terrible economics even if access were possible.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- REALISTICALLY: ALMOST NOBODY. Market access closed with only 3 licenses granted total as of 2025.

- Considering acquisition of existing licensed operator at favorable valuation (under 3x annual EBITDA given market constraints). Conduct extensive due diligence on actual profitability.

- Major Asian iGaming group seeking geographic diversification and willing to accept 3-5 year ROI timeline despite small market size. Must have $2M+ capital available.

- Operator with existing infrastructure in India, Bangladesh, or Nepal where Bhutan operations could be incremental addition to regional footprint with shared services reducing costs.

- Company with specific strategic interest in Buddhist-majority markets or unique cultural expertise in responsible gambling promotion in religiously conservative societies.

❌ Definitely Avoid If You Are:

- ANY NEW OPERATOR SEEKING LICENSING – Only 3 licenses exist with no indication more will be granted. Market access essentially impossible.

- Seeking profitable operations within 18-24 months – Economics require 24-36 months minimum for positive ROI even with flawless execution.

- Casino-focused operator expecting significant revenue – Total market only $27M across ALL product categories. Casino games just one segment.

- Cryptocurrency-focused platform – Crypto completely banned, eliminating core payment method and appeal to crypto-native users.

- Startup or small operator with under $2M capital – $1M capital requirement held in escrow plus $370K+ setup costs plus $570K-810K annual operating costs require substantial financial backing.

- Operators seeking scalable growth markets – Population 771,000 with 2.3% penetration creates absolute ceiling of ~40,000 potential users even at 5% penetration. No path to meaningful scale.

- Companies requiring remote operation – Mandatory physical presence with local office, resident staff, partnerships with local entities eliminates remote operation possibility.

- Operators needing quick licensing – 6-9 month timeline plus office setup extends time to market to 9-12 months minimum.

- Affiliates promoting offshore/unlicensed operators – Legal action against affiliates of unlicensed operators creates prosecution risk not worth tiny market potential.

- Payment processors handling crypto gambling – Cryptocurrency banned creates regulatory risk for processors facilitating crypto transactions.

- Any operator prioritizing ROI and profitability – Same $1.37M investment deployed in UK, Malta, Ontario, or other established markets would generate 5-10x higher returns with lower risk and complexity.

⚠️ BOTTOM LINE: Market access closed, economics terrible, market too small – avoid completely unless acquiring existing licensed operator at steep discount. This is a closed oligopoly where entry barriers (only 3 licenses ever granted) make discussion of market entry purely theoretical. For the 3 existing operators, market provides modest but viable business if costs tightly controlled. For everyone else, pretend this market doesn’t exist and deploy capital in markets with actual growth potential and reasonable economics. Rating of 5.6/10 reflects legal framework and player access, but 4.8/10 Operator Ease Score accurately represents reality: this market is largely inaccessible and economically marginal even if access were possible.