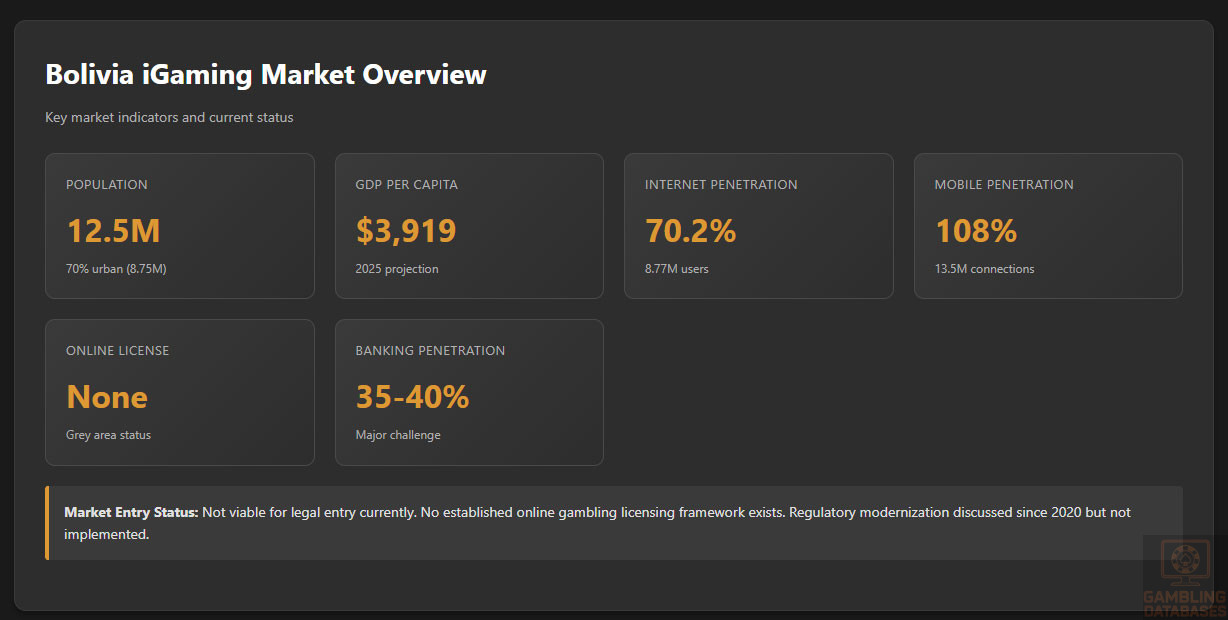

Bolivia presents a complex and challenging landscape for iGaming operators, characterized by highly restrictive gambling regulations and an undefined online licensing framework. With a population of 12.5 million and growing internet penetration reaching 70.2%, the market demonstrates underlying digital potential.

This analysis provides comprehensive insights into Bolivia’s current gambling environment, demographic composition, technological infrastructure, and the realistic prospects for market entry by international iGaming operators seeking opportunities in South American markets.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Legal Status – Online Gambling | Grey Area / Undefined | No established licensing framework |

| Legal Status – Land-Based | Highly Restricted | Only one licensed casino operating |

| Regulatory Authority | AJ (Autoridad de Fiscalización del Juego) | Established 2010 under Law No. 060 |

| Online License Available | No | No defined application process exists |

| License Application Cost | Not Established | Framework not yet implemented |

| License Duration | Not Established | Determined by AJ on case basis |

| GGR Tax Rate – Land-Based | 30% | For licensed land-based casinos |

| GGR Tax Rate – Online | 25% (proposed) | Not yet implemented |

| Corporate Income Tax | 25% | Flat rate for all businesses |

| Total Population | 12.5 million | 2025 estimate |

| Urban Population | 70% | 8.75 million urban residents |

| Median Age | 25.2 years | Young demographic profile |

| GDP (Total) | $47 billion USD | 2024 estimate |

| GDP Per Capita | $3,919 USD | 2025 projection |

| GDP Growth Rate | 2.5% – 3.0% | 2025 forecast |

| Internet Penetration | 70.2% | 8.77 million internet users |

| Mobile Penetration | 108% | 13.5 million mobile connections |

| Smartphone Penetration | 65% – 70% | Predominantly Android devices |

| Social Media Users | 7.63 million | 61.1% of population |

| Mobile Internet Speed | 10.75 Mbps | Median download speed |

| Fixed Internet Speed | 47.72 Mbps | Median download speed |

| Online Banking Penetration | 35% – 40% | Growing digital payment adoption |

| Gambling Tax Revenue (2021) | 30 million BOB ($4.4M USD) | Down from 47 million BOB in 2020 |

| Estimated Online Market Size | Unknown | Study commissioned by AJ in 2023 |

| Market Entry Difficulty | Very High | No legal pathway currently exists |

| Ease of Doing Business Rank | 150 out of 190 | World Bank ranking (archived) |

| Market Entry Timeline | Indefinite | Awaiting regulatory framework |

| Recommended Market Status | Monitor Only | Not viable for entry currently |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

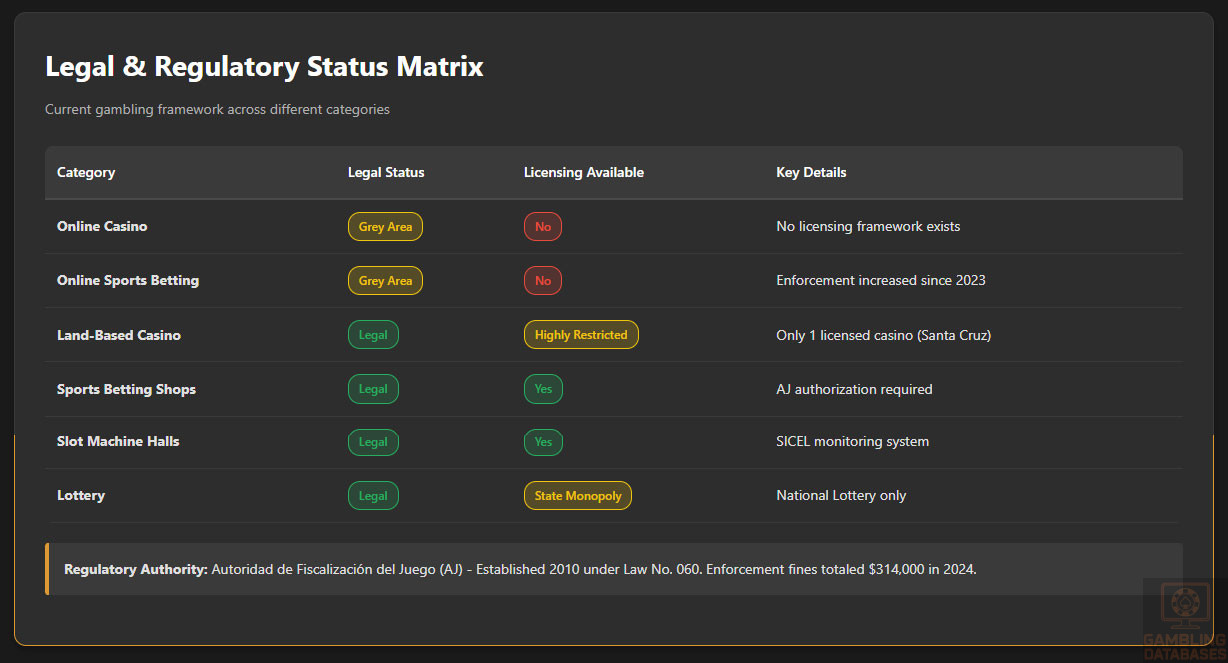

Bolivia’s gambling sector operates under Law No. 060, enacted in 2010, which established the regulatory foundation for all gambling activities. The legislation created the Autoridad de Fiscalización del Juego (AJ) as the primary oversight body responsible for licensing, supervision, and enforcement.

The legal framework is characterized by its highly restrictive nature, with all unauthorized gambling activities explicitly prohibited and subject to severe penalties. The law focuses primarily on land-based operations, while online gambling exists in a legal grey area with no clear regulatory pathway.

Before 2010, gambling regulation was minimal, with only the National Lottery of Bolivia (Lotería Nacional de Bolivia, LNB) established in 2002 providing some oversight. The current system represents a more structured but extremely limited approach to gambling regulation.

The regulatory environment has shown minimal evolution since implementation, despite repeated announcements about modernization efforts and plans to address the online gambling sector that emerged during the COVID-19 pandemic.

Land-Based Gambling Activities

Casino Operations: Bolivia currently licenses only one land-based casino, located in Santa Cruz de la Sierra. This severely restricted market presents minimal competition but also indicates the government’s cautious approach to gambling expansion. The licensed casino operates under strict conditions with daily regulatory oversight.

Sports Betting Venues: Land-based sports betting is legal and regulated by the AJ. Sports betting shops can be found in various locations throughout major cities, offering betting options on popular sports including soccer, basketball, and tennis. These operations must obtain proper authorization and operate within defined parameters.

Slot Machine Halls: Slot machine operations require specific licensing from the AJ. The regulatory authority conducts regular inspections and has implemented an Online Control System (SICEL) similar to Colombia’s remote monitoring infrastructure to oversee slot machine operations and ensure compliance.

Lottery Operations: The National Lottery remains a state-controlled monopoly and represents the most established form of legal gambling in Bolivia. Lottery games enjoy broader social acceptance and face fewer restrictions compared to other gambling activities.

Online Gambling Framework

Current Legal Status: Online gambling operates in a legal grey area in Bolivia. Law No. 060 explicitly prohibits unauthorized gambling activities, including online operations, but fails to provide a clear licensing procedure for online gambling operators.

This ambiguity has created a situation where the law technically prohibits online gambling, yet foreign operators continue to accept Bolivian players with minimal enforcement action. The lack of clarity creates significant legal uncertainty for any operator considering market entry.

Prohibited Activities: All online gambling activities not expressly authorized by the state are prohibited. However, the absence of a licensing framework means that essentially no online gambling can be legally authorized under current legislation.

Enforcement Approach: The AJ has increased its enforcement efforts, particularly since 2023, when it announced intensified controls on unauthorized online gambling platforms. In 2024, the authority issued fines totaling $314,000 against illegal operators.

However, enforcement remains primarily focused on domestic operators and visible promotions rather than blocking access to international platforms. Internet Service Provider (ISP) blocking of unlicensed operators has not been systematically implemented.

Licensed Operators and Market Players

Land-Based Market: The land-based casino market is dominated by the single licensed casino in Santa Cruz de la Sierra. The exact identity and ownership structure of this operator is not widely publicized. Sports betting shops operate through multiple smaller operators with local licenses.

Lottery Market: The National Lottery of Bolivia (LNB) maintains monopoly control over lottery operations. As a state entity, it faces no private competition and represents the most established gambling operation in the country.

Online Market Players: The online gambling market is served exclusively by international operators licensed in other jurisdictions such as Curaçao, Malta, and Gibraltar. These operators accept Bolivian players but operate without local authorization.

Major international brands serving the Bolivian market include operators focused on Latin American markets. However, specific market share data is unavailable due to the unregulated nature of online operations.

Market Concentration: The legal market is highly concentrated, with the state lottery dominating and only one casino licensed. The grey-market online sector likely represents a significant portion of total gambling activity but operates without transparency or regulatory oversight.

Competitive Landscape: Competition in the legal market is virtually non-existent due to licensing restrictions. The online grey market features competition among international operators, but Bolivian players have limited local options and face challenges with payment processing and customer support.

Licensing Framework and Requirements

Application Process and Eligibility

Regulatory Authority Contact: The Autoridad de Fiscalización del Juego (AJ) serves as the sole licensing authority. However, as of 2025, no formal process exists for obtaining online gambling licenses. The authority has offices in La Paz.

Online Licensing Status: There is no established process for obtaining an online gambling license in Bolivia. The AJ has discussed implementing online licensing procedures since 2020, but no timeline or specific requirements have been published.

Land-Based Licensing: For land-based operations, applicants must submit comprehensive documentation including business plans, ownership structures, management information, technical specifications of gaming equipment, and evidence of financial capacity. Background checks on directors and key personnel are mandatory.

Application Timeline: For land-based licenses, the process involves thorough operational inspections and audits by the AJ before approval. The timeline is determined on a case-by-case basis, with the authority conducting extensive due diligence.

Financial Requirements: Specific financial guarantee amounts and minimum capital requirements vary by license type and are determined by the AJ during the application process. Online gambling financial requirements have not been established.

Application Fees: License application fees for land-based operations are not publicly disclosed and appear to be negotiated individually. No fee structure exists for online gambling licenses.

Local Presence and Operational Requirements

Physical Presence: Land-based gambling operators must maintain a physical presence in Bolivia, including offices and operational facilities. The single licensed casino operates from its premises in Santa Cruz de la Sierra.

Online Presence Requirements: Requirements for online operators have not been defined. However, based on discussions in 2020, any future framework would likely require local representation, similar to requirements in neighboring countries.

Domain and Hosting: No specific requirements exist for domain registration or server location for online gambling operations, as the licensing framework remains undefined. Future regulations may mandate .bo domain usage or local server hosting.

Personnel Requirements: Land-based operators must employ local staff and comply with Bolivian labor laws, which limit foreign employees to 15% of total workforce. Management positions may require Bolivian nationals or residents.

Foreign Ownership: Bolivia generally allows 100% foreign ownership of businesses, including in most gambling activities. However, restrictions apply in strategic sectors, and gambling regulations may impose additional requirements.

Local Partnership Requirements: While not explicitly mandated by general business law, the restrictive licensing environment and single casino operation suggest that local partnerships or relationships with government entities may be practically necessary.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification: The legal gambling age in Bolivia is 18 years. All gambling operators must verify customer age before allowing participation. Land-based venues check identification documents, while online age verification requirements remain undefined.

KYC/AML Standards: Land-based operators must comply with Bolivia’s anti-money laundering regulations, which require identity verification and transaction monitoring. The Financial Services Supervisory Authority (ASFI) oversees financial crime prevention.

Responsible Gambling Measures: The AJ has expressed concern about problem gambling and unauthorized operations. However, specific mandatory responsible gambling requirements for operators are not clearly defined in published regulations.

Self-Exclusion Systems: No national self-exclusion system currently exists in Bolivia. Individual land-based operators may maintain their own exclusion lists, but this is not standardized or centrally coordinated.

Player Information Disclosure: Requirements for displaying odds, return-to-player percentages, and responsible gambling information are not clearly specified in available regulatory documentation.

Session Limits and Loss Limits: Mandatory session time limits, deposit limits, or loss limits have not been implemented in Bolivia’s gambling regulations. Future online gambling framework may incorporate such protections.

Financial Monitoring and Reporting

Transaction Monitoring: Land-based operators must monitor transactions exceeding $10,000 USD and report suspicious activities to prevent money laundering. This applies to both gambling operations and general financial transactions in Bolivia.

Reporting Requirements: Licensed operators must submit regular reports to the AJ, though the specific frequency and format of reporting obligations are not publicly detailed. The authority conducts regular inspections and audits.

Audit Procedures: The AJ conducts thorough operational inspections and financial audits of licensed operators. Companies with annual sales exceeding $170,000 USD must submit audited financial statements to the commercial registry.

Data Retention: Specific data retention requirements for gambling operators are not detailed in publicly available regulations. General business record-keeping requirements under Bolivian law apply.

Taxation Structure and Financial Obligations

Player Taxation

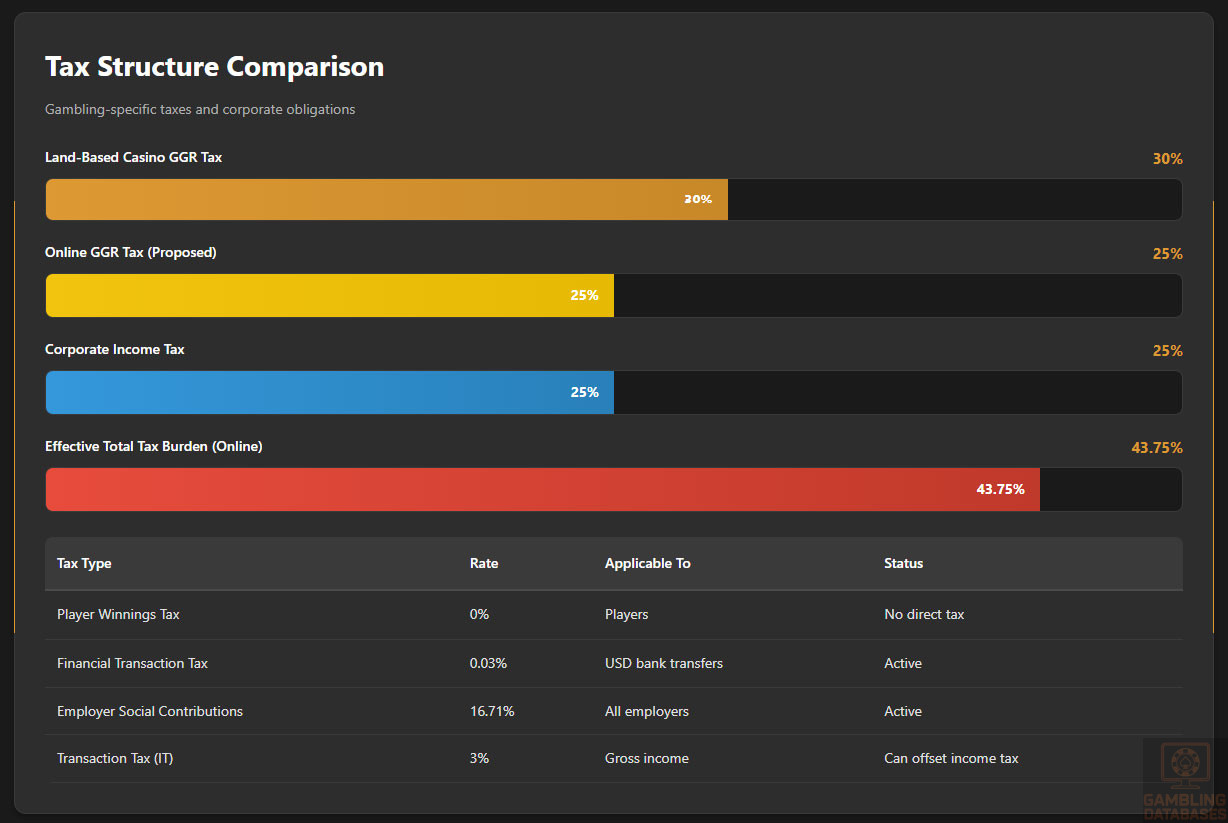

Winnings Tax Rate: Bolivia does not currently impose direct taxation on player winnings from gambling activities. This differs from some neighboring countries that tax gambling proceeds.

Withholding Procedures: No withholding tax on gambling winnings is applied at source. Players are subject to Bolivia’s personal income tax system, which uses a flat rate of 13% on income.

Player Obligations: Individual players are theoretically required to declare gambling winnings as income, but enforcement of this provision is minimal and compliance rates appear low.

Tax-Free Thresholds: No specific tax-free threshold exists for gambling winnings. Standard personal income tax thresholds and deductions apply to all income sources.

Operator Taxation

GGR Tax – Land-Based Casinos: Licensed land-based casinos pay a 30% tax on Gross Gaming Revenue. This represents the primary gambling-specific tax obligation for casino operators.

GGR Tax – Online Operations: The proposed framework discussed in 2020 suggested a 25% GGR tax rate for online gambling operators. However, this has not been implemented and remains unconfirmed.

Corporate Income Tax: All gambling operators are subject to Bolivia’s flat corporate income tax rate of 25% on profits, in addition to any gambling-specific taxes.

Operational Fees: License renewal fees and other operational charges exist but are not publicly disclosed. The AJ determines these on a case-by-case basis.

Turnover Tax: Bolivia may impose additional transaction-based taxes depending on the specific structure of operations. Financial transaction taxes of 0.03% apply to certain banking transfers.

| Tax Type | Rate | Applicable To | Status |

|---|---|---|---|

| Land-Based Casino GGR Tax | 30% | Licensed casinos | Active |

| Online GGR Tax (Proposed) | 25% | Online operators | Not implemented |

| Corporate Income Tax | 25% | All gambling businesses | Active |

| Player Winnings Tax | 0% | Players | No direct tax |

| Financial Transaction Tax | 0.03% | USD bank transfers | Active |

| Employer Social Contributions | 16.71% | All employers | Active |

Gambling Market Financial Performance

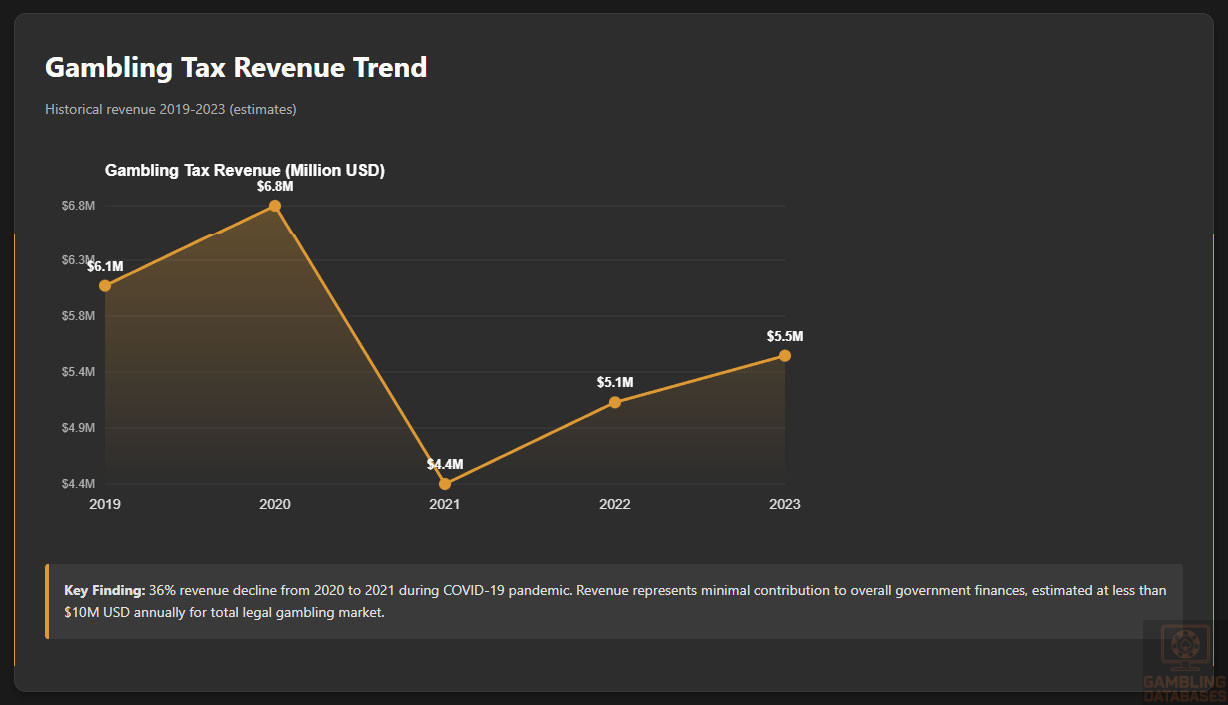

Tax Revenue Trends: Gambling tax revenue in Bolivia declined significantly from 47 million bolivianos ($6.8M USD) in 2020 to 30 million bolivianos ($4.4M USD) in 2021, representing a 36% decrease.

This decline occurred during the COVID-19 pandemic period and reflects reduced land-based gambling activity. The revenue also represents a minimal contribution to overall government finances.

Market Size Estimation: The total legal gambling market in Bolivia is estimated to generate less than $10 million USD annually in operator revenue, based on tax collection data. This represents one of the smallest regulated gambling markets in South America.

Online Market Size: The size of the grey-market online gambling sector is unknown. The AJ commissioned a study in 2023 to determine online gambling consumption in major cities, but results have not been publicly released.

| Year | Tax Revenue (Million BOB) | Tax Revenue (Million USD) | YoY Change |

|---|---|---|---|

| 2019 | 42 | 6.1 | – |

| 2020 | 47 | 6.8 | +11.9% |

| 2021 | 30 | 4.4 | -36.2% |

| 2022 | Estimated 35 | 5.1 | +16.7% (est) |

| 2023 | Estimated 38 | 5.5 | +8.6% (est) |

Advertising and Marketing Restrictions

Permitted Channels: Bolivia has not established comprehensive advertising regulations specific to gambling. Land-based operators appear to conduct limited marketing through traditional channels, though the single casino operation reduces the need for competitive advertising.

Content Restrictions: Specific content guidelines for gambling advertising have not been publicly detailed. General advertising standards prohibiting false claims and protecting minors apply.

Promotional Limitations: Restrictions on bonus offers, wagering requirements, and promotional terms have not been codified in available regulations. This represents an area that would likely be addressed in any future online gambling framework.

Sponsorship Regulations: Sports sponsorship by gambling operators is not clearly regulated. Football clubs and sports organizations in Bolivia have not prominently featured gambling sponsorships compared to markets with established industries.

Affiliate Marketing: No specific regulations govern gambling affiliate marketing in Bolivia. The undefined online licensing framework means affiliate operations exist in the same grey area as operators themselves.

Protection of Minors: Gambling advertising must not target minors, consistent with the 18+ age requirement. However, detailed restrictions on advertising placement, timing, and content have not been established.

Recent Regulatory Changes and Their Impact

2020 Modernization Proposal: In July 2020, then-AJ Executive Director Juan Carlos Antonio Abrego presented proposals to amend Law No. 060, introducing online gambling regulation and modernized sanctioning regimes. The proposal aimed to boost the economy and generate employment.

However, these amendments were not implemented, and the regulatory framework remains unchanged. This represents a significant missed opportunity for market development.

2023 Enforcement Intensification: In April 2023, current AJ Executive Director Jessica Saravia Atristain announced increased controls on unauthorized online gambling platforms, describing the pandemic-era growth of illegal sites as a priority concern.

The authority committed to conducting a market study in major cities and implementing campaigns to reduce unauthorized business promotions. In 2024, fines totaling $314,000 were issued against illegal operators.

2025 Criminal Enforcement: In July 2025, the AJ initiated criminal and administrative proceedings against an unlicensed online sports betting platform, marking a notable shift toward more aggressive enforcement. The authority pledged further legal action against illicit platforms.

Impact on Market Entry: These developments have not created a pathway for legal market entry but have increased operational risk for unauthorized operators. The combination of enforcement without licensing options creates an inhospitable environment.

Enforcement Mechanisms and Penalties

Penalty Structure: Law No. 060 establishes severe penalties for unauthorized gambling operations, though specific fine amounts and penalty structures are not detailed in publicly available documentation. The $314,000 in fines issued in 2024 demonstrates active enforcement.

License Suspension/Revocation: The AJ has authority to suspend or revoke licenses for non-compliance. Given the single licensed casino, examples of such actions are not publicly documented.

Criminal Penalties: The 2025 initiation of criminal proceedings against an unlicensed operator indicates that illegal gambling can result in criminal charges beyond administrative fines. Specific criminal penalties under Bolivian law can include imprisonment.

ISP Blocking: While the AJ has discussed blocking unauthorized gambling websites, systematic implementation of ISP-level blocking has not been confirmed. Technical infrastructure for widespread site blocking may be limited.

Payment Processor Restrictions: Bolivia’s banking system faces U.S. dollar scarcity and includes transaction monitoring requirements. However, specific restrictions targeting gambling payment processing have not been implemented systematically.

Recent Enforcement Examples: Beyond the 2024 fines and 2025 criminal proceedings, the authority destroyed over 540kg of illegal gambling equipment in May 2025, exporting it as electronic waste to the United States.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Total Population: Bolivia’s population stands at approximately 12.5 million in 2025, representing one of the smaller populations in South America. The country has experienced steady but modest population growth of around 1.4% annually.

This demographic scale limits the total addressable market for gambling operators compared to larger regional markets like Brazil, Mexico, or Argentina. However, increasing urbanization and digital connectivity are expanding the reachable consumer base.

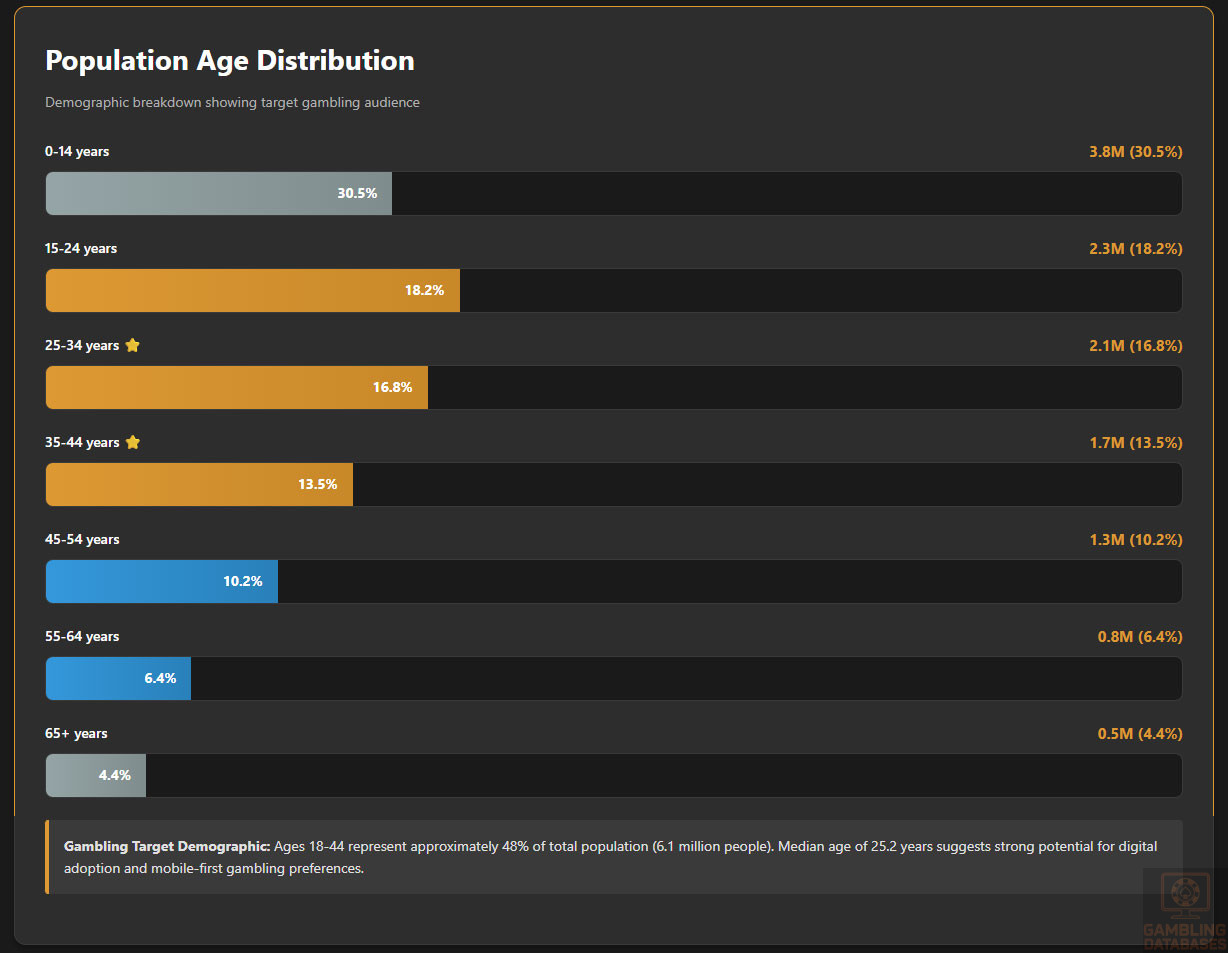

Age Distribution: Bolivia has a notably young population with a median age of 25.2 years. The age structure shows significant concentration in younger demographics, which typically represents the core gambling audience in digital markets.

| Age Group | Percentage of Population | Approximate Number |

|---|---|---|

| 0-14 years | 30.5% | 3.8 million |

| 15-24 years | 18.2% | 2.3 million |

| 25-34 years | 16.8% | 2.1 million |

| 35-44 years | 13.5% | 1.7 million |

| 45-54 years | 10.2% | 1.3 million |

| 55-64 years | 6.4% | 0.8 million |

| 65+ years | 4.4% | 0.5 million |

Gender Distribution: Bolivia has a relatively balanced gender ratio with approximately 49.5% male and 50.5% female population. Life expectancy stands at approximately 72 years, with women living slightly longer than men at 74 years versus 70 years.

Implications for Gambling: The concentration of population in the 18-44 age range (approximately 48% of total population or 6.1 million people) represents the primary target demographic for online gambling. The young median age suggests potential for digital adoption and mobile-first gambling preferences.

Geographic Distribution

Urbanization Rate: Approximately 70% of Bolivia’s population lives in urban areas, equating to 8.75 million urban residents. This represents a significant shift from historical rural population dominance and continues to trend upward.

Urban concentration is crucial for gambling market development, as cities offer better internet infrastructure, higher incomes, and greater exposure to digital entertainment options.

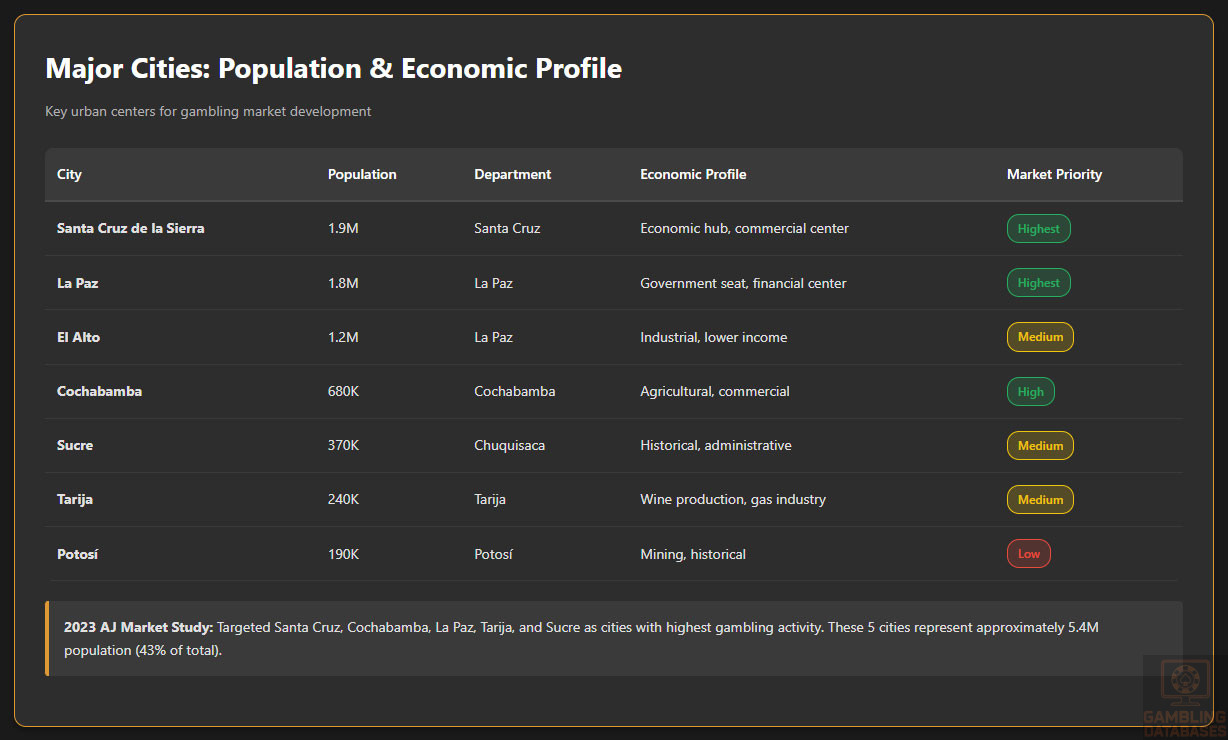

Major Population Centers: Bolivia’s population is concentrated in several key cities, with significant regional economic differences affecting purchasing power and market potential.

| City | Population | Region | Economic Profile |

|---|---|---|---|

| Santa Cruz de la Sierra | 1.9 million | Santa Cruz Department | Economic hub, commercial center |

| La Paz (administrative) | 1.8 million | La Paz Department | Government seat, financial center |

| El Alto | 1.2 million | La Paz Department | Industrial, lower income |

| Cochabamba | 680,000 | Cochabamba Department | Agricultural, commercial |

| Sucre (constitutional capital) | 370,000 | Chuquisaca Department | Historical, administrative |

| Tarija | 240,000 | Tarija Department | Wine production, gas industry |

| Potosí | 190,000 | Potosí Department | Mining, historical |

Regional Economic Differences: Santa Cruz represents Bolivia’s wealthiest region with higher GDP per capita and more developed commercial infrastructure. La Paz serves as the political and financial center with concentrated middle-class population.

The AJ’s 2023 market study specifically targeted Santa Cruz, Cochabamba, La Paz, Tarija, and Sucre as cities with the highest gambling activity, confirming these urban centers as key markets.

Internet Access Patterns: Urban areas enjoy significantly better internet connectivity than rural regions. Fixed broadband infrastructure is concentrated in major cities, while mobile internet provides primary connectivity in smaller towns and rural areas.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

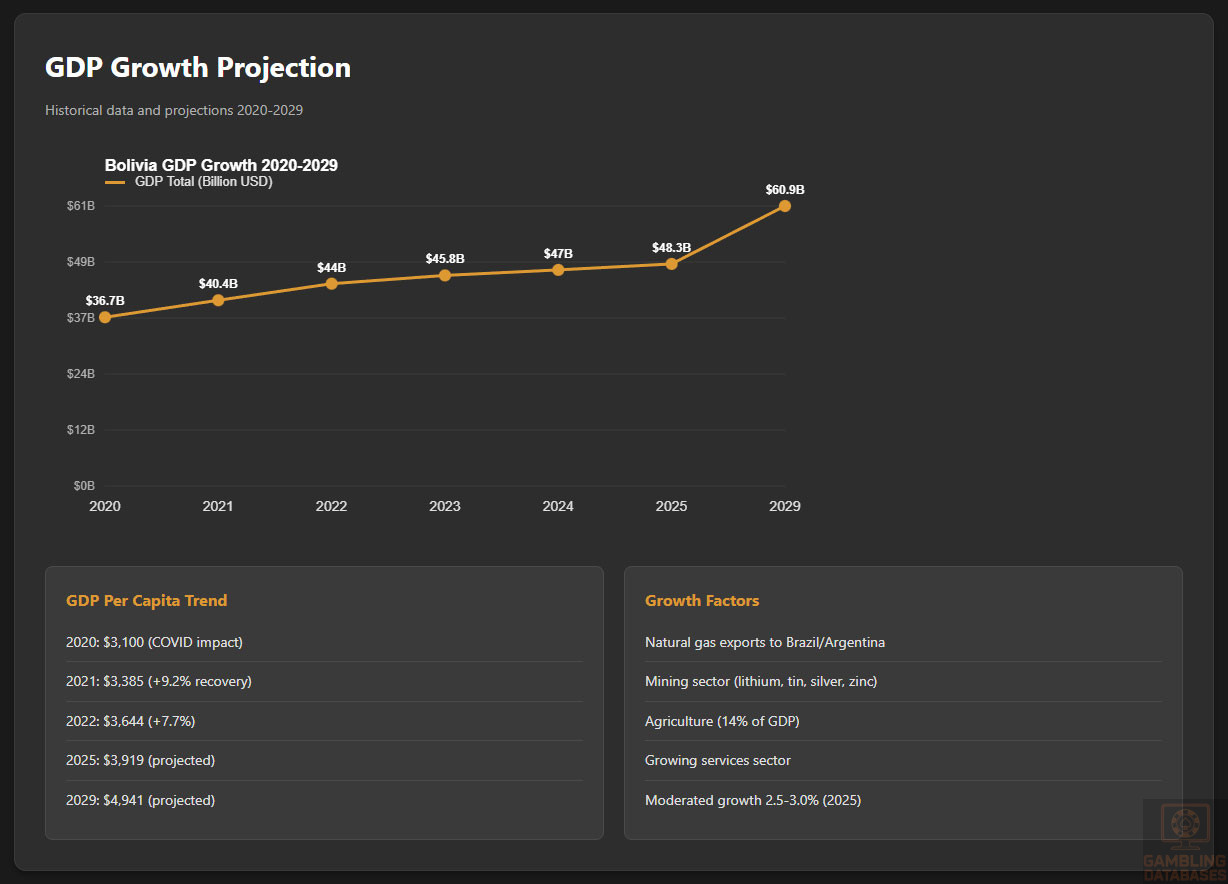

Total GDP: Bolivia’s economy is valued at approximately $47 billion USD in total GDP for 2024-2025. This represents one of the smaller economies in South America, though the country has made progress in economic development over recent decades.

GDP Per Capita: Bolivia’s GDP per capita stands at approximately $3,919 USD in 2025, placing it among the poorest countries in South America. This represents a significant constraint on consumer spending power for discretionary entertainment like gambling.

For comparison, this is substantially lower than regional neighbors: Chile ($17,000 USD), Argentina ($12,000 USD), Peru ($7,500 USD), and Colombia ($7,200 USD). Only Paraguay has comparable GDP per capita in the region.

GDP Growth Trends: Bolivia experienced 3.61% GDP growth in 2022 and 6.11% in 2021 following pandemic recovery. However, growth has moderated to 2.5-3.0% projected for 2025.

| Year | GDP Total (Billion USD) | GDP Per Capita (USD) | Growth Rate |

|---|---|---|---|

| 2020 | 36.7 | 3,100 | -8.74% |

| 2021 | 40.4 | 3,385 | +6.11% |

| 2022 | 44.0 | 3,644 | +3.61% |

| 2023 | 45.8 | 3,750 | +2.8% (est) |

| 2024 | 47.0 | 3,820 | +2.5% (est) |

| 2025 | 48.3 | 3,919 | +2.7% (proj) |

| 2029 | 60.9 | 4,941 | +26% cumulative (proj) |

Economic Sector Composition: Bolivia’s economy is heavily dependent on natural resources, particularly natural gas exports to Brazil and Argentina. Mining (tin, silver, zinc, lithium) represents a major sector. Agriculture accounts for approximately 14% of GDP, while services comprise the largest sector.

The government maintains significant state control over key industries, which has deterred some foreign investment. Manufacturing remains underdeveloped compared to larger South American economies.

Employment and Wages: Average monthly wages in Bolivia are approximately $729 USD, though this varies significantly by sector and region. Urban wages are higher than rural, and formal sector employment offers better compensation than informal work.

Unemployment rates have remained relatively low at 3-5%, but underemployment and informal sector participation are high. Approximately 44% of workers are engaged in agriculture, often in subsistence farming.

Inflation Trends: Bolivia has maintained relatively stable inflation in recent years at 2-4% annually, a significant improvement from hyperinflation that exceeded 20,000% in 1985. Currency stability has improved but U.S. dollar scarcity has emerged as a concern since 2014.

Income and Wealth Distribution

Income Inequality: Bolivia has made progress in reducing poverty, with extreme poverty declining from 38% in 2006 to 18% by 2019. However, significant income inequality persists with wealth concentrated in urban centers and certain regions.

Average Household Income: Average monthly household income is estimated at $850-1,200 USD in urban areas, with significant variation based on employment sector and region. Rural household incomes are substantially lower at $400-600 USD monthly.

Disposable Income Constraints: With average monthly wages around $729 USD and basic living costs consuming a large portion of household budgets, disposable income for entertainment and gambling remains limited for most Bolivians.

This economic reality significantly constrains the viable target market for gambling operators to a relatively small percentage of the population with higher incomes.

Middle Class Size: Bolivia’s middle class has grown but remains smaller than in neighboring countries. Estimates suggest 20-25% of the population can be classified as middle class, representing approximately 2.5-3.0 million people.

This segment, concentrated in Santa Cruz, La Paz, and Cochabamba, represents the primary viable market for online gambling services.

| Income Bracket (Monthly USD) | Percentage of Population | Approximate Number | Gambling Potential |

|---|---|---|---|

| Below $300 | 35% | 4.4 million | Very Low |

| $300-$600 | 30% | 3.8 million | Low |

| $600-$1,200 | 20% | 2.5 million | Moderate |

| $1,200-$2,500 | 10% | 1.3 million | Good |

| Above $2,500 | 5% | 0.6 million | High |

Market Size and Growth Projections

Current Legal Market Size: Based on gambling tax revenue of 30-38 million bolivianos ($4.4-5.5M USD) annually, the legal gambling market is estimated to generate $8-12 million USD in total operator revenue. This represents one of the smallest regulated markets in Latin America.

Grey Market Online Gambling: The size of unauthorized online gambling is unknown. The AJ commissioned a market study in 2023 but has not released findings. Conservative estimates suggest the grey market could represent $15-30 million USD annually based on regional patterns.

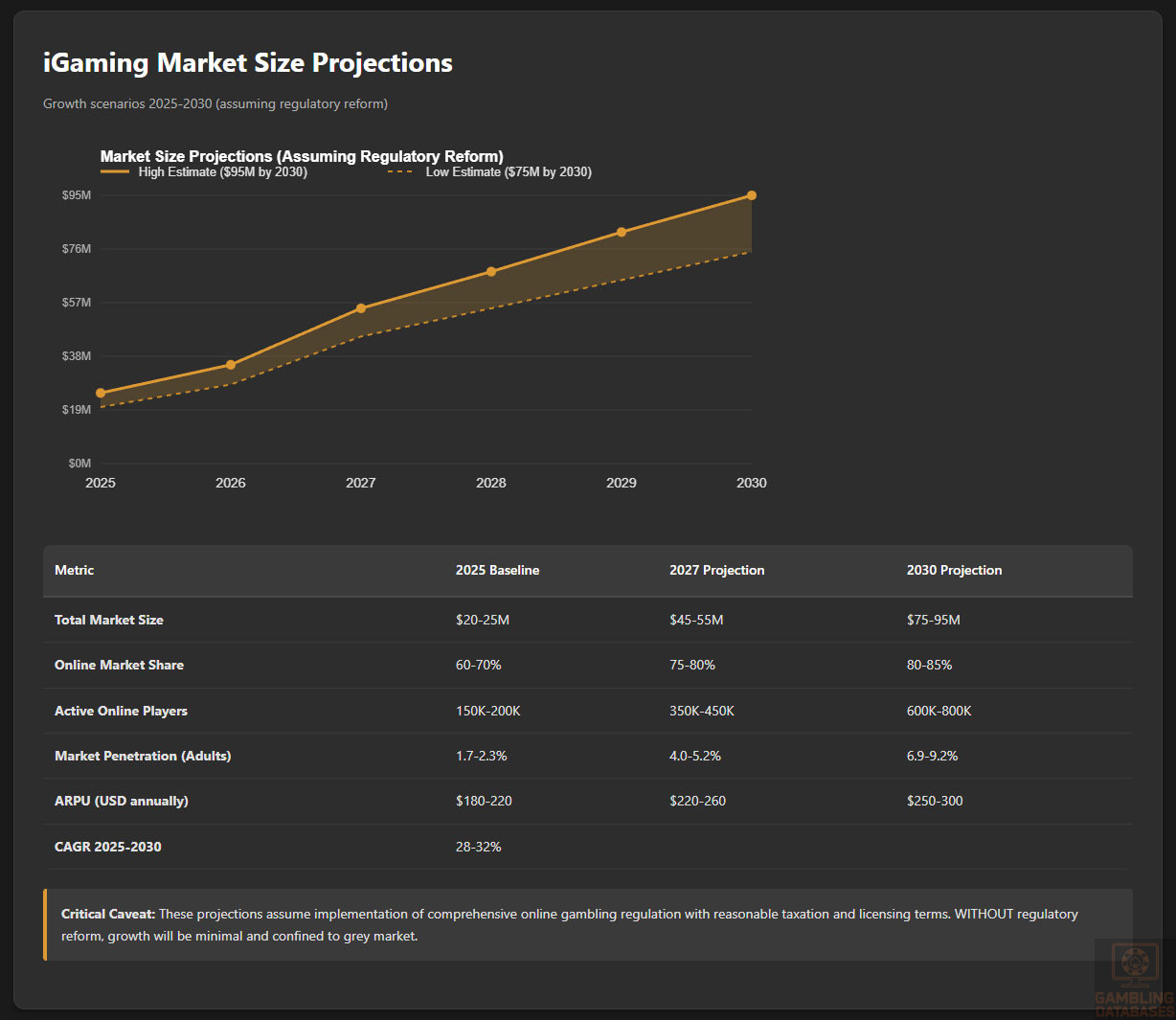

Total Addressable Market: If Bolivia were to implement comprehensive online gambling regulation with appropriate licensing, the total market could potentially reach $50-80 million USD annually within 3-5 years of implementation.

This estimate is based on: adult population (8.7 million), gambling participation rates in similar markets (15-25%), average spending per active player ($150-300 annually), and economic constraints.

Growth Projections: Without regulatory reform, the legal market will remain stagnant. If online licensing is implemented, the market could experience 20-30% annual growth for 3-5 years as grey market activity transitions to licensed operators and new players enter.

| Metric | 2025 Baseline | 2027 Projection | 2030 Projection |

|---|---|---|---|

| Total Market Size (Million USD) | 20-25 | 45-55 | 75-95 |

| Online Market Share | 60-70% | 75-80% | 80-85% |

| Active Online Players | 150,000-200,000 | 350,000-450,000 | 600,000-800,000 |

| Market Penetration (Adults) | 1.7-2.3% | 4.0-5.2% | 6.9-9.2% |

| ARPU (USD annually) | 180-220 | 220-260 | 250-300 |

| CAGR (2025-2030) | – | – | 28-32% |

Important Caveat: These projections assume implementation of comprehensive online gambling regulation with reasonable taxation and licensing terms. Without regulatory reform, growth will be minimal and confined to the grey market.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy Rates: Bolivia has achieved a literacy rate of approximately 92-94% for adults, representing significant progress in education access. Youth literacy rates are higher at 98-99%, indicating improvements in educational infrastructure.

However, literacy rates vary by region and gender, with rural areas and older populations showing lower rates. Indigenous language speakers may have limited Spanish literacy despite functional literacy in native languages.

Education Levels: Primary education completion rates have improved significantly, reaching approximately 95%. Secondary education completion is lower at 70-75%, while tertiary education enrollment remains limited at 20-25% of the relevant age cohort.

The education system faces challenges with quality, particularly in rural areas and for indigenous populations. This affects workforce skill development and digital literacy preparation.

Digital Literacy: Digital literacy is growing rapidly, particularly among younger urban populations. However, significant gaps exist between urban and rural areas, and between younger and older age groups.

Smartphone adoption has driven practical digital skills development, with many Bolivians learning to navigate apps and digital services through mobile devices rather than computers.

Language Skills: Spanish is the primary official language, spoken by the majority of the population. Indigenous languages including Quechua, Aymara, and Guarani are also official languages and widely spoken, particularly in rural areas.

English proficiency is low among the general population, concentrated among educated urban elites and younger professionals. This necessitates Spanish-language gambling platforms for mass market appeal.

Cultural and Social Factors

Communication and Language

Primary Languages: Spanish dominates in business and urban settings. However, approximately 36% of the population speaks Quechua, 27% speaks Aymara, and smaller percentages speak other indigenous languages as their primary tongue.

Successful gambling operators would need to provide services in Spanish as a minimum, with potential consideration for indigenous language support in specific regions to maximize market penetration.

Internet Language Preferences: Spanish is the dominant language for internet content consumption. Social media, e-commerce, and digital services operate primarily in Spanish. English-only platforms face significant adoption barriers.

Business Communication Norms: Business communication in Bolivia values personal relationships and face-to-face interaction. Trust building is important, and formal documentation is expected. Bureaucratic processes often require physical presence and paper documentation despite digitalization efforts.

Cultural Attitudes

Gambling Acceptance: Cultural attitudes toward gambling in Bolivia are mixed. Traditional lottery games enjoy broad social acceptance and participation across economic classes. However, casino gambling and sports betting carry more negative stigma.

Indigenous cultural values and Catholic religious influence contribute to ambivalence about gambling. This cultural backdrop partially explains the government’s restrictive approach to licensing.

Religious Influences: Bolivia is predominantly Catholic (approximately 70% of population), with growing Evangelical Protestant presence (15-20%). Both traditions include segments that view gambling negatively on moral grounds.

However, religious opposition has not prevented lottery participation or sports betting, suggesting that attitudes are nuanced rather than absolutist. Social gambling for small stakes is culturally accepted.

Trust in Foreign Brands: Bolivians have mixed attitudes toward foreign companies. Economic nationalism has grown under recent governments, with preference for state-owned enterprises over foreign private investment in key sectors.

International brands in consumer goods, technology, and entertainment have established presence, but building trust requires local partnerships and community engagement. Concerns about data privacy and financial security are significant.

Risk Tolerance: Economic volatility and historical inflation have created a culture with experience in financial risk. However, low average incomes mean most Bolivians have limited capacity to absorb gambling losses.

This suggests potential market segments: higher-income players willing to take risks, and lower-income players seeking lottery-style games with small stakes and large potential wins.

Entertainment Preferences: Football (soccer) dominates as the primary entertainment passion, with strong following of domestic leagues and international competitions. Other popular sports include basketball and volleyball.

Traditional festivals, music, and family-oriented activities are central to entertainment culture. Digital entertainment adoption is growing rapidly among youth but competes with traditional social activities.

Problem Gambling and Social Considerations

Prevalence Data: Comprehensive data on problem gambling prevalence in Bolivia is not available. The AJ has expressed concern about gambling addiction and commissioned studies on gambling consumption, but findings have not been publicly released.

In the absence of regulated online gambling, problem gambling rates are likely lower than in markets with established industries. However, grey market operations provide no player protections.

At-Risk Populations: Young males aged 18-35 in urban areas represent the demographic most likely to engage in online gambling, based on patterns in similar markets. Limited disposable income paradoxically increases risk of gambling-related harm for lower-income participants.

Government Response: The AJ has not implemented comprehensive problem gambling prevention programs or treatment services. The emphasis has been on prohibition rather than harm reduction through regulation.

Social Responsibility Infrastructure: Bolivia lacks the treatment facilities, counseling services, and support organizations for problem gamblers found in more developed gambling markets. This represents a significant gap that would need to be addressed in any regulatory framework.

Underage Gambling: Enforcement of age restrictions in land-based venues appears inconsistent. The lack of online regulation means no systematic age verification for internet gambling. This represents a child protection concern.

Political Structure and Governance

Government System: Bolivia is a unitary presidential republic with executive, legislative, and judicial branches. The president holds significant power. The country has experienced political instability historically, including a crisis in 2019-2020.

Political Stability: Political tensions remain elevated, with divisions along regional, ethnic, and ideological lines. Economic challenges and declining gas revenues create fiscal pressures that influence policy decisions.

For businesses, political instability creates regulatory uncertainty and potential for sudden policy changes. The gambling sector’s low priority means it receives inconsistent attention from policymakers.

Corruption Perception: Bolivia ranks 113th out of 180 countries on Transparency International’s Corruption Perceptions Index (2023), indicating significant corruption challenges. Businesses report that interaction with government officials often involves facilitation payments.

This environment complicates licensing processes and regulatory compliance, as formal requirements may differ from informal expectations. Legal certainty is limited.

International Relations: Bolivia maintains independent foreign policy and has strained relations with the United States. The country is a member of the Andean Community and associate member of MERCOSUR, providing trade access to regional markets.

Bolivia is not part of major trade agreements with European Union or other developed markets, limiting some business facilitation mechanisms available in other countries.

Technology Adoption and Digital Behavior

Internet and Digital Usage

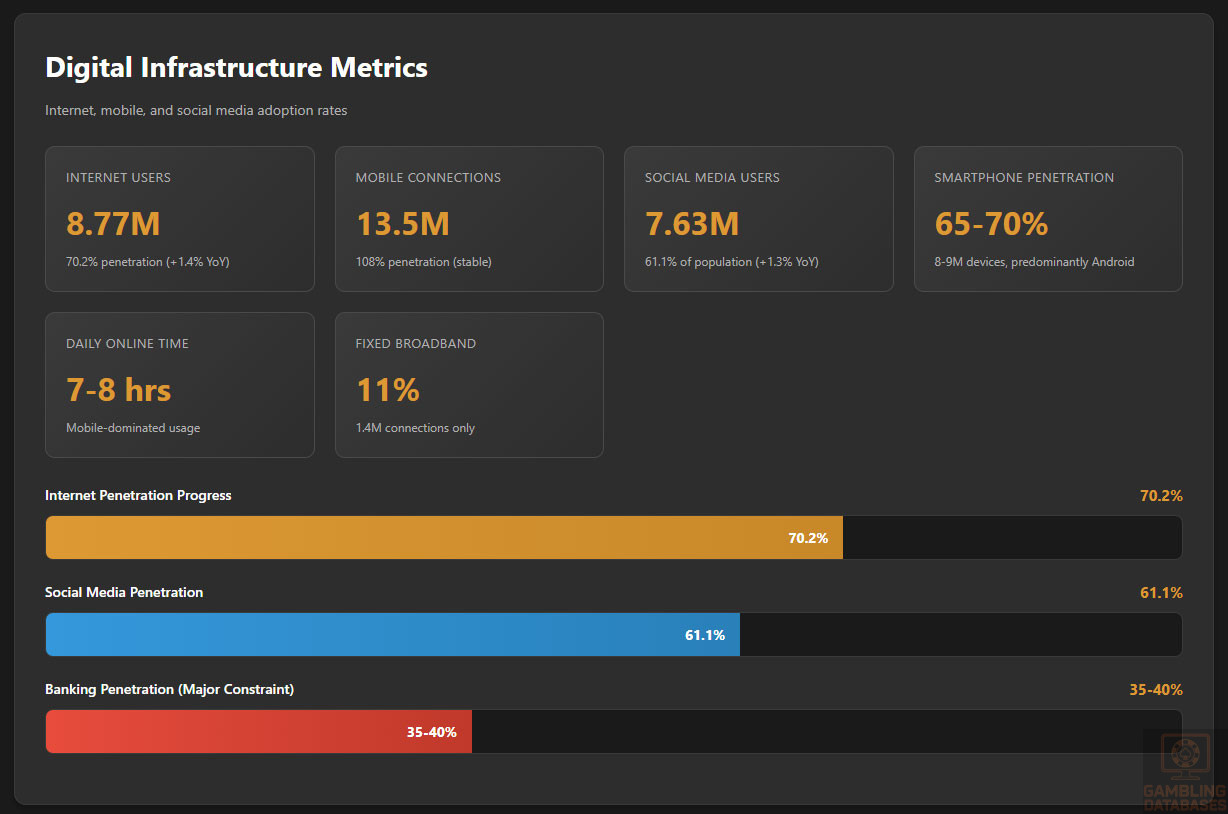

Internet Penetration: Bolivia’s internet penetration reached 70.2% in January 2025, representing 8.77 million internet users. This reflects significant growth, with 119,000 new users (+1.4%) added in the previous year.

While penetration lags behind developed markets (80-95%), Bolivia has achieved meaningful digital connectivity that supports online services including potential gambling platforms.

Daily Usage Patterns: Bolivian internet users spend an average of 7-8 hours per day online, comparable to regional averages. Mobile devices dominate access, with users spending more time on mobile internet than desktop.

Peak usage occurs in evening hours (18:00-23:00), representing optimal time for gambling platform activity and marketing.

Social Media Engagement: Bolivia had 7.63 million social media users in January 2025, representing 61.1% of the population. Facebook dominates as the primary platform, followed by Instagram, TikTok, and YouTube.

Social media represents a key channel for customer acquisition, community building, and promotional activities for gambling operators. Facebook advertising reach increased 1.3% between October 2024 and January 2025.

E-commerce Participation: E-commerce adoption is growing but remains limited compared to developed markets. Cash on delivery remains popular due to limited trust in online payments. Credit card penetration is low, creating payment challenges for online services.

The e-commerce market is valued at a fraction of regional leaders, but growth rates are strong as digital trust develops and payment infrastructure improves.

| Metric | Value | Year-over-Year Change |

|---|---|---|

| Internet Users | 8.77 million (70.2%) | +119,000 (+1.4%) |

| Mobile Connections | 13.5 million (108%) | Stable |

| Social Media Users | 7.63 million (61.1%) | +100,000 (+1.3%) |

| Mobile Internet Speed | 10.75 Mbps | +0.48 Mbps (+4.7%) |

| Fixed Internet Speed | 47.72 Mbps | +15.22 Mbps (+46.8%) |

| Smartphone Penetration | 65-70% | Growing steadily |

Digital Payment Behavior

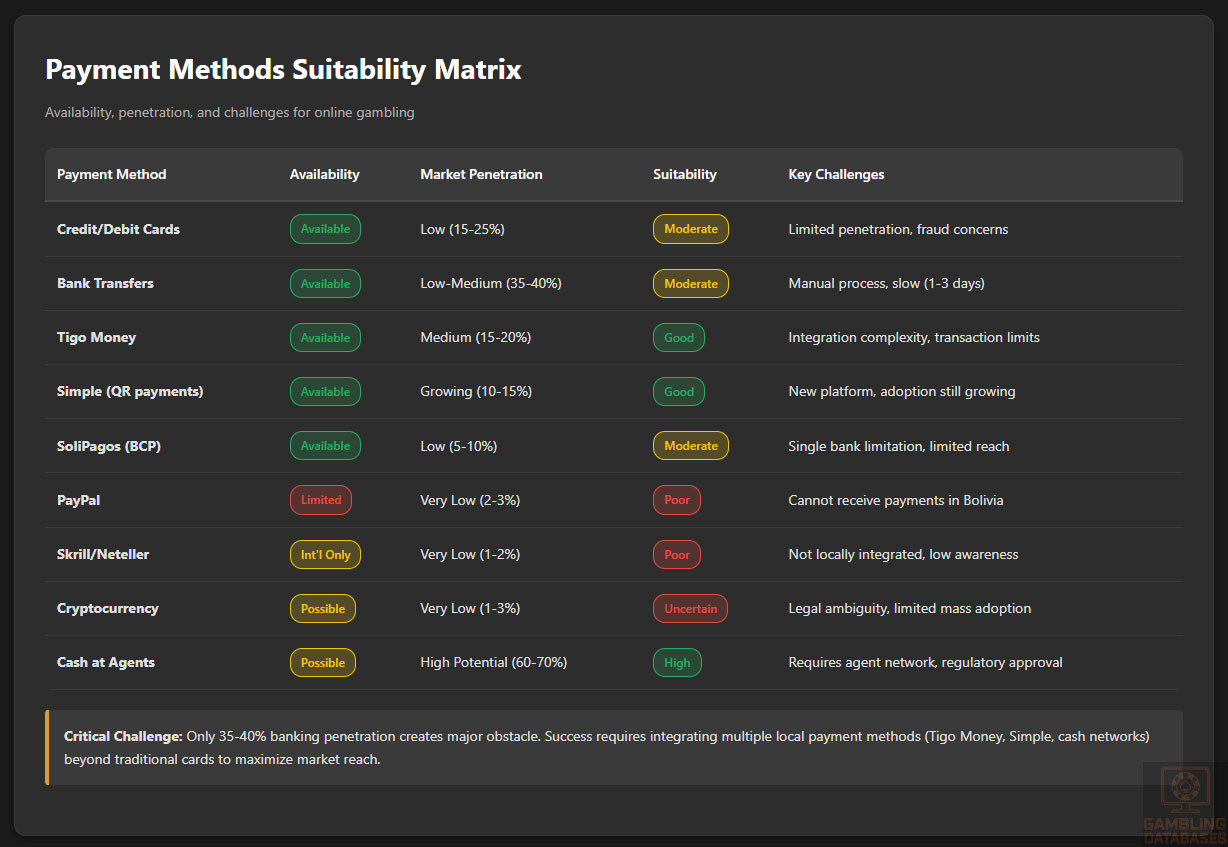

Payment Method Preferences: Cash remains dominant in Bolivia, representing over 95% of transactions in many contexts. Digital payment adoption is growing in urban areas but faces significant barriers including limited banking access and trust issues.

Banking Penetration: Only 35-40% of Bolivians have bank accounts, creating a major challenge for online gambling operators requiring deposit and withdrawal mechanisms. The unbanked population relies on cash and informal financial services.

Credit and Debit Cards: Card penetration is low, with debit cards more common than credit cards. Visa and Mastercard are the primary networks. Card usage is concentrated among middle and upper-income urban populations.

| Payment Method | Market Share | Notes |

|---|---|---|

| Credit Cards | 37% | Primarily urban, middle/upper income |

| Prepaid Cards | 31% | Growing alternative to bank accounts |

| E-wallets | 18% | Tigo Money, Simple, SoliPagos |

| Bank Transfer | 6% | Simple platform, manual transfers |

| Mobile Payments | 6% | QR code systems growing |

| Cash on Delivery | 2% | Still relevant for some transactions |

Digital Wallets: Local digital wallet services are emerging as important payment solutions. Tigo Money (mobile operator-based), Simple (bank consortium platform using QR codes), and SoliPagos (Banco de Crédito de Bolivia) offer alternatives to traditional banking.

These platforms are gaining traction for bill payments, transfers, and small purchases. Integration with these local payment methods would be essential for gambling operators to maximize market reach.

International Payment Services: PayPal has limited functionality in Bolivia, with restrictions on receiving payments for Bolivian businesses. Bolivian companies cannot charge foreign buyers using PayPal. Other international e-wallets like Apple Pay, Google Pay, and Samsung Pay have minimal presence.

Cryptocurrency Adoption: Cryptocurrency use exists in Bolivia but faces legal ambiguity. The Central Bank issued warnings against cryptocurrency use in 2014, though enforcement is limited. Some Bolivians use cryptocurrencies for international transfers and inflation hedging.

For gambling, cryptocurrency could offer payment solution benefits, but legal uncertainty and limited adoption among mass market users restrict viability.

Transaction Security Concerns: Trust in online payments remains a barrier. Bolivians express concerns about card fraud, data privacy, and unauthorized charges. This creates preference for cash on delivery or payment at physical locations even for online purchases.

Gaming and Gambling Preferences

Current Market Participation

Gambling Participation Rates: Precise data on gambling participation is unavailable due to the unregulated nature of online gambling and limited research. The AJ’s commissioned study has not released findings publicly.

Based on regional patterns and lottery popularity, estimated gambling participation rates range from 15-25% of adults annually, with most activity concentrated in lottery and informal sports betting.

Online Gambling Adoption: The percentage of the population engaged in online gambling through grey market international operators is unknown but likely represents 1-3% of adults (87,000-261,000 people).

This low penetration reflects payment barriers, limited awareness, language issues with international sites, and economic constraints rather than lack of interest.

Popular Activities: Lottery represents the most popular gambling activity with broad social acceptance and accessibility. Sports betting, particularly on football, represents significant grey market activity. Casino games have limited legal availability but show demand based on international platform usage.

Consumer Behavior Patterns

Average Spending: Due to low incomes, average spending per active gambling participant is likely $150-300 USD annually, significantly lower than in developed markets. High-value players represent a small percentage of the market.

Platform Preferences: Mobile devices dominate internet access (Android holds 94% of mobile OS market share), suggesting mobile-first gambling would be essential for market success. Desktop gambling would represent a small minority of activity.

Preferred Game Types: Football betting is the most popular sports betting category. For casino games, slots appeal to broad audiences due to simple gameplay, while table games attract smaller sophisticated player segments.

Lottery-style games with low cost entry and large jackpot potential align with local gambling culture and economic realities.

Bonus Sensitivity: Price-sensitive Bolivian consumers would likely show high responsiveness to bonuses, promotions, and free play opportunities. Welcome bonuses and deposit matches would be important acquisition tools.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Internet Penetration Quality: Bolivia’s 70.2% internet penetration represents meaningful coverage, but quality and reliability vary significantly between urban and rural areas. Urban centers enjoy relatively stable connectivity while rural regions face infrastructure gaps.

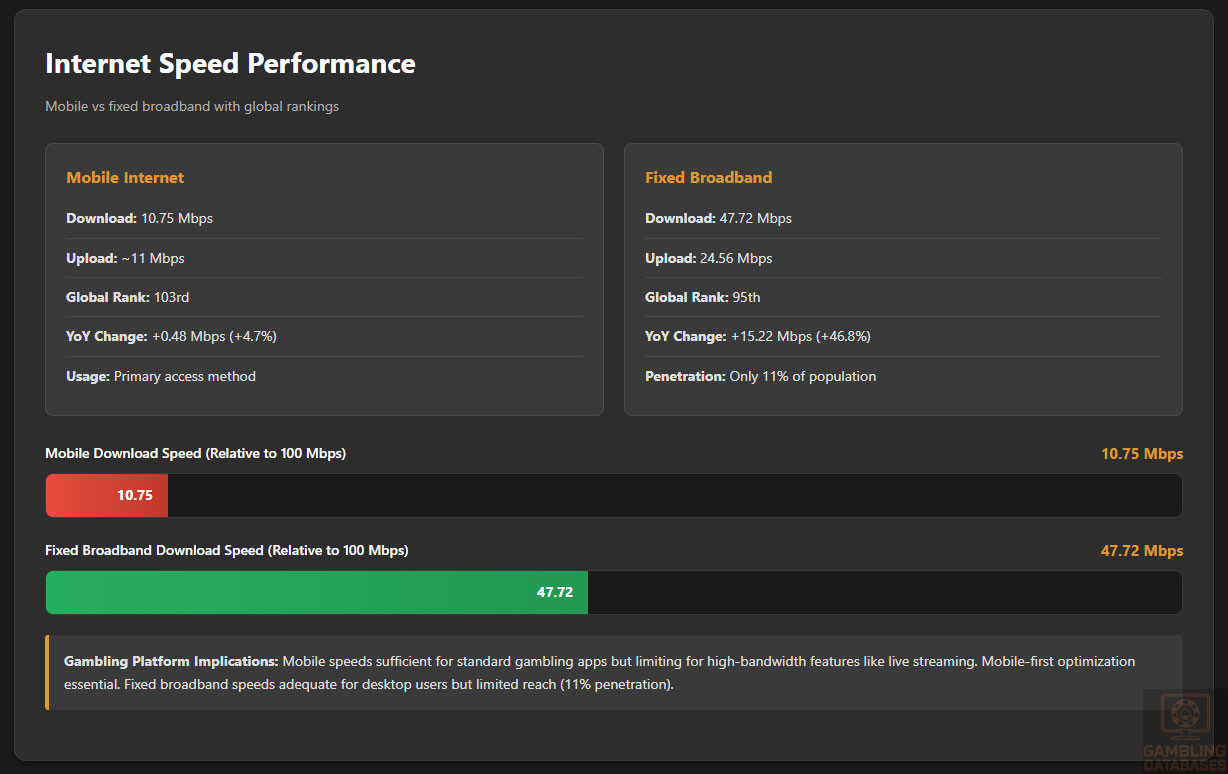

The country ranks 95th globally for fixed broadband speeds and 103rd for mobile internet speeds, indicating below-average performance compared to international standards but acceptable for basic online services.

Fixed Broadband vs Mobile Internet: Mobile internet dominates connectivity in Bolivia. Fixed broadband penetration is only 11% of the population, with approximately 1.4 million fixed connections. Mobile broadband serves as the primary internet access method for most users.

This mobile-first connectivity pattern requires gambling platforms to prioritize mobile optimization and minimize data usage to accommodate users with limited data plans.

Internet Speeds: Median mobile internet download speed stands at 10.75 Mbps, sufficient for most mobile gambling applications but limiting for high-bandwidth features like live streaming. Fixed internet offers better performance at 47.72 Mbps median download speed.

Upload speeds are slower, with mobile upload at approximately 11 Mbps and fixed broadband upload at 24.56 Mbps. These speeds support standard gambling platform functionality but require optimization.

| Connection Type | Download Speed | Upload Speed | Global Ranking | YoY Change |

|---|---|---|---|---|

| Mobile Internet | 10.75 Mbps | 11 Mbps | 103rd | +0.48 Mbps (+4.7%) |

| Fixed Broadband | 47.72 Mbps | 24.56 Mbps | 95th | +15.22 Mbps (+46.8%) |

Network Reliability: Network uptime and reliability are generally adequate in major cities but can be inconsistent. Power outages and infrastructure limitations affect service continuity, particularly outside primary urban areas.

Infrastructure Investment: Bolivia has invested in telecommunications infrastructure development, including fiber optic network expansion and connectivity to neighboring countries. The country established a fiber connection to the Pacific Ocean via Peru, improving international bandwidth.

However, investment levels remain below regional leaders, and rural connectivity programs face funding and implementation challenges.

Urban-Rural Connectivity Gap: Significant disparities exist between urban and rural internet access. Cities like Santa Cruz and La Paz enjoy relatively good connectivity, while remote valleys and rural areas have minimal infrastructure.

This geographic digital divide limits the addressable market for online gambling to primarily urban populations, reinforcing the concentration on major cities.

5G and Future Technology Deployment

4G Coverage: 4G LTE networks cover major urban areas and principal transportation corridors. The three major mobile operators (Entel, Tigo, Viva) have deployed 4G infrastructure in population centers, reaching approximately 60-70% of the population.

4G connectivity provides adequate speeds for mobile gambling applications, including live dealer games and sports betting with real-time updates.

5G Rollout Status: 5G deployment in Bolivia is in early stages or planning phases. The country lags behind regional leaders like Brazil, Chile, and Colombia in 5G adoption. Commercial 5G services are not widely available as of 2025.

Near-term gambling platform development should not depend on 5G availability, though future infrastructure improvements will enhance user experience capabilities.

Future Infrastructure Plans: The government has announced plans to expand rural connectivity and improve telecommunications infrastructure. Space agency initiatives aim to boost satellite-based internet in rural areas.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Mobile Network Operators: Bolivia has three primary mobile network operators competing in the market. Market dynamics include both state-influenced and private operators.

| Operator | Ownership | Market Position | Technology |

|---|---|---|---|

| Entel (Empresa Nacional de Telecomunicaciones) | State-owned | Market leader | 4G LTE, expanding coverage |

| Tigo (Telefónica/Millicom) | Private (International) | Strong competitor | 4G LTE, established network |

| Viva (NuevaTel) | Private | Third player | 4G LTE, urban focus |

Network Quality by Operator: Entel, as the state operator, maintains the most extensive geographic coverage including rural areas. Tigo and Viva focus primarily on urban markets with competitive pricing and data packages.

Quality and coverage vary by region, with all operators performing best in major cities. Rural coverage is dominated by Entel’s infrastructure.

Mobile Data Costs: Mobile data pricing in Bolivia is relatively affordable compared to income levels. Average monthly mobile phone contract costs approximately $20.40 USD, including voice, SMS, and data.

Prepaid plans dominate the market, with users purchasing data packages as needed. Typical packages offer 1-5 GB for $5-15 USD, with costs declining as data usage grows nationally.

Mobile Payment Integration: Mobile operators have launched financial services, particularly Tigo Money, which enables mobile-based payments, transfers, and bill payments. This operator-based financial infrastructure provides important payment channels for online services.

Device Penetration

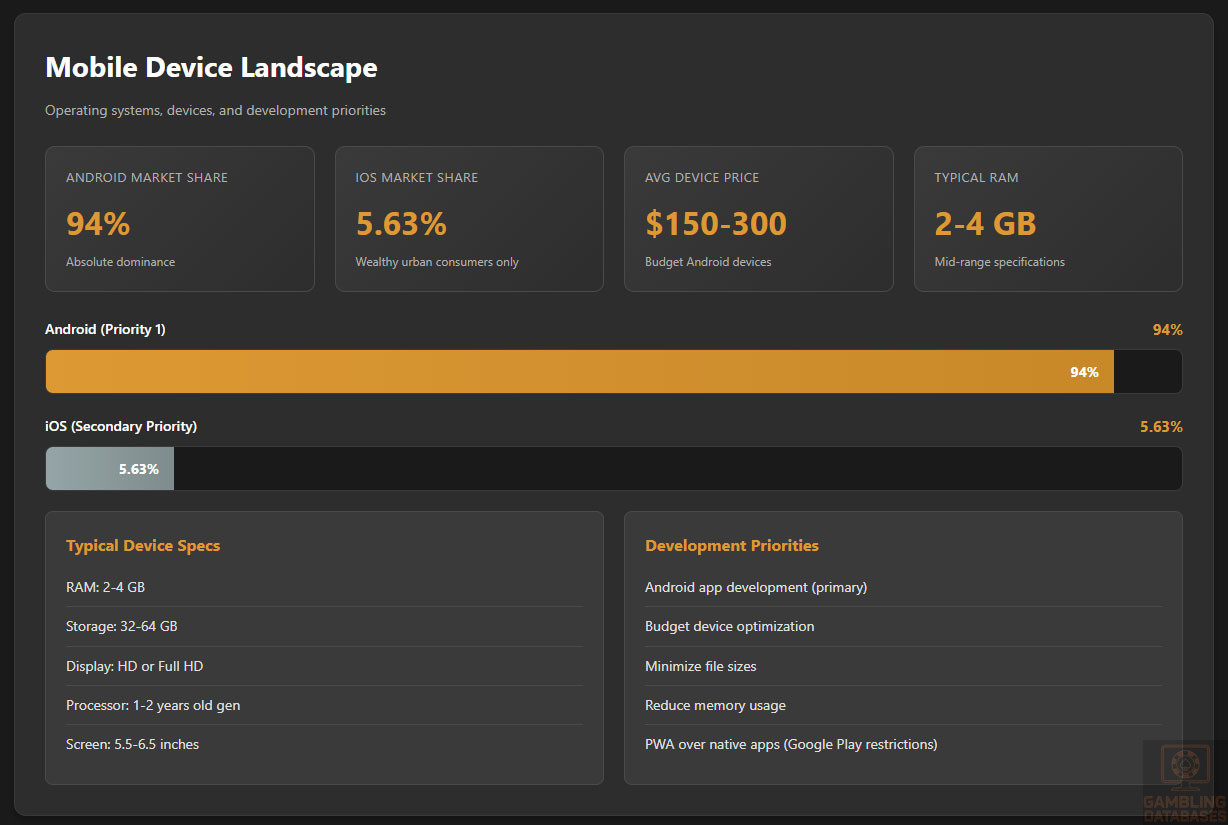

Smartphone Adoption: Smartphone penetration reaches approximately 65-70% of the population, representing 8-9 million devices. This high adoption rate, despite low incomes, reflects device affordability improvement and financing availability.

Smartphone penetration is higher in urban areas (80-85%) compared to rural regions (40-50%), aligning with internet access patterns.

Smartphones Per Capita: With 13.5 million mobile connections and 12.5 million population, Bolivia has 108% mobile penetration. Many individuals own multiple devices or SIM cards, though not all connections include data services.

Device Preferences: Budget Android devices dominate the market. Chinese manufacturers (Xiaomi, Huawei, Samsung budget lines) are popular due to affordable pricing and acceptable performance.

Premium devices like iPhones remain limited to high-income consumers, representing less than 6% of the market.

Android vs iOS Market Share: Android absolutely dominates Bolivia’s mobile OS market with 94% share in 2024. iOS holds only 5.63% market share, concentrated among wealthy urban consumers.

This near-monopoly Android environment means gambling operators must prioritize Android app development and ensure web platforms work seamlessly on Android browsers.

| Metric | Value | Implications for Gambling |

|---|---|---|

| Smartphone Penetration | 65-70% | Strong mobile-first market |

| Android Market Share | 94% | Prioritize Android development |

| iOS Market Share | 5.63% | iOS secondary priority |

| Average Device Price | $150-300 | Budget device optimization needed |

| Typical Screen Size | 5.5-6.5 inches | Mobile-optimized interfaces essential |

Average Device Specifications: Typical Bolivian smartphones feature mid-range specifications: 2-4 GB RAM, 32-64 GB storage, HD or Full HD displays, and processors from 1-2 years prior generation.

Gambling platforms must optimize for these specifications, ensuring smooth performance on devices that are not cutting-edge. File sizes, memory usage, and processing requirements should be minimized.

Mobile Usage Patterns: Bolivians spend majority of internet time on mobile devices. Average daily mobile internet usage is 6-7 hours, encompassing social media, messaging, entertainment, and increasingly, e-commerce.

Peak mobile usage occurs during evening hours and weekends, representing optimal times for gambling engagement and promotional activities.

Financial Services and Payment Infrastructure

Banking System Structure

Major Banks: Bolivia’s banking sector includes approximately 12 commercial banks, with market concentration among the largest institutions. Major players include Banco de Crédito de Bolivia (BCP), Banco Nacional de Bolivia (BNB), and Banco Económico.

State-owned Banco Unión provides commercial banking services with government backing. The banking sector is regulated by the Financial Services Supervisory Authority (ASFI).

Banking Penetration: Only 35-40% of Bolivians hold bank accounts, representing significant underbanking. Urban populations have higher banking access (50-60%) compared to rural areas (15-25%).

This low banking penetration creates major challenges for online gambling operations requiring deposit and withdrawal mechanisms through traditional banking channels.

Digital Banking Adoption: Digital banking services are available from major banks, with mobile banking apps and online platforms. However, adoption remains limited, with many account holders preferring in-branch transactions.

Younger urban consumers show higher digital banking adoption, representing the demographic most likely to engage with online gambling.

Credit and Lending Markets: Credit availability is limited, with high interest rates and strict lending criteria. Credit card penetration is low, estimated at 15-20% of adults. Debit cards are more common but still limited to bank account holders.

ATM Infrastructure: ATM density is concentrated in urban centers. Cash withdrawals remain the primary banking service for many account holders. ATM fees and transaction limits can affect cash-based gambling funding strategies.

Payment Processing Options

Available Payment Methods: For online gambling operations, payment method availability and integration would be critical challenges in Bolivia.

| Payment Method | Availability | Market Penetration | Suitability | Challenges |

|---|---|---|---|---|

| Credit/Debit Cards (Visa, Mastercard) | Available | Low (15-25%) | Good for existing users | Limited penetration, fraud concerns |

| Bank Transfers | Available | Low-Medium (35-40%) | Moderate | Manual process, slow, requires banking |

| Tigo Money | Available | Medium (15-20%) | Good | Integration complexity, limits |

| Simple (QR payments) | Available | Growing (10-15%) | Good potential | New platform, adoption growing |

| SoliPagos (BCP) | Available | Low (5-10%) | Moderate | Single bank, limited reach |

| PayPal | Limited | Very Low (2-3%) | Poor | Cannot receive in Bolivia, restrictions |

| Skrill/Neteller | Available internationally | Very Low (1-2%) | Poor | Not locally integrated, awareness low |

| Cryptocurrency | Possible | Very Low (1-3%) | Uncertain | Legal ambiguity, limited adoption |

| Cash Deposit at Agents | Possible | High potential (60-70%) | High | Requires agent network, regulatory approval |

Processing Fees: Payment processing fees in Bolivia vary by method. Card transactions typically incur 3-5% merchant fees. Bank transfers may have fixed fees of $1-3 per transaction. Digital wallet fees depend on the specific platform.

For gambling operations, these fees represent significant costs that must be factored into business models, particularly given lower average transaction values in the Bolivian market.

Transaction Processing Times: Bank transfers can take 1-3 business days to process. Card transactions are typically instantaneous for deposits but may take 3-7 days for withdrawals. Digital wallets offer faster processing but with transaction limits.

International Payment Capabilities: Bolivia faces challenges with international payment processing due to U.S. dollar scarcity and banking system limitations. International wire transfers are possible but expensive and slow.

For gambling operators based internationally, establishing local payment processing partnerships would be essential rather than relying on international payment gateways.

Regulatory Restrictions on Gambling Payments: Explicit restrictions on payment processing for gambling transactions have not been systematically implemented. However, the undefined legal status of online gambling creates ambiguity for payment processors.

Banks and payment providers may refuse gambling-related transactions due to reputational risk or unclear regulatory status. This represents a significant operational challenge.

Chargebacks and Disputes: Consumer protection mechanisms in Bolivia are developing. Chargeback processes exist for card transactions but are less established than in developed markets. Dispute resolution can be slow and unpredictable.

E-commerce and Digital Economy

Digital Market Development

E-commerce Market Size: Bolivia’s e-commerce market is emerging but remains small compared to regional leaders. Total e-commerce value is estimated at $200-300 million USD annually, representing less than 1% of retail sales.

However, growth rates are strong at 15-25% annually as digital trust develops and younger consumers embrace online shopping.

Online Retail Penetration: E-commerce represents approximately 0.5-0.8% of total retail, significantly lower than regional averages of 3-5%. Cash-based economy, low banking penetration, and trust barriers slow adoption.

Consumer Trust in Online Transactions: Trust in online transactions remains a significant barrier. Many Bolivians express concerns about fraud, product quality, delivery reliability, and payment security.

Cash on delivery remains popular for e-commerce, reducing payment risk for consumers. Building trust through secure payment methods, clear policies, and responsive customer service would be essential for gambling operators.

Popular E-commerce Platforms: International platforms like Amazon have limited presence. Regional platforms and local marketplaces dominate, including classified sites for peer-to-peer sales. Social media (particularly Facebook) serves as important e-commerce channel.

Digital Services Consumption: Streaming services (Netflix, Spotify), mobile apps, and digital content consumption are growing among urban youth. This demonstrates increasing comfort with recurring digital payments and subscription models.

Business Environment and Regulatory Framework

Ease of Business Operations

World Bank Rankings: Bolivia ranked 150th out of 190 countries in the World Bank’s archived Doing Business rankings, indicating significant challenges for business operations. The country scores poorly on starting a business, enforcing contracts, and dealing with construction permits.

Business Registration Processes: Starting a business in Bolivia requires navigating multiple government agencies and procedures. The process involves company name reservation, articles of incorporation, tax registration, municipal licenses, and labor registration.

Total steps number 13-15 procedures, taking approximately 40-50 days to complete under optimal circumstances. In practice, delays and complications are common.

Bureaucratic Challenges: Bolivia’s business environment is characterized by heavy bureaucracy, inconsistent enforcement of regulations, and discretionary decision-making by officials. Corruption remains a significant constraint.

Facilitation payments are often expected to expedite processes. Personal relationships and local knowledge are important for navigating regulatory systems.

Foreign Investment Policies: Bolivia generally allows 100% foreign ownership in most sectors. However, restrictions apply in strategic industries including natural resources, telecommunications (within certain parameters), and areas within 50 km of international borders.

Gambling has not been explicitly classified as a restricted sector, but the highly limited licensing suggests practical restrictions exist regardless of formal policy.

Operational Costs: Business operational costs in Bolivia are lower than in developed markets but quality and reliability challenges exist. Office rent in prime La Paz locations ranges from $10-20 per square meter monthly. Utility costs are relatively low but service can be inconsistent.

| Expense Category | Low Range | High Range | Notes |

|---|---|---|---|

| Office Rent (100 sqm, prime) | 1,000 | 2,000 | La Paz/Santa Cruz business districts |

| Utilities (electricity, water, internet) | 150 | 300 | Office space |

| Salaries – Manager | 1,200 | 2,500 | Experienced professional |

| Salaries – Technical Staff | 800 | 1,500 | IT, customer service |

| Salaries – Support Staff | 400 | 800 | Administrative, entry level |

| Legal/Accounting Services | 500 | 1,500 | Ongoing compliance |

Labor Market Conditions: Bolivia has a labor force of approximately 5.5 million workers. Unemployment is officially low (3-5%) but underemployment is high. Average wages are low by regional standards at approximately $729 USD monthly.

Skilled technical workers (IT, software development, data analysis) are limited. Competition for qualified personnel is significant, particularly for specialized roles required in gambling operations.

Corporate Structure and Registration

Available Entity Types

Limited Liability Company (SRL – Sociedad de Responsabilidad Limitada): The most common entity for small to medium businesses. Requires minimum 2 shareholders and 1 director of any nationality. Minimum capital of $1 USD (nominal), though practical capital requirements are higher.

SRLs offer liability protection and are simpler than corporations. Annual audited financial statements are required if sales exceed $170,000 USD.

Corporation (SA – Sociedad Anónima): Suitable for larger operations. Requires minimum 3 directors (one must be Bolivia resident), 3 shareholders, company secretary, and resident agent. Minimum paid-up capital is $100 USD.

Corporations face more regulatory requirements but allow easier ownership transfer and can issue different share classes. Sales exceeding $160,000 require annual audits.

Branch Office: Foreign companies can establish branches 100% owned by parent company. Scope of operations defined by parent company. Requires registered office in Bolivia and appointed manager with power of attorney.

Branches face similar tax obligations as local companies but cannot engage in activities beyond parent company’s scope.

Representative Office: Can be 100% foreign owned but cannot conduct income-generating activities. Limited to market research and promoting parent company business. All expenses must be met through foreign currency remittances.

Recommended Structure for iGaming: An SRL or SA would be appropriate for gambling operations if licensing becomes available. SRL offers simplicity for initial market entry. SA may be preferable if planning significant operations or eventual public listing.

Registration Requirements

Registration Timeline: Company registration through SEPREC (Servicio Plurinacional de Registro de Comercio) takes approximately 2-4 weeks if documentation is complete. However, total business setup including tax registration, municipal licenses, and labor registration extends to 40-50 days minimum.

For gambling operations, additional licensing procedures would substantially extend timelines, though these remain undefined.

Registration Costs: Company registration fees are approximately $200-300 USD depending on company size and structure. Additional costs include notary fees ($100-200), legal assistance ($500-1,500), and translation services for foreign documents ($100-300).

Total initial setup costs typically range from $1,500-3,000 USD for basic company formation, excluding industry-specific licensing.

Required Documentation: Articles of incorporation, shareholder identification documents, proof of registered office address, and power of attorney for directors. Foreign documents must be apostilled and translated to Spanish by court-certified translators.

Foreign Ownership Rules: 100% foreign ownership is permitted in most sectors including gambling (subject to obtaining licenses). No minimum Bolivian ownership requirements exist in general business law.

Minimum Capital Requirements: Nominal minimum capital requirements ($1-100 USD depending on entity type) are not practically meaningful. Gambling licenses, if issued, would likely require substantial financial guarantees and working capital.

Ongoing Compliance: Annual commercial registry filings, tax returns, audited financial statements (if exceeding thresholds), and license renewals. Compliance requirements can be burdensome with multiple government agencies requiring separate filings and documentation.

Taxation Framework

Corporate Income Tax Structure

Standard Corporate Tax Rate: Bolivia applies a flat 25% corporate income tax rate on profits. This is moderate by regional standards (Chile 27%, Colombia 35%, Brazil 34%, Peru 29.5%).

Tax Calculation Base: Corporate tax is calculated on net profits after deducting allowable business expenses. Transfer pricing rules apply for transactions with related parties to prevent profit shifting.

Special Industry Rates: Mining companies face 12.5% surtax. Financial institutions, insurance companies, and stockbrokers pay 25% surtax, effectively increasing their rate to 50%. Gambling-specific surtaxes are not currently defined beyond the GGR taxes.

Economic Zones and Incentives: Bolivia does not offer special economic zones with reduced tax rates for iGaming or technology companies. Tax incentives are limited and primarily focused on specific industrial sectors.

Tax Holidays: No tax holidays are available for new businesses in gambling sector. Some investment incentives exist for manufacturing and agricultural sectors but are limited.

International Tax Treaties: Bolivia has limited double taxation treaties. Treaties exist with Argentina, Germany, Spain, Sweden, and United Kingdom. This limits tax planning options for international gambling operators.

| Tax Type | Rate | Base | Comments |

|---|---|---|---|

| Corporate Income Tax | 25% | Net Profit | Flat rate for all sectors |

| Transaction Tax (IT) | 3% | Gross Income | Can be offset against income tax |

| Value Added Tax (VAT) | 13% | Sale of Goods/Services | May not apply to gambling stakes |

| Withholding Tax – Dividends | 12.5% | Dividend Payments | Remittance to foreign shareholders |

| Withholding Tax – Royalties | 12.5% | Royalty Payments | Software licenses, IP |

| Financial Transaction Tax | 0.03% | USD Bank Transfers | Applies to foreign currency transfers |

Transfer Pricing Rules: Bolivia has implemented transfer pricing regulations requiring documentation for related party transactions. Arms-length principle applies. Documentation requirements create compliance burden for international operations.

Withholding Taxes: Dividends paid to foreign shareholders face 12.5% withholding tax. Interest and royalty payments to foreign entities also incur 12.5% withholding. This affects profit repatriation strategies.

VAT Applicability: Bolivia applies 13% Value Added Tax to most goods and services. However, gambling stakes are typically not subject to VAT (the gambling-specific GGR taxes apply instead). VAT treatment of online gambling would need clarification in any licensing framework.

Personal Income Tax

Individual Tax Rates: Bolivia uses a flat 13% personal income tax rate on employment income and other qualifying income. This is among the lowest personal income tax rates in Latin America.

Tax Residents: Individuals spending more than 183 days in Bolivia during a calendar year are considered tax residents and taxed on worldwide income. Non-residents are taxed only on Bolivian-source income.

Employer Obligations: Employers must withhold income tax from employee salaries and remit to tax authorities. Monthly withholding and reporting requirements apply.

Social Security Contributions: Employers must contribute 16.71% of gross salary to social security programs. Employees contribute 12.71%. These rates are high relative to base wages and represent significant employment costs.

| Component | Employer % | Employee % | Total % |

|---|---|---|---|

| Social Security | 16.71% | 12.71% | 29.42% |

| Income Tax Withholding | – | 13% | 13% |

| Total Employment Cost | 116.71% | – | – |

Foreign Employee Taxation: Foreign employees working in Bolivia are subject to same income tax and social security contributions. The 15% limit on foreign employees in any company means most staff must be Bolivian nationals.

Market Entry Considerations

Recommended Entry Strategies

Current Market Reality: Given the absence of online gambling licensing framework, legal market entry is not currently possible. The following recommendations assume future regulatory implementation.

Monitor and Wait Approach: The most prudent strategy for 2025 is to monitor Bolivian regulatory developments while focusing resources on markets with established frameworks. Bolivia should remain on watch list but not active entry target.

If Licensing Becomes Available: Once clear licensing procedures are established, recommended entry strategies would include:

1. Local Partnership Model: Partner with established Bolivian businesses or lottery operators to navigate regulatory environment and leverage existing relationships. This reduces political risk and provides local market knowledge.

2. White Label Solution: For smaller operators, white label partnerships with established platform providers reduce technical investment and time-to-market. Focus resources on licensing, payments, and customer acquisition.

3. Technology Platform Licensing: Provide gambling platform technology and services to licensed Bolivian entities rather than directly operating. This reduces regulatory burden while generating revenue.

Payment Provider Selection: Critical success factor. Must integrate multiple local payment methods (Tigo Money, Simple, bank transfers, cash deposit networks) to maximize market access beyond banking population.

Localization Requirements: Spanish language is mandatory for all customer-facing content. Consider indigenous language support for specific regions. Customer service must be available in Spanish with local cultural understanding.

Marketing Channels: Focus on digital marketing through Facebook, Instagram, and TikTok given high social media engagement. Football sponsorships and partnerships could provide brand visibility if regulations permit.

Typical Costs and Timelines

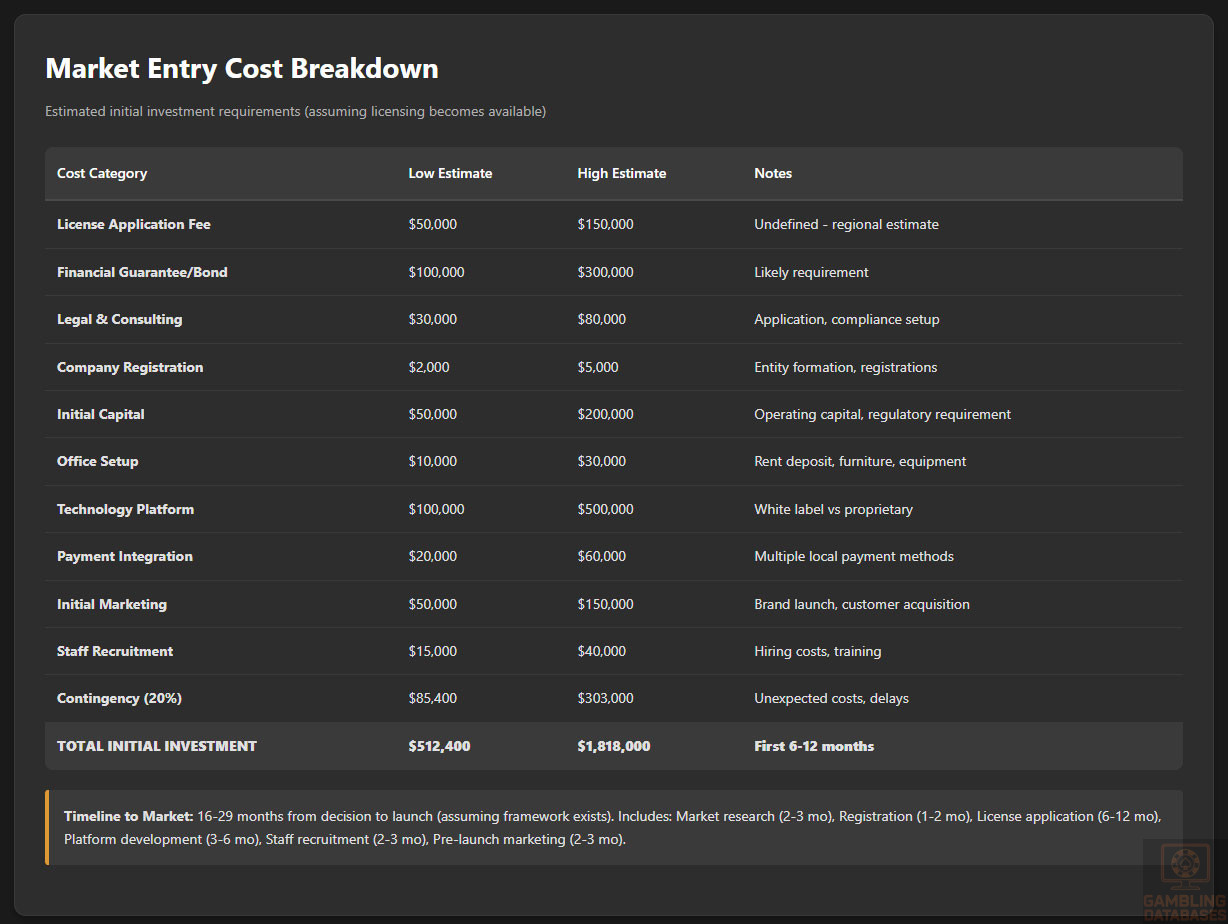

Initial Setup Investment Breakdown: The following estimates assume licensing framework implementation and represent order-of-magnitude costs.

| Cost Category | Low Estimate | High Estimate | Notes |

|---|---|---|---|

| License Application Fee | 50,000 | 150,000 | Undefined – estimate based on regional comparisons |

| Financial Guarantee/Bond | 100,000 | 300,000 | Likely requirement for license |

| Legal and Consulting Fees | 30,000 | 80,000 | Licensing application, compliance setup |

| Company Registration | 2,000 | 5,000 | Entity formation, registrations |

| Initial Capital Requirement | 50,000 | 200,000 | Operating capital, regulatory requirement |

| Office Setup | 10,000 | 30,000 | Rent deposit, furniture, equipment |

| Technology Platform | 100,000 | 500,000 | White label vs proprietary development |

| Payment Integration | 20,000 | 60,000 | Multiple local payment methods |

| Initial Marketing Budget | 50,000 | 150,000 | Brand launch, customer acquisition |

| Initial Staff Recruitment | 15,000 | 40,000 | Hiring costs, training |

| Contingency (20%) | 85,400 | 303,000 | Unexpected costs, delays |

| Total Initial Investment | 512,400 | 1,818,000 | First 6-12 months |

Operational Cost Estimates (Monthly): Ongoing operational expenses for a licensed gambling operation in Bolivia.

| Expense Category | Monthly Low | Monthly High | Annual (Low-High) |

|---|---|---|---|

| Staff Salaries (15-25 employees) | 15,000 | 30,000 | 180,000 – 360,000 |

| Office Rent and Utilities | 2,000 | 4,000 | 24,000 – 48,000 |

| Technology and Platform Costs | 10,000 | 25,000 | 120,000 – 300,000 |

| Payment Processing Fees (3-5% of GGR) | 5,000 | 20,000 | 60,000 – 240,000 |

| Marketing and Customer Acquisition | 20,000 | 60,000 | 240,000 – 720,000 |

| Legal and Compliance | 3,000 | 8,000 | 36,000 – 96,000 |

| Customer Support | 4,000 | 10,000 | 48,000 – 120,000 |

| Taxes and License Fees | Variable | Variable | Based on revenue |

| Miscellaneous/Administrative | 3,000 | 8,000 | 36,000 – 96,000 |

| Total Monthly Operating | 62,000 | 165,000 | 744,000 – 1,980,000 |

Timeline Expectations: Estimated time requirements for market entry process, assuming regulatory framework exists.

| Phase | Duration | Key Activities |

|---|---|---|

| Market Research and Planning | 2-3 months | Regulatory analysis, market study, business plan |

| Company Registration | 1-2 months | Entity formation, tax registration, legal setup |

| License Application Process | 6-12 months | Documentation, background checks, AJ review |

| Platform Development/Integration | 3-6 months | Technology setup, payment integration, testing |

| Staff Recruitment and Training | 2-3 months | Hiring, onboarding, system training |

| Marketing and Pre-Launch | 2-3 months | Brand development, marketing campaigns, partnerships |

| Total Time to Market | 16-29 months | From decision to launch |

Resource Requirements: Minimum staffing and expertise needed for viable operation.

Minimum Staff Headcount: 15-25 employees initially, scaling to 30-50 within first year depending on customer volume. Mix of technical, operational, customer service, and administrative roles.

Key Positions Required:

- General Manager / Country Director (Bolivia resident, regulatory relationships)

- Compliance Officer (AJ liaison, regulatory reporting)

- Technical Manager (platform management, IT infrastructure)

- Payment Operations Manager (transaction processing, reconciliation)

- Customer Service Team Lead + 5-10 agents (Spanish speaking, local cultural knowledge)

- Marketing Manager (digital marketing, local partnerships)

- Risk and Fraud Analyst (transaction monitoring, AML compliance)

- Finance Manager (accounting, tax compliance, financial reporting)

- Legal Counsel (ongoing compliance, contract management)

Technology Stack Requirements: Gambling platform (proprietary or white label), payment gateway integrations, customer management system, sports betting odds feeds (if applicable), fraud detection systems, reporting and analytics tools.

Success Factors and Challenges

Key Success Enablers

1. Payment Method Diversity: Success critically depends on integrating multiple local payment methods beyond credit cards. Tigo Money, Simple platform, cash deposit networks, and bank transfers must all be available to reach mass market.

Operators who solve payment accessibility will have significant competitive advantage in Bolivia’s underbanked market.

2. Mobile-First Approach: With 94% Android market share and mobile-dominated internet usage, gambling platforms must be optimized for budget Android devices with limited data plans and processing power.