Bosnia and Herzegovina presents a complex yet emerging opportunity for iGaming operators, characterized by a fragmented regulatory landscape divided between two entities with distinct gambling frameworks. The market operates under dual regulatory systems, with the Federation of Bosnia and Herzegovina and Republika Srpska maintaining separate licensing regimes and taxation structures.

Despite regulatory challenges and modest market size, the country demonstrates growing internet penetration, increasing smartphone adoption, and a young population segment receptive to digital entertainment, positioning it as a potential entry point for operators targeting the Balkan region.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Gambling Legal Status | Legal with restrictions | Dual regulatory system across two entities |

| Online Gambling Status | Partially regulated | Different frameworks in FBiH and RS |

| Regulatory Bodies | Entity-level authorities | No unified national framework |

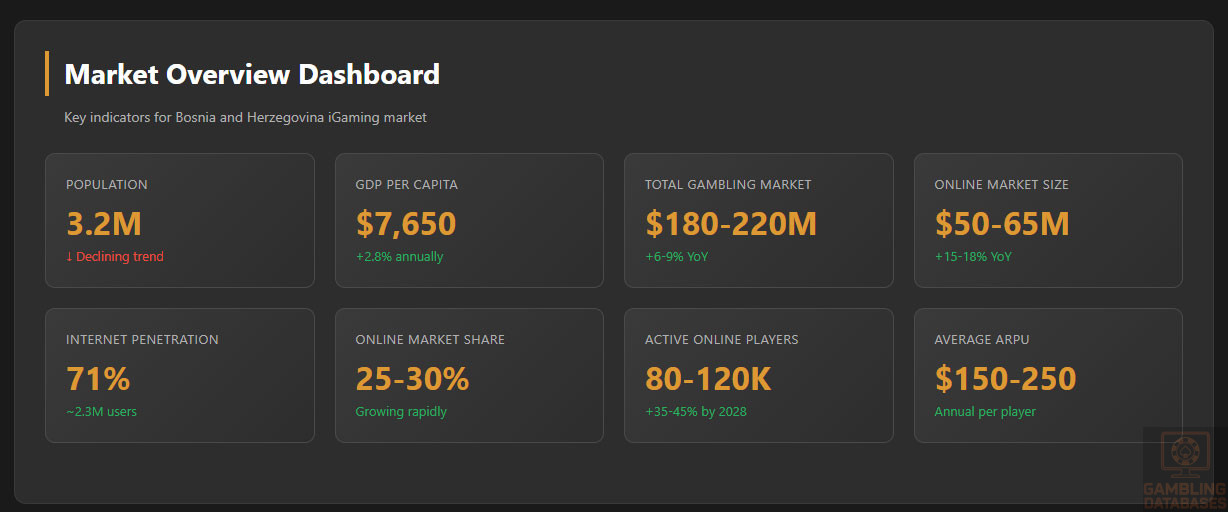

| Population | 3.2 million | Declining population trend |

| Median Age | 43.5 years | Aging population structure |

| Urban Population | 49% | Balanced urban-rural distribution |

| GDP Total | 24.5 billion USD | 2024 estimate |

| GDP Per Capita | 7,650 USD | Lower-middle income economy |

| GDP Growth Forecast | 2.8% annually | 2025-2027 projection |

| Average Monthly Income | 550-650 USD | Varies by entity and sector |

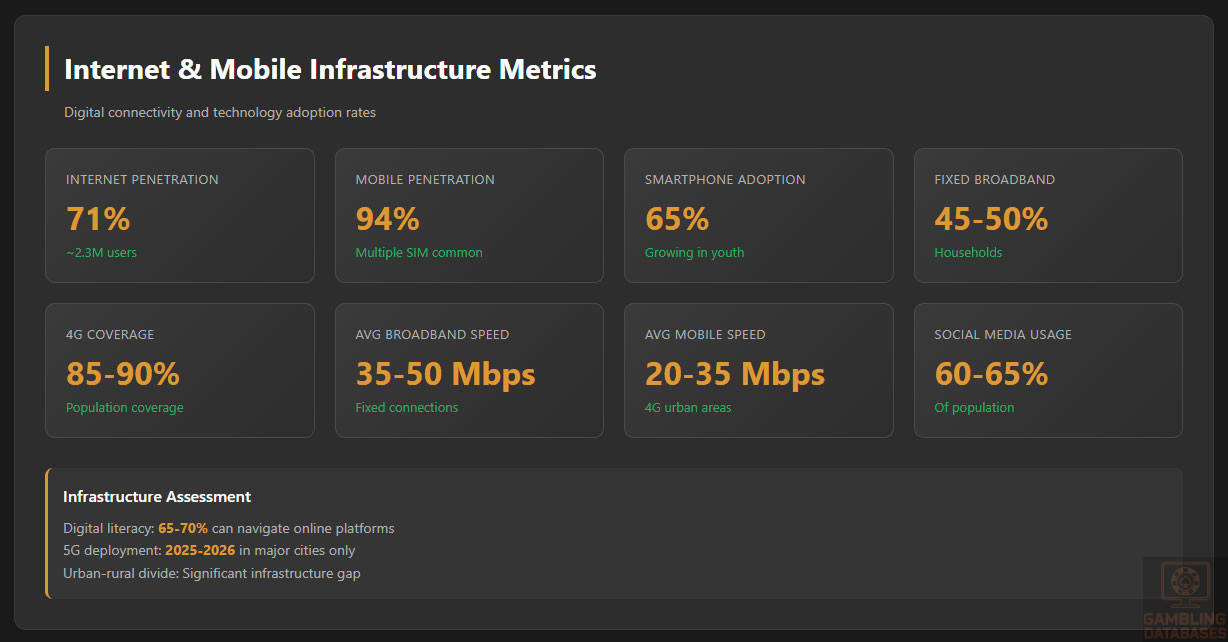

| Internet Penetration | 71% | Approximately 2.3 million users |

| Mobile Penetration | 94% | Multiple SIM ownership common |

| Smartphone Adoption | 65% | Growing among younger demographics |

| License Cost (FBiH) | 50,000-100,000 BAM | 26,000-52,000 USD annually |

| License Cost (RS) | 30,000-80,000 BAM | 15,600-41,600 USD annually |

| GGR Tax Rate (FBiH) | 10% | Plus municipal taxes |

| GGR Tax Rate (RS) | 5-10% | Varies by game type |

| Corporate Income Tax | 10% | Among lowest in Europe |

| Total Gambling Market Size | 180-220 million USD | 2024 estimate, all channels |

| Online Market Share | 25-30% | Approximately 50-65 million USD |

| Market Growth CAGR | 8-12% | 2025-2028 online segment projection |

| Online Gambling Participation | 8-12% | Of adult population |

| Average ARPU | 150-250 USD | Annual per active player |

| Mobile Gaming Share | 55-60% | Of online gambling revenue |

| Sports Betting Share | 70% | Dominant gambling vertical |

| Time to License | 6-12 months | From complete application |

| Minimum Capital Requirement | 50,000-100,000 BAM | Varies by entity and license type |

| Doing Business Rank | 90th globally | World Bank ranking |

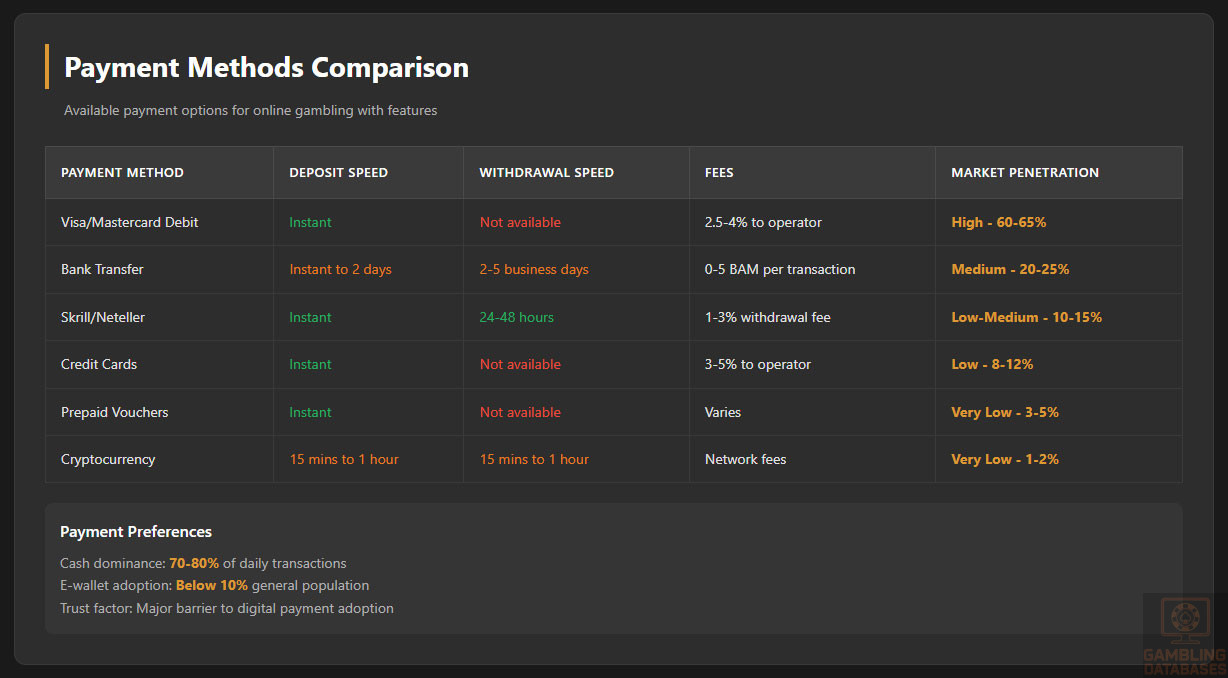

| Payment Method Preference | Cash, cards, e-wallets | Digital payments growing |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Bosnia and Herzegovina operates under a unique constitutional structure that creates a fragmented gambling regulatory environment. The country comprises two autonomous entities: the Federation of Bosnia and Herzegovina and Republika Srpska, each maintaining independent legislative authority over gambling activities within their territories. This dual system results in parallel regulatory frameworks, different licensing procedures, and varying tax structures, requiring operators to navigate multiple jurisdictions even within a single small market.

The absence of a unified national gambling law means that operators seeking comprehensive market coverage must obtain separate licenses from each entity. Additionally, the Brčko District, a self-governing administrative unit, maintains its own gambling regulations, further complicating the regulatory landscape. This fragmentation creates both challenges and opportunities, as operators can strategically choose their entry point based on more favorable regulatory conditions in one entity while potentially expanding to the other later.

Land-Based Gambling Activities

Casino Operations: Both entities permit casino operations under regulated frameworks requiring specific licenses and compliance with technical standards. The Federation of Bosnia and Herzegovina authorizes casino licenses for establishments offering table games, electronic gaming machines, and related gambling activities. Casinos must maintain physical premises meeting prescribed standards, employ certified gaming staff, and implement comprehensive player monitoring systems. Minimum investment thresholds and facility requirements vary by canton within the Federation.

Sports Betting Venues: Land-based sports betting represents the most popular and widespread gambling activity in Bosnia and Herzegovina. Both entities license betting shops extensively, with hundreds of retail locations operating across the country. The Federation requires sports betting operators to obtain licenses at the cantonal level, creating multiple regulatory touchpoints for operators seeking broad geographic coverage. License requirements include premises standards, betting terminal specifications, and connection to centralized monitoring systems.

In Republika Srpska, sports betting licenses are issued by the entity-level authorities with more streamlined procedures compared to the cantonal system in the Federation. Operators must maintain physical betting locations, employ trained staff, and implement real-time reporting systems connecting all betting terminals to regulatory oversight platforms. The high density of betting shops in urban areas reflects strong consumer demand for sports wagering opportunities.

Slot Machine Halls and Gaming Parlors: Electronic gaming machines operate under separate licensing categories in both entities. Gaming halls dedicated to slot machines require specific authorizations distinct from casino licenses. The Federation regulates the number of machines per location, technical specifications for gaming devices, and payout percentages. Operators must use certified gaming equipment meeting technical standards and maintain server-based monitoring systems.

Republika Srpska imposes limits on machine density and requires gaming halls to implement player identification systems and loss tracking mechanisms. The entity has established zones where gaming halls can operate and restricts their proximity to schools and religious institutions. Both entities require operators to purchase gaming machine permits in addition to facility licenses, creating multiple fee obligations.

Lottery Operations: Lottery activities operate under state monopoly or exclusive concession models in both entities. The Federation authorizes lottery operations through entity-level concessions, with the official lottery operator holding exclusive rights for traditional lottery products, instant win games, and related activities. Republika Srpska similarly maintains a lottery monopoly system with a designated operator.

Online Gambling Framework

Digital Gaming Regulations: The online gambling regulatory framework in Bosnia and Herzegovina remains underdeveloped compared to land-based gambling legislation. The Federation of Bosnia and Herzegovina has begun implementing online gambling regulations, permitting licensed operators to offer digital betting and gaming services. However, the regulatory framework lacks the comprehensive detail found in more mature markets, creating ambiguity around technical requirements, player protection standards, and compliance procedures.

Online gambling licenses in the Federation cover sports betting and casino gaming delivered via internet platforms and mobile applications. Licensed operators must demonstrate technical capability, maintain servers within approved jurisdictions, and implement geolocation verification to restrict services to authorized territories. The regulatory framework requires online operators to meet similar player protection standards as land-based venues, including age verification, self-exclusion capabilities, and responsible gambling tools.

Republika Srpska has taken steps toward regulating online gambling, with legislation authorizing digital gambling services under entity oversight. The regulatory approach focuses primarily on online sports betting, which dominates player interest. Casino gaming, poker, and other online gambling verticals face more restrictive treatment, with unclear authorization pathways. Operators must obtain specific licenses for online operations, which remain separate from land-based authorizations.

Prohibited Activities and Restrictions: Both entities maintain prohibitions on certain gambling activities and impose restrictions on online gambling operations. Skill games with gambling characteristics face regulatory scrutiny, with authorities distinguishing between games of chance requiring licenses and lawful skill-based competitions. Online poker rooms and peer-to-peer betting exchanges operate in regulatory gray zones, with unclear authorization pathways.

Fantasy sports platforms and social gaming applications with real-money elements have emerged without clear regulatory oversight, creating uncertainty for operators considering these verticals. Cryptocurrency gambling faces restrictions related to broader digital asset regulations, with authorities requiring transparency around payment methods and maintaining skepticism toward anonymous gambling transactions. Both entities prohibit gambling services targeting minors and impose restrictions on gambling advertising content and placement.

Regulatory Body Structure and Oversight: The Federation of Bosnia and Herzegovina distributes gambling regulatory authority across cantonal governments, creating a decentralized oversight structure. Each canton maintains its own gambling regulatory body or assigns gambling oversight to existing administrative departments. This creates significant complexity for operators seeking Federation-wide coverage, as they must engage with multiple regulatory authorities, each with distinct procedures and requirements.

Republika Srpska centralizes gambling regulation under entity-level authorities, providing more streamlined oversight compared to the Federation’s cantonal system. The entity’s gambling regulatory body maintains responsibility for licensing, compliance monitoring, and enforcement across all gambling activities in Republika Srpska territory. This centralized approach simplifies regulatory engagement for operators but still requires separate authorization from Federation authorities for cross-entity operations.

Licensed Operators and Market Players

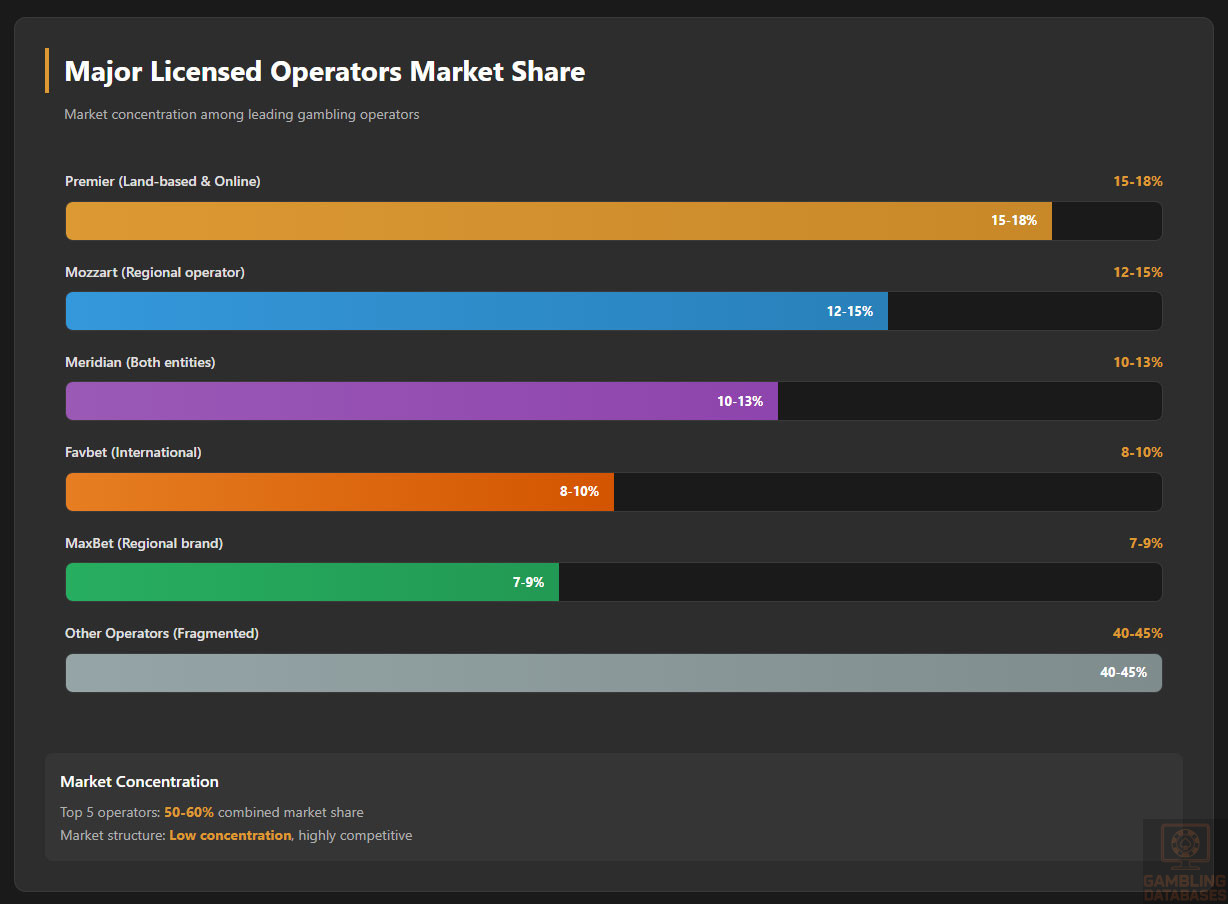

Market Structure and Licensed Operators: The Bosnia and Herzegovina gambling market hosts a mix of domestic operators with deep local market knowledge and international operators leveraging regional scale and brand recognition. The land-based betting sector features intense competition, with numerous licensed operators maintaining extensive retail networks. Premier, Mozzart, Meridian, and other regional brands operate betting shop chains across both entities, competing for market share in urban centers and secondary cities.

Online gambling operations include both domestic operators transitioning from land-based to digital channels and international platforms securing local licenses to enter the market legally. The competitive landscape remains fragmented, with no single operator dominating across all verticals and territories. Market leadership positions vary by entity, with different operators achieving prominence in the Federation versus Republika Srpska.

International Operators and Market Entry Strategies: Several international gambling groups have entered the Bosnia and Herzegovina market through acquisition of local operators, partnership arrangements, or direct licensing applications. Regional operators from neighboring Serbia, Croatia, and Slovenia have leveraged their Balkan presence to expand into Bosnia and Herzegovina, bringing established brands and operational expertise. These operators typically employ localized marketing strategies, sponsor popular football clubs, and adapt their product offerings to local preferences.

Entry strategies vary based on regulatory complexity and market opportunities in each entity. Some international operators have chosen to establish presence in one entity initially, using it as a foundation for potential expansion to the other entity. Others have pursued simultaneous licensing in both entities despite the additional complexity and cost. White-label arrangements and technology platform partnerships have enabled smaller operators to enter the market without developing proprietary gaming platforms.

Market Share and Competitive Dynamics: Market concentration in Bosnia and Herzegovina remains relatively low, with the top five operators collectively holding approximately 50-60 percent of the total gambling market. Sports betting operators dominate market share given the vertical’s popularity, with leading betting brands capturing 15-20 percent individual market shares in their strongest territories. Online operations show even more fragmentation, with no single operator holding more than 10-15 percent of the digital gambling market.

Competition focuses heavily on betting shop density and location quality in the land-based segment, with operators competing for prime retail positions in city centers and near transportation hubs. Online competition emphasizes mobile application quality, odds competitiveness, and promotional offers. Customer acquisition costs remain manageable compared to Western European markets, but retention proves challenging given the small market size and intense promotional competition among operators.

| Operator | License Type | Market Presence | Estimated Market Share |

|---|---|---|---|

| Premier | Land-based and online betting | Both entities, extensive retail network | 15-18% |

| Mozzart | Sports betting (retail and online) | Regional operator, strong in RS | 12-15% |

| Meridian | Betting shops and digital platforms | Both entities, growing online presence | 10-13% |

| Favbet | Online and retail betting | International operator, selective presence | 8-10% |

| MaxBet | Betting and gaming | Regional brand, land-based focus | 7-9% |

| Others | Various licenses | Fragmented smaller operators | 40-45% |

Licensing Framework and Requirements

Application Process and Eligibility

Regulatory Authority Engagement: Prospective operators must identify the appropriate regulatory authority based on their intended operational territory. In the Federation of Bosnia and Herzegovina, operators must engage with cantonal-level gambling authorities if operating physical establishments or the entity-level authority for online gambling licenses. Contact information and application procedures vary by canton, requiring operators to research specific requirements for their target cantons.

Republika Srpska centralizes licensing through entity-level authorities, simplifying initial regulatory engagement. Operators should initiate contact with the relevant ministry or gambling regulatory department early in their planning process to clarify current requirements, as regulations and procedures evolve. Regulatory authorities typically require preliminary consultations where operators present their business plans and proposed operations before submitting formal applications.

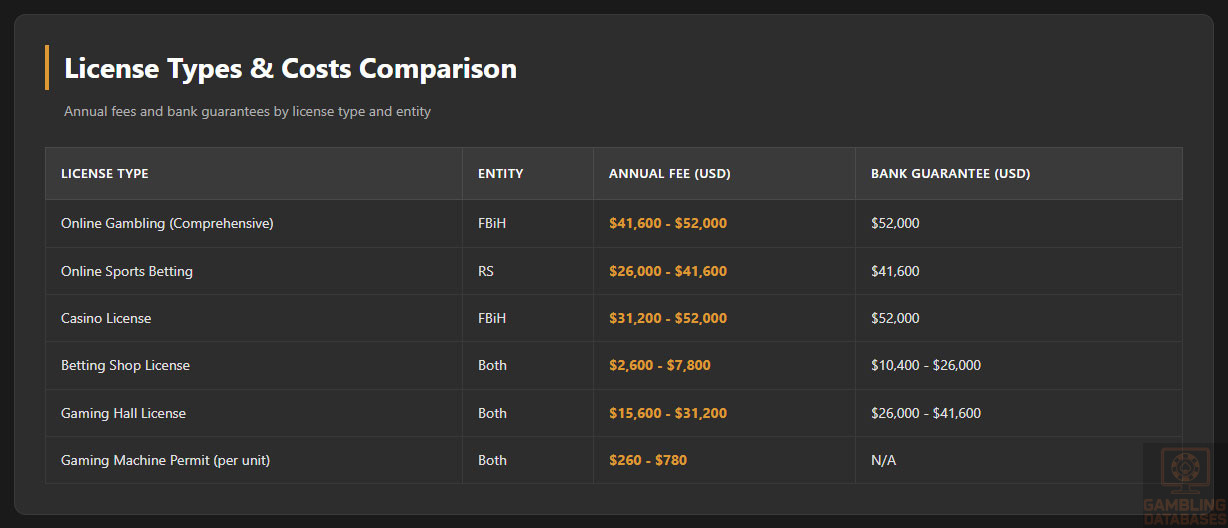

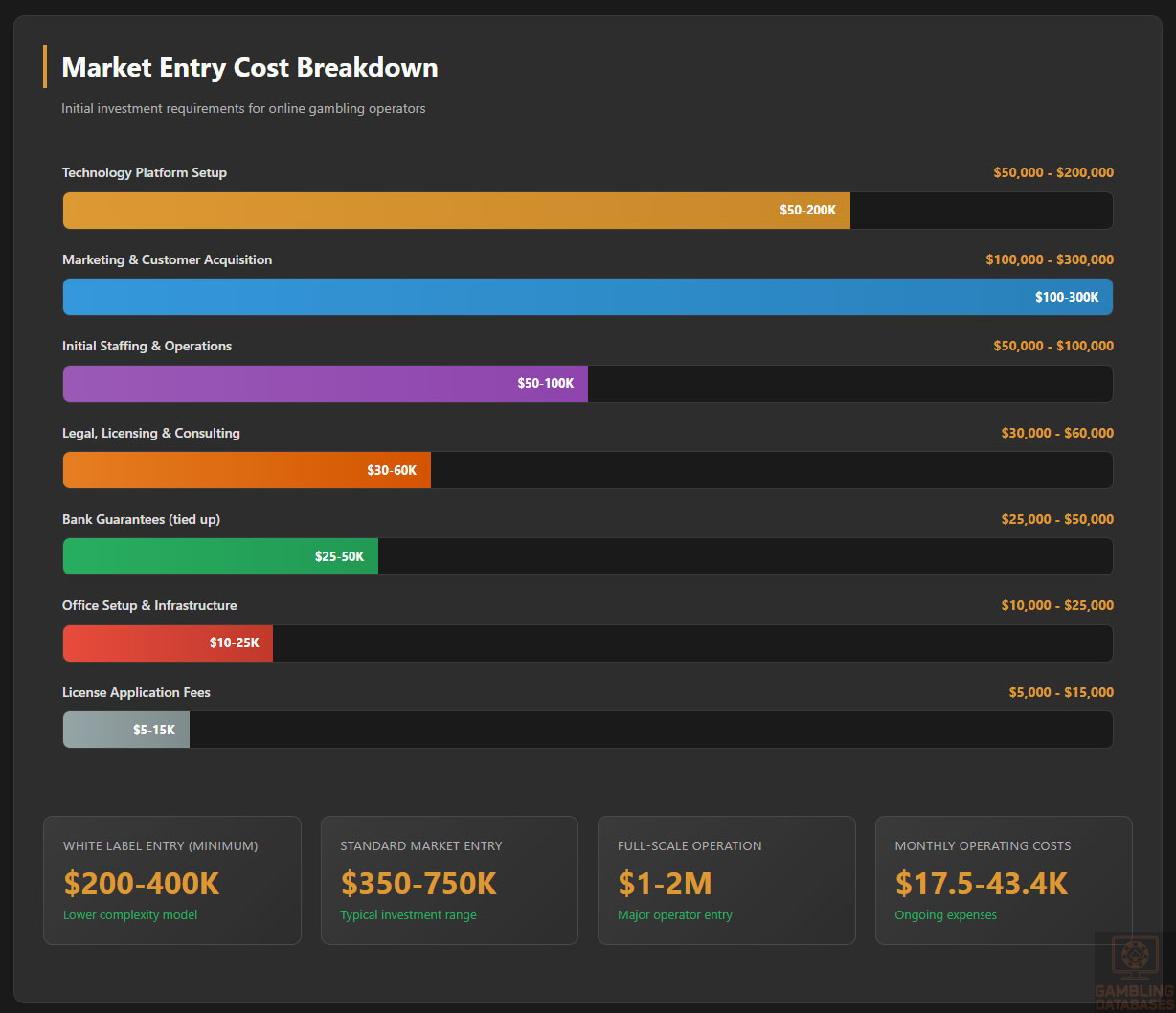

Financial Requirements and Guarantees: License applications require substantial financial documentation demonstrating the operator’s capability to conduct gambling operations responsibly. The Federation of Bosnia and Herzegovina typically requires bank guarantees ranging from 50,000 to 100,000 BAM depending on license type and scope. Online gambling licenses sit at the higher end of this range, while single betting shop licenses require lower guarantees.

Republika Srpska imposes similar financial guarantee requirements, with amounts varying based on operational scale. Operators planning extensive retail networks face higher aggregate guarantee requirements across all licensed locations. Bank guarantees must come from recognized financial institutions, typically banks operating within Bosnia and Herzegovina or international banks with local correspondent relationships. Guarantees remain in force throughout the license validity period and may be called upon for regulatory violations or unpaid obligations.

Minimum capital requirements apply to the licensed entity itself, separate from bank guarantees. Operators must demonstrate sufficient capitalization to sustain operations, meet player obligations, and cover potential liabilities. The Federation typically requires minimum capital of 50,000 to 100,000 BAM for corporate entities holding gambling licenses. Republika Srpska imposes similar minimum capital thresholds, with specific amounts depending on the license category and anticipated operational scale.

Technical Standards and Certifications: Gambling equipment and software platforms must meet technical standards established by regulatory authorities. Gaming machines require certification from approved testing laboratories confirming compliance with random number generation standards, payout percentage requirements, and security specifications. Both entities maintain lists of acceptable testing laboratories, typically including international certification bodies recognized across multiple jurisdictions.

Online gambling platforms must undergo technical evaluation covering game fairness, data security, player protection mechanisms, and system integrity. Operators must provide detailed technical documentation describing their platform architecture, security measures, and player data protection protocols. Some licenses require operators to use certified gaming content from approved providers, while others permit proprietary games subject to certification processes.

| License Type | Entity | Annual Fee (BAM) | Annual Fee (USD) | Bank Guarantee |

|---|---|---|---|---|

| Online Gambling (Comprehensive) | FBiH | 80,000-100,000 | 41,600-52,000 | 100,000 BAM |

| Online Sports Betting | RS | 50,000-80,000 | 26,000-41,600 | 80,000 BAM |

| Casino License | FBiH | 60,000-100,000 | 31,200-52,000 | 100,000 BAM |

| Betting Shop License | Both | 5,000-15,000 | 2,600-7,800 | 20,000-50,000 BAM |

| Gaming Hall License | Both | 30,000-60,000 | 15,600-31,200 | 50,000-80,000 BAM |

| Gaming Machine Permit (per unit) | Both | 500-1,500 | 260-780 | N/A |

Background Check Procedures and Timelines

Due Diligence Requirements: Regulatory authorities conduct comprehensive background investigations on license applicants, covering beneficial owners, directors, and key management personnel. Individuals with ownership stakes exceeding specified thresholds undergo detailed scrutiny, typically those holding 5 percent or more of company equity. Background checks examine criminal records, financial history, previous gambling industry involvement, and regulatory compliance records in other jurisdictions.

Applicants must provide extensive documentation including police clearance certificates, financial statements, business references, and detailed curriculum vitae for key personnel. Documents originating outside Bosnia and Herzegovina require notarization, apostille certification, and official translation into the local language. The authentication process adds time and cost to application preparation, particularly for international operators assembling documentation from multiple jurisdictions.

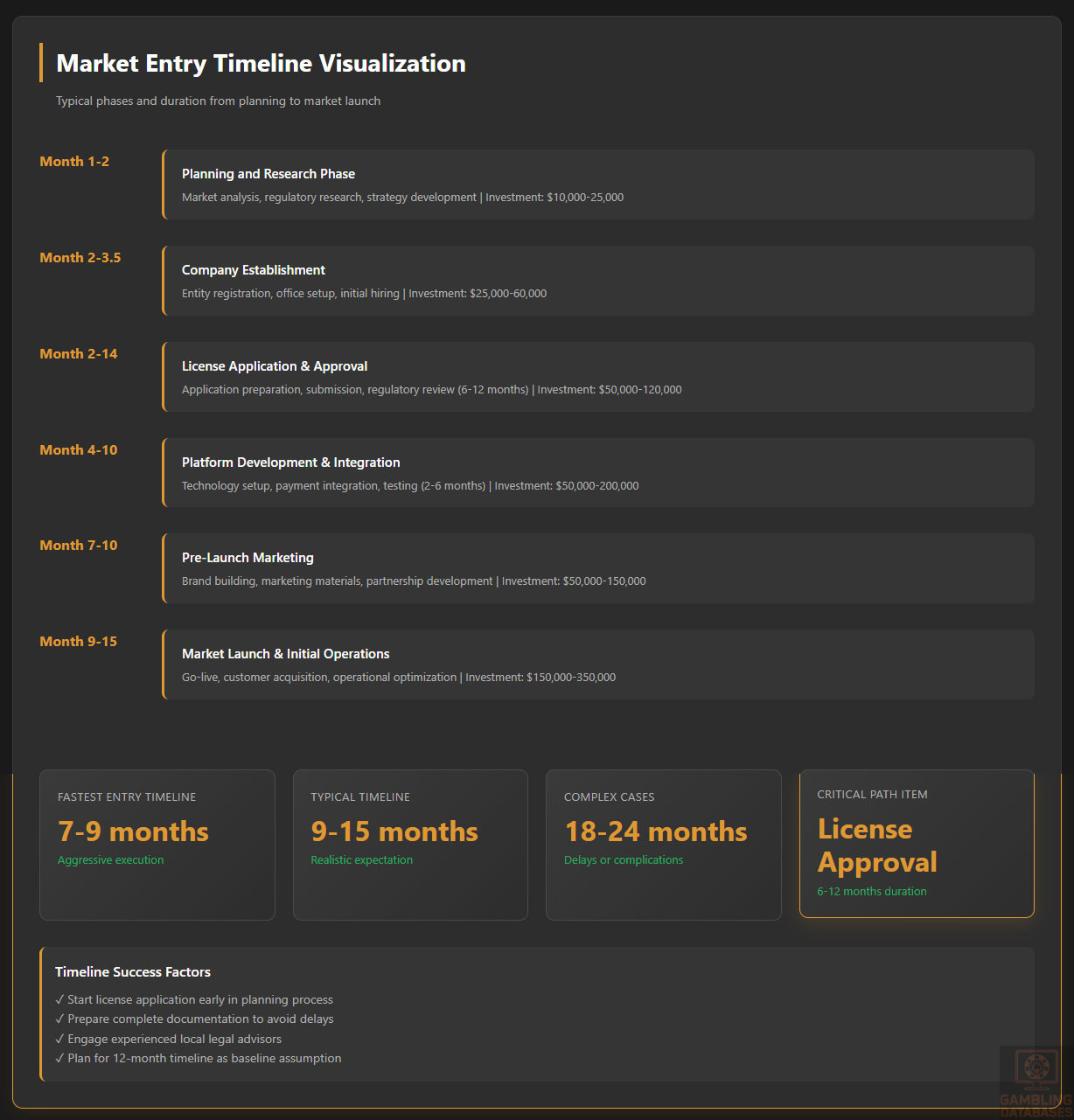

Background check timelines vary considerably based on application complexity and the number of individuals requiring investigation. Simple applications with few stakeholders and domestic ownership may complete background checks within 2-3 months. Complex applications involving multiple international beneficial owners, corporate ownership structures, and extensive gambling industry histories can extend background investigations to 6-9 months. Authorities may request additional information or clarification during reviews, further extending timelines.

Application Processing Timeline: Complete license applications in the Federation of Bosnia and Herzegovina typically require 6-12 months from submission to final approval, assuming no significant complications or deficiencies. Cantonal authorities process land-based establishment licenses, with timelines varying by canton based on administrative capacity and application volume. Entity-level online gambling licenses follow more complex review procedures, contributing to longer processing periods.

Republika Srpska maintains similar overall timelines, with complete applications requiring 6-10 months for final approval. The entity’s centralized regulatory structure potentially enables slightly faster processing compared to the Federation’s cantonal system, though actual timelines depend heavily on application quality and completeness. Incomplete applications or those requiring substantial clarification can extend well beyond these typical ranges, potentially reaching 18-24 months in problematic cases.

Local Presence and Operational Requirements

Physical Presence Mandates: Both entities require licensed gambling operators to maintain physical business presence within their respective territories. Operators must establish registered legal entities incorporated under Bosnia and Herzegovina law, either as limited liability companies or other recognized corporate forms. The registered entity must maintain a physical office address within the licensing territory, not merely a virtual office or mail forwarding service.

Office requirements vary by license type and operational scale. Online gambling operators must maintain functional offices with adequate staff to conduct business operations, respond to regulatory inquiries, and handle customer service functions. While regulations do not always specify minimum office sizes or staff counts, authorities expect operational substance matching the license scope. Operators running extensive online gambling platforms require larger facilities and more substantial local teams than small-scale betting operations.

Land-based gambling establishments inherently satisfy physical presence requirements through their gaming venues. However, operators must maintain administrative offices separate from customer-facing gambling facilities for corporate functions, regulatory compliance, and financial operations. Multi-site operators often centralize administrative functions in a single office location while maintaining the required physical presence at each licensed gambling venue.

Domain and Hosting Requirements: Online gambling regulations address technical infrastructure requirements, though specifics vary between entities and evolve as authorities refine their approaches. The Federation of Bosnia and Herzegovina requires online operators to use approved domains, typically mandating .ba country-code top-level domains or specific subdomain structures for licensed gambling operations. Domain registration must reflect the licensed entity, establishing clear attribution for regulatory and enforcement purposes.

Server and hosting requirements remain less strictly defined than in some European markets. Authorities generally do not mandate server physical location within Bosnia and Herzegovina, recognizing the impracticality for the small market. However, operators must ensure regulatory authorities can access systems for monitoring and inspection purposes. Data retention requirements may necessitate maintaining certain records on servers within Bosnia and Herzegovina or European Union territories with acceptable data protection standards.

Personnel and Management Obligations: Licensed operators must employ qualified personnel meeting regulatory standards for key positions. Gaming managers, compliance officers, and technical staff often require specific certifications or demonstrated competency. Some licenses mandate that key management positions be filled by individuals physically present in Bosnia and Herzegovina, preventing purely remote management structures.

Staff training requirements cover responsible gambling, anti-money laundering procedures, and customer service standards. Operators must document training programs and maintain records demonstrating employee competency. Customer-facing staff in land-based venues require particular attention to age verification procedures, intoxicated patron identification, and problem gambling recognition. Online operators must similarly train staff handling customer communications and account verification processes.

Foreign Ownership Restrictions: Bosnia and Herzegovina generally permits foreign ownership of gambling operators without absolute prohibitions, though practical considerations and regulatory preferences influence ownership structures. Neither entity imposes strict caps on foreign ownership percentages for most gambling license categories. However, authorities may scrutinize applications from entirely foreign-owned entities more closely than those with local ownership participation.

Some operators pursue joint ventures or partnership structures with local businesses to facilitate market entry and regulatory approval. Local partners provide market knowledge, regulatory relationships, and cultural understanding that international operators lack. However, partnership arrangements introduce complexity around profit sharing, operational control, and exit strategies. Operators must carefully structure arrangements to protect their interests while satisfying regulatory preferences for local involvement.

Compliance Obligations and Monitoring

Player Protection and Identification

Age Verification Requirements: Both entities mandate strict age verification procedures to prevent underage gambling. The minimum legal gambling age stands at 18 years throughout Bosnia and Herzegovina. Operators must verify player ages before permitting gambling participation, both in land-based venues and online platforms. Land-based establishments must request government-issued identification from any patron appearing younger than 25 years, implementing age verification at entry points and gaming positions.

Online operators face more complex age verification challenges given the remote nature of transactions. Registration processes must capture identification document information, with operators verifying authenticity through document checks and data validation. Leading practices include identity verification services cross-referencing provided information against official databases and document authentication technology detecting fraudulent identification.

Operators bear liability for permitting underage gambling, facing penalties including fines, license suspension, and potential criminal charges for serious violations. Regulatory authorities conduct mystery shopping exercises and compliance audits examining age verification procedures. Documented policies, staff training records, and verification logs provide evidence of compliance efforts during regulatory inspections.

KYC and Anti-Money Laundering Compliance: Bosnia and Herzegovina gambling operators must comply with anti-money laundering regulations aligned with international standards. Know Your Customer procedures require operators to identify and verify customer identities, understand the nature of customer relationships, and monitor transactions for suspicious activity. Enhanced due diligence applies to high-value customers, politically exposed persons, and transactions from higher-risk jurisdictions.

Customer identification requirements mandate collection of full names, dates of birth, addresses, and identification document details. Operators must verify provided information through reliable sources, maintaining verification records throughout customer relationships and for specified periods after account closures. Source of funds inquiries become necessary when customer transaction patterns or volumes raise questions about fund origins.

Transaction monitoring obligations require operators to implement systems detecting unusual patterns that may indicate money laundering. Large cash deposits, rapid high-volume betting with minimal gambling activity, and structured transactions designed to evade reporting thresholds warrant enhanced scrutiny. Operators must file suspicious transaction reports with financial intelligence units when detecting activity suggesting money laundering or terrorist financing.

Responsible Gambling Measures: Regulatory frameworks require operators to implement responsible gambling protections addressing problem gambling risks. Self-exclusion programs allow players to voluntarily ban themselves from gambling activities for specified periods. Both entities require operators to maintain self-exclusion registries and prevent excluded individuals from gambling during exclusion periods. Land-based operators must train staff to recognize self-excluded individuals and deny them access to gaming areas.

Online operators must implement technical controls preventing self-excluded players from accessing gambling platforms. Account closure procedures, IP address blocking, and payment method restrictions help enforce exclusions. Some regulations require operators to participate in shared self-exclusion databases enabling exclusions across multiple operators, though implementation across Bosnia and Herzegovina’s fragmented regulatory landscape remains incomplete.

Deposit limits, loss limits, and session time limits empower players to control their gambling behavior. While not universally mandated across all license types, leading operators offer these tools voluntarily or in response to specific regulatory requirements. Reality checks interrupting play sessions to inform players of elapsed time and losses sustained help maintain player awareness during extended gambling sessions.

Mandatory Player Information Disclosures: Operators must provide players with clear information about gambling risks, odds of winning, and available support resources for problem gambling. Terms and conditions must use plain language explaining betting rules, payout structures, and bonus conditions. Misleading advertising or promotional materials violate consumer protection standards and gambling regulations.

Online platforms must display prominent warnings about gambling addiction risks, links to problem gambling support organizations, and clear information about self-exclusion options. House edges, return-to-player percentages, and game rules should be readily accessible to players before they commit to wagering. Transparency requirements extend to payment processing, with operators clearly communicating deposit methods, withdrawal procedures, processing timelines, and applicable fees.

Financial Monitoring and Reporting

Transaction Monitoring Systems: Licensed operators must implement transaction monitoring systems capable of tracking all gambling activity, financial transactions, and player account movements. Land-based operators connect betting terminals and gaming machines to centralized monitoring platforms providing real-time visibility to regulatory authorities. These systems capture bet placement, outcomes, payouts, and operator hold percentages across all gaming devices.

Online operators similarly must implement comprehensive transaction logging capturing all player interactions, bets placed, game outcomes, deposits, withdrawals, and account balance changes. Audit trails must be tamper-proof and maintained for regulatory inspection. Authorities may conduct remote monitoring or require regular data feeds providing visibility into operator activities without requiring physical inspections.

Reporting Requirements and Schedules: Regulatory authorities impose periodic reporting obligations providing visibility into operator activities and market performance. Monthly reports typically include gross gaming revenue, number of active players, total amounts wagered, and payouts to players. Reports break down activity by game type, allowing authorities to analyze market composition and identify trends.

Ad hoc reporting obligations arise when authorities investigate specific issues or respond to complaints. Operators must provide requested information within prescribed timeframes, which may range from immediate provision for urgent matters to several weeks for comprehensive data requests. Failure to submit accurate and timely reports constitutes license violations potentially resulting in penalties.

Audit and Inspection Procedures: Regulatory authorities maintain rights to audit operator activities and inspect facilities without advance notice. Audits examine financial records, player transaction data, responsible gambling program implementation, and technical system compliance. Inspectors may visit land-based establishments to observe operations, interview staff, and examine equipment. Online operators receive requests for system access, data extracts, and documentation evidencing compliance with technical and operational standards.

Operators must cooperate fully with regulatory inspections, providing requested information and access to personnel, systems, and records. Obstruction of regulatory inspections represents serious violations potentially resulting in license revocation. Third-party audits from independent accounting firms or technical testing laboratories supplement regulatory inspections, with operators often required to commission periodic independent assessments of their operations.

Taxation Structure and Financial Obligations

Player Taxation

Tax on Winnings: Bosnia and Herzegovina does not impose comprehensive taxation on gambling winnings at the player level. Individual players generally do not face withholding requirements or tax declaration obligations for gambling winnings from licensed operators. This approach aligns with many European jurisdictions that tax gambling operators rather than individual players, simplifying tax administration and reducing compliance burdens on casual gamblers.

However, professional gamblers or individuals deriving substantial income from gambling may face income tax obligations on their gambling-related earnings. Tax authorities may examine individuals whose primary income source appears to be gambling, potentially classifying substantial gambling winnings as taxable income. The threshold between recreational gambling and taxable gambling income remains somewhat ambiguous, with determinations made on case-by-case bases.

Large single-event winnings occasionally trigger reporting requirements, though specific thresholds and procedures vary between entities. Operators paying out substantial winnings may request identification information for reporting purposes, particularly when anti-money laundering obligations intersect with large transactions. Players winning jackpots or tournament prizes occasionally face tax inquiries, though systematic withholding remains uncommon.

Operator Taxation

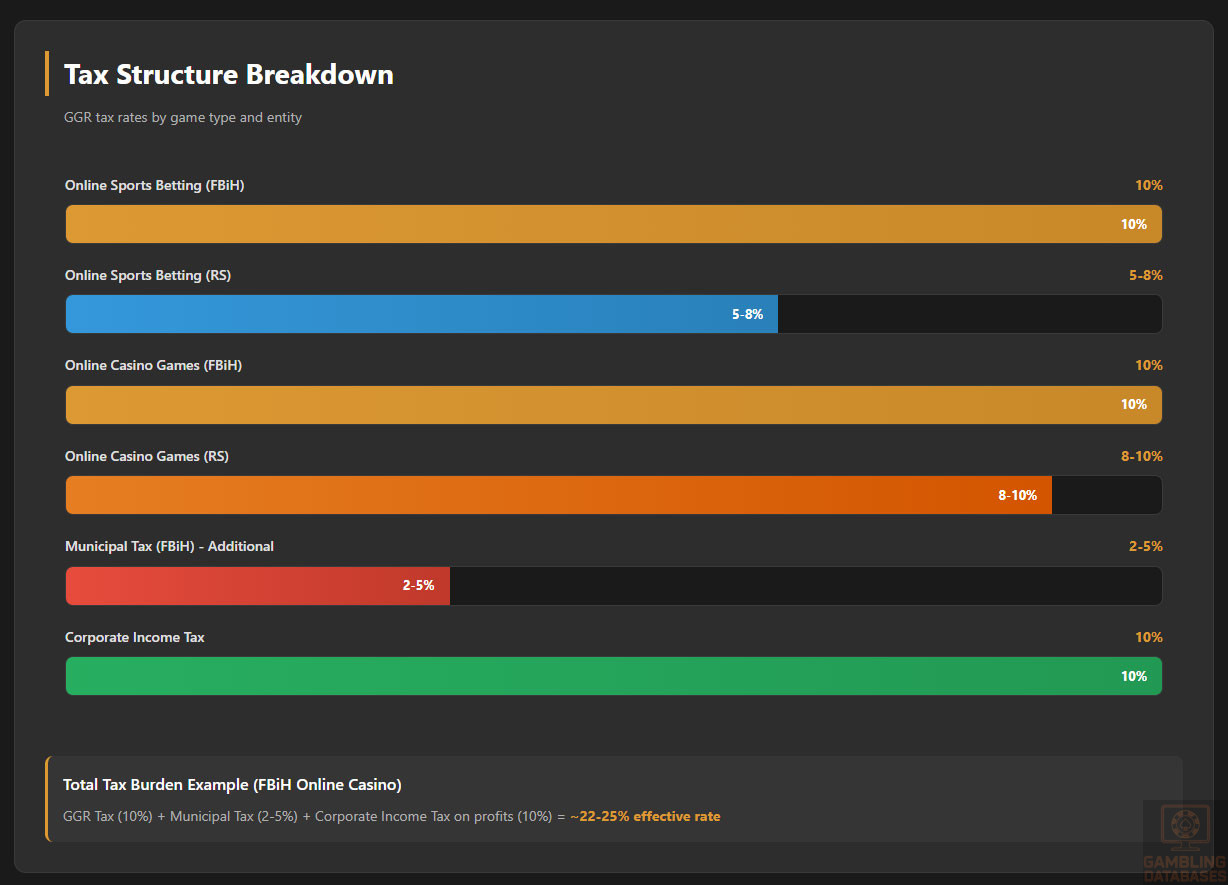

Gross Gaming Revenue Taxation: The primary gambling-specific tax burden falls on operators through gross gaming revenue taxation. The Federation of Bosnia and Herzegovina imposes a 10 percent GGR tax rate on licensed gambling operations. GGR represents total amounts wagered minus payouts to players, before deducting operational expenses. This calculation method ensures taxation on operator revenue rather than turnover, aligning with international best practices.

Republika Srpska implements variable GGR tax rates depending on gambling activity type. Sports betting typically faces 5-8 percent GGR taxation, while casino gaming and slots may incur 8-10 percent rates. The entity periodically adjusts rates through legislative amendments, creating some uncertainty around long-term tax obligations. Online gambling operations generally face similar tax rates to their land-based equivalents, though specific treatment continues evolving.

Tax calculation methodologies require careful attention to ensure accurate compliance. Operators must maintain detailed records supporting GGR calculations, including total wagers accepted, all payouts made, and adjustments for voided bets or cancelled transactions. Bonus costs and promotional expenses typically do not reduce taxable GGR, with bonuses considered operator marketing expenses rather than player payouts. Free bet costs may receive different treatment depending on specific regulatory guidance.

| Game Type | FBiH GGR Tax | RS GGR Tax | Additional Fees |

|---|---|---|---|

| Online Sports Betting | 10% | 5-8% | Municipal taxes may apply |

| Online Casino Games | 10% | 8-10% | License fees separate |

| Land-Based Betting | 10% | 5-8% | Municipal taxes 2-5% |

| Casino Table Games | 10% | 8-10% | Facility-based fees |

| Slot Machines/EGMs | 10% | 8-10% | Per-machine fees |

| Lottery Products | Varies | Varies | Monopoly concessions |

Corporate Income Tax: Beyond gambling-specific taxes, licensed operators pay corporate income tax on their profits. Bosnia and Herzegovina maintains a competitive 10 percent corporate income tax rate, among the lowest in Europe. This rate applies to all corporate entities operating in the country, including gambling operators. The low corporate tax burden partially offsets higher gambling-specific taxes and regulatory costs.

Tax base calculations follow standard accounting principles, allowing deduction of legitimate business expenses from gross revenues to determine taxable profits. Gambling taxes paid represent deductible expenses reducing corporate income tax obligations. International operators structuring operations across multiple jurisdictions must navigate transfer pricing requirements ensuring that profits are appropriately allocated to Bosnia and Herzegovina operations rather than shifted to lower-tax jurisdictions.

Municipal and Other Taxes: Local municipalities in the Federation of Bosnia and Herzegovina levy additional taxes on gambling operations within their territories. Municipal gambling taxes typically range from 2-5 percent of GGR, adding to entity-level tax burdens. Operators must register with municipal authorities and comply with local tax payment schedules separate from entity-level obligations. The aggregate tax burden combining entity and municipal taxes can reach 12-15 percent of GGR in the Federation.

Republika Srpska generally does not impose municipal gambling taxes beyond entity-level obligations, simplifying tax compliance for operators in that territory. However, municipalities may levy standard business taxes, real estate taxes, and utility fees applicable to all businesses regardless of industry. Land-based venues pay property taxes based on facility valuations, while all operators incur standard employment-related taxes and social contributions.

Gambling Market Financial Performance

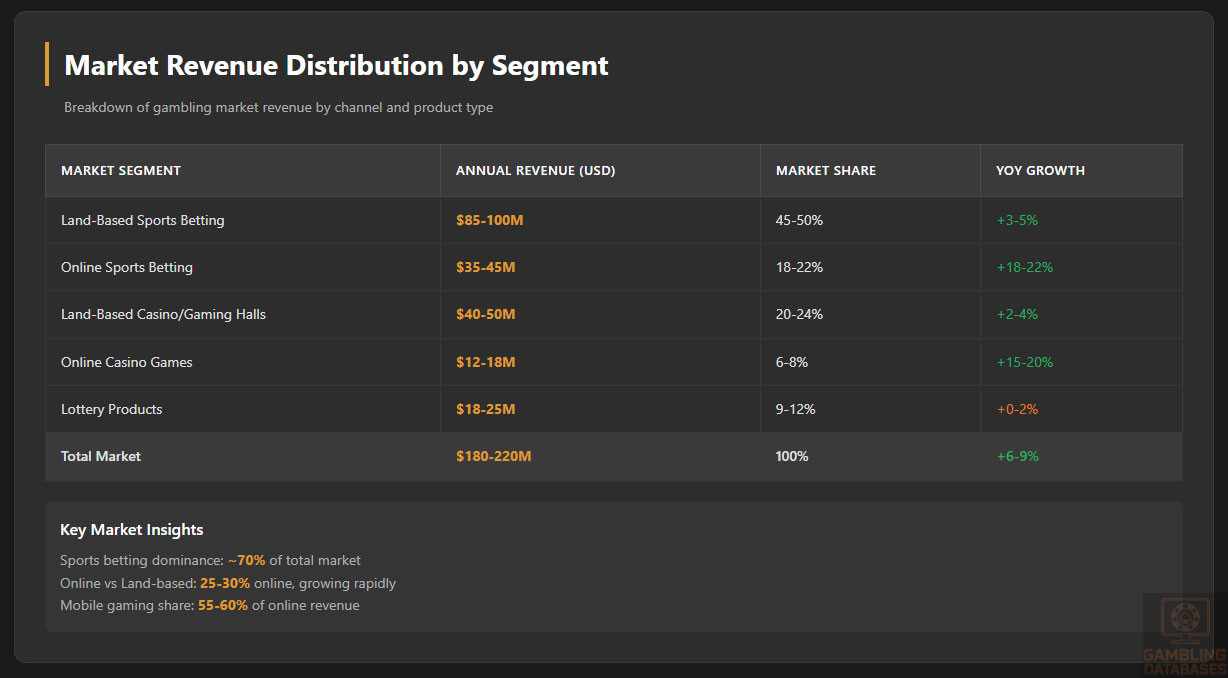

Market Revenue and Growth Trends: The total Bosnia and Herzegovina gambling market generates approximately 180-220 million USD annually across all channels and operators. Land-based gambling activities account for roughly 70-75 percent of total market revenue, reflecting the traditional dominance of retail betting shops and gaming halls. Sports betting represents the single largest segment, contributing approximately 60 percent of total gambling revenue given Bosnian consumers’ strong preferences for sports wagering.

Online gambling has grown rapidly over recent years, reaching 50-65 million USD in annual revenue representing 25-30 percent of the total market. The COVID-19 pandemic accelerated digital adoption as land-based venues faced closures and capacity restrictions, permanently shifting some consumer behavior toward online channels. Annual growth rates for online gambling range from 15-20 percent, significantly exceeding land-based market growth of 2-5 percent annually.

Casino gaming including table games and electronic gaming machines contributes approximately 25-30 percent of total market revenue. The casino segment shows more modest growth than sports betting, constrained by limited tourism inflows and domestic consumer preferences favoring sports wagering over casino products. Lottery operations maintain steady but declining market share, representing approximately 10-15 percent of gambling revenue with minimal growth given the mature nature of lottery markets.

Tax Revenue Generation: Gambling taxes contribute 20-30 million USD annually to government revenues across both entities, representing a meaningful but not transformational revenue source. The Federation of Bosnia and Herzegovina collects higher absolute gambling tax revenues given its larger population and more extensive gambling market, though per-capita gambling tax contributions remain modest compared to Western European benchmarks.

Republika Srpska’s lower tax rates partially offset by high gambling participation rates result in meaningful gambling tax revenues for the entity’s budget. The gambling sector’s tax contribution has grown steadily over recent years as online gambling expansion and land-based market maturation generate increasing revenues. However, gambling taxes represent only 1-2 percent of total government revenue, limiting authorities’ fiscal dependence on the sector.

Municipal gambling tax collections in the Federation vary significantly based on local gambling venue density and operational scale. Sarajevo and other major cities collect substantial municipal gambling taxes, while rural municipalities with limited gambling presence receive minimal gambling-related revenue. This geographic variation creates different municipal attitudes toward gambling regulation, with some municipalities actively encouraging gambling operations to enhance tax collections while others restrict licensing to limit social impacts.

| Market Segment | Annual Revenue (USD millions) | Market Share | YoY Growth Rate |

|---|---|---|---|

| Land-Based Sports Betting | 85-100 | 45-50% | 3-5% |

| Online Sports Betting | 35-45 | 18-22% | 18-22% |

| Land-Based Casino/Gaming Halls | 40-50 | 20-24% | 2-4% |

| Online Casino Games | 12-18 | 6-8% | 15-20% |

| Lottery Products | 18-25 | 9-12% | 0-2% |

| Total Market | 180-220 | 100% | 6-9% |

Advertising and Marketing Restrictions

Permitted Advertising Channels: Bosnia and Herzegovina permits gambling advertising across multiple channels with varying restrictions by medium and entity. Television advertising faces the most comprehensive regulation, with both entities restricting gambling advertisements during certain time periods to minimize exposure to minors. The Federation typically prohibits gambling advertising on television between 6:00 AM and 10:00 PM, limiting commercials to late evening and overnight hours when younger audiences are less likely to be watching.

Republika Srpska implements similar television advertising restrictions with some variation in specific time windows and content requirements. Radio advertising faces less stringent timing restrictions but must include responsible gambling warnings and avoid content appealing to minors. Print media including newspapers and magazines can generally carry gambling advertisements with content restrictions around imagery and messaging that might attract underage interest.

Online advertising operates in a less regulated environment, with fewer restrictions on digital display advertising, search engine marketing, and social media promotions. However, operators must ensure online advertising does not target minors through content selection, placement on youth-oriented websites, or use of appealing imagery and themes. Affiliate marketing arrangements between operators and promotional websites remain permitted, with operators bearing responsibility for affiliate compliance with advertising standards.

Content Restrictions and Guidelines: Advertising content must not present gambling as a solution to financial problems, social success pathway, or necessary activity for social acceptance. Advertisements cannot portray excessive gambling as socially acceptable or glamorize problem gambling behaviors. Use of celebrities, sports figures, or cultural icons in advertising faces scrutiny, particularly when these individuals have substantial youth followings that might increase underage appeal.

All gambling advertisements must include responsible gambling messaging, typically warnings that gambling involves risks and players should gamble responsibly. Contact information for problem gambling support organizations should appear in advertising materials. Advertisements cannot make misleading claims about winning odds, suggest guaranteed returns, or minimize the risks inherent in gambling activities. Terms and conditions for bonuses and promotions must be clearly disclosed with no hidden requirements or unrealistic wagering conditions.

Sponsorship Regulations: Gambling operators actively sponsor football clubs, sports leagues, and sporting events throughout Bosnia and Herzegovina, representing major marketing investments. The Federation and Republika Srpska generally permit gambling sponsorships with some content restrictions. Sponsored teams and athletes cannot promote gambling to minors or use youth-oriented imagery in sponsorship materials. Stadium signage and jersey sponsorships must comply with general advertising content standards.

Controversy occasionally arises around gambling sponsorship’s prominence in Bosnian sports, with some advocacy groups calling for restrictions similar to tobacco advertising bans. However, gambling operators remain major sports sponsors given limited corporate sponsorship alternatives in the small economy. Sports betting operators particularly leverage sponsorships to build brand awareness and associate their brands with popular football clubs and competitions.

Bonus and Promotion Restrictions: Welcome bonuses, free bets, and promotional offers face increasing regulatory scrutiny across both entities. Authorities have begun limiting bonus amounts, requiring transparent wagering requirements, and restricting promotional mechanics that might encourage excessive gambling. Maximum bonus values help prevent operators from using unsustainable promotions to acquire customers, while clear wagering requirements ensure players understand what’s required to withdraw bonus-related winnings.

Some restrictions prohibit promotional offers targeting players who have self-excluded or shown problem gambling behaviors. Operators must not send promotional communications to self-excluded individuals or those who have requested no marketing contact. Bonus terms must be clearly presented before players accept offers, with no hidden conditions or unfair requirements that make bonus fulfillment virtually impossible.

Recent Regulatory Changes and Their Impact

Regulatory Evolution 2022-2025: Bosnia and Herzegovina’s gambling regulatory framework has experienced ongoing development over recent years as authorities respond to market changes and online gambling growth. The Federation implemented revised online gambling regulations clarifying licensing requirements and compliance obligations for digital operators. These amendments addressed previous regulatory ambiguities that created uncertainty for operators considering market entry.

Republika Srpska similarly updated gambling legislation enhancing online gambling oversight and strengthening player protection requirements. Amendments introduced clearer technical standards for online platforms, mandatory responsible gambling tools, and enhanced financial monitoring obligations. The entity also adjusted tax rates for certain gambling activities, though changes remained modest compared to dramatic tax increases seen in some European markets.

Enhanced Player Protection Requirements: Recent regulatory changes across both entities strengthened player protection obligations for licensed operators. New requirements mandate comprehensive self-exclusion systems, enhanced age verification procedures, and mandatory responsible gambling training for staff. Online operators must implement reality checks interrupting play sessions and informing players of time elapsed and losses incurred.

Deposit limit requirements enable players to set daily, weekly, or monthly deposit caps preventing excessive spending. While some operators voluntarily offered these tools previously, new regulations mandate their availability across all licensed platforms. Enhanced protection for vulnerable players includes requirements to identify potential problem gambling behaviors and intervene with account restrictions, mandatory cooling-off periods, or direct contact to offer support resources.

Advertising and Bonus Restrictions: Regulatory amendments have progressively tightened advertising and promotional activity restrictions. New rules limit television advertising to late-night hours exclusively, expanding previous restrictions that permitted some daytime advertising. Content standards became more stringent, requiring prominent responsible gambling warnings and prohibiting testimonials suggesting gambling success or financial gain.

Bonus restrictions introduced caps on welcome offer values and requirements for transparent presentation of wagering conditions. Some proposed amendments would prohibit certain promotional mechanics considered particularly risky, such as loss rebates that might encourage players to chase losses. The regulatory direction clearly favors enhanced consumer protection even at the cost of limiting operator marketing flexibility.

Impact on Operator Costs and Strategy: Regulatory changes have increased operator compliance costs through enhanced monitoring system requirements, mandatory responsible gambling tool implementation, and stricter reporting obligations. Smaller operators face particular challenges absorbing compliance costs that represent larger proportional burdens relative to their revenues. Some marginal operators have exited the market unable to justify continued operations under more stringent regulatory requirements.

Marketing restrictions have forced operators to adjust customer acquisition strategies, emphasizing brand building over aggressive promotional offers. The limitation on television advertising hours concentrates gambling commercials in late-night time slots, potentially reducing their effectiveness while increasing competition for limited advertising inventory. Operators increasingly focus on digital marketing channels, sponsorship activations, and retention of existing customers rather than aggressive new customer acquisition.

Enforcement Mechanisms and Penalties

Penalty Structures: Regulatory authorities maintain graduated penalty structures addressing compliance violations. Minor infractions typically result in warnings and requirements to remedy issues within specified timeframes. Repeated or more serious violations trigger financial penalties proportional to violation severity and operator size. Fine amounts range from several thousand BAM for minor infractions to hundreds of thousands BAM for serious compliance failures.

License suspension represents a more severe penalty, temporarily halting operator activities until compliance issues are resolved. Suspensions create substantial financial harm given revenue losses during suspension periods and reputational damage with customers and business partners. License revocation constitutes the ultimate penalty, permanently terminating an operator’s authorization to conduct gambling activities. Revoked licenses may not be reinstated, requiring operators to submit entirely new applications if seeking to re-enter the market.

Recent Enforcement Actions: Regulatory authorities have demonstrated increasing willingness to enforce compliance requirements, imposing penalties on both domestic and international operators. Recent enforcement actions have targeted inadequate age verification procedures, failures to implement self-exclusion systems effectively, and violations of advertising restrictions. Some operators faced license suspensions for serious anti-money laundering compliance failures, sending strong signals about regulatory expectations.

Enforcement trends indicate authorities prioritizing player protection violations over technical compliance issues. Operators permitting underage gambling, failing to identify problem gambling behaviors, or violating self-exclusion requirements face particularly serious consequences. Financial penalties have increased in recent years, with authorities imposing fines large enough to impact operator profitability and motivate compliance investments.

Unlicensed Operator Enforcement: Both entities actively combat unlicensed gambling operations through multiple enforcement mechanisms. Internet service provider blocking prevents consumer access to offshore gambling websites operating without local licenses. Payment processor restrictions complicate financial transactions between Bosnian consumers and unlicensed operators, reducing the appeal of offshore alternatives. Authorities periodically publish lists of blocked websites and warn consumers about gambling with unlicensed operators.

Criminal penalties apply to individuals operating unlicensed gambling activities within Bosnia and Herzegovina. Police raid illegal gambling establishments, confiscate equipment, and file criminal charges against operators. While enforcement focuses primarily on land-based illegal gambling venues, authorities have begun pursuing individuals promoting offshore gambling websites within Bosnia and Herzegovina. However, practical enforcement challenges limit effectiveness against sophisticated international online operators targeting Bosnian consumers from foreign jurisdictions.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Total Population and Growth Trends: Bosnia and Herzegovina has a population of approximately 3.2 million people, experiencing gradual decline over recent decades due to emigration, low birth rates, and aging demographics. The population peaked in the early 1990s before declining through conflict-related population losses and sustained emigration waves. Current demographic trends show continued slow population decrease of approximately 0.5-1.0 percent annually, driven primarily by youth emigration to Western Europe seeking better economic opportunities.

This declining population trend presents challenges for market growth, limiting the potential customer base for gambling operators. However, the negative demographic trajectory may stabilize as emigration rates potentially moderate and economic conditions gradually improve. Operators must account for shrinking population when projecting long-term market growth, recognizing that revenue increases will depend more on increasing gambling participation rates and spending per player rather than population expansion.

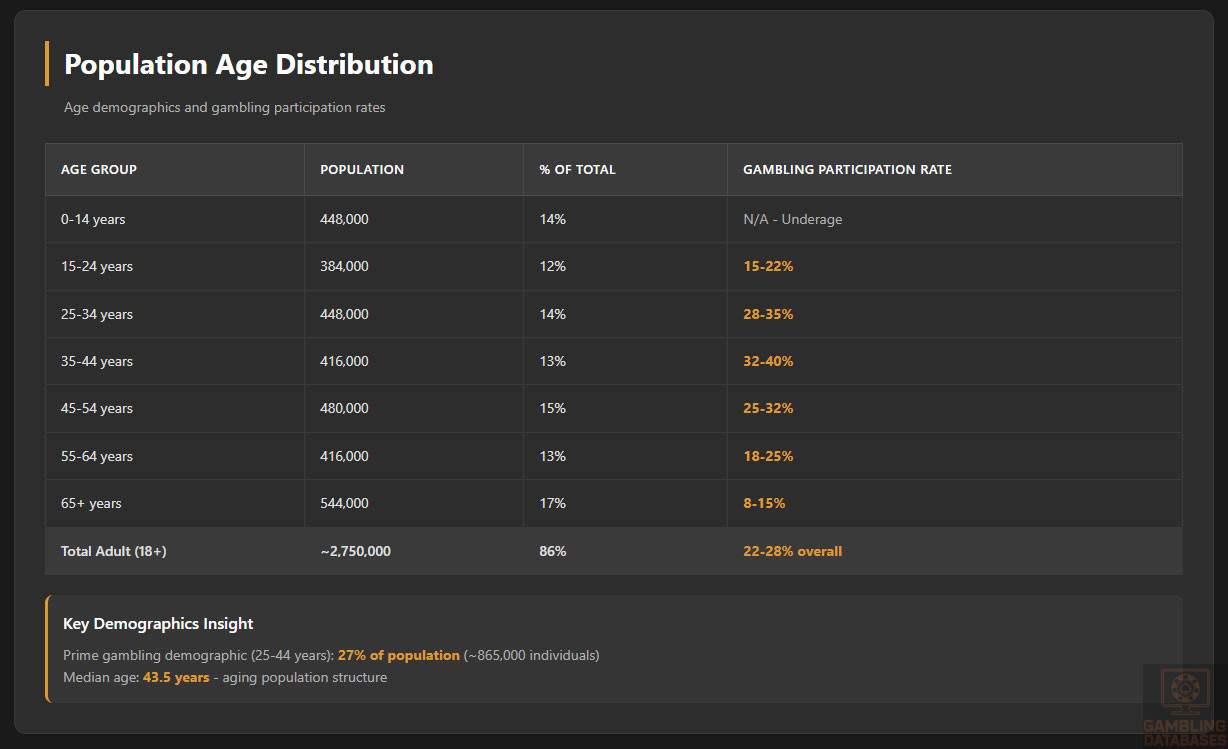

Age Distribution and Market Implications: Bosnia and Herzegovina displays an aging population structure with median age around 43.5 years, significantly higher than the global median. The age distribution skews older, with substantial population concentrations in middle-aged and senior categories while younger age groups represent diminishing proportions of total population. Approximately 14 percent of the population falls under age 15, while 17 percent exceeds 65 years old.

The 25-44 age bracket, representing prime gambling demographics, comprises approximately 27 percent of the population or roughly 865,000 individuals. This cohort demonstrates highest gambling participation rates and spending levels, making them primary targets for operator marketing. The 45-64 age group represents another 28 percent of population with significant gambling interest, particularly for land-based betting and traditional casino games. Younger adults aged 18-24 account for roughly 9 percent of population, showing growing interest in online gambling and mobile betting platforms.

| Age Group | Population (thousands) | Percentage of Total | Gambling Participation Rate |

|---|---|---|---|

| 0-14 years | 448 | 14% | N/A – Underage |

| 15-24 years | 384 | 12% | 15-22% |

| 25-34 years | 448 | 14% | 28-35% |

| 35-44 years | 416 | 13% | 32-40% |

| 45-54 years | 480 | 15% | 25-32% |

| 55-64 years | 416 | 13% | 18-25% |

| 65+ years | 544 | 17% | 8-15% |

| Total Adult Population (18+) | ~2,750 | 86% | 22-28% overall |

Gender Distribution and Life Expectancy: Bosnia and Herzegovina maintains relatively balanced gender distribution with slight female majority, approximately 51 percent female and 49 percent male. Life expectancy averages around 77 years, with women living approximately 4-5 years longer than men on average. Gender differences in gambling participation show typical patterns, with men demonstrating higher overall gambling participation rates and spending levels particularly for sports betting.

Male gambling participation rates reach 35-45 percent of the adult male population, while female participation ranges from 12-18 percent. However, female participation in online gambling has grown more rapidly than male participation in recent years, narrowing gender gaps particularly among younger demographics. Women show stronger preferences for casino games, slots, and lottery products compared to male-dominated sports betting participation.

Geographic Distribution

Urban and Rural Population Patterns: Bosnia and Herzegovina displays balanced urban-rural distribution with approximately 49 percent urban population and 51 percent rural population. This distribution differs from more urbanized European countries, reflecting the country’s mountainous terrain, historical settlement patterns, and limited industrialization. However, urban areas concentrate economic activity, internet infrastructure, and gambling venues despite representing only half the population.

Rural areas face challenges including limited internet access, lower income levels, and reduced entertainment options compared to cities. Gambling participation rates in rural areas lag urban levels, though land-based betting shops have penetrated even smaller towns given the popularity of sports betting. Online gambling adoption shows stronger urban concentration, with rural players facing connectivity limitations and lower digital literacy rates.

Major Population Centers: Sarajevo, the capital and largest city, has a population of approximately 275,000 in the core city and 420,000 in the greater metropolitan area. As the political, economic, and cultural center, Sarajevo concentrates gambling activities with numerous betting shops, casinos, and the highest online gambling participation rates. The city’s younger, more educated, and higher-income population represents prime gambling demographics.

Banja Luka, the largest city in Republika Srpska with approximately 185,000 residents, serves as the entity’s administrative and economic center. The city hosts substantial gambling infrastructure including multiple casinos, extensive betting shop networks, and growing online gambling adoption. Tuzla, the third-largest city with around 110,000 residents, represents another significant gambling market with established operator presence and competitive market dynamics.

Mostar, Zenica, Bijeljina, and other secondary cities with populations ranging from 40,000 to 95,000 comprise important regional markets. These cities host gambling venues and demonstrate solid gambling participation, though at lower absolute volumes than major urban centers. Operators targeting comprehensive market coverage must establish presence in these secondary cities beyond just focusing on Sarajevo and Banja Luka.

| City | Population | Entity | Gambling Venues | Market Characteristics |

|---|---|---|---|---|

| Sarajevo | 275,000 (420,000 metro) | FBiH | High density | Largest market, high online adoption |

| Banja Luka | 185,000 | RS | High density | RS capital, strong betting culture |

| Tuzla | 110,000 | FBiH | Moderate-high | Industrial center, working-class demographics |

| Zenica | 95,000 | FBiH | Moderate | Industrial city, betting shops dominant |

| Mostar | 85,000 | FBiH | Moderate | Tourism potential, mixed market |

| Bijeljina | 75,000 | RS | Moderate | Border city, some cross-border traffic |

| Prijedor | 67,000 | RS | Low-moderate | Regional center, developing market |

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

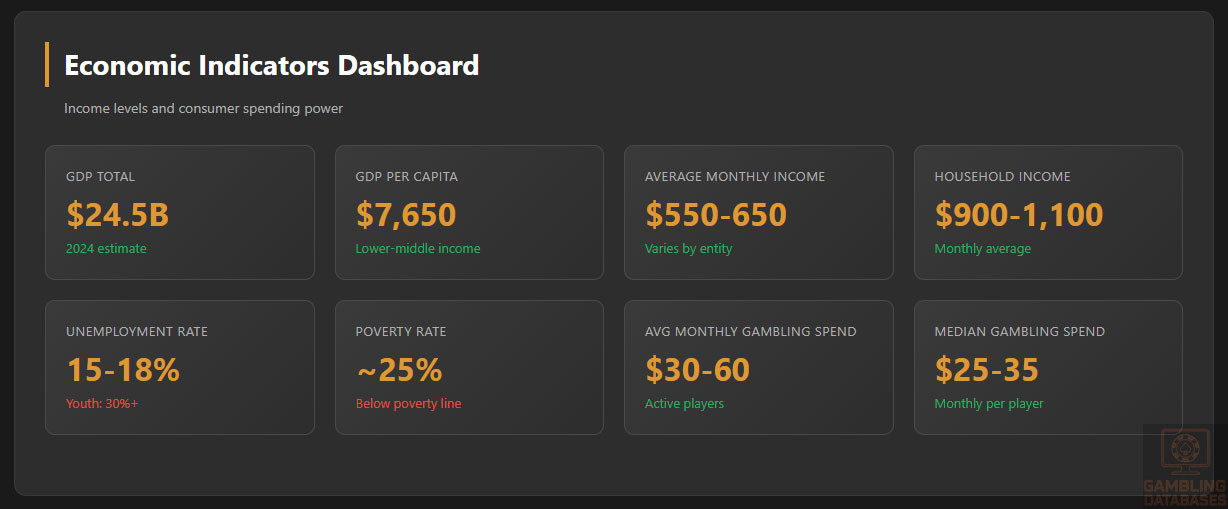

Current Economic Output: Bosnia and Herzegovina’s economy generates approximately 24.5 billion USD in annual GDP, positioning it as a lower-middle income country by World Bank classifications. GDP per capita stands around 7,650 USD, significantly below European Union averages but comparable to other Western Balkan economies. The economy relies heavily on services sector contributing approximately 60 percent of GDP, with industry representing 25 percent and agriculture 8 percent.

Economic growth has remained modest but positive in recent years, averaging 2-3 percent annually. Growth faces constraints from political fragmentation, limited foreign investment, infrastructure deficiencies, and continued emigration of working-age population. However, remittances from diaspora workers in Western Europe provide meaningful economic support, supplementing domestic income and sustaining consumption levels above what GDP figures alone suggest.

GDP Growth Forecasts: Economic projections for 2025-2027 anticipate continued modest growth of 2.5-3.5 percent annually, driven by services sector expansion, gradual infrastructure improvements, and potential EU accession progress. Tourism development, particularly in Sarajevo and Herzegovina region, could provide growth stimulus. However, demographic decline and continued emigration limit growth potential, as shrinking working-age population constrains economic expansion.

The gambling market’s growth potential exceeds overall GDP growth rates as online gambling adoption accelerates and gambling participation increases. Market analysts project iGaming revenue growing 8-12 percent annually over the next 3-5 years, significantly outpacing general economic growth. This divergence reflects gambling’s transition from primarily land-based to increasingly digital channels and rising smartphone penetration enabling convenient gambling access.

Employment and Wage Levels: Unemployment rates in Bosnia and Herzegovina remain elevated compared to EU standards, officially reported around 15-18 percent though real rates likely exceed official statistics when accounting for underemployment and discouraged workers. Youth unemployment poses particular challenges, exceeding 30 percent and driving emigration among younger demographics. High unemployment suppresses wage growth and limits consumer spending power.

Average monthly wages vary substantially between entities, sectors, and skill levels. The Federation reports average monthly net wages around 600-650 USD, while Republika Srpska averages slightly lower at 550-600 USD. Public sector employees typically earn higher wages than private sector workers, while wages in Sarajevo exceed other regions. However, significant portions of economic activity occur in grey economy not reflected in official wage statistics.

Income and Wealth Distribution

Household Income Levels: Average household monthly income approximates 900-1,100 USD across Bosnia and Herzegovina, though significant regional and demographic variation exists. Urban households generally earn 20-30 percent more than rural households. Remittances from family members working abroad supplement many household incomes, providing crucial financial support particularly in rural areas and economically depressed regions.

Median household income sits somewhat below average figures, around 800-900 USD monthly, indicating right-skewed income distribution with relatively small high-income populations pulling averages upward. The concentration of higher incomes in Sarajevo and other major cities creates geographic wealth disparities. Disposable income after essential expenses limits discretionary spending capacity for many households, constraining gambling spending potential for lower and middle-income consumers.

Income Inequality and Distribution: Bosnia and Herzegovina displays moderate income inequality with Gini coefficient around 0.33-0.36, lower than many developed economies but indicating meaningful wealth concentration. Approximately 25 percent of the population lives below national poverty lines, struggling with basic needs and having minimal discretionary spending capacity. The middle class represents roughly 40-50 percent of population, with sufficient income for modest discretionary spending including occasional gambling.

Higher-income households comprising perhaps 15-20 percent of population concentrate in urban areas and professional occupations. This segment demonstrates highest gambling spending capacity and participation rates. However, the relatively small wealthy population limits total addressable market for premium gambling products. Operators must focus on middle-income mass market players rather than relying on high-roller segments given wealth distribution patterns.

Consumer Spending Patterns: Bosnian households allocate large portions of income to necessities including housing, food, and utilities, leaving limited discretionary spending. Average household spending on entertainment and recreation represents approximately 5-8 percent of total expenditure. Within entertainment spending, gambling competes with dining out, cultural events, sports activities, and other leisure pursuits for limited discretionary budgets.

Monthly household spending on gambling among participating households averages approximately 30-60 USD, though significant variation exists from occasional small-stakes bettors spending 10-15 USD monthly to regular players wagering 150-300 USD monthly. Higher-income players and problem gamblers skew averages upward, while median spending sits lower around 25-35 USD monthly among active gambling participants. Spending concentrates around major sporting events, particularly European football competitions and international tournaments.

Market Size and Growth Projections

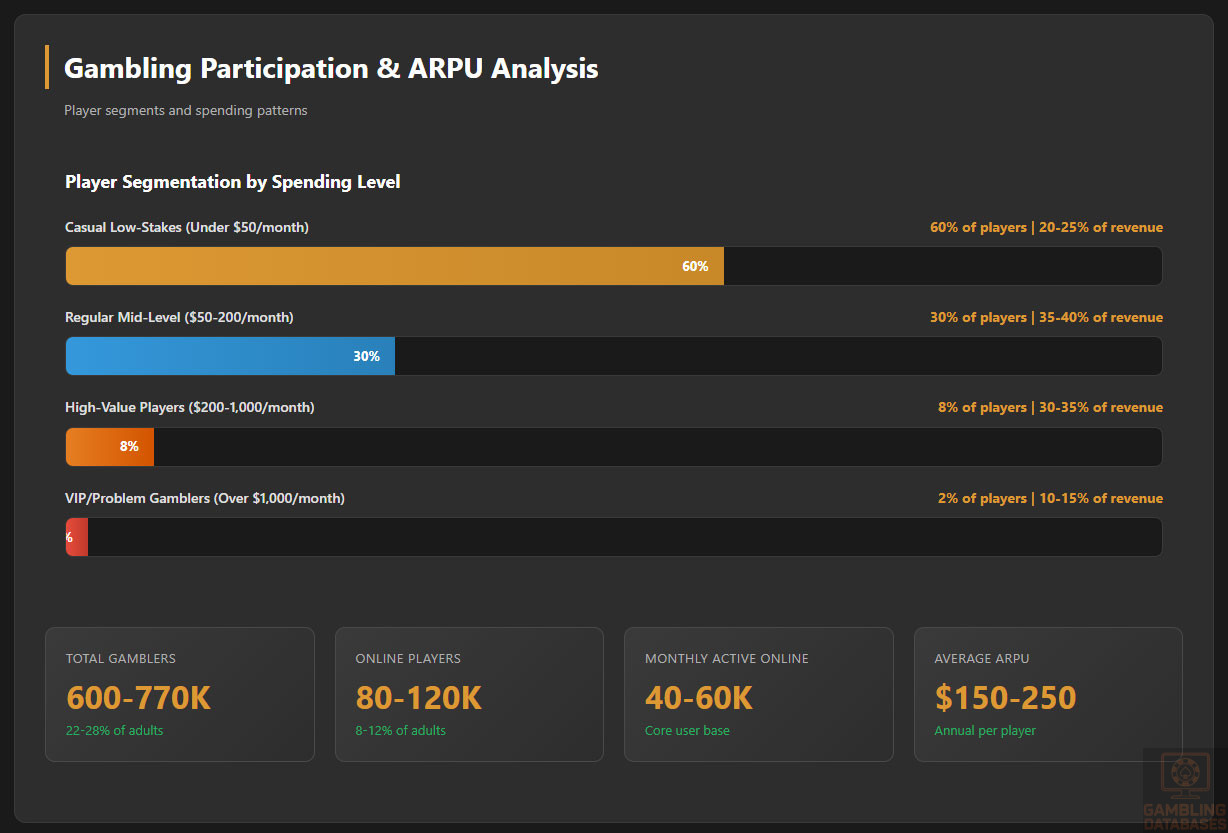

Current Market Revenue Analysis: The Bosnia and Herzegovina iGaming market generates approximately 50-65 million USD in annual revenue from online gambling activities, representing 25-30 percent of the total gambling market. Online sports betting dominates digital gambling revenue contributing 65-70 percent of online totals, reflecting strong consumer preference for sports wagering. Online casino games including slots, table games, and live dealer products contribute 25-30 percent of online revenue.

The total addressable market includes approximately 250,000-350,000 adults who gamble at least occasionally, representing 9-13 percent of the adult population. Among these participants, roughly 80,000-120,000 individuals engage in online gambling with varying frequency. Active monthly online gambling participants number approximately 40,000-60,000, representing the core customer base generating the majority of online gambling revenue. This relatively small active player base concentrates revenue, with top 20 percent of players generating 60-70 percent of total revenue.

Historical Revenue Growth: Online gambling revenue has grown substantially over the past 3-5 years, with compound annual growth rates of 18-25 percent. Growth accelerated significantly during 2020-2021 as COVID-19 restrictions closed land-based venues and drove digital adoption. While growth rates have moderated from pandemic peaks, they remain robust at 12-18 percent annually as digital gambling continues displacing land-based activities and new players enter online gambling markets.

Land-based gambling revenue growth has stagnated or declined slightly in recent years, with modest 0-3 percent annual growth failing to keep pace with inflation. The channel shift from retail betting shops to online platforms explains divergent growth trajectories. Some land-based operators have closed unprofitable locations while expanding online operations, recognizing changing consumer preferences. Total market growth averaging 6-9 percent annually reflects the mix of declining land-based and rapidly growing online segments.

Revenue Forecasts 2025-2028: Market analysts project online gambling revenue reaching 75-95 million USD by 2028, representing compound annual growth of 10-14 percent. Growth drivers include continued smartphone adoption, improved internet infrastructure, expanding payment method options, and generational shifts as younger digitally-native consumers enter gambling markets. Sports betting revenue should grow 8-12 percent annually, while online casino gaming may achieve 15-20 percent growth from its smaller base.

Total gambling market revenue including both online and land-based channels should reach 220-260 million USD by 2028, growing 5-8 percent annually. Online gambling’s market share will expand to 35-40 percent of total gambling revenue by 2028 as digital channels continue gaining ground. Land-based revenue may stabilize or decline slightly in absolute terms as venue closures offset per-venue revenue growth, with the channel increasingly serving older demographics less comfortable with digital alternatives.

| Year | Online Revenue (USD millions) | Total Market (USD millions) | Online Market Share | YoY Growth Rate |

|---|---|---|---|---|

| 2024 (Actual) | 50-65 | 180-220 | 27-30% | 15-18% |

| 2025 (Projected) | 58-72 | 192-232 | 29-31% | 12-15% |

| 2026 (Projected) | 65-81 | 202-242 | 31-34% | 11-14% |

| 2027 (Projected) | 70-88 | 210-250 | 33-36% | 10-13% |

| 2028 (Projected) | 75-95 | 220-260 | 35-38% | 10-12% |

User Base Growth Projections: The active online gambling user base should expand from current 80,000-120,000 individuals to 120,000-170,000 by 2028, representing 35-45 percent growth. Monthly active users will grow from 40,000-60,000 to 65,000-95,000 over the same period. Growth will come from conversion of land-based-only players to omnichannel users, attraction of younger adults entering gambling age, and increased female participation in online gambling.

However, population decline limits user base expansion potential. Growth depends on increasing gambling participation rates among existing population rather than population growth adding new potential customers. Operators must focus on activation of currently non-gambling adults and increasing engagement among occasional gamblers to drive user base growth given demographic constraints.

Average Revenue Per User Trends: ARPU currently ranges from 150-250 USD annually per active online gambling participant, though significant variation exists between casual small-stakes players and high-value customers. ARPU has grown modestly over recent years as players increase gambling frequency and spending per session. However, competitive pressures and bonus costs limit ARPU expansion, with operators sacrificing some revenue per player to acquire and retain customers in competitive markets.

ARPU projections suggest moderate growth to 180-280 USD annually by 2028, representing 4-6 percent annual increases. Growth will come from players shifting more gambling spending from land-based to online channels where they tend to gamble more frequently given accessibility. Cross-selling casino products to sports bettors and vice versa should increase per-customer revenue. However, ARPU growth faces headwinds from income constraints and competitive promotional intensity.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy and Educational Attainment: Bosnia and Herzegovina maintains high literacy rates exceeding 98 percent among adults, reflecting historical emphasis on education during Yugoslav period. Primary and secondary school enrollment reaches nearly universal levels, ensuring baseline educational foundations across the population. However, educational quality varies significantly between urban and rural areas, with city schools generally offering superior facilities and instruction.

Tertiary education completion rates approximate 20-25 percent of the adult population, below European Union averages but reasonable for the region. University graduates concentrate in urban areas, particularly Sarajevo which hosts multiple universities. Vocational and technical education provides pathways for non-university-bound students, though quality and labor market relevance vary. Brain drain affects educational outcomes as many highly educated individuals emigrate after completing studies.

Digital Literacy and Technology Skills: Digital literacy levels vary considerably by age, education, and urban-rural location. Younger adults under 35 demonstrate relatively strong digital skills, comfortable navigating websites, using mobile applications, and conducting online transactions. Middle-aged adults show more variable digital competency, with educated urban professionals highly digital-literate while older rural residents struggle with technology. Senior citizens generally display limited digital skills, preferring traditional channels for banking, shopping, and entertainment.

Approximately 65-70 percent of adults demonstrate sufficient digital literacy to navigate online gambling platforms without significant difficulty. However, building trust in online transactions and overcoming concerns about payment security require operator effort beyond just technical accessibility. Digital literacy improvements as younger generations age should expand the potential online gambling customer base over time, while current older demographics remain more oriented toward land-based gambling venues.

Language Skills and Communication: Bosnian, Croatian, and Serbian represent the three official languages, which are mutually intelligible and collectively understood across the population. Linguistic fragmentation creates some complexity for operators, as ethnic groups have sensitivities around language designation. Most operators use neutral language or offer content in all three variants to avoid alienating customer segments. English proficiency remains limited outside educated urban populations and younger adults, requiring operators to provide comprehensive local language customer support and content.

Cultural and Social Factors

Communication and Language Preferences

Language in Business and Digital Contexts: Operators must provide gambling platforms, customer service, and marketing materials in local languages to effectively serve the market. English-only platforms face significant adoption barriers given limited English proficiency across much of the population. Translation quality matters greatly, as poor translations damage credibility and create confusion around terms and conditions, bonus requirements, and betting rules.

Customer service availability in local languages represents a competitive differentiator, with players preferring operators offering support in their preferred language variant. Live chat, email support, and telephone assistance should all accommodate local language needs. Social media marketing and content must similarly use appropriate local languages and avoid linguistic choices that might alienate segments of the ethnically diverse population.

Cultural Attitudes Toward Gambling

Social Acceptance of Gambling: Gambling enjoys relatively high social acceptance in Bosnia and Herzegovina, particularly sports betting which many view as a legitimate entertainment activity and social pastime. Betting shops serve as gathering places where men watch sports and discuss betting strategies, creating social dimensions beyond pure gambling. However, casino gambling faces more mixed perceptions, with some viewing it as morally questionable or associated with vice and excess.

Religious influences on gambling attitudes vary across the population. Muslim populations, representing approximately 51 percent of the total, show diverse attitudes ranging from complete abstinence based on religious principles to active participation viewing gambling as personal choice. Orthodox Christian populations around 31 percent and Catholic populations around 15 percent similarly display varied attitudes. Overall, religious opposition to gambling does not prevent substantial market participation, though it influences some individuals’ choices and creates social stigma in certain communities.

Gender and Gambling Culture: Gambling in Bosnia and Herzegovina historically skewed heavily male, particularly for sports betting and casino gambling. Land-based betting shops cater primarily to men, with gender ratios often exceeding 80-90 percent male in retail venues. This male-dominated culture can discourage female participation in land-based gambling despite no formal restrictions.

Online gambling presents opportunities to reach female audiences in more comfortable, private environments. Women demonstrate growing online gambling participation, particularly for casino games, slots, and bingo-style products. Operators targeting female players should emphasize welcoming brand positioning, avoid masculine sports-focused marketing stereotypes, and provide customer service approaches that appeal to women. Breaking the male-dominated gambling culture could significantly expand the total addressable market.

Risk Tolerance and Gambling Preferences: Bosnian gamblers generally display moderate risk tolerance, preferring relatively conservative betting strategies with frequent small-stakes wagers rather than infrequent large bets. Sports betting appeal stems partly from beliefs that knowledge and skill can improve outcomes, even though randomness ultimately dominates results. Accumulator bets combining multiple selections with higher odds attract players seeking bigger potential payouts from small stakes.

Casino gambling preferences lean toward slots and simple games rather than complex table games requiring substantial rules knowledge. Live dealer games have gained popularity as they combine online convenience with social interaction and perceived fairness from visible dealers. Lottery products remain popular for their simplicity and very small stake requirements, accessible even to lowest-income populations.

Problem Gambling and Social Considerations