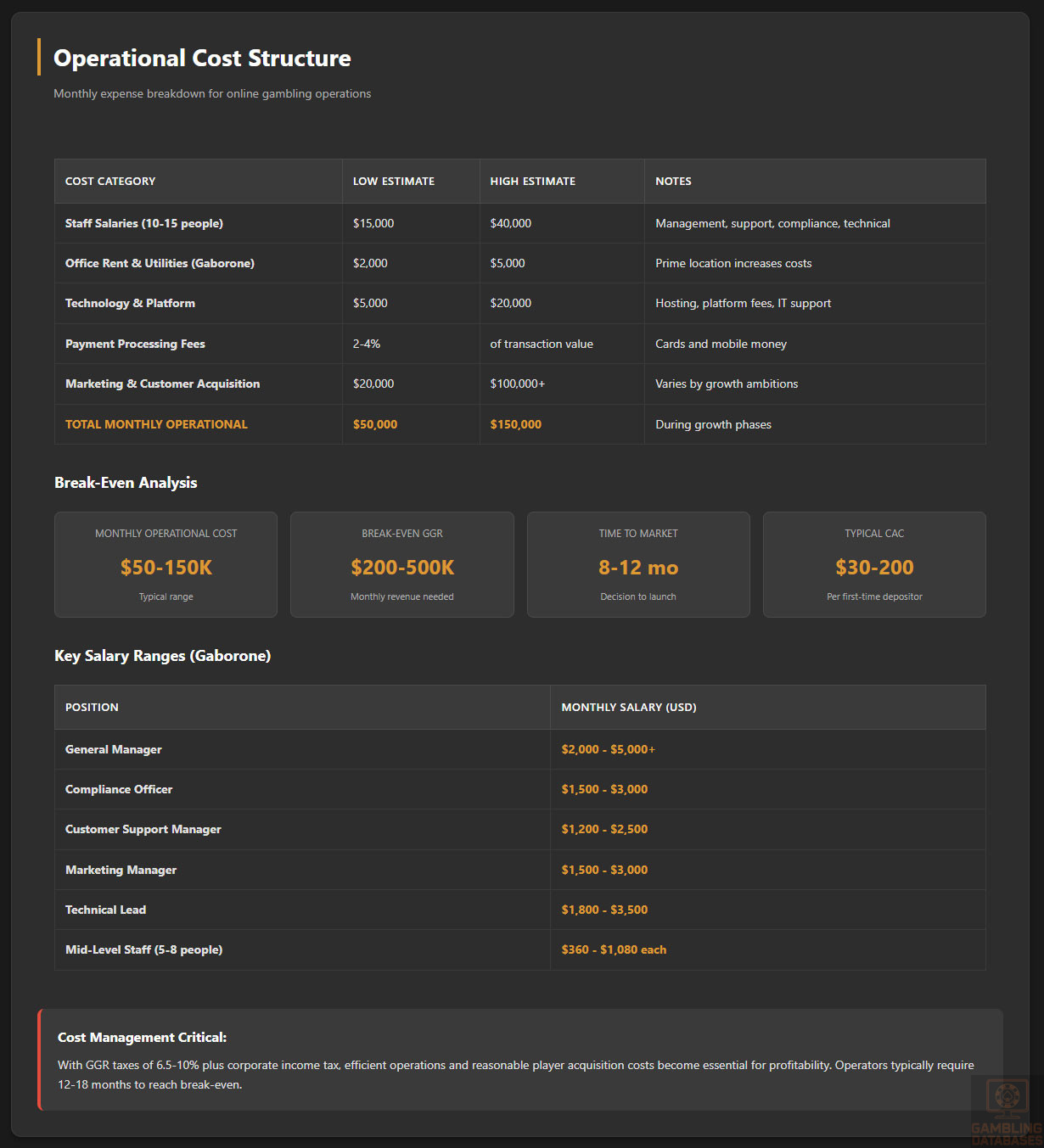

Botswana presents a developing opportunity for iGaming operators within the Southern African market. The country maintains a well-structured regulatory framework for land-based gambling through the Botswana Gambling Authority, established under the Gambling Act of 2012. Online gambling remains unregulated, creating both challenges and opportunities for international operators seeking market entry.

With an internet penetration rate of 81.4% and a population of 2.56 million, Botswana demonstrates strong digital infrastructure compared to regional peers. The nation’s stable political environment, diamond-driven economy with GDP per capita of approximately $8,159, and growing mobile money adoption create favorable conditions for digital gambling expansion, despite the current regulatory gap for online operations.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

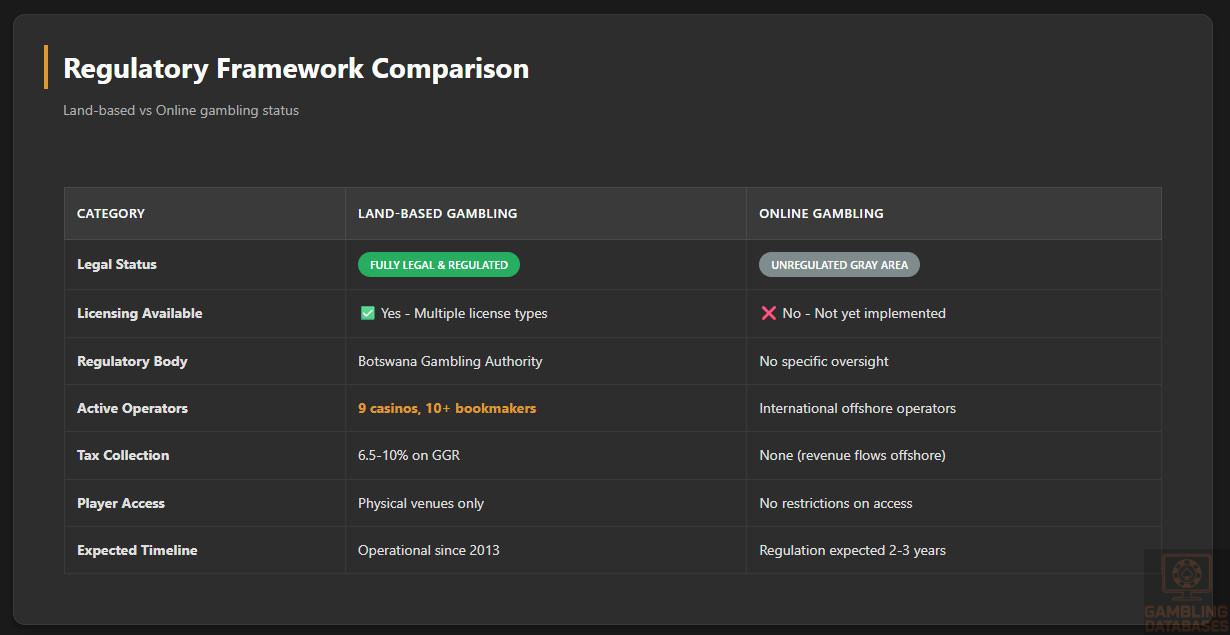

| Online Gambling Legal Status | Unregulated Gray Area | No specific legislation for online gambling |

| Land-Based Gambling Status | Fully Legal & Regulated | 9 licensed casinos, bookmakers operational |

| Regulatory Authority | Botswana Gambling Authority | Established 2012, operational since 2013 |

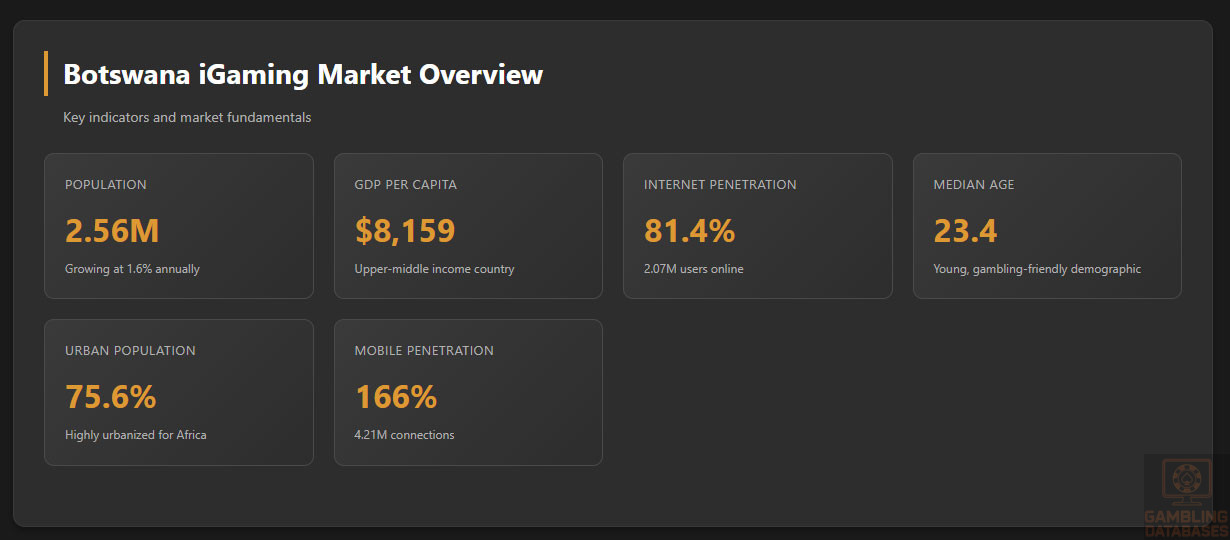

| Total Population (2025) | 2.56 million | Growing at 1.6% annually |

| Median Age | 23.4 years | Young, gambling-friendly demographic |

| Urban Population | 75.6% | Highly urbanized for Africa |

| GDP (2024) | $18-20 billion USD | Diamond-driven economy |

| GDP Per Capita (2025) | $8,159 USD | Upper-middle income country |

| Internet Penetration | 81.4% | 2.07 million users, top in Africa |

| Mobile Penetration | 166% | 4.21 million connections |

| Smartphone Penetration | High (estimated 70%+) | Primary internet access device |

| Social Media Users | 1.30 million (51.1%) | Strong digital engagement |

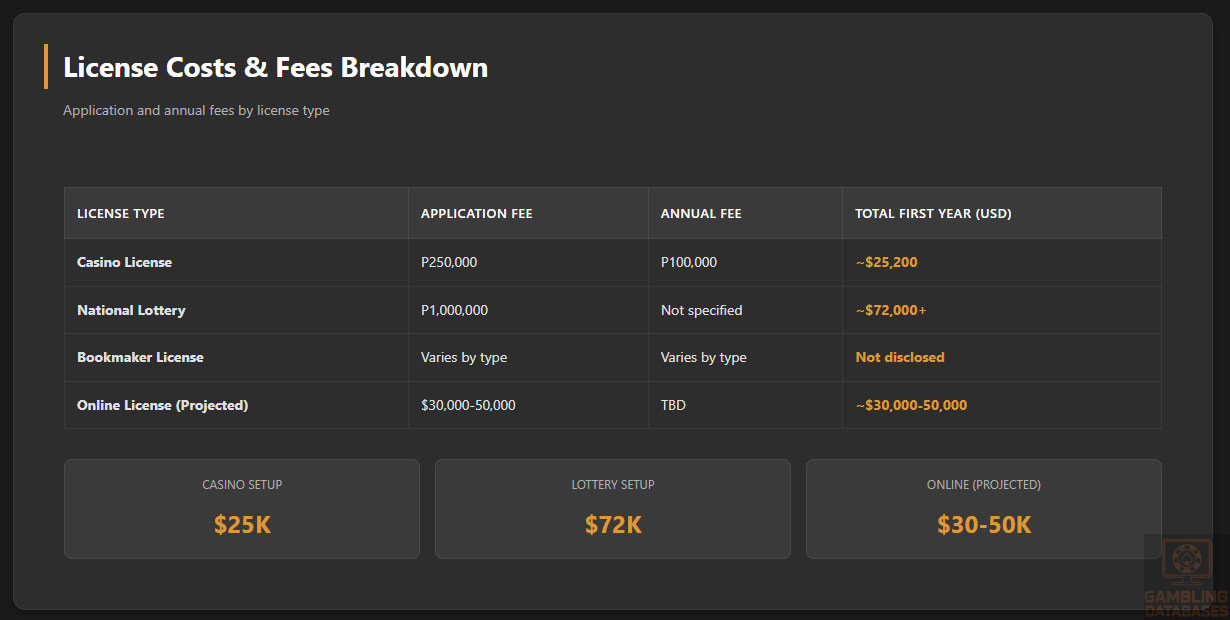

| Casino License Fee | P250,000 application | Plus P100,000 annual fee |

| Lottery License Fee | P1 million | For national lottery operator |

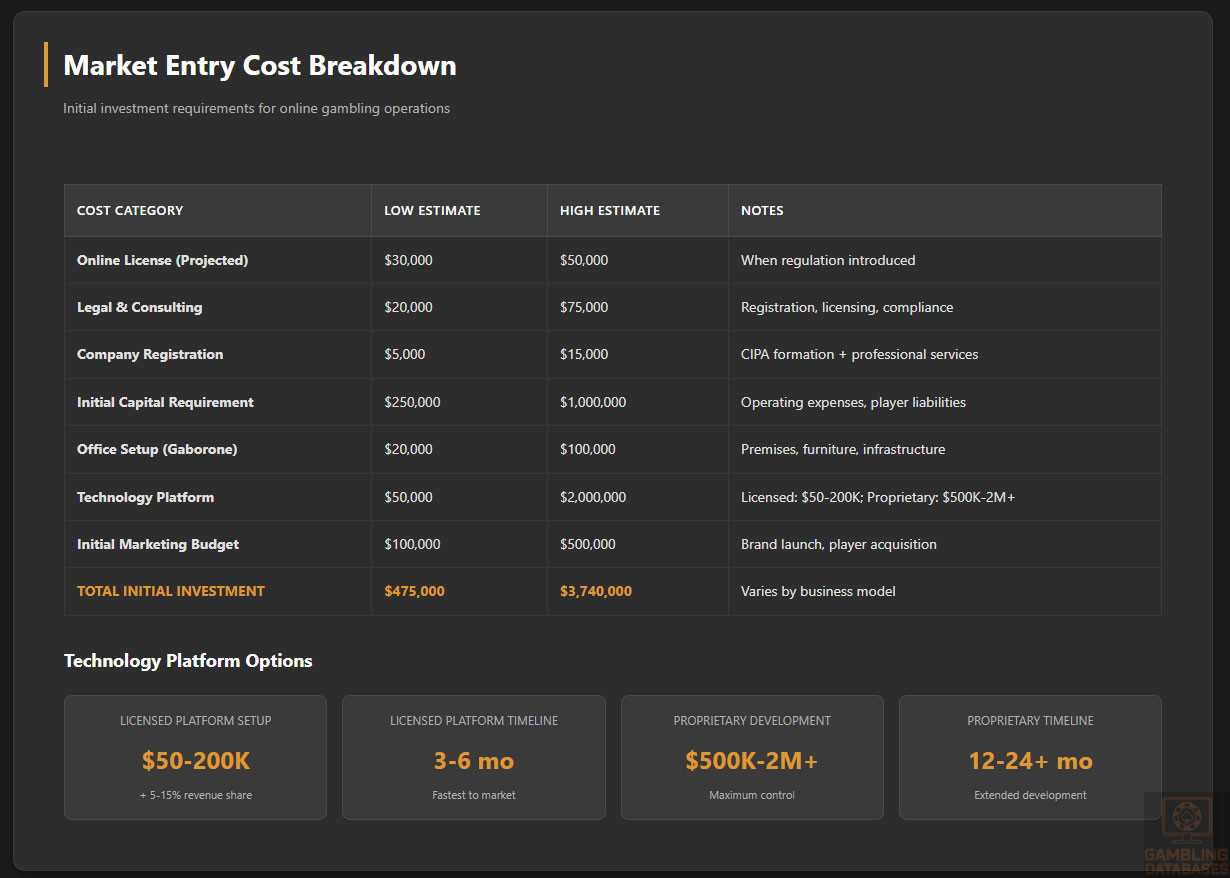

| Estimated Online License Cost | $30,000-$50,000 USD | If/when online licensing introduced |

| Casino Tax Rate | 10% on gross wins | Monthly payment |

| Bookmaker Tax Rate | 6.5% on gross wins | Competitive regional rate |

| Corporate Income Tax | Standard rate applicable | Varies by business structure |

| Legal Gambling Age | 18 years | Standard African requirement |

| Licensed Land Casinos | 9 active | Concentrated in Gaborone |

| Licensed Bookmakers | 10 new licenses issued (2025) | Market expanding rapidly |

| Official Currency | Botswana Pula (BWP) | Stable, managed by central bank |

| Primary Languages | English, Setswana | English widely used in business |

| Literacy Rate | 88.5% | High for sub-Saharan Africa |

| Employment Rate | 72.4% | Unemployment at 27.6% |

| Doing Business Rank | Upper-middle performance | Relatively stable environment |

| Corruption Perception | 3rd least corrupt in Africa | Strong governance standards |

| Market Entry Timeline | 4-6 months (land-based) | Online: No current pathway |

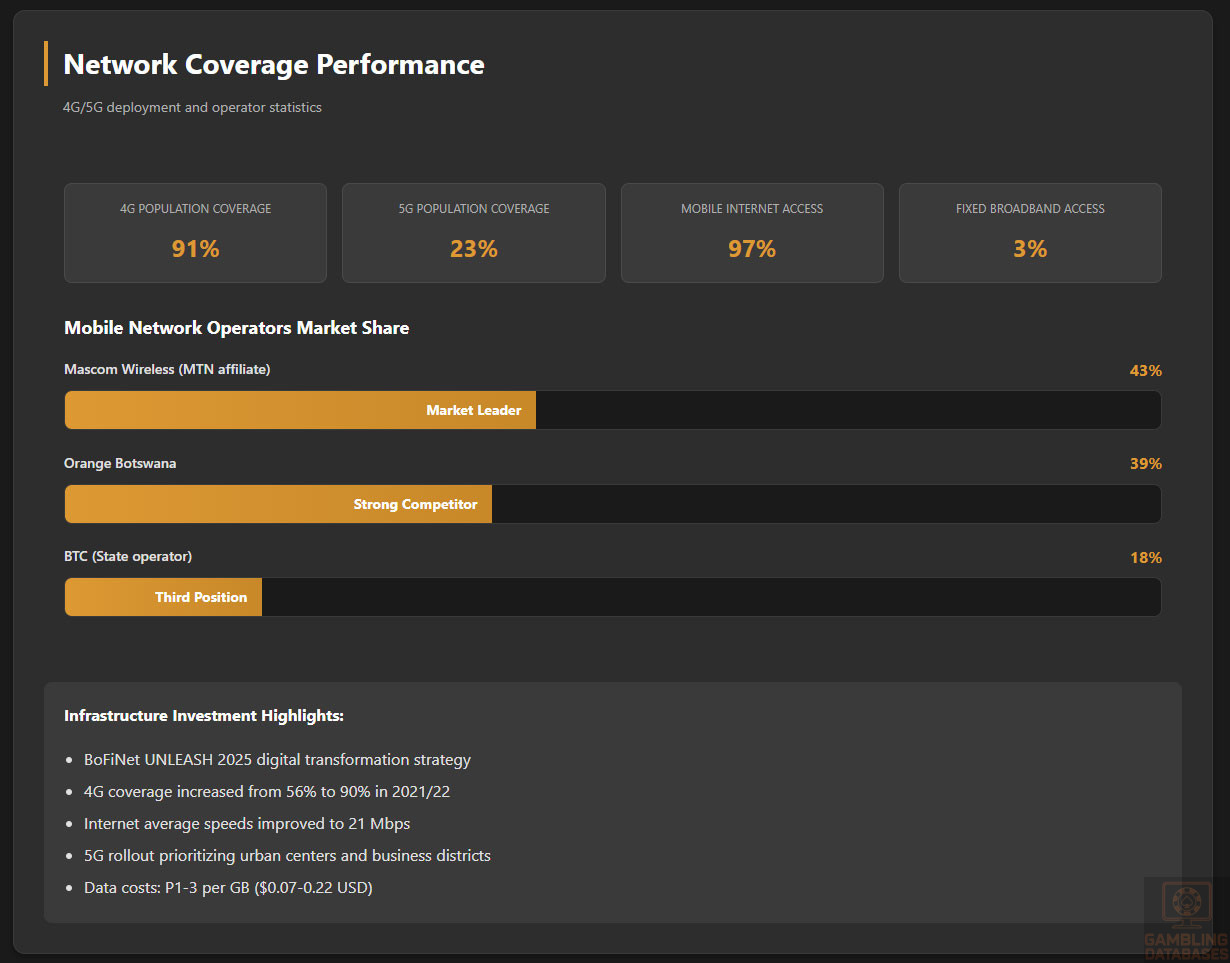

| Mobile Network Coverage (4G) | 91% population | Strong mobile infrastructure |

| 5G Network Coverage | 23% population | Expanding rapidly |

| Average Internet Speed | 15.6 Mbps download | Adequate for gaming |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Botswana’s gambling industry operates under a dual regulatory framework that clearly distinguishes between land-based and online gambling activities. The Gambling Act of 2012, which came into full effect on June 1, 2013, replaced the outdated Casino Act (1971) and Lotteries and Betting Act (1966). This modern legislation established the Botswana Gambling Authority as the primary regulatory body responsible for licensing, monitoring, and enforcing gambling regulations throughout the country.

The regulatory framework demonstrates a progressive approach to land-based gambling while maintaining silence on online operations. This regulatory gap creates an interesting market dynamic where international online operators can potentially serve Botswana players without local licensing, though they operate without explicit legal protection. The government has indicated interest in regulating online gambling, but no concrete legislative proposals have been implemented as of 2025.

Land-Based Gambling Activities

Land-based gambling in Botswana encompasses several distinct categories, each subject to specific licensing requirements and operational standards:

- Casino Operations: Nine licensed casinos currently operate in Botswana, predominantly located in the capital city Gaborone. These establishments offer traditional casino games including table games, electronic gaming machines, and associated entertainment facilities. Casino licenses authorize specific games listed in the license and are subject to strict operational requirements.

- Sports Betting Venues: The bookmaking sector has experienced significant expansion, with the Gambling Authority issuing 10 new national bookmaker licenses in 2025. Six operators have already launched operations, creating approximately 400 new jobs. Bookmakers offer betting on football (the most popular sport), rugby, cricket, basketball, and international sporting events.

- Limited Payout Machines (LPMs): These gaming devices are regulated separately from full casino slot machines and can be placed in various licensed establishments. LPM regulations govern payout limits, placement restrictions, and operational standards to prevent problem gambling.

- Bingo Establishments: Both electronic and manual bingo operations are permitted under specific licensing. Bingo licenses authorize the operation of bingo games with defined prize structures and operational parameters.

Online Gambling Framework

Online gambling exists in a regulatory gray area in Botswana. The Gambling Act of 2012 makes no specific mention of internet gambling, interactive gaming, or remote betting operations. This legislative silence creates several important implications for market participants.

Botswana residents can access international online casinos, sportsbooks, poker sites, and lottery platforms without legal restriction. The government does not block access to offshore gambling websites, nor does it prosecute players for participating in online gambling. However, no domestic operators hold licenses specifically for online gambling operations, and the Gambling Authority lacks explicit jurisdiction over internet-based gaming.

Several factors suggest online regulation may be forthcoming. The government has expressed interest in capturing tax revenue from online gambling activity. Industry observers expect amendments to the Gambling Act to address online operations within the next 2-3 years. Brazil’s recent licensing framework, which issued 173 online operator licenses, serves as a potential model for Botswana’s regulatory evolution.

Licensed Operators and Market Players

The Botswana gambling market features a mix of domestic and international operators, with clear market concentration patterns:

Land-Based Casino Operators:

- Major casino resorts concentrated in Gaborone serve both domestic and tourist markets

- Several 24-hour operations cater to international visitors

- Hotel-casino combinations dominate the upscale market segment

- Smaller casinos operate in regional centers with limited hours

- Foreign investment permitted with appropriate licensing and local partnerships

Sports Betting Operators:

- BetXplosion – One of the newly licensed bookmakers launched in 2025

- Mix of local and South African-backed operators entering the market

- Retail betting shops expanding across urban centers

- Mobile betting applications increasingly popular among licensed operators

- Estimated market share data not publicly available due to recent licensing expansion

International Online Operators:

- Bet365 – Well-known international brand accepting Botswana players

- Major offshore operators licensed in Malta, Curacao, and other jurisdictions

- No publicly disclosed player volume or market share data

- Payment processing through international methods as local banks cannot explicitly support unlicensed operators

The licensed operator landscape is evolving rapidly. The Gambling Authority’s 2025 licensing round demonstrates clear government intent to expand legal gambling operations, create employment, and capture additional tax revenue. The Authority projected that the expanded gambling sector could support over 2,300 jobs across casinos, betting shops, and LPM operations.

Licensing Framework and Requirements

Application Process and Eligibility

The Botswana Gambling Authority manages all licensing applications through a structured process designed to ensure operator suitability, financial stability, and commitment to responsible gambling. The Authority operates under the Ministry of Trade and Industry’s oversight while maintaining operational independence.

Regulatory Authority Details:

- Official Name: Botswana Gambling Authority (BGA)

- Establishment: 2012 (operational from June 1, 2013)

- Legal Basis: Gambling Act of 2012

- Primary Functions: Licensing, compliance monitoring, revenue collection, responsible gambling promotion

- Board Composition: Seven members appointed by the Minister, including legal professionals, community representatives, and industry experts

- Contact: Official website at gamblingauthority.co.bw

Financial Requirements:

- Casino License Application Fee: P250,000 (approximately $18,000 USD)

- Casino Annual License Fee: P100,000 (approximately $7,200 USD)

- Lottery Operator License: P1,000,000 (approximately $72,000 USD) for application

- Bookmaker License Fees: Specific amounts vary by license type (national vs. regional)

- Bank guarantees or bonds required to demonstrate financial sustainability

- Proof of minimum capitalization requirements for different license categories

- Operating capital sufficient for at least six months of operations

- Financial statements audited by recognized accounting firms

Technical Standards and Certifications:

- Gaming equipment must meet international standards for fairness and randomness

- Electronic gaming machines require certification from approved testing laboratories

- Software providers must demonstrate compliance with recognized gaming standards

- Random Number Generator (RNG) certification for electronic games

- Secure server infrastructure meeting data protection standards

- Player account management systems with audit trail capabilities

- Responsible gambling tools including self-exclusion functionality

- Age verification systems to prevent underage gambling

Background Check Procedures:

All applicants and key personnel undergo comprehensive background investigations. The process typically requires 3-4 months for completion and examines criminal history, financial standing, business reputation, and prior gambling industry involvement. Disqualifying factors include criminal convictions, bankruptcy within specified timeframes, previous license revocations, and undisclosed conflicts of interest.

Local Presence and Operational Requirements

Botswana’s licensing framework imposes specific local presence obligations to ensure regulatory oversight and economic benefit to the country:

Physical Presence Mandates:

- Registered office in Botswana required for all license holders

- Dedicated management presence within the country

- Minimum staffing levels depending on license type and operation scale

- Physical premises meeting health, safety, and accessibility standards

- For casinos: Specific architectural and security requirements for gaming floors

- For bookmakers: Retail locations meeting accessibility and visibility standards

Domain and Hosting Requirements:

Currently, Botswana does not mandate .bw domain registration or local server hosting for land-based operations, as online gambling lacks explicit regulation. However, when online licensing is introduced, typical requirements are expected to include local domain registration, data hosting within Botswana or approved jurisdictions, and technical infrastructure enabling regulatory access for compliance monitoring.

Personnel and Management Obligations:

- Key personnel including general managers, compliance officers, and financial controllers require individual licensing

- Citizenship preferences for certain positions, though foreign expertise accepted in specialized roles

- Training requirements for staff handling customer funds, operating gaming equipment, and implementing responsible gambling measures

- Designated compliance officer responsible for regulatory adherence

- Money laundering reporting officer as required under financial intelligence legislation

Foreign Ownership Restrictions:

Foreign investors can participate in Botswana’s gambling industry, subject to standard company registration requirements. The Gambling Act does not impose explicit foreign ownership caps for gambling licenses, though practical considerations favor local partnerships. Foreign operators often establish joint ventures with Botswana citizens or companies to navigate regulatory processes, access local market knowledge, and build government relationships.

The Companies Act governs corporate structure and foreign investment generally. Registration with the Companies and Intellectual Property Authority (CIPA) is mandatory before applying for gambling licenses. Foreign companies must appoint local directors meeting residency requirements and maintain statutory registers accessible in Botswana.

Compliance Obligations and Monitoring

Player Protection and Identification

Botswana’s gambling regulations emphasize player protection, responsible gambling, and prevention of underage participation. These requirements apply strictly to land-based operations and would likely extend to online operators when licensing is introduced.

Age Verification Requirements:

- Minimum gambling age: 18 years throughout Botswana

- Mandatory identification checks at casino entrances and betting shop counters

- Accepted identification documents: National identity cards, passports, driver’s licenses

- Prohibition on allowing minors on gaming floors, even if accompanied by adults

- Staff training requirements for identifying and refusing service to underage individuals

- Penalties for operators allowing underage gambling including fines and license suspension

KYC/AML Compliance Standards:

- Customer identification and verification for all account registrations

- Enhanced due diligence for high-value transactions exceeding defined thresholds

- Source of funds verification for large deposits or unusual transaction patterns

- Ongoing monitoring of customer transactions for suspicious activity

- Reporting obligations to the Financial Intelligence Agency for suspicious transactions

- Record retention requirements: Minimum five years for transaction records and customer identification documents

- Staff training on money laundering detection and prevention

- Designated compliance personnel responsible for AML program implementation

Responsible Gambling Measures:

- Mandatory display of responsible gambling information in prominent locations

- Problem gambling helpline numbers and resources readily available

- Self-exclusion program allowing individuals to ban themselves from gambling establishments

- Staff training to identify signs of problem gambling behavior

- Prohibition on credit provision for gambling purposes

- Restrictions on ATM placement near gaming areas

- Limitations on advertising targeting vulnerable populations

- Contributions to problem gambling treatment and prevention programs

The Gambling Authority employs a Responsible Gambling Manager who oversees industry-wide initiatives. Portia Diteko, the current manager, has emphasized that responsible gaming protects both players and operators by ensuring sustainable industry growth. The Authority has implemented the Problem Gambling Severity Index (PGSI) for assessing at-risk behavior.

Financial Monitoring and Reporting

Transaction Monitoring Systems:

Licensed operators must implement robust financial monitoring systems tracking all gambling transactions, customer deposits and withdrawals, prize payouts, and promotional bonuses. These systems must generate audit trails accessible to regulatory inspectors and flag transactions meeting suspicious activity criteria or exceeding reporting thresholds.

Reporting Requirements and Schedules:

- Monthly financial returns detailing gross gaming revenue, payouts, and tax calculations

- Quarterly compliance reports addressing responsible gambling, customer complaints, and regulatory adherence

- Annual audited financial statements prepared by approved accounting firms

- Real-time reporting of suspicious transactions to financial intelligence authorities

- Incident reports for security breaches, customer disputes, or operational irregularities

Audit and Inspection Procedures:

- Regular scheduled inspections by Gambling Authority compliance officers

- Unannounced spot checks to verify operational compliance

- Gaming equipment testing and certification verification

- Financial record reviews and reconciliation audits

- Customer protection measure effectiveness assessments

- Staff qualification and training verification

- Security system adequacy reviews

Operators must provide inspectors immediate access to premises, records, and systems. Failure to cooperate with audits or inspections can result in penalties including fines, license suspension, or revocation. The Gambling Authority’s Compliance and Monitoring Services unit conducts these oversight activities systematically.

Taxation Structure and Financial Obligations

Player Taxation

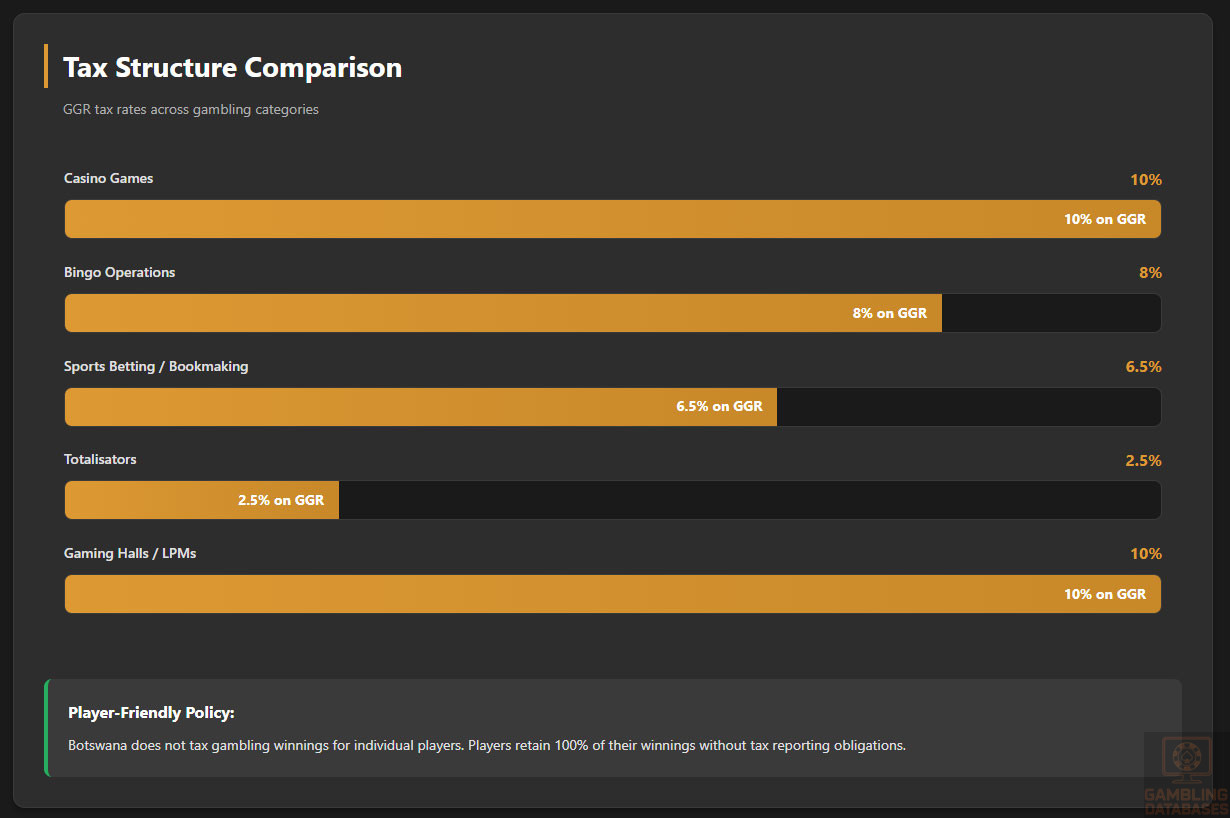

Botswana does not currently impose taxes on gambling winnings for individual players. This player-friendly approach differs from jurisdictions like South Africa where winnings above certain thresholds face withholding taxes. Players retain 100% of their winnings without tax reporting obligations or withholding deductions.

This policy creates competitive advantages for Botswana operators compared to regional competitors who must withhold player winnings taxes. It also simplifies compliance for operators who do not need to implement withholding systems or issue tax documentation to winning players.

Operator Taxation

Operators face multiple taxation obligations based on gambling activity type, revenue generation, and corporate structure:

Gross Gaming Revenue (GGR) Tax Rates by Game Type:

- Casino Games: 10% monthly tax on gross wins (total player losses minus total player wins)

- Sports Betting/Bookmaking: 6.5% on gross wins – competitive rate encouraging market entry

- Bingo Operations: 8% on gross wins

- Gaming Halls/LPMs: 10% on gross wins

- Totalisators: 2.5% on gross wins

These GGR taxes apply specifically to gambling activities and are calculated monthly. Payment typically occurs within specified timeframes following month-end, with penalties for late submission. The Gambling Authority’s Funds Disbursement Agency collects all gambling-specific taxes and levies.

Corporate Income Tax:

Beyond gambling-specific taxes, operators remain subject to standard Botswana corporate income taxation on net profits. Corporate tax rates vary depending on company size, industry classification, and potential incentive qualifications. Gambling operators should expect standard corporate rates applicable to similar-sized businesses in the service sector.

Additional Financial Obligations:

- License renewal fees paid annually to maintain operational authorization

- Investigation fees for background checks when key personnel change

- Inspection fees potentially charged for compliance audits

- Transfer fees when licenses change ownership or location

- Contributions to problem gambling prevention and treatment funds

Gambling Market Financial Performance

Comprehensive market revenue data for Botswana’s gambling sector remains limited in public sources. The government does not publish detailed annual gambling revenue reports like more mature markets. Available information suggests the following market characteristics.

The land-based casino and betting sector has shown consistent growth since 2013 when the Gambling Act came into effect. The 2025 expansion with 10 new bookmaker licenses indicates government confidence in continued market growth and revenue generation potential. Casino operations concentrated in Gaborone serve both domestic players and international tourists visiting for business or safari tourism.

Tax revenues from gambling contribute to government budgets, though exact figures are not published separately from general tax collections. The Gambling Authority’s funds disbursement function allocates gambling tax revenues according to government priorities including infrastructure development, social programs, and administrative costs.

The absence of online gambling regulation means significant potential tax revenue flows to offshore operators beyond Botswana’s reach. Industry observers estimate substantial online gambling activity by Botswana residents on international platforms, representing forgone tax revenue that motivates regulatory interest in online licensing.

Advertising and Marketing Restrictions

Botswana imposes targeted advertising restrictions designed to protect minors and promote responsible gambling while allowing operators reasonable promotional freedom:

Permitted Advertising Channels:

- Television advertising allowed with time restrictions avoiding children’s programming hours

- Radio advertising permitted with similar protections

- Print media advertising in adult-focused publications

- Outdoor advertising subject to location restrictions

- Online advertising on websites and social media platforms

- Sponsorships of sporting events and teams permitted with approval

Content Restrictions and Guidelines:

- Prohibition on content suggesting gambling solves financial problems

- Restrictions on claims of guaranteed winnings or easy money

- Mandatory responsible gambling messaging in advertisements

- Prohibition on using celebrities or influences popular with minors

- Requirements to display legal gambling age prominently

- Restrictions on advertising content glamorizing excessive gambling

Location and Placement Restrictions:

- Prohibition on outdoor advertising near schools, playgrounds, and youth facilities

- Restrictions on advertising directed at educational institutions

- Limitations on promotional materials in locations frequented by minors

- Prohibitions on advertising on children’s media platforms

The Gambling Authority can refer advertising matters to the Botswana Communications Regulatory Authority (BOCRA) for additional oversight. Operators must submit significant advertising campaigns for pre-approval to ensure compliance with content and placement restrictions.

Recent Regulatory Changes and Their Impact

Botswana’s gambling regulatory environment has evolved significantly since the Gambling Act’s 2013 implementation, with notable developments accelerating in 2024-2025:

2024-2025 Regulatory Developments:

- Bookmaker License Expansion (May 2025): The Gambling Authority issued 10 new national bookmaker licenses, dramatically expanding the legal sports betting market. Six operators launched immediately, three more expected within weeks, and one withdrew. This expansion created approximately 400 direct jobs and signals government commitment to regulated gambling growth.

- Responsible Gambling Framework Strengthening (2024-2025): The Authority enhanced responsible gambling requirements including mandatory Problem Gambling Severity Index (PGSI) implementation, expanded self-exclusion program accessibility, enhanced training requirements for staff, and increased problem gambling awareness campaigns.

- Technology Integration Requirements (Ongoing): The Authority, led by Board Chairman Marvin Torto, encouraged operators to adopt AI monitoring tools for detecting illicit player behaviors, preventing money laundering, protecting against problem gambling, and enhancing overall compliance effectiveness.

- Illegal Gambling Crackdown (2024-2025): Increased enforcement efforts targeting unlicensed land-based operations, community reporting programs for illegal gambling machines, and protection of licensed operators from illegal competition.

Impact on Operators:

The bookmaker licensing expansion creates significant opportunities for new market entrants while intensifying competition for existing operators. The relatively low 6.5% tax rate on sports betting makes Botswana attractive compared to neighbors like South Africa. Enhanced responsible gambling requirements increase operational costs but provide long-term sustainability and social acceptance benefits.

The regulatory emphasis on technology and AI tools suggests future requirements may mandate sophisticated compliance systems. Operators investing early in advanced monitoring and player protection technologies position themselves favorably for ongoing regulatory evolution.

Anticipated Future Regulatory Changes:

Industry stakeholders widely expect online gambling regulation within the next 2-3 years. The government’s 2025 licensing expansion demonstrates comfort with gambling sector growth and revenue generation. Brazil’s recent comprehensive online licensing (173 operators) provides a potential regulatory model. Expected elements of future online gambling regulation may include:

- Dedicated online casino and sports betting license categories

- Local server hosting or data localization requirements

- .bw domain registration mandates for licensed operators

- Enhanced player verification and KYC standards for remote gambling

- Specific responsible gambling tools required for online platforms

- Competitive tax rates designed to encourage license applications over offshore operations

Enforcement Mechanisms and Penalties

The Botswana Gambling Authority maintains comprehensive enforcement powers to ensure regulatory compliance and protect public interests:

Penalty Structures:

- Financial Penalties: Fines ranging from P5,000 to substantial amounts depending on violation severity

- License Suspension: Temporary operating prohibition for serious violations with remediation requirements

- License Revocation: Permanent license cancellation for egregious violations or repeated non-compliance

- Criminal Prosecution: Certain violations constitute criminal offenses punishable by imprisonment or substantial fines

- Seizure of Equipment: Authority to confiscate gaming equipment or assets involved in illegal operations

- Director Disqualification: Prohibition on key personnel holding future gambling industry positions

Recent Enforcement Actions: The Gambling Authority has intensified enforcement against unlicensed operations, particularly targeting illegal gaming machines in retail locations and unlicensed betting operations. The Authority relies on community reporting to identify illegal operations, as local residents often know where unlicensed gambling occurs. Licensed operators have complained that illegal online sites affect their market share, prompting increased regulatory attention to enforcement mechanisms.

Compliance Trends: Most licensed operators demonstrate strong compliance with regulations, resulting in relatively few court cases regarding gambling law violations. The industry’s general adherence to licensing requirements reflects the regulatory framework’s clarity and the Authority’s effective oversight. Operators understand that maintaining good standing protects their significant license investments and ensures continued operational authorization.

ISP Blocking and Payment Restrictions: While Botswana does not currently block access to offshore gambling websites or restrict payment processors from handling international gambling transactions, these enforcement tools may be implemented when online gambling regulation is introduced. Many jurisdictions use ISP-level blocking to prevent access to unlicensed operators and payment processing restrictions to limit unlicensed gambling financial flows.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

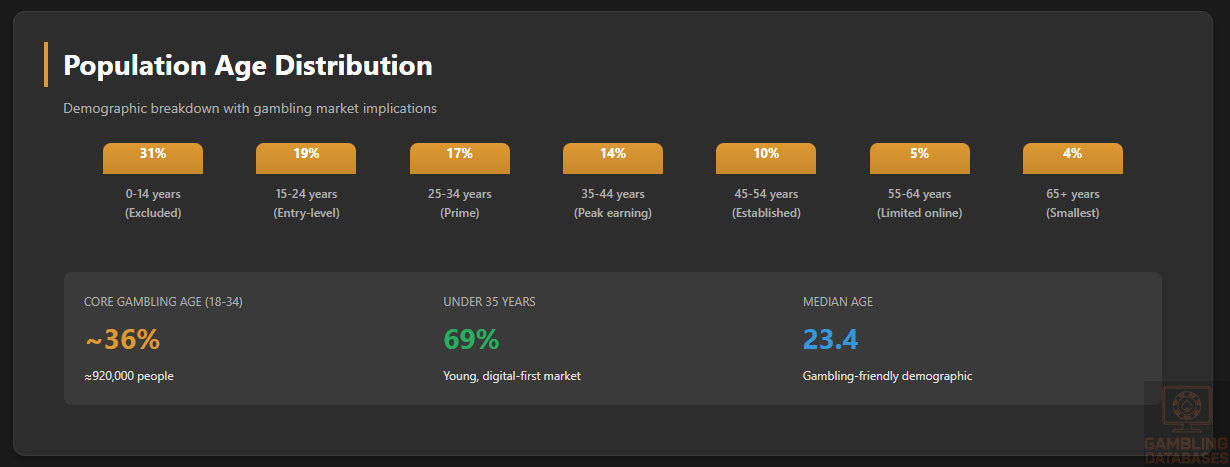

Botswana’s population of 2.56 million people creates a compact but lucrative market for gambling operators. The population has grown steadily at approximately 1.6% annually, with projections indicating continued gradual growth through 2030. This growth rate, while modest, suggests stable market expansion opportunities for gambling operators establishing long-term positions.

The median age of 23.4 years positions Botswana favorably for gambling market development. Young adults typically demonstrate higher gambling participation rates, greater comfort with digital platforms, and more willingness to adopt new entertainment options compared to older demographics. This youthful population profile suggests strong potential for online gambling adoption when regulatory frameworks permit licensed operations.

Gender distribution is relatively balanced at approximately 50.3% female and 49.7% male. Life expectancy stands at 58.1 years overall, with males at 58.8 years and females at 57.3 years. These figures reflect the ongoing impact of HIV/AIDS, which affects approximately 20-25% of the adult population. However, Botswana has made significant progress in HIV treatment and prevention, earning WHO certification for eliminating mother-to-child HIV transmission.

| Age Group | Percentage of Population | Gambling Market Implications |

|---|---|---|

| 0-14 years | ~31% | Excluded from gambling; future market potential |

| 15-24 years | ~19% | Entry-level gambling demographic; mobile-first |

| 25-34 years | ~17% | Prime gambling demographic; highest engagement |

| 35-44 years | ~14% | Peak earning years; higher value players |

| 45-54 years | ~10% | Established income; preference for land-based |

| 55-64 years | ~5% | Limited online adoption; loyalty-focused |

| 65+ years | ~4% | Smallest gambling segment; traditional preferences |

The age distribution reveals that approximately 69% of Botswana’s population is under 35 years old, creating a predominantly young market well-suited for digital gambling platforms. The 18-34 age bracket, representing the core gambling demographic, comprises roughly 36% of the total population or approximately 920,000 people. This represents the primary target market for both land-based and online gambling operations.

Geographic Distribution

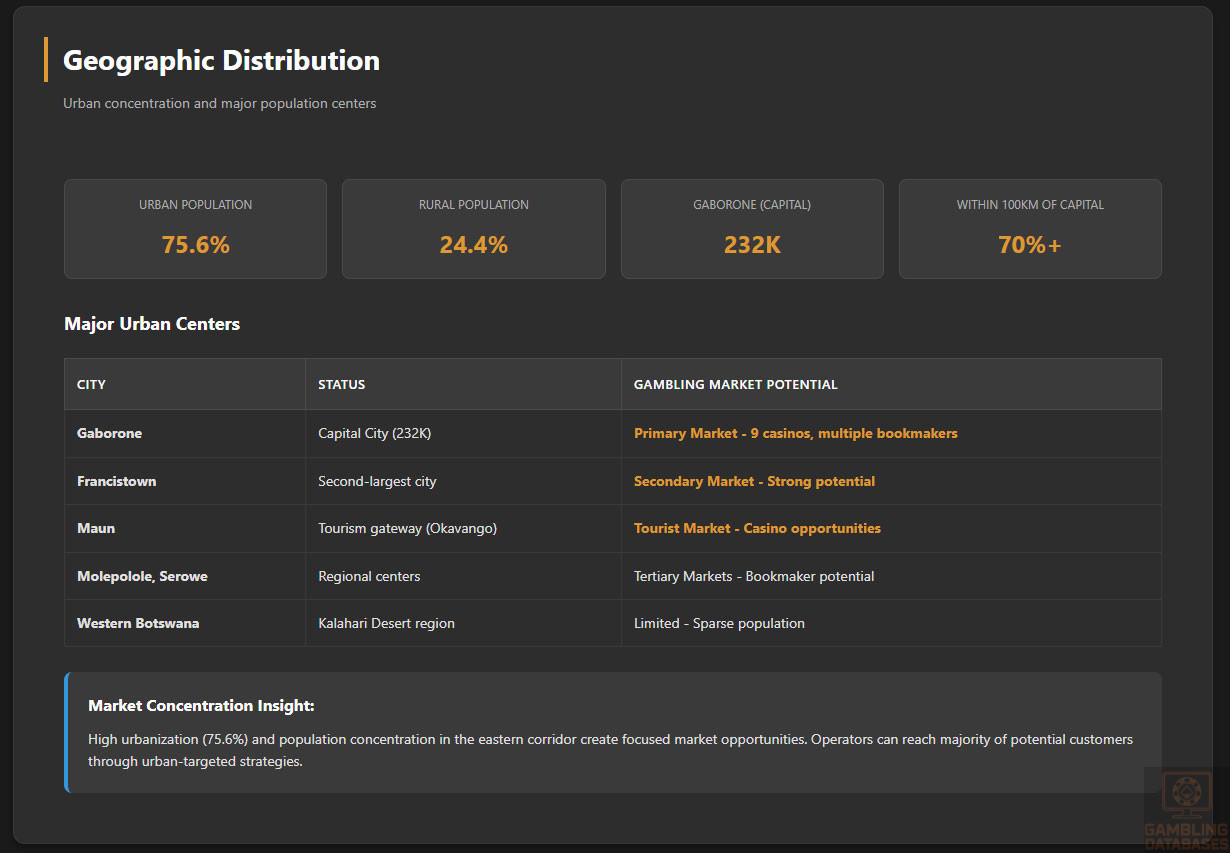

Botswana exhibits exceptional urbanization for sub-Saharan Africa, with 75.6% of the population living in urban areas. This urban concentration simplifies market entry strategies, as operators can reach the majority of potential customers through urban-focused marketing and distribution channels. The urbanization rate continues growing at approximately 2.3% annually, suggesting ongoing migration from rural to urban areas.

Gaborone, the capital city, serves as the primary gambling market with approximately 232,000 residents representing more than 10% of the national population. The city hosts the majority of Botswana’s nine licensed casinos and numerous bookmaker locations. Beyond Gaborone, major population centers include Francistown (the second-largest city), Molepolole, Maun (gateway to the Okavango Delta tourism region), Serowe, Selebi-Phikwe, Kanye, Mochudi, Mahalapye, and Palapye. These cities create secondary markets for gambling operations, though with smaller revenue potential than the capital.

More than 70% of the population lives within 100 kilometers of Gaborone, creating a concentrated market corridor in the eastern portion of the country. This geographic concentration reduces operational costs for physical infrastructure while creating intense competition for market share in key urban areas. The western portion of Botswana, dominated by the Kalahari Desert, remains sparsely populated with limited gambling market potential.

Regional economic differences impact gambling participation patterns. Urban areas demonstrate higher disposable incomes, greater internet access, and more exposure to gambling opportunities compared to rural regions. However, mobile money penetration is bridging urban-rural gaps, potentially enabling rural residents to participate in online gambling when regulations permit licensed operations.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

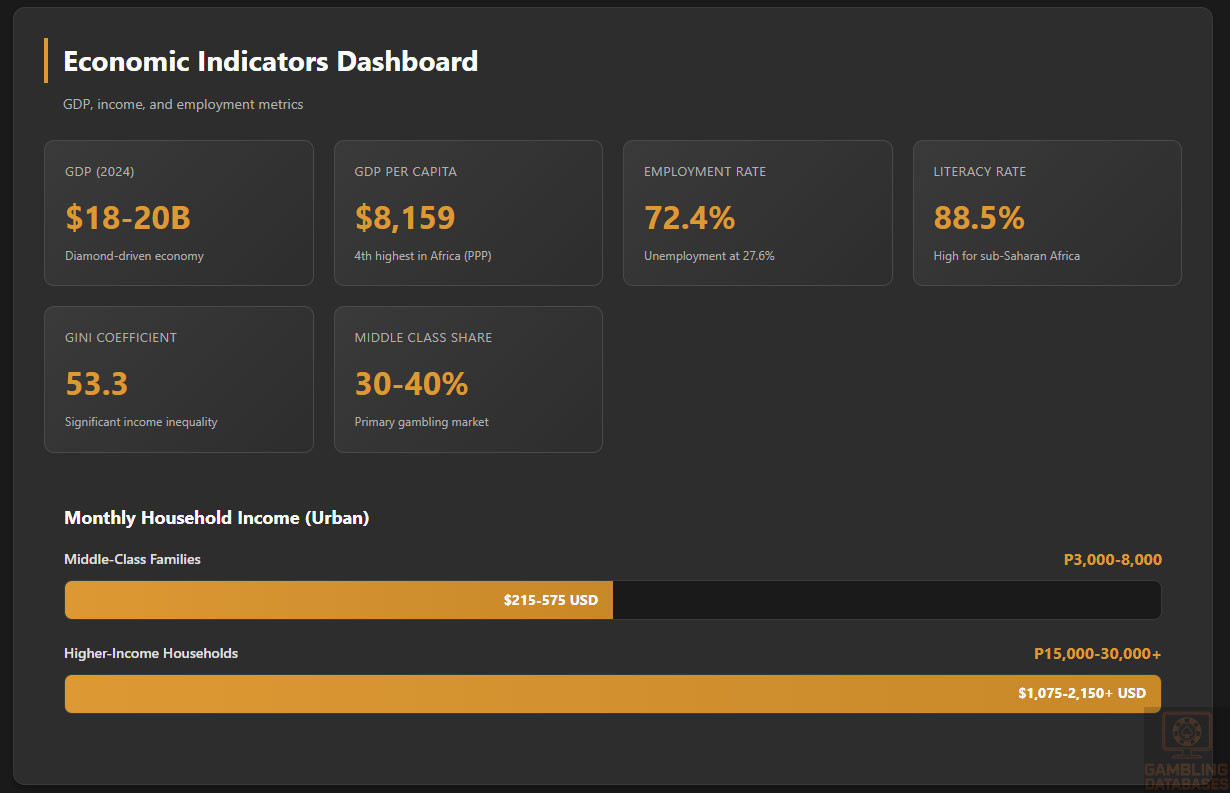

Botswana’s economy demonstrates remarkable success compared to regional neighbors, built on diamond mining, prudent fiscal management, and stable governance. The country’s GDP reached approximately $18-20 billion USD in 2024, with GDP per capita of $8,159 in 2025. This positions Botswana as an upper-middle-income country and the fourth-highest GDP per capita in Africa on a purchasing power parity basis.

The economy has historically averaged 5% annual growth over the past decade, though recent years have shown more modest expansion. GDP growth forecasts for 2025-2027 project 3-4% annual increases, reflecting reduced mineral revenues, global economic conditions, and domestic economic diversification efforts. The government’s Economic Transformation Program aims to reduce diamond dependency and expand services, tourism, and technology sectors.

Diamond mining contributes approximately 30-35% of GDP and 50% of government revenue through the Debswana Diamond Company (50% government, 50% De Beers joint venture). This resource dependence creates economic volatility linked to global diamond demand, though Botswana has managed mineral wealth more effectively than many resource-rich developing nations. The government maintains substantial foreign exchange reserves and has historically run budget surpluses, though recent fiscal deficits reflect spending pressures and reduced mineral revenues.

Tourism represents approximately 10-13% of GDP, driven by the Okavango Delta, Chobe National Park, and Central Kalahari Game Reserve attractions. The sector creates gambling market opportunities through casino resort operations serving international visitors. Agriculture contributes less than 2% of GDP despite employing significant rural populations, reflecting challenging climatic conditions and poor soils limiting agricultural productivity.

Income and Wealth Distribution

Understanding income distribution is critical for assessing gambling market potential and player value segmentation. Average household income in Botswana varies significantly between urban and rural areas, with monthly household income in urban centers ranging from P3,000-P8,000 ($215-$575 USD) for middle-class families. Higher-income households in Gaborone and other major cities may earn P15,000-P30,000+ ($1,075-$2,150+ USD) monthly.

Botswana faces significant income inequality despite relatively high GDP per capita. The Gini coefficient stands at 53.3, indicating substantial wealth concentration. This inequality reflects urban-rural divides, formal vs. informal employment gaps, and educational attainment differences. For gambling operators, income inequality suggests market segmentation strategies targeting different income brackets with appropriate products, bet limits, and promotional strategies.

The middle class, estimated at 30-40% of urban populations, represents the primary gambling market. This demographic possesses sufficient discretionary income for entertainment spending while lacking wealth levels that make gambling financially insignificant. Higher-income segments, while smaller in absolute numbers, contribute disproportionately to gambling revenue through higher-value play and premium product preferences.

Unemployment stands at 27.6%, creating affordability challenges for significant population segments. Employment remains skewed toward low-productivity sectors, with many workers in informal employment lacking stable incomes. These economic realities constrain gambling market size, as large population segments lack discretionary spending capacity. However, employed urban residents, government workers, and private sector professionals demonstrate gambling participation comparable to regional markets.

Market Size and Growth Projections

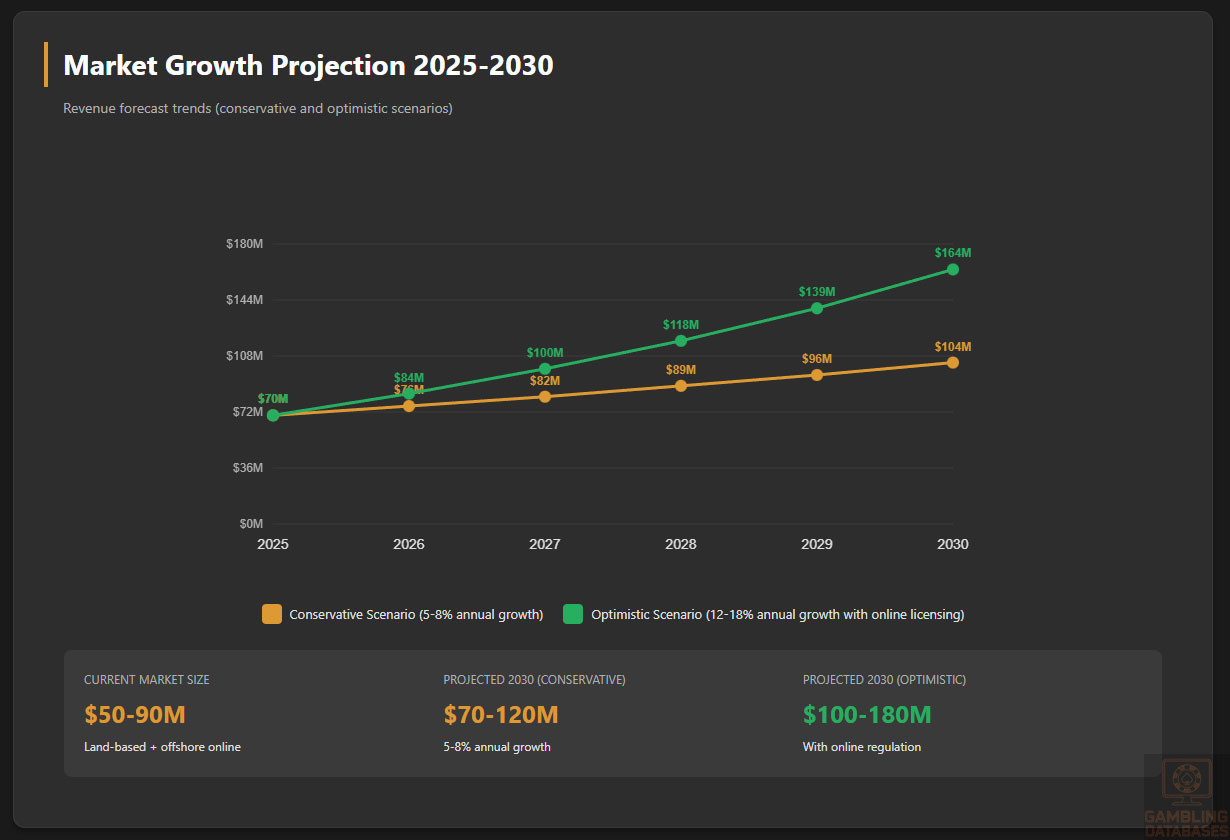

Estimating Botswana’s current and projected iGaming market size requires synthesizing limited public data with regional benchmarks and demographic analysis. The land-based gambling market, encompassing nine casinos and expanding bookmaker operations, generates estimated annual revenues of $30-50 million USD based on operator counts, population size, and regional comparisons.

The online gambling market served by offshore operators remains unquantified in official statistics but likely represents $20-40 million USD in annual gross gaming revenue based on internet penetration, population size, and international operator market presence. These figures suggest total gambling market size (land-based plus offshore online) of approximately $50-90 million USD annually.

When Botswana introduces online gambling licensing, the regulated online market could capture 60-70% of current offshore activity while stimulating additional participation through legal protection and local payment method integration. This suggests potential regulated online market revenue of $15-30 million USD initially, growing as more players transition from offshore operators and new participants enter the market.

Market growth projections depend heavily on regulatory developments, economic conditions, and technological adoption. Conservative scenarios project 5-8% annual market growth through 2030, driven by population growth, rising incomes, and increasing digital adoption. Optimistic scenarios incorporating online licensing implementation suggest 12-18% annual growth as new products, licensed operators, and enhanced player protections expand market participation.

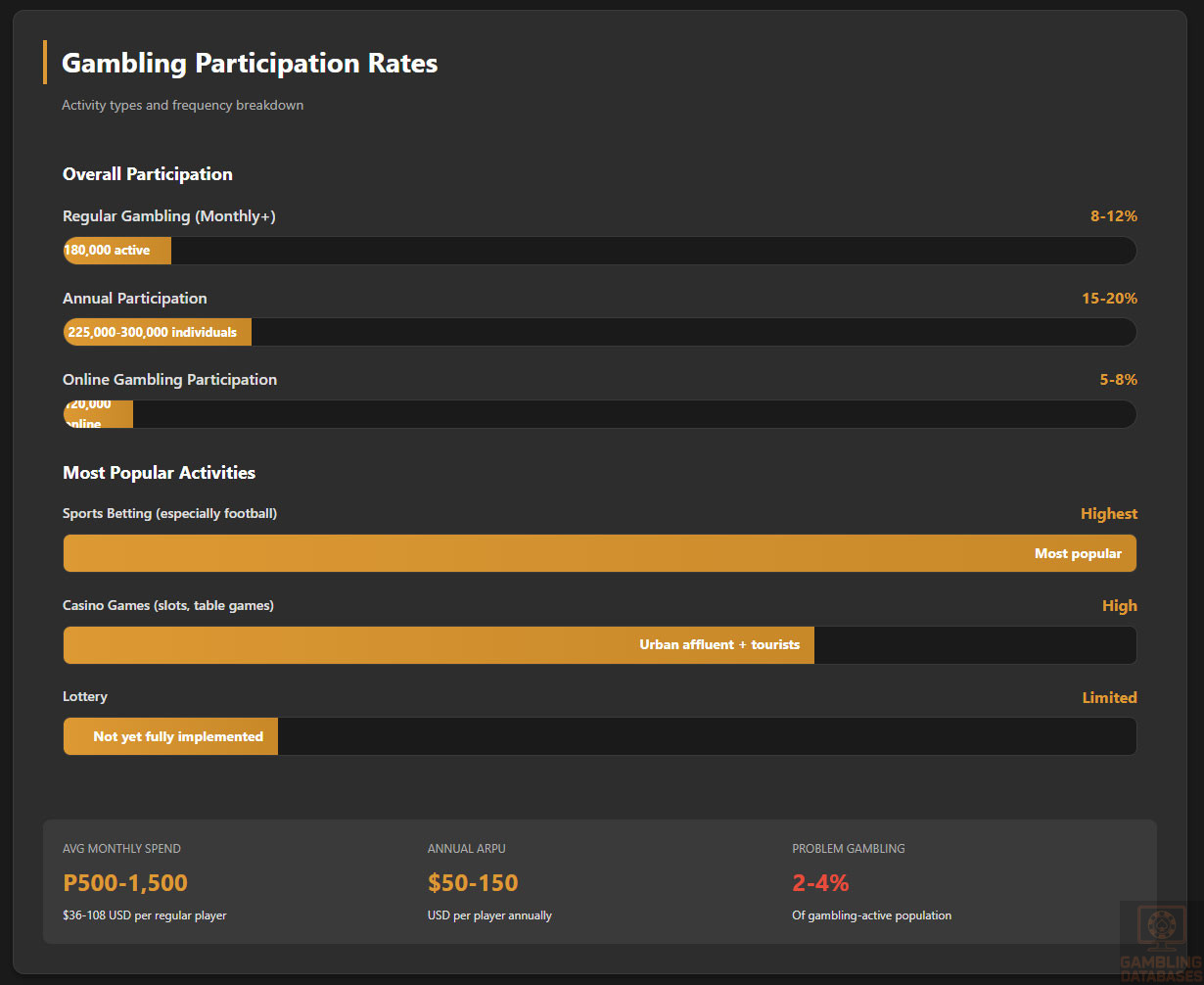

Average Revenue Per User (ARPU) in Botswana likely ranges from $50-150 USD annually for online gambling participants, comparable to South African emerging market segments. ARPU varies significantly by player segment, with casual players contributing $30-60 USD annually while committed players may wager $300-1,000+ USD annually. Land-based casino players typically demonstrate higher ARPU than online players due to tourism segment participation and premium product preferences.

Market penetration rates for gambling currently estimated at 8-12% of the adult population for regular participation (monthly or more frequently) and 15-20% for annual participation. These figures align with developing market norms where gambling remains primarily urban entertainment rather than mass-market activity. Online gambling penetration specifically may reach 5-8% of the adult population currently using offshore operators, with significant growth potential when local licensing enables broader participation.

Education, Skills, and Digital Literacy

Educational Foundation

Botswana maintains impressive educational attainment for sub-Saharan Africa, with overall literacy rates of 88.5% (88.0% male, 88.9% female). This high literacy facilitates gambling participation as players can understand game rules, terms and conditions, and responsible gambling information. Educational infrastructure includes universal primary education, widespread secondary education access, and growing tertiary enrollment.

Primary education completion rates exceed 90%, while secondary education completion reaches approximately 60-70% of cohorts. Tertiary education enrollment, including universities, polytechnics, and vocational training, has expanded significantly. The University of Botswana and numerous technical colleges produce graduates with skills applicable to gambling industry employment including IT, finance, customer service, and management roles.

Digital literacy is growing rapidly, particularly among younger cohorts educated during the smartphone era. Urban youth demonstrate comfortable facility with mobile applications, social media platforms, e-commerce, and digital entertainment. This digital fluency translates directly to online gambling adoption potential, as familiar interface patterns and payment methods reduce adoption barriers.

English language proficiency is widespread, as English serves as the official language of government, business, and education alongside Setswana. This linguistic advantage simplifies market entry for international operators, as English-language platforms require no translation. However, incorporating Setswana language options could enhance localization and appeal to specific market segments preferring native language interactions.

Cultural and Social Factors

Communication and Language

Setswana and English serve as Botswana’s primary languages, with English dominating business, government, and urban communication while Setswana remains prevalent in rural areas and informal settings. Most urban residents speak both languages fluently, code-switching based on context. Internet content consumption occurs predominantly in English, as most websites, applications, and digital services use English interfaces.

For gambling operators, English-language platforms suffice for the majority of the target market. However, customer support should ideally offer both English and Setswana options to accommodate player preferences and resolve issues effectively. Marketing materials incorporating Setswana phrases or cultural references can enhance localization and brand resonance, even when primary platform language remains English.

Cultural Attitudes

Gambling acceptance in Botswana reflects complex cultural dynamics. Traditional Setswana culture did not include gambling in the modern commercial sense, though informal betting on games and competitions occurred. The introduction of formal gambling through casinos and betting shops represents relatively recent cultural adoption, primarily in urban areas.

Urban populations, particularly younger demographics, demonstrate generally positive attitudes toward gambling as legitimate entertainment. The government’s regulated approach, including licensing expansion and responsible gambling emphasis, signals official acceptance of gambling’s economic and recreational roles. Sports betting particularly resonates with football enthusiasts, as Botswana has strong sporting culture and passionate support for local and international teams.

However, certain cultural and religious segments view gambling skeptically. Christian denominations, which represent the majority religious affiliation in Botswana, vary in gambling acceptance. Some denominations tolerate gambling as personal choice while others discourage participation as contrary to principles of stewardship and financial prudence. Muslim and Hindu minorities, present primarily in urban areas, bring diverse gambling perspectives based on religious teachings and cultural backgrounds.

Foreign brand perception is generally positive in Botswana. The country maintains strong international ties, particularly with South Africa, the United Kingdom, and the United States. International brands across various sectors successfully operate in Botswana, and consumers often perceive foreign products and services as high-quality. This attitude extends to gambling operators, where international brands may enjoy prestige advantages over purely local operations.

Risk tolerance indicators suggest moderate comfort with financial risk among urban populations. Small-scale entrepreneurship is common, and investment in informal savings schemes (stokvels) demonstrates willingness to pool resources for potential gains. However, economic volatility and employment insecurity encourage cautious financial management for many households, limiting gambling spend to discretionary entertainment budgets rather than primary income allocation.

Problem Gambling and Social Considerations

Problem gambling prevalence in Botswana lacks comprehensive epidemiological data, as systematic population studies have not been published. However, the Gambling Authority recognizes problem gambling as a significant concern requiring regulatory attention and intervention. The Authority employs a dedicated Responsible Gambling Manager and has implemented the Problem Gambling Severity Index (PGSI) for assessing at-risk behaviors.

Available evidence suggests problem gambling affects approximately 2-4% of the gambling-active population, comparable to international norms for emerging markets. At-risk gambling behaviors, including frequent play exceeding financial means, chasing losses, and gambling-related family conflicts, may affect an additional 5-8% of regular gamblers. These estimates translate to several thousand individuals experiencing gambling-related harm requiring intervention or support.

Demographic patterns indicate young males aged 25-40 represent the highest-risk group for problem gambling. This demographic demonstrates higher gambling participation rates, greater risk-taking propensity, and less developed financial management skills compared to older cohorts or female demographics. Urban residents face higher problem gambling risks than rural populations due to greater gambling availability and exposure.

Underage gambling remains a concern despite 18+ age restrictions. Enforcement at land-based venues has improved with enhanced ID checking and staff training, but offshore online operators accessible to Botswana residents often lack robust age verification. When online licensing is introduced, strong age verification requirements will be critical for protecting minors from gambling harm.

Government response to problem gambling includes several initiatives. The Gambling Authority provides helpline resources, though dedicated treatment facilities remain limited. The Authority is developing partnerships with mental health services and community organizations to expand support availability. Licensed operators must contribute to problem gambling prevention funds and implement responsible gambling measures including self-exclusion programs, deposit limits, and staff training.

Social responsibility requirements for operators emphasize prevention through education, early intervention through player monitoring, and treatment referral through support partnerships. The Gambling Authority has indicated that protecting players serves operator interests by ensuring sustainable industry growth rather than short-term revenue extraction that creates social backlash and regulatory tightening.

Political Structure and Governance

Botswana maintains a stable democratic system and ranks as one of Africa’s most successful democracies. The country gained independence in 1966 and has held regular free elections every five years since. The Botswana Democratic Party (BDP) governed continuously from independence until 2024, when the Umbrella for Democratic Change coalition won power. This peaceful transfer demonstrates democratic maturity and institutional stability.

President Duma Boko assumed office in November 2024 following October elections. The new government has emphasized economic transformation, job creation, and service sector development. These priorities align favorably with gambling industry expansion, as the sector creates employment and generates tax revenue. The government’s Economic Transformation Program launched in August 2025 aims to diversify beyond diamond dependency, potentially creating openness to gambling sector growth.

Political stability rankings position Botswana favorably within Africa. The country avoids political violence, maintains peaceful transitions of power, and demonstrates respect for rule of law. Corruption levels remain relatively low, with Botswana ranking as the third least corrupt nation in Africa on Transparency International’s Corruption Perceptions Index. These governance strengths create predictable business environments and reduce regulatory uncertainty.

Regulatory consistency characterizes Botswana’s approach to business oversight. The Gambling Authority operates with relative independence while maintaining government accountability. Policy changes occur through transparent legislative processes rather than arbitrary administrative actions. This predictability allows operators to make long-term investments with confidence in regulatory stability.

International relations impact gambling business minimally, as Botswana maintains positive relationships with major economies. The country participates in the Southern African Development Community (SADC) and maintains close ties with South Africa, its largest trading partner and source of significant tourist traffic. These regional connections facilitate cross-border operations and market integration. Botswana is not an EU member but maintains positive relations with European nations supporting tourism and investment flows.

Technology Adoption and Digital Behavior

Internet and Digital Usage

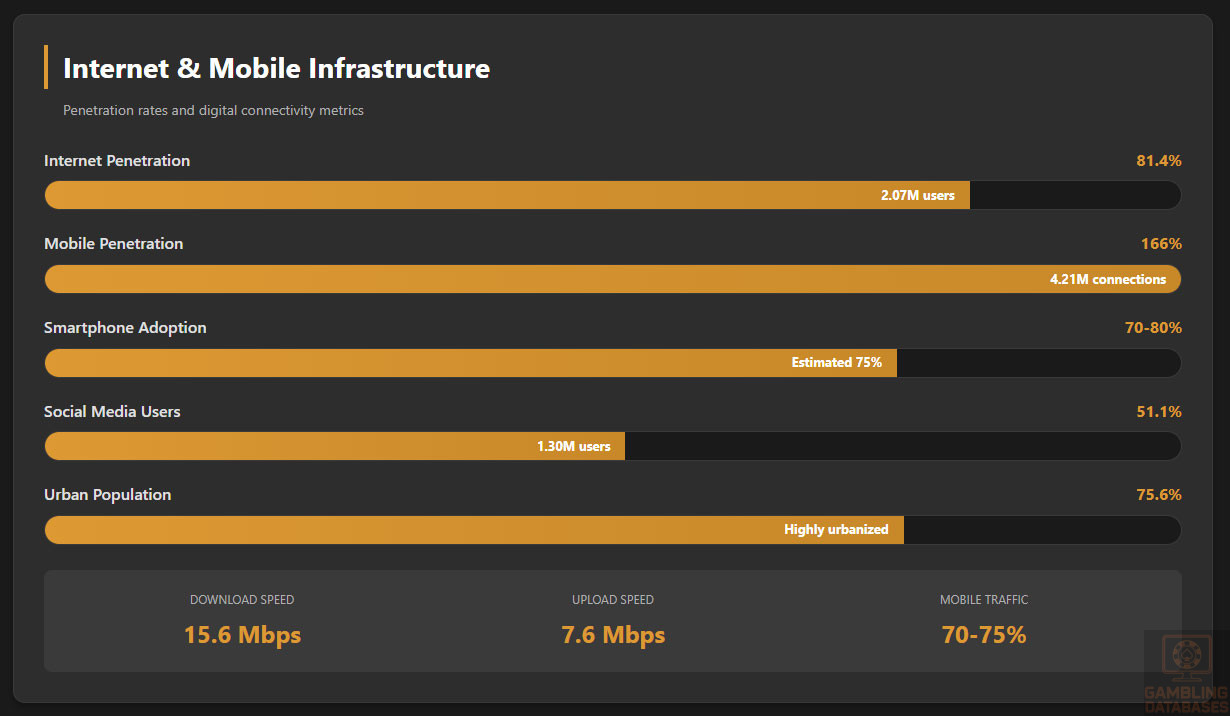

Botswana demonstrates exceptional internet penetration for Africa at 81.4%, with 2.07 million users in a population of 2.56 million. This penetration rate ranks among Africa’s highest, comparable to South Africa (78%) and approaching Mauritius levels. The figure represents dramatic growth from 42% in 2019 and 61% in 2022, indicating rapid digital expansion that facilitates online gambling market development.

Daily internet usage averages several hours per day for active users, with young urban residents spending 4-6 hours online through smartphones, computers, and tablets. Usage patterns emphasize social media, messaging applications, content streaming, and increasingly e-commerce. This digital engagement suggests comfortable familiarity with online platforms translating readily to gambling applications.

Mobile devices dominate internet access, with smartphones serving as the primary means of connectivity for the majority of users. Approximately 70-80% of internet traffic occurs via mobile devices, reflecting Africa-wide patterns where mobile infrastructure developed faster than fixed broadband. This mobile-first reality requires gambling operators to prioritize mobile-optimized platforms and potentially develop dedicated mobile applications for iOS and Android.

Social media engagement is substantial, with 1.30 million social media user identities (51.1% of population) as of January 2025. Popular platforms include Facebook, Instagram, WhatsApp, and TikTok. These platforms serve as primary communication channels, news sources, and entertainment venues for young Batswana. Gambling operators can leverage social media for marketing, customer engagement, and brand building, though advertising restrictions will apply.

E-commerce participation has grown significantly, with the e-commerce market projected to reach $538 million USD by 2027 from $246 million in 2022. This growth indicates increasing consumer comfort with online transactions, digital payments, and remote service delivery. As e-commerce adoption expands, barriers to online gambling participation diminish.

Digital Payment Behavior

Payment method preferences in Botswana reflect the transitional state between cash-based and fully digital payment systems. Cash remains dominant, particularly in rural areas and for daily transactions, but digital payment adoption is accelerating rapidly in urban centers. For gambling operators, understanding payment preferences and offering appropriate options is critical for market penetration.

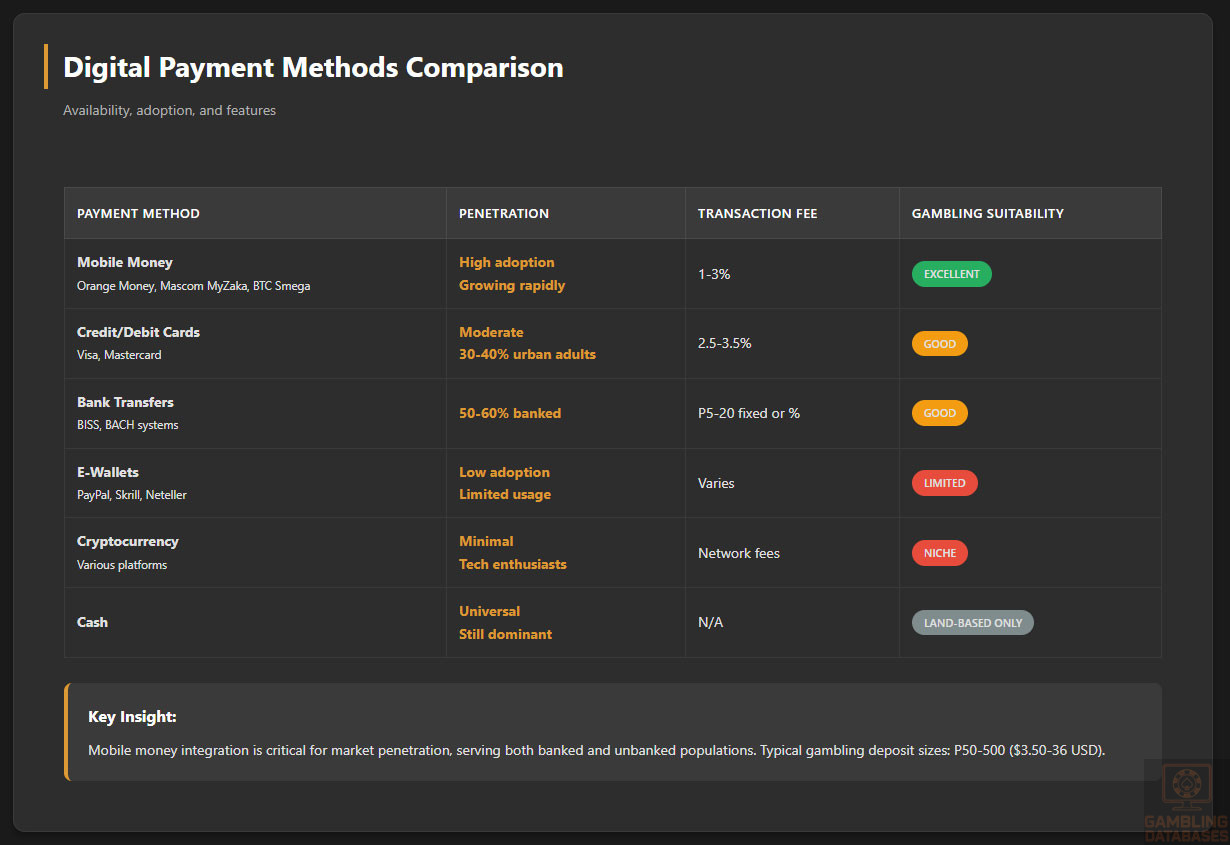

Credit and debit card penetration remains moderate, with cards used primarily by middle-class and affluent urban residents. Visa and Mastercard are widely accepted in cities, though many rural areas lack card payment infrastructure. Banks issue both debit and credit cards, though credit access is selective. For online gambling, card payments would serve the affluent segment but exclude significant population portions without banking relationships.

Mobile money has emerged as a transformative payment channel bridging the banked and unbanked populations. Orange Money, Mascom MyZaka, and BTC Smega represent the primary mobile money providers, enabling person-to-person transfers, bill payments, merchant payments, and savings functions without bank account requirements. PosoMoney, operated by BotswanaPost, offers interoperable services working across all mobile networks.

Mobile money adoption has surged from limited usage in 2015 to widespread use in 2025, particularly among younger demographics and urban populations. Transaction fees are lower than traditional banking charges, making mobile money attractive for small-value payments common in gambling contexts. Online gambling operators would benefit significantly from integrating mobile money payment options to access broader market segments beyond cardholders.

Bank transfers through the Botswana Interbank Settlement System (BISS) and Botswana Automated Clearing House (BACH) facilitate larger transactions, including salary payments and business settlements. Real-time payment systems are emerging, enabling instant transfers rather than batch processing delays. These systems could support gambling deposits and withdrawals, though mobile money likely offers superior user experience for typical transaction sizes.

Cryptocurrency adoption remains limited and highly niche in Botswana. While services like Plisio exist, cryptocurrency awareness and usage concentrate among small technology-savvy populations. Regulatory status is unclear, with no explicit prohibition or authorization. For gambling operators, cryptocurrency payment options would serve minimal market segments currently but could become relevant as digital currency adoption grows.

Average transaction sizes for gambling deposits would likely range from P50-P500 ($3.50-$36 USD), reflecting modest discretionary spending budgets for most players. Higher-value players might deposit P1,000-P5,000 ($72-$360 USD) or more, but these represent smaller market segments. Payment systems must accommodate both small casual player transactions and larger committed player deposits efficiently.

Trust in online payment systems has grown as e-commerce expands and digital payment infrastructure matures. However, fraud concerns persist, requiring gambling operators to implement secure payment processing, clear transaction confirmations, and responsive customer support addressing payment issues. Partnerships with established local payment providers can enhance trust through brand recognition and local regulatory compliance.

Gaming and Gambling Preferences

Current Market Participation

Gambling participation rates in Botswana reflect the sector’s growth trajectory and cultural acceptance evolution. Approximately 8-12% of the adult population engages in regular gambling (monthly or more frequently), translating to roughly 120,000-180,000 active players. Annual participation rates, including occasional players, may reach 15-20% of adults or 225,000-300,000 individuals.

Online gambling participation specifically, using offshore operators, likely represents 5-8% of adults or 75,000-120,000 players. This suggests substantial existing online gambling activity that could transition to licensed local operators when regulatory frameworks permit. The gap between overall gambling participation and online-specific participation indicates significant land-based gambling preference among current participants.

Sports betting emerges as the most popular gambling activity in Botswana, driven by passionate football fandom and expanding bookmaker availability. Football betting dominates, with English Premier League, UEFA Champions League, La Liga, and local Botswana Premier League matches attracting significant wagering. Rugby, cricket, basketball, and international events like the Olympics also generate betting interest.

Casino games appeal primarily to affluent urban residents and tourists visiting Gaborone’s casino resorts. Table games including blackjack, roulette, and poker attract experienced players and high-rollers, while slot machines and electronic gaming machines serve broader audiences seeking casual entertainment. Live dealer games, where available online through offshore operators, blend casino atmosphere with online convenience, appealing to players seeking authentic experiences without physical casino visits.

Lottery participation remains limited due to the absence of a fully implemented national lottery. The Gambling Act authorizes lottery operations, and a P1 million license has been issued, but comprehensive lottery operations have not launched. When introduced, lottery products could attract mass-market participation given low entry costs and wide appeal across demographic segments.

Consumer Behavior Patterns

Average spending per gambling participant in Botswana likely ranges from P500-P1,500 monthly ($36-$108 USD) for regular players, with significant variation based on income level and gambling intensity. Casual players may wager P100-P300 monthly ($7-$22 USD), while committed players might spend P3,000-P10,000+ monthly ($215-$720+ USD). Annual per-player spending thus ranges from approximately $50-150 USD for the overall player base, with core segments contributing substantially more.

Betting patterns emphasize moderate stakes aligning with middle-class discretionary budgets. Typical sports bets range from P20-P100 ($1.50-$7 USD) for casual players and P100-P500 ($7-$36 USD) for committed bettors. Casino slot machine play typically occurs at P1-P5 per spin for casual players and P5-P20 per spin for regular players. Table game bets vary widely but generally align with modest entertainment budgets rather than high-roller levels.

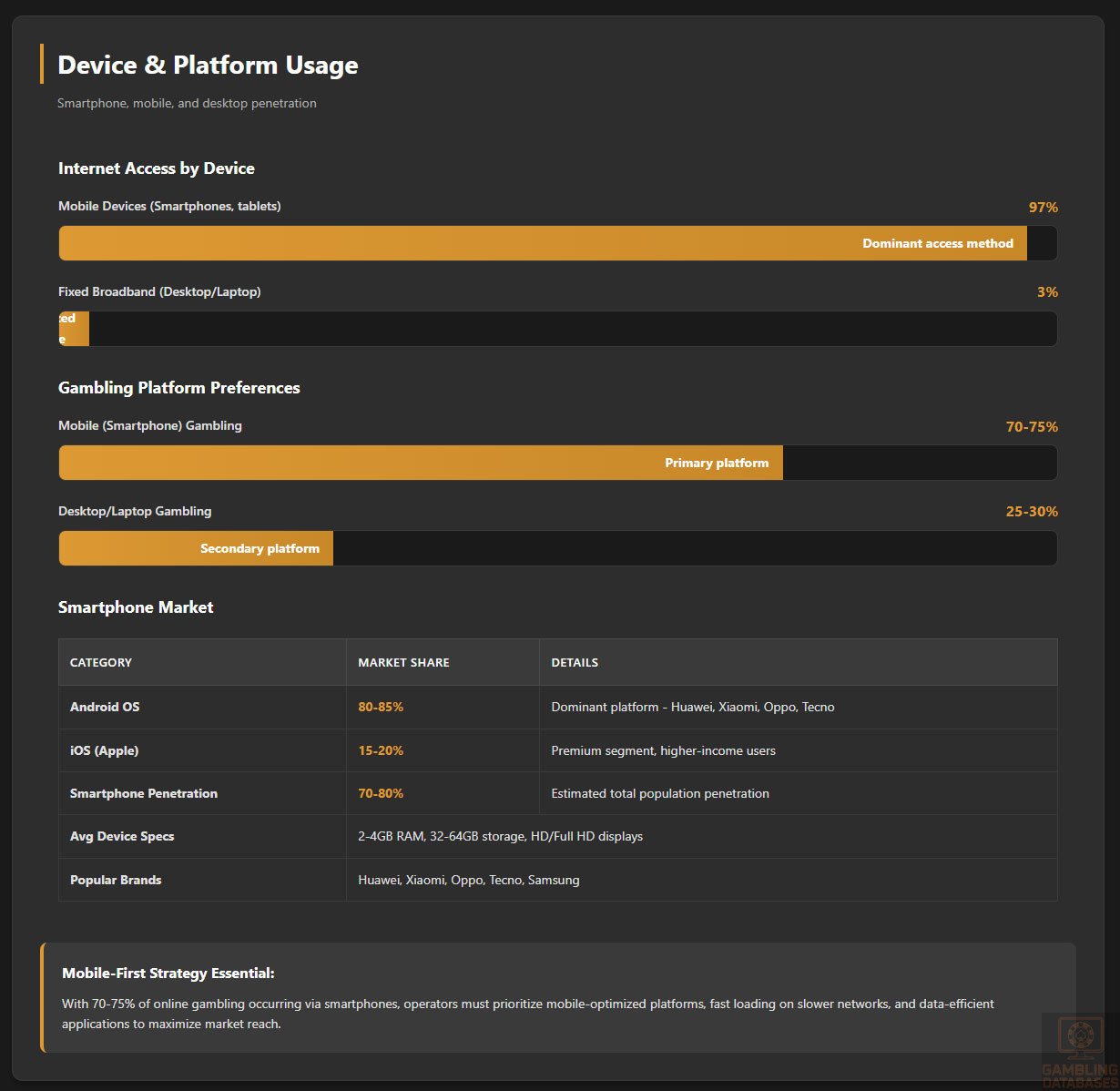

Platform preferences demonstrate strong mobile orientation. Approximately 70-75% of online gambling activity occurs via smartphones, with desktop/laptop usage accounting for 25-30% of sessions. This mobile dominance requires operators to ensure excellent mobile user experiences, fast loading times on slower networks, and data-efficient applications minimizing mobile data consumption.

Session lengths vary by product type. Sports betting sessions often remain brief (5-15 minutes) for placing pre-match bets, though live betting during matches can extend sessions to 90+ minutes matching game duration. Casino gaming sessions typically last 20-60 minutes for casual play, with dedicated players sometimes engaging for several hours. Mobile platform limitations (battery life, data costs) encourage shorter sessions compared to desktop usage patterns.

Retention and loyalty patterns suggest moderate player stickiness in Botswana’s developing market. First-month retention rates likely reach 30-40% for online gambling operators, declining to 15-25% by month three. Annual retention rates may stabilize around 20-30% for operators offering competitive products and localized experiences. Building loyalty requires culturally relevant marketing, local payment methods, responsive customer support, and competitive bonuses.

Bonus sensitivity is high among Botswana players, as welcome bonuses and promotions significantly influence operator selection and trial decisions. However, complex wagering requirements or restrictive terms can alienate players accustomed to straightforward transactions. Operators should balance attractive bonus offers with clear, achievable terms that allow players to realistically benefit from promotions.

Game type preferences by age reveal distinct patterns. Younger players (18-30) favor sports betting, particularly football, and faster-paced casino games like slots and crash games. Middle-aged players (30-45) show more diverse preferences including sports betting, slots, and table games, with some interest in poker. Older players (45+) who gamble demonstrate preferences for traditional casino games, slower-paced slots, and familiar betting patterns rather than new gaming innovations.

Deposit and withdrawal frequency patterns reflect trust-building processes and financial management approaches. New players often make small initial deposits (P100-P200 / $7-14 USD) to test platform reliability before committing larger amounts. Established players may maintain account balances rather than depositing per session, topping up weekly or monthly. Withdrawal requests typically occur after significant wins or when players want to secure profits, with processing speed critically important for satisfaction and trust.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Botswana’s internet infrastructure demonstrates impressive quality for the region, supporting online gambling operations effectively. The 81.4% penetration rate combines with expanding network coverage and improving speeds to create favorable conditions for digital service delivery. However, infrastructure remains uneven between urban and rural areas, with cities enjoying superior connectivity compared to remote regions.

Fixed broadband versus mobile internet breakdown heavily favors mobile connectivity. Approximately 97% of internet access occurs via mobile networks, with only 3% through fixed broadband connections. This mobile dominance reflects Africa-wide patterns where mobile infrastructure deployment proved faster and more economically viable than fixed-line expansion. Gambling operators must optimize for mobile networks rather than assuming high-speed fixed broadband availability.

Average internet speeds reached 15.6 Mbps download and 7.6 Mbps upload as of February 2025, positioning Botswana 143rd globally for fixed broadband speeds and 138th for upload speeds. While modest by developed market standards, these speeds suffice for online gambling applications including video streaming for live dealer games, real-time sports betting odds updates, and interactive gaming experiences. Mobile network speeds vary significantly by location and network operator but generally support gambling applications adequately in urban areas.

Network reliability has improved substantially with infrastructure investments by major operators. Urban areas generally experience reliable connectivity with uptime exceeding 95%, though rural areas face more frequent outages and connectivity gaps. Gambling operators should implement offline modes or session recovery features accommodating temporary disconnections common on mobile networks.

Infrastructure investment continues through government initiatives and private operator expansion. BoFiNet, the state-owned fiber network operator, is implementing its UNLEASH 2025 digital transformation strategy, upgrading existing sites, erecting new towers, and expanding fiber coverage. During the 2021/22 financial year, 4G population coverage increased from 56% to 90%, and internet average speeds improved from previous levels to 21 Mbps through these infrastructure enhancements.

5G and Future Technology Deployment

Current 4G/5G coverage shows Botswana in early 5G adoption stages. As of 2023, 5G coverage reached 23% of the population, concentrated in major urban centers including Gaborone, Francistown, and key commercial districts. Meanwhile, 4G coverage has reached 91% of the population, providing widespread access to high-speed mobile internet suitable for bandwidth-intensive applications.

The 5G rollout timeline suggests gradual expansion over the next 3-5 years, prioritizing business districts, tourism zones, and densely populated urban areas before extending to secondary cities and rural regions. Mobile network operators including Mascom Wireless (MTN affiliate), Orange Botswana, and Botswana Telecommunications Corporation (BTC) are investing in 5G infrastructure as part of competitive strategies and government digital transformation goals.

Future infrastructure plans emphasize universal connectivity, reduced data costs, and enhanced network capacity. The government’s digital transformation agenda targets bringing remaining offline populations online through public Wi-Fi programs, satellite connectivity for remote areas, and continued mobile network expansion. These initiatives will expand the addressable market for online gambling as more citizens gain internet access.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Three primary mobile network operators serve Botswana’s market: Mascom Wireless (43% market share, MTN affiliate), Orange Botswana (39% market share, Orange Group affiliate), and Botswana Telecommunications Corporation – BTC (18% market share, semi-privatized state operator). This competitive market structure drives network quality improvements, pricing competition, and service innovation benefiting consumers and digital service providers.

Network operator market share has remained relatively stable, with Mascom maintaining leadership through superior network coverage and customer service reputation. Orange Botswana competes aggressively on pricing and data packages, while BTC leverages government relationships and nationwide infrastructure. All three operators have invested in 4G expansion and begun 5G deployment in major centers.

Coverage quality varies by operator and geography. Mascom generally provides the most reliable coverage across urban and rural areas, justifying its market leadership. Orange offers competitive urban coverage with some rural gaps. BTC maintains acceptable coverage but faces customer service and network quality challenges compared to private competitors. Gambling operators should test platform performance across all three networks to ensure acceptable user experiences regardless of carrier choice.

Data costs have declined significantly over the past five years due to competitive pressures and regulatory encouragement. Current pricing ranges from approximately P1-3 per GB ($0.07-0.22 USD) depending on package size, promotions, and operator. These costs remain meaningful for budget-conscious consumers but no longer prohibit regular internet usage. Gambling operators should optimize data efficiency to minimize player costs and enable longer session durations without excessive data consumption.

Mobile payment integration represents a critical competitive advantage for gambling operators. All three mobile network operators offer mobile money services enabling direct carrier billing or wallet-based transactions. Integration with Orange Money, Mascom MyZaka, and BTC Smega allows operators to reach beyond banked populations and offer familiar payment methods reducing friction in deposit processes.

Device Penetration

Smartphone adoption in Botswana has reached high levels, with estimates suggesting 70-80% of the population owns smartphones. This penetration creates a large addressable market for mobile gambling applications and mobile-optimized websites. Feature phone usage persists among older demographics and lower-income segments but declines steadily as smartphone prices decrease and second-hand markets expand.

Multiple device ownership is common, with the 166% mobile connection rate (4.21 million connections for 2.56 million people) indicating many individuals maintain multiple SIM cards for different operators, taking advantage of promotional rates or coverage variations. For gambling operators, this multi-SIM behavior necessitates robust anti-fraud systems detecting multiple accounts while avoiding false positives on legitimate users with several devices.

Device preferences favor mid-range Android smartphones from Chinese manufacturers including Huawei, Xiaomi, Oppo, and Tecno. These brands offer affordable pricing (P1,000-P3,000 / $72-215 USD) suitable for middle-class budgets while providing adequate performance for gaming applications. Premium brands like Samsung and Apple serve affluent segments but represent smaller market shares. Android dominates with approximately 80-85% market share, while iOS captures 15-20% primarily among higher-income urban professionals.

Average device specifications among the mass market include 2-4 GB RAM, 32-64 GB storage, HD or Full HD displays, and mid-range processors. These specifications support modern gambling applications adequately, though operators should optimize resource usage for lower-end devices to maximize market reach. Testing on entry-level devices ensures compatibility across the device spectrum rather than optimizing solely for premium hardware.

Mobile internet usage patterns show extensive smartphone integration into daily life. Urban residents use smartphones for social media, messaging, content streaming, mobile money transactions, and increasingly e-commerce. Average daily usage ranges from 3-5 hours for typical users and 5-8 hours for heavy users. Data consumption averages 5-10 GB monthly for regular users, with heavy users consuming 15-30 GB monthly when affordable packages are available.

Financial Services and Payment Infrastructure

Banking System Structure

Botswana’s banking sector demonstrates strong stability and reasonable penetration by African standards. Major banks operating in the country include First National Bank Botswana (FNB), Standard Chartered Bank Botswana, Barclays Bank Botswana (now Absa), Stanbic Bank Botswana, Bank of Baroda, and Access Bank Botswana. These institutions provide comprehensive banking services to individual and corporate customers throughout urban areas.

Market share distribution favors established banks with long-standing operations. FNB and Standard Chartered maintain significant market positions through branch networks, digital banking platforms, and corporate banking relationships. Newer entrants like Access Bank compete through innovative products and aggressive customer acquisition strategies. Total bank count stands at approximately 8-10 commercial banks, creating adequate competition while maintaining system stability.

Digital banking adoption has accelerated rapidly, with most banks offering internet banking portals and mobile banking applications. Services include account management, funds transfers, bill payments, and increasingly advanced features like cardless ATM withdrawals and mobile wallet integration. For gambling operators, partnerships with established banks can facilitate payment processing, though banks may hesitate to explicitly support gambling transactions without clear regulatory frameworks.

Account penetration rates indicate approximately 50-60% of adults hold bank accounts, concentrated among employed urban residents. This leaves 40-50% of the adult population unbanked, relying on cash transactions, mobile money services, or informal savings mechanisms. For gambling market penetration, serving both banked and unbanked populations requires diverse payment method offerings including mobile money and alternative payment processors.

Credit and lending markets remain relatively conservative, with banks employing strict lending criteria and requiring substantial documentation. Credit card availability is limited compared to developed markets, with cards issued primarily to salaried employees and high-income professionals. Personal loan availability has expanded but faces high interest rates reflecting risk premiums in developing markets. This credit market structure limits credit-based gambling but protects vulnerable players from accumulating gambling-related debt.

Payment Processing Options

Available payment methods for iGaming in Botswana span traditional banking channels, mobile money platforms, and emerging digital payment solutions. When online gambling licensing is introduced, operators will need comprehensive payment integrations serving diverse market segments with varying banking relationships and technology adoption levels.

Credit and debit card processing through Visa and Mastercard networks serves the banked, middle-class segment. Card penetration remains moderate, with estimates suggesting 30-40% of urban adults hold debit cards and 10-15% hold credit cards. Payment processing fees typically range from 2.5-3.5% for domestic cards, with higher fees for international card transactions. Gambling operators require merchant accounts explicitly permitting gambling transactions, which may face scrutiny from acquiring banks until regulatory clarity exists.

E-wallet options remain limited compared to mature markets. International e-wallets like PayPal, Skrill, and Neteller are available to Botswana residents but face limited local adoption due to registration complexities and funding challenges. These services primarily serve users engaged in international e-commerce or freelancing rather than mass-market consumers. For gambling operators, e-wallets may facilitate international player segments but offer limited utility for core domestic market penetration.

Bank transfer systems including real-time payment infrastructure and automated clearing house (ACH) equivalents enable direct bank-to-bank transactions. The Botswana Interbank Settlement System (BISS) handles high-value interbank transfers, while the Botswana Automated Clearing House (BACH) processes bulk payments including salaries. Emerging instant payment systems enable real-time settlements rather than batch processing delays, improving user experience for gambling deposits and withdrawals.

Cryptocurrency acceptance remains minimal and largely unregulated in Botswana. While crypto payment processors like Plisio exist, actual usage concentrates among technology enthusiasts and individuals engaged in international crypto markets. Regulatory status is ambiguous, with no explicit prohibition or authorization. For gambling operators, crypto payments would serve niche segments currently but may become relevant as digital currency adoption grows and regulatory frameworks clarify.

Processing fees vary significantly by payment method and transaction volume. Mobile money transactions typically incur fees of 1-3% depending on transaction size, making them cost-effective for typical gambling deposit amounts. Bank transfers may involve fixed fees (P5-20 / $0.35-1.40 USD) or percentage fees depending on bank and transfer type. Card processing fees of 2.5-3.5% represent standard merchant service costs. Cryptocurrency transactions involve network fees plus processor margins but avoid traditional banking intermediaries.

Transaction processing timelines differ markedly across payment methods. Mobile money transactions typically settle instantly, enabling immediate play upon deposit. Card transactions usually process within seconds to minutes. Bank transfers may require several hours for same-day processing or next business day for batch settlements. Withdrawals to mobile money can be instant, while bank withdrawals typically require 1-3 business days. Players prioritize fast deposits and withdrawals, making processing speed a competitive differentiator.

International payment capabilities matter for operators accepting deposits from Botswana players using international accounts or serving expatriate populations. Standard international payment processors handle cross-border transactions, though currency conversion fees and correspondent banking charges increase costs. Operators should support Botswana Pula (BWP) pricing and settlements to avoid currency conversion friction and provide transparent pricing to local players.

Regulatory restrictions on gambling payments currently remain minimal due to online gambling’s unregulated status. Banks and payment processors operate without explicit prohibitions or authorizations regarding gambling transactions. When online licensing is introduced, clearer frameworks will likely mandate that only licensed operators can access local payment infrastructure, blocking transactions to unlicensed offshore operators. This regulatory development could significantly shift competitive dynamics toward licensed local operators.

Chargebacks and dispute resolution procedures follow standard banking practices. Card transactions permit chargebacks under dispute conditions, requiring operators to maintain clear transaction records and terms of service documentation. Mobile money platforms typically offer fewer chargeback rights but include dispute resolution procedures for alleged fraud or unauthorized transactions. Operators should implement responsive customer service addressing payment issues promptly to minimize disputes and maintain payment processor relationships.

E-commerce and Digital Economy

Digital Market Development

E-commerce in Botswana has experienced significant growth, with the market expanding from $246 million USD in 2022 to projected $538 million USD by 2027. This represents compound annual growth exceeding 15%, driven by improved internet infrastructure, smartphone adoption, digital payment proliferation, and changing consumer behaviors accelerated by COVID-19 pandemic experiences with online shopping.

Online retail penetration remains modest at approximately 8-12% of total retail sales, indicating substantial growth runway as more consumers adopt online shopping behaviors. Urban populations drive e-commerce adoption, purchasing electronics, fashion, household goods, and increasingly groceries through online platforms. Rural e-commerce remains limited due to delivery infrastructure challenges and lower internet penetration.