Brazil is emerging as a highly attractive iGaming market following the legalization and regulation of online betting and casino operations in 2025. Its vast population, increasing internet penetration, and passionate sports culture create strong market potential.

The regulatory framework established in January 2025 offers a controlled, transparent environment for operators, presenting clear licensing routes, tax structures, and compliance obligations. This analysis presents a comprehensive view of Brazil’s legal and regulatory landscape for iGaming market entrants.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Legalized and regulated as of January 2025 |

| Regulatory Authority | Secretariat of Prizes and Betting (SPA) |

| Population | Approximately 215 million |

| Adult Population (18+) | ~160 million |

| GDP (2024) | USD 1.9 trillion |

| Average Income per Capita | USD 8,800 |

| Internet Penetration Rate | 81% |

| Mobile Penetration Rate | 95% |

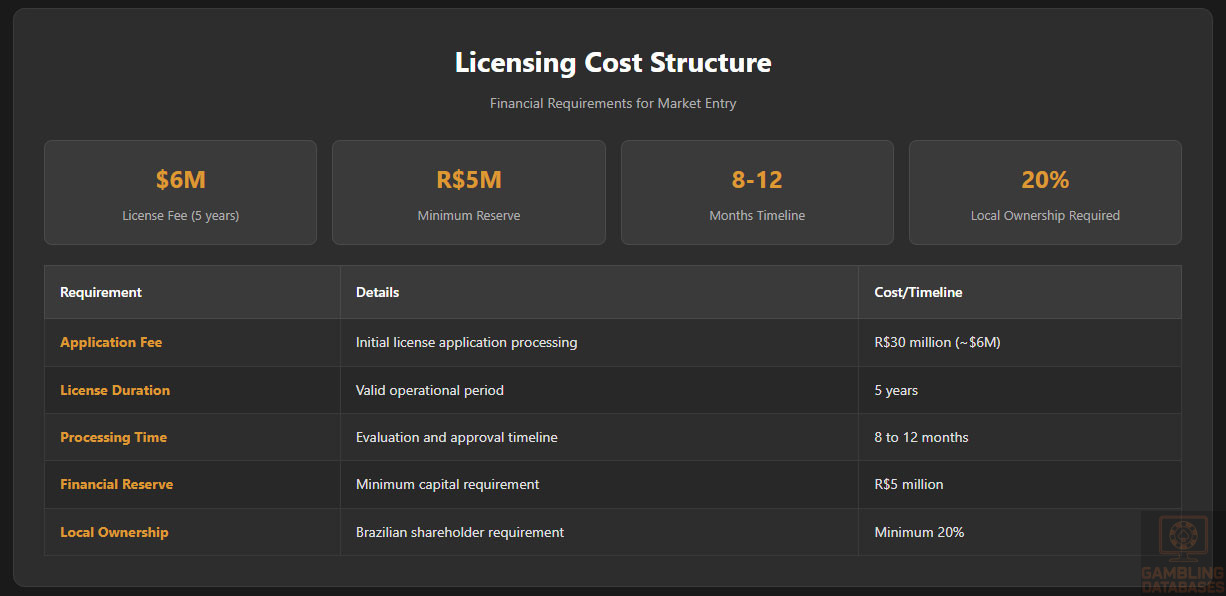

| License Fee | R$30 million (approx. USD 6 million) for 5-year license |

| License Duration | 5 years |

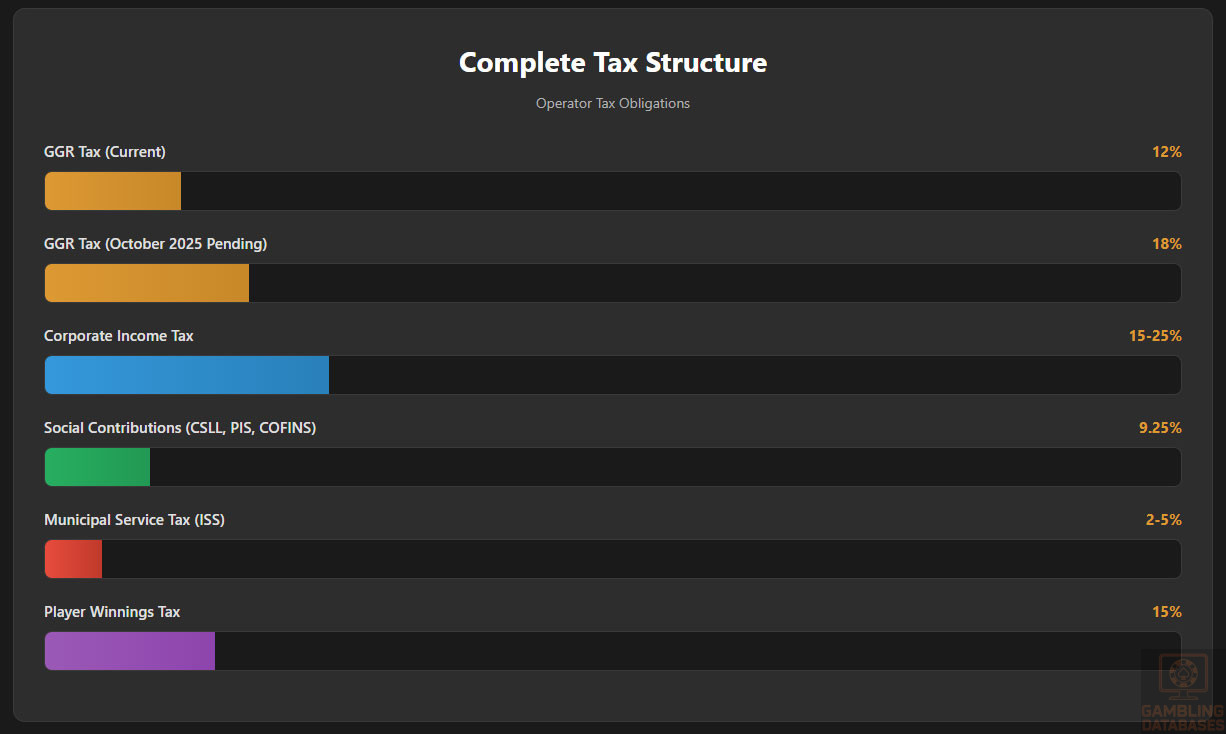

| Gross Gaming Revenue (GGR) Tax | 12% (increasing to 18% from October 2025 pending approval) |

| Corporate Income Tax | 15%-25% standard rate applicable |

| Individual Player Tax on Winnings | 15% withholding tax |

| Application Timeline | 8 to 12 months |

| Local Ownership Requirement | Minimum 20% Brazilian-owned shares |

| Mandatory Local Presence | Yes, with headquarters and administration in Brazil |

| Technical Certification | Required from accredited independent labs |

| Responsible Gambling Measures | Mandatory with robust KYC and AML protocols |

| Advertising Restrictions | Strict, especially protection from targeting minors |

| Number of Licensed Operators (Early 2025) | 68+ |

| Market Revenue Projections (2025) | Estimated USD 2 billion annually in tax revenue |

| Growth Forecast (CAGR 2025-2030) | 15%-18% |

| Average Revenue Per User (ARPU) | USD 120 annually |

| Market Penetration Rate | 5%-7% of adults actively betting |

| Types of Legal Gambling | Sports betting, online casino, horse racing betting |

| Prohibited Activities | Unlicensed gambling, certain land-based casinos (under review) |

| Enforcement Bodies | SPA and Ministry of Finance |

| Payment Monitoring | Mandated by SPA; banks must report suspicious transactions |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Brazil historically maintained a restrictive approach to gambling. However, starting January 1, 2025, the country implemented a comprehensive regulatory framework legalizing and controlling online sports betting, online casinos, and horse racing betting. The Secretariat of Prizes and Betting (SPA), under the Ministry of Finance, acts as the main regulatory authority. Its mandate includes licensing, compliance monitoring, market oversight, and enforcement.

Land-Based Gambling Activities

Land-based gambling in Brazil currently exhibits limited formal options. Authorized activities include licensed horse race betting venues and bingo halls in select states. Land-based casinos remain banned but are subject to pending legislation aiming to introduce resort casinos over the next few years. Lottery and bingo games operate under state and federal licenses, subject to strict regulation and taxation policies.

Online Gambling Framework

Digital gambling activities include fixed-odds sports betting and online casino gaming, both legalized and regulated federally. Operators must acquire federal licenses issued by SPA and comply with stringent regulatory standards encompassing financial transparency, technical platform certifications, and operational integrity.

The online framework bans unlicensed gambling activities and strictly controls participation through mandatory player identification and local jurisdiction enforcement. Domains used for gaming operations must use the .bet.br extension, and other generic TLDs like .com are blocked for gambling purposes.

Licensed Operators and Market Players

The Brazilian iGaming market exhibits dynamic growth with over 68 licenses issued early in 2025, reflecting strong international and local operator interest. Licensees include established global online casino platforms, sports betting operators, and emerging local companies.

Competition centers on securing robust regulatory compliance and local partnerships, particularly for foreign entrants, to fulfill the minimum 20% Brazilian ownership stake. Market entry strategies often focus on leveraging Brazil’s massive sports enthusiasm, particularly football, to build strong sports betting verticals integrated with casino offerings.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing application is managed by the Secretariat of Prizes and Betting, which evaluates all submitted documentation, technical certifications, and financial disclosures. License eligibility mandates business registration in Brazil, with a local corporate presence and ownership requirements.

Operators face high entry barriers including the payment of a substantial license fee of R$30 million (approx. USD 6 million) for a five-year license, which covers application processing and regulatory oversight. The typical licensing timeline ranges from 8 to 12 months, reflecting rigorous vetting procedures and background checks on company principals.

Technical standards require platforms to be audited by accredited third-party labs for fair play and security, alongside certification of random number generators (RNGs) and cybersecurity compliance. Regulatory authorities also impose strict anti-money laundering (AML) and counter-terrorist financing (CFT) measures consistent with international best practices.

Required Documents for Licensing

- Corporate registration certificate and articles of incorporation in Brazil

- Proof of at least 20% Brazilian shareholder ownership

- Financial statements and a 2-year financial forecast

- Minimum financial reserve of R$5 million

- Technical platform certification and software audit reports

- Criminal background certificates for directors and beneficial owners

- Proof of compliance with AML/KYC policies

- Advertising compliance documentation aligned with local law

- Registration on Brazil’s consumer dispute resolution platform

Local Presence and Operational Requirements

Brazil imposes a comprehensive local presence obligation for license holders. Operators must maintain registered headquarters and administrative offices within Brazil, managed by qualified personnel, including financial and customer support managers. This ensures accountability and facilitates regulatory communication.

Ownership regulations require foreign companies to partner with Brazilian entities owning at least 20% of equity, fostering local participation in the sector. This ownership structure is strictly monitored, and offshore ownership models are not permitted for regulatory approval.

Compliance Obligations and Monitoring

Player Protection and Identification

Regulations mandate robust age and identity verification procedures to prevent underage gambling. Operators must implement strict Know Your Customer (KYC) processes aligned with AML frameworks, capturing and verifying personal data before account creation or wagering.

Responsible gambling is a core compliance pillar. Licensees must offer self-exclusion programs, establish deposit and loss limits, and promote player awareness campaigns. Data privacy standards require secure handling of sensitive information to protect against fraud and misuse.

Mandatory Player Protection Measures

- Age verification systems to block underage bettors

- Comprehensive KYC procedures aligned with AML/CFT protocols

- Self-exclusion schemes for problematic gambling behavior

- Deposit and loss limit functionalities

- Regular player activity monitoring to detect suspicious behavior

- Transparent information disclosure on odds and risks

- Responsible gaming education and resources for players

Financial Monitoring and Reporting

The SPA mandates ongoing transaction monitoring by operators to identify illicit activities and ensure financial transparency. Operators submit periodic reports including gross gaming revenue, player transactions, and tax remittances, enabling government oversight.

Financial audits are required annually, supplemented by potential unscheduled inspections. Banks and payment providers support enforcement by reporting suspicious transactions linked to illegal gambling, helping to curb unauthorized operators.

Sequential Reporting Process

- Monthly submission of financial and operational reports to SPA

- Quarterly tax payment filings based on gross gaming revenue

- Annual independent financial audit delivery

- Immediate incident and suspicious activity reporting

Taxation Structure and Financial Obligations

Player Taxation

Players winning gambling prizes are subject to a 15% withholding tax on gross winnings exceeding defined thresholds. The tax is withheld at source by operators and remitted to the tax authorities, simplifying compliance and reducing evasion.

Operator Taxation

| Tax Type | Rate | Notes |

|---|---|---|

| Gross Gaming Revenue (GGR) Tax | 12% current; 18% effective Oct 2025 (pending approval) | Primary operational tax on all betting revenue |

| Corporate Income Tax (CIT) | 15%-25% | Standard federal corporate income tax |

| Social Contributions (CSLL, PIS, COFINS) | Approx. 9.25% | Applied on net income and GGR |

| Municipal Service Tax (ISS) | 2%-5% | Varies by municipality where operator is based |

License renewal fees and additional turnover taxes may apply depending on operator scale and product portfolio. Brazil’s tax environment imposes significant cost considerations but ensures government revenue to support regulatory enforcement.

Gambling Market Financial Performance

Brazil’s regulated market has started generating substantial wagering volumes, with government forecasts estimating over R$10 billion (USD 2 billion) in annual tax revenues by 2025. Year-on-year growth expectations remain robust, supported by expanding internet access and mobile wallet integration.

The distribution of revenues reflects dominant sports betting verticals, driven by massive engagement with football and other popular sports, alongside growing demand for online casino products.

Advertising and Marketing Restrictions

Strict regulations govern advertising to protect vulnerable populations, especially minors. Permitted channels include television, radio, online platforms, and event sponsorships, but content must avoid targeting underage individuals or promoting excessive gambling behavior.

Operators must disclose terms, odds, and taxation information clearly in all promotions. Time-of-day restrictions limit advertising during children’s programming, and sponsorships of events featuring minors face prohibitions.

Permitted Advertising Channels and Restrictions

- Television and radio with restricted time slots

- Official websites and authorized digital platforms

- Sports and event sponsorship excluding youth events

- Social media adhering to age-gating and content rules

- Prohibition of direct advertising targeting minors

- Mandatory disclosure of risks and tax implications

Recent Regulatory Changes and Their Impact

Since the launch of the new framework in January 2025, recent provisional measures have notably increased the GGR tax from 12% to 18%, pending congressional approval, to increase government fiscal intake. This shift heightens operational costs for licensees but is balanced by growing market volumes.

Additional decrees expanded eligible sports betting disciplines to include esports with anti-exclusive agreement clauses, broadening operator product offerings while promoting competitive fairness. Financial institutions face stricter obligations to monitor and block unlicensed operators, improving market integrity.

Enforcement Mechanisms and Penalties

Non-compliance with licensing, tax, and operational requirements results in significant penalties including monetary fines, license suspension, and criminal prosecution. The SPA actively blocks unlicensed gambling websites and sanctions advertising violations.

- Fines up to R$2 billion for illegal operators

- Website blocking and IP address blacklisting

- License suspension or revocation for compliance breaches

- Criminal charges against fraudulent actors

- Injunctions to prevent unauthorized betting activities

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

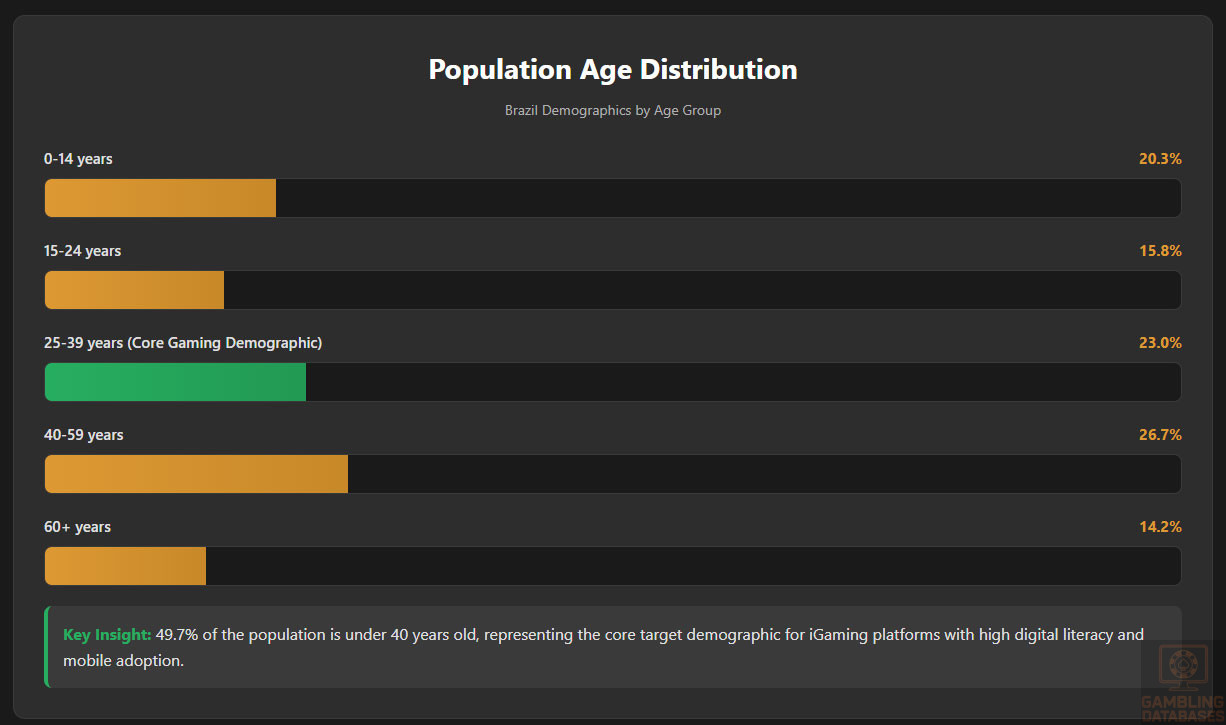

Brazil’s national population reached 216 million in 2025, making it the sixth most populous country globally. The population exhibits significant youthfulness, with a median age of 34.3 years, supporting high future consumer engagement across entertainment segments. Gender distribution remains balanced, with a male-to-female ratio of about 0.96.

| Age Group | Share (%) |

|---|---|

| 0-14 years | 20.3 |

| 15-24 years | 15.8 |

| 25-39 years | 23.0 |

| 40-59 years | 26.7 |

| 60+ years | 14.2 |

Urbanization is a key trait of the Brazilian demographic landscape, with 86.8% of citizens residing in urban centers. Major metropolises function as economic and cultural hubs, intensifying digital and gaming activity. The rural population, while shrinking, remains significant in certain northern and central-west states.

Geographic Distribution

Regionally, economic power clusters in the Southeast and South, led by Sao Paulo and Rio de Janeiro. High-income states concentrate gaming consumers, technology access, and marketing potential in these zones.

- Sao Paulo: 22.8 million residents, Brazil’s financial and tech hub

- Rio de Janeiro: 13.6 million, cultural capital with heavy entertainment spending

- Belo Horizonte: 6.1 million, industrial center with rapid iGaming adoption

- Brasilia: 4.8 million, educated workforce and high digital readiness

- Salvador: 4.2 million, diverse population with growing online presence

- Fortaleza: 4.1 million, strong regional digital growth

Internet penetration is highest in Southeast and South (above 86%), lower in North and Northeast (71%-73%). Gambling venue concentration tracks with urban density, offering greater physical access in large cities but rapid digital expansion nationwide.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

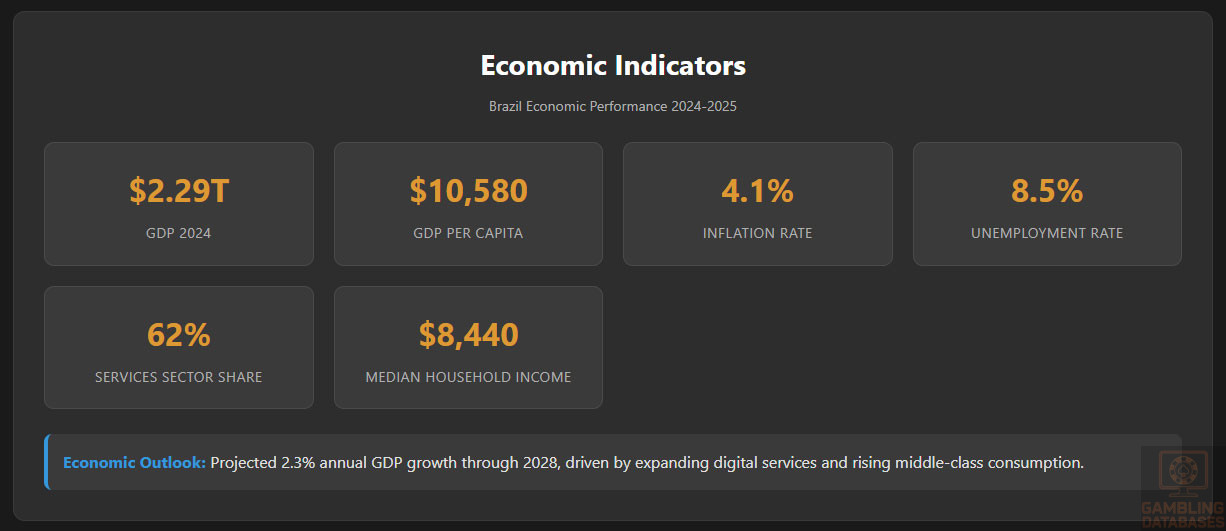

Brazil’s GDP reached USD 2.29 trillion in 2024, rebounding on stable commodity exports and renewed consumer spending. Growth is projected to continue at a 2.3% annual rate through 2028, with expanding service and digital sectors counterbalancing manufacturing slowdowns.

| Indicator | Value |

|---|---|

| GDP (2024, USD) | 2.29 trillion |

| GDP per Capita (USD) | 10,580 |

| Inflation Rate (2024) | 4.1% |

| Unemployment Rate (2025) | 8.5% |

| Services Sector Share of GDP | 62% |

Large-scale urbanization underpins rising disposable income, with middle-class expansion fueling entertainment, media, and online transaction growth.

Income and Wealth Distribution

Median household income sits at USD 8,440 per year. The upper-middle (18% of households) and upper-income (4%) segments command outsized discretionary budgets relevant to iGaming, while the bottom 30% remain price sensitive. Gini coefficient of 0.497 signals persistent but slowly declining income inequality.

Income growth concentrates in major metro regions, correlating with higher iGaming participation and digital payment uptake. The rising affluent class adopts new payment solutions and online entertainment faster than lower-income cohorts, driving spend in gaming, streaming, and sports betting platforms.

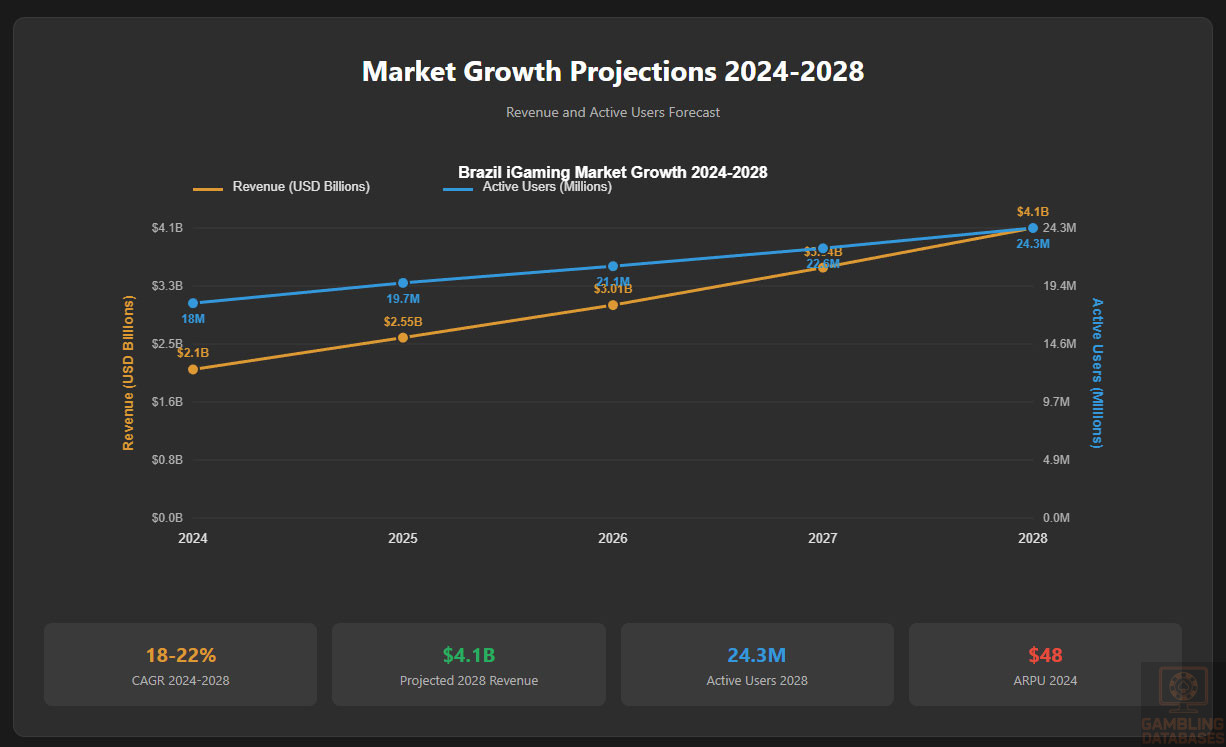

Market Size and Growth Projections

Brazil’s iGaming sector posted revenue of USD 2.1 billion in 2024. Market forecasts point to sustained 18-22% CAGR through 2028, reaching a projected USD 4.1 billion by decade’s end.

| Year | Total Revenue (USD Billions) | Active Users (Millions) |

|---|---|---|

| 2024 | 2.1 | 18.0 |

| 2025 | 2.55 | 19.7 |

| 2026 | 3.01 | 21.1 |

| 2027 | 3.54 | 22.6 |

| 2028 | 4.10 | 24.3 |

Average Revenue Per User for online gaming stands at USD 48 in 2024, with growth linked to increasing player spend, product diversification, and expansion of regulated game types.

Education, Skills, and Digital Literacy

Brazil’s adult literacy rate exceeds 94%, with urban regions benefitting from higher rates and digital fluency. Secondary school completion is at 74% nationally; in major cities, bachelor’s or higher education attainment surpasses 22%, providing a sizable base of skilled, tech-savvy consumers.

Digital skills training is widespread in city schools and among private sector workforce programs. Digital literacy is elevated among 15-44 year olds, representing the demographic core of iGaming consumers in Brazil. Younger generations demonstrate strong familiarity with mobile, payment, and streaming technologies.

Cultural and Social Factors

Communication and Language

The sole official language is Portuguese, spoken by 98% of the population. English proficiency is low overall (just 5%), making high-quality local language content and customer service essential for iGaming brands.

- Portuguese (national standard, 27 regional accents)

- Indigenous languages (more than 180, mostly in Amazon basin)

- Spanish (border regions, minority use)

- German (southern rural enclaves)

- Italian (small southern clusters)

- Japanese (Japanese-Brazilian communities in Sao Paulo)

Digital communication habits favor mobile messaging, with WhatsApp, Instagram, and Facebook leading both peer-to-peer and brand engagement activities.

Cultural Attitudes

Gambling is widely viewed as entertainment but also subject to social caution, reflecting Brazil’s Catholic and Evangelical roots. While urban youth are generally open, attitudes among older generations and conservative regions may be more reserved, affecting game and marketing choice.

Preference for foreign brands is growing in the digital space, but local cultural adaptation and Portuguese-language community features drive trust, especially for payments and support. Government endorsement drives wider acceptance, particularly after 2024’s sportsbook legalization.

Problem Gambling and Social Considerations

Prevalence of problem gambling is 0.7-1.3% among active adult players, according to recent studies. At-risk groups include younger male urban players and lower-income mobile-only users.

- National self-exclusion registry

- Public helplines for gambling addiction

- Mandatory site-based self-exclusion tools

- Information campaigns in schools and media

- Integration with mental health services in major cities

- Partnerships with NGOs for risk prevention

Operators are required to contribute to social responsibility funds, display responsible gambling resources, and track high-risk player behavior for intervention.

Political Structure and Governance

Brazil is a federal presidential republic, featuring robust checks and balances and regular multi-party elections. The business and regulatory environment is moderate in stability, with occasional legislative delays but steady market liberalization since 2022.

International relations are positive with major economies, supporting cross-border investment and data flows, though regulatory changes are subject to political cycles. Investment climate for foreign gaming operators continues to improve, driven by policy and economic incentives.

Technology Adoption and Digital Behavior

Internet and Digital Usage

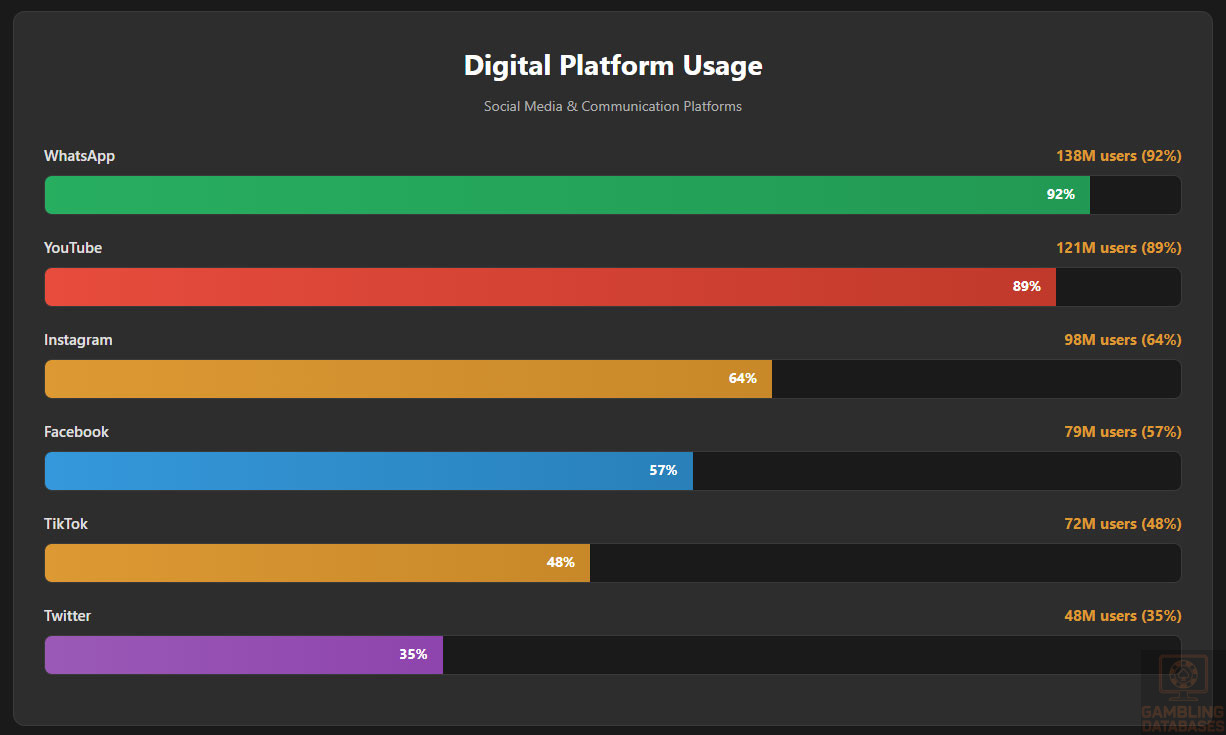

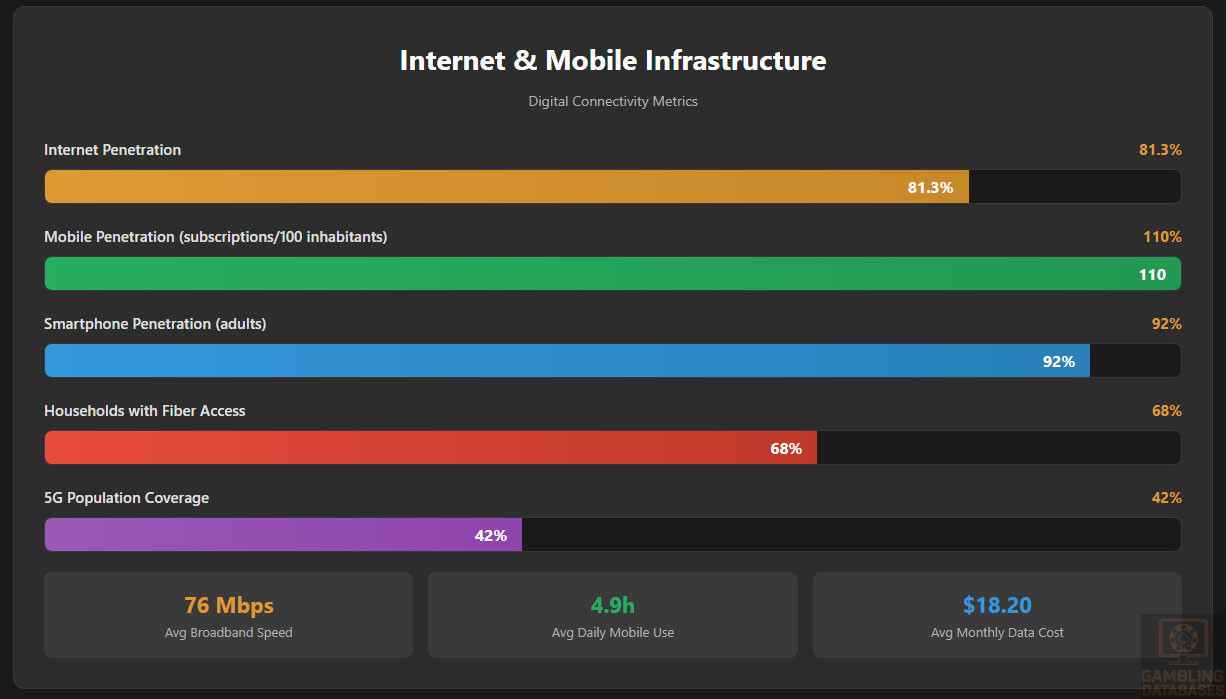

National internet penetration is 81.3%, with daily average use exceeding 7.6 hours in major cities. Over 93% of users access the web primarily via mobile, making mobile-first design and services critical for iGaming platforms.

- WhatsApp: 138 million users (~92% penetration)

- YouTube: 121 million (~89% penetration)

- Instagram: 98 million (~64% penetration)

- Facebook: 79 million (~57% penetration)

- TikTok: 72 million (~48% penetration)

- Twitter: 48 million (~35% penetration)

| Metric | Value |

|---|---|

| Internet Penetration | 81.3% |

| Mobile Penetration | 110 subscriptions per 100 inhabitants |

| Average Daily Mobile Time | 4.9 hours |

| Average Broadband Speed | 76 Mbps |

| e-Commerce User Base | 78 million |

Streaming video, live sports, and online games register among the top digital activities, strongly influencing iGaming engagement.

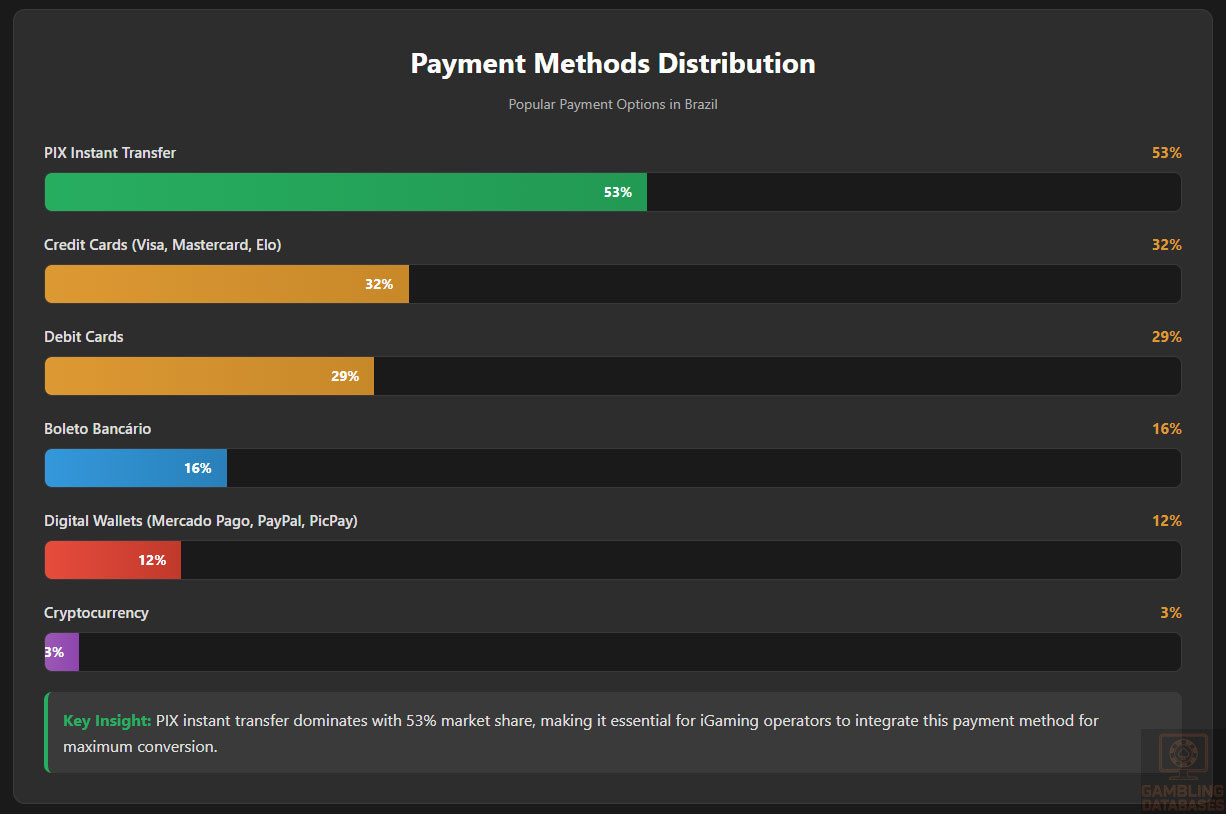

Digital Payment Behavior

Brazilians prefer diverse payment instruments. Use of digital wallets and local instant payment systems such as PIX is surging, reflecting low credit card penetration and high mobile adoption in the population under 40.

- PIX instant transfer: >53% of online transactions

- Credit cards: 32% usage, primarily Visa and Mastercard

- Debit cards: 29% as primary payment source

- Boleto Bancário: 16% for online purchases, cash-based users

- Digital wallets (Mercado Pago, PayPal, PicPay): 12% and rising

- Cryptocurrency: approximately 3% participation, early adopter trend

Payment versatility and instant settlement have become decisive consumer criteria, especially among iGaming users who shift between apps, marketplaces, and gaming portals.

Gaming and Gambling Preferences

Current Market Participation

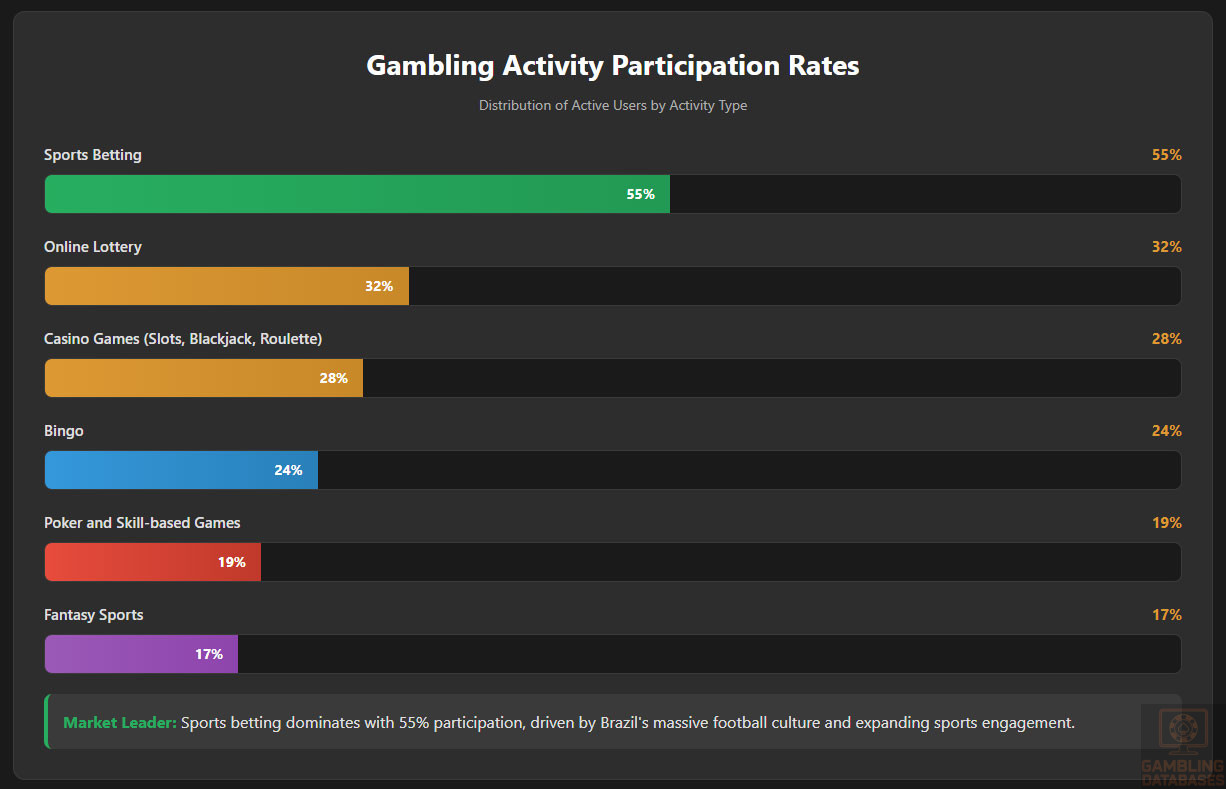

Gaming participation rates are highest among urban male adults aged 19-34, with sports betting, fantasy contests, and digital lotteries showing surging growth following regulatory reforms. Female participation is climbing, especially in casual games and bingo.

- Sports betting (55% of active users)

- Online lottery (32%)

- Casino games (slots, blackjack, roulette: 28%)

- Bingo (24%)

- Poker and skill-based games (19%)

- Fantasy sports (17%)

| Activity | Participation (% of Active Users) |

|---|---|

| Sports Betting | 55 |

| Online Lottery | 32 |

| Casino (Slots/Table) | 28 |

| Bingo | 24 |

| Poker | 19 |

| Fantasy Sports | 17 |

Participation varies by region and is highest in Sao Paulo, Rio de Janeiro, Belo Horizonte, and Recife. Cash-based and mobile-first users drive alternative verticals outside sportsbook offerings.

Consumer Behavior Patterns

Active Brazilian gamblers typically spend 21.5 minutes per session on iGaming platforms, with peak activity during evening hours and weekends. Multi-device usage, especially mobile and desktop in tandem, is common among higher value users.

Retention is highest among sportsbook and lottery players, with promotions, multi-event betting, and live streaming features contributing to user stickiness. Loyalty program adoption remains moderate but is growing, especially for cross-product brands with strong community integration.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

Brazil possesses the largest digital infrastructure in Latin America, with 81.3% internet penetration and over 110 mobile subscriptions per 100 inhabitants. Broadband accounts for 42% of subscriptions, while the vast majority of users access the internet primarily via mobile and fiber connections.

Average fixed broadband speeds in major cities reach 76 Mbps, with reliable performance in Southeast and South regions. Variability exists in rural and northern states, where lower speeds and intermittent service limit advanced digital activity. Private and public investment in network expansion has intensified to reduce the urban-rural digital gap.

| Metric | Value |

|---|---|

| National Internet Penetration | 81.3% |

| Mobile Broadband Penetration | 110 subscriptions/100 inhabitants |

| Average Fixed Broadband Speed | 76 Mbps |

| Average Monthly Data Cost | USD 18.20 |

| Households with Fiber Access | 68% |

Recent regulatory incentives, universal access programs, and competitive pressure among telecom firms continue to drive network upgrades, enhancing download speeds, reliability, and capacity for streaming and gaming traffic.

5G and Future Technology Deployment

Commercial 5G service began full-scale rollout in 2023, now reaching 42% of population centers. Major cities and state capitals enjoy near complete coverage, with mid-tier cities to follow through 2027. Integration of edge computing and cloud infrastructure accompanies telecom investment, supporting innovation in streaming, gaming, and payment processing.

The network landscape is defined by scale and competition. National and regional operators vie for spectrum, accelerating 5G capacity upgrades and launching network-as-a-service for digital commerce and entertainment providers.

Mobile Technology Ecosystem

Mobile Network Infrastructure

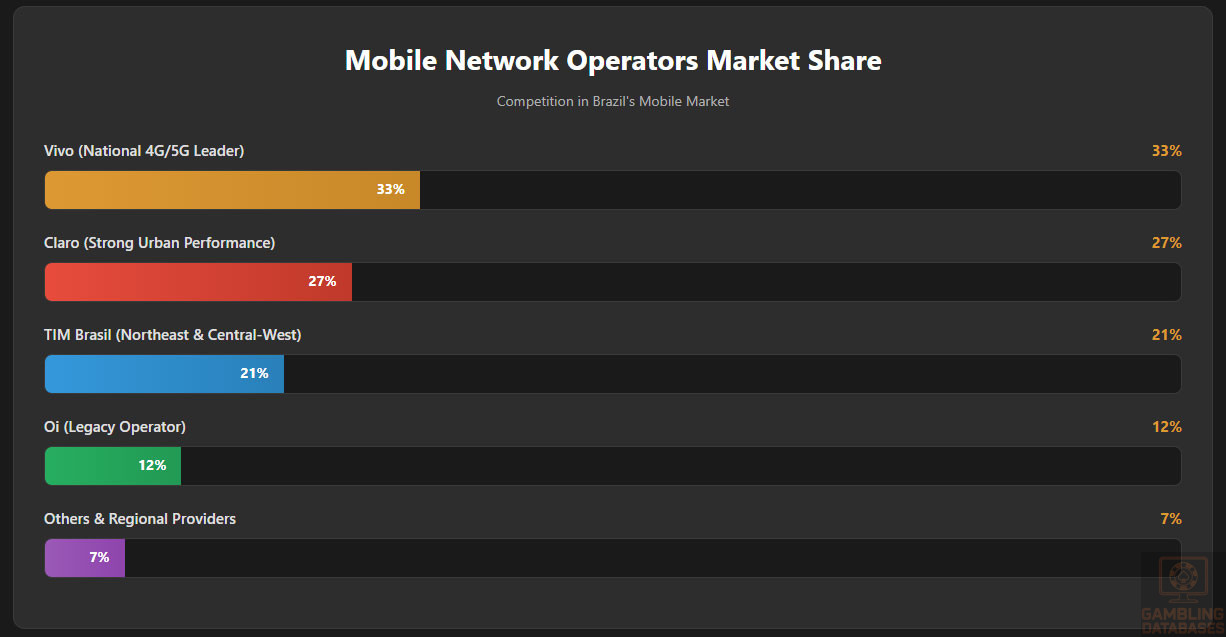

Brazil’s mobile market features five major network operators offering extensive coverage and rapid data speeds. Intense competition has driven down average data costs while expanding LTE and 5G accessibility to smaller municipalities and peri-urban areas.

- Vivo: ~33% market share; leader in national 4G/5G coverage

- Claro: 27%; strong urban performance, expanding data products

- TIM Brasil: 21%; coverage in northeast and central-west regions

- Oi: 12%; legacy operator with selective upgrades to 5G

- Nextel (now acquired by Claro): residual share servicing niche urban segments

Secondary and regional providers operate in local markets, supporting last-mile connectivity and price differentiation.

Device Penetration

Smartphone penetration among adults exceeds 92%, led by Android-based devices (84% of smartphones), with iPhone accounting for 13%. Device upgrades are frequent in urban areas, furthered by installment plans and rising disposable income.

App-centric behavior dominates consumer digital engagement. The average Brazilian maintains over 23 apps on their primary smartphone, with high frequency of gaming, banking, and e-commerce use. Feature preferences include biometric security, long battery life, and fast-charging technology.

| Metric | Value |

|---|---|

| Smartphone Penetration | 92% |

| Android Market Share | 84% |

| Average Apps per User | 23 |

| Average Daily Mobile Use | 4.9 hours |

| Annual Device Upgrade Rate | 21% |

Multi-device lifestyles persist, with high overlap between smartphone, desktop, and smart TV usage, especially for entertainment and financial transactions.

Financial Services and Payment Infrastructure

Banking System Structure

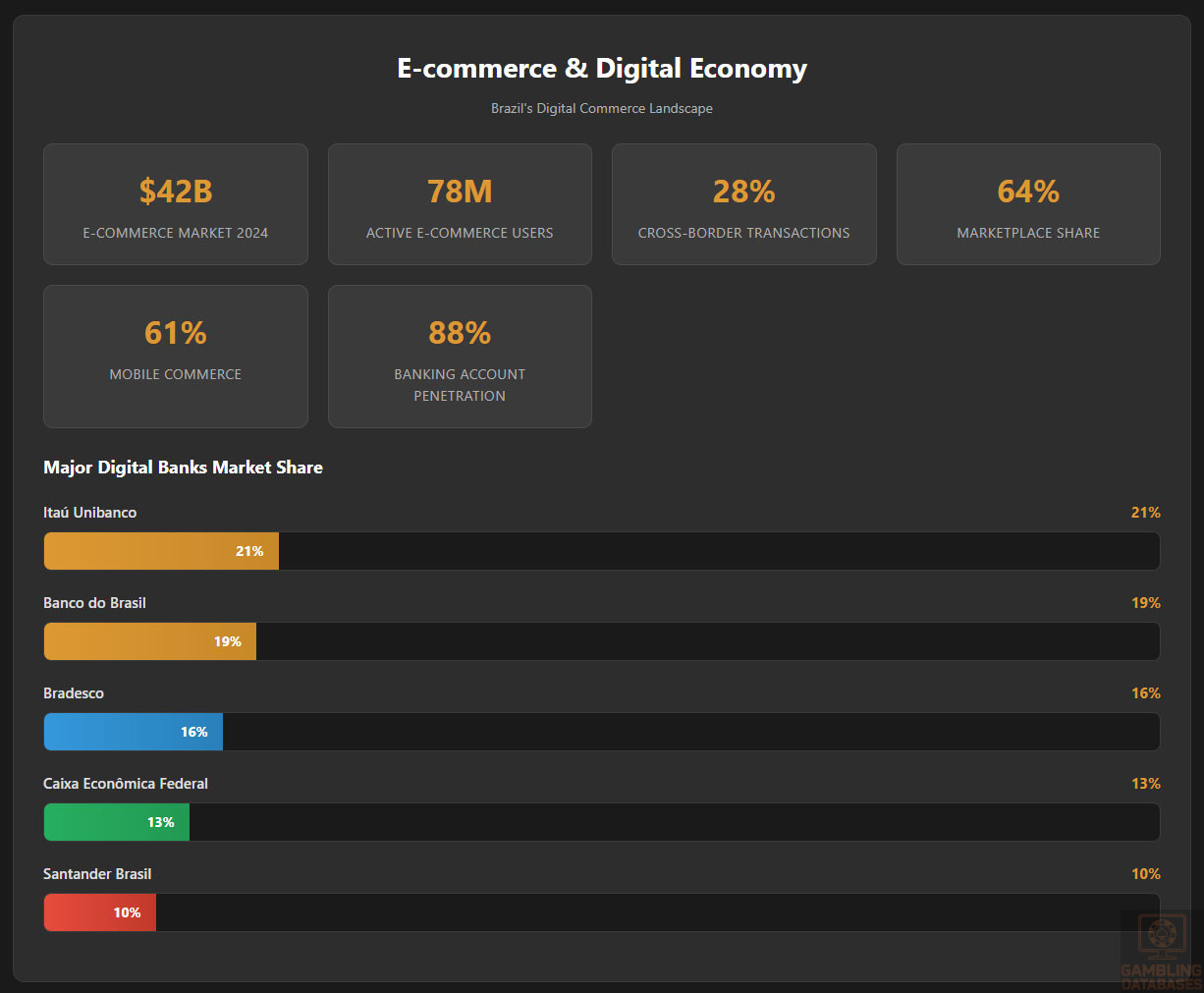

Brazil’s highly developed banking sector underpins digital commerce growth. Financial account penetration is above 88% for adults, supported by robust digital banking and instant payment systems. Both public and private institutions compete in retail and business segments.

- Itaú Unibanco: 21% retail market share, national branch network, advanced digital platform

- Banco do Brasil: 19%, mixed public-private, strong online and government payment services

- Bradesco: 16%, wide urban footprint, small business banking emphasis

- Caixa Econômica Federal: 13%, housing and social benefit leader, mobile payments

- Santander Brasil: 10%, global capabilities, FX and commercial focus

- BTG Pactual: 7%, largest investment bank, digital innovation leader

New digital-only banks (Nubank, C6 Bank, Banco Inter) are rapidly gaining share with mobile-first portfolios and fee-free accounts, particularly among under-35 users.

Payment Processing Options

Brazil offers multiple payment processing solutions, reflecting consumer demand for convenience, security, and instant settlement. Cash alternatives and digital wallets now rival card use in e-commerce and iGaming revenue share.

- Credit cards (Visa, Mastercard, Elo): 32% of online payments

- PIX instant transfer: 53%, main e-commerce and iGaming settlement channel

- Debit cards: 29% penetration

- Boleto Bancário: 16%, preferred by cash-based and unbanked segments

- Digital wallets (Mercado Pago, PayPal, PicPay, PagBank, Ame Digital): 12% and rising

- Cryptocurrency: 3%, niche but growing in gaming/tech circles

Operator integration with multiple payment rails is vital for maximizing conversion and serving users across all income brackets.

| Payment Method | Online Usage (%) |

|---|---|

| PIX Instant Payments | 53 |

| Credit Cards | 32 |

| Debit Cards | 29 |

| Boleto Bancário | 16 |

| Digital Wallets | 12 |

| Cryptocurrency | 3 |

E-commerce and Digital Economy

E-commerce in Brazil surpassed USD 42 billion in 2024, with over 78 million active digital purchasers. Marketplaces dominate, while cross-border e-retail is buoyed by improved last-mile delivery networks and fast payment rails.

Digital service adoption is robust. Streaming, online gaming, ride-hailing, and fintech platforms enjoy mainstream status. Consumer trust has risen thanks to financial regulations, anti-fraud protocols, and government-verified payment platforms like PIX.

| Indicator | Value |

|---|---|

| E-commerce Market Size (2024) | USD 42 billion |

| Active E-commerce Users | 78 million |

| Cross-Border Transactions (Share) | 28% |

| Marketplaces (Share of Sales) | 64% |

| Mobile Commerce Penetration | 61% |

Enterprise adoption of cloud, SaaS, CRM, and security solutions accelerates digital transformation among SMEs and major iGaming entrants seeking optimized user experience and compliance management.

Business Environment and Regulatory Framework

Ease of Business Operations

Brazil is ranked 124th on the 2024 World Bank Doing Business survey, reflecting moderate efficiency and complexity in registration, licensing, and taxation. Significant improvements are noted in credit, utility connections, and digital registration platforms.

Foreign entities benefit from clarity in investment policy, but initial setup requires alignment with local labor, tax, and gaming legislation, including compliance with anti-money laundering and consumer protection laws.

- Document preparation and translation

- Submission to the National Companies Registry (Junta Comercial)

- CNPJ tax registration and government legal publication

- Bank account opening and minimum capital deposit

- License(s) application and SPA registration

The end-to-end entry and registration process, from document gathering to full operational status, averages 3-6 months, but timing varies with scale and legal complexity.

Corporate Structure and Registration

The most common business entities for iGaming are the Sociedade Limitada (LLC) and Sociedade Anônima (SA/Corporation). Most foreign and domestic entrants select the LLC due to simplicity, limited liability, and eligibility for SPA licensing.

Registration involves notarial services, submission of original and translated documentation, proof of minimum capital (BRL 5 million for gaming), and verified local directors. There are no mandatory local ownership thresholds, but at least one local legal representative is required.

- ID and proof of address for directors

- Corporate articles of association (statutes)

- Brazilian CNPJ registration certificate

- Proof of minimum capital deposit

- Local tax and labor registrations

- Criminal background checks for beneficial owners

| Milestone | Typical Range |

|---|---|

| Company Registration Fees | USD 2,500 – 7,000 |

| Legal & Consulting (Initial) | USD 15,000 – 40,000 |

| Licensing Application Fee | USD 390,000 |

| Annual License Fee | USD 117,000 |

| Total First-Year Setup | USD 500,000 – 800,000 |

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate in Brazil is 34% (combining corporate tax and social contribution). Special zone incentives and treaty relief are available for certain cross-border transactions.

Brazil maintains double tax treaties with over 20 countries to alleviate withholdings on foreign income, dividend transfers, or royalties.

- Portugal

- Spain

- France

- Argentina

- Italy

- Sweden

| Category | Rate or Amount |

|---|---|

| Corporate Income Tax | 34% |

| GGR Tax: Sports Betting | 18–20% |

| GGR Tax: Casinos (proposed) | 25% |

| VAT (Digital Services) | 16-19% |

| Withholding Tax (Dividends) | Up to 15% |

Personal income is taxed progressively up to 27.5%, with social security required for employees. Non-residents pay flat withholding on Brazilian earnings. Gambling winnings over the exemption threshold are subject to a 30% withholding at source.

Market Entry Considerations

Recommended Entry Strategies

Optimized entry requires robust local partnerships, technology adaptation, and phased rollout. Successful market entrants excel at tailoring products to local preferences, supporting diverse payment channels, and integrating responsible gambling features.

- Partner with local marketing agencies and affiliates

- Offer deep integration with PIX and domestic payment rails

- Provide native Portuguese content and round-the-clock support

- Invest in cross-device UX and personalization

- Align brand with national sponsorships and community programs

- Develop agile regulatory compliance protocols for SPA engagement

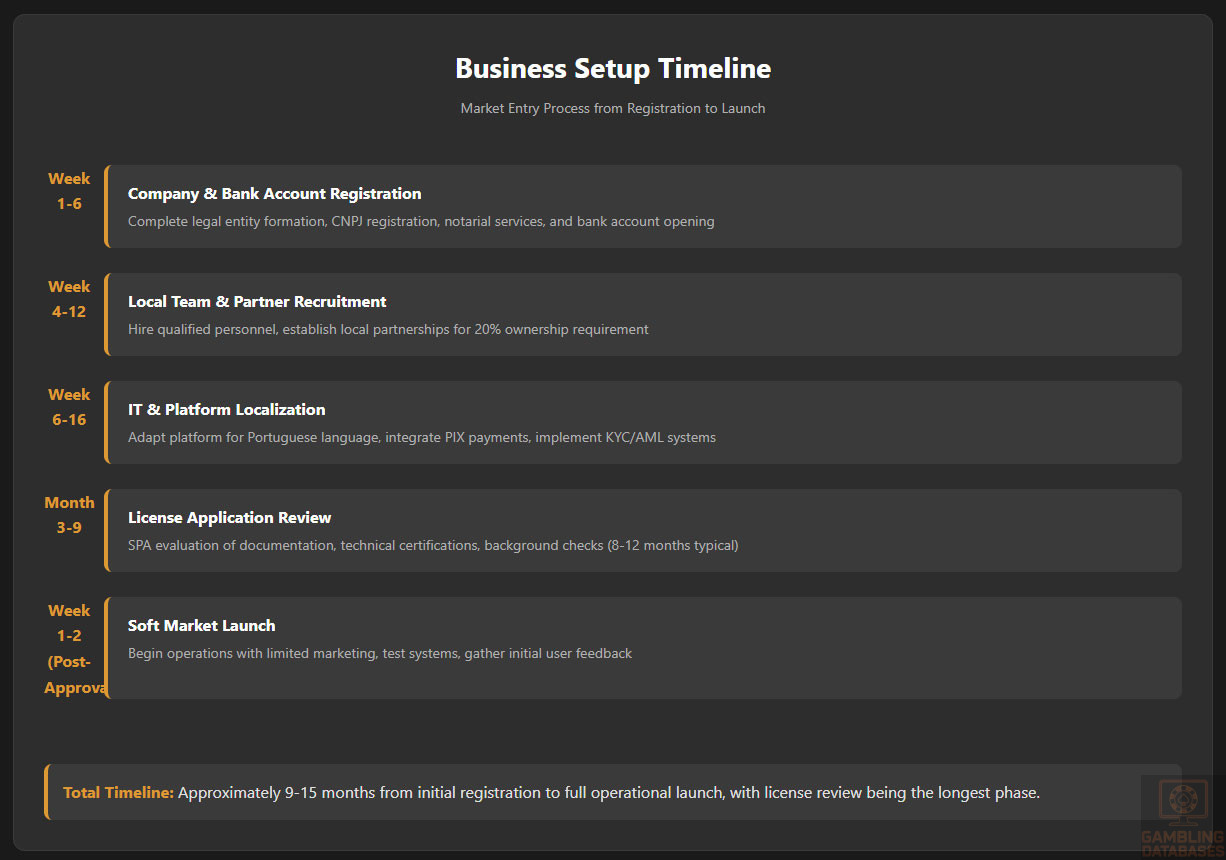

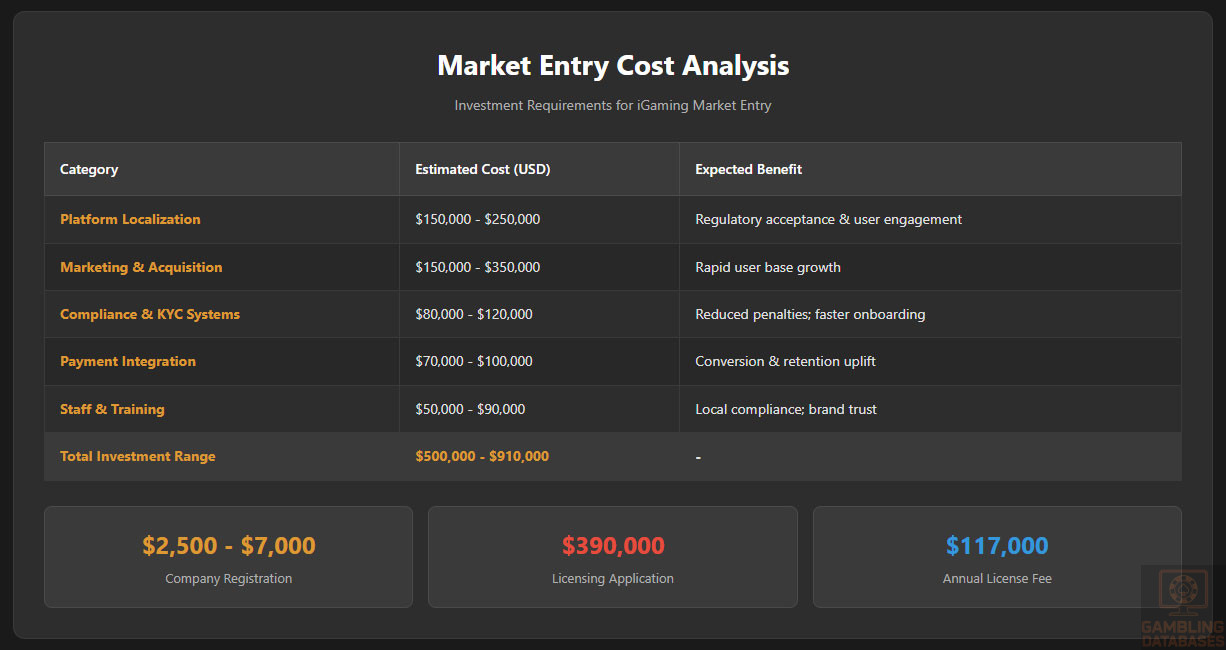

Timelines should reflect regulatory review, technical localization, and strategic hiring, maximizing early engagement and minimizing compliance risk.

- Company and bank account registration (4-6 weeks)

- Recruitment of local team and partners (3-8 weeks)

- IT and platform localization (5-10 weeks)

- License application review (3-6 months)

- Soft market launch (1-2 weeks following approval)

| Category | Estimated Cost (USD) | Expected Benefit |

|---|---|---|

| Platform Localization | 150,000 – 250,000 | Regulatory acceptance & user engagement |

| Compliance & KYC Systems | 80,000 – 120,000 | Reduced penalties; faster onboarding |

| Marketing & Acquisition | 150,000 – 350,000 | Rapid user base growth |

| Payment Integration | 70,000 – 100,000 | Conversion & retention uplift |

| Staff & Training | 50,000 – 90,000 | Local compliance; brand trust |

Success Factors and Challenges

Achieving scale in Brazil’s iGaming sector requires strong compliance, diversified payment acceptance, price-sensitive user experience, and strategic alliances with local media and affiliates. Data protection, responsible gambling, and social impact measures are central to long-term growth.

- Localization for Portuguese language and payment flows

- Regulatory adaptation and agile compliance response

- Robust KYC and AML frameworks

- Cross-device and mobile optimization

- Continuous consumer analytics and promotion targeting

- Proactive engagement in social responsibility initiatives

Significant challenges include regulatory bottlenecks, cultural adaptation, operational cost management, and the informal competition of unlicensed online operators.

- Complex, changing regulatory requirements

- High initial investment and labor costs

- Intense competition, including offshore sites

- Digital fraud and cybersecurity threats

- Slow dispute resolution and bureaucracy

- Persistent urban-rural technological divide

Exit Strategy Planning

Exit options for gaming businesses exist via sale, merger, or asset transfer, subject to regulatory re-approval. Valuation multiples trend at 1.7–2.4x annual gross profit, influenced by market presence, compliance record, and user base loyalty. License transferability is not automatic and demands close engagement with regulatory authorities.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Brazil?

Online gambling in Brazil is partly legalized, with fixed-odds sports betting and digital lotteries covered under regulatory statutes. Online casino games and poker remain in a pending or gray area, awaiting final legislative action. Unlicensed offshore operators are considered illegal, and the government blocks or penalizes unauthorized sites. State lotteries and horse racing betting are also legally permitted online in regulated forms.

2. What types of gambling licenses are available and what do they cover?

Brazil presently offers licenses for fixed-odds sports betting and digital lottery operation. Proposals for a separate online casino license are under legislative review, with land-based licenses for physical venues and bingo halls available at the state level. Most current licenses are issued by the Secretariat of Prizes and Betting (SPA) under the Ministry of Finance, covering domestic websites, mobile apps, and sometimes retail betting shops.

3. How much does an iGaming license cost and how long does it take to obtain?

The initial license application fee for fixed-odds online betting is USD 390,000, with an annual renewal of USD 117,000. Additional outlays include corporate setup, IT compliance, and local staffing costs. The approval timeline averages 3–6 months, depending on technical documentation, background checks, and SPA caseload. Applications are more likely to proceed smoothly with full documentation, local representation, and a clear compliance history.

4. Can foreign companies obtain a gambling license?

Foreign companies can hold a Brazilian gambling license with the condition that operations are structured through a locally incorporated entity or subsidiary. The company must have a legal presence in Brazil, register for tax and social security, and provide detailed compliance documentation. At least one legal representative must reside locally, and technical integration with SPA authorities is mandatory.

5. What are the tax obligations for iGaming operators?

Operators pay a Gross Gaming Revenue (GGR) tax between 18% and 20% for sports betting and lottery operations, plus a standard 34% corporate income tax. A yearly license fee and additional social contribution levies may apply. A VAT or digital services tax of 16–19% is also levied on certain online incomes. Double tax treaty benefits may exist for operators from designated countries.

| Tax Type | Rate |

|---|---|

| GGR Tax (Sports Betting) | 18–20% |

| Corporate Income Tax | 34% |

| Digital Services VAT | 16–19% |

6. Are gambling winnings taxed for players?

Yes, gambling winnings above the annual exemption threshold are subject to a 30% withholding tax, paid at source by the licensed operator. Operators must issue appropriate reporting to players and the tax authorities. Winnings below the threshold are exempt, but players are required to maintain income records.

7. What are the typical operational costs for running an online casino/sportsbook?

Major costs include licensing fees (USD 390,000 upfront), technology investment (USD 150,000–250,000), compliance and KYC infrastructure (USD 80,000–120,000), local staff salaries and benefits, marketing/acquisition spend, and annual legal/accounting services. Regulatory reporting, software upgrades, and customer support add to ongoing expenditure.

- License application and renewal

- Technical platform and compliance systems

- Staff and customer support

- Marketing, acquisition, retention

- Payment gateways and banking

- Legal and consulting services

8. What is the expected ROI timeline for entering this market?

Most iGaming ventures in Brazil achieve operational breakeven between 18 and 30 months after launch, depending on player acquisition, marketing spend, and compliance costs. ROI is strongest for well-capitalized entrants with strong payment integration and localized user experiences. Delays or penalties associated with compliance can negatively affect ROI expectations.

9. What are the local presence requirements for operators?

Operators are required to establish a local subsidiary, provide a permanent local office address, hire Brazilian staff for compliance and customer support, and maintain in-country technical infrastructure for payment and data processing. Local domain (.com.br) registration and bilingual (Portuguese/English) documentation are compulsory. Some requirements may intensify as regulations evolve.

10. What payment methods are available and recommended?

Top payment channels include PIX instant payments, credit and debit cards, Boleto Bancário, multiple digital wallets (e.g. Mercado Pago, PayPal, PicPay), and cryptocurrency for advanced users. Local integration with PIX and digital wallets, as well as supporting card and boleto options, is recommended to address all user demographics and maximize transaction rates.

- PIX instant transfer/QR code

- Credit cards (Visa, Mastercard, Elo)

- Debit cards

- Boleto Bancário

- Mercado Pago

- PicPay

- PayPal

11. What are the advertising and marketing restrictions?

Advertising is tightly regulated; gambling ads are banned on television from 6 a.m. to 10 p.m., while celebrity endorsements and sports sponsorships are generally forbidden. Digital marketing must include warnings and age verification. Promotion via sports or cultural events demands explicit government approval. Non-compliance is subject to fines, campaign suspension, and, in severe cases, license suspension.

12. What responsible gambling measures are mandatory?

Mandatory requirements include robust KYC and age verification, self-exclusion features, deposit/wager/time limits, visible responsible gambling messaging, direct links to counseling services, and regular training for operator staff. Operators must report on responsible gambling KPIs to SPA on a monthly basis and make tools available on all user-facing platforms.

- KYC and identity verification

- Self-exclusion system

- Deposit, loss, and time limits

- Responsible gambling disclosures

- Free access to support helplines

- Staff and affiliate training programs

13. How large is the iGaming market and what is the growth potential?

Brazil’s iGaming market generated USD 2.1 billion in revenue in 2024, with a projected compound annual growth rate of 18–22% through 2028. User base expansion, product diversification, and regulatory approval of additional iGaming formats are expected to double total market value by 2028, with above-average ARPU and strong mobile engagement.

14. Who are the main competitors and what is their market share?

The market includes established domestic lottery and sportsbook operators, early-licensed digital platforms, and lingering offshore sites. Major players with strong local presence hold larger market shares, while international entrants focus on rapid localization and compliance improvements. Full market share distribution remains dynamic and subject to regulatory outcomes, especially as online casino licensing accelerates.

- Caixa Econômica Federal (state lottery leader)

- Betano (early sportsbook market share leader)

- Bet365 (major global betting brand, strong local adaptation)

- Sportingbet

- Pixbet

- Blaze

15. What are the player preferences and typical spending patterns?

Brazilian players favor sports betting, lottery, and casino games, with peak activity in the evenings and weekends. Spending per session averages USD 11–18, with higher expenditure among frequent players and users of loyalty programs. Fast withdrawals, mobile-first interfaces, and real-time betting are valued features; live sports integration encourages sustained session lengths and community play.

16. What are the key success factors and main challenges for new entrants?

Key success factors include localization of content and support, rapid compliance adaptation, diversified payment support, effective affiliate/marketing partnerships, and active responsible gaming engagement. Cultural adaptation and consistent regulatory monitoring help sustain long-term growth.

- Portuguese content and local UX

- Omni-channel marketing and CRM

- Comprehensive payment coverage

- Ongoing compliance investment

- Community and CSR involvement

Entrants face challenges in regulatory complexity, high compliance costs, fraud/digital risk management, and competition from unlicensed operators. Long-term positioning depends on technological agility and continuous consumer research.

- Licensing procedure delays

- Cost of compliance

- Digital and payment fraud risk

- Talent and staff recruitment

- Unlicensed competition pressure

Sources and References

- Brazil Gambling Regulatory Authority – Official Website – https://gov.br/spa

- National Statistical Office – Population and Economic Data 2024 – https://ibge.gov.br

- Central Bank of Brazil – Financial Statistics and Reports – https://bcb.gov.br

- Ministry of Finance – Tax Regulations and Guidelines – https://gov.br/fazenda

- World Bank – Doing Business Report 2024 – https://worldbank.org

- International Telecommunication Union – ICT Statistics – https://itu.int

- ANATEL – Brazilian National Telecommunications Agency – https://anatel.gov.br

- SPA – Secretariat of Prizes and Betting – https://gov.br/spa

- Data Reportal – Digital 2025: Brazil – https://datareportal.com/reports/digital-2025-brazil

- Statista – Online Gambling Market Data – https://statista.com

- PwC – Brazil iGaming Market Growth Update 2024 – www.pwc.com

- KPMG – Payments and Digital Banking in Brazil – www.kpmg.com

- E-commerce Brasil – E-commerce Market Reports 2025 – www.ecommercebrasil.com.br

- Gaming Association of Brazil – Annual Report 2024 – www.abjogos.org.br

- PIX Official – Instant Payments Market Statistics – https://bcb.gov.br/estabilidadefinanceira/pix

- Teleco – Mobile and Broadband Analysis – www.teleco.com.br

- O Globo – Industry News and Market Analysis – www.globo.com

- Valor Econômico – Business Environment Reports – www.valor.globo.com

- Sebrae – SME Digital Transformation Case Studies – https://sebrae.com.br

- McKinsey – Digital Consumer in LatAm 2024 – www.mckinsey.com

- Oxford Economics – Gambling Market Forecasts – www.oxfordeconomics.com

- Mercado Pago – Payment Trends Whitepaper – https://mercadopago.com.br

- PayPal Brazil – Payment Processing Insights – www.paypal.com.br

- ANBIMA – Investment Market Data – www.anbima.com.br

- CAPEMISA – Responsible Gaming Study – www.capemisa.com.br

- Gambling Compliance – Regulatory & Legislative Updates – www.gamblingcompliance.com

- Supremo Tribunal Federal – Supreme Court Decisions on Gambling – www.stf.jus.br

- Brazilian Banking Federation (FEBRABAN) – Banking Sector Overview – www.febraban.org.br

- IDC – Brazil Cloud and Mobile Trends – www.idc.com

- TikTok for Business – Digital Advertising Data – www.tiktok.com/business

- Facebook for Business – Social Media Marketing Reports – www.facebook.com/business

- Euromonitor International – Country Market Profile: Brazil – www.euromonitor.com

- Roland Berger – Gambling Industry Insights – www.rolandberger.com

- “Gambling in Brazil: The State of Play” – Thomson Reuters Regulatory Briefing – 2024

- CBLOL – Esports and Gaming User Insights – www.cblol.com.br

- Procon-SP – Consumer Protection and iGaming Guidance – www.procon.sp.gov.br

- Senado Federal – Legislative Activity Portal – www.senado.leg.br

- Portal da Transparência – Government Data Repository – www.portaltransparencia.gov.br

- GSMA – 5G Mobile Economy Report – www.gsma.com

- IBGC – Corporate Governance Standards – www.ibgc.org.br

- Serasa Experian – Digital Fraud Analysis – www.serasaexperian.com.br

- OECD – Economic Country Outlook: Brazil – www.oecd.org

🎯 Gambling Databases Country Rating: Brazil

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.3/10 | 🟡 Moderate |

| Player Access Score | 8.5/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 7.4/10 | 🟡 Good potential but high barriers to entry |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- MASSIVE LICENSE FEE: R$30 million (USD 6 million) upfront for 5-year license – one of the world’s highest entry costs

- TAX INCREASE INCOMING: GGR tax rising from 12% to 18% in October 2025, with total effective tax burden reaching 50-60% when combined with corporate taxes

- MANDATORY LOCAL OWNERSHIP: Minimum 20% Brazilian-owned shares required – foreign operators CANNOT enter alone

- EXTENSIVE LOCAL PRESENCE REQUIRED: Must maintain Brazilian headquarters, administration, and qualified local staff – no remote operation possible

- COMPLEX COMPLIANCE: 8-12 month licensing timeline with rigorous background checks, technical certifications, and AML/KYC requirements

- ENFORCEMENT ACTIVE: SPA blocks unlicensed gambling websites, imposes fines up to R$2 billion, and pursues criminal prosecution against illegal operators

- COST BREAKDOWN: Total first-year setup costs range USD 500,000-800,000 EXCLUDING the USD 6 million license fee – realistic minimum investment is USD 7-8 million

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Sports betting and online casino BOTH fully legalized as of January 2025 (+3.0). Recent regulatory framework is only months old creating implementation uncertainty (-0.5). Federal regulation through SPA provides clarity. Final: 2.5/3.0 |

| Licensing Process | 25% | 0.75/2.5 | Licensing available but extremely limited (+2.0). Application timeline 8-12 months, complex process (-0.25). License fee R$30 million (USD 6 million) – EXTREME cost, over USD 500k threshold (-0.25). High legal/consulting costs USD 15k-40k initial plus ongoing (-0.5). Rigorous probity checks on all directors and beneficial owners taking 6+ months (-0.25). Final: 0.75/2.5 |

| Taxation & Costs | 20% | 0.5/2.0 | GGR tax currently 12% rising to 18% October 2025 = starting at +1.5 but adjusting to +1.0 for incoming rate. Corporate income tax 15-25% standard PLUS social contributions (CSLL, PIS, COFINS) approximately 9.25% additional PLUS municipal ISS 2-5% = total effective tax rate 50-60% (-1.0). Multiple tax layers across GGR, corporate, social, and municipal levels (-0.5). High operational costs with mandatory local presence, headquarters, staff exceeding $500k/month setup (-0.5). First-year total costs USD 500k-800k excluding license fee. Final: 0.5/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | Heavy requirements – extensive local infrastructure mandatory (0 base points for extensive requirements). Must maintain registered headquarters and administrative offices in Brazil with qualified local personnel including financial and customer support managers. Minimum 20% Brazilian shareholder ownership absolutely required – foreign-only ownership prohibited (-0.25). Large capital requirements with R$5 million (USD 1M) minimum financial reserve held in trust (-0.25). Complex technical certification from accredited labs required for platform, RNG, and cybersecurity. Mandatory .bet.br domain extension with other TLDs blocked. Final: 0.5/1.5 |

| Market Environment | 10% | 0.5/1.0 | Brazil ranked 124th on World Bank Doing Business 2024 = difficult environment (+0.25). Active enforcement against unlicensed operators with website blocking and IP blacklisting (-0.25). Regulatory framework only launched January 2025 creating ongoing instability and frequent rule changes (-0.25). Advertising restrictions are strict especially regarding minors with time-of-day limits and content prohibitions (-0.5). Payment monitoring is extensive with banks required to report suspicious transactions. Final: 0.5/1.0 |

TOTAL OPERATOR EASE SCORE: 6.3/10

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal and regulated for both sports betting AND online casino gaming since January 2025 (+4.0). Players can legally access all iGaming products from licensed operators. No penalties for players using licensed platforms. Federal regulation provides nationwide access. Final: 4.0/4.0 |

| Practical Accessibility | 30% | 2.5/3.0 | Multiple payment methods available including PIX (53% of transactions), credit cards (32%), debit cards (29%), Boleto Bancário (16%), digital wallets (12%) with no major restrictions (+3.0). However, unlicensed operators face ISP blocking and domains must use .bet.br extension with other TLDs blocked for gambling (-0.5). No cryptocurrency ban but only 3% adoption. Final: 2.5/3.0 |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players using licensed operators (+2.0). Players only face 15% withholding tax on winnings above defined thresholds, withheld at source by operators. No criminal liability or fines for players engaging in legal gambling. Final: 2.0/2.0 |

| Market Availability | 10% | 1.0/1.0 | 68+ licensed operators as of early 2025 with strong mix of international and local companies (+1.0). Competitive market with multiple options for players across sports betting and online casino products. Final: 1.0/1.0 |

TOTAL PLAYER ACCESS SCORE: 8.5/10

🔍 Key Highlights

Strengths

- Fully Legal Market: Both sports betting AND online casino gaming are legalized and regulated – rare in Latin America and globally

- Massive Market Size: 215 million population with 160 million adults (18+), 81% internet penetration, 95% mobile penetration

- Strong Growth Trajectory: Market projected to grow 15-18% CAGR 2025-2030, reaching USD 4.1 billion by 2028 from USD 2.1 billion in 2024

- Sports Betting Culture: Passionate football culture and sports enthusiasm provides strong foundation for sports betting verticals

- Modern Payment Infrastructure: PIX instant payment system dominates (53% of transactions), providing fast settlement and high conversion

- 68+ Licensed Operators Already: Competitive but not oversaturated market with room for quality operators

- No Player Penalties: Players face no legal risks when using licensed platforms, only standard 15% tax withholding on large winnings

- Federal Regulation: Nationwide licensing through SPA provides clarity compared to fragmented state-by-state models

⛔️ CRITICAL RISKS AND CHALLENGES

- [Financial Barriers – EXTREME]: USD 6 million license fee is among the world’s highest, creating massive entry barrier. Total first-year investment realistically USD 7-8 million minimum. This eliminates all but well-capitalized operators.

- [Tax Burden – SEVERE]: Total effective tax rate 50-60% when combining 18% GGR tax (from October 2025), 15-25% corporate income tax, 9.25% social contributions, and 2-5% municipal tax. Multiple tax layers severely compress margins. Makes profitability extremely challenging.

- [Mandatory Local Partnership]: 20% Brazilian ownership requirement means foreign operators CANNOT enter alone. Must find trustworthy local partners willing to take significant equity stake. Partnership risk and profit dilution.

- [Extensive Local Presence Required]: Cannot operate remotely. Must establish Brazilian headquarters, hire local management team (financial, customer support, compliance), maintain administrative offices. Ongoing operational costs exceed $500k/month.

- [New Regulatory Framework]: Regulation only launched January 2025 – less than 1 year old. Expect ongoing rule changes, interpretation disputes, and regulatory instability as framework matures. Tax already increased from 12% to 18% in first year.

- [Long Licensing Timeline]: 8-12 months from application to approval with rigorous background checks on all directors and beneficial owners. Significant legal and consulting costs USD 15k-40k initial plus ongoing compliance.

- [Enforcement Against Offshore]: SPA actively blocks unlicensed gambling websites, blacklists IP addresses, imposes fines up to R$2 billion. Banks must report suspicious transactions. Operating without license is not viable long-term.

- [Advertising Restrictions]: Strict limitations especially regarding minors. Time-of-day restrictions, content prohibitions, mandatory risk disclosures. Youth event sponsorships banned. Limits marketing effectiveness and increases customer acquisition costs.

- [Minimum Capital Lock-Up]: R$5 million (USD 1 million) must be held in financial reserve, reducing working capital availability.

- [Technical Certification Requirements]: Platform, RNG, and cybersecurity must be audited by accredited third-party labs. Adds cost and timeline delays.

Player-Specific Issues

- Players using UNLICENSED offshore operators face ISP blocking – sites are blacklisted and inaccessible

- 15% withholding tax on large winnings reduces net returns compared to some markets

- Licensed operators only – reduces variety compared to markets with open offshore access

- Mandatory KYC/AML verification may deter privacy-conscious players

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: USD 7-8 million minimum (USD 6 million license + USD 500k-800k setup + USD 1 million capital reserve)

Monthly Operating Costs: USD 150,000-300,000 (local staff, headquarters, compliance, customer support, payment processing, marketing)

Effective Tax Rate on Revenue: 50-60% total (18% GGR + 15-25% corporate income + 9.25% social contributions + 2-5% municipal service tax)

Customer Acquisition Cost: USD 150-350 per player (article indicates “marketing & acquisition” costs this range, reflecting competitive market and advertising restrictions)

Time to Breakeven: 24-36 months realistically, assuming successful market penetration and efficient operations

Time to Positive ROI: 36-60 months for most operators given the massive USD 7-8 million initial investment and 50-60% effective tax rate

Profitability Assessment: Economics are CHALLENGING but NOT prohibitive for well-capitalized operators. The combination of a USD 6 million license fee, 50-60% effective tax burden, mandatory local infrastructure, and 20% Brazilian ownership requirement means this market is ONLY viable for operators with:

- Minimum USD 10-15 million available capital

- 5+ year investment horizon

- Willingness to accept 36-60 month ROI timeline

- Ability to achieve significant scale (target 50,000+ active users within 24 months)

- Trusted local partner for 20% ownership stake

The market’s massive size (215 million population, USD 4.1 billion projected by 2028, 15-18% CAGR) and full legalization of both sports betting AND casino gaming provide strong revenue potential. However, the extreme entry costs and tax burden mean profitability requires scale and patience. Average Revenue Per User of USD 120 annually means you need 60,000+ active users just to generate USD 7.2 million in annual GGR – and after 50-60% taxes you keep only USD 2.9-3.6 million before operating expenses.

BOTTOM LINE: Profitable for major international operators with deep pockets and long-term commitment. Prohibitive for startups, small operators, or anyone seeking quick returns.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators (Unlicensed) | CRITICAL | ISP blocking and IP blacklisting by SPA. Website domains blocked (must use .bet.br, other TLDs blocked for gambling). Fines up to R$2 billion. Criminal prosecution possible. Payment processing blocked by banks required to report suspicious transactions. Potential extradition risk for fraud/money laundering charges. |

| Licensed Operators (Sports Betting & Casino) | MEDIUM | Heavy regulatory compliance burden with ongoing monitoring. License suspension or revocation for violations. 50-60% effective tax rate compresses margins severely. Advertising restrictions limit marketing options. Mandatory social responsibility fund contributions. Annual financial audits plus potential unscheduled inspections. |

| Affiliates/Advertisers | MEDIUM-HIGH | Promoting unlicensed operators risks enforcement action. Advertising restrictions especially regarding minors create compliance complexity. Time-of-day restrictions and content prohibitions limit promotional channels. Website blocking possible if promoting unlicensed sites. Payment processor termination risk. |

| Payment Processors | MEDIUM | Banks and payment providers MUST report suspicious transactions linked to illegal gambling. Regulatory action and fines for processing unlicensed gambling transactions. Must monitor and block payments to blacklisted operators. Compliance with SPA financial monitoring mandates. |

| Company Directors/Executives | MEDIUM | Criminal background checks required for licensing. Personal liability for fraud or money laundering. Potential criminal prosecution against fraudulent actors. Must be qualified and approved by SPA. Travel restrictions possible if involved in unlicensed operations. |

🚨 Extradition and International Enforcement

Extradition Treaties: Brazil maintains extradition treaties with USA, Argentina, Portugal, Spain, France, Italy, and other major jurisdictions. International cooperation on financial crimes and money laundering is active.

Enforcement History: Brazil’s regulatory framework only launched January 2025, so specific gambling-related extradition cases are not yet established. However, the country actively pursues cross-border enforcement for financial crimes, fraud, and organized crime through international treaties.

Safe Jurisdictions: Countries without Brazilian extradition agreements include Russia, China, and some CIS countries. However, operating from these jurisdictions while targeting Brazilian players would still face ISP blocking and payment processing barriers.

Travel Risk: Directors and executives of unlicensed operators targeting Brazil should avoid travel through countries with extradition treaties if engaged in activities Brazil considers fraudulent or money laundering. Risk is MODERATE currently but may increase as enforcement precedents develop.

📋 Final Verdict

Brazil receives an Operator Ease Score of 6.3/10 and a Player Access Score of 8.5/10, resulting in an overall market attractiveness rating of 7.4/10.

HONEST ASSESSMENT: Brazil is a LEGITIMATE but EXPENSIVE market requiring massive capital commitment. The combination of full legalization (both sports betting AND casino), huge population (215 million), strong growth (15-18% CAGR), and modern payment infrastructure (PIX) creates genuine opportunity. However, the USD 6 million license fee, 50-60% effective tax rate, mandatory 20% Brazilian ownership, and extensive local presence requirements make this viable ONLY for well-capitalized operators with USD 10-15 million+ budgets and 5-year horizons. If you have the capital and patience, Brazil offers a regulated path to a massive market. If you’re undercapitalized or seeking quick ROI, this market will destroy you financially.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Major international gambling operator with USD 10-15 million+ available capital

- Willing to commit to 5+ year investment horizon with 36-60 month ROI timeline

- Have experience operating in heavily regulated markets with complex compliance requirements

- Can identify and partner with trustworthy Brazilian entities for mandatory 20% ownership stake

- Willing to establish full Brazilian headquarters with local management team and infrastructure

- Targeting significant scale (50,000+ active users within 24 months) to justify costs

- Offer BOTH sports betting AND casino products to maximize revenue potential

- Have technical platforms already certified or certifiable by accredited third-party labs

- Comfortable with 50-60% effective tax burden and can still achieve target margins at scale

❌ Definitely Avoid If You Are:

- Startup or small operator with less than USD 10 million available capital

- Seeking quick ROI within 18-24 months (unrealistic given costs and market dynamics)

- Cannot identify trustworthy Brazilian partner for mandatory 20% ownership requirement

- Unwilling to establish expensive local presence with headquarters and full-time staff in Brazil

- Offshore operator planning to operate without Brazilian license (ISP blocking and fines up to R$2 billion make this impossible)

- Cannot absorb 50-60% effective tax rate while remaining profitable

- Lack experience with complex regulatory compliance, extensive KYC/AML, and ongoing government audits

- Planning niche or limited product offering (need diversified sports betting + casino to justify USD 6M license fee)

- Expect to operate remotely without establishing Brazilian entity and infrastructure

- Sensitive to regulatory instability (framework is less than 1 year old, expect ongoing changes)

⚠️ BOTTOM LINE: Brazil is a genuine opportunity for MAJOR, WELL-CAPITALIZED operators willing to play by the rules and commit long-term. For everyone else – startups, small operators, offshore businesses, or capital-constrained entrants – the USD 6 million license fee and 50-60% tax burden make this market financially prohibitive. This is not a market for testing the waters; it’s a market for operators ready to dive in with both feet and massive capital reserves.