Bulgaria represents an emerging and rapidly growing iGaming market in Southeast Europe with exceptional potential for operators seeking EU market access. The country offers a well-regulated gambling framework, competitive taxation at 20% GGR, and a digitally connected population of 6.7 million with 87% internet penetration.

With online gambling revenue reaching EUR 561 million in 2024 and projected annual growth exceeding 10%, Bulgaria combines attractive market fundamentals with favorable entry conditions including no local presence requirements for EU operators and straightforward five-year licensing.

Executive Summary: Key Market Indicators

| Indicator | Value | Notes |

|---|---|---|

| Online Gambling Legal Status | Fully Legal & Regulated | All forms permitted except traditional lotteries (state monopoly) |

| Regulatory Authority | National Revenue Agency (NRA) | Since August 2020, replacing State Commission on Gambling |

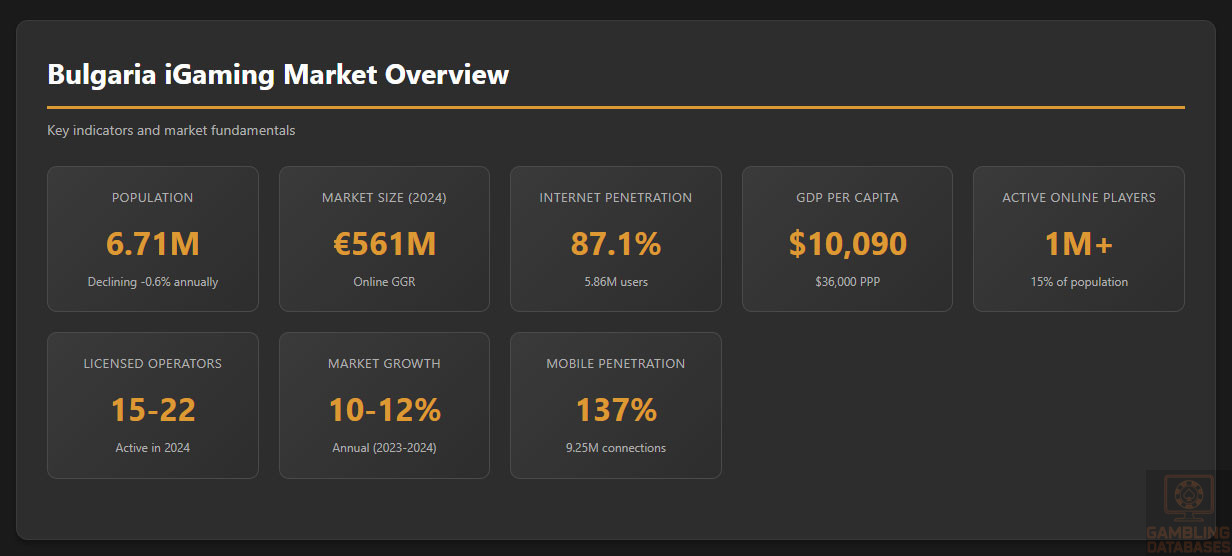

| Population (2025) | 6.71 million | Declining at -0.6% annually |

| Median Age | 44.8 years | Aging population, mature gambling demographic |

| Urban Population | 77.1% | 5.18 million urban residents |

| GDP (2024) | USD 107 billion | Nominal; USD 229 billion PPP |

| GDP Per Capita (2024) | USD 10,090 nominal | USD 36,000 PPP; 43% of EU average nominal |

| GDP Growth (Q1 2025) | 3.1% YoY | Above EU average, strong domestic demand |

| Average Monthly Salary | EUR 1,262 gross | December 2024 data |

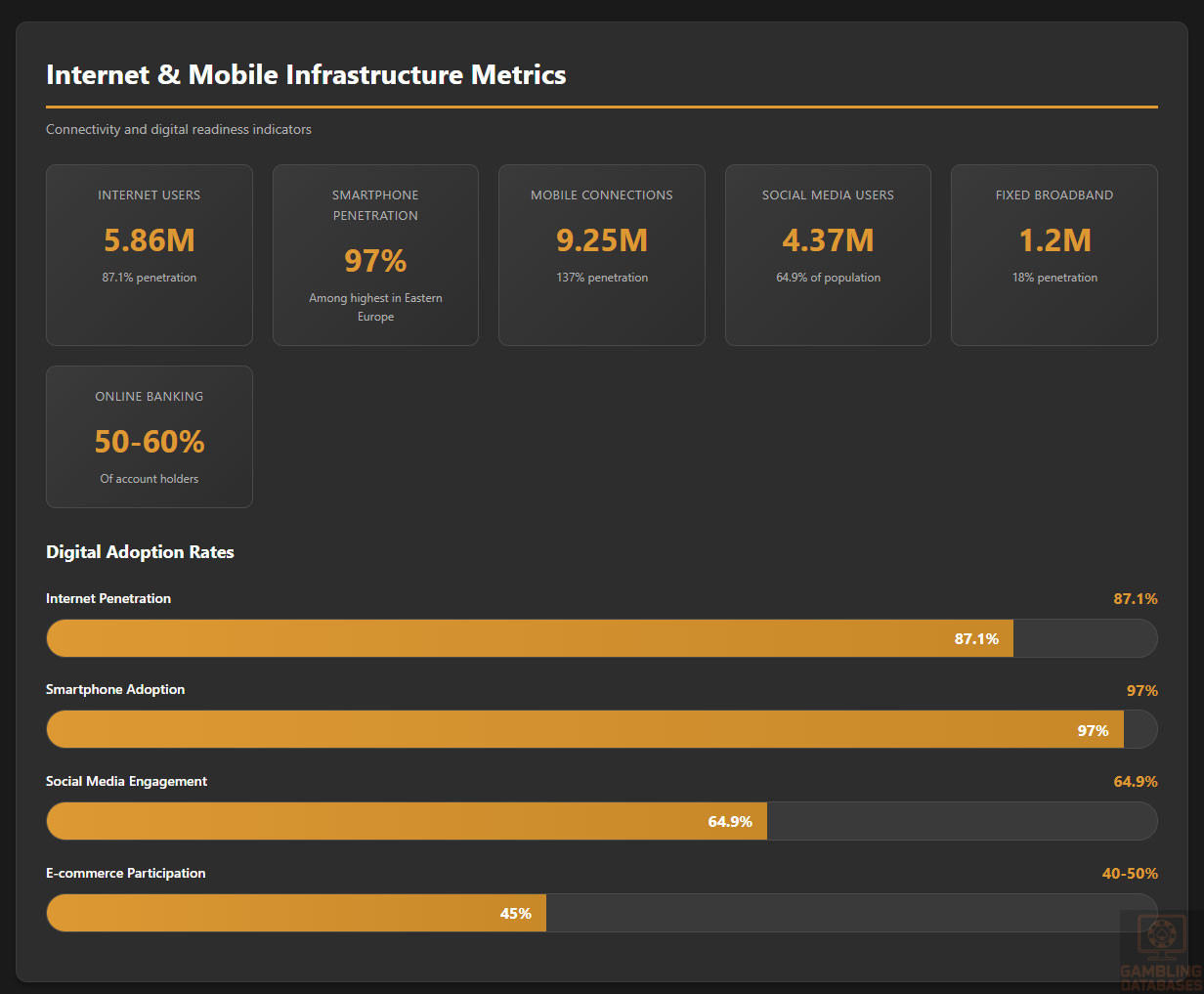

| Internet Penetration | 87.1% | 5.86 million internet users (January 2025) |

| Mobile Penetration | 137% | 9.25 million active connections |

| Smartphone Penetration | 97% | Among highest in Eastern Europe |

| Mobile Internet Speed | 172.49 Mbps median | Increased 82% year-over-year |

| Fixed Broadband Speed | 85.36 Mbps median | Ranked 68th globally |

| 5G Coverage | Expanding | Widespread 4G coverage nationwide |

| Online Gambling Market Size (2024) | EUR 561 million GGR | BGN 1.1 billion; bets minus winnings |

| Total Gambling Market (2025) | USD 820 million projected | Including land-based operations |

| Market Growth Rate (2023) | 12% YoY | Slowing from 50% growth in 2021-2022 |

| Market CAGR (2025-2029) | 2.1% overall; 4.8% online | Conservative estimates |

| Online Casino Growth | 30% YoY projected | Fastest growing segment |

| Sports Betting Growth | 12-20% YoY projected | Strong football betting culture |

| Active Online Players | 1+ million | 15% of total population |

| Online Gambling Penetration | 5.7% in 2024 | Expected to reach 6.5% by 2029 |

| Average Revenue Per User (ARPU) | EUR 390-411 annually | USD 390k projected for 2024 |

| Female Players | 40% of bettors | Higher than regional average |

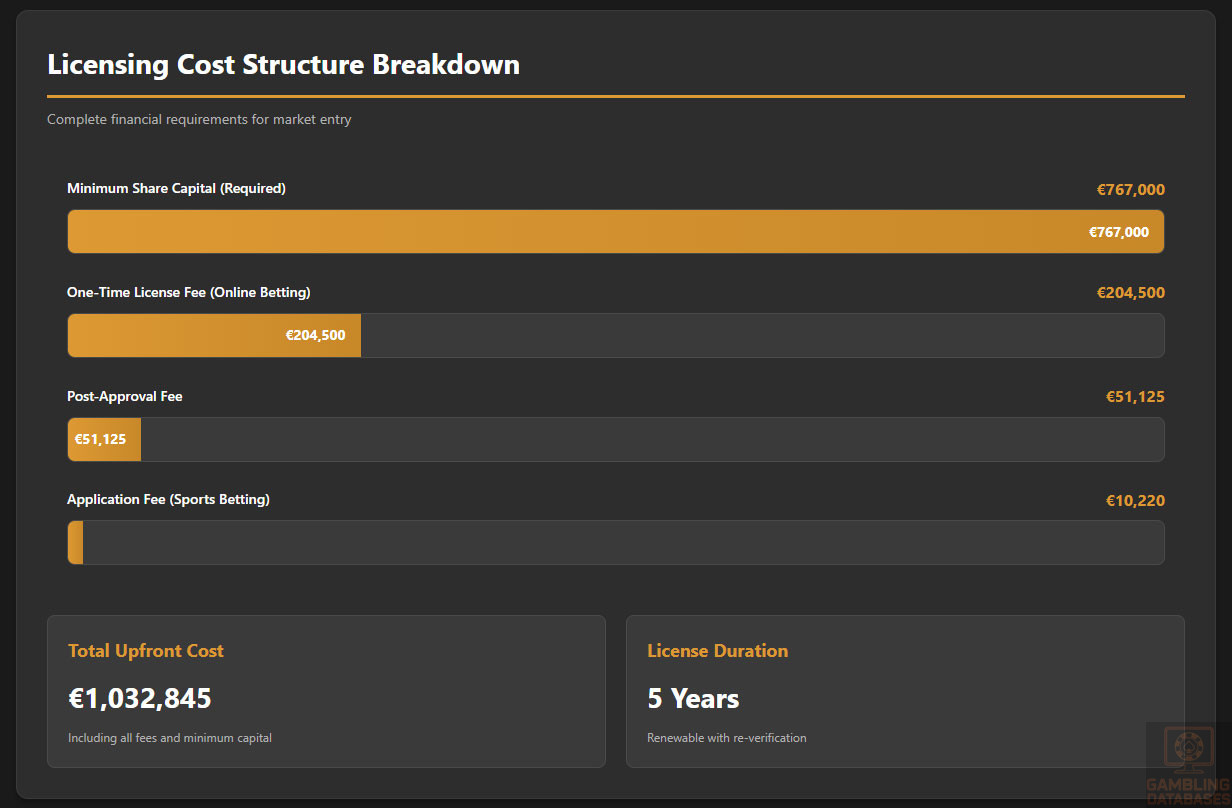

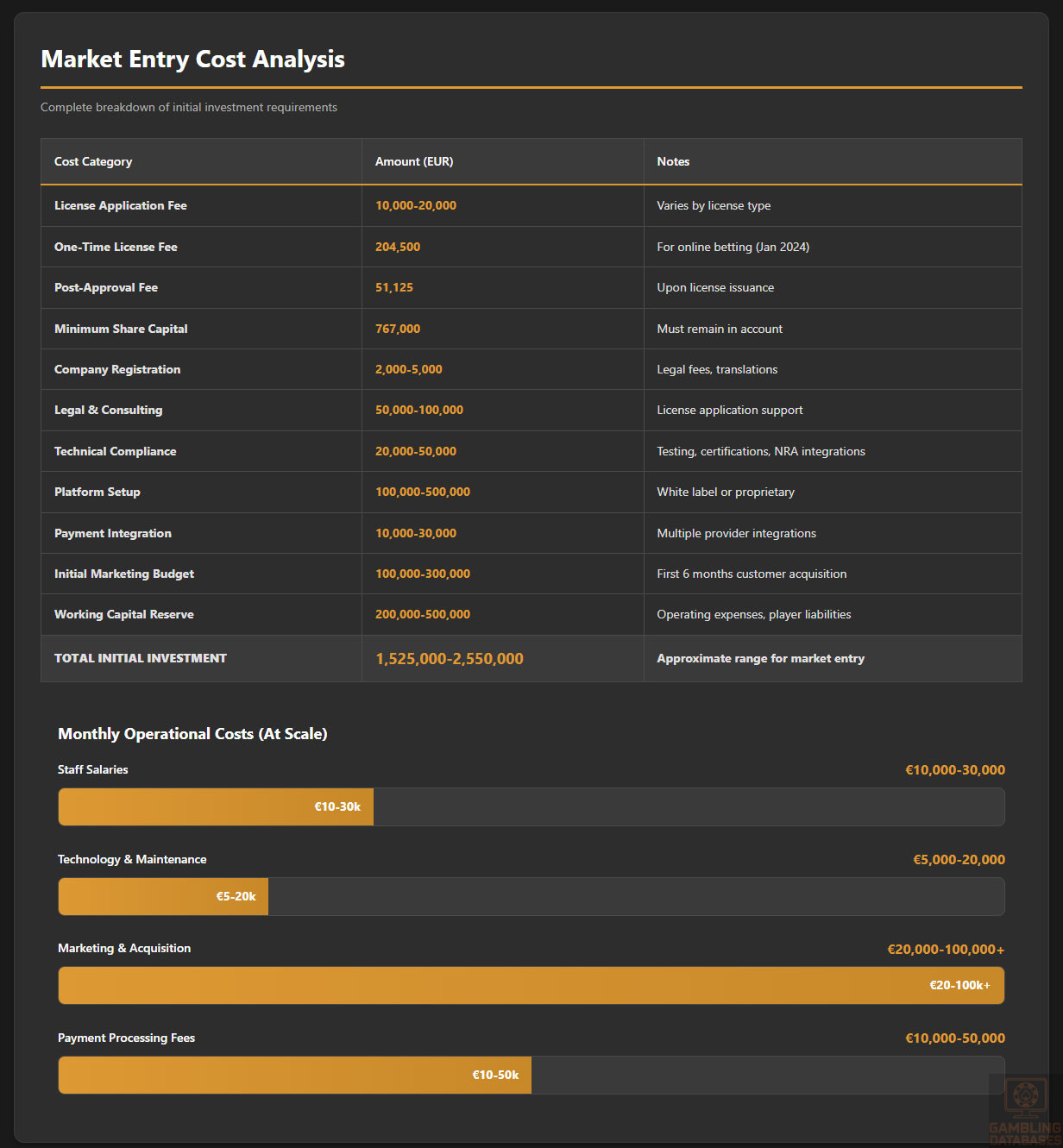

| License Application Fee | BGN 20,000 (EUR 10,220) | For online sports betting; varies by type |

| One-Time License Fee | BGN 400,000 (EUR 204,500) | As of January 2024 for online betting |

| Additional Post-Approval Fee | BGN 100,000 (EUR 51,125) | One-off payment upon approval |

| License Duration | 5 years | Renewable |

| Minimum Share Capital | BGN 1.5 million (EUR 767,000) | Paid-in capital requirement |

| GGR Tax Rate | 20% | Increased from 15% in 2024 |

| Corporate Income Tax | 10% | Flat rate, lowest in EU |

| Player Winnings Tax | 0% for licensed operators | 20% for unlicensed/foreign operators |

| Annual Tax Revenue from Gambling | BGN 200 million projected (2024) | EUR 102 million approximately |

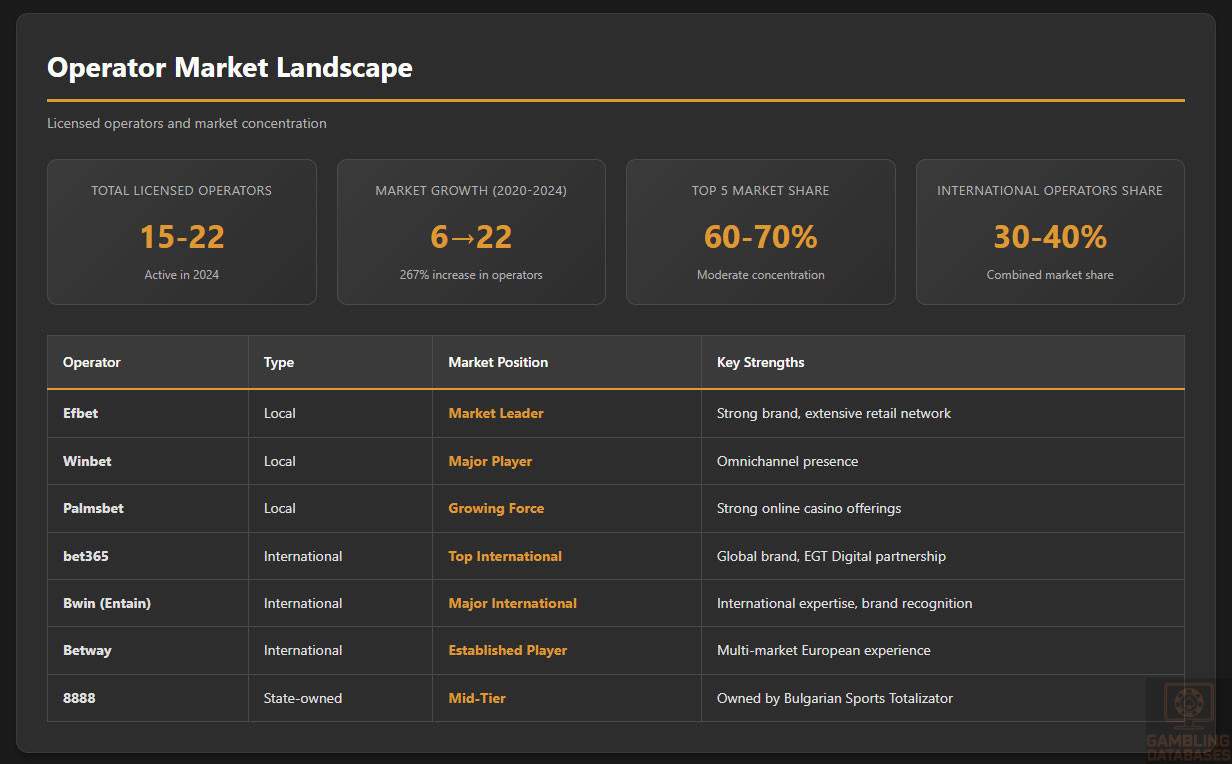

| Number of Licensed Operators | 15-22 active | Grew from 6 in 2020 to 22 in 2024 |

| Market Concentration | Moderate | Top 5 operators control ~60-70% share |

| Local Presence Requirement | Not mandatory for EU operators | Authorized representative required if non-Bulgarian |

| Server Location Requirement | EU/EEA/Switzerland | Central computer systems must be in approved territories |

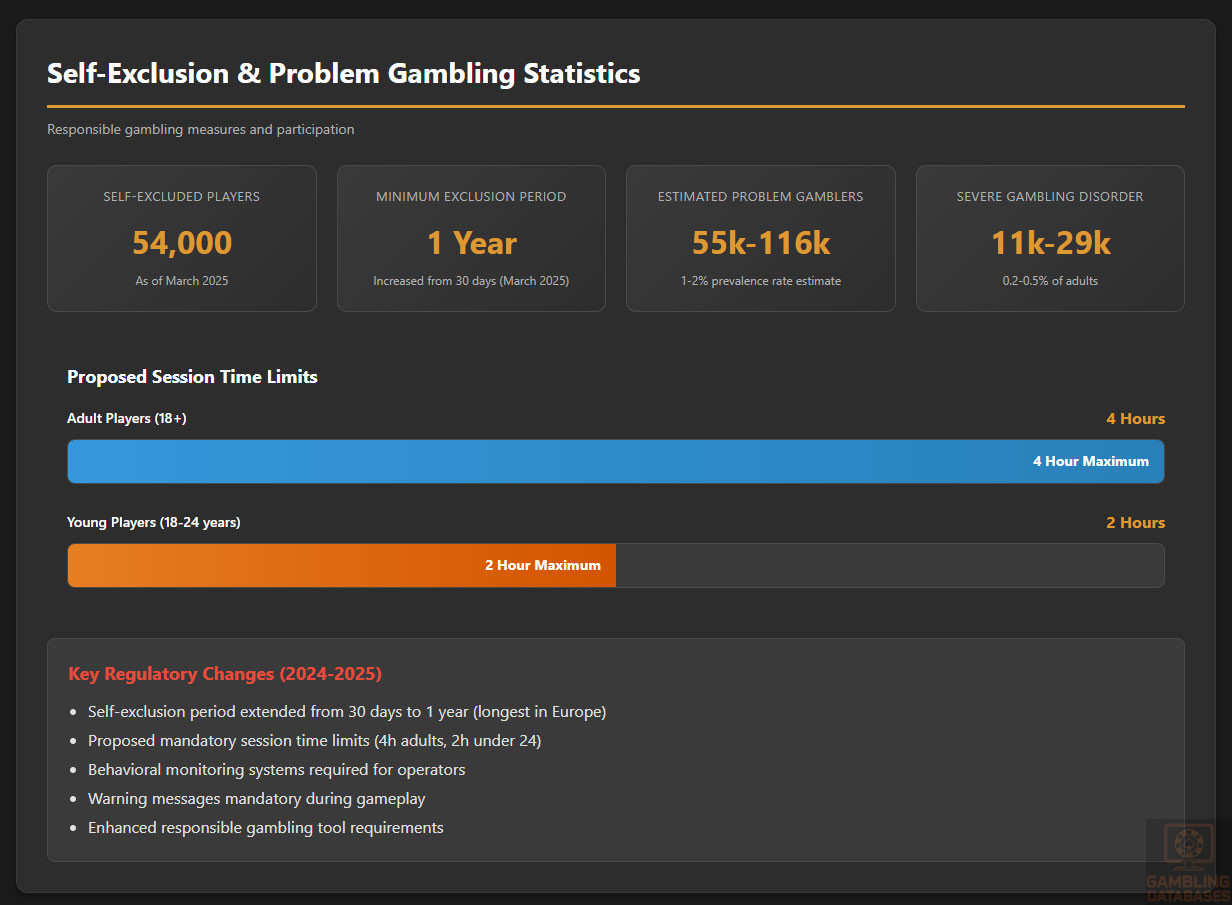

| Self-Exclusion Registrations | 54,000 people | Minimum 1-year exclusion period (as of March 2025) |

| Problem Gambling Rate | Data limited | Government increasing focus on responsible gambling |

| Advertising Restrictions | Severe limitations since May 2024 | Ban on TV, radio, print, most online media |

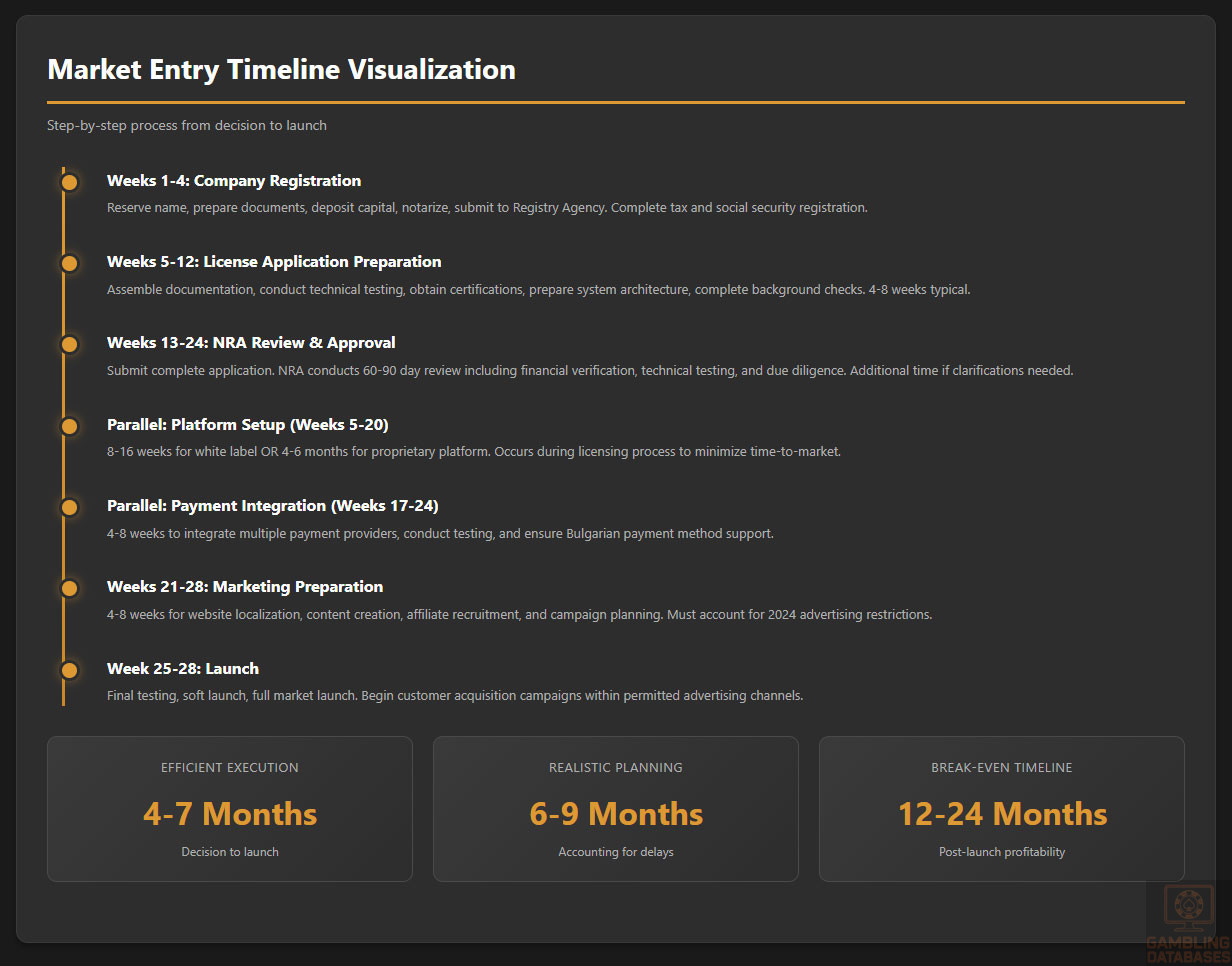

| Time to Market | 4-6 months | Including company setup and licensing |

| Application Review Period | 60-90 days | After submission of complete documentation |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Bulgaria operates a comprehensive and well-defined regulatory framework for gambling activities governed primarily by the Gambling Act of 2012. The regulatory environment underwent significant modernization in August 2020 when oversight responsibilities transferred from the State Commission on Gambling to the National Revenue Agency, enhancing integration between gambling regulation and fiscal policy. This transition marked a strategic shift toward more streamlined enforcement and improved revenue collection mechanisms.

The Bulgarian gambling market represents a mature yet still-growing sector within Southeast Europe. As an EU member state since 2007, Bulgaria maintains regulatory autonomy in gambling matters, as the sector remains largely exempt from EU-wide harmonization. This allows the country to craft policies tailored to its domestic market conditions while benefiting from EU single market principles for licensing and operations.

Land-Based Gambling Activities

Land-based gambling in Bulgaria encompasses a diverse range of activities including traditional casinos, sports betting shops, slot machine halls, bingo parlors, and lottery operations. Casino operations require specific licensing and must meet stringent facility standards including minimum gaming floor space, security systems, and surveillance infrastructure. The country hosts numerous casinos in major urban centers, particularly Sofia, Plovdiv, Varna, and Burgas, catering to both local players and tourists visiting Black Sea resorts.

Sports betting venues have proliferated throughout Bulgaria, with physical betting shops operating under dedicated licenses. Following regulatory changes in late 2023 that reduced tax rates for physical sports betting outlets, the market has seen renewed investment in retail betting infrastructure. This segment experienced significant restructuring after 2020 when the government revoked licenses of major operators, creating opportunities for new market entrants.

Slot machine halls operate under separate licensing requirements with specific regulations governing machine-to-floor-space ratios, payout percentages, and technical standards. All gaming equipment must be registered with the Bulgarian Institute of Metrology and undergo regular testing to ensure compliance with fairness and technical specifications. Distance requirements introduced in May 2024 mandate that billboards and gambling establishments maintain at least 300 meters separation from educational institutions and playgrounds, affecting location strategies for new venues.

Bingo and keno operations are permitted under the gambling framework, with venues subject to capacity restrictions and operational standards. These activities have maintained steady popularity, particularly among older demographic segments. The regulatory environment requires operators to implement comprehensive player identification systems, maintain transaction records, and submit regular operational reports to the NRA.

Online Gambling Framework

Online gambling in Bulgaria is fully legal and regulated, with the Gambling Act defining it as any game of chance where players bet directly using the internet or other electronic communication means. Licensed operators can offer a comprehensive range of online gambling products including sports betting, casino games, poker, and instant lotteries. The framework permits both pre-match and live betting on sporting events, online slot games, table games, live dealer games, and various forms of casino entertainment.

A critical distinction exists for lottery products: traditional lottery games are subject to state monopoly following amendments in February 2021, with only the state-owned Bulgarian Sports Totalizator holding the exclusive right to operate classic number-draw lotteries. However, instant lotteries, bingo, keno, and raffle games remain available to private operators, creating opportunities in these adjacent verticals. This monopoly reflects the government’s strategy to maintain control over the most stable gambling revenue stream while opening competitive segments to private investment.

The regulatory framework imposes several technical requirements specific to online operations. Central computer systems that control gaming operations must be located within the EU, EEA member states, or Switzerland. All data related to player registration, identification, bets placed, and winnings paid must be stored within Bulgaria and transmitted in real-time to NRA servers for monitoring purposes. This data localization requirement ensures regulatory oversight while creating technical infrastructure obligations for operators.

Online operators must implement sophisticated player protection systems including self-exclusion mechanisms, session time tracking, and responsible gambling tools. Recent regulatory developments include proposed session time limits of four hours for adults and two hours for players under 24 years old, representing Bulgaria’s adoption of hard-limit approaches similar to emerging European trends. These requirements demand significant investment in compliance technology and player monitoring systems.

Licensed Operators and Market Players

The Bulgarian online gambling market has experienced remarkable expansion in operator numbers, growing from just six licensed operators at the beginning of 2020 to between 15 and 22 active operators by 2024. This rapid growth was catalyzed by the 2020 revocation of licenses held by companies associated with gambling tycoon Vasil Bozhkov, which eliminated major market players and created immediate opportunities for new entrants. The resulting market opening triggered 50% year-over-year growth in 2021 and 2022 before stabilizing to more sustainable 10-12% growth rates.

The market demonstrates moderate concentration with several dominant local operators commanding significant market share alongside international brands. Major local players include Efbet, widely considered the market leader with the strongest brand recognition and extensive retail network. Winbet represents another significant Bulgarian operator with robust online and land-based presence. Palmsbet has established itself as a growing force particularly in online casino offerings.

International operators have successfully entered the market with bet365, one of the world’s largest gambling operators, establishing operations through partnership with EGT Digital to offer localized content from Bulgarian providers. Bwin, part of the Entain group, brings international expertise and brand recognition. Betway, operating under Malta-based GMBS Ltd and part of Super Group, leverages its multi-market European experience. These international entrants typically capture 30-40% combined market share, with local operators retaining dominant positions.

The competitive landscape includes several mid-tier operators such as 8888 (owned by state lottery Bulgarian Sports Totalizator), Alphawin (operating both online and gaming halls), Betmarket (new local entrant), Inbet, Palms Bet, and Sesame (Telematic Interactive Bulgaria, publicly listed). Market positioning strategies vary with some operators focusing on sports betting excellence, others emphasizing casino game variety, and several pursuing omnichannel approaches combining online platforms with physical venue networks.

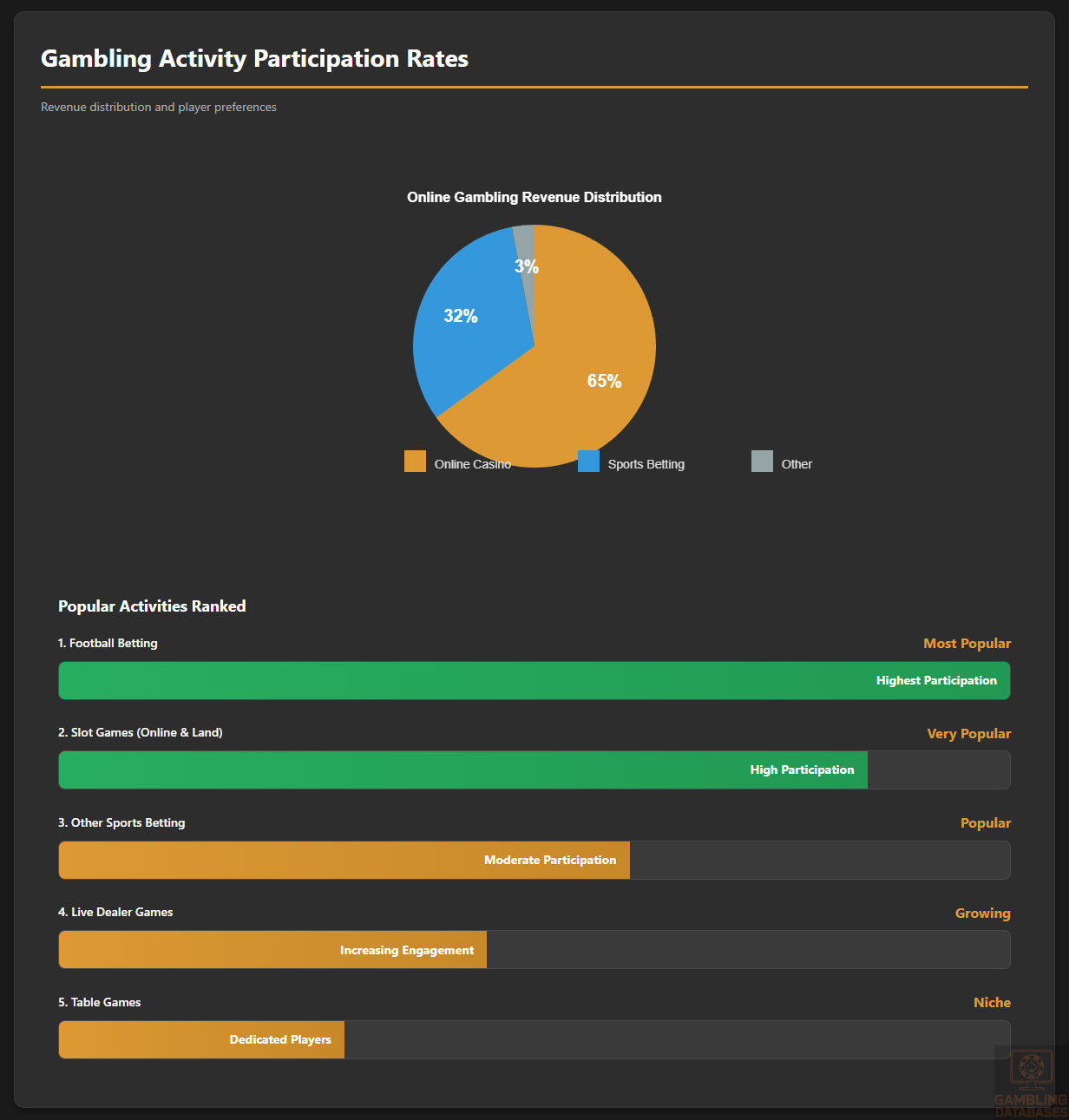

Market share distribution shows online casinos generating approximately two-thirds of total online gambling revenue, while sports betting accounts for 30-35%. This represents a distinctive market characteristic as many European markets show higher sports betting penetration. The casino-dominant revenue mix reflects strong player preference for slot games, live dealer offerings, and table games, creating opportunities for operators with comprehensive casino content libraries and exclusive game partnerships.

Licensing Framework and Requirements

Application Process and Eligibility

The National Revenue Agency serves as the sole licensing authority for all gambling activities in Bulgaria. The NRA operates under the Ministry of Finance framework and handles license applications, compliance monitoring, enforcement actions, and tax collection. Operators seeking market entry must engage directly with the NRA through formal application procedures that demand comprehensive documentation and financial disclosures. Contact information includes the official NRA website and dedicated gambling regulation departments accessible through their Sofia headquarters.

Financial requirements represent the most substantial barrier to entry. Applicants must demonstrate paid-in share capital of at least BGN 1.5 million (approximately EUR 767,000 or USD 835,000), which must be verified through bank statements and audited financial reports. This capital requirement applies regardless of the gambling activity type, establishing a significant entry threshold that effectively limits market access to well-capitalized entities. The capital must be maintained throughout the license period and cannot be withdrawn below minimum thresholds.

Application fees vary by gambling activity type. For online sports betting licenses, the government examination fee is BGN 20,000 (approximately EUR 10,220). Other online gambling activities incur fees ranging from BGN 5,000 to BGN 35,000 (EUR 2,555 to EUR 17,895) depending on the specific license category. Following approval, operators must pay an additional one-time post-approval fee of BGN 100,000 (EUR 51,125). As of January 2024, a substantial one-time state licensing fee of BGN 400,000 (approximately EUR 204,500) applies specifically to online betting operations, representing a significant increase from previous levels.

Technical standards and certifications constitute critical approval requirements. Gaming equipment including central computer systems, control local servers, communication equipment, and gaming software must undergo testing and registration with the Bulgarian Institute of Metrology. Each software version requires separate registration before deployment. Testing methodology follows specific NRA-approved protocols ensuring fairness, randomness, security, and accurate transaction recording. Operators must provide detailed technical documentation including system architecture, data flow diagrams, security protocols, and disaster recovery plans.

Background check procedures apply to all beneficial owners, directors, and key management personnel. Criminal record certificates must be obtained from all jurisdictions where individuals have resided for significant periods during the preceding five years. The NRA investigates financial backgrounds to ensure applicants have not been involved in bankruptcy proceedings, tax violations, or previous gambling license revocations. This reliability assessment aims to prevent criminal elements from infiltrating the gambling sector and ensures only reputable operators receive licenses.

The application review timeline spans 60 to 90 days from submission of complete documentation. This period allows the NRA to conduct thorough due diligence including verification of financial capacity, technical system testing, background checks, and assessment of operational procedures. Incomplete applications or requests for additional information can extend this timeline. Upon completion of the review, the NRA Director issues a formal decision either approving or rejecting the license application. Rejections are appealable to the Sofia Administrative Court, providing legal recourse for applicants who believe decisions were improperly made.

Local Presence and Operational Requirements

Bulgaria’s regulatory framework distinguishes between domestic and foreign operators in its local presence requirements. Companies registered in Bulgaria face no additional representation obligations. However, operators registered in other EU member states, EEA countries, or Switzerland must appoint an authorized representative with an address in Bulgaria. This representative must hold power of attorney with sufficient scope to conclude contracts on behalf of the foreign entity and represent them before Bulgarian state authorities and courts. Importantly, this authorized representative cannot serve as a commercial representative under Bulgarian commerce law, requiring genuine authority and responsibility.

Domain and hosting requirements mandate that central computer systems and communication equipment be physically located within the European Union, European Economic Area, or Switzerland. This provision allows operators to leverage existing EU infrastructure rather than establishing dedicated Bulgarian data centers. However, all data related to gambling services including player registration, identification, betting transactions, and winnings must be stored within Bulgaria and transmitted in real-time to NRA servers. This creates a hybrid approach where core systems can be EU-hosted but Bulgarian data repositories must exist for regulatory access.

Banking requirements specify that operators must maintain accounts in banks licensed in Bulgaria or other EU member states, EEA countries, or Switzerland that operate in Bulgaria. These accounts are used exclusively for depositing player bets and paying winnings. Cash payments for winnings are restricted to BGN 5,000 (approximately EUR 2,555), with higher amounts requiring bank transfer payments. This limitation reduces money laundering risks while ensuring traceable financial flows for regulatory oversight.

Personnel and management obligations focus primarily on the authorized representative for foreign operators rather than requiring extensive Bulgarian staff. Operators can structure their businesses to centralize operations in other EU jurisdictions while maintaining the required representative function in Bulgaria. This flexibility reduces operational costs compared to jurisdictions demanding full local teams. However, practical considerations around customer support, payment processing partnerships, and marketing often lead operators to establish more substantial local presence than minimum requirements mandate.

Foreign ownership faces no restrictions for EU, EEA, and Swiss entities, creating a level playing field within the European single market. This open approach contrasts with some jurisdictions that require local partnership shares or impose nationality restrictions on ownership. Bulgarian citizens and non-EU foreign investors face the same eligibility criteria as EU operators once they establish appropriate corporate structures within the EU/EEA/Switzerland framework. This regulatory neutrality within the European context facilitates international investment while maintaining control through licensing standards.

Compliance Obligations and Monitoring

Player Protection and Identification

Age verification requirements mandate that all gambling participants must be at least 18 years old. Operators must implement robust age verification systems that confirm player age before permitting account registration or gambling activity. Acceptable verification methods include government-issued identification documents, passport verification, and integration with national identification databases. The verification process must occur at the point of registration and cannot be deferred to withdrawal stages, ensuring minors cannot access gambling services even temporarily.

Know Your Customer and Anti-Money Laundering compliance follows comprehensive standards aligned with EU AML directives. Licensed operators are designated as obliged entities under the Bulgarian Measures Against Money Laundering Act, subjecting them to extensive due diligence requirements. Operators must verify player identities, assess risk profiles, monitor transaction patterns for suspicious activity, and report potential money laundering to the NRA’s Anti-Money Laundering Unit formed in 2023. Enhanced due diligence applies to high-value transactions, politically exposed persons, and players from high-risk jurisdictions.

Responsible gambling measures have become increasingly stringent through recent legislative amendments. Operators must provide self-exclusion mechanisms allowing players to block access to gambling services. Following changes effective March 27, 2025, the minimum self-exclusion period increased from 30 days to one full year, representing one of Europe’s longest mandatory exclusion periods. As of March 2025, nearly 54,000 people had registered for self-exclusion through the national program administered by the NRA. Players can apply for exclusion either in person at NRA offices or online, with operators required to check the exclusion list in real-time before permitting gambling activity.

Session time limits and loss limits represent emerging regulatory requirements. Draft legislation for 2025 proposes mandatory session limits of four hours for adult players and two hours for players under 24 years of age. Additional behavioral monitoring requirements will mandate operators to identify signs of problem gambling including extended play sessions, chasing losses, and dramatic bet size increases. When concerning patterns emerge, operators must intervene through warning messages, temporary cooling-off period suggestions, and referrals to gambling support resources.

Mandatory player information disclosures require operators to clearly communicate odds, payout percentages, house advantages, and game rules. Terms and conditions must be presented in Bulgarian language with transparent explanation of bonus wagering requirements, withdrawal processes, and fees. Warning messages about gambling addiction risks must appear prominently on websites, in marketing materials, and during gameplay. Operators must provide easy access to responsible gambling tools including deposit limits, loss limits, reality checks, and contact information for gambling addiction support services.

Financial Monitoring and Reporting

Transaction monitoring systems must operate continuously to detect suspicious financial activity and potential money laundering. Operators must implement automated monitoring rules that flag unusual deposit patterns, rapid turnover of funds, structured transactions designed to avoid reporting thresholds, and other indicators of financial crime. All flagged transactions require review by designated compliance officers with authority to suspend accounts, request additional documentation, or file suspicious activity reports with the NRA.

Reporting requirements to the NRA operate on real-time, daily, and periodic bases depending on the information type. Real-time data transmission includes all bets placed, outcomes determined, and winnings paid, allowing the NRA to maintain comprehensive oversight of gambling activity. Monthly reports must detail total bets received, total winnings paid, gross gaming revenue, player account balances, and tax calculations. Quarterly reports provide more detailed financial information including revenue by game type, player demographics, and operational statistics.

Audit and inspection procedures authorize the NRA to conduct on-site and remote audits of operator systems, financial records, and compliance procedures. Operators must grant NRA officials access to all relevant data, systems, and documentation upon request. Annual financial audits by licensed auditing firms are mandatory, with audit reports submitted to the NRA demonstrating financial stability and accurate tax reporting. Technical audits verify gaming systems continue to meet fairness and security standards throughout the license period.

Data retention requirements mandate preservation of all gambling-related data for specified periods after transactions occur. Player registration information, betting history, financial transactions, communications, and compliance documentation must remain accessible for regulatory inspection. These retention obligations create significant data storage requirements but ensure the NRA can investigate complaints, verify tax calculations, and conduct enforcement actions based on comprehensive historical records.

Taxation Structure and Financial Obligations

Player Taxation

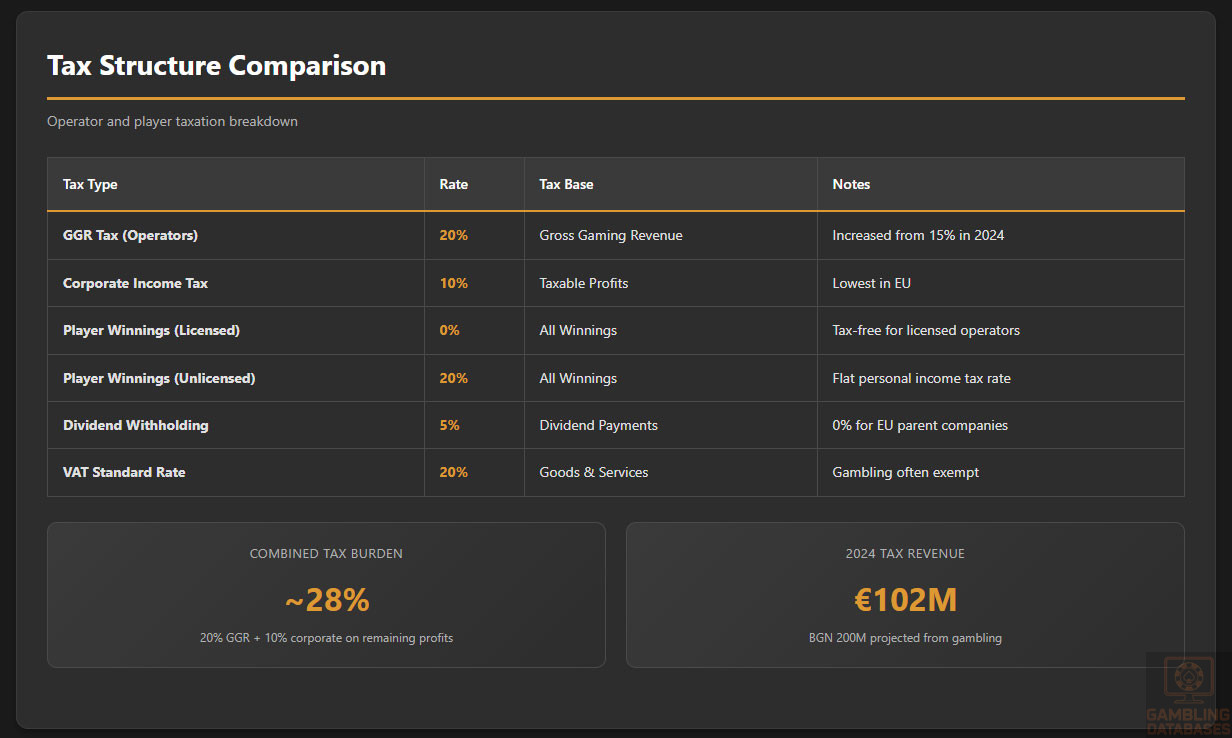

Players using licensed Bulgarian operators enjoy tax-free winnings regardless of amount. This zero-tax structure for licensed operator winnings creates a competitive advantage for regulated market operators and incentivizes players to use licensed platforms rather than offshore alternatives. The tax exemption applies to all forms of gambling including sports betting, casino games, poker, and lottery products offered by licensed entities.

However, a critical distinction exists for unlicensed operators. Winnings from unlicensed operators or from operators licensed in non-EU member states are subject to personal income taxation at Bulgaria’s flat 20% rate. Players are legally obligated to declare such winnings in their annual tax returns and pay applicable taxes. This creates a significant financial disincentive for using offshore operators while simultaneously increasing enforcement complexity as the government must rely substantially on player self-reporting for international gambling winnings.

Withholding procedures apply when operators pay winnings from unlicensed or foreign sources. While licensed operators have no withholding obligations, banks and financial institutions may flag large incoming transfers from known gambling operators for tax reporting purposes. The government has enhanced cooperation with financial institutions to identify players receiving substantial winnings from international sources, though enforcement remains challenging given the cross-border nature of online gambling.

Tax-free thresholds do not apply to licensed operator winnings – all amounts from BGN 1 to unlimited sums remain tax-exempt for players. This unlimited exemption differs from some jurisdictions that impose taxation above certain winning thresholds. The policy reflects Bulgaria’s strategy to maximize licensed operator appeal and channel gambling activity into the regulated market where operator taxation generates government revenue while protecting consumers through regulatory oversight.

Operator Taxation

Gross Gaming Revenue taxation represents the primary gambling tax burden on operators. As of January 2024, the GGR tax rate increased to 20% from the previous 15% rate. GGR is calculated as total bets received minus total winnings paid to players, representing the operator’s gross profit before operational expenses. This 20% rate applies uniformly across online gambling activities including sports betting, casino games, and poker. The rate increase reflects government efforts to boost tax revenues from the growing gambling sector while remaining competitive with regional jurisdictions.

Net Gaming Revenue considerations do not apply in Bulgaria’s tax framework, which focuses exclusively on GGR as the tax base. Operators cannot deduct operational expenses, marketing costs, technology investments, or other business expenditures when calculating gambling tax obligations. This gross-basis taxation creates higher effective tax rates compared to jurisdictions permitting expense deductions but provides simplicity and predictability in tax calculations while minimizing disputes over deductible expense classifications.

Fixed operational taxes include the substantial one-time license fees. The BGN 400,000 (EUR 204,500) one-time fee for online betting licenses effective January 2024 represents a significant upfront cost that must be amortized over the five-year license period. Additional annual license maintenance fees apply with amounts varying by license type. The BGN 100,000 (EUR 51,125) post-approval fee paid upon license issuance adds to initial capital requirements.

Corporate income tax applies to gambling operators at Bulgaria’s flat 10% rate on taxable profits after deducting gambling taxes and operational expenses. This 10% corporate tax rate represents the lowest in the European Union, providing a meaningful competitive advantage. The combined effective tax burden includes the 20% GGR tax plus 10% corporate income tax on remaining profits, plus social security contributions on employee salaries. When fully loaded, the tax structure remains competitive with many European jurisdictions while generating substantial government revenues.

License renewal fees apply at the end of five-year license periods. Operators seeking renewal must pay fees comparable to initial licensing costs though specific renewal fee structures remain at NRA discretion. The renewal process involves re-verification of financial capacity, technical compliance, and operational standards but typically proceeds more efficiently than initial applications given established track records.

Gambling Market Financial Performance

| Year | Online GGR (BGN Million) | Online GGR (EUR Million) | YoY Growth | Tax Revenue (BGN Million) |

|---|---|---|---|---|

| 2020 | ~440 | ~225 | Market opening | ~66 |

| 2021 | ~660 | ~337 | ~50% | ~99 |

| 2022 | ~1,000 | ~511 | ~50% | 251.2 |

| 2023 | ~1,100 | ~562 | ~10-12% | ~165-220 |

| 2024 | 1,100 | 561 | ~0-5% | ~200 projected |

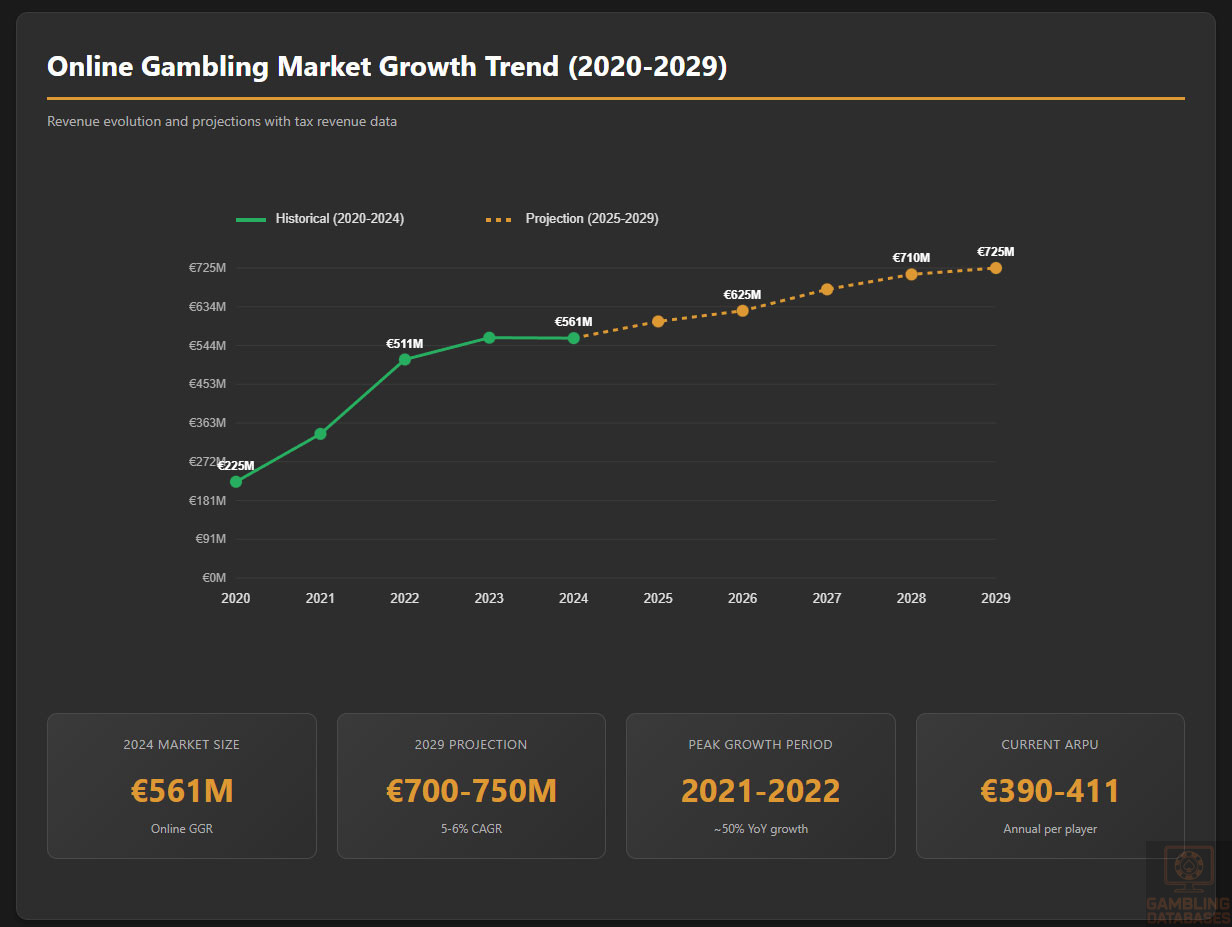

The Bulgarian online gambling market reached BGN 1.1 billion (EUR 561 million) in gross gaming revenue during 2024, representing stabilization after explosive growth in previous years. This figure represents the total amount wagered minus winnings paid to players, effectively measuring operator gross profit before expenses. The market demonstrated exceptional expansion in 2021 and 2022 with approximately 50% year-over-year growth, catalyzed by the removal of dominant operators and regulatory market opening that created opportunities for new entrants.

Growth rates moderated significantly in 2023 and 2024 to approximately 10-12% and near-zero respectively, indicating market maturation as operator numbers stabilized and competitive intensity increased. This growth deceleration reflects natural market evolution as early rapid expansion gives way to sustainable long-term growth patterns. Industry participants expect renewed growth acceleration as international operators increase market investment and product innovation drives player engagement.

Total gambling market size including both online and land-based operations is estimated to exceed EUR 2 billion in total turnover, with online activities representing approximately 25-30% of total gambling revenue. The substantial land-based sector includes traditional casinos, gaming halls, sports betting shops, and state lottery operations. Land-based gambling recovered from COVID-19 impacts and continues growing albeit at slower rates than online channels, with physical venues maintaining strong positions in tourist destinations and major urban centers.

Revenue distribution by gambling type shows online casinos commanding dominant market share at approximately 65-67% of online gambling revenue. This casino-heavy mix distinguishes Bulgaria from many European markets where sports betting often dominates. Sports betting accounts for 30-35% of online revenue, reflecting strong football betting culture and interest in international sporting events. The remaining revenue comes from poker, bingo, and other game categories.

Tax revenues generated for government coffers reached BGN 251.2 million in 2022 and were projected at BGN 200 million for 2024, representing substantial contributions to the national budget. The decline from 2022 to 2024 reflects tax rate changes, enforcement patterns, and market dynamics rather than revenue reduction. With the 2024 increase to 20% GGR tax rates, government revenues are expected to grow significantly in 2025 and beyond, providing resources for social programs, regulatory enhancement, and problem gambling treatment initiatives.

Year-over-year growth trends indicate Bulgarian online gambling transitioned from explosive expansion phase (2021-2022) through rapid growth (2023) to market maturation (2024). Future projections suggest sustained growth rates of 5-12% annually through 2029, driven by continued internet penetration increases, smartphone adoption, payment method improvements, and product innovation. Conservative estimates project the market reaching EUR 186-231 million by 2027-2029, though these figures may prove understated given current momentum.

Advertising and Marketing Restrictions

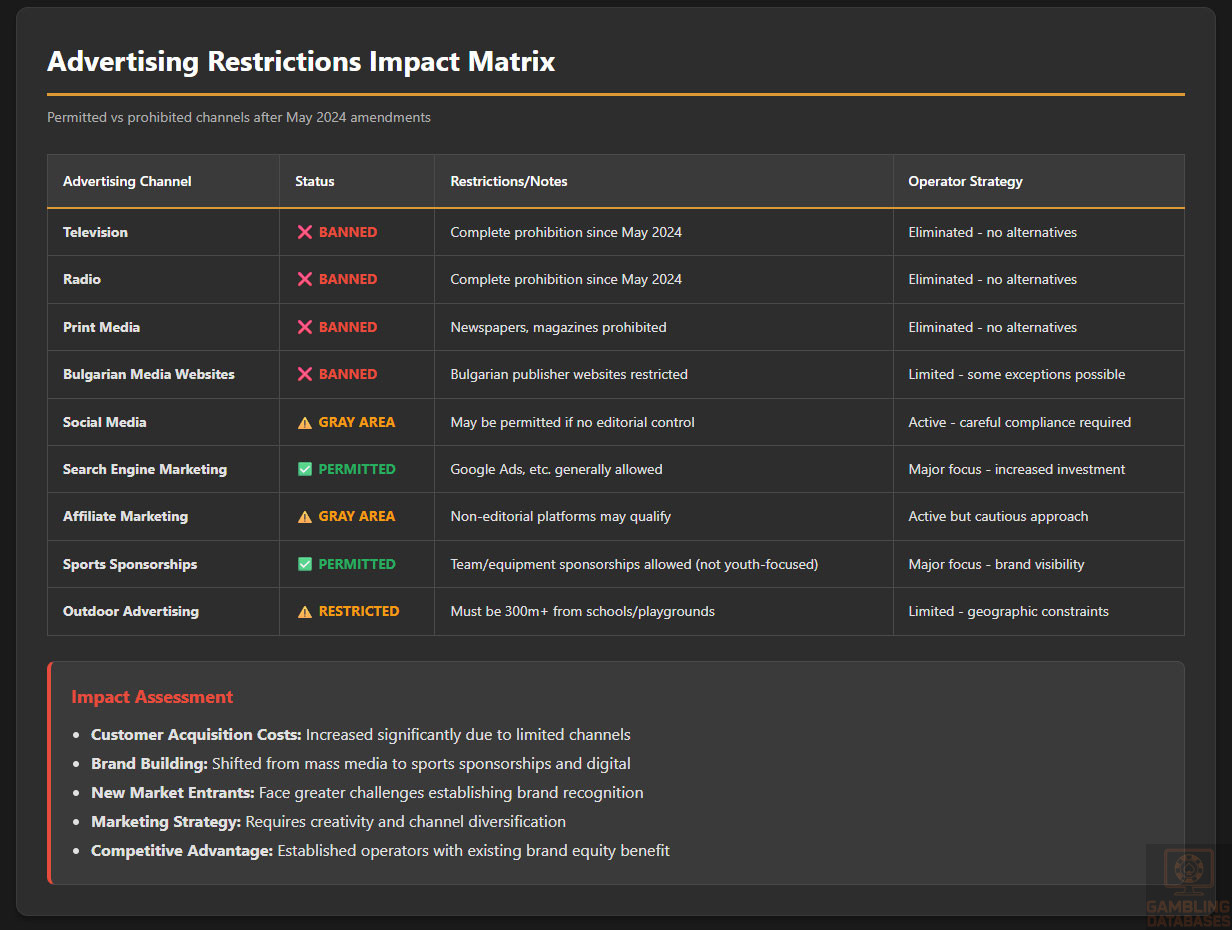

Bulgaria implemented severe gambling advertising restrictions effective May 18, 2024, through comprehensive amendments to the Gambling Act. These restrictions represent some of Europe’s most stringent advertising limitations and fundamentally reshape how operators can acquire customers and build brand awareness. The regulatory changes reflect growing political and social pressure to reduce gambling’s public visibility and perceived normalization, particularly among younger populations.

Permitted advertising channels have been dramatically restricted. Traditional broadcast media including television and radio face complete bans on gambling advertisements regardless of time of day or program content. Print media including newspapers, magazines, and other publications similarly cannot carry gambling advertising. Most significantly, online media websites operated by Bulgarian publishers fall under the advertising prohibition, eliminating major digital advertising channels that operators previously relied upon for customer acquisition.

The definition of prohibited online media generated significant uncertainty initially, with the National Revenue Agency issuing clarifying guidance in September 2024. The NRA decision indicated restrictions target Bulgarian media outlets and their websites rather than the entire internet. Social media platforms like Facebook, Instagram, and TikTok may fall outside the prohibition scope depending on whether they exercise editorial control over content or merely distribute user-generated content. The NRA’s case-by-case approach creates interpretation challenges but suggests social media advertising may remain viable.

Affiliate marketing platforms exist in a gray area under current interpretations. The NRA guidance suggests platforms without editorial responsibility that simply facilitate connections between advertisers and publishers might avoid the strictest prohibitions. However, operators must carefully assess compliance risks when engaging affiliates given evolving enforcement patterns and potential for regulatory guidance changes. Conservative compliance approaches favor limiting affiliate relationships or requiring contractual terms that shift legal risk to affiliate partners.

Outdoor advertising faces geographical restrictions rather than complete prohibition. Billboards and other outdoor advertising materials must maintain at least 300 meters distance from educational institutions and playgrounds. This zoning requirement complicates outdoor campaign planning and limits placement options in urban areas with dense school networks. Operators must conduct detailed geographic analysis before outdoor campaigns to ensure compliance while maximizing visibility to target demographics.

Sponsorship regulations permit gambling operators to place branding on sports equipment, materials, and products unless the sponsorship targets minors or occurs at venues primarily used by children. Sports team sponsorships remain viable, creating opportunities for brand building through association with popular football clubs and sporting events. However, operators must carefully structure sponsorship agreements to ensure appropriate audience targeting and avoid youth-focused properties.

Content restrictions mandate that all permitted advertising must include prominent warnings about gambling addiction risks. Messages must clearly communicate that gambling involves financial risk and provide contact information for gambling addiction support services. Promotional content cannot suggest gambling solves financial problems, guarantees winning outcomes, or targets vulnerable populations. Youth appeal elements including cartoon characters, celebrity endorsements popular with minors, and placement near children’s content face strict prohibition.

Promotional limitations extend beyond advertising placement to regulate bonus offers and incentive structures. While specific bonus caps have not been imposed, operators must ensure promotional terms are transparent, fair, and not misleading. Wagering requirements must be clearly disclosed with realistic achievement probabilities. The regulatory environment suggests possible future restrictions on bonus generosity or structure, following patterns seen in jurisdictions like Germany and the Netherlands.

Time restrictions for television and radio advertising are moot given the complete broadcast advertising ban. However, should regulations liberalize in the future, watershed restrictions limiting gambling advertising to late evening hours would likely apply consistent with European norms. Current prohibition reflects political determination to minimize gambling’s cultural presence rather than merely protect vulnerable viewing hours.

Marketing to minors faces absolute prohibition with severe penalties for violations. Operators must implement age-gating on all digital properties, verify user ages before displaying gambling content, and avoid any messaging, imagery, or channel selection that could appeal to persons under 18. The regulatory focus on youth protection intensified in recent years given concerns about gambling normalization among younger generations increasingly exposed to online content.

Recent Regulatory Changes and Their Impact

The May 2024 regulatory amendments represent the most significant gambling law changes since the 2012 Gambling Act’s enactment. These amendments fundamentally altered the operational landscape for gambling operators with particular focus on advertising restrictions, player protection enhancement, and unlicensed operator suppression. The changes reflect growing political pressure to address perceived gambling harms while maintaining the regulated market’s viability.

The advertising ban detailed above constitutes the most visible and impactful change. Operators report dramatic increases in customer acquisition costs as traditional advertising channels closed. Marketing budgets shifted toward permitted channels including social media, search engine marketing, affiliate partnerships, and sponsorships. Brand building through sports sponsorships gained importance as direct response advertising options contracted. Total gambling industry television advertising spending declined 13% year-over-year in 2023 anticipating these restrictions.

Player protection measures expanded substantially through several mechanisms. The March 2025 increase in minimum self-exclusion periods from 30 days to one year represents Europe’s longest mandatory exclusion. This change aims to ensure self-excluded players have adequate time away from gambling to address problematic behavior rather than quickly re-entering after brief cooling-off periods. The nearly 54,000 registered self-excluded players cannot access licensed gambling services, creating a significant excluded customer base.

Session time limits expected to take effect during 2025 will mandate maximum four-hour gambling sessions for adults and two-hour limits for players aged 18-24. These hard limits require sophisticated technical implementation to track session duration across devices and platforms while permitting breaks that reset timers. Operators must invest in compliance technology and player education about limit mechanisms while potentially experiencing revenue impacts from reduced play duration.

Mandatory behavioral monitoring obligations will require operators to implement systems identifying problem gambling indicators. When systems detect concerning patterns including extended play, chasing losses, or dramatic bet increases, operators must intervene through warning messages, mandatory breaks, or account restrictions. This shift from passive responsible gambling tools to active intervention represents significant compliance burden increase while potentially improving player outcomes.

The 2024 tax rate increase from 15% to 20% on gross gaming revenue directly impacts operator profitability and pricing strategies. The five percentage point increase represents a 33% relative increase in tax burden, requiring operators to improve operational efficiency, adjust bonus generosity, or accept reduced margins. The increased rates generated immediate government revenue increases while creating competitive pressure particularly on smaller operators with limited scale economies.

Distance requirements for physical gambling establishments and advertising create operational constraints for land-based operators planning new venues or advertising campaigns. The 300-meter buffer from schools and playgrounds significantly reduces available locations in urban areas. Some existing operations found themselves non-compliant with new distance rules, though grandfather provisions typically provide protection for established facilities.

Unlicensed operator suppression intensified through multiple enforcement mechanisms. Internet service providers must block access to unlicensed gambling websites under NRA orders. Payment institutions cannot process transactions to or from unlicensed operators. Postal operators and couriers cannot facilitate payments related to unlicensed gambling. These multi-layered restrictions aim to channel gambling activity into the regulated market while protecting consumers from unregulated offshore operators.

Impact on operator costs and business strategy has been substantial. Marketing expense shifted from broad-reach television advertising to more targeted digital channels, requiring strategy adaptation and potentially reducing total addressable market reach. Compliance technology investments increased significantly to implement monitoring systems, session limits, and enhanced data reporting. Smaller operators face particular pressure from increased costs while lacking scale to efficiently absorb these burdens.

Upcoming regulatory changes remain under discussion with potential further restrictions on loss limits, mandatory deposit limits, and enhanced verification requirements. The regulatory trajectory suggests continuing tightening of operational requirements aligned with broader European player protection trends. Operators must maintain flexible compliance infrastructure capable of adapting to evolving requirements while engaging constructively with regulatory development processes.

Enforcement Mechanisms and Penalties

The National Revenue Agency employs comprehensive enforcement powers to ensure gambling law compliance. Enforcement actions range from administrative warnings and fines through license suspensions to permanent license revocations depending on violation severity and repetition patterns. The NRA maintains authority to conduct announced and unannounced inspections, access operator systems and records, interview personnel, and require remedial actions within specified timeframes.

Penalty structures for licensed operators include financial fines calculated based on violation severity and resulting harm. Minor technical violations may incur fines of BGN 10,000-50,000 (EUR 5,000-25,000), while serious violations including player protection failures, tax evasion, or money laundering can result in fines exceeding BGN 500,000 (EUR 255,000). Repeated violations escalate penalty severity with the NRA empowered to impose increasingly harsh sanctions on operators demonstrating compliance failures.

License suspension represents an intermediate sanction allowing the NRA to temporarily halt operator activities while investigating serious violations or requiring compliance improvements. Suspensions typically last 30-90 days during which operators cannot accept bets or process new registrations but must maintain player account access for withdrawals. Suspended operators lose revenue during the suspension period while maintaining operational costs, creating significant financial pressure to achieve swift compliance.

License revocation constitutes the ultimate enforcement action, permanently terminating operator market access. Revocations occur for severe violations including criminal activity, systematic regulatory breaches, fraud, money laundering facilitation, or failure to remedy suspension-triggering violations. Revoked operators must cease all gambling activities, return player funds, settle outstanding tax obligations, and cannot reapply for licensing within specified exclusion periods. The 2020 revocations of major operators associated with Vasil Bozhkov demonstrate the government’s willingness to take drastic enforcement actions.

Recent enforcement actions focused heavily on unlicensed operator suppression. The NRA maintains a public blacklist of prohibited gambling websites with court orders requiring ISP blocking. As of 2024, hundreds of unlicensed websites face access restrictions, though enforcement effectiveness varies given players’ ability to use VPNs or access through mobile apps. Payment processor restrictions create more effective barriers by preventing Bulgarian bank cards and payment methods from funding unlicensed gambling accounts.

Compliance enforcement trends indicate increasing regulatory sophistication and willingness to impose meaningful sanctions. The formation of the NRA’s Anti-Money Laundering Unit in 2023 enhanced financial crime detection and enforcement capacity. Regular audits of player protection systems, verification procedures, and responsible gambling tool implementation demonstrate regulatory focus on consumer protection rather than merely revenue collection. Operators report more frequent NRA communications, inspection notices, and compliance inquiries compared to earlier years.

ISP blocking of unlicensed operators operates through court order mechanisms. The NRA identifies unlicensed gambling websites operating without Bulgarian licenses, obtains court orders mandating access blocking, and directs all Bulgarian ISPs to implement blocks. While technically straightforward, enforcement faces practical challenges given the ease of website migration to new domains and player ability to circumvent blocks through VPN services or Tor browsers.

Payment processor restrictions create more effective enforcement by cutting financial flows. Banks and payment service providers operating in Bulgaria must screen transactions for gambling-related activity and reject payments to unlicensed operators. The NRA provides guidance on identifying gambling transactions through merchant category codes, known operator accounts, and transaction pattern analysis. Financial institutions face their own penalties for facilitating illegal gambling transactions, incentivizing robust screening programs.

Criminal penalties for illegal gambling operations apply primarily to unlicensed operators rather than licensed entities committing regulatory violations. Operating gambling services without appropriate licenses constitutes a criminal offense under Article 327 of the Penal Code, carrying imprisonment sentences of one to four years plus financial penalties. Prosecution targets organized illegal gambling operations, particularly those involving money laundering, fraud, or other criminal activity. Individual players using unlicensed services typically face no criminal liability though tax evasion for undeclared winnings remains prosecutable.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

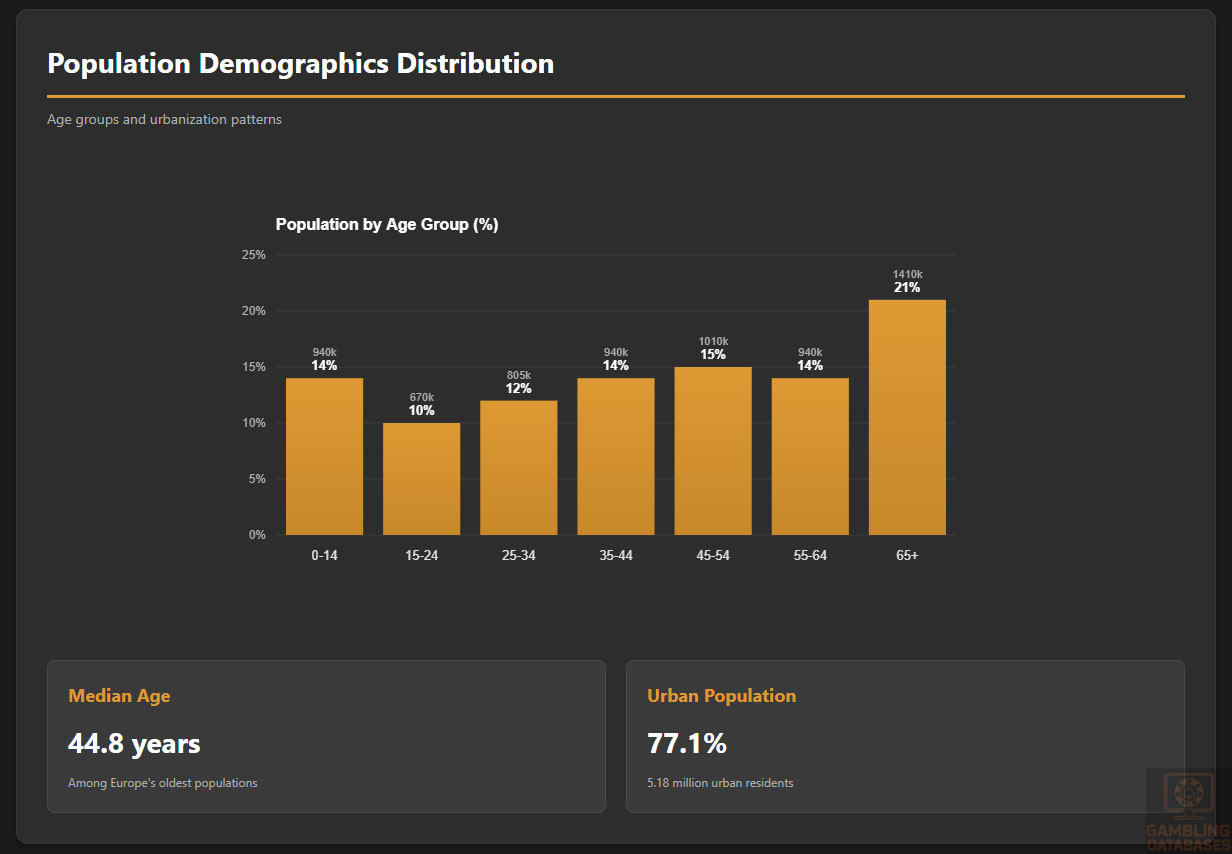

Bulgaria’s population stands at approximately 6.71 million people as of mid-2025, representing a small but significant market within Southeast Europe. The population has been declining steadily for decades, with current annual decreases of approximately 0.6% driven by low birth rates, aging demographics, and emigration to Western European countries. This declining population trajectory creates challenges for market growth but does not negate opportunities given increasing gambling participation rates and rising disposable incomes among remaining residents.

Age distribution reveals a mature population structure with implications for gambling market development. Persons aged 0-14 represent approximately 14% of the population (940,000 people), while the crucial 15-24 demographic comprises roughly 10% (670,000). The 25-34 age bracket, prime gambling demographic, accounts for approximately 12% (805,000). The 35-44 cohort represents 14% (940,000), while 45-54 year-olds comprise 15% (1.01 million). The 55-64 demographic accounts for 14% (940,000), and persons 65 and older represent 21% (1.41 million), highlighting significant population aging.

The median age of 44.8 years positions Bulgaria among Europe’s oldest populations, exceeded only by countries like Italy, Germany, and Portugal. This aging demographic structure suggests gambling operators should target mature audiences rather than youth-focused strategies. The substantial population segments in 35-64 age ranges represent prime gambling customers with established careers, disposable income, and leisure time for gambling entertainment. Marketing strategies emphasizing sophisticated entertainment, reliability, and responsible gambling likely resonate more effectively than youth-oriented approaches.

Gender ratios show approximately 946 men per 1,000 women, reflecting higher female life expectancy and demographic patterns common throughout Eastern Europe. The female population surplus grows more pronounced in older age brackets where life expectancy differentials accumulate. For gambling operators, the gender distribution suggests opportunities in female-focused game categories and marketing approaches, particularly given data showing approximately 40% of online gambling activity comes from female players, higher than many markets assume.

Life expectancy stands at 73.6 years overall, with male life expectancy at 70 years and female life expectancy at 77.4 years. These figures fall below Western European averages, reflecting healthcare system challenges and socioeconomic factors. The relatively short life expectancy combined with late retirement ages creates a smaller elderly leisure class compared to wealthier EU nations, though improving economic conditions may extend both life expectancy and healthy retirement years over the coming decade.

Geographic Distribution

Urban population concentration reaches 77.1%, with approximately 5.18 million people residing in cities and towns. This high urbanization rate facilitates internet infrastructure deployment, payment service availability, and marketing reach compared to predominantly rural markets. Urban dwellers typically demonstrate higher internet usage, greater digital payment adoption, and stronger gambling participation rates than rural populations, concentrating the addressable market in manageable geographic footprints.

Major cities and population centers include Sofia, the capital and largest city with approximately 1.3 million residents in the metropolitan area. Sofia serves as the economic, cultural, and technological hub with highest incomes and most developed digital infrastructure. Plovdiv, Bulgaria’s second city, hosts approximately 340,000 people and represents an important secondary market. Varna on the Black Sea coast has roughly 335,000 residents and significant tourism-related gambling activity.

Burgas, another Black Sea coastal city, contains approximately 202,000 people with seasonal population increases during summer tourism peaks. Ruse, located on the Danube River bordering Romania, has around 145,000 residents. Stara Zagora in central Bulgaria hosts approximately 138,000 people. Pleven in northern Bulgaria contains roughly 107,000 residents, while Sliven in southeast Bulgaria has about 96,000 people. Dobrich in northeastern Bulgaria rounds out the major urban centers with approximately 90,000 inhabitants.

Regional economic differences create income and gambling participation disparities across Bulgaria. Sofia and the southwestern region demonstrate highest GDP per capita, most developed services sectors, and greatest concentration of higher-income professionals. Coastal areas benefit from tourism revenues generating seasonal economic activity and gambling demand spikes during summer months. Northern and central regions face greater economic challenges with higher unemployment and lower wages, though cost of living advantages partially offset income differentials.

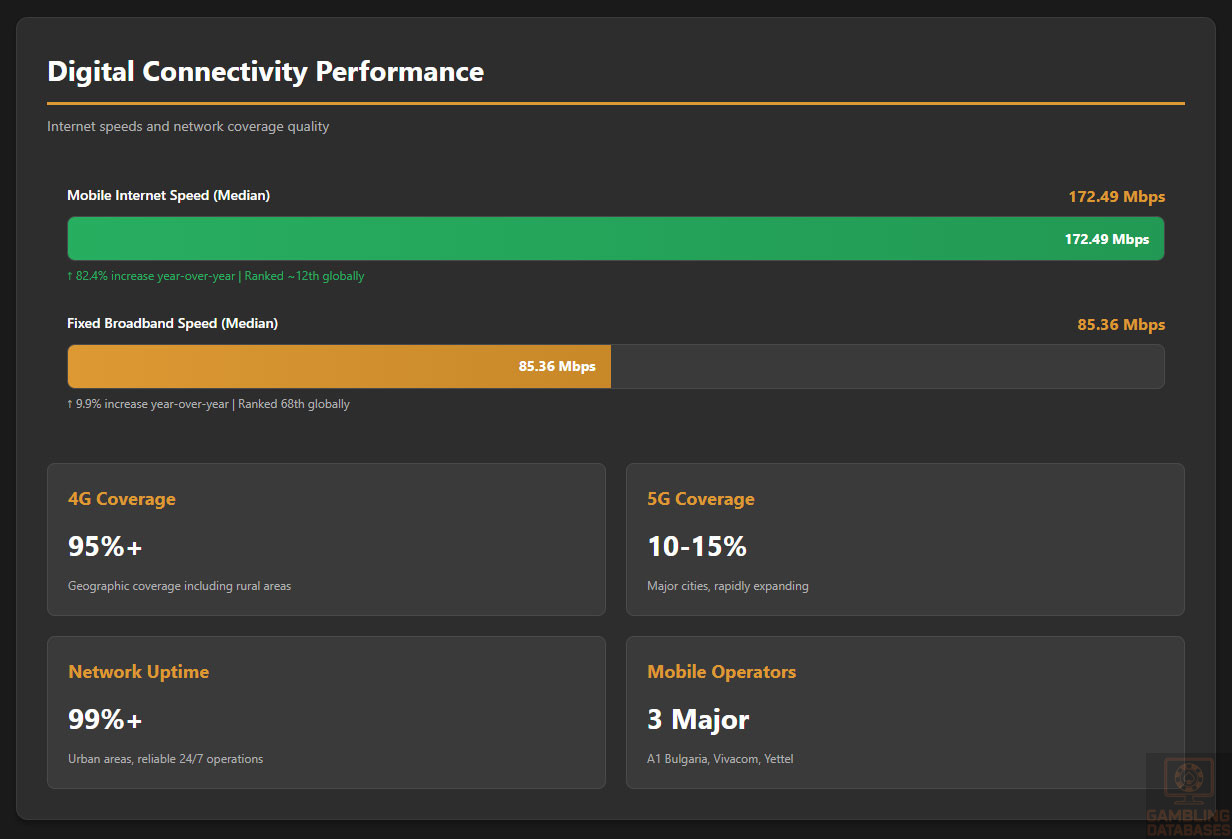

Internet access geographic patterns show near-universal coverage in urban areas with 95%+ penetration rates, while rural areas lag significantly with penetration rates potentially 20-30 percentage points lower. This digital divide concentrates the online gambling addressable market even more heavily in urban areas beyond what population distribution alone suggests. Mobile internet expansion has improved rural connectivity substantially in recent years, with 4G coverage extending to most inhabited areas and creating previously unavailable gambling access in underserved regions.

Concentration of gambling venues by region follows population and economic patterns. Sofia hosts the highest density of land-based casinos, gaming halls, and sports betting shops reflecting population concentration and tourist traffic. Black Sea coastal areas show elevated gambling venue density supporting seasonal tourism activity. Regional cities maintain smaller gambling infrastructures proportional to local populations, while rural areas rely primarily on online access given limited physical venue economic viability in low-density areas.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

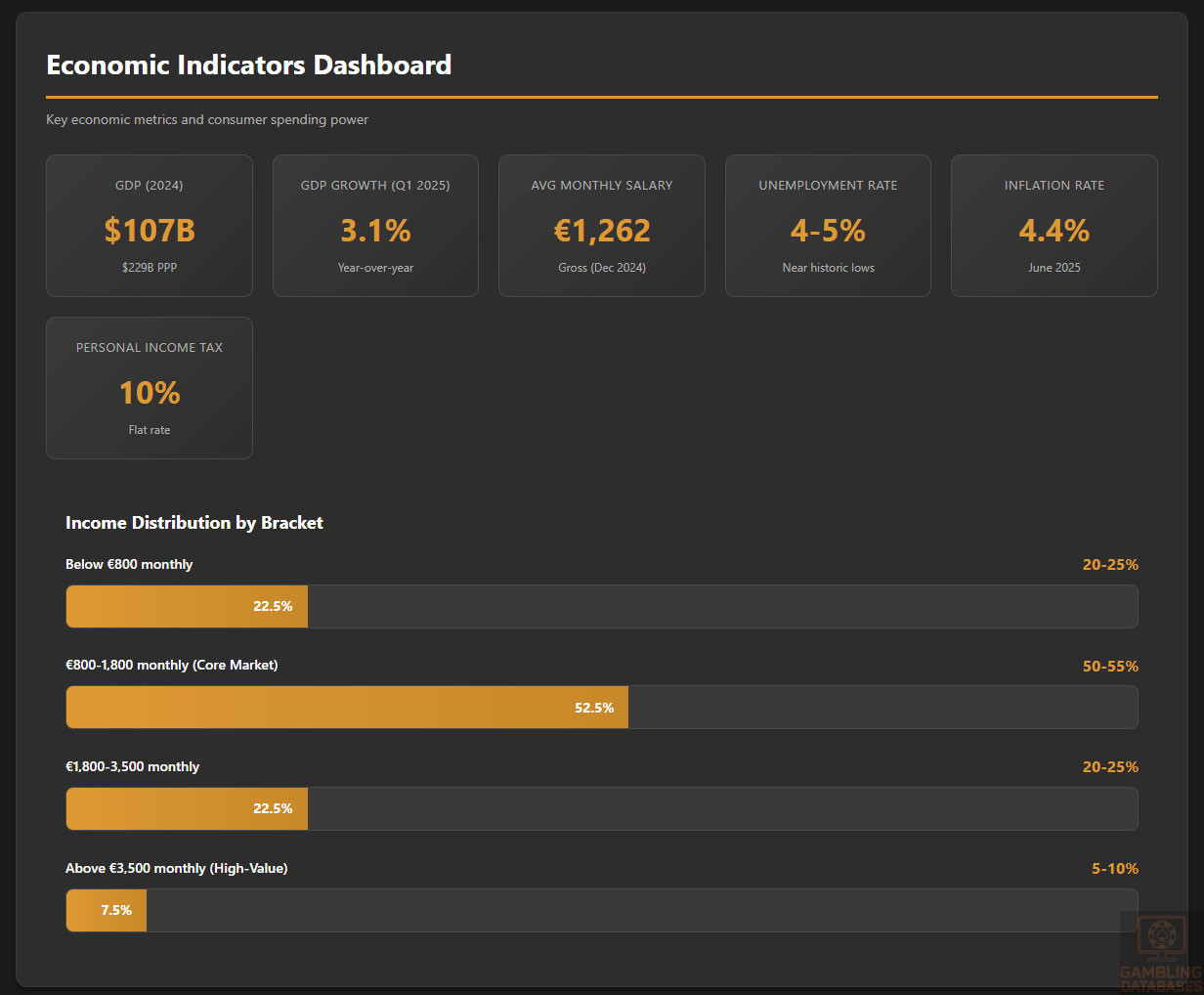

Bulgaria’s current GDP reaches approximately USD 107 billion in nominal terms for 2024, representing meaningful economic scale despite relatively small population. On a purchasing power parity basis accounting for lower Bulgarian living costs, GDP expands to approximately USD 229 billion, demonstrating that real economic output exceeds nominal dollar measurements. This PPP adjustment reflects that Bulgarian consumers’ actual purchasing power and living standards exceed what raw income figures suggest when comparing to higher-cost Western European markets.

GDP per capita stands at USD 10,090 in nominal terms for 2024, positioning Bulgaria in the upper-middle income category but substantially below Western European levels. On a PPP basis, GDP per capita reaches approximately USD 36,000, representing 70% of the EU average on PPP terms but only 43% on nominal terms. This disparity indicates Bulgarians enjoy better real living standards than dollar income comparisons suggest, important for understanding consumer discretionary spending capacity for gambling and entertainment.

GDP growth forecasts show Bulgaria maintaining expansion rates above EU averages over the coming years. First quarter 2025 growth reached 3.1% year-over-year, exceeding the eurozone average and demonstrating economic resilience. Growth is driven primarily by domestic demand including consumption and investment, while external trade showed weakness in early 2025. Forecasts suggest GDP growth of 2.5-3.5% annually through 2027-2029, supporting continued gambling market expansion through rising incomes and consumer spending capacity.

GDP per capita trends show steady improvement over the past decade, with Bulgaria narrowing its income gap with Western Europe though substantial differentials remain. Real wage growth exceeding inflation creates genuine income increases supporting discretionary spending. The trajectory suggests continued convergence toward EU income levels over the next decade, though complete parity remains decades away. For gambling operators, the improving income trends support market growth optimism despite population decline headwinds.

Economic sector composition shows services dominating at approximately 65-70% of GDP, reflecting Bulgaria’s transition from agriculture and heavy industry toward modern service economy. Industry including manufacturing, construction, and mining contributes roughly 25-30% of GDP. Agriculture’s share has declined to approximately 4-5% of GDP though remaining important for rural employment. The services-heavy economy supports gambling market development as disposable income and leisure time increase with service sector job growth.

Employment rates have improved substantially in recent years, with unemployment falling to approximately 4-5% in 2024-2025, near historically low levels. This tight labor market drives wage growth and improves household financial security, supporting consumer spending on discretionary categories including gambling. However, labor shortages in some sectors create inflationary pressures and may constrain economic growth if unfilled positions limit business expansion.

Wage levels demonstrate significant regional variation with Sofia averaging EUR 1,500-1,800 gross monthly salaries for professional positions while regional cities average EUR 800-1,200. The national average gross monthly salary reached EUR 1,262 in December 2024, representing steady increase from previous years. Net salaries after taxes and social contributions average approximately 75% of gross figures. Double-digit wage growth in recent years has outpaced inflation, creating real income gains supporting gambling spending increases.

Inflation trends showed relative stability through most of the 2010s before accelerating in 2022-2023 during the European energy crisis and supply chain disruptions. Inflation reached 4.4% in June 2025, moderating from earlier peaks but remaining above the 2% target typical for stable economies. The National Bank of Bulgaria’s currency board maintaining a fixed exchange rate to the euro provides monetary stability and inflation discipline, though limiting independent monetary policy tools for managing economic fluctuations.

Income and Wealth Distribution

Average household income reaches approximately EUR 1,500-1,800 monthly on a gross basis nationally, with substantial regional variation between Sofia’s higher incomes and smaller cities’ lower earnings. Household income includes wages, pensions, social benefits, and other income sources. Multi-earner households in Sofia metropolitan area may achieve EUR 3,000-4,000 monthly household income, while single-earner households in regional areas may earn EUR 800-1,200 monthly, illustrating the wide income distribution.

Median household income sits somewhat below average figures, indicating positively skewed income distribution where high earners pull averages upward. The median household likely earns EUR 1,200-1,400 monthly, representing typical Bulgarian family circumstances more accurately than averages influenced by high-income outliers. For gambling market sizing, median income metrics provide better guidance on mass market spending capacity while high-income segments represent premium player targets.

Income inequality measures including the Gini coefficient position Bulgaria in moderate inequality territory within European context. The Gini coefficient of approximately 0.38-0.40 indicates less extreme inequality than the United States but more than Scandinavian countries. Wealth inequality exceeds income inequality as property ownership, investments, and inherited wealth concentrate more heavily than earnings. This inequality creates market segmentation opportunities with distinct products and marketing for mass market versus high-value players.

Disposable income trends show steady improvement as wage growth outpaces inflation and tax burden remains relatively low. Bulgarian personal income tax follows a 10% flat rate, among Europe’s lowest, leaving more income available for consumption. Social security contributions reduce take-home pay but at lower rates than Western European countries. The combination of rising wages, low taxes, and moderate cost inflation creates genuine disposable income growth supporting gambling market expansion.

Consumer spending patterns show Bulgarians allocating substantial portions of income to necessities including housing, food, and utilities, with smaller discretionary spending shares than wealthier countries. However, absolute discretionary spending increases as incomes rise faster than necessity costs. Entertainment, leisure, and gambling represent emerging expenditure categories growing faster than overall consumption as Bulgarian consumers adopt Western European lifestyle patterns. The trend supports optimism about gambling market growth potential as economic development continues.

Percentage of population by income bracket creates distinct market segments. Approximately 20-25% of households earn below EUR 800 monthly, representing limited gambling market potential given constrained budgets. The bulk of the population, roughly 50-55%, earns EUR 800-1,800 monthly, comprising the core mass-market gambling segment. Approximately 20-25% earn EUR 1,800-3,500 monthly, representing attractive mid-market players with meaningful discretionary budgets. The top 5-10% earning above EUR 3,500 monthly constitute the high-value player segment meriting premium service approaches.

Middle class size and growth represent critical market development indicators. Bulgaria’s middle class, defined as households with income sufficient for comfortable living beyond necessities, comprises approximately 40-50% of the population and grows steadily. This expanding middle class drives consumption of discretionary services including entertainment, dining, travel, and gambling. The middle class growth trajectory supports sustained gambling market expansion even amid population decline, as participation rates and spending per player increase faster than population decreases.

Market Size and Growth Projections

| Metric | 2024 | 2025 | 2027 | 2029 | CAGR |

|---|---|---|---|---|---|

| Online Gambling Revenue (EUR Million) | 561 | 590-610 | 650-700 | 700-750 | 5-6% |

| Online Casino Revenue (EUR Million) | 365-375 | 475-490 | 550-600 | 600-650 | 10-12% |

| Sports Betting Revenue (EUR Million) | 170-195 | 190-215 | 210-240 | 230-260 | 6-8% |

| Total Gambling Market (USD Million) | ~800 | 820-850 | 900-950 | 950-1,000 | 3-4% |

| Active Online Players (Thousands) | 1,000-1,050 | 1,050-1,100 | 1,150-1,200 | 1,200-1,300 | 4-5% |

| Market Penetration Rate | 5.7% | 6.0% | 6.3% | 6.5-6.8% | – |

| ARPU (EUR) | 390-411 | 420-450 | 470-510 | 520-560 | 6-7% |

Current iGaming market revenue reached EUR 561 million in gross gaming revenue for 2024, representing total bets minus player winnings. This figure excludes the substantial amounts wagered, which industry representatives estimate at several billion euros annually when considering bet volumes. The GGR metric provides the most meaningful measurement of market size as it represents actual operator revenue available to cover expenses, taxes, and generate profits. Converting to US dollars at current exchange rates, the market approximates USD 600 million.

Historical revenue growth demonstrates explosive expansion from 2020 through 2022 following market liberalization. Starting from approximately EUR 225 million in 2020, the market more than doubled to EUR 511 million in 2022, representing compound annual growth exceeding 50%. This exceptional growth resulted from increased operator competition following license revocations that removed dominant players, improved product offerings, enhanced payment options, and rising consumer comfort with online gambling during COVID-19 lockdowns that accelerated digital adoption.

Growth rates moderated significantly in 2023-2024 to approximately 10-12% and near-zero respectively, indicating market maturation as operator numbers stabilized around 15-22 active platforms and competitive intensity increased. The growth deceleration reflects natural market evolution as penetration rates approach sustainable levels and easy growth opportunities become exhausted. However, this maturation should not be interpreted as market stagnation but rather transition to stable long-term growth patterns typical of developed gambling markets.

Revenue forecasts for the next 3-5 years project compound annual growth rates of 5-6% for total online gambling, potentially reaching EUR 700-750 million by 2029. However, this conservative estimate may understate growth potential given continued internet penetration increases, smartphone adoption among older demographics, payment method improvements, and product innovation including live dealer games and gamification features. More optimistic scenarios suggest EUR 800-850 million potential by 2029 if market conditions remain favorable.

Expected CAGR varies significantly by product category. Online casinos, representing two-thirds of current revenue, are projected to grow at 10-12% annually through 2029, potentially reaching EUR 600-650 million. This rapid casino growth reflects Bulgarian player preference for slot games, live dealer experiences, and table games while benefiting from continuous content innovation by game providers. Sports betting growth rates of 6-8% annually appear more modest but still healthy, potentially reaching EUR 230-260 million by 2029 supported by football betting culture and expanding sports coverage.

Projected user base growth shows active online gamblers increasing from approximately 1.0-1.05 million in 2024 to 1.2-1.3 million by 2029, representing 4-5% annual growth. This user growth derives from several sources: younger cohorts reaching gambling age with high digital adoption, older demographics gaining confidence with online platforms, improved mobile experiences reducing technical barriers, and enhanced payment options increasing accessibility. The relatively modest user growth compared to revenue growth indicates rising spending per player drives much of the market expansion.

Average Revenue Per User currently stands at EUR 390-411 annually and is projected to increase to EUR 520-560 by 2029, representing 6-7% annual ARPU growth. Rising ARPU reflects increasing player engagement, improved cross-selling between sports betting and casino products, enhanced loyalty programs encouraging sustained play, and real income growth supporting larger entertainment budgets. Operators successfully migrating customers from low-value sports betting to higher-margin casino games contribute substantially to ARPU expansion.

Market penetration rates measure the percentage of adults participating in online gambling annually. Current penetration of 5.7% positions Bulgaria below Western European leaders like UK (15%+) but comparable to Southern and Eastern European peers. Penetration is projected to reach 6.5-6.8% by 2029 through continued normalization of online gambling, improved trust in digital payments, and enhanced responsible gambling measures addressing safety concerns that deter some potential players. Double-digit penetration rates appear achievable long-term as the market matures.

Online versus land-based revenue split currently favors land-based operations at approximately 70-75% of total gambling revenue, with online comprising 25-30%. This distribution reflects Bulgaria’s relatively early stage in the online transition compared to markets like UK where online represents 50%+ of total gambling. The split is projected to shift toward 40-45% online by 2029 as digital channels capture increasing share, though land-based operations will maintain majority given the tourism-driven casino sector and retail betting shop networks’ continued viability.

Market size comparison with regional neighbors provides useful context. Romania, with roughly three times Bulgaria’s population, operates a larger online gambling market of approximately EUR 800-900 million. Greece, with 50% larger population, shows comparable online market size to Bulgaria due to regulatory restrictions limiting market development. Serbia’s market approximates EUR 300-400 million despite similar population, reflecting less developed regulatory framework. Bulgaria’s market size per capita positions favorably within the Balkan region, suggesting relatively mature market development.

Education, Skills, and Digital Literacy

Educational Foundation

Literacy rates in Bulgaria reach exceptionally high levels at 98.4% overall, with minimal gender disparity. Male literacy stands at 98.7% while female literacy reaches 98.1%, both representing near-universal reading and writing capability. This educational foundation, inherited from the socialist era’s emphasis on public education, ensures gambling operators can utilize text-based communications, written terms and conditions, and complex game rules without concerning about basic literacy barriers that affect less developed markets.

Education levels show strong completion rates through secondary school. Primary education completion reaches near 100% as compulsory education laws ensure basic schooling. Secondary education completion, including gymnasium and vocational schools, reaches approximately 85-90% of relevant age cohorts. Tertiary education, including universities and specialized colleges, shows completion rates of approximately 30-35%, positioning Bulgaria in the middle range among European countries for higher education attainment.

Digital literacy indicators demonstrate Bulgaria’s relatively advanced technological capabilities despite lower economic development. The population shows strong computer skills development, with younger cohorts exhibiting near-universal digital competency. Approximately 70-75% of adults demonstrate at least basic digital skills including internet navigation, email usage, online shopping, and digital service access. This digital comfort level supports online gambling adoption as players possess the technical skills to register accounts, deposit funds, navigate game lobbies, and manage their gambling activity online.

Workforce skill levels reflect the educational system’s emphasis on STEM subjects and technical training. Bulgaria produces substantial numbers of engineering, IT, mathematics, and science graduates, contributing to the country’s growing technology sector. Language skills, particularly English, have improved significantly among younger generations, though older demographics may show limited foreign language proficiency. Russian remains widely understood among older cohorts due to historical educational emphasis during the socialist period.

Technology adoption readiness appears high relative to income levels, with Bulgarians demonstrating eagerness to adopt new digital services and platforms. Smartphone penetration reaching 97% exemplifies this adoption tendency. Social media usage rates exceed 60% of population, indicating comfort with digital platforms. E-commerce participation grows rapidly as payment security concerns diminish and delivery infrastructure improves. This technology adoption mindset creates favorable conditions for online gambling market development as consumers readily trial new platforms and services.

English language proficiency varies substantially by generation and urban/rural geography. Younger urban residents, particularly in Sofia, demonstrate good-to-excellent English skills through school education, media consumption, and workplace requirements in internationally-oriented companies. Middle-aged populations show moderate English capabilities, often sufficient for basic communication but not complex discussions. Older demographics typically demonstrate limited English proficiency, relying primarily on Bulgarian with Russian as a secondary language. For gambling operators, Bulgarian-language platforms, customer support, and marketing materials remain essential despite some English capability in target demographics.

Cultural and Social Factors

Communication and Language

Primary languages used in daily life center overwhelmingly on Bulgarian, a South Slavic language using Cyrillic script. Approximately 85% of the population speaks Bulgarian as their native language and primary communication medium. Turkish serves as the primary language for approximately 8-9% of the population, concentrated in certain regions and representing the largest minority language. Romani languages are spoken by approximately 4-5% of the population, though many Roma also speak Bulgarian. Small minorities speak Russian, Armenian, and other languages.

Internet language preferences show strong Bulgarian dominance with users expecting websites, apps, and digital services to provide Bulgarian-language interfaces and content. While younger, educated demographics may navigate English-language sites, mass market reach requires Bulgarian localization. This creates essential requirements for gambling operators to provide Bulgarian-language platforms, game interfaces, customer support, terms and conditions, and marketing materials. Machine translation proves insufficient given gambling’s specialized terminology and the importance of clear, accurate communication for regulatory compliance and customer satisfaction.

Business communication norms combine formal and informal elements depending on relationship stage and context. Initial business contacts typically follow relatively formal patterns using titles and surnames, though relationships may become more casual once established. Email and messaging apps serve as primary business communication channels supplementing phone calls. Written communication standards expect correct grammar and spelling, with careless writing potentially signaling unprofessionalism. For gambling operators, professional Bulgarian-language business communication supports partnerships with payment providers, affiliates, and service vendors.

Language requirements for gambling websites extend beyond basic translation to encompass cultural localization. Game names, bonus promotions, marketing messages, and customer communications must resonate with Bulgarian cultural references and language usage patterns. Terms and conditions require particular attention as regulatory compliance demands precise legal language while consumer protection requires clear explanations accessible to players with limited legal expertise. Customer support in Bulgarian proves essential as players expect native-language assistance, particularly when resolving payment issues or disputes.

Cultural Attitudes

Gambling acceptance levels in Bulgarian society show moderate-to-high tolerance for gambling as entertainment. Historical gambling traditions dating to Ottoman era and socialist-period sports betting created cultural familiarity. The 1993 legalization and subsequent market development normalized gambling as a mainstream leisure activity. However, recent concerns about gambling prevalence, advertising visibility, and problem gambling have prompted public debate and regulatory responses including the 2024 advertising restrictions. This suggests gambling occupies a contested cultural space with mainstream acceptance coexisting alongside growing criticism.

Religious influences on gambling perception remain limited despite Bulgaria’s Orthodox Christian heritage. Approximately 59% of the population identifies as Eastern Orthodox, though active religious practice rates fall significantly lower. The Orthodox Church does not maintain strong institutional opposition to gambling comparable to some other Christian denominations, resulting in limited religious barriers to gambling participation. Muslim population segments, comprising roughly 8%, may show lower gambling participation due to religious prohibitions, though enforcement varies by individual observance level and community norms.

Risk tolerance indicators suggest Bulgarians demonstrate moderate-to-high risk acceptance in gambling contexts. Economic uncertainty and income volatility throughout post-communist transition period may have cultivated risk-taking tendencies as survival strategies. The substantial casino segment dominance over sports betting, despite Bulgaria’s strong football culture, suggests player preference for chance-based games over skill-influenced betting. However, this risk tolerance exists within entertainment context rather than financial investment, with most players gambling recreational amounts rather than life-changing sums.

Entertainment preferences and habits emphasize social activities, sports, and increasingly digital entertainment. Football dominates sports interest with passionate followings for national team and domestic league clubs. Volleyball, basketball, and winter sports also maintain audiences. Television remains important entertainment medium though internet streaming and social media increasingly compete for attention. Dining out, cafe culture, and social gatherings represent important leisure activities. For gambling operators, aligning with entertainment preferences through sports sponsorships, social gaming features, and positioning gambling as entertainment rather than income opportunity resonates with cultural attitudes.

Social gambling versus solitary gambling preferences show Bulgarians engaging in both patterns. Land-based casinos and betting shops provide social environments where gambling occurs alongside conversation and camaraderie. However, online gambling’s convenience supports solitary play, particularly for casino games where social interaction plays minimal role. Live dealer games offering chat functionality and multiplayer poker rooms create hybrid social-digital experiences appealing to players seeking community alongside convenience. The diversity of gambling motivations and contexts suggests operators should offer both social and solitary gaming options.

Problem Gambling and Social Considerations