Burkina Faso presents a cautiously emerging opportunity in the iGaming sector with an evolving regulatory framework primarily focused on land-based gambling. While online gambling regulation remains undeveloped, the country’s growing economy, increasing internet penetration, and government licensing initiatives create a foundation for market entry.

The regulatory environment balances traditional gaming operations with modern trends, making Burkina Faso a viable target for operators willing to navigate a hybrid system and pending online legislation.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Legalized for land-based; online unregulated but not explicitly prohibited |

| Gambling Regulatory Authority | Commission Nationale des Jeux de Hasard (CNJH) |

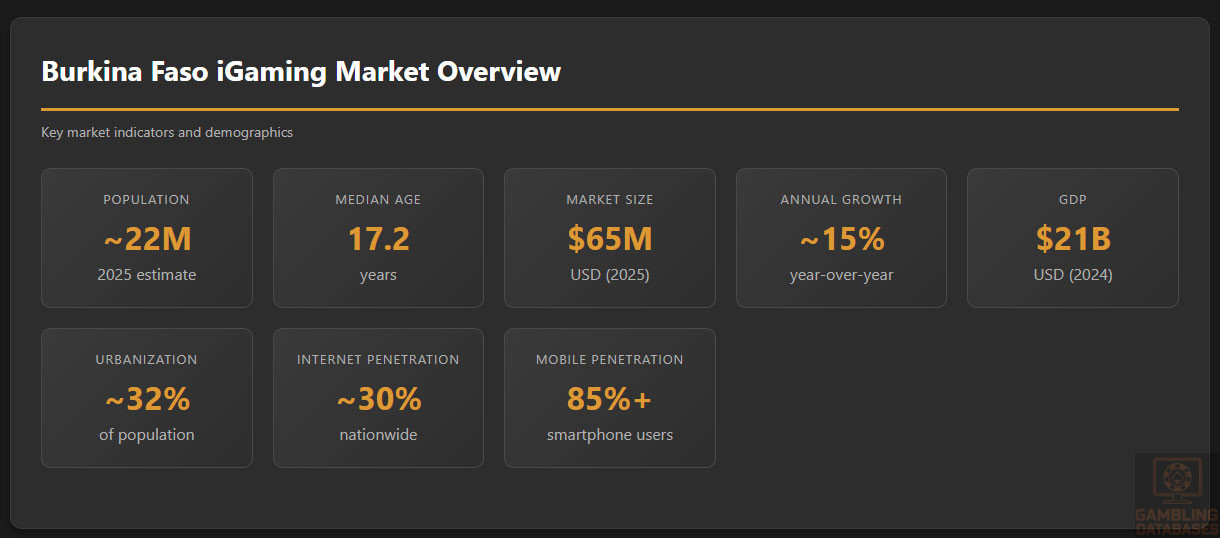

| Population | ~22 million (2025 estimate) |

| Median Age | 17.2 years (very young population) |

| Urbanization Rate | ~32% |

| GDP (Nominal) | Approx. $21 billion USD (2024) |

| GDP Growth Rate (CAGR) | 5.5% (projected) |

| GDP Per Capita | ~$950 USD (2024) |

| Internet Penetration Rate | ~30% |

| Mobile Penetration Rate | 85%+ |

| Land-Based Operator Licensing Cost | Approx. $30,000 – $50,000 USD |

| Online Operator Licensing Cost | Proposed but unregulated; expected similar to land-based |

| Gaming Tax Rate | Unified 5% on Gross Gaming Revenue (as of 2025) |

| Other Taxes on Operators | Corporate income tax applies separately |

| Player Taxation | No direct tax on winnings |

| Licensing Application Timeline | 4-6 months typical |

| Minimum Legal Gambling Age | 18 years |

| Market Size (Estimate 2025) | $65 million USD |

| Growth Rate (Annual) | ~15% |

| Average Revenue Per User (ARPU) | Estimated $30-$40 USD |

| Local Presence Requirement | Local company registration mandatory for operators |

| Foreign Ownership Restrictions | Allowed with local entity incorporation |

| Responsible Gambling Measures | Mandatory age checks, self-exclusion options |

| Compliance Monitoring | Regular inspections, audits by CNJH |

| Advertising Restrictions | Content limitations and channel restrictions apply |

| Payment Systems | Mobile money widespread; international cards accepted |

| Technology Infrastructure | Improving digital infrastructure enabling online access |

| Enforcement Penalties | License suspension, fines, potential criminal sanctions |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling in Burkina Faso is legally regulated for land-based activities, including casinos, sports betting, lotteries, and slot machine halls. The regulatory framework was established by Law No. 024-96/AN in 1996 and has since evolved with the creation of governmental oversight bodies and taxation policies.

While land-based gambling enjoys clear legal status and a structured licensing regime, online gambling currently operates in a regulatory grey zone. Online operators do not face explicit prohibitions but are not directly regulated either. The government reserves the right to block unlicensed online gambling platforms, and future legal provisions are anticipated to bring online gambling under formal regulation.

Land-Based Gambling Activities

Burkina Faso supports a variety of land-based gambling formats. Casinos operate primarily in major cities with a limited number of licensed operators maintaining physical venues. Sports betting is widespread and offered both through retail outlets and on-site at race tracks. Lotteries are run under a government monopoly through LONAB (Loterie Nationale Burkinabé).

Slot machine halls and gaming arcades exist but are tightly controlled. The government maintains a licensing and inspection regime to ensure compliance with regulations, including age restrictions and responsible gaming measures.

Online Gambling Framework

The legal framework for online gambling is currently undeveloped. Neither explicit legalization nor prohibition exists. International operators typically provide online sports betting and casino services targeting local players, often through partnerships or local company registrations.

Potential licensing requirements for online operators will likely mirror land-based regulations, including mandatory registration, taxation compliance, responsible gaming policies, and technical security standards. The CNJH is expected to extend its oversight to online platforms once new legislation is enacted.

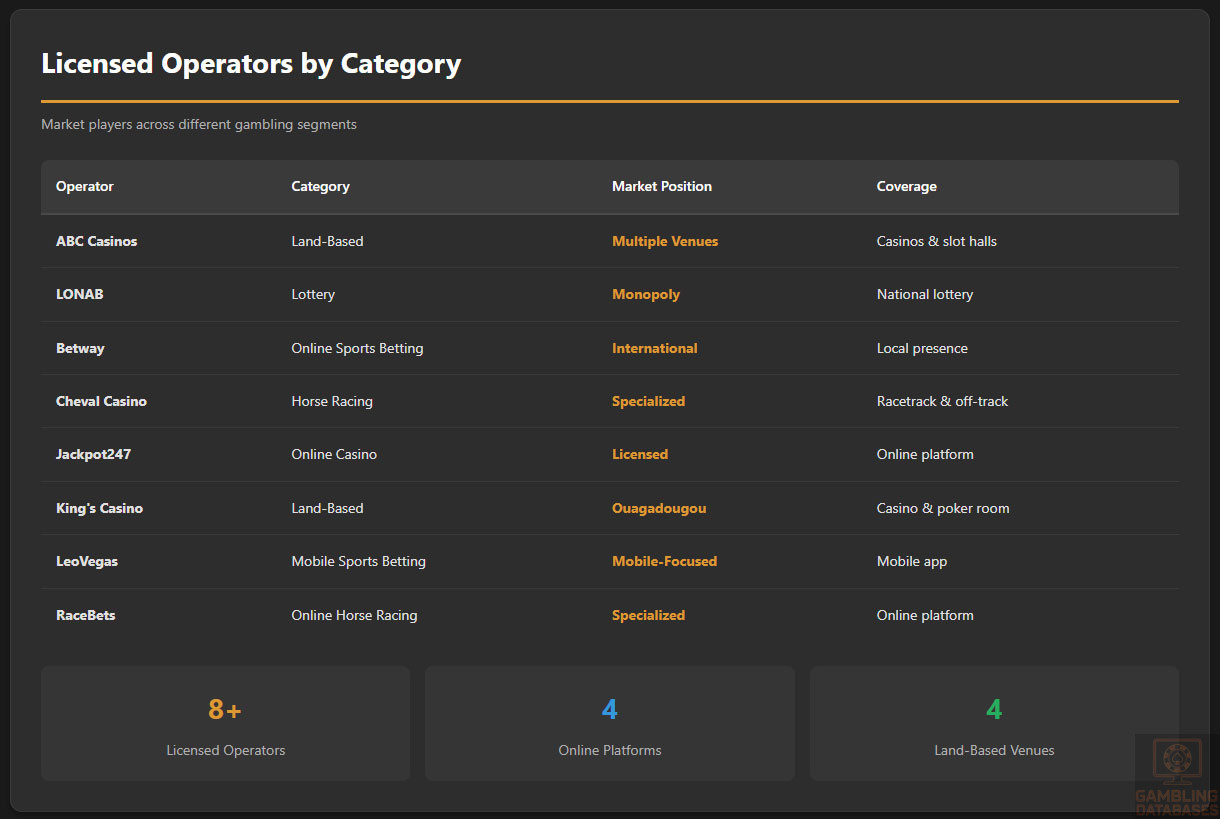

Licensed Operators and Market Players

The licensed gambling market includes a mix of domestic and international operators primarily focused on land-based gaming and sports betting. Operators must be registered locally under Burkinabé commercial law to receive a license.

Market competition is moderate with several key players offering physical venues and others operating online sports betting platforms legally or in a grey area supplemented by local entity registration. The government supports market growth through licensing reforms and international collaborations aimed at adopting global best practices.

- ABC Casinos – operates multiple land-based venues including casinos and slot halls

- Betway – international online sports betting with local presence

- LONAB – national lottery operator with monopoly on lottery products

- Cheval Casino – horse racing betting at racetrack and multiple off-track sites

- Jackpot247 – licensed online casino platform

- King’s Casino – land-based casino and poker room in Ouagadougou

- LeoVegas – mobile-focused sports betting app

- RaceBets – online horse race betting platform

Licensing Framework and Requirements

Application Process and Eligibility

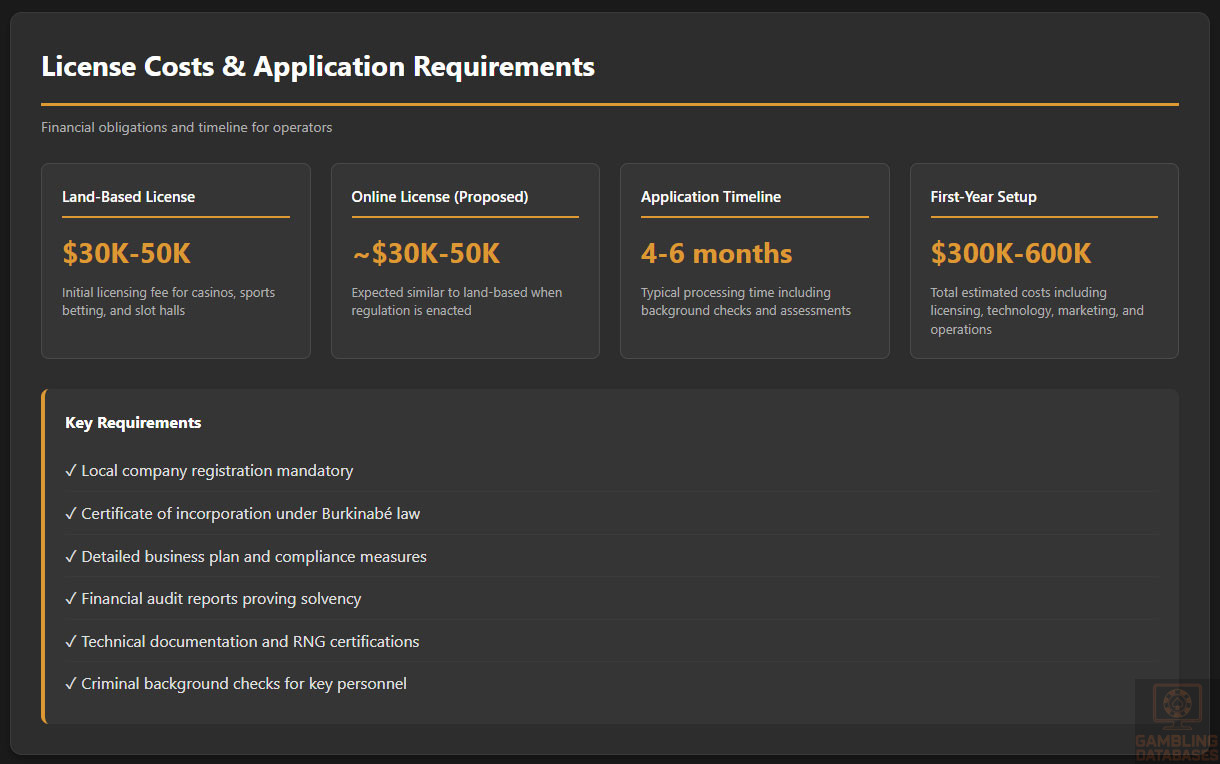

The licensing authority is the Commission Nationale des Jeux de Hasard (CNJH), which administers the application, vetting, and issuance of gambling licenses. Applicants must register a company locally, submit detailed business plans, and demonstrate financial solvency.

Licensing fees depend on the type of operation and typically range between $30,000 and $50,000. The application review process generally takes 4 to 6 months, involving background checks and technical assessments of the gambling platform security. Licenses cover land-based casinos, sports betting, lotteries, and potentially online gambling pending regulatory updates.

The required documents generally include:

- Certificate of company incorporation under Burkinabé law

- Business plan highlighting market strategy and compliance measures

- Financial audit reports proving solvency

- Technical documentation of gaming software and RNG certifications

- Criminal background checks and integrity declarations for key personnel

- Proof of minimum capital deposit in a recognized bank

Local Presence and Operational Requirements

Operators are required to establish a local legal entity with all commercial registration obligations met under Burkinabé law. Physical presence in the country is generally necessary for land-based licenses and strongly recommended for online operators.

Further operational requirements include maintenance of local servers or approval for offshore hosting, regular submission of financial and operational reports to CNJH, and appointment of local compliance officers.

Foreign ownership is permitted but subject to regulatory approval, and operators may need to partner with local firms to meet compliance expectations.

Compliance Obligations and Monitoring

Player Protection and Identification

Burkina Faso mandates a comprehensive set of player protection requirements aimed at responsible gambling and anti-money laundering. The minimum legal gambling age is 18 years.

Operators must perform age verification and identity checks for all players, monitor suspicious betting patterns, and provide tools for self-exclusion and betting limits.

- Mandatory KYC verification and age checks

- Anti-money laundering compliance consistent with local and FATF-related standards

- Provision of responsible gambling policies including self-exclusion

- Regular training of staff to identify problem gambling

- Information disclosure on the risks of gambling and available support services

Financial Monitoring and Reporting

Operators are required to monitor all financial transactions to ensure transparency and prevent fraudulent activity. Regular reporting to the CNJH includes tax declarations, transaction logs, and audit reports.

- Submit quarterly financial reports covering all gaming revenue

- Provide detailed tax filings aligned with the unified 5% GGR tax

- Undergo periodic independent audits of gaming operations and finances

- Report suspicious transactions or use of illicit funds immediately to regulatory authorities

Taxation Structure and Financial Obligations

Player Taxation

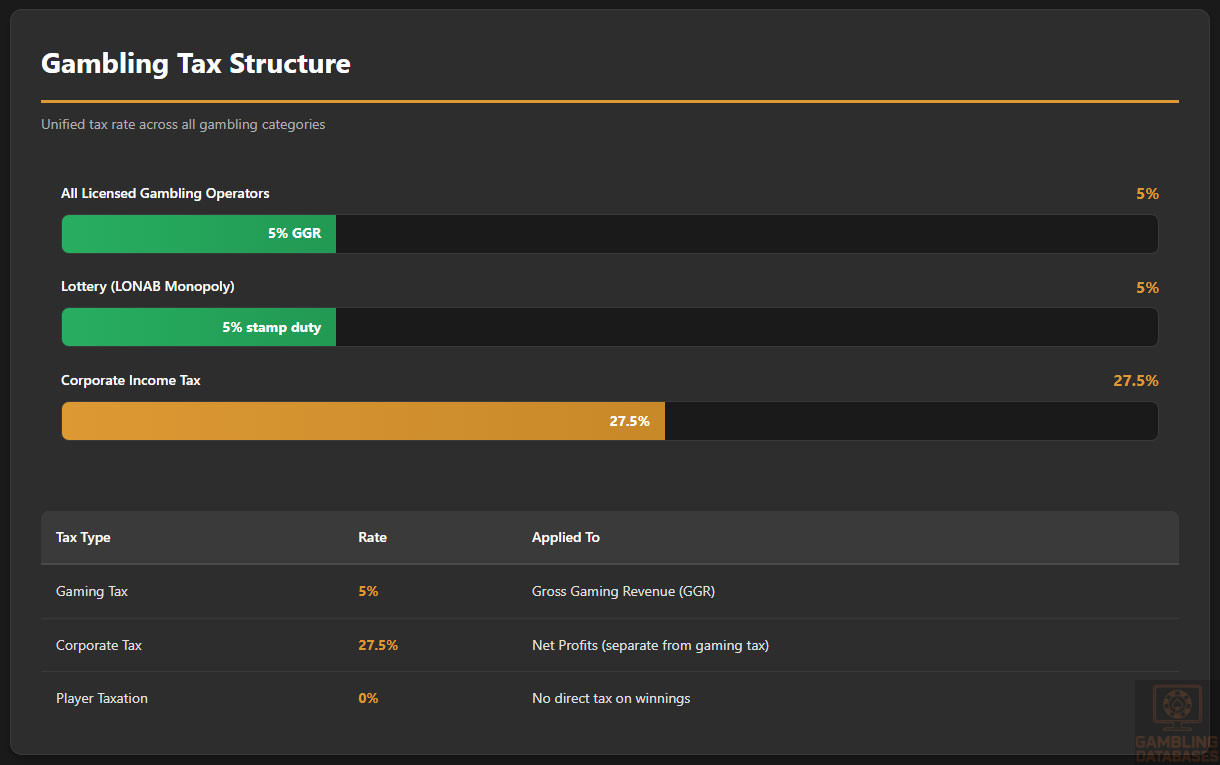

Players are not directly taxed on their gambling winnings in Burkina Faso. All tax obligations fall on the operators.

Operator Taxation

| Game Type | Tax Rate (GGR) |

|---|---|

| All Licensed Gambling Operators (land-based and online) | 5% |

| Lottery (LONAB Monopoly) | 5% stamp duty |

Besides the gambling tax, operators are also subject to ordinary corporate income tax. Licensing fees and annual renewal payments are additional financial obligations.

Gambling Market Financial Performance

The total wagered amount was estimated at over 64 billion FCFA in 2021, with gambling revenues growing approximately 15% annually. Tax revenues from gambling contribute to public service funding and infrastructure development. Increasing digital penetration and mobile betting adoption promise continued revenue growth.

Advertising and Marketing Restrictions

Advertising gambling in Burkina Faso is subject to content restrictions prohibiting misleading claims and targeting minors. Marketing channels, including broadcast and digital media, face limitations to ensure responsible promotion of gambling products.

- Prohibition of advertising targeting individuals under 18

- Restrictions on incentives and bonuses advertisements

- Limitation on gambling promotion during certain hours on broadcast channels

- Mandatory display of responsible gambling messages in ads

- Ban on false, exaggerated payout claims

Recent Regulatory Changes and Their Impact

In 2024-2025, Burkina Faso amended its tax framework to unify the various gambling tax categories under a single 5% gross gaming revenue rate. This change broadens the tax base and simplifies compliance.

Although online gambling regulation remains pending, proposals suggest the eventual imposition of licensing and taxation paralleling land-based rules. These reforms will likely increase operator costs but also create a clearer legal environment for investment.

Enforcement Mechanisms and Penalties

Regulatory authorities actively conduct inspections and compliance audits. Enforcement measures include financial penalties, license suspensions, and potential criminal charges against operators violating statutory obligations. Conformance to anti-money laundering and responsible gambling policies is closely monitored.

- Fines for operating without a valid license

- Suspension or revocation of gambling licenses for repeated violations

- Seizure of illegal gaming equipment

- Criminal prosecution for fraud or money laundering

- Public warnings and reputational sanctions

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

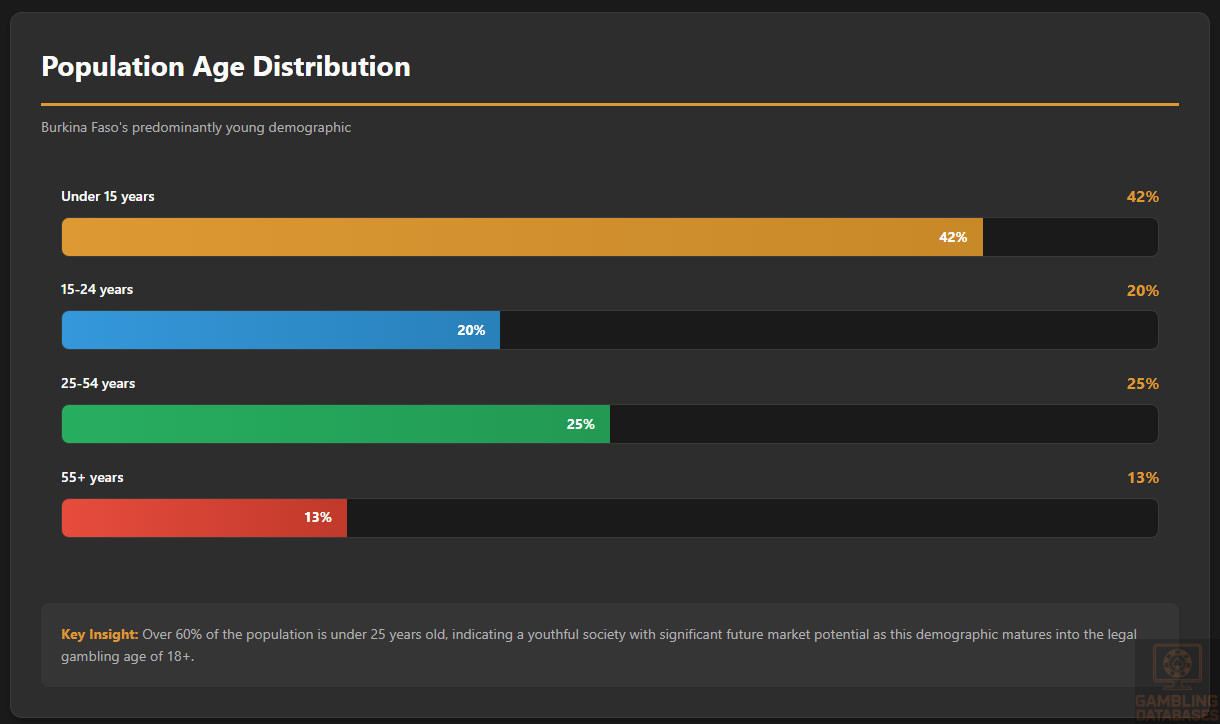

Burkina Faso has a population of approximately 22 million people in 2025, characterized by a predominantly young demographic with a median age of about 17.2 years. The age distribution is heavily skewed towards children and teenagers, with over 60% under 25 years old, indicating a youthful society.

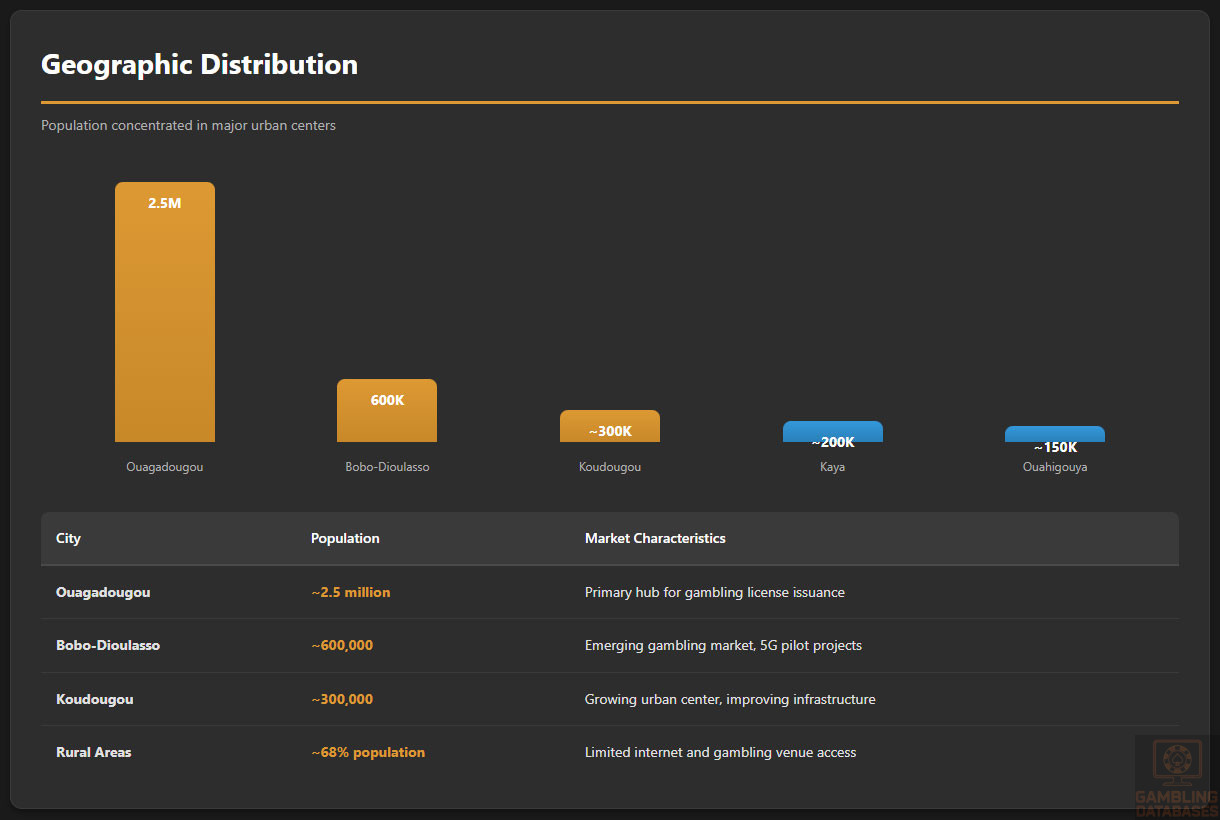

The gender ratio remains balanced, with a slight female majority. Urban areas account for roughly 32% of the population, concentrated mainly in Ouagadougou, Bobo-Dioulasso, and Koudougou. The majority of the population resides in rural regions, with limited internet and gambling venue access.

| Age Group | Population Percentage |

|---|---|

| Under 15 years | 42% |

| 15-24 years | 20% |

| 25-54 years | 25% |

| 55+ years | 13% |

Geographic Distribution

Major cities like Ouagadougou and Bobo-Dioulasso are the primary hubs for economic activity and gambling venues. Regional disparities are significant, with urban centers benefiting from better internet infrastructure and higher income levels.

- Ouagadougou – population ~2.5 million, focus for gambling license issuance

- Bobo-Dioulasso – population ~600,000, emerging gambling market

- Kaya – smaller city with growing sports betting presence

- Ouahigouya and Fada Nürel – rural towns with limited access

- Regional economic differences influence consumer participation in gambling activities, with urban areas demonstrating higher engagement due to better infrastructure

Gambling venues are mainly concentrated in these key cities, with internet access improving rapidly in urban regions, thereby facilitating online gambling prospects among younger populations.

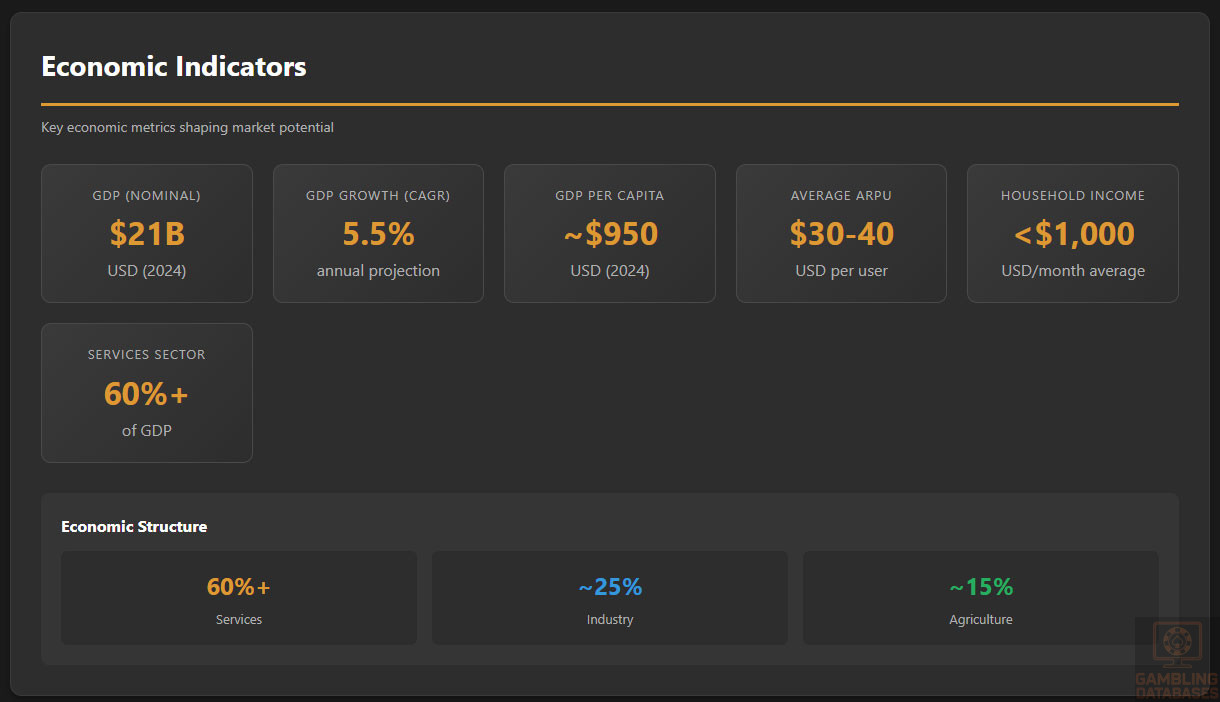

Economic Indicators and Consumer Spending Power

Burkina Faso’s GDP stands at around $21 billion USD, with a projected growth rate of approximately 5.5% annually. The economy relies heavily on agriculture, industry, and services, with the latter accounting for more than 60% of GDP.

The country’s *income distribution* remains uneven, with average household income estimated at less than $1,000 USD per month. Disposable income is limited, especially in rural regions, though urban centers see higher spending capabilities, especially on entertainment and gambling.

Current consumer spending patterns reflect a cautious approach, with a higher propensity for mobile and informal digital payment methods. The growth of the middle class, albeit limited, is gradually increasing market potential for gambling services.

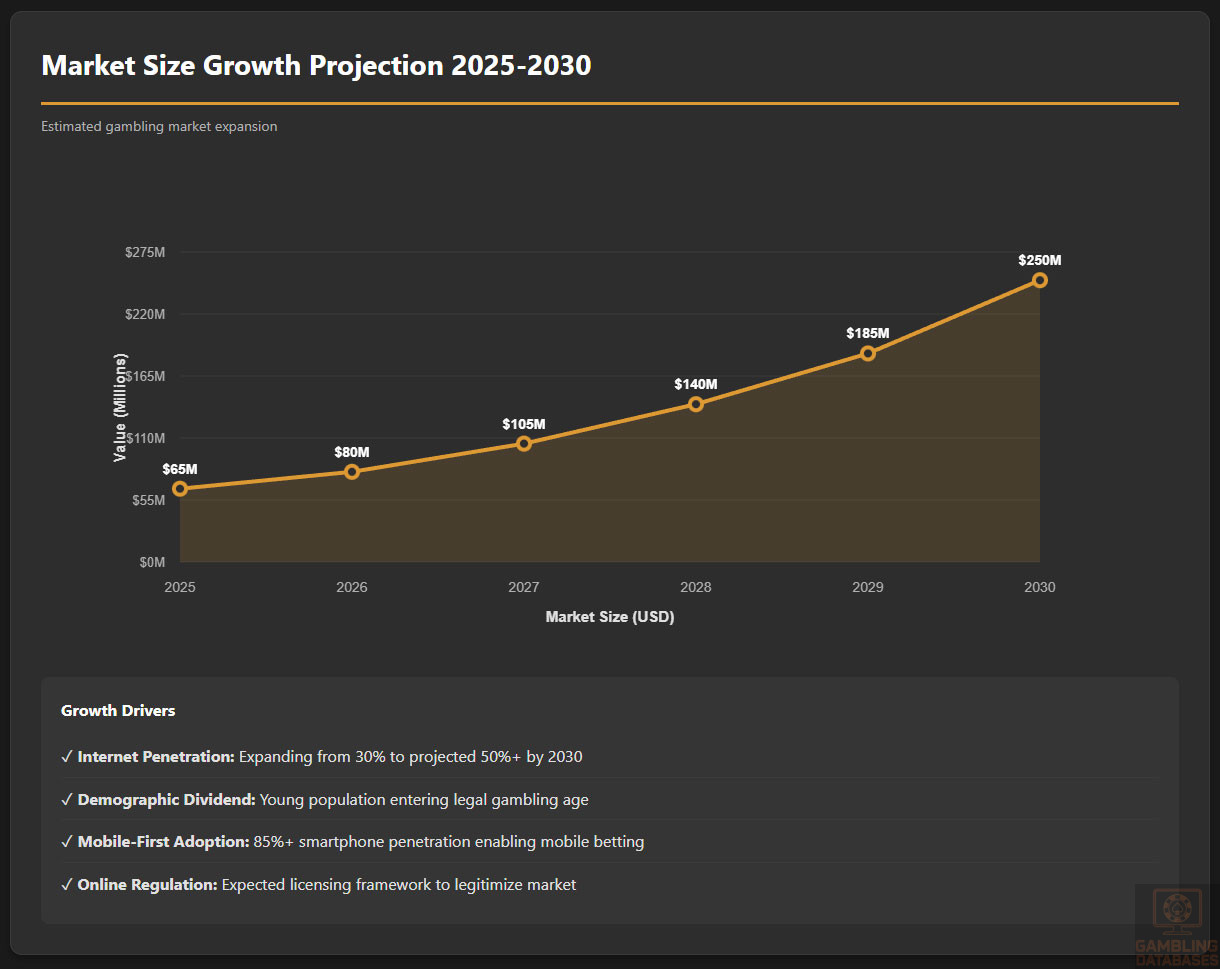

Market Size and Growth Projections

The existing gambling market is estimated at over €110 million ($130 million USD), predominantly driven by land-based betting and lotteries. Historical growth has averaged about 12-15% per year, with forecasts predicting continued expansion.

The online gambling sector remains nascent but promising, with expectations of tripling in size over the next five years. The total addressable market could reach approximately $250 million USD by 2030, fueled by internet penetration and demographic trends.

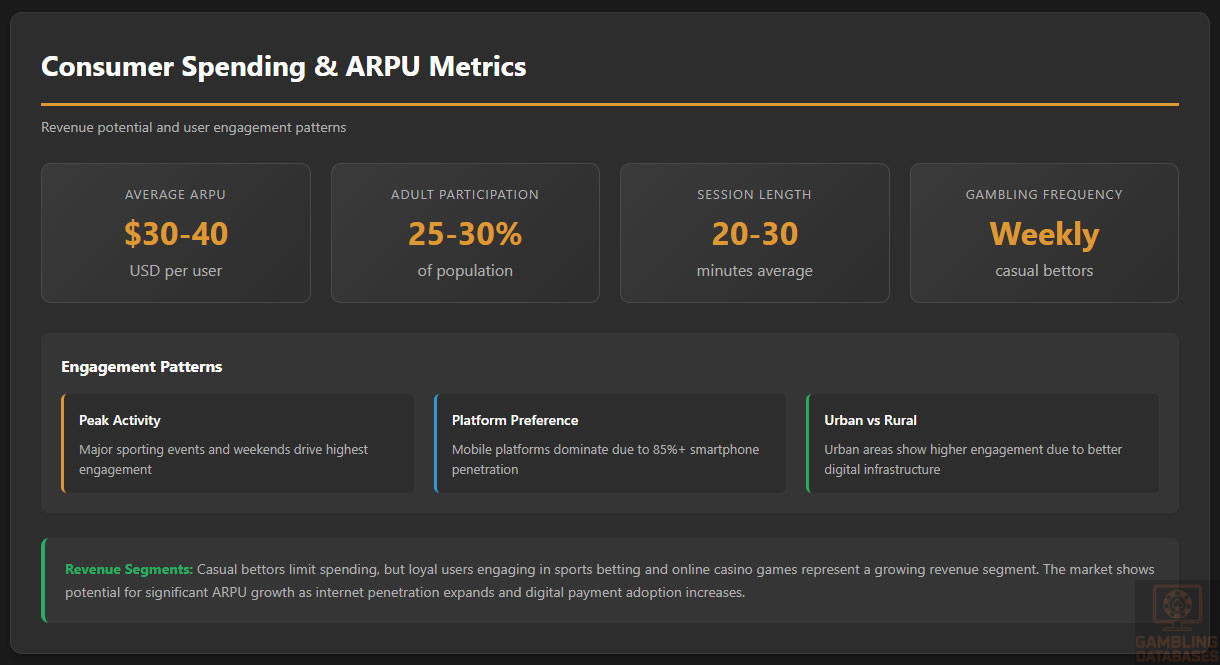

Projected ARPU (Average Revenue Per User) is around $30-$40 USD, with user engagement peaking during major sporting events and weekends.

Education, Skills, and Digital Literacy

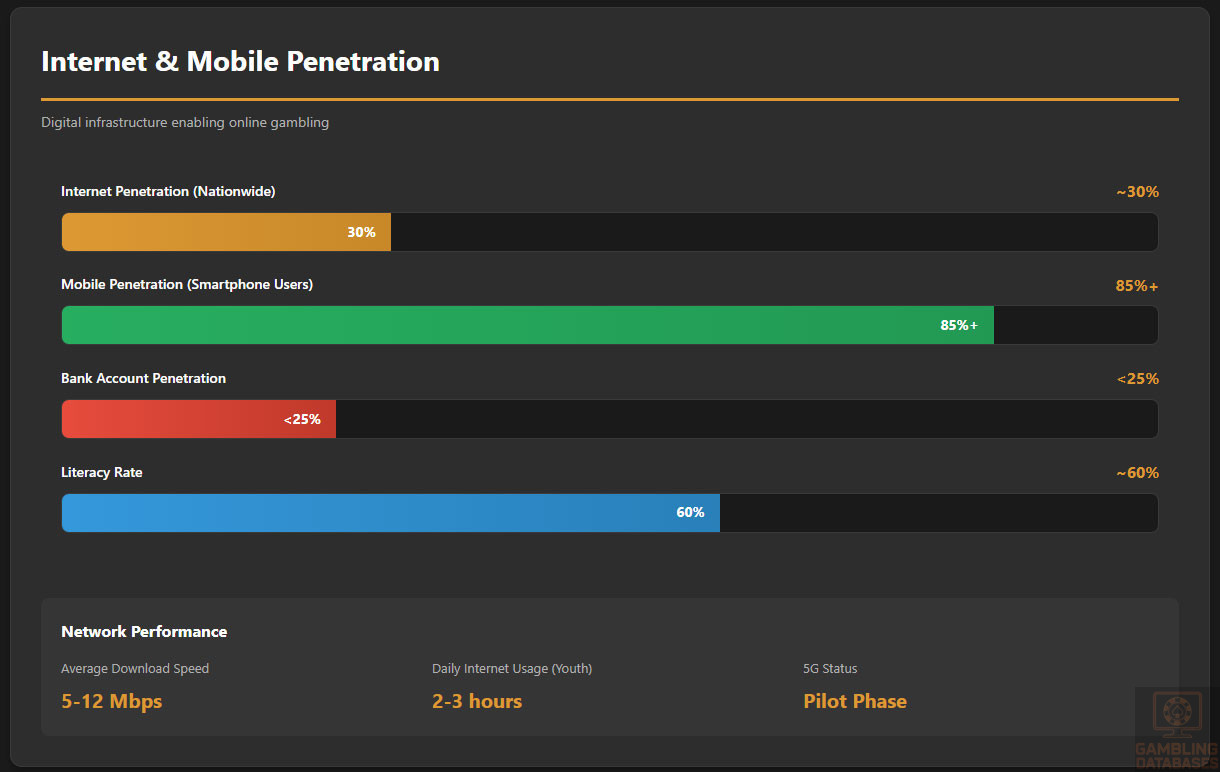

Literacy levels are around 60%, with higher literacy among urban youth. Educational attainment is improving, with more young people completing secondary education and some pursuing tertiary studies.

Digital literacy is growing, especially among those aged 15-34, driven by increased mobile internet access. Youths often access social media and entertainment platforms daily, creating a foundation for digital gambling exposure.

Workforce skills are primarily in agriculture, trade, and public administration, though digital skills in software use and basic online transactions are spreading rapidly among urban populations.

Cultural and Social Factors

Communication and Language

The dominant language is French, used officially and in education, but local languages such as Moore, Dioula, and Fula are widely spoken. Internet communication commonly occurs in French and local dialects, influencing marketing strategies and platform localization.

Cultural Attitudes

Gambling enjoys moderate social acceptance, especially as a form of entertainment linked to community festivals and sports. Religious influences, mainly Islam, promote caution around gambling, although it remains culturally ingrained in many regions.

Foreign gambling brands are perceived as modern and reliable, attracting urban populations, although some social stigma persists among rural communities.

Social Responsibility and Problem Gambling

- Gambling addiction awareness programs

- Responsible gambling policies mandated for licensed operators

- Self-exclusion options introduced by some online platforms

- Public campaigns to educate about gambling risks

- Support services and counseling centers available in urban areas

Problem gambling prevalence remains low but is monitored vigilantly by authorities to mitigate social harm.

Political Structure and Governance

Burkina Faso operates as a semi-presidential republic with stable governance structures designed to promote economic development. Political stability has improved following recent reforms, but regional security concerns influence investor confidence.

The government demonstrates a cautious but open approach to regulating gambling, balancing economic growth with social stability and compliance with international standards.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration is increasing, reaching approximately 30% of the population, primarily in urban centers. Daily internet usage among youth averages 2-3 hours, with social media and mobile apps widely used.

- Facebook and WhatsApp are dominant social platforms

- YouTube is popular among younger users for entertainment

- Twitter and TikTok are expanding rapidly among urban youth

- Online streaming and gaming are critical digital behaviors

- Smartphone adoption exceeds 85%, facilitating mobile betting

Digital Payment Behavior

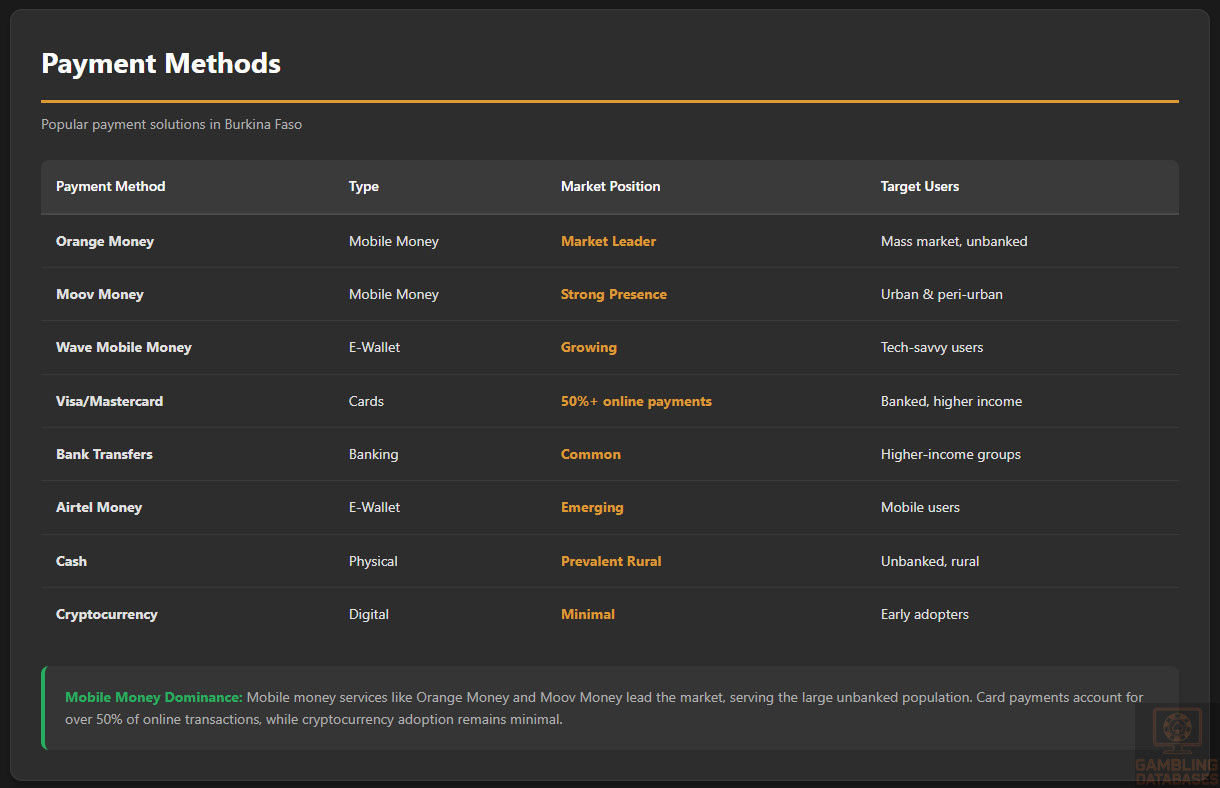

Payment methods are shifting towards mobile wallets and digital transactions, especially in urban areas. Credit and debit cards account for over 50% of online payments, with mobile money increasing rapidly.

- Mobile money services like Orange Money and Moov Money lead the market

- Bank transfers remain common among higher-income groups

- E-wallets such as Wave and Airtel Money are gaining popularity

- Cryptocurrency adoption remains minimal but shows potential

- Cash remains prevalent in rural regions due to limited digital infrastructure

Gaming and Gambling Preferences

Current Market Participation

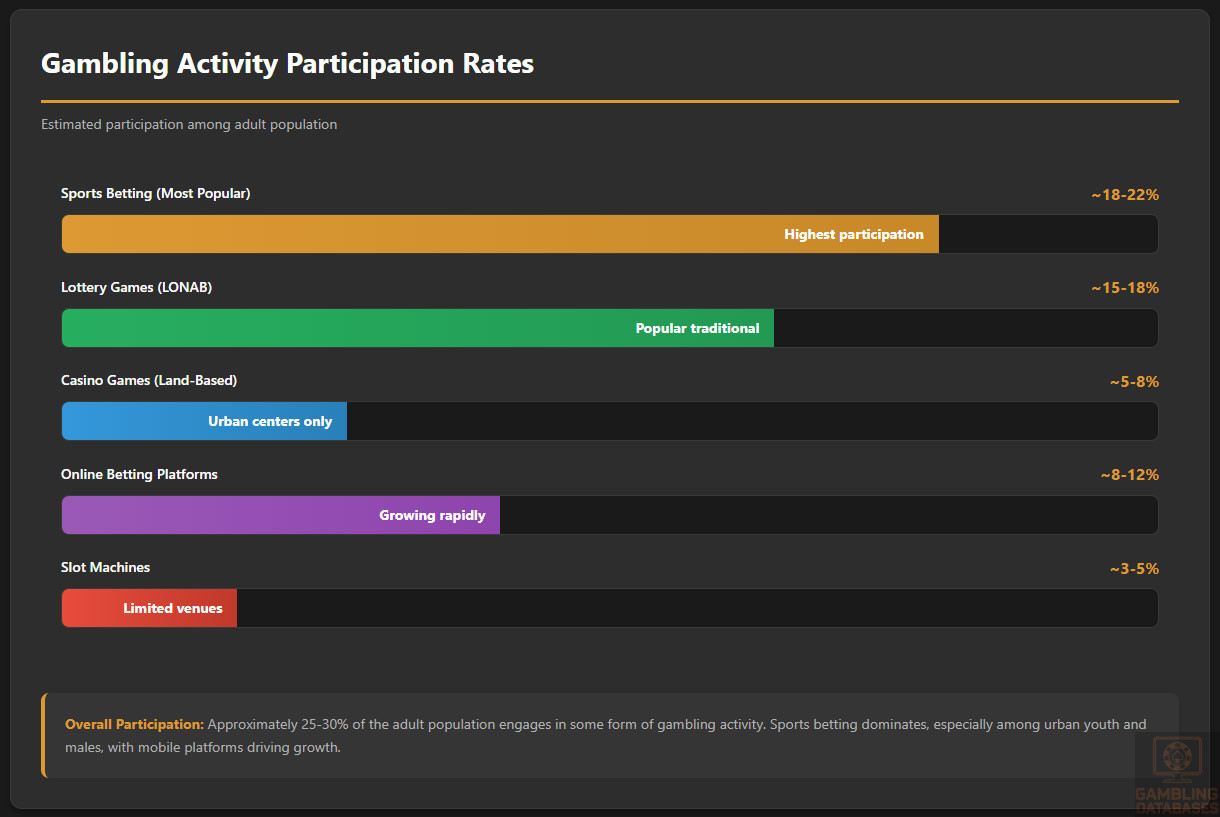

Participation in gambling activities is estimated at about 25-30% of the adult population. Sports betting, lotto, and informal betting are the most popular, especially among youth and males.

- Sports betting (most popular)

- Lottery games

- Casino card games in land venues

- Slot machines, mostly in urban clubs

- Online betting platforms

Consumer Behavior Patterns

Gambling spending peaks during major sporting events, with casual bettors participating weekly. Mobile platforms dominate, with session lengths averaging 20-30 minutes. Engagement is higher in urban areas due to better digital infrastructure and entertainment options.

Casual bettors tend to limit their spendings, but loyal users engaging in sports betting or online casino games represent a growing revenue segment for operators.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Internet penetration in Burkina Faso remains moderate at approximately 30% nationwide, with broadband access concentrated mainly in urban centers. Mobile networks dominate internet connectivity due to limited fixed-line infrastructure. Average download speeds range from 5 to 12 Mbps, reflecting ongoing network development and variable reliability across regions.

Government and private sector investments have focused on expanding fiber optic networks and improving backbone connectivity. Rural areas still face connectivity challenges limiting digital service reach but are gradually catching up with expanding mobile coverage.

5G and Future Technology Deployment

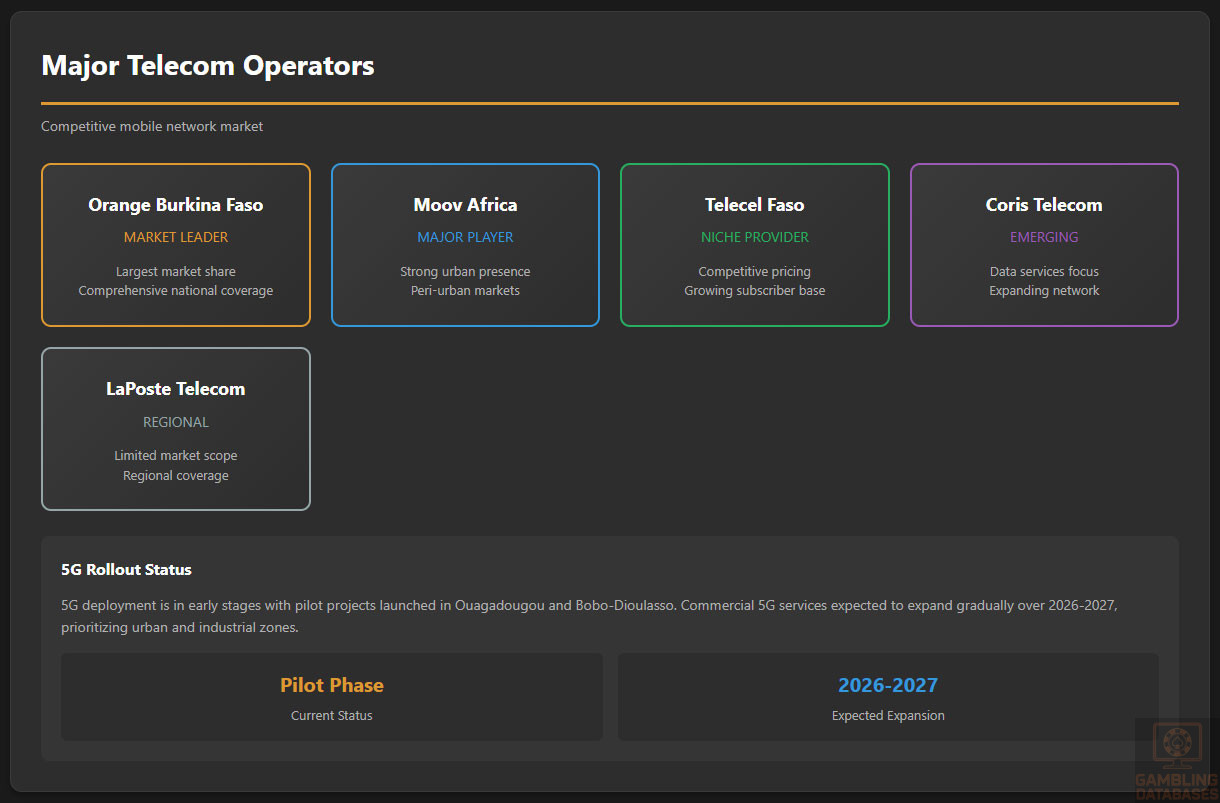

5G rollout is in the early stages with pilot projects initiated in Ouagadougou and Bobo-Dioulasso. Commercial 5G services are expected to expand gradually over 2026-2027, prioritizing urban and industrial zones. The main telecom operators are actively upgrading network infrastructure to support future digital economy needs and enhance mobile data capacity.

Simultaneously, satellite internet services and alternative technologies are being explored to bridge rural connectivity gaps and expand the digital inclusion agenda.

Mobile Technology Ecosystem

The mobile network market is competitive, led by several key operators with extensive coverage and diverse service offerings. Mobile data costs are moderate but remain a barrier for low-income consumers in rural areas. Smartphone penetration exceeds 85% among urban users, fueling mobile-first digital behaviors and online gambling engagement.

- Orange Burkina Faso – largest market share, comprehensive national coverage

- Moov Africa – strong presence in urban and peri-urban markets

- Telecel Faso – niche provider with competitive pricing

- Coris Telecom – emerging operator focused on data services

- LaPoste Telecom – regional operator with limited market scope

Device preferences trend towards mid-range Android smartphones, favored for affordability and app compatibility. Increasing availability of budget devices supports growing smartphone adoption among younger demographics.

Financial Services and Payment Infrastructure

The banking sector includes a mix of commercial banks and microfinance institutions facilitating business and consumer transactions. While traditional bank account penetration remains relatively low at under 25%, mobile money platforms dominate daily financial services, especially for unbanked populations.

- Coris Bank – leading commercial bank with digital platforms

- BCEAO Burkina Faso – central banking services and regulation

- NSIA Bank – regional bank focused on SMEs

- Banque Atlantique – retail banking and mobile integration

- Ecobank Burkina Faso – pan-African banking network presence

Popular payment methods include international cards (Visa, Mastercard), mobile money services (Orange Money, Moov Money), bank transfers, e-wallets, and cash-on-delivery for e-commerce.

- Orange Money

- Moov Money

- Wave Mobile Money

- Visa/Mastercard debit and credit cards

- Bank wire transfers

E-commerce and Digital Economy

E-commerce in Burkina Faso is growing but remains underdeveloped relative to regional peers. Trust in online retail is gradually increasing, supported by expanding internet access and improved payment infrastructure. Local platforms offer electronics, fashion, and digital services primarily via mobile apps and websites optimized for lower bandwidth.

Digital service adoption, including entertainment streaming and mobile gaming, is gaining momentum, creating a favorable environment for the development of online gambling products tailored to local consumer expectations.

Business Environment and Regulatory Framework

Burkina Faso ranks modestly in global ease of doing business indices, with ongoing reforms aimed at simplifying company registration and tax compliance. Foreign direct investment is encouraged, particularly in IT and financial services sectors, supported by bilateral treaties and membership in the West African Economic and Monetary Union (WAEMU).

The business registration process requires a blend of local legal expertise and administrative navigation, with increasing digitization of public services reducing turnaround times.

- Prepare and notarize incorporation documents, including apostille for foreign certifications (2-3 weeks)

- Submit registration to the Trade and Companies Registry (processing ~1 week)

- Obtain tax identification and social security registration (3-5 business days)

- Open corporate bank account and deposit statutory capital (1-2 weeks)

- Receive final confirmation and operating permits (2-4 days)

Corporate Structure and Registration

Common business entity types are Limited Liability Companies (LLCs), Joint Stock Companies (SAs), and Branch offices of foreign companies. LLCs are preferred by small and medium-sized operators for liability protection and simplified governance. SAs are suited for larger investment projects requiring access to capital markets. Branch offices provide operational flexibility but are subject to full local compliance.

Foreign ownership is generally permitted without restrictions but requires full compliance with registration and tax laws.

Required registration documents include:

- Articles of Incorporation and company bylaws

- Proof of registered office address

- Identification documents for all directors and shareholders

- Tax clearance certificates

- Bank statements confirming capital deposits

- Proof of compliance with anti-money laundering requirements

Taxation Framework

The standard corporate income tax rate is 27.5%, with exemptions and reduced rates available in designated economic zones. Tax treaties with multiple countries aim to prevent double taxation and encourage cross-border investment.

- France

- Belgium

- Senegal

- Ivory Coast

- Mali

- Luxembourg

Personal income tax follows a progressive scale reaching up to 30%, with mandatory social security contributions. Withholding taxes apply on dividends, interest, and royalties, impacting foreign investors.

Market Entry Considerations

Recommended entry strategies highlight partnerships with local firms, acquisitions of land-based operators, and deployment of mobile-first platforms focusing on sports betting and lottery segments. Leveraging mobile money integration and local payment solutions enhances user acquisition and retention.

- Form joint ventures with established local gambling companies

- Acquire existing physical venue operators for rapid market access

- Launch mobile betting platforms optimized for local infrastructure

- Implement localized marketing campaigns respecting cultural norms

- Comply proactively with evolving regulatory requirements

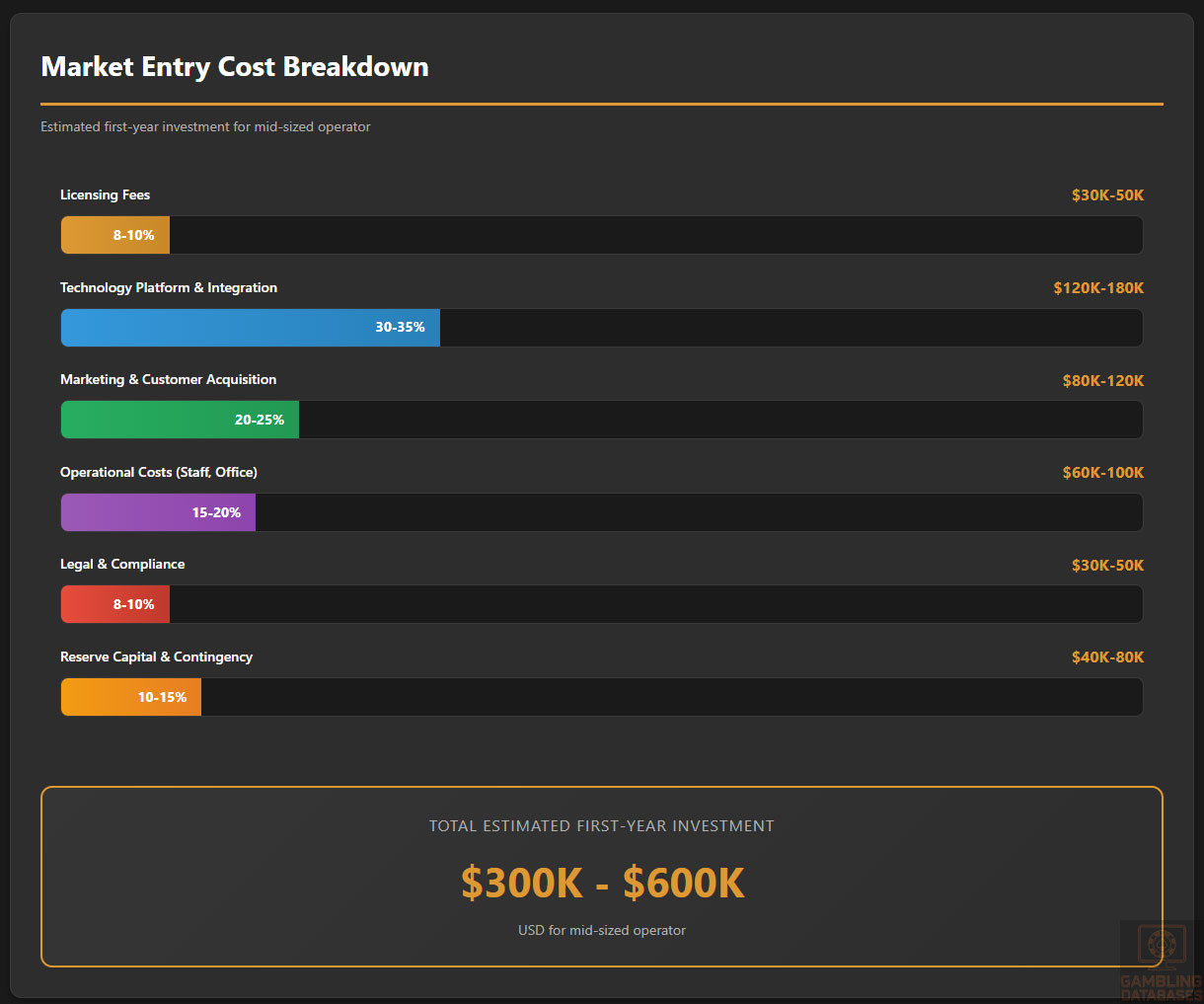

Initial setup investments vary but typically encompass licensing fees, technology deployment, marketing, and operational staffing. Estimated first-year costs range between $300,000 and $600,000 for a mid-sized operator.

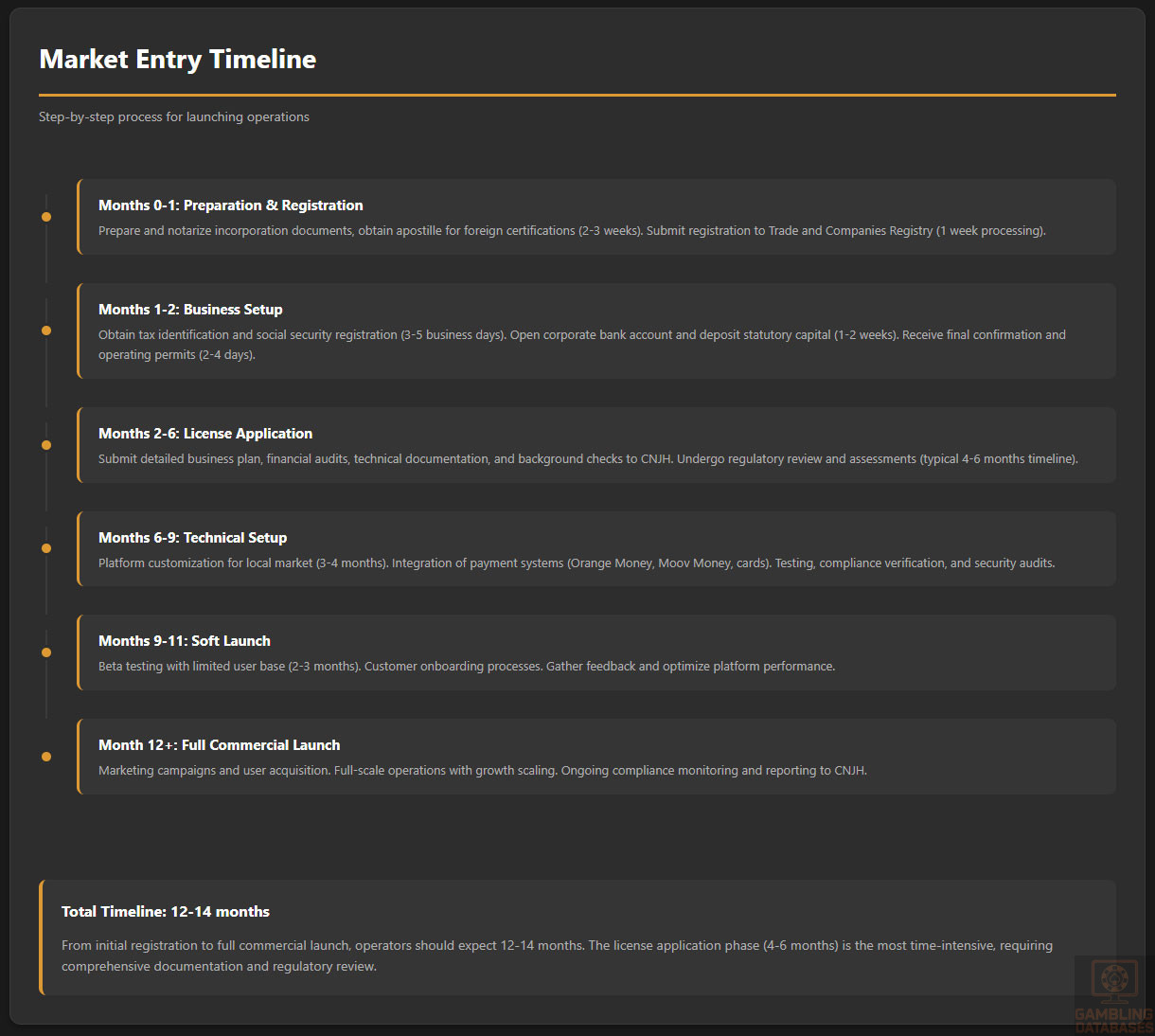

Business timelines include license application and approval (4-6 months), platform customization and testing (3-4 months), and launch phases supported by marketing campaigns (2-3 months).

- License application and regulatory approvals

- Technical and market preparation

- Soft launch and customer onboarding

- Full commercial launch and growth scaling

Key success factors include understanding local consumer behavior, robust compliance, technological adaptability, and competitive pricing. Major challenges encompass infrastructure gaps, payment system complexity, and occasional political uncertainties.

- Strong local partnerships and regulatory relations

- Flexible technology platforms optimized for mobile

- Effective payment and withdrawal systems integration

- Compliance with AML and responsible gaming protocols

- Adaptation to rapid market and regulatory changes

Exit strategy planning involves license transfer provisions, secondary market liquidity for gambling assets, and valuation dependent on user base growth and regulatory status.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Burkina Faso?

Online gambling currently operates in a regulatory grey area. While not explicitly legalized, it is not prohibited. The government is developing a legal framework to formally regulate online operators, anticipated to require licensing and taxation similar to land-based entities. Operators typically partner with local firms and seek CNJH approval to mitigate risks.

2. What types of gambling licenses are available and what do they cover?

Licenses cover land-based casinos, sports betting, lotteries, and slot machine operations. Although no formal online gambling license exists yet, proposals suggest its introduction soon. Licenses authorize operation within specified venues or platforms, with regulatory oversight covering compliance, taxation, and responsible gaming implementation.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing fees generally range from $30,000 to $50,000 depending on scope. The application evaluation process usually spans four to six months and involves background checks, technical assessments, and financial vetting. License renewal and annual fees apply thereafter.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain licenses but must establish a local legal entity. Foreign ownership is permitted with no explicit restrictions, providing regulatory compliance is met. Partnering with local entities eases market entry and aligns with government expectations.

5. What are the tax obligations for iGaming operators?

Operators pay a unified 5% gross gaming revenue tax, supplemented by standard corporate income tax around 27.5%. Additional fees include licensing and renewal costs. Compliance with local tax filing and audit requirements is mandatory.

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue Tax | 5% |

| Corporate Income Tax | 27.5% |

| Licensing Fees | Varies ($30,000-$50,000) |

6. Are gambling winnings taxed for players?

No direct taxation is imposed on players’ gambling winnings. The government taxes operators only, making winnings tax-free for end users.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, technology platform expenses, marketing, staffing, payment processing fees, and compliance costs. Marketing and customer acquisition often represent the largest variable expense, followed by software licensing and regulatory payments.

8. What is the expected ROI timeline for entering this market?

ROI typically materializes over 2-3 years, influenced by effective market penetration and operational efficiency. Initial costs are offset gradually with growth in user base and betting volumes. Strategic partnerships and local knowledge expedite returns.

9. What are the local presence requirements for operators?

Operators must establish a local entity registered under Burkinabé law. Physical offices and appointed compliance officers are typically required, especially for land-based operations. Online operators are expected to comply similarly as regulations evolve.

10. What payment methods are available and recommended?

Mobile money services dominate, including Orange Money and Moov Money. International cards (Visa, Mastercard), bank transfers, and e-wallets are also supported, with mobile money favored for convenience and penetration among lower-income populations.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors and must include responsible gambling messages. Bonuses and promotions are regulated, and gambling ads on broadcast media are limited to certain times. Misleading claims are prohibited to protect consumers.

12. What responsible gambling measures are mandatory?

Operators must verify player age, provide self-exclusion options, monitor for problem gambling indicators, conduct staff training, and disclose gambling risks. These measures align with international best practices for consumer protection.

13. How large is the iGaming market and what is the growth potential?

The current market size exceeds $130 million, with projections expecting growth to $250 million by 2030. This expansion is driven by digital infrastructure improvements and favorable demographics, especially youth engagement with mobile platforms.

14. Who are the main competitors and what is their market share?

Key competitors include ABC Casinos, Betway, LONAB, and national lottery operators. Land-based firms dominate revenue, while online sportsbooks and mobile betting platforms capture a growing market share in urban centers.

15. What are the player preferences and typical spending patterns?

Sports betting leads in popularity, followed by lotteries and casino card games. Players primarily engage via mobile devices, with spending concentrated around major sports events, preferring small to moderate wagers.

16. What are the key success factors and main challenges for new entrants?

Success depends on local partnerships, technology adaptability, compliance diligence, and tailored marketing. Challenges include infrastructure gaps, payment system integration, fluctuating regulatory landscape, and cultural sensitivities.

Sources and References

- Commission Nationale des Jeux de Hasard (CNJH) – Official Gambling Authority Burkina Faso

- National Institute of Statistics and Demography (INSD) Burkina Faso – Population Reports 2024

- World Bank – Doing Business Report 2024 – Burkina Faso

- International Telecommunication Union – ICT Statistics 2025

- Central Bank of West African States (BCEAO) – Financial Reports 2025

- Ministry of Finance Burkina Faso – Tax Regulation Publications 2025

- Orange Burkina Faso – Annual Telecom Report 2025

- Moov Africa – Market Share and Network Performance Data 2025

- LONAB – National Lottery Reports 2024

- Global Betting and Gambling Consultants – Africa Market Analysis 2025

- African Development Bank – Economic Outlook Burkina Faso 2024-2026

- GSMA Intelligence – Mobile Networks in Africa 2025

- United Nations Development Programme (UNDP) – Digital Literacy Survey 2024

- Burkina Faso Ministry of Commerce – Business Registration Guidelines 2025

- World Economic Forum – Global Competitiveness Report 2024

- International Monetary Fund – Country Report Burkina Faso 2024

- KPMG Africa – Tax and Regulatory Guide 2025

- PwC Africa – Financial Services Report 2025

- TechnoAfrica Insights – Burkina Faso Telecom Infrastructure 2025

- Cambridge Economic Research – Gambling Market Projections 2025

- Gaming Association of West Africa – Regulatory Review 2025

- LexAfrica Legal – Gambling Law and Compliance 2025

- African Casino Review – Market Competitor Analysis 2024

- Africa Digital Economy Report 2025 – African Union Publications

- Bureau of Economic Analysis – Consumer Spending Patterns 2025 Burkina Faso

- Local News Outlets – Gambling Legislative Updates 2024-2025

🎯 Gambling Databases Country Rating: Burkina Faso

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 4.9/10 | 🟡 Moderate (Emerging market with significant challenges) |

| Player Access Score | 5.3/10 | 🟡 Partially Legal (Land-based legal, online grey area) |

| Overall Market Attractiveness | 5.1/10 | 🟡 Emerging Frontier Market (High risk, limited immediate returns) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Online gambling operates in a REGULATORY GREY ZONE with no explicit legalization. Current operations are unregulated and subject to potential future crackdowns or blocking.

- Government reserves the right to block unlicensed online gambling platforms at any time without notice. No formal online licensing framework exists as of 2025.

- Extremely limited market size ($65 million total, 2025) means customer acquisition costs will remain high relative to potential revenue.

- GDP per capita of only $950 USD creates severe constraints on player spending power and ARPU ($30-40), making profitability extremely challenging.

- Internet penetration at only 30% with average speeds of 5-12 Mbps limits addressable market to urban centers only.

- Banking penetration under 25% means heavy reliance on mobile money, which can be restricted or regulated at any time.

- Political instability and regional security concerns create ongoing investment risk. Recent governance reforms show improvement but uncertainty remains.

- No established legal precedent for online gambling means you’re operating in a regulatory vacuum. Future laws could be punitive.

- Mandatory local company registration and physical presence requirements increase operational complexity and costs for unregulated online operations.

- Very young population (median age 17.2 years, 42% under 15) creates significant responsible gambling compliance challenges and reputational risks.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.8/3.0 | Land-based gambling fully legal (+1.5). Online gambling NOT EXPLICITLY LEGALIZED, operates in grey zone (0 points for online). Government reserves right to block unlicensed online platforms (-0.5). No formal online licensing framework available (-0.25). Total deductions significantly reduce score. Final: 0.8/3.0 |

| Licensing Process | 25% | 1.3/2.5 | Limited licensing available only for land-based operations (+1.0). Application cost $30-50k is relatively accessible (+0.5). However, 4-6 month timeline is moderate (0). Online licensing framework DOES NOT EXIST, creating massive uncertainty (-0.5). Mandatory local company registration adds complexity (-0.25). Foreign ownership allowed but requires regulatory approval creates delays (-0.25). No clear path for online operators (-0.25). Final: 1.3/2.5 |

| Taxation & Costs | 20% | 1.8/2.0 | Unified 5% GGR tax rate is exceptionally favorable (+2.0). However, additional 27.5% corporate income tax applies separately (-0.25). Total effective tax rate approximately 30-32% after all obligations. Estimated first-year setup costs $300k-600k for mid-sized operator remain significant for market size (-0.25). High customer acquisition costs relative to low ARPU ($30-40) create profitability challenges but not explicitly penalized here. Final: 1.8/2.0 |

| Operational Requirements | 15% | 0.8/1.5 | Mandatory local company registration required (+0). Physical presence “generally necessary” for land-based, “strongly recommended” for online adds costs (+0.5). Local servers or offshore hosting approval creates technical barriers (-0.25). Appointment of local compliance officers required (-0.1). Heavy reliance on mobile money (85%+ banking unbanked) creates payment infrastructure risk (-0.25). Limited payment method diversity (-0.25). Capital deposit requirements in recognized banks create barriers. Final: 0.8/1.5 |

| Market Environment | 10% | 0.2/1.0 | Burkina Faso ranks poorly in global ease of doing business indices (+0.25 for difficult environment). Recent political reforms show improvement but regional security concerns persist (-0.25). Advertising content restrictions and channel limitations present (-0.25). Regulatory framework for online gambling remains undeveloped, creating uncertainty (-0.25). Market size only $65M total severely limits opportunity (-0.25). Very low internet penetration (30%) restricts addressable market. Extremely low GDP per capita ($950) constrains consumer spending. Final: 0.2/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.0/4.0 | Land-based gambling fully legal and accessible (+2.0). Online gambling exists in grey area – not explicitly prohibited but not regulated (+1.0). International operators provide online services but without legal clarity. Government can block platforms at any time (-0.5). No formal online licensing means players accessing offshore sites face regulatory uncertainty (-0.5). Players not currently penalized but this could change. Final: 2.0/4.0 |

| Practical Accessibility | 30% | 2.0/3.0 | Mobile money widespread (Orange Money, Moov Money, Wave) provides access (+1.5). International cards (Visa, Mastercard) accepted (+0.5). Bank transfers available (+0.25). However, banking penetration under 25% severely limits formal payment access (-0.5). Internet penetration only 30% restricts online access to urban minority (-0.5). Average internet speeds 5-12 Mbps create technical barriers (-0.25). Rural areas have minimal connectivity (-0.25). No evidence of systematic ISP blocking currently (+0.25). Final: 2.0/3.0 |

| Player Penalties | 20% | 1.5/2.0 | No direct taxation on player winnings (+1.0). No evidence of penalties for players using offshore sites (+1.0). Minimum legal age 18 years enforced for land-based. However, unclear legal status for online gambling means players face regulatory uncertainty (-0.5). Government reserves right to implement penalties in future. Final: 1.5/2.0 |

| Market Availability | 10% | 0.8/1.0 | Multiple land-based operators licensed and operating (+0.5). Several international online operators serve market (Betway, LeoVegas, Jackpot247) (+0.3). However, no formal online licensing means limited truly “legal” online options. Land-based venues concentrated only in major cities (Ouagadougou, Bobo-Dioulasso). 68% of population in rural areas has minimal access (-0.25). Market concentration limits player choice. Final: 0.8/1.0 |

🔍 Key Highlights

Strengths (Limited)

- Very Low Tax Rate: Unified 5% GGR tax is among the lowest globally, with reasonable 27.5% corporate tax creating approximately 30-32% total effective rate – significantly better than most regulated markets.

- No Online Prohibition: Unlike many markets, online gambling is not explicitly banned, creating potential opportunity once regulation is formalized.

- Growing Digital Infrastructure: Internet penetration increasing, mobile penetration exceeds 85%, smartphone adoption strong in urban areas, providing foundation for digital gambling growth.

- Young Population: Median age 17.2 years means large cohort entering legal gambling age (18+) over next 5-10 years, creating long-term growth potential if market develops.

- Mobile Money Dominance: Widespread mobile payment infrastructure (Orange Money, Moov Money, Wave) provides payment rails for unbanked population.

- Market Growth Rate: 15% annual growth in gambling market shows increasing consumer interest despite economic constraints.

- Foreign Ownership Allowed: No explicit restrictions on foreign operators, though local registration mandatory.

⛔️ CRITICAL RISKS AND CHALLENGES

- [Online Regulatory Vacuum:] Online gambling operates in COMPLETE REGULATORY GREY ZONE with no licensing framework, no legal protections, and risk of sudden blocking or criminalization. You are operating without legal cover.

- [Microscopic Market Size:] Total market only $65 million USD (2025) across ALL gambling products. For context, this is smaller than a single successful online casino brand in regulated EU markets. Extremely limited revenue opportunity.

- [Crushing Economics:] GDP per capita $950 USD means disposable income essentially non-existent. ARPU only $30-40 USD makes customer acquisition costs prohibitive. Most operators need $200+ ARPU to be profitable.

- [Severe Infrastructure Limitations:] Internet penetration only 30%, concentrated in urban areas. Average speeds 5-12 Mbps. 68% of population in rural areas has minimal/no connectivity. You can only serve small urban minority.

- [Banking Exclusion:] Banking penetration under 25% means 75% of population unbanked. Heavy reliance on mobile money which can be restricted by government or telcos at any time without recourse.

- [Political and Security Risks:] Regional security concerns, recent political instability, and governance challenges create ongoing investment risk. Government could implement punitive regulations at any time.

- [Responsible Gambling Nightmare:] 42% of population under 15 years old. Very young population (median 17.2) creates massive responsible gambling challenges. Age verification extremely difficult with limited ID infrastructure.

- [No Legal Precedent:] Zero established case law or regulatory precedent for online gambling. First movers face all the risk with no legal clarity. Future regulations could be retroactively punitive.

- [Local Presence Mandatory:] Must establish local company, maintain physical presence, appoint local compliance officers. High overhead costs for tiny market opportunity.

- [Payment Processing Risk:] Limited payment method diversity. No cryptocurrency mention suggests it may not be viable. International card processors may restrict gambling transactions.

- [Customer Acquisition Impossibility:] In a $65M total market with $30-40 ARPU, advertising restrictions, and limited digital reach, acquiring customers profitably is nearly impossible for new entrants.

- [Market Already Saturated:] Multiple international brands (Betway, LeoVegas) plus local operators already serve the small addressable market. Late entrants face entrenched competition for microscopic player base.

Player-Specific Issues

- Players CANNOT legally access online casino gaming under formal regulation – only grey market offshore sites available.

- Banking exclusion (75% unbanked) severely limits payment options – mobile money dependency creates vulnerability.

- Internet access limited to 30% of population – rural majority cannot access online gambling even if legal.

- No consumer protections for online gambling – players using offshore sites have zero legal recourse.

- Future regulatory changes could criminalize player activity – currently no penalties but no guarantees.

- Low income ($950 GDP per capita) makes gambling unaffordable for most population – creates predatory optics.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $300,000 – $600,000 for mid-sized operator (licensing, tech, marketing, staffing)

Monthly Operating Costs: $40,000 – $80,000 (staff, compliance, tech, local presence, servers, support)

Effective Tax Rate on Revenue: 30-32% (5% GGR + 27.5% corporate income tax calculated on net income)

Customer Acquisition Cost: Estimated $80-150 for a market with $30-40 ARPU. This ratio is UNSUSTAINABLE.

Addressable Market: 30% internet penetration × 22M population × 18+ age × 25-30% gambling participation = approximately 1.3-1.6 million potential online players. In a $65M total market, this means online gambling likely represents $15-25M maximum annually.

Time to Breakeven: 36-48 months MINIMUM, assuming favorable conditions and no major regulatory changes

Time to Positive ROI: 48-60+ months, assuming you survive regulatory uncertainty

Profitability Assessment: Economics are PROHIBITIVE for virtually all operators. With ARPU of only $30-40 USD in a market where GDP per capita is $950, customer acquisition costs of $80-150 consume almost all first-year revenue per player. The total addressable online market of $15-25M annually means even capturing 10% market share generates only $1.5-2.5M in gross gaming revenue annually – before the 5% gambling tax and 27.5% corporate tax. After paying $480k-960k in annual operating costs, breakeven requires 50%+ market share in a market already served by Betway, LeoVegas, and other established brands. Unless you have $2M+ capital to burn for 5+ years while building brand in a microscopic market, stay away. This is a frontier market for patient, well-capitalized operators willing to accept 5-7 year investment horizons with high risk of total loss if regulation turns hostile.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators (No Local License) | ⚠️ HIGH | Operating in complete regulatory vacuum. Government reserves right to block platforms at any time. No legal protections. Future regulations could be retroactively punitive. Zero legal recourse if blocked or prosecuted. Banking/payment rails can be cut off instantly. |

| Licensed Land-Based Operators | 🟡 MEDIUM | Clear licensing framework and legal status. However, 4-6 month licensing process, mandatory local presence costs, and limited market size ($65M total) create profitability challenges. Regulatory compliance burden significant relative to market opportunity. |

| Online Operators Seeking Local Registration | ⚠️ HIGH | No formal online licensing framework exists. Cannot obtain legal license for online operations. Must operate in grey zone with local entity registration but no gambling license. Exposed to sudden regulatory changes. First movers bear all risk of establishing precedent. |

| Affiliates/Advertisers | 🟡 MEDIUM | Advertising restrictions apply (content limitations, no targeting minors, channel restrictions). No evidence of prosecution for promoting offshore sites currently, but legal status unclear. Future regulations could criminalize affiliate marketing for unlicensed operators. |

| Payment Processors | 🟡 MEDIUM | Mobile money dominance means telco partnerships critical but vulnerable to regulatory pressure. Banking sector can restrict gambling transactions. No cryptocurrency framework mentioned. Processing for grey-market online gambling creates compliance risk. |

| Company Directors/Executives | 🟡 MEDIUM-HIGH | Mandatory local presence and local compliance officer appointments create personal exposure. Directors of companies operating in regulatory grey zone face potential future prosecution if laws change. Travel risk moderate but increasing if operating without clear legal status. |

🚨 Extradition and International Enforcement

Extradition Treaties: Burkina Faso has extradition agreements with France (former colonial power), and as ECOWAS member cooperates with West African nations. Limited extradition relationships with USA, UK, EU beyond France. Not a major concern currently but could develop.

Enforcement History: No documented cases of international prosecution or extradition specifically for online gambling offenses. However, regulatory framework is new and evolving. Absence of precedent means no protection – first cases could establish harsh standards.

WAEMU Membership: As member of West African Economic and Monetary Union, Burkina Faso coordinates financial regulation with Benin, Ivory Coast, Mali, Niger, Senegal, Togo. Gambling regulations could harmonize across region, extending enforcement reach.

Safe Jurisdictions: Countries without extradition agreements include most of Asia, Russia, China, CIS countries. However, operating from these jurisdictions creates other banking and payment processing challenges.

Travel Risk: LOW to MODERATE. Currently minimal risk for executives of offshore gambling operators. However, this could change rapidly if Burkina Faso formalizes online gambling laws and begins enforcement. French connections create potential EU travel complications if prosecuted.

International Banking Risk: MODERATE. Operating in regulatory grey zone may cause international banks and payment processors to restrict accounts. Compliance departments at major financial institutions may flag Burkina Faso gambling operations as high-risk.

📋 Final Verdict

Burkina Faso receives an Operator Ease Score of 4.9/10 and a Player Access Score of 5.3/10, resulting in an overall market attractiveness rating of 5.1/10.

HONEST ASSESSMENT:

Burkina Faso represents a FRONTIER MARKET with frontier-level risks and microscopic rewards. While the 5% gambling tax is attractive and online gambling is not explicitly prohibited, the complete absence of online licensing framework means operators are flying blind in a regulatory vacuum. The crushing economic reality – $950 GDP per capita creating $30-40 ARPU, a total market size of only $65 million, internet penetration of just 30%, and 75% banking exclusion – makes profitable operations nearly impossible for all but the most patient, well-capitalized operators. You are investing $300k-600k to chase a $15-25M online gambling market (at most) where Betway and LeoVegas already operate, requiring 5-7 years to maybe break even, with constant risk that the government implements punitive regulations. Unless you have $2M+ to burn building long-term brand in West Africa as a loss leader for regional expansion, avoid this market. The risk-reward ratio is abysmal.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Major pan-African operator with $5M+ capital treating Burkina Faso as small piece of broader West African strategy, willing to accept losses for 5+ years while building regional brand.

- Established land-based operator in neighboring ECOWAS countries seeking to expand physical casino/betting shop presence to Ouagadougou and Bobo-Dioulasso with clear licensing path.

- Mobile money or telecom company with existing infrastructure in Burkina Faso able to integrate gambling at minimal incremental cost.

- Patient institutional investor with 7-10 year investment horizon betting on future GDP growth, internet penetration reaching 60-70%, and favorable online gambling regulation eventually emerging.

- Willing to operate ONLY land-based gambling (casinos, sports betting shops) with clear legal licensing, avoiding online grey zone entirely.

❌ Definitely Avoid If You Are:

- Online casino-focused operator seeking quick ROI – no legal licensing framework, grey market operations, microscopic market, terrible economics. Complete non-starter.

- Startup or small operator with less than $2M capital – you will run out of money before achieving scale. Market is too small and customer acquisition too expensive.

- Seeking breakeven within 36 months – impossible given market size, ARPU, and customer acquisition costs. Minimum 48-60 months required.

- Risk-averse operator requiring legal certainty – online gambling regulatory vacuum creates unacceptable legal risk. No licenses available for online operations.

- Cryptocurrency or fintech gambling operator – no crypto framework mentioned, banking penetration only 25%, payment infrastructure extremely limited.

- Affiliate or media company focused on gambling advertising – advertising restrictions apply, microscopic market means minimal revenue opportunity, future liability risk as regulations develop.

- Operator requiring 50+ Mbps internet speeds and 70%+ penetration – infrastructure simply doesn’t exist. Average speeds 5-12 Mbps, penetration 30%, concentrated in 2-3 cities only.

- Operator requiring $100+ ARPU for unit economics – impossible in market where GDP per capita is $950 and ARPU is $30-40. Economics don’t work.

- International operator without local partnerships – mandatory local registration, physical presence, compliance officers, and local knowledge requirements make solo entry nearly impossible.

⚠️ BOTTOM LINE: Burkina Faso is a frontier market suitable ONLY for well-capitalized operators with 5-7 year horizons treating it as a long-term brand-building exercise in emerging West Africa, not a profit center. The microscopic market size ($65M total), crushing economics ($950 GDP per capita, $30-40 ARPU), regulatory vacuum for online gambling, and severe infrastructure limitations make this one of the least attractive iGaming markets globally for immediate returns. If you need to ask whether you should enter this market, the answer is no.