Burundi presents a nascent yet evolving iGaming landscape with significant growth potential driven by increasing internet penetration and a youthful demographic. The country’s regulatory environment remains in development, with existing gambling laws primarily regulating land-based activities. Understanding Burundi’s legal framework, licensing procedures, and market restrictions is crucial for any operator aiming to establish a presence in this emerging frontier.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Gambling | Partially regulated, licensing for land-based only |

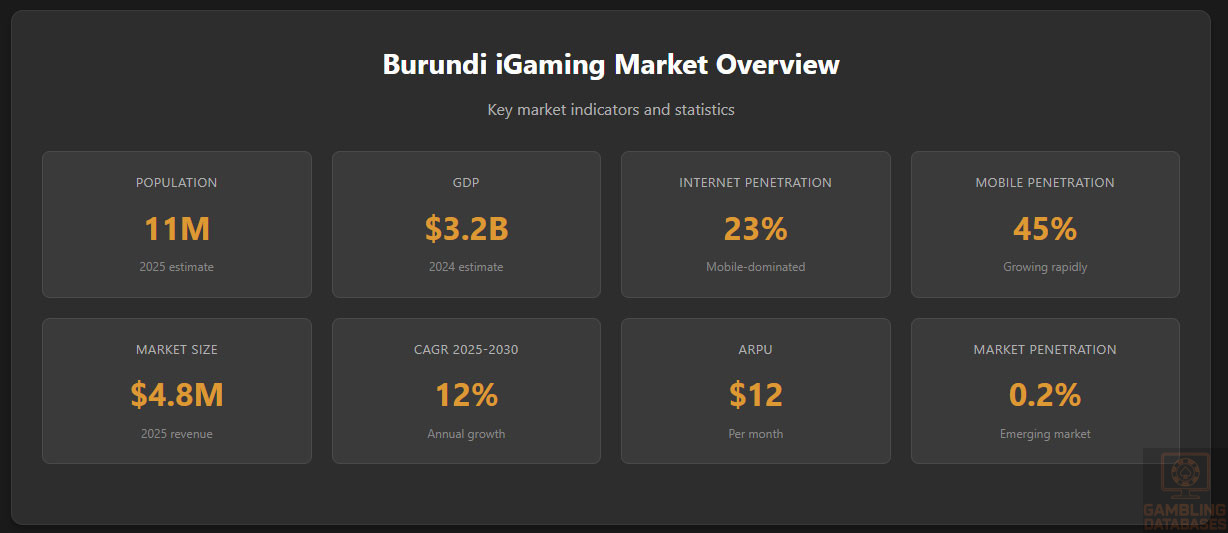

| Population | 11 million (2025 est.) |

| GDP | $3.2 billion (2024 est.) |

| Internet Penetration | 23% |

| Mobile Penetration | 45% |

| Licensing Costs | $20,000 – $50,000 |

| GGR Tax Rate | 15% |

| Market Size | Minimal, emerging market |

| CAGR (2025-2030) | 12% |

| Average Revenue Per User (ARPU) | $12/month |

| Market Penetration | 0.2% |

| Regulatory Authority | Burundi National Gambling Board |

Regulatory Framework and Legal Environment

Current Gambling Regulation Status

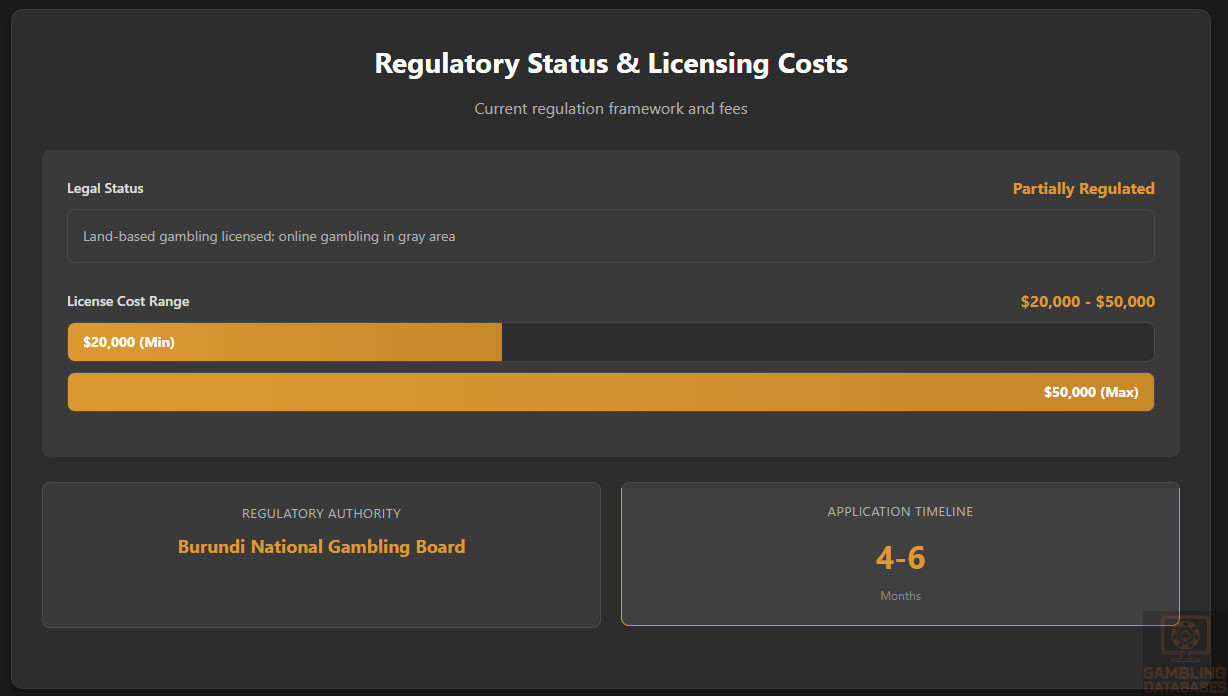

Burundi’s gambling laws are primarily focused on land-based activities, with online gambling falling into a regulatory gray area. The existing legal framework addresses casino operations, sports betting, and slot machine halls but does not specifically encompass digital platforms. The government has expressed interest in establishing a formal regulatory structure for online gambling, but comprehensive laws are yet to be enacted.

Land-Based Gambling Activities

Currently, Burundi licenses land-based casinos, sports betting outlets, and slot machine halls, primarily in urban centers such as Bujumbura. These activities are regulated under the 2018 Gambling Act, which stipulates licensing requirements, operational standards, and taxation. There are over a dozen licensed land-based operators, with a market characterized by limited competition and a small number of venues.

Online Gambling Framework

Online gambling remains largely unregulated, with no specific legislative acts addressing digital betting or casino platforms. The government’s stance is cautious, prioritizing control over unlicensed operators. While some foreign companies attempt to operate online, there is no formal licensing regime, raising legal uncertainties and potential compliance challenges for entrants.

Licensed Operators and Market Players

The Burundi gambling market features a small group of licensed land-based operators, including both domestic entities and regional players. The dominant market share is held by a few established brands with longstanding operations. The competitive landscape is limited but poised for expansion as regulations evolve to accommodate digital gambling.

Licensing Framework and Requirements

Application Process and Eligibility

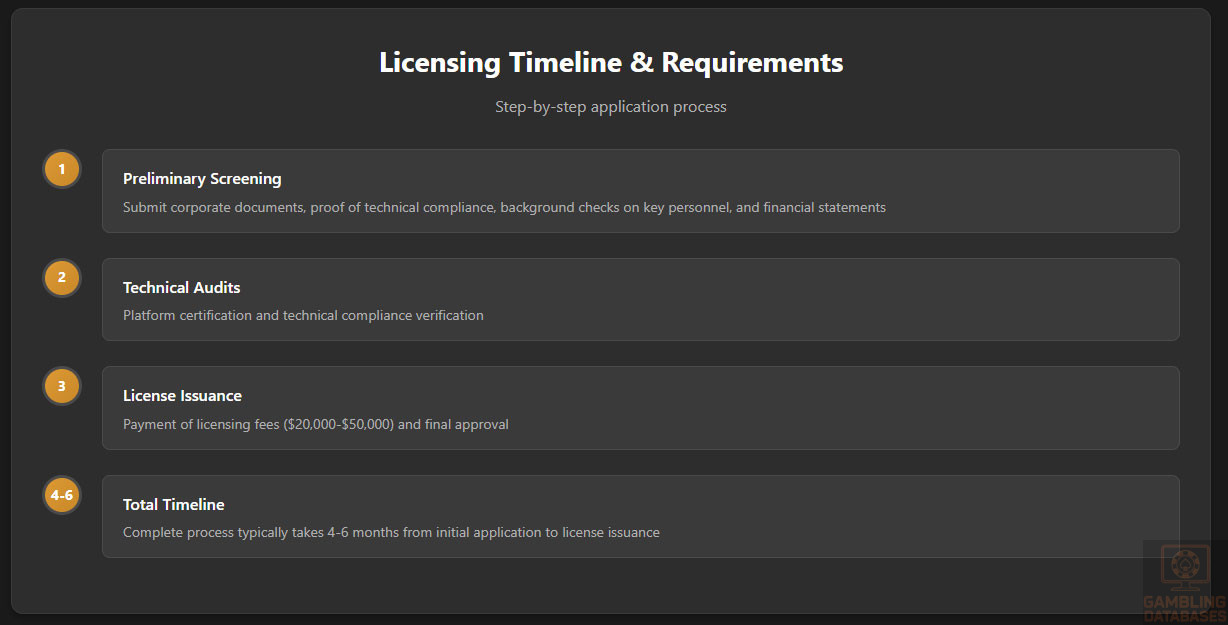

The Burundi National Gambling Board oversees licensing, requiring applicants to submit comprehensive documentation and pass technical and financial evaluations. The application process involves several stages, including preliminary screening, technical audits, and license issuance, typically taking 4–6 months.

- Corporate registration and legal documents

- Proof of technical compliance and platform certification

- Background checks on key personnel

- Financial statements demonstrating minimum capital

- Payment of licensing fees ($20,000–$50,000)

Local Presence and Operational Requirements

Operators must establish a local office and appoint a local authorized representative to facilitate communication with authorities. Foreign ownership restrictions limit majority control by non-residents. Additionally, operators are required to maintain local banking relationships and ensure compliance with domain registration mandates.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators are mandated to implement age verification, KYC procedures, and AML measures. Responsible gambling policies include self-exclusion options, spending limits, and public awareness campaigns. Disclosure of responsible gambling information must be prominently displayed and accessible to players.

- Mandatory age verification at registration

- AML and anti-fraud procedures

- Self-exclusion system implementation

- Real-time transaction monitoring

- Reporting suspicious activities

Financial Monitoring and Reporting

Licensed operators are obligated to maintain transparent financial records and submit regular reports to authorities. This includes tracking all financial transactions, wagering activities, and payouts. Audit requirements enforce compliance with tax obligations and operational standards, with quarterly submissions mandated.

- Monthly transaction logs submission

- Annual financial audits by certified auditors

- Tax remittance reports

- Dispute resolution documentation

Taxation Structure and Financial Obligations

Player Taxation

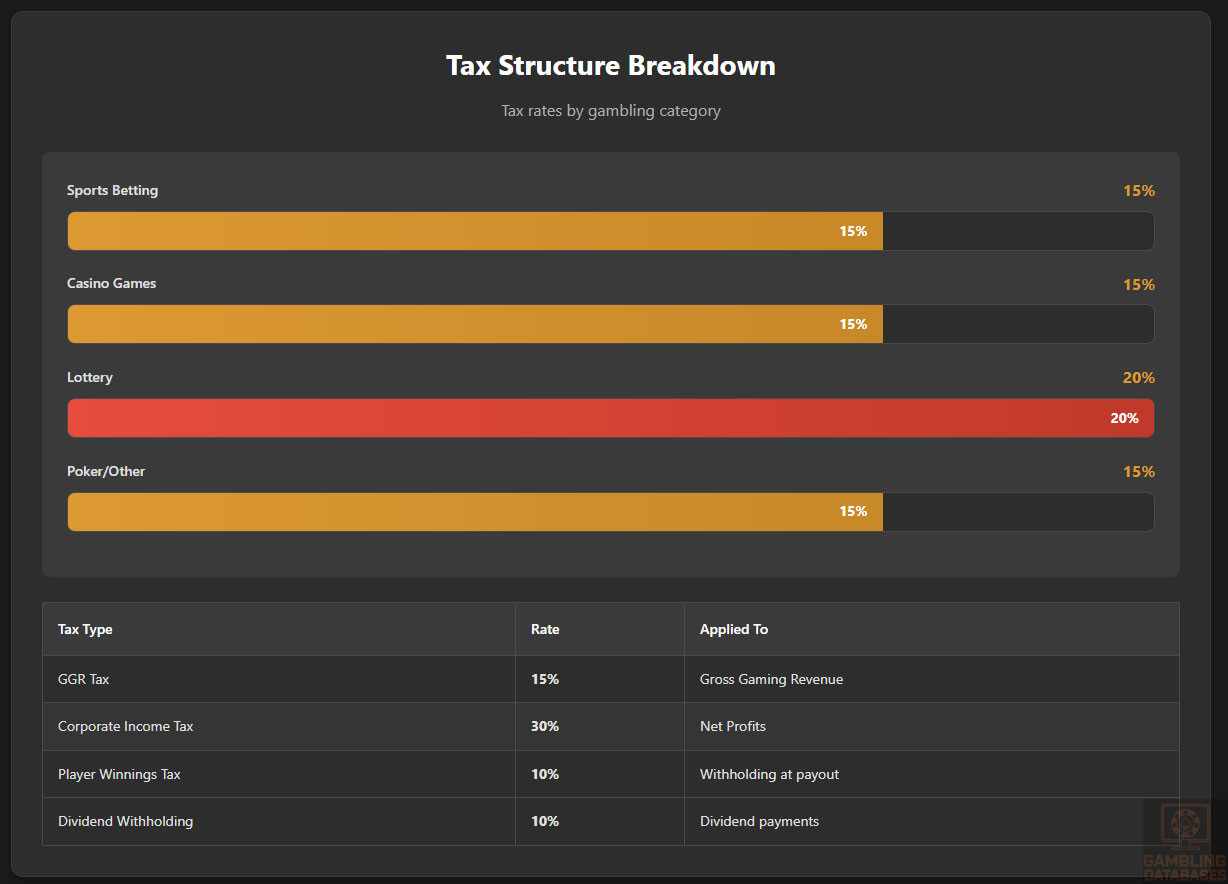

Winnings from gambling are subject to a flat withholding tax of 10%, deducted at source by operators before payout. There are minimum thresholds for taxable winnings, and players are required to declare large wins in their annual tax filings.

Operator Taxation

Operators pay a gross gaming revenue (GGR) tax of 15%, based on monthly revenue. License renewal costs range from $20,000 to $50,000, with additional fixed operational taxes for specific game categories. Corporate income tax is set at 30% on profits.

| Game Type | Tax Rate |

|---|---|

| Sports Betting | 15% |

| Casino Games | 15% |

| Lottery | 20% |

| poker/Other | 15% |

Gambling Market Financial Performance

Although data remains scarce, total wagers in Burundi are estimated at a few million dollars annually, with revenues mainly derived from land-based operators. Market growth is expected as digital infrastructure improves and regulations potentially broaden, with a CAGR forecast of approximately 12% through 2030.

Advertising and Marketing Restrictions

Advertising is limited to approved channels such as licensed venues, radio, and government-approved media. There are strict content restrictions, prohibiting misleading claims and promoting irresponsible gambling behavior. Sponsorships are permissible but subject to regulatory approval, with marketing activities confined to specific times and platforms.

- Restrictions on online ads

- Ban on targeting minors

- Prohibition of misleading promotions

- Selective sponsorship permissions

Recent Regulatory Changes and Their Impact

Any recent amendments have focused on tightening operational standards for land-based venues and potential plans for online regulation. The introduction of a digital licensing framework remains under discussion, which could significantly alter market entry costs and compliance obligations.

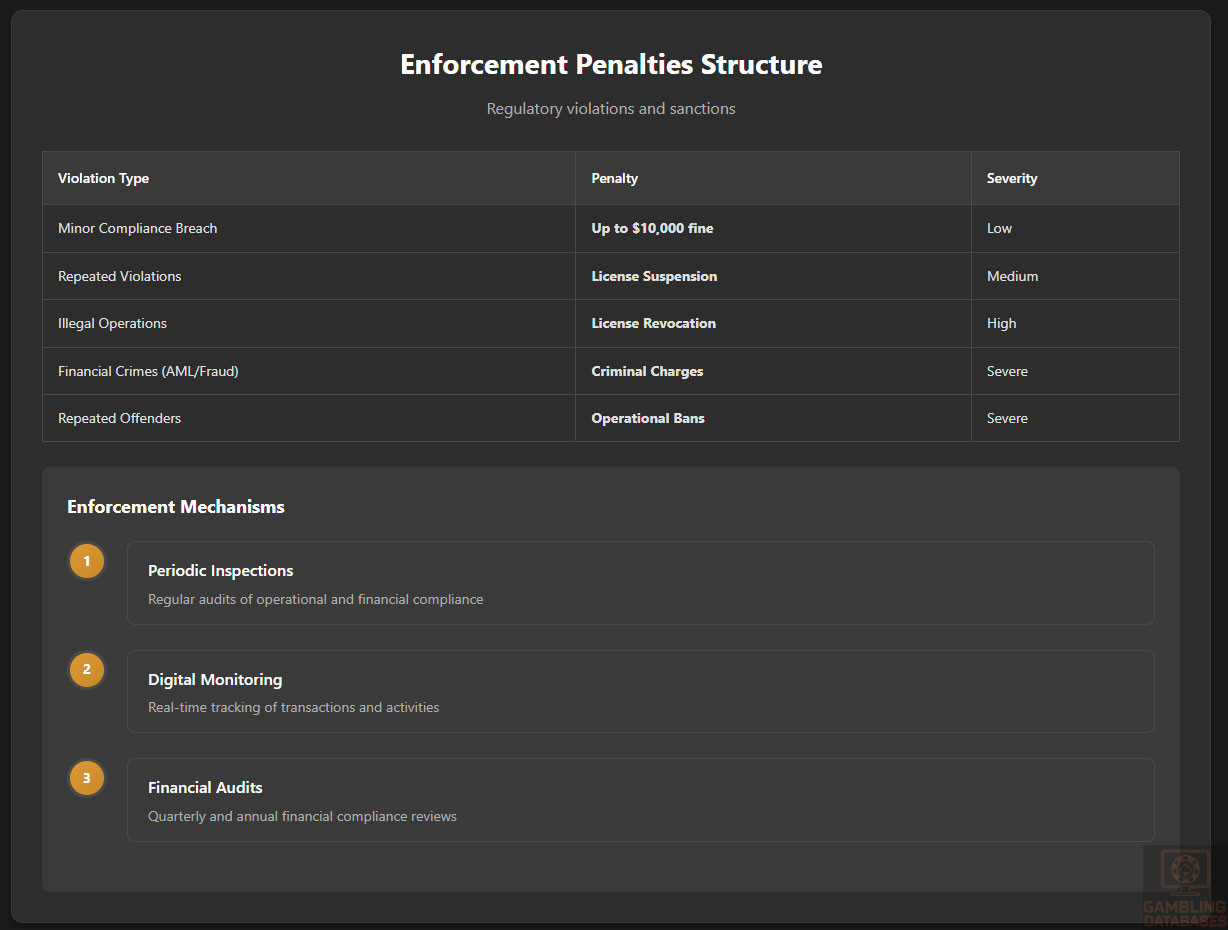

Enforcement Mechanisms and Penalties

Enforcement is carried out through periodic inspections, audits, and digital monitoring. Penalties range from fines to license suspensions, with a focus on compliance enforcement for financial crimes, illegal operations, and breaches of responsible gambling policies.

- Fines up to $10,000

- License suspension or revocation

- Criminal charges for severe violations

- Operational bans for repeat offenders

Demographics and Consumer Analysis

Population Demographics and Distribution

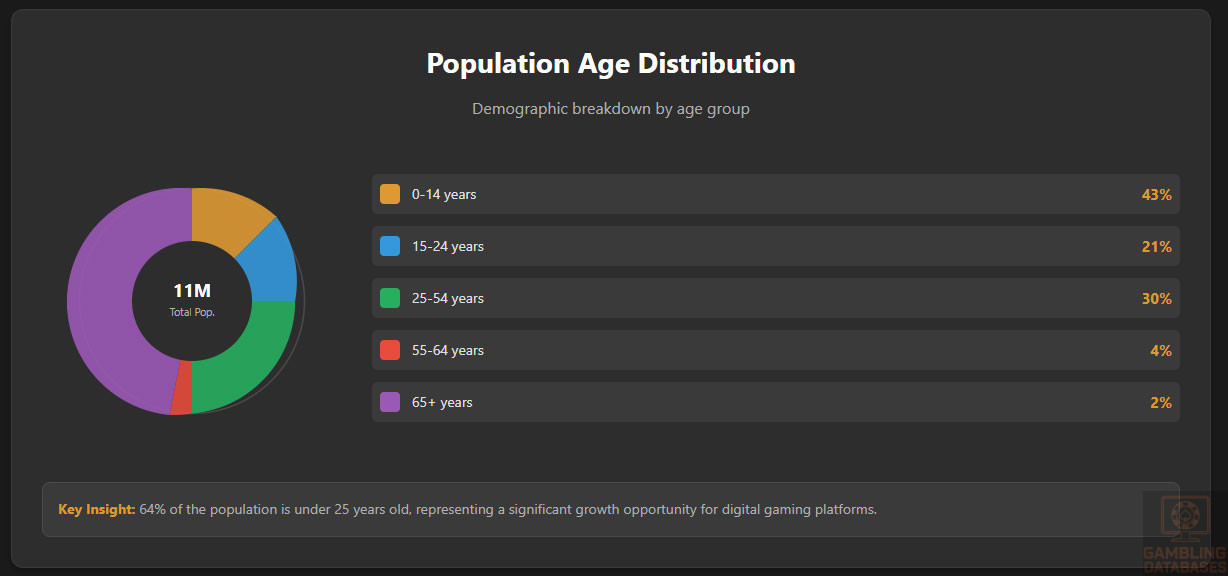

Burundi has a population of approximately 11 million as of 2025, marked by a young demographic profile. The median age is around 18 years, reflecting a predominantly youthful society. The gender ratio is slightly skewed towards females, with approximately 97 males per 100 females. Urbanization remains limited, with roughly 13% of the population residing in urban areas and the majority living in rural regions engaged in subsistence agriculture.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 43% |

| 15-24 years | 21% |

| 25-54 years | 30% |

| 55-64 years | 4% |

| 65 years and over | 2% |

The concentrated youth cohort represents a potential growth segment for iGaming, given rising digital engagement. Urban population centers act as hubs for internet connectivity and gambling venue concentration, setting the stage for focused market penetration strategies.

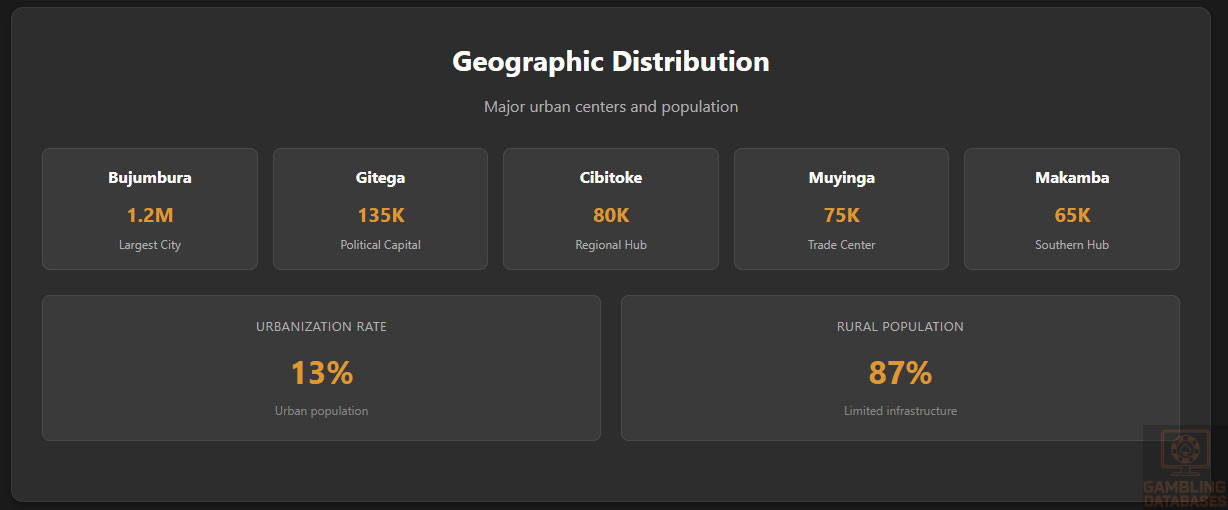

Geographic Distribution

Burundi’s economic and population distribution is heavily centered around key urban areas along the western border with Lake Tanganyika. Internet access and gambling infrastructure exhibit strong regional disparities, favoring urban hubs.

- Bujumbura: Largest city, population approximately 1.2 million, main commercial center

- Gitega: Political capital, population about 135,000, growing urban development

- Cibitoke: Regional economic activities, population near 80,000

- Muyinga: Agricultural trade center, population around 75,000

- Makamba: Southern hub, population about 65,000

Internet penetration is significantly higher in Bujumbura and Gitega, where broadband and mobile network infrastructure are more developed. Most licensed gambling venues are concentrated in these urban nodes, limiting access in rural provinces where the majority of the population resides.

Economic Indicators and Consumer Spending Power

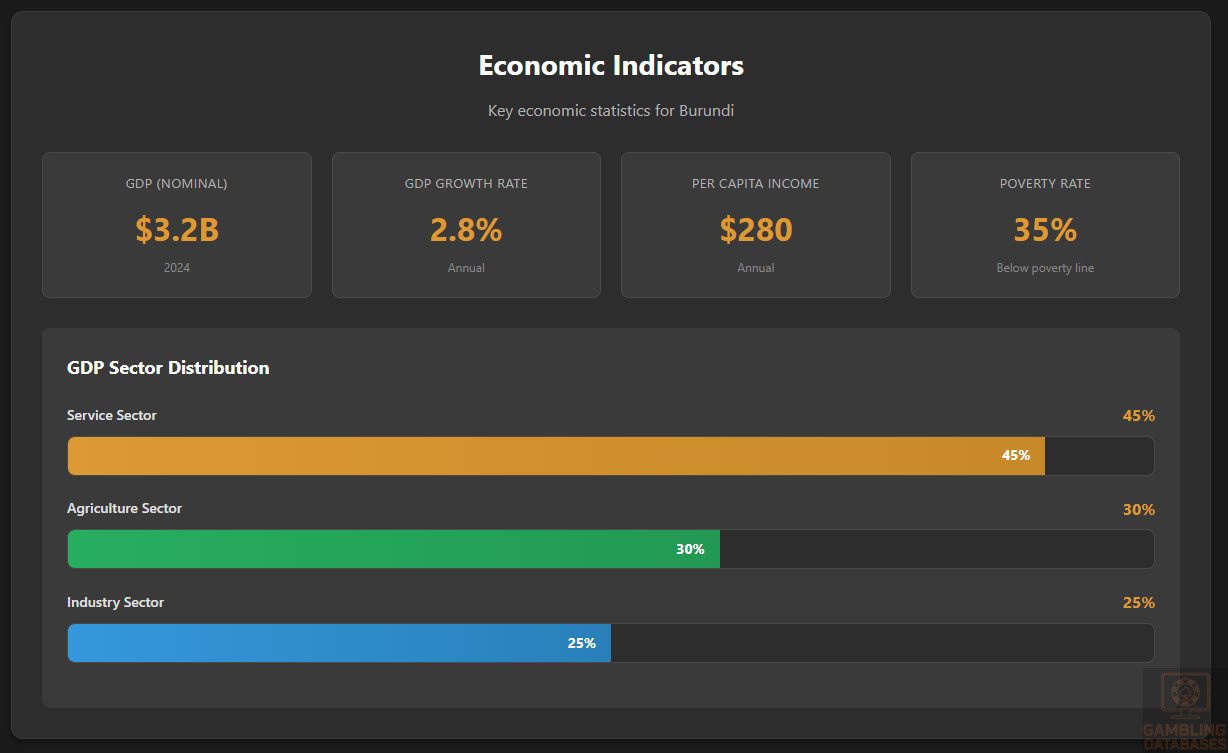

Burundi’s economy remains one of the least developed globally, with a GDP of around $3.2 billion as of 2024. The economy grows at a moderate pace estimated at 2.8% annually, driven mainly by agriculture, which accounts for over 30% of GDP. The service sector is gradually expanding, contributing about 45%, including trade, telecommunications, and financial services.

Per capita income is low, estimated at roughly $280 annually, with significant disparities between urban and rural households. Rising remittances and microenterprise growth contribute modestly to disposable income. Consumer spending on discretionary entertainment, including gambling, remains constrained but shows upward momentum in urban middle-class segments.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $3.2 billion |

| GDP Growth Rate | 2.8% |

| Per Capita Income | $280 |

| Agriculture Sector | 30% |

| Service Sector | 45% |

| Industry Sector | 25% |

Income and Wealth Distribution

Income inequality remains pronounced, with the top 20% of households capturing nearly 60% of total income. Urban households experience better economic conditions, with median income reaching up to four times rural averages. Approximately 35% of the population lives below the national poverty line, which limits widespread disposable income for entertainment spending.

Market Size and Growth Projections

The current iGaming market in Burundi is embryonic, with total estimated revenues below $5 million annually, dominated by informal and land-based activity. However, with increasing internet access and demographic shifts, the sector is projected to grow at a compound annual growth rate (CAGR) of approximately 12% through 2030.

User base expansion is expected to primarily arise from the 15-34 age group, with the average revenue per user (ARPU) increasing from $12 to an anticipated $18 by 2030. Market penetration remains low at around 0.2%, suggesting significant room for expansion upon regulatory clarity and technology adoption.

| Metric | 2025 | 2030 (Forecast) |

|---|---|---|

| Total Market Revenue | $4.8 million | $9.5 million |

| User Base | 400,000 | 900,000 |

| ARPU | $12 | $18 |

| Market Penetration | 0.2% | 0.8% |

| CAGR | 12% | – |

Education, Skills, and Digital Literacy

Burundi’s literacy rate is approximately 68%, with significant regional disparities favoring urban populations. Secondary education enrollment has improved but remains below regional averages. Digital literacy is emerging, with growing smartphone use catalyzing internet access, mainly among youth.

Workforce skills relevant to the iGaming sector, such as IT and customer service, remain underdeveloped but show gradual enhancement through vocational training programs and government initiatives supporting digital economy growth.

Cultural and Social Factors

Communication and Language

Burundi’s official languages are Kirundi, French, and English. Kirundi is the dominant local language spoken by nearly the entire population, while French serves as the language of administration and business. English is increasingly used in education and digital content, especially among younger, tech-savvy demographics.

- Kirundi: Spoken natively by 98%

- French: Official and administrative language

- English: Growing digital and business usage

- Swahili: Regional trade and communication

- Other local dialects with minor prevalence

Cultural Attitudes

Gambling is treated ambivalently, combining traditional social reservations with growing acceptance among urban youth as a form of entertainment. Religious influences, particularly from Christian and Muslim communities, advocate for caution and social responsibility regarding gambling.

Foreign brand perceptions are generally positive, associating international operators with professionalism and higher service standards, provided they adhere to local cultural norms and regulatory requirements.

Problem Gambling and Social Considerations

There is limited formal data on problem gambling prevalence, but estimates suggest a low to moderate incidence, primarily among younger males. Government agencies and NGOs have begun addressing social risks, emphasizing prevention and treatment programs, although resources remain scarce.

- Awareness campaigns on gambling risks

- Self-exclusion and counseling services

- Youth education programs

- Collaboration with religious institutions

- Support helplines and NGO initiatives

Political Structure and Governance

Burundi operates a presidential representative democratic republic with relative political stability since 2020 reforms. Regulatory consistency remains a challenge due to institutional capacity constraints. The government actively seeks investment while cautiously managing digital economy growth, balancing openness with regulatory prudence.

Technology Adoption and Digital Behavior

Internet and Digital Usage

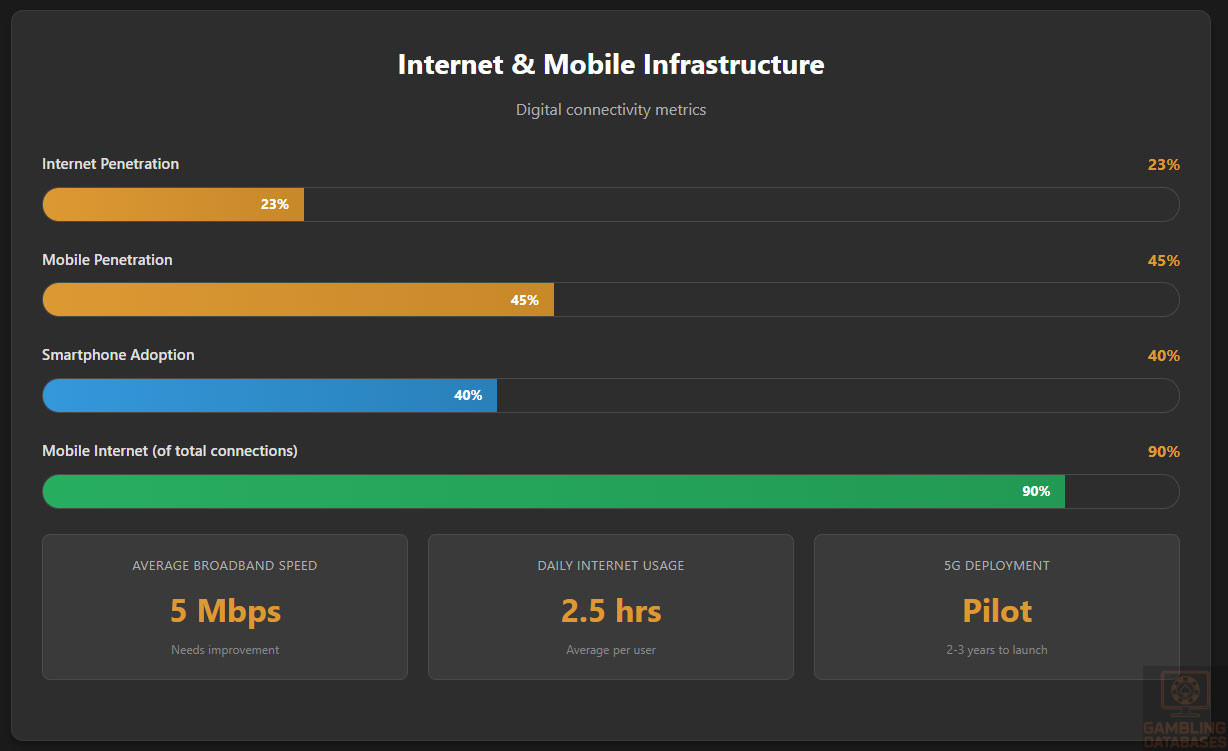

Internet penetration is approximately 23%, with mobile broadband being the primary access mode. Daily internet usage averages 2.5 hours, predominantly for social media, messaging, and entertainment.

- Facebook: Leading platform with 78% internet user penetration

- WhatsApp: Widely used for communication, especially mobile

- YouTube: Popular for video consumption and entertainment

- Instagram: Growing rapidly among younger segments

- TikTok: Emerging platform for short-form content

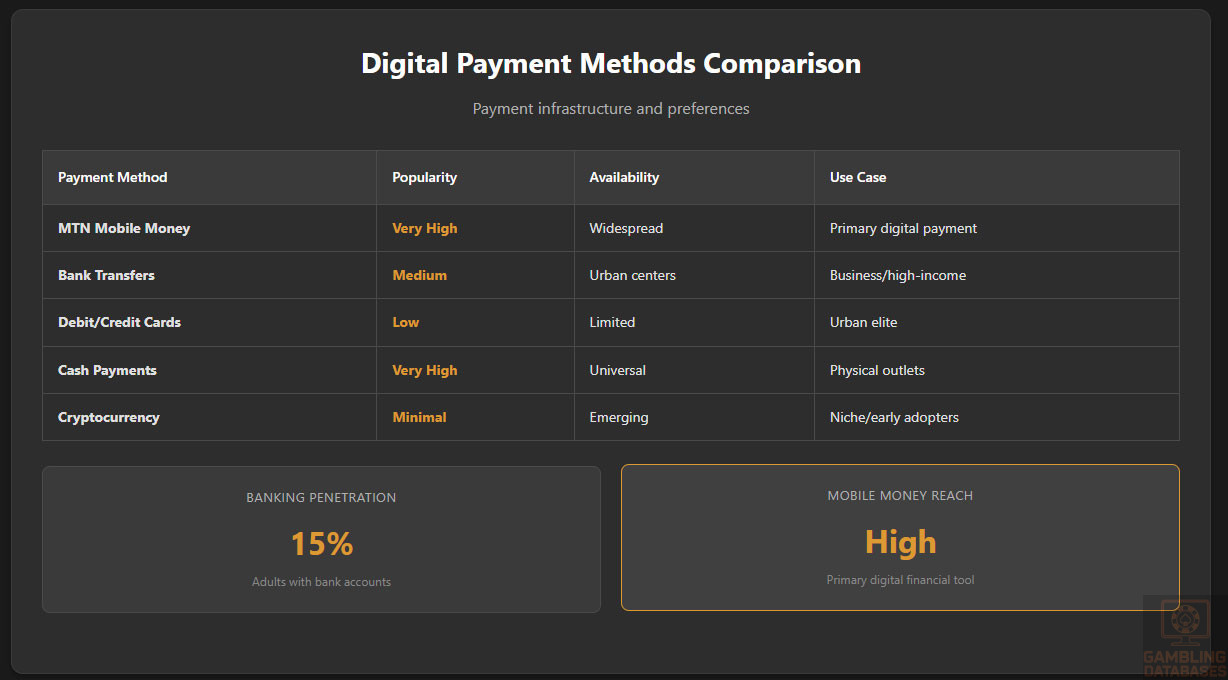

Digital Payment Behavior

Payment preferences favor mobile money solutions due to low banking penetration. E-wallets and mobile payment services are increasingly popular, facilitating online transactions in urban areas. Cryptocurrency adoption is minimal but showing early signs of interest among niche users.

- Mobile Money (e.g., MTN Mobile Money)

- Bank Transfers

- Debit/Credit Cards (limited penetration)

- Cash Payments at physical outlets

- Emerging interest in P2P crypto transactions

Gaming and Gambling Preferences

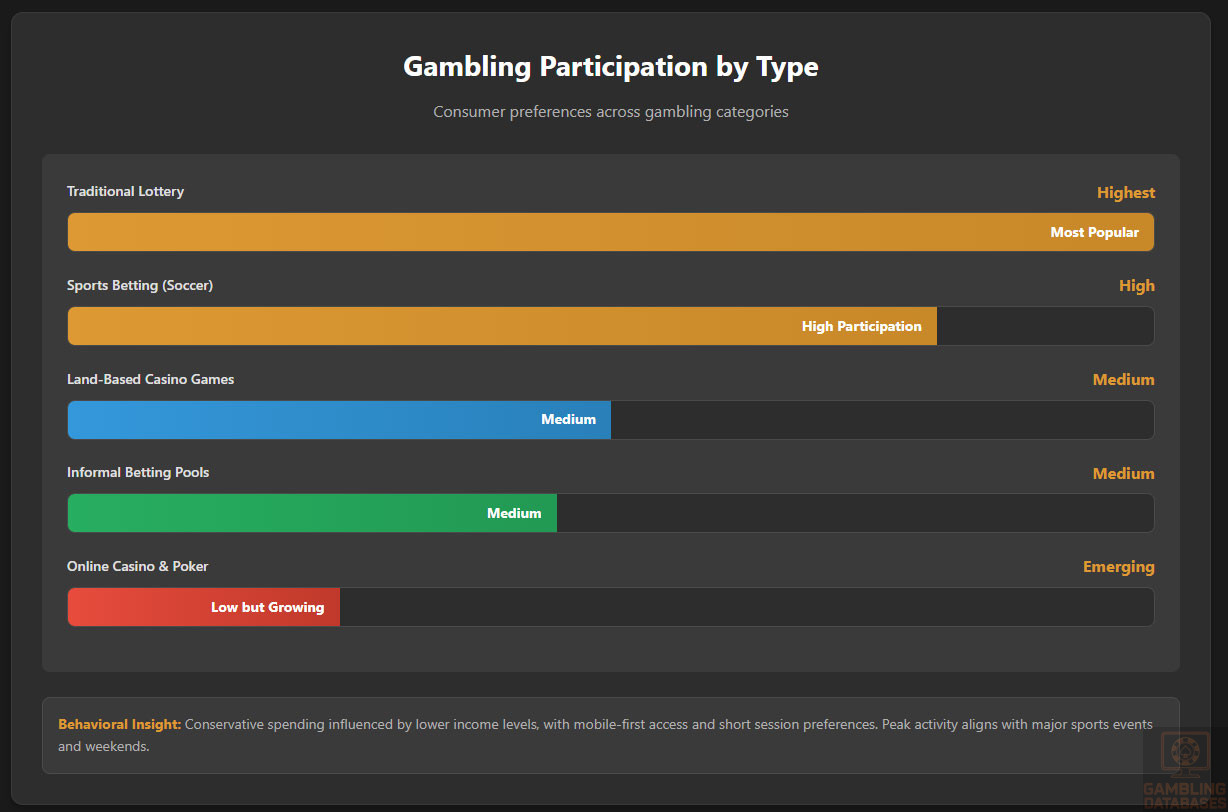

Current Market Participation

Gambling participation is currently limited, with land-based betting and lottery activities dominating. Online gambling participation remains marginal but is growing steadily among urban youth and working adults.

- Traditional lottery (highest participation)

- Sports betting (notably soccer)

- Land-based casino games

- Informal betting pools

- Emerging online casino and poker platforms

Consumer Behavior Patterns

Spending on gambling is conservative, influenced by lower income levels but rising with disposable income growth. Players prefer mobile access and short session times, aligning with digital consumption habits. Retention hinges on localized content, payment convenience, and reliable customer support.

Peak gambling activity aligns with major sports events and weekend evenings, with loyalty programs increasingly used to drive engagement. Operators focusing on mobile-first experiences and vernacular language interfaces are positioned to gain competitive advantage.

Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Burundi’s internet penetration stands at roughly 23%, dominated by mobile broadband rather than fixed-line connections. Average broadband speeds remain low, around 5 Mbps, reflecting underdeveloped fiber optic and copper networks. Network reliability varies significantly, with frequent outages outside urban centers. Investment in digital infrastructure has increased moderately, backed by government initiatives and international aid, focusing on expanding backbone connectivity and reducing costs.

Mobile internet predominates, accounting for over 90% of connections, while fixed broadband usage is minimal due to cost and infrastructure constraints. The government’s digital agenda prioritizes improving broadband quality to support services such as e-commerce and digital entertainment, including iGaming.

5G and Future Technology Deployment

5G rollout in Burundi is in nascent stages, with pilot projects initiated in Bujumbura by select operators. Full commercial deployment is anticipated within the next 2-3 years, pending regulatory approvals and infrastructure investments. Operators face challenges including spectrum allocation and financial constraints but view 5G as critical for enabling faster, more reliable mobile internet and digital service innovation.

The telecommunications sector is dominated by a handful of players, collectively shaping the network landscape as the country transitions towards next-generation technology.

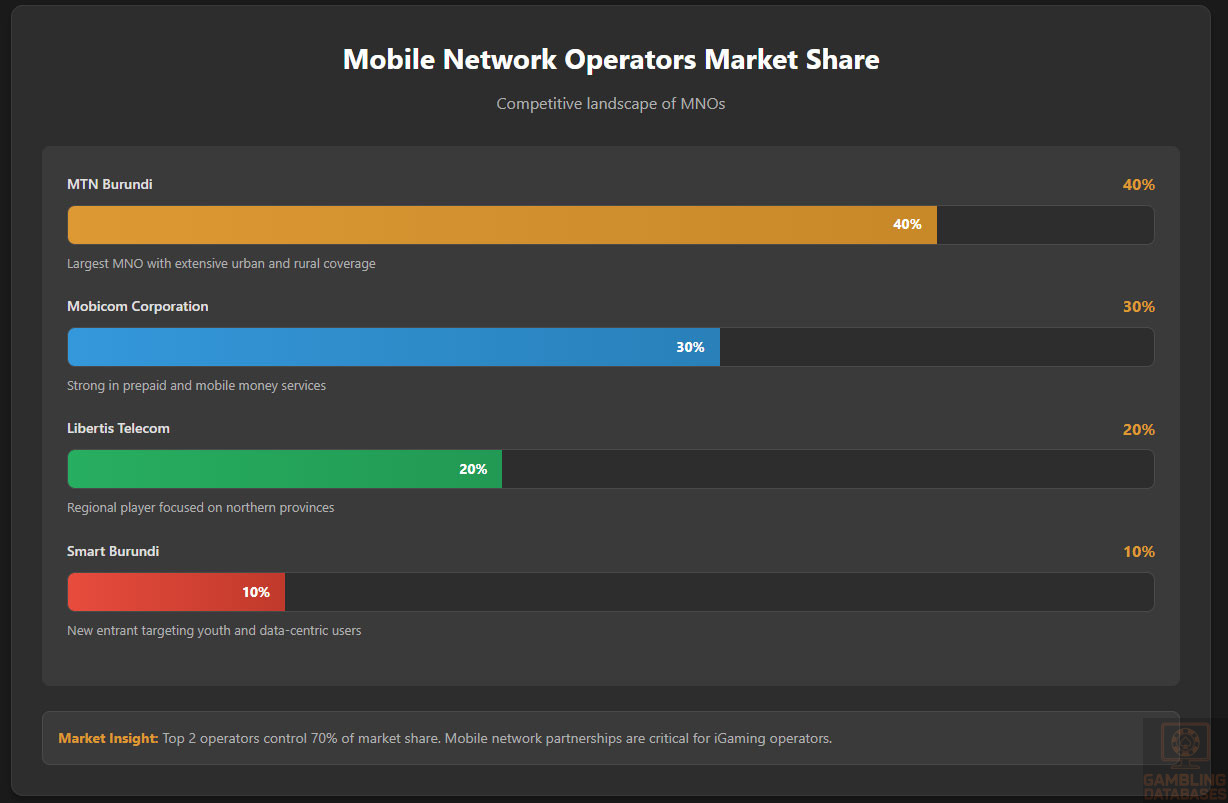

Mobile Technology Ecosystem

There are four major mobile network operators (MNOs) competing in Burundi, providing GSM and LTE services with varying geographic coverage and customer bases. Market share is concentrated with the two largest operators controlling approximately 70% of subscriptions, while smaller providers focus on niche regional markets.

- MTN Burundi: Largest MNO with ~40% market share and extensive urban and rural coverage

- Mobicom Corporation: 30% share, strong in prepaid and mobile money services

- Libertis Telecom: Regional player with 20% focus on northern provinces

- Smart Burundi: New entrant targeting youth and data-centric users

Data pricing remains relatively high compared to regional peers but shows a downward trend as competition intensifies. Coverage gaps still exist in rural and border areas, limiting overall digital inclusion.

Smartphone adoption is growing, with an estimated 40% of mobile users owning a smartphone, primarily low-cost Android devices. Market preferences favor affordable models with reliable internet capabilities. Mobile usage patterns confirm dominant demand for social media, messaging, and video content, forming a critical channel for iGaming engagement.

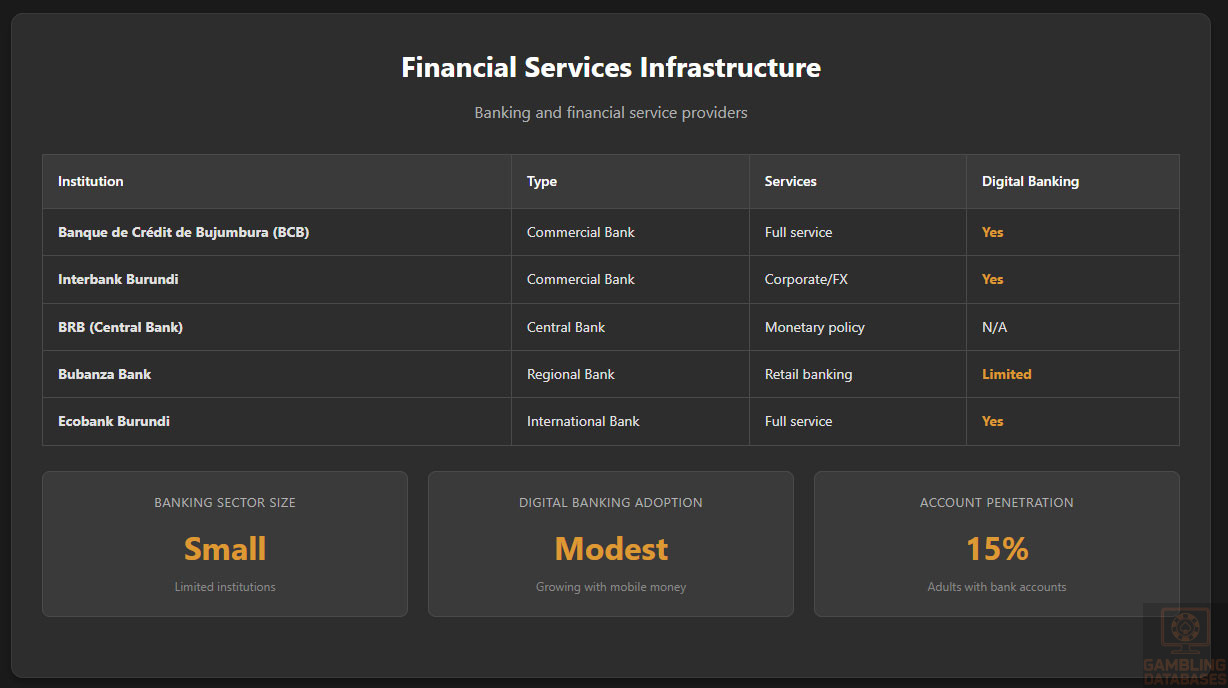

Financial Services and Payment Infrastructure

The banking sector is characterized by a small number of commercial banks, with limited penetration outside urban centers. Digital banking adoption is modest but growing, driven by mobile money services expanding financial inclusion. Approximately 15% of adults hold bank accounts, though mobile wallets reach a larger share of the population.

- Banque de Crédit de Bujumbura (BCB): Leading commercial bank with comprehensive digital banking platform

- Interbank Burundi: Strong in corporate banking and foreign exchange services

- BRB (Banque de la République du Burundi): Central bank overseeing monetary policy and payments

- Bubanza Bank: Regional focus with retail banking services

- Ecobank Burundi: International presence with digital banking solutions

Payment processing solutions include mobile money (MTN Mobile Money and others), bank transfers, debit/credit cards with limited penetration, and cash-based alternatives for e-commerce and gambling deposits. Cryptocurrency adoption remains exploratory with small communities engaging in peer-to-peer transactions.

- Mobile Money: Most widely used digital payment method for online and offline transactions

- Bank Transfers: Used primarily by businesses and higher-income consumers

- Debit/Credit Cards: Limited adoption, mostly Visa and Mastercard

- Cash Payments: Common for deposits and withdrawals at physical points

- Cryptocurrency (small scale): Emerging but unregulated

E-commerce and Digital Economy

Burundi’s e-commerce sector is in early development with online retail penetration below 5%. Consumer trust and logistical challenges constrain broader adoption. However, digital services such as mobile money, digital content, and utility payments have laid foundational infrastructure for expanding digital commerce.

Growing smartphone ownership and improved mobile data coverage are expected to stimulate e-commerce growth, creating opportunities for integrated digital entertainment and iGaming platforms to capture emerging consumer demand.

Business Environment and Regulatory Framework

The World Bank ranks Burundi in the lower tier for ease of doing business, reflecting regulatory complexity, limited infrastructure, and bureaucratic inefficiencies. Despite challenges, recent reforms aim to simplify company registration and enhance investor protections.

- Preparation and notarization of company documents (2-3 weeks)

- Submission and approval by the Companies Registry (5-7 business days)

- Tax registration and securing tax identification number (3-5 days)

- Opening corporate bank account and depositing required capital (1-2 weeks)

- Final registration confirmation and certificate issuance (2-3 days)

Foreign investment is welcomed but must adhere to restrictions on ownership in certain sectors, including gambling. Operational costs remain relatively low but fluctuate with infrastructural deficits and import dependencies.

Corporate Structure and Registration

Business entity types available include Limited Liability Companies (LLCs), corporations, and branch offices for foreign firms. LLCs are the most common due to flexible governance and limited shareholder liability. Branch offices are subject to regulatory scrutiny and primarily used for establishing local presence without full incorporation.

- LLC: Popular for SMEs and local operations

- Corporation: Suitable for larger investments and shareholders

- Branch Office: Foreign firms with regional management

- Partnerships: Used for joint ventures

- Sole Proprietorships: Limited use in iGaming due to regulatory demands

Registration typically requires submission of proof of corporate existence, tax compliance certificates, identification for shareholders and directors, a business plan, and evidence of local address.

- Article of Incorporation

- Tax Identification Number

- Proof of local office address

- Identification documents of shareholders and directors

- Business plan outlining activities and financial projections

Taxation Framework

The corporate income tax rate in Burundi is set at 30%, with reduced rates or exemptions available within special economic zones. Tax treaties exist with neighboring countries to avoid double taxation, facilitating cross-border trade and investment. Personal income tax follows a progressive rate structure, with withholding requirements on certain payments.

- Democratic Republic of Congo

- Rwanda

- Tanzania

- Kenya

- Uganda

Social security contributions and tax residency rules apply for employees and operators, requiring careful regulatory compliance.

Market Entry Considerations

Recommended market entry strategies emphasize partnerships with local entities to navigate regulatory and cultural landscapes. Leveraging mobile-first platforms and integrating mobile payment options are critical. Establishing a local presence with compliance advisors is advised to streamline licensing and operational setup. Market entry can be phased, starting with sports betting before expanding into digital casino gaming.

- Joint ventures with local operators

- White-label partnerships for licensing ease

- Targeted digital marketing focused on urban youth

- Mobile payment integration prioritizing local wallets

- Compliance consulting to manage evolving regulations

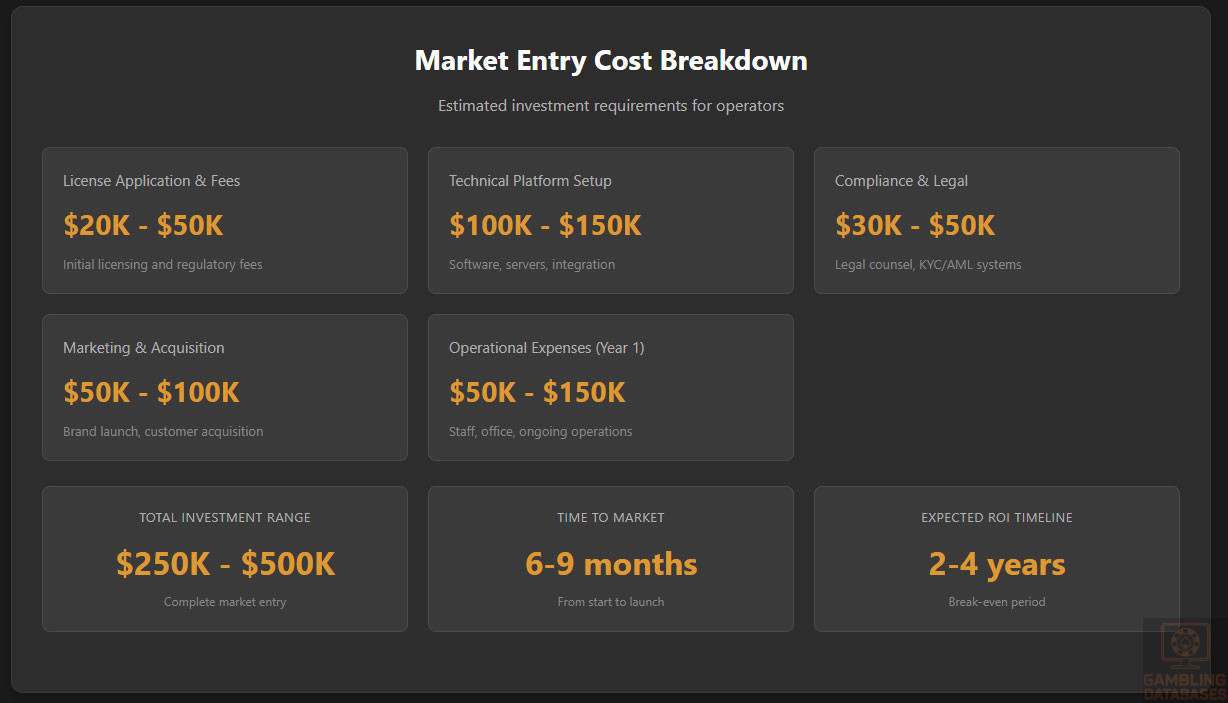

Initial capital requirements and operational budgets vary but average setup costs range between $250,000 and $500,000, including licensing, technical integration, and marketing. Time to market typically spans 6-9 months depending on regulatory responsiveness and infrastructure deployment.

| Cost Category | Estimated Cost (USD) |

|---|---|

| License Application and Fees | $20,000 – $50,000 |

| Technical Platform Setup | $100,000 – $150,000 |

| Compliance and Legal | $30,000 – $50,000 |

| Marketing and Customer Acquisition | $50,000 – $100,000 |

| Operational Expenses (First Year) | $50,000 – $150,000 |

Key success factors include cultural adaptation, robust mobile experience, regulatory compliance, and reliable customer service. Major challenges involve limited digital infrastructure, regulatory uncertainty, and payment system constraints.

Exit strategies should consider secondary market valuation for licenses and partnerships.

- Strong local partnerships

- Mobile-first technology adoption

- Clear regulatory engagement

- Robust AML and KYC adherence

- Culturally relevant marketing campaigns

- Infrastructure limitations

- Regulatory delays

- Low banking penetration

- Payment interoperability issues

- Market fragmentation

FAQ: Frequently Asked Questions

1. Is online gambling legal in Burundi?

Online gambling in Burundi is currently unregulated, creating a legal gray area. While land-based gambling activities are regulated and licensed, digital platforms operate without a formal regime, posing risks for operators. The government is reviewing laws to incorporate online gambling regulation, but until enacted, offshore operators face uncertainty. Caution is advised, with emphasis on compliance readiness for upcoming legislation.

2. What types of gambling licenses are available and what do they cover?

Burundi offers licenses primarily for land-based casinos, sports betting venues, and lottery operations. Online gambling licenses do not yet exist formally. Operators typically obtain general gaming licenses covering physical operations, requiring compliance with financial, technical, and operational standards. Expansion into digital licenses is anticipated but currently unavailable, limiting lawful online market participation.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing fees range between $20,000 and $50,000, reflecting operational scope and game types. The application process spans approximately 4 to 6 months, including documentation review and platform audits. Delays can occur due to regulatory capacity constraints. Early engagement with authorities is recommended to streamline approvals.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply but must establish a local presence and comply with ownership restrictions limiting majority foreign control. Partnerships or joint ventures with local entities are common to satisfy regulatory requirements. Full transparency on beneficial ownership, financial probity, and technical standards is mandatory.

5. What are the tax obligations for iGaming operators?

Operators are subject to a gross gaming revenue tax of 15% plus corporate income tax at 30%. License renewal fees and fixed operational taxes apply depending on game categories. Compliance with tax reporting is critical to avoid sanctions. Structured payments and audits are part of the regulatory oversight.

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue Tax | 15% |

| Corporate Income Tax | 30% |

| License Renewal Fees | $20,000 – $50,000 |

| Withholding Tax on Dividends | 10% |

6. Are gambling winnings taxed for players?

Yes, winnings are subject to a flat withholding tax of 10%, deducted at payout by the operator. Large winnings must be declared in annual tax filings. This system simplifies tax collection but requires operators to maintain accurate records and ensure withholding compliance.

7. What are the typical operational costs for running an online casino or sportsbook?

Key cost categories include licensing, technical platform development and maintenance, marketing, compliance, and staffing. Operators should budget for initial setup and recurring expenses such as software licensing fees, customer support, fraud prevention, and payment processing. These costs can vary widely depending on scale and market focus.

- License fees and renewals

- Software procurement and hosting

- Marketing and player acquisition

- Compliance and regulatory reporting

- Operational staffing and customer service

8. What is the expected ROI timeline for entering this market?

Return on investment is generally projected within 2 to 4 years, contingent on market acceptance and regulatory stability. Early movers benefit from limited competition but face infrastructure challenges. A phased investment approach aligned with regulatory developments reduces risks and improves ROI visibility.

9. What are the local presence requirements for operators?

Operators must establish a physical office in Burundi and appoint a local representative. This facilitates regulatory communications, tax compliance, and operational oversight. Maintaining local bank accounts and employing Burundi-based personnel are typically required to demonstrate genuine local commitment.

10. What payment methods are available and recommended?

Mobile money services lead digital payments, supported by bank transfers and limited card usage. Cash remains significant for deposits and withdrawals at physical points. Operators should integrate popular mobile wallets for seamless user experience and consider emerging payment technologies cautiously.

- MTN Mobile Money

- AirTel Money

- Bank Wire Transfers

- Visa and Mastercard (limited)

- Cash-based transactions

11. What are the advertising and marketing restrictions?

Advertising is restricted to prevent targeting minors and prohibits misleading claims about winning probabilities. Marketing must avoid promoting excessive gambling and adhere to time restrictions on broadcast media. Sponsorships require regulatory approval, ensuring campaigns are socially responsible and culturally sensitive.

12. What responsible gambling measures are mandatory?

Operators must implement robust KYC and AML procedures, provide self-exclusion tools, set deposit and bet limits, display responsible gambling information prominently, and engage in public awareness initiatives. These measures protect consumers and mitigate social risks associated with gambling expansion.

13. How large is the iGaming market and what is the growth potential?

The iGaming market is currently small but growing at around 12% CAGR, driven by increasing internet adoption and a youthful population. With regulatory evolution and mobile technology uptake, revenue could double to approximately $10 million by 2030. Penetration remains low, indicating significant future opportunities.

14. Who are the main competitors and what is their market share?

The market is dominated by a handful of established land-based operators, with limited online presence. Regional players hold significant shares, but foreign entrants are beginning to explore partnerships. Competitive dynamics are expected to intensify with formal online licensing.

15. What are the player preferences and typical spending patterns?

Players favor traditional lottery and sports betting, particularly football. Mobile accessibility and localized content are critical. Average spend is modest but steadily increasing, with peak activity during major sports seasons. Retention depends on trust, payment convenience, and entertaining game variety.

16. What are the key success factors and main challenges for new entrants?

Success depends on navigating regulations, local partnerships, technological adaptation, strong mobile payment integration, and culturally relevant marketing. Challenges include infrastructural gaps, payment limitations, limited digital literacy, regulatory ambiguity, and competition from informal operators. Preparedness and adaptability are vital for sustainable growth.

- Regulatory compliance and local expertise

- Mobile-first platform design

- Strong customer support and security

- Culturally tailored content and marketing

- Robust responsible gambling policies

- Underdeveloped infrastructure

- Limited banking access

- Regulatory uncertainties

- Competition from unlicensed operators

- Payment method fragmentation

Sources and References

- Burundi Gambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Burundi – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Africa Digital Infrastructure Report 2024 – International Telecommunication Union

- Africa Mobile Network Market Analysis 2024 – GSMA Intelligence

- Burundi National Gambling Board Annual Report 2024

- Burundi Ministry of Commerce – Business Registration Guide 2024

- East African Community Tax Treaties Documentation

- International Monetary Fund – Burundi Country Report 2024

- GSMA Mobile Money Deployment Tracker 2024

- Africa Online Payment Methods 2024 – Industry Report

- Burundi Telecommunications Authority – Spectrum and Licensing Data 2024

- Local NGO Reports on Gambling and Social Impact (2024)

- World Economic Forum – Digital Economy Africa Report 2024

- International Finance Corporation – SME Financing in Burundi

- Burundi Ministry of Health – Responsible Gambling Initiatives 2024

- Global Gaming Expo – Africa Trends 2024

- Regional E-commerce Development Reports – UNCTAD 2024

- Country Credit Risk Profile – Moody’s 2024

- Burundi Investment Promotion Agency – Market Entry Guidelines 2024

- Burundi Central Bank – Payment Systems Overview 2024

- Burundi National Internet Agency – Infrastructure Development Updates

- International Labour Organization – Burundi Employment and Skills Data 2024

- Burundi Ministry of Youth and ICT – Digital Literacy Programs Overview 2024

- United Nations Development Program – Burundi Human Development Report 2024

- East African Community – Regional Economic Outlook 2024

- Various news articles from regional media outlets covering regulatory changes 2023-2025