Cambodia presents a unique opportunity in the Southeast Asian iGaming market through its emerging casino sector and strategic location. Although land-based gambling flourishes under a governed licensing regime, online gambling remains restricted.

This analysis offers a detailed examination of Cambodia’s regulatory environment, licensing, fiscal obligations, and compliance mandates pertinent to market entry.

| Metric | Value |

|---|---|

| Gambling Legal Status | Land-based casinos legal; online gambling banned |

| Regulatory Authority | Commercial Gambling Management Commission (CGMC) |

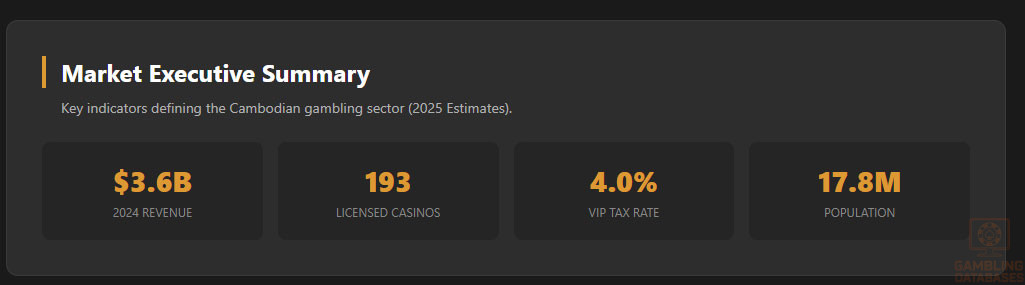

| Number of Licensed Casinos | Approx. 193 licensed casinos (2025) |

| Population | 16.9 million (2025 est.) |

| GDP | Approx. $30.5 billion USD (2025 est.) |

| GDP per Capita | $1,803 USD (2025 est.) |

| Internet Penetration | 75% of population |

| Mobile Penetration | 110% (SIM subscriptions per 100 people) |

| Licensing Application Fee | Varies; license capital requirements $100M-$200M USD |

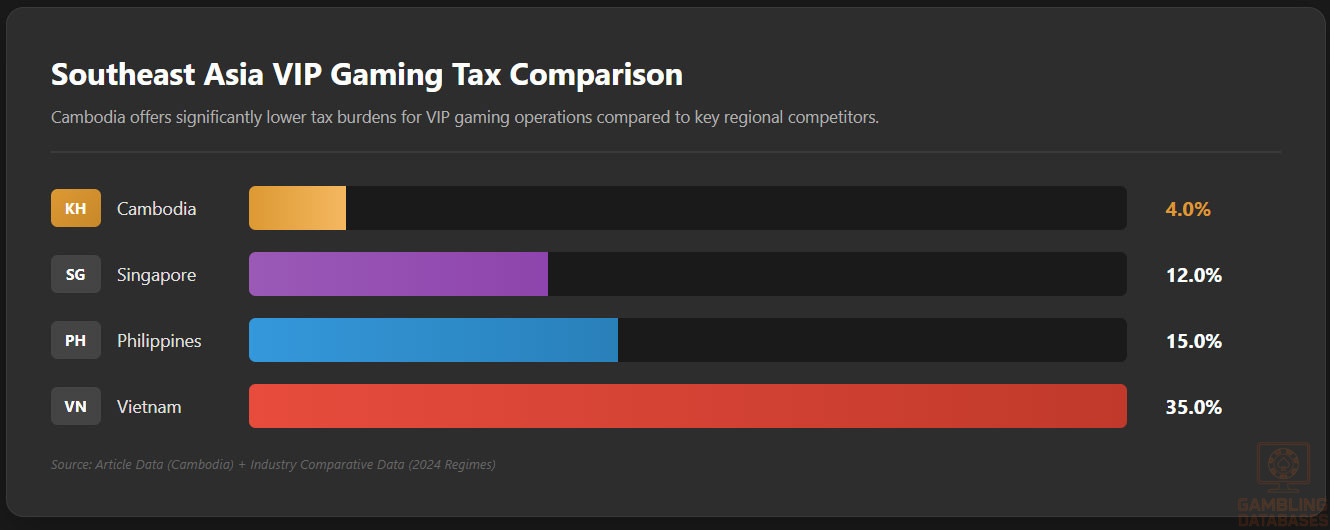

| GGR Tax Rate | 7% standard; VIP gaming 4% |

| Additional Taxes | 10% VAT on gross revenue; 1% monthly income tax prepayment |

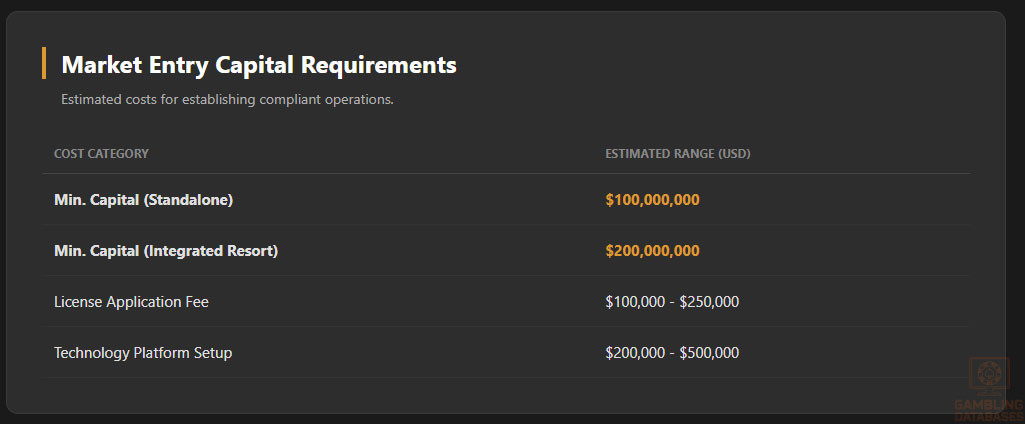

| Minimum Capital Requirements | $100M USD (standalone casino); $200M USD (integrated resort) |

| License Application Timeline | Up to 60 days decision period |

| Market Entry Barriers | High capital requirement, land zoning restrictions, local partnerships recommended |

| Foreign Ownership Rules | Permitted with government approval; encouraged local partnerships |

| Compliance Offices | 13 onsite regulator offices established in licensed casinos |

| Player Age Restriction | Minimum 21 years |

| Online Gambling Status | Prohibited; strict enforcement against illegal operations |

| Advertising Restrictions | Permitted with government oversight; content and channel restrictions apply |

| Market Size 2024 | $3.6 billion USD in gaming-related revenue |

| Growth Forecast CAGR | 8.6% (2020-2026 projection) |

| Average Revenue Per User (ARPU) | Data not publicly disclosed |

| Strategic Zones for Casinos | Promoted zones: Sihanoukville, Koh Kong; prohibited in religious/cultural zones |

| Enforcement Measures | License suspensions, fines, casino closures |

| Regulatory Changes 2023-2025 | Introduction of VAT on gaming revenue, onsite regulator offices, online gambling ban reinforcement |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

The Cambodian gambling industry operates under a dual framework that formally permits land-based casinos, integrated resorts, and limited betting activities while imposing a strict ban on online gambling. The primary regulatory body is the Commercial Gambling Management Commission (CGMC), responsible for licensing, monitoring, and enforcement.

Land-based gambling is concentrated in designated gaming zones primarily located in coastal provinces such as Sihanoukville and border areas like Poipet that attract international visitors. The Kingdom has established three types of zones: prohibited, promoted, and favored zones, to safeguard cultural sites and religious areas, notably around Angkor Wat.

Land-Based Gambling Activities

Land-based operations include:

- Casino resorts hosting table games and slot machines, mostly catering to tourists and VIP clientele

- Betting venues primarily focused on sports and horse racing in limited areas

- Integrated resorts combining hospitality, entertainment, and gambling under a single license structure

- Lottery operations legally permitted nationwide

Casinos are largely foreign-owned but operate under strict licensing conditions, including capital requirements and government oversight. Locals are prohibited from gambling within these establishments.

Online Gambling Framework

The Cambodian government enforces an outright ban on all online gambling platforms. The prohibition extends to license issuance, operational activities, and promotion. Despite the ban, Cambodia has seen illegal online operators, prompting active crackdowns by authorities. CGMC works closely with law enforcement to suppress unauthorized digital gambling activities.

Licensed Operators and Market Players

The market is characterized by approximately 193 licensed casinos, of which a significant share are integrated resorts. Major operators include international hotel-casino groups and regional casino companies. Competitive dynamics favor operators able to meet rigorous capital, operational, and compliance standards with emphasis on VIP customer acquisition.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing process is overseen by the CGMC, which evaluates applications within a 60-day timeframe after submission. Applicants must demonstrate robust financial capacity, corporate governance, and operational expertise.

Technical standards mandate that all gaming hardware and software be sourced from licensed suppliers and be under 10 years old.

License applicants must submit a comprehensive packet of documents, including:

- Legal company registration and tax compliance certificates

- Proof of minimum capital adequacy ($100M standalone casino; $200M integrated resort)

- Business plan detailing operational, financial, and market strategies

- Technical documentation covering gaming platforms and random number generator (RNG) certifications

- Background checks for all senior management and beneficial owners

- Risk management and internal control policies

- Physical premises approvals and infrastructure details

Local Presence and Operational Requirements

Operators must maintain a physical presence in Cambodia through registered offices and gaming venues located within approved zones. There are no absolute foreign ownership bans, but government approval is mandatory, and partnerships with local entities are strongly encouraged to navigate regulatory and cultural environments effectively.

- Onsite management staffed by personnel approved by regulators

- Physical infrastructure compliant with safety and operational standards

- Use of Cambodian domain names for digital marketing linked to licensed properties

- Strict adherence to operational hours and gaming zone limitations

- Collaboration with authorities on compliance and reporting

Compliance Obligations and Monitoring

Player Protection and Identification

Operators are required to implement strict Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures. The minimum player age is 21 years. Responsible gambling measures include self-exclusion programs, deposit limits, and public awareness campaigns to mitigate gambling-related harm.

- Mandatory age verification with government-issued IDs

- Continuous monitoring of suspicious transactions

- Provision of responsible gambling tools and counseling access

- Transparent disclosure of game rules and payout rates

- Data protection and privacy compliance

Financial Monitoring and Reporting

Licensed operators must submit monthly financial reports detailing gaming revenues, taxes paid, and customer transaction data. Audits are conducted regularly to ensure compliance with tax obligations and anti-fraud measures.

- Submission of monthly gross gaming revenue and tax payments

- Annual audited financial statements filed with the CGMC

- Periodic on-site inspections and compliance audits

- Immediate reporting of any suspicious or illegal activities

Taxation Structure and Financial Obligations

Player Taxation

Cambodia does not currently impose taxation on individual player winnings. All fiscal liabilities related to gambling are borne by operators under a gross gaming revenue (GGR) tax regime.

Operator Taxation

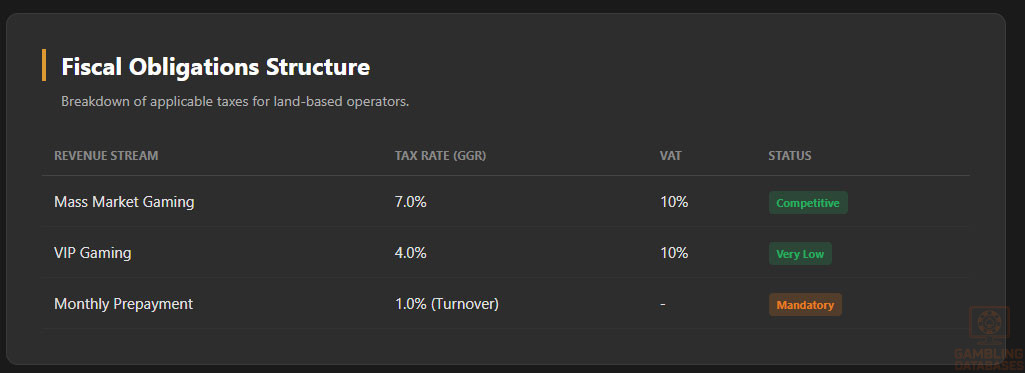

Operators face a structured tax environment comprising a 7% GGR tax on standard land-based gambling revenue. VIP gaming activities have a reduced GGR tax of 4%. An additional 10% value-added tax (VAT) applies to all gambling revenue, effective from January 2025. Monthly income tax prepayments at 1% are also mandatory.

| Game Type | GGR Tax Rate | Additional Taxes |

|---|---|---|

| Mass Market Gaming | 7% | 10% VAT; 1% monthly income tax prepayment |

| VIP Gaming | 4% | 10% VAT; 1% monthly income tax prepayment |

| Online Gambling | Prohibited | Not applicable |

License renewal fees and turnover-based taxes are also part of the fiscal regime, although specifics vary by license holder. The tax burden increased notably since the end of a two-year VAT deferral period in late 2024.

Gambling Market Financial Performance

The Cambodian gaming market generated approximately $3.6 billion in revenue in 2024, primarily from land-based casinos. Year-over-year growth is supported by a tourism rebound and increased high-roller activity in coastal and border regions.

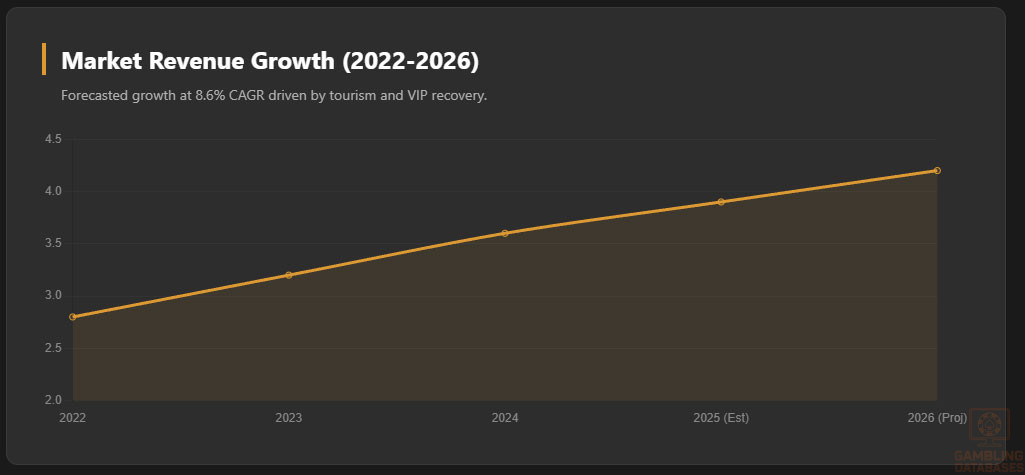

The market forecast predicts an 8.6% compound annual growth rate (CAGR) through 2026, driven by investment in integrated resorts and infrastructure.

Advertising and Marketing Restrictions

Advertising of gambling products is allowed under stringent conditions that prohibit targeting minors or promoting gambling as a solution to financial problems. Permissible channels include regulated digital platforms, casino premises, and select broadcast media. Sponsorship of public events faces government scrutiny to prevent indirect marketing to vulnerable groups.

- Advertising content must disclose risks associated with gambling

- Time restrictions on broadcast advertising to protect minors

- Prohibition of misleading or deceptive claims

- Restrictions on bonuses and promotional offers

- Mandatory regulatory approval for major campaigns

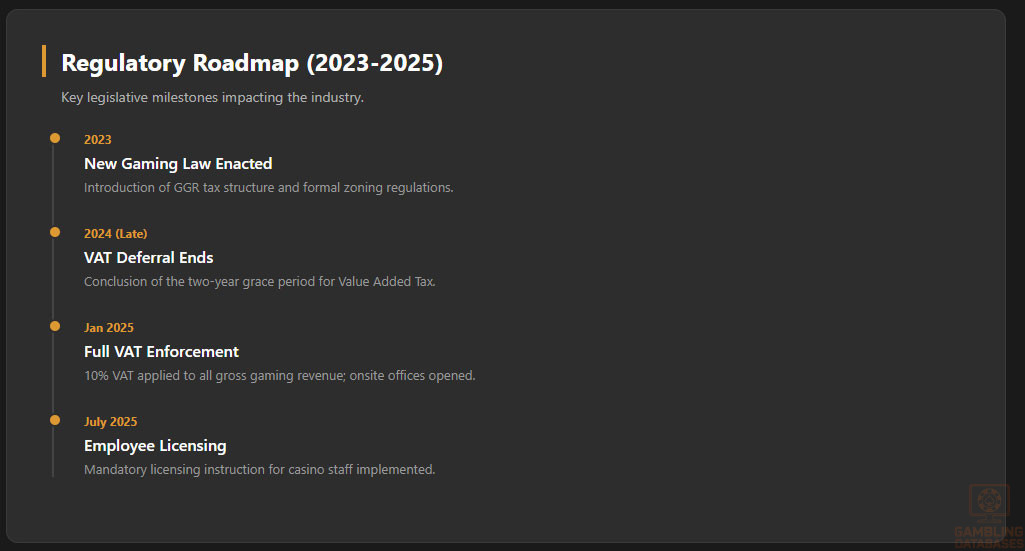

Recent Regulatory Changes and Their Impact

- 2023: New gaming law enacted introducing GGR tax and zoning regulations.

- 2024: VAT on gross gaming revenue deferred until end of year.

- 2025 (Jan): VAT obligation of 10% enforced; compliance offices established onsite.

- 2025 (July): Instruction for casino employee licensing implemented.

These changes have increased operational costs for licensed operators and reinforced regulatory supervision, resulting in enhanced market credibility and investor confidence despite the higher tax rates.

Enforcement Mechanisms and Penalties

The CGMC enforces compliance through a graduated penalty system including written warnings, suspension, and license revocation. Operators found enabling illegal online activities face severe fines and potential criminal prosecution. The regulator’s onsite presence enhances real-time compliance monitoring, reducing violations and fostering a transparent business environment.

- Issuance of formal warnings for minor infractions

- Suspension of gaming operations pending corrective measures

- Permanent revocation of licenses for serious breaches

- Fines scaled according to severity and recurrence

- Coordination with police for criminal cases involving illegal gambling

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

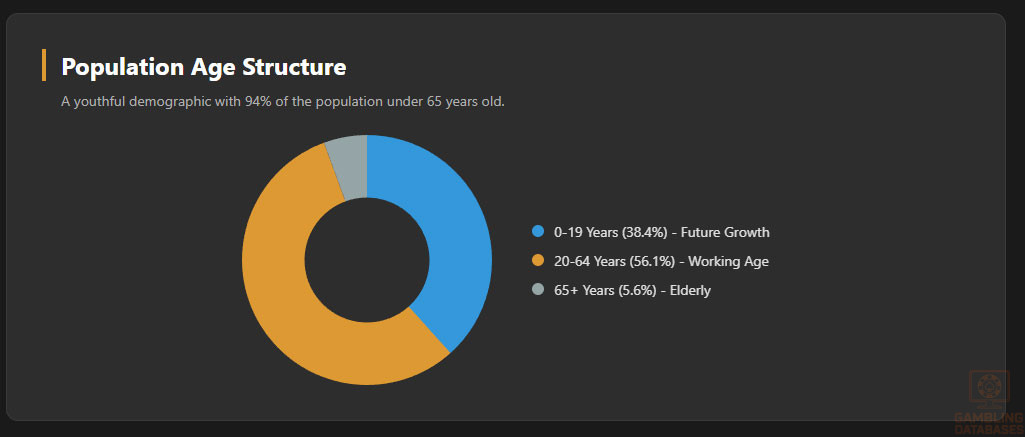

Cambodia’s total population in 2025 is estimated at approximately 17.8 million people, exhibiting steady growth at a rate of about 1.2% annually. The population structure is youthful, with a median age of 29.4 years, reflecting a dynamic workforce and consumer base poised for expansion in sectors like entertainment and digital services.

The gender ratio slightly favors females, with approximately 956 men per 1,000 women. Around 38.4% of the population is aged 19 or younger, while the working-age group (20 to 64 years) makes up 56.1% of the population. The elderly (65 years and older) represent a small 5.6% segment, minimizing age-related market constraints.

| Age Group | Population (%) | Population (Millions) |

|---|---|---|

| 0-19 years | 38.4% | ~6.8 |

| 20-64 years | 56.1% | ~10.0 |

| 65+ years | 5.6% | ~1.0 |

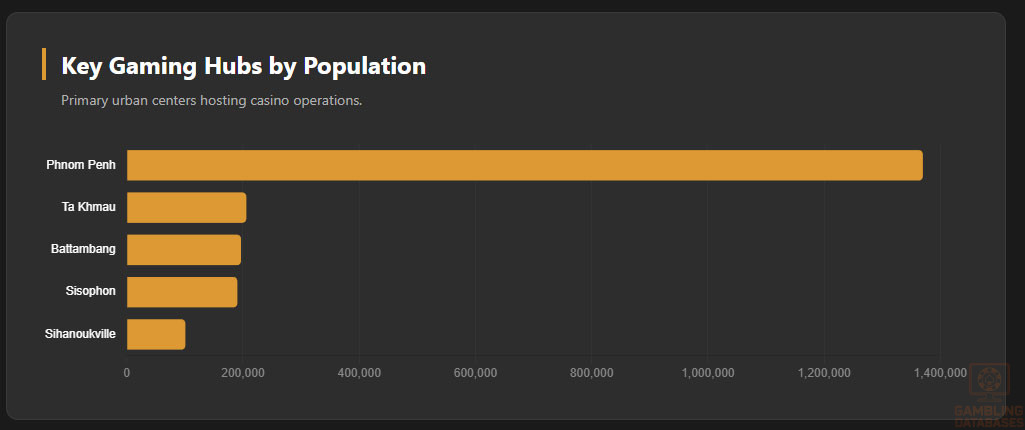

Urbanization is moderate, with about 23.6% of the population residing in urban areas primarily concentrated in Phnom Penh and other provincial capitals.

While rural areas remain home to the majority, increasing infrastructure and digital connectivity fuel urban growth and consumer market development.

- Phnom Penh – approximately 1.37 million inhabitants

- Ta Khmau – 205,813 residents

- Battambang – 196,729 residents

- Sisophon – 190,416 residents

- Siem Reap – 189,363 residents

- Sihanoukville – 100,952 residents

Major gambling venues are heavily clustered around Phnom Penh, Sihanoukville, and border towns like Poipet, coinciding with these urban and tourist-centric regions.

Economic Indicators and Consumer Spending Power

Cambodia’s economy has maintained robust growth despite regional uncertainties, with a 2025 GDP forecast near $30.5 billion USD and annual growth poised around 4.8%-5.8%, slightly down from previous optimistic projections.

The economy is diversified, balancing manufacturing, agriculture, tourism, and a growing digital economy. Growth drivers include foreign direct investment concentrated in industrial zones, infrastructure projects, and an increasingly service-oriented sector.

GDP per capita stands at roughly $1,803 USD, with disposable income showing a positive trend although unevenly distributed. Urban areas exhibit higher income levels and consumer spending power, while rural income remains constrained by agricultural dependence.

Consumer spending reflects gradual increases in discretionary expenditure, with a growing middle class showing demand for entertainment, including gambling-related activities and digital services.

| Indicator | Value |

|---|---|

| GDP (nominal) | $30.5 billion USD |

| Real GDP Growth Rate | 4.8% – 5.8% |

| GDP per Capita | $1,803 USD |

| Inflation Rate | Approx. 2.8% |

| Urban Population Share | 23.6% |

| Unemployment Rate | Approx. 0.6% (official) |

Income and Wealth Distribution

Income distribution in Cambodia remains skewed, with significant disparities between urban and rural populations. The wealthier urban middle class drives consumption in entertainment and luxury sectors, while lower-income rural groups prioritize essentials.

Household income levels indicate rising median incomes in the key cities, with disposable income growth supported by employment gains in manufacturing and services. However, inequality reduces spending potential across large rural segments.

This economic contrast impacts gambling market penetration, which is primarily urban-focused due to higher disposable income and access to entertainment facilities.

Market Size and Growth Projections

The Cambodian gambling market reached approximately $3.6 billion USD in 2024 revenues, primarily from land-based casinos. Market forecasts anticipate a compound annual growth rate (CAGR) of 8.6% between 2022 and 2026, driven by increasing tourism and VIP player activity.

The user base remains relatively niche, focused on affluent tourists and foreign gamblers, with average revenue per user (ARPU) undisclosed but significantly higher than regional counterparts due to VIP segmentation.

| Year | Market Revenue (Billion USD) | Growth Rate (%) |

|---|---|---|

| 2022 | 2.8 | – |

| 2023 | 3.2 | 14.3% |

| 2024 | 3.6 | 12.5% |

| 2025 | 3.9 | 8.3% |

| 2026 | 4.2 | 7.7% |

Education, Skills, and Digital Literacy

Cambodia exhibits improving literacy rates exceeding 80%, with higher education rates concentrated in urban centers. Digital literacy is rapidly increasing among youth and working-age adults, supported by expanding internet access and mobile device penetration.

A growing skilled workforce supports sectors such as IT, finance, and services, enhancing Cambodia’s appeal for digital and tech-driven industries, including iGaming operators looking for local talent in support and customer services.

Cultural and Social Factors

Communication and Language

The official language is Khmer, widely spoken across the country. English is increasingly common in business and tourism sectors, particularly in urban areas and among younger populations. Chinese languages, especially Mandarin, are also used, reflecting significant Chinese investment and visitor presence.

- Khmer (Official and Predominant)

- English (Business and Tourism)

- Mandarin Chinese (Investor and Tourist Communities)

- French (Residual Influence, Government)

- Vietnamese and Minority Languages (Border Regions)

Cultural Attitudes

Gambling is viewed by the local population largely as a foreign-oriented activity, with strong cultural and religious reservations. Buddhism’s influence discourages gambling among locals, contributing to legal restrictions prohibiting Cambodian nationals from casino gambling.

Foreign brands and operators are generally well accepted in urban and tourist areas, especially where casinos support local employment and infrastructure development. Entertainment preferences among younger Cambodians trend towards digital and mobile gaming rather than traditional gambling.

Problem Gambling and Social Considerations

Though comprehensive data on problem gambling prevalence is limited, the government acknowledges social risks associated with gambling activities and enforces strict measures to protect at-risk groups. Mandatory responsible gambling programs accompany casino licenses.

- Government-funded public awareness campaigns

- Self-exclusion and voluntary exclusion programs in casinos

- Dealer and staff training on responsible gambling

- Collaboration with NGOs providing counseling services

- Regular compliance monitoring of player protection policies

Political Structure and Governance

Cambodia operates as a constitutional monarchy with a stable government focused on economic modernization and foreign investment attraction. Regulatory consistency has improved, though challenges remain in enforcement capacity and transparency.

Political stability supports sustainable business growth, while international relations, particularly with ASEAN partners and China, enhance market access and investor confidence.

Technology Adoption and Digital Behavior

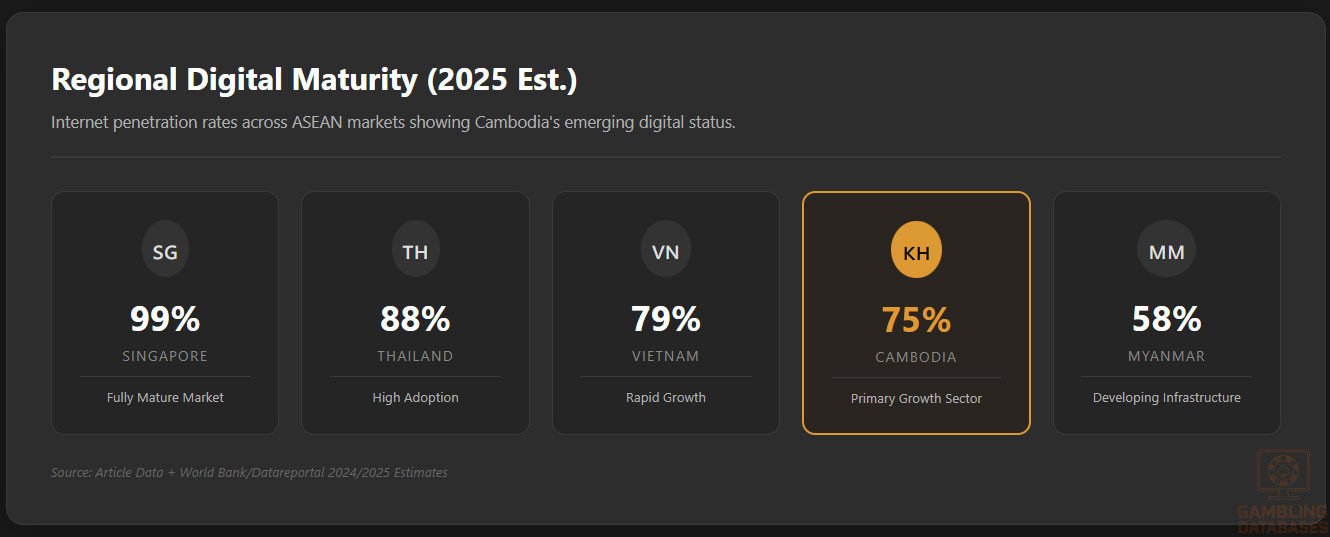

Internet and Digital Usage

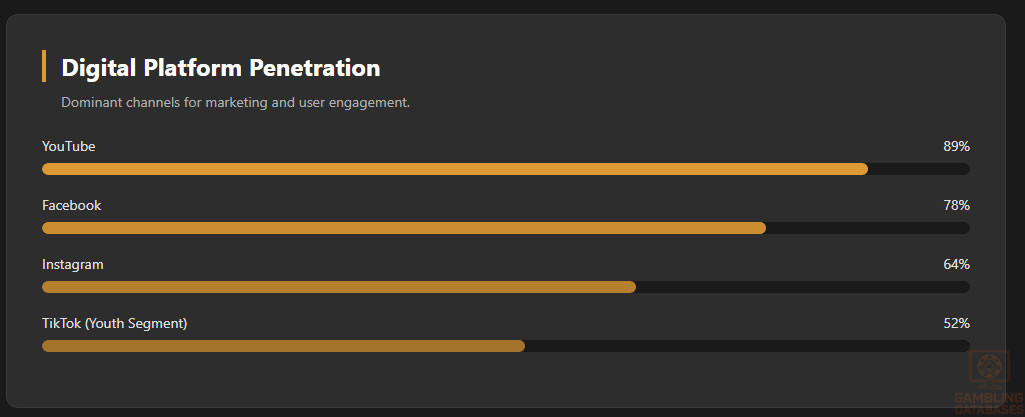

Internet penetration stands at around 69.6% of the population in 2025, with daily usage averaging several hours, particularly among youth. Mobile adoption is widespread, with cellular connections exceeding the total population at over 143%, reflecting multiple device ownership per user.

High-speed broadband access is increasing, with median fixed internet download speeds rising substantially. Social media and messaging platforms dominate digital interaction and content consumption.

- Facebook: 78% penetration, daily usage 2.3 hours

- Instagram: 64% penetration, popular among 18-34

- YouTube: 89% penetration, average watch time 45 minutes

- TikTok: Rapid growth at 52% among under-25 users

- Twitter: 31% penetration, news-focused audience

- LinkedIn: 28% professional networking penetration

Digital Payment Behavior

Cambodia’s digital payment ecosystem rapidly expands, driven by mobile wallets, QR code payments, and digital banking linked to local banks. Cash and US Dollar usage remain prominent, but digital payments gain traction among younger and urban consumers.

- ABA Pay: leading digital wallet with broad acceptance

- Wing Money: popular for P2P and online bill payments

- TrueMoney and Pi Pay: rising wallet platforms

- QR Code Payments: widely adopted in retail and services

- Digital Banking: supported by ACLEDA and Canadia Banks

Gaming and Gambling Preferences

Current Market Participation

Participation is dominated by foreign tourists and VIP high rollers. Among local Cambodians, gambling participation is minimal due to legal prohibitions. Popular gambling activities abroad and in casinos focus on table games, slot machines, and sports betting, with poker and baccarat prevalent among VIP clients.

- Casino Table Games (Baccarat, Blackjack)

- Slot Machines

- Sports Betting (Primarily Soccer and Boxing)

- Poker

- Lotteries

Consumer Behavior Patterns

Customers favor premium service experiences and privacy, with longer session durations typical for VIP clientele. Peak activity aligns with holiday seasons and tournament weeks. Retention focuses on personalized service, loyalty programs, and high-limit gaming options, while digital gaming platforms remain limited due to legal restrictions.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Cambodia’s internet penetration reached approximately 70% in 2025, predominantly driven by mobile broadband rather than fixed connections. Average broadband speeds in urban centers have improved to around 18 Mbps, yet nationwide connectivity remains uneven due to infrastructure gaps in rural regions.

Investment in fibers optics and undersea cable connections from China and Japan is expanding the digital backbone, with government-backed initiatives targeting improved rural access and network reliability. Despite progress, challenges such as frequent power outages and reliance on foreign transit networks limit consistent high-speed access outside major cities.

5G and Future Technology Deployment

5G rollout is underway, led primarily by major telecom operators focusing on Phnom Penh and key economic zones. By late 2025, coverage reached over 30% of the population in urban centers, with plans to expand to 60% by 2027. This deployment underpins Cambodia’s ambitions in digital services and smart city projects.

Mobile Technology Ecosystem

Mobile networks dominate Cambodia’s digital landscape, with a strong subscriber base exceeding the total population due to multi-SIM ownership. Smartphone penetration is growing rapidly, fostering a young, digitally savvy consumer segment attractive to iGaming and digital entertainment sectors.

- Metfone: Largest operator with roughly 45% market share, extensive rural coverage.

- Smart Axiata: Largest urban presence, 4G and 5G-ready, about 40% market share.

- Cellcard: Cambodian-owned, 20% market share, broad urban and rural reach.

- Seatel: Specialized 4G provider, niche market focus.

- Cootel: First 4G LTE operator, expanding urban coverage.

Data costs have decreased over recent years, strengthening mobile internet adoption and fueling digital payment and e-commerce growth.

Financial Services and Payment Infrastructure

Cambodia’s banking sector features a diverse mix of local and foreign banks supporting expanding digital financial services. Digital banking adoption is increasing with a growing number of accounts offering mobile app access and real-time transactions.

- ACLEDA Bank: Largest retail bank, significant digital expansion.

- Canadia Bank: Strong corporate and consumer banking services.

- BIDV Cambodia: Vietnam-backed with solid SME lending.

- Foreign banks: Support cross-border payments and FX services.

- Specialized digital banks: Emerging focus on mobile-first offerings.

Payment processing is increasingly digital, with cash still dominant but mobile wallets and QR code payments rapidly gaining. Cross-border remittances and e-commerce payments also mostly use digital channels.

- Mobile wallets: ABA Pay, Wing, TrueMoney.

- QR payments fueled by merchant adoption in cities.

- Bank transfers via National Bank of Cambodia’s ‘Fast Payment’ system.

- Card payments gaining traction in urban retail and hospitality.

- Paypal and international remittance platforms

E-commerce and Digital Economy

The e-commerce market is valued at approximately $1.1 billion USD in 2025, with expectations to grow to nearly $1.8 billion by 2029. Key sectors include apparel, electronics, and groceries, supported by rising internet penetration and smartphone adoption.

Domestic and international platforms compete, with increasing consumer trust evidenced by improved logistics, secure payments, and government promotion programs fostering digital trade integration in the ASEAN marketplace.

Business Environment and Regulatory Framework

Cambodia ranks moderately on the World Bank’s Ease of Doing Business index, with streamlined business registration but remaining challenges in tax compliance and contract enforcement. Foreign direct investment policies are favorable, with incentives for export-oriented and ICT sectors.

- Name reservation and business registration through the CamDX platform (5-10 days processing).

- Approval by the Ministry of Commerce and linkage to tax registration (3-5 days).

- Opening local bank accounts and depositing required capital (1-2 weeks).

- Obtaining relevant sector-specific licenses and permits.

Operational costs remain competitive, though infrastructure and talent acquisition present considerations. Compliance requirements focus on tax reporting, employee health and safety, and industry-specific regulations such as gambling licenses.

Corporate Structure and Registration

Common entity types include Limited Liability Companies (LLCs), Joint Stock Companies (Corporations), and Branch Offices of foreign firms. LLCs are preferred for flexibility and limited liability protection, while branches suit multinational corporations seeking operational presence.

Registration requires company articles, proof of office lease, director and shareholder identification, and tax documentation. Foreign ownership is permitted but subject to government approval, often accompanied by local partnership recommendations for regulatory navigation.

- Articles of Incorporation (Khmer and English)

- Shareholder and director ID/passports

- Lease agreement for registered office

- Tax registration certificates

- Power of attorney or authorization letters (if applicable)

Taxation Framework

The corporate income tax rate standard is 20%, with benefits such as exemptions or reductions for SMEs and companies operating under Qualified Investment Projects. Cambodia applies a territorial taxation principle taxing residents on worldwide income and non-residents only on Cambodian-sourced revenue.

- Reduced tax rates available for agricultural and SMEs

- 5-30% rates in special sectors like natural resources and insurance

- Monthly corporate income tax prepayments of 1% on turnover

- Penalties for late filing range from 10% to 40% of unpaid taxes plus interest

- Tax treaties include ASEAN countries, China, Japan, and others

Personal income tax is progressive, ranging from 0% to 20%, alongside social security contributions. Compliance mandates quarterly filings and withholding taxes for certain payments.

Market Entry Considerations

Recommended entry strategies focus on forming local partnerships, utilizing existing casino licenses for land-based operations, and leveraging digital platforms for marketing and payment processing. Foreign direct investment requires navigating regulatory approvals and capital investment mandates.

- Partnering with established local operators to gain market insight

- Investing in integrated resort development to meet licensing requirements

- Adopting compliant gambling platforms and KYC/AML technologies

- Implementing digital payment solutions aligned with Cambodian consumer habits

- Engaging with regulatory bodies proactively to ensure compliance

| Cost Category | Estimated Cost |

|---|---|

| License Application Fees | $100,000 – $250,000 |

| Company Registration and Legal Fees | $10,000 – $30,000 |

| Office Lease (Annual) | $15,000 – $45,000 |

| Staff Salaries (Annual) | $100,000 – $300,000 |

| Technology Platform Setup | $200,000 – $500,000 |

| Marketing and Compliance | $50,000 – $150,000 |

- Preparation and submission of application documents (1-2 months)

- Licensing authority review and due diligence (up to 60 days)

- Physical office setup and local staffing (1-3 months)

- Regulatory compliance integration and launch (3-6 months)

Key success factors include robust compliance infrastructures, tailored product offerings for VIP clientele, and strong local relationships. Challenges stem from regulatory complexity, infrastructure limitations outside urban centers, and competitive pressures from neighboring jurisdictions.

- Strong local regulatory knowledge

- High capital availability

- Effective KYC/AML implementation

- Superior client relationship management

- Integration with local payment systems

FAQ: Frequently Asked Questions

1. Is online gambling legal in Cambodia?

Online gambling is strictly prohibited under Cambodian law. The government bans all online gaming operations, with no licensing framework available for digital gambling platforms. Enforcement actions include fines, license revocations, and criminal charges. Land-based casinos remain legal but online operators must stay outside Cambodia’s jurisdiction or risk penalties.

2. What types of gambling licenses are available and what do they cover?

Licenses primarily cover land-based casino operations and integrated resorts. Specific licenses include general casino gaming, VIP gaming zones, and lottery operations. Online gambling licenses are not issued. License holders are regulated under the Commercial Gambling Management Commission with compliance obligations such as responsible gambling and taxation.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing costs vary but generally require a capital commitment of at least $100 million USD for standalone casinos and $200 million for integrated resorts. Application fees are typically between $100,000 and $250,000. The approval process can take up to 60 days, with additional time required for establishment of operational infrastructure.

4. Can foreign companies obtain a gambling license?

Foreign ownership is permitted but subject to government approval and encouraged local partnerships. The regulatory environment necessitates strong compliance with capital requirements and operational mandates. Foreign companies often partner with Cambodian entities to fulfill local presence obligations and navigate cultural and regulatory complexity.

5. What are the tax obligations for iGaming operators?

Operators pay a 7% gross gaming revenue (GGR) tax on standard gaming and a 4% rate for VIP gaming. Additionally, a 10% VAT applies to all revenue as of 2025, along with a 1% monthly income tax prepayment.

Corporate income tax at 20% applies to overall profits. Compliance requires timely monthly and annual financial reporting.

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue (Standard) | 7% |

| Gross Gaming Revenue (VIP) | 4% |

| Value-Added Tax (VAT) | 10% |

| Monthly Income Tax Prepayment | 1% |

| Corporate Income Tax | 20% |

6. Are gambling winnings taxed for players?

No direct taxation is imposed on gambling winnings for individual players. Tax obligations rest with operators under gross gaming revenue taxation. This policy further incentivizes player participation by removing withholding tax burdens from individual winners.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, technology platform setup, staff salaries, compliance and legal services, marketing, and payment processing agreements. High capital investment is required upfront, especially for physical casino components when applicable. Ongoing costs depend on regulatory compliance and market scale.

8. What is the expected ROI timeline for entering this market?

Return on investment typically spans 3 to 5 years, depending on scale, market positioning, and regulatory adherence. Initial heavy capital outlay and operating expenses delay profitability, yet growing tourism and regulated VIP segments underpin strong revenue potential over time.

9. What are the local presence requirements for operators?

Operators must maintain a registered office in Cambodia, employ locally approved management, and operate within licensed zones. Foreign companies usually form joint ventures with local firms to satisfy regulatory and cultural expectations. Physical presence facilitates compliance and government liaison.

10. What payment methods are available and recommended?

Cambodian consumers predominantly use a mix of cash, mobile wallets, bank transfers, and card payments. Mobile wallets such as ABA Pay and Wing are widespread, especially in urban areas. E-wallets and QR code payments facilitate rapid transaction processing in casinos and related services.

11. What are the advertising and marketing restrictions?

Advertising is regulated to prevent targeting minors, misleading claims, or excessive promotion of gambling benefits. Casino operators must secure prior government approvals for major marketing campaigns. Content must disclose risks and promote responsible gambling.

12. What responsible gambling measures are mandatory?

Operators must implement age verification, self-exclusion programs, deposit limits, staff training on responsible gambling, and consumer awareness campaigns. Compliance monitoring ensures adherence to these requirements to protect vulnerable players.

13. How large is the iGaming market and what is the growth potential?

The Cambodian iGaming market, dominated by land-based operations, generated $3.6 billion in 2024 with an 8.6% CAGR forecast through 2026. Growth is supported by increasing tourism, infrastructural investments, and regulatory stability. However, online iGaming remains prohibited.

14. Who are the main competitors and what is their market share?

Market leaders include prominent integrated resorts and international casino groups operating over 190 licensed venues. Competition hinges on VIP player acquisition, service excellence, and compliance robustness. Foreign operators hold significant shares via partnerships or ownership.

15. What are the player preferences and typical spending patterns?

Players favor table games such as baccarat and blackjack, with slot machines heavily used by mass-market segments. VIP customers contribute disproportionately to revenues with high-stakes gaming and personalized services. Peak activity occurs during holidays and entertainment events.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, capital adequacy, strong local partnerships, and tailored product offerings. Challenges involve infrastructure constraints outside urban areas, complex licensing requirements, competition from regional hubs, and strict enforcement of online gambling prohibitions.

- Regulatory expertise and compliance frameworks

- Substantial upfront capital investment

- Robust KYC/AML capabilities

- Strong local market intelligence

- Efficient payment processing integration

- Infrastructure gaps in rural areas

- Limited online gaming legalization

- Complex application and approval processes

- Competitive regional market pressure

- Dependence on tourism fluctuations

Sources and References

- Gambling Regulation in Cambodia – iGaming Today

- Cambodia Commercial Gambling Management Commission (CGMC) Official Documents

- Cambodia Gambling Market Forecast 2020-2026 – 6W Research

- Digital 2025 Cambodia Report – DataReportal

- Cambodia Population and Demographics – Worldometers

- Cambodia Economic Update 2025 – Cambodia Securities Exchange

- Cambodia Internet Infrastructure Outlook 2025 – Loma Technology

- Cambodia Mobile Network Operators Overview – Tech Junction

- Cambodia Banking Sector Report 2025 – Cambodia Investment Review

- Top Payment Methods in Cambodia – Wise.com

- Business Registration Guide Cambodia – Ministry of Commerce via CamDX

- Corporate Income Tax Cambodia – PwC Tax Summaries

- Cambodia E-commerce Market Analysis – Statista

- National Bank of Cambodia Reports

- World Bank Doing Business Reports 2024

- ASEAN Regulatory Frameworks Comparative Studies

- Cambodia Ministry of Finance Tax Reports 2025

- International Telecommunication Union – Cambodia ICT Statistics

- Cambodia Digital Economy and Smart City Initiatives – Government Publications

- News Articles on Cambodia Gambling Regulation and Market – Various

🎯 Gambling Databases Country Rating: Cambodia

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.5/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 2.0/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 1.3/10 | High-Risk / Prohibited for Online |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE ONLINE PROHIBITION: While land-based casinos are legal, the Cambodian government enforces an outright ban on all online gambling platforms. There is no legal mechanism to obtain an online license.

- MANDATORY ONSITE REGULATORS: New 2025 regulations established 13 onsite regulator offices within casinos to monitor activity, making “grey” operations from within licensed land-based venues virtually impossible to hide.

- HIGH CAPITAL BARRIERS: Even for land-based entry (the only legal route), minimum capital requirements are $100,000,000 USD for standalone casinos and $200M for integrated resorts.

- AGGRESSIVE ENFORCEMENT: The Commercial Gambling Management Commission (CGMC) actively works with police to raid illegal online setups. Penalties include immediate license revocation, asset seizure, and criminal charges.

- NEW TAX BURDENS (2025): Introduction of a 10% VAT on gross gaming revenue (effectively a turnover tax) plus a 1% monthly income tax prepayment significantly degrades profit margins for any gambling entity.

- LOCAL PLAYER BAN: It is strictly illegal for Cambodian citizens to gamble. The market is legally restricted 100% to foreigners and tourists.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Illegal with enforcement (-1.0). Online gambling is explicitly prohibited. While land-based is legal, this assessment focuses on iGaming. Deductions: Online casino prohibition (-1.5), Active enforcement and raids (-0.5). |

| Licensing Process | 25% | 0.0/2.5 | No licensing available (0). There is no license for online operators. Land-based licenses require $100M-$200M capital (-0.25 for extreme cost). Final score cannot be negative, floored at 0. |

| Taxation & Costs | 20% | 0.5/2.0 | High Tax Burden. Even if operation were legal, the fiscal regime is heavy. 7% GGR (Mass) + 10% VAT (new) + 1% Revenue Tax = Effective rate approx 18-20% of GGR, but VAT on gaming is administratively burdensome and costly. Deductions: High operational costs/capital ($100M entry ticket) (-0.5). New VAT implementation (-0.5). |

| Operational Requirements | 15% | 0.0/1.5 | Excessive requirements (0). Online operations are banned. Land-based requires massive infrastructure. Deductions: Mandatory onsite regulator presence (-0.25), $100M+ capital requirement (-0.25). |

| Market Environment | 10% | 0.0/1.0 | Difficult environment (100+) (+0.25). Deductions: Regulatory instability (frequent changes 2023-2025 including new taxes) (-0.25), Active enforcement against online sector (-0.25). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.5/4.0 | Illegal for Locals. Cambodian citizens are strictly prohibited from gambling (-1.5). Online is illegal for everyone (-1.5). Only foreign tourists in physical zones have legal status. |

| Practical Accessibility | 30% | 1.0/3.0 | Limited accessibility. While VPNs work, the government monitors suspicious financial transactions. ISP blocking is active for known illegal operators. Deductions: Active blocking (-0.5), Banking surveillance (-0.5). |

| Player Penalties | 20% | 1.0/2.0 | Fines possible (+1.0). Locals caught gambling face fines and potential detention. Foreigners are generally left alone if playing online privately, but have no consumer protection. |

| Market Availability | 10% | 0.0/1.0 | No access (0). There are zero licensed online operators. Players are forced to the black market. |

🔍 Key Highlights

Strengths (For Land-Based Only)

- Strategic Location: Proximity to Thailand and Vietnam drives physical traffic to border casinos (Poipet, Bavet).

- Low Labor Costs: Operational staffing costs are significantly lower than regional competitors like Singapore or Macau.

- Tourism Growth: 8.6% CAGR projected for the sector, driven by physical integrated resorts.

⛔️ CRITICAL RISKS AND CHALLENGES

- Product Prohibitions: Online gambling is 100% banned. There is no legal loophole for iGaming.

- Financial Barriers: $100M USD minimum capital requirement makes market entry impossible for non-institutional players.

- Fiscal Aggression: The 2025 introduction of 10% VAT on gaming revenue significantly erodes margins. This is on top of GGR tax and 1% monthly revenue tax.

- Regulatory Surveillance: The establishment of 13 onsite CGMC offices inside casinos indicates a move toward “police state” monitoring of gambling activities.

- Banking Restrictions: Strict AML/KYC and government monitoring of transaction flows make processing payments for illegal online sites difficult.

- Local Exclusion: The entire local population (16.9 million) is legally fenced off from the market.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $100,000,000+ USD (Land-based only).

Monthly Operating Costs: High (Physical infrastructure, 100+ staff required).

Effective Tax Rate on Revenue: Approx. 18-25% (7% GGR + 10% VAT + 1% Turnover Tax + Corporate Tax).

Customer Acquisition Cost: N/A for online (Illegal). High for land-based (Junket/VIP commissions).

Time to Breakeven: 5-7 years (Physical Resort Model).

Profitability Assessment: IMPOSSIBLE FOR ONLINE OPERATORS. For iGaming, this market does not exist legally. Attempting to operate illegally involves high risks of asset seizure and arrest. For land-based operators, profitability is possible but requires massive capital and navigating a complex, high-corruption environment with rising tax rates.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Online Casino Operators | 🔴 Critical | Criminal prosecution, asset seizure, immediate shutdown, blacklisting. |

| Land-Based Operators | 🟡 Medium | Regulatory volatility, increasing tax burden, strict compliance audits. |

| Affiliates/Advertisers | 🔴 High | Promotion of illegal gambling is a criminal offense; severe fines. |

| Payment Processors | 🔴 High | Money laundering charges for processing gambling transactions; license loss. |

| Company Directors | 🔴 Critical | Personal liability for illegal operations; high risk of detention if in-country. |

🚨 Extradition and International Enforcement

Extradition Treaties: Cambodia has active extradition treaties with China, Thailand, and Vietnam. Cooperation with Chinese authorities is particularly strong regarding gambling crackdowns.

Enforcement History: Frequent joint operations with Chinese and Thai police to raid illegal online gambling compounds. Hundreds of foreign nationals are deported annually for involvement in illegal gambling rings.

Safe Jurisdictions: None within the region. Cambodia actively cooperates with ASEAN and Chinese law enforcement.

Travel Risk: EXTREME for operators of unlicensed Asian-facing sites. Entering Cambodia puts you within reach of Chinese/Thai law enforcement requests.

📋 Final Verdict

Cambodia receives an Operator Ease Score of 0.5/10 and a Player Access Score of 2.0/10, resulting in an overall market attractiveness rating of 1.3/10.

HONEST ASSESSMENT: Cambodia is a “physical only” jurisdiction that poses extreme danger to online operators. The government has drawn a hard line: land-based resorts are welcome (if you have $100M), but online gambling is criminalized and actively policed. With the 2025 tax hikes (VAT) and onsite regulatory offices, the environment is becoming stricter, not looser. Do not attempt to operate an online casino or sportsbook targeting Cambodia.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major international hotel/resort developer with $200M+ USD capital.

- Willing to build physical infrastructure in Sihanoukville or Poipet.

- Focused exclusively on foreign VIP/Junket tourism, not local players.

❌ Definitely Avoid If You Are:

- An Online Operator: iGaming is strictly illegal.

- Targeting Local Players: Locals are banned; no revenue base.

- Under-Capitalized: Cannot meet the $100M minimum investment.

- A Crypto Operator: Digital assets for gambling are highly scrutinized.

- Affiliate Marketer: No legal brands to promote; high legal risk.

⚠️ BOTTOM LINE: Cambodia is closed for iGaming business; it is exclusively a playground for massive land-based developers and offers zero opportunity for digital operators.

The article’s discussion on regulatory frameworks in the gambling industry necessitates an examination of the jurisdictional variations, particularly in regions like Europe, where the European Gaming and Betting Association (EGBA) plays a crucial role. For instance, the UK’s Gambling Commission and Malta’s Gaming Authority have implemented stringent measures to ensure compliance, with a focus on anti-money laundering (AML) and know-your-customer (KYC) protocols, which has led to a significant reduction in illicit activities, with some operators reporting a 25% decrease in suspicious transactions. Furthermore, the implementation of the General Data Protection Regulation (GDPR) has also had a profound impact on the industry, with operators required to maintain data protection standards, adhering to the 72-hour deadline for reporting data breaches, and ensuring transparency in their data processing practices, which has resulted in enhanced customer trust and loyalty, with a notable example being the operator, Bet365, which has seen a 15% increase in customer retention rates.

Regarding the mention of the European Gaming and Betting Association (EGBA), it’s worth noting that their efforts in promoting a safe and regulated environment for online gambling have been instrumental in shaping the industry’s standards. The implementation of robust AML and KYC protocols, as well as adherence to GDPR, are indeed crucial for maintaining integrity and trust. For example, a study by the EGBA found that 75% of operators reported an improvement in their AML and KYC processes after implementing the association’s guidelines. Additionally, the importance of transparency in data processing practices cannot be overstated, as it directly impacts customer loyalty and retention, with a recent survey indicating that 80% of customers consider data protection a key factor in their choice of operator.

Thanks for the insight, the EGBA’s guidelines have indeed been a benchmark for many operators. I’d like to add that the role of technology, such as AI-powered monitoring systems, in enhancing AML and KYC processes should not be underestimated, with some operators reporting a 30% reduction in false positives. Furthermore, the use of blockchain technology has also shown promise in improving the transparency and security of transactions, with a recent pilot study demonstrating a 99% reduction in transaction disputes.

That’s a valuable point, the integration of technology is certainly a key factor in the evolution of regulatory compliance in the gambling industry. The use of AI and blockchain can significantly enhance the efficiency and security of operations, and it will be interesting to see how these technologies continue to shape the industry’s future, with potential applications in areas such as responsible gaming and customer protection. A recent report by the International Association of Gaming Advisors highlighted the potential of AI in identifying problem gamblers, with a 90% accuracy rate in detecting early signs of problematic behavior.