Cameroon’s iGaming market presents a promising opportunity fueled by growing internet penetration and evolving regulatory efforts. Although land-based gambling is well regulated, the online gambling sector is currently under regulatory transition with recent government initiatives to tighten oversight and streamline licensing.

This article provides a detailed analysis of Cameroon’s regulatory framework and legal environment for iGaming market entrants. It outlines prevailing laws, licensing mandates, taxation structures, compliance requirements, and enforcement mechanisms pivotal for successful market entry.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Population | 27 million (approx.) |

| GDP (nominal) | ~$40 billion USD |

| Internet Penetration Rate | ~45% |

| Mobile Penetration Rate | 85% |

| Legal Gambling Framework Established | Law No. 2015/012 (July 2015) |

| Regulatory Authority | Ministry of Territorial Administration |

| Online Gambling Legal Status | Legal with authorization/licensing required |

| License Types | Concession, Authorization, Declaration |

| License Duration | 5 to 10 years |

| License Application Fee | $10,000 – $20,000 |

| Minimum Bank Guarantee (Online License) | 200 million CFA (~$330,000) |

| Gross Gaming Revenue Tax Rate (GGR) | 15% for casinos, 25% for other games |

| Fixed Annual Tax per Slot Machine | 100,000 CFA (~$165) |

| Supplementary Tax on GGR | 10% |

| Electronic Money Transfer Tax | 1% + 4 CFA per transaction |

| Average Market Growth Rate (2025-2029 CAGR) | 5.2% |

| Projected Market Volume 2029 | US$134.1 million |

| Number of Licensed Land-Based Operators | ~18 (Casinos, Betting Houses, Gaming Halls) |

| Market Penetration (Online Gambling) | Increasing, driven by digital adoption |

| License Approval Timeline | 4-6 months |

| Local Presence Requirement | Mandatory representation in Cameroon |

| Exclusive Payment Aggregator | INTOUCH Cameroun (since Jan 2025) |

| Advertising Restrictions | Permitted with conditions; Google allows ads since Aug 2025 |

| Responsible Gambling Measures | Mandatory for land-based operators, evolving online |

| Player Protection | KYC and AML required, online protections limited |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

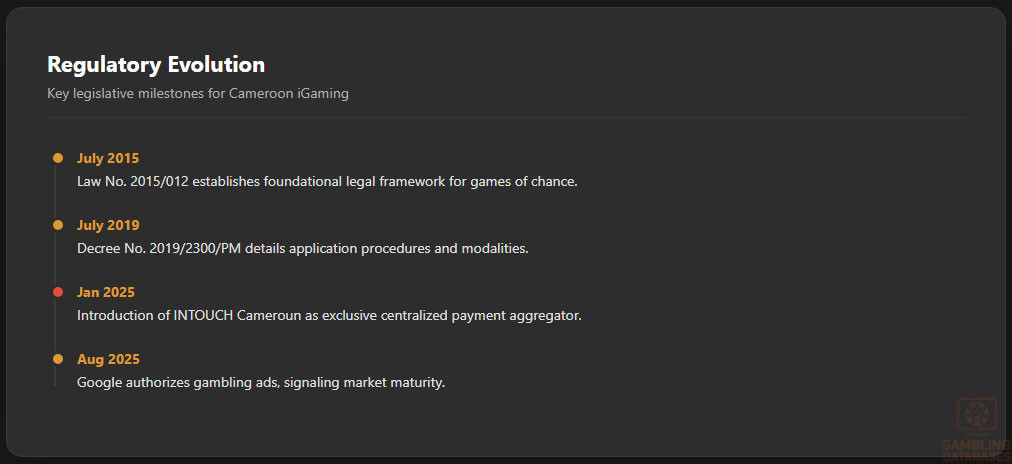

Gambling in Cameroon is governed primarily by the Law No. 2015/012 of July 16, 2015, which provides the foundational legal framework regulating entertainment games, games of chance, and money games. This law was further refined by Decree No. 2019/2300/PM enacted on July 18, 2019, that specifically details application procedures and operational modalities for gambling activities across the country.

Land-based gambling activities have long been established and regulated, covering casinos, sports betting venues, and gaming halls. However, online gambling, despite being formally recognized as legal under the 2015 law, remains in an emerging and somewhat ambiguous state with regulatory efforts still catching up to market realities.

Land-Based Gambling Activities

Cameroon licenses and regulates a range of land-based gambling entities, including seven casinos, seven betting and lottery houses, and four dedicated gaming machine halls. Most of these venues are concentrated in the major urban centers of Yaoundé and Douala, serving a sizable domestic gambling population. Gaming machine businesses pay fixed annual fees per machine, differentiated by size and type.

Online Gambling Framework

Online gambling is legal in Cameroon but requires specific authorization from the Ministry of Territorial Administration. The legal framework mandates that operators secure an authorization license to offer online betting or gaming services. Any operator functioning without such authorization faces penalties including imprisonment or substantial fines.

Furthermore, since January 30, 2025, Cameroon introduced a centralized system that mandates all online gambling financial transactions pass through a single government-approved payment aggregator, INTOUCH Cameroun. This control mechanism aims to enhance regulatory oversight, combat fraud, and ensure proper cash flow monitoring within the online gaming ecosystem.

Despite these advances, online player protections remain less developed relative to the land-based sector, leaving a grey area especially for operators licensed abroad but marketing to Cameroonian players.

Licensed Operators and Market Players

The Cameroonian gambling market hosts approximately 18 licensed land-based operators across casinos, betting houses, and gaming halls. These license holders form the backbone of the regulated gambling ecosystem. Online licensed operators are fewer, as the process and regulatory clarity continue advancing.

Market dynamics reveal opportunities for international entrants able to comply with stringent licensing and integrate with INTOUCH Cameroun for payment processing. Competition focuses heavily on sports betting and expanding digital platforms, with investments anticipated to grow in online casino and virtual lottery offerings.

Licensing Framework and Requirements

Application Process and Eligibility

The gambling licensing authority is the Ministry of Territorial Administration, overseeing both land-based concession licenses and online authorization regimes. Operators must meet rigorous financial and technical requirements aligned with international best practices.

Applications include submission of corporate documents demonstrating financial stability, including a minimum bank guarantee of 200 million CFA for online gaming, alongside technical certifications for gaming platforms. Application fees range from $10,000 to $20,000, with total license durations between 5 to 10 years depending on the license type.

The licensing procedure typically takes between four to six months and involves a thorough review to ensure compliance with legal, financial, and operational standards.

Local Presence and Operational Requirements

All operators must maintain a physical or legal presence in Cameroon, necessitating registration of a local subsidiary or representation. This requirement ensures accountability and facilitates regulatory enforcement. Foreign ownership is permitted but subject to full compliance with Cameroonian business laws and regulatory oversight.

The exclusive designation of INTOUCH Cameroun as the payment aggregator also implies integration requirements for authorized online operators, mandating technical alignment with the centralized payment monitoring infrastructure.

Compliance Obligations and Monitoring

Player Protection and Identification

Regulations enforce strict Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols for licensing applicants and operational licensees. Age verification and responsible gambling initiatives are mandated for land-based operators, with ongoing development to extend similar protections for online players.

- Mandatory age verification to prevent underage gambling

- Comprehensive KYC procedures to identify and verify player identities

- Anti-money laundering checks integrated into transaction monitoring

- Responsible gambling education and prevention programs required

- Self-exclusion mechanisms available for players at risk

Information disclosure and transparency towards players constitute additional compliance pillars, albeit evolving especially for online platforms.

Financial Monitoring and Reporting

Operators must routinely submit detailed financial reports to the regulatory authority covering revenue streams, wager volumes, and tax obligations. The Ministry mandates rigorous transaction monitoring underpinned by the centralized payment system to ensure transparency.

- Monthly submission of financial statements including wager and payout data

- Quarterly compliance audits with technical and financial verifications

- Annual renewal applications with updated organizational compliance information

- Immediate reporting of suspicious or irregular transactions as per AML laws

Taxation Structure and Financial Obligations

Player Taxation

Players in Cameroon are generally not subject to direct taxation on gambling winnings under current laws. However, indirect taxation arises from transactional levies applied to deposits and withdrawals. Such taxes are integrated within the operational framework to capture revenue passively through financial flows.

Operator Taxation

| Game Type | Tax Rate / Fee |

|---|---|

| Casino Gross Gaming Revenue (GGR) | 15% |

| Other Games’ GGR (e.g., betting, lotteries) | 25% |

| Annual Slot Machine Fee | 100,000 CFA (~$165) per machine |

| Supplementary Tax on GGR | 10% |

| Electronic Money Transfer Tax (related to gambling) | 1% + 4 CFA per transaction |

Operators additionally pay corporate income tax under Cameroon’s general taxation regime, with licensing renewal fees applying regularly. Turnover taxes and fixed fees on equipment augment the tax burden.

Gambling Market Financial Performance

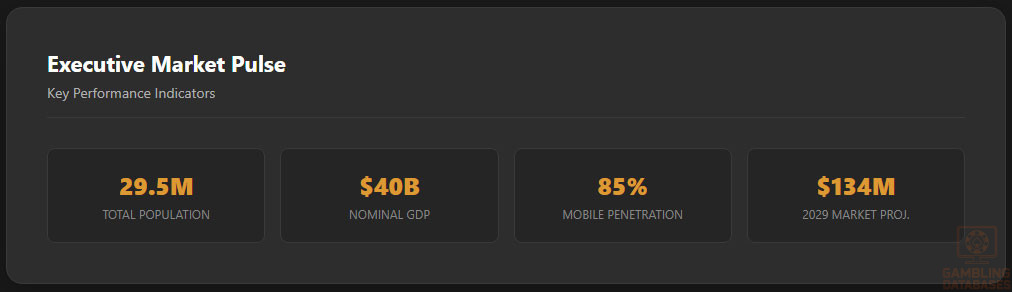

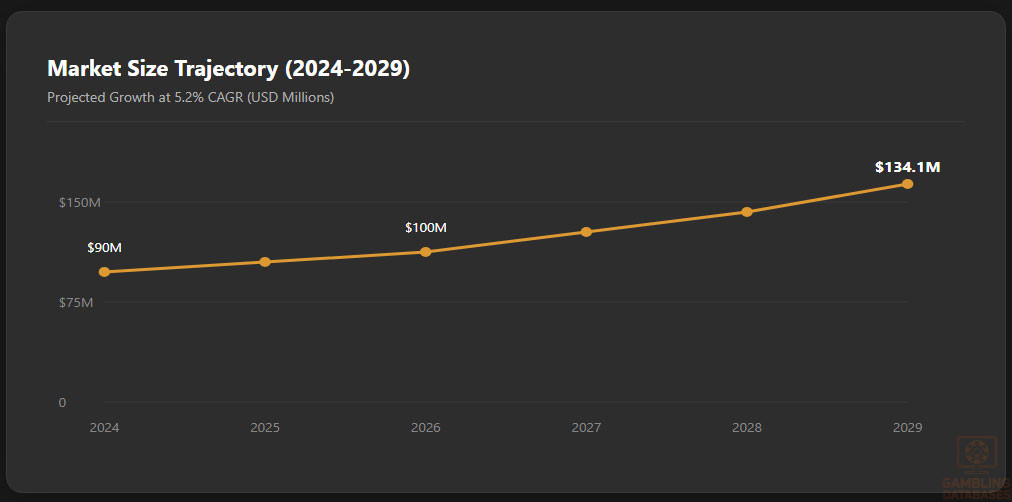

The Cameroonian market has displayed steady growth with wagering volumes expected to reach approximately US$134.1 million by 2029, growing at an annual compound rate of 5.2%. Revenue diversification between land-based and digital platforms underpins the evolving market landscape. Tax revenues from gambling constitute an increasing portion of national government revenues.

Advertising and Marketing Restrictions

Advertising for gambling activities in Cameroon is permitted but regulated to ensure consumer protection and prevent promotion targeting minors. From August 2025, Google has authorized gambling ads in Cameroon, reflecting progressive openness to regulated marketing activities.

- Advertising must avoid content encouraging excessive gambling

- All promotions require clear terms and conditions disclosure

- Targeting minors and vulnerable groups is strictly prohibited

- Broadcasting times for gambling ads may be restricted to certain hours

- Sponsorship of events by gambling operators must comply with regulatory guidelines

Recent Regulatory Changes and Their Impact

In early 2025, Cameroon implemented a centralized control system for online gambling payments via INTOUCH Cameroun, a move aimed at improving financial oversight and consumer protection.

The 2025 Finance Bill further introduced taxes on electronic money transfers related to gambling transactions, expanding fiscal revenues from the sector. These regulatory developments raise compliance costs but enhance market transparency and operator accountability, attracting more responsible investment.

Enforcement Mechanisms and Penalties

The regulatory regime enforces strict penalties including fines, license suspensions, and imprisonment for non-compliance with licensing or operational laws. Enforcement actions target illegal operators, fraud, money laundering, and breaches of player protection protocols.

- Fines up to 25 million CFA for unauthorized gambling operations

- Imprisonment terms of 6 months to 2 years for severe violations

- License revocations and suspensions for regulatory breaches

- Seizure of assets and equipment used in illegal gambling activities

- Close collaboration with financial institutions to enforce payment controls

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

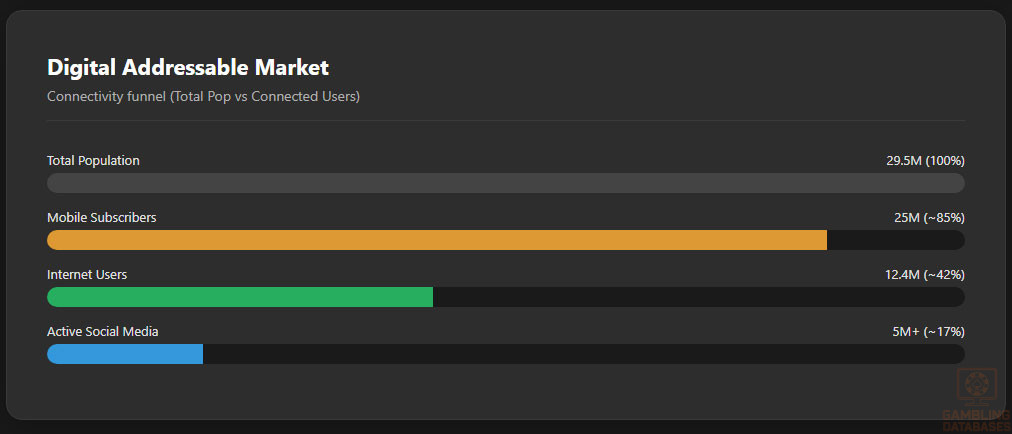

As of early 2025, Cameroon’s population is estimated at approximately 29.5 million people. The country presents a youthful demographic profile, with a median age of about 18 years, indicating a large proportion of the population is under 25. The gender ratio is relatively balanced, with females representing roughly 50.2% and males 49.8%.

The age distribution demonstrates significant population segments within younger cohorts, supporting a dynamic and potentially tech-savvy consumer base. Urbanization trends show that approximately 60.2% of the population resides in urban centers, while the rural population accounts for 39.8%, highlighting areas of concentrated consumer activity and access disparities.

| Age Group | Percentage of Total Population |

|---|---|

| 0-4 years | 15.1% |

| 5-12 years | 21.3% |

| 13-17 years | 11.4% |

| 18-24 years | 13.2% |

| 25-34 years | 14.6% |

| 35-44 years | 10.8% |

| 45-54 years | 6.9% |

| 55-64 years | 3.9% |

| 65 years and above | 2.8% |

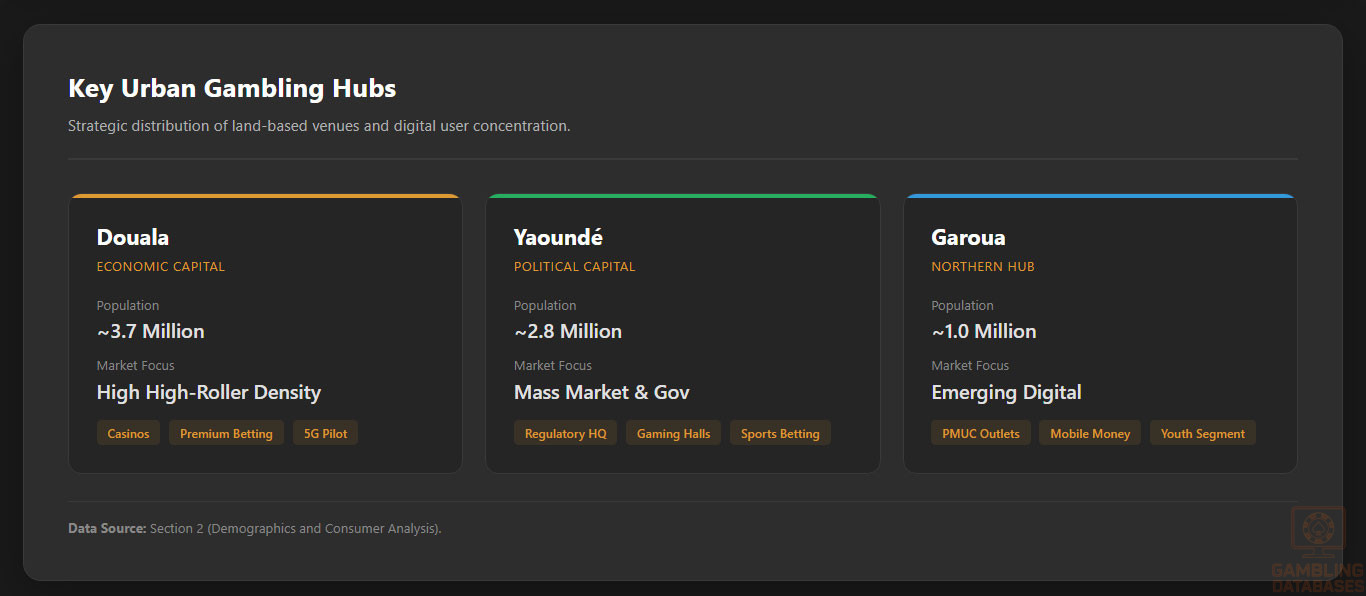

Population density concentrates mainly in urban hubs such as Yaoundé, Douala, and Garoua, with these cities representing key economic and social centers where gambling venues and digital infrastructure are most accessible.

- Yaoundé – Capital city, approx. 2.8 million inhabitants

- Douala – Economic hub, approx. 3.7 million inhabitants

- Garoua – Northern key city, approx. 1 million inhabitants

- Bafoussam – Western region, approx. 720,000 inhabitants

- Maroua – Northern region, approx. 500,000 inhabitants

Internet penetration correlates strongly with these urban centers where access and adoption are highest, which influences gambling venue concentration and online gambling activity distribution.

Economic Indicators and Consumer Spending Power

Cameroon’s GDP experienced a growth rate of approximately 3.5% in 2024, with forecasts indicating a stable medium-term growth averaging around 3.9% annually through 2028. The nominal GDP stands near $40 billion, driven by the service sector’s expansion, which accounts for over 50% of GDP.

Consumer spending is buoyed by steady improvements in disposable incomes alongside declining inflation rates, which reached about 4.5% in 2024. The per capita income remains modest but is showing gradual upward trends, supporting increasing engagement in discretionary spending such as gaming.

| Indicator | Value |

|---|---|

| GDP Growth Rate 2024 | 3.5% |

| Projected Average GDP Growth (2025-28) | 3.9% |

| Nominal GDP | ~$40 billion |

| Inflation Rate 2024 | 4.5% |

| Per Capita Income (approx.) | $1,350 |

Income distribution reveals significant disparities, with a majority in lower to middle income brackets while a smaller wealthy segment leads consumer trends in urban zones. Household consumption patterns indicate increasing penetration of mobile services and online retail, feeding into the digital entertainment market growth trajectory.

Market Size and Growth Projections

The gambling market in Cameroon is actively expanding, supported by rising internet adoption and urban consumer growth. The market size was estimated to be around $90 million in 2024, with projections to surpass $130 million by 2029, reflecting a compound annual growth rate (CAGR) near 5.2%.

Online gambling segments are the fastest-growing, driven by digital platform proliferation and mobile access. Average revenue per user (ARPU) is rising steadily due to increased consumer spending power and engagement levels.

| Year | Market Size (USD millions) | Annual Growth Rate (%) | ARPU (USD) |

|---|---|---|---|

| 2024 | 90 | – | 7.5 |

| 2025 | 95 | 5.5 | 8.0 |

| 2026 | 100 | 5.3 | 8.3 |

| 2027 | 110 | 6.0 | 8.7 |

| 2028 | 120 | 5.9 | 9.0 |

| 2029 | 134.1 | 5.2 | 9.3 |

Education, Skills, and Digital Literacy

Cameroon has made substantial progress in literacy rates, currently estimated at around 77% nationally, with higher rates in urban centers. Educational attainment varies widely, but there is a growing emphasis on technical and digital skills development, facilitated through public and private sector initiatives.

Digital literacy is improving, particularly among youth who constitute a significant share of the online population. This enhances the potential for online gambling engagement as users become more adept at navigating web and mobile platforms.

Cultural and Social Factors

Communication and Language

Cameroon is linguistically diverse, with over 250 native languages spoken nationwide. The official languages are French and English, with French predominant in the majority of regions and English primarily in the Northwest and Southwest.

- French: Spoken by approximately 80% of the population

- English: Spoken by about 20%, mainly in Anglophone regions

- Fang

- Betï

- Fulfulde

Online content consumption and digital communications primarily use French and English, shaping marketing and platform localization strategies.

Cultural Attitudes

Gambling is generally culturally accepted as a form of entertainment and social activity across Cameroon, particularly in urban and younger demographics. Religious and traditional beliefs influence attitudes in some regions, with some communities more conservative regarding gambling activities.

Foreign brands in the entertainment and digital sectors face moderate receptiveness, especially when engaging in community-driven campaigns that align with local values. There is rising interest in digital entertainment, including gaming and sports betting, reflecting changing leisure preferences.

Problem Gambling and Social Considerations

Problem gambling prevalence remains relatively low but is a growing concern due to increased accessibility of digital gambling channels. The government and civil society have begun implementing measures to mitigate risks related to addiction and financial harm.

- Public awareness campaigns on responsible gambling

- Support services including counseling for at-risk players

- Regulatory mandates for operator responsible gaming programs

- Self-exclusion options in licensed gambling platforms

- Collaboration with NGOs to monitor gambling harms

Social responsibility requirements for operators include mandatory contributions towards player protection programs and public education efforts.

Political Structure and Governance

Cameroon is a unitary republic with a strong presidential system. Political stability has improved, with consistent regulatory frameworks fostering confidence among investors. The government maintains strategic international partnerships, enhancing trade and regulatory alignment within Central Africa and beyond.

The regulatory environment benefits from a centralized administration, ensuring consistent application of laws relevant to gambling and digital consumer protection.

Technology Adoption and Digital Behavior

Internet and Digital Usage

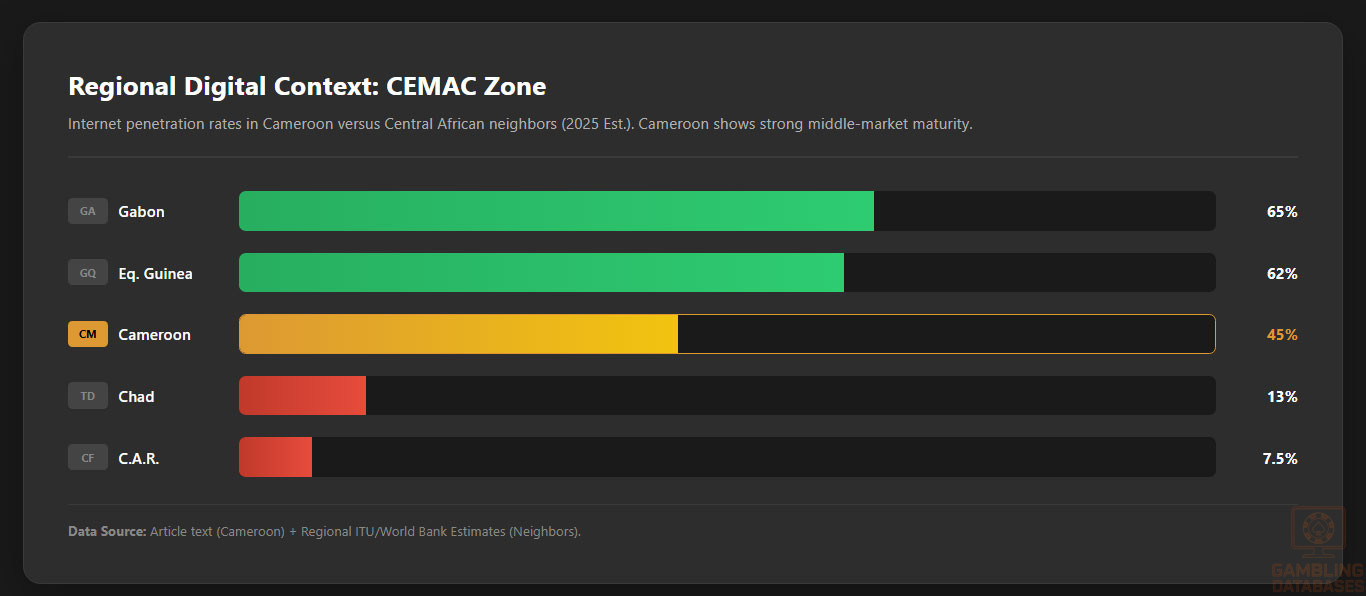

Cameroon’s internet penetration stood near 42% in early 2025, with rapid growth driven by expanding 4G mobile networks, which cover over 70% of the population. Daily internet usage averages roughly 4 hours, fueled by mobile access and social media engagement.

- Facebook: dominating with over 5 million active users

- WhatsApp: widely used for communication and commerce

- TikTok: rapidly growing among youth audience

- Instagram: popular for visual storytelling and brand engagement

- YouTube: major platform for video consumption and entertainment

Digital Payment Behavior

Digital payments increasingly facilitate online transactions with growing adoption of mobile money services. Payment method preferences lean towards mobile wallets, bank transfers, and card payments, while cryptocurrency use remains limited but emerging among niche user segments.

- Mobile Money (e.g., MTN Mobile Money, Orange Money)

- Bank Transfers

- Credit/Debit Cards

- E-wallets

- Cash payments as fallback in rural areas

Gaming and Gambling Preferences

Current Market Participation

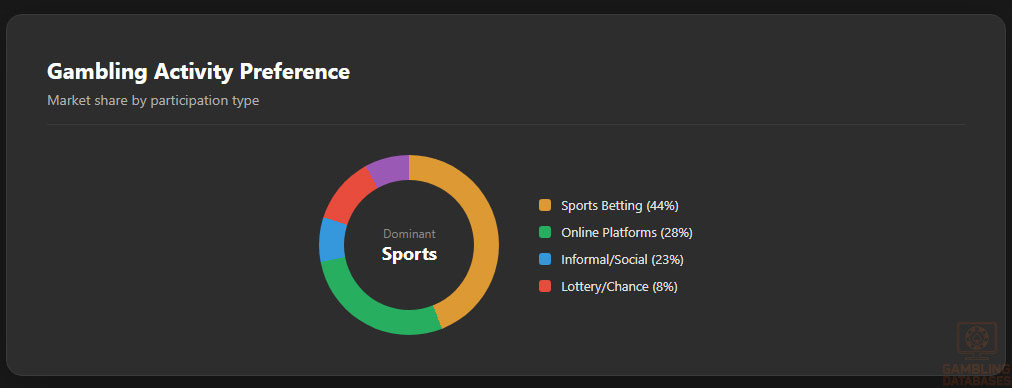

- Sports Betting – approximately 44% participation annually

- Informal Betting Among Friends and Communities – about 23%

- Online Sports Betting Via Platforms and Apps – roughly 28%

- Lotteries and Games of Chance – around 8%

- Casino Games – emerging, smaller but growing segment

Sports betting remains the dominant gambling activity, heavily influenced by football and other popular sports. Online platforms rapidly gain traction driven by smartphone usage and mobile broadband availability.

Consumer Behavior Patterns

Cameroonian consumers typically display episodic gambling with increased activity during major sporting events and holidays. Peak betting times align with evenings and weekends. Average session durations are improving with digital ease of access, while mobile platforms enhance retention through notifications and in-app engagement.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

As of early 2025, Cameroon’s population is estimated at approximately 29.5 million people. The country presents a youthful demographic profile, with a median age of about 18 years, indicating a large proportion of the population is under 25. The gender ratio is relatively balanced, with females representing roughly 50.2% and males 49.8%.

The age distribution demonstrates significant population segments within younger cohorts, supporting a dynamic and potentially tech-savvy consumer base. Urbanization trends show that approximately 60.2% of the population resides in urban centers, while the rural population accounts for 39.8%, highlighting areas of concentrated consumer activity and access disparities.

| Age Group | Percentage of Total Population |

|---|---|

| 0-4 years | 15.1% |

| 5-12 years | 21.3% |

| 13-17 years | 11.4% |

| 18-24 years | 13.2% |

| 25-34 years | 14.6% |

| 35-44 years | 10.8% |

| 45-54 years | 6.9% |

| 55-64 years | 3.9% |

| 65 years and above | 2.8% |

Population density concentrates mainly in urban hubs such as Yaoundé, Douala, and Garoua, with these cities representing key economic and social centers where gambling venues and digital infrastructure are most accessible.

- Yaoundé – Capital city, approx. 2.8 million inhabitants

- Douala – Economic hub, approx. 3.7 million inhabitants

- Garoua – Northern key city, approx. 1 million inhabitants

- Bafoussam – Western region, approx. 720,000 inhabitants

- Maroua – Northern region, approx. 500,000 inhabitants

Internet penetration correlates strongly with these urban centers where access and adoption are highest, which influences gambling venue concentration and online gambling activity distribution.

Economic Indicators and Consumer Spending Power

Cameroon’s GDP experienced a growth rate of approximately 3.5% in 2024, with forecasts indicating a stable medium-term growth averaging around 3.9% annually through 2028. The nominal GDP stands near $40 billion, driven by the service sector’s expansion, which accounts for over 50% of GDP.

Consumer spending is buoyed by steady improvements in disposable incomes alongside declining inflation rates, which reached about 4.5% in 2024. The per capita income remains modest but is showing gradual upward trends, supporting increasing engagement in discretionary spending such as gaming.

| Indicator | Value |

|---|---|

| GDP Growth Rate 2024 | 3.5% |

| Projected Average GDP Growth (2025-28) | 3.9% |

| Nominal GDP | ~$40 billion |

| Inflation Rate 2024 | 4.5% |

| Per Capita Income (approx.) | $1,350 |

Income distribution reveals significant disparities, with a majority in lower to middle income brackets while a smaller wealthy segment leads consumer trends in urban zones. Household consumption patterns indicate increasing penetration of mobile services and online retail, feeding into the digital entertainment market growth trajectory.

Market Size and Growth Projections

The gambling market in Cameroon is actively expanding, supported by rising internet adoption and urban consumer growth. The market size was estimated to be around $90 million in 2024, with projections to surpass $130 million by 2029, reflecting a compound annual growth rate (CAGR) near 5.2%.

Online gambling segments are the fastest-growing, driven by digital platform proliferation and mobile access. Average revenue per user (ARPU) is rising steadily due to increased consumer spending power and engagement levels.

| Year | Market Size (USD millions) | Annual Growth Rate (%) | ARPU (USD) |

|---|---|---|---|

| 2024 | 90 | – | 7.5 |

| 2025 | 95 | 5.5 | 8.0 |

| 2026 | 100 | 5.3 | 8.3 |

| 2027 | 110 | 6.0 | 8.7 |

| 2028 | 120 | 5.9 | 9.0 |

| 2029 | 134.1 | 5.2 | 9.3 |

Education, Skills, and Digital Literacy

Cameroon has made substantial progress in literacy rates, currently estimated at around 77% nationally, with higher rates in urban centers. Educational attainment varies widely, but there is a growing emphasis on technical and digital skills development, facilitated through public and private sector initiatives.

Digital literacy is improving, particularly among youth who constitute a significant share of the online population. This enhances the potential for online gambling engagement as users become more adept at navigating web and mobile platforms.

Cultural and Social Factors

Communication and Language

Cameroon is linguistically diverse, with over 250 native languages spoken nationwide. The official languages are French and English, with French predominant in the majority of regions and English primarily in the Northwest and Southwest.

- French: Spoken by approximately 80% of the population

- English: Spoken by about 20%, mainly in Anglophone regions

- Fang

- Betï

- Fulfulde

Online content consumption and digital communications primarily use French and English, shaping marketing and platform localization strategies.

Cultural Attitudes

Gambling is generally culturally accepted as a form of entertainment and social activity across Cameroon, particularly in urban and younger demographics. Religious and traditional beliefs influence attitudes in some regions, with some communities more conservative regarding gambling activities.

Foreign brands in the entertainment and digital sectors face moderate receptiveness, especially when engaging in community-driven campaigns that align with local values. There is rising interest in digital entertainment, including gaming and sports betting, reflecting changing leisure preferences.

Problem Gambling and Social Considerations

Problem gambling prevalence remains relatively low but is a growing concern due to increased accessibility of digital gambling channels. The government and civil society have begun implementing measures to mitigate risks related to addiction and financial harm.

- Public awareness campaigns on responsible gambling

- Support services including counseling for at-risk players

- Regulatory mandates for operator responsible gaming programs

- Self-exclusion options in licensed gambling platforms

- Collaboration with NGOs to monitor gambling harms

Social responsibility requirements for operators include mandatory contributions towards player protection programs and public education efforts.

Political Structure and Governance

Cameroon is a unitary republic with a strong presidential system. Political stability has improved, with consistent regulatory frameworks fostering confidence among investors. The government maintains strategic international partnerships, enhancing trade and regulatory alignment within Central Africa and beyond.

The regulatory environment benefits from a centralized administration, ensuring consistent application of laws relevant to gambling and digital consumer protection.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Cameroon’s internet penetration stood near 42% in early 2025, with rapid growth driven by expanding 4G mobile networks, which cover over 70% of the population. Daily internet usage averages roughly 4 hours, fueled by mobile access and social media engagement.

- Facebook: dominating with over 5 million active users

- WhatsApp: widely used for communication and commerce

- TikTok: rapidly growing among youth audience

- Instagram: popular for visual storytelling and brand engagement

- YouTube: major platform for video consumption and entertainment

Digital Payment Behavior

Digital payments increasingly facilitate online transactions with growing adoption of mobile money services. Payment method preferences lean towards mobile wallets, bank transfers, and card payments, while cryptocurrency use remains limited but emerging among niche user segments.

- Mobile Money (e.g., MTN Mobile Money, Orange Money)

- Bank Transfers

- Credit/Debit Cards

- E-wallets

- Cash payments as fallback in rural areas

Gaming and Gambling Preferences

Current Market Participation

- Sports Betting – approximately 44% participation annually

- Informal Betting Among Friends and Communities – about 23%

- Online Sports Betting Via Platforms and Apps – roughly 28%

- Lotteries and Games of Chance – around 8%

- Casino Games – emerging, smaller but growing segment

Sports betting remains the dominant gambling activity, heavily influenced by football and other popular sports. Online platforms rapidly gain traction driven by smartphone usage and mobile broadband availability.

Consumer Behavior Patterns

Cameroonian consumers typically display episodic gambling with increased activity during major sporting events and holidays. Peak betting times align with evenings and weekends. Average session durations are improving with digital ease of access, while mobile platforms enhance retention through notifications and in-app engagement.

Spending behavior trends indicate cautious but growing investment in gambling, often motivated by both entertainment and income opportunity. Platform preferences lean toward user-friendly, local-language options integrating mobile money payment systems.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Cameroon’s internet penetration stood at approximately 42% in 2025, reflecting continuous expansion driven largely by mobile broadband. Fixed broadband remains limited, constrained by infrastructure costs and geographic challenges, whereas mobile internet dominates connectivity.

Average mobile broadband speeds range from 10 Mbps to 25 Mbps in urban centers, providing generally sufficient performance for digital entertainment including online gambling. Network reliability varies, with occasional disruptions in rural areas, but urban regions benefit from ongoing infrastructure investments.

Government and private sector initiatives are steadily enhancing fiber optic and 4G network deployment to boost coverage and reduce latency, critical for live gaming platforms and secure transactions.

5G and Future Technology Deployment

5G infrastructure rollout in Cameroon is in early pilot phases, primarily focused on urban areas such as Douala and Yaoundé. Major telecommunications operators plan progressive expansions targeting full commercial availability by 2027.

This technology is expected to dramatically improve latency and capacity, enabling real-time interactive gaming experiences. The government views 5G as strategic for digital economy growth and is facilitating spectrum allocation processes.

Mobile Technology Ecosystem

Cameroon’s mobile network sector is competitive, with four dominant operators providing over 90% market share collectively. Market penetration exceeds 85%, with high smartphone adoption rates fostering mobile-based internet usage.

- MTN Cameroon – largest operator with ~40% market share

- Orange Cameroon – strong second with ~30% share

- Camtel – state-owned operator with ~15% market share

- Nexttel – growing presence with ~10%

- Other local MVNOs and niche operators

Data costs remain among the more affordable in Central Africa, encouraging mobile-first digital engagement responsible for much of Cameroon’s online gambling traffic.

Smartphone adoption exceeds 60% of mobile subscribers, with mid- and low-range devices popular due to affordability. User patterns show a preference for Android OS driven by extensive app ecosystems and cost efficiency.

Financial Services and Payment Infrastructure

Cameroon’s banking sector is growing but remains under-penetrated with less than 40% of the adult population holding bank accounts. Digital banking services, however, are rapidly expanding through mobile money platforms, which have become critical for financial inclusion.

- National Bank of Cameroon – largest retail bank with extensive branch network

- Afriland First Bank – focused on SME and personal banking

- BGFIBank Cameroon – regional subsidiary with corporate banking expertise

- Société Générale Cameroon – international bank offering digital products

- Ecobank Cameroon – pan-African bank with digital payment solutions

Payment processing accommodates a variety of methods, including mobile money, card payments (Visa and Mastercard), bank transfers, and emerging e-wallet services. These form the backbone for secure and flexible iGaming transactions.

- Mobile Money (MTN Mobile Money, Orange Money) – dominant payment channel

- International and local debit/credit cards

- Bank wire transfers for higher-value transactions

- E-wallet solutions integrated into major platforms

- Cash payments as fallback for unbanked populations

E-commerce and Digital Economy

Cameroon’s e-commerce sector is growing steadily alongside improvements in internet connectivity and payment infrastructure. Online retail penetration stands at about 15%, with high growth potential supported by increasing smartphone ownership and urban consumer trends.

Digital services such as mobile entertainment, fintech, and online education are well established and exhibit consumer trust levels rising gradually. These digital economy segments share infrastructure and market dynamics similar to online gambling, easing market entry challenges for iGaming operators.

Business Environment and Regulatory Framework

Cameroon ranks moderately in ease of doing business, with recent reforms simplified registration procedures and stronger protections for investors. However, bureaucratic delays and infrastructure inconsistencies remain challenges for rapid scale.

Business registration is commonly completed within 2 to 4 weeks, subject to document preparation and government processing efficiency. Foreign investment is welcomed and incentivized, especially in technology and services sectors, but cross-border regulatory compliance can be demanding.

- Prepare and notarize company incorporation documents

- Register with the Central Commercial Registry

- Obtain tax identification and social security registrations

- Open corporate bank accounts and deposit capital

- Secure sector-specific operational licenses as required

Corporate Structure and Registration

Business entities commonly used include Limited Liability Companies (LLCs), corporations, and branch offices for foreign firms. LLCs tend to be recommended for startups due to lower capital requirements and operational flexibility.

Foreign investors can wholly own ventures but must comply with national laws requiring local presence and adherence to tax and labor regulations. Registration costs are moderate but require careful documentation and local expert involvement.

- Certificate of incorporation

- Articles of association

- Proof of physical office address

- Tax registration certificate

- Proof of bank account and capital deposit

Taxation Framework

Corporate income is taxed at a standard rate of 30%, with reduced rates and tax holidays applicable in designated special economic zones. Cameroon holds Double Taxation Avoidance Agreements with multiple countries, easing international operations.

- France

- Belgium

- China

- Germany

- United Arab Emirates

- South Africa

Personal income tax rates are progressive up to 35%, with obligatory social security contributions and withholding taxes for employees and contractors.

Market Entry Considerations

Optimal market entry strategies include partnerships with local operators, leveraging mobile money payment integration, and adopting bilingual platform offerings (French and English). Compliance with INTOUCH Cameroun’s payment aggregation is essential for operators targeting online gaming consumers.

- Form joint ventures or partnerships with established local companies

- Integrate mobile money payment systems comprehensively

- Develop multilingual platforms to serve diverse linguistic groups

- Establish local offices to meet regulatory physical presence mandates

- Invest in responsible gambling measures and player protection

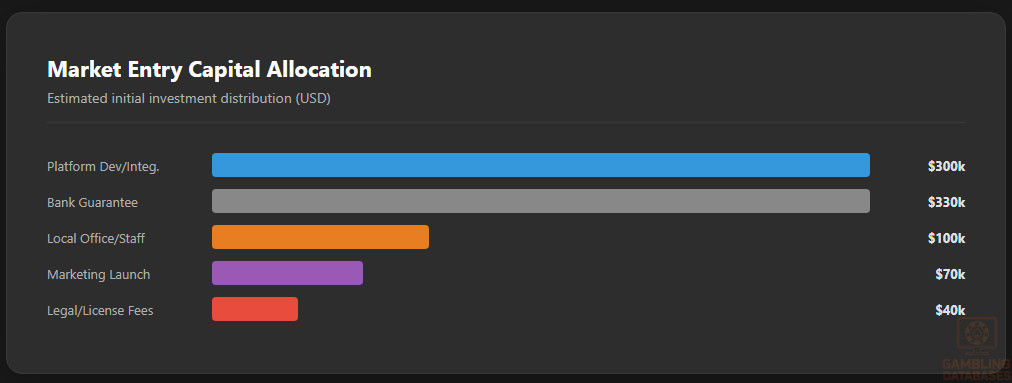

Initial setup costs notably comprise licensing fees, platform development, local staffing, marketing, and compliance programs, summing to several hundred thousand USD for comprehensive market entry.

| Category | Estimated Cost |

|---|---|

| Licensing Fees | $15,000 – $25,000 |

| Platform Development and Integration | $150,000 – $300,000 |

| Local Office Setup and Staffing | $50,000 – $100,000 |

| Marketing and Advertising | $30,000 – $70,000 |

| Compliance and Legal Advisory | $20,000 – $40,000 |

- Document preparation and submission (2 weeks)

- Regulatory review and background checks (1-2 months)

- Licensing decision and payment of fees (1 month)

- Onboarding to payment aggregator and platform launch (1 month)

Exit strategies involve considerations of limited secondary market liquidity for licenses and potential government restrictions on license transfers, though well-structured ownership arrangements and local partnerships mitigate risks.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Cameroon?

Online gambling is legal in Cameroon provided operators secure authorization licenses from the Ministry of Territorial Administration. The regulatory framework requires compliance with financial, technical, and operational standards, including integration with the country’s centralized payment system. Unlicensed operations are illegal and subject to heavy penalties. The market is still maturing, with online gambling expanding rapidly alongside mobile internet access.

2. What types of gambling licenses are available and what do they cover?

Cameroon offers several license categories including concession licenses for land-based casinos, authorization licenses for online and remote gaming, and declarations for smaller-scale activities like lottery operations. Each license category targets specific gambling verticals and imposes distinct compliance obligations. Online licenses mandate technical assessments and financial guarantees. This tiered licensing structure supports diverse operational models while ensuring regulatory oversight.

3. How much does an iGaming license cost and how long does it take to obtain?

License fees vary by type but typically range from $10,000 to $25,000, with a licensing period generally between 5 and 10 years. The application process spans approximately 4 to 6 months, encompassing document submission, financial vetting, technical reviews, and background checks. Applicants should anticipate additional time for payment system integration. Early engagement with regulators facilitates smoother approvals.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to obtain gambling licenses provided they establish a legal presence in Cameroon, which may involve registering a local subsidiary or appointing a representative. They must comply with all local regulatory, tax, and operational requirements, including mandated partnerships for payment processing. Full foreign ownership is permitted but subject to regulatory scrutiny ensuring integrity and local economic contribution.

5. What are the tax obligations for iGaming operators?

Operators are subject to a gross gaming revenue tax of 15% for casino games and 25% for other games such as sports betting. Additional levies include a 10% supplementary tax on gross revenues and fixed annual fees per gaming machine where applicable. Tax liabilities are supplemented by corporate income tax at 30%. Compliance with electronic money transfer levies is also required.

6. Are gambling winnings taxed for players?

Players in Cameroon generally do not pay direct taxes on gambling winnings under current laws. However, indirect taxation occurs via financial transaction levies embedded in deposit and withdrawal processes. This tax treatment seeks to simplify enforcement while ensuring government revenue capture from gambling activities.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include platform licensing and software fees, payment processing charges, local staffing and office expenses, marketing and advertising investments, and ongoing compliance costs for reporting and responsible gambling measures. Infrastructure costs for connectivity and security also represent significant investments. These expenses collectively require careful budgeting to ensure sustainable operation.

8. What is the expected ROI timeline for entering this market?

Market entry ROI timelines usually range between 18 and 36 months, depending on scale and market penetration. Initial investment recovery is driven by licensing, setup, and marketing outlays, with revenue growth supported by product diversification and brand development. Efficient compliance and payment integrations accelerate revenue realization.

9. What are the local presence requirements for operators?

Operators must maintain a local legal presence, which typically entails registering a subsidiary or appointing an in-country representative. This presence ensures regulatory compliance, facilitates audits, and enables active engagement with the centralized payment infrastructure. Physical office requirements align with national business laws and strengthen operator accountability.

10. What payment methods are available and recommended?

Recommended payment methods include mobile money solutions like MTN Mobile Money and Orange Money, widely adopted by consumers for ease and accessibility. International debit and credit cards (Visa, Mastercard) are accepted alongside bank wire transfers for larger transactions. E-wallets and cash options serve niche and rural segments. Integration with the government-mandated payment processor INTOUCH Cameroun is mandatory for online operators.

11. What are the advertising and marketing restrictions?

Advertising gambling products must avoid targeting minors or vulnerable groups and comply with content restrictions banning misleading or aggressive promotions. Advertising channels must provide clear terms and conditions for all offers. Gambling operators can advertise on permitted digital platforms, including Google since August 2025, but must observe broadcasting time restrictions and responsible messaging standards.

12. What responsible gambling measures are mandatory?

Mandatory measures include age verification systems, player identity authentication procedures, provision of self-exclusion tools, clear responsible gambling messaging, and operator contributions to awareness and support programs. These requirements extend progressively to online platforms to align with global best practices in player protection.

13. How large is the iGaming market and what is the growth potential?

The Cameroonian iGaming market was valued at approximately $90 million in 2024 and is forecast to grow to $134 million by 2029, reflecting a CAGR of around 5.2%. Growth is driven primarily by increasing digital penetration, mobile adoption, and evolving consumer preferences for convenient entertainment options such as sports betting and online casino games.

14. Who are the main competitors and what is their market share?

The market features a mix of local licensed operators dominating land-based and traditional sports betting, and a growing number of online platforms targeting urban consumers. Key players include established operators such as Pari Mutuel Urbain Camerounais (PMUC) and newer entrants leveraging technology and payment platform integration. Market share is fragmented but consolidating with increasing regulatory clarity.

15. What are the player preferences and typical spending patterns?

Players favor sports betting, particularly football, driven by social engagement and entertainment. Online participation is concentrated during major sporting events and weekends, with average spend per user increasing annually. Platform convenience, payment flexibility, and bilingual interfaces contribute to player retention and higher spending levels over time.

16. What are the key success factors and main challenges for new entrants?

Success relies on regulatory compliance including adherence to licensing and payment aggregation mandates, strong local partnerships, efficient bilingual platform delivery, and robust responsible gambling practices. Challenges include navigating regulatory complexities, competition with established operators, infrastructure inconsistencies, and consumer trust development. Market entrants must also address payment integration and marketing restrictions strategically.

- Compliance with local licensing and payment procedures

- Effective multi-language customer support

- Innovative mobile-first platform design

- Strong marketing aligned with regulatory guidelines

- Investment in responsible gambling and player protection

- Regulatory delays and bureaucratic processes

- Infrastructure and network reliability issues

- Competition from informal and unlicensed operators

- Limited banking penetration impacting payments

- Cultural sensitivities around gambling promotions

Sources and References

- Cameroon Ministry of Territorial Administration – Gambling Regulatory Framework

- Cameroon Finance Law 2025 – Taxation and Licensing Updates

- Official Government Gazette – Decree No. 2019/2300/PM

- INTOUCH Cameroun – Official Website for Centralized Payment System

- World Bank – Cameroon Economic Update 2025

- International Telecommunication Union – ICT Data for Cameroon 2025

- MTN Cameroon – Market Share and Network Statistics 2025

- Orange Cameroon – Digital Infrastructure Reports 2025

- National Institute of Statistics Cameroon – Population and Demographic Data 2025

- Statista – Cameroon Gambling Market Forecasts 2024-2029

- TGM Research – Gambling and Sports Betting Survey in Cameroon 2022

- Worldometers – Cameroon Population and Demographics 2025

- Cameroon Central Bank Publications – Financial and Payment Statistics 2025

- PWC Cameroon – Tax Facts and Figures 2025

- Cameroon Digital 2025 Report – DataReportal

- Business in Cameroon News – MTN Internet Users Data 2025

- Internews – Digital Security Situational Analysis Cameroon 2021

- GS StatCounter – Cameroon Social Media Usage 2025

- Lawzana – Gambling License Procedure Overview Cameroon

- Miranda Law Firm – Legal Insights on Cameroon Gambling Regulation

- IGaming Afrika – Industry Reports on Cameroon Gambling Market

- Focus Group News – Betting and Gambling Legal Analysis Africa 2025

- CMS Law – Expert Guide to Gambling Laws in Africa: Cameroon

- Trading Economics – Cameroon Internet Usage Statistics 2024

- African Development Bank – Cameroon Economic Reports 2025

- Google Ads Policy Announcements – Gambling Ads in Cameroon 2025

- Global Gaming Reports – Market Analysis and Trends 2024-2025

- Tnet Ltd – Top Social Media Platforms in Cameroon 2025

- PwC Ghana Publications – Regional Gambling Taxation Analysis 2025

- Cameroon National Assembly – Legislative Publications 2025

🎯 Gambling Databases Country Rating: Cameroon

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.2/10 | [🟡 Moderate 5-7] |

| Player Access Score | 9.2/10 | [🟢 Fully Legal] |

| Overall Market Attractiveness | 7.2/10 | [High Potential but High Tax Burden] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- [Punitive Tax Stack:] Total GGR tax reaches 35% (25% standard + 10% supplementary), PLUS a 1% tax on all electronic money transfers, severely eroding margins.

- [Mandatory Payment Centralization:] Since Jan 2025, ALL online gambling transactions must pass through INTOUCH Cameroun. This creates a single point of failure and ensures 100% government visibility on revenue.

- [High Capital Lock-up:] Applicants must provide a bank guarantee of 200 million CFA (~$330,000 USD), a significant barrier for smaller entrants.

- [Local Presence Mandatory:] You cannot operate remotely. A registered local subsidiary and physical office are strict requirements for licensing.

- [Ambiguous Online Framework:] While recognized by law, the online sector is in “regulatory transition,” meaning rules are subject to sudden change by the Ministry of Territorial Administration.

- [Strict Enforcement Capabilities:] The centralization of payments via INTOUCH gives the government the technical ability to instantly block payments to unauthorized operators.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.1/3.0 | Full product legality (Sports + Casino) (+3.0). Deductions: “Ambiguous” regulatory state during transition (-0.4); Mandatory centralized payment aggregator creates strict surveillance environment (-0.5). Final: 2.1/3.0. |

| Licensing Process | 25% | 1.5/2.5 | Accessible licensing (+2.0). Application fees are low (<$20k) (+0.5). CRITICAL DEDUCTIONS: Significant bank guarantee (~$330k) creates capital barrier (-0.5); Timeline 4-6 months is standard but bureaucratic (-0.25); Mandatory local incorporation adds complexity (-0.25). Final: 1.5/2.5. |

| Taxation & Costs | 20% | 0.5/2.0 | Base GGR tax is 25% + 10% Supplementary = 35% (-0.5 points). Corporate tax ~30%. CRITICAL DEDUCTION: New 2025 Finance Bill adds 1% + 4 CFA tax on ALL electronic transfers, effectively a turnover tax (-1.0). Total effective tax burden is extremely high. Final: 0.5/2.0. |

| Operational Requirements | 15% | 0.6/1.5 | Moderate requirements base (+1.0). Deductions: Mandatory local subsidiary/presence (-0.2); Mandatory integration with INTOUCH Cameroun aggregator (-0.2). Final: 0.6/1.5. |

| Market Environment | 10% | 0.5/1.0 | Moderate business environment (+0.5). Google Ads permitted (+0.1). Deductions: Infrastructure inconsistencies (-0.1). Final: 0.5/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal (+4.0). Players face no penalties for participating in licensed gambling activities. |

| Practical Accessibility | 30% | 2.5/3.0 | High mobile penetration (85%) (+2.0). Dominant payment methods (Mobile Money) are widely available (+0.5). Deduction: Crypto usage limited/niche (-0.0). No active ISP blocking of offshore sites currently reported (-0.0). Final: 2.5/3.0. |

| Player Penalties | 20% | 2.0/2.0 | No fines or criminal penalties for players. |

| Market Availability | 10% | 0.7/1.0 | Approx 18 land-based licensees, fewer online. Market is growing but not yet saturated with licensed options (+0.7). |

🔍 Key Highlights

Strengths

- High Mobile Penetration: 85% mobile penetration with widespread use of Mobile Money makes player deposits/withdrawals frictionless.

- Clear Legal Status: Unlike many African nations, online gambling is explicitly recognized by Law No. 2015/012.

- Advertising Access: Google allows gambling ads (since Aug 2025), significantly lowering barriers to entry for marketing.

⛔️ CRITICAL RISKS AND CHALLENGES

- [Profit-Killing Taxation:] The combination of 25% GGR, 10% supplementary tax, and the new 1% transfer tax creates one of the heaviest fiscal burdens in the region.

- [Payment Monopoly:] The requirement to use INTOUCH Cameroun as the exclusive payment aggregator removes operator autonomy over payment processing and exposes all data to the state.

- [Capital Requirements:] The ~$330,000 bank guarantee is a high “entry ticket” that freezes working capital.

- [Local Bureaucracy:] Mandatory physical presence means you are subject to local labor laws, corporate taxes, and administrative hurdles.

- [Regulatory Fluidity:] The sector is in “transition,” meaning the Ministry can change licensing modalities or fees with little notice.

Player-Specific Issues

- [Data Privacy:] With all transactions routed through a government-mandated aggregator, player financial privacy is non-existent.

- [Payment Options:] Heavy reliance on Mobile Money; credit cards and other international methods are less effective.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $400,000 – $500,000 (Includes $330k bank guarantee + $20k license fee + setup).

Monthly Operating Costs: $50,000 – $100,000 (Local office, staff, marketing).

Effective Tax Rate on Revenue: Over 45% (35% GGR + 1% Transaction Tax + Corporate Tax).

Customer Acquisition Cost: Moderate ($10 – $30), aided by Google Ads availability.

Time to Breakeven: 24 – 36 months.

Profitability Assessment: DIFFICULT. While the market volume is growing, the government takes nearly half of the revenue through various tax layers. This market is volume-dependent. Small operators will struggle to cover the $330k guarantee and fixed costs. Only viable for well-capitalized operators aiming for long-term market share dominance.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [High] | [Payment blocking via INTOUCH aggregator is highly effective; penalties for unauthorized operation include imprisonment.] |

| Licensed Sports Betting Operators | [Medium] | [Regulatory volatility; high tax compliance burden; audit risks via centralized payment system.] |

| Affiliates/Advertisers | [Medium] | [Must comply with strict advertising standards; potential fines for promoting unauthorized entities.] |

| Payment Processors | [Critical] | [Operating outside the INTOUCH aggregator system is illegal and subject to severe financial penalties.] |

| Company Directors/Executives | [Medium] | [Local directors face personal liability for tax non-compliance or AML failures.] |

🚨 Extradition and International Enforcement

Extradition Treaties: Cameroon has extradition agreements with France and several neighboring African states (CEMAC region). Treaties with the UK and USA are limited or case-specific but exist.

Enforcement History: Enforcement is primarily domestic, focusing on shutting down unauthorized physical venues and blocking payments. International extradition for gambling offenses is rare but financial crimes (AML) can trigger Interpol cooperation.

Safe Jurisdictions: Enforcement reach is weak outside of Central/West Africa and France.

Travel Risk: Low for offshore operators, but local directors must remain compliant to avoid detention.

📋 Final Verdict

Cameroon receives an Operator Ease Score of 5.2/10 and a Player Access Score of 9.2/10, resulting in an overall market attractiveness rating of 7.2/10.

HONEST ASSESSMENT: Cameroon offers a high-volume, legally clear market that is unfortunately hampered by greed-driven taxation. While player access is excellent and mobile adoption is high, the government’s decision to stack a 10% supplementary tax on top of a 25% GGR tax—plus a transaction tax—makes margins razor-thin. The mandatory $330,000 bank guarantee and requirement to use a single government-controlled payment aggregator (INTOUCH) effectively shuts out startups. This is a playground for large, established African operators (like PMUC), not for new entrants seeking quick ROI.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major Pan-African operator with existing infrastructure in CEMAC countries.

- Capable of locking up $330,000 in a bank guarantee without cash flow issues.

- Willing to accept lower margins (10-15% net) in exchange for high volume.

- Able to set up a physical office in Douala or Yaoundé.

❌ Definitely Avoid If You Are:

- A bootstrap startup or small-cap operator (the bank guarantee will kill you).

- Reluctant to share all transaction data with the government (INTOUCH integration is mandatory).

- Looking for a low-tax jurisdiction (35% GGR + Transaction taxes is prohibitive).

- An offshore operator hoping to fly under the radar (Centralized payments make blocking easy).

⚠️ BOTTOM LINE: Legal and growing, but the fiscal regime and capital requirements make it a “pay-to-play” market reserved for well-funded heavyweights.

Looking at the cost breakdown of operating a sportsbook in New Jersey, I’ve noticed that the licensing fees can range from $100,000 to $500,000 annually, depending on the type of license. For example, a sports wagering license can cost around $100,000, while a casino license can cost upwards of $400,000. Additionally, operators must also consider the costs of maintaining a physical presence in the state, including rent, utilities, and staffing. According to a study by the New Jersey Division of Gaming Enforcement, the total revenue from sports betting in 2020 was over $6 billion, with a tax revenue of around $50 million. This suggests that despite the high costs, there is still a significant potential for profit in the New Jersey sports betting market.

Regarding the cost breakdown of operating a sportsbook in New Jersey, it’s worth noting that the licensing fees are just one aspect of the overall costs. Operators must also consider the costs of compliance, marketing, and customer acquisition. According to a report by the American Gaming Association, the total cost of compliance for sports betting operators in the US can range from 10% to 20% of total revenue. This highlights the need for operators to carefully manage their costs in order to remain competitive in the market.

Thanks for the insight on compliance costs. Can you elaborate on how operators can manage these costs effectively?

Operators can manage compliance costs by implementing robust AML and KYC procedures, as well as investing in regulatory technology (RegTech) solutions. These solutions can help automate compliance processes and reduce the risk of non-compliance.

I’m curious about the impact of payment methods on the online gambling experience. For instance, does the use of e-wallets like PayPal or Skrill affect the overall user experience? Are there any specific regulations or restrictions on payment methods in certain jurisdictions? I’ve heard that some operators are now offering cryptocurrencies like Bitcoin as a payment option – what are the implications of this for the industry?

The impact of payment methods on the online gambling experience is a crucial aspect of the industry. Research has shown that the use of e-wallets can improve the overall user experience by providing faster and more secure transactions. However, there are also regulatory considerations to take into account, such as anti-money laundering (AML) and know-your-customer (KYC) requirements. In terms of cryptocurrencies, their use is still relatively limited in the online gambling industry, but they do offer potential benefits such as increased security and anonymity.