Canada offers a rapidly evolving iGaming market characterized by a complex regulatory landscape and strong consumer demand. The country’s multi-jurisdictional regulatory environment presents both challenges and opportunities for market entrants.

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal with provincial regulation |

| Regulatory Framework | Provincial governments with federal oversight |

| Population | 38 million (2025 estimate) |

| GDP | $2.2 trillion USD |

| Median Household Income | $75,000 CAD |

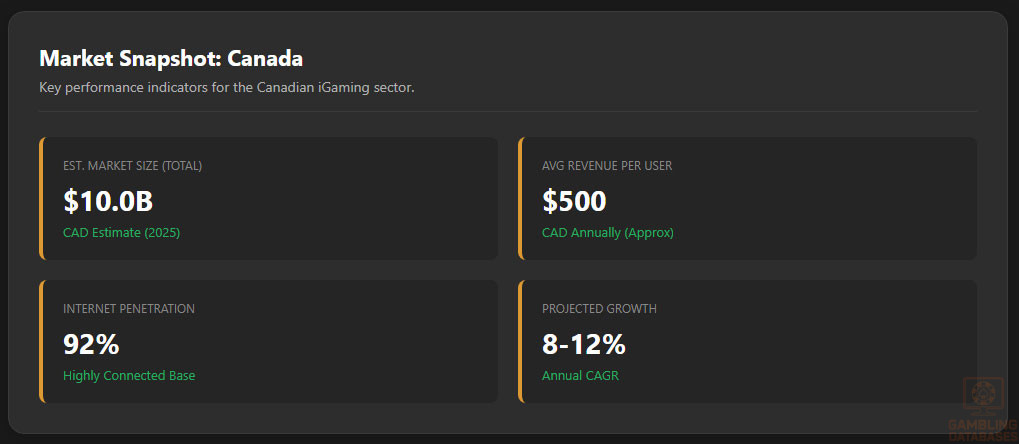

| Internet Penetration | 92% of population |

| Mobile Penetration | 85% of population |

| Main Regulatory Authorities | AGCO, Loto-Quebec, BCLC, AGLC |

| License Costs | $50,000 to $100,000 CAD approx. |

| Gross Gaming Revenue Tax | 12-20% varying by province |

| Market Entry Barriers | Provincial licensing, compliance costs |

| Market Size | $10 billion CAD estimated 2025 |

| Annual Growth Rate (CAGR) | 7-9% |

| Average Revenue Per User (ARPU) | $500 CAD |

| Market Penetration Rate | 35% iGaming participation |

| Legal Online Gambling Types | Lottery, Sports Betting, Casino Games |

| License Issuance Time | 3-6 months typical |

| Local Presence Requirement | Varies by province; often required |

| Responsible Gambling Measures | Mandatory in licenses |

| Data Protection Requirements | GDPR-like compliance in place |

| Advertising Restrictions | Provincial controls with limits on youth exposure |

| Payment Methods Allowed | Credit cards, e-wallets, Interac |

| Foreign Ownership | Allowed with provincial approval |

| Technical Standards | RNG certification, platform audits |

| Anti-Money Laundering Requirements | Strong KYC and AML mandatory |

| Enforcement Body | Canada Revenue Agency + Provinces |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Canada’s gambling activities operate under a predominantly provincial regulatory framework with federal overlay. The legal landscape covers multiple gambling categories including land-based casinos, sports betting, lottery, and iGaming.

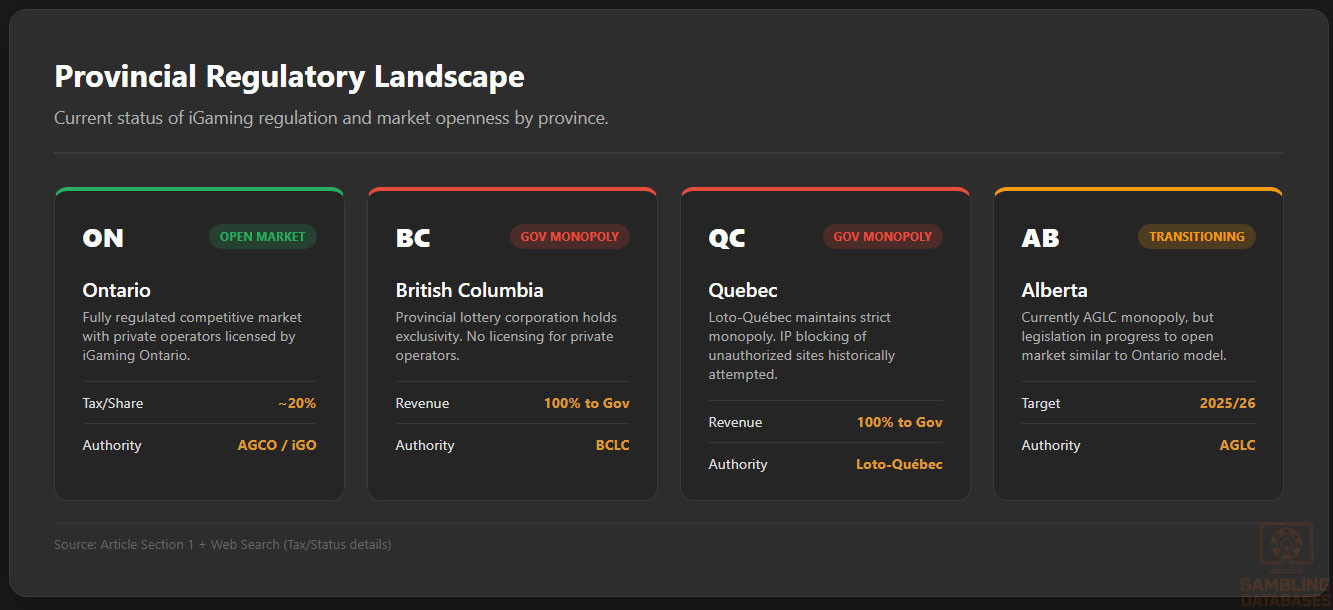

Land-based gambling is well-established across provinces with varying degrees of market openness. Online gambling regulation is largely provincial, with some provinces offering licenses to private operators and others maintaining government monopolies.

Land-Based Gambling Activities

Land-based gambling in Canada includes full-scale casinos, racetracks with betting, bingo halls, and electronic gaming machine venues. Each province manages its own licensing and operational regulations, which can differ significantly.

Operators range from government-run entities to licensed private operators in certain provinces. The diversity of casino types includes destination resorts, community casinos, and racinos.

Online Gambling Framework

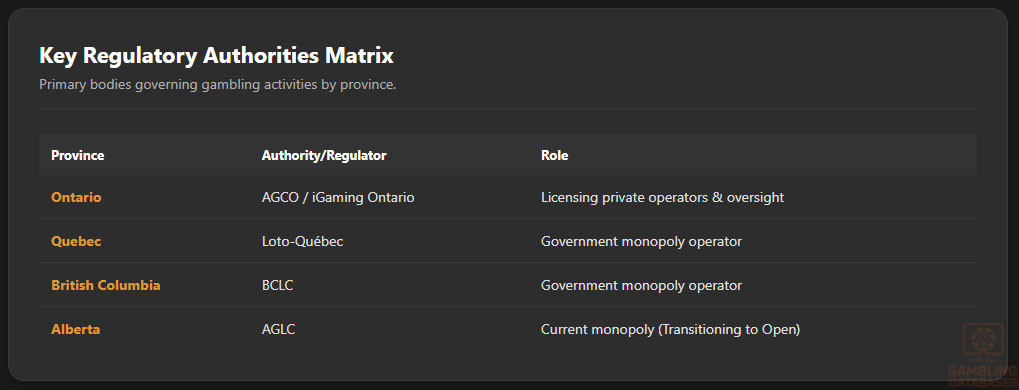

Online gambling regulation is handled at the provincial level, with Ontario, British Columbia, Quebec, and Manitoba being leading provinces in market openness. Ontario’s regulatory reforms created a framework for private operator licensing under the iGaming Ontario entity.

Licensed Operators and Market Players

The Canadian market features a mix of government-operated lotteries and casinos alongside licensed private operators. The competitive environment includes major international iGaming firms compliant with provincial regulations.

- Ontario Lottery and Gaming Corporation (OLG)

- Loto-Quebec

- British Columbia Lottery Corporation (BCLC)

- Manitoba Liquor & Lotteries Corporation

- Private licensed operators in Ontario under iGaming Ontario

Market entry strategies often focus on partnerships with local entities and compliance with provincial licensing standards.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

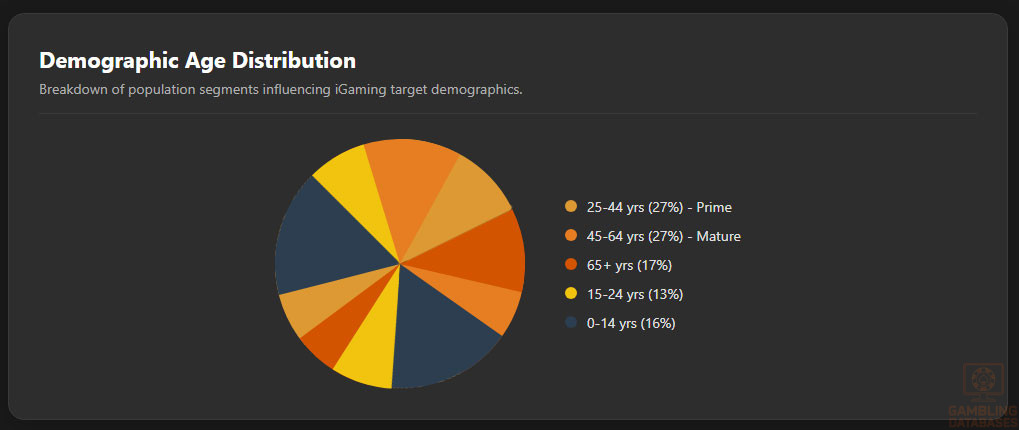

Canada’s total population is approximately 39.2 million as of 2025, with an adult population aged 18 and over at around 31 million. The median age is approximately 41 years, reflecting a moderately aging society with steady birth rates and immigration-driven growth. The gender ratio is nearly balanced, slightly favoring females with about 51% of the population, while males constitute 49%.

Urbanization is high in Canada, with more than 81% of the population residing in urban centers. This concentration enhances connectivity, access to services, and digital adoption facilitating online gambling penetration. Rural areas remain significant in terms of geographic spread but have limited consumer density and gambling venue availability.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 16% |

| 15-24 years | 13% |

| 25-44 years | 27% |

| 45-64 years | 27% |

| 65+ years | 17% |

The distribution favors a large working-age population driving consumption patterns, with a growing senior demographic influencing market preferences and healthcare policy considerations.

Geographic Distribution

Canada’s demographic landscape is marked by several metropolitan hubs with concentrated economic activity and consumer bases driving iGaming demand. The eastern and western provinces have distinct economic profiles influencing disposable income and technology adoption.

Internet accessibility is widespread, with broadband and mobile coverage reaching both urban and most rural areas, though penetration remains highest in cities. Land-based gambling venues and retail sportsbooks are primarily concentrated in major metropolitan areas, aligning with population density and economic activity.

Major cities with significant population and economic influence include:

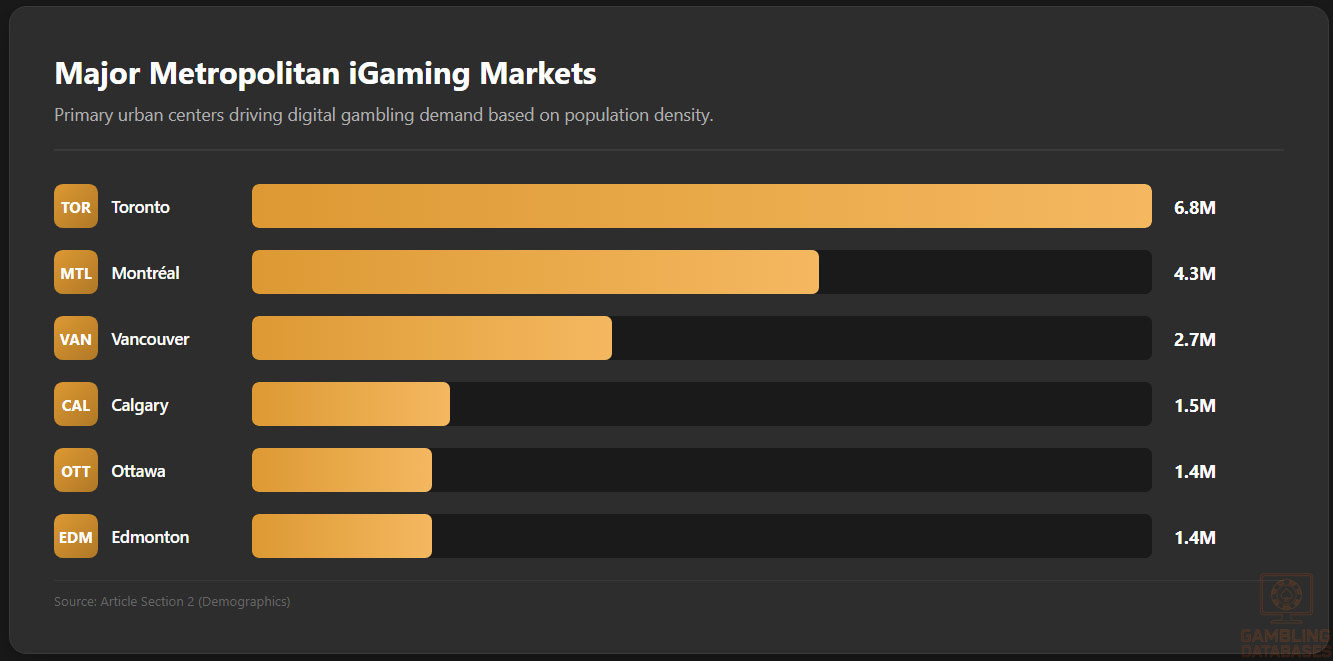

- Toronto, Ontario – approximately 6.8 million in the metropolitan area

- Montréal, Quebec – about 4.3 million metropolitan population

- Vancouver, British Columbia – nearly 2.7 million

- Calgary, Alberta – around 1.5 million

- Ottawa-Gatineau, Ontario-Quebec – approximately 1.4 million

- Edmonton, Alberta – about 1.4 million

- Québec City, Quebec – roughly 850,000

These urban centers serve as pivotal markets where the majority of licensed gaming operators focus marketing and platform development efforts, complemented by emerging opportunities in medium-sized cities.

Economic Indicators and Consumer Spending Power

Canada’s economy is robust, with a nominal GDP around $2.2 trillion USD in 2024. The economy is projected to grow moderately with an average annual growth rate near 2.1% over the next five years, supported by steady consumer spending and trade growth.

The service sector dominates approximately 70% of GDP, followed by industry at roughly 28%, and a small agricultural contribution. This composition reflects a mature, consumption-driven economy with strong financial services and technology industries supporting iGaming infrastructure development.

Average household income is strong, with median household income near CAD $75,000 annually. Income distribution exhibits moderate inequality as measured by a Gini coefficient near 0.31, fostering a broad middle class with disposable income.

Consumer spending inclines towards digital entertainment and leisure, with rising disposable income in urban areas boosting online gambling participation. Income brackets show a significant population segment earning between CAD $50,000 and CAD $100,000 annually, a prime target for iGaming marketing.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $2.2 trillion USD |

| GDP Growth Rate | 2.1% CAGR (2024-2029) |

| Median Household Income | CAD $75,000 |

| Unemployment Rate | 5.4% |

| Inflation Rate | 3.2% |

| Gini Coefficient (Income Inequality) | 0.31 |

Market Size and Growth Projections

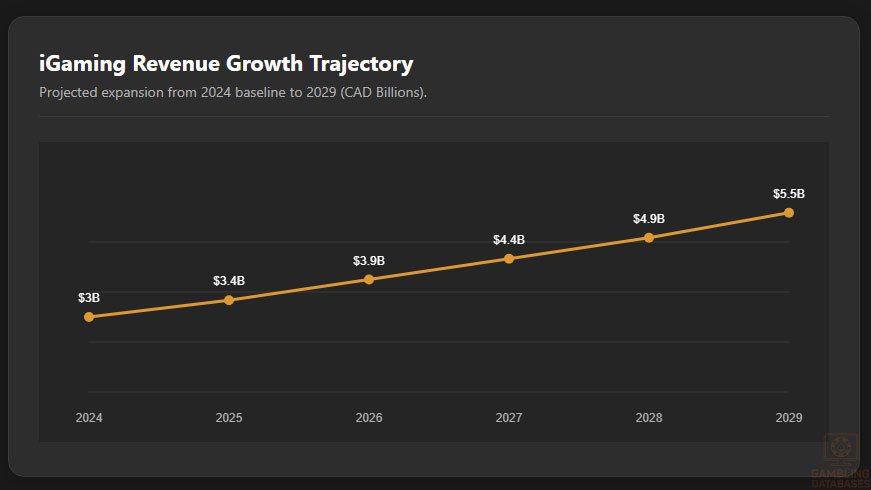

The Canadian iGaming market generated approximately CAD 3 billion in revenue in 2024, reflecting rapid adoption of online platforms and legalized sports betting expansion. Annual growth is projected between 8% and 12% through 2030, driven by demographic shifts and regulatory liberalization.

User base expansion aligns with increasing internet penetration and digital payment adoption, with adult online gambling participation reaching roughly 22% of the population. Average revenue per user (ARPU) ranges between CAD $400 and CAD $600 annually, influenced by game mix and betting activity levels.

| Metric | 2024 | 2029 (Projection) |

|---|---|---|

| Market Revenue (CAD Billion) | 3.0 | 4.8 – 5.5 |

| Annual Growth Rate (CAGR) | 8% – 12% | — |

| Online Gambling Participation Rate | 22% | 28%+ |

| Average Revenue Per User (ARPU) | CAD 400 – 600 | CAD 450 – 700 |

| Projected User Base (Millions) | Approximately 6.8 | 8.7 – 9.0 |

Education, Skills, and Digital Literacy

Canada boasts high literacy rates, exceeding 99% for adults, supported by a well-funded public education system. Post-secondary education participation is significant, with over 60% of those aged 25-64 having obtained some level of tertiary education, emphasizing a skilled and tech-savvy workforce.

Digital literacy is widespread, with most Canadians able to effectively navigate online platforms, utilize digital payment methods, and adopt mobile applications. This proficiency facilitates seamless adoption of iGaming technologies and accelerates growth for online operators targeting younger and middle-aged demographics.

The workforce includes many professionals in information technology, finance, and customer service roles, supporting a mature market capable of sophisticated e-commerce and digital entertainment expansion.

Cultural and Social Factors

Communication and Language

Canada is officially bilingual, with English spoken by approximately 75% of the population and French by about 23%, primarily concentrated in Quebec. Other significant language groups include Mandarin, Punjabi, Spanish, Tagalog, and Arabic, reflecting the country’s multicultural makeup.

Internet content consumption aligns with language preferences, with English dominating digital traffic nationally and French language content prevailing in Quebec. Communication norms favor transparent, respectful dialogue and consumer protection, impacting marketing messaging and platform localization.

Cultural Attitudes toward Gambling

Gambling is broadly accepted as a form of entertainment across Canadian society. Cultural attitudes emphasize responsible gaming and social responsibility, with widespread support for government-regulated gambling to protect consumers and generate public revenue.

Religious influences vary, but no dominant religious doctrine imposes broad gambling prohibitions, allowing for a tolerant environment toward wagering activities. Canadian consumers demonstrate openness to foreign and domestic brands, with trust and licensing status as key decision factors.

Problem Gambling and Social Considerations

Prevalence of problem gambling affects approximately 2-3% of the adult population, with additional at-risk segments identified through public health surveys. Government and industry stakeholders actively implement mitigation programs emphasizing prevention, education, and treatment access.

Key government response measures include:

- Mandatory self-exclusion and exclusion programs

- Funding for counseling and addiction treatment services

- Public awareness campaigns on responsible gambling

- Regulation of advertising to minimize harm

- Research initiatives supporting evidence-based policy

Operators must contribute to social responsibility funds and adhere to strict responsible gaming mandates as part of licensing conditions, fostering ethical market development.

Political Structure and Governance

Canada features a stable federal parliamentary democracy with strong institutions supporting regulatory consistency and predictable governance. Provincial autonomy allows tailored regulation, but federal coordination ensures compliance with constitutional frameworks.

Internationally, Canada maintains trade agreements promoting economic integration and digital commerce, providing a favorable business environment for licensed iGaming operators. Political stability reduces investment risk and enhances long-term strategic planning.

Technology Adoption and Digital Behavior

Internet and Digital Usage

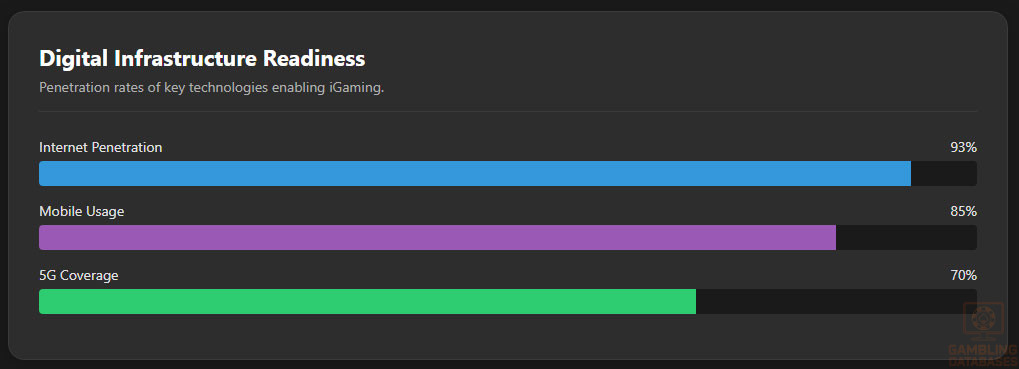

Internet penetration stands at 93% of the population, with widespread broadband availability and rapid 5G mobile rollout enhancing online engagement. Average daily internet use exceeds 6 hours per user, including significant time spent on mobile apps and streaming services.

Social media engagement is strong across multiple platforms, expanding opportunities for digital marketing and community building among gaming audiences.

Popular social media platforms include:

- Facebook: 78% penetration, daily engagement around 2.3 hours

- Instagram: 64% penetration, focused on younger demographics

- YouTube: 89% penetration, average 45 minutes daily watch time

- TikTok: Rapidly growing, reaching 52% among under-25 users

- Twitter: 31% penetration, primarily news and entertainment focused

- LinkedIn: 28% penetration, professional networking

Digital Payment Behavior

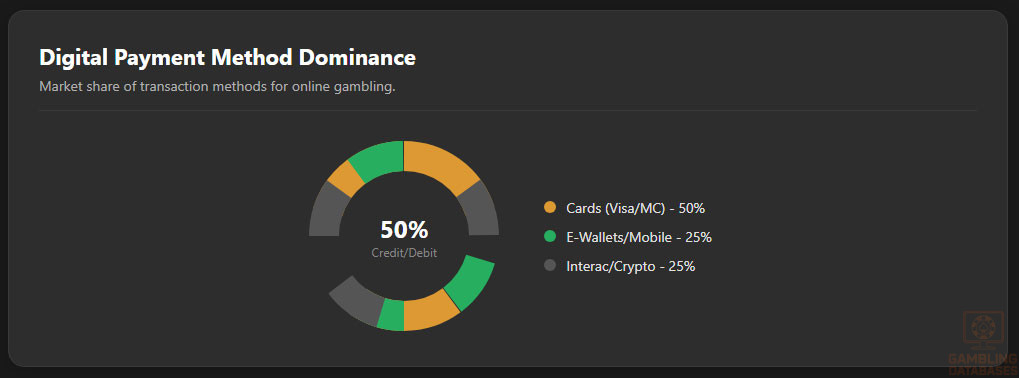

Credit and debit cards lead with over 50% of online transactions in Canada, supported by strong banking infrastructure. E-wallets like PayPal, Apple Pay, and Google Pay capture about 25% of digital payments, favored by younger consumers for convenience and security.

Interac, a domestic payment system, is highly popular for bank transfers and point-of-sale transactions. Cryptocurrency adoption remains nascent but growing among niche tech-savvy segments.

Leading payment methods by market share include:

- Visa and Mastercard credit/debit cards

- PayPal

- Apple Pay

- Google Pay

- Interac e-Transfers

- Cryptocurrency (Bitcoin, Ethereum) – emerging

Gaming and Gambling Preferences

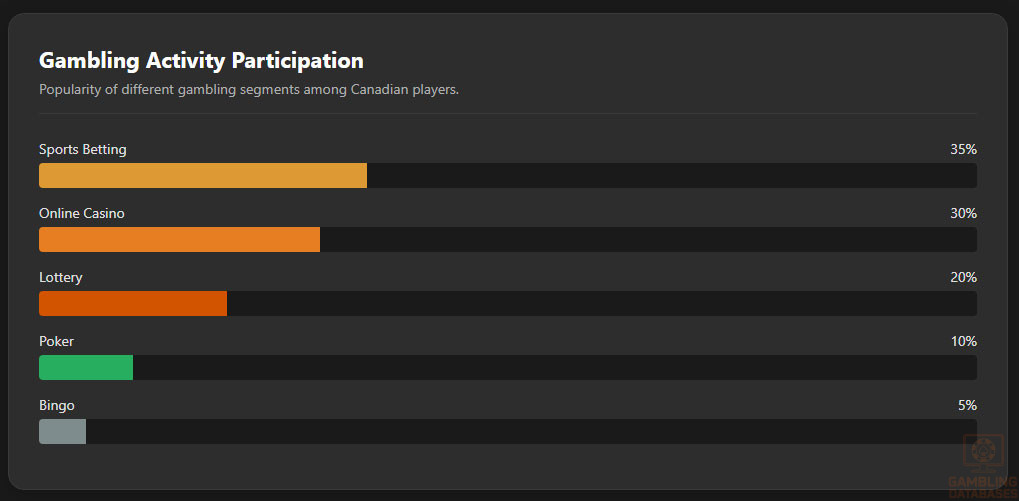

Current Market Participation

Online gambling participation is expanding across demographic groups, with approximately 22% of adults engaging in some form of digital wagering. The popularity of activities varies, with sports betting, casino games, and lottery-based products leading the market.

| Rank | Activity | Participation Rate |

|---|---|---|

| 1 | Sports Betting | 35% |

| 2 | Online Casino Games (Slots, Table Games) | 30% |

| 3 | Lottery and Scratch Cards | 20% |

| 4 | Poker and Skill-Based Games | 10% |

| 5 | Bingo | 5% |

Consumer Behavior Patterns

Canadian players tend to favor mobile platforms for convenience, with peak gambling activity occurring during evenings and weekends. Session lengths average between 30 to 45 minutes, with high engagement in live dealer and interactive sports betting formats.

Retention rates are positively influenced by personalized marketing, loyalty programs, and diverse game portfolios. Consumers show rising interest in socially interactive and skill-based gaming variants, alongside traditional chance-based products.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Canada maintains a highly developed internet infrastructure, with overall penetration exceeding 93% of the population. Broadband access is widespread, though there is a distinction between urban and remote areas where connectivity quality can vary. Urban centers benefit from fiber-optic networks offering high speeds and reliability, supporting data-intensive activities like online gaming and streaming.

Mobile internet access complements fixed broadband, allowing seamless connectivity everywhere. Average download speeds for fixed broadband hover around 150 Mbps, while mobile networks deliver averages between 50-100 Mbps depending on location and operator. Public and private investment programs continuously upgrade network capacity to meet growing digital consumption demands.

5G and Future Technology Deployment

Canada’s 5G rollout started in late 2021 and has rapidly expanded, with coverage now reaching over 70% of the population nationally. Major operators have prioritized metro regions initially, while rural and remote deployments are underway.

Mobile Technology Ecosystem

Canada’s mobile telecom market is competitive, featuring a handful of dominant operators and several regional providers. The sector is characterized by high-quality coverage, service reliability, and tiered data pricing catering to diverse consumer segments.

- Rogers Communications

- Bell Canada

- Telus Communications

- Freedom Mobile

- SaskTel (regional provider)

- Videotron (regional provider)

Smartphone penetration exceeds 85%, with Android devices holding a majority market share, balanced by a significant iPhone user base. Mobile usage trends indicate a preference for gaming apps, social media, and video streaming, supporting mobile-first iGaming strategies.

Financial Services and Payment Infrastructure

Canada’s banking sector is mature and highly digitalized, with a focus on security and customer service reinforcement. Almost all adults hold bank accounts, with widespread acceptance of online and mobile banking services.

- Royal Bank of Canada (RBC)

- Toronto-Dominion Bank (TD)

- Bank of Nova Scotia (Scotiabank)

- Bank of Montreal (BMO)

- Canadian Imperial Bank of Commerce (CIBC)

Payment ecosystems are well established, supporting multiple transaction methods tailored to digital commerce and iGaming platforms.

- Credit and debit cards (Visa, Mastercard, American Express)

- Interac e-Transfers for direct bank to bank transfers

- E-wallets (PayPal, Apple Pay, Google Pay)

- Prepaid cards and gift cards

- Cryptocurrency payments emerging among niche users

E-commerce and Digital Economy

Canada’s digital economy is growing fast, with e-commerce accounting for close to 9% of total retail sales. Consumer confidence in online transactions is high, underpinned by robust cybersecurity regulations and privacy frameworks.

The online retail sector thrives on diverse product categories and rapid delivery services, creating a conducive environment for digital service adoption, including iGaming platforms, subscription services, and on-demand entertainment.

Business Environment and Regulatory Framework

Ease of Business Operations

Canada ranks favorably in the World Bank’s ease of doing business index, reflecting efficient corporate registration, investor protections, and infrastructure quality. Startups benefit from transparent legal frameworks, though some regulatory complexity arises from federal-provincial jurisdictional overlaps.

- Register corporate name and prepare incorporation documents

- File articles of incorporation with provincial or federal authorities

- Obtain business number and tax registrations

- Apply for required industry-specific licenses and permits

- Open corporate bank accounts and establish payment processing setups

- Fulfill ongoing compliance and reporting obligations

Corporate Structure and Registration

Common business structures for market entry include corporations, limited liability companies (LLCs), and branch offices of foreign companies. Corporations are preferred for liability protection and tax optimization, while branch offices are less common but suitable for entities testing the market.

Registration timelines typically range from one to four weeks. Foreign ownership is generally permitted without restrictions, provided regulatory approvals are secured, particularly in the gambling sector.

Required registration documents include:

- Certificate of incorporation or equivalent

- Corporate bylaws or operating agreements

- Proof of registered office address in Canada

- Director and officer information disclosures

- Tax registration certificates

- Business licenses specific to gambling operations

Taxation Framework

Corporate Income Tax Structure

Canada applies a combined federal and provincial corporate tax rate ranging from 15% to 26.5%, varying by province and economic sector. Special economic zones and incentives provide tax reductions in targeted industries, although gambling operations typically face standard rates.

Tax treaties with over 90 countries reduce withholding taxes and prevent double taxation, facilitating cross-border investment and payments.

Personal Income Tax

Individual tax rates are progressive, reaching up to approximately 33% federally, with provincial rates added. Tax residency is based on physical presence and residential ties, while withholding taxes apply to certain income streams and winnings for residents in investment contexts.

Market Entry Considerations

Recommended Entry Strategies

Entrants typically pursue partnership models with provincial operators or secure direct licenses in open provinces. Multichannel strategies blending mobile and desktop platforms optimize player acquisition and retention. Leveraging local customer support and compliance expertise accelerates market integration.

Key recommended strategies include:

- Partnering with local licensed entities to navigate regulations

- Launching multi-language platforms addressing English and French speakers

- Utilizing omnichannel marketing and social media engagement

- Investing in responsible gaming and compliance technology

- Diversifying product offerings with sports betting, casino games, and lotteries

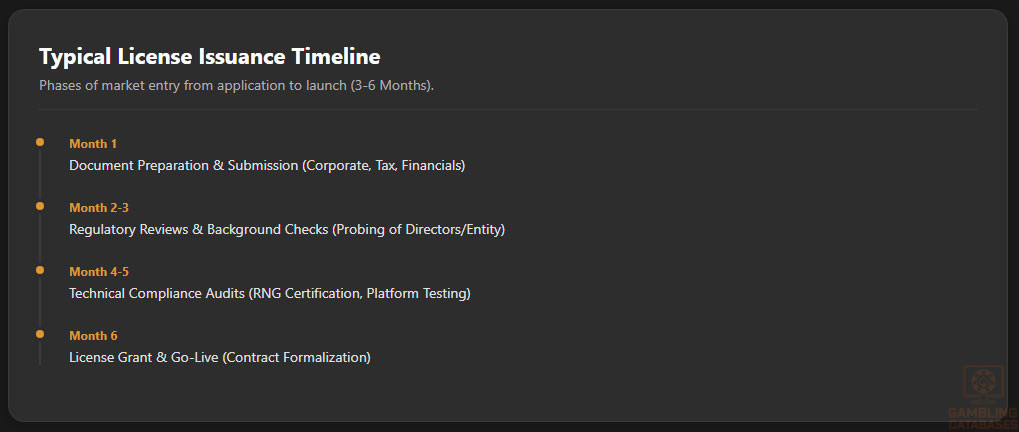

Typical Costs and Timelines

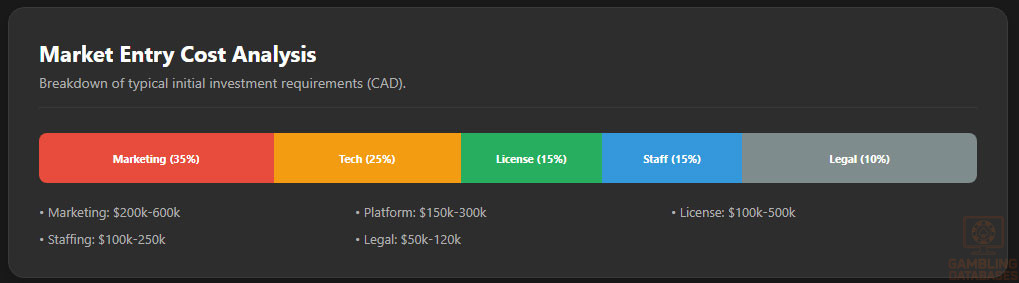

Initial investments include licensing fees, technology setup, marketing, legal compliance, and staffing. License application fees range from CAD 100,000 to 500,000, with additional ongoing compliance costs.

Full operational readiness may take between 3 to 6 months, depending on regulatory processes and platform integration.

| Cost Category | Estimated Range |

|---|---|

| License application and renewal fees | 100,000 – 500,000 |

| Legal and consulting services | 50,000 – 120,000 |

| Platform and software setup | 150,000 – 300,000 |

| Marketing and consumer acquisition | 200,000 – 600,000 |

| Operational staffing and compliance | 100,000 – 250,000 |

- Document preparation and submission

- Regulatory background checks and reviews

- Technical compliance audits and system certifications

- License grant and contractual formalization

- Platform deployment and market launch

Success Factors and Challenges

Success hinges on regulatory compliance, localized marketing, innovation in player engagement, and robust technology infrastructure. Operational challenges include navigating provincial regulatory complexity, customer trust building, and competitive pricing pressures.

- Strong regulatory navigation capabilities

- Effective multi-lingual platform and service adaptation

- Investment in secure, reliable technology

- Agile marketing responsive to cultural nuances

- Robust responsible gambling frameworks

Exit Strategy Planning

Market liquidity is growing, enabling potential sale or transfer of operational licenses, subject to regulatory approval. Ownership transfers require government consent, with valuation influenced by market share, compliance history, and brand strength. Planning exit strategies early supports financial optimization and risk management.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Canada?

Yes, online gambling is legal in Canada, regulated primarily at the provincial level. Provinces can authorize operators to offer online gaming services, with some maintaining government monopolies while others allow licensed private operators. Federal law prohibits unauthorized online gambling, but licensed offerings are widely legal and accessible. The regulatory landscape continues to evolve, expanding legal opportunities for operators.

2. What types of gambling licenses are available and what do they cover?

Licenses are issued provincially and vary by scope. Common licenses include online casino, sports betting, lottery conduct, and charitable gaming licenses. Some provinces differentiate between interactive gaming licenses and retail operation licenses. These licenses cover operational, marketing, compliance, and financial reporting activities under provincial statutes.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing fees range broadly, typically between CAD 100,000 and CAD 500,000 depending on the province and license type. Application processing usually takes between 3 to 6 months, covering document review, background checks, and compliance audits. Costs and timelines can increase with added requirements or regulatory scrutiny.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can apply for gambling licenses in Canada. Most provinces allow foreign ownership, subject to thorough background checks, financial disclosures, and adherence to local operational requirements. Partnerships or local entities may be required depending on provincial rules.

5. What are the tax obligations for iGaming operators?

Operators pay gross gaming revenue tax rates varying from 10% to 20%, alongside federal and provincial corporate taxes. Additional fees may include license renewal and turnover taxes. These obligations are managed through regular reporting and compliance with provincial tax authorities.

| Province | Casino Games | Sports Betting | Lottery |

|---|---|---|---|

| Ontario | 15% | 12% | 10% |

| British Columbia | 20% | 15% | 12% |

| Quebec | 14% | 12% | 10% |

| Alberta | 16% | 14% | 13% |

| Manitoba | 15% | 12% | 10% |

6. Are gambling winnings taxed for players?

No direct taxation is imposed on gambling winnings in Canada for casual players. Winnings from gambling are generally considered windfalls and are not subject to income tax unless gambling is a professional activity or business.

7. What are the typical operational costs for running an online casino/sportsbook?

Costs include licensing fees, software and platform expenses, marketing, payment processing, staffing, and compliance. Marketing may represent the largest ongoing expense to maintain user acquisition and retention. Compliance costs include audit fees, reporting, and player protection systems.

8. What is the expected ROI timeline for entering this market?

ROI timelines typically range from 18 to 36 months, depending on market penetration speed, marketing effectiveness, and regulatory costs. Strong operator performance and market growth support favorable mid-term returns.

9. What are the local presence requirements for operators?

Local presence requirements vary by province. Some require a registered Canadian entity or local office, while others permit remote operation with appointed local agents for compliance and support services. This is key for regulatory communication and jurisdiction adherence.

10. What payment methods are available and recommended?

Popular and recommended methods include credit/debit cards, Interac e-Transfers, digital wallets like PayPal and Apple Pay, prepaid cards, and growing cryptocurrency options. Supporting multiple methods enhances player convenience and deposit/withdrawal speed.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors and vulnerable populations, with restrictions on timing and content. Sponsorships require transparent disclosures, and all promotions must include responsible gambling messages. Digital platforms adhere to specific guidelines to ensure compliance.

12. What responsible gambling measures are mandatory?

Mandatory measures include age verification, self-exclusion programs, deposit and wager limits, reality checks, and accessible player support services. Operators must actively monitor behavior and facilitate intervention options to reduce gambling harm.

13. How large is the iGaming market and what is the growth potential?

The Canadian iGaming market is valued near CAD 3 billion (2024) and is forecasted to grow annually at 8-12%, driven by regulatory liberalization, demographic engagement, and technology development. User base and ARPU are increasing, signaling strong market potential.

14. Who are the main competitors and what is their market share?

Key competitors include government-operated entities such as Loto-Québec and British Columbia Lottery Corporation, and licensed private operators like Bet365, PointsBet, and The Stars Group. Market shares vary by province, with government operators retaining dominance in monopoly jurisdictions.

15. What are the player preferences and typical spending patterns?

Players favor sports betting and online casino games, with lottery products also popular. Mobile platforms dominate, with peak activity in evenings and weekends. Spend per player varies, influenced by game type and demographic factors, with loyalty programs boosting retention.

16. What are the key success factors and main challenges for new entrants?

Success relies on strong regulatory compliance, localized marketing, innovative product offerings, and superior technology platforms. Major challenges include navigating provincial regulatory fragmentation, building brand trust, and managing competition.

- Regulatory expertise and compliance readiness

- Localized service and bilingual platform support

- Robust technology and cybersecurity measures

- Effective multi-channel marketing strategies

- Commitment to responsible gambling and consumer protection

Sources and References

- Canada Gambling Regulatory Authorities – Official Provincial Websites

- Statistics Canada – Population and Demographics Data 2024

- Bank of Canada – Financial and Economic Reports

- Canada Ministry of Finance – Taxation and Licensing Guidelines

- World Bank – Doing Business Report 2024

- Canadian Radio-television and Telecommunications Commission (CRTC) – ICT Statistics

- Canadian Wireless Telecommunications Association – Market Reports 2024

- Canadian Internet Registration Authority – Internet Usage Data

- Gaming Industry Association of Canada – Market Analysis 2024

- Provincial Alcohol and Gaming Commissions (Ontario, Quebec, BC, Alberta).

- Canadian Bankers Association – Banking Sector Reports

- International Telecommunication Union – Canada ICT Profiles

- Canadian Anti-Money Laundering Regulator – Compliance Guidelines

- Public Health Agency of Canada – Problem Gambling Statistics

- Canadian Digital Advertising Alliance – Marketing Regulation Overview

- Legal frameworks and licensing acts (Federal and Provincial)

- Industry reports by H2 Gambling Capital and Eilers & Krejcik Gaming

- Canada’s Ministry of Innovation, Science and Economic Development – Digital Economy Data

- Canadian Payments Association – Payment Systems Reports

- Canadian Competition Bureau – Market Structure Analyses

- Canadian E-commerce Association – Digital Market Growth Data

- IT and Cybersecurity standards bodies in Canada

- Academic research on Canadian gambling behavior and economic trends

- News and industry media including Canadian Gaming Business Magazine

- International taxation treaties and agreements registered by the Canada Revenue Agency

- Provincial Health and Social Services Ministries – Gambling Harm Mitigation

- Telecommunication providers’ public coverage and performance reports

- Legal consulting and market entry advisory firms specialized in Canadian gaming

- Canadian Chamber of Commerce – Business Environment Studies

- Statistics Canada – Household Income and Spending Surveys

- Consumer behavior analysis reports from Nielsen and Ipsos Canada

- Provincial Lottery and Gaming Corporations annual financial reports

- Sports wagering market data from provincial regulators

- Cryptocurrency adoption and regulation reports in Canada

- Mobile device market penetration data from IDC and Statista

- Canada Revenue Agency – Corporate and Individual Tax Guidelines

🎯 Gambling Databases Country Rating: Canada

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.5/10 | 🟡 Moderate |

| Player Access Score | 10.0/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 8.2/10 | 🟢 High Potential (But Complex) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Provincial Fragmentation: Canada is NOT a single jurisdiction. Ontario has an open license model (iGaming Ontario), while provinces like BC, Quebec, and Manitoba maintain government-run monopolies (BCLC, Loto-Quebec).

- Grey Market Crackdowns: While historically lenient, the text notes “penalties for operators running unlicensed sites.” As Ontario regulates, tolerance for grey market operations in other provinces is diminishing.

- Local Presence Requirements: Local presence is “often required” depending on the province, adding significant operational overhead.

- Advertising Restrictions: Strict provincial controls limit youth exposure and marketing content, with increasing pressure to ban celebrity endorsements.

- Extradition Risk: Canada has robust extradition treaties with the USA and UK. Executives of grey-market operators violating criminal codes could face legal jeopardy.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.0/3.0 | Full product legality (+3.0). Deduction: Massive provincial fragmentation (-0.5); Monopolies in BC/Quebec limit private entry outside Ontario (-0.5). Final: 2.0/3.0. |

| Licensing Process | 25% | 1.5/2.5 | Accessible licensing in Ontario (+2.0). Application costs favorable (~$50k-$100k) (+0.5). Deduction: Licensing unavailable for private operators in monopoly provinces (-1.0). Final: 1.5/2.5. |

| Taxation & Costs | 20% | 1.5/2.0 | GGR Tax 12-20% falls into favorable 15-25% bracket (+1.5). No excessive deductions; this is a tax-competitive market compared to Europe. |

| Operational Requirements | 15% | 0.75/1.5 | Moderate requirements (+1.0). Deduction: Local presence often required (-0.25). Deduction: Complex multi-jurisdictional compliance overhead (-0.25). Deducted for mandatory RG measures (-0). Final: 0.5/1.5. |

| Market Environment | 10% | 0.75/1.0 | Excellent business environment (+1.0). Deduction: Strict advertising restrictions and saturation in Ontario (-0.25). Final: 0.75/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal and regulated (+4.0). Players face no legal risks for participation. |

| Practical Accessibility | 30% | 3.0/3.0 | Excellent accessibility (+3.0). Interac, Credit Cards, and E-wallets widely accepted. No ISP blocking affecting player experience significantly. |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players (+2.0). |

| Market Availability | 10% | 1.0/1.0 | 5+ licensed operators (+1.0). High market competition and choice. |

🔍 Key Highlights

Strengths

- High Player Value: Median household income of $75k CAD and 92% internet penetration create a high-ARPU environment ($500 CAD avg).

- Tax Competitiveness: 12-20% GGR tax is significantly lower than European counterparts (often 30-50%).

- Payment Ecosystem: Interac is a dominant, secure, and gambling-friendly payment method that simplifies deposits/withdrawals.

⛔️ CRITICAL RISKS AND CHALLENGES

- The “Two Canadas” Problem: Operators must treat Ontario (regulated, private license) and the Rest of Canada (Monopolies/Grey) as completely different business models.

- Compliance Costs: Meeting RG (Responsible Gambling) standards, KYC, and AML requirements in a “complex regulatory landscape” is expensive.

- Saturation: Ontario is flooded with major international brands; CAC is rising rapidly.

- Monopoly Barriers: In provinces like Quebec and BC, private operators cannot technically obtain a local license, forcing them into a grey operating model or B2B partnerships.

Player-Specific Issues

- Players in monopoly provinces (e.g., Quebec) technically have fewer “locally licensed” private options than Ontarians, though offshore access remains open.

- Geo-location technology must be precise to prevent players crossing provincial borders (virtually) where regulations differ.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: CAD $350,000 – $800,000 (Licensing + Legal + Tech Setup).

Monthly Operating Costs: High. Compliance staff and local directors add to wage bills.

Effective Tax Rate on Revenue: ~20% (Very Favorable).

Customer Acquisition Cost: Rising ($300 – $600 CAD). Intense competition in Ontario drives this up.

Time to Breakeven: 18-24 Months.

Profitability Assessment: VIABLE BUT COMPETITIVE. Unlike high-tax jurisdictions, the underlying economics (20% tax) are sound. However, the sheer number of entrants in Ontario means only those with strong retention strategies and deep marketing pockets will survive. The “Rest of Canada” offers revenue but carries increasing legal risk.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Medium/High | No license in Ontario = Blacklist. Operating in other provinces is legally grey but facing increased scrutiny and potential ISP blocking/payment blocking in future. |

| Licensed Sports Betting Operators | Low | Full legal protection in Ontario. Compliance burden is high but manageable. |

| Affiliates/Advertisers | Medium | Strict advertising standards. Promoting unlicensed brands in Ontario attracts heavy fines. |

| Payment Processors | Low | Banks and Interac work willingly with licensed entities. |

| Company Directors/Executives | Medium | Local presence requirements create personal liability jurisdiction. Extradition treaties exist. |

🚨 Extradition and International Enforcement

Extradition Treaties: Canada has active extradition treaties with the USA, UK, Australia, and EU nations.

Enforcement History: Canada generally targets money laundering and organized crime rather than pure gambling offenses, but the legal framework exists to prosecute unlicensed operators, especially if they ignore cease-and-desist orders from provincial regulators.

Safe Jurisdictions: None. If you operate in Canada, you should be licensed in Canada (specifically Ontario) or compliant with provincial monopolies.

📋 Final Verdict

Canada receives an Operator Ease Score of 6.5/10 and a Player Access Score of 10.0/10, resulting in an overall market attractiveness rating of 8.2/10.

HONEST ASSESSMENT: Canada is currently one of the most attractive iGaming markets globally due to high consumer spending and reasonable tax rates (~20%). However, it is a fragmented regulatory minefield.

Ontario is a “pay-to-play” regulated market with high competition, while the rest of the country remains a mix of government monopolies and grey-market operations. Entering without a substantial budget for compliance and local partnerships is a recipe for failure.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A mid-to-large operator with $2M+ capital ready for Ontario licensing.

- Capable of navigating complex multi-jurisdictional compliance.

- Able to offer localized payment solutions (Interac is mandatory for success).

❌ Definitely Avoid If You Are:

- An offshore operator hoping to run “under the radar” in Ontario (You will be blacklisted).

- Under-capitalized (High CAC and legal fees will drain funds quickly).

- Unwilling to establish a local presence or adhere to strict Responsible Gambling audits.

- Solely relying on crypto payments (Niche adoption only).

⚠️ BOTTOM LINE: Canada is a gold mine for professional, licensed operators, but a trap for those expecting a simple, unified market. Focus on Ontario first, but prepare for a street fight over market share.