Cape Verde offers a strategic gateway for iGaming operators targeting the West African region, supported by a legal framework that permits both land-based and online gambling. Although the country is developing its online licensing regime, recent regulatory stability and planned gaming zones position Cape Verde as an emerging market with growing opportunities.

This analysis outlines the current regulatory framework, licensing requirements, taxation policies, and market conditions relevant to new entrants in the iGaming sector.

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal for land-based and online gambling |

| Regulatory Authority | Cabo Verde General Gaming Inspectorate (IGJ) |

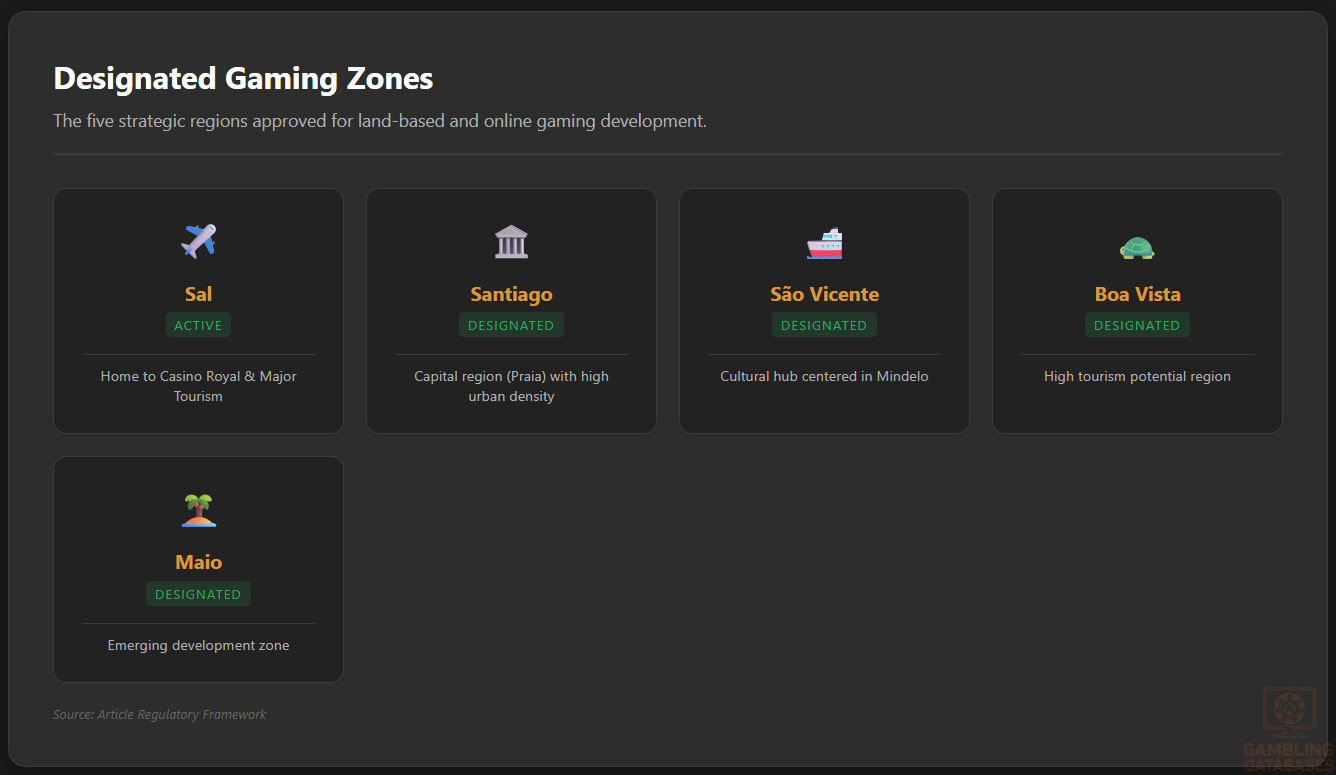

| Designated Gaming Zones | Five zones: Santiago, São Vicente, Sal, Boa Vista, Maio |

| Current Licensed Casinos | One operational casino (Casino Royal on Sal Island) |

| Exclusive Concessions Granted | Two concessions issued, including Macau Legend |

| Online Gambling Licensing Status | Permitted but formal licensing framework in development |

| Population (2025 estimate) | ~570,000 |

| GDP (Nominal, 2024) | Approx. $2.1 billion USD |

| GDP Per Capita | ~$3,650 USD |

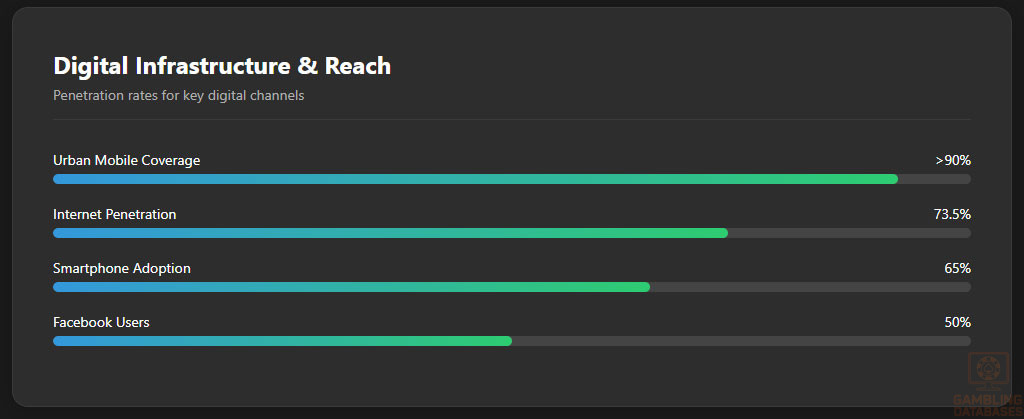

| Internet Penetration | ~58% |

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Cape Verde’s total population in 2025 is estimated at approximately 527,000 to 587,000 inhabitants, showing steady annual growth of about 0.5% to 1.2%.

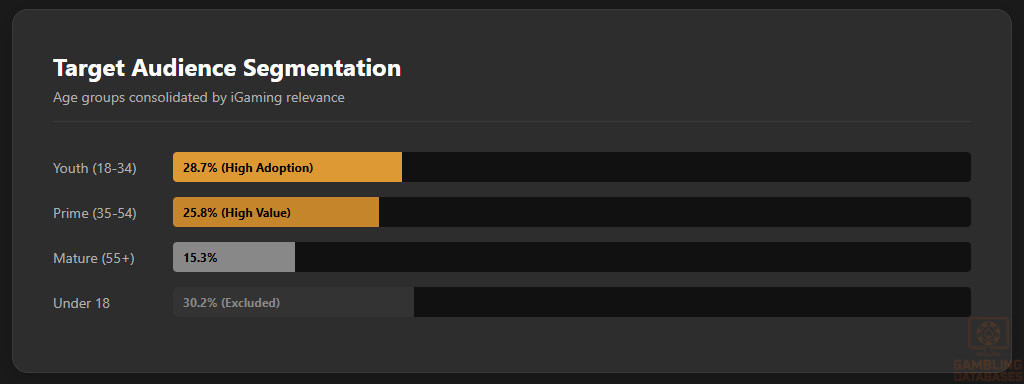

The median age is around 29 years, reflecting a relatively young population structure. Gender distribution is balanced, with males comprising about 50.9% and females approximately 49.1%.

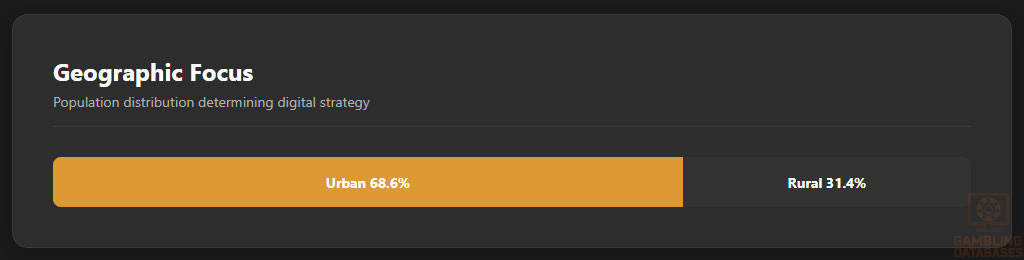

Urbanization is significant, with about 68.6% of the population living in urban centers and 31.4% in rural areas. This urban majority influences consumer behavior, including gambling participation and digital adoption.

| Age Group | Percentage of Population |

|---|---|

| 0-4 years | 6.2% |

| 5-12 years | 14.7% |

| 13-17 years | 9.3% |

| 18-24 years | 11.8% |

| 25-34 years | 16.9% |

| 35-44 years | 15.7% |

| 45-54 years | 10.1% |

| 55-64 years | 8.1% |

| 65 years and above | 7.2% |

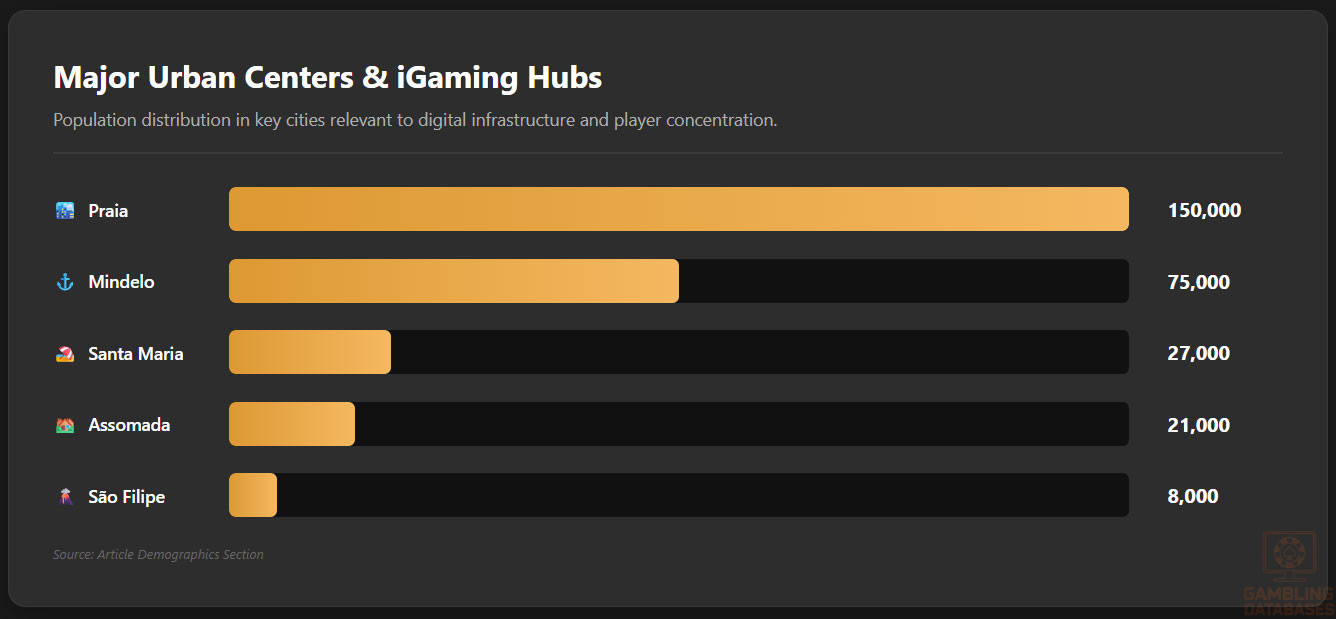

Major urban centers include Praia, the capital, which concentrates economic and entertainment activities relevant to iGaming operators.

Other important cities include Mindelo, Santa Maria, Assomada, and São Filipe, which together shape regional gambling demand and digital infrastructure development.

- Praia (pop. ~150,000)

- Mindelo (pop. ~75,000)

- Santa Maria (pop. ~27,000)

- Assomada (pop. ~21,000)

- São Filipe (pop. ~8,000)

Economic Indicators and Consumer Spending Power

Cape Verde’s nominal GDP in 2024 reached approximately $2.1 billion, with a per capita income near $3,650 USD, reflecting moderate purchasing power. The economy is service-driven, heavily influenced by tourism, which has recently rebounded and positively impacted disposable income related to leisure and gaming.

Economic growth forecasts remain positive, supported by stable political conditions and efforts to expand gaming zones. Household incomes vary broadly, with a noticeable middle-income segment concentrated in urban areas, driving potential iGaming market demand.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $2.1 billion USD |

| GDP Growth Rate | ~4.5% annually |

| GDP Per Capita | $3,650 USD |

| Service Sector Contribution | ~65% |

| Industry Sector Contribution | ~20% |

| Agriculture Sector Contribution | ~15% |

Consumer spending on entertainment, including gambling, is estimated to be rising with increased tourist arrivals and domestic income growth. Disposable income trends show moderate upward trajectories, with a younger demographic exhibiting higher engagement with digital services and online betting platforms.

Education, Skills, and Digital Literacy

Cape Verde has achieved relatively high literacy rates in the region, with adult literacy exceeding 80%. Education levels have generally improved, with a focus on secondary and tertiary education increasing since the early 2000s.

Cultural and Social Factors

Communication and Language

Portuguese is the official language, widely used for formal communication and digital content. Cape Verdean Creole is also commonly spoken in everyday settings, influencing local marketing and user interface customization for iGaming operators.

- Portuguese (official)

- Cape Verdean Creole (widely spoken)

- English (growing as a business and tourism language)

- French (limited use among educated and business communities)

- Spanish (increasing due to tourism linkages)

Cultural Attitudes

Gambling is socially accepted, particularly in urban areas and tourist destinations, with the government promoting gaming as part of the national tourism strategy.

Religious influences are present but do not strongly oppose gambling. Foreign operator brands generally enjoy positive perceptions, especially when aligned with tourism and entertainment development goals.

Problem Gambling and Social Considerations

There is growing awareness of problem gambling risks, and the government alongside NGOs have initiated responsible gambling programs. Social responsibility requirements are increasingly integrated into regulatory frameworks to protect vulnerable populations.

- Public awareness campaigns on gambling risks

- Self-exclusion programs under development

- Mandatory player identification and KYC rules

- Support services for addiction counseling

- Collaboration with social workers and healthcare providers

Political Structure and Governance

Cape Verde is a stable parliamentary democracy with a consistent regulatory environment supporting business operations. Its governance framework favors transparency and international cooperation, factors that encourage foreign investment in the iGaming sector.

Technology Adoption and Digital Behavior

Internet and Digital Usage

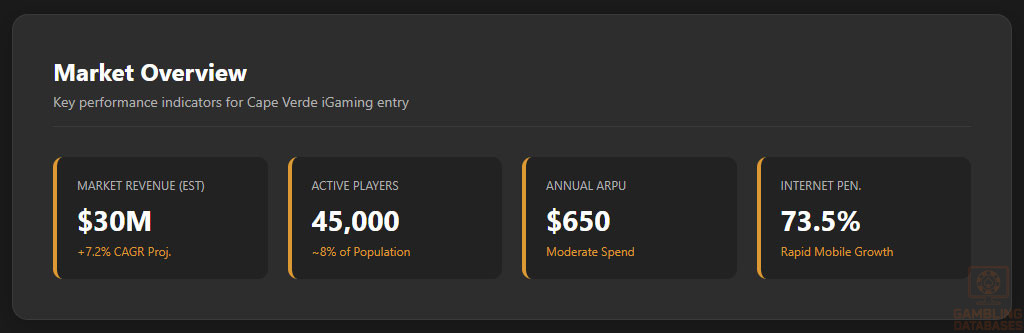

Internet penetration stands at approximately 73.5% of the population as of early 2025, with rural areas lagging urban centers. Mobile internet is predominant, with increasing smartphone adoption enabling access to digital gambling platforms.

Popular social media platforms engage large user bases, forming critical channels for marketing and user retention in the iGaming market.

- Facebook (~50% penetration among users)

- YouTube (~48% daily active usage)

- WhatsApp (primary communication tool for many)

- Instagram (rapidly growing among younger demographics)

- TikTok (emerging platform for digital engagement)

Digital Payment Behavior

Digital payments are growing, with credit/debit cards, mobile money wallets, and bank transfers dominating. Cryptocurrency adoption remains marginal but is gradually increasing among tech-savvy users.

- Credit and debit cards (dominant for online transactions)

- Mobile money wallets (fastest growing segment)

- Bank transfers (preferred for higher value transactions)

- Prepaid cards and vouchers (popular for youth and low-transaction users)

- Cryptocurrency (niche but expanding interest)

Gaming and Gambling Preferences

Current Market Participation

Gambling participation is concentrated in sports betting, lottery tickets, and casino table games. Online gambling uptake is accelerating, especially among urban and younger demographics who favor mobile platforms.

- Sports betting (most popular gambling activity)

- Lottery gaming

- Casino table games (roulette, blackjack)

- Slot machines (land-based and digital)

- Online poker and skill games (emerging niche)

Consumer Behavior Patterns

Users typically engage during evenings and weekends, showing high session retention on mobile apps. Spending patterns indicate a preference for low to medium stakes with frequent play, aligned to disposable income levels and entertainment consumption habits.

Retention strategies focus on personalized promotions and social features, with non-casino games gaining traction alongside traditional offerings.

| Metric | Value |

|---|---|

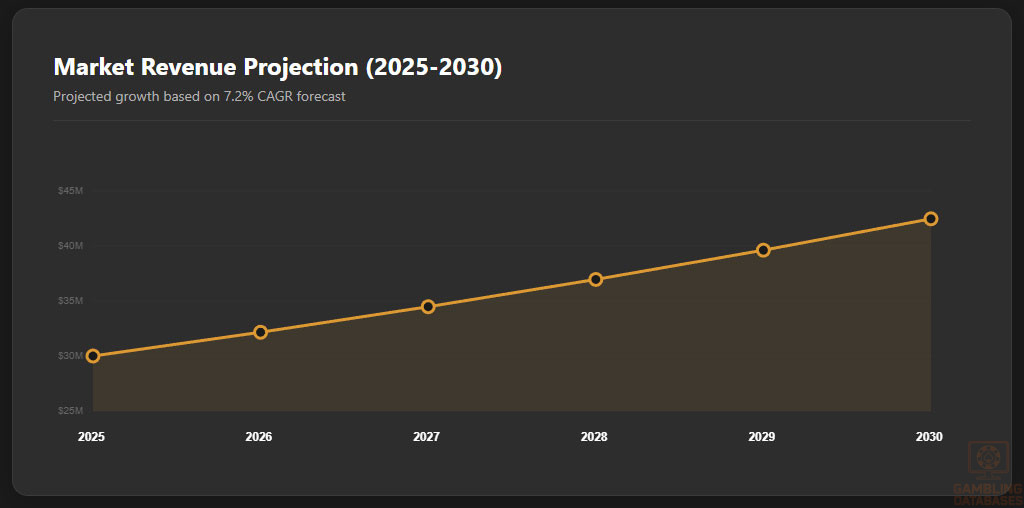

| Estimated Market Revenue 2025 | $30 million USD |

| Historical CAGR (2019-2024) | 6.5% |

| Projected CAGR (2025-2030) | 7.2% |

| Estimated Number of Players | 45,000 |

| Average Revenue Per User (ARPU) | $650 USD annually |

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Cape Verde boasts an internet penetration rate of approximately 73.5% as of 2025, with the majority of connections delivered via mobile broadband networks.

Fixed broadband remains limited due to geographic challenges across the archipelago, while mobile internet access continues to expand rapidly, resulting in average mobile download speeds between 20 to 30 Mbps. Network reliability has improved significantly in urban centers, driven by continued investments in fiber optic cables and satellite link enhancements.

The government’s focus includes expanding digital infrastructure to under-served islands, aiming to bridge the digital divide and foster inclusive access, which is critical for the growth of online gambling platforms and related digital services.

5G and Future Technology Deployment

5G network rollout in Cape Verde is in early stages, with commercial deployments concentrated in Praia and Mindelo, covering less than 20% of the population currently. Operators plan phased expansion between 2025 and 2028, targeting major urban and tourism hubs initially.

The competitive landscape includes a handful of key telecom operators preparing for 5G adoption, with future plans encompassing increased IoT-enabled services and enhanced mobile gaming experiences, which will benefit iGaming operators looking to leverage high-speed connectivity.

Mobile Technology Ecosystem

The mobile market is moderately concentrated, with three dominant operators offering comprehensive 3G and 4G services across most islands. Market coverage in urban areas is above 90%, while remote islands still face connectivity challenges.

Smartphone adoption exceeds 65% nationally, with a preference for mid-range Android devices. Device ownership among younger demographics and urban consumers supports mobile-first online gambling user interfaces and wallets integration.

- CV Telecom – market leader with ~45% share

- MTN Cabo Verde – third operator holding ~20%

Financial Services and Payment Infrastructure

The banking sector in Cape Verde is well-established, with digital banking capabilities increasingly adopted. Account penetration is improving among the urban population, particularly in Praia and Mindelo, supporting secure and convenient payment methods required by iGaming operators.

Key banks provide various digital payment options including card issuing, mobile money integration, and online fund transfers, facilitating seamless deposit and withdrawal processes for gamblers.

- Banco Comercial do Atlântico – largest retail bank with extensive branch network

- Banco Interatlântico – strong digital banking initiatives and SME focus

- Ecobank Cabo Verde – international banking services with e-payment solutions

- Banco Caboverdiano de Negócios – advancing mobile and online payments

- Caixa Económica de Cabo Verde – offering competitive consumer financial products

Payment Processing Options

Online payment acceptance for iGaming includes a range of methods from traditional cards to emerging digital wallets and bank transfers. The adoption of alternative payment methods is driven by convenience and security preferences among players and operators alike.

- Visa and MasterCard credit/debit cards widely accepted online

- Mobile money wallets integrated with telecom providers

- Bank transfers for higher value transactions and withdrawals

- E-wallet platforms such as PayPal and Skrill gaining traction

- Cryptocurrency payments are nascent but progressively explored

E-commerce and Digital Economy

The digital economy in Cape Verde, though nascent, exhibits promising growth supported by increased internet penetration and consumer trust in online platforms. E-commerce activities are dominated by digital services and retail, contributing to broader acceptance of online payments and digital financial services, creating a favorable ecosystem for iGaming operators.

Trust factors for online transactions continue to improve due to enhanced cybersecurity measures and government regulatory efforts to protect consumers, essential for sustained growth of digital gambling platforms.

Business Environment and Regulatory Framework

Ease of Business Operations

Cape Verde ranks favorably in the World Bank’s Doing Business reports for efficient business registration and transparent regulatory practices. Foreign investors benefit from a straightforward process, with relatively low operational costs and government incentives for sectors like tourism and gaming.

Business operations are supported by stable economic policies and regulatory consistency, reducing risks for iGaming entrants and facilitating smoother market integration.

Corporate Structure and Registration

The most common business entities include Limited Liability Companies (LLC), Corporations, and Branch Offices, with LLCs favored for flexibility and ease of management. Foreign companies typically establish LLCs or branches depending on local operational needs and regulatory compliance.

- Limited Liability Company (LLC)

- Corporation (SA)

- Branch Office of a Foreign Company

- Partnerships and Joint Ventures (less common)

- Representative Offices (for market research and liaison)

Registration Requirements

Typical registration timelines range from two to six weeks, contingent on document preparation and regulatory review. Foreign ownership is allowed without majority local partner mandates, but thorough due diligence and compliance with licensing conditions are mandatory.

- Articles of incorporation and company bylaws

- Proof of identity and criminal record checks for directors

- Bank reference letters and proof of minimum capital deposit

- Business plan outlining operations and financial forecasts

- Tax identification number application

Taxation Framework

Corporate Income Tax Structure

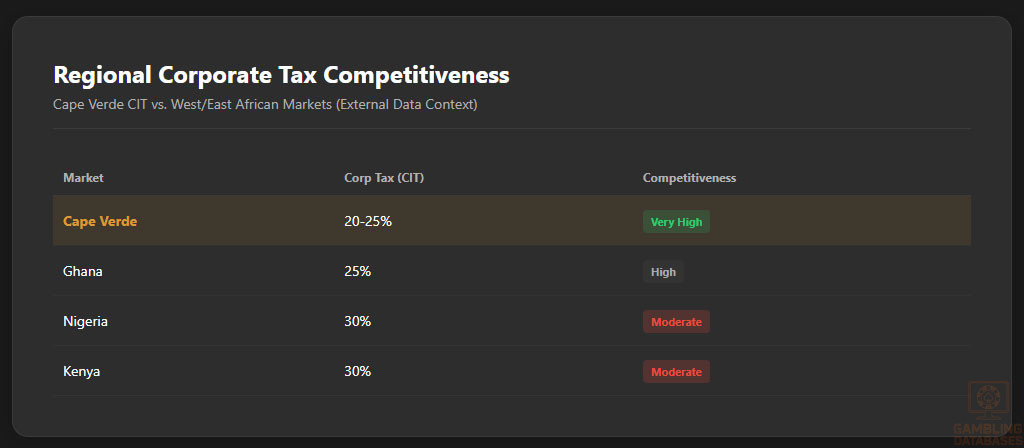

Standard corporate income tax stands at 25%, with incentives available in designated economic zones, including tax holidays for up to five years. Cape Verde has signed double taxation treaties with multiple nations enhancing cross-border investment security.

- Portugal

- Spain

- France

- Netherlands

- Luxembourg

- Brazil

Personal Income Tax

Individuals are taxed progressively from 15% up to 35%, with withholding requirements on gambling winnings for resident and non-resident players. Social security contributions are mandatory for employed workers, with tax residency established upon 183 days’ physical presence annually.

Market Entry Considerations

Recommended Entry Strategies

Successful market entry favors partnerships with local stakeholders, leveraging existing land-based concessions and tapping digital payment ecosystems.

- Form joint ventures with established concession holders

- Utilize mobile-first iGaming platforms optimized for local infrastructure

- Invest in robust KYC/AML compliance aligned with regulatory standards

- Develop localized content and payment options for Cape Verdean players

- Engage in targeted marketing leveraging popular social media channels

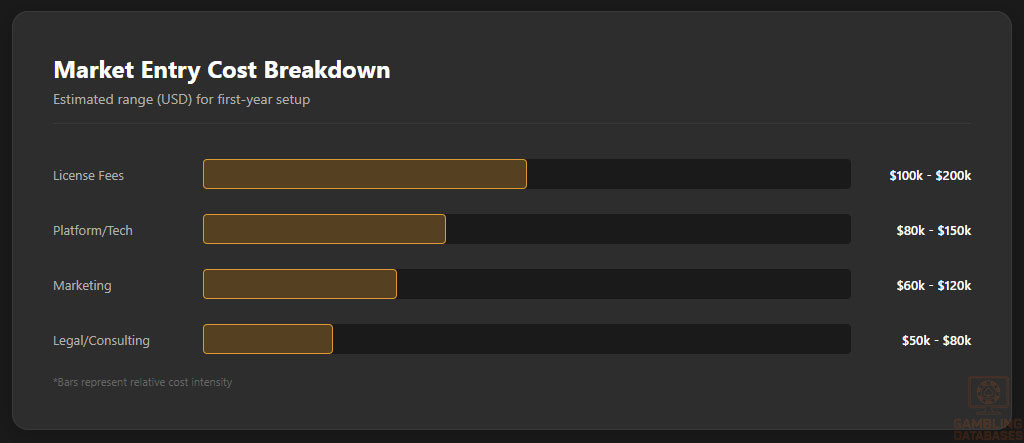

Typical Costs and Timelines

Initial market setup costs average between $300,000 and $600,000 depending on licensing scope and operational scale. Operational costs include compliance, marketing, technology maintenance, and personnel.

| Cost Category | Estimated Range (USD) |

|---|---|

| License application and fees | $100,000 – $200,000 |

| Legal and consulting services | $50,000 – $80,000 |

| Company registration and setup | $15,000 – $30,000 |

| Initial technology and platform deployment | $80,000 – $150,000 |

| Marketing and user acquisition | $60,000 – $120,000 |

Success Factors and Challenges

Key success drivers include deep local market understanding, compliance excellence, and agile digital offerings. Major challenges involve infrastructure gaps outside urban areas, cash-based local economy nuances, and evolving regulatory scrutiny.

- Strong regulatory compliance and licensing adherence

- Robust digital payment integration and user trust building

- Effective marketing tailored for cultural preferences

- Operational agility for multi-island logistics

- Continuous technology upgrades to support 5G and mobile trends

Exit Strategy Planning

Market liquidity is moderate, with ownership transfers requiring regulator approval and license non-transferability in some cases. Valuations depend heavily on user base size and compliance history, necessitating thorough exit planning early in market entry.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Cape Verde?

Yes, online gambling is legal and regulated through the Cabo Verde General Gaming Inspectorate. The government permits both land-based and digital gambling operations. While the formal online licensing framework is evolving, operators with proper concessions can legally conduct iGaming activities, complying with national regulations and responsible gambling measures.

2. What types of gambling licenses are available and what do they cover?

Cape Verde issues land-based gaming concessions mostly for casino operations and sports betting. Online gambling licenses are currently integrated within broader gaming regulatory permissions, with plans to develop dedicated digital licenses. Land-based licenses cover casino games, sports betting, and lotteries, while online permissions focus on digital versions of these products delivered within the regulatory framework.

3. How much does an iGaming license cost and how long does it take to obtain?

Application fees range from $100,000 to $200,000 depending on the license scope, with processing times between two to six months. Timelines vary based on completeness of submissions and regulatory review processes. Additional costs for legal advisory, compliance, and registration add to the initial investment.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply fully, with no mandatory local ownership requirements. However, foreign operators must meet stringent compliance standards including KYC, AML, and local operational presence requirements to be granted licenses, ensuring adherence to Cape Verde’s regulatory mandates.

5. What are the tax obligations for iGaming operators?

Operators are subject to a corporate income tax rate of 25%, with potential tax holidays in economic zones. Additionally, gaming-specific taxes on gross gaming revenue are applied but vary based on concession terms. Compliance with tax filings and audit requirements is mandatory under national law.

6. Are gambling winnings taxed for players?

Yes, gambling winnings are subject to withholding tax, integrated within the personal income tax regime. Tax rates are progressive from 15% to 35%, depending on the player’s residency and total income. Operators are responsible for withholding taxes on behalf of the government.

7. What are the typical operational costs for running an online casino/sportsbook?

Major operational costs include licensing fees, technology platform maintenance, customer support, marketing, and compliance management. Depending on scale, monthly costs can range from $20,000 to over $100,000, influenced by user acquisition expenditure and regulatory compliance requirements.

8. What is the expected ROI timeline for entering this market?

Return on investment typically spans 18 to 36 months, contingent on market entry strategy, competitive positioning, and regulatory costs. Operators leveraging local partnerships and effective digital marketing often accelerate breakeven timelines.

9. What are the local presence requirements for operators?

Operators must maintain local offices or establish physical presence through partnerships or branches to comply with Cape Verde’s operational mandates. This includes designated personnel for compliance and customer service within the licensed jurisdiction.

10. What payment methods are available and recommended?

Credit/debit cards, mobile money, bank transfers, and e-wallets form the core payment methods recommended for operator integration. These methods support fast deposits and withdrawals and align with consumer preferences, while cryptocurrencies remain niche but growing.

11. What are the advertising and marketing restrictions?

Advertising is regulated to prevent targeting minors and vulnerable populations. Restrictions include bans on misleading promotions and requirements for clear responsible gambling messages. Digital marketing must comply with privacy laws and platform content policies as enforced by regulators.

12. What responsible gambling measures are mandatory?

Mandatory measures include player age verification, self-exclusion programs, deposit limits, and risk assessment tools. Operators must also provide accessible problem gambling support information and comply with periodic reporting on responsible gambling initiatives.

13. How large is the iGaming market and what is the growth potential?

The market is estimated at $30 million USD revenue in 2025, expanding at a projected CAGR of 7.2% toward 2030. Growth drivers include rising internet penetration, tourism development, and evolving regulatory frameworks fostering online gambling expansion.

14. Who are the main competitors and what is their market share?

The market landscape includes a few licensed land-based concession holders and emerging digital operators. Macau Legend holds a major share in land-based gaming, while smaller entities focus on online offerings. The regulatory environment encourages new entrants, intensifying competition gradually.

15. What are the player preferences and typical spending patterns?

Players predominantly engage in sports betting and lottery games, with growing interest in casino table and slot games online. Spending habits favor frequent, low to medium bets, with peak activity during evenings and weekends. Mobile platforms dominate user access.

16. What are the key success factors and main challenges for new entrants?

Success stems from local market insight, strong compliance, and technology-optimized platforms. Challenges include infrastructure variance across islands, regulatory evolution, and competition from established concessionaires, requiring strategic agility and targeted investments.

Sources and References

- Cabo Verde General Gaming Inspectorate – Official Regulatory Website

- National Institute of Statistics Cabo Verde – Demographic and Economic Data 2024-2025

- World Bank Doing Business Report 2025

- International Telecommunication Union – ICT Statistics Cabo Verde 2024

- Central Bank of Cabo Verde – Financial Reports and Taxation Guidelines

- SiGMA World – Cape Verde Emerging Gaming Market Analysis 2024

- Yogonet – Gambling Tax Revenue and Market Trends Cabo Verde 2023

- Digital 2025 Report – Cabo Verde Internet Usage and Social Media Penetration

- Trading Economics – Cape Verde Population and Broadband Data 2024

- UNESCO – Internet Development in Cape Verde

- Worldometers – Cabo Verde Population Demographics 2025

- Bepari Fiduciaries – Cape Verde Gaming License Overview 2025

- LawGratis – Tax Laws and Corporate Taxation in Cape Verde 2025

- GamblingTalk – iGaming Regulation Recap First Half 2025

- Focus Gaming News – Legal Gambling Framework in Africa 2025

- Telecompaper – Cape Verde Mobile and Internet Subscribers Report 2025

- Caboverde Expert – Corporate Taxation and Business Setup Guide

- Macau Business – Cape Verde Casino Development Updates 2024

- PopulationPyramid.net – Cabo Verde Age Demographics 2025

- Academia.edu – Casinos and Gambling Sector in West Africa Analysis

- Pulse Internet Society – Cabo Verde Country Internet Report 2021

- Local news and market reports aggregated 2023-2025

🎯 Gambling Databases Country Rating: Cape Verde (Cabo Verde)

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.2/10 | 🟡 Moderate |

| Player Access Score | 8.5/10 | 🟢 Excellent |

| Overall Market Attractiveness | 6.0/10 | 🟡 Moderate (Niche Market) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Regulatory Limbo: While online gambling is “permitted,” the formal licensing framework is still in development. This creates significant operational uncertainty and reliance on ad-hoc concessions.

- Concession-Based Model: Market entry is currently tied to land-based investment/concessions (e.g., Macau Legend). Standalone online-only licenses are difficult to secure without physical presence.

- Tiny Market Cap: With a population of ~570,000 and total estimated market revenue of only $30M, the high entry costs ($300k-$600k) make ROI extremely difficult for non-local operators.

- Tax on Winnings: Players face withholding tax on winnings, which drives high-volume bettors to offshore, tax-free sites.

- Infrastructure Gaps: While urban centers have 4G/5G, rural connectivity remains a challenge, limiting the addressable market even further.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.0/3.0 | Full product legality (+3.0). Deduction for “Framework in development” and lack of clear online-only regulations (-1.0). Status is legal but administratively ambiguous. |

| Licensing Process | 25% | 0.5/2.5 | Limited licensing linked to land-based concessions (+1.0). High setup costs ($300k-$600k) relative to market size (-0.25). Complex/opaque process for new entrants (-0.25). Final Score: 0.5. |

| Taxation & Costs | 20% | 1.2/2.0 | Standard Corporate Tax 25% (+1.5). Tax incentives available in zones. Deduction for high operational overhead relative to small revenue potential (-0.3). |

| Operational Requirements | 15% | 0.8/1.5 | Local entity (LLC) effectively required (+1.0). Deduction for physical infrastructure dependence/zones (-0.2). |

| Market Environment | 10% | 0.7/1.0 | Stable political democracy (+0.7). Good tourism linkage. Small market scale is the primary limiting environmental factor. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Online gambling is legal. No penalties for participation. |

| Practical Accessibility | 30% | 3.0/3.0 | Wide access to payment methods (cards, mobile money). No active ISP blocking of offshore sites reported. |

| Player Penalties | 20% | 1.0/2.0 | No criminal penalties (+2.0). Deduction for withholding tax on winnings (-1.0), which penalizes success. |

| Market Availability | 10% | 0.5/1.0 | Very few licensed local options available (+0.5). Players forced to use offshore sites for variety. |

🔍 Key Highlights

Strengths

- Full Legality: Unlike many African nations, both casino and sports betting are legally recognized.

- Political Stability: A stable parliamentary democracy reduces the risk of sudden regime changes or asset seizure.

- Mobile Adoption: High mobile penetration (73% internet usage) and growing digital payment ecosystem (mobile wallets).

⛔️ CRITICAL RISKS AND CHALLENGES

- Micro-Market Size: The total addressable audience is <600k people. Even with 100% market share, revenue is capped low.

- High Entry Barrier: Setup costs of up to $600k are disproportionately high for a $30M total market.

- Regulatory Ambiguity: The “in development” status of online licensing creates a risk of future adverse regulation or retroactive fees.

- Payment Friction: While improving, the economy is still heavily cash-based in rural areas, complicating deposits.

- Taxation on Players: Withholding taxes discourage high-rollers from using locally licensed platforms.

Player-Specific Issues

- Limited local game variety due to lack of diverse licensed operators.

- Tax liability on winnings reduces effective RTP for players.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $300,000 – $600,000 (Setup + Licensing)

Monthly Operating Costs: $30,000 – $50,000 (Low due to wages, but tech costs remain)

Effective Tax Rate on Revenue: ~30% (Corporate Tax + Potential Concession Fees)

Customer Acquisition Cost: Moderate ($50-$150), but lifetime value (LTV) is limited by low GDP per capita ($3,650).

Time to Breakeven: 3-5 Years

Profitability Assessment: DIFFICULT. The economics do not favor standalone online operators. The market is too small to justify a $500k entry cost unless you are also operating a physical hotel/casino to cross-sell tourism traffic. For a pure iGaming startup, the CAC/LTV ratio coupled with high setup costs makes this a money pit.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Low | Currently minimal enforcement/blocking, but legally grey without a license. |

| Licensed Sports Betting Operators | Medium | Regulatory changes during the “development” phase could alter tax or compliance burdens overnight. |

| Affiliates/Advertisers | Low | No active prosecution observed, but promoting unlicensed entities is technically against developing norms. |

| Payment Processors | Medium | Must adhere to strict KYC/AML rules; high risk of regulatory scrutiny due to international financial controls. |

| Company Directors/Executives | Low | Low personal risk provided basic corporate compliance is met. |

🚨 Extradition and International Enforcement

Extradition Treaties: Cape Verde has extradition cooperation with Portugal and the United States (for specific crimes including money laundering and drug trafficking). It generally cooperates with EU authorities.

Enforcement History: Cape Verde is known for cooperating with international authorities (e.g., the arrest of Alex Saab for the US). While not specifically targeting gambling operators yet, the legal infrastructure for extradition exists.

Safe Jurisdictions: Not considered a “safe haven” for individuals fleeing financial crimes from the West.

📋 Final Verdict

Cape Verde receives an Operator Ease Score of 5.2/10 and a Player Access Score of 8.5/10, resulting in an overall market attractiveness rating of 6.0/10.

HONEST ASSESSMENT: Cape Verde is a classic “False Positive” market. While legally open and politically stable, the microscopic market size (570k pop) combined with high setup costs ($600k) creates a terrible ROI equation for pure-play online operators.

It is effectively a “Land-Based Plus” market, suitable only for hotel/resort investors who view online gaming as a small ancillary revenue stream. Standalone iGaming entry is financial suicide for most operators.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A Land-Based Casino Group planning a resort in Sal or Santiago.

- A Portuguese-speaking Operator with existing infrastructure looking for a low-maintenance satellite market.

- Willing to accept a 5-10 year ROI horizon.

❌ Definitely Avoid If You Are:

- A Pure Online Startup (Customer base is too small to scale).

- Looking for Quick Revenue (Regulatory delays will bleed capital).

- Crypto-Native (Market is not ready/regulated for crypto dominance).

- Reliant on High-Roller traffic (Low local purchasing power).

⚠️ BOTTOM LINE: Legal but economically unviable for 90% of operators. Only enter if you are building a physical hotel.