China presents a uniquely challenging environment for iGaming operators, characterized by strict regulatory controls and a predominantly prohibitive legal landscape for private gambling ventures. Despite these challenges, its vast population and growing digital infrastructure attract attention from global gaming entities looking for strategic opportunities within adjacent markets and controlled sectors.

The current regulatory framework severely restricts online gambling activities, permitting only state-run lotteries and offering minimal space for private iGaming operations. Navigating these constraints requires keen understanding of the legal environment, compliance obligations, and potential indirect market entry strategies.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Restricted; only state lotteries legal, private and online gambling banned |

| Population | ~1.4 billion |

| Urban Population Percentage | 64% |

| GDP (Nominal) | Approx. $19.9 trillion (2024) |

| GDP Per Capita | Approx. $14,200 |

| Internet Penetration | ~75% |

| Mobile Penetration | ~98% with 1.6 billion mobile connections |

| State Lottery Market Size | Over $60 billion annually |

| Online Gambling Licensing | No private licensing framework; prohibitively restricted |

| Regulatory Authority | Multiple including Ministry of Finance (lotteries), Ministry of Public Security, NPPA (gaming content) |

| Gaming Approval Regulator (Digital) | National Press and Publication Administration (NPPA) |

| License Application Timeline | Not applicable for private operators |

| Operator Tax Rates (State-run) | Variable; typically high tax and revenue sharing for state lotteries |

| Player Taxation | No official taxes on winnings (state lotteries excluded) |

| Market Entry Barriers | Extremely high due to legal prohibition and enforcement |

| Legal Online Gambling Options | State lotteries only |

| Land-based Casinos | Only in Macau Special Administrative Region (excluded from mainland) |

| Online Gambling Prohibition Enforcement | Active blocking of offshore domains and prosecutions |

| Recent Regulatory Changes | Increased youth protection, real-name verification, gaming content control since 2023 |

| Average Revenue Per User (ARPU) – State Lotteries | Approx. $42 |

| Technology Infrastructure Index | High 4G/5G coverage; ongoing expansion of broadband |

| Business Environment Index | Moderate; foreign investment restricted in gambling sectors |

| Legal Sports Betting Status | Not permitted (except limited state-backed lotteries) |

| Advertising Restrictions | Severe bans on gambling ads in all media including online |

| Crackdown on Illegal Gambling | Frequent raids, VPN restrictions, online domain blacklisting |

| Regulatory Reporting Requirements | Applicable only to state-approved lotteries and related entities |

| Foreign Ownership Restrictions | Absolute ban on foreign ownership in gambling operators |

| Legal Framework Complexity | Very high due to overlapping authorities and ambiguous enforcement |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

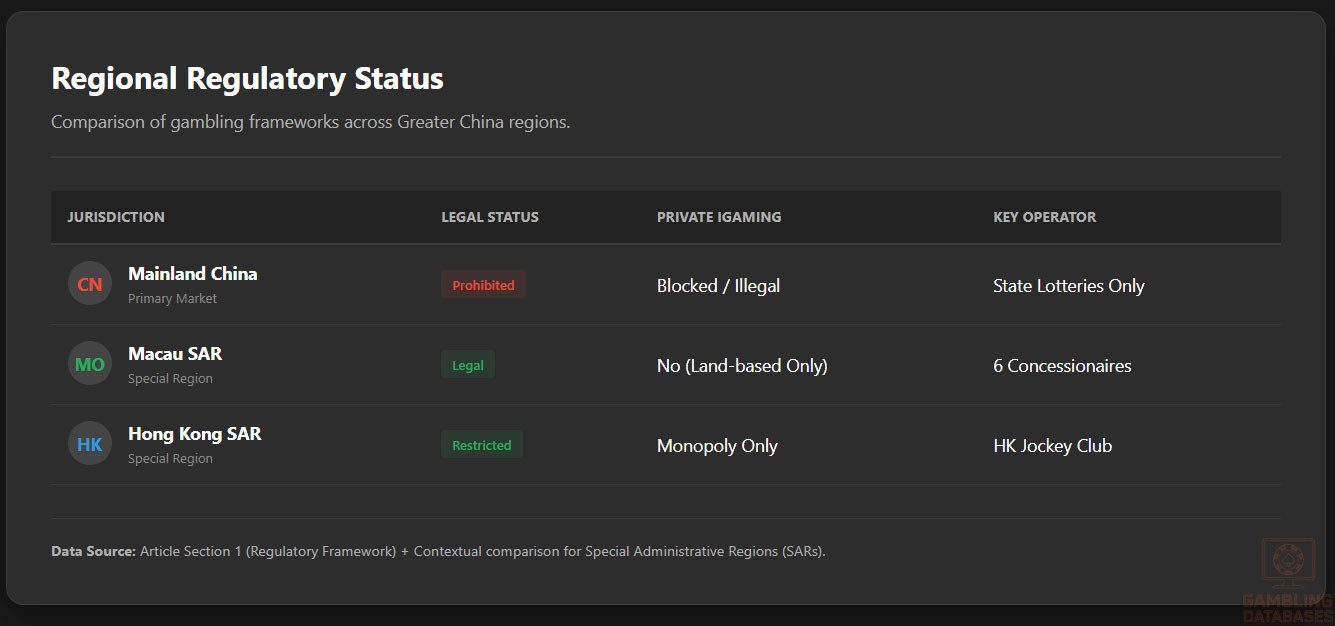

China’s gambling sector remains one of the most tightly controlled worldwide, with a legal regime that prohibits nearly all forms of private gambling, both land-based and online, across mainland China. The government permits only two state-run lotteries — the Welfare Lottery and the Sports Lottery — which operate under strict state supervision through the Ministry of Finance. Other forms of gambling including casinos, sports betting, poker, and slot machines are illegal, making market entry for private iGaming operators effectively impossible within the mainland.

The Chinese government also prohibits all forms of online gambling, including online casinos, poker, sports betting, and lottery sales by private or offshore operators. The Ministry of Public Security actively enforces anti-online gambling legislation by blocking access to offshore gambling websites and prosecuting individuals involved in illegal gambling activities. Recent enhancements to regulatory controls involve sophisticated internet surveillance and restrictions on virtual private networks (VPNs) to prevent access to illicit platforms.

Land-Based Gambling Activities

Within mainland China, the only legal land-based gambling activities are the state-operated welfare and sports lotteries. These lotteries are widespread, with physical sales outlets often integrated into convenience stores and kiosks.

There is no legal private casino presence or legal sports betting establishments. Moreover, gambling-like entertainment venues that do not involve actual betting but simulate gambling, such as mahjong parlors and certain video game arcades, face stringent scrutiny and frequent regulatory interventions to prevent illegal gambling.

Macau remains the sole Chinese jurisdiction where large-scale licensed casinos operate, but its regulatory environment is separate and not applicable to mainland market entry strategies for private operators.

Online Gambling Framework

China’s online gambling framework is prohibitive and uncompromising. The central government has not established any licensing regime for online casinos, sportsbooks, or poker rooms for private entities. Online betting is explicitly forbidden, with enforcement mechanisms including website blocking, account suspension, and criminal charges for operators and participants.

The National Press and Publication Administration (NPPA) oversees digital gaming content approvals and enforces regulations targeting gaming addiction, underage gambling, and online transaction authenticity. Platforms must implement real-name authentication systems, spending caps for minors, and comply with content censorship. These regulations extend to online games that promote gambling elements, which are routinely banned or censored by authorities.

Licensed Operators and Market Players

The gambling landscape in mainland China is a monopoly dominated by government entities, specifically the Welfare Lottery and the Sports Lottery organizations. No licenses exist for private operators to offer any form of gambling services, online or offline, within the territory. Private companies attempting to target the Chinese market via online platforms operate in a legal gray zone and face significant risk of enforcement actions.

Multinational gaming companies, such as Tencent and NetEase, participate legally in the broader gaming industry but must comply with stringent NPPA approvals and cannot offer real money gambling. Their involvement in the iGaming space is largely limited to entertainment-focused games without wagering or betting mechanics.

Licensing Framework and Requirements

Application Process and Eligibility

For mainland China, there is no established application process or eligibility criteria for private gambling licenses because they are not issued. The lawful operation of gambling activities is restricted to designated government-authorized bodies for lottery issuance.

For online games subject to NPPA approval, companies must submit detailed content for review, including compliance with technical standards, censorship guidelines, and payment system regulations. While this does not constitute a gambling license, it governs the digital environment in which game-related monetization occurs.

Local Presence and Operational Requirements

Foreign or private operators seeking to engage with the Chinese market must understand that there are strict prohibitions against foreign ownership or operation of gambling businesses within the mainland. Establishing a physical presence for gambling operations is not legally recognized and will not provide authorization or protection. Partnerships or joint ventures in related digital entertainment fields require compliance with cultural and regulatory content restrictions but do not extend to gambling activities.

Compliance Obligations and Monitoring

Player Protection and Identification

The Chinese government mandates rigorous player protection measures primarily enforced through digital real-name verification protocols, especially in online games. The NPPA enforces age verification and spending limits for minors to curb gambling addiction and ensure compliance with social responsibility objectives.

Responsible gambling frameworks require operators (within the permitted game content domain) to provide mechanisms for spending caps, session time restrictions, self-exclusion options, and transparency in user data handling. These measures are embedded within the broader gaming regulatory structure overseen by the NPPA, rather than focused solely on gambling applications.

Financial Monitoring and Reporting

State lottery operators must comply with extensive financial monitoring and reporting obligations under the Ministry of Finance and Public Security oversight. These include regular audits, detailed revenue reporting, and compliance with anti-money laundering (AML) regulations.

For private digital platforms, financial transparency is enforced indirectly via content approval and payment system authorization, with technical audits and security certifications ensuring transaction integrity and compliance with legal statutes.

Taxation Structure and Financial Obligations

Player Taxation

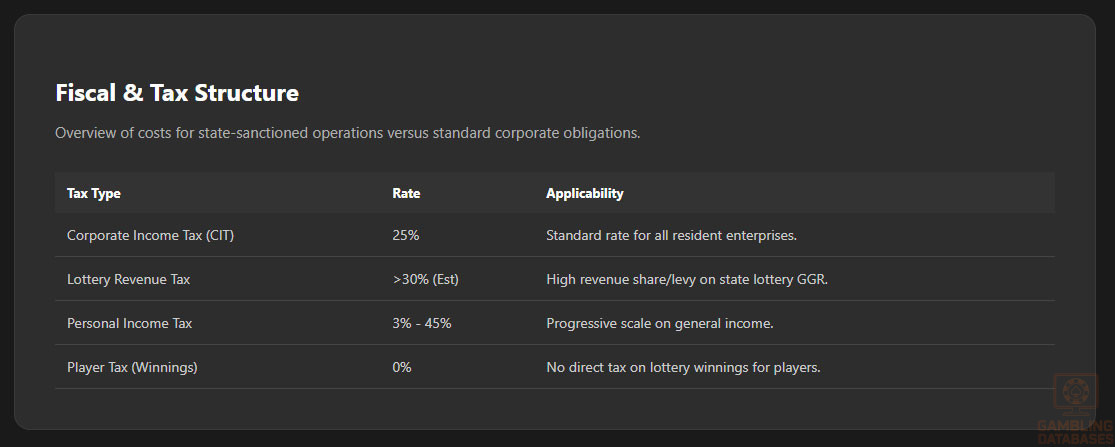

There is no official taxation on player winnings in mainland China for the state lotteries or any other permitted activity. Players do not bear direct tax obligations on lottery winnings.

Operator Taxation

| Tax Type | Applicable Rate / Description |

|---|---|

| Lottery Revenue Tax | High state-imposed revenue sharing; estimated effective tax rates exceed 30% |

| Corporate Income Tax | Standard 25% applied to state lottery operators |

| License Renewal / Fees | Not applicable to private operators; state lottery fees managed centrally |

| Turnover Tax | None formally levied beyond revenue sharing |

Gambling Market Financial Performance

The state lottery market represents the only legal gambling revenue source within mainland China, generating an estimated annual turnover exceeding $60 billion. This sector experiences steady growth aided by digital sales expansion and government promotion. Operator revenues are subject to high taxation and mandatory revenue sharing with the government budget.

Growth in illicit online gambling channels, despite enforcement efforts, reflects persistent demand but does not translate into legitimate market revenue or regulatory acceptance.

Advertising and Marketing Restrictions

Advertising of gambling services is heavily restricted in mainland China. All forms of commercial promotions for gambling, including lotteries, online betting, and casinos, are banned across traditional and digital media. The government employs strict content controls, censorship, and sanctions against violations.

- Prohibition of gambling ads on television, radio, and print media

- Online platform restrictions and content blocking for gambling promotion

- No sponsorship of sports or entertainment events by gambling operators

- Ban on advertising targeting minors or using misleading claims

- Strict penalties for unauthorized promotional activities

Recent Regulatory Changes and Their Impact

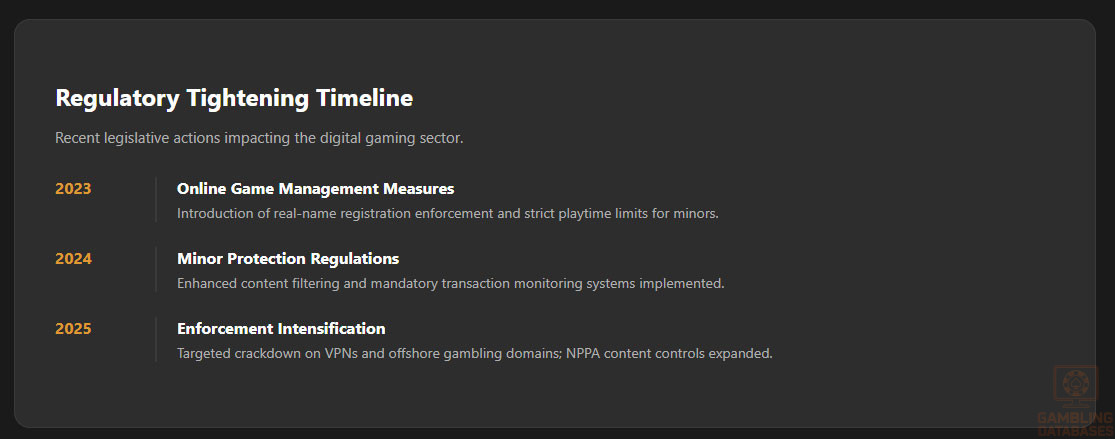

- 2023: Introduction of the Measures for Online Game Management requiring real-name registration and limiting minors’ playtime and spending

- 2024: Implementation of Regulations on the Protection of Minors Online with enhanced content filtering and transaction monitoring

- 2024-2025: Expansion of NPPA gaming content controls with new publication licensing requirements

- 2025: Intensified internet enforcement against unauthorized gambling platforms and VPN circumvention

These reforms have raised operational barriers, increased compliance costs, and heightened enforcement risks for any entities touching gambling-related activities. Publicly listed gaming companies have experienced volatility due to these regulatory dynamics.

Enforcement Mechanisms and Penalties

The Chinese government enforces gambling laws vigorously through a combination of internet censorship, blocking offshore domains, financial transaction monitoring, and criminal prosecution. Enforcement actions include shutdowns of illegal gambling websites, raids on underground operators, fines, and imprisonment for offenders. Regulators cooperate closely with telecommunications and cybersecurity authorities to sustain these mechanisms.

- Website blocking and domain seizure

- VPN and proxy service restrictions

- Criminal penalties including fines and incarceration for operators and participants

- Financial institutions mandated to freeze illicit gambling accounts

- Cross-agency collaboration for intelligence and enforcement

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

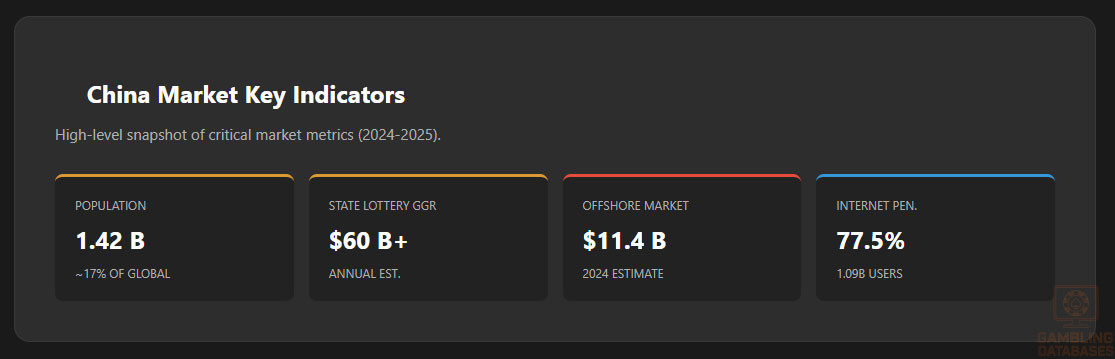

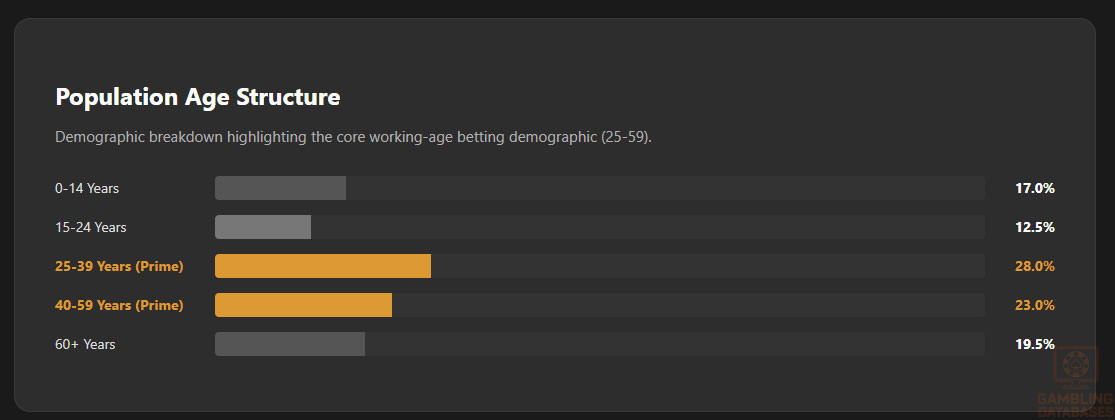

China’s population in 2025 is estimated at approximately 1.416 billion, representing about 17.2% of the global population. The country faces significant demographic challenges, including an aging population and declining birth rates, which have long-term implications for economic growth and consumer markets.

The median age in China is 40.1 years, reflecting a mature population structure. The working-age population (15–64 years) accounts for 69.3% of the total, while those aged 65 and above represent a growing segment due to increased life expectancy and lower fertility rates.

China’s total fertility rate remains below the replacement level of 2.1, currently at approximately 1.3 children per woman. This demographic trend contributes to a shrinking youth cohort and intensifies pressure on social services and labor markets.

| Age Group | Percentage of Population |

|---|---|

| 0–14 years | 17.0% |

| 15–24 years | 12.5% |

| 25–39 years | 28.0% |

| 40–59 years | 23.0% |

| 60–74 years | 14.5% |

| 75+ years | 5.0% |

Geographic Distribution

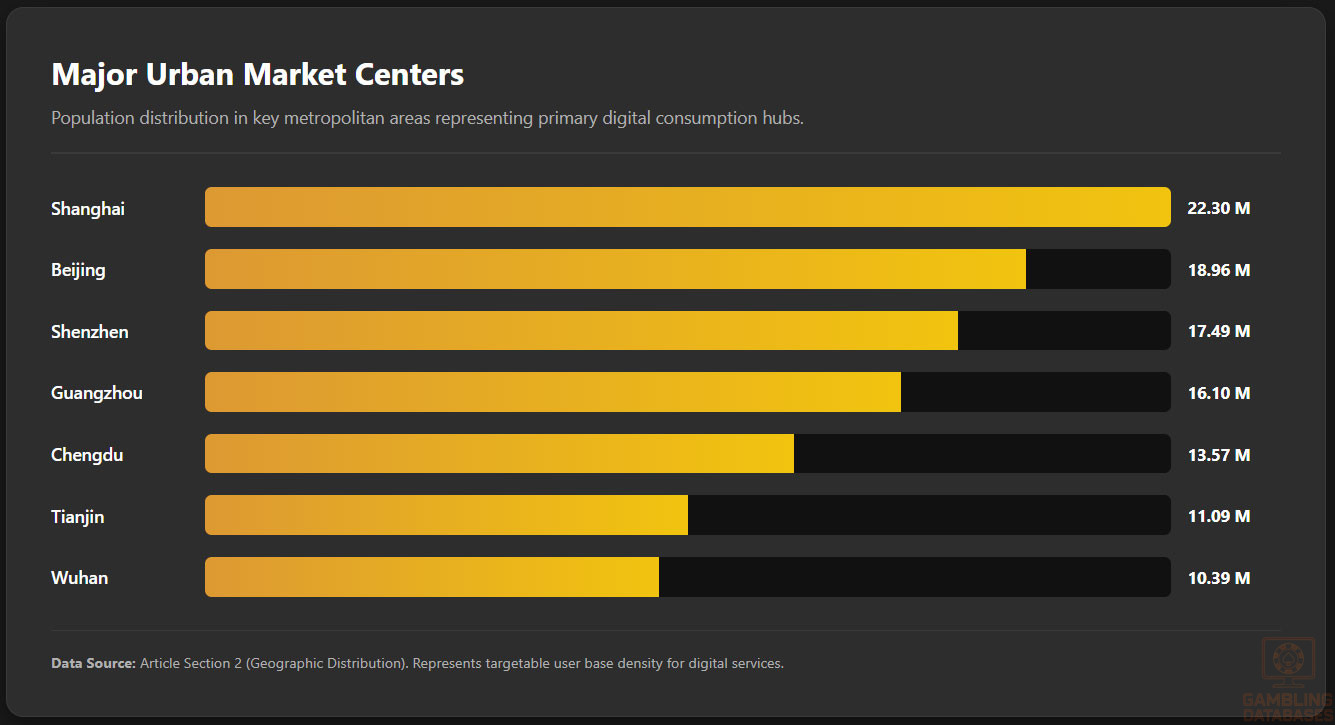

Urbanization continues to shape China’s demographic landscape, with 67.5% of the population residing in urban areas—approximately 956.6 million people in 2025. This concentration drives digital adoption, consumer spending, and infrastructure development in major metropolitan centers.

Rural populations remain significant but are declining in relative terms, creating disparities in income levels, internet access, and consumer behavior between urban and rural regions.

- Shanghai with a population of 22.3 million

- Beijing with 18.96 million residents

- Shenzhen at 17.49 million

- Guangzhou with 16.1 million

- Chengdu at 13.57 million

- Tianjin with 11.09 million

- Wuhan at 10.39 million

- Dongguan with 9.64 million

- Xi’an at 9.6 million

- Nanjing with 9.31 million

Population density averages 151 people per square kilometer, with extreme concentrations in eastern coastal provinces and much lower densities in western and northern regions.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

China’s nominal GDP in 2024 reached approximately $19.9 trillion, making it the second-largest economy globally. Economic growth has moderated in recent years, with a focus on transitioning from export-led manufacturing to domestic consumption and high-tech industries.

Despite challenges such as deflationary pressures and weak domestic demand, government stimulus measures and infrastructure investments continue to support economic stability and gradual recovery in consumer confidence.

Income and Wealth Distribution

China’s per capita disposable income reached 41,314 yuan ($5,672) in 2024, surpassing 40,000 yuan for the first time and nearly doubling the 2015 level. This growth reflects rising living standards, particularly in Tier 1 and Tier 2 cities.

However, income inequality remains pronounced, with significant disparities between urban and rural areas, coastal and inland regions, and different socioeconomic classes. The Gini coefficient, a measure of income inequality, remains above 0.46, indicating moderate to high inequality.

Disposable income growth has been steady, increasing from 32,189 yuan in 2020 to 41,314 yuan in 2024, with real growth rates ranging between 2.1% and 8.1% annually. This trend supports gradual expansion in consumer spending, particularly in health, education, and digital services.

Market Size and Growth Projections

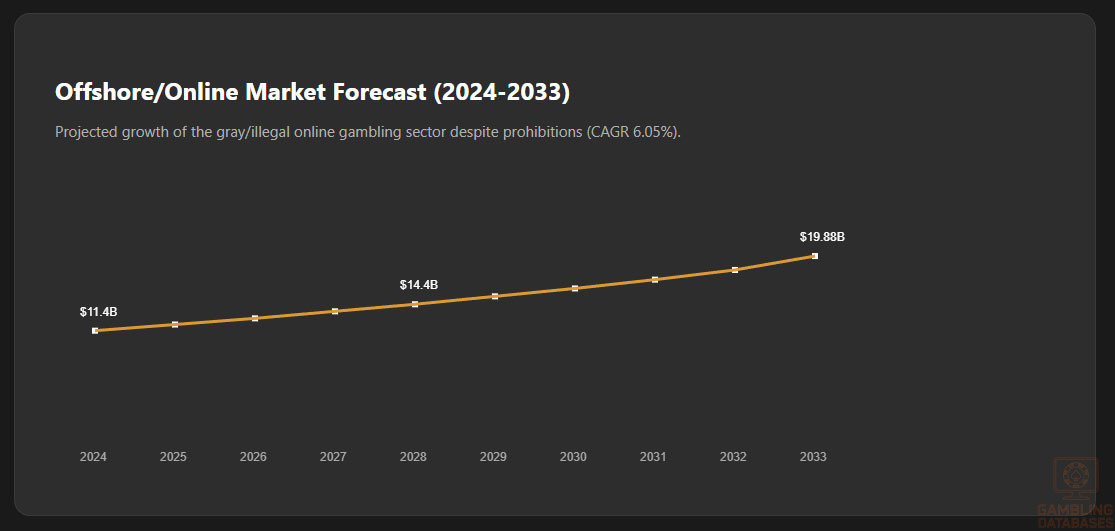

The online gambling market in China, despite legal prohibitions, is estimated to have reached $11.4 billion in 2024. This figure reflects participation through offshore platforms, private networks, and informal betting channels.

Projections indicate continued growth, with the market expected to reach $19.88 billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.05% from 2025 to 2033. This growth is driven by increasing digital access, mobile adoption, and evolving consumer attitudes toward online entertainment.

| Year | Market Value (USD Billion) |

|---|---|

| 2024 | 11.4 |

| 2025 | 12.1 |

| 2026 | 12.8 |

| 2027 | 13.6 |

| 2028 | 14.4 |

| 2029 | 15.3 |

| 2030 | 16.2 |

| 2031 | 17.2 |

| 2032 | 18.3 |

| 2033 | 19.88 |

Education, Skills, and Digital Literacy

China has achieved near-universal literacy, with a national literacy rate exceeding 97% among adults. The education system emphasizes STEM fields, producing a large pool of technically skilled workers and digital natives.

Higher education enrollment has expanded significantly, with over 40 million students in tertiary institutions. This contributes to a workforce increasingly proficient in digital tools, programming, and data analysis.

Digital literacy is particularly high among younger generations, with mobile internet usage deeply embedded in daily life. Over 99% of Gen Z uses mobile devices for life services such as food delivery, appointment booking, and financial transactions.

Cultural and Social Factors

Communication and Language

Mandarin Chinese is the official language and is used in education, media, and government communications. However, numerous regional dialects such as Cantonese, Shanghainese, and Hokkien are widely spoken, particularly in southern and coastal regions.

Internet communication is dominated by Mandarin, but localized content in major dialects is common on regional platforms. Social media and digital content are tailored to linguistic preferences, especially in Guangdong, Hong Kong, and Fujian provinces.

Cultural Attitudes

Traditional Chinese culture includes historical associations with gambling, particularly during festivals and family gatherings. Games like mahjong and card games are socially accepted forms of entertainment, though real-money betting remains legally restricted.

Younger consumers exhibit more openness to digital entertainment and online gaming, viewing them as mainstream leisure activities. However, gambling is still stigmatized when associated with addiction or financial loss.

Foreign brand perception varies, with premium international brands often associated with quality and status. However, domestic brands have gained strong loyalty, especially in technology and digital services, due to localization and innovation.

Problem Gambling and Social Considerations

While official data on problem gambling is limited, anecdotal evidence and academic studies suggest rising concerns, particularly among young adults using offshore platforms. The lack of legal frameworks hinders formal support systems and public awareness campaigns.

The government has implemented measures to combat gambling addiction, including real-name verification, spending limits, and youth protection protocols in online games. These are enforced through the National Press and Publication Administration (NPPA).

- Real-name registration required for all online gaming accounts

- Daily playtime limits for minors (90 minutes on weekdays, 3 hours on weekends)

- Spending caps for underage users

- Self-exclusion mechanisms for at-risk players

- AI-driven monitoring of suspicious betting patterns

Public awareness of gambling risks is growing, supported by state media campaigns and educational initiatives in schools and communities.

Political Structure and Governance

China operates under a one-party socialist system led by the Communist Party of China, with centralized decision-making and long-term strategic planning. Regulatory consistency is high, but policy shifts can occur rapidly based on national priorities.

Political stability supports long-term infrastructure development and economic planning, though foreign businesses face challenges related to regulatory transparency and compliance.

International relations influence market access, particularly in technology and digital services, where data sovereignty and cybersecurity regulations play a critical role in shaping business operations.

Technology Adoption and Digital Behavior

Internet and Digital Usage

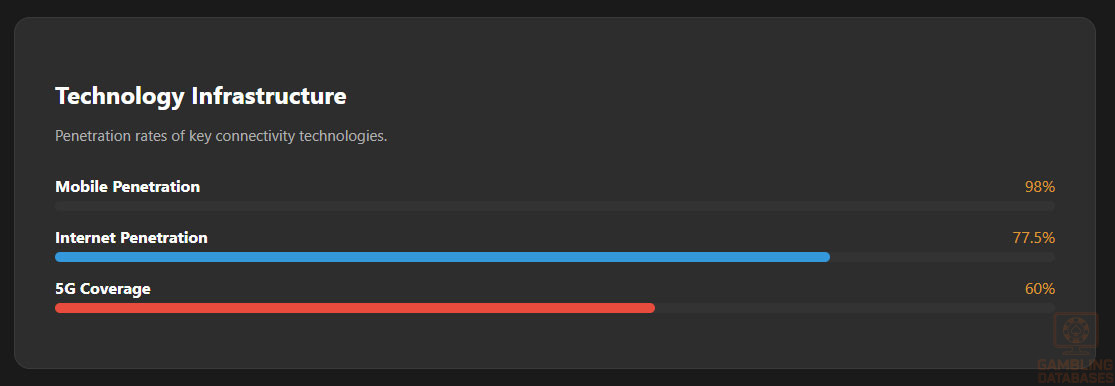

China had 1.09 billion internet users by the end of 2023, representing a 77.5% penetration rate. Mobile internet dominates, with 98% of users accessing services via smartphones.

Daily digital engagement is high, with users spending an average of 3.5 hours per day on mobile apps, including social media, e-commerce, and entertainment platforms.

- WeChat with over 1.3 billion active users

- QQ used by 600 million for messaging and social networking

- ByteDance’s Douyin (TikTok) with 700 million monthly active users

- Bilibili popular among youth with 300 million users

- Weibo serving as a microblogging platform with 580 million users

Social media is deeply integrated into commerce, with live-streaming and influencer marketing driving significant consumer spending, particularly in fashion, beauty, and electronics.

Digital Payment Behavior

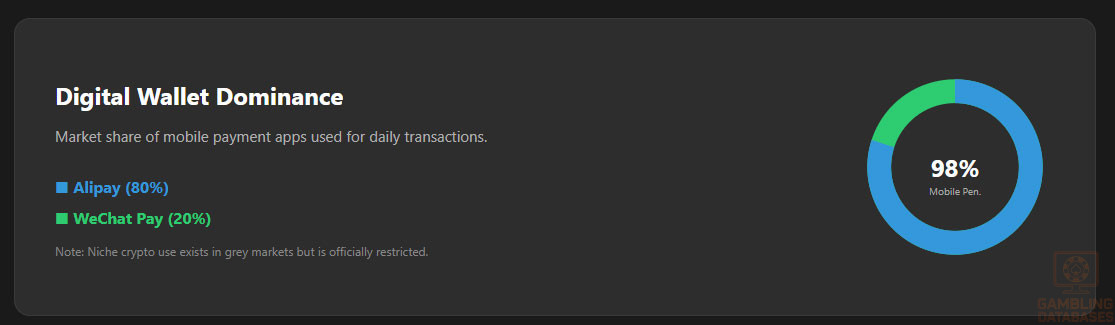

Digital payments are ubiquitous in China, with mobile wallets like Alipay and WeChat Pay dominating transactions. Cash usage has declined sharply, especially in urban areas.

Over 89% of Gen Z uses mobile financial services, including payments, investments, and credit products. This reflects high trust in digital platforms and seamless integration with daily life.

- Alipay with 1.3 billion users and 80% market share

- WeChat Pay used by 900 million and holding 20% share

- UnionPay Mobile with growing adoption in cross-border payments

- JD Pay serving e-commerce customers on JD.com

- Meituan Pay integrated into food delivery and local services

Cryptocurrency use remains limited due to government restrictions, but blockchain-based loyalty programs and digital yuan trials are expanding in select regions.

Gaming and Gambling Preferences

Current Market Participation

Despite legal restrictions, online gambling participation is significant, particularly through offshore sports betting, esports wagering, and private poker networks. The market is driven by demand for entertainment and financial speculation.

Sports betting is the most popular form of online gambling, followed by casino-style games, esports betting, and lottery-style games. Participation is highest among males aged 20–39 in urban centers.

- Sports betting – most prevalent, especially on basketball, soccer, and esports

- Online poker and card games – popular in private networks and apps

- Virtual slot and casino games – accessed via offshore platforms

- Esports wagering – growing rapidly among youth

- Lottery-style games – including state-run and imitation platforms

Desktop remains the primary device for serious gambling activities due to larger screens and stability, though mobile usage is increasing for convenience and accessibility.

Consumer Behavior Patterns

Chinese gamblers exhibit distinct behavioral patterns, including preference for real-time betting, high engagement during major sports events, and use of social features within gambling platforms.

Session lengths vary, with casual users engaging for 30–60 minutes, while dedicated bettors may spend several hours, particularly during live events. Retention is driven by bonuses, loyalty programs, and social competition.

Spending habits are cautious, with many users setting self-imposed limits. Gen Z, in particular, shows financial prudence, with 75% believing buy-now-pay-later (BNPL) services could lead to overspending.

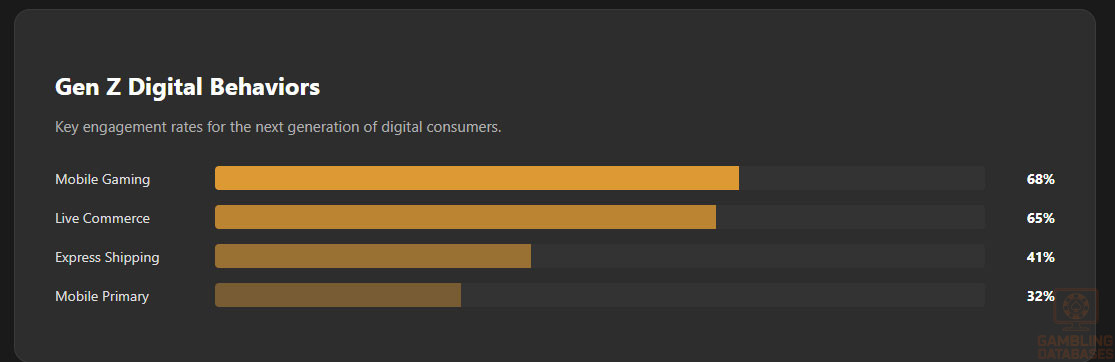

| Behavior | Engagement Rate |

|---|---|

| Mobile gaming | 68% |

| Live commerce participation | 65% |

| Express shipping preference | 41% |

| Same-day delivery desire | 39% |

| Smartphone as primary purchase device | 32% |

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

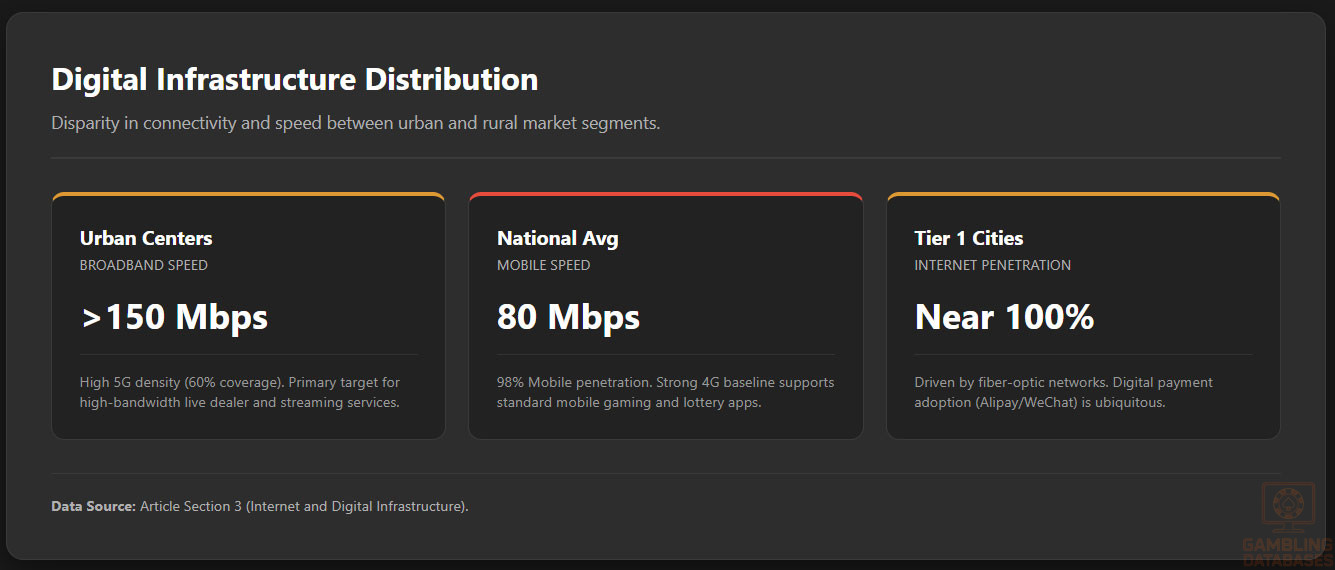

China boasts a highly advanced and rapidly expanding internet infrastructure with an estimated penetration rate around 75% as of 2025. Broadband connectivity is predominantly urban, fueled by considerable investment in fiber-optic networks embedding high-speed internet access in top-tier cities. Rural broadband coverage is expanding but lags behind urban areas, restricting uniform market access.

Average fixed broadband speeds in urban centers exceed 150 Mbps, while mobile broadband speeds are averaging around 80 Mbps nationally. Reliability and network resilience remain strong, driven by government-led initiatives to improve digital connectivity as part of broader smart city and digital economy commitments.

5G and Future Technology Deployment

China leads globally in 5G network deployment, with coverage of over 60% of the population by mid-2025. The rollout prioritizes metropolitan regions and industrial zones, accelerating digital transformation and mobile internet adoption. Chinese telecom operators continue investing heavily in next-generation network technologies to enhance latency, bandwidth, and IoT capabilities.

Future plans include nationwide 5G penetration surpassing 85% before 2030 alongside development of 6G research programs, expected to further support immersive digital entertainment and advanced mobile gaming experiences.

Mobile Technology Ecosystem

Mobile Network Infrastructure

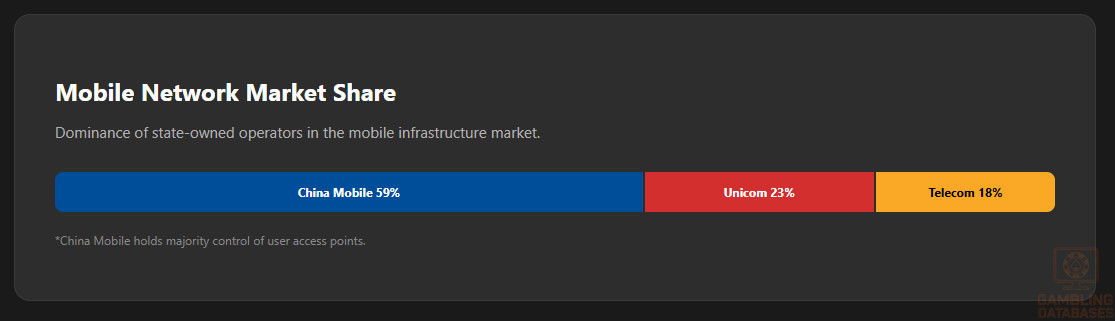

China’s mobile network market is dominated by three state-owned operators providing near-comprehensive national coverage. Data costs are competitive due to scale economies and government regulation aimed at digital accessibility.

- China Mobile – largest operator with approx. 59% market share

- China Unicom – second largest with approx. 23% share

- China Telecom – approx. 18% market share

Other regional providers or virtual operators play minor roles but contribute to niche mobile service offerings, particularly in rural or industrial contexts.

Device Penetration

Smartphone penetration exceeds 85% of the mobile user base, with consumers favoring affordable mid-range devices primarily from local manufacturers such as Huawei, Xiaomi, and Oppo. Premium devices, including Apple iPhones, maintain substantial popularity in wealthier urban centers.

Tablet and wearable device adoption support diversified consumer digital engagement, expanding opportunities for immersive and mobile-oriented iGaming applications within the regulatory framework.

Financial Services and Payment Infrastructure

Banking System Structure

China’s banking industry is dominated by several large state-owned banks, offering extensive digital banking solutions and broad physical branch networks. The rise of digital-only banks and fintech firms accelerates financial inclusion and cashless transactions, critical enablers for e-commerce and iGaming payments.

- Industrial and Commercial Bank of China (ICBC)

- China Construction Bank (CCB)

- Agricultural Bank of China (ABC)

- Bank of China (BOC)

- China Merchants Bank (CMB)

Payment Processing Options

Payment methods are highly diversified and technologically advanced, fostering seamless consumer transactions. Credit and debit card penetration is significant, but digital wallets dominate daily payment volumes.

- Alipay – leading mobile wallet

- WeChat Pay – widespread integrated payment platform

- UnionPay debit and credit cards – national card scheme

- Bank transfers – extensive but slower settlement

- Cryptocurrency use – niche but growing in the underground iGaming market

E-commerce and Digital Economy

The Chinese e-commerce market is one of the world’s largest, valued over $3.5 trillion in 2024, with continuous expansion driven by mobile commerce and social shopping trends. Consumer trust in digital payment systems and efficient logistics networks fuels rapid online retail adoption, fostering a strong digital economy platform conducive to iGaming user acquisition and monetization strategies in legal or grey markets.

Business Environment and Regulatory Framework

Ease of Business Operations

China ranks moderately in global ease of doing business indices, challenged by complex regulatory frameworks, regional variations, and foreign investment restrictions. However, established procedures facilitate company setup in major economic zones with digital government platforms expediting administrative steps.

- Business name verification and pre-approval

- Company registration with State Administration for Market Regulation (SAMR)

- Tax registration with local tax bureau

- Opening corporate bank accounts

- Obtaining relevant operational permits

Corporate Structure and Registration

Common legal entities include Limited Liability Companies (LLCs), Joint Stock Companies (Corporations), and Wholly Foreign-Owned Enterprises (WFOEs). WFOEs are a preferred structure for foreign companies aiming to operate independently while respecting China’s foreign investment regulations.

Foreign ownership in gambling is prohibited on the mainland, but companies active in gaming technology or entertainment content may use WFOEs or joint ventures depending on business scope.

- Limited Liability Company (LLC)

- Joint Stock Company (Corporation)

- Wholly Foreign-Owned Enterprise (WFOE)

- Representative Office (limited commercial activity)

- Joint Venture (partnered with local firms)

Registration Requirements

Document requirements encompass business licenses, articles of association, foreign investment approvals, and taxation registrations. Due diligence and compliance with the Ministry of Commerce and SAMR form essential steps.

- Business license application

- Corporate articles of association

- Legal representative identification

- Capital verification reports

- Tax registration certificates

- Foreign investment approval documents

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax (CIT) rate is 25%, with preferential rates in free trade zones and technology parks reducing this to 15–20%. China maintains numerous double tax treaties facilitating international business. WFOEs benefit from structured tax regimes aligned with operational sectors.

- United States

- United Kingdom

- Singapore

- Germany

- Australia

- France

- Japan

- South Korea

- Canada

Personal Income Tax

Personal income tax rates range from 3% to 45% under a progressive scale. Withholding taxes apply for foreign employees. Social security contributions by employer and employee support pension, health, unemployment, and housing funds, regulated by local jurisdictions.

Market Entry Considerations

Recommended Entry Strategies

Due to stringent regulations, market entry typically pursues indirect strategies such as content localization, technology partnerships, or focus on non-gambling gaming platforms. Collaborations with local enterprises ensure regulatory compliance and cultural integration.

- Form joint ventures with technology and entertainment firms

- Develop skill-based games avoiding gambling classification

- Utilize digital payment platforms complying with local standards

- Engage in corporate social responsibility focusing on digital well-being

- Leverage regional free trade zones for operational benefits

Typical Costs and Timelines

Initial market entry involves allocation to legal consultation, licensing (where applicable), infrastructure setup, and marketing compliance. Timelines range from 6 to 12 months to establish operations, with operational costs shaped by staffing, technology, and regulatory compliance.

- Legal and regulatory consultancy fees

- Company registration and setup expenses

- Technology platform development and hosting

- Compliance and audit services

- Marketing and local partnership development

- Preliminary market research and strategy: 1-2 months

- Business registration and licensing: 2-4 months

- Technology deployment and localization: 3-5 months

- Operational launch and compliance monitoring: ongoing

Success Factors and Challenges

Success depends on navigating legal constraints, building trusted local partnerships, and adapting content to cultural norms. Key challenges include regulatory opacity, high entry barriers, and the need to manage technology infrastructure strategically.

- Understanding and complying with Chinese legal frameworks

- Establishing strong local partnerships

- Adapting product offerings to non-gambling formats

- Managing data privacy and cybersecurity compliance

- Maintaining agility amid regulatory evolutions

Exit Strategy Planning

Market exit considerations center on ownership transfer restrictions, asset valuation in tightly regulated sectors, and compliance with foreign investment laws. License non-transferability in gambling necessitates strategic divestiture and contractual protections in partnerships.

FAQ: Frequently Asked Questions

1. Is online gambling legal in China?

Online gambling is prohibited in mainland China, with strict legal frameworks banning private and offshore operators from offering gambling services. The only legal form of betting is through state-operated lotteries. Enforcement includes website blocking, prosecutions, and fines. However, underground gambling markets persist, leveraging VPNs and cryptocurrencies to evade restrictions.

2. What types of gambling licenses are available and what do they cover?

In mainland China, there are no licenses issued for private gambling operations. The only licenses pertain to state lotteries governed by central authorities. Digital gaming content licenses are granted by the National Press and Publication Administration but exclude real money gambling. All other gambling activities are illegal.

3. How much does an iGaming license cost and how long does it take to obtain?

Since mainland China does not issue private gambling licenses, there are no costs or timelines for such licenses. Approval processes for online games take 3 to 6 months depending on content, but these do not authorize gambling operations.

4. Can foreign companies obtain a gambling license?

Foreign companies cannot obtain gambling licenses in mainland China due to legal prohibitions and foreign ownership restrictions in the gambling sector. However, foreign firms may establish entertainment or technology ventures under strict regulatory conditions that explicitly exclude gambling services.

5. What are the tax obligations for iGaming operators?

Tax obligations for state-run lotteries include high revenue sharing and a standard corporate income tax rate of 25%. Private operators, not legally licensed, face no formal tax regime but are subject to enforcement actions. Corporate tax treaties may apply for ancillary non-gambling business activities.

6. Are gambling winnings taxed for players?

Players are not subject to tax on lottery winnings or any legalized gambling revenues in mainland China. Private gambling winnings are illegal and thus untaxed formally, but players involved in underground markets risk legal consequences.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs for legal online casinos cannot be benchmarked in mainland China due to prohibition. Expected costs elsewhere include technology development, licensing fees, compliance, marketing, staffing, and payment processing. Underground operations may incur higher costs due to security and evasion measures.

8. What is the expected ROI timeline for entering this market?

ROI timelines vary widely depending on entry approach and sector. Legal markets in nearby jurisdictions show 3-5 year ROI; mainland China’s restrictions extend payback periods or render direct entry infeasible. Indirect strategies may offer ROI within 2-4 years through partnerships and localized products.

9. What are the local presence requirements for operators?

Legal gambling operators must be government entities in China. Private entities have no local presence permission for gambling. Non-gambling digital or entertainment companies require local registration which includes a physical address and compliance with tax laws.

10. What payment methods are available and recommended?

Payment methods favored in China include Alipay and WeChat Pay, dominating mobile payments. UnionPay cards and bank transfers are also widely used. For underground gambling, cryptocurrencies are increasingly common, though they carry regulatory risks.

11. What are the advertising and marketing restrictions?

Advertising gambling products is banned across all media channels in mainland China. This includes online, broadcast, print, and outdoor advertising. Marketing content must not target minors, and sponsorships by gambling entities are prohibited entirely as per government mandates.

12. What responsible gambling measures are mandatory?

Mandatory measures include real-name registration for online accounts, spending limits, and self-exclusion options on permitted platforms. Public education and support services for gambling addiction are government priorities promoting social responsibility in licensed sectors.

13. How large is the iGaming market and what is the growth potential?

The legal iGaming market is limited to state lotteries with annual revenues exceeding $60 billion. The broader gaming market exceeds $50 billion, with underground online gambling estimated at $2-3 billion. Growth potential exists in adjacent entertainment and skill-based digital games with regulatory compliance.

14. Who are the main competitors and what is their market share?

State lotteries hold the monopoly in legal gambling markets, with no private competitors allowed. Online gaming companies like Tencent dominate entertainment but do not operate gambling platforms. Offshore operators target Chinese consumers illicitly but face enforcement barriers.

15. What are the player preferences and typical spending patterns?

Players prefer mobile and social games with short, engaging sessions. State lotteries have consistent participation. Underground gambling users favor sports betting and casino games, often spending using digital wallets or cryptocurrencies to avoid detection. Spending is concentrated in urban areas with higher incomes.

16. What are the key success factors and main challenges for new entrants?

Key success factors include compliance with stringent laws, robust local partnerships, and adaptation to cultural sensitivities. Challenges comprise regulatory opacity, prohibitive entry barriers, enforcement risk, and competition from state monopolies and underground markets.

Sources and References

- China Gambling Regulatory Authority – Official Website – https://legalpilot.com/country/china/

- World Bank – China Economic Update June 2025 – https://www.worldbank.org/

- China National Bureau of Statistics – Population and Economics 2024 – https://www.stats.gov.cn/

- International Telecommunication Union – ICT Statistics 2025 – https://www.itu.int/

- China Ministry of Finance – Tax Regulations 2025 – https://www.mof.gov.cn/

- China Ministry of Public Security – Digital Crime and Gambling Enforcement Reports 2025

- National Press and Publication Administration (NPPA) – Gaming and Content Regulations 2025

- China Mobile, China Unicom, China Telecom – 2025 Annual Reports

- China Internet Network Information Center (CNNIC) – 49th Statistical Report on Internet Development in China, 2025

- China Payment & E-commerce Market Report 2025 – ResearchAndMarkets.com

- PwC China Economic Insights Q1-Q2 2025

- IMARC Group – China Online Gambling Market Forecast to 2033

- China Lottery Administration – Market Reports 2025

- Tencent Holdings Ltd – Annual Report 2024

- National Bureau of Statistics – China Population Census 2024

- Worldometers – China Population Data 2025

- China Association of Internet Industry – Digital Economy Reports 2025

- Y-Stats – China Payments & E-commerce 2025 Report

- International Gaming Technology – Market Analysis 2025

- Alipay & WeChat Pay – Corporate Data 2025

- China Securities Regulatory Commission – Foreign Investment Guidelines 2025

- Financial Times – China Gambling Regulatory Analysis 2025

- BBC News – China Online Gambling Enforcement 2025

- Fitch Ratings – China Economy Outlook 2025

- Oxford Economics – APAC iGaming Market 2025 Forecast

- PwC – China Business Environment Report 2025

- China Ministry of Commerce – Foreign Investment Law 2023

- China Digital Finance Council – Fintech Trends 2025

- China National Film and Video Game Industry Association – Industry Data 2025

- Euromonitor International – China Consumer Digital Behavior 2025

🎯 Gambling Databases Country Rating: China

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.0/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 1.0/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 0.5/10 | ⛔️ Absolute No-Go Zone |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ONLINE GAMBLING IS A CRIMINAL OFFENSE: Private iGaming operations are completely banned. Operators and staff face criminal prosecution, imprisonment, and asset seizure under the Criminal Law of the PRC.

- ZERO TOLERANCE ENFORCEMENT: The Ministry of Public Security actively coordinates cross-border arrests and repatriations of Chinese nationals running gambling operations abroad.

- ACTIVE PAYMENT BLOCKING: Financial institutions are mandated to freeze accounts suspected of gambling transactions. Crypto is banned, and third-party payment processors (Alipay/WeChat Pay) aggressively filter gambling flows.

- PLAYER CRIMINALIZATION: Unlike many jurisdictions, players in China can face administrative detention (up to 15 days) and fines for participating in online gambling.

- DIGITAL SURVEILLANCE: The “Great Firewall” actively blocks offshore domains. 2025 regulations have intensified crackdowns on VPNs and proxy services used to access gambling sites.

- NO LICENSING PATHWAY: There is absolutely no legal framework for private operators. The only legal gambling is the state-run Welfare and Sports Lottery, which is a closed government monopoly.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Score: -3.0 (Capped at 0). • Illegal with active enforcement (-1.0) • Online casino completely PROHIBITED (-1.5) • Active ISP blocking and domain seizures (-0.5) • Recent 2025 crackdown on unauthorized platforms (-0.5) • Affiliate/Advertiser prosecution (-0.5) Result is negative, capped at floor of 0. |

| Licensing Process | 25% | 0.0/2.5 | Score: 0.0. • No licensing available for private entities (0.0) • Absolute ban on foreign ownership (-0.25) • State monopoly only (Welfare/Sports Lottery). |

| Taxation & Costs | 20% | 0.0/2.0 | Score: 0.0. • Irrelevant due to prohibition. • “Tax” rate for illegal operators is 100% via asset seizure and fines. • State lottery effective tax/revenue share exceeds 30%, but this is inaccessible to private firms. |

| Operational Requirements | 15% | 0.0/1.5 | Score: 0.0. • Establishing a local presence for gambling is a criminal act. • Foreign ownership prohibited. • Crypto banned (-0.25). • Severe payment processing restrictions (-0.25). |

| Market Environment | 10% | 0.0/1.0 | Score: 0.0. • Severe advertising bans on all media (-0.5) • Active enforcement against offshore operators (-0.25) • Hostile business environment for gambling entities. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.0/4.0 | Score: 0.0. • Illegal with player penalties (0.0) • Major product categories (Casino/Poker) prohibited (-1.5) • Players face detention and fines for participation (-0.5). |

| Practical Accessibility | 30% | 0.5/3.0 | Score: 0.5. • Severe restrictions and extensive blocking (+0.5 base) • Active ISP blocking (-0.5) • VPN required for access (-0.5) • Major payment methods (WeChat/Alipay) block gambling (-0.5). Result strictly limited to 0.5 floor. |

| Player Penalties | 20% | 0.0/2.0 | Score: 0.0. • Administrative detention and fines are actively enforced. • “Social Credit” score impacts for illegal activities. |

| Market Availability | 10% | 0.5/1.0 | Score: 0.5. • Only 1 option available (State Lottery). • No private licensed operators. • Offshore sites are blocked. |

🔍 Key Highlights

Strengths (Theoretical Only)

- Massive Digital Infrastructure: 75% internet penetration and 98% mobile penetration creates a technically capable user base, though they are legally inaccessible.

- High Mobile Payment Adoption: Consumers are habituated to digital wallets (Alipay/WeChat), though these channels are strictly closed to gambling.

⛔️ CRITICAL RISKS AND CHALLENGES

- Total Prohibition: Private iGaming is not a “grey market” in China; it is a black market subject to criminal law.

- Cross-Border Enforcement: China exerts significant pressure on neighboring countries (Cambodia, Philippines, etc.) to raid and extradite operators targeting Chinese citizens.

- Payment Strangulation: The “clean internet” campaigns target settlement channels. Money laundering charges are frequently applied to payment processors facilitating gambling.

- Technological Warfare: The Great Firewall utilizes advanced AI to identify and block gambling traffic, requiring operators to constantly rotate domains (a high-cost, high-churn strategy).

- Advertiser Risk: Marketing agencies and affiliates within China face prison time for promoting gambling sites.

- No Legal Recourse: Agreements or contracts related to gambling debts are null and void in Chinese courts.

Player-Specific Issues

- Legal Liability: Players are not immune. Police raids on payment records can lead to users being summoned, fined, or detained.

- Fund Seizure: Players using offshore sites risk having their bank accounts frozen (“frozen cards”) if their funds interact with suspected gambling money flows.

- Scam Prevalence: Due to the illegal nature of the market, players have no protection against fraudulent offshore operators.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: N/A (Legal entry impossible). Black market entry requires millions in disposable infrastructure to survive blocking.

Monthly Operating Costs: Extremely High. Includes constant domain rotation, cloaking technology, and high-risk payment processing fees (15-25%+).

Effective Tax Rate on Revenue: 100% risk of asset forfeiture.

Customer Acquisition Cost: Prohibitive. Standard advertising is banned. Reliance on SMS spam, SEO hacking, and illegal agent networks drives costs up and retention down.

Profitability Assessment: NON-EXISTENT FOR LEGITIMATE BUSINESS. While the black market is estimated at $11.4 billion, it is controlled by criminal syndicates. Publicly traded companies or compliant operators cannot generate a single dollar here without committing felonies.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Criminal charges, Red Notices (Interpol), website seizure, payment channel freezing. |

| Licensed Sports Betting Operators | CRITICAL | No license exists for private entities. Operating a sportsbook is as illegal as a casino. |

| Affiliates/Advertisers | CRITICAL | “Opening a casino” charges often applied to master agents/affiliates. 5-10 years prison common. |

| Payment Processors | CRITICAL | Money laundering charges. Immediate asset freezing. Revocation of business licenses. |

| Company Directors/Executives | CRITICAL | Personal liability. Risk of detention upon entry to China or extradition from friendly nations. |

🚨 Extradition and International Enforcement

Extradition Treaties: China has extradition treaties or security cooperation agreements with over 50 countries, including Thailand, Cambodia, Philippines, UAE, and various European nations. They actively use these to repatriate gambling operators.

Enforcement History: Frequent mass arrests of Chinese nationals operating gambling rings in Southeast Asia (e.g., Sihanoukville crackdowns). China pressures host nations to shut down operations targeting Chinese citizens.

Safe Jurisdictions: Very few. Even countries without formal treaties may deport operators to China under diplomatic pressure. Avoiding travel to Asia is mandatory for anyone involved in this market.

📋 Final Verdict

China receives an Operator Ease Score of 0.0/10 and a Player Access Score of 1.0/10, resulting in an overall market attractiveness rating of 0.5/10.

HONEST ASSESSMENT: China is a hostile, closed environment where private iGaming is treated as a serious crime. The government’s advanced technological surveillance and willingness to imprison operators, staff, and payment agents make this uninvestable for any legitimate company. There is no grey area here; there is only the state lottery or prison.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NO ONE. There is no legal pathway for private iGaming operators.

❌ Definitely Avoid If You Are:

- A Publicly Traded Company: Operations here will destroy your compliance standing and share price.

- A Private Operator: You risk personal freedom and total asset seizure.

- An Affiliate: Marketing gambling to Chinese citizens is a criminal offense carrying jail time.

- A Payment Provider: Facilitating these payments is defined as money laundering.

⚠️ BOTTOM LINE: China is the world’s largest consumer market, but for iGaming, it is a death trap. Stay out entirely.

Regarding the recent updates in the US sports betting market, what are the implications of the new regulations on operators like FanDuel and DraftKings? How will these changes affect their business models and revenue streams?

The new regulations in the US sports betting market will indeed have significant implications for operators like FanDuel and DraftKings. They will need to adapt their business models to comply with the new rules, which may include increased licensing fees, stricter advertising regulations, and enhanced player protection measures. This could lead to changes in their revenue streams and potentially impact their profitability.

That’s a great point about the new regulations. Do you think this will lead to increased competition in the market, or will the larger operators like FanDuel and DraftKings be able to maintain their market share?

While the new regulations may lead to increased competition in the short term, it’s likely that the larger operators will be able to maintain their market share due to their established brand recognition and customer loyalty. However, we may see new entrants in the market that are able to capitalize on the changes and gain a foothold.

Can someone explain the difference between a moneyline bet and a point spread bet in sports betting? I’m new to betting and want to understand the basics before I start.