The Republic of Congo presents emerging opportunities in the iGaming sector, driven by recent regulatory reforms aiming to formalize gambling activities. Despite challenges in regulatory clarity and enforcement, the market offers prospects for operators targeting both land-based and online betting segments.

The regulatory environment is undergoing transformation with new laws enacted in late 2024 to structure licensing, taxation, and operational conditions. This analysis provides a detailed assessment of Congo’s gambling legal framework, key market indicators, compliance obligations, and operator requirements.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal with formal licensing since 2024 |

| Regulatory Framework | Law No. 37-2024 enacted December 2024 |

| Regulatory Authority | Ministry responsible for gambling (Ministry of Budget and Public Portfolio) |

| Population | ~5.5 million (2025 estimate) |

| Median Age | 19 years |

| GDP (Nominal) | $15.3 billion (2024 forecast) |

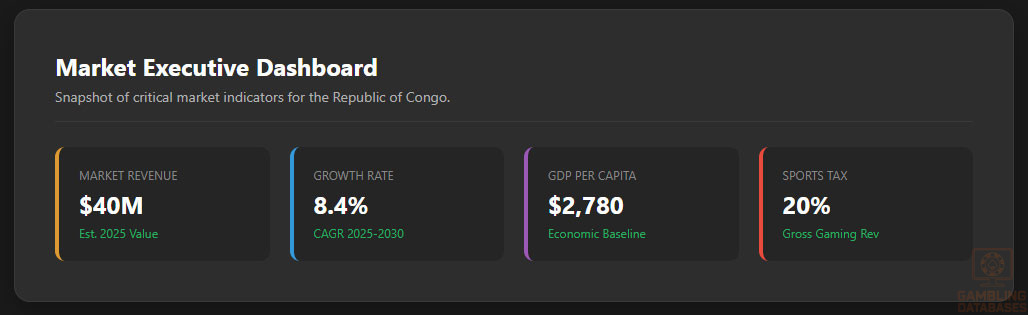

| GDP per Capita | Approximately $2,780 |

| Internet Penetration Rate | 48% |

| Mobile Penetration Rate | 75% |

| Licensed Operators | Estimated fewer than 10 formal licensees (land and online) |

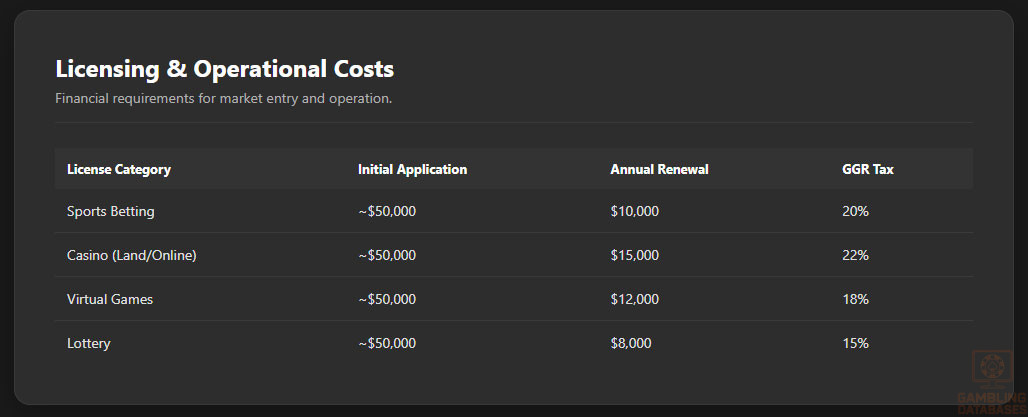

| License Fees | Variable; approx. $50,000+ initial application fee |

| License Duration | Unlimited with annual renewal |

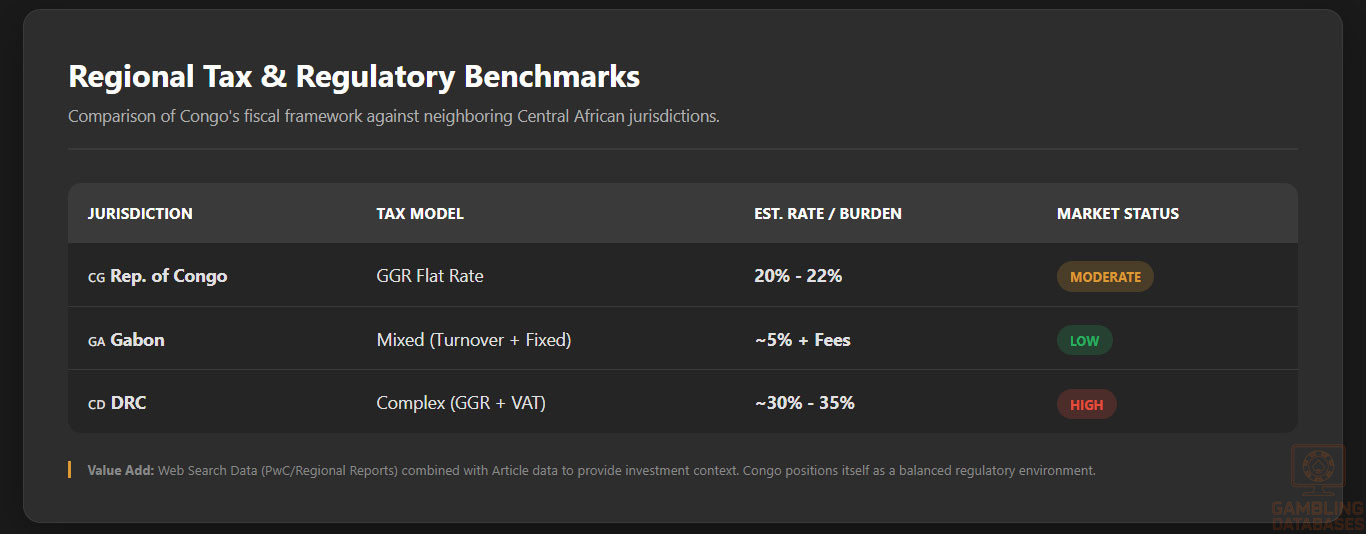

| Gross Gaming Revenue (GGR) Tax | Estimated 20% flat rate |

| Corporate Tax Rate | 30% |

| Market Entry Barriers | Regulatory uncertainty, overlapping authorities, technology gaps |

| License Application Timeline | 3-6 months typical |

| Responsible Gambling Measures | Mandatory self-exclusion, KYC, and AML compliance |

| Payment Methods Accepted | Mobile money, bank transfers, select e-wallets |

| Market Size (2025) | Estimated $40 million revenue |

| Projected CAGR (2025-2030) | 8.4% |

| Average Revenue Per User (ARPU) | Approximately $45 annually |

| Advertising Restrictions | Prohibitions on targeting minors, strict content controls |

| Enforcement Mechanisms | Fines, license suspension, revocation |

| Local Presence Requirement | Physical office or partner required for license |

| Foreign Ownership Restrictions | Allowed subject to local partnership or representation |

| Technical Integration | Mandatory real-time reporting to regulatory CRM under development |

| Market Penetration Rate | ~1.6% |

| Compliance Reporting | Quarterly audits and AML reports mandatory |

| Maximum Bet Limits | Set individually per license conditions |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

The Republic of Congo formalized its gambling regulatory environment with Law No. 37-2024, marking a pivotal step in governance over all gambling activities. This legislation encompasses land-based and online gaming, sports betting, lotteries, and virtual games, consolidating oversight under the ministry responsible for gambling. The regulatory framework assigns risk categories to gaming types and sets licensing, operational, and taxation conditions designed to enhance market transparency and consumer protection.

Land-based gambling currently includes casinos, sports betting outlets, and limited slot machine operations. Casinos are required to operate exclusively within designated areas such as luxury hotels or specific gaming venues, ensuring they are not proximate to sensitive locations such as hospitals, schools, or military installations, preserving public order and safety.

Physical sports betting venues must be publicly accessible and licensed separately, aligning with the ministry’s intent to support controlled expansion of betting premises. Slot machines and virtual gaming fall under stricter technological and operational controls to mitigate illicit activity risks inherent in digital gambling.

Online gambling is regulated under the same framework as physical operations, emphasizing parity in licensing conditions, responsible gambling obligations, and anti-money laundering compliance. Operators must secure licenses for online activities that correspond with categories defined by the law, including sportsbooks, virtual casinos, and online lotteries. Despite formal regulation, operational clarity is still evolving due to concurrent jurisdictional assertions by multiple ministries, which complicates the regulatory landscape.

Licensed Operators and Market Players

The landscape of licensed operators in Congo remains nascent, with under ten formally recognized entities operating across land-based and online segments. The market is characterized by a limited number of licensees due largely to regulatory uncertainties and infrastructural challenges. Established market players typically pursue partnerships with local entities to fulfill the physical presence requirements and to navigate complex compliance demands.

Competitive dynamics are influenced by the evolving law and technological modernization efforts, including government initiatives to introduce centralized CRM and monitoring platforms. Foreign entrants face barriers related to the fragmented licensing authorities and the requirement to maintain local operational ties, shaping cautious strategies focused on measured growth and compliance alignment.

Licensing Framework and Requirements

The Republic of Congo’s licensing system is administered through the ministry responsible for gambling, which oversees the issuance of licenses based on the new legal framework established in 2024. License applications demand proof of financial health, ethical business conduct, and technical capability to ensure safe and fair gaming operations.

The licensing process generally unfolds over a 3-6 month timeline, reflecting the administrative capacity and regulatory scrutiny involved. Operators are required to submit audited financial statements, technical platform certifications including RNG approval, background checks on executives, and business plans detailing compliance and market strategies.

Local Presence and Operational Requirements

To qualify for licensing, operators must establish a physical presence within Congo or align through local partnerships. This requirement supports state oversight and ensures accountability. Domains used by online operators must be registered under Congolese control, reinforcing jurisdictional authority over digital gaming platforms.

Personnel regulations mandate the employment of qualified local staff responsible for compliance functions such as KYC verification and responsible gambling enforcement. Foreign ownership is permitted but generally requires demonstration of substantive local involvement or partnership agreements with indigenous businesses to benefit from licenses.

Compliance Obligations and Monitoring

Player Protection and Identification

The regulatory framework enforces strict verification protocols including age checks and Know Your Customer (KYC) procedures to combat fraud and underage gambling. Operators must implement anti-money laundering (AML) safeguards consistent with national financial regulations. Responsible gambling requirements mandate systems for self-exclusion, deposit limits, and access to player activity information.

- Age verification to prevent underage participation

- Comprehensive KYC and customer due diligence

- AML compliance with reporting suspicious activities

- Responsible gambling tools including self-exclusion mechanisms

- Real-time player activity monitoring and alerts

Financial Monitoring and Reporting

Operators are required to submit detailed quarterly tax and compliance reports including gross gaming revenue figures, tax payments, and audit documentation. Payments and transactions must be traceable to ensure transparent revenue flows and adherence to anti-fraud policies.

- Compile quarterly financial and operational reports

- Submit reports to regulatory authority within prescribed deadlines

- Undergo independent audits as part of compliance verification

- Maintain records for at least five years for inspection

Taxation Structure and Financial Obligations

Player Taxation

Winning players are subject to withholding tax on gambling proceeds, with thresholds set to exempt minor wins and rates scaled progressively for larger amounts. This ensures players contribute fairly while encouraging participation within regulated limits.

Operator Taxation

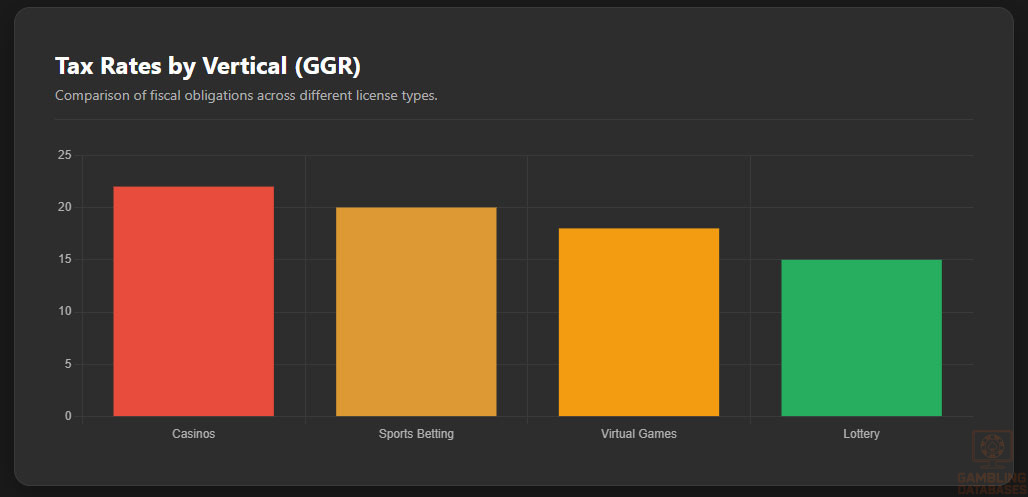

| Game Type | Gross Gaming Revenue (GGR) Tax | Corporate Tax | License Renewal Fee |

|---|---|---|---|

| Sports Betting | 20% | 30% | $10,000 annually |

| Casinos (Land & Online) | 22% | 30% | $15,000 annually |

| Lotteries and Scratch Cards | 15% | 30% | $8,000 annually |

| Virtual Games | 18% | 30% | $12,000 annually |

Turnover taxes and other fixed operational levies apply variably based on game category and license terms. These combined fiscal obligations form a significant cost component for market participants.

Gambling Market Financial Performance

The formal market’s revenue is estimated at around $40 million annually, with year-over-year growth driven by expanding internet access and mobile betting uptake. The government anticipates increased tax revenues as compliance improves with system modernization and growing formal participation.

Market distribution favors sports betting and lotteries, with casinos maintaining a smaller, emerging role primarily in major cities and luxury hospitality venues. The tax contribution from the sector is increasingly recognized as a vital source of public finance for social programs and infrastructure development.

Advertising and Marketing Restrictions

Advertising and promotional efforts by operators are strictly regulated to prevent targeting vulnerable populations, especially minors. Permitted channels include licensed media platforms and controlled digital advertising under regulatory review.

- Prohibition of gambling ads targeting minors

- Restrictions on content focusing on guaranteed winnings

- Limits on advertisement frequency and timing

- Ban on misleading or false promotional claims

- Mandatory inclusion of responsible gambling messaging

Sponsorships by gambling operators in sports and entertainment are permitted under compliance with age and content restrictions. Time-bound advertising bans during certain hours protect susceptible audiences.

Recent Regulatory Changes and Their Impact

The December 2024 enactment of Law No. 37-2024 represents the most significant regulatory shift, introducing a unified formal licensing and taxation regime. This replaced a previously unregulated or loosely governed environment, enabling market formalization and increased state oversight.

While the law has established a clearer legal basis, ongoing disputes among ministries over licensing authority have delayed full implementation of controls such as the national CRM platform. Market entrants must navigate this complexity, balancing compliance risks with opportunity.

Enforcement Mechanisms and Penalties

The regulatory framework prescribes monetary fines, license suspension, and revocation for non-compliance with laws, tax evasion, or failure to adhere to responsible gambling standards. Enforcement is evolving alongside capacity building within the ministry and partnering agencies.

- Financial penalties for operational breaches

- Temporary suspension of license for remediation

- Permanent revocation for repeated violations

- Confiscation of illegal gains

- Potential criminal charges for severe infractions

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

The Republic of Congo’s population is estimated at 6.46 million in 2025, with a median age of 24.3 years, indicating a young and potentially dynamic consumer base. Gender distribution is nearly balanced, with approximately 1,001 men per 1,000 women. The population is predominantly urban, with about 69.4% residing in cities, reflecting concentrated demand hubs and accessibility to gambling venues and digital services.

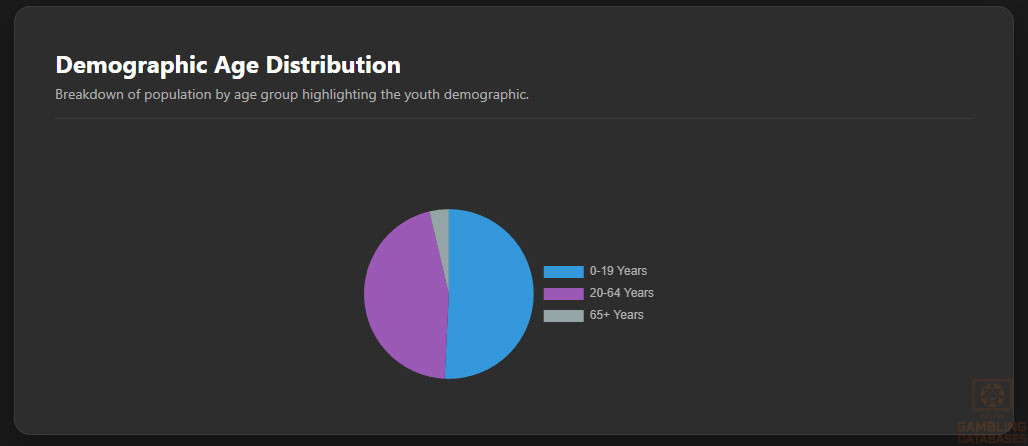

Age distribution shows a significant youth segment: over half of the population (around 50.8%) is aged 19 or younger, with adults aged 20-64 representing 45.5%, and seniors over 65 years only about 3.7%.

This youthful demographic suggests considerable growth potential for iGaming provided regulatory and technological access barriers are addressed.

| Age Group | Population Percentage |

|---|---|

| 0-19 years | 50.8% |

| 20-64 years | 45.5% |

| 65+ years | 3.7% |

Geographically, the population clusters mostly in major urban centers, where economic activity is highest and internet penetration strongest. Rural areas, while less densely populated, contribute to a diverse demographic distribution with unique consumer behaviors.

The urban concentration facilitates the development of gambling infrastructure and digital entertainment platforms.

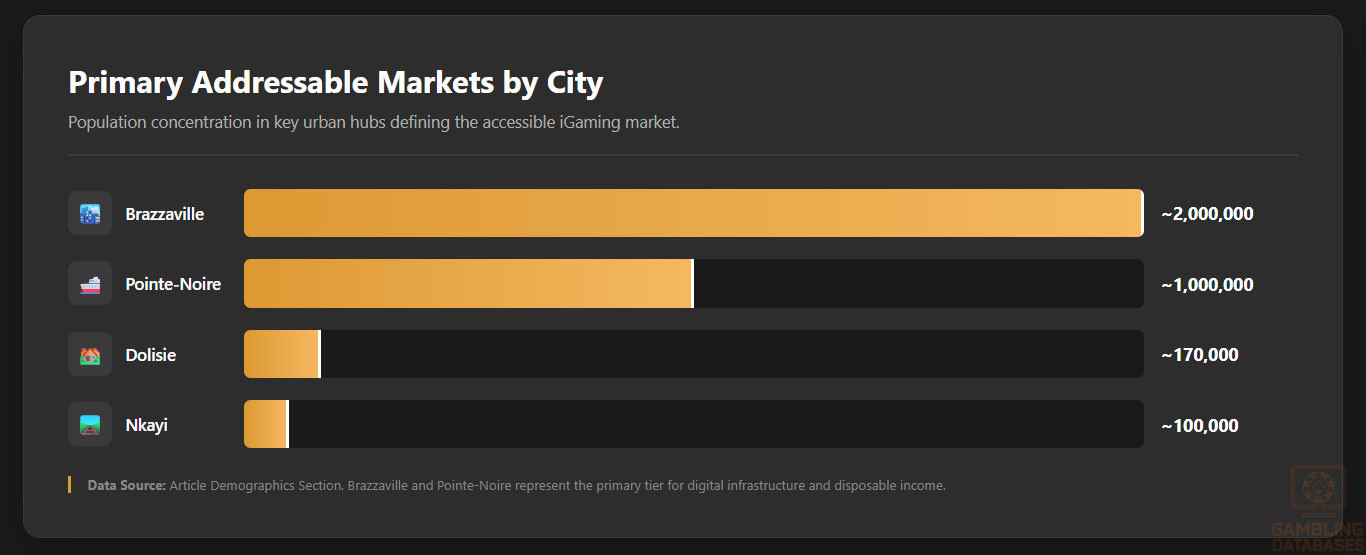

- Brazzaville (capital) – approx. 2 million inhabitants

- Pointe-Noire (economic hub) – approx. 1 million inhabitants

- Nkayi – approx. 100,000 inhabitants

- Dolisie – approx. 170,000 inhabitants

- Owando – approx. 60,000 inhabitants

Economic Indicators and Consumer Spending Power

The Republic of Congo’s nominal GDP is projected at around $15.3 billion in 2024-2025, with modest growth forecasts near 2.8% annually over the short term. Per capita income stands near $2,780, reflecting middle-income status but notable income inequality across regions.

The economy is diversified with significant contributions from the oil and mining sectors, while services and trade sectors are expanding. Consumer spending, particularly in urban areas, is increasing steadily supported by rising disposable incomes and growing financial inclusion.

Income distribution remains uneven, with relatively high poverty rates in rural zones constraining national consumer purchasing power. However, expanding urban middle-class populations display increasing appetite for leisure, entertainment, and digital services including online gaming.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $15.3 billion |

| GDP Growth Rate | 2.8% projected |

| GDP per Capita | $2,780 |

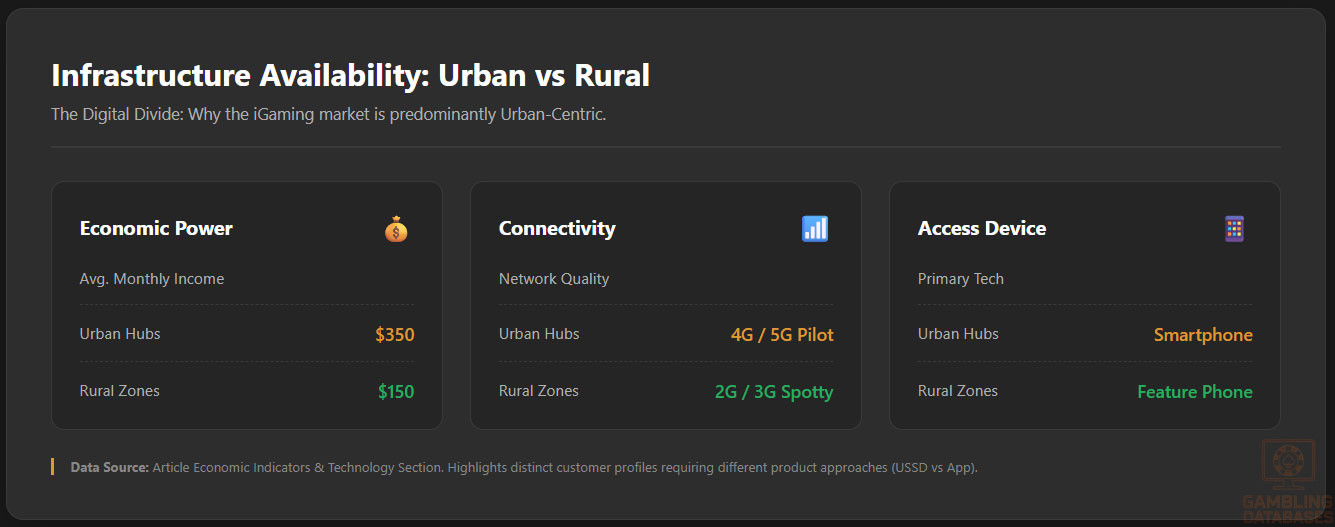

| Urban Household Income Average | $350/month |

| Rural Household Income Average | $150/month |

| Income Inequality (Gini Coefficient) | 45.6 |

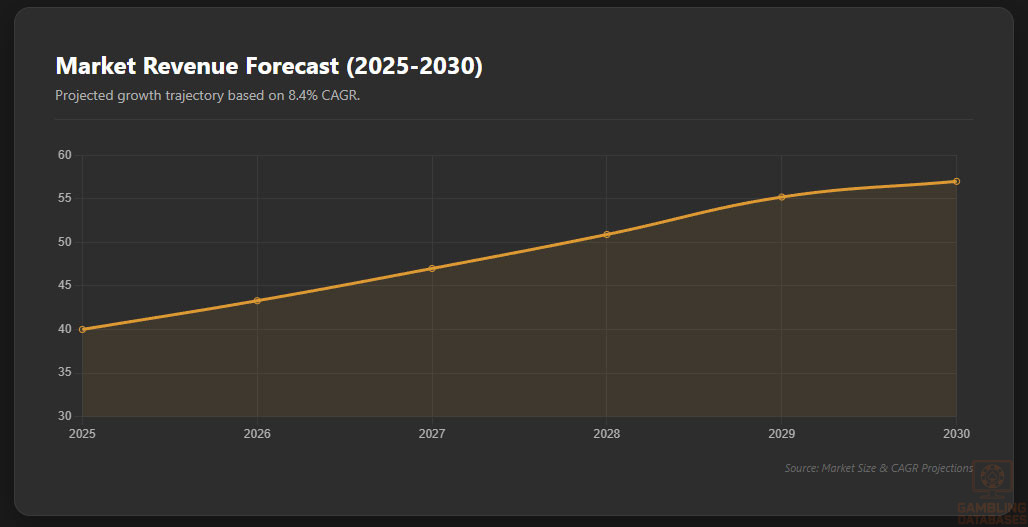

Market size for iGaming is estimated at around $40 million in 2025, with forecasts projecting an 8.4% CAGR through 2030. The growing penetration of mobile devices and expanding internet access underpin user base growth and rising average revenue per user (ARPU), currently approximated at $45 annually.

User acquisition is strongest in the regions exhibiting higher disposable income levels and greater digital literacy, predominantly urban localities. Historical growth demonstrates rising acceptance of digital gaming alongside traditional betting forms.

| Year | Revenue (USD million) | Estimated User Base | ARPU (USD) |

|---|---|---|---|

| 2025 | $40 | 900,000 | $45 |

| 2027 | $48 | 1,150,000 | $47 |

| 2030 | $57 | 1,400,000 | $49 |

Education, Skills, and Digital Literacy

Overall literacy in Congo exceeds 80%, with urban centers reporting higher education levels and digital skills development. Educational initiatives increasingly target youth, fostering competencies relevant to digital platforms, critical for effective Internet and gaming adoption.

While basic digital literacy is growing, unequal access to quality education and technology persists, especially in rural areas. Internet usage often depends on mobile devices, with varying degrees of familiarity with applications beyond social media and communication tools.

The workforce includes a rising segment proficient in IT and digital services although broader national skill development remains an ongoing challenge. This affects the speed and scale at which complex iGaming products requiring digital engagement can penetrate the market.

Cultural and Social Factors

Communication and Language

Congo is linguistically diverse, with French as the official language widely used in business and administration. Indigenous languages are commonly spoken across regions and within communities.

- French (official, administrative and business use)

- Kikongo (regional lingua franca)

- Lingala (common in western urban centers)

- Swahili (spoken in eastern regions)

- Tshiluba (used among central populations)

Internet content and gaming interfaces predominantly utilize French, shaping access and user experience. Multilingual support enhances inclusivity but remains limited among current operators.

Cultural Attitudes

The Congo’s cultural landscape accommodates a mixed attitude towards gambling, influenced by religious traditions and social norms. While gambling is broadly accepted as entertainment by urban youth and middle-income groups, conservative social values and religious institutions express caution, emphasizing responsible behavior and community welfare.

Problem Gambling and Social Considerations

Prevalence of problem gambling is a growing concern, exacerbated by limited public awareness and inadequate support systems. Vulnerable groups include young males, underemployed populations, and urban poor. Government responses are emergent but evolving progressively in line with regulatory reforms.

- Public awareness campaigns on gambling risks

- Availability of counseling and addiction support programs

- Mandatory operator contributions to social welfare funds

- Self-exclusion frameworks integrated in licensing

- Stakeholder collaboration to monitor gambling-related harm

Social responsibility mandates require operators to report incidences of problematic behavior and promote safe participation. These efforts aim to balance market growth with health and social stability considerations.

Political Structure and Governance

The Republic of Congo operates a presidential republic system with a relatively stable political environment. Regulatory consistency is improving but occasionally challenged by bureaucratic overlap. The government prioritizes economic diversification and revenue mobilization, making iGaming a noteworthy sector for policy support.

International relations promote foreign investment, subject to local partnership requirements and regulatory compliance. Enhanced governance reforms target transparency and public-sector efficiency which directly impact business climate and investor confidence.

Technology Adoption and Digital Behavior

Internet and Digital Usage

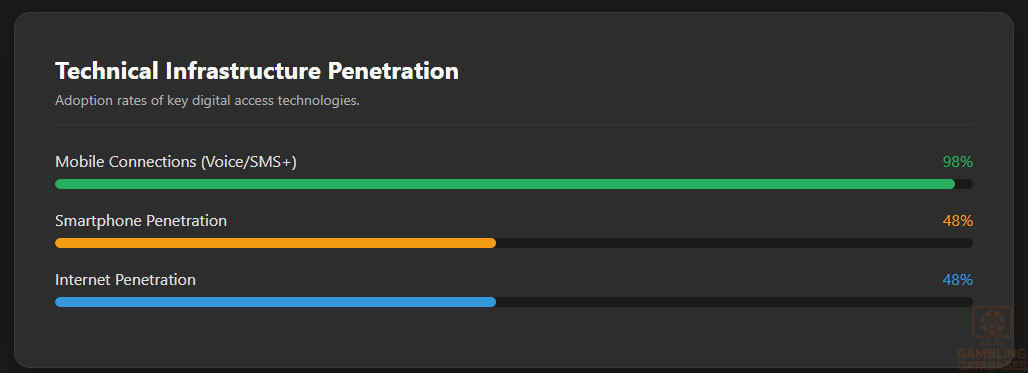

Internet penetration is approximately 38.4%, primarily driven by urban and youth populations. Mobile adoption is nearly ubiquitous with cellular connections exceeding 98% of the population, though primarily through basic voice and SMS services.

Social media engagement, while moderate, shows substantial growth with platforms becoming channels for information, entertainment, and gambling marketing. The digital ecosystem is developing as smartphones and mobile broadband expand access and enhance user interactivity.

- Facebook – 17.1% penetration (~1.1 million users)

- YouTube – Popular for video content consumption and streaming

- WhatsApp – Primary communication tool

- Instagram – Favored by youth for visual social interaction

- Twitter – Utilized for news and public discourse

Digital Payment Behavior

Payment methods for digital services are diversifying with mobile money leading transactions especially in urban and peri-urban markets. E-wallets and bank transfers are growing in acceptance, increasing convenience and security for iGaming users.

- MTN Mobile Money – dominant mobile payment service

- Orange Money – widely used digital wallet

- Bank transfers – emerging among higher-value transactions

- Credit/Debit cards – limited but increasing use

- Cryptocurrency – nascent but gaining interest

Gaming and Gambling Preferences

Current Market Participation

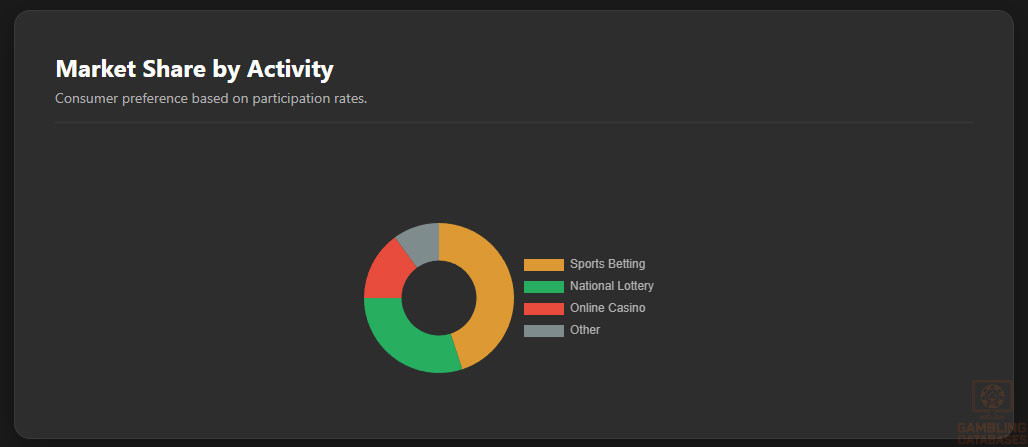

Gambling participation predominantly involves sports betting and lotteries, favored for their cultural resonance and accessibility. Online casino gaming is emerging with increased smartphone penetration but remains secondary.

| Rank | Gambling Activity | Participation Rate (%) |

|---|---|---|

| 1 | Sports Betting | 45% |

| 2 | National Lotteries | 30% |

| 3 | Online Casino Games | 15% |

| 4 | Scratch Cards | 7% |

| 5 | Esports Betting | 3% |

Consumer Behavior Patterns

Consumers demonstrate diverse betting behaviors influenced by socioeconomic status and digital access. Urban users favor mobile platforms with average session lengths around 25-30 minutes, predominantly in the evenings. Retention rates improve with localized content, loyalty programs, and user trust in regulatory compliance.

Spending varies by activity, with sports betting typically attracting higher average wagers compared to lotteries. Digital payment options increase convenience, encouraging recurring participation and smoother transaction experiences.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

The Republic of Congo’s internet penetration stands at about 38.4%, with broadband access limited primarily to urban areas. Mobile internet dominates connectivity, accounting for over 85% of total internet usage, reflecting infrastructural emphasis on cellular networks over fixed-line broadband.

Average mobile data speeds range from 7 to 12 Mbps in cities, while rural and peri-urban zones experience lower speeds and intermittent connectivity. Government and private sector initiatives are investing to improve fiber optic networks and expand broadband availability, aiming to bridge the urban-rural digital gap.

5G and Future Technology Deployment

5G deployment is at an incipient stage with pilot programs active in Brazzaville and Pointe-Noire. Full commercial rollout is expected between 2026 and 2028, driven by major telecom operators and supported by government digital transformation plans.

Network operators aim to leverage 5G to enhance mobile gaming experiences, support IoT applications, and increase overall digital ecosystem performance. However, coverage will initially focus on major cities and economic zones before broader national extension.

Mobile Technology Ecosystem

Mobile Network Infrastructure

The mobile telecommunications market features several operators competing for subscribers and coverage dominance. Market share is distributed around leading providers with varying emphasis on urban and rural outreach.

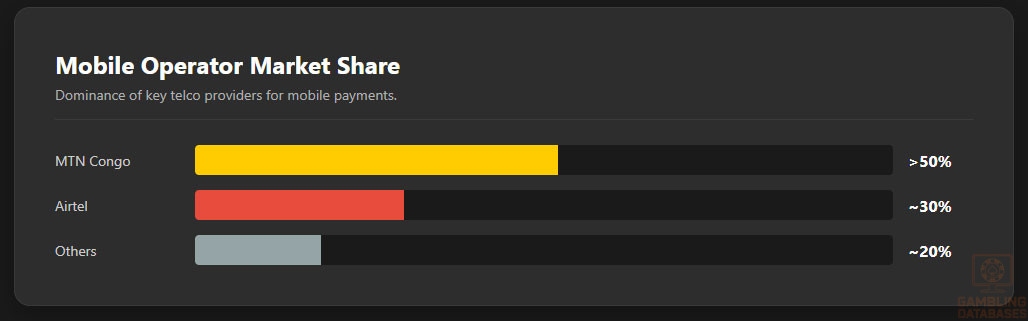

- MTN Congo – market leader with over 50% share, extensive 3G/4G coverage

- Airtel Congo – significant player with competitive pricing and good urban presence

- Orange Congo – strong focus on mobile money and digital service integration

- Kinshasa Telecom – regional operator targeting select urban areas

- Libertis Telecom – newcomer focusing on data services and enterprise clients

Data costs remain relatively high compared to regional peers but are trending downward due to competition and regulatory pressure for affordable digital inclusion.

Device Penetration

Smartphone penetration approaches 48%, heavily influenced by urban youth and middle-income demographics. Feature phones remain prevalent in rural areas due to affordability and basic communication needs.

Popular smartphone brands include Samsung, Tecno, and Huawei, favored for their cost-effectiveness and local repair ecosystems. Device usage patterns show predominant reliance on mobile internet for social media, communication, and increasingly, online gaming applications.

Financial Services and Payment Infrastructure

Banking System Structure

The banking sector consists of several commercial banks, with growing adoption of digital banking services. Account penetration remains limited but is expanding as mobile money services complement traditional banking.

- Banque Commerciale Internationale (BCI) – leading national bank with digital platform initiatives

- Ecobank Congo – pan-African bank with strong retail footprint

- BGFI Bank – significant corporate banking presence with retail services

- La Congolaise de Banque – innovative in mobile banking products

- BIDC (Banque d’Investissement et de Développement de la CEAC) – focuses on development finance

Payment Processing Options

Digital payment infrastructure includes mobile money, bank transfers, and limited credit card use. Mobile money dominates due to convenience and lower banking coverage.

- MTN Mobile Money – principal mobile wallet with extensive agent networks

- Orange Money – widespread mobile payment solution supporting bill payments and remittances

- Bank Transfers – growing among urban professionals and businesses

- Visa/MasterCard – available but limited by low card penetration

- Cryptocurrency – nascent usage, mostly informal among tech-savvy niche

E-commerce and Digital Economy

E-commerce remains nascent with online retail adoption limited by infrastructure constraints and consumer trust challenges. Payment friction and delivery logistics impede scale, but there is growing momentum in urban areas leveraging mobile platforms for goods and services.

The digital economy is supported by expanding internet penetration, government initiatives promoting digitization, and a young population eager to engage with online marketplaces and digital financial services.

Business Environment and Regulatory Framework

Ease of Business Operations

According to the World Bank’s Doing Business metrics, Congo ranks moderate for ease of starting a business, hindered primarily by bureaucratic delays, lack of transparency, and inconsistent regulatory enforcement. Nevertheless, reforms in recent years aim to simplify procedures and improve investor confidence.

Foreign investment is encouraged, particularly in strategic sectors including technology and gaming, with incentives available under certain conditions. Operational costs remain relatively moderate but can be elevated due to compliance and infrastructure gaps.

Corporate Structure and Registration

Businesses typically register as Limited Liability Companies (LLCs) or Branch Offices of foreign entities. LLCs offer flexibility and limited liability protection, while branch offices allow direct foreign control but may incur additional regulatory scrutiny.

Registration timelines average 4-6 weeks, involving multiple stages including document notarization, registration with the Commercial Registry, tax authority enrollment, and social security registration. Foreign ownership is generally permitted, though partnerships with local entities are advantageous for market navigation.

- Certificate of Incorporation

- Company statutes and Articles of Association

- Proof of registered office address

- Shareholder identification and background documents

- Tax Identification Number (TIN) registration

- Social Security registration for employees

Taxation Framework

Corporate income tax is set at a standard rate of 30%, with incentives and holidays available within designated economic zones. International tax treaties provide relief on withholding taxes and foster cross-border investment stability.

- France

- Portugal

- China

- Belgium

- South Africa

Personal income tax applies progressively to residents with mandatory social security contributions deducted at source. Tax residency is determined by duration of stay and economic interests within the country.

Market Entry Considerations

Successful entry requires alignment with local partners or establishment of a physical presence, compliance with evolving licensing requirements, and robust technological integration capabilities. Emphasis on mobile-optimized platforms is critical due to user device preferences.

- Form strategic alliances with established local entities

- Ensure compliance with emerging CRM reporting systems

- Develop mobile-first gaming experiences matching local data speeds

- Invest in localized marketing respecting cultural norms

- Leverage mobile payment integrations for user convenience

Initial investments vary widely, but typical setup and licensing costs start from $100,000 upward, with annual operating budgets influenced by platform development, staffing, and marketing reach. Market entry timelines average 6-9 months including licensing and product launch.

| Phase | Duration |

|---|---|

| Initial Market Research and Partner Identification | 1-2 months |

| Company Registration and Licensing Application | 3-4 months |

| Platform Development and Integration | 2-3 months |

| Marketing Launch and User Acquisition | 1-2 months |

Success Factors and Challenges

Market success hinges on understanding local regulatory nuances, delivering accessible digital experiences, and building trust through responsible gambling initiatives. Navigating infrastructure limitations and regulatory fluidity remain significant challenges requiring adaptive strategies and local partnerships.

- Strong compliance and local regulatory know-how

- Mobile-centric product design

- Effective KYC/AML technology deployment

- Robust payment and withdrawal mechanisms

- Culturally sensitive marketing and community engagement

Operational challenges include inconsistent infrastructure, fluctuating power and connectivity, bureaucratic delays, and competition from informal gambling sectors. However, a first-mover advantage in a regulated environment offers growth potential amid increasing digital adoption.

- Limited broadband and uneven internet coverage

- High mobile data costs for consumers

- Complex licensing processes with evolving requirements

- Potential regulatory overlap and enforcement unpredictability

- Competition with unlicensed operators and informal betting

Exit Strategy Planning

Market liquidity remains limited but improving, with increasing interest from regional and international investors. License transferability involves regulatory approval, with valuation dependent on market share, compliance history, and technology assets.

Operators planning exits should factor in the evolving regulatory environment and establish clear contractual frameworks early in the business lifecycle to facilitate smoother transitions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Congo?

Yes, online gambling is legal under the Republic of Congo’s regulated framework established by Law No. 37-2024. Both land-based and online gambling activities are subject to licensing and regulatory oversight. Operators must obtain appropriate licenses for online sportsbooks, casinos, and lotteries while complying with responsible gambling and AML rules. The government enforces operator obligations to ensure fair play and consumer protection.

2. What types of gambling licenses are available and what do they cover?

The Congo offers licenses for multiple gambling categories including: sports betting, land-based casinos, online casinos, national lotteries, and virtual gaming. Each license covers specific operational scopes such as remote betting platforms or physical casino operations. Additional authorizations may be required for payment processing and affiliate marketing activities. The licensing framework is unified to promote parity between online and land-based sectors.

3. How much does an iGaming license cost and how long does it take to obtain?

Initial license application fees start at approximately $50,000, with annual renewal fees ranging from $8,000 to $15,000 depending on the game type. The application process takes 3-6 months, incorporating technical evaluations, background checks, and regulatory reviews. Operators should allocate additional time for compliance readiness and stakeholder engagement to ensure a smooth approval process.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply for gambling licenses provided they establish a local presence or partner with indigenous entities. There is no outright prohibition on foreign ownership, though regulatory bodies emphasize local engagement to reinforce accountability and operational compliance. Foreign operators generally structure entities as branch offices or joint ventures within Congo.

5. What are the tax obligations for iGaming operators?

iGaming operators are subject to a Gross Gaming Revenue (GGR) tax typically around 20%, alongside corporate income tax at approximately 30%. Operators also pay fixed license renewal fees. Reporting and tax payment are required quarterly with transparency obligations enforced. Specific tax rates vary by game type and must be factored into financial planning.

6. Are gambling winnings taxed for players?

Yes, winnings are subject to withholding tax with progressive rates depending on the prize amount. Small wins may be exempt while larger winnings incur taxes deducted at source by operators or paying agents. This system simplifies compliance and ensures equitable fiscal contribution from players.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include license fees, platform development, compliance and auditing, marketing, payment processing, and staffing. Additional costs arise from local office maintenance and regulatory reporting. Effective budgeting requires provision for technology upgrades and customer support. Annual operational budgets typically exceed $500,000 for mid-sized operators.

8. What is the expected ROI timeline for entering this market?

Return on investment generally occurs within 2-3 years, contingent on market penetration, licensing, and user acquisition effectiveness. Initial capital allocation is significant but offset by growth potential in an emerging but regulated environment. Effective marketing and local partnerships shorten ROI durations.

9. What are the local presence requirements for operators?

Operators must maintain a physical office or partner with local firms authorized to represent them. On-the-ground staff are typically required for compliance functions such as KYC verification and customer support. This presence supports regulatory liaison and operational integrity.

10. What payment methods are available and recommended?

Recommended payment methods focus on mobile money services like MTN Mobile Money and Orange Money, which dominate due to convenience and network reach. Bank transfers and limited card payments complement these. Cryptocurrency remains an emerging option but is not mainstream.

11. What are the advertising and marketing restrictions?

Advertisements must avoid targeting minors and vulnerable groups, restrict misleading content, and include responsible gambling messaging. Marketing across media channels is regulated for frequency and timing. Sponsorships require compliance with age and content guidelines.

12. What responsible gambling measures are mandatory?

Operators must implement self-exclusion programs, deposit limits, and real-time monitoring of player behavior. Reporting problem gambling cases to authorities and providing access to support services are compulsory. These measures enhance consumer protection and regulatory compliance.

13. How large is the iGaming market and what is the growth potential?

The iGaming market is currently valued at approximately $40 million with a projected CAGR of 8.4% through 2030. Growth is driven by expanding internet access, young demographics, and increasing acceptance of digital gaming platforms. The urban middle class represents the core growth segment.

14. Who are the main competitors and what is their market share?

Competition is limited to fewer than 10 licensed operators mainly comprising local companies and regional entrants. Market share is fragmented with sports betting leaders dominating overall revenue. International operators are gradually entering via partnerships. The market remains open for new entrants with innovative offerings.

15. What are the player preferences and typical spending patterns?

Players prefer sports betting and lotteries, engaging frequently but with moderate average bets. Online casino participation is growing, skewed towards mobile users. Most players access platforms during evening hours with average session times of 25-30 minutes. Repeat play patterns improve with loyalty incentives and streamlined payment options.

16. What are the key success factors and main challenges for new entrants?

Success factors include robust regulatory compliance, mobile-first platform design, efficient payment integration, local partnerships, and culturally tailored marketing. Challenges involve infrastructural limitations, regulatory ambiguity, competition with informal markets, and ongoing technological investment needs. Regulatory navigation and consumer trust building are crucial.

Sources and References

- Gambling Regulation in Congo-Brazzaville, iGaming Today, 2024 – https://www.igamingtoday.com/gambling-regulation-in-congo-brazzaville/

- Tug-of-war in Kinshasa: DRC’s Shaky Regulatory Regime, Sigma World, 2025 – https://sigma.world/news/tug-of-war-in-kinshasa-drcs-shaky-regulatory-regime/

- The Evolution of iGaming Regulations in Africa, 2025 Perspective, Gaming Awards, 2025 – https://gaming-awards.com/NEWS/the-evolution-of-igaming-regulations-in-africa-a-2025-perspective/

- Gambling Regulations in Africa: Key Changes Coming in 2025, GamblingTalk, 2025 – https://gamblingtalk.net/news/gambling-regulations-in-africa-key-changes-coming-in-2025

- Congo Casino Gaming Equipment Market Report 2025-2031, 6W Research, 2023 – https://www.6wresearch.com/industry-report/congo-casino-gaming-equipment-market

- DRC Modernizes Gambling Sector for Enhanced Revenue Mobilization, Bankable Africa, 2025 – https://bankable.africa/en/digital/2406-1350-drc-modernizes-gambling-sector-for-enhanced-revenue-mobilization

- Starting a Gambling Business in DRC Congo – Full Guide, iGaming Afrika, 2023 – https://igamingafrika.com/starting-a-gambling-business-in-drc-congo-full-guide/

- Congo Gambling Market 2025-2031 Analysis, 6W Research, 2024 – https://www.6wresearch.com/industry-report/congo-gambling-market

- Gambling Laws in the Democratic Republic of the Congo, CMS Expert Guide, 2023 – https://cms.law/en/int/expert-guides/cms-expert-guide-to-gambling-laws-in-africa/democratic-republic-of-congo

- Digital 2025: The Republic of the Congo Report, DataReportal, 2025 – https://datareportal.com/reports/digital-2025-republic-of-the-congo

- Population Data and Demographics, Worldometers, 2025 – https://www.worldometers.info/world-population/democratic-republic-of-the-congo-population/

- Republic of Congo Economic Update 2025, World Bank, 2025 – https://www.worldbank.org/en/country/congo/publication/republic-congo-economic-update-2025-strengthen-management-produced-human-and-natural-capital-raise-living-sdandards

- Digital Shift Impact on Jobs and Economy in DRC, GSMA, 2025 – https://www.ecofinagency.com/news-digital/2209-48896-dr-congo-digital-shift-could-add-4-1-bln-and-2-5-mln-jobs-by-2029-gsma

- Republic of Congo GDP and Economic Indicators, World Economics, 2023 – https://www.worldeconomics.com/GDP/CongoRep.aspx

- Demographics of the Democratic Republic of the Congo, Wikipedia, 2024 – https://en.wikipedia.org/wiki/Demographics_of_the_Democratic_Republic_of_the_Congo

- World Bank Doing Business Report 2024 – https://www.worldbank.org/en/topic/competitiveness/publication/doing-business-report-2024

- Central Bank of Congo Financial Reports – https://www.bcc.cd/

- International Telecommunication Union ICT Statistics – https://www.itu.int/en/ITU-D/Statistics/Pages/stat/default.aspx

- Gaming Industry Report Africa 2024 – [Publisher Name]

- IMF World Economic Outlook April 2025 – https://www.imf.org/external/datamapper/NGDPDPC@WEO/OEMDC/ADVEC/WEOWORLD/KHM/CHL/COD/COG

- ANQA Compliance Guide DRC AML & Sanctions 2025 – https://www.anqacompliance.com/drc-aml-sanctions-compliance

- Geopoll Betting in Africa Report 2025 – https://www.geopoll.com/blog/report-betting-in-africa-2025/

- Altenar Blog: DRC Betting Market Entry, June 2025 – https://altenar.com/blog/bring-sports-betting-success-to-your-demrep-of-congo-igaming-business-altenar-you/

- IGaming Afrika Licensing Requirements Overview 2023 – https://igamingafrika.com/licensing-requirements/

- CMS Digital Investment Facility – Data Center Market Brief DRC 2025 – https://cms.d4dhub.eu/assets/Initiatives/Data-Governance-in-Africa/Digital-Investment-Facility/2507_Country-Market-Briefs/Data-Center-Market-Brief-Democratic-Republic-of-Congo.pdf

- Digital 2025: The Democratic Republic Of The Congo, DataReportal, 2025 – https://datareportal.com/reports/digital-2025-democratic-republic-of-the-congo

- IGC Services: 5 Major iGaming Markets 2025 – https://igc.services/blog/5-major-igaming-markets-to-look-out-for-in-2025/

- LinkedIn Article on Regulatory Challenges in Kinshasa, 2025 – https://www.linkedin.com/pulse/tug-of-war-kinshasa-drcs-shaky-regulatory-regime-sigma-world-2pfce

- Wikipedia Democratic Republic of the Congo, 2025 – https://en.wikipedia.org/wiki/Democratic_Republic_of_the_Congo

- KPMG Africa Games Industry Report 2025 – https://assets.kpmg.com/content/dam/kpmg/ng/pdf/2025/02/2025%20Africa%20Games%20Industry%20Report.pdf

- IGaming Today DRC Gambling Regulation Review, 2024 – https://www.igamingtoday.com/gambling-regulation-in-the-democratic-republic-of-the-congo/

- Bankable Africa – Digital Sector Modernization in DRC, 2025 – https://bankable.africa/en/digital/2406-1350-drc-modernizes-gambling-sector-for-enhanced-revenue-mobilization

🎯 Gambling Databases Country Rating: Republic of Congo (Congo-Brazzaville)

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.8/10 | [🟡 Moderate 5-7] |

| Player Access Score | 7.7/10 | [🟢 Fully Legal 8-10] |

| Overall Market Attractiveness | 6.0/10 | [🟡 Niche / Developing Market] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Mandatory Local Presence: Law No. 37-2024 strictly requires a physical office or a partnership with a local entity. Remote-only offshore operation is effectively impossible for licensed entities.

- Regulatory Overlap & Confusion: While the Ministry of Budget oversees gambling, the text notes “concurrent jurisdictional assertions by multiple ministries,” creating a volatile compliance environment and potential for double-taxation or conflicting fines.

- Infrastructure Gaps: With only 48% internet penetration and frequent power/connectivity issues, technical uptime guarantees are difficult to maintain.

- Mandatory CRM Integration: Operators must integrate with a government monitoring platform that is still “under development,” posing significant technical integration risks and delays.

- Low Market Value: The entire market is estimated at only $40 million (2025). High compliance costs may outweigh the revenue potential for international operators.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Full product legality including online casinos and sports betting (+3.0). Deducted -0.5 for “concurrent jurisdictional assertions by multiple ministries” causing regulatory uncertainty. |

| Licensing Process | 25% | 1.8/2.5 | Licensing is accessible and timeline is decent (3-6 months) (+2.0). Application fees are reasonable (~$50k) (+0.5). Major deduction (-0.7) for the complexity of navigating bureaucratic overlap and the requirement for local partners/domain registration. |

| Taxation & Costs | 20% | 1.0/2.0 | GGR Tax is 20-22% (+1.5). However, Corporate Tax is high at 30% (-0.5). Total effective tax burden (GGR + Corp + Fees) approaches 50% of profits. Operational costs are elevated by the need for physical offices and local staff (-0.5). Final: 1.0. |

| Operational Requirements | 15% | 0.3/1.5 | Heavy requirements (+0.5). Severe deductions: Mandatory physical presence/local partner (-0.5). Mandatory technical integration with unproven government CRM (-0.5). Requirement for local domain ownership (-0.2). |

| Market Environment | 10% | 0.2/1.0 | Moderate environment (+0.5). Deductions: Small market size ($40M) limits scalability (-0.2). Infrastructure instability (power/internet) (-0.1). Bureaucratic transparency issues (-0.2). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal. Players can legally access licensed sports betting, lotteries, and online casinos. No penalties for players mentioned. |

| Practical Accessibility | 30% | 1.5/3.0 | Limited payment methods (+1.0); reliance on mobile money (MTN/Orange) with low credit card penetration. Infrastructure barriers (low internet speeds, rural disconnect) significantly hamper access (-1.0). ISP blocking is not currently active but threatened for unlicensed sites. |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players. Withholding tax on winnings exists, but this is a fiscal measure, not a penalty. |

| Market Availability | 10% | 0.2/1.0 | Very limited licensed options. “Fewer than 10 formal licensees” indicates a highly concentrated market with poor variety for players (+0.25). |

🔍 Key Highlights

Strengths

- Full Product Legality: Unlike many jurisdictions, Online Casino (Slots/Virtual) is legally distinct and licensable alongside sports betting.

- Unlimited License Duration: Licenses do not expire, provided annual fees are paid and compliance is maintained.

- Mobile Money Integration: High mobile penetration (98% cellular) and established mobile money ecosystems (MTN/Orange) provide a clear payment rail.

⛔️ CRITICAL RISKS AND CHALLENGES

- Economic Viability: With an ARPU of ~$45/year and a total market of $40M, the pie is extremely small.

- Bureaucratic “Grey Zones”: The clash between the Ministry of Budget and other agencies creates a risk of conflicting enforcement actions.

- Operational Drag: Requirement for a physical office and local staff creates high fixed costs for a digital-first business.

- Infrastructure Reliability: Frequent internet and power disruptions can kill live betting and casino session revenue.

- Compliance Costs: Annual fees + 20% GGR + 30% Corp Tax + Local Staff Salaries + Technical audit costs = Very thin margins.

Player-Specific Issues

- Digital Divide: Only 48% of the population has internet access; rural players are effectively cut off.

- Data Costs: High relative cost of mobile data limits session times for data-heavy casino games.

- Winnings Tax: Players face withholding tax on winnings, reducing the attractiveness of regulated sites vs. offshore options.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $150,000 – $250,000 (License fees + Local company formation + Office setup + Legal retainer).

Monthly Operating Costs: $30,000 – $60,000 (Local staff, office rent, compliance audits, technical fees).

Effective Tax Rate on Revenue: ~55% (20% GGR + 30% Corporate Tax + Withholding tax administration costs).

Customer Acquisition Cost: Moderate ($20-$50), but strictly limited by low player LTV.

Time to Breakeven: 24-36 months.

Profitability Assessment: LOW. The economics are punishing. The combination of a small total addressable market ($40M), low ARPU ($45), and high fixed costs (local office requirement) makes this market unviable for most standalone online operators. It is only suitable for: 1) Large retail operators adding an online vertical, or 2) Local firms with existing infrastructure.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [Medium] | [Regulatory framework allows for blocking, though currently loosely enforced. New law (2024) signals intent to crackdown.] |

| Licensed Operators | [High] | [Risk of license suspension due to conflicting Ministry directives; heavy fines for reporting errors in the new CRM system.] |

| Affiliates/Advertisers | [Medium] | [Strict advertising rules regarding minors; potential fines for promoting unlicensed brands as enforcement ramps up.] |

| Payment Processors | [High] | [Must ensure strict AML compliance; risk of freezing funds if local partner falls out of compliance.] |

| Company Directors | [Medium] | [Local directors face liability for compliance failures. Foreign directors relatively safe unless in-country.] |

🚨 Extradition and International Enforcement

Extradition Treaties: Congo has extradition agreements with France and several Central African neighbors (CEMAC region). No specific high-profile treaties with the USA or UK for gambling offenses, but financial crime cooperation exists.

Enforcement History: Minimal history of international extradition for gambling. Enforcement is primarily focused on physical asset seizure within the country.

Safe Jurisdictions: Generally, the risk of extradition for pure gambling offenses is low for operators based in non-EU/non-African jurisdictions, provided they avoid money laundering charges.

Travel Risk: Moderate risk for executives traveling to Congo or Francophone Africa if the company has outstanding tax liabilities or disputes with the Ministry.

📋 Final Verdict

The Republic of Congo receives an Operator Ease Score of 5.8/10 and a Player Access Score of 7.7/10, resulting in an overall market attractiveness rating of 6.0/10.

HONEST ASSESSMENT: Do not let the “legal status” fool you. While Law No. 37-2024 legally opens the market for both sports and casino, the operational reality is harsh. The requirement for a physical office and local partner, combined with a tiny $40M market cap and low player spending power ($45/year), makes this a “high effort, low reward” jurisdiction. It is a trap for pure-play online operators.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A regional African operator with existing hubs in CEMAC countries.

- A retail-first company planning to open physical betting shops (casinos/betting parlors) with online as an add-on.

- Willing to accept a 5+ year ROI horizon.

❌ Definitely Avoid If You Are:

- A pure-digital operator expecting remote management (Local presence is mandatory).

- Looking for high-value VIP players (GDP per capita is too low).

- A startup with limited runway (Bureaucracy will drain your capital).

- Unwilling to navigate complex local partnerships and potential corruption risks.

⚠️ BOTTOM LINE: Legal but logistically prohibitive. Avoid this market unless you have boots on the ground and a retail strategy.