Cyprus offers a strategic gateway for iGaming expansion, featuring a robust regulatory environment and growing digital infrastructure. The country’s regulatory framework supports both land-based and online gaming, presenting diverse market opportunities.

| Metric | Value |

|---|---|

| Legal Gambling Status | Fully regulated with unified licensing |

| Regulatory Authority | Cyprus Gaming and Casino Supervision Commission (CGCSC) |

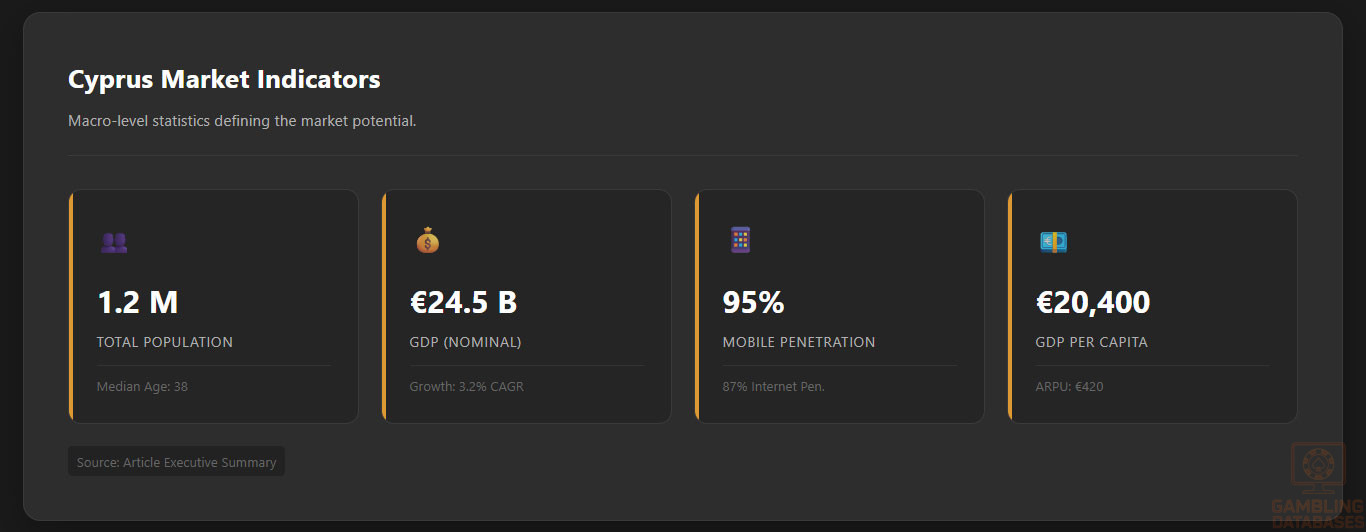

| Population | 1.2 million |

| GDP (nominal) | €24.5 billion |

| GDP per capita | €20,400 |

| Internet Penetration | 87% |

| Mobile Penetration | 95% |

| Number of Licensed Operators | 8 online, 4 land-based casinos |

| License Application Fee | €30,000 – €150,000 |

| Annual License Fee | €50,000+ depending on turnover |

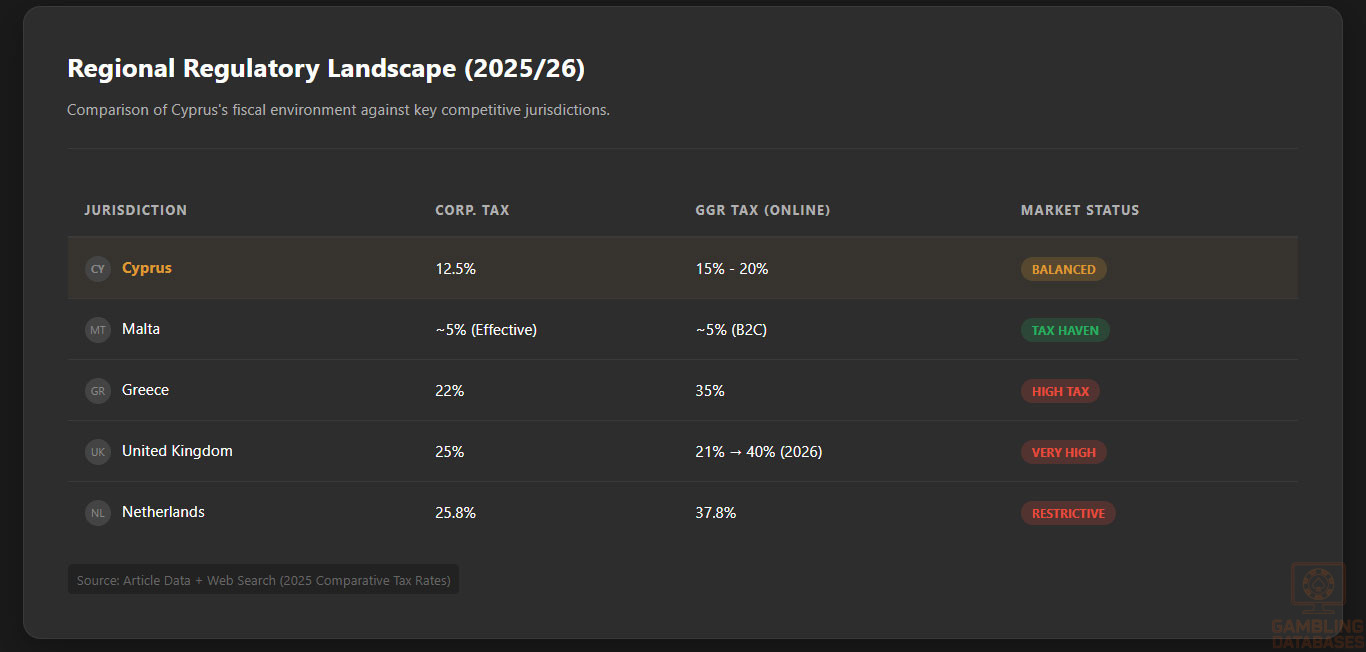

| Gross Gaming Revenue Tax | 15%-20% depending on game type |

| Corporate Tax Rate | 12.5% |

| Market Size | €350 million (2025 est.) |

| Market Growth Forecast CAGR | 8.5% (2025-2030) |

| Average Revenue Per User (ARPU) | €420 |

| Online Market Share | 60% of total gaming revenue |

| Land-Based Market Share | 40% |

| Licensing Timeline | 3-6 months |

| KYC/AML Compliance | Strict, EU aligned |

| Advertising Restrictions | Targeted and limited |

| Responsible Gambling Requirements | Mandatory interventions and self-exclusion |

| Currency Restrictions | Euro only |

| Data Protection | GDPR compliance mandatory |

| Foreign Ownership | Allowed with conditions |

| Physical Presence Requirement | Official Cyprus registered entity required |

| Technology Infrastructure Quality | High broadband and mobile network coverage |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Cyprus maintains a comprehensive regulatory framework encompassing both land-based and online gambling. The government instituted the Cyprus Gaming and Casino Supervision Commission (CGCSC) as the central regulatory authority overseeing all gaming operations.

Land-based casinos are under strict surveillance, and online gambling is permitted under licensing schemes designed to align with EU directives and ensure consumer protection.

Land-Based Gambling Activities

Land-based gambling in Cyprus includes four major casinos, licensed sports betting venues, and regulated slot machine halls. These venues operate under stringent licensing terms that enforce operational integrity, customer protection, and anti-money laundering controls. The variety of gambling options includes table games, sports betting, and electronic gaming machines.

Online Gambling Framework

Cyprus regulates online gambling comprehensively with a unified licensing system introduced in 2021. Operators offering online casino games, sports betting, and lotteries must secure licenses from CGCSC.

Licensed Operators and Market Players

The Cyprus iGaming market hosts a modest number of licensed online operators, including both local startups and international brands. Competition is moderately concentrated, with market shares divided between established operators and emerging entrants targeting niche segments.

Market entry strategies often involve partnerships with local entities and investment in digital marketing to foster brand recognition and player acquisition.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing application follows a structured multi-step process overseen by the CGCSC. Applicants must submit comprehensive corporate documentation, audited financial statements covering the past three years, detailed business plans with market strategies, and technical certifications including RNG and platform security.

Background checks on directors and beneficial owners are mandatory, ensuring integrity and compliance. The process generally spans 3 to 6 months, with application fees ranging from €30,000 to €150,000 depending on the license category and scope.

Required documentation for licensing includes:

- Corporate registration certificate

- Financial statements audited for the past 3 years

- Business plan with market strategy

- Technical documentation including RNG certification

- KYC and AML policies

- Proof of minimum capital deposit

- Background checks for directors and shareholders

- Security and data protection policies

Local Presence and Operational Requirements

Operators are mandated to establish a registered entity or local branch within Cyprus to maintain a physical presence. This includes maintaining compliance and responsible gambling teams physically located in Cyprus.

The gaming website domain must be registered under Cyprus jurisdiction, facilitating regulatory control and legal accountability. Foreign ownership is permitted, but local partnership or direct registration ensures smoother regulatory engagement and operational stability.

Compliance Obligations and Monitoring

Player Protection and Identification

Cyprus enforces rigorous player protection standards requiring online operators to implement EU-standard KYC and AML policies. Player identity verification includes document authentication, source of funds checks, and continuous transaction monitoring. Responsible gambling measures are mandatory, aiming to mitigate problem gambling through proactive interventions.

Key responsible gambling measures include:

- Self-exclusion programs

- Deposit and loss limits

- Time limits on play

- Access to counselling and support services

- Mandatory player information disclosures

Financial Monitoring and Reporting

Operators must continuously monitor financial transactions, with robust anti-fraud and AML systems in place. Reporting to regulators occurs quarterly, supplemented by annual audits verifying compliance and revenue accuracy. The CGCSC conducts random audits to reinforce regulatory adherence.

Reporting follows a multi-step sequence involving transaction logging, internal reviews, submission to regulatory bodies, and verification checks ensuring transparency and fiscal responsibility.

Taxation Structure and Financial Obligations

Player Taxation

Players generally are not taxed on gambling winnings from licensed operators. Taxation on winnings applies primarily to unlicensed or private gambling activities, creating a clear legal distinction that supports licensed market participation and consumer confidence.

Operator Taxation

Gross Gaming Revenue (GGR) taxes vary by game type, ranging from 15% on lotteries to 20% on casino games. Annual license renewal fees depend on turnover brackets, complemented by a corporate income tax rate fixed at 12.5%. This tax framework balances government revenue needs with industry competitiveness, fostering sustainable market growth.

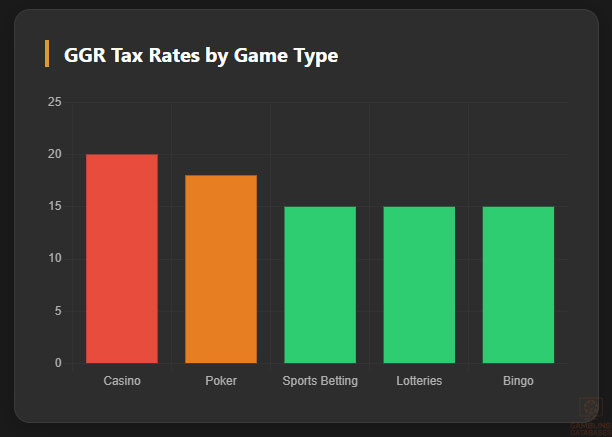

| Game Type | GGR Tax Rate |

|---|---|

| Casino Games | 20% |

| Sports Betting | 15% |

| Lotteries | 15% |

| Poker | 18% |

| Bingo | 15% |

Gambling Market Financial Performance

The Cyprus gambling market demonstrates consistent growth, particularly through its online segment. Total wagers and tax revenues have increased steadily, fueled by expanded internet and mobile penetration and a growing player base.

The average annual growth rate is projected at 8.5%, supported by modern technology infrastructure and investor interest. Payout ratios maintain a balance conducive to operator profitability and player satisfaction.

Advertising and Marketing Restrictions

Advertising in Cyprus gambling is permitted but tightly regulated. Campaigns can utilize traditional media and digital platforms, subject to strict content controls designed to prevent misleading messages and protect vulnerable populations.

Advertising channel categories include:

- Television

- Radio

- Internet ads with specified restrictions

- Sponsorships of sporting and cultural events

- Print media

Content restrictions enforce:

- No misleading claims or guarantees

- No targeting of minors

- No promotion of excessive or irresponsible gambling

- Prohibition on advertising unlicensed operators

- No use of aggressive or intrusive marketing tactics

Recent Regulatory Changes and Their Impact

Recent amendments in 2023 introduced a modernized unified licensing system, increased compliance standards, and adjusted tax rates moderately upward.

These reforms raised operational costs for licensees but strengthened market transparency, player safeguards, and regulatory oversight. Operators have adapted by enhancing compliance infrastructure and evolving marketing strategies to align with new norms.

Enforcement Mechanisms and Penalties

The CGCSC employs a multi-faceted enforcement approach combining administrative penalties and legal sanctions. Penalties include substantial fines, license suspensions or revocations, and potential criminal prosecution for fraudulent practices. Operators may also face mandatory corrective actions or public warnings, fostering a culture of compliance and integrity in the industry.

- Fines for operating without a license

- Suspension or revocation of licenses

- Criminal prosecution for fraud

- Mandatory corrective actions imposed

- Public warnings and blacklists

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

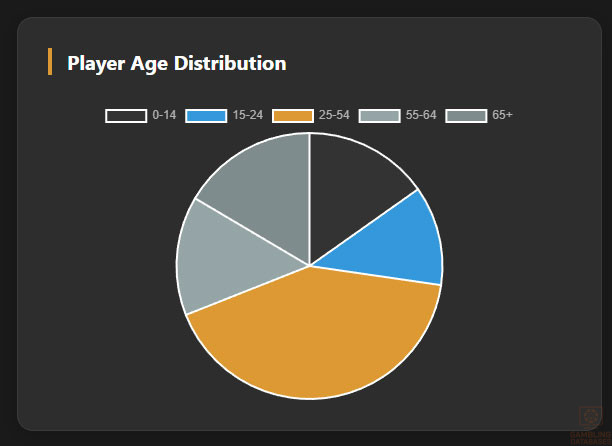

Cyprus has a total population of approximately 1.2 million inhabitants with a median age of 38 years. The age distribution indicates a balanced population pyramid, with a slightly larger proportion of adults aged 25 to 54. Gender distribution is almost even, with males constituting 49% and females 51% of the population.

Urbanization trends show that over 70% of the population resides in urban areas, particularly in major metropolitan centers. Rural population remains significant, especially in inland and southern regions, supporting traditional livelihoods but with growing digital connectivity facilitating remote engagement with iGaming platforms.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 15.2% |

| 15-24 years | 12.1% |

| 25-54 years | 41.7% |

| 55-64 years | 14.5% |

| 65 years and over | 16.5% |

Internet penetration closely follows urban population concentration, with coastal and metropolitan regions demonstrating near-universal broadband and mobile access.

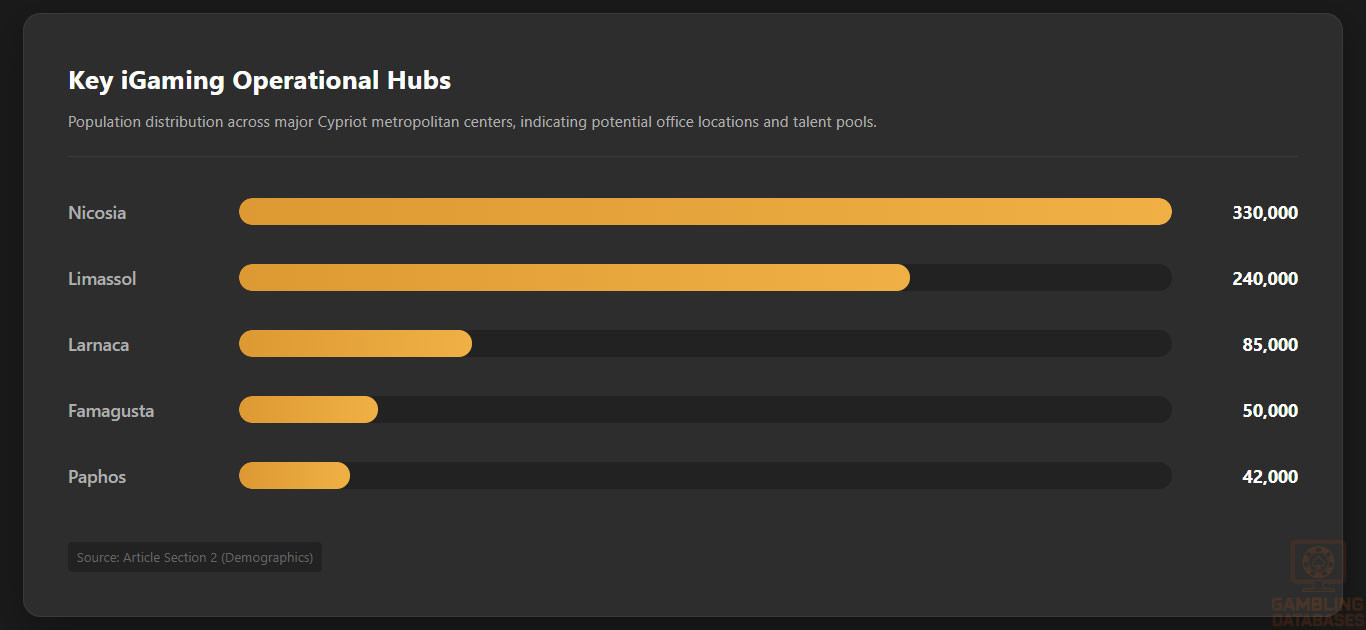

The availability of licensed gambling venues parallels these demographic footholds, concentrating in urban hubs such as Nicosia, Limassol, and Larnaca.

- Nicosia: approximately 330,000 inhabitants including metropolitan area

- Limassol: around 240,000 inhabitants

- Larnaca: roughly 85,000 inhabitants

- Famagusta: near 50,000 inhabitants

- Paphos: 42,000 inhabitants

Economic Indicators and Consumer Spending Power

Cyprus’ economy posted a nominal GDP of approximately €24.5 billion in 2025, reflecting steady growth driven by services, tourism, and financial sectors. The country enjoys an annual GDP growth forecast averaging around 3.2% over the next five years, enhancing consumer spending capability.

Per capita income stands at approximately €20,400 with a relatively equitable income distribution. Median household income supports moderate disposable income, enabling discretionary spending on entertainment and online gaming. The wealth distribution indicates a middle-income majority with vibrant upper-middle-class segments.

Household expenditure data reveals rising allocation towards digital entertainment and leisure activities, supported by increasing credit card and e-wallet penetration. These economic dynamics bode well for expanding the iGaming market with a consumer base equipped for regular online participation.

| Indicator | Value |

|---|---|

| GDP (nominal) | €24.5 billion |

| GDP Growth Forecast (2025-2030 CAGR) | 3.2% |

| GDP per Capita | €20,400 |

| Median Household Income | €18,300 |

| Consumer Spending on Leisure | 6.5% of Household Budget |

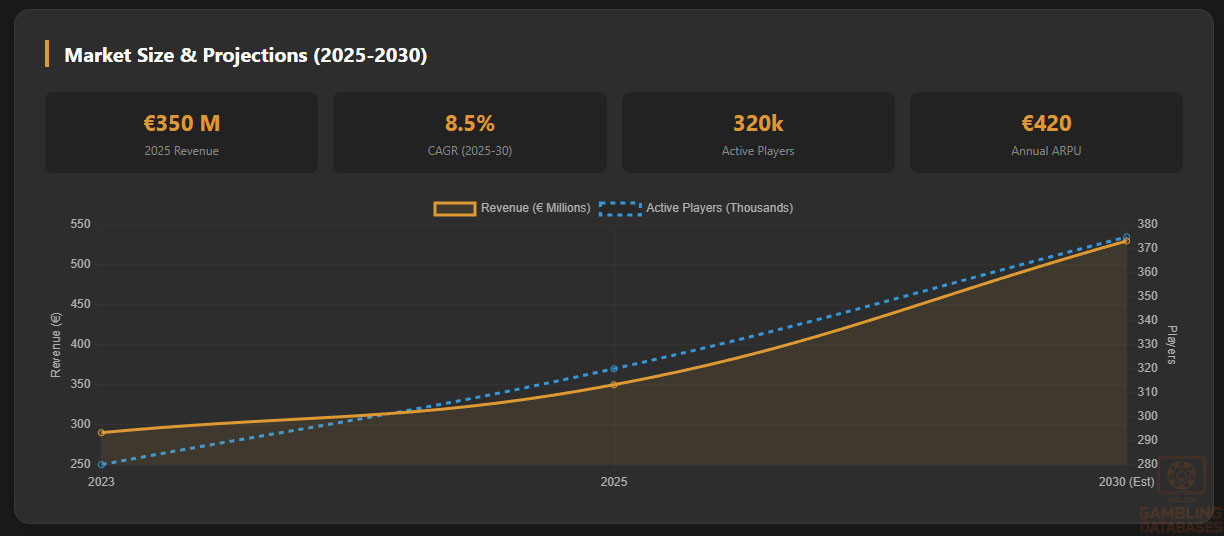

Market Size and Growth Projections

The projected gross gaming revenue (GGR) for Cyprus in 2025 is approximately €350 million. Historical growth has averaged 7.8% annually, driven mainly by expanding online gambling adoption and improved regulatory clarity. Forecast CAGR for 2025-2030 stands at 8.5%, signaling robust market potential.

User base expansion is expected to reach over 370,000 active gambling participants by 2030, fueled by internet and mobile penetration trends. The average revenue per user (ARPU) is estimated at around €420 annually, reflecting a mature market with increasing adaptation of new game categories.

| Metric | 2023 | 2025 | 2030 (Forecast) |

|---|---|---|---|

| Gross Gaming Revenue (€ million) | 290 | 350 | 530 |

| Active Players (thousands) | 280 | 320 | 375 |

| Average Revenue Per User (€) | 410 | 420 | 460 |

| Market CAGR (%) | 7.8% | 8.5% | 7.2% |

Education, Skills, and Digital Literacy

Cyprus features a high literacy rate above 97%, with a well-educated workforce. Secondary education completion rates are high, accompanied by growing tertiary education enrollment, particularly in technology and business disciplines. Digital literacy is widespread, supported by government initiatives promoting ICT skills and digital inclusion.

Cultural and Social Factors

Communication and Language

Cyprus officially recognizes Greek and Turkish as primary languages. English usage is widespread across business and online environments serving as a lingua franca. Internet content consumption heavily favors English and Greek languages, facilitating international operator access and marketing.

- Greek (official, 78% of population)

- Turkish (official, 18% of population)

- English (widely used, especially in business and digital media)

- Russian (growing minority community and online presence)

- Other European languages (small percentages among expatriates)

Cultural Attitudes and Gambling Perception

Gambling holds moderate social acceptance in Cyprus, with a clear regulatory framework instilling legitimacy. Religious and cultural influences, mainly from Greek Orthodox Christianity, traditionally promote conservative attitudes but generally do not prohibit gambling given responsible practices.

Foreign gaming brands are largely accepted, particularly those licensed domestically and recognized for consumer protection. Entertainment consumption trends show a growing enthusiasm for digital gaming, sports betting, and lottery participation, reflecting a shift towards online leisure activities.

Problem Gambling and Social Considerations

Problem gambling prevalence in Cyprus aligns with European averages, with approximately 1.5% of adults exhibiting signs of gambling-related harm. At-risk populations include young adults and individuals with pre-existing addictive behaviors.

Government and industry responses include mandated contributions to addiction counseling, awareness campaigns, and support services. Social responsibility frameworks encourage operators to implement self-exclusion programs and funds for treatment initiatives.

- Mandatory funding for addiction counseling centers

- National awareness campaigns on responsible gambling

- Operator obligations for self-exclusion systems

- Training programs for staff on identifying at-risk gamblers

- Collaboration with healthcare providers and NGOs

Political Structure and Governance

Cyprus operates a stable presidential republic with a democratic political system known for regulatory consistency and pro-business policies. The government promotes foreign investment and adheres to EU regulations, providing a predictable environment for iGaming operators. Its international relations support cross-border cooperation within the EU gambling regulatory framework.

Technology Adoption and Digital Behavior

Internet and Digital Usage

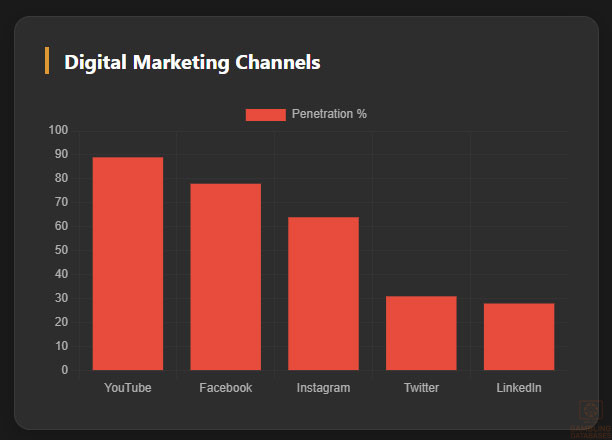

Internet penetration exceeds 87% of the population, with daily internet usage averaging 6.8 hours, underscoring a highly connected society. Mobile network coverage reaches over 95%, encompassing 4G and expanding 5G infrastructure. Social media engagement is robust, particularly among younger demographics, essential for marketing digital gaming products.

Popular social media platforms by market share include:

- Facebook – 78% penetration with extensive daily user engagement

- Instagram – 64% penetration, favored for visual and influencer content

- YouTube – 89% penetration with high video consumption rates

- TikTok – rapidly growing platform especially among under-25 users

- Twitter – 31% penetration, mainly used for news and trends

- LinkedIn – 28% penetration, prominent in professional networking

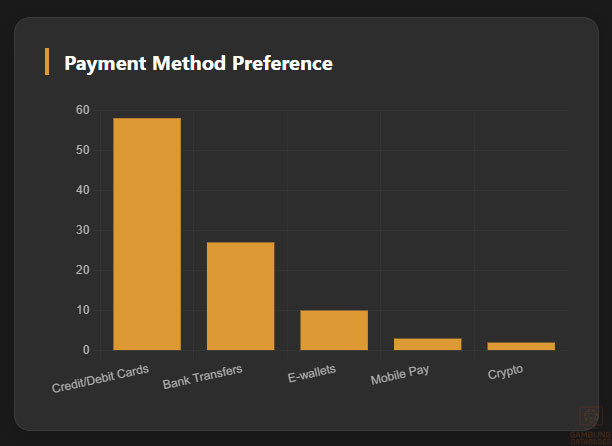

Digital Payment Behavior

The Cypriot market embraces diverse digital payment solutions aligned with iGaming transaction requirements. Credit and debit cards remain dominant, but e-wallets and mobile payments gain strong adoption, particularly among younger and urban consumers. Cryptocurrency usage is emergent, with growing acceptance among progressive operators facilitating blockchain transactions.

Primary digital payment methods, by market share, include:

- Visa/MasterCard credit and debit cards (58%)

- Bank transfers (27%)

- E-wallets such as PayPal, Skrill, Neteller (10%)

- Mobile payment solutions (3%)

- Cryptocurrency payments (2%, growing rapidly among niche players)

Gaming and Gambling Preferences

Current Market Participation

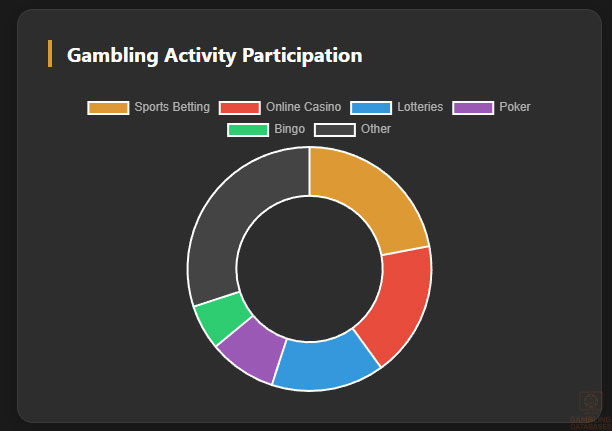

Approximate participation rates among adults show that roughly 35% engage in some form of gambling activity annually. Sports betting is the most popular segment, followed by online casino games, lotteries, and poker. Traditional land-based gambling retains loyal patronage but is increasingly complemented by digital alternatives.

- Sports betting (22% participation)

- Online casino games (18%)

- Lotteries (15%)

- Poker (9%)

- Bingo (6%)

Consumer Behavior Patterns

Cypriot players generally favor platforms offering local language options, fast payouts, and mobile-friendly interfaces. Peak gaming activity occurs during evenings and weekends, with session lengths averaging 40 to 60 minutes. Operators report high retention rates when integrating responsible gambling tools and personalized player engagement.

Spending patterns indicate moderate monthly budgets averaging €35 to €50, with higher spenders concentrated in the 25-44 age group. Digital payment flexibility and trust in licensed operators significantly influence consumer loyalty and participation frequency.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Cyprus boasts an advanced internet infrastructure, with broadband penetration exceeding 80% and mobile internet access near 95%. The average fixed broadband speed is approximately 150 Mbps, supporting high-quality streaming and real-time gaming. Mobile broadband coverage includes widespread 4G availability, ensuring consistent internet performance across urban and suburban areas.

Investment in fiber-optic networks has steadily improved connection reliability and reduced latency, essential for seamless online gaming experiences. Infrastructure resilience is bolstered by regulated service providers committed to maintaining high uptime and quick restoration times.

5G and Future Technology Deployment

The rollout of 5G networks in Cyprus began in late 2023, progressing rapidly through major cities and expanding to suburban and some rural regions by mid-2025. Full 5G coverage of urban centers like Nicosia and Limassol is expected by 2026, promising ultra-low latency that will enhance mobile gaming and live betting.

Network operators are collaborating with government agencies to deploy 5G infrastructure supporting smart city initiatives and IoT development. This next-generation technology will be a key driver for new iGaming technologies and innovative player engagement solutions.

Mobile Technology Ecosystem

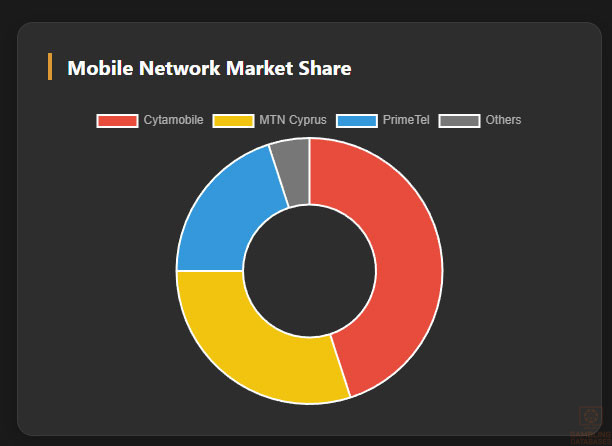

The Cypriot mobile market is highly competitive, with three primary operators commanding the majority of subscribers and data traffic. These providers offer extensive 4G networks and rapidly expanding 5G services, fostering an environment conducive to mobile-first gambling platforms.

- Cytamobile-Vodafone – market leader with around 45% market share and extensive nationwide coverage

- MTN Cyprus – strong presence accounting for around 30% market share with competitive pricing

- PrimeTel – focused on data-driven plans, holding 20% market share

- Smaller regional and MVNO providers covering niche segments and prepaid users

- Emerging digital-only operators targeting young demographics with app-based services

Smartphone adoption stands at over 85%, with preferences trending towards mid-to-high-end Android devices, supported by increasing iOS market penetration. Mobile devices dominate consumer internet usage patterns, making mobile-optimized gambling interfaces essential for market entry success.

Financial Services and Payment Infrastructure

The banking sector in Cyprus is well developed, offering a variety of digital banking platforms with near-universal access to online banking and mobile payment services. Most Cypriots hold at least one bank account, providing a strong foundation for financial transactions linked to gaming activities.

- Bank of Cyprus – leading bank with comprehensive digital offerings and wide branch network

- Hellenic Bank – second largest with focus on corporate and retail banking

- Eurobank Cyprus – international banking services with strong e-commerce support

- Alpha Bank Cyprus – notable for SME lending and digital innovation

- RCB Bank – specialization in corporate and private banking

Payment processing options are broad, encompassing cards, e-wallets, bank transfers, and emerging digital currency acceptance. Integration of diverse payment methods that accommodate local preferences and regulatory requirements is critical for operator success.

- Credit/debit cards (Visa, MasterCard) widely accepted for deposits and withdrawals

- E-wallets such as PayPal, Skrill, Neteller preferred by younger demographics

- Bank transfers popular for larger transactions and withdrawals

- Mobile payment systems gaining traction for convenience and speed

- Cryptocurrency payments accepted by select forward-looking operators

E-commerce and Digital Economy

Cyprus’ digital economy is expanding rapidly, with e-commerce accounting for an increasing share of retail transactions. Consumers exhibit growing trust in online payment methods, supported by robust data protection and consumer rights frameworks compliant with EU standards.

Digital service adoption extends across entertainment, financial services, and retail, enhancing the readiness of the population to engage in regulated online gambling. The rise of influencer marketing and digital payment solutions further propels online commercial activities.

Business Environment and Regulatory Framework

Ease of Business Operations

Cyprus ranks favorably in global ease of doing business indices, particularly for startup registration and regulatory transparency. The government maintains progressive foreign investment policies encouraging iGaming and digital enterprises.

The business registration process involves:

- Preparation and notarization of incorporation documents, including apostille certification for foreign entities

- Submission to the Department of Registrar of Companies for incorporation approval

- Registration with the Tax Department to obtain a Tax Identification Number

- Opening a corporate bank account with required minimum capital deposit

- Final confirmation and issuance of business license certificates

Corporate Structure and Registration

Common legal entities include Limited Liability Companies (LLCs), Branch Offices of foreign companies, and Public Limited Companies. The LLC is preferred for iGaming businesses due to flexibility, limited liability, and ease of compliance.

Foreign ownership is allowed without restrictions, subject to full regulatory disclosure and adherence to anti-money laundering policies. Corporate compliance requirements include annual financial reporting, tax filing, and audit obligations enforced consistently by Cypriot authorities.

Required registration documents typically comprise:

- Articles of incorporation and memorandum of association

- Proof of registered office address in Cyprus

- Identification documents for directors and shareholders

- Tax registration forms and declarations

- Bank account opening confirmation and capital deposit proof

- Compliance and KYC/AML policy documentation

Taxation Framework

The standard corporate income tax rate in Cyprus is 12.5%. Special economic zones offer tax incentives and holiday periods for qualifying activities, including technology and innovation sectors relevant to iGaming. Cyprus benefits from an extensive network of double tax treaties facilitating cross-border investment.

Key treaty countries include:

- United Kingdom

- Germany

- Russia

- France

- United Arab Emirates

- China

- Switzerland

- USA

Personal income tax rates are progressive, with withholding on gambling-related incomes applied selectively. Social security contributions and residency rules ensure compliance with EU labor and tax frameworks.

Market Entry Considerations

Successful market entry in Cyprus requires combining local partnership or entity registration with competitive digital platforms optimized for compliance and user experience. Leveraging technology to ensure fast payment processing, local language support, and responsible gambling tools is critical.

Recommended entry strategies include:

- Forming strategic partnerships with existing Cypriot operators for market access

- Licensing an independent entity to ensure regulatory compliance and local presence

- Utilizing mobile-first platforms to capture growing smartphone user base

- Implementing multi-channel marketing aligned with local content restrictions

- Investing in robust KYC/AML and responsible gambling technologies to exceed regulatory standards

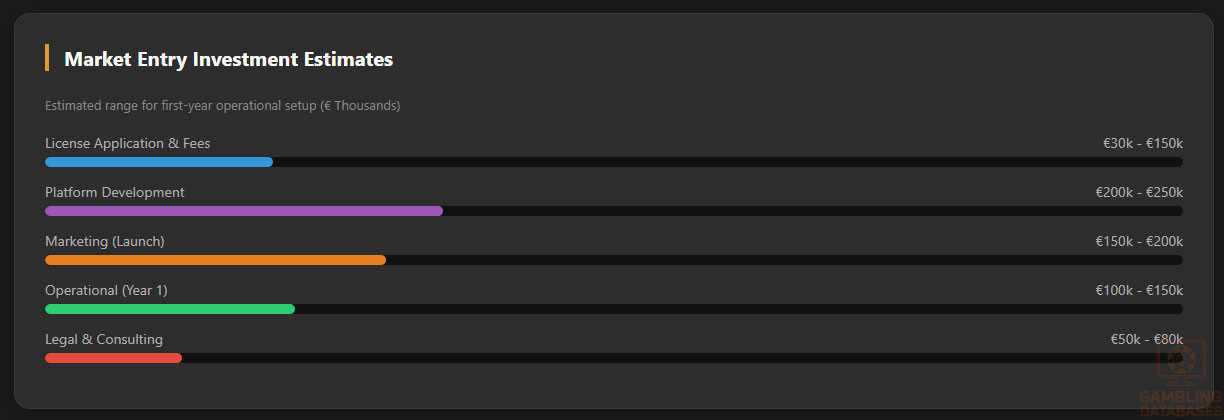

Typical cost factors include licensing fees, legal compliance, platform setup, marketing, staffing, and operational budgets.

Initial setup usually requires an investment of at least €600,000, with ongoing costs related to compliance and customer acquisition.

| Cost Category | Estimated Cost |

|---|---|

| License Application and Fees | 30 – 150 |

| Legal and Consulting Services | 50 – 80 |

| Company Registration and Setup | 15 – 25 |

| Technology Platform Development | 200 – 250 |

| Marketing and Customer Acquisition | 150 – 200 |

| Operational Expenses (First Year) | 100 – 150 |

Market entry timelines vary from 4 to 8 months, contingent on licensing efficiency, technology integration, and marketing rollout.

- Preliminary assessments and document gathering – 1 month

- License application submission and review – 3 to 6 months

- Technology and platform integration – overlapping 2 to 4 months

- Marketing and launch preparations – 1 to 2 months

Key success factors include regulatory compliance, strong local partnerships, digital innovation, and consumer trust-building. Challenges include navigating complex licensing, maintaining cybersecurity standards, and competing with established international operators.

- Robust compliance frameworks

- Investment in mobile technology and UX

- Localized content and marketing

- High-quality customer support

- Effective payment processing

- Adaptation to evolving regulations

Exit strategies should consider license transfer regulations, asset valuation, and market liquidity. Early planning is essential to maximize investment returns and facilitate ownership transitions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Cyprus?

Yes, online gambling in Cyprus is fully legal and regulated under the Cyprus Gaming and Casino Supervision Commission (CGCSC). Licensed operators can offer online casino games, sports betting, and lotteries. Unauthorized gambling activities are prohibited with strict enforcement and penalties to protect consumers and ensure market integrity.

2. What types of gambling licenses are available and what do they cover?

Cyprus offers a unified iGaming license covering multiple gambling categories including online casinos, sports betting, poker, lotteries, and bingo. Licenses are issued by CGCSC and require compliance with technical, financial, and operational standards. The framework supports multi-product operators under single licenses for streamlined market access.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees range from €30,000 to €150,000 depending on the scope. Annual license fees depend on turnover, starting at €50,000. The typical licensing process takes between 3 to 6 months, including background checks, document reviews, and technical validations.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain a Cyprus gambling license by establishing a registered entity or branch within the country. Full disclosure of ownership and management is required, as well as compliance with KYC, AML, and data protection regulations. Foreign ownership is permitted without restrictions but must meet regulatory standards.

5. What are the tax obligations for iGaming operators?

Operators are subject to Gross Gaming Revenue (GGR) taxation ranging from 15% to 20% depending on the game type, alongside corporate income tax of 12.5%. Annual license fees and compliance costs also apply. The tax system is designed to be competitive while ensuring significant revenue contributions to the government.

6. Are gambling winnings taxed for players?

Generally, players are not taxed on winnings from licensed operators in Cyprus. Winnings taxation primarily applies to unlicensed or private gambling activities. This policy supports player participation and market transparency.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, technology platform maintenance, staffing, marketing, compliance monitoring, and payment processing. Initial setup can require €600,000 or more. These costs vary with market scale and platform complexity.

8. What is the expected ROI timeline for entering this market?

ROI timelines fluctuate but generally range from 18 to 36 months, depending on customer acquisition efficiency, market penetration, and cost control. Strategic marketing and superior technology shorten the break-even period.

9. What are the local presence requirements for operators?

Operators must establish a registered company or branch in Cyprus with physical offices for compliance staff. This ensures regulatory oversight and effective local management of responsible gambling and KYC procedures.

10. What payment methods are available and recommended?

Recommended payment methods include credit/debit cards, e-wallets like PayPal and Skrill, bank transfers, mobile payments, and emerging cryptocurrency options. Offering multiple options enhances player convenience and regulatory compliance.

11. What are the advertising and marketing restrictions?

Advertising must avoid misleading claims, not target minors, and exclude unlicensed operator promotions. Permitted channels include television, radio, internet, sponsorships, and print media, all subject to content and timing restrictions enforcing responsible promotion.

12. What responsible gambling measures are mandatory?

Mandatory measures include self-exclusion programs, deposit and loss limits, time limits on play, player information disclosures, and access to counselling and support. Operators must implement robust frameworks to protect vulnerable populations and ensure compliance.

13. How large is the iGaming market and what is the growth potential?

The Cyprus iGaming market is estimated at €350 million in gross revenue for 2025, with an expected CAGR of 8.5% through 2030. Growing internet penetration and regulatory clarity support expanding user bases and revenue growth.

14. Who are the main competitors and what is their market share?

The market features a mix of local operators and international brands competing primarily in online casino and sports betting verticals. Market shares tend to be concentrated among 5 to 8 major players offering multi-product portfolios and strong regional presence.

15. What are the player preferences and typical spending patterns?

Players prefer mobile-friendly platforms featuring popular games like sports betting and online slots. Average monthly spending ranges between €35 and €50, with peak activity during evenings and weekends. Trust in payment security and regulatory compliance heavily influences player loyalty.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, strong local partnerships, superior user experience, and effective marketing. Challenges include navigating licensing complexity, competing against established operators, ensuring cybersecurity, and adapting to evolving regulations.

Sources and References

- Cyprus Gaming and Casino Supervision Commission – Official Website – https://www.cgcsr.gov.cy

- Cyprus Statistical Service – Demographic and Economic Data 2025 – https://www.cystat.gov.cy

- Central Bank of Cyprus – Financial Reports and Banking Information – https://www.centralbank.cy

- Department of Registrar of Companies – Registration Procedures – https://www.mcit.gov.cy

- Ministry of Finance Cyprus – Taxation Rules and Guidelines – https://www.mof.gov.cy

- World Bank – Doing Business 2024 Report – https://www.worldbank.org

- International Telecommunication Union – ICT and Internet Data – https://www.itu.int

- Cyprus Telecommunication Authority – Network Infrastructure Updates – https://www.cyta.com.cy

- European Gaming and Betting Association – Market Analysis Reports 2024

- Gaming Industry Research Group – Global Market Trends Report 2024

- Cyprus Ministry of Digital Governance – Digital Economy Strategy – https://www.digitalcyprus.gov.cy

- Cyprus Chamber of Commerce and Industry – Business Environment Analysis – https://www.ccci.org.cy

- International Monetary Fund – Country Reports and Economic Analysis – https://www.imf.org

- Cyprus Ministry of Health – Addiction Prevention and Responsible Gambling Programs

- United Nations Development Programme – Social and Economic Development Reports

- European Commission – Consumer Protection and Data Privacy Regulations

- Cyprus Investment Promotion Agency – Foreign Investment Guidelines

- Global Mobile Network Report 2024 – Market Competition and Coverage Analysis

- PayTech Industry Reports – Payment Methods and Digital Wallet Adoption

- Academic Journals on iGaming Regulation and Market Dynamics in Europe

- Industry News Outlets on Cyprus Gambling Sector Developments 2023-2025

- Local Media Reports on Gambling Advertising and Social Impact Studies

🎯 Gambling Databases Country Rating: Cyprus

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.8/10 | 🟡 Moderate |

| Player Access Score | 9.8/10 | 🟢 Excellent |

| Overall Market Attractiveness | 7.5/10 | 🟡 Good (But High Entry Barrier) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Physical Presence Mandate: Operators MUST establish a registered entity, local branch, and maintain compliance/responsible gambling teams PHYSICALLY within Cyprus. This creates a massive overhead for a market of only 1.2 million people.

- High Entry CapEx: Estimated setup costs exceed €600,000 due to licensing fees, local incorporation, office setup, and technical compliance.

- Strict Financial Audits: Quarterly reporting and annual audits are mandatory. The regulator (CGCSC) conducts random audits.

- Limited Market Size: With only ~370,000 active players projected by 2030, the Total Addressable Market (TAM) is small. Competition is concentrated among 8 existing giants.

- EU Compliance & GDPR: Full adherence to strict EU Anti-Money Laundering (AML) and Data Protection (GDPR) laws is non-negotiable.

- Unlicensed Operation Penalties: Operating without a license leads to blacklisting, fines, and potential criminal prosecution for fraud.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.8/3.0 | Full product legality (Casino + Sports) (+3.0). Deduction for “Strict surveillance” and rigid administrative oversight (-0.2). Final: 2.8/3.0 |

| Licensing Process | 25% | 1.5/2.5 | Accessible process but costly. Base (+2.0). Deduction for fees up to €150k initially + €50k annual (-0.25). Deduction for lengthy 3-6 month timeline and complex background checks (-0.25). Final: 1.5/2.5 |

| Taxation & Costs | 20% | 1.3/2.0 | GGR Tax is 20% for Casino / 15% Sports (+1.5). Corporate tax is 12.5%. Total effective tax burden approaches 30%+ (-0.2). Deduction for high operational costs (local staff/office) in a small market (-0.5). Final: 0.8/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | Base (+1.5). CRITICAL DEDUCTION: Mandatory physical presence (office + staff) is a severe burden for a 1.2m population market (-0.75). Requirement for local domain and strict EU-aligned KYC (-0.25). Final: 0.5/1.5 |

| Market Environment | 10% | 0.7/1.0 | Stable EU jurisdiction (+1.0). Deduction for advertising restrictions (no aggressive marketing, content controls) (-0.2). Deduction for small market cap limits scalability (-0.1). Final: 0.7/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal. Players can access sports betting, casino, poker, and lottery legally through licensed sites. No deductions. |

| Practical Accessibility | 30% | 3.0/3.0 | Excellent infrastructure (95% mobile penetration, 5G). Multiple payment methods (Cards, E-wallets, Instant Banking). No blocking of licensed sites. |

| Player Penalties | 20% | 2.0/2.0 | No taxes on player winnings from licensed operators. No legal penalties for players. |

| Market Availability | 10% | 0.8/1.0 | 8 Licensed online operators (+1.0). Slight deduction because market is concentrated and variety is lower than massive markets like UK/Malta (-0.2). |

🔍 Key Highlights

Strengths

- Regulatory Clarity: A unified licensing system (CGCSC) covers all verticals (Casino, Sports, Lottery), providing legal certainty.

- High Player Value: Average Revenue Per User (ARPU) is €420, indicating a spending-capable demographic.

- Infrastructure: 95% mobile penetration and rapidly expanding 5G coverage support high-quality mobile gaming.

- Tax Stability: 12.5% Corporate Tax is one of the lowest in the EU (though GGR tax is separate).

⛔️ CRITICAL RISKS AND CHALLENGES

- Small Market / High Overhead: The #1 Risk. You are forced to set up a physical office and hire local staff for a market of only 1.2 million people. The economics often fail for smaller operators.

- High GGR Tax: 20% GGR tax on casino games is significant. Combined with operational costs, margins are thin.

- Market Saturation: 8 established operators already hold 60% of the online market share. Breaking in requires significant marketing spend.

- Strict Compliance: EU-standard AML/KYC and mandatory responsible gambling interventions (self-exclusion, loss limits) increase operational friction.

- Payment Limits: Euro-only currency restrictions and strict banking oversight can complicate processing for non-EU entities.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €600,000 – €800,000 (License, Entity Setup, Tech, First Year Office/Staff).

Monthly Operating Costs: €100,000+ (Due to mandatory local staff, compliance teams, and office rent).

Effective Tax Rate on Revenue: ~32.5% (20% GGR + 12.5% Corporate Tax).

Customer Acquisition Cost: Moderate (€100-200), but rising due to ad restrictions and competition.

Time to Breakeven: 24 – 36 Months.

Profitability Assessment: DIFFICULT FOR STARTUPS. The math is brutal for small players. To cover the fixed costs of a local office and staff, plus a €600k setup, you need significant market share immediately. This market is viable only for:

- Large international groups expanding their footprint.

- Companies using Cyprus as a B2B hub who also run a B2C arm.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | High | EU jurisdiction means strong enforcement capabilities. ISP blocking is active. Payments to unauthorized entities can be blocked by local banks. |

| Licensed Operators | Medium | Strict regulatory audits. Risk of fines for AML failures or responsible gambling lapses. License revocation is a real threat for non-compliance. |

| Affiliates/Advertisers | Medium | Advertising unauthorized operators is prohibited. Strict content rules (no targeting minors, no misleading claims). |

| Payment Processors | High | Must adhere to strict EU anti-money laundering directives. Processing for unlicensed gambling is illegal. |

| Company Directors | Medium | Background checks are mandatory. Directors of licensed entities are personally accountable for compliance failures. |

🚨 Extradition and International Enforcement

Extradition Treaties: Cyprus is an EU member state. It has active European Arrest Warrant (EAW) agreements with all EU nations. It also maintains extradition treaties with the USA, UK, Russia, and Australia.

Enforcement History: Cyprus actively cooperates with international bodies (Interpol, Europol) regarding financial crimes and fraud. While gambling-specific extradition is rare, “fraud” charges related to unregulated gambling are a potential vector for prosecution.

Safe Jurisdictions: None within the EU/Western sphere.

📋 Final Verdict

Cyprus receives an Operator Ease Score of 6.8/10 and a Player Access Score of 9.8/10, resulting in an overall market attractiveness rating of 7.5/10.

HONEST ASSESSMENT: Cyprus is a “Gold-Plated Trap.” It looks excellent on paper—fully legal, EU regulated, high player value. However, the requirement to establish a physical presence with local staff for a tiny population of 1.2 million destroys the unit economics for 90% of operators. Unless you are a massive Tier-1 operator who can absorb high fixed costs for strategic reasons, the ROI here is agonizingly slow.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major multinational operator (Entain, Flutter, etc.) expanding your EU footprint.

- Able to invest €1M+ upfront with a 3-year breakeven horizon.

- Already operating a B2B business in Cyprus (tech/support) and want to add a B2C vertical using existing resources.

❌ Definitely Avoid If You Are:

- A startup or mid-sized operator looking for quick cash flow.

- An offshore operator hoping to run “grey” (Enforcement is strict).

- Unable to commit to a physical office and local employees.

- Focused purely on high-margin Casino without a Sportsbook product (20% tax hurts).

⚠️ BOTTOM LINE: Excellent legal framework, but the “Physical Presence vs. Market Size” ratio makes it financially unviable for anyone but the biggest players.

Looking at the sports betting market in New York, I’m curious about the impact of natural systems on betting trends. Can we apply outdoor approaches to understand player behavior?

Regarding the application of natural systems to sports betting, it’s an intriguing concept. While direct correlations might be challenging to establish, understanding the psychological and sociological aspects of betting can indeed benefit from insights into human behavior in natural environments. For instance, examining how outdoor activities influence decision-making could provide unique perspectives on betting trends.

Thanks for the insight. I’ve been considering how outdoor environments might influence betting decisions, possibly through stress reduction or enhanced cognitive functions. Do you think there’s a potential for developing betting strategies based on these natural influences?

That’s an interesting point about natural influences on betting decisions. While it’s speculative, exploring the psychological effects of natural environments on risk-taking and decision-making could offer novel insights into betting behavior. It might be worthwhile to look into studies on environmental psychology and its potential applications in sports betting analysis.

Tried to analyze betting data from a recent Knicks game, but the numbers just didn’t add up. What am I missing? Is there a specific tool or method I should be using to get more accurate results?

About your question on analyzing betting data, it seems like there might be a few factors at play that could be affecting your results. Firstly, ensure you’re accounting for all variables, including team performance, player injuries, and even external factors like weather for outdoor games. Secondly, consider utilizing more advanced statistical tools or consulting with a sports analyst to refine your method. There are also several online platforms and forums, such as those found on GamblingDatabases.com, where you can find detailed guides and discussions on sports betting analysis.