Denmark’s iGaming market is a mature, well-regulated ecosystem driven by a progressive regulatory framework and dynamic digital adoption. The country combines rigorous consumer protections with a transparent licensing regime, making it an attractive destination for operators seeking a stable and innovative European market.

With strong mobile penetration and a growing online casino segment, Denmark offers significant growth potential amidst evolving regulatory advancements focused on player safety, market integrity, and competitive fairness.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Fully Regulated, Licensed Framework |

| Regulatory Authority | Danish Gambling Authority (Spillemyndigheden) |

| Population | 5.9 million |

| GDP per Capita | ~USD 65,000 |

| Internet Penetration | 98% |

| Mobile Penetration | 93% |

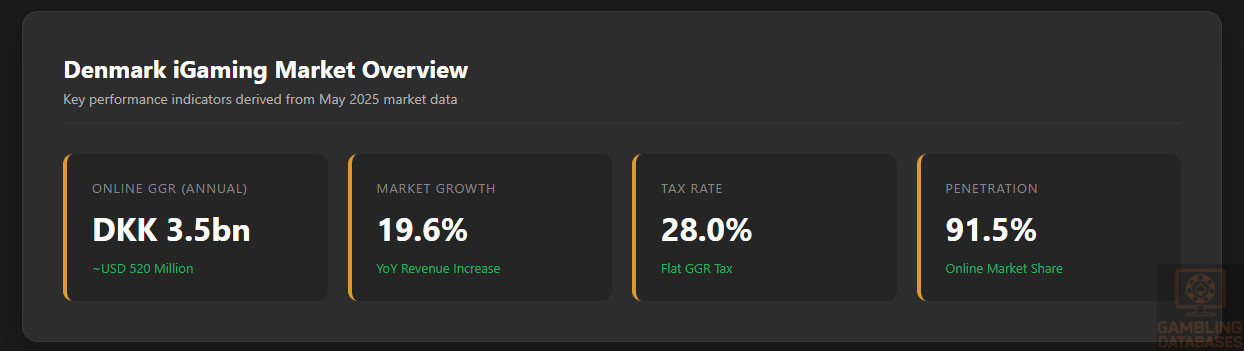

| Online Gambling Market Size (Annual GGR) | DKK 3.5 billion (~USD 520 million) |

| Total Gambling Market Revenue (May 2025) | DKK 683 million (~USD 101 million) |

| Online Casino Revenue (May 2025) | DKK 389 million (+39.9% YoY) |

| Sports Betting Revenue (Annual 2024) | DKK 2.2 billion |

| Top Gaming Vertical | Online Slots (78.9% of online casino revenue) |

| License Application Fee | DKK 327,500 (~USD 49,000) |

| Operator Gross Gaming Revenue Tax Rate | 28% |

| Average License Approval Time | 3-6 Months |

| Local Presence Requirement | Physical presence in Denmark or EU/EEA, or local representative |

| Compliance Monitoring | Regular audits, RNG certification, AML compliance |

| Player Protection Measures | Mandatory KYC, self-exclusion, anti-money laundering |

| Advertising Restrictions | Strict promotional limits including bonus caps |

| Market Penetration Online | 91.5% of total gambling activity |

| Growth Forecast (CAGR 2024-2026) | 6-8% |

| Average Revenue Per User (ARPU) | DKK 4,500 (~USD 675) annually |

| Number of Licensed Operators (2025) | 41 licensed operators |

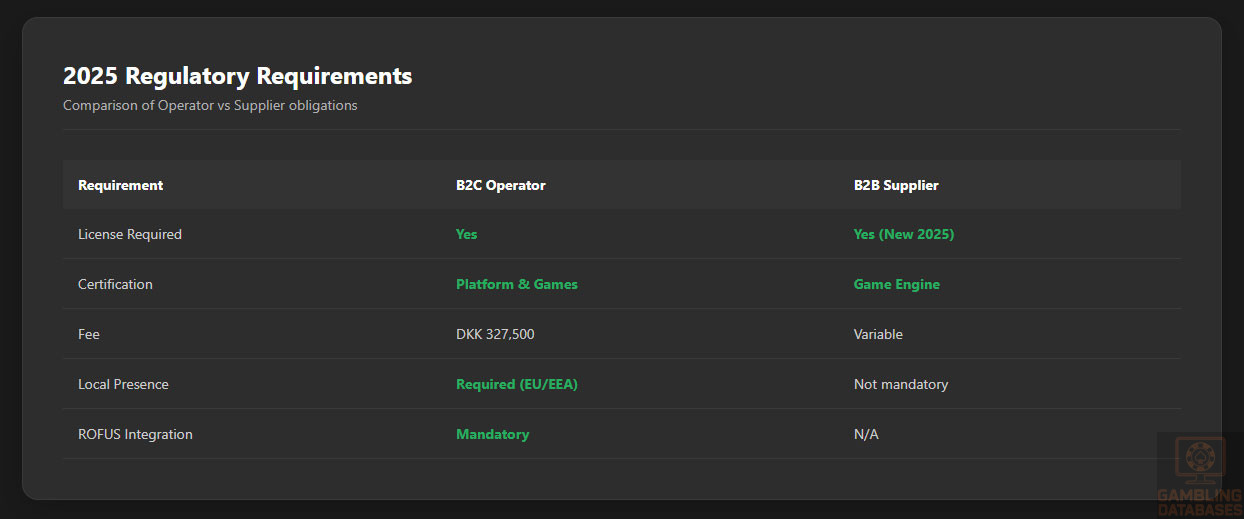

| Supplier Licensing Requirement | Mandatory from January 1, 2025 |

| Game Supplier Certification | Dual certification mandatory from July 1, 2025 |

| Responsible Gambling Tools | National self-exclusion register (ROFUS), StopSpillet helpline |

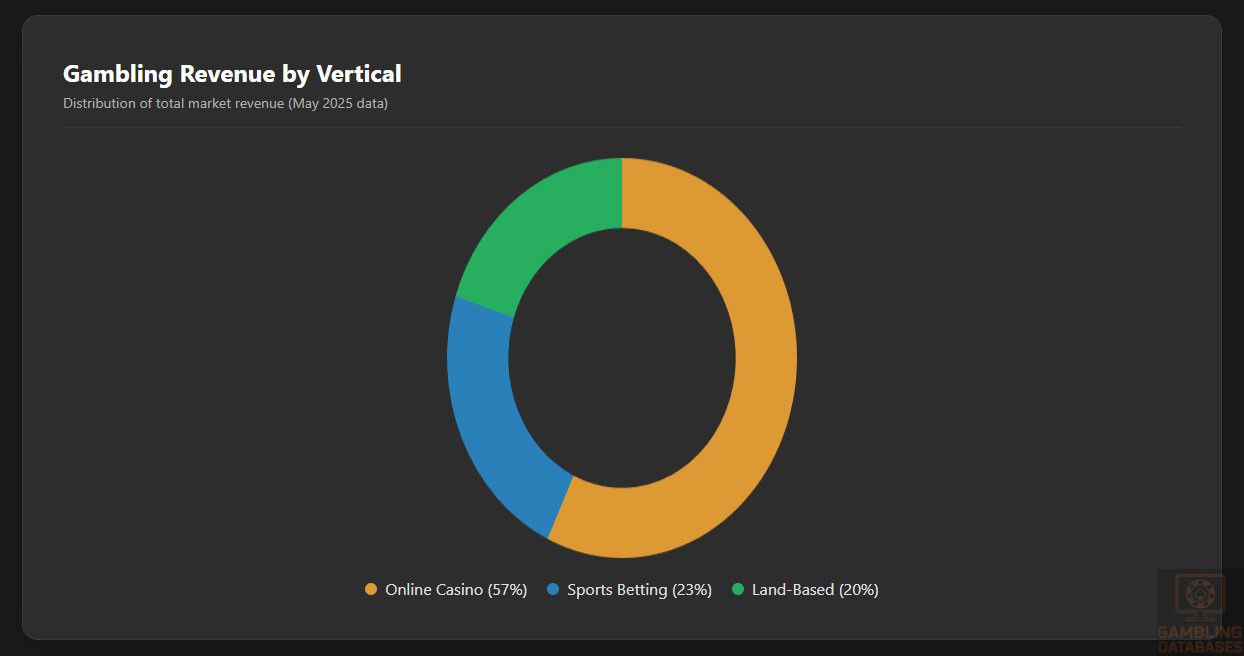

| Market Share – Online Casino | ~57% of total gambling revenue |

| Market Share – Sports Betting | ~23% |

| Market Share – Land-Based Slots & Casinos | ~20% |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Denmark maintains a comprehensive regulatory framework covering all categories of gambling, including land-based casino operations, sports betting, lotteries, online gaming, and electronic gaming machines. The Danish Gambling Authority (Spillemyndigheden) is the central regulatory body overseeing the licensing, compliance control, and market integrity within this sector.

The regulatory regime enforces strict consumer protection through measures such as mandatory licensing for all operators, advanced player identification, and AML compliance. The market is transparent and adheres to EU regulations, ensuring cross-border cooperation and regulatory harmonization.

Land-Based Gambling Activities

Land-based gambling in Denmark is well established with licensed casinos, sports betting shops, and slot machine halls operating under stringent regulatory oversight.

Casinos are typically located in major urban centers and are often integrated with hotel and entertainment complexes. Sports betting venues concentrate around populous areas with legal authorization for in-person betting. Slot machine operations are heavily regulated, with defined limits on the number and type of machines allowed.

Online Gambling Framework

The online gambling sector in Denmark operates under a robust licensing framework introduced in 2012 and continuously updated to reflect technological and market developments. Digital gaming operators must secure licenses from Spillemyndigheden to provide online casino, poker, sports betting, and other gaming services.

Activities prohibited in the online space include unlicensed gambling offers, unauthorized advertising, and any forms promoting underage or irresponsible gambling behaviors.

Licensed Operators and Market Players

The competitive landscape comprises both established domestic operators and major international entities. The state-owned Danske Spil leads the market, maintaining a strong multi-channel presence across land-based and online verticals. International operators such as Kindred Group, bet365, LeoVegas, and PokerStars actively compete, leveraging advanced technology and marketing strategies focused on mobile and online user acquisition.

The market features a high degree of digital innovation with mobile gaming accounting for 67% of play. The operator competition centers around technology differentiation, compliance with evolving regulatory standards, and responsible gambling measures that foster consumer trust.

| Operator Name | Primary Verticals | Market Position |

|---|---|---|

| Danske Spil | Lottery, Sports Betting, Casino | Market Leader, State-Owned |

| Kindred Group | Online Casino, Sports Betting | Major International Operator |

| bet365 | Sports Betting, Online Casino | Top Sports Betting Operator |

| LeoVegas | Casino, Sports Betting | Growing Mobile Presence |

| Kaizen Gaming | Sports Betting | Emerging Sponsor & Market Player |

| Royal Casino | Land-Based & Online Casino | Local Hybrid Operator |

| PokerStars | Poker, Casino | Niche Market Specialist |

Licensing Framework and Requirements

Application Process and Eligibility

The Danish Gambling Authority administers licensing for all gambling sectors, requiring detailed applications demonstrating financial stability, technical capability, and compliance readiness. Applicants must provide substantial documentation to prove operational integrity and reliable consumer protection mechanisms.

License applications are subject to a non-refundable fee of approximately DKK 327,500, with combined licenses covering multiple gaming verticals requiring higher fees. The typical approval period ranges from 3 to 6 months, depending on completeness and operator responsiveness.

Game suppliers seeking to provide software and gaming content to licensed operators must also obtain a supplier license, a mandatory requirement effective from January 1, 2025. This framework includes rigorous inspection and testing of gaming platforms and RNG certification by accredited labs.

The eligibility criteria for applicants emphasize transparency, financial soundness, compliance with anti-money laundering (AML) standards, and adherence to consumer protection laws, including responsible gambling protocols.

- Corporate registration and ownership verification

- Financial viability evidence and three-year audited financial statements

- Detailed business and market strategy plans

- Technical documentation including RNG and game fairness certifications

- Criminal background checks for key personnel

- AML and KYC procedure manuals

Local Presence and Operational Requirements

Operators must establish a legal presence within Denmark or the broader European Economic Area (EEA), or appoint a local representative to ensure compliance with Danish gambling laws. This includes hosting servers in compliant jurisdictions and maintaining records accessible to regulators.

Operational obligations include staffing qualified compliance officers, implementing secure player data management systems, and facilitating effective communication channels with the Danish Gambling Authority.

Foreign ownership is permissible without significant restrictions, provided all regulatory obligations are met. Partnerships with Danish entities are common to enhance local market penetration and regulatory trust.

- Registered office within Denmark or EEA

- Designated compliance officer resident in Denmark or EEA

- Operational control over gaming offerings

- Secure data handling and anti-fraud procedures

- Compliance reporting and audit cooperation

Compliance Obligations and Monitoring

Player Protection and Identification

Denmark enforces stringent player protection standards emphasizing age verification, responsible gambling, and anti-money laundering requirements. All operators must implement robust KYC procedures to verify player identity and prevent underage gambling.

Self-exclusion mechanisms are mandatory and integrated with the national ROFUS register, enabling players to voluntarily restrict access across all licensed operators. Additionally, operators must provide clear information and tools for responsible gambling, including deposit limits and reality checks.

- Mandatory age verification at registration and betting points

- KYC documentation for identity confirmation

- Integration with the national self-exclusion system (ROFUS)

- AML transaction monitoring and suspicious activity reporting

- Provision of responsible gambling tools and information

Financial Monitoring and Reporting

Operators are required to maintain transparent financial records and submit regular reports to Spillemyndigheden covering gross gaming revenue, player transactions, and AML compliance. These reports ensure ongoing oversight of market integrity and operator solvency.

The sequential reporting requirements include monthly GGR declarations, AML incident reports, and annual financial audits by approved accountants. The Danish Gambling Authority reserves the right to conduct on-site inspections and demand additional documentation at any time.

- Monthly gross gaming revenue (GGR) report submission

- Quarterly anti-money laundering activity reports

- Annual audited financial statements

- Ad hoc compliance and operational audits upon request

Taxation Structure and Financial Obligations

Player Taxation

Players in Denmark are generally exempt from taxation on gambling winnings, shifting the tax burden to operators. This tax policy supports player engagement and aligns with broader European taxation standards.

Operator Taxation

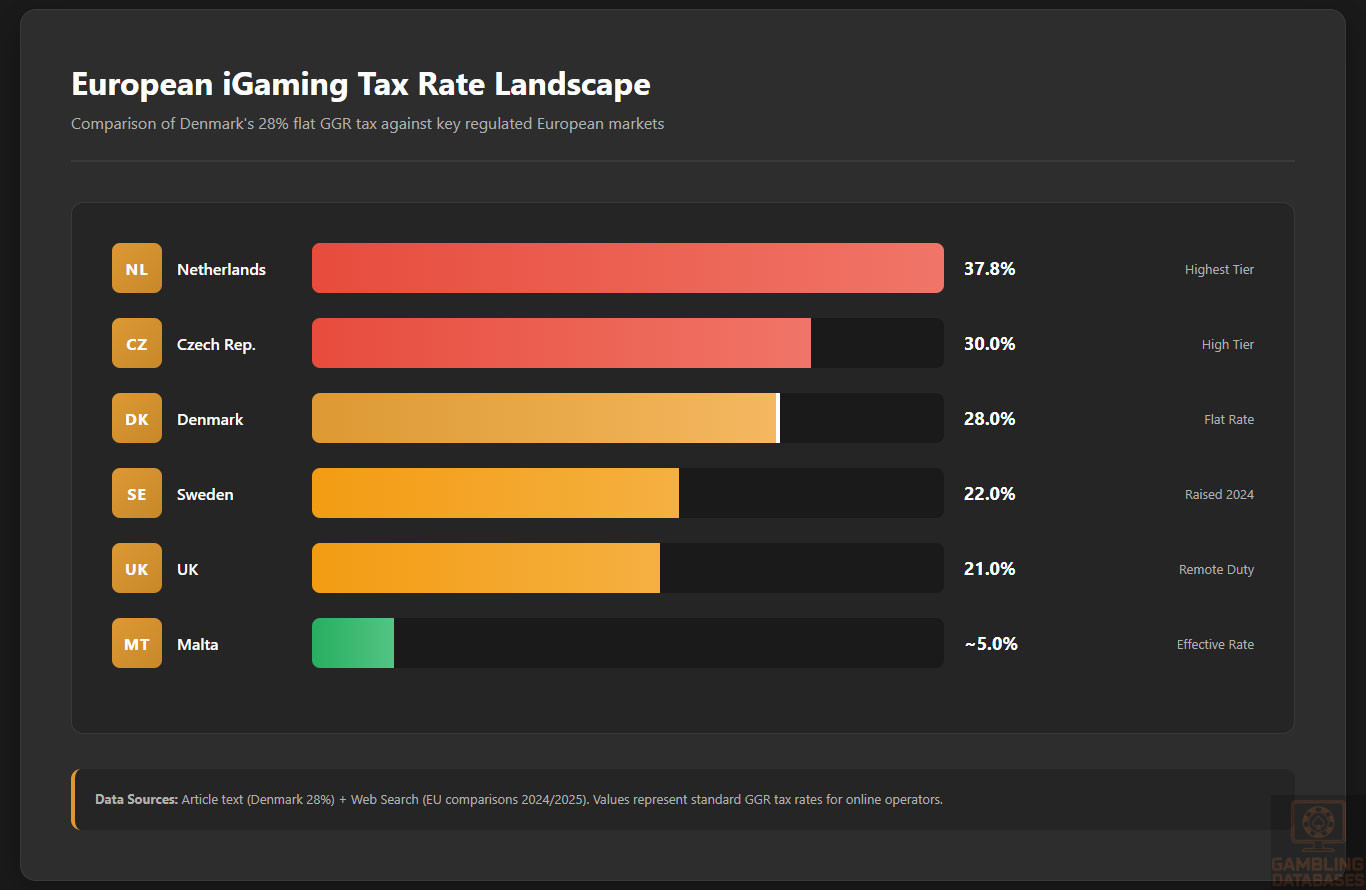

Operators pay a gross gaming revenue (GGR) tax applied at 28%, which is among the higher rates across European regulated markets. The tax includes all gaming verticals and applies irrespective of the operator’s country of incorporation. There are no separate turnover taxes, but license renewal fees are charged periodically, depending on the license type.

| Game Type | Tax Rate |

|---|---|

| Online Casino | 28% GGR |

| Sports Betting | 28% GGR |

| Lottery | 28% GGR |

| Land-Based Gambling | 28% GGR |

Gambling Market Financial Performance

The Danish gambling market demonstrated consistent growth, with a 19.6% year-on-year increase in May 2025 total gambling revenue reaching DKK 683 million. The online casino segment was the largest contributor, increasing by 39.9% to DKK 389 million during the same period.

Sports betting and land-based casinos maintained steady revenue streams, together constituting roughly 43% of the market’s total revenue. Tax revenues from the gambling sector provide a substantial contribution to the Danish state budget, reflecting the market’s healthy fiscal footprint.

Advertising and Marketing Restrictions

Marketing and advertising for licensed gambling operators are tightly regulated to ensure transparency and consumer protection. Promotional spending caps limit bonuses to DKK 1,000 per player per campaign, and advertisements must include clear warnings about gambling risks.

Operators are restricted from targeting minors and vulnerable groups, with digital channels under periodic review to prevent misleading claims or unauthorized promotions. Sponsorship deals are permitted but monitored for compliance with ethical standards.

- Bonus and promotional spending cap of DKK 1,000 per player

- Advertising must carry responsible gambling messages

- Prohibition on advertising targeting minors

- Restrictions on timing and frequency of gambling ads

- Strict oversight of sponsorships and partnerships

Recent Regulatory Changes and Their Impact

Significant amendments in 2025 include the introduction of mandatory supplier licensing and dual certification, which increase market transparency and regulatory clarity. These changes place additional compliance responsibilities on B2B providers and operators alike.

Advertising rules have become more restrictive, instituting spending caps and enhanced disclosure obligations. Enhanced player protection measures such as strengthened self-exclusion protocols have also been integrated, reinforcing Denmark’s commitment to responsible gaming.

Enforcement Mechanisms and Penalties

The Danish Gambling Authority enforces compliance through a range of measures including fines, license suspensions, and revocations. Penalties are imposed for breaches such as unlicensed operations, failure to comply with AML regulations, and misleading advertising.

- Monetary fines for regulatory breaches

- Temporary license suspensions for serious non-compliance

- Permanent license revocation for repeated offenses

- Operational restrictions imposed to halt unlawful activity

- Public warning notices to increase market transparency

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Denmark’s population reached 6.0 million in 2025, reflecting steady growth and demographic stability. The median age stands at 42.6 years, with women averaging 43.5 years and men 41.7 years, indicating a mature and aging population structure.

Gender distribution is nearly balanced, with 50.3% of the population being female. Life expectancy is high, with men living an average of 79.9 years and women 83.7 years, among the highest in Europe.

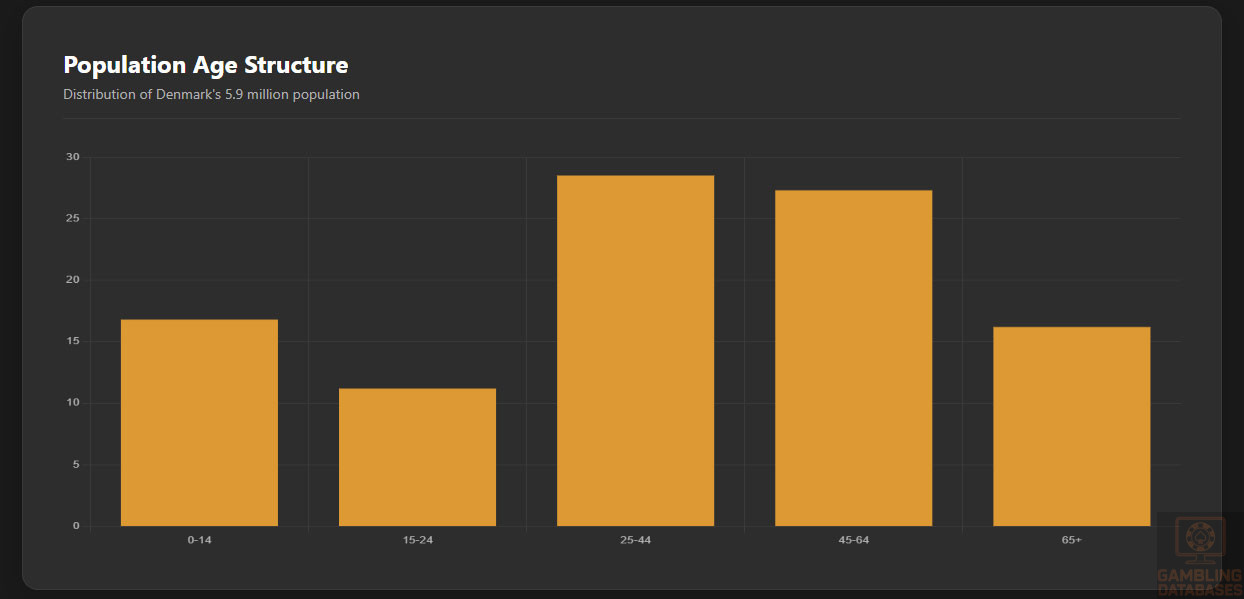

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 16.8% |

| 15-24 years | 11.2% |

| 25-44 years | 28.5% |

| 45-64 years | 27.3% |

| 65+ years | 16.2% |

Geographic Distribution

Urbanization is pronounced in Denmark, with 87.4% of the population residing in urban areas, totaling approximately 5.25 million people. The country has a population density of 141 people per square kilometer, reflecting efficient land use and concentrated development.

Internet access is nearly universal, with 97% of households having home internet, facilitating widespread digital engagement and online service adoption, including iGaming.

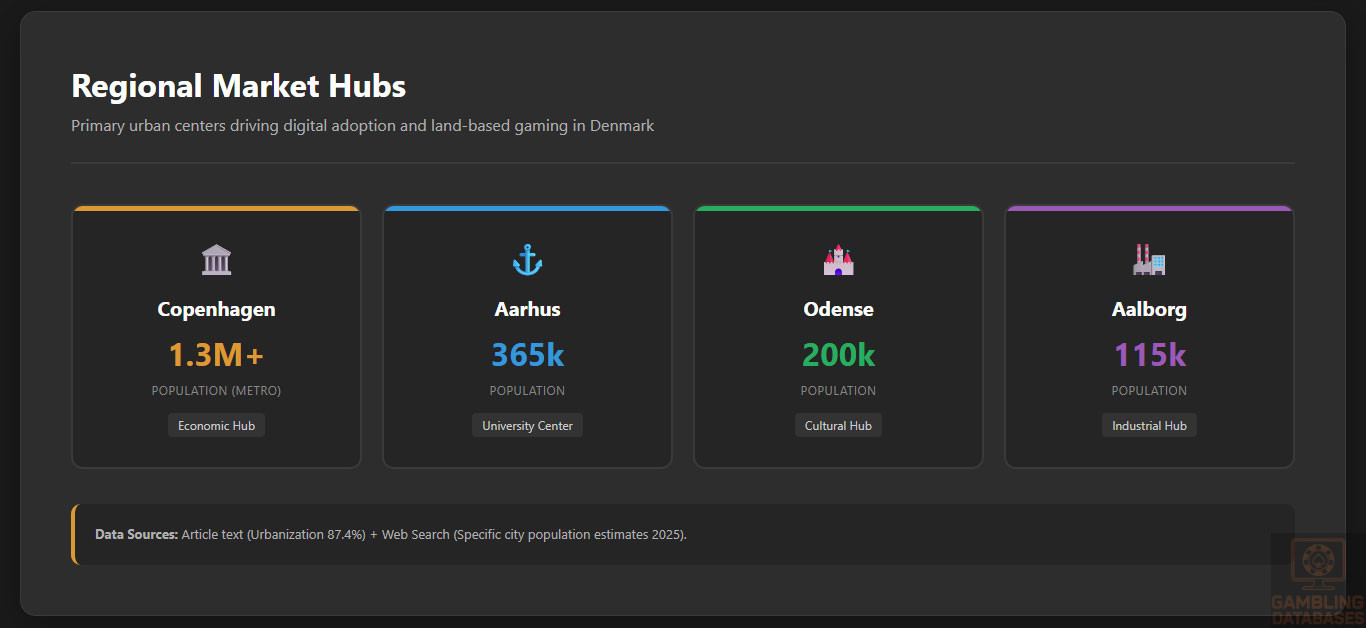

- Copenhagen – 1.3 million residents, economic and cultural hub

- Aarhus – 365,000 residents, second-largest city and educational center

- Odense – 200,000 residents, birthplace of Hans Christian Andersen

- Aalborg – 115,000 residents, industrial and port city

- Esbjerg – 75,000 residents, energy and fishing industry center

- Roskilde – 50,000 residents, historical and festival city

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Denmark’s economy is robust, with a GDP per capita of approximately USD 65,000, placing it among the wealthiest nations globally. The service sector dominates, accounting for 75% of GDP, followed by industry at 22% and agriculture at 3%.

The country maintains strong economic stability, with low unemployment and high labor participation, supporting consistent consumer spending and digital service adoption.

Income and Wealth Distribution

The average monthly income before taxes is DKK 48,572, reflecting strong purchasing power. Median net worth in 2023 was DKK 730,094, indicating solid household wealth accumulation.

Disposable income remains high, with Danes spending significantly on leisure, travel, and digital entertainment, creating favorable conditions for iGaming market expansion.

Market Size and Growth Projections

The Danish iGaming market continues to expand, with total gambling revenue reaching DKK 683 million in May 2025, a 19.6% year-on-year increase. Online casino revenue alone hit DKK 389 million, up 39.9% from the previous year.

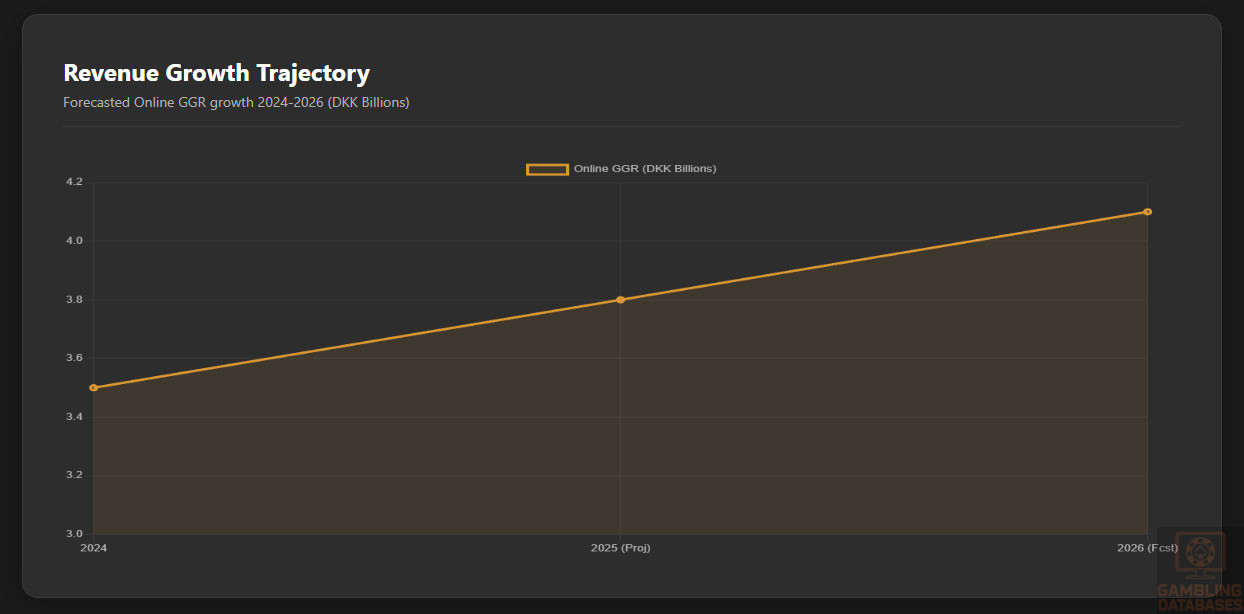

Annual online GGR was DKK 3.5 billion in 2024, with projections indicating sustained growth at a CAGR of 6-8% through 2026. The average revenue per user (ARPU) is estimated at DKK 4,500 annually.

| Year | Total Gambling Revenue (DKK) | Online GGR (DKK) | CAGR |

|---|---|---|---|

| 2024 | 11.0 billion | 3.5 billion | 5.6% |

| 2025 (Projected) | 12.1 billion | 3.8 billion | 8.6% |

| 2026 (Forecast) | 13.1 billion | 4.1 billion | 7.9% |

Education, Skills, and Digital Literacy

Denmark boasts high educational attainment, with 90% of adults aged 16-74 using social media and 83% of youth aged 16-19 actively using AI tools. Digital literacy is widespread, supported by universal internet access and strong public education.

The workforce is highly skilled, with a strong emphasis on technology, innovation, and digital services, fostering a favorable environment for online gaming and fintech adoption.

Cultural and Social Factors

Communication and Language

Danish is the official language, but English proficiency is exceptionally high, with over 86% of the population fluent. This facilitates seamless access to international iGaming platforms and content.

Online communication is predominantly in Danish, but multilingual support is common among licensed operators, enhancing accessibility for diverse user groups.

Cultural Attitudes

Gambling is widely accepted in Denmark, viewed as a legitimate form of entertainment with strong regulatory oversight. The culture emphasizes fairness, transparency, and responsible play.

Foreign brands are well-received, particularly those demonstrating compliance with local regulations and responsible gambling standards. Entertainment preferences lean toward digital and mobile-first experiences.

Problem Gambling and Social Considerations

Approximately 21.7% of Danes aged 15 and over have gambled online in the past year. While overall participation is high, problem gambling remains a concern, with targeted interventions in place.

The government supports multiple initiatives to mitigate gambling harm, including national self-exclusion (ROFUS), helplines, and public awareness campaigns.

- National self-exclusion register (ROFUS) for cross-operator blocking

- StopSpillet helpline offering counseling and support

- Public education campaigns on responsible gambling

- Mandatory operator contributions to research and treatment

- Real-time monitoring of player behavior for risk detection

Political Structure and Governance

Denmark is a stable parliamentary democracy with consistent regulatory policies and strong rule of law. The government maintains a proactive stance on consumer protection and market integrity.

International relations are strong, with active participation in EU regulatory frameworks, ensuring alignment with broader European standards and cross-border cooperation.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration is 98%, with 97% of households having home access. Mobile penetration is 93%, and digital engagement is high across all age groups.

Online activity is dominated by social media, streaming, and e-commerce, with strong adoption of mobile-first services.

- YouTube – 89% penetration, 45 minutes daily average

- Facebook – 78% penetration, primary for news and social interaction

- Instagram – 64% penetration, popular among 18-34 demographic

- TikTok – 52% penetration, rapidly growing among under-25 users

- LinkedIn – 28% penetration, used for professional networking

Digital Payment Behavior

Digital payments are highly developed, with credit and debit cards dominating online transactions. E-wallets and mobile payment solutions are gaining traction, especially among younger users.

Cryptocurrency adoption remains limited but is monitored for future integration potential.

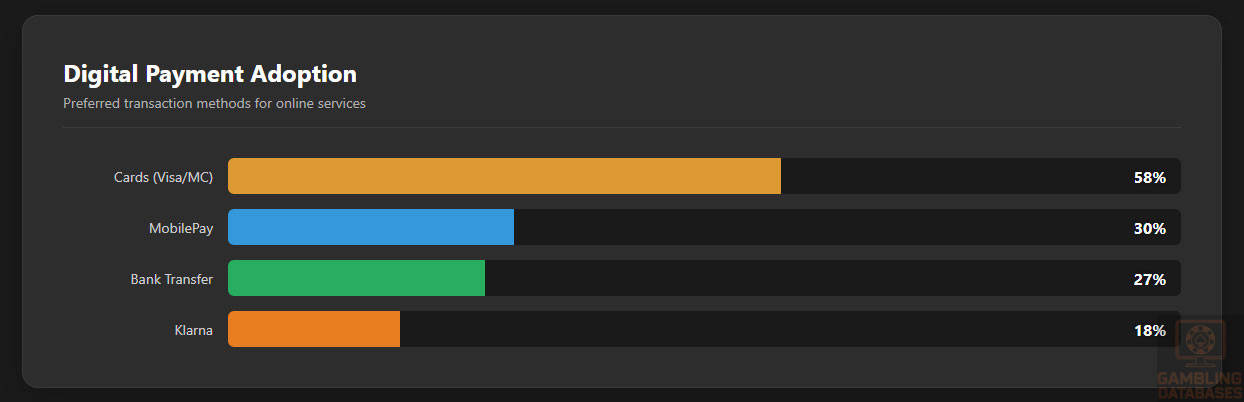

- Visa and Mastercard – 58% of online transactions

- MobilePay – 30% adoption, leading domestic e-wallet

- Bank transfers – 27% of payment volume

- Klarna – 18% usage, popular for installment payments

- Paysafecard – 12% usage, common in gaming and youth segments

Gaming and Gambling Preferences

Current Market Participation

Online gambling participation is highest among younger demographics, with 53% of online casino players under 36 and 57% of online bettors under 36. Men dominate account registrations, accounting for 72% of online casino and 84% of online betting accounts.

Mobile is the preferred platform, with 67% of play occurring on smartphones, reflecting a strong mobile-first culture.

- Online Slots – 78.9% of online casino revenue

- Sports Betting – 23% of total gambling revenue

- Live Casino – growing segment with high engagement

- Poker – niche but loyal player base

- Lottery – stable participation, especially among older demographics

Consumer Behavior Patterns

Spending habits show strong engagement during weekends and major sports events. Session lengths average 28 minutes, with high retention rates among registered users.

Players favor transparency, fair odds, and responsible gambling tools, with increasing demand for personalized experiences and loyalty rewards.

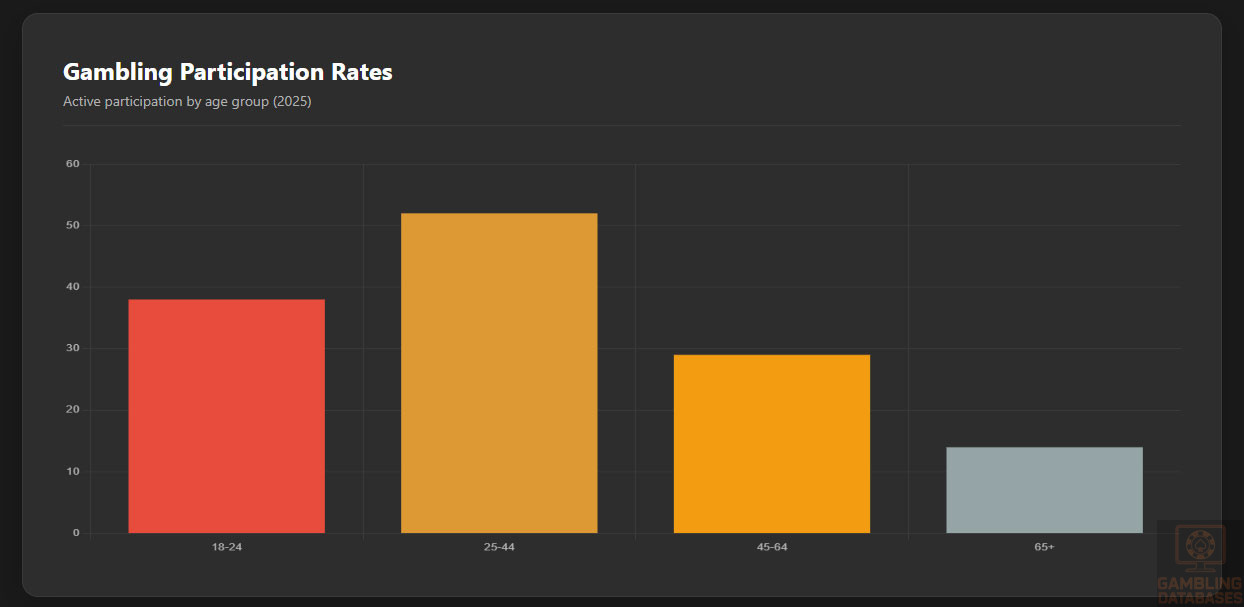

| Demographic | Participation Rate | Primary Vertical |

|---|---|---|

| 18-24 years | 38% | Online Slots, Mobile Betting |

| 25-44 years | 52% | Sports Betting, Live Casino |

| 45-64 years | 29% | Lottery, Land-Based Slots |

| 65+ years | 14% | Lottery, Bingo |

| Male | 48% | Sports Betting, Poker |

| Female | 36% | Online Slots, Bingo |

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Denmark features near-universal internet penetration exceeding 98%, supported by advanced broadband and mobile networks. Fixed broadband services provide stable high-speed connectivity with average download speeds surpassing 200 Mbps, fostering seamless digital experiences essential for iGaming platforms.

Mobile broadband complements fixed lines, with 4G LTE coverage reaching over 99% of the population. National investments into fiber optic infrastructure ensure Denmark remains one of the most connected countries in Europe, supporting low latency and high reliability critical for interactive gaming and streaming services.

5G and Future Technology Deployment

The country has initiated a comprehensive 5G rollout that covers more than 75% of populated areas as of 2025. Operators have accelerated deployment with government facilitation, focusing on urban and suburban coverage initially, with rural expansion planned within the next three years.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Denmark’s mobile market is competitive and mature, served by several operators offering comprehensive national coverage. Market shares are distributed among large network providers, with a focus on high data throughput, improved customer service, and value-added mobile applications.

- TDC Group (Danmark’s largest operator, ~38% market share)

- Telenor Denmark (~25% market share)

- Telia Denmark (~23% market share)

- 3 Denmark (~10% market share)

- Smaller MVNOs capturing the remaining market segment

Device Penetration

Smartphone penetration is extensive, with approximately 85% of Danes owning smartphones, predominantly high-end models from Apple and Samsung. Device usage trends indicate a preference for iOS-based gaming due to seamless app ecosystems, though Android dominates in market share by volume.

Tablet and wearable devices also gain traction, supporting mobile gaming’s growth as players increasingly engage in flexible, on-the-go gaming sessions. High device affordability and frequent upgrades contribute to a digitally savvy consumer base.

Financial Services and Payment Infrastructure

Banking System Structure

Denmark’s banking sector is stable and highly digitalized, dominated by a mix of traditional big banks and innovative fintech players. Digital banking adoption is nearly universal, with over 90% of account holders using mobile or online banking services.

- Danske Bank (largest institution with extensive digital services)

- Nykredit Bank (focus on mortgages and digital financial products)

- Nordea Bank Danmark (strong corporate and retail presence)

- Jyske Bank (regional and SME-focused operations)

- Spar Nord Bank (local banking services with digital expansion)

Payment Processing Options

The payment landscape offers extensive options for secure transactions, including card payments, e-wallets, and instant bank transfers tailored to Danish consumer preferences. Payment service providers integrate seamlessly with iGaming operators to ensure fast deposits and withdrawals.

- Credit and Debit Cards (Visa, Mastercard)

- MobilePay (dominant mobile wallet in Denmark)

- Bank Transfers (Trustly, Dankort Online)

- E-wallets (PayPal, Skrill, Neteller)

- Cryptocurrency options (emerging but limited)

E-commerce and Digital Economy

Denmark ranks among the leaders in European e-commerce, with over 85% of the population making online purchases annually. Consumer trust in digital payment, delivery logistics, and data security underpins this vibrant ecosystem.

This digital economy maturity supports the iGaming sector by promoting secure payments, customer retention strategies, and digital marketing efficacy. Extensive use of analytics and personalized content further drive consumer engagement.

Business Environment and Regulatory Framework

Ease of Business Operations

Denmark is highly ranked internationally for ease of doing business, characterized by streamlined registration processes, transparent regulatory frameworks, and active foreign investment encouragement. Regulatory agencies maintain open communication channels for market entrants.

Costs associated with market entry and operational continuity remain moderate compared to other Western European countries, reflecting efficient bureaucratic practices and a competitive service sector.

Corporate Structure and Registration

Common business entity types include the private limited company (ApS), public limited company (A/S), and branch offices of foreign companies. The private limited company (ApS) is most frequently used for iGaming startups due to limited liability, simplified administration, and favorable tax treatment.

Entities must comply with Danish Financial Statements Act and coordinate with tax and gambling authorities to maintain licensing compliance. The legal framework encourages transparency, corporate governance, and responsible ownership.

Registration Requirements

Establishing a company involves several standard steps, with a typical timeline of 3-6 weeks from preparation to registration completion. Foreign ownership is fully permitted, with no equity restrictions, provided regulatory licenses are secured.

- Valid identification and passports of shareholders and directors

- Articles of Association and Memorandum of Understanding

- Proof of registered office address in Denmark or EEA

- Bank confirmation of capital deposit (minimum capital: DKK 40,000 for ApS)

- Tax registration certificates for corporate tax and VAT

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate is a flat 22%, competitive within the EU context. Denmark offers no specific tax holidays for the gaming sector, but companies benefit from extensive double taxation treaties enhancing international operations.

- United States

- Germany

- United Kingdom

- France

- Sweden

- Norway

- Netherlands

Personal Income Tax

Personal income tax in Denmark is progressive, with rates reaching up to 55.9% including municipal taxes and social contributions. Tax residency is defined by physical presence over six months or domicile, influencing employee and executive compensation structures.

Market Entry Considerations

Recommended Entry Strategies

Successful entry depends on strategic partnerships with local operators, robust compliance programs, and technology innovation aligning with Danish consumer preferences. Leveraging mobile-first platforms and responsible gambling features enhances market acceptance.

- Form alliances with established Danish operators

- Invest in localized marketing and customer support

- Implement advanced player protection and KYC solutions

- Adopt scalable, cloud-based gaming platforms

- Focus on mobile gaming due to dominant user behavior

Typical Costs and Timelines

Market entry demands significant upfront investment, especially in licensing, technology, and marketing. Ongoing operational costs also require prudent financial planning for compliance and user acquisition. The time from market entry decision to launch typically spans 6-9 months.

- License application fees: DKK 327,500 (~USD 49,000)

- Technology platform setup and certification: USD 150,000 – 300,000

- Marketing and user acquisition initial spend: USD 200,000+

- Compliance and audit costs annually: USD 50,000+

- Operational overhead including staffing and office: USD 100,000+

Success Factors and Challenges

Key success factors include regulatory compliance, technological adaptability, and effective localization. Challenges lie in navigating complex licensing requirements, aggressive market competition, and managing responsible gambling obligations.

- Strong compliance with Danish Gambling Authority regulations

- Innovative mobile gaming and user experience design

- Efficient KYC and AML operation integration

- Effective marketing under advertising restrictions

- Maintaining player trust through responsible gambling initiatives

Exit Strategy Planning

License transferability is restricted; thus, exit strategies typically involve asset sale or share transfer compliant with regulatory approval. Market valuation depends on revenue, compliance history, and market position, with liquidity influenced by Denmark’s stable yet competitive environment.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Denmark?

Yes, online gambling is fully legal and regulated in Denmark under the Danish Gambling Act. All operators providing online services must obtain licenses from the Danish Gambling Authority. The regulatory framework ensures player protection through strict licensing conditions, KYC requirements, and responsible gambling measures.

2. What types of gambling licenses are available and what do they cover?

Denmark offers unified licenses that cover multiple gambling verticals including online casino, sports betting, lottery, and land-based operations. Additionally, from 2025, suppliers providing software to operators must hold a separate supplier license to ensure comprehensive market oversight and integrity.

3. How much does an iGaming license cost and how long does it take to obtain?

The license application fee is currently DKK 327,500 (~USD 49,000), non-refundable. The approval timeline usually ranges from 3 to 6 months depending on application completeness and responsiveness. This process includes a thorough review of financial, technical, and compliance capabilities.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are fully eligible to apply for gambling licenses, provided they comply with Danish regulatory requirements including local presence or appointing a Danish representative. There are no restrictions on foreign ownership, facilitating international operator participation in the market.

5. What are the tax obligations for iGaming operators?

Operators must pay a gross gaming revenue tax at a flat rate of 28% on all gaming activities. This tax applies equally to online casinos, sports betting, lotteries, and land-based gaming. License renewal fees and compliance-related costs are additional obligations to consider.

| Activity | Tax Rate |

|---|---|

| Online Casino | 28% |

| Sports Betting | 28% |

| Lottery | 28% |

| Land-Based Gambling | 28% |

6. Are gambling winnings taxed for players?

No, players in Denmark do not pay taxes on gambling winnings. The tax liability rests solely with the operator, which simplifies player engagement and incentivizes participation within the licensed market.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs typically include licensing fees, technology platform expenses, marketing budgets, compliance and audit costs, along with staff salaries. These combined can amount to several hundred thousand USD annually, depending on market scale and marketing intensity.

- License and regulatory fees

- Technology licensing and maintenance

- Advertising and promotional budgets

- Compliance and auditing expenses

- Customer support and operational staffing

8. What is the expected ROI timeline for entering this market?

Return on investment can vary but generally ranges between 2-4 years, factoring in market entry costs and competitive landscape. Operators focusing on mobile innovation and responsible gambling often achieve faster growth and improved retention.

9. What are the local presence requirements for operators?

Operators must have legal presence within Denmark or another EEA country. Alternatively, appointing a Danish-based representative ensures compliance oversight. Physical presence is not mandatory but facilitates regulatory communication and operational transparency.

10. What payment methods are available and recommended?

Recommended payment methods include credit/debit cards, MobilePay, bank transfers via Trustly or Dankort Online, and e-wallets such as PayPal and Skrill. These options align with consumer preferences for fast, secure transactions suitable for iGaming platforms.

11. What are the advertising and marketing restrictions?

Marketing campaigns must adhere to strict limits including maximum bonus offers capped at DKK 1,000 per player and mandatory display of responsible gambling messages. Advertising targeting minors or vulnerable populations is prohibited, and promotional frequency is regulated.

12. What responsible gambling measures are mandatory?

Operators must integrate comprehensive measures such as mandatory age verification, self-exclusion via the national ROFUS system, deposit limits, reality checks, and AML compliance. These protections support player welfare and market integrity.

- Age verification and KYC at registration

- Self-exclusion registry integration

- Deposit and loss limits

- Reality and time checks

- Anti-money laundering monitoring

13. How large is the iGaming market and what is the growth potential?

The iGaming market in Denmark is valued at over DKK 3.5 billion (~USD 520 million) with sustained CAGR around 7%. Growth is propelled by mobile adoption, expanding game verticals, and continuous regulatory improvements fostering operator and player confidence.

14. Who are the main competitors and what is their market share?

The Danish market is led by the state-owned Danske Spil, followed by international operators such as Kindred Group, bet365, LeoVegas, and PokerStars. Together, these entities hold a dominant share, with competition based on technology innovation, user experience, and localized marketing.

- Danske Spil (Market leader)

- Kindred Group

- bet365

- LeoVegas

- PokerStars

15. What are the player preferences and typical spending patterns?

Danish players favor online slots and sports betting, with mobile platforms favored for convenience. Spending trends indicate moderate but steady wagering, with retention driven by personalized offers and a trusted regulatory environment promoting responsible play.

16. What are the key success factors and main challenges for new entrants?

Success factors include strong regulatory compliance, effective localization, robust technology platforms, and proactive responsible gambling policies. Challenges involve navigating licensing complexities, competitive market saturation, and strict advertising limitations.

- Compliance with Danish Gambling Authority

- Localization of marketing and customer support

- Advanced mobile gaming experience

- Efficient KYC/AML processes

- Adaptability to evolving regulations

Sources and References

- Denmark Gambling Authority – Official Website – http://www.spillemyndigheden.dk

- National Statistical Office Denmark – Population and Economic Data 2025 – https://www.dst.dk

- Central Bank of Denmark – Financial Statistics and Reports – https://www.nationalbanken.dk

- Ministry of Taxation Denmark – Tax Regulations and Guidelines – https://www.skat.dk

- World Bank – Doing Business Report 2024 – https://www.doingbusiness.org

- International Telecommunication Union – ICT Statistics – https://www.itu.int

- Denmark Digital Economy Report 2024 – Danish Ministry of Digitalization

- iGaming Industry Review – SiGMA Europe 2025 Report

- Euromonitor International – Denmark Online Gambling Market Report 2025

- Gaming Compliance Journal – Denmark Regulatory Update 2025

- Telecoms.com – Denmark 5G Rollout 2025

- Payment Systems Worldwide – Denmark Edition 2025

- Danish Ministry of Business and Growth – Company Registration Guidelines 2025

- European Gaming & Betting Association (EGBA) – Regulatory Trends 2025

- European Commission – Gambling and Digital Services Overview 2024

- Nordic Economic Outlook 2024 – OECD

- Danish Financial Supervisory Authority – Consumer Finance Reports 2025

- International Monetary Fund – Denmark Country Report 2024

- GlobalData – Denmark Mobile Market Trends 2025

- Social Media Usage Statistics Denmark – We Are Social Report 2025

- Responsible Gambling Council Denmark – Annual Report 2025

- Local News – Denmark iGaming Market Growth – 2025

- Mobile Network Operators Denmark – Market Share Analysis 2025

- Investment Denmark – Foreign Direct Investment Reports 2024

- Gaming Commission Finland & Denmark Joint Regulatory Updates 2025

- Danish Ministry of Finance – Economic Forecast April 2025

- Online Casino Reports – Denmark Market Insights 2025

- Danish Gambling Advertising Code – Regulatory Authority Publication 2025

- Crypto Adoption Reports – Denmark Analysis 2025

- European Mobile Payment Solutions Report 2025

- Nordic Tech Innovation Forum – Gaming Technology 2025

🎯 Gambling Databases Country Rating: Denmark

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.1/10 | 🟡 Moderate |

| Player Access Score | 10.0/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 8.0/10 | 🟢 High Stability / High Competition |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Bonus Caps Kill Acquisition: Strict promotional limits (cap of DKK 1,000 / ~$145 per player) severely restrict traditional acquisition strategies.

- New Mandatory Supplier Licensing (2025): As of Jan 1, 2025, game suppliers must hold their own licenses. This increases supply chain costs and administrative friction.

- Dual Certification Requirement: Effective July 2025, independent certifications are required for both suppliers and B2C operators, doubling compliance overhead.

- High Effective Tax Burden: While GGR tax is 28%, the addition of 22% corporate tax and high local labor costs creates a heavy financial load.

- Market Saturation: With 41 licensed operators serving a population of only 5.9 million, market share is entrenched; displacing incumbents is extremely expensive.

- Active Blocking: The Danish Gambling Authority actively monitors and blocks unlicensed offshore domains and payments.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | Full product legality (+3.0). Both sports betting and online casino (including slots) are fully regulated and legal. No grey areas. |

| Licensing Process | 25% | 1.75/2.5 | Accessible licensing (+2.0). Application fee ~$49k (+0.5). Approval 3-6 months. Deduction: New mandatory supplier licensing adds administrative complexity to the supply chain (-0.25). |

| Taxation & Costs | 20% | 0.25/2.0 | 28% GGR Tax (+1.0). Critical Deductions: High corporate tax (22%) results in high effective tax rate (-0.5). Extremely high labor/operational costs in Denmark (-0.25). |

| Operational Requirements | 15% | 0.75/1.5 | Moderate requirements (+1.0). Local representative required. Deduction: Dual certification (supplier + operator) starting July 2025 adds significant technical burden (-0.25). |

| Market Environment | 10% | 0.35/1.0 | Excellent business environment (+1.0). Critical Deductions: Severe advertising restrictions and bonus caps (-0.4). High market saturation/concentration (-0.25). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal (+4.0). Players can legally access all forms of online gambling via licensed sites without fear of prosecution. |

| Practical Accessibility | 30% | 3.0/3.0 | Multiple payment methods (+3.0). MobilePay, Visa, Mastercard, and bank transfers are widely available. High internet/mobile penetration ensures seamless access. |

| Player Penalties | 20% | 2.0/2.0 | No penalties (+2.0). Players are not criminalized, and winnings from licensed operators are tax-exempt. |

| Market Availability | 10% | 1.0/1.0 | 41 licensed operators (+1.0). Players have a vast selection of legal, high-quality domestic and international brands. |

🔍 Key Highlights

Strengths

- Regulatory Clarity: One of Europe’s most transparent and predictable licensing regimes.

- High Player Value: High GDP (~$65k) and ARPU (~$675) make individual players very valuable.

- Digital Maturity: 98% internet penetration and 93% mobile adoption create a seamless environment for mobile-first operators.

⛔️ CRITICAL RISKS AND CHALLENGES

- Advertising Limits: The DKK 1,000 bonus cap makes it nearly impossible to compete on “free money” offers, forcing competition on product quality and brand—areas where incumbents dominate.

- Supply Chain Friction: The new 2025 supplier licensing rules mean you can only use software from licensed B2B providers, potentially limiting game variety or increasing vendor costs.

- Financial Barriers: The combination of 28% GGR tax, corporate tax, and high cost of living (wages, office) requires a substantial capital runway.

- Active Enforcement: The regulator (Spillemyndigheden) is aggressive. Misleading ads or AML failures result in public warnings and fines.

- Player Protection: ROFUS (self-exclusion) is mandatory. If a player is on this list, you strictly cannot onboard them, reducing the addressable market.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $500,000 – $800,000 (License fees, legal, tech compliance, initial marketing)

Monthly Operating Costs: High. Specialized local staff or representatives are expensive in Denmark.

Effective Tax Rate on Revenue: ~45-50% (28% GGR + 22% Corporate Tax + Employment Taxes)

Customer Acquisition Cost: High ($300+), exacerbated by marketing restrictions.

Time to Breakeven: 24-36 months.

Profitability Assessment: Hard Mode. While the market is stable, the margins are squeezed by taxes and the inability to aggressively acquire players via bonuses. This market favors established brands with organic traffic or deep pockets for brand-building. Small operators will struggle to survive the CAC/LTV ratio.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | 🔴 High | ISP blocking, payment blocking, public blacklisting by Spillemyndigheden. |

| Licensed Operators | 🟡 Medium | Regulatory fines for AML/KYC failures or marketing breaches. New dual certification adds compliance risk. |

| Affiliates/Advertisers | 🟡 Medium | Strict rules on promoting only licensed brands. Promoting unlicensed sites can lead to prosecution. |

| Payment Processors | 🔴 High | Processing for unlicensed sites is strictly prohibited and actively monitored. |

| Company Directors | 🟡 Medium | Personal liability exists for gross negligence regarding AML and responsible gambling compliance. |

🚨 Extradition and International Enforcement

Extradition Treaties: Denmark is a member of the EU and has robust extradition treaties with the USA, UK, Canada, Australia, and all EU member states.

Enforcement History: Denmark actively cooperates with EU regulators. While they focus on blocking and fines for offshore entities, cross-border legal action is possible for serious fraud or money laundering offenses.

Safe Jurisdictions: None within the Western sphere. Enforcement is coordinated across the EEA.

📋 Final Verdict

Denmark receives an Operator Ease Score of 6.1/10 and a Player Access Score of 10.0/10, resulting in an overall market attractiveness rating of 8.0/10.

HONEST ASSESSMENT: Denmark is a “Gold Standard” market that is legally safe but commercially brutal. The regulatory framework is perfect, but the entry barriers—specifically the bonus caps, high taxes, and new supplier licensing rules—make it a graveyard for under-capitalized operators. You will not get rich quick here. It is a volume and retention play suited only for professional, well-funded companies.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A Tier-1 international operator with a recognizable brand.

- Able to sustain 2-3 years of negative ROI to build market share.

- Technologically advanced with mobile-first proprietary tech.

- Compliant with stringent EU AML and RG standards.

❌ Definitely Avoid If You Are:

- A “Bonus Casino” relying on high-deposit matches to acquire players.

- Under-capitalized (less than $2M runway).

- A white-label operator with no control over your supply chain (due to supplier license rules).

- Looking for a low-tax, high-margin unregulated environment.

- An offshore operator hoping to fly under the radar (you will be blocked).

⚠️ BOTTOM LINE: Enter Denmark only if you want a long-term, low-margin, high-stability asset in your portfolio; avoid if you need aggressive growth or quick profits.

The recent(ish) hike in the tax rate from 20% to 28% has definitely reshaped the competitive landscape here. While Denmark remains a model market for stability, the increased cost base has made it significantly harder for smaller, niche brands to enter. It is increasingly becoming a game for the large, multi-national groups that can absorb the margin compression.