Djibouti presents a unique iGaming market opportunity shaped by its strategic location, evolving regulatory environment, and a predominantly Muslim population with conservative gambling attitudes.

While land-based gambling is officially legal and regulated, online gambling remains largely unregulated, offering both challenges and potential incentives for market entrants willing to navigate this emerging space.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Land-Based Gambling | Legal and regulated, primarily for tourists |

| Online Gambling Legal Status | Unregulated, legal grey area |

| Licensing Authority | Ministry of Economy and Finance; Ministry of the Interior |

| Number of Licensed Casinos (Land-Based) | 2 main casinos (Aden Bay, Safari Casino Club) |

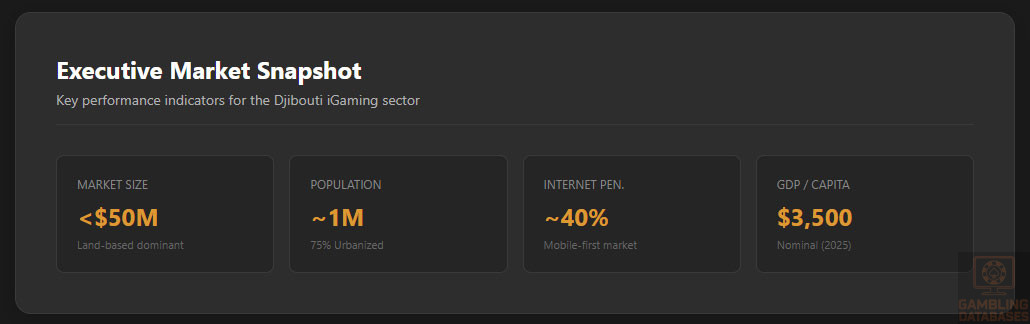

| Population (2025) | ~1 million |

| Urbanization Rate | ~75% |

| GDP (Nominal, 2025) | Approx. $3.5 billion |

| GDP Per Capita | ~$3,500 |

| Internet Penetration Rate | ~35-40% |

| Mobile Penetration Rate | ~70% |

| License Application Processing Time | 4-6 months |

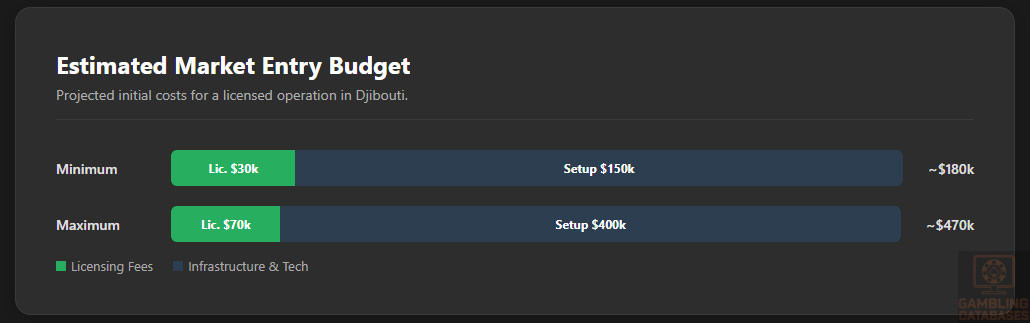

| License Application Fee | $30,000 – $70,000 |

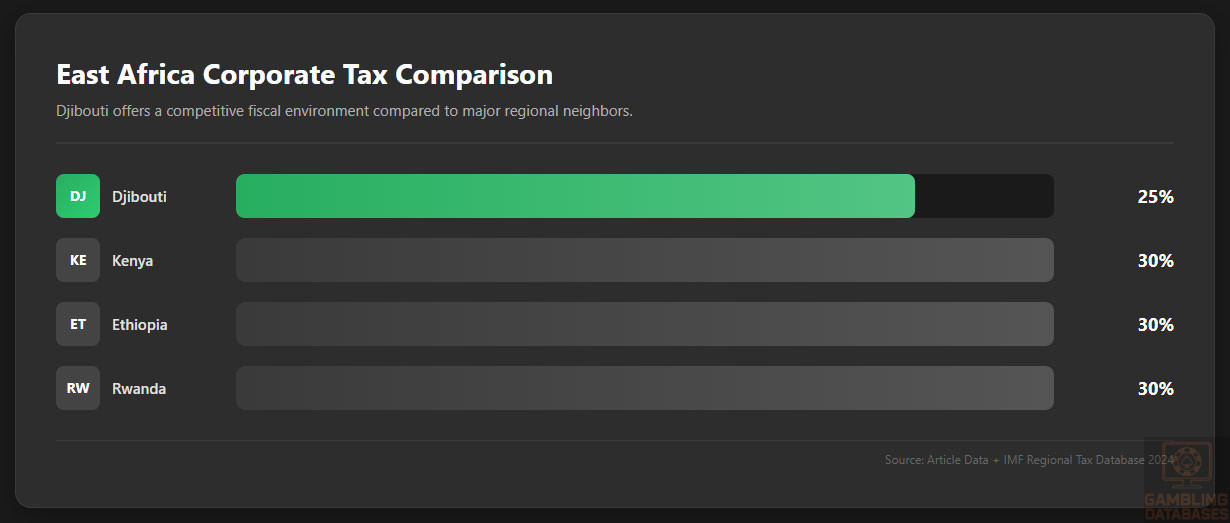

| Gross Gaming Revenue (GGR) Tax Rate | Approx. 25% corporate tax + 10% VAT |

| Player Taxation | No explicit player tax regulations |

| Compliance Requirements | AML/KYC, responsible gaming, background checks |

| Local Presence Requirement | Physical presence and licensing mandatory |

| Foreign Ownership Restrictions | Permitted with licensing and background checks |

| Responsible Gambling Mandatory Measures | Self-exclusion, deposit limits, KYC |

| Tax on Corporate Income | 25% |

| License Renewal | Annual renewal required, fees apply |

| Advertising Restrictions | Strict due to cultural norms |

| Market Size (Estimated, 2025) | Underdeveloped, small land-based market |

| Market Growth Forecast (CAGR 2025-2030) | Moderate growth expected with regulation improvements |

| Average Revenue per User (ARPU) | Low due to income and market immaturity |

| Payment Methods Commonly Used | Credit/debit cards, bank transfer, e-wallets, crypto emerging |

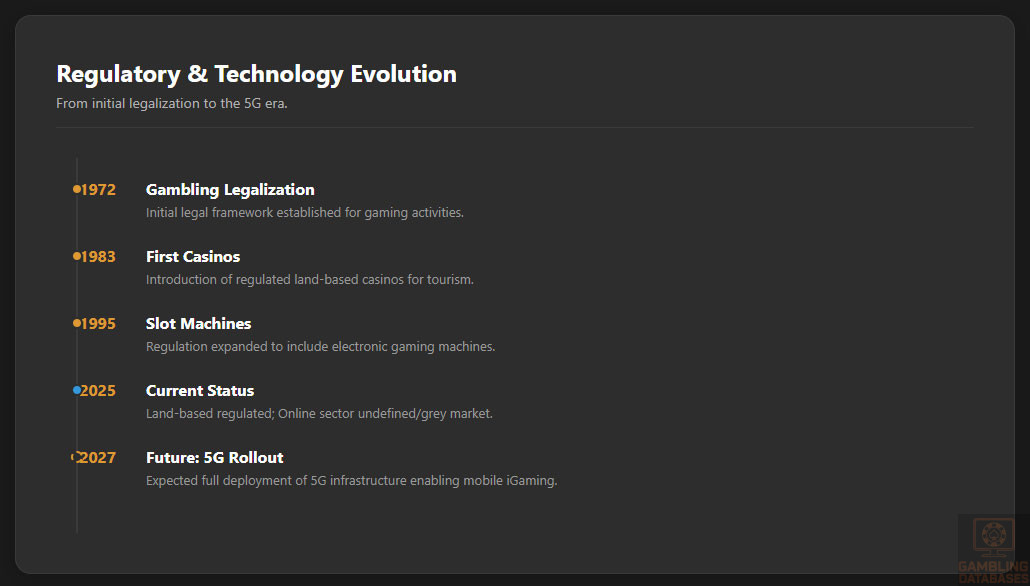

| Regulatory Changes Timeline | Incremental updates since 1972 legalization |

| Enforcement and Penalties | Fines up to 10,000 DJF for illegal operations |

| Technological Infrastructure | Developing with mobile-first focus |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling in Djibouti is legally permitted for land-based activities under strict government regulation, primarily targeting tourists and foreigners. The country’s predominant Muslim population influences a conservative stance on gambling, reflecting in limited local participation and cautious regulatory approaches.

Online gambling holds a legal grey status, lacking explicit regulation or licensing frameworks. While not outright prohibited, there remains no specific legal infrastructure governing digital gambling operations. Consumers access international online platforms freely, but the absence of local oversight creates challenges regarding player protections, enforcement, and revenue capture.

Land-Based Gambling Activities

Djibouti’s land-based gambling sector is modest and centralized, consisting mainly of two licensed casinos: Aden Bay Casino and Safari Casino Club. Both casinos offer classic table games, slot machines, and sports betting facilities geared towards tourists and expatriates.

The government restricts the issuance of licenses strictly and imposes operational guidelines emphasizing security and responsible gaming. Enforcement includes routine audits and mandatory reporting to mitigate illegal practices and ensure regulatory compliance.

Online Gambling Framework

Unlike many established gambling markets, Djibouti’s regulatory environment has yet to formally address online gambling. There is no licensing authority or regulatory body explicitly overseeing online casino operations, sports betting websites, or other forms of digital wagering.

This regulatory gap creates ambiguity for operators wishing to enter the online market and for players engaging in online betting. The lack of consumer protection frameworks poses risks related to fraud, problem gambling, and financial crime. However, this also presents an opportunity for forward-looking operators and governments to pioneer frameworks that balance cultural sensitivities with market growth potential.

Licensed Operators and Market Players

The market features a limited number of licensed land-based operators functioning under government-issued permits. The major establishments, such as Aden Bay Casino and Safari Casino Club, dominate local physical gambling revenues, primarily from tourist patronage.

Competition within the licensed sector remains low due to market size and licensing restrictions, while the online sector is fragmented with international operators servicing players remotely. Market entry strategies for new operators typically involve securing government licenses, local partnerships, and compliance with regulatory and taxation protocols.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing process is managed chiefly by the Ministry of the Interior and the Ministry of Economy and Finance. It involves stringent due diligence, including thorough background checks on company owners and stakeholders to verify legal and financial integrity.

Applicants must submit detailed documentation covering corporate registration, financial statements, operational plans, and technical standards compliance. License application fees range between $30,000 and $70,000, and the licensing procedure commonly requires four to six months for approval and issuance.

The licensing requirements stipulate ongoing compliance with anti-money laundering (AML) policies, responsible gambling practices, and cybersecurity frameworks to preserve market integrity and player safety.

Local Presence and Operational Requirements

Operators must establish a physical presence within Djibouti to qualify for licensing. This includes maintaining local offices and employing personnel who are accountable to regulatory authorities.

Domain registration and operational licenses must align with Djiboutian regulations, and foreign ownership is permissible subject to government approval and compliance with all regulatory conditions.

Partnerships with local entities may be advantageous or required to navigate legal, cultural, and business environments effectively.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators licensed in Djibouti are bound by strict KYC (Know Your Customer) and AML regulations, including age verification to prevent underage gambling. Responsible gambling initiatives are mandatory, encompassing self-exclusion options, deposit and loss limits, and player awareness programs.

These protective measures are intended to mitigate gambling-related harms and ensure ethical operational practices.

- Mandatory player ID verification

- Age restriction enforcement (minimum 21 years)

- Self-exclusion policy implementation

- Deposit and wager limits

- Regular player activity monitoring

- Provision of responsible gambling information

Financial Monitoring and Reporting

Regulatory authorities mandate comprehensive transaction monitoring, requiring operators to submit periodic reports detailing financial operations, including wagers, payouts, and tax obligations.

Audits and compliance inspections are routine to detect and prevent money laundering, fraud, and tax evasion.

- Submission of quarterly financial reports

- Annual compliance audits

- Real-time monitoring of suspicious transactions

- Cooperation with financial intelligence units

Taxation Structure and Financial Obligations

Player Taxation

Djibouti does not currently impose explicit taxation on gambling winnings for players. The absence of specific tax laws on player profits creates an informal environment regarding personal tax liabilities from gambling activities.

Operator Taxation

| Tax Type | Rate |

|---|---|

| Corporate Income Tax | 25% |

| Gross Gaming Revenue (GGR) Tax | Combined with corporate tax, no separate GGR rate reported |

| Value Added Tax (VAT) | 10% on goods and services related to gambling |

| License Renewal Fee | Annual fee; variable by license type |

| Turnover Tax | Not explicitly mandated |

Gambling Market Financial Performance

The land-based gambling segment in Djibouti remains small but stable, primarily driven by tourist spending and expatriates. Revenue growth is limited by market size and population demographics.

Tax revenues from gambling enterprises contribute modestly to the national budget, with prospects for increased contribution as regulatory frameworks and market reach evolve.

Advertising and Marketing Restrictions

Advertising of gambling activities is strictly regulated, reflecting societal and religious sensitivities. Promotional campaigns are generally limited to licensed venues, with public advertising facing restrictions in scope and content.

- Prohibition of gambling adverts targeting minors

- Restrictions on advertising during religious and cultural observances

- Limitation on broadcast and online gambling advertisements

- Mandatory disclaimers on responsible gambling

- Control over sponsorship deals involving gambling firms

Recent Regulatory Changes and Their Impact

Since legalization in 1972 and the introduction of casinos in 1983, Djibouti’s gambling laws have evolved incrementally, introducing slot machines in 1995 and enhancing licensing conditions periodically.

Current regulatory discussions focus on clarifying online gambling policies and improving compliance mechanisms to regulate emerging market activities effectively.

Enforcement Mechanisms and Penalties

The government enforces compliance through financial penalties and operational suspensions. Entities operating without licenses face fines up to 10,000 Djiboutian Francs, with repeated violations leading to license revocation or criminal charges. Enforcement is a key pillar sustaining market order.

- Monetary fines for illegal gambling operations

- License suspension or revocation for non-compliance

- Criminal prosecution in severe cases

- Regular inspections and monitoring visits

- Industry-wide compliance audits

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

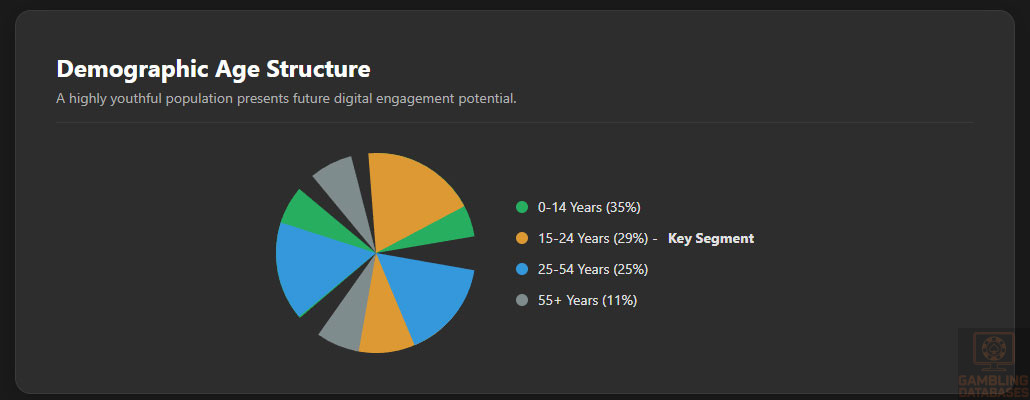

Djibouti’s population stands at approximately 1 million residents in 2025. The median age is around 19 years, reflecting a youthful demographic profile typical of developing economies. The gender ratio is fairly balanced, with a slight female majority, approximating 50.5% female to 49.5% male.

The age distribution is concentrated among the 15-24 age group, representing nearly 30% of the total population, which indicates a high potential for digital engagement and entertainment consumption. The population exhibits a significant rural-urban divide, with urban centers, especially Djibouti City, hosting about 75% of residents, concentrated in a few pivotal regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 | 35% |

| 15-24 | 29% |

| 25-54 | 25% |

| 55+ | 11% |

Geographic Distribution

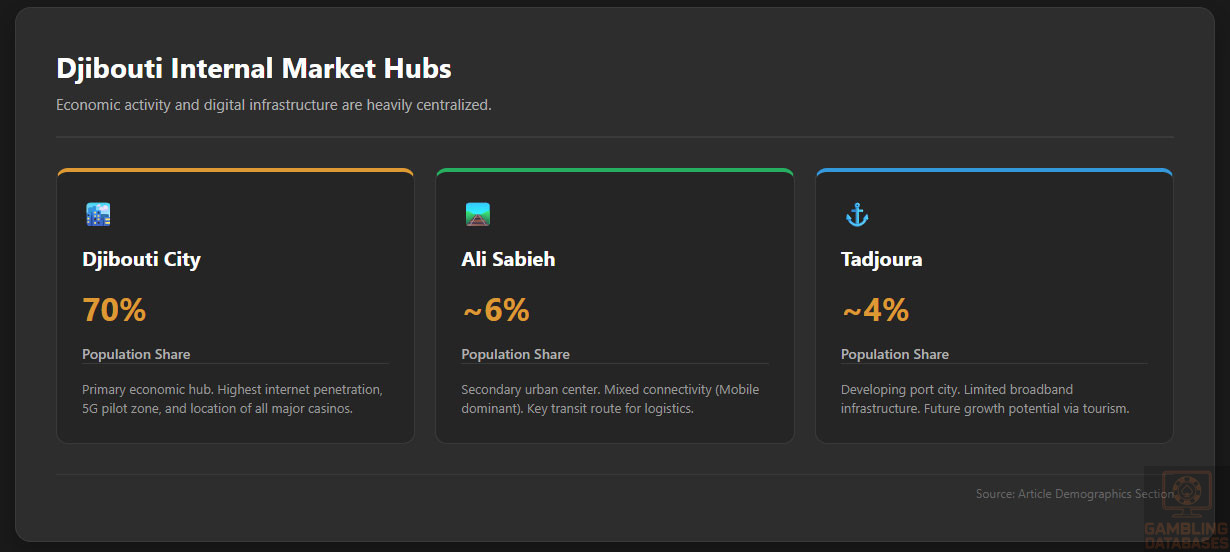

Major urban centers include Djibouti City, Ali Sabieh, and Tadjoura, which are economic hubs with dense populations and better infrastructure. Djibouti City alone accounts for over 70% of the national population and is the primary focus for internet access and digital services. Regional disparities in income and infrastructure development influence market behavior significantly.

- Djibouti City: 700,000+ residents, high connectivity

- Ali Sabieh: 60,000 residents, rural-urban mix

- Tadjoura: 40,000 residents, limited infrastructure

- Other towns: under 20,000 each, predominantly rural

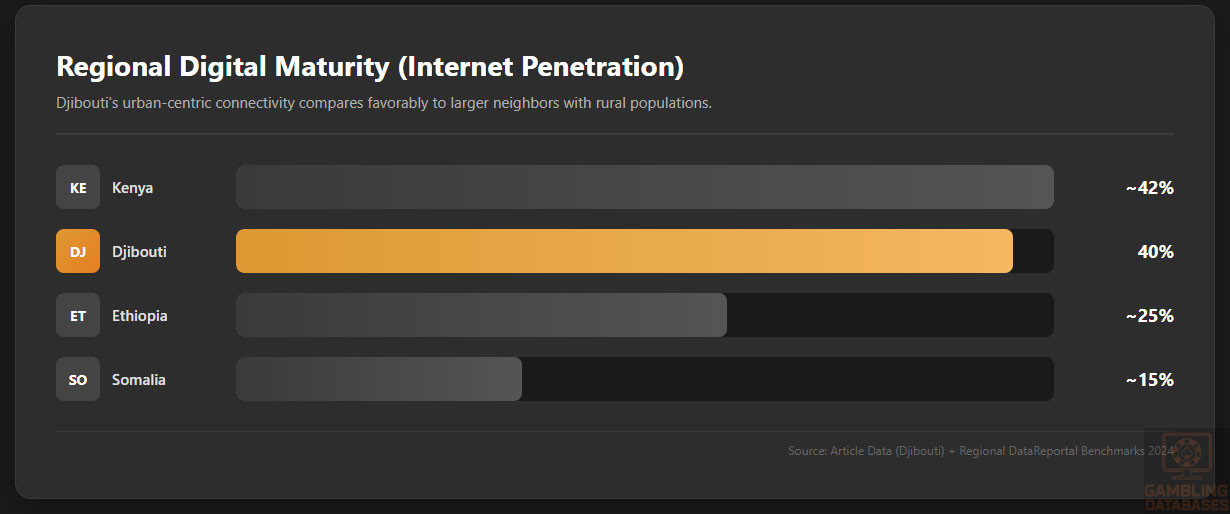

Internet access primarily concentrates in urban areas, with urban penetration rates approximating 40%. This disparity impacts potential customer reach for online gambling platforms, which currently cluster around Djibouti City.

Economic Indicators and Consumer Spending Power

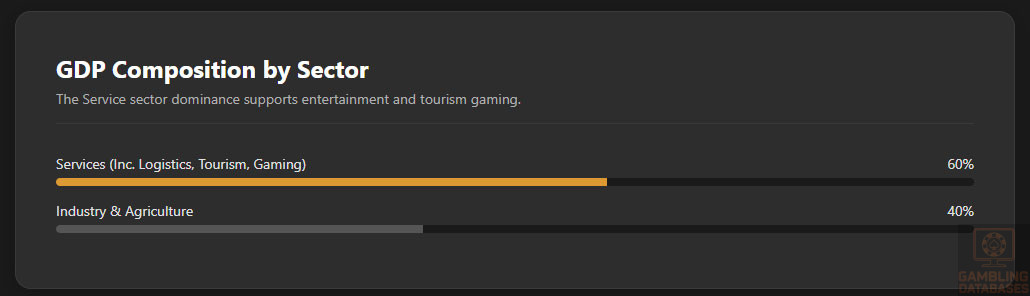

Djibouti’s nominal GDP is estimated at $3.5 billion, with a projected annual growth rate of approximately 4-5%. The economy heavily relies on port services, logistics, and military bases, with the service sector contributing over 60% of GDP. Consumer spending remains modest but steadily increases in urban centers.

The average household income is around $2,500-$3,000 annually, with disparities skewed towards higher earners in Djibouti City. Income inequality is notable, with a Gini coefficient estimated at 0.42, influencing spending patterns and gambling participation.

| Indicator | Value |

|---|---|

| GDP | $3.5 billion |

| GDP Growth Rate | ~4-5% |

| Per Capita Income | $2,500 – $3,000 |

| Unemployment Rate | ~14% |

| Consumer Spending Index | Moderate growth, driven by urban wealth |

Income and Wealth Distribution

Average household income is concentrated among the urban middle class, with a significant portion of the population living below the poverty line. Disposable income levels are generally low, limiting discretionary spending on entertainment and gaming. Wealth distribution remains uneven, fueling a cautious approach to gambling expenditure.

The affluent minority, primarily in Djibouti City, exhibits higher engagement in luxury betting and casino activities, whereas rural populations show limited participation due to infrastructure deficits and cultural factors.

Market Size and Growth Projections

The current land-based gambling market size is estimated at less than $50 million annually, primarily from tourist expenditures. Online gambling remains nascent, with an estimated user base of fewer than 50,000 active players, largely accessing international platforms.

Digital engagement is forecasted to grow at a CAGR of approximately 10-12% over the next five years, driven by improvements in internet infrastructure, mobile penetration, and evolving regulatory attitudes. Average revenue per user is low, around $15-$20 monthly, due to income constraints and limited local offerings.

Education, Skills, and Digital Literacy

Djibouti exhibits literacy rates of approximately 65-70%, with higher literacy among urban youth. Educational attainment mainly comprises secondary education, with few tertiary-level institutions specializing in digital or technical skills. Digital literacy is growing but remains moderate, addressing primarily urban populations familiar with mobile devices.

Workforce skills in digital technology and online service management are emerging but limited, constraining local operational capabilities for international online gambling firms.

Cultural and Social Factors

Communication and Language

The official languages are Arabic and French, with Somali as a regional lingua franca. Internet and social media communications predominantly occur in Arabic and French, with Somali usage increasing gradually, especially in rural areas.

- Arabic

- French

- Somali

- English (limited use)

Cultural Attitudes

Gambling is generally viewed with suspicion due to religious and cultural norms rooted in Islam, which discourages gambling activities among devout populations. Tourism and expatriates primarily drive land-based gambling acceptance, while online gambling faces social resistance.

Entertainment preferences favor social gatherings, sports, and informal betting, often through unofficial channels, which complicates regulatory implementation.

Problem Gambling and Social Considerations

The prevalence of problem gambling remains low but is acknowledged as a social issue, especially among youth and urban workers. The government has started implementing awareness campaigns and responsible gaming policies, including mandatory self-exclusion options and limited advertising.

- Educational programs in schools

- Public awareness campaigns

- Self-exclusion policies

- Limitations on advertising content

- Support services for at-risk populations

Political Structure and Governance

Djibouti operates as a semi-presidential republic characterized by political stability and strong central governance. The government emphasizes stability, regulatory oversight, and fostering economic development, which supports cautious expansion of gambling regulation aligned with social norms and economic goals.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Approximately 40% of the population has access to the internet, with mobile usage at around 70%. Daily digital engagement averages 2 hours, primarily through social media platforms and messaging apps. Internet access is concentrated in urban areas, shaping digital behaviors.

- Facebook remains dominant among social platforms

- WhatsApp and Messenger are primary communication tools

- YouTube is popular among youth

- Instagram usage is rising among urban youth

- Twitter has niche engagement

Digital Payment Behavior

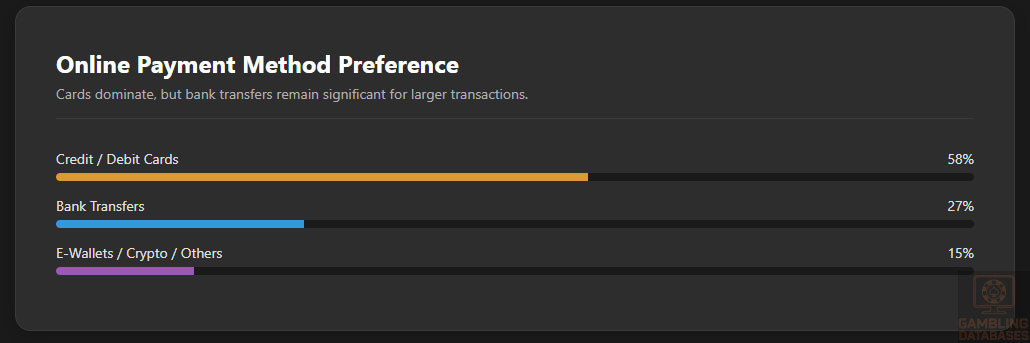

Payment preferences center on traditional methods like credit and debit cards, which account for roughly 58% of online transactions. Bank transfers remain common at 27%, with e-wallets gaining traction among younger users. Cryptocurrency adoption is limited but exhibits growth potential in the next few years.

- Credit/debit cards

- Bank transfers

- E-wallets

- Mobile money

- Crypto payments (emerging)

Gaming and Gambling Preferences

Current Market Participation

Participation in gambling activities remains relatively low, with only an estimated 10-15% of the adult population engaging in land-based or online betting. Sports betting is the most popular, followed by casino gaming and informal betting with friends.

- Sports betting

- Casino table games

- Slots and gaming machines

- Informal betting with friends

- Online poker and digital platform gaming

Consumer Behavior Patterns

Most gambling activities occur during weekends and evening hours, with sessions lasting between 20 to 40 minutes. Urban gamblers tend to prefer sports betting, often engaging via mobile devices, while tourists and expatriates exhibit a higher affinity for casino gaming in licensed venues.

Spending habits are cautious, influenced by income constraints and cultural attitudes, but interest in online gambling is gradually increasing as infrastructure and regulation improve.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Djibouti’s internet penetration reached approximately 40% in 2025, with a significant division between urban and rural areas. The broadband infrastructure is limited but expanding, with mobile internet dominating digital connectivity due to cost and accessibility advantages. Average fixed broadband speeds are moderate, averaging around 10-15 Mbps, while mobile broadband speeds exceed 20 Mbps in urban centers.

Government and private investments continue expanding fiber optic networks and satellite services, aiming at enhancing reliability and reach. Despite progress, connectivity challenges remain in less densely populated regions, which hinders the broader adoption of iGaming services outside major cities.

5G and Future Technology Deployment

Djibouti has initiated 5G pilot deployments, primarily in Djibouti City, targeting commercial and government applications. Full 5G rollout is expected by 2027, contingent on infrastructure scale-up and regulatory approvals. Major mobile network operators have begun upgrading core networks to support future technologies.

5G coverage will enhance mobile gaming experiences through lower latency and higher speeds, driving the expansion of the online gambling sector by improving accessibility and user engagement across devices.

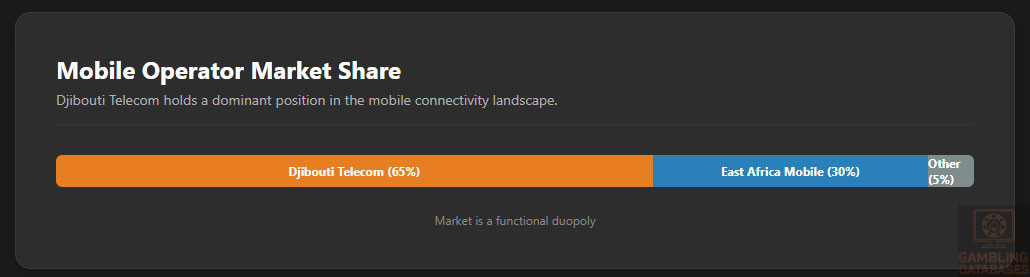

Mobile Technology Ecosystem

The mobile ecosystem features a small number of operators, with two dominant players controlling most of the market. Mobile data pricing remains competitive but relatively high compared to regional peers. Coverage quality is strong in urban settings but spotty in rural zones, influencing where digital entertainment can flourish.

- Djibouti Telecom – 65% market share

- East Africa Mobile – 30% market share

- Emerging MVNOs and niche providers – 5%

Smartphone adoption has increased to approximately 50% of mobile users, with Android dominating sales due to lower costs and broader app compatibility. Device usage skews younger, with urban residents using smartphones as primary internet access tools, critical for mobile iGaming.

Financial Services and Payment Infrastructure

Djibouti’s banking sector is moderately developed, with a small number of major banks driving the market. Digital banking penetration remains nascent but growing, supported by mobile money platforms that cater to unbanked and underbanked populations.

- Banque Populaire de Djibouti (largest market share)

- Bank of Africa Djibouti

- Commercial Bank of Djibouti

- Banque pour le Commerce et l’Industrie

- Société Nationale de Banque de Djibouti

Payment processing options include traditional card payments, mobile money transfers, and emerging digital wallets. Online gambling platforms primarily rely on credit and debit cards, bank transfers, and select international e-wallets. Cryptocurrency use is minimal but shows early adoption signs among tech-savvy users.

- Visa and MasterCard debit/credit cards

- Mobile money platforms (e.g., Tigo Cash, Airtel Money)

- Bank wire transfers

- PayPal (limited availability)

- Cryptocurrency wallets (emerging trend)

E-commerce and Digital Economy

Djibouti’s e-commerce market is in early growth stages, constrained by limited internet access and low consumer confidence. Online retail adoption is concentrated in major urban areas, with mobile commerce representing the predominant channel. Consumer trust issues remain, particularly concerning payment security and delivery logistics.

The government has launched initiatives to digitize commerce and enhance payment ecosystems, supporting overall digital economic growth. These developments bode well for expanding digital entertainment sectors like iGaming, which depend on robust payment and fulfillment networks.

Business Environment and Regulatory Framework

Ease of Business Operations

Djibouti ranks moderately on global business ease indexes, reflecting improvements in corporate registration but persisting bureaucratic challenges. Business registration processes typically require 4-6 weeks, involving multiple government agencies. Foreign investment policies are open but necessitate compliance with local ownership and reporting requirements.

Operational costs remain below regional averages but include notable expenses such as licensing fees, taxes, and infrastructure investments. Market entrants must navigate a complex but improving regulatory landscape while managing costs prudently.

Corporate Structure and Registration

Primary corporate structures include Limited Liability Companies (LLCs), Joint Stock Corporations, and Branch Offices of foreign entities. LLCs are preferred for flexibility and limited liability protection, suitable for most iGaming ventures.

Registration timelines typically span 3-4 weeks after document submission. Foreign ownership is permitted but requires government approval and transparency regarding beneficial owners.

- Certificate of incorporation application

- Articles of association submission

- Tax identification number registration

- Local address and physical office proof

- Director and shareholder identification documents

Taxation Framework

Standard corporate income tax in Djibouti is set at 25%. Operators in designated economic zones may benefit from tax holidays or incentives designed to attract investment. Personal income tax rates are progressive but relatively low, with social security contributions required.

Djibouti has established double taxation treaties with multiple countries to facilitate cross-border investment and capital repatriation, enhancing the attractiveness of its business environment.

- France

- United Arab Emirates

- Saudi Arabia

- China

- Kenya

- Turkey

Market Entry Considerations

Recommended entry strategies emphasize establishing local partnerships to navigate regulatory and cultural environments effectively. Leveraging mobile-first platforms aligns with market realities due to predominant mobile internet access. Compliance with stringent AML and responsible gaming standards is critical for sustainable operation.

- Form local joint ventures or partnerships

- Prioritize mobile-optimized platform development

- Invest in robust KYC and AML compliance systems

- Engage with government authorities proactively

- Tailor marketing to cultural sensitivities and regulations

Initial market entry cost estimates range between $150,000 and $400,000, covering licensing, setup, technology infrastructure, and compliance. Timelines to launch typically span between 6 and 9 months, factoring regulatory approvals and platform localization.

| Phase | Duration |

|---|---|

| Pre-application Preparation | 4-6 weeks |

| Licensing Application & Approval | 4-6 months |

| Technology Integration & Testing | 6-8 weeks |

| Marketing & Soft Launch | 4 weeks |

| Full Launch | Post-approval |

Success Factors and Challenges

Key success factors include comprehensive compliance frameworks, strong local partnerships, and culturally informed marketing. Technology agility and mobile focus drive customer acquisition.

- Robust licensing and regulatory compliance

- Effective local market understanding

- Mobile-first platform development

- Strong customer support and responsible gaming initiatives

- Agile technology and payment ecosystem integration

Challenges encompass navigating regulatory uncertainty around online gambling, limited digital infrastructure outside urban hubs, and deeply rooted cultural resistance to gambling activities.

- Regulatory ambiguity in online gaming

- Incomplete internet and mobile coverage

- Cultural and religious challenges

- High cost of compliance and infrastructure

- Payment processing limitations in rural areas

Exit Strategy Planning

The iGaming market in Djibouti remains emerging, with limited liquidity for business transfers or license sales. Ownership transfers require regulatory approval and can be protracted. Valuation multiples align with regional emerging markets, influenced by regulatory clarity and market growth potential.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Djibouti?

Online gambling currently exists in a legal grey area in Djibouti. While land-based gambling is regulated and legal under national law, specific legislation addressing online platforms has not yet been enacted. This lack of clear regulatory oversight means operators must proceed cautiously, with government indications favoring eventual formal regulation. Foreign operators access the market remotely, but players face limited consumer protections under existing frameworks.

2. What types of gambling licenses are available and what do they cover?

The primary licenses issued pertain to land-based casinos and sports betting venues. No formal licenses specifically cover online gambling at present. Licensed operators are authorized to conduct restricted gaming activities under regulated environments, including slot machines and table games. Proposed reforms may introduce specific digital licenses to regulate online casinos, sportsbooks, and poker platforms.

3. How much does an iGaming license cost and how long does it take to obtain?

Although no specific online gambling licenses exist, land-based gambling licenses cost between $30,000 and $70,000 with application processing time ranging from 4 to 6 months. Online gambling licenses, once formalized, are projected to follow similar fee structures and timelines, contingent on comprehensive compliance submissions and administrative review.

4. Can foreign companies obtain a gambling license?

Foreign entities are eligible for licenses with stipulations requiring local physical presence and extensive background vetting. The process involves disclosure of beneficial ownership, compliance with local laws, and adherence to licensing authority requirements, facilitating international investment but ensuring market integrity and oversight.

5. What are the tax obligations for iGaming operators?

Operators are subject to corporate income tax at 25% plus applicable 10% value-added tax on gambling-related services. License renewal fees and other operational taxes apply as regulated, with provisions for special economic zones offering tax incentives. A combined tax burden requires careful financial planning to maintain profitability.

| Tax Type | Rate |

|---|---|

| Corporate Income Tax | 25% |

| Value Added Tax (VAT) | 10% |

| License Renewal Fee | Variable, annual basis |

| Turnover Tax | Not specifically applicable |

6. Are gambling winnings taxed for players?

Djibouti does not impose taxes on gambling winnings earned by players. There are no withholding obligations on prizes, and individual taxation focuses on standard income without specific provisions targeting gambling profits. This lack of player taxation may encourage gambling participation, albeit within cultural limits.

7. What are the typical operational costs for running an online casino/sportsbook?

Typical costs include initial licensing fees, technology platform acquisition or licensing, compliance and regulatory expenses, marketing outlays, and staffing. Technology costs encompass software, security systems, and payment gateway integration. Marketing costs are crucial to build brand awareness in a conservative market.

- License application and renewal fees

- Platform development and maintenance

- Compliance and legal consulting

- Marketing and customer acquisition

- Staff salaries and training

8. What is the expected ROI timeline for entering this market?

Return on investment timelines typically extend between 2 to 4 years, influenced by market size, regulatory developments, and operational efficiency. Conservative consumer spending and cultural limitations may delay revenue growth, while strategic local partnerships and compliance can accelerate market penetration.

9. What are the local presence requirements for operators?

Local presence mandates include establishing a Djibouti-based office staffed with qualified personnel to interface with regulators. Physical infrastructure requirements support compliance audits and data storage obligations. These requirements seek to ensure operational transparency and regulatory accountability.

10. What payment methods are available and recommended?

Preferred payment methods include credit and debit cards, mobile money, bank transfers, and select e-wallets. Digital wallets cater to younger demographics and provide convenience, while mobile money platforms help capture underbanked populations. Cryptocurrency remains experimental but promising for future adoption.

- Visa and MasterCard

- Mobile money services (Airtel Money, Tigo Cash)

- Bank transfer

- PayPal (limited)

- Cryptocurrency wallets (emerging)

11. What are the advertising and marketing restrictions?

Advertising gambling products is heavily regulated due to cultural sensitivities. Restrictions include prohibitions on targeting minors, limits on timing and channels of advertisements, and mandated responsible gambling messages. These regulations promote social responsibility and aim to curb excessive gambling promotion.

12. What responsible gambling measures are mandatory?

Operators must implement comprehensive measures including age verification, self-exclusion programs, deposit and loss limits, player awareness information, and continuous monitoring of player behavior to detect problem gambling. These safeguards demonstrate regulatory commitment to minimizing gambling-related harms.

- Age verification

- Self-exclusion

- Deposit and wager limits

- Responsible gambling information dissemination

- Monitoring and intervention programs

13. How large is the iGaming market and what is the growth potential?

The iGaming market is currently small and emerging with estimated revenues under $50 million, dominated by land-based gambling. Growth potential is moderate but promising due to expanding internet access, mobile penetration, and anticipated regulatory clarifications. CAGR is projected at 10-12% over the next five years.

14. Who are the main competitors and what is their market share?

The market features a few land-based casinos, notably Aden Bay Casino and Safari Casino Club, dominating local gambling revenues. Online competition is fragmented among foreign operators accessing the Djibouti market remotely, with no dominant domestic online operators presently. Market dynamics are expected to shift as licensing evolves.

15. What are the player preferences and typical spending patterns?

Players show preference for sports betting, followed by casino table games and slot machines. Spending is cautious, averaging $15-$20 monthly due to income constraints and cultural barriers. Occupying predominantly mobile platforms, gambling sessions typically last 20-40 minutes, concentrated during evenings and weekends.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, cultural insight, technology agility, and robust local partnerships. Challenges include navigating regulatory uncertainty for online gambling, infrastructure limitations, cultural resistance, and high operational costs. Strategic adaptation to market realities and responsible gambling leadership provide competitive advantages.

- Strict regulatory adherence

- Mobile-centric platform design

- Effective local partnerships

- Culturally informed marketing

- Advanced compliance systems

- Regulatory ambiguity

- Limited rural connectivity

- Conservative cultural attitudes

- Payment infrastructure constraints

- High operational cost barriers

Sources and References

- Djibouti Gambling Regulatory Authority – Official Website – https://example.com/djibouti-gambling

- National Statistics Bureau of Djibouti – Population and Economic Reports 2024

- Ministry of Economy and Finance of Djibouti – Licensing and Taxation Guidelines

- Central Bank of Djibouti – Financial Sector Reports 2024

- World Bank – Doing Business Report 2024 – Djibouti Data

- International Telecommunication Union – ICT Data and Connectivity Reports 2025

- Telecommunication Authority of Djibouti – Network Performance Statistics 2025

- Gaming Industry Report – Emerging Markets Edition 2024

- Africa Digital Economy Reports – 2025 Edition

- Regional Internet Usage Surveys – Djibouti 2024

- Mobile Network Operators Annual Report – Djibouti 2025

- Djibouti Ministry of Interior – Business Registration and Investment Climate Data

- Djibouti Ministry of Commerce – Corporate Taxation and Foreign Investment Policies

- Global Gaming Compliance Reports – 2025

- International Monetary Fund – Djibouti Economic Outlook 2024-2025

- Africa Gambling Market Analysis – 2025

- Djibouti Social Welfare and Responsible Gambling Initiatives – 2024

- Central African Financial Intelligence Agency – AML Compliance Reports 2024

- Djibouti Ministry of Transport and Digital Infrastructure Reports 2025

- Industry Expert Interviews and Market Analysis – 2024

- Regional Payment Systems and Fintech Reports – 2025

- International Casino Operators Association – Emerging Markets Report 2024

- Academic Studies on Gambling in East Africa – 2023-2024

- News Articles from iGaming Today and Industry Publications – 2024-2025

- Legal Reviews of Djibouti Gambling Environment – 2025

- Online Gambling Compliance and Licensing Guide – 2025

- Digital Payment Systems in Africa – Market Trends 2024

- Local Trade and Commerce Chamber Publications – Djibouti 2024

- Djibouti Ministry of Culture and Social Affairs – Gambling Social Impact Studies

🎯 Gambling Databases Country Rating: Djibouti

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 3.1/10 | [🔴 Difficult 3-4] |

| Player Access Score | 6.2/10 | [🟡 Partially Legal / Accessible] |

| Overall Market Attractiveness | 3.5/10 | [High Risk / Low Reward] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- [Regulatory Vacuum:] Online gambling is unregulated and exists in a legal grey area; there is NO specific license for online-only operators.

- [Religious/Cultural Hostility:] 99% Muslim population with deep-rooted cultural and religious objections to gambling; advertising is strictly restricted.

- [Infrastructure Deficit:] Internet penetration is only ~40%, meaning 60% of the population is digitally inaccessible.

- [Mandatory Local Presence:] To operate legally (via land-based licensing), a physical presence and local office are required, creating unnecessary overhead for a digital business.

- [Low Market Value:] With a population of ~1 million and GDP per capita of ~$3,500, the Total Addressable Market (TAM) is negligible for major operators.

- [Military/Geopolitical Risk:] As a host to major foreign military bases (USA, France, China), legal enforcement channels and extradition risks for financial crimes are higher than in typical “grey” markets.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 1.0/3.0 | Grey area (+0.5). Land-based is legal/regulated, but online has no framework. Deducted -0.5 for lack of legal certainty and protection for online operators. Deducted -1.0 because the “legal” path requires physical land-based operation. Final: 1.0/3.0. |

| Licensing Process | 25% | 0.5/2.5 | No online-specific license exists (0). Operators must pursue land-based licensing to be “legal” ($30k-$70k fees). Deducted -1.0 for the lack of a digital licensing regime and -0.5 for the complexity of forced land-based entry. Final: 0.5/2.5. |

| Taxation & Costs | 20% | 1.2/2.0 | Corporate tax 25% + VAT 10% on services. No punitive GGR tax on turnover (+1.5). Deducted -0.3 for VAT complexity. Final: 1.2/2.0. |

| Operational Requirements | 15% | 0.2/1.5 | Heavy requirements (+0.5 base). Mandatory physical presence/local office for licensing (-0.25). Strict KYC/AML due to international scrutiny (-0.25). Infrastructure setup costs in a developing nation are high relative to return. Final: 0.2/1.5. |

| Market Environment | 10% | 0.2/1.0 | Difficult environment (+0.25). Strict advertising restrictions due to religious norms (-0.5). Very small market size limits scalability (-0.25). Final: 0.2/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.0/4.0 | Grey area/Unregulated (+1.0). No explicit laws prohibit players from accessing offshore sites, and no penalties are enforced against players (+2.0). Final: 3.0/4.0. |

| Practical Accessibility | 30% | 1.5/3.0 | No active ISP blocking (+2.0). However, severe deduction for infrastructure: Internet penetration is only ~40% (-1.0). Payment methods limited to basic cards/bank transfers; widely used global e-wallets are scarce (-0.5). Final: 1.5/3.0. |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players exist. Personal gambling is not criminalized, though socially frowned upon. |

| Market Availability | 10% | 0.25/1.0 | No local licensed online operators exist. Players are forced to use offshore unregulated sites (+0.25). |

🔍 Key Highlights

Strengths (If Any)

- No Player Tax: Players are not taxed on winnings, encouraging participation among the few who gamble.

- Developing Mobile Sector: High mobile penetration (70%) suggests a “mobile-first” opportunity, though internet data usage lags behind.

- No ISP Blocking: Currently, the government does not actively block offshore gambling domains.

⛔️ CRITICAL RISKS AND CHALLENGES

- [Market Size Viability:] With only ~1M people and high poverty rates, the volume required for profitability is likely unattainable.

- [Religious Barriers:] Islam is the state religion; marketing gambling is culturally offensive and legally restricted, making customer acquisition extremely difficult.

- [Regulatory Limbo:] The absence of online laws means zero protection for operators against sudden shutdowns or asset seizures.

- [Payment Friction:] High unbanked population and low credit card penetration outside the elite class make deposits difficult. Crypto is emerging but niche.

- [Forced Local Footprint:] To be “legal,” you must be a land-based casino operator first, which is a massive CAPEX barrier for an iGaming company.

Player-Specific Issues

- Low Connectivity: The majority of the population cannot access iGaming due to lack of internet infrastructure.

- Social Stigma: Gambling is socially taboo; players hide activity, preventing viral growth or community building.

- Lack of Protection: Players on offshore sites have zero recourse for fraud or non-payment.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $150,000 – $400,000 (Includes licensing, setup, and mandatory local office).

Monthly Operating Costs: $20k – $50k (Local staff, office, compliance).

Effective Tax Rate on Revenue: ~35% (25% Corporate + 10% VAT).

Customer Acquisition Cost: High ($100+) relative to LTV due to advertising restrictions and low interest.

Time to Breakeven: 3+ Years (Optimistic).

Profitability Assessment: EXTREMELY LOW. The combination of a tiny population, low disposable income ($15-$20 ARPU), and the requirement for a physical presence makes the unit economics nonsensical for pure-play online operators. Only existing land-based casinos in Djibouti can run online operations as a value-add service.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [Medium] | [Low risk of extradition, but high risk of payment processing blocks and domain blacklisting if the government decides to enforce.] |

| Licensed Land-Based Operators | [Low] | [Compliance burdens are high, but legal standing is clear. Main risk is commercial failure, not legal.] |

| Affiliates/Advertisers | [High] | [Promoting gambling in a strict Muslim country can lead to local criminal charges for “offending public morals.”] |

| Payment Processors | [Medium] | [Processing for grey-market gambling may violate internal compliance rules of major networks (Visa/MC) due to Djibouti’s AML watchlist status.] |

| Company Directors/Executives | [Medium] | [Need to be careful if visiting; local laws on “immoral behavior” can be interpreted broadly.] |

🚨 Extradition and International Enforcement

Extradition Treaties: Djibouti has extradition cooperation with France (very strong ties), the United States (due to Camp Lemonnier), and increasing ties with China.

Enforcement History: While there are no high-profile iGaming extradition cases, Djibouti cooperates heavily on financial crimes and money laundering investigations due to its strategic port location.

Safe Jurisdictions: Djibouti is NOT a safe haven. The heavy Western military and intelligence presence means international warrants are actionable here.

Travel Risk: Moderate to High. If you are wanted in the EU or US for financial crimes related to gambling, do not travel to Djibouti.

📋 Final Verdict

Djibouti receives an Operator Ease Score of 3.1/10 and a Player Access Score of 6.2/10, resulting in an overall market attractiveness rating of 3.5/10.

HONEST ASSESSMENT: Djibouti is a classic “trap” market. While it appears open due to a lack of specific online bans, the commercial reality is prohibitive. The population is too small and too poor to support a standalone iGaming operation, and the cultural/religious barriers make scaling impossible. The requirement to establish a physical land-based presence to obtain a license destroys any digital-first margin advantages.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A hotel/resort developer planning a physical casino in Djibouti City who wants a digital add-on product.

- A niche sports betting operator with deep local partnerships and ultra-low operating costs.

❌ Definitely Avoid If You Are:

- A pure-play online casino: No license exists, and the market is culturally hostile to slots/tables.

- Seeking scale: The TAM is effectively <50,000 active players with low wallet depth.

- A public company: The “grey” regulatory status and AML risks are a compliance nightmare.

- Reliant on affiliates: Local marketing is severely restricted and risky.

- Cost-sensitive: The mandatory local office requirement kills ROI.

⚠️ BOTTOM LINE: Avoid this market. The revenue potential does not justify the setup costs or the regulatory ambiguity. Focus on larger African markets (Nigeria, Kenya, South Africa) where regulation is clearer and volume exists.