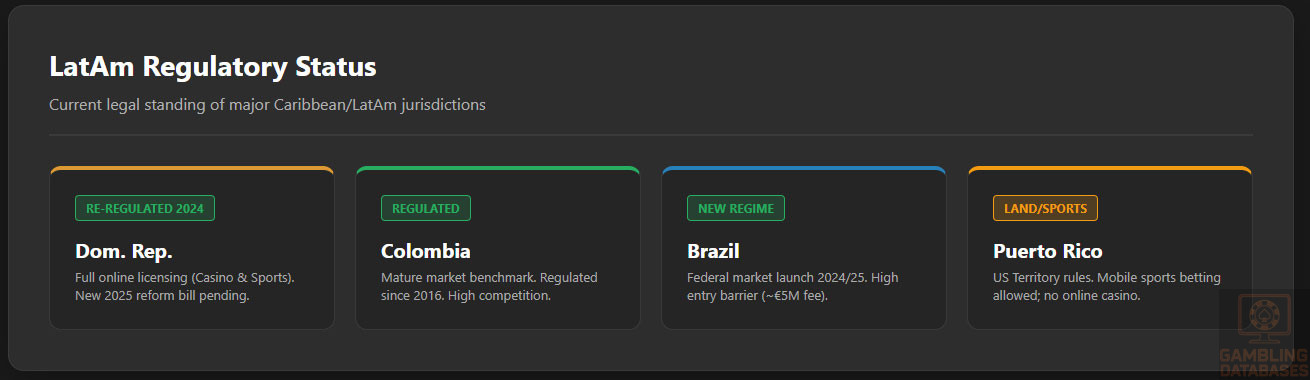

The Dominican Republic is emerging as a promising destination for iGaming operators in 2025, driven by a newly established regulatory framework and favorable market conditions. With formal online gambling regulation introduced in 2024, the country offers structured licensing and taxation systems set to attract new entrants.

Strong internet penetration, a robust tourism industry, and a well-established land-based gambling sector combine to create an attractive environment for iGaming market development. The recent regulatory overhaul signals increased government oversight and a push for industry modernization.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Fully regulated for land-based and online gambling |

| Key Regulatory Authority | Directorate of Casinos and Games of Chance (DCJA), proposed DGJA |

| Regulatory Framework Enactment | Online gambling regulated since 2024 (Resolution No.136-2024) |

| License Validity | 5 years, non-transferable for first 3 years |

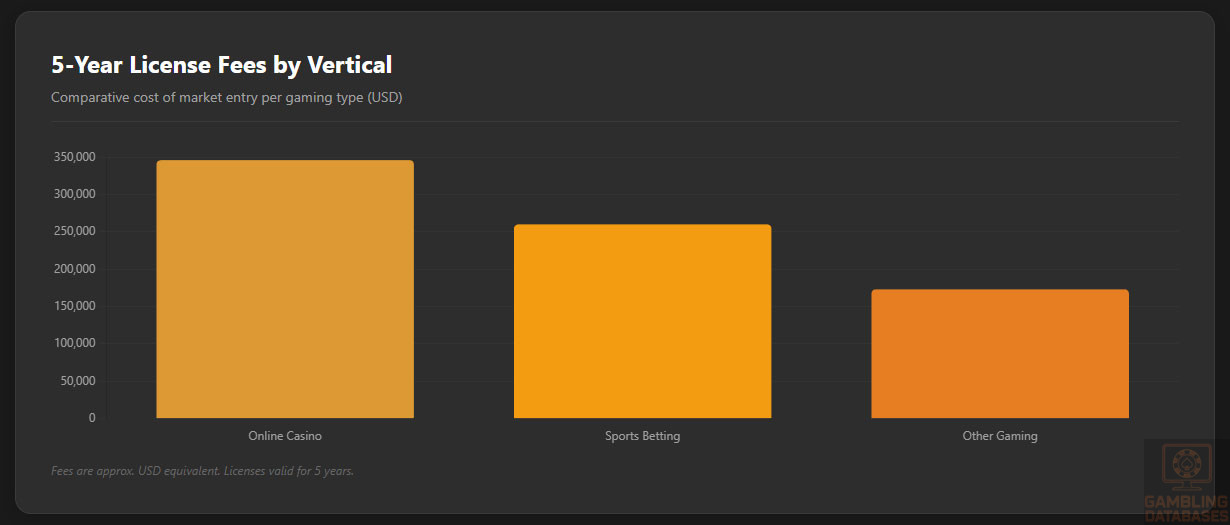

| License Fees (Online Casinos) | Approx. USD 346,000 per 5-year license |

| License Fees (Sports Betting) | Approx. USD 260,000 per 5-year license |

| License Fees (Other Online Gaming) | Approx. USD 173,000 per 5-year license |

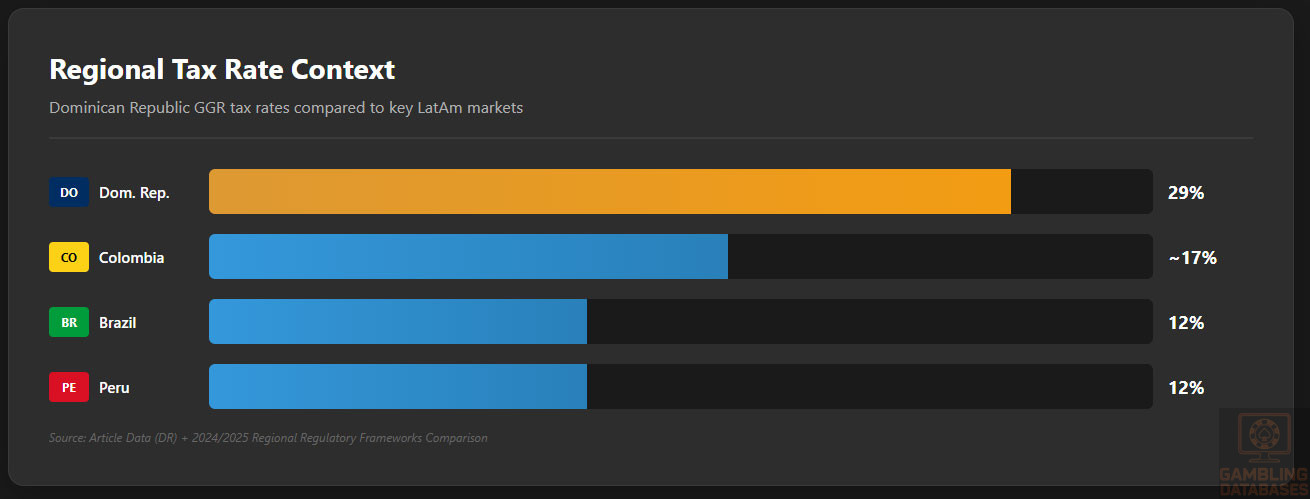

| Tax Rate on Gross Gaming Revenue (Land-Based Casinos) | 29% |

| Slot Machine Tax on Gross Sales | 5% monthly |

| Tax Rate Increase | From 25% to 29% for all income generating companies (2024) |

| Corporate Income Tax for Licensed Gambling Companies | 0% |

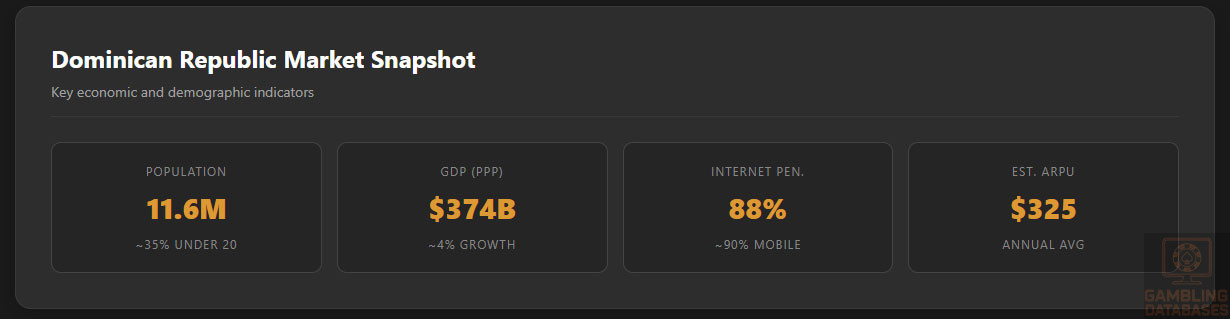

| Population | Approx. 11 million |

| Internet Penetration Rate | 75%-80% |

| Mobile Penetration Rate | ~90% |

| Market Size (Estimated Revenue) | Mid-sized regional market with growth potential |

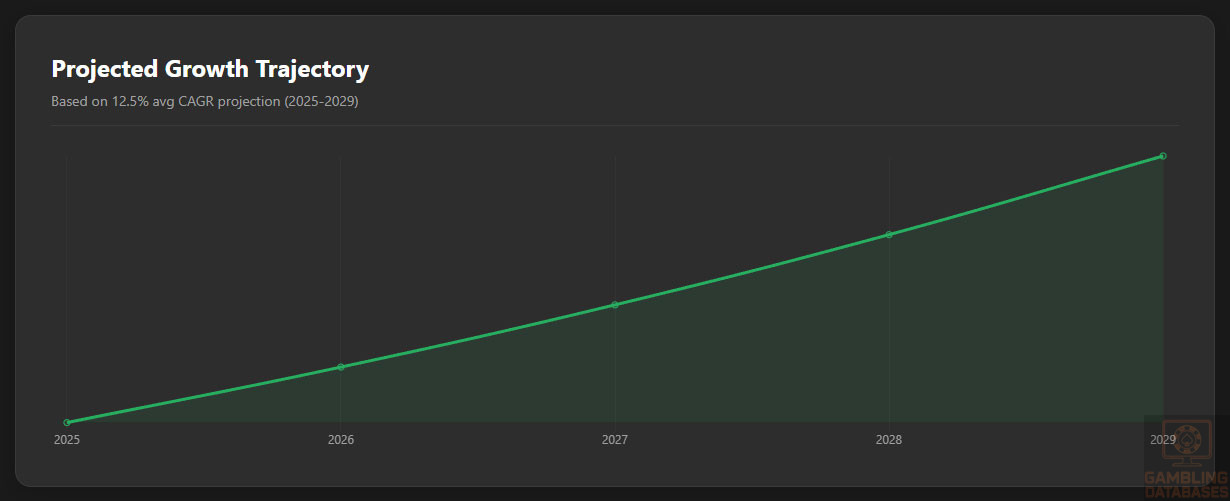

| iGaming Market Growth Forecast (CAGR) | Projected 10%-15% annual growth over next 5 years |

| Average Revenue Per User (ARPU) | Estimated USD 300-350 annually |

| Licensed Land-Based Casinos | ~60, mostly resort-based |

| Licensing Timeline | 6 months or more from application to approval |

| Foreign Ownership Restrictions | Allowed with local presence and operational requirements |

| Responsible Gambling Obligations | Mandatory self-exclusion, session time limits, visible warnings |

| Advertising Restrictions | Distance regulations, content limits, sponsorship rules |

| Recent Regulatory Changes | New gambling reform bill (2025), proposed new regulator DGJA |

| Payment Systems Requirements | Local banking integration and financial compliance mandatory |

| Market Entry Barriers | High licensing fees, infrastructure compliance, local presence requirements |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

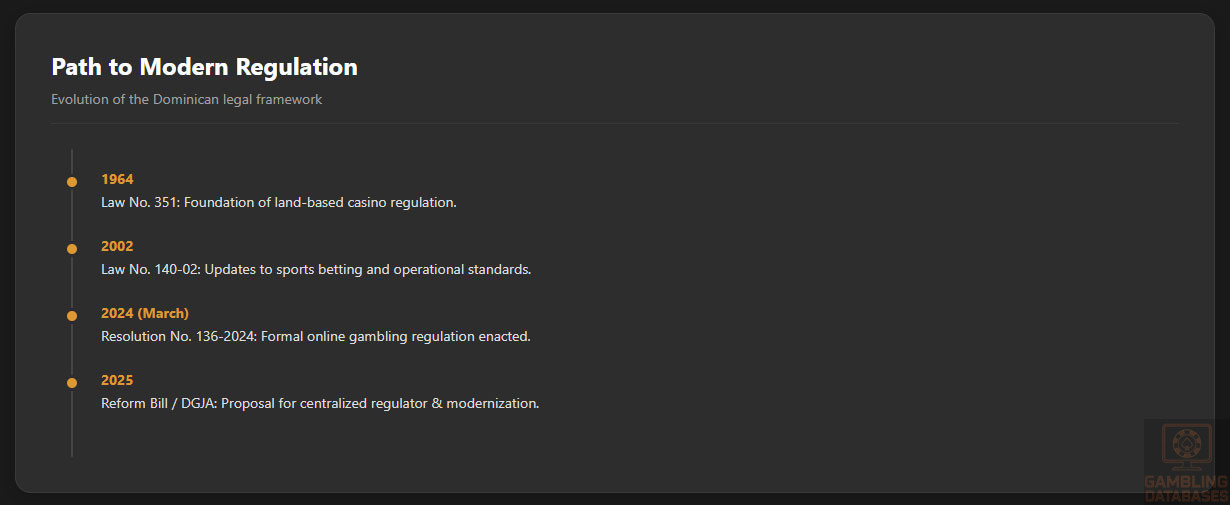

The Dominican Republic maintains a fully regulated gambling sector encompassing land-based and online activities. Historically, gambling regulation has centered on land-based casinos and retail sports betting, closely linked to the country’s tourism industry and cultural affinity for baseball betting. The sector is governed by longstanding national laws (Law No. 351 of 1964, Law No. 140-02, and amendments) complemented recently by progressive regulations focused on digital gaming.

The Directorate of Casinos and Games of Chance (DCJA), under the Ministry of Finance, administers these regulations. There is a concurrent legislative proposal to establish the General Directorate of Games of Chance (DGJA) to centralize and enhance regulatory functions across all gambling verticals.

Land-Based Gambling Activities

Land-based gambling is predominantly centered on casinos integrated within four- and five-star hotel resorts, which are incentivized to operate gaming facilities aimed at tourists. Approximately 60 licensed casinos operate nationwide, with significant venues located in Punta Cana, Santo Domingo, and Santiago.

Retail sports betting remains widespread, particularly on baseball, and is conducted through authorized betting kiosks and venues. Slot machine halls are allowed at casinos, hotels with one- to three-star ratings, and regulated sportsbook outlets. The government enforces geographical restrictions to maintain social safeguards around vulnerable locations such as schools and hospitals, mandating minimum distances between gambling venues and these sensitive sites.

Online Gambling Framework

The 2024 regulation introduced criteria for online operator licensing, including technical standards for platforms, game fairness (random number generators), data security, and anti-money laundering (AML) compliance. Online casinos, sportsbooks, and other permitted formats must secure a license valid for five years, renewable subject to compliance review. Licenses cannot be transferred within the first three years to ensure operator stability.

The regulation prohibits unauthorized remote gambling operations and imposes specific restrictions on game types and wagering formats. Operators are mandated to implement responsible gambling measures such as self-exclusion and session time-tracking, ensuring consumer protection. Oversight includes monitoring adherence to advertising rules, financial reporting obligations, and periodic audits.

Licensed Operators and Market Players

The Dominican Republic’s online gambling market remains nascent but growing rapidly with an expanding license framework encouraging new entrants. Historically, very few online licenses were issued, with mature operators like Flutter Entertainment holding exclusive rights. The adoption of the new regulation dissolves monopolistic barriers, inviting competitive participation from international and local companies.

Market dynamics involve strong competition for tourism-focused operators and integrated hotel-casino enterprises. Entry strategies emphasize compliance with local presence mandates, technological infrastructure deployment domestically, and adherence to robust financial and customer protection standards. The licensing cost and rigorous application process act as moderate barriers but add market credibility and operational certainty.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing authority, currently the DCJA, reviews applications for both land-based and online gaming operations. The process involves demonstrating financial solvency, technical compliance, and transparency of ownership. A comprehensive due diligence process includes criminal background checks and validation of beneficial owners.

Applicants must submit a detailed business plan, platform technical documentation, and evidence of responsible gaming programs. There is a required minimum capital deposit in a licensed financial institution. Application fees range depending on the license type, with online casino licenses costing approximately USD 346,000 for a five-year term.

The timeline for license approval typically spans six months or more, reflecting thorough examination procedures. The authority requires continued compliance audits to maintain licensure.

Local Presence and Operational Requirements

Foreign operators must establish a legal entity within the Dominican Republic and maintain physical presence through offices or hosting facilities. Gaming servers and IT infrastructure must be based domestically to comply with data sovereignty and permanent establishment rules. Authorities require licensed operators to maintain a close relationship with local banking partners to ensure proper financial monitoring.

Personnel with expertise in compliance, security, and customer service must be employed locally to guarantee ongoing regulatory adherence and support consumer protections. Foreign ownership is permitted but subject to transparency and operational alignment with local regulations.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators are mandated to implement stringent age verification processes ensuring all players are at least 18 years old. Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures require verified identity documentation and ongoing customer risk assessment.

Responsible gambling is a focus, with mandatory measures including:

- Self-exclusion systems accessible to players

- Session duration tracking visible to users

- Betting limits customizable by players

- Permanent display of responsible gambling notices on platforms

- Provision of links to support organizations for gambling addiction

Financial Monitoring and Reporting

The regulatory authority enforces rigorous financial reporting protocols. Operators must submit monthly reports detailing gross gaming revenues, tax liabilities, and player transactions.

Audit procedures include examination of transaction logs, payout ratios, and compliance with tax withholdings. The reporting cycle involves the following steps:

- Preparation of monthly revenue and transaction summaries by operators

- Submission to the Directorate of Casinos and Games of Chance

- Verification and cross-checking with independent auditors

- Issuance of compliance confirmation or enforcement actions if discrepancies arise

Taxation Structure and Financial Obligations

Player Taxation

Players are subject to taxation on gambling winnings exceeding RD$50,000 with automatic withholding mechanisms at the point of payout. The tax withholding rate for winnings surpassing this threshold is set at 15%.

Operator Taxation

| Gaming Segment | Tax Rate |

|---|---|

| Land-Based Casinos (Gross Gaming Revenue) | 29% |

| Slot Machines (Gross Sales) | 5% monthly |

| Online Casinos (Projected) | Expected similar to land-based, pending regulation finalization |

| Sports Betting (Online & Land-Based) | Variable fees plus GGR tax pending new framework |

| License Renewal Fee | Determined per license type, typically 50% of initial fee |

Corporate income tax exemptions apply to licensed gambling companies, reducing the effective tax burden but reinforcing compliance obligations. Operators must also pay fixed monthly fees based on the number of gaming tables and machines for land-based casinos.

Gambling Market Financial Performance

The Dominican gambling market demonstrates steady growth supported by expanding land-based operations and the advent of regulated online platforms. Total wagered amounts have increased annually, reflecting growing player bases and rising average bet sizes.

Tax revenues from gambling activities contribute substantially to public finances, with year-over-year increases reported for casino and lottery segments. Online gaming is anticipated to significantly augment government revenues as new operators enter under the updated regulatory regime.

Advertising and Marketing Restrictions

Advertising of gambling services is subject to specific content and venue restrictions to protect vulnerable populations. Regulations prohibit gambling ads near schools, healthcare facilities, places of worship, and government offices.

Recent Regulatory Changes and Their Impact

In 2024 and 2025, the Dominican Republic implemented significant regulatory reforms to modernize and expand gambling oversight. The introduction of Resolution 136-2024 created a clear legal basis for online gambling licensing.

A bill proposing the establishment of the DGJA aims to consolidate regulatory activities and enhance enforcement, with potential to improve market transparency and reduce fraud. The reforms are expected to increase operator costs due to stricter compliance but also to open market access and boost legitimacy.

Enforcement Mechanisms and Penalties

The regulatory framework includes robust enforcement tools to ensure compliance, with penalties for violations ranging from fines to license suspension or revocation. The Directorate is empowered to conduct investigations and audits, impose sanctions, and refer criminal matters to judicial authorities.

- Fines for unauthorized operations or violations of license terms

- License suspension or revocation for repeated breaches

- Penalties for advertising infractions

- Seizure of illegal equipment and gaming revenue

- Criminal prosecution for fraud or money laundering offenses

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

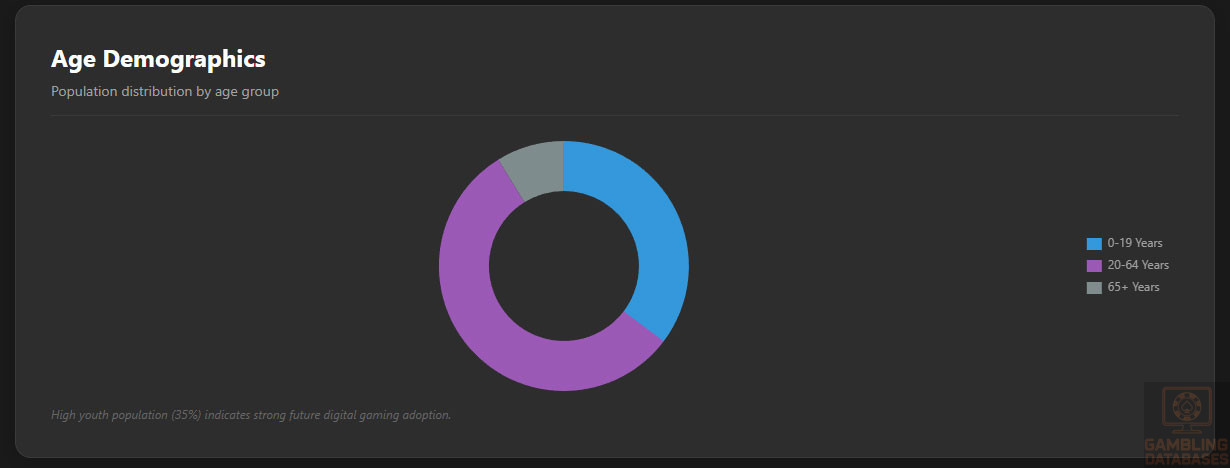

The Dominican Republic’s population in 2025 is estimated at approximately 11.6 million, with a median age of 32 years and a nearly balanced gender ratio of around 987 men per 1,000 women. The age distribution shows a youthful society with about 35% under 20 years, while 56% fall between 20 and 64 years, and roughly 9% are aged 65 and above.

Urbanization is pronounced, with over 85% of the population residing in urban areas. Population density stands at approximately 241 persons per square kilometer. The demographic profile reflects steady natural growth alongside net negative migration, resulting in gradual population increase and an aging trend in coming years.

| Age Group | Population % |

|---|---|

| 0-19 years | 35.3% |

| 20-64 years | 55.9% |

| 65+ years | 8.8% |

Major population centers concentrate around the capital Santo Domingo, Santiago, and tourism hubs like Punta Cana. Internet and gambling venue access correlate strongly with these urban centers, where infrastructure and economic activity are most developed.

- Santo Domingo: Approx. 3 million inhabitants

- Santiago de los Caballeros: Over 1 million residents

- La Romana

- Punta Cana

- Puerto Plata

Economic Indicators and Consumer Spending Power

The Dominican Republic has demonstrated robust economic growth, with a projected GDP of about USD 374 billion (PPP) in 2025 and an annual growth rate near 4%. The economy is service-driven but maintains substantial industry and agriculture sectors. Improvements in infrastructure and foreign investment underpin this positive trajectory.

Average household income ranges widely, reflecting disparities between urban and rural regions. The emergence of a growing middle class alongside reduced poverty levels has improved disposable income, fueling consumer spending particularly in urban areas where the iGaming market is concentrated.

Market size for iGaming remains mid-tier but shows strong year-on-year growth projected at 10-15% CAGR, supported by expanding internet access and tourism. Estimated ARPU in the iGaming sector is between USD 300-350 annually, supported by increasing penetration and consumer engagement.

| Metric | Value |

|---|---|

| GDP (PPP) | USD 374 Billion |

| GDP Growth Rate | Approx. 4% |

| Per Capita Income | USD 3,200 (approx.) |

| Unemployment Rate | ~5% |

| Inflation Rate | ~3.5% |

Education, Skills, and Digital Literacy

Literacy rates in the Dominican Republic are high, exceeding 93% among adults, with widespread primary and secondary education coverage. Digital literacy is growing, boosted by increased internet penetration and government initiatives to expand IT skills training. The workforce garners increasing capabilities suited to technology-driven sectors including gaming and eCommerce.

Cultural and Social Factors

Communication and Language

Spanish is the official and primary language of communication, used predominantly online and offline. English is spoken in business and tourist areas. The country has limited linguistic diversity, with Spanish dominating all media and digital content consumption.

Cultural Attitudes

Gambling enjoys moderate social acceptance, especially in tourist hubs and among younger populations. Religious influences, primarily Catholicism, impose some social restrictions, but cultural attitudes are generally tolerant, facilitating the growth of gaming and betting sectors.

Foreign brands are viewed positively, particularly those associated with trust and digital innovation, which attracts younger tech-savvy consumers who favor online gambling platforms over traditional betting venues.

Problem Gambling and Social Considerations

Problem gambling prevalence remains low but is under increased scrutiny with the expansion of the online market. Government and NGOs have initiated multiple programs to mitigate risks, including educational campaigns, addiction support services, and regulatory mandates for operators to promote responsible gambling.

- Mandatory self-exclusion programs

- Gambling addiction counseling services

- Public awareness and prevention campaigns

- Regulatory monitoring of operator compliance

- Collaboration with healthcare providers for support

Political Structure and Governance

The Dominican Republic is a stable representative democracy with consistent governance frameworks promoting foreign investment and business transparency. Regulatory consistency has improved post-2024 gambling reforms, fostering a reliable environment for market entrants.

Technology Adoption and Digital Behavior

Internet and Digital Usage

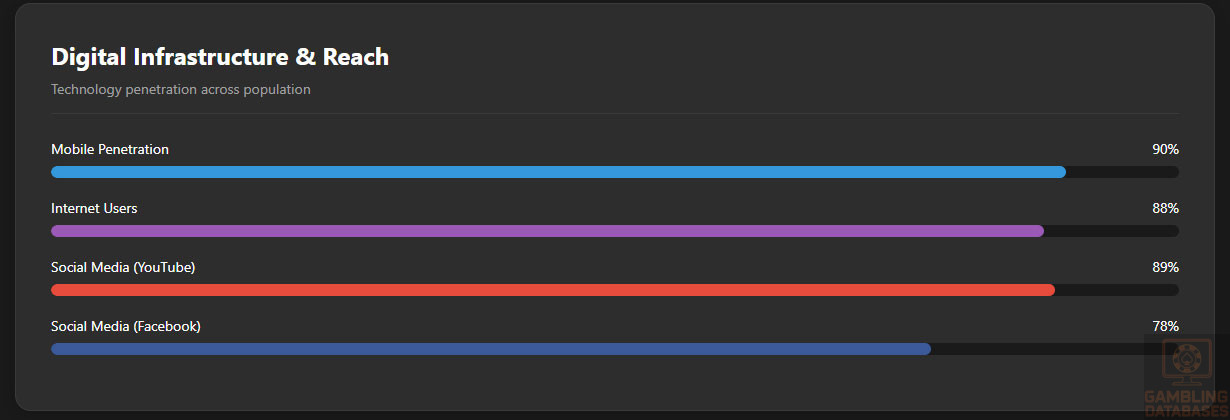

Internet penetration stands at approximately 88% of the population, driven by robust mobile broadband expansion. Median mobile internet speeds approach 40 Mbps, with fixed broadband slightly faster, enabling smooth streaming and gaming experiences.

Mobile connections exceed 90% of the population, with multiple device ownership common. Daily average internet use surpasses 3 hours, reflecting high digital engagement and social media activity.

- Facebook – 78% penetration among internet users

- Instagram – 64% among youth demographics

- YouTube – 89% reach with high watch times

- TikTok – Rapid growth, 52% under age 25

- Twitter – 31% penetration, news-focused audience

- LinkedIn – 28% of professionals using for networking

Digital Payment Behavior

The digital payment landscape is diverse yet dominated by debit and credit cards, comprising the majority of online transactions. Bank transfers and mobile payment solutions have grown, supported by local banking integration and secure platforms. Cryptocurrency adoption remains niche but is gradually increasing among younger users.

- Debit and credit cards—leading online payment method

- Bank transfers—widely used for bill payments and remittances

- Mobile wallets—gaining traction with growing smartphone usage

- Cash payments—still common for many retail transactions

- Electronic Fund Transfers (EFT)—used in business and gig economy

Gaming and Gambling Preferences

Current Market Participation

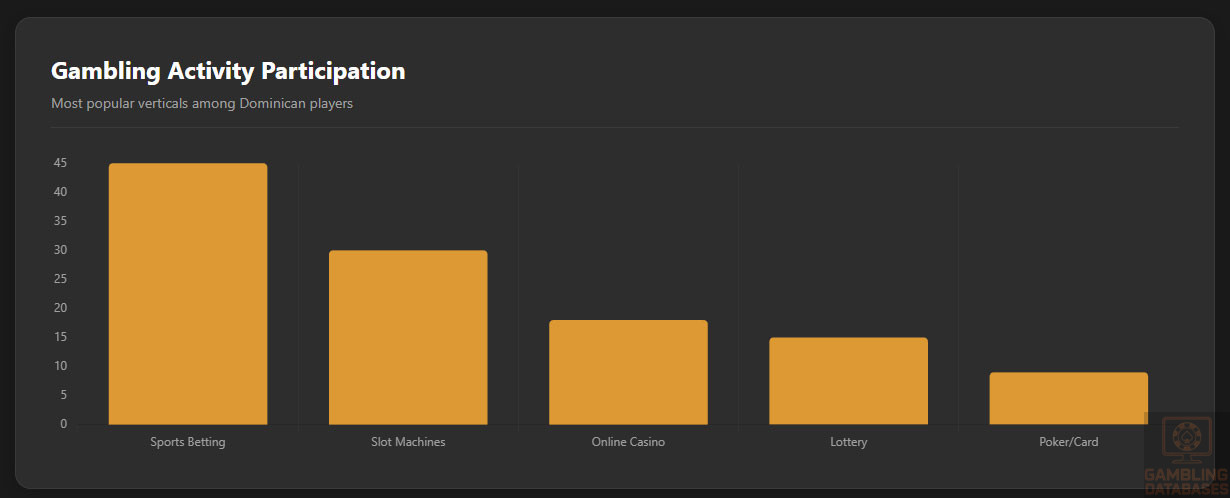

Gambling participation in the Dominican Republic centers around sports betting, casino games, and lottery products. Sports betting, especially on baseball, dominates activity, followed by slot machines and online casino games in urban areas.

| Rank | Activity | Participation % |

|---|---|---|

| 1 | Sports Betting | 45% |

| 2 | Slot Machines | 30% |

| 3 | Online Casino Games | 18% |

| 4 | Lottery | 15% |

| 5 | Poker and Card Games | 9% |

Consumer Behavior Patterns

Dominican players tend to favor mobile platforms due to high smartphone penetration and reliable mobile data coverage. Peak gambling hours occur in the evenings and weekends, aligning with leisure time post-work. Session lengths vary, with online casino users tending toward medium-length sessions of 30-45 minutes, while sports bettors may engage briefly but frequently.

Retention rates are bolstered by localized promotions, loyalty programs, and cultural engagement through sports sponsorships. The consumer base shows openness to novel game types and cross-channel experiences combining social and real-money gambling.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

The Dominican Republic exhibits solid internet penetration, reaching approximately 88% of the population by 2025. Fixed broadband access remains less prevalent compared to mobile broadband, reflecting infrastructural and economic preferences. Mobile broadband connections outnumber fixed lines by nearly 3:1, driven by extensive 4G network coverage and affordable data plans.

Average mobile broadband speeds reach near 40 Mbps, sufficient for high-quality streaming and online gaming. National investments have improved network backbone capacity and fiber optic expansion, enhancing reliability and reducing latency, crucial for iGaming platform performance.

5G and Future Technology Deployment

5G rollout began in early 2025, with initial deployment concentrated in major urban areas such as Santo Domingo, Santiago, and key tourist zones. Operators plan phased expansion targeting 75% population coverage within two years, prioritizing business districts and high-traffic public areas.

The competitive telecom landscape encourages rapid 5G adoption to maintain market share and service quality. Future technology investments include plans for enhanced IoT ecosystems and broader fiber-to-the-home (FTTH) penetration, which will bolster digital economy growth.

Mobile Technology Ecosystem

The mobile ecosystem is vibrant, supported by multiple network operators and high smartphone adoption rates. Over 90% of the population owns at least one smartphone, predominantly mid-range Android devices, with iOS adoption concentrated in affluent urban consumers.

- Claro (América Móvil) – Market leader with approx. 45% share

- Altice Dominicana – Holding about 30% of mobile subscriptions

- Viva (now part of Altice) – Remaining operational spectrum merged

- Smaller MVNOs serve niche segments

- New entrants focusing on data plans and youth markets

Data costs are competitive, averaging USD 0.50 per GB, supporting high consumption levels. Mobile wallets and banking apps are frequently used, aligned to convenience-seeking consumer segments.

Financial Services and Payment Infrastructure

The Dominican banking sector is stable and growing, with widespread digital banking adoption. Most adults hold bank accounts, and online banking penetration rises steadily thanks to mobile app innovation and fintech partnerships.

- Banco Popular Dominicano – Largest bank, strong digital platform

- BHD León – Prominent retail and corporate banking services

- Banco de Reservas – State-owned, extensive branch network

- Scotiabank Dominicana – International banking with strong remittance services

- Banesco Dominicana – Regional bank focused on digital payments

Payment processing includes credit/debit cards issued by Visa, Mastercard, and local schemes. E-wallets such as PayPal and local solutions (e.g., T-Pago) are establishing footholds. Bank transfers remain popular for bill payments and larger transactions, while cash still dominates many retail payments.

- Debit and credit card transactions dominate online payments

- Bank transfers preferred for high-value transactions

- Mobile wallets growing among tech-savvy users

- Cash payments remain significant in rural areas

- Cryptocurrency utilization is minimal but emerging

E-commerce and Digital Economy

The ecommerce market is expanding rapidly, reaching an estimated value of USD 3 billion in 2025 with projected annual growth exceeding 15%. Consumer trust in online payments is improving with better fraud protection and digital identity verification tools.

Retail platforms such as Amazon, MercadoLibre, and local e-commerce sites are popular, with increasing cross-border trade. The digital services economy, including gaming and entertainment subscriptions, continues to attract younger consumers, driving online spending behavior aligned with iGaming trends.

Business Environment and Regulatory Framework

The Dominican Republic ranks favorably in the World Bank’s Ease of Doing Business report, excelling in starting a business, registering property, and protecting minority investors. Foreign investment policies are welcoming, with a free trade zone regime offering tax incentives to qualifying companies, including gaming enterprises.

Business registration is generally straightforward, backed by digitized government services facilitating company incorporation and tax registration.

- Prepare and notarize incorporation documents within 2-3 weeks

- Register company with the Mercantile Registry within 5-7 business days

- Register for tax identification with the DGII within 3-5 days

- Open corporate bank account and deposit minimum capital over 1-2 weeks

- Obtain municipal licenses and operating permits within 2-4 weeks

Corporate Structure and Registration

Common entity types include Limited Liability Companies (SRL), Corporations (SA), and Branch Offices for foreign entities. LLCs offer flexibility and limited liability protections, widely favored by small and medium enterprises.

Corporations suit larger businesses seeking capital markets or institutional investment. Branch offices allow foreign companies to operate directly but face stricter regulatory scrutiny and local agent requirements.

- Articles of incorporation and by-laws notarized and filed

- Taxpayer registration (RNC) from DGII

- Proof of address and unique taxpayer identification

- Registration of legal representative and tax agent

- Payment of registration fees and municipal permits

Taxation Framework

The corporate income tax rate in the Dominican Republic is generally 27%. Special economic zones and free trade zones enjoy tax holidays ranging from 5 to 15 years, often applicable to sectors including technology and gaming. Bilateral tax treaties with over 20 countries facilitate reduced withholding taxes and international tax planning efficiency.

- United States

- Canada

- Spain

- France

- United Kingdom

Personal income tax applies on a progressive scale from 15% to 25%, with mandatory social security contributions. Tax residency rules require paying taxes on worldwide income for those residing over 183 days annually.

Market Entry Considerations

Optimal market entry strategies involve establishing local partnerships with financial institutions and service providers to comply with regulatory and operational requirements. Leveraging mobile-first platforms tailored to Dominican consumer behaviors enhances market penetration.

- Forming joint ventures with local entities for compliance ease

- Utilizing domestic bank partnerships for payment processing

- Adapting marketing strategies to local cultural preferences

- Investing in responsible gaming infrastructure from launch

- Phased geographic expansion starting from high-density urban areas

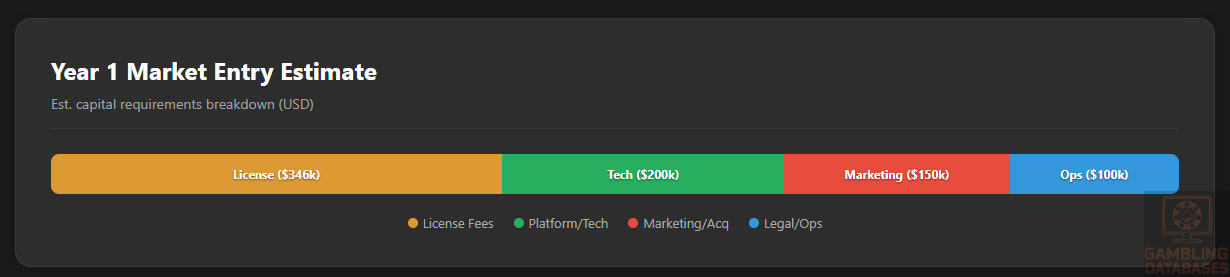

Initial investment commitments cover licensing fees, technology infrastructure, staffing, regulatory compliance, and marketing. Return on investment is expected in 2 to 4 years depending on scale and market conditions. Ongoing challenges include navigating evolving regulation, currency fluctuations, and local competition.

| Cost Category | Estimated Amount |

|---|---|

| License Fees (5-year license) | 346,000 |

| Legal and Consulting Services | 50,000-80,000 |

| Technology Platform Setup | 150,000-250,000 |

| Marketing and Customer Acquisition | 100,000+ |

| Operational Staff and Office Expenses | 80,000-120,000 annually |

FAQ: Frequently Asked Questions

1. Is online gambling legal in the Dominican Republic?

Yes, online gambling was formally regulated in 2024 with the introduction of Resolution No. 136-2024. This legislation outlines the legal framework encompassing online casinos, sports betting, and other remote gaming activities. Operators must obtain a valid license from the Directorate of Casinos and Games of Chance, and comply with regulatory, technical, and financial obligations to operate legally.

2. What types of gambling licenses are available and what do they cover?

Licenses are issued for several categories including:

- Land-Based Casinos

- Online Casinos

- Sports Betting (online and retail)

- Lotteries and Bingo

- Slot Machine Operations

Each license type defines permitted games, operational scope, tax structures, and compliance requirements, ensuring tailored regulation across gaming sectors.

3. How much does an iGaming license cost and how long does it take to obtain?

Obtaining an iGaming license for online casinos typically costs around USD 346,000 for a five-year term. Sports betting licenses are cheaper, around USD 260,000. The application and approval process can take 6 months or longer due to comprehensive due diligence and technical assessments.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are eligible provided they establish a legal entity within the Dominican Republic, maintain local operational presence, and comply with ownership transparency rules. Foreign ownership is unrestricted though operational personnel must be locally engaged.

5. What are the tax obligations for iGaming operators?

Operators are subject to a gross gaming revenue tax of approximately 29% for land-based activities, with expected similar rates for online operations. They also pay annual license renewal fees and fixed operational taxes related to equipment and venue size. Corporate income tax exemptions exist for licensed operators under certain conditions.

6. Are gambling winnings taxed for players?

Yes, players must pay 15% tax on winnings exceeding RD$50,000, collected at the payout source by licensed operators. This withholding reduces evasion risks and ensures compliance with fiscal policy.

7. What are the typical operational costs for running an online casino or sportsbook?

Major operational costs include platform licensing and maintenance, regulatory compliance, payment processing fees, employee salaries, and marketing expenses. Legal and consulting fees for initial setup and ongoing audits also contribute to budgets.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines vary but generally fall between 2 to 4 years post-launch. Factors include market penetration speed, marketing efficacy, regulatory costs, and client retention. Early investment in local partnerships and responsible gaming infrastructure improves ROI prospects.

9. What are the local presence requirements for operators?

Operators must establish a legal entity and maintain domain hosting and data servers physically within Dominican territory. Regulatory personnel requirements include compliance officers and customer support staff resident locally.

10. What payment methods are available and recommended?

The preferred payment methods include debit and credit cards, local bank transfers, and mobile wallets. Cash payments remain relevant in rural zones, while cryptocurrency is emerging but not yet mainstream. Operators should integrate local payment ecosystems for optimal market acceptance.

11. What are the advertising and marketing restrictions?

Advertising must exclude minors and vulnerable populations, prohibiting placements near schools and religious sites. Content must be truthful, avoiding misleading claims, and sponsorships are subject to content restrictions and time limitations. Digital ads require compliance with data privacy mandates.

12. What responsible gambling measures are mandatory?

Mandatory measures include self-exclusion systems, session time-tracking, bet limit options, and prominently displayed responsible gambling messages. Operators must provide links to support organizations and adhere to regulatory monitoring protocols to protect consumers.

13. How large is the iGaming market and what is the growth potential?

The Dominican iGaming market is mid-sized with estimated revenues in tens of millions USD, projected to grow at 10-15% annually over the next five years. Increased internet penetration, tourism, and regulatory clarity underpin expansion, attracting new entrants and diversified offerings.

14. Who are the main competitors and what is their market share?

The market features a handful of established operators including key international brands and regional players. Market leadership is fluid as new licenses issue post-2024 reforms, fostering competition around innovative platforms and localized services.

15. What are the player preferences and typical spending patterns?

Players favor sports betting, particularly on baseball, alongside slot machines and online casino games. Mobile devices dominate access, with peak activities during evenings and weekends. Spending is concentrated in urban centers, with preferences for localized promotions and loyalty rewards.

16. What are the key success factors and main challenges for new entrants?

Key success factors include robust compliance adherence, strong local partnerships, effective mobile-optimized platforms, and culturally relevant marketing.

- Operational agility to adapt to regulatory changes

- Investment in player protection and responsible gambling

- Innovative payment integrations

- Understanding consumer behavior for product tailoring

- Management of currency and inflation risk

Main challenges encompass high licensing costs, competition from incumbent operators, and navigating complex reporting and auditing requirements.

Sources and References

- Directorate of Casinos and Games of Chance, Dominican Republic Official Site

- Resolution No. 136-2024 – Online Gambling Regulatory Framework

- Dominican Republic Ministry of Finance – Taxation Codes

- World Bank – Doing Business Report 2024

- International Telecommunication Union (ITU) – ICT Data 2025

- Dominican Republic National Statistical Office – Population and Demographics 2025

- Central Bank of Dominican Republic – Economic and Financial Reports 2025

- Dominican Republic Ministry of Tourism – Market Reports 2024

- Dominican Republic Gambling Regulatory Reform Bill 2025

- Vixio Gambling Compliance Reports 2024-2025

- SoftSwiss iGaming Trends Report 2025

- DataReportal – Digital 2025 Dominican Republic Report

- Worldometers – Dominican Republic Population Data 2025

- Trading Economics – Dominican Republic Economic Indicators

- Statista – Dominican Republic Casino Market Forecast

- Dominican Republic Telecommunications Authority – Network Data 2025

- Banco Popular Dominicano – Corporate Services Overview

- BHD León – Retail Banking and Digital Channels

- Scotiabank Dominicana – Financial Services 2025

- Banesco Dominicana – Payment Systems Landscape

- MercadoLibre – E-commerce Growth Dominican Republic

- Dominican National Institute of Statistics – Education and Literacy Data

- Global Gaming Business News (GGB) – Caribbean Market Updates

- Dominican Ministry of Labor – Workforce Skills Reports

- Dominican Republic National Problem Gambling Program – Public Health Reports

- Dominican Tourism Board – Visitor Demographics and Spending Patterns

- Dominican Republic Free Trade Zone Regulatory Authority

- Various Industry Whitepapers on Caribbean iGaming

- Local Dominican News Outlets – Gambling Reform Coverage 2024-2025

- Academic Publications on Caribbean Digital Economy and Culture

- Dominican Republic Central Electoral Board – Population Census Data

- Dominican Credit Bureau – Consumer Finance Reports 2024

- Dominican Supreme Court – Legal Framework on Gambling and Licensing

- International Gaming Regulations Annual Review 2025

- Caribbean Telecommunications Regulatory Commission – Market Reports

- Dominican Republic Ministry of Social Services – Responsible Gambling Initiatives

- Dominican Republic Transparency and Anti-Fraud Authorities

🎯 Gambling Databases Country Rating: Dominican Republic

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.0/10 | [🟡 Moderate 5-7] |

| Player Access Score | 9.5/10 | [🟢 Fully Legal] |

| Overall Market Attractiveness | 7.7/10 | [High Potential but Capital Intensive] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- High Financial Barrier to Entry: License fees are exorbitant for a regional market (approx. USD $346,000 for online casinos per 5-year term), excluding setup costs.

- Strict Local Presence Mandate: Operators MUST establish a physical office, local legal entity, and host servers/IT infrastructure domestically. Remote operation is impossible.

- Player Tax Friction: A mandatory 15% withholding tax on winnings over RD$50,000 creates a strong incentive for high-volume players to use black-market offshore sites.

- Regulatory Instability: The market is currently undergoing a transition with the proposed creation of the DGJA; enforcement protocols and final tax interpretations are still settling.

- Advertising Restrictions: Strict distance regulations and content limits restrict marketing channels, particularly near schools and public institutions.

- Non-Transferable Licenses: Licenses cannot be transferred for the first three years, locking capital and preventing quick exits or acquisitions.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | [Full legality (+3.0). Both online sports betting and online casinos are fully regulated under Resolution No. 136-2024. No product prohibitions.] |

| Licensing Process | 25% | 1.5/2.5 | [Accessible (+2.0). Deduction for High Cost: Fees exceed USD $300k, placing it in the >€250k deduction bracket (0 points awarded for cost). Deduction for Timeline: Approval takes 6+ months (-0.5). Final: 1.5/2.5] |

| Taxation & Costs | 20% | 1.0/2.0 | [GGR Tax is 29% (+1.0 for 25-35% bracket). 0% Corporate Tax is a benefit, but the Player Winnings Tax (15%) reduces liquidity and player retention (-0.5). High operational costs due to local presence requirements (-0.5). Final: 1.0/2.0] |

| Operational Requirements | 15% | 0.25/1.5 | [Heavy requirements (+0.5). Deduction for Mandatory Local Presence: Physical office, servers, and staff required (-0.25). Final: 0.25/1.5] |

| Market Environment | 10% | 0.25/1.0 | [Moderate environment (+0.5). Deduction for Regulatory Instability: New 2024/2025 reforms and proposed DGJA regulator create uncertainty (-0.25). Final: 0.25/1.0] |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | [Fully legal (+4.0). Players face no legal risks for participating in licensed online gambling.] |

| Practical Accessibility | 30% | 3.0/3.0 | [High accessibility (+3.0). Multiple payment methods available (Cards, Bank Transfer). High mobile penetration (~90%). No blocking of legal sites.] |

| Player Penalties | 20% | 1.5/2.0 | [Fines possible (+1.5). While not a criminal penalty, the mandatory 15% tax withholding on winnings >RD$50k acts as a financial penalty on success, reducing the score.] |

| Market Availability | 10% | 1.0/1.0 | [5+ licensed operators (+1.0). The market has ~60 land-based casinos and a growing number of online licenses being issued.] |

🔍 Key Highlights

Strengths

- Full Legal Clarity: Unlike many LATAM regions, both casino and sports betting are explicitly legal and regulated.

- 0% Corporate Tax: Licensed gambling companies are exempt from corporate income tax, significantly improving net margins if GGR tax is managed.

- Strong Tourism Synergy: Integration with a robust tourism sector provides cross-selling opportunities for operators with land-based partners.

⛔️ CRITICAL RISKS AND CHALLENGES

- High Front-Loaded Costs: ~$346,000 license fee + mandated physical infrastructure makes the “entry ticket” expensive compared to Curacao or Anjouan.

- Player Tax Leakage: The 15% tax on winnings is a major competitive disadvantage against offshore operators who do not withhold tax.

- Infrastructure Burden: Requirement for domestic servers and data residency complicates technical setups for international operators.

- Regulatory Flux: The transition from DCJA to the proposed DGJA may lead to administrative delays and changing enforcement priorities.

- Strict Advertising: Distance-based restrictions limits physical advertising, and content rules are tightening.

Player-Specific Issues

- Withholding Tax: Players winning over approx. USD $850 will lose 15% immediately, discouraging high-rollers.

- Geo-Restrictions: Strict location verification is required to ensure players are within DR borders.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: USD $600,000 – $800,000+ (License fees, local incorporation, office lease, server hardware, legal retainers).

Monthly Operating Costs: USD $80,000 – $150,000 (Local staff wages, office rent, compliance audits, technical maintenance).

Effective Tax Rate on Revenue: 29% of GGR (Plus 5% on slots sales if applicable). While Corporate Tax is 0%, the high GGR tax eats directly into gross margin.

Customer Acquisition Cost: USD $150 – $300 (Moderate, but rising due to competition from established land-based brands).

Time to Breakeven: 3 – 4 Years (Longer than average due to high upfront license amortization).

Profitability Assessment: Economics are tight for pure-play online startups. The 29% GGR tax is high. Viability depends entirely on volume. This market is best suited for operators who can cross-sell to tourists or have sufficient capital to weather the first 3 years of license amortization. Small operators will struggle to cover the fixed costs.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [High] | [New regulations explicitly prohibit unauthorized remote gambling. Increased risk of ISP blocking and payment processing interdiction.] |

| Licensed Operators | [Medium] | [Compliance burden is high; risk of fines for AML failures or responsible gambling breaches (session limits).] |

| Affiliates/Advertisers | [Medium] | [Strict advertising distance/content rules. Promoting unlicensed sites is becoming riskier under new reforms.] |

| Company Directors | [Medium] | [Local presence requirement exposes directors to direct jurisdiction of Dominican courts.] |

🚨 Extradition and International Enforcement

Extradition Treaties: The Dominican Republic has an active extradition treaty with the United States (updated 2016), Spain, and other nations. The country cooperates on financial crimes and money laundering.

Enforcement History: The DR has a history of extraditing individuals to the US for fraud and money laundering. Operating an illegal gambling ring that touches US financial systems could lead to extradition requests.

Travel Risk: High for executives of unlicensed operations if they enter the country, given the local focus on “cleaning up” the industry.

📋 Final Verdict

The Dominican Republic receives an Operator Ease Score of 6.0/10 and a Player Access Score of 9.5/10, resulting in an overall market attractiveness rating of 7.7/10.

HONEST ASSESSMENT: The Dominican Republic offers a fully legal, stable environment, but the price of admission is steep. The requirement for a physical local footprint (office, servers, staff) combined with $300k+ license fees and a 29% GGR tax makes this a “pay-to-play” market for established entities, not startups.

While the 0% corporate tax is an attractive sweetener, the 15% player withholding tax is a “poison pill” that will make retention of high-value players difficult against offshore competitors.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A regional LATAM operator with existing Spanish-language support and infrastructure.

- A land-based casino brand looking to digitize an existing player database.

- Well-capitalized ($2M+ funding) and looking for a “White Market” license to boost valuation.

❌ Definitely Avoid If You Are:

- A remote-first company unwilling to set up a physical office and hire local staff.

- A bootstrapped startup (License fees alone will bankrupt you).

- Looking for a low-tax jurisdiction (29% GGR is significant).

- Focused purely on high-rollers (15% tax on winnings will kill your VIP retention).

⚠️ BOTTOM LINE: A legitimate, high-potential market for mid-to-large enterprises, but financially and operationally illogical for small operators or startups.