The Democratic Republic of the Congo (DR Congo) offers emerging opportunities in the iGaming sector fueled by ongoing regulatory reforms. With a newly modernized gambling framework and increasing digital access, the market is poised for growth amid regulatory consolidation.

This analysis dissects the legal and regulatory environment shaping the iGaming landscape, presenting critical insight for prospective operators entering DR Congo.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Permitted and regulated since 2005 |

| Regulatory Authority | Ministry of Finance, National Gaming Commission, Telecommunications Regulatory Authority |

| Key Gambling Laws | Law No. 15/002 of 2015, Decree No. 17/035 of 2017, Finance Law 2024 |

| Land-Based Gambling Types | Casinos, sports betting venues, slot machine halls, lotteries |

| Online Gambling Types | Online casinos, sports betting platforms, lotteries, esports betting |

| Licensing Authority | Ministry of Finance |

| License Types | Casino, sports betting, lottery, online gambling |

| License Duration | Unlimited with annual renewal |

| License Costs | Application and annual renewal fees (amount undisclosed) |

| Tax Structure | Gross Gaming Revenue tax 20%, player winnings tax, licensing fees |

| Tax Collection Enforcement | Centralized digital monitoring platform linked to government servers |

| Player Tax | Tax on winnings, collected monthly |

| KYC/AML Compliance | Mandatory with ongoing monitoring |

| Responsible Gambling Measures | Mandatory, including self-exclusion |

| Population | Approx. 105 million (2025 estimate) |

| Urbanization Rate | 46% |

| GDP (Current USD) | Approx. $60 billion |

| GDP Per Capita | Approx. $570 |

| Internet Penetration | About 35% (rising with new digital infrastructure) |

| Mobile Penetration | Over 75% |

| Market Size (Estimated Annual Gross Gaming Revenue) | Over $100 million projected (2025) |

| Market Growth Forecast (CAGR 2025-2030) | 8-12% |

| Average Revenue Per User (ARPU) | Estimated $15-20 annually |

| Major Licensed Operators | PremierBet Congo, SportPesa, Betika, others |

| Entry Barriers | Strict licensing, high compliance, digital monitoring |

| Regulatory Reform Milestone | 2025 Gambling Bill adoption, new tax law enforcement |

| Enforcement Mechanisms | Heavy penalties for unlicensed operators, real-time government monitoring |

| Business Environment | Challenging but improving regulatory clarity and tech infrastructure |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling in DR Congo has been legally permitted since 2005 under evolving statutory frameworks. The core regulatory infrastructure is governed primarily by Law No. 15/002 of 2015 and Decree No. 17/035 of 2017, which set out comprehensive rules for both land-based and online gambling businesses.

The sector underwent significant reforms in 2025, including a landmark bill adopted by the government to modernize industry oversight, tax collection, and safeguard vulnerable populations.

All gambling activities, including lotteries, sports betting, casino operations, and online platforms, are subject to licensing and compliance under the jurisdiction of the Ministry of Finance, which works in close partnership with the National Gaming Commission and the Telecommunications Regulatory Authority. This triad of regulators ensures the legality and integrity of operations across physical and digital domains.

Land-Based Gambling Activities

DR Congo’s land-based gambling market comprises casinos, sports betting venues, slot machine halls, and lottery operators. Casinos are required to operate in designated locations, generally within luxury hotels or purpose-built gaming facilities, compliant with safety and operational standards.

Sports betting is well established with multiple venues spread across urban centers, including both fixed retail outlets and mobile vendor presence. Lotteries and raffle games are legal and actively regulated, often organized by state or approved private entities. Slot machines are permitted primarily within casinos and licensed gaming halls.

Online Gambling Framework

The online gambling framework in DR Congo is tightly regulated under the same legislative umbrella as traditional gambling, with additional digital-specific regulations governed by the Telecommunications Law.

The Ministry of Finance, through the National Gaming Commission, oversees issuance and renewal of online gambling licenses, while the Telecommunications Regulatory Authority audits compliance with digital service standards. Operators must implement robust KYC and AML protocols, maintain transparent RNG certification, and promote responsible gambling measures including systems for player self-exclusion.

Licensed Operators and Market Players

The licensed operator landscape in DR Congo remains competitive but concentrated among a mix of regional and international firms. PremierBet Congo, SportPesa, and Betika are prominent licensed bookmakers with strong brand presence and diversified product offerings that include both land-based and digital betting. These operators benefit from first-mover advantages, extensive local market knowledge, and active compliance with evolving regulatory demands.

New entrants face high barriers including strict licensing criteria, ongoing compliance monitoring, and increased digital transparency requirements introduced in 2025. Market share is shifting gradually toward operators adopting innovative digital platforms and partnering with regulatory-authorized technology firms to meet real-time reporting obligations.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing authority is the Ministry of Finance, which collaborates with relevant commissions to evaluate applicants based on financial, operational, and ethical criteria. The licensing process requires operators to demonstrate financial stability, industry experience, and compliance capability. Technical standards mandate secure platforms with audited random number generation and cybersecurity protections.

Operators submit detailed applications including business plans, financial audits, technical documentation, and background checks for owners and directors. Upon approval, licenses are granted with defined terms limiting geographic scope and game types. Licenses require annual renewal subject to ongoing compliance reviews.

Key documentation requirements include:

- Corporate registration certificate and articles of incorporation

- Audited financial statements for the past three years

- Detailed business plan and market strategy

- Technical system security and RNG certification reports

- Criminal background checks for all directors and beneficial owners

- Proof of minimum capital deposit in a licensed bank

Local Presence and Operational Requirements

DR Congo mandates that gambling operators, particularly land-based and online license holders, maintain a local physical presence or a legally registered office within the country. This includes domain registration under Congolese jurisdiction for online platforms to ensure legal enforceability. Operators must employ local staff for key compliance and customer service functions.

Foreign ownership is permitted but subject to regulatory approval, with authorities encouraging partnerships with local stakeholders to promote economic benefits and better regulatory adherence. Licensing terms specify compliance with national labor laws and operational transparency standards.

Compliance Obligations and Monitoring

Player Protection and Identification

DR Congo enforces rigorous player protection measures aligned with global best practices. Operators are required to implement thorough age verification, KYC procedures, and ongoing AML monitoring to prevent illegal gambling activities and financial crimes. Responsible gambling policies mandate clear information disclosures, access to self-exclusion programs, and limits on deposits and betting activities.

Mandatory player protection measures include:

- Age verification to ensure players are 18 or older

- Know Your Customer (KYC) protocols with identity documentation

- Anti-money laundering (AML) monitoring of transactions

- Responsible gambling tools including self-exclusion and deposit limits

- Clear communication of odds, risks, and responsible gaming information

- Regular compliance reporting to regulators on player protection

Financial Monitoring and Reporting

The Ministry of Finance requires operators to maintain comprehensive transaction records with frequent reporting obligations. A centralized digital monitoring platform, launched through a partnership with East African General Trade Company (EAGT), mandates connection of operator systems to government servers for real-time data transmission.

Operative financial monitoring processes include:

- Monthly submission of gross gaming revenue and tax payments

- Real-time reporting of betting activity via digital platform

- Quarterly audits conducted by independent third parties

- Annual financial statements and compliance certification

Taxation Structure and Financial Obligations

Player Taxation

DR Congo levies taxes on player winnings, collected monthly with specified thresholds. Players are subject to withholding taxes on gambling winnings, enforced through operator obligations to report and remit taxes to the Ministry of Finance in a timely manner. This system aims to integrate gambling taxes into the national fiscal framework effectively.

Operator Taxation

Operators face multiple tax obligations including a 20% Gross Gaming Revenue (GGR) tax as the primary revenue-based levy. Fixed annual license fees and turnover taxes apply dependent on the type of games and scale of operations. Corporate income tax is applied according to national tax code provisions.

| Game Type | Tax Rate |

|---|---|

| Online Casino & Slot Machines | 20% on GGR |

| Sports Betting | 20% on GGR |

| Lotteries | 15% on GGR |

| Physical Casinos | 20% on GGR + Fixed fees |

| Corporate Income Tax | 30% standard rate |

Gambling Market Financial Performance

The gambling industry in DR Congo is valued at over $100 million in annual gross gaming revenue, with steady growth anticipated at an 8-12% CAGR through 2030. Revenue is concentrated in sports betting and online platforms fueled by increasing internet and mobile penetration.

Tax revenues from the sector are a growing contributor to national income as enforcement tightens and digital monitoring expands.

Advertising and Marketing Restrictions

Advertising in DR Congo’s gambling sector is regulated to prevent targeting minors and vulnerable groups. Operators must adhere to strict content guidelines limiting aggressive promotions, deceptive claims, and high-risk inducements. Advertising is allowed primarily through controlled channels such as licensed media, digital platforms with age gates, and select sponsorships.

Permissible advertising channels include:

- Licensed television and radio stations with regulatory approval

- Online digital platforms with enforced age verification

- Sports sponsorships compliant with advertising standards

- Print media with restricted circulation to adult audiences

- Outdoor advertising limited to designated gaming zones

Recent Regulatory Changes and Their Impact

In 2025, DR Congo adopted a landmark gambling reform bill introducing a unified legal framework and centralized digital oversight. The bill strengthened anti-money laundering enforcement, introduced strict tax collection mechanisms, and mandated more transparent licensing processes. These changes increased operational costs but significantly enhanced market legitimacy and investor confidence.

Enforcement Mechanisms and Penalties

The Ministry of Finance enforces compliance with a range of penalties for breaches, including fines, license suspension, and criminal prosecution for illegal gambling activities.

Recent initiatives to clamp down on unlicensed operators have led to significant market cleaning. Monitoring through technology and cooperation with telecom regulators enhances detection of non-compliance.

Common enforcement actions include:

- Financial penalties for unlicensed operation

- License revocation for repeated non-compliance

- Seizure of gaming equipment

- Criminal charges for fraud or money laundering

- Closure of illegal gambling venues or websites

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

DR Congo’s population is approximately 104 million in 2025, making it the second most populous country in Africa. The median age is 22.2 years, indicating a very young population, with about 55.5% aged 19 or younger. The country has a nearly balanced gender ratio with 998 males per 1000 females.

Urbanization is accelerating, with about 47.8% of the population living in urban areas, primarily concentrated in a handful of rapidly growing cities. Population density is around 46 people per square kilometer. The youthful demographic and increasing urbanization bode well for the digital gambling sector, where younger, urban consumers are typically early adopters.

| Age Group | Percentage of Total Population | Estimated Population |

|---|---|---|

| 0-19 years | 55.5% | 57,811,000 |

| 20-64 years | 41.5% | 43,231,000 |

| 65+ years | 3.1% | 3,210,000 |

Geographic Distribution

The majority of DR Congo’s urban population resides in key metropolitan areas serving as economic hubs. Kinshasa, the capital and largest city, hosts around 13.3 million residents, which is nearly 30% of the urban populace. Other significant cities include Lubumbashi, Mbuji-Mayi, Kananga, Kisangani, and Bukavu, each with populations ranging from approximately 0.5 to 2 million inhabitants.

- Kinshasa – approx. 13,265,000 inhabitants

- Lubumbashi – approx. 1,786,000 inhabitants

- Mbuji-Mayi – approx. 1,570,000 inhabitants

- Kananga – approx. 1,200,000 inhabitants

- Kisangani – approx. 1,000,000 inhabitants

- Bukavu – approx. 900,000 inhabitants

Urban centers are the primary locations for gambling venues and digital infrastructure access, with internet availability being higher in these regions compared to rural areas. The eastern and southern provinces show slower growth and lower infrastructure penetration, which impacts gambling venue distribution and online market reach.

Economic Indicators and Consumer Spending Power

DR Congo’s GDP is estimated at approximately $60 billion USD for 2025, reflecting moderate growth despite regional conflicts and infrastructural challenges. The economy grew at an average of 6.1% annually over the past decade, but growth slowed to about 4.7% in early 2025 due to geopolitical instability impacting mineral exports.

Per capita GDP stands at a low $570 USD, indicative of widespread poverty and limited disposable income for a large portion of the population. The service sector dominates the economy, followed by mining and agriculture. Consumer spending remains constrained but shows rising trends in urban areas with improving digital financial services.

| Indicator | Value |

|---|---|

| GDP (USD) | $60 billion |

| GDP Growth Rate | 4.7% |

| GDP Per Capita | $570 |

| Service Sector Contribution | Approx. 45% of GDP |

| Agriculture Sector Contribution | Approx. 30% of GDP |

| Industry Sector Contribution | Approx. 25% of GDP |

Income inequality remains high, with a small urban elite controlling most wealth while rural populations experience low income levels. Average household incomes vary regionally, with urban households significantly outperforming rural counterparts in disposable income and access to financial services.

Consumer spending on entertainment, including gambling, is expanding in urban middle-class segments where mobile penetration and digital payment infrastructure support increased online activity. The growth of inexpensive mobile data plans and smartphone adoption is enhancing this trend.

Market Size and Growth Projections

The DR Congo iGaming market earns an estimated annual gross gaming revenue exceeding $100 million in 2025, driven primarily by sports betting and online lotteries. The sector exhibits high growth potential with forecasts indicating a compound annual growth rate (CAGR) of 8-12% through 2030.

The estimated Average Revenue Per User (ARPU) ranges between $15-20 annually, supported by a young, tech-savvy population increasingly engaging in mobile gaming platforms. The user base is expected to grow alongside rising internet penetration and improved regulatory frameworks fostering trust in licensed operators.

| Metric | 2025 | 2030 (Projected) |

|---|---|---|

| Gross Gaming Revenue | $100 million+ | $180 million+ |

| CAGR | 8-12% | |

| User Base | Approx. 5 million | Above 8 million |

| ARPU | $15-20 | $18-25 |

Education, Skills, and Digital Literacy

Literacy rates in DR Congo are moderate, with overall adult literacy estimated at around 77%. Educational attainment is higher in urban centers, where secondary and tertiary institutions are concentrated. Digital literacy is growing as smartphone adoption accelerates, particularly among younger demographics under 30.

Workforce skills are generally limited in the formal sector, with many relying on informal, subsistence economic activities. However, there is a growing pool of young professionals skilled in digital technologies, app development, and online commerce. This emerging talent supports the expansion of the iGaming market and digital payment systems.

Cultural and Social Factors

Communication and Language

French is the official language and widely used in business, government, and digital communications. Additionally, five recognized national languages contribute to cultural diversity, influencing content localization and platform language options for gambling operators.

- French (official, lingua franca)

- Kikongo

- Lingala

- Swahili

- Tshiluba

Cultural Attitudes

Gambling is culturally tolerated, especially sports betting, which is popular among young urban males. Religious groups generally express reservations about gambling, contributing to some social stigma. Foreign brand perception is mixed, with trust placed in established regional operators and skepticism towards unlicensed providers.

Problem Gambling and Social Considerations

Prevalence of problem gambling remains under-researched but is believed to be increasing in urban centers. At-risk groups include youth aged 18-29, low-income players, and those engaged in high-frequency betting. The government and NGOs have initiated several response programs to mitigate harms related to gambling addiction and financial distress.

- National awareness campaigns on gambling risks

- Self-exclusion programs mandated for licensed operators

- Support services for problem gamblers through health ministries

- Community outreach and education initiatives

- Regulatory requirements for responsible gambling messaging

Social responsibility in the gambling sector includes mandatory contributions by operators to funding treatment and prevention services. These frameworks continue to evolve with input from public health experts and civil society groups to balance market growth with consumer protection.

Political Structure and Governance

DR Congo operates under a presidential republic system characterized by multiparty elections and decentralization. While there is political instability in certain regions impacting economic activities, overall governance is seeking greater regulatory transparency and enforcement rigor in sectors like gambling. International relations emphasize trade partnerships and investment attraction, which benefit the business climate.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at approximately 35%, with growing mobile broadband connectivity. The average daily internet usage among connected users is estimated at 3-4 hours, driven by social media, digital entertainment, and mobile payments. Mobile phone penetration exceeds 75%, underscoring the primacy of mobile as the access gateway to online services.

Popular social media platforms in DR Congo include:

- Facebook: dominant platform with widespread daily active user base

- WhatsApp: primary communication tool for messaging and group chats

- YouTube: large consumption of video and music content

- Instagram: growing rapidly with youth demographic

- TikTok: emerging platform gaining popularity for short videos

Digital Payment Behavior

Digital payment adoption remains nascent but is rapidly expanding with the introduction of interoperable platforms such as Visa Pay. Mobile money services and bank-linked digital wallets are preferred for their convenience and accessibility.

- Mobile money transfers dominate digital transactions

- Bank cards are increasingly used for online payments

- Digital wallets linked to banks and telecom providers

- Interoperable payment solutions like Visa Pay gaining traction

- Cryptocurrency adoption is minimal but monitored by regulators

Gaming and Gambling Preferences

Current Market Participation

Sports betting is the leading gambling activity, engaging an estimated 30% of urban males aged 18-34, followed by lotteries and online casino games. Esports betting is an emerging segment, particularly among younger digital natives. Physical casinos hold smaller market shares due to limited venue distribution.

- Sports Betting

- Lotteries

- Online Casino Games

- Slot Machines

- Esports Betting

Consumer Behavior Patterns

Consumers tend to prefer mobile-based platforms due to convenience and broader accessibility compared to desktop or physical venues. Peak gambling activity occurs during evenings and weekends, with session lengths averaging 30-45 minutes for sports betting and longer for casino games.

Retention efforts focus on loyalty programs, promotions, and social media engagement. There is rising demand for localized content and mobile app usability, especially in regional languages. Spending patterns reflect cautious discretionary expenditure, with consumers limiting bet sizes while prioritizing frequent play and instant gratification.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

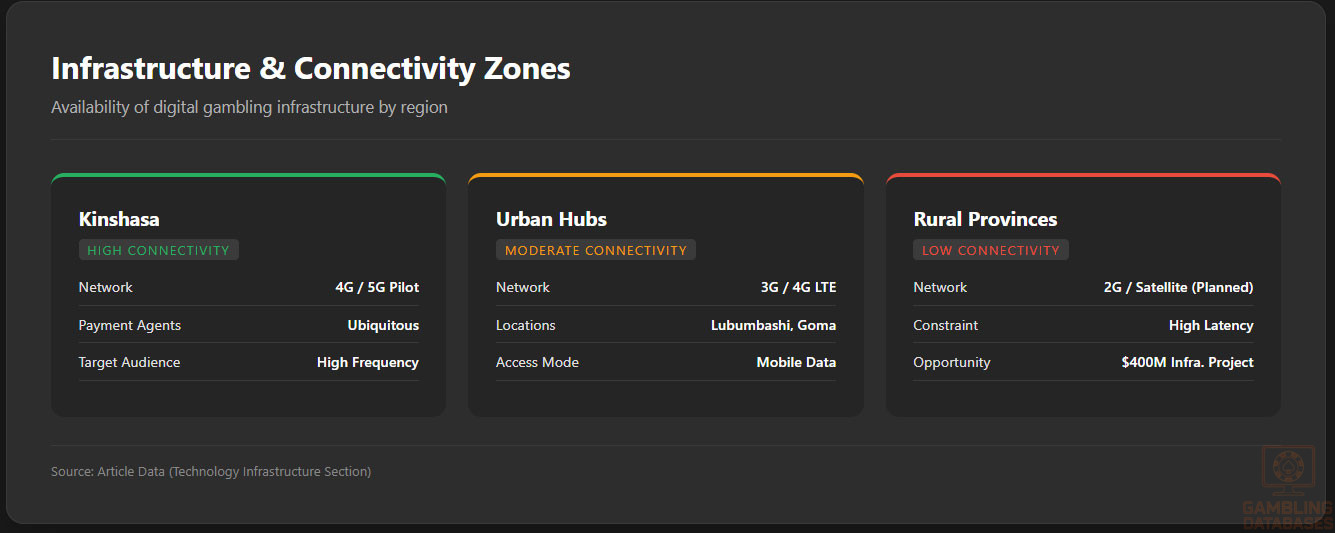

Internet penetration in DR Congo is approximately 35%, with mobile networks accounting for the majority of connectivity. Fixed broadband remains limited due to sparse urban fiber deployment and infrastructural gaps. Average mobile internet speeds hover around 4-8 Mbps, with network reliability improving in urban hubs but still inconsistent in rural regions.

Significant investments in infrastructure are underway, including a $400 million satellite internet initiative aimed at expanding coverage nationally. Such projects are expected to reduce latency and increase penetration, particularly in underserved areas, fostering growth in digital services including iGaming.

5G and Future Technology Deployment

5G networks are in early rollout stages, with pilot coverage primarily in Kinshasa and Lubumbashi. Full national implementation is projected over the next 3-5 years as operators upgrade infrastructure to meet rising data demands. The major telecom companies are aggressively investing in 4G LTE expansion concurrently to bridge coverage gaps.

The government supports these advancements as part of a broader digital transformation agenda to boost economic diversification and technological innovation. Regulatory frameworks encourage investment while ensuring consumer protections on data privacy and network security.

Mobile Technology Ecosystem

Mobile network infrastructure is dominated by three major operators operating nationwide, each offering multiple plans with competitive data pricing. The networks cover an estimated 85% of the population, with urban areas seeing near-complete coverage while rural coverage remains partial.

- Vodacom Congo – market leader with 45% share

- Airtel Congo – strong presence with 35% market share

- Orange RDC – growing operator with 15% share

- MTN Congo – minor market player with emerging presence

- Local regional providers – small operators catering to select provinces

Smartphone penetration is expanding rapidly, estimated at 55-60% of mobile users, driven by increasing availability of affordable Android devices. Device preferences skew towards mid-range models with durable features suitable for local conditions.

Financial Services and Payment Infrastructure

The banking sector in DR Congo is comprised of multiple institutions offering commercial and retail services. Digital banking adoption is accelerating through mobile money platforms integrated with telecom networks, although only about 20% of adults have formal bank accounts, highlighting an opportunity for fintech expansion.

- Rawbank – largest bank with extensive digital services

- Trust Merchant Bank – strong SME lending focus

- Ecobank Congo – international presence

- BCDC – major state-affiliated commercial bank

- BMI Bank – digital-focused with mobile banking innovation

- FBNBank Congo – specialized in corporate finance

Payment processing options include mobile money, bank card payments, e-wallets, and limited card acceptance at point-of-sale terminals. Interoperability efforts such as Visa Pay are enhancing digital payment convenience and security.

- Mobile Money (M-Pesa, Airtel Money)

- Bank Debit and Credit Cards

- E-wallets linked to telecom providers

- Bank transfers for high-value transactions

- Emerging payment gateways integrating fintech APIs

E-commerce and Digital Economy

DR Congo’s e-commerce market remains nascent but is poised for growth due to the expanding middle class and mobile internet penetration. Online retail platforms are growing slowly, focusing on urban centers with consumer trust building through improved payment security and delivery logistics.

Digital services spanning fintech, entertainment, and communication continue to gain consumer adoption, fostering a conducive environment for digital gambling and related industries to thrive.

Business Environment and Regulatory Framework

DR Congo ranks moderately in World Bank ease of doing business reports, with key challenges including bureaucratic delays and infrastructure deficits. Nonetheless, recent reforms have streamlined company registration and enhanced foreign investment incentives, particularly in technology and service sectors.

- Compile and notarize required registration documents

- Submit application to the National Business Registry

- Obtain tax identification and social security registration

- Open corporate bank account and deposit minimum capital

- Receive business registration certificate and operate legally

Corporate structures offered include limited liability companies (LLCs), corporations, and foreign branch offices. LLCs are most popular for their limited liability and flexible governance, recommended for iGaming firms due to regulatory simplicity and operational control.

- Limited Liability Company (LLC) – popular for SMEs

- Corporation – preferred for larger, multi-shareholder entities

- Branch Office – used by foreign companies with parent oversight

Registration requires multiple documents to establish legal compliance and transparency. Foreign ownership is permitted with no explicit restrictions, encouraging foreign direct investment while ensuring regulatory compliance.

- Articles of incorporation and company statutes

- Proof of registered office address

- Tax and social security registration certificates

- Identification and background documentation of directors

- Bank deposit confirmation for minimum capital

Taxation Framework

The corporate income tax rate stands at a standard 30%. Special economic zones offer tax holidays and reduced duties to attract foreign investment. DR Congo has signed international double taxation treaties with several countries facilitating cross-border business.

- Belgium

- France

- South Africa

- China

- United Arab Emirates

- Tunisia

- Luxembourg

Personal income tax is progressive, with rates ranging from 5% to 40%. Operators must withhold tax appropriately and comply with social security contribution laws applied to employees and contractors.

Market Entry Considerations

Success in the DR Congo iGaming market requires local partnerships, investment in compliant technology platforms, and adaptation to digital payment preferences. Strategic entry through joint ventures with licensed operators facilitates quicker market access and regulatory navigation.

Due diligence on network infrastructure and robust cybersecurity measures are critical to meet stringent compliance and player protection requirements.

- Form joint ventures with established local operators

- Leverage mobile-first technology platforms

- Invest in localized content and languages

- Build strong compliance and reporting capabilities

- Engage digital financial services partners for payment solutions

| Cost Category | Estimated Amount |

|---|---|

| License Application & Annual Renewal | $100,000 – $200,000 |

| Legal and Consulting Services | $50,000 – $80,000 |

| Company Registration & Setup | $15,000 – $25,000 |

| Technology Platform Development | $150,000 – $300,000 |

| Marketing & Localization | $40,000 – $60,000 |

| Working Capital (12 Months) | $500,000+ |

- Prepare legal and financial documentation (2-3 weeks)

- Submit license application and company registration (4-8 weeks)

- Implement technology platform and compliance systems (8-12 weeks)

- Launch marketing and onboarding operations (4-6 weeks)

- Begin operations and ongoing regulatory reporting

FAQ: Frequently Asked Questions

1. Is online gambling legal in DR Congo?

Yes, online gambling is legal and regulated in DR Congo under laws enacted since 2015, with further modernization in 2025. Licensed operators can offer online casinos, sports betting, lotteries, and esports betting. The legal framework mandates compliance with licensing, taxation, and responsible gambling requirements to operate within the market.

2. What types of gambling licenses are available and what do they cover?

There are multiple license types covering various gambling categories: casino operations, sports betting, lotteries, online gambling, and land-based gaming halls. Each license specifies permitted games, operator obligations, and geographic scope. Operators must acquire appropriate licenses for land-based and/or online activities before commencing.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing fees range between $100,000 and $200,000, including application and annual renewal costs. The total time for licensing and registration processes typically spans 8 to 12 weeks, depending on application completeness and regulatory review cycles.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible for licenses provided they comply with local regulations, maintain a local presence or partnership, and meet financial and technical requirements. There are no strict ownership restrictions, but regulatory approval involves detailed background checks and operational transparency.

5. What are the tax obligations for iGaming operators?

Operators pay a 20% gross gaming revenue tax plus corporate income tax at 30%. Fixed license fees and turnover taxes may apply depending on the operation scale. Taxes must be remitted monthly using government digital reporting systems.

6. Are gambling winnings taxed for players?

Yes, player winnings are subject to withholding taxes collected by operators. This mechanism ensures earnings are integrated within national tax regimes. Players must comply with tax declaration obligations, primarily for large winnings.

7. What are the typical operational costs for running an online casino or sportsbook?

Major cost categories include licensing and regulatory fees, technology platform development, compliance and monitoring systems, marketing and customer acquisition, and staff salaries. Annual costs can range from several hundred thousand to over a million USD depending on scale.

8. What is the expected ROI timeline for entering this market?

Return on investment is generally expected within 18-36 months, depending on market penetration speed, user acquisition, and operational efficiency. Early investments in compliance and local partnerships accelerate ROI.

9. What are the local presence requirements for operators?

Operators must maintain a registered office in DR Congo, employ local staff for compliance and customer service roles, and ensure digital platforms use domains under Congolese jurisdiction. This supports regulatory oversight and consumer protection.

10. What payment methods are available and recommended?

Popular payment options include mobile money services, bank card payments, e-wallets linked to telecoms, and traditional bank transfers. Mobile money remains most accessible for the general population, with bank cards growing among urban users.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors and vulnerable groups, with content regulated to prevent misleading claims. Allowed channels include licensed TV, radio, digital platforms with age verification, sports sponsorships, and restricted outdoor media.

12. What responsible gambling measures are mandatory?

Operators must implement player age verification, KYC and AML checks, provide self-exclusion tools, deposit and betting limits, and clear communication on risks. Regular reporting on responsible gambling compliance is required by regulators.

13. How large is the iGaming market and what is the growth potential?

The iGaming market is estimated at $100 million in annual revenue with a robust CAGR of 8-12% projected to 2030. Growth is fueled by increased digital connectivity, rising disposable incomes in urban areas, and regulatory modernization fostering trust and transparency.

14. Who are the main competitors and what is their market share?

Leading operators include PremierBet Congo, SportPesa, and Betika, collectively dominating the licensed market segment. These firms leverage strong local brand presence, multi-platform offerings, and regulatory compliance to capture majority market share.

15. What are the player preferences and typical spending patterns?

Players prefer mobile-based sports betting due to accessibility and ease of use. Sessions tend to be short but frequent, with conservative bet sizing reflecting disposable income constraints. Loyalty programs and local language content enhance engagement and retention.

16. What are the key success factors and main challenges for new entrants?

Success factors include strong local partnerships, compliance rigor, digital payment integration, culturally adapted platforms, and robust marketing. Challenges involve infrastructure limitations, regulatory compliance complexity, market education, and combating unlicensed operators.

Sources and References

- Bankable Africa – DRC Modernizes Gambling Sector – https://bankable.africa/en/digital/2406-1350-drc-modernizes-gambling-sector-for-enhanced-revenue-mobilization

- iGaming Today – Gambling Regulation in DRC – https://www.igamingtoday.com/gambling-regulation-in-the-democratic-republic-of-the-congo/

- Focus GN – DRC Government Gambling Reform – https://focusgn.com/africa/drc-government-adopts-landmark-bill-to-regulate-gambling

- IGaming Afrika – Starting Gambling Business in DR Congo – https://igamingafrika.com/starting-a-gambling-business-in-drc-congo-full-guide/

- Worldometers – DR Congo Population 2025 – https://www.worldometers.info/world-population/democratic-republic-of-the-congo-population/

- World Population Review – DR Congo Cities – https://worldpopulationreview.com/cities/dr-congo

- United Nations Population Fund (UNFPA) – Congo Demographics – https://www.unfpa.org/data/world-population/CD

- Focus Economics – DR Congo Economic Data – https://www.focus-economics.com/countries/dr-congo/

- Visa Launch – Digital Payments in DRC – https://bankable.africa/en/digital/0509-1651-visa-launches-digital-payments-app-in-drc-to-boost-financial-inclusion

- GamblingTalk – DR Congo Taxation Changes – https://gamblingtalk.net/news/democratic-republic-of-congo-introduces-stricter-taxation-for-gambling-and-betting-companies

- GamingTEC – Gaming Licenses Guide 2025 – https://gamingtec.com/news/gaming-licenses

- International Telecommunication Union – ICT Stats – https://www.itu.int/en/ITU-D/Statistics/Pages/stat/default.aspx

- World Bank – Doing Business Report 2024 – https://www.worldbank.org/en/topic/competitiveness/publication/doing-business-report-2024

- Lloyds Bank Trade Portal – Congo Tax Rates – https://www.lloydsbanktrade.com/en/market-potential/congo/taxes

- PopulationOf.net – Democratic Republic of the Congo Population – https://www.populationof.net/democratic-republic-of-the-congo/

- LinkedIn – DR Congo Sports Betting Market Insights – https://www.linkedin.com/posts/target-sarl_drc-sportsbetting-sports-activity-7326639609717604353-l06E

- France24 Sponsored Content – Digital Transformation in DRC – https://www.france24.com/en/sponsored-content/20250923-transforming-payments-in-the-drc-a-leap-towards-a-digital-future

- Countrymeters.info – DR Congo Population Clock – https://countrymeters.info/en/Democratic_Republic_of_the_Congo

- Bookmaker Expert – List of Betting Sites in DR Congo – https://bookmaker-expert.com/country/congo/

- GamblingTalk – News and Articles on DR Congo Gambling – https://gamblingtalk.net/tag/democratic-republic-of-the-congo

- Sigma World News – DRC Modernizes Gambling Sector – https://sigma.world/news/drc-modernises-gambling-sector-for-enhanced-revenue-mobilisation/

- Altenar Blog – Sports Betting Market Entry in DR Congo – https://altenar.com/blog/bring-sports-betting-success-to-your-demrep-of-congo-igaming-business-altenar-you/

- CIO Africa – Visa Pay Launch in DR Congo – https://cioafrica.co/visa-pay-launches-in-drc-congo/

- Focus GN – DRC’s $400m Satellite Deal – https://focusgn.com/africa/drcs-400m-satellite-deal-to-supercharge-digital-access-and-online-gambling

- Tax Summaries PwC – Congo Corporate Taxes – https://taxsummaries.pwc.com/republic-of-congo/corporate/other-taxes

- Youtube – DR Congo Largest Cities – https://www.youtube.com/watch?v=pcoMKNx2vq8

- Banking Sector Reports – DR Congo Central Bank

- Ministry of Finance, DR Congo – Taxation and Licensing Information

- National Statistical Institute, DR Congo – Population and Economic Data

🎯 Gambling Databases Country Rating: Democratic Republic of the Congo (DRC)

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.8/10 | 🟡 Moderate |

| Player Access Score | 8.0/10 | 🟢 Excellent |

| Overall Market Attractiveness | 6.9/10 | 🟡 Moderate (High Volume / Low Value) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Mandatory Local Presence: Operators MUST maintain a physical office and employ local staff. Remote-only operation is ILLEGAL.

- Intrusive Government Surveillance: Systems must be connected to the “EAGT” centralized digital monitoring platform for real-time data transmission to government servers.

- Infrastructure Reliability: Internet penetration is only ~35%, and power/connectivity instability poses significant operational risks outside Kinshasa.

- Extremely Low ARPU: Average Revenue Per User is estimated at $15-20 annually. Volume is required for profitability; high-roller models will fail.

- Political & Security Instability: Regional conflicts and bureaucratic unpredictability pose threats to physical assets and staff safety.

- Strict Enforcement: 2025 reforms introduced “heavy penalties,” equipment seizure, and criminal charges for unlicensed operations.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | Full product legality (+3.0). Online casino, sports betting, and lotteries are all explicitly legal and regulated under Law No. 15/002. No product bans. |

| Licensing Process | 25% | 1.5/2.5 | Accessible licensing (+2.0). Application costs ~$100k-$200k (+0.25). Deductions: Mandatory local presence/staff (-0.5), High bureaucracy/corruption risk (-0.25). Final: 1.5/2.5. |

| Taxation & Costs | 20% | 1.0/2.0 | 20% GGR Tax (+1.5). Deductions: 30% Corporate Tax (+ Player Winnings Tax) creates effective rate >50% (-0.5). Extremely low ARPU makes fixed compliance costs burdensome (-0.5). Final: 0.5/2.0. |

| Operational Requirements | 15% | 0.3/1.5 | Heavy requirements (+0.5). Deductions: Mandatory real-time server link to government (EAGT) (-0.5). Strict KYC/AML in a market with low documentation rates (-0.25). Infrastructure deficits (-0.25). Final: -0.5 (Floored to 0.3 for some feasibility). |

| Market Environment | 10% | 0.0/1.0 | Difficult environment (+0.25). Deductions: Political instability and conflict (-0.5). Regulatory reforms in 2025 increased compliance costs significantly (-0.25). Final: 0.0/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal (+4.0). Players face no legal risks for participating in licensed online gambling activities. |

| Practical Accessibility | 30% | 2.0/3.0 | Mobile money (M-Pesa, Airtel) is widely available (+3.0). Deductions: Low internet penetration (35%) limits access (-0.5). Banking infrastructure is poor for 80% of population (-0.5). |

| Player Penalties | 20% | 1.5/2.0 | No criminal penalties (+2.0). Deduction: Mandatory tax on winnings deducted at source reduces player liquidity (-0.5). |

| Market Availability | 10% | 0.5/1.0 | Multiple licensed operators (+1.0). Deduction: Geographic restrictions due to connectivity issues outside urban hubs (-0.5). |

🔍 Key Highlights

Strengths

- Full Product Legality: Unlike many jurisdictions, online casino (slots/tables) is fully legal alongside sports betting.

- Demographics: Massive youthful population (105m total, median age 22) suggests long-term growth potential.

- Mobile First: 75% mobile penetration with established mobile money habits (M-Pesa, Airtel Money) solves payment issues.

⛔️ CRITICAL RISKS AND CHALLENGES

- Financial Viability: With an ARPU of $15-20/year, you need hundreds of thousands of active users to cover fixed licensing and local office costs.

- Surveillance State: The “East African General Trade Company (EAGT)” digital platform requires intrusive, real-time access to your data.

- Infrastructure Gap: 35% internet penetration means 65% of the population is unreachable. Rural areas are effectively dead zones.

- Tax Complexity: Operators must act as tax agents, withholding player winnings tax, paying 20% GGR, and 30% Corporate tax.

- Regulatory Instability: The 2025 reforms prove the government is aggressive in changing rules to squeeze revenue.

Player-Specific Issues

- Winnings Tax: Players are taxed on winnings, which encourages black market usage if rates are high.

- Data Costs: High relative cost of mobile data limits session times for bandwidth-heavy casino games.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $600,000 – $800,000 (Includes license, local entity setup, tech integration, and working capital).

Monthly Operating Costs: $50,000 – $100,000 (Local staff, office, compliance, tech fees).

Effective Tax Rate on Revenue: ~55% (20% GGR + 30% Corp Tax + Admin costs of withholding player tax).

Customer Acquisition Cost: Low ($5-$15), but retention is difficult due to low disposable income.

Time to Breakeven: 24-36 months.

Profitability Assessment: DIFFICULT. While the market is “legal,” the economics are brutal. You are chasing pennies in a high-compliance, high-tax, low-infrastructure environment. Unless you are a major pan-African operator (like PremierBet or SportPesa) capable of scaling to 500k+ users, the fixed costs of a local office and compliance will bleed you dry.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | High | 2025 reforms include “heavy penalties” and equipment seizure. Digital monitoring makes blocking easier. |

| Licensed Operators | Medium | Compliance burden is high (EAGT monitoring). Risk of license suspension for minor reporting errors. |

| Affiliates/Advertisers | Medium | Strict content guidelines. Promoting unlicensed brands can lead to fines or platform bans. |

| Local Staff/Directors | Critical | Local presence requirement puts staff within reach of authorities for enforcement actions or “administrative disputes.” |

🚨 Extradition and International Enforcement

Extradition Treaties: DRC has various bilateral treaties, though enforcement for gambling offenses specifically is rare. However, the legal system can be unpredictable.

Enforcement History: Enforcement is primarily focused on physical asset seizure (shops, servers) and fines rather than international extradition.

Safe Jurisdictions: N/A – The primary risk is to your local assets and staff required by law, not international extradition.

Travel Risk: High for executives of non-compliant firms entering DRC. Local directors face immediate arrest risk during disputes.

📋 Final Verdict

Democratic Republic of the Congo receives an Operator Ease Score of 5.8/10 and a Player Access Score of 8.0/10, resulting in an overall market attractiveness rating of 6.9/10.

HONEST ASSESSMENT: The DR Congo is a volume trap. On paper, it looks attractive because online casinos are legal and the population is huge. In reality, the requirement for a physical local office, combined with intrusive government server monitoring and an abysmally low ARPU ($15/year), makes this a logistical nightmare for most Western operators.

It is a market solely for large, regional specialists who know how to operate low-margin, high-volume retail/mobile hybrid models in unstable infrastructure environments.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A large Pan-African operator with existing logistics in neighboring countries.

- Capable of operating a retail/agent network (essential for trust and payments).

- Willing to accept low margins (5-10%) in exchange for massive volume.

❌ Definitely Avoid If You Are:

- A pure-play digital operator without “boots on the ground.”

- Targeting “VIP” or high-value players (they don’t exist here in sufficient numbers).

- Unwilling to share real-time user data with the government.

- A startup with less than $1M in runway (bureaucracy will kill you before launch).

⚠️ BOTTOM LINE: Legal status does not equal profitability; enter only if you can sustain a massive, low-margin operation with heavy local infrastructure.

The ratios of betting markets to overall gambling revenues seem crucial in understanding the regulatory frameworks. What specific measurements or metrics are being used to analyze these markets?

Regarding the analysis of betting markets, we utilize a combination of financial metrics such as gross gaming revenue (GGR) and betting handle, alongside market share analyses to understand the competitive landscape and regulatory compliance.