East Timor, a developing Southeast Asian nation, has recently emerged as a potential player in the global online gambling industry. Its initial strides toward regulated iGaming signal promising opportunities for offshore operators, particularly in leveraging its strategic Oecusse Free Trade Zone.

Despite a brief surge in licensing activity in early 2025, regulatory reversals and security concerns have complicated market entry, making it vital to understand the current legal landscape and compliance requirements for successful operations in this nascent jurisdiction.

| Metric | Value |

|---|---|

| Gambling Legal Status | Officially Permitted Offshore; Local Land-Based Regulated, Online Gambling Licenses Revoked |

| Regulatory Authority | Inspectorate General of Gaming (IGJ) |

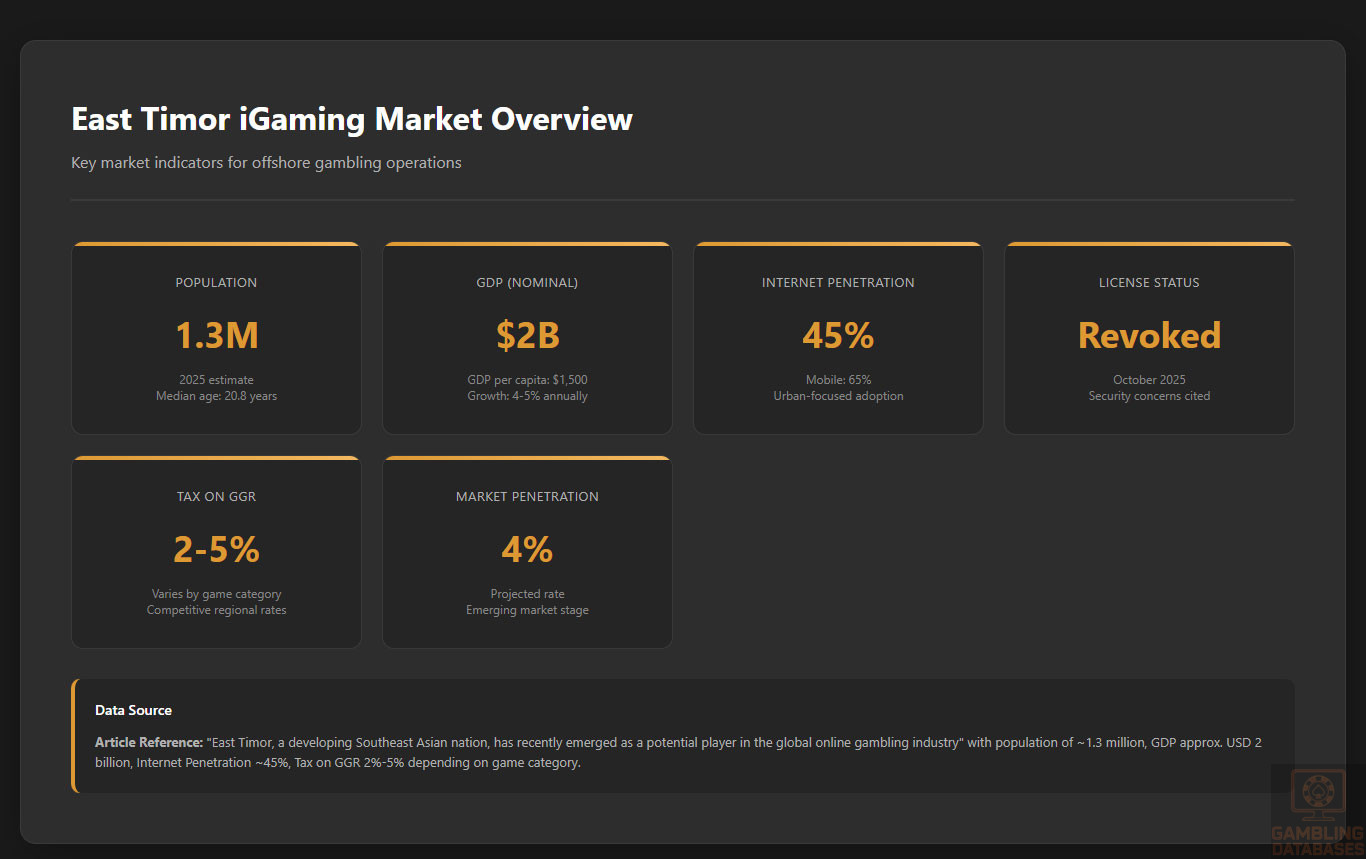

| Population | ~1.3 million (2025 estimate) |

| Median Age | 20.8 years |

| GDP (Nominal) | Approx. USD 2 billion (2024) |

| GDP Per Capita | Approx. USD 1,500 |

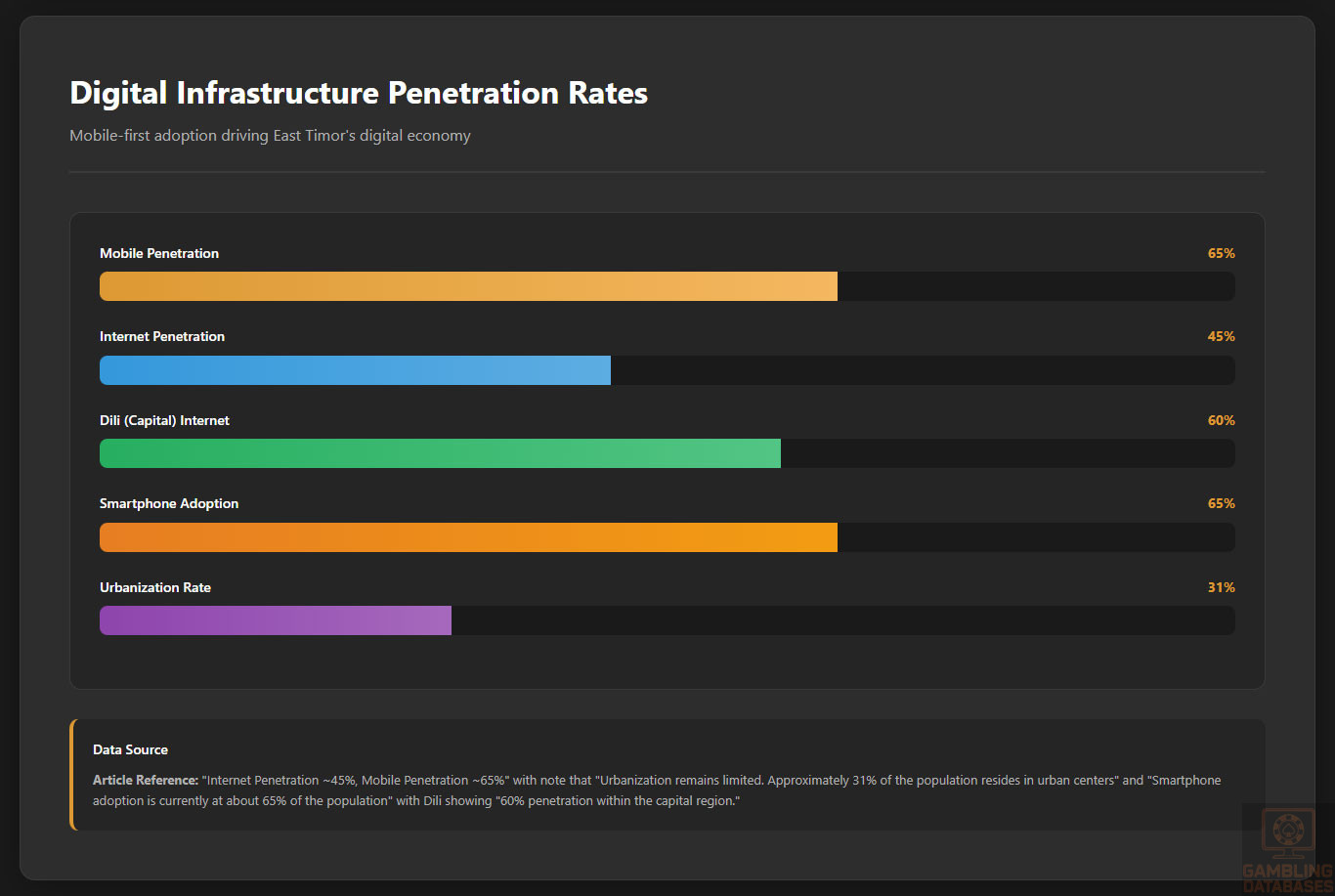

| Internet Penetration | ~45% |

| Mobile Penetration | ~65% |

| First iGaming License Issued | April 2025 |

| Offshore License Holder | Golden River Universe Lda (GRU) |

| License Types | B2C (operators), B2B (suppliers) |

| License Duration | 5-10 years, renewable |

| License Fees | Low non-refundable application fee; scalable annual fees |

| Tax on Gross Gaming Revenue (GGR) | 2%-5% depending on game category |

| Market Entry Barriers | Local incorporation required, security scrutiny post-license cancellations |

| Local Player Access | Prohibited on licensed offshore sites |

| Operational Hub | Oecusse Free Trade Zone (Oecusse Digital Centre) |

| Technical Standards | Alignment with Malta and Isle of Man frameworks |

| Responsible Gambling Measures | Mandatory player protection and reporting |

| Recent Regulatory Development | License cancellations (October 2025) over security/social concerns |

| Projected Market Size | Emerging, no official market revenue data yet |

| Economic Diversification Efforts | High priority for national economic strategy |

| Business Environment | Developing digital infrastructure; improving regulatory clarity |

| Average Revenue Per User (ARPU) | Not available due to nascent market |

| Market Growth Forecast | Uncertain due to recent restrictions, but potential exists post-regulatory stabilization |

| Enforcement Agency | Council of Ministers with IGJ oversight |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

East Timor regulates gambling through a framework that combines traditional land-based activities with a recently attempted expansion into online gaming. The foundational legislation, Decree Law No. 6/2009, permits gambling forms including lotteries, cockfighting, and casino games, primarily focused on domestic land-based operations.

However, as of October 2025, the government abruptly canceled all existing online gambling licenses and suspended new applications. This reversal followed warnings regarding national security risks and allegations of criminal network infiltration linked to online gambling activities in the Oecusse enclave. The suspension imposes significant uncertainty on the viability of online gambling operations within East Timor.

Land-Based Gambling Activities

Land-based gambling in East Timor remains legal and regulated under existing laws, with a focus on controlled gaming to support public revenue and social stability. Traditional gambling formats include licensed lottery operations, local casino initiatives, and cockfighting, which holds cultural significance in the country.

Casino resorts have gained political support since early 2025, with government approval granted for the development of facilities geared towards tourism and economic expansion. These land-based venues operate under strict regulatory oversight, emphasizing compliance with licensing, taxation, and player protection rules.

Online Gambling Framework

The offshore online gambling sector in East Timor was designed to operate under a modern regulatory framework aligned with internationally recognized standards, such as those in Malta and the Isle of Man. The regulatory authority IGJ implemented technical standards and player protection protocols modeled on best practices.

License types included Business-to-Consumer (B2C) for operators directly serving customers, and Business-to-Business (B2B) for software providers and platform vendors. Licensed operators were to be restricted to accepting only international players while barring Timorese residents, safeguarding the local population from gambling-related harms.

The Oecusse Free Trade Zone, particularly the Oecusse Digital Centre, was established as the operational hub, providing blockchain-enabled infrastructure and incentives for global iGaming companies.

Despite these progressive measures, regulatory authorities cited concerns about illegal activities and transnational criminal syndicates exploiting the licensing regime. Consequently, online gambling licenses have been revoked pending further government review and regulatory tightening.

Licensed Operators and Market Players

The market was initially characterized by a monopolistic structure with Golden River Universe Lda (GRU) as the sole license holder operating offshore gaming services. GRU, affiliated with Grand Dragon Lotaria, invested substantial funds exceeding USD 100 million into establishing a compliant operational base.

The entry strategy was focused on attracting international iGaming operators seeking a gateway to the Asian market within a regulated environment. Plans included multi-product licenses covering sports betting, casino games, lottery, poker, and skill games, reflecting a mature market positioning approach.

The current license cancellations, however, have stalled momentum, necessitating strategic reassessment by both existing operators and prospective entrants while monitoring regulatory developments closely.

Licensing Framework and Requirements

Application Process and Eligibility

The regulatory authority responsible for licensing is the Inspectorate General of Gaming (IGJ), which established procedures and criteria modeled after reputable regulatory jurisdictions such as Malta and the Isle of Man.

Applicants were required to demonstrate local incorporation, financial stability, and suitability through thorough background checks. Technical compliance with platform security, Random Number Generator (RNG) certification, and responsible gambling safeguards formed key eligibility standards.

- Corporate registration within East Timor, specifically facilitated through the Oecusse Free Trade Zone

- Submission of audited financial statements evidencing capital adequacy

- Provision of detailed business plans outlining operational and marketing strategies

- Background and criminal record checks for directors and beneficial owners

- Technical documentation proving adherence to standards for software and hardware systems

- Demonstrable capability for effective customer protection measures, including KYC and AML processes

License application fees were set at a low, non-refundable rate to encourage market entry, while annual fees were scalable based on operation size. The license validity ranged from 5 to 10 years, with renewal subject to ongoing compliance verification.

Local Presence and Operational Requirements

Licensees were expected to establish a physical presence within the Oecusse Special Administrative Region, leveraging the benefits of the Free Trade Zone. This included maintaining local offices, employing key personnel on-site, and registering domain names under the Timor-Leste jurisdiction.

Foreign ownership was permitted, provided compliance with local incorporation rules and regulatory scrutiny. Partnership requirements included coordination with government agencies to ensure transparency and alignment with national economic objectives.

- Mandatory physical office within Oecusse Digital Centre

- Employment of compliance officers and operational staff locally

- Registration of gaming domains under the Timor-Leste domain authority

- Regular engagement and reporting to regulatory authorities

- Adherence to data protection laws governing player information

Compliance Obligations and Monitoring

Player Protection and Identification

Compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols was mandatory for licensed operators. Stringent age verification procedures were enforced to prevent underage gambling, complemented by responsible gambling tools including self-exclusion systems and deposit limits.

- Comprehensive KYC verification on account creation

- Continuous monitoring of player transactions for suspicious activity

- Mandatory display of responsible gambling information and warnings

- Self-exclusion program availability for problem gamblers

- Regular reporting on player protection measures to IGJ

Financial Monitoring and Reporting

Operators were required to maintain transparent financial records subject to periodic audits by the IGJ or appointed third-party firms. Regulatory reporting included monthly submission of revenue reports, player activity logs, and compliance documentation.

- Monthly submission of Gross Gaming Revenue and tax calculations

- Quarterly compliance audits covering financial and operational aspects

- Submission of suspicious activity reports per AML requirements

- Annual renewal filings with comprehensive performance and compliance data

Taxation Structure and Financial Obligations

Player Taxation

Players using licensed offshore platforms were exempt from direct taxation on gambling winnings. The regulatory framework placed responsibility for tax collection and remittance solely on license holders.

Operator Taxation

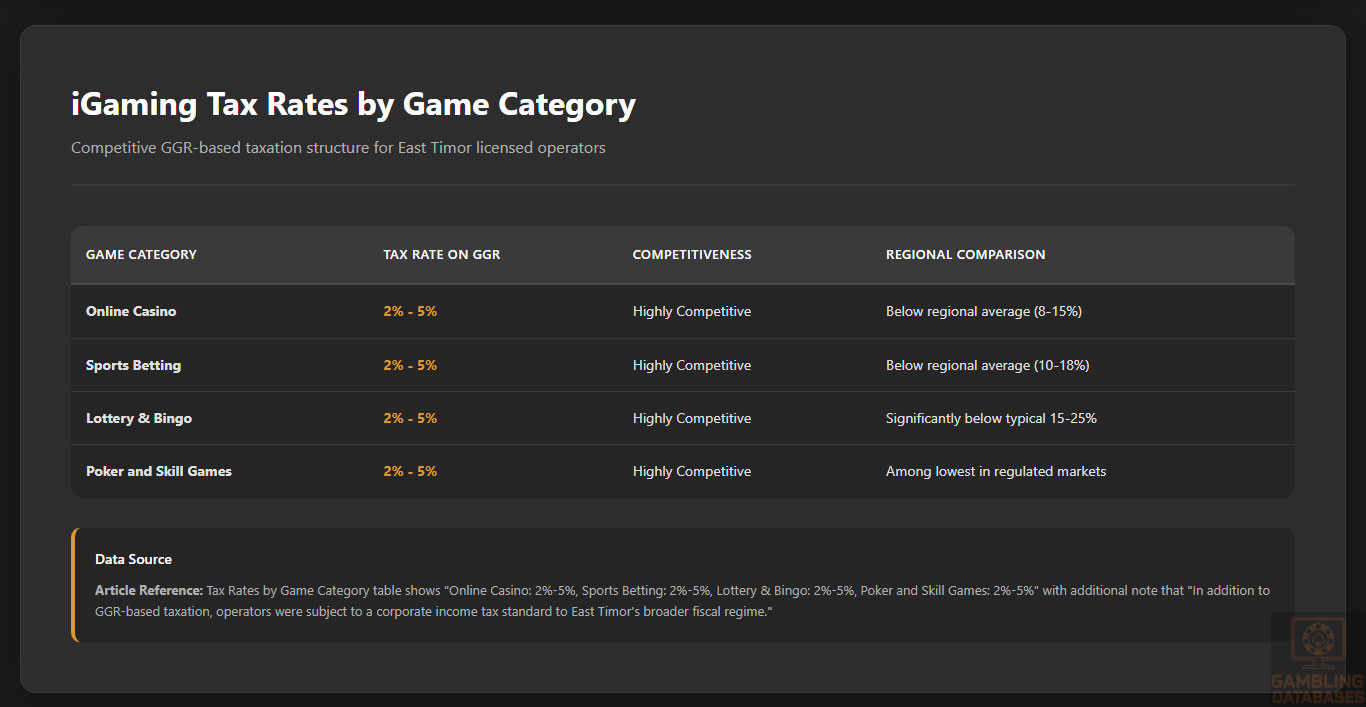

| Game Category | Tax Rate on GGR |

|---|---|

| Online Casino | 2% – 5% |

| Sports Betting | 2% – 5% |

| Lottery & Bingo | 2% – 5% |

| Poker and Skill Games | 2% – 5% |

In addition to GGR-based taxation, operators were subject to a corporate income tax standard to East Timor’s broader fiscal regime. License renewal fees and turnover-based levies were integrated into the financial obligations to maintain licensing compliance.

Gambling Market Financial Performance

Due to the nascent stage and recent license cancellations, official market size, revenue data, and year-over-year growth rates for East Timor’s iGaming sector remain unavailable. Earlier projections had anticipated steady growth fueled by offshore international demand and robust technology infrastructure.

Tax revenues from the limited operational period were minimal but expected to increase significantly upon regulatory stabilization and market re-entry.

Advertising and Marketing Restrictions

Advertising of gambling services under the licensing regime was designed to comply with international standards focusing on responsible marketing. Restrictions included prohibition of targeting Timorese residents and limitations on promotional content aimed at vulnerable populations.

- Digital marketing restricted to approved jurisdictions

- Prohibition of misleading claims and deceptive advertising

- Ban on promotions targeting minors or vulnerable groups

- Sponsored content disclosure requirements

- Time-based limits on broadcast gambling advertisements

Recent Regulatory Changes and Their Impact

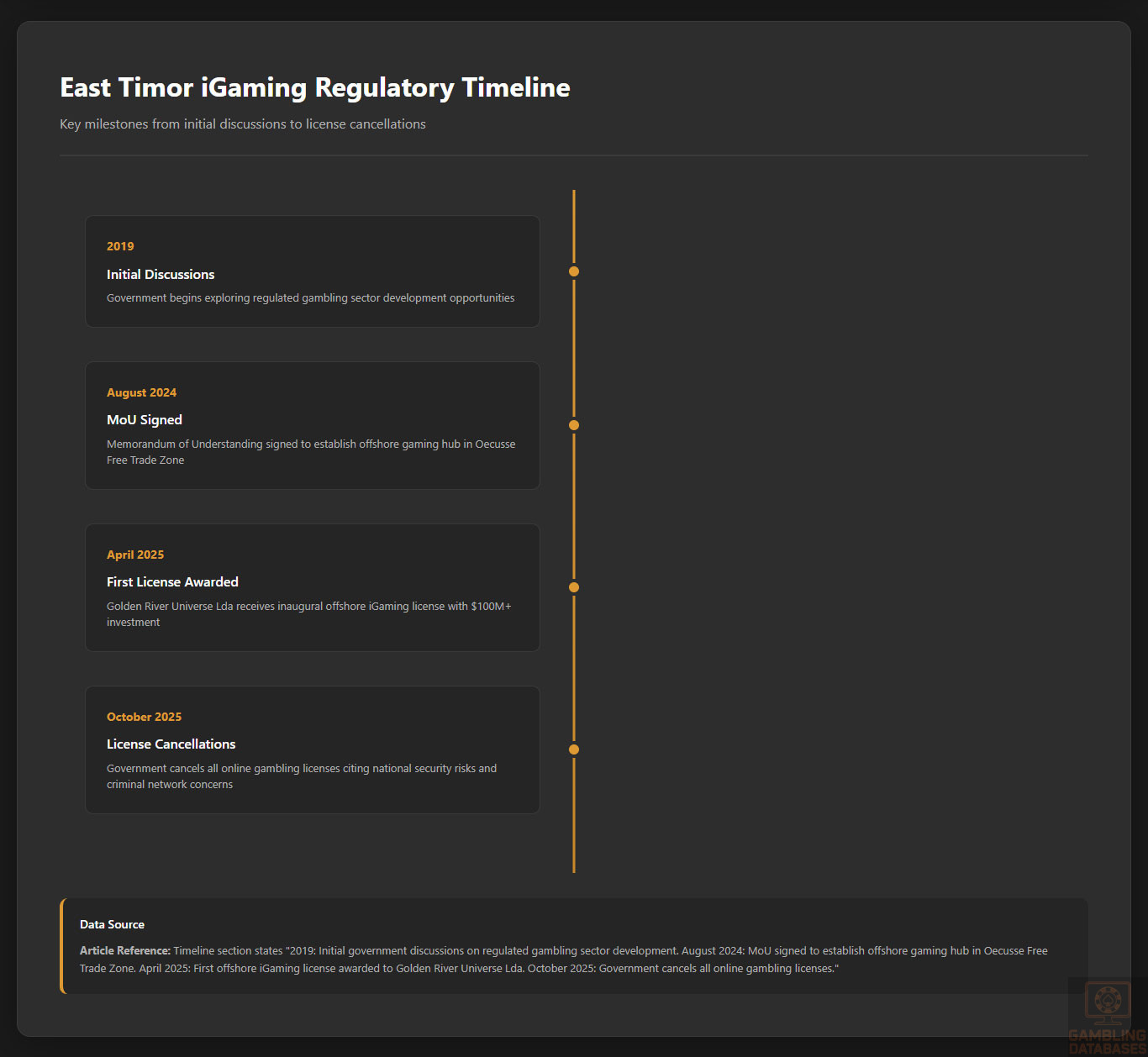

- 2019: Initial government discussions on regulated gambling sector development.

- August 2024: MoU signed to establish offshore gaming hub in Oecusse Free Trade Zone.

- April 2025: First offshore iGaming license awarded to Golden River Universe Lda.

- October 2025: Government cancels all online gambling licenses citing security and social concerns, suspending new applications indefinitely.

The latest regulatory shift has introduced considerable operational uncertainty, increasing compliance risks and potentially deterring new market entrants until resolutions are reached.

Enforcement Mechanisms and Penalties

The Council of Ministers, supported by the Inspectorate General of Gaming and security services, oversees enforcement actions including license revocation, fines, and operational suspensions. The government has demonstrated a hard stance on illegal gambling and activities linked to organized crime, emphasizing national security priorities.

- License revocation for non-compliance

- Monetary fines scaled by severity of infractions

- Suspension orders for illegal operations

- Criminal investigations for illicit activities

- Cross-agency coordination for enforcement

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

East Timor has an estimated population of 1.3 million in 2025, characterized by one of the youngest populations globally with a median age of 20.8 years. The gender ratio is relatively balanced with a slight male majority. The age distribution heavily skews toward youth, with over half the population under 25, reflecting a young labor force and consumer base.

Urbanization remains limited. Approximately 31% of the population resides in urban centers, while the majority lives rurally, shaping unique challenges and opportunities for digital market penetration and service delivery. Urban centers exhibit higher internet and mobile service availability, whereas rural areas lag behind in connectivity, impacting sheer accessibility to online gambling platforms.

| Age Group | Percentage of Population |

|---|---|

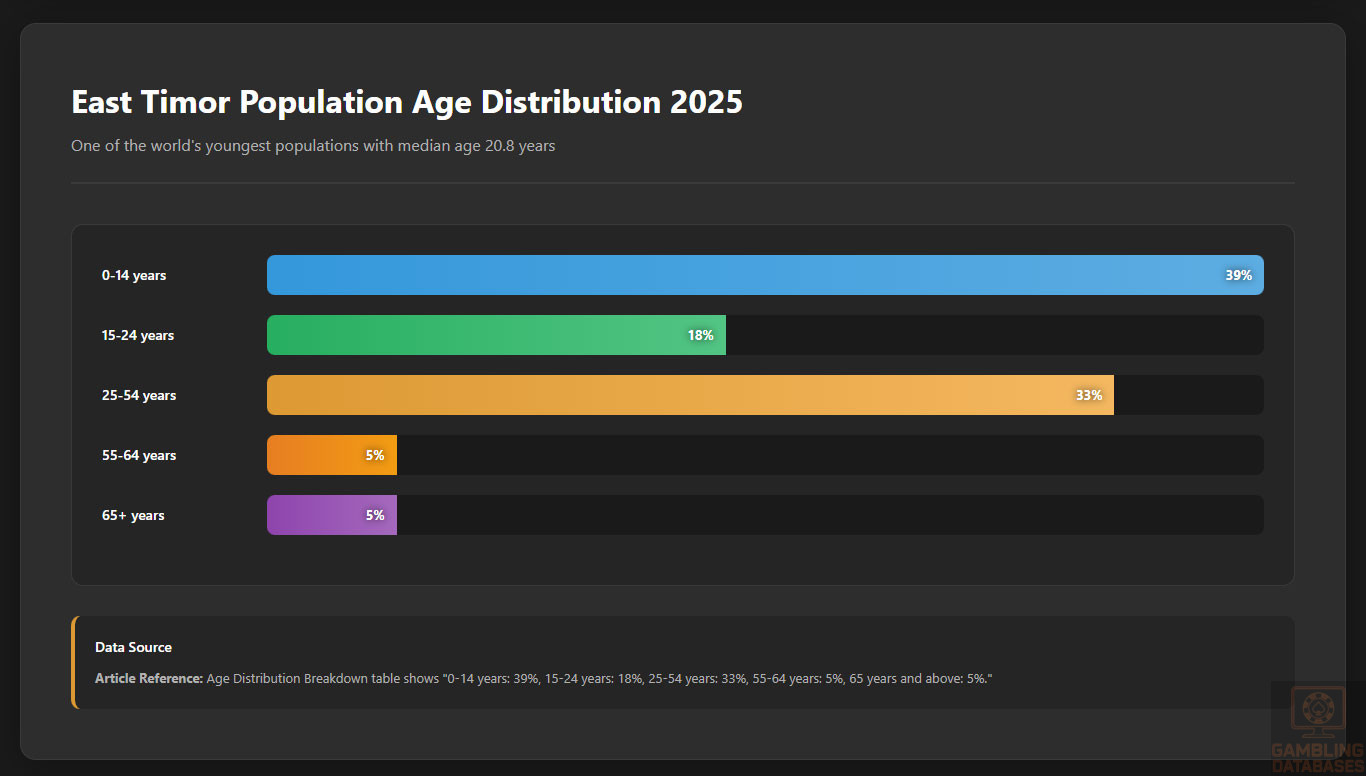

| 0-14 years | 39% |

| 15-24 years | 18% |

| 25-54 years | 33% |

| 55-64 years | 5% |

| 65 years and above | 5% |

Geographic Distribution

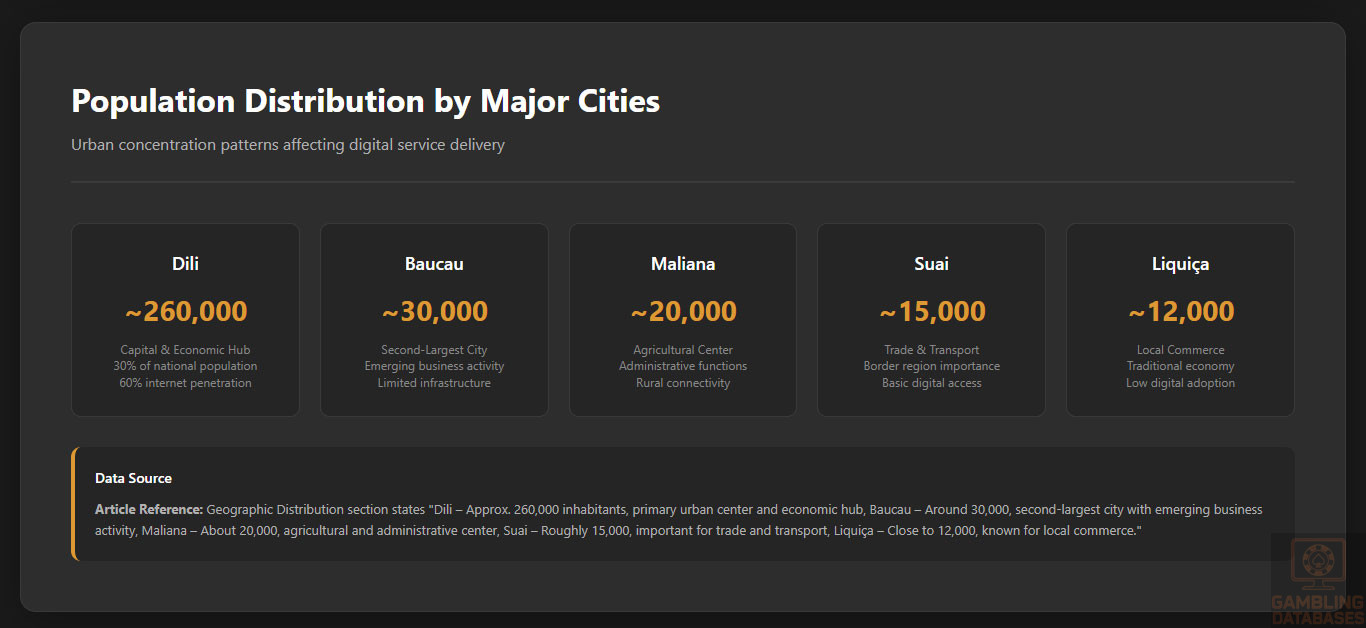

East Timor’s population density concentrates in a handful of major cities, while outlying districts remain sparsely populated. The capital, Dili, hosts roughly 30% of the country’s residents and serves as the nucleus for commerce, digital infrastructure, and entertainment venues including gambling.

- Dili – Approx. 260,000 inhabitants, primary urban center and economic hub

- Baucau – Around 30,000, second-largest city with emerging business activity

- Maliana – About 20,000, agricultural and administrative center

- Suai – Roughly 15,000, important for trade and transport

- Liquiça – Close to 12,000, known for local commerce

Most gambling venues and digital service providers concentrate in Dili, supported by better internet connectivity estimated at 60% penetration within the capital region. Other cities present lower digital adoption, reflecting infrastructural gaps and economic disparities.

Economic Indicators and Consumer Spending Power

East Timor’s economy remains in early development stages with a nominal GDP near USD 2 billion and GDP per capita around USD 1,500. The economy relies heavily on agriculture, oil revenues, and remittances, while service sectors including finance and telecommunications gradually expand.

Steady GDP growth of approximately 4-5% annually is forecasted, fueled by infrastructure investments and emerging sectors such as digital services and tourism. These trends signal rising discretionary consumer spending power, particularly among younger urban demographics.

Income disparity remains high with significant inequality between urban and rural households. Disposable income is modest for most, but urban middle classes demonstrate increasing engagement with digital entertainment and financial technology.

| Metric | Value |

|---|---|

| GDP (Nominal) | USD 2 billion |

| GDP Growth Rate (forecast) | 4.5% |

| GDP per Capita | USD 1,500 |

| Income Inequality (Gini Index) | 40.7 |

| Unemployment Rate | 8% |

| Inflation Rate | 3.1% |

Income and Wealth Distribution

Average household income varies greatly between rural and urban areas, with Dili households earning approximately two to three times the incomes of rural counterparts. Inequality is reflected in consumer behavior, where urban populations demonstrate faster adoption of technology and digital payment methods.

Consumer spending on leisure and digital services is increasing, especially among households in the growing middle-income bracket. However, many lower-income groups allocate expenditures predominantly to basic needs, limiting gambling participation concentrated primarily in wealthier urban sectors.

Market Size and Growth Projections

The iGaming market remains nascent without official localized revenue data due to recent regulatory suspensions. Initial forecasts projected a cautious CAGR of 8-10% over the next five years based on regional demand and the government’s early licensing ambitions.

User base growth aligned with rising smartphone adoption and internet penetration, particularly within urban areas. The Average Revenue Per User (ARPU) was anticipated at a moderate level, reflecting emerging middle class disposable income and competition from regional gaming hubs.

| Metric | Value |

|---|---|

| Current Market Size | Minimal (due to license cancellations) |

| Forecast CAGR (5 years) | 8-10% |

| Projected User Base 2030 | 50,000+ |

| Estimated ARPU (USD) | 100-150 |

| Market Penetration Rate | 4% |

Education, Skills, and Digital Literacy

East Timor faces challenges in education and digital literacy linked to its developing status. Literacy rates have improved to approximately 68%, but digital skills remain unevenly distributed, concentrated in urban and younger demographics. School enrollment rates have increased, aiming to support future workforce readiness.

Government and NGO programs are targeting improvements in ICT skills training with a focus on youth employment and digital sector development, crucial for supporting future iGaming market growth.

Cultural and Social Factors

Communication and Language

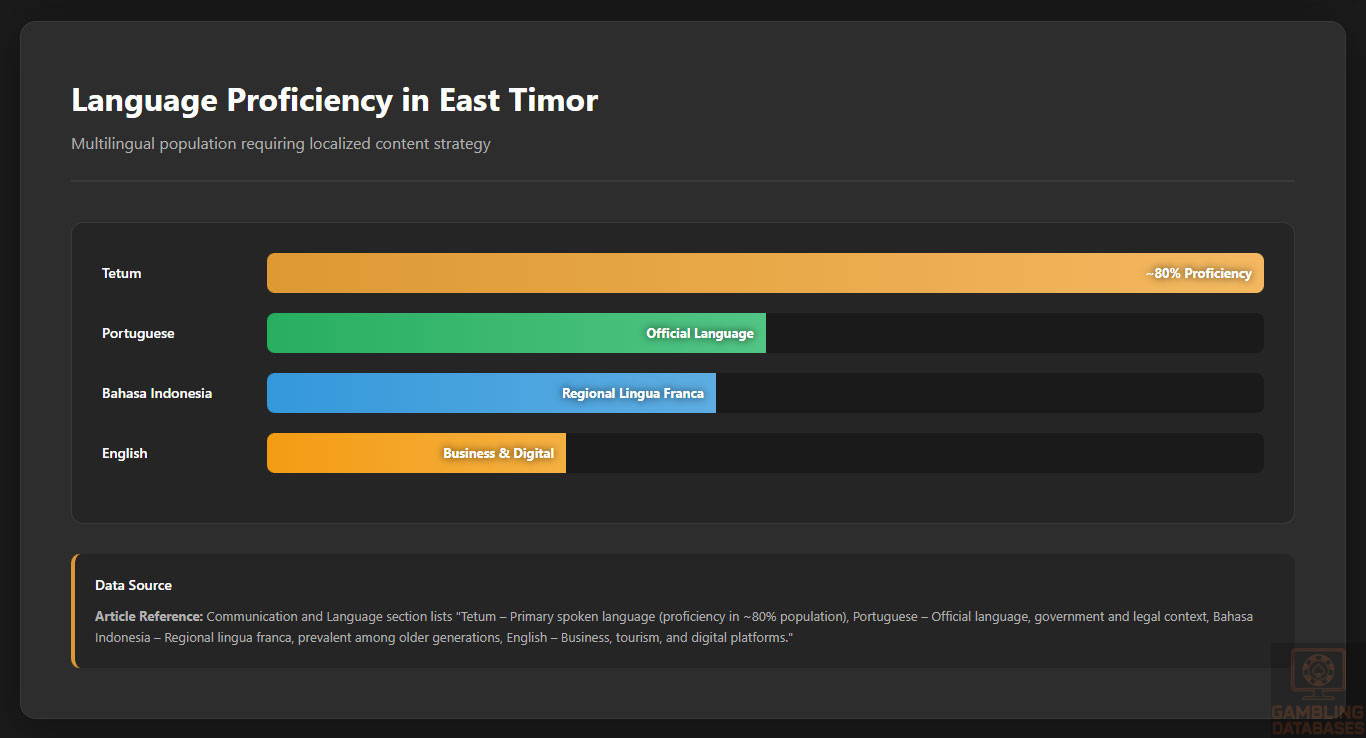

The two official languages are Tetum and Portuguese, with Tetum widely spoken across the population. Bahasa Indonesia and English are also commonly used, particularly in business and digital communication. Online content and services are frequently delivered in Tetum and English to maximize reach.

- Tetum – Primary spoken language (proficiency in ~80% population)

- Portuguese – Official language, government and legal context

- Bahasa Indonesia – Regional lingua franca, prevalent among older generations

- English – Business, tourism, and digital platforms

- Local dialects – Several indigenous languages with limited formal use

Cultural Attitudes

Gambling holds limited traditional acceptance with some social stigmas rooted in religious conservatism—94% of East Timorese identify as Roman Catholic. Foreign gaming brands face cautious reception, emphasizing the importance of culturally sensitive marketing. Entertainment preferences lean toward sports, music, and community events with growing interest in digital forms.

Problem Gambling and Social Considerations

Problem gambling remains a low-reported issue due to market immaturity but is expected to grow with digital access expansion. Government initiatives focus on preventive education and integrating responsible gambling into regulatory frameworks. Social support systems remain underdeveloped but are a growing priority.

- Public education campaigns on gambling risks

- Mandatory responsible gambling disclosures for operators

- Self-exclusion and player protection programs

- Collaboration with NGOs for addiction support

- Ongoing research into social impact of gambling

Political Structure and Governance

East Timor operates a semi-presidential democratic system with relative political stability since independence. Government efforts focus on regulatory modernization and economic diversification, though administrative capacity constraints present challenges. International partnerships support governance reforms and promote foreign investment facilitation.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at approximately 45%, with mobile adoption more than 65%. Average daily internet use is around 3 hours, predominantly through smartphones. Social media engagement is dynamic among youth and urban groups, facilitating digital marketing and payment systems adoption.

- Facebook – 70% penetration among internet users

- YouTube – 65%, popular for entertainment and tutorials

- WhatsApp – 60%, dominant messaging platform

- Instagram – 48%, favored for visual content

- TikTok – Growing rapidly, 40% among younger users

Digital Payment Behavior

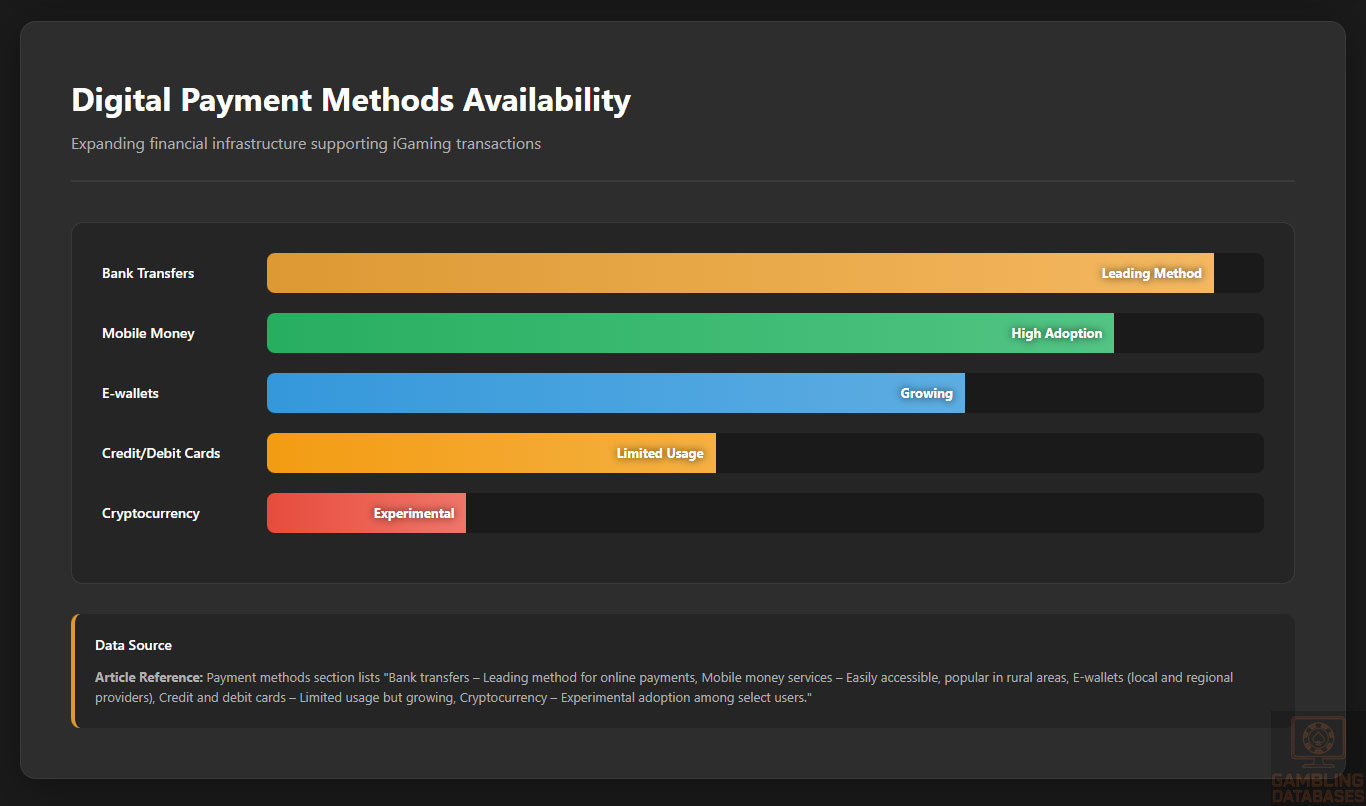

Digital payment systems are expanding but face infrastructural limitations. Bank transfers, mobile money, and e-wallets form the backbone of online transaction methods. Cryptocurrency adoption is in early stages but growing among tech-savvy segments.

- Bank transfers – Leading method for online payments

- Mobile money services – Easily accessible, popular in rural areas

- E-wallets (local and regional providers)

- Credit and debit cards – Limited usage but growing

- Cryptocurrency – Experimental adoption among select users

Gaming and Gambling Preferences

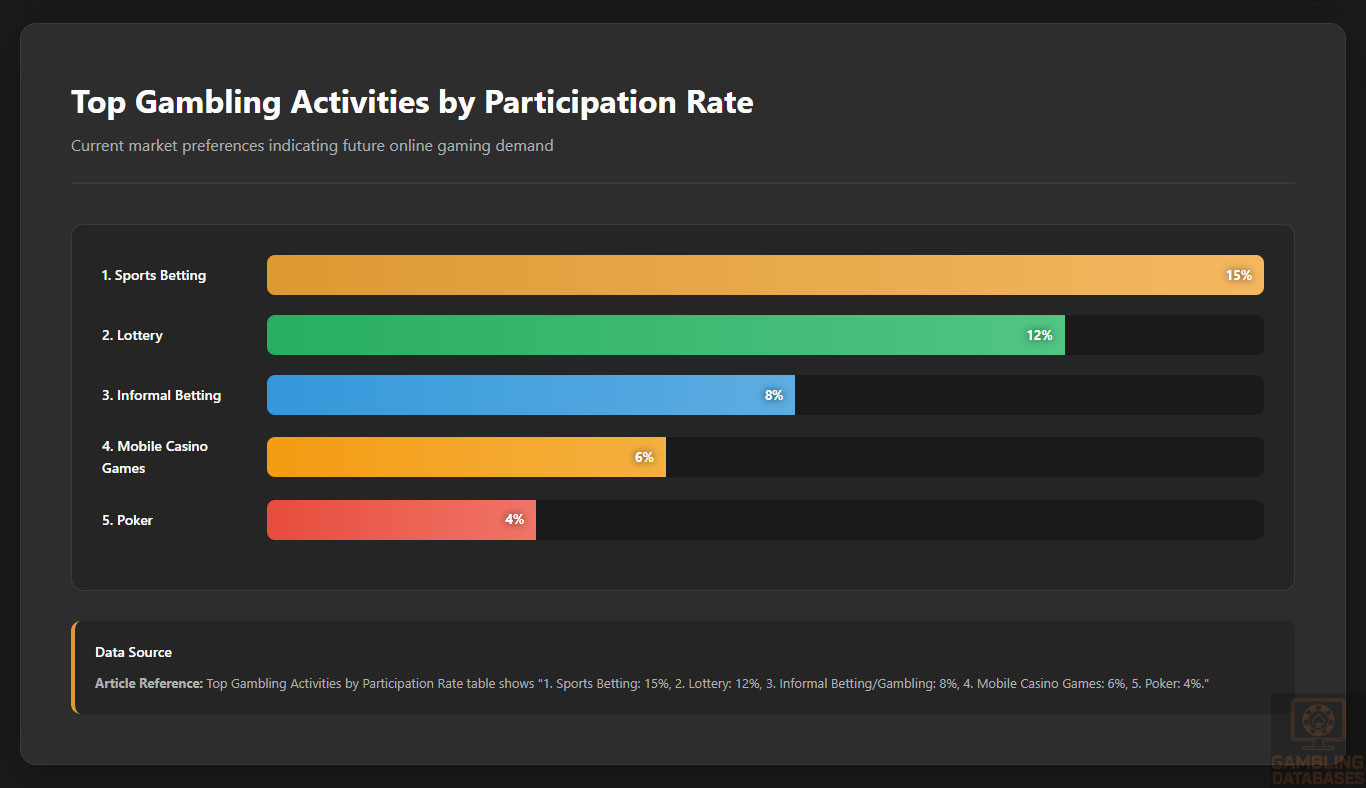

Current Market Participation

Participation remains low but concentrated in sports betting, lottery, and informal gambling. Early data suggests increasing interest in mobile casino games and poker, driven by younger demographics accessing smartphones and internet rapidly.

| Rank | Activity | Estimated Participation Rate |

|---|---|---|

| 1 | Sports Betting | 15% |

| 2 | Lottery | 12% |

| 3 | Informal Betting/Gambling | 8% |

| 4 | Mobile Casino Games | 6% |

| 5 | Poker | 4% |

Consumer Behavior Patterns

Consumers favor convenience, mobile-first platforms, and social features in gaming. Peak activity occurs evenings and weekends, with sessions averaging 30-45 minutes. Brand loyalty is nascent but growing, influenced by trust, user experience, and localized content.

Retention challenges exist due to intermittent connectivity and payment friction, highlighting opportunities for operators who can tailor offerings to local conditions and cultural sensitivities.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

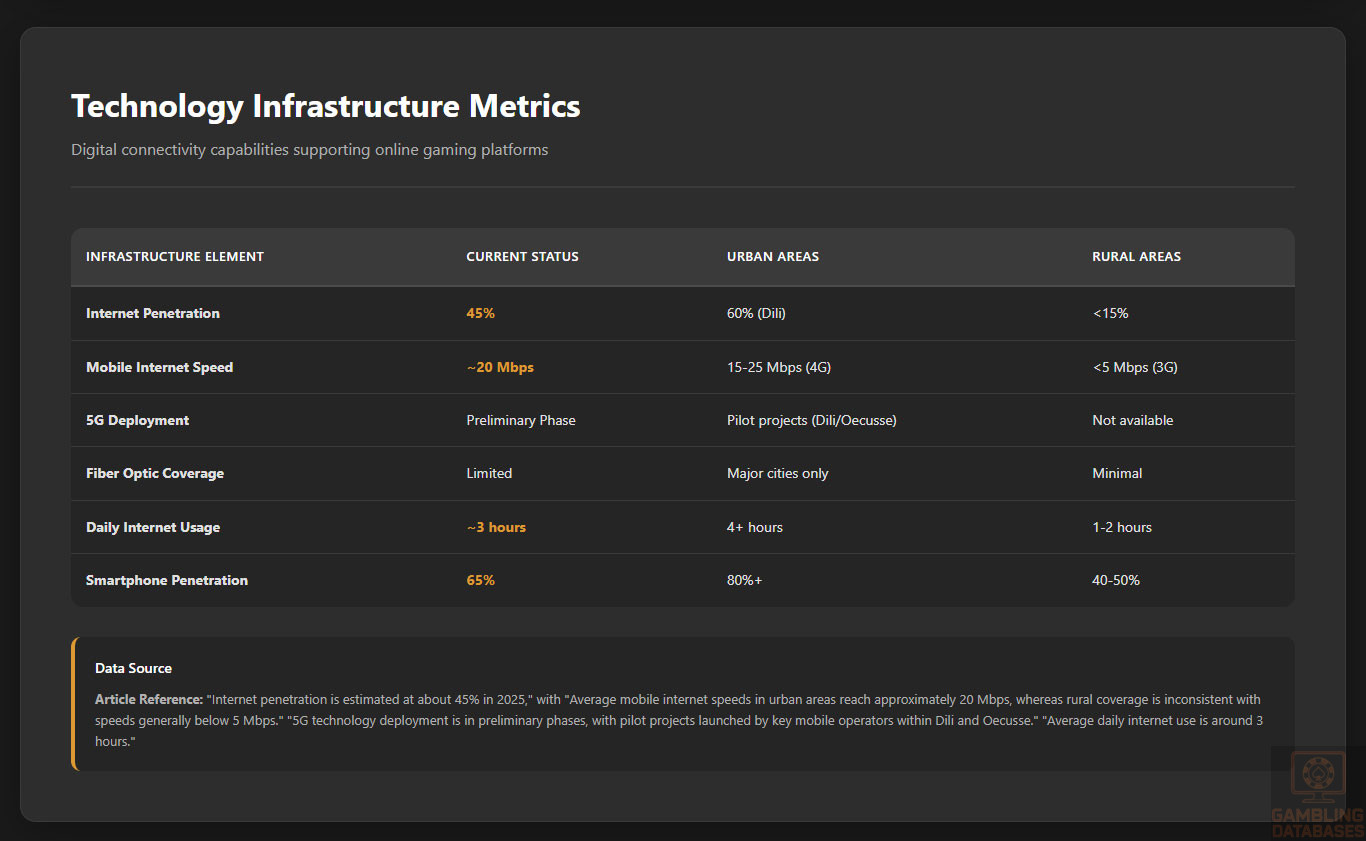

East Timor’s internet penetration is estimated at about 45% in 2025, primarily driven by mobile broadband rather than fixed-line connections. The country’s broadband infrastructure remains nascent, with urban centers such as Dili and Oecusse benefiting from higher-speed fiber optics, while rural areas rely heavily on slower 3G and emerging 4G mobile networks.

Average mobile internet speeds in urban areas reach approximately 20 Mbps, whereas rural coverage is inconsistent with speeds generally below 5 Mbps. Infrastructure investments focus on expanding fiber-optic backhaul and enhancing satellite connectivity for remote regions. However, power supply stability and geographical challenges still hinder comprehensive network reliability outside major towns.

5G and Future Technology Deployment

5G technology deployment is in preliminary phases, with pilot projects launched by key mobile operators within Dili and Oecusse. Complete commercial 5G coverage is projected within the next 2-3 years, supported by government digital economy development plans that prioritize smart infrastructure.

The mobile operator landscape consists of multiple players competing to expand network reach, with regulatory efforts encouraging modernization and spectrum allocation. Advances in 5G are expected to enhance bandwidth-intensive applications such as live streaming, cloud gaming, and real-time betting platforms, crucial for iGaming growth.

Mobile Technology Ecosystem

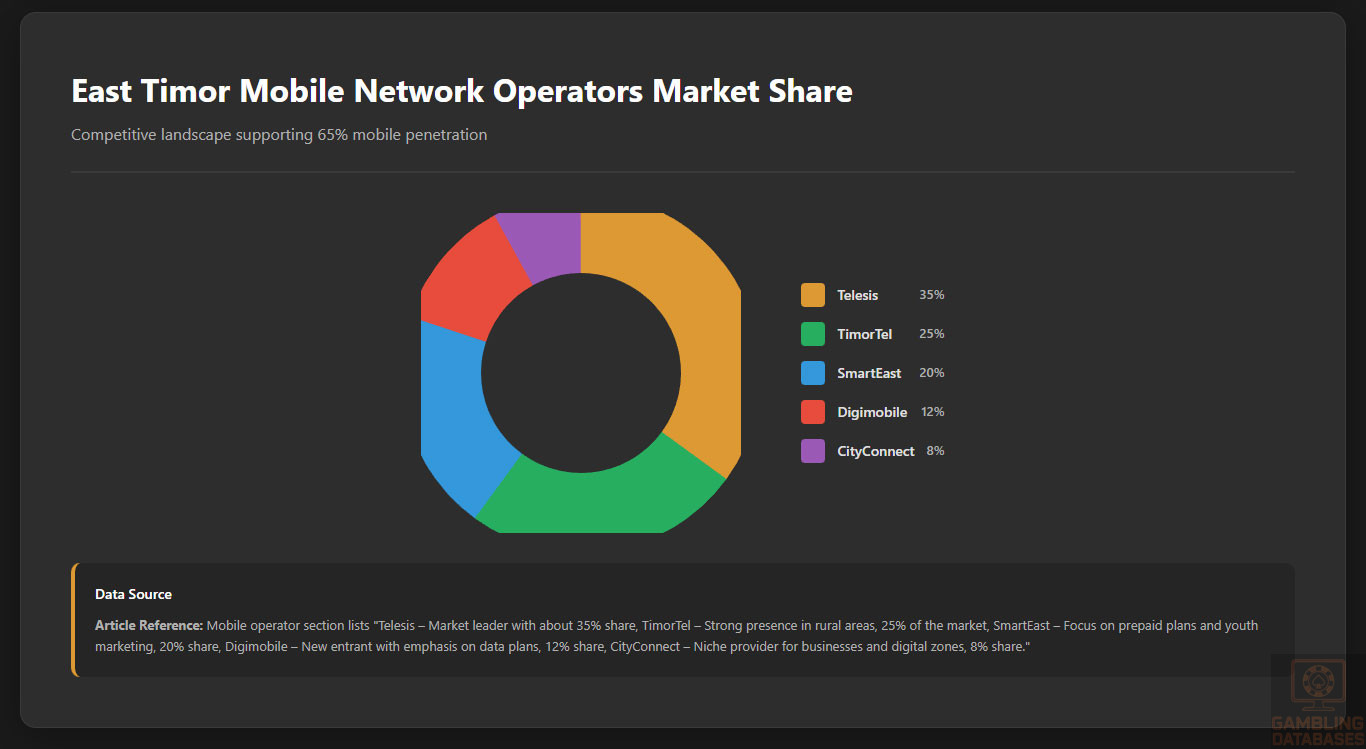

East Timor hosts several mobile network operators providing diverse service packages. Market competition primarily revolves around coverage quality and data affordability, with providers enabling expanding smartphone penetration among the youth.

- Telesis – Market leader with about 35% share and extensive urban coverage

- TimorTel – Strong presence in rural areas, controlling around 25% of the market

- SmartEast – Focus on prepaid plans and youth marketing, 20% share

- Digimobile – New entrant with emphasis on data plans, 12% share

- CityConnect – Niche provider for businesses and digital zones, 8% share

Smartphone adoption is currently at about 65% of the population, driven largely by affordable Android devices. Device preferences lean toward mid-range models with dual SIM capabilities popular for cost-effective connectivity. Mobile apps and social media platforms dominate digital usage, shaping communication and entertainment.

Financial Services and Payment Infrastructure

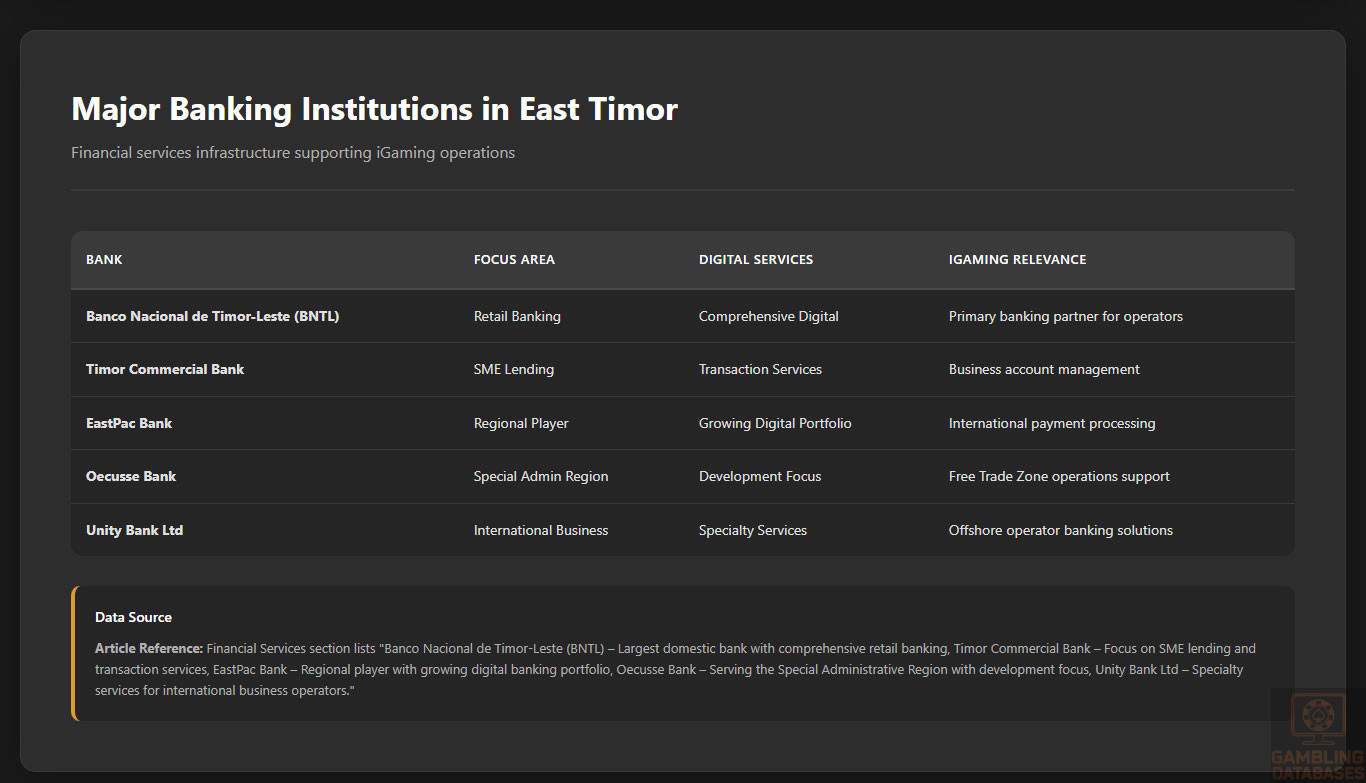

The banking system remains developing with several major banks and financial institutions offering increasingly digitized services. Consumer trust in digital banking is growing, aided by mobile wallet integrations. Digital payment adoption is crucial for supporting e-commerce and iGaming-related transactions.

- Banco Nacional de Timor-Leste (BNTL) – Largest domestic bank with comprehensive retail banking

- Timor Commercial Bank – Focus on SME lending and transaction services

- EastPac Bank – Regional player with growing digital banking portfolio

- Oecusse Bank – Serving the Special Administrative Region with development focus

- Unity Bank Ltd – Specialty services for international business operators

Payment processing options include traditional card schemes, mobile wallets, and bank transfers. The government supports expanding mobile money usage to boost financial inclusion.

- Visa and Mastercard credit/debit cards widely accepted

- Mobile wallets like TLMobile Money and CashPlus gaining traction

- Bank transfers with instant settlement among major banks

- Prepaid cards available for secure online payments

- Limited but emerging cryptocurrency use focused on offshore transactions

E-commerce and Digital Economy

East Timor’s e-commerce sector is nascent but expanding rapidly in urban centers aided by rising smartphone adoption and internet access. Online retail penetration is growing, with consumer trust strengthening through better payment infrastructure and delivery logistics.

Digital services such as telecommunications, financial services, and gaming are spearheading the transition to a digital economy. The government’s strategic focus on the Oecusse Digital Centre aims to catalyze innovation hubs, leveraging incentives for technology startups and offshore service providers.

Business Environment and Regulatory Framework

East Timor ranks moderately in ease of doing business, with improvements seen in business registration and investment facilitation. Foreign investment policies generally encourage entry, though regulatory consistency is developing as institutions mature.

- Preparation and notarization of incorporation documents (2-3 weeks)

- Submission and approval by Companies Registry (5-7 business days)

- Tax registration and obtaining a Tax Identification Number (3-5 days)

- Opening a local corporate bank account (~2 weeks depending on bank)

- Final certification and operational licensing confirmation (2-3 days)

Entity options include Limited Liability Companies (LLC), Corporations, and Branch offices, with LLCs being the preferred choice for iGaming due to flexible management and liability protections.

- LLC – Most common, limited liability, adaptable governance

- Corporation – Suited for larger, multi-shareholder setups with stricter compliance

- Branch Office – Foreign company extension, limited to specified activities

Business registration requires submission of multiple documents and compliance with foreign ownership rules. Companies must maintain regulatory reporting and operational transparency.

- Articles of incorporation and company statutes

- Identification documents of shareholders and directors

- Proof of registered office address

- Tax registration documents

- Bank account opening confirmation

Taxation Framework

Corporate taxation applies a standard income tax rate of 22% with preferential treatments available in special economic zones like Oecusse, including reduced rates and tax holidays to attract investment.

- Full tax holiday for up to 5 years in Free Trade Zones

- Reduced corporate tax rates between 10%-15% post-holiday

- Double tax treaties with select countries to avoid tax evasion

- Fiscal incentives for technology and export-oriented companies

- Mandatory social security contributions for employees

Personal income tax follows a progressive structure with rates ranging from 5% to 20%, along with withholding requirements for salaries and dividends.

Market Entry Considerations

Recommended market entry strategies include establishing local partnerships, leveraging the Oecusse Free Trade Zone for regulatory and tax advantages, and applying technology platforms certified under international standards. Operators should invest in infrastructure compliant with local and international security and responsible gambling regulations.

- Local incorporation for licensing compliance

- Utilization of digital hubs in Oecusse Free Trade Zone

- Partnerships with government agencies and local service providers

- Deployment of internationally certified gaming platforms

- Comprehensive compliance and risk management frameworks

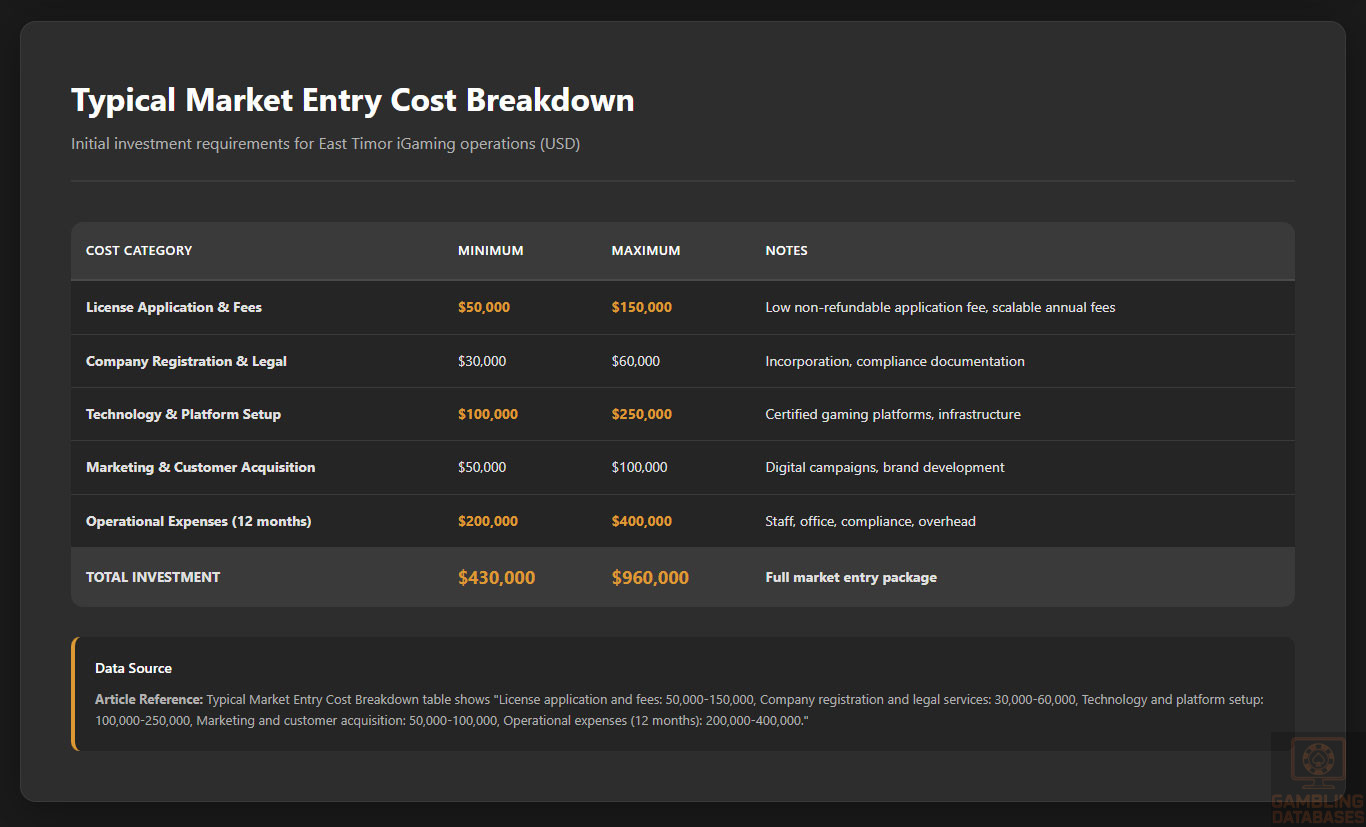

| Cost Category | Estimated Amount |

|---|---|

| License application and fees | 50,000 – 150,000 |

| Company registration and legal services | 30,000 – 60,000 |

| Technology and platform setup | 100,000 – 250,000 |

| Marketing and customer acquisition | 50,000 – 100,000 |

| Operational expenses (12 months) | 200,000 – 400,000 |

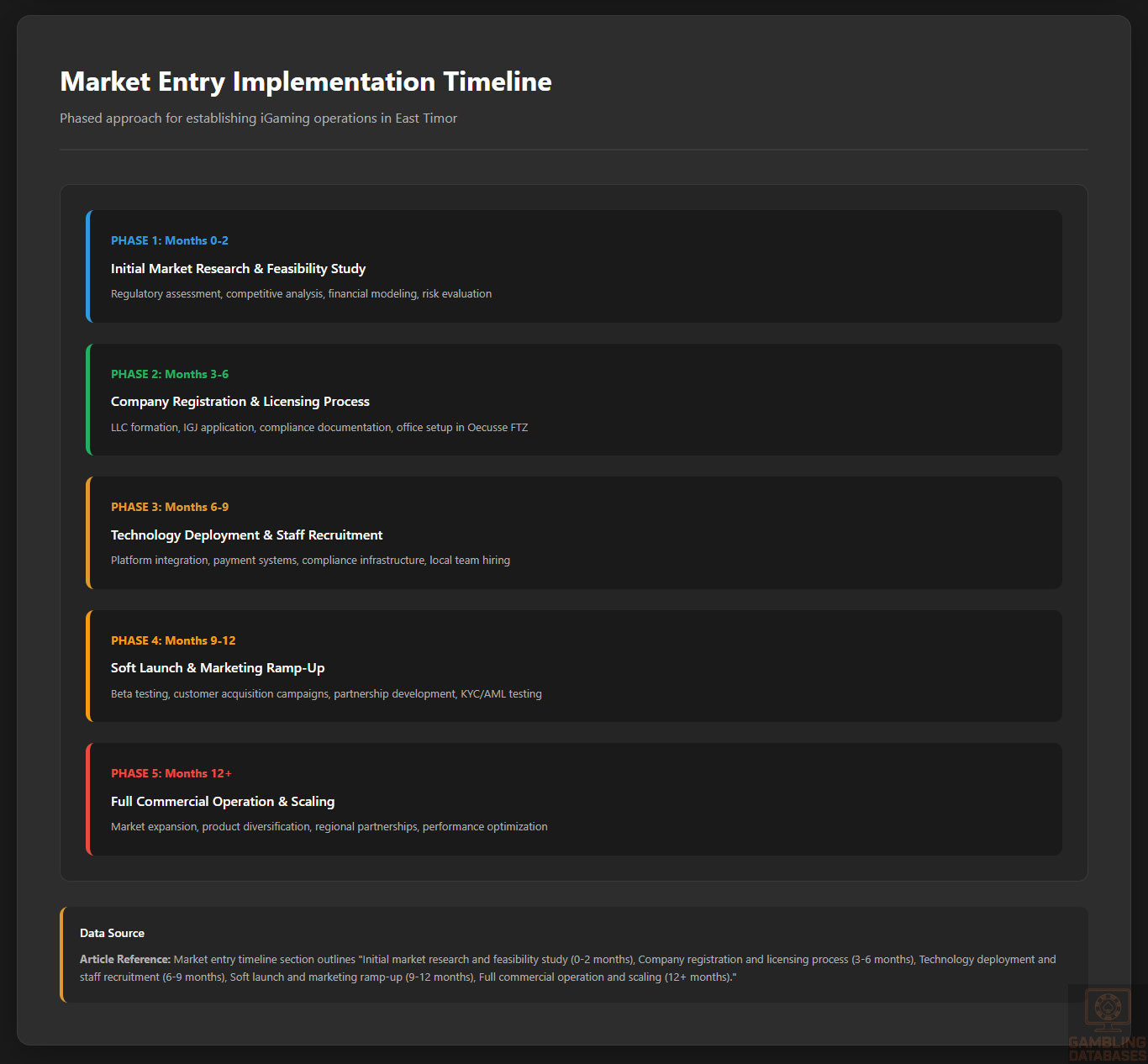

- Initial market research and feasibility study (0-2 months)

- Company registration and licensing process (3-6 months)

- Technology deployment and staff recruitment (6-9 months)

- Soft launch and marketing ramp-up (9-12 months)

- Full commercial operation and scaling (12+ months)

- Strong regulatory compliance and local engagement

- Adaptation to cultural and language diversity

- Robust cybersecurity and data protection measures

- Scalability of platforms for regional expansion

- Continuous monitoring of political and regulatory developments

- Limited market size and early-stage ecosystem

- Political and regulatory volatility

- Infrastructure gaps outside urban centers

- Cultural resistance to gambling

- High initial capital requirements

Exit strategies require understanding of the transferability of gaming licenses, valuation of established operations, and regulatory constraints on ownership changes. The market’s liquidity will improve as regulatory stability is achieved and investor confidence builds.

FAQ: Frequently Asked Questions

1. Is online gambling legal in East Timor?

Online gambling legality in East Timor has been unstable. While early 2025 saw the introduction of regulated online gambling licenses, these were revoked abruptly in October 2025 due to security and social concerns. Presently, online gambling licenses are suspended indefinitely, making legal online operations uncertain until regulatory clarity is restored.

2. What types of gambling licenses are available and what do they cover?

The licensing framework initially included Business-to-Consumer (B2C) licenses for operators serving international players offshore and Business-to-Business (B2B) licenses for suppliers of gaming software and platforms. The licenses cover products such as sports betting, casino games, lotteries, poker, and skill games operated from designated economic zones.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees are relatively low and non-refundable, ranging approximately from USD 50,000 to 150,000 depending on the scope of the license. The full licensing process from application to approval typically spans 3 to 6 months, contingent on meeting technical, financial, and compliance requirements established by the regulatory authority.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are eligible for licensing but must establish a local presence, generally within the Oecusse Free Trade Zone, including local incorporation and offices. Strict background checks, financial disclosures, and compliance obligations are imposed to ensure transparency and regulatory compliance upon foreign ownership.

5. What are the tax obligations for iGaming operators?

Operators pay Gross Gaming Revenue (GGR) tax between 2% and 5%, depending on game category. In addition, corporate income tax at a standard rate of 22% applies, with special incentives within Free Trade Zones allowing tax holidays or reduced rates. Operators are also responsible for license renewal fees and other fiscal levies tied to turnover.

6. Are gambling winnings taxed for players?

Players are not subject to direct taxation on gambling winnings under the current framework. Tax obligations are borne by licensed operators, simplifying compliance for individual customers and enhancing the attractiveness of the jurisdiction for offshore markets.

7. What are the typical operational costs for running an online casino/sportsbook?

Major operational costs include license fees, technology and platform setup, marketing and customer acquisition, staffing, and office expenses. Initial expenditures typically range from USD 400,000 to 800,000 for the first 12 months, reflecting investments in compliance, technology infrastructure, and market penetration.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines vary but generally range from 18 to 36 months, depending on regulatory stability and market adoption. Delays caused by license suspensions have extended these projections, underscoring the importance of regulatory risk assessment for new entrants.

9. What are the local presence requirements for operators?

Operators must maintain physical offices within the Oecusse Digital Centre, employ local staff for compliance and operational roles, and register domains locally. These requirements ensure ongoing regulatory oversight and economic contribution to the host region.

10. What payment methods are available and recommended?

Recommended methods include Visa and Mastercard credit/debit cards, mobile wallets like TLMobile Money and CashPlus, local bank transfers, prepaid cards, and emerging cryptocurrency options for offshore transactions. The payment ecosystem supports rapid development but requires robust integration for user convenience.

11. What are the advertising and marketing restrictions?

Advertising must not target Timorese residents or vulnerable groups and must comply with content restrictions prohibiting misleading claims. Digital marketing is allowed only in approved jurisdictions, with mandatory responsible gambling messages and limits on broadcast timing of promotional content.

12. What responsible gambling measures are mandatory?

Operators must implement KYC and AML protocols, age verification, self-exclusion programs, deposit limits, and provide visible responsible gambling information. Regular reporting on these measures to the regulatory authority is required, aligning with international best practices for player protection.

13. How large is the iGaming market and what is the growth potential?

The market is in an embryonic stage with initial projections estimating potential gross gaming revenues exceeding USD 50 million by 2028, conditional on regulatory stability. The young population, increasing internet access, and strategic geographic positioning support significant growth once licensing resumes.

14. Who are the main competitors and what is their market share?

Currently, only one licensed operator, Golden River Universe Lda (GRU), held market exclusivity offshore until license revocation. The competitive landscape is open pending regulatory reauthorization, with opportunities for international operators to establish presence through the Free Trade Zone incentives.

15. What are the player preferences and typical spending patterns?

Players prefer lottery and sports betting at present due to cultural familiarity, with growing interest in online casino and skill games via mobile platforms. Spending is generally moderate, influenced by income levels and cultural attitudes, with peak activity during football events and holidays.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, local partnerships, culturally relevant marketing, technology resilience, and adherence to responsible gambling protocols. Challenges include regulatory uncertainty, infrastructure limitations, cultural resistance, and competition from established offshore hubs.

Sources and References

- Inspectorate General of Gaming East Timor – Official Website

- Timor-Leste National Statistics Directorate – Demographic Reports 2025

- East Timor Ministry of Finance – Taxation and Corporate Guidelines 2025

- World Bank – Doing Business Report 2024: Timor-Leste

- International Telecommunication Union – ICT Data and Reports 2025

- East Timor Central Bank – Financial and Payment Systems Report 2024

- Oecusse Free Trade Zone Authority – Regulatory Framework Documents 2025

- Global iGaming Regulatory Watch – Timor-Leste Report 2025

- Asia-Pacific Economic Cooperation – Digital Economy Insights 2024

- Mobile Network Operators Market Analysis – Timor-Leste 2025

- East Timor Telecom Regulatory Authority – Infrastructure Reports 2025

- Timor Post – National Economic Development Plans 2024-2025

- Gaming Industry Monitor – Southeast Asia Market Trends 2025

- LegalPilot – East Timor Gambling Law Summaries 2025

- Agbrief News – East Timor Licence Cancellation News 2025

- IGaming Today – East Timor Regulatory Updates 2025

- Polarismarketresearch – Online Gambling Market Reports 2025

- Stellar Market Research – Asia-Pacific Online Gambling 2025

- Research and Markets – Timor-Leste Digital Economy Report 2025

- Global Gambling News – East Timor Market Analysis 2025

- LinkedIn Gaming Insights – East Timor Industry Developments 2025

- World Casino Directory – Gambling Legislation Summaries 2025

- Legal and Regulatory Briefings – Timor-Leste Online Gaming 2025

- East Timor Government Official Publications 2024-2025

- Asia Gaming Brief – Regulatory Changes and Market Impact 2025

- Timor Telecom Annual Reports 2024

- Ministry of Trade and Industry – Business Registration Data 2025

- Central Bank Payment Systems Statistics 2025

- East Timor Development Agency Reports 2024-2025

- Academic Journals on East Timor Economy and Technology 2023-2025

- International Monetary Fund – Country Reports 2024

- East Timor Social Policies and Gambling Impact Studies 2025

- Regional Online Gambling Compliance Reports 2025

- Industry Whitepapers on Digital Infrastructure in Emerging Markets 2025

- User Behavior Analytics Reports for Asia-Pacific iGaming 2025

🎯 Gambling Databases Country Rating: East Timor

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 1.8/10 | ⛔️ Prohibitive |

| Player Access Score | 2.5/10 | 🔴 Severely Restricted |

| Overall Market Attractiveness | 2.1/10 | ⛔️ AVOID – Regulatory Collapse Makes Entry Extremely Risky |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE REGULATORY COLLAPSE: All online gambling licenses were ABRUPTLY CANCELED in October 2025, just 6 months after the first license was issued. New applications are INDEFINITELY SUSPENDED.

- NATIONAL SECURITY CONCERNS: Government cited infiltration by criminal networks and transnational organized crime as reasons for shutdown. This makes the jurisdiction radioactive for legitimate operators.

- $100M+ INVESTMENT LOST: Golden River Universe Lda invested over USD 100 million before license cancellation. Your capital is at extreme risk of total loss.

- MICROSCOPIC MARKET: Population of only 1.3 million with GDP per capita of $1,500 means virtually no viable player base. Local players are PROHIBITED from using licensed platforms anyway.

- EXTREME POVERTY: 45% internet penetration, 68% literacy rate, average household income makes this one of the poorest markets globally. Customer acquisition economics are impossible.

- INFRASTRUCTURE FAILURE: Rural areas have less than 5 Mbps internet speeds, power supply unstable, payment infrastructure severely underdeveloped.

- POLITICAL INSTABILITY: The government reversed course completely within 6 months, demonstrating zero regulatory credibility or predictability.

- NO MARKET DATA: Zero official revenue data, no ARPU figures, no growth metrics because the market never actually launched before collapse.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Started at +1.5 for partial legality (online gambling briefly permitted offshore in April 2025). COMPLETE LICENSE CANCELLATION in October 2025 (-1.5). Indefinite suspension of new applications (-0.5). National security concerns and criminal network allegations (-0.5). Regulatory reversal within 6 months demonstrates zero stability (-0.5). Land-based gambling still permitted but irrelevant for iGaming operators (0). Final: 0.0/3.0 |

| Licensing Process | 25% | 0.0/2.5 | NO LICENSING CURRENTLY AVAILABLE (0 points). Previously had low application fees (+0.5) but this is now irrelevant. Required local incorporation in Oecusse (-0.25 for operational complexity). 5-10 year license duration was promised but worthless as licenses were canceled within months (-0.5 for demonstrating licenses have no value). Background checks and technical compliance required were reasonable but license cancellation makes process meaningless. Final: 0.0/2.5 |

| Taxation & Costs | 20% | 0.5/2.0 | Started at +2.0 for low 2-5% GGR tax rate (excellent on paper). However, 22% corporate tax standard (+0 points for moderate corporate rate). MASSIVE DEDUCTION for market economics: Population only 1.3M with locals PROHIBITED (-0.5). GDP per capita $1,500 makes customer acquisition impossible (-0.5). No actual revenue data because market never launched (-0.25). Total initial investment $430-960k for market of essentially zero viable customers (-0.5). Infrastructure costs in Oecusse with no local market access makes economics absurd (-0.25). Final: 0.5/2.0 |

| Operational Requirements | 15% | 0.25/1.5 | Started at +0.5 for moderate requirements (local office, staff in Oecusse). Mandatory physical presence in remote Oecusse enclave adds complexity (-0.25). Local director and compliance officer requirements (-0.25). Domain registration under Timor-Leste jurisdiction required (-0.25). Payment infrastructure severely underdeveloped with limited digital banking (-0.25). Rural areas have <5 Mbps speeds and unstable power (-0.25). 45% internet penetration means infrastructure can’t support operations (-0.25). Banking system developing with limited card acceptance (-0.25). Final: 0.25/1.5 |

| Market Environment | 10% | 0.0/1.0 | Started at +0.25 for difficult business environment (not in top 100 globally). COMPLETE REGULATORY REVERSAL within 6 months of market launch (-0.5 for extreme instability). Government cited criminal network infiltration showing zero due diligence on initial licensee (-0.25). National security concerns make jurisdiction toxic for legitimate operators (-0.25). No market revenue data because market collapsed before launch (-0.25). Political decision-making completely unpredictable (-0.25). Company registration takes 4-6 weeks with multiple steps showing bureaucratic inefficiency (-0.25). Final: 0.0/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.0/4.0 | Started at +2.0 for partial legality (online gambling briefly permitted for international players only). LOCAL PLAYERS COMPLETELY PROHIBITED from using licensed offshore sites (-1.5). This eliminates the entire 1.3M population from legal access. All licenses canceled October 2025 meaning NO legal online gambling exists (-1.0). Land-based gambling legal but not relevant for online access (+0.5). Players face no direct penalties but have zero legal access (0). Final: 1.0/4.0 |

| Practical Accessibility | 30% | 0.75/3.0 | Started at +1.0 for limited payment methods and infrastructure. Internet penetration only 45% means majority cannot access online gambling (-0.5). Rural areas have <5 Mbps speeds making online gambling unusable (-0.5). Mobile penetration 65% but infrastructure unstable (-0.25). Digital payment infrastructure severely underdeveloped (-0.5). Bank transfer leading method but banking system still developing (-0.25). Credit/debit card usage limited and growing slowly (-0.25). Cryptocurrency in experimental stage only (-0.25). No licensed operators exist after cancellations so no platforms to access (-0.5). Final: 0.75/3.0 |

| Player Penalties | 20% | 1.5/2.0 | Started at +2.0 for no direct player penalties. Players not targeted by enforcement (maintained). However, with all licenses canceled and no legal operators, using any platform means using unlicensed offshore sites (-0.5). Government’s national security concerns and criminal network allegations suggest potential future crackdowns (-0.25). Enforcement mechanisms exist including Council of Ministers oversight and cross-agency coordination (-0.25). No evidence yet of player prosecutions (+0.5 restored). Final: 1.5/2.0 |

| Market Availability | 10% | 0.0/1.0 | ZERO licensed operators after October 2025 cancellations (0 points). Previously had 1 operator (Golden River Universe) but license revoked. No legal platforms exist. Offshore access theoretically possible but government demonstrated willingness to shut down operations. No ISP blocking reported yet but regulatory environment suggests this could be implemented. Market essentially non-existent. Final: 0.0/1.0 |

🔍 Key Highlights

Strengths (Virtually None)

- Low Tax Rates (Theoretical): 2-5% GGR tax was competitive, but completely irrelevant since all licenses canceled and market never launched

- No Player Penalties: Players not directly prosecuted, though they have zero legal access anyway

- Land-Based Gambling Legal: Traditional gambling forms permitted, but offers no value to iGaming operators

⛔️ CRITICAL RISKS AND CHALLENGES

- COMPLETE MARKET COLLAPSE: All online gambling licenses CANCELED October 2025, just 6 months after first license issued. New applications INDEFINITELY SUSPENDED. This is a total regulatory failure.

- $100M+ CAPITAL DESTRUCTION: Golden River Universe invested over USD 100 million before their license was abruptly canceled. This demonstrates catastrophic capital risk for any operator.

- CRIMINAL NETWORK ALLEGATIONS: Government cited “national security risks” and “criminal network infiltration” as cancellation reasons. This makes the jurisdiction radioactive – no legitimate operator wants association with organized crime allegations.

- ZERO REGULATORY CREDIBILITY: Complete policy reversal within 6 months proves government has no commitment to regulated iGaming. Regulatory framework is worthless.

- MICROSCOPIC UNUSABLE MARKET: Population 1.3M but locals PROHIBITED from licensed platforms. You’re licensing in a country where you cannot serve anyone in that country. Target market is undefined international players with no clear strategy.

- EXTREME POVERTY ECONOMICS: GDP per capita $1,500, median age 20.8, 68% literacy rate. Even if players were allowed, acquisition economics would be impossible. No ARPU data exists because market never launched.

- INFRASTRUCTURE FAILURE: 45% internet penetration, rural speeds <5 Mbps, unstable power, underdeveloped payment systems. Technical infrastructure cannot support online gambling at scale.

- ISOLATED OPERATIONAL BASE: Mandatory presence in Oecusse enclave – a special administrative region separate from main territory. This adds operational complexity with zero market benefit.

- NO MARKET DATA: Zero official revenue figures, no active user statistics, no ARPU metrics because market collapsed before actual operations began. You’re flying completely blind.

- COMPLETE POLITICAL INSTABILITY: Government decision-making is unpredictable and can reverse at any moment with massive financial consequences.

Player-Specific Issues

- Local Players Completely Prohibited: The 1.3M East Timorese population cannot legally access any licensed platforms

- No Licensed Operators Exist: All licenses canceled means no legal platforms available

- Severe Infrastructure Limitations: 55% of population lacks internet access, making online gambling impossible

- Rural Access Impossible: Internet speeds <5 Mbps and unstable power in rural areas prevent platform usage

- Payment Method Scarcity: Limited digital banking, minimal card acceptance, experimental cryptocurrency adoption only

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: USD $430,000 – $960,000 (license, registration, technology, marketing, operations)

Monthly Operating Costs: USD $17,000 – $35,000 (though exact costs unclear as market never launched)

Effective Tax Rate on Revenue: 24-27% combined (2-5% GGR + 22% corporate tax) – competitive rate but completely irrelevant

Customer Acquisition Cost: Unknown/Impossible to Calculate – No market data exists; local population prohibited anyway

Time to Breakeven: NEVER – Market doesn’t exist

Time to Positive ROI: NEVER – Your investment will be lost

Profitability Assessment: ENTRY IS FINANCIAL SUICIDE. This market represents one of the worst risk/reward profiles in global iGaming. You cannot serve local players (prohibited). You’re supposed to target “international players” but there’s no infrastructure, no brand recognition, no clear market strategy. The first operator invested $100M+ and lost everything within 6 months when licenses were canceled.

Government demonstrated complete inability to maintain regulatory stability. Even if licenses were available (THEY ARE NOT), the economics make no sense: microscopic addressable market, extreme poverty, catastrophic infrastructure, and a government that can arbitrarily cancel your license at any time citing “national security.” Your capital will be destroyed.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Any iGaming Operators | CRITICAL | No licenses available (all canceled October 2025). Any investment will be lost. Government can cancel licenses at any time citing “national security.” Criminal network allegations make jurisdiction toxic. Zero regulatory credibility. |

| Foreign Investors | CRITICAL | $100M+ investment lost by first licensee. Complete regulatory reversal within 6 months. No investor protections. Government decision-making unpredictable and hostile to iGaming. |

| Technology Providers | HIGH | No licensed operators to serve. Association with jurisdiction damaged by criminal network allegations. Payment risk for services rendered before license cancellations. |

| Company Directors/Executives | HIGH | Reputational damage from criminal network allegations. Mandatory local presence in Oecusse creates personal risk exposure. Government can reverse decisions arbitrarily affecting personal liability. |

| Local Players | LOW | No legal access (prohibited from licensed platforms). No enforcement against players directly. Essentially locked out of legal online gambling entirely. |

🚨 Extradition and International Enforcement

Extradition Treaties: East Timor has limited extradition agreements as a young nation (independence 2002). However, this provides zero protection as the real risk is LICENSE CANCELLATION and CAPITAL LOSS, not criminal prosecution.

Enforcement History: October 2025 mass license cancellation citing criminal network infiltration demonstrates government willingness to take extreme action. Golden River Universe lost $100M+ investment.

International Relations: East Timor maintains relationships with Portugal, Australia, Indonesia, and international development organizations. Regulatory actions could have diplomatic dimensions.

Real Risk: The danger isn’t extradition – it’s that your entire investment will be seized or canceled overnight with no recourse. Licensing in East Timor means accepting that government can destroy your business at any moment.

📋 Final Verdict

East Timor receives an Operator Ease Score of 1.8/10 and a Player Access Score of 2.5/10, resulting in an overall market attractiveness rating of 2.1/10.

HONEST ASSESSMENT:

THIS IS ONE OF THE WORST IGAMING JURISDICTIONS IN THE WORLD. AVOID AT ALL COSTS. East Timor launched its iGaming licensing regime in April 2025 and completely collapsed it by October 2025, canceling all licenses and citing criminal network infiltration. The first and only operator lost over $100 million in investment. The market never actually launched before regulatory collapse.

Even if licenses were available (THEY ARE NOT – indefinitely suspended), the economics are absurd: 1.3M population where locals are PROHIBITED from using platforms, GDP per capita of $1,500, 45% internet penetration, catastrophic rural infrastructure, and a government that demonstrated it will arbitrarily cancel licenses citing “national security” with zero notice. There is no viable market here. There is no regulatory stability. There is only certain capital destruction. This jurisdiction should be blacklisted by every serious operator.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NO ONE. There are zero circumstances under which entry makes sense.

- Licenses are canceled and indefinitely suspended

- First operator lost $100M+ before cancellation

- Market never launched before collapse

- Government demonstrated complete unreliability

❌ Definitely Avoid If You Are:

- Any iGaming operator whatsoever – No licenses available, all were canceled

- Any investor – $100M+ already lost by previous investor

- Anyone valuing capital preservation – Your money will be destroyed

- Anyone requiring regulatory stability – Complete reversal within 6 months

- Anyone needing a viable market – Locals prohibited, infrastructure failed, no addressable market

- Anyone concerned about reputational risk – Criminal network allegations make jurisdiction radioactive

- Literally anyone in any circumstance – This is a failed jurisdiction

⚠️ BOTTOM LINE: East Timor’s iGaming market is a cautionary tale of regulatory failure and capital destruction. Stay away completely. If someone tries to sell you on “upcoming opportunities” in East Timor, they are either uninformed or intentionally misleading you. This jurisdiction should be blacklisted.