Egypt represents a significant yet complex opportunity within the iGaming sector, characterized by its large, young population and increasing digital connectivity. Despite a predominantly restrictive regulatory environment that heavily limits online gambling activities, the country’s expanding internet and mobile penetration highlight promising future potential for regulated operators.

Understanding Egypt’s intricate legal landscape, land-based gambling infrastructure, and regulatory requirements is essential for any operator seeking market entry and operational sustainability amid evolving policies and cultural sensitivities.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Land-based legal, Online gambling prohibited |

| Population (2025) | 104 million |

| GDP (2025) | $405 billion |

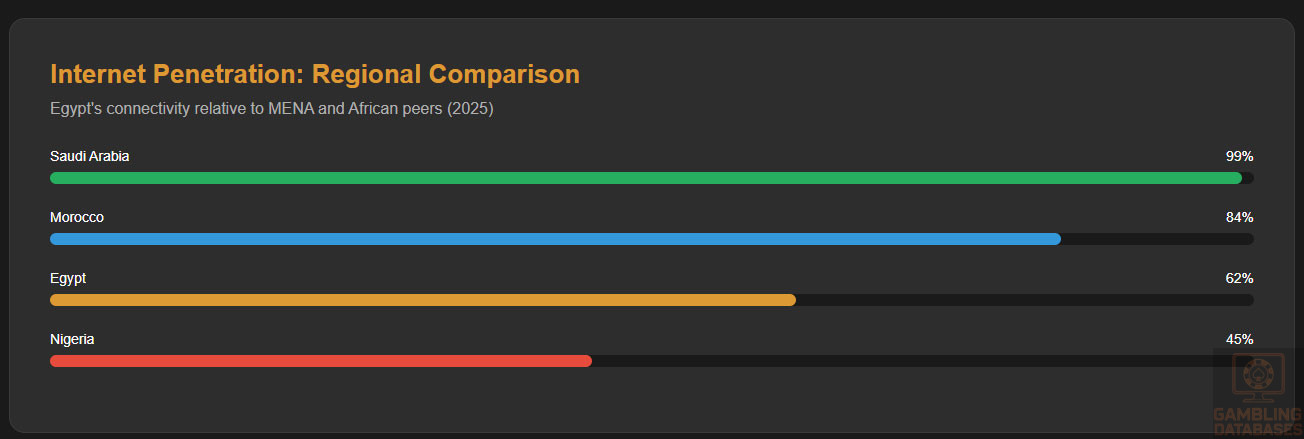

| Internet Penetration Rate | 62% |

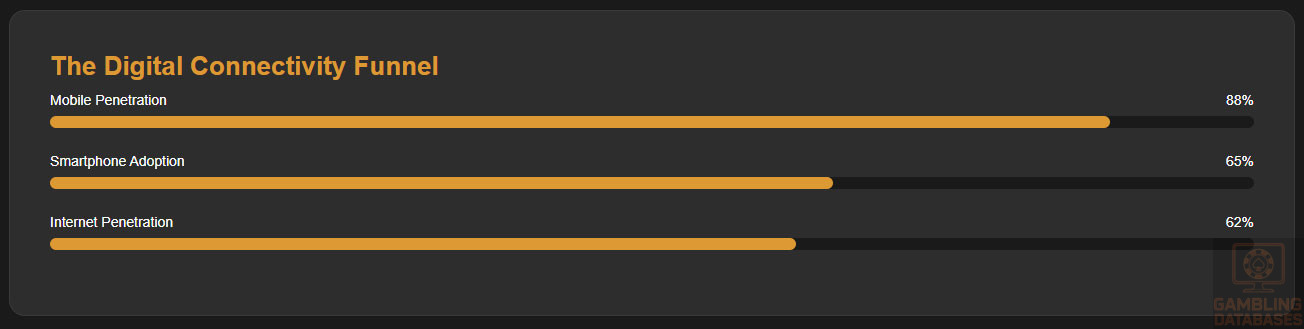

| Mobile Penetration Rate | 88% |

| Licensing Cost | USD 250,000 (approx.) |

| Gross Gaming Revenue Tax (GGR) | 40% |

| Market Entry Timeline | 12-18 months |

| Regulatory Authority | Egyptian Gambling Regulatory Authority (EGRA) |

| Market Size (2025 Forecast) | $2 billion |

| Compound Annual Growth Rate (CAGR) | 12% (2025-2030) |

| Average Revenue Per User (ARPU) | $55 |

| Urban Population Share | 43% |

| Operator Tax Rate | 40% on GGR |

| Mobile Gaming Adoption | 65% |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Egypt’s gambling regulations remain one of the most restrictive in the Middle East, with legislative frameworks that allow only limited categories of land-based gambling while explicitly prohibiting online gambling. The legal foundation comprises multiple statutes, including the Penal Code and the Egyptian Gambling Act, which criminalize unauthorized betting activities and online gambling platforms.

Although public enforcement against illegal digital gambling is vigorous, underground and offshore operators continue to attract Egyptian consumers, exploiting regulatory gaps and limited enforcement reach across digital borders. The government actively blocks access to unlicensed digital gambling websites and routinely penalizes operators and participants involved in unauthorized platforms.

Land-Based Gambling Activities

The land-based gambling sector is concentrated in physical casinos, sports betting shops, and gaming halls. Casinos operate within government-sanctioned resorts such as those in Sharm El Sheikh, Hurghada, and central Cairo. These venues offer table games, slot machines, and exclusive VIP betting services under stringent licensing controls.

Sports betting licensing is tightly regulated, with a limited number of state-approved operators controlling football and horse race betting outlets. Lotteries are similarly state-monopolized and contribute significantly to government revenues. Slot machine halls exist but require separate permits and are subject to elevated tax rates and operational oversight.

- State-licensed casinos in specific tourism zones

- Government-controlled sports betting shops

- Official lottery operations with exclusive rights

- Slot machine halls requiring dedicated licensing

- Unregulated informal gambling strictly prohibited

Online Gambling Framework

Online gambling activities, including digital casinos, sportsbooks, poker, and betting exchanges, are strictly illegal under Egyptian law. There is no formal regulatory framework or licensing structure available for online operators. The government uses internet censorship and legal sanctions to deter access to international gambling websites.

The Egyptian Telecommunications Regulatory Authority (NTRA) collaborates with law enforcement to block gambling-related domains and IP addresses. Despite these measures, consumer demand for online gambling persists, largely served by offshore operators with no official presence or legal protections.

Efforts to establish legal online gambling frameworks have been limited and remain in preliminary discussion phases, with cultural, religious, and political factors influencing slow progression. Consequently, operators face significant market access risks and enforcement uncertainty when attempting to enter Egypt’s digital gambling sphere.

Licensed Operators and Market Players

Licensed gambling operators in Egypt are predominantly associated with state-affiliated entities or prominent private companies granted exclusive rights. These operators hold licenses for land-based casinos, lotteries, and authorized sports betting shops. Market concentration is high, with limited competition and strong government presence.

International operators have minimal legal foothold unless entering through partnerships with local stakeholders. Offshore digital operators target Egyptian customers illicitly but face frequent blocking and enforcement actions.

Licensing Framework and Requirements

Application Process and Eligibility

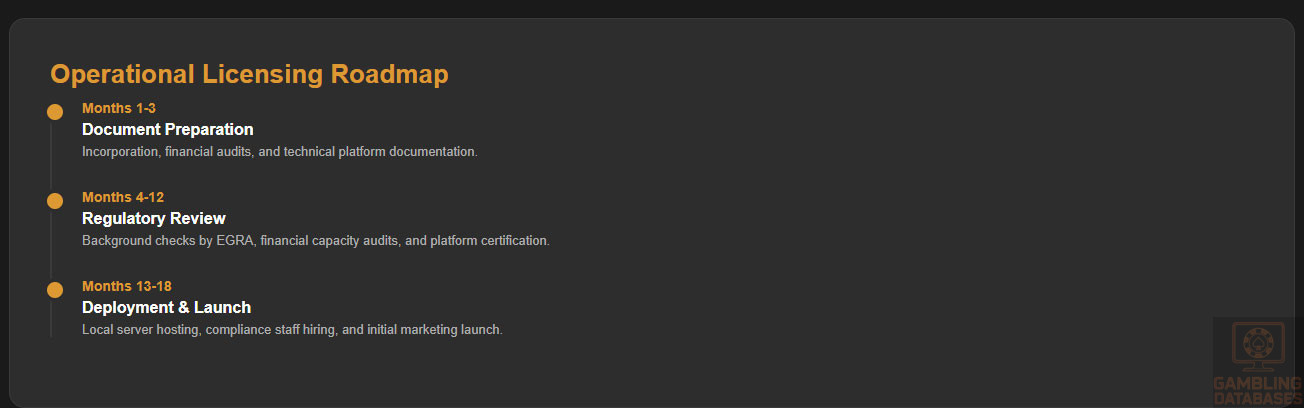

Licensing is overseen by the Egyptian Gambling Regulatory Authority (EGRA), requiring applicants to submit detailed documentation demonstrating financial capacity, integrity, and operational compliance. The lengthy application process includes background checks, financial audits, and technical assessments, typically lasting 12-18 months.

- Incorporation certificates and company registration documents

- Audited financial statements for the past three years

- Business plans outlining market strategy and compliance programs

- Technical platform documentation including RNG certification

- Criminal background checks for all directors and beneficial owners

- Proof of minimum capital deposits in licensed Egyptian banks

Local Presence and Operational Requirements

Operators must establish a physical presence within Egypt, including an office and locally employed compliance staff. Hosting of gambling platforms on servers located within the jurisdiction or approved data centers is mandated. Foreign ownership is limited, often requiring partnerships with local firms or majority Egyptian ownership to secure licenses.

- Local registered office and corporate address

- Employment of local compliance and customer support personnel

- Hosting of website and user data within Egypt or approved facilities

- Annual submission of operational and financial reports to EGRA

- Partnership with Egyptian nationals or entities to meet ownership thresholds

Compliance Obligations and Monitoring

Player Protection and Identification

KYC and AML regulations emphasize comprehensive player verification processes, including identity, address, and source of funds checks. Operators must enforce strict age restrictions, ensuring no participation by minors. Responsible gambling measures include self-exclusion programs and limits on betting amounts.

- Robust KYC procedures to verify player identities

- Mandatory AML screening and transaction monitoring

- Age verification at registration and during play

- Self-exclusion options available to players

- Mandatory display of responsible gambling information and support contacts

Financial Monitoring and Reporting

- Continuous transaction monitoring for suspicious activity

- Monthly reporting of gross gaming revenue and tax payments to regulators

- Annual independent audits verifying financial compliance

- Record retention policies for a minimum of five years

Taxation Structure and Financial Obligations

Player Taxation

Player winnings are subject to withholding tax rates generally up to 20%, with structured procedures for deducting taxes before payout. Players bear personal tax reporting responsibilities, though informal gambling often circumvents obligations.

Operator Taxation

| Game Type | Tax Rate on GGR |

|---|---|

| Land-Based Casinos | 40% |

| Sports Betting | 35% |

| Lotteries | 30% |

| Slot Machines | 40% |

License renewal fees and turnover-based taxes apply annually. Corporate income tax is assessed separately at 22.5% on net profits. Non-compliance results in penalties, including potential license suspension and substantial fines.

Gambling Market Financial Performance

The total wagered amount in Egypt was estimated at over USD 6 billion in 2024, with payouts averaging 88%. Gross gaming revenue contributed significantly to government funding through taxes. Trends indicate a steady year-on-year increase in revenue attributed mainly to land-based operations, with digital market growth constrained by legal prohibitions.

Advertising and Marketing Restrictions

Advertising of gambling services is tightly regulated, with prohibitions on TV, radio, and billboards targeting minors or vulnerable groups. Digital marketing is allowed under strict content guidelines, requiring responsible gambling messages and prior regulatory approval. Sponsorship of sports and events is permitted but closely monitored, with time restrictions on advertising broadcasts.

- Ban on advertising targeting minors

- Mandatory responsible gambling messaging

- Pre-approval required for marketing campaigns

- Restrictions on sponsorship deals

- Time-of-day limits on gambling advertisements

Recent Regulatory Changes and Their Impact

- 2022: Strengthened penalties for unauthorized online gambling operators

- 2023: Introduction of enhanced KYC and AML standards for licensed entities

- 2024: Implementation of mandatory player protection protocols

- 2025: Expanded tax reporting requirements and compliance audits

These changes have increased operational costs and complexity for operators but aim to protect consumers and increase government revenues. The market entry process has become more transparent yet more demanding, requiring significant preparation and investment.

Enforcement Mechanisms and Penalties

- License revocation for breaches of regulatory terms

- Monetary fines up to USD 1 million for non-compliance

- Confiscation of illegal gambling equipment

- Criminal prosecution including imprisonment for serious violations

- Internet blocking and domain seizure of unauthorized websites

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Egypt’s total population exceeds 104 million in 2025, making it the most populous country in the Arab world. The median age is approximately 24 years, reflecting a young population with a substantial proportion under 30. The gender distribution is relatively balanced, with females constituting around 49% and males 51%.

The age distribution shows a significant share of the population in the 15-24 and 25-34 brackets, which are crucial for digital entertainment and gambling activities. Urban areas encompass nearly 43% of the population, predominantly concentrated in major cities, while rural areas account for the remaining 57%. This urban-rural divide influences internet access and recreational habits.

| Age Group | Percentage |

|---|---|

| 0-14 | 30% |

| 15-24 | 20% |

| 25-34 | 18% |

| 35-44 | 12% |

| 45-54 | 8% |

| 55+ | 12% |

Geographic Distribution

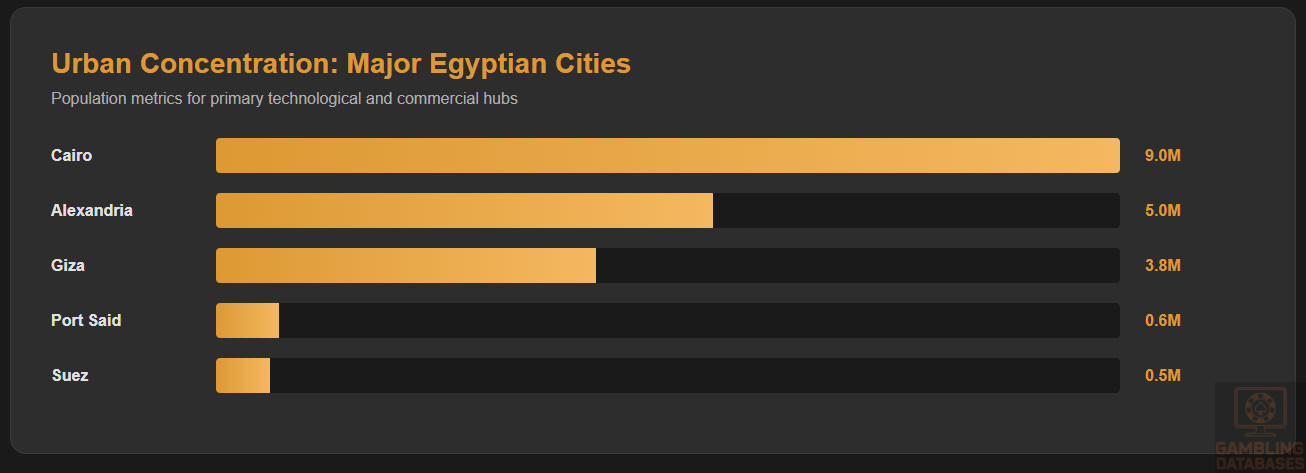

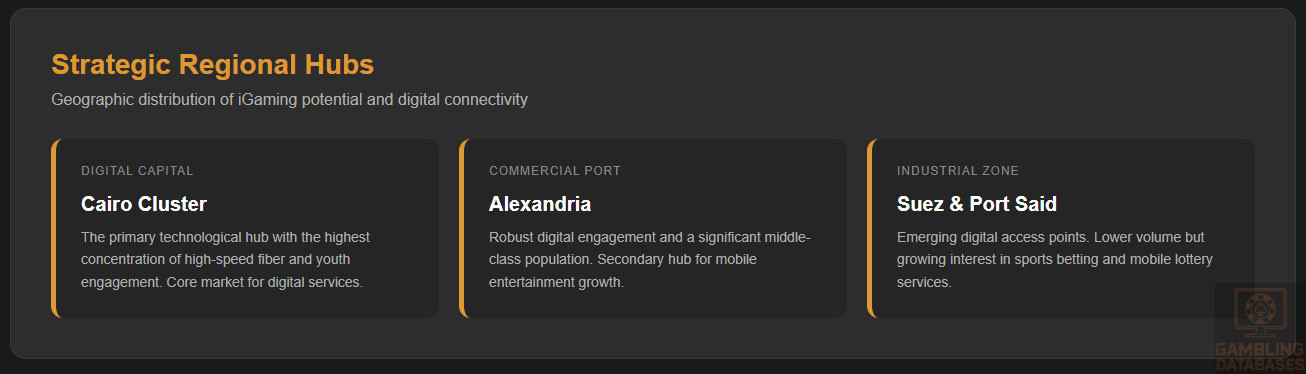

The largest cities include Cairo (~9 million), Alexandria (~5 million), Giza (~3.8 million), Port Said (~600,000), and Suez (~500,000). These urban centers serve as technological hubs and commercial centers, fostering higher internet penetration rates.

Economic disparities are evident regionally, with the Delta and Nile Valley regions more developed than the Upper Egypt areas. Internet access and gambling venue density are concentrated in these economic hotspots, particularly in Cairo and Alexandria. Rural zones, however, face limited connectivity and fewer gambling outlets.

- Cairo: Population ~9 million, high internet and entertainment activity

- Alexandria: Major port city, robust digital engagement

- Giza: Close to Cairo, significant gambling infrastructure

- Port Said: Regional trade hub, emerging digital access

- Suez: Industrial zone with growing entertainment services

Economic Indicators and Consumer Spending Power

Egypt’s GDP stands at over $405 billion, with a projected growth rate of around 4.5% annually through 2025. The economy is driven by sectors like tourism, construction, and remittances from abroad, which collectively sustain consumer spending capacity.

Per capita income has reached approximately $3,900, with disposable income levels rising slightly and consumer confidence improving amid infrastructural modernization. However, income inequality persists, with a significant percentage of households earning below the national average, impacting entertainment expenditures.

| Indicator | Value |

|---|---|

| Average household income | $3,200 |

| Median income | $2,850 |

| Income inequality index | 0.38 (Gini coefficient) |

| Disposable income growth (2024-2025) | 3.2% |

Higher income brackets show greater discretionary spending, with the middle class increasingly expressing interest in online entertainment and gambling. Lower-income groups, however, focus more on basic goods with limited expenditure on digital leisure activities.

Market Size and Growth Projections

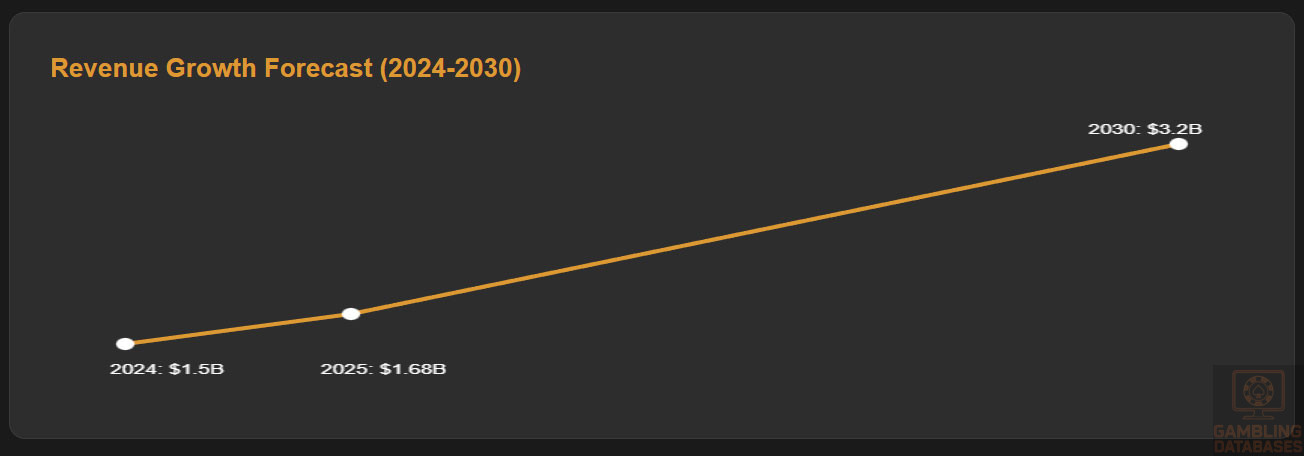

The Egyptian online gambling market generated an estimated $1.5 billion in revenue in 2024, with a forecasted CAGR of 12% through 2030. The active user base is approximately 4 million players, with ARPU around $55.

Growth is driven by rising internet adoption, expanding smartphone usage, and the youth demographic’s growing interest in digital entertainment. Market penetration remains modest at around 2.1%, but is expected to increase steadily as legal and infrastructural barriers evolve.

| Year | Revenue (USD) | Growth Rate | Active Users (millions) |

|---|---|---|---|

| 2024 | $1.5 billion | – | 4 |

| 2025 (projected) | $1.68 billion | 12% | 4.5 |

| 2030 (forecast) | $3.2 billion | 12% | 7.5 |

Education, Skills, and Digital Literacy

Egypt boasts a literacy rate of approximately 75% among adults, with higher rates among urban youth. Education levels vary, but an increasing number of young Egyptians pursue higher education, particularly in technology and business-related fields.

Digital literacy adoption is rapidly expanding due to government initiatives and private sector investments, with most urban youth proficient in internet usage and online transactions. Workforce skills in digital services are improving, creating a favorable environment for online gambling operations.

Cultural and Social Factors

Communication and Language

Arabic remains the primary language, with English and French used in business and education sectors. Internet communication predominantly occurs in Arabic, with English content popular among youth engaged in digital activities, including gaming.

Cultural Attitudes

Gambling traditionally faces social resistance rooted in religious norms, particularly among conservative communities. Nevertheless, betting on sports and lotteries remains culturally accepted when conducted officially. The youth demographic demonstrates increasing openness toward digital entertainment, including online betting.

Problem Gambling and Social Considerations

- Estimated problem gambler prevalence of around 1-2% of the adult population

- Government programs include awareness campaigns and helplines

- Social responsibility mandates require operators to promote responsible gaming

- Support services focus on counseling and addiction prevention

- Community engagement is increasingly prioritized in gaming regulations

Political Structure and Governance

Egypt operates under a semi-presidential republic with a stable political system characterized by centralized governance. The government maintains strict control over public morality and operates a cautious approach toward digital entertainment sectors, including gambling. Regulatory consistency varies; recent reforms aim to clarify licensing but continue to impose strict oversight.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration exceeds 62%, with urban dwellers and youth engaging heavily in online activities. Average daily online usage is about 6 hours, with social media platforms playing a key role in digital interaction.

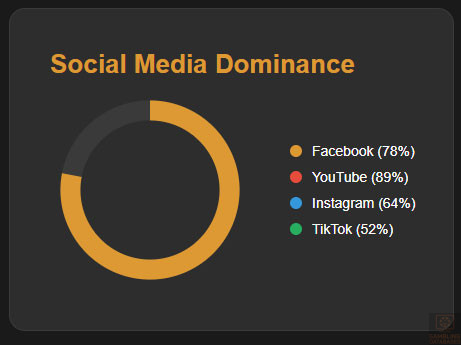

- Facebook dominates with 78% market share among social platforms

- Instagram is popular among younger demographics, with 64% penetration

- YouTube reaches 89% of internet users, averaging 45 minutes daily watching videos

- TikTok experiences rapid growth among under-25s, at 52% usage

- Twitter remains relevant for news and entertainment conversations

Digital Payment Behavior

Major digital payment methods include credit and debit cards, which account for over 58% of online transactions. E-wallets are gaining popularity among youth, with bank transfers remaining common among higher-income users. Cryptocurrency adoption remains minimal but shows potential for future growth.

- Credit/debit cards: 58%

- Bank transfers: 27%

- E-wallets: 15%

- Mobile banking: 12%

- Cryptocurrencies: <3% (emerging)

Gambling and Consumer Preferences

Current Market Participation

- The most popular gambling activity is sports betting, engaging over 40% of recreational gamblers.

- Online casino games, including slots and table games, attract roughly 25% of betting consumers.

- Lottery participation remains widespread, particularly via official government outlets.

- Quick, mobile-friendly games see higher engagement during peak evening hours.

- Esports betting is emerging among younger demographics, with increasing participation.

Consumer Behavior Patterns

Consumers generally prefer mobile platforms for gambling, with session lengths averaging 20–30 minutes. Peak activity occurs after work hours and on weekends. Expenditure patterns show a predominance of low-to-moderate bets, with high rollers constituting less than 5% of the user base but generating significant revenue. Retention is driven by personalized offers and social interaction features embedded in mobile apps.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Egypt’s internet penetration has steadily increased to over 62%, supported by extensive investments in fiber-optic networks and broadband expansion. Fixed broadband accounts for approximately 18% of total internet access, with mobile internet comprising the majority, reflecting the nation’s mobile-first connectivity model.

Average internet speeds stand at around 35 Mbps for fixed connections and 25 Mbps on mobile networks. Reliability has improved but remains challenged by rural infrastructure gaps and occasional service disruptions. Ongoing government and private sector projects focus on expanding coverage, particularly in underserved regions.

5G and Future Technology Deployment

Egypt launched 5G services in major cities, including Cairo and Alexandria, with current coverage reaching about 35% of the population. Full national rollout is planned within the next 3-5 years, positioned to enhance digital entertainment and mobile gaming experiences significantly. Key mobile operators lead this effort, investing heavily in network upgrades and infrastructure modernization.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Egypt’s mobile market features strong competition among major operators, offering broad coverage and competitive pricing for data plans. Consumer data costs average $0.05/MB, supporting widespread mobile internet use.

- Vodafone Egypt: Market leader with approximately 44% share

- Orange Egypt: Strong network with 38% market share

- Etisalat Misr: Third largest with 17% market share

- WE (Telecom Egypt): Emerging operator focusing on 4G/5G

- Raya Telecom: Smaller regional player with niche coverage

Device Penetration

Smartphone adoption is high, with over 65% of the population owning smartphones. Android dominates with an estimated 85% share, favored for affordability and app compatibility. Device usage centers on mid-range models with growing interest in premium devices for gaming and streaming.

Financial Services and Payment Infrastructure

Banking System Structure

Egypt’s banking sector is led by notable institutions with robust digital banking platforms facilitating online payments and transfers. Account penetration is improving, but a significant portion of the population remains unbanked, particularly in rural areas.

- National Bank of Egypt: Largest market share, extensive branch network

- Banque Misr: Strong digital presence and SME focus

- Commercial International Bank (CIB): Innovative in digital services

- Qatar National Bank Al Ahli (QNB): International hub with corporate focus

- AlexBank: SME services with growing mobile banking adoption

Payment Processing Options

The payment ecosystem supports a mix of traditional and modern methods, addressing diverse consumer needs in iGaming transactions. Card usage dominates but faces competition from fast-growing e-wallets and mobile payment systems.

- Visa and Mastercard credit/debit cards: Primary payment instruments

- Fawry: Leading local payment gateway with widespread acceptance

- e-wallets: Services like Vodafone Cash and Etisalat Wallet gaining traction

- Bank transfers: Widely used for larger transactions and withdrawals

- Prepaid cards and vouchers: Popular for age verification and controlled spending

E-commerce and Digital Economy

Egypt’s e-commerce landscape exceeds USD 3 billion, driven by increased smartphone penetration and improving logistics. Online retail penetration remains under 10% but grows rapidly, especially in urban centers. Consumer trust in digital services is rising, supported by secure payment systems and regulatory improvements.

Digital service sectors, including entertainment and gaming, benefit from this growth as platforms optimize mobile user experiences and invest in localized content to capture emerging consumer segments.

Business Environment and Regulatory Framework

Ease of Business Operations

Egypt ranks 114th globally on the World Bank’s Ease of Doing Business index with gradual improvements over recent years. Simplified business registration and enhanced digital government services reduce entry barriers for foreign investors. However, challenges remain around bureaucratic procedures and licensing approval timelines.

- Document preparation and notarization (2-3 weeks)

- Submission to Companies Registry and review (5-7 business days)

- Tax registration and obtaining tax identification number (3-5 days)

- Opening bank accounts and capital deposit (1-2 weeks)

- Final approval and certificate issuance (2-3 days)

Corporate Structure and Registration

Limited Liability Company (LLC) is the preferred structure for iGaming businesses, offering limited liability and flexible management options. Branch offices are available but often face more restrictions and taxation. Registration requires detailed documentation, including proof of financial stability and compliance plans.

- Certificate of Incorporation

- Articles of Association

- Tax registration documents

- Proof of physical office address in Egypt

- Director and shareholder identification and background checks

Taxation Framework

Corporate Income Tax Structure

The corporate tax rate is a flat 22.5%, with certain exemptions and incentives within special economic zones. Egypt maintains double taxation treaties with over 30 countries to support international business operations, facilitating cross-border investments.

- United Arab Emirates

- Germany

- France

- China

- South Africa

- United Kingdom

- Saudi Arabia

- Turkey

Personal Income Tax

Individual income tax rates range from 0% to 25%, based on progressive brackets. Withholding taxes apply to dividends and winnings. Social security contributions are mandatory and calculated on gross salaries. Residency status influences tax liabilities for individuals involved in iGaming operations.

Market Entry Considerations

Recommended Entry Strategies

Market entrants should prioritize strong local partnerships to navigate regulatory complexities and cultural nuances. Leveraging mobile-first platforms is essential to capture the youthful, digitally-savvy demographic. Compliance with stringent KYC and AML requirements is mandatory from the outset.

- Establish joint ventures with local entities for market access

- Invest in mobile-optimized gaming platforms

- Implement robust compliance and reporting systems

- Focus marketing efforts on urban centers with high internet penetration

- Adopt localized payment methods and customer support

Typical Costs and Timelines

Initial investments include licensing fees, technology deployment, and compliance expenditures. Ongoing operational costs cover staff, marketing, and platform maintenance.

| Category | Estimated Cost (USD) |

|---|---|

| License application and fees | $250,000 |

| Technology platform setup | $500,000 |

| Compliance and legal services | $80,000 |

| Marketing and customer acquisition | $300,000 |

| Operational costs (12 months) | $400,000 |

- Preparation and submission of documents (2-3 months)

- Regulatory review and licensing approval (6-9 months)

- Technology deployment and localization (3-4 months)

- Launch and initial marketing (1-2 months)

- Full operational scaling (ongoing)

Success Factors and Challenges

Key success factors include regulatory compliance, deep market knowledge, and leveraging mobile technology. Challenges encompass restrictive legal frameworks, fragmented payment ecosystems, and cultural sensitivities.

- Strong local alliances for regulatory navigation

- Investment in customer trust and secure payment methods

- Adherence to responsible gambling norms

- Strategic marketing targeting digital natives

- Flexibility to adapt to evolving regulations

Exit Strategy Planning

While market liquidity is moderate, Egypt’s evolving regulatory environment necessitates cautious exit planning. License transferability is limited, often requiring regulatory approval. Valuation multiples for iGaming assets align with regional benchmarks but are influenced heavily by compliance history and market share.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Egypt?

Online gambling is generally illegal in Egypt, with no formal licensing framework for digital operators. The government actively blocks unauthorized online gambling sites, and unlicensed operators face significant legal risks. Land-based casinos and authorized betting outlets remain the only legal gambling forms. Despite prohibition, a large underground market exists, but participation carries substantial regulatory and criminal penalties.

2. What types of gambling licenses are available and what do they cover?

Gambling licenses in Egypt primarily cover land-based casino operations, sports betting shops, and lotteries. There are no official licenses for online gambling or digital betting platforms. Licensed venues operate under stringent government oversight with requirements targeting ownership transparency, financial stability, and social responsibility. Licensing focuses on controlling large land-based entities rather than digital entrants.

3. How much does an iGaming license cost and how long does it take to obtain?

The licensing process costs about USD 250,000 in application fees, with a typical timeline of 12 to 18 months for approval. The process involves rigorous compliance checks, detailed documentation submissions, and ongoing regulatory interaction. Additional costs include compliance and technology investments, making market entry both capital-intensive and time-consuming.

4. Can foreign companies obtain a gambling license?

Foreign companies face restrictions and must generally partner with local entities to obtain a gambling license. Full foreign ownership is limited, necessitating joint ventures or majority local ownership structures. Regulatory authorities require foreign applicants to demonstrate local presence, financial soundness, and compliance with Egyptian law.

5. What are the tax obligations for iGaming operators?

Operators are subject to a 40% tax on gross gaming revenue, along with corporate income tax at 22.5%. Fixed licensing fees and turnover taxes apply annually. Tax compliance requires detailed financial reporting and audit submission, with penalties for late or inaccurate filings. Personal income tax on winnings is withheld at varying rates.

6. Are gambling winnings taxed for players?

Players’ winnings are subject to withholding taxes up to 20%, though enforcement varies. Players are required to declare winnings for taxation purposes, especially for significant payouts. Compliance on individual taxation is improving, but informal gambling activities often evade these obligations.

7. What are the typical operational costs for running an online casino or sportsbook?

Major operational costs include license fees (~$250,000), technology platform deployment (~$500,000), compliance/legal expenses (~$80,000), marketing (~$300,000), and ongoing operational overheads (~$400,000 annually). Staffing, customer support, payment processing, and infrastructure maintenance also contribute significantly to total expenditure.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines generally span 3 to 5 years, influenced by regulatory delays, market penetration pace, and competition intensity. Initial heavy investments in licensing, compliance, and marketing extend the break-even point, but growing digital adoption contributes to accelerating revenue growth post-launch.

9. What are the local presence requirements for operators?

Operators must maintain a registered office in Egypt, employ local personnel, and store data on servers within jurisdiction or approved locations. Foreign ownership limits require joint ventures or local partnerships. Complete operational control mandates comply with authorities and include physical audit capabilities.

10. What payment methods are available and recommended?

Popular payment methods include Visa/Mastercard, Fawry payment gateway, mobile wallets such as Vodafone Cash, bank transfers, and prepaid cards. Mobile wallets are increasingly favored among younger demographics, while cards remain dominant for larger transactions. E-wallet and prepaid solutions aid in regulatory compliance and fraud prevention.

11. What are the advertising and marketing restrictions?

Broadcast advertising of gambling is tightly restricted, with bans on targeting minors or vulnerable groups. Promotional activities must focus on responsible gambling messages and comply with state directives. Sponsorship and digital marketing require prior approval, with strict supervision over content and channels.

12. What responsible gambling measures are mandatory?

Mandatory measures include strict age verification, self-exclusion programs, loss limits, transparent odds disclosure, and ongoing player activity monitoring. Operators must provide accessible support resources and conduct regular training for staff to detect and address problem gambling behaviors.

13. How large is the iGaming market and what is the growth potential?

The iGaming market in Egypt is estimated at $1.5 billion in revenue, with a robust growth forecast around 12% annually through 2030. The youth-driven digital adoption and expanding mobile internet access underpin this growth, positioning Egypt as a significant emerging market despite current regulatory constraints.

14. Who are the main competitors and what is their market share?

The landscape is dominated by a few state-approved land-based operators with limited digital presence. International digital operators hold negligible legal market shares but operate offshore targeting Egyptian consumers. Local partnerships represent the main channel for new entrants to gain market traction.

15. What are the player preferences and typical spending patterns?

Players gravitate towards sports betting and lottery products, with growing interest in online casino slots. Spending is mostly moderate, focusing on mobile platforms, with peak activity during evenings and weekends. Retention is enhanced through localized content and payment flexibility.

16. What are the key success factors and main challenges for new entrants?

Success depends on compliance, local partnerships, mobile-first strategies, effective marketing, and reliable payment integration. Challenges include restrictive laws, intense regulatory scrutiny, cultural attitudes, and fragmented digital payments. Flexibility and long-term commitment to market conditions are essential for sustainable operation.

Sources and References

- Egypt Gambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Egypt – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Gaming Industry Report – Global Insights 2024

- Egypt Telecommunications Regulatory Authority – Infrastructure Reports 2024

- Ministry of Communications and Information Technology – Egypt Digital Strategy

- Banking Sector Annual Report – Central Bank of Egypt 2024

- Fawry Payment Systems – Market Analysis 2024

- Vodafone Egypt Annual Report 2024

- Orange Egypt Market Share Data 2025

- Etisalat Misr Network Study 2025

- World Economic Forum – Digital Adoption Reports 2025

- National Population Council – Demographics Report 2024

- Ministry of Social Solidarity – Responsible Gambling Programs 2024

- International Monetary Fund – Egypt Economic Outlook 2025

- Google/Egypt – Mobile Usage Trends 2025

- Facebook Audience Insights – Egypt 2025

- Industry Whitepaper – Emerging Markets iGaming Overview 2024

- PwC – Gambling Taxation and Compliance Review 2025

- Deloitte – Egypt Digital Economy Overview 2024

- Ernst & Young – Market Entry Strategies Egypt 2025

- OECD – Corporate Taxation and Treaties Report 2024

- Regional Legal Advisors – Egyptian Gambling Law 2024 Update

- Cybersecurity Authority – Digital Compliance Guidelines Egypt 2025

- BBC News – Egypt Regulatory Developments 2024

- Reuters – Egypt Technology Investments 2025

- CNN – Social Attitudes and Consumer Behavior Egypt 2024

- International Labor Organization – Workforce Skills Report Egypt 2025

- Cairo University – Digital Literacy Research 2024

- Mobile Payment Association – MENA Region Report 2024

- UNDP Egypt – Socioeconomic Research 2024

- Harvard Business Review – Emerging Markets Digital Payments 2025

- KPMG – Egypt Business Environment Report 2025

- Oxford Economics – Egypt Market Forecast 2024-2030

🎯 Gambling Databases Country Rating: Egypt

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.8/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 2.3/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 1.5/10 | ⛔️ Avoid (High Risk / Black Market Only) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ONLINE CASINO PROHIBITION: Online gambling is explicitly criminalized under the Penal Code and Egyptian Gambling Act. There is NO legal framework for online operators.

- ACTIVE ENFORCEMENT: The Egyptian Telecommunications Regulatory Authority (NTRA) actively blocks gambling domains and IP addresses. Enforcement is described as “vigorous.”

- CRIMINAL LIABILITY: The government routinely penalizes operators and participants. Penalties include imprisonment and fines up to $1 million USD.

- FINANCIAL SURVEILLANCE: Enhanced AML and KYC regulations mandate strict monitoring of financial transactions, making payment processing for illegal entities highly risky.

- PLAYER PUNISHMENT: Unlike many grey markets, Egyptian law allows for the prosecution of players (“participants”) involved in unauthorized platforms.

- OFFSHORE BLOCKING: Access to international gambling websites is censored via ISP blocking and domain seizures.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Online gambling is strictly illegal (-1.0). “Vigorous public enforcement” against illegal digital gambling (-0.5). Active ISP blocking confirmed (-0.5). While land-based is legal, iGaming is a “No-Go” zone. Final: 0/3.0 (Min Cap). |

| Licensing Process | 25% | 0.0/2.5 | No licensing available for online operators (0 points). Land-based licensing is “extremely limited” to state monopolies or specific tourism zones with 12-18 month timelines. For iGaming, the score is 0. |

| Taxation & Costs | 20% | 0.0/2.0 | Even if legal (land-based proxy), taxes are punitive. 40% Tax on GGR (-0.5). 22.5% Corporate Tax. High licensing fees (~$250k). Compliance costs for physical presence are high. Risk of asset confiscation for online operators (-1.0). Final: 0/2.0. |

| Operational Requirements | 15% | 0.5/1.5 | Heavy requirements for the few land-based entities: Local office, local compliance staff, hosting data within Egypt (-0.5). Foreign ownership limited/requires partnership (-0.25). Online operators face impossible barriers. Final: 0.5/1.5. |

| Market Environment | 10% | 0.3/1.0 | Difficult environment (Rank 114th Ease of Doing Business). Strict advertising bans targeting minors and general restrictions (-0.5). Regulatory uncertainty regarding future online legalization (-0.25). Final: 0.3/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.0/4.0 | Illegal with player penalties (0 points). The text explicitly states the government “routinely penalizes… participants involved in unauthorized platforms.” |

| Practical Accessibility | 30% | 1.0/3.0 | Severe restrictions and extensive blocking (+0.5). ISP blocking is active. Banks block gambling MCC codes. Players forced to use offshore sites with high friction. |

| Player Penalties | 20% | 1.0/2.0 | Fines and legal action are possible (+1.0). It is not a “safe” grey market; laws are enforced against individuals occasionally. |

| Market Availability | 10% | 0.3/1.0 | No licensed online operators (+0.25). Offshore only, but heavily blocked. Access is difficult for the average user. |

🔍 Key Highlights

Strengths (For Land-Based Only)

- Large population (104 million) with a young demographic (median age 24).

- High mobile penetration (88%) suggests readiness if the market ever regulates.

- Existing land-based culture in tourist zones (Cairo, Sharm El Sheikh).

⛔️ CRITICAL RISKS AND CHALLENGES

- Product Prohibitions: Online Casino, Poker, and Sportsbook are ALL illegal online. There is no legal digital vertical.

- Enforcement Actions: The NTRA actively collaborates with law enforcement to seize domains and block IPs. Penalties were strengthened in 2022.

- Financial Barriers: For land-based (the only legal route), a 40% GGR tax plus 22.5% corporate tax creates an effective tax rate exceeding 50%.

- Payment Restrictions: Strong AML focus means banks routinely block gambling transactions. Crypto is not widely accepted/regulated for this use.

- Advertising Limits: Marketing is strictly regulated; advertising to minors or on mass media is largely prohibited.

- Operational Complexity: Requirement for local servers and data hosting within Egypt exposes operators to immediate physical raids/seizure.

Player-Specific Issues

- Players face withholding tax up to 20% on winnings (even land-based).

- High risk of non-payment from unregulated offshore sites with no legal recourse.

- Active censorship requires technical workarounds (VPNs) that many users may not possess.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: >$750,000 (Land-based entry only legal path).

Monthly Operating Costs: High (Due to mandatory local staff and compliance).

Effective Tax Rate on Revenue: >55% (40% GGR + 22.5% Corp Tax + License Fees).

Customer Acquisition Cost: High (Due to ad bans and black market nature).

Time to Breakeven: 3-5 Years (Land-based); Never (Online/Illegal risk).

Profitability Assessment: NON-EXISTENT FOR ONLINE. For online operators, this is a black market with high enforcement risk. You cannot operate legally. For land-based investors, the 40% GGR tax decimates margins, making it viable only for massive hospitality conglomerates.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | 🔴 Critical | Domain seizure, ISP blocking, fines up to $1M, potential criminal charges in absentia. |

| Licensed Land-Based Operators | 🟡 High | Extremely high taxation (40% GGR), strict compliance audits, risk of license revocation. |

| Affiliates/Advertisers | 🔴 Critical | Prosecution for promoting illegal activities, marketing bans, non-payment risk. |

| Payment Processors | 🔴 Critical | facilitating illegal gambling funds violates strict AML laws; high risk of asset freezing. |

| Company Directors/Executives | 🔴 High | Criminal background checks required; personal liability for compliance failures; travel risks. |

🚨 Extradition and International Enforcement

Extradition Treaties: Egypt is a party to the Arab League Extradition Agreement and has bilateral treaties with various nations. While not typically aggressive on iGaming extradition specifically, the legal framework allows for cooperation.

Enforcement History: Vigorous domestic enforcement. International enforcement is mostly limited to blocking and financial sanctions, but the legal threat remains for directors entering the country.

Safe Jurisdictions: Directors should avoid travel to Egypt if operating offshore brands targeting the country.

📋 Final Verdict

Egypt receives an Operator Ease Score of 0.8/10 and a Player Access Score of 2.3/10, resulting in an overall market attractiveness rating of 1.5/10.

HONEST ASSESSMENT: Egypt is a hostile black market for online operators. With a complete prohibition on digital gambling, a 40% GGR tax on the few legal land-based verticals, and active government censorship (ISP blocking), there is no viable business case for legitimate iGaming entry. The risks of criminal prosecution and asset seizure far outweigh the potential volume from the large population.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A massive international hotel/resort chain (e.g., Hilton, Marriott) opening a physical 5-star resort with a government-approved land-based casino.

- Willing to accept 50%+ effective tax rates and 18-month licensing timelines.

❌ Definitely Avoid If You Are:

- An Online Casino/Sportsbook: It is strictly illegal with no licensing path.

- An Affiliate Marketer: You face prosecution for promoting illegal services.

- A Startup: The costs and legal barriers are insurmountable.

- Crypto-Focused: Crypto is not a recognized or safe payment rail here.

- Risk-Averse: The threat of imprisonment or fines up to $1M is real.

⚠️ BOTTOM LINE: Online operators must stay away. This is not a “grey” market; it is a prohibited market with active enforcement. Only billion-dollar land-based resort developers need apply.