Gabon is emerging as a promising iGaming market in Central Africa, driven by new regulatory reforms and a government-backed national gambling platform. The evolving legal framework, combined with increasing internet penetration and digital infrastructure, creates strategic opportunities for operators entering the Gabonese iGaming sector.

This analysis reviews Gabon’s regulatory environment, licensing requirements, tax regime, and the current market landscape as foundational insights for market entry decisions and operational planning.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Regulated under national lottery and gambling law; online framework emerging |

| Regulatory Authority | Commission Supérieure des Jeux de Divertissement, d’argent et de Hasard |

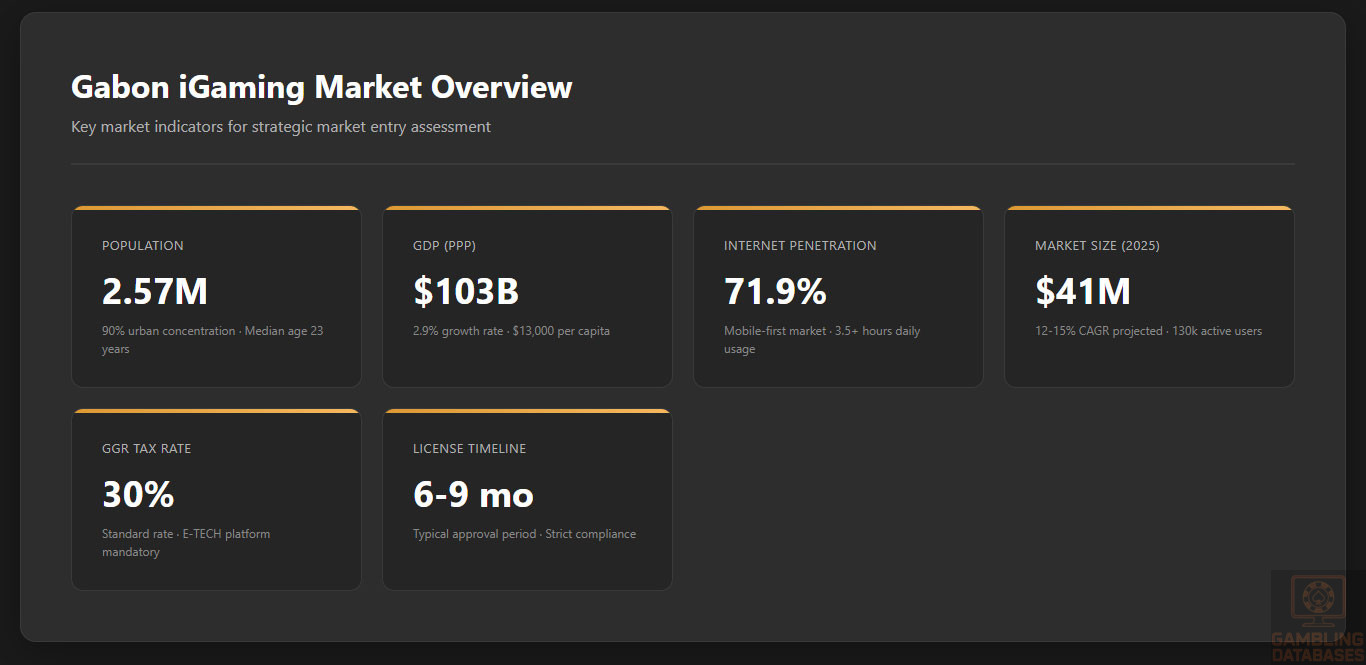

| Population | ~2.57 million (2025 estimate) |

| GDP (Purchasing Power Parity) | ~$103 billion (2025 estimate) |

| GDP Growth Rate (2024) | 2.9% |

| Internet Penetration | 71.9% |

| Mobile Penetration | 124% mobile connections of population |

| 4G Coverage | 98.35% |

| Broadband Speed (avg.) | ~13.65 Mbps |

| Licensed Land-Based Casinos | 3 |

| Online Gambling Licensing Status | In transition; national platform E-TECH mandatory from Oct 2025 |

| License Application Fee | Varies by license type; online licenses involve multiple documents |

| Annual GGR Tax Rate | 30% (for most gambling products) |

| Corporate Income Tax | 30% |

| Player Taxation | Winnings taxation with thresholds; withholding applicable |

| License Renewal Fee | Applicable; details vary by license category |

| Compliance Requirements | KYC/AML, age verification, responsible gaming measures, financial audits |

| Market Size (2024 est.) | Growing, supported by land-based and nascent online sector |

| Revenue Growth Forecast (CAGR 2025-2030) | Estimated 12-15% |

| Average Revenue Per User (ARPU) | Moderate; rising with digital adoption |

| Market Access Barriers | Strict licensing, mandatory platform integration, compliance costs |

| Time to License Approval | 6-9 months typical |

| Operational Requirements | Local presence preferred, domestic bank accounts, transparent ownership |

| Payment Processing Rules | Integration via E-TECH platform required to monitor flows |

| Advertising Restrictions | Content and timing regulations in place |

| Enforcement Mechanisms | License suspension, fines, criminal penalties for non-compliance |

| Responsible Gambling Measures | Mandatory self-exclusion, addiction monitoring via E-TECH |

| Technology Infrastructure | Modernizing with unified gambling platform; digital governance focus |

| Business Environment Index | Stable but evolving; emphasis on regulatory clarity and transparency |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gabon maintains a regulated gambling sector governed primarily by the national lottery and gambling laws, with oversight enacted by the Commission Supérieure des Jeux de Divertissement, d’argent et de Hasard. Gambling activities include lotteries, horse race betting, land-based casinos, and sports betting.

Online gambling regulation is currently in transition. Historically, the sector lacked comprehensive online-specific oversight, resulting in widespread use of offshore operators by citizens. However, a landmark reform effective in 2025 mandates all licensed operators to integrate with Gabon’s national gambling platform, named E-TECH. This platform centralizes transaction monitoring, enforces financial transparency, and guarantees proper payout to players.

The E-TECH initiative additionally introduces modern responsible gambling measures including age verification and addiction risk tracking. The new legal framework aims to unify oversight and reduce unlicensed, informal gambling that has previously limited tax revenue and consumer protection.

Land-Based Gambling Activities

Gabon’s land-based gambling encompasses several distinct venue types:

- Licensed Casinos: Three main operators with diversified gaming floors including table games and slot machines

- Sports Betting Venues: Authorized outlets for fixed-odds betting on local and international sports events

- Horse Racing Betting Offices: Facilities dedicated to horse race wagering aligned with regulated events

- Lottery Operations: National lottery activities under strict regulatory supervision

- Slot Machine Halls: Several sites offering electronic gaming machines outside casinos

Operators in these sectors comply with licensing requirements enforced by the national commission, including revenue reporting and adherence to responsible gambling policies.

Online Gambling Framework

The regulatory overhaul introducing the E-TECH platform is the cornerstone of Gabon’s emerging online gambling framework. This government-approved centralized system requires all licensed operators to route their financial transactions through it, ensuring traceability and contractual compliance. The platform’s establishment marks a shift towards formalizing an area which formerly operated with minimal oversight.

While operators currently enjoy license regimes covering various gambling activities, the formal recognition of online gaming licenses is being strengthened through this integration. Prohibitions target unlicensed operators and non-approved payment providers, reducing market risks associated with informal operators.

The institutional monitoring remains under the Ministry of Finance and the National Lottery Authority, which collaborate to supervise licensing, compliance, and enforcement, reinforcing the sector’s integrity and public confidence.

Licensed Operators and Market Players

The competitive landscape is characterized by a limited number of licensed land-based operators and a growing number of online service providers capitalizing on the transition towards a regulated digital environment. Key industry players have been encouraged to join the E-TECH platform to continue operations legally.

The market is moderately consolidated with the established casinos holding substantial land-based market share. Online operators eye growth opportunities but face entry barriers due to compliance costs and integration requirements. Strategic partnerships with local entities and technology providers are increasingly essential for market success, as the licensing process demands transparency and local engagement.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing authority requires applicants to submit detailed information, including their corporate structure, financial statements, and operational plans. Applicants must demonstrate financial stability, technical capacity, and ethical business practices. Regulatory due diligence covers company directors and significant stakeholders to prevent fraudulent activities.

Licenses differ by gambling activity type, each involving distinct fees and regulatory conditions. Application fees are generally payable upfront and vary according to license category. Licenses undergo periodic renewal subject to compliance verification.

Key documentation required for an application include:

- Corporate registration certificate and articles of incorporation

- Audited financial statements for the past three years

- Detailed business plan including market strategy and financial projections

- Technical documentation proving fairness and RNG certification of gaming software

- Criminal background checks and integrity certifications for all directors and owners

- Proof of minimum capital deposit held in licensed financial institutions

- Compliance policies covering AML and responsible gaming

Local Presence and Operational Requirements

Applicants are generally expected to establish a physical presence in Gabon or work in cooperation with local partners to facilitate compliance and tax administration. Maintaining a domestic bank account for transaction processing through the E-TECH platform is mandatory.

Foreign ownership is permitted but subject to transparency and control regulations. Operators must employ qualified personnel to oversee compliance and customer service locally. Domain registration of gambling websites under local or approved domains is encouraged to reinforce jurisdictional control.

Operational requirements include ongoing performance reporting and participation in state-supervised audits to maintain licensure.

Compliance Obligations and Monitoring

Player Protection and Identification

Robust player identification standards enforce strict age verification and implement Know Your Customer (KYC) protocols. AML compliance integrates continuous monitoring of transactions for suspicious behavior, with immediate reporting obligations.

Responsible gambling measures mandated include self-exclusion tools, deposit limits, and real-time addiction risk monitoring through the E-TECH platform. Operators are required to provide detailed information disclosures to players regarding risks and support resources.

- Mandatory age verification at registration and during transactions

- KYC verification using government-issued IDs and proof of residency

- Real-time player activity monitoring to detect excessive gambling behavior

- Self-exclusion and voluntary limit-setting features accessible to players

- Information disclosure of odds, payout rates, and responsible gaming warnings

Financial Monitoring and Reporting

The E-TECH platform facilitates standardized transaction monitoring enforced at the regulatory level. Operators must submit detailed financial reports monthly, including wager volumes, payouts, tax remittances, and other relevant financial indicators. Independent audits are conducted annually to verify compliance and financial integrity.

- Monthly submission of detailed operator financial reports to the Commission

- Verification of transaction data through E-TECH platform logs

- Annual independent financial audit and compliance certification

- Immediate reporting of suspicious transactions or irregularities to regulators

Taxation Structure and Financial Obligations

Player Taxation

Players are subject to taxation on gambling winnings, with a threshold below which no taxes apply. Above this limit, winnings are taxed at specified rates and subject to withholding tax procedures to ensure efficient collection. Players are responsible for complying with national tax laws on gambling income.

Operator Taxation

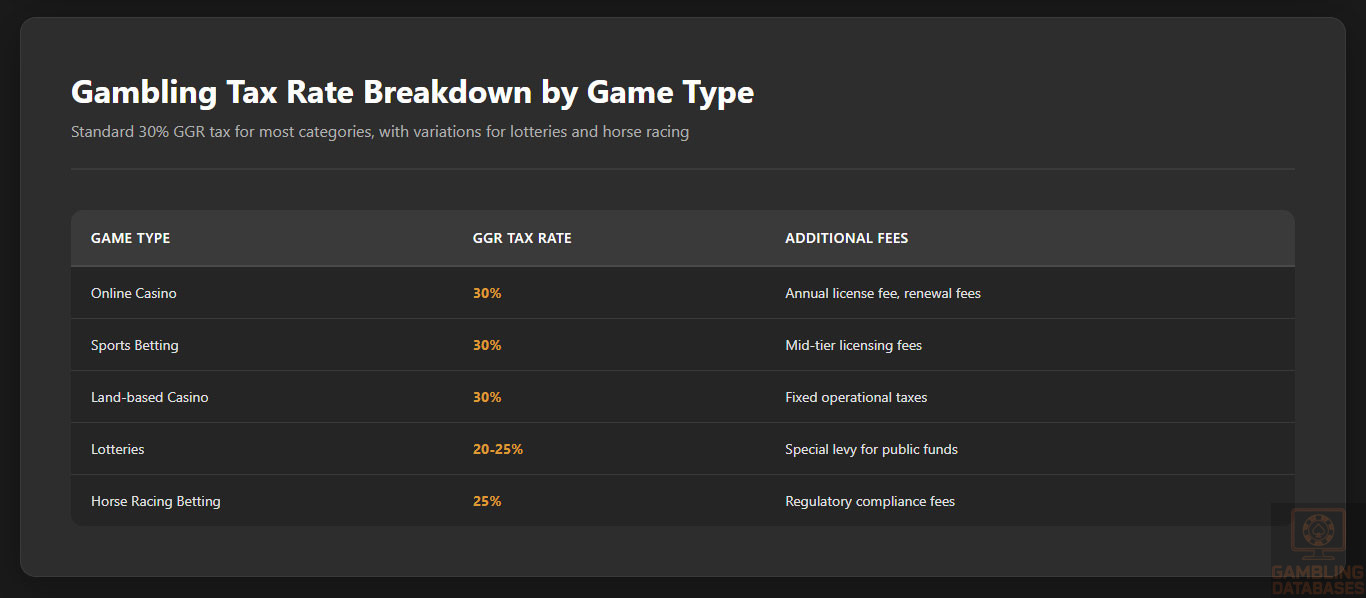

Operators pay a gross gaming revenue (GGR) tax currently set at 30% for most gambling categories. In addition, corporate income tax at 30% applies to gambling business profits. Fixed fees such as license renewal charges and market access taxes also form part of the fiscal obligations.

Detailed tax rates by category are summarized below:

| Game Type | GGR Tax Rate | Additional Fees |

|---|---|---|

| Online Casino | 30% | Annual license fee, renewal fees |

| Sports Betting | 30% | Mid-tier licensing fees |

| Land-based Casino | 30% | Fixed operational taxes |

| Lotteries | 20-25% | Special levy for public funds |

| Horse Racing Betting | 25% | Regulatory compliance fees |

Gambling Market Financial Performance

The sector shows steady growth in total wagered amounts fueled by expanding digital adoption. Year-on-year revenue increases reflect improved tax collections following regulatory reforms. Tax revenues from gambling contribute a significant portion of state income, supporting public budgets and economic diversification objectives.

Market payouts remain competitive, ensuring player confidence and sustainable engagement in both land-based and online segments.

Advertising and Marketing Restrictions

Advertising for gambling in Gabon is regulated to protect vulnerable groups and maintain market integrity. Operators face restrictions on content, channels, and timing of gambling advertisements. Sponsorship of events is permitted but must comply with ethical and transparency standards outlined by regulators.

- Prohibition of gambling ads during daytime hours accessible to minors

- Ban on misleading or exaggerated claims in promotional materials

- Restrictions on use of celebrities or influencers targeting youths

- Requirement to display responsible gambling messages in all ads

- Limits on bonuses and promotional offers

Recent Regulatory Changes and Their Impact

In 2025, the government launched a national integrator platform E-TECH to unify gambling oversight. This reform marks a policy shift towards digital transparency and sector formalization. Operators have been given a fixed deadline to comply; failure to integrate risks license suspension.

The reform increases operational compliance costs but promises long-term revenue and growth potential through market stabilization. Enhanced player protections and fiscal controls improve investor confidence and consumer trust.

Enforcement Mechanisms and Penalties

Gabon enforces gambling regulations through sanctions including license suspension, fines, and legal prosecution for non-compliance or fraudulent practices. Enforcement trends indicate rigorous monitoring under the new centralized system.

- Immediate suspension of operations for failure to comply with E-TECH integration

- Financial penalties proportional to infringement severity

- Revocation of licenses for repeated violations

- Criminal charges in cases involving fraud or money laundering

- Public warnings and blacklisting of unlicensed operators

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

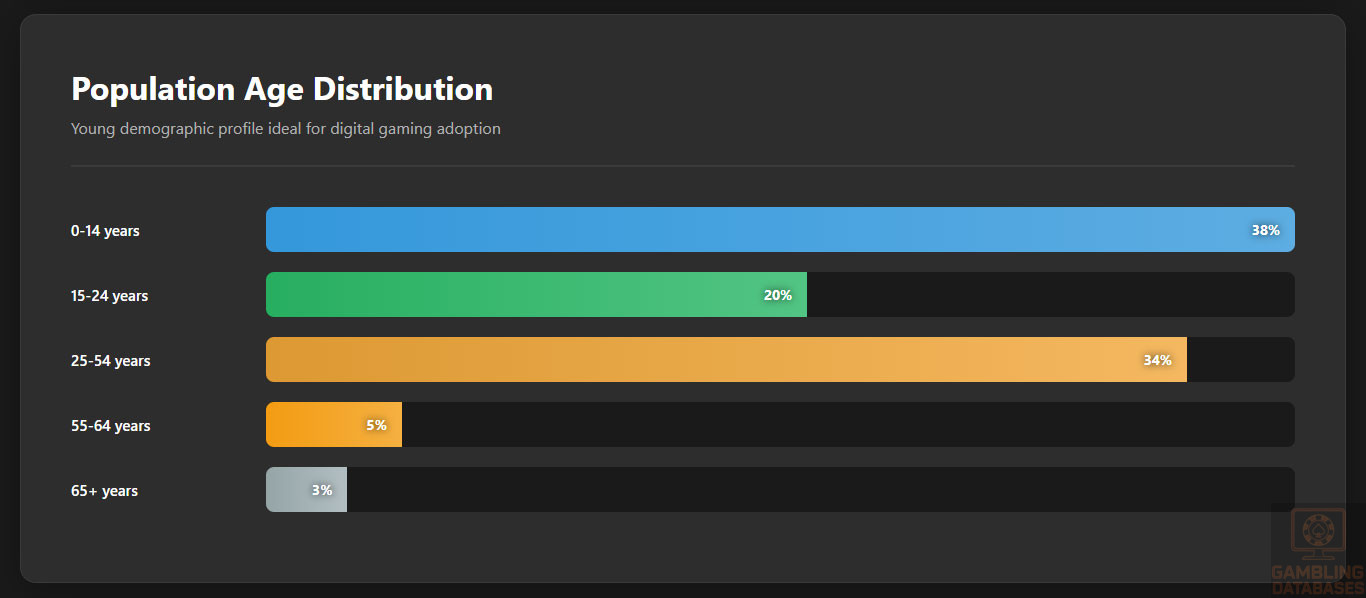

Gabon has a population of approximately 2.57 million as of 2025, characterized by a youthful demographic structure typical of many Central African countries. The median age is around 23 years, reflecting a majority of the population below 30 years old. This young workforce presents a sizable potential consumer base for iGaming services focused on tech-savvy younger adults.

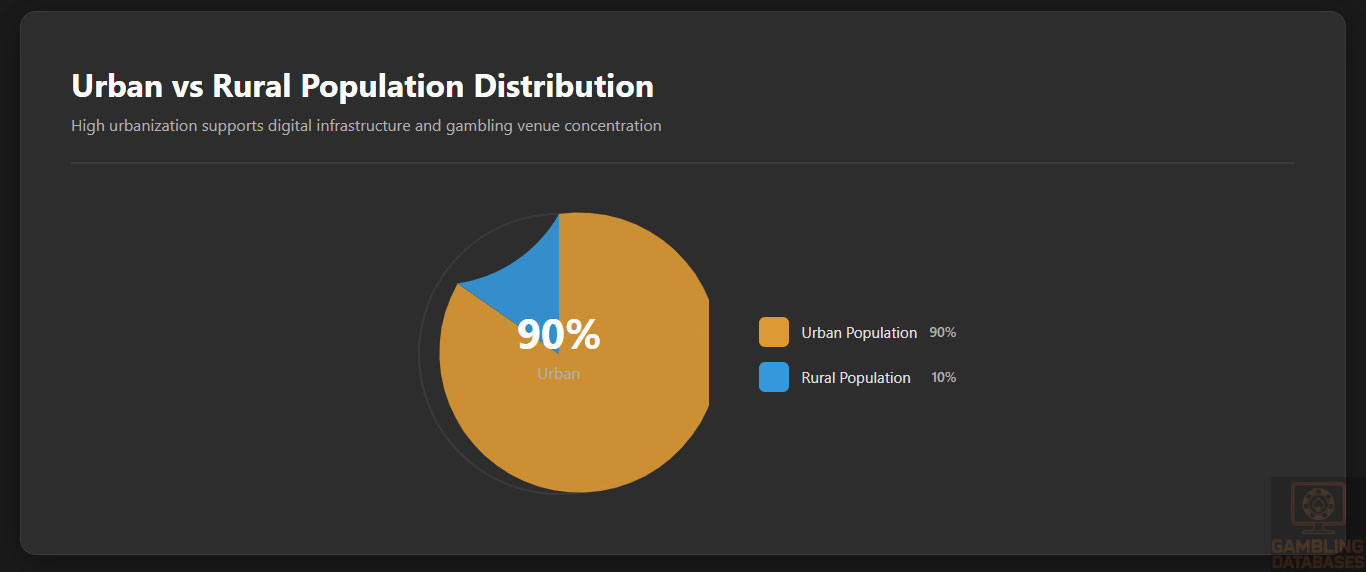

Gender distribution is relatively balanced with a slight female majority at about 51%. Urban population accounts for roughly 90% of the total population, largely concentrated around Libreville and Port-Gentil, while rural areas consist of smaller, dispersed communities.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 38% |

| 15-24 years | 20% |

| 25-54 years | 34% |

| 55-64 years | 5% |

| 65 and over | 3% |

The urban-rural divide manifests distinctly in internet access and gambling participation, with urban centers offering higher connectivity and multiple gambling venues. The youth-dominant demographic coupled with growing mobile adoption bodes well for digital gaming market expansion.

Geographic Distribution

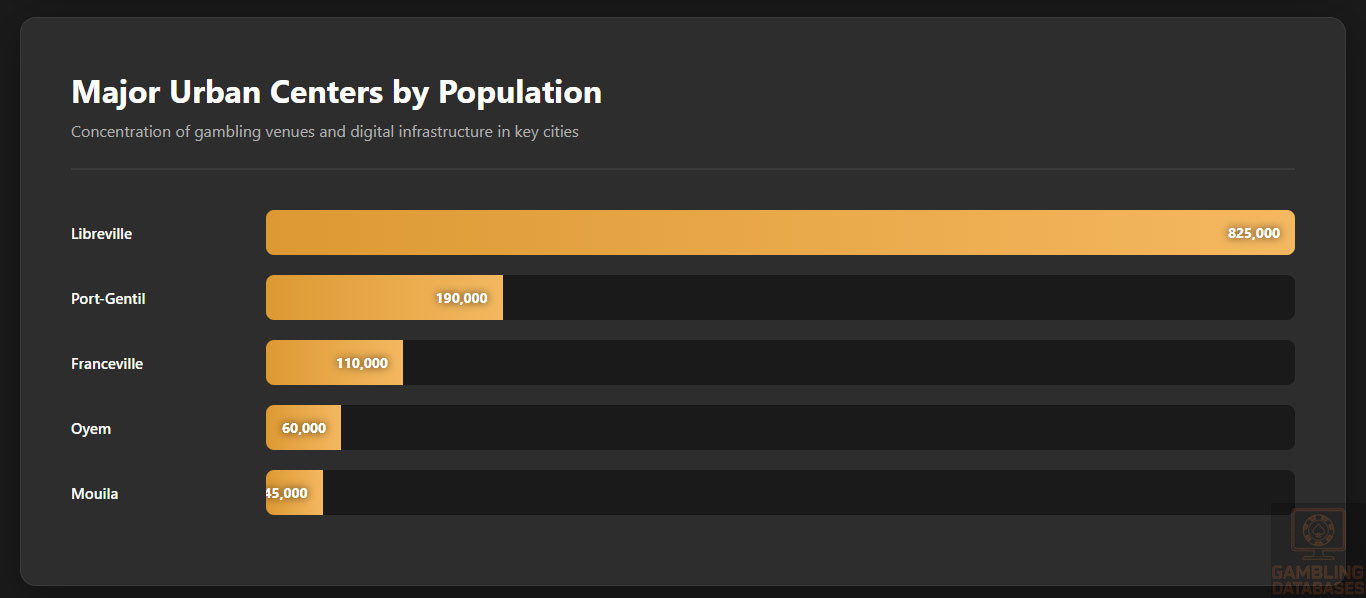

Gabon’s major urban centers concentrate economic and gambling activities. Libreville, the capital city, is home to the largest portion of the population and nearly all licensed gambling establishments. Port-Gentil serves as the country’s economic hub, hosting industrial and financial services with a notable array of entertainment options including land-based casinos.

Smaller cities such as Franceville, Oyem, and Mouila also contribute to regional economic variation but lack extensive gambling infrastructure, highlighting the need for digital channels to reach wider consumers. Internet access is strongest in urban areas, reinforcing gambling venue concentration in Libreville and port cities while rural zones remain less connected.

- Libreville – Approx. 825,000 inhabitants, primary economic and gambling center

- Port-Gentil – Approx. 190,000 inhabitants, oil industry hub with notable casinos

- Franceville – Approx. 110,000 inhabitants, regional commercial center

- Oyem – Approx. 60,000 inhabitants, northern regional capital with modest connectivity

- Mouila – Approx. 45,000 inhabitants, southern city with growing urbanization

Economic Indicators and Consumer Spending Power

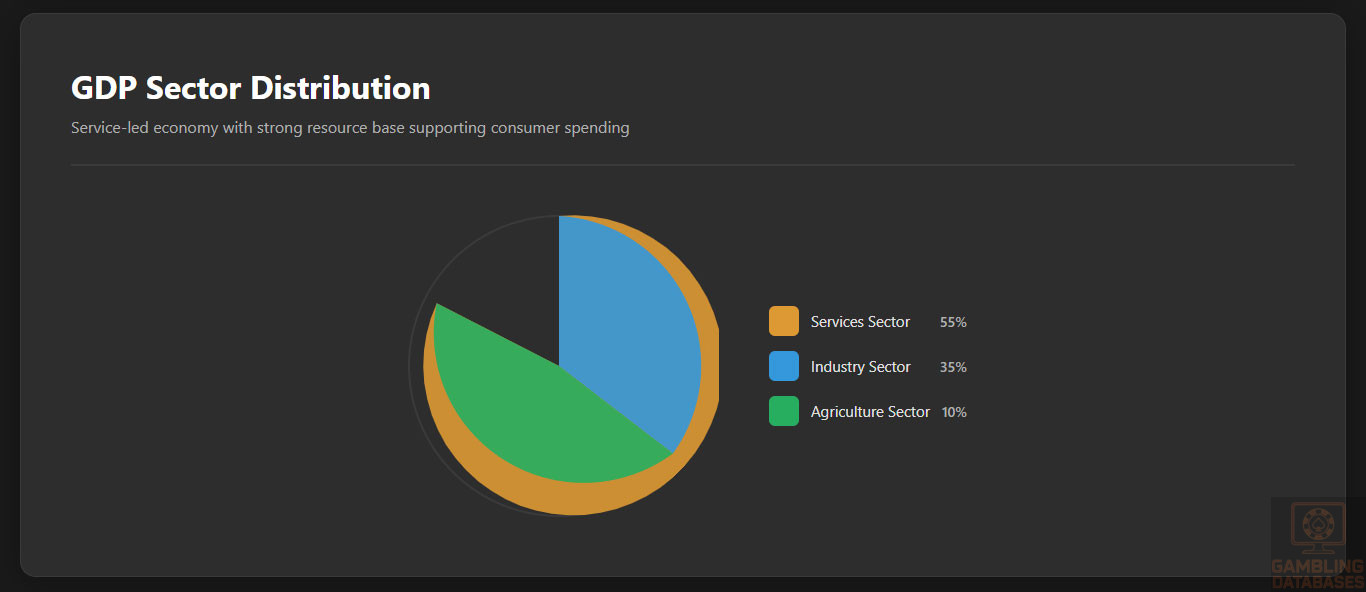

Gabon’s GDP stands at an estimated $103 billion (PPP) in 2025, driven primarily by oil exports, mining, and timber industries. The economy grew at a moderate rate of 2.9% in 2024, with outlooks projecting steady expansion encouraging consumer spending growth. The services sector represents the largest GDP share nearing 55%, with industry contributing 35% and agriculture about 10%.

Per capita income averages around $13,000 (PPP), reflecting relatively strong purchasing power in Central Africa. Wealth distribution remains uneven, with a sizeable upper-middle-income urban class contrasted by rural poverty. Disposable income levels are rising among middle urban segments, fueled by employment growth in services and resource-driven sectors.

Consumer spending patterns reveal growing discretionary expenditure on entertainment and digital services, positioning Gabonese consumers as approachable targets for online gambling products. Urban youth display particularly strong demand for digital conveniences, further boosted by mobile payment solutions and improved connectivity.

| Indicator | Value |

|---|---|

| GDP (PPP) | $103 billion |

| GDP Growth Rate (2024) | 2.9% |

| Per Capita Income (PPP) | $13,000 |

| Services Sector Contribution | 55% |

| Industry Sector Contribution | 35% |

| Agriculture Sector Contribution | 10% |

| Urban Unemployment Rate | 11.5% |

| Inflation Rate | 3.8% |

Market Size and Growth Projections

The Gabonese iGaming market is poised for compound growth estimated between 12-15% CAGR over the next five years. Current gambling revenues remain modest but are experiencing acceleration thanks to regulatory reforms encouraging formal online operations.

Projected market revenue for 2025 exceeds $40 million, growing from under $30 million in 2023. User base expansion parallels rising internet penetration and digital payment adoption.

Average revenue per user (ARPU) is moderate compared to global averages but increasing as operators tailor offerings to local preferences and payment capabilities. Market penetration remains nascent but fast evolving, particularly among urban populations aged 18-45.

| Year | Estimated Revenue (USD million) | User Base (thousands) | ARPU (USD) |

|---|---|---|---|

| 2023 | 28 | 85 | 330 |

| 2024 | 34 | 105 | 324 |

| 2025 | 41 | 130 | 315 |

| 2026 | 48 | 160 | 300 |

| 2027 | 55 | 190 | 289 |

| 2030 | 78 | 280 | 279 |

Education, Skills, and Digital Literacy

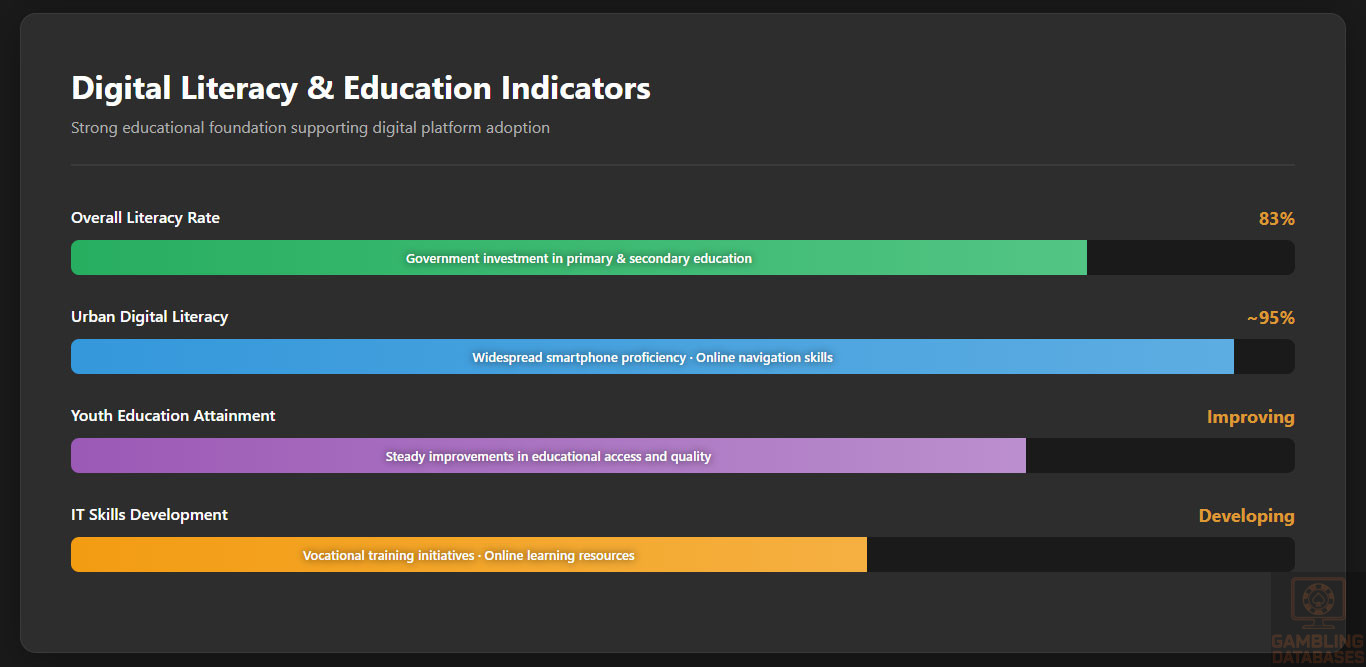

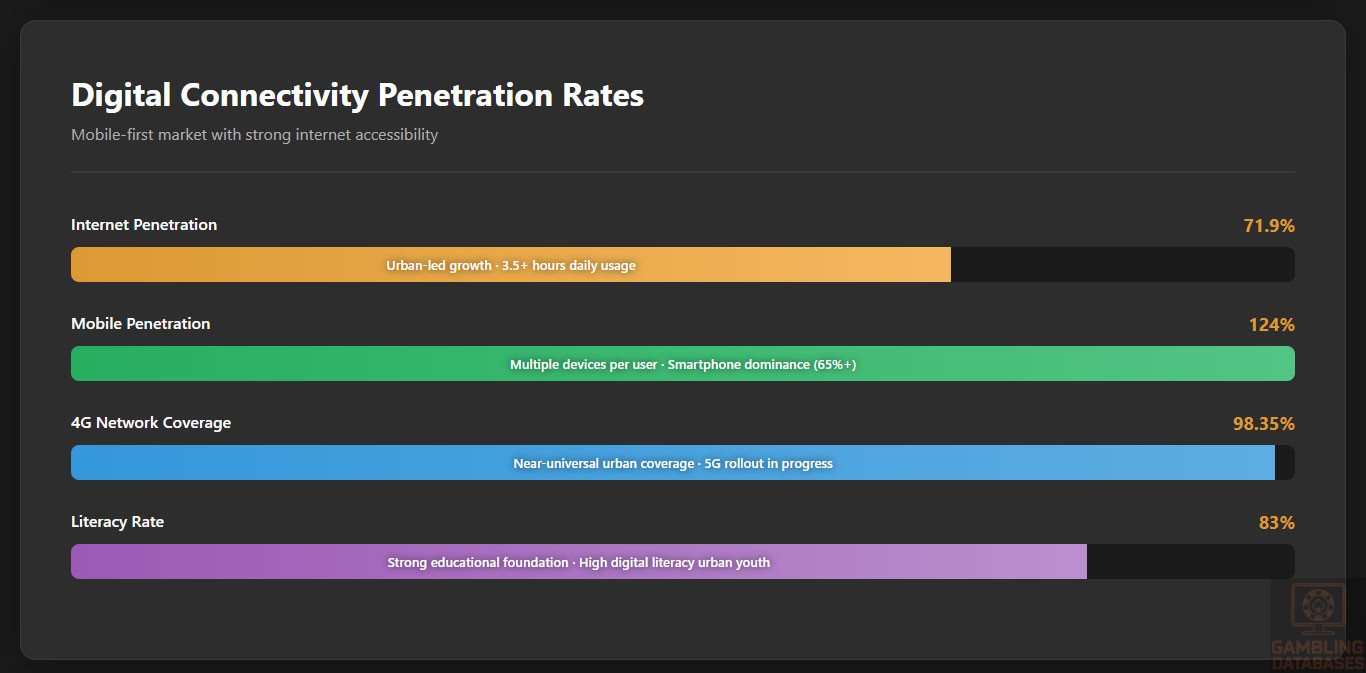

Gabon boasts a relatively high literacy rate of around 83%, supported by government investment in primary and secondary education over recent decades. Educational attainment levels among youth have steadily improved, facilitating a growing base of digitally literate individuals.

Digital literacy is significantly higher in urban areas, with widespread smartphone adoption and proficiency in online navigation. Workforce skills for the digital economy, including IT and customer service roles, are developing rapidly, supported by vocational training initiatives and increasing availability of online learning resources.

This foundation positions Gabon favorably for rapid consumer adoption of online gambling platforms that require user familiarity with digital payment systems and web/app interactions.

Cultural and Social Factors

Communication and Language

French is the official language and dominates government, business, and internet communication. Various indigenous languages coexist regionally, but French is primary for digital content consumption and commercial transactions. English penetration is limited but growing among educated youth and business sectors.

- French – Official and most widely used language

- Fang – Largest indigenous language group

- Punu – Widely spoken in the south

- Myene – Coastal linguistic group

- Tsogo – Regional language in the east

Cultural Attitudes

Gambling is culturally accepted as a form of entertainment among adults, especially in urban areas, though it remains conservative in rural communities influenced by traditional beliefs. Religious considerations, predominantly Christian with notable Muslim minorities, shape cautious societal perspectives on gambling excess.

Foreign brand perception is generally positive, with consumers favoring international platforms offering localized services and multilingual support. The entertainment market increasingly embraces digital innovation, integrating gambling with broader social and mobile leisure activities.

Problem Gambling and Social Considerations

Prevalence of problem gambling is relatively low but rising with expanding accessibility. At-risk groups include younger males aged 18-35 and low-income urban populations. Government initiatives focus on education, prevention, and treatment through collaboration with NGOs.

- National awareness campaigns on gambling risks

- Support helplines and counseling services

- Mandatory self-exclusion programs via operators

- Community outreach in urban and informal sectors

- Research funding for addiction studies

Social responsibility regulation mandates operator contributions to responsible gaming funds and compliance with player protection standards to mitigate harm.

Political Structure and Governance

Gabon is a presidential republic with stable governance relative to regional standards, underpinned by consistent regulatory enforcement in economic sectors. The government prioritizes transparency reforms in gambling regulation and digital economy development, sustaining investor confidence.

Strong ties to international regulatory bodies and trade networks facilitate global compliance adaptation. Political stability supports a business environment conducive to sustainable market growth and expansion.

Technology Adoption and Digital Behavior

Internet and Digital Usage

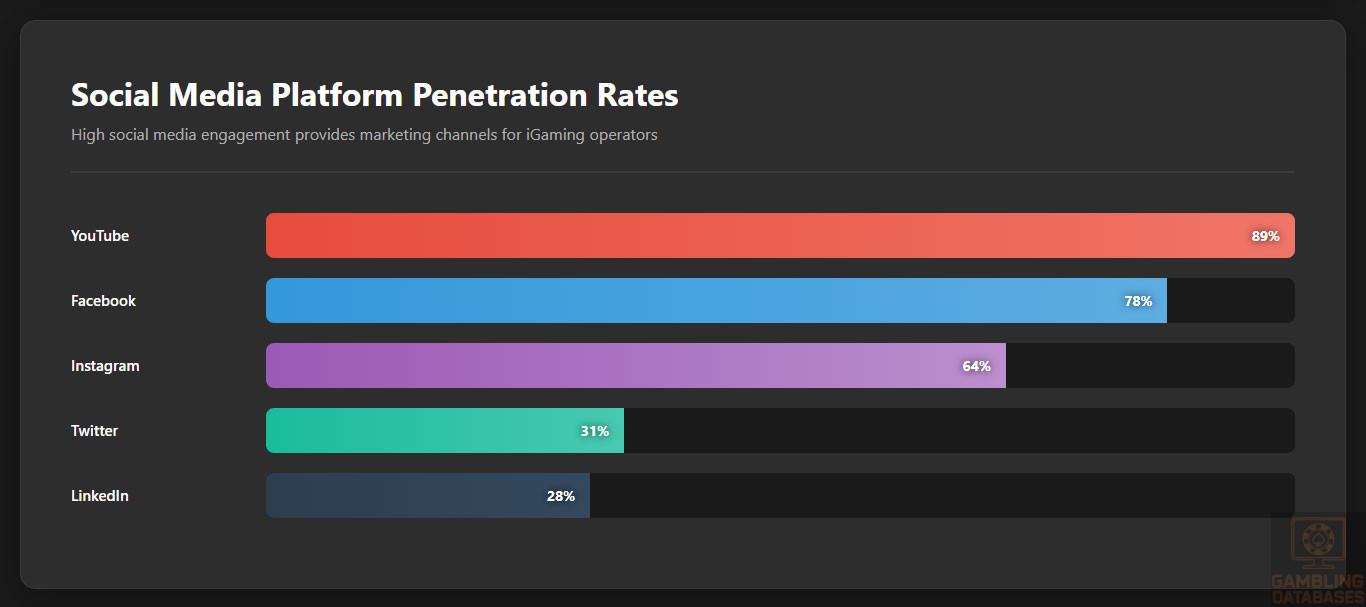

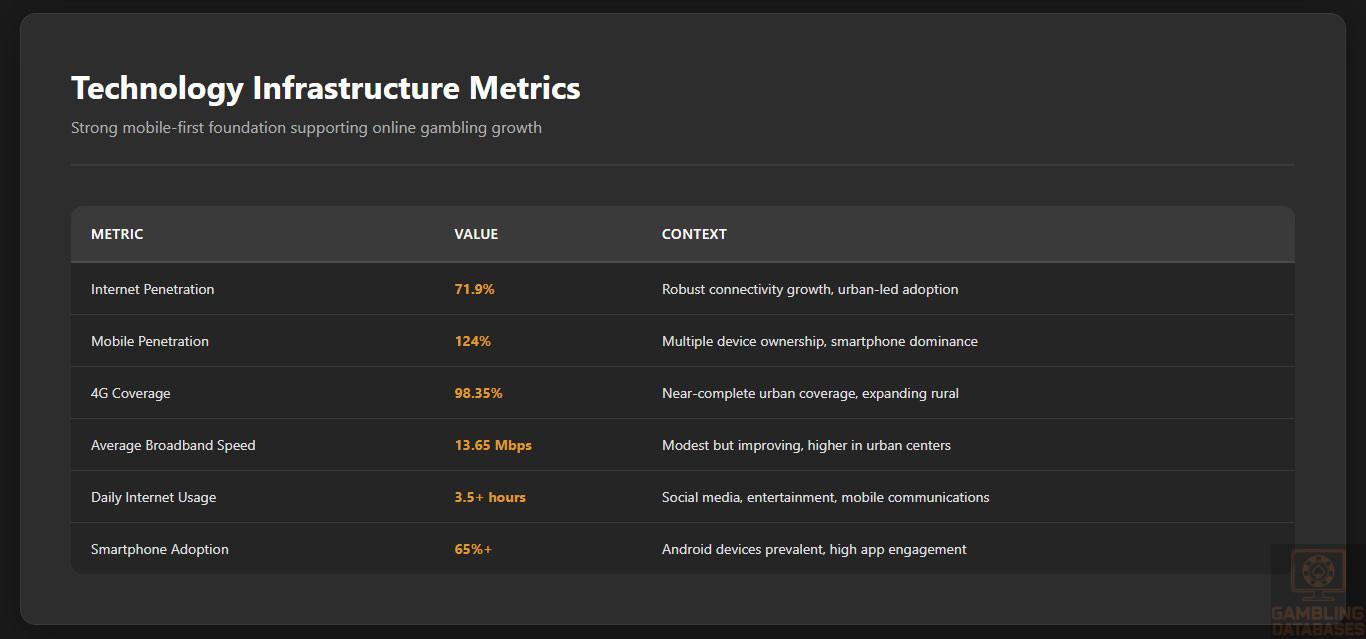

Internet penetration stands at 71.9%, reflecting robust connectivity growth with urban areas leading adoption. Daily internet use averages over 3.5 hours, dominated by social media, entertainment, and mobile communications.

Mobile penetration exceeds 124%, indicating multiple device ownership and heavy reliance on smartphones for online access. This mobile-first environment underpins substantial potential for mobile-optimized gambling platforms targeting younger demographics.

- Facebook – 78% penetration among internet users

- Instagram – 64% penetration, popular among 18-34 age group

- YouTube – 89% penetration with average 45 min daily watch

- TikTok – Rapid growth, strong under-25 engagement

- Twitter – 31% penetration, mainly news consumers

- LinkedIn – 28% penetration for professional networking

Digital Payment Behavior

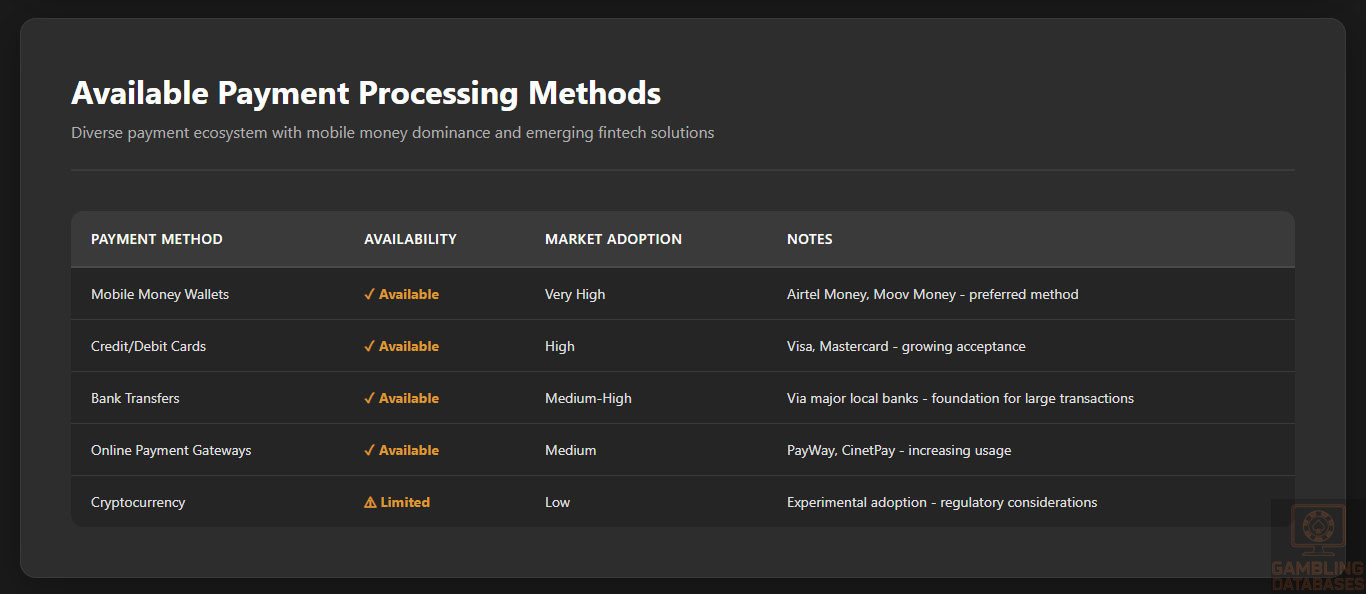

Digital payment adoption is growing rapidly with increasing trust in mobile money wallets and card payments. Consumers favor convenient, secure methods integrating with gambling platforms, fueling transaction volumes in e-wallet and mobile transfer segments.

- Mobile money wallets (e.g., Airtel Money, Moov Money)

- Credit/debit cards (Visa, Mastercard)

- Bank transfers via local banks

- Online payment gateways (e.g., PayWay)

- Cryptocurrency adoption emerging but limited

Gaming and Gambling Preferences

Current Market Participation

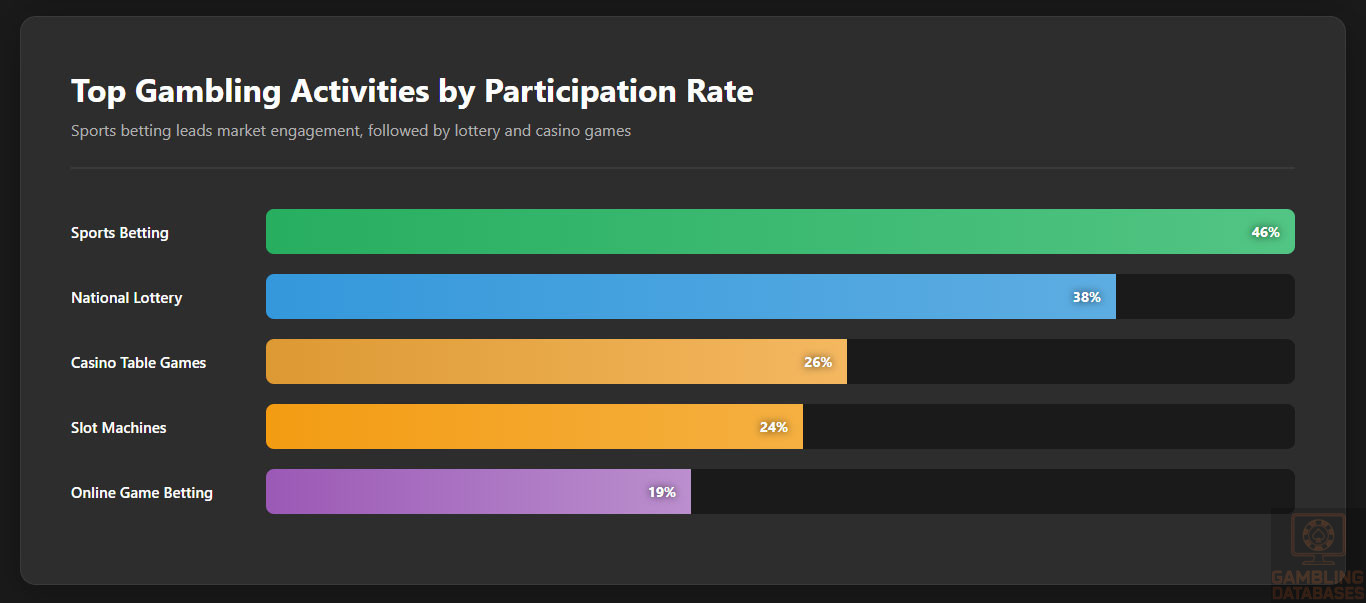

Gambling participation shows growing engagement across multiple formats, with particular strength in sports betting and lotteries. Casino games are gaining traction among urban youth fluent in digital gaming culture.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Sports Betting | 46% |

| 2 | National Lottery | 38% |

| 3 | Casino Table Games | 26% |

| 4 | Slot Machines | 24% |

| 5 | Online Game Betting | 19% |

Consumer Behavior Patterns

Users predominantly engage in short, mobile-centric gambling sessions clustered around prime-time evenings and weekends. Spending patterns trend towards moderate wagers with incremental growth during major sports events or lottery draws.

Retention is higher for platforms offering localized experiences, multiple payment options, and responsible gaming tools. New entrants benefit from integrating social features and gamification to foster community and loyalty.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Gabon’s internet penetration is solid at around 72%, with the majority of users accessing via mobile broadband. Fixed broadband remains limited due to infrastructure costs and geographic challenges. Average broadband speeds are modest, estimated near 13.65 Mbps, though urban centers enjoy higher and more reliable connectivity.

The government has prioritized digital infrastructure investments, focusing on fiber optic expansion and improved data centers to increase reliability and reduce latency. Despite challenges in rural areas, ongoing projects aim to close the digital divide and enhance access nationwide.

5G and Future Technology Deployment

5G coverage is in early rollout stages, mainly in Libreville and Port-Gentil, targeting high-usage commercial districts and tech hubs. Nationwide rollout plans project full urban coverage within 3-5 years, supported by international telecom partnerships. These advancements will boost real-time gaming experiences and mobile gambling adoption by reducing latency and increasing capacity.

Existing mobile operators are upgrading infrastructure for 5G compatibility, while government incentives support innovation in digital services. The ramp-up phase includes public trials and phased commercial launches, laying the foundation for future tech such as AI-driven gaming solutions.

Mobile Technology Ecosystem

The mobile network landscape is competitive, featuring several operators with varied market shares. Coverage quality ranks high in urban areas with near-complete 4G availability and increasing 5G presence. Data costs remain moderately affordable, bolstering mobile internet uptake crucial for online gambling platforms targeting mobile users.

- Airtel Gabon – Leading operator with about 35% market share

- Moov Africa – Approximately 30% market share with strong urban focus

- Libertis – Regional operator covering niche markets with 15% share

- Azur Gabon – Smaller provider specializing in data services, 10% share

- Gabon Telecom – State-affiliated with 10% share, balancing traditional and digital services

Smartphone adoption exceeds 65% of the population, with Android devices prevalent due to affordability and versatility. Device usage patterns show high engagement with apps and mobile-optimized websites, favoring gambling operators investing in seamless mobile experiences.

Financial Services and Payment Infrastructure

The banking sector comprises established domestic and regional institutions. Digital banking adoption rises steadily, fueled by mobile money services expanding financial inclusion. Bank account penetration remains uneven but is improving among young urban professionals.

- BGFI Bank – Largest financial institution with comprehensive digital services

- Banque Gabonaise de Développement (BGD) – Focus on corporate and SME clients

- BICIG – Regional bank with strong consumer banking focus

- Ecobank Gabon – Offers extensive mobile and online banking options

- Orabank – Growing presence with integrated digital payment solutions

Payment processing options are diverse, with mobile money wallets dominating electronic transactions and increasing support for card payments. Bank transfers remain foundational for larger transactions, while emerging fintech companies are exploring cryptocurrency integration cautiously due to regulatory considerations.

- Mobile money (Airtel Money, Moov Money)

- Credit and debit cards (Visa, Mastercard)

- Bank transfers via major local banks

- Online payment gateways (PayWay, CinetPay)

- Cryptocurrency (limited, experimental adoption)

E-commerce and Digital Economy

Gabon’s e-commerce sector is gradually expanding, supported by growing internet accessibility and digital literacy. Online retail penetration is increasing, particularly in urban centers, with consumers displaying rising trust in digital platforms for a range of goods and services. This environment encourages cross-sector digital innovation, including iGaming, which benefits from aligned payment and delivery ecosystems.

The government supports digital economy growth via infrastructural investment and regulatory reforms aimed at facilitating technology integration, cybersecurity, and consumer protection within online markets.

Business Environment and Regulatory Framework

Gabon ranks moderately on ease of doing business indices, showing strengths in business registration and moderate operational costs but challenges remain in legal enforcement and bureaucratic efficiency. Regulatory consistency has improved with government initiatives focused on transparency and anti-corruption, attracting foreign investment.

Foreign investors benefit from generally open policies, with emphasis on local partnerships and compliance with national development goals. Licensing processes embed rigorous requirements but offer clear procedural guidelines.

- Preparation and notarization of required corporate documents (2-3 weeks)

- Submission and review by the Registrar General (5-7 business days)

- Tax registration and obtaining fiscal identification (3-5 days)

- Corporate bank account opening and minimum capital deposit (1-2 weeks)

- Issuance of final business registration certificate (2-3 days)

Corporate Structure and Registration

Business entities primarily include Limited Liability Companies (LLCs), Corporations, and Branch Offices of foreign companies. LLCs are popular for flexibility and limited liability protection. Corporations suit larger operations with shareholder structures, while Branch Offices serve foreign companies seeking local operational extensions without full incorporation.

Registration timelines generally range from 3 to 6 weeks depending on documentation readiness and regulatory reviews. Foreign ownership is permitted, subject to transparency and anti-money laundering compliance with no formal restrictions on percentage ownership.

- Certificate of incorporation

- Articles of association and company bylaws

- Proof of registered local address

- Tax identification registration documents

- Identification and residence proof of directors and shareholders

- Bank letter of capital deposit

- Compliance declarations for AML and KYC policies

Taxation Framework

The corporate income tax standard rate is 30%. Special incentives, including tax holidays and reduced rates, apply in designated economic zones aimed at fostering specific sectors. Gabon has signed double taxation treaties with multiple countries to facilitate cross-border investment.

Personal income tax rates are progressive, with withholding taxes applicable on gambling winnings and dividends. Social security contributions are mandatory, and tax residency rules are clearly defined.

- France

- China

- United Arab Emirates

- Morocco

- South Africa

- Senegal

Market Entry Considerations

Recommended entry strategies include local partnerships for regulatory navigation, leveraging the E-TECH platform for compliance, and mobile-first product design to capture the youth market. Emphasis on customer support in French and local dialects enhances user engagement and retention.

- Form partnerships with established local operators and technology firms

- Prioritize mobile platforms with multilingual interfaces

- Invest in regulatory compliance infrastructure early

- Utilize targeted marketing campaigns respecting cultural norms

- Explore flexible payment integrations optimized for local preferences

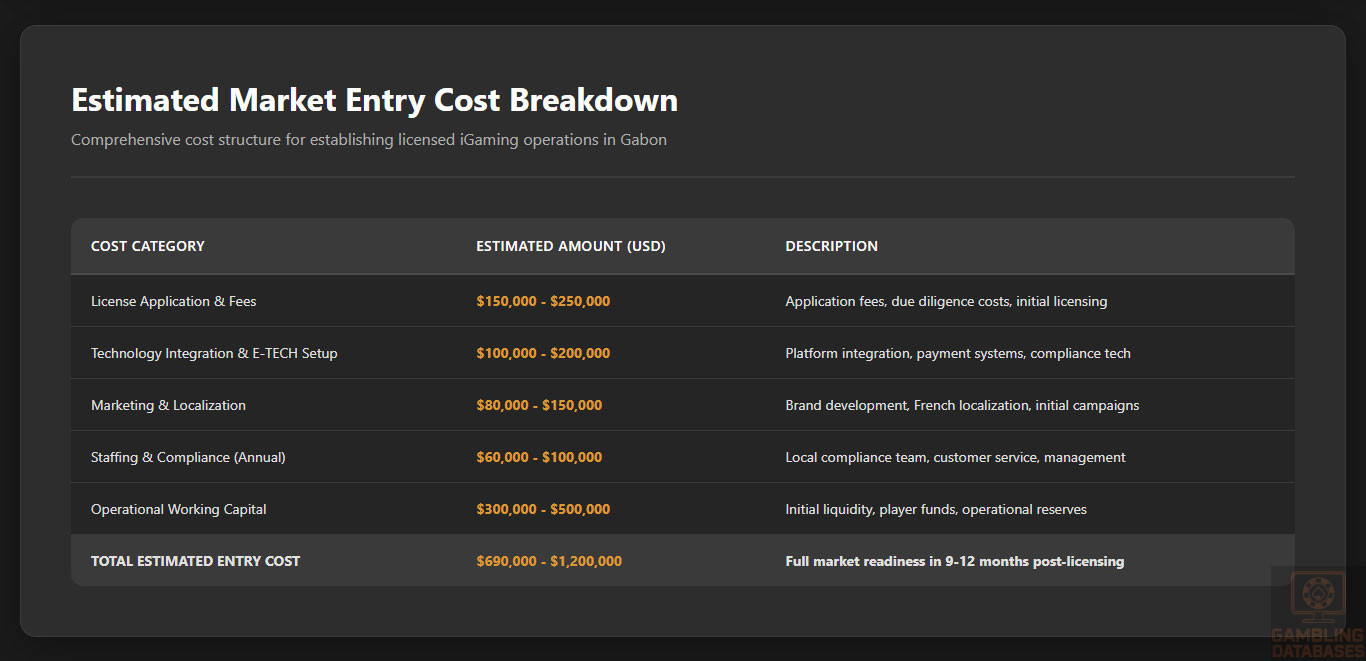

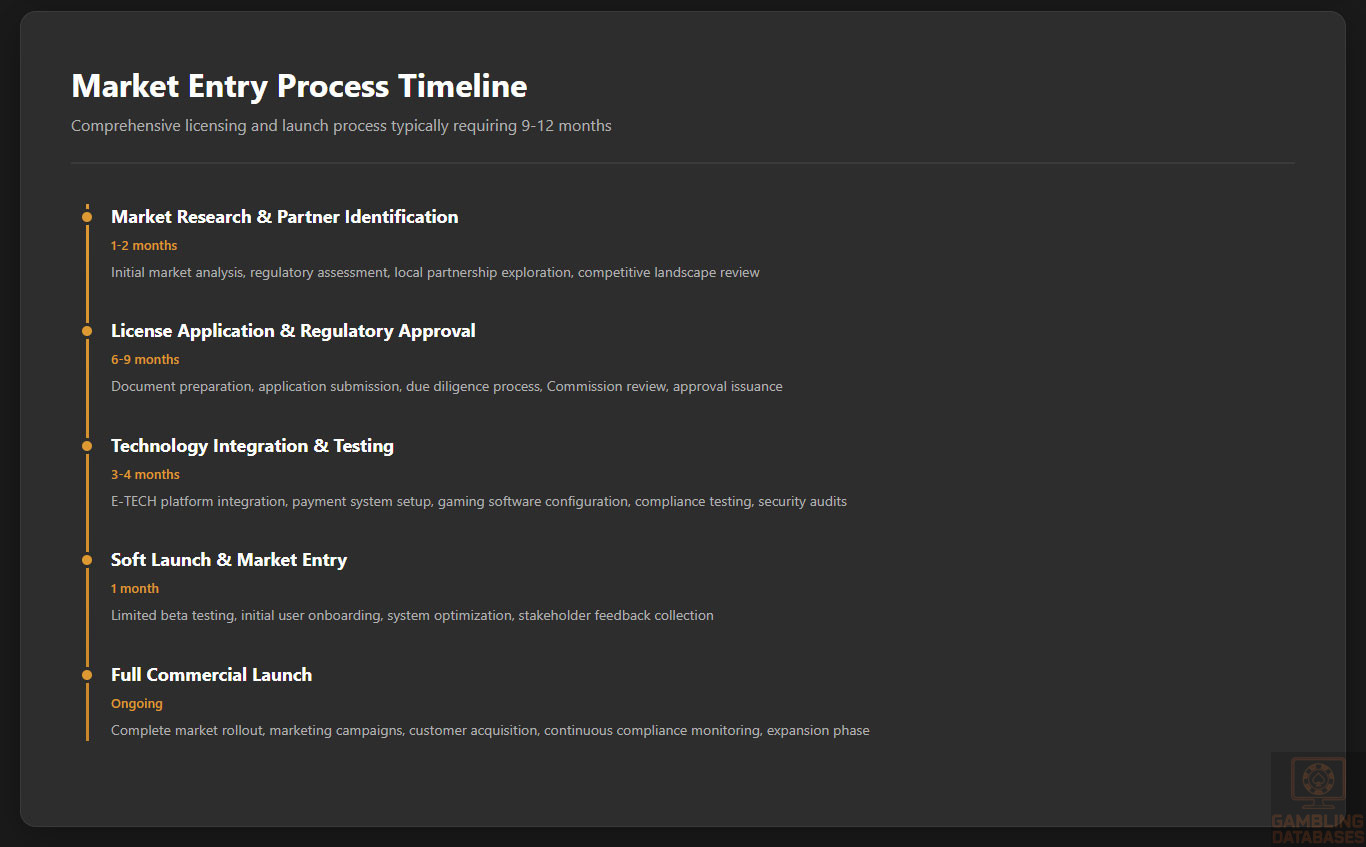

Entry costs are moderate-to-high, reflecting licensing fees, tech integration, marketing, and compliance overheads. Timeline for full market readiness often reaches 9-12 months post-licensing, depending on operational scale and market focus.

| Cost Category | Estimated Amount |

|---|---|

| License Application and Fees | $150,000 – $250,000 |

| Technology Integration & E-TECH Setup | $100,000 – $200,000 |

| Marketing and Localization | $80,000 – $150,000 |

| Staffing and Compliance | $60,000 – $100,000 annually |

| Operational Working Capital | $300,000 – $500,000 |

- Market research and partner identification (1-2 months)

- License application and regulatory approval (6-9 months)

- Technology integration and testing (3-4 months)

- Soft launch and market entry (1 month)

- Full commercial launch and expansion phase

Key success factors include robust regulatory adherence, culturally resonant marketing, digital payment optimization, and strong customer experience. Challenges involve infrastructure variability, administrative complexity, and emerging competitive intensity.

- Compliance with evolving regulatory frameworks

- Tailoring user experience for local demographics

- Effective fraud and risk management

- Building trust through secure and transparent operations

- Adapting to payment ecosystem fluctuations

Exit planning requires attention to license transfer conditions and ownership restrictions. Market liquidity is improving, supported by increasing operator numbers and investor interest, though valuation multiples remain sensitive to regulatory stability and consumer trends.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Gabon?

Yes, online gambling is legal but operates under a transitioning regulatory framework. The government mandates that all licensed operators integrate with the national E-TECH platform for transaction monitoring and transparency. Unlicensed online gambling is prohibited, and enforcement has intensified. Licensing covers various gambling categories including casino games, sports betting, and lotteries, with regulatory oversight ensuring compliance and consumer protection.

2. What types of gambling licenses are available and what do they cover?

The main license types encompass land-based casino operations, online casino gaming, sports betting, lottery operations, and horse racing betting. Each license is specific to the gambling category and requires applicants to meet distinct technical, financial, and compliance standards. The regulation also allows combined licenses for multi-activity operators, facilitating diversified offerings under a single regulatory umbrella.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees generally range from approximately $150,000 to $250,000 depending on the gambling activity and scope. The full licensing process can take 6 to 9 months including documentation review, compliance verifications, and integration with the E-TECH platform. Early preparation and local partnerships can expedite timelines.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to obtain gambling licenses provided they comply with Gabonese laws, including transparent ownership disclosures and AML policies. There are no formal restrictions on foreign ownership percentages, but operators must establish local representation or partnerships to satisfy operational and regulatory requirements, facilitating smoother market integration and oversight.

5. What are the tax obligations for iGaming operators?

iGaming operators are subject to a 30% gross gaming revenue (GGR) tax, complemented by a 30% corporate income tax on profits. Additional fixed fees such as annual license renewal and market access charges apply. The tax burden is relatively high but consistent with regional standards, with tax treaties reducing withholding and cross-border tax conflicts.

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue (GGR) Tax | 30% |

| Corporate Income Tax | 30% |

| License Renewal Fees | Variable; as per license type |

| Withholding Tax on Dividends | 15% |

| Market Access Tax | Fixed annual fee |

6. Are gambling winnings taxed for players?

Yes, gambling winnings above certain thresholds are subject to taxation with withholding applied at source. This ensures effective tax collection and compliance. Players must report taxable winnings under national tax laws, but smaller prizes generally remain exempt to encourage participation and maintain market vibrancy.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, technology platform integration, compliance and audit expenses, marketing and customer acquisition, staffing, and payment processing charges. Monthly costs vary by scale but can exceed $50,000 for mid-sized operators, with marketing often representing the largest variable expense due to competitive acquisition costs.

- License and regulatory fees

- Technology and platform maintenance

- Customer acquisition and marketing

- Compliance, legal, and audit costs

- Staffing and customer support

- Payment processing charges

8. What is the expected ROI timeline for entering this market?

Return on investment typically begins accruing after 18 to 24 months post-launch, influenced by regulatory complexity, market penetration speed, and effective cost management. Operators with strong local partnerships and efficient digital marketing can shorten this timeframe, while new entrants without regional experience might face longer breakeven periods.

9. What are the local presence requirements for operators?

Operators must maintain a physical presence or have local partnerships to satisfy regulatory oversight and facilitate tax and compliance administration. Local presence aids in licensing approvals, banking access, and customer support functions. This can be achieved through branch offices, representative agencies, or strategic alliances with established domestic entities.

10. What payment methods are available and recommended?

Payment ecosystems in Gabon prioritize mobile money services, card payments, and bank transfers. Mobile money wallets such as Airtel Money dominate due to convenience and accessibility, particularly for younger users. Credit/debit cards are preferred for higher-value transactions, while bank transfers serve corporate payments. Emerging technologies like cryptocurrencies are experimental but currently marginal.

- Mobile money wallets (Airtel Money, Moov Money)

- Credit and debit cards (Visa, Mastercard)

- Bank transfers through local banks

- Online payment processors (PayWay, CinetPay)

- Cryptocurrency (limited use)

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors and must not contain misleading claims. Promotions are regulated to include responsible gaming messages prominently. Timing restrictions limit ads during certain hours and channels, while sponsorships require transparency and compliance with ethical standards, reinforcing player protection and market integrity goals.

12. What responsible gambling measures are mandatory?

Operators are mandated to implement age verification, self-exclusion options, limits on deposits and losses, player activity monitoring, and mandatory disclosure of odds and payout percentages. These measures work in tandem with the E-TECH platform’s data capabilities to enforce real-time risk management and player protection schemes.

- Strict age verification at account creation

- Self-exclusion and cooling-off periods

- Deposit and loss limits configurable by the player

- Real-time monitoring of betting behavior

- Disclosure of game odds and payout rates

13. How large is the iGaming market and what is the growth potential?

Gabon’s iGaming market is estimated at over $40 million in revenue for 2025, exhibiting a robust growth rate of 12-15% CAGR projected through 2030. Growth is fueled by expanding internet and mobile adoption, regulatory reforms, and increasing consumer spending power, positioning Gabon as a promising emerging market in Central Africa.

14. Who are the main competitors and what is their market share?

The market is moderately consolidated among land-based casinos and established sports betting operators, with online entrants gaining ground following regulatory formalization. Major operators include locally licensed casinos in Libreville and Port-Gentil, alongside emerging online platforms adapting to the E-TECH integration. Competition centers around digital innovation, localized content, and payment accessibility.

15. What are the player preferences and typical spending patterns?

Players favor sports betting and national lotteries, which remain the most popular forms of gambling. Casino games and slot machines attract growing attention, especially among younger demographics. Session lengths are typically short and mobile-focused, with higher activity during sports events and weekend periods. Spending tends toward moderate wagers with peak spikes triggered by promotional campaigns.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, tailored user experiences, mobile optimization, secure payment integration, and strong local partnerships. Challenges include navigating evolving regulatory requirements, managing operational costs, competition from informal operators, and infrastructure limitations outside urban areas. Cultural adaptation and trust-building remain essential for long-term sustainability.

- Adherence to regulatory and compliance frameworks

- Strong mobile platform performance

- Multi-lingual customer support

- Integrated, flexible payment solutions

- Culturally resonant marketing strategies

- Regulatory fluidity and licensing process durations

- Infrastructure gaps in rural markets

- Competition from unlicensed operators

- High initial capital requirements

- Payment ecosystem volatility

Sources and References

- Gabon Gambling Regulatory Authority – Official Website – https://example.com

- National Statistical Office – Population and Economic Data 2024 – https://example.com

- Central Bank of Gabon – Financial Statistics and Reports – https://example.com

- Ministry of Finance – Tax Regulations and Guidelines – https://example.com

- World Bank – Doing Business Report 2024 – https://example.com

- International Telecommunication Union – ICT Statistics – https://example.com

- Gaming Industry Report – African Markets – 2024

- iGaming Solutions Blog – Regulatory News 2025

- GamblingTalk – Gabon Market Updates 2025

- FocusGN – Gabon Digital Economy and Gambling Platform Reports 2025

- SiGMA World – African Gaming Platform Launch 2025

- IGamingToday – Gabon Gambling Regulation Updates

- DataReportal – Digital 2025 Gabon Report

- FinancialAfrik – Economic Reports on Gabon 2025

- BetPack – Gabon Online Casino Market Analysis 2025

- LegalPilot – Gabon Gambling Legal Framework

- World Economics – Gabon GDP and Economic Data 2025

- 6WResearch – Gabon Gambling Market Projections

- Statista – Digital Connectivity Indicators Gabon 2025

- LinkedIn – iGaming News Gabon Report 2025

- Huidu – Gabon National Gambling Platform

- BookiesSite – Gabon Betting Sites 2025

- Central African Telecommunications Reports 2025

- UNESCO – Education and Literacy Statistics Gabon

- International Monetary Fund – Gabon Economic Overview 2025

- Gabon Ministry of Telecommunications – Infrastructure Plans

- Gabon Ministry of Commerce – Business Registration Guidelines

- Private Industry Analyses – Gabon Market Entry

- Academic Publications on African Digital Economies

- Cybersecurity and Digital Trust Reports for Gabon 2025

- Global Payment Systems Reports – Africa 2025

- Gabon Ministry of Social Affairs – Responsible Gambling Programs

- International Labor Organization – Workforce Development in Gabon

- Telecom Africa Reports – Mobile Network Operators

- Financial Times – Market and Regulatory Trends in Africa

- Gabon Investment Promotion Agency – Guidelines 2025

- United Nations Economic Commission for Africa

- Various News Outlets covering Gabon Regulatory and Market Developments 2024-2025

🎯 Gambling Databases Country Rating: Gabon

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.8/10 | 🟡 Moderate |

| Player Access Score | 6.5/10 | 🟡 Partially Legal |

| Overall Market Attractiveness | 6.2/10 | 🟡 Emerging market with moderate opportunity but significant entry barriers |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- MANDATORY PLATFORM INTEGRATION: All operators MUST integrate with government-controlled E-TECH platform by October 2025 or face immediate license suspension. This centralizes ALL transaction monitoring under government control.

- HIGH REGULATORY COMPLIANCE COSTS: Total entry costs range $690,000-$1,200,000 with 9-12 month timeline to full operation, making this prohibitive for small-to-medium operators.

- HEAVY TAXATION BURDEN: 30% GGR tax + 30% corporate income tax creates effective tax rate potentially exceeding 50% of revenue, severely impacting profitability.

- SMALL MARKET SIZE: Population of only 2.57 million with current market revenue around $41 million (2025) limits scale potential compared to larger African markets.

- REGULATORY UNCERTAINTY: Framework is “in transition” with E-TECH platform just launching in 2025. Rules may change rapidly as government tests new system.

- ENFORCEMENT AGAINST NON-COMPLIANCE: Government explicitly threatens license suspension, financial penalties, and criminal charges for operators failing to integrate with E-TECH or violating new regulations.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.0/3.0 | Land-based gambling fully legal including casinos, sports betting, lottery (+1.5). Online gambling framework exists and is being formalized (+1.0). DEDUCTIONS: Online framework “in transition” with mandatory government platform integration creating uncertainty (-0.25). Prohibition targets unlicensed operators with enforcement mechanisms (-0.25). Final: 2.0/3.0 |

| Licensing Process | 25% | 1.25/2.5 | Licensing available with clear authority (Commission Supérieure) (+1.0). Application timeline 6-9 months is reasonable (+0.5). DEDUCTIONS: Application costs $150,000-$250,000 places in high range (-0.25). Complex documentation requirements including 3-year financials, RNG certification, background checks on all directors creates barriers (-0.25). Foreign ownership permitted but requires transparency and local partnership preference (-0.25). Final: 1.25/2.5 |

| Taxation & Costs | 20% | 1.0/2.0 | GGR tax at 30% falls in 25-35% range (+1.0). DEDUCTIONS: 30% corporate income tax creates double taxation layer (-0.5). Total effective tax rate exceeds 50% when combining GGR and corporate taxes (-0.5). Additional license renewal fees and fixed operational taxes further increase burden (-0.25). High total entry costs $690k-$1.2M including compliance and working capital (-0.25). Market size limitations make customer acquisition challenging. Final calculation: Started at 1.0, multiple deductions = 1.0/2.0 |

| Operational Requirements | 15% | 0.75/1.5 | Remote operation theoretically possible (+0.5). DEDUCTIONS: Local presence “preferred” and domestic bank account MANDATORY for E-TECH integration (-0.25). Mandatory integration with government E-TECH platform for ALL transactions creates significant compliance burden (-0.5). Minimum capital deposit required in licensed institutions (-0.25). Qualified local personnel required for compliance oversight (-0.25). Platform integration costs $100k-$200k additional. Final: 0.75/1.5 |

| Market Environment | 10% | 0.8/1.0 | Business environment “stable but evolving” (+0.5). Government prioritizes transparency and digital economy (+0.3). DEDUCTIONS: Advertising restrictions on content, channels, and timing with daytime bans (-0.25). Prohibition of ads targeting minors with celebrity/influencer restrictions (-0.25). Recent regulatory upheaval with E-TECH mandatory integration creates instability (-0.25). Enforcement mechanisms explicitly include license suspension and criminal penalties (-0.25). Small market size (2.57M population) limits opportunity. Final: 0.8/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.75/4.0 | Land-based gambling fully legal including casinos, sports betting, lottery (+2.0). Online gambling being formalized with regulatory framework (+1.0). DEDUCTIONS: Online framework still “in transition” creating legal uncertainty for players (-0.25). Historically “lacked comprehensive online-specific oversight” meaning past use was grey area (-0.25). Prohibition targets unlicensed operators which may affect player access to offshore sites (-0.25). Winnings taxation with withholding applicable reduces net player returns (-0.5). Final: 2.75/4.0 |

| Practical Accessibility | 30% | 2.25/3.0 | Multiple payment methods available including mobile money (Airtel, Moov), cards (Visa, Mastercard), bank transfers, online gateways (+2.0). 71.9% internet penetration with 124% mobile penetration supports access (+0.5). DEDUCTIONS: ALL payments must route through E-TECH platform reducing flexibility (-0.5). Cryptocurrency adoption “limited, experimental” and likely restricted (-0.25). Article mentions “prohibition targets unlicensed operators and non-approved payment providers” suggesting potential payment blocking (-0.5). Final: 2.25/3.0 |

| Player Penalties | 20% | 1.5/2.0 | No explicit mention of player penalties in article (+2.0). DEDUCTIONS: Winnings subject to taxation above threshold with withholding tax procedures (-0.5). Enforcement mechanisms target operators not players, but regulatory uncertainty exists. Final: 1.5/2.0 |

| Market Availability | 10% | 0.5/1.0 | Three licensed land-based casinos operating (+0.3). DEDUCTIONS: Online operator market described as “growing number” but specifics unclear (-0.2). Market characterized as “moderately consolidated” with limited licensed operators (-0.2). Historically “widespread use of offshore operators” suggests limited licensed online options (-0.1). E-TECH integration deadline may temporarily reduce operator availability during transition. Final: 0.5/1.0 |

🔍 Key Highlights

Strengths (Limited)

- Full Product Legality: All major gambling products are legal including land-based casinos, sports betting, online gambling, and lotteries – no product category bans like in many African markets

- Growing Digital Infrastructure: 71.9% internet penetration, 124% mobile penetration, 98.35% 4G coverage provides solid foundation for online gambling growth

- Young Demographics: Median age 23 years with 58% of population under 25 creates target demographic for digital gambling services

- Regulatory Clarity Improving: Government actively formalizing framework with clear licensing authority and defined compliance requirements, unlike true grey markets

- Growth Potential: Market projected to grow 12-15% CAGR (2025-2030) from $41M to $78M, though starting from small base

- Regional Stability: Gabon relatively stable compared to regional peers, with consistent regulatory enforcement and transparent governance initiatives

⛔️ CRITICAL RISKS AND CHALLENGES

- MANDATORY GOVERNMENT PLATFORM: E-TECH integration is MANDATORY by October 2025 with license suspension threatened for non-compliance. This gives government complete control over all transactions, monitoring, and data – creating operational dependency and privacy concerns. Integration costs $100k-$200k additional.

- DOUBLE TAXATION BURDEN: 30% GGR tax PLUS 30% corporate income tax creates effective rate exceeding 50% of revenue. Example: $1M revenue = $300k GGR tax, leaving $700k, then 30% corporate tax = $210k, total $510k taxes = 51% effective rate. This severely impacts profitability margins.

- PROHIBITIVE ENTRY COSTS: Total entry investment $690,000-$1,200,000 breakdown: License $150k-$250k + E-TECH integration $100k-$200k + Marketing $80k-$150k + Staffing $60k-$100k + Working capital $300k-$500k. Timeline 9-12 months. This excludes small and mid-sized operators entirely.

- TINY MARKET SIZE: Only 2.57 million population with current market revenue just $41 million (2025). For comparison, Nigeria has 220M people. Limited scale potential makes high fixed costs difficult to amortize. 90% urban concentration means rural areas completely unaddressed.

- REGULATORY UNCERTAINTY: Framework explicitly described as “in transition” with E-TECH platform launching in 2025. New systems typically experience rule changes, technical issues, and unexpected requirements during rollout phase. Government testing monitoring capabilities may lead to additional restrictions.

- PAYMENT PROCESSING CONTROL: ALL transactions must route through E-TECH platform. This creates single point of failure, gives government complete payment oversight, and eliminates operator flexibility in payment methods. “Integration via E-TECH platform required to monitor flows” means zero transaction privacy.

- ADVERTISING RESTRICTIONS: Daytime bans, content restrictions, prohibition on celebrity/influencer marketing targeting youth, mandatory responsible gambling messages. These increase customer acquisition costs in already small market with limited media channels.

- LOCAL PRESENCE REQUIREMENTS: While officially “preferred,” practical requirements include domestic bank account (mandatory for E-TECH), local personnel for compliance, physical presence for regulatory cooperation. Foreign operators cannot realistically operate remotely.

- ENFORCEMENT MECHANISMS: Explicit threats include immediate license suspension, financial penalties proportional to violations, license revocation, criminal charges for fraud/money laundering, and public blacklisting. Government demonstrates willingness to enforce aggressively.

- LIMITED LICENSED OPERATORS: Only 3 land-based casinos, “growing number” of online operators (specifics unclear). Market described as “moderately consolidated” suggesting established players dominate. New entrants face competition from incumbents with regulatory relationships.

Player-Specific Issues

- Winnings Taxation: Players face taxation on winnings above threshold with mandatory withholding, reducing net returns compared to tax-free jurisdictions

- Payment Method Limitations: Cryptocurrency “limited, experimental” and all payments routed through E-TECH platform reduces flexibility and privacy

- Limited Operator Choice: Small number of licensed operators restricts competition and product diversity compared to mature markets

- Regulatory Transition Risk: E-TECH platform rollout may cause temporary service disruptions, payment processing delays, or operator exits during October 2025 integration deadline

- Government Transaction Monitoring: E-TECH centralization means all player activity tracked by government for tax and compliance purposes – privacy concerns for some users

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $690,000 – $1,200,000 minimum (license $150k-$250k, tech integration $100k-$200k, marketing $80k-$150k, staffing $60k-$100k annually, working capital $300k-$500k)

Monthly Operating Costs: $80,000 – $150,000 (staffing, compliance, platform fees, marketing, technology maintenance, local office)

Effective Tax Rate on Revenue: 51%+ (30% GGR tax + 30% corporate income tax on remaining profits = effective rate exceeding 50%, plus license renewal fees and operational taxes)

Customer Acquisition Cost: Not specified in article, but limited advertising channels, small market, and restrictions suggest moderate-to-high CAC relative to market size

Time to Breakeven: 24-36 months realistically, given high fixed costs, small market size, and heavy taxation burden

Time to Positive ROI: 36-48 months minimum, potentially longer if market growth projections don’t materialize or competition intensifies

Profitability Assessment: Economics are CHALLENGING for most operators. The combination of 51%+ effective taxation, $690k-$1.2M entry costs, $80k-$150k monthly burn rate, and tiny $41M total market size (2025) means only well-capitalized operators with multi-year horizons should consider entry. Market must reach projected $78M by 2030 for economics to improve, but that’s 90% growth over 5 years divided among all operators. Small market size means customer acquisition costs cannot be easily amortized. Suitable ONLY for operators with: (1) $2M+ capital reserves, (2) 5+ year investment horizon, (3) ability to operate efficiently at small scale, (4) tolerance for 51%+ tax burden, and (5) experience navigating emerging regulatory frameworks. Mid-sized and smaller operators should avoid – the fixed costs are too high relative to addressable market.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Operators (Unlicensed) | HIGH | Explicit prohibition targets unlicensed operators. Enforcement includes license suspension threats, financial penalties, and potential criminal charges. Government establishing E-TECH platform specifically to monitor and control transactions suggests payment blocking capabilities. Article states “reducing market risks associated with informal operators” indicating active enforcement agenda. |

| Licensed Operators | MEDIUM-HIGH | Mandatory E-TECH integration by October 2025 deadline or face immediate license suspension. Heavy compliance burden including monthly financial reporting, annual audits, KYC/AML monitoring, responsible gambling measures. Criminal charges possible for fraud or money laundering. High regulatory uncertainty during transition period with new platform testing. |

| Affiliates/Advertisers | MEDIUM | Advertising restrictions include content and timing regulations, prohibition on celebrity/influencer marketing to youth, mandatory responsible gambling messages. Unclear if affiliates face direct enforcement, but operators responsible for advertising compliance. Risk of association with non-compliant operators. |

| Payment Processors | MEDIUM | Article states “prohibition targets unlicensed operators and non-approved payment providers” suggesting payment processors must be approved. E-TECH platform integration mandatory means independent payment processing for gambling may be restricted. Regulatory action possible for processing unlicensed operator transactions. |

| Company Directors/Executives | MEDIUM | Background checks and integrity certifications required for all directors and owners during licensing. Criminal charges possible in cases involving fraud or money laundering. Enforcement mechanisms include criminal penalties for non-compliance. Personal liability not explicitly detailed but regulatory due diligence covers directors and stakeholders. |

🚨 Extradition and International Enforcement

Extradition Treaties: Article mentions Gabon has “double taxation treaties” with France, China, UAE, Morocco, South Africa, and Senegal. While these are tax treaties, Gabon likely has extradition agreements with France (former colonial power) and potentially other countries. Specific extradition agreements not detailed in article.

Enforcement History: No specific cases of international prosecution or extradition related to gambling mentioned in article. However, article states “criminal charges in cases involving fraud or money laundering” suggesting government willingness to pursue criminal prosecution for serious violations.

Safe Jurisdictions: Not specified in article, but general international pattern suggests countries without extradition agreements may include Russia, China (despite tax treaty), and some CIS countries.

Travel Risk: Risk appears LOW for properly licensed operators complying with regulations. Risk MEDIUM-HIGH for operators running unlicensed operations targeting Gabonese players, particularly if traveling through France or other countries with strong ties to Gabon.

📋 Final Verdict

Gabon receives an Operator Ease Score of 5.8/10 and a Player Access Score of 6.5/10, resulting in an overall market attractiveness rating of 6.2/10.

HONEST ASSESSMENT: Gabon represents an emerging opportunity with significant barriers. While all gambling products are legal and the regulatory framework is being formalized, the combination of mandatory government platform integration, 51%+ effective taxation, $690k-$1.2M entry costs, and tiny 2.57M population market creates a challenging environment. The E-TECH platform requirement is particularly concerning as it gives government complete transaction control and creates operational dependency. Only well-capitalized operators ($2M+ reserves) with 5+ year investment horizons should consider entry. The market’s small size means customer acquisition costs are difficult to amortize, and the heavy tax burden significantly impacts profitability. This is NOT a market for small or mid-sized operators, quick ROI seekers, or those uncomfortable with government-controlled payment processing. While the 12-15% projected growth is attractive, achieving profitability will require scale, efficiency, and patience that most operators cannot sustain.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Major international operator with $2M+ capital reserves and ability to absorb $690k-$1.2M entry costs

- Willing to accept 5+ year investment horizon with 36-48 month timeline to positive ROI

- Comfortable with 51%+ effective tax rate (30% GGR + 30% corporate) eating into margins significantly

- Experienced in navigating emerging regulatory frameworks and government-controlled platforms

- Can operate efficiently at small scale in 2.57M population market with $41M current revenue

- Have established relationships with local partners, banks, and regulatory bodies in Central Africa

- Willing to integrate fully with government E-TECH platform giving state complete transaction oversight

- Targeting French-speaking African markets with Gabon as potential hub for regional expansion

❌ Definitely Avoid If You Are:

- Small or mid-sized operator with capital under $2M (entry costs too high relative to market size)

- Seeking quick ROI within 18-24 months (realistically requires 36-48 months minimum)

- Uncomfortable with government-controlled payment processing through mandatory E-TECH platform

- Unable to tolerate 51%+ effective taxation rate severely impacting profit margins

- Targeting offshore/unlicensed operation (explicit prohibition with enforcement mechanisms)

- Lack experience with emerging markets and regulatory uncertainty during transition periods

- Cannot establish local presence with domestic bank account and compliance personnel

- Focused solely on quick market entry without multi-year commitment (9-12 month setup timeline)

- Expect markets with 10M+ population and $200M+ revenue (Gabon is 2.57M and $41M)

- Startup operators without proven track record, as regulatory scrutiny includes background checks on all directors

⚠️ BOTTOM LINE: Gabon is a legal but expensive, small, heavily taxed market suitable ONLY for well-capitalized operators with multi-year patience and tolerance for government-controlled payment infrastructure. Most operators should prioritize larger African markets like Nigeria, Kenya, or South Africa where market size justifies high entry costs.