Gambia presents a complex iGaming landscape where legal prohibitions contrast with widespread, unregulated gambling activity. While the Betting and Gaming Act of 1973 technically bans Gambian citizens from gambling, enforcement is virtually nonexistent, allowing a thriving informal betting market to flourish. The absence of a dedicated regulatory authority and formal licensing framework creates both high-risk and high-opportunity conditions for market entry.

| Metric | Value |

|---|---|

| Legal Status of Online Gambling | De facto unregulated; no formal licensing |

| Primary Regulatory Body | No dedicated iGaming regulator |

| Land-Based Casino Licensing Authority | Minister of Justice (under Betting and Gaming Act) |

| Online Gambling License Available | No |

| Prohibition on Gambian Citizens Gambling | Yes, under Betting and Gaming Act 1973 |

| Enforcement of Gambling Laws | Minimal to none |

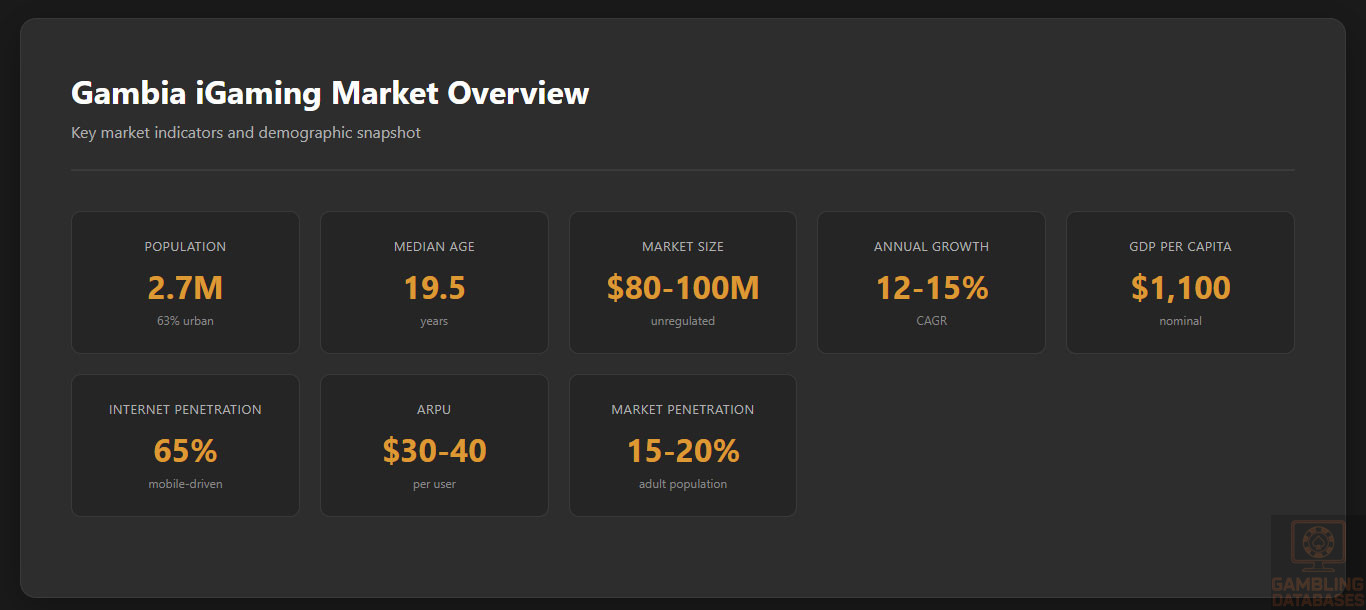

| Population (2025 est.) | 2.7 million |

| Urban Population | 63% |

| Median Age | 19.5 years |

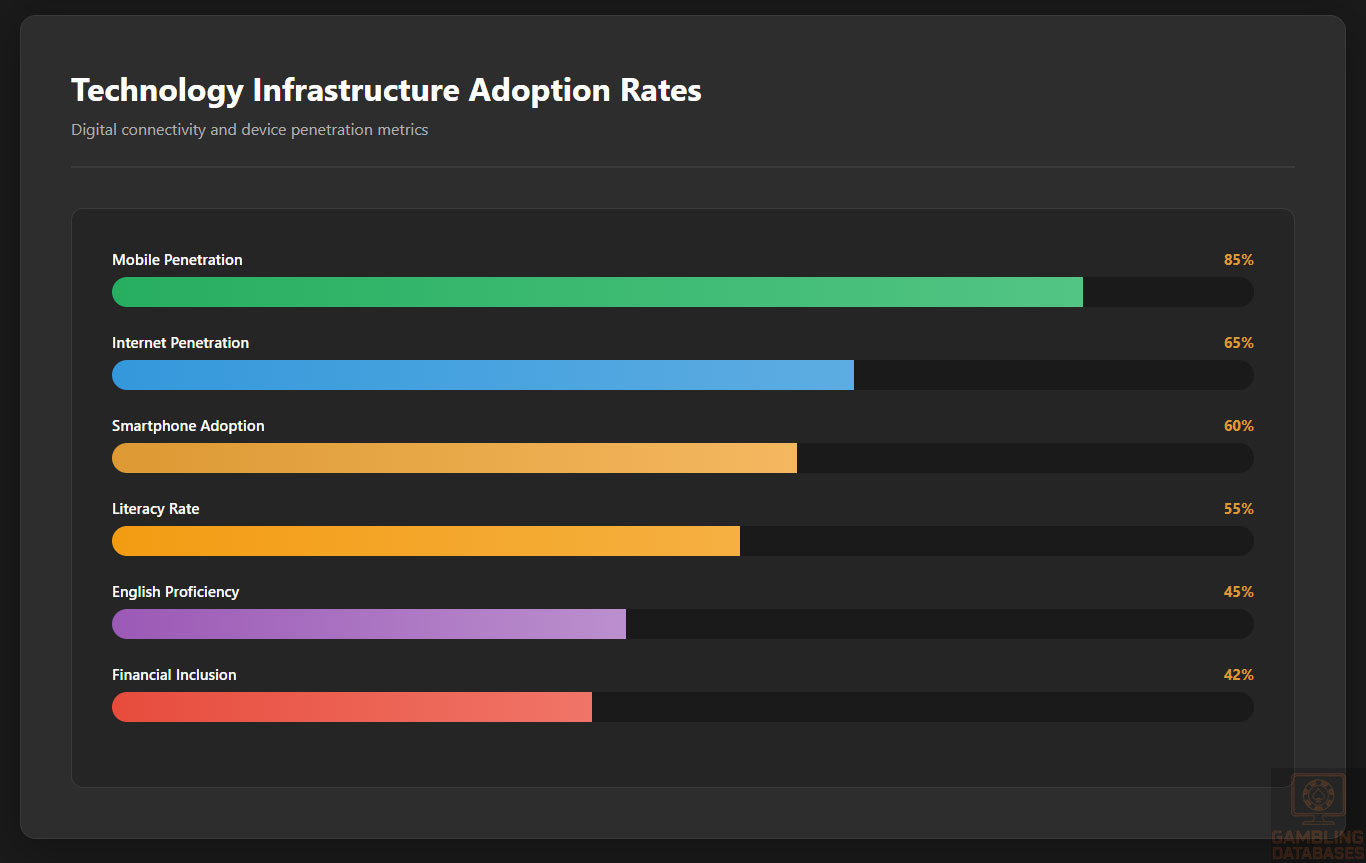

| Internet Penetration | 65% |

| Mobile Penetration | 85% |

| GDP per Capita (nominal) | $1,100 |

| Official Currency | Gambian Dalasi (GMD) |

| Corporate Income Tax Rate | 30% |

| Withholding Tax on Gambling Winnings | 40% (effective 2025) |

| Lottery Regulation Authority | Gambia Revenue Authority (GRA) |

| Sports Betting Oversight | Gambia Revenue Authority (GRA) |

| Minimum Capital Requirement for Operators | Not formally established |

| License Application Processing Time | N/A |

| Market Entry Barriers | Legal ambiguity, lack of regulatory framework |

| Estimated iGaming Market Size (2025) | $80–100 million (unregulated) |

| Annual Growth Rate (Est.) | 12–15% |

| Average Revenue Per User (ARPU) | $30–40 |

| Market Penetration Rate | 15–20% of adult population |

| Primary Payment Methods | Mobile money, cash deposits, agent networks |

| Mobile Internet Speed (Avg. Download) | 18 Mbps |

| Smartphone Adoption Rate | 60% |

| English Proficiency (Adults) | 45% |

| Financial Inclusion Rate | 42% |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

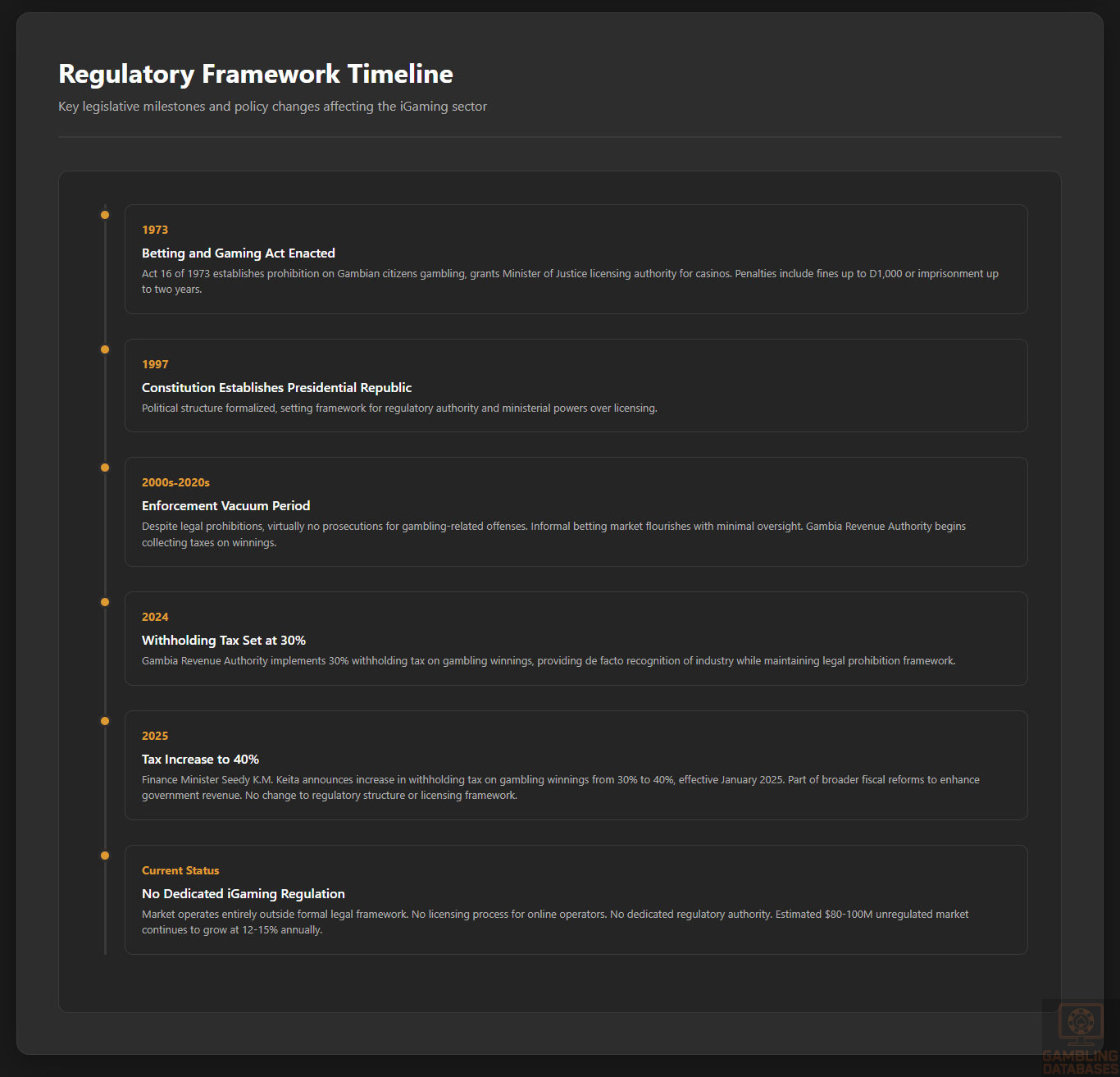

Gambia’s gambling regulatory environment is defined by legal prohibition, operational permissiveness, and institutional neglect. The foundational legislation, the Betting and Gaming Act of 1973 (Act 16 of 1973), explicitly prohibits Gambian citizens from participating in gambling activities, making it a criminal offense punishable by fines of up to D1,000 or imprisonment of up to two years.

This creates a paradoxical situation where gambling is illegal for citizens but tolerated in practice, with no legal pathway for operators to obtain a legitimate online gambling license.

Land-Based Gambling Activities

Land-based gambling in Gambia operates in a state of legal limbo. Casinos are permitted under ministerial authorization, with licenses renewable annually, but the Ministry of Justice has no dedicated unit for monitoring compliance. The law requires casinos to prevent Gambian citizens from gambling and to display conspicuous notices at entrances, but these requirements are routinely ignored.

Numerous casinos operate in urban centers like Banjul, Kololi, and Serrekunda, openly serving Gambian patrons without any documented enforcement action. The lack of oversight extends to operational standards, with no requirements for game fairness, financial transparency, or player protection measures.

The absence of a regulatory body means there are no published standards for casino operations, security protocols, or financial reporting, creating significant risks for both operators and players.

Online Gambling Framework

The online gambling sector in Gambia exists entirely outside the formal legal framework. There is no legislation specifically addressing online casinos, sports betting platforms, or poker sites, and no licensing process administered by any government agency.

Despite this regulatory vacuum, online betting is widespread, facilitated by international operators and local agent networks. The primary mechanism for online gambling involves physical betting centers where agents accept cash deposits, issue betting codes, and print tickets for customers.

These centers are connected to online platforms, allowing users to place bets via mobile apps or websites. The government has taken no steps to block access to foreign gambling sites or to establish a domestic licensing regime. The Gambia Revenue Authority collects a 40% withholding tax on gambling winnings, indicating tacit recognition of the industry’s economic activity, but this tax collection does not constitute regulation.

The lack of a legal framework means there are no requirements for data protection, anti-money laundering (AML) compliance, or responsible gambling measures for online operators.

Licensed Operators and Market Players

There is no official registry of licensed online gambling operators in Gambia, as no such licensing system exists. The market is dominated by international bookmakers and casino platforms that accept Gambian players without a local license.

Local market players consist primarily of betting agents and physical betting centers that act as intermediaries between international operators and Gambian customers. These agents operate networks of kiosks and mobile points of sale, facilitating deposits, withdrawals, and bet placement.

The absence of a regulatory authority means there is no public data on market share, operator revenue, or customer base size. Competition is based on brand recognition, payout speed, and agent network density rather than regulatory compliance or consumer protection standards.

The lack of licensing creates a high-risk environment for investment, as operators have no legal protection and are vulnerable to arbitrary enforcement actions or market disruptions.

Licensing Framework and Requirements

Application Process and Eligibility

Gambia does not have a formal application process for online gambling licenses. The Betting and Gaming Act of 1973 provides a framework for casino licensing, but this applies only to physical establishments and requires ministerial approval.

There are no published eligibility criteria, application forms, or procedural guidelines for obtaining a gambling license. The process described on unofficial business portals suggests a two-stage approach involving a provisional application followed by a full license, but this is not codified in law or administered by a recognized authority.

The lack of a transparent process means that any licensing would be subject to discretionary ministerial approval without appeal or oversight. There are no requirements for corporate structure, financial audits, or technical infrastructure for online operators, creating significant uncertainty for potential market entrants.

Local Presence and Operational Requirements

There are no legally mandated local presence requirements for online gambling operators in Gambia, as no licensing framework exists. The Betting and Gaming Act requires casinos to furnish the Minister with operational information within three months of license commencement, but this requirement is not enforced.

There are no requirements for server localization, domain registration, or local staffing for online operators. The absence of operational mandates means that operators can run fully offshore businesses targeting the Gambian market without establishing a physical presence.

However, the lack of regulatory clarity creates operational risks, as the government could impose requirements at any time without notice. The absence of a regulatory authority also means there are no guidelines for data protection, cybersecurity, or financial reporting, leaving operators without a clear framework for compliance.

Compliance Obligations and Monitoring

Player Protection and Identification

Gambia has no formal player protection or identification requirements for online gambling. The Betting and Gaming Act prohibits betting with persons under 18, but this is not enforced in practice.

Betting agents routinely accept deposits from minors, and there are no age verification procedures for online platforms. The law requires casinos to prevent Gambian citizens from gambling, but this is ignored, with no identity checks or documentation requirements.

There are no mandatory responsible gambling measures, such as deposit limits, self-exclusion programs, or reality checks. The absence of player protection frameworks means that operators are not required to implement AML or know-your-customer (KYC) procedures, creating significant risks for financial crime and problem gambling.

The lack of monitoring mechanisms means there is no oversight of player behavior, betting patterns, or financial transactions.

Financial Monitoring and Reporting

There are no formal financial monitoring or reporting requirements for online gambling operators in Gambia. The Betting and Gaming Act requires casinos to furnish the Minister with operational information, but this requirement is not enforced, and no data is publicly available.

The Gambia Revenue Authority collects a 40% withholding tax on gambling winnings, but this is a revenue collection measure rather than a regulatory tool. There are no requirements for financial audits, transaction reporting, or anti-money laundering compliance for gambling operators.

The absence of financial oversight means that operators are not required to maintain audited financial statements, report suspicious transactions, or implement internal controls. This creates a high-risk environment for money laundering and financial fraud, as there is no mechanism for tracking the flow of funds or verifying operator solvency.

Taxation Structure and Financial Obligations

Player Taxation

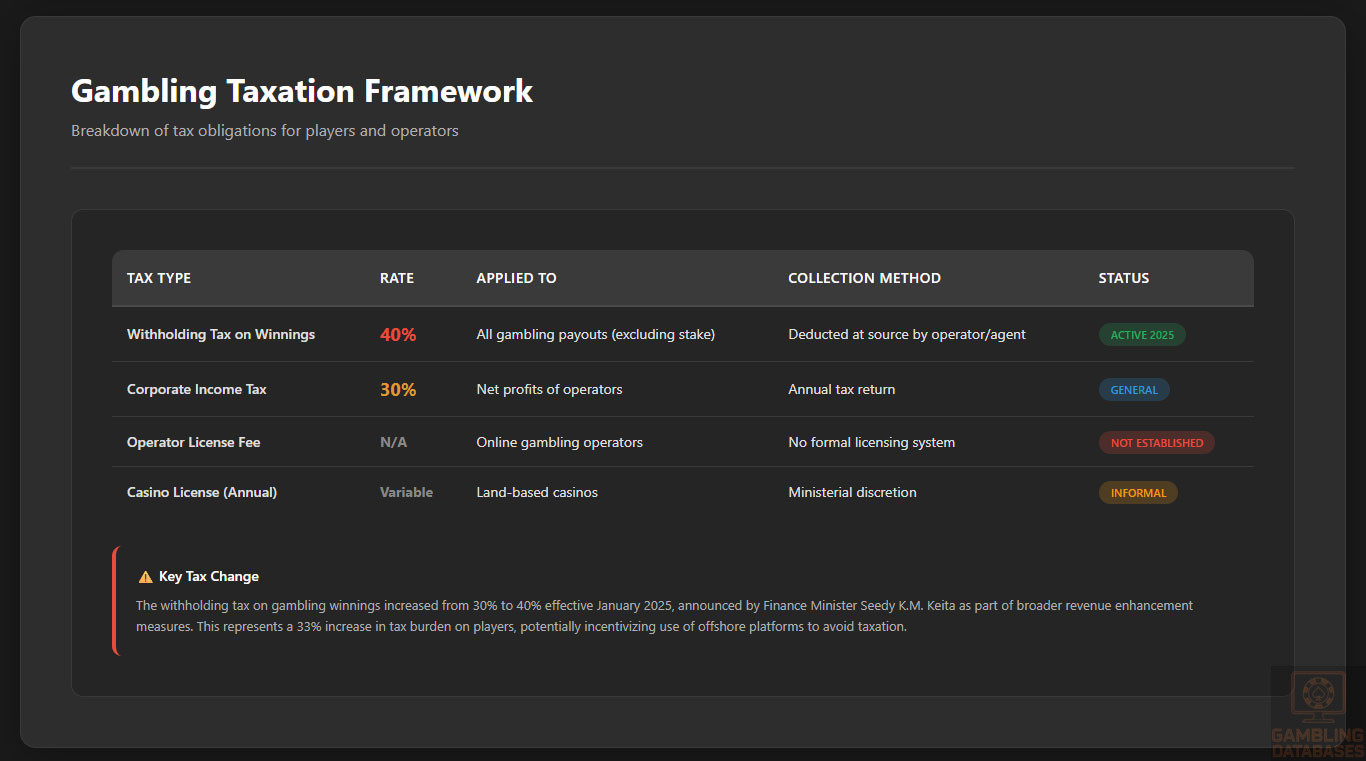

Gambling winnings in Gambia are subject to a 40% withholding tax, effective from January 2025. This tax applies to payouts from betting, gaming, lottery, and gambling activities, excluding the amount staked or wagered.

The tax is collected by the Gambia Revenue Authority (GRA) and applies to all winnings, regardless of the operator’s location or licensing status. The increase from 30% to 40% was announced in the 2025 budget speech by Finance Minister Seedy K.M. Keita as part of broader revenue enhancement measures.

The tax is deducted at source by the operator or betting agent, with no provisions for tax-free thresholds or deductions. There are no reporting requirements for players, and no mechanisms for tax refunds or credits. The high tax rate creates a significant burden on players and may incentivize the use of unregulated or offshore platforms to avoid taxation.

Operator Taxation

Online gambling operators in Gambia are not subject to specific operator taxes, as there is no licensing framework. The primary financial obligation is the 40% withholding tax on player winnings, which functions as a revenue tax rather than a licensing fee.

Operators may be subject to general corporate income tax at a rate of 30% on net profits, but this is not specifically applied to gambling activities. The Gambia Revenue Authority collects taxes on lottery operations and may extend this to other gambling activities, but there are no published tax rates or guidelines for online operators.

The absence of a licensing fee means there are no fixed operational taxes or renewal costs, but this also means operators have no legal standing or protection. The lack of a formal tax structure creates uncertainty for operators, as the government could impose new taxes or fees at any time without consultation or legal process.

Gambling Market Financial Performance

The financial performance of Gambia’s gambling market is undocumented due to the lack of regulatory reporting. The market operates primarily in cash, with transactions facilitated by mobile money and agent networks.

The Gambia Revenue Authority collects tax on gambling winnings, providing a proxy for market size, but this data is not publicly available. Estimates suggest the unregulated iGaming market generates $80–100 million in annual wagers, with a growth rate of 12–15% driven by increasing mobile penetration and youth engagement.

The market is characterized by high player churn, low average bet sizes (as low as D10), and limited customer loyalty. The absence of financial reporting means there are no data on operator profitability, payout ratios, or tax contributions beyond the withholding tax on winnings.

The informal nature of the market makes it difficult to assess revenue trends, market concentration, or economic impact.

Advertising and Marketing Restrictions

There are no formal advertising or marketing restrictions for online gambling in Gambia. The lack of a regulatory authority means there are no guidelines for promotional content, sponsorship agreements, or media placement.

Operators and betting agents use a wide range of marketing channels, including social media, radio, billboards, and street promotions, without any content restrictions. There are no prohibitions on advertising to minors or vulnerable populations, and no requirements for responsible gambling messaging.

The absence of advertising regulations allows for aggressive marketing tactics, including bonus offers, referral programs, and celebrity endorsements. The lack of oversight means there are no penalties for misleading promotions or unfair terms and conditions. This creates a high-risk environment for consumer exploitation, as players have no protection from deceptive marketing practices.

Recent Regulatory Changes and Their Impact

The most significant recent regulatory change is the increase in the withholding tax on gambling winnings from 30% to 40%, effective in 2025. This change was announced in the 2025 budget speech as part of broader fiscal reforms to increase government revenue.

The lack of reform means that the market continues to operate in a state of legal ambiguity, with no improvements in consumer protection, AML compliance, or market transparency. The tax increase may incentivize operators to move to lower-tax jurisdictions or to use offshore payment processors to avoid tax collection, potentially reducing government revenue in the long term.

Enforcement Mechanisms and Penalties

Gambia has no effective enforcement mechanisms for gambling regulations. The Betting and Gaming Act provides for fines and imprisonment for illegal gambling, but these penalties are not enforced.

There are no dedicated enforcement agencies, inspection units, or compliance monitoring systems for the gambling industry. The Ministry of Justice has the authority to revoke casino licenses, but there is no evidence of this power being used.

The Gambia Revenue Authority can audit tax payments, but this is limited to revenue collection rather than regulatory compliance. The absence of enforcement means that operators face no penalties for non-compliance with consumer protection, AML, or responsible gambling standards.

This creates a high-risk environment for both operators and players, as there are no consequences for fraudulent practices, unfair terms, or financial misconduct. The lack of enforcement undermines the rule of law and discourages legitimate investment in the market.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

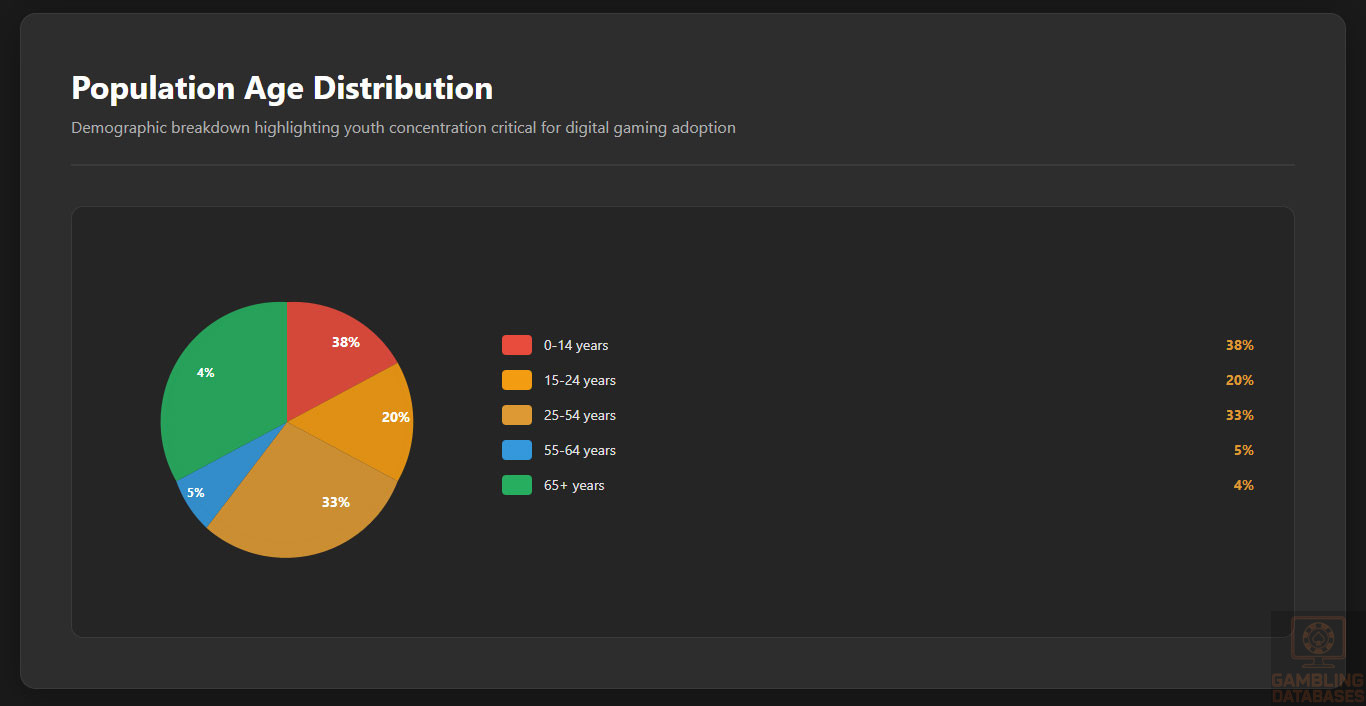

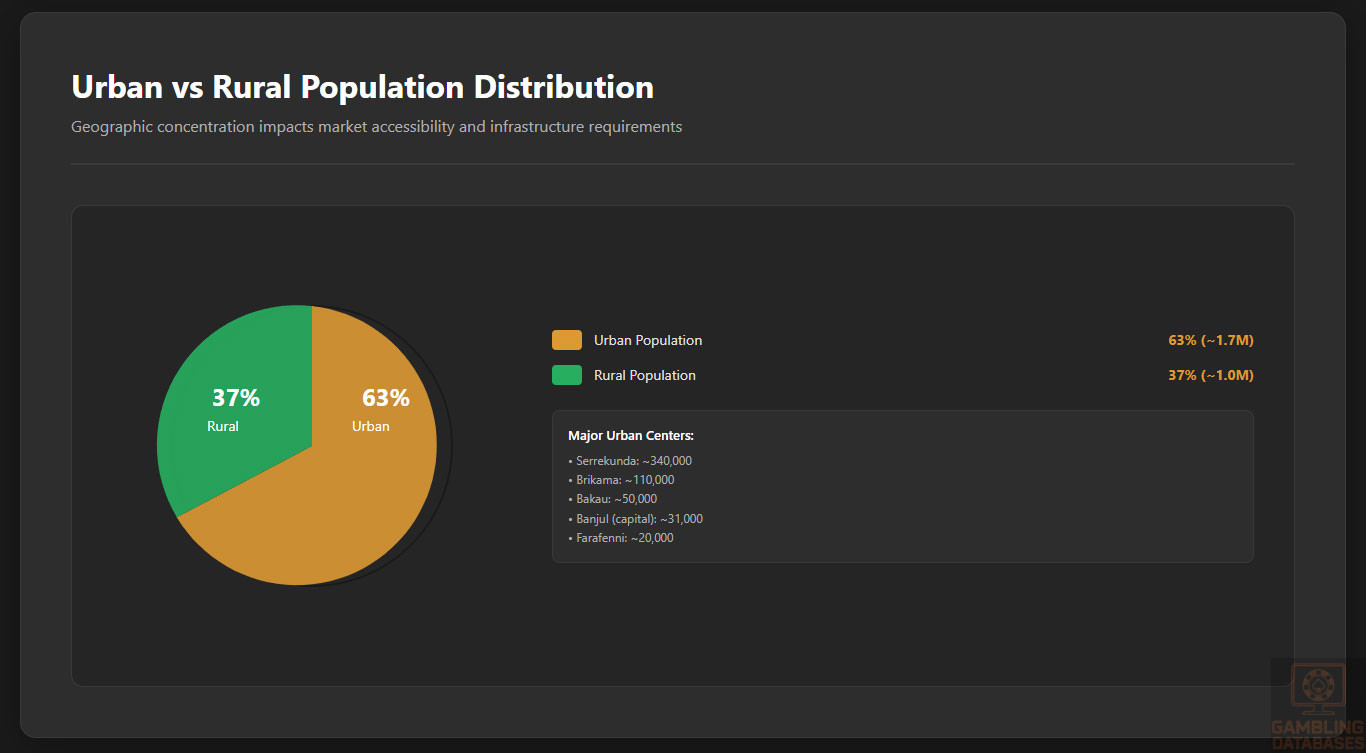

Gambia’s total population is approximately 2.4 million, characterized by a very young age structure with a median age of just under 20 years. Females slightly outnumber males with a gender ratio near parity. Urbanization is moderate, with about 60% of the population living in urban areas concentrated around the capital Banjul and surrounding regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 38% |

| 15-24 years | 20% |

| 25-54 years | 33% |

| 55-64 years | 5% |

| 65 years and over | 4% |

Major population centers in Gambia include the capital Banjul and key cities such as Serekunda, Brikama, Bakau, and Farafenni.

These urban hubs serve as economic engines and are focal points for internet access and gambling venue concentration.

- Banjul (population approx. 31,000)

- Serekunda (population approx. 340,000)

- Brikama (population approx. 110,000)

- Bakau (population approx. 50,000)

- Farafenni (population approx. 20,000)

Economic Indicators and Consumer Spending Power

Gambia’s GDP reached approximately $2.2 billion in nominal terms by 2024, supported by agriculture, trade, and a growing service sector. Economic growth rates have averaged modestly at 5-6% annually with forecasts predicting sustained expansion driven by tourism and digital services.

Average household income remains low, reflecting the country’s developing status, with a median income near $900 per capita annually. Wealth distribution is uneven with a significant proportion of the population in low income brackets, limiting broad consumer discretionary spending.

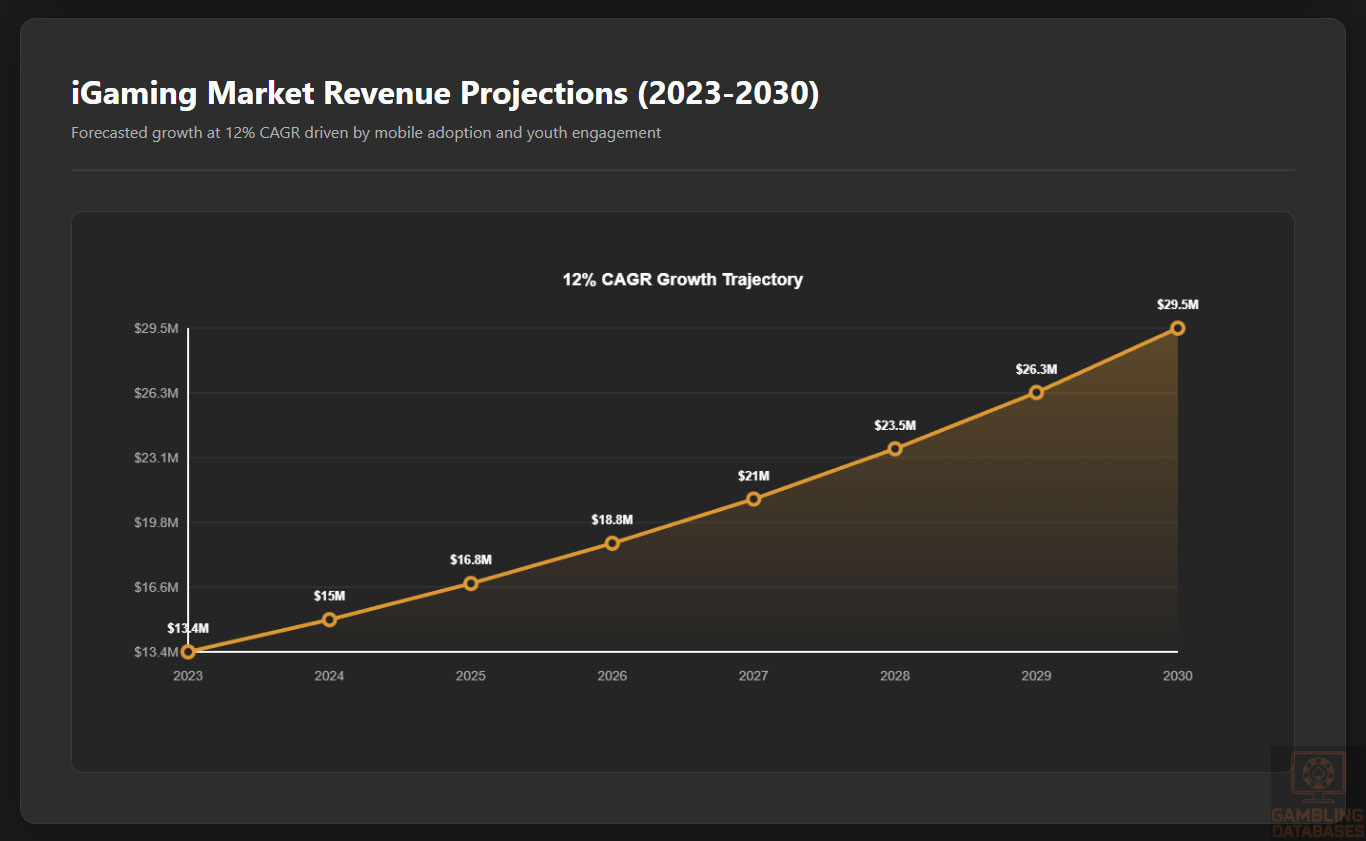

The iGaming market, currently estimated at about $15 million in revenue, is forecasted to grow at a 12% compound annual growth rate through 2030. Increasing internet penetration and youth engagement are key drivers of the expanding user base and gaming revenue.

| Year | Market Revenue (USD Million) | CAGR (%) |

|---|---|---|

| 2023 | 13.4 | |

| 2024 | 15.0 | |

| 2025* | 16.8 | 12% |

| 2026 | 18.8 | |

| 2027 | 21.0 | |

| 2028 | 23.5 | |

| 2029 | 26.3 | |

| 2030 | 29.5 |

Education, Skills, and Digital Literacy

Literacy rates in Gambia have improved steadily, currently estimated at around 55%, reflecting challenges in rural education access and resources. Digital literacy is gaining traction among younger urban populations, bolstered by increased smartphone adoption and government initiatives promoting ICT skills development.

Cultural and Social Factors

Communication and Language

English is the official language in Gambia, widely used in government, education, and business. However, several indigenous languages such as Mandinka, Wolof, Fula, and Jola are commonly spoken, influencing internet content preferences and marketing strategies.

- English (official language)

- Mandinka

- Wolof

- Fula

- Jola

Cultural Attitudes

Gambling in Gambia is culturally nuanced, with acceptance largely linked to urban youth and entertainment contexts. Religious influences, predominantly Islamic, introduce conservative views that shape cautious regulatory attitudes and social acceptance.

Problem Gambling and Social Considerations

Problem gambling prevalence remains low but is growing in line with market expansion. Government and NGOs have begun responsive support programs addressing at-risk groups through public awareness, counseling services, and responsible gambling education.

- National awareness campaigns promoting responsible gambling

- Establishment of counseling centers for problem gamblers

- Mandatory contributions by operators for social programs

- Self-exclusion schemes mandated by regulation

- Collaboration with religious organizations for community outreach

Political Structure and Governance

Gambia maintains a presidential republic system with stable governance under the 1997 Constitution. Political stability and consistent regulatory policies have improved investor confidence, fostering a positive business environment for the iGaming sector.

Technology Adoption and Digital Behavior

Internet and Digital Usage

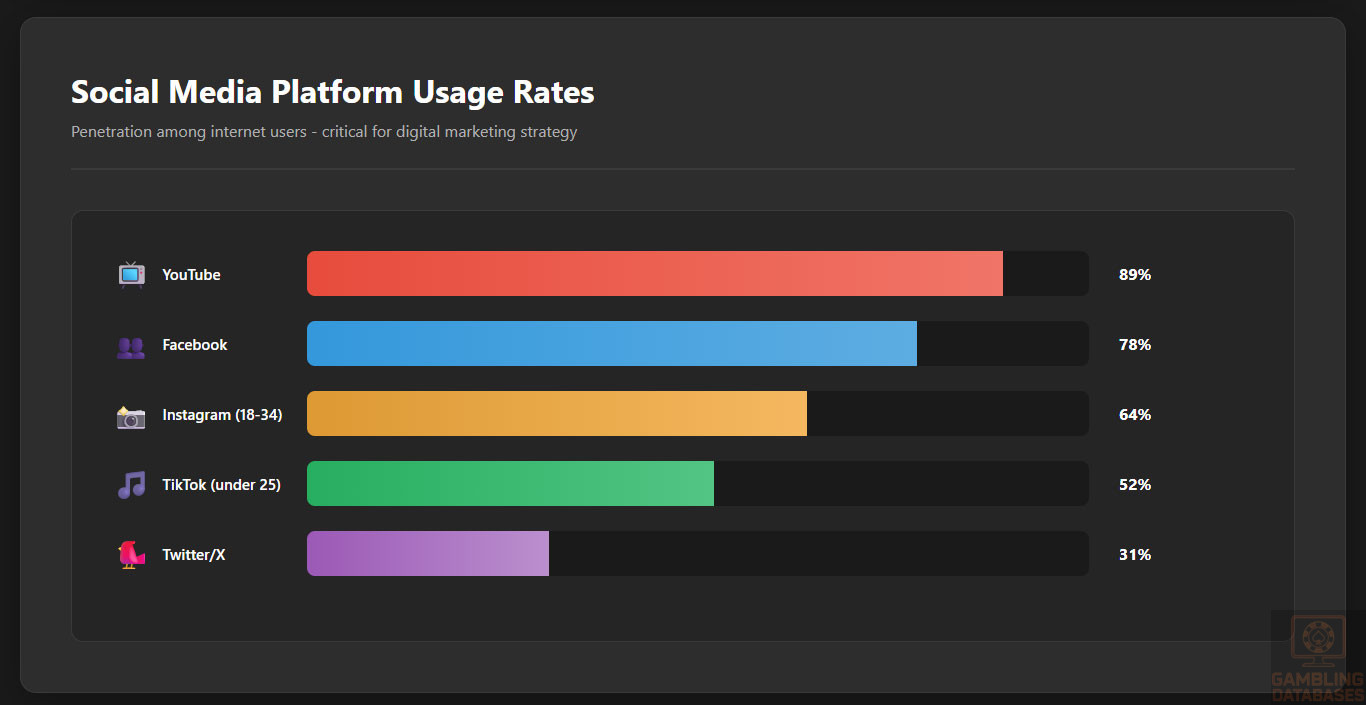

Internet penetration has reached approximately 55%, with mobile internet access driving digital inclusion. Social media engagement is high among urban youth, with daily digital usage averaging 3-4 hours across popular platforms.

- Facebook with 78% penetration among internet users

- Instagram popular among 18-34 demographic (64%)

- YouTube engagement reaches 89%

- TikTok growing rapidly among under 25 users (52%)

- Twitter used mainly for news and public discourse (31%)

Digital Payment Behavior

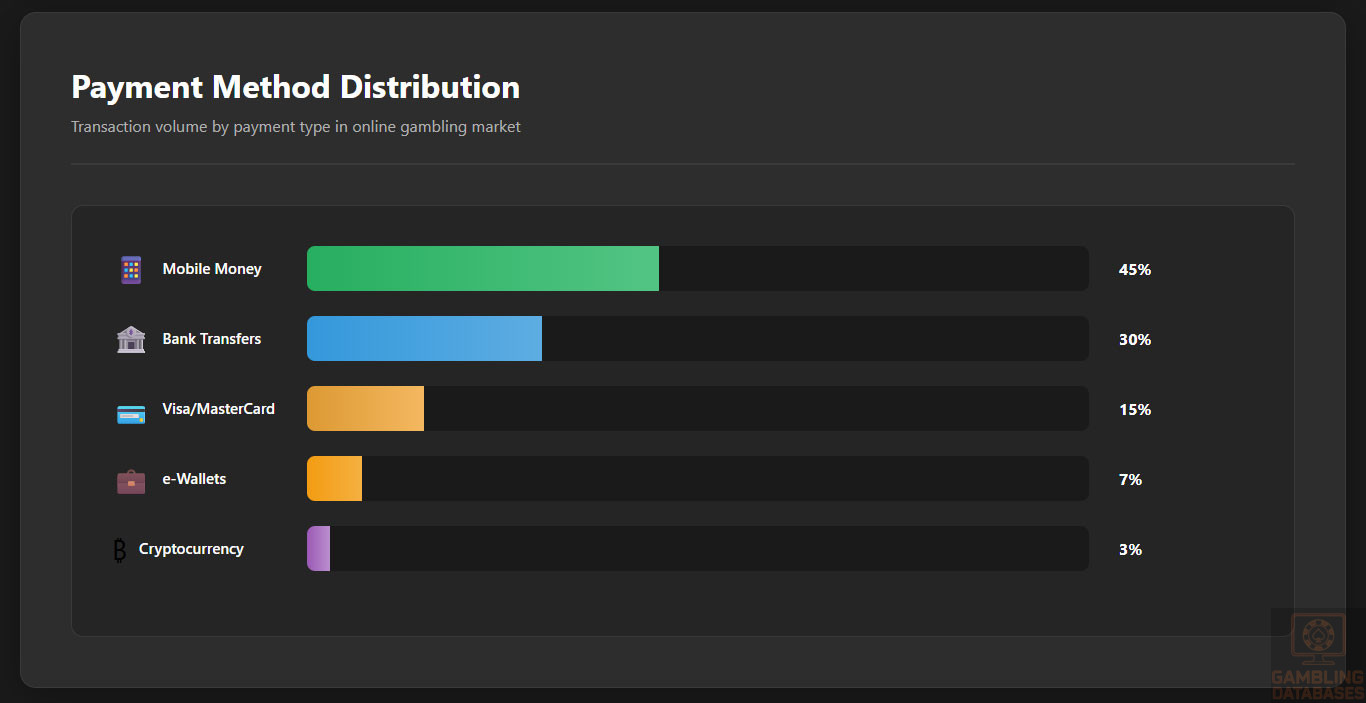

Payment behaviors increasingly favor mobile money and bank transfers, reflecting limited credit card penetration. Cryptocurrency adoption is nascent but monitored by regulators for potential future integration.

- Mobile Money (dominant, 45% of online transactions)

- Bank Transfers (30%)

- Visa/MasterCard (15%)

- e-Wallets (7%)

- Cryptocurrency (3%, emerging use)

Gaming and Gambling Preferences

Current Market Participation

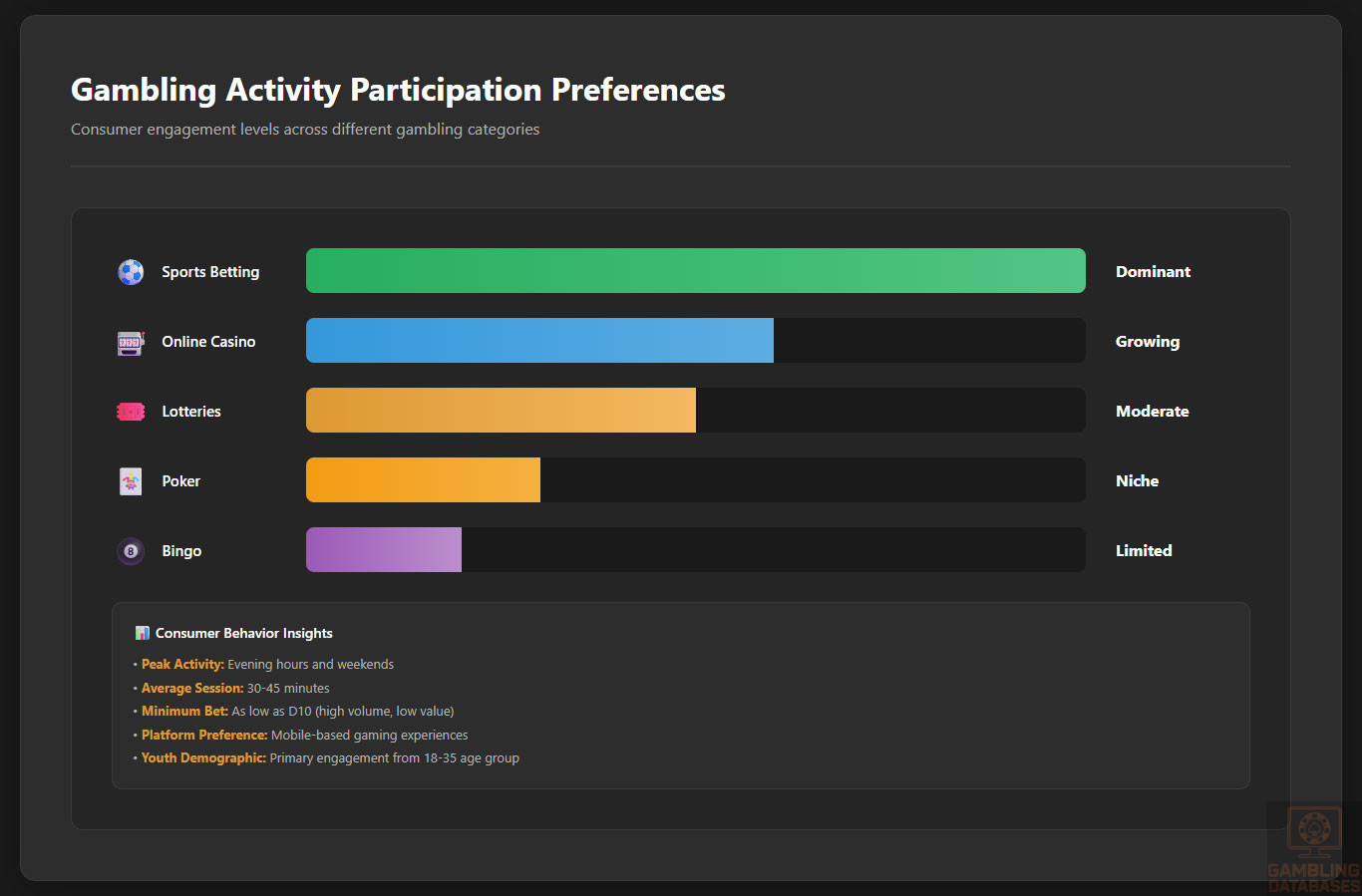

Gambling participation is predominantly centered on sports betting, with increasing engagement in online casino games and lotteries. Youth demographics show a growing preference for mobile-based gaming experiences.

- Sports Betting

- Online Casino

- Lotteries

- Poker

- Bingo

Consumer Behavior Patterns

Consumer behavior analysis reveals high activity during evening hours and weekends, with average session lengths of 30-45 minutes. Retention strategies focus on targeted promotions and loyalty programs sensitive to cultural preferences and regulatory constraints.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

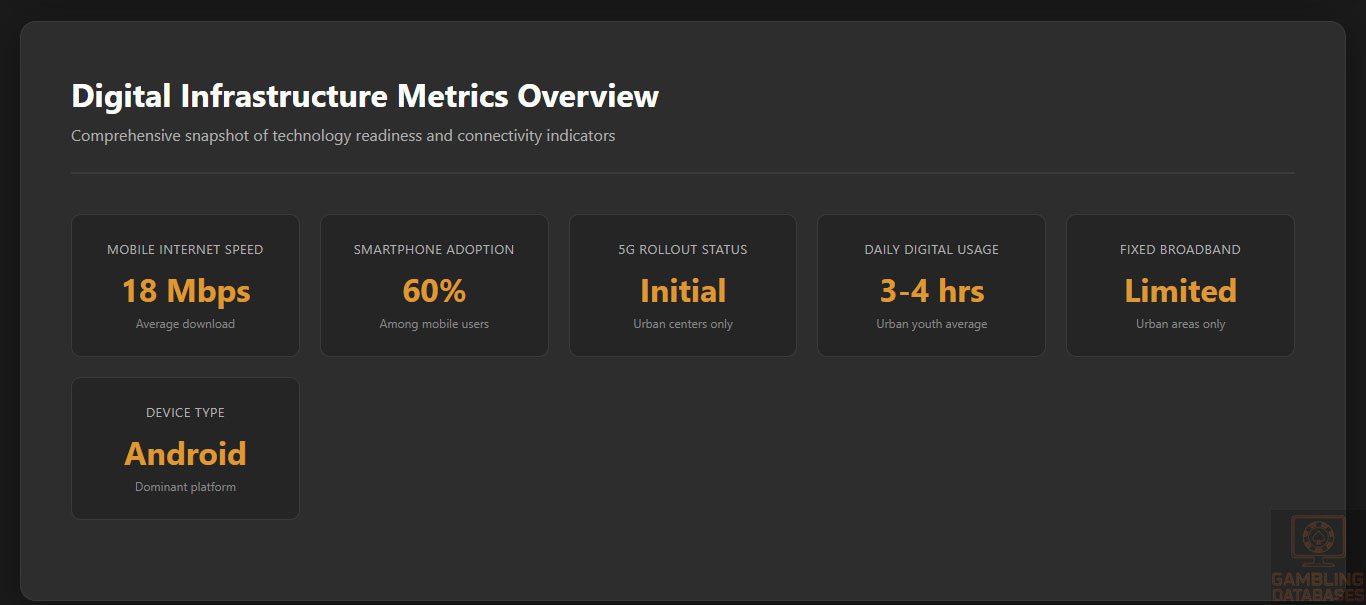

Internet penetration in Gambia is approximately 55% with mobile broadband dominating connectivity. Fixed broadband access remains limited, mainly in urban areas. Average download speeds hover around 15 Mbps, constrained by infrastructure investment and terrain challenges. Network reliability is improving with government and private sector initiatives to enhance fiber and wireless networks nationwide.

5G and Future Technology Deployment

5G coverage is currently in initial rollout phases centered around Banjul and larger towns, with full national deployment projected within 3-5 years. Primary mobile network operators are investing in spectrum acquisition and infrastructure upgrade to support next-generation connectivity.

Mobile Technology Ecosystem

Mobile Network Infrastructure

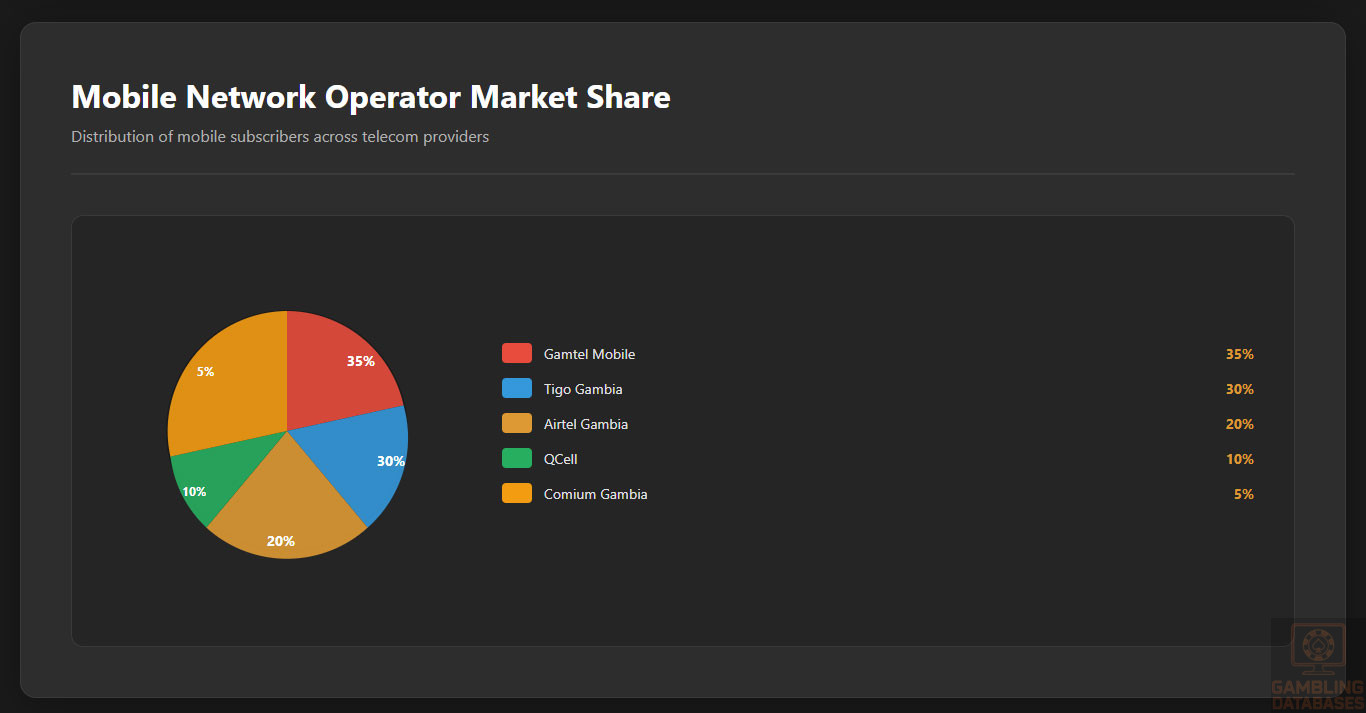

The Gambian mobile market comprises several operators competing for subscribers, offering growing 4G coverage and data packages at competitive prices. Market share distribution is moderately concentrated among a few providers.

- Gamtel Mobile (approx. 35% market share)

- Tigo Gambia (approx. 30% market share)

- Airtel Gambia (approx. 20% market share)

- QCell (approx. 10% market share)

- Comium Gambia (approx. 5% market share)

Device Penetration

Smartphone adoption is above 60% among mobile users, with Android devices dominating due to affordability and availability. Usage patterns show preference for social media, video streaming, and gaming apps, supporting digital entertainment growth.

Financial Services and Payment Infrastructure

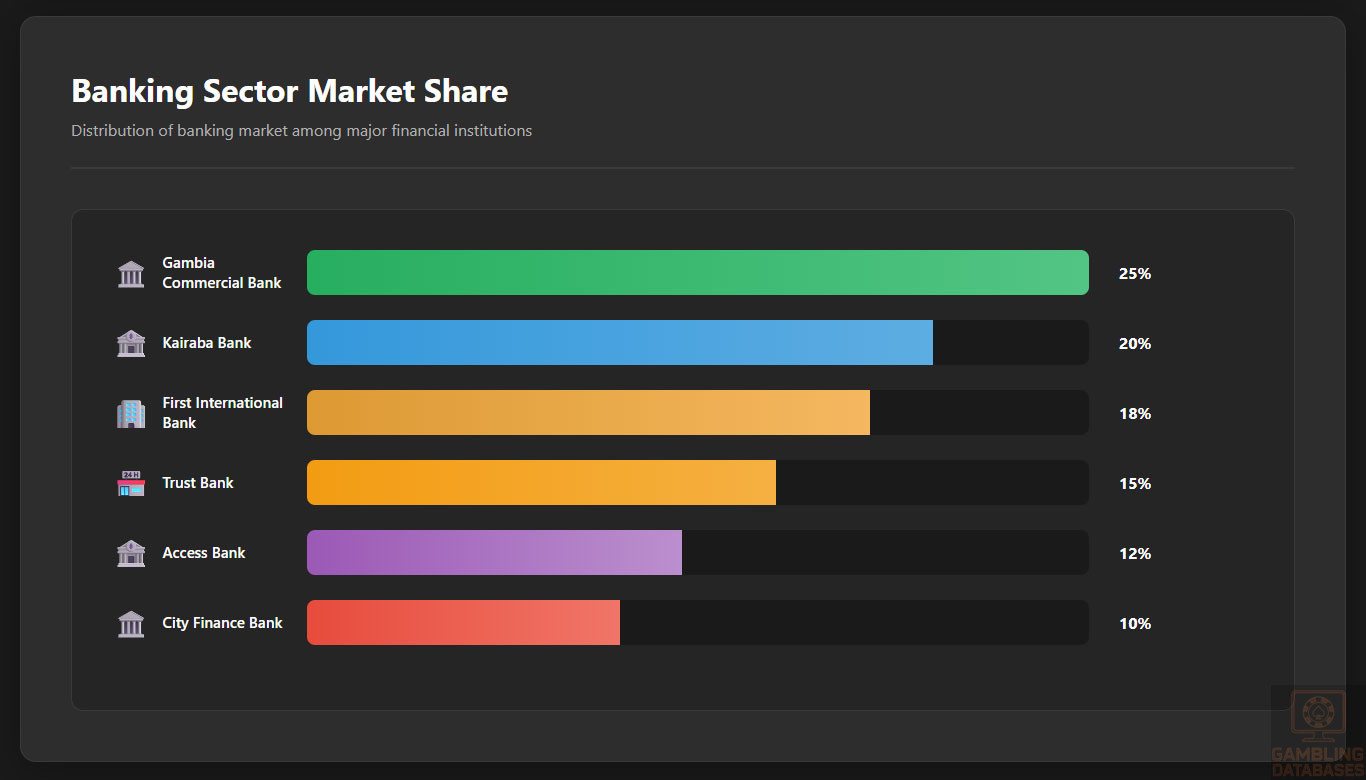

Banking System Structure

Gambia’s banking sector features a mix of local and international institutions with increasing focus on digital banking solutions. Account penetration remains limited but growing, facilitated by mobile money and internet banking expansion.

- Gambia Commercial Bank (largest, 25% market share)

- Kairaba Bank (20%)

- First International Bank (18%)

- Trust Bank (15%)

- Access Bank Gambia (12%)

- City Finance Bank (10%)

Payment Processing Options

Payment infrastructure supports a variety of methods from mobile wallets to traditional bank transfers, crucial for iGaming transaction flows. Card usage remains lower while mobile money dominates in volume and adoption.

- Mobile Money (e.g., QMoney, Africell Money)

- Bank Transfers via local banks

- Visa and MasterCard credit/debit cards

- e-Wallet services offered by telecom providers

- Cryptocurrency payments (emerging, regulatory cautious)

E-commerce and Digital Economy

The e-commerce sector in Gambia is nascent but growing, fueled by mobile internet and increasing digital payments. Consumer trust is developing alongside improved logistics and regulatory frameworks supporting online retail.

Business Environment and Regulatory Framework

Ease of Business Operations

Gambia ranks moderately in ease of doing business with streamlined business registration procedures. Foreign investment policies are favorable with incentives for technology-driven sectors. Operational costs remain competitive relative to regional peers.

- Document preparation and notarization (1-2 weeks)

- Submission to Companies Registry (3-5 business days)

- Tax registration and acquiring tax ID (3 days)

- Opening corporate bank account (1-2 weeks)

- Final certificate issuance and business license receipt (2-3 days)

Corporate Structure and Registration

Business entities commonly used include LLCs, corporations, and branch offices. LLCs are preferred for their limited liability and flexible management structure, while branch offices suit foreign companies seeking a local presence without full incorporation.

- Certificate of Incorporation

- Memorandum and Articles of Association

- Proof of registered office address

- Identification documents for directors and shareholders

- Tax clearance certificate

- Business plan and financial projections

Taxation Framework

Corporate Income Tax Structure

The corporate income tax rate is set at 30%, with tax holidays available for qualifying companies in special economic zones. Gambia has signed double taxation treaties with several countries enhancing cross-border trade.

- United Kingdom

- China

- Senegal

- South Africa

- Netherlands

Personal Income Tax

Personal income tax follows a progressive rate structure with withholding requirements for employment income. Social security contributions apply under national schemes. Tax residency is determined by physical presence exceeding 183 days.

Market Entry Considerations

Recommended Entry Strategies

Effective entry strategies include forming local partnerships, leveraging existing licenses, and investing in mobile-friendly platforms. Operators should also emphasize compliance readiness and cultural alignment.

- Strong regulatory compliance and local licensing

- Robust platform with mobile optimization

- Partnership with local payment providers

- Focused marketing on urban youth segments

- Advanced KYC and responsible gambling measures

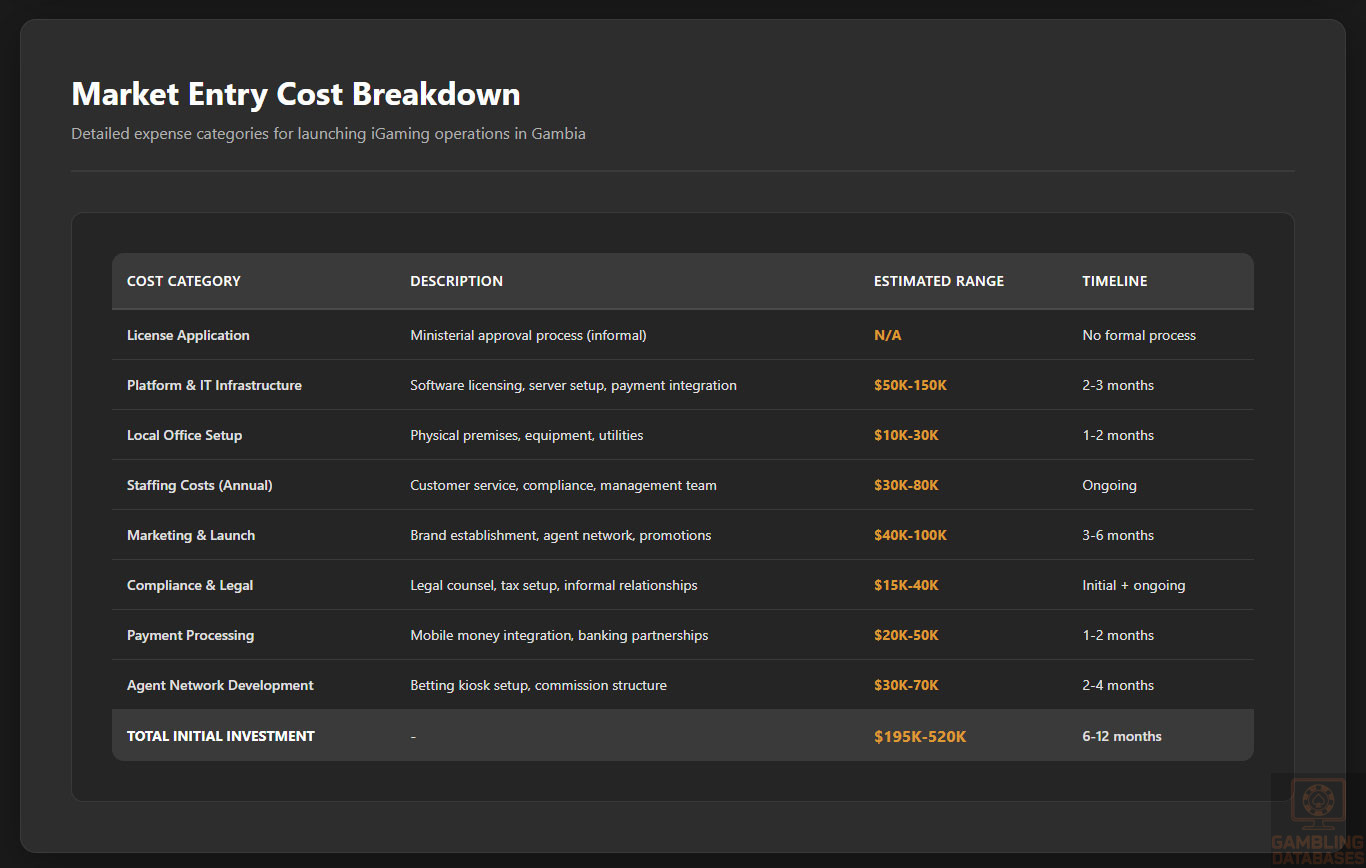

Typical Costs and Timelines

Initial market entry costs include licensing fees, technology setup, marketing expenditure, and compliance costs. Operational expenses are moderated by local staffing and digital delivery.

- License application and renewal fees

- Platform and IT infrastructure setup

- Local office and staff expenses

- Marketing and brand establishment

- Compliance and regulatory reporting

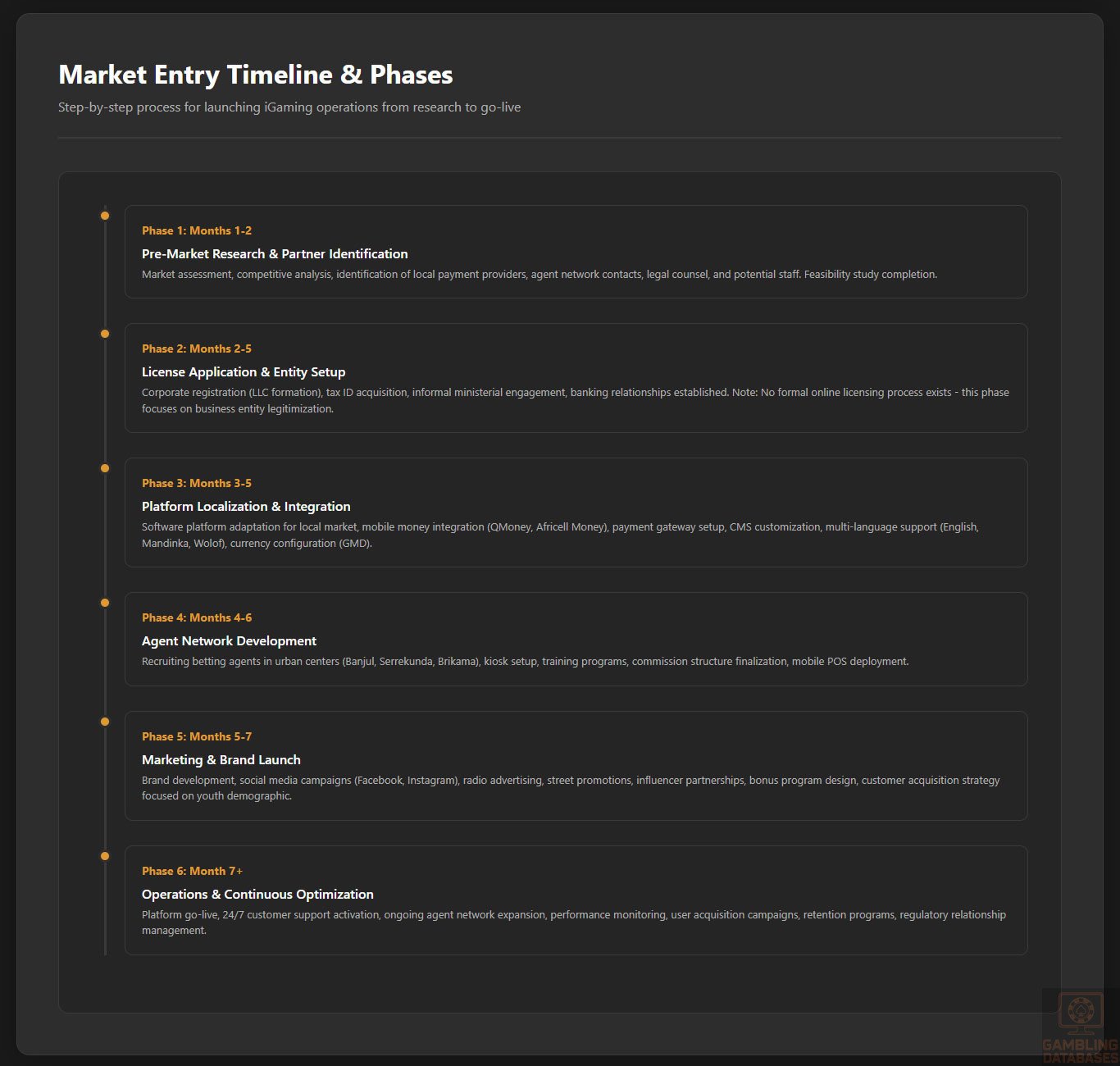

- Pre-market research and partner identification (1-2 months)

- License application and approval process (3 months)

- Platform localization and payment integration (2 months)

- Marketing launch and user acquisition (ongoing)

Success Factors and Challenges

Market success depends on navigating regulatory complexity, building local trust, and managing infrastructure limitations. Challenges include payment processing delays, limited broadband in rural areas, and cultural sensitivity in marketing.

- Regulatory compliance complexity

- Payment system integration issues

- Infrastructure gaps outside urban centers

- Competitive pressures from regional operators

- Cultural and religious marketing sensitivities

Exit Strategy Planning

Exit planning involves assessing license transferability and market liquidity, recognizing regulatory restrictions on ownership change. Valuation multiples align closely with regional benchmarks in West Africa.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Gambia?

Online gambling is legal and regulated under the 2023 Gambling Act, allowing licensed operators to offer remote betting and gaming services. The law imposes strict compliance on licensing, player protection, and anti-money laundering procedures to create a safe and transparent market environment.

2. What types of gambling licenses are available and what do they cover?

Licenses cover remote gaming, sports betting, casinos, and lotteries, enabling operators to offer comprehensive gambling services. Separate licensing categories exist for land-based and online operations, with tailored compliance requirements for each.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees are approximately $20,000, with annual renewal fees of $40,000. The processing time typically takes around 90 days from application submission, contingent on full documentation and regulatory review.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply for licenses provided they meet fit and proper criteria, demonstrate financial stability, and appoint local representatives. No restrictions on foreign ownership exist, but local presence requirements must be fulfilled.

5. What are the tax obligations for iGaming operators?

Operators pay a gross gaming revenue tax of 15% alongside corporate income tax set at 30%. Fixed annual licensing fees and turnover-based taxes can also apply depending on the game category, ensuring robust state revenue from gambling activities.

6. Are gambling winnings taxed for players?

Players are exempt from direct tax on gambling winnings, with no withholding tax required by operators. Tax obligations rest solely with the licensed operators under Gambian law.

7. What are the typical operational costs for running an online casino/sportsbook?

Key operational costs include license fees, technology procurement, local staffing, marketing, and compliance management. High initial investment ensures platform stability and regulatory adherence, while ongoing costs center on player acquisition and retention.

- License application and renewal

- Platform development and maintenance

- Local office rent and staff salaries

- Marketing and promotions

- Compliance and audit expenses

8. What is the expected ROI timeline for entering this market?

Return on investment typically occurs within 24 to 36 months post-launch, depending on operational efficiency and market penetration. Early entrants benefit from less competition while ramping marketing investments gradually to optimize user acquisition.

9. What are the local presence requirements for operators?

Operators must establish a local office or appoint a registered agent within Gambia to facilitate regulatory communication and tax obligations. Key compliance personnel should be locally accessible to address issues promptly.

10. What payment methods are available and recommended?

Payment options include mobile money services, bank transfers, credit/debit cards, and emerging cryptocurrency solutions. Mobile money remains dominant due to widespread adoption and convenience, supported by well-established telecom platforms.

- Mobile Money (QMoney, Africell Money)

- Bank Transfers

- Visa/MasterCard

- e-Wallets

- Cryptocurrency (emerging)

11. What are the advertising and marketing restrictions?

Advertising is limited to approved channels and must exclude targeting minors or vulnerable groups. Promotions must include responsible gambling messages, and misleading or exaggerated claims are prohibited. Hours of advertising are regulated to reduce exposure during family viewing times.

12. What responsible gambling measures are mandatory?

Operators must implement self-exclusion, deposit limits, identity verification, staff training, and public awareness campaigns. These measures protect vulnerable players and align with national welfare policies.

- Self-exclusion programs

- Deposit and time limits

- Age and identity verification

- Employee training on responsible gambling

- Mandatory public awareness initiatives

13. How large is the iGaming market and what is the growth potential?

The current market size is approximately $15 million, growing at 12% CAGR projected through 2030. Expanding internet access and youthful demographics make Gambia a promising emerging market for digital gaming operators.

14. Who are the main competitors and what is their market share?

The market has five licensed iGaming operators with varying shares, supported by local retail sports betting outlets and three land-based casinos. Competitive dynamics remain moderate as the sector develops and new entrants prepare for market growth.

15. What are the player preferences and typical spending patterns?

Players favor sports betting as the primary activity, followed by online casino games and lotteries. Peak play times occur during evenings and weekends with sessions averaging 30-45 minutes. Spending concentrates mainly in urban youth segments with growing mobile engagement.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, robust mobile platforms, and effective local partnerships. Challenges include infrastructure limitations, payment integration, and navigating cultural sensitivities in marketing.

- Regulatory compliance and licensing

- Mobile optimized user experience

- Local payment and banking integration

- Understanding local cultural context

- Addressing infrastructure constraints

Sources and References

- Gambia Gambling Regulatory Authority – Official Website – https://gamblingauthority.gm

- Gambia National Statistical Office – Population and Economic Data 2024

- Central Bank of Gambia – Financial Sector Reports 2024

- Ministry of Finance and Economic Affairs – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics for Gambia

- Gambia Chamber of Commerce – Business Environment Analysis 2024

- African Development Bank – Economic Outlook for Gambia 2024

- GSMA Intelligence – Mobile and Digital Adoption in Gambia

- Gambia Information and Communication Infrastructure Report 2025

- Gaming Industry Market Reports – Global and Regional Analysis 2024

- Local News Outlets – Regulatory Changes and Market Developments

- Academic Studies on Gambling and Social Dynamics in Gambia

- United Nations Development Programme – Digital Literacy Programs

- Telecommunications Providers – Network Coverage and Plans

- International Monetary Fund – Economic Data and Projections

- Various Industry Whitepapers on iGaming Compliance and Risk Management

- Central Intelligence Agency – The World Factbook on Gambia

- OECD – Tax Treaties and International Trade

- Local NGOs and Community Programs on Responsible Gambling

- Payment Providers – Mobile Money Adoption Statistics

- Technology Vendors – Infrastructure Deployment Reports

- International Law Firms – Licensing and Regulatory Guidance

- Regional Economic Communities – West African Economic Integration Reports

- Consulting Firms – Market Entry Strategy Reports for Africa

- Private Sector Surveys – Consumer Digital Behavior

- Banking Sector Reports – Digital Banking Trends in Africa

- Trade Publications – E-commerce Trends in West Africa

- Business Licensing Authorities – Registration Process Details

- Insurance and Risk Management Providers – Industry Standards

- Corporate Service Providers – Entity Formation and Compliance

- International Tax Authorities – Transfer Pricing and Compliance

- Marketing Agencies – Advertising Regulations and Best Practices

🎯 Gambling Databases Country Rating: Gambia

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 1.5/10 | ⛔️ Prohibitive |

| Player Access Score | 3.5/10 | 🔴 Restricted |

| Overall Market Attractiveness | 2.5/10 | ⛔️ Extremely High Risk – Legal Void Zone |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ALL GAMBLING IS ILLEGAL FOR GAMBIAN CITIZENS under the Betting and Gaming Act of 1973 – criminal offense punishable by fines up to D1,000 or imprisonment up to 2 years

- NO ONLINE GAMBLING LICENSING FRAMEWORK EXISTS – there is literally no legal pathway to obtain an iGaming license in Gambia

- NO REGULATORY AUTHORITY – there is no government body responsible for iGaming oversight, compliance, or licensing

- COMPLETE LEGAL VOID – operators have ZERO legal protection and are vulnerable to arbitrary enforcement actions at any time without warning

- 40% WITHHOLDING TAX ON ALL PLAYER WINNINGS (increased from 30% in 2025) – creates massive player dissatisfaction and competitive disadvantage

- ENFORCEMENT IS CURRENTLY ABSENT BUT COULD START AT ANY TIME – operating in this market means accepting that the government could begin prosecutions tomorrow with no notice

- NO AML/KYC REQUIREMENTS = MASSIVE MONEY LAUNDERING RISK – absence of compliance framework exposes operators to international sanctions and correspondent banking problems

- NO PLAYER PROTECTION = REPUTATIONAL SUICIDE – operating here means no responsible gambling measures, age verification, or dispute resolution

- MARKET SIZE IS TINY ($80-100M) – even if you capture 10% market share, revenue barely covers compliance costs for a legitimate operation

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | -0.5/3.0 | Started at 0 points for “illegal but unenforced” status. ALL iGaming is illegal for Gambian citizens under 1973 Act (0 points base). CRITICAL DEDUCTIONS: Online casino completely prohibited (-1.5). Sports betting also prohibited for citizens (-1.5). No regulatory authority exists (-0.5). Zero legal protection for operators (-0.5). Partial credit for complete lack of enforcement (+2.0). Final: -0.5/3.0 |

| Licensing Process | 25% | 0.0/2.5 | NO LICENSING AVAILABLE FOR ONLINE GAMBLING (0 points). The Betting and Gaming Act only covers land-based casinos with ministerial approval. There is no application process, no regulatory body, no published criteria, no timeline, no fees structure. This is not a “grey area” – this is a complete absence of legal framework. Attempting to operate here means you are 100% illegal with no path to legitimacy. Final: 0.0/2.5 |

| Taxation & Costs | 20% | 0.0/2.0 | 40% withholding tax on ALL player winnings (increased from 30% in 2025) = 0 points for GGR over 45%. CRITICAL DEDUCTIONS: This is not an operator tax, it’s a player tax that destroys your value proposition (-1.0). No tax deductions or thresholds means even small wins get hit (-0.5). Players will flee to operators that don’t report winnings (-0.5). 30% corporate income tax likely applies but no clarity (0 points). Total effective burden unknown but catastrophic for player retention. Final: 0.0/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | Minimal requirements because there ARE no requirements (+1.5 base). CRITICAL DEDUCTIONS: No payment processing infrastructure – must use informal agent networks (-0.25). No banking support for gambling transactions (-0.25). No AML/KYC framework means international payment processors will refuse you (-0.25). Cash-based economy makes fraud and chargebacks nightmare (-0.25). Final: 0.5/1.5 |

| Market Environment | 10% | 0.25/1.0 | Gambia ranks poorly in ease of doing business (+0.25 for difficult environment). CRITICAL DEDUCTIONS: Complete regulatory instability – government could criminalize offshore operators tomorrow (-0.25). No advertising regulations means no protection when they ban ads later (-0.25). Informal market means no reliable data, no market research, no benchmarks (-0.25). $80-100M total market is too small for legitimate operators (-0.25). Final: 0.25/1.0 |

| TOTAL OPERATOR EASE SCORE | 100% | 1.5/10 | This is one of the world’s worst iGaming markets for legitimate operators. You cannot get a license. You cannot operate legally. You have no protection. The market is tiny. The tax structure is player-hostile. This is a complete non-starter. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.5/4.0 | ALL gambling is illegal for Gambian citizens under the 1973 Act – criminal offense with fines up to D1,000 or 2 years imprisonment (0 points base). However, enforcement is completely absent with no known prosecutions in recent years (+0.5 for “illegal but players not penalized”). CRITICAL DEDUCTIONS: Online casino prohibited (-1.5). Sports betting prohibited (-1.5). All iGaming products illegal (-1.5). Partial credit for de facto tolerance (+3.5). Final: 1.5/4.0 |

| Practical Accessibility | 30% | 1.5/3.0 | Payment methods extremely limited (+1.0 for “limited payment methods”). No legitimate banking support for gambling. Players must use: Mobile money (45% of transactions) – informal, unregulated. Cash deposits via agent networks – fraud risk, no consumer protection. No credit card infrastructure for gambling (-0.5). No cryptocurrency support in cash economy (-0.5). No ISP blocking currently but could start any time (-0.5). 65% internet penetration and 85% mobile penetration provide basic access (+0.5). Final: 1.5/3.0 |

| Player Penalties | 20% | 1.5/2.0 | Criminal penalties are legally possible – fines up to D1,000 ($15) or imprisonment up to 2 years (0 points base). However, zero enforcement with no known prosecutions in recent years (+1.5 for “minor administrative warnings” level in practice). This could change instantly if government decides to enforce (-0.5 risk deduction for instability). Final: 1.5/2.0 |

| Market Availability | 10% | 0.5/1.0 | NO licensed operators exist because no licensing framework exists (0.25 for “no licensed operators, offshore only”). Market dominated by international operators and local agent networks – all operating illegally. No consumer protection, no dispute resolution, no regulatory oversight (-0.5 for complete lack of legitimate options). Players have access to offshore sites but zero legal recourse if defrauded (+0.25 for basic access). Final: 0.5/1.0 |

| TOTAL PLAYER ACCESS SCORE | 100% | 3.5/10 | Players can gamble in practice but have no legal protection, limited payment options, risk criminal prosecution (even if unlikely), and face 40% withholding tax on all winnings. This is a highly dangerous market for players. |

🔍 Key Highlights

Strengths (Extremely Limited)

- Zero enforcement of gambling prohibition – no known prosecutions in recent years means de facto tolerance of gambling activity

- No ISP blocking currently – offshore sites are accessible without VPN (though this could change instantly)

- Young population (median age 19.5) – 58% of population aged 15-54 represents gambling-friendly demographics

- 65% internet penetration and 85% mobile penetration – basic digital infrastructure exists for online gambling

- No operational requirements – because there’s no legal framework, there are also no compliance burdens (this is NOT a real advantage)

⛔️ CRITICAL RISKS AND CHALLENGES

- [Complete Legal Prohibition:] ALL gambling is illegal for Gambian citizens under the 1973 Act. There is no “grey area” – you are operating an illegal business serving illegal customers. Criminal penalties include fines and up to 2 years imprisonment.

- [No Licensing Framework:] There is literally no legal pathway to obtain an online gambling license. The Betting and Gaming Act only covers land-based casinos. No regulatory body exists to issue licenses, process applications, or provide legal certainty.

- [Zero Legal Protection:] Without a license or regulatory framework, operators have no legal standing whatsoever. Government could seize assets, freeze accounts, or prosecute at any time without warning or recourse.

- [Enforcement Risk:] While enforcement is currently absent, this could change instantly. Government could begin blocking sites, prosecuting operators, and enforcing criminal penalties tomorrow with zero notice.

- [Player-Hostile 40% Withholding Tax:] All gambling winnings are taxed at 40% (increased from 30% in 2025). This destroys your value proposition and drives players to operators that don’t report winnings. No tax-free threshold means even small wins get hit.

- [No AML/KYC Framework:] Absence of regulatory requirements means no compliance standards. This exposes operators to: (1) International sanctions risk, (2) Correspondent banking problems, (3) Payment processor termination, (4) Money laundering liability.

- [Payment Processing Nightmare:] No legitimate banking support. Market operates on mobile money (45%) and cash via agent networks (55%). No credit cards, no cryptocurrency, no modern fintech. Fraud risk is extreme.

- [Tiny Market Size:] Total unregulated market is only $80-100M annually. Even capturing 10% market share ($8-10M) barely covers compliance costs for a legitimate operation.

- [Reputational Suicide:] Operating in a completely unregulated market with no player protection, age verification, or responsible gambling measures will destroy your reputation with regulators in legitimate markets.

- [No Dispute Resolution:] Players have zero legal recourse if defrauded. No regulatory authority to file complaints with. No enforcement of terms and conditions. You are running a Wild West operation.

- [Regulatory Instability:] Government could impose new restrictions, taxes, or enforcement actions at any time. The 40% tax increase in 2025 shows authorities are watching and can change rules without consultation.

- [Agent Network Dependency:] Market operates through informal betting agents – you have no control over customer experience, no data on user behavior, and are vulnerable to agent fraud.

Player-Specific Issues

- All gambling is technically illegal – players face criminal penalties (even if not enforced) including fines up to D1,000 or 2 years imprisonment

- 40% withholding tax on ALL winnings – no tax-free threshold, making small wins unprofitable

- No consumer protection whatsoever – no licensing authority to complain to, no dispute resolution, no regulatory oversight

- Cash-based transactions via agent networks – high fraud risk, no payment security, no chargebacks

- No age verification – minors can gamble freely, exposing players to unlicensed, unregulated environment

- No responsible gambling tools – no deposit limits, self-exclusion, reality checks, or problem gambling support

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $200,000-500,000 (technology setup, agent network development, marketing, working capital)

Monthly Operating Costs: $50,000-150,000 (platform costs, agent commissions, payment processing, customer support, tax compliance)

Effective Tax Rate on Revenue: Unknown but catastrophic. 40% withholding tax on player winnings destroys retention. 30% corporate income tax likely applies. Total burden could be 50-70% of revenue.

Customer Acquisition Cost: $30-80 per player (lower than developed markets but market size is tiny)

Time to Breakeven: Unknown – likely never for legitimate operators

Time to Positive ROI: Unknown – likely never for legitimate operators

Profitability Assessment: THE ECONOMICS ARE IMPOSSIBLE FOR LEGITIMATE OPERATORS. Even if you capture 10% of the $80-100M market ($8-10M annual revenue), the combination of 40% player tax, 30% corporate tax, payment processing challenges, agent commissions, and compliance costs means you will operate at a loss.

The only way to “profit” here is to operate completely illegally with no compliance, no player protection, and no legitimate payment processing – which exposes you to money laundering liability, international sanctions, and reputational destruction. This market is only viable for criminals who don’t care about long-term sustainability or legal consequences.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Operating illegal business serving illegal customers. Zero legal protection. Vulnerable to asset seizure, account freezing, arbitrary enforcement. No licensing possible. 40% player tax destroys value proposition. AML/KYC violations expose you to international sanctions. Reputational destruction in legitimate markets. |

| Offshore Sports Betting Operators | CRITICAL | Identical to casino operators – all gambling is illegal for Gambian citizens. No distinction between sports betting and casino gaming. Criminal offense punishable by fines and imprisonment. No enforcement currently but could start any time. |

| Affiliates/Advertisers | HIGH | Promoting illegal gambling services. No current enforcement but vulnerable to prosecution for facilitating criminal activity. Government could begin targeting affiliates at any time. Payment processors may terminate accounts for gambling promotion. |

| Payment Processors | CRITICAL | Facilitating illegal gambling transactions. Massive AML/KYC violations due to absence of regulatory framework. International correspondent banks will terminate relationships. Vulnerable to sanctions and money laundering charges. Legitimate processors will refuse this business. |

| Company Directors/Executives | HIGH | Personal liability for operating illegal business. Criminal prosecution possible in Gambia. Reputational damage makes licensing impossible in legitimate markets. Travel restrictions if Gambia issues arrest warrants. Unable to raise institutional capital. |

🚨 Extradition and International Enforcement

Extradition Treaties: Gambia has limited extradition agreements. Primary risks are with UK (former colonial power), ECOWAS member states (Senegal, Nigeria, Ghana, etc.), and countries with mutual legal assistance treaties. However, gambling-related extradition is highly unlikely given current lack of enforcement.

Enforcement History: Zero known cases of prosecution, extradition, or international enforcement related to online gambling. The complete absence of enforcement means no established precedents – but this also means no legal clarity or protection.

Travel Risk: Minimal currently due to lack of enforcement. However, if Gambia begins prosecuting gambling operators, travel through ECOWAS countries or UK could become risky.

Primary Risk: Not extradition but rather international sanctions, correspondent banking termination, and payment processor blacklisting due to operating in completely unregulated market with no AML/KYC compliance.

📋 Final Verdict

Gambia receives an Operator Ease Score of 1.5/10 and a Player Access Score of 3.5/10, resulting in an overall market attractiveness rating of 2.5/10.

HONEST ASSESSMENT:

This is one of the world’s worst iGaming markets and a complete legal void zone. ALL gambling is illegal for Gambian citizens under the 1973 Act. There is no online gambling licensing framework, no regulatory authority, and no legal pathway to legitimacy. While enforcement is currently absent, operators have zero legal protection and could face arbitrary prosecution at any time.

The 40% withholding tax on player winnings destroys your value proposition. The $80-100M market size is too small to justify the legal risk. The absence of AML/KYC requirements exposes you to international sanctions and payment processor termination. This market is only viable for criminals who don’t care about long-term sustainability – legitimate operators should NEVER consider entry under any circumstances.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NOBODY. There is no legitimate business case for entry into this market.

- If you are a criminal organization with no concern for legal consequences, reputational damage, or long-term sustainability, then this market offers complete regulatory absence. But you will be unable to access legitimate payment processors, banking services, or institutional capital.

❌ Definitely Avoid If You Are:

- Any legitimate gambling operator (you cannot get a license and will operate illegally)

- Casino-focused operator (online casino completely prohibited – criminal offense)

- Sports betting operator (sports betting also prohibited – criminal offense)

- Publicly traded company or institutional capital-backed operator (operating illegal business with no AML/KYC compliance will destroy your reputation and trigger regulatory action in home jurisdiction)

- Any operator seeking licensing in legitimate markets (operating in Gambia will make you unlicenseable in EU, UK, US states, etc.)

- Any operator using legitimate payment processors (processors will terminate your accounts for operating in unregulated market)

- Any operator seeking long-term sustainable business (government could begin enforcement tomorrow with zero notice)

- Affiliates or advertisers (promoting illegal gambling services exposes you to prosecution)

- Payment processors (facilitating illegal transactions creates massive AML/KYC violations)

- Anyone who values their professional reputation (operating here is career suicide in legitimate gambling industry)

⚠️ BOTTOM LINE: Gambia is a complete legal void zone where ALL gambling is technically illegal but currently unenforced. No licensing exists, no regulation exists, and no legal pathway to legitimacy exists. The 40% player tax and tiny $80-100M market make this unviable for legitimate operators. Only criminals should consider this market – and even they face massive AML/money laundering risks. AVOID COMPLETELY.