Georgia presents a promising opportunity for iGaming operators due to its evolving regulatory environment and expanding digital infrastructure. The country is actively reforming gambling laws to accommodate both land-based and online markets, aiming to attract foreign investment while ensuring robust player protection.

The regulatory framework balances strict compliance with competitive taxation, creating a business-friendly environment. Key attractions include streamlined licensing processes, relatively low tax rates for foreign player revenues, and a growing internet user base.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal under regulated framework for land-based and online gambling |

| Regulatory Authority | Ministry of Finance |

| License Duration | 1 to 5 years depending on activity |

| Population | 3.7 million (approx.) |

| Adult Gambling Age | 25+ for Georgians, 18+ for foreigners |

| GDP (Nominal) | ~$20 billion USD |

| Average Income per Capita | ~$4,500 USD per year |

| Internet Penetration | ~80% |

| Mobile Penetration | >90% |

| Online Gambling License Fee | From GEL 250,000 to 1,000,100 (~US$85,000–370,000) |

| Land-Based Casino License Fee | Varies; application fees up to $700 for expedited service |

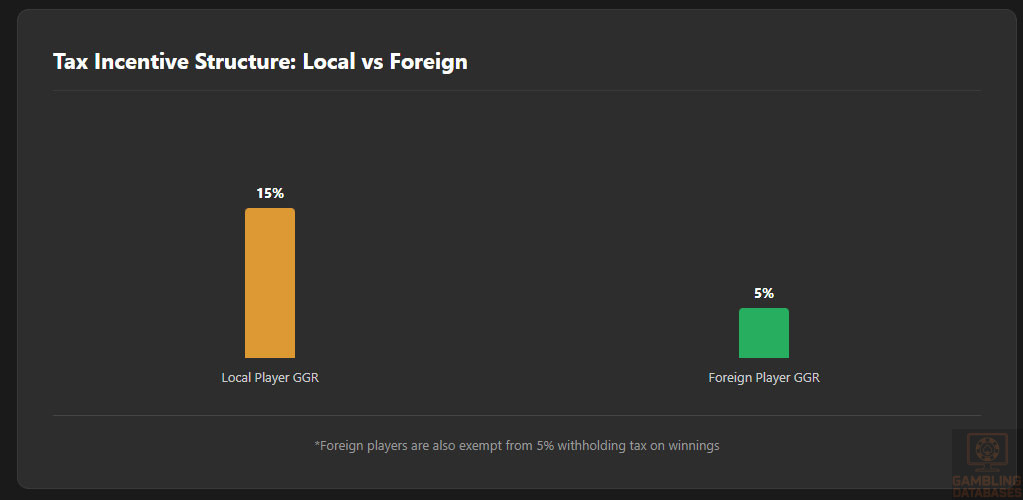

| Gross Gaming Revenue Tax (Local Players) | 15% |

| Gross Gaming Revenue Tax (Foreign Players) | 5% |

| Player Winning Tax | 5% withheld by operator for local players; exempt for foreign players |

| License Renewal Fees | Applicable; varies by gambling activity |

| Minimum Capital Requirement | Specified per license type; generally moderate |

| License Application Processing Time | 1 to 20 working days, fees vary accordingly |

| Market Size (Online Revenue 2025) | $204 million USD (projected) |

| Annual Market Growth Rate (CAGR 2025-2031) | 7.8% |

| Average Revenue Per User (ARPU) | Estimated $55 USD |

| Land-Based Casino Venues | Licensed casinos, gambling clubs, slot clubs, bingo halls |

| Online Gambling Segments Licensed | Online casino, slots, online sports betting |

| Local Presence Requirements | Company registration in Georgia mandatory for license |

| Operational Compliance | KYC, AML, real-time platform monitoring, data protection |

| Advertising Restrictions | Television/radio restricted 6 AM to midnight; sponsorships permitted; online ads on licensed platforms only |

| Responsible Gambling Measures | Mandatory KYC, self-exclusion, user limit settings, public messaging |

| Enforcement and Penalties | Fines, license revocations, criminal charges for illegal operations |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling in Georgia is legal and regulated across multiple forms, including land-based casinos, sports betting venues, slot machine halls, and online gambling platforms. Licensing and oversight are managed by the Ministry of Finance, which issues permits for both physical and digital operations.

Operators are required to comply with specific age restrictions, with a notable distinction between Georgian citizens (minimum age 25) and foreign players (minimum age 18). Responsible gambling frameworks mandate identity verification, the implementation of self-exclusion programs, and public awareness campaigns to curb addiction and fraudulent activity.

Land-Based Gambling Activities

Georgia’s land-based gambling sector includes licensed casinos, dedicated gambling clubs, slot machine halls, and bingo venues. Each type operates under regulated licenses with distinct requirements for compliance, reporting, and taxation.

Casinos must meet capital and operational standards coordinated by the Ministry of Finance, with business plans and internal controls scrutinized during licensing. Gambling clubs and slot halls have tailored regulations reflecting their unique operational models, including limits on the number and location of machines.

Sports betting remains primarily land-based but is in transition due to legislative initiatives exploring expansion into legalized online sports betting. Physical outlets must adhere to rigorous KYC and anti-money laundering protocols.

Online Gambling Framework

The online gambling segment in Georgia is regulated within an evolving legal framework that distinguishes between various gaming activities such as online casinos, slots, and betting. Licenses are granted for up to five years and subject to comprehensive compliance requirements.

Licensed operators must register locally, demonstrating economic presence and meeting financial and technological criteria. Platforms are mandated to incorporate real-time monitoring linked to state surveillance systems to ensure integrity and compliance.

Recent legal amendments include provisions for offshore operation licenses that allow operators to serve foreign players with differentiated tax rates and expanded domain usage, including multi-domain permissions specifically aimed at Georgian and international audiences.

Licensed Operators and Market Players

The market includes a mix of established local operators and international companies targeting both domestic and foreign players. Licensing terms favor operators with demonstrable financial capacity and technical infrastructure capable of meeting Georgia’s compliance standards.

Competitive dynamics are influenced by tax structures where revenues from Georgian players are taxed higher than those generated from foreign clientele, encouraging operators to segment their offerings accordingly. Market entry strategies typically focus on gaining quick regulatory approvals and investing in robust KYC/AML systems.

Licensing Framework and Requirements

Application Process and Eligibility

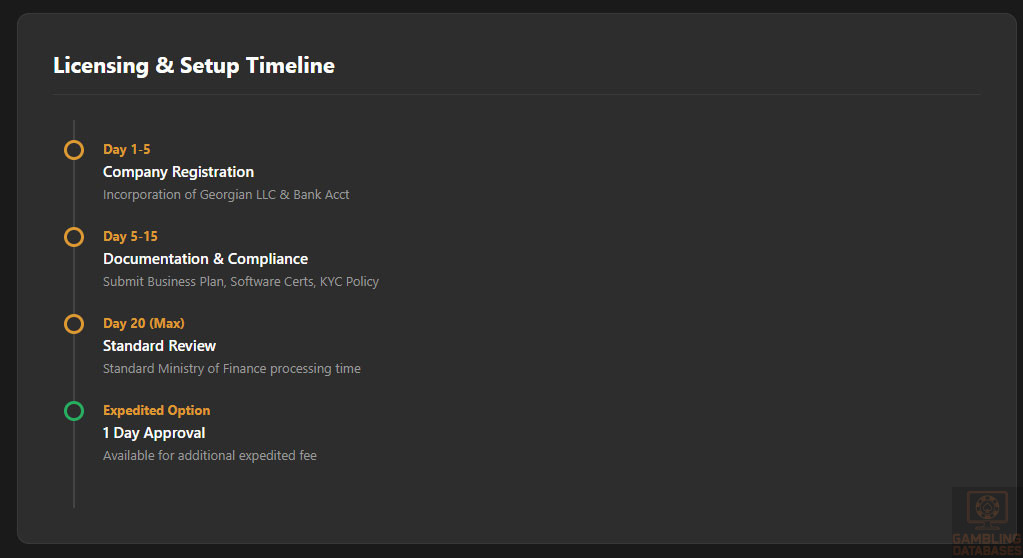

The Ministry of Finance administers gambling licenses, requiring applicants to submit detailed documentation and adhere to strict application guidelines. The fee structure varies according to the license type and desired processing speed, with expedited review available for higher fees.

- License application form

- Certificate of company registration in Georgia

- Proof of fee payment and source of funds documentation

- Business plan including financial projections

- Technical documentation of gaming systems and software certification

- Criminal background checks of owners and key personnel

- Compliance policies for KYC, AML, and responsible gambling

- Proof of capital availability and operational readiness

The application process ranges from free 20 working days review to a 1-day expedited approval at an additional fee. Eligibility criteria prohibit applicants in tax debt or with criminal records among key stakeholders.

Local Presence and Operational Requirements

A physical company registration in Georgia is mandatory for all license applicants, ensuring economic presence and accountability. While direct ownership by foreign entities is permitted, operational management and control must comply with local regulations.

Operators must maintain licenses with domains registered under Georgian jurisdiction, with recent regulations allowing up to two domains per license to differentiate Georgian and international audiences. Personnel involved in management and compliance functions must be adequately qualified and adhere to state-imposed standards.

- Company registration in Georgia required

- Local technical support and compliance teams recommended

- Platform domains registered for Georgian jurisdiction

- Dual-domain licenses for segmented markets (Georgian vs. foreign)

- Ongoing reporting and audit obligations

Compliance Obligations and Monitoring

Player Protection and Identification

Georgia enforces rigorous player protection measures including mandatory verification of identity through tiered KYC checks. Operators must screen players against politician and sanctions lists and conduct enhanced due diligence for high turnover accounts.

- Identity verification during registration (KYC)

- Screening against PEP and sanctions lists

- Enhanced due diligence for accounts exceeding GEL 5,000 turnover

- Self-exclusion options and player-set limits

- Responsible gambling messaging on platforms and venues

Self-exclusion programs are integrated with national registries to prevent problem gambling, and operators must provide easy access to user control settings and withdrawal options consistent with data protection laws.

Financial Monitoring and Reporting

Operators are required to implement real-time transaction monitoring linked to state services for immediate detection of suspicious activity. Regular reporting to the Ministry of Finance includes financial audits, tax filings, and compliance certifications.

- Submission of periodic financial and compliance reports

- Real-time data integration with government monitoring systems

- Internal and external audits for financial and operational integrity

- Reporting of suspicious transactions to financial authorities

Taxation Structure and Financial Obligations

Player Taxation

Players domiciled in Georgia are subject to a 5% tax levy on winnings, withheld by operators at payout. Foreign players are exempt from this withdrawal tax, incentivizing international participation.

Operator Taxation

| Category | Local Players Tax Rate | Foreign Players Tax Rate |

|---|---|---|

| Online Casino | 15% | 5% |

| Online Slots | 15% | 5% |

| Online Sports Betting | 15% | 5% |

| Land-Based Gambling | Standard 15% | N/A |

Corporate income tax applies according to standard rates, with license renewal and business fees assessed periodically. Operators targeting foreign markets benefit from a significantly reduced tax burden on revenues generated outside Georgia.

Gambling Market Financial Performance

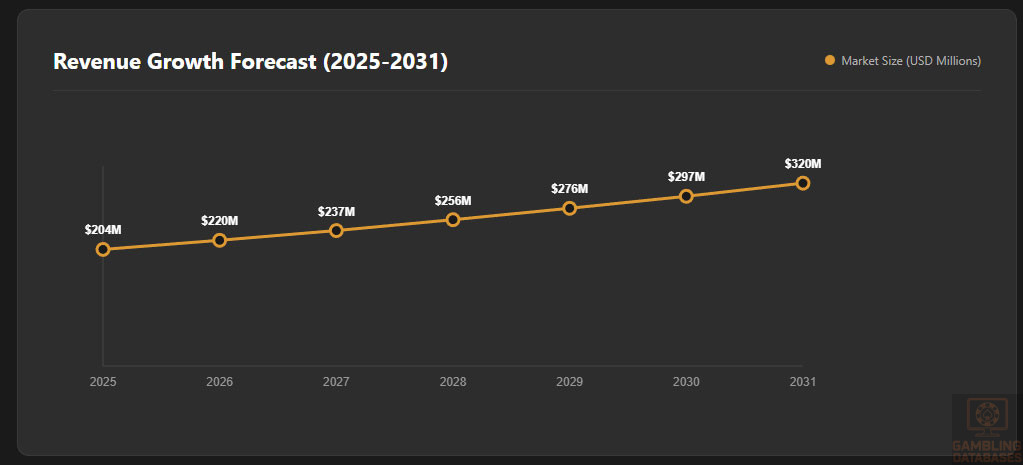

The iGaming market in Georgia is projected to reach $204 million in revenue by 2025, growing annually at a CAGR of 7.8% through 2031. Revenues are increasing due to regulatory stability, improved licensing clarity, and growing online user engagement.

Tax revenue from gambling contributes significantly to government budgets, supporting social and educational programs aimed at mitigating gambling risks. Operators report improved profitability linked to favorable tax differentiation between local and foreign player income.

Advertising and Marketing Restrictions

Advertising gambling activities in Georgia is permitted but strictly regulated. Broadcast advertising on television and radio is banned between 6 AM and midnight except on PIN-protected channels or public-interest programming.

- Permitted advertising at licensed venues

- Allowed at airports and customs zones

- Online advertising restricted to licensed platforms

- Sponsorships by gambling operators are widely used and regulated

- Advertising must not target minors or portray gambling as quick wealth

Online and offline promotional activities must align with responsible gambling principles, avoiding misleading claims or incentivizing excessive play.

Recent Regulatory Changes and Their Impact

Recent reforms effective December 2024 introduced offshore online gambling licenses, allowing operators to run two domains—one dedicated to Georgians and one to foreign players with tax advantages. Stake acceptance in EUR and USD expanded operator flexibility.

This regulatory evolution aims to make Georgia competitive relative to offshore jurisdictions, enhancing transparency and compliance while expanding market size and operator choice.

Enforcement Mechanisms and Penalties

Strict penalties apply for noncompliance, including license suspension, revocation, and financial fines. Illegal gambling operations may be subject to misdemeanor or felony charges with imprisonment up to five years depending on severity.

- Fines for unauthorized gambling activities

- License suspension or revocation for regulatory breaches

- Criminal charges for illegal commercial gambling

- Asset seizures and extended probation for serious offenses

- Penalties intensify for repeat violations or large-scale operations

The regulatory environment favors licensed, compliant operators while deterring illicit activity through robust enforcement and monitoring systems.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Georgia’s total population stands at approximately 3.7 million, characterized by a relatively balanced gender ratio and an increasing urbanization trend. The median age is about 38 years, reflecting a mature population with a steady working-age majority, important for disposable income generation and iGaming participation.

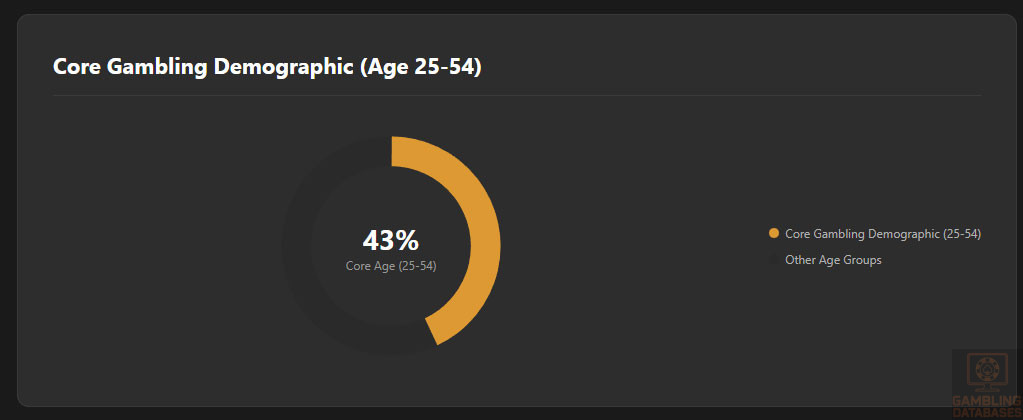

The age distribution shows a slight decline in the youth segment, compensated by a significant adult population aged 25-54, which represents the core gambling demographic. Gender distribution is nearly equal, with a slight female majority, though men tend to dominate gambling participation rates.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 16% |

| 15-24 years | 14% |

| 25-54 years | 43% |

| 55-64 years | 14% |

| 65+ years | 13% |

Urban residency accounts for roughly 58% of the population, with the remaining 42% living in rural areas. This urban concentration supports access to gambling venues and high-speed internet, enhancing online gambling opportunities alongside traditional land-based options.

Geographic Distribution

Major population centers concentrate in western and central Georgia, with Tbilisi as the dominant metropolitan hub, followed by secondary cities supporting regional economies. These cities serve as focal points for gambling venue density and internet connectivity infrastructure.

- Tbilisi – approximately 1.1 million residents

- Batumi – around 154,000 residents

- Kutaisi – about 147,000 residents

- Zugdidi – near 100,000 residents

- Rustavi – roughly 125,000 residents

- Gori – close to 50,000 residents

Internet access in urban areas exceeds rural regions by over 20%, with gambling venues predominantly located in cities. The infrastructural disparity underscores the need for focused market strategies tailored to urban consumers while considering gradual rural penetration via mobile platforms.

Economic Indicators and Consumer Spending Power

Georgia’s economy exhibits steady growth with a nominal GDP near $20 billion and a projected annual growth rate of 4.1%. The services sector dominates at nearly 60%, supplemented by industry at 28% and agriculture around 12%, indicating a diversified economic base supportive of consumer spending on leisure activities like gambling.

Per capita income stands at an average of $4,500 USD with disposable income rising moderately, driven by wage growth in urban centers. While income inequality exists with a Gini coefficient around 38, the emerging middle class fuels demand for entertainment and digital services, including iGaming.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $20 billion USD |

| GDP Growth Rate (2025 Forecast) | 4.1% |

| Average Per Capita Income | $4,500 USD |

| Gini Index (Income Inequality) | 38 |

| Inflation Rate | 3.2% |

| Unemployment Rate | 15% |

Consumer spending shows a preference for digital goods and leisure activities, with the gaming sector benefiting from rising disposable incomes in urban youth and middle-aged adults. Market growth is reinforced by expanding credit availability and increased digital payment adoption.

Market Size and Growth Projections

The Georgian iGaming market revenue is forecasted to reach $204 million USD in 2025, with sustained growth supported by regulatory reforms. Operating growth projections indicate a compound annual growth rate (CAGR) of 7.8% through 2031, reflecting rising user adoption and expanded game offerings.

Average Revenue Per User (ARPU) is estimated around $55 USD, consistent with emerging market benchmarks. User base expansion is driven by digital infrastructure improvements and increased social acceptance, with online casinos and sports betting dominating revenue shares.

| Metric | Value |

|---|---|

| 2025 Market Revenue | $204 million USD |

| 2026 Projected Revenue | $220 million USD |

| 2027 Projected Revenue | $237 million USD |

| CAGR (2025-2031) | 7.8% |

| Estimated User Base (2025) | 3.7 million |

| Average Revenue Per User (ARPU) | $55 USD |

Education, Skills, and Digital Literacy

Georgia boasts a literacy rate exceeding 99%, with a substantial portion of the population attaining secondary or higher education levels. Digital literacy has increased substantially, driven by government initiatives and private sector engagement, facilitating widespread use of mobile and internet technologies critical for online gambling engagement.

Workforce skills are increasingly aligned with IT and service sectors, with an emerging talent pool in software development and digital marketing fostering innovation within the iGaming industry.

Cultural and Social Factors

Communication and Language

Georgian is the official language, spoken by nearly the entire population. Russian remains widely used, especially among older and rural demographics. English proficiency is growing among younger and urban populations, particularly affecting digital content consumption and cross-border iGaming marketing.

- Georgian (official, 87%)

- Russian (spoken by 40% approx.)

- English (growing, particularly 18-35 age group)

- Azerbaijani (minority language)

- Armenian (minority language)

Cultural Attitudes

Gambling is traditionally viewed with mixed attitudes. While entertainment and sport betting gain social acceptance, religious and conservative groups express caution. The government’s strong regulatory stance and promotion of responsible gambling support public trust and mitigate stigma associated with gaming activities.

Problem Gambling and Social Considerations

Problem gambling prevalence is estimated at 3-4%, with at-risk groups including young adults and lower-income brackets. The government and NGOs have launched several intervention programs focused on education, counseling, and rehabilitation.

- Public awareness campaigns on gambling risks

- National helplines and counseling services

- Self-exclusion databases integrated with licensed operators

- Mandatory contribution from operators to social responsibility funds

- Community outreach programs and school education initiatives

Social responsibility frameworks enforce operator contributions and compliance with harm minimization strategies, embedding player protection in the market culture.

Political Structure and Governance

Georgia operates as a parliamentary republic with stable governance conducive to foreign business investment. Regulatory consistency is a government priority, supported by transparent legislative processes and international cooperation, which fosters a predictable environment for market entrants.

Strong international relations with European and neighboring countries support integration of advanced regulatory and technological standards in the iGaming sector.

Technology Adoption and Digital Behavior

Internet and Digital Usage

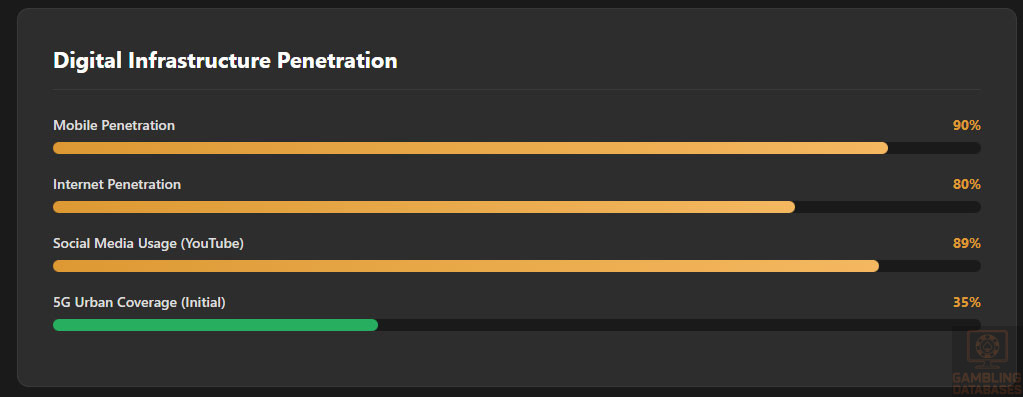

Internet penetration in Georgia exceeds 80%, with daily usage averaging 5 hours across devices. Mobile internet access outpaces fixed broadband due to widespread smartphone adoption, exceeding 90% mobile penetration.

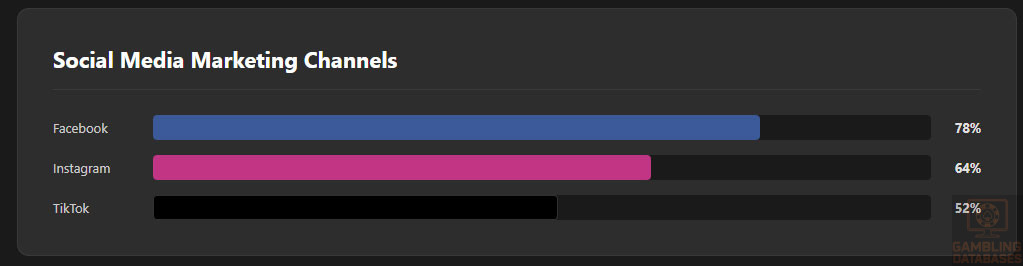

- Facebook – 78% penetration, strong daily engagement

- Instagram – 64% penetration, popular among young adults

- YouTube – 89% penetration, high video consumption

- TikTok – rapid growth, 52% among users under 25

- Twitter – 31% penetration, primarily news and sports followers

- LinkedIn – 28% among professionals and business users

Digital Payment Behavior

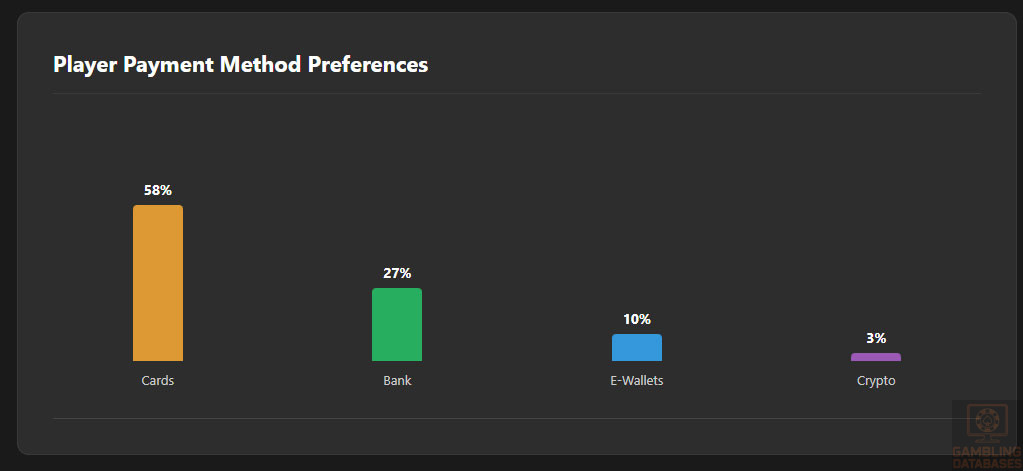

Digital payments are increasingly popular for online gaming transactions. Credit and debit cards dominate, followed by bank transfers and growing usage of e-wallets and mobile payment solutions. Cryptocurrency adoption is nascent but emerging within tech-savvy segments.

- Visa/MasterCard cards – 58% of online payments

- Bank transfers – 27% of user transactions

- E-wallets (e.g., Skrill, Neteller) – 10% and growing

- Mobile payments (via telecom operators) – expanding rapidly

- Emerging cryptocurrencies usage – ~3% among young users

Gaming and Gambling Preferences

Current Market Participation

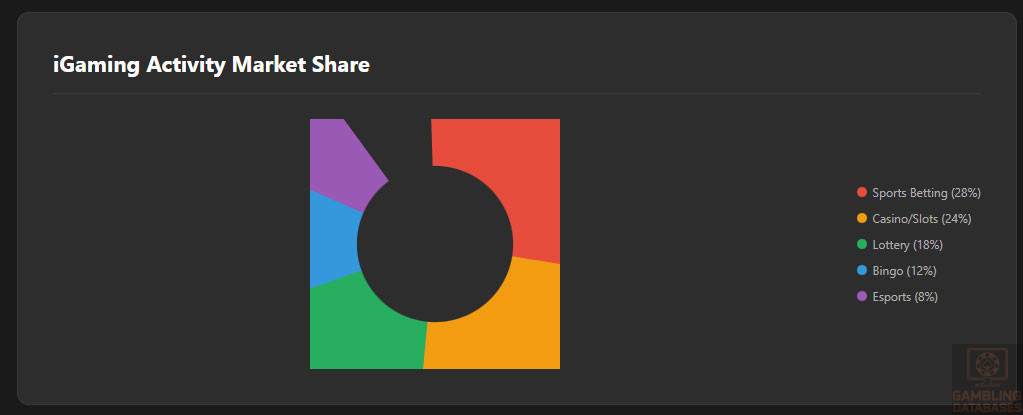

Gambling activity participation ranges broadly, with an estimated 40% of adults having engaged in some form of gambling within the past year. Online casino games, sports betting, and lottery dominate consumer preferences, reflecting diversified interests across urban and semi-urban regions.

- Sports Betting – 28% participation

- Online Casino Games (slots, table games) – 24%

- Lottery and Instant Win Games – 18%

- Bingo and Social Casino Games – 12%

- Esports Betting – 8%

Consumer Behavior Patterns

Players favor mobile platforms for flexibility, with peak playing hours in evenings and weekends. Session lengths average 45 minutes, with a growing trend toward social and live dealer games enhancing engagement. Retention rates improve with personalized offers and loyalty programs.

Spending patterns show cautious but steady growth, with average monthly bets aligning with disposable income trends, emphasizing the importance of tailored local market strategies and responsible gaming initiatives.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Georgia has achieved a significant milestone in internet penetration, reaching over 80% of the population. Fixed broadband subscriptions constitute around 18%, while mobile broadband dominates, exceeding 75% due to the widespread accessibility of mobile devices and competitive mobile data pricing. Average internet speeds stand at approximately 45 Mbps for fixed lines and 27 Mbps for mobile networks, reflecting ongoing investments in infrastructure and network modernization.

The reliability of internet services has improved substantially with government and private sector collaboration, enhancing both urban and rural connectivity. Fiber-optic networks are progressively deployed, supporting high-capacity data transfer essential for streaming and online gaming user experience. Increased public and private infrastructure investments lay a strong foundation for scalable growth in digital sectors, including iGaming.

5G and Future Technology Deployment

Georgia is in the early to mid-stage rollout of 5G technologies, focusing first on urban centers like Tbilisi, Batumi, and Kutaisi. Telecommunications providers have launched initial commercial 5G networks covering about 35% of urban populations with plans to expand coverage to 65% by 2027.

The government supports 5G deployment through regulatory incentives and spectrum auctions, aiming to ensure competitive operator participation. Emerging 5G infrastructure will facilitate ultra-low latency and high bandwidth essential for advanced iGaming solutions such as live dealer streaming and augmented reality gaming platforms.

Mobile Technology Ecosystem

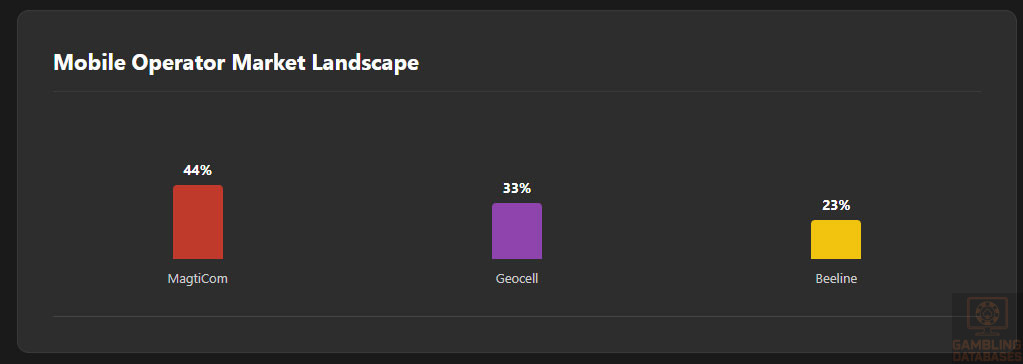

Georgia’s mobile ecosystem comprises multiple network operators delivering extensive coverage nationwide. Smartphone penetration exceeds 85%, with Android devices dominating the market followed by steadily increasing iOS adoption due to rising consumer purchasing power and affinity for premium devices.

- MagtiCom – Market leader with over 44% market share and extensive 4G/5G coverage

- Geocell – Significant competitor holding around 33% market share, focuses on customer service and rural expansion

- Beeline Georgia – Covers approximately 23% of subscribers, emphasizing competitive pricing

- Adjara Group – Regional provider with niche service areas

- Mobile Virtual Network Operators (MVNOs) – Emerging, targeting budget-conscious consumers

Mobile data costs remain competitive, supporting high daily consumption and enabling seamless streaming critical for online gambling platforms. Device usage patterns reveal a preference for mid-range smartphones with increasing adoption of mobile payment technologies.

Financial Services and Payment Infrastructure

The Georgian banking sector is diverse, incorporating both local and international institutions that support a modern digital payments ecosystem. Digital banking has seen rapid adoption, with online account penetration exceeding 60% of the adult population and significant growth in mobile wallet users driven by convenience and security.

- TBC Bank – Largest bank holding over 30% market share, leading digital innovation

- Bank of Georgia – Strong nationwide presence with robust mobile banking offerings

- Liberty Bank – Focus on SME and retail banking, expanding digital product suite

- Cartu Bank – Known for private banking and international partnerships

- Procredit Bank – Emerging leader in sustainable finance and digital transformation

Payment processing options have diversified to support multi-channel commerce. Credit and debit cards are widely accepted; e-wallets and bank transfer services are increasingly common for iGaming transactions, facilitating rapid deposits and withdrawals.

- Visa and MasterCard cards – Dominant for online payments

- Skrill, Neteller, Payoneer – Popular e-wallet providers with quick transfers

- Bank transfers – Used for high-value transactions with strong security

- Mobile payment solutions integrated with telecom operators

- Cryptocurrency payment gateways – Early adoption growing among tech-savvy segments

E-commerce and Digital Economy

Georgia’s e-commerce sector is expanding rapidly, supported by improving logistics, payment infrastructure, and consumer trust. Online retail penetration has surpassed 40% among urban residents, complemented by active adoption of digital services such as entertainment, food delivery, and financial technology.

Consumer behavior indicates increasing preference for convenience and mobile-based transactions, contributing to a fertile environment for digital games and iGaming markets. Digital economy growth is augmented by government-backed innovation hubs and favorable regulatory frameworks.

Business Environment and Regulatory Framework

The World Bank ranks Georgia among the top 10 countries globally for ease of doing business, reflecting efficient administrative processes and progressive business laws. Registering a company is straightforward, taking typically less than five business days with minimal bureaucratic hurdles and low fees.

- Prepare and notarize required incorporation documents

- Submit registration with the National Agency of Public Registry

- Obtain tax identification number and register with the Revenue Service

- Open a corporate bank account and deposit the minimum required capital

- Complete licensing applications if applicable for regulated activities

Foreign direct investment is actively encouraged with no restrictions on foreign ownership or capital repatriation, enhancing appeal to international iGaming operators. Operating costs vary across industries but remain competitive relative to regional peers, with labor costs and office rents moderate and predictable.

Corporate Structure and Registration

Common corporate entities for market entry include Limited Liability Companies (LLC), Joint Stock Companies, and Branch Offices. The LLC is the preferred structure due to operational flexibility, liability protection, and streamlined governance requirements.

Registration requires comprehensive compliance with local legislation, including submission of articles of association, shareholder information, and proof of corporate address. Foreign ownership is unrestricted, though regulatory licenses for gambling impose additional operational requirements.

- Articles of Incorporation

- Founders’ identification documents

- Proof of registered office

- Tax registration certificates

- Bank account opening confirmation

- Licensing documentation (if applicable)

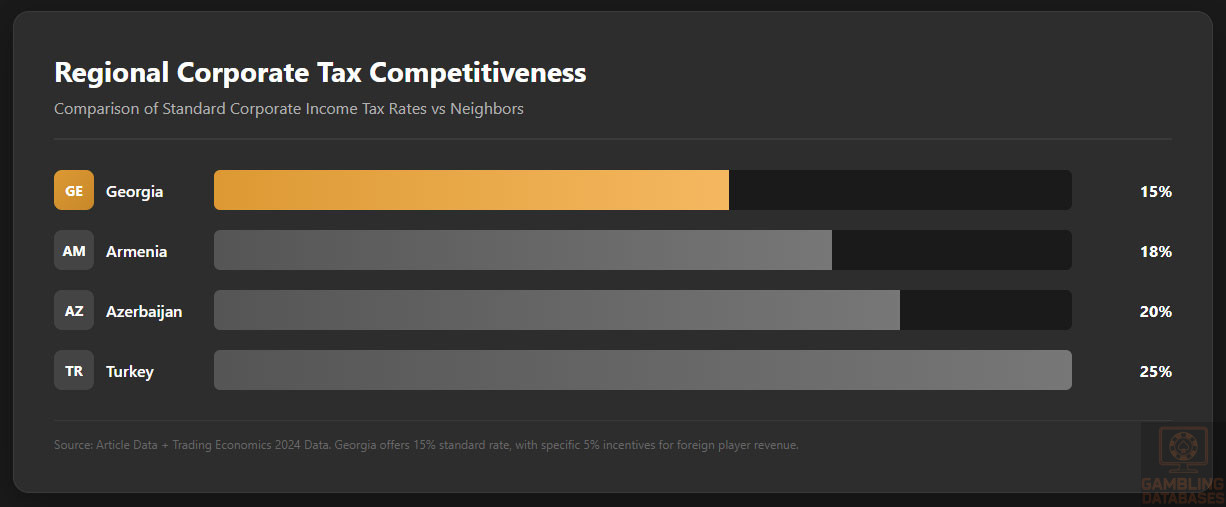

Taxation Framework

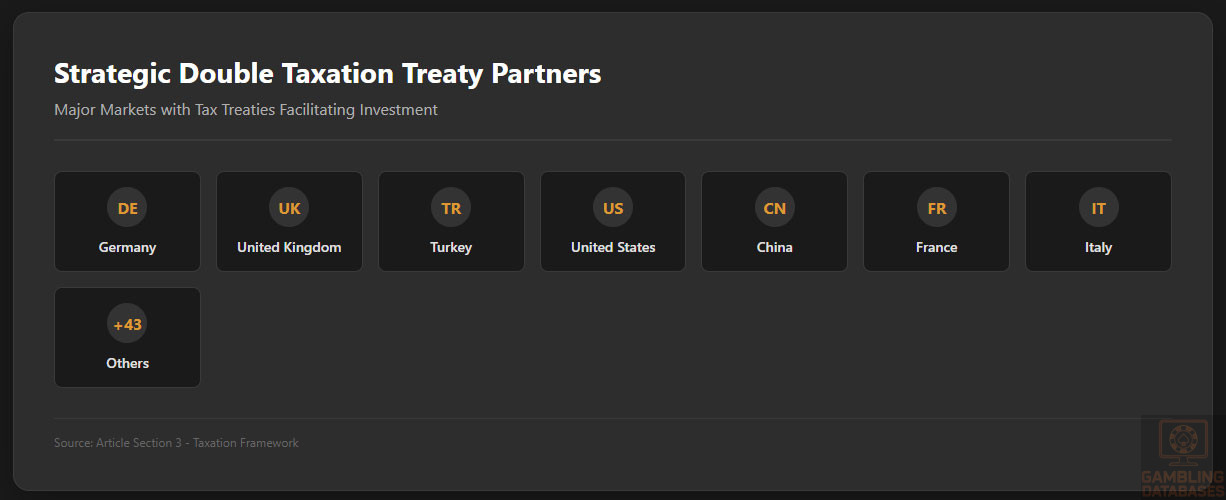

Corporate income tax in Georgia is set at a flat rate of 15% on distributed profits, with numerous incentives including tax holidays for special economic zones and preferential treatment for IT companies. International treaties with over 50 countries mitigate double taxation risks, fostering cross-border trade and investment.

- Germany

- United Kingdom

- Turkey

- Russia

- United States

- China

- France

- Italy

Personal income tax is also flat at 20%, with additional social security contributions levied. Residency rules encourage foreign experts’ relocation through favorable taxation agreements and exemptions. Withholding taxes apply variably, especially on dividends and interest payments.

Market Entry Considerations

Optimal entry into Georgia’s iGaming sector involves strategic partnerships with local entities, navigating licensing intricacies, and investing in robust KYC/AML technology. Leveraging mobile platforms and aligning marketing efforts with cultural norms are critical for success.

- Establishing a Georgian-registered LLC for licensing eligibility

- Partnering with experienced local operators for market insights

- Implementing advanced compliance and player protection systems

- Utilizing dual-domain licensing to target both local and foreign players

- Investing in mobile-first, multi-lingual platform development

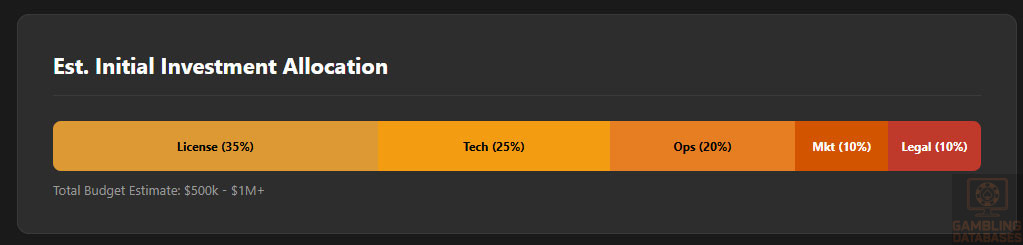

Initial investment requirements span licensing fees, technology procurement, staffing, and marketing, with timelines from application to launch realistic within 6-9 months.

- License application fees: US$85,000–370,000 depending on scope

- Setup and legal consultancy costs: $50,000–80,000

- Office and operational expenses for first year: $150,000–250,000

- Marketing budget initial phase: $100,000+

- Technology platform development and certification: $200,000+

| Cost Category | Estimated Range (USD) |

|---|---|

| License Fees | $85,000–$370,000 |

| Legal & Consulting | $50,000–$80,000 |

| Office Setup & Operations | $150,000–$250,000 |

| Marketing & Customer Acquisition | $100,000+ |

| Technical Infrastructure & Certification | $200,000+ |

The most common challenges include navigating regulatory updates, establishing local compliance capacity, and managing player acquisition costs in a competitive online market. Companies with a deep understanding of local culture and responsiveness to regulatory changes achieve superior market positioning and compliance sustainability.

- Adapting to evolving licensing requirements

- Ensuring rigorous KYC/AML compliance

- Attracting and retaining players amid rising competition

- Balancing tax efficiency with full compliance

- Integrating multi-channel marketing respecting advertising restrictions

Exit strategies are considered through asset and license transfer possibilities, with valuation dependent on brand strength, compliance record, and active user base. Georgia’s transparent regulatory system facilitates orderly ownership transitions under set conditions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Georgia?

Yes, online gambling is fully legal and regulated in Georgia. Operators must obtain appropriate licenses issued by the Ministry of Finance, which oversees compliance with strict regulations including player protection, KYC/AML obligations, and tax reporting. The law permits both Georgian and foreign operators to serve distinct player segments under a dual-domain licensing framework, ensuring legal clarity and business opportunity.

2. What types of gambling licenses are available and what do they cover?

Georgia issues licenses covering a broad spectrum of gambling activities:

- Land-based casino operation

- Online casino games including slots and table games

- Sports betting platforms (both online and land-based)

- Bingo halls and lottery games

- Offshore licenses for operators serving only foreign players

This structured licensing allows market segmentation and targeted regulation based on player geography and game type.

3. How much does an iGaming license cost and how long does it take to obtain?

License fees range from GEL 250,000 to GEL 1,000,100 (~US$85,000–370,000) depending on the gambling category and application urgency. Standard processing time is up to 20 working days, with expedited reviews available within 1 to 5 days for additional fees. Timely compliance with document submission and background checks influences overall timelines.

4. Can foreign companies obtain a gambling license?

Foreign companies can obtain licenses but must register a local legal entity in Georgia. This requires company registration, tax payer identification, and compliance with local physical presence regulations. While there are no restrictions on foreign ownership, operational control and licensing approval demand adherence to Georgian laws and regulations.

5. What are the tax obligations for iGaming operators?

Operators pay a 15% gross gaming revenue (GGR) tax on revenues from Georgian players and a reduced rate of 5% on revenues from foreign players. Corporate income tax is 15% on distributed profits. License renewal fees and turnover-based levies may also apply, making tax planning critical for profitability.

| Tax Type | Local Player Revenue | Foreign Player Revenue |

|---|---|---|

| Gross Gaming Revenue Tax | 15% | 5% |

| Corporate Income Tax | 15% | 15% |

| License Renewal Fee | Varies | Varies |

6. Are gambling winnings taxed for players?

Players domiciled in Georgia are subject to a 5% tax on winnings, withheld at the source by operators. Foreign players are exempt from this player-level tax, which incentivizes cross-border gaming participation and supports operator differentiation strategies.

7. What are the typical operational costs for running an online casino/sportsbook?

Key operational costs include licensing fees, technology platform procurement and maintenance, staffing, marketing and customer acquisition, and compliance costs related to KYC and AML systems. Depending on scale, monthly operational expenses can range from $50,000 to well over $200,000, underscoring the importance of optimized resource allocation.

8. What is the expected ROI timeline for entering this market?

Return on investment typically occurs within 18 to 36 months post-launch, influenced by market penetration speed, regulatory adherence, and marketing effectiveness. Early investments in compliance and player trust building accelerate profitability while mitigating the risk of penalties and operational disruptions.

9. What are the local presence requirements for operators?

Operators must legally register a company in Georgia and maintain a physical office or representative. Additionally, local technical support and compliance staff are recommended to ensure real-time regulatory adherence. Dual-domain licenses require domain registrations adhering to Georgian jurisdiction authenticity guidelines.

10. What payment methods are available and recommended?

Preferred payment methods include credit/debit cards (Visa, MasterCard), e-wallets (Skrill, Neteller), bank transfers, mobile payments via telecoms, and emerging cryptocurrencies. Operators benefit from multi-option integrations ensuring convenience, security, and low transaction times for diverse user demographics.

11. What are the advertising and marketing restrictions?

Advertising is permitted but regulated with restrictions on broadcast times (banned 6 AM–midnight), bans against targeting minors, and a requirement for truthful, responsible gambling messaging. Sponsorships are widely used but must avoid promoting excessive gambling behaviors or unrealistic winning expectations.

12. What responsible gambling measures are mandatory?

Operators must implement comprehensive responsible gambling standards including mandatory KYC verification at registration, self-exclusion options, player-deposit limits, regular messaging on gambling risks, and contributions to social responsibility and addiction treatment funds.

13. How large is the iGaming market and what is the growth potential?

Georgia’s iGaming market is projected to generate over $204 million in revenue by 2025 with strong growth prospects at a CAGR close to 7.8% through 2031. Expanding internet access, increasing digital literacy, and progressive regulations underpin sustained market expansion and investor interest.

14. Who are the main competitors and what is their market share?

The market features a mix of local operators and international entrants leveraging offshore licenses. While no single entity dominates overwhelmingly, leading firms capture approximately 20-25% of revenues each, competing vigorously through technology, licensing, and regional marketing strategies.

15. What are the player preferences and typical spending patterns?

Players favor sports betting and online casino games, with average monthly spend around $55. Peak engagement occurs during evening hours and weekends, supported by mobile platforms that offer convenience and immersive experiences. Loyalty programs and personalized promotions significantly boost retention.

16. What are the key success factors and main challenges for new entrants?

Successful market entry depends on:

- Strong regulatory compliance processes

- Effective multi-lingual marketing and localized content

- Robust KYC/AML frameworks

- Adaptive technology infrastructure and platform reliability

- Competitive pricing and bonus strategies balanced with responsible gambling

Main challenges include regulatory complexity, competitive pressures, and evolving player expectations requiring ongoing innovation and operational agility.

Sources and References

- GeorgiaGambling Regulatory Authority – Official Website – https://4h.agency/everything-else/tpost/cf4ofse1c1-complete-guide-to-gambling-laws-licenses

- Ministry of Finance of Georgia – Licensing and Tax Regulations – https://ybcase.com/en/fintech/igornaa-licenzia-v-gruzii

- iGaming Today – Georgia Market Research Report – https://www.igamingtoday.com/georgia-market-research-report/

- National Statistical Office of Georgia – Population and Economic Data – https://www.geostat.ge/en

- Central Bank of Georgia – Financial and Digital Payment Statistics – https://www.nbg.gov.ge/

- International Telecommunication Union – ICT Statistics for Georgia – https://www.itu.int/en/ITU-D/Statistics/

- World Bank – Doing Business Report 2024 – https://www.worldbank.org/en/programs/business-enabling-environment

- TBC Bank – Annual Reports and Market Data – https://www.tbcbank.ge/

- Bank of Georgia – Industry Analysis – https://bankofgeorgia.ge/

- MagtiCom – Mobile Market Share and Coverage – https://www.magti.ge/

- Geocell – Telecommunications Reports – https://www.geocell.ge/

- Ministry of Economy and Sustainable Development of Georgia – Technology and Business Environment – https://economy.ge/

- Legal 500 – Georgia Gambling Law Guide – https://www.legal500.com/guides/chapter/georgia-gambling-law/

- Orbitax – Taxation Updates for Georgia – https://orbitax.com/news/country/article/Georgia-Increases-Taxation-of–54710

- Yogonet – News on Georgian Gambling Regulation – https://www.yogonet.com/international/news/2025/07/30/113165-georgia-lawmakers-reopen-study-on-casino-sports-betting-and-racing-legalization

- Altenar – Guide to iGaming Licences – https://altenar.com/blog/gaming-licences-which-one-should-you-get-in-2024/

- Sigma World – Georgian Gambling Association Statements – https://sigma.world/news/georgian-gambling-associations-stance-on-future-of-regulation-in-jurisdiction/

- Focus GN – Enforcement and Penalties News – https://focusgn.com/two-charged-over-illegal-gambling-business-in-georgia

- CNews.AM – Local Market Updates – https://cnews.am/business/news-from-igaming-georgia-lets-follow-and-see-if-it-will-work-or-not/

- International Monetary Fund (IMF) – Georgia Economic Reports – https://www.imf.org/en/Countries/GEO

- Georgia Today – Taxation and Market Insights – https://georgiatoday.ge/georgia-introduces-favorable-tax-treatment-for-online-gambling-operators-targeting-foreign-players/

- YbCase – FinTech and Payment System Analysis – https://ybcase.com/en/fintech

- 2WPower – Licensing Services in Georgia – https://2wpower.com/en/licensing/georgia

- Lawstrust – Step-by-step Licensing Guide – https://lawstrust.com/en/licence/gambling/ge

- Legal Justia – Georgia Gambling Codes – https://law.justia.com/codes/georgia/2022/title-16/chapter-12/article-2/part-1/

- Esports Insider – Market Development News – https://esportsinsider.com/2025/07/georgia-lawmakers-discuss-potential-sports-betting-legalisation

- Yogonet – Industry Competitive Analysis – https://www.yogonet.com/international/news/

- Central Statistical Office – Internet and Digital Usage Reports – https://www.geostat.ge/en

- International Data Corporation (IDC) – Market Technology Reports

- Global Gaming Reports – Industry Trends

- Transparency International – Business Environment Analysis

- Academic Journals on Digital Economy in Georgia

- Private Consultancies – Market Entry Strategy Reports

🎯 Gambling Databases Country Rating: Georgia

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 8.2/10 | 🟢 Excellent |

| Player Access Score | 8.8/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 8.5/10 | 🟢 High Potential (Specific Strategy Required) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Strict Advertising Curfew: TV and radio advertising is BANNED between 6 AM and Midnight. This severely limits mass-market acquisition strategies during peak hours.

- High Age Barrier for Locals: The minimum gambling age for Georgian citizens is 25 years old. This eliminates the lucrative 18-24 demographic entirely for the local market.

- Mandatory Player Tax: Operators must withhold 5% tax on ALL winnings for local players. This increases friction, lowers effective RTP, and encourages black market usage.

- Criminal Liability: Operating without a license is not just a fine; it can lead to felony charges and imprisonment up to 5 years.

- State Surveillance: Licensed platforms must integrate with real-time government monitoring systems. There is zero privacy for operator data; the Ministry of Finance sees everything instantly.

- Physical Presence: You cannot operate remotely. A physical company registration in Georgia and distinct domain registration are mandatory.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | All major verticals (Sports, Casino, Slots) are fully legal (+3.0). No product bans. Final: 3.0/3.0 |

| Licensing Process | 25% | 2.0/2.5 | Fast processing (1-20 days) (+2.0). Costs are reasonable (~$85k start) (+0.5). Deduction: Mandatory local physical company and bureaucracy (-0.5). Final: 2.0/2.5 |

| Taxation & Costs | 20% | 2.0/2.0 | GGR tax is excellent: 15% for locals, 5% for foreigners (+2.0). Note: While attractive, the administrative burden of player withholding tax is significant, but the low headline rate keeps this score high. Final: 2.0/2.0 |

| Operational Requirements | 15% | 0.7/1.5 | Moderate requirements (+1.0). Deductions: Real-time state surveillance integration (-0.25), Mandatory local director/company structure (-0.25), Strict KYC/AML turnover checks (-0.25), Dual domain requirement for tax segregation (-0.05). Final: 0.7/1.5 |

| Market Environment | 10% | 0.5/1.0 | Good business rank (+1.0). Deductions: Severe advertising restrictions (6AM-Midnight ban) (-0.25), Small total market size ($204m is low volume) (-0.25). Final: 0.5/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.5/4.0 | Fully legal (+4.0). Deduction: Restrictive age limit (25+) for locals excludes a major demographic (-0.5). Final: 3.5/4.0 |

| Practical Accessibility | 30% | 3.0/3.0 | Excellent internet/mobile penetration (90%+) (+2.0). Multiple payment methods including crypto emerging and cards (+1.0). No major blocking reported. Final: 3.0/3.0 |

| Player Penalties | 20% | 1.3/2.0 | No criminal penalties for playing (+2.0). Deduction: 5% mandatory tax on winnings withheld at source acts as a financial penalty/disincentive (-0.7). Final: 1.3/2.0 |

| Market Availability | 10% | 1.0/1.0 | Competitive mix of local and international operators available. Final: 1.0/1.0 |

🔍 Key Highlights

Strengths

- Tax Efficiency for Foreign Revenue: The 5% GGR tax on foreign players is world-class, making Georgia an excellent hub for targeting the wider region legally.

- Speed to Market: Licensing can take as little as 1 day (expedited) to 20 days, which is incredibly fast compared to EU jurisdictions (6-12 months).

- Banking Access: A regulated environment allows for stable banking relationships within Georgia’s sophisticated banking sector (TBC, Bank of Georgia).

⛔️ CRITICAL RISKS AND CHALLENGES

- Demographic Cap: The 25+ age restriction for Georgian citizens significantly reduces the lifetime value (LTV) and pool of local players.

- Marketing Handcuffs: The broadcast ban (6 AM – Midnight) forces operators into digital-only or sponsorship heavy strategies, increasing digital CPMs.

- Market Size: With a total projected market of only $204M USD (2025), the local ceiling is very low. High competition for a small pie.

- Surveillance: The government has a “backdoor” into your platform via the mandatory real-time monitoring system. Data privacy from the state is non-existent.

- Player Tax Friction: The 5% tax on winnings irritates players and makes offshore/crypto casinos (which ignore this) more attractive to high rollers.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $200,000 – $350,000 (License fees, legal setup, local office).

Monthly Operating Costs: $50,000 – $100,000 (Staff, compliance, monitoring fees, office).

Effective Tax Rate on Revenue: ~15-20% (Includes GGR tax + Corporate Tax).

Profitability Assessment:

For a local-only strategy, profitability is DIFFICULT due to the small population (3.7M), age restrictions, and crowded market. The volume simply isn’t there for new entrants to scale easily.

However, as a hub for foreign operations (utilizing the “Offshore” license with 5% tax), the economics are EXCELLENT. The low tax rate and reputable banking make it a viable alternative to Curacao or Malta for operators targeting the CIS/Eastern European region, provided they handle the dual-domain structure correctly.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Unlicensed/Offshore Operators | 🔴 High/Critical | Criminal charges (up to 5 years prison), domain blocking, and blacklisting. Georgia actively enforces its borders. |

| Licensed Operators | 🟢 Low | High compliance burden (surveillance/reporting) but legal protection is strong if taxes are paid. |

| Affiliates | 🟡 Medium | Must stick to licensed brands. Promoting unlicensed sites can lead to domain blocks and potential fines. |

| Company Directors | 🟡 Medium | Personal liability for compliance failures. Criminal background checks are strict. |

🚨 Extradition and International Enforcement

Extradition Treaties: Georgia is aspiring to join the EU and has strong cooperation with USA, UK, and EU member states. It is NOT a safe haven for operators avoiding Western justice.

Enforcement History: The government frequently cooperates with Interpol and regional neighbors (Turkey, Azerbaijan) regarding illegal gambling and money laundering investigations.

Travel Risk: High for executives of unlicensed platforms. Entering Georgia (or transiting) could lead to arrest if an international warrant exists.

📋 Final Verdict

Georgia receives an Operator Ease Score of 8.2/10 and a Player Access Score of 8.8/10, resulting in an overall market attractiveness rating of 8.5/10.

HONEST ASSESSMENT: Georgia is a “White Market” gem disguised as a small CIS jurisdiction. While the local market is too small and restrictive (25+ age limit) to support many new entrants, the regulatory framework for targeting foreign players is outstanding due to the 5% tax rate. It is a strictly regulated environment—expect government surveillance and bureaucracy—but it offers a rare combination of full product legality, low taxes, and fast licensing.

Entry is recommended primarily for operators intending to use Georgia as a low-tax hub for international traffic, rather than those solely focused on the local Georgian player base.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- An operator targeting CIS/Eastern Europe needing a Tier-2 “White” license.

- Able to manage a dual-domain structure (Local vs. Foreign).

- Willing to establish a physical office and hire local staff.

- Looking for a low-tax (5%) jurisdiction with reputable banking access.

❌ Definitely Avoid If You Are:

- A “lean” startup wanting 100% remote operations (Physical presence is mandatory).

- Focused exclusively on the local Georgian market (Market size is capped and crowded).

- Unwilling to share real-time data with the government (Surveillance is mandatory).

- Relying on TV/Radio advertising for acquisition (Banned during day/evening).

- Operating without a license (Prison time is a real threat).

⚠️ BOTTOM LINE: Come for the 5% foreign tax rate and banking; stay away if you are an unlicensed cowboy or expect to get rich solely from the small local population.