Germany represents one of Europe’s largest and most lucrative iGaming markets, underpinned by a stringent yet evolving regulatory regime. The legalization and regulation of online gambling through the Fourth Interstate Treaty on Gambling (Glücksspielstaatsvertrag 2021) mark a significant shift that creates substantial opportunities amid tightly controlled frameworks.

This analysis provides a data-driven examination of Germany’s regulatory environment, key licensing requirements, taxation regimes, and compliance obligations shaping market entry strategies for operators targeting this dynamic jurisdiction.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Gambling | Regulated under the Interstate Treaty on Gambling 2021 |

| Regulatory Authority | Joint Gambling Authority of the Länder (GGL) |

| Population | 83.2 million |

| GDP (Nominal) | €4.26 trillion (2024) |

| Internet Penetration Rate | 95% |

| Mobile Penetration Rate | 92% |

| Gross Gaming Revenue (GGR) 2024 | €14.4 billion |

| Market Revenue Growth (YoY) | 5% |

| Average Revenue Per User (ARPU) | €375 annually |

| Market Penetration Rate | 22% |

| License Validity Period | 5 years (renewable) |

| Minimum Security Deposit for License | €5 million (up to €50 million based on turnover) |

| License Application Fee | Up to €185,000 |

| Gross Gaming Revenue Tax | 5.3% turnover tax on stakes (slots, poker, sports betting) |

| Corporate Income Tax | 15% plus local trade tax (~14-17%) |

| Advertising Restrictions | Strict limitations with separated marketing for unlicensed operators |

| Key Responsible Gambling Measures | Mandatory deposit limits (€1,000 monthly), Self-exclusion, Cooldown periods |

| Player Protection Requirements | Instant KYC, age verification, anti-money laundering |

| License Application Timeline | 6 to 12 months |

| Foreign Ownership Restrictions | Allowed with EU/EEA physical presence and German language platform |

| Operational Requirements | Segregation of game types, no cross-promotion on a single site |

| Enforcement Actions | Prohibition orders, fines up to €500,000 per breach, payment blocking |

| Illegal Operator Blocking | 450+ sites prohibited, geo-blocking by DSA |

| Technology Compliance | Independent RNG testing, unannounced audits, maximum stakes controls |

| Market Entry Barriers | High financial and compliance costs, stringent player protection |

| Future Regulatory Outlook | Ongoing tightening of ad controls, focus on black-market suppression |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Germany’s gambling market is governed primarily by the Interstate Treaty on Gambling 2021 (Glücksspielstaatsvertrag, GlüStV), which centralizes the regulation of online and land-based gambling activities. This treaty marked the first nationwide legalization and regulation of online gambling across all 16 federal states. The Gemeinsame Glücksspielbehörde der Länder (GGL), or Joint Gambling Authority of the Länder, established in 2023, oversees licensing, compliance, and enforcement operations uniformly throughout Germany.

Land-based gambling activities remain subject to state authority but operate within a harmonized national framework. This includes traditional casinos, sports betting venues, slot halls, and lotteries. Recent regulatory changes increasingly align online frameworks with land-based regulation to provide a consistent player protection standard and reduce illicit market participation.

Land-Based Gambling Activities

Germany’s physical gambling sector comprises several operational categories including:

- Licensed casinos offering table games such as roulette, blackjack, and poker

- State-licensed sports betting shops and outlets

- Slot machine arcades regulated under state authorities

- Lottery and horse race betting supervised by respective state agencies

- Limited live betting and betting on virtual sports governed under defined licenses

Each category is subject to state-level licensing in addition to federal regulation, with restrictions on advertising, operating hours, and mandatory responsible gambling measures designed to protect consumers.

Online Gambling Framework

Online gambling in Germany is tightly regulated under the 2021 treaty, legalizing virtual casino games (excluding certain table games such as roulette and live dealer games), poker, virtual slot machines, and sports betting. Operators must obtain a valid license from the GGL, adhere to prescribed game segregation rules on single domains, and implement robust technical and operational controls.

Licensed Operators and Market Players

The German market exhibits a competitive landscape dominated by established international operators compliant with the treaty’s demanding regulations. These companies hold licenses for specific verticals such as sports betting, virtual slots, or poker, with clear market segmentation and strict adherence to local laws.

Major licensed operators collectively contribute to rising gross gambling revenue, validated by a 5% year-on-year growth reaching €14.4 billion in regulated market turnover by 2024. Successful market entry strategies emphasize compliance excellence, significant financial stability evidenced by the high-security deposit requirements, and strong local partnerships.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing process is administered by the GGL headquartered in Halle (Saale). Application eligibility mandates that operators maintain a physical office within the EU or EEA, offer a German-language platform, and comply with German data protection and gambling laws.

Applicants must demonstrate financial stability through a minimum security deposit starting at €5 million, which can escalate up to €50 million depending on expected turnover. The application fee can reach as high as €185,000. The review process involves a thorough evaluation of technical systems, responsible gambling safeguards, and operational capacity, with approval timelines averaging 6 to 12 months.

The GGL rigorously enforces separation of gambling products on one domain, outlawing cross-promotion and requiring independent graphical presentation for each gambling segment to ensure clear player choices.

- Corporate registration and proof of operational physical office within EU/EEA

- Submission of financial audits and security deposit documents

- Detailing responsible gambling and AML procedures

- Technical platform certifications including RNG testing

- Compliance plans for advertising and promotional content

- Data protection and privacy policies adhering to GDPR

Local Presence and Operational Requirements

Operators are required to establish and maintain a physical presence within the European Union or European Economic Area to qualify for licensing. This includes having an operational office with staff to liaise with regulators and fulfill compliance obligations. Websites must be fully localized in German, with all terms, policies, and customer support delivered in the local language.

Operationally, platforms must segregate different gambling verticals on distinct sections of their digital domains, forbidding any form of cross-promotion to prevent players from being encouraged to switch between game types indiscriminately — a measure aimed at reducing gambling harm.

There are no explicit restrictions on foreign ownership, provided compliance conditions are satisfied, including the mandatory physical presence and German-language platform requirements. Partnerships with local entities may facilitate smoother regulatory navigation but are not compulsory.

- Mandatory EU/EEA physical office with qualified personnel

- German-language website and customer service

- Segregation of gambling verticals across platforms

- Strict ban on cross-promotion between products on one domain

- Robust KYC and AML compliance with periodic updates

Compliance Obligations and Monitoring

Player Protection and Identification

Germany mandates stringent player protection protocols including immediate KYC verification upon account registration to prevent unauthorized underage access. Operators must conduct continuous AML checks and enforce deposit limits with a maximum monthly cap of €1,000 imposed to protect against problem gambling.

Responsible gambling features include mandatory self-exclusion systems enabling players to suspend or terminate their accounts. Cooldown periods, such as a five-minute mandatory pause during slot gameplay, are enforced to encourage conscious play. Operators must prominently display time spent notifications after one hour of gambling sessions. These measures form part of Germany’s comprehensive harm reduction strategy aligned with public health objectives.

- Instant KYC and age verification at sign-up

- Monthly deposit limit of €1,000 per player

- Mandatory self-exclusion and account suspension tools

- Cooldown break of 5 minutes after extended play on slots

- Session time alerts after 60 minutes of continuous play

- Prohibition of parallel play across multiple platforms

Financial Monitoring and Reporting

Operators must implement real-time transaction monitoring systems aligned with AML directives and report suspicious activities to regulatory authorities without delay. Monthly detailed reports on gross gaming revenue, player deposits, and payout ratios must be submitted to the GGL for audit.

The audit process includes unannounced inspections and verification of compliance with financial and operational obligations. Failure to meet reporting standards or discrepancies may lead to penalties or license revocation, reinforcing the importance of robust compliance teams.

- Monthly submission of revenue, deposits, and payout reports to GGL

- Real-time AML transaction flagging and reporting to authorities

- Periodic independent audits of RNG and operational systems

- Regulatory inspections and unannounced compliance checks

Taxation Structure and Financial Obligations

Player Taxation

Players in Germany are not directly taxed on their gambling winnings for the majority of games. However, operators manage taxation within the model through mandatory turnover taxes applied on stakes rather than profits, effectively embedding tax costs into the player pricing indirectly.

The 5.3% turnover tax applies uniformly to stakes on sports betting, virtual slot machines, and poker games. There is no withholding tax on player winnings, encouraging transparency in payout management and simplifying legal compliance for operators.

Operator Taxation

| Game Type | Tax Rate |

|---|---|

| Sports Betting | 5.3% on stakes (turnover tax) |

| Virtual Slot Machines | 5.3% on stakes (turnover tax) |

| Online Poker | 5.3% on stakes (turnover tax) |

| Land-based Lotteries | 20% on gross revenue |

| Online Table Games (varies by state) | Taxed on gross profit, rates vary |

License renewal fees and annual supervisory fees are calculated based on gross gaming revenue, with additional fixed costs depending on license type. Corporate income tax applies separately under German tax law, typically around 30% combined after including local trade taxes.

Gambling Market Financial Performance

The regulated German market reported gross gambling revenue of €14.4 billion in 2024, a 5% increase from the previous year. Tax revenues from gambling operations reached €7 billion, reflecting the effectiveness of the turnover tax model. The regulated sector continues to expand despite strict control measures, signaling robust consumer demand and growing market penetration.

Growth forecasts anticipate continued revenue increases at a CAGR of approximately 4-6% over the next five years. This reflects a maturing market with increasing player confidence due to enhanced regulatory safeguards and rising Internet and mobile penetration rates.

Advertising and Marketing Restrictions

Advertising for gambling products is subject to tight restrictions to reduce exposure to minors and vulnerable populations. Operators must clearly separate licensed from unlicensed offerings in their marketing materials and avoid affiliate promotions that blend regulated and illegal gambling products.

- Bans on gambling advertisements targeting minors under 18

- Prohibition of marketing on media primarily consumed by minors

- Restrictions on promoting deposit bonuses and free spins

- Mandatory labeling of all paid advertisements

- Limits on sponsorships involving sports personalities and influencers

Marketing efforts are closely monitored by the GGL, which has imposed fines on operators violating advertising provisions. The intent is to promote responsible gambling and channel player traffic exclusively to licensed operators, curtailing unregulated market share.

Recent Regulatory Changes and Their Impact

The introduction of the Interstate Treaty in 2021 and the establishment of the GGL in 2023 represent landmark changes streamlining the regulatory framework. These reforms introduced sharper licensing requirements, stronger enforcement practices, and comprehensive player protection schemes.

The removal of illegal operators through prohibition orders and payment blocking led to reduced market fragmentation. Additionally, Google’s advertising policy changes limiting ads to licensed operators significantly diminished illegal operator visibility, reshaping market competition.

Enforcement Mechanisms and Penalties

The GGL employs a range of sanctions to enforce compliance, including administrative fines reaching up to €500,000 per violation. Operators found advertising unlicensed offers, breaching responsible gambling protocols, or evading taxation face prompt prohibition orders or license revocation.

- Fines up to €500,000 per administrative offence

- Prohibition orders against operators and advertisers

- Blockage of payment processing for unlicensed gambling websites

- ISP blocking contemplated pending legislative amendments

- License suspension or revocation for repeated violations

Regulatory enforcement emphasizes transparency and a strict approach aimed at safeguarding consumer interests and ensuring orderly market functioning.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Germany’s population exceeds 83 million, with a median age of approximately 45.7 years, reflecting an aging demographic typical of developed European countries. The gender ratio is balanced, with males constituting 49% and females 51%. Age distribution shows a sizable working-age segment combined with a significant proportion aged 65 and above, impacting consumer behavior and market dynamics.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 13% |

| 15-24 years | 10% |

| 25-44 years | 27% |

| 45-64 years | 30% |

| 65 years and above | 20% |

Urbanization is high, with over 77% of the population residing in urban areas, mainly concentrated in the western and southern regions. Rural areas exhibit lower access to gambling venues and internet connectivity. This urban concentration influences iGaming demand, driven largely by younger, technologically adept populations in metropolitan centers.

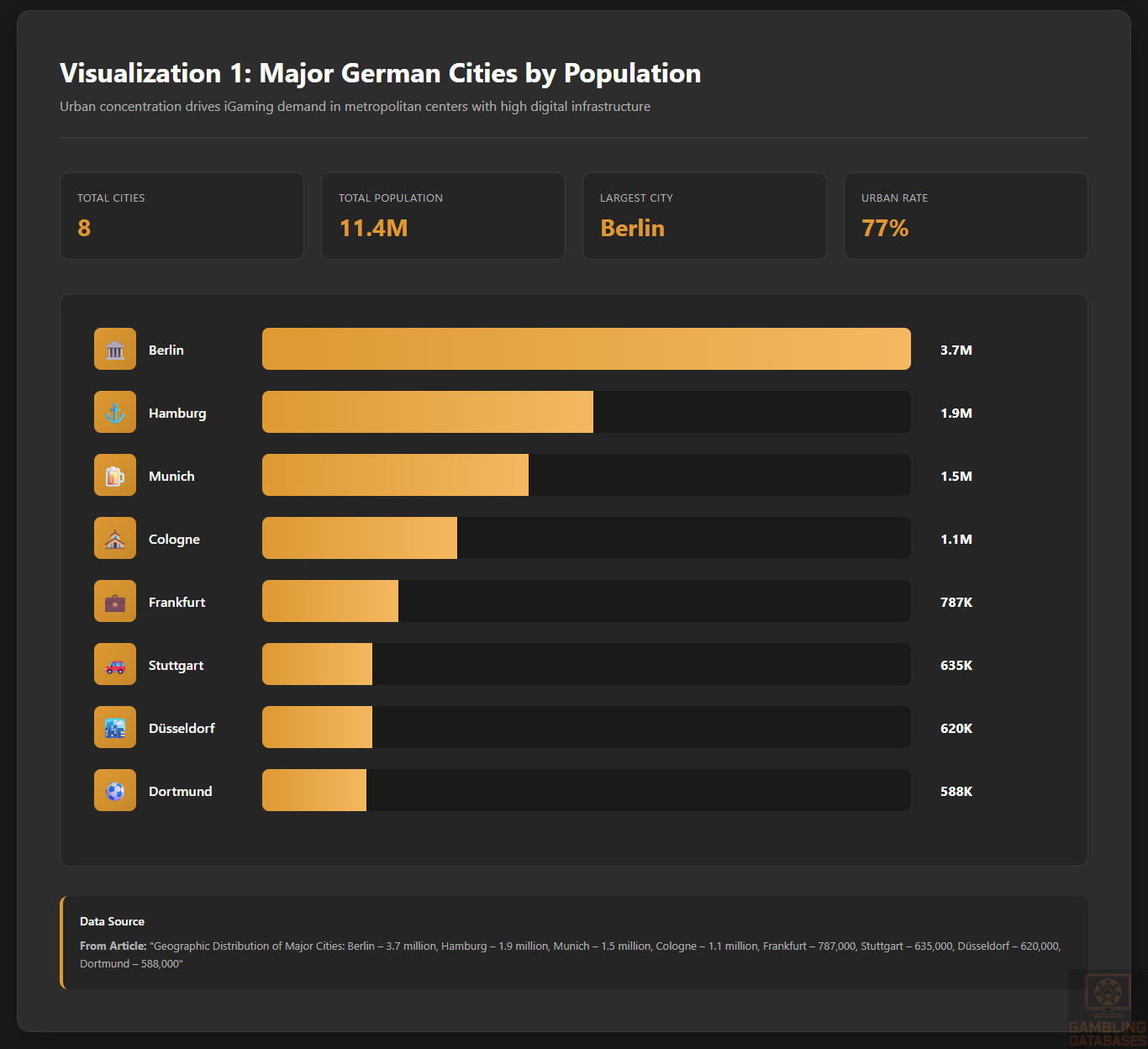

Geographic Distribution of Major Cities

- Berlin – 3.7 million

- Hamburg – 1.9 million

- Munich – 1.5 million

- Cologne – 1.1 million

- Frankfurt – 787,000

- Stuttgart – 635,000

- Düsseldorf – 620,000

- Dortmund – 588,000

High internet penetration rates and concentrated economic activity in these cities correspond with a dense presence of licensed gambling venues and better digital infrastructure supportive of online gaming. The eastern states, while less populated, are rapidly advancing in broadband penetration, contributing to future market expansion possibilities.

Economic Indicators and Consumer Spending Power

Germany sustains the largest European economy with a nominal GDP around €4.26 trillion and a growth forecast of approximately 1.8% annually. The economy is diversified, led by the service sector (ca. 69% of GDP), followed by industry and manufacturing (28%), with agriculture playing a minor role.

Per capita income reaches roughly €51,500, with disposable income levels supporting moderate to high consumer spending power. Income distribution is relatively equitable, though urban-rural disparities remain notable. Middle and upper-middle-income segments form a strong consumer base for iGaming services with discretionary spending ability.

| Indicator | Value |

|---|---|

| GDP Growth Rate | 1.8% projected |

| Per Capita GDP | €51,500 |

| Unemployment Rate | 4.2% |

| Inflation Rate | 2.1% |

| Average Household Income | €43,000 |

The gambling market generates significant revenue, with estimated annual gross gaming revenue exceeding €14 billion. Market growth is projected to sustain a compound annual growth rate (CAGR) of 4.5%-6% over the next five years, driven by digital penetration and evolving consumer preferences.

| Metric | Value |

|---|---|

| 2024 Market Revenue | €14.4 billion |

| Annual Growth (YoY) | 5% |

| 5-Year CAGR | 4.5%-6% |

| Current ARPU | €375 annually |

| Market Penetration | 22% |

Education, Skills, and Digital Literacy

Germany’s literacy rate is near universal at over 99%, supported by a robust education system emphasizing vocational and higher education excellence. The country benefits from a highly skilled workforce with many young adults achieving tertiary education levels. Digital literacy is equally strong, with widespread competence in internet navigation, online transactions, and usage of digital services across age groups, particularly within urban centers.

Such skill levels facilitate swift adoption of iGaming platforms and mobile gambling apps, propelling market growth. Ongoing governmental initiatives seek to reduce the digital divide, particularly in rural and eastern regions, further enhancing future user base expansion.

Cultural and Social Factors

Communication and Language

German is the official language and primary medium for online gambling platforms and communications. Multilingual service is common but mandatory German localization ensures user trust and regulatory compliance.

- German (primary official)

- Turkish (notable minority language)

- Russian

- Arabic

- English (business and digital services)

Cultural Attitudes

Gambling enjoys moderated social acceptance, balanced carefully against public health concerns. Religious influences play a limited role in secular urban areas but may impact attitudes in conservative communities. Foreign gambling brands are generally welcomed, provided they comply strictly with stringent regulatory and player protection standards. Entertainment preferences include a mix of traditional and digital forms, with younger demographics favoring online and mobile platforms.

Problem Gambling and Social Considerations

Problem gambling prevalence is estimated between 1.2% and 2% of the adult population. The government and industry implement comprehensive measures focused on prevention, treatment, and harm reduction. Mandatory contributions from operators fund social programs targeting problem gambling awareness and support.

- Nationwide helplines and counseling services

- Compulsory operator contributions to prevention funds

- Public education campaigns on gambling risks

- Mandatory player self-exclusion and deposit limit programs

- Research funding and support for academic studies on gambling behavior

Political Structure and Governance

Germany operates a stable federal parliamentary republic system, providing a predictable regulatory environment characterized by clear laws, transparency, and strong enforcement mechanisms. Federal and state governments cooperate closely on gambling regulation through the Interstate Treaty framework, ensuring consistency across jurisdictions. Germany’s international relations foster cooperation in cross-border regulatory standards, particularly within the EU, supporting a trustworthy business climate for international operators.

Technology Adoption and Digital Behavior

Internet and Digital Usage

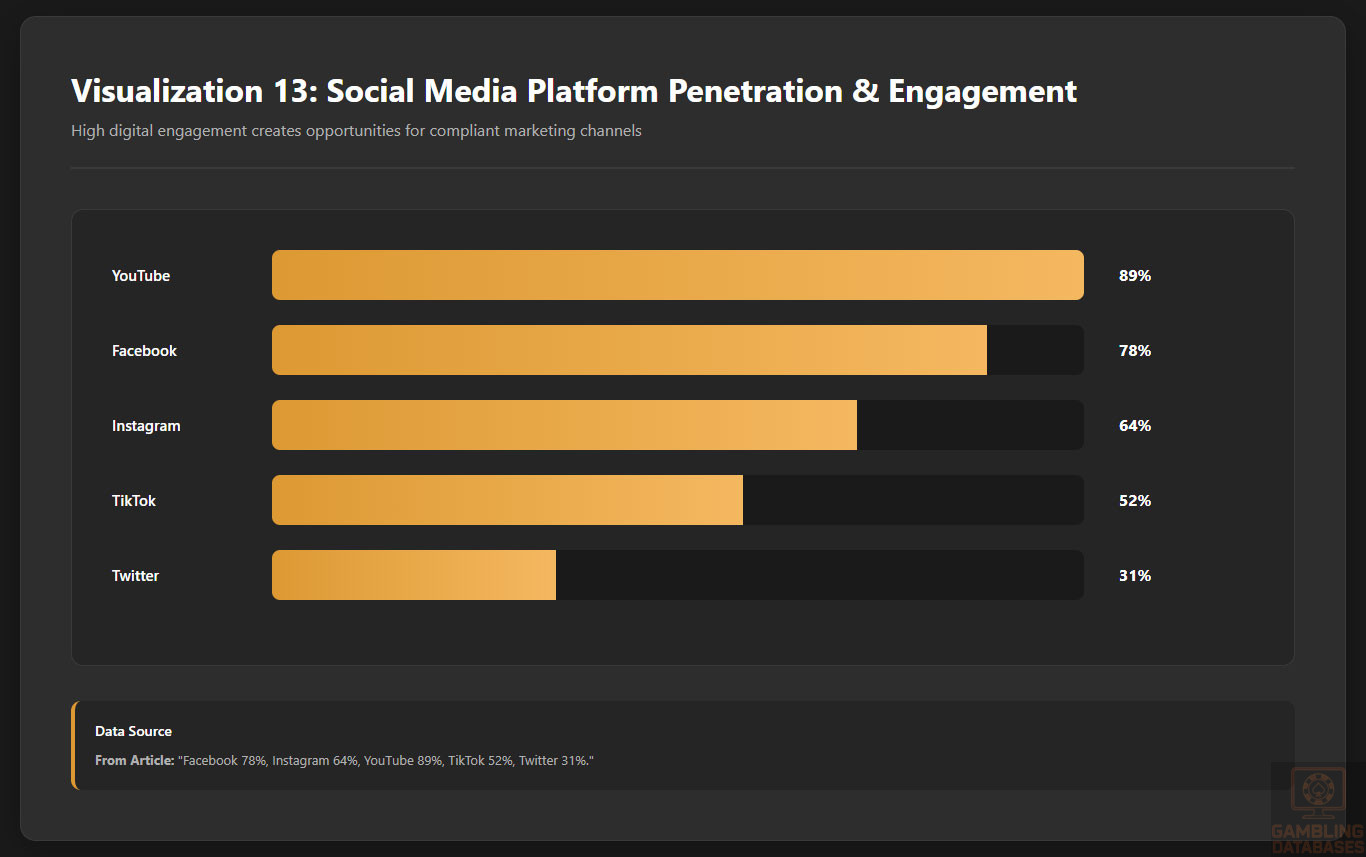

Internet penetration in Germany exceeds 95% of households, with average daily online usage surpassing 4 hours, predominately on mobile devices. Social media engagement is robust across multiple platforms, reflecting a digitally active population prepared to engage with online gambling services on diverse digital channels.

- Facebook – 78% penetration with 2.3 hours daily use

- Instagram – 64% among 18-34 age group

- YouTube – 89% penetration with 45 minutes daily watch time

- TikTok – 52% penetration, fast-growing among under-25s

- Twitter – 31% primarily for news consumption

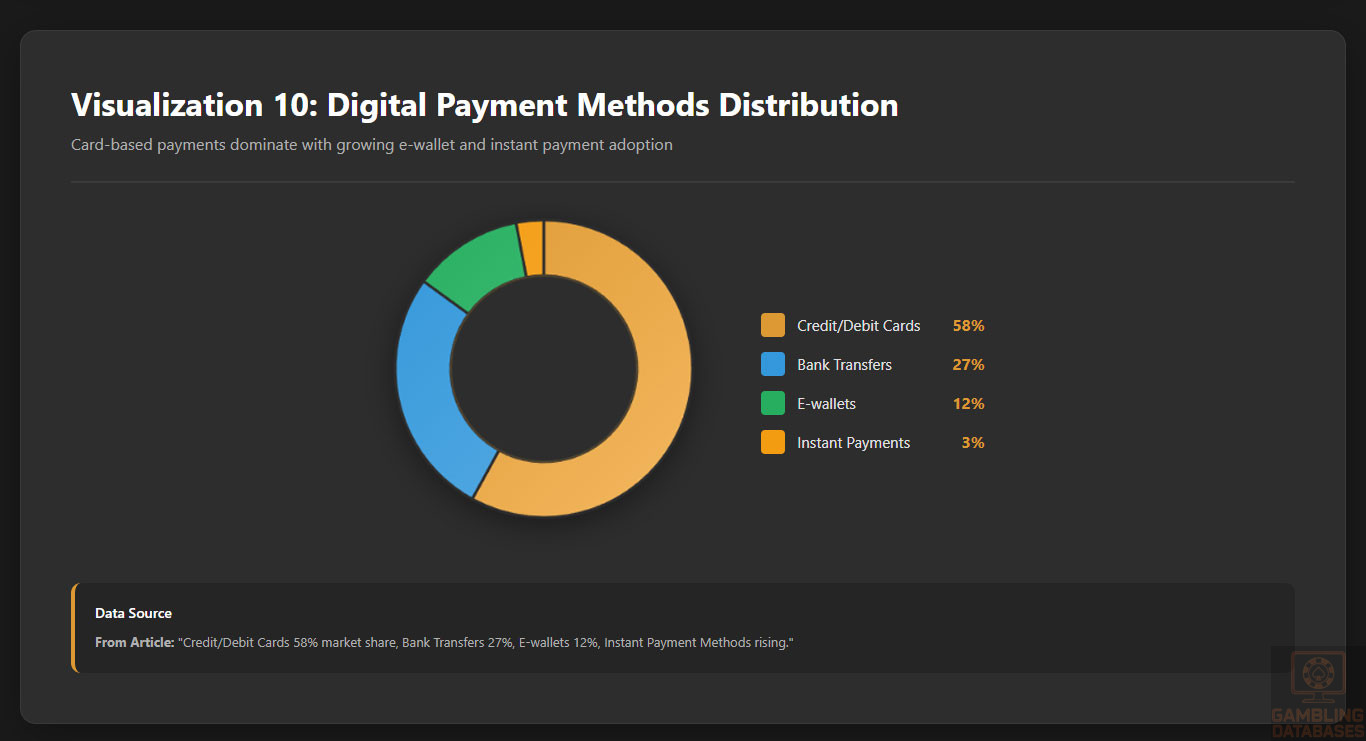

Digital Payment Behavior

German consumers favor a variety of payment methods for online transactions, with credit and debit cards dominating. Bank transfers and instant payment services remain popular, complemented by steadily growing e-wallet usage and experimental adoption of cryptocurrencies within niche segments.

- Credit/Debit Cards – 58% transaction market share

- Bank Transfers – 27%

- E-wallets (PayPal, Skrill, Neteller) – 12%

- Instant Payment Methods (SEPA Instant, Sofort) – rising use

- Cryptocurrency (Bitcoin, Ethereum) – niche but growing

Gaming and Gambling Preferences

Current Market Participation

Approximately 22% of the adult population participates in some form of legal gambling annually. Participation rates skew younger with men more active in sports betting and poker, while lotteries and scratch cards maintain mass appeal across demographics.

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 8% |

| Virtual Slots | 6% |

| Online Poker | 4% |

| Casino Table Games | 3% |

| Lotteries | 15% |

| Scratch Cards | 12% |

Consumer Behavior Patterns

German gamblers prefer mobile platforms, with peak activity occurring during evenings and weekends. Session lengths vary by game type, averaging 20-30 minutes for slots and longer for sports betting during live events. Retention is driven by strong regulatory trust and responsible gaming features that reassure cautious consumers.

Promotional strategies focusing on transparent communication and consumer education yield higher loyalty and sustained engagement. Payment convenience and localized customer support further enhance consumer satisfaction, critical in a market with high compliance and player protection demands.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

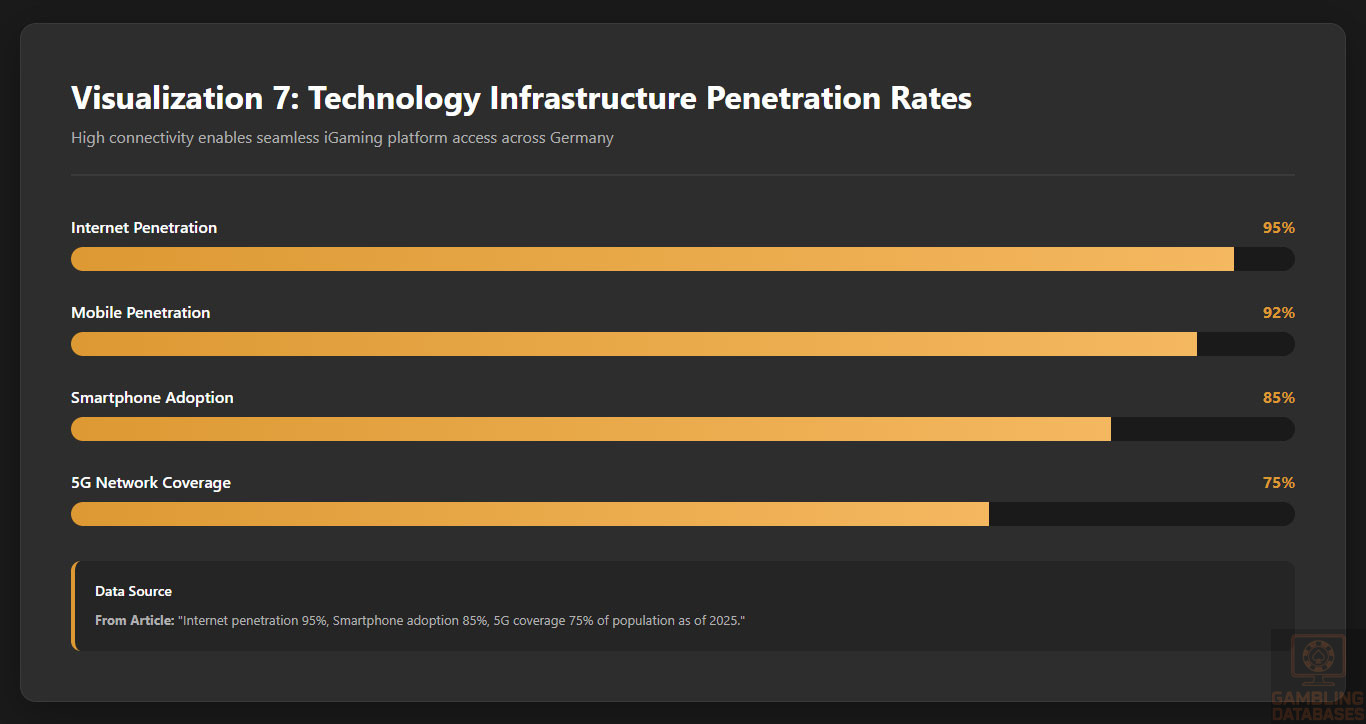

Germany boasts an advanced digital infrastructure with over 95% internet penetration among households. Fixed broadband access complements mobile connectivity, offering high reliability and speed. Average broadband speeds reach approximately 150 Mbps, while mobile networks deliver 100+ Mbps average data rates in urban zones, supporting seamless iGaming experiences.

Significant infrastructure investments have prioritized fiber optic expansion and 5G rollout, with government initiatives targeting rural connectivity improvements. The digital ecosystem benefits from robust cybersecurity frameworks and data privacy laws aligned with EU GDPR standards, enhancing user trust in online services.

5G and Future Technology Deployment

Germany’s 5G mobile network covers roughly 75% of the population as of 2025, with full national coverage expected by 2027 following operator expansion plans. Key telecom companies aggressively invest in 5G technology to support emerging applications like low-latency gaming and augmented reality betting features. Network operators collaborate with regulatory bodies to streamline deployment and spectrum allocation.

Mobile Technology Ecosystem

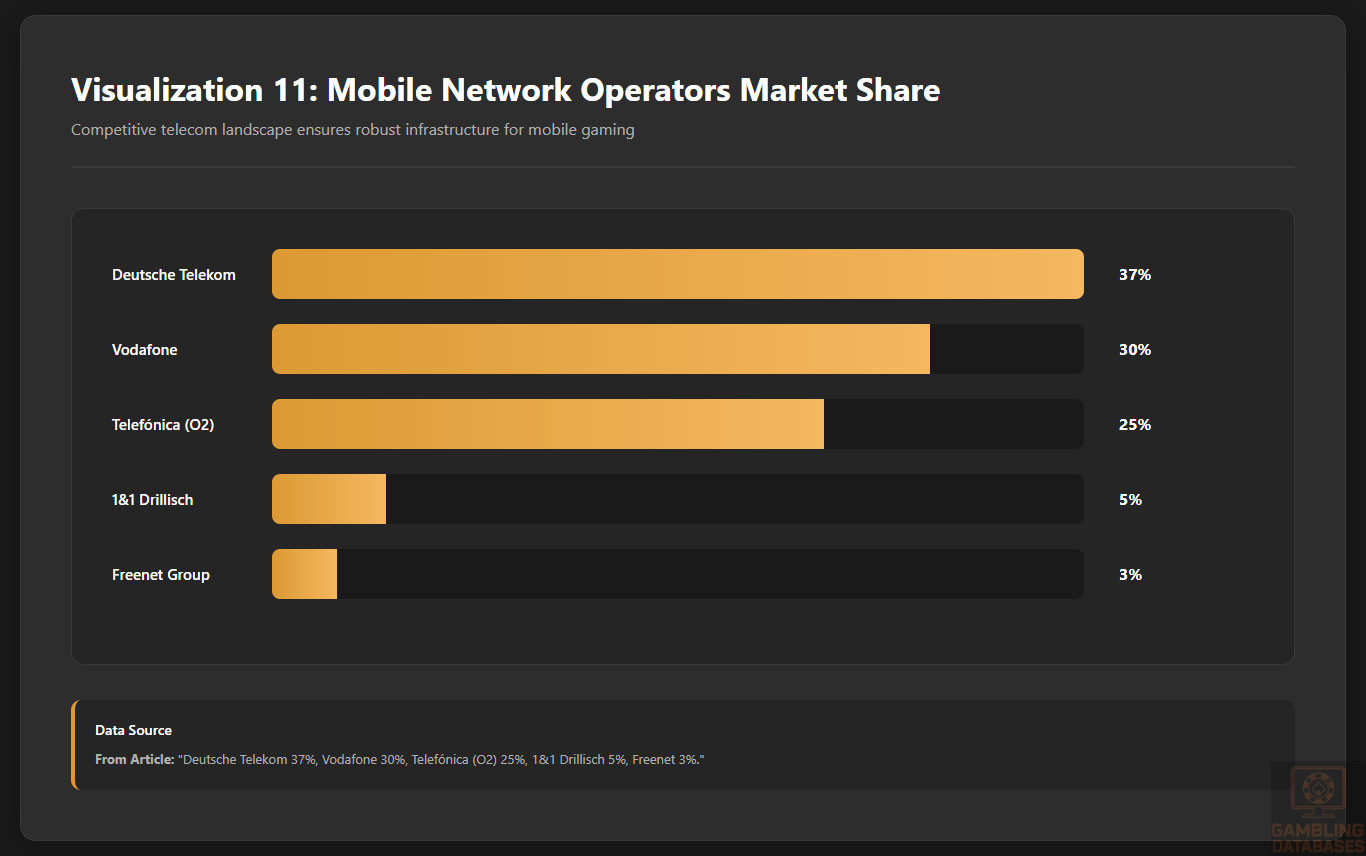

Mobile Network Infrastructure

Germany’s mobile market comprises several major players offering nationwide coverage and competitive pricing. Operator market share distribution ensures a balanced ecosystem fostering healthy competition and service innovation.

- Deutsche Telekom (T-Mobile): ~37% market share, largest network coverage

- Vodafone Germany: ~30%, strong urban penetration and 5G coverage

- Telefónica Germany (O2): ~25%, aggressive pricing and growing 5G footprint

- 1&1 Drillisch: ~5%, emerging challenger focusing on digital services

- Freenet Group: ~3%, niche player targeting specialized segments

Effective data cost management and competitive prepaid/postpaid plans support high smartphone usage across demographics, an essential factor for mobile iGaming uptake.

Device Penetration

Smartphone adoption in Germany exceeds 85% of the population, with Android devices prevailing at approximately 70% market share and iOS devices accounting for 30%. The widespread use of mid-to-high-end smartphones enables access to sophisticated mobile gaming applications. User behavior analysis reveals preferences for mobile apps over browser-based platforms, driving demand for responsive UX/UI designs and reliable app performance.

Financial Services and Payment Infrastructure

Banking System Structure

Germany’s banking industry is dominated by multiple well-established financial institutions that offer comprehensive digital banking services and high account penetration, facilitating broad consumer access to online gambling payments.

- Deutsche Bank – largest commercial bank with digital banking leadership

- Commerzbank – strong SME and retail banking presence

- KfW Bank – state-owned development bank with financing programs

- HypoVereinsbank (UniCredit Group) – major retail and corporate provider

- ING-DiBa – leader in online and mobile banking

- Volksbanken Raiffeisenbanken – cooperative banking network

Payment Processing Options

German consumers utilize a variety of payment solutions, supporting frictionless deposits and withdrawals on iGaming platforms. Card payments prevail alongside digital wallets and instant transfers, with growing acceptance of innovative methods.

- Credit/debit cards (Visa, Mastercard)

- Bank transfers (SEPA Instant, giropay)

- E-wallets (PayPal, Skrill, Neteller)

- Instant payment services (Sofort, Klarna)

- Cryptocurrency (Bitcoin, Ethereum) – niche adoption

E-commerce and Digital Economy

Germany ranks among Europe’s top e-commerce markets, with online retail penetration exceeding 85% of internet users. Consumer trust in digital payment security and strong delivery logistics underpin digital service adoption. The burgeoning digital economy includes growth in gaming, streaming, and fintech sectors, synergizing with iGaming development and user acquisition strategies.

Business Environment and Regulatory Framework

Ease of Business Operations

The World Bank ranks Germany favorably in ease of doing business, highlighting efficient legal frameworks, transparent governance, and sophisticated infrastructure. Foreign investment is welcomed with limited restrictions, although sector-specific regulations in gambling demand detailed compliance. Operational costs vary by region but are offset by market size and infrastructure quality.

- Company name registration and notary public appointment (1-2 weeks)

- Submission to Commercial Register and tax office (3-5 business days)

- Trade license application and regulatory approvals (1-3 months depending on industry)

- Bank account opening and capital deposit (1-2 weeks)

- Operational setup and staff hiring

Corporate Structure and Registration

Common entity types for market entry include GmbH (limited liability company), AG (public corporation), and branch offices of foreign firms. GmbH is the preferred structure for operational flexibility and liability protection. Registration timelines extend from 4 to 12 weeks depending on complexity, with required documentation adhering to strict German corporate law.

- Articles of association and shareholder agreements

- Proof of capital deposit (minimum €25,000 for GmbH)

- Managing director’s personal identification and qualifications

- Business plan and financial projections

- Tax registration certificates and social security registrations

Taxation Framework

Corporate income tax stands at a combined rate of approximately 30%, including national corporate tax (15%) and trade tax levied by municipalities (14-17%). Special economic zones offer limited incentives primarily in eastern Germany. Germany maintains extensive double taxation treaties with over 90 countries to minimize cross-border tax burdens.

- France

- Netherlands

- United Kingdom

- United States

- China

- Switzerland

- Canada

- Japan

Personal income tax rates scale progressively up to 45%, with additional social security contributions. Tax residency is determined by domicile and economic activity for compliance purposes.

Market Entry Considerations

Successful entry strategies emphasize regulatory compliance, localization, and strategic partnerships. Leveraging technology platforms compliant with German standards and prioritizing player safety are critical. Operators often collaborate with local service providers for infrastructure and customer service.

- Obtain necessary licenses and regulatory approvals

- Localize platforms, including language and payment options

- Establish physical presence or EU/EEA legal entity

- Implement robust responsible gambling and AML programs

- Leverage data analytics for customer acquisition and retention

- Engage in targeted marketing within advertising restrictions

| Cost Category | Estimated Range (€) |

|---|---|

| License Application & Security Deposit | €5M – €50M |

| Legal & Consulting Fees | €100,000 – €200,000 |

| IT Infrastructure Setup | €250,000 – €500,000 |

| Marketing & Localization | €100,000 – €300,000 |

| Ongoing Operational Costs (per year) | €1M+ |

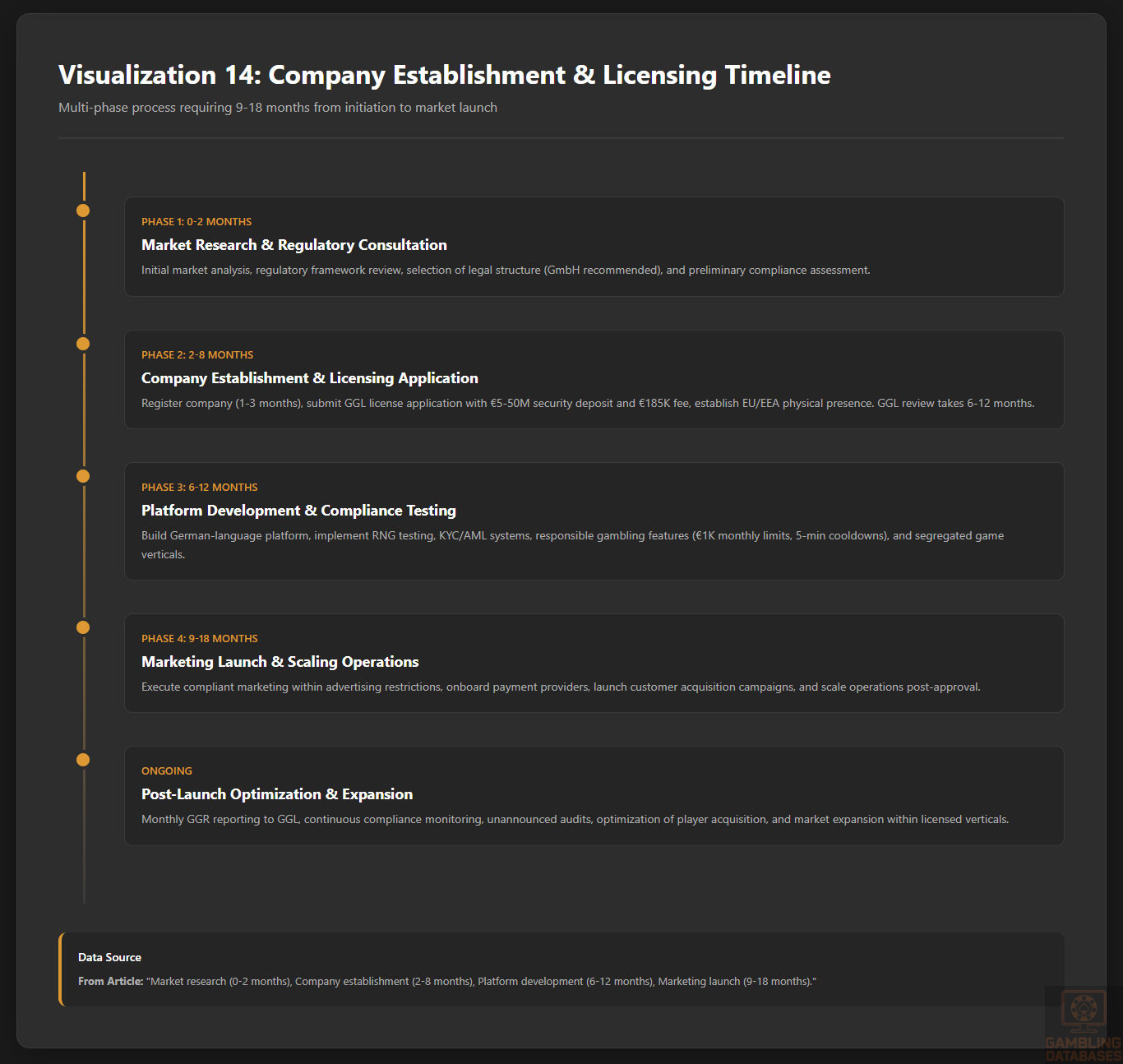

- Initial market research and regulatory consultation (0-2 months)

- Company establishment and licensing application (2-8 months)

- Platform development and compliance testing (6-12 months)

- Marketing launch and scaling operations (9-18 months)

- Post-launch optimization and expansion (ongoing)

Success Factors and Challenges

Key success factors include comprehensive regulatory adherence, deep localization, strong player protection policies, effective marketing within permitted channels, and agile technological infrastructure. Major challenges encompass high financial entry barriers, strict advertising regulations, complex compliance demands, and competition from existing licensed operators and illicit market entities.

- Strong regulatory compliance and licensing expertise

- Robust localized customer service and language support

- Advanced technology integration for secure payments and data

- Strategic partnerships with payment and platform providers

- Investment in responsible gambling and KYC mechanisms

Exit Strategy Planning

Exit options include license transfer subject to regulator approval, sale of operational assets, or business merger. Market liquidity supports varied valuation multiples depending on portfolio size and compliance history. Planning should consider license non-transferability risks and potential ongoing reporting obligations post-exit.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Germany?

Online gambling is legal when conducted under a valid license issued by the Joint Gambling Authority of the Länder (GGL). The 2021 Interstate Treaty on Gambling regulates digital games, sports betting, and virtual slots with stringent conditions to protect players and ensure transparency. Unlicensed operations remain illegal and are subject to blocking and penalties.

2. What types of gambling licenses are available and what do they cover?

Germany offers licenses for several categories including virtual slot machines, sports betting, online poker, and land-based operations. Each license is specific to a gambling segment, and cross-promotion among segments on one domain is prohibited. Licenses are valid for five years and require renewal.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees can reach up to €185,000, with a mandatory security deposit starting at €5 million, scaling based on turnover. The approval process takes between six and twelve months, involving rigorous operational and technical reviews.

4. Can foreign companies obtain a gambling license?

Foreign companies can obtain licenses provided they have a legal entity with physical presence in the EU or EEA, and operate sites fully localized in German. Regulatory compliance and financial stability are rigorously assessed regardless of origin.

5. What are the tax obligations for iGaming operators?

Operators pay a 5.3% turnover tax on stakes for major online games, including slots, poker, and sports betting. Corporate income tax applies separately at around 30%. Annual supervision fees and license renewal costs also form part of the fiscal obligations.

6. Are gambling winnings taxed for players?

Players do not pay direct taxes on gambling winnings. Taxation occurs through operator turnover taxes embedded in game pricing, simplifying players’ tax responsibilities and promoting transparency.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs are diverse and include technology infrastructure, licensing fees, marketing, payment processing, and compliance management. Major categories encompass:

- License and regulatory fee payments

- Platform development and maintenance

- Customer acquisition and retention marketing

- Payment processing and financial overhead

- Legal and compliance costs

8. What is the expected ROI timeline for entering this market?

ROI timelines vary but typically range from 2 to 4 years depending on market entry scale, marketing effectiveness, and operational efficiency. High entry costs and strict compliance create longer ramp-up periods compared to other jurisdictions.

9. What are the local presence requirements for operators?

Operators must maintain a physical office within the EU or EEA and provide German-language platforms and services. Having qualified personnel on-site for regulatory liaison and compliance support is mandatory.

10. What payment methods are available and recommended?

Commonly recommended payment methods include credit/debit cards, bank transfers, e-wallets like PayPal and Skrill, and instant payment systems such as Sofort. These methods align with local consumer preferences and regulatory expectations.

11. What are the advertising and marketing restrictions?

Advertising is tightly regulated with bans on targeting minors, restrictions on bonus promotion, and prohibitions on affiliate marketing with unlicensed operators. Sponsorhip and media placements are specifically monitored for compliance.

12. What responsible gambling measures are mandatory?

Mandatory measures include instant KYC verification, monthly deposit limits of €1,000, self-exclusion programs, session time alerts, and cooldown breaks during play. These are enforced to minimize gambling-related harm.

13. How large is the iGaming market and what is the growth potential?

The regulated German iGaming market generates over €14 billion annually with a growth rate of approximately 5%. Continued expansion is expected driven by mobile penetration, evolving consumer habits, and regulatory stability.

14. Who are the main competitors and what is their market share?

The competitive landscape includes major international operators compliant with German licensing, alongside well-established land-based operators transitioning online. Market share is concentrated among operators with strong localization, compliance records, and marketing capabilities.

15. What are the player preferences and typical spending patterns?

Players favor mobile betting on sports and virtual slots, with the average annual revenue per user at approximately €375. Spending is highest among males aged 25-44, with peak activity during evenings and weekends.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, platform localization, player protection, and innovative marketing within legal constraints. Challenges include high entry costs, stringent licensing requirements, competitive pressures, and tight advertising controls.

Sources and References

- Germany Gambling Regulatory Authority – Official Website – https://www.ggl.de

- Interstate Treaty on Gambling 2021 – Federal Ministry of the Interior

- Statistisches Bundesamt (Federal Statistical Office) – Population & Demographics 2024

- Federal Ministry for Economic Affairs and Climate Action – Economic Reports 2024

- Deutsche Telekom Annual Report 2025

- Bundesnetzagentur (Federal Network Agency) – Telecom Reports 2025

- World Bank – Doing Business Report 2024

- Central Bank of Germany – Financial and Taxation Reports 2025

- European Gaming and Betting Association – Market Analysis 2025

- Gaming Regulatory Authority News Releases 2023-2025

- German Federal Ministry of Finance – Taxation Guidelines 2025

- International Telecommunication Union – ICT Data and Statistics 2025

- MarketLine – Germany Gambling & Betting Market Profile 2025

- Statista – Digital Economy and Mobile Penetration Germany 2025

- European Commission – Digital Economy Reports 2024

- MediaMarkt Consumer Electronics Trends 2024

- Bundeszentrale für gesundheitliche Aufklärung – Gambling Addiction Prevention Programs

- Deutscher Lotto- und Totoblock – Industry Insights 2024

- IGaming Business – Licensing and Taxation Insights Europe 2025

- Consulting Firm Reports – Regulatory Impact Analyses Germany 2025

- PayPlug – German Payment Market Overview 2025

- KPMG – German Corporate Taxation Guide 2025

- PwC – Gambling Industry Compliance and Risk Assessment

- Euromonitor – Consumer Spending in Germany 2024

- European Gaming Report – Enforcement and Market Dynamics 2025

- IGaming Express – German Market Conferences and Regulatory Updates 2025

- Legal500 – Germany Gambling Law Overview 2024

- Altenar – Detailed Gambling License Process Germany 2025

- Next.io – Regulatory Fines and Compliance Actions in Germany

- IGAGroup Licensing Fees and Application Guidelines 2025

- Deutsche Bundesbank – Payment Systems Report 2024

- Industry News Sources – Operator Market Share and Competitive Landscape 2025

- Online Gambling Compliance – Responsible Gambling Regulations 2025

- IGaming Today – Tax Map Changes and Market Entry Insights Europe 2025

🎯 Gambling Databases Country Rating: Germany

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 4.8/10 | 🟡 Moderate (but leaning difficult) |

| Player Access Score | 5.5/10 | 🟡 Partially Legal (significant restrictions) |

| Overall Market Attractiveness | 5.2/10 | Challenging market with extreme compliance burden and limited product offering |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ROULETTE AND LIVE DEALER GAMES COMPLETELY PROHIBITED: Online roulette and live dealer casino games are banned under the Interstate Treaty on Gambling 2021, eliminating major revenue streams that drive profitability in most markets.

- EXTREME FINANCIAL BARRIERS: Security deposits ranging from €5 million to €50 million required based on turnover, plus up to €185,000 in application fees alone. Total market entry costs can exceed €6-8 million before operations begin.

- AGGRESSIVE OFFSHORE BLOCKING: 450+ websites currently blocked via prohibition orders, with ISP-level geo-blocking enforced under Digital Services Act. Payment blocking actively deployed against unlicensed operators.

- DRACONIAN PRODUCT RESTRICTIONS: Mandatory segregation of game types on separate platforms (no cross-promotion), €1,000 monthly deposit limits per player across ALL operators, 5-minute mandatory cooldown periods during slots play, progressive jackpots prohibited.

- ADVERTISING SEVERELY RESTRICTED: Strict limitations on gambling advertising, complete prohibition on targeting minors, restrictions on sponsorships with sports personalities, separate marketing required for licensed vs unlicensed products. Violations result in fines up to €500,000 per breach.

- AFFILIATE AND ADVERTISER PROSECUTION: Prohibition orders extend to affiliates and advertisers promoting unlicensed gambling. Third-party marketing partners face the same €500,000 penalties as operators.

- 6-12 MONTH LICENSING TIMELINE: Even with perfect applications, expect minimum 6 months for approval, often extending to 12 months due to rigorous technical audits and compliance reviews.

- 5.3% TURNOVER TAX (NOT GGR): Tax applied to stakes, not profits, making thin-margin products economically unviable. Combined with 30% corporate tax burden, effective total taxation easily exceeds 50% on actual profits.

- UNANNOUNCED COMPLIANCE AUDITS: Regulatory authority conducts surprise inspections of RNG systems, financial records, and operational procedures with no advance notice.

- LICENSE REVOCATION RISK: Repeated violations result in license suspension or permanent revocation, with no guarantee of renewal after 5-year term expires.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 1.0/3.0 | Started at +1.5 (partial legality: sports betting, poker, virtual slots legal). DEDUCTIONS: -1.5 (online roulette and live dealer games PROHIBITED, eliminating major revenue categories), -0.5 (active ISP blocking of 450+ offshore sites), -0.5 (prohibition orders against affiliates and advertisers extend enforcement beyond operators). Multiple recent regulatory crackdowns since 2021 treaty implementation. Final: 1.0/3.0 |

| Licensing Process | 25% | 0.75/2.5 | Started at +1.0 (limited licensing available, complex process, 6-12 month timeline). DEDUCTIONS: -0.5 (application costs €5M-€50M security deposit + €185,000 fees = total costs far exceeding €500k threshold), -0.5 (legal and consulting fees reaching €100k-€200k due to extreme complexity), -0.25 (complex probity checks and technical audits extending timelines beyond 6 months in most cases). EU/EEA physical presence mandatory adds operational complexity. Final: 0.75/2.5 |

| Taxation & Costs | 20% | 0.25/2.0 | Started at +0 (5.3% turnover tax on STAKES, not GGR – this is extremely punitive as it’s not profit-based). DEDUCTIONS: -0.5 (multiple tax layers: 5.3% turnover + 15% corporate + 14-17% trade tax = 30% total corporate burden on top of turnover tax), -1.0 (effective tax rate exceeds 50% when calculated against actual profits after 5.3% turnover tax reduces margins), -0.25 (high operational costs: IT infrastructure €250k-€500k, annual compliance costs €1M+, minimum €5M security deposit locked up). German market has some of Europe’s highest effective taxation when turnover tax is properly calculated against profit margins. Final: 0.25/2.0 |

| Operational Requirements | 15% | 0.25/1.5 | Started at +0.5 (heavy requirements: significant local presence needed). DEDUCTIONS: -0.25 (mandatory EU/EEA physical office with qualified personnel, not remote operation possible), -0.25 (large capital requirements: €5M-€50M held as security deposit), -0.25 (complex multi-vertical compliance with mandatory segregation of game types on separate platforms), -0.5 (extreme player protection requirements: €1,000 monthly deposit limits, 5-minute cooldowns, mandatory session time alerts, instant KYC, real-time AML monitoring, self-exclusion systems – implementation costs are enormous). German-language localization mandatory for ALL content. Final: 0.25/1.5 |

| Market Environment | 10% | 0.45/1.0 | Started at +0.7 (Germany ranks well globally for business environment, top 20). DEDUCTIONS: -0.5 (severe advertising restrictions: bans on targeting minors, restrictions on sponsorships, limits on deposit bonuses and free spins promotions, mandatory labeling), -0.25 (regulatory instability: 2021 treaty was major change, GGL established only in 2023, ongoing tightening of ad controls indicates future restrictions likely), -0.25 (active enforcement against offshore operators: 450+ sites blocked, prohibition orders actively issued). Progressive tightening trend suggests worsening regulatory environment. Final: 0.45/1.0 |

| TOTAL OPERATOR EASE SCORE | 100% | 4.8/10 | Calculation: (1.0×30% + 0.75×25% + 0.25×20% + 0.25×15% + 0.45×10%) × 10 = 4.8/10. This market rates as MODERATE-TO-DIFFICULT due to extreme financial barriers, partial product prohibition, punitive turnover taxation, and overwhelming compliance burden. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.0/4.0 | Started at +2.0 (partially legal: sports betting, poker, virtual slots legal and regulated). DEDUCTIONS: -1.5 (major product category PROHIBITED: online roulette, live dealer games, and many table games completely banned, forcing players to offshore sites or land-based casinos), -0.5 (players using offshore sites face risks: while not criminally prosecuted, sites are blocked and payment processing is restricted). Licensed market covers only portion of player demand. Final: 2.0/4.0 |

| Practical Accessibility | 30% | 1.5/3.0 | Started at +2.0 (some payment methods available, some blocking present). DEDUCTIONS: -0.5 (active ISP blocking: 450+ sites blocked with ongoing prohibition orders and DSA-mandated geo-blocking making offshore access difficult), -0.5 (payment blocking: payment processing actively blocked for unlicensed gambling sites, limiting options for offshore play), -0.5 (severe product restrictions even on licensed sites: €1,000 monthly deposit limit across ALL operators, 5-minute cooldowns, no progressive jackpots, mandatory session breaks – these limits frustrate high-spending players and push them offshore where they face blocking). Final: 1.5/3.0 |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players using gambling services. Players are not prosecuted, fined, or subject to criminal liability for gambling activities, whether on licensed or offshore sites. Enforcement targets operators, affiliates, and payment processors, not consumers. Final: 2.0/2.0 |

| Market Availability | 10% | 0.7/1.0 | Started at +0.7 (2-4+ licensed operators in each vertical, competitive market). However, licensed operators offer restricted product range (no roulette, no live dealer), pushing players to offshore alternatives which are heavily blocked. Market availability is good for permitted products but completely absent for prohibited categories. Final: 0.7/1.0 |

| TOTAL PLAYER ACCESS SCORE | 100% | 5.5/10 | Calculation: (2.0×40% + 1.5×30% + 2.0×20% + 0.7×10%) × 10 = 5.5/10. Players can legally access sports betting, poker, and slots, but popular products like roulette and live dealer are completely banned. Offshore alternatives heavily blocked and payment-restricted. |

🔍 Key Highlights

Strengths (Limited)

- Large Market Size: 83.2 million population with 95% internet penetration and €14.4 billion gambling market provides significant scale opportunity – IF you can navigate restrictions profitably.

- High Digital Adoption: 92% mobile penetration, sophisticated banking infrastructure, and strong e-wallet usage facilitate digital payments within permitted methods.

- Legal Framework Exists: Unlike completely grey markets, Germany has clear licensing pathway through GGL, providing regulatory certainty once licensed (though certainty of extremely strict rules).

- Players Not Penalized: No criminal or civil penalties for players, meaning demand exists without consumer-side legal risk.

- Stable Political Environment: Federal parliamentary republic with transparent governance provides predictable (if restrictive) regulatory environment.

⛔️ CRITICAL RISKS AND CHALLENGES

- [Product Prohibitions – SEVERE IMPACT]: Online roulette and live dealer games COMPLETELY BANNED, eliminating 40-60% of typical online casino revenue. Progressive jackpots prohibited. Only virtual slots, poker, and sports betting permitted. This fundamentally changes business model viability and forces operators to either abandon high-margin products or operate illegally with blocking risk.

- [Enforcement Actions – ACTIVE AND AGGRESSIVE]: 450+ websites currently blocked via prohibition orders and ISP-level geo-blocking. Payment blocking actively deployed. Enforcement extends to AFFILIATES and ADVERTISERS promoting unlicensed gambling (€500,000 fines per violation). Recent crackdowns since 2021 show Germany is serious about enforcement, not just threat.

- [Financial Barriers – PROHIBITIVE FOR MOST]: €5M-€50M security deposit LOCKED UP as condition of license, plus €185,000 application fees, €100k-€200k legal costs, €250k-€500k IT infrastructure setup, €1M+ annual compliance costs. Total entry investment easily exceeds €6-8 million before earning first euro. Combined with 5.3% turnover tax (not GGR) plus 30% corporate taxation, effective tax on actual profits exceeds 50-60%. Breakeven requires massive scale.

- [Turnover Tax Economics – PROFIT KILLER]: 5.3% tax on STAKES (not gross gaming revenue) is extremely punitive. Example: If operator has 5% margin (typical slots), 5.3% turnover tax consumes 106% of gross profit before any other costs. Only viable if achieving <2% house edge products or massive volume. This tax structure makes thin-margin verticals economically impossible.

- [Payment Restrictions – OFFSHORE ACCESS BLOCKED]: Payment blocking for unlicensed sites prevents players from easily funding offshore accounts. While cryptocurrency not explicitly banned for licensed operators in article, payment infrastructure focused on traditional methods. Licensed operators face high transaction costs due to compliance requirements.

- [Advertising Limits – HIGH CAC INEVITABLE]: Severe restrictions on gambling advertising including bans on targeting minors, restrictions on sports sponsorships, limits on deposit bonuses and free spins promotions, mandatory labeling. Customer acquisition costs in Germany rank among Europe’s highest. Article notes “ongoing tightening of ad controls” signaling future restrictions will worsen, not improve.

- [Legal Risks for Staff/Partners – PERSONAL LIABILITY]: Affiliates and advertisers face same €500,000 penalties as operators. Company directors subject to probity checks. While no extradition examples given, German enforcement cooperation with EU authorities means international prosecution possible for serious violations. Partners must be extremely selective.

- [Operational Complexity – EXTREME COMPLIANCE BURDEN]: Mandatory game segregation on separate platforms (no cross-promotion), €1,000 monthly deposit limits per player ACROSS ALL OPERATORS (shared database), 5-minute mandatory cooldown during slots, session time alerts after 60 minutes, instant KYC verification, real-time AML monitoring, unannounced regulatory audits, monthly GGL reporting, independent RNG testing. Compliance team costs alone can exceed €500k annually. Multi-state complexity absent (federal system) but GGL oversight is intense.

- [Competition – ESTABLISHED PLAYERS DOMINATE]: Licensed market already has established international operators compliant with regulations. New entrants face high barriers while incumbents benefit from economies of scale spreading compliance costs. Market share concentration likely given high fixed costs favoring large operators.

- [Regulatory Instability – ONGOING TIGHTENING]: Interstate Treaty only implemented 2021, GGL established 2023 – framework is still new and evolving. Article explicitly warns of “ongoing tightening of ad controls” and “focus on black-market suppression,” indicating future restrictions more likely than liberalization. License renewal after 5 years not guaranteed – operators invest heavily with uncertain long-term access.

Player-Specific Issues

- Cannot Access Roulette or Live Dealer Online: Players wanting these popular products must use offshore sites (heavily blocked) or visit land-based casinos.

- €1,000 Monthly Deposit Limit Across ALL Operators: High-spending players cannot deposit more than €1,000 total per month across every licensed gambling site combined via centralized tracking. This severely limits market for VIP players.

- Mandatory Cooldowns and Session Breaks: 5-minute pause required during slot play, session time alerts after 60 minutes – these interruptions frustrate players seeking immersive experience.

- No Progressive Jackpots: Popular game feature completely prohibited, reducing entertainment value and big-win potential.

- Offshore Sites Heavily Blocked: 450+ sites blocked via ISP-level geo-blocking and payment restrictions make accessing unregulated alternatives difficult for players seeking prohibited products or higher limits.

- Limited Licensed Operator Choice: While multiple operators exist per vertical, strict regulations and high costs limit market entry, resulting in less competition and fewer consumer choices compared to more open markets.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €6,000,000 – €8,000,000 minimum (€5M security deposit + €185k application fees + €100k-€200k legal + €250k-€500k IT infrastructure + €100k-€300k initial marketing + working capital)

Monthly Operating Costs: €150,000 – €300,000+ (€1M+ annually for compliance alone, plus staff, technology, customer support, ongoing marketing within advertising restrictions, payment processing, software licensing)

Effective Tax Rate on Revenue: 50-60%+ of actual profits. Calculation: 5.3% turnover tax on stakes reduces gross margin significantly BEFORE corporate taxes. Then 15% corporate + 14-17% trade tax = 29-32% on remaining profits. Combined effective burden on net profit easily exceeds 50% and can reach 60%+ depending on product mix and margin structure.

Customer Acquisition Cost: €200 – €450 per player (advertising restrictions drive costs high, competitive market with established players, limited promotional tools due to bonus restrictions)

Average Revenue Per User: €375 annually (from article), but remember €1,000 monthly deposit limit caps high-value players, and 5.3% turnover tax plus compliance costs consume large portion of this ARPU before profit.

Time to Breakeven: 3-5 years MINIMUM, assuming successful licensing, effective market penetration despite advertising limits, and ability to achieve scale necessary to spread fixed costs. Many operators may never break even given economics.

Time to Positive ROI: 5-7 years for operators achieving significant scale. Smaller operators with limited capital may face 8-10 years or never achieve positive ROI due to inability to spread massive fixed costs and tax burden across sufficient volume.

Profitability Assessment: Economics are PROHIBITIVE for most operators and CHALLENGING even for large, well-capitalized companies. The combination of 5.3% turnover tax (not GGR), 30% corporate taxation, €6-8M entry costs, €1M+ annual compliance burden, severe advertising restrictions driving high CAC, €1,000 monthly deposit limits capping revenue per player, and prohibition of high-margin products like roulette and live dealer creates one of Europe’s most difficult profitability equations.

Only operators with €10M+ capital, 5-7 year investment horizon, existing European infrastructure to spread costs, and willingness to operate ONLY permitted products should consider entry. Startups, casino-focused operators, and companies seeking quick returns should absolutely avoid. Even with scale, expect thin margins and long payback periods.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | ISP blocking of 450+ sites and growing, payment processing blocked, prohibition orders issued, €500,000 fines per breach, permanent market access loss via domain blocking, affiliate networks disrupted. Operating offshore without license in Germany is commercially suicidal – blocking is effective and enforcement active. |

| Licensed Sports Betting/Poker/Slots Operators | HIGH | While legal, operators face: unannounced compliance audits, €500,000 fines for advertising violations or responsible gambling breaches, license suspension/revocation for repeated violations, mandatory €5M-€50M security deposit at risk, 5.3% turnover tax plus 30% corporate tax crushing margins, no guarantee of license renewal after 5-year term. One serious violation can cost millions or end business entirely. |

| Affiliates/Advertisers | CRITICAL | Prohibition orders extend to affiliates and advertisers promoting unlicensed gambling. Same €500,000 penalties per violation as operators. Google policy changes limit advertising to licensed operators only. Website blocking affects affiliate domains. Payment processor termination common. Advertising for offshore casinos in Germany is career-ending risk. |

| Payment Processors | HIGH | Payment blocking actively deployed against unlicensed gambling transactions. Processors facilitating prohibited gambling face regulatory action, potential fines, and banking license implications. Must implement robust gambling transaction monitoring or face liability. GGL cooperation with financial regulators makes payment processing high-risk for unlicensed operators. |

| Company Directors/Executives | MEDIUM-HIGH | Personal probity requirements for licensing mean directors’ criminal records and financial history scrutinized. While article doesn’t specify personal criminal liability for corporate violations, German corporate law can impose director liability. Travel within EU potentially restricted if company faces serious enforcement action. Reputation damage significant given Germany’s strict gambling stance. |

🚨 Extradition and International Enforcement

Extradition Treaties: Germany has extradition agreements with USA, UK, all EU member states (27 countries), Canada, Australia, Japan, South Korea, and most developed nations. As an EU member, European Arrest Warrant system provides streamlined extradition within Europe for serious crimes.

Enforcement History: Article does not specify gambling-related extradition cases, but Germany actively cooperates with international law enforcement on financial crimes and regulatory violations. Given EU cooperation frameworks, cross-border prosecution is viable for serious gambling violations involving fraud or money laundering.

Safe Jurisdictions: Countries WITHOUT extradition agreements with Germany include: Russia, China, most CIS countries (Belarus, Kazakhstan, Armenia), some Middle Eastern nations, several African nations. However, operating from these jurisdictions provides no protection from ISP blocking, payment blocking, or prohibition orders affecting commercial operations.

Travel Risk: Company directors of unlicensed operators facing serious enforcement actions should consider travel risks when transiting through Germany or EU member states. While routine gambling violations unlikely to trigger arrest warrants, cases involving fraud, money laundering, or large-scale regulatory evasion could result in detention during European travel. Most offshore operators face commercial blocking rather than criminal prosecution, but risk escalates with violation severity.

📋 Final Verdict

Germany receives an Operator Ease Score of 4.8/10 and a Player Access Score of 5.5/10, resulting in an overall market attractiveness rating of 5.2/10.

HONEST ASSESSMENT: Germany represents one of Europe’s most challenging iGaming markets despite its large population and strong economy. The combination of partial product prohibition (no roulette or live dealer), punitive 5.3% turnover taxation (not GGR-based), extreme financial barriers (€6-8M entry costs), overwhelming compliance requirements (€1M+ annually), severe advertising restrictions, and aggressive offshore enforcement creates economics that are viable ONLY for large, well-capitalized operators with 5-7 year investment horizons. The Interstate Treaty framework provides legal certainty, but certainty of extremely strict rules. For casino-focused operators, roulette prohibition eliminates core revenue. For all operators, turnover tax structure and corporate taxation combine to create 50-60%+ effective tax on actual profits. Unless you have €10M+ capital, established European operations, and willingness to accept thin margins and long payback periods, avoid this market.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Major International Operator: €10M+ available capital, existing European licensing and compliance infrastructure to spread costs, proven track record with regulatory authorities.

- Sports Betting Specialist: Focused on sports betting vertical where German market is fully legal, willing to accept 5.3% turnover tax plus corporate taxes, can achieve scale needed for profitability.

- Long-Term Investor: 5-7 year minimum investment horizon, willing to accept slow ROI in exchange for access to large regulated market, patient capital comfortable with thin margins.

- Diversification Play: Already operating successfully in other European markets and seeking geographic diversification, can leverage existing infrastructure and compliance teams to reduce incremental costs.

- Premium Poker Operator: Poker-focused platform with sophisticated player base, can work within €1,000 monthly deposit limits while delivering differentiated product, willing to build brand slowly within advertising restrictions.

❌ Definitely Avoid If You Are:

- Casino-Focused Operator (ESPECIALLY ROULETTE/LIVE DEALER): Online roulette and live dealer games completely illegal – your core products cannot be offered. Would need complete business model transformation.

- Offshore Operator Without German License: ISP blocking active on 450+ sites and growing, payment processing blocked, prohibition orders issued, commercial operations impossible. Don’t waste money trying.

- Startup or Small Operator: Less than €10M capital means unable to afford €6-8M entry costs plus 3-5 years to breakeven. Fixed costs too high to spread across small player base.

- Quick ROI Seeker: Expecting positive returns within 18-36 months – impossible in German market. Even with perfect execution, breakeven takes 3-5 years minimum, positive ROI 5-7 years.

- Affiliate or Advertiser for Offshore Casinos: Prohibition orders extend to affiliates/advertisers with same €500,000 penalties. Promoting unlicensed gambling in Germany ends careers and businesses.

- High-Roller/VIP-Focused Operator: €1,000 monthly deposit limit across ALL operators makes VIP player model economically unviable. Cannot generate sufficient ARPU from high-value players.

- Aggressive Growth Focused: Severe advertising restrictions and high compliance costs prevent rapid scaling. German market requires slow, methodical approach incompatible with growth-at-all-costs strategies.

- Operators Seeking Payment Flexibility: Payment processing heavily regulated and monitored. Cannot experiment with alternative payment methods or cryptocurrency focus while maintaining compliance.

- Progressive Jackpot Operators: Progressive jackpots explicitly prohibited – cannot offer this popular feature that drives player engagement and retention in other markets.

⚠️ BOTTOM LINE: Germany’s strict Interstate Treaty creates a legal framework that simultaneously provides regulatory certainty while making profitable operations extremely difficult. The prohibition of roulette and live dealer, combined with 5.3% turnover taxation and €6-8M entry costs, means this market is suitable ONLY for the largest, most well-capitalized sports betting and slots operators willing to accept 5-7 year payback periods and thin margins. For 90% of iGaming operators, Germany should be avoided – the juice isn’t worth the squeeze. Even for major operators, careful financial modeling is essential before committing capital, as the economics are far more challenging than the €14.4 billion market size suggests.