Ghana presents a growing opportunity for iGaming operators driven by increasing internet penetration and a favorable demographic profile. The country’s regulatory landscape is evolving with clear licensing frameworks that support both land-based and online gambling activities. Understanding Ghana’s legal environment is key for strategic market entry and sustainable operation.

| Metric | Value |

|---|---|

| Gambling Legal Status | Licensed and regulated |

| Primary Regulatory Authority | Ghana Gaming Commission |

| Population (2025 estimate) | 33.4 million |

| Adult Population (18+) | 58% of total population |

| GDP (Nominal, 2024) | $80 billion USD |

| GDP Per Capita (2024) | $2,400 USD |

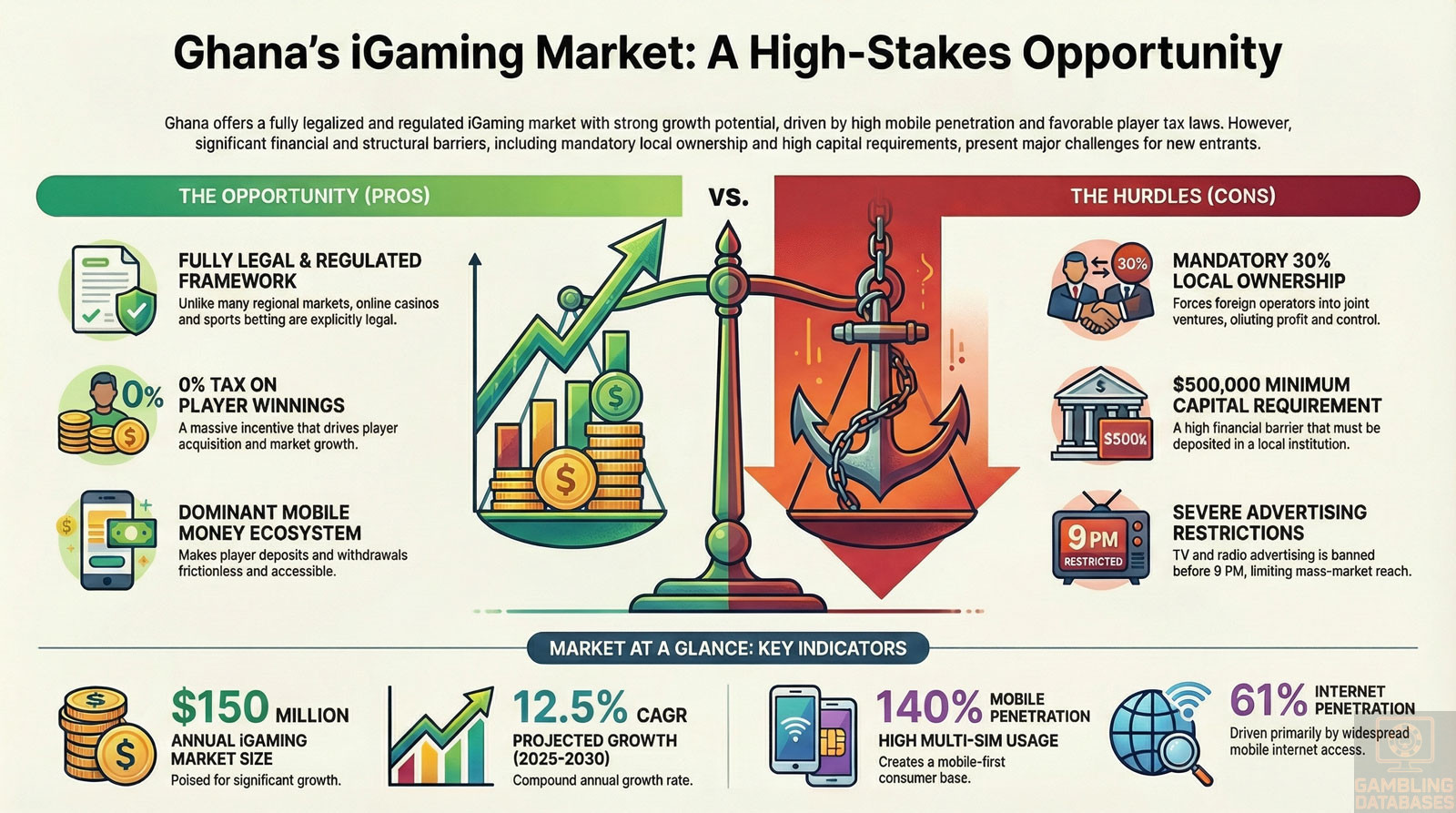

| Internet Penetration Rate | 61% |

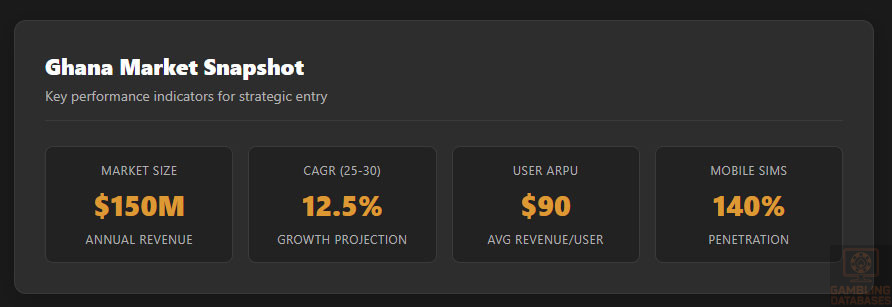

| Mobile Penetration Rate | 140% (active SIM cards) |

| Average Broadband Speed | 18 Mbps |

| Smartphone Penetration | 52% of population |

| Annual iGaming Market Size | $150 million USD |

| iGaming Market CAGR (2025-2030) | 12.5% |

| Average Revenue Per User (ARPU) | $90 USD |

| Total Licensed Operators | 12 |

| Land-Based Casinos Licensed | 7 |

| Sports Betting Operators Licensed | 25 |

| License Application Fee | $20,000 USD |

| Annual License Renewal Fee | $10,000 USD |

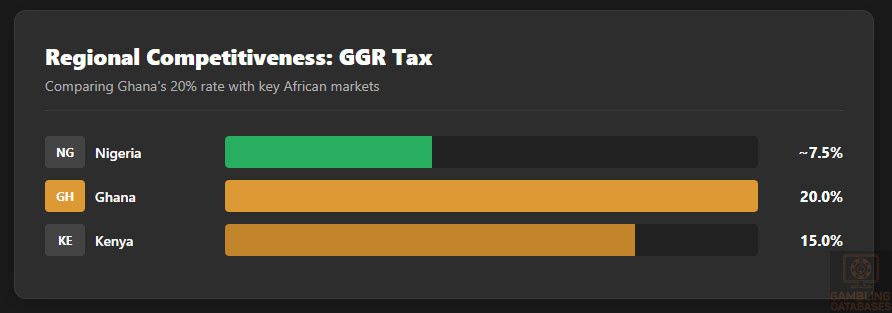

| Gross Gaming Revenue (GGR) Tax Rate | 20% |

| Corporate Tax Rate | 25% |

| Withholding Tax on Player Winnings | 0% |

| Minimum Capital Requirement | $500,000 USD |

| Typical Licensing Timeline | 3-6 months |

| Local Ownership Requirement | Minimum 30% Ghanaian ownership |

| Mandatory Responsible Gambling Measures | Yes |

| KYC/AML Compliance Requirements | Strict enforcement |

| Advertising Restrictions | Time and content restrictions |

| Enforcement and Penalties | Fines, license suspension, criminal sanctions |

| Currency Restrictions | GHS preferred for local operations |

| Payment Methods Popularity | Mobile money, cards, e-wallets |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

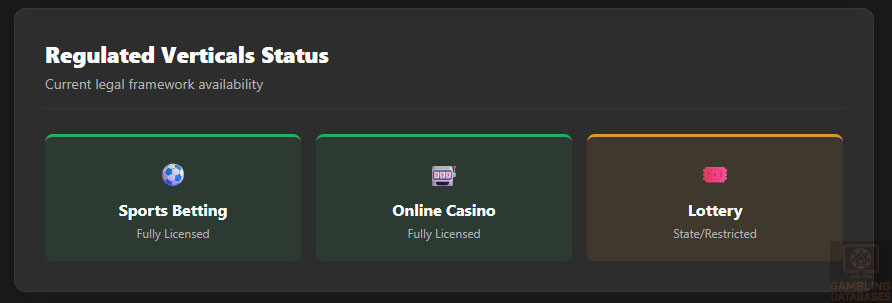

Ghana’s gambling industry is regulated primarily under the Gaming Act, which oversees all forms of betting and gaming activities including land-based and online operations. Gambling in Ghana is legal and regulated, covering casinos, sports betting, lottery, and gaming machines.

Land-based gambling remains a significant part of the market, with licensed casinos, sports betting shops, slot machine halls, and other physical gaming venues operating under strict regulatory supervision. The legislation mandates comprehensive controls over licensing, operations, and advertising to ensure market transparency and player protection.

Land-Based Gambling Activities

Casino operations are authorized in specific licensed venues with oversight from the Ghana Gaming Commission. Sports betting shops are widespread, with numerous operators licensed to offer betting services across the country.

Slot machine halls and electronic gaming machines are permitted under regulated conditions, with operators required to comply with technical standards and reporting obligations. Additionally, the government allows lottery-based gaming, which is also regulated under the Gaming Act.

Online Gambling Framework

Online gambling is fully legal and regulated in Ghana, requiring operators to obtain a specific online gaming license from the Ghana Gaming Commission. The framework prohibits certain activities such as unlicensed gambling, underage participation, and fraudulent practices. Operators must comply with robust technical standards, data security protocols, and ongoing auditing requirements to maintain licences.

The regulatory framework is designed to foster a competitive market environment while protecting consumers and ensuring responsible gambling practices. The Commission exerts close oversight on online operators, including mandatory reporting and compliance checks.

Licensed Operators and Market Players

The competitive landscape consists of a range of licensed operators including established local enterprises and regional international groups. Market concentration shows a balance between larger operators with extensive reach and smaller niche providers focused on specific game verticals. Entry strategies often involve partnerships with local stakeholders to meet ownership requirements and leverage market knowledge.

Currently, there are 12 licensed operators with a range of offerings from sports betting to full casino platforms. This diverse market structure supports innovation and competitive pricing, benefitting consumers with varied preferences.

Licensing Framework and Requirements

Application Process and Eligibility

The Ghana Gaming Commission is the sole licensing authority responsible for issuing gambling licenses in the country. Applicants must meet stringent financial, technical, and integrity standards to qualify. The process involves submission of multiple documents, background checks, and review of business plans.

Key steps in the application and eligibility process include:

- Submission of formal application to the Ghana Gaming Commission

- Provision of corporate registration certificates and governance documents

- Financial statements audited by recognized firms for the past three years

- Presentation of technical and security system documentation, including RNG certification

- Completion of criminal background checks for all directors and beneficial owners

- Proof of minimum capital requirement deposit in a licensed financial institution

Application fees are set at $20,000 USD with additional fees for annual renewal at $10,000 USD. License decisions typically take between 3 to 6 months.

Local Presence and Operational Requirements

Operators are required to maintain a local physical presence or a registered office within Ghana. Domains used for online operations must be registered locally or comply with Commission standards. Managers and key personnel must demonstrate relevant qualifications and experience in gaming operations.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators must implement strict player identification protocols to prevent underage gambling and ensure compliance with anti-money laundering (AML) standards. Age verification is mandatory for all participants with a minimum legal age of 18 years.

Responsible gambling measures are enforced, requiring operators to provide self-exclusion options, limit bet sizes, and offer information on problem gambling resources. Transparency in terms and conditions is mandated, ensuring players understand risks and rights.

- Mandatory age verification for all players

- Robust KYC (Know Your Customer) processes

- AML compliance including transaction monitoring

- Self-exclusion schemes available to players

- Limits on deposit amounts and bet sizes

- Disclosure of fair gaming practices and odds

Financial Monitoring and Reporting

Operators are subject to rigorous financial reporting obligations designed to prevent fraud and money laundering. Regular transaction monitoring is mandatory, with suspicious activities reported to regulatory authorities.

The reporting process includes multiple steps starting from internal audits to submission of quarterly financial statements and annual compliance reports to the Commission.

- Perform internal audits of all gambling transactions

- Prepare quarterly financial reports with detailed operational data

- Submit annual compliance reports and audit certificates

- Respond to Commission inquiries and regulatory inspections

Taxation Structure and Financial Obligations

Player Taxation

Players do not incur direct taxation on gambling winnings, as there is no withholding or income tax applied on individual prizes. This policy encourages participation and attracts more users to the legal market.

Operator Taxation

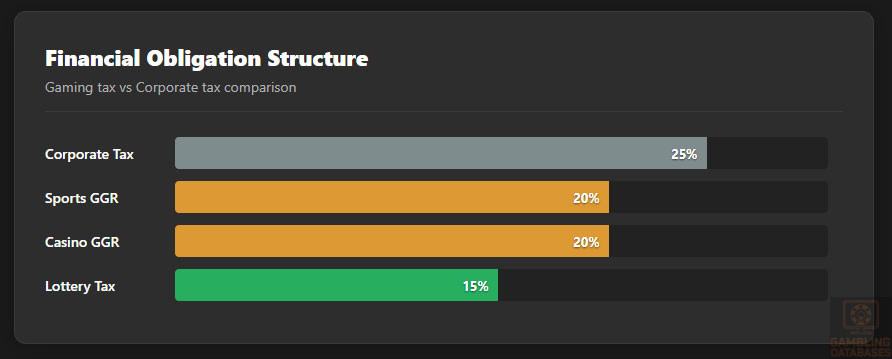

| Game Type | Tax Rate |

|---|---|

| Sports Betting | 20% |

| Casino Games | 20% |

| Lottery and Bingo | 15% |

| Other Games | 20% |

Besides gross gaming revenue (GGR) taxes, operators must also pay corporate income tax at 25%. License renewal fees at $10,000 USD apply annually, and turnover-based taxes are calculated as part of gross revenue assessments.

Gambling Market Financial Performance

The Ghanaian gambling market has shown steady growth with total wagers reaching over $750 million USD annually. Operator revenues have increased in line with market expansion, supported by rising internet accessibility and mobile payment integration.

Tax revenues from gambling activities contribute significantly to government budgets, funding social initiatives and regulatory enforcement. Market forecasts predict a compound annual growth rate (CAGR) of 12.5% over the next five years, supported by digital adoption and regulatory stability.

Advertising and Marketing Restrictions

Advertising in gambling is regulated with clear restrictions on the times, channels, and content to which operators can market their services. The objective is to reduce exposure to minors and vulnerable populations while allowing reasonable brand visibility.

- Television and radio advertising allowed only between 9 PM and midnight

- Online advertising must exclude minors and prohibited content

- Sponsorship agreements require prior regulatory approval

- Bonuses and promotions must be transparent and fair

- Direct marketing via SMS or email is limited in frequency and scope

Recent Regulatory Changes and Their Impact

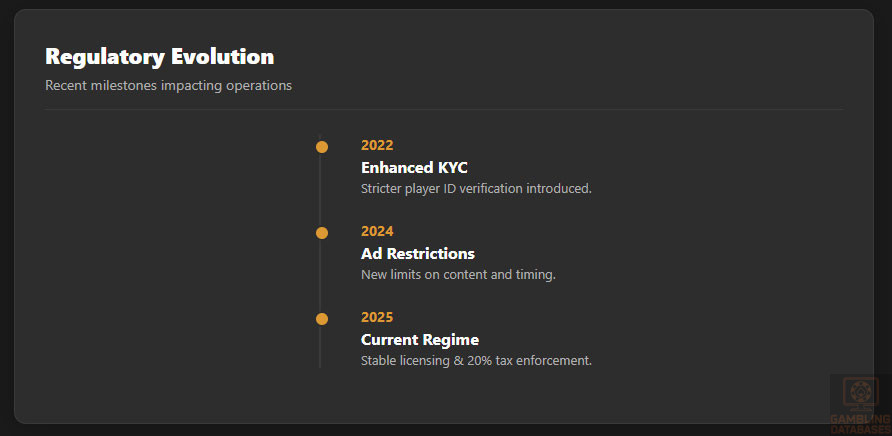

The Ghana Gaming Commission implemented several regulatory updates between 2022 and 2025, focusing on tightening KYC requirements and enhancing responsible gambling measures. These changes increased operational costs for operators but improved market integrity and consumer trust.

Enforcement Mechanisms and Penalties

Compliance enforcement is rigorous, with penalties for violations including substantial fines, license suspensions, and potential criminal charges in cases of fraud or major breaches. The Commission actively monitors operators and conducts audits to ensure adherence to legal and ethical standards.

- Monetary fines for regulatory non-compliance

- Temporary suspension of licenses

- Permanent revocation of licenses for severe breaches

- Criminal prosecution for fraudulent activities

- Public warnings and blacklisting of operators

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

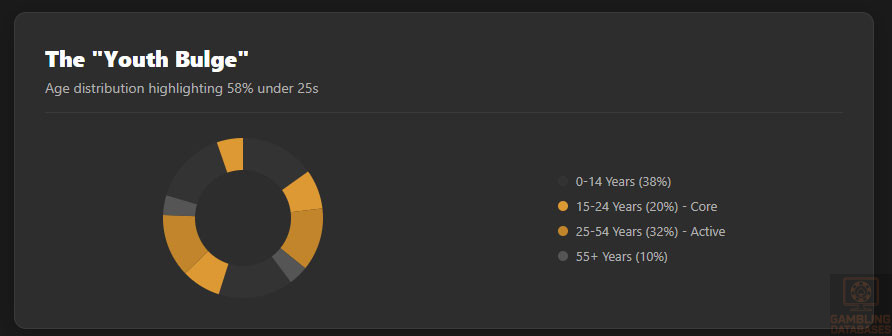

Ghana’s total population stands at approximately 33.4 million as of 2025, with a youthful demographic profile. The median age is 21 years, reflecting a large segment of the population under 30 years. Gender distribution is nearly balanced, with males accounting for 50.3% and females 49.7%. The population is predominantly rural, with about 43% living in urban centers and the remainder in rural areas.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 38% |

| 15-24 years | 20% |

| 25-54 years | 32% |

| 55-64 years | 5% |

| 65 years and over | 5% |

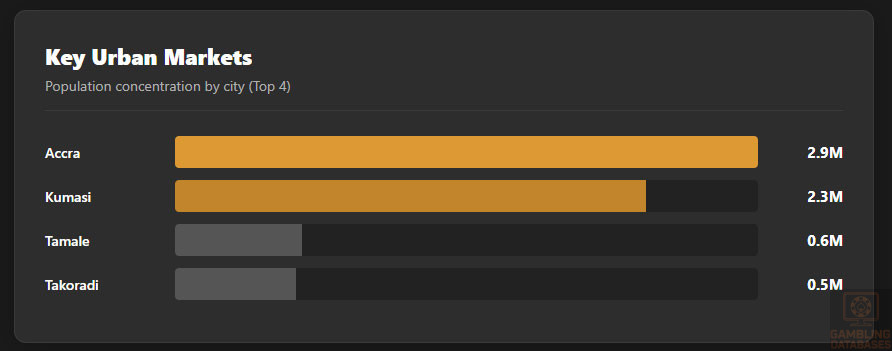

The urban population is concentrated in a few key metropolitan areas that drive economic activity and digital adoption. Internet infrastructure and gambling venue availability are markedly higher in urban settings, shaping consumer access and behavior.

- Accra – approximately 2.9 million residents (capital and largest city)

- Kumasi – around 2.3 million inhabitants, key commercial hub

- Takoradi – 550,000 residents, major port city

- Tema – 500,000 residents, industrial and shipping center

- Tamale – 600,000 inhabitants, regional center in the north

Economic Indicators and Consumer Spending Power

Ghana’s economy has shown steady expansion, with nominal GDP reaching $80 billion USD in 2024. The service sector dominates at roughly 50%, followed by industry at 30% and agriculture at 20%, reflecting ongoing diversification.

Per capita income is around $2,400 USD, underpinning rising consumer spending, particularly in urban markets. Disposable income varies widely with income inequality, yet a growing middle class is emerging, intensifying demand for digital entertainment and gambling services.

| Indicator | Value |

|---|---|

| GDP Growth Rate (2024) | 4.5% |

| Per Capita Income | $2,400 USD |

| Service Sector Contribution | 50% |

| Industry Sector Contribution | 30% |

| Agriculture Sector Contribution | 20% |

| Middle Class Growth Rate | 6.5% annually |

The iGaming consumer base is projected to grow significantly due to this expanding economic vitality. Market revenue is forecasted to reach $150 million in 2025, with a user base increasing annually by 10%, supported by digital financial access.

Education, Skills, and Digital Literacy

Ghana has a literacy rate of over 79% with continuing improvements driven by education reforms. Secondary education enrollment rates exceed 70%, and tertiary education is increasing, particularly in urban areas.

Digital literacy is improving rapidly, with over half of the population demonstrating basic to intermediate skills in using mobile and internet technologies. The workforce is developing skills relevant to digital commerce and entertainment sectors, including the iGaming industry.

Cultural and Social Factors

Communication and Language

Ghanaians predominantly speak English, which is the official language and primary language of internet and digital content. Several ethnic languages are widely spoken, including Akan, Ewe, and Ga, shaping localized marketing approaches.

- Akan (Twi, Fante dialects)

- Ewe

- Ga-Dangme

- Hausa

- English (official and widely used in business and digital)

Cultural Attitudes

The country exhibits generally positive attitudes toward gambling as a form of entertainment, mostly concentrated among the youth and urban populations. Religious groups occasionally express caution, influencing advertising restrictions and responsible gambling efforts. Foreign iGaming brands are increasingly welcomed due to their enhanced offerings and trustworthiness compared to informal operators.

Problem Gambling and Social Considerations

Problem gambling is recognized as a social issue, with an estimated prevalence rate of around 3% of the adult population. Various support programs and regulatory measures exist to mitigate harm and promote responsible gaming.

- Government-sponsored awareness campaigns

- Self-exclusion registry managed by regulators

- Mandatory responsible gambling education for operators

- Helpline and counseling services for affected individuals

- Collaboration with NGOs for addiction prevention

Political Structure and Governance

Ghana is a stable democracy with a multi-party political system and strong regulatory institutions. Political stability supports consistent enforcement of gambling laws and encourages foreign investment. The government actively pursues transparent regulatory reforms to enhance business environment predictability.

Technology Adoption and Digital Behavior

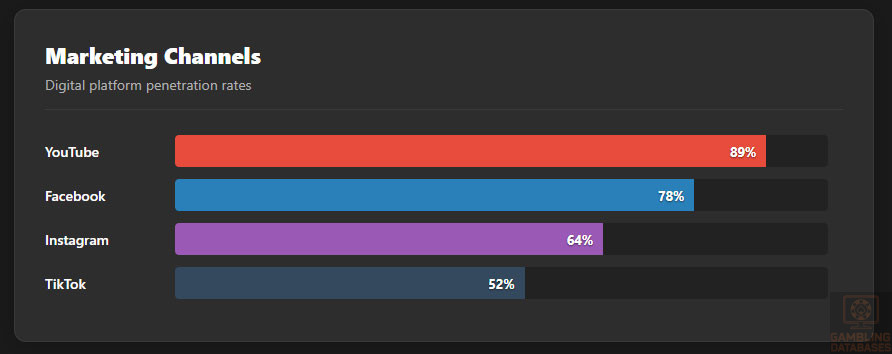

Internet penetration reached 61%, with average daily user time at over 4 hours, making digital platforms key channels for consumer engagement in entertainment and gambling. Mobile phone adoption exceeds 140% due to multi-SIM use.

- Facebook dominates social media usage with 78% penetration

- YouTube strong with 89% penetration, especially for video content

- Instagram popular among younger demographics, 64% penetration

- TikTok growing rapidly among under-25 users at 52%

- Twitter used by 31% primarily for news and information

Digital Payment Behavior

Mobile money is the preferred payment method for digital transactions, including gambling, driven by widespread agent networks and ease of use. Card payments and e-wallets also have significant market shares, with growing adoption of cryptocurrency primarily among younger users.

- Mobile money (MTN Mobile Money, Vodafone Cash)

- Debit and credit cards (Visa, MasterCard)

- E-wallets (Skrill, Neteller)

- Bank transfers

- Cryptocurrency (in limited use, growing)

Gaming and Gambling Preferences

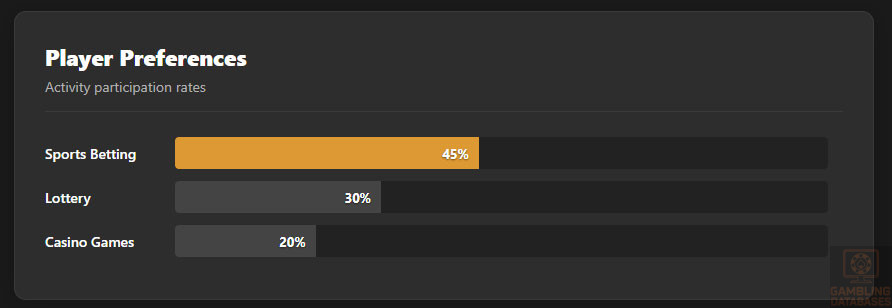

Participation in gambling activities is broadening, with the majority of players engaged in sports betting, followed by lottery and casino games. Online platforms have notably increased access and convenience, especially for urban young adults.

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 45% |

| Lottery | 30% |

| Casino Games | 20% |

| Slot Machines | 15% |

| Poker | 10% |

- Sports Betting

- Lottery

- Casino Games

- Slot Machines

- Poker

Consumer behavior trends indicate peak gambling activity during weekends and major sports events, with average session lengths around 45-60 minutes. Retention is supported by bonuses, user-friendly interfaces, and localized payment options.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Ghana’s internet penetration stands at 61%, a combination of broadband and mobile connectivity. Fixed broadband access remains limited, concentrated mainly in urban centers, while mobile internet is the dominant mode of connectivity nationwide. Average broadband speeds hover around 18 Mbps, with improvements driven by infrastructure investments and international submarine cable access.

Network reliability is mixed, with urban areas experiencing consistent service and rural regions facing intermittent coverage issues. Ongoing government and private sector initiatives are focused on expanding fiber optic networks and improving last-mile connectivity to support growing digital demand, especially for streaming and real-time gaming applications.

5G and Future Technology Deployment

5G deployment is in its initial phase, with pilot projects underway in Accra and Kumasi. Nationwide 5G coverage is expected within the next 3-5 years, with operators investing heavily in spectrum licenses and infrastructure upgrades. The Ghana government supports rollout through public-private partnerships, anticipating significant enhancements in mobile broadband speed, latency, and capacity.

Major mobile network operators are actively upgrading their networks to 5G standard to capture the young, tech-savvy demographic that drives digital entertainment and iGaming growth. These advancements are anticipated to elevate user experience and encourage new product innovations.

Mobile Technology Ecosystem

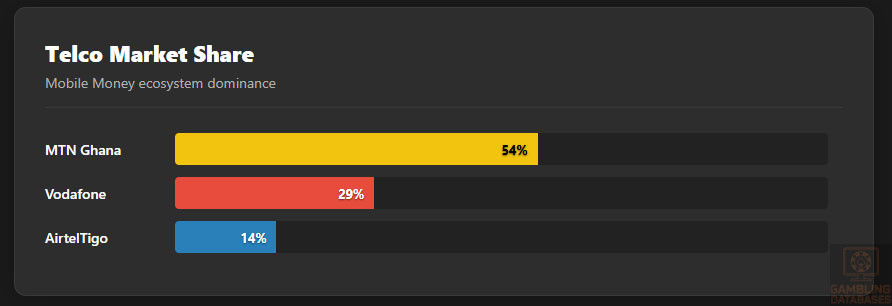

Ghana hosts several mobile network operators providing competitive services across the country. Market share is distributed primarily among leading providers, with coverage extending broadly in urban and peri-urban areas. Data costs have declined in recent years, making mobile internet more accessible for the mass market.

- MTN Ghana – market leader with over 54% share

- Vodafone Ghana – approximately 29% market share

- AirtelTigo – roughly 14% share, catering to niche rural segments

- Local MVNOs and emerging smaller operators

- Expanding 4G and initial 5G service zones

Smartphone penetration is estimated at 52%, driven by affordable device availability and increasing consumer preference for mobile-first digital experiences. Android devices dominate the market, favored for cost-effectiveness and broad service compatibility, while Apple devices hold premium segments primarily in urban centers.

Financial Services and Payment Infrastructure

Ghana’s banking sector comprises traditional banks and emerging digital-only institutions, promoting broad financial inclusion. Mobile banking adoption is particularly strong, with widespread mobile money usage transforming payment behaviors across demographics. Digital transaction infrastructure is reliable, with expanding agent networks supporting cash-in/cash-out operations.

- Ghana Commercial Bank – largest market share, extensive branch network

- Ecobank Ghana – pan-African bank with strong SME digital services

- Stanbic Bank Ghana – focus on corporate banking and digital innovation

- Barclays Bank Ghana (ABSA) – significant retail banking presence

- Access Bank Ghana – growing digital banking portfolio

Payment processing in the iGaming sector leverages multiple channels, including mobile money services, card payments, and e-wallets, providing convenience and security for consumers. Bank transfers remain essential, particularly for large transactions, while cryptocurrency adoption is growing among younger, tech-savvy demographics.

- Mobile Money (MTN Mobile Money, Vodafone Cash)

- Debit/Credit Cards (Visa, MasterCard)

- E-wallets (Skrill, Neteller)

- Bank Transfers

- Cryptocurrency (limited but expanding use)

E-commerce and Digital Economy

Ghana’s digital economy has seen rapid expansion alongside improvements in internet and mobile infrastructure. Online retail penetration is increasing, particularly for electronics, fashion, and consumer goods. Trust in digital payment systems is rising, facilitated by regulatory frameworks protecting consumers and encouraging e-commerce growth.

Digital services such as streaming, online gaming, and financial technology are driving consumer adoption of digital platforms. The expansion of logistics and delivery services supports e-commerce growth, which indirectly enhances opportunities for digital gambling operators.

Business Environment and Regulatory Framework

Ghana ranks favorably in the World Bank’s Ease of Doing Business index, particularly in areas of starting a business, registering property, and enforcing contracts. The business registration process is streamlined but requires compliance with specific foreign investment regulations and licensing standards.

- Prepare and notarize all incorporation documents

- Submit registration to the Registrar General’s Department

- Register for tax identification numbers with Ghana Revenue Authority

- Open corporate bank accounts and deposit minimum capital

- Apply for sector-specific licenses, including gaming licenses

Corporate Structure and Registration

Available corporate entities include Limited Liability Companies (LLCs), public corporations, and branch offices for foreign companies. LLCs are preferred for their flexibility and limited liability. Foreign ownership is permitted but subject to minimum 30% local ownership for certain regulated sectors including gambling.

Registration timelines vary but generally complete within 4-8 weeks. Required documents include incorporation certificates, shareholder agreements, financial statements, and proof of capital deposit.

- Certificate of Incorporation

- Company Regulations and Articles of Association

- Tax Identification Number (TIN) registration

- Proof of address for registered office

- Evidence of minimum capital deposit

Taxation Framework

Corporate income tax applies at a standard rate of 25%, with special economic zones offering concessions and tax holidays. Ghana holds treaties with multiple countries to avoid double taxation, facilitating cross-border operations.

- United Kingdom

- Germany

- China

- South Africa

- United States

Personal income tax is progressive, with withholding taxes on dividends and royalties. Social security contributions are mandatory for employees and employers. Tax residency is determined by physical presence exceeding 183 days annually.

Market Entry Considerations

Successful entry into Ghana’s iGaming market requires understanding local market dynamics, regulatory compliance, and partnership building. Strategies often include joint ventures or acquiring existing licenses through local entities to comply with ownership rules.

- Establish local partnerships to meet ownership requirements

- Invest in mobile-optimized platforms given device usage patterns

- Implement robust KYC/AML systems per regulatory standards

- Leverage mobile money and e-wallet integrations for payments

- Adapt marketing strategies to cultural and regulatory constraints

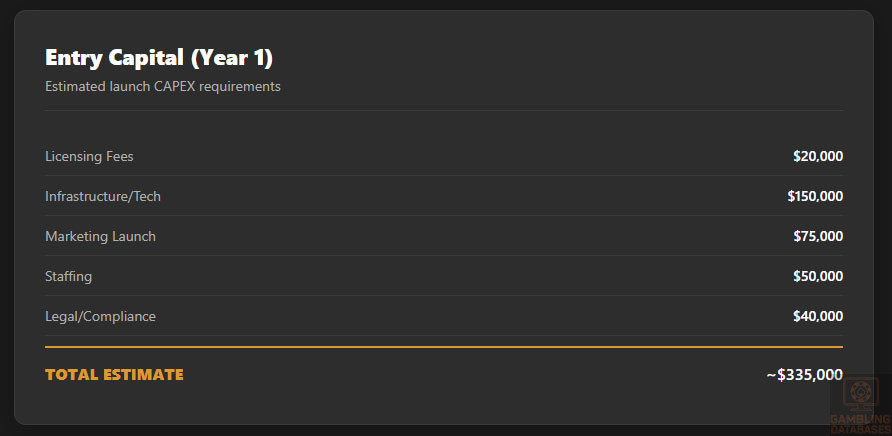

Initial setup costs encompass licensing, infrastructure, marketing, and personnel expenses. Expected timelines from registration to launch average 6 to 12 months, with continuous monitoring required to maintain compliance.

| Cost Category | Estimated USD |

|---|---|

| Licensing Fees | $20,000 |

| Infrastructure Setup | $150,000 |

| Marketing & Promotion | $75,000 |

| Legal and Compliance | $40,000 |

| Personnel and Training | $50,000 |

FAQ: Frequently Asked Questions

1. Is online gambling legal in Ghana?

Online gambling is fully legal and regulated by the Ghana Gaming Commission. Operators must obtain appropriate licenses, meet compliance standards, and adhere to responsible gambling regulations. Unlicensed gambling is prohibited with strict enforcement.

2. What types of gambling licenses are available and what do they cover?

Licenses cover various categories including sports betting, casino operations, lottery, and online gaming platforms. Each license type mandates specific regulatory compliance in operation, financial reporting, and player protection to maintain market integrity and consumer trust.

3. How much does an iGaming license cost and how long does it take to obtain?

Application fees are approximately $20,000 with annual renewals around $10,000. The review period averages 3-6 months depending on completeness of documentation and regulatory workload, with thorough background checks and audits integral to the process.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply for licenses but must comply with local ownership mandates, typically requiring at least 30% Ghanaian stakeholder involvement. Partnering with local entities facilitates compliance and integration into the regulatory framework.

5. What are the tax obligations for iGaming operators?

Operators are subject to a gross gaming revenue tax of 20%, alongside a corporate income tax of 25%. Additional taxes and fees may apply based on jurisdictional regulations and specific license terms, requiring detailed financial reporting and compliance.

6. Are gambling winnings taxed for players?

Players do not incur direct taxation on winnings. Ghana currently exempts gambling prizes from personal income tax, promoting wider legalized participation and reducing incentive for illicit gambling.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, technology infrastructure, marketing, personnel, compliance, and payment processing. Technology investment is substantial, with marketing necessary to build brand presence in a competitive market.

8. What is the expected ROI timeline for entering this market?

Return on investment varies but typically ranges between 24 to 36 months, contingent on market penetration speed, operational efficiency, and adaptation to consumer preferences and regulatory compliance.

9. What are the local presence requirements for operators?

Operators must establish a registered presence or branch in Ghana, including a physical office, to facilitate regulatory oversight and compliance. Key personnel must be locally accessible and experienced in gaming operations.

10. What payment methods are available and recommended?

Mobile money solutions dominate digital payments, supported by cards, e-wallets, bank transfers, and emerging cryptocurrency options. Integrating multiple payment methods expands customer reach and simplifies user transactions.

11. What are the advertising and marketing restrictions?

Advertising is limited by time of day and content to protect minors and vulnerable populations. Operators must ensure transparency, avoid misleading promotions, and seek prior regulatory approval for sponsorships and major campaigns.

12. What responsible gambling measures are mandatory?

Operators are required to implement age verification, self-exclusion options, deposit and bet limits, and provide problem gambling resources and support. Compliance with these standards is closely monitored by regulators.

13. How large is the iGaming market and what is the growth potential?

The Ghanaian iGaming market is valued at around $150 million with a projected CAGR of 12.5% over the next five years. Growth is driven by expanding internet access, mobile penetration, and increasing consumer acceptance.

14. Who are the main competitors and what is their market share?

The market features a mix of local operators and international entrants, with approximately 12 licensed iGaming providers. Market share varies widely, with leaders leveraging technology and brand trust to maintain competitive advantages.

15. What are the player preferences and typical spending patterns?

Sports betting is the dominant activity, followed by lottery and casino games. Players prefer mobile platforms with localized payment options and value bonuses and promotions. Peak activity aligns with sporting events and weekends.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, effective local partnerships, payment integration, strong marketing, and customer service. Challenges include navigating licensing processes, competitive pricing, infrastructure limitations, and cultural sensitivity.

Sources and References

- Ghana Gaming Commission – Official Regulatory Authority Website – https://www.gamingcommission.gov.gh

- Ghana Statistical Service – Population and Economic Data Reports 2024 – https://www.statsghana.gov.gh

- Central Bank of Ghana – Financial Sector Reports – https://www.bog.gov.gh

- Ministry of Finance Ghana – Taxation Laws and Guidelines – https://www.mofep.gov.gh

- World Bank – Doing Business Report 2024 – https://www.worldbank.org/en/topic/doingbusiness

- International Telecommunication Union – Ghana ICT Statistics – https://www.itu.int/en/ITU-D/Statistics

- Ghana Chamber of Commerce – Business Environment Reports

- Africa Digital Economy Report 2024 – Industry Publisher

- Mobile Network Operator Publications (MTN Ghana, Vodafone Ghana)

- Financial Inclusion Reports – GSMA Intelligence 2024

- Gambling Industry Market Analysis – Global Gaming Report 2024

- Academic Publications on Gambling Behavior in Ghana

- Tax Authority Publications – Ghana Revenue Authority

- Telecommunications Infrastructure Reports – Ghana Ministry of Communications

- Local News Media Coverage on Gambling Regulation and Market Developments

- International Monetary Fund Country Report Ghana 2024

- Digital Payment Systems Review – Ghana Market 2025

- Reports from NGOs on Responsible Gambling Ghana

- Online Retail and E-commerce Market Reports 2025

- Investment Climate Reports – Ghana Investment Promotion Centre

- Public Health Data – Gambling Addiction Statistics Ghana

- Technology Adoption and Consumer Behavior Studies

- Legal Framework Summaries – Ghana Updated Laws 2025

- Infrastructure and Network Deployment Progress Reports

- World Economic Forum Competitiveness Report 2024

- Emerging Trends in African iGaming – Market Research Reports

🎯 Gambling Databases Country Rating: Ghana

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 7.0/10 | [🟡 Moderate 5-7] |

| Player Access Score | 9.5/10 | [🟢 Fully Legal] |

| Overall Market Attractiveness | 7.5/10 | [Accessible but requires local partnerships] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Mandatory Local Ownership: Foreign entities are REQUIRED to have a minimum 30% Ghanaian ownership stake. This forces joint ventures and introduces significant partner risk and profit dilution.

- Advertising Restrictions: TV and radio advertising is BANNED outside the hours of 9:00 PM to Midnight, severely limiting mass-market brand awareness campaigns.

- Capital Requirements: A minimum capital requirement of $500,000 USD must be deposited, which is a high barrier for smaller entrants.

- Strict KYC Enforcement: Recent regulatory tightening has increased operational costs regarding player identification and data security compliance.

- License Revocation Risk: The Gaming Commission actively enforces compliance; operators face license suspension or revocation for failure to meet reporting or technical standards.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | Full product legality (+3.0). Both sports betting and online casinos are fully regulated and legal. No deductions for prohibited verticals. |

| Licensing Process | 25% | 1.75/2.5 | Accessible licensing (+2.0). Application costs under €100k (+0.5). Deduction: Foreign investment barrier/Local partner requirement (-0.5). Deduction: Process takes 3-6 months (-0.25). Final: 1.75. |

| Taxation & Costs | 20% | 1.5/2.0 | GGR tax is 20% (+1.5). Note: Corporate tax is 25%. While GGR tax is reasonable, the combined burden is significant but not punitive enough for major deductions. Final: 1.5. |

| Operational Requirements | 15% | 0.5/1.5 | Heavy requirements (+0.5). Deduction: $500k minimum capital requirement (-0.25). Deduction: Mandatory local presence and 30% local ownership structure adds significant complexity and risk (-0.75). Bonus for clear payment channels (+0.5). Final: 0.5. |

| Market Environment | 10% | 0.25/1.0 | Moderate environment (+0.5). Deduction: Strict advertising time restrictions (9PM-12AM) (-0.25). Final: 0.25. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal and regulated (+4.0). Players can legally access sports betting, casinos, and lottery without fear of prosecution. |

| Practical Accessibility | 30% | 3.0/3.0 | Multiple payment methods (+3.0). Mobile money (MTN, Vodafone) is ubiquitous. No blocking of payments or widespread ISP blocking of major sites reported. |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players (+2.0). Tax on winnings is 0%, making it highly attractive for players. |

| Market Availability | 10% | 0.5/1.0 | 12 Licensed operators (+1.0). Deduction: Market is somewhat concentrated with only 12 licensed operators relative to population size (-0.5). Final: 0.5. |

🔍 Key Highlights

Strengths

- Zero Player Tax: 0% withholding tax on player winnings is a massive driver for player retention and market growth.

- Clear Legal Status: Unlike many African nations, online casino is explicitly legal and regulated, not a grey area.

- Mobile Penetration: 140% mobile penetration with established mobile money habits makes deposits/withdrawals frictionless.

⛔️ CRITICAL RISKS AND CHALLENGES

- [Partnership Risk:] The mandatory 30% local ownership rule creates a “forced marriage” scenario. If your local partner fails or disputes arise, your license is at risk.

- [Capital Lockup:] $500,000 USD minimum capital requirement is dead money that must sit in a local institution.

- [Advertising Limits:] The ban on daytime TV/Radio ads (before 9 PM) makes mass-market acquisition slower and forces reliance on digital channels.

- [Market Size Cap:] While growing, the total market is currently only ~$150M. With 12 operators, the average slice is small ($12.5M revenue). ARPU is $90/year, which is low compared to Western standards.

- [Compliance Costs:] Strict KYC and technical standards (RNG certification, audits) are enforced, raising the barrier to entry above typical “grey market” levels.

Player-Specific Issues

- Players face minimal issues, but the limited number of licensed operators (12) means less variety in bonuses and odds compared to saturated markets.

- Offshore access is technically prohibited but individual players are rarely penalized.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $600,000 – $800,000 USD (Includes $500k capital deposit + $20k license + setup).

Monthly Operating Costs: Moderate. Local wages are lower, but compliance and technical infrastructure costs are fixed globally.

Effective Tax Rate on Revenue: ~40% (20% GGR + 25% Corporate Tax on profits). Note: You also give up 30% of dividends to your local partner.

Customer Acquisition Cost: Moderate. Ad restrictions increase difficulty, but lack of player tax helps retention.

Profitability Assessment: The economics are viable but tight. The market volume ($150M) is not massive. You are competing for a relatively small pie with established players. The 30% local ownership requirement effectively reduces your ROI by a third. This market is best for regional African operators expanding their footprint, rather than single-market entries.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [Medium] | [Regulatory framework prohibits unlicensed operations; risk of blacklisting and potential ISP blocking measures.] |

| Licensed Sports Betting Operators | [Low] | [Stable regulatory environment, provided KYC and reporting obligations are met.] |

| Affiliates/Advertisers | [Medium] | [Must comply with strict time-based advertising restrictions (9 PM – 12 AM). Promoting unlicensed brands carries risk.] |

| Payment Processors | [Low] | [Mobile money is integrated and legal. High volume of transactions.] |

| Company Directors/Executives | [Medium] | [Criminal background checks required. Responsibility for strict AML compliance falls on directors.] |

🚨 Extradition and International Enforcement

Extradition Treaties: Ghana is a Commonwealth nation and has extradition arrangements with the UK, USA, Canada, and Australia. It is not a safe haven for financial criminals.

Enforcement History: The Ghana Gaming Commission actively suspends licenses for non-compliance but international extradition for pure gambling offenses is rare. However, money laundering charges (AML) are taken very seriously.

Travel Risk: Low for licensed operators. High for operators attempting to bypass the 30% local ownership rule through fraudulent fronting.

📋 Final Verdict

Ghana receives an Operator Ease Score of 7.0/10 and a Player Access Score of 9.5/10, resulting in an overall market attractiveness rating of 7.5/10.

HONEST ASSESSMENT: Ghana offers a stable, fully regulated environment with legal online casino and sports betting, which is rare in Africa. However, the mandatory 30% local ownership requirement is a “poison pill” for many international operators, forcing them into joint ventures that dilute control and profit. While the 0% player tax is excellent for retention, the small total market size ($150M) limits the upside. Enter only if you have a trusted local partner and patience.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A Pan-African operator with existing regional infrastructure.

- Willing to cede 30% equity to a Ghanaian partner.

- Able to lock up $500,000 USD in capital immediately.

- Focused on high-volume, low-margin mobile betting.

❌ Definitely Avoid If You Are:

- A solo international operator unwilling to form a Joint Venture.

- Looking for a “wild west” market with zero compliance (KYC is strict here).

- Under-capitalized (Costs >$600k to open doors).

- Expecting massive immediate returns (Market size is limited).

⚠️ BOTTOM LINE: A solid, legally safe market for serious players, but the 30% local partner tax and $500k capital requirement make it mathematically unattractive for small-to-mid-sized offshore operators.