Greece presents a notable opportunity for iGaming operators due to its sizable population and evolving regulatory landscape. The country has established a comprehensive legal framework to oversee digital gambling activities, balancing market growth with rigorous compliance standards. As one of the emerging markets in Europe, Greece’s regulatory environment and consumer base make it an attractive, yet complex, jurisdiction for market entry strategies.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal status of online gambling | Licensed & regulated |

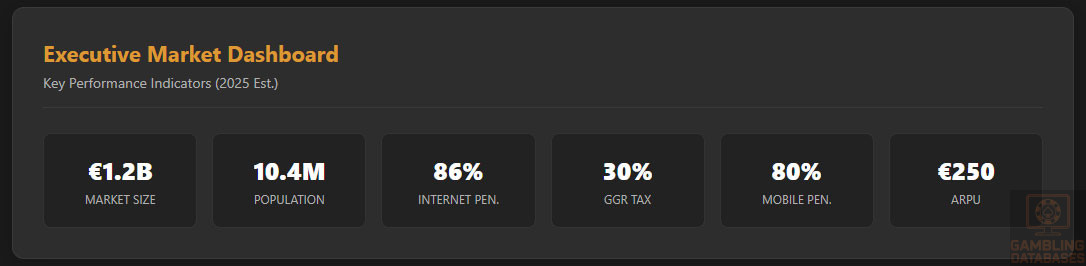

| Population | 10.4 million (2025 est.) |

| GDP | $200 billion (2025 est.) |

| Internet penetration rate | 86% |

| Mobile penetration rate | 80% |

| License application cost | €50,000 |

| Annual license fee | €25,000 – €50,000 |

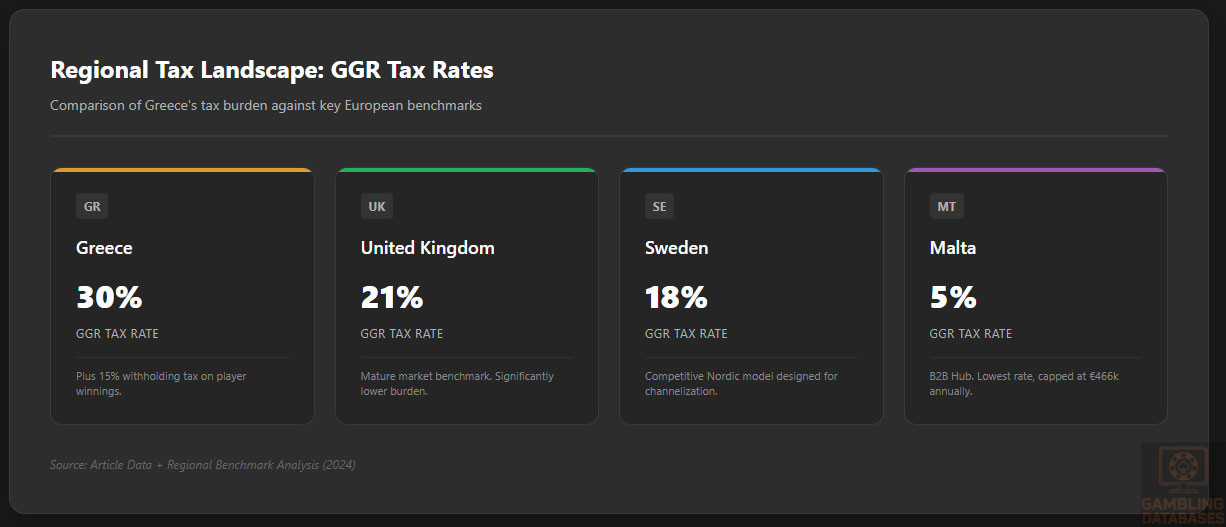

| Tax on GGR | 30% |

| Market size (projected annual revenue) | €1.2 billion |

| Market CAGR (2025-2030) | 8% |

| ARPU | €250 |

| Market penetration rate | ~60% |

| Average time for license issuance | 6-9 months |

| Number of licensed operators | 15+ |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Greece has developed a comprehensive legal and regulatory framework that governs all sectors of gambling, both land-based and online. The Hellenic Gaming Commission (HGC) acts as the sole regulatory authority responsible for licensing, monitoring, and enforcing compliance across all gambling activities. The framework explicitly covers casinos, sports betting, lotteries, slot machines, and all forms of digital gambling under unified regulatory oversight.

The online gambling sector is governed by a dedicated and robust licensing regime introduced in 2021, which modernized previous fragmented legislation to align with European Union directives. This regime mandates licenses for all digital gaming operators targeting Greek consumers, requiring adherence to strict regulatory, technical, and operational conditions to ensure market integrity and player security.

Online Gambling Framework

The HGC’s licensing system for online gambling enforces rigorous technical and procedural standards, including platform certification, secure data handling, and anti-fraud measures. This framework covers online sports betting, casino gaming, poker, virtual games, skill games, and lottery services, creating a broad regulated environment for all iGaming verticals.

Licensing is compulsory; any operator conducting activities without a proper license faces strong sanctions including hefty fines, service blacklisting, and criminal proceedings. The regulatory provisions also emphasize strong Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance, requiring operators to verify player identities before allowing access and continuously monitor transactions to detect suspicious activities.

Responsible gambling is a core component of the framework. Licensed operators must integrate player protection mechanisms such as self-exclusion, loss limits, and warnings about gambling risks. These measures complement strict advertising codes aimed at preventing the promotion of gambling to minors and vulnerable groups.

Licensed Operators and Market Players

The Greek iGaming market consists of a limited yet expanding roster of licensed operators, including major international casino brands and local firms authorized to provide services. The market exhibits a moderately competitive environment, with key players holding multiple licenses to operate across different verticals, thus maximizing portfolio diversity and market reach.

Leading operators leverage their compliance capabilities and local partnerships to establish trusted brand positions and expand market share. Market entry strategies commonly involve acquiring licenses from exiting operators or partnering with domestic companies to fulfill legal requirements and facilitate smoother regulatory approvals. The HGC enforces continuous monitoring of operators, conducting audits and compliance checks to maintain high standards across the sector.

Licensing Framework and Requirements

The Greek licensing procedure for online gambling involves a multi-stage application process managed by the HGC. Prospective operators must submit extensive documentation validating their corporate history, financial soundness, ownership structure, and technical capabilities.

- Legal entity registration in Greece or within the European Union, ensuring jurisdictional transparency

- Proof of platform certification and technical compliance, including Random Number Generator (RNG) testing and cybersecurity audits

- Submission of audited financial statements demonstrating minimum capitalization levels appropriate to the scale of operations

- Criminal background checks for directors, beneficial owners, and executive management to verify integrity and suitability

- Payment of non-refundable application fees, currently set at €50,000, alongside annual license renewal fees

The application review period typically spans 6 to 9 months and includes rigorous background investigations, technical inspections, and compliance assessments. Upon approval, licensees receive specific terms covering their operational scope and compliance obligations.

Local Presence and Operational Requirements

Licensed operators are required to establish a physical presence in Greece, either by setting up a local office or by engaging in binding partnerships with Greek entities. This presence ensures effective regulatory oversight and access to local market intelligence. Additionally, operators must register Greek Internet domains and maintain customer support services operating in the Greek language at minimum.

Foreign ownership is permitted without restrictions; however, regulatory approval is mandatory. Ownership structures involving foreign stakeholders necessitate enhanced transparency and compliance with domestic laws to uphold operational accountability and market fairness.

Compliance Obligations and Monitoring

Player protection measures constitute a regulatory cornerstone. Operators must enforce strict age verification, ensuring all players are at least 18 years old, backed by KYC protocols utilizing government-issued identification and electronic verification processes. AML compliance mandates continuous transaction monitoring, flagging, and reporting suspicious activities to authorities as part of an integrated risk management strategy.

Operators are also obligated to maintain accessible self-exclusion programs allowing players to voluntarily restrict or cease gambling activity. Transparency is enforced through the publication of return-to-player (RTP) percentages and comprehensive game odds disclosures, promoting informed and responsible player choices.

- Enforcement of mandatory age and identity verification before gameplay

- AML policies requiring in-depth transaction tracking and reporting

- Availability of self-exclusion and player-imposed spending/time limits

- Transparent publication of game fairness and RTP data

- Regular compliance reporting submitted to the HGC on a monthly or quarterly basis

The HGC performs financial and operational audits, examining gross gaming revenue (GGR) declarations, tax remittances, and adherence to technical standards. Non-compliance triggers a range of penalties, including financial sanctions, license suspension, and revocations.

Taxation Structure and Financial Obligations

Players’ winnings are taxed with a flat withholding rate of 15%, automatically deducted at payout to ensure efficient tax collection. Operators face a gross gaming revenue tax of 30%, uniformly applied across all licensed gaming verticals including online casino, sports betting, poker, and virtual games, which contributes significantly to state revenues.

Annual license fees are standardized at €50,000, reflecting costs associated with regulatory oversight and administrative processes. Additional taxes and levies may apply based on turnover thresholds and specific operator activities, necessitating detailed financial planning and reporting.

| Game Type | Tax Rate |

|---|---|

| Online casino GGR | 30% |

| Sports betting GGR | 30% |

| Poker & Virtual Games | 30% |

The market projects consistent revenue growth underpinned by increasing internet penetration, smartphone adoption, and digital payment integration, with anticipated CAGR around 8% through 2030. Advertising activities are tightly regulated to restrict exposure to minors and vulnerable populations, limiting marketing to defined hours and approved channels primarily encompassing digital media.

Recent 2022 reforms intensified regulatory supervision by expanding mandatory responsible gambling measures, tightening anti-fraud controls, and increasing penalties for breaches. Enforcement mechanisms now include immediate license suspension capabilities, fines scaling with violation severity, and public disclosure of compliance failures to ensure transparency and deter misconduct.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

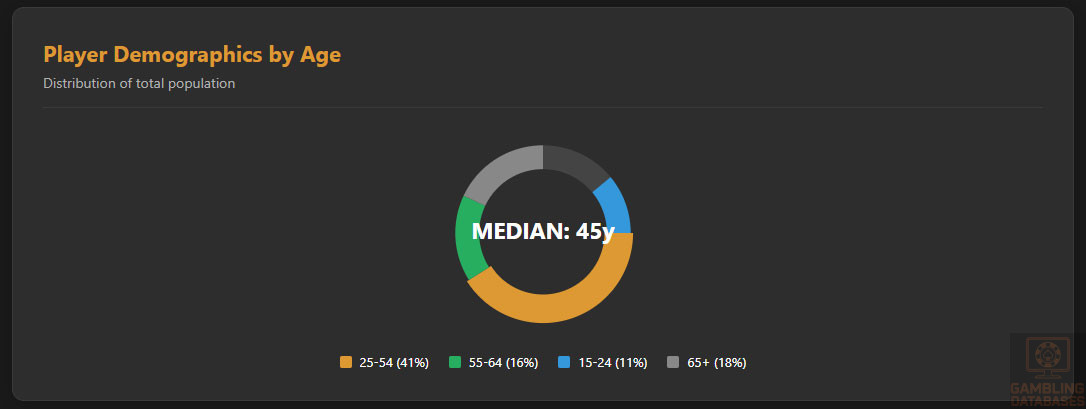

Greece has a total population of approximately 10.4 million as of 2025, with demographic characteristics shaped by aging trends and urban concentration. The median age stands near 45 years, reflecting an older population relative to other European nations.

Gender distribution is balanced, with a slight majority of females at 51%. Urban areas host about 80% of the population, dominated by Athens and Thessaloniki, underscoring the urban-centric nature of consumer markets.

| Age Group | Population Share (%) |

|---|---|

| 0-14 years | 14% |

| 15-24 years | 11% |

| 25-54 years | 41% |

| 55-64 years | 16% |

| 65 years and above | 18% |

The rural population, concentrated mainly in northern and island regions, comprises about 20% of the total. Internet access is widespread in urban centers while more remote areas exhibit lower penetration rates. Gambling venues including casinos and betting shops are predominantly located in metropolitan locations, aligning with population density and disposable income levels.

Geographic Distribution

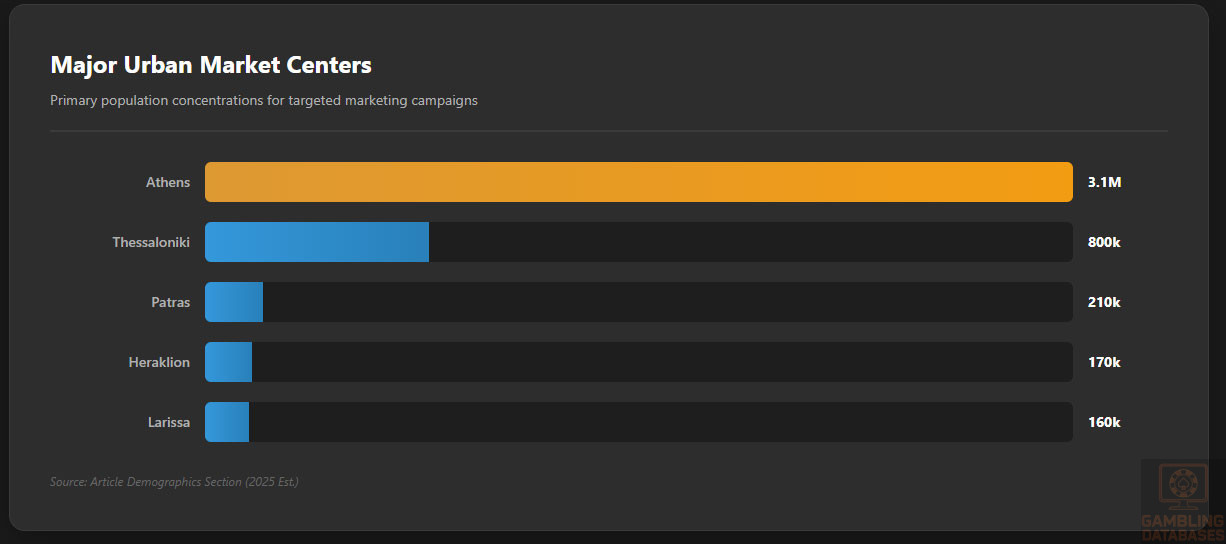

Greece’s geographic population distribution highlights significant economic disparities among regions. The Athens metropolitan area alone accounts for around 3.1 million residents, serving as the country’s political, economic, and cultural hub. Thessaloniki, Greece’s second-largest city, hosts about 800,000 people and supports a vibrant commercial landscape.

- Athens – 3.1 million

- Thessaloniki – 800,000

- Patras – 210,000

- Heraklion – 170,000

- Larissa – 160,000

- Volos – 145,000

- Ioannina – 112,000

These urban centers exhibit higher internet connectivity rates, exceeding 90%, and act as focal points for gambling activity, both online and land-based. Peripheral regions see lower digital engagement but show gradual improvements in infrastructure, enhancing potential market reach outside the core cities.

Economic Indicators and Consumer Spending Power

Greece’s GDP currently ranks around $200 billion, with growth forecast at approximately 2.5% annually over the next five years. The economy is primarily service-oriented, accounting for about 75% of GDP, followed by industry (20%) and agriculture (5%). Domestic consumption forms a significant driver, supported by improving labor market conditions and rising consumer confidence.

Household income displays marked variation, with average disposable income near €18,000 annually but a median closer to €15,000, indicating income disparities. The Gini coefficient sits at 0.34, reflecting moderate inequality. Wealth distribution and consumer spending patterns are strongly influenced by urban-rural divides and age demographics, with younger urban cohorts showing higher engagement in digital entertainment.

Market Size and Growth Projections

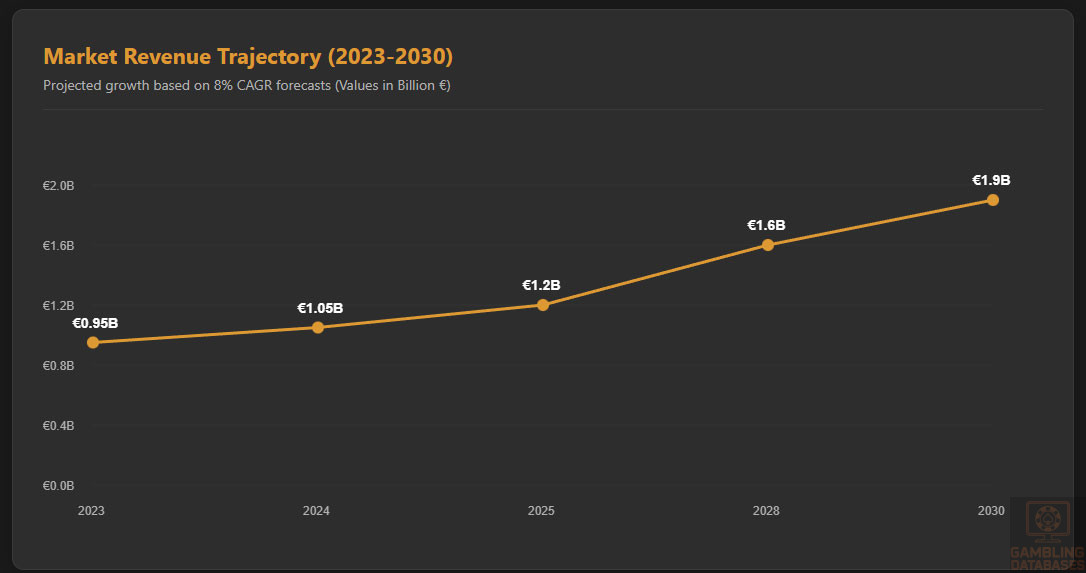

The iGaming market in Greece has demonstrated robust expansion, with current estimated revenues around €1.2 billion. Historical CAGR measured near 7.5% in recent years, with forecasts projecting growth rates accelerating to 8% through 2030. The user base currently includes roughly 4.8 million active gamblers, representing a market penetration of close to 46% of the adult population.

| Year | Market Revenue (Billion €) | User Base (Million) | CAGR (%) |

|---|---|---|---|

| 2023 | €950 | 4.1 | 7.5 |

| 2024 | €1.05 | 4.4 | 7.5 |

| 2025 (Current) | €1.2 | 4.8 | 8.0 |

| 2028 (Forecast) | €1.6 | 5.6 | 8.0 |

| 2030 (Forecast) | €1.9 | 6.1 | 8.0 |

The average revenue per user (ARPU) stands at around €250, influenced by strong participation in sports betting and online casinos. Growth drivers include rising smartphone adoption, improved digital payment mechanisms, and evolving player preferences towards mobile gaming platforms.

Education, Skills, and Digital Literacy

Greece boasts a high literacy rate of over 97%, underpinned by a robust public education system emphasizing both general and technical education. University enrollment rates are rising, with growing programs focused on IT, finance, and digital skills development. Workforce skills reflect increasing digital literacy, especially among younger populations, fueling demand for online services including iGaming.

Government initiatives promote lifelong learning and skill upgrading, aiming to align workforce competencies with evolving technology trends. Digital literacy campaigns have improved internet usability awareness, significantly benefiting e-commerce and online entertainment sectors.

Cultural and Social Factors

Communication and Language

The official language is Greek, spoken by over 98% of the population. English proficiency is widespread, especially in urban and tourist areas, facilitating international market operations and customer support. Internet usage predominantly occurs in Greek and English, with digital content consumption favoring bilingual access.

Cultural Attitudes

Gambling in Greece is traditionally accepted as a form of entertainment, with a cultural openness tempered by strong religious influences that advocate moderation. Foreign brand acceptance is generally positive, particularly among younger consumers, who favor international operators known for advanced platforms and diverse game offerings.

Entertainment preferences increasingly lean towards digital formats, with social and mobile gaming rapidly gaining popularity alongside traditional betting. The hospitality and tourism sectors further stimulate demand for gambling-related entertainment during peak seasons.

Problem Gambling and Social Considerations

Government monitoring identifies approximately 3% of adult gamblers as problem gamblers, with at-risk populations including younger males and urban residents. Social responsibility frameworks require operators to contribute to prevention programs and fund support services targeting addiction.

- Mandatory operator contributions to problem gambling research

- Government-funded helplines and counseling services

- Public awareness campaigns focused on youth

- Self-exclusion program oversight by regulators

- Collaboration with NGOs for rehabilitation support

Political Structure and Governance

Greece operates as a parliamentary republic with stable democratic governance supporting regulatory consistency. The political environment favors alignment with EU directives and international standards, providing a reliable framework for foreign business investment. Strong institutional frameworks and transparent regulatory procedures enhance the business climate.

Technology Adoption and Digital Behavior

Internet and Digital Usage

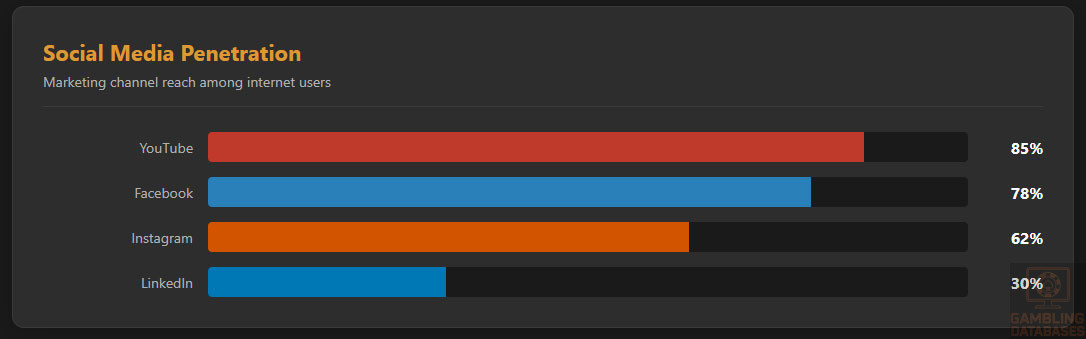

Internet penetration in Greece is approximately 86%, with average daily usage exceeding 5 hours. Mobile internet accounts for 80% of all connections, driven by smartphone proliferation and affordable data plans. Digital engagement includes strong social media usage, with platforms playing key roles in marketing and player interaction.

- Facebook with 78% penetration among internet users

- Instagram at 62%, dominant among youth

- YouTube reaching 85%, high video consumption

- TikTok expanding rapidly, especially under age 25

- LinkedIn utilized by 30% of professionals

Digital Payment Behavior

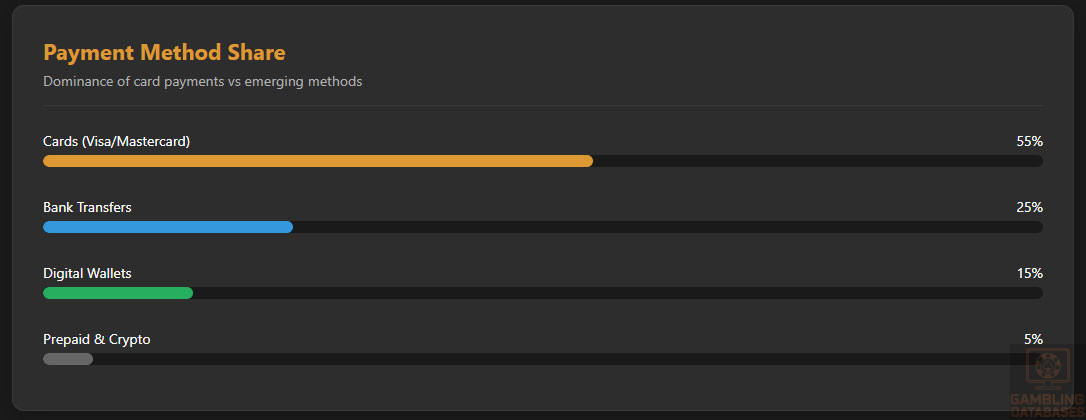

Payment preferences are evolving with increased adoption of digital wallets and instant banking solutions complementing traditional credit and debit cards. Cryptocurrency acceptance remains limited but is emerging among tech-savvy consumer segments and international operators.

- Credit/Debit cards: 55% market share

- Bank transfers: 25%

- Digital wallets (PayPal, Skrill, Neteller): 15%

- Prepaid cards: 3%

- Cryptocurrency: Emerging under 2%

Gaming and Gambling Preferences

Current Market Participation

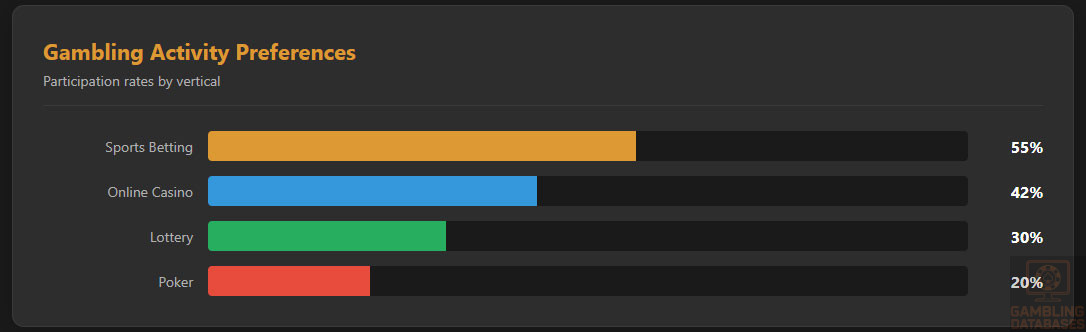

The most popular gambling activities in Greece include sports betting, online casino games, and lottery participation, reflecting broad consumer interest across formats.

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 55% |

| Online Casino Games | 42% |

| Lottery | 30% |

| Poker | 20% |

| Slot Machines (Land-based) | 15% |

Consumer Behavior Patterns

Greek consumers demonstrate strong preference for mobile gaming, with peak activity during evening hours. Average session lengths vary by product, with casino games averaging 45 minutes per session and sports betting lasting 30 minutes. Retention strategies heavily focus on personalized offers and loyalty programs, which are well received by the market. Spending habits reflect a balanced mix of casual and high-stakes players, with significant seasonal fluctuation tied to major sporting events and holidays.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

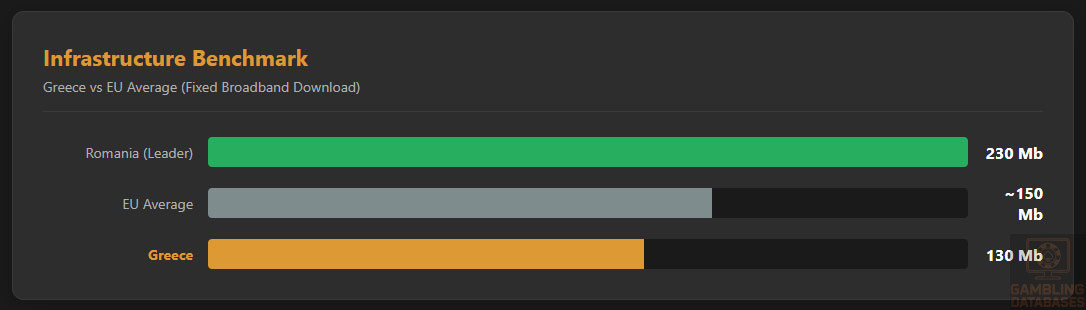

Greece exhibits robust internet penetration at approximately 86%, with a broadband-to-mobile ratio favoring mobile connectivity due to widespread smartphone use. Average fixed broadband download speeds reached around 130 Mbps, with upload speeds near 55 Mbps, reflecting ongoing investments in fiber and cable technology. Mobile internet sees average LTE download speeds exceeding 75 Mbps, supported by significant upgrades to 4G infrastructure.

Network reliability is solid in urban areas, while some rural locations experience slower connection speeds and limited redundancy. Investments from private telecom operators, in partnership with government digitalization programs, focus on expanding high-speed access and reducing latency to support data-intensive services, including iGaming platforms.

5G and Future Technology Deployment

5G rollout in Greece began in 2023, reaching about 45% population coverage by 2025, primarily in major cities and economically strategic zones. Full nationwide 5G deployment is projected by 2027, supported by multiple network operators expanding infrastructure investment. The technological landscape favors low-latency, high-bandwidth connectivity essential for real-time gaming and streaming applications.

Government policy encourages private-public collaboration and spectrum allocation conformity with EU standards. The continued rollout supports vertical adoption in sectors such as entertainment, enhancing user experience for mobile and online gamblers.

Mobile Technology Ecosystem

Greece hosts a competitive mobile market with three principal mobile network operators dominating coverage and subscriber base. These operators leverage advanced LTE and nascent 5G networks to offer comprehensive national and urban coverage at competitive price points, fostering high consumer mobile data usage.

- Cosmote: Market leader with ~47% subscription share and extensive 5G network deployment

- Vodafone Greece: Approximately 33% market share, strong urban coverage and business solutions

- Wind Hellas: Holding about 20% market share, aggressive pricing strategy with growing 5G footprint

Device penetration is high, with smartphone ownership surpassing 85% among adults. Popular devices range from mid-tier Android smartphones, favored for affordability, to premium iPhone models among higher income groups. Mobile usage patterns prioritize social media, video streaming, and increasingly mobile gaming, fueling demand for seamless gambling experiences on handheld devices.

Financial Services and Payment Infrastructure

The Greek banking sector comprises well-established institutions offering modern digital banking services, including mobile and online platforms with high account penetration. Digital banking adoption exceeds 70%, with consumer preferences shifting towards instant payments and integrated wallets facilitating online transactions.

- National Bank of Greece: Largest retail network, digital services driving market retention

- Piraeus Bank: Strong SME focus with expanding digital payment options

- Eurobank: Pioneering mobile-first banking solutions

- Alpha Bank: Significant corporate client base and digital innovation investments

- Attica Bank: Niche market with growing digital offerings

Payment processing options encompass a wide range of methods suited to iGaming, from classic credit/debit cards to e-wallets and bank transfers. Emerging payment trends include peer-to-peer instant payments and contactless technologies enhancing transaction speed and security.

- Credit/Debit cards (Visa, Mastercard)

- E-wallets (PayPal, Skrill, Neteller)

- Bank transfers with immediate settlement

- Prepaid cards (Paysafecard)

- Emerging cryptocurrency acceptance (Bitcoin, Ethereum)

E-commerce and Digital Economy

The Greek e-commerce market has grown steadily with online retail capturing approximately 12% of total retail sales in 2024. Consumer trust in digital services continues to strengthen with enhanced cybersecurity regulations and consumer protection laws. Digital service adoption extends beyond retail into entertainment and financial services, underpinning the iGaming sector’s growth.

Business Environment and Regulatory Framework

Ease of Business Operations

Greece ranks in the top half of EU countries in the World Bank Ease of Doing Business Index, reflecting improvements in business registration and licensing processes. Regulatory reforms have reduced company registration times and simplified tax compliance. Foreign investment is welcomed but subject to scrutiny in strategic sectors, ensuring regulatory compliance and market stability.

- Preparation and notarization of incorporation documents (2-3 weeks)

- Submission and approval by the General Commercial Registry (5-7 business days)

- Tax Authority registration and VAT number issuance (3-5 days)

- Opening a corporate bank account and depositing minimum capital (1-2 weeks)

- Completion with social security registrations and compliance filings (2-3 days)

Corporate Structure and Registration

Common corporate entities include Limited Liability Companies (LLC), Societe Anonymes (Corporation), and branch offices of foreign companies. LLCs are preferred by SMEs and new entrants due to simpler governance and lower initial capital requirements. Branch offices serve international operators seeking direct market presence without separate legal personality.

- Minimum share capital for LLC: €4,500

- Minimum share capital for Corporation: €24,000

- Branch offices require parent company documentation and local representative

- Mandatory presence of a local director or management under specific circumstances

- Compliance with Greek GAAP for financial reporting

Registration timelines vary but generally span 3-6 weeks from initial filing to operational readiness. Foreign ownership is unrestricted in most sectors, including iGaming, while compliance with regulatory licenses is mandatory for market participation.

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate in Greece is 22% as of 2025. Special economic zones offer incentives including tax holidays and reduced rates for qualifying entities. Greece maintains double taxation treaties with over 60 countries, facilitating international business and investment attraction.

- Germany

- United Kingdom

- France

- Italy

- Cyprus

- Netherlands

- Belgium

- Switzerland

Personal Income Tax

Personal income tax rates are progressive, with brackets ranging from 9% to 44%. Employers withhold taxes on salaries, and social security contributions are mandatory, varying by employment type. Tax residency is defined by physical presence exceeding 183 days or center of economic interests within Greece.

Market Entry Considerations

Recommended Entry Strategies

Successful market entry into Greece’s iGaming sector typically involves establishing strong local partnerships, leveraging licensed platforms, and customizing products to meet local consumer preferences. Multichannel marketing, mobile-first approaches, and compliance agility are critical for long-term sustainability.

- Form joint ventures or partnerships with established local operators

- Obtain direct licensing or acquire existing license holders

- Invest in mobile-optimized platforms and localized content

- Implement robust compliance and responsible gambling measures

- Utilize data analytics to tailor marketing and player retention

Typical Costs and Timelines

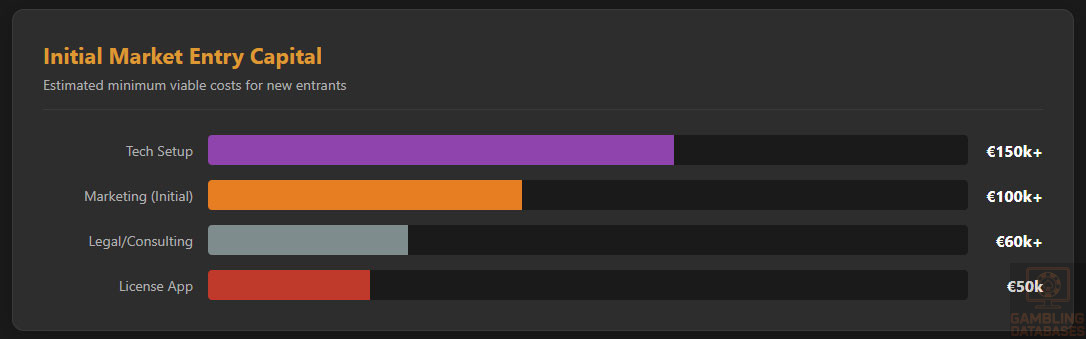

Initial market entry costs include licensing fees, legal and consultancy expenses, technology integration, and marketing budgets. Operating expenses depend on platform scale, staff, and compliance investments. Average license processing times range from 6 to 9 months, with break-even expected within 2-3 years under competitive execution.

- License application fee: €50,000

- Annual license renewal: €50,000

- Legal and consultancy fees: €60,000 – €100,000

- Technology and platform setup: €150,000 – €300,000

- Initial marketing budget: €100,000+

Success Factors and Challenges

Key success enablers include stringent regulatory compliance, superior user experience, agile marketing, and strong customer support. Challenges encompass intense competition, regulatory changes, tax obligations, and cultural adaptation.

- Regulatory agility and transparent communication with authorities

- Localized customer service and responsible gambling initiatives

- Robust cybersecurity and data protection measures

- Continuous platform innovation and mobile optimization

- Effective fraud prevention and payment processing reliability

Exit strategies focus on market valuation optimization, license transferability, and partnerships ensuring operational continuity. Legal transfer of licenses is possible but subject to regulatory approval and compliance audits.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Greece?

Yes, online gambling is fully legal and regulated by the Hellenic Gaming Commission. Operators must obtain licenses to offer sports betting, casino games, poker, and other digital gaming services. Unlicensed activities are prohibited and subject to enforcement actions.

2. What types of gambling licenses are available and what do they cover?

The Greek regulatory framework offers licenses covering:

- Online sports betting

- Online casino gaming

- Poker and skill games

- Lottery and virtual games

- Land-based casino operations

Each license type mandates specific compliance and operational standards tailored to activity categories.

3. How much does an iGaming license cost and how long does it take to obtain?

The initial license application fee is approximately €50,000, with annual renewal fees ranging from €25,000 to €50,000 depending on market segment. The licensing process generally takes between 6 to 9 months, including document reviews, audits, and compliance verification.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply for Greek gambling licenses but must meet local regulatory requirements including establishing operational presence or partnering with Greek entities. All applicants undergo extensive background checks and technical evaluations.

5. What are the tax obligations for iGaming operators?

Operators pay a gross gaming revenue tax of 30% on all licensed gambling activities. Additionally, corporate income tax at 22% applies to net profits. Licensing and operational fees are also mandated annually, contributing to the fiscal environment.

6. Are gambling winnings taxed for players?

Yes, player winnings are subject to withholding tax at 15%, deducted at source by operators. This includes winnings from sports betting, casino games, and lottery. Players are not required to declare winnings separately on their tax returns.

7. What are the typical operational costs for running an online casino or sportsbook?

Operational costs include licensing fees, technology infrastructure, marketing, compliance personnel, payment processing fees, and customer support. Marketing and technology tend to be the largest expenses, with operational costs varying significantly based on scale.

8. What is the expected ROI timeline for entering this market?

ROI timelines vary but typically span 2 to 3 years from market entry. Success depends on efficient license acquisition, compliant operations, strong marketing execution, and player retention effectiveness.

9. What are the local presence requirements for operators?

Operators must maintain local offices or partner with Greek entities. Presence includes domain registration, local staff for customer service, and fulfillment of regulatory reporting and compliance functions within Greece.

10. What payment methods are available and recommended?

Popular payment methods include credit/debit cards, e-wallets such as PayPal and Skrill, bank transfers, prepaid cards, and emerging cryptocurrency options. Operators typically offer multiple payment channels to enhance player convenience and transaction security.

11. What are the advertising and marketing restrictions?

Marketing is restricted to prevent targeting minors and limiting aggressive promotions. Advertising via print, TV, radio, and digital media is regulated, with bans on 24-hour promotions during certain hours and compulsory responsible gambling messaging.

12. What responsible gambling measures are mandatory?

Operators must provide self-exclusion tools, player spending limits, age verification, informational disclosures, and support contact accessibility. Contribution to national problem gambling programs is also required.

13. How large is the iGaming market and what is the growth potential?

The Greek iGaming market is valued at approximately €1.2 billion, with an annual CAGR of 8%. Growth prospects remain strong due to increasing digital adoption, mobile penetration, and regulatory modernization.

14. Who are the main competitors and what is their market share?

The market features 15+ licensed operators, with three dominant players holding over 60% combined market share. Competition centers on service quality, compliance, and local market understanding.

15. What are the player preferences and typical spending patterns?

Players prefer sports betting and online casino games, with peak activity during evenings and major sports events. Spending patterns range from casual low-stakes users to high rollers, supported by mobile platforms and bonuses.

16. What are the key success factors and main challenges for new entrants?

Success hinges on regulatory compliance, local partnerships, mobile optimization, superior customer experience, and adaptive marketing. Challenges include regulatory complexity, competitive intensity, tax burden, and cultural nuances.

Sources and References

- Hellenic Gaming Commission – Official Website – https://www.gamingcommission.gov.gr

- National Statistical Authority of Greece – Population and Economic Data 2025 – https://www.statistics.gr

- Bank of Greece – Financial Reports and Statistics – https://www.bankofgreece.gr

- Ministry of Finance Greece – Tax Regulations and Guidelines – https://www.minfin.gr

- World Bank – Ease of Doing Business Report 2024 – https://www.worldbank.org

- International Telecommunication Union – ICT Statistics 2024 – https://www.itu.int

- Greek Telecommunications Authority – Market Overview Reports 2024

- European Commission – Digital Economy and Society Index – 2024

- Gaming Intelligence Report – Greek Market Analysis 2024

- Mobile Network Operators Annual Reports – Cosmote, Vodafone, Wind Hellas 2024

- Central Bank of Greece – Payment Systems Report 2024

- Greek Ministry of Digital Governance – 5G Rollout Plan 2023-2027

- European Gambling and Betting Association – Regulatory Updates 2024

- OECD – Greece Economic Outlook 2025

- Greek Association for Responsible Gambling – Annual Review 2024

- European Commission – Gambling Advertising Regulations 2023

- Greek Ministry of Labor – Workforce and Education Report 2024

- Greek Consumer Protection Authority – Online Retail Statistics 2024

- International Monetary Fund – Greece Country Report 2024

- Academic Study – Digital Literacy and Gaming Behavior in Greece 2025

- Greek Tax Authority Publications – Corporate and Personal Taxation 2024

- European Online Payment Providers Association – Market Penetration Data 2024

- Greek Ministry of Culture – Social and Cultural Trends Report 2024

- Local News Archives – Gambling Market Developments 2024-2025

- Consultancy Reports – iGaming Market Entry and Licensing Strategies 2025

- Greek Chamber of Commerce – Business Registration Guidelines 2025

- Greek Ministry of Digital Transformation – E-commerce Growth Report 2024

- Tech Industry Analysis – Greece Digital Infrastructure 2025

- Greek Ministry of Health – Problem Gambling Prevention Programs 2024

🎯 Gambling Databases Country Rating: Greece

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.0/10 | 🟡 Moderate 5-7 |

| Player Access Score | 7.5/10 | 🟢 Fully Legal (But Taxed) |

| Overall Market Attractiveness | 6.8/10 | High Entry Barrier / Stable but Expensive |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- PUNITIVE TAXATION: Operators face a 30% GGR tax on top of a 22% corporate tax. This creates an extremely high break-even threshold.

- PLAYER WINNINGS TAX: Players are subject to a 15% withholding tax on winnings. This reduces player retention and lifetime value (LTV) compared to other EU markets.

- MANDATORY LOCAL PRESENCE: You strictly require a local office or a binding partnership with a Greek entity, plus Greek language support.

- ACTIVE BLACKLISTING: The Hellenic Gaming Commission (HGC) actively maintains a blacklist of unlicensed operators and enforces ISP blocking.

- CRIMINAL LIABILITY: Operating without a license can lead to criminal proceedings against directors and seizures of assets.

- EU EXTRADITION: As an EU member state, Greece has robust extradition treaties with all major Western jurisdictions.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | Full legality for sports betting, casino, and poker. The framework is clear and established under the HGC. No deductions for legality, but strict compliance is enforced. |

| Licensing Process | 25% | 1.25/2.5 | Licenses are available but the process is slow (6-9 months, -0.5) and bureaucratically complex. Application fees (€50k) and renewals (€50k) are significant. Strict probity checks on all directors (-0.25). Final: 1.25 |

| Taxation & Costs | 20% | 0.5/2.0 | Severe Deduction: 30% Tax on GGR (-1.0). When combined with 22% Corporate Tax, the effective tax rate exceeds 50%. High operational costs (local office, Greek staff) further reduce margins. Final: 0.5 |

| Operational Requirements | 15% | 0.75/1.5 | Requires physical local presence or partnership (-0.25). Must have Greek domain and Greek-speaking support. Strict KYC/AML from day one. Financial guarantees required. Final: 0.75 |

| Market Environment | 10% | 0.5/1.0 | Stable EU environment (+0.5). However, market is concentrated with 15+ established operators, and advertising is strictly regulated regarding hours and content (-0.25). Final: 0.5 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Players can legally access all forms of iGaming (Sports, Casino, Poker) through licensed sites. No legal gray areas for the player. |

| Practical Accessibility | 30% | 2.0/3.0 | Payment methods are good (Cards, PayPal, Skrill). However, ISP blocking of offshore sites is active (-0.5). Crypto is not standard for licensed sites (-0.5). |

| Player Penalties | 20% | 1.0/2.0 | Major Deduction: While not a “fine” for illegal play, the mandatory 15% tax on player winnings is a financial penalty that degrades the user experience significantly (-1.0). |

| Market Availability | 10% | 0.5/1.0 | 15+ licensed operators give reasonable choice, but the high tax barriers prevent a flood of niche competition. Offshore alternatives are blocked. |

🔍 Key Highlights

Strengths

- Full Product Legality: Unlike many jurisdictions, Online Casino and Sports Betting are both fully legal and regulated.

- High Connectivity: 86% internet penetration and high mobile usage make digital delivery easy.

- Clear Rules: The HGC provides a specific, albeit strict, rulebook. No “grey market” ambiguity.

⛔️ CRITICAL RISKS AND CHALLENGES

- Taxation is the Profit Killer: A 30% GGR tax is among the highest in Europe. This necessitates high volume to cover fixed costs.

- Player Winnings Tax: The 15% withholding tax on winnings makes Greek licensed operators less competitive regarding odds/RTP compared to black-market offshore sites, yet offshore sites are blocked.

- Slow Licensing: A 6-9 month wait time means you are burning cash on overhead (local office, staff) long before you take a bet.

- Advertising Restrictions: Marketing is tightly controlled, protecting minors but making customer acquisition harder for new entrants.

- Local Presence: You cannot run this remotely. You need boots on the ground in Greece.

Player-Specific Issues

- Winnings Tax: Players lose 15% of their profits immediately.

- ISP Blocking: Players attempting to use non-taxed offshore sites will face blocking screens.

- KYC Friction: Identity verification is mandatory before play, not just at withdrawal.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €350,000 – €500,000 (License, Legal, Tech, Local Setup)

Monthly Operating Costs: €50,000 – €100,000 (Staff, Office, Compliance, Hosting)

Effective Tax Rate on Revenue: ~52% (30% GGR + 22% Corporate Tax)

Customer Acquisition Cost: Moderate to High (€150 – €300) due to ad restrictions.

Time to Breakeven: 2.5 – 3 Years

Profitability Assessment: DIFFICULT. The 30% GGR tax is a massive hurdle. This market is only viable for operators who can achieve significant scale to dilute the fixed costs of compliance and local presence. Small boutique casinos will bleed money here.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | 🔴 High | ISP blocking, blacklisting, potential criminal charges, inability to process payments via standard EU channels. |

| Licensed Operators | 🟡 Medium | Regulatory compliance risk (fines for KYC/AML breaches), risk of license revocation for non-compliance. |

| Affiliates/Advertisers | 🟡 Medium | Strict advertising codes; promoting unlicensed sites can lead to fines and domain blocking. |

| Company Directors | 🟡 Medium | Personal liability for compliance failures; background checks are invasive. |

🚨 Extradition and International Enforcement

Extradition Treaties: Greece is a member of the European Union and NATO. It holds active extradition treaties with the USA, UK, Canada, Australia, and all EU member states.

Enforcement History: Greece cooperates fully with Europol and Interpol. Cross-border financial crimes related to gambling (money laundering) are prosecuted aggressively.

Travel Risk: Executives of blacklisted/illegal offshore operators risk arrest if entering Greece or transiting through Greek airports.

📋 Final Verdict

Greece receives an Operator Ease Score of 6.0/10 and a Player Access Score of 7.5/10, resulting in an overall market attractiveness rating of 6.8/10.

HONEST ASSESSMENT: Greece is a stable, fully regulated European market, but the cost of entry is steep. The 30% GGR tax combined with mandatory local presence requirements makes it a “pay-to-play” jurisdiction reserved for well-capitalized international brands. It is NOT suitable for startups or operators looking for quick, low-cost market entry. The 15% tax on player winnings also creates a unique friction point that depresses player value compared to other EU nations.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major Tier-1 operator with deep pockets (€10M+ capital).

- Looking for a legally watertight EU license and accepting lower margins (10-15% net).

- Willing to commit to a 5-year ROI horizon.

- Capable of setting up a physical office in Athens.

❌ Definitely Avoid If You Are:

- A startup or small operator with limited budget.

- An offshore operator trying to target Greeks without a license (you will be blocked).

- Expecting high margins (taxes will eat over 50% of your gross profit).

- A crypto-focused casino (regulatory framework is fiat-centric).

⚠️ BOTTOM LINE: Enter Greece only if you have the capital to survive a 50%+ effective tax rate and a 3-year wait for profitability.

A critical nuance in the Greek market is the impact of the tiered tax on player winnings. While the regulation provides safety, the taxation on withdrawals creates a significant friction point that often pushes high-volume players toward the grey market. Balancing strict compliance with player retention strategies here is much harder than in other EU jurisdictions.