Grenada represents a promising gateway for iGaming operators targeting the Caribbean market. The nation has established a comprehensive regulatory framework that balances strong control with incentives for growth.

Its legal environment supports diverse gambling activities inclusive of online casinos, betting, and lotteries, under strict supervision to ensure fairness and compliance. This analysis covers Grenada’s regulatory landscape, licensing processes, and operational requirements for market entry.

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal for land-based and online gambling |

| Regulatory Authority | Grenada Gaming Commission |

| Key Gambling Legislation | Gambling, Lotteries, and Betting Act 1966; Casino Gaming Act 2014; Gaming Act 2016 |

| Recent Regulatory Change | Casino Gaming Amendment Bill 2022 |

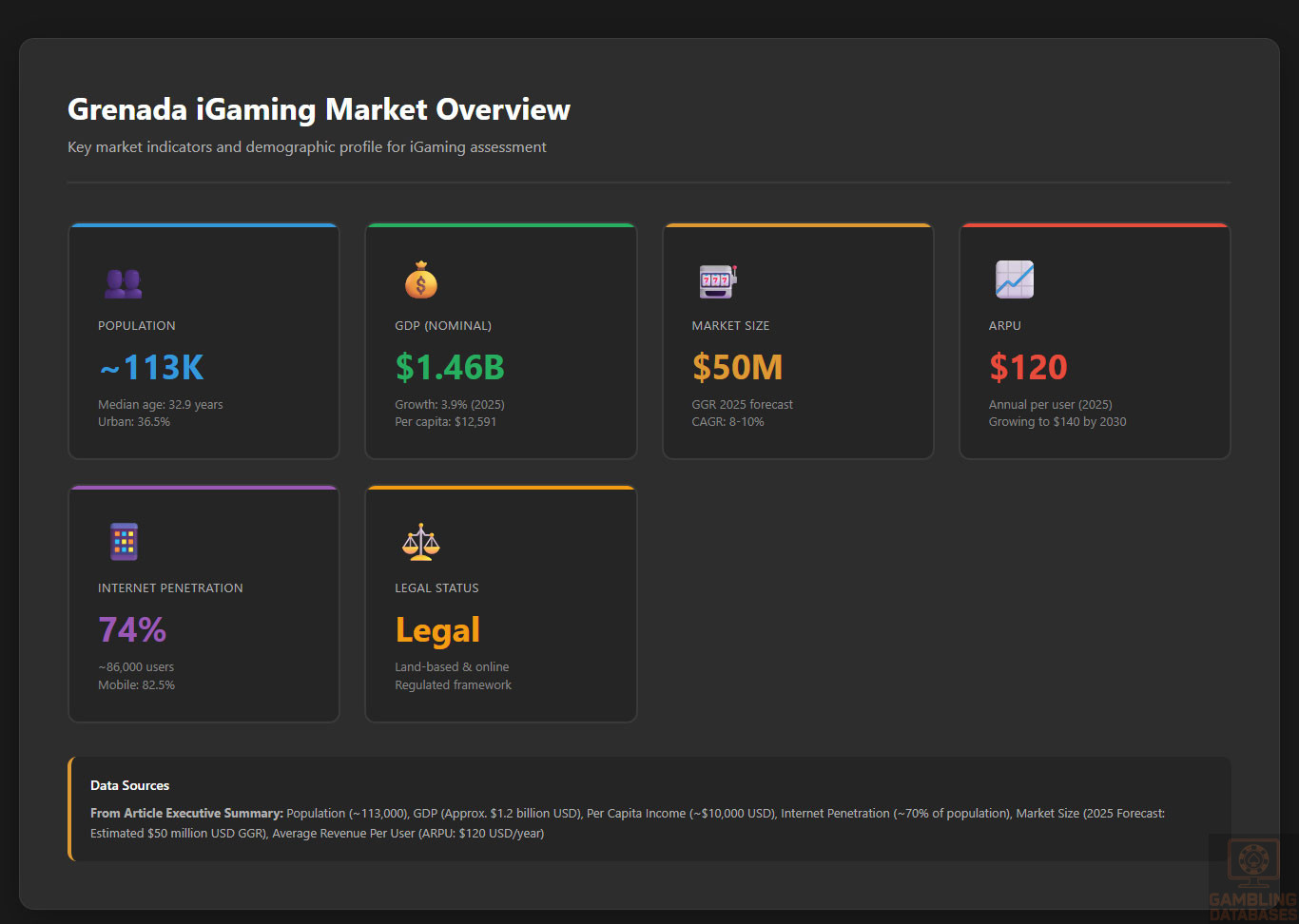

| Population | ~113,000 |

| GDP (Nominal) | Approx. $1.2 billion USD |

| Per Capita Income | ~$10,000 USD |

| Internet Penetration | ~70% of population |

| Mobile Penetration | Over 90% |

| License Types | Land-based, Online Gambling, Betting |

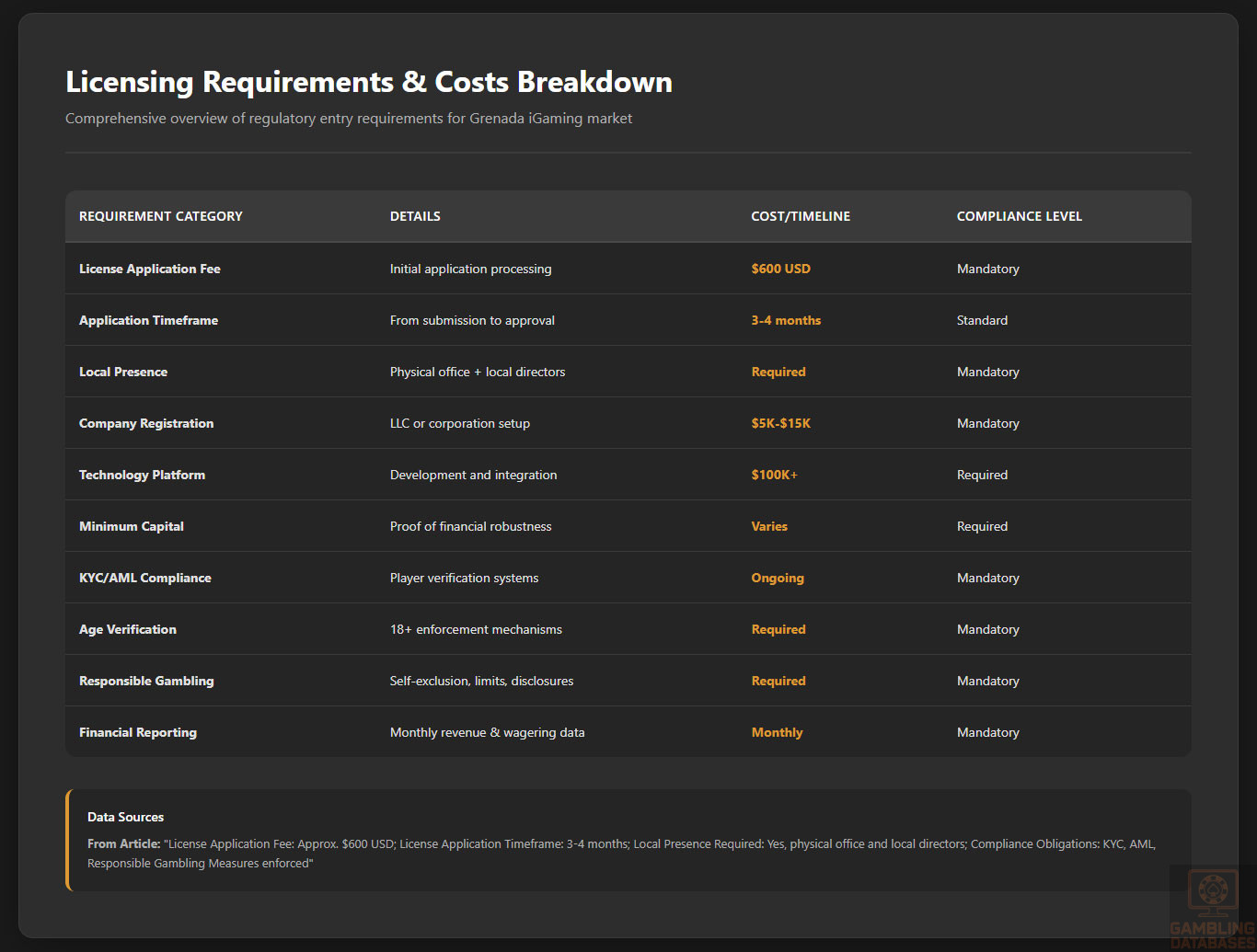

| License Application Timeframe | 3-4 months |

| License Application Fee | Approx. $600 USD |

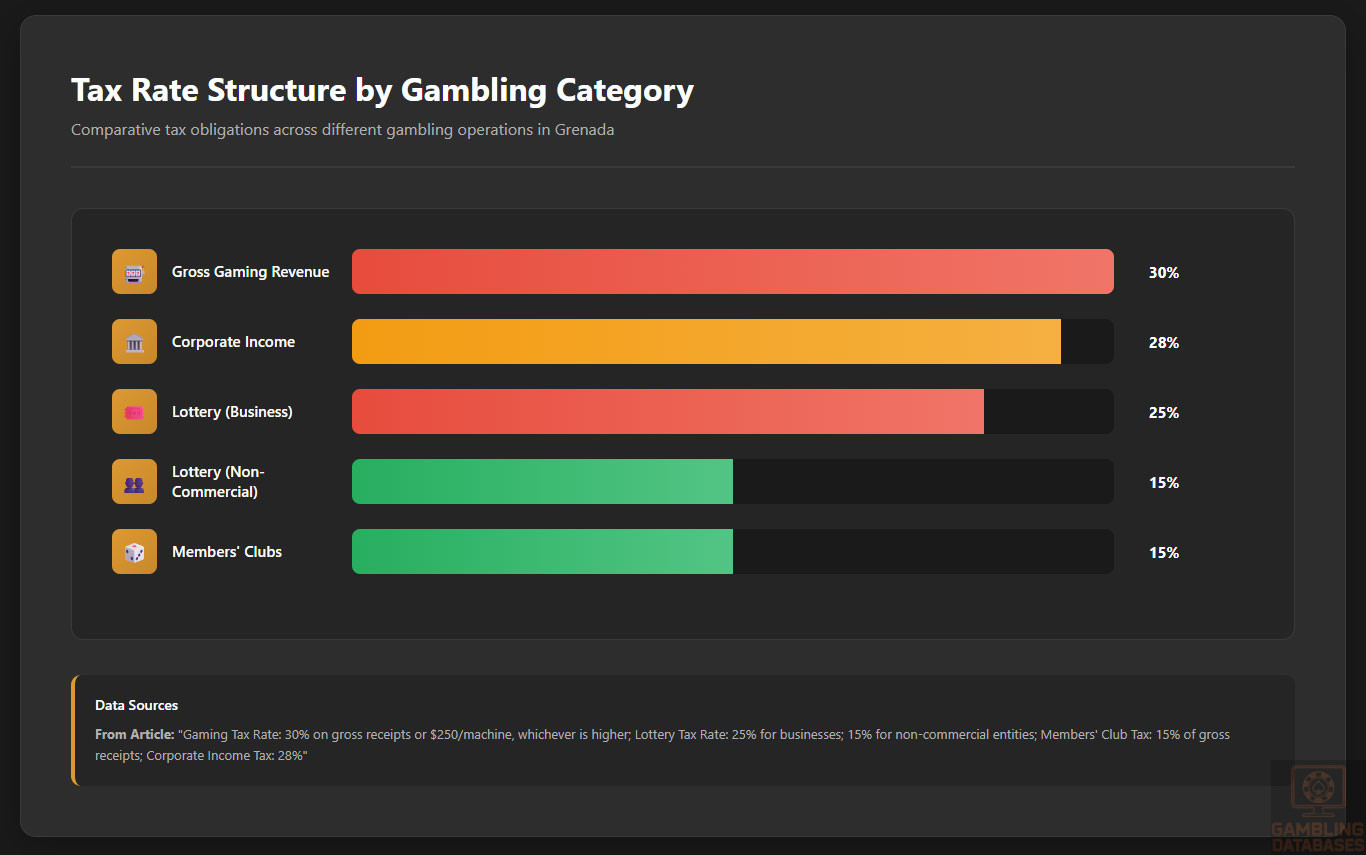

| Gaming Tax Rate | 30% on gross receipts or $250/machine, whichever is higher |

| Lottery Tax Rate | 25% for businesses; 15% for non-commercial entities |

| Members’ Club Tax | 15% of gross receipts |

| Minimum Capital Requirement | Varies; often capital proof required |

| Local Presence Required | Yes, physical office and local directors |

| Foreign Ownership Restrictions | Allowed but under stringent regulatory scrutiny |

| Compliance Obligations | KYC, AML, Responsible Gambling Measures enforced |

| Player Age Limit | 18 years |

| License Renewal Fee | Varies, typically higher than initial application |

| Market Entry Barriers | Strong regulatory enforcement, licensing fees, compliance costs |

| Market Size (2025 Forecast) | Estimated $50 million USD GGR |

| Projected CAGR | 8-10% over 5 years |

| Average Revenue Per User (ARPU) | $120 USD/year |

| Technology Infrastructure | Modern broadband, mobile-optimized |

| Business Environment | Favorable investment climate, moderate bureaucracy |

| Enforcement Mechanisms | Fines, license revocation, criminal penalties |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling in Grenada is fully legal, encompassing land-based and online activities. The regulatory framework stems from foundational legislation established in 1966 and has evolved through successive acts, notably the Casino Gaming Act of 2014 and the Gaming Act of 2016. These laws collectively govern all facets of gambling, ensuring stringent control, consumer protection, and operational transparency.

Land-Based Gambling Activities

Land-based gambling in Grenada includes casinos, sports betting venues, licensed slot machine halls, bingo operations, and lotteries. Casino operations are supervised under the Casino Gaming Act and are subject to strict licensing and operational standards.

Sports betting venues offer bookmaker services with oversight to prevent illegal or unlicensed betting. Slot machine halls operate under individual machine licensing requirements, necessitating a minimum tax or percentage of gross receipts. Bingo and lottery games are also regulated with separate tax considerations that differ for commercial and non-commercial entities.

Online Gambling Framework

The online gambling environment is regulated under the Gaming Act provisions, with the Grenada Gaming Commission acting as the primary licensing and supervisory body. Online operators must obtain explicit licenses ensuring compliance with technical standards, fairness measures, and anti-fraud mechanisms.

The framework prohibits unauthorized gambling activities and enforces rigorous KYC (Know Your Customer) and AML (Anti-Money Laundering) protocols. Online platforms are obligated to maintain data security, promote responsible gambling, and regularly submit compliance reports to the Commission.

Licensed Operators and Market Players

The licensed operator landscape in Grenada is competitive yet tightly regulated. Key market players include several local and international entities holding licenses for both land-based and digital gambling services. The competitive dynamics emphasize compliance reliability, technological innovation, and market reputation.

While no public comprehensive list exceeds five licensed large operators, the market is characterized by a mixture of local casinos and international companies specializing in online gaming. Entry strategies typically involve partnership with local stakeholders to meet physical presence requirements and navigate the regulatory environment effectively.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing process is governed by the Grenada Gaming Commission and entails financial robustness, technical capability, and adherence to regulatory standards. Applicants undergo scrutiny regarding their corporate structure, financial health, and operational transparency.

Application fees are moderate at an estimated $600, with the approval process spanning approximately three to four months. Applicants must meet eligibility requirements, including compliance with capital requirements and demonstrate the ability to maintain secure and fair gaming environments.

The documentation submitted typically covers corporate registration, financial audits, business plans, technical system certifications, and background checks for all principals involved.

Local Presence and Operational Requirements

Operators are mandated to establish a physical presence in Grenada, including a registered office and local directors or responsible officers. This ensures regulatory oversight and responsiveness to local compliance demands.

Domain ownership and control requirements exist to guarantee that online operations are clearly associated with Grenada-licensed entities. Personnel obligations include employing qualified staff to uphold operational integrity, compliance, and customer support functions.

Foreign ownership is permissible but strictly scrutinized to ensure no circumvention of regulatory requirements occurs. Partnerships with local stakeholders or entities often facilitate smoother regulatory approval and operational integration.

Compliance Obligations and Monitoring

Player Protection and Identification

Grenada enforces robust player protection measures encompassing age verification to restrict participation to those 18 and older. KYC standards obligate operators to verify identity, source of funds, and ongoing transaction monitoring to deter money laundering and fraud.

Responsible gambling measures include mandatory self-exclusion systems, deposit limits, and clear disclosure of game odds and terms. Operators must provide accessible tools for players to manage gambling behavior responsibly under Commission guidelines.

- Age verification protocols

- Comprehensive KYC and AML compliance

- Self-exclusion programs availability

- Deposit and loss limits enforcement

- Transparent game fairness disclosures

- Staff training on responsible gambling

Financial Monitoring and Reporting

Operators must maintain transparent and auditable financial records submitted periodically to the Gaming Commission. Transaction monitoring systems are required for real-time detection of suspicious activities.

Reporting obligations include monthly financial statements, detailed wagering data, anti-money laundering audit reports, and annual compliance certifications. These ensure ongoing regulatory adherence and tax compliance.

- Submission of monthly revenue and wagering reports

- Provision of AML audit findings quarterly

- Annual submission of audited financial statements

- Immediate notification of any suspicious activity

- Regular compliance review meetings with regulators

Taxation Structure and Financial Obligations

Player Taxation

Players are generally not liable for withholding taxes on winnings. The tax burden primarily rests with operators, with the framework designed to encourage participation while ensuring market sustainability through business taxation.

Operator Taxation

| Category | Tax Rate | Details |

|---|---|---|

| Gross Gaming Revenue (GGR) Tax | 30% | On gross receipts for most gambling activities or $250 per gaming machine, whichever is higher |

| Lottery Tax | 25% (businesses); 15% | Non-commercial organizations and members’ clubs |

| Members’ Clubs | 15% | Gross receipts from gaming activities for members |

| License Renewal Fees | Varies | Typically higher than initial application fees |

| Corporate Income Tax | 28% | Applies to operating companies |

Gambling Market Financial Performance

The gambling sector in Grenada contributes significantly to government revenues through gaming taxes and license fees. Total wagered amounts have grown steadily, driven by increasing online engagement and expanding tourism-related casino activities.

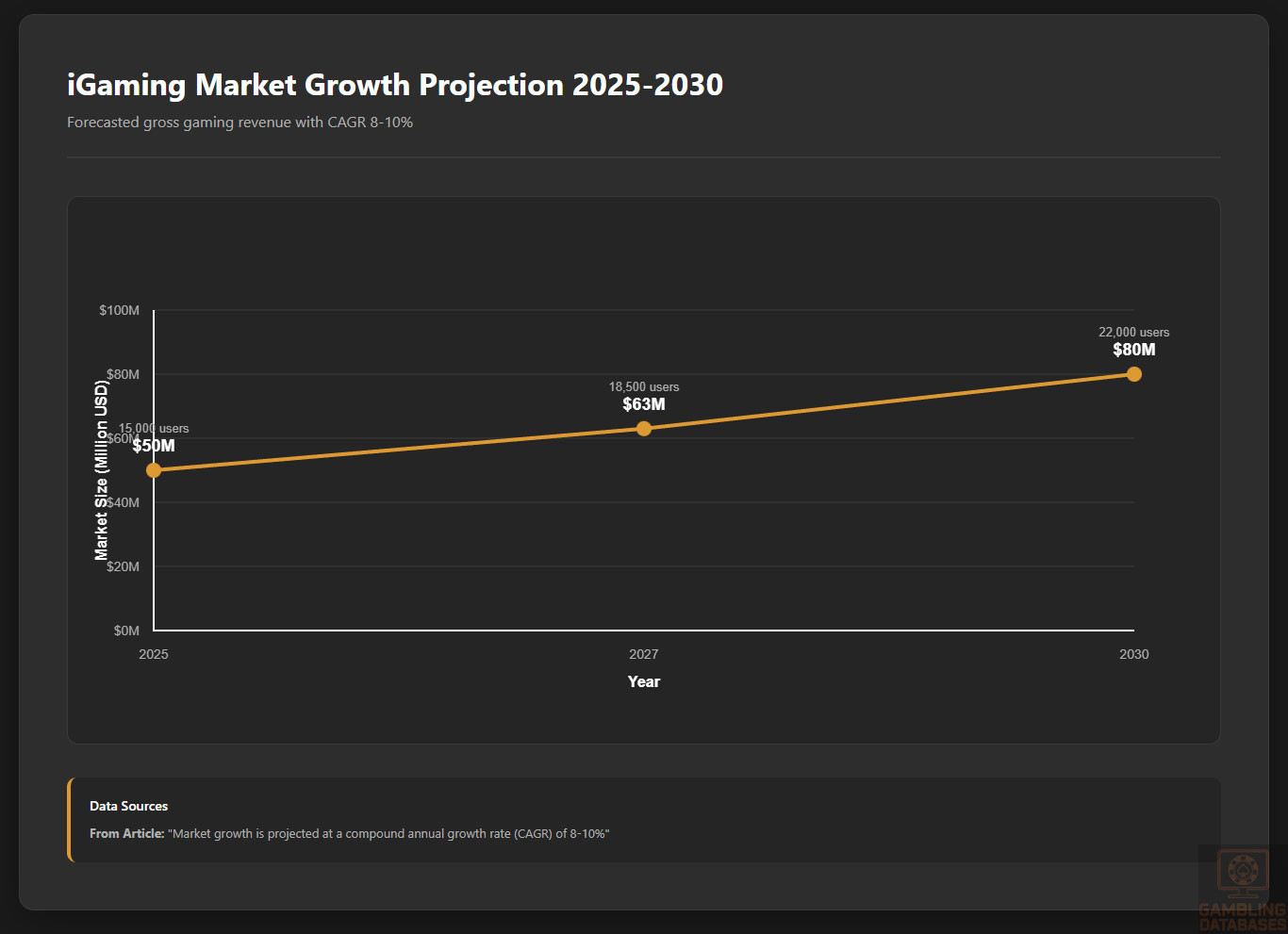

Revenue trends indicate a robust upward trajectory with a projected market size of $50 million gross gaming revenue in 2025 and an estimated CAGR of 8-10% over the next five years. Tax revenues support further regulatory and social programs aimed at gambling harm reduction and economic diversification.

Advertising and Marketing Restrictions

Advertising of gambling services in Grenada is permitted but strictly regulated to ensure ethical promotion. Restrictions include prohibitions on targeting minors, false or misleading claims, and limitations on advertising during certain hours.

- Prohibition on targeting underage audiences

- Restrictions on aggressive or misleading advertising

- Limitations on bonuses and promotional terms

- Strict guidelines on sponsorships and endorsements

- Mandatory disclosure of responsible gambling messages

Recent Regulatory Changes and Their Impact

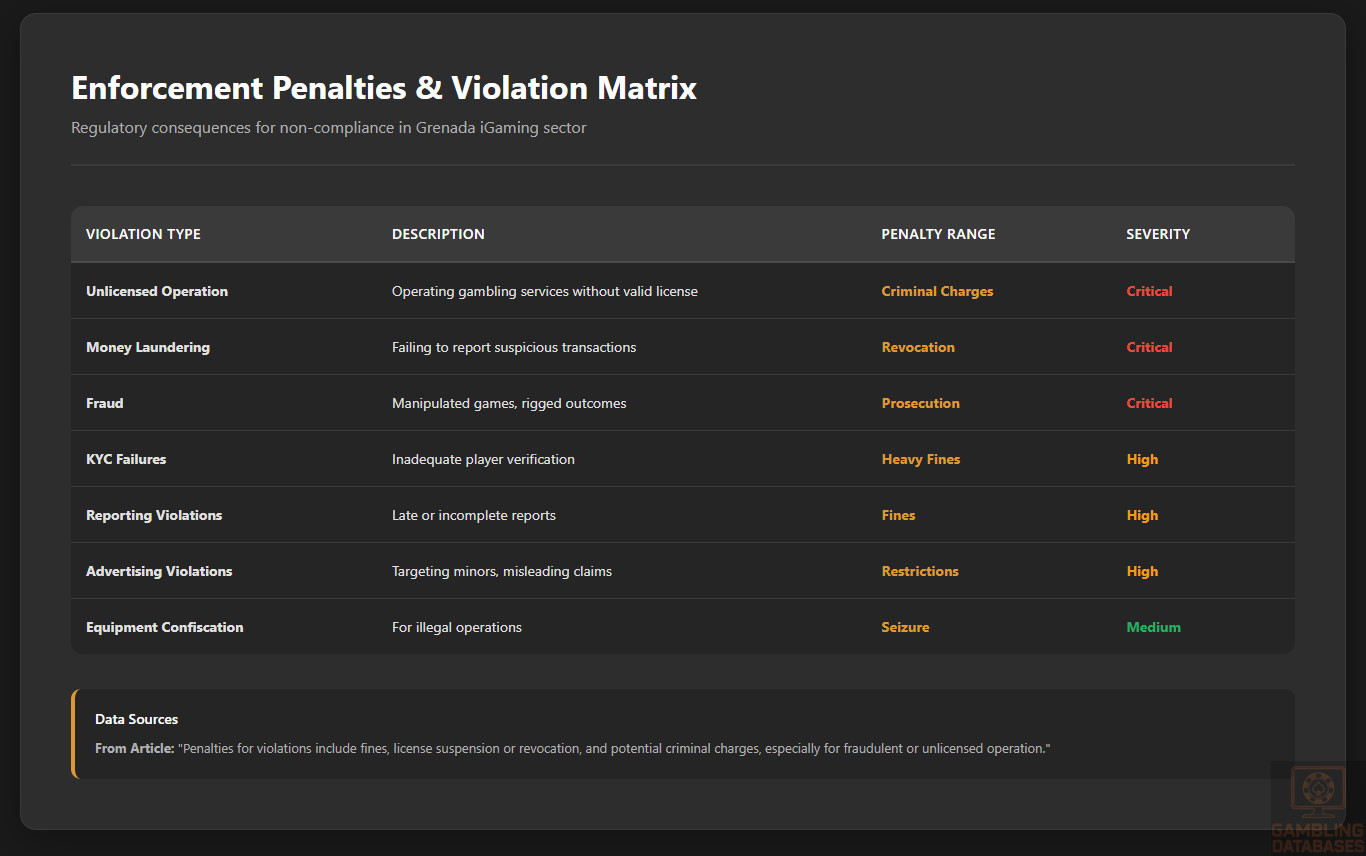

The 2022 Casino Gaming Amendment Bill brought heightened penalties for unauthorized gambling, expanded licensing revocation terms, and defined “beneficial owner” more comprehensively. These changes have increased the compliance costs for operators by emphasizing transparency and accountability.

Market strategies have shifted toward more rigorous KYC processes, enhanced reporting systems, and local engagement to secure and maintain licenses. The regulatory clarity benefits the long-term viability of the sector, enhancing investor and player confidence.

Enforcement Mechanisms and Penalties

Grenada employs robust enforcement to maintain a legal and fair gambling environment. Penalties for violations include fines, license suspension or revocation, and potential criminal charges, especially for fraudulent or unlicensed operation.

- Monetary fines escalating with severity of infraction

- Suspension or revocation of gambling licenses

- Confiscation of equipment for illegal operations

- Criminal prosecution for fraud and money laundering

- Restrictions on advertising for non-compliant operators

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

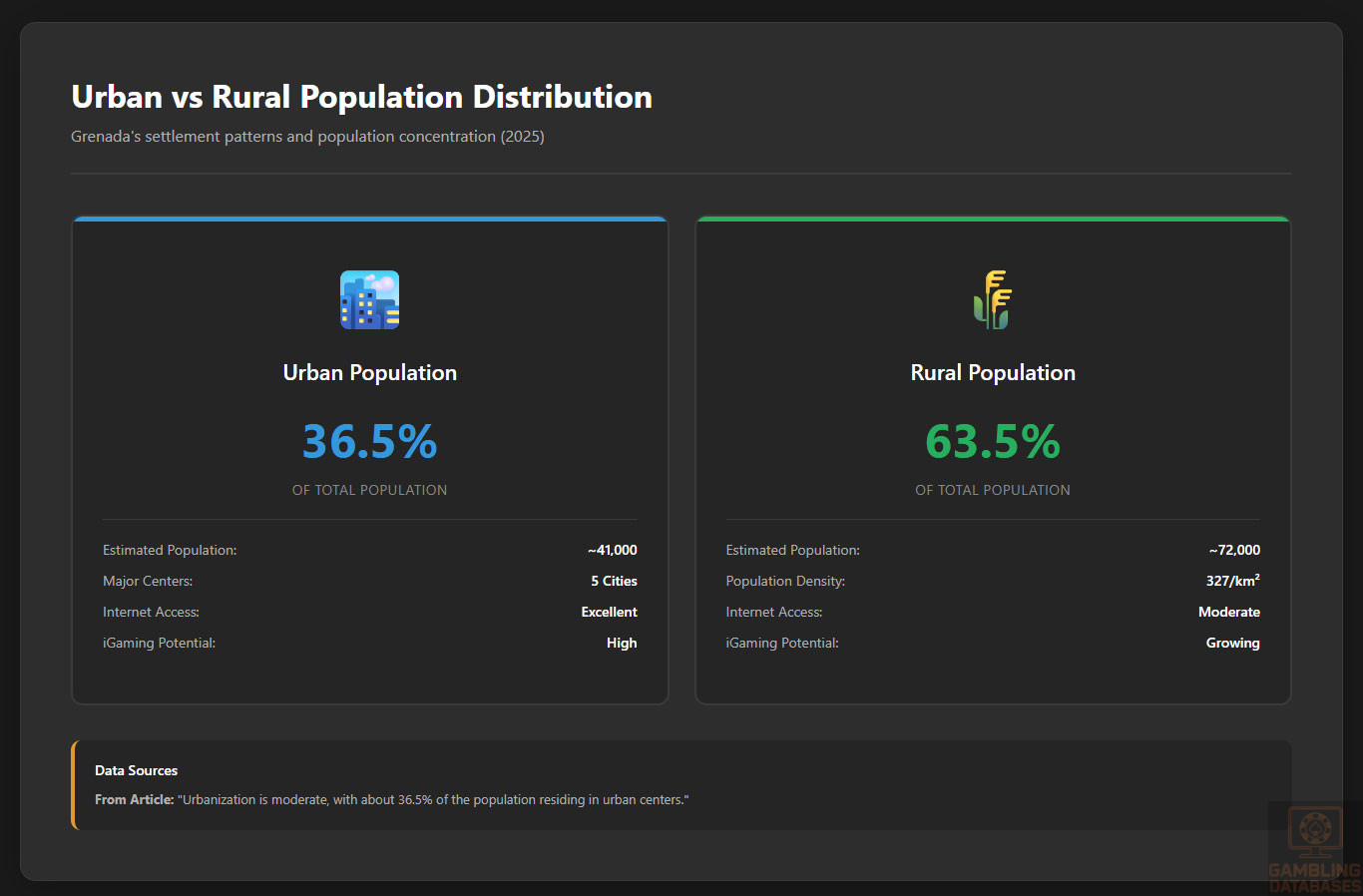

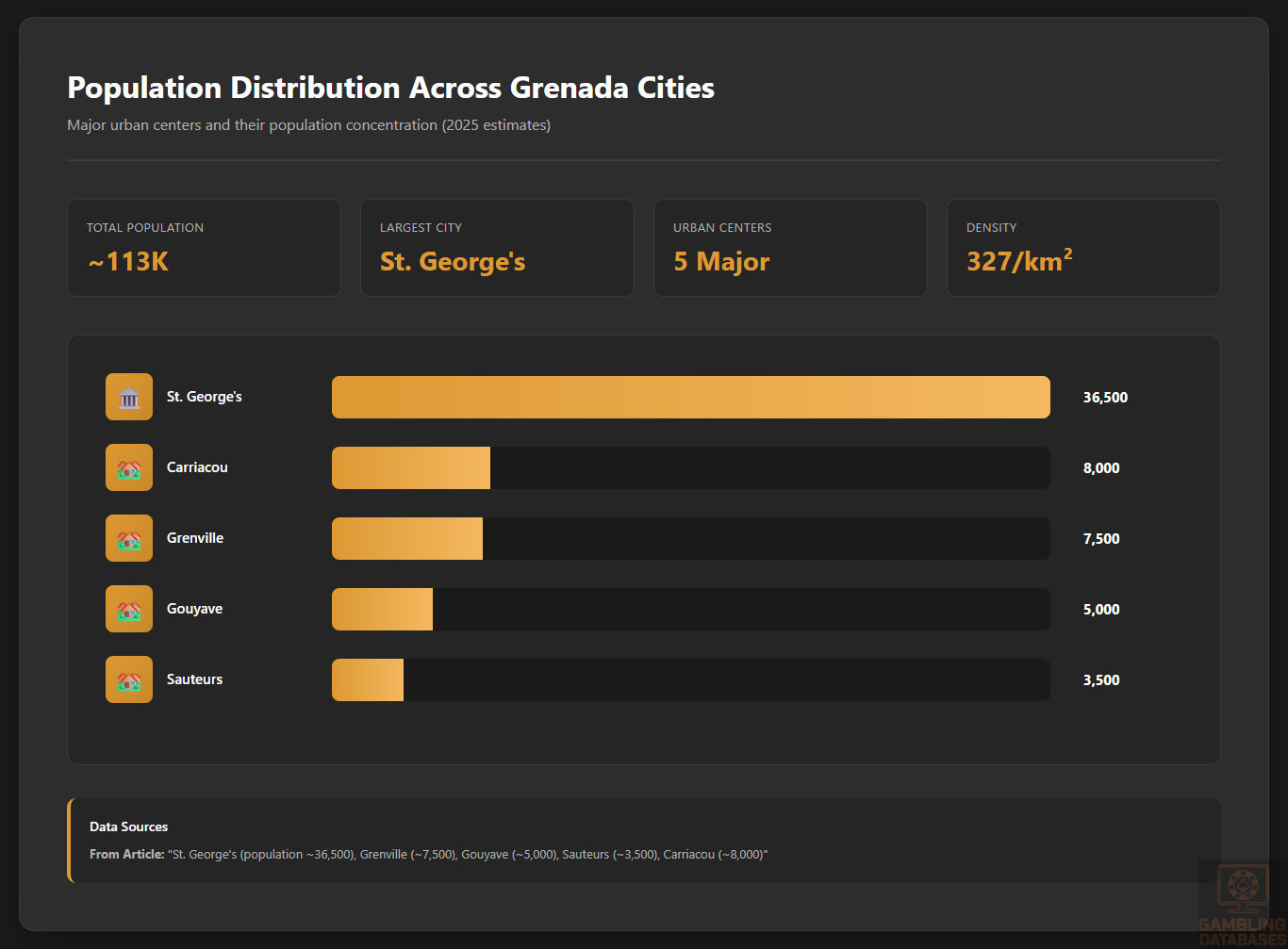

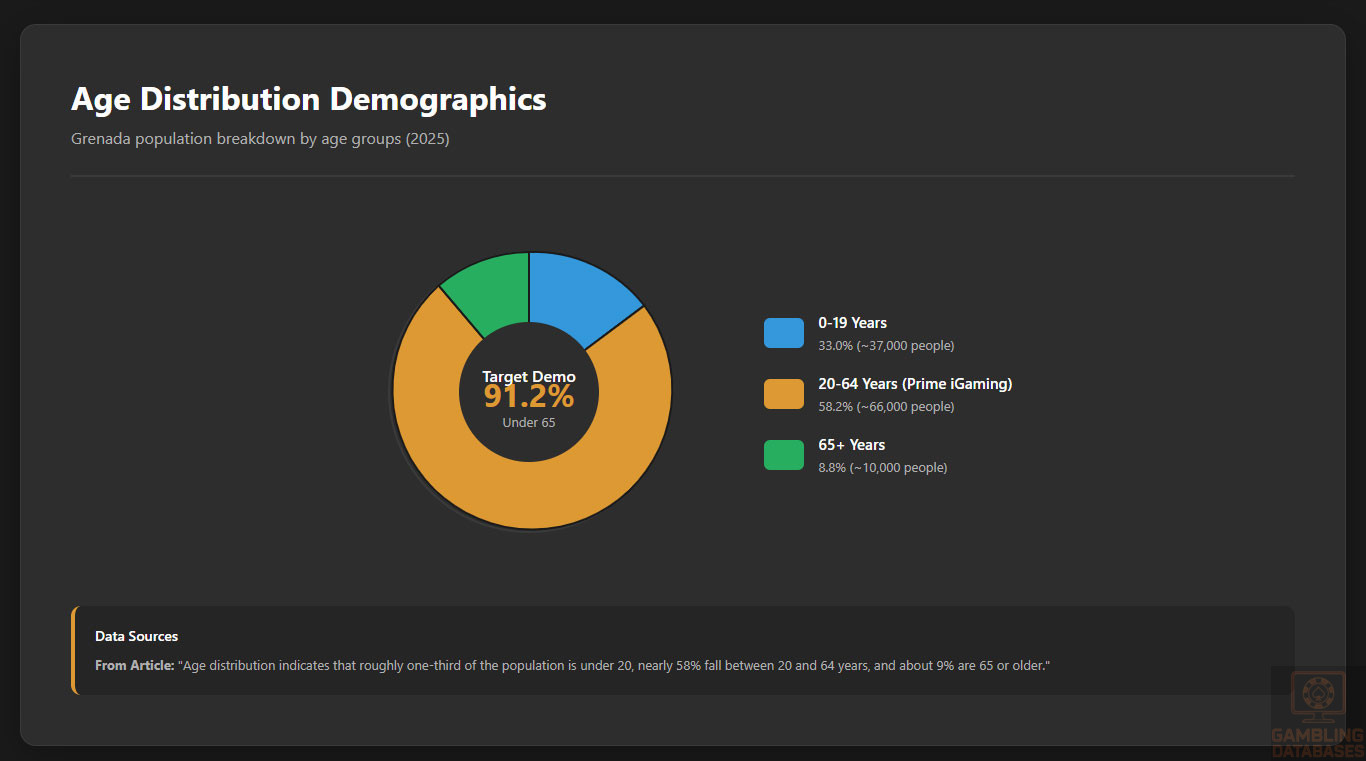

Grenada’s population in 2025 is approximately 111,000 people, with a relatively balanced gender ratio of 1,018 males per 1,000 females. The median age stands at 32.9 years, reflecting a moderately young but maturing population. Age distribution indicates that roughly one-third of the population is under 20, nearly 58% fall between 20 and 64 years, and about 9% are 65 or older.

Urbanization is moderate, with about 36.5% of the population residing in urban centers. The population density is high at around 327 people per square kilometer, concentrated mainly in Grenada’s larger towns and economic hubs, fostering local demand for entertainment and digital services including iGaming.

| Age Group | Population % |

|---|---|

| 0-19 years | 33.0% |

| 20-64 years | 58.2% |

| 65+ years | 8.8% |

Geographic Distribution

The population is distributed primarily across Grenada island and the smaller islands of Carriacou and Petite Martinique. The capital, St. George’s, is the largest city and commercial hub, hosting nearly 36,500 residents and a significant portion of iGaming consumers and internet infrastructure.

Other towns like Grenville, Gouyave, and Sauteurs serve as secondary economic centers. Internet access and gambling venue concentration are strongest in urban centers, benefitting from better broadband and mobile network coverage, while rural areas experience lower penetration rates.

- St. George’s (population ~36,500)

- Grenville (~7,500)

- Gouyave (~5,000)

- Sauteurs (~3,500)

- Carriacou (~8,000)

Economic Indicators and Consumer Spending Power

Grenada’s GDP is estimated at approximately $1.46 billion USD in 2025 with a growth forecast of 3.9%, supported mainly by tourism, manufacturing, and services. The economy is projected to maintain steady growth at around 3.1% annual GDP increase through 2027.

The GDP per capita stands near $12,591 USD, reflecting moderate consumer spending power with improvements in income distribution. Inflation remains low and stable, fostering a favorable environment for discretionary spending in entertainment sectors such as iGaming.

| Indicator | 2025 (Estimate) | 2026 (Forecast) | 2027 (Forecast) |

|---|---|---|---|

| GDP (billion USD) | 1.46 | 1.54 | 1.62 |

| GDP Growth Rate (%) | 3.9 | 3.3 | 2.7 |

| GDP per Capita (USD) | 12,591 | 13,196 | 13,748 |

| Inflation Rate (%) | 1.3 | 2.0 | 2.0 |

Income and Wealth Distribution

Average household income is modestly rising, supporting gradual increases in disposable income. Income inequality remains a challenge, with a significant portion of the population in lower income brackets while urban professionals and tourism-related workers hold moderate to high earnings.

Consumer spending is increasingly directed towards digital entertainment, mobile services, and leisure, aligning with rising internet accessibility and smartphone adoption. The middle-income group exhibits the strongest growth potential for iGaming participation, driven by young adults and working professionals.

Market Size and Growth Projections

The iGaming market in Grenada is in an emergent phase, with estimated gross gaming revenue of approximately $50 million USD in 2025. The user base is expected to expand steadily, attracting 15-20% of the adult population as active gamblers within five years.

Market growth is projected at a compound annual growth rate (CAGR) of 8-10%, fueled by increasing smartphone penetration, improved internet infrastructure, and evolving consumer preferences towards online gambling platforms.

| Year | Market Size (Million USD) | Estimated Active Users | ARPU (USD/year) |

|---|---|---|---|

| 2025 | 50 | 15,000 | 120 |

| 2027 | 63 | 18,500 | 125 |

| 2030 | 80 | 22,000 | 140 |

Education, Skills, and Digital Literacy

Grenada exhibits strong literacy rates, with adult literacy exceeding 95%, reflecting a well-educated workforce complemented by sound educational infrastructure. Digital literacy is expanding rapidly, particularly among youth and working-age adults, facilitated by government and private sector initiatives.

Workforce skills in IT and customer service sectors support the growth of tech-driven industries including online gambling. The availability of educated, digitally proficient talent enhances Grenada’s attractiveness as a viable iGaming hub.

Cultural and Social Factors

Communication and Language

English is the official language and predominates in government, education, and commercial activities. Local dialects and Creole languages thrive culturally but have limited presence online, making English the primary medium for iGaming communication and marketing.

- English (official and business language)

- Grenadian Creole English (widely spoken informally)

- French Creole (cultural communities)

- Spanish (minor presence)

- Other Caribbean dialects (limited)

Cultural Attitudes

Gambling is generally accepted socially, often associated with leisure and tourism. Religious influences encourage moderation but do not significantly restrict gambling activities. Foreign brand entry is met with cautious optimism, with preference for operators demonstrating compliance and social responsibility.

Entertainment preferences align with interactive digital experiences, favoring mobile-friendly gaming, promotions, and live events that connect the local user base with global platforms.

Problem Gambling and Social Considerations

The prevalence of problem gambling remains low but monitored actively by health and regulatory bodies. At-risk populations primarily include youth and low-income groups.

The government and NGOs have implemented multiple response programs addressing gambling addiction, focusing on awareness, treatment accessibility, and social reintegration.

- National responsible gambling awareness campaigns

- Access to counseling and support services

- Self-exclusion program promotion

- Training for gambling operators on social responsibility

- Collaboration with health agencies for research and monitoring

Political Structure and Governance

Grenada operates a stable parliamentary democracy within the Commonwealth framework, benefiting from consistent regulatory policies. Government commitment to economic diversification supports favorable business environments and regulatory clarity in gaming sectors.

Political stability and progressive international relations foster investor confidence and provide a sound platform for long-term iGaming market development.

Technology Adoption and Digital Behavior

Internet and Digital Usage

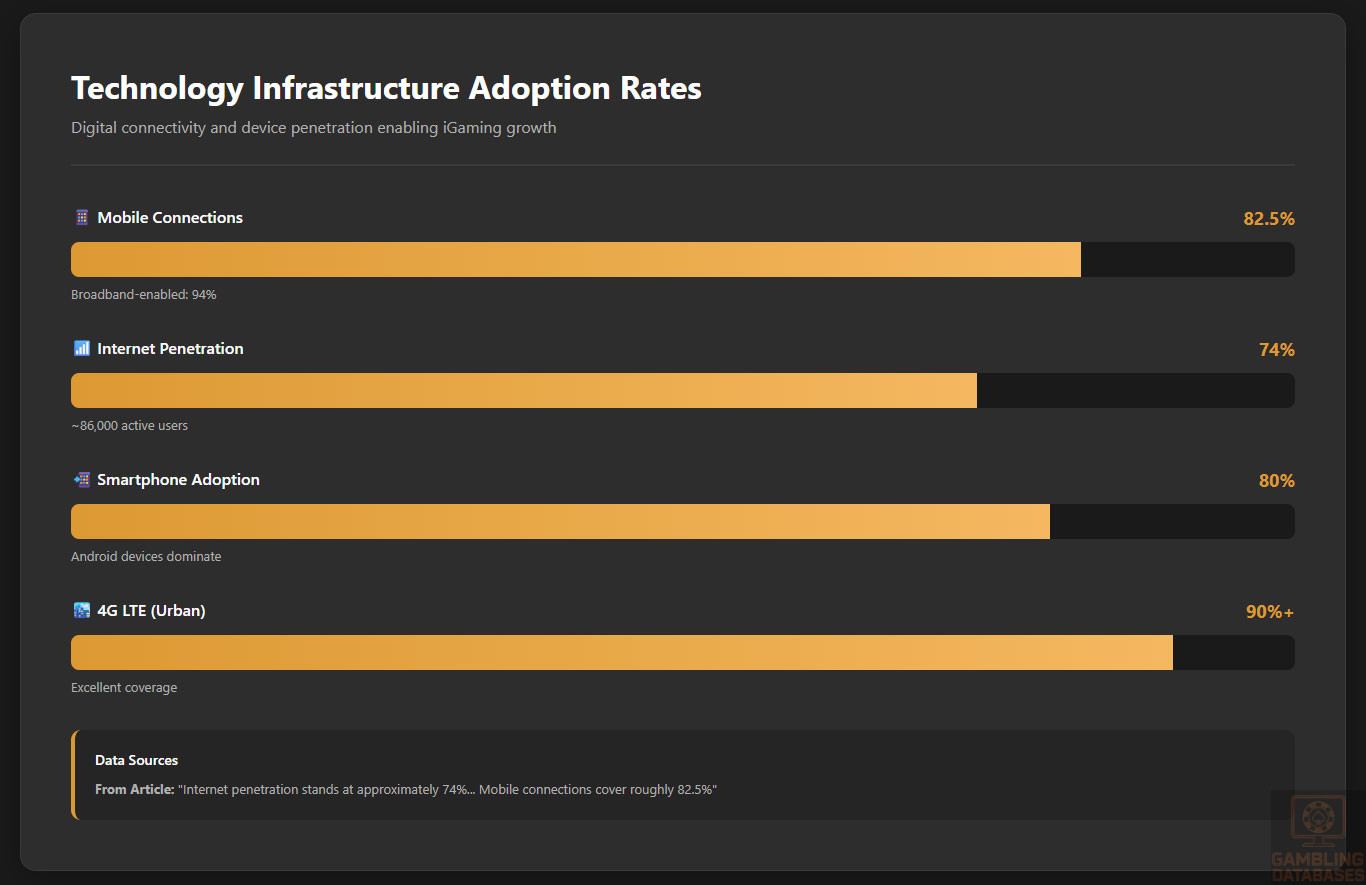

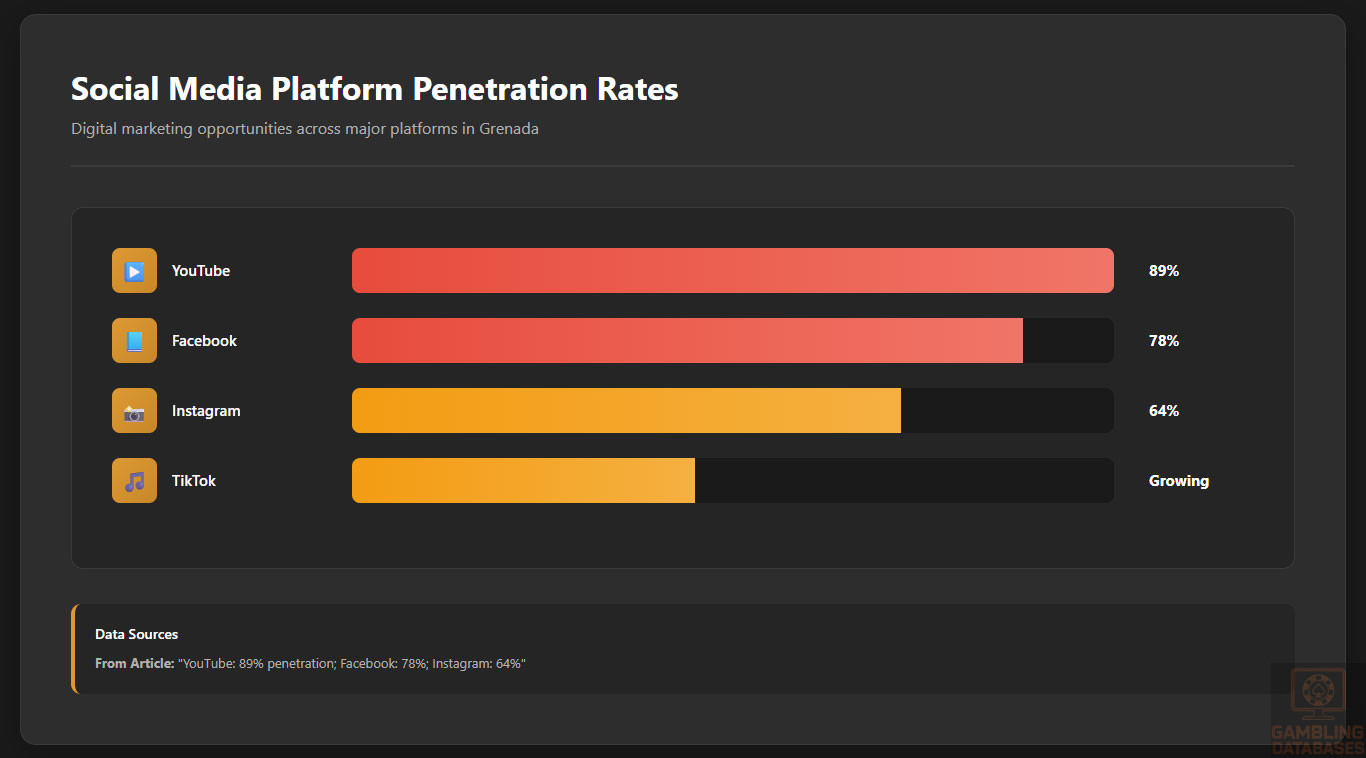

Internet penetration in Grenada stands at approximately 74%, with over 86,000 users. Mobile connections cover roughly 82.5% of the population, with broadband-enabled devices accounting for more than 94% of mobile connections. Daily internet usage averages several hours among active users, driven by social media, mobile apps, and streaming entertainment.

Social media platforms enjoy widespread popularity, acting as primary channels for community, marketing, and customer engagement in gambling sectors.

- Facebook: 78% penetration among internet users

- Instagram: 64% of youth and young adults

- YouTube: 89% penetration, preferred content platform

- TikTok: Rapid growth among under-25 demographic

- Twitter and LinkedIn: Moderate usage for news and professional networking

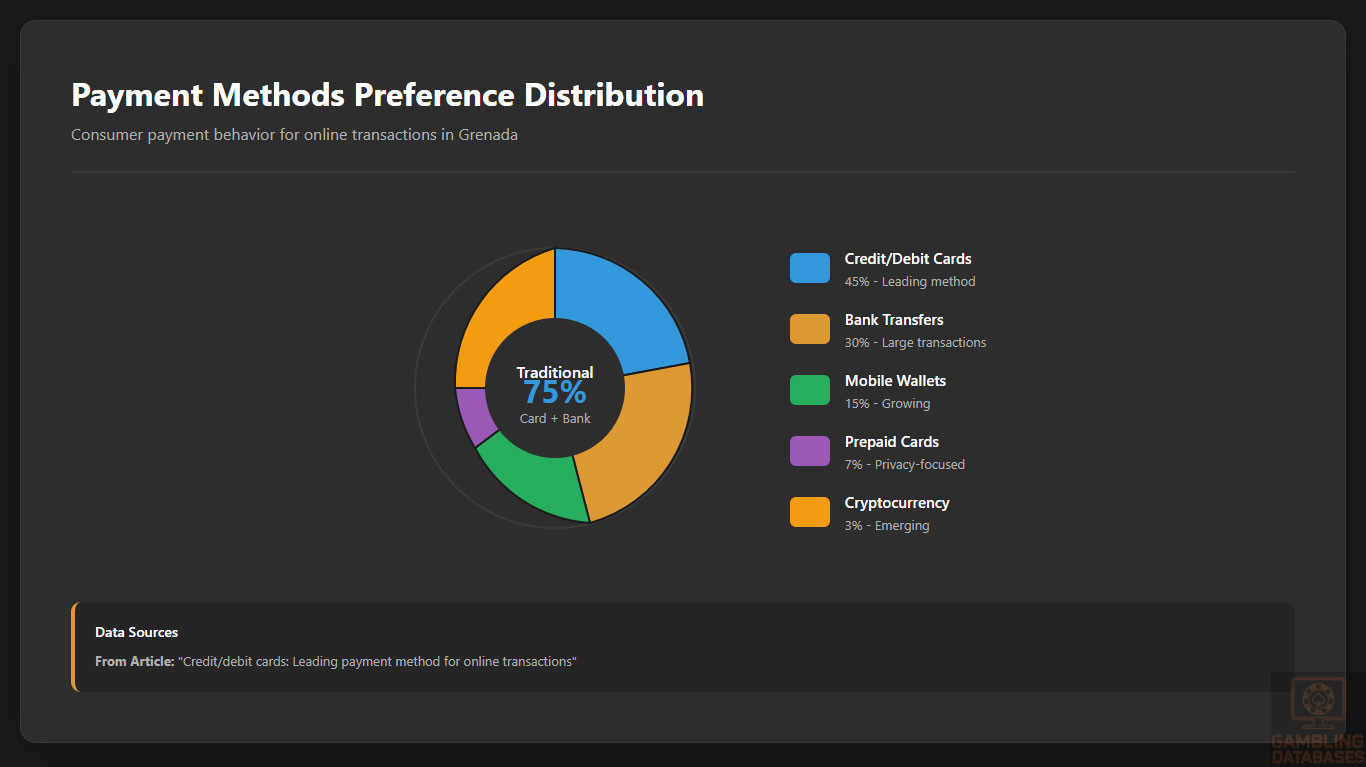

Digital Payment Behavior

Payment methods in Grenada emphasize convenience and security, with digital wallets, cards, and bank transfers dominant. Cryptocurrency adoption is nascent but growing gradually, particularly among younger and tech-savvy consumers.

- Credit/debit cards: Leading payment method for online transactions

- Bank transfers: Frequently used for larger sums and bill payments

- Mobile money wallets: Increasingly popular among youth

- Prepaid cards: Used for privacy-focused transactions

- Cryptocurrency payments: Emerging with cautious adoption

Gaming and Gambling Preferences

Current Market Participation

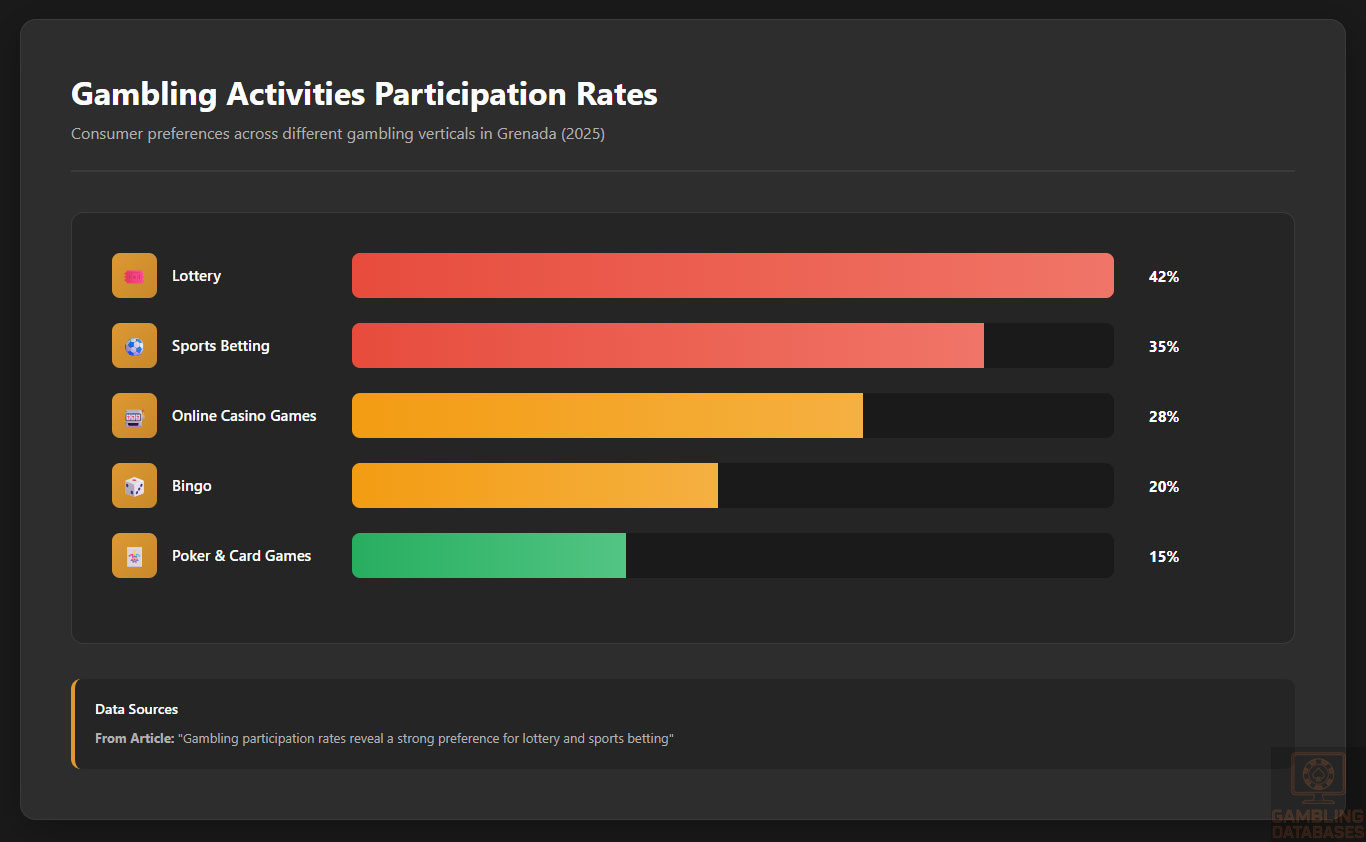

Gambling participation rates reveal a strong preference for lottery and sports betting, followed by online casino games and bingo. Mobile gaming platforms attract younger demographics, while traditional venues maintain traction among older adults.

| Rank | Activity | Participation (%) |

|---|---|---|

| 1 | Lottery | 42% |

| 2 | Sports Betting | 35% |

| 3 | Online Casino Games | 28% |

| 4 | Bingo | 20% |

| 5 | Poker and Card Games | 15% |

Consumer Behavior Patterns

Spending habits indicate moderate expenditure on gambling, with users favoring platforms offering loyalty programs and flexible betting limits. Peak activity typically occurs during evenings and weekends, aligning with social leisure times.

Session lengths center around 30-45 minutes, with high retention rates noted on mobile-optimized platforms providing live dealer and interactive game options. Responsible gambling tools and personalized marketing positively influence continued consumer engagement.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

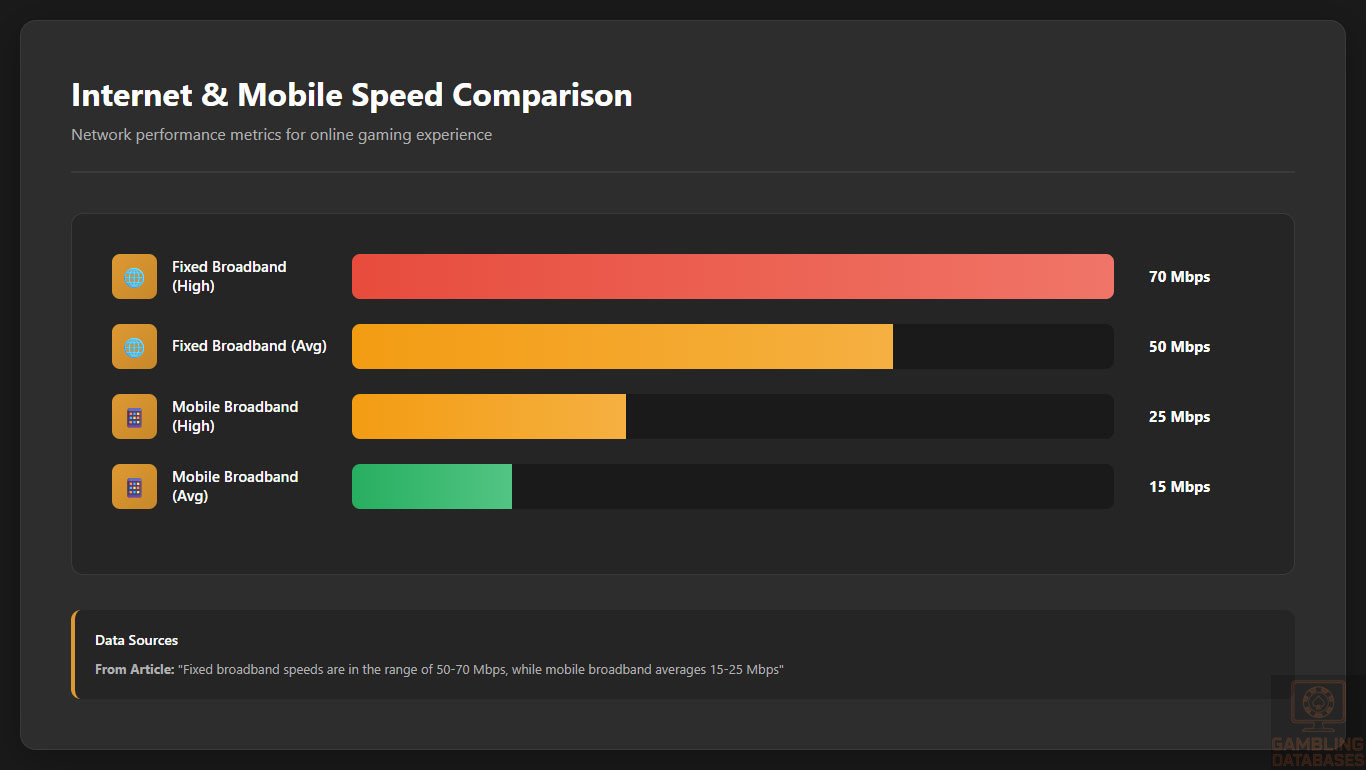

Grenada’s internet penetration is estimated at approximately 74% of the population, with modern broadband infrastructure complemented by widespread mobile internet access. Broadband and fiber-optic deployments are focused largely in urban centers such as St. George’s, supporting reliable high-speed connections suitable for online gaming and streaming.

Average fixed broadband speeds are in the range of 50-70 Mbps, while mobile broadband averages 15-25 Mbps with growing improvements. Network reliability is generally strong, although rural and remote areas occasionally face connectivity challenges. Continued investment in infrastructure by telecommunications providers aims to enhance coverage and service quality nationwide.

5G and Future Technology Deployment

5G rollout in Grenada is in initial phases with pilot programs launched in 2024 in major cities. Full commercial deployment is expected by late 2025 or early 2026, supported by multiple mobile network operators collaborating with technology vendors. This evolution will boost latency reduction and bandwidth, critically strengthening real-time gaming and streaming experiences.

Government policies encourage adoption of future technologies, including IoT and expanded fiber networks, positioning Grenada as a forward-looking digital economy hub within the Caribbean region.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Grenada hosts a competitive mobile operator market, with three primary providers controlling approximately 95% of subscriptions. Market shares are roughly split with one dominant operator holding just over 50%, and the two competitors sharing the remainder. Coverage quality is excellent in urban and suburban areas with over 90% 4G LTE availability, while data costs remain average for the Caribbean region.

- Digicel Grenada: Largest market share, extensive 4G and pilot 5G coverage

- FLOW Grenada: Strong presence with expanding fiber-to-cell sites

- Carib Surf: Niche provider focusing on rural broadband and data services

Device Penetration

Smartphone adoption in Grenada has surged, with more than 80% of the population owning smartphones as of 2025. Market trends favor mid-range Android devices favored for their affordability and app ecosystem, though premium devices hold sway among urban professionals. Mobile usage patterns emphasize social media, video content, and increasingly, mobile gaming, laying a solid foundation for iGaming platform engagement.

Financial Services and Payment Infrastructure

Banking System Structure

Grenada’s banking sector is well-established with four major institutions covering bulk retail and commercial banking needs. Digital banking services have expanded rapidly in recent years, with over 70% of the adult population holding at least one active bank account. The sector supports online transactions robustly, enabling seamless payment processing for e-commerce and digital entertainment platforms.

- Grenada Co-operative Bank

- Republic Bank (Grenada) Limited

- Bank of Saint Lucia Grenada Branch

- First Caribbean International Bank

- St. George’s Bank (smaller regional player)

Payment Processing Options

Online and mobile payment options feature prominently in Grenada’s payment ecosystem, with card payments and e-wallet services leading the volume on digital platforms.

- Visa and Mastercard credit/debit cards widely accepted

- Mobile money and e-wallets like Digicel’s Mobile Money and FLOW’s wallet

- Bank transfers for larger transactions or withdrawals

- Prepaid cards available for online usage and security

- Cryptocurrency adoption is emerging but still limited

E-commerce and Digital Economy

Grenada’s digital economy is growing steadily, supported by rising internet and smartphone penetration. E-commerce adoption is rising, with online retail growing due to enhanced logistics and payment solutions. Trust in digital transactions improves through regulatory safeguards, and digital services such as streaming, digital content, and gaming present expanding market opportunities.

Business Environment and Regulatory Framework

Ease of Business Operations

Grenada is ranked moderately on global ease of doing business indices, with a streamlined process for company registration and investment approvals. Foreign investment policies are open with incentives for technology and service sectors, though some bureaucratic hurdles remain, particularly in licensing and tax compliance.

Operational costs are competitive relative to regional standards, with lower office rental and labor costs compared to larger Caribbean nations.

Corporate Structure and Registration

Business entities in Grenada primarily include Limited Liability Companies (LLC), corporations, and foreign branch offices. LLCs are favored for their flexibility and limited liability protection, suitable for technology and gaming operations. Corporations are more regulated with stricter reporting requirements, while branch offices facilitate foreign company presence with operational oversight from the parent entity.

Registration Requirements

Company registration timelines range from 2 to 4 weeks, depending on document completeness and regulatory approval speed. Costs are moderate and include government filing fees, legal services, and licensing-related expenses. Foreign ownership is permitted with no maximum restrictions but requires transparent disclosure and compliance.

- Certificate of Incorporation

- Memorandum and Articles of Association

- Proof of registered office address

- Director and shareholder identification documents

- Tax registration documents

Taxation Framework

Corporate Income Tax Structure

Grenada applies a flat corporate income tax rate of 28% with certain tax holidays and incentives for new technology-focused companies. Special economic zones offer reduced tax rates and accelerated depreciation benefits. The government maintains double taxation treaties with regional and international partners improving cross-border business viability.

- United States

- United Kingdom

- Canada

- France

- Barbados

- Trinidad and Tobago

Personal Income Tax

Personal income tax rates range progressively from 10% to 30%. Withholding tax is applied to dividend and interest payments under specified conditions. Social security contributions are mandatory, contributing to employee benefits and health security. Residency rules are aligned with international standards to prevent tax evasion and ensure compliance.

Market Entry Considerations

Recommended Entry Strategies

Strategies for market entry emphasize partnerships with local entities for regulatory compliance and market insight. Investing in mobile-first platforms optimized for Caribbean consumers and building strong customer support enhances competitiveness. Leveraging social media for marketing and responsible gambling measures supports brand trust and regulatory goodwill.

- Form local partnerships for licensing and operations

- Develop mobile-optimized gaming platforms

- Implement comprehensive responsible gambling programs

- Engage in targeted social media and digital marketing

- Focus on player data protection and compliance transparency

Typical Costs and Timelines

Initial market entry requires capital allocation spanning license fees, legal and consulting expenses, technology deployment, and marketing. Operational costs involve staffing, regulatory compliance, and continuous platform maintenance.

- License and application fees: Approximately $600 to $10,000+

- Company registration and legal setup: $5,000–$15,000

- Technology platform development and integration: $100,000+

- Marketing and player acquisition: Variable, start-around $50,000

- Operational costs (annual): $150,000+

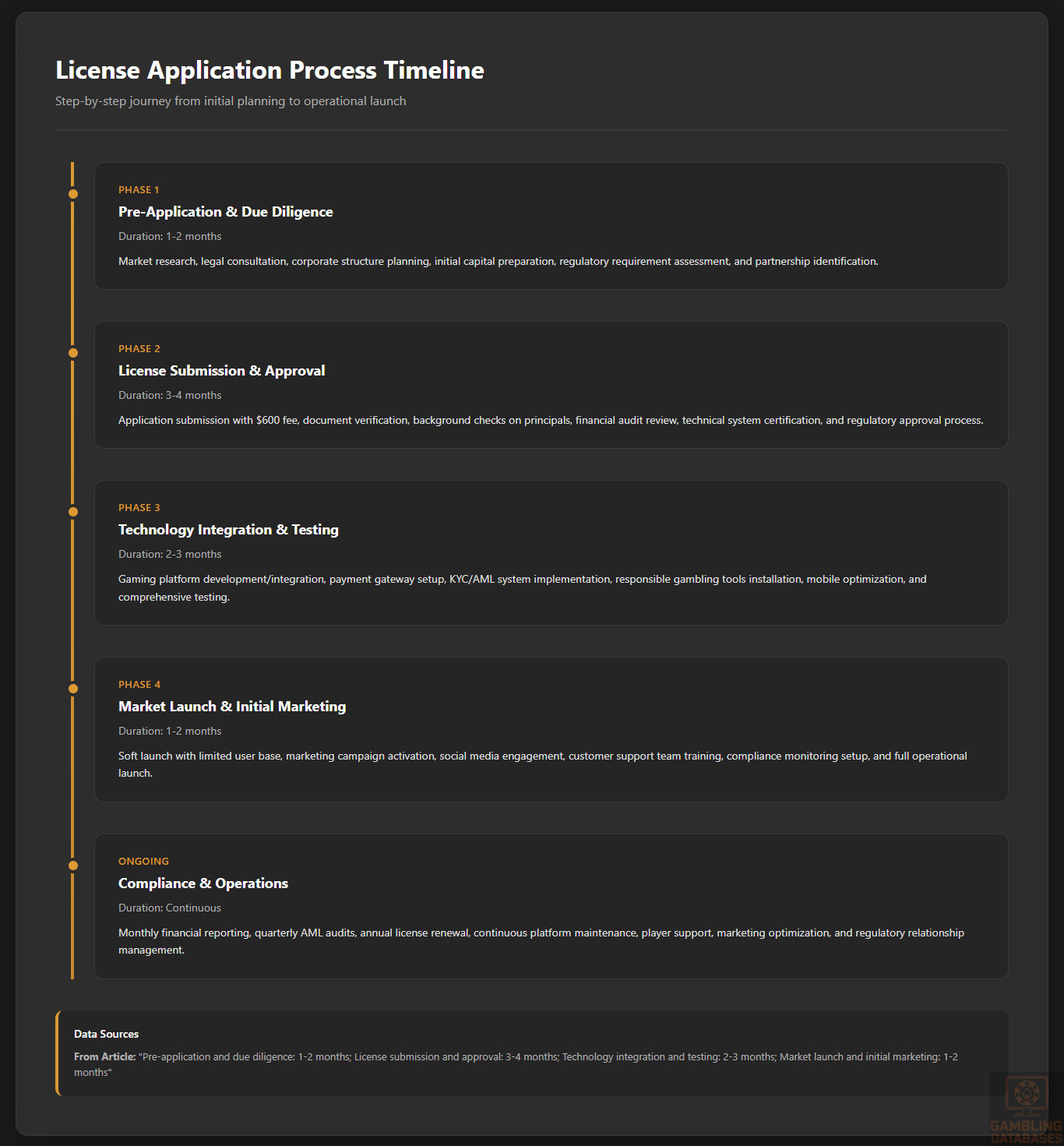

| Phase | Duration |

|---|---|

| Pre-application and due diligence | 1-2 months |

| License submission and approval | 3-4 months |

| Technology integration and testing | 2-3 months |

| Market launch and initial marketing | 1-2 months |

| Ongoing compliance and operations | Continuous |

Success Factors and Challenges

Key success drivers include regulatory compliance, local market understanding, technological innovation, effective marketing, and strong consumer trust. Challenges stem from bureaucratic delays, competition, infrastructure limitations in rural zones, and balancing regulatory cost pressures with profitability.

- Strong regulatory engagement and transparency

- Robust, user-friendly gaming platforms

- Targeted marketing tuned to cultural preferences

- Investment in data security and player protection

- Adaptability to evolving legal and market conditions

Exit Strategy Planning

Grenada’s regulatory framework supports ownership transfers and secondary market liquidity with conditions for prior regulatory approval. License portability is limited, requiring reapplication or transfer consent. Valuation multiples align with Caribbean digital market norms, influenced by operational performance and regulatory good standing.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Grenada?

Yes, online gambling is legal and regulated by the Grenada Gaming Commission. The legal framework provides licenses for online casinos, sports betting, and other digital gaming services. Operators must comply with strict regulatory standards including KYC, AML, and responsible gambling requirements to operate legally.

2. What types of gambling licenses are available and what do they cover?

Licenses in Grenada include land-based casino licenses, online gaming licenses, sports betting licenses, and lottery licenses. Each license covers specific activities and requires adherence to regulations governing operations, technical standards, and financial reporting. Licensing is open to domestic and foreign entities meeting all criteria.

3. How much does an iGaming license cost and how long does it take to obtain?

Application fees typically start around $600, with total costs varying based on license scope and application complexity. The approval process generally takes 3 to 4 months, factoring document submission, background checks, and regulatory review. Renewal fees tend to be higher, with ongoing compliance costs factored in.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to obtain gambling licenses provided they meet local regulatory requirements, including disclosure of beneficial ownership and establishing a physical presence. Partnerships with local stakeholders are common to streamline compliance and market penetration.

5. What are the tax obligations for iGaming operators?

iGaming operators in Grenada are subject mainly to a gross gaming revenue tax of approximately 30%, alongside corporate income tax at 28%. Special rates apply to lotteries and members’ clubs. Additional operational taxes may include license renewal fees and transaction reporting responsibilities.

6. Are gambling winnings taxed for players?

Players are generally not taxed on gambling winnings in Grenada. The tax liability falls on operators, aligning with the government’s objective to encourage participation while securing revenue through business taxation rather than player taxation.

7. What are the typical operational costs for running an online casino or sportsbook?

Operational costs encompass license fees, technology platform maintenance, staffing, marketing, regulatory compliance, and payment processing fees. These costs vary significantly based on scale but typically start at several hundred thousand USD annually for mid-sized operations.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines depend on market penetration and operational efficiency but generally range between 18 to 36 months. Early focus on compliance, trust-building, and mobile user acquisition accelerates breakeven points and profit realization.

9. What are the local presence requirements for operators?

Operators must establish a physical office in Grenada, appoint local directors or responsible officers, and maintain substantial operational activities domestically. This ensures regulatory oversight and alignment with local economic development objectives.

10. What payment methods are available and recommended?

Recommended payment methods include credit/debit cards (Visa, Mastercard), mobile money wallets, bank transfers, prepaid cards, and emerging cryptocurrency options. Offering a diverse range of secure, user-friendly payment options enhances player satisfaction and regulatory compliance.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors, false claims, and misleading offers. Promotions should comply with responsible gambling guidelines and regulatory approval. Marketing channels are monitored for compliance with content restrictions and sponsorship transparency rules.

12. What responsible gambling measures are mandatory?

Mandatory measures include age verification, self-exclusion options, deposit and loss limits, staff training on responsible gambling, and clear disclosure of game odds. Operators must provide players with tools to manage gambling behavior responsibly and submit regular compliance reports.

13. How large is the iGaming market and what is the growth potential?

The Grenada iGaming market is projected at $50 million USD in 2025, with a CAGR of 8-10% over five years driven by increasing digital access and consumer acceptance. Expanding internet penetration and improving infrastructure underpin robust growth opportunities.

14. Who are the main competitors and what is their market share?

The competitive landscape is composed of several local casinos and international operators licensed in Grenada. Market share is fragmented, with a few dominant online operators holding around 60% combined, while smaller providers compete in niches such as sports betting and lotteries.

15. What are the player preferences and typical spending patterns?

Players favor lottery and sports betting most, followed by online casinos and bingo. Spending is moderate but growing, focusing on mobile platforms with loyalty incentives and flexible betting limits. Evening and weekend usage peaks align with leisure time availability.

16. What are the key success factors and main challenges for new entrants?

Success hinges on regulatory compliance, local market knowledge, technology agility, and robust player protection. Challenges include navigating regulatory complexities, competition intensity, limited rural infrastructure, and managing compliance costs without sacrificing growth.

Sources and References

- Grenada Gaming Commission – Official Regulatory Authority

- Government of Grenada – Legal Framework Documents

- National Statistical Office of Grenada – Population and Economic Data 2025

- Central Bank of Grenada – Financial Reports and Banking Data

- Ministry of Finance, Grenada – Taxation and Licensing Information

- World Bank – Ease of Doing Business Reports 2024

- International Telecommunication Union – ICT Statistics 2025

- Digital 2025: Grenada – DataReportal Report

- Caribbean Telecommunications Union – Network Infrastructure Data

- Market Research Reports – Caribbean iGaming Industry 2024-2025

- KPMG Grenada – Tax and Regulatory Updates 2025

- IMF DataMapper – Grenada Economic Indicators 2025

- World Population Review – Grenada Demographics 2025

- Digicel Grenada – Mobile Network Information

- FLOW Grenada – Telecommunications Coverage

- Republic Bank Grenada – Commercial Banking Services

- First Caribbean International Bank – Digital Banking Statistics

- Grenada Ministry of Digital Transformation – Technology Initiatives

- Global Gaming Industry Reports 2024-2025

- Local News Outlets – Recent Regulatory Changes and Market Analysis

- Gaming Technology Providers – Platform and Compliance Solutions

- International Monetary Fund – Caribbean Economic Outlook 2025

- Caribbean Development Bank – Infrastructure Investment Reports

- UN Economic Commission for Latin America and the Caribbean

- World Economic Forum – Regional Competitiveness Reports

- Academic Journals on Caribbean Digital Markets and Gambling Behavior

- Industry Conferences and Webinars – Caribbean iGaming Trends 2025

- OECD Tax Policy Reviews – Grenada

- Emerging Technology Providers – 5G and Network Expansion Reports

- Grenada Ministry of Health and Social Services – Responsible Gambling Programs

- Caribbean Lottery and Betting Associations Reports

- Local NGO Reports on Gambling Addiction and Social Impact

- Global Payment Processing Firms – Market Analysis for Grenada

🎯 Gambling Databases Country Rating: Grenada

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.8/10 | 🟡 Moderate |

| Player Access Score | 7.5/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 6.7/10 | 🟡 Moderate potential, but small market with significant operational requirements |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- TINY MARKET SIZE: Population of only ~113,000 means maximum addressable market of 15,000-22,000 active players by 2030. Market scale makes profitability extremely challenging for most operators.

- HIGH EFFECTIVE TAX BURDEN: 30% gaming tax + 28% corporate income tax creates total effective rate approaching 50% on gross gaming revenue.

- MANDATORY LOCAL PRESENCE: Physical office, local directors, and operational staff required in Grenada – increasing fixed costs in micro-market.

- LIMITED PROFIT POTENTIAL: Estimated total market GGR of only $50 million USD in 2025 across ALL operators. With limited players and high taxes, only niche operators or regional consolidators should consider entry.

- STRINGENT COMPLIANCE: Comprehensive KYC/AML obligations, responsible gambling measures, monthly reporting, and quarterly audits create ongoing operational burden.

- ELEVATED ENTRY COSTS: Total setup costs $250,000-$500,000+ for licensing, legal, technology, and compliance – disproportionately high relative to tiny market potential.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Full product legality for both land-based and online gambling including casinos, sports betting, and lotteries (+3.0). Comprehensive regulatory framework under Gaming Act 2016 and Casino Gaming Act 2014. However, recent 2022 amendments increased penalties and expanded regulatory definitions creating additional compliance burden (-0.5). Final: 2.5/3.0 |

| Licensing Process | 25% | 1.5/2.5 | Accessible licensing process available through Grenada Gaming Commission (+2.0). Application timeline 3-4 months is reasonable. Low application fee of approximately $600 USD (+0.5). HOWEVER: Stringent scrutiny of foreign ownership despite being permitted (-0.25). Mandatory physical presence and local directors required (-0.25). Complex probity checks and financial audits extend timeline (-0.25). Capital proof requirements vary but often substantial (-0.25). Final: 1.5/2.5 |

| Taxation & Costs | 20% | 0.5/2.0 | Gaming tax rate of 30% on gross receipts (+1.0 for 25-35% bracket). Corporate income tax 28% creates total effective tax burden of approximately 50% when combined (-0.5 for multiple tax layers). Licensing fees, while initially low ($600), increase substantially for renewals. Operational costs disproportionately high for micro-market: office rental, local staff, compliance costs exceed $150,000 annually minimum (-0.5). Total setup costs $250,000-$500,000+ create high barrier relative to market size with only $50M total GGR (-0.5). Final: 0.5/2.0 |

| Operational Requirements | 15% | 0.75/1.5 | Heavy requirements significantly reduce score (+0.5 base for extensive infrastructure needed). Mandatory registered physical office in Grenada required (-0.25). Local directors or responsible officers mandatory (-0.25). Domain ownership and control requirements for online operations add complexity (-0.25). Ongoing compliance obligations include monthly financial reports, quarterly AML audits, annual certifications creating continuous operational burden. Staff must be employed locally for compliance, support, and regulatory liaison. Final: 0.75/1.5 |

| Market Environment | 10% | 0.55/1.0 | Moderate business environment with favorable investment climate (+0.5 for moderate ranking). Parliamentary democracy provides political stability. Regulatory framework is clear post-2022 amendments. HOWEVER: Advertising restrictions exist prohibiting targeting minors, limiting hours, requiring responsible gambling messages (-0.15). Recent 2022 regulatory amendments intensified penalties and expanded enforcement (-0.15). Small market with limited infrastructure outside urban centers creates operational challenges (-0.15). Moderate bureaucracy despite streamlined registration. Final: 0.55/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal and regulated gambling environment for all products including online casinos, sports betting, and lotteries (+4.0). Comprehensive legal framework supports player participation across all gambling categories. No product prohibitions. Players face no legal penalties for gambling activities. Age restriction of 18+ is standard and reasonable. No deductions warranted. |

| Practical Accessibility | 30% | 2.0/3.0 | Good but not excellent accessibility. Multiple payment methods available including Visa/Mastercard, bank transfers, mobile money wallets, prepaid cards (+2.0 base). Internet penetration 74% supports online access. Mobile penetration over 90% with 80% smartphone adoption. HOWEVER: Cryptocurrency adoption nascent and not widely supported (-0.5). Rural areas face connectivity challenges reducing accessibility for ~63.5% of population outside urban centers (-0.5). No ISP blocking reported (+0.5 bonus). Final: 2.0/3.0 |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players engaging in legal gambling activities (+2.0). Regulatory enforcement targets operators, not consumers. Players protected under consumer protection framework with responsible gambling measures. No fines, criminal penalties, or administrative sanctions against players. Perfect score – no deductions. |

| Market Availability | 10% | 0.5/1.0 | Limited licensed operator landscape reduces player choice. Market characterized by mixture of local casinos and international online operators, but article notes “no public comprehensive list exceeds five licensed large operators” (+0.5 for 2-4 operators estimated). Competitive market is “tightly regulated” limiting new entries. Small market size naturally restricts operator diversity. Players have access but limited competitive options compared to larger markets. Final: 0.5/1.0 |

🔍 Key Highlights

Strengths (Limited)

- Full Product Legality: All major gambling categories legal (online casino, sports betting, lottery) without product restrictions – rare in Caribbean

- Clear Regulatory Framework: Well-defined laws under Gaming Act 2016 provide operational certainty

- No Player Penalties: Legal framework protects players, creating consumer confidence

- Low Initial Application Fee: $600 USD application cost is nominal compared to most jurisdictions

- Reasonable Licensing Timeline: 3-4 months approval process faster than many competing markets

- Political Stability: Parliamentary democracy with consistent regulatory policy supports long-term planning

- High Digital Penetration: 74% internet and 90% mobile penetration supports online gambling adoption

⛔️ CRITICAL RISKS AND CHALLENGES

- CATASTROPHICALLY SMALL MARKET: Population of only 113,000 creates total addressable market of maximum 15,000-22,000 active gamblers by 2030. Total market GGR estimated at only $50 million in 2025 across ALL operators. Market scale fundamentally limits revenue potential regardless of execution quality.

- PUNISHING EFFECTIVE TAX RATE: 30% gaming tax + 28% corporate income tax = approximately 50% total effective tax burden on gross gaming revenue. This makes profitability extremely challenging even with operational efficiency.

- DISPROPORTIONATE FIXED COSTS: Mandatory physical office, local directors, compliance staff, and ongoing reporting create $150,000+ annual fixed costs in market generating only $50M total GGR. Fixed cost burden as percentage of potential revenue is among highest globally.

- HIGH ENTRY BARRIERS RELATIVE TO OPPORTUNITY: Total setup costs $250,000-$500,000+ (licensing, legal, technology, compliance) represent 0.5-1% of TOTAL MARKET SIZE. ROI timeline extends to 5+ years making entry economically questionable for most operators.

- STRINGENT LOCAL PRESENCE REQUIREMENTS: Physical office plus local directors/officers mandatory – cannot operate remotely. This eliminates cost efficiencies available in remote licensing jurisdictions.

- COMPLEX COMPLIANCE BURDEN: Monthly financial reports, quarterly AML audits, annual certifications, ongoing KYC/AML monitoring, responsible gambling implementations create continuous operational overhead disproportionate to market scale.

- LIMITED PAYMENT INFRASTRUCTURE: Cryptocurrency largely unsupported. Rural areas (63.5% of population) face connectivity challenges. Banking system limited to 4-5 major institutions reducing payment processing options.

- INCREASED REGULATORY SCRUTINY: 2022 amendments intensified penalties and expanded definitions. Trend toward stricter enforcement increases compliance risk and operational costs.

- RESTRICTED OPERATOR LANDSCAPE: Fewer than 5 major licensed operators suggests regulatory authority limits market entries, increasing barriers for new applicants.

- INFRASTRUCTURE LIMITATIONS: Broadband speeds 50-70 Mbps adequate but not exceptional. Rural connectivity problems. 5G rollout only in pilot phase, full deployment late 2025/early 2026.

Player-Specific Issues

- Limited Operator Choice: Fewer than 5 major licensed operators reduces competitive pricing and product innovation

- Rural Access Challenges: 63.5% of population outside urban centers face connectivity limitations

- Nascent Cryptocurrency Support: Modern payment methods largely unavailable, limiting payment flexibility

- Small Market = Limited Liquidity: Poker rooms, peer-to-peer betting, and other liquidity-dependent products unlikely to thrive

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $250,000-$500,000+ (licensing $600-$10,000+, legal/consulting $5,000-$15,000, technology $100,000+, marketing $50,000+, setup costs)

Monthly Operating Costs: $15,000-$25,000+ ($150,000-$300,000 annually including office, staff, compliance, technology maintenance, ongoing marketing)

Effective Tax Rate on Revenue: ~50% (30% gaming tax + 28% corporate income tax on remaining profits)

Customer Acquisition Cost: $120-$200 estimated (small market means limited organic growth, requiring paid acquisition)

Average Revenue Per User: $120 USD/year (2025), growing to $140 by 2030

Time to Breakeven: 4-6 years minimum (assuming successful customer acquisition and retention)

Time to Positive ROI: 6-8 years realistically (market size constraints limit scaling)

Profitability Assessment: Economics are EXTREMELY CHALLENGING and suitable only for specific strategic scenarios. With total market GGR of only $50 million across all operators, even capturing 10% market share yields only $5 million annual GGR. After 30% gaming tax ($1.5M), operating costs ($200,000+), and corporate tax on profits, margins are razor-thin. The 50% effective tax rate combined with high fixed costs and limited scaling potential makes this market economically viable ONLY for: (1) Regional operators consolidating Caribbean licenses for brand presence, (2) Technology providers seeking regulatory sandbox for product testing before larger market launches, (3) Niche operators targeting specific player segments with ultra-low CAC through existing relationships. For typical online casino or sportsbook operators seeking profitable expansion, Grenada’s economics simply don’t work – the market is too small to justify the costs and complexity.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Licensed Operators (All Products) | Low | Well-defined regulatory framework. Main risks: compliance failures leading to fines/license suspension, changing regulations increasing costs, market size limits profitability not legal risk |

| Unlicensed/Offshore Operators | High | 2022 amendments intensified penalties for unlicensed operations. Fines, potential criminal prosecution, equipment confiscation. Regulatory enforcement active and increasing |

| Affiliates/Advertisers | Low-Medium | Must comply with advertising restrictions (no minor targeting, limited hours, responsible gambling messages). Non-compliance risks fines and advertising restrictions. Licensed operator affiliates face minimal risk if compliant |

| Payment Processors | Low | Licensed operators supported by local banking system. Processors for unlicensed operators face regulatory action risk. Standard financial compliance required |

| Company Directors/Executives | Low-Medium | Local directors required creating personal compliance responsibility. Directors of compliant licensed operators face minimal risk. Executives of unlicensed operations face potential criminal penalties under 2022 amendments |

🚨 Extradition and International Enforcement

Extradition Treaties: As Commonwealth member, Grenada maintains extradition agreements with UK, Canada, and participates in regional Caribbean extradition frameworks. Limited broader international extradition network compared to major economies.

Enforcement History: No documented cases of international gambling-related extraditions from Grenada. Enforcement focuses on domestic compliance within jurisdiction. Regional cooperation primarily addresses money laundering and financial crimes rather than gambling-specific offenses.

Practical Risk Assessment: Low for licensed operators operating within regulatory framework. Grenada’s small size and limited international enforcement resources mean cross-border gambling prosecutions extremely rare. However, 2022 amendments signal increasing regulatory seriousness about unlicensed operations.

Travel Risk: Minimal for executives of properly licensed operations. Directors of unlicensed operations theoretically face local prosecution risk but practical enforcement limited by jurisdiction size and resources.

📋 Final Verdict

Grenada receives an Operator Ease Score of 5.8/10 and a Player Access Score of 7.5/10, resulting in an overall market attractiveness rating of 6.7/10.

HONEST ASSESSMENT: Grenada offers full product legality and clear regulations, but the market’s catastrophic size makes it economically unviable for most operators. With only 113,000 population and $50 million total market GGR, even significant market share generates insufficient revenue to justify $250,000-$500,000 entry costs, $150,000+ annual operating expenses, and 50% effective tax burden. The 6-8 year ROI timeline assumes perfect execution in a market too small to support multiple profitable operators. This is a “regulatory win, economic fail” scenario where everything is legal but nothing makes financial sense except for ultra-specific strategic situations.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry ONLY If You Are:

- Regional Caribbean consolidator building portfolio of Caribbean licenses for brand presence and regulatory credibility across multiple small markets

- Technology provider seeking low-cost regulatory sandbox to test products, processes, and compliance systems before launching in larger markets

- Niche operator with existing Caribbean player base who can add Grenada at marginal cost while serving nearby islands

- Operator with ultra-low customer acquisition costs through existing relationships, partnerships, or land-based presence in Grenada

- Prepared for 6-8 year investment horizon with no expectation of meaningful ROI in first 5 years

- Wealthy enough to treat this as brand-building expense rather than profit center ($500,000+ investment you can afford to write off)

❌ Definitely Avoid If You Are:

- Seeking profitable market expansion – market size simply cannot support traditional operator economics

- Startup or small operator with limited capital (under $2 million) – fixed costs consume disproportionate resources

- Expecting ROI within 3-5 years – market scale makes this timeline impossible

- Focused solely on online casino or sportsbook without regional portfolio strategy – isolated Grenada license doesn’t justify costs

- Unwilling to establish physical presence – mandatory local office and directors required, no remote operation possible

- Expecting to scale rapidly – maximum addressable market of 15,000-22,000 players caps growth regardless of execution

- Looking for low-cost licensing jurisdiction – despite $600 application fee, total costs and ongoing compliance make this expensive relative to market opportunity

- Cryptocurrency-focused operator – crypto infrastructure nascent and largely unsupported in market

- Expecting efficient remote operations – local presence requirements eliminate cost efficiencies

⚠️ BOTTOM LINE: Grenada is legally permissive but economically prohibitive – a micro-market where everything is allowed but almost nothing is profitable. Only enter with clear strategic rationale beyond direct market ROI, such as regional portfolio building or regulatory testing. For 95% of operators, your capital and resources will generate far superior returns in almost any other market.